Embed Size (px)

Citation preview

PAGE 72 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

04

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

Islamic banking in its present form though can be traced back to four decades back; how-ever, it has its values embedded in the ethics of Islamic society of 1400 years ago. Islamic finance is not just about prohibition of interest, its inherent strengths of being based on real economic activity, devoid of excessive leveraging, uncertainty, and speculation while encour-aging investment disclosure and imprudent risk taking has attracted the world to this alternate financial system. Consequently, Islamic finance today exists around the globe catering not only to the financial needs of Muslims but also to non-Muslim clientele. However, it was imper-ative to have distinct global infrastructure for Islamic financial industry to spur and sustain its growth. In this background along with growing number of institutions, many international and multinational organisations have emerged aimed at developing conducive and standardised regulatory framework for the development of Islamic finance industry.

Multilateral institutions have played an important role in the development Islamic finance by building an enabling environment for Islamic finance to flourish and ensuring a level play-ing field with conventional finance. This chapter highlights key developmental roles of sev-eral multilateral institutions and standard-setting bodies that have established exclusively for Islamic finance industry namely Islamic Development Bank (IDB) Group, Islamic Financial Services Board (IFSB), Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), International Islamic Financial Market (IIFM) and International Islamic Liquidity Management Corporation (IILM). The role of World Bank as the most active infrastructure organisation of global regulatory environment, which has started working for Islamic finance industry, is also highlighted.

Islamic Development Bank Group The Islamic Development Bank Group (IDB Group) is a South-South multilateral devel-

opment finance institution established on October 20, 1975 with the objective to foster the economic development and social progress of member countries and Muslim communities individually and collectively, in accordance with the principles of Shari’a (Islamic Law). To fulfil its objective IDB Group is engaged in a wide range of activities including:

ŀŀ Project financing in the public and private sectors;

PAGE 73GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

ŀŀ Development assistance for poverty alleviation;

ŀŀ Technical assistance for capacity-building;

ŀŀ Economic and trade cooperation among member countries;

ŀŀ Trade financing;

ŀŀ SME financing;

ŀŀ Resource mobilization;

ŀŀ Direct equity investment in Islamic financial institutions;

ŀŀ Insurance and reinsurance coverage for investment and export credit;

ŀŀ Research and training programmes in Islamic economics and banking;

ŀŀ Awqaf investment and financing;

ŀŀ Special assistance and scholarships for member countries and Muslim communities in non-member countries;

ŀŀ Emergency relief; and

ŀŀ Advisory services for public and private entities in member countries.

The IDB Group is located in Jeddah, Kingdom of Saudi Arabia, with four regional offices in Morocco, Malaysia, Kazakhstan and Senegal, and 15 field representatives in selected member countries. The IDB Group comprises of five entities, namely:

i. Islamic Development Bank (IDB);

ii. Islamic Research and Training Institute (IRTI);

iii. Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC);

iv. Islamic Corporation for the Development of the Private Sector (ICD); and

v. International Islamic Trade Finance Corporation (ITFC).

Islamic Development Bank (IDB)

The vision of IDB is to become a world-class development bank, inspired by Islamic princi-ples to transform the landscape of comprehensive human development in the Muslim world. To achieve its objective, IDB provides (i) financial resources for development activities in member countries and (ii) technical assistance for capacity building and scholarships for human capital development while it manages special funds and mobilizes resources through Shari’a-com-pliant instruments. To become a member of IDB, a country is required to fulfil following the conditions:

ŀŀ must become a member of the Organization of Islamic Cooperation (OIC);

ŀŀ should pay the first instalment of its minimum subscription to the Capital Stock of IDB; and

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 74 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

ŀŀ must accept such terms and conditions that may be decided by IDB Board of Gover-nors.

At present, membership of IDB stands at 56 countries from four continents (Africa, Asia, Europe, and South America).

Islamic Research and Training Institute (IRTI)

IRTI was established in 1981 as the research and training arm of IDB in helping the trans-formation of IDB Group into a world-class knowledge-based organisation. Towards this end, key objectives of IRTI are as follows:

ŀŀ Undertake research, training and knowledge-creation activities on Islamic economics, banking and finance;

ŀŀ Organize seminars and conferences on various subjects in collaboration with national, regional and international institutions;

ŀŀ Undertake information management activities such as developing information sys-tems for use in Islamic economics, banking and finance; and

ŀŀ Maintaining databases on experts as well as trade information and promotion.

Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC)

The ICIEC1 was established in 1994 with the following objectives:

ŀŀ Increase the scope of trade transactions from the member countries of the Organiza-tion of Islamic Cooperation (OIC);

ŀŀ Facilitate foreign direct investments into member countries; and

ŀŀ Provide reinsurance facilities to Export Credit Agencies (ECAs) in member countries.

ICIEC fulfils these objectives by providing appropriate Shari’a-compatible solutions like export credit insurance and reinsurance to cover non-payment of export receivables, invest-ment insurance and reinsurance against country risks stemming mainly from currency incon-vertibility and transfer restrictions, expropriation, war and civil disturbance, breach of contract and noncompliance with sovereign financial obligations. Moreover, ICIEC manages IDB Group Investment Promotion Technical Assistance Program (ITAP), set up in 2005 to unlock the development potential of member countries through a comprehensive and integrated program of foreign investment promotion and technical assistance.

Islamic Corporation for the Development of the Private Sector (ICD)

The ICD was established in 1999 to support the economic development of its member countries through financing private sector development in accordance with the principles of Shari’a; and advise governments and private organisations to encourage the establishment, expansion and modernization of private enterprises. At present, its membership comprises of 52 IDB member countries from the continents of Africa, Latin America, Asia and Europe.

1. The ICIEC membership comprises of 40 IDB member countries from continents of Africa, Asia and Europe.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 75GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

International Islamic Trade Finance Corporation (ITFC)

The ITFC was established in 2007 and presently comprises of 37 members from Africa and Europe. The main objective of ITFC is to promote trade among OIC member countries. ITFC works towards achieving this through trade finance and Trade Cooperation & Promotion Program (TCPP). Being a member of the IDB Group, ITFC has unique access to governments in its member countries and therefore it works efficiently as a facilitator to mobilize private and public resources towards achieving its objectives of fostering economic development through trade.

Achievements of IDB Group

IDB Group has played pivotal role in establishing and strengthening Islamic financial industry in the world. Its significant achievements mainly include:

ŀŀ Supportive role in establishment of infrastructural organisations like Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), General Council of Islamic Banks and Financial Institutions (GCIBAFI), International Islamic Financial Market (IIFM), Islamic International Rating Agency (IIRA) and International Islamic Liquidity Management Corporation (IILMC), etc

ŀŀ Equity investment for establishing more than 30 Islamic banks and Islamic financial institutions (IFIs) across various jurisdictions

ŀŀ Issuance of sukuk program. The first resource mobilization was the issuance of a maiden sukuk in 2003. In 2005, IDB established a US$1 billion Medium Term Note (MTN) Program to tap the global capital market resources in more regular and organ-ized basis. The program allows IDB to issue sukuk in various currency denominations

Islamic Financial Services Board (IFSB)The IFSB is an international standard setting body for Islamic financial industry. It was

inaugurated in November 2002 with the signing of the Articles of Agreement by founding mem-bers including Bahrain Monetary Agency, Bank Indonesia, Bank Markazi Jomhouri Iran, Cen-tral Bank of Kuwait, Bank Negara Malaysia, State Bank of Pakistan, Saudi Arabian Monetary Agency, Bank of Sudan and Islamic Development Bank. The organisation became operational in March 2003 in Kuala Lumpur, Malaysia, under the specially enacted law; Financial Services Board Act 2002, which gives IFSB the immunities and privileges akin to that of international organisations and diplomatic missions. Over the years membership of IFSB has grown to 189 consisting of 65 regulatory and supervisory authorities, 8 international inter-governmental organisations and 116 market players. With respect to three categories of membership of IFSB (see Box 5.1), 30 fall into the category of Full Membership, 28 Associate Membership and 131 Observer Membership.

