Embed Size (px)

DESCRIPTION

PCE – Part C Life Insurance. Revision 01 (25/11/2011). LIFE INSURANCE PRELIMINARIES. CHAPTER 21. LIFE INSURANCE PRELIMINARIES. Characteristics of Life Insurance Products Basic Principles of Insurance as Applied to Life Insurance Risk Covered by Life Insurance. - PowerPoint PPT Presentation

Citation preview

AIA confidential and proprietary information. Not for distribution.

AIA.COM

PCE – Part C Life Insurance

• Revision 01 (25/11/2011)

AIA confidential and proprietary information. Not for distribution.

2

LIFE INSURANCE PRELIMINARIES

CHAPTER 21

AIA confidential and proprietary information. Not for distribution.

3

• Characteristics of Life Insurance Products

• Basic Principles of Insurance as Applied to Life

Insurance

• Risk Covered by Life Insurance

LIFE INSURANCE PRELIMINARIES

AIA confidential and proprietary information. Not for distribution.

4

CHARACTERISTICS OF LIFE INSURANCE PRODUCTS

Long Term Contracts

Principle of Uberrima Fides

Aleatory Contracts

AIA confidential and proprietary information. Not for distribution.

5

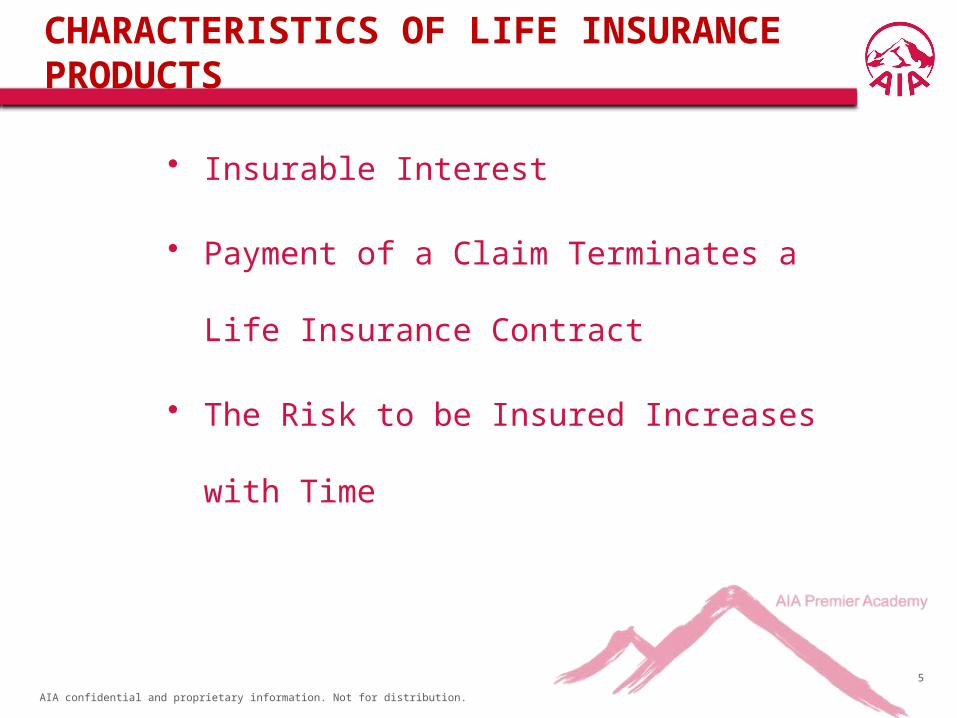

• Insurable Interest

• Payment of a Claim Terminates a Life

Insurance Contract

• The Risk to be Insured Increases with Time

CHARACTERISTICS OF LIFE INSURANCE PRODUCTS

AIA confidential and proprietary information. Not for distribution.

6

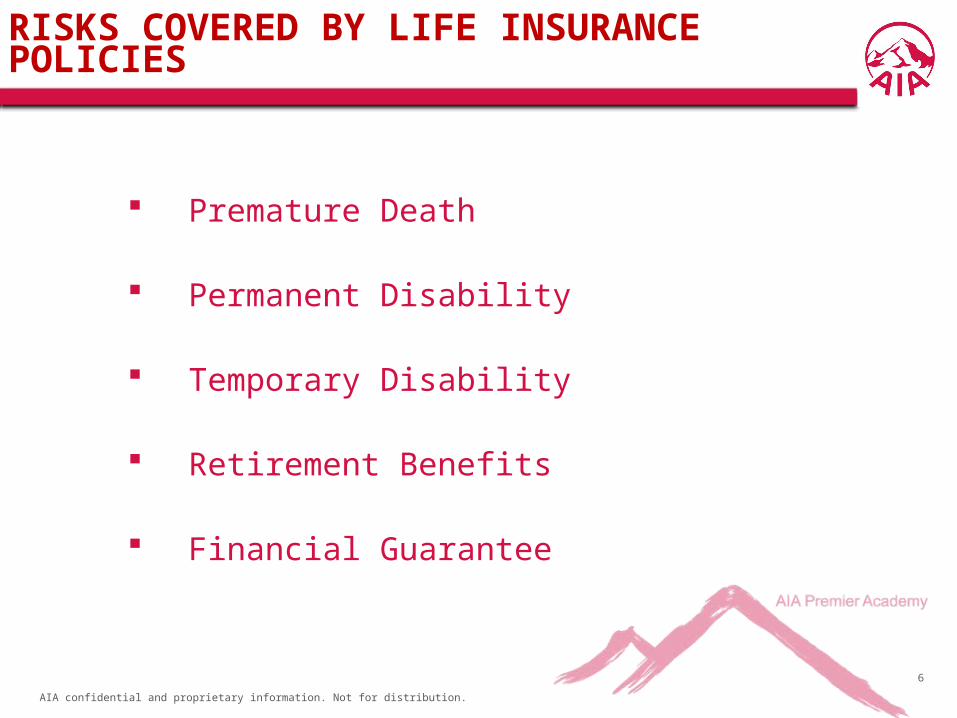

RISKS COVERED BY LIFE INSURANCE POLICIES

Premature Death

Permanent Disability

Temporary Disability

Retirement Benefits

Financial Guarantee

AIA confidential and proprietary information. Not for distribution.

7

LIFE INSURANCE PRODUCTS &

FAMILY TAKAFUL BUSINESS

CHAPTER 22

AIA confidential and proprietary information. Not for distribution.

8

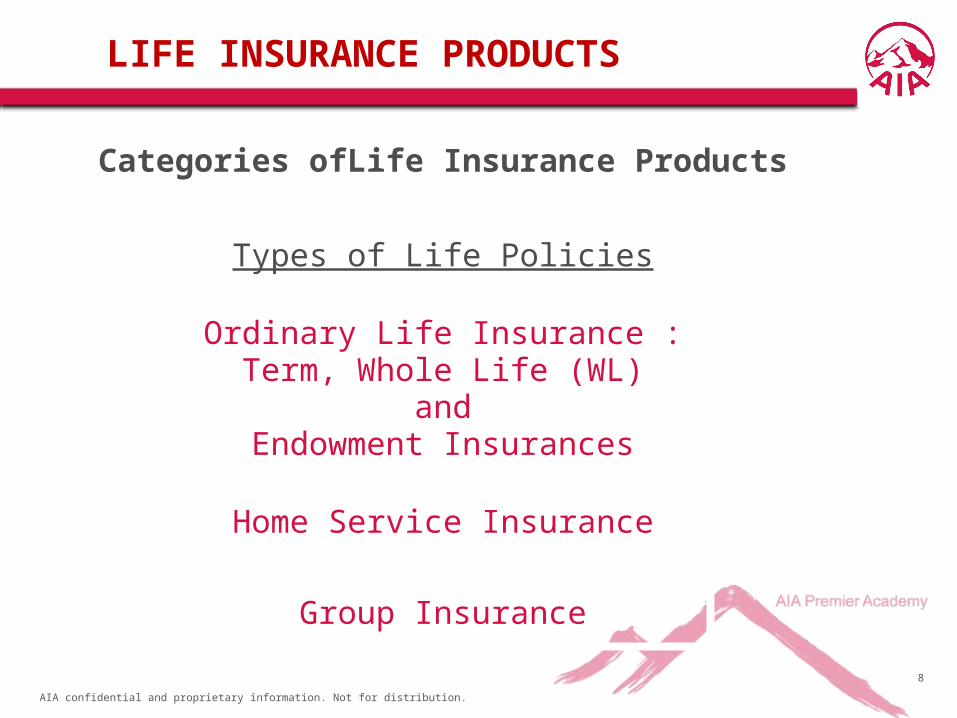

LIFE INSURANCE PRODUCTS

Categories ofLife Insurance Products

Group Insurance

Home Service Insurance

Ordinary Life Insurance :Term, Whole Life (WL)

andEndowment Insurances

Types of Life Policies

AIA confidential and proprietary information. Not for distribution.

9

Family Takaful Business

Miscellaneous Policies :Children’s Insurances and Joint-Life Insurance

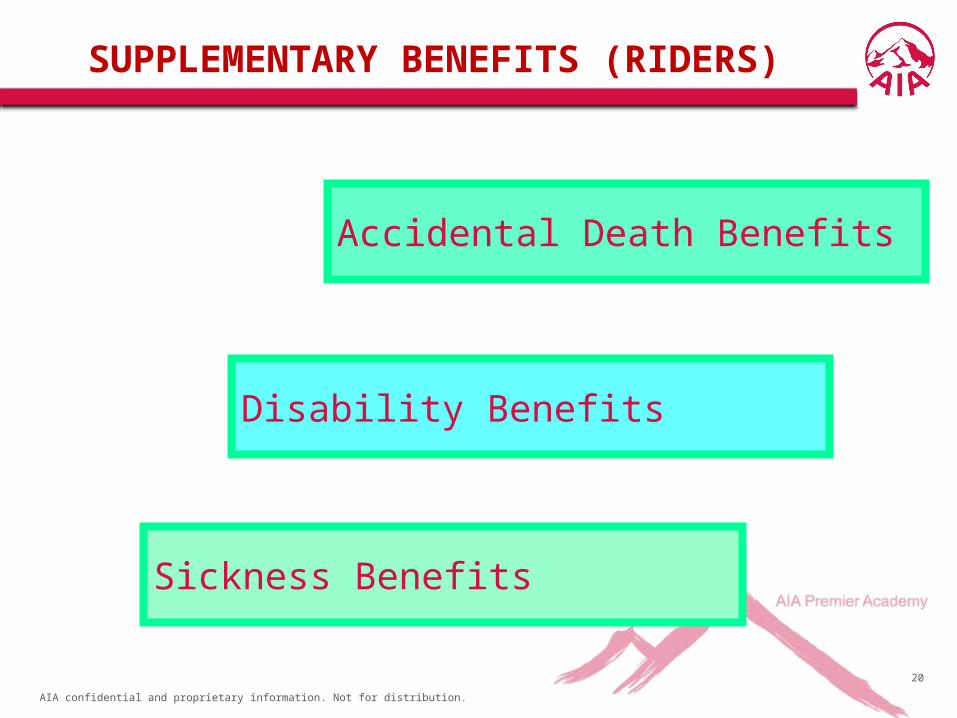

Supplementary Benefits (Riders)

