Embed Size (px)

Citation preview

PETROL AD

AUDITOR'S REPORT ANDFINANCIAL STATEMENTS

December 31, 2004

P E T R O L A D

Contents

Petrol AD

Auditor's report Page 2

Financial statements as of December 31, 2004 Page 4

Notes to the financial statements Page 9

Deloitte Deloitte Audit Ltd. AeAOum Ogum OOfl55, Al. Stambolijski Blvd. 6yA. ,,AA. CmaM6oAuucku" 55Sofia 1000 Cocfiuf! 1000Bulgaria BbAaapua

Tel. +359 (0) 2 980 8500 OupMeno geAO 10638/96Fax +359 (0) 2 980 0436 npu Co4>uucku apagcku ct>gwww.deloitte.bg 6aHko6a cwemka: MHT BANK kog 14591458

CMemka 6 AeBa: 1000270610

AUDITOR'S REPORT

TO THE SHAREHOLDERS OFPETROL AD

1. We have audited the accompanying non-consolidated balance sheet of Petrol AD(the "Company") as of December 31, 2004 and the related non-consolidated statements of income, cashflows and changes in equity for the year then ended. These non-consolidated financial statements are theresponsibility of the Company's management. Our responsibility is to express an opinion on the non-consolidated financial statements, based solely on our audit.

2. Except as discussed in paragraph 3 below, we conducted our audit in accordance withInternational Standards on Auditing. Those standards require that we plan and perform the audit to obtainreasonable assurance about whether the non-consolidated financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includes assessing the accounting principles usedand significant estimates made by management, as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

3. As disclosed in Note 4 to the accompanying non-consolidated financial statements, in 2004 theCompany has recognized income under fuel supply agreement signed with a supplier (the "Supplier"). Itincludes an increase of the Company's remuneration under this agreement, which to recover the incurredoperating expenses and discounts given to customers at the amount of BGN 17,901 thousand. TheManagement of Petrol AD believes that the amount of BGN 17,901 thousand should be included in thecalculation of the Company's remuneration set in accordance with this agreement and its net balancewith the Supplier. We were not provided with documentation or other evidence confirming the agreementof Supplier with this adjustment and therefore, we are not able to confirm the validity and the valuationof the revenue recognized at the amount of BGN 17,901 thousand. Additionally, we did not receiveconfirmation for the outstanding balance with the Supplier, reported as a net liability at the amount ofBGN 7,143 thousand as of December 31, 2004. As a result of the above, we were not able to confirm,through other alternative procedures, the validity, valuation and representation of the recognized revenuefrom sales and related trade payables reflecting the transactions with this Supplier, as reported in theaccompanying non-consolidated financial statements.

Audit* Tax* Consulting'Financial Advisory* A member ofDeloitte Touche Tohmatsu

4. In our opinion, except for the effect of such adjustments, if any, as might have been determinednecessary had we been able to satisfy ourselves about the validity, valuation and representation of therecognized revenue from sales and related trade payables reflecting the transactions with the Supplier, asdiscussed in paragraph 3 above, the Company's non-consolidated financial statements present fairly, inall material respects, the financial position of the Company as of December 31, 2004, and the results ofits operations, changes in cash flows and shareholders' equity for the year then ended, in accordance withInternational Financial Reporting Standards.

5. Without further qualifying our opinion, we draw attention to the fact that plant and equipmentwith carrying amount of BGN 2,212 thousand as of December 31, 2003, which are non-operating, havebeen disclosed in the non-consolidated financial statements of the Company as of December 31, 2003,prepared in accordance with International Financial Reporting Standards. These fixed assets have beenreported at their historical cost, which may differ form their recoverable amount. As a result our auditor'sreport dated March 25, 2004 on the non-consolidated financial statements of the Company as ofDecember 31, 2003 contained qualification with regards to the fair presentation of these assets. Asdisclosed in Note 14 to the accompanying non-consolidated financial statements, these plant andequipment have been impaired in 2004.

Deloitte Audit Ltd.

Sylvia PenevaManaging DirectorRegistered Auditor

March 31,2005Sofia

Petrol AD

Financial Statements

as of December 31, 2004

Financial statements as of December 31, 2004

Petrol AD

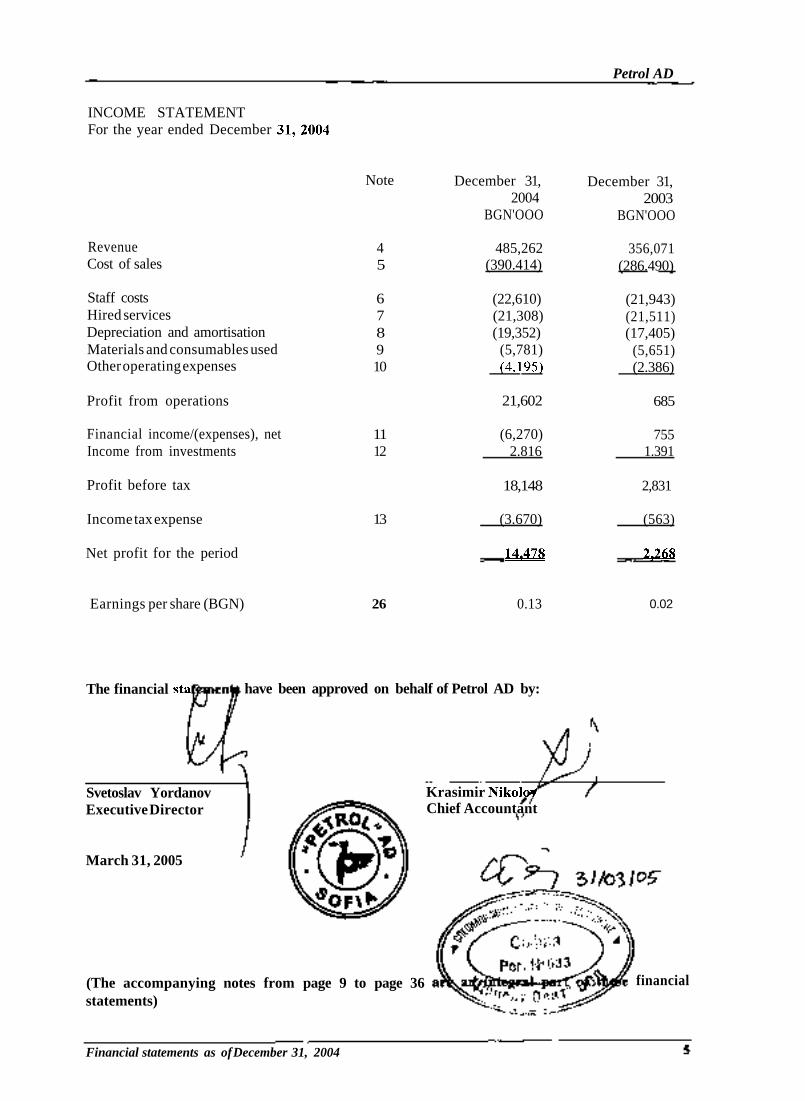

INCOME STATEMENTFor the year ended December 31, 2004

RevenueCost of sales

Staff costsHired servicesDepreciation and amortisationMaterials and consumables usedOther operating expenses

Profit from operations

Financial income/(expenses), netIncome from investments

Profit before tax

Income tax expense

Net profit for the period

Note

45

678910

1112

13

December 31,2004

BGN'OOO

485,262(390.414)

(22,610)(21,308)(19,352)

(5,781)(4.195)

21,602

(6,270)2.816

18,148

(3.670)

14T478

December 31,2003

BGN'OOO

356,071(286.490)

(21,943)(21,511)(17,405)

(5,651)(2.386)

