Embed Size (px)

Citation preview

18

CHAPTER 2

INDUSTRIAL SICKNESS IN INDIA AND

REVIEW OF LITERATURE

2.1 INTRODUCTION

This chapter covers two broad topics - Industrial Sickness in India and

Review of Literature. In the first section, an overview of industrial sickness in

India is provided. Legal framework and reorganization of sick units are also

discussed in the first section. The second section of this chapter is devoted to

the review of previous research studies. Such a review provides a glimpse of

already established sickness prediction models and the financial ratios used as

discriminators and predictors. In all, this chapter provides the basic theoretical

framework.

2.2 INDUSTRIAL SICKNESS IN INDIA

Corporate distress is a global phenomenon. It can involve any of the

three main stages namely bad corporate performance, corporate bankruptcy and

industrial sickness. Firms that perform poorly are likely to enter corporate

bankruptcy when they fail to pay their debt obligations. The definition of

industrial sickness in India is beyond bankruptcy and it refers to the firms

persistently making losses and survive, even after such accumulated losses

have exceeded net worth many times (Goswami, 1996)1. Financial distress is

defined as “the inability of a firm to pay its financial obligations as they

mature” (Beaver, 1966)2. Similar definitions of financial distress were

proposed by Andrade and Kalpan (1998)3 and Brown, James and

19

Mooradian (1993)4 who interpreted financial distress as a crucial event, the

occurrence of which separates the time of a company’s financial health from

the period of financial illness and requires corrective actions in order to

overcome the troubled situation.

The term ‘bankruptcy’ is used in research studies carried out in USA.

Bankruptcy is a legal event taking place at a definite point of time and is

undoubtedly a conclusive evidence of the firm having failed. In practice,

bankruptcy is the culmination of failure. Failure, in the economic sense, occurs

prior to bankruptcy proceedings. Platt and Platt (2006)5 found that financial

distress and bankruptcy were not same process, explaining the reason why

many fiancially distressed firms do not ultimately file for bankruptcy

protection.

India has coined her own terminology as ‘industrial sickness’ or

‘corporate sickness’ (Banjerjee, 2005)6. In general, bankruptcy is defined as

the inability of a company to continue its current operations due to high debt

obligations (Pongstat, Ramage and Lawrence, 2004)7. Some of the research

studies including Beaver (1966)2, have defined bankruptcy according to the

rationale and scope of their study, rather than following any general definition.

In the present study, the definition of sick industrial unit as proposed by Sick

Industrial Companies (Special Provisions) Act, 1985 (SICA) has been

considered. The terms ‘sickness’ and ‘bankruptcy’ have been used

interchangeably in this study.

20

2.2.1 Operational Definition of Sick Industrial Unit:

According to Sick Industrial Companies (Special Provisions) Repeal

Act, 2003, Sick Industrial Company means an industrial company which has at

the end of any financial year accumulated losses exceeding 50 per cent of peak

net worth during the last four years or has failed to repay installment of its

debts or creditors in 3 consecutive quarters.

Any of the above two conditions is sufficient to consider a company

sick.

It may be noted here that industrial companies existing immediately

before the commencement of Sick Industrial Companies (Special Provisions)

Act, 1985 (1 of 1986) commonly known as SICA and are registered for at least

last five years, have accumulated losses equal to or exceeding its entire net

worth, will also be treated as sick units. Sick Industrial Companies (Special

Provisions) Act, 1985 (SICA) was repealed and replaced by Sick Industrial

Companies (Special Provisions) Repeal Act, 2003.

The definition of a sick unit by RBI is that a firm which incurs cash loss

for one year and in the judgment of the bank is likely to incur further losses for

the current year as well as for the following year. It highlights a common

factor, namely sustenance of cash loss and erosion of Net Worth (Panigrahy

and Mishra, 1993)8.

As per section 2(46AA) of Companies Act 1956 ‘Sick Industrial

Company’ means an industrial company, which has at the end of any financial

year, accumulated losses exceeding 50% of average net worth during four

21

years; or has failed to repay debts to its creditor(s) in three consecutive quarters

on demand made in writing for such repayment.

Net worth means sum total of paid up capital and free reserves. Free

reserves includes all reserves created out of profits and security premium

account but does not include reserves created out of revaluation of assets and

depreciation reserves. Sick Industrial Companies (Special Provisions) Act,

1985 (SICA) deals with industrial sickness and it applies to industrial

undertakings both in public and private sectors.

The Act pertains to the following:

(a) The industries specified in the First schedule to the Industries

(Development and Regulation) Act, 1951 except the industries relating to ships

and other vessels drawn by power;

(b) Not being "small scale industrial undertakings or ancillary industrial

undertakings" as defined in Section 3(j) of the IDR Act.

(c) The criteria to determine sickness in an industrial company are (i) the

accumulated losses of the company to be equal to or more than its net worth i.e.

its paid up capital plus its free reserves (ii) the company should have completed

five years after incorporation under the Companies Act, 1956 (iii) it should

have 50 or more workers on any day of the 12 months preceding the end of the

financial year with reference to which sickness is claimed and (iv) it should

have a factory license.

2.2.2. History of Industrial Sickness in India:

Industrial sickness in India has become an important matter of concern,

22

in the light of its increasing magnitude in terms of number of sick units,

outstanding bank credit involved and number of workers affected. The total

number of sick industrial units in large, medium and small scale rose from

17,150 at the end of June 1979 to 92,559 at the end of December 1984. The

total amount of bank credit outstanding against these sick units rose from

Rs.1,283.43 crores at the end of June 1979 to Rs.3,218 crores at the end of

December 1984 (Yadav, 1986)9. During 1982-89, outstanding credit to sick

units has risen from Rs.2,585 crores to Rs.9,353 crores. The number of sick

units have increased at a modest rate of 4.8% per year, the amount of

outstanding credit locked in these companies have grown at 17.65% during

1982-89 and the real outstanding bank credit has risen by 11% per year over

inflation (Kapila and Kapila, 1995)10

. Industrial sickness in India has resulted

in an accumulated loss of more than Rs.23,000 crores during 1987-96 and has

left about 1.2 million workers in uncertainty.

According to BIFR performance review report of 1996, the cumulative

losses of 1,447 sick companies registered with the board added up to Rs.23,793

crores against the total net worth of Rs.8,981 crores up to December 1996.

Total accumulated losses of the Central and Public sector undertakings attained

Rs.15,392 crores and about 6,10,000 workers were affected. As on March

2001, the total number of sick units in the portfolio of scheduled commercial

banks stood at 2,52,947 involving an outstanding bank credit of about

Rs.25,775 crores. The major industries affected by sickness are textiles,

engineering goods and jute (Mukherjee and Ghose, 2002)11

.

