Embed Size (px)

Citation preview

PinguinLutosa NV PinguinLutosa NV

Small caps conferenceSmall caps conference

30/11/201030/11/2010

The information contained herein shall not constitute or form any part of any offer or invitation to subscribe for, underwrite or otherwise acquire, or any solicitation of any offer to purchase or subscribe for, securities including in the United States, Australia, Canada of Japan.

The information contained herein is not for publication or distribution into the United States, Australia, Canada or Japan. Neither this announcement nor any copy of it may be taken or distributed or published, directly or indirectly, in the United States, Australia, Canada or Japan.

The material set forth herein is for informational purposes only and is not intended, and should not be construed, as an offer of securities for sale into United States or any other jurisdiction. Securities may not be offered or sold in the United States absent registration under the U.S. Securities Act of 1933, as amended (the “Securities Act”) or an exemption from registration. The securities of the company described herein have not been and will not be so registered. There will be no public offer of securities in the United States, Australia, Canada or Japan.

Disclosure

I. Who we are?II. Operational update ecialistIII. Financial update IV. Cecab (D’aucy Frozen Foods)V. Q & A

Agenda

Who we are?Who we are?

Herwig Dejonghe, CEO Herwig Dejonghe, CEO

5

■ Specialised in the development, production and sales of:

■ Frozen products

■ Vegetables

■ Fries & potato specialities

■ Ready-to-use culinary preparations (ready meals)

■ Pre-fried chilled chips (BBD 21 days) & pasteurised potatoes

■ Dehydrated potato flakes

Who we are?

6

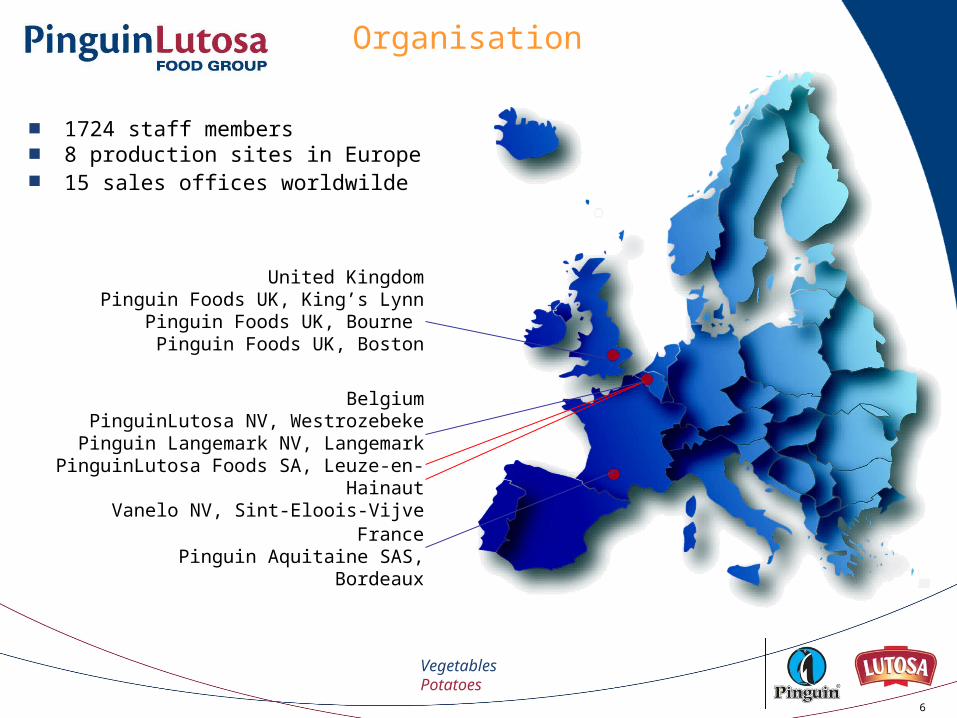

■ 1724 staff members■ 8 production sites in Europe■ 15 sales offices worldwilde

VegetablesPotatoes

Organisation

FrancePinguin Aquitaine SAS, Bordeaux

BelgiumPinguinLutosa NV, Westrozebeke

Pinguin Langemark NV, LangemarkPinguinLutosa Foods SA, Leuze-en-Hainaut

Vanelo NV, Sint-Eloois-Vijve

United KingdomPinguin Foods UK, King’s Lynn

Pinguin Foods UK, Bourne Pinguin Foods UK, Boston

7

Strategy

■ 3 basics

Operational excellence

Quality assurance

Sustainable development

■ 5 key-objectives

Customer-staff-supplier satisfaction

Innovation

Internationalisation

Profitable growth

Brand awareness

Operational updateOperational update

Herwig Dejonghe, CEOHerwig Dejonghe, CEO

Growing conditions and crops

UK & Belgium: • Long winter, cold spring caused late start of the early crops of peas,

cauliflower and potatoes.

• Extremely hot start of summer at the end of June and first half of July gives a short pea season and stops early potatoes growing.

• Fresh but rather dry weather from half July to end of August brings good growing conditions for the bean crop but too late for root crops like carrots and potatoes, which will result in smaller products and as such lower yields per acre. From the start of September to the first week of October the weather was cool and wet. The combination of first too dry and then too wet was also a disaster for the second crop of spinach . For potatoes it causes even secondary growth for the autumn crop which increases the risk on glassy potatoes.

• After some dry weather from the second week of October which was good to harvest, excessive rainfall at the end of October and first half of November caused big problems to harvest and increases risk of rotting potatoes.

France:• Excellent growing conditions for sweet corn, beans and carrots.

Market conditions: vegetables

• Reduction of planned acreage for 2010 with 5 % all over Europe to correct for the good crops of the last years and the high stocks.

• Good sales because of cold and long winter reduces stocks to healthy levels at the start of the new season in July.

• Contract negotiations running from May to end of September in difficult conditions, leading to high price pressure from customers. Biggest pressure in France and in UK. The market goes for price drops of about 8%, we succeed to limit the decrease to 4% in those countries. In other markets we maintain old seasons price level by strong resistance and product mix optimisation.

• Problematic crops in East-Europe (Poland and Hungary) due to extreme rainfall cause shortages for sweet corn, cauliflower and onions.

Market conditions: potatoes

• From end of April 2010 prices of old crop potatoes increase from 75 euro/ton to 95 euro/ton.

• The late crop of early potatoes causes price increases up to 200 euro/ton and low availability. Hope is then that prices will drop to 100 euro/ton for the autumm crop but due to smaller potatoes prices remain high on 130 euro/ton.

• The problematic harvest circumstances continue to put pressure on availability and prices remain high in October and November.

• Bad crops in Russia and Eastern Europe increases demand for fresh potatoes.

• Competitors open contract negotiations in August with too low prices as they are hoping for lower prices from autumm crop. We resist and even show the way for higher prices as we see the same scenario as the 2006 crop situation.

• Today competitors are going for higher prices forced by reality.

• Demand for deep-frozen potato products remains very high in Europe and even more overseas.

Financial updateFinancial updateSteven D’haene, CFOSteven D’haene, CFO

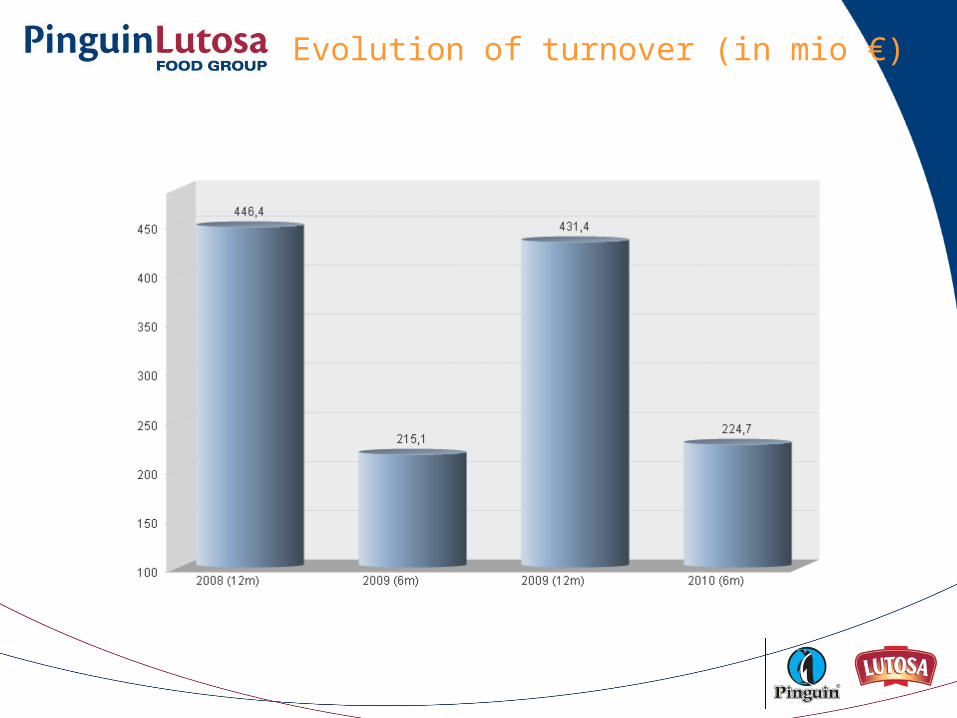

Evolution of turnover (in mio €)

