Embed Size (px)

Citation preview

November 14,2013| Strictly private and confidential

In Pod We Trust Ross Colbert, Rabobank International

National Automatic Merchandising Association

P

2

Agenda

Introduction

Outlook on US Market for Single Cup Coffee 3

Today’s presentation will cover the following:

A brief look at Global Market for Single Cup Coffee 2

An introduction to Rabobank 1

2

Q & A 4

3

Introduction to Rabobank

Section I

3

4

M&A Advisory

Global Client

Solutions

Credit

Products

Global

Financial

Markets

Trade &

Commodity

Finance

F&A

Research &

Advisory

Fundamentals

Highest rated

Privately owned bank

Total Assets: $992bn

(December 2012)

> 10 million clients

Rabobank - Strong Fundamentals & Full Product Suite

Food & Agri Research & Advisory

Relationship Management/ Wholesale Banking

M&A Advisory

Safest Privately Owned Bank in the World (August 2013)

29th-largest bank worldwide by total assets (July 2013)

Global Financial Markets

Highest rated privately owned bank based on new ratings system (2011)

5

Rabobank… The Financial Link in the Global Food Chain

19/20 19 of the Top 20 Global Beverage companies are Rabobank clients

100 clients around the globe 100

$6.0 billion in commitments to the global beverage industry

6 6

Introduction to Rabobank

Strategic relationships throughout the global coffee, tea and cocoa sectors

Multinational coffee traders Diversified traders and processors

Roasters, consumer packaged goods and OCS companies

7

A year ago we forecasted…

8

2013 – A Transformational Year in Coffee!

$10.5 billion in new capital

9

Consumer confidence has moved lower since May

10

Small Business Optimism is at pre-recession level

DEC 2007

11

The Beverage Honesty Index

12

Global Coffee Pod Market

Section II

13

Consumers now demand

convenience, variety and

premium/quality taste, both at-

home and out-of-home

Changing consumption patterns and

recent hardware innovations are helping to drive

growth in the single-serve coffee

market

Increasing consumption in

emerging markets

Key coffee market drivers

Strategic considerations in global coffee demand

Shift from multi-serve to single-serve

Premiumization

Growing out-of-home offering

Growing demand in emerging markets

Product innovation

Consumers willing to pay more for convenience

Gourmet coffee shops continue to lose ground in specialty coffee to quick-service restaurants (“QSR”)

Growth focused on differentiation, brands and quality

Premiumization within R&G

Premium offerings also supported by fair trade, health benefits, organic and origin

At-home and out-of-home consumption changed by single-serve systems

Format innovations driving value growth in mature markets

Emerging markets to reach 50% of global coffee consumption by 2020¹

Growth in instant coffee driven largely by emerging countries

Innovation driving market share gains and gross profits

Consumer preference for convenience and quality driving innovation in single-serve R&G brewing technology

Regional differences in retail coffee value and volume

Western Europe continues to lead both value and volume sales of coffee

Asia Pacific second in value but trailing North America, Eastern Europe and Latin America in RTD retail volume

Coffee market fundamentals

8

Source: Rabobank

14

Coffee preferences vary greatly by region

• In 2012, North America and Western Europe, combined, accounted for over 90% of the global pod market

• North American is increasing at a much faster rate, recording 105% value growth in 2012, compared to Western Europe’s 12% increase.

• At over US$5 billion, the market for fresh coffee pods in Western Europe is still almost twice as large that of the North America.

Source: Euromonitor International/ Rabobank

15

• Fresh coffee pods are most successful in Western Europe and North America - high per capita consumption of fresh coffee & high income regions,

• Pods are actually benefiting from the recession - consumers are not spending money in cafes but purchasing pod coffee machines in order to replicate the café experience at home for a better value.

Pod market is geographically concentrated

Source: Euromonitor International

16

Global coffee value is driven by pod growth

• Between 2007 and 2012, pods expanded in value by an average annual rate of 26%, or 8 x faster than the remaining coffee categories combined.

• Pod penetration limited almost entirely to higher income markets like Western Europe and North America.

Source: Euromonitor International, Rabobank

17

Nespresso maintains widest global presence

Source: Euromonitor International

• Coffee styles are different around the world, and single cup formats remain fragmented.

