Embed Size (px)

Citation preview

PETROGAS GLOBALAnnual Report 2014

PETROGAS GLOBAL Annual Report 2014 3

PETROGAS GLOBALAnnual Report 2014

5

9

Chairman’s Review

The Applegreen Story

15

Directors’ Report and Financial Statements

PETROGAS GLOBAL Annual Report 2014 Chairman’s Review5

Chairman’s Review

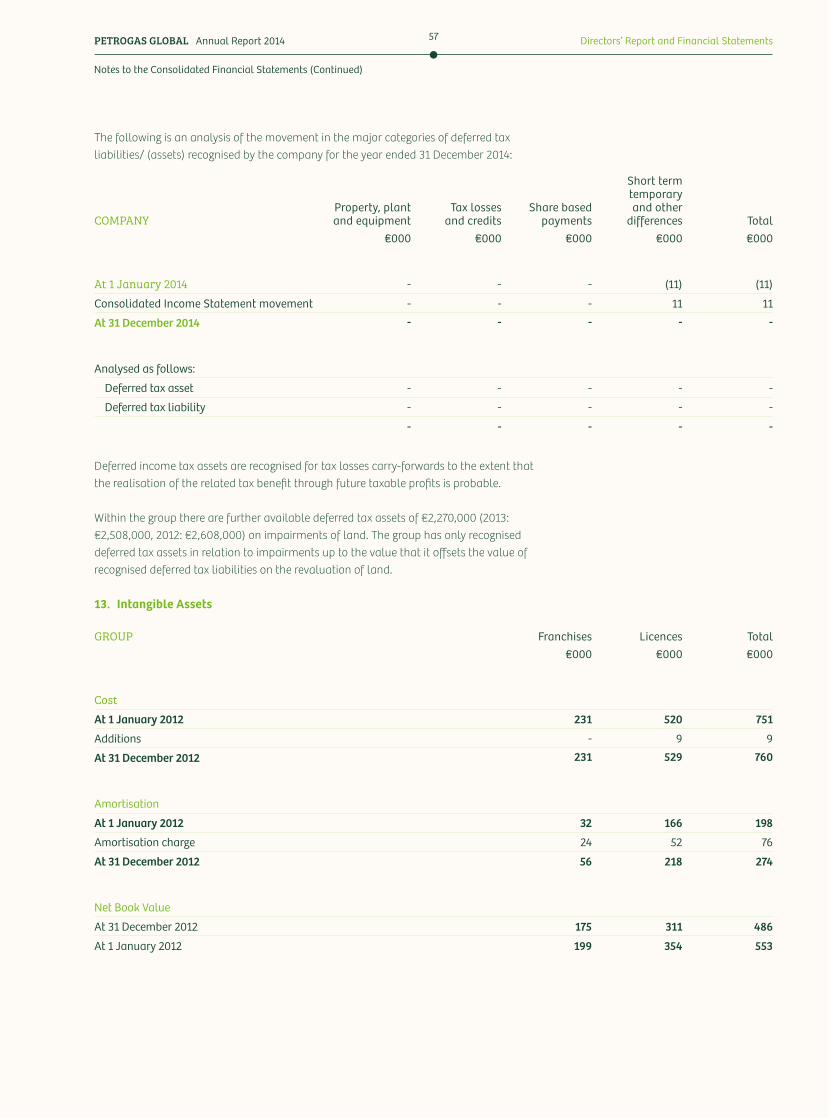

It was a refreshing change to be able to concentrate on

growing our business

We now have great momentum in our business

and we look forward to continuing to work with

you all and hopefully we will all enjoy

a successful journey together.

After many years of ba!ling against recessionary headwinds the storm abated in 2014 and we were able to fully exploit the skills and expertise of our talented staff.

6Chairman’s Review

Robert C EtchinghamChairman

PETROGAS GLOBAL Annual Report 2014 7

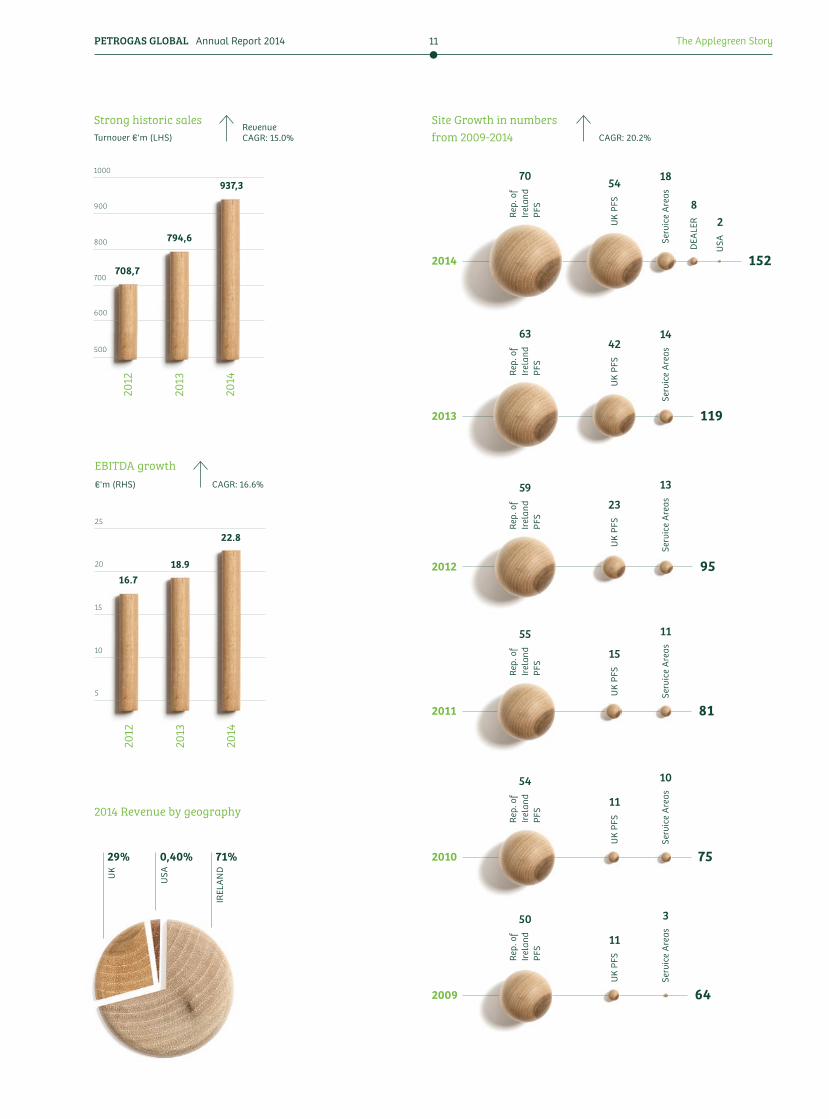

It was a year in which revenue for the Group grew by c. 18% compared to 2013 which resulted in a 20% increase in adjusted EBITDA. This was delivered through the upgrade and rebrand of 18 sites and in particular the addition of 31 new locations for the group across Ireland and the UK as well as 2 sites in a new market for the group in 2014, Long Island in the United States.

The upgrade programme comprised 10 in the Republic of Ireland and 8 in the United Kingdom. This involved the rebranding of the facility as Applegreen, significant upgrade to the internal facility and in particular the enhancement of the food offer. 17 new Subways units were added as part of this programme.

The expansion in the UK and Irish estate was made up by the following:

• Two new Motorway Service Areas (MSA) - the first opened in June on the M11 in Wicklow and the second in October on the M7 in Birdhill, Tipperary. Each of these were greenfield developments on property acquired by the Group.

• Two smaller service areas which had a significant food offer were developed and opened in Lemybrien, Co. Waterford in August and Swords in November.

• Seven Petrol Filling stations (‘PFS’) were also added in the Republic of Ireland as well as twelve new sites in the UK

• We commenced a dealer programme during the year whereby we sell fuel under our brand at sites owned by third parties and at the end of 2014 there were 8 dealer sites in operation.

A key feature of our development has been the development of the food offer within our business both through the development of partnerships with international food brands and the development of our own aCafe and Bakewell offers. At the end of 2014 in addition to our own brand food offer, which is present in the majority of our sites, we also had 12 Burger Kings, 8 Costa Coffees and 32 Subways in operation.

Chairman’s Review

Apart from the dealer project referred to above we also launched a commercial fuel card, LowFuelCard, which was well received by the market. As referred to above a further new initiative was the establishment of a small presence in Long Island, United States. This provides the group with a potential platform for expansion, in the medium term, in the north east of the United States.

Since the year end we have continued to develop and grow the business. In April we opened the first MSA in Northern Ireland on the M2 North of Belfast on one of four sites we acquired on the region’s motorway network. We have also developed two smaller service areas in the west of Ireland and added 10 other locations across Ireland, the UK and the U.S. We have also further developed our food business with the addition of 14 branded units across the estate. This included two new food offerings following the conclusion of franchise agreements with Chopstix and Greggs. Two Chopstix and four Greggs units were opened since year end.

As a business, we are fortunate to be operating at a time of unprecedented change in the forecourt industry. There are many and varied opportunities for our team to exploit and we commenced a major 'ramp up' of our activities during 2014, with a record capital investment programme. The Board continues to consider the appropriate levels of investment for future years and our options for funding them. This will be the major theme for us in 2015, as we are commi"ed to continuing to grow our earnings.

Finally on behalf of the Board I would like to thank the able and commi"ed group of employees, licensees, consultants and suppliers who have made the Applegreen business such a success over the years. We now have great momentum in our business and we look forward to continuing to work with you all and hopefully we will all enjoy a successful journey together.

PETROGAS GLOBAL Annual Report 2014 The Applegreen Story9

There are many and varied opportunities for our

team to exploit and we commenced a major

'ramp up' of our activities during 2014, with

a record capital investment programme.

The Applegreen Story

As a business, we are fortunate to be

operating at a time of unprecedented change

10The Applegreen Story

A key feature of our development has been the development of the food offer within our business.

PETROGAS GLOBAL Annual Report 2014 11 The Applegreen Story

2014 Revenue by geography

71%

IREL

AN

D

29%

UK

0,40%

USA

Site Growth in numbers from 2009-2014

2014

2013

2012

2011

2010

2009

82

18

14

13

11

10

3

70 54

42

23

15

11

11

DEA

LER

USASe

rvic

e A

reas

Serv

ice

Are

asSe

rvic

e A

reas

Serv

ice

Are

asSe

rvic

e A

reas

Serv

ice

Are

as

Rep.

of

Irel

and

PFS

Rep.

of

Irel

and

PFS

Rep.

of

Irel

and

PFS

Rep.

of

Irel

and

PFS

Rep.

of

Irel

and

PFS

Rep.

of

Irel

and

PFS

UK

PFS

UK

PFS

UK

PFS

UK

PFS

UK

PFS

UK

PFS

CAGR: 20.2%

152

119

95

81

75

64

RevenueCAGR: 15.0%Turnover €'m (LHS)

Strong historic sales20

12

2013

2014

1000

900

800

700

600

500

708,7

794,6

937,3

CAGR: 16.6%€'m (RHS)

EBITDA growth

2012

2013

2014

25

20

15

10

5

18.916.7

22.8

63

59

55

54

50

12

64Stations

Open 6 Motorway Service Areas (MSA)

Outsource transaction processing to EXL

in India

75Stations

Petrogas launches the Applegreen

brand

24Stations

Open first forecourt

in UK

53Stations

Distribution Centre opens

2005

2008

2009

2010

The Applegreen Story

Sausage Rolls sold 2014 - Total weight 64 Tones, Same weight as

10.5 Elephants.

The volume of coffee sold was 1,049,644 Litres, Enough coffee

to fill 583 fire trucks.

The Applegreen Story

13PETROGAS GLOBAL Annual Report 2014

Fuel card and dealer offering launched

Opened 2 sites in the USA

152Stations

157,000 loyalty card holders

95Stations

Launch loyalty card programme

81Stations

Complete refinance of business

Acquire 4 MSAsites in NI

119Stations2011

2012

2013

2014

Also our fries tonnage sold is the equivalent weight of 2 Boeing 757 Aircrafts.

The number of cookies sold in 2014 was 341726. Placed side by side they would be twice the height of Mount Everest.

If you place our whopper buns sold edge to edge they

would be taller than the Trump Tower in 2014.

The Applegreen Story

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements15

Directors’ Report

&Financial

Statements

Directors’ Report and Financial Statements 16

Contents

Directors’ Report / 17

Statement of Directors’ Responsibilities / 21

Independent Auditors’ Report to the Members of Petrogas Global Limited / 22

Consolidated Income Statement / 25

Consolidated Statement of Comprehensive Income / 26

Consolidated Statement of Financial Position / 27

Company Statement of Financial Position / 28

Consolidated Statement of Changes in Equity / 29

Company Statement of Changes in Equity / 30

Consolidated Statement of Cash Flows / 31

Company Statement of Cash Flows / 32

Notes to the Consolidated Financial Statements / 33

Directors and Other Information / 89

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements17

The directors present their annual report together with the audited group financial statements of Petrogas Global Limited for the year ended 31 December 2014.

Principal activities and review of the businessThe principal activity of the group is the operation of service stations throughout Ireland, the UK and the USA under the Applegreen brand. The details of the company’s subsidiaries and substantial undertakings are disclosed in Note 28. There has been no change in the principal activities of the subsidiary companies during the financial year.

The highlights of the group’s financial statements include:

• The growth in turnover of 18 % (2013: 12%) arose due to the expansion of the estate in Ireland and more particularly in the UK.

• During the year the company continued to open new trading sites including new motorway service areas on the M11 in Wicklow and the M7 at Birdhill. Works continued on two further motorway service areas on the M1 and M2 in Northern Ireland, one of which opened in March 2015.