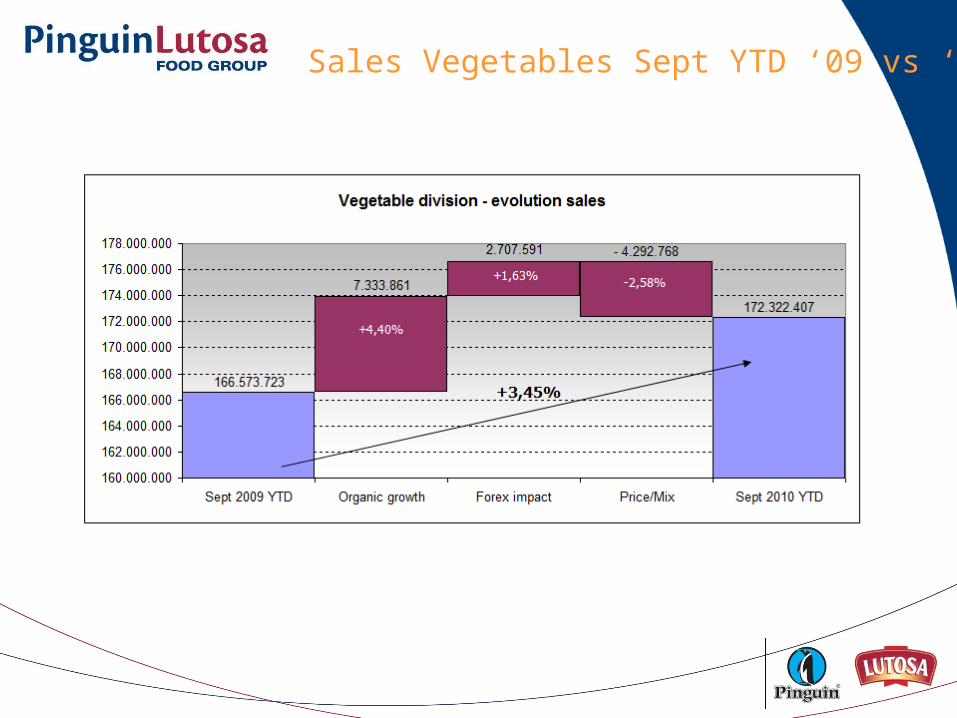

Sales Vegetables Sept YTD ‘09 vs ‘10

+4,40%

+4,40%

+1,63% - 2.58%

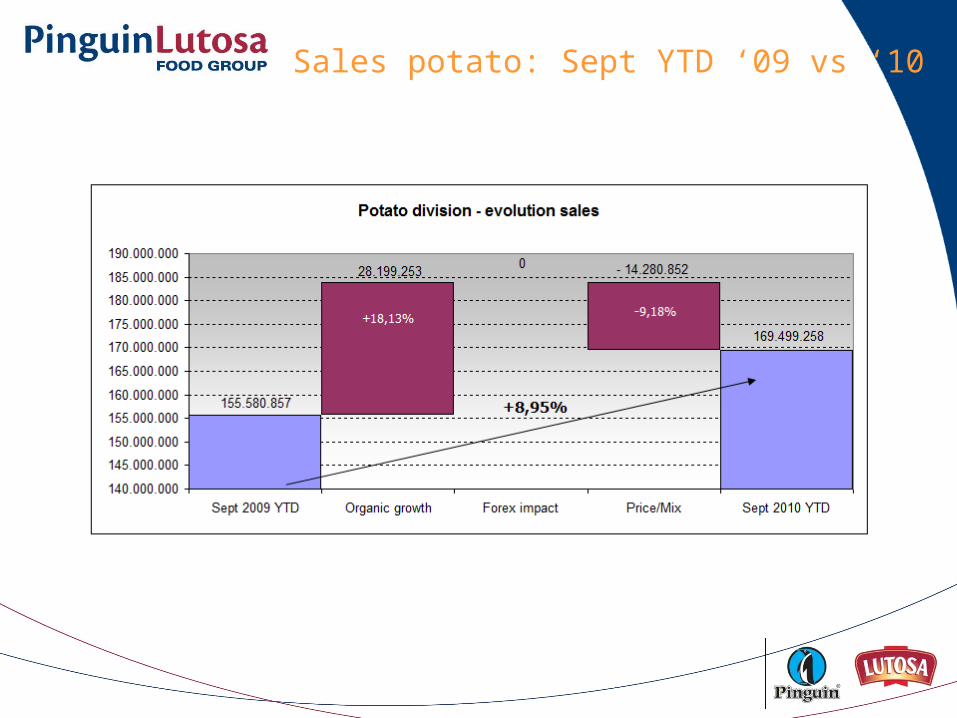

Sales potato: Sept YTD ‘09 vs ‘10

+4,40%

+4,40%

+1,63% - 2.58%

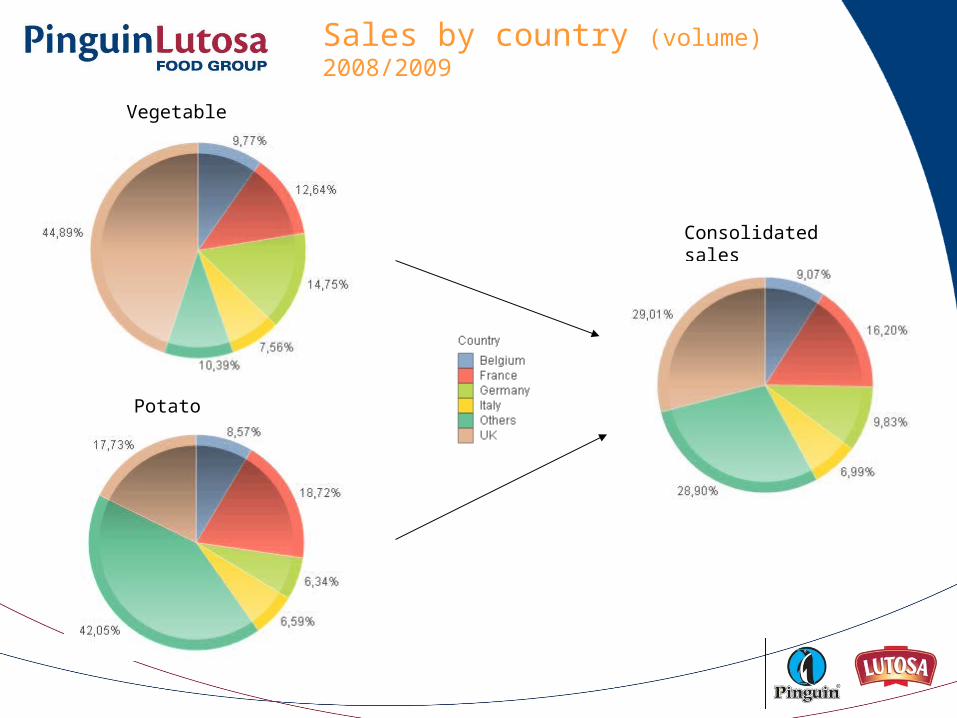

Sales by country (volume) 2008/2009

Consolidated sales

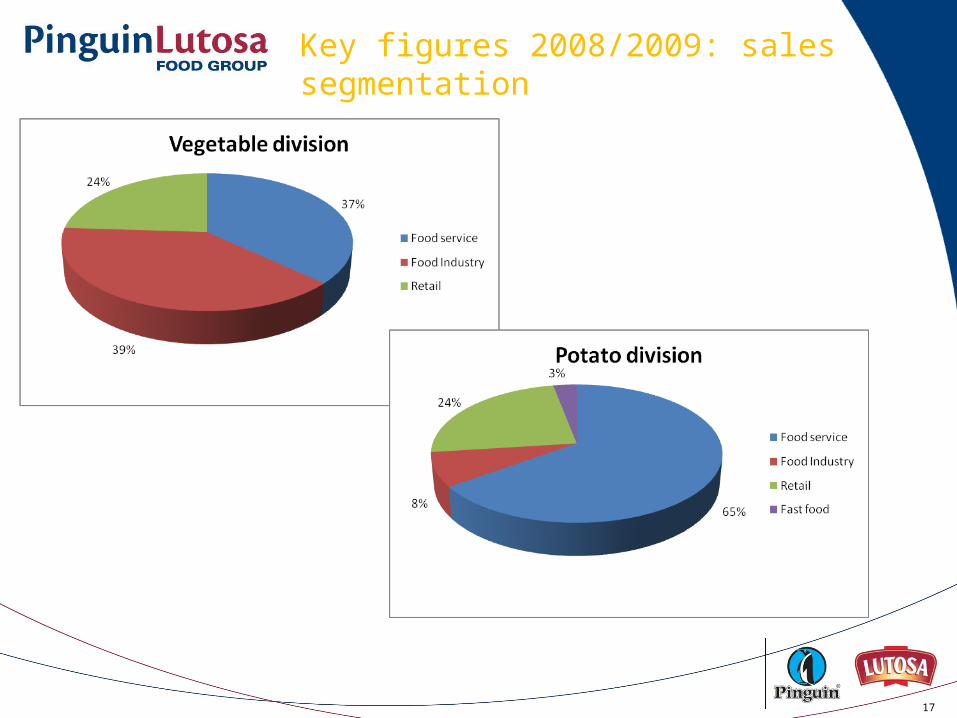

Vegetable division

Potato division

17

Key figures 2008/2009: sales segmentation

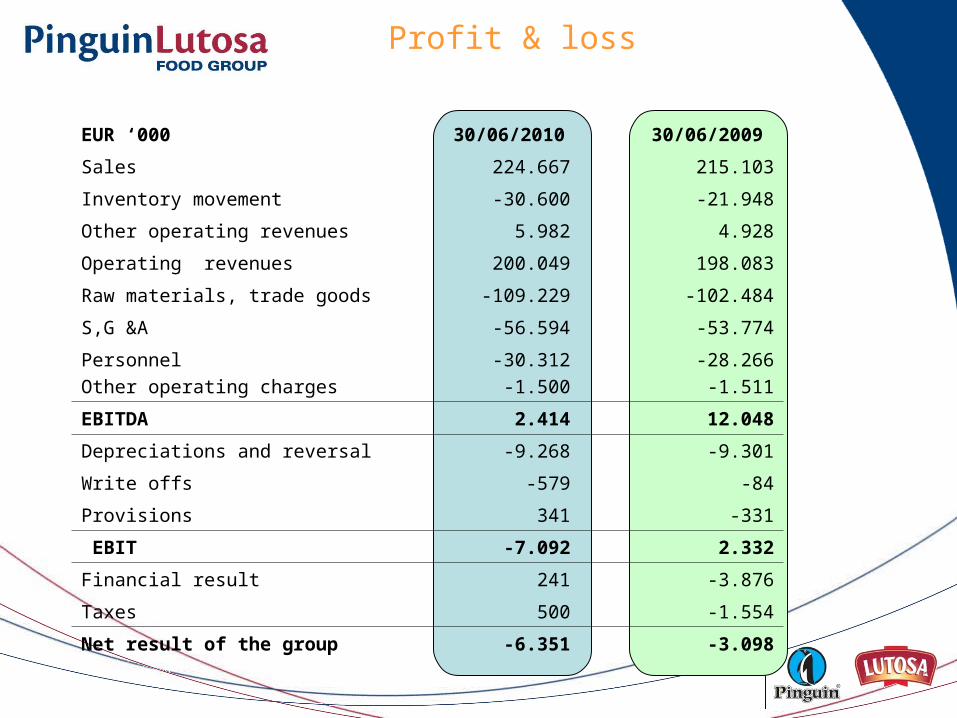

EUR ‘000 30/06/2010 30/06/2009

Sales 224.667 215.103

Inventory movement -30.600 -21.948

Other operating revenues 5.982 4.928

Operating revenues 200.049 198.083

Raw materials, trade goods -109.229 -102.484

S,G &A -56.594 -53.774

PersonnelOther operating charges

-30.312-1.500

-28.266-1.511

EBITDA 2.414 12.048

Depreciations and reversal -9.268 -9.301

Write offs -579 -84

Provisions 341 -331

EBIT -7.092 2.332

Financial result 241 -3.876

Taxes 500 -1.554

Net result of the group -6.351 -3.098

Profit & loss

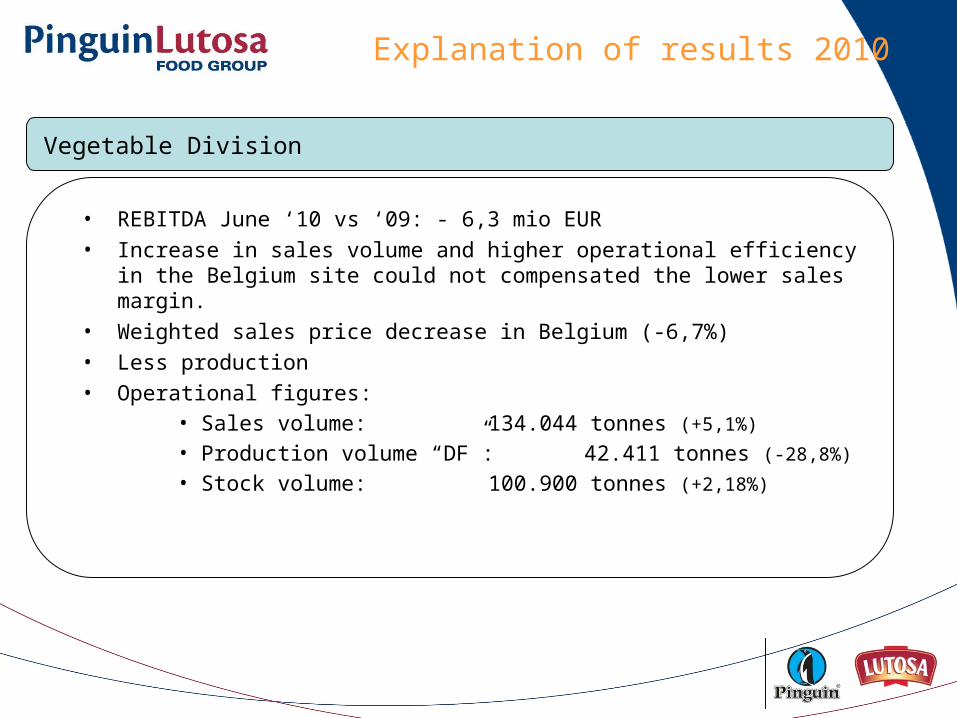

Explanation of results 2010

Vegetable Division

• REBITDA June ‘10 vs ‘09: - 6,3 mio EUR• Increase in sales volume and higher operational efficiency in the

