Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

30 September 2014

Asia Pacific/Philippines

Equity Research

Casinos & Gaming (Hotels/Restaurants/Gaming PH (Asia))

Philippine Gaming Sector ASSUMING COVERAGE

All the right cards

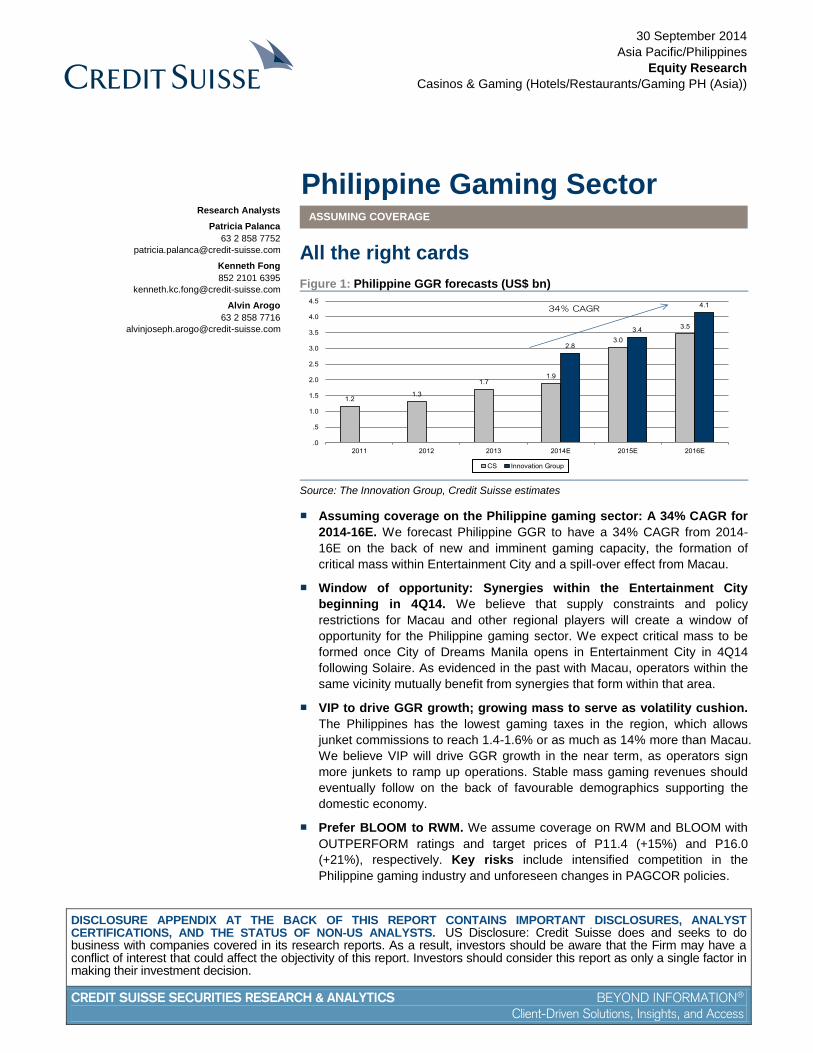

Figure 1: Philippine GGR forecasts (US$ bn)

1.21.3

1.71.9

3.0

3.5

2.8

3.4

4.1

.0

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014E 2015E 2016E

CS Innovation Group

34% CAGR

Source: The Innovation Group, Credit Suisse estimates

■ Assuming coverage on the Philippine gaming sector: A 34% CAGR for

2014-16E. We forecast Philippine GGR to have a 34% CAGR from 2014-

16E on the back of new and imminent gaming capacity, the formation of

critical mass within Entertainment City and a spill-over effect from Macau.

■ Window of opportunity: Synergies within the Entertainment City

beginning in 4Q14. We believe that supply constraints and policy

restrictions for Macau and other regional players will create a window of

opportunity for the Philippine gaming sector. We expect critical mass to be

formed once City of Dreams Manila opens in Entertainment City in 4Q14

following Solaire. As evidenced in the past with Macau, operators within the

same vicinity mutually benefit from synergies that form within that area.

■ VIP to drive GGR growth; growing mass to serve as volatility cushion.

The Philippines has the lowest gaming taxes in the region, which allows

junket commissions to reach 1.4-1.6% or as much as 14% more than Macau.

We believe VIP will drive GGR growth in the near term, as operators sign

more junkets to ramp up operations. Stable mass gaming revenues should

eventually follow on the back of favourable demographics supporting the

domestic economy.

■ Prefer BLOOM to RWM. We assume coverage on RWM and BLOOM with

OUTPERFORM ratings and target prices of P11.4 (+15%) and P16.0

(+21%), respectively. Key risks include intensified competition in the

Philippine gaming industry and unforeseen changes in PAGCOR policies.

Research Analysts

Patricia Palanca

63 2 858 7752

Kenneth Fong

852 2101 6395

Alvin Arogo

63 2 858 7716

30 September 2014

Philippine Gaming Sector 2

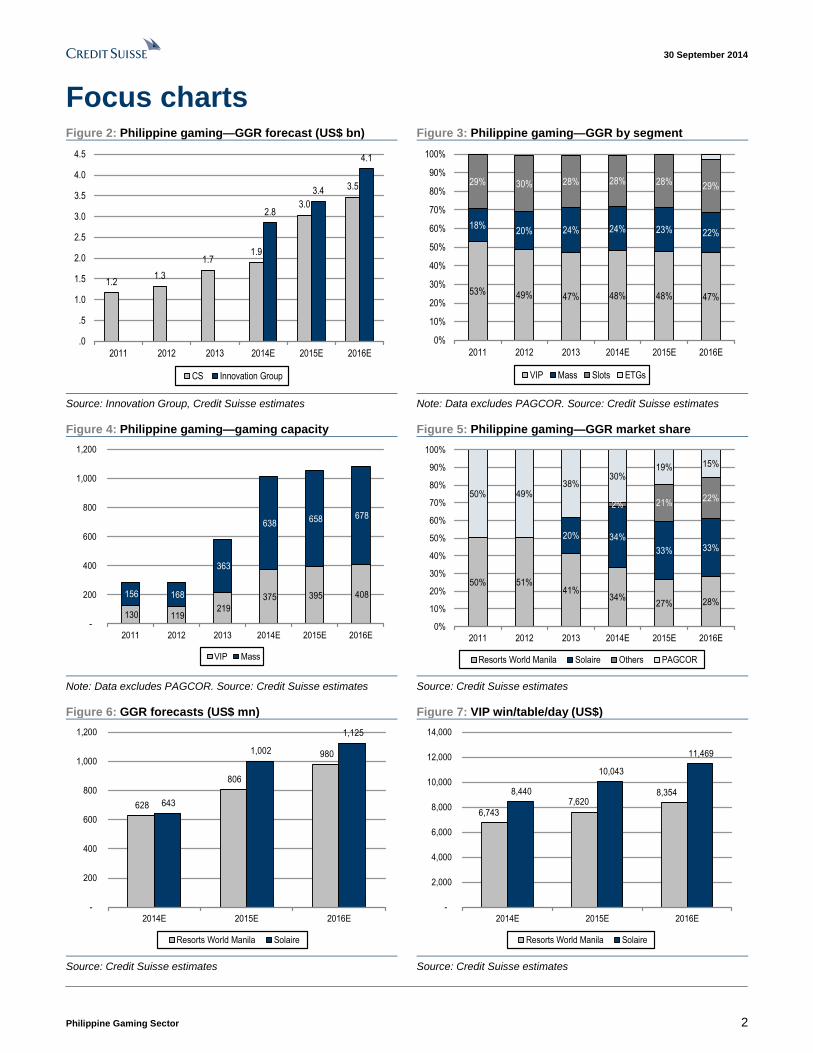

Focus charts Figure 2: Philippine gaming—GGR forecast (US$ bn) Figure 3: Philippine gaming—GGR by segment

1.21.3

1.71.9

3.0

3.5

2.8

3.4

4.1

.0

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014E 2015E 2016E

CS Innovation Group

53% 49% 47% 48% 48% 47%

18%20% 24% 24% 23% 22%

29% 30% 28% 28% 28% 29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014E 2015E 2016E

VIP Mass Slots ETGs

Source: Innovation Group, Credit Suisse estimates Note: Data excludes PAGCOR. Source: Credit Suisse estimates

Figure 4: Philippine gaming—gaming capacity Figure 5: Philippine gaming—GGR market share

130 119 219

375 395 408 156 168

363

638 658 678

-

200

400

600

800

1,000

1,200

2011 2012 2013 2014E 2015E 2016E

VIP Mass

50% 51%41%

34%27% 28%

20% 34%

33% 33%

2% 21%22%50% 49%

38%30%

19% 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014E 2015E 2016E

Resorts World Manila Solaire Others PAGCOR

Note: Data excludes PAGCOR. Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 6: GGR forecasts (US$ mn) Figure 7: VIP win/table/day (US$)

628

806

980

643

1,002

1,125

-

200

400

600

800

1,000

1,200

2014E 2015E 2016E

Resorts World Manila Solaire

6,743 7,620

8,354 8,440

10,043

11,469

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2014E 2015E 2016E

Resorts World Manila Solaire

Source: Credit Suisse estimates Source: Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 3

All the right cards A 34% CAGR in GGR from 2014-16E

We estimate Philippine gross gaming revenue (GGR) to double from US$1.7 bn in 2013 to

US$3.5 bn in 2016E, or a CAGR of 34% over 2014-16E. A total of 440 tables (+76% from

now) will be added in 4Q14 with the opening of City of Dreams Manila and Solaire's Phase 1A

expansion.

Window of opportunity: Synergies within

Entertainment City beginning in 4Q14

We believe that the limited number of new casino projects and additional gaming supply

within the region will provide a window of opportunity for the Philippine gaming industry.

We expect it to receive spill-over from Macau, as Chinese VIP players look outside of

Macau, at least in the near term, on the back of newly implemented policy restrictions.

Also, new gaming capacity in Macau will only open by mid-2015 at the earliest. Macau's

gaming table expansion is limited to 3% YoY growth for the next ten years. Likewise,

Genting Highlands remains the sole venue for legalised casino gambling in Malaysia and

the Singapore casino gaming market is still limited to a duopoly through 2017. It is our

view that the Philippines is well-positioned to capitalise on the constrained capacity of

regional competitors. City of Dreams Manila and Solaire's Phase1A expansion are

scheduled to be launched in 4Q14 and should be able to build critical mass in the area as

was witnessed in the past with Macau. We expect that the two integrated resorts will also

derive benefits from the strong retail base of Melco's partner in CoD Manila, the SM group.

The group's largest mall—SM Mall of Asia—generates average foot traffic of around

200,000 people daily and is roughly 1km away from CoD Manila.

VIP to drive GGR growth; growing mass to serve as

volatility cushion

The Philippines has the lowest gaming taxes in the region, which allows junket

commissions to reach 1.4-1.6% or as much as 14% over that of Macau. Moreover, the

Philippines is also relatively more attractive versus its regional counterparts due to: (1) the

imminent supply of gaming capacity; (2) a shorter travel time from China; and (3) evident

government support of gaming and tourism. According to a study by the United Nations,

the Philippines will also enter a "demographic window" by 2015 whereby most of the

population will be of working age (15-65 years old). We expect that such favourable

demographics will eventually provide earnings stability in the form of mass gaming

revenues and soften the earnings volatility from the VIP segment.

Prefer BLOOM (+21%) over RWM (+15%)

We assume coverage on RWM and BLOOM with OUTPERFORM ratings and target

prices of P11.4 and P16.0, respectively. BLOOM has the first mover advantage inside

Entertainment City and should benefit from the synergies with the opening of CoD Manila

in 4Q14. We believe most of the forecast growth in the industry will be captured by the

new players—Solaire and CoD Manila—and we expect RWM and PAGCOR-owned

casinos to lose some market share. We estimate BLOOM will achieve leading market

share by 2015E. Despite a lack of catalysts and low margins for RWM, we retain an

OUTPERFORM rating, as the company has substantial expansion plans, albeit not in the

near term. Key risks include intensified competition in the Philippine gaming industry and

unforeseen changes in PAGCOR policies.

Philippine GGR to double to

US$3.5 bn in 2016E

Critical mass to build up in

the Entertainment City as

synergies form within the

area

The VIP segment to drive

near-term growth while the

mass market gradually

builds up

BLOOM is well-positioned to

capitalise on the industry

positives that we see on the

horizon

30 September 2014

Philippine Gaming Sector 4

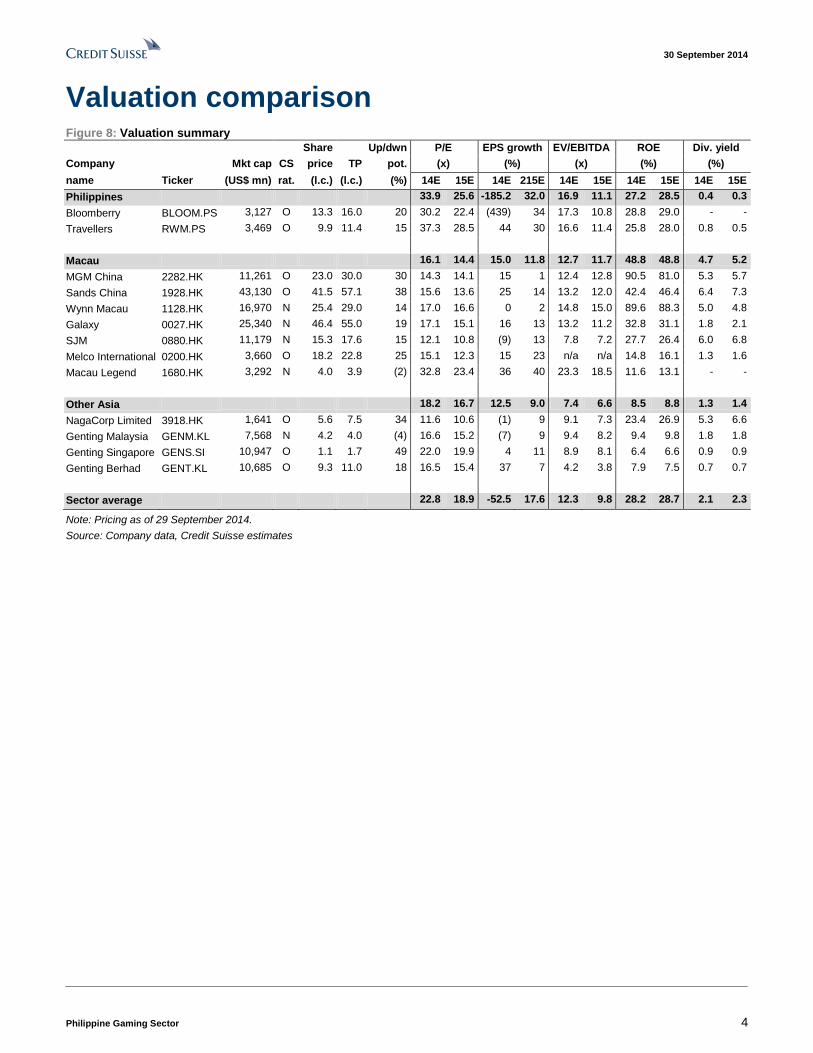

Valuation comparison Figure 8: Valuation summary

Share Up/dwn P/E EPS growth EV/EBITDA ROE Div. yield

Company Mkt cap CS price TP pot. (x) (%) (x) (%) (%)

name Ticker (US$ mn) rat. (l.c.) (l.c.) (%) 14E 15E 14E 215E 14E 15E 14E 15E 14E 15E

Philippines 33.9 25.6 -185.2 32.0 16.9 11.1 27.2 28.5 0.4 0.3

Bloomberry BLOOM.PS 3,127 O 13.3 16.0 20 30.2 22.4 (439) 34 17.3 10.8 28.8 29.0 - -

Travellers RWM.PS 3,469 O 9.9 11.4 15 37.3 28.5 44 30 16.6 11.4 25.8 28.0 0.8 0.5

Macau 16.1 14.4 15.0 11.8 12.7 11.7 48.8 48.8 4.7 5.2

MGM China 2282.HK 11,261 O 23.0 30.0 30 14.3 14.1 15 1 12.4 12.8 90.5 81.0 5.3 5.7

Sands China 1928.HK 43,130 O 41.5 57.1 38 15.6 13.6 25 14 13.2 12.0 42.4 46.4 6.4 7.3

Wynn Macau 1128.HK 16,970 N 25.4 29.0 14 17.0 16.6 0 2 14.8 15.0 89.6 88.3 5.0 4.8

Galaxy 0027.HK 25,340 N 46.4 55.0 19 17.1 15.1 16 13 13.2 11.2 32.8 31.1 1.8 2.1

SJM 0880.HK 11,179 N 15.3 17.6 15 12.1 10.8 (9) 13 7.8 7.2 27.7 26.4 6.0 6.8

Melco International 0200.HK 3,660 O 18.2 22.8 25 15.1 12.3 15 23 n/a n/a 14.8 16.1 1.3 1.6

Macau Legend 1680.HK 3,292 N 4.0 3.9 (2) 32.8 23.4 36 40 23.3 18.5 11.6 13.1 - -

Other Asia 18.2 16.7 12.5 9.0 7.4 6.6 8.5 8.8 1.3 1.4

NagaCorp Limited 3918.HK 1,641 O 5.6 7.5 34 11.6 10.6 (1) 9 9.1 7.3 23.4 26.9 5.3 6.6

Genting Malaysia GENM.KL 7,568 N 4.2 4.0 (4) 16.6 15.2 (7) 9 9.4 8.2 9.4 9.8 1.8 1.8

Genting Singapore GENS.SI 10,947 O 1.1 1.7 49 22.0 19.9 4 11 8.9 8.1 6.4 6.6 0.9 0.9

Genting Berhad GENT.KL 10,685 O 9.3 11.0 18 16.5 15.4 37 7 4.2 3.8 7.9 7.5 0.7 0.7

Sector average 22.8 18.9 -52.5 17.6 12.3 9.8 28.2 28.7 2.1 2.3

Note: Pricing as of 29 September 2014.

