Embed Size (px)

DESCRIPTION

Citation preview

January 2013

Japanese Equities

1Japanese EquitiesPictet Asset Management

Japan is cheap versus history…

Source: Bloomberg

Dividend Yield / Price-to-Book

0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0

0.5

1.0

1.5

2.0

2.5

3.0

TOPIX Dividend Yield TOPIX Price to Book

Despite the ‘Abe-nomics’

rally, the market remains

cheap…

2Japanese EquitiesPictet Asset Management

… and other markets…

Source: Bloomberg

Dividend Yield… although the rally has

(just) closed the yield

advantage over the US

market.

0

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

TOPIX Dividend Yield S&P 500 Dividend Yield

3Japanese EquitiesPictet Asset Management

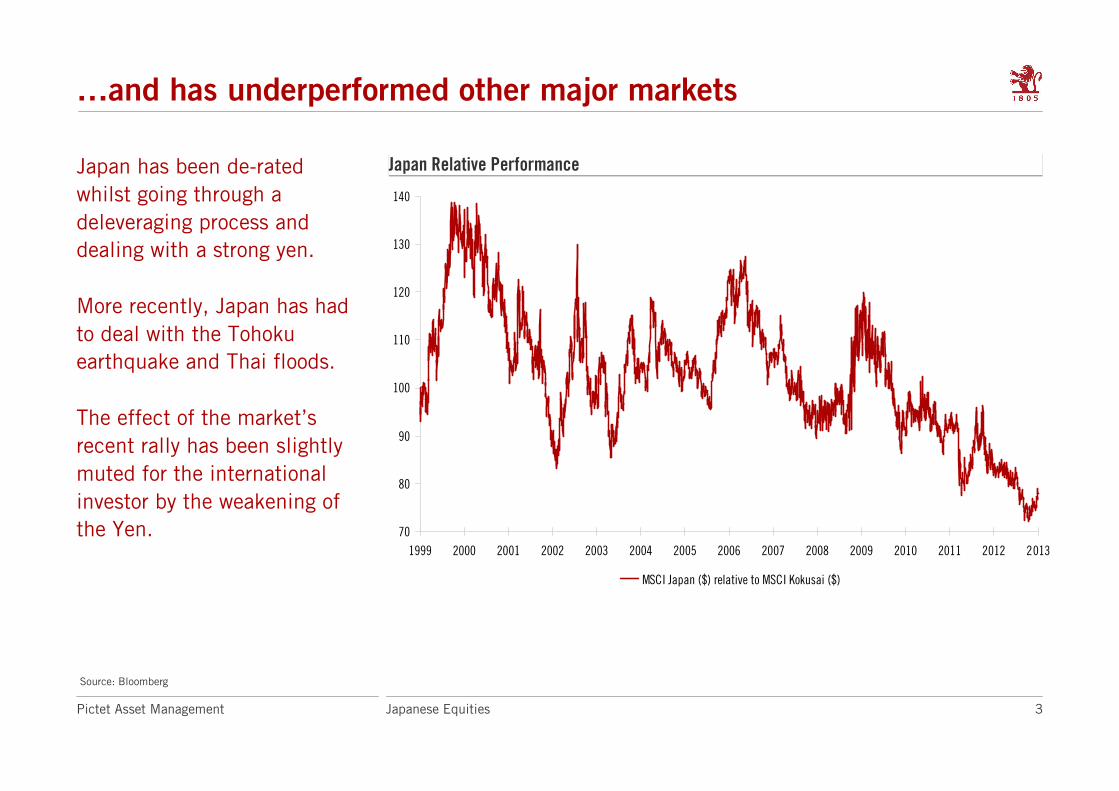

…and has underperformed other major markets

Japan Relative PerformanceJapan Relative Performance

Source: Bloomberg

Japan has been de-rated

whilst going through a

deleveraging process and

dealing with a strong yen.

More recently, Japan has had

to deal with the Tohoku

earthquake and Thai floods.

The effect of the market’s

recent rally has been slightly

muted for the international

investor by the weakening of

the Yen. 70

80

90

100

110

120

130

140

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

MSCI Japan ($) relative to MSCI Kokusai ($)

4Japanese EquitiesPictet Asset Management

… although Spain may be cheaper …

Source: Haver Analytics, Datastream, GSAM* Length of series varies: most DMs 30+ years, others 15 years.

CAPE ratios – deviation from historical averageCAPE ratios – deviation from historical average

