Embed Size (px)

Citation preview

Completion Report

Program Number: 39516 Loan Numbers: 2387, 2584 January 2013

Philippines: Local Government Financing and Budget Reform Program Cluster

CURRENCY EQUIVALENTS

Currency Unit – peso (P)

Subprogram 1 At Appraisal At Program Completion (30 October 2007) (09 April 2008) P1.00 = $0.027 $0.024 $1.00 = P44.02 P41.40 ¥1.00 = $0.008 $0.010 $1.00 = ¥114.177 ¥102.655

Subprogram 2

At Appraisal At Program Completion (6 October 2009) (31 March 2010) P1.00 = $0.021 $0.022 $1.00 = P46.61 P45.14

ABBREVIATIONS

ADB – Asian Development Bank AFD

APIS BIR

– – –

Agence Française de Développement annual poverty indicator survey Bureau of Internal Revenue

BLGF – Bureau of Local Government Finance CCD – Coordination Committee on Decentralization CLUP

DBM – –

comprehensive land use planning Department of Budget and Management

DENR DILG DMF

– – –

Department of Environment and Natural Resources Department of Interior and Local Government design and monitoring framework

DOF – Department of Finance FIES – family income and expenditure survey GDP – gross domestic product GFC – global financial crisis GFI

GPRA HUC

– – –

government financial institution Government Procurement Reform Act highly urbanized cities

IRA – internal revenue allotment LGC

LGFBR LGFPMS LGPMS LGU

– – – – –

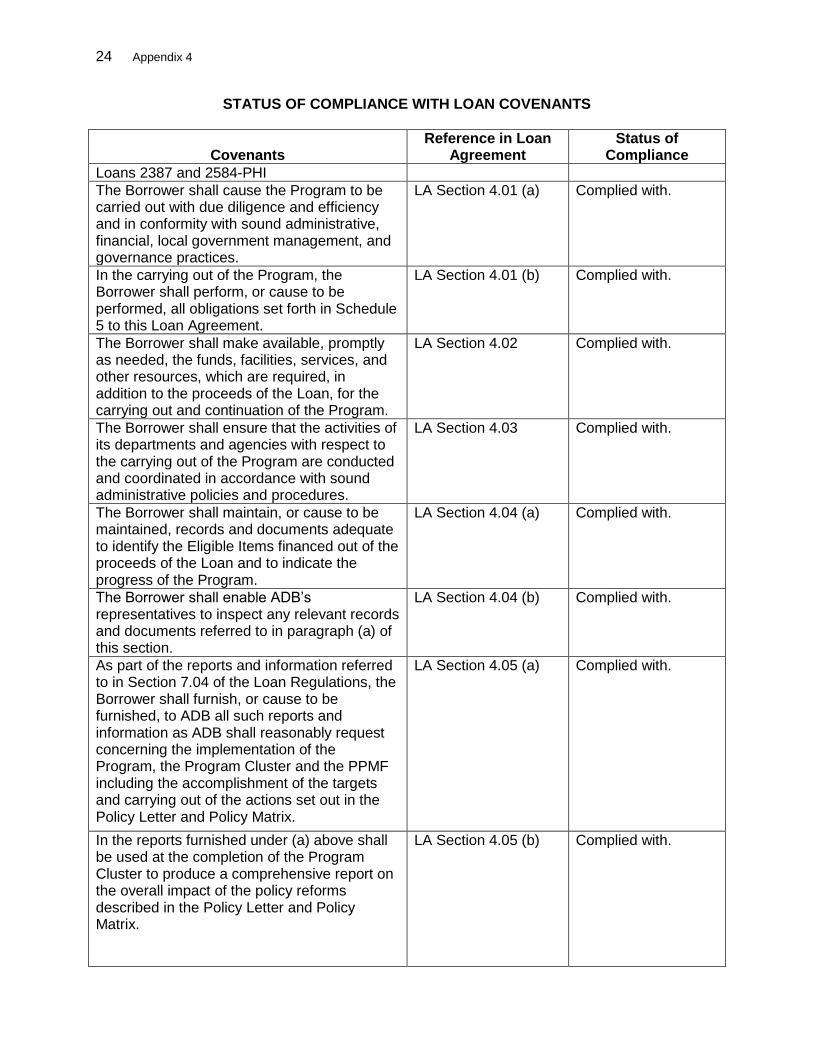

local government code Local Government Financing and Budget Reform local government financial performance management system local government performance management system local government unit

MDFO – Municipal Development Fund Office MDG

MPI MTPDP

– – –

Millennium Development Goal multidimensional poverty index Medium-Term Philippine Development Plan

NDHS NEDA

– –

national demographic and health survey National Economic and Development Authority

NGA – national government agency ODA – official development assistance PDAF – Priority Development Assistance Fund PDF

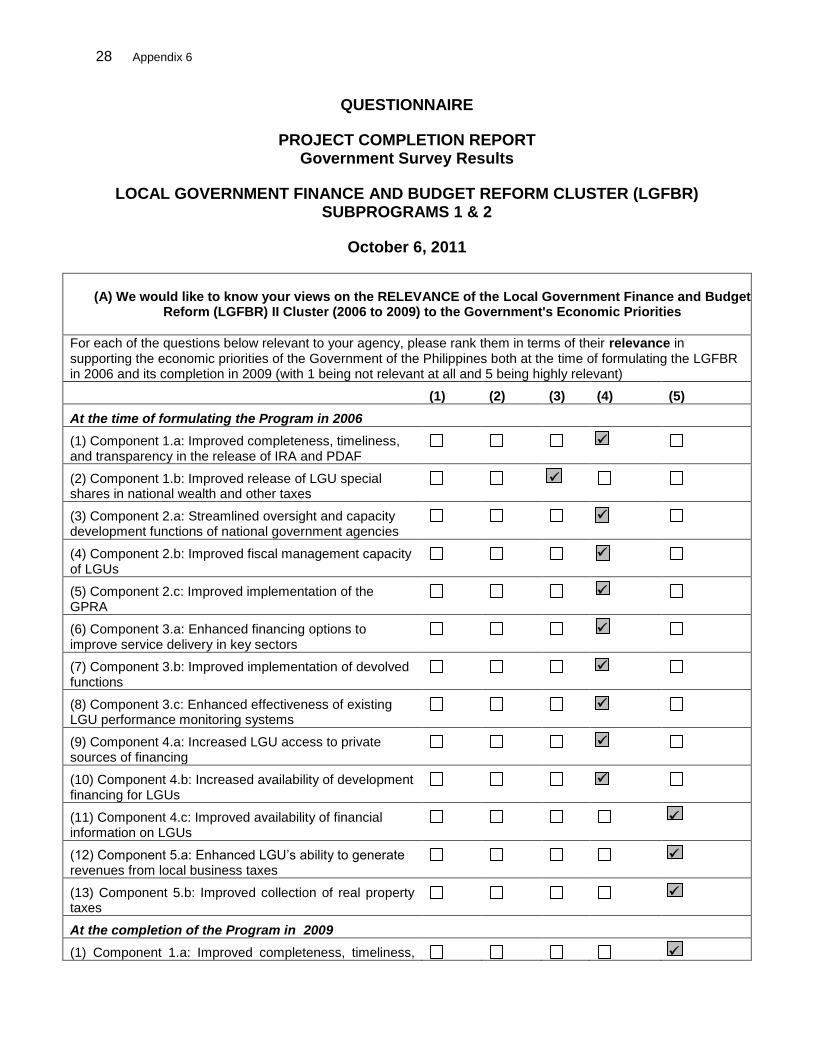

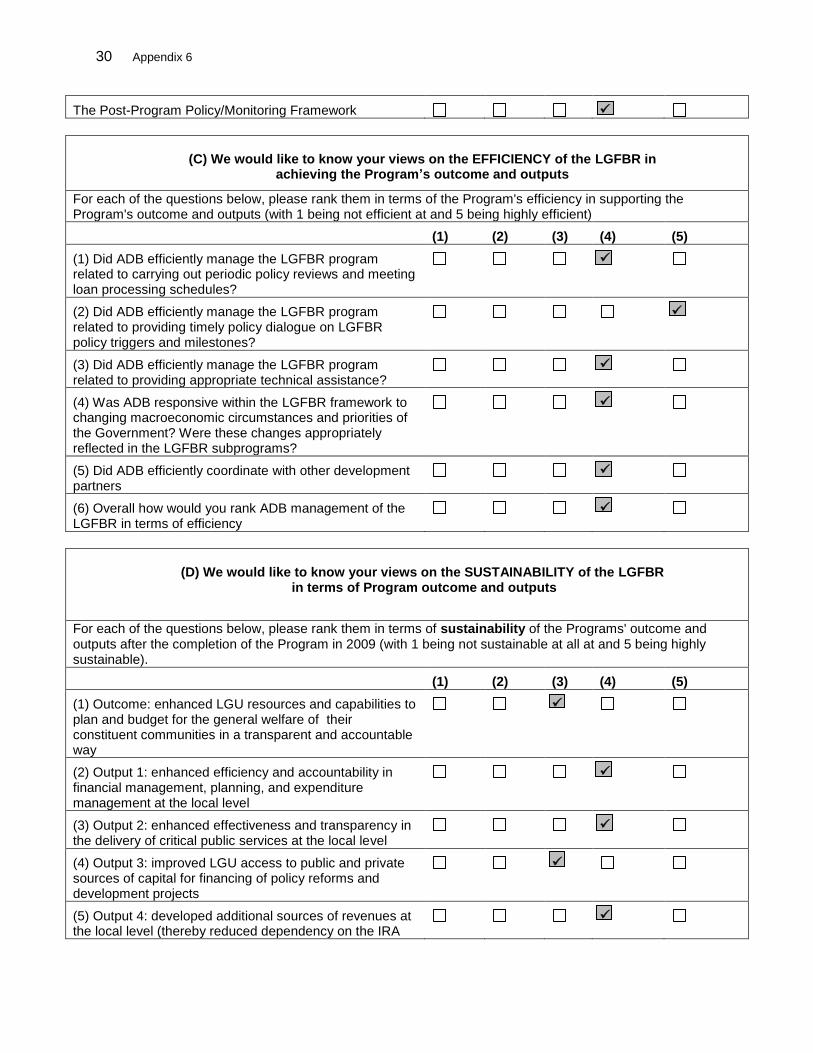

PFM – –

Philippines Development Forum public financial management

PROLEND SIE

– –

program lending facility statement of income and expenditures

SRE TA

– –

statement of receipts and expenditures technical assistance

NOTES

(i) The fiscal year (FY) of the Government and its agencies ends on 31 December. (ii) In this report, "$" refers to US dollars.

