Embed Size (px)

Citation preview

Please refer to Disclosures and Disclaimers at the end of the Research Report.

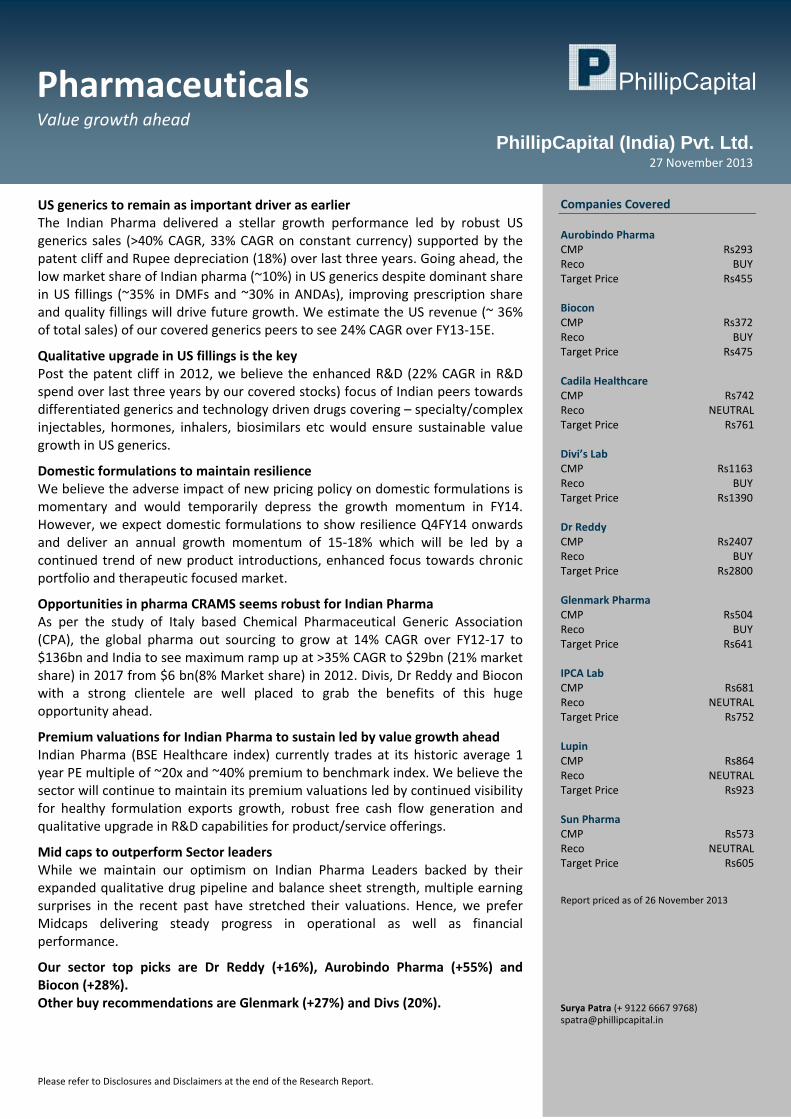

Pharmaceuticals Value growth ahead

27 November 2013PhillipCapital (India) Pvt. Ltd.

US generics to remain as important driver as earlier The Indian Pharma delivered a stellar growth performance led by robust US generics sales (>40% CAGR, 33% CAGR on constant currency) supported by the patent cliff and Rupee depreciation (18%) over last three years. Going ahead, the low market share of Indian pharma (~10%) in US generics despite dominant share in US fillings (~35% in DMFs and ~30% in ANDAs), improving prescription share and quality fillings will drive future growth. We estimate the US revenue (~ 36% of total sales) of our covered generics peers to see 24% CAGR over FY13‐15E.

Qualitative upgrade in US fillings is the key Post the patent cliff in 2012, we believe the enhanced R&D (22% CAGR in R&D spend over last three years by our covered stocks) focus of Indian peers towards differentiated generics and technology driven drugs covering – specialty/complex injectables, hormones, inhalers, biosimilars etc would ensure sustainable value growth in US generics.

Domestic formulations to maintain resilience We believe the adverse impact of new pricing policy on domestic formulations is momentary and would temporarily depress the growth momentum in FY14. However, we expect domestic formulations to show resilience Q4FY14 onwards and deliver an annual growth momentum of 15‐18% which will be led by a continued trend of new product introductions, enhanced focus towards chronic portfolio and therapeutic focused market.

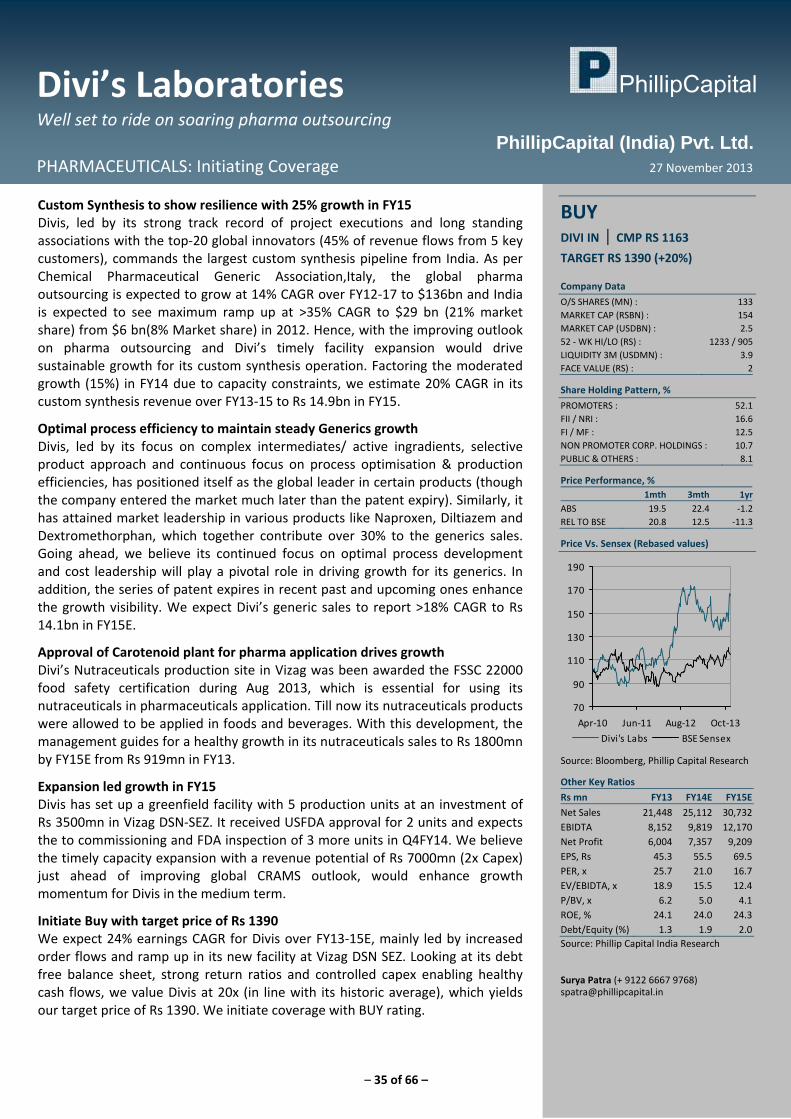

Opportunities in pharma CRAMS seems robust for Indian Pharma As per the study of Italy based Chemical Pharmaceutical Generic Association (CPA), the global pharma out sourcing to grow at 14% CAGR over FY12‐17 to $136bn and India to see maximum ramp up at >35% CAGR to $29bn (21% market share) in 2017 from $6 bn(8% Market share) in 2012. Divis, Dr Reddy and Biocon with a strong clientele are well placed to grab the benefits of this huge opportunity ahead.

Premium valuations for Indian Pharma to sustain led by value growth ahead Indian Pharma (BSE Healthcare index) currently trades at its historic average 1 year PE multiple of ~20x and ~40% premium to benchmark index. We believe the sector will continue to maintain its premium valuations led by continued visibility for healthy formulation exports growth, robust free cash flow generation and qualitative upgrade in R&D capabilities for product/service offerings.

Mid caps to outperform Sector leaders While we maintain our optimism on Indian Pharma Leaders backed by their expanded qualitative drug pipeline and balance sheet strength, multiple earning surprises in the recent past have stretched their valuations. Hence, we prefer Midcaps delivering steady progress in operational as well as financial performance.

Our sector top picks are Dr Reddy (+16%), Aurobindo Pharma (+55%) and Biocon (+28%). Other buy recommendations are Glenmark (+27%) and Divs (20%).

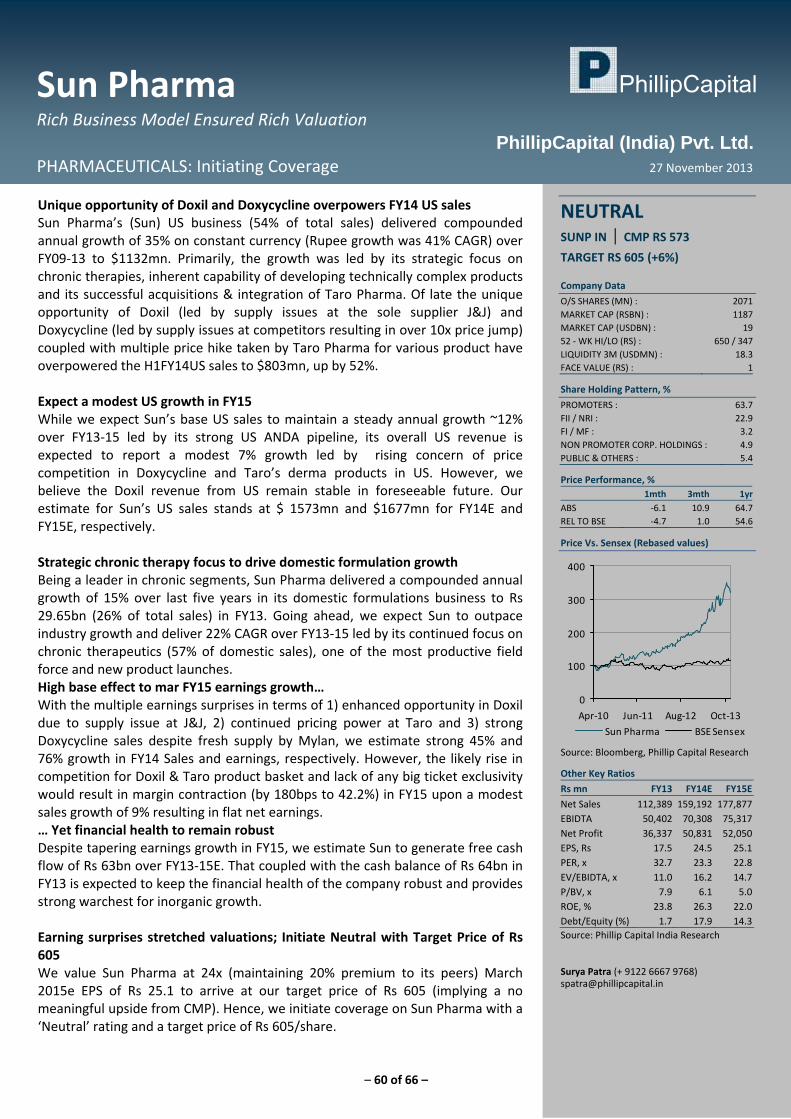

Companies Covered Aurobindo Pharma CMP Rs293Reco BUYTarget Price Rs455 Biocon CMP Rs372Reco BUYTarget Price Rs475 Cadila Healthcare CMP Rs742Reco NEUTRALTarget Price Rs761 Divi’s Lab CMP Rs1163Reco BUYTarget Price Rs1390 Dr Reddy CMP Rs2407Reco BUYTarget Price Rs2800 Glenmark Pharma CMP Rs504Reco BUYTarget Price Rs641 IPCA Lab CMP Rs681Reco NEUTRALTarget Price Rs752 Lupin CMP Rs864Reco NEUTRALTarget Price Rs923 Sun Pharma CMP Rs573Reco NEUTRALTarget Price Rs605 Report priced as of 26 November 2013 Surya Patra (+ 9122 6667 9768) [email protected]

2 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Table of Contents US generics to remain as important driver as earlier∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 3

Strategic Shift in Fillings to improve the quality of income ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 5

US patent cliff is behind us but peak patent expiry opportunities in

advanced markets yet to follow ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 7

Domestic formulations to maintain its resilience ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 8

Emerging markets ‐ Offers growth visibility albeit diverse complexities ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 10

CRAMS offers strong growth visibility ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 12

Indian Pharma trades at historic average valuation multiples∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 14

Companies Section Aurobindo Pharma ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 19