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

US

Mexic

oInd

ones

ia

Korea UK

India

China

Turke

y

Braz

ilGe

rman

y

Franc

e

Russ

ia

Japa

n

Spain Ita

ly

CAPE deviation from historical average*

5Japanese EquitiesPictet Asset Management

We are positive on Japanese Equities

• Valuations are extremely low

• Japan still has world-leading technology

• The domestic economy is resilient

• No credit given for restructuring efforts

• The banking system is healthy

• The corporate sector is becoming bolder

Nothing new – Japan’s been

cheap for a while…

… but a lot of the old saws

about the Japanese economy

are no longer true…

… and the corporate sector is

very different to 2002 – when

it was trading above current

valuations

6Japanese EquitiesPictet Asset Management

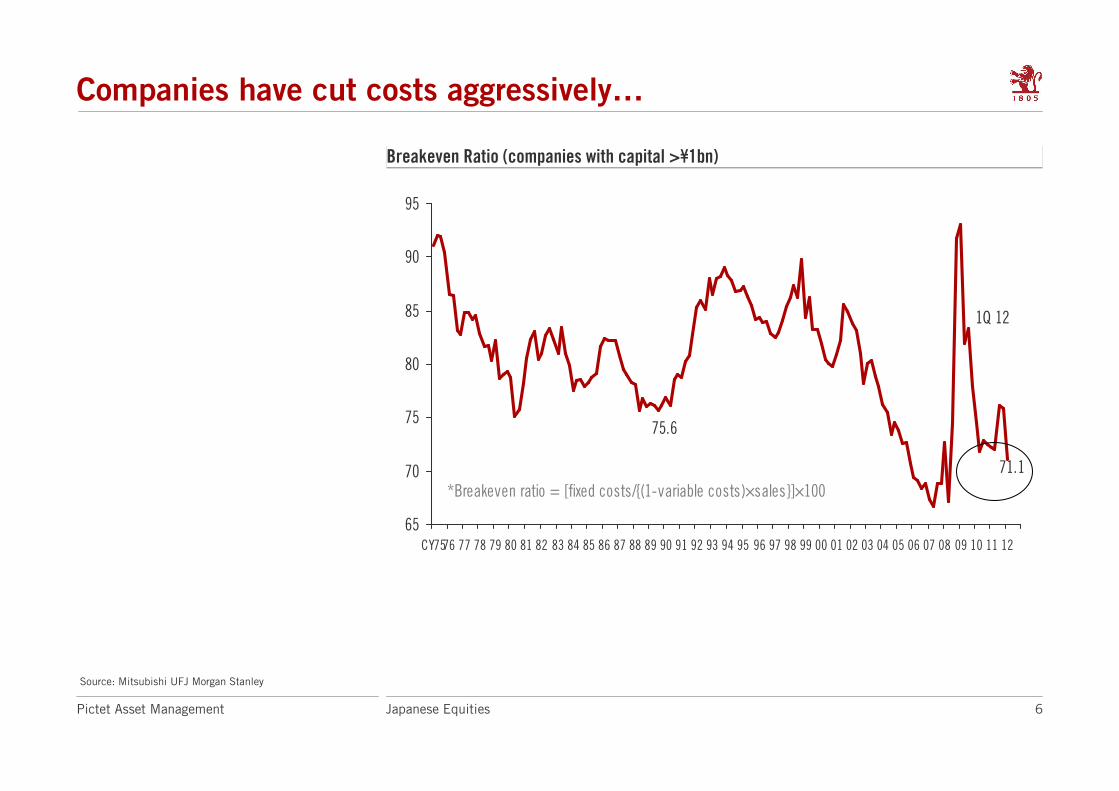

Companies have cut costs aggressively…

75.6

71.1

65

70

75

80

85

90

95

CY7576 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

*Breakeven ratio = [fixed costs/{(1-variable costs)×sales}]×100

1Q 12

Breakeven Ratio (companies with capital >¥1bn)Breakeven Ratio (companies with capital >¥1bn)

Source: Mitsubishi UFJ Morgan Stanley

7Japanese EquitiesPictet Asset Management

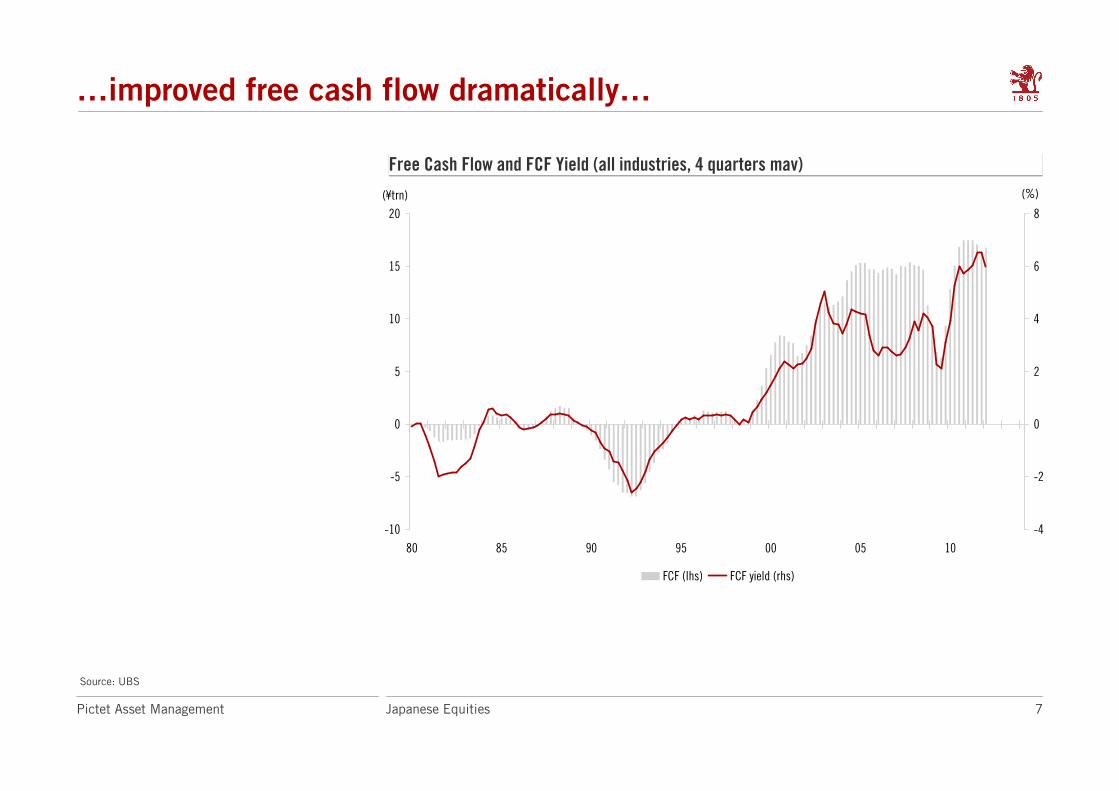

…improved free cash flow dramatically…

Source: UBS

Free Cash Flow and FCF Yield (all industries, 4 quarters mav)Free Cash Flow and FCF Yield (all industries, 4 quarters mav)

-10

-5

0

5

10

15

20

80 85 90 95 00 05 10

-4

-2

0

2

4

6

8

FCF (lhs) FCF yield (rhs)

(¥trn) (%)

8Japanese EquitiesPictet Asset Management

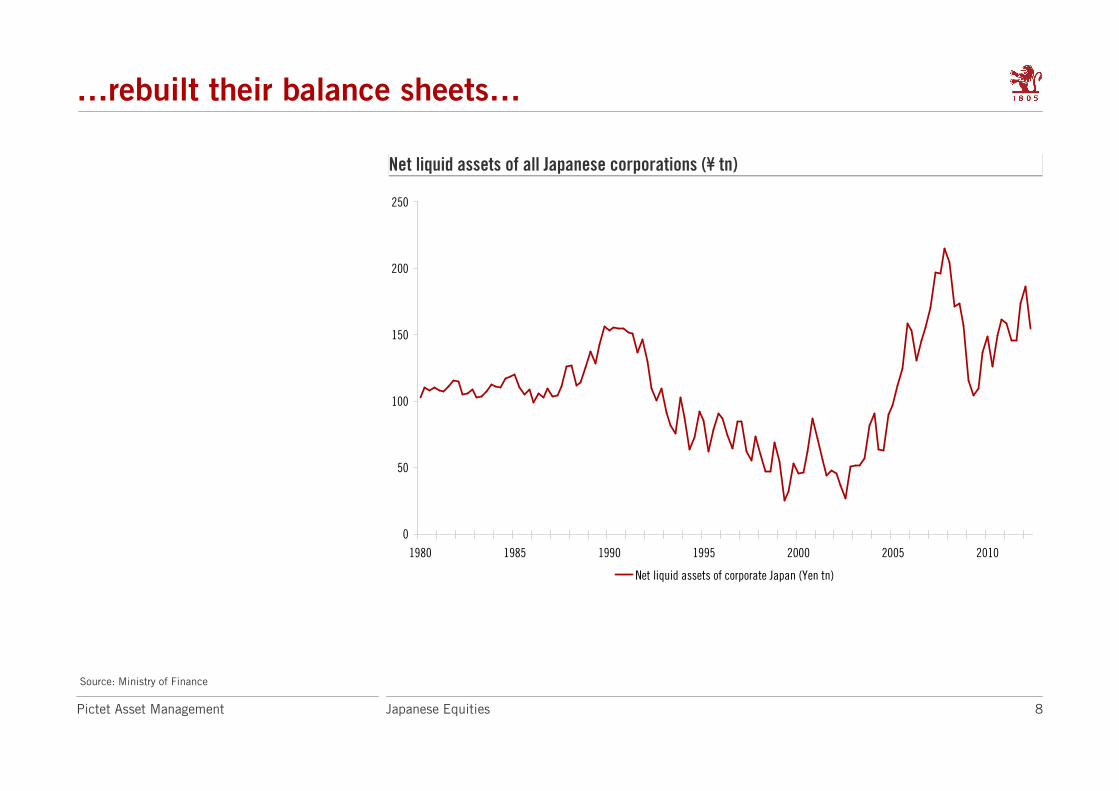

…rebuilt their balance sheets…

Source: Ministry of Finance

Net liquid assets of all Japanese corporations (¥ tn)Net liquid assets of all Japanese corporations (¥ tn)