685

7551.391

2,831

(563)

2,268

Earnings per share (BGN) 26 0.13 0.02

The financial sta have been approved on behalf of Petrol AD by:

Svetoslav YordanovExecutive Director

March 31, 2005

Krasimir NikolwrChief Accountant

(The accompanying notes from page 9 to page 36statements)

financial

Financial statements as of December 31, 2004

Petrol AD

BALANCE SHEETAs at December 31, 2004

Non-current assetsProperty, plant and equipmentInvestmentsInvestment propertyIntangible assetsGoodwill

Total non-current assets

Current assetsTrade and other receivables, netInventoriesFinancial assets available for saleCash and cash equivalents

Total current assets

Current liabilitiesTrade and other payablesShort-term loans and borrowingsProvisionsObligations under finance leases

Total current liabilities

Non-current liabilitiesLong term loans and borrowingsCorporate bond loanDeferred taxObligations under finance leases

Total non-current liabilities

Total net assets

Capital and reservesShare capitalRevaluation reserveStatutory reserveRetained earnings

Total capital and reserves

Note

14151614

17181920

21222324

22221324

25

December 31,2004

BGN'OOO

205,80328,40018,312

1,426_

253,941

44,47923,47416,2974,304

88,554

46,28519,703

1,10031

67,119

57,61114,7859,224

76

81,696

193.680

109,25058,5299,005

16,896

193.680

December 31,2003

BGN'OOO

210,369111,617

19,5502,117

16

343,669

34,32826,63413,8938,926

83,781

146,47117,538

1,11037

165,156

55,55214,78512,989

110

83.436

178.858

109,25057,692

8,6813.235

178.858

(The accompanying notes from page 9 to page 36 are an integral part of these financialstatements)

Financial statements as of December 31, 2004

Petrol AD

CASH FLOW STATEMENTFor the year ended December 31,2004

Cash flows from operating activities

Proceeds from clients and other partiesPayments to suppliers and other partiesPayments to employees, net

Cash generated from operations

Income tax paid

Net cash from operating activities

Cash flows from investing activities

Purchase of property, plant and equipmentAcquisition of financial assets available for saleProceeds on disposal of property, plant and equipmentProceeds on disposal of financial assets available for saleDeposits openedDividends receivedAcquisition of investments

Net cash used in investing activities

Cash flows from financing activities

Proceeds from borrowingsProceeds from corporate bond loanRepayments of borrowingsInterest paidDividends paidOther proceeds of financing activities, net

Net cash used in financing activities

Net increase/(decrease) in cash and cash equivalents

Cash and cash equivalents at the beginning of periodEffect of foreign exchange rate changes

Cash and cash equivalents at the end of period

December 31,2004

BGN'OOO

611,688(561,841)

(21.928)

27,919

(769)

27,150

(34,913)(2,029)

8,68423,181

(25,518)3,079

(27,516)

241,705

(237,313)(6,574)(2,169)

128

(4,223)

(4,589)

8,926(33)

December 31,2003

BGN'OOO

410,589(391,134)

(20.855)

(1,400)

(2.127)

(3,527)

(34,370)(766)

38321,042

1,103(14.096)

(26,704)

351,14014,997

(326,665)(2,619)

36,853

6,622

2,987(683)

(The accompanying notes from page 9 to page 36 are an integral part of these financialstatements.)

Financial statements as of December 31, 2004

Petrol AD

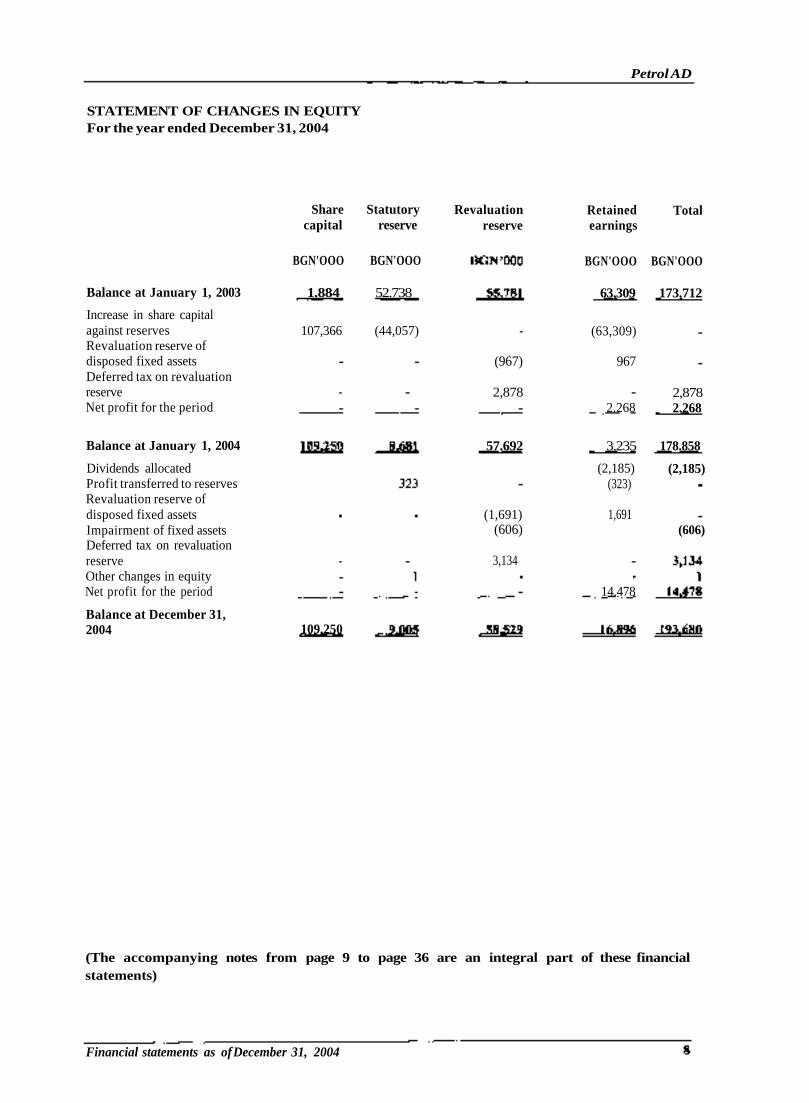

STATEMENT OF CHANGES IN EQUITYFor the year ended December 31, 2004

Balance at January 1, 2003

Increase in share capitalagainst reservesRevaluation reserve ofdisposed fixed assetsDeferred tax on revaluationreserveNet profit for the period

Share Statutorycapital reserve

BGN'OOO BGN'OOO

1.884 52.738

107,366 (44,057)

Revaluationreserve

(967)

2,878

Retainedearnings

Total

BGN'OOO BGN'OOO

63,309 173.712

(63,309)

967

2.2682,8782.268

Balance at January 1, 2004

Dividends allocatedProfit transferred to reservesRevaluation reserve ofdisposed fixed assetsImpairment of fixed assetsDeferred tax on revaluationreserveOther changes in equityNet profit for the period

Balance at December 31,2004 109.250

57.692

(1,691)(606)

3,134

3.235

(2,185)(323)

1,691

14.478

178.858

(2,185)

(606)

(The accompanying notes from page 9 to page 36 are an integral part of these financialstatements)

Financial statements as of December 31, 2004

Petrol AD

Notes to the Financial Statements

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

1. GENERAL

Petrol AD (the Company) is a joint-stock company, registered at the Sofia City Court. Based on aShare Purchase Agreement of 1999 Naftex Petrol AD acquired 51% of the Company's shares. Asof December 31, 2004 majority shareholder of Petrol AD is Petrol Holding AD (former NaftexBulgaria Holding AD) with 83.44% ownership of the share capital. The remaining part of theCompany's shares is ownership of other legal entities, the state - through the Ministry of Economyand of individual shareholders.

