Embed Size (px)

Citation preview

Phaunos Timber Fund LimitedMeeting with DWS13 September 2018

Background

2

• Phaunos Timber Fund Limited (the Company) launched in December2006 to invest in a diversified portfolio of timberland and timber-relatedinvestments. The Investment Manager at launch was FourWinds CapitalManagement (FWCM)

• In December 2013, the Company terminated the managementagreement with FWCM

• The Board engaged Stafford Capital Partners Limited (Stafford) toprovide a review of the Company’s assets and the results were publishedin June 2014

• Following the review, Stafford were appointed as investment managerand sought to turn around the Company's performance including thesale of the higher risk assets

• In June 2017, at the Company’s AGM, a resolution that the Companycontinue for a further five years was not approved by shareholders

• In July 2017, Stafford announced its intention to step down as managerwith effect from February 2018

• In August 2017, at a general meeting of the Company, shareholdersapproved a revised investment objective and policy to implement amanaged wind-down of the portfolio

• Each of the Directors that were in place resigned following the generalmeeting

• The existing directors were all appointed in H2 2017 with the mandateto dispose of the asset portfolio and return capital to shareholders

• Since then the Company received a firm cash offer from Stafford atUS$0.49 per share as well as a possible all-stock offer from CatchMark atUS$0.57 per share

• Stafford’s offer was rejected and the Company is currently evaluatingCatchMark’s offer

• In the meantime the Company is progressing with the disposal of itsasset portfolio and announced on 5 September 2018 that it had openeda virtual dataroom to bidders for the Matariki and Latam assets

-60

-50

-40

-30

-20

-10

0

10

0.3

0.5

0.7

0.9

1.1

% D

isco

un

t(-)

/ P

rem

ium

(+

)

Pri

ce (

US

$)

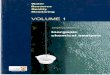

Phaunos NAV per share vs share price

NAV Event Share Price Discount

Stafford

appointed Stafford

tendered

Stafford

resignation

FourWinds

appointment

terminated

1,2

1 Please note that the NAV does not take into account the Indicative Bids received for assets which are subject to a sales process under the Asset Realisation Process

The graph shows the Going Concern NAV from 30 May 2008 to 31 December 2016. With effect from 31 December 2016 the NAV was prepared on a break-up basis to reflect the wind-down status of the Company

2

Portfolio Overview

3

Matariki 74% of Portfolio Value (PV)

New Zealand

• The Company holds a 23.01% interest

• One of the largest and highest quality forestry assets in New Zealand with approximately 120,000 plantable hectares of FSC certified plantations

• Radiata Pine is the dominant species grown

• Mainly serves New Zealand, China, South Korea, Japan and India

• 82% EBITDA CAGR since 2015, driven by significant growth in export demand

LatAm Portfolio 18% of PV

Brazil / Uruguay

• 100% interest in Eucateca (Eucalyptus), Brazil− 7,500 plantable hectares in Mato Grosso− Most standing timber ready for harvest

• 100% interest in Eucateca (Teak), Brazil− 1,700 plantable hectares of teak plantation− All trees planted in 2009

• 100% interest in Mata Mineira, Brazil− 9,650 plantable hectares of fast-growing,

Eucalyptus forest in Minas Gerais• 100% interest in Pradera Roja, Uruguay

− 3,000 plantable hectares of mostly Eucalyptus− Half cutting rights sold for next five years

Aurora Forestal 5% of PV

Uruguay

• The Company holds a 23.57% interest

• Integrated business comprising 11,000 plantable hectares of pine forestland and a sawmill with production capacity of approximately 225,000 m3 per annum

GreenWood Tree Farm Fund 4% of PV

US - Fund Interest

• The fund is in liquidation with three remaining assets− an outstanding loan note receivable− a parcel of timberland in Portland, Oregon− a pending legal claim, substantially settled

Asset Realisation Process

4

▪ The Asset Realisation Process was formally launched in late 2017 covering the entire portfolio

▪ Matariki and the LatAm Portfolio reflecting 92% of the portfolio value are subject to an asset sale process managed by PöyryCapital

▪ The Asset Realisation Range reflects bids received in late June 2018 and subsequently confirmed in late July and early Augustthis year, all in US dollars

▪ All bidders have been provided with preliminary information including information memoranda, appraisal reports and otherrelevant forestry and financial information

▪ All bidders are highly credible and well-capitalised international investors in timber assets

▪ All bidders for Matariki are experienced in dealing with the New Zealand Overseas Investment Office and have a detailedunderstanding of what is required to effectively navigate the consent process

▪ The Asset Realisation Process is expected to be substantially complete by Q3 2019

▪ Aurora Forestal (5% of Portfolio Value) and GreenWood Tree Farm Fund (4% of Portfolio Value) are subject to separatedisposal/liquidation processes, respectively

▪ On 27 July 2018, the Company’s interest in NTP was realised at marginally above its reported NAV as at 31 December 2017

Asset Realisation Range of US$0.54 – US$0.60 per share

The Board of Phaunos is committed to returning all sales proceeds from the Asset Realisation Process as they are received, after allowing for cash reserves to wind-down the Company

Asset Realisation Process (cont.)