0

50

100

150

200

250

1980 1985 1990 1995 2000 2005 2010

Net liquid assets of corporate Japan (Yen tn)

9Japanese EquitiesPictet Asset Management

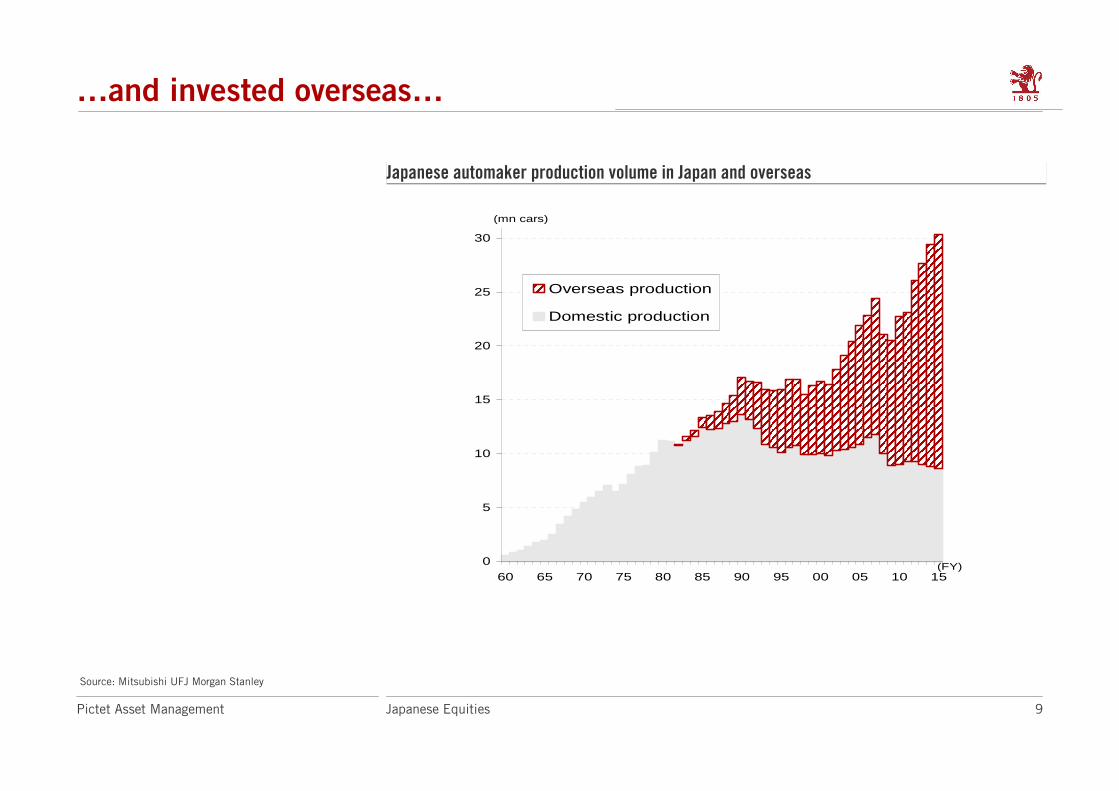

Japanese automaker production volume in Japan and overseasJapanese automaker production volume in Japan and overseas

…and invested overseas…

0

5

10

15

20

25

30

60 65 70 75 80 85 90 95 00 05 10 15

Overseas production

Domestic production

(mn cars)

(FY)

Source: Mitsubishi UFJ Morgan Stanley

10Japanese EquitiesPictet Asset Management

…where returns are higher

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

88 90 92 94 96 98 00 02 04 06 08 10

Overseascorporation

Domesticcorporation

(FY)

(%)

<Recurring profit margin>

RP margin for domestic corporations and overseas subsidiaries/affiliates

Source: Mitsubishi UFJ Morgan Stanley, Ministry of Economy

Japan is doing much more

than just moving factories to

China.

Over the last two years,

Japanese companies have

represented more than 10%

of all cross-border M&A

(by value).

Japanese companies are

second only to the Americans

in making cross-border deals.

11Japanese EquitiesPictet Asset Management

The export mix has changed dramatically

Export values by destination

1

2

3

4

5

6

7

8

90 92 94 96 98 00 02 04 06 08 10 12

To developed countries To EM countries

(JPY trn, sa)

Emerging markets are now

the key driver of exports

Source: DB Global Markets Research, Ministry of Finance

12Japanese EquitiesPictet Asset Management

Japan is highly competitive

Unit Labour Costs (rebased 100 in 2000, FX adjusted)

Insert here your graphs

and tables

70

90

110

130

150

170

190

210

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Japan Germany Korea UK USA Italy Spain

Employee cost (US$ PPP adjusted)

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Japan Germany Korea UK USA Italy Spain

