Embed Size (px)

Citation preview

Country Profile 2004

PhilippinesThis Country Profile is a reference work, analysing thecountry’s history, politics, infrastructure and economy. It isrevised and updated annually. The Economist IntelligenceUnit’s Country Reports analyse current trends and provide atwo-year forecast.

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where itslatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

Copyright© 2004 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5979

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Philippines 1

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Contents

Philippines

3 Basic data

4 Politics4 Political background6 Recent political developments8 Constitution, institutions and administration9 Political forces12 International relations and defence

15 Resources and infrastructure15 Population16 Education17 Health17 Natural resources and the environment18 Transport, communications and the Internet20 Energy provision

21 The economy21 Economic structure22 Economic policy26 Economic performance29 Regional trends

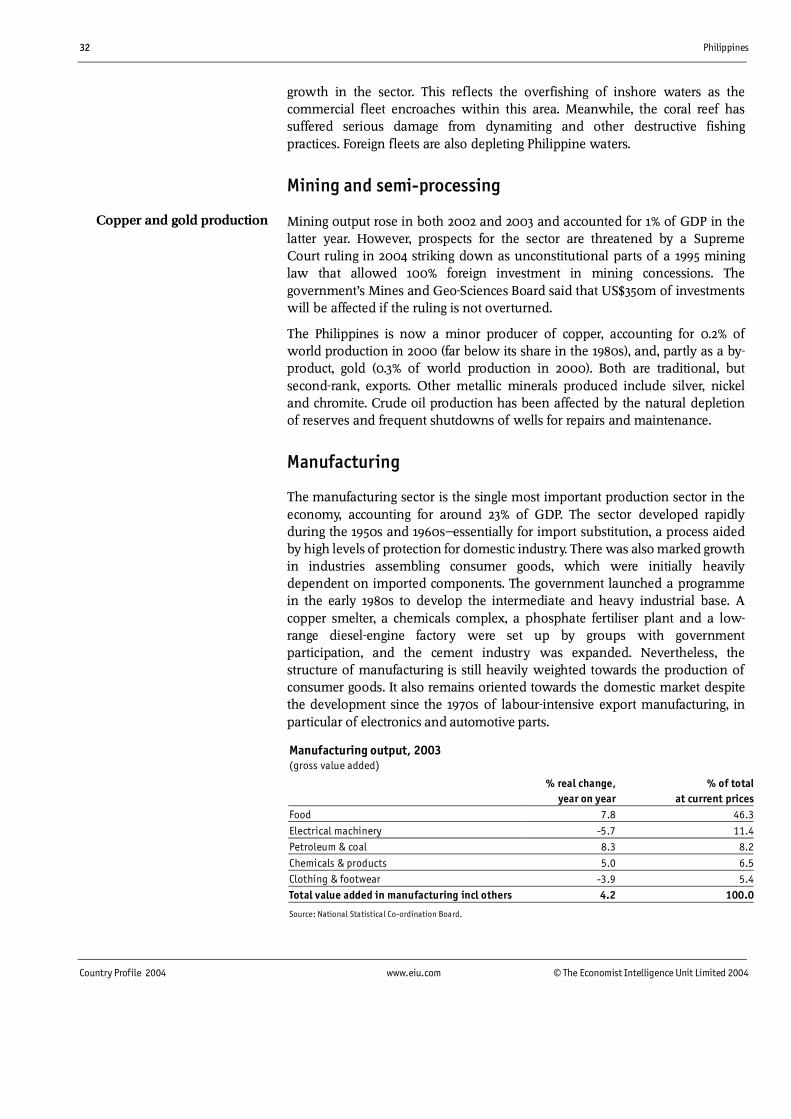

30 Economic sectors30 Agriculture32 Mining and semi-processing32 Manufacturing34 Construction34 Financial services37 Other services

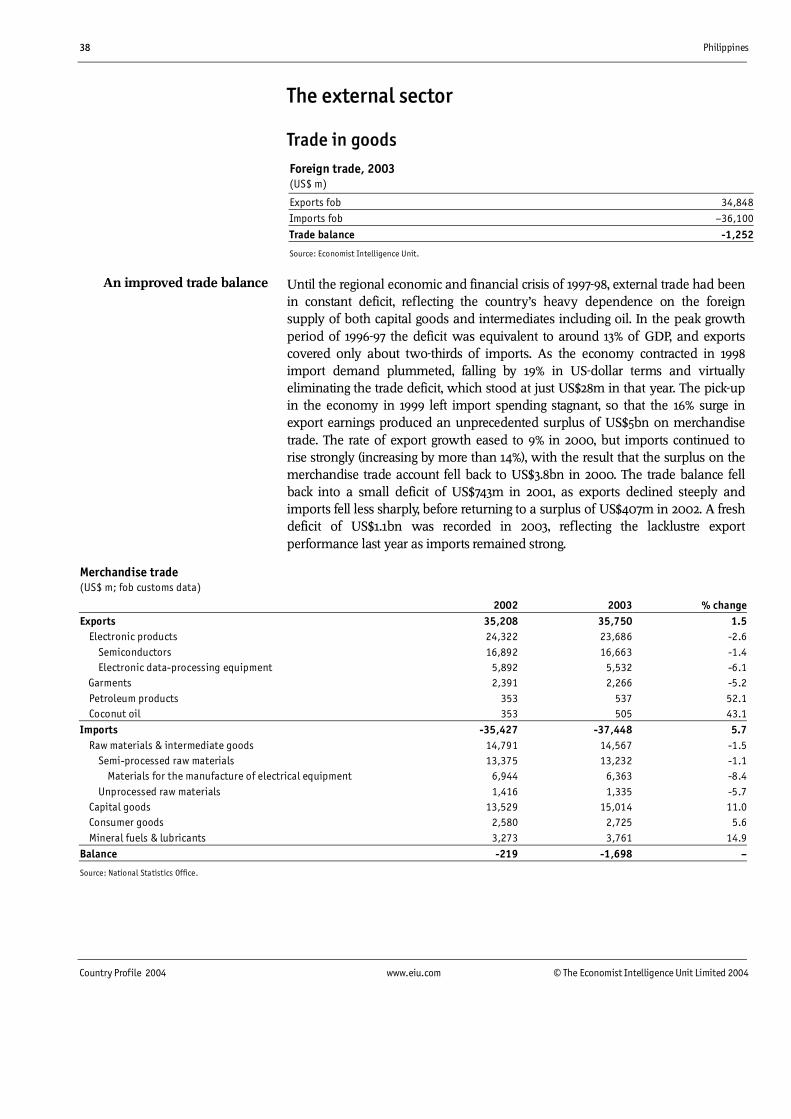

38 The external sector38 Trade in goods40 Invisibles and the current account41 Capital flows and foreign debt42 Foreign reserves and the exchange rate

44 Regional overview44 Membership of organisations

47 Appendices47 Sources of information48 Reference tables48 Population48 Labour force48 Structure of employment49 Transport statistics

2 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

49 Energy consumption by source49 Outstanding public-sector debt50 Government revenue and expenditure50 Money supply and credit50 Interest rates51 Gross domestic product51 Gross domestic product by expenditure52 Gross domestic product by sector52 Prices52 Meat production53 Production of major crops53 Output of wood products53 Private construction54 Mineral production54 Manufacturing production54 Philippines Stock Exchange indicators55 Visitor arrivals by country/region of residence55 Exports55 Imports56 Key commodity exports56 Main trading partners57 Balance of payments, IMF series58 Balance of payments, national series59 External debt59 Net official development assistance60 Foreign reserves60 Exchange rates

Philippines 3

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Philippines

Basic data

300,179 sq km

82.7m (mid-2004 official estimate)

Population in ‘000 (2000)

Metropolitan Manila Davao 1,147(National Capital Region) 9,933 Cebu 719 of which: Zamboanga 602 Manila (capital) 1,581 Cagayan de Oro 462 Quezon City 2,174 Bacolod 429 Kalookan 1,178 General Santos City 412 Pasig 582 Iloilo 366 Valenzuela 485 Las Pinas 473 Paranaque 450 Makati 449

Tropical

Hottest month, May, 24-34°C; coldest month, January, 21-30°C (average dailyminimum and maximum); driest month, February, 13 mm average rainfall;wettest month, July, 432 mm average rainfall

Tagalog, English and Spanish; many local dialects

Metric system; also some local units

Peso (P)=100 centavos. Average exchange rate in 2003: P54.2:US$1. Exchangerate on July 14th 2004: P55.82:US$1

Eight hours ahead of GMT

January-December

January 1st; April 8th, Maundy Thursday; April 9th, Good Friday; May 1st,Labour Day; June 12th, Independence Day; August 31st, National Heroes’ Day;November 1st, All Saints’ Day; November 30th, Bonifacio Day; December 25th,Christmas Day; December 30th, Rizal Day

Land area

Population

Main towns

Weather in Manila(altitude 14 metres)

Languages

Weights and measures

Currency

Time

Fiscal year

Public holidays in 2004

Climate

4 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Politics

The Philippines is a pluralist democracy modelled on the US, with an executivepresidency, a bicameral Congress and a Supreme Court that can rule on theconstitutionality of government actions. In January 2001 Gloria MacapagalArroyo, then vice-president, replaced the incumbent president, Joseph Estrada,in a civilian coup backed by the military. She served out the remainder of hissix-year term before winning re-election in her own right in the May 10th 2004presidential election. The congressional elections held on the same dayproduced a large pro-administration majority, headed by the president’s party,Lakas ng Edsa-National Union of Christian Democrats (Lakas), in the House ofRepresentatives (the lower house) and gave the president a larger majority inthe Senate (the upper house).

Political background

The Philippine islands, inhabited by Malay peoples, were a colony of Spainfrom the late 1500s until the end of the 19th century. In the early 19th centurythat export crops sugar, coconuts, abaca (Manila hemp) and tobacco weredeveloped. At the same time a Chinese entrepreneurial class evolved, marryinginto the indigenous population and forming an elite based on land ownership.Spanish colonial rule ended in December 1898 after the US intervened in apopular rebellion that had broken out two years earlier. Spain ceded thePhilippines to the US. Under US colonial rule democratic institutions wereintroduced, Filipinos increasingly took over all political and bureaucraticpositions, and English-language education was extended throughout thecountry. In 1934 the Philippines became an internally self-governingcommonwealth, with full independence scheduled for July 4th 1946. Thetransition to independence was interrupted by the Japanese invasion ofDecember 1941. The Japanese occupation and the battle for liberation, inwhich local guerrilla groups played a significant role, destroyed much of thePhilippines’ physical infrastructure.

The independent republic, inaugurated on schedule in 1946, maintainedpreferential economic relations with the US. The constitution was modelled onthat of the US and, as in Washington, power tended to alternate between twoparties, the Nationalists and the Liberals. The fairly peaceful alternation in powerwithin the political elite was interrupted in September 1972 as the president,Ferdinand Marcos, neared the end of his second term. Citing the threat from“subversive forces”, Mr Marcos imposed martial law.

For the next 13 years until 1986 the Philippines experienced “constitutionalauthoritarianism”. In a series of elections the president and the party that he hadcreated, the New Society Movement (Kilusan Bagong Lipunan), consistentlyrecorded overwhelming popular support, whether or not the oppositionparticipated in the electoral exercise. This owed something to the virtualmonopoly over the media exercised by the president and his close associates, butmore to manipulation and outright cheating at the polls. With many of its leaders

The colonial andcommonwealth periods

An independent republicclosely tied to the US

The Marcos autocracy

Philippines 5

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

in detention or voluntary exile, the moderate opposition seemed unable tomobilise feeling against the administration and its abuses of power. The mosteffective opposition came from the communist New People’s Army (NPA), whichwas active in rural areas, and from the southern areas, where a secessionistMuslim movement had been active since before the introduction of martial law.