Organisational Structure

All members form the General Assembly, but the Council is the senior executive and policy making body. Two main offices work under Council, namely the Secretariat and Technical Committee. The Secretariat is the permanent administrative body, which is headed by a full-time Secretary-General appointed by the Council while Technical Committee is responsible for advising the Council on technical issues. Technical Committee consists of up to fifteen persons selected by the Council and each member gets a term of three years. Working Groups, Task Force and Editing Committee work under Technical Committee.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 76 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

BOX 4.1:CATEGORIES OF MEMBERSHIP AT IFSB

The IFSB has three categories of membership;

i. Full Membership: This category is available to the supervisory authority responsible for the supervision of the banking industry, securities and/or insurance/Takâful indus-tries of each sovereign country that recognises Islamic financial services, whether by legislation or regulation or by established practice, and international inter-governmental organisations that have an explicit mandate for promoting Islamic finance.

ii. Associate Membership: This category is available to any central bank, monetary authority or financial supervisory or regulatory organisation or international organisa-tion involved in setting or promoting standards for the stability and soundness of inter-national and national monetary and financial systems which does not qualify or does not seek to become IFSB Full member.

iii. Observer Membership: This category is available to any:

a. national, regional or international professional or industry association;

b. institution that offers Islamic financial services; or

c. firm or organisation that provides professional services, including accounting, legal, rating, research or training services to any aforementioned institutions in (a) and (b)

Source: IFSB Website

Functions

IFSB is aimed at enhancing the soundness and stability of Islamic financial services indus-try through issuing global prudential standards and guiding principles broadly covering areas like banking, capital market and insurance. The procedure of preparing standards and guide-lines has been defined by the Council (see Box 5.2 for Steps of Issuing Standard). Since its inception, the IFSB has issued twenty-four Standards, Guiding Principles and Technical Note for the Islamic financial services industry. The published documents are on the areas of:

1. Risk Management (IFSB-1)

2. Capital Adequacy (IFSB-2)

3. Corporate Governance (IFSB-3)

4. Transparency and Market Discipline (IFSB-4)

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 77GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

5. Supervisory Review Process (IFSB-5)

6. Governance for Collective Investment Schemes (IFSB-6)

7. Special Issues in Capital Adequacy (IFSB-7)

8. Guiding Principles on Governance for Islamic Insurance (Takaful) Operations (IFSB-8)

9. Conduct of Business for Institutions offering Islamic Financial Services (IIFS) (IFSB-9)

10. Guiding Principles on Shari'a Goverance System (IFSB-10)

11. Standard on Solvency Requirements for Takaful (Islamic Insurance) Undertakings (IFSB-11)

12. Guiding Principles on Liquidity Risk Management (IFSB-12)

13. Guiding Principles on Stress Testing (IFSB-13)

14. Standard on Risk Management for Takaful (Islamic Insurance) Undertakings (IFSB-14)

15. Revised Capital Adequacy Standard (IFSB-15)

16. Revised Guidance on Key Elements in the Supervisory Review Process (IFSB-16)

17. Core Principles for Islamic Finance Regulations (IFSB-17)

18. Recognition of Ratings on Shari'a-Compliant Financial Instruments (GN-1)

19. Guidance Note in Connection with the Risk Management and Capital Adequacy Standards: Commodity Murabahah Transactions (GN-2)

20. Guidance Note on the Practice of Smoothing the Profits Payout to Investment Account Holders (GN -3)

21. Guidance Note in Connection with the IFSB Capital Adequacy Standard: The Deter-mination of Alpha in the Capital Adequacy Ratio (GN-4)

22. Guidance Note on the Recognition of Ratings by External Credit Assessment Institu-tions (ECAIS) on Takaful and ReTakaful Undertakings (GN-5)

23. Quantitative Measures for Liquidity Risk Management (GN-6)

24. Development of Islamic Money Markets (TN-1)

In addition, the IFSB is actively involved in the promotion of awareness of issues that are relevant or have an impact on the regulation and supervision of the Islamic financial services

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 78 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

BOX 4.2:STEPS OF ISSUING STANDARD

ŀŀ Working Groups (WG) are formed by the Technical Committee (TC) for drafting of stand-ards/guidelines. Since members of the WG render their services on part-time basis, therefore a full-time project manager is assigned to each WG. In addition to the project manager, each WG is also assigned a part-time consultant who is well knowledgeable in the international standard/guideline that is relevant to the standard/guideline that is being prepared.

ŀŀ The General Secretariat in consultation with the Technical Committee (TC) and other relevant regulatory bodies and organisations compile a list of the standards/guidelines that it deems necessary to be prepared. However, Council approves the final list.

ŀŀ Each WG meets to discuss the initial study of the standard/guideline assigned to it. The WG may require that the initial study should be revised and resubmitted in light of the comments made by its members.

ŀŀ The WG submits the revised document to the TC for discussion, amendment, and approval. The project manager and the consultant use the document approved by the TC as the basis for the preparation of a draft.

ŀŀ A workshop may be held on the topic of each standard/guideline to be prepared. This enables the WG to embark on an engagement process with the various relevant supervi-sory and regulatory bodies (both members and non-members of the IFSB) and elicit their views on the issues raised in the document approved by the TC.

ŀŀ Based on the feedback from the workshop the WG provides the project manager with guidelines to prepare an exposure draft of the standard/guideline to submit to the TC.

ŀŀ The TC then discusses and amends the draft of the exposure draft to submit to the body of Shari’a scholars (in accordance with Article 30 (e)) for endorsement that the document complies with Shari’a rules and principles.

ŀŀ The WG then addresses the remarks of the body of Shari’a scholars, if any, and ask the project manager and the consultant to revise the draft of the exposure draft accordingly. The WG discusses, amends and approves the revision made by the project manager and the consultant to submit the revised draft to the body of the Shari’a scholars for endorsement.

ŀŀ The revised document is submitted to the TC which discusses and amends the revised draft of the exposure draft before its approval for issuance as an Exposure Draft (ED).

ŀŀ The ED is posted on the website of the IFSB for comments by all interested parties within stipulated time by WG. In cases where it is deemed appropriate, the TC shall decide to hold public hearing(s). The WG attends the public hearing and receives the comments of the participants on the ED and respond to their queries.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 79GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

industry. This mainly takes the form of international conferences, seminars, workshops, train-ings, meetings and dialogues.

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI)

AAOIFI, formerly known as Financial Accounting Organization for Islamic Banks and Financial Institutions, was established in accordance with the Agreement of Association, which was signed by Islamic financial institutions on February 26, 1990 in Algiers. AAOIFI as an international autonomous non-profit making corporate body was registered on March 27, 1991 in the State of Bahrain. The organisation was mandated to enhance the confidence of users of the financial statements of Islamic financial institutions (IFIs) and to encourage these users to invest in these institutions and to use their services. AAOIFI key objectives are:

1. To develop accounting and auditing thoughts relevant to IFIs;

2. To disseminate accounting and auditing thoughts relevant to IFIs and its applications through training, seminars, publication of periodical newsletters, carrying out and commissioning of research and other means;

3. To prepare, promulgate and interpret accounting and auditing standards for IFIs; and

4. To review and amend accounting and auditing standards for IFIs.

AAOIFI is supported by 200 institutional members from 40 countries including central banks, IFIs, and other participants from the international Islamic banking and finance industry, worldwide (see Box 5.3 for membership categories at AAOIFI). The governance structure of AAOIFI can be grouped into two broader categories - General Assembly consisting of Board of

ŀŀ The project manager together with the consultant analyse all the com-ments received on the ED and present them to the WG with suggestion as to the necessary revision to the ED.

ŀŀ The revised ED is again referred to the body of Shari’a scholars to endorse the compliance of the document with Shari’a rules and principles before its submis-sion to the TC for discussion and amendment, if any.

ŀŀ The TC then decides whether the revision made in the ED warrants that the ED should be distributed for further comments or not.

ŀŀ The TC presents the revised ED to the Council for consideration and formal adoption.