• A major project to replace our existing site IT software continues and is expected to be fully completed in 2015.

• The group commenced trading in the USA on 9 April 2014 from two sites in Long Island. Performance to date has been encouraging.

• The group launched two new business streams during the year – a commercial fuel card business and a dealer operated network. Both streams have performed well during the year.

Results and dividendsThe directors do not recommend the payment of a dividend (2013: €nil; 2012 €nil).

Current tradingThe group continues to trade profitably.

Directors’ Report

2013 2013 2012

€000 €000 €000

Revenue 937,322 794,623 708,718

Profit for the year 12,279 14,650 6,853

Gross assets 176,659 131,920 134,740

Equity 17,655 3,329 (11,368)

Directors’ Report and Financial Statements 18

Events since the year end and future developmentsSince the year end, the group has opened four new sites in Ireland, two in the USA and one in the UK. In March 2015, the group entered into new banking arrangements with its senior lenders. These new agreements extend the maturity of the group’s debt and make additional facilities available to the group.

The group has entered into franchise arrangements with two new food offerings, Chopstix and Greggs, with the first sales taking place inMarch 2015 and April 2015 respectively.

Principal risks and uncertaintiesThe group’s general business activities may be affected by risks associated with all companies in the fuel distribution and retail sector. The group has identified the following risks specific to its business:

• The group operates in a highly competitive market, with competitors drawn from local and large scale multi-national corporations. To mitigate this risk, we focus on delivering superior service at a competitive cost to our customers. To facilitate this at a profitable level, we aim to have the best economies of scale in the industry with central purchasing and distribution.

• In the event of another economic decline the group may experience decreased customer demand.

• The group expands the business through a strategy of service station and site acquisitions and lease arrangements. The group’s growth may be hindered should it be unable to find a*ractive acquisitions or source the required financial facilities in the current banking environment.

• The storage and dispensing of hydrocarbon fuels can give rise to environmental damage and the cost of any clean-up can be considerable. The group has procedures in place to mitigate these risks, including fuel stock management and reconciliations.

• Severe weather conditions can impact average traffic volumes which would directly impact on the demand for the group’s products.

• The group operates in a highly regulated and legally stringent environment. Changes in environmental, health and safety, or governmental laws or regulations could result in significant additional costs to the group.

• Changes in the stability of financial institutions may lead to higher costs to be borne by the group. An increase in the costs associated with the group’s debt or an increase in financing costs could hinder the group’s growth.

• The financial crisis has heightened the need for effective capital management and the risk of insufficient liquidity can undermine an entity’s ability to develop and manage a robust business model. The group manages the risk of insufficient liquidity by liaising with its bankers regularly to ensure the availability of sufficient liquidity to allow the group to manage its growth aspirations effectively.

• The group currently operates in Pound Sterling and US Dollars as well as Euro. Any changes in the foreign exchange rate relative to the Euro could impact the group adversely.

Directors’ Report (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements19

The directors take such actions as they deem appropriate to minimise the group’s exposure to identified risks. The group’s financial risks are set out in note 24 to the financial statements.

DirectorsThe present members of the board of the company and those who held office during the year are:

Robert EtchinghamJoseph Barre#Michael O’LoughlinEugene Moore (appointed 11 February 2014)Paul Lynch (appointed 19 August 2014)Martin Southgate (appointed 11 February 2014)Brian Geraghty (appointed 19 August 2014)

In accordance with the articles of association of the company, the directors are not required to retire by rotation.

Interests of the directors/secretary in the groupDetails of the directors’ and secretary’s shareholdings, interests and transactions with the group are provided in note 28 to the financial statements.

Political donationsNo political donations were made during the current or prior year.

Books of accountThe measures taken by the directors to ensure compliance with the requirements of Section 202, Companies Act 1990, regarding proper books of account are the implementation of necessary policies and procedures for recording transactions, the employment of competent accounting personnel with appropriate expertise and the provision of adequate resources to the finance function. The books of account are maintained at the company’s head office, Block 17, Joyce Way, Parkwest, Dublin 12, and at various subsidiary offices.

AuditorsPricewaterhouseCoopers Chartered Accountants were appointed as auditors to the group during 2013. In Accordance with Section 160(2) of The Companies Acts 1963 to 2013, PricewaterhouseCoopers will continue in office.

Joseph Barrett

Paul Lynch

On behalf of the directors30 April 2015

Directors’ Report (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements21

Statement of Directors’ Responsibilities

The directors are responsible for preparing the Directors’ Report and the financial statements inaccordance with applicable Irish law. Under that law, the directors have elected to prepare the financial statements in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union.

Company law requires the directors to prepare financial statements for each financial year which give a true and fair view of the state of affairs of the company and of the group, and of the profit or loss of the group for that year. In preparing these financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the company will continue in business.

The directors confirm that they have complied with the above requirements in preparing the financial statements.

The directors are responsible for keeping proper books of account that disclose with reasonable accuracy at any time the financial position of the company and enable them to ensure that the financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union and Irish statute law

comprising the Companies Acts 1963 to 2013, and the European Communities (Companies: Group Accounts) regulations 1992.

The directors are also responsible for safeguarding the assets of the company and the group and hence for taking responsible steps for the prevention and detection of fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the corporate and financial information included on the company and group’s website. Legislation in Ireland governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

Joseph Barrett

Paul Lynch

On behalf of the directors30 April 2015

Directors’ Report and Financial Statements 22

Independent Auditors’ Report to the Members of Petrogas Global Limited

We have audited the financial statements of Petrogas Global Limited for the year ended 31 December 2014 which comprise the Consolidated Income Statement, the Consolidated Statement of Comprehensive Income, the Consolidated Statement of Financial Position, the Company Statement of Financial Position, the Consolidated Statement of Changes in Equity, the Company Statement of Changes in Equity, the Consolidated Statement of Cash Flows, the Company Statement of Cash Flows and the related notes. The financial reporting framework that has been applied in their preparation is Irish law and International Financial Reporting Standards (IFRSs) as adopted by the European Union and, as regards the parent company financial statements, as applied in accordance with the provisions of the Companies Acts 1963 to 2013.

Respective responsibilities of directors and auditorsAs explained more fully in the Directors’ Responsibilities Statement set out on page 6, the directors are responsible for the preparation of the financial statements giving a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with Irish law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

This report, including the opinions, has been prepared for and only for the company’s members as a body in accordance with Section 193 of the Companies Act, 1990 and for no other

purpose. We do not, in giving these opinions, accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

Scope of the audit of the financial statementsAn audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the group’s and the parent company’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the Directors’ Report to identify material inconsistencies with the audited financial statements. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Opinion on financial statementsIn our opinion:

• the group financial statements give a true and fair view, in accordance with IFRSs as adopted by the European Union, of the state of the group’s affairs as at 31 December 2014 and of its profit and cash flows for the year then ended;

• the parent company financial statements give a true and fair view, in accordance with IFRSs as adopted by the European Union as applied in accordance with the provisions of the Companies Acts 1963 to 2013, of the state of the parent company’s affairs as at 31 December 2014 and cash flows for the year then ended; and

• the financial statements have been properly prepared in accordance with the requirements of the Companies Acts 1963 to 2013.

Matters on which we are required to report by the Companies Acts 1963 to 2013• We have obtained all the information

and explanations which we consider necessary for the purposes of our audit.

• In our opinion proper books of account have been kept by the parent company.

• The Company Statement of Financial Position is in agreement with the books of account.

• In our opinion the information given in the Directors’ Report is consistent with the financial statements.

• The net assets of the parent company, as stated in the Company Statement of Financial Position, are more than half of the amount of its called-up share capital and, in our opinion, on that basis there did not exist at 31 December 2014 a financial situation which under Section 40 (1) of the Companies (Amendment) Act, 1983 would require the convening of an

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements23

extraordinary general meeting of the parent company.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the provisions in the Companies Acts 1963 to 2013 which require us to report to you if, in our opinion, the disclosures of directors’ remuneration and transactions specified by law are not made.

Kevin Egan for and on behalf of PricewaterhouseCoopers Chartered Accountants and Statutory Audit Firm Dublin

30 April 2015

Independent Auditors’ Report to the Members of Petrogas Global Limited (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements25

Year to 31 December

Year to 31 December

Year to 31 December

Notes 2014 2013 2012

€000 €000 €000

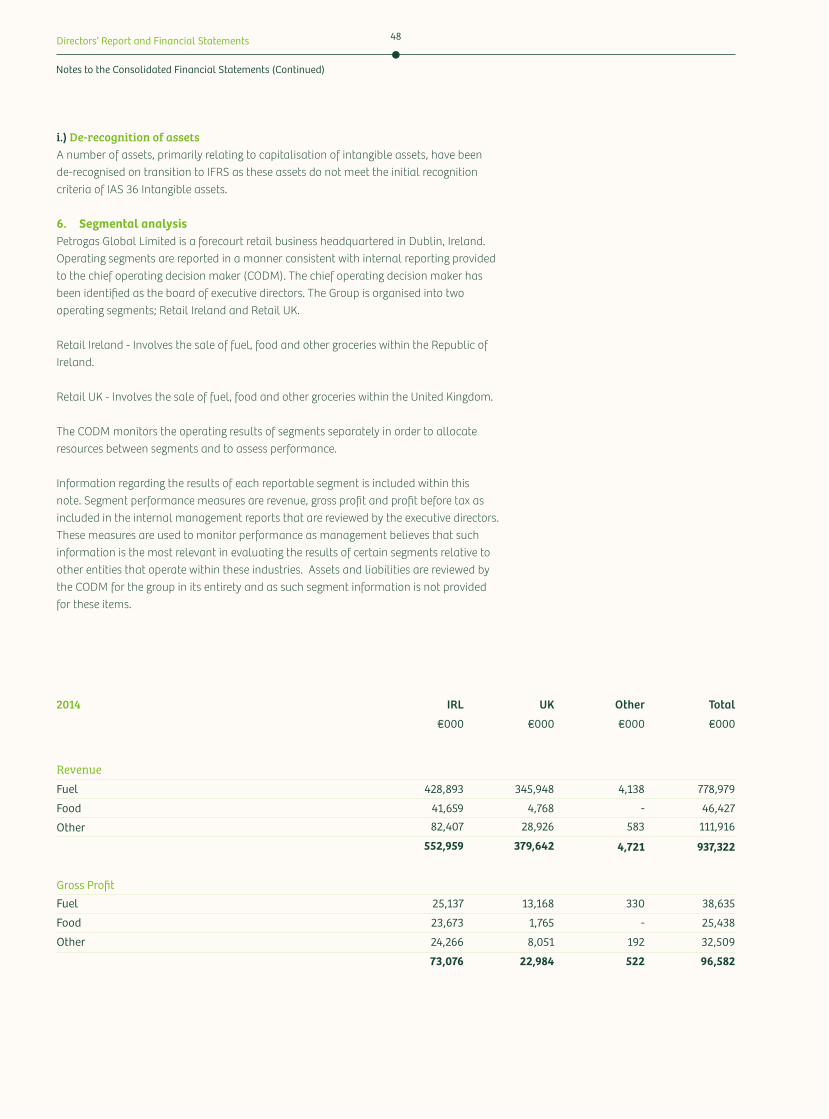

Revenue 937,322 794,623 708,718

Cost of Sales (840,740) (718,511) (639,509)

Gross assets 96,582 76,112 69,209

Selling and distribution costs (63,903) (50,240) (45,672)

Administrative expenses (16,238) (10,761) (11,738)

Other income 8 974 670 520

Finance costs 11 (2,885) 75 (5,028)Finance income 11 417 357 428Share of loss of associates - - (441)

Profit before income tax 14,947 16,213 7,278

Income tax expense 12 (2,668) (1,563) (425)

Profit for the year 12,279 14,650 6,853

Earnings per share from continuing operations a&ributable to the owners of the parent company during the year