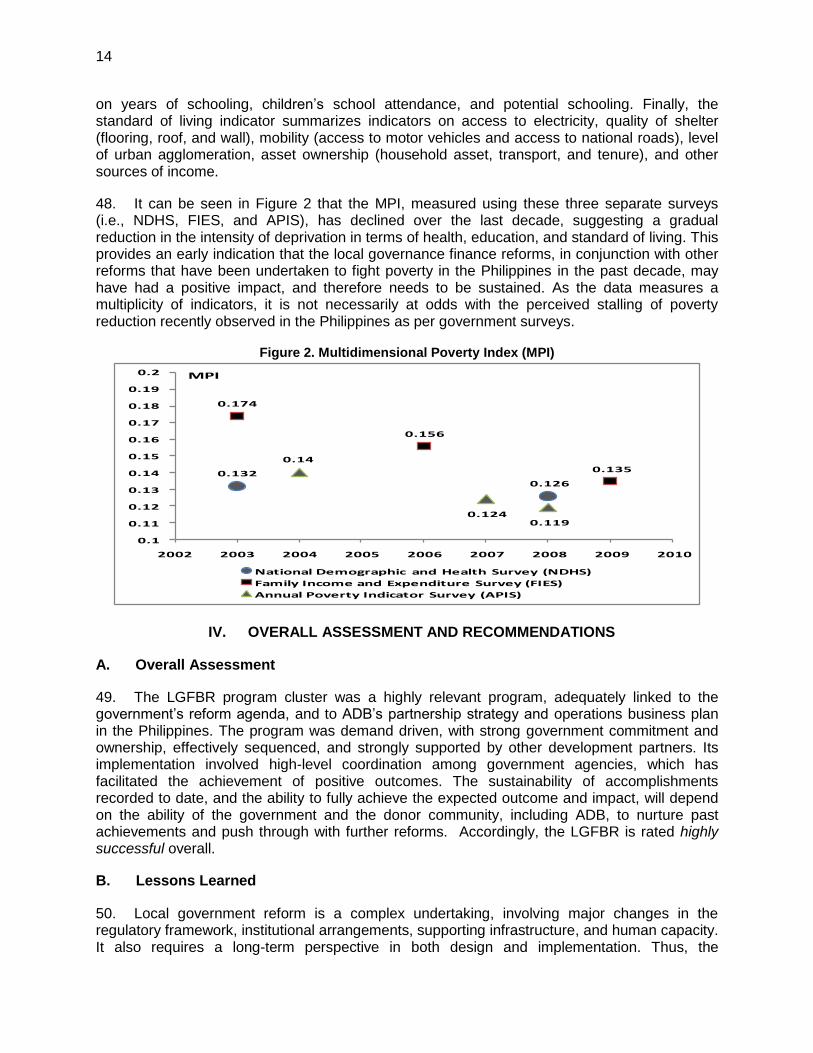

Vice President S. Groff, Operations 2 Director General K. Senga, Southeast Asia Department (SERD) Director S. Hattori, Public Management, Financial Sector, and Trade Division, SERD Team leader J.L. Gomez Reino, Senior Public Management Specialist, SERD Team members R. Anglingkusumo, Financial Sector Economist, SERD

R. Aquino, Associate Project Analyst, SERD K.M. Sanchez, Operations Assistant, SERD

R. Ramilla-Siquijor, Operations Assistant, SERD S. Tukuafu, Principal Financial Sector Specialist, SERD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS

Page

BASIC DATA

I. PROGRAM DESCRIPTION 1

II. EVALUATION OF DESIGN AND IMPLEMENTATION 2

A. Relevance of Design and Formulation 2 B. Program Outputs 3 C. Program Costs and Disbursements 8 D. Program Schedule 8 E. Implementation Arrangements 8 F. Conditions and Covenants 8 G. Related Technical Assistance 8 H. Consultant Recruitment and Procurement 10 I. Performance of the Borrower and the Executing Agency 10 J. Performance of the Asian Development Bank 10

III. EVALUATION OF PERFORMANCE 11

A. Relevance 11 B. Effectiveness in Achieving Outcome 11 C. Efficiency in Achieving Outcome and Outputs 13 D. Preliminary Assessment of Sustainability 13 E. Impact 13

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 14

A. Overall Assessment 14 B. Lessons Learned 15 C. Recommendations 15

APPENDIXES

1. Design and Monitoring Framework 16 2. Performance of Local Government Financing and Budget Reform Program, Subprogram 1 – Triggers 19 3. Performance of Local Government Financing and Budget Reform Program, 22 Subprogram 2 – Triggers 4. Status of Compliance with Loan Covenants 24 5. Post-LGFBR Program Monitoring Framework 27 6. Project Completion Report: Government Survey Results 28

i

BASIC DATA: LOCAL GOVERNMENT FINANCING AND BUDGET REFORM PROGRAM CLUSTER, SUBPROGRAM 1

A. Loan Identification

1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

Philippines 2387 Local Government Financing and Budget Reform Program (Subprogram 1) Republic of the Philippines Department of Finance (DOF) ¥34,253,100,000 equiv $300,000,000 1382

B. Loan Data

1. Fact-finding – Date Started – Date Completed

2. Appraisal – Date Started – Date Completed 3. Loan Negotiations – Date Started – Date Completed 4. Date of Board Approval 5. Date of Loan Agreement 6. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 7. Closing Date – In Loan Agreement – Actual – Number of Extensions 8. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years) 9. Terms of Relending (if any) – Interest Rate – Maturity (number of years) – Grace Period (number of years) – Second-Step Borrower

15 May 2007 6 June 2007

10 July 2007 27 July 2007 11 December 2007 11 December 2007 13 December 2007 22 February 2008 7 April 2008 7 April 2008 - 31 Mar 2008 9 April 2008 1 LIBOR-based lending rate 15 years 3 years Not Applicable Not Applicable Not Applicable Not Applicable

ii

10. Disbursements a. Dates

Initial Disbursement

09 April 2008

Final Disbursement

09 April 2008

Time Interval

-

Effective Date

07 April 2008

Original Closing Date

31 March 2008

Time Interval

-

b. Amount

Category or Subloan

Original

Allocation

Last Revised

Allocation

Amount

Canceled

Net Amount Available

Amount

Disbursed

Undisbursed

Balance

Local Government

Financing and Budget

Reform Program

¥34,253 million

None - ¥34,253 million

¥34,253 million

-

USD Equivalent

$300 million - $300 million $337.552 million

-

11. Local Costs (Financed) - Amount ($) None - Percent of Local Costs None - Percent of Total Cost None C. Program Data

1. Program Cost

Cost Appraisal Estimate Actual1

Foreign Exchange Cost $300,000,000 $337,552,086

Total

2. Financing Plan

Cost Appraisal Estimate Actual

Implementation Costs

ADB-Financed

Single Tranche $300,000,000 $337,552,086

Total $300,000,000 $337,552,086

ADB = Asian Development Bank

1 US$ equivalent of the actual loan disbursements of ¥34,253,100,000.

iii

3. Cost Breakdown by Program Component

Component Appraisal Estimate Actual

Single Tranche $300,000,000 $337,552,086

4. Program Schedule

Item Appraisal Estimate Actual

Other Milestones

Single Tranche $300,000,000 $337,552,086

Total $300,000,000 $337,552,086

5. Program Performance Report Ratings

Implementation Period

Ratings

Development Objectives

Implementation Progress

07 Apr 2008–30 Apr 2008 S S S = satisfactory.

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Members

a

Fact-Finding 15 May–06 June 2007 05 80 a, b, c, d, e

Appraisal 10–27 July 2007 04 72 a, b, c, f

a a – public sector management specialist , b – country specialist, c – senior capacity development specialist,

d – social security specialist, e – financial management specialist, f – staff consultant.

