Embed Size (px)

Citation preview

The Future Royal Bank of Scotland N.V.

Investor Presentation January 2010

Slide 2

Important Information

This document has been prepared solely for use at the presentation to RBS Clients in January 2010 (the “Presentation”). By attending the meeting where

the Presentation is made, or by reading this document containing the Presentation slides, you agree to be bound by the following limitations.

This document and the information contained herein is strictly confidential, is being provided to you solely for your information and for use at the

Presentation. Accordingly, neither this document nor its contents may be reproduced or published or further distributed or passed on to any other

person in whole or in part, by any medium or in any form, for any purpose. If you have received this document in error, you are instructed to dispose of it

immediately.

Certain sections in this document contain „forward-looking statements‟ as that term is defined in the United States Private Securities Litigation Reform Act of 1995,

such as statements that include the words „expect‟, „estimate‟, „project‟, „anticipate‟, „believes‟, „should‟, „intend‟, „plan‟, „probability‟, „risk‟, „Value-at-Risk (VaR)‟,

„target‟, „goal‟, „objective‟, „will‟, „endeavour‟, „outlook‟, „optimistic‟, „prospects‟ and similar expressions or variations on such expressions. Such statements are subject

to risks and uncertainties.

Important factors that could cause actual results to differ materially from those estimated by the forward-looking statements contained in this document include, but

are not limited to: the extent and nature of future developments in the credit markets, including the sub-prime market, and their impact on the financial industry in

general and the Group in particular; the effect on the Group‟s capital of write downs in respect of credit market exposures; general economic conditions in the UK and

in other countries in which the Group has significant business activities or investments, including the United States; the monetary and interest rate policies of the Bank

of England, the Board of Governors of the Federal Reserve System and other G7 central banks; inflation; deflation; unanticipated turbulence in interest rates, foreign

currency exchange rates, commodity prices and equity prices; changes in UK and foreign laws, regulations and taxes; changes in competition and pricing

environments; natural and other disasters; the inability to hedge certain risks economically; the adequacy of loss reserves; acquisitions or restructurings; technological

changes; changes in consumer spending and saving habits; and the success of the Group in managing the risks involved in the foregoing.

The forward-looking statements contained in this document speak only as of the date of this document, and the Group does not undertake to update any forward-

looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

The information, statements and opinions contained in this document do not constitute a public offer under any applicable legislation or an offer to sell or solicitation of

an offer to buy any securities or financial instruments or any advice or recommendation with respect to such securities or other financial instruments.

Slide 3

Table of Contents

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

Slide 4

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

Slide 5

Separate existing key

ABN AMRO platforms

shared between RBS

and Dutch State-owned

partner

22 July 2009 30 September 2009

Filing of documents

with the Amsterdam

Chamber of Commerce

De-merge majority of the

Dutch State-owned

assets to new ABN

AMRO Bank N.V..

Existing ABN AMRO

Bank renamed RBS N.V.

Separate new ABN

AMRO Bank N.V. from

joint holding company.

New Banking

and payments

IT platform

implemented

Preparation of

legal

demerger process

Preparation of

regulatory

approvals

Execution of legal

demerger

Execution of legal

separation

Major technical separation completed on schedule

Novation of selected traded product portfolios from existing ABN AMRO Bank N.V. to RBS plc is progressing according to plan and will complete by Q3 2010

Legal Demerger and Separation subject to all legal processes and regulatory approvals

Highlights

Q1 2010 Two months after demerger

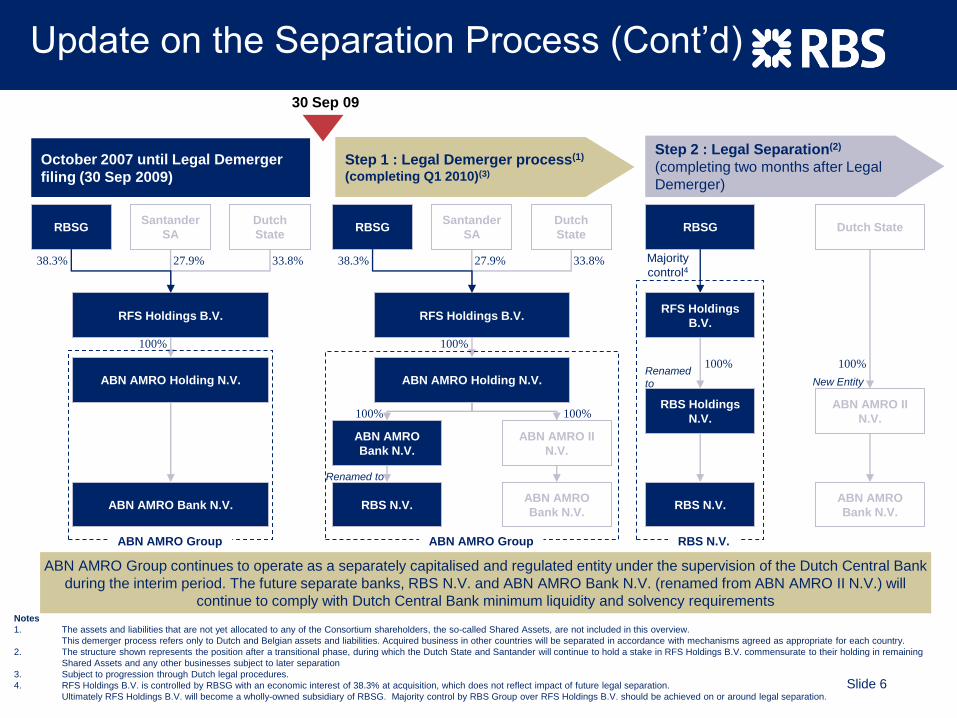

Update on the Separation Process

Slide 6

October 2007 until Legal Demerger

filing (30 Sep 2009)

Step 1 : Legal Demerger process(1)

(completing Q1 2010)(3)

Step 2 : Legal Separation(2)

(completing two months after Legal

Demerger)

30 Sep 09

Notes

1. The assets and liabilities that are not yet allocated to any of the Consortium shareholders, the so-called Shared Assets, are not included in this overview.

This demerger process refers only to Dutch and Belgian assets and liabilities. Acquired business in other countries will be separated in accordance with mechanisms agreed as appropriate for each country.

2. The structure shown represents the position after a transitional phase, during which the Dutch State and Santander will continue to hold a stake in RFS Holdings B.V. commensurate to their holding in remaining

Shared Assets and any other businesses subject to later separation

3. Subject to progression through Dutch legal procedures.

4. RFS Holdings B.V. is controlled by RBSG with an economic interest of 38.3% at acquisition, which does not reflect impact of future legal separation.

Ultimately RFS Holdings B.V. will become a wholly-owned subsidiary of RBSG. Majority control by RBS Group over RFS Holdings B.V. should be achieved on or around legal separation.

RBSGSantander

SA

Dutch

State

RFS Holdings B.V.

ABN AMRO Holding N.V.

ABN AMRO Bank N.V.

38.3% 27.9% 33.8%

100%

100%

RBSGSantander

SA

Dutch

State

RFS Holdings B.V.

ABN AMRO Holding N.V.

ABN AMRO

Bank N.V.

38.3% 27.9% 33.8%

100%

100%

RBS N.V.

ABN AMRO II

N.V.

ABN AMRO

Bank N.V.

100%

RBSG Dutch State

RBS Holdings

N.V.

Majority

control4

100%

RBS N.V.

ABN AMRO II

N.V.

ABN AMRO

Bank N.V.

100%

RFS Holdings

B.V.

ABN AMRO Group ABN AMRO Group RBS N.V.

ABN AMRO Group continues to operate as a separately capitalised and regulated entity under the supervision of the Dutch Central Bank

during the interim period. The future separate banks, RBS N.V. and ABN AMRO Bank N.V. (renamed from ABN AMRO II N.V.) will

continue to comply with Dutch Central Bank minimum liquidity and solvency requirements

Update on the Separation Process (Cont‟d)