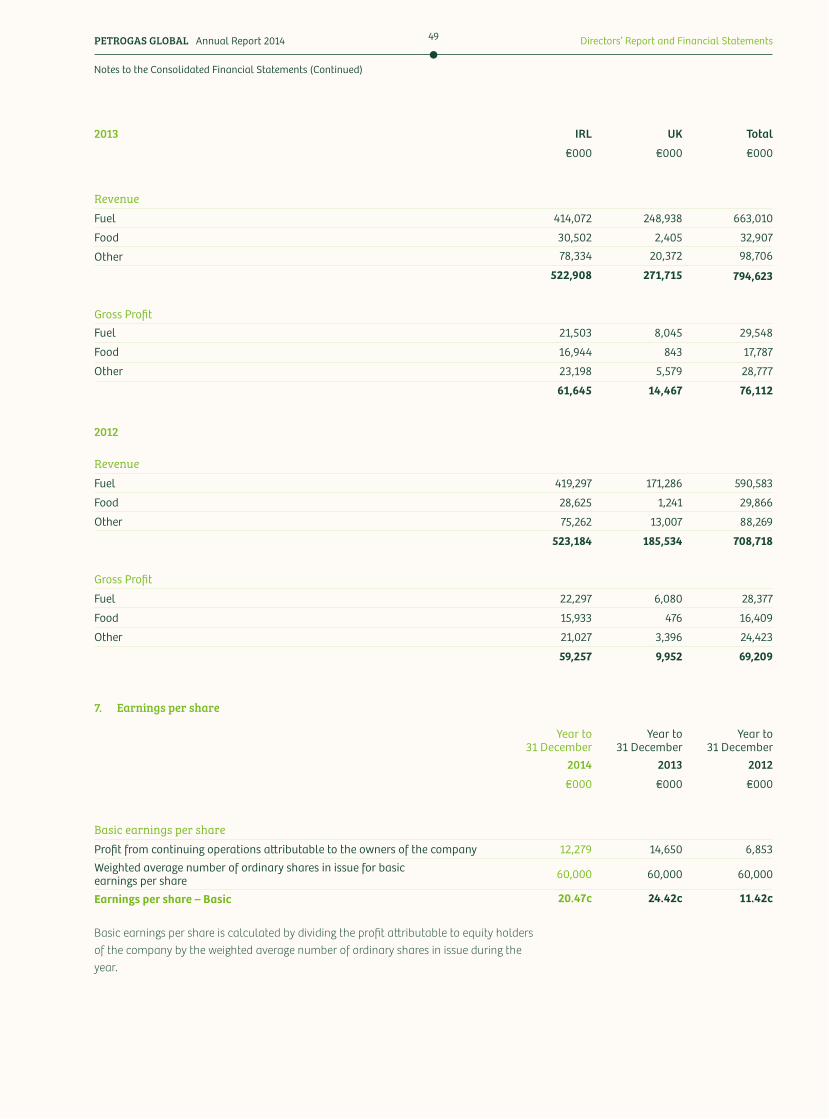

Earnings per share – Basic 20.47c 24.42c 11.42c

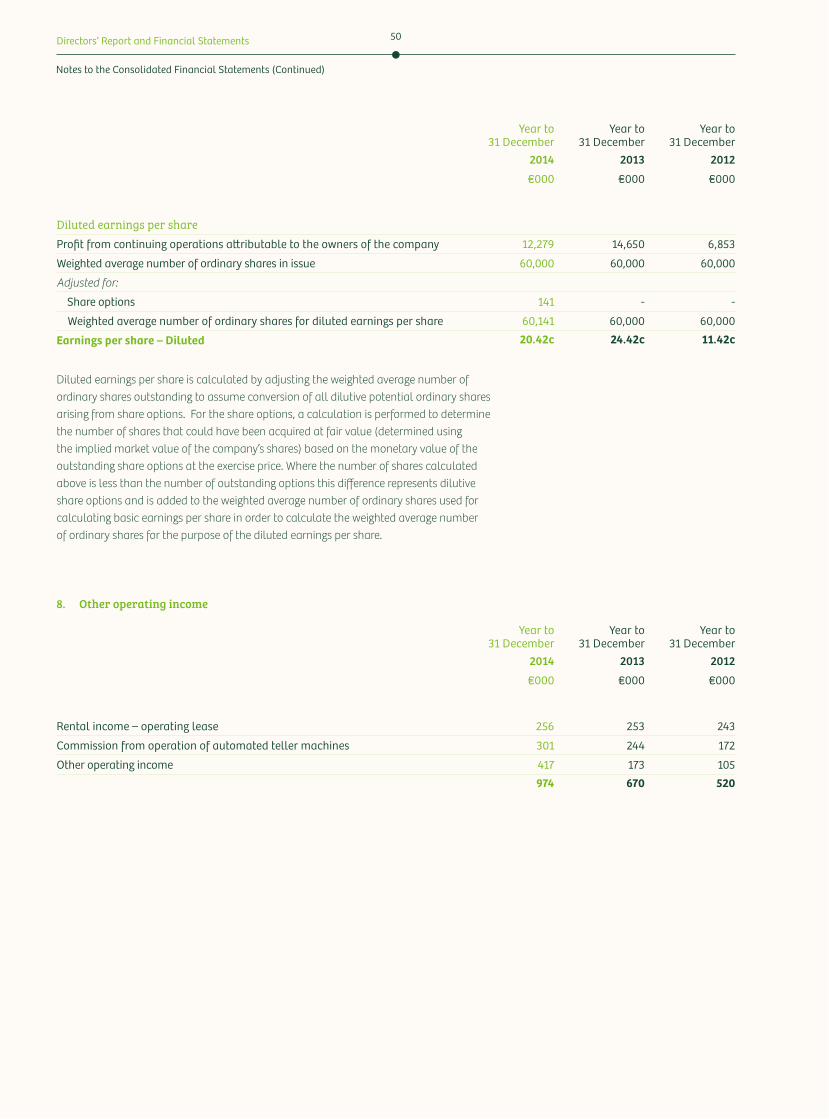

Earnings per share – Diluted 20.42c 24.42c 11.42c

Non-GAAP measure: Reconciliation of Profit before income tax to Earnings before tax, interest, depreciation and amortisation (EBITDA), net foreign exchange loss/(gain), share based payments and other non-recurring gains and losses (Adjusted EBITDA)

Profit before income tax 14,947 16,213 7,278

Depreciation 9 5,604 4,080 3,687

Amortisation 9 116 89 76

Net impairment charge 9 293 - 1,266

Net finance cost/(income) 11 2,468 (432) 4,600

EBITDA 23,428 19,950 16,907

Net foreign exchange loss/(gain) 9 (205) 601 (140)

Share based payments 29 332 - -

Profit on disposal of assets 9 (2,872) (1,621) (507)

Share of loss of associates 16 - - 441

Other non-recurring losses 9 2,093 - -

Adjusted EBITDA 22,776 18,930 16,701

Consolidated Income StatementYear ended 31 December 2014

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

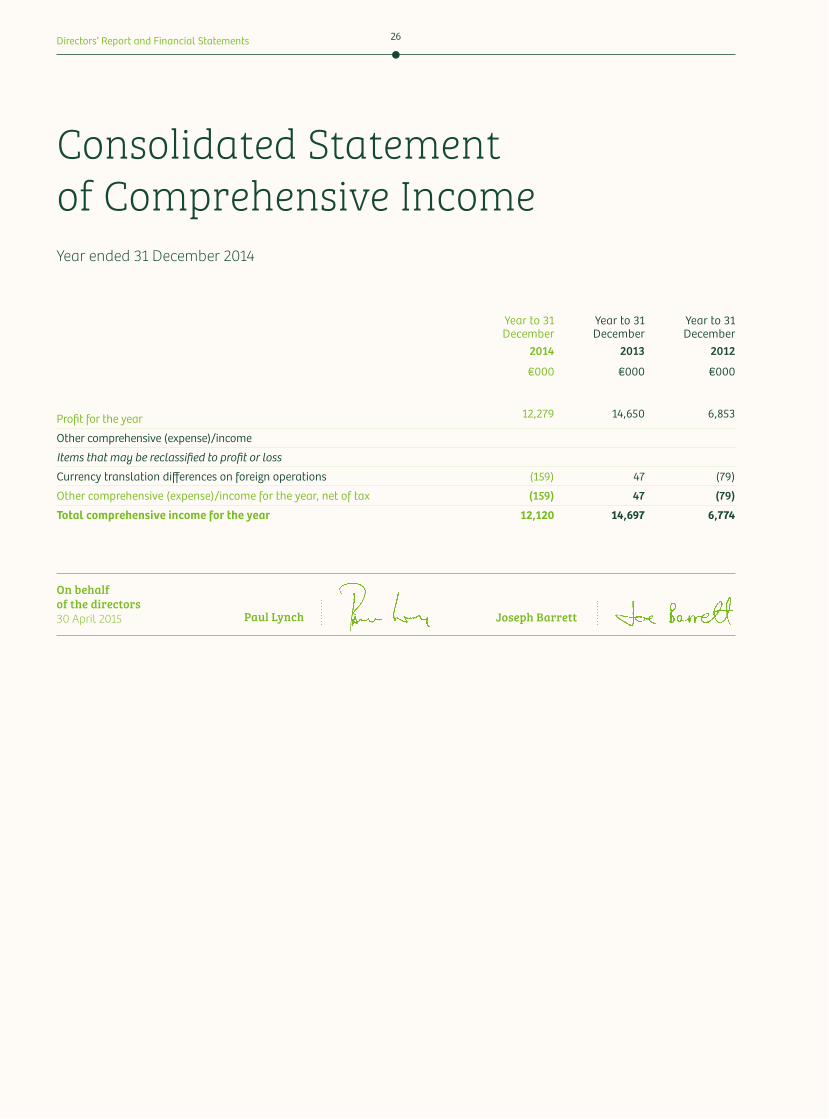

Directors’ Report and Financial Statements 26

Year to 31 December

Year to 31 December

Year to 31 December

2014 2013 2012 €000 €000 €000

Profit for the year 12,279 14,650 6,853

Other comprehensive (expense)/income

Items that may be reclassified to profit or loss

Currency translation differences on foreign operations (159) 47 (79)

Other comprehensive (expense)/income for the year, net of tax (159) 47 (79)

Total comprehensive income for the year 12,120 14,697 6,774

Consolidated Statement of Comprehensive IncomeYear ended 31 December 2014

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements27

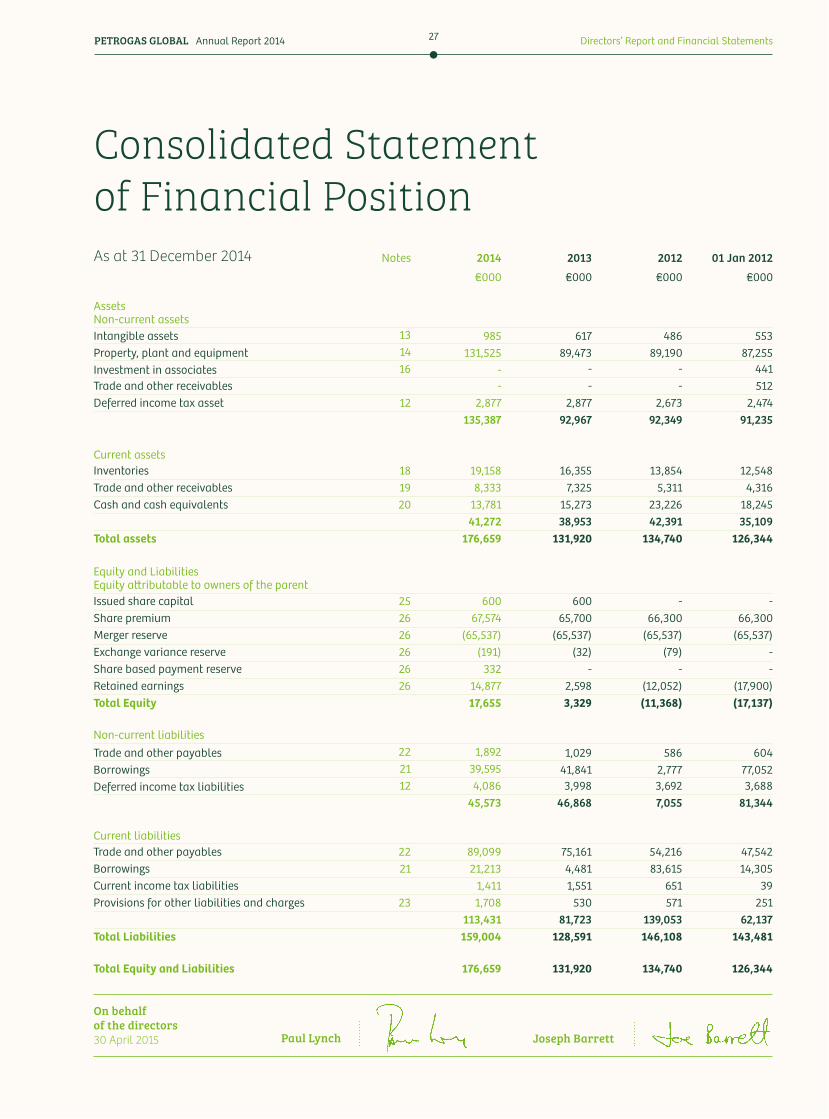

Consolidated Statement of Financial PositionAs at 31 December 2014 Notes 2014 2013 2012 01 Jan 2012

€000 €000 €000 €000

Assets Non-current assetsIntangible assets 13 985 617 486 553Property, plant and equipment 14 131,525 89,473 89,190 87,255Investment in associates 16 - - - 441Trade and other receivables - - - 512Deferred income tax asset 12 2,877 2,877 2,673 2,474

135,387 92,967 92,349 91,235

Current assetsInventories 18 19,158 16,355 13,854 12,548Trade and other receivables 19 8,333 7,325 5,311 4,316Cash and cash equivalents 20 13,781 15,273 23,226 18,245

41,272 38,953 42,391 35,109Total assets 176,659 131,920 134,740 126,344

Equity and LiabilitiesEquity a&ributable to owners of the parentIssued share capital 25 600 600 - -Share premium 26 67,574 65,700 66,300 66,300Merger reserve 26 (65,537) (65,537) (65,537) (65,537)Exchange variance reserve 26 (191) (32) (79) -Share based payment reserve 26 332 - - -Retained earnings 26 14,877 2,598 (12,052) (17,900)Total Equity 17,655 3,329 (11,368) (17,137)

Non-current liabilitiesTrade and other payables 22 1,892 1,029 586 604Borrowings 21 39,595 41,841 2,777 77,052Deferred income tax liabilities 12 4,086 3,998 3,692 3,688

45,573 46,868 7,055 81,344

Current liabilitiesTrade and other payables 22 89,099 75,161 54,216 47,542Borrowings 21 21,213 4,481 83,615 14,305Current income tax liabilities 1,411 1,551 651 39Provisions for other liabilities and charges 23 1,708 530 571 251