Effective from July 1, 1998 Petrol AD is registered as a public company in the Public Register ofFinance Supervisory Commission.

The main activity of Petrol AD comprises retail of oil products and non-oil products and services.The Company is one of the oldest commercial companies in Bulgaria and owns the largest networkof fuel-filling stations. In 2004, the Company operates 450 gas stations located all over thecountry. The total number of employees of the Company as of December 31, 2004 and December31,2003 is 3,561 and 3,544.

2. BASIS FOR PREPARATION OF THE FINANCIAL STATEMENTS

2.1. General

The accompanying financial statements for the year ended December 31, 2004 have been preparedin all material respects in accordance with International Financial Reporting Standards (IFRS) andinterpretations issued by the International Accounting Standards Board, and approved by theCouncil of Ministers of Republic of Bulgaria.

These financial statements have been prepared under the historical cost convention and do notrepresent consolidated financial statements in accordance with Art. 37, Para 2 of the AccountancyAct. The Company also prepares consolidated financial statements in accordance withInternational Accounting Standard (IAS) 27 - Consolidated Financial Statements and Accountingfor Investments in Subsidiaries and the Accountancy Act of Republic of Bulgaria. The principalaccounting policies are set out below.

2.2. Reporting currency

According to the Bulgarian accounting legislation the Company keeps its records and prepares itsfinancial statements in the national currency of the Republic of Bulgaria - the Bulgarian lev.Effectively January 1, 1999, Bulgarian lev was fixed to the EUR at a rate BGN 1.95583 = EUR 1.

These financial statements are presented in thousands of Bulgarian leva ("BGN'000").

Financial statements as of December 31, 2004 10

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

2.3. Subsidiary companies

A subsidiary is an enterprise that is controlled by the parent company. Control is the power togovern the financial and operating policies of an enterprise so as to obtain benefits from itsactivities.

As of December 31, 2004 and December 31, 2003 the Company has the following subsidiaries:

Subsidiary Main Activity Investment as of Investment as ofDecember 31, December 31,

2004 2003

Petrol Trans Express EOOD Transport services 100.0% 100.0%Petrol Technics EOOD Repairs and maintenance of

fuel-filling stations 100.0% 100.0%Petrol Storage EOOD Storage of fuels 100.0% 100.0%Petrol Trade EOOD Trade 100.0% 100.0%BPI EAD Trade with oil products and

property rental 100.0% 100.0%Naftex Petrol OOD Wholesales with oil

products 100.0% 100.0%Petrol Card Service EOOD Fleet card operator 100.0% 50.0%TranslotoAD Lottery 99.9% 99.9%Eurocapital Bulgaria AD Investing activities 99.8% 99.8%Vratzata OOD Recreation services 99.4% 99.4%Transat AD Data maintenance and

transfer through a satellite - 98.0%Trans Telecom OOD Telecommunication

services - 95.0%

In these financial statements, investments in subsidiaries are stated at cost of acquisition.

In July 2004 the Petrol AD acquired 100% of the share capital of Petrol Card Service EOOD(PCS). In prior periods, this subsidiary was a joint venture between Petrol AD and Union TankEckstein, Germany. The cost of acquisition of the 50% of Petrol Card Service is BGN 509thousand.

As a result of the reorganization policy adopted within Petrol Holding AD (the majorityshareholder of the Company), in prior periods the Management Board of the Company had takendecisions for the disposal of Transloto AD, Eurocapital Bulgaria AD, Vratzata OOD, Transat AD,Trans Telecom OOD and Petrol Card Service EOOD. As at December 31, 2004 the Company haseffectively disposed of the subsidiaries Transat AD and Trans Telecom OOD, which have beentransferred to Transhold AD - subsidiary of the majority shareholder of the Company, at cost. As aresult of these deals, the Company has not generated any loss. The rest of the subsidiaries forwhich there is decision for their disposal are presented in these financial statements as financialassets available for sale (see also note 20).

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

2.4. Interests in associates

An associate is an enterprise over which the Company is in a position to exercise significantinfluence, but not control, through participation in the financial and operating policy decisions ofthe investee.

In these financial statements investments in associates are stated at cost of acquisition.

As of December 31, 2004 and December 31, 2003 the Company has the following associates:

Associate Main Activity Investment as of Investment as ofDecember 31, December 31,

2004 2003

Petrol Engineering AD Fiscal system maintenance 40.0% 40.0%Varna Business Services OOD Training, consultation and 36.7%

hotel servicePetrol Card Service EOOD Fleet card operator - 50.0%

In March 2004, Petrol AD participated in the increase of share capital of Varna Business ServicesOOD - subsidiary of Company's majority shareholder through an in-kind contribution of tangiblefixed assets with book value of BGN 2,184 thousand as of March 31, 2004. The total value of thisinvestment was in the amount of BGN 2,205 thousand, set by the independent expert valuersappointed by the Court.

2.5. Foreign currency

Transactions in foreign currency are initially recorded at the official rate of exchange of theBulgarian National Bank (BNB) as of the date of the transaction. The foreign exchange ratedifferences, arising upon the settlement of these monetary positions or at restatement of thesepositions at rates, different from those when initially accounted for, are reported as financialincome or financial expenses for the period in which they arise. In these financial statements, thefinancial instruments denominated in foreign currency as of December 31, 2004 are restated at theclosing exchange rate of BNB.

The closing exchange rate of Bulgarian lev against the USD for the periods, covered by thesefinancial statements is as follows:

December 31,2004: $ 1 = BGN 1.43589December 31,2003: $ 1 = BGN 1.54856

2.6. Accounting estimates and reasonable assumptions

The presentation of financial statements in accordance with International Financial ReportingStandards requires management to make certain accounting estimates and reasonable assumptionsthat affect some of the reported amounts of assets, liabilities, revenues and expenses. Theseestimates and assumptions are based on the best estimate of management as of the date of theconsolidated financial statements. The actual results could differ from those estimates.

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

3.1. Property, plant and equipment and intangible non-current assets

Property, plant and equipment are carried at cost, including its purchase price and all additionalcosts related to their acquisition, less any accumulated depreciation and accumulated impairmentlosses, or at revalued amount.

Intangible fixed assets are carried at cost, including their purchase price and all additional costsrelated to their acquisition, less any accumulated amortization and accumulated impairment losses.

Assets under construction are carried at cost, including their purchase price and all additional costsrelated to their acquisition, less accumulated impairment losses.

Depreciation and amortisation on non-current assets other than land and properties underconstruction, is charged so as to write off the cost over their estimated useful lives, using thestraight-line method at the following rates:

Buildings 4%Plant and equipment 4%, 30% and 50%Vehicles 10% and 25%Fixtures and fittings 15%Intangible non-current assets 15% and 50%

First depreciation charge for the newly acquired assets is provided in the month following themonth of the acquisition.

Subsequent expenditure related to property, plant and equipment is capitalized if it is probable theCompany to obtain future economic benefits higher than the benefit from the originally assessedstandard profitability of the asset. All subsequent expenses are recognized as expenditures for theperiod when they arose.

Assets held under finance leases are depreciated over their expected useful lives on the same basisas owned assets or, where shorter, the term of the relevant lease.

The gain or loss arising on the disposal or retirement of an asset is determined as the differencebetween the sales proceeds and the carrying amount of the asset and is charged to the income forthe period of the disposal.

3.2. Investment property

Investment property is property (land, building or part of building, or both) held by the Companyto earn rentals or for capital appreciation, or for both.

In these financial statements investment property is stated at cost less any accumulateddepreciation and any impairment losses thereon.

