Embed Size (px)

Citation preview

Pension Policy in Central and East Europe: Reforms and

Reversals

IGOR GUARDIANCICH

CONVERSATIONS ON EUROPECenter for European Studies – European Union

CenterThursday, January 19, 4 pm1636 International Institute

1

Structure of the presentation

1. The ‘new pension orthodoxy’ Averting the Old-Age Crisis Criticism and reassessment

2. Pension privatization in Central and East Europe

Diffusion and variation

3. The financial crisis as dual exogenous shock Impact of the crisis Impact of the Stability and Growth Pact Reform reversals

4. Theoretical implications Croatia, Hungary, Poland and Slovenia compared

2

Part I - The ‘new pension orthodoxy'3

The World Bank’s three pillars

Redistributive plus

coinsurance

Savings plus coinsurance

Savings plus coinsurance

Objectives

Means-tested, minimum pension

guarantee, or flat

Personal savings plan or

occupational plan

Personal savings plan or

occupational plan

Form

Tax-financedRegulated fully

funded Fully fundedFinancing

Mandatory publicly managed

(first) pillar

Mandatory privately managed

(second) pillar

Voluntary (third) pillar

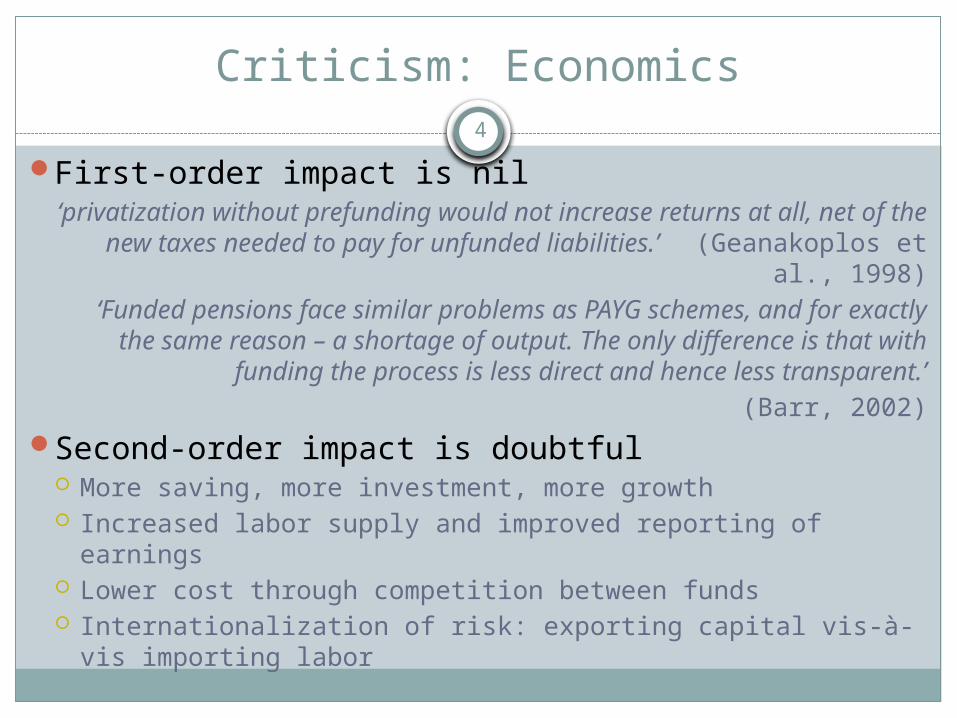

Criticism: Economics4

First-order impact is nil‘privatization without prefunding would not increase returns at

all, net of the new taxes needed to pay for unfunded liabilities.’ (Geanakoplos et al., 1998)

‘Funded pensions face similar problems as PAYG schemes, and for exactly the same reason – a shortage of output. The only difference is that with funding the process is less direct and

hence less transparent.’(Barr, 2002)

Second-order impact is doubtful More saving, more investment, more growth Increased labor supply and improved reporting of earnings Lower cost through competition between funds Internationalization of risk: exporting capital vis-à-vis

importing labor

Criticism: Politics5

The backlash of losers‘too often the Bank has not addressed sufficiently the

primary goal of a pension system to reduce poverty and provide adequate retirement income within a fiscal

constraint. It has also focused insufficient attention on the income of the aged.’(World Bank, IEG, 2006)

Persistence of moral hazard private funds are tempting for politicians, as they

accumulate many years of contributions (as opposed to less than one year in PAYG plans);

renationalization as quick budget fix (Argentina, Hungary).