iv

BASIC DATA: LOCAL GOVERNMENT FINANCING AND BUDGET REFORM PROGRAM CLUSTER, SUBPROGRAM 2

A. Loan Identification

1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

Philippines 2584 Local Government Financing and Budget Reform Program (Subprogram 2) Republic of the Philippines Department of Finance (DOF) $225 million 1382

B. Loan Data

1. Fact finding – Date Started – Date Completed

2. Appraisal – Date Started

– Date Completed

3. Loan Negotiations – Date Started – Date Completed

4. Date of Board Approval 5. Date of Loan Agreement

6. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions

7. Closing Date – In Loan Agreement – Actual – Number of Extensions

8. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years)

9. Terms of Relending (if any)

01 June 2009 16 June 2009

27 July 2009 5 August 2009

03 September 2009 03 September 2009

26 November 2009 08 December 2009

28 December 2009 28 December 2009 -

31 March 2010 31 March 2010 -

LIBOR-based lending rate 15 years 3 years

NA

10. Disbursements a. Dates

Initial Disbursement

29 December 2009

Final Disbursement

29 December 2009

Time Interval

0

Effective Date

29 December 2009

Original Closing Date

29 December 2009

Time Interval

0

v

b. Amount

Category or Subloan

Original Allocation

Last Revised

Allocation

Amount Canceled

Net Amount Available

Amount Disbursed

Undisbursed Balance

1 $225 million None - $225 million $225 million

Total $225 million - $225 million $225 million

11. Local Costs (Financed) - Amount ($) None - Percent of Local Costs None - Percent of Total Cost None

C. Program Data

1. Program Cost

Cost Appraisal Estimate Actual

Foreign Exchange Cost $441,000,000 $441,000,000

Total $441,000,000 $441,000,000

2. Financing Plan

Cost Appraisal Estimate Actual

Implementation Costs

ADB-Financed

Single Tranche

AFD-Financed

$225,000,000

$216,000,000

$225,000,000

$216,000,000

Total $441,000,000 $441,000,000 ADB = Asian Development Bank

3. Cost Breakdown by Program Component

Component Appraisal Estimate Actual

ADB-Financed (Single Tranche)

AFD-Financed

$225,000,000

$216,000,000

$225,000,000

$216,000,000

Total $441,000,000 $441,000,000

4. Program Schedule

Item Appraisal Estimate Actual

Other Milestones

ADB-Financed (Single Tranche)

AFD-Financed

Total

$225,000,000

$216,000,000

$441,000,000

$225,000,000

$216,000,000

$441,000,000

vi

HS = highly satisfactory, S = satisfactory.

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of Members

a

Fact-Finding

Appraisal

1–16 June 2009

27 July –5 Aug 2009

4

4

64

40

a, b, c, f

a, b, c, f

a a – public sector management specialist , b – country specialist, c – senior capacity development specialist,

d – social security specialist, e – financial management specialist, f – staff consultant.

5. Program Performance Report Ratings

Implementation Period

Ratings

Development Objectives

Implementation Progress

28 Dec 2009–31 Dec 2009 S S

01 Jan 2010–31 Mar 2010 S S

I. PROGRAM DESCRIPTION

1. Background. In the mid 2000s, under the umbrella of the Medium-Term Philippine Development Plan (MTPDP) 2004–2010, the Government of the Philippines initiated a wide-ranging and comprehensive program of reforms to address the long-standing problems of poverty and unemployment, and achieve the Millennium Development Goals (MDGs).1 The Philippines Development Forum (PDF)2 in 2007 reiterated the government‟s commitment to poverty reduction, through nurturing local growth, fostering local economic development, and promoting better service delivery by local governments. More specifically, the government sought to strengthen poverty reduction efforts by continuing with its reforms in fiscal management and service delivery by local government units (LGUs) .3

2. Local government reform in the Philippines had started a decade and a half earlier with the enactment of the Local Government Code (LGC) in 1991. The LGC provided a comprehensive framework for local autonomy and decentralization. It re-assigned various service delivery responsibilities from the national government to LGUs and expanded the scope of local government taxing powers. As a result, the LGC opened up new sources of development financing, and stressed the key role played by LGUs in local development dynamics. The Local Government Financing and Budget Reform (LGFBR) program cluster has been an integral part of local government reforms. Prior to the LGFBR program, local government reforms had produced a number of well-performing LGUs. Yet, there was also considerable scope for improving the ability of LGUs to be more responsive to local development challenges. Areas that were perceived as reform priorities included (i) clearer and more streamlined expenditure assignments between national government agencies (NGAs) and LGUs, (ii) wider alternatives for LGUs‟ resource mobilization, (iii) increased capacity of LGUs in tax administration, budgeting, and financial management, (iv) better structures, procedures, and information systems for NGAs to exercise their oversight roles in LGUs‟ activities, and (v) a stronger legal and institutional framework for decentralization.

3. The need to enhance the pace of local government reform increased in 2008–2009, on the back of the global financial crisis (GFC). Hit by reduced access to capital markets, decreased remittances, and weakened global demand for exports, GDP growth slowed sharply and poverty reduction came to a halt. The deteriorating external environment and its impact on the domestic economy brought to the forefront the critical role that LGUs could play in cushioning the impact of the GFC, stimulating domestic demand, and sustaining the government‟s economic development agenda. It was envisaged that the effectiveness of the fiscal stimulus package in supporting growth and sustaining poverty reduction could be enhanced by strengthening the effectiveness and efficiency of LGUs in planning, funding, and delivering key government services at the local level.

4. Program’s impact, outcome, and outputs. The LGFBR program cluster was expected to increase the efficiency and effectiveness of LGUs in delivering basic public services to their constituent communities. To bring about this expected impact, the program cluster‟s outcome

1

Government of the Republic of the Philippines, National Economic Development Authority. 2004. Medium-Term Philippines Development Plan (MTPDP) 2004–2010. Manila.

2 The Philippines Development Forum or PDF is the primary mechanism of the Government for facilitating

substantive policy dialogue among stakeholders on the country‟s development agenda. Co-chaired by the Government (Department of Finance) and the World Bank, comprises representatives from development partners, civil society, academia, private sector, and the legislature.

3 LGUs comprise highly urbanized cities, independent component cities, provinces, component cities, municipalities,

and barangays (villages).

2

was the enhanced resources and capacities of LGUs to plan and budget for the general welfare of their constituent communities in a transparent and accountable way.

5. The scope of the program included reforms to (i) improve the release of LGU shares in national government revenues; (ii) implement a financial reporting system; (iii) improve the local government performance measurement system; (iv) facilitate access of LGUs to development credit financing; and (v) improve the collection of local business and real property taxes. The Design and Monitoring Framework (DMF) of the LGFBR program is presented in Appendix 1. Policy measures undertaken under subprogram 1 and 2 are presented in Appendix 2 and 3, respectively.

6. Financing and cofinancing. The program cluster comprised two single tranche loans (or subprograms) from 2006 to 2010. Each subprogram was funded from the ordinary capital resources of the Asian Development Bank (ADB). Subprogram 1 ($300 million) was approved by ADB‟s Board on 26 December 2007, and subprogram 2 ($225 million) on 26 November 2009. Agence Française de Developpement (AFD) provided an additional $216 million equivalent for subprogram 2 through a collaborative cofinancing arrangement. Subprogram 1 (2006–2008) was implemented with a well-defined, medium-term framework specified at the outset, including reforms prior to Board consideration.4 Subprogram 2 (2009–2010) was implemented based on the medium-term framework specified under subprogram 1, with adequate room for flexibility in the program‟s design to accommodate the progress made under subprogram 1 and changes in the external environment resulting from the GFC.5

II. EVALUATION OF DESIGN AND IMPLEMENTATION

A. Relevance of Design and Formulation

7. The design of the LGFBR program was highly relevant. The program was aligned with the government‟s reform agenda, as conceived in the MTPDP, to reduce poverty by emphasizing the effectiveness and efficiency of local governments in delivering basic public services. Through the government-led PDF, ADB and the government jointly defined the policy measures implemented under the LGFBR.6 The program cluster consolidated key fiscal, expenditure, budget, and planning reforms in local governance under five key policy areas (described in subsection II.B below). The program also pursued capacity building initiatives, coordination among oversight agencies, and transparency in local fiscal governance.

8. The LGFBR program was also aligned with a core element of ADB‟s country strategy and program 2005–2007 for the Philippines, and it was the first policy program that addressed major policy issues surrounding local governance.7 Complementing the broader policy support provided by the Development Policy Support Program, the LGFBR program was central to

4 ADB. 2007. Report and Recommendation of the President to the Board of Directors: Proposed Program Loan and

Technical Assistant Grant to the Republic of Philippines: Local Government Financing and Budget Reform Program Cluster (Subprogram 1). Manila (Loan 2387-PHI).

5 ADB. 2009. Report and Recommendation of the President to the Board of Directors: Proposed Program Loan to the Republic of Philippines for Subprogram 2: Local Government Financing and Budget Reform Program Cluster. Manila (Loan 2584-PHI).

6 PDF is a forum that serves as a venue for dialogue on core development issues, including those concerning local

governments (finance, capacity development, performance benchmarking, and policy reforms on devolution). 7 ADB. 2005. Country Strategy and Program: Philippines, 2005–2007. Manila.