These properties, that are used partially for Company's operations and partially to earn rentals andit is impossible to be reported separately, are presented in compliance with IAS 16 - Property,plant and equipment.

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3.2. Investment property (Continued)

Depreciation on investment property is charged so as to write off the cost, other than land, overtheir estimated useful lives, using the straight-line method, on the following bases:

Buildings 4%Plant and equipment 30%Fixtures and fittings 15%

3.3. Impairment

At each balance sheet date, the Company reviews the carrying amounts of its tangible andintangible assets to determine whether there is any indication that those assets have suffered animpairment loss. If any such indication exists, the recoverable amount of the asset is estimated inorder to determine the extent of the impairment loss (if any). Where it is not possible to estimatethe recoverable amount of an individual asset, the Company estimates the recoverable amount ofthe cash-generating unit to which the asset belongs.

Recoverable amount is the greater of net selling price and value in use.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than itscarrying amount, the carrying amount of the asset (cash generating unit) is reduced to itsrecoverable amount. Impairment losses are expensed to the income statement immediately, unlessthe relevant asset is carried at a revalued amount, in which case the impairment loss is treated as adecrease of the revaluation reserve.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash -generating unit) is increased to the revised estimate of its recoverable amount, but so that theincreased carrying amount does not exceed the carrying amount that would have been determinedhad no impairment loss been recognised for the asset (cash-generating unit) in prior years. Areversal of an impairment loss is recognised as income immediately, unless the relevant asset iscarried at a revalued amount, in which case the reversal of the impairment loss is treated as arevaluation increase.

3.4. Investments

Investments in subsidiary and associate companies are carried at cost, less any accumulatedimpairment losses in compliance with IAS 27 - Consolidated Financial Statements and Accountingfor Investments in Subsidiaries and IAS 28 - Accounting for Investments in Associates.

3.5. Inventories

Materials and goods for resale are stated at the lower of cost and net realisable value. Costcomprises purchase price, transportation, customs duties and other related costs. Net realisablevalue represents the estimated selling price less all estimated cost to be incurred in selling anddistribution. Upon consumption, materials and goods for resale are stated using the followingmethods:

Crude oil - Specific identification price of each deliveryFuel and other goods for resale - Weighted average priceMaterials - Weighted average price

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3.6. Financial instruments

Financial assets and financial liabilities are recognized in the Company's balance sheet only whenthe Company becomes a party to the contractual provisions of the instrument.

3.6.1. Trade and other receivables

Trade and other receivables are stated at their amortised cost. As at the balance sheet date, theCompany prepares review of all significant outstanding balances in order to determine if there isany impairment.

3.6.2. Cash and cash equivalents

For the purposes of cash flow presentation, cash and cash equivalents represent unrestricted cashon hand and in bank accounts.

3.6.3. Trade and other payables

Trade and other payables are stated at their amortised cost.

3.6.4. Financial assets available for sale

Financial assets available for sale are recognised on a trade-date basis and are initially measured atcost, including transaction costs. At subsequent reporting dates, financial assets available for saleare measured at fair value, except where market price quotations for these financial assets are notavailable and other methods for reasonable fair value definition are not applicable. Financial assetsavailable for sale where no fair value exists are states at cost, adjusted by any impairment losses.

3.6.5. Loans and borrowings

Short-term and long-term interest-bearing bank loans and overdrafts and the issued corporate bondloan are recorded at the proceeds received, net of direct issue costs. Finance charges, includingpremiums payable on settlement or redemption and direct issue costs, are accounted for on anaccrual basis to the profit and loss account using the effective interest method and are added to thecarrying amount of the instrument to the extent that they are not settled in the period in which theyarise.

3.6.6. Risk assessment and risk management

Interest rate risk

Information about maturity and effective interest rates on loans granted to the Company ispresented in Note 22 to the financial statements. Interest rates are pegged to EUROLIBOR andSOFIBOR, whilst the corporate bond loan issued by the Company bears a fixed interest rate.Therefore the Company is exposed to interest risk in case of considerable increase in floatinginterest rates and/or significant decrease in the fixed interest rate. The Company does not usespecial financial instruments for interest risk hedging, but the Management believes that thepossibility for interest rate negative movement is negligible and the interest rate risk which theCompany is exposed to is insignificant.

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3.6. Financial instruments (Continued)

3.6.6. Risk assessment and risk management

Currency risk

The Company is party to loan contracts and performs transactions denominated in US dollars.Therefore it is exposed to risk of possible appreciation of the US dollar against Bulgarian lev,which could result in an exchange loss for the Company. The Company does not use specialfinancial instruments for currency risk hedging, but it is secured to a reasonable extent against thisrisk as the national currency is fixed to the EUR (see also Note 2.4), and the risk of materialdepreciation of the EUR against USD is minimal.

Credit risk

Financial assets that potentially expose the Company to a credit risk are primarily its tradereceivables. Basically, the Company is exposed to credit risk, in case the clients do not meet theirpayment obligations. Company's policy is directed primarily to sales of goods and services in cash,as well as deferred payment sales to clients with appropriate credit standing.

Credit risk of cash at banks is minimal as the Company deals with local and foreign banks withhigh credit rating.

3.7. Lease

Assets held under finance leases are recognised as assets of the Company at their fair value at thedate of acquisition or, if lower, at the present value of the minimum lease payments. Thecorresponding liability to the lessor is included in the balance sheet as a finance lease obligation.

Lease payments are apportioned between finance charges and reduction of the lease obligation soas to achieve a constant rate of interest on the remaining balance of the liability.

Finance lease originates depreciation charge for amortizable assets, as well as financial expensesfor every reporting period. The depreciation policy with regards to the leased assets is incompliance with the policy applied to the own assets.

3.8. Deferred income and expense

Deferred income and expense in the Company's balance sheet represents income and expense,which is paid in the current, but refers to future accounting periods - advertising, insurance,subscription, rent, etc.

Financial statements as of December 31, 2004 '"

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3.9. Income tax

Income tax expense represents the sum of the tax currently payable and deferred tax.

The tax currently payable is based on taxable profit for the year. Taxable profit differs from netprofit as reported in the income statement because it excludes items of income or expense that aretaxable or deductible in other years and it further excludes items that are never taxable ordeductible. The Company's liability for current tax is calculated using tax rates that have beenenacted or substantively enacted by the balance sheet date.

Deferred tax liabilities are recognised for taxable temporary differences arising on investments insubsidiaries and associates, except where the Company is able to control the reversal of thetemporary difference and it is probable that the temporary difference will not reverse in theforeseeable future.

Deferred tax is the tax expected to be payable or recoverable on differences between the carryingamount of assets and liabilities in the financial statements and the corresponding tax basis used inthe computation of taxable profit, and is accounted for using the balance sheet liability method.Deferred tax liabilities are generally recognised for all taxable temporary differences and deferredtax assets are recognised to the extent that it is probable that taxable profits will be availableagainst which deductible temporary differences can be utilised. Such assets and liabilities are notrecognised if the temporary difference arises from goodwill or from the initial recognition (otherthan in a business combination) of other assets and liabilities in a transaction that affects neitherthe tax profit nor the accounting profit.

The carrying amount of deferred tax assets is reviewed at each balance sheet date and reduced tothe extent that it is no longer probable that sufficient taxable profit will be available to allow all orpart of the asset to be recovered.

Deferred tax is calculated at the tax rates that are expected to apply in the period when the liabilityis settled or the asset realised. Deferred tax is charged or credited in the income statement, exceptwhen it relates to items charged or credited directly to equity, in which case the deferred tax is alsodealt with in equity.