23

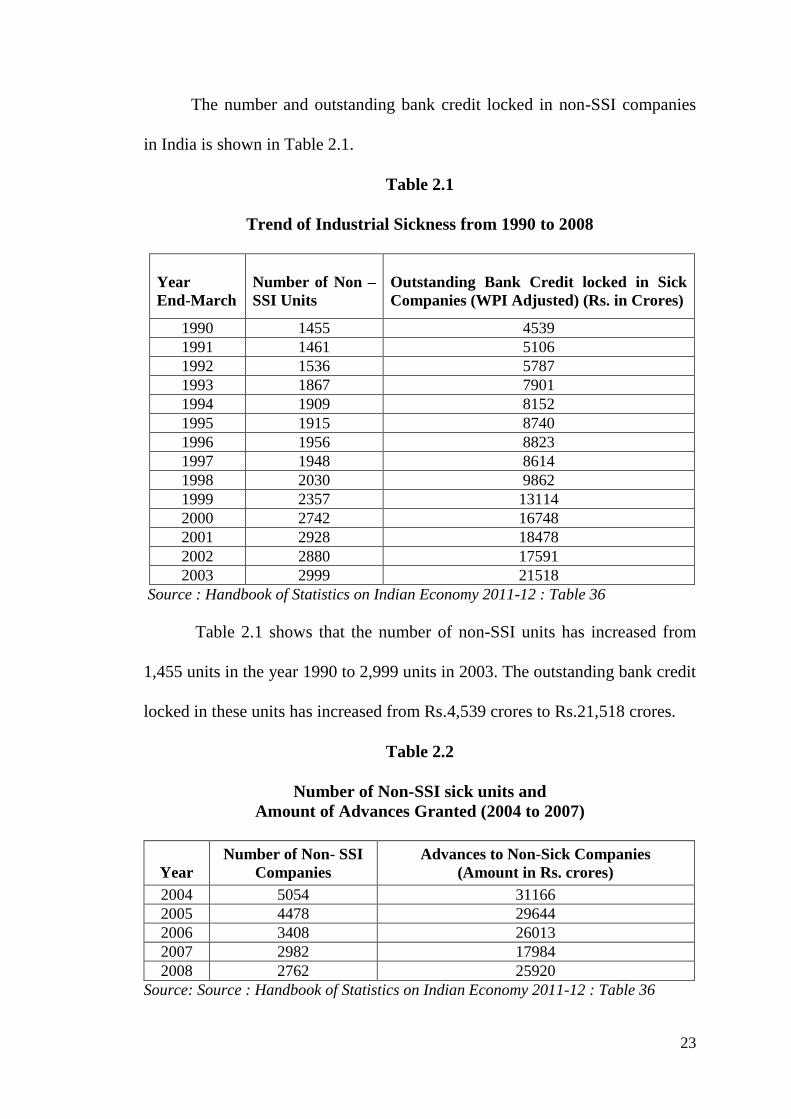

The number and outstanding bank credit locked in non-SSI companies

in India is shown in Table 2.1.

Table 2.1

Trend of Industrial Sickness from 1990 to 2008

Year

End-March

Number of Non –

SSI Units

Outstanding Bank Credit locked in Sick

Companies (WPI Adjusted) (Rs. in Crores)

1990 1455 4539

1991 1461 5106

1992 1536 5787

1993 1867 7901

1994 1909 8152

1995 1915 8740

1996 1956 8823

1997 1948 8614

1998 2030 9862

1999 2357 13114

2000 2742 16748

2001 2928 18478

2002 2880 17591

2003 2999 21518

Source : Handbook of Statistics on Indian Economy 2011-12 : Table 36

Table 2.1 shows that the number of non-SSI units has increased from

1,455 units in the year 1990 to 2,999 units in 2003. The outstanding bank credit

locked in these units has increased from Rs.4,539 crores to Rs.21,518 crores.

Table 2.2

Number of Non-SSI sick units and

Amount of Advances Granted (2004 to 2007)

Year

Number of Non- SSI

Companies

Advances to Non-Sick Companies

(Amount in Rs. crores)

2004 5054 31166

2005 4478 29644

2006 3408 26013

2007 2982 17984

2008 2762 25920

Source: Source : Handbook of Statistics on Indian Economy 2011-12 : Table 36

24

Table No.2.2 indicates that the number of sick non-SSI units has been

decreasing from 5,054 units in the year 2004 to 2762 in the year 2007. The

advances to these sick units also have decreased from Rs.31166 crores in 2004

to 17,984 in 2007, but has increased to Rs.25,920 in the year 2008.The

accumulated losses and the number of workers affected were the highest in the

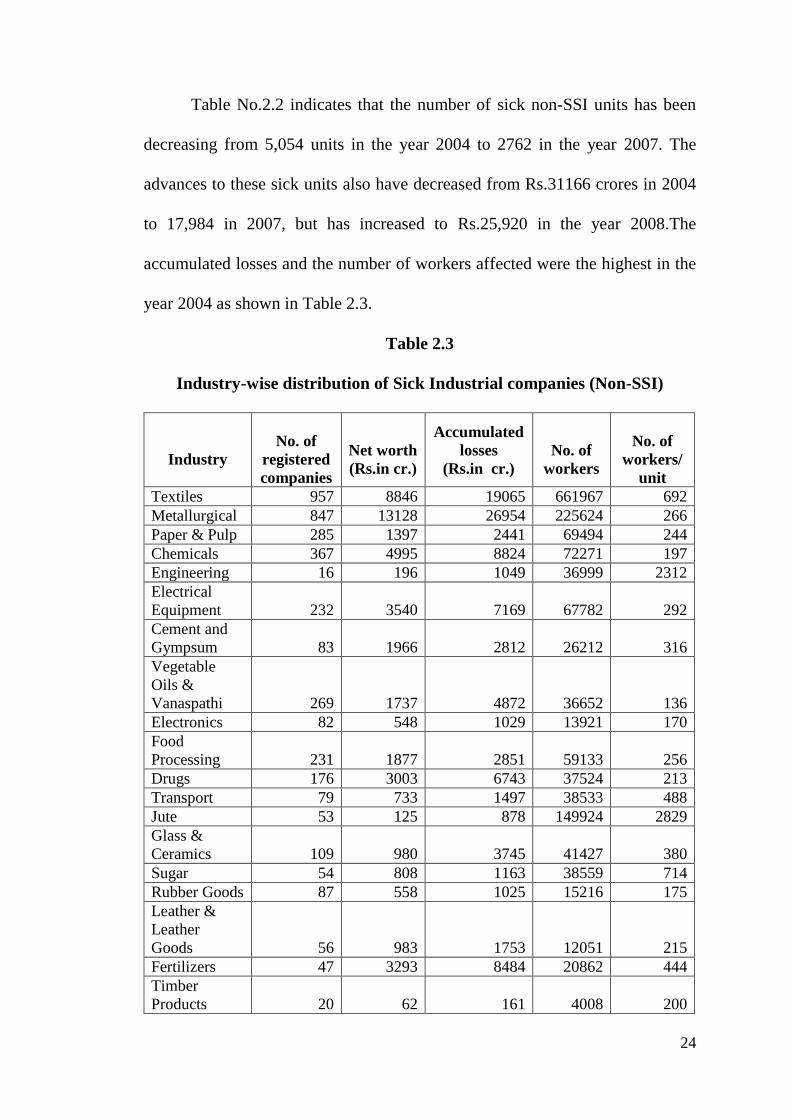

year 2004 as shown in Table 2.3.

Table 2.3

Industry-wise distribution of Sick Industrial companies (Non-SSI)

Industry

No. of

registered

companies

Net worth

(Rs.in cr.)

Accumulated

losses

(Rs.in cr.)

