Embed Size (px)

Citation preview

Pietro Modiano - Deputy CEO, Head of Wholesale Banking Division

European Road Show

2nd-4th April 2002

UNICREDITO ITALIANOWholesale Banking Division

Dario Frigerio - CEO, Pioneer Global AM

2

Agenda

UCI’s Wholesale Banking Division - P. Modiano

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

3

Italian Banking

Wholesale Banking

New Europe Banking

WHOLESALE BANKING IN UCI’S ORGANISATIONAL CHART

4

Italian & New Europe Banking

Indirect UBM + TLUBM + TL Pioneer

2001 REVENUE CONTRIBUTION*

A POWERFUL CONTRIBUTION TO THE GROUP’S DIVERSIFICATION

*Net of Corporate Centre negative contribution

GEOGRAPHIC DIVERSIFICATION

30% of Pioneer’s revenues generated out of Italy

REVENUE DIVERSIFICATION

5.8%2.0% 4.7%

87.5%

5

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

6

THE CONTEXT

UNSATISFIED DEMAND IN ITALY OF INVESTMENT BANKING PRODUCTS & SERVICES

AS A CONSEQUENCE OF:

Global players targeting only large corporate customers & big deals

Local players unprepared and in a phase of transition

UBM FILLS THE GAP...

7SNOWBALL EFFECT

Successful recruitment

Immediate self-financing

An attractive projectStart-upStable managementUniCredito brand & customer baseGood strategy

Good priority selectionFirst corporate and retail derivatives ... ...then corporate finance

…leveraging on:

THE CONTEXT

8

THE CHALLENGE

The best Italian engineering and manufacturing center of high value added financial products (primary capital markets, derivatives, corporate finance)

The best market provider for the Group’s network

The most dynamic and high quality merchant bank for Italian large & mid-corporate customers

BEING RECOGNISED AS:

9

OUR ANSWER:UBM BUSINESS MODEL

Global quality in terms of:

Domestic focus

Flexible and dynamic approach to business, organised by segments:

product innovation (SPIN, Corporate derivatives, Kilovar®)

time to market risk management

mid corporate institutional

large corporate

retail

10

UBM IDENTITY CARD

CONCEIVED IN 1997 BORN AS CREDITO ITALIANO DIVISION 1998 BORN AS A BANK 2000 UBM

2001 TLab FY 01 N. OF EMPLOYEES 566 FY 01 REVENUES 601.3 (mln

Euro) FY 01 ROE 55% FY 01 C/I Ratio 35%

INVESTMENT BANKING

SALES & TRADING

UCI’s investment bank turning out:

Complex financial instruments marketed to corporate and institutional customers

Branded derivatives and services (such as TLX) for the retail market through TradingLab

3 BUSINESS LINES 1 SUBSIDIARY (100%)

11

KEY HIGHLIGHTS

1998 1999 2000 2001

278.5391.2

444.0

601.3

165.5

37%35%

Operating Income

Total Revenues

Operating Costs**

Cost Income ratio

+40.5%

+35%

210.1+27%

1998 1999 2000 2001

1998 1999 2000 2001

1998 1999 2000* 2001

67%

55%

ROE

2000 2001***

*** Euro 156 mln Capital increase in 2001

322.7

132.1

101.363.8

68.3

231.4

31%

48%

** Estimates for 1998 & 1999

* First year of full operation

(Euro mln)

12

2000 % ch.2001

HIGH GROWING REVENUES, COSTS UNDER CONTROL

C/I Ratio at excellent level (35%), despite significant investments and increased headcount (566, +181 vs. 2000)

Tot. Staff Costs: +48%. Cost per employee: +1%

High growing, recurring, non-cyclical and stress-proof Trading Profits generated by:

CorporateLab TradingLab Institutional deriv. Securities

business

By

natu

reB

yb

usin

ess lin

e

Net Interest margin

Trading profits

Total revenues

Net Commissions

35.0

357.0

52.0

n.s.

+47

+44

0.4

525.8

75.1

444.0 +35601.3

Staff costs

Operating income

Net provisions & other costs

Tax expenses

Other costs

-62.3

278.5

-16.7

155.8

-106.0

-103.2

+48

+40

+22

+39

+46

+14

-92.1

391.2

-20.3

216.6

-154.3

-118.0

Net income

Sales & Trading (incl.Institut.Deriv.)