Source: OECD

13Japanese EquitiesPictet Asset Management

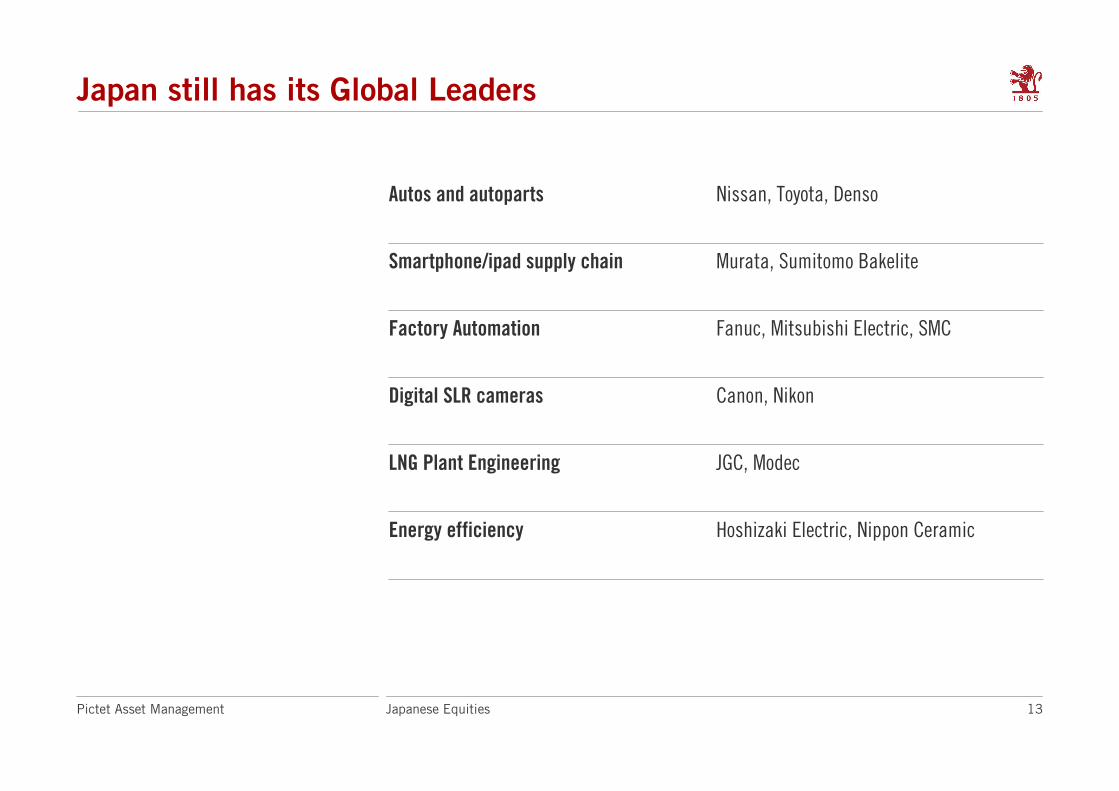

Japan still has its Global Leaders

Hoshizaki Electric, Nippon CeramicEnergy efficiency

JGC, ModecLNG Plant Engineering

Canon, NikonDigital SLR cameras

Fanuc, Mitsubishi Electric, SMCFactory Automation

Murata, Sumitomo BakeliteSmartphone/ipad supply chain

Nissan, Toyota, DensoAutos and autoparts

14Japanese EquitiesPictet Asset Management

It’s not just an export story

Non-manufacturing profit marginsProfit margins have improved

sharply in non-manufacturing

sectors

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Current Profit Margin of Non-Manufacturing Sector (ex-electric utilities)

Source: BNP Paribas, Ministry of Finance

15Japanese EquitiesPictet Asset Management

The domestic economy is relatively robust

Source: Bloomberg

The recovery from the

earthquake and Thai floods

has been impressive

This is before the impact of

reconstruction really takes

hold

SME Confidence indices in Japan and USSME Confidence indices in Japan and US

50

60

70

80

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Shoko Chukin Small Business Confidence Index NFIB Small Business Optimism Index

16Japanese EquitiesPictet Asset Management

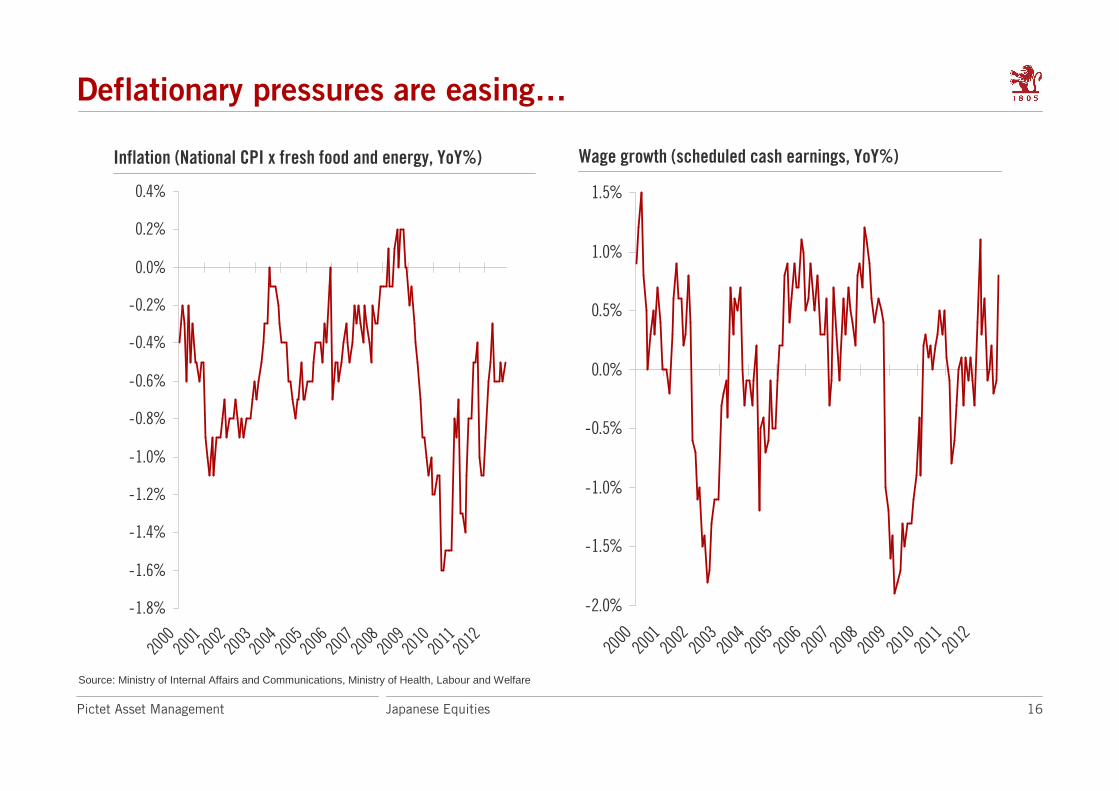

Deflationary pressures are easing…

Source: Ministry of Internal Affairs and Communications, Ministry of Health, Labour and Welfare

Inflation (National CPI x fresh food and energy, YoY%) Wage growth (scheduled cash earnings, YoY%)