Deferred tax is calculated at the tax rates that are expected to apply in the period when the liabilityis settled or the asset realised. Deferred tax is charged or credited in the income statement, exceptwhen it relates to items charged or credited directly to equity, in which case the deferred tax is alsodealt with in equity.

Deferred tax assets and liabilities are offset when they relate to income taxes levied by the sametaxation authority and the Company intends to settle its current tax assets and liabilities on a netbasis.

In accordance with the tax legislation enforceable as of the date of these consolidated financialstatements, the tax rates to be applied for calculation of tax liabilities of the Company are asfollows:

2005 2004 2003

Corporate income tax (profit tax) 15.0 % 19.5 % 23.5 %

Financial statements as of December 31, 2004 *7

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

3.10. Income and expenses recognition

Revenues and expenses are accounted for on an accrual basis, regardless the cash payment. Theyare reported in compliance with the matching concept.

Interest income and expense is accrued on a time basis, by reference to the principal outstandingand at the effective interest rate applicable.

Dividend income from investments is recognized when the shareholders' rights to receive paymenthave been established.

3.11. Borrowing costs

All borrowing costs are recognised in net profit or loss in the period in which they are incurred.

4. REVENUE

An analysis of the Company's revenue is as follows:

December 31,2004

BGN'OOO

432,58835,860

9,7583,5781,8911,338

249

December 31,2003

BGN'OOO

321,89222,248

3835,1611,9121,7062.769

Sales of goodsSales of servicesSales of materials and fixed assetsRental incomeRental income from investment propertiesSales of electricityOther sales

Total

According to the terms of fuel supply agreement, in the revenue for the year ended December 31,2004, the Company has recognized income amounting to BGN 41,170 thousand. This amountincludes reduction in revenue amounting to BGN 4,038 thousand. In the calculation of thisreduction is included an amount of BGN 17,901 thousand, which represents increase of theCompany's remuneration for incurred operating expenses and discounts given to customers. TheManagement of the Company believes that the amount of BGN 17,901 thousand must be includedin the calculation of Company's remuneration according to this contract and in the closing balanceof trade accounts payable with this supplier, amounting to BGN 7,143 thousand. As at the date ofapproval of these financial statements, the Company is still negotiating the adjustment of BGN17,901 thousand with the counterparty. If agreement is not reached, the Company will be requiredto reverse this adjustment, thereby reducing revenue, shareholders' equity and profit before tax,and increasing trade and other payables, by BGN 17,901 thousand.

Financial statements as of December 31, 2004 18

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

4. REVENUE (CONTINUED)

Revenue from sales of goods comprises:

Gasoline A95 HDiesel oilGasoline A92 HLPGLubricants and other goods in filling stationsGasoline A98 HIndustrial oilCrude oil

Total

December 31,2004

BGN'OOO

135,536132,36098,19032,97024,321

6,2852,643

283

December 31,2003

BGN'OOO

91,78280,24096,61520,36019,3456,7856,495

270

5. COST OF SALES

Cost of sales can be analyzed as follows:

Cost of goods soldCost of materials and fixed assets sold

Total

December 31,2004

BGN'OOO

388,1052.309

December 31,2003

BGN'OOO

286,283207

Cost of goods sold comprises:

Gasoline A95 HDiesel oilGasoline A92 HLPGLubricants and other goods in filling stationsGasoline A98 HIndustrial oilCrude oil

Total

December 31,2004

BGN'OOO

122,094119,40588,95127,17022,078

5,5752,550

282

December 31,2003

BGN'OOO

81,83469,14087,04917,35819,2285,7115,694

269

Financial statements as of December 31, 2004 19

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

6. STAFF COSTS

Staff costs comprise the following:

Salaries and wagesSocial security expensesFood allowancesRecreation and sport activitiesSocial aid, transportation and other expensesMedicaments and medical services

Total

December 31,2004

BGN'OOO

16,4385,0211,112

2612

1

December 31,2003

BGN'OOO

15,5175,0521,120

2919

206

7. HIRED SERVICES

Hired services comprise the following:

Repairs and maintenance of fixed assetsTransportationTelephone, fax and similar expensesSecurityConsulting servicesState and municipal taxesCash collection servicesRent of buildings and automobilesInsuranceAdvertisingOther expenses

Total

December 31,2004

BGN'OOO

5,3842,5762,5232,1112,0191,9581,5531,471

469212

1.032

December 31,2003

BGN'OOO

4,4371,0801,3752,2784,7042,4191,1341,636

768579

1.101

21.511

8. DEPRECIATION AND AMORTISATION

Expenses for depreciation and amortization include:

Depreciation of tangible fixed assetsDepreciation of investment propertiesAmortisation of intangible fixed assetsAmortisation of goodwill

Total

The increase in depreciation expense in 2004 compared to 2003 is due to the significant capitalexpenditures made by the Company in compliance with its intensive investment program, whichlead to an increase in the value of tangible fixed assets.

December 31,2004

BGN'OOO

17,2941,317

7365

December 31,2003

BGN'OOO

14,7321,3401,327

6

Financial statements as of December 31, 2004 20

NOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

Petrol AD

9. MATERIALS AND CONSUMABLES USED

Expenses for materials and consumables comprise:

ElectricityOffice consumablesWorking clothesWater supplyFuel and other oil consumablesSpare partsHeatingOther expenses

Total

December 31,2004

BGN'OOO

2,4771,417

50034820012574

640

December 31,2003

BGN'OOO

2,2961,084

759377230139169597

10. OTHER OPERATING EXPENSES

Other operating expenses comprise:

Impairment of assetsWithholding and other taxesFixes assets and materials wastedBusiness tripsProperty tax and automobile taxEntertainmentShortages of assetsOther expenses

Total

December 31,2004

BGN'OOO

2,56644239321221118410177

4,195

December 31,2003

BGN'OOO

15162963631520410962280

11. FINANCIAL INCOME/(EXPENSES), NET

Net effect from change in exchange ratesInterest expensesInterest incomeOther financial expenses, net

Total

December 31,2004

BGN'OOO

160(6,424)

213(219)

December 31,2003

BGN'OOO

Financial statements as of December 31, 2004 21

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

12. INCOME FROM INVESTMENTS

Income from investments includes dividends received and the results of operations with thefollowing investees:

Eurocapital Bulgaria ADPetrol Card Service OODVarna Business Services OOD

Total

December 31,2004

BGN'OOO

1,7541,036

26

2.816

December 31,2003

BGN'OOO

1,102289

1.391

13. INCOME TAX

Income tax expense in the income statement is as follows:

Current tax:

Deferred tax:Effect from change in tax ratesEffect from change in temporary differences

Total

December 31,2004

BGN'OOO

4,301

December 31,2003

BGN'OOO

1,054

132(623)

Deferred tax assets and liabilities are attributable to the following balance sheet items:

Liabilities Assets Net

December 31, December 31, December 31, December 31, December 31, December 31,

Fixed assets

Trade and otherreceivablesInventories

Provisions

Net tax assets/(liabilities)

2004

BGN'OOO

(10,448)

2003

BGN'OOO

(14,030)

2004

BGN'OOO

918

1401

165

r 10.448^ (14.030^ 1.224

2003

BGN'OOO

724

1001

216

1,041

2004

BGN'OOO

(9,530)

1401

165

2003

BGN'OOO

(13,306)

1001

216

Financial statements as of December 31, 2004 22

NOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

13. INCOME TAX (CONTINUED)

Movement of deferred tax assets and liabilities for the period is as follows:

Petrol AD

Fixed assetsTrade and otherreceivablesInventoriesProvisions

Total

Balance atDecember 31,

2003BGN'OOO

(13,306)

1001

216

Recognized inthe result for

the yearBGN'OOO

643

39

631

Recognized inthe reserves for

the yearBGN'OOO

3,134

3T134

Balance atDecember 31,

2004BGN'OOO

(9,529)

1391

165

Deferred tax assets and liabilities on taxable and deductible temporary differences as ofDecember 31, 2004 are calculated using the effective tax rate for corporate income tax for 2005 at15.0% (see also Note 3.9).