Biocon ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 24

Cadila ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 30

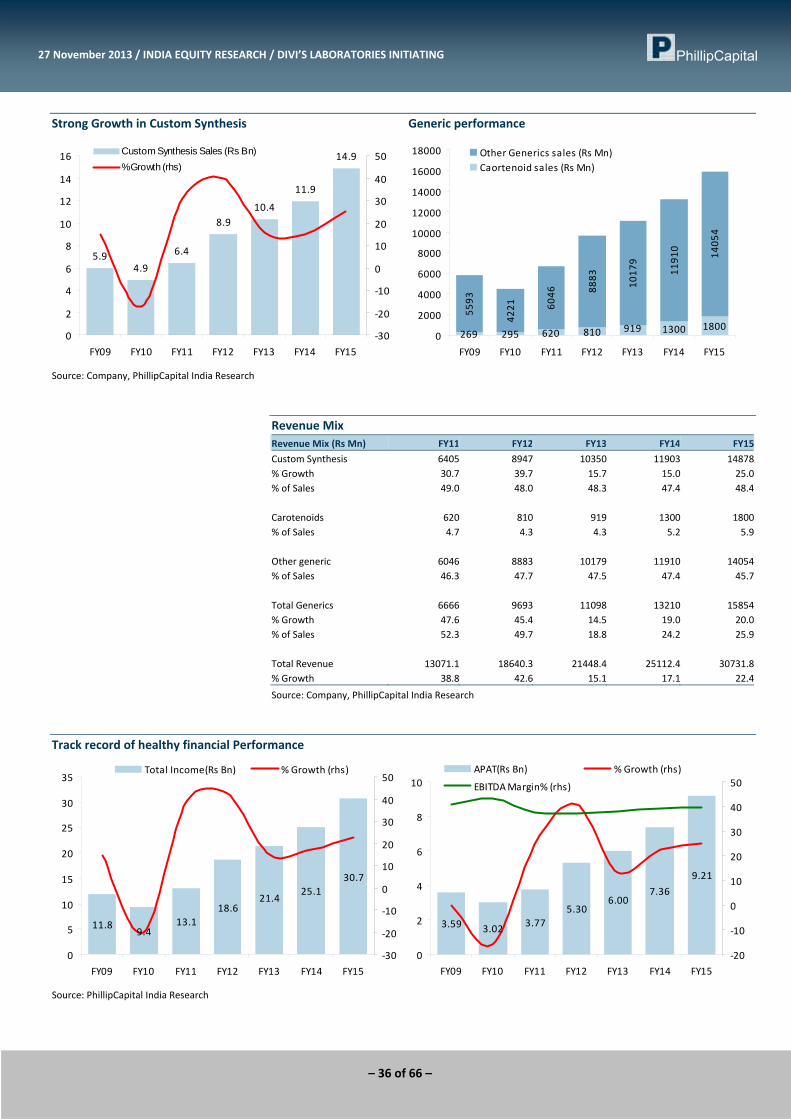

Divi’s Lab ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 35

Dr Reddy’s Lab ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 39

Glenmark ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 44

IPCA ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 49

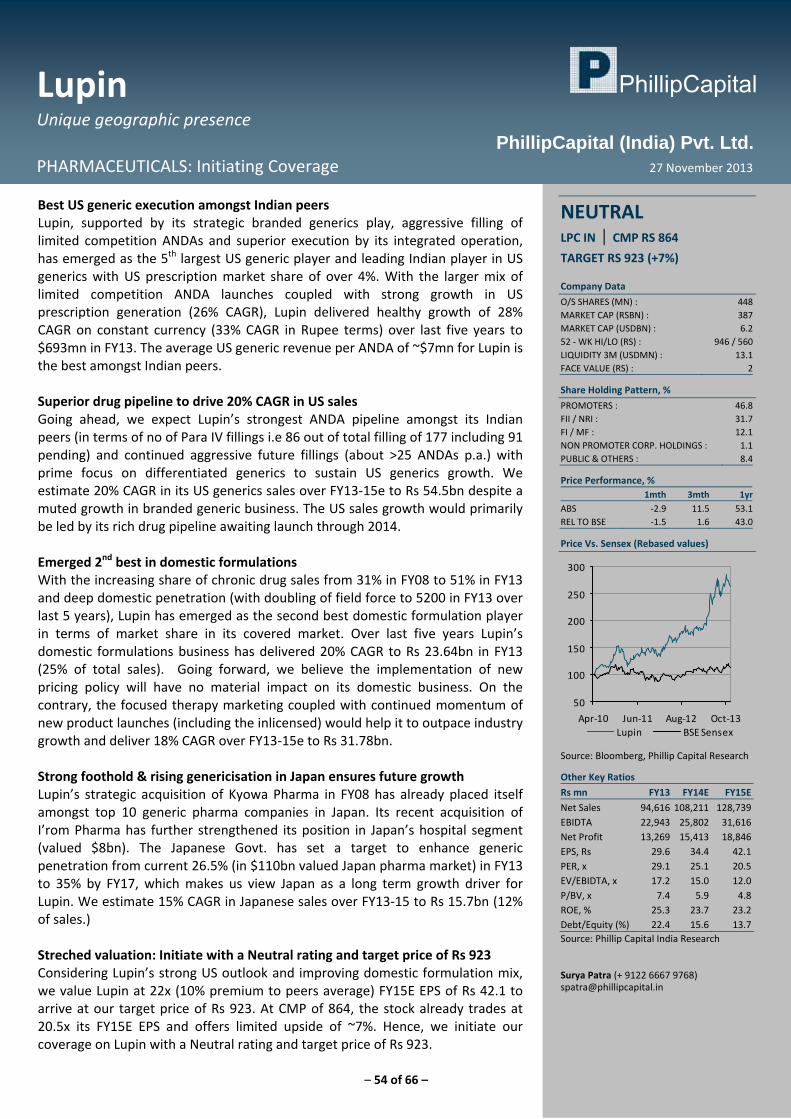

Lupin ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 54

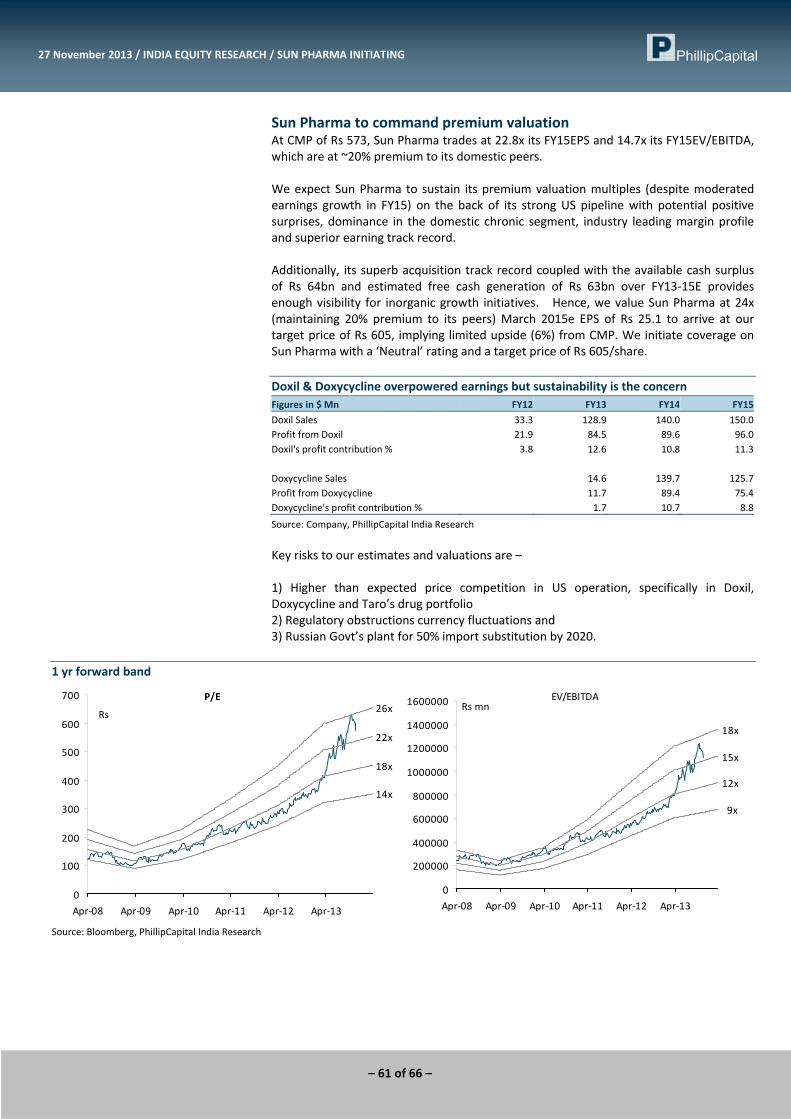

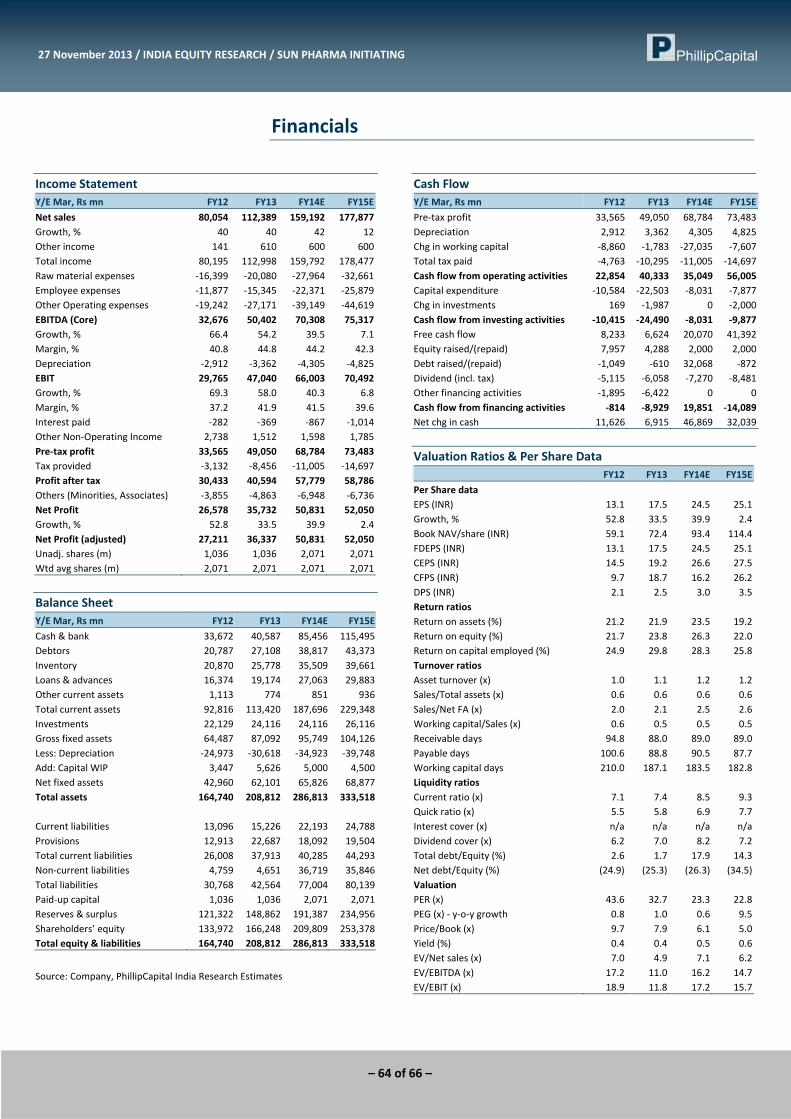

Sun Pharma ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 60

3 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

US Generics to remain key growth driver as earlier Indian Pharma delivered a stellar growth performance led by robust US generics sales supported by the patent cliff over last three years. Additionally, the depreciating Rupee against US Dollar has further facilitated the growth momentum. In fact, our coverage stocks delivered a compounded annual growth of 40% over FY11‐FY13 to Rs 188bn.

Patent cliff coupled with Rupee depreciation strengthened Indian Pharma performance

64.1 68.192.6

128.9

188.5

0

40

80

120

160

200

FY2009 FY2010 FY2011 FY2012 FY2013

Gross US Generic Sales of our covered stocks (Rs Bn)

40%

4.3

40.8

30.7 30.4

6.2

36.039.2

46.2

‐10

0

10

20

30

40

50

FY2010 FY2011 FY2012 FY2013

% Growth in US Generic Sales in $ mn% Growth in US Generic Sales in Rs mn% of Re depreciation

Source: PhillipCapital India Research

US generics to remain a key growth driver despite Patent cliff: US Patent cliff during 2012 has certainly overpowered the growth of Indian Pharma in over last three years and there may be moderation in the patent expiry cycle. However, the relatively low share of Indian companies in the US generics market implies good long‐term potential. Patent Expiry trend of blockbuster drugs in US

1916

19 20

35

15

1922

17

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross value of patents expiries ($ bn)

Linear (Gross value of patents expiries ($ bn) )

Source: Company, USFDA

Despite having a dominant share in US DMFs fillings (~35%) and ANDA fillings (~30%) and most cost effective generic offering, the generic market share of Indian pharma is still low at ~10%.

4 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Steady rising dominance of Indian Pharma in US generics space both in terms of drug fillings and prescription market share

308.7

381.3450.1

534.2

644

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012

0

2

4

6

8

10

12

14

16

18

Cumulative Prescription count by top 8 Indian peers in US (M n Nos)

Share of top 8 Indian Peers in to tal Rx in US

425 433 437490

311

105 94 103 11484

0

100

200

300

400

500

600

2009 2010 2011 2012 YTD 2013

15

17

19

21

23

25

27

29

Total ANDA Approvals (Nos.)ANDA approvals for Indian peers(Nos.)% Share of India (RHS)

Source: USFDA, IMS Health, PhillipCapital India Research

Going ahead, we expect the strong ANDA pipeline as well as enhanced focus towards development and filling of niche/complex/differentiated generics by leading Indian pharma peers and increased demand for cost effective generics (forte of Indian peers) will drive increased generic market share and ultimate growth for Indian Pharma. Positioning of US generic players in terms of pending ANDA pipeline

325

190172

143 133110 99 91

72 62 53 44 41

0

50

100

150

200

250

300

350

Mylan

Actavis

Sandoz

Teva Su

n

Aurobindo

Cadila

Lupin

Par

Dr Reddy

Glenmark

Impax

Apotex

Source: Hikma presentation, PhillipCapital India Research

Strong Pipeline of ANDAs by Indian Peers Pending ANDA fillings Total ANDA Pending Para IV Target ANDA p.a. Remarks

Sun Pharma 453 133 30 25‐30 Majority of future pipeline is differentiated and technology driven drugs Dr Reddy 201 65 38 20 70% of future generic is differentiated Lupin 177 91 86 ~25 Majority of current and future pipeline is niche generics Cadila 160 89 12 30 ~20% of the pending fillings are differentiated Glenmark 140 53 26 20 Key focus being limited completion drugs in hormones, derma, Oncology Aurobindo 281 110 10 30‐35 30% of pending ANDAs are injectables and over 50% of future filling would

be injectables covering opthalmics, oncology and penems IPCA 37 20 0 12‐15 Complete backward integration & optimal process development is key

Source: Company, PhillipCapital India Research

5 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

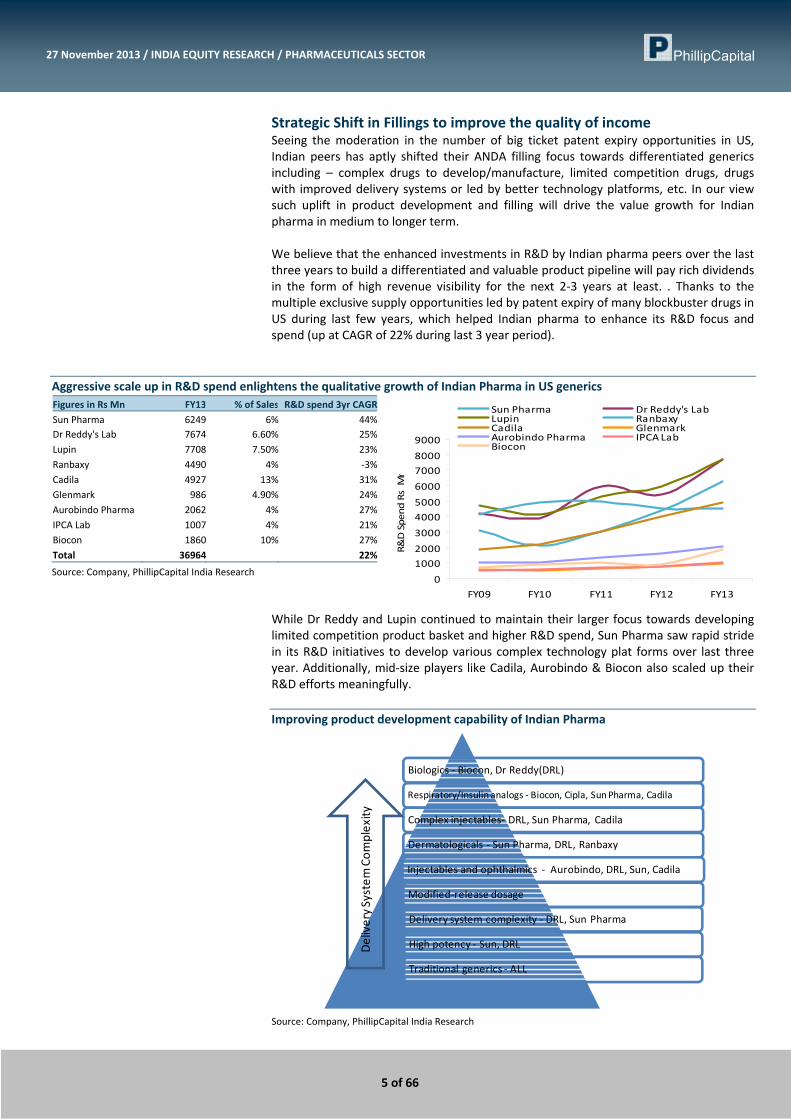

Strategic Shift in Fillings to improve the quality of income Seeing the moderation in the number of big ticket patent expiry opportunities in US, Indian peers has aptly shifted their ANDA filling focus towards differentiated generics including – complex drugs to develop/manufacture, limited competition drugs, drugs with improved delivery systems or led by better technology platforms, etc. In our view such uplift in product development and filling will drive the value growth for Indian pharma in medium to longer term. We believe that the enhanced investments in R&D by Indian pharma peers over the last three years to build a differentiated and valuable product pipeline will pay rich dividends in the form of high revenue visibility for the next 2‐3 years at least. . Thanks to the multiple exclusive supply opportunities led by patent expiry of many blockbuster drugs in US during last few years, which helped Indian pharma to enhance its R&D focus and spend (up at CAGR of 22% during last 3 year period).

Aggressive scale up in R&D spend enlightens the qualitative growth of Indian Pharma in US generics Figures in Rs Mn FY13 % of Sales R&D spend 3yr CAGRSun Pharma 6249 6% 44%Dr Reddy's Lab 7674 6.60% 25%Lupin 7708 7.50% 23%Ranbaxy 4490 4% ‐3%Cadila 4927 13% 31%Glenmark 986 4.90% 24%Aurobindo Pharma 2062 4% 27%IPCA Lab 1007 4% 21%Biocon 1860 10% 27%Total 36964 22%

Source: Company, PhillipCapital India Research

While Dr Reddy and Lupin continued to maintain their larger focus towards developing limited competition product basket and higher R&D spend, Sun Pharma saw rapid stride in its R&D initiatives to develop various complex technology plat forms over last three year. Additionally, mid‐size players like Cadila, Aurobindo & Biocon also scaled up their R&D efforts meaningfully. Improving product development capability of Indian Pharma

Biologics ‐ Biocon, Dr Reddy(DRL)

Respiratory/Insulin analogs ‐ Biocon, Cipla, Sun Pharma, Cadila

Complex injectables‐ DRL, Sun Pharma, Cadila

Dermatologicals ‐ Sun Pharma, DRL, Ranbaxy

Injectables and ophthalmics ‐ Aurobindo, DRL, Sun, Cadila

Modified‐release dosage

Delivery system complexity ‐ DRL, Sun Pharma

High potency ‐ Sun, DRL

Traditional generics ‐ ALL

Delivery System

Com

plexity

Source: Company, PhillipCapital India Research

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

FY09 FY10 FY11 FY12 FY13

Sun Pharma Dr Reddy's LabLupin RanbaxyCadila GlenmarkAurobindo Pharma IPCA LabBiocon

R&D Spend Rs Mn

6 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Implementation of GDUFA in US could result in volume growth; Could lead to intense price competition for plain vanilla generics: US Food and Drug Administration has implemented the Generic Drug User Fee Act (GDUFA) On Oct. 1, 2012 with an objective of clearing the clearing the backlog of pending ANDA/drug approvals of over 2700 ANDAs and expediting the approval (both drug and facility) timeline.

Steady rising backlog of pending ANDAs… …extended ANDA Approval timeline beyond 30 months

891

1216 13091441

16301912

2500

29333054

0

500

1000

1500

2000

2500

3000

3500

2005 2006 2007 2008 2009 2010 2011 2012 2013

No of ANDAs

16 1719

22

27 2830

0

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012

Months

Source: USFDA

The set goal of GDUFA relating to ANDA backlog clearing Period of filling No of ANDAs Goal

Backlog till 1st Oct 2012 ~2700 90% (i.e.~ 2340)of backlog to be reviewed & approved by end of FY17

Filling during FY13 1013

Filling during FY14 1063

Focus is to expedite review of 1) Paragraph IV filed on the day 1 of NCE exclusivity,

2) Shortage based drugs applications

Filling during FY15 1063 60% (i.e. ~600) to be reviewed & approved in 15months period of submission

Filling during FY16 1010 75% (i.e. ~750) to be reviewed & approved in 15months period of submission

Filling during FY17 959 90% (i.e.~850) to be reviewed & approved in 10 months period of submission

Source: USFDA

As per the set GDUFA target, USFDA to clear 90% of pending ANDAs as of 1st Oct 2012 (i.e about 2700) and a majority of ANDA fillings over FY13‐17 will be reviewed and approved by FY17. This indicates over 5000 ANDAs will be reviewed and approved over a period of 5 years (i.e FY13 to FY17), which implys about over 1000 ANDAs per annum compared to about 450 annual ANDA approval over last five years. Thus the doubling rate of ANDA approvals could result in a substantial volume growth in plain vanilla US generics as we believe a major chunk of current ANDA back log is plain vanilla. This could result in more price competition. However, we believe the GDUFA implementation will favour Indian Pharma on two grounds like 1) it will reduce approval timeline of recently filled complex and limited competition drugs basket and 2) helps Indian pharma to grab better market share due to its cost competency and dominance in the share of fillings. Finally, We estimate our covered stocks would maintain a steady constant currency growth of 18% over FY13‐15 led by strong ANDA pipeline coupled with rising share of complex and differentiated generics despite a significantly high base. More specifically, we believe Sun Pharma, Dr Reddy, Lupin and Aurobindo would outpace the industry growth.