• Nespresso continues to be the leader in global pod value share with nearly 26% share

• #2 Keurig is closing in fast – despite a far more limited market in North America.

18

• After North America, Latin America was the fastest growing region for coffee in 2012.

• In 2012, pods accounted for only 2% of the Latin America fresh coffee market, recording US$154 million in sales, with a presence in only six countries: Argentina, Brazil, Chile, Columbia, Mexico and Uruguay.

• The price of a cup of pod coffee in Latin America was more than 3x the price of any of the types of non-pod coffee.

• While Brazil accounts for 69% of Latin American pod sales, pods still made up only 2% of the Brazilian fresh coffee market in 2012.

Opportunities in Latin America

Source: Euromonitor International

19

• By registering patents for every aspect of the Nespresso system, Nestlé aimed to prevent other companies from manufacturing Nespresso-compatible pods With so many layers of protection, other companies have struggled to compete with Nespresso for share of the pod category.

• However, while Nespresso maintains the widest global penetration of any major pod brand, its presence in the rapidly growing North American market remains limited.

• Since 2009, Nespresso’s share in North America has declined from 5% to 3%.

Nespresso’s will be challenged outside of Europe

Source: Euromonitor International

20

Top Five Global Pod Brands: Value 2012

Rank Brand Company % value

share 2012

1 Nespresso Nestlé 25.8

2 Keurig GMCR 14.7

3 Senseo DE Master Blenders 1753

8.6

4 Nescafé Dolce Gusto

Nestlé 8.0

5 Tassimo Mondelez 6.6

Total 63.6

Top Five Global Pod Brands: Volume 2012

Rank Brand Company % volume

share 2012

1 Senseo DE Master Blenders 1753

17.7

2 Nespresso Nestlé 14.5

3 Keurig GMCR 7.4

4 Nescafé Dolce Gusto

Nestlé 6.2

5 Tassimo Mondelez 5.6

Total 51.4

Consolidated among top five brands

Source: Euromonitor International

21

US Coffee Pod Market Trends

Section III

22 Source: Euromonitor International

US market is over 25% of global retail value of pods

23

Channel %

Supercenters (WalMart) 33%

Supermarkets & Grocery 19%

Convenience 1%

Drugstores 2%

Department Stores 4%

Warehouse Clubs 10%

Home Retailers 9%

Office Supply Stores 8%

Natural Food Stores 3%

Internet 10%

Dollar Stores 1%

Single serve across multiple retail channels

Measured Channels

59%

Unmeasured Channels

41%

Source: Packaged Facts, Feb 2013

Unmeasured channel volume may be as high as 65% of total volume

Excluding: • Foodservice – QSR • Office Coffee Service • Hospitality & Leisure