3

ADB‟s country operations business plan 2009–2010, which strongly underscored the role of decentralization and good local governance as outlined in the MTPDP.8 B. Program Outputs

9. The expected outputs of the LGFBR program were grouped into five components or policy objectives: (i) improved completeness, timeliness, and transparency of releases of LGU shares in national government revenues; (ii) enhanced efficiency and accountability in financial management, planning, and expenditure management at the local level; (iii) enhanced effectiveness and transparency of critical public services at the local level; (iv) improved LGU access to public and private sources of capital for financing of policy reforms and development projects; and (v) reduced dependence on national transfer through additional sources of revenue developed at the local level. This subsection summarizes the sector analysis underpinning the program design at the time of processing, and the measures implemented under the cluster.

1. Intergovernmental fiscal relations: improved completeness, timeliness, and transparency of releases of LGU shares in national government revenues.

10. Government transfers to LGUs are of three types: (i) formula-based block grants (i.e., the internal revenue allotment (IRA); (ii) origin-based share in national government revenues (i.e., share in national wealth and other taxes); and (iii) ad hoc categorical grants. The IRA is the most significant revenue source, especially for the lower income class LGUs.9 Under the LGC, the aggregate IRA of LGUs is set at 40% of the actual internal revenue tax collections of the government three years prior to the current year.10

11. The effectiveness of national transfers to LGUs was constrained by several obstacles. (i) The quarterly IRA releases were not performed in a reliable manner. Despite the

provisions of the LGC, the government retained considerable discretion in appropriating and releasing IRA. This turned the IRA into a highly unpredictable revenue source for LGUs when the government‟s fiscal position was unfavorable. At the same time, this limited LGUs‟ ability to budget and plan effectively. It also hampered LGUs‟ access to financial markets, since creditors made LGUs rely heavily on the IRA deposits as collateral.

(ii) IRA allocations did not fix the substantial vertical and horizontal fiscal imbalances in LGU financing. Transfers did not adequately cover the cost of devolved functions, and discriminated between certain groups of LGUs, with provinces and municipalities complaining of unfavorable treatment.

(iii) Widespread complaints were reported on the non-transparent allocation of the Priority Development Assistance Fund (PDAF). The PDAF is allocated to members of Congress for discretionary spending at the LGU level, and if these non-IRA grants are not channeled to local investments in a transparent way, they can potentially undermine LGU planning for strategic use of the funds.

8

ADB. 2008. Country Operations Business Plan: Philippines, 2009–2010. Manila. 9

Bureau of Local Government Finance classifies LGUs in 6 classes based on a four year average of their regular income with 1 being the wealthiest.

10 The aggregate IRA is then divided among different local government levels as follows: 23% to provinces, 23% to cities, 34% to municipalities, and 20% to barangays. The IRA share of each tier of local government is then apportioned to individual LGUs within each level based on population (50%), land area (25%), and equal sharing (25%).

4

(iv) The release of LGU shares in national wealth taxes was neither timely nor complete. The reasons for this were: (i) problems in accurately estimating tax collections from natural resources since actual tax collections for the immediately preceding year are not yet known when the General Appropriation Act is prepared; and (ii) lack of information on the location of the taxable entity.

12. The government undertook reforms in intergovernmental fiscal relations to improve the ability of LGUs to plan and budget their resources:

(i) The reforms improved the completeness, timeliness, and transparency of the release of LGU shares in national government revenues. Republic Act 9358 was passed in 2006, providing for „automatic appropriation‟ of the IRA from 2007. The predictability and transparency in the release of the IRA was further improved by the timely estimation and certification of the IRA shares by the Bureau of Internal Revenue (BIR), and distribution of the Local Budget Memorandum (LBM) to LGUs by June of every year, announcing their IRA share for the coming year. To improve the transparency framework, the government, through the Department of Budget and Management (DBM), also posted on its website the IRA share of each of the 43,704 local governments in line with the formulas prescribed by the LGC, and the releases of the PDAF. This enhanced transparency framework has allowed citizens to monitor the amount each LGU is receiving from the government and reduced uncertainty in fiscal planning at the local level.

(ii) The reforms improved the release of LGU special shares in national wealth and other taxes. The LGFBR program supported the issuance and implementation of Joint Circular 2006–1, which provided a multidepartment framework for the release of LGU shares of national wealth in mining, forestry, and energy royalties. In addition, Joint Circular 2009–1 has streamlined the documentary procedure and delineated departments‟ responsibilities for the prompt release of LGUs‟ share of mining taxes.11 With these actions, over the medium term, the amount of transfer resources flowing to LGUs has increased and the uncertainty over the releases of LGU shares of national wealth has been reduced.

2. Enhanced efficiency and accountability in financial management, planning, and expenditure management.

13. The LGFBR noted that the efficiency and accountability in financial management, planning, and expenditure management at the local level could be improved by addressing several key challenges. First, local planning and expenditure management needed to be improved by linking financial and budget reporting to local development planning. Second, the planning links between regions and provinces were weak as coordination between government and LGU planning units was lacking. Investment planning at the local level was formulated independently of regional and national investment plans and vice versa. Third, revenue estimates during budget formulation were very poor, distorting the integrity of local budgeting. In addition, LGUs‟ reporting and procurement practices were totally inadequate. Accordingly, the objectives of this policy area were to (i) streamline the oversight and capacity development functions of NGAs,(ii) improve the fiscal management capacity of LGUs, and (iii) improve implementation of the Government Procurement Reform Act (GPRA).

11

The Joint Circular was issued by the Department of Finance (DOF), DBM, Department of Interior and Local Government (DILG), and Department of Environment and Natural Resources (DENR).

5

14. To streamline the oversight and capacity development functions of NGAs, the LGFBR program aimed to enhance local transparency and accountability in financial management, planning, and expenditure management. It attempted to improve debt management and the information base for LGU performance measurement and credit rating, and to improve also the competency of local financial managers. Specifically, the program supported: (i) the issuance of a Joint Circular 2007-1 to institutionalize a coordinated framework on harmonizing local planning, investment programming, revenue administration, budgeting, and expenditure management;12 (ii) the issuance of an updated budget operations manual, with 90% of LGUs trained in its use; (iii) the completion and distribution of provincial planning guidelines and the training of local officials in using the guidelines to enable them to plan, identify, prepare, and prioritize critical programs and projects, and raise and allocate resources; and (iv) the preparation of provincial development and physical framework plans and a provincial development investment program using the guidelines on provincial and local planning and expenditure management. Under the LGFBR, the government was also able to: (i) implement the updated budget operations manual for provinces (81) and highly urbanized cities (HUCs) (28); (ii) complete and implement a debt monitoring system at the provincial, city, and municipal levels; and (iii) issue the barangay operations manual.

15. To improve the fiscal management capacity of LGUs, the LGFBR program supported: (i) the development, computerization, and implementation of the statement of receipts and expenditures (SRE) financial reporting system, and harmonization of the SRE with the new government accounting system; (ii) 2,551 mandatory and demand-driven training programs for 494 LGUs in project management, operations and maintenance, planning, and investment programming; and (iii) the development and implementation of a competency certification system for local treasurers. On this last measure, the government also provided assistance to the Mayors Development Center for the distance training of treasurers, the training of 228 LGUs in standardized project financing, and other demand-driven training. Over the medium term, these measures have improved the timeliness and accuracy of financial information for LGU financial managers, and the overall fiscal and financial management systems.

16. To improve implementation of the GPRA, the LGFBR program aimed to improve procurement efficiency and transparency at the local level, including the barangay level. To achieve this, the program: (i) provided training courses on the GPRA to 86% of all LGUs; (ii) prepared and pilot tested simplified procurement procedures for LGUs; (iii) developed and implemented the barangay procurement manual; and (iv) simplified procurement procedures and bidding documents. All LGUs implemented the GPRA with the help of the simplified guide to the Generic Procurement Manual.

3. Performance Measurement and Service Delivery: enhanced effectiveness and transparency of critical public services at the local level.

17. Development of an adequate framework for providing resources, including through private financing, based on LGU‟s performance in the delivery of local services, was identified as a reform priority. To address this issue, a two-track reform was implemented under the LGFBR to develop a framework for performance-based grants and simultaneously provide a link for improving the availability of credit financing to LGUs (see Program Output 4 described below). More specifically, this key policy area sought to: (i) enhance financing options as a way to improve infrastructure and the provision of social services at the local level; and (ii) improve

12

The Joint Memorandum Circular was agreed upon by the DOF, DBM, DILG, and the National Economic and Development Authority (NEDA).

6

efficiency in the devolution of key functions and services, and enhance the effectiveness of existing LGU performance monitoring systems, thus increasing private sector confidence in lending to LGUs.

18. To enhance financing options for improved service delivery in key sectors, the LGFBR program supported the government‟s plan to improve LGUs‟ access to development credit, which would likely lead to improvements in the environment, local urban infrastructure, health, and rural and agricultural services. The program also assisted the government in completing a study on performance-based grants for LGUs, and in adopting a framework for such grants. The program supported the institutionalization of a coordination body, the Coordination Committee on Decentralization (CCD), at the national level to address recurrent and future issues on decentralization. The program expanded the coverage of the Local Government Performance Management System (LGPMS) and introduced the system to all LGUs. The system provided LGUs with a tool to assess their strengths and weaknesses in the performance of their roles and responsibilities. Indicators included in the system were derived largely from the LGC and measured performance in four key areas: governance, administration, social services, and economic development. The program also supported the integration of the Local Government Financial Performance Monitoring System (LGFPMS) into the LGPMS, enriching the performance monitoring framework for local governments in the country with the inclusion of financial performance indicators.