Effective tax rate for the period is presented in the table below:

Profit before taxApplicable tax rate

Income tax expense at applicable tax rate

Tax effect from permanent differencesTax effect from temporary differences

Income tax expense

Effective tax rate

December 31,2004

BGN'OOO

18,14819.5%

December 31,2003

BGN'OOO

2,83123.5%

665

389(491)

19.9%

Financial statements as of December 31, 2004 23

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

14. FIXED ASSETS

Movement of property, plant and equipment for the period is as follows:

Cost

As of December 31, 2003AdditionsDisposalsImpairment lossAs of December 31, 2004

Accumulated Depreciation

As of December 31, 2003Charge for the periodDisposalsAs of December 31, 2004

Land andbuildingsBGN'OOO

113,3153,122

(3,834)(694)

111.909

29,2851,856

(1.235129.906

Plant andequipment

BGN'OOO

127,56726,086(1,624)(1.0911

150.938

40,24711,843

(1.259150.831

Motor Fixtures Assets under Totalvehicles and fittings construction

BGN'OOO BGN'OOO BGN'OOO BGN'OOO

11,9042,368

(3,470)

10.802

6,7291,124

(•3.32414.529

17,0153,909(139)

20.784

4,6952,472(12817.039

21,524 291,32515,691 51,176

(33,540) (42,607)(1,786)

3,675 298,108

80,95617,295(5,946)92.305

Net book value as ofDecember 31, 2003Net book value as ofDecember 31, 2004 100.107

12.320

In fixed assets' disposals for the year ended December 31, 2004 is included the in-kindcontribution in the share capital of Varna Business Services OOD, amounting to BGN 2,205thousand (see also note 15).

Movement of intangible assets for the period is as follows:

Cost

As of December 31, 2003AdditionsDisposalsAs of December 31, 2004

Accumulated Amortization

As of December 31, 2003Charge for the periodDisposalsAs of September 30, 2004

Net book value as ofDecember 31, 2003

Net book value as ofDecember 31, 2004

Patents andlicenses

BGN'OOO

1,22813

(1.158)83

461141

(561)41

42

Software Other Assets under Totalconstruction

BGN'OOO BGN'OOO BGN'OOO BGN'OOO

2,568 347 500 4,643392 16 223 644

(2.2141 - - (3.372)746 363

1,949 116541 53

(2,211)279 169

619 J31

467 194

723 1,915

2,526735

(2.772)489

500 2,117

Financial statements as of December 31, 2004 24

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

14. FIXED ASSETS (CONTINUED)

As some of the Company's storage facilities are not operating at full capacity as at December 31,2004 the Management of Petrol AD took decision to impair their book value with the amount ofBGN 1,682 thousand. As a result, the effectiveness and the cash generated by the rest of thestorage facilities have increased.

As of December 31, 2004 and December 31, 2003 tangible fixed assets with total net book value ofBGN 66,144 thousand and BGN 70,178 thousand, respectively, are pledged as collateral for loansgranted to the Group and to related parties.

15. INVESTMENTS

Subsidiary companies:

Naftex Petrol OOD (see also Note2.2)BPI BADPetrol Trans Express EOODPetrol Technics EOODPetrol Trade EOODPetrol Storage EDDOVratzata OOD (see also Note 19)Transat AD (see also Note 20)

Associated companies:

Petrol Engineering ADVarna Business Services ADPetrol Card Service OOD

Total

December 31, 2004

% of BGN'OOOcapital

100.00%100.00%100.00%100.00%100.00%100.00%

40.00%36.7%

15,5549,821

650505050

100.00%100.00%100.00%100.00%100.00%100.00%

26.175

202,205

December 31, 2003

%OT

Kanmajia XHJI. JIB.

100,9669,821

650505050

40.00%

50.00%

111.587

20

10

30

As per a decision of Varna Regional Court, on July 12, 2004 the share capital of Naftex PetrolOOD has been decreased from BGN 95,412 thousand to BGN 10,000 thousand. This share capitalreduction aimed to increase the profitability of the subsidiary by releasing cash funds and decreasethe paid in capital to the current needs of Naftex Petrol OOD.

On August 2, 2004, according to a decision of Varna Regional Court, the share capital of VarnaBusiness Services OOD - subsidiary of the Company's majority shareholder was increasedthrough an in-kind contribution of tangible fixed assets in the amount of BGN 2,205 thousand. Inthese financial statements this increase is presented as disposal of fixed assets and increase ininvestments in associates (see also note 14).

Financial statements as of December 31, 2004 25

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

16. INVESTMENT PROPERTY

As of December 31, 2004 as investment properties are presented a hotel complex with carryingamount of BGN 12,582 thousand and two administrative buildings with carrying amount of BGN5,730 thousand.

Movement of investment properties for the year is as follows:

Cost

As of December 31, 2003AdditionsDisposalsAs of December 31, 2004

Accumulated Depreciation

As of December 31, 2003Charge for the periodAs of December 31, 2004

Net book value as of December31, 2003

Net book value as of December31,2004

Land andBuildingsBGN'OOO

18,977

18,977

Plant andEquipment

BGN'OOO

1,86726

L893

Fixtures andFittings

BGN'OOO

1,73859

1,791

951

603

Total

BGN'OOO

1,433685

2.118

916374

L290

683258941

3,0321,3174.349

850

December 31,2004

BGN'OOO

33,4387,203

563558387115

2.215

December 31,2003

BGN'OOO

14,3116,273

6883,020

7994,9804.257

17. TRADE AND OTHER RECEIVABLES, NET

Receivables from related partiesTrade receivables, net of impairment lossesLitigations and writs, net of impairment lossesAdvances to suppliersPrepaid expensesRecoverable taxesOther receivables

Total

Receivables from related parties as of December 31, 2004 and 2003 are further disclosed in Note27.

Receivables from related parties as of December 31, 2004 include cash deposit opened withmajority shareholder of the Company - Petrol Holding AD at the amount of BGN 25,518thousand. This cash deposit is highly liquid and there are movements on its balance in very shortperiods of time.

Company's management considers that the carrying amount of trade and other receivablesapproximates their fair value as of December 31, 2004.

Financial statements as of December 31, 2004 26

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31,2004

18. INVENTORIES

December 31, December 31,2004 2003

BGN'OOO BGN'OOO

GasolineLubricants and other goods for resaleDiesel oilRaw materialsLPGOils at petrol basesIndustrial fuelOther goods for resale

Total

As of December 31, 2004 and December 31, 2003 inventories amounting to BGN 19,459 thousandand BGN 22,272 thousand respectively, represent oil products and other goods for resale at the gasstations delivered under purchase agreement but not invoiced by the supplier as at the period end.According to the terms of the purchase contract, significant risks are transferred from the supplierto the Company. Applying the substance over form accounting principle the Company adopted thepolicy to recognise such inventories in the balance sheet (see also Note 21).

19. FINANCIAL ASSETS AVAILABLE FOR SALE

December 31, 2004 December 31, 2003

%of BGN'OOO % of capital BGN'OOOcapital

Eurocapital Bulgaria AD 99.80% 12,853 99.80% 12,853TranslotoAD 99.99% 2,700 99.99% 700VratzataOOD 99.42% 225 99.42% 225Petrol Card Service OOD 100.00% 519Trans Telecom OOD - - 95.00% 66TransatAD - - 98.00% 49

As at December 31, 2004 as financial assets available for sale amounting to BGN 16,297 thousandare presented investments in subsidiaries for which there is decision of the Management Board ofthe Company for their disposal (see also note 2.2). Thus, the effectiveness of the core business ofthe Company - retail of fuel and non-fuel products and related services - will be increased.