24

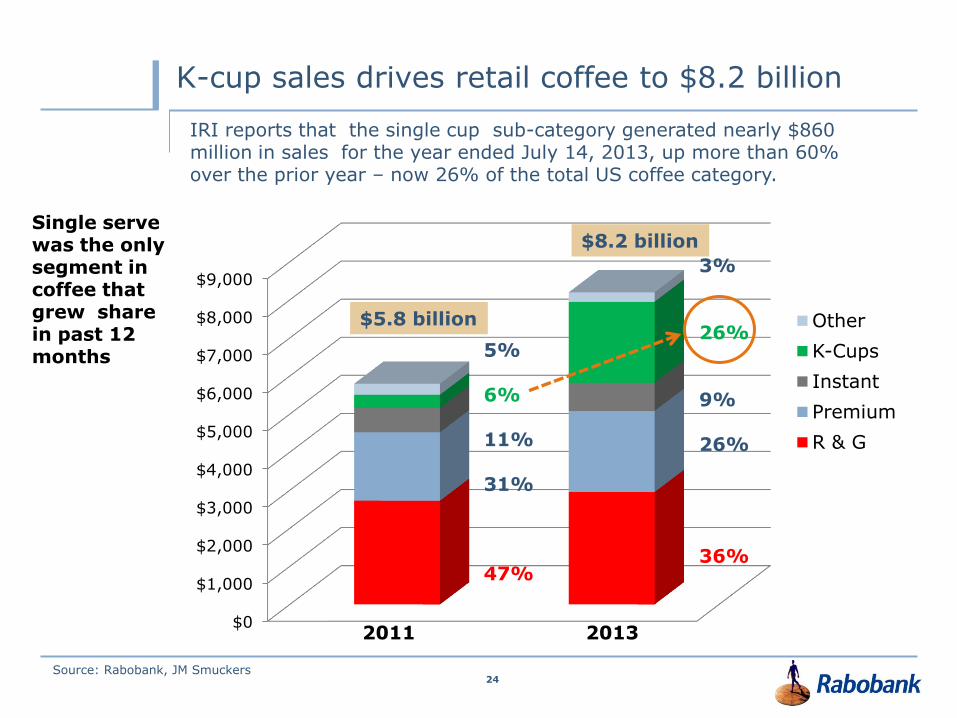

K-cup sales drives retail coffee to $8.2 billion

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

Other

K-Cups

Instant

Premium

R & G

5% 6% 11% 31% 47%

3% 26% 9% 26% 36%

2011 2013

IRI reports that the single cup sub-category generated nearly $860 million in sales for the year ended July 14, 2013, up more than 60% over the prior year – now 26% of the total US coffee category.

$5.8 billion

$8.2 billion Single serve was the only segment in coffee that grew share in past 12 months

Source: Rabobank, JM Smuckers

25

US Single serve retail market dominated by GMCR

Source: SymphonyIRI Rabobank, industry reports

• GMCR remains clear leader in US despite share loss

• Private label has estimated 8% share of single serve market

• Folgers also losing out to Kraft & Private Label brands

• Top 3 brands total over 73% of K-Cup sales

53.0

19.0

14.3

0

0

3.4 3.7

6.6

K-Cup Sales Dec 2012

Green Mountain

J.M. Smucker

Starbucks

Kraft

Peets

Eight O'Clock

Caribou

Private Label, Others

45.1

14.3

14.2

5.4

1.3 5.0

3.1 11.6

K-Cup Sales Sep 2013

26

Volume Share of K-Cups

K-Cup Volume Share in Food-Drug-Mass Channels

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 19-May 16-Jun 14-Jul 11-Aug 8-Sep

Caribou 7% 5% 4% 4% 3% 3% 3% 3% 3% 3% 3%

Eight O'Clock 0% 0% 1% 3% 4% 5% 6% 5% 5% 6% 6%

Green Mountain 60% 61% 60% 53% 49% 46% 45% 45% 47% 43% 45%

JM Smucker 22% 20% 20% 20% 19% 16% 17% 15% 15% 15% 15%

Starbucks 8% 11% 11% 11% 10% 11% 10% 11% 9% 11% 11%

GMCR-licensed 97% 97% 96% 91% 86% 81% 81% 81% 79% 78% 79%

Kraft 0% 0% 0% 0% 3% 5% 5% 5% 6% 6% 6%

Peet's 0% 0% 0% 0% 0% 0% 0% 0% 0% 1% 1%

Private Label /

Other 3% 3% 4% 9% 11% 14% 14% 14% 14% 15% 15%

Unlicensed 3% 3% 4% 9% 14% 19% 19% 19% 21% 22% 21%

Source: Symphony IRI.

27

• In past twelve months the category growth rate has slowed by over 62%

• Last three months in 55-46% range, likely even slower in Oct/Nov period.

• Outlook for volume growth in 2014 is +25-30% range

Category Volume Growth has slowed

0%

20%

40%

60%

80%

100%

120%

140%

Source: Symphony IRI

+124%

+46%

28

K-Cup Retail Price Segmentation

LTM Sep 2013

Volume

(K-cups) Sales

$/K-

cup

Peet’s 6,247791 5,362,042

$0.86 Starbucks 381,009,478 305,558,556 $0.80

Caribou 124,839,036 77,239,073 $0.62 Green Mountain 1,776,926,748 1,067,858,908 $0.60

JM Smucker 640,123,449 378,172,298 $0.59 Kraft 123,007,740 72,045,947 $0.59

Eight O‘ Clock 165,379,036 89,781,065 $0.54 Private Label / Other 421,720,527 190,852,043 $0.45 Total 3,639,253,805 2,186,869,932 $0.60