No. of

workers

No. of

workers/

unit

Textiles 957 8846 19065 661967 692

Metallurgical 847 13128 26954 225624 266

Paper & Pulp 285 1397 2441 69494 244

Chemicals 367 4995 8824 72271 197

Engineering 16 196 1049 36999 2312

Electrical

Equipment 232 3540 7169 67782 292

Cement and

Gympsum 83 1966 2812 26212 316

Vegetable

Oils &

Vanaspathi 269 1737 4872 36652 136

Electronics 82 548 1029 13921 170

Food

Processing 231 1877 2851 59133 256

Drugs 176 3003 6743 37524 213

Transport 79 733 1497 38533 488

Jute 53 125 878 149924 2829

Glass &

Ceramics 109 980 3745 41427 380

Sugar 54 808 1163 38559 714

Rubber Goods 87 558 1025 15216 175

Leather &

Leather

Goods 56 983 1753 12051 215

Fertilizers 47 3293 8484 20862 444

Timber

Products 20 62 161 4008 200

25

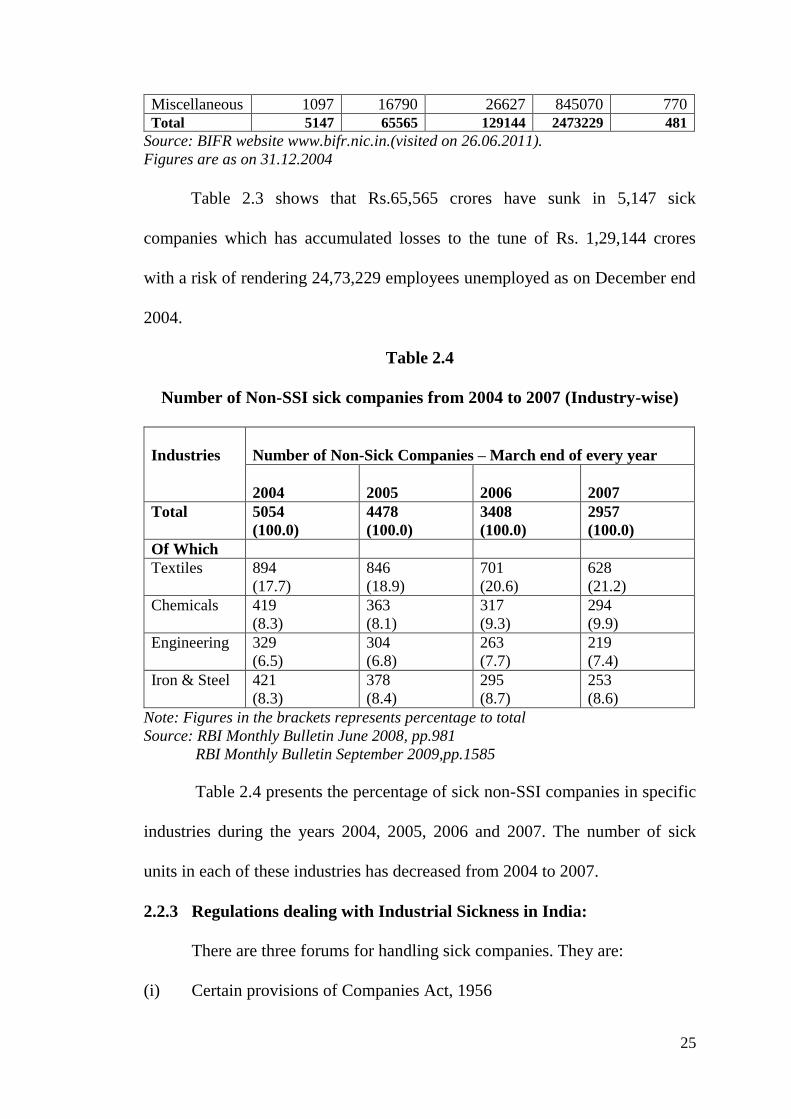

Miscellaneous 1097 16790 26627 845070 770

Total 5147 65565 129144 2473229 481

Source: BIFR website www.bifr.nic.in.(visited on 26.06.2011).

Figures are as on 31.12.2004

Table 2.3 shows that Rs.65,565 crores have sunk in 5,147 sick

companies which has accumulated losses to the tune of Rs. 1,29,144 crores

with a risk of rendering 24,73,229 employees unemployed as on December end

2004.

Table 2.4

Number of Non-SSI sick companies from 2004 to 2007 (Industry-wise)

Industries

Number of Non-Sick Companies – March end of every year

2004

2005

2006

2007

Total 5054

(100.0)

4478

(100.0)

3408

(100.0)

2957

(100.0)

Of Which

Textiles 894

(17.7)

846

(18.9)

701

(20.6)

628

(21.2)

Chemicals 419

(8.3)

363

(8.1)

317

(9.3)

294

(9.9)

Engineering 329

(6.5)

304

(6.8)

263

(7.7)

219

(7.4)

Iron & Steel 421

(8.3)

378

(8.4)

295

(8.7)

253

(8.6)

Note: Figures in the brackets represents percentage to total

Source: RBI Monthly Bulletin June 2008, pp.981

RBI Monthly Bulletin September 2009,pp.1585

Table 2.4 presents the percentage of sick non-SSI companies in specific

industries during the years 2004, 2005, 2006 and 2007. The number of sick

units in each of these industries has decreased from 2004 to 2007.

2.2.3 Regulations dealing with Industrial Sickness in India:

There are three forums for handling sick companies. They are:

(i) Certain provisions of Companies Act, 1956

26

(ii) Sick Industries Companies Act, 1985 (SICA) and this was replaced by

Sick Industrial Companies (Special Provisions) Repeal Act, 2003.

(iii) Board for Industrial and Financial Reconstruction (BIFR) for revival and

rehabilitation of sick companies and High Court for winding up.

The details of each of these forums have been discussed below.

(i) Companies Act, 1956:

The major amendments to the Companies Act 1956 include Companies

Amendment Act, 1988 and the Companies Amendment Act, 2002. The basic

intention behind incorporation of the new provisions (section 424A to 424L) in

Companies Act 1956 with regard to sick companies was to close the loopholes

in Sick Industrial Companies Act. The proposed Companies Bill 2011 contains

provisions with regard to revival/winding up of companies from section 253 to

259.

(ii) Sick Industrial Companies (Special Provisions) Act, 1985 (SICA)

The broad objectives of SICA are:

1. Timely detection of sick and potentially sick companies

2. Speedy determination of preventive, remedial measures by expediting

the revival of potentially viable units or closure of unviable units ( Sick

Industrial Company) and

3. Expeditious enforcement of the measures and thus by revival of the sick

unit, idle investments will become productive and by closure, the locked

up investments in unviable units would get released for productive use

elsewhere.

27

(iii) Board for Industrial and Financial Reconstruction (BIFR):

The Government of India set up Board for Industrial and Financial

Reconstruction (BIFR) in January 1987 (operational from May 15, 1987), under

the purview of Sick Industrial Companies (Special Provisions) Act, 1985

(SICA) for determining the preventive ameliorative remedial and other

measures which were required to be taken in respect of sick industrial

companies. It has been established as a quasi-judicial body in the Department of

Economic Affairs, Ministry of Finance, for revival and rehabilitation of

potentially sick undertakings and for closure/liquidation of non-viable and sick

industrial companies.

BIFR deals with medium and large scale sick industrial companies as

heavy investments are sunk in such industries. In December 2004, the

Government established a Board for Reconstruction of Public Sector Enterprises

(BRPSE) to advice on revival /restructuring of sick and loss-making CPSEs.

The Board of directors will be responsible for reporting sickness of industrial

companies to BIFR under the provisions of SICA within 60 days from the date

of finalization of duly audited accounts of the company. The Central or State

Government or RBI or public financial institution or scheduled bank, if have

sufficient reasons to believe that accumulated losses have resulted in an erosion

of 50 per cent of its peak net worth during the immediately preceding four

financial years, then it can report the matter to BIFR. If BIFR, upon its own

knowledge, has reasons to believe that accumulated losses have resulted in an

erosion of 50 per cent of its peak net worth during the immediately preceding

28

four financial years, then also BIFR can initiate enquiry regarding sickness.

On receipt of such a reference, BIFR will conduct an inquiry and

ascertain whether the company is sick or not. For this purpose, the Board may,

through any operating agency, cause to prepare with respect to the sick

company:

a. A complete inventory of that company which includes all assets and

liabilities as well as all books of accounts, registers, maps, plans, records,

documents of title or ownership of property and all other documents of

whatsoever nature relating thereto;

b. A list of shareholders and creditors (showing separately the list of

secured creditors and unsecured creditors);

c. A valuation report in respect of the shares and assets of the company;

d. An estimate of its reserve price, lease rent or share exchange ratio; and

Performa accounts, where no up-to-date audited accounts are available.

On the basis of such an enquiry, if BIFR is convinced that the company

has become sick, it will either give reasonable time to the company concerned

to make its net worth positive or it will appoint an operating agency consisting

of certain banks and financial institutions to prepare a package for the revival of