4. Improved LGU access to public and private sources of capital for the financing of policy reforms and development projects.

19. Given the expanded responsibilities of LGUs to provide a wide range of services to local constituents, such as services in basic infrastructure and health, they require access to both public and private sources of financing. Aligned to this, the government‟s long-term vision was for the capital market and private lending to play a vital role in local government financing, in order to diversify the sources of development credit for LGUs. Not all LGUs were able to borrow from banks because of their lack of creditworthiness. However, cities had better access to credit financing because of their creditworthiness. Thus, cities accounted for 54 percent of total outstanding LGU loans in 2004, while provinces accounted for 18.8 percent, and municipalities for 25.8 percent. Most LGUs relied primarily on Government Financial Institutions (GFIs) and the Municipal Development Fund Office (MDFO) to finance the development of infrastructure, capital investment, and a portion of operating expenses. In 2006, GFIs provided around 76% of LGU development credit financing and the MDFO 7%. The GFIs had an advantage in the LGU credit market because of their role as LGU depository banks. In the event of a default in the payment of interest and amortization of the principal, the GFI, through a “back-to-back” agreement with the LGU, can debit the LGU‟s IRA depository account in the GFI. This created a structural impediment to private banks‟ entry into the market for lending to LGUs.

20. The LGFBR program supported the government‟s agenda to: (i) improve LGU access to private sources of financing, thus increasing LGUs‟ ability to finance investments; (ii) increase the availability of development financing for LGUs to achieve service delivery objectives; and (iii) improve availability of financial information on LGUs to provide private investors with more accurate information for assessing their creditworthiness.

21. To improve LGU access to private sources of financing, the LGFBR helped in the adoption of the LGU financing framework as a national policy, and of the national government–LGU cost sharing policy for the evaluation and processing of projects involving devolved activities for LGUs financed by MDFO. The program also supported the issuance of guidelines

7

for LGUs to open depository accounts in private banks. As a result, the DOF issued department order no. 27-05, allowing private, thrift, rural, and cooperative banks to act as LGU depository banks. With the aim of increasing the availability of development financing for LGUs, the program supported the Program Lending (PROLEND) facility, as a program lending facility, providing concessional credit financing to LGUs. The LGFBR also assisted in (i) the design of a government financing window for projects supporting the MDGs, and (ii) the establishment of a Disaster Calamity Fund. As regards financial information on LGUs, the program supported the revision of the income classification system for LGUs, which considers only LGUs‟ own-source revenues as an indicator, and integrated the system with the LGPMS. The LGFBR has assisted also in the computerization of the SRE financial reporting system and its harmonization with the New Government Accounting System, and the development of a debt certification system. These activities provide potential creditors and investors with a better picture of the LGUs‟ own-source revenue-generation capacity.

5. Development of additional sources of revenue at the local level, thereby reducing dependence on the IRA.

22. The LGFBR design noted that LGUs‟ own source of revenue for development financing was limited, thus creating dependency on the IRA. In 2006, tax revenue accounted for only 25 percent of total LGU income. To generate additional revenues, the LGUs imposed a huge array of taxes, fees, and charges, with low collection rates and high administrative costs. The lack of professional staff and inadequate automation were the constraints faced by LGUs in their tax administration activities. These constraints affected all aspects of tax administration, including poor taxpayer registration, inadequate tax law enforcement, and the lack of records and audit, resulting in widespread tax delinquencies. This was further aggravated by the lack of implementing guidelines governing local taxation. Hence, there was a need to focus on taxes, fees, and charges that had high yield potential, and on improving their administration and collection.

23. The LGFBR supported the government in achieving two key reform objectives: (i) enhancing LGUs‟ ability to generate revenues from local business taxes; and (ii) improving the collection of real property taxes. Under the first objective, an executive order was issued requiring the BIR and its regional offices to provide tax information to LGUs. Interpretation of the situs of tax rule for banks under Local Finance Circular 1–93 on the levying of a local business tax was revised in 2007. In addition, guidelines were issued on the situs of tax rule for mining firms in regard to the local business tax. A manual on creating a business taxpayers database and billing and collection system for LGUs was developed and distributed. In addition, 72 LGUs were trained under MDFO‟s Local Government Finance and Development project (LOGOFIND) and 11 LGUs availed of loans under the Business Tax Enhancement Program of MDFO‟s LOGOFIND initiative.

24. Under the second objective, the following was achieved: (i) 1,002 LGUs were trained under MDFO‟s LOGOFIND on revenue mobilization and updating the local revenue code;(ii) 60 LGUs availed of loans for real property tax improvements under MDFO‟s LOGOFIND projects; (iii) valuation standards for equipment and machinery were issued as an addendum to the assessors‟ manual; and (iv) valuation training on machinery and equipment was completed for 70 LGUs. The manual includes revised valuation standards, a code of ethics, mass appraisal, and market values as the basis for valuation. With the implementation of the updated manual on valuation standards for machinery and equipment, the collection of property taxes was expected to improve.

8

C. Program Costs and Disbursements

25. The cost of the LGFBR program cluster was $525 million. This was funded from ADB‟s ordinary capital resources and consisted of two single-tranche loans of ¥34,263,100 or $300 million equivalent for subprogram 1 and $225 million for subprogram 2. The first tranche of ¥34,263,100 was valued at $337,552,086 on 9 April 2008 and was released on April 7, 2008. The second tranche of $225 million for subprogram 2 was released on December 28, 2009. AFD provided additional financing of $216 million for subprogram 2 through a collaborative cofinancing arrangement with ADB.

D. Program Schedule

26. The implementation period for subprogram 1 was from January 2006 to 31 December 2007, while subprogram 2 was implemented from January 2008 to 31 December 2009. The loan accounts were closed on 9 April 2008 for subprogram 1 after one extension and 31 March 2010 for subprogram 2.

E. Implementation Arrangements

27. DOF was the executing agency responsible for the overall implementation of the two subprograms, including compliance with the policy actions, program administration, disbursements, and maintenance of all program records. An LGFBR program coordination committee (the Committee) was established at the start of subprogram 1. It was chaired by the undersecretary of DOF and its members were officials from the implementing agencies, namely BLGF, MDFO, DILG, DBM, and NEDA. The committee was responsible for coordinating the implementation of LGFBR program policy actions with agencies supporting the program and met quarterly to monitor progress and oversee implementation of the program.

F. Conditions and Covenants

28. The program cluster accomplished 42 policy triggers. The status of compliance with the policy triggers for each subprogram is shown in Appendix 2 and 3. In addition to the policy triggers, both subprograms had additional covenants on administering the program, all of which were complied with (Appendix 4).

G. Related Technical Assistance

29. Two accompanying advisory TA projects, were approved to complement the LGFBR program.13 The TA 7019 project that accompanied subprogram 1, funded by the Japan Special Fund, was designed to support implementation of the LGFBR program cluster by (i) building institutional capacity in the development and implementation of a medium-term reform agenda in local government financing and governance; (ii) providing the government with just-in-time policy advice; and (iii) facilitating achievement of the delivery targets and commitments in the LGFBR‟s policy matrix. The total cost estimate was $1.1 million, with ADB providing $0.8 million and the government the balance of $0.3 million for the remuneration and per diem of local consultants ($180,000) and office accommodation, transport, and other costs ($120,000). Actual disbursements amounted to $742,230 and the project was closed on 25 August 2010. The

13

ADB. 2007. Technical Assistance to the Republic of the Philippines for Local Government Financing and Budget Reform Program. Manila. (TA 7019) and ADB. 2009. Technical Assistance to the Republic of the Philippines for Support to Local Government Financing. Manila. (TA 7451).

9

executing agency for the TA was DILG. A project steering committee consisted of DILG, DOF, DBM, NEDA, and representatives of the League of Provinces, League of Municipalities, and League of Cities. DILG coordinated with DBM, DOF, NEDA, the LGU Leagues, and participating LGUs. The project steering committee met every quarter to review the written assessment of implementation progress and recommendations prepared by a technical committee, and discussed the review with ADB.

30. The TA was rated successful,14 as it delivered a wide range of useful outputs and well-targeted activities for improved local fiscal management. The outputs of the TA were organized under three main components.15

(i) Component I. A Coordination Committee on Decentralization (CCD) was established to strengthen the institutional coordination of decentralization reforms. The CCD promoted, coordinated, and oversaw the decentralization reforms, including the changes envisaged in the LBFGR policy matrix. The CCD has been very successful in defining a coordinated agenda of reforms and ensuring adequate dialogue across stakeholders, including government agencies, LGUs and development partners.

(ii) Component II. Planning and budgeting management capacity at the city level has been strengthened through the implementation of: (i) an enhanced guide to Comprehensive Development Plan (CDP) preparation, (ii) training modules and session guides for the conduct of courses on CDP preparation, (iii) a cross-reference guide on suggested tools and techniques for planning, investment programming, and plan monitoring and evaluation, extracted from the various manuals and guidebooks prepared by the relevant NGAs, and (iv) reports on the consultations among all stakeholders on the harmonization of the Comprehensive Land Use Plan (CLUP) and CDP.