-1.8%

-1.6%

-1.4%

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

200020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

200020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

17Japanese EquitiesPictet Asset Management

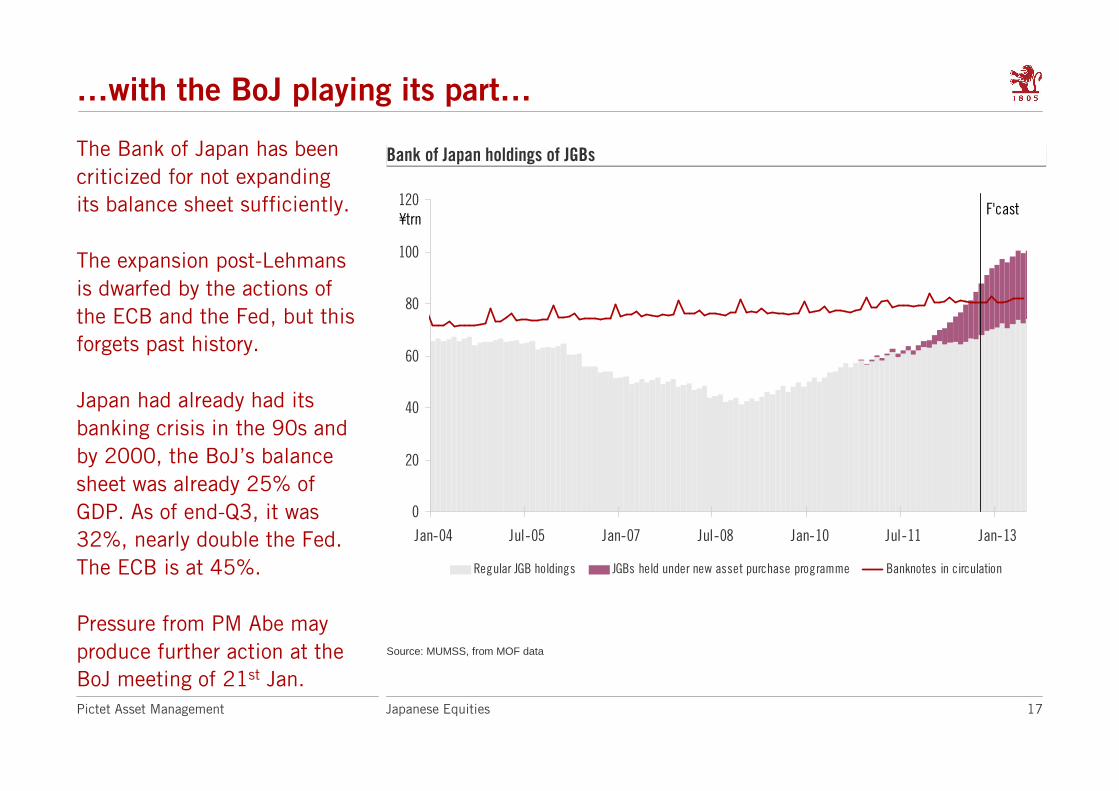

…with the BoJ playing its part…

Source: MUMSS, from MOF data

Bank of Japan holdings of JGBsBank of Japan holdings of JGBs

0

20

40

60

80

100

120

Jan-04 Jul-05 Jan-07 Jul-08 Jan-10 Jul-11 Jan-13

Regular JGB holdings JGBs held under new asset purchase programme Banknotes in circulation

¥trnF'cast

The Bank of Japan has been

criticized for not expanding

its balance sheet sufficiently.

The expansion post-Lehmans

is dwarfed by the actions of

the ECB and the Fed, but this

forgets past history.

Japan had already had its

banking crisis in the 90s and

by 2000, the BoJ’s balance

sheet was already 25% of

GDP. As of end-Q3, it was

32%, nearly double the Fed.

The ECB is at 45%.

Pressure from PM Abe may

produce further action at the

BoJ meeting of 21st Jan.

18Japanese EquitiesPictet Asset Management

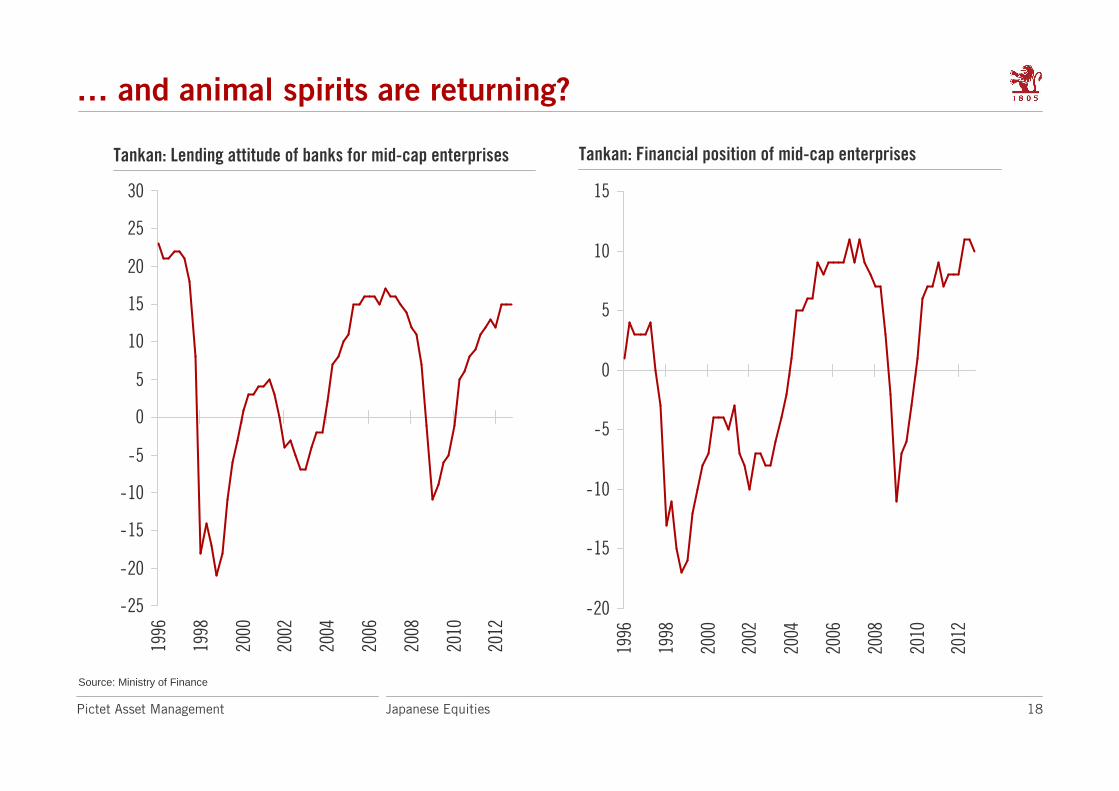

… and animal spirits are returning?

Source: Ministry of Finance

Tankan: Lending attitude of banks for mid-cap enterprises Tankan: Financial position of mid-cap enterprises