113,431 81,723 139,053 62,137Total Liabilities 159,004 128,591 146,108 143,481

Total Equity and Liabilities 176,659 131,920 134,740 126,344

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

Directors’ Report and Financial Statements 28

Company Statement of Financial PositionAs at 31 December 2014

Notes 2014 2013 2012 01 Jan 2012

€000 €000 €000 €000

Assets

Non-current assetsFinancial assets 17 122,441 107,110 66,300 66,300

Deferred income tax assets 12 - 11 - -

122,441 107,121 66,300 66,300

Current assets

Trade and other receivables 19 1,959 4,048 1,005 -

1,959 4,048 1,005 -

Total assets 124,400 111,169 67,305 66,300

Equity and Liabilities

Issued share capital 25 600 600 - -

Share premium 26 67,574 65,700 66,300 66,300

Retained earnings 26 704 (85) - -

Share based payment reserve 26 332 - - -

Total Equity 69,210 66,215 66,300 66,300

Non-current liabilities

Borrowings 21 35,997 38,575 - -35,997 38,575 - -

Current liabilitiesTrade and other payables 22 364 3,767 1,005 -

Borrowings 21 18,829 2,373 - -

Current income tax liabilities - 239 - -

19,193 6,379 1,005 -

Total Liabilities 55,190 44,954 1,005 -

Total Equity and Liabilities 124,400 111,169 67,305 66,300

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements29

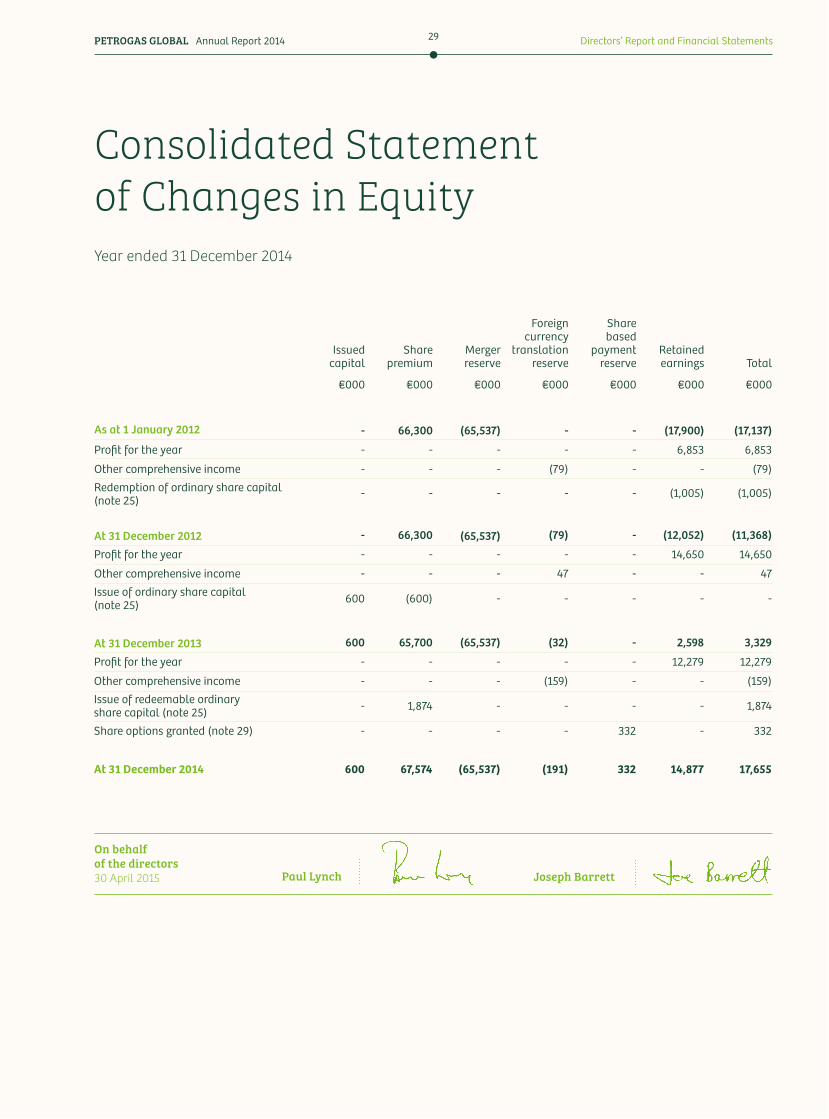

Consolidated Statement of Changes in EquityYear ended 31 December 2014

Issued capital

Share premium

Merger reserve

Foreign currency

translation reserve

Share based

payment reserve

Retainedearnings Total

€000 €000 €000 €000 €000 €000 €000

As at 1 January 2012 - 66,300 (65,537) - - (17,900) (17,137)

Profit for the year - - - - - 6,853 6,853

Other comprehensive income - - - (79) - - (79)Redemption of ordinary share capital (note 25)

- - - - - (1,005) (1,005)

At 31 December 2012 - 66,300 (65,537) (79) - (12,052) (11,368)

Profit for the year - - - - - 14,650 14,650

Other comprehensive income - - - 47 - - 47Issue of ordinary share capital (note 25) 600 (600) - - - - -

At 31 December 2013 600 65,700 (65,537) (32) - 2,598 3,329

Profit for the year - - - - - 12,279 12,279

Other comprehensive income - - - (159) - - (159)Issue of redeemable ordinary share capital (note 25) - 1,874 - - - - 1,874

Share options granted (note 29) - - - - 332 - 332

At 31 December 2014 600 67,574 (65,537) (191) 332 14,877 17,655

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

Directors’ Report and Financial Statements 30

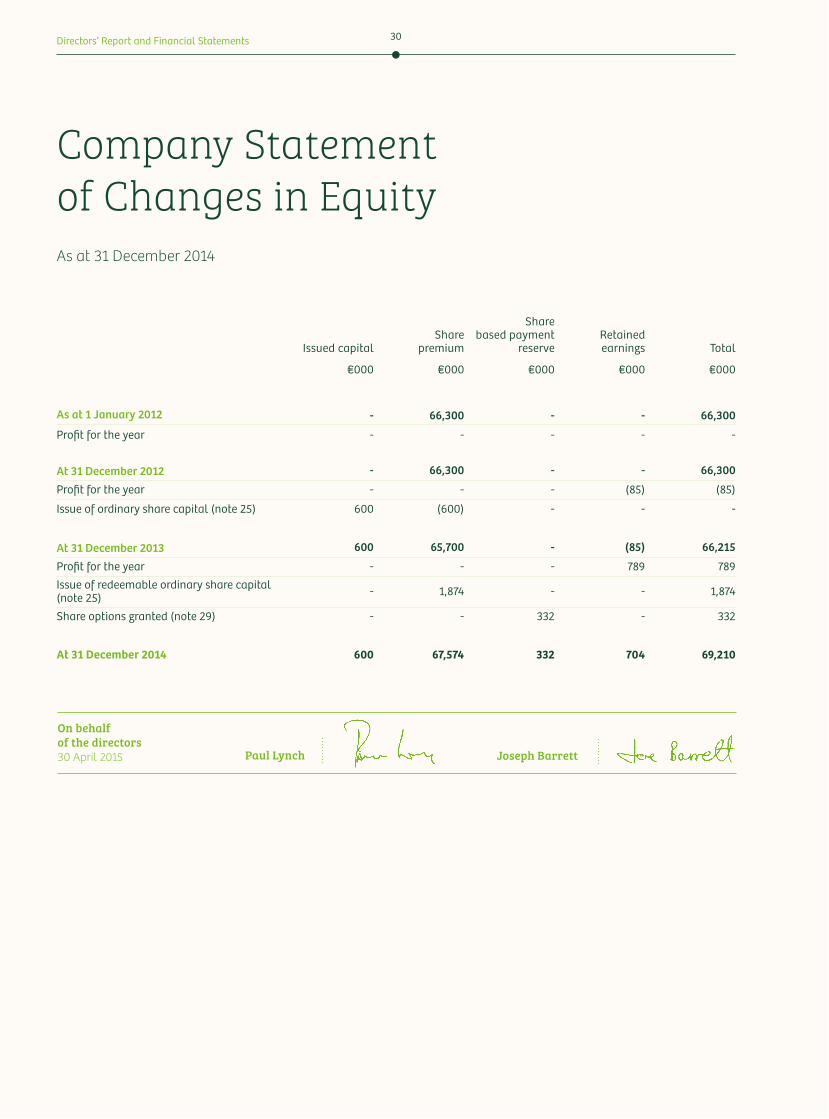

Company Statement of Changes in EquityAs at 31 December 2014

Issued capitalShare

premium

Share based payment

reserveRetainedearnings Total

€000 €000 €000 €000 €000

As at 1 January 2012 - 66,300 - - 66,300

Profit for the year - - - - -

At 31 December 2012 - 66,300 - - 66,300

Profit for the year - - - (85) (85)

Issue of ordinary share capital (note 25) 600 (600) - - -

At 31 December 2013 600 65,700 - (85) 66,215

Profit for the year - - - 789 789Issue of redeemable ordinary share capital (note 25) - 1,874 - - 1,874

Share options granted (note 29) - - 332 - 332

At 31 December 2014 600 67,574 332 704 69,210

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements31

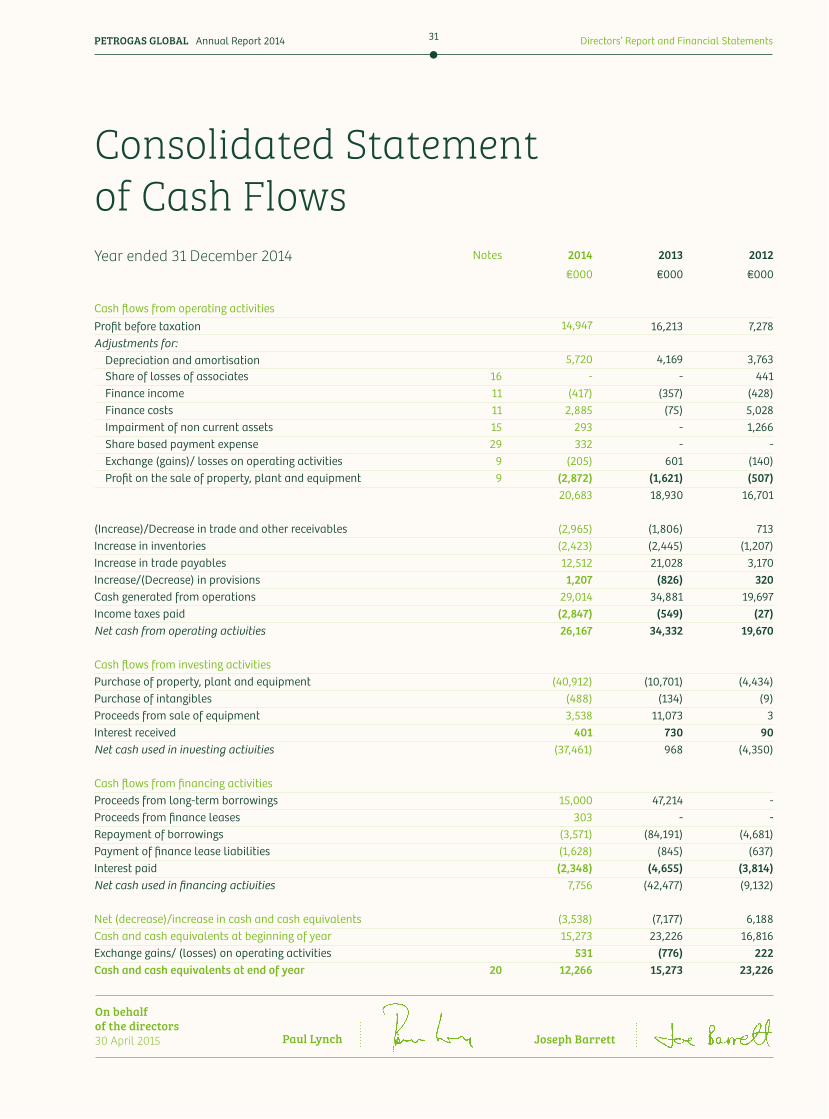

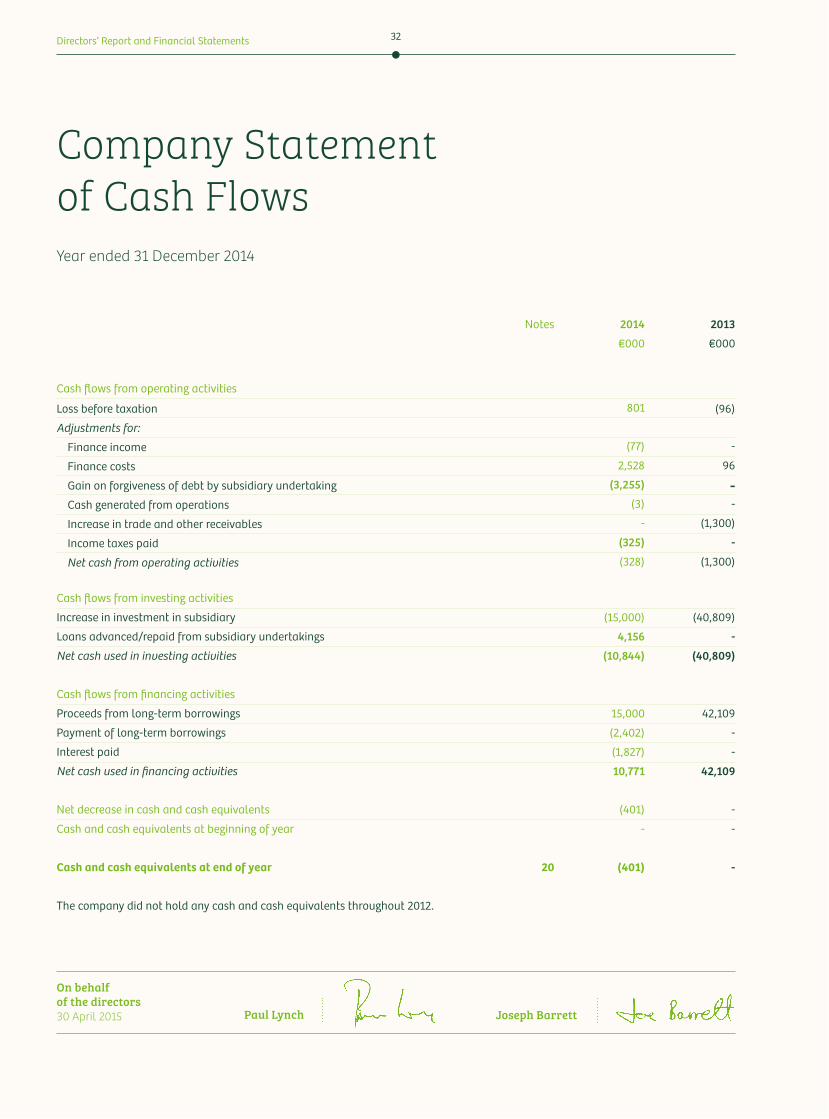

Consolidated Statement of Cash FlowsYear ended 31 December 2014 Notes 2014 2013 2012