Investment & Corporate Banking

196.9

114.9

38.5

+1

+14

+34

198.7

130.7

51.4

CorporateLab (Corporate Derivatives) 93.7 +135220.5

TradingLab (Retail Derivatives)

(Euro mln)

13

LEADING INVESTMENT BANK IN ITALY BY REVENUES AND NET INCOME

(*) Year end figures as at June, 30th 2001(**) Excluding IMIWeb Bank

2001 REVENUES(Euro mln)

601.3

UBM+TLAB Mediobanca

513.3 (*)

Banca IMI

198 (**)

Interbanca

305

UBM 403

TL198

2001 NET INCOME(Euro mln)

216.6

151.2 (*)

31 (**)

116

UBM+TLAB Mediobanca Banca IMIInterbanca

14

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

15(1) Risk Adjusted P&L = Average Daily P&L/Standard Deviation of Daily P&L

UBM AND TRADINGLAB: A TRACK RECORD OF SOLIDITY AND STRONG GROWTH

Solid Economic Model Not only the 35% growth of

Average daily Trading Net Revenues achieved in 2001 is confirmed in the first months of 2002...

…but also the Risk Adjusted P&L shows a similar growing pattern rising from Euro 1.1 mln in 2000 to Euro 1.3 mln in 2001 and to Euro 1.8 mln in 2002

The shift to the right of the distribution curves of the daily P&Ls measures the growth of UBM

The asymmetry toward the right of the distribution of P&Ls shows the prevalence of positive results

2001

1.512.04

2000

+35%

Euro mln

Average daily Trading Net Revenues

and Risk Adj P&L(1)

Jan-Feb 2002

3.86+89%

UBM + TL Daily P&L distribution

0%

5%

10%

15%

20%

25%

-4.00

-3.20

-2.40

-1.60

-0.80

0.00

0.80

1.60

2.40

3.20

4.00

4.80

5.60

6.40

7.20

8.00

Daily P&L

Fre

qu

ency

1998 1999 2000 2001

UBM + TL Daily P&L distribution

0%

5%

10%

15%

20%

25%

-4.00

-3.20

-2.40

-1.60

-0.80

0.00

0.80

1.60

2.40

3.20

4.00

4.80

5.60

6.40

7.20

8.00

Daily P&L

Fre

qu

ency

1998 1999 2000 2001

1.11.3

1.8

16

Limited impact of bad market conditions: non-correlation between revenue sources (corporate derivatives vs. retail derivatives)

LOW CORRELATION WITH MARKET TRENDS AND ...

… ABSENCE OF OVERSHOOTING IN SITUATIONS OF EXTREME VOLATILITY

Extreme market movements do not affect P&L

Extreme movements

-5

-3

-1

1

3

5

7

-8% -6% -4% -2% 0% 2% 4% 6% 8%

MIB30 - Returns

Dai

ly P

&L

-5

-3

-1

1

3

5

7

-8% -6% -4% -2% 0% 2% 4% 6% 8%

MIB30 - Returns

Dai

ly P

&L

Correlation between revenues sources and market

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

weeks

Dai

ly a

vg P

&L

on w

eekl

y ba

sis

-

10,000

20,000

30,000

40,000

50,000

60,000

Dai

ly M

IB30

avg

val

ue o

n w

eekl

y ba

sis

Logarithmic interpolated curves

Mib30 Index Corporate Derivatives revenues Retail Derivatives revenues

17

2001 Average daily VAR(1)

4.3% down vs 2000 (Euro 4.4 mln vs Euro 4.6 mln)

11 Trading days with negative P&L before September 11th; 16 after September 11th; no negative daily P&Ls in 2002 up to end of February

No negative outliner

RESILIENCE TO MARKET STRESS PROVED BY STABILITY OFPOSITIVE DAILY P&Ls FROM TRADING ACTIVITIES

UBM+TL Daily VAR(1) and P&L (Jan. 2001 - Feb. 2002)

Euro mln

UB

M+

TL D

aily V

AR

an

d P

&L

Daily P&L VaR

(1)Figure relates to UBM and TL combined; calculation made with a 98-99% asymmetric double tail confidence interval. P&L net of accounting adjustments as of 31.12.2001

More and more efficient use of VaR Channel: Avg Daily P&L / Avg Daily VaR Ratio from 17% in 1999 to 23% in 2001

Avg Daily P&L / Avg Daily VaR

21%

1999 2000 2001

23%

17%

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

P&L without end of year devaluations

18

EXCELLENT QUALITY IN PROCESS CONTROL...