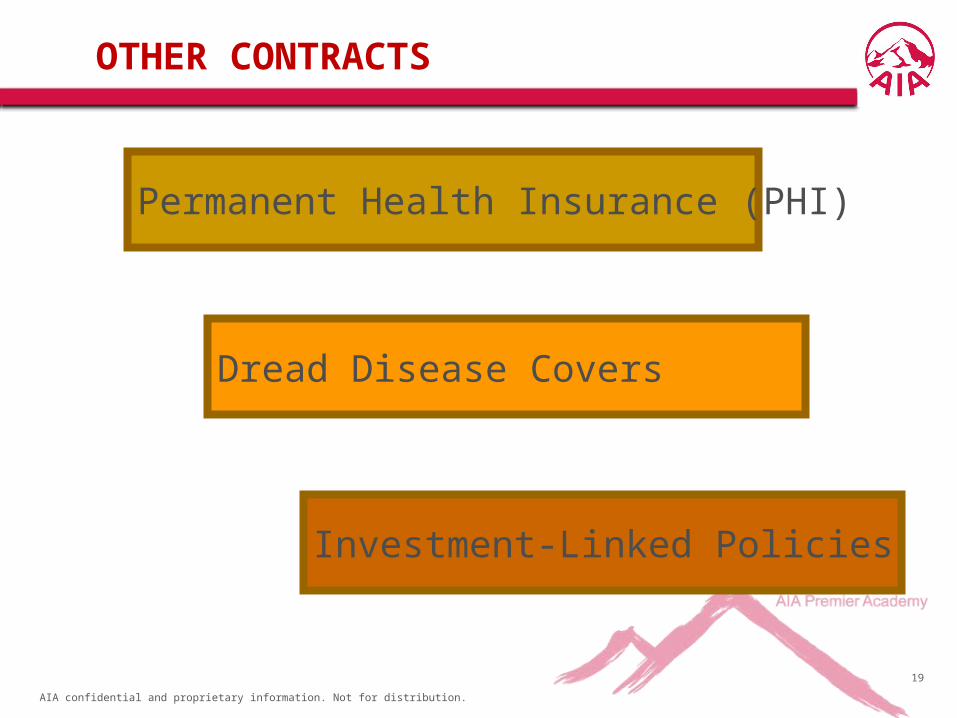

Other Contracts :Permanent Health Insurance (PHI),

Dread Disease Coversand Investment-Linked Policies

LIFE INSURANCE PRODUCTS

AIA confidential and proprietary information. Not for distribution.

10

CATEGORIES OF LIFE INSURANCE PRODUCTS

Participating Contracts (Par)

Non-participating Contracts (Non-par)

AIA confidential and proprietary information. Not for distribution.

11

TYPES OF LIFE POLICIES

Home Service

Group Insurance

Ordinary

AIA confidential and proprietary information. Not for distribution.

12

ORDINARY LIFE INSURANCE

Term Insurance Whole Life (WL)

AnnuitiesEndowment

AIA confidential and proprietary information. Not for distribution.

13

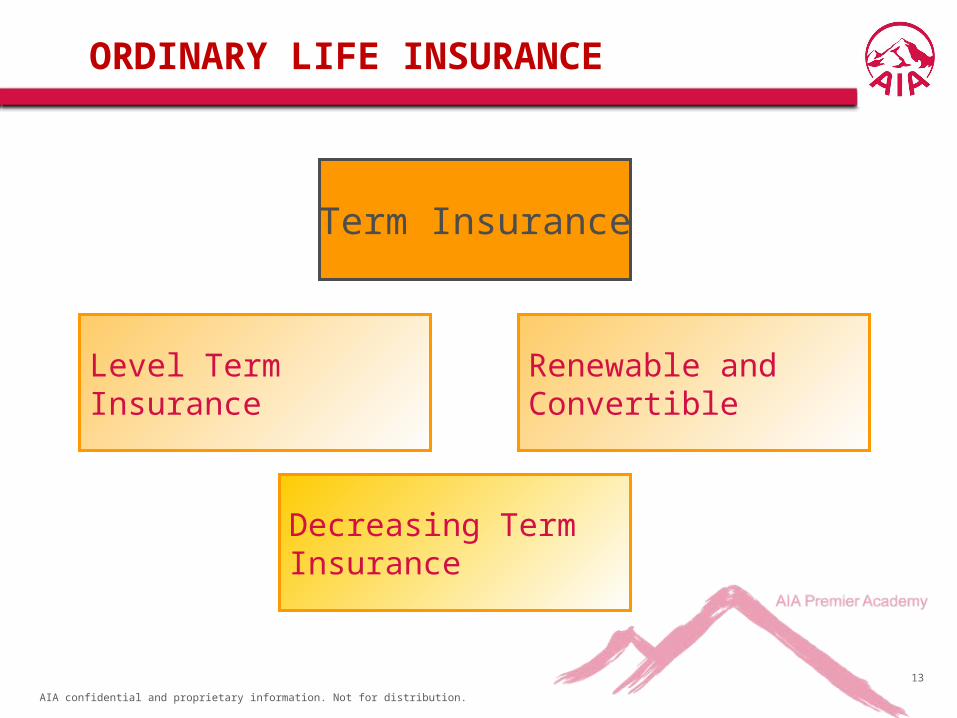

ORDINARY LIFE INSURANCE

Term Insurance

Level TermInsurance

Decreasing TermInsurance

Renewable andConvertible

AIA confidential and proprietary information. Not for distribution.

14

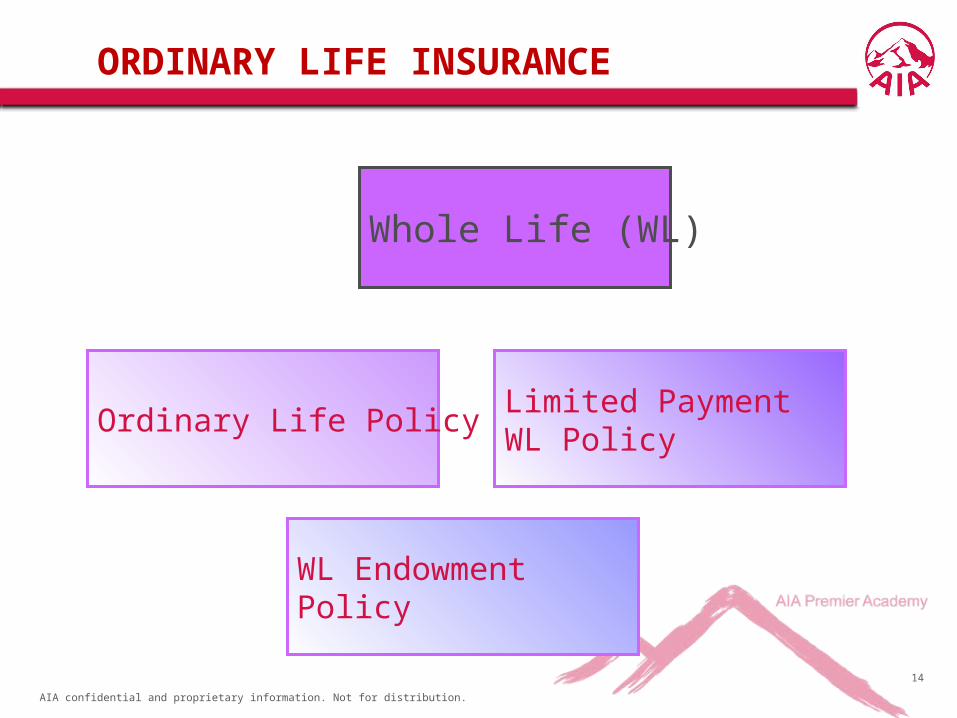

ORDINARY LIFE INSURANCE

Ordinary Life PolicyLimited PaymentWL Policy

WL EndowmentPolicy

Whole Life (WL)

AIA confidential and proprietary information. Not for distribution.

15

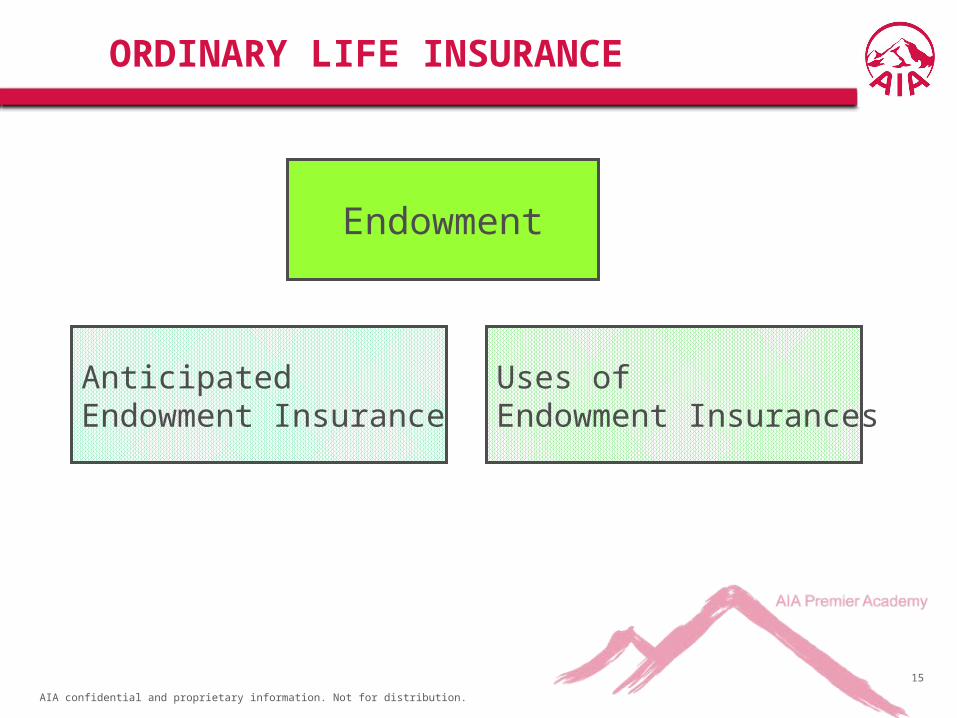

ORDINARY LIFE INSURANCE

AnticipatedEndowment Insurance

Uses ofEndowment Insurances

Endowment

AIA confidential and proprietary information. Not for distribution.

