Embed Size (px)

Citation preview

Peter Schnedlitz, Dirk Morschett,Thomas Rudolph, Hanna Schramm-Klein, Bernhard Swoboda (Eds.)

European Retail Research

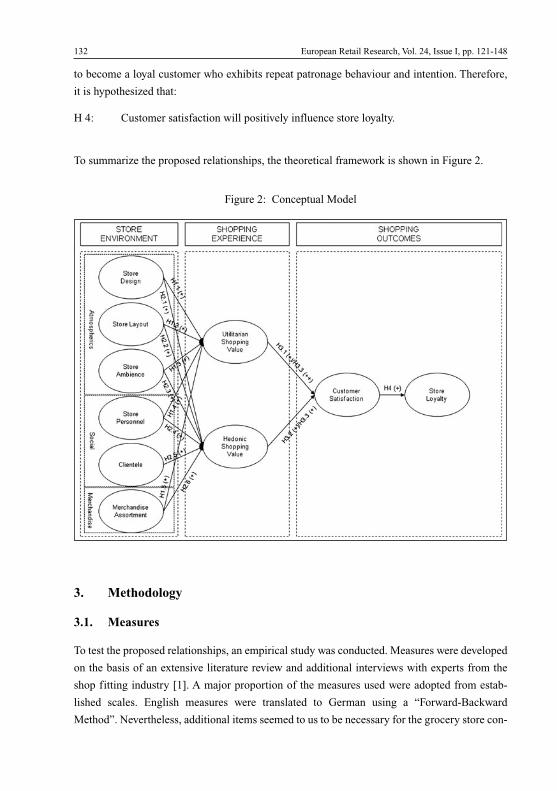

GABLER RESEARCH EditorsDirk Morschett, University of Fribourg, Switzerland, [email protected] Rudolph, University of St. Gallen, Switzerland, [email protected] Schnedlitz, Vienna University of Economics and Business, Austria, [email protected] Schramm-Klein, Siegen University, Germany, [email protected] Swoboda, University of Trier, Germany, [email protected]

EDITORIAL ADVISORY BOARDIn the editorial advisory board, a number of distinguished experts in retail research from different countries support the editors:

– Steve Burt, University of Stirling, UK– Michael Cant, University of South Africa, South Africa– Gérard Cliquet, University of Rennes I, France– Enrico Colla, Negocia, France– Ulf Elg, Lund University, Sweden– Martin Fassnacht, WHU - Otto Beisheim School of Management, Germany– Marc Filser, University of Dijon, France– Thomas Foscht, University of Graz, Austria– Juan Carlos Gázquez Abad, University of Almeria, Spain– Arieh Goldman, Hebrew University, Israel (†)– David Grant, University of Hull, UK– Andrea Gröppel-Klein, Saarland University, Germany– Herbert Kotzab, Copenhagen Business School, Denmark– Michael Levy, Babson College, USA– Cesar M. Maloles III, California State University, USA– Peter J. McGoldrick, Manchester Business School, Manchester University, UK– Richard Michon, Ryerson University, Canada– Dirk Möhlenbruch, University Halle-Wittenberg, Germany– Heli Paavola, University of Tampere, Finland– Luca Pellegrini, IULM University Milan, Italy– Barry Quinn, University of Ulster, Northern Ireland– Will Reijnders, Tilburg University, The Netherlands– Thomas Reutterer, Vienna University of Economics and Business, Austria– Jonathan Reynolds, Oxford, UK– Sharyn Rundle-Thiele, University of Southern Queensland, Australia– Brenda Sternquist, Michigan State University, USA– Gilbert Swinnen, Universiteit Hasselt, Belgium– Ikuo Takahashi, Keio University, Japan– Waldemar Toporowski, University of Goettingen, Germany– Volker Trommsdorff, Technical University Berlin, Germany– Gianfranco Walsh, Koblenz-Landau University, Germany– Barton Weitz, University of Florida, USA– Joachim Zentes, Saarland University, Germany

Peter Schnedlitz, Dirk Morschett,Thomas Rudolph, Hanna Schramm-Klein, Bernhard Swoboda (Eds.)

European Retail Research 2010 | Volume 24 Issue I

RESEARCH

Bibliographic information published by the Deutsche Nationalbibliothek

The Deutsche Nationalbibliothek lists this publication in the Deutsche Nationalbibliografi e;

detailed bibliographic data are available in the Internet at http://dnb.d-nb.de.

”Jahrbücher zur Handelsforschung“ were fi rst published at:

Physica-Verlag (1986-1988)

Gabler Verlag (1989-1999/2000)

BBE-Verlag (2000/01-2004)

Kohlhammer Verlag (2005-2007)

The 24th Volume Issue I is sponsored by

1st Edition 2010

All rights reserved

© Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2010

Editorial Offi ce: Ute Wrasman | Sabine Schöller

Gabler Verlag is a brand of Springer Fachmedien.

Springer Fachmedien is part of Springer Science+Business Media..

www.gabler.de

No part of this publication may be reproduced, stored in a retrieval system

or transmitted, in any form or by any means, electronic, mechanical, photo-

copying, recording, or otherwise, without the prior written permission of the

copyright holder.

Registered and/or industrial names, trade names, trade descriptions etc. cited in this publica-

tion are part of the law for trade-mark protection and may not be used free in any form or by

any means even if this is not specifi cally marked.

Umschlaggestaltung: KünkelLopka Medienentwicklung, Heidelberg

Printed on acid-free paper

Printed in Germany

ISBN 978-3-8349-2254-0

Preface of the Editors

EUROPEAN RETAIL RESEARCH is a new bi-annual that is in the tradition of the reputable

and distinguished book series „Handelsforschung“ (Retail Research) which has been published

by Prof. Dr. Volker Trommsdorff in Germany for more than two decades. With Volume 22

appearing in 2008, Prof. Trommsdorff handed over this publication to a team currently consist-

ing of retail researchers from Austria, Germany and Switzerland. The aim of the publication is

to publish interesting manuscripts of high quality with a focus on retail researchers and lectur-

ers, retail students and retail executives. As it has always been, retail executives are part of the

target group and the knowledge transfer between retail research and retail management remains

a part of the publication’s concept. Following the international development in the field of retail

research and publication, the new team has decided to introduce some changes and extensions

to the concept:

- Language - articles will appear in English

- Content - manuscripts will be double-blind reviewed and the book will invite manuscripts

from a wider regional context but with a focus on Europe

- Institutional - a permanent team of editors will be supported by an Editorial Advisory Board

Frequency - EUROPEAN RETAIL RESEARCH will be published in two parts per year, Issue I

in spring and Issue II in fall. The review process will support the authors in enhancing the qual-

ity of their work and will offer the authors a reviewed book as a publication outlet. Part of the

concept is an only short delay between manuscript submission and final publication, so the

book is intended to become a quick publication platform. Therefore the deadlines are always

fixed. Issue I (publication in April): submission deadline: End of August, notification of accept-

ance: End of October, re-submission of revised manuscript: End of January. Issue II (publica-

tion in October): submission deadline: End of February, notification of acceptance: End of

April, re-submission of revised manuscript: End of June. An electronic database with all pub-

lished articles will be prepared and will be available with an adequate delay after the printed

edition.

EUROPEAN RETAIL RESEARCH welcomes manuscripts on original theoretical or conceptu-

al contributions as well as empirical research – based either on large-scale empirical data or on

the casestudy method. Following the state of the art in retail research, articles on any major

issues that concern the general field of retailing and distribution are welcome, e.g.

- different institutions in the value chain, e.g. customers, retailers, wholesalers, traders, service

companies such as logistics service providers, but also manufacturers’ distribution activities,

- different value chain processes, esp. marketing-orientated processes (e.g. innovation, customer

relationship management, category management), supply chain processes (e.g. purchasing,

logistics), organisational processes, informational or financial management processes,

V

- different aspects of retail management and retail marketing, e.g. retail corporate and compet-

itive strategies, incl. internationalisation, retail formats, e-commerce, customer behaviour,

branding and store image, retail location, assortment, pricing, service, communication, in-

store marketing, human resource management,

- different aspects of distribution systems, e.g. sales management, key account management, ver-

tical integration, alliances and networks, channel power, conflicts and multi channel strategies.

However, EUROPEAN RETAIL RESEARCH is also interested in manuscripts that focus on

wholesaling, distribution concepts, specific strategies or country markets and we accept that

non-English literature is used to. Basically, we are considering different types of papers. Arti-

cles can be based on large-scale empirical data, on the case-study method or on conceptual

issues:

- Research articles should provide a relevant and significant contribution to theory and prac-

tice; they are theoretically well grounded and methodologically on a high level.

- Manuscripts submitted as more practice- or conceptual-based articles show new questions,

issues, solutions and contributions from practice or conceptual issues. These papers are

selected based on relevance and continuing importance to the future retail research communi-

ty as well as on originality.

Manuscripts are reviewed with the understanding that they are substantially new, have not been

previously published in English and in whole, have not been previously accepted for publica-

tion, are not under consideration by any other publisher, and will not be submitted elsewhere

until a decision is reached regarding their publication in EUROPEAN RETAIL RESEARCH.

The only exceptions are papers in conference proceedings that we treat as work-in-progress.

Furthermore, the editors invite articles from specific authors, which address the retailing situa-

tion in a specific European country. Those articles will also be double blind reviewed.

Contributions should be submitted in English language in Microsoft Word format by e-mail to

the current EUROPEAN RETAIL RESEARCH managing editor or to info@european-retail-

research.org. Questions or comments regarding this publication are very welcome. They may be

sent to one of the editors or to the above mentioned e-mail-address.

Full information for prospective contributors is available at: http://www.european-retail-

research.org. For ordering an issue please contact the German publisher “Gabler Research”

(www.gabler.de).

We are extremely grateful for editorial assistance provided by Eva Lienbacher, Robert Zniva and

Ruth Angerer.

Fribourg, St. Gallen, Siegen, Trier and Vienna, Summer 2010

Dirk Morschett; Thomas Rudolph; Hanna Schramm-Klein; Bernhard Swoboda

Peter Schnedlitz (managing editor for Volume 24 Issue I)

VI Preface of the Editors

Contents

Interactive Web 2.0 Applications in the Multi-Channel Marketing for Retailers.................. 1

Dirk Möhlenbruch, David Elias Blunck and Falk Ritschel

How to Maintain a Process Perspective on Retail Internationalization: The IKEA Case ..... 27

Anna Jonsson

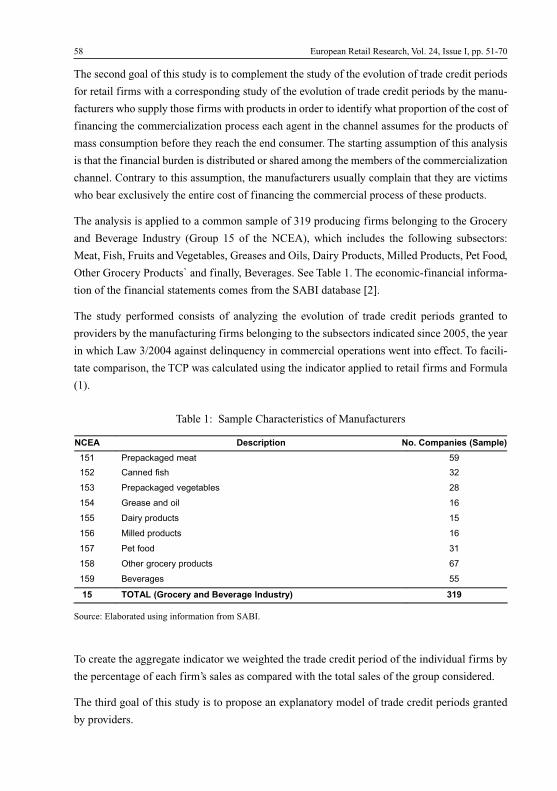

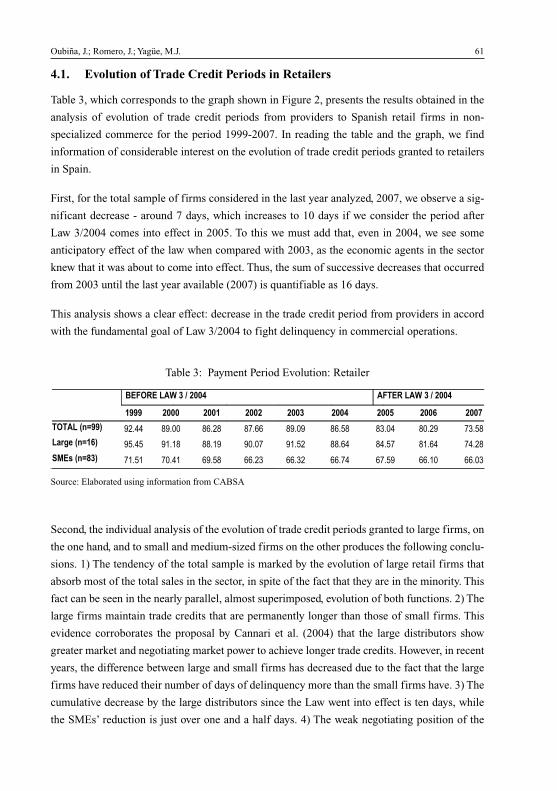

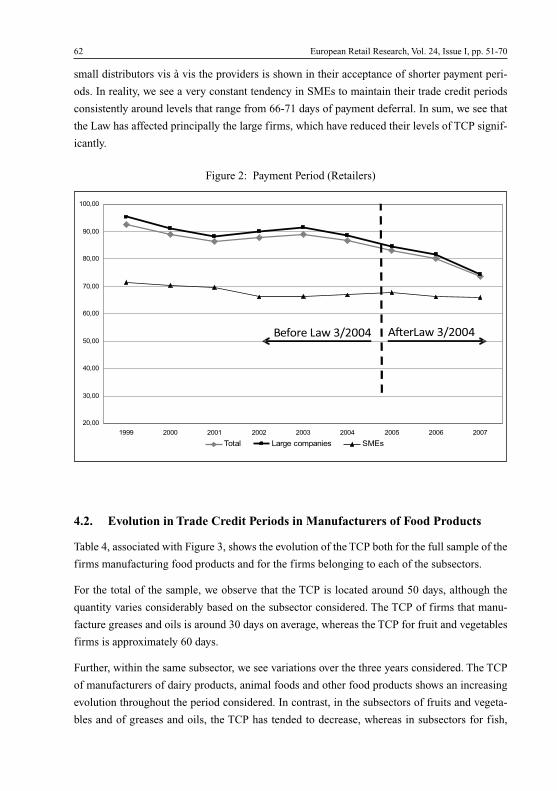

Trade Credit Periods in Retail Commerce for Products of Mass Consumption:An Application to Spanish Legislation.................................................................................. 51