such sick industrial units. When BIFR is of the opinion that the sick industrial

unit is not likely to make its net worth exceed its accumulated losses within a

reasonable time and it is just and equitable that the company should be wound

up, then BIFR will forward its opinion for winding up of the sick unit to the

concerned High Court. The High Court will take final decision at its discretion

29

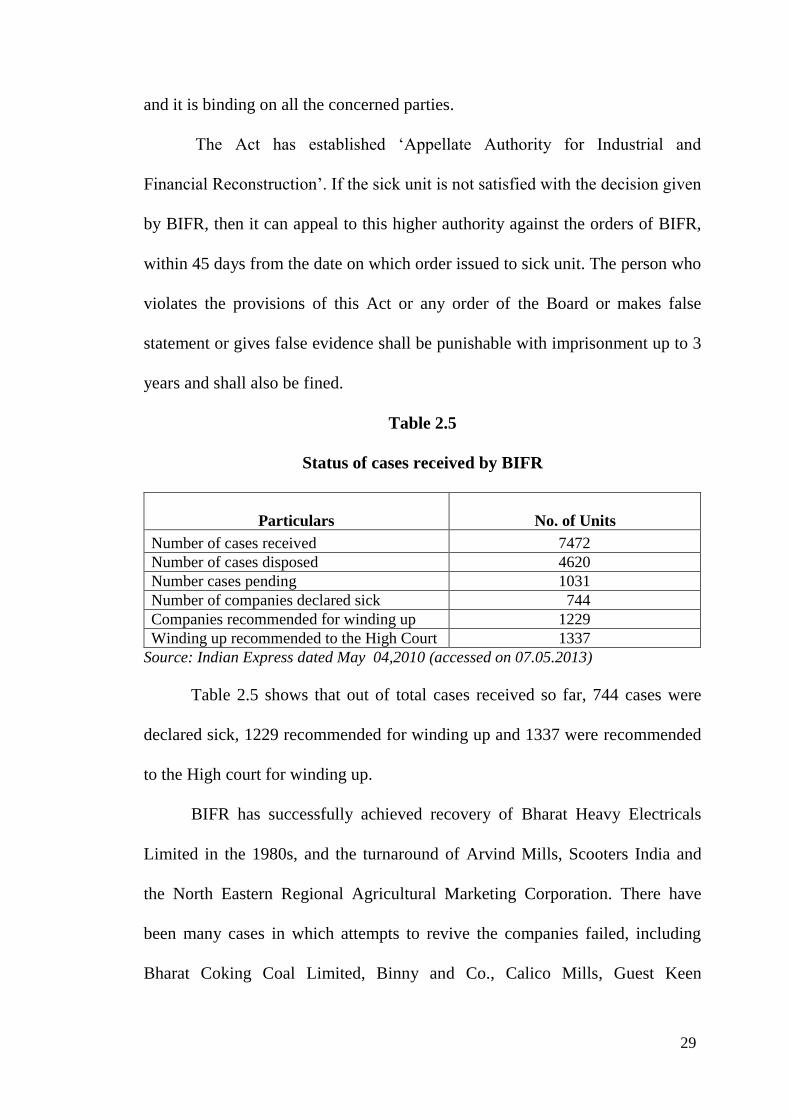

and it is binding on all the concerned parties.

The Act has established ‘Appellate Authority for Industrial and

Financial Reconstruction’. If the sick unit is not satisfied with the decision given

by BIFR, then it can appeal to this higher authority against the orders of BIFR,

within 45 days from the date on which order issued to sick unit. The person who

violates the provisions of this Act or any order of the Board or makes false

statement or gives false evidence shall be punishable with imprisonment up to 3

years and shall also be fined.

Table 2.5

Status of cases received by BIFR

Particulars

No. of Units

Number of cases received 7472

Number of cases disposed 4620

Number cases pending 1031

Number of companies declared sick 744

Companies recommended for winding up 1229

Winding up recommended to the High Court 1337

Source: Indian Express dated May 04,2010 (accessed on 07.05.2013)

Table 2.5 shows that out of total cases received so far, 744 cases were

declared sick, 1229 recommended for winding up and 1337 were recommended

to the High court for winding up.

BIFR has successfully achieved recovery of Bharat Heavy Electricals

Limited in the 1980s, and the turnaround of Arvind Mills, Scooters India and

the North Eastern Regional Agricultural Marketing Corporation. There have

been many cases in which attempts to revive the companies failed, including

Bharat Coking Coal Limited, Binny and Co., Calico Mills, Guest Keen

30

Williams, Hindustan Cables, Metal Box Company and Wyman Gordon (Kazmi,

2008)12

. The reasons include insufficient resources, delays and lack of political

willingness to take tough decisions. The BIFR in practice has been often

prolonging the life of unviable companies for years together at taxpayer expense

(Baijal, 2008)13

.

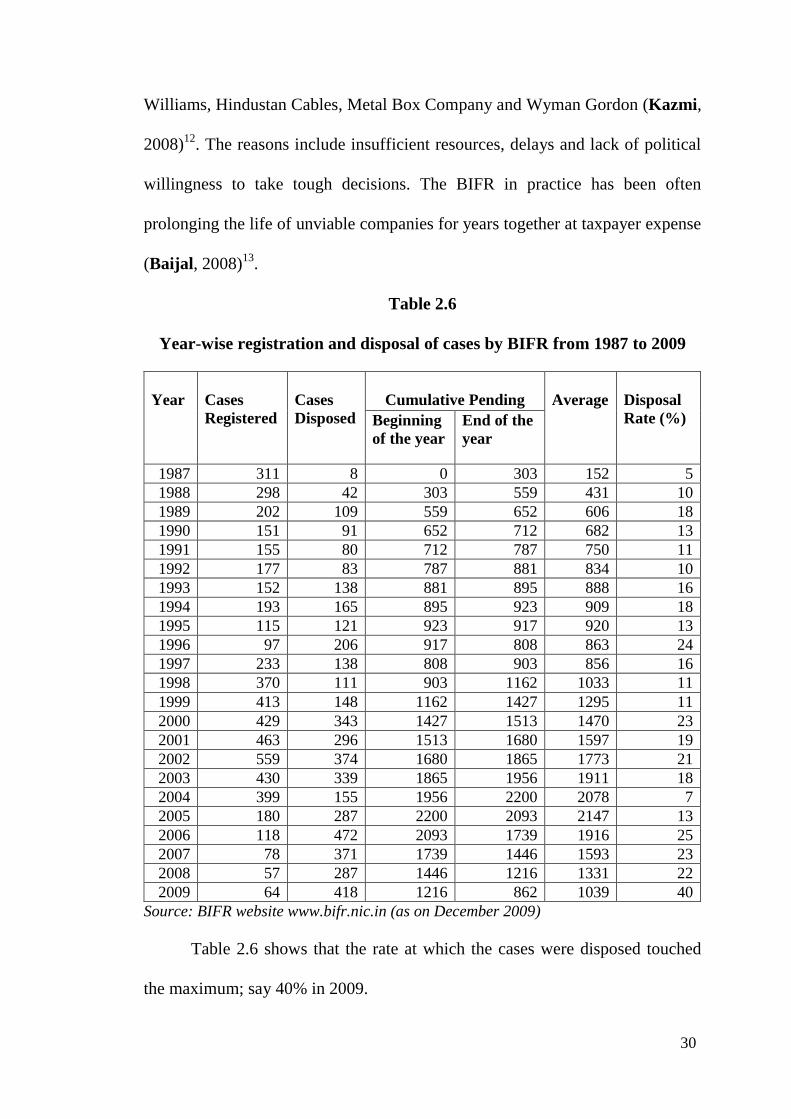

Table 2.6

Year-wise registration and disposal of cases by BIFR from 1987 to 2009

Year

Cases

Registered

Cases

Disposed

Cumulative Pending

Average

Disposal

Rate (%)

Beginning

of the year

End of the

year

1987 311 8 0 303 152 5

1988 298 42 303 559 431 10

1989 202 109 559 652 606 18

1990 151 91 652 712 682 13

1991 155 80 712 787 750 11

1992 177 83 787 881 834 10

1993 152 138 881 895 888 16

1994 193 165 895 923 909 18

1995 115 121 923 917 920 13

1996 97 206 917 808 863 24

1997 233 138 808 903 856 16

1998 370 111 903 1162 1033 11

1999 413 148 1162 1427 1295 11

2000 429 343 1427 1513 1470 23

2001 463 296 1513 1680 1597 19

2002 559 374 1680 1865 1773 21

2003 430 339 1865 1956 1911 18

2004 399 155 1956 2200 2078 7

2005 180 287 2200 2093 2147 13

2006 118 472 2093 1739 1916 25

2007 78 371 1739 1446 1593 23

2008 57 287 1446 1216 1331 22

2009 64 418 1216 862 1039 40

Source: BIFR website www.bifr.nic.in (as on December 2009)

Table 2.6 shows that the rate at which the cases were disposed touched

the maximum; say 40% in 2009.

31

The number of cases registered with BIFR in years 2010, 2011 and 2012

were 72, 73 and 80 units respectively. (Source: www.bifr.nic.in as on 06.05.13)

The Companies (Amendment) Bill 2001 proposed to set up a National

Company Law Tribunal (NCLT) and a National Company Law Appellate

Tribunal (NCLAT) which would take over the functions of the BIFR and other

bodies in order to speed up the process of winding down sick companies. The

government considered that the BIFR had not met its objective of preventing

industrial sickness and hence the bill was introduced. The Sick Industrial

Companies (Special Provisions) Repeal Act, 2003 replaced SICA and sought to

dissolve the BIFR and the Appellate Authority for Industrial and Financial

Reconstruction (AAIFR) and replace them by the NCLT and NCLAT.