Renamed

to New Entity

Renamed to

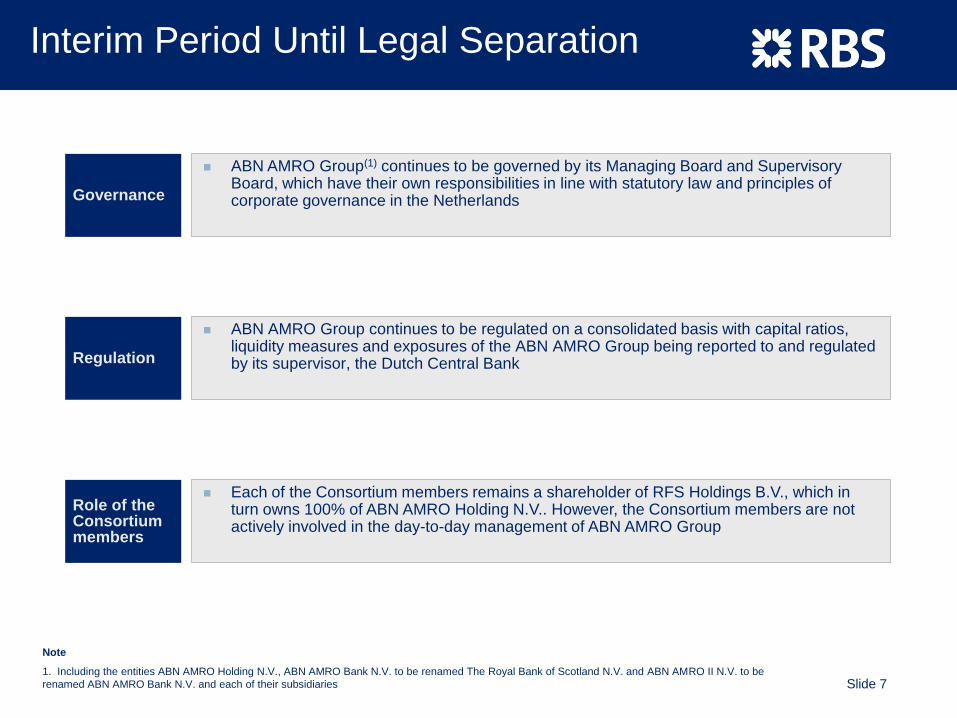

Slide 7

ABN AMRO Group continues to be regulated on a consolidated basis with capital ratios, liquidity measures and exposures of the ABN AMRO Group being reported to and regulated by its supervisor, the Dutch Central Bank

Governance

Regulation

Role of the Consortium members

ABN AMRO Group(1) continues to be governed by its Managing Board and Supervisory Board, which have their own responsibilities in line with statutory law and principles of corporate governance in the Netherlands

Each of the Consortium members remains a shareholder of RFS Holdings B.V., which in turn owns 100% of ABN AMRO Holding N.V.. However, the Consortium members are not actively involved in the day-to-day management of ABN AMRO Group

Note

1. Including the entities ABN AMRO Holding N.V., ABN AMRO Bank N.V. to be renamed The Royal Bank of Scotland N.V. and ABN AMRO II N.V. to be

renamed ABN AMRO Bank N.V. and each of their subsidiaries

Interim Period Until Legal Separation

Slide 8

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

Slide 9

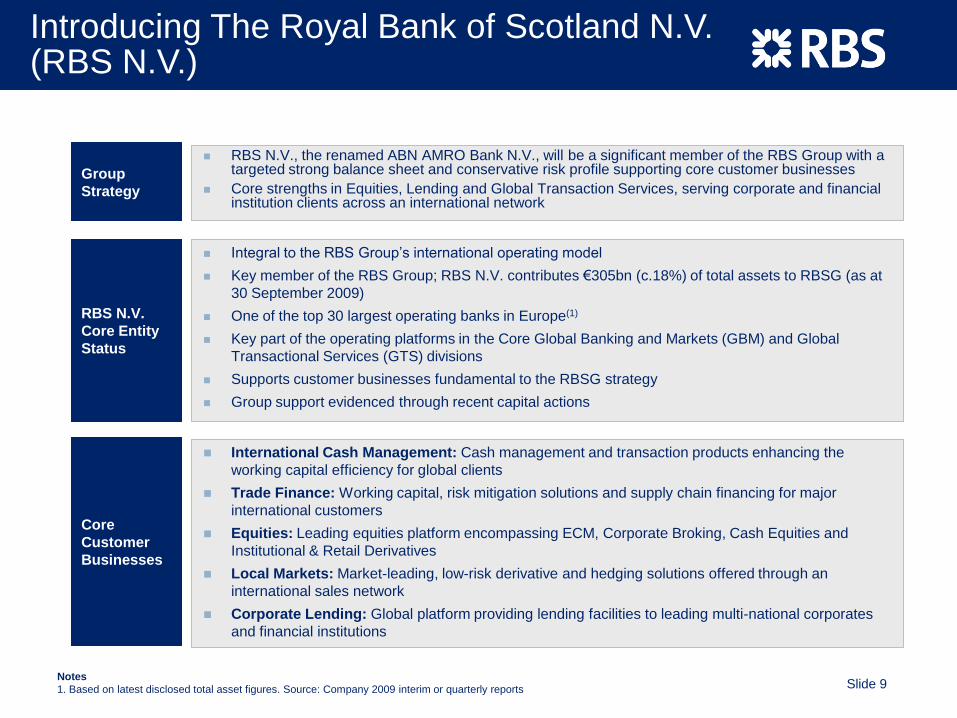

RBS N.V., the renamed ABN AMRO Bank N.V., will be a significant member of the RBS Group with a targeted strong balance sheet and conservative risk profile supporting core customer businesses

Core strengths in Equities, Lending and Global Transaction Services, serving corporate and financial institution clients across an international network

Group

Strategy

Integral to the RBS Group‟s international operating model

Key member of the RBS Group; RBS N.V. contributes €305bn (c.18%) of total assets to RBSG (as at

30 September 2009)

One of the top 30 largest operating banks in Europe(1)

Key part of the operating platforms in the Core Global Banking and Markets (GBM) and Global

Transactional Services (GTS) divisions

Supports customer businesses fundamental to the RBSG strategy

Group support evidenced through recent capital actions

RBS N.V.

Core Entity

Status

Core

Customer

Businesses

International Cash Management: Cash management and transaction products enhancing the

working capital efficiency for global clients

Trade Finance: Working capital, risk mitigation solutions and supply chain financing for major

international customers

Equities: Leading equities platform encompassing ECM, Corporate Broking, Cash Equities and

Institutional & Retail Derivatives

Local Markets: Market-leading, low-risk derivative and hedging solutions offered through an

international sales network

Corporate Lending: Global platform providing lending facilities to leading multi-national corporates

and financial institutions

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Notes

1. Based on latest disclosed total asset figures. Source: Company 2009 interim or quarterly reports

Slide 10

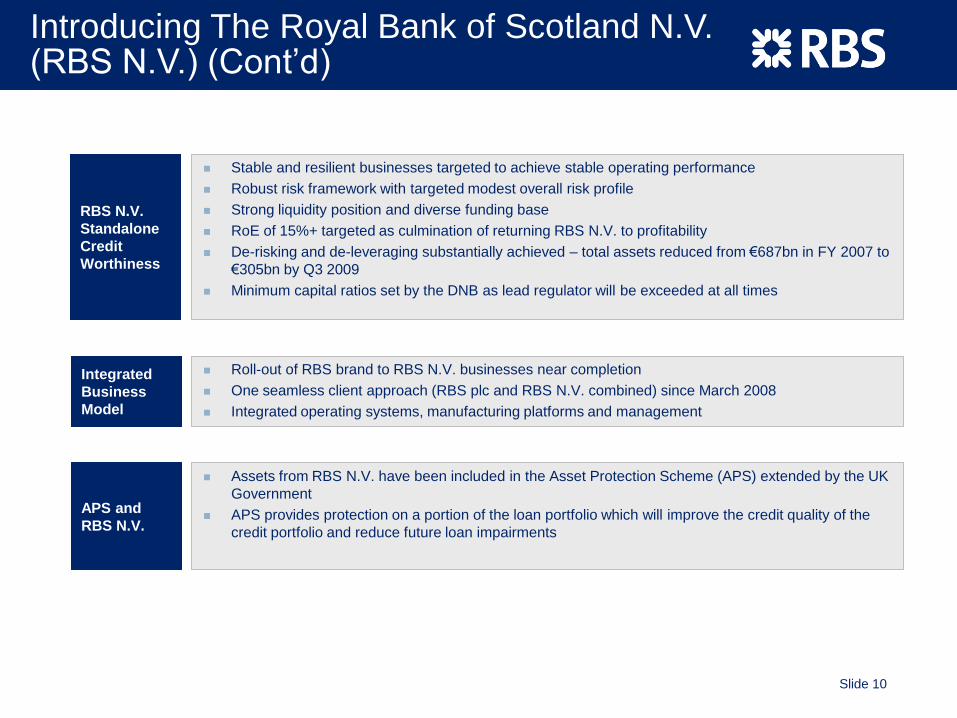

Roll-out of RBS brand to RBS N.V. businesses near completion

One seamless client approach (RBS plc and RBS N.V. combined) since March 2008

Integrated operating systems, manufacturing platforms and management

Integrated

Business

Model

Assets from RBS N.V. have been included in the Asset Protection Scheme (APS) extended by the UK

Government

APS provides protection on a portion of the loan portfolio which will improve the credit quality of the

credit portfolio and reduce future loan impairments

APS and

RBS N.V.

Stable and resilient businesses targeted to achieve stable operating performance

Robust risk framework with targeted modest overall risk profile

Strong liquidity position and diverse funding base

RoE of 15%+ targeted as culmination of returning RBS N.V. to profitability

De-risking and de-leveraging substantially achieved – total assets reduced from €687bn in FY 2007 to

€305bn by Q3 2009

Minimum capital ratios set by the DNB as lead regulator will be exceeded at all times

RBS N.V.