Javier Oubiña, Jaime Romero and María Jesús Yagüe

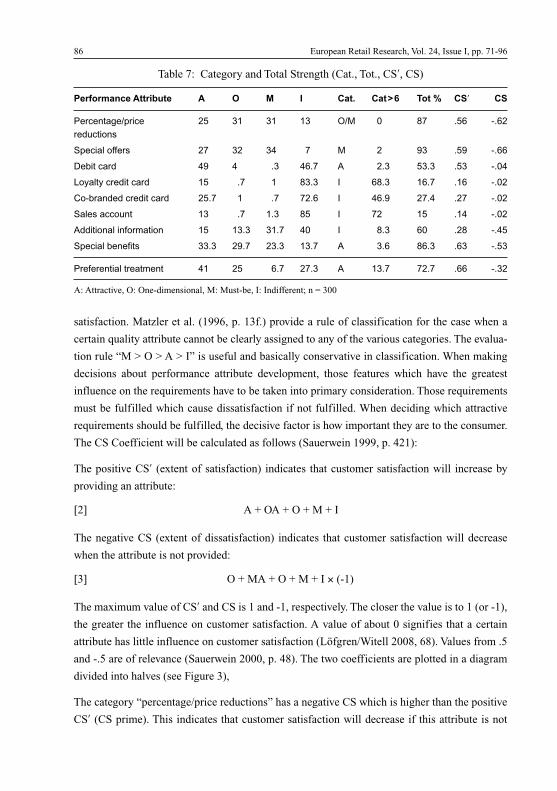

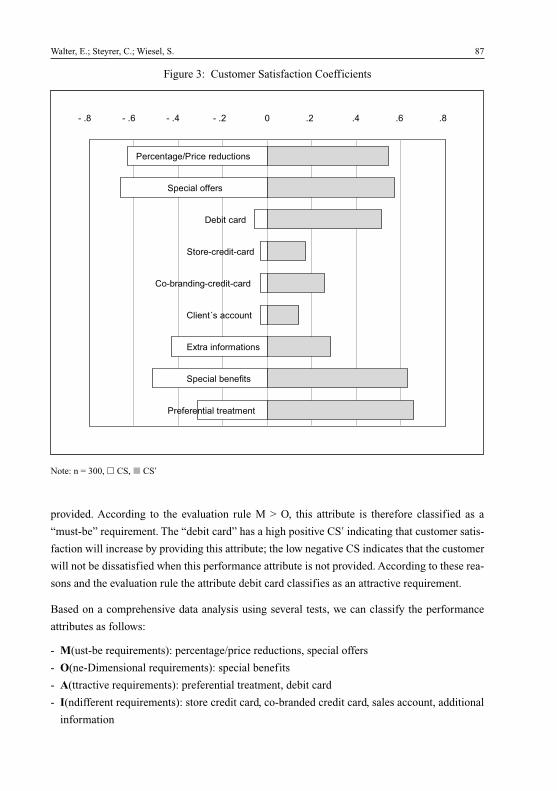

Customer Satisfaction with Loyalty Card Programs in the Austrian Clothing Retail Sector- an Empirical Study of Performance Attributes Using Kano’s Theory ................................ 71

Eva Walter, Claudia Steyrer and Stefan Wiesel

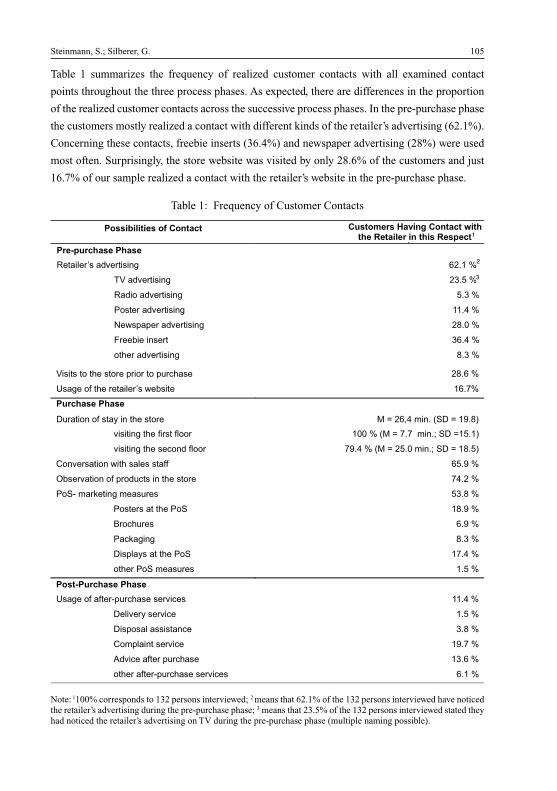

Clustering Customer Contact Sequences - Results of a Customer Survey in Retailing........ 97

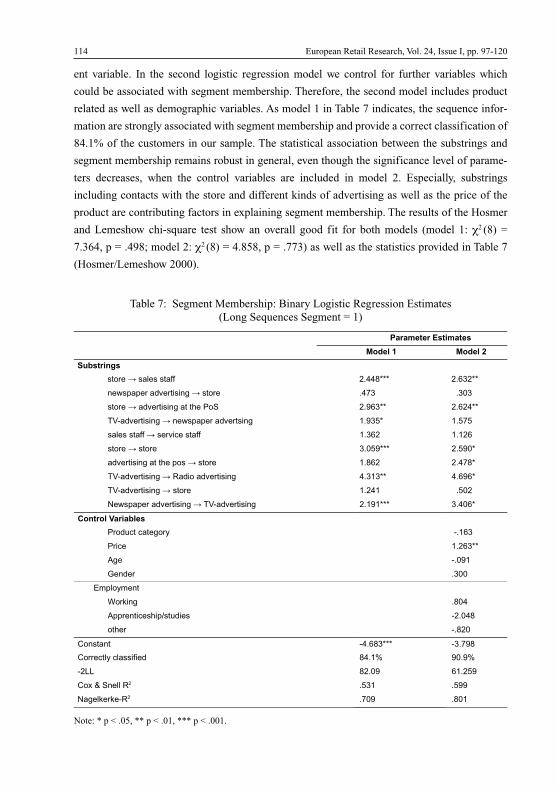

Sascha Steinmann and Günter Silberer

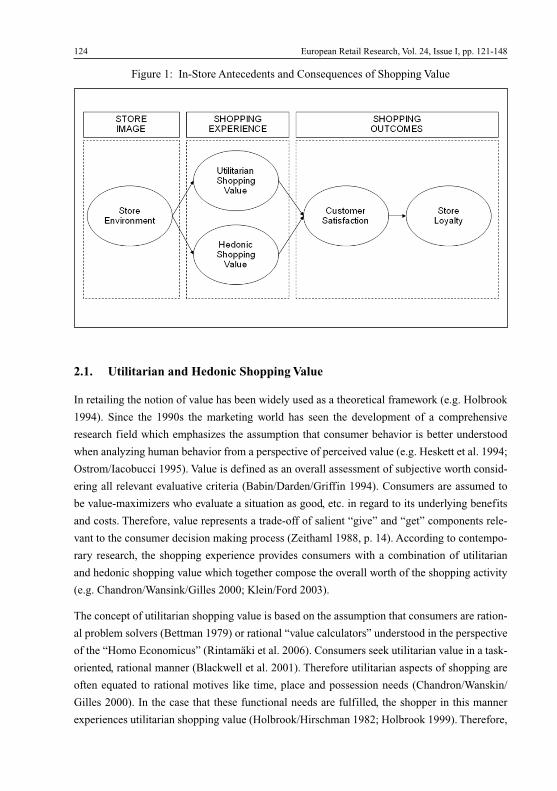

The In-Store Antecedents and Consequences of Perceived Shopping Valuefor Regularly Purchased Products ......................................................................................... 121

Wolfgang Weitzl and Robert Zniva

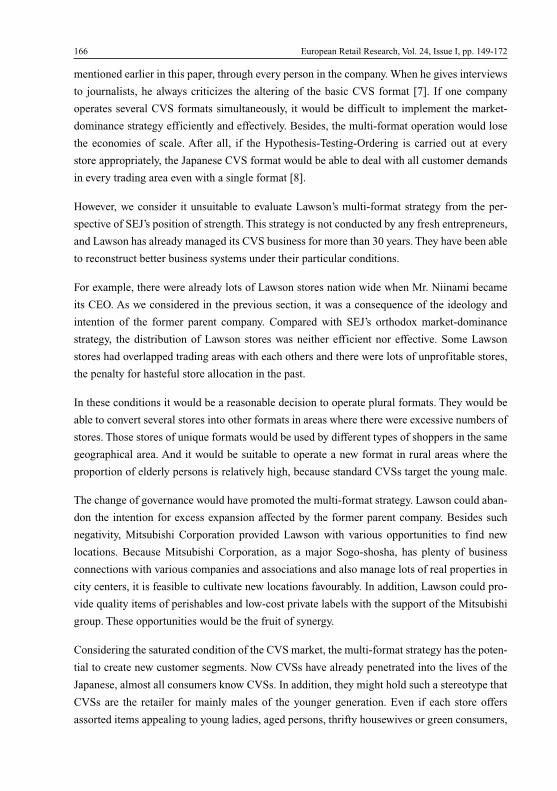

Strategic Differentiation in the Japanese Convenience Store Business.The Example of Lawson’s Format Variation.......................................................................... 149