Source: Symphony IRI

• Premium brands (Peets & SBX) priced at 33% to 43% premium over GMCR

• Private Label/Other priced at 25% discount to GMCR

29

K-Cup prices appear to have stabilized

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

Caribou Eight O'Clock Green Mountain

JM Smucker Kraft Peet's

Starbucks Private Label / Other Total

Source: Symphony IRI

30

Private label pods are expanding

• The expiration of Keurig patents in 2012 and overturned legal challenges to Nespresso exclusivity in Germany has resulted in a host of new private label brands using the Keurig and Nespresso formats.

• In the US, key retailers including Safeway, Wegmans, SuperValue, Kroger and Costco have entered the pod category using the K-cup format. Over time, it is likely that US retailer /unlicensed brands will increase from current 8%-10% to 12% share of the pod category.

Source: Euromonitor International, industry sources

Private label penetration still low in US – expected to reach 12% share in 2014

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Netherlands Germany Switzerland Portugal Italy US

Coffee Pods - Private Label Share

8%

12%

31

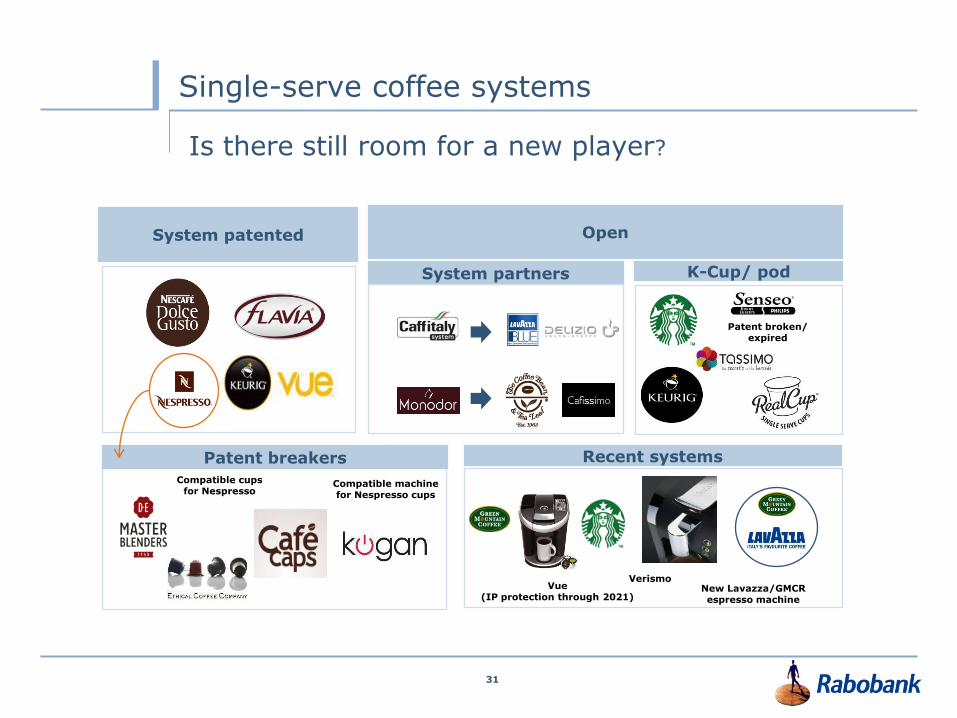

Single-serve coffee systems

System partners

Compatible machine for Nespresso cups

Compatible cups for Nespresso

System patented Open

K-Cup/ pod

Recent systems Patent breakers

Patent broken/ expired

Is there still room for a new player?

Verismo Vue

(IP protection through 2021) New Lavazza/GMCR espresso machine

32

“Make way for McCafé” in supermarkets in 2014

2009 2007 2013 2014

• McCafé was created and launched in Melbourne Australia in 1994 • McDonalds launched their very successful national US McCafe platform in 2009. • McCafe Premium Roast in bags began testing in Canada in November 2012 • October 2013, McDonald’s announced partnership with Kraft for retail distribution of McCafe

Premium in US supermarkets in 2014. • Kraft deal includes McCafe Single Cup launch, expected to be in Tassimo brewer format.