ŀŀ The Council may adopt and approve for issuance the ED in the form of a stand-ard/guideline.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 80 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Trustees, the Executive Committee and the General Secretariat; and Technical Boards, namely the Accounting Board, the Shari’a Board, and the Governance and Ethics Board.

A total of 88 standards have been issued so far (see Box 5.4 for Process of Standard Devel-opment & Revision), which includes 48 on Shari’a, 26 on accounting, 5 on auditing, 7 on gov-ernance and 2 codes of ethics. AAOIFI has gained assuring support for the implementation of its standards, which are now adopted in the Kingdom of Bahrain, Dubai International Financial Centre, Jordan, Lebanon, Qatar, Sudan and Syria. The relevant authorities in Australia, Indo-nesia, Malaysia, Pakistan, Kingdom of Saudi Arabia, and South Africa have issued guidelines that are based on AAOIFI’s standards and pronouncements. AAOIFI is also making efforts to enhance the industry’s human resources base and governance structures. In this regard the most significant is the professional qualification programs such as the “Certified Shari'a Advisor & Auditor (CSAA) targeted at equipping candidates with the requisite technical under-standing and professional skills on Shari’a compliance and review processes and the Corporate Compliance Program. In addition, AAOIFI also conducts workshops, seminars and confer-ences to raise awareness as part of its promotional activities for Islamic banking and finance.

BOX 4.3:CATEGORIES OF MEMBERSHIP AT AAOIFI

Founding Members: This category consists of IFIs that are signatories to the Agreement establishing AAOIFI, and those that have been subsequently accepted as founding members. These are the Islamic Development Bank, Dallah Al Baraka, Faysal Group (Dar Al Maal Al Islami), Al Rajhi Banking & Investment Corporation, Kuwait Finance House, and Albukhary Foundation.

Associate Members

This category comprise of

A. IFIs and companies that comply with Islamic Shari’a rules and principles in all their transactions.

B. Islamic Fiqh academies and learning institutions.

Associate members shall have the right to participate in the meetings of the General Assem-bly but without a right to vote. They shall also have the right to take part in AAOIFI’s events and receive AAOIFI’s publications at special rates. An associate member is entitled to enjoy the rights of the founding members provided the following terms are satisfied:

A. File an application in this respect.

B. Obtain an initial approval by the Board of Trustees of this application.

C. Fulfill all the financial obligations of the founding members from the date of the initial approval.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 81GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

BOX 4.4:PROCESS IN STANDARDS DEVELOPMENT & REVISION

In carrying out the standards development and revision processes of AAOIFI standards, the relevant standards board works with AAOIFI General Secretariat and, if deemed necessary with external consultants. The relevant standards board may also form committees or working groups, in coordination with the General Secretariat, to assist with the board’s work programs. Such committees or working groups may comprise of representatives of the relevant standards boards together with other representatives of the international Islamic finance industry stake-holders. Major steps of the process are as follows;

ŀŀ The relevant standards board, in coordination with the General Secretariat, formulates a tentative work program or agenda to include potential new standard to be developed, or existing standard to be reviewed. During this process suggestions and feedback from the international Islamic finance industry as well as members of AAOIFI standards boards are incorporated.

(D) Issuance of a final resolution on this application by the General Assembly.

Members comprising of regulatory and supervisory authorities

These members comprise of regulatory and supervisory authorities that supervise IFIs. Members representing regulatory and supervisory authorities have the right to par-ticipate and vote in the meetings of the General Assembly. They also have the right to take part in AAOIFI’s events and receive AAOIFI’s publications at AAOIFI’s members’ rates.

Observer Members

This category comprise of

A. Organizations and associations responsible for regulating the accounting and auditing profession and/or those responsible for preparing accounting and audit-ing standards.

B. Practicing certified accounting and auditing firms that have interest in the accounting and auditing practices of IFIs.

C. Financial institutions engaged in financial activities of Islamic institutions.

D. Users of financial statements of IFIs.

Observer members have the right to participate in the meetings of the General Assembly but without a right to vote. They also have the right to take part in AAOIFI’s events and receive AAOIFI’s publications at special rates.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 82 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

ŀŀ Members of the General Secretariat and/or external consultant/s prepare the preliminary study or research that is discussed with the relevant commit-tee or working group (if applicable) and the relevant standards board.

ŀŀ Subsequently, a consultation note is prepared that outlines proposed major points of a new standard, or proposed major changes to an existing standard. Feedback of relevant committee or working group (if applicable) and the relevant standards board on consultation note is solicited.

ŀŀ After the agreement of relevant standards board on consultation note, it is released to the international Islamic finance industry and beyond, for comments and suggestions. The consultation note may also be submitted to technical workshops, public hearing meetings and/or similar forum.

ŀŀ After incorporating comments and suggestions an exposure draft of the stand-ard is developed which is subject to discussions with the relevant committee or working group (if applicable) and the relevant standards board.

ŀŀ After the agreement of relevant standards board on exposure draft, it is released to the international Islamic finance industry and beyond, for comments and suggestions. The exposure draft may also be submitted to technical workshops, public hearing meetings or/and similar forum.

ŀŀ Subsequent to the exposure draft, a final new or revised standard will be pre-pared which is discussed with the relevant committee or working group (if appli-cable), and approval by the relevant standards board.

ŀŀ Upon approval by the relevant standards board, the final standard is then issued to the international Islamic finance industry.

However, issued standards are subject to continuous review. Revision to the stand-ards is carried out, through the above processes, as and when necessary.

International Islamic Financial Market (IIFM) Founded in 2002 and restructured in 2007, the International Islamic Financial Market

(IIFM) is responsible for developing Shari’a-compliant financial contracts and product tem-plates relating to Islamic capital and money market, trade finance and corporate finance. The creation of IIFM, as a standard-setting organisation, has been linked to a joint effort led by six founding member countries to strengthen an Islamic global prudential Shari’a-compliant standard agreements regime. This is being done through financial documentation and product templates standardization, independent Shari’a enhancement and guidelines for new products and, transparency in transactions and financial contracts as well as legal certainty in case of unexpected adverse events.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 83GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

IIFM has issued seven standard agreements/products covering areas of Islamic Cross Currency Swap2, Master Collateralized Murabahah Agreement, Inter-Bank Unrestricted Mas-ter Investment Wakalah Agreement, Islamic Profit Rate Swap , Tahawwut (Hedging) Master Agreement, Master Agreements for Treasury Placement (see Box 5.5 for the brief overview of standard agreements/products) while projects in progress include Product Templates on Islamic Foreign Exchange Forward, Islamic Credit Support Arrangement, Risk Participation Agreement (funded and unfunded) and Sukuk standardization.

The realization of objectives of IIFM, indeed, requires hard work and continuous coop-eration with financial institutions, regulators, legal experts and other market participants worldwide especially since the standards issued by the Islamic main standard-setting bodies are voluntary. This implies that these standards are offered for adoption without being man-dated in law. Some standards become mandatory when they are adopted by regulators as the legal requirements in some jurisdictions. For example, for liquidity management, the Central Bank of Bahrain launched a new Shari’a-compliant Wakalah liquidity management tool aimed at absorbing excess liquidity of local Islamic retail banks. The master agreement has been developed based on IIFM’s Inter-Bank Unrestricted Master Investment Wakalah Agreement (published in 2013). Saudi Arabian Monetary Agency (SAMA) has also commissioned all the Islamic banks in the Kingdom to adopt the Tahawwut (Hedging) Master Agreement (published in 2010) in their Shari’a-compliant hedging transactions.

As evidenced above, IIFM plays an important role through the formation of Islamic finan-cial policies in many jurisdictions across the globe through its standardization of the Shari’a compliant agreements and product templates. However, IIFM is aware of the challenges to achieve a general consensus in the industry in the formation of Islamic financial policies. In this regard, IIFM has adopted a simple strategy in order to enhance its role in the formation of the Islamic financial policy across the globe. Major components of the strategy are as follows:

1. To get countries to agree to introduce the standards published by IIFM to the financial institutions in their respective jurisdictions, and let these institutions to commit to a level playing field with regard to these standards.