Ari Huuhka, Nobutoshi Shimizu and Martti Laaksonen

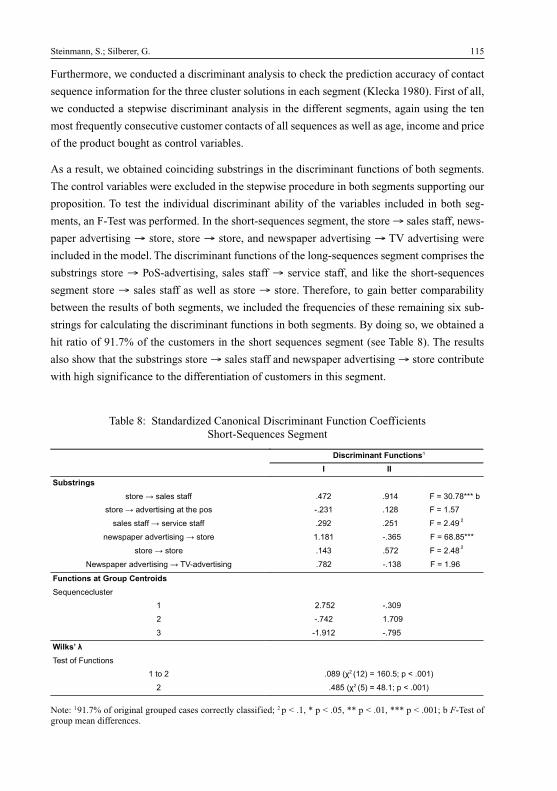

Country Reports

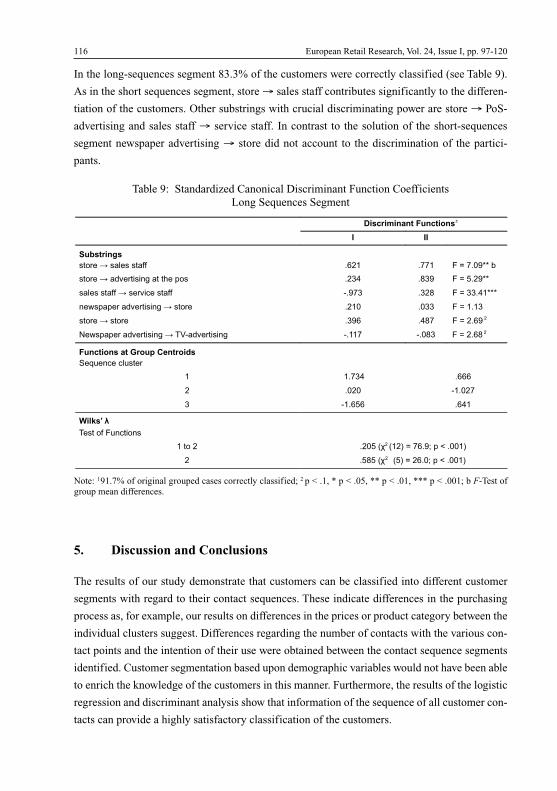

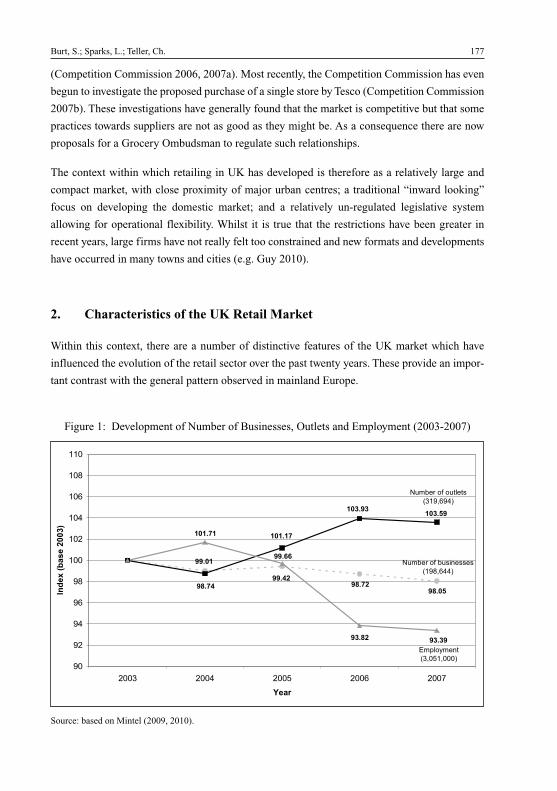

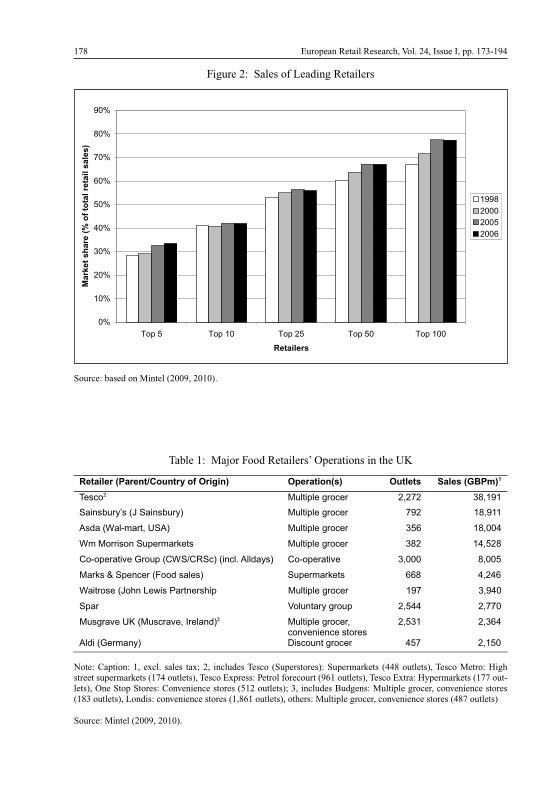

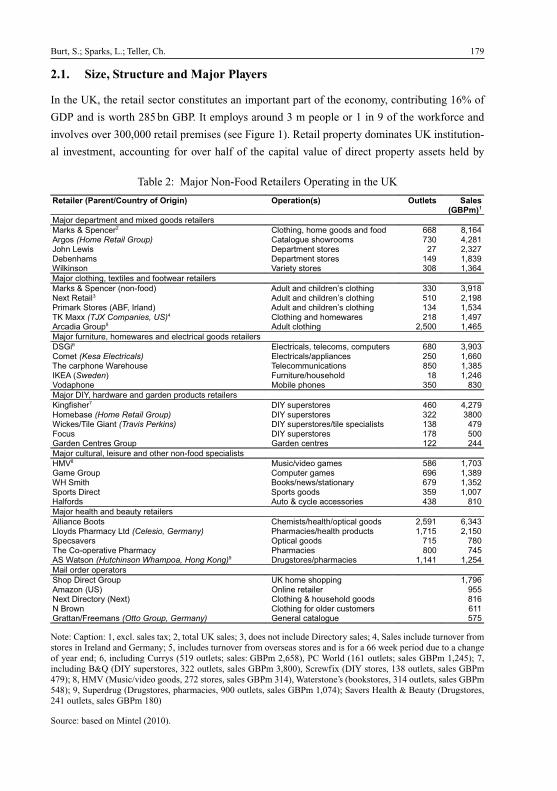

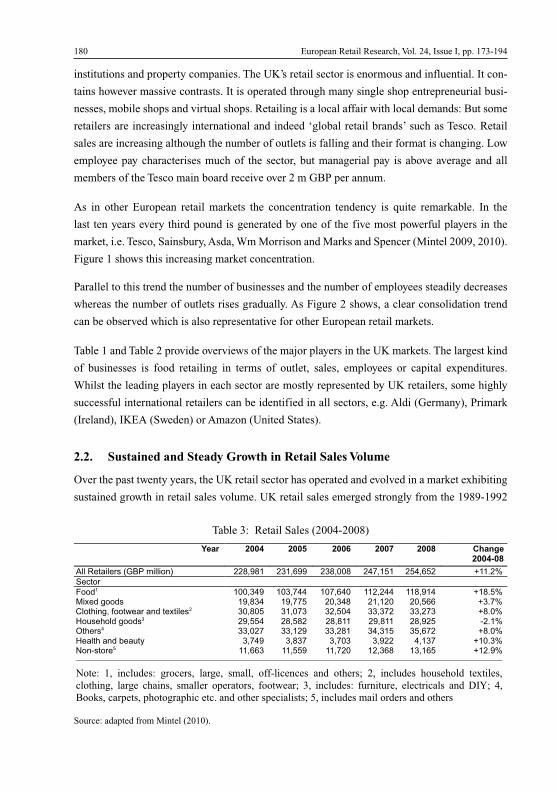

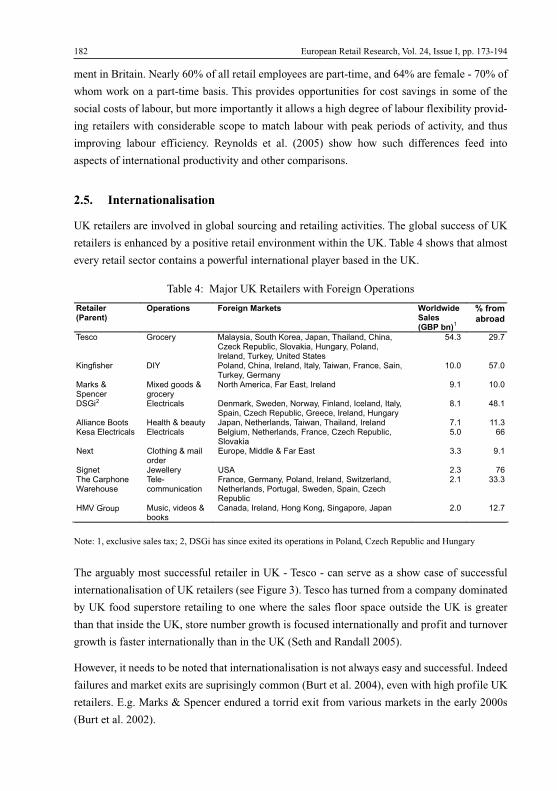

Retailing in the United Kingdom - a Synopsis...................................................................... 173