Source: Company data, Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 5

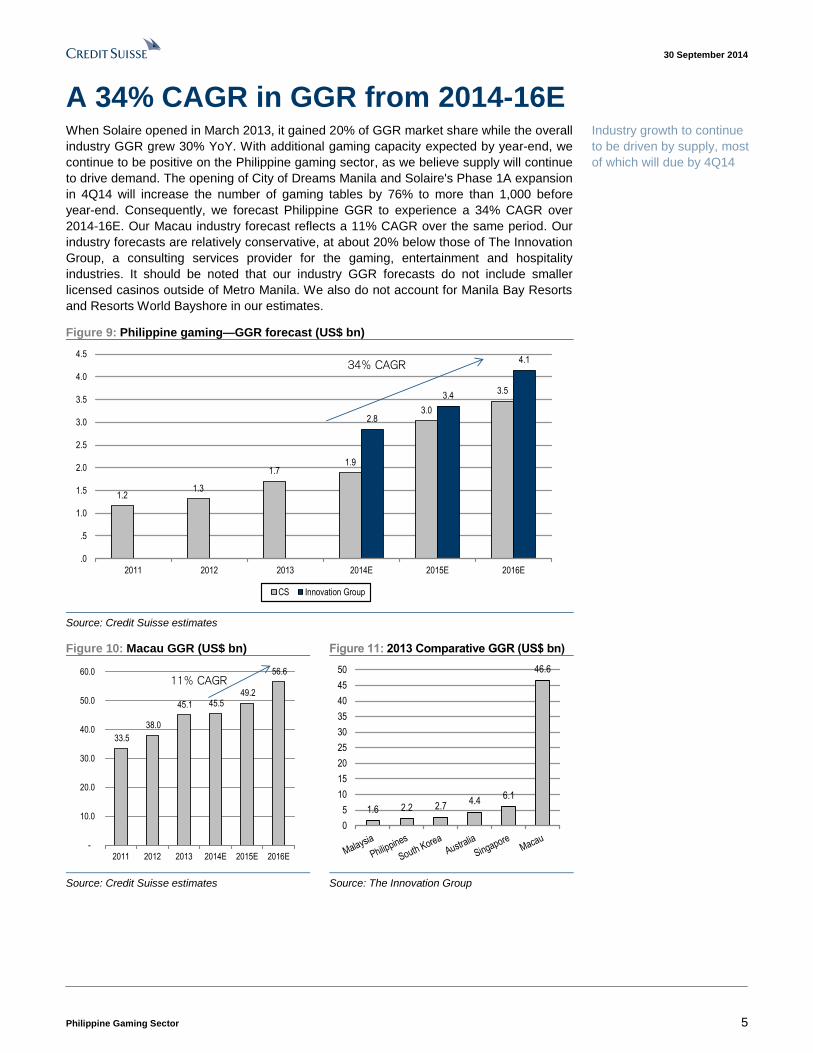

A 34% CAGR in GGR from 2014-16E When Solaire opened in March 2013, it gained 20% of GGR market share while the overall

industry GGR grew 30% YoY. With additional gaming capacity expected by year-end, we

continue to be positive on the Philippine gaming sector, as we believe supply will continue

to drive demand. The opening of City of Dreams Manila and Solaire's Phase 1A expansion

in 4Q14 will increase the number of gaming tables by 76% to more than 1,000 before

year-end. Consequently, we forecast Philippine GGR to experience a 34% CAGR over

2014-16E. Our Macau industry forecast reflects a 11% CAGR over the same period. Our

industry forecasts are relatively conservative, at about 20% below those of The Innovation

Group, a consulting services provider for the gaming, entertainment and hospitality

industries. It should be noted that our industry GGR forecasts do not include smaller

licensed casinos outside of Metro Manila. We also do not account for Manila Bay Resorts

and Resorts World Bayshore in our estimates.

Figure 9: Philippine gaming—GGR forecast (US$ bn)

1.21.3

1.71.9

3.0

3.5

2.8

3.4

4.1

.0

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014E 2015E 2016E

CS Innovation Group

34% CAGR

Source: Credit Suisse estimates

Figure 10: Macau GGR (US$ bn) Figure 11: 2013 Comparative GGR (US$ bn)

33.5

38.0

45.1 45.5 49.2

56.6

-

10.0

20.0

30.0

40.0

50.0

60.0

2011 2012 2013 2014E 2015E 2016E

11% CAGR

1.6 2.2 2.74.4

6.1

46.6

0

5

10

15

20

25

30

35

40

45

50

Source: Credit Suisse estimates Source: The Innovation Group

Industry growth to continue

to be driven by supply, most

of which will due by 4Q14

30 September 2014

Philippine Gaming Sector 6

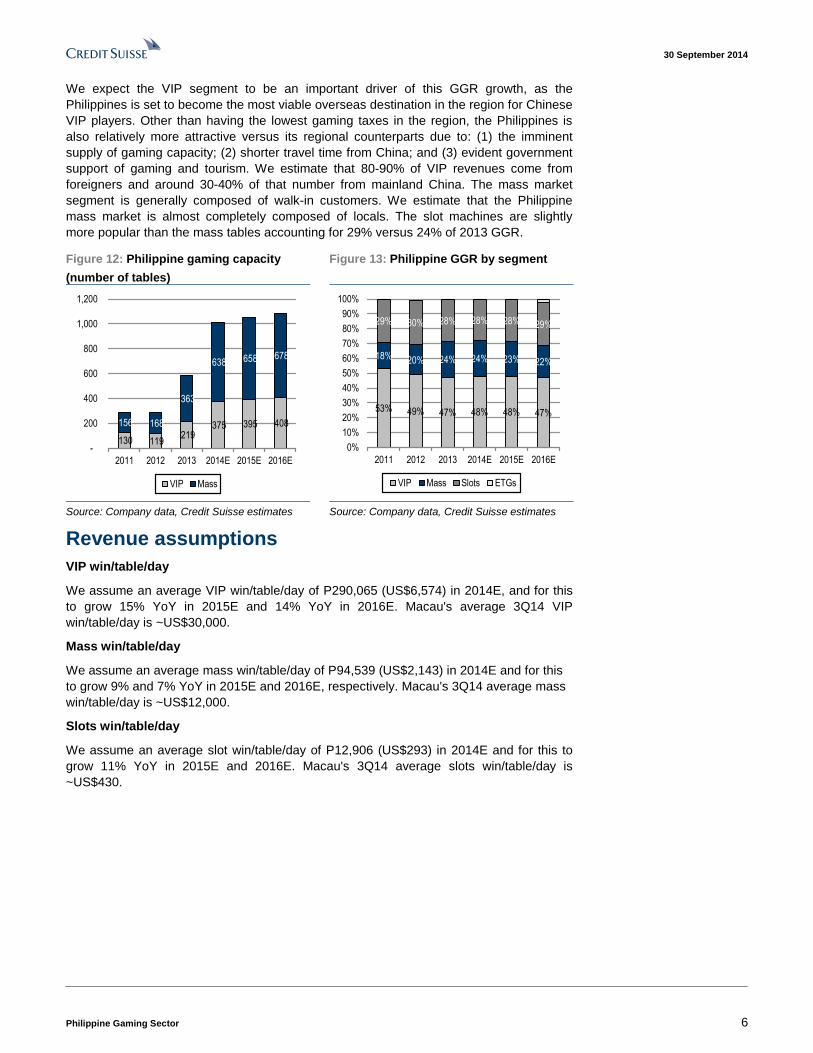

We expect the VIP segment to be an important driver of this GGR growth, as the

Philippines is set to become the most viable overseas destination in the region for Chinese

VIP players. Other than having the lowest gaming taxes in the region, the Philippines is

also relatively more attractive versus its regional counterparts due to: (1) the imminent

supply of gaming capacity; (2) shorter travel time from China; and (3) evident government

support of gaming and tourism. We estimate that 80-90% of VIP revenues come from

foreigners and around 30-40% of that number from mainland China. The mass market

segment is generally composed of walk-in customers. We estimate that the Philippine

mass market is almost completely composed of locals. The slot machines are slightly

more popular than the mass tables accounting for 29% versus 24% of 2013 GGR.

Figure 12: Philippine gaming capacity

(number of tables)

Figure 13: Philippine GGR by segment

130 119 219

375 395 408 156 168

363

638 658 678

-

200

400

600

800

1,000

1,200

2011 2012 2013 2014E 2015E 2016E

VIP Mass

53% 49% 47% 48% 48% 47%

18% 20% 24% 24% 23% 22%

29% 30% 28% 28% 28% 29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014E 2015E 2016E

VIP Mass Slots ETGs

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Revenue assumptions

VIP win/table/day

We assume an average VIP win/table/day of P290,065 (US$6,574) in 2014E, and for this

to grow 15% YoY in 2015E and 14% YoY in 2016E. Macau's average 3Q14 VIP

win/table/day is ~US$30,000.

Mass win/table/day

We assume an average mass win/table/day of P94,539 (US$2,143) in 2014E and for this

to grow 9% and 7% YoY in 2015E and 2016E, respectively. Macau's 3Q14 average mass

win/table/day is ~US$12,000.

Slots win/table/day

We assume an average slot win/table/day of P12,906 (US$293) in 2014E and for this to

grow 11% YoY in 2015E and 2016E. Macau's 3Q14 average slots win/table/day is

~US$430.

30 September 2014

Philippine Gaming Sector 7

Figure 14: Philippine gaming—GGR forecasts (P mn)

GGR (P mn) 2011 2012 2013 2014E 2015E 2016E

Resorts World Manila 25,428 28,058 30,004 27,714 34,754 42,225

YoY 10% 7% -8% 25% 21%

VIP 13,475 13,708 15,120 13,030 15,968 19,241

YoY 2% 10% -14% 23% 20%

Mass 4,544 5,683 6,117 6,093 7,150 8,260

YoY 25% 8% 0% 17% 16%

Slots 7,358 8,639 8,758 8,313 11,344 14,419

YoY 17% 1% -2% 36% 27%

Breakdown

VIP 53% 49% 50% 47% 46% 46%

Mass 18% 20% 20% 22% 21% 20%

Slots 29% 31% 29% 30% 33% 34%

Solaire 14,774 28,366 43,192 48,479

YoY 52% 52% 12%

VIP 6,096 14,271 26,070 29,770

YoY 0% 85% 83% 14%

Mass 4,627 7,050 7,747 7,927

YoY 0% 21% 10% 2%

Slots 4,051 7,045 9,375 10,782

YoY 0% 38% 33% 15%

Breakdown

VIP 41% 50% 60% 61%

Mass 31% 25% 18% 16%

Slots 27% 25% 22% 22%

Others 25,010 27,479 27,583 26,323 52,478 57,928

Total 50,438 55,537 72,361 82,403 130,425 148,631

YoY 10% 30% 14% 58% 14%

Source: Company data, Credit Suisse estimates

Valuation versus Macau

Considering the different gearing ratios and capex schedules, we use EV/EBITDA for peer

comparison. Bloomberry's 2015E EV/EBITDA of 10.8x and Traveller's 11.4x are both at a

discount to Macau's 11.7x. At a 2015E P/E of 25.4x, Philippine gaming names are trading

at a 44% premium to the Philippine Stock Exchange Index (PSEi). This is a lower premium

compared to Macau, which is trading at a 2015E P/E of 14.7x or a premium of 47% to the

Hang Seng Index (HSI). However, since the Philippine operators are still heavy on capex

this year, it will take some time before they yield any significant dividend.

Figure 15: Philippine gaming versus Macau

Company Mkt cap Share TP P/E (x) EV/EBITDA (x) Dividend yield (%)

name (US$ mn) price (l.c.) (l.c.) 2014E 2015E 2016E 2014E 2015E 2016E 2014E 2015E 2016E

Philippines 33.9 25.6 19.9 16.9 11.1 9.0 0.4 0.3 0.4

Bloomberry 3,127 13.3 16.0 30.2 22.4 18.1 17.3 10.8 9.1 - - -

Travellers 3,469 9.9 11.4 37.3 28.5 21.5 16.6 11.4 8.9 0.8 0.5 0.7

Macau 16.1 14.4 12.5 12.7 11.7 9.8 4.7 5.2 5.8

Note: Priced as of 29 September 2014. Source: Company data, Credit Suisse estimates

Our valuations are at a

slight discount to Macau

30 September 2014

Philippine Gaming Sector 8

Window of opportunity: Synergies within Entertainment City beginning in 4Q14 Critical mass in the Entertainment City formed by

mutualism

The gambling behaviour in Macau suggests that players normally visit two to three

properties per trip. Solaire, post its Phase1A expansion, will have 10,000 sq m of retail

space. The expansion will coincide with the opening of City of Dreams in 4Q14 and

together, these projects should be able to build critical mass in the area, benefiting both

casino operators. Solaire and CoD Manila are already in talks to provide a shuttle service

to increase connectivity between their respective properties.

We have witnessed this kind of relationship in the past among the casino operators in

Macau. Sands Macau was the first casino to open in Macau after the gaming industry was

liberalised by the government in 2002. We saw GGR increase by 23% YoY to US$7.1 bn

in 2006 when Wynn Macau opened two years after Sands Macau. GGR increased further

by 47% YoY when the Venetian and MGM Grand opened in 2007.

Figure 16: Macau gaming tables versus GGR

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gaming tables GGR ($ bn)

Sands

Wynn

Venetian

MGM Grand

Grand Lisboa

City of DreamsGalaxy

Sands

Cotai

Source: Credit Suisse research

We expect critical mass to

build up in Entertainment

City, as Solaire and City of

Dreams Manila mutually

benefit from their close

proximity

30 September 2014

Philippine Gaming Sector 9

Figure 17: Philippine gaming tables versus GGR

-

200

400

600

800

1,000

1,200

.0

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014E 2015E 2016E

Gaming tables GGR ($bn)

CoD Manila

Solaire Phase 1A

Manila Bay

Resorts

Solaire Phase 1

Source: Credit Suisse estimates

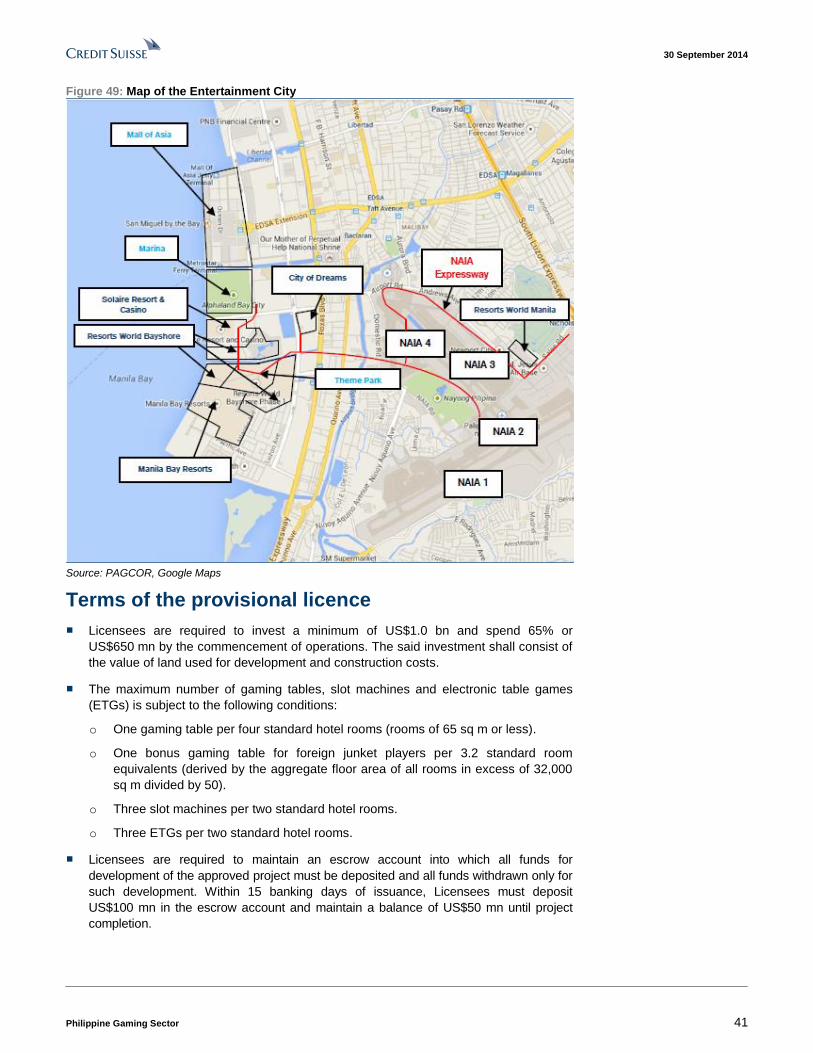

New airport and infrastructure developments to

increase connectivity to Entertainment City

Within the next two months, several foreign carriers, including Delta Airlines, KLM Royal

Dutch Airlines, Emirates Airlines, Singapore Airlines and Cathay Pacific, will be transferred to

NAIA Terminal 3 from the congested NAIA Terminal 1. This should alleviate travel pains and

encourage more near-term tourist arrivals. For the long run, government is also reviewing

proposals for a new airport. There are three possible airport sites being considered:

■ Reclaimed land in the Manila Bay area. San Miguel, the proponent of this site,

claims it can finish construction within five years. The design was drafted by US

engineering and design firm Aecom Technology Corp.