16

ORDINARY LIFE INSURANCE

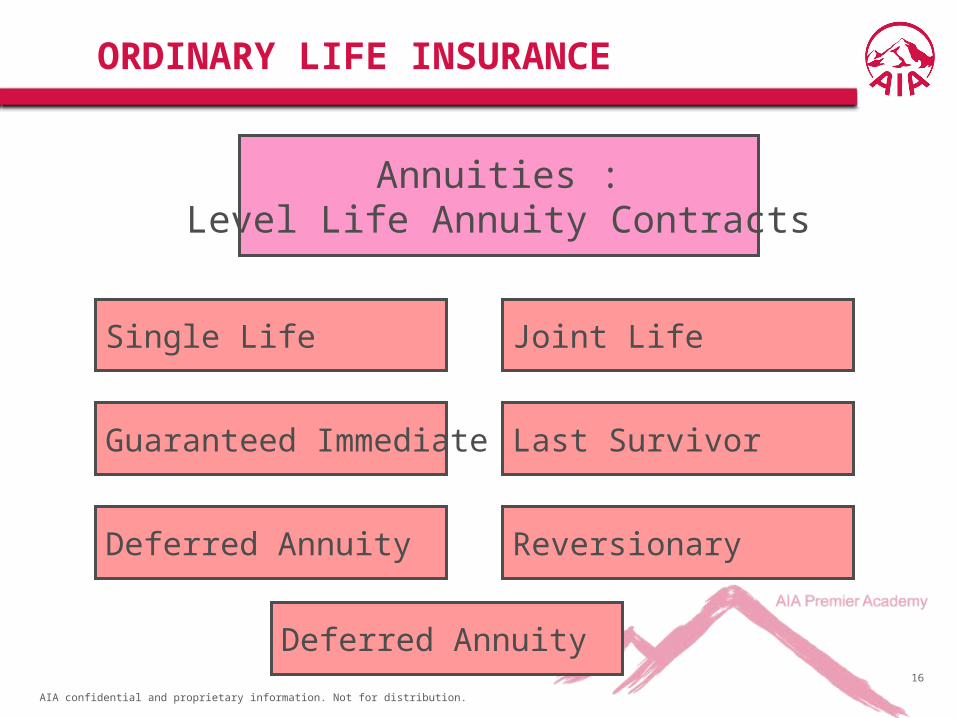

Annuities :Level Life Annuity Contracts

Deferred Annuity

Guaranteed Immediate

Reversionary

Last Survivor

Joint LifeSingle Life

Deferred Annuity

AIA confidential and proprietary information. Not for distribution.

17

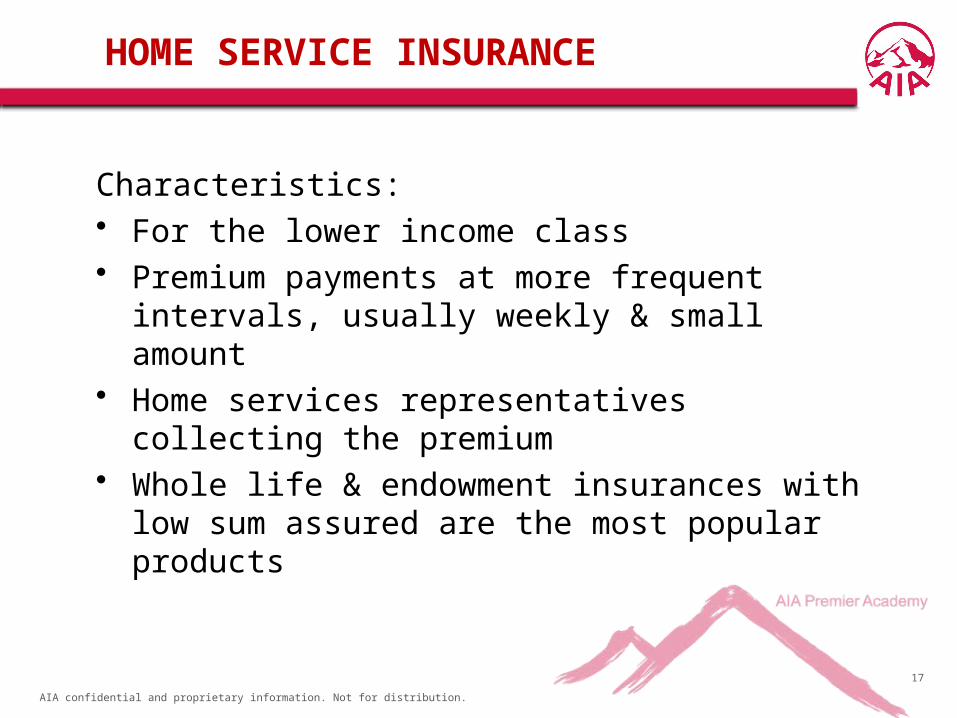

Characteristics:• For the lower income class • Premium payments at more frequent intervals,

usually weekly & small amount• Home services representatives collecting the

premium• Whole life & endowment insurances with low sum

assured are the most popular products

HOME SERVICE INSURANCE

AIA confidential and proprietary information. Not for distribution.

18

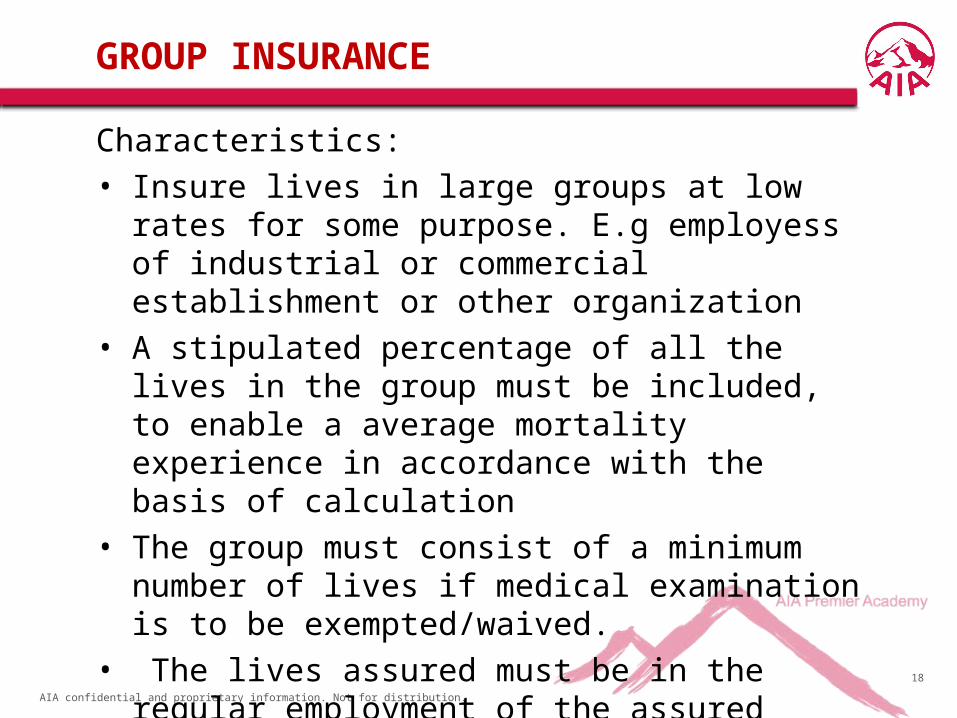

GROUP INSURANCE

Characteristics:• Insure lives in large groups at low rates for some

purpose. E.g employess of industrial or commercial establishment or other organization

• A stipulated percentage of all the lives in the group must be included, to enable a average mortality experience in accordance with the basis of calculation

• The group must consist of a minimum number of lives if medical examination is to be exempted/waived.

• The lives assured must be in the regular employment of the assured employer

AIA confidential and proprietary information. Not for distribution.

19

OTHER CONTRACTS

Permanent Health Insurance (PHI)

Dread Disease Covers

Investment-Linked Policies

AIA confidential and proprietary information. Not for distribution.

20

SUPPLEMENTARY BENEFITS (RIDERS)

Accidental Death Benefits

Disability Benefits

Sickness Benefits

AIA confidential and proprietary information. Not for distribution.

21

MISCELLANEOUS POLICIES

Children’sInsurance

Protected

Educational P

oliciesC

hildren’s

Deferred A

ssuranceJoint LifeInsurance

AIA confidential and proprietary information. Not for distribution.

22

FAMILY TAKAFUL BUSINESS

Types

Participant’s Accounts (PA) andParticipant’s Special Account (PSA)

OperationBenefits

AIA confidential and proprietary information. Not for distribution.

23

POLICY CONDITIONS

CHAPTER 23

AIA confidential and proprietary information. Not for distribution.

24

POLICY CONDITIONS

• Definition of a Policy

• Privileges and Conditions

– Privileges

– Restrictive Conditions

– Conditions Explaining the Contract

• Policy Transactions

• Policy Alterations

AIA confidential and proprietary information. Not for distribution.

25

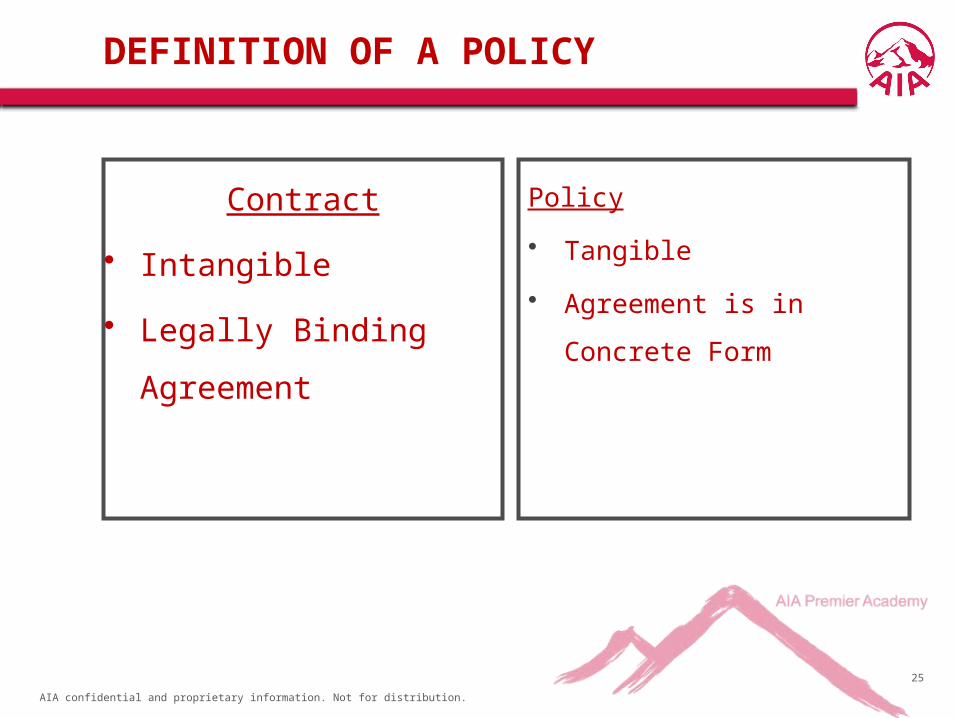

DEFINITION OF A POLICY

Contract

• Intangible

• Legally Binding

Agreement

Policy

• Tangible

• Agreement is in Concrete

Form

AIA confidential and proprietary information. Not for distribution.

26

PRIVILEGES AND CONDITIONS

• Days of Grace• Surrender Value• Policy Loans• Paid-up Policy• Non-forfeiture Conditions•Automatic Premium Loan•Paid-up Policy•Extended Term Assurance

• Reinstatement Condition

AIA confidential and proprietary information. Not for distribution.