5

Matariki (74% of Portfolio Value)

▪ Process letters for phase 2 sent to selected bidders andaccess provided to a virtual data room

▪ Site visits to commence soon

▪ Binding offers due in early November

▪ Timing subject to consent from New Zealand OverseasInvestment Office and Rayonier claims (see later)

▪ Completion of Matariki disposal estimated between Q12019 and Q3 2019

LatAm Portfolio (18% of Portfolio Value)

▪ Selected bidders have been provided with access to avirtual data room

▪ Phase 2 to include site visits, inventory checks andmeetings with local forest management and operators

▪ Completion of disposal expected between Q4 2018 toQ1 2019

Aurora Forestal (5% of Portfolio Value)

▪ The Company has exercised its right to initiate avoluntary exit pursuant to the shareholder agreement

▪ The Company is also in discussions with the majorityshareholder to negotiate a disposal of its interest

▪ The negotiations are progressing well and variousoptions are being explored to effect an exit

GreenWood Tree Farm Fund (4% of Portfolio Value)

▪ The disposal of this asset is subject to a separateliquidation procedure

▪ GTFF is currently in the process of realising theremaining three assets in the portfolio

▪ Expressions of interest and/or non-binding bids havebeen received for all assets in the portfolio

Stafford Offer – timeline to date1

6

5 June

Possible all cash offerStafford announced a possible all cash offer of US$0.49 for

the entire issued and to be issued share capital of Phaunos

21 August

14 August

Firm cash offer for PhaunosStafford announced an all cash offer of US$0.49, valuing Phaunos’ entire issued and to

be issued share capital at approximately US$244.2 million

Publication of Offer Document Stafford publish their offer document containing the terms of

the Offer and acceptance conditions

31 July

Phaunos publish Rejection of Stafford’s OfferBoard publish their Response Circular stating that they believe the Stafford

offer undervalues Phaunos and recommend shareholders to take no action

First Closing Date

3 July

22 August

Stafford announce Extension of OfferValid acceptances of 14.21% received by first closing date. Second closing date set for

5 September, terms of the offer remain unchanged

Second Closing Date

6 September

Stafford announce Second Extension of OfferValid acceptances of 14.24% received by second closing date. Third

closing date set for 13 September, terms of the offer remain unchanged

5 September

Further information, including all documents relating to the offer by Stafford can be found at http://www.phaunostimber.com/offer-from-stafford/1

Stafford’s Offer

7

Reject Stafford’s Offer – Extract Maximum Value

The Board believe that Stafford’s Offer undervalues Phaunos and that there is significant upside from the Asset Realisation Process compared to Stafford’s Offer. Accordingly, the Board have recommended that shareholders should take no action in relation to Stafford’s Offer

Next steps

Stafford’s Offer

Stafford have offered US$0.49 per share

This values the Company below the updated asset realisation range of US$0.54-US$0.60 and therefore the Board strongly believes that Stafford’s Offer does not provide an attractive exit opportunity for Shareholders and that the Asset Realisation Process is the best strategy for maximising shareholder value over a reasonable timeframe

US$0.60

US$0.54

US$0.49

Stafford’s Offer

Updated Asset Realisation

Range

The Updated Asset Realisation Range, based on Indicative Bids received in US dollars, represents a 10% to 22% upside to Stafford’s Offer

13 September Next closing date

15 September Latest date for Stafford to revise their offer

29 September Latest date for the offer to be declared

unconditional as to acceptances

• CatchMark announced that it was evaluating a potential offer to acquire Phaunos Timber Fund in a stock-for-stocktransaction

• CatchMark's potential offer values Phaunos at US$0.57 per share to be paid in new shares of CatchMark common stock

CatchMark Possible Offer

8

6 September – CatchMark publish Possible Offer announcement

Who are CatchMark?