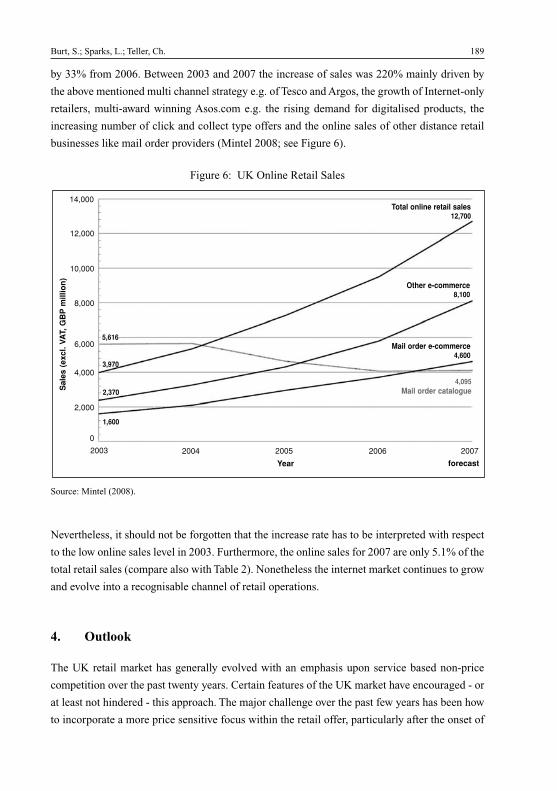

Steve Burt, Leigh Sparks and Christoph Teller

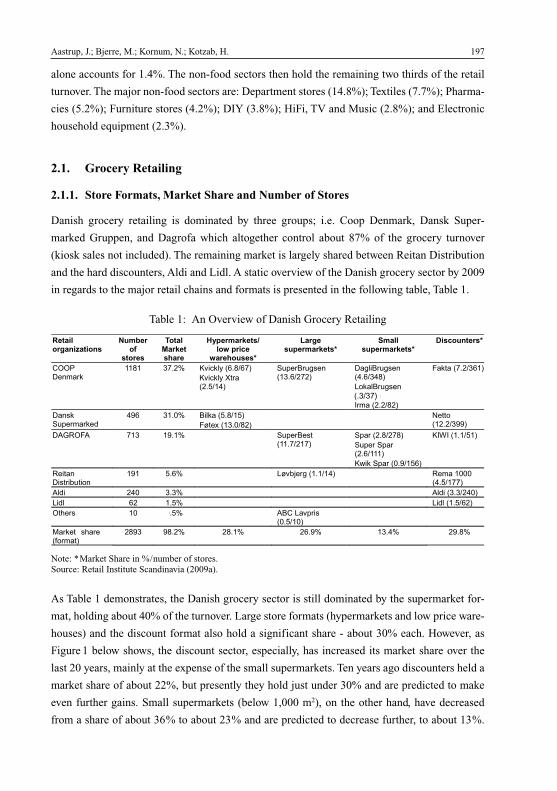

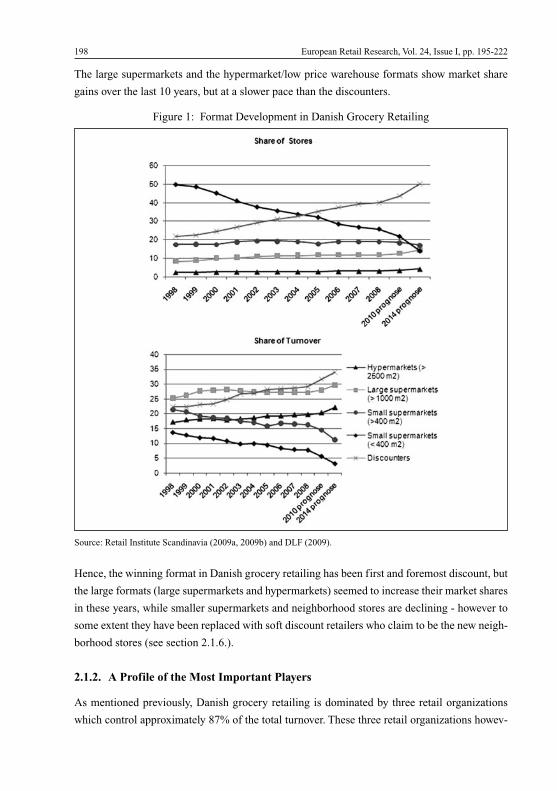

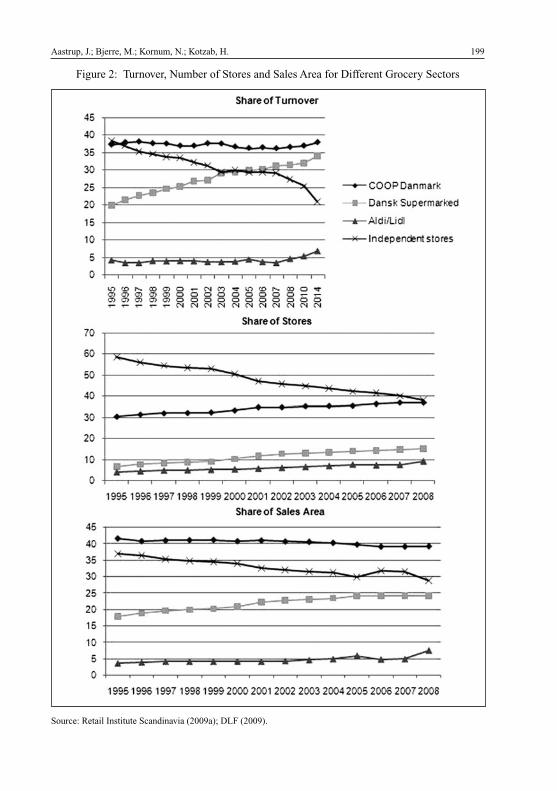

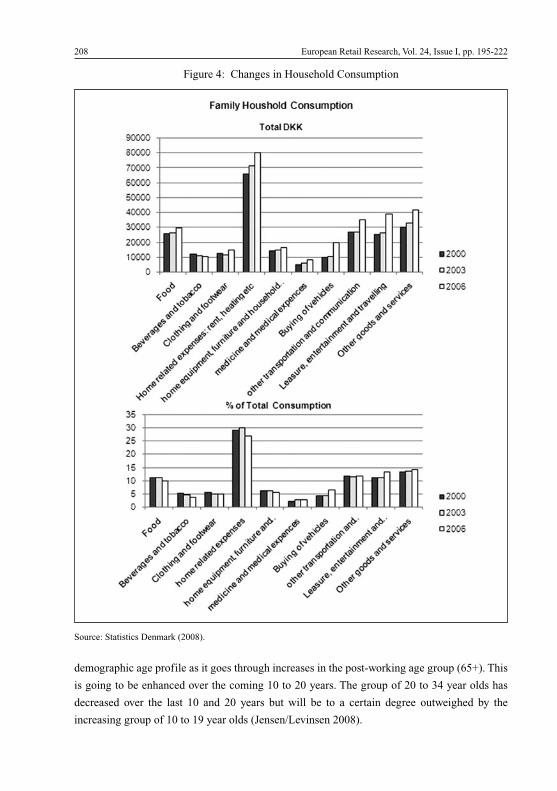

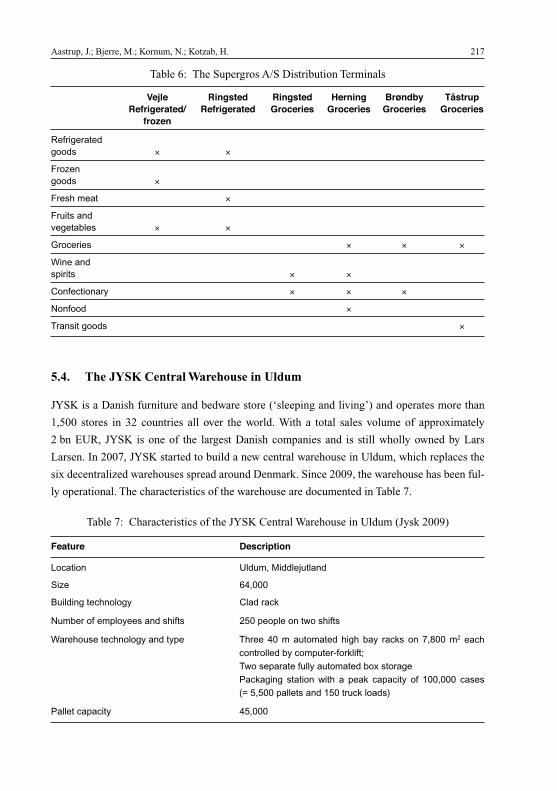

The Danish Retail Market: Overview and Highlights ........................................................... 195

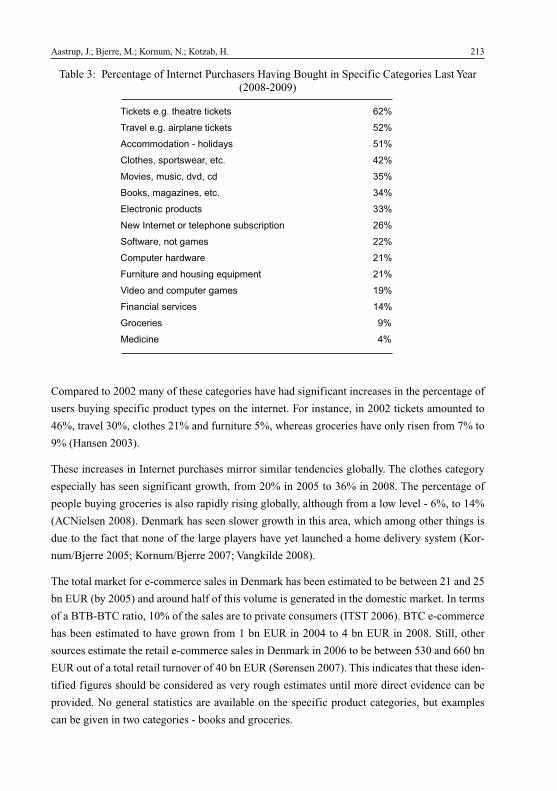

Jesper Aastrup, Mogens Bjerre, Niels Kornum and Herbert Kotzab

EUROPEAN

RETAIL

RESEARCHVol. 24, Issue I, 2010, pp. 1-222

Interactive Web 2.0 Applications in the Multi-Channel Marketingfor Retailers

Dirk Möhlenbruch, David Elias Blunck and Falk Ritschel

AbstractThis literature review recapitulates the state of the art knowledge about the characteristics ofWeb 2.0 instruments and deduces application options for multi-channel marketing by retailers.The different instruments of Web 2.0 and the theoretical foundations of multi-channel market-ing are introduced. The authors assign the specific Web 2.0 applications through the instrumen-tal areas of retailing by confronting their particular features and functions with the specificchances, risks, goals and the operational and strategic demands (needs) of multi-channel man-agement. This systematization gives retailers the chance to choose their instrumental assign-ments strategically, based on their specific goals in multi-channel marketing.

KeywordsRetailing, Multi-Channel Marketing, Web 2.0, Cross-Channel

Dirk Möhlenbruch (corresponding author)Department of Business Administration, Martin-Luther-University Halle-Wittenberg, Halle, Germany(Tel: ++49 345 5523391; E-mail: [email protected]).

David Elias BlunckInstitute for Innovation and Entrepreneurship, Martin-Luther-University Halle-Wittenberg, Halle,Germany.

Falk RitschelDepartment of Business Administration, Martin-Luther-University Halle-Wittenberg, Halle, Germany.

Received: September 3, 2009Revised: February 23, 2010Accepted: February 25, 2010

EUROPEAN

RETAIL

RESEARCHVol. 24, Issue I, 2010, pp. 1-26

1. Introduction

The discussion about Multi-Channel-Systems in retail business might not be new - but it

has gained momentum against the background of consolidations and mergers, the develop-

ment of information and communication technologies (ICT) and experiences of disillusion-

ment with pure e-commerce players (Dohmann et al. 2002; Barth et al. 2007). This is

additionally evidenced by the increasing number of academic publications and the gain in

importance of multi-channel distribution in retail-practice - where many pure e-players have

augmented their structure of distribution with alternative channels (Tang/Xing 2001; Schögel

et al. 2004).

Despite the lively discussions on the part of academic researchers and the growth of experience

in practice, there is still an unsatisfactorily low level of knowledge - which might be the reason

why companies often fail in the realization or achieve only suboptimal levels of channel inte-

gration - even though the domination of multi-channel companies in the B2C e-commerce sec-

tor (with the exception of a few companies, e.g. eBay or Amazon) implies a great potential for

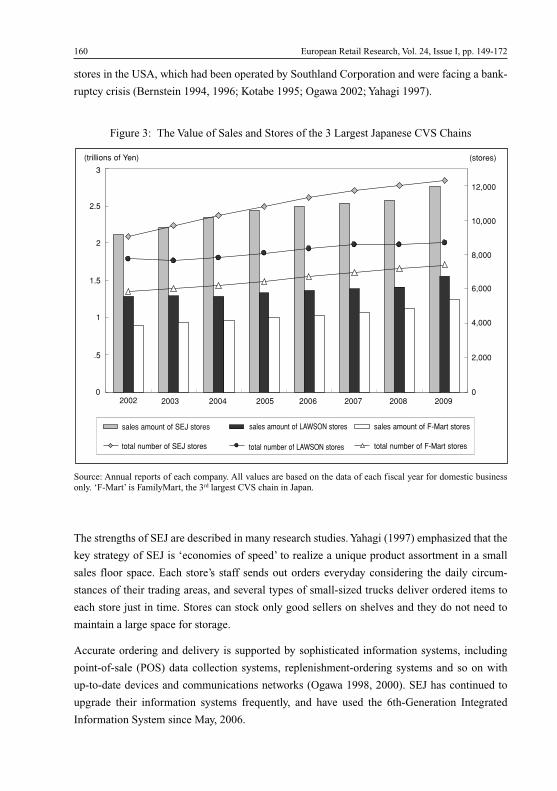

success (Hudetz/Baal 2005; Emrich 2008). For this reason most authors seem to agree upon the

potential as well as the relevance of multi-channel distributors. Hudetz/Baal identify multi-

channel companies “a good starting base to get even more dominant in the future” (Hudetz/Baal

2005, p. 136). Emrich agrees that multi-channel strategies might become “crucial to survive”

(Emrich 2008, p. 1), and Ahlert/Hesse (2003) substantiate with empirical studies the preference

that customers have for multi-channel distributors.

The ability to establish, integrate and uplink different distribution and communication channels

becomes one of the main challenges in retail management. This applies especially against the

background of the enormous intensity of competition in this field. Even though there is an

undisputedly high impact of the internet on the buying decisions of consumers, many retail

companies use this important medium not as a strategically integrated interactive communica-

tion and customer-retention tool, but more like an encrypted business card (Silberer 2002). In

this context, Web 2.0 and its applications gain importance but are often disputed as controver-

sial. Neither Web 2.0 nor its applications can be limited to a single technology - in fact it should

be understood as new perceptions and uses of the internet, with a strong leaning towards inter-

action (Thackeray/Neiger 2009). While roles on the internet have been separated in the past

between the active content producers and passive content consumers, today the use of inter-

active instruments - like wikis, blogs, virtual communities and RSS feeds for example - allows

not only new business models in e-commerce but enables a close and interactive dialog between

companies and their relevant stakeholders (Kollmann/Häsel 2007).

Despite the already-mentioned range of scientific and practical-oriented specific literature

about the topics of Web 2.0 and multi-channel marketing and against the background of the

2 European Retail Research, Vol. 24, Issue I, pp. 1-26

importance of the online-channel, surprisingly little attention has been paid to the specific

potentials of Web 2.0 applications in multi-channel marketing in the retail business, and Web

2.0 is still in an experimental stage in practice (Marfleet 2008; Ailawadi et al. 2009). This arti-

cle therefore describes the necessary theoretical backgrounds of multi-channel marketing and

Web 2.0, displays the characteristics of the specific instruments, and confronts their particular

features and functions with the explicit chances, risks, goals and operational- as well as strate-

gic demands of multi-channel management to deduce a systemization of application fields of

Web 2.0 applications through the different instrumental areas of retailing. This gives retailers

the chance to choose their instrumental assignments strategically based on their specific goals

in multi-channel marketing.

2. Theoretical Background of Multi-Channel Retailing

The complexity and heterogeneity of retailing, combined with inconsistent market structures

(Zentes/Morschett 2005) are important reasons that a comprehensive characterization of the

market environment cannot be carried out in adequate dimensions. We will therefore limit the

description to the spurring factors with the highest influence on the general development in

retail business (Barth et al. 2007) and on Multi-Channel-Business in particular (Ahlert/Hesse

2003; Bachem 2004). Increasing mobility and the development of ICT (which, among other

things, leads to new marketing channels and increasing capacities in the back end) expand the

competitive situation in retail business to an additional geographical level (Purper 2007). The

intensity of competition increases the need for a consistent orientation toward customer require-

ments, market demarcation, and boosts accelerated tendencies towards consolidation processes

in reseller markets (Zboralski/Gemünden 2004; Weinberg/Purper 2006). Accordingly, the

changes in society’s values - which precede the changes in buying behavior - have a higher

impact on developments in the retail business. There has been a lively scientific discussion

about changes in consumer behavior for quite some time, but the dynamics as well as the

dimensions of those developments present themselves in a new quality (Foscht/Swoboda 2007).