27

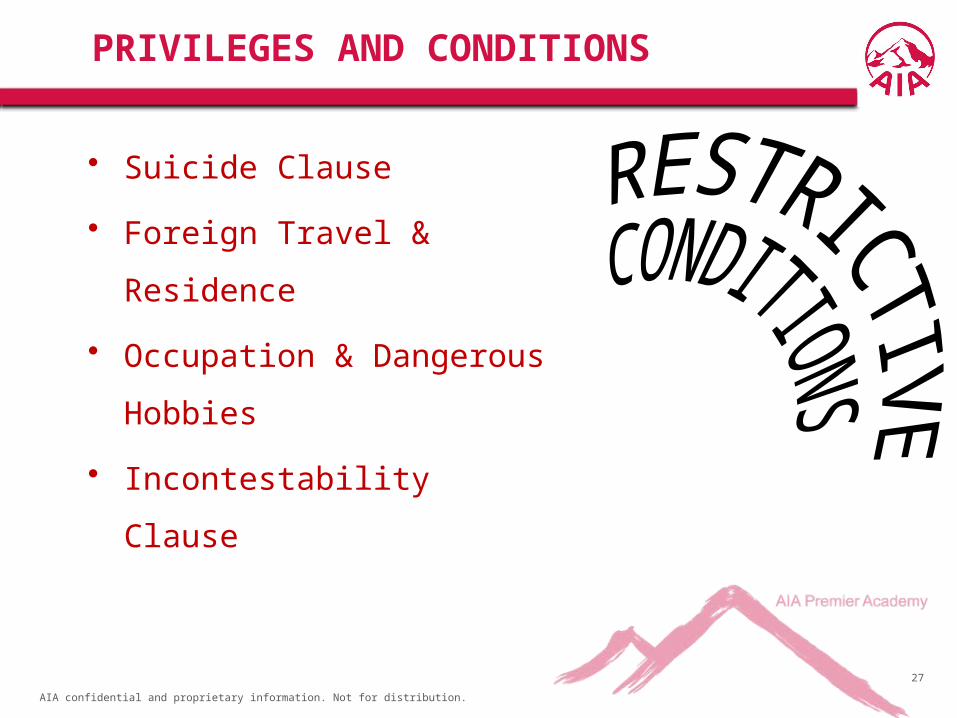

• Suicide Clause

• Foreign Travel & Residence

• Occupation & Dangerous

Hobbies

• Incontestability Clause

PRIVILEGES AND CONDITIONS

AIA confidential and proprietary information. Not for distribution.

28

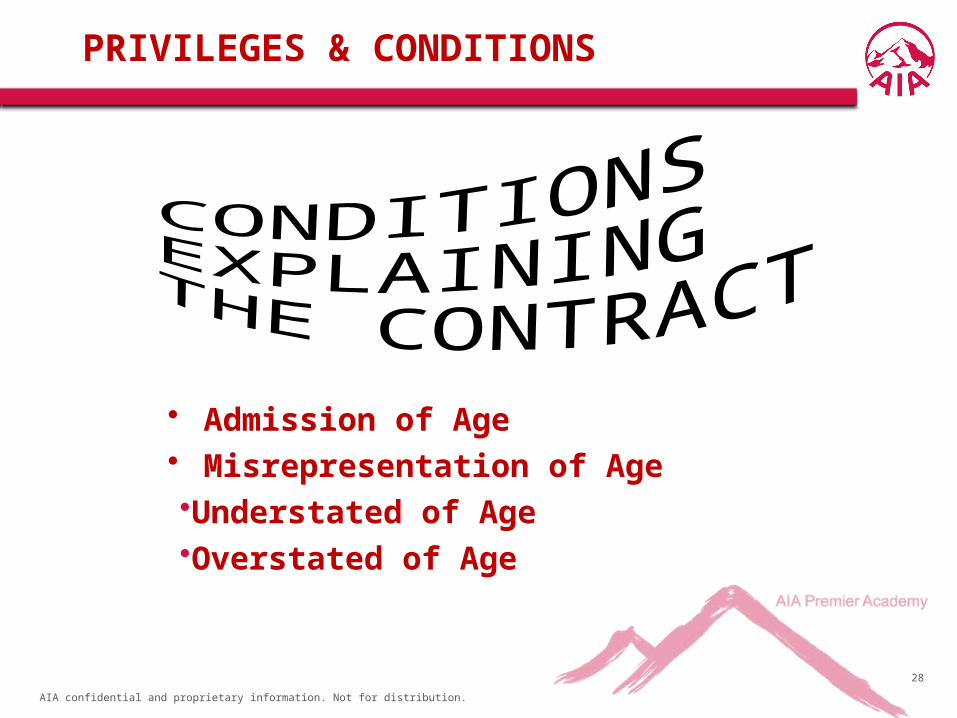

• Admission of Age• Misrepresentation of Age•Understated of Age•Overstated of Age

PRIVILEGES & CONDITIONS

AIA confidential and proprietary information. Not for distribution.

29

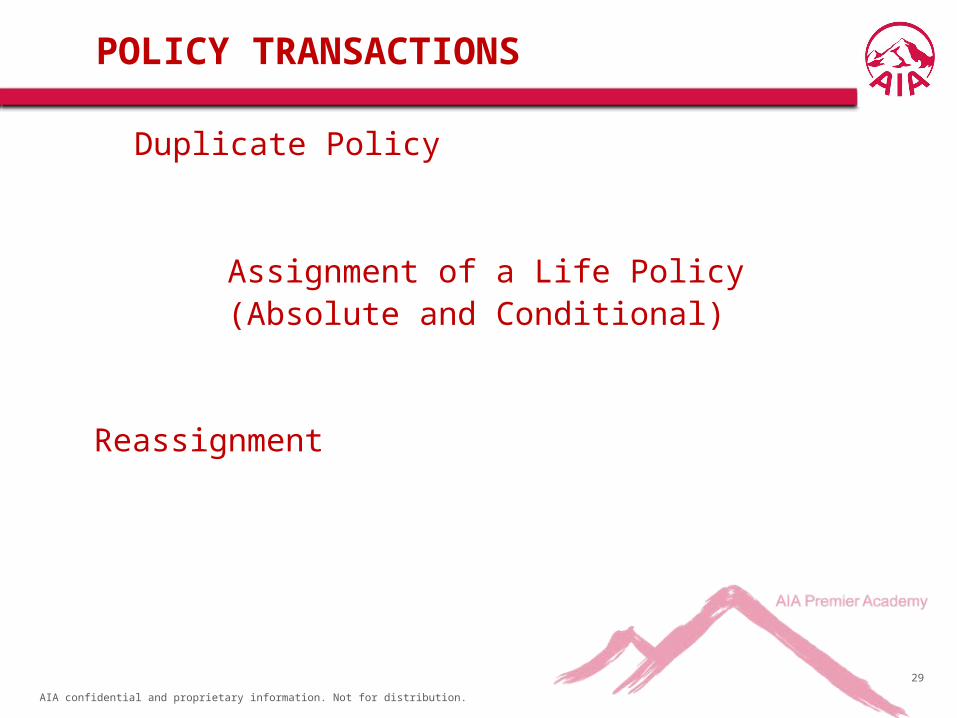

POLICY TRANSACTIONS

Duplicate Policy

Assignment of a Life Policy(Absolute and Conditional)

Reassignment

AIA confidential and proprietary information. Not for distribution.

30

POLICY ALTERATIONS

• Address• Name• Mode of Payment• Sum Insured• Beneficiary• Term of Insurance• Policy Altered to Paid-up• Class of Policy• Removal of Extra Premium

AIA confidential and proprietary information. Not for distribution. 31

PRACTICE OF LIFE INSURANCE:

NEW BUSINESS-SELECTION OF LIVES AND

OTHER ISSUES

AT & D- Center for Learning Excellence

CHAPTER 24

AIA confidential and proprietary information. Not for distribution.

32

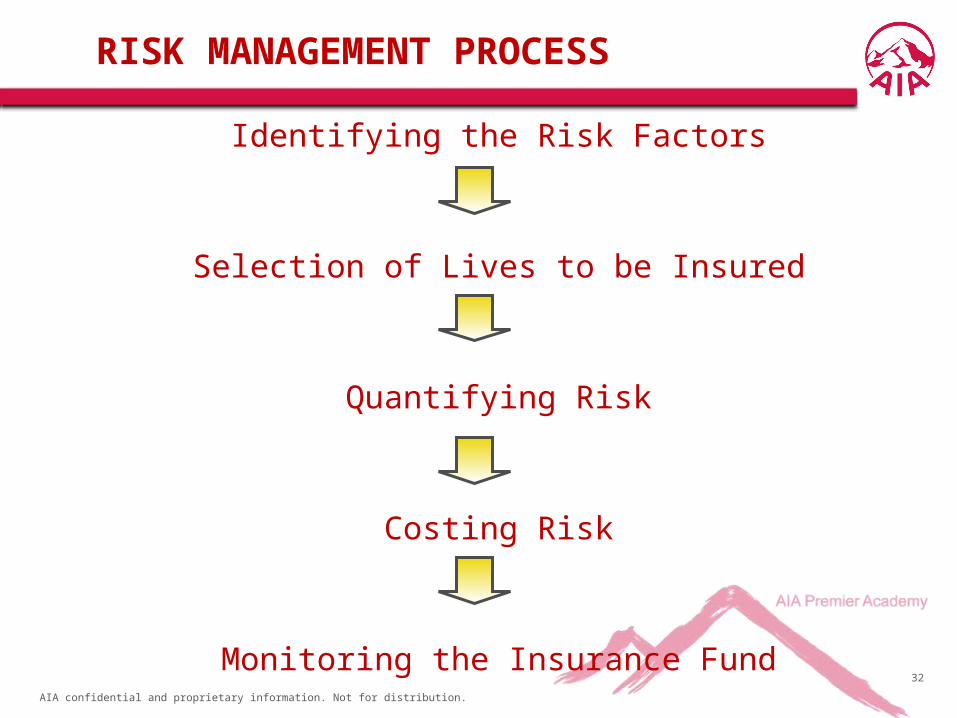

RISK MANAGEMENT PROCESS

Identifying the Risk Factors

Selection of Lives to be Insured

Quantifying Risk

Costing Risk

Monitoring the Insurance Fund

AIA confidential and proprietary information. Not for distribution.