Standalone

Credit

Worthiness

Introducing The Royal Bank of Scotland N.V. (RBS N.V.) (Cont‟d)

Slide 11

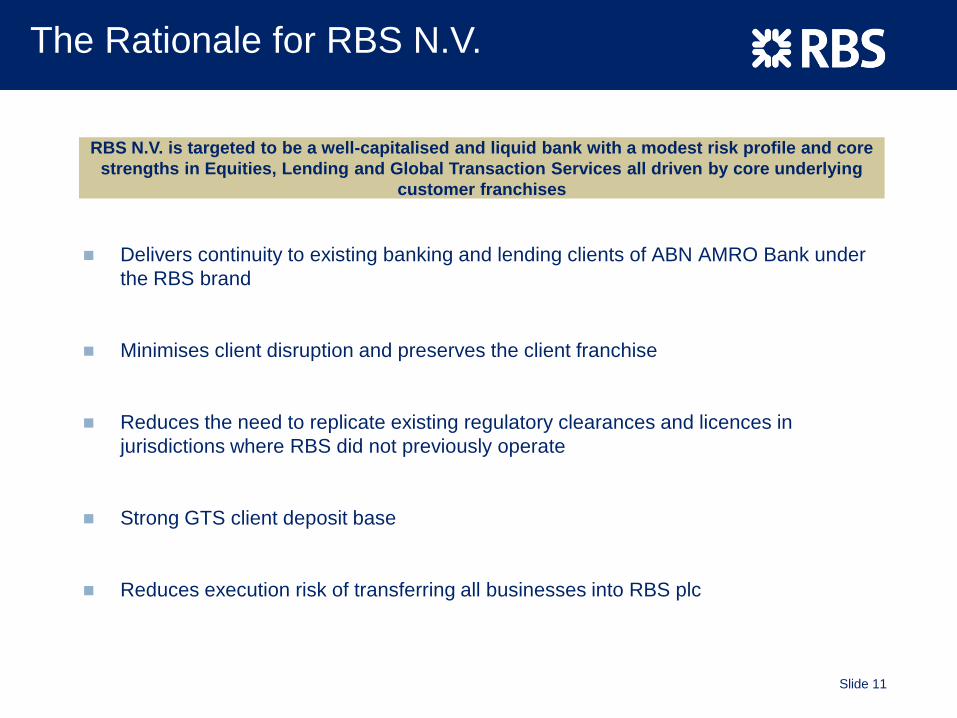

Delivers continuity to existing banking and lending clients of ABN AMRO Bank under

the RBS brand

Minimises client disruption and preserves the client franchise

Reduces the need to replicate existing regulatory clearances and licences in

jurisdictions where RBS did not previously operate

Strong GTS client deposit base

Reduces execution risk of transferring all businesses into RBS plc

RBS N.V. is targeted to be a well-capitalised and liquid bank with a modest risk profile and core

strengths in Equities, Lending and Global Transaction Services all driven by core underlying

customer franchises

The Rationale for RBS N.V.

Slide 12

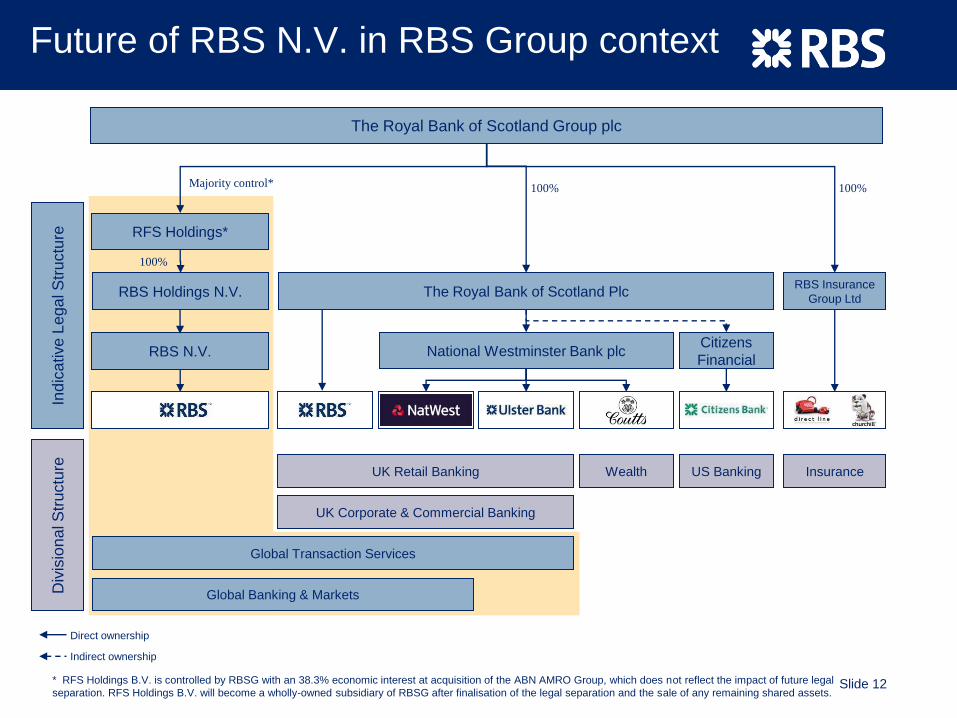

Future of RBS N.V. in RBS Group context

The Royal Bank of Scotland Group plc

RFS Holdings*

The Royal Bank of Scotland PlcRBS Insurance

Group Ltd

RBS N.V. National Westminster Bank plcCitizens

Financial

Ind

icative

Le

ga

l S

tructu

reD

ivis

ion

al S

tructu

re

100%

UK Retail Banking

UK Corporate & Commercial Banking

Insurance

100%

US BankingWealth

100%

Direct ownership

Indirect ownership

Global Banking & Markets

Global Transaction Services

* RFS Holdings B.V. is controlled by RBSG with an 38.3% economic interest at acquisition of the ABN AMRO Group, which does not reflect the impact of future legal

separation. RFS Holdings B.V. will become a wholly-owned subsidiary of RBSG after finalisation of the legal separation and the sale of any remaining shared assets.

Majority control*

RBS Holdings N.V.

Slide 13

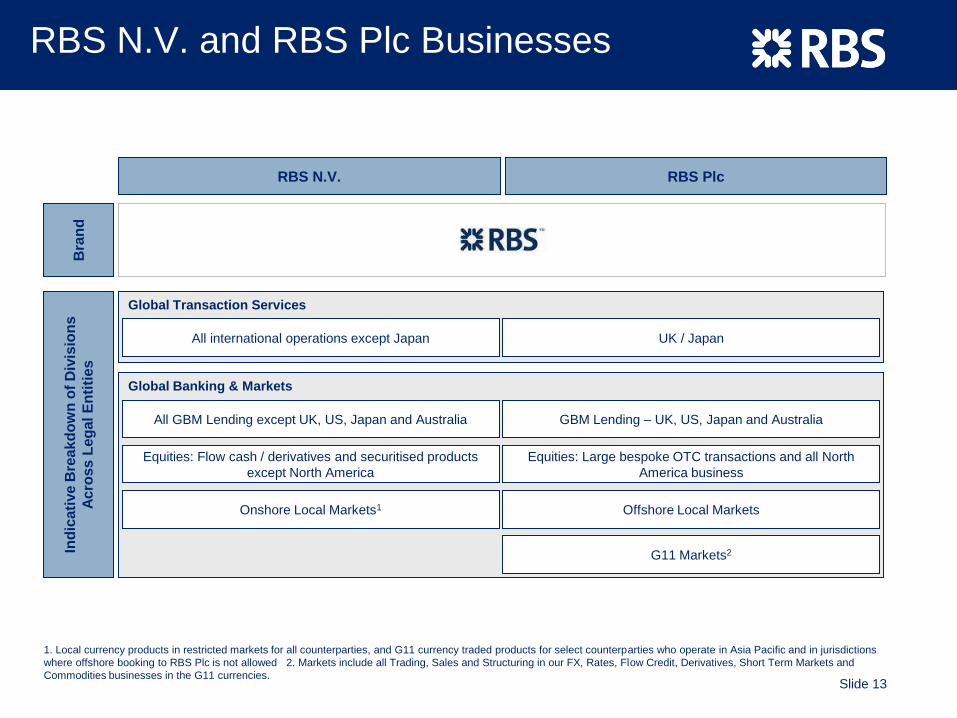

RBS N.V. RBS Plc

Bra

nd

Ind

icati

ve

Bre

ak

do

wn

of

Div

isio

ns

Ac

ross

Leg

al E

nti

tie

s

Global Transaction Services

All international operations except Japan UK / Japan

Global Banking & Markets

All GBM Lending except UK, US, Japan and Australia GBM Lending – UK, US, Japan and Australia

Equities: Flow cash / derivatives and securitised products

except North America

Equities: Large bespoke OTC transactions and all North

America business

Onshore Local Markets1 Offshore Local Markets

G11 Markets2

1. Local currency products in restricted markets for all counterparties, and G11 currency traded products for select counterparties who operate in Asia Pacific and in jurisdictions

where offshore booking to RBS Plc is not allowed 2. Markets include all Trading, Sales and Structuring in our FX, Rates, Flow Credit, Derivatives, Short Term Markets and

Commodities businesses in the G11 currencies.