The situation changed radically in August 1983, when Benigno Aquino, theopposition leader regarded as the most credible alternative to Mr Marcos, wasassassinated minutes after his return from exile and while under military escort.A series of massive demonstrations followed in which the disenchantment ofthe urban middle class, and notably the business community, was expressed forthe first time. To reassert his own supremacy, Mr Marcos called an earlypresidential election for February 1986. In a close-run contest he was narrowlydefeated by the candidate of a temporarily united opposition, Corazon Aquino,Mr Aquino’s widow. The attempt by Mr Marcos to hold on to power set off acoup attempt by the military, backed by the deputy chief of staff, Fidel Ramos,and the defence minister. This received critically important backing fromMrs Aquino’s People’s Power movement and the local Catholic Church. Underpressure from the US, Mr Marcos went into voluntary exile in Hawaii, where hedied in 1989.

Under the new regime civil liberties were restored, political prisoners werereleased and an attempt was made to negotiate with the NPA. A newconstitution, drawn up by a convention appointed by Mrs Aquino, largelyrestored the set-up that existed before 1972, but with new controls on thepresidency based on the experience of the Marcos years. From July 1986 therewas a series of attempted coups, and rumours of coups, in which elements ofthe military were involved. In all cases the loyalty of the then chief-of-staff,Mr Ramos, was critical. Meanwhile, the reform hopes of the early days faded.The much-vaunted land reform was stalled by bureaucratic delay and landlordopposition, widespread corruption continued and the government wasperceived as ineffectual.

Mr Ramos won the mid-1992 presidential election. Within months of coming tothe power, he had built up a large pro-government majority in Congress,secured a cessation of hostilities by dissident military groups and begun theprocess of peace negotiations with both communist and Muslim secessionistrebels. A ceasefire was agreed with the Muslim rebels in late 1993, and thecommunist insurgency began to weaken as fissures within the leadershipemerged and active membership fell. However, deep-rooted economic andsocial problems remained largely unresolved. The president came underincreasing pressure from some of his supporters to stand for a second term in 1998.However, this would have required a revision of the 1987 constitution (seeConstitution, institutions and administration), and was strongly opposed by theCatholic Church, opposition politicians and some prominent members of thebusiness community, all of whom feared a drift to a constitutionally riggedautocracy on the Marcos precedent. The persistent speculation about thepresident’s intentions was only put to rest when Mr Ramos endorsed thesecretary-general of Lakas as his nominee for the presidency in November 1997.

The return to a free democracy

Political stability underFidel Ramos

6 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Recent political developments

In the presidential election of May 1998 the administration’s candidate was beatenby a wide margin by the popular vice-president and former film star, JosephEstrada. Mr Estrada, who was backed by an alliance of the two opposition parties,the Nationalist People’s Coalition (NPC) and Laban ng Demokratikong Pilipino(Laban, or Struggle for a Democratic Philippines; the pro-administration partyunder Mrs Aquino), won 40% of the vote in a field of ten candidates. The Lakascandidate for the vice-presidency, Gloria Macapagal Arroyo, won even moreresoundingly, with 50% support. The coalition backing Mr Estrada won onlyaround 60 of the 208 directly elected seats in the House of Representatives, but asthe party of the presidential incumbent, renamed Laban ng Masang Pilipino(LAMP, Struggle of the Filipino Masses), it attracted enough defections from Lakasto build a large majority in the lower house by end-1998.

The worst fears of a lurch towards populist policies under the self-proclaimed“president for the poor” were not borne out in the first two years of the Estradaadministration as it maintained the macroeconomic targets and liberalisingstance of its predecessor. However, policy formulation and implementationwere often incoherent and unco-ordinated. Cronyism re-emerged on a majorscale, and the president himself was implicated in a stockmarket scandal inJanuary 2000. Although the president boosted his personal popularity bylaunching an all-out attack in March 2000 on Muslim rebels in Mindanao,sentiment in the business community, both foreign and domestic, deterioratedfurther as allegations of corruption by the president came to light. Theseculminated in October 2000 when a disaffected presidential crony claimed thatMr Estrada had been receiving multi-million-peso monthly pay-offs from theproceeds of illegal gambling as well as a slice of government funds for tobaccoindustry support.

On November 13th 2000 the House of Representatives voted through articles ofimpeachment on four counts: bribery, graft and corruption, betrayal of publictrust and culpable violation of the constitution. However, on January 16th 2001pro-Estrada senators won a vote in the Senate rejecting as inadmissibleevidence that could have led to Mr Estrada’s impeachment. The opposition wasnot prepared to accept a de facto acquittal on these terms. Mass streetdemonstrations immediately began, on the pattern of February 1986, and as in1986 civilians and the military came together. The heads of all the armedservices and of the national police joined the call for the president to resign.Besieged in the presidential palace, Mr Estrada agreed to leave the premisesalthough he refused to resign formally. He was deemed by the Supreme Courtto have abandoned the office of president, and Gloria Macapagal Arroyo wassworn in as president on January 20th 2001.

The ouster of Mr Estrada prompted a rebound of confidence among thepolitical and business elite. In May 2001 followers of the deposed presidentattempted to storm the presidential palace after Mr Estrada was arrested on acharge of “economic plunder” a capital offence. The administration secured astrong popular mandate in the congressional election in mid-May 2001, with a

Joseph Estrada is electedpresident by a wide margin

Inefficiency and corruptionlead to Mr Estrada’s ouster

The new governmentgradually gains legitimacy

Philippines 7

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

sizeable majority in the House of Representatives and a slim, but viable,majority in the Senate. Hopes that Ms Macapagal Arroyo’s first administrationwould achieve rapid progress on economic reform were, however,disappointed, as the government grappled with the ballooning budget deficitinherited from the Estrada government and the security situation in the southof the country remained dire. Ms Macapagal Arroyo has come to relyincreasingly heavily on the US in counter-insurgency activities within thePhilippines. In the wake of the September 11th 2001 terrorist attacks in the US,Abu Sayyaf, an extremist Muslim rebel group in Mindanao (see Political forces)was linked by the US to the al-Qaida terrorist network. This paved the way fora resumption of US military aid, in the form both of hardware and of technicalassistance, agreed in December 2001, and the deployment of US personnel onthe ground from January 2002 in support of the Philippine military’s campaignagainst the rebels.

On December 30th 2002 Ms Macapagal Arroyo announced that she would notrun for a second presidential term. However, many political analysts continuedto expect her to contest the May 10th 2004 presidential election, and she finallyreversed her decision in November 2003. In the final year of her first term inoffice, there was a gradual increase in political instability as pro-Estrada forcesreadied themselves to right what they saw as the wrong of January 2001. InJuly 2003 junior officers mutinied in the Makati financial district of Manila, butthe attempted coup was quickly defeated, and Ms Macapagal Arroyo managedto hold the government together in the run-up to the elections. Her main rivalwas a film star and political novice, Fernando Poe, an associate of Mr Estrada.Mr Poe initially rode high in the opinion polls, but the candidacy of PanfiloLacson, the police chief in Mr Estrada’s administration, split the oppositionvote, allowing Ms Macapagal Arroyo to win re-election by a margin of around1m votes on May 10th. She was sworn in for a fresh six-year term on June 30th,despite the fact that Mr Poe’s supporters continued to contest the legitimacy ofthe result. Ms Macapagal Arroyo can claim some improvement in negotiationswith insurgent rebels both Muslim separatist groups in Mindanao and theCommunist Party of the Philippines and peace talks with a number of groupsare likely to take place in the near future.

Important recent events

March 2000

The government launches a campaign that clears the most active Muslimsecessionist movement at that time, the Moro Islamic Liberation Front (MILF), out ofits bases in Mindanao.

November 2000

The House of Representatives (the lower house) votes to approve the articles ofimpeachment of the president, Joseph Estrada, on charges of bribery and corruption.

January 2001

Mr Estrada is removed from office after mass street demonstrations demanding hisresignation are backed by the military high command. His vice-president, GloriaMacapagal Arroyo, becomes president.

Ms Macapagal Arroyo wins asecond term

8 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

May 2001

Mid-term elections give the administration a comfortable majority in the House ofRepresentatives and a narrow majority in the Senate (the upper house).

August 2001

A ceasefire is agreed with the MILF, as the preliminary to peace negotiations.

January 2002

US forces return to the Philippines to assist the military campaign against a smallextremist Muslim rebel group, Abu Sayyaf.

June 2002

The defection of one senator ends the government’s majority in the upper house.The government regains its majority in July, when opposition senators cross the floorto the government side.

December 2002

Ms Macapagal Arroyo announces that she will not stand for a new term in the 2004presidential election. But speculation continues that she will do so.

May 2003

The Philippines is declared a Major Non-NATO Ally during a visit by Ms MacapagalArroyo to the US. Both countries commit themselves to crushing the Abu Sayyafguerrilla group.

July 2003

An attempted coup by more than 300 junior officers and soldiers in the Makatifinancial district of Manila is crushed, but security-related jitters continue.

November 2003

Fernando Poe, a film star with no political experience, announces his candidacy inthe 2004 presidential election. Ms Macapagal Arroyo reverses her decision not tostand for re-election.

May 2004

Ms Macapagal Arroyo wins re-election and has the support of an enhanced majorityin the Senate.

Constitution, institutions and administration

The constitution introduced in 1987 provides for a single six-year presidentialterm. The president is chief executive, head of state and commander-in-chief.The legislature is bicameral, with a Senate of 24 members elected “at large” (ona nationwide ballot), and a House of Representatives composed of 212members directly elected by district and up to 52 members chosen by partylist. Senators have six-year terms and representatives three-year terms. Thepresident may not abolish Congress, and the presidential veto can beoverridden by a two-thirds majority in the legislature. The judiciary, which isindependent of the executive, rules on the constitutionality of presidentialdecrees. A permanent, independent commission oversees compliance with abill of rights contained in the constitution.

A structure on the US model

Philippines 9

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

The president selects the members of the cabinet, but, in line with theseparation of powers, they must be from outside Congress. All cabinet appoint-ments require congressional approval, but, once approved, an incumbent canbe removed only by the president. The National Economic DevelopmentAuthority (NEDA), headed ex officio by the planning secretary, co-ordinatespolicy and decisions in all areas relevant to the economic development plan.

The institutional structure is transparent, but its operation is far from open. Thisstems from the deeply entrenched patronage system that pervades Philippinesociety, where a favour granted requires a favour in return. Although this canhave a benign aspect, preserving social stability in the short term, it seriouslyundermines the quality of policy formulation and implementation.

Traditionally, government in the Philippines has been highly centralised.However, the 1987 constitution made provision for the establishment ofautonomous regions in two areas with distinct historical and culturalheritages the Cordillera region of northern Luzon, and Mindanao if the localpopulation voted by referendum for such status. Both autonomous regionshave been established, although the autonomous region in Mindanao is limitedto the five provinces (out of 13) in Mindanao that voted for inclusion. Theautonomous authorities have powers in the areas of personal and propertyrelations, regional and urban planning, education, and economic and socialdevelopment. The Local Government Code of 1991 also devolved some fiscalpowers, in the form of the oversight and control of government spending, tolocal governments.

Political forces

Political parties in the Philippines are based on personalities rather thanideologies. All those represented in Congress support the existing political andsocial structures, espouse a market economy (until it threatens sectoralinterests), and are nationalistic, to varying degrees. There are thus continualshifts in allegiance. The president tends to attract a greater following inCongress than the election results would indicate, at least in the early years ofhis term. In the final years of a presidential term of office the parties tend tosplinter as presidential hopefuls emerge and the president has only limitedpatronage to offer.

After the congressional elections in May 2004 the three major partiesrepresented in Congress were as follows.

The president’s party is Lakas ng Edsa-National Union of Christian Democrats(Lakas), which was formed in 1992 to support the presidential candidacy ofMr Ramos. Its strength in Congress was eroded after the May 1998 election,which brought Joseph Estrada to power, but surged once more in the 2001 mid-term election following Ms Macapagal Arroyo’s assumption of the presidency.Lakas won 91 of 212 directly elected seats in the House of Representatives in theMay 2004 election.