Focus on the role of either internal or external players of the process

Focus on key control activities supported by detailed technical documentation

Focus on correlation between business process, support process, control and administrative process

… AS WELL AS IN RISK CONTROLS (1)

Distinctive skills High-profile team

Proprietary product development

In house development of sophisticated risk-management instruments and value-added products

Risk Management tools Proprietary pricing models Proprietary VaR engine On line real-time calculation

(1) See Annex for a flowchart example

Low volatility of trading profits Low cyclical variance

Sustainability

19

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

20

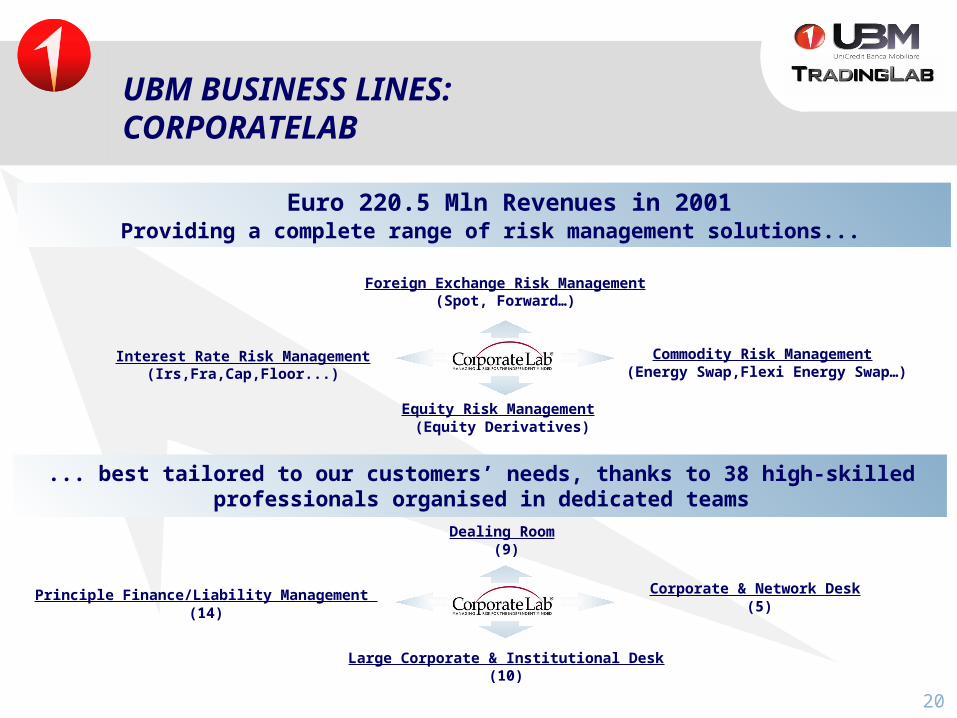

UBM BUSINESS LINES: CORPORATELAB

Providing a complete range of risk management solutions...

Equity Risk Management (Equity Derivatives)

Foreign Exchange Risk Management (Spot, Forward…)

Commodity Risk Management (Energy Swap,Flexi Energy Swap…)

Interest Rate Risk Management (Irs,Fra,Cap,Floor...)

... best tailored to our customers’ needs, thanks to 38 high-skilled professionals organised in dedicated teams

Large Corporate & Institutional Desk (10)

Principle Finance/Liability Management (14)

Corporate & Network Desk (5)

Dealing Room (9)

Euro 220.5 Mln Revenues in 2001

21

Innovation, pricing, sale and management of risk related to derivatives products for corporate customers

Italian leader in liability management for middle-market companies and public sector entities

More than 4,000 repeat customers served through UCI network

More than 250 key customers directly managed

CORPORATELAB: THE REVENUE STREAM

(*) Management accounts for 1998 and 1999

NET REVENUES (*)

(Euro mln)

1998

35.2

50.4

93.7

1999 2000

CAGR + 84%

220.5

2001

350-400

2004

22

UCI has relationships with more than 80,000 corporate customers in the Italian market, representing more than 50% of the whole system financing requirements. Customers will rise up to 92,000 in 2004 thanks to the new Corporate Bank (S3 Project)

The upside potential for CorporateLab is represented by more than 35,000 companies with revenues higher than Euro 5 mln

2004 target is to reach 10% of total UCI’s corporate customers, moving from 4,000 to more than 9,200