(iii) Component III. Revenue generation and service delivery was enhanced through the improved implementation of the Local Governance Performance Management System (LGPMS). This was achieved through the improvements to the LGPMS manual, and through the widespread use of LGPMS data. In addition, the TA 477816 assisted in refining the LGPMS system design, and the system for monitoring and analyzing overall LGU performance. This TA initiated work on a number of key areas further developed with the LGFBR.

31. The TA 7451 project accompanying subprogram 2 was estimated at $1 million, with ADB financing $0.7 million from the Technical Assistance Special Fund. Total actual disbursements amounted to $0.607 million. The TA provided analytical inputs, system development, and institutional capacity building support to BLGF, MDFO, and DBM to further strengthen their capabilities to support LGUs in effecting key local resource mobilization, expenditure management, and service delivery reforms. This TA was completed in September 2012, and its associated TA completion report will be prepared in 2013. The TA has been very successful in providing continuity to reforms incorporated in the LGFBR‟s post program partnership framework.

14

ADB. 2011. Local Government Financing and Budget Reform Program (TA 7019). Technical Assistance Completion Report. Manila.

15 See ADB TA 7019 – PHI: Local Government Financing and Budget Reform Project, Final Report (Volume 1: Main Report and Appendices), Chapter 3, pp 9-24.

16 ADB. 2006. Technical Assistance to the Republic Philippines for Local Governance and Fiscal Management Project (formerly Strengthening LGU Management and Administration). Manila (TA 4778).

10

H. Consultant Recruitment and Procurement

32. Implementation of the TA under subprogram 1 took place from August 2008 to May 2010 with a total of 73.77 person-months of national consultants. The consultants were mostly engaged under ADB‟s contract with a consulting firm (Poyry IDP Consult, Inc.), but with the addition of three individual experts. The TA delivered most of the expected outputs and the performance of the consultants was satisfactory. The TA under subprogram 2 was also implemented by Poyry IDP Consult, Inc, from September 2010 to September 2012, with a total input of 64 person-months. I. Performance of the Borrower and the Executing Agency

33. The performance of the government is rated highly satisfactory. Through the CCD and the PDF, the government continued to refine its long-term vision for decentralization and reforms in local public financial management. Government ownership of the program was very strong, as shown by the number of quality policy triggers and measures completed on time during the program cluster period.

34. The commitment of the DOF (the executing agency) and the implementing agencies was also commendable, given the substance of the reforms undertaken by these agencies, which in many cases required solid inter-agency coordination to accomplish. The issuance of Joint Memorandum Circulars orchestrated by the DOF is one example of the strong cooperation among the implementing agencies. Other instances include the two-track reform under the Performance Measurement and Service Delivery component, which led to the adoption of performance-based grants and links to credit financing. The concerted efforts on interlinked components aimed at improving the availability of timely and accurate financial information systems for fiscal and financial management at the local level were equally commendable. These reforms continue to be pursued and refined by the oversight agencies.

35. In addition, the final subprogram 1 TA report indicates that the TA was used effectively by the DOF and implementing agencies to provide local officials with useful practical knowledge, tools, and skills that would further strengthen their capacity in designing, funding, and delivering quality government services at the local level. J. Performance of the Asian Development Bank

36. The performance of ADB has been highly satisfactory. During the processing of the program cluster, ADB staff conducted ample two-way dialogue and policy consultations with the DOF and implementing agencies to ensure that the program was demand driven, with solid government ownership. ADB also worked proactively with other donors, resulting in cofinancing from AFD, which continues to be a close partner in reforms for the forthcoming cluster. The design of the TA projects was also relevant and effective in helping the government accomplish the policy measures of the program cluster.

37. As part of the project completion review, ADB requested the government to provide its assessment of the program through a survey questionnaire completed by the implementing agencies. Overall, the government rated the program favorably in terms of relevance, efficiency, effectiveness, and likely sustainability. The full results of the survey are presented in Appendix 6.

11

III. EVALUATION OF PERFORMANCE

A. Relevance

38. The program cluster was highly relevant to the government‟s reform agenda. The program‟s ultimate objective of increased efficiency and effectiveness of basic public services delivered at the local level was in line with the government‟s long-term vision for reform, as articulated by the MTPDP and the PDF. The LGFBR took into account the need to improve the ability of LGUs to be more responsive to local development challenges, by addressing the obstacles faced by LGUs in accessing financial resources. The LGFBR helped to ensure the efficient delivery of devolved functions, by building the institutional capacity of LGUs to plan and budget for the better delivery of key public services to their constituents. The program also complemented the broader policy objective of continued fiscal consolidation and public debt sustainability, provided by the Development Policy Support Program.

39. The relevance of the program was also characterized by a well-designed framework. The five key policy objectives were harmoniously interlinked, and they reinforced each other to bring about the main objective of enhanced governance and better delivery of public services through increased financial resources, improved fiscal management, and an effective performance management system.

40. The government‟s assessment based on the project completion review questionnaire shows that most implementing agencies rated the program as relevant or highly relevant both at the time of formulation and after its completion. This reflects the government‟s favorable view of the use of LGFBR-type reforms as a strategy to foster local growth and advance local development. The government‟s responses to the survey questionnaire also show that the implementing agencies plan to retain some of the key features of the LGFBR program for similar initiatives in the future. These include continued efforts to develop accountability and transparency systems, and increase local sources of revenue.

B. Effectiveness in Achieving Outcome

41. The program is rated effective in achieving the outcome.17 Overall, the program has built a strong foundation for improved flows of financial resources into the LGUs. The program contributed to improved completeness, timeliness, and transparency in the release of LGU shares of national government revenues and grants. It has also strengthened the framework for improving LGU access to private sources of capital for development projects, and supported measures aimed at developing LGUs‟ own revenue sources. The reform on intergovernmental fiscal transfers was a difficult decision on the part of the government, because the change in legislation made the IRA releases not just "automatic" but "automatically appropriated." This effectively meant that the government retained no legal loophole to withhold any portion of the IRA or delay its release. The only other item that enjoys a similar status, in terms of being an automatic budget appropriation, is the payment of external debt obligations. On the non-financing side, the program helped build the institutional preconditions for improved efficiency and accountability of financial management, planning, and expenditure management at the local level. The adoption of the LGPMS, improvements in the competency of local officials, and enhancement of the financial reporting frameworks at the local level are some of the key accomplishments of the reforms. In due time, the reforms may generate even wider benefits.

17

ADB. 2006. Technical Assistance to the Republic Philippines for Local Governance and Fiscal Management Project (formerly Strengthening LGU Management and Administration). Manila (TA 4778).

12

Table 1. LGUs’ Sources of Revenues 2006-2009

(In million pesos)

Year IRA Loans and Borrowings

Business Tax

Real Property

Total Local Sources

2007

147,239

5,065

26,130

27,387

79,403

2008 171,861 5,197 28,880 29,799 89,552

2009 189,374 10,603 30,907 30,185 92,731 Source: SIE on BLGF website

Figure 1. LGUs’ Expenditures by Service Categories (Aggregated, cumulative, in million pesos)

- 20,000 40,000 60,000 80,000 100,000 120,000

Economic Services

Health Nutrition and Population Control

General Public Services

Social Security /Social Services & Welfare

Education, Culture & Sports/ Manpower Development

Housing and Community Development

Labor and Employment

Total Expenditures

2009

2008

2007

Source: SIE on BLGF website, data for 2009 are preliminary

42. The reforms have helped LGUs to obtain greater and more stable financial resources. LGUs have also improved their capacity to plan and budget for the general welfare of their constituents in a transparent and accountable manner. Consolidated data from LGUs indicate that local government revenues have continued to increase in cumulative terms. Though revenue from IRA remains the biggest portion, LGUs were able to increase non-IRA resources from loans and borrowings and local revenue sources (Table 1). In terms of LGUs‟ access to private credit, the data showed that higher borrowing levels were recorded in 19 provinces between 2006 and 2009. Over the same period, real revenues grew strongly in all provinces and cities, regardless of their income base.

43. Between 2007 and 2009 LGUs‟ expenditures concentrated on economic services; health nutrition and population control; general public services; and social security and social services and welfare (Figure 1). Some modest improvements in financial management were observed during implementation of the LGFBR. Data provided by Commission on Audit for 2008 showed a decrease of 22.6% in the number of fraud cases relative to 2006, with the amount of money involved in each case declining by nearly 15% from 2006 to 2008.18 44. The government‟s own assessment, based on the results of the survey questionnaire

18

Based on the assessment provided in the report and recommendation of the President (RRP) for subprogram 2.

13

during project completion review, shows that, overall, the program is viewed as effective. In particular, the component on developing local sources of revenue was singled out as highly effective.

C. Efficiency in Achieving Outcome and Outputs

45. The program is rated efficient in achieving its outcome and outputs, as it was efficiently managed by the DOF, implementing agencies, and ADB. The design of the program cluster, including the use of expected prior actions for subsequent subprograms enveloped by a medium-term framework, enabled the program to be implemented efficiently. All policy triggers were accomplished within the original time frame. Through the TA, the CCD was formed to pursue reforms collectively, and the capacity of local officials was enhanced, thereby contributing to the success of the program. Based on the project completion review survey, the government has rated the project as efficient.