Parties based aroundpersonalities

Lakas

Two autonomous regions

10 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The Nationalist People’s Coalition (NPC) was originally formed to support thepresidential candidacy of Eduardo Cojuangco (a former Marcos crony) in 1992.In the 1998 election it backed Mr Estrada’s presidential candidacy and was thelargest component of the pro-administration coalition, Laban ng MasangPilipino (LAMP, now defunct). The NPC remained part of the pro-administration coalition led by Lakas under Ms Macapagal Arroyo, and won 58seats in the May 2004 election. Altogether pro-administration parties won 181of the 212 directly elected seats in the May poll.

Laban ng Demokratikong Pilipino (Laban, Struggle for a Democratic Philippines)was formed in 1988 to back the Aquino presidency. After the 1992 election itsposition as the largest party in the House of Representatives soon collapsedowing to defections to the new administration party, Lakas. The party gave itssupport to Mr Estrada in 1998 after its leader, Edgardo Angara, abandoned hisown presidential ambitions to run for the vice-presidency. The LDP is currentlythe largest opposition party in the House of Representatives, although it wononly 15 seats in the May 2004 election.

Outside the mainstream of congressional politics are political forces for whichideology is the determining factor, as follows.

The National Democratic Front (NDF) is the umbrella organisation for theMaoist Communist Party and its military wing, the New People’s Army (NPA).The Philippines has a long tradition of rural rebellion, and the NPA, founded in1969, took up the fight waged by the Hukbalahap rebel movement in Luzon inthe mid-1950s. The NPA expanded rapidly under martial law, the number of itsregulars rising to an estimated 25,000 by mid-1985. It was then thought tocontrol one-fifth of villages and to be active in 60 of the 75 provinces, as well asin the Manila region. Its attachment to the Maoist dogma that revolution mustcome from the countryside meant that it played no role as an organisation inthe overthrow of Mr Marcos. The post-Marcos regimes have eroded its popularbase by offering amnesties, the legalisation of the Communist Party (in late1992), and land and jobs to surrendering rebels, while maintaining an activemilitary campaign. Peace negotiations with the government are intermittentlyunder way, although a full resolution of the NDF insurgency may take sometime to reach.

Another more heavily armed but less cohesive rebel movement is that of theMuslim secessionists in Mindanao. In the past, the main rebel group was theMoro National Liberation Front (MNLF). The Moro Islamic Liberation Front(MILF) has been more active in recent years. The secessionist movement has ahistory stretching back several centuries. There is no easy solution to demandsfor secession or autonomy for Mindanao, since migration from Luzon and theVisayas in the 1950s and 1960s has created a Christian majority or near-parity in a number of provinces in the region.

A referendum on autonomy was held in Mindanao in August 2001, but it failed toproduce an agreement that the whole of Mindanao should come under thecontrol of an autonomous administration. The MILF has taken part in peace talkswith the government, and these are expected to continue, but hardliners within

The NPC

Laban

The NDF rebels

The rebels in Mindanao

Philippines 11

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

the rebel movement may delay progress towards a peace accord. A more extremegroup, Abu Sayyaf, periodically kidnaps foreigners for ransom and is not open tothe possibility of dialogue with the government.

Another important political force is that represented by the Catholic Church. Itplayed an active part in the civilian opposition to the Marcos regime, andhelped the military rebellion that brought Mrs Aquino to power by bringing thepopulation out on to the streets of Manila in its support. The church also tookthe lead in demands for Mr Estrada’s resignation in the wake of the corruptionallegations in late 2000. The church has given its blessing to the disputedvictory of Ms Macapagal Arroyo in the May 2004 presidential election.

Main political figures

Gloria Macapagal Arroyo

President, brought to power in January 2001 in a civilian coup backed by the military.She had been elected vice-president in May 1998, with more than 50% of the vote. Shecompleted the presidential term of the ousted president, Joseph Estrada, and wonre-election in her own right in May 2004. Ms Macapagal Arroyo’s first term wasdisappointing in terms of economic reform. Her supporters hope that she will movemore determinedly to implement a reform agenda over the next six years.

Noli de Castro

Elected as vice-president in May 2004. Despite having served as a senator, Mr deCastro is a former TV broadcaster, and this constituted his chief appeal to theelectorate.

Fidel Ramos

A former president and retired general, Mr Ramos continues to play the role of elderstatesman. His influence may be crucial in encouraging the new administration toimplement its reform agenda.

Joseph Estrada

The former president, elected in May 1998 for a six-year term with strong popularbacking. Deposed in January 2001 after the collapse of his impeachment trial inthe Senate, he remains under arrest on charges of perjury and economic plunder.

Fernando Poe

A film star and associate of Mr Estrada, Mr Poe failed to win the presidency inMay 2004 and continues to dispute the result.

Raul Roco

A former education secretary, Mr Roco topped opinion polls at one stage in therecent presidential election campaign. Concerns over his health and a lack of financeled his campaign to collapse in the spring. He came fourth in the poll.

Panfilo Lacson

A former police chief in the Estrada administration, Mr Lacson insisted on mountinga separate presidential bid to that of Mr Poe, thus splitting the opposition vote andhanding victory to Ms Macapagal Arroyo. Mr Lacson is surrounded by accusations

The Catholic Church

12 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

that the Presidential Anti-Crime Commission murdered 11 criminals while heheaded it.

Organised labour has little power in the Philippines. Only around one in fiveworkers was a member of a trade union in the late 1990s, although the ratewas significantly higher in multinational firms, where union membership wasaround one in three. A tiny proportion (only 4% of the 11.8m salaried workersin the mid-1990s) were covered by collective-bargaining agreements. Thisreflects the weak bargaining position of workers in a labour-surplus economy.

International relations and defence

A continuing foreign policy priority has been the strengthening of relationswith fellow members of the Association of South-East Asian Nations, orASEAN (see Regional overview: Membership of organisations). Membershipof this organisation gives the Philippines a regional identity independent ofrelations with the US. Another priority for the Philippine government isparticipation in a regional force to counterbalance China, which is seen as athreat, notably in the dispute over the Spratly Islands in the South China Sea.

The US has maintained a special relationship, both political and economic,with the Philippines since the latter’s independence in 1946. The USadministration has on a number of occasions played a pivotal role in domesticpolitical affairs, inducing Mr Marcos to leave the country in February 1986 andbacking the Aquino administration against coup attempts (on one occasionwith military aircraft). The Philippines was home to two of the most importantUS military bases outside US territory, the naval facility at Subic Bay and thenearby air base at Clark Field. The non-renewal of the lease on the militarybases when it expired in 1991 was the most open sign of the Philippines’emerging “Asian” identity. However, the US “war on terror” and thePhilippines’ own problems with Muslim insurgents have led to a closermilitary relationship between the US and the Philippines over the past fewyears. The US has awarded the Philippines Major Non-NATO Ally status, andUS troops and hardware arrived in 2002 to support the campaign against AbuSayyaf. The US remains a leading source of private investment in thePhilippines, reflecting links forged during the colonial period and the earlydecades of independence; it has by far the largest Filipino community outsidethe Philippines; and its culture remains the dominant foreign influence withinthe Philippines.

Armed forces and paramilitary, 2003Armed forces 106,000 Army 66,000 Navy (incl 8,000 marines) 24,000 Air force 16,000Paramilitary 84,000 Philippine National Police (PNP) 40,500 Coastguard 3,500 Civil Armed Force Geographical Units (part-time) 40,000

Source: International Institute for Strategic Studies, The Military Balance, 2003-2004.

Weak trade unions

Relations with the US

Regional issues

Philippines 13

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Security risk in the Philippines

I. Armed conflict

Armed conflict is a regular and disturbing feature of the domestic political scene inthe Philippines. Over the years, several groups of armed rebels have been active inthe large southern island of Mindanao, seeking the creation of an independent stateon the island. The two principal secessionist movements are the Moro NationalLiberation Front (MNLF) and the Moro Islamic Liberation Front (MILF). (Moro is theterm traditionally used to describe the Muslim population of the southern islands ofthe Philippines.) The Philippine military has been battling with the rebels for nearlythree decades, although a peace agreement was signed with the MNLF in 1996. Aseparate ceasefire was reached with the MILF in August 2001, but armed conflict hascontinued. Negotiations for a permanent settlement are likely to be resumed at somepoint in the near future.In 2003 the military also found itself in pitched battles with yet another Mindanaorebel group, Abu Sayyaf. A small extremist Islamist organisation, Abu Sayyaf claimsto be fighting for an independent Muslim state, but in fact appears more interested inkidnapping tourists and local residents for ransom. Abu Sayyaf is famously brutal:more than a few of its kidnap victims have been beheaded. Some members of thegroup have reportedly been trained at camps in Afghanistan run by Osama binLaden’s al-Qaida terrorist network. The Philippine military intensified its campaignagainst Abu Sayyaf after an American tourist was killed in mid-2001, and thecampaign has received backing in the form of both hardware and personnel fromthe US as part of its “war on terrorism”. This involvement has enhanced thePhilippine military’s ability to flush out Abu Sayyaf in the difficult terrain of therebel group’s island base, Basilan, but could be counterproductive if it is perceived asanti-Muslim and so provokes terrorist acts in other parts of Mindanao. This area ofthe Philippines is clearly unsafe, for foreigners as well as local residents.It is important to note, however, that the Muslim insurgency is far removed from thepolitical and business centre of Manila. Investors who avoid the disputed regions areunlikely to be affected significantly by the secessionist movements and the military’sattempts to subdue them.The challenge from the communist guerrilla movement, the New People’s Army(NPA), is much reduced but not defunct. The NPA’s activities are essentially confinedto attacking the security forces and local political leaders, but are more widelyspread, notably in Luzon, and thus are closer to the country’s economic hub. As withthe MILF, peace negotiations with the NPA are likely to be resumed in the nearfuture.Externally, the Philippines faces no serious threat. The government maintains itsterritorial claim to some of the Spratly Islands, and occasionally has minorconfrontations with China over the presence of shipping in the area and the buildingof semi-permanent structures. However, there is little chance of armed conflictbetween the two countries.

II. Civil unrest

Large public demonstrations in the Philippines are commonplace; indeed, thecountry’s so-called People’s Power movement has brought down two governmentsin the past 15 years, most recently in January 2001. Such protests are not particularlyviolent, but are disruptive to the normal functioning of business in the capital.

14 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Violence is not, however, uncommon. The run-up to the May 2004 presidential andcongressional elections was characterised by protests and a total of around 150election-related deaths. Supporters of Fernando Poe, the film star who failed in hisbid for the presidency in May, may continue to protest in the streets. Protests overeconomic issues are common, and demonstrations against the US military presencein support of the campaign against Abu Sayyaf are also likely to persist until thewithdrawal of US troops.

III. Crime

Street crime is a serious problem in the Philippines, particularly in metropolitanManila. According to official statistics, incidents of serious crime in 2002 were 107.8 per100,000 population (a rate of 25 or less per 100,000 is considered low). This was wellbelow the recorded peak of 313.6 per 100,000 in 1984, but higher than the rate of 98.8per 100,000 in 2001. The authorities acknowledge that 18 murders, on average, arecommitted in the country every day. Kidnappings, rapes and drug-related crimes arealso frequent. The high level of crime is a major reason why foreign investors shun thePhilippines, and is a factor in the fall in tourist visits in recent years from the peak of2.2m in 1999. The problem is made worse by the apparent complicity of some policeofficials in criminal enterprises.

IV. Organised crime

Violent drug-trafficking organisations are well established in the Philippines, and thenarcotic trade is massive. The huge sums to be earned in the drug trade attractpoliticians, law enforcement officials and leading business figures, and undermineattempts to reduce official corruption. A leading opposition senator has beenaccused of having co-operated with one of the drug gangs while he headed thenational police, and of ordering the murder of several Chinese nationals who fellfoul of the group. The government has created a new National Anti-CrimeCommission and has designated an “anti-crime czar”, but they have had fewsuccesses so far. Organised crime is not confined to drugs, however; it alsoencompasses gambling, prostitution, kidnapping, smuggling and extortion.Organised criminal gangs are believed to launder money through a network of localbanks. The Philippines has been cited by the Financial Action Task Force (FATF) of theGroup of Seven as “non-co-operative” in anti-money-laundering efforts. Legislationagainst money-laundering was introduced in 2003, but the Philippines remains on theFATF’s blacklist.