However, legal hurdles prevent the constitution of NCLT.

2.2.4 Factors causing Industrial Sickness:

Industrial Sickness may be due to change in government policy, over

spending on essentials, absence of control on borrowings, dishonest practices

on the part of the management. The reasons for such sickness may vary from

unit to unit. The business failure may have been caused by a plethora of

reasons. The factors causing industrial sickness could be internal and external.

The external factors usually affect all the industrial units in the same group and

the internal factors affect a particular unit only, not the entire industry

(Srivastava and Yadav, 1986)14

.

32

When the causes of corporate bankruptcy are identified, preventive

measures can be undertaken and failure rates can be reduced (Abdelsamad

and Kindling, 197815

; Larson and Clute, 197816

)

The internal factors includes inadequate management, inappropriate

technology, sub-optimal plant and/or factors external to the organization, like

increased competition, economic condition, input shortages, changes in

government policies, or disturbed industrial relations. The major reasons for

industrial sickness are financial reasons, managerial inability, government

laws, technological changes, reduced product demand, and marketing related

problems (Singh and Singh, 2011)17

.

Hambrick and D’Aveni (1992)18

when examined top management

teams in bankrupt firms noticed that bankruptcy was associated with a

dominant CEO, high top management team turnover, small top management

teams with lower percentage of members with expertise in marketing/sales,

operations, production and R&D.

Argenti (1976)19

found that features associated with companies failure

could be categorized into three categories namely, inherent defects in the

actual organization and financial structure of the company (ii) management

mistakes and (iii) symptoms of deterioration and thus supported the fact that

lack of financial expertise among top management team members was

associated with bankruptcy.

33

A firm would be in a crisis situation when already weakened by poor

management, lack of control and inefficiency is subjected to adverse

movements in market demand and commodity prices, price competition

(Slatter, 1984)20

.

This part of the chapter has discussed the trend of industrial sickness in

India and the outstanding bank credit due to the lenders including banks and

financial institutions. The efforts being made by various legal regulations have

been dealt in detail. The factors affecting industrial performance have gained

serious attention of the researchers, who explore various techniques of

predicting the symptoms of corporate bankruptcy in order to prevent companies

from falling sick. In this direction, the present study attempts to identify the

financial ratios that reveal symptoms of sickness and thus focus on developing

sickness prediction models using various analytical tools.

2.3 REVIEW OF LITERATURE

This part provides an outline of previous research works on

discriminators and predictors of corporate bankruptcy. Failure prediction

models including Altman’s Model and new sickness prediction models

developed using Multi Discriminant Analysis (MDA) and Logit analysis have

been discussed. The academic literature on corporate bankruptcy is an

extensive area for research work and has definite conclusions indicating that

financial ratios significantly predict corporate failure. Most of the studies have

concluded that Multiple Discriminant Analysis (MDA) performs well and

certain other research studies have found that Logit analysis was better than

34

Altman’s model and MDA. An overview of these related studies is provided

below.

2.3.1 Financial Ratios as Discriminators and Predictors of Corporate

Bankruptcy:

Karami, Hosseini, Attaran and Hosseini (2012)21

employed

independent sample t-test to 18 financial ratios of 45 bankrupted and 45 non-

bankrupted firms from various industries and found that there were significant

differences in two groups and those ratios such as liquidity (Current

Assets/Current Liabilities), leverage (Total Liabilities/Total Assets) and

profitability (Return On Assets, Net Income/Fixed Assets, Operating

Income/Total Assets) were appropriate measures for classifying bankrupt from

non-bankrupt.

Leksrisakull and Evans ( 2005)22

selected a sample of 89 non-failed

and 46 failed firms and employed 37 financial ratios classified into five

categories, namely leverage, profitability, turnover, liquidity and others. It was

found that the significance of the Wilks’ Lambda statistic indicating that the

five variables - market value of equity/ total debt, earnings before interest and

tax/total assets, retained earnings/ total assets, sales/total assets and working

capital to total assets - were significant discriminators.

Samarakoon and Hasan (2003)23

tested for the difference between the

means of the variables belonging to 13 distressed and 13 non-distressed firms

of same size belonging to the same industry, using the paired t-test. It was

found that the means of the variables namely working capital to total assets,

35

retained earnings to total assets, earnings before interest and taxes to total

assets, market value of equity to book value of total liabilities, book value of

equity to book value of total liabilities and sales to total assets in the distressed

sample were vastly lower than the means in the non-distressed sample. Also the

results of the paired t-test showed that the mean differences in variables

between the two groups were extremely significant.

Gupta (1983)24

examined a sample containing 20 sick and 21 non sick

textile companies during 1962-64 to identify the lead indicators of sickness

using 63 financial ratios. Using Discriminant analysis, it was found that net

worth to short and long term debt and all outside liabilities to tangible assets

were useful. The study revealed that five ratios were found to have the highest

predictive value and the least classification error when applied to a

homogeneous group. They were: Earnings Before Depreciation, Interest and

Tax (EBDIT)/Net Sales, Operating Cash Flow (OCF)/Net Sales, EBDIT/Total

Gross Assets, OCF/Total gross Assets and EBDIT/Interest + 0.25 (Debt). The

study also revealed that in early years of the company, the predictive power of

OCF and EBDIT was more or less the same and in the later years, OCF become

important as sick firms rely more and more on borrowed funds.

Green (1978)25

stated that financial ratios have been regarded as

indicators of corporate health revealing liquidity, leverage, activity and

profitability and one could evaluate its future likelihood of success.

Weibel (1973)26

constructed a sample of 36 failed swiss firms from

1960 to 1971 and matched them to a like number of non-failed firms in terms

36

of age, size and line of business. The researcher analyzed ratios of these two

groups using univariate statistical parametric and non-parametric tests, and

found that many of the individual ratios were non-normal. He used cluster

analysis and found that six other ratios including liquidity measures were

effective in discriminating among the paired groups and also found that

inventory turnover and debt to asset ratios were good individual predictors.

Beaver (1966)27

compared the mean values of 30 ratios of 79 failed and

79 non-failed firms in 38 industries and the results of the univariate analysis

showed empirical evidence that cash flow/total debt exhibit statistically

significant warnings prior to business failure. The researcher found that Net

Income to Total Debt had the highest predictive ability (92% accuracy one year

prior to failure), followed by Net Income to Sales (91%) and Net Income to Net

Worth, Cash Flow to Total Debt and Cash Flow to Total Assets (each with

90% accuracy) and suggested that the possibility of using multiple ratios

simultaneously may have higher predictive ability than single ratios.

Winakor and Smith (1935)28

analysed financial ratios of 183 failed

firms belonging to different industries in a follow-up study to the BBR’s 1930

publication. The results of the study indicated that Working capital to total

assets was a better predictor than both cash to total assets and current ratio. It

was found out that current assets to total assets ratio dropped as the firm

approached bankruptcy.

Patrick (1932)29

the pioneer in the field of corporate failure, examined

whether there was significant difference in the ratios between failed and non-

37

failed firms at least three years prior to failure. The researcher selected 19

companies randomly which had failed during the period of 1920-1929 and

matched with 19 successful companies using financial soundness, asset size,

sales volume, product line and fiscal year as matching criteria. The study

showed that the net worth to debt and net profits to net worth were the best

indicators of failure among the ratios used.

In 1930, the Bureau of Business Research (BBR)30

published a bulletin

containing a study analyzing 24 ratios of 29 firms to determine common

characteristics of failing firms. When the ratios of each firm were compared

with the average ratios, eight ratios were considered as indicators of “growing

sickness” of a firm. They were: Working capital to total assets, Surplus and

Reserves to total assets, Net worth to fixed assets, Fixed assets to total assets,

current ratio, Net worth to total assets, Sales to total assets and cash to total

assets. It claimed that Working capital to total assets ratio was a more valuable

indicator than current ratio.

Zulkarnain et al. (2001)31

Lennox (1999)32

, Ohlson (1980)33

and

Libby (1975)34

revealed that profitability was an important determinant of

bankruptcy. The companies with large profits naturally have a lower

probability of bankruptcy; hence, the relationship between profitability and

corporate sickness is negative. The company’s short term solvency must be

measured to find out its ability to meet short term financial obligations.