€000 €000 €000

Cash flows from operating activitiesProfit before taxation 14,947 16,213 7,278Adjustments for: Depreciation and amortisation 5,720 4,169 3,763 Share of losses of associates 16 - - 441 Finance income 11 (417) (357) (428) Finance costs 11 2,885 (75) 5,028 Impairment of non current assets 15 293 - 1,266 Share based payment expense 29 332 - - Exchange (gains)/ losses on operating activities 9 (205) 601 (140) Profit on the sale of property, plant and equipment 9 (2,872) (1,621) (507)

20,683 18,930 16,701

(Increase)/Decrease in trade and other receivables (2,965) (1,806) 713Increase in inventories (2,423) (2,445) (1,207)Increase in trade payables 12,512 21,028 3,170Increase/(Decrease) in provisions 1,207 (826) 320Cash generated from operations 29,014 34,881 19,697Income taxes paid (2,847) (549) (27)Net cash from operating activities 26,167 34,332 19,670

Cash flows from investing activitiesPurchase of property, plant and equipment (40,912) (10,701) (4,434)Purchase of intangibles (488) (134) (9)Proceeds from sale of equipment 3,538 11,073 3Interest received 401 730 90Net cash used in investing activities (37,461) 968 (4,350)

Cash flows from financing activitiesProceeds from long-term borrowings 15,000 47,214 -Proceeds from finance leases 303 - -Repayment of borrowings (3,571) (84,191) (4,681)Payment of finance lease liabilities (1,628) (845) (637)Interest paid (2,348) (4,655) (3,814)Net cash used in financing activities 7,756 (42,477) (9,132)

Net (decrease)/increase in cash and cash equivalents (3,538) (7,177) 6,188Cash and cash equivalents at beginning of year 15,273 23,226 16,816Exchange gains/ (losses) on operating activities 531 (776) 222Cash and cash equivalents at end of year 20 12,266 15,273 23,226

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

Directors’ Report and Financial Statements 32

Company Statement of Cash FlowsYear ended 31 December 2014

Notes 2014 2013

€000 €000

Cash flows from operating activities

Loss before taxation 801 (96)

Adjustments for:

Finance income (77) -

Finance costs 2,528 96

Gain on forgiveness of debt by subsidiary undertaking (3,255) - Cash generated from operations (3) -

Increase in trade and other receivables - (1,300)

Income taxes paid (325) -

Net cash from operating activities (328) (1,300)

Cash flows from investing activities

Increase in investment in subsidiary (15,000) (40,809)

Loans advanced/repaid from subsidiary undertakings 4,156 -

Net cash used in investing activities (10,844) (40,809)

Cash flows from financing activities

Proceeds from long-term borrowings 15,000 42,109

Payment of long-term borrowings (2,402) -

Interest paid (1,827) -

Net cash used in financing activities 10,771 42,109

Net decrease in cash and cash equivalents (401) -

Cash and cash equivalents at beginning of year - -

Cash and cash equivalents at end of year 20 (401) -

The company did not hold any cash and cash equivalents throughout 2012.

On behalf of the directors30 April 2015 Joseph BarrettPaul Lynch

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements33

Notes to the Consolidated Financial Statements

1. Statement of complianceThe consolidated financial statements of Petrogas Global Limited have been prepared in accordance with International Financial Reporting Standards (IFRS) and their interpretations approved by the International Accounting Standards Board (IASB) as adopted by the European Union (EU) and those parts of the Companies Acts, 1963 to 2013 applicable to companies reporting under IFRS. IFRS as adopted by the EU differ in certain respects from IFRS as issued by the IASB. Both the company and the group financial statements have been prepared in accordance with IFRS as adopted by the EU and references to IFRS hereafter should be construed as references to IFRS as adopted by the EU.

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the group’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements are disclosed in note 3.

In presenting the parent company financial statements together with the group financial statements, the company has availed of the exemption in Section 148(8) of the Companies Act 1963 not to present its individual Income Statement and related notes that form part of the approved Company financial statements. The Company has also availed of the exemption from filing its individual Income Statement with the Registrar of Companies as permi*ed by Section 7(1A) of the Companies (Amendment) Act 1986.

The Company’s result for the financial year, determined in accordance with IFRS, is a profit for the year of €789,000 (2013: €(85,000), 2012: €nil).

2. Basis of accountingFor all periods up to and including 31 December 2013 the group prepared its financial statements in accordance with applicable Irish law and Generally Accepted Accounting Practice in Ireland including the accounting standards issued by the Financial Reporting Council and published by The Institute of Chartered Accountants in Ireland.

These are the group’s first consolidated financial statements prepared in accordance with IFRS. The accounting policies set out in note 2.2 have been applied in preparing the financial statements for the year ended 31 December 2014, the comparative information presented in these financial statements for the years ended 31 December 2013 and 31 December 2012 and in the preparation of the opening IFRS Statement of Financial Position at 1 January 2012 (the group’s date of transition). In preparing its opening IFRS Statement of Financial Position, the group has adjusted the amounts reported previously in financial statements prepared with Irish GAAP. An explanation of how the transition from Irish GAAP to IFRS has affected the group’s financial position, financial performance and cash flows is set out in note 5.

Directors’ Report and Financial Statements 34

The consolidated financial statements have been prepared on a historical cost basis. The consolidated financial statements are presented in Euro (€) and all values are rounded to the nearest thousand (€000), except where otherwise stated.

2.1 Basis of consolidationThe consolidated financial statements comprise the financial statements of the group and its subsidiaries as at 31 December 2014.

Subsidiaries are consolidated from the date of acquisition, being the date on which the group obtains control, and continue to be consolidated until the date when such control ceases. The group controls an entity when the group is exposed to, or has rights to, variable returns from its involvement with the entity, and has the ability to affect those returns through its control over the entity. Subsidiaries are accounted for using the acquisition method as at the acquisition date i.e. when control is transferred to the group. The financial statements of the subsidiaries are prepared for the same reporting period as the parent company using consistent accounting policies.

The consideration transferred for the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred by the former owners of the acquiree and the equity interests issued by the group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. The group recognises any non-controlling interest in the acquiree on an acquisition-by-acquisition basis, either at fair value or at the non-controlling interest’s proportionate share of the recognised amounts of the acquiree’s identifiable net assets.

Acquisition-related costs are expensed as incurred.

All intra-group balances, transactions, unrealised gains and losses resulting from intra-group transactions and dividends are eliminated in full.

Associates are all entities over which the group has significant influence. Significant influence is the power to participate in the financial and operating policy decisions of the investee, but is not control or joint control, generally accompanying a shareholding of 20-50% of the voting rights. Investments in associates are accounted for using the equity method of accounting. Under the equity method, the investment is initially recognised at cost and the carrying amount increased or decreased to recognise the investor’s share of the profit or loss of the investee after the date of acquisition.

2.2 Significant accounting policiesThe following are significant accounting policies applied by the group in preparing its consolidated financial statements:

AssociatesThe group’s share of post-acquisition profit or loss is recognised in the Income Statement, and its share of post-acquisition movements in other comprehensive income is recognised in other comprehensive income with a corresponding adjustment to the carrying amount of the investment. When the group’s share of losses in an associate equals or exceeds its equity interest in the associate and any other long term interests, the group does not recognise further losses, unless it has incurred legal or constructive obligations or made payments on behalf of the associate.

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements35

The group determines at each reporting date whether there is any objective evidence that the investment in the associate is impaired. If this is the case, the group calculates the amount of impairment as the difference between the recoverable amount of the associate and its carrying value and recognises the amount adjacent to ‘share of profit / (loss)’ of associates in the Income Statement.

Profits and losses resulting from upstream and downstream transactions between the group and its associates are recognised in the group’s financial statements only to the extent of unrelated investors’ interests in the associates. Unrealised losses are eliminated unless the transaction provides evidence of an impairment of the asset transferred. Accounting policies of associates have been changed where necessary to ensure consistency with the policies adopted by the group. Investment in associates is shown separately on the group Statement of Financial Position.

TurnoverTurnover from the sale of goods in the course of ordinary activities is measured at the fair value of consideration received or receivable, excluding value added tax and net of returns, trade discounts and including duty on goods to external customers.

Revenue is recognised when the significant risks and rewards of ownership have been transferred to the customer, it is probable that economic benefits will flow to the group, the associated costs can be measured reliably, there is no continuing managerial involvement with the goods, and the amount of revenue can be measured reliably. If it is probable that discounts will be granted and the amount can be measured reliably, then the discount is recognised as a reduction of revenue as the sales are recognised.

Retail sales The group’s revenue is earned from fuel, shop and restaurant sales throughout its network of service stations in Ireland, the UK and the USA. Sales of goods are recognised when the group sells a product to the customer. Retail sales are usually in cash or by credit card. Due to the nature of the products sold, the group does not experience material levels of returns.

Gross versus net presentationWhen deciding the most appropriate basis for presenting revenue or costs of revenue, both the legal form and substance of the agreement between the group and its business partners are reviewed to determine each party’s respective role in the transaction. Where the group’s role in a transaction is that of principal, revenue is recognised on a gross basis. This requires revenue to comprise the gross value of the transaction billed to the customer, after trade discounts, with any related expenditure charged as an operating cost. Where the group’s role in a transaction is that of an agent, revenue is recognised on a net basis with revenue representing the margin earned.

Customer loyalty programmesThe group operates a customer loyalty programme whereby points are awarded on the sale of goods. Revenue is recorded at the amount of the consideration received or receivable less the fair value of the points awarded. The fair value of the points awarded is deducted from the consideration received on the initial purchase and carried forward as a liability until the points are redeemed.

Interest incomeInterest income is recognised using the effective interest rate method when it is probable that income will flow to the group. When a loan or receivable is impaired, the group reduces the carrying amount to its recoverable amount, being the estimated future cash

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 36

flow discounted at the original effective interest rate of the instrument, and continues unwinding the discount as interest income. Interest income on impaired loans and receivables is recognised using the original effective interest rate.

Segmental information Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the board of directors that makes strategic decisions.

Going concernThe group’s forecasts and projections, taking account of reasonably possible changes in trading performance, show that the group expects to operate within the level of its current banking facilities. The directors are confident that the group has adequate resources to continue in operational existence for the foreseeable future. The group therefore continues to adopt the going concern basis in preparing its consolidated financial statements.

Foreign currenciesItems included in the financial statements of each of the group’s entities are measured using the currency of the primary economic environment in which the entity operates (the functional currency). The consolidated financial statements are presented in Euro (€), which is the group’s presentation currency.

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions or valuation where items are re-measured. Foreign exchange gains and losses resulting from the se*lement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the Income Statement.

Foreign exchange gains and losses that relate to borrowings and cash and cash equivalents are presented in the Income Statement within finance costs. All other foreign exchange gains and losses are presented in the Income Statement within administrative expenses.

The results and financial position of all the group entities that have a functional currency different from the presentation currency are translated into the presentation currency as follows:

(a) assets and liabilities for each Statement of Financial Position presented are translated at the closing rate at the date of that Statement of Financial Position;

(b) income and expenses for each Income Statement are translated at average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the rate on the dates of the transactions); and

(c) all resulting exchange differences are recognised in other comprehensive income.