CORPORATELAB: UPSIDE POTENTIAL

2001

4,000

80,000

9,200

92,000

2004

CLab UCI CLab UCI

Corporate Customers +15%

+130%

~35,000S>5 Euro

mln

~45,000S<5 Euro

mln

~40,000S>5 Euro

mln

~52,000S<5 Euro

mln

~2,600S>5 Euro

mln~1,400

S<5 Euro mln

~2,800S<5 Euro

mln

~6,400S>5 Euro

mln

The new Corporate Bank will determine an increased focus on relationships with selected growth of customers’ portfolio and a rise in specialization and sales force training

New product development (e.g. QES)

Development of the same distribution model in New Europe

23

CORPORATELAB: BUSINESS DIVERSIFICATION

Leader in Asset & Liability Management for domestic Public Sector Entities and Institutions

110 mandates

131 deals

More than Euro2 bn notional

NEW PRODUCTS... ... & NEW MARKETS

Quality Energy Solutions: the first Italian reality in Energy Risk Management

Risk Management

Hedging

Consulting

Oil

Natural Gas

Electric Power

24

INVESTMENT & CORPORATE BANKING: THE MODEL

INTEGRATION OF LENDING ACTIVITY AND CORPORATE FINANCE: A UNIQUE MODEL IN ITALY

(A small JP Morgan-Chase)

Corporate Banking

Corporate FinanceEquity Capital Market

Structured Finance

Merger & Acquisitions

Corporate Lending

Fixed Income Origination & Syndication

Investment Banking

Relationship Management Euro 51.4 mln

Revenues in 2001

57 Professionals, of which 30 hired in 2001

25

2H01: UBM assumed the governance of the relationships with UCI’s Large Corporate customers (Revenues exceeding Euro 250 mln)

Direct Structured Finance activity

Transactional services and loans through UCI’s network

Euro 19.4 mln revenues, mainly from Syndication Financing (leading role in the most significant deals in Italy)

UCI’s network profitability up to 28%, with stable amount of outstanding loans

Strategic goals: leveraging on UBM’s capabilities and customer understanding to reduce plain vanilla loans of the whole UCI Group and to increase Corporate finance, Leverage finance and M&A Activities

INVESTMENT & CORPORATE BANKING: FOCUS ON LARGE CORPORATE

26

EQUITY

Fourth-ranking among Italian intermediaries in domestic equity capital market

Leadership in STAR segment (small-to mid-cap companies on MTA)

FIXED INCOME

First position in both Eurobond and all currency bookrunner rankings

Top ranking specialist in the Italian Government Bond market and specialist in French Treasury Bonds

4.5% mkt share in MTS and 3.6% mkt share in Euro-MTS

RANKING FIRST IN FIXED INCOME AMONG ITALIAN PEERS, TOP POSITION IN THE EQUITY SEGMENT

Giacomelli

€37 mlnIPO2001

Joint Global Coordinator&

Sponsor

BPCI

€365 mlnSecondary Offering

2001Lead Manager

De Longhi

€128 mlnIPO2001

Joint Global Coordinator&

Sponsor

due 2021

Joint Bookrunner

EUR 215,772,000

5.3% NotesFloating Rate Notes

11% Notes

Joint Bookrunner

PLZ 100,000,000

due 2002 due 2005

Joint Bookrunner

EUR 1,500,000,000

Floating Rate Notes Callable

EUR 500,000,000

6,80% Notes

due 2008

Joint Bookrunner

EUR 300,000,000

8.364% Notes Subordinated Tier I

Perpetual

Joint Bookrunner

BANCA POPOLARE DIBERGAMO

CREDITO VARESINO

C

Joint Bookrunner

EUR 1,000,000,000

Subordinated LT II

due 2011 6% Notes

Floating Rate Notes NC5

27

UBM BUSINESS LINES: SALES & TRADING

Euro 130.7 mln Revenues in 2001Generated minimising proprietary trading by 147 professionals organised

in a traditional market-oriented structure

Government Bonds

Debt Syndication

Spread products

Repo Desk

Emerging Markets

Forex & Treasury

Research

Derivatives &

Structured products

Fixed Income

Sales/Trading

Old style options

Institutional sales

Stock lending

Foreign Markets

Research

Equity

Derivatives &

Structured products

Prime Brokerage

28

UBM BUSINESS LINES: TRADINGLAB - THE SUBSIDIARY FOR RETAIL DERIVATIVES

Euro 198.7 mln Revenues in 2001

Covere

d

Warr

an

ts

Ben

ch

mark

s

Revers

e

Con

vert

ible

s

Eq

uit

y-L

inked

B

on

ds

Oth

er

Instr

um

en

ts

TLXKILOVAR®

TRADINGLAB.COMCUSTOMER SERVICE & TRADINGLAB & MY MONEY

engineering, producing and distributing innovative financial products and services dedicated to