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

1996

1998

2000

2002

2004

2006

2008

2010

2012

-20

-15

-10

-5

0

5

10

15

1996

1998

2000

2002

2004

2006

2008

2010

2012

19Japanese EquitiesPictet Asset Management

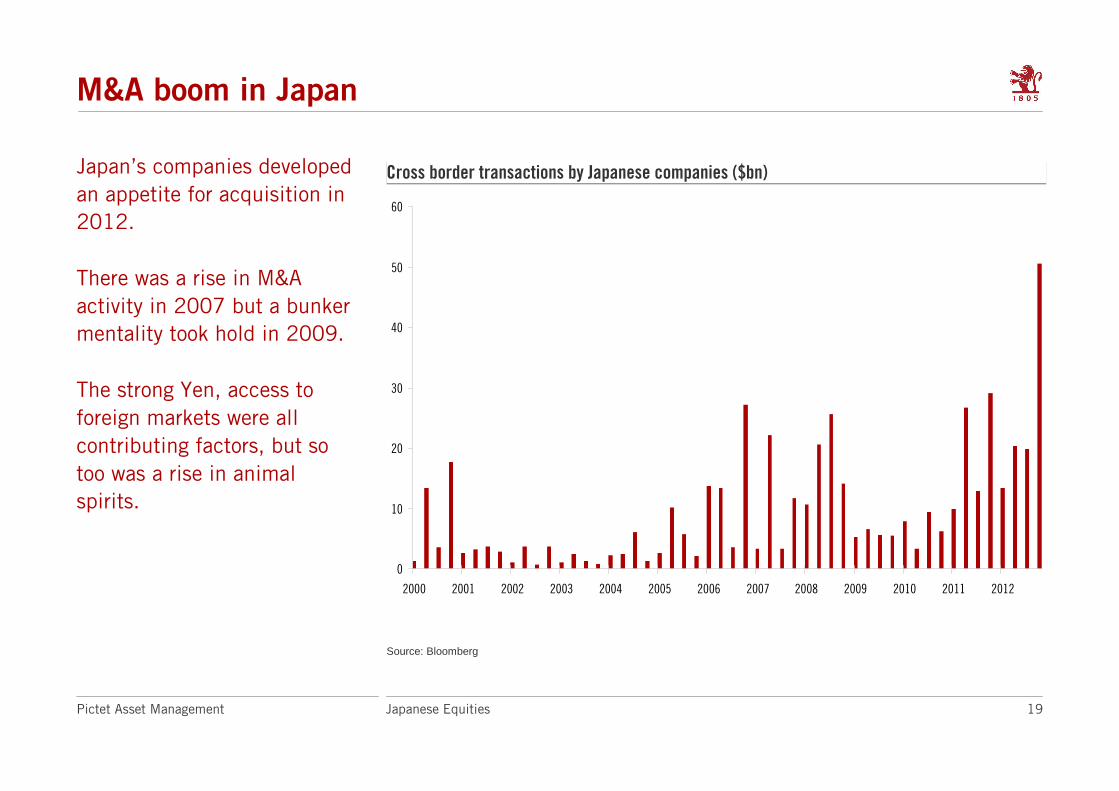

M&A boom in Japan

Source: Bloomberg

Cross border transactions by Japanese companies ($bn)Cross border transactions by Japanese companies ($bn)Japan’s companies developed

an appetite for acquisition in

2012.

There was a rise in M&A

activity in 2007 but a bunker

mentality took hold in 2009.

The strong Yen, access to

foreign markets were all

contributing factors, but so

too was a rise in animal

spirits.

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

20Japanese EquitiesPictet Asset Management

Dangerous debt position?

Source: OECD

Gross Government Debt as % GDP Net Government Debt as % GDP

0

50

100

150

200

Japa

n US UKGe

rman

yFra

nce

Austr

iaIta

lySp

ainPo

rtuga

lIre

land

Gree

ce0

20

40

60

80

100

120

140

Japa

n US UKGe

rman

yFra

nce

Austr

iaIta

lySp

ainPo

rtuga

lIre

land

Gree

ce

21Japanese EquitiesPictet Asset Management

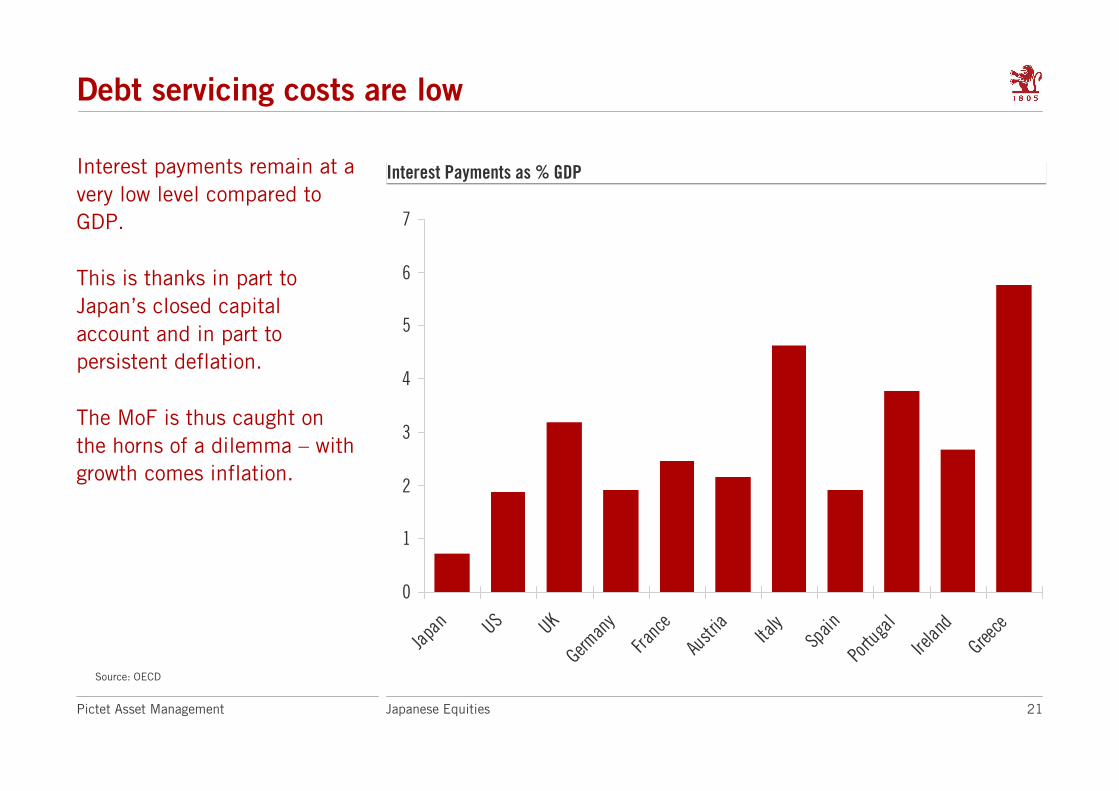

Debt servicing costs are low

Source: OECD

Interest Payments as % GDPInterest Payments as % GDP

0

1

2

3

4

5

6

7

Japa

n US UKGe

rman

y

Franc

e

Austr

ia

Italy

Spain

Portu

gal

Irelan

d

Gree

ce

Interest payments remain at a

very low level compared to

GDP.

This is thanks in part to

Japan’s closed capital

account and in part to

persistent deflation.

The MoF is thus caught on

the horns of a dilemma – with

growth comes inflation.