7 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

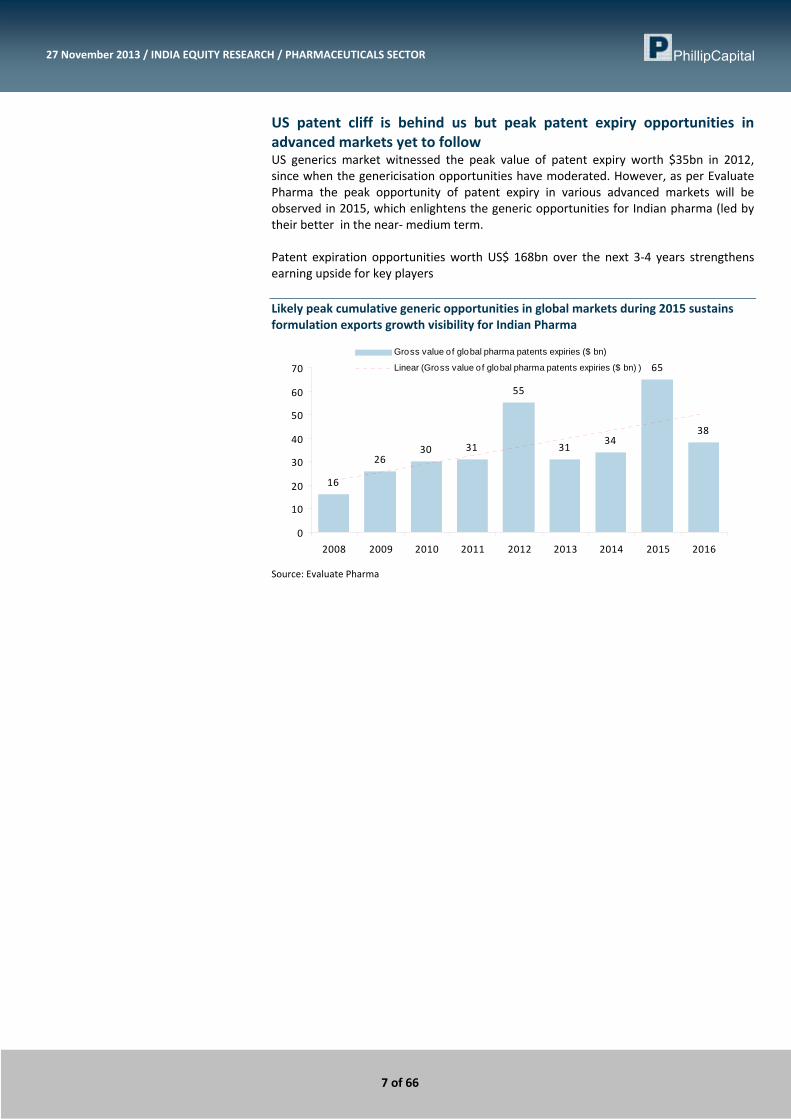

US patent cliff is behind us but peak patent expiry opportunities in advanced markets yet to follow US generics market witnessed the peak value of patent expiry worth $35bn in 2012, since when the genericisation opportunities have moderated. However, as per Evaluate Pharma the peak opportunity of patent expiry in various advanced markets will be observed in 2015, which enlightens the generic opportunities for Indian pharma (led by their better in the near‐ medium term. Patent expiration opportunities worth US$ 168bn over the next 3‐4 years strengthens earning upside for key players Likely peak cumulative generic opportunities in global markets during 2015 sustains formulation exports growth visibility for Indian Pharma

16

2630 31

55

3134

65

38

0

10

20

30

40

50

60

70

2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross value of global pharma patents expiries ($ bn)

Linear (Gross value of global pharma patents expiries ($ bn) )

Source: Evaluate Pharma

8 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

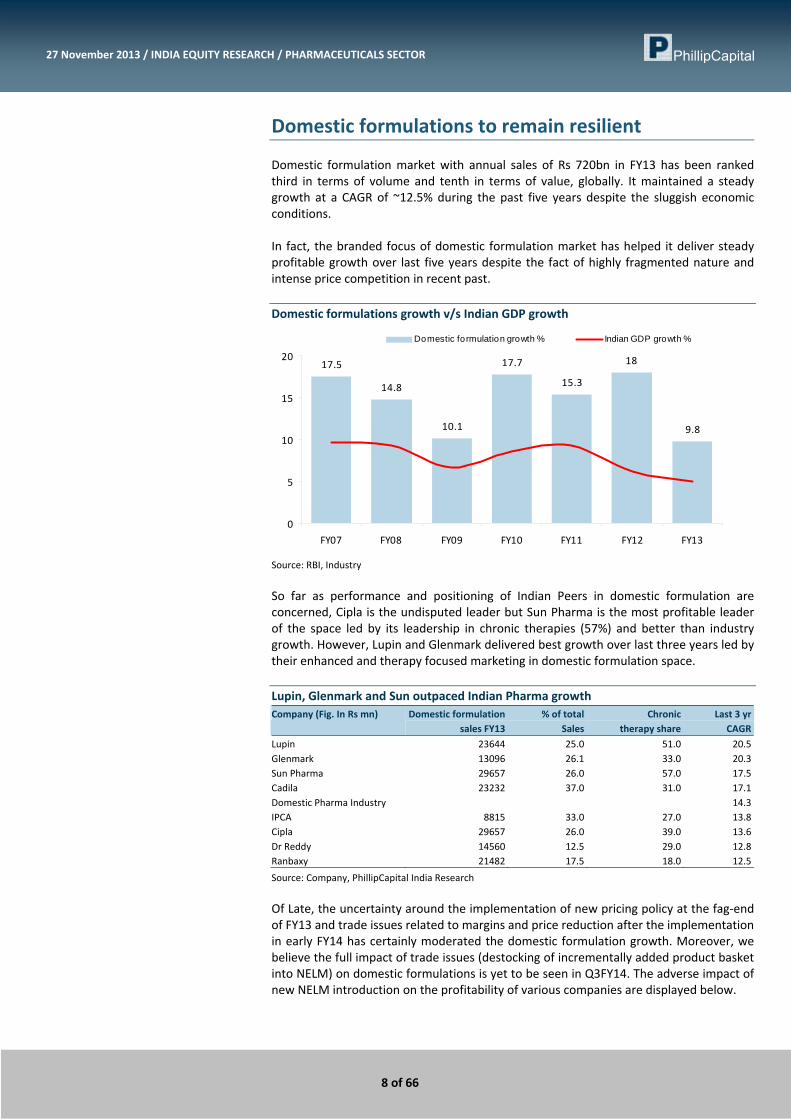

Domestic formulations to remain resilient Domestic formulation market with annual sales of Rs 720bn in FY13 has been ranked third in terms of volume and tenth in terms of value, globally. It maintained a steady growth at a CAGR of ~12.5% during the past five years despite the sluggish economic conditions. In fact, the branded focus of domestic formulation market has helped it deliver steady profitable growth over last five years despite the fact of highly fragmented nature and intense price competition in recent past. Domestic formulations growth v/s Indian GDP growth

17.5

14.8

10.1

17.7

15.3

18

9.8

0

5

10

15

20

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Domestic formulation growth % Indian GDP growth %

Source: RBI, Industry

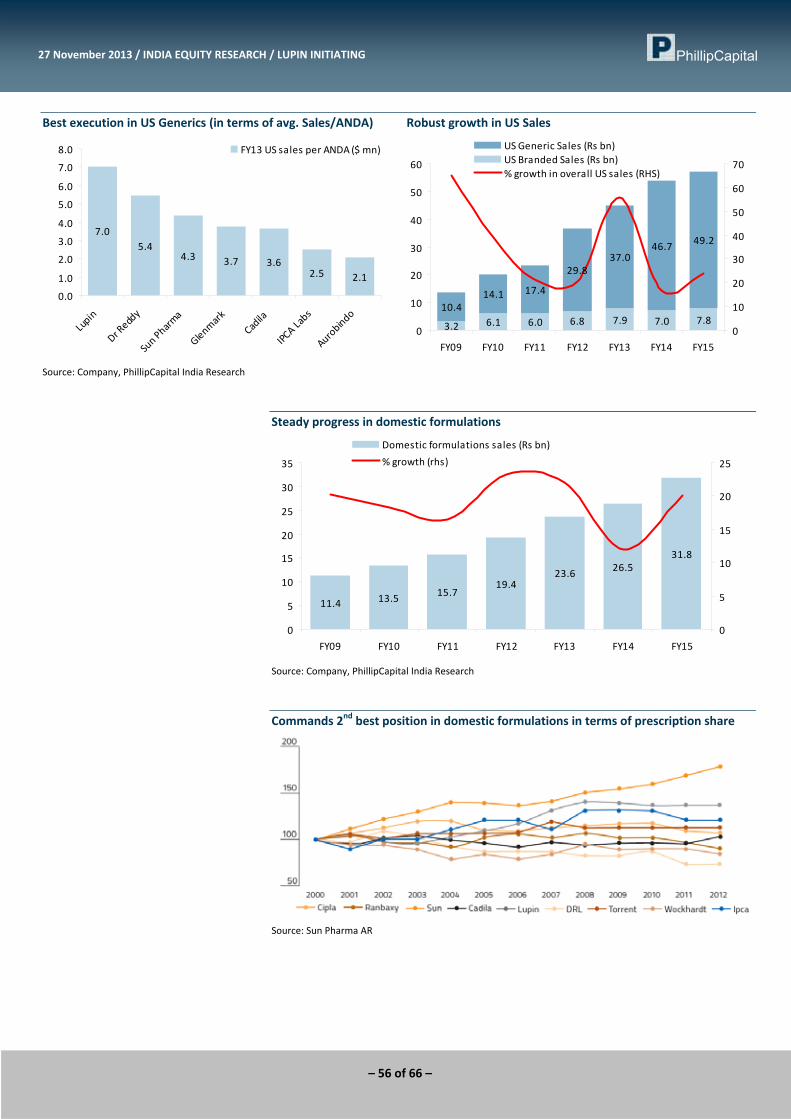

So far as performance and positioning of Indian Peers in domestic formulation are concerned, Cipla is the undisputed leader but Sun Pharma is the most profitable leader of the space led by its leadership in chronic therapies (57%) and better than industry growth. However, Lupin and Glenmark delivered best growth over last three years led by their enhanced and therapy focused marketing in domestic formulation space. Lupin, Glenmark and Sun outpaced Indian Pharma growth Company (Fig. In Rs mn) Domestic formulation

sales FY13% of total

Sales Chronic

therapy shareLast 3 yr

CAGR

Lupin 23644 25.0 51.0 20.5Glenmark 13096 26.1 33.0 20.3Sun Pharma 29657 26.0 57.0 17.5Cadila 23232 37.0 31.0 17.1Domestic Pharma Industry 14.3IPCA 8815 33.0 27.0 13.8Cipla 29657 26.0 39.0 13.6Dr Reddy 14560 12.5 29.0 12.8Ranbaxy 21482 17.5 18.0 12.5

Source: Company, PhillipCapital India Research

Of Late, the uncertainty around the implementation of new pricing policy at the fag‐end of FY13 and trade issues related to margins and price reduction after the implementation in early FY14 has certainly moderated the domestic formulation growth. Moreover, we believe the full impact of trade issues (destocking of incrementally added product basket into NELM) on domestic formulations is yet to be seen in Q3FY14. The adverse impact of new NELM introduction on the profitability of various companies are displayed below.

9 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Impact of new pricing policy on Indian Pharma Company Domestic formulation

sales FY13Price

impact %Absolute revenue

loss (Rs mn)Impact on FY14

Margin%

Cipla 36813 3.0 1104 130bpsCadila 23232 3.9 900 120bpsLupin 23644 2.0 470 50bpsIPCA 8815 1.7 150 50bpsDr Reddy 14560 3.0 440 40bpsSun Pharma 29657 1.7 500 30bpsGlenmark 13096 0.5 65 20bps

Source: Company, PhillipCapital India Research

In our view, Cipla and Cadila due to their relatively larger share of revenue from domestic formulation and that too from acute therapies would see maximum adverse impact on their profitability. Given the fact and relatively slow growth in acute therapy drug basket, we believe Cipla and Cadila might underperform the domestic formulation industry growth in near future. Chronic therapies outpace acute therapies in growth

18.9

15.814.5

12.9 12.7 12.6 12.6 11.6 11 10.4 9.9

02468

101214161820

Diabetes

Cardiac

Neuropathy

Derma

Gynaecology

Industry

Gastro

Anti invective

Pain Mgt.

Respiratory

Vitamins

Growth (%

)

Source: Sun Pharma AR

Sun leads in domestic pharma in terms of prescription share

Source: Sun Pharma AR

However, we believe the above mentioned adverse impact of new pricing policy is just a momentary for just FY14 and would depress the growth momentum of Indian Pharma in FY14. More specifically, we expect domestic formulations to show its resilience Q4FY14 onwards and deliver an annual growth momentum of 15‐18% which will be led by continued trend of new product introductions, enhanced focus towards chronic portfolio, therapeutic focused market. Also, the Indian macro factors like – 1) rising healthcare spend, 2) rising income levels, 3) rapid urbanisation and 4) steady progressing health insurance penetration would maintain the continued growth momentum.

10 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Emerging markets ‐ Offers growth visibility albeit diverse complexities While the developed pharma markets seem matured led by series of patent expires and generic penetration reaching almost peak beyond 75%, the developing markets emerged as the key growth engine for global pharma. As per IMS Health, the pharmerging economies (including ‐ Brazil, Russia, China, India, Mexico and South Africa) are expected to deliver highest growth at a CAGR of 12‐15% to reach US$ 345‐375 billion in 2016 from US$ 193.6 billion in 2011. The market size is expected to almost double during 2012‐16. In fact, about 75% of incremental growth in global pharma during 2012‐16 to be driven by emerging markets. The key growth drivers for these markets are ‐ rising income levels, increased access to medicines, high out of pocket spending and government focus on generics. Also the branded generic nature of the market ensures better value growth. Given the fact of rapid progress in the emerging markets, Indian pharma peers led by their strong cost advantage, better understanding of these markets( due to similarity to Indian market), rapid progress in product registrations are well placed to exploit the highest growth in the emerging markets. Selective Indian peers like – Ranbaxy, Dr Reddy, Cipla, Glenmark etc have already achieved meaningful foothold in various emerging markets including – Russia, South Africa, Latin American markets. Typically Out‐of‐pocket expenditure in the emerging markets is high in comparison to developed markets

46% 39% 32% 29%11% 13%

11%16%

13%6% 43%

15%

43% 45%55%

65%46%

72%

0%

20%

40%

60%

80%

100%

120%

APAC LatAm ME & Africa Europe EM USA EUS

General government expenditureOther private health expenditureOut‐of‐pocket

Source: IMS Health

Emerging markets offer highest growth visibility Economy 2011 2016 CAGR (%)

Pharmerging 193.6 345‐375 12‐15 China 66.7 155‐165 15‐18 Tier 2 59.9 100‐110 12‐15 Brazil 29.9 42‐52 12‐15 Russia 15.7 23‐33 10‐13 India 14.3 24‐34 14‐17 Tier 3 67 90‐100 7‐10l

Source: IMS Health

11 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

While there is strong growth visibility for emerging markets, the varying business dynamics of different markets are the key challenge for pharma peers. Though, the local conditions vary by country, the core challenges remain broadly comparable: • understanding stakeholders and their changing needs • political, economic, and intellectual property risk • immature regulatory frameworks • launching new products • finding the right partners/distributors Hence, in order to tackle the unknown challenges and to capture the maximum growth opportunity in the emerging markets most of Indian peers have adopted partnership model. The key emerging market alliances by India pharma peers are – Dr Reddy‐Glaxo, Sun Pharma‐Merck, Cipla‐Dr Reddy, Cadila Healthcare – Abbott etc. Going ahead, we expect Indian pharma peers led by their cost competitiveness, rapid drug registrations and alliances to outpace industry growth and grow in the range on 18‐20% in near future.

12 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

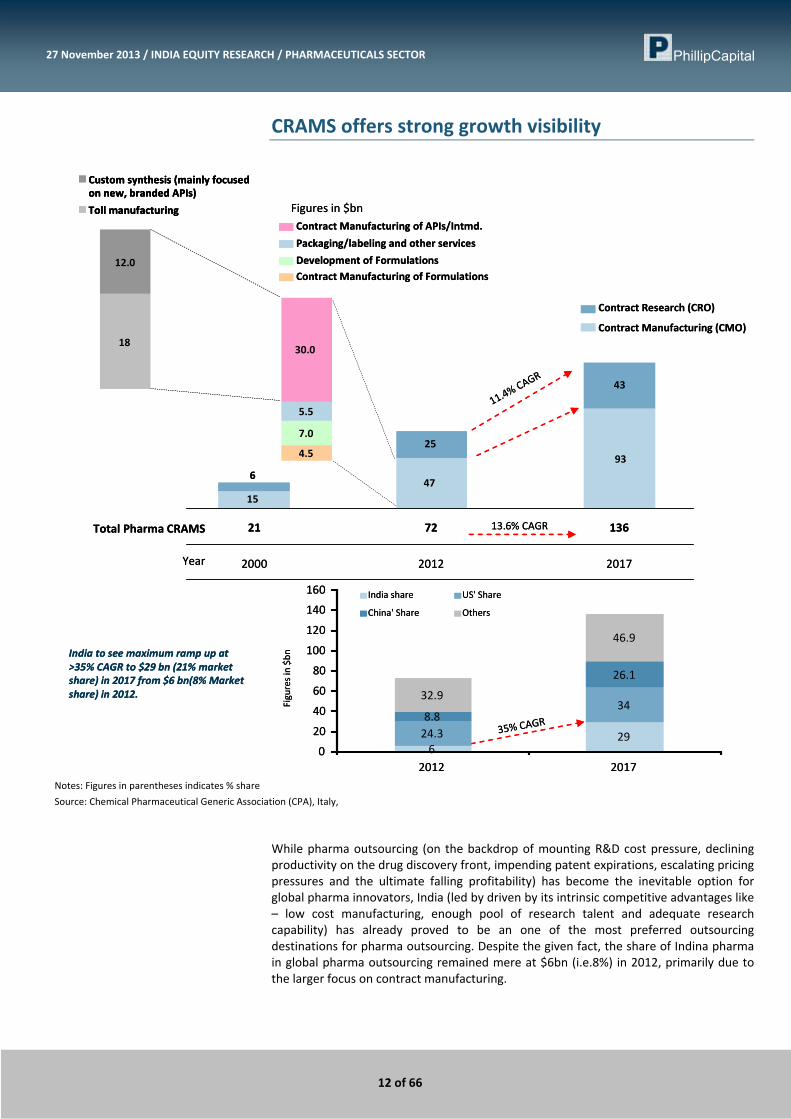

CRAMS offers strong growth visibility

2000 2012 2017

Contract Research (CRO)

Contract Manufacturing (CMO)

4.5

7.0

5.5

30.0

Contract Manufacturing of APIs/Intmd.

Packaging/labeling and other services

Development of FormulationsContract Manufacturing of Formulations

18

12.0

Custom synthesis (mainly focusedon new, branded APIs)

Toll manufacturing

1547

93

43

25

21 72 136Total Pharma CRAMS

11.4%

CAGR

35% CAGR

13.6% CAGR

Year

6

Figures in $bn

India to see maximum ramp up at >35% CAGR to $29 bn (21% market share) in 2017 from $6 bn(8% Market share) in 2012.

62924.3

348.8

26.1

32.9

46.9

0

20

40

60

80

100

120

140

160

2012 2017

India share US' Share

China' Share Others

Figures in $bn

2000 2012 2017

Contract Research (CRO)

Contract Manufacturing (CMO)

4.5

7.0

5.5

30.0

Contract Manufacturing of APIs/Intmd.

Packaging/labeling and other services

Development of FormulationsContract Manufacturing of Formulations

18

12.0

Custom synthesis (mainly focusedon new, branded APIs)

Toll manufacturing

18

12.0

Custom synthesis (mainly focusedon new, branded APIs)

Toll manufacturing

1547

93

43

25

21 72 136Total Pharma CRAMS

11.4%

CAGR

35% CAGR

13.6% CAGR

Year

6

Figures in $bn

India to see maximum ramp up at >35% CAGR to $29 bn (21% market share) in 2017 from $6 bn(8% Market share) in 2012.

62924.3

348.8

26.1

32.9

46.9

0

20

40

60

80

100

120

140

160

2012 2017

India share US' Share

China' Share Others

Figures in $bn

Notes: Figures in parentheses indicates % share

Source: Chemical Pharmaceutical Generic Association (CPA), Italy,

While pharma outsourcing (on the backdrop of mounting R&D cost pressure, declining productivity on the drug discovery front, impending patent expirations, escalating pricing pressures and the ultimate falling profitability) has become the inevitable option for global pharma innovators, India (led by driven by its intrinsic competitive advantages like – low cost manufacturing, enough pool of research talent and adequate research capability) has already proved to be an one of the most preferred outsourcing destinations for pharma outsourcing. Despite the given fact, the share of Indina pharma in global pharma outsourcing remained mere at $6bn (i.e.8%) in 2012, primarily due to the larger focus on contract manufacturing.