RBS N.V. and RBS Plc Businesses

Slide 14

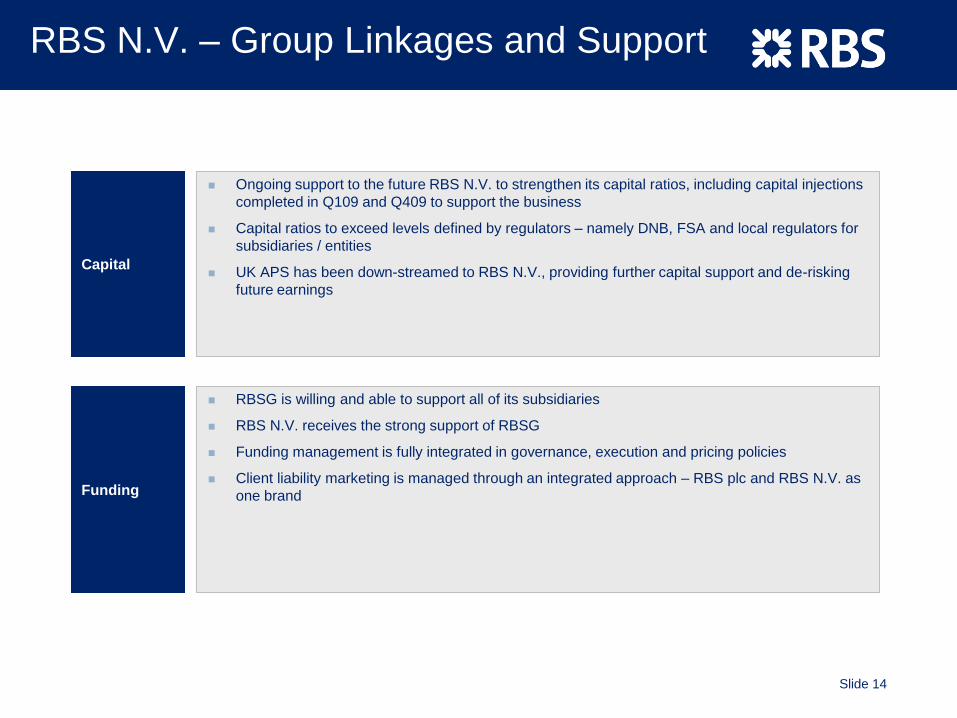

RBS N.V. – Group Linkages and Support

Ongoing support to the future RBS N.V. to strengthen its capital ratios, including capital injections

completed in Q109 and Q409 to support the business

Capital ratios to exceed levels defined by regulators – namely DNB, FSA and local regulators for

subsidiaries / entities

UK APS has been down-streamed to RBS N.V., providing further capital support and de-risking

future earnings

Capital

RBSG is willing and able to support all of its subsidiaries

RBS N.V. receives the strong support of RBSG

Funding management is fully integrated in governance, execution and pricing policies

Client liability marketing is managed through an integrated approach – RBS plc and RBS N.V. as

one brandFunding

Slide 15

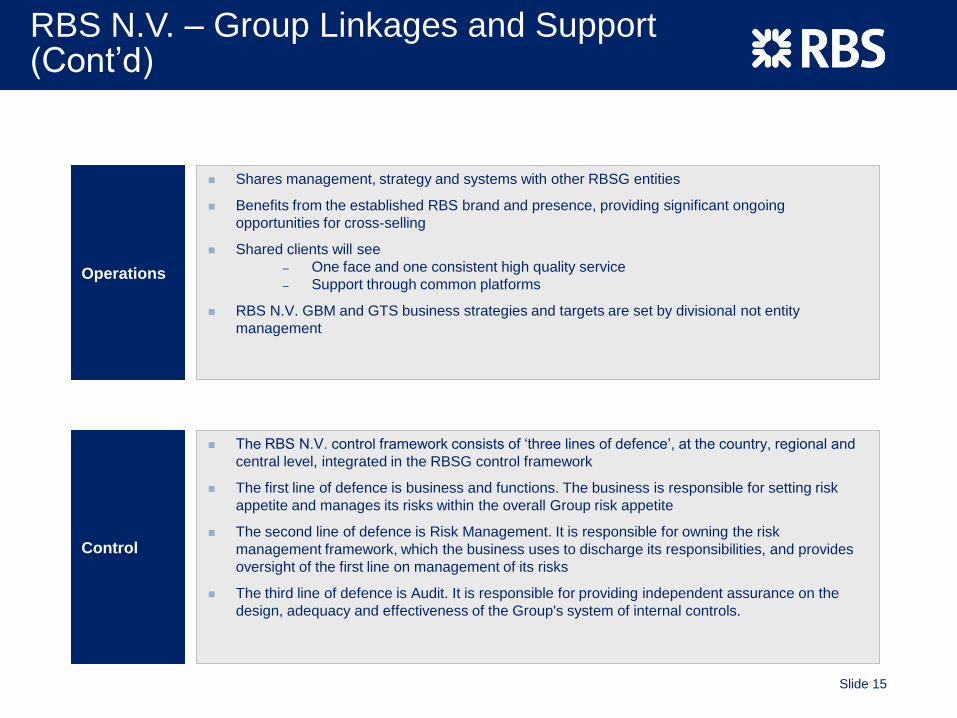

Shares management, strategy and systems with other RBSG entities

Benefits from the established RBS brand and presence, providing significant ongoing

opportunities for cross-selling

Shared clients will see

– One face and one consistent high quality service

– Support through common platforms

RBS N.V. GBM and GTS business strategies and targets are set by divisional not entity

management

Operations

The RBS N.V. control framework consists of „three lines of defence‟, at the country, regional and

central level, integrated in the RBSG control framework

The first line of defence is business and functions. The business is responsible for setting risk

appetite and manages its risks within the overall Group risk appetite

The second line of defence is Risk Management. It is responsible for owning the risk

management framework, which the business uses to discharge its responsibilities, and provides

oversight of the first line on management of its risks

The third line of defence is Audit. It is responsible for providing independent assurance on the

design, adequacy and effectiveness of the Group's system of internal controls.

Control

RBS N.V. – Group Linkages and Support(Cont‟d)

Slide 16

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

Slide 17

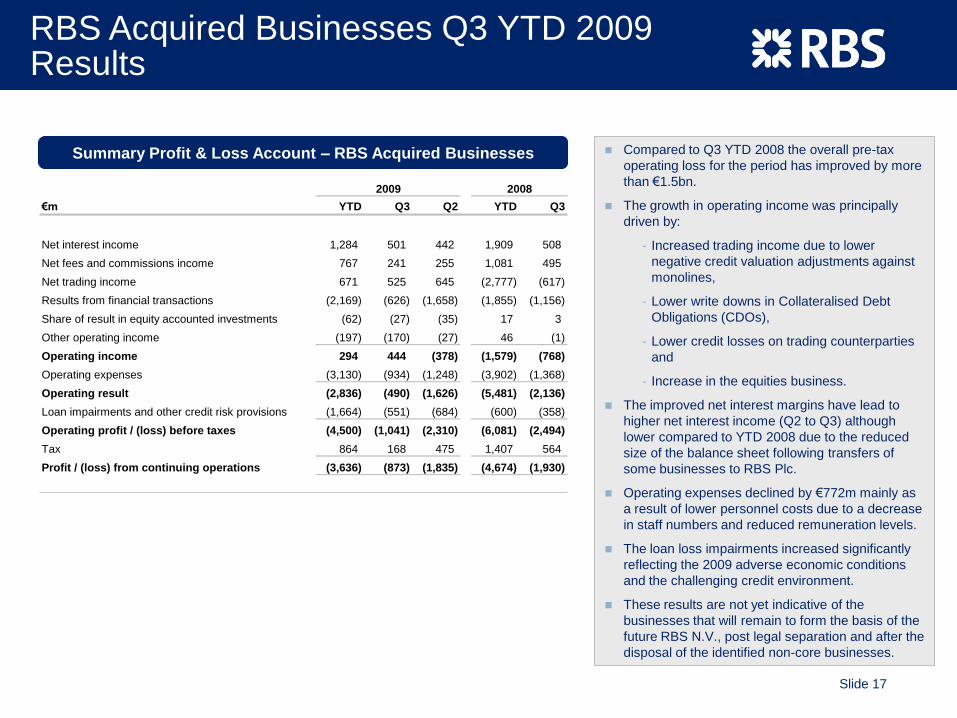

RBS Acquired Businesses Q3 YTD 2009 Results

Summary Profit & Loss Account – RBS Acquired Businesses Compared to Q3 YTD 2008 the overall pre-tax

operating loss for the period has improved by more

than €1.5bn.