■ Reclaimed land in Sangley Point. The proposal by the Japan International

Cooperation Agency (JICA) identifies Sangley Point, a former US Air Force base in

Manila Bay, as a possible site for a new airport. JICA estimates that the airport can

handle 66 mn passengers a year by 2025 and 100 mn by 2040.

■ Clark International Airport. Clark, now a civilian airport, is also a former US Air Force

base 60 miles north of Manila. JICA recommends that Clark serves as a secondary

airport catering to Central and Northern Luzon.

The two major road infrastructure projects that will increase connectivity to the

Entertainment City are:

■ NAIA Expressway. The NAIA Expressway, a US$345 mn public private partnership

(PPP) project, consists of a four-lane, 7.75 km elevated expressway and a 2.22 km

feeder road that will give access to NAIA Terminals I, II and III and connect the airport

to the Skyway ,the Manila-Cavite Toll Expressway and Entertainment City. The

Department of Public Works and Highways (DPWH) estimates that the project will be

completed by 2016. However, San Miguel, the winning bidder of this project, expects

this to be operational by mid-2015.

■ LRT 1 Extension. The LRT Line 1 South Extension Project consists of the

construction of an estimated 11.7 km length from LRT Line 1 terminus at the Baclaran

Terminal (close to the Entertainment City) to Bacoor Cavite. The entire length of the

integrated LRT 1 upon completion will be about 32.4 km. This should increase access

to Entertainment City from towns south of Metro Manila. The target completion period

for this project is 3Q18.

Improvements in airport and

infrastructure to help

encourage tourist arrivals

30 September 2014

Philippine Gaming Sector 10

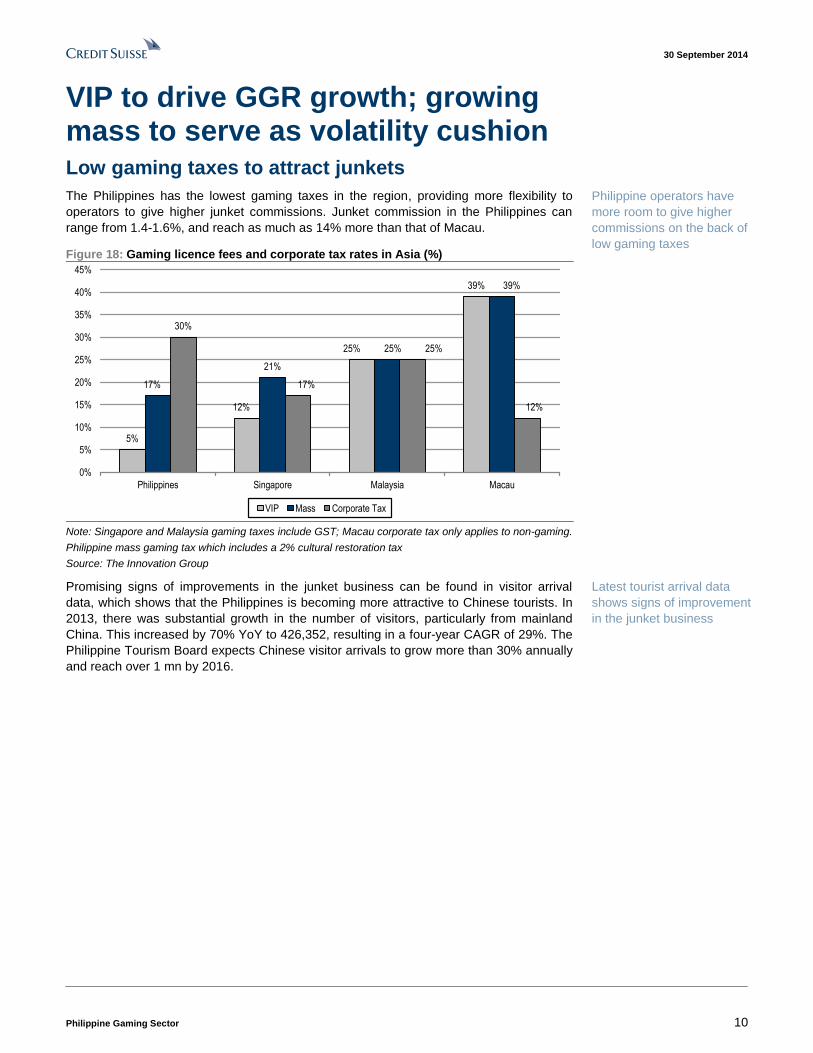

VIP to drive GGR growth; growing mass to serve as volatility cushion Low gaming taxes to attract junkets

The Philippines has the lowest gaming taxes in the region, providing more flexibility to

operators to give higher junket commissions. Junket commission in the Philippines can

range from 1.4-1.6%, and reach as much as 14% more than that of Macau.

Figure 18: Gaming licence fees and corporate tax rates in Asia (%)

5%

12%

25%

39%

17%

21%

25%

39%

30%

17%

25%

12%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Philippines Singapore Malaysia Macau

VIP Mass Corporate Tax

Note: Singapore and Malaysia gaming taxes include GST; Macau corporate tax only applies to non-gaming.

Philippine mass gaming tax which includes a 2% cultural restoration tax

Source: The Innovation Group

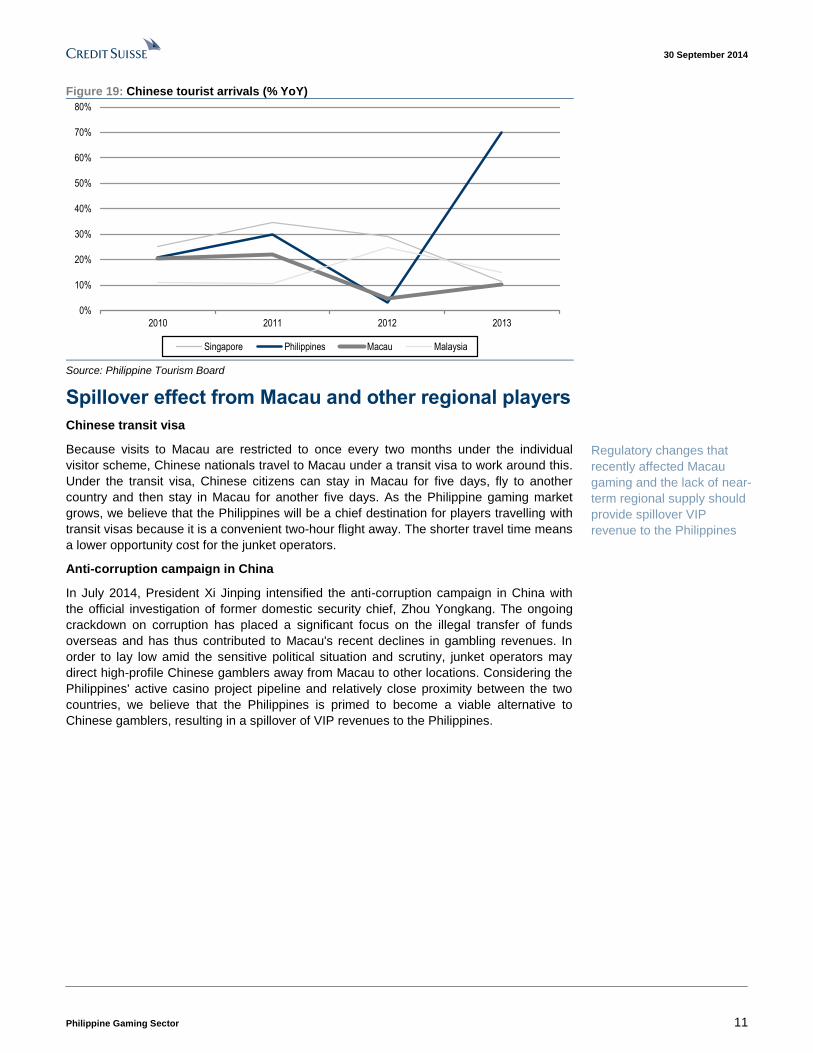

Promising signs of improvements in the junket business can be found in visitor arrival

data, which shows that the Philippines is becoming more attractive to Chinese tourists. In

2013, there was substantial growth in the number of visitors, particularly from mainland

China. This increased by 70% YoY to 426,352, resulting in a four-year CAGR of 29%. The

Philippine Tourism Board expects Chinese visitor arrivals to grow more than 30% annually

and reach over 1 mn by 2016.

Philippine operators have

more room to give higher

commissions on the back of

low gaming taxes

Latest tourist arrival data

shows signs of improvement

in the junket business

30 September 2014

Philippine Gaming Sector 11

Figure 19: Chinese tourist arrivals (% YoY)

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013

Singapore Philippines Macau Malaysia

Source: Philippine Tourism Board

Spillover effect from Macau and other regional players

Chinese transit visa

Because visits to Macau are restricted to once every two months under the individual

visitor scheme, Chinese nationals travel to Macau under a transit visa to work around this.

Under the transit visa, Chinese citizens can stay in Macau for five days, fly to another

country and then stay in Macau for another five days. As the Philippine gaming market

grows, we believe that the Philippines will be a chief destination for players travelling with

transit visas because it is a convenient two-hour flight away. The shorter travel time means

a lower opportunity cost for the junket operators.

Anti-corruption campaign in China

In July 2014, President Xi Jinping intensified the anti-corruption campaign in China with

the official investigation of former domestic security chief, Zhou Yongkang. The ongoing

crackdown on corruption has placed a significant focus on the illegal transfer of funds

overseas and has thus contributed to Macau's recent declines in gambling revenues. In

order to lay low amid the sensitive political situation and scrutiny, junket operators may

direct high-profile Chinese gamblers away from Macau to other locations. Considering the

Philippines' active casino project pipeline and relatively close proximity between the two

countries, we believe that the Philippines is primed to become a viable alternative to

Chinese gamblers, resulting in a spillover of VIP revenues to the Philippines.

Regulatory changes that

recently affected Macau

gaming and the lack of near-

term regional supply should

provide spillover VIP

revenue to the Philippines

30 September 2014

Philippine Gaming Sector 12

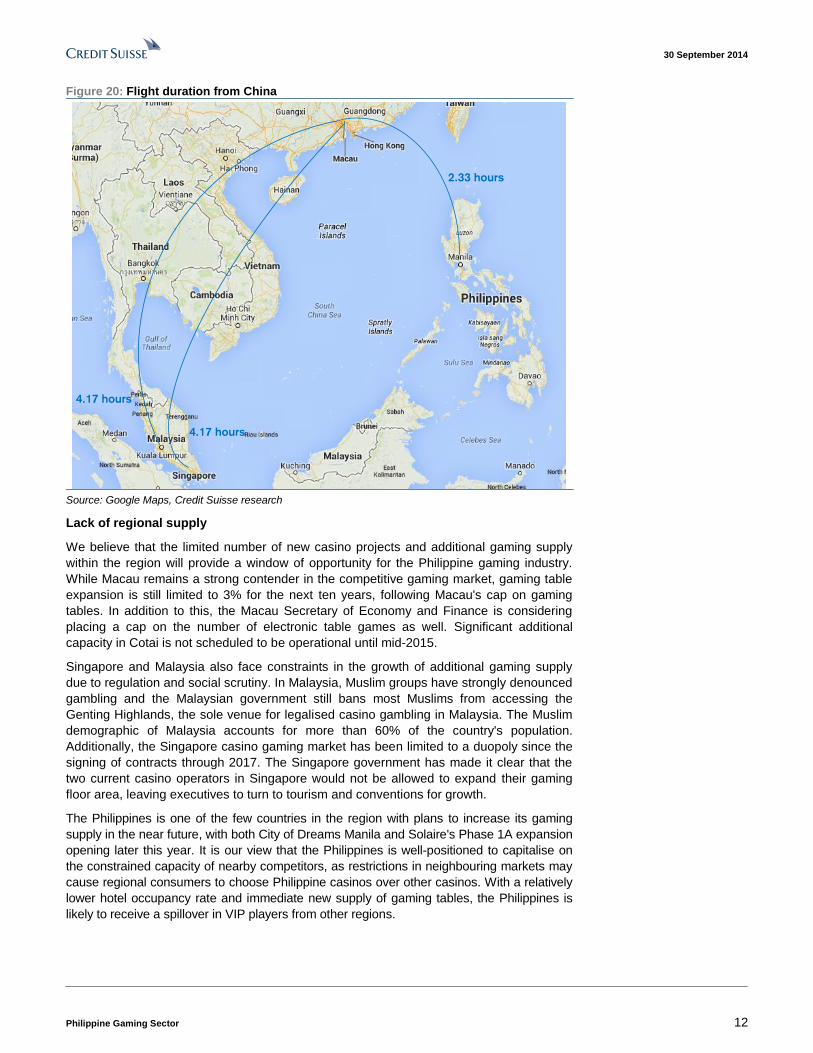

Figure 20: Flight duration from China

2.33 hours

4.17 hours

4.17 hours

Source: Google Maps, Credit Suisse research

Lack of regional supply

We believe that the limited number of new casino projects and additional gaming supply

within the region will provide a window of opportunity for the Philippine gaming industry.

While Macau remains a strong contender in the competitive gaming market, gaming table

expansion is still limited to 3% for the next ten years, following Macau's cap on gaming

tables. In addition to this, the Macau Secretary of Economy and Finance is considering

placing a cap on the number of electronic table games as well. Significant additional

capacity in Cotai is not scheduled to be operational until mid-2015.

Singapore and Malaysia also face constraints in the growth of additional gaming supply

due to regulation and social scrutiny. In Malaysia, Muslim groups have strongly denounced

gambling and the Malaysian government still bans most Muslims from accessing the

Genting Highlands, the sole venue for legalised casino gambling in Malaysia. The Muslim

demographic of Malaysia accounts for more than 60% of the country's population.

Additionally, the Singapore casino gaming market has been limited to a duopoly since the

signing of contracts through 2017. The Singapore government has made it clear that the

two current casino operators in Singapore would not be allowed to expand their gaming

floor area, leaving executives to turn to tourism and conventions for growth.

The Philippines is one of the few countries in the region with plans to increase its gaming

supply in the near future, with both City of Dreams Manila and Solaire's Phase 1A expansion

opening later this year. It is our view that the Philippines is well-positioned to capitalise on

the constrained capacity of nearby competitors, as restrictions in neighbouring markets may

cause regional consumers to choose Philippine casinos over other casinos. With a relatively

lower hotel occupancy rate and immediate new supply of gaming tables, the Philippines is

likely to receive a spillover in VIP players from other regions.