13 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

However, with the improved focus on building R&D capability, enhanced and quality service offerings at competitive cost, Indian Pharma is well placed to grab a meaningful chunk of huge global pharma outsourcing opportunity. As per the study of Italy based Chemical Pharmaceutical Generic Association (CPA), the global pharma out sourcing to grow at 14% CAGR over FY12‐17 to $136bn and India to see maximum ramp up at >35% CAGR to $29 bn (21% market share) in 2017 from $6 bn(8% Market share) in 2012. Given the fact, we believe Indian peers like – Divi’s Lab, Dr Reddy, Biocon etc led by their research capability and strong clientele base are well positioned to make the maximum out of the huge foreseeable pharma outsourcing opportunity. Additionally, better execution track record by Indian pharma peers in contract manufacturing and recent quality concerns around Chinese (key competitor of Indian Pharma) pharma operation coupled with relatively higher service charges to lead Indian pharma outpace China.

14 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Indian Pharma trades at historic average valuation multiples Indian Pharma represented by BSE Healthcare Index saw its dream run and has grossly outperformed the benchmark index – SENSEX over last three year period. It has gradually raised its premium valuation to about 40% currently over SENSEX during the said period. In our view, 1) strong visibility of formulation exports especially to US led by patent cliff resulting in multiple exclusive supply opportunities, 2) powering free cashflow generation and 3) investment favour due to defensive nature helped Indian pharma to outbid the benchmark index. Additionally, the favouring Rupee depreciation against US Dollar further powered the earnings growth as the exports account over 50% of the gross Indian Pharma revenue.

Indian Pharma currently trades at historic average PE BSE Healthcare index trades at over 40% premium to SENSEX

10

15

20

25

30

35

Apr‐08Jul‐08

Oct‐08

Jan‐09

Apr‐09Jul‐09

Oct‐09

Jan‐10

Apr‐10Jul‐10

Oct‐10

Jan‐11

Apr‐11Jul‐11

Oct‐11

Jan‐12

Apr‐12Jul‐12

Oct‐12

Jan‐13

Apr‐13Jul‐13

Oct‐13

HC Index 1yr fwd PE Historic Avg PE

19.2x

‐

50

100

150

200

250

Jan‐08 Jan‐09 Jan‐10 Jan‐11 Jan‐12 Jan‐13

BSE_SENSEX BSE HC Index

Source: BSE, PhillipCapital India Research

At the current level the pharma index is trading at its historic average 1 year PE multiple of ~20x. We believe the sector should command its premium valuation multiples led by continued visibility for healthy formulation exports growth, robust free cash flow generation and enhanced build up in R&D capability over last couple of years. Thanks to the multiple exclusive supply opportunities led by patent expiry of many blockbuster drugs in US during last few years, which helped Indian pharma to enhance its R&D focus and spend.

15 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

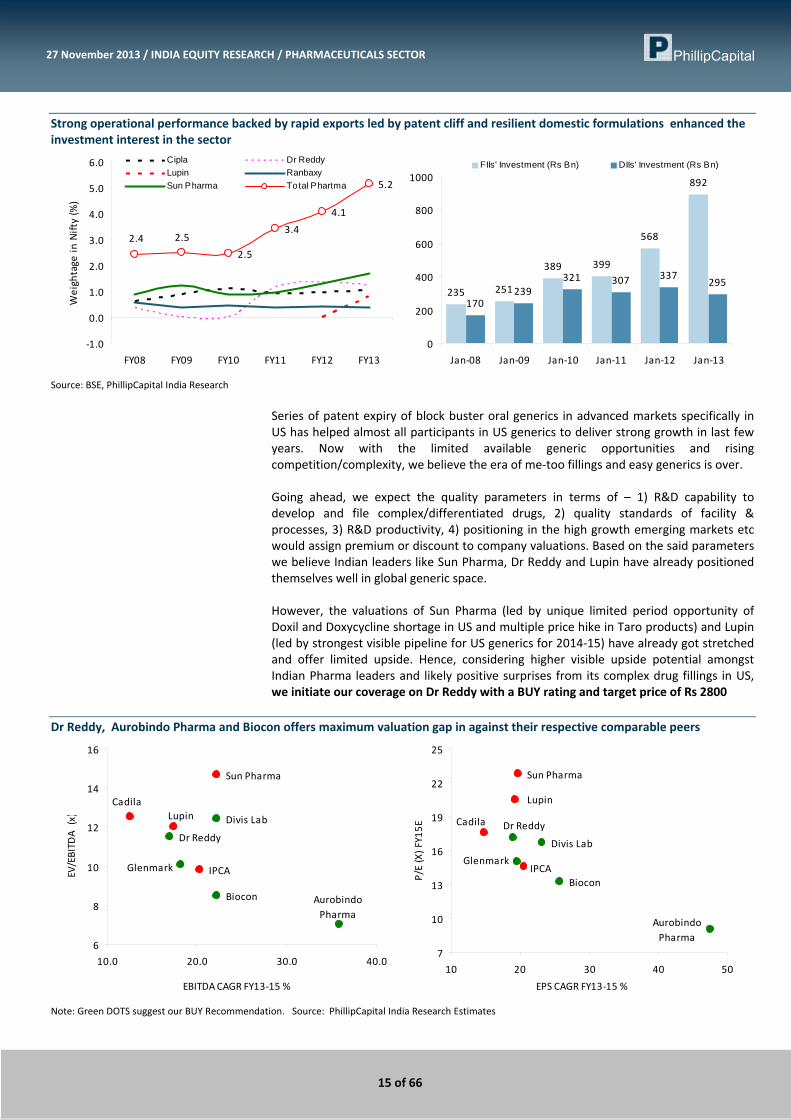

Strong operational performance backed by rapid exports led by patent cliff and resilient domestic formulations enhanced the investment interest in the sector

2.5

3.4

4.1

5.2

2.4 2.5

‐1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

FY08 FY09 FY10 FY11 FY12 FY13

Weightage

in Nifty (%)

Cipla Dr ReddyLupin RanbaxySun Pharma Total Phartma

235 251

389 399

568

892

170239

321 307 337295

0

200

400

600

800

1000

Jan‐08 Jan‐09 Jan‐10 Jan‐11 Jan‐12 Jan‐13

FIIs' Investment (Rs Bn) DIIs' Investment (Rs Bn)

Source: BSE, PhillipCapital India Research

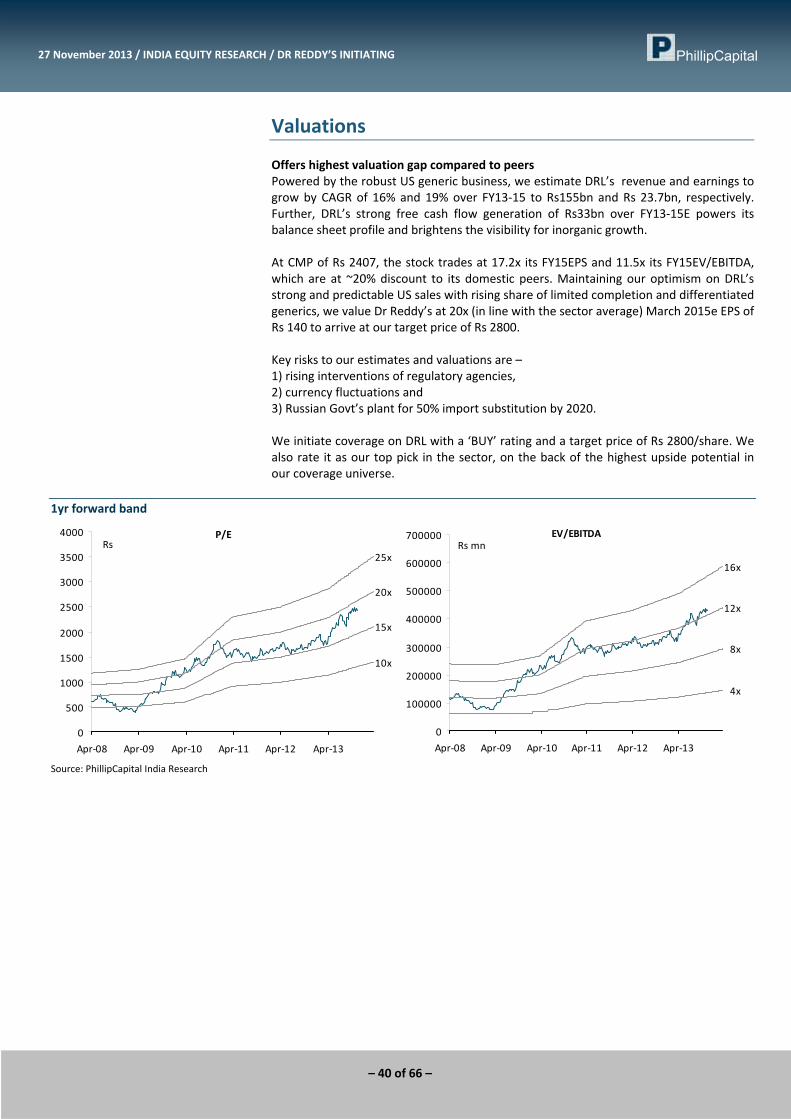

Series of patent expiry of block buster oral generics in advanced markets specifically in US has helped almost all participants in US generics to deliver strong growth in last few years. Now with the limited available generic opportunities and rising competition/complexity, we believe the era of me‐too fillings and easy generics is over. Going ahead, we expect the quality parameters in terms of – 1) R&D capability to develop and file complex/differentiated drugs, 2) quality standards of facility & processes, 3) R&D productivity, 4) positioning in the high growth emerging markets etc would assign premium or discount to company valuations. Based on the said parameters we believe Indian leaders like Sun Pharma, Dr Reddy and Lupin have already positioned themselves well in global generic space. However, the valuations of Sun Pharma (led by unique limited period opportunity of Doxil and Doxycycline shortage in US and multiple price hike in Taro products) and Lupin (led by strongest visible pipeline for US generics for 2014‐15) have already got stretched and offer limited upside. Hence, considering higher visible upside potential amongst Indian Pharma leaders and likely positive surprises from its complex drug fillings in US, we initiate our coverage on Dr Reddy with a BUY rating and target price of Rs 2800

Dr Reddy, Aurobindo Pharma and Biocon offers maximum valuation gap in against their respective comparable peers

Sun Pharma

Dr Reddy

IPCA

Divis Lab

Biocon

LupinCadila

Glenmark

Aurobindo Pharma

6

8

10

12

14

16

10.0 20.0 30.0 40.0

EBITDA CAGR FY13‐15 %

EV/EBITD

A (x)

Sun Pharma

Divis Lab

Biocon

Dr Reddy

Lupin

Cadila

GlenmarkIPCA

Aurobindo Pharma

7

10

13

16

19

22

25

10 20 30 40 50

EPS CAGR FY13‐15 %

P/E (X) FY15E

Note: Green DOTS suggest our BUY Recommendation. Source: PhillipCapital India Research Estimates

16 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

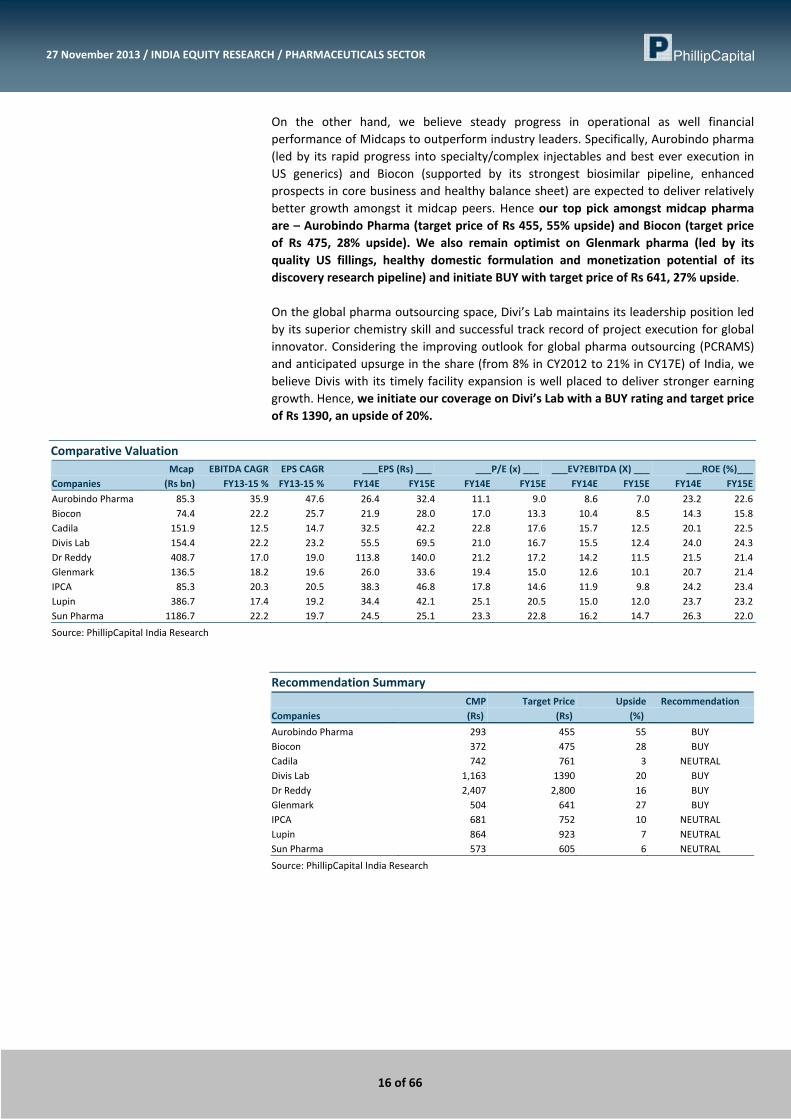

On the other hand, we believe steady progress in operational as well financial performance of Midcaps to outperform industry leaders. Specifically, Aurobindo pharma (led by its rapid progress into specialty/complex injectables and best ever execution in US generics) and Biocon (supported by its strongest biosimilar pipeline, enhanced prospects in core business and healthy balance sheet) are expected to deliver relatively better growth amongst it midcap peers. Hence our top pick amongst midcap pharma are – Aurobindo Pharma (target price of Rs 455, 55% upside) and Biocon (target price of Rs 475, 28% upside). We also remain optimist on Glenmark pharma (led by its quality US fillings, healthy domestic formulation and monetization potential of its discovery research pipeline) and initiate BUY with target price of Rs 641, 27% upside. On the global pharma outsourcing space, Divi’s Lab maintains its leadership position led by its superior chemistry skill and successful track record of project execution for global innovator. Considering the improving outlook for global pharma outsourcing (PCRAMS) and anticipated upsurge in the share (from 8% in CY2012 to 21% in CY17E) of India, we believe Divis with its timely facility expansion is well placed to deliver stronger earning growth. Hence, we initiate our coverage on Divi’s Lab with a BUY rating and target price of Rs 1390, an upside of 20%.

Comparative Valuation Mcap EBITDA CAGR EPS CAGR ___EPS (Rs) ___ ___P/E (x) ___ ___EV?EBITDA (X) ___ ___ROE (%)___Companies (Rs bn) FY13‐15 % FY13‐15 % FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E

Aurobindo Pharma 85.3 35.9 47.6 26.4 32.4 11.1 9.0 8.6 7.0 23.2 22.6Biocon 74.4 22.2 25.7 21.9 28.0 17.0 13.3 10.4 8.5 14.3 15.8Cadila 151.9 12.5 14.7 32.5 42.2 22.8 17.6 15.7 12.5 20.1 22.5Divis Lab 154.4 22.2 23.2 55.5 69.5 21.0 16.7 15.5 12.4 24.0 24.3Dr Reddy 408.7 17.0 19.0 113.8 140.0 21.2 17.2 14.2 11.5 21.5 21.4Glenmark 136.5 18.2 19.6 26.0 33.6 19.4 15.0 12.6 10.1 20.7 21.4IPCA 85.3 20.3 20.5 38.3 46.8 17.8 14.6 11.9 9.8 24.2 23.4Lupin 386.7 17.4 19.2 34.4 42.1 25.1 20.5 15.0 12.0 23.7 23.2Sun Pharma 1186.7 22.2 19.7 24.5 25.1 23.3 22.8 16.2 14.7 26.3 22.0

Source: PhillipCapital India Research

Recommendation Summary CMP Target Price Upside Recommendation Companies (Rs) (Rs) (%)

Aurobindo Pharma 293 455 55 BUY Biocon 372 475 28 BUY Cadila 742 761 3 NEUTRAL Divis Lab 1,163 1390 20 BUY Dr Reddy 2,407 2,800 16 BUY Glenmark 504 641 27 BUY IPCA 681 752 10 NEUTRAL Lupin 864 923 7 NEUTRAL Sun Pharma 573 605 6 NEUTRAL

Source: PhillipCapital India Research

17 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

This page is intentionally left blank.

18 of 66

27 November 2013 / INDIA EQUITY RESEARCH / PHARMACEUTICALS SECTOR

Compa

nies Section

– 19 of 66 –

Aurobindo Pharma Gaining ground in US generics

PHARMACEUTICALS: Initiating Coverage 27 November 2013

PhillipCapital (India) Pvt. Ltd.