Belgium site could not compensated the lower sales margin.• Weighted sales price decrease in Belgium (-6,7%)• Less production• Operational figures:

• Sales volume: 134.044 tonnes (+5,1%)

• Production volume “DF”: 42.411 tonnes (-28,8%)

• Stock volume: 100.900 tonnes (+2,18%)

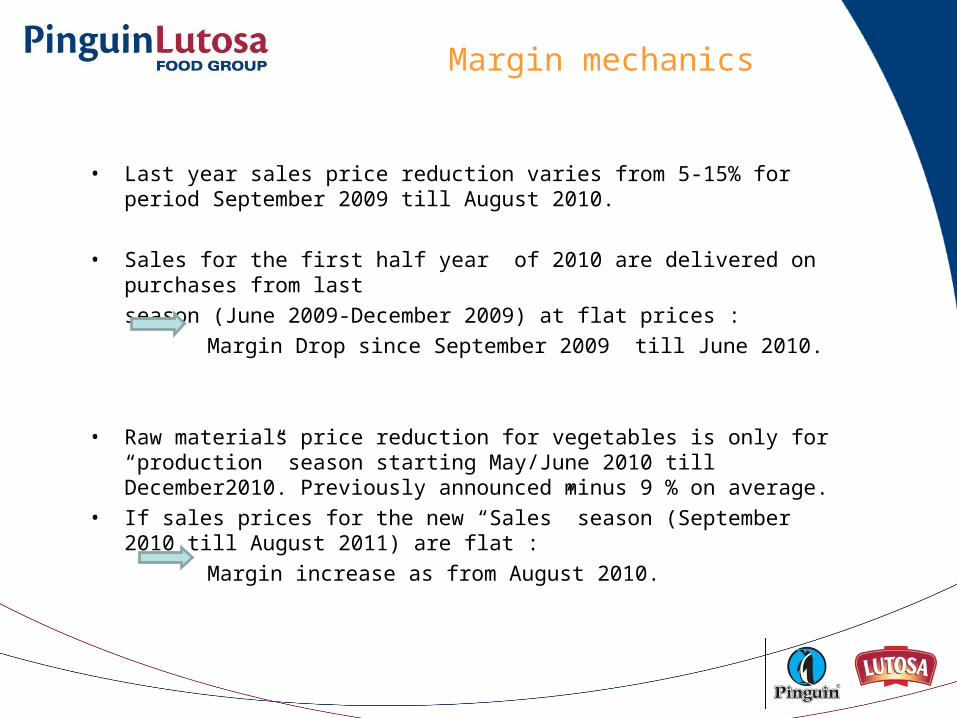

• Last year sales price reduction varies from 5-15% for period September 2009 till August 2010.

• Sales for the first half year of 2010 are delivered on purchases from lastseason (June 2009-December 2009) at flat prices :

Margin Drop since September 2009 till June 2010.

• Raw materials price reduction for vegetables is only for “production” season starting May/June 2010 till December2010. Previously announced minus 9 % on average.

• If sales prices for the new “Sales” season (September 2010 till August 2011) are flat :

Margin increase as from August 2010.

Margin mechanics

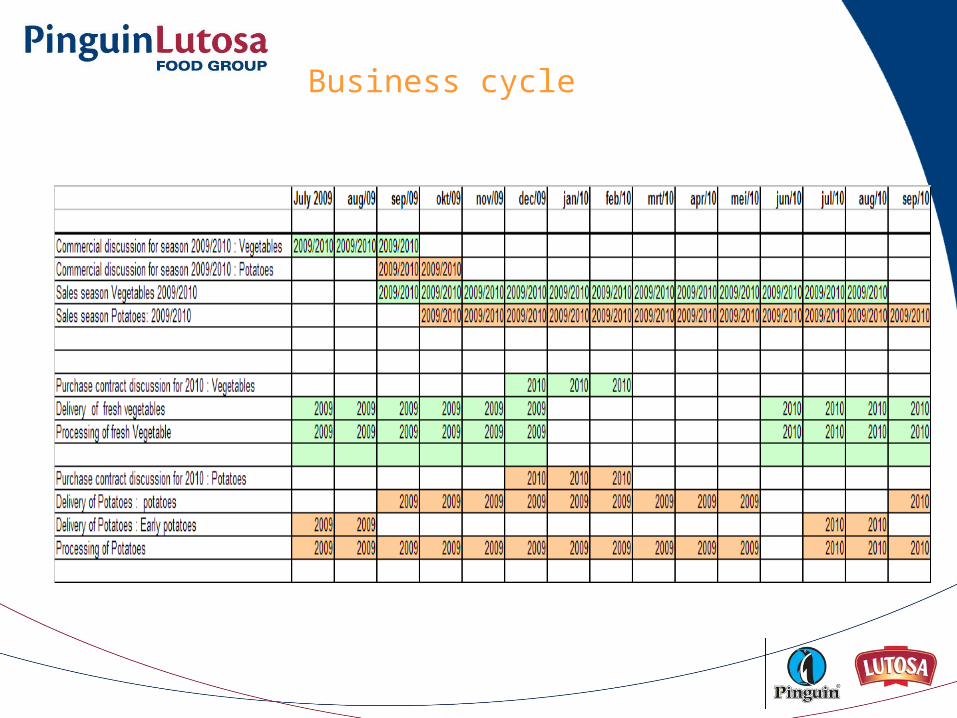

Business cycle

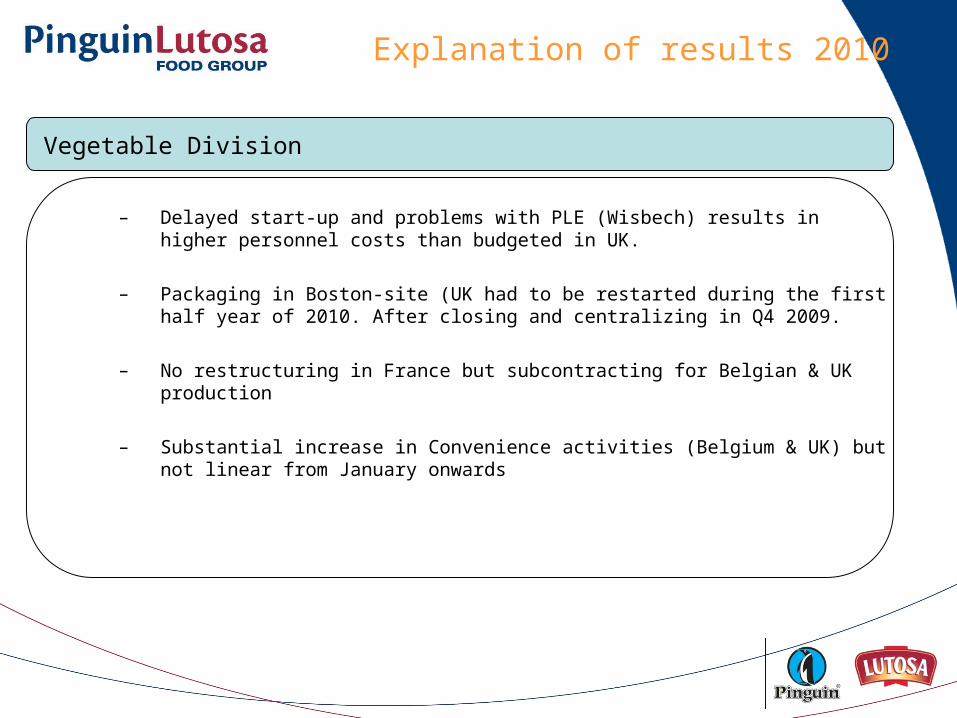

Explanation of results 2010

Vegetable Division

– Delayed start-up and problems with PLE (Wisbech) results in higher personnel costs than budgeted in UK.

– Packaging in Boston-site (UK had to be restarted during the first half year of 2010. After closing and centralizing in Q4 2009.