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

20. CASH AND CASH EQUIVALENTS

Cash equivalentsCash at banksCash in hand

O6uio

December 31,2004

BGN'OOO

3,96723899

December 31,2003

BGN'OOO

1,6397,103

184

21. TRADE AND OTHER PAYABLES

Trade payablesPayables to related partiesPayables to the State BudgetPayables to the employeesAdvances from customersSocial security payableDeferred incomeOther payables

Total

December 31,2004

BGN'OOO

December 31,2003

BGN'OOO

41,39397,780

1,1981,2372,255

53666

2.006

Payables to related parties as of December 31, 2004 and December 31, 2003 are further disclosedin Note 27.

From the total amount of trade payables, as of December 31, 2004 and December 31, 2003, BGN19,459 thousand and BGN 22,272 thousand, respectively, represent liabilities for delivered, but notinvoiced fuels (see Note 18).

22. LOANS AND BORROWINGS

The interest rates on interest-bearing bank loans and borrowings granted to the Company vary inthe range between SOFIBOR/LIBOR/EURIBOR + 2.5 points and SOFIBOR/LIBOR/EURIBOR +4.5 points.

These loans and borrowings are secured by mortgage and pledge of non-current assets amountingto BGN 19,073 thousand.

Financial statements as of December 31, 2004 28

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

22. LOANS AND BORROWINGS (CONTINUED)

In November 2003 Petrol AD issued registered, non-materialised, ordinary, interest bearing andfreely transferable corporate bonds at a total amount of BGN 15,000 thousand and nominal valueof BGN 1,000 per one bond. The corporate bond has a term of 5 years. The interest rate of thebond is 8.375% per annum. It is secured by a corporate guarantee, issued by the majorityshareholder of the Company. Interest payments are payable twice per year, at every six months.

Further details about the loans and borrowings granted to the Company and the terms andconditions thereof are presented below:

Short-term

ExpressbankExpressbankExpressbankBBVA Spain

ING BankING BankDSK Bank

Total

Total

Corporate bondFirst issue

Total

Currency/ December 31, 2004Face value Book valueThousand BGN'OOO Currency'OOO

December 31, 2003 MaturityBook value Month/

BGN'OOO Currency'OOO BGN'OOO

EUR 5,500USD 1,500EUR 3,500EUR 4,245

BGN 7,000BGN 2,360EUR 2,200

10,7462,1511,4162,033

1,868629860

EUR 5,494USD 1,498EUR 724EUR 1,039

BGN 1,868BGN 629EUR 440

10,7572,322

-1,746

1,853-

860

EUR 5,500USD 1,500

-EUR 893

BGN 1,853-

EUR 440

12/200412/20042/2004

Accordingto schedule

9/200712/20079/2007

Long-term

DSK BankBulgarian PostBankExpressbankBBVA Spain

ING BankING BankPireos BankDSK Bank

EUR 10,000

EUR 9,000EUR 3,500EUR 4,245

BGN 7,000BGN 2,360EUR 7,000EUR 2,200

19,558

10,3534,2493,597

3,2281,259

13,6461.721

EUR 10,000

EUR 5,293EUR 2, 172EUR 1,839

BGN 3,228BGN 1,259EUR 6,977EUR 880

19,557

15,8426,8455,630

5,096--

2.582

EUR 10,000

EUR 8, 100EUR 3,500EUR 2,878

BGN 5,096--

EUR 1,320

12/2008

09/200812/2008

Accordingto schedule

9/200712/200712/20073/2009

BGN 15,000 14,785 BGN 14,785 14,785 BGN 14,785 11/2008

Financial statements as of December 31, 2004 29

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

23. PROVISIONS

Provisions for salaries on unused annual leavesProvisions for social insurance on unused annual

leaves

O6mo

Movement of provisions for the period is as follows:

Balance at beginning of period

Accrued during the periodUtilized during the period

Balance at end of period

24. OBLIGATIONS UNDER FINANCE LEASES

December 31,2004

BGN'OOO

830

270

December 31,2003

BGN'OOO

854

256

December 31,2004

BGN'OOO

1,110

800(810)

1.100

l t l t O

December 31,2003

BGN'OOO

1,321

939(1.150)

1 ,110

Minimum leasepayments

Present value ofminimum lease

payments

December December31, 2004 31, 2003

BGN'OOO BGN'OOO.

December December31, 2004 31, 2003

BGN'OOO BGN'OOO

Amounts payable under finance leases:

Within one yearIn the second to fifth years inclusive

Less: Future finance charges

Present value of lease obligations

Less: Amount due for settlement within12 months (shown under currentliabilities)

Amount due for settlement after 12months

3882

120(13)

47124

171(24)

3176

107_

37110

147-

=142 107

76

147

J37)

110

The average lease term is 4 years. For the year ended December 31, 2004 the average effectiveborrowing rate was 8%. All leases are on a fixed repayment monthly basis.

The fair value of the Company's lease obligations approximates their carrying amount.

Financial statements as of December 31, 2004 30

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

25. SHARE CAPITAL

The share capital as of December 31, 2004 and 2003 amounts to BGN 109,250 thousanddistributed in 109,249,612 registered and non-materialised shares with face value of BGN 1 each.

Shareholders of Petrol AD as of December 31, 2004 and 2003 are as follows:

December 31, 2004 December 31, 2003% of share capital % of share capital

Petrol Holding AD 83.44 78.24RosOilEOOD 9.31 14.22Ministry of Economics 1.19 3.42Other shareholders 6.06 4.12

Total inn.nn ioo.no

26. EARNINGS PER SHARE

As of December 31, 2004 and 2003 basic earnings per share are calculated by dividing the netprofit, reported for the period by the weighted average number of ordinary shares held at the samedate. As of December 31, 2004 and 2003, basic earnings per share from newly registered sharecapital of Petrol AD are as follows:

December 31, 2004 December 31, 2003

Number of shares (thousand) 109,250 109,250Profit for the period (BGN'000) 14.478 2.268

Earnings per share (BNG) 0.13 0.02

As at December 31, 2004 and December 31, 2003 the closing market price of the Company'sshares at the Bulgaria Stock Exchange is BGN 3.21 and BGN 3.96, respectively.

27. RALATED PARTIES

In 2004 the Company has performed various transactions with related parties. The transactionsperformed refer primarily to:

• Purchase and sale of fuels and oil products;• Loan granted for investments;• Purchase of tangible fixed assets;• Technical assistance for maintenance of fiscal electronic systems;• Supply of materials;• Security;• Reconstruction and modernisation of gas stations;• Rents;• Banking and financial services;• Legal consulting.

The transactions with related parties do not differ materially from the normal market conditions.