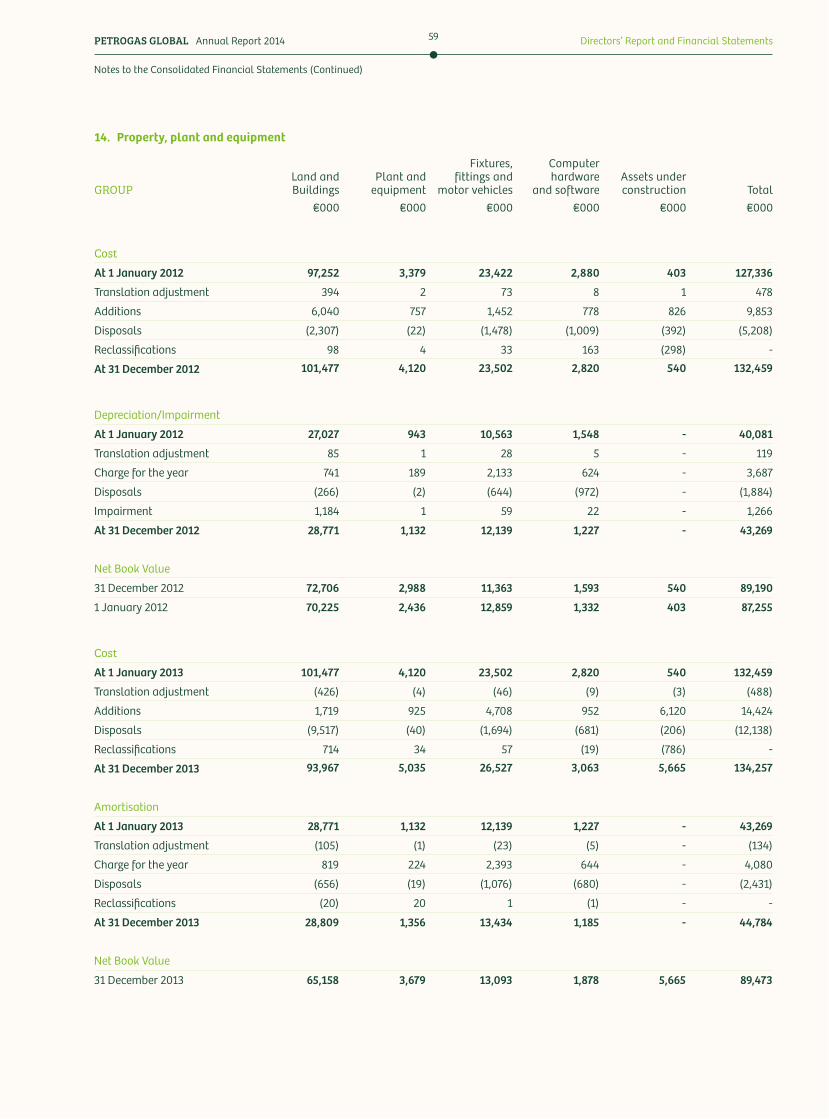

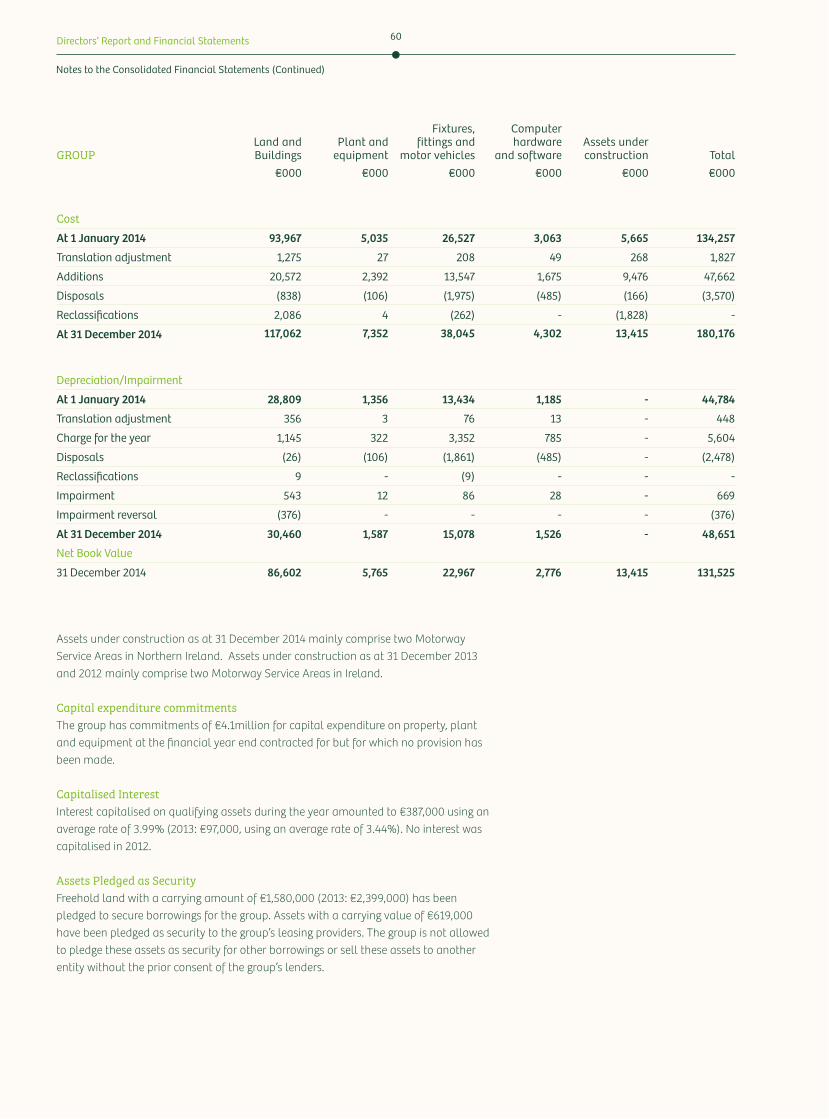

Property, plant & equipmentProperty, plant and equipment is stated at cost, less accumulated depreciation and accumulated impairment losses. The initial cost of an asset comprises its purchase price or construction cost plus any costs directly a*ributable to bringing the asset into the location and condition necessary for it to be capable of operating in a manner intended by management.

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements37

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the group and the cost of the item can be measured reliably.

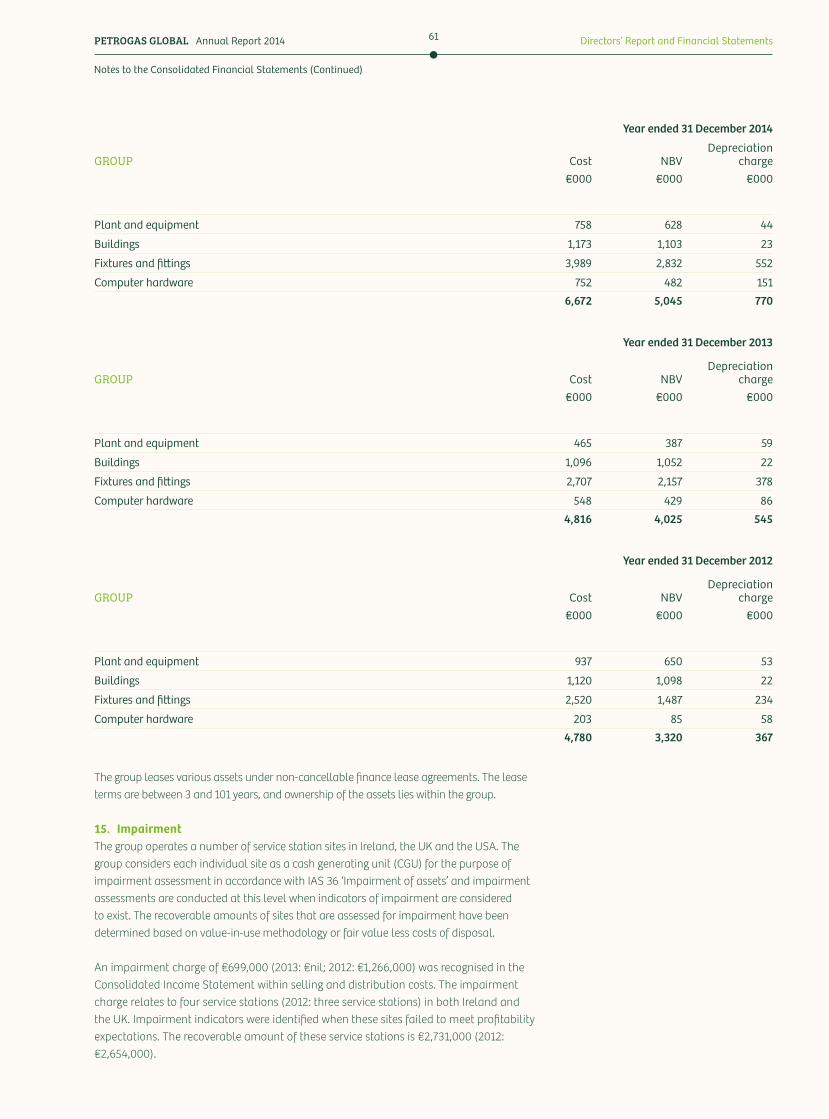

Property, plant and equipment is depreciated on a straight-line basis over its expected useful life. The typical useful lives of the group’s property, plant and equipment are:

Freehold property Over 50 years

Leasehold improvements Over the term of the lease

Plant and equipment 20 years

Fixtures & fi&ings 10 years

Motor vehicles 5 years

Computer hardware and software 5 years

Freehold land is not depreciated.

The expected useful lives of property, plant and equipment are reviewed and adjusted, if appropriate, at each financial year end.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected to arise from its use. Any gain or loss arising on de-recognition of the asset is recorded in the Income Statement in the period the asset is derecognised.

An asset’s carrying amount is wri*en down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Assets under construction Capitalisation of costs in respect of constructing an asset commences when it is probable that future economic benefits associated with the asset will flow to the group and the costs are directly a*ributable to the related asset and required to bring the asset into working condition. The cost of self-constructed assets includes:

• the cost of materials and labour;• any other costs directly a*ributable to bringing the assets to a working condition for

their intended use;• an estimate of the costs associated with the removal of the asset or restoration of the

site when the group has an obligation.

Assets under construction are not depreciated.

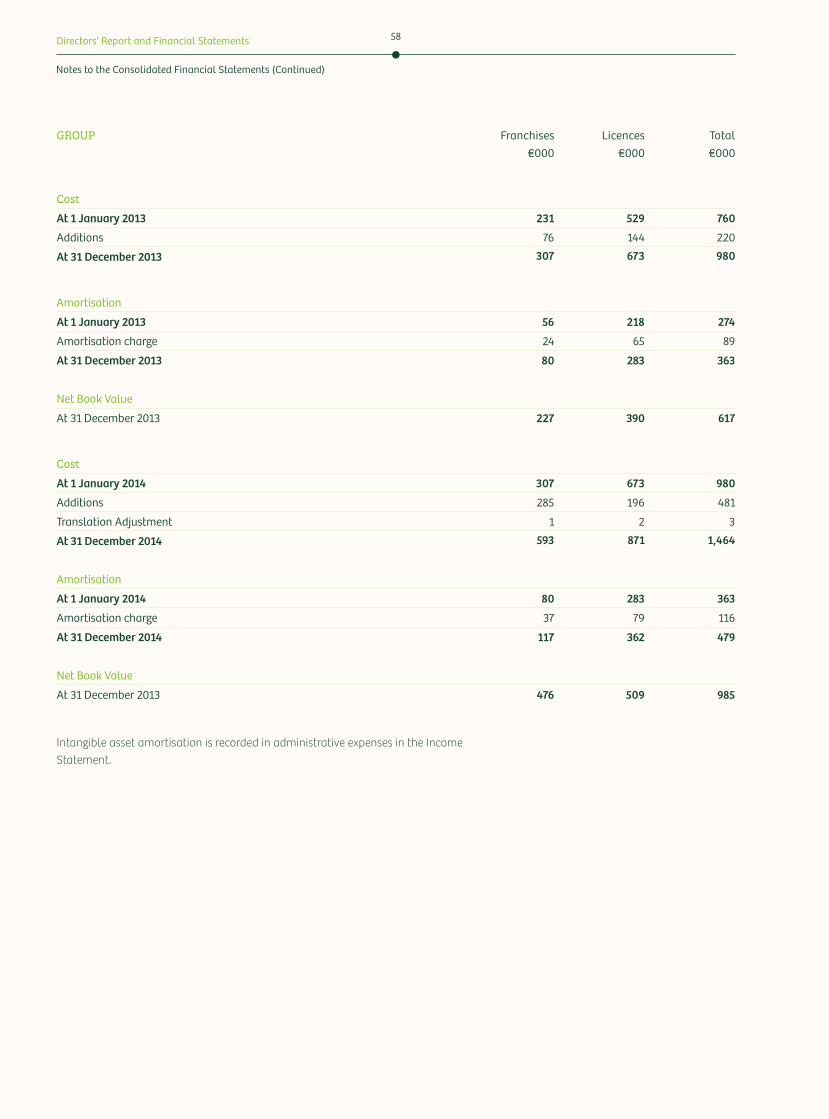

Intangible assetsIntangible assets include i) franchise licences for the operation of franchised operations throughout the group’s retail network and ii) wine and off licence fees in respect of those retail stores that sell alcohol.

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 38

Franchises 5-25 years

Licences 10 years

Intangible assets acquired are initially capitalised at cost and amortised using the straight-line basis over their useful lives as follows;

Impairment of non-financial assets

The carrying amounts of the group’s property, plant and equipment, and intangible assets are reviewed at each reporting date to determine whether there is any indication of impairment. If events or changes in circumstances indicate that the carrying value of property, plant and equipment, or intangible assets may not be recoverable, the group carries out an impairment test.

When testing for impairment assets are grouped together into the smallest group of assets that is largely independent of the group’s other cash generating streams. The recoverable amount in respect of the cash generating units (CGUs) is the higher of its fair value less cost of disposal and the value in use.

Value in use is determined by discounting to present value the estimated future cash flows expected to be derived from the CGU. The discount rate used is the company’s weighted average cost of capital reflecting current market assessments of the time value of money and the risks specific to the CGU.

To the extent that the carrying amount exceeds the recoverable amount, the asset is impaired and is wri*en down. Any impairment loss arising is recognised in the Consolidated Income Statement.

Prior impairments of non-financial assets (other than goodwill) are reviewed for possible reversal at each reporting date.

Financial assetsClassification The group classifies its financial assets in the following categories: at fair value through profit or loss, loans and receivables, and available for sale. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition.

Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except for maturities greater than 12 months after the end of the reporting period. These are classified as non-current assets. The group’s loans and receivables comprise trade and other receivables and cash and cash equivalents in the Statement of Financial Position. Loans and receivables are initially recognised at fair value and subsequently at amortised cost using the effective interest rate method less any impairment losses.

Investments in subsidiariesInterests in subsidiary undertakings are measured at cost less provisions for impairment in value on the company Statement of Financial Position. The company carries out an impairment test if events or changes in circumstances indicate that the carrying value

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements39

of the investment in a subsidiary may not be recoverable. The recoverable amount is determined by comparing the carrying value of the investment in the subsidiary against the higher of its fair value less costs to dispose and its value in use. The value in use is determined by discounting estimated future cash flows expected to be derived from the financial asset, to net present value.

Impairment of financial assets The group assesses at the end of each reporting period whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a loss event) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated.