While the debates about brand- and price-related behavior have been supplemented since the

early 1990s by terms like “hybrid customer”, “smart shopper”, “bargain shopper”, “variety

seeking” and “convenience orientation” is the phenomenon of “multi-optional consumers”

increasingly mentioned in modern marketing literature (Hurth 2002; Foscht/Swoboda 2007).

Those types of consumers follow different acting principles at once and change their behaviors

and group memberships as well, which results in multi-optional buying behavior and shifts

between different distribution channels during a single buying process (Wegener 2008; Ahlert/

Hesse 2003). Their differentiated needs are not limited to the actual transaction but range over

the whole buying process including pre- and post-buying phases (Möhlenbruch/Schmieder

2002). These developments have a great impact on multi-channel distribution and lead to the

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 3

necessity of meeting the differentiated needs of consumers during the various phases of a buy-

ing process through the implementation of an integrated multi-channel system (Hurth 2002;

Kilcourse 2008; Kwon/Lennon 2009).

Even though multi-channel marketing is not a new phenomenon (Möhlenbruch/Schmieder

2002; Barth et al. 2007.) the scientific literature does not offer a standardized definition

(Schramm-Klein 2003; Hudetz/Baal 2005; Wirtz 2008). In fact there are a multitude of terms

and definitions dealing with sales and communications via several channels which appear sim-

ilar at a first glance, but often differ in meaning (Wirtz 2008). Multi-channel marketing of

retailers is defined in this paper as “market oriented management of retailers using a multitude

of parallel and integrated information, communication, and distribution channels” (Möhlen-

bruch/Schmieder 2004, p. 104). This includes the strategic planning and operational application

of the whole marketing-mix of retailers with the objective to develop new distribution channels

or to strengthen existing ones, respectively. While strategic retail management establishes new

potentials for success, operational retail management is geared to tap the full potential of exist-

ing chances for success and defines the operational instruments to serve as strategic pillars

(Ahlert 2002).

The integration of different channels with an otherwise homogeneous system allows retailers to

meet the multi-optional behavior of consumers and their differentiated needs during the respec-

tive phases of a buying process (Schramm-Klein 2003; Möhlenbruch/Schmieder 2004). There

are potentials for integrated multi-channel systems, especially during the initiation phase, for

upscale products and distance selling (Baal/Hudetz 2007). Additional customer acquisition,

retention and win-back potentials open up through the integration of distance channels, the

expansion of market areas and the chance to meet the channel-specific preferences of cus-

tomers (Schröder 2005). Furthermore, empirical studies prove a higher loyalty of consumers to

integrated Multi-Channel-Systems (compared to mono- or multiple-channel retailers) and high-

er turnover per customer and therefore invalidating the fear of channel cannibalization

(Ahlert/Hesse 2003; Baal/Hudetz 2004; Wegener 2008). According to these findings, multi-

channel retailing allows for increasing market share at the expense of competitors’ (Schramm-

Klein 2003; Schröder 2005). The combination of different channels can also build trust and

enlarge the perceived service competence. Additionally, the integration of innovative channels

can help to vitalize the brand image and demarcate markets (Wegener 2008). Last, but not least,

the potential to decrease costs in communication and market research through direct- and indi-

vidual customer approaches and an active navigation of interaction to the most efficient chan-

nel should be mentioned (Schröder 2005). On the other hand, channel conflicts and a lack of

channel flexibility are potential risks of multi-channel strategies (Kilcourse 2008). If synergetic

effects and goodwill transfer are seen as important goals of an integrative branding of market-

ing channels it is obvious that negative experiences can also have unwanted effects on the whole

4 European Retail Research, Vol. 24, Issue I, pp. 1-26

system (Hurth 2002). Imperfect channel integration can complicate communication with cus-

tomers and can lead to confusion in cases of incoherent goods and services, image positions,

levels of prices, and service quality in the respective channels (Möhlenbruch/Schmieder 2002;

Ahlert/Hesse 2003; Kreutzer 2008).

Integrative planning, monitoring and controlling of different channels and their differentiated

sale- and handling processes, combined with the necessary rearrangement of cross-channel

customer contacts, implies a high coordination effort and often leads to the limiting of integra-

tion efforts to standardized purchase transactions (Ahlert/Hesse 2003; Wegener 2008). Realiz-

ing the already mentioned potentials for success, however, requires increased effectiveness of

market cultivation as well as using efficiency- and synergy effects (Bachem 2004). While the

first is dependent on a consistent perception of the retail brand in all channels, integrated mer-

chandise planning, control systems and customer relationship management system are basic

prerequisites for the second (Hurth 2002; Böing et al. 2003). This requires a corresponding

infrastructure, cross-channel coordination of the marketing-mix, and a relocation of channel-

specific marketing budgets (Hansen/Madlberger 2007). The knowledge of customer needs and

their basic trends gains importance in the specific market environment of retailing (Möhlen-

bruch et al. 2007; Promondo 2007). Multi-channel retailers have to use all contact points with

their customers to gather relevant information concerning buying behavior and have to combine

this with a comprehensive and differentiated picture of consumers (Schröder 2005). In chapter

3 we will analyze the specific contributions of Web 2.0 applications to the already mentioned

requirements, tasks and goals of multi-channel marketing.

3. Foundations of Web 2.0

The internet and associated technologies are developing rapidly. Consequently, the portfolio of

technical resources for the effective and efficient ascertainment, archiving, processing, and

transmission of data, information and knowledge is continuously growing. Accordingly, the

electronic realization of business processes through electronic media has obtained more and

more economic relevance for an increasing number of vendors in the last years (Lihotzky

2003). Many of the technological changes are summarized under the term “Web 2.0”, which is

not yet precisely defined. Most of the attempts to define Web 2.0 go back to a definition of

O’Reilly, who understands the term more as an approach than a technology (O’Reilly 2005).

Even though there is no precise definition, most publications seem to agree in the characteriza-

tion of the central idea of Web 2.0: Internet users transform from passive consumers of mostly

static content to active, content producing and distributing participants (Kreutzer/Merkle 2008).

According to O’Reilly (2005), there are a number of other characteristic requirements for appli-

cations belonging to the term Web 2.0:

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 5

- The application is net based; only a web browser is essential.

- The content is not static but is going to be dynamically generated. It will change depending

on the input of the user.

- There are possibilities for users to generate content by themselves.

- Role and authorization models enable the differentiation of who is enabled to view which

content and who is allowed to edit the information.

- Users own their data and are able to edit it by themselves. There are possibilities for personal-

ized content and layout.

- Users are able to comment on articles by other people and communicate among each other.

- A strong community feeling is going to develop between users.

Since economic and technical principles are as important for Web 2.0 applications as socio-

economic, psychological and legal aspects, it’s safe to say that the limitation of the phenomenon

Web 2.0 to specific instruments or technologies is not valid. In fact it is rather based on a modi-

fied attitude towards electronic media on the whole and the internet in particular (Kollmann/

Häsel 2007; Möhlenbruch et al. 2007). To discuss the specific potentials of Web 2.0 applications

for multi-channel marketing for retailers later on, it first seems necessary to take a closer look at

the paradigms and underlying motivational structures of internet users. Due to the dynamic

changes in electronic media the following explanations can make no claim to be complete.

Efficient search-engines, open interfaces and usability of web-based software gain in impor-

tance by enabling user self-service and orientation (Alby 2008; Kreutzer/Merkle 2008; Töpfer

et al. 2008). This technological development combined with growing user participation enable

new possibilities for personalization and individualization and therefore a consequent orienta-

tion on the differentiated consumer needs (Schenk 2007). Moreover, internet applications are

increasingly based on user-generated content and have to open themselves for participation

(O’Reilly 2005; Schenk 2007). At the same time Web 2.0 is changing the proportions between

individuality and collectivity, culminating in a virtual collective intelligence which is learning

with every new participator (Richard 2008). Additional benefits in terms of knowledge quality

improvement are generated through collaborative inspection, systematization and validation of

information on the internet (Kollmann/Häsel 2007). Those benefits increase, according to Met-

calfe’s Law, with the number of active internet users (network effects) which develop a sense of

community over the time (Möhlenbruch et al. 2008). Nevertheless, Web 2.0 applications have

to be understood as a part of a continuous development process which is not an expression of

defective planning but of inherent adaption flexibility (Kollmann/Häsel 2007). Simplicity and

lightweight user interfaces of net-based software applications have relatively low hardware

requirements for end-user devices and boost an increasing convergence of the internet, tele-

vision and mobile telephony (Kollmann/Häsel 2007). Open interfaces and technologies like

AJAX enable the combination of separated (knowledge) resources as well as the cross-linking

of interactive information and collaboration (O’Reilly 2005; Souders 2007).

6 European Retail Research, Vol. 24, Issue I, pp. 1-26

It has to be mentioned that user generated content and the joint development of open source

software create specific problems concerning copyrights. On the one hand it is essential to pro-

vide open licenses to benefit from the collective cooperation in communities but on the other

hand there are growing concerns of users about the (commercial) use of personalized data, con-

tent and applications (O’Reilly 2005). But it’s not enough to limit the view on new technologi-

cal options of participating users, in fact it’s necessary to take a closer look at the motivation of

users to participate and provide information and content (Schenk 2007). Self-expression and

image cultivation by publishing, for example, one’s own interests, opinions or achievements are

the driving factors for providing user generated content (Mühlenbeck/Skibicki 2008). This is

closely connected to a general talkativeness of some individual users and their desires for (vir-

tual) contacts. Needs can be satisfied through Web 2.0 in manifold ways (Sassenberg 2008).

Furthermore there are a lot of platforms like Second Life or Weblin which allow users a tem-

porarily escape from reality (escapism) and enable them to present themselves in a way they are

prevented from doing in real life (Kreutzer/Merkle 2008). Since the number of active partici-

pants in Web 2.0 is much lower in proportion to passive content consumers, and the quality of

additional benefits and network effects depends on the amount and quality of user-generated

content, provider and other business models should try to satisfy the commercial motives of

users in order to reward their content supply (Drüner et al. 2007). While searching for relevant

information during buying decisions reduces transaction costs, consumer-generated content

helps the social orientation and reduces the social risks of buying decisions. Moreover, there is

a strong bonding phenomenon inside social communities, even for passive users who often pro-

vide each other additional technical assistance for the use of products or services (Hennig-Thu-

rau 2005). The paradigms described above lead to a number of applications often linked to the

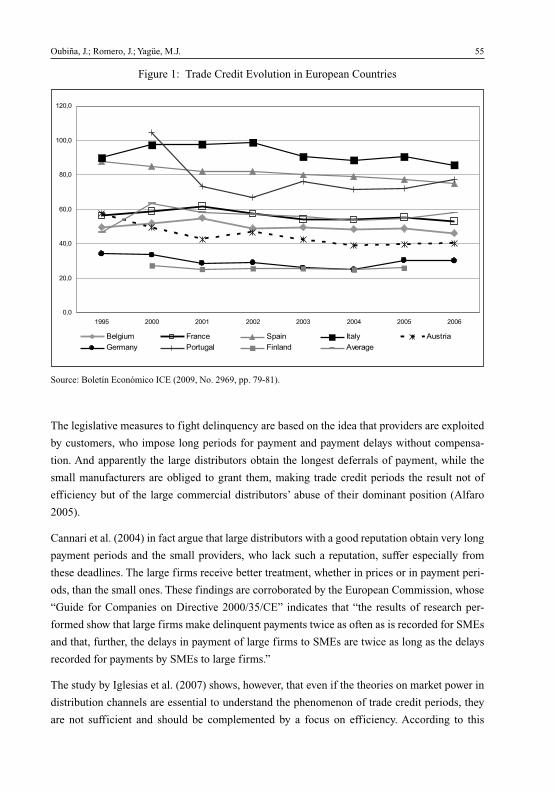

term Web 2.0 (see Figure 1).

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 7

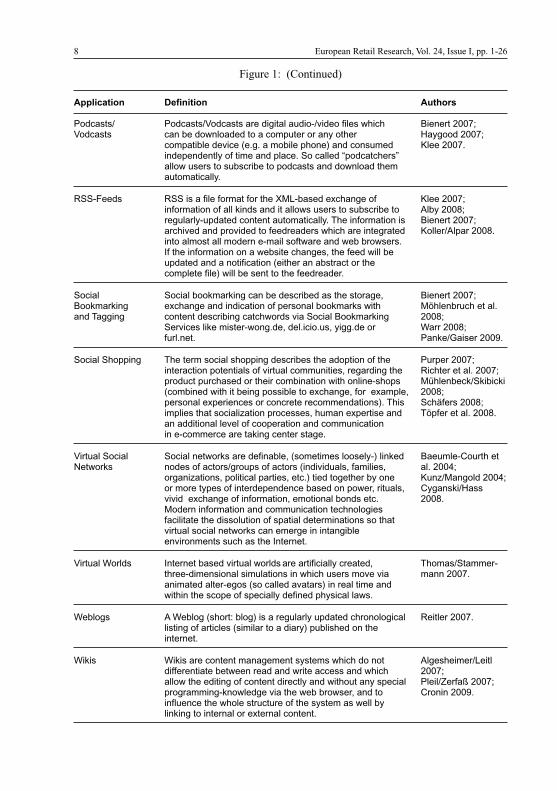

Figure 1: Description of Web 2.0 Applications

Application Definition Authors

Customer Reviews Virtual opinion platforms are special forms of virtual Richter et al. 2007;and Virtual Opinion communities and offer users features to evaluate revue Baumgarth 2008;Platforms and/or comment the service-performance or product Enderle/Wirtz 2008;

quality. Customer reviews are able to influence the Töpfer et al. 2008.buying decision process and enable companies tocommunicate a high level of transparency.