The growth in operating income was principally

driven by:

- Increased trading income due to lower

negative credit valuation adjustments against

monolines,

- Lower write downs in Collateralised Debt

Obligations (CDOs),

- Lower credit losses on trading counterparties

and

- Increase in the equities business.

The improved net interest margins have lead to

higher net interest income (Q2 to Q3) although

lower compared to YTD 2008 due to the reduced

size of the balance sheet following transfers of

some businesses to RBS Plc.

Operating expenses declined by €772m mainly as

a result of lower personnel costs due to a decrease

in staff numbers and reduced remuneration levels.

The loan loss impairments increased significantly

reflecting the 2009 adverse economic conditions

and the challenging credit environment.

These results are not yet indicative of the

businesses that will remain to form the basis of the

future RBS N.V., post legal separation and after the

disposal of the identified non-core businesses.

2009 2008

€m YTD Q3 Q2 YTD Q3

Net interest income 1,284 501 442 1,909 508

Net fees and commissions income 767 241 255 1,081 495

Net trading income 671 525 645 (2,777) (617)

Results from financial transactions (2,169) (626) (1,658) (1,855) (1,156)

Share of result in equity accounted investments (62) (27) (35) 17 3

Other operating income (197) (170) (27) 46 (1)

Operating income 294 444 (378) (1,579) (768)

Operating expenses (3,130) (934) (1,248) (3,902) (1,368)

Operating result (2,836) (490) (1,626) (5,481) (2,136)

Loan impairments and other credit risk provisions (1,664) (551) (684) (600) (358)

Operating profit / (loss) before taxes (4,500) (1,041) (2,310) (6,081) (2,494)

Tax 864 168 475 1,407 564

Profit / (loss) from continuing operations (3,636) (873) (1,835) (4,674) (1,930)

Slide 18

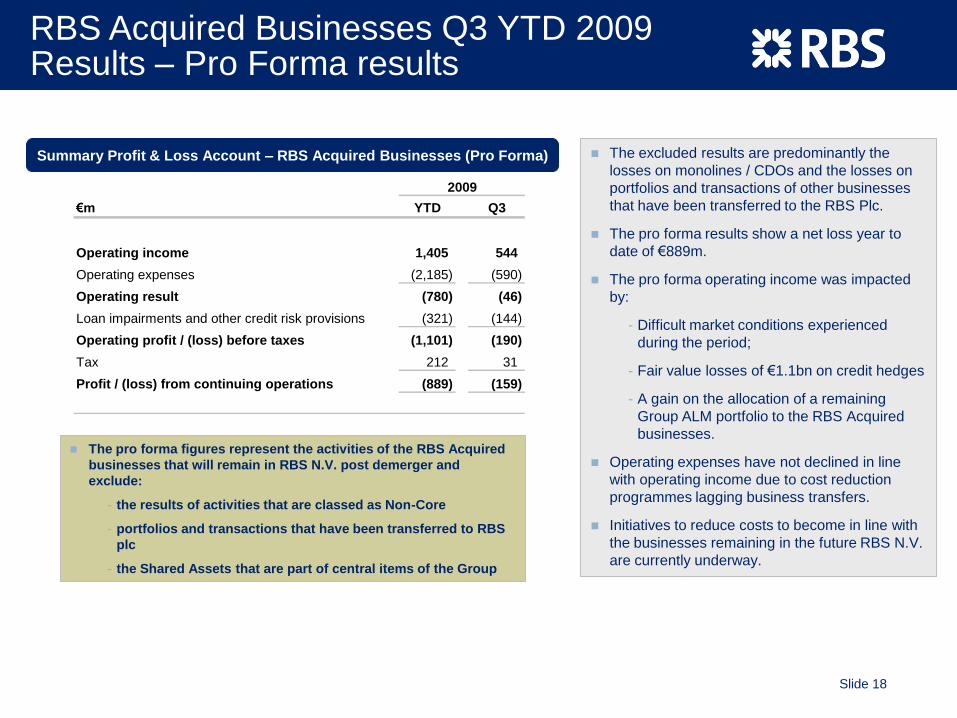

RBS Acquired Businesses Q3 YTD 2009 Results – Pro Forma results

The pro forma figures represent the activities of the RBS Acquired

businesses that will remain in RBS N.V. post demerger and

exclude:

- the results of activities that are classed as Non-Core

- portfolios and transactions that have been transferred to RBS

plc

- the Shared Assets that are part of central items of the Group

Summary Profit & Loss Account – RBS Acquired Businesses (Pro Forma) The excluded results are predominantly the

losses on monolines / CDOs and the losses on

portfolios and transactions of other businesses

that have been transferred to the RBS Plc.

The pro forma results show a net loss year to

date of €889m.

The pro forma operating income was impacted

by:

- Difficult market conditions experienced

during the period;

- Fair value losses of €1.1bn on credit hedges

- A gain on the allocation of a remaining

Group ALM portfolio to the RBS Acquired

businesses.

Operating expenses have not declined in line

with operating income due to cost reduction

programmes lagging business transfers.

Initiatives to reduce costs to become in line with

the businesses remaining in the future RBS N.V.

are currently underway.

2009

€m YTD Q3

Operating income 1,405 544

Operating expenses (2,185) (590)

Operating result (780) (46)

Loan impairments and other credit risk provisions (321) (144)

Operating profit / (loss) before taxes (1,101) (190)

Tax 212 31

Profit / (loss) from continuing operations (889) (159)

Slide 19

Total Assets (€bn)

De-risking and de-leveraging of the business has resulted in a 36% reduction of the balance

sheet in the last nine months

5 12 15

212

92

52

56 55

66

39 46

120

99 80

23

1618

100

FY 2008 H1 2009 Q3 2009

Cash at central banks Financial assets for trading

Financial investments Loans to banks

Loans to customers Other

36%

Balance Sheet Progress – FY 2008 to Q32009

478

322305

Well on track to be a strong and stable banking

franchise

Significant initiatives have been undertaken to de-

risk and de-leverage the business and develop a

sustainable model

Balance sheet reduced through:

- reduction in Trading Assets due to novations,

netting of derivatives

- reduction in Reverse Repo agreements

- reduction due to roll-off of transactions to RBS

plc

- reduction through maturing loans and transfers

to RBS plc

Significant strengthening of the liquidity reserve

with over €15bn of cash balances held with central

banks

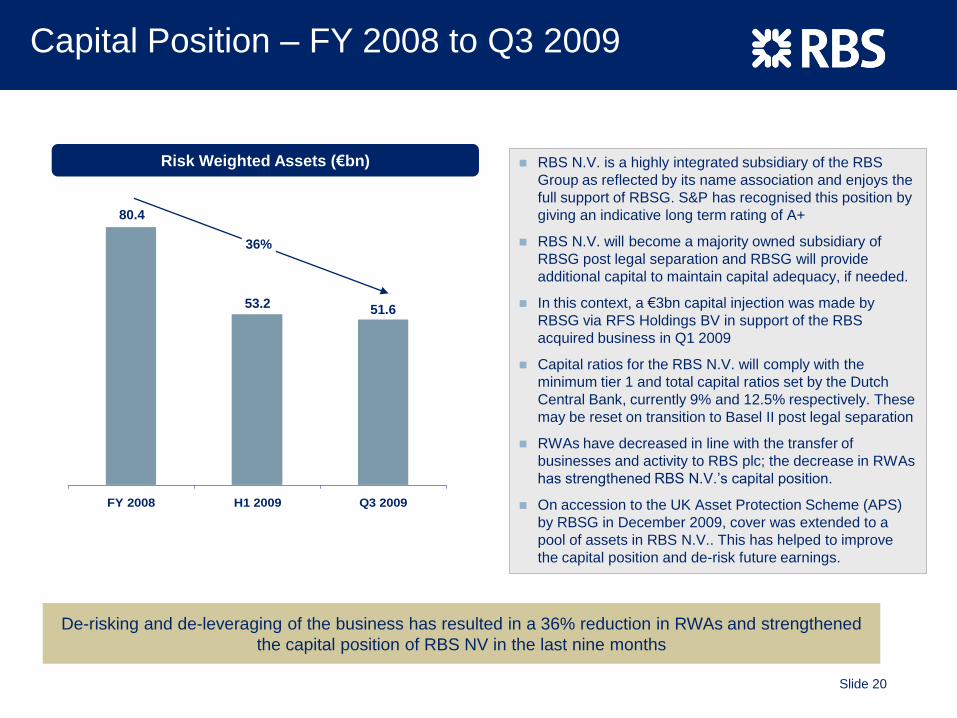

Slide 20

FY 2008 H1 2009 Q3 2009

Cash at central banks

Risk Weighted Assets (€bn)

De-risking and de-leveraging of the business has resulted in a 36% reduction in RWAs and strengthened

the capital position of RBS NV in the last nine months

36%

Capital Position – FY 2008 to Q3 2009

80.4

53.2 51.6

RBS N.V. is a highly integrated subsidiary of the RBS

Group as reflected by its name association and enjoys the

full support of RBSG. S&P has recognised this position by

giving an indicative long term rating of A+

RBS N.V. will become a majority owned subsidiary of

RBSG post legal separation and RBSG will provide

additional capital to maintain capital adequacy, if needed.