38

Majority of the studies including Mohamed, Li, and Sanda (2001)35

,

Zmijewski (1984)36

, Ohlson (1980)37

, Deakin (1972)38

and Beaver (1966)27

found that Debt related ratios significantly determine corporate failure.

2.3.2 Corporate Bankruptcy Prediction Models:

Datta (2012)39

found that the financial ratios used in various models

including Altman’s (1968) model were so complicated that it become difficult

to operationalize them in the Indian context and concluded that the existing

models might not provide a robust set of financial ratios for analyzing firm

level sickness. Thus models were developed based on MDA and Logit analysis

and the validity of these two models were checked by considering a panel data

of 50 ‘healthy’ companies and 50 ‘sick’ companies and found them robust. The

Discriminant model correctly classified 97% before one year, 95% before two

years, 93% before three years, 90% before four years and 86% before five

years of original grouped companies whereas using the predictive model

developed, with probability of 0.72, 97% of the companies have been found to

be correctly classified into their respective predetermined group.

Uchenna and Okelue (2012)40

used a sample of 11 Nigerian firms and

employed parametric t-test to test the hypothesis if there is no significant

difference between the failure/success factor (Z) of Nigerian manufacturing

firms and the corporate bankruptcy model using multi discriminant analysis

model. The study indicated that there is no significant difference between the

failure/success factor (Z) of Nigerian manufacturing firms and the multi

discriminant analysis model outcome.

39

Rashid and Abbas (2011)41

considered a sample of companies

belonging to non-financial sector of Pakistan which became bankrupt over the

time period 1996-2006 and matched non-bankrupt firms in the same industry.

Using statistical t-test, it was found out that there was a significant difference

between the two populations means for three financial variables namely EBIT

to total assets, market value of equity to book value of debt, and equity to long

term debt. The Multivariate Discriminant Analysis concluded that EBIT to

current liabilities ratio, sales to total assets ratio and cash flow ratio were found

highly significant at 5% significance level. Twenty four financial ratios

covering profitability, liquidity, leverage, and turnover ratios were examined

for a five-year period prior to bankruptcy. The researchers used discriminant

analysis to produce a parsimonious model of three variables viz. sales to total

assets, EBIT to current liabilities, and cash flow ratio. The estimates showed

that firms having Z-value below zero falls into the “bankrupt” whereas the

firms with Z-value above zero fall into the “non-bankrupt” category and the

model achieved 76.9% prediction accuracy.

Kosmidis , Venetaki , Stavropoulos and Terzidis (2011)42

developed

a model for the prediction of financial distress using 27 financially

distressed and 27 financially viable companies with 41 financial ratios. T-tests

and univariate discriminant analysis were employed to identify the most

significant factors for the financial viability of companies. The empirical

results of the study indicated that the Logit model was more accurate than

the MDA model in terms of correct classification.

40

Yap, Yong and Poon (2010)43

used 32 failed companies with matching

32 non-failed companies and developed a failure prediction model to improve

the predictive abilities for company failures using 16 financial ratios for 64

companies in Malaysia. A strong discriminant function was constructed using

multi discriminant analysis wherein seven ratios were found to be significant in

its discriminating power and the model had good predictive abilities with

accuracy rates of 90% on average for the analysis sample and 89% on average

for the hold-out sample for the five years prior to actual failure. The results of

the study revealed that the ratios measuring liquidity and profitability were

most useful in predicting a company’s success or failure.

Hlahla (2010)44

developed a bankruptcy prediction model for South

African companies listed on the Johannesburg Stock Exchange. The study used

a sample of 14 failed and 14 non-failed firms and 64 financial ratios as

independent variables in a Multi Discriminant Model. Times Interest Earned,

Cash to Debt, and working capital to turnover ratios were identified as

significant ratios. The results of the study showed that the Times Interest

Earned had greater discriminating power followed by cash to debt ratio and

working capital turnover ratio. The overall classification accuracy of the model

was found to be 75.3 per cent.

Ahmad, Azhar and Wan-Abu-Bakar (2010)45

investigated whether a

model utilizing cash-flow ratios in combination with other categories of

financial ratios result in a model superior to a model that does not include cash-

flow ratios. A sample of 4607 non-failed firms and 2260 failed firms for a

41

period of 5 years from 1998 to 2002 with 41 financial ratios as independent

variables was employed using logistic regression. The study considered all the

firms to be included in the analysis and the matched pair design was not

adopted. Two models were constructed, first model containing activity,

liquidity, leverage and profitability ratios along with operating cash flow based

ratios. The operating cash flow to current liabilities, operating cash flow to total

assets and operating cash flow to total debts were the cash flow ratios. The

second model is similar to the first one, except that it excluded operating cash

flow based ratios. It was found that the first model had a better association

between the independent variables and the dependent variable than the second

model and the overall accuracy was 68.30 per cent and 66.90 for the two

models respectively. The results asserted that a model utilizing cash flow ratios

served as the best warning signals of bankruptcy.

Angelina (2009)46

developed a model using Discriminant Analysis to

investigate into the prediction of sickness in the textile industries in India,

considering 70 textile industries, of which 39 being sick, 31 non-sick between

the years 1996 and 2006, using 25 financial ratios. Sick firms were taken on the

basis of those who have made a request for sickness with the BIFR or those

experiencing serious financial difficulties. The study revealed that that in the

case of isolated data set, the discriminant function was able to predict and

correctly classify 76.9%, 87.2% and 89.7% of the observations in the Non-sick

group and 83.9%, 80.6% and 83.9% respectively of the observations in the Sick

group in the first, second and third year prior to the event. The function

42

predicted 73.1% of the observations correctly in the Non-sick group for 1 and 2

years prior to sickness taken together and 82.3% of the observations in the Sick

group. The prediction for 1,2 and 3 years prior to sickness taken together was

78.6% of the observations correctly in the Non-sick group and 79.6% of the

observations in the Sick group observations correctly.

Gerantonis, Vergos and Christopoulos (2009)47

analyzed whether

Altman Z-Score model can predict correctly company failures for a period of

up to three years prior to sickness. The researcher found that this model was

useful in identifying financially troubled companies that may fail up to 2 years

before bankruptcy as it matches both accounting data and market value.

Chowdhury and Barua (2009)48

used Z score model to predict risk of

financial distress of Z category companies listed in Dhaka Stock Exchange

(DSE). The results suggested that ninety percent of the companies were

suffering from financial distress risk due to very poor management capability

and operating inefficiency. The Altman’s Z score model, though may not be

fully applicable for companies in Bangladesh, still it has proved its strong

validity and correctness in predicting distressful status of the Z category

companies. The researchers have acknowledged that the Altman Z score (1968)

model to predict the financial distress of publicly traded manufacturing firms

may not be the best technique to apply for companies operating in Bangladesh

as the rules of accounting treatment, the rules of accounting information

disclosure, and the governance structure may not be perfectly commensurate

with the companies considered by Altman (1968) in his model and thus they

43

opted to develop a new model to predict the financial distress for the

companies operated and traded in Bangladesh capital market both in DSE and

CSE.

Abdullah, Hallim, Ahmad and Rus (2008)49

considered a sample of 52

distressed and non-distressed companies. Among ten determinants of corporate

performance examined, the ratio of debt to total assets was found to be a

significant predictor of corporate distress regardless of the methodology used.

In addition, net income growth was another significant predictor in MDA,

whereas the return on assets was an important predictor when the logistic

regression and hazard model methodologies were used.

Bellovary, Giacomino and Akers (2007)50

have summarized and

analyzed the existing research on bankruptcy prediction studies from 1930’s,

when studies focused on the use of simple ratio analysis to predict future

bankruptcy, to the present. Investigation of model type by decade showed that

the primary method began to shift to Logit analysis in the 1980's.

Ugurlu and Aksoy (2006)51

identified predictors of corporate financial

distress, with help of the discriminant and Logit models, using a sample of 27

failed and 27 non-failed manufacturing firms during the period 1996-2003,

which included a period of high economic growth (1996-1999) followed by an

economic crisis period (2000-2002). The results of the study identified the

same number of significant predictors out of the total variables analyzed, using

the discriminant and Logit models, and six of these are common in both. The

ratio of EBITDA to total asset was found to be the most important predictor of

44

financial distress in both models. The Logit model identified operating profit

margin and the proportion of trade credit within total claims ratios as the

second and third most important predictors respectively. It was also found that

the discriminant model had lesser power and predictive accuracy during the

four years period prior to bankruptcy than the Logit model.