30 September 2014

Philippine Gaming Sector 13

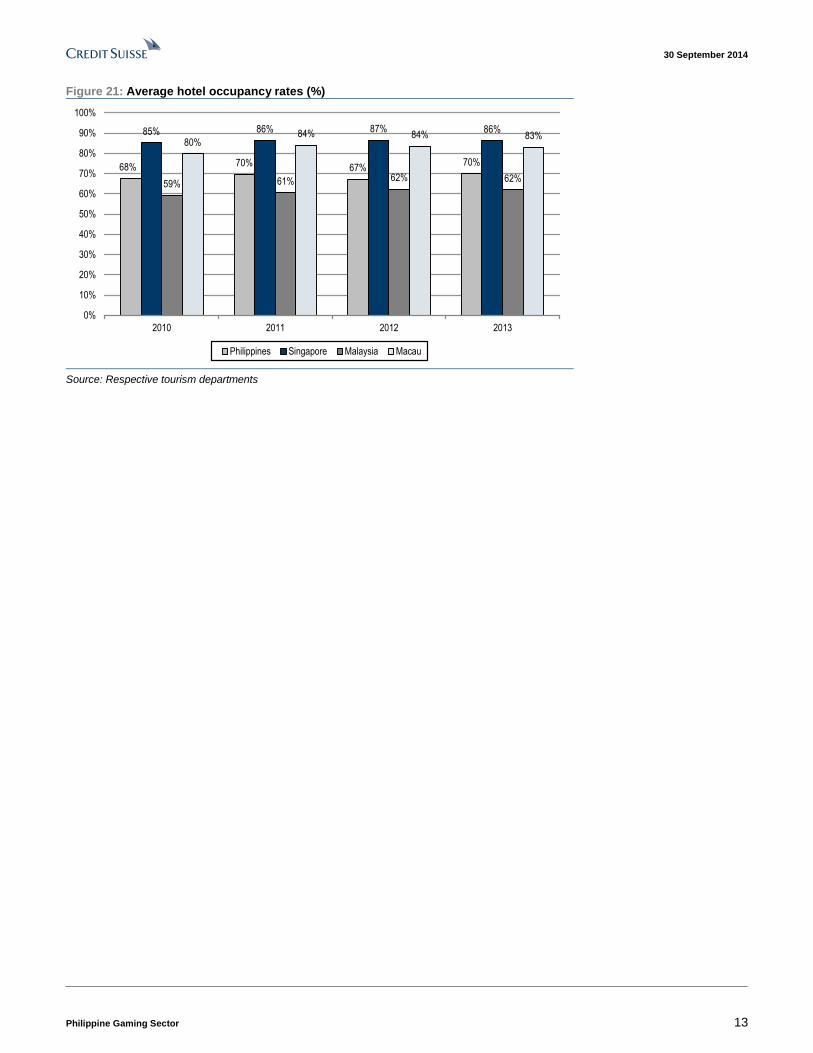

Figure 21: Average hotel occupancy rates (%)

68% 70%67%

70%

85% 86% 87% 86%

59% 61% 62% 62%

80%84% 84% 83%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013

Philippines Singapore Malaysia Macau

Source: Respective tourism departments

30 September 2014

Philippine Gaming Sector 14

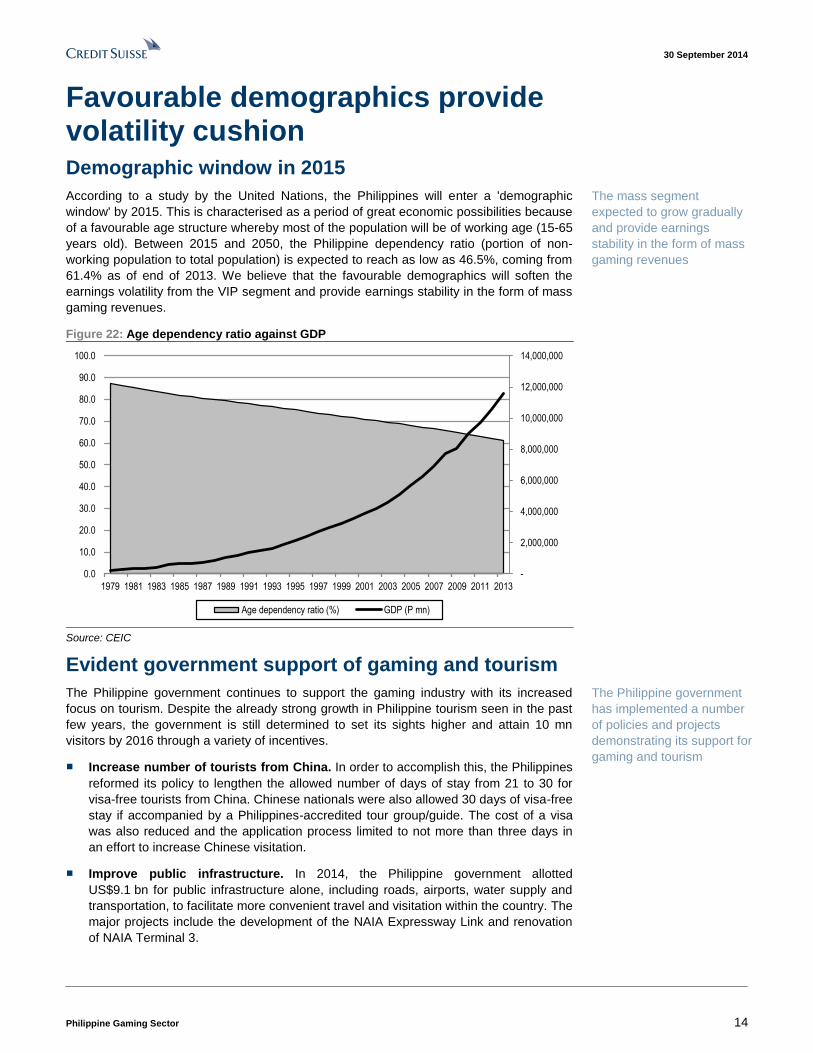

Favourable demographics provide volatility cushion Demographic window in 2015

According to a study by the United Nations, the Philippines will enter a 'demographic

window' by 2015. This is characterised as a period of great economic possibilities because

of a favourable age structure whereby most of the population will be of working age (15-65

years old). Between 2015 and 2050, the Philippine dependency ratio (portion of non-

working population to total population) is expected to reach as low as 46.5%, coming from

61.4% as of end of 2013. We believe that the favourable demographics will soften the

earnings volatility from the VIP segment and provide earnings stability in the form of mass

gaming revenues.

Figure 22: Age dependency ratio against GDP

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Age dependency ratio (%) GDP (P mn)

Source: CEIC

Evident government support of gaming and tourism

The Philippine government continues to support the gaming industry with its increased

focus on tourism. Despite the already strong growth in Philippine tourism seen in the past

few years, the government is still determined to set its sights higher and attain 10 mn

visitors by 2016 through a variety of incentives.

■ Increase number of tourists from China. In order to accomplish this, the Philippines

reformed its policy to lengthen the allowed number of days of stay from 21 to 30 for

visa-free tourists from China. Chinese nationals were also allowed 30 days of visa-free

stay if accompanied by a Philippines-accredited tour group/guide. The cost of a visa

was also reduced and the application process limited to not more than three days in

an effort to increase Chinese visitation.

■ Improve public infrastructure. In 2014, the Philippine government allotted

US$9.1 bn for public infrastructure alone, including roads, airports, water supply and

transportation, to facilitate more convenient travel and visitation within the country. The

major projects include the development of the NAIA Expressway Link and renovation

of NAIA Terminal 3.

The mass segment

expected to grow gradually

and provide earnings

stability in the form of mass

gaming revenues

The Philippine government

has implemented a number

of policies and projects

demonstrating its support for

gaming and tourism

30 September 2014

Philippine Gaming Sector 15

■ Increase number of flights and air seats. The Philippines recently signed air service

agreements with Australia, Canada, France, Singapore, New Zealand, Myanmar, Italy,

Brazil, Japan, Macau, South Africa and Israel to increase flights to and from these

countries. Under the new air service pact, the Philippines and Macau have more seat

entitlements, up 56% from 4,500 seats to 7,020 seats. Philippine Airlines and Cebu

Pacific aim to increase seat entitlements to Singapore as well.

■ Marketing campaigns. The Department of Tourism's highly publicised promotion

campaign "It's more fun in the Philippines" was rolled out in 2012 and helped attract a

record 4.27 mn visitors that year. To supplement the campaign, the Department of

Tourism recently released four television commercials featuring Manila, Cebu, Davao

and Boracay.

We believe that these favourable government initiatives to support tourism will directly

benefit the Philippine gaming industry and provide it with a competitive advantage over

casinos in Singapore and Malaysia. It should also be noted that in April 2013, the Bureau

of Internal Revenue (BIR) issued a revenue memorandum circular (RMC) stating that the

Philippine Amusement and Gaming Corporation (PAGCOR), its contractees and licensees

are no longer exempt from corporate tax. Rather than breach the mutually agreed upon

provisions of the licence agreements, PAGCOR issued guidelines for a temporary 10%

income tax allocation (ITA) measure whereby the 25% and 15% licence fees were

reduced to 15% and 5%, respectively, inasmuch as 10% of licence fees was allocated for

income tax on gaming. The parties will revert to the original licence fee structure if the BIR

action is permanently restrained, corrected or withdrawn. This temporary measure to

neutralise the burden of additional tax liabilities on gaming operators can be viewed as

further proof of the Philippine government's favourable support of the gaming industry.

30 September 2014

Philippine Gaming Sector 16

Prefer BLOOM (+21%) over RWM (+15%) We assume coverage on RWM and BLOOM with OUTPERFORM ratings and DCF-based

target prices of P11.4 and P16.0, respectively.

Review of 1H14 results

RWM's 1H14 EBITDA stood at P4.7 bn, which accounts for only 40% of full-year

consensus estimates. This may pose downward earning revisions, which can limit price

appreciation in the near term. On the other hand, BLOOM's 1H14 results came in line with

expectations after analysts raised consensus estimates following strong 1Q14 results. We

see further boosts in 2H14 and in 2015, as synergies form between City of Dreams Manila

and Solaire's Phase 1A expansion, and critical mass starts to build in the area.

Figure 23: RWM vs BLOOM—1H14 EBITDA (P mn) vs 2014E CS and consensus forecasts

4,686 4,474

9,198 9,694

11,698

8,967

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

RWM BLOOM

1H14 CS Consensus

Source: Company data, Credit Suisse estimates

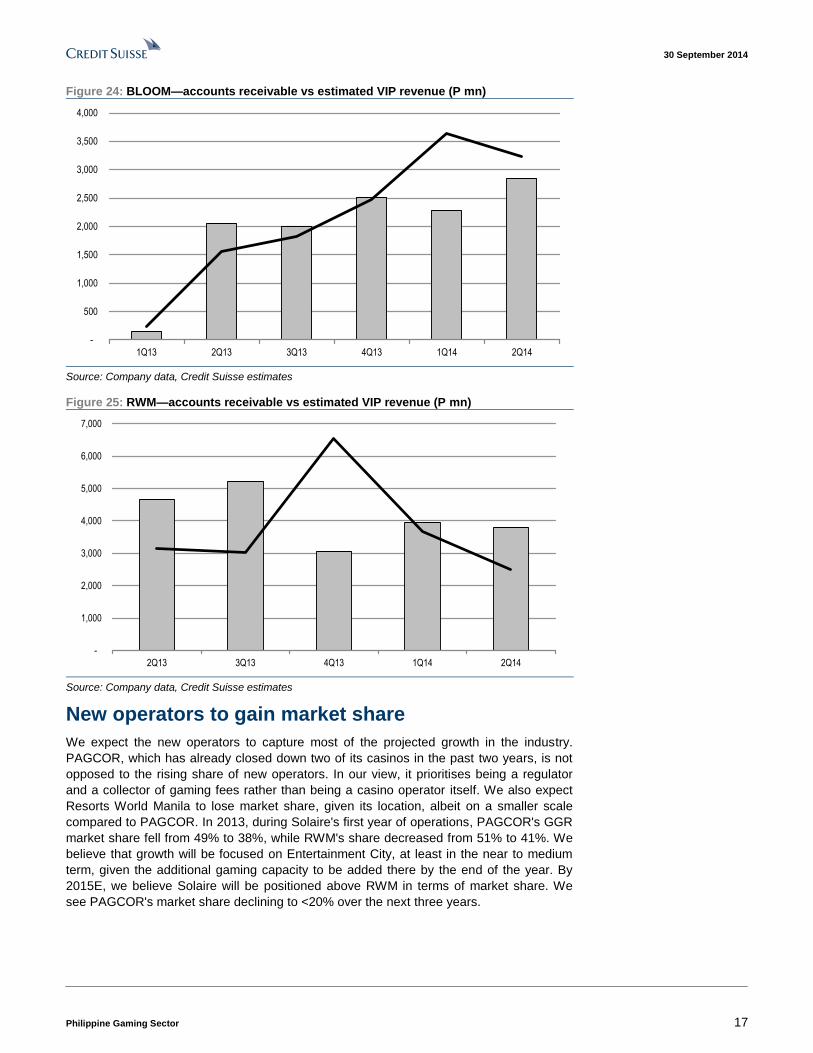

We believe the strong VIP revenue growth that Solaire recorded in 1H14 is on the back of

a credit extension to the junkets. This is reflected in the growth of its accounts receivable,

which appears to be continuously increasing. Based on the historical performance of

Macau casino operators, credit extension tends to yield the most revenue growth in the

first six months and tapers off thereafter. We believe that fresh credit injections, which we

see as a continuing trend for BLOOM, will be able to support its VIP growth momentum in

the near to medium term. On the other hand, RWM's accounts receivable seem to have

peaked in 3Q13 and hence we expect its VIP volume growth to slow down.

30 September 2014

Philippine Gaming Sector 17

Figure 24: BLOOM—accounts receivable vs estimated VIP revenue (P mn)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

Source: Company data, Credit Suisse estimates

Figure 25: RWM—accounts receivable vs estimated VIP revenue (P mn)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2Q13 3Q13 4Q13 1Q14 2Q14

Source: Company data, Credit Suisse estimates

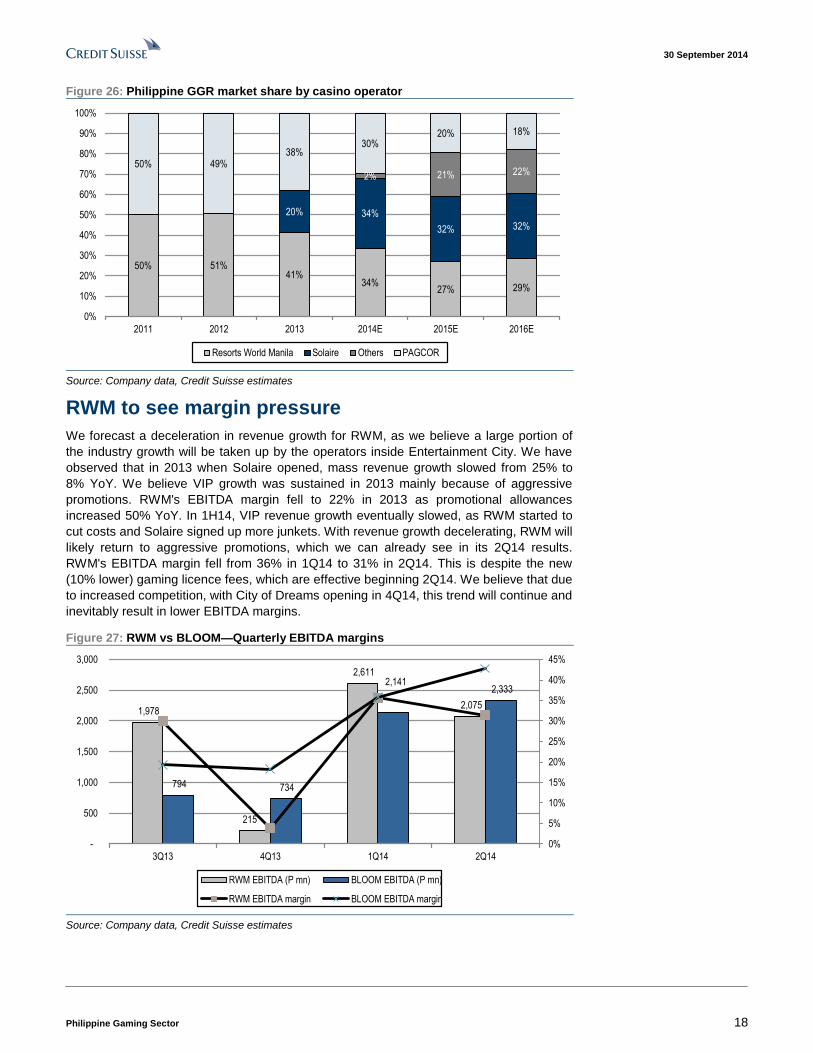

New operators to gain market share

We expect the new operators to capture most of the projected growth in the industry.