D. Preliminary Assessment of Sustainability

46. The LGFBR program is considered most likely to be sustainable. Under the program, the government has strengthened the institutional framework for the increased efficiency and effectiveness of basic public services delivered by LGUs. Supporting systems, such as the competency certification of local officials, and improved performance management and financial reporting systems have been developed. LGUs have also benefited from new regulations for better access to public and private sources of capital for development financing; and important enhancements to local revenue assignments have been conducted. Moreover, the TA projects have helped implementing agencies and LGUs to internalize concepts, ideas, and tools for efficient and effective fiscal management, development planning, and service delivery at the local level, all of which will contribute to the sustainability of the reforms. To date, reforms are continuously being pursued by the oversight agencies through the CCD and the PDF. The likelihood of highly sustainable results will continue with the implementation of the post LGFBR program framework (Appendix 5) and additional support from the donor community.

E. Impact

47. To monitor the progress of the program in achieving its expected outcome, the multidimensional poverty index (MPI), developed jointly by the United Nations Development Programme and NEDA, is used.19 The MPI measures the level of multiple deprivations in health, education, and standard of living that are simultaneously experienced by the poor. It can be seen as a composite index of overall well-being as perceived by the poor. For measuring poverty in the Philippines, three surveys are used as inputs to the MPI: the National Demographic and Health Survey (NDHS), the Family Income and Expenditure Survey (FIES), and the Annual Poverty Indicator Survey (APIS). Based on these surveys, sub-indicators are developed to measure the degree of deprivation with respect to: (i) education, (ii) health, and (iii) living standards. The health indicator summarizes indicators on child mortality, access to water and sanitation, nutrition, and food poverty. The education indicator summarizes indicators

19

The Multidimensional Poverty Index (MPI), developed in 2010 by the Oxford Poverty & Human Development Initiative and the United Nations Development Programme uses a number of variables in addition to traditional income measures to determine poverty. An application to the Philippines can be found in: Balisacan, Arsenio M. 2011. What has really happened to poverty in the Philippines? New measures, evidence and policy implications. Presentation material. United Nations Development Programme and NEDA, downloadable at www.undp.org.ph. Data source in Figure 5 is Balicasan, Arsenio M. (2011).

14

on years of schooling, children‟s school attendance, and potential schooling. Finally, the standard of living indicator summarizes indicators on access to electricity, quality of shelter (flooring, roof, and wall), mobility (access to motor vehicles and access to national roads), level of urban agglomeration, asset ownership (household asset, transport, and tenure), and other sources of income.

48. It can be seen in Figure 2 that the MPI, measured using these three separate surveys (i.e., NDHS, FIES, and APIS), has declined over the last decade, suggesting a gradual reduction in the intensity of deprivation in terms of health, education, and standard of living. This provides an early indication that the local governance finance reforms, in conjunction with other reforms that have been undertaken to fight poverty in the Philippines in the past decade, may have had a positive impact, and therefore needs to be sustained. As the data measures a multiplicity of indicators, it is not necessarily at odds with the perceived stalling of poverty reduction recently observed in the Philippines as per government surveys.

Figure 2. Multidimensional Poverty Index (MPI)

0.1320.126

0.174

0.156

0.1350.14

0.1240.119

0.1

0.11

0.12

0.13

0.14

0.15

0.16

0.17

0.18

0.19

0.2

2002 2003 2004 2005 2006 2007 2008 2009 2010

National Demographic and Health Survey (NDHS)

Family Income and Expenditure Survey (FIES)

Annual Poverty Indicator Survey (APIS)

MPI

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

49. The LGFBR program cluster was a highly relevant program, adequately linked to the government‟s reform agenda, and to ADB‟s partnership strategy and operations business plan in the Philippines. The program was demand driven, with strong government commitment and ownership, effectively sequenced, and strongly supported by other development partners. Its implementation involved high-level coordination among government agencies, which has facilitated the achievement of positive outcomes. The sustainability of accomplishments recorded to date, and the ability to fully achieve the expected outcome and impact, will depend on the ability of the government and the donor community, including ADB, to nurture past achievements and push through with further reforms. Accordingly, the LGFBR is rated highly successful overall.

B. Lessons Learned

50. Local government reform is a complex undertaking, involving major changes in the regulatory framework, institutional arrangements, supporting infrastructure, and human capacity. It also requires a long-term perspective in both design and implementation. Thus, the

15

government‟s continuous commitment to reform, its ownership of the program, and collaborative support by the donor community are all necessary elements in designing local government reform through a programmatic approach. The LGFBR program cluster shows that ADB, through continuous dialogue with the government and collaborative financing with other donors, was able to develop a well-designed program that is sufficiently demand driven. Substantial reforms were accomplished, which laid a stronger foundation for achieving the program‟s objective of more effective delivery of key government services at the local level. The program‟s success and likely sustainability can be attributed also to the TA activities undertaken during implementation, which have strengthened the capacity of local officials in carrying out reforms. C. Recommendations

1. Program Related

51. Future Monitoring. Sustaining the key achievements of the LGFBR should be a key priority of ADB and the government going forward. The successful implementation of policy measures linked to the post-LGFBR program framework has provided continuity to the first two subprograms, and has paved the way for the processing of the next subprogram in support of fiscal decentralization and local government finance reforms. In addition, a joint assessment by ADB, the government, and AFD as cofinancier is being conducted to monitor the sustainability of the outputs and fine-tune the design of the next stage of reforms to ensure further improvements in all outcome and impact indicators. Considering the effective role that TA activities have played in sustaining policy reforms and building capacity, it would be useful to continue to provide TA so that post-program outcomes can be achieved smoothly and preparations can be made for the next program, which is already included in the country operations business plan for 2013–2015. 52. Further Action and Follow Up. Based on the project completion survey, the government has recommended some features that could be added to the next program, such as: (i) harmonization of fiscal accounts and reports by LGUs, (ii) rationalization of the functional and revenue assignments of LGUs, (iii) improvement in intergovernmental transfers to LGUs by incorporating performance and equity, and (iv) guidelines on public–private partnerships. All these policy reforms are currently at the core of the policy dialogue being conducted, and for some of them, such as the public–private partnerships, ADB already has initiatives in place. 53. Additional Assistance and Timing of PPER. ADB is currently processing a new cluster of policy-based loans in support of local government finance reforms in Philippines, including co-financing from the AFD. A first joint assessment of the implementation of the post-program partnership framework has been completed and serves as the basis of the current policy dialogue. The new cluster is expected to be approved by ADB Board in September 2013. As such, the PPER would probably would benefit of the analysis conducted and can proceed once processing is completed.

2. General

54. Future initiatives in support of Government‟s reforms should underline ADB‟s involvement in the review and eventual reform of the system of intergovernmental relations, specifically the Local Government Code of 1991 and the Local Government Financing Framework. To that extent, intense policy dialogue with all government counterparts will be required. Future programs of assistance should equally aim to ensure co-financing from other development partners as was the case of earlier ADB program loans.

16 Appendix 1

DESIGN AND MONITORING FRAMEWORK

Design Summary

Performance Targets/Indicators Monitoring Mechanism/ Update to Subprogram 2

Assumptions and Risks

Impact

Increased efficiency and effectiveness of basic public services delivered by LGUs to their constituent communities

More than half of the aggregate LGU indicators improve by one-fifth to one-tenth of 2007 results by 2012: (i) ratio of health facilities to population, (ii) access to basic services such as water and electricity, (iii) sanitation conditions, (iv) extent of solid waste collection and disposal, and (v) presence of sewerage facilities.

The Multidimensional Poverty Index (MPI), measuring deprivation in terms of health, education and standard of living, has continued to decline since 2003. The NDHS dimension of the MPI declined from 0.132 in 2003 to 0.126 in 2008. The FIES dimension declined steadily from 0.174 in 2003 to 0.156 in 2008 and 0.135 in 2009. The API dimension declined from 0.14 in 2004 to 0.124 in 2007 and 0.119 in 2008. (See also Figure 2 and sub-section III.E. in the main text).

Assumption

LGUs use enhanced resources for investments in basic public services.

Risk

Key government agencies at all levels of government may be preoccupied by measures to mitigate the impact of the global financial crisis on the economy and vulnerable groups. This may leave limited resources to implement the agreed program.

Outcome

LGUs avail themselves of enhanced resources and capacity to plan and budget for the general welfare of their constituents in a transparent and accountable way

Real local government revenues, including access to public and private sources of credit, increase by at least 4% annually at all levels of government from 2007 in two-thirds of all provinces and highly urbanized cities and in most LGUs in the fourth to sixth income classes.

Real expenditures for service delivery increase by at least 2% annually from 2008 in two-thirds of provinces, highly urbanized cities, and in most LGUs in the fourth to sixth income classes.

The number of fraudulent cases reported by COA decreases by at least 20% at all sub-national levels.

BLGF‟s SIE data indicate that LGUs‟ sources of revenues have continued to increase in cumulative terms between 2007 and 2009. The cumulative IRA figure increased by 30% (from 83.7 billion pesos to 108.8 billion pesos) between 2007 and 2009 despite the GFC. There have been early signs of more diversified sources of revenues. The data between 2006 and 2009 show that new loans or borrowings were recorded in 19 provinces

(See also Table 1 and subsection III.B. in the main text).

BLGF‟s SIE data indicate that LGUs have continued to increase spending for key services. (See Figure 1 and subsection III.B. in the main text).