CatchMark Timber Trust, is a self-administered and self-managed timberland REIT traded on the New York Stock

Exchange. Further information can be found at http://www.catchmark.com/

6 September – Phaunos publish response to announcement

• The Board noted that the possible offer represents a significant premium of 16.3% to the offer by Stafford CapitalPartners of US$0.49 per share

• The Board explained that it intends to engage with CatchMark to fully understand its proposal and will consider it indue course

5pm 22 September CatchMark deadline to have either announced a firm intention to make an offer for the fund or that it does not intend to make an offer

• Rayonier own the remaining interest in Matariki

• On 27 August the Board were made aware that Rayonier has issued proceedings in the Auckland High Court alleging abreach by Phaunos of confidentiality, notice and consultation obligations in the shareholders agreement

• The substance of Rayonier's complaint relates to the inclusion within the Company's circular, published on 14 August2018 in response to Stafford's takeover offer, of a valuation report on Matariki, as was required by Rule 29 of the UKTakeover Code

• Rayonier has asserted that it is entitled to acquire Phaunos' interest in Matariki for NZD225m (c.US$152m), reflecting adiscount to what Rayonier believes to be the fair market value of Phaunos' interest in Matariki

• Phaunos believes that Rayonier's claims are without merit and that the Acquisition Notice is invalid

• Phaunos intends to defend itself vigorously against the claims brought by Rayonier and take whatever further steps itdeems necessary in order to protect its interests

• Consequently, Phaunos will continue to progress the Asset Realisation Process in accordance with its strategy

Rayonier Proceedings

9

Summary

10

Pri

ce U

S$

0.60

0.59

0.58

0.57

0.56

0.55

0.54

0.53

0.52

0.51

0.50

0.49

0.48

Stafford Offer

Asset

Realisation

Range

CatchMark

Possible Offer

Investment Policy

The managed wind-down will be effected with a view to the Companyrealising all of its investments in a manner that achieves a balancebetween maximising the value from the Company's investments andmaking timely returns of capital to Shareholders

Stafford’s Offer

The US$0.54-US$0.60 asset realisation range represents a 10% to 22% upside to Stafford’s offer

The Board strongly believes that Stafford’s Offer does not provide an attractive exit opportunity for Shareholders and that the Asset Realisation Process is the best strategy for maximising shareholder value over a reasonable timeframe

CatchMark Possible Offer

• The CatchMark offer represents a significant premium of 16.3 per cent. to the offer by Stafford Capital Partners of US$0.49 per Phaunos share

• The Board intends to engage with CatchMark to understand fully its proposal and will consider it in due course

• There can be no certainty that any firm offer for the Company will be made nor as to the terms on which any firm offer might be made

Questions and Feedback

11

Q&A

Disclaimer

12

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN, INTO OR

FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OR

REGULATIONS OF SUCH JURISDICTION

This presentation (including any oral briefing and any question-and-answer in connection with it) relates to the all-cash offer by Stafford Capital Partners

Limited (via Mahogany Bidco Limited) ("Stafford") for the entire issued and to be issued share capital of Phaunos Timber Fund Limited ("PTFL"); and the

possible all-stock offer by CatchMark Timber Trust, Inc ("CatchMark") (each an "Offer" and together, the "Offers").

By attending (whether in person, by telephone or webcast) this presentation or by reading the presentation slides you agree to the conditions set out

below.

You should conduct your own independent analysis of PTFL, Stafford, CatchMark and each Offer, including consulting your own independent advisers in

order to make an independent determination of the suitability, merits and consequences of each Offer.

This presentation shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any

jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

Responsibility

The directors of PTFL accept responsibility for the information contained in this presentation and, to the best of their knowledge and belief (having taken all

reasonable care to ensure that such is the case), the information contained in this presentation is in accordance with the facts and does not omit anything

likely to affect the import of such information.

Publication of this presentation

A copy of this presentation will be available subject to certain restrictions relating to persons resident in restricted jurisdictions on Phaunos website at

http://www.phaunostimber.com/ during the course of the Offer.

Forward-looking statements

This presentation contains certain forward-looking statements, including statements regarding the Offers, Phaunos's plans, objectives and expected

performance. Such statements relate to events and depend on circumstances that will occur in the future and are subject to risks, uncertainties and

assumptions. There are a number of factors which could cause actual results and developments to differ materially from those expressed or implied by such

forward looking statements, including, among others the enactment of legislation or regulation that may impose costs or restrict activities, the re-

negotiation of contracts or licences, fluctuations in demand and pricing in the timber industry, fluctuations in exchange controls, changes in government

policy and taxations, industrial disputes and war and terrorism. These forward-looking statements speak only as at the date of this presentation.

Further information, including all documents related to the Offers, can be found at: http://www.phaunostimber.com/.