33

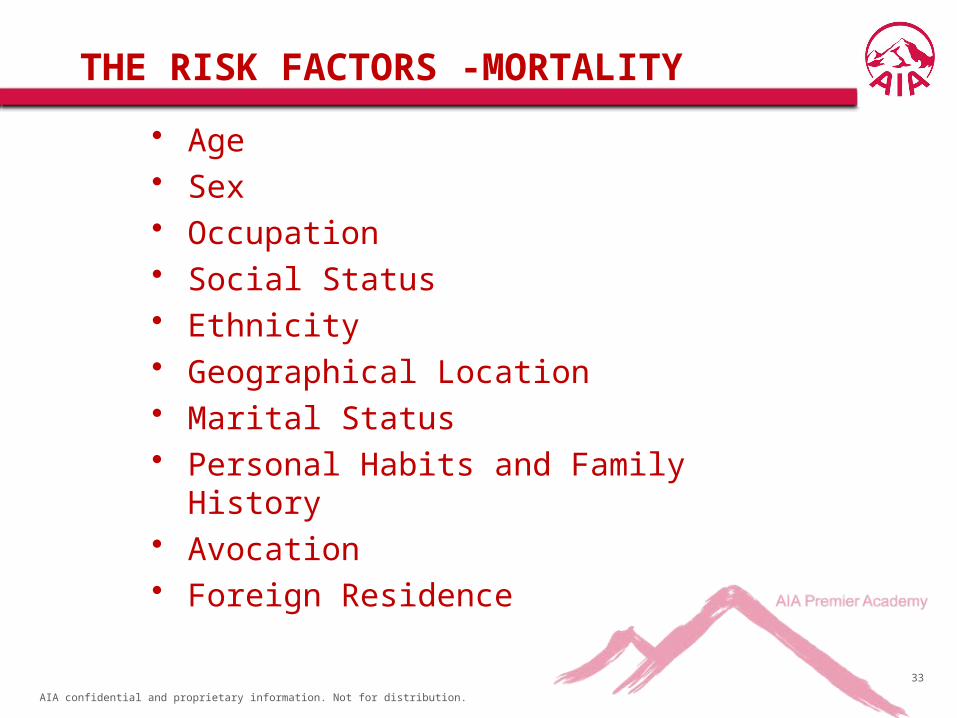

THE RISK FACTORS -MORTALITY

• Age• Sex• Occupation• Social Status• Ethnicity• Geographical Location• Marital Status• Personal Habits and Family History• Avocation• Foreign Residence

AIA confidential and proprietary information. Not for distribution.

34

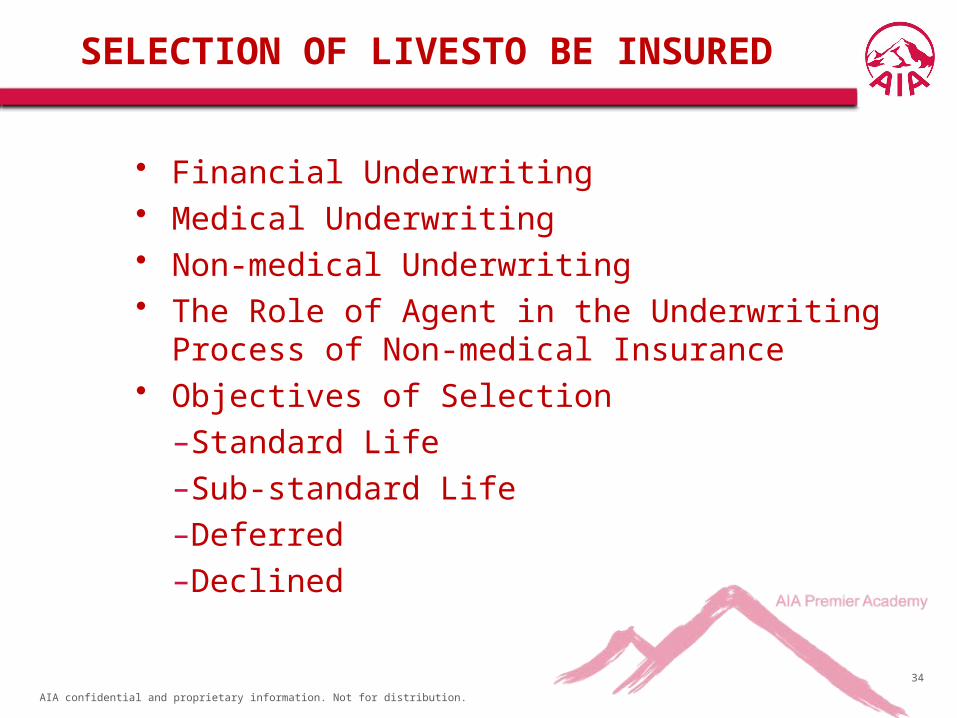

SELECTION OF LIVESTO BE INSURED

• Financial Underwriting• Medical Underwriting• Non-medical Underwriting• The Role of Agent in the Underwriting Process of

Non-medical Insurance• Objectives of Selection

–Standard Life–Sub-standard Life–Deferred–Declined

AIA confidential and proprietary information. Not for distribution.

35

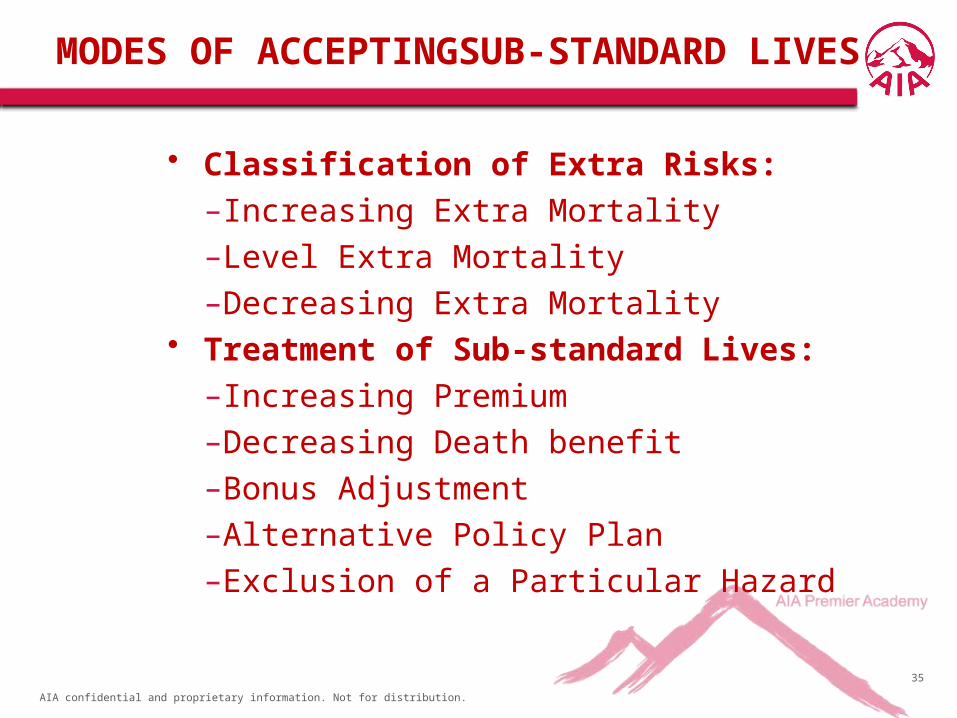

MODES OF ACCEPTINGSUB-STANDARD LIVES

• Classification of Extra Risks:–Increasing Extra Mortality–Level Extra Mortality–Decreasing Extra Mortality

• Treatment of Sub-standard Lives:–Increasing Premium–Decreasing Death benefit–Bonus Adjustment–Alternative Policy Plan–Exclusion of a Particular Hazard

AIA confidential and proprietary information. Not for distribution.

36

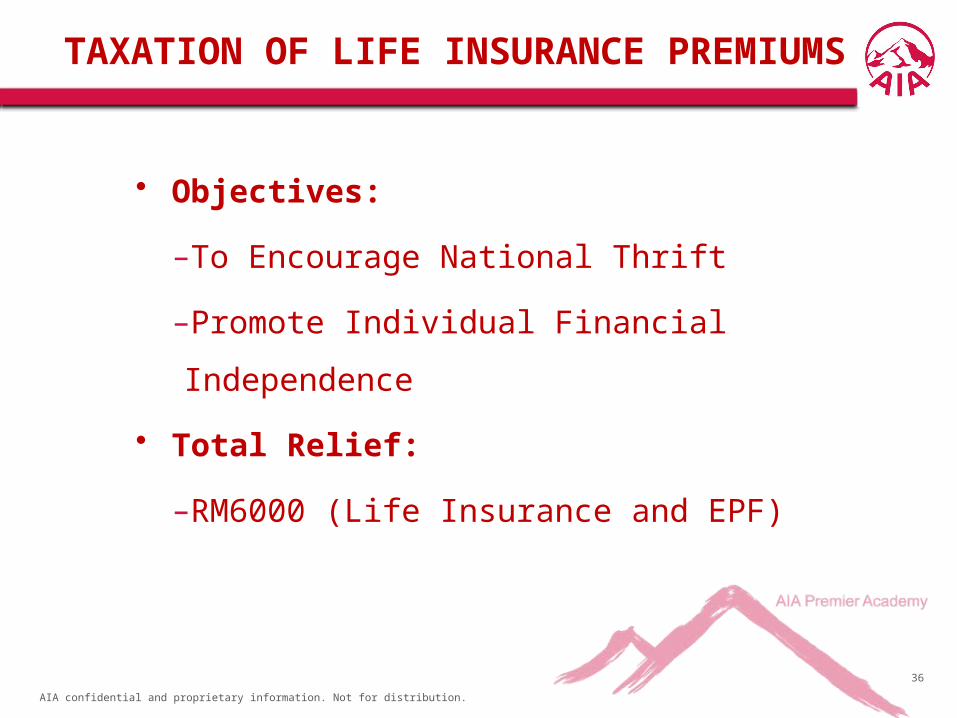

TAXATION OF LIFE INSURANCE PREMIUMS

• Objectives:

–To Encourage National Thrift

–Promote Individual Financial Independence

• Total Relief:

–RM6000 (Life Insurance and EPF)

AIA confidential and proprietary information. Not for distribution.

37

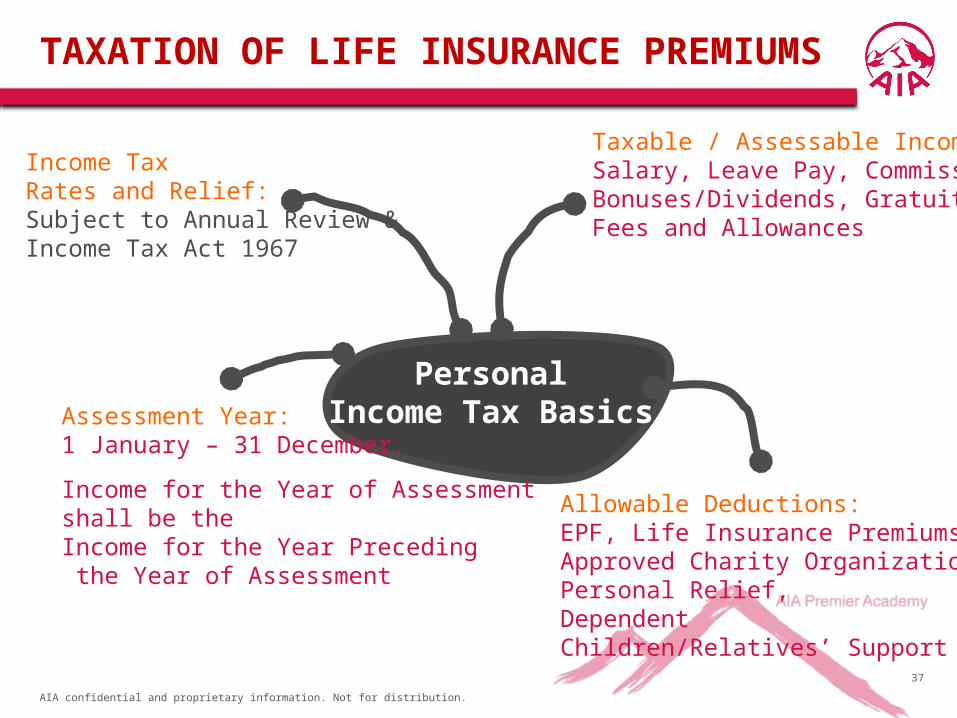

TAXATION OF LIFE INSURANCE PREMIUMS

PersonalIncome Tax Basics

Income Tax Rates and Relief:Subject to Annual Review &Income Tax Act 1967

Assessment Year:1 January – 31 December.