Data provided by COA for 2008 show that the number of fraudulent cases has decreased, with the amount of money involved in each case declining by nearly 15% (See subsection III.B. in the main text).

Assumption

Mechanisms are in place in LGUs at all levels to provide incentives to make use of enhanced resources and capacities to plan and budget for the general welfare of constituent communities.

Risk

Delays may be experienced in engaging oversight agencies and LGUs because of the election scheduled in May 2010.

Appendix 1 17

Design Summary

Outputs

1. Completeness, timeliness, and transparency of release of LGU share in national government revenues is improved.

2. Enhanced efficiency and accountability in local financial management, planning, and expenditure management

3. Enhanced effectiveness and transparency in the delivery of critical local public services

Performance Targets/Indicators

Passage of Republic Act 9358;

IRA release to LGUs amounts to P183 billion in 2007 and P210 billion in 2008

Predictability of annual IRA release ensured by DBM in time for preparation of LGU budgets from 2007

Documentary requirements on the release of the LGUs‟ share in the proceeds from the development and utilization of national wealth in mining, forestry, and energy reduced from five to two by December 2007.

Requirements for the release of the special share of LGUs in mining taxes further reduced by BIR by December 2008

Capacity development for LGUs in planning, revenue mobilization, expenditure management, and budgeting harmonized by 2010

Committee for implementation of the competency certification system for local treasurers officially named and convened by BLGF by January 2011

Improved training skills available for the comprehensive development plan by January 2011

Implementation of the performance-based incentive policy included in the design of at least one sector program with national Government and ODA funding by January 2011

Use of the Special Education Fund improved by January 2011

Efficiency and transparency of performance data improved

Monitoring Mechanism/ Update to Subprogram 2

Copy of the Republic Act.

Official certification from BIR

Local budget memorandum for the indicative IRA to the LGUs for the ensuing budget year by June of the current year for 2007–2010 Certification of posting from DBM and DBM website

Copy of joint circular

Copy of BIR memorandum order Copy of joint memorandum circular providing the schedule of joint capacity development initiatives

The Competency Certification System has been finalized and is under review by the BLGF Management.

Certification from MDFO

Updated guidelines by DBM in coordination with the DepEd, DILG, and COA DILG Website.

Assumptions and Risks

Assumption

There is no political pressure on DBM to ignore the provisions of Republic Act 9358 or to suppress transparency on IRA releases Risk

Financial crisis leading to unmanageable public sector deficit

Assumption

Oversight agencies‟ limited understanding of capacity-building roles for LGUs

Risk

Incentive for coordination among oversight agencies may weaken over time

Assumption

Sector agencies and donors remain committed to implementing the performance-based incentive policy

Risk

Financial crisis results in a decrease in transfers

18 Appendix 1

4. Improved LGU access to public and private sources of capital for financing policy reforms and development projects

5. Additional local sources of revenue developed, thereby reducing dependency on IRA

for at least 90% of provinces, cities, and municipalities by January 2011

Guidance availability by January 2011 to ensure that ODA funds are used in a way that does not crowd out private sector financing

Operational efficiency of MDFO improved by January 2011

PROLEND policy improved by January 2011

MDFO-PGB increases the amount in the MDG fund and other projects for achieving the MDGs as the number of interested LGUs increases

BLGF creditworthiness rating system available on the internet by January 2011

Transparency of local business taxpayer database improved by January 2011

Qualification standards for local assessors enforced by January 2011

Improved regulation for the establishment of local economic enterprises available by January 2011

Copy of guidelines submitted by DOF

MDFO-PGB resolution on rationalization plan of MDFO provided by MDFO, setting up MDFO as an attached agency of DOF

MDFO-PGB resolution provided by MDFO

MDG fund allocation provided by DOF

Implementation of the creditworthiness system will be done in 2012.

The procedure for building up the database has been finalized under the subprogram 2 TA for Support to Local Government Financing. The database is being rolled out in 2012.

The Real Estate Service Act became effective on July 30, 2009.

The real estate service profession is now under the supervision of the Professional Regulatory Board of Real Estate Service (PRBRES) through the Professional Regulation Commission (PRC). Only licensed real estate professionals are appointed to the position of government assessors and assistant assessors. Copy of joint memorandum circular of BLGF, DBM and DILG.

Assumption

Priority funding will not be affected. The willingness of LGUs to provide quality performance data increases over time.

Risk

Private sector financing does not grow with the increased availability of financial information on LGUs.

Assumptions

Business tax revenue base of LGUs is sufficient to justify collection cost

LGUs are increasingly willing to use property-evaluation methods

Risk

Government may run out of resources for capacity development planned for the program

API = Annual Poverty Indicator, BIR = Bureau of Internal Revenue, BLGF = Bureau of Local Government Finance, COA = Commission on Audit, DBM = Department of Budget and Management, DepEd = Department of Education, DILG = Department of Interior and Local Government, DOF = Department of Finance, FIES = Family Income and Expenditure Survey, GFC = Global Financial Crisis, IRA = internal revenue allotment; LGU = local government unit, MDFO = Municipal Development Fund Office, MDG = Millennium Development Goal, MPI = Multidimensional Poverty Index, NDHS = National Demographic and Health Survey, PGB = Policy Governing Board. Source: Asian Development Bank.

Appendix 2 19

PERFORMANCE OF LOCAL GOVERNMENT FINANCING AND BUDGET REFORM PROGRAM, SUBPROGRAM 1 – TRIGGERS

Original Triggers in Subprogram 1 Document, Appendix 3

Performance

A. Intergovernmental Fiscal Relations: Improving Completeness, Timeliness, and Transparency in the Release of LGU Shares in National Government Revenues and Grants

1. Republic Act 9358 passed providing automatic appropriation of IRA.

Accomplished. Local budget memorandum (LBM) no. 52, issued on 5 January 2007, authorized the distribution of the IRA share of LGUs amounting to P183 million.

2. IRA share of local government units (LGUs) estimated timely by Bureau of Internal Revenue (BIR) for 2007 at P183 billion.

Accomplished. LBM no. 57, issued on 11 July 2008, certifies LGU shares of IRA for distribution in 2009 at P210.7 billion. LBM are issued to guide the preparation of LGU budgets for the following year.

3. BIR certified an IRA of P210 billion for release in 2008.

Accomplished. DOF-DBM-DILG-DENR joint memorandum circular no. 2009-1, issued on 31 March 2009, streamlined the documentary procedure to just one document and delineated agencies‟ responsibilities in promptly releasing LGU shares of mining taxes.

4. Uploading of the Priority Development Assistance Fund (PDAF) releases on the DBM website

5. Framework adopted on the release of LGUs‟ share in the proceeds from the development and utilization of national wealth in mining, forestry, energy and mining royalties reducing the documentary requirements from 5 to 2 (Joint Circular 2006-1).

Accomplished. Framework was adopted and releases started in 2008 from taxes collected in 2007.

B. Fiscal Management, Planning, and Public Expenditure Management: Enhancing Efficiency and Accountability in Financial Management, Planning, and Expenditure Management at the Local Level

1. Coordinated framework developed among Department of Finance (DOF), DBM, Department of Interior and Local Government (DILG), and National Economic Development Authority (NEDA) on the harmonization of local planning, investment programming, revenue administration, budgeting, and expenditure management (Joint Memorandum Circular 2007-1).

Accomplished. Local treasury operations manual completed and distributed to all LGUs.

2. Issuance of Updated Budget Operations Manual (UBOM), with 90 percent of LGUs trained in its use.

Accomplished. 23 provinces have prepared the provincial development and physical framework plan and the provincial development investment program using the provincial planning guidelines.

3. Statement of Receipts and Expenditures (SRE, formerly Statement of Income and

Accomplished. SRE financial reporting implemented by treasurers at all LGU levels.

20 Appendix 2

Expenditures) financial reporting system harmonized with New Government Accounting System (NGAS) completed and computerization achieved.

4. 2,551 mandatory and demand driven trainings conducted for 513 LGUs in the areas of project management, operation and maintenance, planning and investment programming.

Accomplished. Competency certification system for all local treasurers completed and implemented.

5. 86 percent of all LGUs trained in the new Government Procurement Reform Act (GPRA).

C. LGU Performance Measurement and Service Delivery: Enhancing Effectiveness and Transparency in the Delivery of Critical Public Services at the Local Level

1. 217 3rd to 6th income class LGUs availed of financing for improved service delivery through investment in urban infrastructure and public services with total loans amounting to P2.25 billion.

Accomplished. Exceeded Target. 270 LGUs availed themselves of financing for investments in environmental and health projects amounting to P3.2 billion.

2. 100 percent of provinces, cities, and municipalities (excluding ARMM) covered by Local Government Performance

Accomplished. Study on performance-based grants (preliminary analytic and design work for the development of a performance-based grant system for LGUs) completed in June 2008.

3. Local Government Financial Performance Monitoring System (LGFPMS) integrated into LGPMS.

Accomplished. Exceeded Target. MDFO-PGB has adopted the policy. In addition, the Development Budget Coordination Committee approved the performance-based incentive policy on 20 February 2009.

D. Credit financing: Improving LGU Access to Public and Private Sources of Capital for Financing of Policy Reforms and Development Projects

1. LGU financing framework as a national policy approved.