Evidence of impairment may include indications that a debtor or a group of debtors are experiencing significant financial difficulty, default or delinquency in interest or principal payments, indicating that they will enter bankruptcy or other financial reorganisation.

For loans and receivables, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced and the amount of the loss is recognised in the Consolidated Income Statement. If a loan or held-to-maturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtor’s credit rating), the reversal of the previously recognised impairment loss is recognised in the Consolidated Income Statement.

Inventory Inventories are stated at the lower of cost and net realisable value. Cost is determined using the first-in, first-out (FIFO) method. Net realisable value is the estimated selling price in the ordinary course of business, less applicable variable selling expenses. Costs of inventories include the transfer from equity of any gains/losses on qualifying cash flow hedges for purchases of raw materials.

Cash and cash equivalents In the consolidated statement of cash flows, cash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly liquid investments with original maturities of three months or less and bank overdrafts. In the Consolidated Statement of Financial Position, bank overdrafts are shown within borrowings in current liabilities.

Trade payablesTrade payables are obligations to pay for goods or services that have been acquired in the ordinary course of business from suppliers. Accounts payable are classified as current liabilities if payment is due within one year or less (or in the normal operating cycle of the business if longer). If not, they are presented as non current liabilities. Trade payables are initially recorded at fair value and subsequently amortised cost using the effective interest rate method.

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 40

Provisions A provision is defined as a liability of uncertain timing or amount. Provisions are recognised when the group has a present legal or constructive obligation as a result of a past event, a reliable estimate of that obligation can be made and it is probable that an outflow of economic benefits will be required to se*le the obligation. Where the effect of the time value of money is material, provisions are discounted to present value, using a pre–tax discount rate that reflects current market assessments of the time value of money and the risks specific to the liability. The amortisation of any discount is recognised as a finance cost in the Income Statement. The amount of a provision is reviewed each year and amended as appropriate.

Defined contribution planThe group operates a defined contribution plan. A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity. The group has no further payment obligations once the contributions have been paid. Obligations for contributions to defined contribution plans are recognised as an employee benefit expense in the Income Statement in the periods during which the related services are received. Prepaid expenses are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

BorrowingsBorrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently carried at amortised cost using the effective interest rate method. Any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the Income Statement over the period of the borrowings using the effective interest method.

Fees paid on the establishment of loan facilities are recognised as transaction costs of the loan to the extent that it is probable that some or all of the facility will be drawn down. In this case, the fee is deferred until the draw-down occurs.

General and specific borrowing costs directly a*ributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale.

Investment income earned on the temporary investment of specific borrowings pending their expenditure on qualifying assets is deducted from the borrowing costs eligible for capitalisation.

All other borrowing costs are recognised in finance costs in the period in which they are incurred.

Share based paymentsThe group launched an equity-se*led, share-based compensation plan in December 2014, under which the entity receives services from employees as consideration for equity instruments (options) of the group. The fair value of the employee services received in exchange for the grant of the options is recognised as an expense. The total amount to be expensed is determined by reference to the fair value of the options granted:

• including any market performance conditions

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements41

• excluding the impact of any service and non-market performance vesting conditions and• including the impact of any non-vesting conditions.

LeasesAssets held by the group under leases which transfer to the group substantially all of the risks and rewards of ownership are classified as finance leases. On initial recognition, assets held under finance leases are included in property, plant and equipment, at the lower of fair value and the present value of the minimum lease payments. Subsequent to initial recognition, the asset is depreciated over the shorter of the lease term or its useful life and otherwise accounted for in accordance with the accounting policy applicable to that asset.

Each lease payment is allocated between the liability and finance charges. The corresponding rental obligations, net of finance charges, are included in current or non current liabilities as appropriate. The interest element of the finance cost is charged to the Income Statement over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period.

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to the Income Statement on a straight-line basis over the period of the lease.

Sale and leasebackA sale and leaseback transaction is one where the group sells an asset and immediately reacquires the use of the asset by entering into a lease with the buyer. The accounting treatment of the sale and leaseback depends upon the substance of the transaction (by applying the lease classification principles described above) and whether or not the sale was made at the asset’s fair value. For sale and finance leasebacks, any profit from the sale is deferred and amortised over the lease term. For sale and operating leasebacks, when the assets are sold at fair value, the profit or loss from the sale is recognised immediately in the Income Statement.

Taxation The tax expense for the period comprises current and deferred tax. Tax is recognised in the Income Statement, except to the extent that it relates to items recognised in other comprehensive income or directly in equity. In this case, the tax is also recognised in other comprehensive income or directly in equity, respectively.

The current income tax charge is calculated on the basis of the tax laws enacted or substantively enacted at the Statement of Financial Position date in the countries where the company and its subsidiaries operate and generate taxable income. Management periodically evaluates positions taken in tax returns with respect to situations in which applicable tax regulation is subject to interpretation. It establishes provisions where appropriate on the basis of amounts expected to be paid to the tax authorities.

Deferred income tax is recognised on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the consolidated financial statements.

No deferred tax is recognised if the temporary difference arises from goodwill or the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss.

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 42

Deferred income tax is recognised in respect of taxable temporary differences associated with investments in associates and interests in joint ventures, except where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future.

Deferred income tax assets are recognised to the extent that it is probable that taxable profit will be available against which the deductible temporary differences can be utilised. The carrying amount of deferred income tax assets is reviewed at each Statement of Financial Position date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all, or part of, the deferred income tax asset to be utilised. Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realised or the liability is se*led, based on tax rates that have been enacted or substantively enacted at the Statement of Financial Position date.

Provision for a corporation tax surcharge assessable on undistributed investment income (in accordance with Section 440, Taxes Consolidation Act 1997) is provided after the time limit of 18 months has elapsed within which a dividend can be paid to avoid such surcharge.

Deferred income tax assets and liabilities are offset when there is a legally enforceable right to offset current tax assets against current tax liabilities and when the deferred income tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where there is an intention to se*le the balances on a net basis.

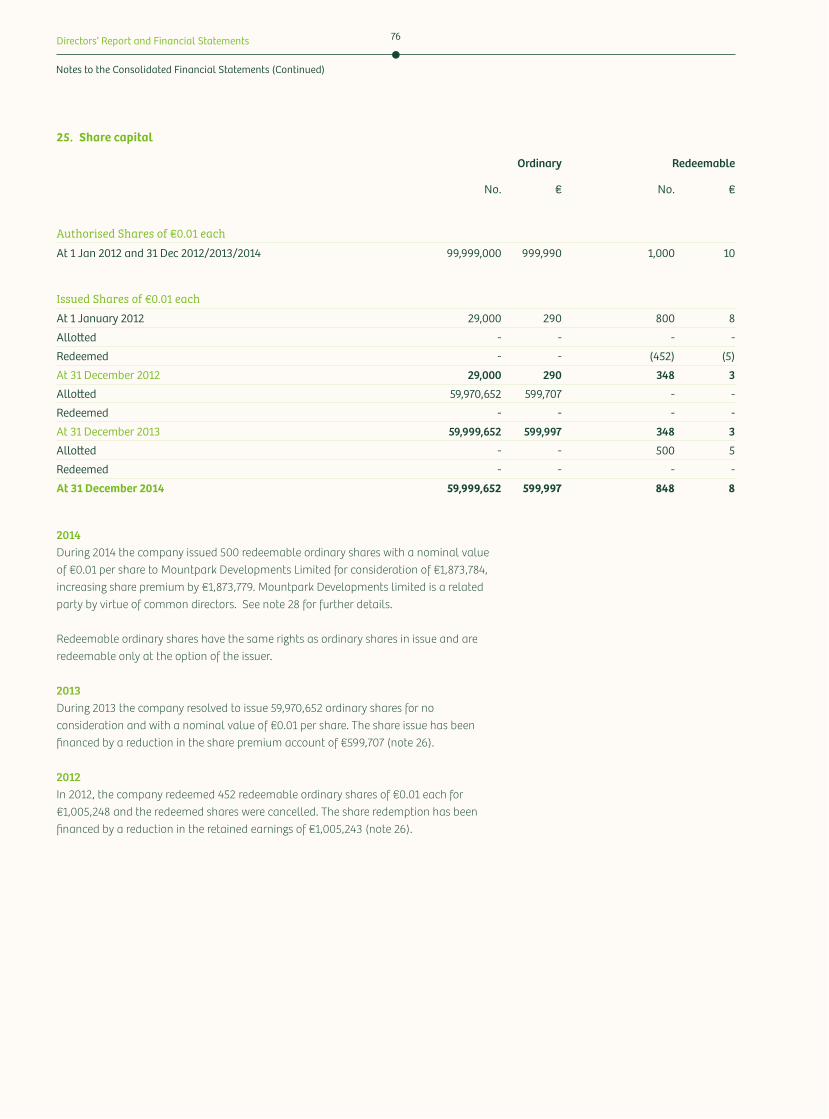

Share capitalOrdinary shares and redeemable ordinary shares that rank pari passu with ordinary shares, carry no preferential dividend right. Redeemable ordinary shares are redeemable only at the option of the issuer and are classified as equity.

3. Significant accounting judgements and estimatesKey assumptions concerning the future, and other key sources of estimation uncertainty, at the Statement of Financial Position date, have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year. The main assumptions and sources of judgement and estimation uncertainty are outlined below:

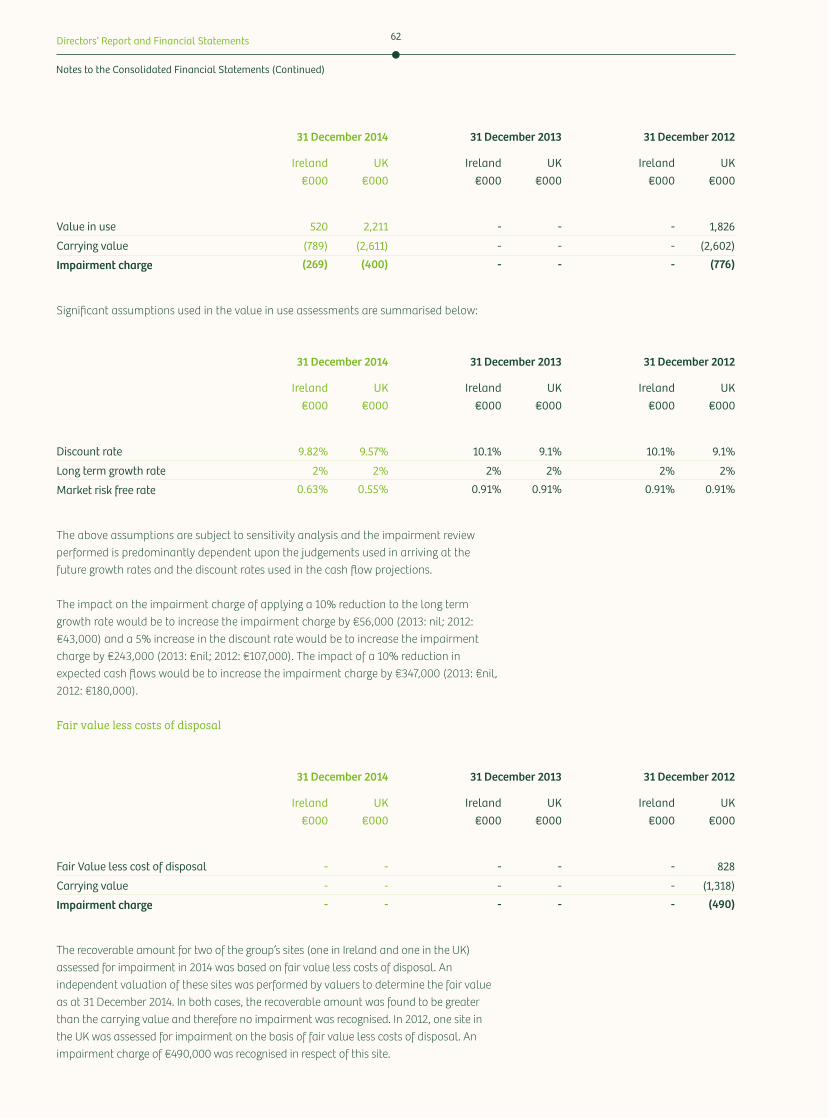

Impairment of non financial assetsThe carrying amounts of the group’s property, plant and equipment, and intangible assets are reviewed at each reporting date to determine whether there is any indication of impairment in accordance with the accounting policy set out in section 2.2 of these financial statements. The recoverable amounts of cash-generating units have been determined based on value-in-use calculations which require the use of estimates. Note 15 details the assumptions used together with an analysis of the sensitivity to changes in key assumptions.

Assets under constructionThe group incurs significant levels of development expenditure on an ongoing basis in respect of the construction of new retail sites and the refurbishment of existing retail sites. Capitalisation of costs directly a*ributable to the asset commences when the group has probable future economic benefits associated with the utilisation of the asset. The determination of the point at which probable future economic benefits associated with the development spend will flow to the group requires management judgement and

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements43

is subject to ma*ers such as planning approval, revisions to planning approval and in the case of publically funded developments, preferred bidder status. Costs incurred in the period before the group determines it has access to the probable future economic benefits that will flow from the asset are expensed in the income statement.

TaxesThe calculation of the group’s total tax charge necessarily involves a degree of estimation and judgement in respect of certain items, where the tax treatment cannot be finally determined until resolution has been reached with the relevant tax authority. The final resolution of some of these items may give rise to material Income Statement and/or cash flow variances.

Assumptions are also made around the assets which qualify for capital allowances and the level of disallowable expenses and this affects the income tax calculation. Provisions may be made for uncertain exposures or recoveries, which can have an impact on both deferred and current tax. Assumptions are also made around the tax net book value of assets to which capital allowances apply, the level of capital allowances, the extent of rollover gains, indexation thereon and the tax base into which they have been rolled.