2. To develop more efficient and effective mechanisms for monitoring and encouraging the adoption of IIFM standard agreements.

3. To encourage the regulators to foster more support for IIFM initiatives so that, it will be able to develop effective international standards.

4. To focus on working with regulators closely to strengthen IIFM role in the formation of Islamic financial policies, not only through the issuance of master standard agree-ments and product templates, but also by organizing topic specific briefing seminars, workshops on IIFM standards, industry consultative meetings and publications.

5. To publish research papers and reports such as consultative papers on important top-ics like Islamic Alternative to Repo, Sukuk Standardization, IIFM Sukuk Reports etc. as a key source of information.

IIFM with its entrusted mandate has a central role to play in pioneering new forms of international cooperation to support a more pluralistic international Islamic financial regula-

2. Two standards are applicable to this product.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 84 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

tory order. However, to achieve its objective IIFM is aware of challenging aspirations which include: developing effective practical mechanisms through its standards development process for implementation, encouraging Shari’a-compliance and harmonization, promoting the devel-opment of effective Shari’a-compliant global financial master agreements and encouraging consensus on their content, establishing its legitimacy within member as well as non-member

BOX 4.5:BRIEF OVERVIEW OF STANDARD AGREEMENT/PRODUCTS ISSUED BY IIFM

By now IIFM has published standards relating to Islamic hedging and liquidity management in response to the most urgent need to have universally acceptable solutions to risk mitigation and liquidity management. The published standards and its brief description are presented below.

IIFM Standard 1: IIFM Master Agreements for Treasury Placement

This was the first ever global standard documentation published in Islamic finance for liquid-ity management purpose. The Master Agreements for Treasury Placement (MATP) comprises of standalone Master Murabahah Agreement and a Master Agency Agreement. The standard documentation involves Commodity Murabahah based on two structures namely: (i) Commodity Murabahah under Agency Agreement, and (ii) Commodity Murabahah based Principle to Prin-ciple. The Agreement was published in 2008 and based on IIFM recent survey MATP is widely used in Islamic inter-bank market particularly involving cross border trades.

IIFM Standard 2: International Swaps and Derivatives Association (ISDA) /IIFM Tahawwut (Hedging) Master Agreement

In March 2010, the Tahawwut Master Agreement (TMA) was jointly published by IIFM and ISDA and marked the introduction of the first globally standardised documentation for OTC Islamic hedging products. TMA is a framework document that provides a globally standardised early termination and close-out mechanism and other legal and Shari'a provisions for privately negotiated and widely accepted Islamic hedging products. The master agreement is designed to facilitate the risk management function of IFIs including providing a legal framework. Under the TMA, Islamic hedging products can be transacted. In order to provide clarity and transparency the TMA also includes an Explanatory Memorandum.

IIFM Standard 4 and IIFM Standard 3: ISDA/IIFM Islamic Profit Rate Swap (IPRS) (Mubadalatul Arbaah) Standard Product Templates

In March 2012, in its efforts to accelerate the use of TMA, IIFM and ISDA jointly published the first hedging product template. The IPRS provides the industry access to robust and well devel-oped product documentation under the TMA. It provides protection to IFIs’ balance-sheet from wide swings in fixed and floating profit rates as well as enabling them to manage their cash-flow risk for various Islamic capital market instruments such as Sukuk. Two sets of IPRS templates have been published; (i) Wa’ad based template that involve a two Sales structure and (ii) Wa’ad based template with a single Sale structure. (The IPRS standard templates also include a product description for guidance purposes).

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 85GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

IIFM Standard 5: IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement

Published on 3rd June 2013, the inter-bank has been specifically designed to pro-vide alternate liquidity management product to the Islamic finance industry in order to reduce over reliance on commodity Murabahah based transactions. The important features of this standard documentation is Wakil’s discretion to invest the funds, use of general treasury pool (segregated and un-segregated asset pool), anticipated profit, early termination, replacement of asset, on-balance sheet accounting assessment, etc., The Unrestricted Wakalah standard includes a detailed operational guidance memorandum on the mechanics of this agreement as well as how it should be applied by the transacting parties. In addition, the operational guidance memo also provides valuable recommen-dations to be taken into consideration at the time of entering into unrestricted Wakalah investment transactions.

IIFM Standard 6: IIFM Master Collateralized Murabahah Agreement (MCMA)

The MCMA was published on 16th November 2014 and it provides a mechanism for access to liquidity on a collateralized basis utilizing Sukuk and other Islamic securities portfolio as collateral. It is an important new tool for IFIs as they seek to address the increased global regulatory focus on liquidity and collateral. Collateralized transactions based on Murabahah provide a level playing field for IFIs by giving them option to tap funds from central banks in case of liquidity short-fall. The MCMA is accompanied by an operational guidance memorandum which covers the operational procedures which may be implemented by potential users of the MCMA.

IIFM Standard 7: ISDA/IIFM Islamic Cross Currency Swap (Himaayah Min Taqallub As‘aar Assarf (ICRCS) Standard Product Template

The ICRCS standard template was published on 26th November 2015 as the second hedging product template under the TMA. With ICRCS the Islamic financial institutions can manage risk in transactions exposed to fluctuations in currencies and rate-of-return mismatches. The ICRCS standard template also includes a product description for guid-ance purposes.

countries and clarifying its relationship with other Islamic global standard-setting organisa-tions.

The International Islamic Liquidity Management Corporation (the IILM)

The IILM was established on October 25, 2010 by central banks, monetary authorities and multilateral organisations and received the status of an international institution under IILM Act 2011 issued by Malaysia. The current shareholders of IILM are from the central banks and monetary agency of Indonesia, Kuwait, Luxembourg, Malaysia, Mauritius, Nigeria, Qatar, Turkey, the United Arab Emirates and the Islamic Development Bank. The organisation is operational under the governance structure comprising of the General Assembly, Governing Board, Board Executive Committee, Board Audit Committee, Board Risk Management Com-mittee and Shari’a Committee. IILM aims at fostering regional and international co-operation by building a robust liquidity management infrastructure at national, regional and international

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 86 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

levels. This is being done by creating a variety of Shari’a-compliant instruments, on commer-cial terms, to suit the varying liquidity needs of IFIs and subsequently, enhancing cross-border investment flows, international linkages and financial stability.

In April 2013, the IILM announced the launch of its inaugural short-term Sukuk Programme, which was rated A-1 by Standard and Poor’s Rating Services. Subsequently, the IILM inaugural Sukuk of US$490 million were issued with a tenor of 3 months and were fully subscribed. The IILM Sukuk Programme marks the first of many things, not only for Islamic finance but also in the conventional space for several reasons. Firstly, it is the first Shari’a-compliant, short-term, highly rated, tradable, US Dollar-denominated instrument in the market. Secondly, it is the first money market instrument backed by sovereign assets in the form of sukuk. Finally, it has the first multi-jurisdictional primary dealer network that facilitates distribution to inves-tors worldwide. The IILM sukuk are expected to complement the intermediate and long-term sukuk currently available in the market.

Role of World Bank as Infrastructure Organisation for Islamic Finance Industry

Multilateral Development Banks (MDBs) have played significant role in the economic and financial development of emerging and low-income countries. In addition to providing direct financial assistance, MDBs, provide advisory services to their clients to facilitate overall eco-nomic development in those countries. The World Bank Group, as the leading MDB on the globe has been providing significant amount of financial assistance to its client countries and helped them through advisory services in establishing the necessary environment that will enable sustainable development in various sectors such as infrastructure, healthcare, edu-cation, and finance. In compliance with the Sustainable Development Goals initiated by the United Nations in 2015, the World Bank has redefined its goals as the eradication of extreme poverty and promotion of shared prosperity.