V. Kidnapping

Kidnapping is rampant in the Philippines, and is carried out by a wide range ofgroups: Islamist insurgents in the southern islands, sophisticated drug gangsthroughout the country and smaller groups of bandits. It is a major concern forcompanies in the Philippines, including foreign firms, and the affluent Chinesebusiness community has been a prime target. In addition, Abu Sayyaf, the notoriousMuslim secessionist group based on the southern island of Basilan, has kidnappeddozens of local residents and tourists, ostensibly for political reasons. When ransomsare not forthcoming, Abu Sayyaf, like other kidnap gangs, has been prepared to carryout its threat to execute hostages. It is widely suspected locally that members of thesecurity forces co-operate with kidnap gangs to extort ransoms. In late 2003Ms Macapagal Arroyo lifted a moratorium on the use of the death penalty, followingthe kidnapping and murder of an executive with a US soft-drinks firm, Coca Cola.

Philippines 15

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

However, no executions have taken place since Ms Macapagal Arroyo cameto power.

VI. Terrorism

Terrorism is a serious concern, although it is mainly confined to the southern islands.Abu Sayyaf carries out bombings, kidnappings and murders that clearly qualify asterrorist acts. The group is included on the US State Department’s list of knownterrorist organisations. Abu Sayyaf claims that some of its members have beentrained by the al-Qaida network in Afghanistan, although Abu Sayyaf seemsmotivated less by religious or political fervour than by financial gain from itskidnappings. The southern Philippines, nonetheless, is now widely regarded as asignificant breeding ground for terrorists, with its large population of alienated,impoverished Muslim youth.

Resources and infrastructure

Population

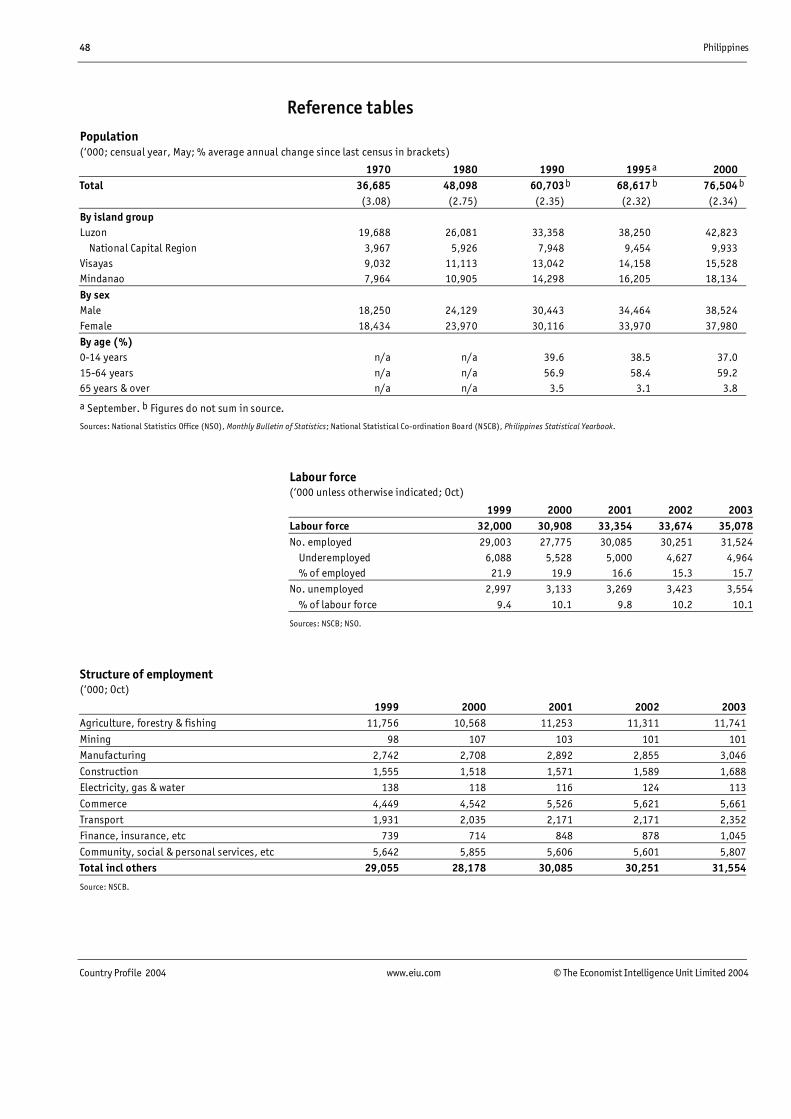

The rate of population growth has been slowing in recent decades (according tonational sources), from an average of 3.1% a year in the 1960s to 2.3% in the1990s. This reflects two trends: a fall in the birth rate and a fall in the death rateas infant mortality rates have declined. Thus the crude birth rate fell from 46per 1,000 in 1960 to 30 in 2000 (when the last census was held) as familyplanning became more widely accepted. Once the government gave its backingto birth control, the percentage of married women of reproductive agepractising contraception rose, reaching a peak of 51% in 1995, and has remainedin the 47-50% range in subsequent years. Meanwhile, life expectancy at birthrose from 53 years in 1960 to 69.5 years in 2001 (according to the HumanDevelopment Report 2003 published by the UN Development Programme, orUNDP) as the infant mortality rate fell from 72 deaths in the first year of life per1,000 live births in 1965 to 29 in 2001. The comparatively high rate ofpopulation growth means that the Philippines has a young population, 37%being under the age of 14 in 2000.

Population by region(‘000, unless otherwise indicated)

Annual average % change2000 1995-2000

LuzonNational Capital Region 9,933 1.06Cordillera Administrative Region 1,365 1.82Ilocos 4,200 2.15Cagayan Valley 2,813 2.25Central Luzon 8,205 3.20Calabarzona 9,321 –Mimaropaa 2,299 –Bicol 4,675 1.68VisayasWestern Visayas 6,209 1.56Central Visayas 5,701 1.08Eastern Visayas 3,610 1.51

Population growth has slowed

16 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

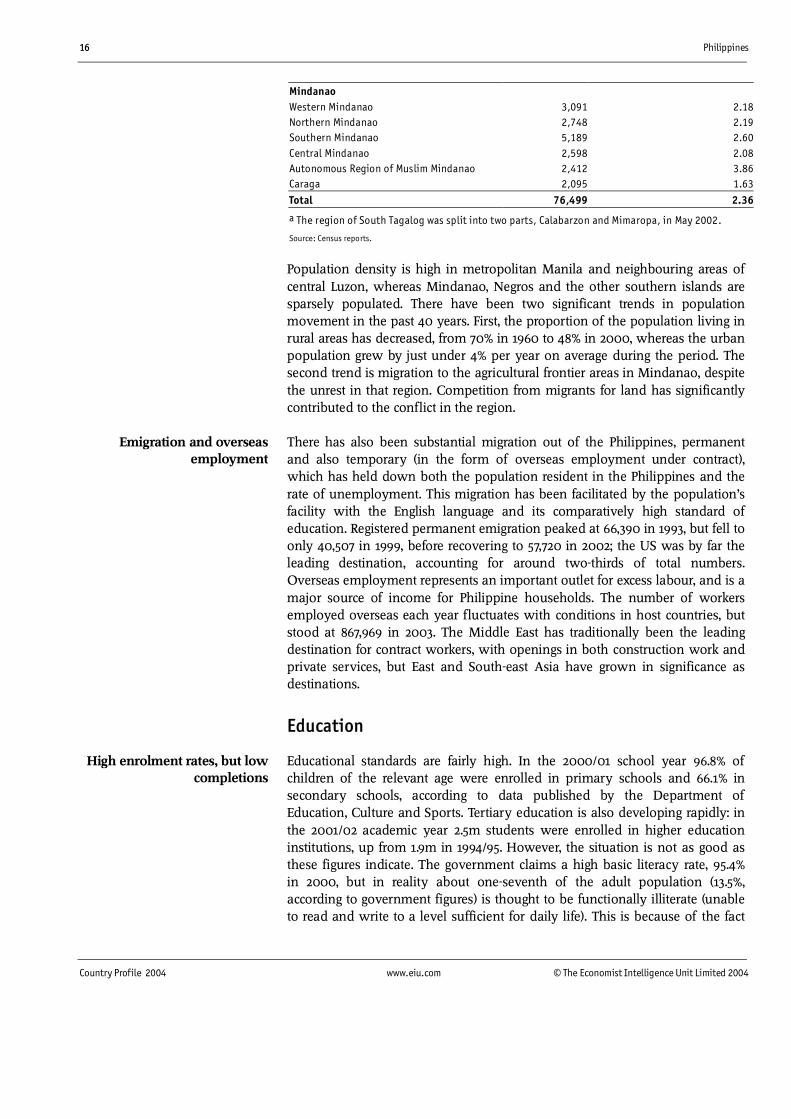

MindanaoWestern Mindanao 3,091 2.18Northern Mindanao 2,748 2.19Southern Mindanao 5,189 2.60Central Mindanao 2,598 2.08Autonomous Region of Muslim Mindanao 2,412 3.86Caraga 2,095 1.63

Total 76,499 2.36

a The region of South Tagalog was split into two parts, Calabarzon and Mimaropa, in May 2002.

Source: Census reports.

Population density is high in metropolitan Manila and neighbouring areas ofcentral Luzon, whereas Mindanao, Negros and the other southern islands aresparsely populated. There have been two significant trends in populationmovement in the past 40 years. First, the proportion of the population living inrural areas has decreased, from 70% in 1960 to 48% in 2000, whereas the urbanpopulation grew by just under 4% per year on average during the period. Thesecond trend is migration to the agricultural frontier areas in Mindanao, despitethe unrest in that region. Competition from migrants for land has significantlycontributed to the conflict in the region.

There has also been substantial migration out of the Philippines, permanentand also temporary (in the form of overseas employment under contract),which has held down both the population resident in the Philippines and therate of unemployment. This migration has been facilitated by the population’sfacility with the English language and its comparatively high standard ofeducation. Registered permanent emigration peaked at 66,390 in 1993, but fell toonly 40,507 in 1999, before recovering to 57,720 in 2002; the US was by far theleading destination, accounting for around two-thirds of total numbers.Overseas employment represents an important outlet for excess labour, and is amajor source of income for Philippine households. The number of workersemployed overseas each year fluctuates with conditions in host countries, butstood at 867,969 in 2003. The Middle East has traditionally been the leadingdestination for contract workers, with openings in both construction work andprivate services, but East and South-east Asia have grown in significance asdestinations.

Education

Educational standards are fairly high. In the 2000/01 school year 96.8% ofchildren of the relevant age were enrolled in primary schools and 66.1% insecondary schools, according to data published by the Department ofEducation, Culture and Sports. Tertiary education is also developing rapidly: inthe 2001/02 academic year 2.5m students were enrolled in higher educationinstitutions, up from 1.9m in 1994/95. However, the situation is not as good asthese figures indicate. The government claims a high basic literacy rate, 95.4%in 2000, but in reality about one-seventh of the adult population (13.5%,according to government figures) is thought to be functionally illiterate (unableto read and write to a level sufficient for daily life). This is because of the fact

Emigration and overseasemployment

High enrolment rates, but lowcompletions

Philippines 17

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

that, although there has been near-universal enrolment at primary-school levelfor more than two decades, the high drop-out rate means that one-third of allpupils do not complete their primary-level education. A similar proportion ofsecondary school students fail to complete secondary-level education.

The national figures also conceal the familiar disparity between Manila and thepoorer provinces: in Manila, the cohort survival rate (pupils completing theirschooling as a proportion of the total intake) in elementary schools was morethan 79%, compared with less than 34% in the Autonomous Region of MuslimMindanao. Overall educational standards have come under pressure owing tounderinvestment, as the sector has fallen victim to the squeeze on governmentspending. The situation in primary education has been compounded by the fallin the state’s proportional contribution to primary-education costs, whereas thestate’s contribution to tertiary education has risen.