22Japanese EquitiesPictet Asset Management

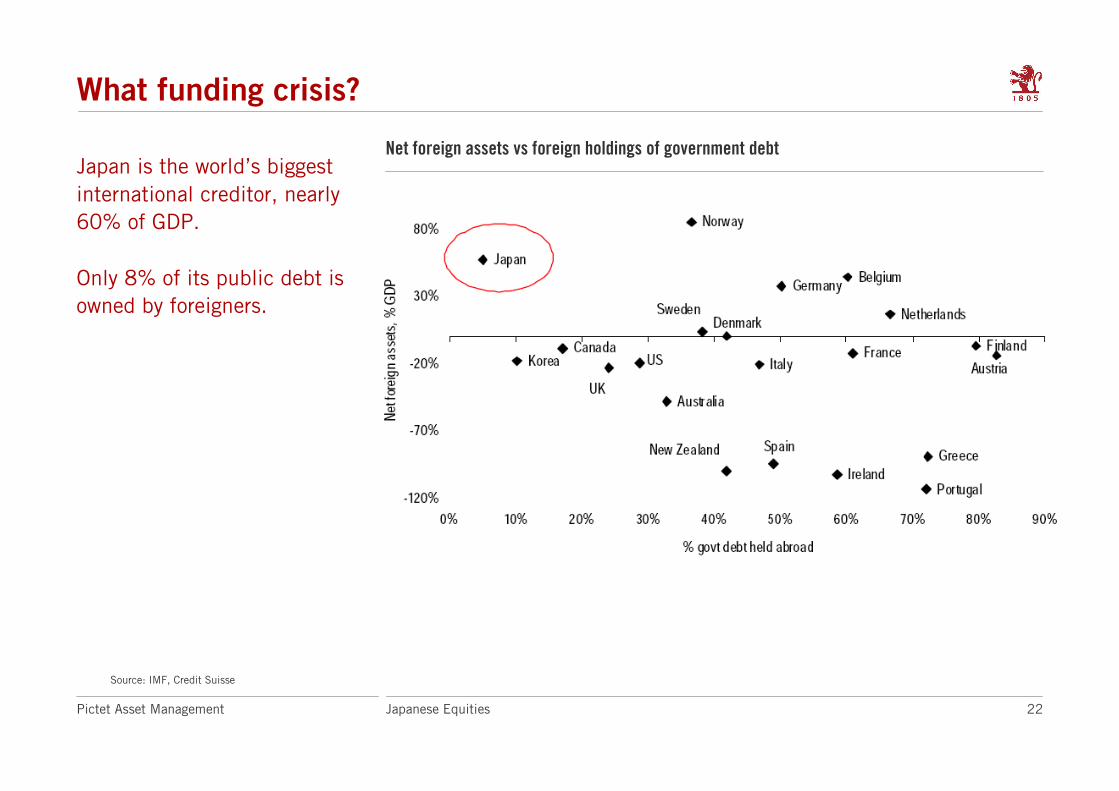

What funding crisis?

Source: IMF, Credit Suisse

Net foreign assets vs foreign holdings of government debtJapan is the world’s biggest

international creditor, nearly

60% of GDP.

Only 8% of its public debt is

owned by foreigners.

23Japanese EquitiesPictet Asset Management

What funding crisis?

• All the ratings agencies have downgraded Japan over the last couple of years

• This looks like they are playing to the crowd…

• While the size of the gross debt is high (225% GDP), the net debt is only about

121% (IMF estimate)

• Almost all debt is held locally – only 8% is held by foreigners

• The private sector has an enormous amount of cash

– The corporate sector has a cash pile equivalent to 30% of GDP

– The household sector holds net savings of about another 4% of GDP

• Japan is the world’s largest net creditor (57% of GDP)

• If the Yen fell to ¥120, then net foreign assets would rise to nearly 90% GDP

• This would enable Japan to retire a significant part of the debt pile.

24Japanese EquitiesPictet Asset Management

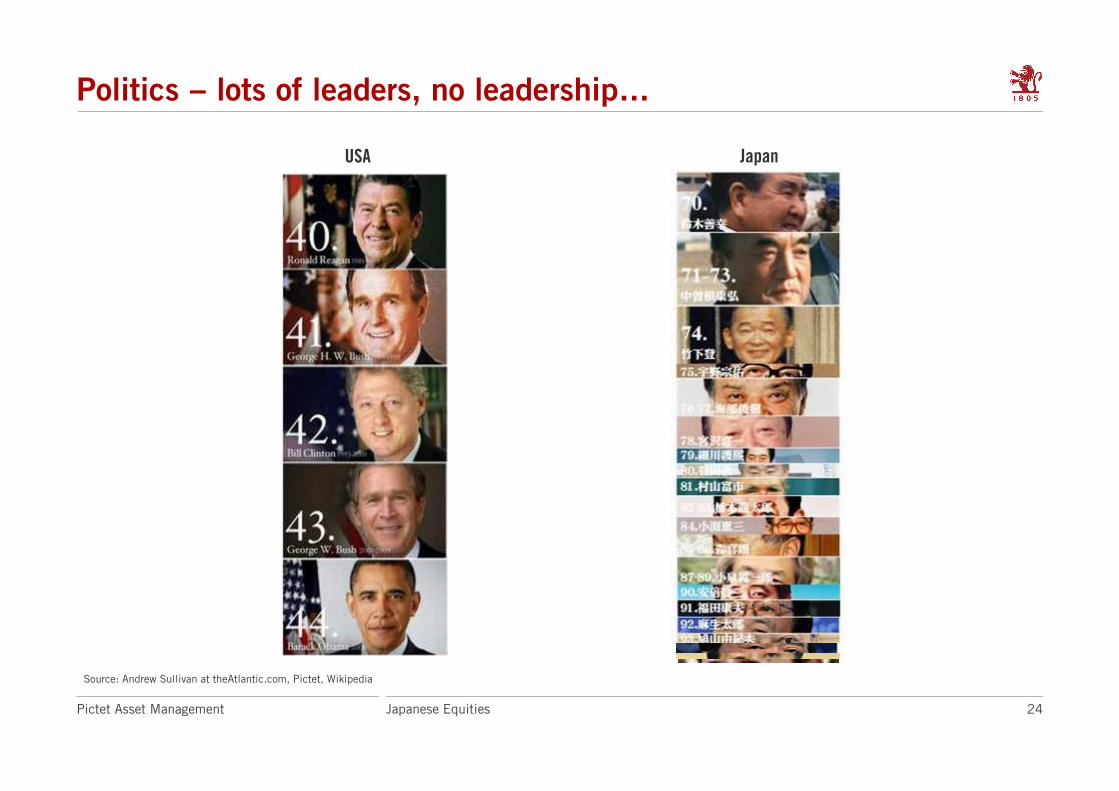

Politics – lots of leaders, no leadership…

Source: Andrew Sullivan at theAtlantic.com, Pictet, Wikipedia

JapanUSA

25Japanese EquitiesPictet Asset Management

Demography – everyone else is on the demographic cliff

Elderly support ratio – number of working age (20-64) per person of pension age (65+)Elderly support ratio – number of working age (20-64) per person of pension age (65+)One of the many headwinds

that Japan has had is the

aging of the population.

What is less well known is

that while Japan has fallen

off the cliff, everyone else is

teetering on the edge.

Japan’s demography is

comparatively stable over the

next several decades.

Demography is everyone

else’s problem.

Source: OECD

0

2

4

6

8

10

12

14

16

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Japan Korea China OECD USA Germany Italy

Western OECD countries

Asia

Projection

26Japanese EquitiesPictet Asset Management

Investors in general still sceptical

• Perception that Japanese companies no longer competitive

– But Sony and Sharp do not represent the whole picture

• Concerns over corporate governance

– Again, Olympus is not typical of corporate Japan

– Recent track record no worse than other regions

• Concerns over government debt and demographics

– Other countries facing similar issues: views on Japan being re-assessed

– Accept that domestic growth is limited but this does not mean equities should be written off

– Understandable concern over currency risk: Sterling and Euro investors have a hedged share class

27Japanese EquitiesPictet Asset Management

Large parts of the market are being totally overlooked

Source: Bloomberg

Stock coverage: Number of analysts S&P 1500 vs. Topix (1672 companies)Percentage of companies with

2 or fewer analysts: US 2%

versus Japan 58% 175

170

237

308

407

172

17

14

0

3

30

107

117

202

244

151

291

527

over 25

21 to 25

16 to 20

11 to 15

6 to 10

3 to 5

2

1

0

USA Japan

28Japanese EquitiesPictet Asset Management

Potential catalysts

• Recovery in domestic demand

– post-earthquake reconstruction to come

• An end to yen appreciation

– the BoJ is playing its part, further pressure from Abe?