PAGCOR, which has already closed down two of its casinos in the past two years, is not

opposed to the rising share of new operators. In our view, it prioritises being a regulator

and a collector of gaming fees rather than being a casino operator itself. We also expect

Resorts World Manila to lose market share, given its location, albeit on a smaller scale

compared to PAGCOR. In 2013, during Solaire's first year of operations, PAGCOR's GGR

market share fell from 49% to 38%, while RWM's share decreased from 51% to 41%. We

believe that growth will be focused on Entertainment City, at least in the near to medium

term, given the additional gaming capacity to be added there by the end of the year. By

2015E, we believe Solaire will be positioned above RWM in terms of market share. We

see PAGCOR's market share declining to <20% over the next three years.

30 September 2014

Philippine Gaming Sector 18

Figure 26: Philippine GGR market share by casino operator

50% 51%41%

34%27% 29%

20% 34%

32% 32%

2% 21% 22%50% 49%

38%30%

20% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014E 2015E 2016E

Resorts World Manila Solaire Others PAGCOR

Source: Company data, Credit Suisse estimates

RWM to see margin pressure

We forecast a deceleration in revenue growth for RWM, as we believe a large portion of

the industry growth will be taken up by the operators inside Entertainment City. We have

observed that in 2013 when Solaire opened, mass revenue growth slowed from 25% to

8% YoY. We believe VIP growth was sustained in 2013 mainly because of aggressive

promotions. RWM's EBITDA margin fell to 22% in 2013 as promotional allowances

increased 50% YoY. In 1H14, VIP revenue growth eventually slowed, as RWM started to

cut costs and Solaire signed up more junkets. With revenue growth decelerating, RWM will

likely return to aggressive promotions, which we can already see in its 2Q14 results.

RWM's EBITDA margin fell from 36% in 1Q14 to 31% in 2Q14. This is despite the new

(10% lower) gaming licence fees, which are effective beginning 2Q14. We believe that due

to increased competition, with City of Dreams opening in 4Q14, this trend will continue and

inevitably result in lower EBITDA margins.

Figure 27: RWM vs BLOOM—Quarterly EBITDA margins

1,978

215

2,611

2,075

794 734

2,141 2,333

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

-

500

1,000

1,500

2,000

2,500

3,000

3Q13 4Q13 1Q14 2Q14

RWM EBITDA (P mn) BLOOM EBITDA (P mn)

RWM EBITDA margin BLOOM EBITDA margin

Source: Company data, Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 19

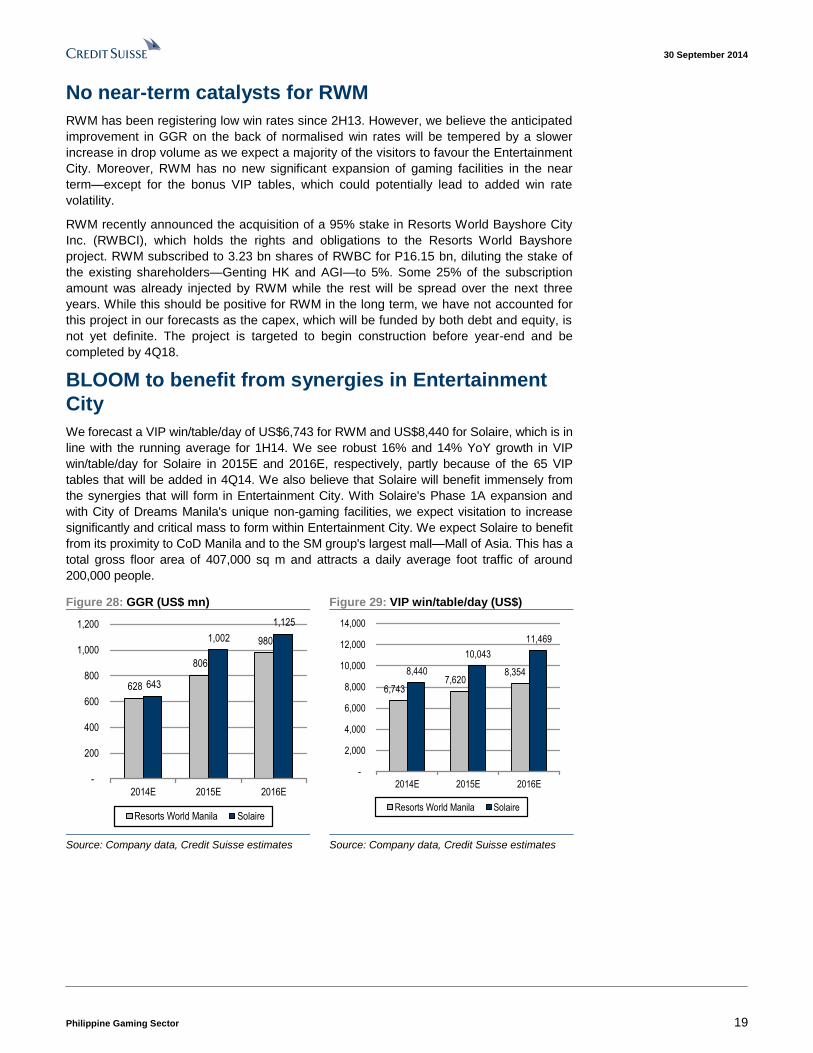

No near-term catalysts for RWM

RWM has been registering low win rates since 2H13. However, we believe the anticipated

improvement in GGR on the back of normalised win rates will be tempered by a slower

increase in drop volume as we expect a majority of the visitors to favour the Entertainment

City. Moreover, RWM has no new significant expansion of gaming facilities in the near

term—except for the bonus VIP tables, which could potentially lead to added win rate

volatility.

RWM recently announced the acquisition of a 95% stake in Resorts World Bayshore City

Inc. (RWBCI), which holds the rights and obligations to the Resorts World Bayshore

project. RWM subscribed to 3.23 bn shares of RWBC for P16.15 bn, diluting the stake of

the existing shareholders—Genting HK and AGI—to 5%. Some 25% of the subscription

amount was already injected by RWM while the rest will be spread over the next three

years. While this should be positive for RWM in the long term, we have not accounted for

this project in our forecasts as the capex, which will be funded by both debt and equity, is

not yet definite. The project is targeted to begin construction before year-end and be

completed by 4Q18.

BLOOM to benefit from synergies in Entertainment

City

We forecast a VIP win/table/day of US$6,743 for RWM and US$8,440 for Solaire, which is in

line with the running average for 1H14. We see robust 16% and 14% YoY growth in VIP

win/table/day for Solaire in 2015E and 2016E, respectively, partly because of the 65 VIP

tables that will be added in 4Q14. We also believe that Solaire will benefit immensely from

the synergies that will form in Entertainment City. With Solaire's Phase 1A expansion and

with City of Dreams Manila's unique non-gaming facilities, we expect visitation to increase

significantly and critical mass to form within Entertainment City. We expect Solaire to benefit

from its proximity to CoD Manila and to the SM group's largest mall—Mall of Asia. This has a

total gross floor area of 407,000 sq m and attracts a daily average foot traffic of around

200,000 people.

Figure 28: GGR (US$ mn) Figure 29: VIP win/table/day (US$)

628

806

980

643

1,002

1,125

-

200

400

600

800

1,000

1,200

2014E 2015E 2016E

Resorts World Manila Solaire

6,743 7,620

8,354 8,440

10,043

11,469

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2014E 2015E 2016E

Resorts World Manila Solaire

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 20

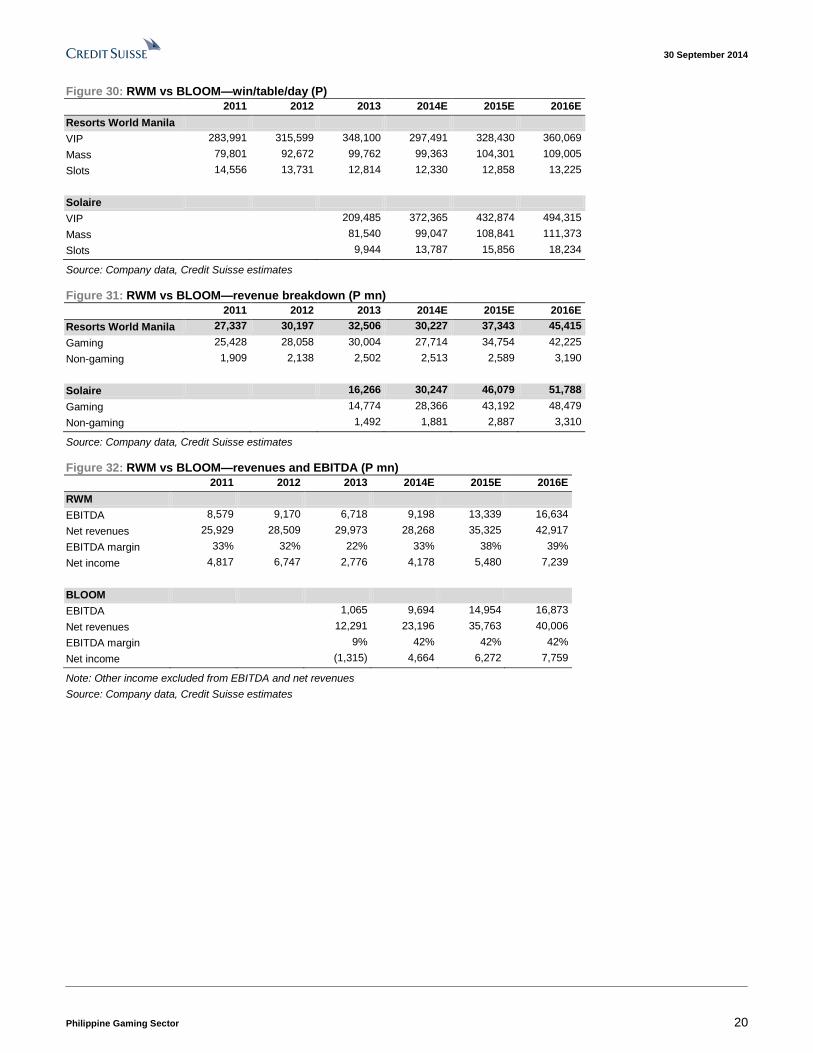

Figure 30: RWM vs BLOOM—win/table/day (P)

2011 2012 2013 2014E 2015E 2016E

Resorts World Manila

VIP 283,991 315,599 348,100 297,491 328,430 360,069

Mass 79,801 92,672 99,762 99,363 104,301 109,005

Slots 14,556 13,731 12,814 12,330 12,858 13,225

Solaire

VIP 209,485 372,365 432,874 494,315

Mass 81,540 99,047 108,841 111,373

Slots 9,944 13,787 15,856 18,234

Source: Company data, Credit Suisse estimates

Figure 31: RWM vs BLOOM—revenue breakdown (P mn)

2011 2012 2013 2014E 2015E 2016E

Resorts World Manila 27,337 30,197 32,506 30,227 37,343 45,415

Gaming 25,428 28,058 30,004 27,714 34,754 42,225

Non-gaming 1,909 2,138 2,502 2,513 2,589 3,190

Solaire 16,266 30,247 46,079 51,788

Gaming 14,774 28,366 43,192 48,479

Non-gaming 1,492 1,881 2,887 3,310

Source: Company data, Credit Suisse estimates

Figure 32: RWM vs BLOOM—revenues and EBITDA (P mn)

2011 2012 2013 2014E 2015E 2016E

RWM

EBITDA 8,579 9,170 6,718 9,198 13,339 16,634

Net revenues 25,929 28,509 29,973 28,268 35,325 42,917

EBITDA margin 33% 32% 22% 33% 38% 39%

Net income 4,817 6,747 2,776 4,178 5,480 7,239

BLOOM

EBITDA 1,065 9,694 14,954 16,873

Net revenues 12,291 23,196 35,763 40,006

EBITDA margin 9% 42% 42% 42%

Net income (1,315) 4,664 6,272 7,759

Note: Other income excluded from EBITDA and net revenues

Source: Company data, Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 21

Key investment risks Regulatory risks

Revision of PAGCOR policies

PAGCOR states that the adjustment of gaming licence fees from 25% to 10% effective

1 April 2014 was done in order to address the BIR action to remove the exemption of

PAGCOR and its licensees from the 30% corporate tax. Any change in the BIR court ruling,

or other government policies affecting PAGCOR will likely result in a change in its

agreement with the licensees.

Suspension of gaming licence

PAGCOR may unilaterally suspend or terminate the provisional licences due to non-

compliance of the licensees with material provisions, failure to remit monthly licence fees

within 30 days of receipt of notice of default, delay in the construction of more than 50% of

schedule or bankruptcy or insolvency.

Implementation of casino entry fee

In September 2014, House Representative Peter Unabia proposed a bill seeking to

impose a P3,500 entrance fee for all Filipinos visiting local casinos. The congressman has

firmly maintained that if passed into law, the bill will prevent financially inadequate citizens

from entering casinos and gambling. Currently, the PAGCOR charter contains no

requirement of an entry fee for any person seeking to play in casinos.

Market risks

PAGCOR issuance of additional gaming licences

PAGCOR is not legally restricted to issue additional gaming licences. A new operator

within Entertainment City may result in increased competition and/or change the dynamics

among the existing operators.

Competition in attracting foreign junkets

Philippine gaming operators will need to provide more enticing incentives, relative to each

other and to regional competitors, in order to attract junket business.

Operational risks

Execution risks

The launch of City of Dreams Manila is slated for 4Q14. Any delays can negatively impact

our forecasts, as well as the public's perception on management's ability to execute.

Delays in infrastructure projects may temper growth

Infrastructure projects that are intended for ease of access to the Entertainment City are

expected to be operational by mid-2015. Significant delays can temper growth in the

medium term.

Negative perception on safety in the Philippines

Incidents that endanger tourists in the country, such as the 2010 bus hostage crisis that

left eight Hong Kong tourists dead, could discourage travel and hinder growth in gaming

revenues, particularly in the VIP segment.

Relations between China and the Philippines

Disputes between China and the Philippines, such as the territorial dispute over

Scarborough Shoal in 2012, can negatively affect visitor arrivals.

30 September 2014

Philippine Gaming Sector 22

Asia Pacific / Philippines

Casinos & Gaming

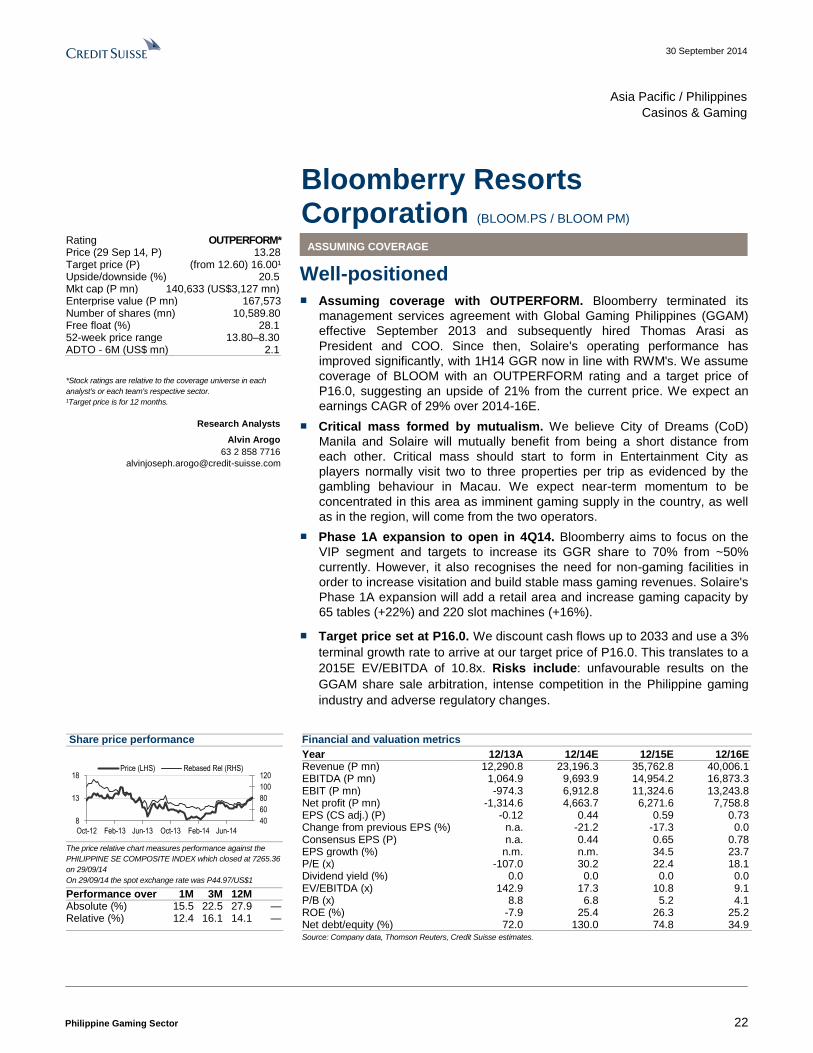

Bloomberry Resorts Corporation (BLOOM.PS / BLOOM PM)

ASSUMING COVERAGE

Well-positioned

■ Assuming coverage with OUTPERFORM. Bloomberry terminated its

management services agreement with Global Gaming Philippines (GGAM)

effective September 2013 and subsequently hired Thomas Arasi as

President and COO. Since then, Solaire's operating performance has

improved significantly, with 1H14 GGR now in line with RWM's. We assume

coverage of BLOOM with an OUTPERFORM rating and a target price of

P16.0, suggesting an upside of 21% from the current price. We expect an

earnings CAGR of 29% over 2014-16E.