Income for the Year of Assessment shall be the Income for the Year Preceding the Year of Assessment

Taxable / Assessable Income:Salary, Leave Pay, Commissions,Bonuses/Dividends, Gratuity,Fees and Allowances

Allowable Deductions:EPF, Life Insurance Premiums,Approved Charity Organization,Personal Relief,DependentChildren/Relatives’ Support

AIA confidential and proprietary information. Not for distribution.

38

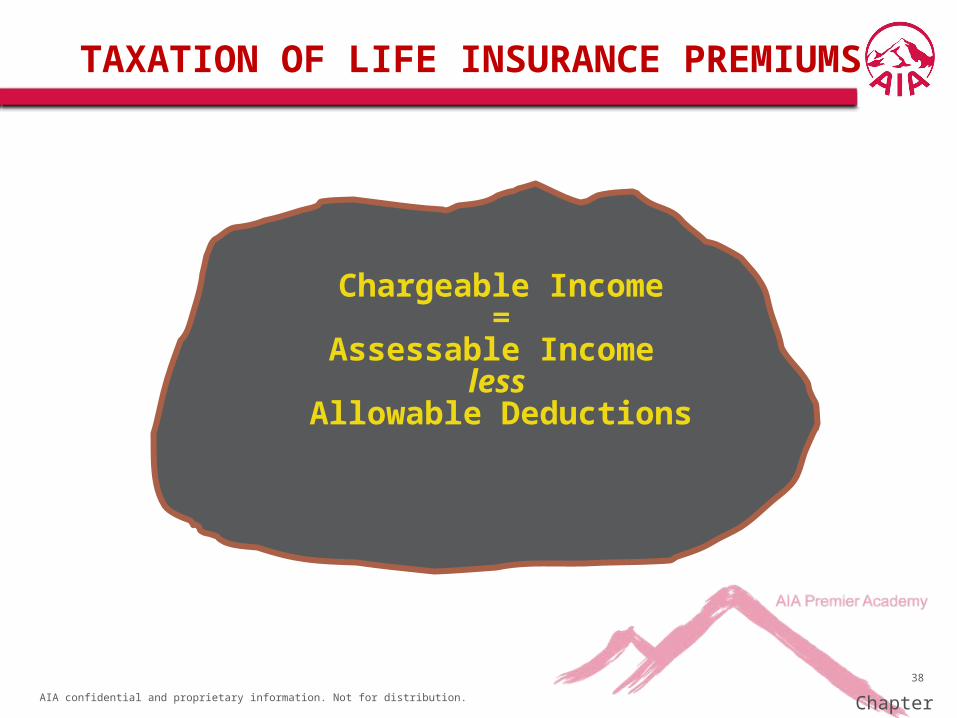

TAXATION OF LIFE INSURANCE PREMIUMS

Chargeable Income =

Assessable Income less

Allowable Deductions

Chapter 19

AIA confidential and proprietary information. Not for distribution.

39

PRACTICE OF LIFE INSURANCE-

NEW BUSINESS-PREMIUM RATING

AT & D- Center for Learning Excellence

CHAPTER 25

AIA confidential and proprietary information. Not for distribution.

40

QUANTIFYING THE RISK

• Pooling of similar risk

• Law of large numbers

• The past forms a guide to the future

AIA confidential and proprietary information. Not for distribution.

41

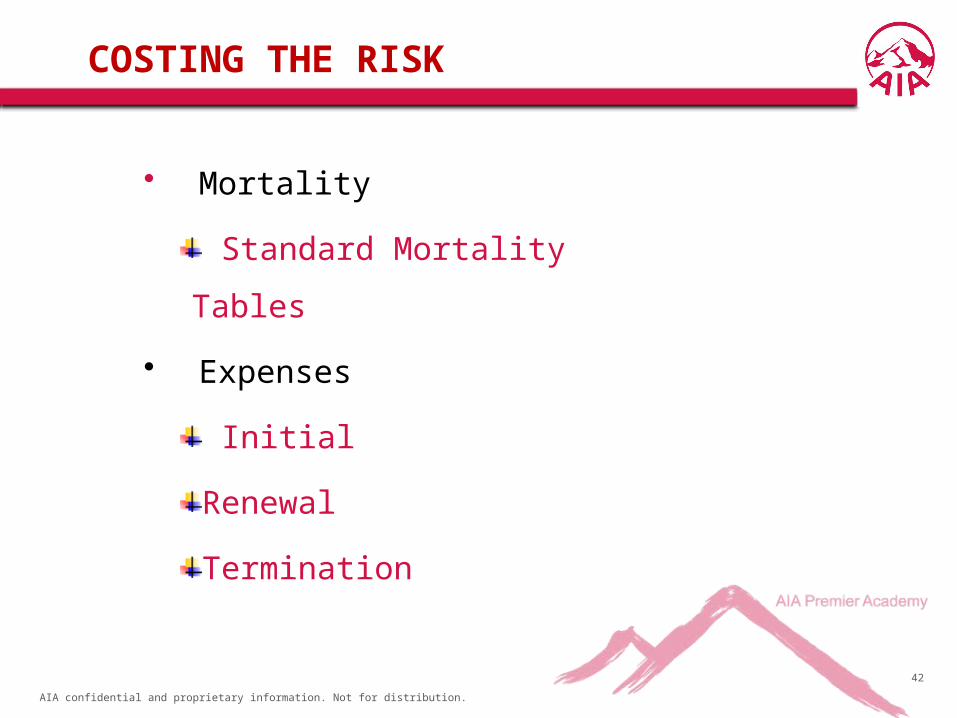

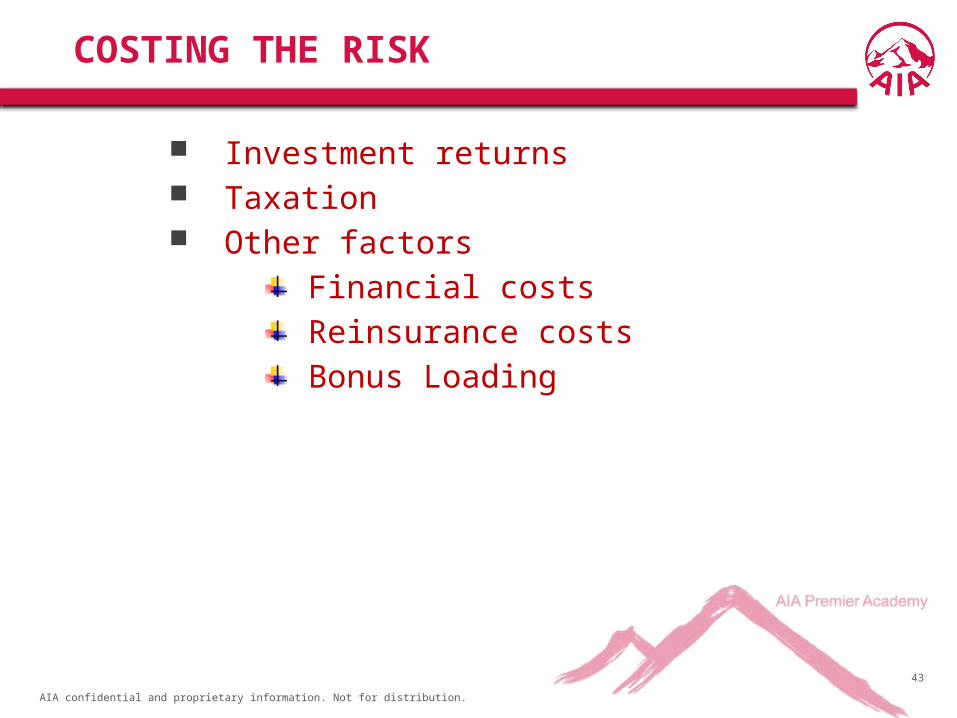

COSTING THE RISK

• Mortality

• Expenses

• Investment returns

• Tax

• Other factors

AIA confidential and proprietary information. Not for distribution.

42

COSTING THE RISK

• Mortality

Standard Mortality Tables

• Expenses

Initial

Renewal

Termination

AIA confidential and proprietary information. Not for distribution.

43

COSTING THE RISK

Investment returns Taxation Other factors

Financial costs Reinsurance costs Bonus Loading

AIA confidential and proprietary information. Not for distribution.

44

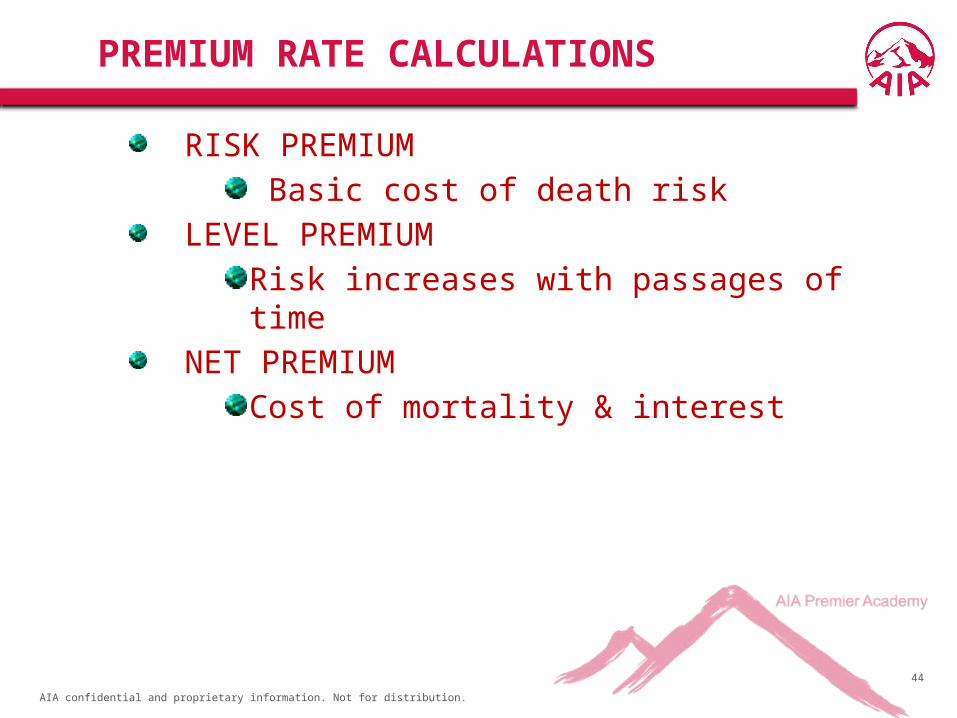

PREMIUM RATE CALCULATIONS

RISK PREMIUM

Basic cost of death risk

LEVEL PREMIUM

Risk increases with passages of time

NET PREMIUM

Cost of mortality & interest

AIA confidential and proprietary information. Not for distribution.