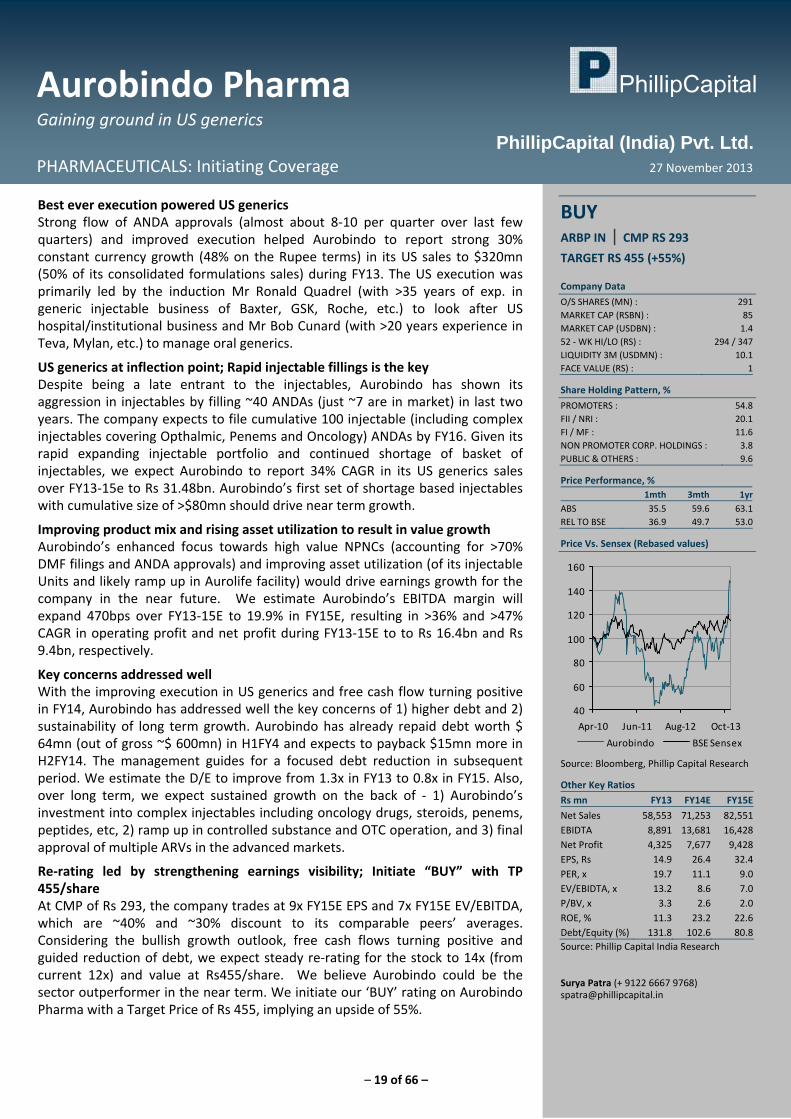

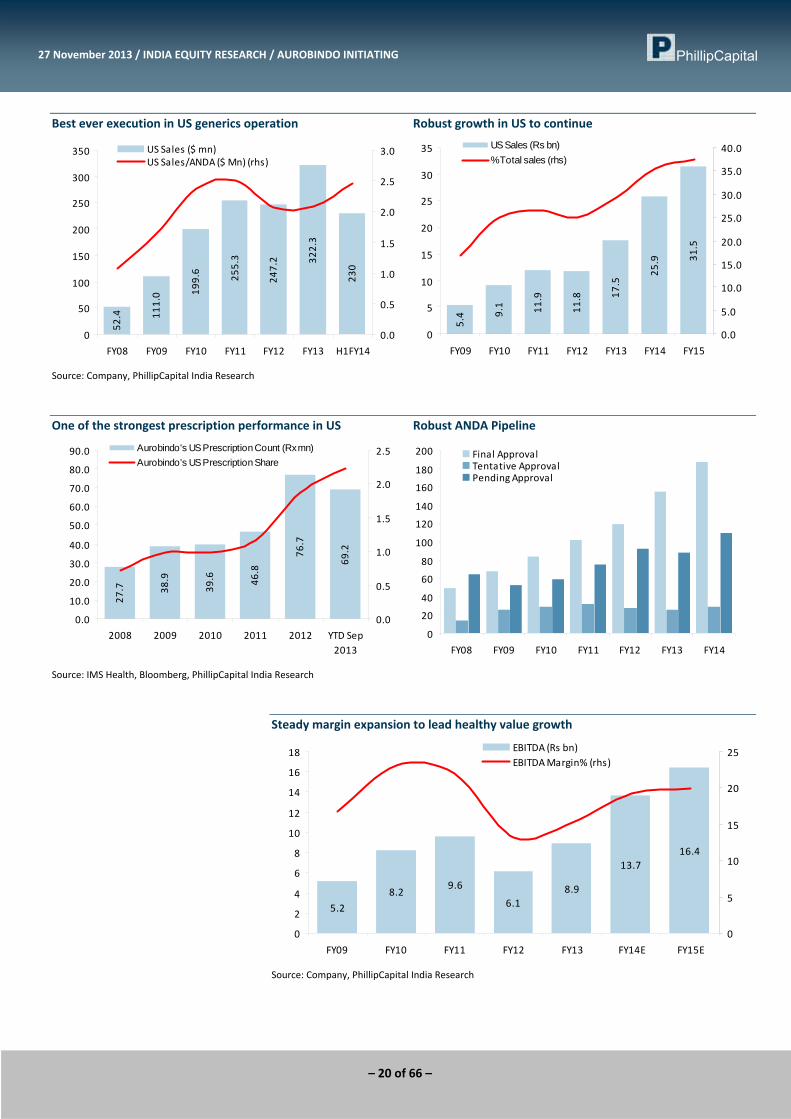

Best ever execution powered US generics Strong flow of ANDA approvals (almost about 8‐10 per quarter over last few quarters) and improved execution helped Aurobindo to report strong 30% constant currency growth (48% on the Rupee terms) in its US sales to $320mn (50% of its consolidated formulations sales) during FY13. The US execution was primarily led by the induction Mr Ronald Quadrel (with >35 years of exp. in generic injectable business of Baxter, GSK, Roche, etc.) to look after US hospital/institutional business and Mr Bob Cunard (with >20 years experience in Teva, Mylan, etc.) to manage oral generics.

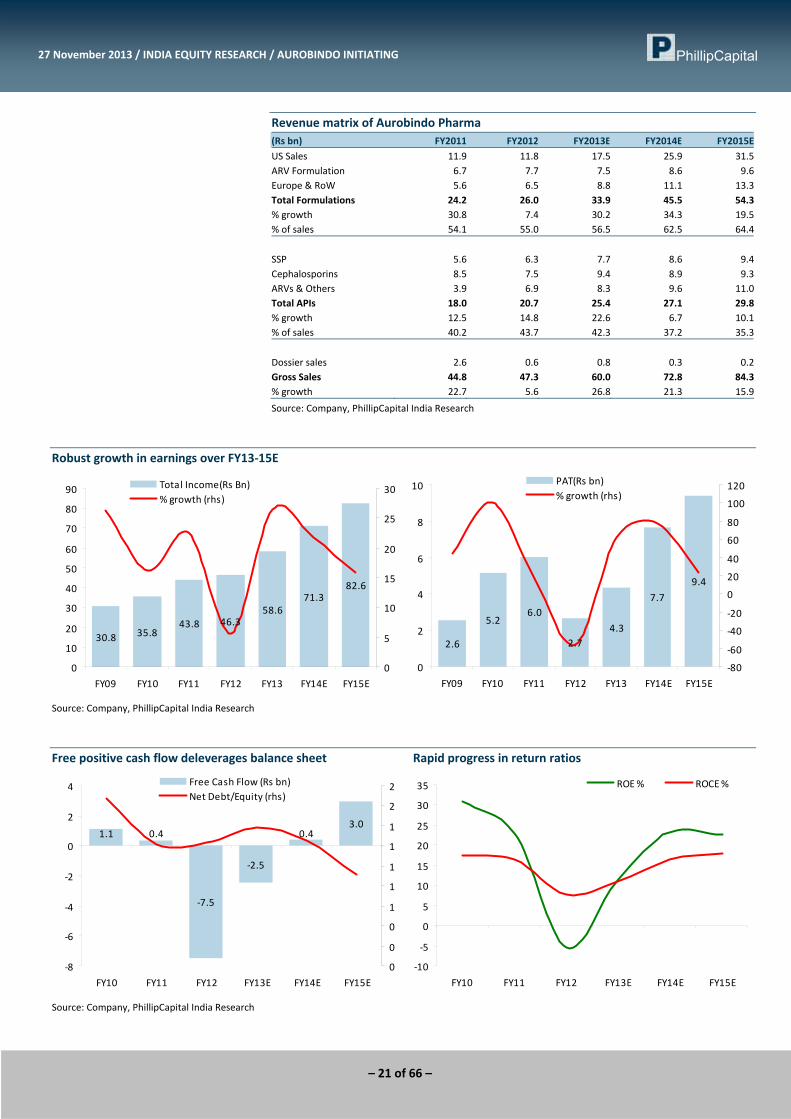

US generics at inflection point; Rapid injectable fillings is the key Despite being a late entrant to the injectables, Aurobindo has shown its aggression in injectables by filling ~40 ANDAs (just ~7 are in market) in last two years. The company expects to file cumulative 100 injectable (including complex injectables covering Opthalmic, Penems and Oncology) ANDAs by FY16. Given its rapid expanding injectable portfolio and continued shortage of basket of injectables, we expect Aurobindo to report 34% CAGR in its US generics sales over FY13‐15e to Rs 31.48bn. Aurobindo’s first set of shortage based injectables with cumulative size of >$80mn should drive near term growth.

Improving product mix and rising asset utilization to result in value growth Aurobindo’s enhanced focus towards high value NPNCs (accounting for >70% DMF filings and ANDA approvals) and improving asset utilization (of its injectable Units and likely ramp up in Aurolife facility) would drive earnings growth for the company in the near future. We estimate Aurobindo’s EBITDA margin will expand 470bps over FY13‐15E to 19.9% in FY15E, resulting in >36% and >47% CAGR in operating profit and net profit during FY13‐15E to to Rs 16.4bn and Rs 9.4bn, respectively.

Key concerns addressed well With the improving execution in US generics and free cash flow turning positive in FY14, Aurobindo has addressed well the key concerns of 1) higher debt and 2) sustainability of long term growth. Aurobindo has already repaid debt worth $ 64mn (out of gross ~$ 600mn) in H1FY4 and expects to payback $15mn more in H2FY14. The management guides for a focused debt reduction in subsequent period. We estimate the D/E to improve from 1.3x in FY13 to 0.8x in FY15. Also, over long term, we expect sustained growth on the back of ‐ 1) Aurobindo’s investment into complex injectables including oncology drugs, steroids, penems, peptides, etc, 2) ramp up in controlled substance and OTC operation, and 3) final approval of multiple ARVs in the advanced markets.

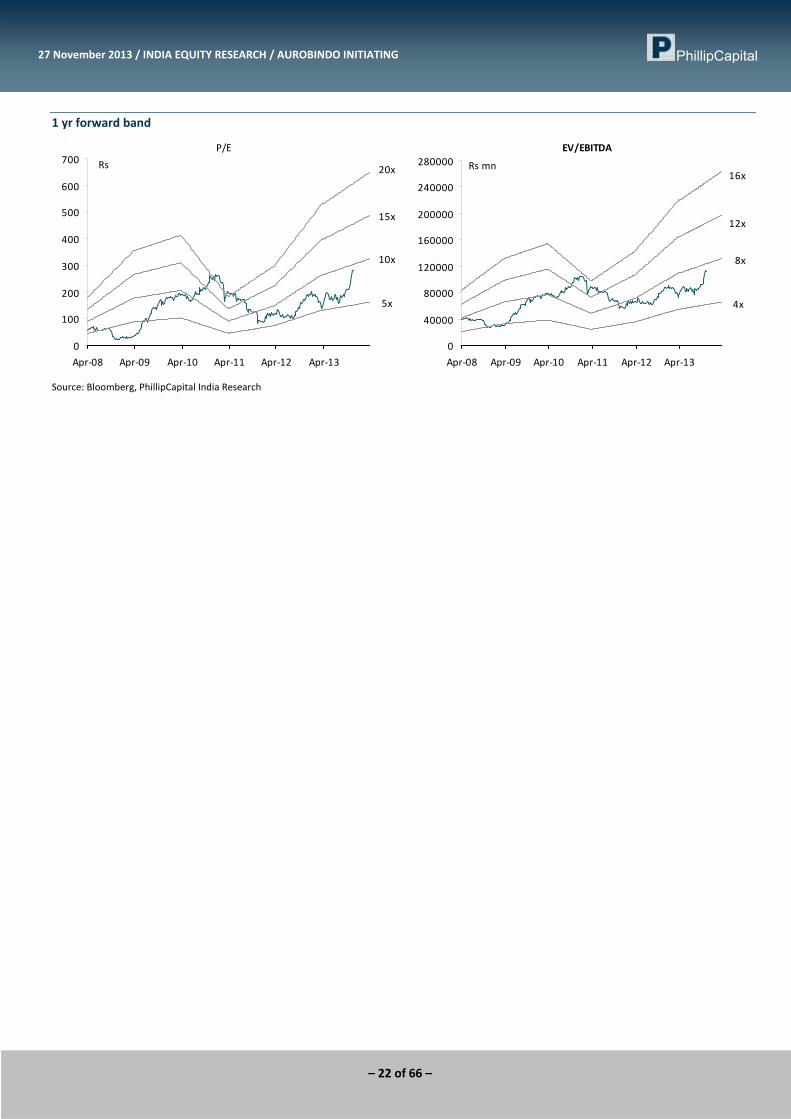

Re‐rating led by strengthening earnings visibility; Initiate “BUY” with TP 455/share At CMP of Rs 293, the company trades at 9x FY15E EPS and 7x FY15E EV/EBITDA, which are ~40% and ~30% discount to its comparable peers’ averages. Considering the bullish growth outlook, free cash flows turning positive and guided reduction of debt, we expect steady re‐rating for the stock to 14x (from current 12x) and value at Rs455/share. We believe Aurobindo could be the sector outperformer in the near term. We initiate our ‘BUY’ rating on Aurobindo Pharma with a Target Price of Rs 455, implying an upside of 55%.

BUY ARBP IN | CMP RS 293

TARGET RS 455 (+55%) Company Data

O/S SHARES (MN) : 291MARKET CAP (RSBN) : 85MARKET CAP (USDBN) : 1.452 ‐ WK HI/LO (RS) : 294 / 347LIQUIDITY 3M (USDMN) : 10.1FACE VALUE (RS) : 1

Share Holding Pattern, %

PROMOTERS : 54.8FII / NRI : 20.1FI / MF : 11.6NON PROMOTER CORP. HOLDINGS : 3.8PUBLIC & OTHERS : 9.6

Price Performance, % 1mth 3mth 1yr

ABS 35.5 59.6 63.1REL TO BSE 36.9 49.7 53.0

Price Vs. Sensex (Rebased values)

40

60

80

100

120

140

160

Apr‐10 Jun‐11 Aug‐12 Oct‐13

Aurobindo BSE Sensex

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY13 FY14E FY15E

Net Sales 58,553 71,253 82,551EBIDTA 8,891 13,681 16,428Net Profit 4,325 7,677 9,428EPS, Rs 14.9 26.4 32.4PER, x 19.7 11.1 9.0EV/EBIDTA, x 13.2 8.6 7.0P/BV, x 3.3 2.6 2.0ROE, % 11.3 23.2 22.6Debt/Equity (%) 131.8 102.6 80.8Source: Phillip Capital India Research Surya Patra (+ 9122 6667 9768) [email protected]

– 20 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / AUROBINDO INITIATING

Best ever execution in US generics operation Robust growth in US to continue 52

.4 111.0 19

9.6

255.3

247.2 322.3

230

0

50

100

150

200

250

300

350

FY08 FY09 FY10 FY11 FY12 FY13 H1FY14

0.0

0.5

1.0

1.5

2.0

2.5

3.0US Sales ($ mn)US Sales/ANDA ($ Mn) (rhs)

5.4 9.1 11.9

11.8 17

.5

25.9 31

.5

0

5

10

15

20

25

30

35

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0US Sales (Rs bn)% Total sales (rhs)

Source: Company, PhillipCapital India Research

One of the strongest prescription performance in US Robust ANDA Pipeline

27.7 38.9

39.6 46.8

76.7

69.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2008 2009 2010 2011 2012 YTD Sep2013

0.0

0.5

1.0

1.5

2.0

2.5Aurobindo's US Prescription Count (Rx mn)Aurobindo's US Prescription Share

0

20

40

60

80

100

120

140

160

180

200

FY08 FY09 FY10 FY11 FY12 FY13 FY14

Final ApprovalTentative ApprovalPending Approval

Source: IMS Health, Bloomberg, PhillipCapital India Research

Steady margin expansion to lead healthy value growth

5.2

8.29.6

6.18.9

13.716.4

0

2

4

6

8

10

12

14

16

18

FY09 FY10 FY11 FY12 FY13 FY14E FY15E

0

5

10

15

20

25EBITDA (Rs bn)EBITDA Margin% (rhs)

Source: Company, PhillipCapital India Research

– 21 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / AUROBINDO INITIATING

Revenue matrix of Aurobindo Pharma (Rs bn) FY2011 FY2012 FY2013E FY2014E FY2015E

US Sales 11.9 11.8 17.5 25.9 31.5ARV Formulation 6.7 7.7 7.5 8.6 9.6Europe & RoW 5.6 6.5 8.8 11.1 13.3Total Formulations 24.2 26.0 33.9 45.5 54.3% growth 30.8 7.4 30.2 34.3 19.5% of sales 54.1 55.0 56.5 62.5 64.4

SSP 5.6 6.3 7.7 8.6 9.4Cephalosporins 8.5 7.5 9.4 8.9 9.3ARVs & Others 3.9 6.9 8.3 9.6 11.0Total APIs 18.0 20.7 25.4 27.1 29.8% growth 12.5 14.8 22.6 6.7 10.1% of sales 40.2 43.7 42.3 37.2 35.3

Dossier sales 2.6 0.6 0.8 0.3 0.2Gross Sales 44.8 47.3 60.0 72.8 84.3% growth 22.7 5.6 26.8 21.3 15.9

Source: Company, PhillipCapital India Research

Robust growth in earnings over FY13‐15E

30.8 35.843.8 46.3

58.671.3

82.6

0

10

20

30

40

50

60

70

80

90

FY09 FY10 FY11 FY12 FY13 FY14E FY15E

0

5

10

15

20

25

30Total Income(Rs Bn)% growth (rhs)

2.6

5.26.0

2.74.3

7.7

9.4

0

2

4

6

8

10

FY09 FY10 FY11 FY12 FY13 FY14E FY15E

‐80

‐60

‐40

‐20

0

20

40

60

80

100

120PAT(Rs bn)% growth (rhs)

Source: Company, PhillipCapital India Research

Free positive cash flow deleverages balance sheet Rapid progress in return ratios

1.1 0.4

‐7.5

‐2.5

0.43.0

‐8

‐6

‐4

‐2

0

2

4

FY10 FY11 FY12 FY13E FY14E FY15E

0

0

0

1

1

1

1

1

2

2Free Cash Flow (Rs bn)Net Debt/Equity (rhs)