Health

Healthcare provision is inadequate. UNDP data show that the Philippines hadonly 124 doctors per 100,000 people in 1990-2002. To some extent, as in thecase of education, this reflects budgetary constraints. Spending on public healthin the Philippines was equivalent to only 1.5% of GDP in 2000, with a further1.8% of GDP spent on private healthcare. However, the situation is exacerbatedby the skewed geographical distribution of health facilities. A disproportionatenumber of doctors are located in the National Capital Region, and the poorroad infrastructure in the rural areas of the poorer provinces limits the access ofa large section of the population to such facilities as do exist.

Natural resources and the environment

The Philippines is one of the largest island groups in the world, numberingmore than 7,100 islands and extending 1,851 km north to south and 1,107 kmeast to west. The topography is varied and includes two mountain ranges inLuzon and several volcanoes, 21 of them active.

The climate is tropical, with some variation in the extent and duration of thedry season. In the western parts of Luzon, Mindoro, Negros and Palawan (thewestern rim) there are two pronounced seasons: dry from November to Apriland wet for the rest of the year. Other regions have rainfall more or less evenlydistributed throughout the year. All are exposed to typhoons, which occur mostfrequently across the middle latitudes of the country. Southern Mindanao isalmost typhoon-free.

The area under crops expanded markedly in the 1970s and reached 12.3m ha in1979/80, mainly as a result of the clearing of virgin forest, particularly inMindanao, where more than one-half of the commercial acreage is located.Bureau of Agricultural Statistics data show that the national cropland area hadrisen to 12.8m has by 2002, but land availability is now a serious constraint inLuzon and some parts of the Visayas. Forests were in the past one of thePhilippines’ main resources, but they have been rapidly depleted (see Economicsectors: Agriculture, forestry and fishing).

Healthcare is substandard

A large island group

18 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The Philippines has extensive fishing resources, both marine and inland, with thelargest area of developed estuarine fishponds in South-east Asia and an exclusivefishing zone of 1.9m sq km. Although neither freshwater fishponds nor most of themarine waters have been fully developed, the productivity of some resources hasbeen deteriorating as rising demand and the use of destructive methods ofexploitation has resulted in overfishing. Few coral reefs remain in good condition,and the mangrove area has halved since the late 1970s.

Mineral resources are widely scattered throughout the islands, but aroundone-quarter of the land area has not been surveyed. At end-1996 there wereestimated reserves of 4.8m tonnes of copper, 1.1m tonnes of nickel, 36,667tonnes of chromite, 226,852 tonnes of gold and 484,696 tonnes of iron. Thepicture is mixed for energy resources. There are large deposits of coal andlignite, with proven reserves of 369m tonnes, of which close to 40% are onSemirara Island, and potential reserves are estimated at 1.6bn tonnes.Commercial deposits of oil off Palawan Island are small and have provedtechnically difficult to exploit and operate. Reserves of gas in the Malampayafield in the same region are substantial, estimated at 2.8trn-3.5trn cu ft (othergas reserves are estimated at 1.8trn cu ft), and are now being exploited.Geothermal resources are large and, as yet, not fully developed.

The Philippines is at significant risk from tropical storms, which can severelydisrupt business operations; an average of around 20 storms hit the countryeach year. Typically, they are more frequent and severe in the northern islands.Volcanic eruptions can be extremely disruptive: the eruption of MountPinatubo in 1991 caused massive damage to a wide area of Luzon north of thecapital and closed Manila airport for a period.

Transport, communications and the Internet

The transport infrastructure is inadequate, having suffered from decades ofunderinvestment. In the liberalised investment environment established by theadministration of the former president, Fidel Ramos, during the 1990s some ofthe most serious shortcomings have begun to be tackled, but development hasbeen concentrated in economic hubs.

The system is essentially bimodal, roads carrying 60% of freight and 80% ofpassenger traffic, and water 40% of freight and 10% of passenger traffic. Airtransport is oriented towards carrying passengers on long-distance inter-islandtravel. The rail network is minimal.

The road network covered 201,834 km at end-2000, of which two-thirds werefeeder and village roads. Less than one-half of the network is all-weather, animportant consideration in view of the climate, and only 21% of all roads arepaved with concrete or asphalt. The condition of the feeder roads is generallypoor, the result of substandard construction, inadequate maintenance and useby overloaded vehicles. Bridges are often weak, if not altogether absent, andsome remote areas have few access roads. Current projects provide for theimprovement of roads in Luzon, including the rehabilitation and modernisation

Fishing

Risk from natural disasters

Minerals

Transport

Philippines 19

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

of the North Luzon highway, much of which is now open to traffic, with theproject as a whole due for completion in February 2005. This work is beingcarried out under build-operate-transfer (BOT) terms, bringing in private capitaland expertise.

The railway network is being gradually extended. The single-line track in theBicol-Manila-La Union corridor in Luzon is in urgent need of rehabilitation, asonly one-fifth of the track is in operation. In addition, there is a modern,elevated rail system in Manila, which is currently being expanded within themetropolitan area.

Given the geography of the Philippines, shipping services and port facilities areof critical importance. In all there are nearly 1,500 ports in operation, but sixManila, Cebu, Iloilo, Cagayan de Oro, Zamboanga and Davao handle over 80%of public port traffic. The inter-island fleet is old, safety regulations are poor andmaritime navigational aids, in particular lighthouses, are inadequate.

There are 87 national airports, of which three Manila, Cebu and GeneralSantos are international. The provision of domestic services has beenimproving as the aviation sector has been liberalised and new airlines haveentered operation. However, after excessive capital spending resulted in afinancial crisis at the privatised national carrier, Philippine Airlines (PAL), in1998, the domestic route network was sharply cut back.

The telecommunications system used to be inadequate and unreliable, andtelephone density stood at only 1 per 100 people in the mid-1980s. Thederegulation of the sector in 1993 transformed the situation. Presidential decreesmandated interconnections between networks and required that internationalgateway operators and mobile telephone companies install telephone systemsin urban and rural areas. The changes ended the monopoly enjoyed by thePhilippine Long Distance Telephone Company (PLDT). As PLDT installed newlines and other operators entered the field, telephone density rose, reaching9.1 per 100 people in 1998 according to the National TelecommunicationsCommission. However, many installed lines are not in use fixed-line densityfell to 8.7 per 100 people in 2002 owing to the vibrancy of the mobile phonemarket. Mobile phone ownership has been expanding rapidly in recent years,with 18m subscribers in June 2003.

There were an estimated 4.1m Internet users in 2002, but ownership ofpersonal computers is limited to wealthy urban households and is estimated atonly 1.7% of the population. The e-commerce market in the Philippines istherefore tiny, estimated at only US$2m-3m in 2000. Although the passage ofthe Electronic Commerce Act in July 2000 should enhance growth in thissector, lax enforcement and the inadequacy of protection for intellectualproperty rights remain severe constraints.

Under the Marcos regime the mass media, with the exception of a few small-circulation and often short-lived newspapers, were controlled by interests closeto the president, and press censorship was exercised by the government. Nowthat the sector has opened up again there is a multiplicity of newspapers 475in 2000 and the Philippine press is a byword for freewheeling comment and

Communications

20 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

speculation. There were 599 broadcasting radio stations in 2000, bothcommercial and non-commercial, of which 270 broadcast on AM wavebandsand 329 on FM. There were 108 television broadcast stations in 2000, of which13 were based in the Metro Manila region.

Energy provision

The Philippines depends to a fairly high degree on foreign energy sources, butsince the oil price rises of the 1970s the government has sought to bring downthe deficit in national supply. The contribution of domestic energy sources hasbeen rising, reflecting investment in geothermal and hydroelectric capacity andthe availability of a wider range of non-conventional sources. This trend wasreinforced with the start-up of gas production from the Malampaya reserves,off Palawan, in October 2001. Domestic oil is not expected to make a significantcontribution, and domestic coal production will continue to be supplementedby imports.

Power generation was previously a state preserve, but the private sector hasbeen brought in over the past decade to remedy shortfalls in supply and capital.When Mr Ramos became president in 1992 the Luzon grid (on which Maniladepends) had a supply deficit of 1,000 mw. This was because a plan for620 mw in nuclear capacity to come on stream in 1986 had lapsed. The newgovernment launched a fast-track programme of electricity expansion, whicheliminated the power shortage by end-1993. At end-1999 power-generatingcapacity was 12,341 mw, up from 6,949 mw at end-1992. Much of the increasecame from plants built under BOT contracts, and the use of such arrangements,as well as of build-own-operate agreements, has become common, being usedalso for the development of capacity that utilises gas from the Malampaya field.The greatest long-term potential for expansion in power-generation capacity liesin geothermal energy. Geothermal power generation on a commercial scalebegan in 1979, and capacity in 2000, at 1,931 mw, was second only to that of theUS. The latest development plan of the Department of Energy envisagesadditional capacity of 990 mw by 2011.

The liberalisation of the energy sector took another, more far-reaching, stepforward in 2001 with the passage of legislation to privatise the state-ownedutility, the National Power Corporation (Napocor). Even so, attempts to sell offNapocor have stumbled, and a major policy challenge for the new governmentelected in May 2004 is to make progress on the sell-off of both generating andtransmission assets.

Energy supply and usage

Philippines 21

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

The economy

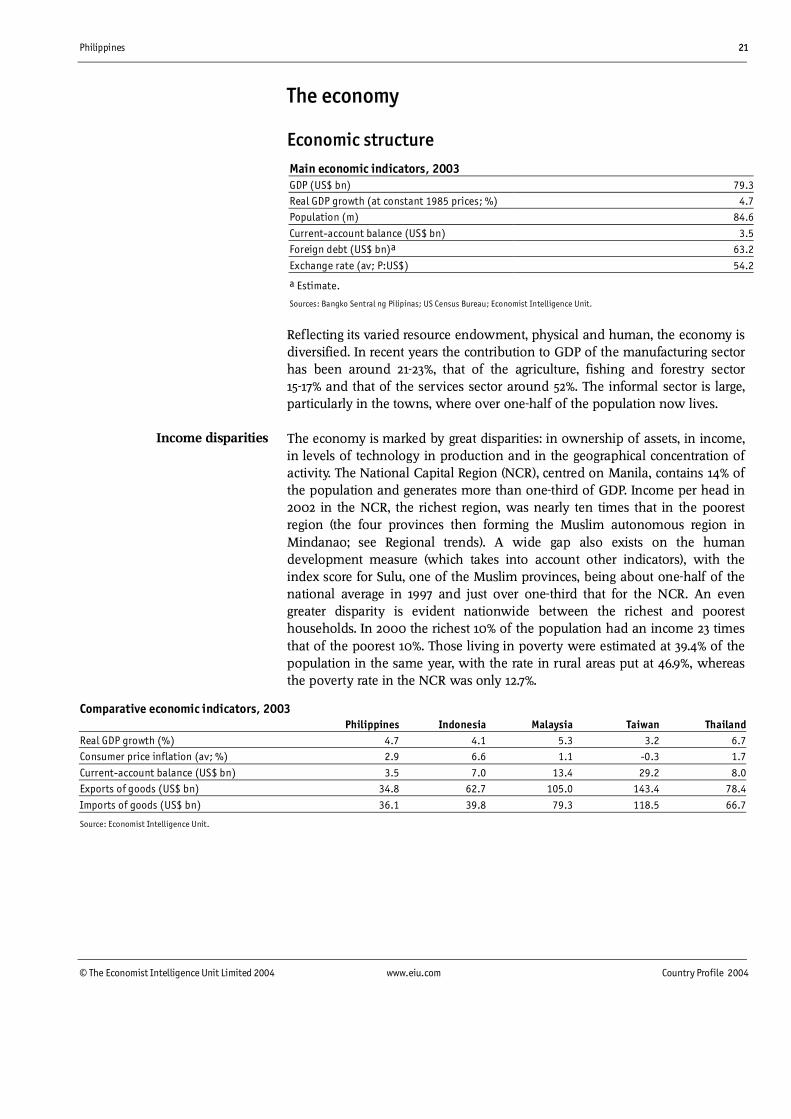

Economic structureMain economic indicators, 2003GDP (US$ bn) 79.3Real GDP growth (at constant 1985 prices; %) 4.7Population (m) 84.6