34

Innovation: Single-serve’s next generation

Growing convergence between single cup coffee & soft drinks

35

From Coffee …to “Keurig 2.0” ?

By Fiscal 2015 GMCR to launch:

Keurig 2.0 Interactive Brewer technology

Four Systems : Hot, Cold, Specialty & Water

Multiple platforms & partners for each system

Global applications & common components

Sustainability built-in

GMCR & Licensed -partner brands for each

3 -year pipeline of innovations

Choice, convenience and consistency drive consumer demand

36

Regional growth potential for pods

Chicago, Miami, Los Angeles , Atlanta and San Francisco among the largest markets - West Coast offers biggest upside

37

How Big Can GMCR Get by 2018?

Source:GMCR report

Model based on growing HHP of brewers through new innovations Increasing at home attachment by new products & occasions

2013

16 mil brewers 18% HHP

1.4 servings

38

GMCR Vision of 2018 is “10x current market”

Source:GMCR report

39

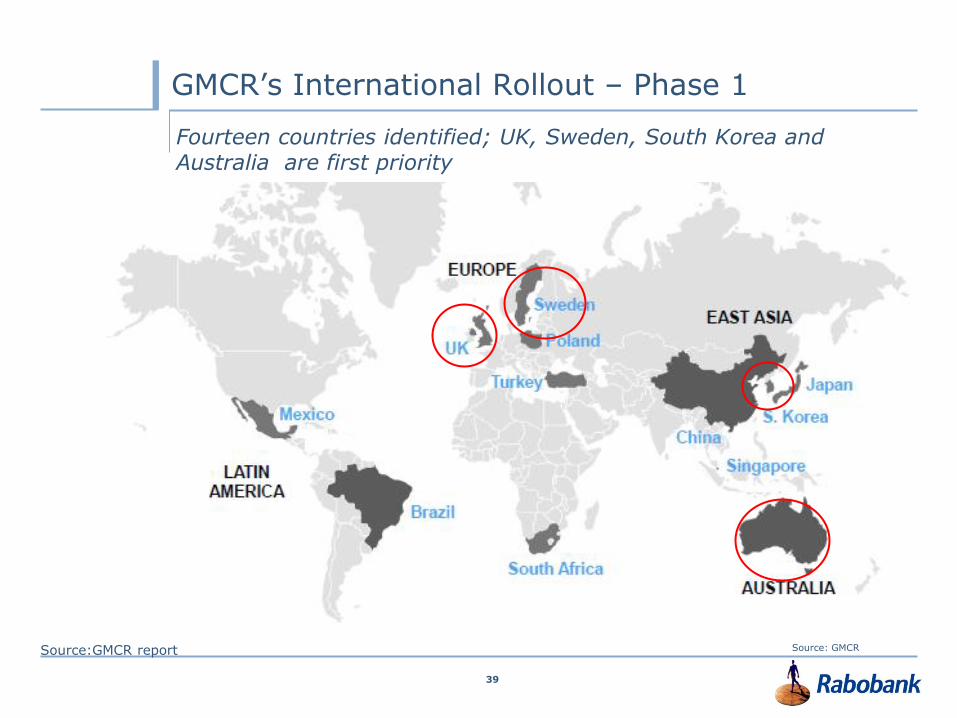

GMCR’s International Rollout – Phase 1

Source: GMCR

Fourteen countries identified; UK, Sweden, South Korea and Australia are first priority

Source:GMCR report

40

1. GMCR

• International rollout (UK, Sweden, S. Korea, Australia)

• Keurig 2.0 - Four systems with new partners in each

1) Hot

2) Cold

3) Specialty

4) Water

2. Other Players: Bevyz, SodaStream, Mars

3. Major appliance deals

4. Strategic partnership in Espresso?

5. Consolidation, M&A

What’s ahead in 2014-2015?

41

ESPRESSO Coffee Beer from Dark Star Brewery!

CONVERGENCE AHEAD?

42

For more information contact:

Ross Colbert, Global Strategist-Beverages

Rabobank International

245 Park Avenue – 36th Floor

New York, NY 10169

Thank You!