131 professionals

Retail Customers

29

Italian leader in Covered Warrants, with 50% mkt share and 1,924 listed instruments as at the end of 2001

880 Covered Warrants listed on Stuggart Exchange

More than Euro 4.5 bn Derivative-linked bond issues

1,558 financial instruments listed on TLX® with a daily trading volume up to Euro 22 mln and 1,900 transactions

TRADINGLAB: THE BUSINESS TREND

… DEVELOPMENT OF A NEW DISTRIBUTION MODEL: TRADINGLAB NETWORK

From a domestic to an European player (focus on countries with similar market features: Germany, France, UK, Benelux, Spain)

Low cost of expansion: centralised and automatic operations (Milan); mainly advertising costs

Opening of TLX® shareholders’ capital to a network of partner banks

47% of 2004 total revenues from non-captive distribution channels

Selling structured products & equity linked notes in the USA through TradingLab USA Inc. (15% of 2004 total revenues)

STABLE MARKET SHARE DESPITE STRONGER

COMPETITION ...

30

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

31

2001-2004 % ch. by business lines

•CORPORATELAB +82%

•INVEST.& CORP.BK. +164%

•SALES & TRADING +76%

•TRADINGLAB +68%

OUTLOOK 2002-2004

2001 2002 2004Total revenues

+26%

601 738

1173

+23%

C/I Ratio

+28%

EBITDA

2001 2002 2004

412495

805

2001 2002 2004

35% 36% 35%

RARORAC

+28%

2001 2002 2004

194

231

378

2001 2002 2004

66% 59% 64%

EVA

+20% +19%

(Euro mln)

02-04CAGR

01-02y/y % ch.

32

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management - D. Frigerio

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

33

New ManagementTeam

Investment ProcessAligned

Positive Net Sales everywhere

THE NEW PIONEER: A RARE STORY OF SUCCESSFULL INTEGRATION IN ASSET MANAGEMENT

New Organisational Structure

34

Operations

Pioneer Global AssetManagement

NEW ORGANISATIONAL STRUCTURE ...

InvestmentsDistribution

Audit

Risk Management

Global Finance

Strategic PlanningCompliance

New Europe

Italy US Intl. Boston

Milan Dublin

Singapore

181 9766

Total number of employees: 1,677(as at 28 February 2002)

56 470 26668 22353 9

17 137

34

Holding Company

New Europe

Italy US Intl.

35

PIONEER GLOBAL ASSET MANAGEMENT

PIONEER USA

PIONEER INTERNATIONAL

... AND NEW TOP QUALITY MANAGEMENT WITH PREVIOUSSUCCESS STORIES

Robert DeNormandie

Daniel T. Geraci

William F. O’Grady

Richard Sardelli

Osbert M. Hood

Steven Graziano

Matteo Perruccio

Avril Ellis

Dominik Kremer

Steve Philips

Edmund Lacis

CFO

President and CEO

Head of Sales

Head of Marketing

COO

Head of Business Development

Head of International Sales and Distribution

Head of Marketing

General manager Germany, Austria, Switzerland

Head of Americas Sales and Distribution

Head of Sales and Distribution Asia

PWC

Fidelity Investments

Fidelity Investments

Fidelity Investments

John Hancock

Pioneer

American Express

Norwich Union and Henderson

Fidelity Investments

EDF Man Invest.

Janus

From

From

From

36

A FULLY INTEGRATED, RESEARCH BASED, GLOBAL INVESTMENT PROCESS ...

BUY DISCIPLINES Define Investment

case What is discounted? Stock, sector,

country weight

Active Portfolio

Management

SELL DISCIPLINES Target price reached Story changes Sector view/macro

environment changes

Better opportunities

Style Focussed

Stock Screening

Bond Valuations

Asset Allocation Model- Sector Allocation

Style Neutral

QUANTITATIVE RESEARCH

FUNDAMENTALRESEARCH

Strategy, ability to implement

Competitive positioning Mgmt assessment Financial strength, Cash generation

Valuation multiples

GROWTH/VALUE

GEOGRAPHIC

LARGE, MID & SMALL CAP

SEPARATE/WRAPSACCOUNTS

INSTITUTIONAL PORTFOLIO

RISK CONTROL

Process and Product

STRUCTURED

37

US High Yield Fund ranking 1st in one year and 3 year rankings

Strategic Income top decile over 2 years

... RESULTING IN TOPPERFORMING FLAGSHIP FUNDS IN KEY SEGMENTS

US Equities

Pioneer Fund outperformed the S&P over each 10 year period since

1928 and is top decile over the last 5 years

Equity Income is top quartile over the last 5 years

Small Cap Value is top quartile over the last 3 years (inception)