In this context, a €3bn capital injection was made by

RBSG via RFS Holdings BV in support of the RBS

acquired business in Q1 2009

Capital ratios for the RBS N.V. will comply with the

minimum tier 1 and total capital ratios set by the Dutch

Central Bank, currently 9% and 12.5% respectively. These

may be reset on transition to Basel II post legal separation

RWAs have decreased in line with the transfer of

businesses and activity to RBS plc; the decrease in RWAs

has strengthened RBS N.V.‟s capital position.

On accession to the UK Asset Protection Scheme (APS)

by RBSG in December 2009, cover was extended to a

pool of assets in RBS N.V.. This has helped to improve

the capital position and de-risk future earnings.

Slide 21

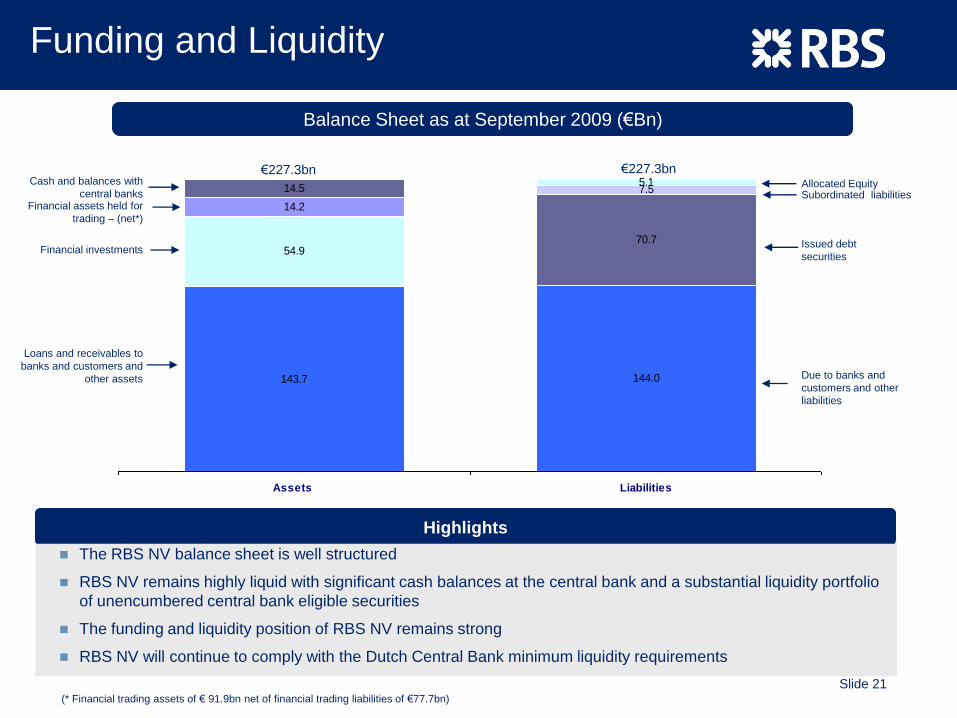

143.7

54.9

14.2

144.0

70.7

7.514.55.1

Assets Liabilities

Highlights

Funding and Liquidity

The RBS NV balance sheet is well structured

RBS NV remains highly liquid with significant cash balances at the central bank and a substantial liquidity portfolio

of unencumbered central bank eligible securities

The funding and liquidity position of RBS NV remains strong

RBS NV will continue to comply with the Dutch Central Bank minimum liquidity requirements

€227.3bn€227.3bn

Balance Sheet as at September 2009 (€Bn)

Cash and balances with

central banks

Loans and receivables to

banks and customers and

other assets

Allocated Equity

Financial assets held for

trading – (net*)

Financial investmentsIssued debt

securities

Subordinated liabilities

Due to banks and

customers and other

liabilities

(* Financial trading assets of € 91.9bn net of financial trading liabilities of €77.7bn)

Slide 22

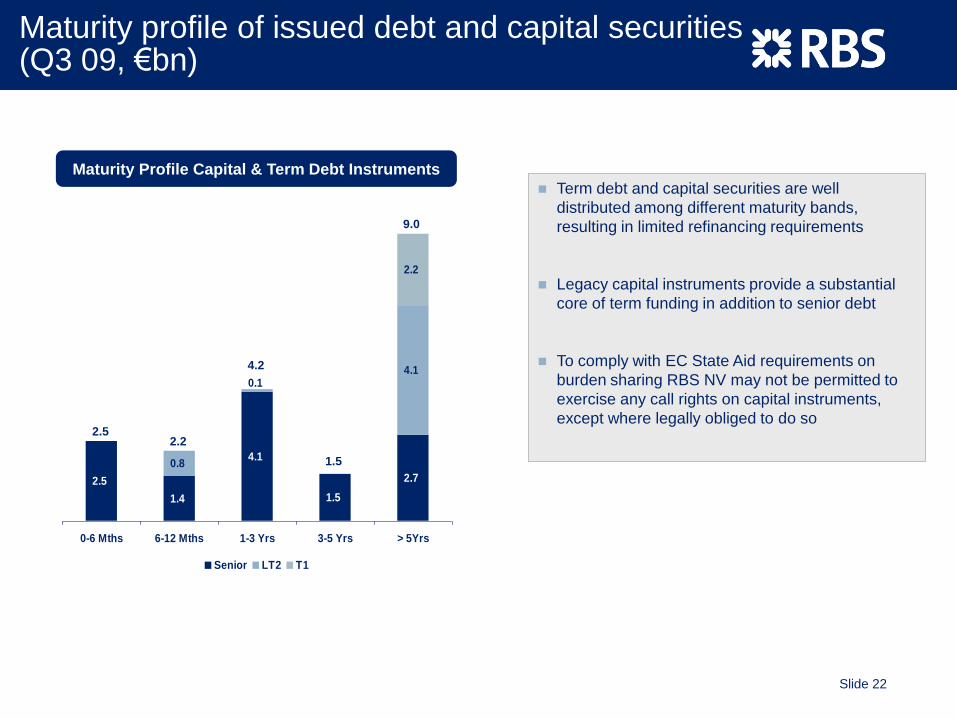

Maturity profile of issued debt and capital securities (Q3 09, €bn)

2.5

1.4

4.1

1.5

2.7

4.1

2.2

0.1

0.8

0-6 Mths 6-12 Mths 1-3 Yrs 3-5 Yrs > 5Yrs

Senior LT2 T1

Maturity Profile Capital & Term Debt Instruments

2.52.2

4.2

1.5

9.0

Term debt and capital securities are well

distributed among different maturity bands,

resulting in limited refinancing requirements

Legacy capital instruments provide a substantial

core of term funding in addition to senior debt

To comply with EC State Aid requirements on

burden sharing RBS NV may not be permitted to

exercise any call rights on capital instruments,

except where legally obliged to do so

Slide 23

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

Slide 24

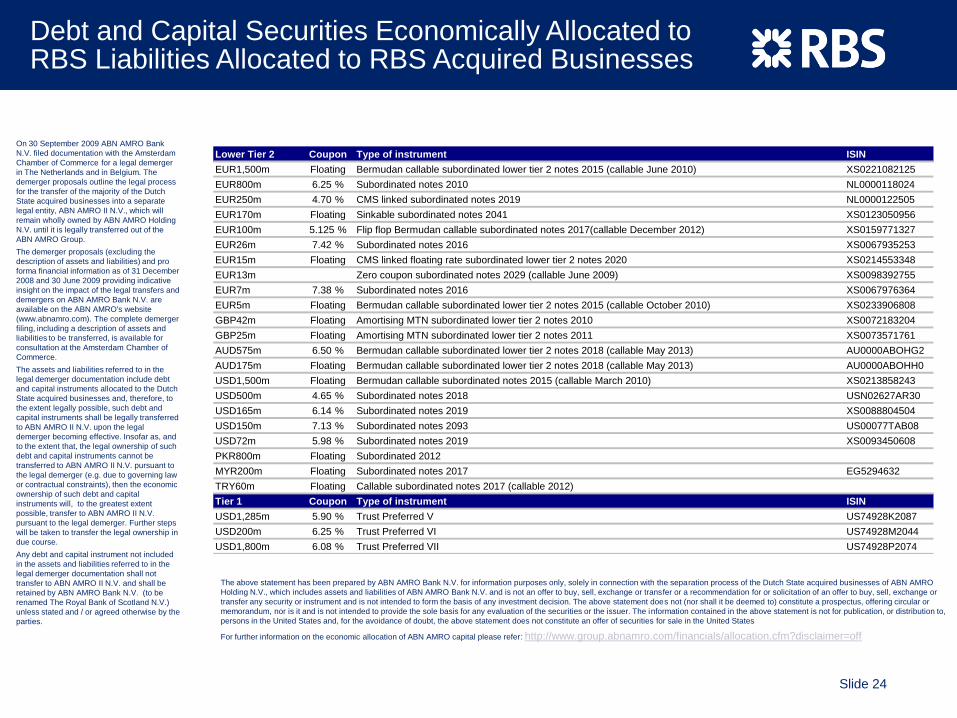

Debt and Capital Securities Economically Allocated to RBS Liabilities Allocated to RBS Acquired Businesses