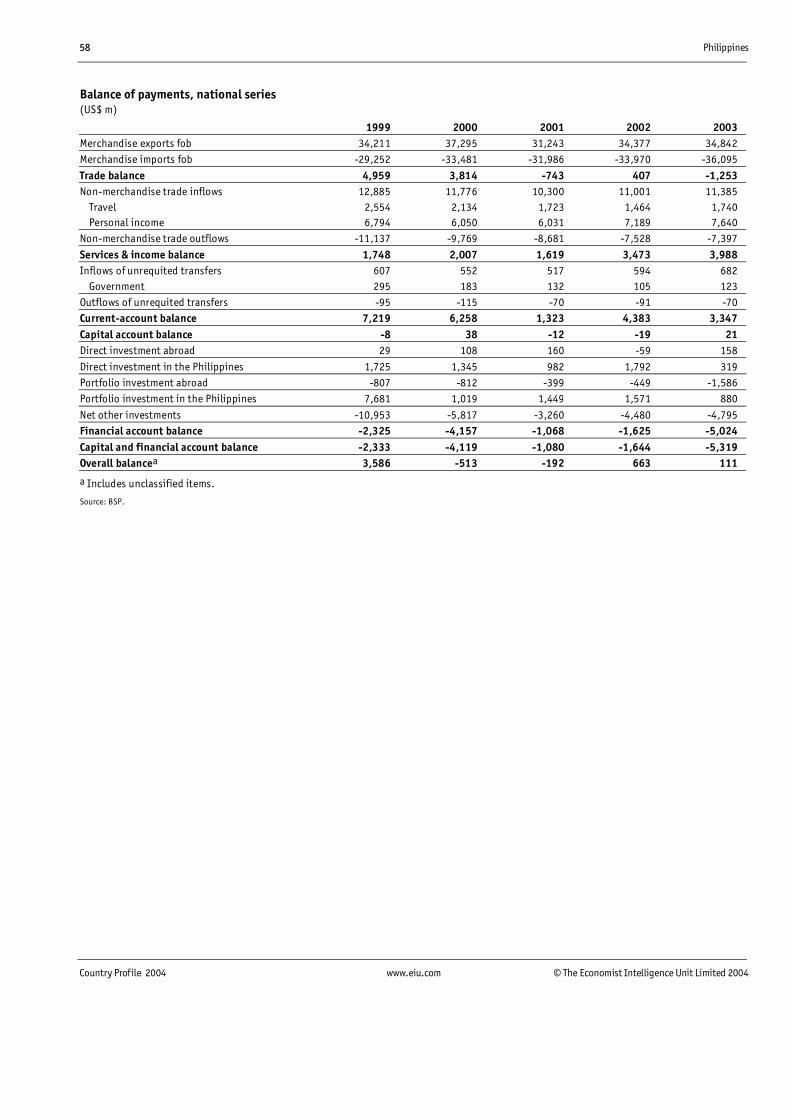

Current-account balance (US$ bn) 3.5Foreign debt (US$ bn)a 63.2

Exchange rate (av; P:US$) 54.2

a Estimate.

Sources: Bangko Sentral ng Pilipinas; US Census Bureau; Economist Intelligence Unit.

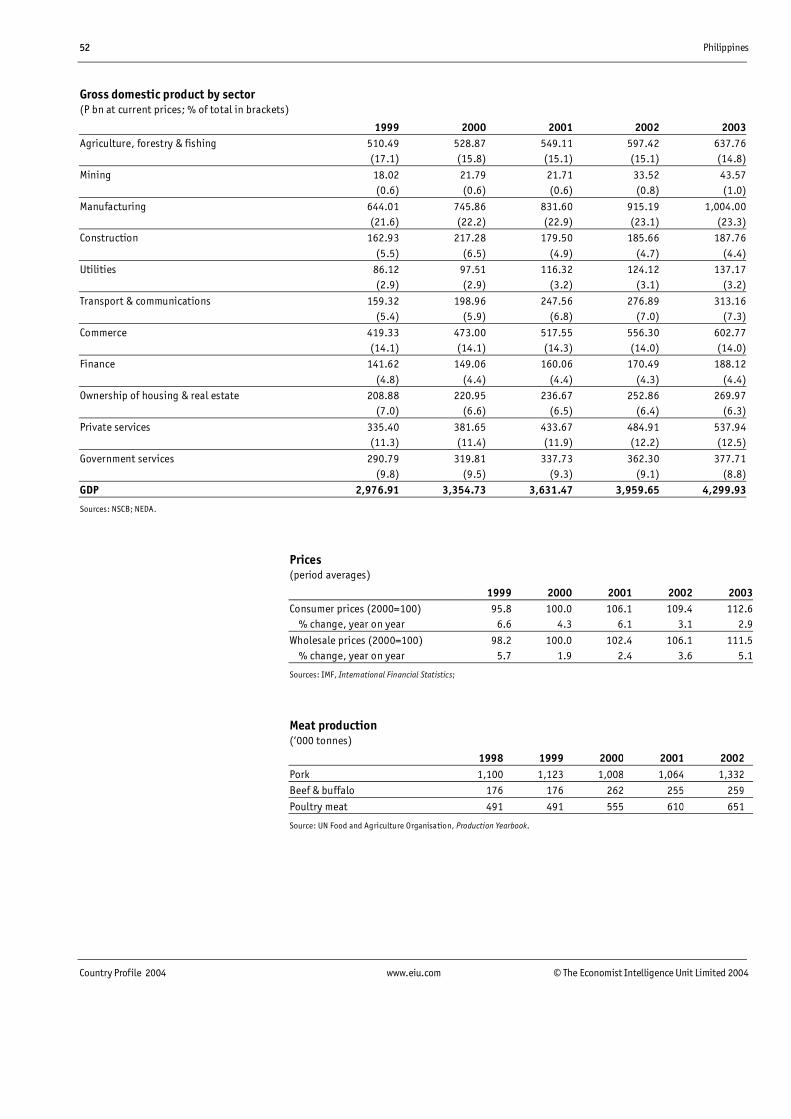

Reflecting its varied resource endowment, physical and human, the economy isdiversified. In recent years the contribution to GDP of the manufacturing sectorhas been around 21-23%, that of the agriculture, fishing and forestry sector15-17% and that of the services sector around 52%. The informal sector is large,particularly in the towns, where over one-half of the population now lives.

The economy is marked by great disparities: in ownership of assets, in income,in levels of technology in production and in the geographical concentration ofactivity. The National Capital Region (NCR), centred on Manila, contains 14% ofthe population and generates more than one-third of GDP. Income per head in2002 in the NCR, the richest region, was nearly ten times that in the poorestregion (the four provinces then forming the Muslim autonomous region inMindanao; see Regional trends). A wide gap also exists on the humandevelopment measure (which takes into account other indicators), with theindex score for Sulu, one of the Muslim provinces, being about one-half of thenational average in 1997 and just over one-third that for the NCR. An evengreater disparity is evident nationwide between the richest and pooresthouseholds. In 2000 the richest 10% of the population had an income 23 timesthat of the poorest 10%. Those living in poverty were estimated at 39.4% of thepopulation in the same year, with the rate in rural areas put at 46.9%, whereasthe poverty rate in the NCR was only 12.7%.

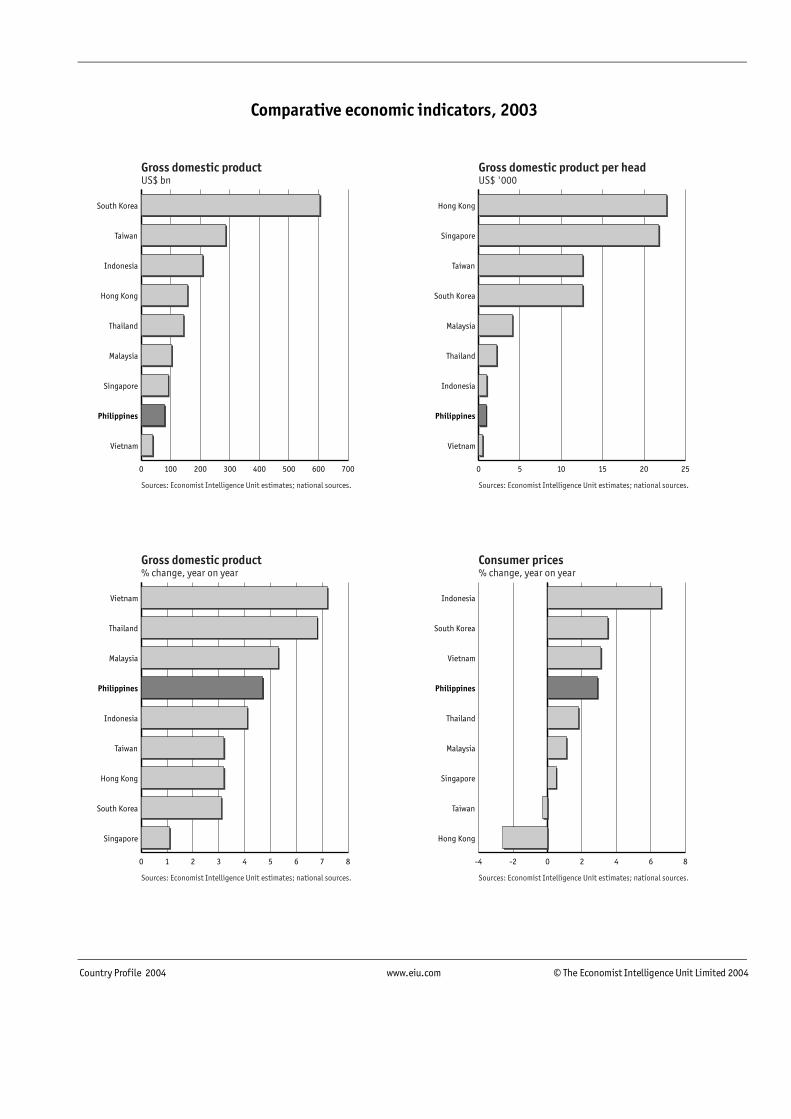

Comparative economic indicators, 2003Philippines Indonesia Malaysia Taiwan Thailand

Real GDP growth (%) 4.7 4.1 5.3 3.2 6.7Consumer price inflation (av; %) 2.9 6.6 1.1 -0.3 1.7

Current-account balance (US$ bn) 3.5 7.0 13.4 29.2 8.0Exports of goods (US$ bn) 34.8 62.7 105.0 143.4 78.4

Imports of goods (US$ bn) 36.1 39.8 79.3 118.5 66.7

Source: Economist Intelligence Unit.

Income disparities

22 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Economic policy

The major economic policy requirement in the Philippines is to raise the levelof budget revenue on a sustainable basis. The low ratio of tax revenue to GDParound 15% in most years has meant that the government has never investedadequately in physical and social infrastructure, generating serious bottlenecksin mobilising the Philippines’ considerable resources. The situation has beenexacerbated by the primacy accorded to achieving fiscal equilibrium, with thespending side bearing the burden of making up revenue shortfalls.