Islamic finance has gained a remarkable momentum during the last decade, especially after the global financial crisis. It has already become systematically important in several coun-tries such as Malaysia, Saudi Arabia, Pakistan, Bahrain, and Indonesia. Furthermore, Islamic finance has been recognised in some non-Muslim developed markets of the World such as the UK and Luxemburg. Due to its core principles of risk sharing and asset-backed/based finance, Islamic finance seems to be a viable tool for promoting economic growth, strengthening sys-temic stability and enhancing the financial inclusion of low-income segments of societies and thereby contributing to the eradication of extreme poverty via boosting shared prosperity.

World Bank Group as the Leading Multilateral Development Institution

Figure 1 below summarizes basic products and services of World Bank Group Institutions (see Box 5.6 for the role of multilateral banks) for its client countries. Under the World Bank Group, the World Bank offers services to public sector while International Finance Corporation (IFC) and Multilateral Investment Guarantee Agency (MIGA) offers services to private sector of client countries. The products offered by the World Bank, can be classified as financial instru-ments intended for development projects, advisory services and analytics. Financial instru-ments that could facilitate development include Investment Project Financing (IPF), Program for Result (PFoR), and Development Policy Financing (DPF). IPF instruments are intended to support specific projects in developing countries, the PFoR type of financing includes the sup-port of government programs with a specific goal and capacity building objective while DPF tools are to sponsor policy and institutional reforms. All of these instruments can be in the form of loans and grants. Advisory services and analytics (ASA) are utilized either as assistance to

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 87GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Figure 1:PRODUCTS AND SERVICES PROVIDED BY WBG INSTITUTIONS

Source: The World Bank Group

ADVISORY SERVICESAND ANALYTICS

Firm Level Advice

PPP Transaction Advice

Quasi-equity Finance

Advice to Governments and

Non-government Institutions

to Improvethe Enabling

Environment

ADVISORY SERVICES

AD

VIS

OR

YS

ER

VIC

ES

DEVELOPMENT FINANCING

INSTRUMENTS

Investment Project

Financing (IPF)

Program for Results (PforR)

Development Policy

Financing (DPF)

PUBLIC SECTOR

Loans

Syndicated Loans

Quasi-equity Finance

Equity Finance

Risk Management Services

Trade Finance and Supply

Chain

Currency Inconvertibility and

Transfer Restriction

Expropriation

War, Terrorism, and Civil

Disturbance

Breach of Contract

Non-honoring of Financial

Obligations

INVESTMENTSERVICES

GUARANTEEPRODUCTS

PRIVATE SECTOR

FIN

AN

CIA

LP

RO

DU

CT

S

a client country or as public service. These services cover a wide range of products, such as reports on key economic and social issues, sector studies, policy notes, knowledge sharing workshops, conferences, evaluations, and training programs together with the collection and compilation of data on various development issues. ASA are financed through the Bank’s own administrative budget and/or donors via Bank Executed Trust Funds or clients themselves through so-called reimbursable Advisory Services (RSA) operations.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 88 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

BOX 4.6:ROLE OF MULTILATERAL INSTITUTIONS

The list of multilateral development banks with either global or regional mandate includes the World Bank Group (WBG), African Development Bank (AfDB), Asian Development Bank (AsDB), European Bank for Reconstruction and Development (EBRD),Inter-American Development Bank (IDB) , and Islamic Development Bank Group (IDBGs). These institutions are established to pro-vide financial support to developing countries for economic development purposes. The con-text of the financial assistance ranges from the support of investment projects in sectors such as energy, transportation, healthcare, agriculture, and technical assistance to implement policy reforms in various areas while the form of the financial assistance can be either through loans, equity investments or guarantees for loans. The significant role of these multilateral development banks is depicted by the premise that the total amount of loan provided by these institutions exceeds US$90 billion during FY 2015.

Figure 2:WORLD BANK GROUP FINANCING IN PARTNER COUNTRIES (AMOUNT OF

COMMITMENTS BY FISCAL YEAR, US$ BILLION)*

0

10

20

30

40

50

60 56.3

51.250.2

58.2 59.8

70

2011 2012 2013 2014 2015

IBRD IDA IFC MIGA

Recipient-Executed Trust Fund WBG Total

Source: World Bank Annual Report, 2015*The data includes IBRD, IDA, IFC, and Recipient-Executed Trust Fund (RETF) commitments, and MIGA

gross issuance.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 89GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

The mandate of IFC mainly covers the support for private sector companies in client countries through loans, syndicated loans, quasi- equity or equity finance, risk management services, and financing trade and supply chain. In addition, IFC has an Asset Management Company for the management of third party capital through investing in IFC operations in developing countries. Furthermore, IFC offers advisory services for firms, for public-private partnership projects, and for governmental and non-governmental institutions to improve the enabling environment that will contribute to private sector development. MIGA, on the other hand, offers guarantee services for investments in client countries against currency incon-vertibility and transfer restrictions, expropriation, war, terror, and civil disturbance, breach of contracts, and non-honouring of financial obligations.

As illustrated in Figure 2, since 2011, the World Bank Group institutions provide, annually, US$55.13 billion financial assistance to client countries on average. International Bank for Reconstruction and Development (IBRD) and International Development Association (IDA) are two main institutions providing more than 70% of annual average financial assistance

Figure 3:DISTRIBUTION OF WORLD BANK GROUP COMMITMENTS BY

REGION FOR FY2015 ( %)

Source: World Bank Annual Report, 2015

16.7%Europe and Central Asia

15% East Asia and Pacific

8.3 %Middle East and North Africa

18.3%South Asia

25.0%Sub-Saharan Africa

16.7% Latin America and the Caribbean

DISTRIBUTIONOF WORLD BANK

GROUPCOMMITMENTSBY REGION FOR

FY2015 ( %)

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 90 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

amount. More than 16% of annual average financial assistance are composed of IFC supports and investments in private sector firms.

When the region wise distribution of financial assistance is analyzed as in the Figure 3, Sub-Saharan Africa appears to take the biggest portion from the WBG operations, which amounts to 25% of financial assistance during financial year 2015. Shares of South Asia, Latin America and Caribbean, Europe and Central Asia, and East Asia and Pacific regions are between 15% and 18% while the Middle East and North Africa region received the lowest portion of the financial assistance.

Islamic Finance: Relevance to World Bank Goals

Islamic finance has experienced a period of remarkable growth worldwide during the last decade. The amount of global Islamic financial assets have reached to $2 trillion dollars cov-ering bank and non-bank financial institutions, capital markets, money markets and insurance (takaful). This corresponds to a cumulative average annual growth rate of around 16% since 2009. The amount of assets are expected to exceed US$3 trillion by 2018.3

3 City UK Report, November 2015 and MIFC, 2015.

Figure 4:POVERTY HEADCOUNT RATIO AT US$1.25 A DAY (PPP) (% OF POPULATION)

15

20

25

30

35

40

45

40.5042.11

36.86

27.60

23.80 23.51

42.4040.82

34.88

25.72

20.3217.54

1990 1995 2000 2005 2010 2014

OIC World

Source: World Development Indicators, the World Bank, authors calculations

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 91GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Figure 5:SURVEY MEAN INCOME PER CAPITA, BOTTOM 40% AND TOTAL POPULATION,

(2005 PPP US$ PER DAY)

Source: World Development Indicators, the World Bank, authors calculations

The fact that Muslims compose one-fifth of the world population (about 1.6 billion) high-lights the growth potential of Islamic finance worldwide. In addition, the data on the level of economic and financial development in Organization of Islamic Cooperation (OIC) member countries suggests that these countries have a long way to go towards achieving the twin goals of the World Bank. Figure 4 indicates the level of extreme poverty throughout the OIC coun-tries and the world through the proportion of population living below US$1.25 a day in terms of purchasing power parity (PPP). From 1990 to 2014, the percentage of population living under the threshold level has decreased from 40.5% to around 23.5% in OIC countries, depicting an average annual reduction of 2.3%. On the other hand, the proportion of population suffering from extreme poverty has decreased from 42.4% to 17.5% level corresponding to around 3.6% average annual reduction in extreme poverty worldwide. This highlights the fact that OIC countries have lagged behind the world average in terms of eradicating extreme poverty and there is a need for policies in OIC countries to address this challenge.