‐10

‐5

0

5

10

15

20

25

30

35

FY10 FY11 FY12 FY13E FY14E FY15E

ROE % ROCE %

Source: Company, PhillipCapital India Research

– 22 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / AUROBINDO INITIATING

1 yr forward band

P/E

5x

10x

15x

20x

0

100

200

300

400

500

600

700

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

Rs

EV/EBITDA

4x

8x

12x

16x

0

40000

80000

120000

160000

200000

240000

280000

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

Rs mn

Source: Bloomberg, PhillipCapital India Research

– 23 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / AUROBINDO INITIATING

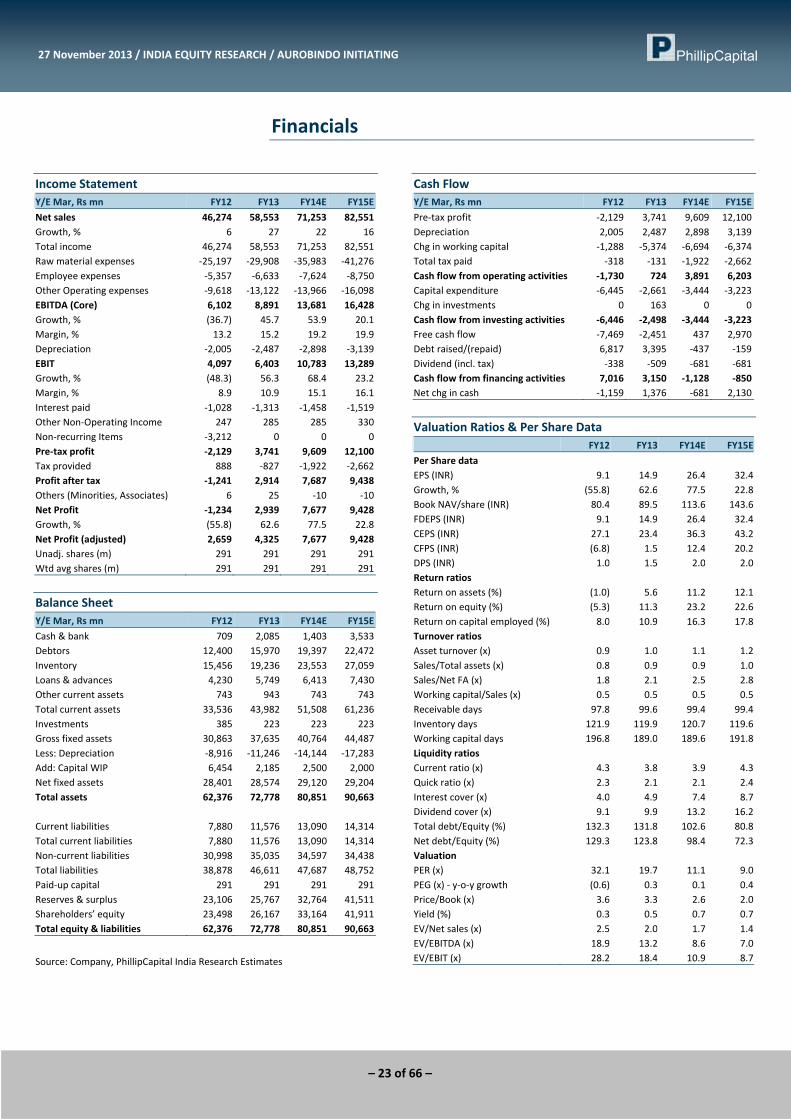

Financials

Income Statement Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Net sales 46,274 58,553 71,253 82,551Growth, % 6 27 22 16Total income 46,274 58,553 71,253 82,551Raw material expenses ‐25,197 ‐29,908 ‐35,983 ‐41,276Employee expenses ‐5,357 ‐6,633 ‐7,624 ‐8,750Other Operating expenses ‐9,618 ‐13,122 ‐13,966 ‐16,098EBITDA (Core) 6,102 8,891 13,681 16,428Growth, % (36.7) 45.7 53.9 20.1Margin, % 13.2 15.2 19.2 19.9Depreciation ‐2,005 ‐2,487 ‐2,898 ‐3,139EBIT 4,097 6,403 10,783 13,289Growth, % (48.3) 56.3 68.4 23.2Margin, % 8.9 10.9 15.1 16.1Interest paid ‐1,028 ‐1,313 ‐1,458 ‐1,519Other Non‐Operating Income 247 285 285 330Non‐recurring Items ‐3,212 0 0 0Pre‐tax profit ‐2,129 3,741 9,609 12,100Tax provided 888 ‐827 ‐1,922 ‐2,662Profit after tax ‐1,241 2,914 7,687 9,438Others (Minorities, Associates) 6 25 ‐10 ‐10Net Profit ‐1,234 2,939 7,677 9,428Growth, % (55.8) 62.6 77.5 22.8Net Profit (adjusted) 2,659 4,325 7,677 9,428Unadj. shares (m) 291 291 291 291Wtd avg shares (m) 291 291 291 291

Balance Sheet Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Cash & bank 709 2,085 1,403 3,533Debtors 12,400 15,970 19,397 22,472Inventory 15,456 19,236 23,553 27,059Loans & advances 4,230 5,749 6,413 7,430Other current assets 743 943 743 743Total current assets 33,536 43,982 51,508 61,236Investments 385 223 223 223Gross fixed assets 30,863 37,635 40,764 44,487Less: Depreciation ‐8,916 ‐11,246 ‐14,144 ‐17,283Add: Capital WIP 6,454 2,185 2,500 2,000Net fixed assets 28,401 28,574 29,120 29,204Total assets 62,376 72,778 80,851 90,663 Current liabilities 7,880 11,576 13,090 14,314Total current liabilities 7,880 11,576 13,090 14,314Non‐current liabilities 30,998 35,035 34,597 34,438Total liabilities 38,878 46,611 47,687 48,752Paid‐up capital 291 291 291 291Reserves & surplus 23,106 25,767 32,764 41,511Shareholders’ equity 23,498 26,167 33,164 41,911Total equity & liabilities 62,376 72,778 80,851 90,663

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Pre‐tax profit ‐2,129 3,741 9,609 12,100Depreciation 2,005 2,487 2,898 3,139Chg in working capital ‐1,288 ‐5,374 ‐6,694 ‐6,374Total tax paid ‐318 ‐131 ‐1,922 ‐2,662Cash flow from operating activities ‐1,730 724 3,891 6,203Capital expenditure ‐6,445 ‐2,661 ‐3,444 ‐3,223Chg in investments 0 163 0 0Cash flow from investing activities ‐6,446 ‐2,498 ‐3,444 ‐3,223Free cash flow ‐7,469 ‐2,451 437 2,970Debt raised/(repaid) 6,817 3,395 ‐437 ‐159Dividend (incl. tax) ‐338 ‐509 ‐681 ‐681Cash flow from financing activities 7,016 3,150 ‐1,128 ‐850Net chg in cash ‐1,159 1,376 ‐681 2,130

Valuation Ratios & Per Share Data FY12 FY13 FY14E FY15E

Per Share data EPS (INR) 9.1 14.9 26.4 32.4 Growth, % (55.8) 62.6 77.5 22.8 Book NAV/share (INR) 80.4 89.5 113.6 143.6 FDEPS (INR) 9.1 14.9 26.4 32.4 CEPS (INR) 27.1 23.4 36.3 43.2 CFPS (INR) (6.8) 1.5 12.4 20.2 DPS (INR) 1.0 1.5 2.0 2.0 Return ratios Return on assets (%) (1.0) 5.6 11.2 12.1 Return on equity (%) (5.3) 11.3 23.2 22.6 Return on capital employed (%) 8.0 10.9 16.3 17.8 Turnover ratios Asset turnover (x) 0.9 1.0 1.1 1.2 Sales/Total assets (x) 0.8 0.9 0.9 1.0 Sales/Net FA (x) 1.8 2.1 2.5 2.8 Working capital/Sales (x) 0.5 0.5 0.5 0.5 Receivable days 97.8 99.6 99.4 99.4 Inventory days 121.9 119.9 120.7 119.6 Working capital days 196.8 189.0 189.6 191.8 Liquidity ratios Current ratio (x) 4.3 3.8 3.9 4.3 Quick ratio (x) 2.3 2.1 2.1 2.4 Interest cover (x) 4.0 4.9 7.4 8.7 Dividend cover (x) 9.1 9.9 13.2 16.2 Total debt/Equity (%) 132.3 131.8 102.6 80.8 Net debt/Equity (%) 129.3 123.8 98.4 72.3 Valuation PER (x) 32.1 19.7 11.1 9.0 PEG (x) ‐ y‐o‐y growth (0.6) 0.3 0.1 0.4 Price/Book (x) 3.6 3.3 2.6 2.0 Yield (%) 0.3 0.5 0.7 0.7 EV/Net sales (x) 2.5 2.0 1.7 1.4 EV/EBITDA (x) 18.9 13.2 8.6 7.0 EV/EBIT (x) 28.2 18.4 10.9 8.7

– 24 of 66 –

Biocon Crowned with biologics

PHARMACEUTICALS: Initiating Coverage 27 November 2013

PhillipCapital (India) Pvt. Ltd.

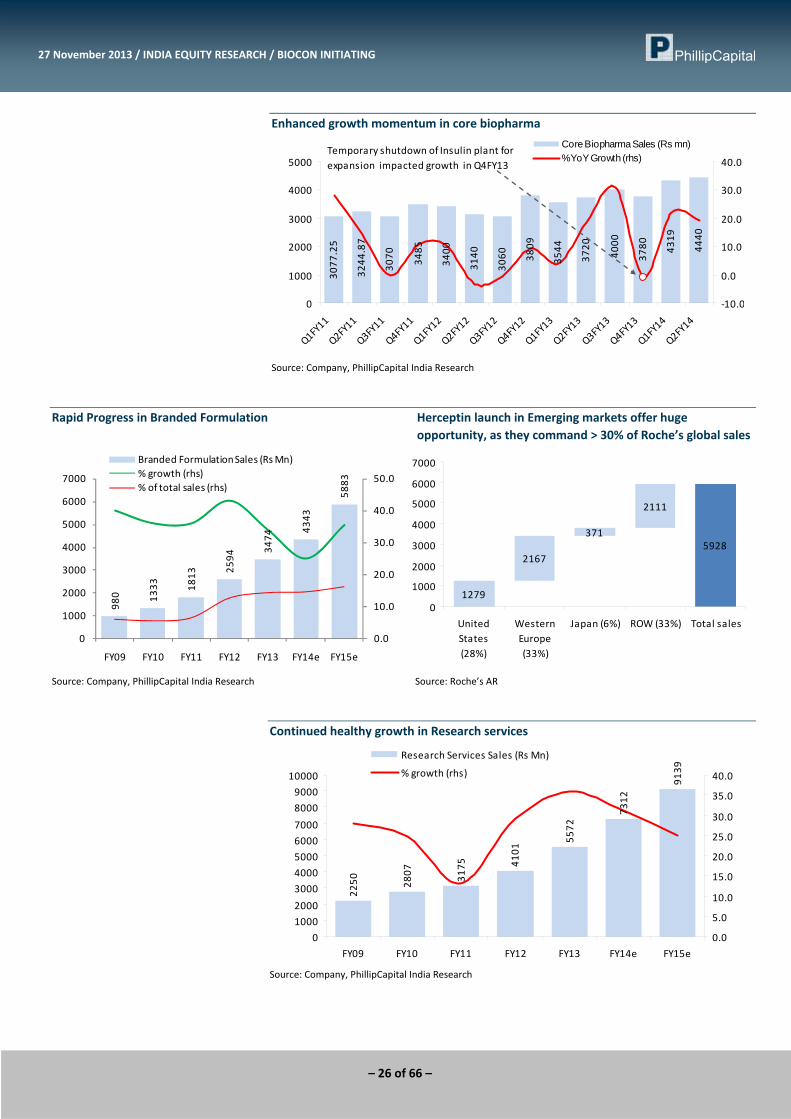

Enhanced growth momentum in core Biopharma Biocon’s core Biopharma business (62% of total sales) including – statins, insulin, immunosuppressant, Orlistat etc has already delivered strong growth of ~20% in FY13 (v/s historical growth trend of ~12‐15%) to Rs 14.9bn. Going forward, 1) the ramp up in insulin in emerging markets (led by capacity expansion effective from mid‐Q2FY14 and deeper geographic penetration into 45 emerging markets) and 2) continued limited competition in Tacrolimus coupled with likely launch of Sirolimus (company already has multiple supply tie‐ups) in Q3FY14 would drive steady growth of >18% CAGR over FY13‐15, despite the flattening sales of statins.

Herceptin launch could drive value growth in branded sales Biocon’s strategic focus on complex formulations, brand positioning and very selective product portfolio has helped its branded formulations (14% of sales) to report 37% CAGR over last five years. Going ahead, its continued focus on differentiated drugs and brand promotion will sustain its growth momentum. Also, the likely launch of world’s first biosimilar version of generic herceptin in India during Q4FY14 (Already got DCGI approval) could drive value growth for Biocon. We believe Biocon would be the only generic player for herceptin (Indian market size Rs 1300mn) for ~15‐18 months after its launch in India and estimate it to generate incremental domestic sales of Rs 600mn (PAT of Rs 160mn) in FY15. In Addition, the huge demand for biosimilar herceptin in emerging markets (valued >$ 2bn) would be the key opportunity for Biocon in medium term. We estimate domestic formulation to report 30% CAGR over FY13‐15 to Rs 5.9bn.

Fresh stream of manufacturing revenue powers Syngene growth Biocon’s Research services operation (Syngene) is the largest Indian CRO with 1500+ Scientists working for 16 of top 20 global innovators. With its continued client expansion (to about 150 now) and improving outlook of global pharma outsourcing, we expect the company to report a growth of 28% CAGR FY13‐15 to Rs 9.13bn. Additionally, a fresh high margin revenue stream of clinical material supply (for 6 Phase III compounds of its partners) commencing from H2FY14 would drive value growth for Syngene.

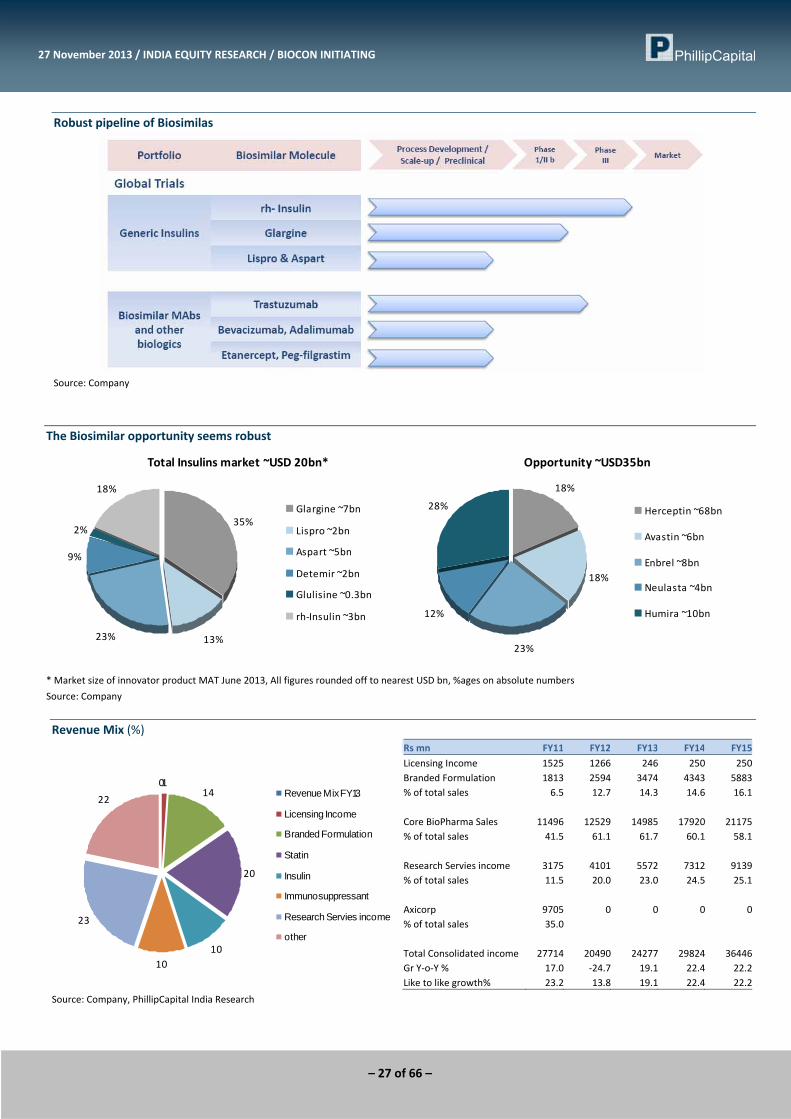

Harmonised dossier filling for Rh‐insulin in Europe and US seems strategically best as 1) the company expects to file from the new state of art facility of Malaysia (which is expected to commence in 2014 earlier than previously guided 2015), 2) the existing old facility can focus on meeting emerging market demand and 3) small delay in product launch in Europe will not erode the product opportunity like in any chemical based generic drug.

Unique biologic/biosimilar pipeline brightens longterm growth Biocon holds the strongest pipeline of of biosimilars (including Rh‐insulin, insulin analogues and five monoclonal antobodies) and biologics (including Itolizumab and IN‐105) amongst Indian peers. The said pipeline projects are in various stages of development and all of them are developed from internal accruals. We believe this pipeline could upgrade Biocon’s financial profile substantially FY16 onwards. In fact, the target opportunities for Biocon’s biosimilar insulin and MAB pipeline are $ 20bn and $35bn respectively.

We expect Biocon to see gradual re‐rating with improved core operating performance and rising visibility of biosimilars in advanced markets going forward. We initiate our coverage on Biocon with BUY rating and a price target of Rs 475 (17x FY15E).

BUY BIOS IN | CMP RS 372

TARGET RS 475 (+28%) Company Data

O/S SHARES (MN) : 200MARKET CAP (RSBN) : 74MARKET CAP (USDBN) : 1.252 ‐ WK HI/LO (RS) : 387 / 253LIQUIDITY 3M (USDMN) : 3.2FACE VALUE (RS) : 5

Share Holding Pattern, %

PROMOTERS : 61.0FII / NRI : 11.7FI / MF : 7.0NON PROMOTER CORP. HOLDINGS : 3.5PUBLIC & OTHERS : 17.0

Price Performance, % 1mth 3mth 1yr

ABS 11.9 8.9 34.3REL TO BSE 13.3 ‐1.0 24.2

Price Vs. Sensex (Rebased values)

60

80

100

120

140

160

Apr‐10 Jun‐11 Aug‐12 Oct‐13Biocon BSE Sensex

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY13 FY14E FY15E

Net Sales 24,263 29,824 36,446EBIDTA 5,701 6,875 8,513Net Profit 3,483 4,371 5,605EPS, Rs 17.4 21.9 28.0PER, x 21.4 17.0 13.3EV/EBIDTA, x 12.3 10.4 8.5P/BV, x 2.8 2.4 2.1ROE, % 18.9 14.3 15.8Debt/Equity (%) 9.9 11.6 12.9Source: Phillip Capital India Research Surya Patra (+ 9122 6667 9768) [email protected]

– 25 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / BIOCON INITIATING

Valuations Expect gradual re‐rating with improved core operating performance and rising visibility of biosimilars in advanced markets We estimate Biocon to deliver sales and profit growth at a CAGR of 21% and 26% over FY13‐15E to Rs 36.6bn and Rs 5.5bn, respectively in FY15. We expect the margins to be maintained in the narrow range of 22‐23% despite higher commitment towards discovery pipeline. At CMP of Rs 372, the company trades at 13.3x FY15E EPS and 8.5x FY15E EV/EBITDA, which are ~20% discount to its comparable peers’ averages. We we value Biocon at 17x (in line with historic valuation multiple) it’s FY15 EPS of Rs 28.0, which yields us our target price of Rs 475/share (implying an upside of 28%). We initiate our coverage on Biocon with BUY rating and a price target of Rs 475. Considering its enhanced growth profile in core operations, robust pipeline of biologi/biosimilar products, likely value unlocking in Syngene by listing it separately, out‐licensing of Rh insulin for advanced markets and strong Balance Sheet position, we expect Biocon to see further re‐rating going forward. However, any substantial delay in the development of its biologic/biosimilar pipeline and any regulatory hurdle in terms of delay in clinical development or facility issues could pose as key risk to our investment thesis.