Financial statements as of December 31, 2004

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

27. RALATED PARTIES (CONTINUED)

During the year ended December 31, 2004 and 2003, the Company entered into thetransactions with related

Related party

Petrol Card ServiceOODPetrol Holding ADNaftex Petrol OODPetrol Trans ExpressEOODPetrol Technics EOOD

Interhotel BulgariaBourgas EOODEurobank ADTranscard AD

KZUADNaftex Security EADCommunication 2002

ADBK Izvor ADNaftex Engineering AD

Varna BusinessServices AD

PFK Naftex ADTransloto ADTransat AD

Jurex Consult ADBPI EAD

Total

parties:

Type of transaction

Trade with fuels

Trade with fuelsTrade with fuelsTransport services

Repairs andmaintenance of fuel-filling stations

Tourist servicesBanking servicesCard paymentservicesRepair worksSecurityMarketing andadvertisement

Trade with fuelsBuilding andengineeringEducation andconvention centre

Trade with fuelsTrade with fuelsData maintenanceand transfer througha satelliteLegal servicesTrade with fuels

December

%oftotal

income

6.05%0.43%2.82%

0.59%

0.22%

0.25%0.91%

0.03%0.03%0.02%

0.02%0.01%

-

-0.01%0.01%

0.01%

0.01%_

31, 2004

%oftotal

expenses

-0.92%

-

1.87%

6.33%

0.04%2.16%

0.47%

2.54%

0.49%-

0.03%

0.26%--

1.49%

0.53%1.42%

18.55%

December

%oftotal

income

9.38%1.81%1.71%

0.60%

0.41%

0.34%0.10%

0.05%0.01%0.01%

0.01%-

-

---

-

0.01%-

14.44%

following

31, 2003

%oftotal

expenses

-4.57%

-

1.62%

5.06%

0.04%0.03%

0.29%0.02%2.67%

0.05%-

-

---

-

0.53%1.56%

16.44%

Financial statements as of December 31, 2004 32

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

27. RELATED PARTIES (CONTINUED)

The outstanding balances with related parties at December 31, 2004 are as follows:

Related Party

Naftex Petrol OODPetrol Technics EOODPetrol Card Service EOODPetrol Trans Express EOODVratzata OODTranscard AD

Interhotel Bulgaria Bourgas EOOD

KZU AD

Petrol Holding ADPetrol Engineering ADNaftex Security BAD

Transat ADCommunication 2002 AD

Eurobank AD

Naftex Engineering AD

BPI EADVarna Business Servisec ADPFC Naftex AD

Jurex Consult AD

Transloto ADTranstelecom OODOther

Total

Type of Relation

SubsidiarySubsidiarySubsidiarySubsidiarySubsidiarySubsidiary of the majorityshareholderSubsidiary of the majorityshareholderCompany with controllingparticipation of the majorityshareholderMajority shareholderAssociated companySubsidiary of the majorityshareholderSubsidiaryAssociated company of themajority shareholderSubsidiary of the majorityshareholderAssociated company of themajority shareholderSubsidiaryAssociated companySubsidiary of the majorityshareholderSubsidiary of the majorityshareholderSubsidiarySubsidiaryMinority shareholders

AmountReceivable

BGN'OOO

302,8881,3181,351

438

604

3

34825,789

96

3177

289

31

14

11

32

43

AmountPayable

BGN'OOO

5,202255

532

19

1

3491

15

31

2,137

59910242

Financial statements as of December 31, 2004 33

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

27. RELATED PARTIES (CONTINUED)

The outstanding balances with related parties at December 31, 2003 are as follows:

Related Party

Naftex Petrol OODPetrol Technics EOODPetrol Card Service EOODPetrol Trans Express EOODVratzata OODTranscard AD

Interhotel Bulgaria Bourgas EOOD

KZUAD

KZU Engineering DZZD

Petrol Holding ADPetrol Engineering ADNaftex Security EAD

Transat ADCommunication 2002 AD

Eurobank AD

Naftex Engineering AD

BPI EADPFC Naftex AD

Transloto ADTranstelecom OODNaftex Fast Food AD

DLA Bottling Company AD

Other

Total

Type of Relation

SubsidiarySubsidiarySubsidiarySubsidiarySubsidiarySubsidiary of the majorityshareholderSubsidiary of the majorityshareholderCompany with controllingparticipation of the majorityshareholder

Company with controllingparticipation of the majorityshareholderMajority shareholderAssociated companySubsidiary of the majorityshareholderSubsidiaryAssociated company of themajority shareholderSubsidiary of the majorityshareholderAssociated company of themajority shareholderSubsidiarySubsidiary of the majorityshareholderSubsidiarySubsidiarySubsidiary of the majorityshareholderSubsidiary of the majorityshareholderMinority shareholders

AmountReceivable

BGN'OOO

7,2632,5341,563

806423

414

334

250

163

11696

9082

7831

2923

1231

AmountPayable

BGN'OOO

72,150883

145

125

3

14,44415

191823

75169

7,735908

105

27

14T311

Financial statements as of December 31, 2004 34

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31, 2004

28. CONTINGENT LIABILITIES

28.1. Contingent liabilities to the State Reserve

According to the Regulation for State and War-time Reserve Storage, adopted by Decree No 312of the Council of Ministers in 1996, Petrol AD has liabilities to the State Reserve by means ofstorage, safeguarding and refreshing of petrol products. While performing such activity, certaincontingent liabilities might arise concerning payment of extra wastage for safekeeping of oilproducts, in case such wastage occurs.

28.2. Contingent liabilities for retirement

According to the Labor code, Petrol AD has liabilities to the personnel when entitled to retirement.The compensation due in accordance with current legislation is calculated based on length ofservice, age and labor category of the respective employee.

As at the date of these financial statements, the average annual turnover of the personnel of theCompany varies between 25% - 30% and the average age of the Company's employees is 35 years.Therefore, these contingent liabilities are significantly deferred in time and the Company has notaccrued any provisions for them. The Management of the Company believes that the amount ofsuch contingent liabilities would be insignificant.

28.3. Contingent liabilities to third parties

As of December 31, 2004, the Company has contingent liabilities for avalised promissory notes forliabilities of related parties in the amount of BGN 129,292 thousand.

29. POST BALANCE SHEET EVENTS

On March 21, 2005 with decision of Varna Regional Court the share capital of Varna BusinessServices OOD was increased with BGN 629 thousand by means of additional in-kind contributionof fixed assets of Petrol AD. After this increase, the Company's ownership in the capital of VarnaBusiness Services OOD reached 42.69%.

In February 2005 the Management Board of Petrol AD took decision general meeting of theCompany's shareholders to be held on April 4, 2005. The agenda of the meeting includesshareholders' approval of the increase of the share capital of Naftex Petrol OOD through in-kindcontribution of Company's fixed assets in all storage facilities, with net book value at December31, 2004 amounting to BGN 61,127 thousand.

Financial statements as of December 31, 2004 35

Petrol ADNOTES TO THE FINANCIAL STATEMENTSFor the year ended December 31,2004

30. ENVIRONMENTAL MATTERS

In relation with the privatization of Petrol AD in 1999, for most of the Company's storage facilitiesand fuel-filling station reports for the environmental impact of the Company's activities had beenprepared and approved by expert council to the Ministry of Environment and Water. Based onthese reports, consents by the Ministry of Environment and Water for the exploitation of allCompany's assets had been issued.

Following its privatisation in 1999, Petrol AD started the implementation of intensive investmentprogram aimed to bring the Company's facilities in line with the requirements of the bestenvironmental practices in Western Europe. Therefore, the Company's outlets are reconstructed tobe in line with the requirements of European Union Directive 94/63/EC which has beenimplemented in Bulgarian legislation in the form of Ordinance No. 16 dated 12 August 1999,which limits the emissions of volatile organic compounds (known as VOCs) connected with thestorage, loading or unloading and transportation of petrol. This Ordinance is issued based on Art.9, Para 1 of the Law on Ambient Air Purity. Before any reconstruction of Company's facility,ecological characteristic is prepared and based on that, the regional inspections of the Ministry ofEnvironment and Water issue reconstruction permission for that facility.

As at the date of these financial statements, the Management of the Company believes, that PetrolAD is in compliance in all material respects with environmental requirements currently applicableto its operations and has no current and contingent liabilities in connection to the environmentallegislation in the Country.

Financial statements as of December 31, 2004 36