Furthermore, as displayed in Figure 5, when income per capita per day for the bottom 40% of the population was used as a measure of shared prosperity, OIC countries appear to have a need for development in terms of this criteria, as well. In 2007, the per capita income

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1.26

2.73

1.47

3.13

1.63

4.16

2.08

5.26

2007 (Bottom 40%) 2007 Total Population

2014 Total Population2014 (Bottom 40%)

OIC World

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 92 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

per day was US$1.26 for the bottom 40% while it was US$2.73 for the whole population in OIC countries. These rates have increased to US$1.47 and US$3.13 respectively in 2014. In absolute terms, these income levels are lagging behind the world averages in both 2007 and 2014.

However, in terms of share, in 2007, a person from the bottom 40% of the population was earning 46.1% of the daily per capita income in OIC countries and in 2014, this ratio increased to 46.9%. In contrast, the proportion of the daily per capita income for the bottom 40% of the income pyramid to that of total population of the world was 39.1% in 2007 and the ratio increased to 39.5% in 2014. In other words, between 2007 and 2014, the improvement, in the income level of the bottom 40% has been better in OIC countries relative to whole population. But as suggested earlier, the absolute terms are still very low and thus, pointing to the need for further development in terms of income inequality.

Another dimension which highlights the possible contribution that Islamic finance could provide is the need for infrastructure investments in MENA countries. It is estimated that by 2020, there will be annual infrastructure investment needs of US$106 billion that corresponds

Figure 6:INFRASTRUCTURE NEED AND INVESTMENT IN MENA (% OF GDP)

Source: World Development Indicators, the World Bank, authors calculations

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Infrastructure Needs (Average, Next Decade)

Total Investment Spending (Average, 2000s)

Oil Importers

Oil

Imp

ort

ers

MENA OtherOil Exporters

GCC

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 93GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Figure 7:SME PENETRATION AS A PERCENTAGE OF TOTAL LENDING

Source: IFC, 2014

to the 6.9% of the annual regional gross domestic product (GDP).4 In terms of block wise annual infrastructure investment needs (see Figure 6), the developing oil exporting countries (OECs) in MENA region are leading with US$48 billion, which corresponds to 11% of their GDP, while this annual need for the oil importing countries and GCC are expected to be 6% and 5% of their GDP respectively. It was also suggested that the main sectors where the infrastructure investment needs are more severe are the electricity and transport, particularly highways in MENA region accounting for about 43% of total infrastructure needs.5 These two sectors are followed by information and communication sectors where infrastructure investments amounting to 9% of regional GDP are required. In addition, 5% of the regional GDP is required to be invested in water and sanitation projects.

Financial inclusion of SMEs is another area that could speed up the realization of the twin goals of the World Bank and Islamic finance can play an instrumental role in this regard, as well. According to the World Bank Global Findex data, only 28% of the adult population (over 15 years of age) living in the OIC countries have an account in a formal financial institution. This ratio is 50% for the whole world. In addition, IFC states that there are more than 37 mil-lion micro, small, and medium sized enterprises (MSMEs) operating in the OIC countries that

4. Estache, et al., 2013. 5. Ianchovichina, et al., 2013.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2.0%

5.0%

7.3%8.0%

12.5%

15.0%16.1%

24.0%

20.3%

Saudi Ara

biaIra

q

Pakista

n

Eqypt

Jord

an

Tunusia

Lebanon

Yemen

Moro

cco

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 94 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

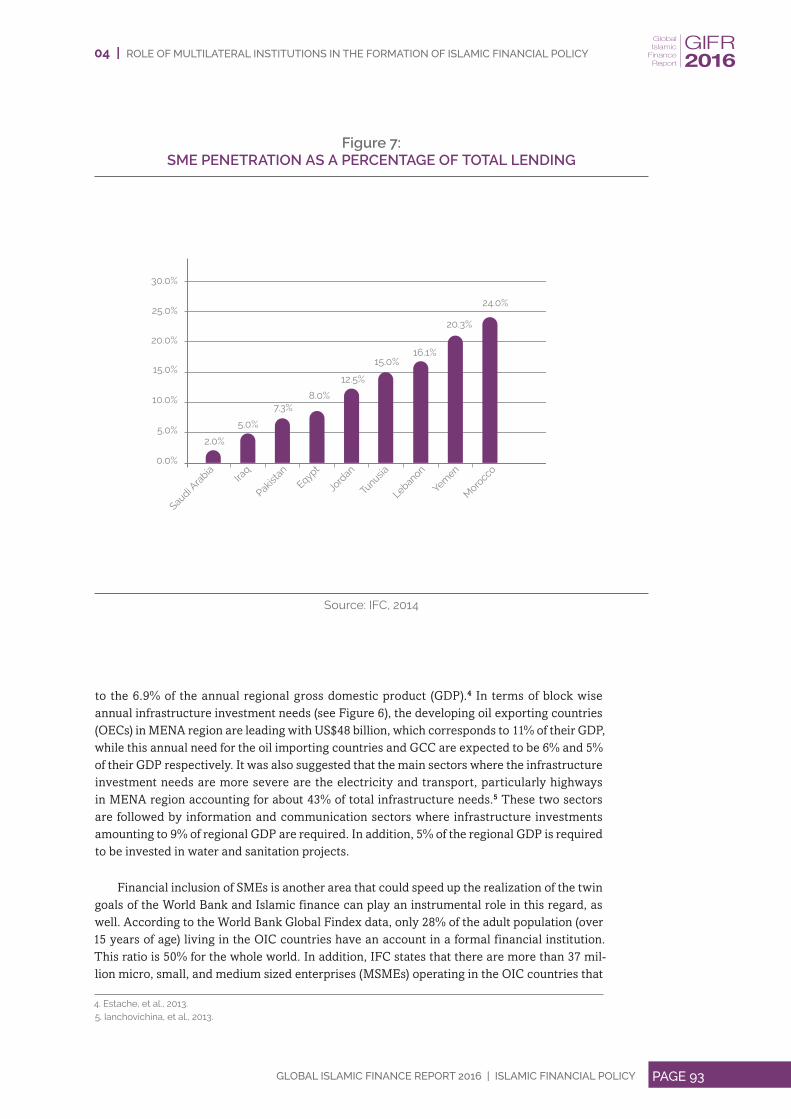

accounts for more than 30% of the total MSMEs worldwide. According to a study conducted by IFC in 2014 in eight MENA countries and Pakistan, the average proportion of SMEs in total lending was estimated as 12.2%. This proportion is quite low for Saudi Arabia, which is just 2% (Figure 7). Even in Morocco, where the proportion of SME penetration in total lending is the highest, the rate is estimated to be only 24%. This explains the dire need to enhance financial inclusion in countries with overwhelmingly Muslim population.

Figure 8 shows how Islamic finance would be relevant in improving financial inclusion and access to finance. The IFC’s survey also reported that a cumulative weighted average of 32.2% of the respondents have suggested that they would prefer Islamic finance products and services rather than using conventional means. The proportion of respondents who expressed their preference ranges from 4% for Lebanon to 90% for Saudi Arabia. When read together with statistics in Figure 9, these survey results have significant implications. For instance, for Saudi Arabia, the SME penetration in total lending is estimated at 2% whereas the preference for Islamic finance is reported at 90% among respondents. This is evident of the huge potential for Islamic finance to contribute towards financial inclusion. The result for Morocco is also interesting. While the SMEs’ share in total lending is 24%, which is the highest amongst the

Figure 8:PREFERENCE FOR SHARI’A-COMPLIANT PRODUCTS (% OF SURVEY DATA)

Source: IFC, 2014

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

4.0%

5.0% 20.0%25.0% 25.0%

35.0%37.0%

90.0%

54.0%

Saudi Ara

biaIra

q

Pakista

n

Eqypt

Jord

an

Tunusia

Lebanon

Yemen

Moro

cco

Cumulative Weighted Average= 32.19%

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 95GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Figure 9:POTENTIAL OF ISLAMIC FUNDING (US$ BILLION)

Source: IFC, 2014

sample countries, the preference for Islamic finance is 54% indicating that there is remarkable potential to improve SMEs access to finance through Islamic finance. Similar conclusions can be claimed for other countries in the study. Based on the analysis of the funding needs of SMEs and the preference for Islamic finance instruments, IFC predicts that there is an Islamic funding opportunity for SMEs between US$8.63 and US$12.98 billion in these MENA countries and also in Pakistan.