1 yr forward band

P/E

6x

12x

18x

24x

0

100

200

300

400

500

600

700

800

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

Rs

EV/EBITDA

5x

8x

11x

14x

0

20000

40000

60000

80000

100000

120000

140000

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

Rs mn

Source: Bloomberg, PhillipCapital India Research

– 26 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / BIOCON INITIATING

Enhanced growth momentum in core biopharma

3077

.25

3244

.87

3070 3485

3400

3140

3060 3809

3544

3720

4000

3780 4319

4440

0

1000

2000

3000

4000

5000

Q1FY11

Q2FY11

Q3FY11

Q4FY11

Q1FY12

Q2FY12

Q3FY12

Q4FY12

Q1FY13

Q2FY13

Q3FY13

Q4FY13

Q1FY14

Q2FY14

‐10.0

0.0

10.0

20.0

30.0

40.0

Core Biopharma Sales (Rs mn)% YoY Growth (rhs)

Temporary shutdown of Insulin plant for expansion impacted growth in Q4FY13

Source: Company, PhillipCapital India Research

Rapid Progress in Branded Formulation Herceptin launch in Emerging markets offer huge opportunity, as they command > 30% of Roche’s global sales

980 1333 1813 25

94

3474

4343

5883

0.0

10.0

20.0

30.0

40.0

50.0

0

1000

2000

3000

4000

5000

6000

7000

FY09 FY10 FY11 FY12 FY13 FY14e FY15e

Branded Formulation Sales (Rs Mn)% growth (rhs)% of total sales (rhs)

1279

2167

371

2111

5928

0

1000

2000

3000

4000

5000

6000

7000

UnitedStates(28%)

WesternEurope(33%)

Japan (6%) ROW (33%) Total sales

Source: Company, PhillipCapital India Research Source: Roche’s AR

Continued healthy growth in Research services

2250 2807 3175 41

01

5572

7312

9139

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY09 FY10 FY11 FY12 FY13 FY14e FY15e

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Research Services Sales (Rs Mn)

% growth (rhs)

Source: Company, PhillipCapital India Research

– 27 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / BIOCON INITIATING

Robust pipeline of Biosimilas

Source: Company

The Biosimilar opportunity seems robust

Total Insulins market ~USD 20bn*

35%

13%23%

9%

2%

18%

Glargine ~7bn

Lispro ~2bn

Aspart ~5bn

Detemir ~2bn

Glulisine ~0.3bn

rh‐Insulin ~3bn

Opportunity ~USD35bn

18%

18%

23%

12%

28% Herceptin ~68bn

Avastin ~6bn

Enbrel ~8bn

Neulasta ~4bn

Humira ~10bn

* Market size of innovator product MAT June 2013, All figures rounded off to nearest USD bn, %ages on absolute numbers

Source: Company

Revenue Mix (%) Rs mn FY11 FY12 FY13 FY14 FY15

Licensing Income 1525 1266 246 250 250Branded Formulation 1813 2594 3474 4343 5883% of total sales 6.5 12.7 14.3 14.6 16.1 Core BioPharma Sales 11496 12529 14985 17920 21175% of total sales 41.5 61.1 61.7 60.1 58.1 Research Servies income 3175 4101 5572 7312 9139% of total sales 11.5 20.0 23.0 24.5 25.1 Axicorp 9705 0 0 0 0% of total sales 35.0 Total Consolidated income 27714 20490 24277 29824 36446Gr Y‐o‐Y % 17.0 ‐24.7 19.1 22.4 22.2Like to like growth% 23.2 13.8 19.1 22.4 22.2

Source: Company, PhillipCapital India Research

0114

20

1010

23

22Revenue Mix FY13

Licensing Income

Branded Formulation

Statin

Insulin

Immunosuppressant

Research Servies income

other

– 28 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / BIOCON INITIATING

Healthy progress in revenue and earnings over FY13‐15E 27

709

2086

5

2485

3

3042

0

3717

50.0

5.0

10.0

15.0

20.0

25.0

0

5000

10000

15000

20000

25000

30000

35000

40000

FY11 FY12 FY13 FY14 FY15

Net Sales (Rs mn)

% growth (Like to like) (rhs)

3756

3131

3483 43

71 5605

0

1000

2000

3000

4000

5000

6000

FY11 FY12 FY13 FY14 FY15

‐10

‐5

0

5

10

15

20

25

30

Adj. Net Profit (Rs mn)

% growth (Like to like) (rhs)

Source: Company, PhillipCapital India Research

Robust cash position despite rising R&D spend

‐569

‐567

6

‐822

5

‐992

2

2591

6723

2284 4046

2082

2429

‐107

54

‐119

23

‐15000

‐10000

‐5000

0

5000

10000

FY10 FY11 FY12 FY13 FY14 FY15

Rs m

n

Net Debt Free Cash flow

10.0

12.0

14.0

16.0

18.0

20.0

FY10 FY11 FY12 FY13 FY14 FY15

ROCE% ROE%

Source: Company, PhillipCapital India Research

– 29 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / BIOCON INITIATING

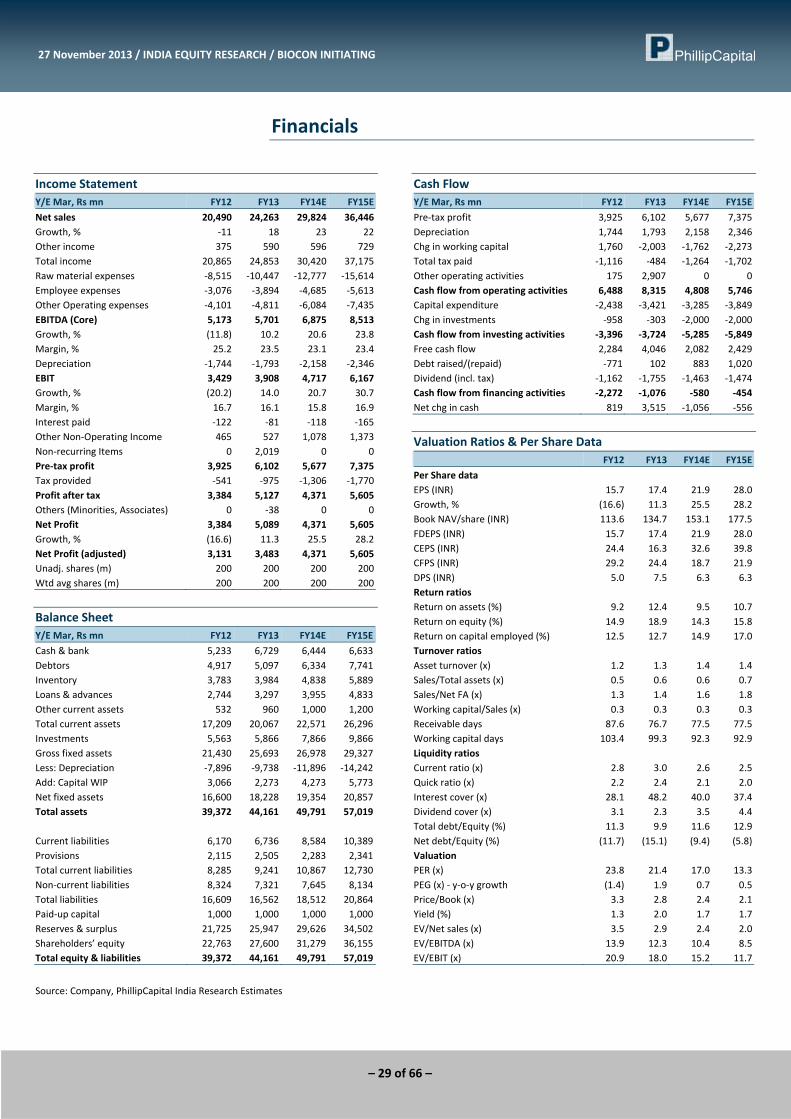

Financials

Income Statement Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Net sales 20,490 24,263 29,824 36,446Growth, % ‐11 18 23 22Other income 375 590 596 729Total income 20,865 24,853 30,420 37,175Raw material expenses ‐8,515 ‐10,447 ‐12,777 ‐15,614Employee expenses ‐3,076 ‐3,894 ‐4,685 ‐5,613Other Operating expenses ‐4,101 ‐4,811 ‐6,084 ‐7,435EBITDA (Core) 5,173 5,701 6,875 8,513Growth, % (11.8) 10.2 20.6 23.8Margin, % 25.2 23.5 23.1 23.4Depreciation ‐1,744 ‐1,793 ‐2,158 ‐2,346EBIT 3,429 3,908 4,717 6,167Growth, % (20.2) 14.0 20.7 30.7Margin, % 16.7 16.1 15.8 16.9Interest paid ‐122 ‐81 ‐118 ‐165Other Non‐Operating Income 465 527 1,078 1,373Non‐recurring Items 0 2,019 0 0Pre‐tax profit 3,925 6,102 5,677 7,375Tax provided ‐541 ‐975 ‐1,306 ‐1,770Profit after tax 3,384 5,127 4,371 5,605Others (Minorities, Associates) 0 ‐38 0 0Net Profit 3,384 5,089 4,371 5,605Growth, % (16.6) 11.3 25.5 28.2Net Profit (adjusted) 3,131 3,483 4,371 5,605Unadj. shares (m) 200 200 200 200Wtd avg shares (m) 200 200 200 200

Balance Sheet Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Cash & bank 5,233 6,729 6,444 6,633Debtors 4,917 5,097 6,334 7,741Inventory 3,783 3,984 4,838 5,889Loans & advances 2,744 3,297 3,955 4,833Other current assets 532 960 1,000 1,200Total current assets 17,209 20,067 22,571 26,296Investments 5,563 5,866 7,866 9,866Gross fixed assets 21,430 25,693 26,978 29,327Less: Depreciation ‐7,896 ‐9,738 ‐11,896 ‐14,242Add: Capital WIP 3,066 2,273 4,273 5,773Net fixed assets 16,600 18,228 19,354 20,857Total assets 39,372 44,161 49,791 57,019 Current liabilities 6,170 6,736 8,584 10,389Provisions 2,115 2,505 2,283 2,341Total current liabilities 8,285 9,241 10,867 12,730Non‐current liabilities 8,324 7,321 7,645 8,134Total liabilities 16,609 16,562 18,512 20,864Paid‐up capital 1,000 1,000 1,000 1,000Reserves & surplus 21,725 25,947 29,626 34,502Shareholders’ equity 22,763 27,600 31,279 36,155Total equity & liabilities 39,372 44,161 49,791 57,019

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Pre‐tax profit 3,925 6,102 5,677 7,375Depreciation 1,744 1,793 2,158 2,346Chg in working capital 1,760 ‐2,003 ‐1,762 ‐2,273Total tax paid ‐1,116 ‐484 ‐1,264 ‐1,702Other operating activities 175 2,907 0 0Cash flow from operating activities 6,488 8,315 4,808 5,746Capital expenditure ‐2,438 ‐3,421 ‐3,285 ‐3,849Chg in investments ‐958 ‐303 ‐2,000 ‐2,000Cash flow from investing activities ‐3,396 ‐3,724 ‐5,285 ‐5,849Free cash flow 2,284 4,046 2,082 2,429Debt raised/(repaid) ‐771 102 883 1,020Dividend (incl. tax) ‐1,162 ‐1,755 ‐1,463 ‐1,474Cash flow from financing activities ‐2,272 ‐1,076 ‐580 ‐454Net chg in cash 819 3,515 ‐1,056 ‐556

Valuation Ratios & Per Share Data FY12 FY13 FY14E FY15E

Per Share data EPS (INR) 15.7 17.4 21.9 28.0Growth, % (16.6) 11.3 25.5 28.2Book NAV/share (INR) 113.6 134.7 153.1 177.5FDEPS (INR) 15.7 17.4 21.9 28.0CEPS (INR) 24.4 16.3 32.6 39.8CFPS (INR) 29.2 24.4 18.7 21.9DPS (INR) 5.0 7.5 6.3 6.3Return ratios Return on assets (%) 9.2 12.4 9.5 10.7Return on equity (%) 14.9 18.9 14.3 15.8Return on capital employed (%) 12.5 12.7 14.9 17.0Turnover ratios Asset turnover (x) 1.2 1.3 1.4 1.4Sales/Total assets (x) 0.5 0.6 0.6 0.7Sales/Net FA (x) 1.3 1.4 1.6 1.8Working capital/Sales (x) 0.3 0.3 0.3 0.3Receivable days 87.6 76.7 77.5 77.5Working capital days 103.4 99.3 92.3 92.9Liquidity ratios Current ratio (x) 2.8 3.0 2.6 2.5Quick ratio (x) 2.2 2.4 2.1 2.0Interest cover (x) 28.1 48.2 40.0 37.4Dividend cover (x) 3.1 2.3 3.5 4.4Total debt/Equity (%) 11.3 9.9 11.6 12.9Net debt/Equity (%) (11.7) (15.1) (9.4) (5.8)Valuation PER (x) 23.8 21.4 17.0 13.3PEG (x) ‐ y‐o‐y growth (1.4) 1.9 0.7 0.5Price/Book (x) 3.3 2.8 2.4 2.1Yield (%) 1.3 2.0 1.7 1.7EV/Net sales (x) 3.5 2.9 2.4 2.0EV/EBITDA (x) 13.9 12.3 10.4 8.5EV/EBIT (x) 20.9 18.0 15.2 11.7

– 30 of 66 –

Cadila Healthcare US generics seems only sweet spot

PHARMACEUTICALS: Initiating Coverage 27 November 2013

PhillipCapital (India) Pvt. Ltd.

Improving visibility on ANDA approvals brightens FY15 US growth Cadila’s quality and cost effective generic drug offerings have made it the 10th largest US generic players and helped it deliver 40% revenue CAGR over the last five years to Rs 15.1bn in FY13. At the same time, the slowing ANDA approvals despite improved ANDA fillings has been the key concern for Cadila in recent past. However, the improved visibility on drug approvals after receipt of complete response from the FDA has brightened the US growth prospects in medium term. The management expects to launch more than 20 products (v/s 7 in FY13) over the next 12‐15 months in the US. We estimate Cadila’s US generics to deliver a compounded annual growth of 21% over FY13‐15 to Rs 22.2bn. Complex technology Initiatives ensures strong future growth but lacks visibility Cadila has rapidly increased it R&D spend at ~70% CAGR over last three years to Rs 4.7bn (7.4% of sales) in FY13, in order to upgrade its drug portfolio to complex technology class including – transdermal, inhalers, controlled release drugs, biologic/biosimilars and NCEs. Such initiatives has certainly enhanced the future growth visibility of Cadila but all those lacks commercial visibility. Domestic formulations to moderated growth despite Lipaglyn launch Cadila, with a strategy to widen its foot hold in domestic formulations acquired Biochem during late FY12, which sharply reduced the share of its chronic therapy from 58% of sales in FY11 to 31% in FY13. Given the fact of lower chronic sales contribution and adverse impact of new pricing policy (~Rs 900mn) we expect moderate revenue growth of 12% CAGR over FY13‐15 (v/s 16% CAGR over FY09‐13) to Rs 29.4bn in FY15. The launch of innovative drug Lipaglyn may not have any major play in near to medium term. Reducing profitability of JVs remain as a concern Super operational excellence and high profitability of its Hospira and Nycomed JV has certainly made Cadila a preffered partner for JVs. But the progressive decline in the cumulative profitability of its JVs, due to increased competition has been a a concern for Cadila in recent past. The cumulative EBITDA margin of its all JVs has, infact, declined from ~60% in FY11 to 45% in FY13. Moreover, the likely muted growth in the JV sales during FY13‐15 is further worrisome. Lacks key earning triggers in near term; Initiate with Neutral rating and target price of Rs 761 Despite improved visibility in US generic launches, we estimate Cadila’s revenue and profits to grow at a moderate CAGR of 15% and 14% over FY13‐15E. Our EPS estimates for FY14E and FY15E stands at Rs 32.5 and Rs 42.2 (against Rs 31.9 in FY13), respectively. At CMP of Rs 742, the stock trades at 17.6x FY15E EPS and 12.5x FY15E EV/EBITDA, which is ~10% discount to its peers. We believe the discount is justified considering no major earnings trigger and concerns over profitability in near term. We value Cadila at 18x FY15 EPS, giving us a price target of Rs 761, implying 3% upside from current levels. We initiate with a Neutral rating and target price of Rs 761/share.