The above statement has been prepared by ABN AMRO Bank N.V. for information purposes only, solely in connection with the separation process of the Dutch State acquired businesses of ABN AMRO

Holding N.V., which includes assets and liabilities of ABN AMRO Bank N.V. and is not an offer to buy, sell, exchange or transfer or a recommendation for or solicitation of an offer to buy, sell, exchange or

transfer any security or instrument and is not intended to form the basis of any investment decision. The above statement does not (nor shall it be deemed to) constitute a prospectus, offering circular or

memorandum, nor is it and is not intended to provide the sole basis for any evaluation of the securities or the issuer. The information contained in the above statement is not for publication, or distribution to,

persons in the United States and, for the avoidance of doubt, the above statement does not constitute an offer of securities for sale in the United States

For further information on the economic allocation of ABN AMRO capital please refer: http://www.group.abnamro.com/financials/allocation.cfm?disclaimer=off

On 30 September 2009 ABN AMRO Bank

N.V. filed documentation with the Amsterdam

Chamber of Commerce for a legal demerger

in The Netherlands and in Belgium. The

demerger proposals outline the legal process

for the transfer of the majority of the Dutch

State acquired businesses into a separate

legal entity, ABN AMRO II N.V., which will

remain wholly owned by ABN AMRO Holding

N.V. until it is legally transferred out of the

ABN AMRO Group.

The demerger proposals (excluding the

description of assets and liabilities) and pro

forma financial information as of 31 December

2008 and 30 June 2009 providing indicative

insight on the impact of the legal transfers and

demergers on ABN AMRO Bank N.V. are

available on the ABN AMRO's website

(www.abnamro.com). The complete demerger

filing, including a description of assets and

liabilities to be transferred, is available for

consultation at the Amsterdam Chamber of

Commerce.

The assets and liabilities referred to in the

legal demerger documentation include debt

and capital instruments allocated to the Dutch

State acquired businesses and, therefore, to

the extent legally possible, such debt and

capital instruments shall be legally transferred

to ABN AMRO II N.V. upon the legal

demerger becoming effective. Insofar as, and

to the extent that, the legal ownership of such

debt and capital instruments cannot be

transferred to ABN AMRO II N.V. pursuant to

the legal demerger (e.g. due to governing law

or contractual constraints), then the economic

ownership of such debt and capital

instruments will, to the greatest extent

possible, transfer to ABN AMRO II N.V.

pursuant to the legal demerger. Further steps

will be taken to transfer the legal ownership in

due course.

Any debt and capital instrument not included

in the assets and liabilities referred to in the

legal demerger documentation shall not

transfer to ABN AMRO II N.V. and shall be

retained by ABN AMRO Bank N.V. (to be

renamed The Royal Bank of Scotland N.V.)

unless stated and / or agreed otherwise by the

parties.

Lower Tier 2 Coupon Type of instrument ISIN

EUR1,500m Floating Bermudan callable subordinated lower tier 2 notes 2015 (callable June 2010) XS0221082125

EUR800m 6.25 % Subordinated notes 2010 NL0000118024

EUR250m 4.70 % CMS linked subordinated notes 2019 NL0000122505

EUR170m Floating Sinkable subordinated notes 2041 XS0123050956

EUR100m 5.125 % Flip flop Bermudan callable subordinated notes 2017(callable December 2012) XS0159771327

EUR26m 7.42 % Subordinated notes 2016 XS0067935253

EUR15m Floating CMS linked floating rate subordinated lower tier 2 notes 2020 XS0214553348

EUR13m Zero coupon subordinated notes 2029 (callable June 2009) XS0098392755

EUR7m 7.38 % Subordinated notes 2016 XS0067976364

EUR5m Floating Bermudan callable subordinated lower tier 2 notes 2015 (callable October 2010) XS0233906808

GBP42m Floating Amortising MTN subordinated lower tier 2 notes 2010 XS0072183204

GBP25m Floating Amortising MTN subordinated lower tier 2 notes 2011 XS0073571761

AUD575m 6.50 % Bermudan callable subordinated lower tier 2 notes 2018 (callable May 2013) AU0000ABOHG2

AUD175m Floating Bermudan callable subordinated lower tier 2 notes 2018 (callable May 2013) AU0000ABOHH0

USD1,500m Floating Bermudan callable subordinated notes 2015 (callable March 2010) XS0213858243

USD500m 4.65 % Subordinated notes 2018 USN02627AR30

USD165m 6.14 % Subordinated notes 2019 XS0088804504

USD150m 7.13 % Subordinated notes 2093 US00077TAB08

USD72m 5.98 % Subordinated notes 2019 XS0093450608

PKR800m Floating Subordinated 2012

MYR200m Floating Subordinated notes 2017 EG5294632

TRY60m Floating Callable subordinated notes 2017 (callable 2012)

Tier 1 Coupon Type of instrument ISIN

USD1,285m 5.90 % Trust Preferred V US74928K2087

USD200m 6.25 % Trust Preferred VI US74928M2044

USD1,800m 6.08 % Trust Preferred VII US74928P2074

Slide 25

Introducing The Royal Bank of Scotland N.V. (RBS N.V.)

Summary Financial Information for RBS N.V.

Update on Separation Process

Debt and Capital Securities allocated to RBS N.V.

Appendices

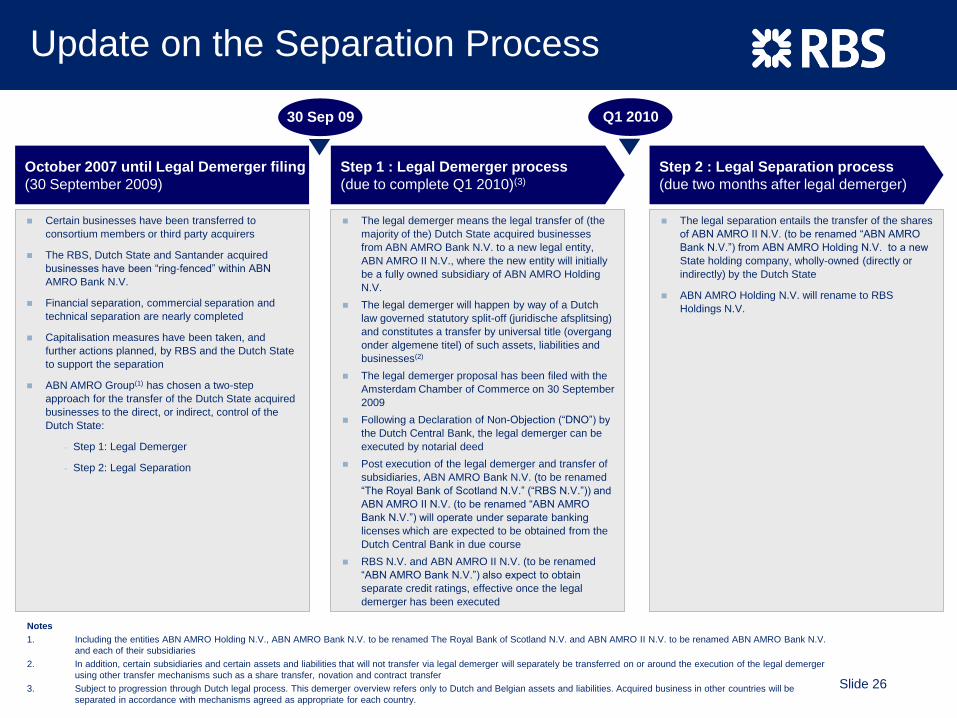

Slide 26

Certain businesses have been transferred to

consortium members or third party acquirers

The RBS, Dutch State and Santander acquired

businesses have been “ring-fenced” within ABN

AMRO Bank N.V.

Financial separation, commercial separation and

technical separation are nearly completed

Capitalisation measures have been taken, and

further actions planned, by RBS and the Dutch State

to support the separation

ABN AMRO Group(1) has chosen a two-step

approach for the transfer of the Dutch State acquired

businesses to the direct, or indirect, control of the

Dutch State:

- Step 1: Legal Demerger

- Step 2: Legal Separation

The legal separation entails the transfer of the shares

of ABN AMRO II N.V. (to be renamed “ABN AMRO

Bank N.V.”) from ABN AMRO Holding N.V. to a new

State holding company, wholly-owned (directly or

indirectly) by the Dutch State

ABN AMRO Holding N.V. will rename to RBS

Holdings N.V.

October 2007 until Legal Demerger filing

(30 September 2009)

Step 1 : Legal Demerger process

(due to complete Q1 2010)(3)

Step 2 : Legal Separation process

(due two months after legal demerger)

The legal demerger means the legal transfer of (the

majority of the) Dutch State acquired businesses

from ABN AMRO Bank N.V. to a new legal entity,

ABN AMRO II N.V., where the new entity will initially

be a fully owned subsidiary of ABN AMRO Holding

N.V.