Criticism: Transition costs6

Transition costs during transition government pays public pensions

while workers accumulate their own funds.Four views

Deduction of transition costs

Counting transition costs

Support for privatization

CEE governments World Bank

Opposition against

privatizationILO (?) IMF

Adapted from Casey and Simonovits (2012)

Part II - Pension privatization in CEE7

The socialist pension systems and transformational crises

8 Three layers

Bismarckian core retirement became the extension of the constitutionally guaranteed right to work

post-war socialist social solidarity PAYG system and reinforced stratification

imported Stalinist centralization monolithic public administration

Crisis under socialism financial strains

low retirement age and long assimilated periods (e.g. maternity leave) benefits calculated according to best- or last-years formulae cross-subsidization of other budget expenditures (e.g. social assistance)

poverty in old age the ‘old portfolio’ problem, due to insufficient indexation

Crisis during the transformation demographic emergency ‘great abnormal pensioner booms’ multiplication of contributors, output decline and tax evasion political exploitation of losers and pampering of core constituencies

Three reform phases9

Refinancing rapid increase in social security contributions (PL 25% in

1981; 38% in 1987-9; 45% in 1990) discontinued due to declining international competitiveness

Retrenchment arbitrary freezing of indexation of all but minimum

benefits struck down by Constitutional Courts (lack of exceptional

circumstances)

Restructuring politically superior, allows for quid-pro-quos resonates with the public (equity as individualization) obfuscates cuts in public pillar

Diffusion and variation10

Different types of privatization Substitutive (KO) Parallel (LT) Mixed (BG, HR, EE – not only carved out, HU – reversed, LV, MC,

PL, RO – stalled, SK – partly reversed) Voluntary (AL, CZ, SI – quasi-mandatory, SR)

Coverage Mandatory for young workers (HU only new workers) Voluntary for intermediate cohorts (PL 30-50; HR 40-50) Not available to older employees (HU rare exception, active errors)

Size Substantial (HU 68/33.5; LV 210/20; PL 7.3/19.52; SK 9/18) Medium (BG 25/23; HR 5/20; EE 4+2/20; LT 2.55.5/18.5; RO

2.56/28) Small (SW 2.5/18.5)

Impact of privatization on deficit/revenues

11

Country Budget balance

Transition cost

Balance if no reform

Lost revenues 2007-60

Bulgaria 0.1 -0.7 0.8 45

Estonia 2.6 -1.3 3.9 64

Latvia -0.3 -0.8 0.5 99

Lithuania -1.0 -0.9 -0.1 43

Hungary -5.0 -1.2 -3.8 93

Poland -1.9 -1.3 -0.6 167

Romania -5.4 -0.3 -5.1 67

Slovakia -1.9 -1.0 -0.9 106

Part III - The financial crisis12

Shrinking demand Most of CEE are small and open economies (<1M – 10M

people). Banks became illiquid in late 2008. Fall in international orders triggered an economic

collapse.Asset bubbles

Hungary and Baltic states had excessive exposure to foreign-denominated mortgages.Country BG HR CZ EE HU LT LV PL RO SK SI

2008 6.2 2.2 3.1 7.5 0.9 2.9 -3.3 5.1 7.3 5.9 3.6

2009 -5.5 -6.0 -4.7 -3.7 -6.8 -14.8

-17.7

1.6 -6.6 -4.9 -8.0

Stability and Growth Pact13

Maastricht criteria for EMU membership: inflation max 1.5 pp higher than the average of 3

lowest-inflation Member States budget deficit <3% of GDP government debt <60% of GDP long-term interest rate max 2.0 pp higher than in 3

lowest-inflation Member States ERM II joined for 2 years prior to accession, no

devaluationStability and Growth Pact (SGP)

Enhanced monitoring procedures Sanctions through Excessive Deficit Procedures (EDPs) Renegotiation and increased flexibility in 2005