Business combinationsFor sites acquired by the group it is necessary to determine whether the substance of the transaction reflects the acquisition of a leasehold/freehold interest in a property or whether it may constitute the acquisition of a business. In the la*er case, the transaction may give rise to goodwill in the group financial statements as well as other identifiable assets and liabilities acquired as part of the acquisition.

Management consider the contract terms and the nature of each site acquired to appropriately conclude whether the sites acquired represent a business combinations or a leasehold/freehold interest in land and buildings. Management reviewed the nature of leasehold acquisitions made in 2014 and concluded they were not business combinations.

Agency versus principal relationshipsThe group evaluates its revenue streams to ensure the most appropriate basis for presenting revenue or costs of revenue is selected. The determination of whether the group is acting as agent or principal requires management judgement and is subject to ma*ers such as the substance of the trading relationship with the counterparty, the legal form and the nature of the risks transferred to the counterparty. The group has considered these requirements and has concluded that it is agent on the sale of lo*ery related products, phone cards and other similar business streams.

Lease classificationThe group enter into a significant number of property leases as part of its expansion strategy and the determination of the appropriate lease classification between finance and operating is considered a key judgment. The determination of whether lease interests represent finance or operating leases requires management judgement and is subject to ma*ers such as contract terms, duration of the lease, nature of the interest/assets leased, the conditions upon which the lease can be exited and the nature of the risks and rewards passed to the group on lease inception.

4. Standards issued but not yet effectiveThe standards and interpretations that are issued but not yet effective up to the date of issuance of the group’s financial statements are disclosed below. The group intends to adopt these standards, if applicable, when they become effective.

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 44

IFRS 9 Financial InstrumentsIFRS 9 Financial Instruments reflects the final phase of the IASB’s work on the replacement of IAS 39 Financial Instruments: Recognition and Measurement and applies to the classification and measurement of financial assets and liabilities as defined in IAS 39, impairment, and the application of hedge accounting. IFRS 9 is effective from 1 January 2018 and is awaiting EU endorsement. The group is currently assessing the impact of IFRS 9.

IFRS 15 Revenue from contracts with customersIFRS 15 Revenue from Contracts with Customers will replace IAS 18 Revenue, IAS 11 Construction Contracts and related interpretations. The new standard is applicable from 1 January 2017 and is subject to EU endorsement. IFRS 15 provides a new five step model to be applied to revenue arising from contracts with customers. The principles in IFRS 15 provide a more structured approach to measuring and recognising revenue and may impact the timing and amount of revenue recognised from contracts with customers. The group is currently assessing the impact of IFRS 15.

There are no other IFRS or IFRIC interpretations that are effective subsequent to the 2014 financial year-end that would have a material impact on the results or financial position of the group.

5. First time adoption of IFRSFor financial reporting periods up to and including 31 December 2013 the group prepared its financial statements in accordance with applicable Irish law and Generally Accepted Accounting Practice in Ireland including the accounting standards issued by the Financial Reporting Council and published by The Institute of Chartered Accountants in Ireland (Irish GAAP). The financial statements for the year ended 31 December 2014 are the first prepared in accordance with IFRS as adopted by the EU. The group has adopted 1 January 2012 as the date of transition to IFRS.

The accounting policies set out in note 2.2 have been applied in preparing the financial statements for the year ended 31 December 2014, the comparative information presented in these financial statements for the years ended 31 December 2013 and 31 December 2012 and in the preparation of the opening Statement of Financial Position at 1 January 2012 (the group’s date of transition). In preparing its opening Statement of Financial Position, the group has adjusted the amounts reported previously in the financial statements prepared under Irish GAAP. An explanation of how the transition from Irish GAAP to IFRS (as adopted by the EU) has affected the group’s financial position, financial performance and cash flows is set out in the following tables and notes.

Exemptions applied Optional exemptions IFRS 1 First-time Adoption of International Financial Reporting Standards (‘IFRS 1’) allows first time adopters certain exemptions from the retrospective application of certain requirements under IFRS. The group has applied the following exemptions:

• The group has elected not to retrospectively apply IFRS 3 Business Combinations to business combinations that occurred before the transition date. Such business combinations have not been restated. Any goodwill arising on such business combinations before the Transition Date has not been adjusted from the carrying value previously reported under Irish GAAP.

• The group has availed of the exemptions in IFRS 1, whereby the deemed cost of certain items of Property, plant and equipment have been calculated as their fair values as at the transition date.

Notes to the Consolidated Financial Statements (Continued)

PETROGAS GLOBAL Annual Report 2014 Directors’ Report and Financial Statements45

• Cumulative currency translation differences for all foreign operations have been set to zero as at the transition date.

• The group has applied the transitional provisions in IAS 23 Borrowing Costs and has capitalised borrowing costs relating to all qualifying assets after the date of transition.

Mandatory exemptions Set out below are the applicable mandatory exceptions in IFRS 1 applied in the conversion from Irish GAAP to IFRS.

• Estimates - IFRS estimates as at 1 January 2012 are consistent with the estimates as at the same date made in conformity with Irish GAAP.

The other compulsory exemptions in IFRS 1 as noted below have not been applied as these are not relevant to the group:

• Derecognition of financial assets and financial liabilities• Non-controlling interests• Hedge accounting

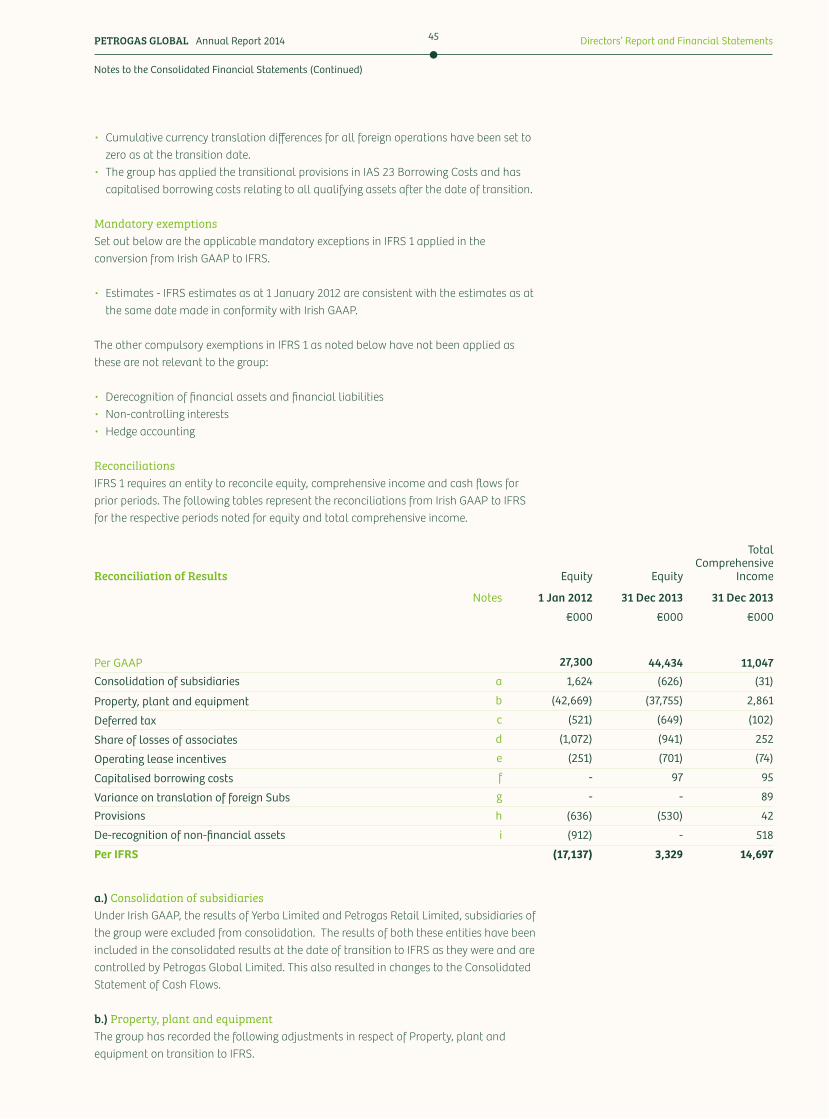

Reconciliations IFRS 1 requires an entity to reconcile equity, comprehensive income and cash flows for prior periods. The following tables represent the reconciliations from Irish GAAP to IFRS for the respective periods noted for equity and total comprehensive income.

Reconciliation of Results Equity Equity

Total Comprehensive

Income

Notes 1 Jan 2012 31 Dec 2013 31 Dec 2013

€000 €000 €000

Per GAAP 27,300 44,434 11,047Consolidation of subsidiaries a 1,624 (626) (31)

Property, plant and equipment b (42,669) (37,755) 2,861

Deferred tax c (521) (649) (102)

Share of losses of associates d (1,072) (941) 252

Operating lease incentives e (251) (701) (74)

Capitalised borrowing costs f - 97 95

Variance on translation of foreign Subs g - - 89

Provisions h (636) (530) 42

De-recognition of non-financial assets i (912) - 518

Per IFRS (17,137) 3,329 14,697

a.) Consolidation of subsidiaries Under Irish GAAP, the results of Yerba Limited and Petrogas Retail Limited, subsidiaries of the group were excluded from consolidation. The results of both these entities have been included in the consolidated results at the date of transition to IFRS as they were and are controlled by Petrogas Global Limited. This also resulted in changes to the Consolidated Statement of Cash Flows.

b.) Property, plant and equipmentThe group has recorded the following adjustments in respect of Property, plant and equipment on transition to IFRS.

Notes to the Consolidated Financial Statements (Continued)

Directors’ Report and Financial Statements 46

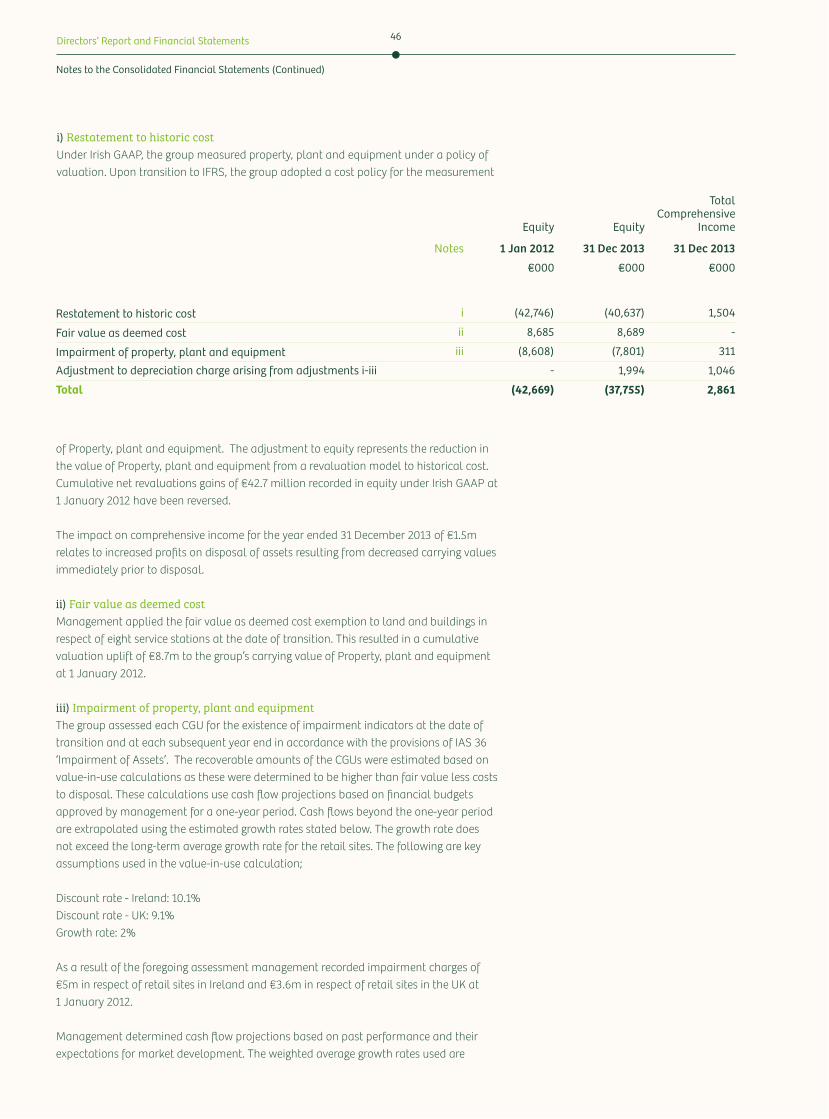

Equity Equity

Total Comprehensive

Income

Notes 1 Jan 2012 31 Dec 2013 31 Dec 2013

€000 €000 €000

Restatement to historic cost i (42,746) (40,637) 1,504

Fair value as deemed cost ii 8,685 8,689 -

Impairment of property, plant and equipment iii (8,608) (7,801) 311

Adjustment to depreciation charge arising from adjustments i-iii - 1,994 1,046

Total (42,669) (37,755) 2,861

i) Restatement to historic costUnder Irish GAAP, the group measured property, plant and equipment under a policy of valuation. Upon transition to IFRS, the group adopted a cost policy for the measurement

of Property, plant and equipment. The adjustment to equity represents the reduction in the value of Property, plant and equipment from a revaluation model to historical cost. Cumulative net revaluations gains of €42.7 million recorded in equity under Irish GAAP at 1 January 2012 have been reversed.

The impact on comprehensive income for the year ended 31 December 2013 of €1.5m relates to increased profits on disposal of assets resulting from decreased carrying values immediately prior to disposal.

ii) Fair value as deemed costManagement applied the fair value as deemed cost exemption to land and buildings in respect of eight service stations at the date of transition. This resulted in a cumulative valuation uplift of €8.7m to the group’s carrying value of Property, plant and equipment at 1 January 2012.