Mashups Mashups are (re-)combinations of different, technically Alpar et al. 2007; independent internet applications (or their content, Alby 2008; respectively) to a new service. The individual services Emrich 2008; are linked on the basis of open interfaces and generate Möhlenbruch et al. added value by connecting different bits of content 2008;(like store locations or transparent price comparison e.g.). Hudson-Smith et al.

2009.

(Continued at p. 8)

8 European Retail Research, Vol. 24, Issue I, pp. 1-26

Figure 1: (Continued)

Application Definition Authors

Podcasts/ Podcasts/Vodcasts are digital audio-/video files which Bienert 2007;Vodcasts can be downloaded to a computer or any other Haygood 2007;

compatible device (e.g. a mobile phone) and consumed Klee 2007.independently of time and place. So called “podcatchers”allow users to subscribe to podcasts and download themautomatically.

RSS-Feeds RSS is a file format for the XML-based exchange of Klee 2007;information of all kinds and it allows users to subscribe to Alby 2008;regularly-updated content automatically. The information is Bienert 2007;archived and provided to feedreaders which are integrated Koller/Alpar 2008.into almost all modern e-mail software and web browsers.If the information on a website changes, the feed will beupdated and a notification (either an abstract or thecomplete file) will be sent to the feedreader.

Social Social bookmarking can be described as the storage, Bienert 2007; Bookmarking exchange and indication of personal bookmarks with Möhlenbruch et al. and Tagging content describing catchwords via Social Bookmarking 2008;

Services like mister-wong.de, del.icio.us, yigg.de or Warr 2008;furl.net. Panke/Gaiser 2009.

Social Shopping The term social shopping describes the adoption of the Purper 2007; interaction potentials of virtual communities, regarding the Richter et al. 2007;product purchased or their combination with online-shops Mühlenbeck/Skibicki(combined with it being possible to exchange, for example, 2008;personal experiences or concrete recommendations). This Schäfers 2008;implies that socialization processes, human expertise and Töpfer et al. 2008.an additional level of cooperation and communicationin e-commerce are taking center stage.

Virtual Social Social networks are definable, (sometimes loosely-) linked Baeumle-Courth etNetworks nodes of actors/groups of actors (individuals, families, al. 2004;

organizations, political parties, etc.) tied together by one Kunz/Mangold 2004;or more types of interdependence based on power, rituals, Cyganski/Hassvivid exchange of information, emotional bonds etc. 2008.Modern information and communication technologiesfacilitate the dissolution of spatial determinations so thatvirtual social networks can emerge in intangibleenvironments such as the Internet.

Virtual Worlds Internet based virtual worlds are artificially created, Thomas/Stammer-three-dimensional simulations in which users move via mann 2007.animated alter-egos (so called avatars) in real time andwithin the scope of specially defined physical laws.

Weblogs A Weblog (short: blog) is a regularly updated chronological Reitler 2007. listing of articles (similar to a diary) published on theinternet.

Wikis Wikis are content management systems which do not Algesheimer/Leitl differentiate between read and write access and which 2007;allow the editing of content directly and without any special Pleil/Zerfaß 2007; programming-knowledge via the web browser, and to Cronin 2009.influence the whole structure of the system as well bylinking to internal or external content.

4. Web 2.0 in Multi-Channel Retailing

Assuming a sustainable influence of Web 2.0 on consumer behavior, suppliers will have to meet

those developments (Graßmann 2004). The differentiation between strategic and operational

fields of Web 2.0 applications in multi-channel retailing, used to systemize the following state-

ments cannot always be mutually exclusive and exhaustive - a problem of demarcation that

Ahlert (2002), using the example of information in retail-management, illustrates that which

“do not per se have a strategic or an operational character”.

4.1. Strategic Potentials

As mentioned before, retailers find themselves in an increasingly dynamic and discontinuous

environment, a situation that requires and complicates long-term strategies at the same time. A

key responsibility of strategic planning is to secure existing potentials and to develop new ones

for success in the already mentioned areas of retail management (Ahlert/Kenning 2007).

4.1.1. Market Research

Marketing decisions require an adequate information background, especially in view of actual

and prospective buying behavior, its principles and variability (Bänsch 2002). A comprehensive

understanding of customer needs and preferences can lead to significant advantages in competi-

tion (Zboralski/Gemünden 2004). Accordingly, the collection of information about customers and

their behavior via interactive media gains importance for retailers (Möhlenbruch/Schmieder

2004). This applies especially for multi-channel retailers which, in the ideal case, manage to col-

lect information about their customers at every contact point (Schröder 2005; Emrich 2008).

Hence Web 2.0 instruments can be used as subjects of research (e.g. the exploration of virtual

communities in view of consumer behavior) and as platforms for research (e.g. investigation of

market acceptance of innovative products) (Kunz/Mangold 2004). User-generated content, espe-

cially, allows deep insights into customer requirements and gives access to information about

(potential) consumers (Drüner et al. 2007; Stampfl 2007). Systematic monitoring of blogs,

forums, tagging platforms or virtual communities delivers information about company-, product-

or brand-image, for example, and allows the researcher to detect social trends, changing lifestyle

concepts or hints about the general change in values (Drüner et al. 2007; Ammann/Bentele 2008).

In addition there are new approaches for the categorization of consumers in the context of cus-

tomer value analyses created through the monitoring of user-generated content in communities,

blogs or forums (Stampfl 2007). The collected data can be used to develop user-, consumption-

and preference-profiles or to identify lead users (Drüner et al. 2007). While the transfer of

industry driven lead-user concepts to consumer goods marketing is considered to be difficult

due to the multitude of potential customers and the wide range of goods and services, the mon-

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 9

itoring of Web 2.0 creates new approaches to lead-user identification in the retail business

(Ernst et al. 2004). Once identified, relevant content of specific users has to be analyzed in view

of use- and object-knowledge, trend leadership and innovativeness. Similar potentials open up

for customer lifetime value analyses. Taking the social position of users in virtual communities

and their influence potentials on other members into account can lead to completely deviant

customer categorizations (compared to a limitation of the examination on the values of, for

example, sales taken place) (Stampfl 2007). Additionally Web 2.0 allows one to contact relevant

(groups of) customers directly after their identification because, unlike traditional market

research and futurology methods, it connects the information directly to its author (Drüner et al.

2007; Herstatt/Sander 2004). Further dialog can be used to gather additional information

regarding innovation processes, for example, or the (de)listing of products and services, how-

ever, the utilization of Web 2.0 instruments for market research creates specific difficulties as

well. First of all it has to be decided whether to choose a (passive) observation of blogs, commu-

nities etc., or an (active) dialog-oriented exploration (Herstatt/Sander 2004). An active

approach would be pointless without the previous identification of suitable interaction partners,

their approval, and the resources required for individual communication. Similar difficulties

result from the complex task of filtering the relevant information from the enormous multitude

of data. This is shown by Koller/Alpar (2008) in an analysis of selected blogs, where less than

0.5% of private posts dealt with companies, but those usually contained valuable information.

While manual filtering requires a lot of time and resources, automatic scanning methods are not

yet able to assure adequate data quality. Once identified, interesting blogs can be monitored rel-

atively resource-friendly via RSS feeds (Koller/Alpar 2008).

Problems in data quality are one of the major points of critique in online market research and have

to be taken into account in results evaluation (Emrich 2008). It has to be questioned whether or

not users of Web 2.0 applications can build representative samples for general analyses of con-

sumer behavior (Kunz/Mangold 2004). This gets even more important when explorations are lim-

ited to company-owned or topic-specific applications to ensure the exclusivity of the results or

the efficiency of the survey (Ernst et al. 2004). The sheer number of more than 60 million

weblogs with more than 1.2 million daily posts in 2007 (Drüner et al. 2007) demonstrates the

potentials for information as well as the difficulty in identifying relevant data. The results have to

be critically examined in view of representativeness as well. Therefore it does not seem to be

advisable to substitute traditional market research methods through the analysis of Web 2.0 appli-

cations. Rather, it is suggested to use their specific potential to get insights on trends or to include

consumers into innovation processes (Herstatt/Sander 2004; Drüner et al. 2007).

4.1.2. Communication

The integration of new media into consistent communication strategies comprehensive to all

channels is one of the main challenges of multi-channel marketing (Möhlenbruch/Schmieder

10 European Retail Research, Vol. 24, Issue I, pp. 1-26

2004). In this regard, the potentials of Web 2.0 range from the direct one-to-one dialog between

companies and their relevant stakeholders as well as internal knowledge transfer, up to the com-

munication between customers amongst each other (Bughin/Manyika 2007; Kreutzer 2008).

There are application fields for RSS feeds in communication policy which, for example, allow

one to build an innovative, customized push channel as well as for communities, whose mem-

bers can be provided with additional information (Möhlenbruch et al. 2008). The user-initiated

subscription of feeds and thereby indicated preferences can be used to customize the communi-

cation with an individual customer across all channels. Blogs and their functions for comment-

ing on posts and linking to other blogs provide a fast and wide platform for communication and

can be an adequate basis for viral marketing campaigns (Langner 2007; Emrich 2008). Such an

advertising message can be placed in forums, blogs or communities and spreads out without

any additional costs to the initiator (Mühlenbeck/Skibicki 2008). Humans in social relation-

ships show, according to the sociological concept of “homophily”, similarities regarding their

level of education, social status and their buying preferences, and spread information mainly to

interested people in their environment (Mangleburg et al. 2004; Stampfl 2007). User-initiated

downloads and RSS subscriptoins of pod- and videocasts reduce waste coverage and allow for

the efficient measuring of diffusion rates simply by counting the numbers of accesses and

downloads (Mühlenbeck/Skibicki 2008). Because the message is delivered by one’s own circle

of acquaintances, viral marketing reduces the defensive demeanor of consumers against classi-

cal advertising messages and is able to increase the probability of cognition (Emrich 2008;

Mühlenbeck/Skibicki 2008). Although viral marketing is not bound to specific media in princi-

ple, Web 2.0 enlarges the possibilities for spreading information with enormous speed and

improved efficiency and allows one to influence personal opinions in the buying process (Hein

2007; Schelske 2007). Additionally, the chance increases that topics from the blogosphere or

virtual communities are adopted into the classic media, because Web 2.0 applications are more

and more included into the research done by the classic media (Töpfer et al. 2008). Neverthe-

less, sufficient added value for multipliers, additional incentives and an appealing presentation

of the content remain substantial conditions for viral marketing (Langner 2007). Besides, a con-

tinuous monitoring is necessary to observe the spreading and to influence the discussion by

active participation in case of need (Schönefeld 2006) and it has to be mentioned that there are

varying channel- and product-specific effects (for example, online purchases are nearly twice

as often influenced by viral marketing as offline purchases) of viral marketing (Riegner 2007).

4.1.3. Harmonization and Integration of Marketing Channels

The integration of different marketing channels into a consistent system is an important area of

responsibility for multi-channel marketing. Extensive knowledge about customers and markets

are fundamental for avoiding channel conflicts (Emrich 2008). The specific potentials of differ-

ent Web 2.0 applications to generate information have been stated already, but blogs and cus-

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 11

tomer diaries, especially, can help to identify critical incidents in view of channel integration

and should be mentioned again.

Against the background of the intangible elements of the retail business, the reliance of cus-

tomers towards a retail brand can be considered a key factor in retail-management

(Zentes/Morschett 2005). Because positive experiences in one marketing channel have effects

on the whole system of channels it can be assumed that the usage of Web 2.0 applications has

cross-channel positives. Those positives are especially based on a high credibility level of user-

generated content (Enderle/Wirtz 2008). In this regard, wikis, blogs and reviews, especially,

seem to be able to convey authenticity, reliability and transparency (Richter et al. 2007). To

meet the consumer’s expectations, particular care must be taken in regard to the safety of user-

specific information and to the non-restrictive publication of even negative opinions (Möhlen-

bruch et al. 2008; Schnieders 2008). At the same time, Web 2.0 applications can be used to sup-

port cross-channel marketing campaigns. Virtual worlds, for instance, could support real events

or product presentations in an interactive, 3-D environment (Thomas/Stammermann 2007).