45

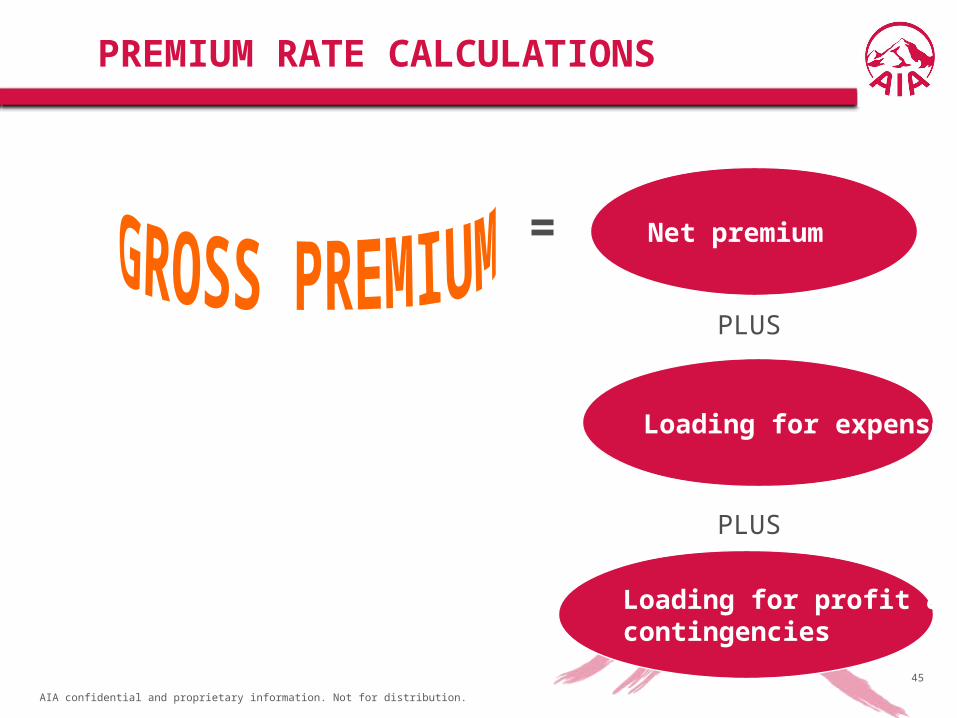

PREMIUM RATE CALCULATIONS

Net premium

Loading for expenses

Loading for profit & contingencies

PLUS

PLUS

=

AIA confidential and proprietary information. Not for distribution.

46

SATISFACTORY PREMIUM RATE STRUCTURE

• ADEQUATE

• COMPETITIVE

• EQUITABLE

• CONSISTENT

• PROFITABLE

AIA confidential and proprietary information. Not for distribution.

47

ADJUSTMENT TO GROSS PREMIUMS IN THE RATEBOOK

• MODE OF PAYMENT

• ADJUSTMENT OF SUM ASSURED

• HEALTH & OCCUPATIONAL EXTRAS

• FEMALE LIVES

AIA confidential and proprietary information. Not for distribution. 48

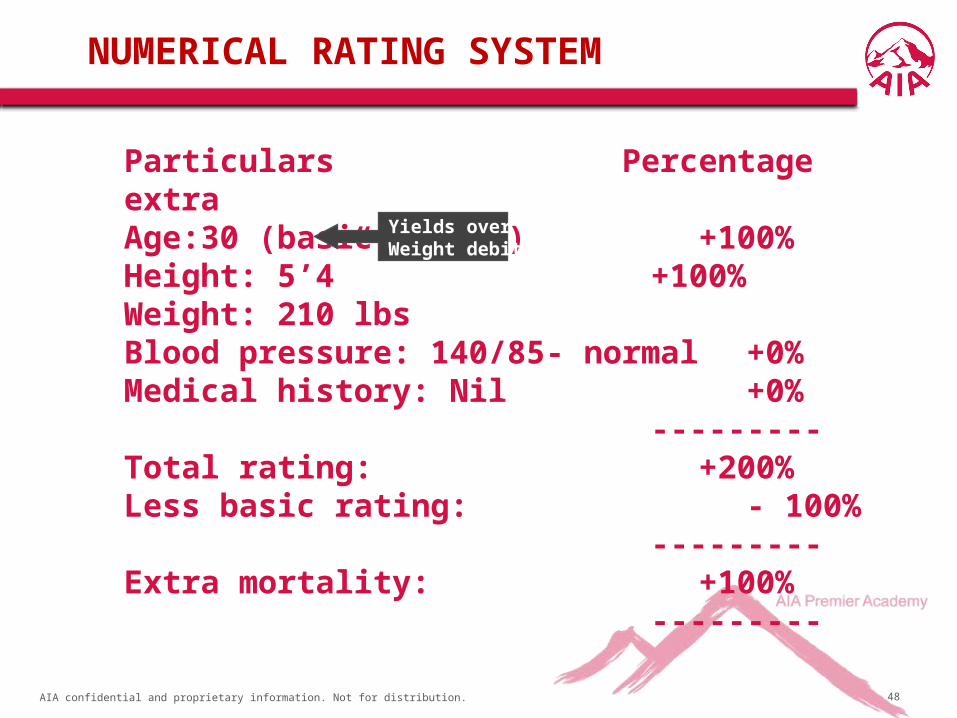

NUMERICAL RATING SYSTEM

Particulars Percentage extraAge:30 (basic rating)+100%Height: 5’4”

+100%Weight: 210 lbsBlood pressure: 140/85- normal +0%Medical history: Nil+0%

---------Total rating:

+200%Less basic rating:

- 100%

---------Extra mortality:+100%

---------

Yields overWeight debit

AIA confidential and proprietary information. Not for distribution.

49

PRACTICE OF LIFE INSURANCE-

MONITORING THE INSURANCE

FUND

AT & D- Center for Learning Excellence

CHAPTER 26

AIA confidential and proprietary information. Not for distribution.

50

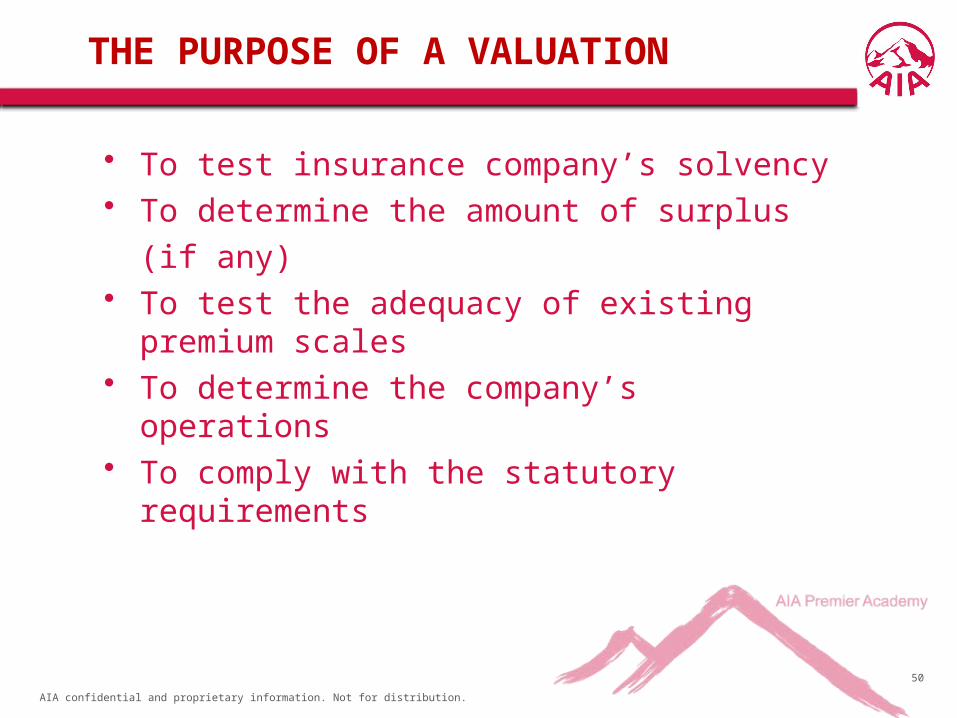

THE PURPOSE OF A VALUATION

• To test insurance company’s solvency• To determine the amount of surplus

(if any) • To test the adequacy of existing premium scales• To determine the company’s operations• To comply with the statutory requirements

AIA confidential and proprietary information. Not for distribution.

51

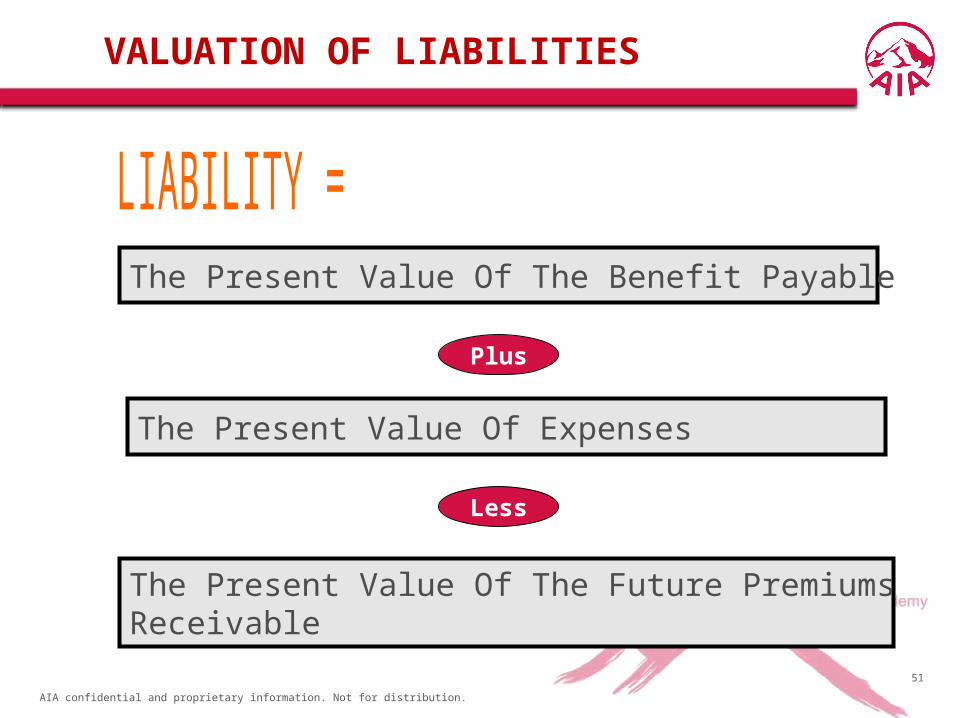

VALUATION OF LIABILITIES

The Present Value Of The Benefit Payable

The Present Value Of Expenses

The Present Value Of The Future Premiums Receivable

Plus

Less

AIA confidential and proprietary information. Not for distribution.