Progress was made under the presidency of Fidel Ramos from 1992 to 1998,with a small surplus registered each year in 1994-97. A complex of factorscontributed. Capital outgoings could be held down as private-sector capital wasbrought in under build-operate-transfer (BOT) contracts, initially to remedy thecritical power shortage in Luzon and subsequently to fund road and commuterrail projects. Income was boosted by the sale of government assets, bothcorporate and physical, which yielded a total of P68.7bn (US$2.5bn) in 1993-96,representing 5% of budget revenue for the period. A new feature in 1996 wasthe achievement of a small surplus before privatisation proceeds, which owedmuch to the fact that interest payments the largest single expenditure itemhad been eroded by the fall in the government’s debt stock. However, the mostsignificant progress made on the fiscal front during Mr Ramos’s presidency wasthe strengthening of the tax base. Value-added tax (VAT) was extended in 1996,while a comprehensive tax reform package, approved in two stages in 1996 and1997, tackled a range of defects in the tax structure. The reforms simplified thesystem of personal and corporate tax, raising thresholds for the former andreducing the range of allowances in both, and rebased the excise system froman ad valorem to a specific levy system. The underlying aim was to reduce boththe scope and the incentive for corruption and evasion, and thereby to increasethe tax take.

The progress achieved in the Ramos years proved short-lived. After a steadynarrowing of the surplus, the budget was back in the red in 1998 to the tune ofP50bn. The deficit more than doubled in 1999, and rose again in both 2000 and2001. A record deficit of P211bn was recorded in 2002, with a minor decrease in2003 leaving the fiscal deficit at a still high 4.6% of GDP. The reason for thereversal was the onset of the Asian economic crisis in 1997. This had animmediate and severe impact on the budget. The depreciation of the peso andthe steep rise in interest rates pushed up the cost of servicing the government’sdebt, at the same time that the slowing of economic growth and the onset ofrecession in 1998 hit tax revenue. Hence GDP growth in 1999 was slower, andmore fitful, than expected, with the result that internal tax receipts were wellbelow expectations. Despite some trimming on the expenditure side, the deficitfar exceeded the target, at P111.7bn.

However, the deterioration cannot all be attributed to poorer GDP results.Economic growth in 2000 was close to the revised official forecast, yet thedeficit of P134.2bn (4% of GDP) was double the target. The results in 2000 werepartly caused by worsening investor sentiment as the political situation

The fiscal priority: enhancingrevenue

A major deterioration by theend of the decade

Progress in the mid-1990s

Philippines 23

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

deteriorated; the government’s privatisation proceeds fell P19bn short of theP22bn target. Moreover, the sharp fall in the peso in October, and the steep risein interest rates aimed at containing the fall, greatly boosted interest outgoingson government debt. The most serious deterioration was in the proceeds of theBureau of Internal Revenue (BIR), which were P43bn below the revised targetand up by only 4.3% compared with 1999, when domestic demand growth wasconsiderably slower. As a result, and despite better than forecast results fromcustoms receipts in both 1999 and 2000, the tax ratio fell from 15.6% of GDP in1998 to 14.9% in 1999 and 13.6% in 2000.

Setting aside the issue of large-scale tax evasion by well-placed individuals, theessential problem lies in the system itself. The comprehensive tax reformintroduced under Mr Ramos has not produced an increase in revenue as apercentage of GDP. A study by the IMF in late 2000 showed that the reform hasbeen broadly revenue-neutral; proceeds from VAT had in fact fallen as apercentage of GDP since 1994 because of the exemptions introduced. A studyby a Philippine think-tank has claimed that tax evasion on personal income taxhas worsened under the simplified structure. It is widely recognised that thesolution lies not in new levies but in improving tax compliance by tighteningup on tax administration and reducing the opportunities for corruption. It wasin part through a reinforced collection effort, aided by a tax amnesty scheme,that the budget deficit in 2001 was held close to the target of P145bn, coming inat P147bn. However, the ratio of the budget deficit to GDP fell only marginally,from 4.1% in 2000 to 4% in 2001.

The government had hoped to begin reining in the budget deficit in 2002, withan elimination of the deficit altogether by 2006. However, poor collection bythe BIR and a P52bn overspend meant that the original forecast for the 2002deficit of P130bn was grossly exceeded. The budget deficit for the year rose toP210.7bn, equivalent to 5.2% of GDP. The government has adjusted its budgetforecasts for the next few years accordingly, and does not now expect fiscalbalance to be achieved until 2009. In 2003 the government held the budgetdeficit just below the target of P202bn at P199.9bn, aided by relatively strongGDP growth and sustained government focus on budgetary results. The deficittarget for 2004 of P197.8bn, although not ambitious, would bring the deficitdown to 4.2% of GDP from 4.6% in 2003, although January-May results indicatethat the government may face some difficulty in meeting this year’smodest target.

Budget targets and results(P bn)

2003 2004Target Actual Target

Revenue 584.1 626.6 671.2 Bureau of Internal Revenue 424.0 425.7 488.6 Bureau of Customs 100.1 106.1 105.2

Expenditure 786.1 826.5 869.0 Interest 223.2 226.4 271.5

Balance -202.0 -199.9 -197.8

Source: Department of Finance.

The ballooning of the deficitdelays a move to fiscal balance

24 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

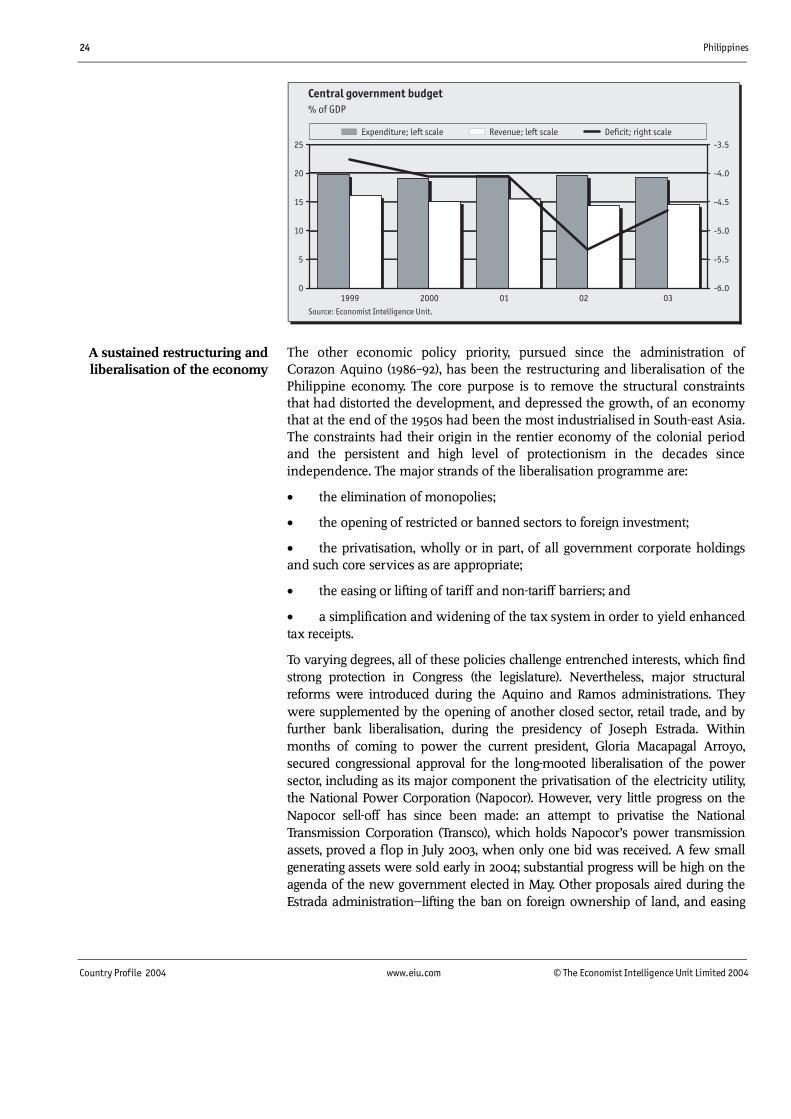

The other economic policy priority, pursued since the administration ofCorazon Aquino (1986 92), has been the restructuring and liberalisation of thePhilippine economy. The core purpose is to remove the structural constraintsthat had distorted the development, and depressed the growth, of an economythat at the end of the 1950s had been the most industrialised in South-east Asia.The constraints had their origin in the rentier economy of the colonial periodand the persistent and high level of protectionism in the decades sinceindependence. The major strands of the liberalisation programme are:

• the elimination of monopolies;

• the opening of restricted or banned sectors to foreign investment;

• the privatisation, wholly or in part, of all government corporate holdingsand such core services as are appropriate;

• the easing or lifting of tariff and non-tariff barriers; and

• a simplification and widening of the tax system in order to yield enhancedtax receipts.

To varying degrees, all of these policies challenge entrenched interests, which findstrong protection in Congress (the legislature). Nevertheless, major structuralreforms were introduced during the Aquino and Ramos administrations. Theywere supplemented by the opening of another closed sector, retail trade, and byfurther bank liberalisation, during the presidency of Joseph Estrada. Withinmonths of coming to power the current president, Gloria Macapagal Arroyo,secured congressional approval for the long-mooted liberalisation of the powersector, including as its major component the privatisation of the electricity utility,the National Power Corporation (Napocor). However, very little progress on theNapocor sell-off has since been made: an attempt to privatise the NationalTransmission Corporation (Transco), which holds Napocor’s power transmissionassets, proved a flop in July 2003, when only one bid was received. A few smallgenerating assets were sold early in 2004; substantial progress will be high on theagenda of the new government elected in May. Other proposals aired during theEstrada administration lifting the ban on foreign ownership of land, and easing

A sustained restructuring andliberalisation of the economy

Philippines 25

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

restrictions on foreign involvement in the media, education and utilities remainon the agenda, but progress will be slow for domestic political reasons.

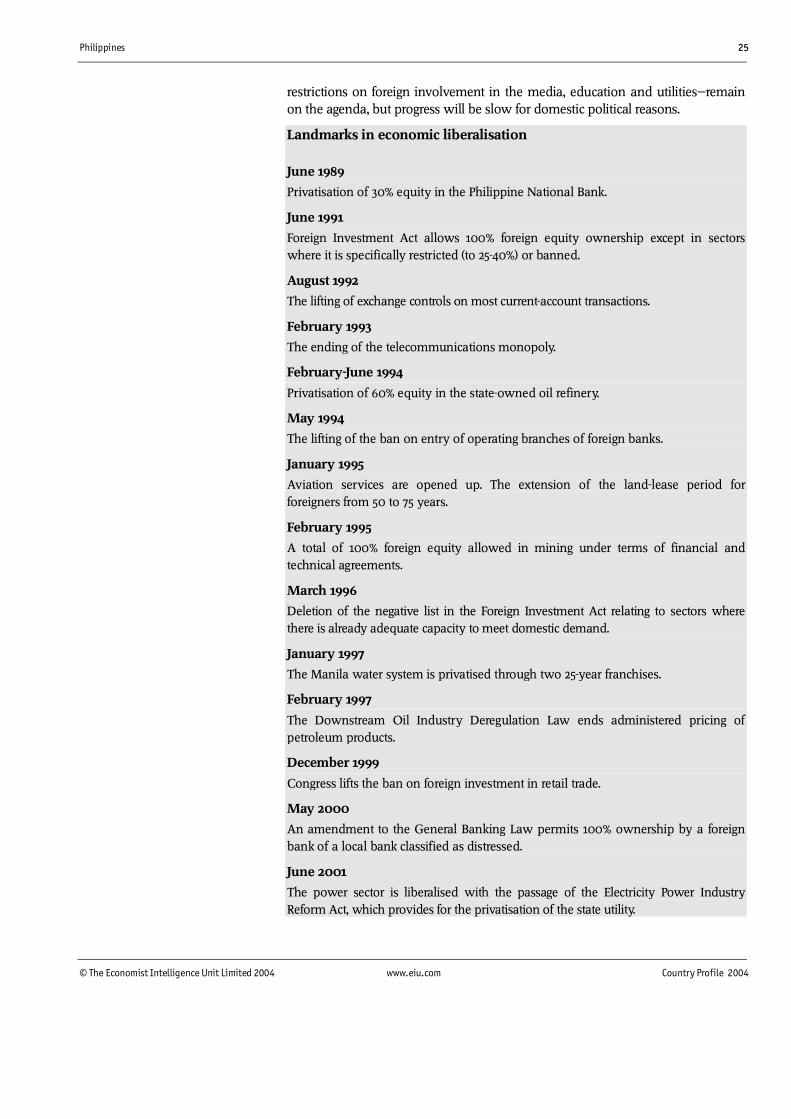

Landmarks in economic liberalisation

June 1989

Privatisation of 30% equity in the Philippine National Bank.