4.1.4. Internal Communication and Knowledge Management

Web 2.0 applications also show great promise for internal communication in complex organiza-

tions facing dynamic environments (Warta 2007). As described before, this characterization

applies especially to multi-channel-retailers. Wikis and blogs for example are able to accelerate

communication and collaboration processes and can be cost-saving alternatives to commercial

knowledge management systems (Algesheimer/Leitl 2007; Drüner et al. 2007). Those instru-

ments are especially able to build location-independent communities of practice, to contribute

to organizational learning and to globalize company-specific knowledge in a decentralized

structure (Zboralski/Gemünden 2004; Schütt 2007).

Internal blogs can be used to announce product decisions and to discuss them with branch man-

agers or suppliers in order to include their field-specific knowledge into decision making. Staff

blogs on internal platforms allow employees to document their work, search problem-specific

information and contact persons or to identify best-practice alternatives inside the organization

(Algesheimer/Leitl 2007). In addition, the amount of internal waste coverage by unspecific e-

mail can be reduced through RSS feeds. Wikis could, too, by the construction of a company-

specific knowledge and information platform or they could serve as a continuous basis for

exchange and collaboration, training or further education (Oeltjen 2005; Bienert 2007; Warta

2007). Their main advantage is the objectification of subjective knowledge resources through

collective validation and improvement of existing information (Müller 2008). Since the neces-

sary software is usually open source, free of charge and easy to use, Web 2.0 instruments are

often more cost-effective than commercial applications (Algesheimer/Leitl 2007). Neverthe-

less, the lower number of potential users of internal wikis limits their growth speed and requires

12 European Retail Research, Vol. 24, Issue I, pp. 1-26

active promotion by the executives to secure a successful implementation. The necessary com-

mitment on the part of the management, however, can be limited because this approach towards

self organized communication and knowledge management defies direct control, makes expert

knowledge available corporation wide and flattens hierarchies (Warta 2007; Müller 2008). To

avoid the misuse of sensitive data, specific access rights for different staff levels and rigid user

administration have to be assured - which erects barriers and reduces the growth speed of inter-

nal wikis even more (Oeltjen 2005).

4.1.5. Acquisition of New Target Groups and Customer Retention Management

Against the background of the dynamic market environment of retail business, retail manage-

ment attaches high importance to the “acquisition of new target groups” and “customer reten-

tion management” objectives (Möhlenbruch/Schmieder 2004). The potential contributions of

Web 2.0 to meet those objectives are mainly based on the ability to enable interactive commu-

nication between retailers and (potential) customers as well as among customers themselves

(Drüner et al. 2007; Ammann/Bentele 2008; Kreutzer/Merkle 2008). This can be illustrated

with the example of a telecommunication company which was able to raise the speed of the

acquisition of new customers up by a factor of five by addressing community members having

contact with steady customers (Stampfl 2007). Web 2.0 is especially able to increase the level of

awareness of retail brands in young target groups with a high affinity for the internet (Wegener

2008; Thomas/Stammermann 2007). Based on the assumption that perceived interactivity of a

website goes along with a more positive brand- and company image and an increasing involve-

ment of users into the communicated content (Gerpott 2004; Lueg et al. 2006), it can be

assumed that there are positive effects of Web 2.0 on customer retention management. Besides

the use of communities (esp. company-owned communities) which are able to increase the den-

sity of communication, design of an interactive brand environment and expanding the customer

relationship on an emotional level; pod- and videocasts, RSS feeds or wikis can affect customer

retention in a positive way (Wirtz 2001; Kunz/Mangold 2004; Möhlenbruch et al. 2008). While

communities enable retailers to provide customers with additional and emotionally charged

information during the post-purchase phase (Klee 2007), wikis and their user generated content

can be used to replace FAQs and act as a first source consulted by customers in case of prob-

lems (Pleil/Zerfaß 2007). Furthermore, the cooperative buying processes in social shopping

enhance the tendency for cross- and re-buying, the recommendations of other community mem-

bers affect trust and customer loyalty, and the emerging social bonds create switching costs

(Hsieh et al. 2005; Möhlenbruch et al. 2008; Verhoef et al. 2009). Additionally, there are inter-

esting perspectives to identify constraining factors for successful customer retention manage-

ment via customer diaries or blogs, respectively. The chronological listing and the detailed

description of customer contacts allow for the identification of crucial experiences and to dis-

play them as whole chains of events. The systematic comparison of different customer diaries

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 13

can provide an overall picture of the customer experience and become the basis for uncovering

drivers of enthusiasm and frustration (Bauer et al. 2008). Those findings can then be transferred

into strategic recommendations to optimize customer experiences. This field of application

gains importance against the background of the heretofore mentioned problems regarding the

integration of different marketing channels into an integrated multi-channel-system and multi-

channel-behavior.

Those positive effects of Web 2.0 instruments for customer retention management and the

acquisition of new target groups come along with the risk of negative expressions of opinions

and spill-over effects on other customers (Herstatt/Sander 2004). Furthermore, attempts at

manipulation of communities can be perceived as annoying by their members (Möhlenbruch et

al. 2008). Multi-channel retailers should also try moderate dosages of the interaction potentials

of Web 2.0 and to regard it as situational to avoid additional negative attitudes caused by cogni-

tive overload (Gerpott 2004). It is also disputable that retailers will always succeed with build-

ing their own virtual communities because their wide product ranges and heterogeneous target

groups reduce the chance to reach a critical mass of community members with equal interests.

To avoid this, thematic networks could be a solution.

4.2. Operational Potentials

Multi-channel marketing includes the operational planning, implementation and evaluation of

all demand-orientated instruments: those that contain merchandise, price and communication

(Barth et al. 2007).

4.2.1. Merchandise

The orientation by retailers on customer value gains importance because of the competitive

environment and high failure rates of market launches for consumer products (Ernst et al. 2004;

Zboralski/Gemünden 2004). There are interesting fields of application for Web 2.0 instruments

in view of the differentiation potentials of merchandise accruing from the analysis of user-gen-

erated content. On the one hand, Web 2.0 enables retailers to detect wishes, needs and trends

(for example, through passive monitoring of communities, blogs, social bookmarking plat-

forms), while on the other hand it allows them to directly integrate customers into product

(range) development processes (Schönefeld 2006; Schnieders 2008). A representative survey

about the buying behavior of Germans regarding distance selling verifies that consumers want

their needs to be taken into account and that they are willing to participate in innovation

processes (Promondo 2007). This would secure the consequent orientation towards customer

value and could contribute to cost efficiency, reduced development times and accelerated mar-

ket launches (Bartl et al. 2004; Algesheimer/Leitl 2007). It additionally communicates close-

14 European Retail Research, Vol. 24, Issue I, pp. 1-26

ness to customers and can therefore have a positive effect on company image and customer

acquisition (Herstatt/Sander 2004).

RSS feeds enable a customized information supply about product availability and additional

services and the information displayed about preferences can be used to optimize the product

line (Möhlenbruch et al. 2008). Accordingly, this can help to optimize goods in stock and gen-

erate cross-selling effects. The German multi-channel retailer “Tchibo” follows an interesting

approach to customer integration into its internal processes with the “Tchibo-Ideas” communi-

ty, www.tchibo-ideas.de, a platform where users can post interesting innovations and participate

in idea competitions. It is intended to check innovative ideas in view of technical feasibility and

to realize them in collaboration with the inventor. Even though Tchibo ideas has engendered no

successful product launch yet, the potentials in principle and the willingness to participate are

proven by the number of 4,500 registered members. But this approach requires the uncondition-

al clarification of patent and copyright issues and it seems to be necessary to offer added value

in monetary form or at least in form of detailed feedback to secure the long lasting participation

of users (Zboralski/Gemünden 2004). The level of openness in a community is a tightrope walk.

Free access opens a community to a wide range of target groups and enlarges the potential for

innovation but this allows access for competitors as well (Ernst et al. 2004). Additionally, the

inclusion of customers into innovation processes can encounter internal opposition which can

manifest itself in specific defense mechanisms of the organization against outside ideas (Bartl

et al. 2004). Furthermore, examples from industry areas hint that there is often not enough

innovation potential inside open communities to actually lead to new products (Herstatt/Sander

2004).

4.2.2. Pricing

The rising importance of electronic business has already had a high impact on price manage-

ment (Wirtz 2001). There are not only new options to orientate pricing more exactly according

to the individual’s willingness to pay, but new ways to realize differentiated prices for cus-

tomized goods and services as well (Weiber/Weber 2002). Insufficient knowledge about the

willingness to pay made such pricing strategies difficult to implement. Monitoring of blogs,

forums and virtual communities can enlarge the basis of information and can simplify such

pricing decisions (Möhlenbruch et al. 2008). Customer oriented pricing can affect the perceived

price-performance risk and helps (along with price transparency and price consultation) to

transfer it to price satisfaction, which strengthens customer loyalty and can result in competitive

advantages (Diller 2005). Following this line of argumentation, customer reviews and rating

functions can increase the perceived price transparency and lower price-performance risks. This

also applies to social shopping, where user-initiated price discussions and collective buying

activities opens up interesting application fields in price policy (Möhlenbruch et al. 2008).

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 15

Nevertheless, passive monitoring in view of pricing can quickly become unprofitable because

companies and their pricing policies are seldom subjects of private blogs, forums or communi-

ties. Because value-added-services increase the perceived quality of buying experiences and

decrease price sensitivity, wikis and mashups can have positive effects in price policy, too, and

raise the probability of transfering website visitors into loyal customers (Panten 2005). Theoret-

ically, it is also possible to receive information about the willingness to pay via RSS feeds and

to inform customers about special offers and prices, but this contains the risk of directly inform-

ing competitors about one’s own actions as well. Research also shows that online-consumers are

less price sensitive provided there is non-price information available on brand, quality and prod-

uct features (Ailawadi et al. 2009).

4.2.3. Communication

The individual need of customers for guidance and advice depends on the breadth and depth of

the product mix and its complexity as well as on the necessity for explanations of the products

themselves (Madlberger 2004). This is the determining factor of the necessity for retailers to

have a counseling service. Research shows that the absence of social interaction is one of the

main reasons why many customers still avoid online shopping (Doolin et al. 2006; van Dolen et

al. 2007; Weathers et al. 2007). The quality of electronic counseling depends on the information

content and its didactic preparation, and therefore concerns web-design aspects and editorial

content creation as well. The ability of some Web 2.0 instruments to let users create content or

to embed third-party content proffers interesting fields of application for mashups, wikis, com-

munities and forums to shift retail functions (in this case counseling) over to the customers

themselves and therefore decreases costs. At the same time, retailers are able to reduce the per-

ceived high buying risks in online purchasing through the high levels of reliability and authen-

ticity shown by consumers to user-generated content (Laroche et al. 2005; Enderle/Wirtz 2008).

It must be mentioned though, that this comes with a loss of control for the retailer, especially

regarding statements made on third-party platforms (Hennig-Thurau 2005). Therefore, it seems

useful for companies to provide those functions on their own platforms in order to retain reac-

tivity and at least a limited amount of control in view of dissatisfied customers who expect

transparency, honesty and a satisfactory problem-solving orientation in cases of criticism

(Schnieders 2008). Those heretofore named fields of application for Web 2.0 in sales promotion

and advertising policy can be demonstrated with two examples: The German DIY-store “Horn-

bach” upgraded its website with discussion forums and podcasts and an extensive virtual

helpdesk where users could help each other (Michael/Rose 2008). Ikeafans.com is also an

example of an independent virtual community where members post decoration suggestions or

examples of use, describe their experiences with the furniture manufacturer or discuss the com-

pany and its policy in different forums. The presence of user generated content shows that com-

munities enable companies to get direct access to the wishes and needs of their potential cus-

16 European Retail Research, Vol. 24, Issue I, pp. 1-26

tomers and even get suggestions for example for visual merchandising or additional fields of

application. The “user-generated help” in cases of product-specific problems generates addi-

tional value for customers and therefore gains relevance in post-purchase marketing (Dellaro-

cas 2006; Enderle/Wirtz 2008; Schnieders 2008).