Sori, Hamid, Nassir and Mohamad (2006)52

selected a set of sample

companies from 6 different industries: 23 companies from the industrial sector,

6 companies from the property sector and 1 company from the consumer,

finance, hotel and mining sectors and used sixty-five ratios as independent

variables which were found to be of non-normal distribution and hence applied

log transformation to approximate the distribution to normal, but found it to be

ineffective for a diversified industry.

Sori, Hamid and Nassir (2006)53

examined the corporate failure before

the 1997 Asian Financial Crisis in three emerging capital markets namely

Malaysia, Singapore and Thailand and thus developed a failure classification

model based on multiple discriminant analysis to classify listed corporations

from these countries for the 1980 to 1996 period. The model was tested on a

sample of 33 Malaysian, 17 Singaporean and 52 Thailand failed firms and

similar number of non-failed firms in the respective countries as a control

sample. The model successfully discriminated between failed and non-failed

listed firms at the rate of 86%, 82% and 71% of Malaysian, Singaporean and

Thailand firms respectively.

45

Charitou, Neophytou and Charalambous (2004)54

examined the

incremental information content of operating cash flows in predicting financial

distress and thus developed reliable failure prediction models for UK public

industrial firms. The results of the study indicated that a parsimonious model

that includes three financial variables, a cash flow, a profitability and a

financial leverage variable which yielded an overall correct classification

accuracy of 83% one year prior to the failure and that the predictive ability of

the Altman model did not perform well when compared to Logit analysis. It

was found that operating cash flows possess discriminatory power when it

comes to predicting failure of UK companies.

Grice and Ingram (2001)55

found that the overall accuracy of the

model was significantly higher for manufacturing firms than non-

manufacturing firms and also that the relation between financial ratios and

financial distress changes over time. The results of the study indicated that

those who employ Altman’s Z-score model should re-estimate the model’s

coefficients rather than relying on those reported by Altman (1968).

Sulaiman, Jili and Sanda (2001)56

tested a Logit model that

distinguishes between the Malaysian firms that did and those that did not seek

court protection from their creditors. The factors which were found to have

significant discriminating power were: debt ratio, interest coverage and total

asset turnover ratio. The Logit model was able to classify accurately 80.7 per

cent of the firms in the estimation sample and 74.4 per cent in the hold out

sample.

46

Sori et al. (2001)57

developed a failure prediction model for Malaysian

industrial sector listed firms which discriminated between 24 failed and non-

failed for the period 1980 to 1996. The model correctly and significantly

classified 91.1% and 89.3% of the failed and non-failed firms respectively.

Also an alternative prediction model was developed based solely on accounting

information which showed similar results. These models predicted failure up to

4 years before the actual event. The variables in the final model implied that

that profits, cash flows, working capital and net worth are important

determinants of firm failures in the Kuala Lumpur Stock Exchange.

Mohamed, Li and Sanda (2001)35

compared MDA and Logit model in

the analysis of bankruptcy. The sample of 26 distressed companies and 79 non-

distressed companies were employed and the results showed that when using

MDA, debt ratio and total assets turnover were found to be significant but

when Logit analysis was used, an additional variable, interest coverage was

also found to be significant, emphasizing the importance of leverage ratio as a

predictor of failure. The Logit model predicted 80.7% of the companies in the

estimation sample and 74.4% in the hold-out sample, whereas the MDA model

predicted 81.1% of the companies in the estimation sample and 75.4% in the

hold-out sample.

Kahya and Theodossiou (1999)58

investigated a sample obtained using

the debt default criteria that included 117 healthy firms and 72 failed firms

whose financial data span the period 1974-91. The CUSUM (Cumulative

Sums) model being viewed as the dynamic time-series extension of LDA

47

resulted in correctly classifying failed firms to the extent of 68% in first year,

49% in second year, 43% in third year and 30% in fourth year prior to failure.

Mossman, Bell, Swartz and Turtle (1998)59

compared four types of

bankruptcy prediction models Altman’s (1968) Z-score model based on

financial ratios; Aziz, Emanuel, and Lawson’s (1988) model comprised of cash

flows; Clark and Weinstein’s (1983) market return model, and Aharony, Jones,

and Swary’s (1980) market return variation model. It was found out that in the

year prior to bankruptcy, the ratio model was the most effective in explaining

the likelihood of bankruptcy and in the three years preceding bankruptcy, the

cash flow model most consistently discriminates between bankrupt and non-

bankrupt firms.

Rujoub, Cook and Hay (1995)60

attempted to examine whether cash

flow data can provide a superior measure to predict bankruptcy over accrual

accounting data. The study used a sample of 33 failed firms and 33 non-failed

firms, matched on the basis of industry type and asset size and employed

eighteen financial ratios based on cash flow data including financial policies

ratio which is equal to cash from financing activities/Total assets. A stepwise

discriminant procedure was employed for selecting the financial ratios that are

most useful in discriminating between bankrupt and non-bankrupt firms and the

results showed that the classification accuracy of cash flow data model is

86.36%,78.79% and 69.70% in one year, at two years and three years prior to

failure respectively. This is higher than that of the model based on accrual data

with 81.82%, 71.21% and 69.70% in one year, two years and three years

48

respectively showing that cash flow data predict bankruptcy better than accrual

accounting data. It was concluded that the classification accuracy of the

combined model comprising of both accrual and cash flow data provide a

superior measure to predict bankruptcy, say, 90.91%, 86.36% and 69.70% in

one year, two years and three years respectively, meaning that the use of cash

flow data in conjunction with accrual accounting data improves the overall

predictive power of accrual accounting data.

Panigrahy and Mishra (1993)61

developed a cash flow variable model

using Multiple Discriminant Analysis (MDA) to predict corporate sickness

using a sample of 45 sick companies matched with 45 non-sick companies on

the basis of size, age, nature of industry and fiscal year of comparison. The sick

companies reported during 1977-87 were drawn at random from 12 different

industry groups and 16 cash flow ratios were employed. The results of the

study indicated that cash flow ratios have 86.67 per cent, 85.56 percent of

correct classification in 1 year and 2 years prior to sickness respectively.

Rais (1990)62

adopted stratified purposive sampling method in selecting

a sample of 18 sick and 18 non sick sugar mills and employed 28 financial

ratios. The researcher developed a discriminant function having five financial

ratios namely profit before tax/capital employed; net profit/net worth; profit

before interest and tax/interest; net profit/net working capital; net sales/net

working capital and net sales/fixed assets using multivariate discriminant

analysis. The accuracy of classification of sick and non-sick sugar mills was

found to be as high as 91%.

49

Gilbert et al (1990)63

investigated the predictive abilities of models

based on two types of samples: 52 bankrupt and 208 non-bankrupt firms and 52

bankrupt and 208 distressed firms during the period 1974-83. Holdout sample

was used to test accuracy of the model. 14 ratios were employed, of which

three were cash flow ratios. On applying stepwise logit, it was found out that

cash flow from operations to total liabilities was significant in classifying

bankrupt and non-bankrupt firms and cash flow from operations to current

liabilities was significant in classifying bankrupt and distressed firms. The

study concluded that cash flow ratios add significantly to prediction accuracy

of accrual models.

Aziz and Lawson (1989)64

compared cash models with Altman’s Z and

Zeta models, and a mixed model comprising cash and accrual variables

employing 49 bankrupt firms matched with 49 non-bankrupt firms up to five

years prior to failure. The researchers compared cash models with Altman’s Z

model and a mixed model comprising cash and accrual variables. It was found

that the cash flow model was more accurate in predicting bankruptcies and

operating cash flow and lender cash flow were the two most significant cash

variables.

Aziz, Emanuel and Lawson (1988)65

developed a Logit model with 6

factors that predicted accuracy levels of 85.7%, 85.7%, 79.6%, 81.3% and

84.8% respectively in 1st, 2

nd, 3

rd, 4

th and 5

th year before failure.

Gahlon and Vigeland (1988)66

compared cash flow profiles with

selected accrual ratios for 60 bankrupt and 204 non-bankrupt firms five years

50

prior to failure. The study resulted in cash flow from operation cash flow after

debt retirement and cash coverage indicating failure as early as the fifth year

prior to failure.