European Equities

All 5 Luxembourg Funds are between first decile and first quartile in

the Micropal ranking since their inception (March ’98 / July ’00)

Credit Funds

38

International

Italy (1)

of which Institutional

New Europe

USA 21,742

81,290

1,044

2,683

Dec. ’01 AuM

+2,863

+596

+408

+1,376

2001Net salesKey figures (Euro mln)

(1) Excluding Proprietary Funds (2) Including Proprietary Funds(3) As at 15.3.2002

2001: POSITIVE NET SALES IN ALL BUSINESS AREAS

TOTAL +5,243

Increasing “Non Captive” share on total AuMs (1)

111,037TOTAL (2)

106,759

Mar. ’02 AuM (3)

Mar. ’02Net sales

81,337

+1,048 5,733

23,006

+576

+65

108,854

113,222

+121

+833

5,915

3,408

1,103

-188

+1,286

Acceleration of positive trend in 2002

Non Captive/Total AuM - Assets Breakdown

25,31%

29,22%30,71%

20%

22%

24%

26%

28%

30%

32%

Year 2000 Year 2001 15 March 2002

39

Total Revenues

2001

Operating costs

Gross operating income

Net Profit(ante minorities)

483.9

378.4

105.6

69.4

(Euro mln)

+3.9% Vs. 2000 pro-forma(1) thanks to successful turnaround of inflows and focus on high margin products (i.e. Capital Guaranteed)

Costs impacted by non recurring restructuring charges, interest expenses(2) and advertising campaigns to relaunch Pioneer brand Gross operating income affected by impact of turnaround costs

Net Profit also affected by increased reserves and very conservative approach to tax provisions(1) Pro-forma based on UCI estimates (not accounting figures) including Pioneer USA results (for the whole 2000) in 2000 Pioneer

Group’s income statement

GOOD INCREASE IN REVENUES (ON A PRO-FORMA BASIS);C/I RATIO AFFECTED BY COSTS OF TURNAROUND

Trend Vs. 2000

Percentage changes over 2000 reported figures are not meaningful because of differences in consolidation perimeter

(2) Interest expenses related to financing of goodwill(3) Gross Operating Income (Euro 105.6 mln) + Interest Expenses (Euro 23.4 mln) + Extraordinary Staff Costs (Euro 4 mln) +

Other Extraordinary Restructuring Costs (Euro 6.4 mln)

Managerial EBIT (3)

139.4 (Ex interest expenses and restructuring costs linked to the acquisition)

40

2002-2004 STRATEGY: FROM A MUTUAL FUND TO A 360° ASSET MANAGER ...

Pioneer has expertise in all these areas and a unique range of funds with a good track record

Pioneer is poised to become a leader in these segments by 2004

High growth/High margin segments

Retirement products and Unit-linked

insurance policies

Third party distribution platformsFocus on affluent and HNW

Separate Accounts including guaranteed wraps

Alternative Products

Other innovative vehicles with mutual funds as

underlying instruments

41

… LEVERAGING ON 5 KEY COMPETITIVE ADVANTAGES

Integrated, global and “institutionalised” investment process

Ensures flexibility and economies of scope for our third party strategy

Leader in packaging and delivering innovative products

A wide product range can be readily combined to deliver sophisticated “ad hoc” solutions in terms of risk control and personalised asset allocation

Comparative advantages with Global Distributors

Only few providers will become global players in this segment; Pioneer is well positioned to enter the group

Great Global Brand adapted to local needs

Global but also flexible enough to adapt quickly to evolving market conditions

Development of Alternative Investments capabilities

Coverage of low volatility segment and synergies in structured products

42

2002-2004 STRATEGY FOCUSED ON RETURN ON ASSETS

Revenues (1)

581

958

+63%

Managerial EBIT 2002 2004

170

449

Managerial C/I Ratio

71%

53%

118

172

Average AuM

49.2

55.8

Revenues on Av. AuM, bp(1) Revenues from pure Asset Management

Managerial EBIT on Av. AuM, bp

2002 2004

14.4

26.1

139

2001

519

73%

2002 2004 2001

2002 2004 2001

111

46.7

2002 2004 2001

2002 2004 2001

Growth drivers: 3% annual Mkt

performance Net sales

02-04CAGR

01-02y/y % ch.