5. Conclusion and Implications

The previous chapters introduced several Web 2.0 instruments and analyzed their fields of

application in multi-channel marketing. The prevailing growth rates in the sector of Web 2.0

suggest that this is not just short-term hype, but rather a sustainable and strident evolution of the

information society, trending towards increasing levels of participation, information, and inte-

gration of internet users and an increasing influence of consumers on goods and services (Rieg-

ner 2007; Rölver/Alpar 2008). The version number in the term Web 2.0 already implies that this

is just an intermediate step in an ongoing development (Schnieders 2008). Even though some

instruments are currently only used by small user groups, it can be assumed that in the course of

the proceeding development of the internet and end-user devices there will be an ongoing diffu-

sion into all classes of population and age groups (Klee 2007). Even though this opens up inno-

vative perspectives for marketing, there is hardly any systematic utilization of potentials. This

might be the result of the dynamic and complex nature of the topic which contributes to the fact

that the innovation potentials of some instruments are widely accepted, but their whole range of

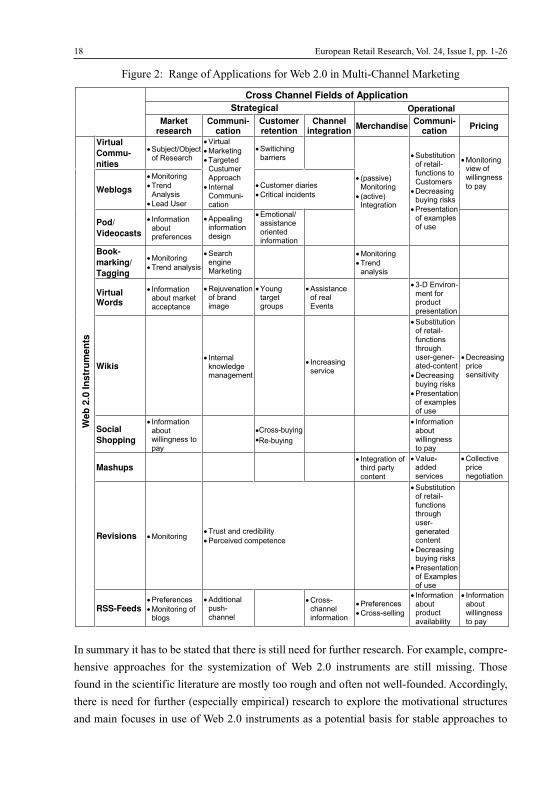

application fields is not yet identified. The following Figure 2 (see p. 18) shows the results of

this paper and categorizes the range of application fields for Web 2.0 instruments.

The potentials of Web 2.0 instruments accrue from the online channel and allow a manifold

strategic and operational cross-channel usage of their effects based on the interaction between

the different channels in integrated systems. It is therefore possible for multi-channel retailers

to create advantages in competition and increase the potentials for success with the addition of

this approach.

A general rating of the performance potentials of single instruments seems impossible against

the background of inhomogeneous target groups and the range of goods and services of multi-

channel retailers and will therefore be avoided. In fact it is advisable to give specific instru-

ments a thorough context sensitive check regarding the product range and the focused target

group. Although some instruments can be used as substitutes, a coordinated and differentiated

implementation of different Web 2.0 applications, in line with the market, can be considered

meaningful (Alpar et al. 2007; Enderle/Wirtz 2008). Their integration into aligned cross-media

communication strategies can even increase their potentials. Additionally, it seems to be appro-

priate to increase the positive effects of virtual communities for example by exclusive (live)

events for members.

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 17

18 European Retail Research, Vol. 24, Issue I, pp. 1-26

Figure 2: Range of Applications for Web 2.0 in Multi-Channel Marketing

Cross Channel Fields of Application

Strategie Operational

Marketresearch

Communi-cation

Customerretention

Channelintegration

Merchandise Communi-

cationPricing

We

b 2

.0 In

str

um

en

ts

Virtual

Commu-

nities

Subject/Objectof Research

Virtual

Marketing

Targeted Custumer Approach

InternalCommuni-cation

Switichingbarriers

(passive)Monitoring

(active) Integration

Substitutionof retail-functions to Customers

Decreasingbuying risks

Presentation of examplesof use

Monitoringview of willingnessto payWeblogs

Monitoring

Trend Analysis

Lead User

Customer diaries

Critical incidents

Pod/

Videocasts

Informationaboutpreferences

Appealing informationdesign

Emotional/assistanceoriented information

Book-

marking/

Tagging

Monitoring

Trend analysis

SearchengineMarketing

Monitoring

Trend analysis

Virtual Words

Informationabout marketacceptance

Rejuvenation of brand image

Young targetgroups

Assistanceof real Events

3-D Environ-ment forproductpresentation

Wikis Internalknowledge management

Increasingservice

Substitutionof retail-functions through user-gener-ated-content

Decreasingbuying risks

Presentation of examplesof use

Decreasingprice sensitivity

Social

Shopping

Informationaboutwillingness topay

Crossbuying

Re-buying

Informationaboutwillingnessto pay

Mashups Integration ofthird partycontent

Value-added services

Collective price negotiation

Revisions Monitoring Trust and credibility

Perceived competence

Substitutionof retail-functions through user-generated content

Decreasingbuying risks

Presentation of Examples of use

RSS-Feeds Preferences

Monitoring ofblogs

Additionalpush-channel

Cross-channel information

Preferences

Cross-selling

Informationaboutproductavailability

Informationaboutwillingnessto pay

In summary it has to be stated that there is still need for further research. For example, compre-

hensive approaches for the systemization of Web 2.0 instruments are still missing. Those

found in the scientific literature are mostly too rough and often not well-founded. Accordingly,

there is need for further (especially empirical) research to explore the motivational structures

and main focuses in use of Web 2.0 instruments as a potential basis for stable approaches to

Strategical

Cross-buyingRe-buying

a systemization of Web 2.0. While some instruments like blogs are used quite frequently and

have already become an important part of corporate communications, other instruments (e.g.

virtual worlds and internal wikis) are still in the stage of development and their fields of

application in multi-channel marketing should be seen as a learning arena. In this regard,

there is a lack of empiric research, e.g. regarding the interrelationship between real and virtu-

al buying behaviors. This applies to market research with Web 2.0 applications and the trans-

fer of lead-user-concepts from the field of industrial goods to consumer goods as well. There

is also a special need for systems for the automatic filtering of relevant posts in forums or

communities (Ernst et al. 2004; Herstatt/Sander 2004). Further difficulties in the practical use

of the described Web 2.0 instruments result from the limited controllability and measurability

of their profit contribution. This applies especially because positive effects will most likely

only appear over time and can hardly be resolved into isolated activities. Because the general-

ly necessary critical mass of participants is often hard to attain and in view of the dynamic

of consumer behavior, the question arises that some instruments like Second Life or other

specific communities might not have enough lasting potential to legitimate long term invest-

ments.

Strategic manipulation by third parties is another risk resulting from handling user-generated

content, reviews and the anonymity of the internet. Dellarocas even models a user-anticipated

manipulation through the retailer in a theoretical game analysis (Dellarocas 2006). Following

these thoughts, companies would actually be forced to manipulate ratings and reviews to match

their anticipated level of manipulation. But this would imply the additional risk of a substantial

loss of image and trust in case of exposure (Enderle/Wirtz 2008). It should also be noted

that, besides of the effects of Web 2.0 on consumer behavior and especially on click behavior,

“traditional” factors like the perceived cost/performance ratio, the urgency of the fulfillment of

demands, the financial situation or buying comfort will not lose their importance (Gerpott

2004).

One of the major tasks of multi-channel marketing in regard to Web 2.0 is therefore to assess

the specific risks and potentials of the different channels and their instruments in view of target

groups and offered goods as well as services, and to derive strategic investment decisions on

that basis. It is essential to consider the resulting changes concerning the increasing transparen-

cy, hierarchical conflicts and the necessary adjustments of company structures and resources.

Capitalization of interaction potentials of the respective Web 2.0 instruments in the context of

multi-channel strategies requires the renunciation of traditional mass-communication and a

new approach towards the identification of target groups. Even though a prognosis as to the

effects of the development of the internet on retail business seems impossible against the back-

ground of its dynamic, it appears that a great deal of adaptability is required to face changes in

the environment for retailers in the era of Web 2.0.

Möhlenbruch, D.; Blunck, D.E.; Ritschel, F. 19

References

Ahlert, D. (2002): Handelsinformationssysteme als Basis des operativen und strategischenHandelsmanagement, in: Möhlenbruch, D.; Hartmann, M. (eds.): Der Handel im Informa-tionszeitalter, Wiesbaden, pp. 53-77.

Ahlert, D.; Hesse, J. (2003): Das Multikanalphänomen - viele Wege führen zum Kunden,in: Ahlert, D.; Hesse, J.; Juliens, J.; Smend, P. (eds.): Multikanalstrategien, Wiesbaden, pp.3-32.

Ahlert, D.; Kenning, P. (2007): Handelsmarketing. Grundlagen der marktorientierten Führungvon Handelsbetrieben, Berlin.

Ailawadi, K.L.; Beachamp, J.P.; Donthu, N.; Gauri, D.K.; Shankar, V. (2009): Communicationand Promotion Decisions in Retailing: A Review and Directions for Future Research, in:Journal of Retailing, Vol. 85, No. 1, pp. 42-55.

Alby, T. (2008): Web 2.0. Konzepte, Anwendungen, Technologien, 3rd ed., Munich.

Algesheimer, R.; Leitl, M. (2007): Unternehmen 2.0, in: Harvard Business Manager, Vol. 29,No. 6, pp. 88-98.

Alpar, P.; Blaschke, S.; Keßler, S. (2007): Web 2.0. Neue erfolgreiche Kommunikationsstrate-gien für kleine und mittlere Unternehmen, Wiesbaden.

Ammann, P.; Bentele, M. (2008): Mit Fallbeispielen den Erfolgsfaktoren des Web 2.0 auf derSpur. Wie Kommunikationsgrenzen im B2B-Geschäft dank neuer Anwendungen überwun-den werden, in: io new management, Vol. 77, No. 9, pp. 44-48.

Baal, S.v.; Hudetz, K. (2004): Online Handel. Kannibalisierung oder Mehrumsatz?, in: ScienceFactory, Vol. 6, No. 3, pp. 1-5.

Baal, S.v.; Hudetz, K. (2007): Dem Kunden auf allen Kanälen begegnen, in: Science Factory,Vol. 9, No. 2, pp. 12-16.

Bachem, C. (2004): Die Rolle von Portalen im Multichannel-Marketing, in: Gentsch, P.; Lee, S.(eds.): Praxishandbuch Portalmanagement, Wiesbaden, pp. 137-156.

Baeumle-Courth, P.; Nieland, S.; Schröder, H. (2004): Wirtschaftsinformatik, Munich.

Bänsch, A. (2002): Käuferverhalten, 9th ed., Munich.

Barth, K.; Hartmann, M.; Schröder, H. (2007): Betriebswirtschaftslehre des Handels, 6th ed.,Wiesbaden.

Bartl, M.; Ernst, H.; Füller, J. (2004): Community Based Innovation - eine Methode zur Ein-bindung von Online Communities in den Innovationsprozess, in: Herstatt, C.; Sander, J.G.(eds.): Produktentwicklung mit virtuellen Communities, Wiesbaden, pp. 141-168.

Bauer, F.; Bössow, O.; Motschmann, K. (2008): Online-Tagebücher: Dem Kundenerleben aufder Spur, in: Planung & Analyse, Vol. 35, No. 1, pp. 40-43.

Baumgarth, C. (2008): Markenpolitik. Markenwirkungen - Markenführung - Markencontrol-ling, 3rd ed., Wiesbaden.

Bienert, J. (2007): Web 2.0 - Die Demokratisierung des Internet, in: IM Information Manage-ment & Consulting, Vol. 22, No. 1, pp. 6-14.

Böing, C.; Jullens, J.; Schrader, M.F. (2003): Customer Relationship Management im Multi-kanalvertrieb, in: Ahlert, D.; Hesse, J.; Jullens, J.; Smend, P. (eds.): Multikanalstrategien,Wiesbaden, pp. 33-65.

20 European Retail Research, Vol. 24, Issue I, pp. 1-26

Bughin, J.; Manyika, J. (2007): How businesses are using Web 2.0: A McKinsey Global Survey,New York.

Cronin, J.J. (2009): Upgrading to Web 2.0: An Experiential Project to Build a Marketing Wiki,in: Journal of Marketing Education, Vol. 31, pp. 66-75.

Cyganski, P.; Hass, B.H. (2008): Potenziale sozialer Netzwerke für Unternehmen, in: Hass, B.;Walsh, G.; Kilian, T. (eds.): Web 2.0, Berlin, pp. 101-120.

Dellarocas, C. (2006): Strategic Manipulation of Internet Opinion Forums: Implications forConsumers and Firms, in: Management Science, Vol. 52, No. 10, pp. 1577-1593.

Diller, H. (2005): Preisethik im Marketing, in: Herrmann, H.; Voigt, K.-I. (eds.): Globalisierungund Ethik, Heidelberg, pp. 35-50.

Dohmann, H.; Fuchs; Khakzar, K. (2002) (eds.): Die Praxis des E-Business. Technische,betriebswirtschaftliche und rechtliche Aspekte, Braunschweig, Wiesbaden.

Dolen, W.M. van; Dabholkar, P.A.; Ruyter, K. de (2007): Satisfaction with Online CommercialGroup Chat: The Influence of Perceived Technology Attributes, Chat Group Characteristics,and Advisor Communication Style, in: Journal of Retailing, Vol. 83, No. 3, pp. 339-358.

Doolin, B.; Dillon, S.; Corner, J.L. (2006): Determinants of Online Purchasing Behaviour, in:Hunter, G.; Tan, F. (eds.): Advanced topics in global information management, Hershey PA.,Vol. 5, pp. 199–225.