– No restructuring in France but subcontracting for Belgian & UK production

– Substantial increase in Convenience activities (Belgium & UK) but not linear from January onwards

Explanation of results 2010

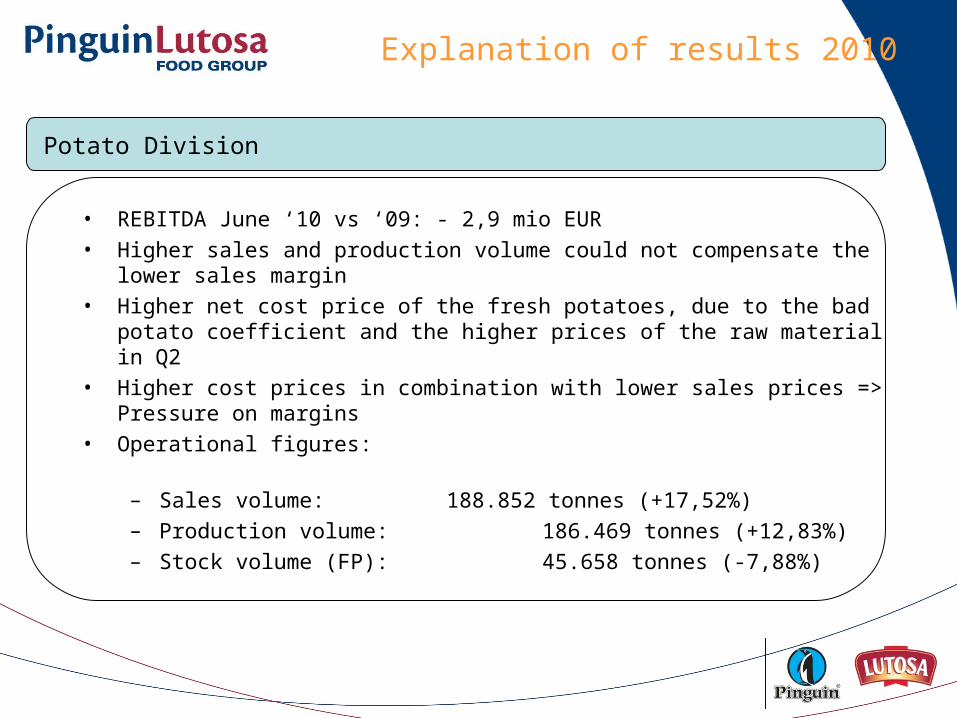

Potato Division

• REBITDA June ‘10 vs ‘09: - 2,9 mio EUR• Higher sales and production volume could not compensate the lower

sales margin• Higher net cost price of the fresh potatoes, due to the bad potato

coefficient and the higher prices of the raw material in Q2• Higher cost prices in combination with lower sales prices => Pressure

on margins• Operational figures:

– Sales volume: 188.852 tonnes (+17,52%)– Production volume: 186.469 tonnes (+12,83%)– Stock volume (FP): 45.658 tonnes (-7,88%)

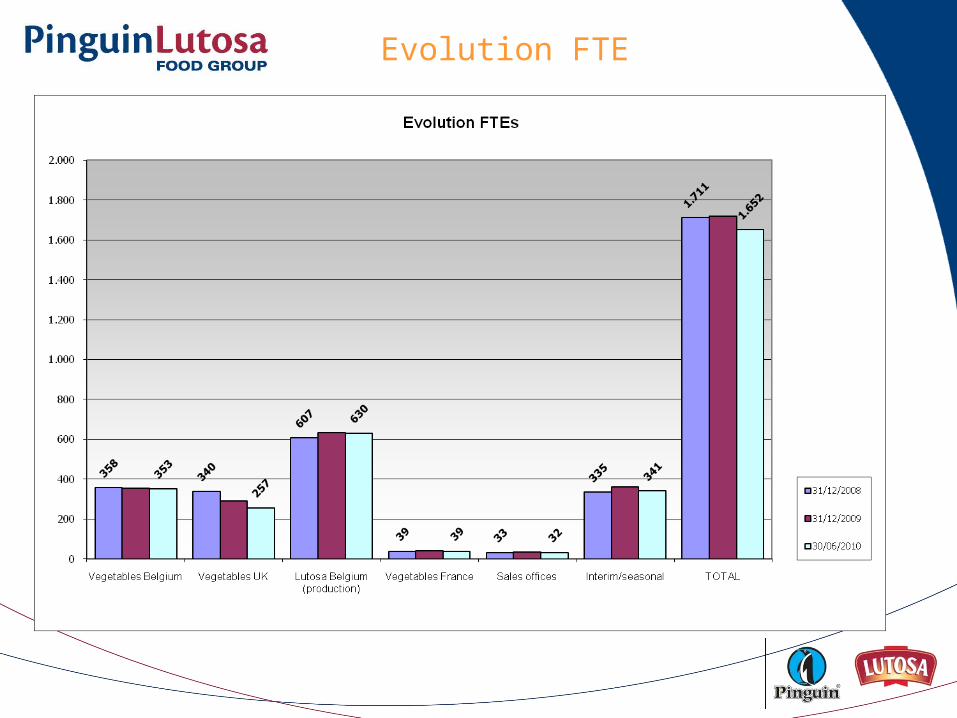

Evolution FTE

30/06/10 Delta 30/06/09

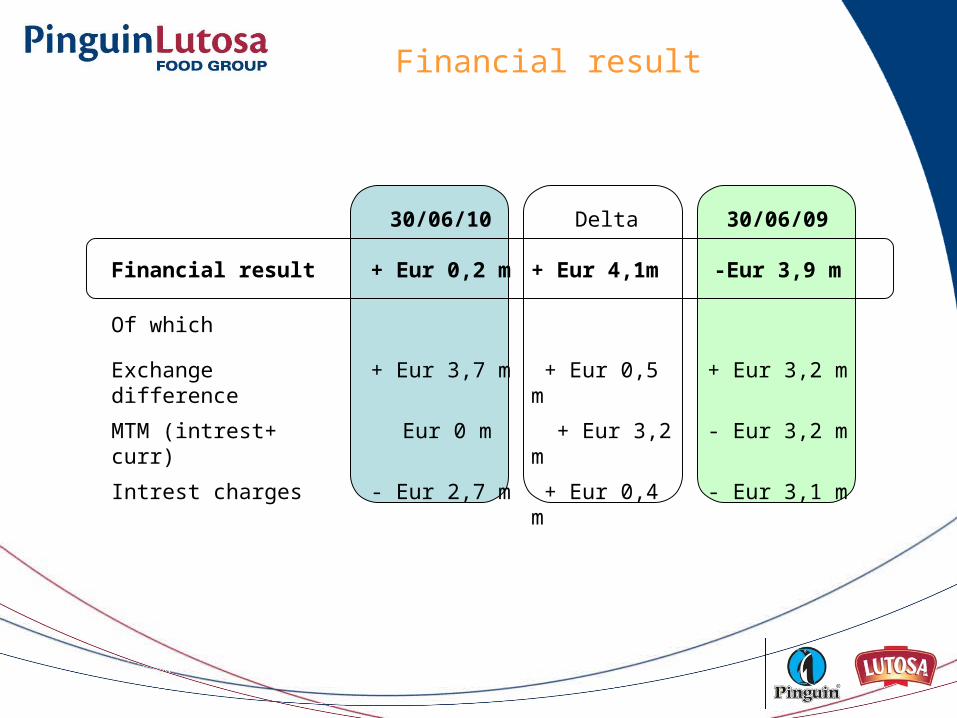

Financial result + Eur 0,2 m + Eur 4,1m -Eur 3,9 m

Of which

Exchange difference + Eur 3,7 m + Eur 0,5 m + Eur 3,2 m

MTM (intrest+ curr) Eur 0 m + Eur 3,2 m - Eur 3,2 m

Intrest charges - Eur 2,7 m + Eur 0,4 m - Eur 3,1 m

Financial result

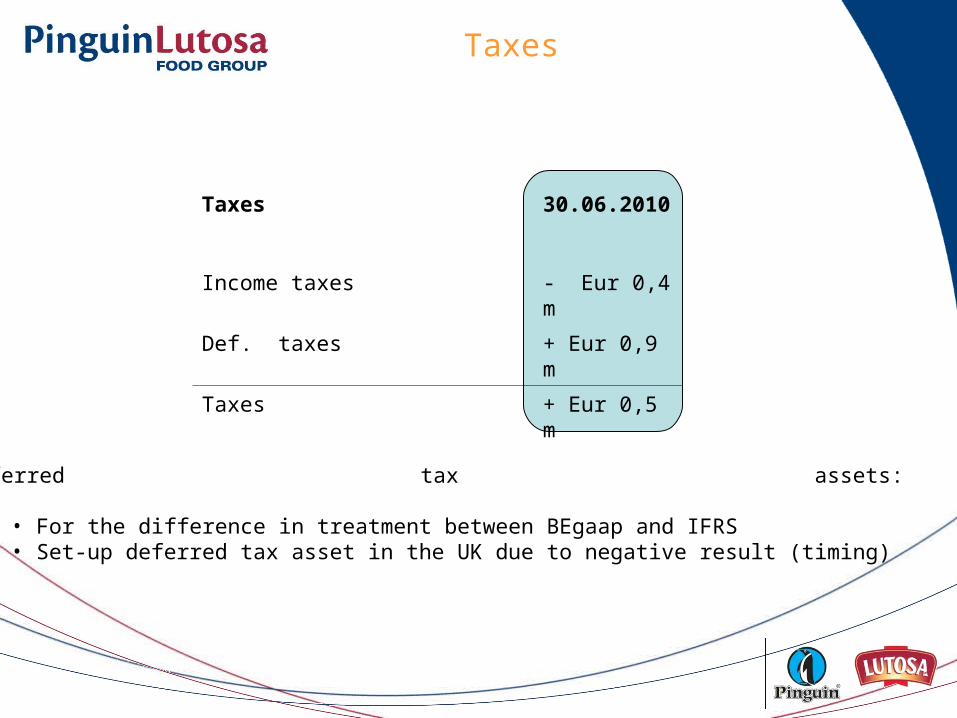

Taxes 30.06.2010

Income taxes - Eur 0,4 m

Def. taxes + Eur 0,9 m

Taxes + Eur 0,5 m

Taxes

Deferred tax assets:

• For the difference in treatment between BEgaap and IFRS • Set-up deferred tax asset in the UK due to negative result (timing)