NEUTRAL CDH IN | CMP RS 742

TARGET RS 761 (+3%) Company Data

O/S SHARES (MN) : 205MARKET CAP (RSBN) : 152MARKET CAP (USDBN) : 2.452 ‐ WK HI/LO (RS) : 925 / 631LIQUIDITY 3M (USDMN) : 1.5FACE VALUE (RS) : 5

Share Holding Pattern, %

PROMOTERS : 74.8FII / NRI : 6.0FI / MF : 9.0NON PROMOTER CORP. HOLDINGS : 4.6PUBLIC & OTHERS : 5.6

Price Performance, % 1mth 3mth 1yr

ABS 11.7 13.1 ‐9.6REL TO BSE 13.1 3.2 ‐19.7

Price Vs. Sensex (Rebased values)

50

100

150

200

Apr‐10 Jun‐11 Aug‐12 Oct‐13

Cadila BSE Sensex

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY13 FY14E FY15E

Net Sales 61,552 70,185 81,137EBIDTA 11,251 11,301 14,234Net Profit 6,701 6,664 8,635EPS, Rs 32.7 32.5 42.2PER, x 22.7 22.8 17.6EV/EBIDTA, x 15.6 15.7 12.5P/BV, x 5.2 4.6 4.0ROE, % 22.2 20.1 22.5Debt/Equity (%) 101.1 95.5 81.8Source: Phillip Capital India Research Surya Patra (+ 9122 6667 9768) [email protected]

– 31 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / CADILA HEALTHCARE INITIATING

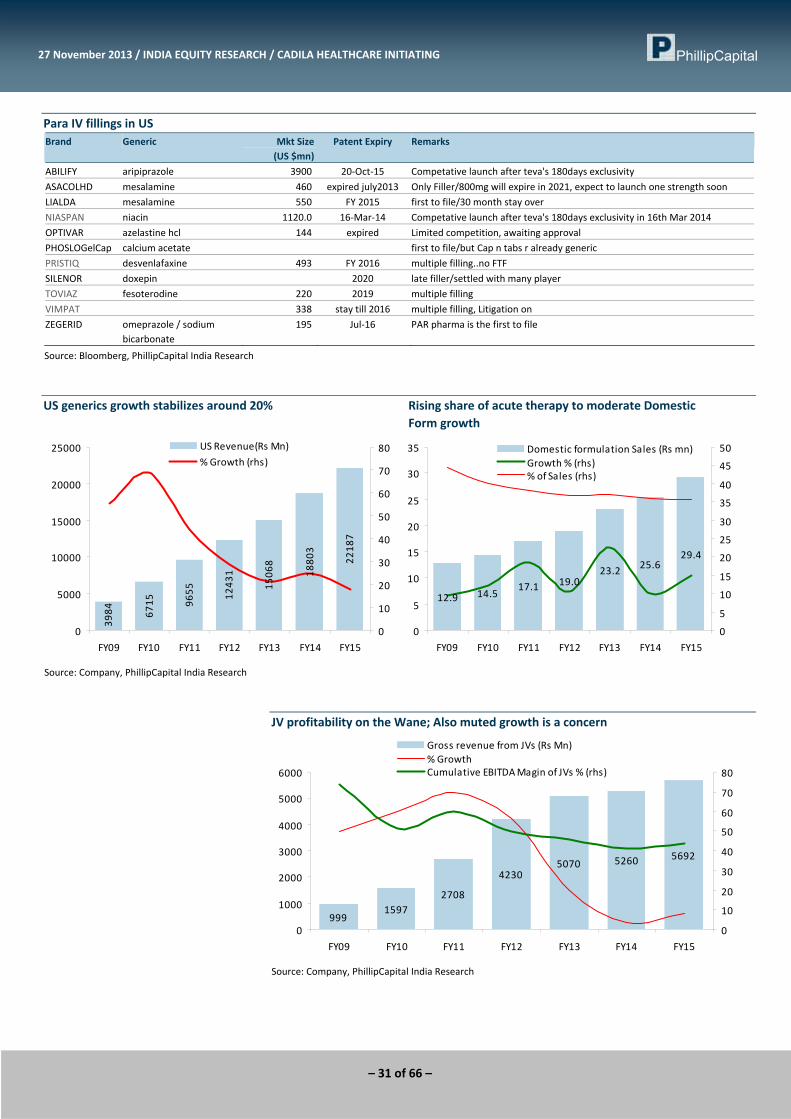

Para IV fillings in US Brand Generic Mkt Size

(US $mn) Patent Expiry Remarks

ABILIFY aripiprazole 3900 20‐Oct‐15 Competative launch after teva's 180days exclusivity

ASACOLHD mesalamine 460 expired july2013 Only Filler/800mg will expire in 2021, expect to launch one strength soon

LIALDA mesalamine 550 FY 2015 first to file/30 month stay over

NIASPAN niacin 1120.0 16‐Mar‐14 Competative launch after teva's 180days exclusivity in 16th Mar 2014

OPTIVAR azelastine hcl 144 expired Limited competition, awaiting approval

PHOSLOGelCap calcium acetate first to file/but Cap n tabs r already generic

PRISTIQ desvenlafaxine 493 FY 2016 multiple filling..no FTF

SILENOR doxepin 2020 late filler/settled with many player

TOVIAZ fesoterodine 220 2019 multiple filling

VIMPAT 338 stay till 2016 multiple filling, Litigation on

ZEGERID omeprazole / sodium bicarbonate

195 Jul‐16 PAR pharma is the first to file

Source: Bloomberg, PhillipCapital India Research

US generics growth stabilizes around 20% Rising share of acute therapy to moderate Domestic Form growth

3984 6715 9655 1243

1

1506

8

1880

3

2218

7

0

5000

10000

15000

20000

25000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0

10

20

30

40

50

60

70

80US Revenue(Rs Mn)

% Growth (rhs)

12.9 14.517.1 19.0

23.2 25.629.4

0

5

10

15

20

25

30

35

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0

5

10

15

20

25

30

35

40

45

50Domestic formulation Sales (Rs mn)Growth % (rhs)% of Sales (rhs)

Source: Company, PhillipCapital India Research

JV profitability on the Wane; Also muted growth is a concern

9991597

2708

42305070 5260 5692

0

1000

2000

3000

4000

5000

6000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0

10

20

30

40

50

60

70

80

Gross revenue from JVs (Rs Mn)% GrowthCumulative EBITDA Magin of JVs % (rhs)

Source: Company, PhillipCapital India Research

– 32 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / CADILA HEALTHCARE INITIATING

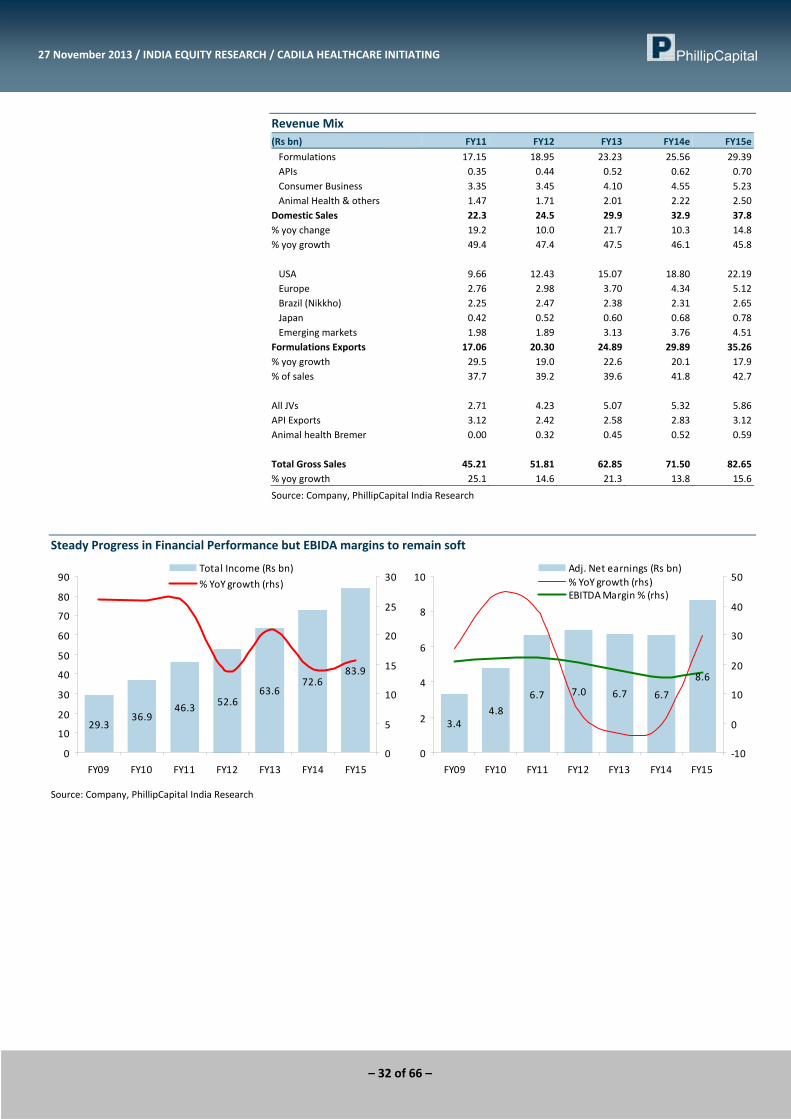

Revenue Mix (Rs bn) FY11 FY12 FY13 FY14e FY15e

Formulations 17.15 18.95 23.23 25.56 29.39 APIs 0.35 0.44 0.52 0.62 0.70 Consumer Business 3.35 3.45 4.10 4.55 5.23 Animal Health & others 1.47 1.71 2.01 2.22 2.50Domestic Sales 22.3 24.5 29.9 32.9 37.8% yoy change 19.2 10.0 21.7 10.3 14.8% yoy growth 49.4 47.4 47.5 46.1 45.8 USA 9.66 12.43 15.07 18.80 22.19 Europe 2.76 2.98 3.70 4.34 5.12 Brazil (Nikkho) 2.25 2.47 2.38 2.31 2.65 Japan 0.42 0.52 0.60 0.68 0.78 Emerging markets 1.98 1.89 3.13 3.76 4.51Formulations Exports 17.06 20.30 24.89 29.89 35.26% yoy growth 29.5 19.0 22.6 20.1 17.9% of sales 37.7 39.2 39.6 41.8 42.7 All JVs 2.71 4.23 5.07 5.32 5.86API Exports 3.12 2.42 2.58 2.83 3.12Animal health Bremer 0.00 0.32 0.45 0.52 0.59 Total Gross Sales 45.21 51.81 62.85 71.50 82.65% yoy growth 25.1 14.6 21.3 13.8 15.6

Source: Company, PhillipCapital India Research

Steady Progress in Financial Performance but EBIDA margins to remain soft

29.336.9

46.3 52.663.6

72.683.9

0

10

20

30

40

50

60

70

80

90

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0

5

10

15

20

25

30Total Income (Rs bn)

% YoY growth (rhs)

3.44.8

6.7 7.0 6.7 6.7

8.6

0

2

4

6

8

10

FY09 FY10 FY11 FY12 FY13 FY14 FY15

‐10

0

10

20

30

40

50Adj. Net earnings (Rs bn)% YoY growth (rhs)EBITDA Margin % (rhs)

Source: Company, PhillipCapital India Research

– 33 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / CADILA HEALTHCARE INITIATING

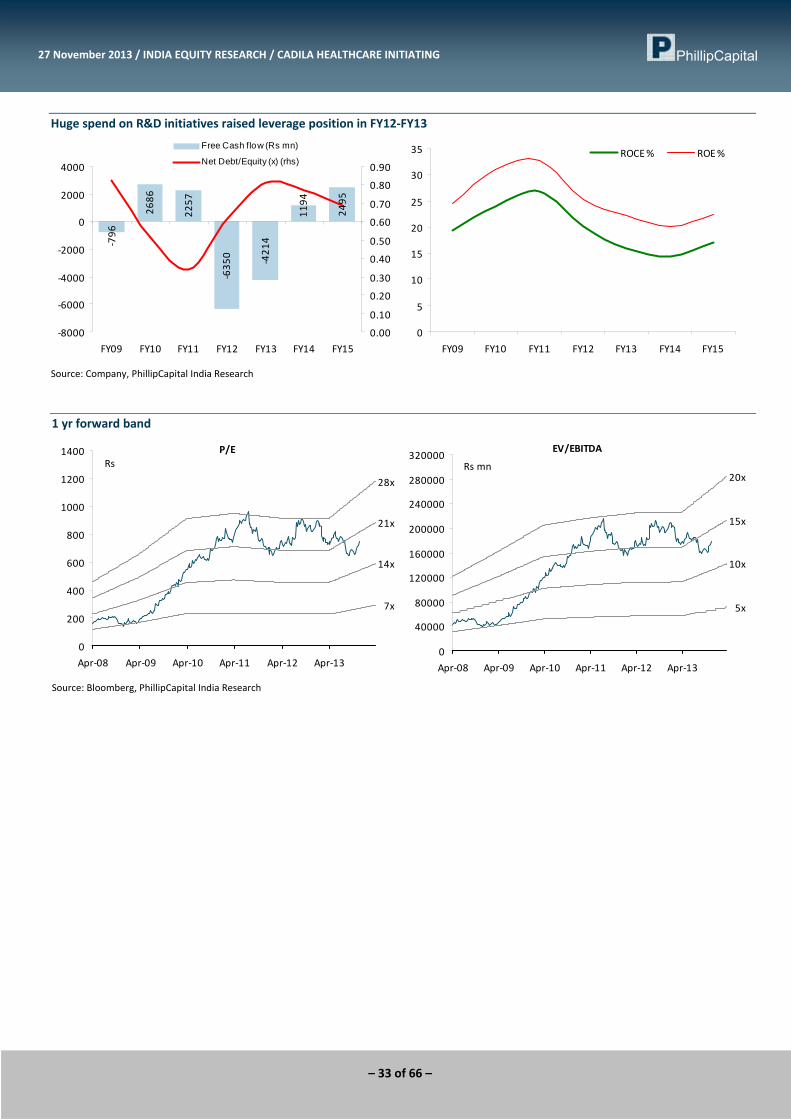

Huge spend on R&D initiatives raised leverage position in FY12‐FY13 ‐796

2686

2257

‐635

0 ‐421

4

1194

2495

‐8000

‐6000

‐4000

‐2000

0

2000

4000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Free Cash flow (Rs mn)

Net Debt/Equity (x) (rhs)

0

5

10

15

20

25

30

35

FY09 FY10 FY11 FY12 FY13 FY14 FY15

ROCE % ROE %

Source: Company, PhillipCapital India Research

1 yr forward band

P/E

7x

14x

21x

28x

0

200

400

600

800

1000

1200

1400

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

RsEV/EBITDA

5x

10x

15x

20x

0

40000

80000

120000

160000

200000

240000

280000

320000

Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12 Apr‐13

Rs mn

Source: Bloomberg, PhillipCapital India Research

– 34 of 66 –

27 November 2013 / INDIA EQUITY RESEARCH / CADILA HEALTHCARE INITIATING

Financials

Income Statement Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Net sales 50,900 61,552 70,185 81,137Growth, % 14 21 14 16Other income 1,733 2,025 2,386 2,759Total income 52,633 63,577 72,571 83,895Raw material expenses ‐16,794 ‐23,202 ‐25,763 ‐29,363Employee expenses ‐7,512 ‐9,042 ‐10,398 ‐11,438Other Operating expenses ‐17,489 ‐20,082 ‐25,110 ‐28,860EBITDA (Core) 10,839 11,251 11,301 14,234Growth, % 5.6 3.8 0.4 26.0Margin, % 21.3 18.3 16.1 17.5Depreciation ‐1,579 ‐1,847 ‐2,132 ‐2,474EBIT 9,260 9,404 9,169 11,760Growth, % 3.0 1.6 (2.5) 28.3Margin, % 18.2 15.3 13.1 14.5Interest paid ‐1,069 ‐1,262 ‐1,424 ‐1,570Other Non‐Operating Income 532 370 508 503Pre‐tax profit 7,942 8,087 8,253 10,693Tax provided ‐1,130 ‐1,188 ‐1,238 ‐1,604Profit after tax 6,812 6,899 7,015 9,089Others (Minorities, Associates) ‐286 ‐364 ‐351 ‐454Net Profit 6,526 6,535 6,664 8,635Growth, % 4.2 (3.6) (0.6) 29.6Net Profit (adjusted) 6,954 6,701 6,664 8,635Unadj. shares (m) 205 205 205 205Wtd avg shares (m) 205 205 205 205

Balance Sheet Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Cash & bank 4,666 5,838 6,081 4,918Debtors 8,863 9,551 11,087 12,817Inventory 10,905 12,136 14,126 16,061Loans & advances 5,377 6,771 7,257 8,390Other current assets 421 669 750 850Total current assets 30,232 34,965 39,301 43,036Investments 242 1,145 1,145 1,145Gross fixed assets 40,229 43,762 51,993 57,533Less: Depreciation ‐11,750 ‐13,506 ‐15,638 ‐18,112Add: Capital WIP 4,839 7,356 4,500 4,500Net fixed assets 33,318 37,612 40,856 43,921Total assets 63,792 73,722 81,302 88,102 Current liabilities 12,379 9,313 11,087 12,817Provisions 3,037 3,118 3,211 3,304Total current liabilities 15,416 12,431 14,298 16,121Non‐current liabilities 21,705 30,711 32,655 32,404Total liabilities 37,121 43,142 46,953 48,526Paid‐up capital 1,024 1,024 1,024 1,024Reserves & surplus 24,712 28,363 32,132 37,360Shareholders’ equity 26,671 30,580 34,348 39,577Total equity & liabilities 63,792 73,722 81,302 88,102

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Pre‐tax profit 7,942 8,087 8,253 10,693Depreciation 1,579 1,847 2,132 2,474Chg in working capital ‐2,019 ‐6,546 ‐2,227 ‐3,074Total tax paid ‐1,072 ‐1,368 ‐1,238 ‐1,604Other operating activities ‐2,474 ‐2,915 0 0Cash flow from operating activities 3,956 ‐895 6,920 8,490Capital expenditure ‐12,261 ‐6,141 ‐5,375 ‐5,540Chg in investments ‐35 ‐903 0 0Cash flow from investing activities ‐12,296 ‐7,044 ‐5,375 ‐5,540Free cash flow ‐6,350 ‐4,214 1,194 2,495Debt raised/(repaid) 10,105 9,186 1,944 ‐251Cash flow from financing activities 10,054 9,111 1,594 ‐706Net chg in cash 1,714 1,172 3,138 2,244

Valuation Ratios & Per Share Data FY12 FY13 FY14E FY15E

Per Share data EPS (INR) 34.0 32.7 32.5 42.2Growth, % 4.2 (3.6) (0.6) 29.6Book NAV/share (INR) 125.9 143.5 161.9 187.5FDEPS (INR) 34.0 32.7 32.5 42.2CEPS (INR) 41.7 41.8 43.0 54.3CFPS (INR) 28.8 8.1 31.3 39.0Return ratios Return on assets (%) 13.6 11.2 10.2 11.9Return on equity (%) 25.3 22.2 20.1 22.5Return on capital employed (%) 20.3 15.9 14.4 17.0Turnover ratios Asset turnover (x) 1.3 1.2 1.2 1.2Sales/Total assets (x) 0.9 0.9 0.9 1.0Sales/Net FA (x) 1.8 1.7 1.8 1.9Working capital/Sales (x) 0.3 0.3 0.3 0.3Receivable days 63.6 56.6 57.7 57.7Working capital days 94.6 117.5 115.1 113.8Liquidity ratios Current ratio (x) 2.4 3.8 3.5 3.4Quick ratio (x) 1.6 2.5 2.3 2.1Interest cover (x) 8.7 7.5 6.4 7.5Total debt/Equity (%) 79.6 101.1 95.5 81.8Net debt/Equity (%) 61.5 81.2 77.1 69.0Valuation PER (x) 21.8 22.7 22.8 17.6PEG (x) ‐ y‐o‐y growth 5.2 (6.2) (41.3) 0.6Price/Book (x) 5.9 5.2 4.6 4.0EV/Net sales (x) 3.3 2.9 2.5 2.2EV/EBITDA (x) 15.5 15.6 15.7 12.5EV/EBIT (x) 18.1 18.7 19.4 15.2

– 35 of 66 –

Divi’s Laboratories Well set to ride on soaring pharma outsourcing

PHARMACEUTICALS: Initiating Coverage 27 November 2013

PhillipCapital (India) Pvt. Ltd.