■ Critical mass formed by mutualism. We believe City of Dreams (CoD)

Manila and Solaire will mutually benefit from being a short distance from

each other. Critical mass should start to form in Entertainment City as

players normally visit two to three properties per trip as evidenced by the

gambling behaviour in Macau. We expect near-term momentum to be

concentrated in this area as imminent gaming supply in the country, as well

as in the region, will come from the two operators.

■ Phase 1A expansion to open in 4Q14. Bloomberry aims to focus on the

VIP segment and targets to increase its GGR share to 70% from ~50%

currently. However, it also recognises the need for non-gaming facilities in

order to increase visitation and build stable mass gaming revenues. Solaire's

Phase 1A expansion will add a retail area and increase gaming capacity by

65 tables (+22%) and 220 slot machines (+16%).

■ Target price set at P16.0. We discount cash flows up to 2033 and use a 3%

terminal growth rate to arrive at our target price of P16.0. This translates to a

2015E EV/EBITDA of 10.8x. Risks include: unfavourable results on the

GGAM share sale arbitration, intense competition in the Philippine gaming

industry and adverse regulatory changes.

Share price performance

40

60

80

100

120

8

13

18

Oct-12 Feb-13 Jun-13 Oct-13 Feb-14 Jun-14

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

PHILIPPINE SE COMPOSITE INDEX which closed at 7265.36

on 29/09/14

On 29/09/14 the spot exchange rate was P44.97/US$1

Performance over 1M 3M 12M Absolute (%) 15.5 22.5 27.9 — Relative (%) 12.4 16.1 14.1 —

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E Revenue (P mn) 12,290.8 23,196.3 35,762.8 40,006.1 EBITDA (P mn) 1,064.9 9,693.9 14,954.2 16,873.3 EBIT (P mn) -974.3 6,912.8 11,324.6 13,243.8 Net profit (P mn) -1,314.6 4,663.7 6,271.6 7,758.8 EPS (CS adj.) (P) -0.12 0.44 0.59 0.73 Change from previous EPS (%) n.a. -21.2 -17.3 0.0 Consensus EPS (P) n.a. 0.44 0.65 0.78 EPS growth (%) n.m. n.m. 34.5 23.7 P/E (x) -107.0 30.2 22.4 18.1 Dividend yield (%) 0.0 0.0 0.0 0.0 EV/EBITDA (x) 142.9 17.3 10.8 9.1 P/B (x) 8.8 6.8 5.2 4.1 ROE (%) -7.9 25.4 26.3 25.2 Net debt/equity (%) 72.0 130.0 74.8 34.9

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (29 Sep 14, P) 13.28 Target price (P) (from 12.60) 16.00¹ Upside/downside (%) 20.5 Mkt cap (P mn) 140,633 (US$3,127 mn) Enterprise value (P mn) 167,573 Number of shares (mn) 10,589.80 Free float (%) 28.1 52-week price range 13.80–8.30 ADTO - 6M (US$ mn) 2.1

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Alvin Arogo

63 2 858 7716

30 September 2014

Philippine Gaming Sector 23

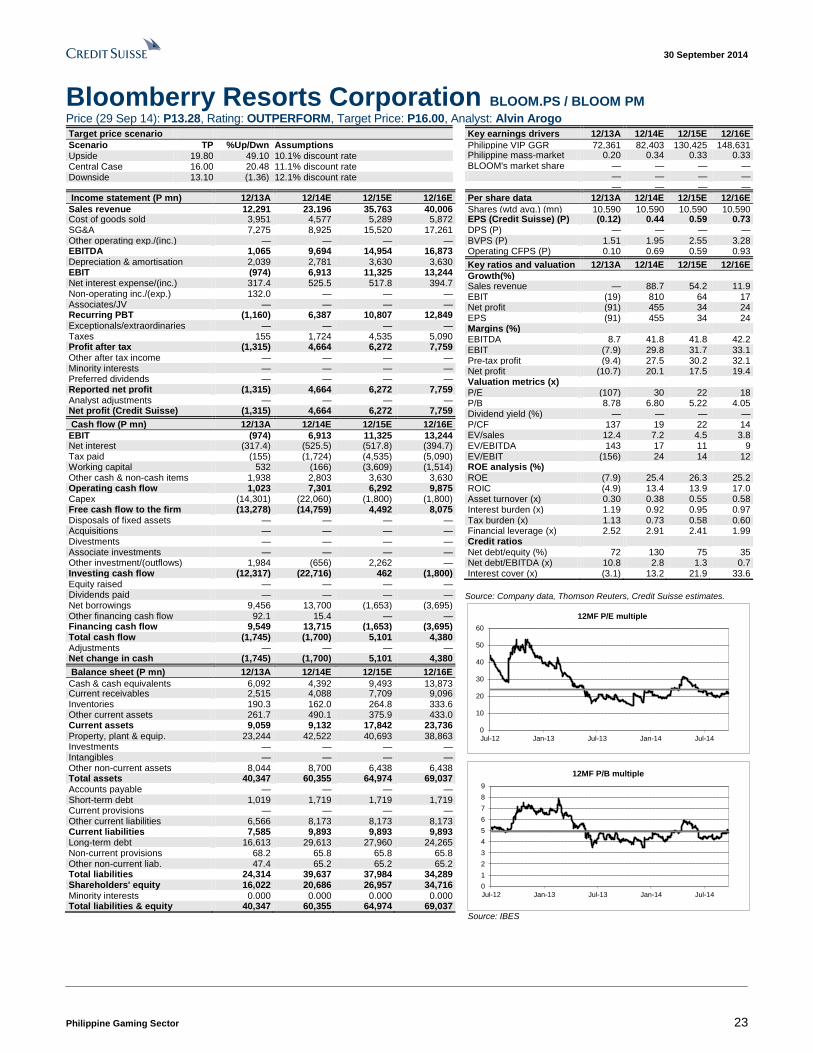

Bloomberry Resorts Corporation BLOOM.PS / BLOOM PM Price (29 Sep 14): P13.28, Rating: OUTPERFORM, Target Price: P16.00, Analyst: Alvin Arogo

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside 19.80 49.10 10.1% discount rate Central Case 16.00 20.48 11.1% discount rate Downside 13.10 (1.36) 12.1% discount rate

Key earnings drivers 12/13A 12/14E 12/15E 12/16E

Philippine VIP GGR 72,361 82,403 130,425 148,631 Philippine mass-market GGR

0.20 0.34 0.33 0.33 BLOOM's market share — — — — — — — — — — — —

Income statement (P mn) 12/13A 12/14E 12/15E 12/16E

Sales revenue 12,291 23,196 35,763 40,006 Cost of goods sold 3,951 4,577 5,289 5,872 SG&A 7,275 8,925 15,520 17,261 Other operating exp./(inc.) — — — — EBITDA 1,065 9,694 14,954 16,873 Depreciation & amortisation 2,039 2,781 3,630 3,630 EBIT (974) 6,913 11,325 13,244 Net interest expense/(inc.) 317.4 525.5 517.8 394.7 Non-operating inc./(exp.) 132.0 — — — Associates/JV — — — — Recurring PBT (1,160) 6,387 10,807 12,849 Exceptionals/extraordinaries — — — — Taxes 155 1,724 4,535 5,090 Profit after tax (1,315) 4,664 6,272 7,759 Other after tax income — — — — Minority interests — — — — Preferred dividends — — — — Reported net profit (1,315) 4,664 6,272 7,759 Analyst adjustments — — — — Net profit (Credit Suisse) (1,315) 4,664 6,272 7,759

Cash flow (P mn) 12/13A 12/14E 12/15E 12/16E

EBIT (974) 6,913 11,325 13,244 Net interest (317.4) (525.5) (517.8) (394.7) Tax paid (155) (1,724) (4,535) (5,090) Working capital 532 (166) (3,609) (1,514) Other cash & non-cash items 1,938 2,803 3,630 3,630 Operating cash flow 1,023 7,301 6,292 9,875 Capex (14,301) (22,060) (1,800) (1,800) Free cash flow to the firm (13,278) (14,759) 4,492 8,075 Disposals of fixed assets — — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) 1,984 (656) 2,262 — Investing cash flow (12,317) (22,716) 462 (1,800) Equity raised — — — — Dividends paid — — — — Net borrowings 9,456 13,700 (1,653) (3,695) Other financing cash flow 92.1 15.4 — — Financing cash flow 9,549 13,715 (1,653) (3,695) Total cash flow (1,745) (1,700) 5,101 4,380 Adjustments — — — — Net change in cash (1,745) (1,700) 5,101 4,380

Balance sheet (P mn) 12/13A 12/14E 12/15E 12/16E

Cash & cash equivalents 6,092 4,392 9,493 13,873 Current receivables 2,515 4,088 7,709 9,096 Inventories 190.3 162.0 264.8 333.6 Other current assets 261.7 490.1 375.9 433.0 Current assets 9,059 9,132 17,842 23,736 Property, plant & equip. 23,244 42,522 40,693 38,863 Investments — — — — Intangibles — — — — Other non-current assets 8,044 8,700 6,438 6,438 Total assets 40,347 60,355 64,974 69,037 Accounts payable — — — — Short-term debt 1,019 1,719 1,719 1,719 Current provisions — — — — Other current liabilities 6,566 8,173 8,173 8,173 Current liabilities 7,585 9,893 9,893 9,893 Long-term debt 16,613 29,613 27,960 24,265 Non-current provisions 68.2 65.8 65.8 65.8 Other non-current liab. 47.4 65.2 65.2 65.2 Total liabilities 24,314 39,637 37,984 34,289 Shareholders' equity 16,022 20,686 26,957 34,716 Minority interests 0.000 0.000 0.000 0.000 Total liabilities & equity 40,347 60,355 64,974 69,037

Per share data 12/13A 12/14E 12/15E 12/16E

Shares (wtd avg.) (mn) 10,590 10,590 10,590 10,590 EPS (Credit Suisse) (P) (0.12) 0.44 0.59 0.73 DPS (P) — — — — BVPS (P) 1.51 1.95 2.55 3.28 Operating CFPS (P) 0.10 0.69 0.59 0.93

Key ratios and valuation 12/13A 12/14E 12/15E 12/16E

Growth(%) Sales revenue — 88.7 54.2 11.9 EBIT (19) 810 64 17 Net profit (91) 455 34 24 EPS (91) 455 34 24 Margins (%) EBITDA 8.7 41.8 41.8 42.2 EBIT (7.9) 29.8 31.7 33.1 Pre-tax profit (9.4) 27.5 30.2 32.1 Net profit (10.7) 20.1 17.5 19.4 Valuation metrics (x) P/E (107) 30 22 18 P/B 8.78 6.80 5.22 4.05 Dividend yield (%) — — — — P/CF 137 19 22 14 EV/sales 12.4 7.2 4.5 3.8 EV/EBITDA 143 17 11 9 EV/EBIT (156) 24 14 12 ROE analysis (%) ROE (7.9) 25.4 26.3 25.2 ROIC (4.9) 13.4 13.9 17.0 Asset turnover (x) 0.30 0.38 0.55 0.58 Interest burden (x) 1.19 0.92 0.95 0.97 Tax burden (x) 1.13 0.73 0.58 0.60 Financial leverage (x) 2.52 2.91 2.41 1.99 Credit ratios Net debt/equity (%) 72 130 75 35 Net debt/EBITDA (x) 10.8 2.8 1.3 0.7 Interest cover (x) (3.1) 13.2 21.9 33.6

Source: Company data, Thomson Reuters, Credit Suisse estimates.

0

10

20

30

40

50

60

Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

12MF P/E multiple

0

1

2

3

4

5

6

7

8

9

Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

12MF P/B multiple

Source: IBES

30 September 2014

Philippine Gaming Sector 24

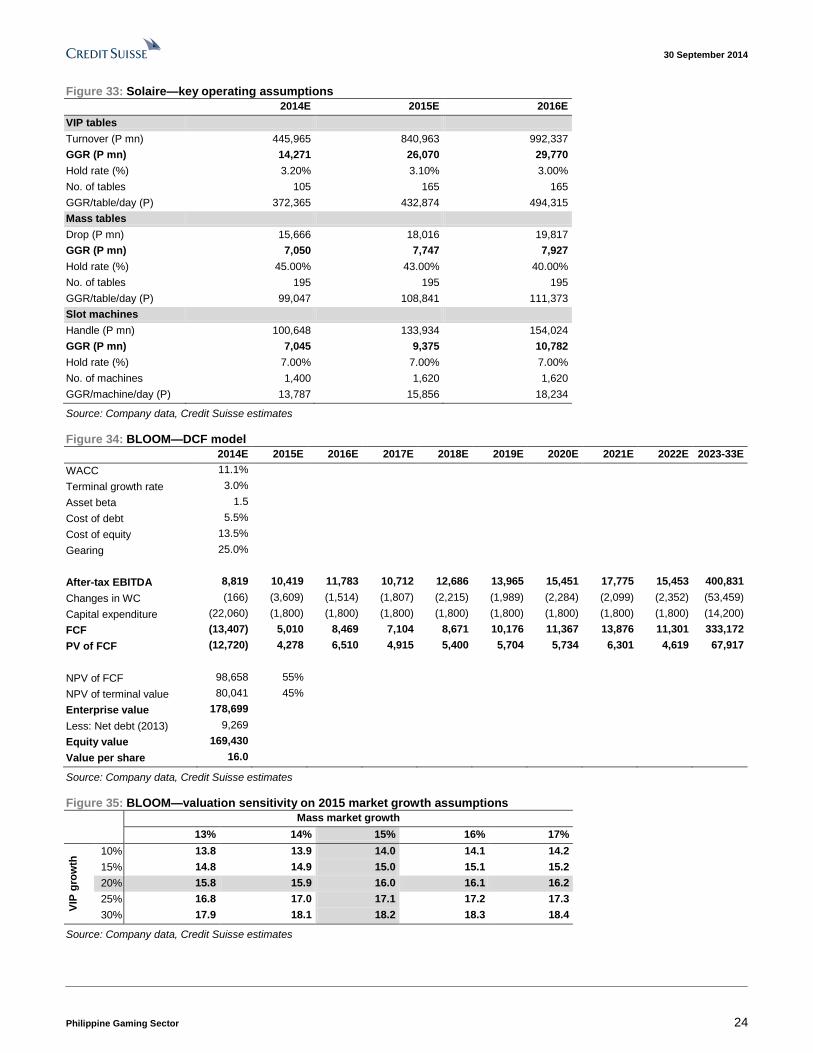

Figure 33: Solaire—key operating assumptions

2014E 2015E 2016E

VIP tables

Turnover (P mn) 445,965 840,963 992,337

GGR (P mn) 14,271 26,070 29,770

Hold rate (%) 3.20% 3.10% 3.00%

No. of tables 105 165 165

GGR/table/day (P) 372,365 432,874 494,315

Mass tables

Drop (P mn) 15,666 18,016 19,817

GGR (P mn) 7,050 7,747 7,927

Hold rate (%) 45.00% 43.00% 40.00%

No. of tables 195 195 195

GGR/table/day (P) 99,047 108,841 111,373

Slot machines

Handle (P mn) 100,648 133,934 154,024

GGR (P mn) 7,045 9,375 10,782

Hold rate (%) 7.00% 7.00% 7.00%

No. of machines 1,400 1,620 1,620

GGR/machine/day (P) 13,787 15,856 18,234

Source: Company data, Credit Suisse estimates

Figure 34: BLOOM—DCF model

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023-33E

WACC 11.1%

Terminal growth rate 3.0%

Asset beta 1.5

Cost of debt 5.5%

Cost of equity 13.5%

Gearing 25.0%

After-tax EBITDA 8,819 10,419 11,783 10,712 12,686 13,965 15,451 17,775 15,453 400,831

Changes in WC (166) (3,609) (1,514) (1,807) (2,215) (1,989) (2,284) (2,099) (2,352) (53,459)

Capital expenditure (22,060) (1,800) (1,800) (1,800) (1,800) (1,800) (1,800) (1,800) (1,800) (14,200)

FCF (13,407) 5,010 8,469 7,104 8,671 10,176 11,367 13,876 11,301 333,172

PV of FCF (12,720) 4,278 6,510 4,915 5,400 5,704 5,734 6,301 4,619 67,917

NPV of FCF 98,658 55%

NPV of terminal value 80,041 45%

Enterprise value 178,699

Less: Net debt (2013) 9,269

Equity value 169,430

Value per share 16.0

Source: Company data, Credit Suisse estimates

Figure 35: BLOOM—valuation sensitivity on 2015 market growth assumptions

Mass market growth

13% 14% 15% 16% 17%

VIP

gro

wth

10% 13.8 13.9 14.0 14.1 14.2

15% 14.8 14.9 15.0 15.1 15.2

20% 15.8 15.9 16.0 16.1 16.2

25% 16.8 17.0 17.1 17.2 17.3

30% 17.9 18.1 18.2 18.3 18.4

Source: Company data, Credit Suisse estimates

30 September 2014

Philippine Gaming Sector 25

Appendix I: Solaire Resort & Casino Project description

Figure 36: Solaire Phase 1

Source: Company data

Total land area: 8.3 hectares

Commencement of operations: 16 March 2013

Total cost: US$1.2 bn (Phase 1 and 1A)

Facilities

■ 488 hotel rooms, suites, and bayside villas.