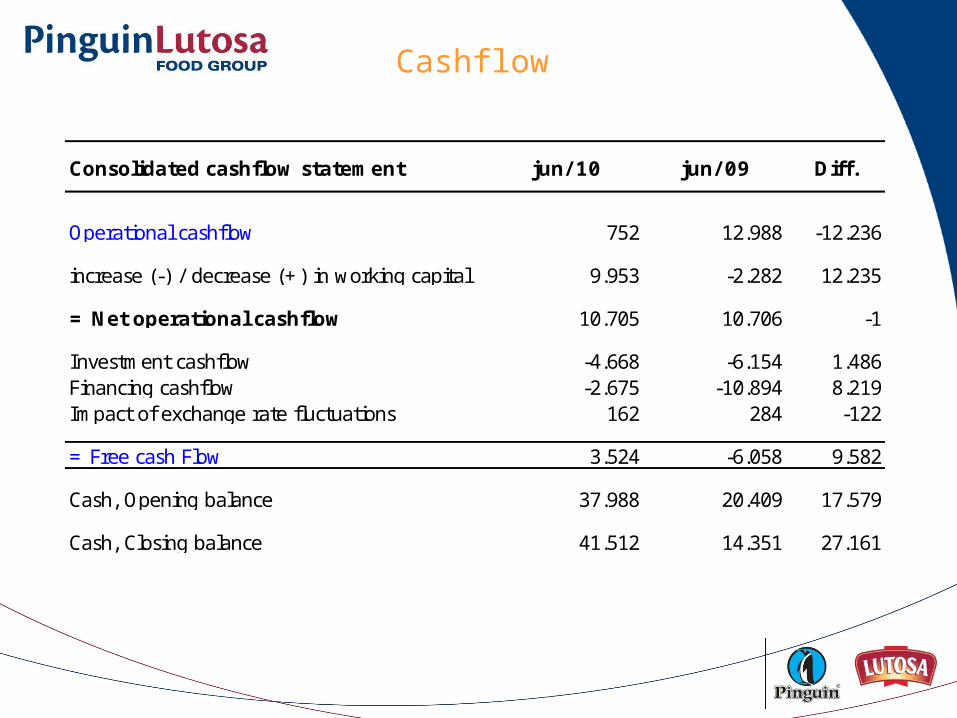

Cashflow

Consolidated cashflow statement jun/ 10 jun/ 09 Diff.

Operational cashflow 752 12.988 -12.236

increase (-) / decrease (+) in working capital 9.953 -2.282 12.235

= Net operational cashflow 10.705 10.706 -1

Investment cashflow -4.668 -6.154 1.486Financing cashflow -2.675 -10.894 8.219Impact of exchange rate fluctuations 162 284 -122

= Free cash Flow 3.524 -6.058 9.582

Cash, Opening balance 37.988 20.409 17.579

Cash, Closing balance 41.512 14.351 27.161

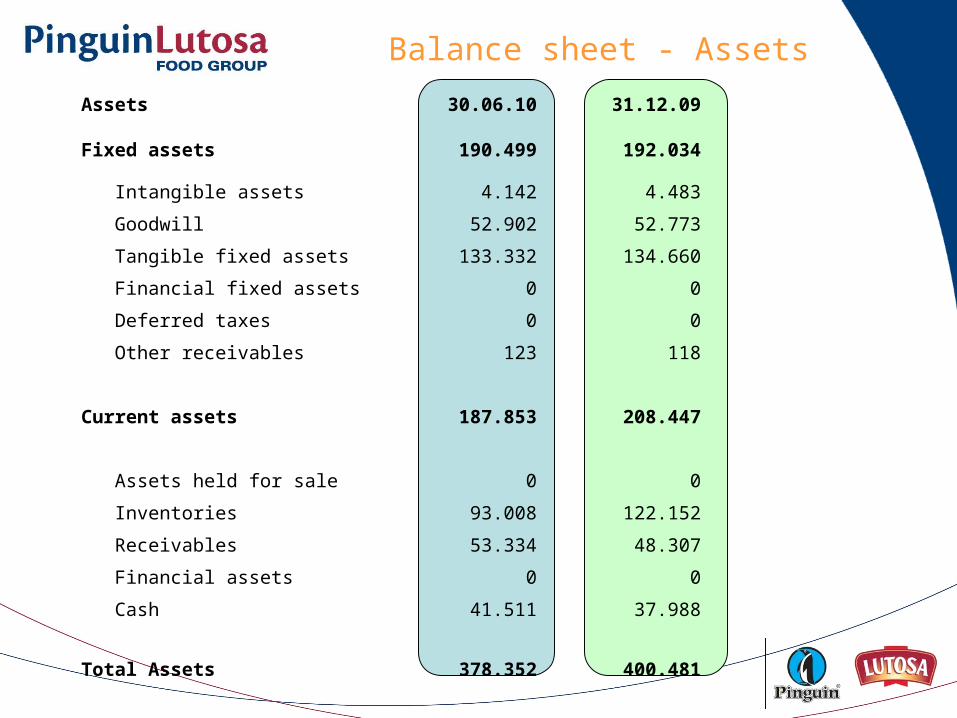

Balance sheet - Assets

Assets 30.06.10 31.12.09

Fixed assets 190.499 192.034

Intangible assets 4.142 4.483

Goodwill 52.902 52.773

Tangible fixed assets 133.332 134.660

Financial fixed assets 0 0

Deferred taxes 0 0

Other receivables 123 118

Current assets 187.853 208.447

Assets held for sale 0 0

Inventories 93.008 122.152

Receivables 53.334 48.307

Financial assets 0 0

Cash 41.511 37.988

Total Assets 378.352 400.481

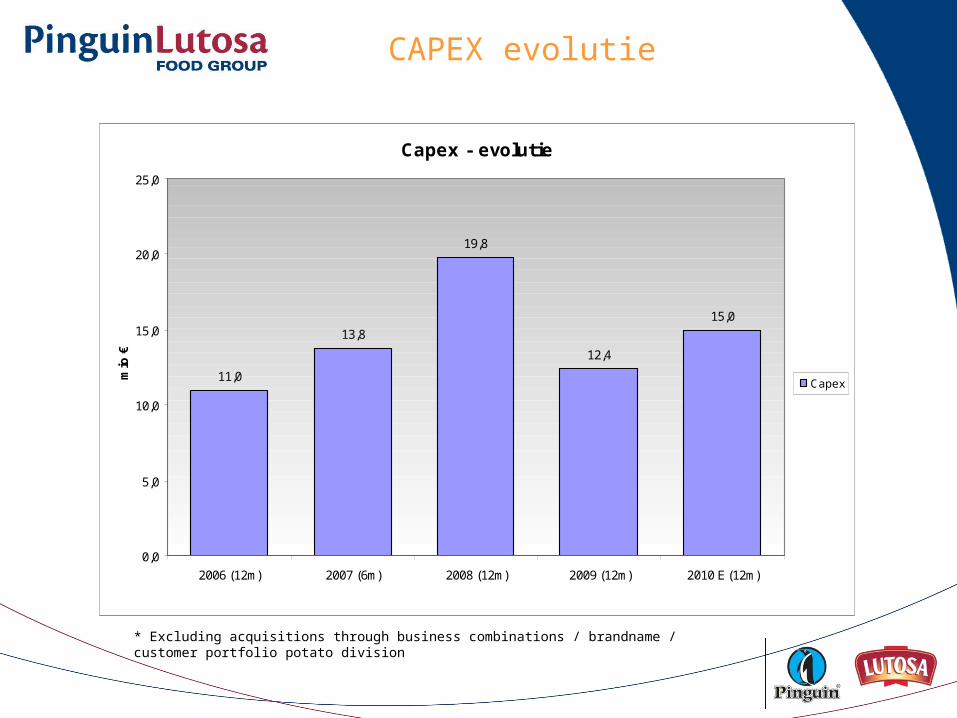

CAPEX evolutie

Capex - evolutie

11,0

13,8

19,8

12,4

15,0

0,0

5,0

10,0

15,0

20,0

25,0

2006 (12m) 2007 (6m) 2008 (12m) 2009 (12m) 2010 E (12m)

mio

€

Capex

* Excluding acquisitions through business combinations / brandname / customer portfolio potato division