+22%

+28%

+12%

+20%

+6%

43

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

44

ITALY: TOP PERFORMER FOR NET SALES IN 2001; PENSION PRODUCTS THE KEY DRIVER OF FUTURE GROWTH

2001 RESULTS

Confirmed leadership in the Institutional segment (Euro 1,048 mln net sales)

Product innovation and time to market the key drivers of 2001 total net sales (Euro 2.863 mln, ex proprietary funds); Capital Guaranteed Products generating Euro 7.46 bn net sales

2002-2004 STRATEGY

Strong involvement in UCI’s S3 project, in order to increase share of wallet of private and affluent customers

New generation of HNW segregated accounts, with a “hedge fund” component - Target: Euro 14 bn AuM and Euro 7 bn net sales by 2004

Launch of Pension Products: Euro 20-25 bn additional AuM by 2004 with an average return of 45-50 bp

Growing presence in “third party platforms” and Institutional segment

45

USA: TURNAROUND IN SALES IN THE FIRST YEAR AFTER ACQUISITION; 2004 TARGETS TO BE REACHED THROUGH A WIDER PRODUCT RANGE AND ENHANCED DISTRIBUTION CAPABILITIES

2002-2004 STRATEGY

Double the number of advisors/ distributors (from 35,000 to 70,000), increasing their productivity by 30%

Sales force reorganisation; development of sales capabilities in Separate Accounts, Alternative Investments, Structured and Retirement products (i.e. Uni-K and 529 plans)

Best performance in Pioneer US’ history for gross and net sales in 2001, despite bad market conditions; excellent trend in 2002 YTD

6291,000

506

1,189

-251

-1,740

1,231

-2,000

-1,000

0

1,000

2,000

1995 1996 1997 1998 1999 2000 2001

PIONEER US - Net Domestic SalesUSD mln

729

2002 (1)

(1) Year-to-date as at 15.3.2002

2001 RESULTS

1,3612,166 2,287

3,430 3,2832,751

3,838

1,000

2,000

3,000

4,000

5,000

1995 1996 1997 1998 1999 2000 2001

PIONEER US - Gross Domestic Sales

0

USD mln

1,330

2002 (1)

46

INTERNATIONAL: 2002 YTD NET SALES ALREADY IN LINE WITH FY2001;NEW THIRD PARTY DISTRIBUTION CHANNELS AND ALTERNATIVE PRODUCTS TO DRIVE GROWTH

-414

596

-1,000

-500

0

500

1,000

2000 2001

PIONEER INTERNATIONAL - Net Sales

Euro mln

576

2002 (1)

New third party distributors, new agreements with Open Platforms and re-branding resulted in a strong net sales turnaround

2001 RESULTS

(1) Year-to-date as at 15.3.2002

2002-2004 STRATEGY New and deeper relations with third

party distributors to boost sales of traditional or alternative funds

Global distribution agreements with at least 7 major global distributors (vs. 3 at end 2001); maximising Pioneer brand awareness for regional HNW/affluent segments open platforms

Leadership in Alternative Investment products with low volatility spectrum

47

NEW EUROPE: LEVERAGING ON EU CONVERGENCE AND UCI’S WIDEAND STRONG NETWORK IN THE REGION

2002-2004 STRATEGY Capitalisation on EU convergence based

on Italian experience

Consolidation of Pioneer’s leadership in the region through close co-operation with UCI’s network

Development in the Pension Product segment

Excellent results in net sales, mainly due to Bank Pekao distribution in Poland

-0.11

45

-100

0

400

1Q01 2Q01

PIONEER NEW EUROPE - Net Sales

Euro mln

367

2002 (1)

300

200

100

3Q01 4Q01

-4.4

65

Tot. 2001: 408 mln

2001 RESULTS

Market leadership in Poland (23.4% mkt. Share(2)) and Czech Republic (6.7% mkt. share(2))

(1) Year-to-date as at 15.3.2002 (2) Mkt. Shares as at 28.2.2002

48

Agenda

UCI’s Wholesale Banking Division

Investment Banking: UBM

Overview & Business Model

The Risk/Return Profile

The Business Lines

Outlook 2002-2004

Pioneer Global Asset Management

Overview & 2002-2004 strategy

Operating Divisions

Conclusion

49

Pioneer has built a factory that is able to address all the risk/return segments:

Expertise and track record are well established in the Bottom-Up Equity segment

The objective is to develop leadership in low volatility Hedge Funds

Guaranteed and Structured products posted out excellent commercial results in Italy

Global Asset Management excellence and sales expertise are the basis for cross-fertilisation

PIONEER VALUE ADDED STRATEGY: SOPHISTICATED PRODUCTS AND CROSS-FERTILISATION OF SALES EXPERTISE

Guaranteed

Products

Credit

Low Volatility Hedge Funds

Bottom Up Equity

Retu

rn

Risk

ENHANCING RESULTS AND REDUCING EXPOSURE TO FINANCIAL CYCLE

THE MISSION:

50

Annexes

51

UBM & TRADINGLAB BEFOREAND AFTER SEPTEMBER, 11th

VaR vs P&L UBM + TL (Sep-Nov 2001)

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

03-s

et-0

1

05-s

et-0

1

07-s

et-0

1

11-s

et-0

1

13-s

et-0

1

17-s

et-0

1

19-s

et-0

1

21-s

et-0

1

25-s

et-0

1

27-s

et-0

1

01-o

tt-0

1

03-o

tt-0

1

05-o

tt-0

1

09-o

tt-0

1

11-o

tt-0

1

15-o

tt-0

1

17-o

tt-0

1

19-o

tt-0

1

23-o

tt-0

1

25-o

tt-0

1

29-o

tt-0

1

31-o

tt-0

1

02-n

ov-0

1

06-n

ov-0

1

08-n

ov-0

1

12-n

ov-0

1

Date

VaR

, P

&L

(m

ln €

)

DAILY P&L

VAR

Positive P&L Trend

Decreasing VaR Trend

EUR 2.5m loss on Sep 11th

VaR increase followed by position cutting

VaR vs P&L UBM + TL (Sep-Nov 2001)

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

03-s

et-0

1

05-s

et-0

1

07-s

et-0

1

11-s

et-0

1

13-s

et-0

1

17-s

et-0

1

19-s

et-0

1

21-s

et-0

1

25-s

et-0

1

27-s

et-0

1

01-o

tt-0

1

03-o

tt-0

1

05-o

tt-0

1

09-o

tt-0

1

11-o

tt-0

1

15-o

tt-0

1

17-o

tt-0

1

19-o

tt-0

1

23-o

tt-0

1

25-o

tt-0

1

29-o

tt-0

1

31-o

tt-0

1

02-n

ov-0

1

06-n

ov-0

1

08-n

ov-0

1

12-n

ov-0

1

Date

VaR

, P

&L

(m

ln €

)

DAILY P&L

VAR

Positive P&L Trend

Decreasing VaR Trend

EUR 2.5m loss on Sep 11th

VaR increase followed by position cutting

52

AN EXAMPLE OF PROCESS AND RISK CONTROL

Mercato OITSistema di Front

OfficeBroker di

EsecuzioneTrader

1Valuta la convenienza

dell'operazione data la propriaesposizione al rischio di mercato

2Trasmette l'ordine albroker via telefono

2Trasmette l'ordine al

broker tramitel'applicativo XTAS/

JPX/GL3

Immette l'ordinesul mercato

4Eseguel'ordine

5Comunica telefonicamente altrader l'eseguito/ attraverso

JPX/GL fornisce a videol'evidenza del'eseguito

5L'applicativo XTAS fornisce avideo l'evidenza dell'eseguito

e trasmette in automatico i datia WSS con un batch periodico

(ogni 15 minuti)

7Summit e WSS

trasmettono i dati dei dealeseguiti e modificati in

giornata a Rolfe & Nolanin batch notturno

trade date +1

trade date

xor

ProcessoGestione

Anagraficheprodotti/ctp

ProcessoHelp Desk

ProcessoAutorizzazione

e controlloBroker

ProcessoControlloRischio dimercato

ProcessoRivalutazioneposizioni a fini

gestionali e det.del P/L in WSS

Presidiano il correttocompleto

trasferimento dei dealtra applicativo XTAS e

Wall Street

6Verifica l'eseguito e lo

carica manualmente suSummit/Wall Street

verificando la correttaregistrazione

xor

ProcessoRivalutazioneposizioni a fini

gestionali e det.del P/L in Summit

a

a

WSS viene alimentato ogni15 minuti con il file messo adisposizione Barclays R&N(broker di regolamento)

La verifica vieneeffettuata per confrontotra WSS e un file Excelcon i deal estratti daXTAS

Listed Derivatives Trading on Foreign Markets flow (example)

Control activity and detailed

documentation

Correlated process