■ Aggregate gaming floor area of 18,500 sq m containing approximately 1,400 slot

machines, 295 gaming tables and 88 ETGs.

■ 15 specialty restaurants and food & beverage outlets.

■ Grand ballroom with 1,000 seats.

■ Spa, fitness centre, and bayview promenade.

Expansion plans

Figure 37: Solaire Phase 1A (Opening date: 4Q14)

Gaming Non-gaming

220 slots 312-room all-suite hotel rooms

65 VIP gaming tables Retail promenade with 40 outlets

1,700-seat performance theatre

Additional F&B offerings

Nightclub, KTV and whisky bar

Spa, gym and salon

3,100 parking spaces

Source: Company data

Figure 38: Solaire Phase 2

Gaming Non-gaming

300 gaming tables Additional three hotels with 1,500 rooms

1,300 electronic gaming machines Event area for 15,000 people

100,000 sq m of exhibition space

35 F&B outlets

Source: Company data

30 September 2014

Philippine Gaming Sector 26

Company history

Bloomberry Resorts Corporation was incorporated in the Philippines and registered with

the Securities and Exchange Commission (SEC) on 3 May 1999. It was primarily engaged

in the manufacture and distribution of consumer communication and electronic equipment

within the Subic Bay Freeport Zone until 2003.

On 9 September 2011, Sureste and Bloomberry Resorts and Hotels, Inc. (BRHI) entered

into a Management Services Agreement (MSA) with Global Gaming Philippines, LLC

(GGAM) for technical assistance on all aspects of planning, design, layout and

construction of the Solaire project. Under the MSA, GGAM was granted the option to

purchase up to 921,184,056 shares of Bloomberry’s outstanding shares from PMHI.

GGAM exercised option to purchase under the MSA on 21 December 2012 and now owns

8.7% of outstanding capital stock in Bloomberry. Effective 12 September 2013, the MSA

with GGAM was terminated allegedly due to material breach by GGAM. GGAM however

alleged that it was BRHI and Sureste that violated the MSA. Both parties currently await

constitution of a three-member arbitration tribunal under the United Nations Commission

International Trade Law (UNCITRAL).

Enrique Razon Jr. indirectly owns 62% of Bloomberry through Prime Metroline Holdings, Inc.

and Sureste Properties, Inc. GGAM owns 8.7% of Bloomberry via Quasar Holdings, Inc.

Senior management

■ Enrique K. Razon, Jr. Chairman and Chief Executive Officer, age 54. Also the

President of Sureste, Chairman and President of International Container Terminal

Services, Inc. (ICTSI), and Chairman, President and Director of a number of ICTSI

subsidiaries and affiliates. He also serves as Chairman and President of Prime

Metroline, Chairman of the Board of Monte Oro Resources and Energy, Inc. and an

independent director of CLSA Exchange Capital Inc. He is a member of the American

Management Association, Management Association of the Philippines, World

Economic Forum and US Philippines Society.

■ Jose Eduardo J. Alarilla. Vice Chairman, age 62. Also President of BRHI, Lakeland

Village Holdings, Inc., Devoncourt Estates Inc., Eiffel House Inc., Manila Holdings and

Management, Inc. and Alpha Allied Holdings Ltd. He is also the President and CEO of

Mega Subic Terminal Services, Inc., Chairman of Mega Equipment International

Corp., as well as director of Monte Oro Resources and Energy, Inc. and International

Cleanvironment Systems Inc. He graduated with a Bachelor of Science degree in

Mechanical Engineering from De La Salle University and a Master’s degree in

Business Management from the Asian Institute of Management.

■ Thomas Arasi. Director, President and Chief Operating Officer from 11 October

2013 to present, age 56. Served as President and Chief Executive Officer of Marina

Bay Sands Pte Ltd. He graduated from Cornell University with a Bachelor of Arts

degree in Hotel and Restaurant Administration.

■ Estella Tuason-Occena. Chief Financial Officer and Treasurer, age 44. Chief

Financial Officer and Treasurer of BRHI as well as Director and Treasurer of Prime

Metroline. She serves as Executive Officer of ICTSI, Chief Financial Officer of Monte

Oro Resources and Energy, Inc., Director and Chief Financial Officer of International

Cleanvironment Systems, Inc., Treasurer of Sureste, Sureste Realty Corporation,

Lakeland Village Holdings Inc., Devoncourt Estates Inc., Achillion Holdings, Inc.,

Bloomberry Cultural Foundation, Inc. and Razon Industries, Inc. She graduated with

distinction from St. Scholastica’s College with a Bachelor's Degree in Commerce and

has an MBA from De La Salle University.

30 September 2014

Philippine Gaming Sector 27

■ Laurence Upton. Senior Vice President for International Marketing from 3 March

2014 to present, age 44. Served as Senior Vice President, VIP International

Marketing in Crown Ltd, Melbourne and was also connected with Star City Pty Ltd in a

number of senior management roles. He also serviced VVIP clients, the world’s largest

gaming customers including international celebrities.

■ Cyrus Sherafat. Senior Vice President for Casino Marketing from 17 March 2014

to present, age 31. Served as Vice President of Casino Marketing in Marina Bay

Sands in Singapore and brings with him ten years of experience in the gaming

industry through various marketing roles. He graduated from Cornell University’s

School of Hotel Administration.

■ Lorraine Koo Man Loo. Senior Vice President for VIP Services, age 37. She was

previously the Senior Manager then Assistant Vice President for Casino Customer

Service of the Galaxy Entertainment Group as well as Senior Executive Host at Marina

Bay Sands in Singapore. She is a graduate of Edith Cowan University in Australia with

a Bachelor of Arts degree in Communications Management.

■ Silverio Benny J. Tan. Corporate Secretary, age 57. He is a Managing Partner of

the law firm Picazo Buyco Tan Fider & Santos as well as Director and Corporate

Secretary of Prime Metroline, Bravo International Port Holdings Inc., Alpha

International Port Holdings Inc., Eiffel House Inc., Cycland Corp., OSA Industries

Philippines Inc. and Negros Perfect Circles Food Corp. Also a director of Celestial

Corporation, Skywide Assets Ltd., Monte Oro Resources and Energy Inc. Minerals

(SL) Ltd., and Dressline Holdings Inc. and its subsidiaries and affiliates. Also the

Corporate Secretary of Mapfre Insular Insurance Corporation, Cebu International

Container Terminal Inc., Sureste, BRHI, Lakeland Village Holdings Inc., and

Devoncourt Estates Inc. and Assistant Corporate Secretary of ICTSI, ICTSI Ltd., and

Monte Oro Resources and Energy, Inc. He graduated with a Bachelor of Arts Major

degree in Political Science, cum laude, from the University of the Philippines College

Iloilo and a Bachelor of Laws degree, cum laude, from the University of the Philippines

College of Law. Atty. Tan placed third in the 1982 Philippine Bar Exams.

■ Christine P. Base. Compliance Officer, age 43. Currently a Securities, Corporate

and Tax Lawyer at Pacis and Reyes, Attorneys and Managing Director of Legis

Forum, Inc. She is also Director and Corporate Secretary of Anchor Land Holdings,

Inc. and Corporate Secretary of Asiasec Equities, Inc., Araneta Properties, Inc. and

several private corporations. She graduated with a Bachelor of Science degree in

Commerce, major in Accounting from De La Salle University and is a Certified Public

Accountant. She earned her degree of Juris Doctor from Ateneo de Manila University

School of Law and is also a member of the Philippine Bar.

■ Christian R. Gonzalez. Director, age 38. Also a Director of Sureste and Prime

Metroline. He is Head of the Asia Pacific Region of International Container Terminal

Services, Inc., as well as Trustee and Auditor of ICTSI Foundation, Inc. He earned his

degree in Business Administration from Pepperdine University in California and his

Bilingual Masters in Business Administration from Instituto de Estudios Superiores de

la Empresa (IESE) Business School in Barcelona, Spain.

■ Donato C. Almeda. Director, age 59. He was President and CEO of Waterfront

Philippines Inc. as well as President of Waterfront Cebu City Hotel, Waterfront Mactan

Hotel, Fort Ilocandia Hotel and Insular Hotel in Davao. He was also the Managing

Director of Waterfront Promotions Ltd. He graduated with a degree in Engineering

from De La Salle University.

30 September 2014

Philippine Gaming Sector 28

■ Carlos C. Ejercito. Independent Director, age 68. Also an Independent Director of

Monte Oro Resources and Energy, Inc. He serves as Chairman and President of

Northern Access Mining Corporation, Forum Cebu Coal Corporation and

Morganhouse Holdings Inc. He is also a Governor of the Management Association of

the Philippines and a member of the Philippine Chamber of Commerce. He earned his

Bachelor’s degree in Business Administration, cum laude, from the University of the

East and is an MBA candidate of the Ateneo Graduate School of Business. He also

attended the Program for Management Development of Harvard Business School.

■ Jon Ramon Aboitiz. Independent Director, age 65. Also an Independent Director of

ICTSI. He is the Chairman of Aboitiz & Co., Inc and Aboitiz Equity Ventures, Inc. He

currently holds a number of varied positions in the Aboitiz Group such as President of

the Aboitiz Foundation, Vice Chairman of Unionbank of the Philippines and Chairman

of the Executive Committee, Risk Management Committee, Compensation and

Remuneration Committee, Nominations Committee, and Corporate Governance

Committee of Unionbank. He also serves as a member of the Board of Advisors of the

Coca-Cola Export Foundation, Trustee of the Philippine Business for Social Progress,

and Trustee of Santa Clara University.

30 September 2014

Philippine Gaming Sector 29

Asia Pacific / Philippines

Casinos & Gaming

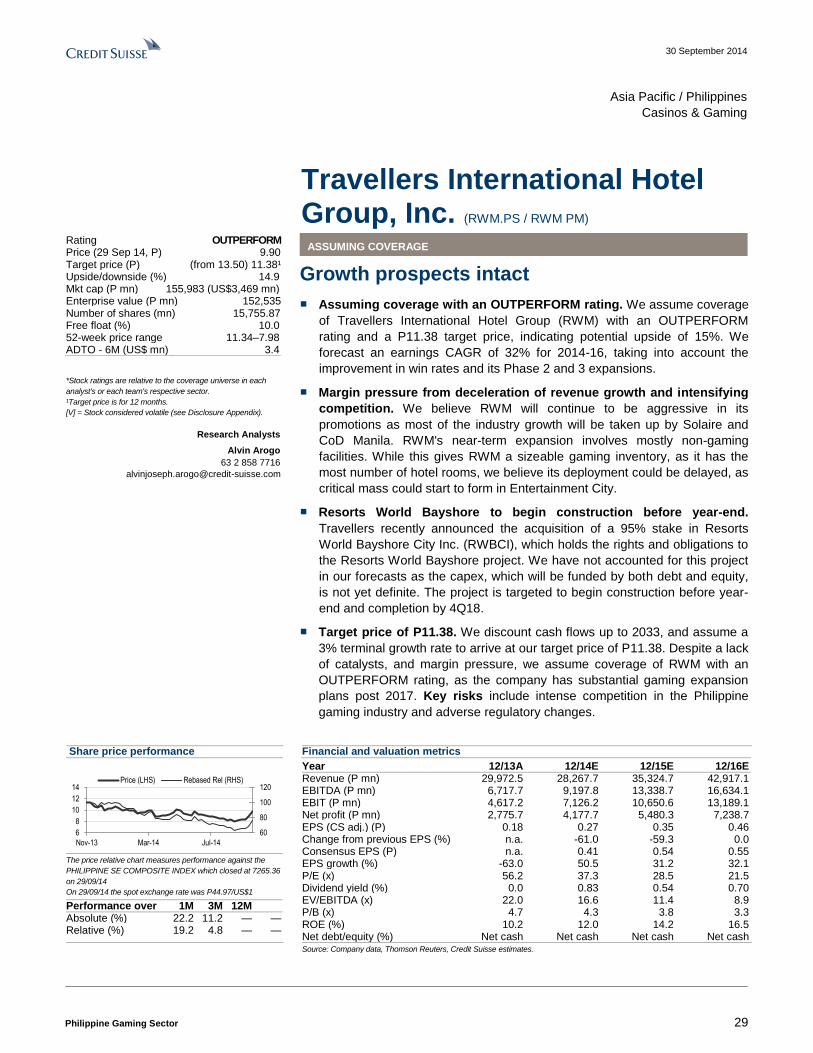

Travellers International Hotel Group, Inc. (RWM.PS / RWM PM)

ASSUMING COVERAGE

Growth prospects intact

■ Assuming coverage with an OUTPERFORM rating. We assume coverage

of Travellers International Hotel Group (RWM) with an OUTPERFORM

rating and a P11.38 target price, indicating potential upside of 15%. We

forecast an earnings CAGR of 32% for 2014-16, taking into account the

improvement in win rates and its Phase 2 and 3 expansions.

■ Margin pressure from deceleration of revenue growth and intensifying

competition. We believe RWM will continue to be aggressive in its

promotions as most of the industry growth will be taken up by Solaire and

CoD Manila. RWM's near-term expansion involves mostly non-gaming

facilities. While this gives RWM a sizeable gaming inventory, as it has the

most number of hotel rooms, we believe its deployment could be delayed, as

critical mass could start to form in Entertainment City.

■ Resorts World Bayshore to begin construction before year-end.

Travellers recently announced the acquisition of a 95% stake in Resorts

World Bayshore City Inc. (RWBCI), which holds the rights and obligations to

the Resorts World Bayshore project. We have not accounted for this project

in our forecasts as the capex, which will be funded by both debt and equity,

is not yet definite. The project is targeted to begin construction before year-

end and completion by 4Q18.

■ Target price of P11.38. We discount cash flows up to 2033, and assume a

3% terminal growth rate to arrive at our target price of P11.38. Despite a lack

of catalysts, and margin pressure, we assume coverage of RWM with an

OUTPERFORM rating, as the company has substantial gaming expansion

plans post 2017. Key risks include intense competition in the Philippine

gaming industry and adverse regulatory changes.