As the leading multilateral development institution, the World Bank also recognizes this increasing importance of Islamic finance and its potential role in achieving the dual goals of the institution. Mobilizing Islamic finance through banking, capital markets, non-bank finan-cial institutions, and other alternative channels may contribute not only to the enhancement of financial and social inclusion worldwide, it may also add up to the enhanced sharing of the wealth for eradicating extreme levels of poverty and for sustainable development. Due to the significant role that Islamic finance could play in helping millions of people to improve their living conditions, World Bank has initiated an Islamic finance program whose components are summarized in the following part. However, before proceeding with the basic components of Islamic finance program, it is worth analysing the case study presented in Box 5.7 that depicts

0.0%

0.5

1.0

1.5

Isla

mic

fu

nd

ing

Op

po

rtu

nit

y (U

SD

Bill

ion

)

2

2.5

3.0

0.05-0.08 0.08-0.100.18-0.30

0.21-0.42

0.58-0.87

0.97-1.22

1.31-2.38

2.62-3.84

2.66-3.99

Potential of Islamic Funding (US$ Billion)

Saudi Ara

biaIra

q

Pakista

n

Eqypt

Jord

an

Tunusia

Lebanon

Yemen

Moro

cco

Low Medium High

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 96 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

a good example of how Islamic finance might be integrated to support the realization of the twin goals of the World Bank Group.

World Bank Islamic Finance Program

The recognition of Islamic finance by the World Bank is reflected by the Islamic Finance Program (IFP) whose components are illustrated in Figure 10. Under the IFP, the first compo-nent is determined as conducting a research program which includes publications, knowledge notes, policy papers, toolkits, case studies and newsletters. The second component is the pub-lication of an annual flagship report that will reflect developments in global Islamic finance industry. Organizing events, seminars, and conferences together with community practices that will increase awareness and knowledge on specific aspects of Islamic finance is third main component of IFP. Moreover, the program is determined to support and facilitate Islamic

BOX 4.7:CAN ISLAMIC FINANCE PROMOTE SOCIALLY RESPONSIBLE OUTCOMES: THE WORLD BANK VACCINE SUKUK CASE

The World Bank Sukuk issuance for the International Finance Facility for Immunization (IFFIm) demonstrates how Sukuk can be used for development purposes and can attract investors from socially responsible investment (SRI) sector. In this respect, the Word Bank has helped the International Finance Facility for Immunization (IFFIm) to issue two Sukuk; one in December 2014 and second in September 2015 for the financing of immunization (Bennett, 2015). IFFIm is an international organisation with primary mission to raise funds for the immunization of children and the development of health systems in poorest countries. The fund raising process for the facility is managed by the World Bank Treasury under the guidelines described by the volunteer Board of Directors of the Facility. With the help of the World Bank, IFFIm has issued two Sukuk for the financing of immunization (Bennett, 2015).

The first Sukuk issuance took place in December 2014 with an issuance amount of $500 million for a three-year maturity. Being the largest issuance by a multination entity, the Sukuk has attracted the attention of investors worldwide. The issuance won few rewards including the Euromoney’s “best innovation in Islamic finance” and the Financial Times’s “best achievement in transformational finance”. Called as Vaccine Sukuk, the Sukuk has been a good example of how economically reasonable issuances can be made for raising funds that are to be used for socially beneficial outcomes. Given the success of the first issuance, the second Vaccine Sukuk issuance took place in September 2015. With an issuance amount of $200 million and maturity of three years, the Sukuk was over-subscribed by 1.6 times attracting not only investors with Shari'a compliancy concerns but also investors from conventional finance side.

Source: • Bennett, M. (2015). “Vaccine Sukuks: Islamic securities deliver economic and social

returns”. Accessible at: http://blogs.worldbank.org/arabvoices/vaccine-sukuks-islamic-securities-deliver-economic-and-social-returns

• Thomson Reuters and Barwa Bank, (2015). “Industry at Crossroads: Sukuk Perceptions and Forecast 2016”.

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 97GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

Figure 10:WORLD BANK ISLAMIC FINANCE PROGRAM COMPONENTS

01

06

03

05

04

02SEMINAR SERIES

Islamic Finance Research Seminars

IF INCLUSION PROGRAM Islamic Micro and SME Finance

07GLOBAL IF DEVELOPMENT CENTER Knowledge Hub

Research and Training

Technical Assist. and Advisory Services

Global Influence through key stakeholders

FLAGSHIP REPORTAnnual Flagship Islamic Finance Development Report

RESERACH PROGRAM

Publications

Knowledge Notes

Policy Papers

Toolkits

Case Studies

Newsletter

COMMUINITY OF PRACTICEKnowledge partnership

Social media outreach

LEARNING CENTERCapacity building

Learning Program for Islamic finance professionals, regulators and policy makers

Annual conference on IF

Source: IFC, 2014

finance inclusion program that will cover practices such as Islamic micro- and SME finance. The most important part of the IFP was the establishment of a global center that will assume the role of a knowledge hub as a learning center to conduct research and provide capacity building activities and technical assistance to client countries.

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 98 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

As a part of the IFP, the Global Islamic Finance Development Center (GIFDC) was estab-lished in Istanbul, Turkey. Launched in October 2013 by the World Bank’s President, the mis-sion of the Center is to develop the awareness and practice of Islamic finance worldwide. The Center is hosted by Borsa Istanbul and is supported by the Turkish authorities of the Prime Ministry Undersecretariat of Treasury, the Central Bank, the Banking Regulation and Supervi-sion Board and the Capital Market Board. Figure 11 broadly defines the role of GIFDC within the World Bank IFP. The GIFDC is expected to contribute to promoting financial inclusion and ensuring global access to financial services from underserved segments such as poor house-holds, SMEs, and agricultural sector via Islamic finance tools and instruments.

The mandate of the GIFDC activities can be categorized under three main headings, namely the financial sector development, research and knowledge hub, and market devel-opment (see Figure 12). In terms of financial sector development, the Center aims to provide technical assistance and prepares reports on strengthening regulatory environment, facilitat-ing standardization of Islamic financial practices and instruments, enhanced corporate gov-ernance and risk management practices for Islamic financial institutions. The second area on which the activities of the Center are focused is conducting research to serve as a knowl-

Figure 11:GIFDC’S ROLE IN WORLD BANK GLOBAL ISLAMIC FINANCE PROGRAM

The volume of Shariah- complaint instruments has been expandind at more than 10 percent annually

GIFDC can help mobilize a creative new source of finance for development

GIFDC can help World bank client countries take advantage of the rapid growth of financial assets that are compliant with Islamic Law

Islamic finance has the potential to focus on vast new resources for development

Shari’a-compliant finance can channel investment to undeserved segments such as poor households, SMEs and agriculture

GIFDC can contribute to the WBG’s goal of promoting financial inclusion and ensuring universal access to financial services

02Knowledge and

Learning

TA & Advisory Services

Guarantees

Research& Training

Global Influence

03

0405

06

01Lending and Investment

ISLAMICFINANCE

PROGRAM

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 99GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

edge hub. For this purpose, the Center organizes conferences, workshops and other capacity building activities with its main stakeholders. In this respect, the Center intends to publish an annual flagship report that will summarize developments in various sectors of Islamic finance in a thematic manner. In addition, the Center has an annual scientific symposium on Islamic finance as one of its f lagship activities. The third category of activities under the mandate of the Center is related to market development. In this area, the Center targets at providing technical assistance to member countries in developing new markets and products to improve Islamic finance practices. The Center also collaborates with its stakeholders to organize work-shops and training programs for this purpose.