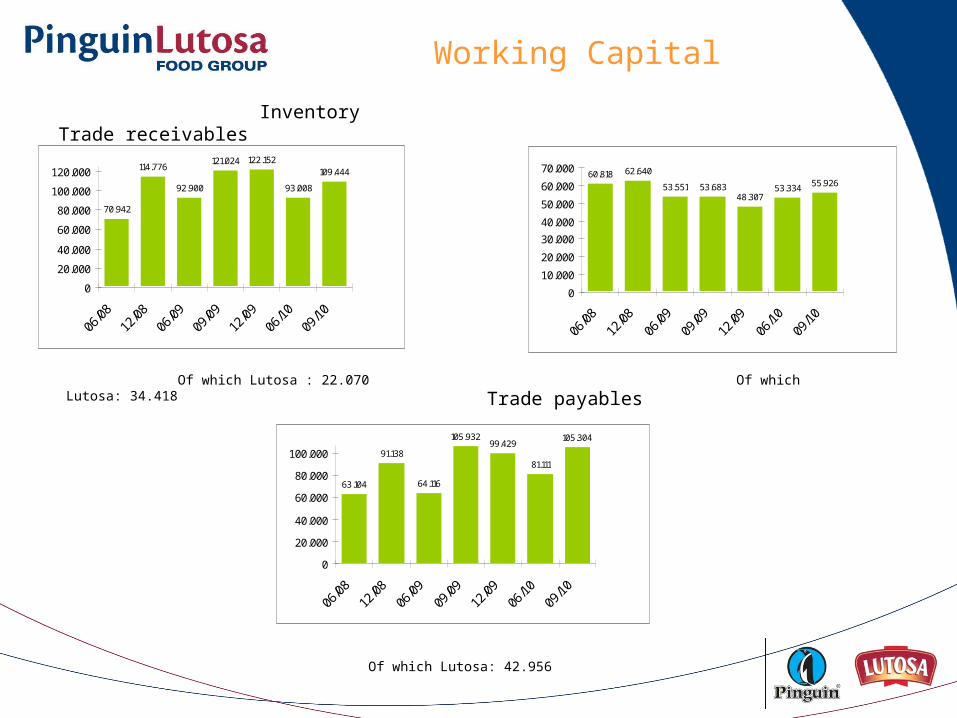

Inventory Trade receivables

Of which Lutosa : 22.070 Of which Lutosa: 34.418

Of which Lutosa: 42.956

Working Capital

Trade payables

70.942

114.776

92.900

121.024 122.152

93.008

109.444

0

20.000

40.000

60.000

80.000

100.000

120.000

06/08

12/08

06/09

09/09

12/09

06/10

09/10

60.818 62.640

53.551 53.68348.307

53.334 55.926

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

06/08

12/08

06/09

09/09

12/09

06/10

09/10

63.104

91.138

64.116

105.93299.429

81.111

105.304

0

20.000

40.000

60.000

80.000

100.000

06/08

12/08

06/09

09/09

12/09

06/10

09/10

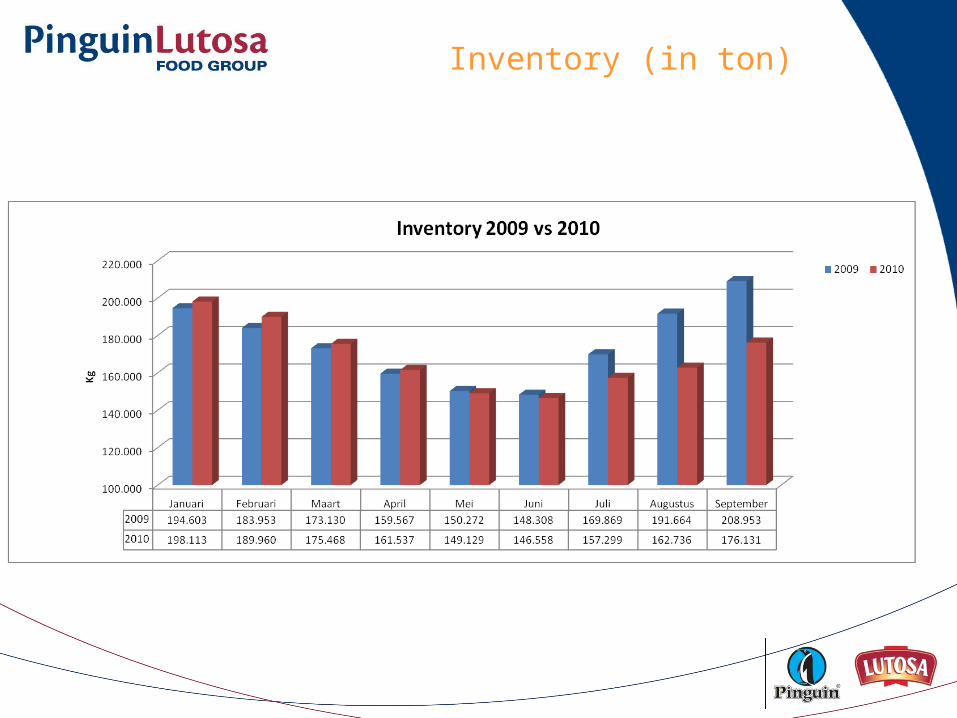

Inventory (in ton)

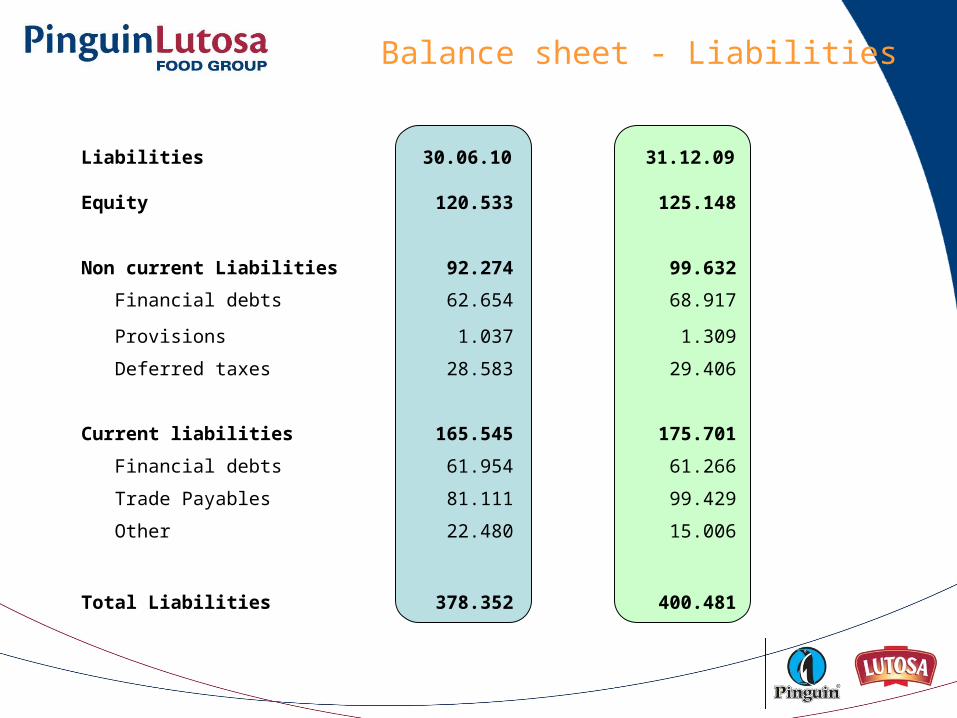

Liabilities 30.06.10 31.12.09

Equity 120.533 125.148

Non current Liabilities 92.274 99.632

Financial debts 62.654 68.917

Provisions 1.037 1.309

Deferred taxes 28.583 29.406

Current liabilities 165.545 175.701

Financial debts 61.954 61.266

Trade Payables 81.111 99.429

Other 22.480 15.006

Total Liabilities 378.352 400.481

Balance sheet - Liabilities

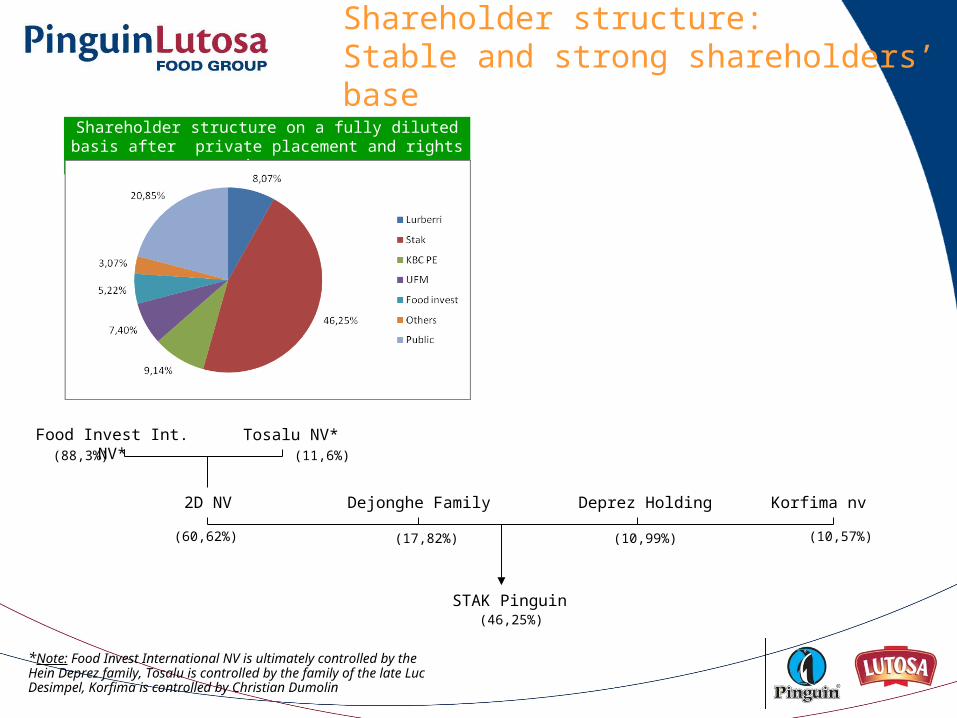

Shareholder structure:Stable and strong shareholders’ base

*Note: Food Invest International NV is ultimately controlled by the Hein Deprez family, Tosalu is controlled by the family of the late Luc Desimpel, Korfima is controlled by Christian Dumolin

Food Invest Int. NV* Tosalu NV*

2D NV Dejonghe Family

(88,3%) (11,6%)

(60,62%) (17,82%)

STAK Pinguin

Shareholder structure on a fully diluted basis after private placement and rights issue

Deprez Holding Korfima nv

(10,99%) (10,57%)

(46,25%)