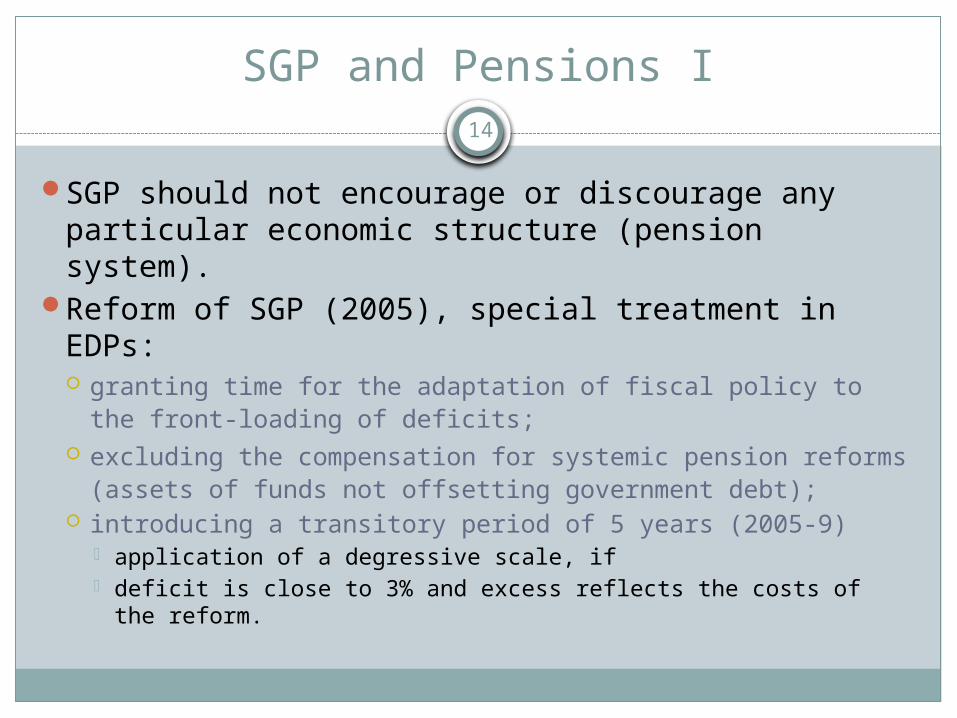

SGP and Pensions I14

SGP should not encourage or discourage any particular economic structure (pension system).

Reform of SGP (2005), special treatment in EDPs: granting time for the adaptation of fiscal policy to the front-

loading of deficits; excluding the compensation for systemic pension reforms

(assets of funds not offsetting government debt); introducing a transitory period of 5 years (2005-9)

application of a degressive scale, if deficit is close to 3% and excess reflects the costs of the reform.

SGP and Pensions II15

Criticism: triggered by expiry of the transition period, soaring budget

deficits; 2nd pillars mature in 40-50 years, 5 years are insufficient; reformers should not be penalized with regards to the

Maastricht criteria.Demand for SGP revision

letter of 8 CEE countries plus Sweden change the statistical treatment of private pension funds; deduct fully the costs of implementing systemic pension reforms

from the budget deficit in the context of the EDP; refusal of interim relief (deviations from accounting rules must

be limited, comparability with similar measures, statistical certainty);

new draft rules allowing for flexibility for virtuous countries.

Reforms and reversals16

Temporary measures many CEE countries froze the indexation of pensions

(wages of public employees, social transfers) during 2010-12

Parametric reforms various CEE countries introduced a number of

‘overdue’ parametric reforms: higher retirement age fewer early retirement venues lower regular indexation

Reversal of privatization governments prefer to spend for Keynesian measures

than for transition costs

Reversals of privatization17

Bulgaria Contributions: frozen at 5% during 2007-14, rising to 7% in 2017Switching back: early retirees brought back to PAYG system

Estonia Contributions: suspended temporarily (employees can pay in 2%)

Hungary Contributions: diverted back to public pillarSwitching back: strong incentives to all pension fund members

Latvia Contributions: reduced from 10% to 2% temporarily

Lithuania Contributions: reduced from 5.5% to 2% temporarily

Poland Contributions: reduced from 7.3% to 2.3%, rising to 3.5% by 2017Switching back: allowed in 2006 for early retirees

Romania Contributions: frozen at 2%

Slovakia Switching back: allowed to all pension fund members, no mandatory entry for new workers

Part IV - Theoretical implications18

Political sustainability Even before the financial crisis there was extreme

heterogeneity with respect to the vulnerability of reforms to changes in power.

Political sustainability of reforms in time, and implementation in general, have so far received insufficient attention.

Two possible variables of interest Political polarization Authority concentration

The majoritarian systems19

Croatia semi-authoritarian system under Tuđman’s HDZ unilateral decision-making in 1998

disproportionalities (Homeland War combatants) obfuscation (2nd pillar unable to compensate for 1st pillar cuts)

reversals, but no elimination of funded pillar (no SGP?)

Hungary super-majority under MSzP-SzDSz (Horn) clientelistic decision-making in 1997

internal affair with successor union MSzOSz opposition parties uninvolved, even SzDSz voted against too much effort for 2nd pillar, 1st pillar amateurish

extreme political budget cycles spectacular reversals all fiscal savings nullified nationalization of the 2nd pillar (only 3% of original members remained)

The consensual democracies 20

Poland after 1997 parliamentary system, checks and balances, SLD-PSL coalition depoliticized Plenipotentiary (Bączkowski, Hausner, Lewicka) and cross-

parliamentary, cross-governmental consensus in 1997-8 professional, innovative Security through Diversity few disproportionalities, but incomplete reforms

marginal reversals, political capital to finalize reforms disappeared, 2nd pillar temporarily reduced

Slovenia only neo-corporatist democracy in CEE unilateral decision-making by LDS (Rop) in 1997-9

impossible to reach an agreement with successor union ZSSS dilution of the White Paper and elimination of 2nd pillar

quasi-mandatory pillar for public employees legislated in 2003 marginal reversals, political capital for further reforms disappeared; failure of the 2010-11 pension reform.

An institutionalist perspective21

High polarization and concentration of authority lower the time and transaction costs of reforms; may reduce the adaptability of reforms to changing

socioeconomic circumstances, due to built-in ‘disproportionalities’;

decrease the resilience of reforms to changes in political power, due to wide ideological swings between subsequent governments.

Low polarization and dispersion of authority increase the time and transaction costs of reforms; may increase the adaptability of reforms, due to inter-

temporal quid-pro-quos; increase the resilience to changes in political power; render future reforms and adjustments difficult.