Dambolena and Shulmen (1988)67

recomputed logit model equivalents

for Altman’s (1968) model and Gentry et al. model using 25 bankrupt firms

and matching 25 non-bankrupt companies. The study revealed that net liquid

balance (equals operating cash flows minus increase in cash investments, plus

increase in long term financial flows) improved the predictive accuracy of both

models especially for non-bankrupt firms. This improvement in predictive

accuracy was greater for the Gentry et al model than for Altman’s model.

Gombola et al (1987)68

computed 21 accrual ratios and three cash flow

ratios namely cash flow from operations/sales, cash flow from operations/assets

and cash flow from operations/debt for 77 failed and matched non-failed firms

and found that non of these cash flow ratios were significant predictors of

failure.

So (1987)69

used eleven financial ratios for ten fiscal years from 1970 to

1979. He found that the distribution of many financial ratios were not normal

and were asymmetrically distributed even after removing the outliers.

Viscione (1985)70

carried out trend analysis of 24 bankrupt firms up to

five years prior to failure and compared cash flow from operations with

selected accrual ratios. He found out that cash flow from operations was not a

strong indicator of financial distress.

51

Casey and Bartczak (1985)71

conducted a study to assess whether

operating cash flow data and related measures lead to more accurate

predictions of bankrupt and non-bankrupt firms and whether operating cash

flow data can increase the accuracy of accrual based multiple discriminant and

Logit models to distinguish between bankrupt and non-bankrupt firms. He used

60 bankrupt and 230 non-bankrupt firms belonging to the same industry during

the period 1971-82 and employed MDA and logit. The results of the study

suggested that operating cash flow data do not provide incremental predictive

power over accrual based ratios.

Gentry, Newbold, and Whitford (1985)72

found that the addition of

cash-based funds flow components to the traditional financial ratios to

discriminate between failed and non-failed companies resulted in significantly

improved predictive performance. A sample of 33 failed and 33 non-failed

firms paired by size and industry classification was used with three techniques

namely, linear discriminant, Probit and Logit analysis and it was found that

MDA classification accuracy and predicted probabilities of failure were

marginally better than Probit and Logit analysis.

Zavgren (1985)73

using a sample of 45 bankrupt and 45 non-bankrupt

firms, developed 7-factor Logit model which resulted in an accuracy of 69%

for holdout sample in all the five years prior to failure.

Taffler (1984)74

examined 24 failed and 49 non-failed companies of the

distribution/retail sector for one year prior to sickness. Using MDA and

adjusted model for prior probabilities and misclassification costs, the results

52

showed that cash flow to total liability was the second most significant

predictor in the model.

Mensah (1983)75

employed 30 bankrupt and matching 30 non-bankrupt

firms with financial ratios up to five years prior to failure. By using MDA and

logit, it was found out that cash flow to net worth was the most significant

variable in historical cost model and this variable was ranked second in specific

price level model.

Largay and Stickney (1980)76

conducted comparison and trend

analysis of cash flow from operations and other accrual variables including

stock price for single case study of W.T.Grant Company. He found out that

cash flow from operations more accurately indicate impending failure up to 10

years prior to WT Grant’s demise.

Ohlson (1980)33

developed a prediction model using a sample of 105

bankruptcy firms and 2058 non-bankrupt firms during the period 1970-1976.

The results of the study revealed that the four factors derived from financial

statements which significantly assessed the probability of bankruptcy were:

(i) size (ii) the financial structure as reflected by a measure of leverage (Total

Liabilities to Total Assets) (iii) some performance measure (Net Income to

Total Assets, and Funds provided by operations to Total Liabilities) and some

measures of current liquidity (Working Capital to Total Assets and Current

Liabilities to Current Assets). The ratios that could very well discriminate

between non-sick and sick companies included net income ratios and sales

53

ratios as the net income and sales of a healthier company grew relatively

rapidly when compared to a sick company.

Sharma and Mahajan (1980)77

presented a general model of failure

prediction for retail firms using MDA and found that the model accuracy was

92%, 78%, 74%, 73% and 77% in the 1st, 2

nd, 3

rd, 4

th and 5

th year respectively

before failure.

Altman, Baidya and Dias (1979)78

utilized Altman (1968) model to

classify Brazilian firms during the period 1973 to 1976. A sample of 23

serious–problem firms was compared with a slightly larger control sample of

healthy firms. A four-variable bankruptcy classification model developed in the

study successfully classified 88 percent of the firms one year prior to serious

problems and as much as 78 percent three years prior.

Moyer (1977)79

used a paired sample of 27 bankrupt and 27 non-

bankrupt firms during 1965-75 and developed nine factor MDA model which

resulted in an accuracy of 89% in predicting corporate failure in each of the

three years prior to failure.

Blum (1974)80

developed a failing company model with reference to

three common denominators underlying the cash-flow framework namely

liquidity, profitability and variability to assess the probability of business

failure. Discriminant analysis was used to test the hypothesis that the model

can distinguish between 115 failed and 115 non-failed samples paired based on

industry, sales and number of employees. The model predicted failures with an

accuracy of approximately 94 percent when failure occurred within one year

54

from the date of prediction, 80 percent for failure two years into the future and,

70 per cent for failure in three, four and five years from the present.

Deakin (1972)38

made an attempt to develop an alternative to the Beaver

and Altman models. A sample of thirty-two failed firms during 1964-1970 and

thirty-two non-failed firms matched in terms of industry and asset size were

considered. In the first test, he adopted a method of analysis similar to Beaver’s

study by applying the dichotomous classification test and percentage error of

each ratio ascertained. In the second test, discriminant analysis technique was

applied using the same sample of data and 14 financial ratios as input to the

discriminant analysis. It was concluded that discriminant analysis could be

used to predict business failure from accounting data as far as three years in

advance with fairly high degree of accuracy. The prediction accuracy

pertaining to failed firms were found to be 77%, 96%, 94%, 91% and 87% in

the 1st, 2

nd, 3

rd, 4

th and 5

th years respectively.

Altman (1968)81

used multivariate discriminant analysis to develop a

five factor model for predicting bankruptcy of manufacturing firms. The ‘Z-

score’ predicted bankruptcy when the firm’s score fell within a certain range.

The discriminant-ratio model proved to be extremely accurate in predicting

bankruptcy correctly to the extent of 95% accuracy for the initial sample one

year before failure. However, the predictive ability of the model subsequently

dropped to 72% accuracy two years before failure, 48%, 29% and 36%

accuracy two years before failure, 48%, 29% and 36% accuracy three, four and

55

five years before failure respectively. The model resulted in 79% accuracy

when tested on a hold sample.

2.4 SUMMARY

From the review of previous research studies, it is observed that the

previous studies have focused more on predictors of bankruptcy rather than

discriminators between failed and non-failed firms. There are limited studies

attempting to determine financial ratios which discriminate between sick and

non-sick companies, though most of the studies focused on determining

predictors of corporate sickness. The studies using both parametric and non-

parametric statistical tests in determining discriminators and predictors with the

help of isolated and non-isolated data set are rare in the present. Earlier studies

have shown contradicting results in determining superior prediction models and

analytical tools in terms of prediction accuracy. Several studies established

superiority of accrual ratios over cash flow ratios in predicting corporate

sickness. They used either parametric or non-parametric tests in determining

discriminators and predictors. Quite a few studies used net worth-related and

cash flow-related measures. Some researchers have developed bankruptcy

prediction models with and without cash flow ratios to determine the predictive

ability of cash flows over accrual ratios; but there are very few studies

comparing these results on the basis of analytical tools used namely, Multiple

Discriminant Analysis, and Logit Analysis. Hence, this study attempts to fill

these gaps.

![WIEN-#2533808-v4-Marko Mobile Payments [Kompatibilitätsmodus] · Mag., LL.M., Akad. Medienfachmann Tel: + 43 / 1 / 51510 – 5090 Fax: + 43 / 1 / 51510 – 665090 E-Mail: roland.marko@wolftheiss.com](https://img.pdfslide.net/doc/110x75/5ec416f7e2fbf52ed91cd7a1/wien-2533808-v4-marko-mobile-payments-kompatibilittsmodus-mag-llm-akad.jpg)