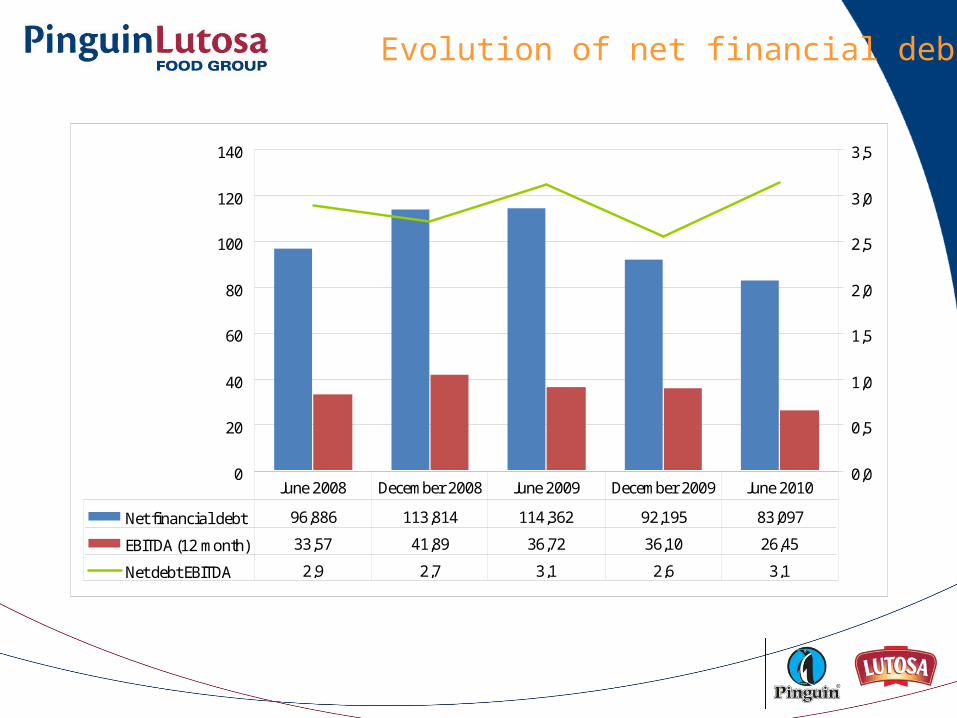

Evolution of net financial debt

0

20

40

60

80

100

120

140

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

Net financial debt 96,886 113,814 114,362 92,195 83,097

EBITDA (12 month) 33,57 41,89 36,72 36,10 26,45

Net debt EBITDA 2,9 2,7 3,1 2,6 3,1

June 2008 December 2008 June 2009 December 2009 June 2010

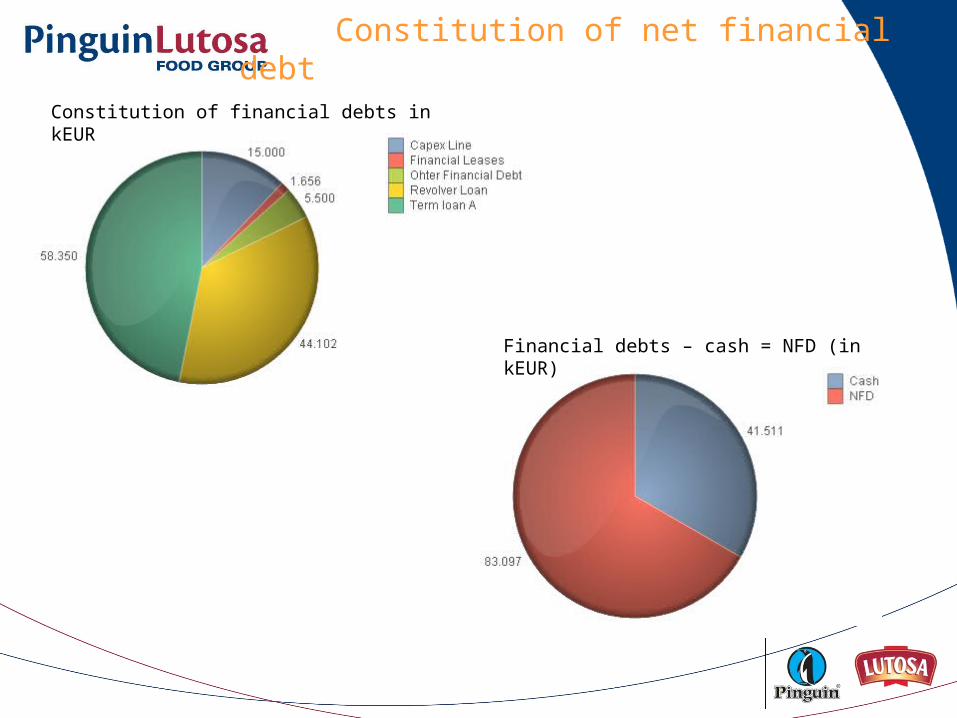

Constitution of net financial debt

Constitution of financial debts in kEUR

Financial debts – cash = NFD (in kEUR)

Cecab (D2f)Cecab (D2f)Herwig Dejonghe, CEOHerwig Dejonghe, CEO

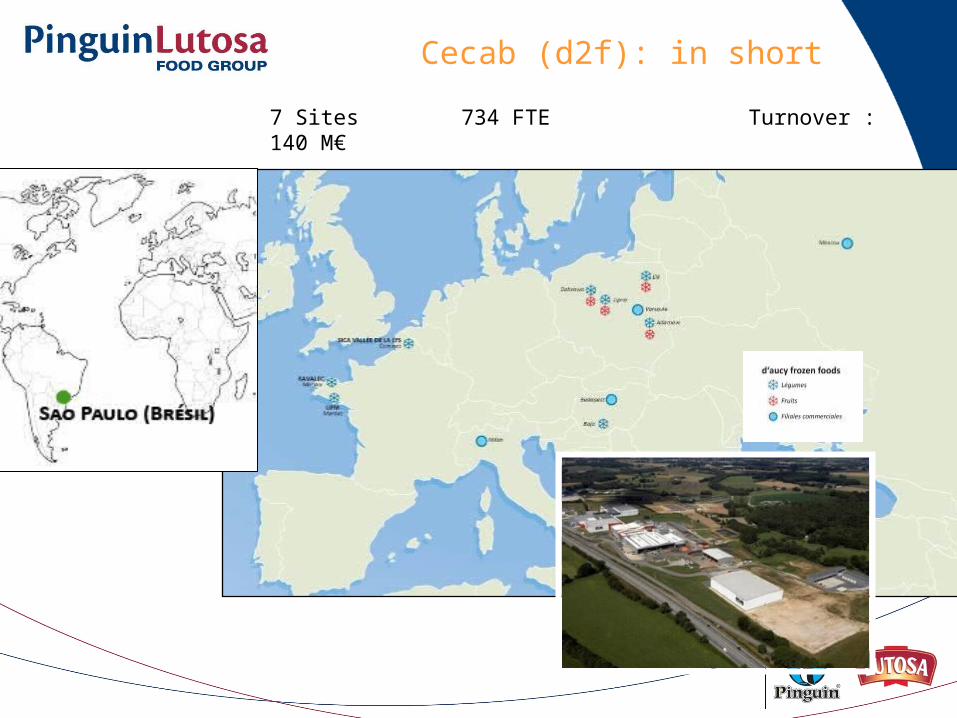

Cecab (d2f): in short

7 Sites 734 FTE Turnover : 140 M€

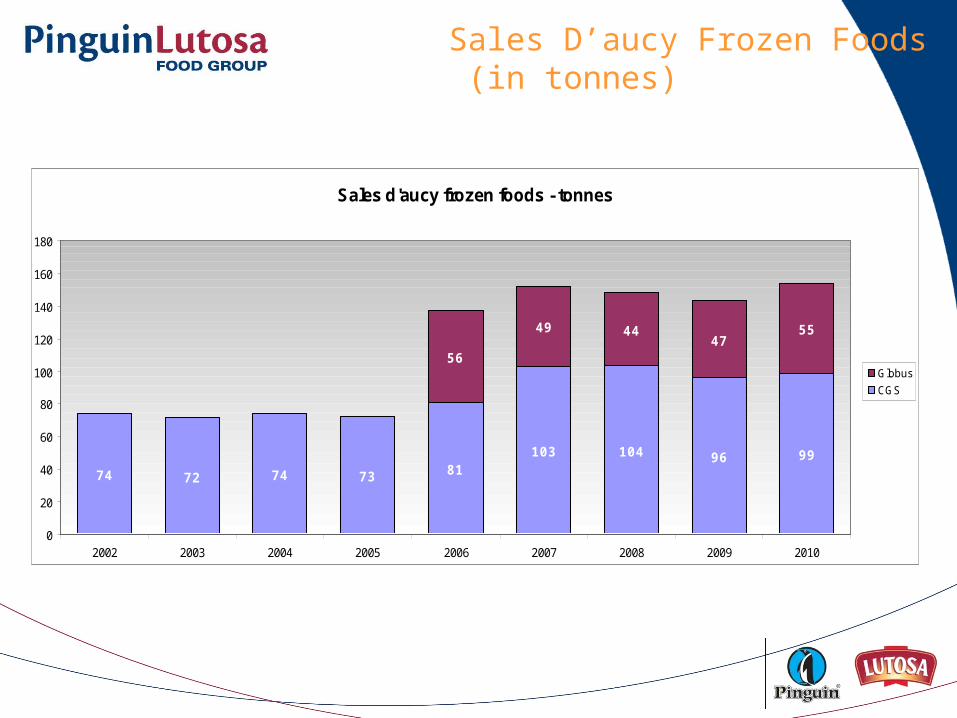

Sales D’aucy Frozen Foods (in tonnes)

Sales d'aucy frozen foods - tonnes

74 72 74 73 81103 104 96 99

56

49 4447

55

0

20

40

60

80

100

120

140

160

180

2002 2003 2004 2005 2006 2007 2008 2009 2010

Globus

CGS

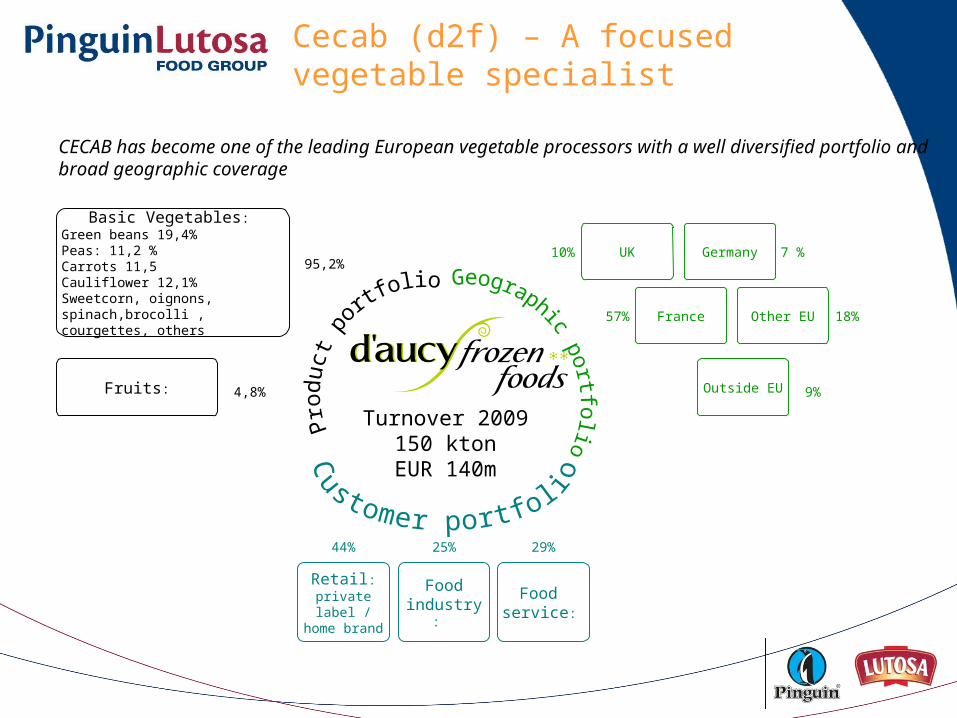

Cecab (d2f) – A focused vegetable specialist

CECAB has become one of the leading European vegetable processors with a well diversified portfolio and broad geographic coverage

Turnover 2009150 kton

EUR 140m

25%44% 29%

10%

57% France

UK Germany

Other EU

Outside EU

7 %

18%

9%

95,2%

4,8%

Basic Vegetables: Green beans 19,4%Peas: 11,2 %Carrots 11,5Cauliflower 12,1%Sweetcorn, oignons, spinach,brocolli , courgettes, others

Fruits:

Food industry:

Retail: private label / home brand

Food service:

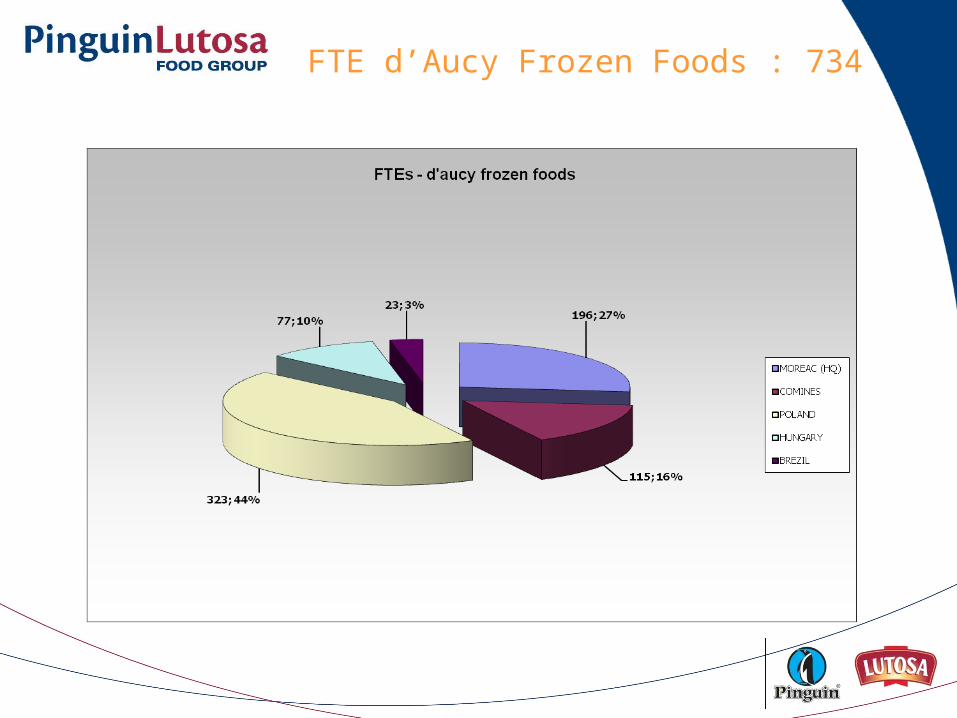

FTE d’Aucy Frozen Foods : 734

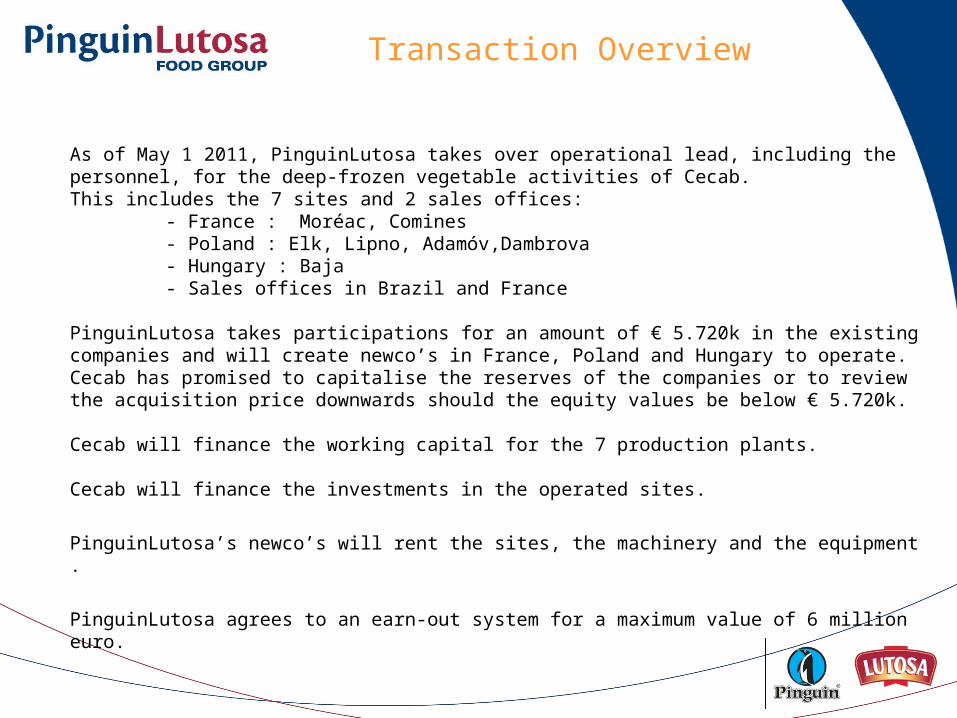

Transaction Overview

As of May 1 2011, PinguinLutosa takes over operational lead, including the personnel, for the deep-frozen vegetable activities of Cecab.This includes the 7 sites and 2 sales offices:

- France : Moréac, Comines- Poland : Elk, Lipno, Adamóv,Dambrova- Hungary : Baja - Sales offices in Brazil and France

PinguinLutosa takes participations for an amount of € 5.720k in the existing companies and will create newco’s in France, Poland and Hungary to operate.Cecab has promised to capitalise the reserves of the companies or to review the acquisition price downwards should the equity values be below € 5.720k.

Cecab will finance the working capital for the 7 production plants.

Cecab will finance the investments in the operated sites.

PinguinLutosa’s newco’s will rent the sites, the machinery and the equipment .

PinguinLutosa agrees to an earn-out system for a maximum value of 6 million euro.

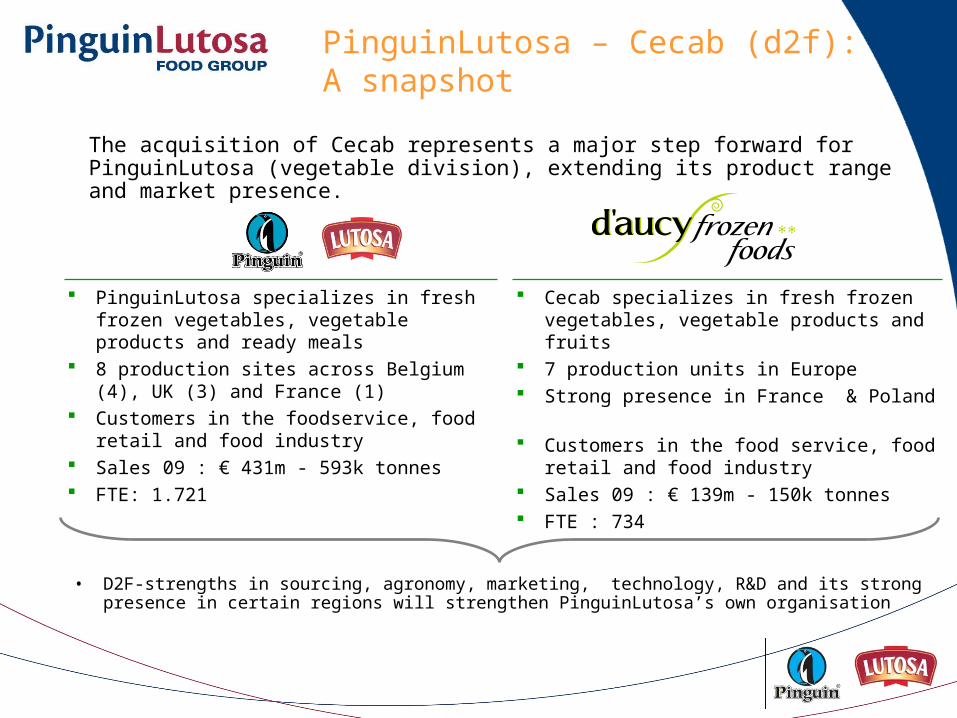

PinguinLutosa – Cecab (d2f): A snapshot

• D2F-strengths in sourcing, agronomy, marketing, technology, R&D and its strong presence in certain regions will strengthen PinguinLutosa’s own organisation

PinguinLutosa specializes in fresh frozen vegetables, vegetable products and ready meals

8 production sites across Belgium (4), UK (3) and France (1)

Customers in the foodservice, food retail and food industry

Sales 09 : € 431m - 593k tonnes FTE: 1.721

Cecab specializes in fresh frozen vegetables, vegetable products and fruits

7 production units in Europe Strong presence in France & Poland

Customers in the food service, food retail and food industry

Sales 09 : € 139m - 150k tonnes FTE : 734

The acquisition of Cecab represents a major step forward for PinguinLutosa (vegetable division), extending its product range and market presence.

Combination PinguinLutosa/Cecab (d2f):makes perfect sense

Better sourcing & closer cooperation with farmers.

Increased purchasing power for other raw materials & services.

Exchange of know-how and best-practice (production, technology, logistics & warehousing and agronomy).

Sales

Purchase and Production

Geographic spread: PinguinLutosa has a better position in the British and German markets who are vital for the Polish and Hungarian operations. Poland and Hungary will be the gateway for the further development of the existing and new product range of PinguinLutosa.

In France, the principal region and activity center of D2F, PinguinLutosa’s presence is rather weak.

Close cooperation possible in Spain, Brazil and Italy.

Combination creates a more complete product offering and improves one-stop shopping with customers.

Cross-selling opportunities will be exploited through leverage of commercial network.

Combination PinguinLutosa/Cecab(d2f) makes perfect sense

Economies of scale.

Dedicated production.

Optimized capacity and investments.

Spread of climatological risks over best production regions. This will enhance our customer service to our industry customers which want security and stability.

PinguinLutosa is considered to be high class in production & efficiency whereas Cecab is considered to be top class in agronomy.

Product range

Optimisation of production and

logistics

The product range of PinguinLutosa is bigger including aromatic herbs and ready meals and potatoes whereas D2F has the know-how and the technology of « légumes cuits » and fruits.

Key investments: highlights

• 2 leading players in deep-frozen vegetables join forces.

• Attractive market outlook.

• Experienced management team.

• PinguinLutosa and d’Aucy frozen vegetable customer portfolios are extremely complementary, only 2% is equal.

• We get a top 3 position in the French deep-frozen vegetable market.

• The presence of processing facilities in Eastern Europe opens new markets.

• The support of Cecab as a partner is a unique strength for our working capital needs and further investments in these countries.

• As Cecab was not used to manage Business Units outside France, the quick wins are present and the potential for better results on medium are high.

• The timing of the deal as to start at 1st of may 2011 is perfect as we are at the start of a new production season.

Outlook MarketsHerwig Dejonghe,

CEO

Outlook markets

• Outlook potato markets:

– Potato markets (raw material) are definitely short and prices will continue to increase. We were aware of this risk and have mainly short-term price agreements with customers so we can adjust our sales prices for higher costs of raw material.

– Consumer demand will remain high.

• Outlook vegetable markets:

– Stocks of most frozen vegetables are reducing and expect to hit historical low levels by end of June 2011.

– Competitors in Germany, Poland and Spain get in to problems because of bad results due to the low market price level and may stop deliveries to customers.

– High wheat prices since August put pressure on negotiations for the new season 2011 to increase prices for comparable crops like peas. Increase of 10 to 15% expected for peas and 25% for sweet corn.

– Consumer demand expected to be high due to low availability of fresh vegetables in retail.

Q&A

New Corporate Website

www.pinguinlutosa.com