June 1991

Foreign Investment Act allows 100% foreign equity ownership except in sectorswhere it is specifically restricted (to 25-40%) or banned.

August 1992

The lifting of exchange controls on most current-account transactions.

February 1993

The ending of the telecommunications monopoly.

February-June 1994

Privatisation of 60% equity in the state-owned oil refinery.

May 1994

The lifting of the ban on entry of operating branches of foreign banks.

January 1995

Aviation services are opened up. The extension of the land-lease period forforeigners from 50 to 75 years.

February 1995

A total of 100% foreign equity allowed in mining under terms of financial andtechnical agreements.

March 1996

Deletion of the negative list in the Foreign Investment Act relating to sectors wherethere is already adequate capacity to meet domestic demand.

January 1997

The Manila water system is privatised through two 25-year franchises.

February 1997

The Downstream Oil Industry Deregulation Law ends administered pricing ofpetroleum products.

December 1999

Congress lifts the ban on foreign investment in retail trade.

May 2000

An amendment to the General Banking Law permits 100% ownership by a foreignbank of a local bank classified as distressed.

June 2001

The power sector is liberalised with the passage of the Electricity Power IndustryReform Act, which provides for the privatisation of the state utility.

26 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

December 2002

The special-purpose asset vehicle law is passed, making it easier for banks to spin offbad loans to asset-management companies.

A key policy change on the monetary side has been the switch to inflationtargeting by the Bangko Sentral ng Pilipinas (BSP, the autonomous central bank)at the beginning of 2001. It had traditionally set interest rates to meet monetarytargets monitored by the IMF, and with an eye to countering sharp fluctuationsin the peso’s value and providing some degree of support when it wasdepreciating rapidly. The target range for 2002 was initially set at 5-6%.

In view of the rapid fall in consumer price inflation during the final months of2001 and the first quarter of 2002, and against a background of slowing growthin money supply and credit and the steep fall in the US federal funds rate in thewake of the September 11th 2001 terrorist attacks, the BSP introduced a markedrelaxation in monetary conditions. Its overnight rates were reduced in everymonth from December 2001 to March 2002, reaching their lowest level sinceSeptember 1995. On June 6th 2003 the BSP restored the tiering system forovernight placements, applying the standard rate of 7% for the first P5bn butlowering the rate to 4% for an additional P5bn and to 1% for deposits aboveP10bn. However, the three-tiered interest rate system was removed on August28th as the BSP sought to defend the peso in the aftermath of the attemptedcoup in July 2003. Overnight borrowing and lending rates, which had beenheld steady since March 2002, were cut by a further 25 basis points in early July2003, to 6.75% and 9% respectively. Rates remain at these levels despite the end-June 2004 increase in the US federal funds rate, as Philippine inflation remainswithin the targeted range.

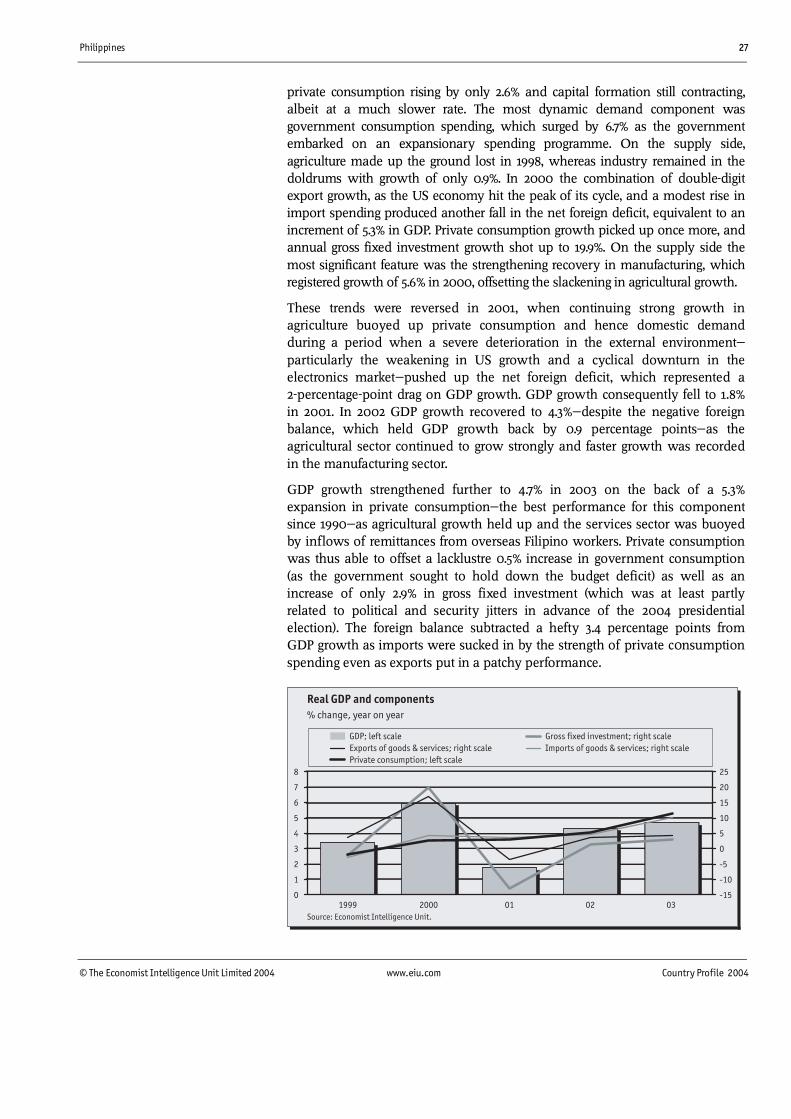

Economic performance

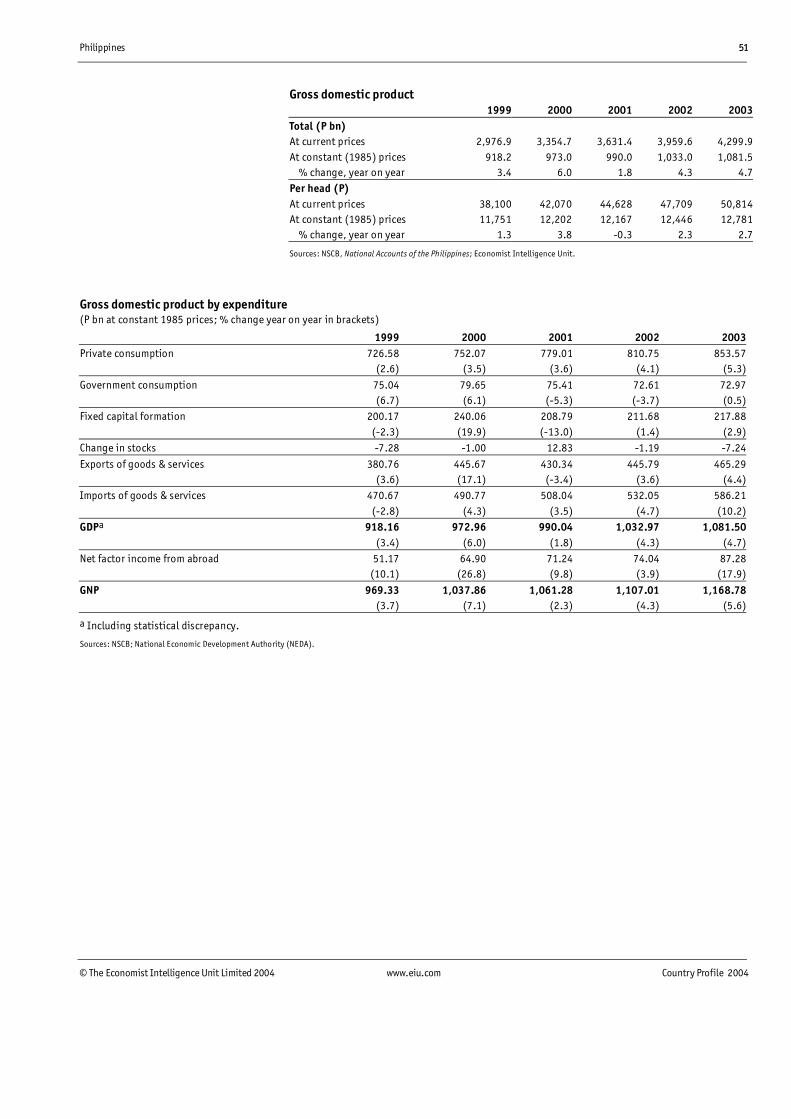

The notable feature of the GDP record in recent years has been the overallresilience of the economy in markedly deteriorating conditions. A sustained periodof accelerating growth in GDP from the mid-1990s on came to an end when thetwo pillars of growth exports and investment were hit by the regional economicand financial crisis of 1997-98. The steep rise in interest rates and in import costs,owing to the rapid devaluation in the peso, caused a sharp contraction in fixedcapital formation in 1998. The 21% contraction in exports (national-accountsmeasure) caused a deterioration in the net foreign balance since the fall inimports although steep was lower, at 14.7%. An aggravating factor on the supplyside was the fall in agricultural output owing to the El Niño weatherphenomenon, which hit the rice and maize crops. GDP consequently fell by 0.6%in 1998, a sharp turnaround compared with growth of 5.8% in 1996 and 5.2% in1997, but a much smaller deterioration than that registered by other economies inthe region.

The recession was also short-lived. The following two years saw a generallystrengthening recovery, with real GDP growth reaching 3.4% in 1999 and 6% in2000. Exports picked up marginally in 1999, but imports continued to decline, if ata much milder pace: as a result the net foreign balance contributed 3% to GDPgrowth in that year. Domestic demand remained sluggish throughout 1999, with

A switch to inflation targeting

A record of resilience indifficult conditions

Philippines 27

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

private consumption rising by only 2.6% and capital formation still contracting,albeit at a much slower rate. The most dynamic demand component wasgovernment consumption spending, which surged by 6.7% as the governmentembarked on an expansionary spending programme. On the supply side,agriculture made up the ground lost in 1998, whereas industry remained in thedoldrums with growth of only 0.9%. In 2000 the combination of double-digitexport growth, as the US economy hit the peak of its cycle, and a modest rise inimport spending produced another fall in the net foreign deficit, equivalent to anincrement of 5.3% in GDP. Private consumption growth picked up once more, andannual gross fixed investment growth shot up to 19.9%. On the supply side themost significant feature was the strengthening recovery in manufacturing, whichregistered growth of 5.6% in 2000, offsetting the slackening in agricultural growth.

These trends were reversed in 2001, when continuing strong growth inagriculture buoyed up private consumption and hence domestic demandduring a period when a severe deterioration in the external environmentparticularly the weakening in US growth and a cyclical downturn in theelectronics market pushed up the net foreign deficit, which represented a2-percentage-point drag on GDP growth. GDP growth consequently fell to 1.8%in 2001. In 2002 GDP growth recovered to 4.3% despite the negative foreignbalance, which held GDP growth back by 0.9 percentage points as theagricultural sector continued to grow strongly and faster growth was recordedin the manufacturing sector.

GDP growth strengthened further to 4.7% in 2003 on the back of a 5.3%expansion in private consumption the best performance for this componentsince 1990 as agricultural growth held up and the services sector was buoyedby inflows of remittances from overseas Filipino workers. Private consumptionwas thus able to offset a lacklustre 0.5% increase in government consumption(as the government sought to hold down the budget deficit) as well as anincrease of only 2.9% in gross fixed investment (which was at least partlyrelated to political and security jitters in advance of the 2004 presidentialelection). The foreign balance subtracted a hefty 3.4 percentage points fromGDP growth as imports were sucked in by the strength of private c0nsumptionspending even as exports put in a patchy performance.

28 Philippines

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Remittance inflows

The importance of the Filipino community abroad