Share price performance

60

80

100

120

6

8

10

12

14

Nov-13 Mar-14 Jul-14

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

PHILIPPINE SE COMPOSITE INDEX which closed at 7265.36

on 29/09/14

On 29/09/14 the spot exchange rate was P44.97/US$1

Performance over 1M 3M 12M Absolute (%) 22.2 11.2 — — Relative (%) 19.2 4.8 — —

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E Revenue (P mn) 29,972.5 28,267.7 35,324.7 42,917.1 EBITDA (P mn) 6,717.7 9,197.8 13,338.7 16,634.1 EBIT (P mn) 4,617.2 7,126.2 10,650.6 13,189.1 Net profit (P mn) 2,775.7 4,177.7 5,480.3 7,238.7 EPS (CS adj.) (P) 0.18 0.27 0.35 0.46 Change from previous EPS (%) n.a. -61.0 -59.3 0.0 Consensus EPS (P) n.a. 0.41 0.54 0.55 EPS growth (%) -63.0 50.5 31.2 32.1 P/E (x) 56.2 37.3 28.5 21.5 Dividend yield (%) 0.0 0.83 0.54 0.70 EV/EBITDA (x) 22.0 16.6 11.4 8.9 P/B (x) 4.7 4.3 3.8 3.3 ROE (%) 10.2 12.0 14.2 16.5 Net debt/equity (%) Net cash Net cash Net cash Net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM Price (29 Sep 14, P) 9.90 Target price (P) (from 13.50) 11.38¹ Upside/downside (%) 14.9 Mkt cap (P mn) 155,983 (US$3,469 mn) Enterprise value (P mn) 152,535 Number of shares (mn) 15,755.87 Free float (%) 10.0 52-week price range 11.34–7.98 ADTO - 6M (US$ mn) 3.4

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Alvin Arogo

63 2 858 7716

30 September 2014

Philippine Gaming Sector 30

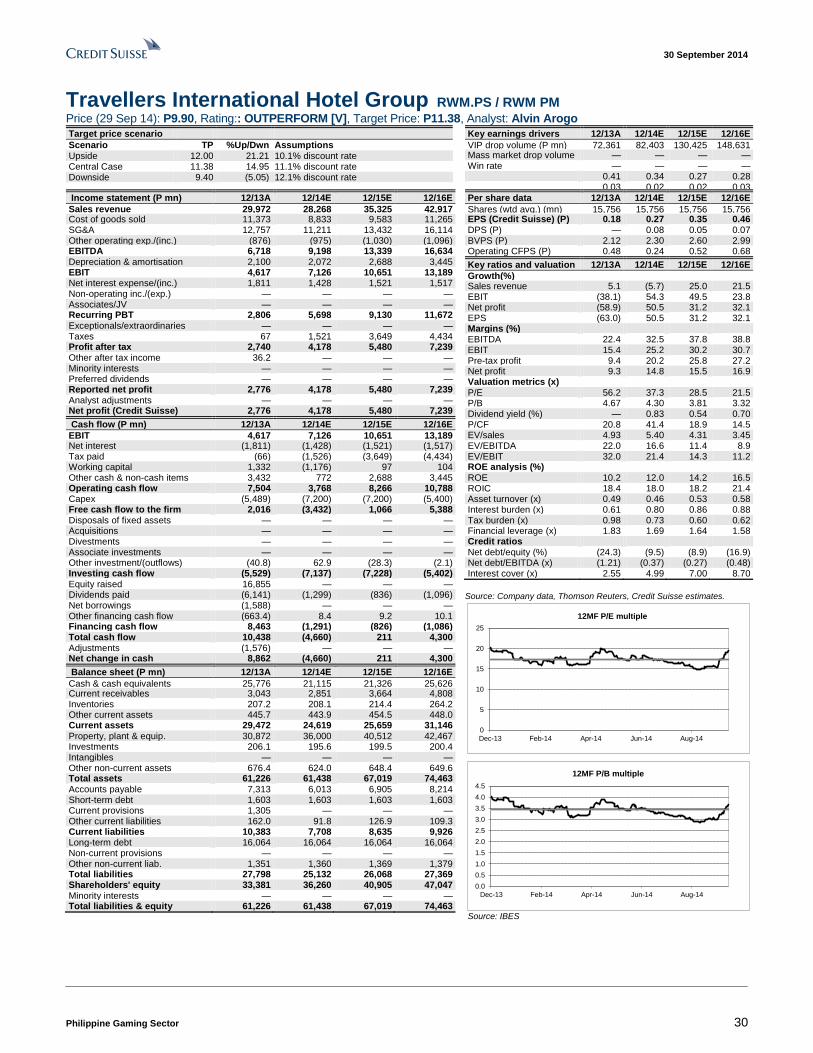

Travellers International Hotel Group RWM.PS / RWM PM Price (29 Sep 14): P9.90, Rating:: OUTPERFORM [V], Target Price: P11.38, Analyst: Alvin Arogo

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside 12.00 21.21 10.1% discount rate Central Case 11.38 14.95 11.1% discount rate Downside 9.40 (5.05) 12.1% discount rate

Key earnings drivers 12/13A 12/14E 12/15E 12/16E

VIP drop volume (P mn) 72,361 82,403 130,425 148,631 Mass market drop volume (P mn)

— — — — Win rate — — — — 0.41 0.34 0.27 0.28 0.03 0.02 0.02 0.03

Income statement (P mn) 12/13A 12/14E 12/15E 12/16E

Sales revenue 29,972 28,268 35,325 42,917 Cost of goods sold 11,373 8,833 9,583 11,265 SG&A 12,757 11,211 13,432 16,114 Other operating exp./(inc.) (876) (975) (1,030) (1,096) EBITDA 6,718 9,198 13,339 16,634 Depreciation & amortisation 2,100 2,072 2,688 3,445 EBIT 4,617 7,126 10,651 13,189 Net interest expense/(inc.) 1,811 1,428 1,521 1,517 Non-operating inc./(exp.) — — — — Associates/JV — — — — Recurring PBT 2,806 5,698 9,130 11,672 Exceptionals/extraordinaries — — — — Taxes 67 1,521 3,649 4,434 Profit after tax 2,740 4,178 5,480 7,239 Other after tax income 36.2 — — — Minority interests — — — — Preferred dividends — — — — Reported net profit 2,776 4,178 5,480 7,239 Analyst adjustments — — — — Net profit (Credit Suisse) 2,776 4,178 5,480 7,239

Cash flow (P mn) 12/13A 12/14E 12/15E 12/16E

EBIT 4,617 7,126 10,651 13,189 Net interest (1,811) (1,428) (1,521) (1,517) Tax paid (66) (1,526) (3,649) (4,434) Working capital 1,332 (1,176) 97 104 Other cash & non-cash items 3,432 772 2,688 3,445 Operating cash flow 7,504 3,768 8,266 10,788 Capex (5,489) (7,200) (7,200) (5,400) Free cash flow to the firm 2,016 (3,432) 1,066 5,388 Disposals of fixed assets — — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) (40.8) 62.9 (28.3) (2.1) Investing cash flow (5,529) (7,137) (7,228) (5,402) Equity raised 16,855 — — — Dividends paid (6,141) (1,299) (836) (1,096) Net borrowings (1,588) — — — Other financing cash flow (663.4) 8.4 9.2 10.1 Financing cash flow 8,463 (1,291) (826) (1,086) Total cash flow 10,438 (4,660) 211 4,300 Adjustments (1,576) — — — Net change in cash 8,862 (4,660) 211 4,300

Balance sheet (P mn) 12/13A 12/14E 12/15E 12/16E

Cash & cash equivalents 25,776 21,115 21,326 25,626 Current receivables 3,043 2,851 3,664 4,808 Inventories 207.2 208.1 214.4 264.2 Other current assets 445.7 443.9 454.5 448.0 Current assets 29,472 24,619 25,659 31,146 Property, plant & equip. 30,872 36,000 40,512 42,467 Investments 206.1 195.6 199.5 200.4 Intangibles — — — — Other non-current assets 676.4 624.0 648.4 649.6 Total assets 61,226 61,438 67,019 74,463 Accounts payable 7,313 6,013 6,905 8,214 Short-term debt 1,603 1,603 1,603 1,603 Current provisions 1,305 — — — Other current liabilities 162.0 91.8 126.9 109.3 Current liabilities 10,383 7,708 8,635 9,926 Long-term debt 16,064 16,064 16,064 16,064 Non-current provisions — — — — Other non-current liab. 1,351 1,360 1,369 1,379 Total liabilities 27,798 25,132 26,068 27,369 Shareholders' equity 33,381 36,260 40,905 47,047 Minority interests — — — — Total liabilities & equity 61,226 61,438 67,019 74,463

Per share data 12/13A 12/14E 12/15E 12/16E

Shares (wtd avg.) (mn) 15,756 15,756 15,756 15,756 EPS (Credit Suisse) (P) 0.18 0.27 0.35 0.46 DPS (P) — 0.08 0.05 0.07 BVPS (P) 2.12 2.30 2.60 2.99 Operating CFPS (P) 0.48 0.24 0.52 0.68

Key ratios and valuation 12/13A 12/14E 12/15E 12/16E

Growth(%) Sales revenue 5.1 (5.7) 25.0 21.5 EBIT (38.1) 54.3 49.5 23.8 Net profit (58.9) 50.5 31.2 32.1 EPS (63.0) 50.5 31.2 32.1 Margins (%) EBITDA 22.4 32.5 37.8 38.8 EBIT 15.4 25.2 30.2 30.7 Pre-tax profit 9.4 20.2 25.8 27.2 Net profit 9.3 14.8 15.5 16.9 Valuation metrics (x) P/E 56.2 37.3 28.5 21.5 P/B 4.67 4.30 3.81 3.32 Dividend yield (%) — 0.83 0.54 0.70 P/CF 20.8 41.4 18.9 14.5 EV/sales 4.93 5.40 4.31 3.45 EV/EBITDA 22.0 16.6 11.4 8.9 EV/EBIT 32.0 21.4 14.3 11.2 ROE analysis (%) ROE 10.2 12.0 14.2 16.5 ROIC 18.4 18.0 18.2 21.4 Asset turnover (x) 0.49 0.46 0.53 0.58 Interest burden (x) 0.61 0.80 0.86 0.88 Tax burden (x) 0.98 0.73 0.60 0.62 Financial leverage (x) 1.83 1.69 1.64 1.58 Credit ratios Net debt/equity (%) (24.3) (9.5) (8.9) (16.9) Net debt/EBITDA (x) (1.21) (0.37) (0.27) (0.48) Interest cover (x) 2.55 4.99 7.00 8.70

Source: Company data, Thomson Reuters, Credit Suisse estimates.

0

5

10

15

20

25

Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

12MF P/E multiple

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

12MF P/B multiple

Source: IBES

30 September 2014

Philippine Gaming Sector 31

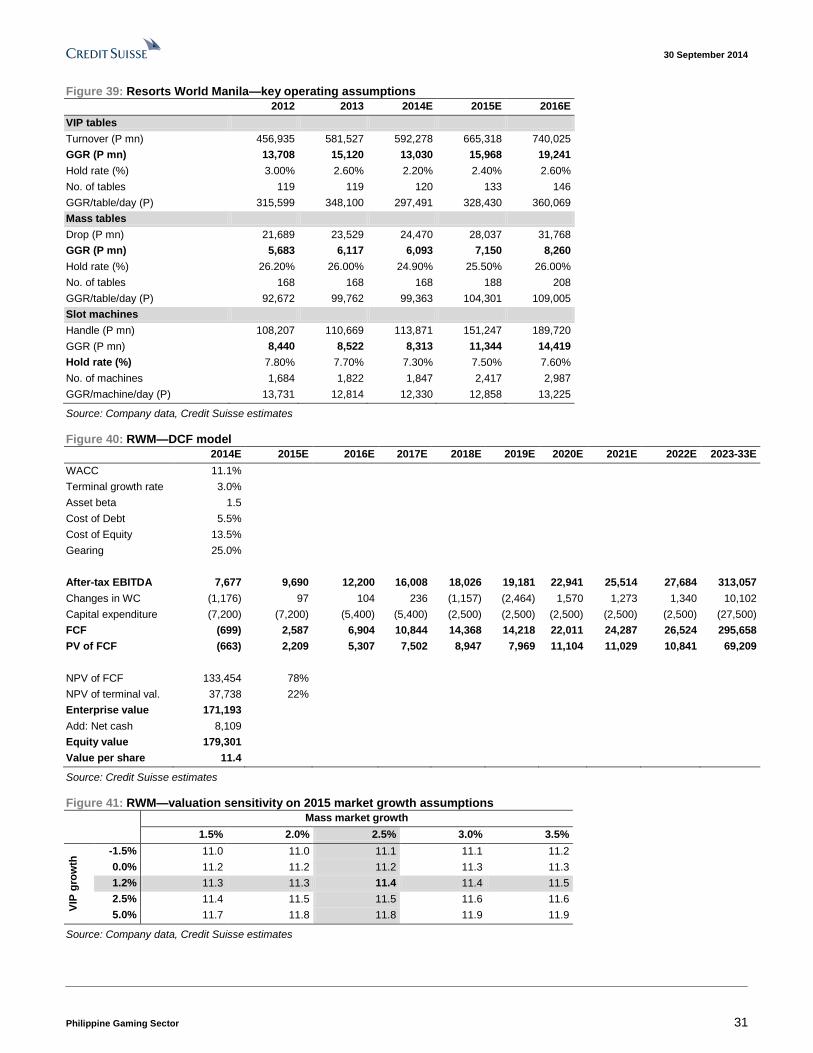

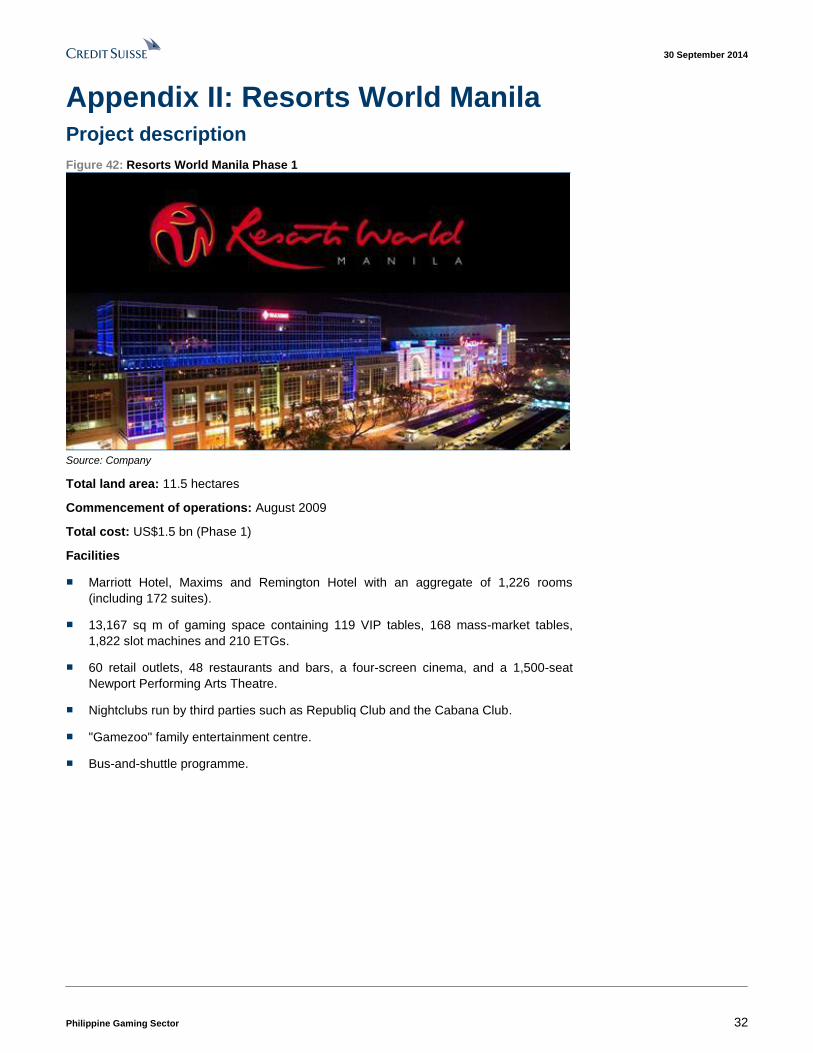

Figure 39: Resorts World Manila—key operating assumptions

2012 2013 2014E 2015E 2016E

VIP tables

Turnover (P mn) 456,935 581,527 592,278 665,318 740,025

GGR (P mn) 13,708 15,120 13,030 15,968 19,241

Hold rate (%) 3.00% 2.60% 2.20% 2.40% 2.60%

No. of tables 119 119 120 133 146

GGR/table/day (P) 315,599 348,100 297,491 328,430 360,069

Mass tables

Drop (P mn) 21,689 23,529 24,470 28,037 31,768

GGR (P mn) 5,683 6,117 6,093 7,150 8,260

Hold rate (%) 26.20% 26.00% 24.90% 25.50% 26.00%

No. of tables 168 168 168 188 208

GGR/table/day (P) 92,672 99,762 99,363 104,301 109,005

Slot machines

Handle (P mn) 108,207 110,669 113,871 151,247 189,720

GGR (P mn) 8,440 8,522 8,313 11,344 14,419

Hold rate (%) 7.80% 7.70% 7.30% 7.50% 7.60%

No. of machines 1,684 1,822 1,847 2,417 2,987

GGR/machine/day (P) 13,731 12,814 12,330 12,858 13,225

Source: Company data, Credit Suisse estimates

Figure 40: RWM—DCF model

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023-33E

WACC 11.1%

Terminal growth rate 3.0%

Asset beta 1.5

Cost of Debt 5.5%

Cost of Equity 13.5%

Gearing 25.0%

After-tax EBITDA 7,677 9,690 12,200 16,008 18,026 19,181 22,941 25,514 27,684 313,057

Changes in WC (1,176) 97 104 236 (1,157) (2,464) 1,570 1,273 1,340 10,102

Capital expenditure (7,200) (7,200) (5,400) (5,400) (2,500) (2,500) (2,500) (2,500) (2,500) (27,500)

FCF (699) 2,587 6,904 10,844 14,368 14,218 22,011 24,287 26,524 295,658

PV of FCF (663) 2,209 5,307 7,502 8,947 7,969 11,104 11,029 10,841 69,209

NPV of FCF 133,454 78%

NPV of terminal val. 37,738 22%

Enterprise value 171,193

Add: Net cash 8,109

Equity value 179,301

Value per share 11.4

Source: Credit Suisse estimates

Figure 41: RWM—valuation sensitivity on 2015 market growth assumptions

Mass market growth

1.5% 2.0% 2.5% 3.0% 3.5%

VIP

gro

wth