The legal demerger will happen by way of a Dutch

law governed statutory split-off (juridische afsplitsing)

and constitutes a transfer by universal title (overgang

onder algemene titel) of such assets, liabilities and

businesses(2)

The legal demerger proposal has been filed with the

Amsterdam Chamber of Commerce on 30 September

2009

Following a Declaration of Non-Objection (“DNO”) by

the Dutch Central Bank, the legal demerger can be

executed by notarial deed

Post execution of the legal demerger and transfer of

subsidiaries, ABN AMRO Bank N.V. (to be renamed

“The Royal Bank of Scotland N.V.” (“RBS N.V.”)) and

ABN AMRO II N.V. (to be renamed “ABN AMRO

Bank N.V.”) will operate under separate banking

licenses which are expected to be obtained from the

Dutch Central Bank in due course

RBS N.V. and ABN AMRO II N.V. (to be renamed

“ABN AMRO Bank N.V.”) also expect to obtain

separate credit ratings, effective once the legal

demerger has been executed

Notes

1. Including the entities ABN AMRO Holding N.V., ABN AMRO Bank N.V. to be renamed The Royal Bank of Scotland N.V. and ABN AMRO II N.V. to be renamed ABN AMRO Bank N.V.

and each of their subsidiaries

2. In addition, certain subsidiaries and certain assets and liabilities that will not transfer via legal demerger will separately be transferred on or around the execution of the legal demerger

using other transfer mechanisms such as a share transfer, novation and contract transfer

3. Subject to progression through Dutch legal process. This demerger overview refers only to Dutch and Belgian assets and liabilities. Acquired business in other countries will be

separated in accordance with mechanisms agreed as appropriate for each country.

30 Sep 09 Q1 2010

Update on the Separation Process

Slide 27

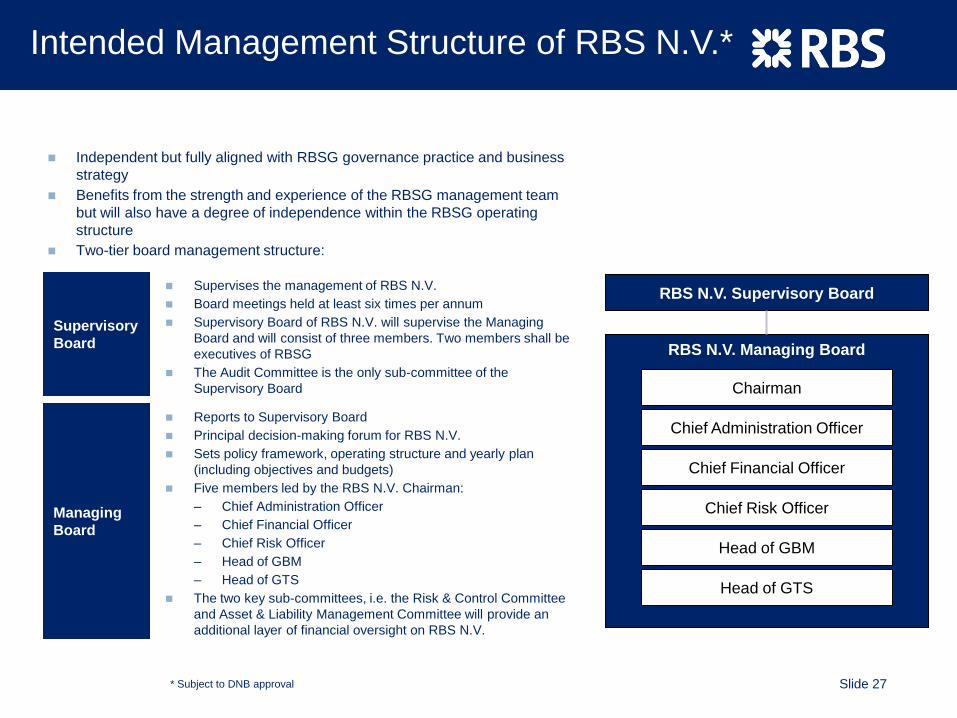

RBS N.V. Managing Board

RBS N.V. Supervisory Board

Chief Financial Officer

Chief Risk Officer

Head of GBM

Chairman

Head of GTS

Independent but fully aligned with RBSG governance practice and business

strategy

Benefits from the strength and experience of the RBSG management team

but will also have a degree of independence within the RBSG operating

structure

Two-tier board management structure:

Supervisory

Board

Managing

Board

Supervises the management of RBS N.V.

Board meetings held at least six times per annum

Supervisory Board of RBS N.V. will supervise the Managing

Board and will consist of three members. Two members shall be

executives of RBSG

The Audit Committee is the only sub-committee of the

Supervisory Board

Reports to Supervisory Board

Principal decision-making forum for RBS N.V.

Sets policy framework, operating structure and yearly plan

(including objectives and budgets)

Five members led by the RBS N.V. Chairman:

– Chief Administration Officer

– Chief Financial Officer

– Chief Risk Officer

– Head of GBM

– Head of GTS

The two key sub-committees, i.e. the Risk & Control Committee

and Asset & Liability Management Committee will provide an

additional layer of financial oversight on RBS N.V.

Intended Management Structure of RBS N.V.*

* Subject to DNB approval

Chief Administration Officer

Slide 28

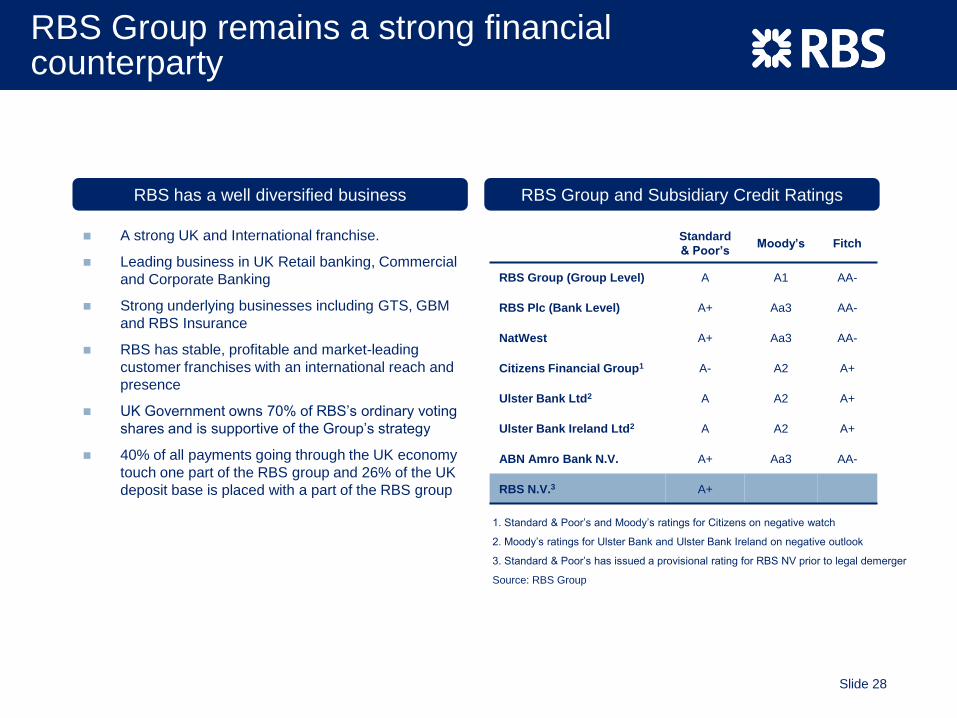

A strong UK and International franchise.

Leading business in UK Retail banking, Commercial

and Corporate Banking

Strong underlying businesses including GTS, GBM

and RBS Insurance

RBS has stable, profitable and market-leading

customer franchises with an international reach and

presence

UK Government owns 70% of RBS‟s ordinary voting

shares and is supportive of the Group‟s strategy

40% of all payments going through the UK economy

touch one part of the RBS group and 26% of the UK

deposit base is placed with a part of the RBS group

RBS has a well diversified business RBS Group and Subsidiary Credit Ratings

Standard

& Poor’sMoody’s Fitch

RBS Group (Group Level) A A1 AA-

RBS Plc (Bank Level) A+ Aa3 AA-

NatWest A+ Aa3 AA-

Citizens Financial Group1 A- A2 A+

Ulster Bank Ltd2 A A2 A+

Ulster Bank Ireland Ltd2 A A2 A+

ABN Amro Bank N.V. A+ Aa3 AA-

RBS N.V.3 A+

1. Standard & Poor‟s and Moody‟s ratings for Citizens on negative watch

2. Moody‟s ratings for Ulster Bank and Ulster Bank Ireland on negative outlook

3. Standard & Poor‟s has issued a provisional rating for RBS NV prior to legal demerger

Source: RBS Group

RBS Group remains a strong financialcounterparty