52

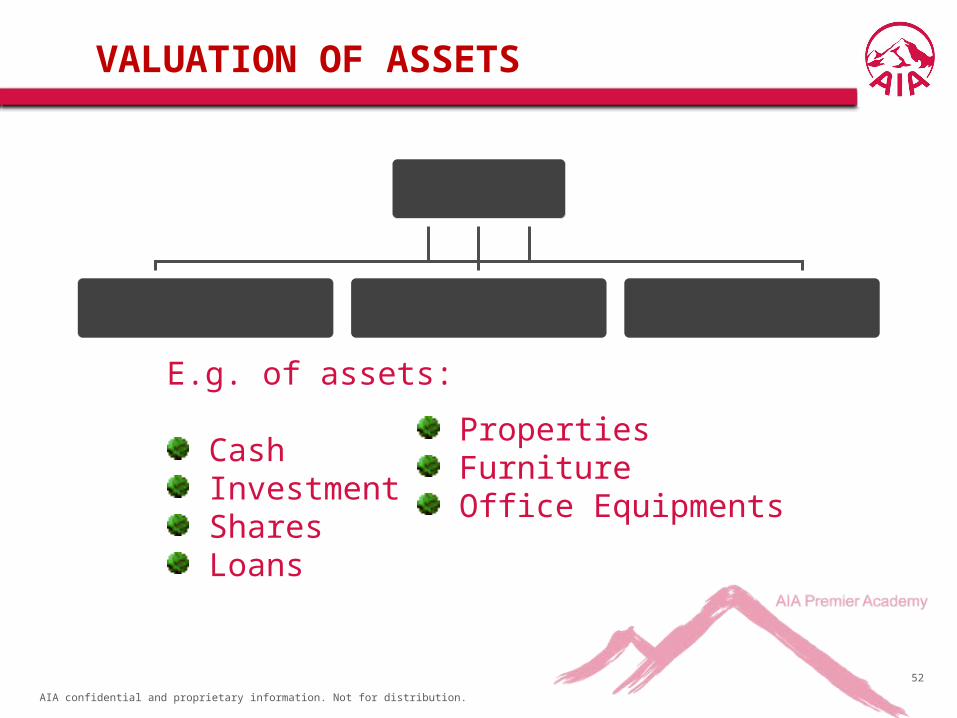

VALUATION OF ASSETS

E.g. of assets:

Cash Investment Shares Loans

Properties Furniture Office Equipments

AIA confidential and proprietary information. Not for distribution.

53

SURPLUS

Sources of surplus include:

• INTEREST

• MORTALITY

• EXPENSE

• MISCELLANEOUS

AIA confidential and proprietary information. Not for distribution.

54

METHODS OF DISTRIBUTION SURPLUS

• Simple Reversionary Bonus• Compound Reversionary Bonus• Cash Bonus• Maturity Bonus or Terminal Bonus• Interim Bonus• Guaranteed Bonus

AIA confidential and proprietary information. Not for distribution.

55

PRACTICE OF LIFE INSURANCE

- POLICY DOCUMENTS

AT & D- Center for Learning Excellence

CHAPTER 27

AIA confidential and proprietary information. Not for distribution.

56

SOURCES OF INFO FOR RISK ASSESSMENT

• PROPOSAL FORM

• MEDICAL REPORT

• ATTENDED PHYSICIAN’S STATEMENT

• AGENT’S REPORT

• PREVIOUS RECORDS

AIA confidential and proprietary information. Not for distribution.

57

THE PROPOSAL FORM

• Personal particulars

• Details of insurance

• Occupation, residence, travel & hazardous

pursuits

• Personal & family history

• Declaration & authorization

AIA confidential and proprietary information. Not for distribution.

58

THE MEDICAL REPORT/SPECIAL EXAMINATIONS

• Height & Weight

• Pulse & blood pressure readings

• Chest & abdomen measurements

• Condition of the:

•Heart

•Lungs

•Nervous system

•Urine analysis

AIA confidential and proprietary information. Not for distribution.

59

ATTENDING PHYSICIAN’S STATEMENT

• Consent of the applicant is required before hand

• Attending physician is required to give specific

answers to queries related to the treatment

AIA confidential and proprietary information. Not for distribution.

60

THE AGENT’S REPORT

• Applicant’s habits

• Appearance

• Character

• Financial status

AIA confidential and proprietary information. Not for distribution.

61

THE PROPOSAL FORM

• Personal particulars

• Details of insurance

• Occupation, Residence, Travel & hazardous pursuits

• Personal & Family history

• Declaration & Authorization

AIA confidential and proprietary information. Not for distribution.

62

POLICY FORM & STRUCTURE

• THE HEADING• THE PREAMBLE• THE OPERATIVE CLAUSE• THE PROVISO• THE SCHEDULE• ATTESTATION• CONDITIONS & PRIVILEDGES

AIA confidential and proprietary information. Not for distribution.

63

ENDORSEMENTS

• Endorsements can be done either at the:

–Time of issue of the policy

–After issue of the policy

AIA confidential and proprietary information. Not for distribution.

64

ENDORSEMENTS- Time if issue of policy

• Premium / Frequency of Payment

• Sum Assured / Mode of Payment

• Special Benefit

• Special Restrictions

AIA confidential and proprietary information. Not for distribution.

65

ENDORSEMENTS- After policy issue

• Mode of payment

• Alterations to the form of the contract

• Imposition / Removal of extra premium

• Surrender of bonus

AIA confidential and proprietary information. Not for distribution.

66

PRACTICE OF LIFE INSURANCE- CLAIMS

AT & D- Center for Learning Excellence

CHAPTER 28

AIA confidential and proprietary information. Not for distribution.

67

CLAIM ARISE

• On the death of the insured

• On maturity of the insurance policy

• Sickness or Disability benefit claims

• Claims arising under supplementary contracts

AIA confidential and proprietary information. Not for distribution.

68

DEATH CLAIMS

• NOTIFICATION OF DEATH

–Policy holder’s name & identity card number

–Policy number

–Address

–Date & cause of death

AIA confidential and proprietary information. Not for distribution.

69

DEATH CLAIMS

• PROOF OF DEATH–A death certificate–A coroner’s report–An order pronouncing a statutory presumption of death–Certificate showing death at sea–Medical certificate by last medical attendant–A certificate evidencing the death of service personnel and war death

AIA confidential and proprietary information. Not for distribution.

70

DEATH CLAIMS

• PROOF OF AGE–Birth certificate–School leaving certificate–Certified extract from baptism register–IC by Malaysian Government–Passport–Statutory declaration (for the elderly)

AIA confidential and proprietary information. Not for distribution.

71

DEATH CLAIMS

• PROOF OF TITLE & SETTLEMENT–A deed of assignment–A probate of will obtained from the court of law

–A letter of administration issued by a court of law

–For a policy effected under Sec 23 of the Civil Law act, the money would be payable to the trustees

AIA confidential and proprietary information. Not for distribution.

72

MATURITY CLAIMS

• NOTIFICATION TO POLICYHOLDER

–Identity form–Survival form–Discharge form

AIA confidential and proprietary information. Not for distribution.

73

MATURITY CLAIMS

• PROOF OF CLAIMS

–Proof of age–Proof of survival–Completion of discharge voucher–The policy document

AIA confidential and proprietary information. Not for distribution.

74

MATURITY CLAIMS

• SETTLEMENT OPTIONS

–By maturity proceeds

–Convert to annuities

–Leave proceeds of maturity as a deposit with insurer at

a pre-determined interest rate

–Draw cash by installments over a number of years

AIA confidential and proprietary information. Not for distribution.

75

LIFE INSURANCE :

SOME MATHEMATICS

AT & D- Center for Learning Excellence

CHAPTER 29

AIA confidential and proprietary information. Not for distribution.

76

CALCULATION

• AGE

• PREMIUM

• INTEREST

• GUARANTEED SURRENDER VALUE

AIA confidential and proprietary information. Not for distribution.

77

CALCULATION

• AGE–Last Birthday–Next Birthday–Nearest Birthday

AIA confidential and proprietary information. Not for distribution.

78

CALCULATION

• PREMIUM–Age–Sex–State of Health–Type of policy–Sum assured–Policy term–Mode of payment

AIA confidential and proprietary information. Not for distribution.

79

CALCULATION

• INTEREST

–Outstanding Premium Charges

–Policy Loan Repayment

AIA confidential and proprietary information. Not for distribution.

80

CALCULATION

• GUARANTEED SURRENDER VALUE–Incorporate value table in the schedules

AIA confidential and proprietary information. Not for distribution.

81AT & D- Center for Learning Excellence

PRACTICE OF INSURANCE

CHAPTER 30

“ETHICS & CODE OF CONDUCT”

AIA confidential and proprietary information. Not for distribution.

82

• Rebating

• Twisting

• Misrepresentation

• Attitude towards competition

CODE OF ETHICS

AIA confidential and proprietary information. Not for distribution.

83

• The practice of sharing an agent’s commission

with the policyholder may be viewed as

discrimination, and the implication of it clouds

the legality of the contract

REBATING

AIA confidential and proprietary information. Not for distribution.

84

• Persuading a policy holder to discontinue or

lapse a present policy in order to buy a new

policy

TWISTING

AIA confidential and proprietary information. Not for distribution.

85

• Constitute telling something that is NOT TRUE.

This statement holds true both when the agent

is representing the insurer to the prospect and

when the agent is representing the applicant to

the company

MISREPRESENTATION

AIA confidential and proprietary information. Not for distribution.

86

• Nothing is gained by casting doubt upon any

company, in which a prospect may have

insurance, or underlying motive of any other

salesman who may at the moment be attempting

to sell to the prospect

ATTITUDE TOWARDS COMPETITION

AIA confidential and proprietary information. Not for distribution.

87

• 7 PRINCIPLES OF THE CODE OF ETHICS &

CONDUCT

•AVOID conflict of interest

•AVOID misuse of position

•PREVENT misuse of information

•ENSURE completeness & accuracy

GUIDELINES ON THE CODE OF CONDUCT

AIA confidential and proprietary information. Not for distribution.

88

• 7 PRINCIPLES OF THE CODE OF ETHICS &

CONDUCT

•ENSURE confidentiality of communication

•ENSURE fair & equitable treatment

•CONDUCT business with utmost good faith &

integrity

GUIDELINES ON THE CODE OF CONDUCT