• An end to deflation

– implications for asset allocation

• A turn in the global cycle

– policy shift in China

29Japanese EquitiesPictet Asset Management

Pictet core Japanese equity funds

The performance target, risk figures and exposures given above provide an indication of the probable characteristics in normal market conditions and are not intended to be legally binding outside of the

Investment Management Agreement

Remain close to 100% investedNet exposure maintained close to 100%Cash

Full market cap spectrum

c.100 holdings: 80 long, 20 short

Topix

4% +

3 – 8%

Long: +4%, Short: -3%

Japanese Equity Opportunities

No “micro” capsExposure

50 – 60 holdingsFocused portfolio

MSCI JapanBenchmark

3% +Alpha target

3 – 7%Ex-ante tracking error

Sectors: +10% active betStocks: +4%

Construction guidelines

Japanese Equity Selection

We manage our funds with a strong bottom-up approach within a sector framework

30Japanese EquitiesPictet Asset Management

Performance – Pictet - Japanese Equity Opportunities (JPY)

Source: Pictet/Performa Global

Annual Performance %

0.00

0.00

0.00

0.00

-1.33

-1.45

6.65

4.28

3.58

3.96

Performance Portfolio Benchmark Difference Portfolio Benchmark

YTD 13.69% 9.73% 3.96% 23.00% 21.70%

Since Inception (31.07.07) -9.49% -11.81% 2.33% 3.58%

1 Year 14.05% 9.87% 4.18% 0.80

3 Years 3.81% -0.23% 4.04%

5 Years -8.15% -10.75% 2.60%

Standard Deviation

Gross Performance in JPY

Benchmark: Topix (TRI)

Portfolio: Pictet- Japanese Equity Opportunities

Reported in JPY

Tracking Error

Information Ratio

Cumulative Performance %

(annualised per 30.11.12)

Risk Figures

(annualised 5 years per 30.11.12)

-60

-40

-20

0

20

2007 (Aug) 2008 2009 2010 2011 2012 (Nov)

- 60

- 40

- 20

0

20

Pictet- Japanese Equity Opportunities Topix (TRI)

31Japanese EquitiesPictet Asset Management

Biographies

Adrian HickeyHead of Japanese Equities

Developed Equities team

Adrian Hickey joined Pictet Asset Management in

2006 and is Head of the Japanese Equities Team.

Adrian has concentrated on Japanese equity fund

management since joining Scottish Equitable in

Edinburgh in 1991. After Scottish Equitable he

spent four years working as a buy-side analyst in

Tokyo with Commerz International Capital

Management. On returning to the UK, Adrian

worked for Edinburgh Fund Managers and Shell

Pensions. Adrian's most recent position before

joining Pictet was Director of Japanese Equities at

Foreign & Colonial in London.

Adrian graduated with a BA (Hons) in Economics

and Economic History from the University of

Birmingham and holds an MA in Philosophy from

Lancaster University.

Sam PerrySenior Investment Manager

Developed Equities team

Sam Perry joined Pictet Asset Management in

1997 and is a Senior Investment Manager

specialising in Japanese equities.

Sam graduated from the University of Oxford with

a first class degree in Philosophy and Psychology.

He later gained a Doctorate in Experimental

Cognitive Psychology, also at Oxford University.

He is also a Chartered Financial Analyst (CFA)

charter holder.

Serena RobinsonSenior Investment Manager

Developed Equities team

Serena Robinson joined Pictet Asset Management

in 2000. She is a Senior Investment Manager

specialising in Japanese equities

She began her finance career at INVESCO in

1999.

Serena graduated from Trinity College Dublin with

a BA in Economics & Business Studies and has a

First Class Master’s degree in Business Studies

from University College Dublin. She is a Chartered

Financial Analyst (CFA) charter holder.

32Japanese EquitiesPictet Asset Management

Biographies

Takeshi Suzuki Senior Investment Analyst

Pictet Asset Management (Japan)

Takeshi Suzuki joined Pictet Asset Management

(Japan) Ltd. as a Senior Investment Analyst in

2001 with a focus on technology sectors

He began his investment career in 1987, joining

Okasan Securities as an institutional salesman,

later becoming an analyst in the research

department.

Takeshi graduated from Rikkyo University with a

BA in Economics. He is a Chartered Financial

Analyst (CFA) charter holder and a Chartered

Member of the Security Analysts Association of

Japan (CMA).

Go ShiinaSenior Investment Analyst

Pictet Asset Management (Japan)

Go Shiina joined Pictet Asset Management (Japan)

Ltd. in 2009, as a Senior Investment Analyst with

a focus on industrial sectors

Before joining Pictet, he spent ten years at

Goldman Sachs Asset Management and began his

career in 1997 as an analyst at Dai-Ichi Kangyo

Bank.

Go graduated with a BA in Economics and Finance

from the University of Tokyo. He is also a

Chartered Member of the Security Analysts

Association of Japan.

Pictet Asset Management (“PAM”) definition: In this document, Pictet Asset Management includes all the operating subsidiaries and divisions of the Pictet group that carry out institutional asset management: Pictet Asset Management SA, a Swiss corporation registered with the Swiss Financial Market Supervisory Authority FINMA, Pictet Asset Management Limited, a UK company authorised and regulated by the Financial Services Authority, and Pictet Asset Management (Japan) Limited, a Japanese company regulated by the Financial Services Agency of Japan.

This document is for distribution to professional investors only. However it is not intended for distribution to any person or entity who is a citizen or resident of any locality, state, country or other jurisdiction where such distribution, publication, or use would be contrary to law or regulation. Information used in the preparation of this document is based upon sources believed to be reliable, but no representation or warranty is given as to the accuracy or completeness of those sources. Any opinion, estimate or forecast may be changed at any time without prior warning. Investors should read the prospectus or offering memorandum before investing in any Pictet managed funds. This document has been issued in Switzerland by Pictet Asset Management SA and/or Pictet & Cie and in the rest of the world by Pictet Asset Management Limited and may not be reproduced or distributed, either in part or in full, without their prior authorisation.

For UK investors, the Pictet and Pictet Total Return umbrellas are domiciled in Luxembourg and are recognised collective investment schemes under section 264 of the Financial Services and Markets Act 2000. Swiss Pictet funds are only registered for distribution in Switzerland under the Swiss Fund Act, they are categorised in the United Kingdom as unregulated collective investment schemes. The Pictet group manages hedge funds, funds of hedge funds and funds of private equity funds which are not registered for public distribution within the European Union and are categorised in the United Kingdom as unregulated collective investment schemes.

For US investors, the Shares of the funds managed by the Pictet Group are being offered to United States tax-exempt investors Shares sold in the United States or to US Persons will only be sold in private placements to accredited investors pursuant to exemptions from SEC registration under the Section 4(2) and Regulation D private placement exemptions under the 1933 Act and qualified clients as defined under the 1940 Act. The Shares of the Pictet funds have not been registered under the 1933 Act and may not, except in transactions which do not violate United States securities laws, be directly or indirectly offered or sold in the United States or to any US Person. The Management Fund Companies of the Pictet Group will not be registered under the 1940 Act.

For more information, please contact

www.pictet.com

Pictet Asset Management SA

Route des Acacias 60, 1211 Geneva 73

Pictet Asset Management Limited

Authorised and regulated by the Financial Services Authority

Moor House, Level 11

120 London Wall

London EC2Y 5ET