The year of 2015 had been a very active and successful one for the Center. Besides complet-ing its establishment process by creating constructive channels of communications with major stakeholders, the Center has undertaken research and activities in the areas under its mandate. In this respect, the inaugural academic Symposium on Islamic finance that was organized in September 2015 together with IDB, Guidance Financial Group and Borsa Istanbul at Bogazici University of Istanbul was a flagship activity of the Center which is intended to be organized in different countries in coming years. The theme of the first Symposium was selected to under-stand the relationship between Islamic finance and shared prosperity. The papers selected for the symposium are going to be published as proceedings in coming months.

Furthermore, a conference on corporate governance for Islamic finance institutions was organized with the General Council for Islamic Banks and Financial Institutions (CIBAFI) in Amman in September. During the conference, suggestions have been made for further enhance-ment of the adoption processes of frameworks of Islamic Financial Services Board (IFSB) and Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) by individ-ual countries in addition to opinion on the requirements for the further development of these international framework themselves. In addition, the annual World Bank and AAOIFI Islamic finance conference was organized in Bahrain. The major objective of these conference series

Figure 12:CORE ACTIVITIES OF GLOBAL ISLAMIC FINANCE DEVELOPMENT CENTER

FINANCIAL SECTORMANAGEMENT

Strengthening Regulatory enviroment

Facilitating Standardization

Enhancing Governance and Transparency

Financial Stability and Risk Management

RESEARCH ANDKNOWLEDGE HUB

Producing quality research on topics with development impact

Knowledge dissemination through international seminars and workshops

Capacity building for emerging markets

MARKETSDEVELOPMENT

Technical and Advisory services for new markets

Collaborate with stakeholders in developing new products and new markets

Standardization of market practices

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 100 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

have been to provide a platform for participants from various segments of Islamic finance to discuss the viability and further enhancement of the standards developed by AAOIFI.

With respect to financial development activities, the Center has been providing the tech-nical expertise and policy advice to the member countries of the World Bank in the areas of developing sukuk markets, implementing financial inclusion strategies through Islamic finance and regulatory framework to introduce Islamic finance. In market development activities, the Center has organized three workshops. These include technical capacity building workshops on topic such as Islamic capital markets, liquidity management, and takaful targeted for mem-ber countries regulatory authorities and policy makers.

During 2015, the Center also played an important role in the Turkish Presidency of G20 by organizing major conferences and preparing policy papers and notes to support the priority areas of investments, SME finance, and financial inclusion. For this purpose, the Center has conducted research studies and two reports were prepared in collaboration with the IDB on the topics of leveraging Islamic finance for SMEs and the analysis of movable collateral in Islamic law. In addition, the Center has organized two conferences under the G20 agenda of Turkey. The first G20 Conference on “Leveraging Islamic Finance for SMEs” was organized in Octo-ber in cooperation with IDB, Republic of Turkey Prime Ministry Undersecretariat of Treasury under the hosting of All Businessmen and Industrialists Association of Turkey (TUMSIAD) in Istanbul. The conference was attended by HE Mr. Recep Tayyip Erdogan, the President of Tukey, Mr. Bertrand Badre, Managing Director of the World Bank, HE Mr. Muhammed Ali, the President of IDB, and Ms. Gloria Grandolini, Senior Director of Finance and Markets Global Practice of the World Bank.

The conference provided a venue for participants from multinational development institu-tions, academia, and private sector to discuss the financing issues regarding SMEs in emerging markets and alternative options to alleviate these issues via Islamic finance instruments. The second conference under the G20 agenda was organized in November on “Mobilizing Islamic Finance for Long-Term Investment Financing” together with Capital Market Board and Borsa Istanbul. Given the fact that investments in infrastructure is one of the main agenda items of G20, this conference contributed to the discussions on how to create alternative modes of financing for infrastructure investment needs, especially in emerging markets.

As a part of the G20 activities, the Center also contributed to the policy note prepared by the World Bank and IMF on how to integrate Islamic finance to global financial system to be submitted to G20 Finance Ministers and Central Banks' Governors' Meeting.6 The note provided a set of policy recommendations at both local and global level to integrate Islamic finance to international financial system. The note also concluded that in order to integrate Islamic finance into financial system at global level, G20 membership could play a construc-tive role, in: (i) establishing a collaborative environment where the Islamic finance standard setters could exchange views on pressing issues, more deployment of these institutions by G20 to improve the standardization of Islamic finance practices, (ii) making these standard setting institutions more active players in international platforms and consultative groups, and (iii) enabling MDBs to transfer their know-how to Islamic finance institutions through policy rec-ommendations, capacity development and integrating Islamic finance tools in their operations.

6. The note is accessible at: http://www.g20.org.tr/wp-content/uploads/2015/09/IMF-WBG-Note-on-Integrating-Is-lamic-Finance-into-Global-Finance.docx

ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY | 04

PAGE 101GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

The Challenge ContinuesIslamic finance, which endorse risk sharing and ensures that the transactions should be

backed by a real economic activity carries a huge potential to contribute to overall economic development, financial stability, and financial inclusion of rather excluded parts of societies, especially, in countries with predominantly Muslim population. However, Islamic finance is still at its infancy level and the total assets which are in compliance with Islamic principles account only for 2% of the overall pool of financial assets in the world. Hence, except for some countries, for Islamic finance to become a systemically significant financial phenomenon worldwide, there is still a long way to go.

One of the main challenges is lack of a comprehensive international regulatory and gov-ernance framework for Islamic finance products and institutions. Despite the competent works of IFSB, IIFM and AAOIFI to establish an internationally recognizable framework for the reg-ulation, supervision, governance and financial reporting of practices of Islamic financial insti-tutions; there is still a gap in terms of the standardization of products and conduct of business. Notwithstanding the many standards, fatwas and resolutions on Islamic financial matters have been published by these international standard setting bodies, not all countries comply with these standards or resolutions. As a result, divergence of opinions among Muslim scholars, particularly between Malaysia and countries of the Middle East, persevere. It is only beneficial for the industry to have a uniform approach in developing Islamic finance as this will remove confusion and misperceptions about Islamic finance, reduce fragmentation, improve confi-dence of all stakeholders and lead to market integration. Having proper regulatory standards and standardisation of documentation, certain products, and practices would lead to greater transparency and consistency, which are essential to ensure sustainable growth of the Islamic financial industry.7 More importantly, this will allow more time for stakeholders, especially scholars, to innovate.8

The involvement of the World Bank in Islamic finance, as the leading MDB of the world, is of crucial importance in terms of increasing awareness of Islamic finance. The World Bank has initiated its Islamic finance program to serve its member countries interested in develop-ing Islamic finance. The most concrete step within the program was the establishment of the World Bank Global Islamic Finance Development Center in Turkey in collaboration with Turk-ish authorities to promote research and best practices of Islamic finance not only within the region but also at a global scale. The creation of this center is a reflection of the global efforts to improve and standardize Islamic finance while contributing to ending poverty and boosting shared prosperity around the world using this increasingly important source of finance.

Referencesŀŀ Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI)

Website, accessible at http://aaoifi.com/?lang=en

ŀŀ Alvi, I. 2009. Standardisation of Documentation in Islamic Finance & Role of the International Islamic Financial Market (IIFM), Islamic Financial Sector Development (IFSD) Forum 2009, Ashgabat, Turkmenistan

7. Yaacob and Smolo, 20118. Alvi, 2009

04 | ROLE OF MULTILATERAL INSTITUTIONS IN THE FORMATION OF ISLAMIC FINANCIAL POLICY

PAGE 102 GLOBAL ISLAMIC FINANCE REPORT 2016 | ISLAMIC FINANCIAL POLICY

ŀŀ Ianchovichina, E., Estache, A., Foucart, R., Garsous, G., & Yepes, T. (2013). Job creation through infrastructure investment in the Middle East and North Africa. World development, 45, 209-222.

ŀŀ IFC, (International Finance Corporation). 2014. “Islamic Banking Opportunities across Small and Medium Enterprises in MENA”.