Embed Size (px)

Citation preview

October 2011

T H E U S E O F F I N A N C I A L D E R I V A T I V E S I N L A T I N A M E R I C A

S T

R I C

T L

Y

P R

I V

A T

E

A N

D

C O

N F

I D

E N

T I A

L

Etienne Lacroix

(1) 212 – 834 - 2260

Introduction

This presentation will attempt to illustrate the evolution of the usage of financial derivatives in global markets and in select

Latin American countries (when data is available)

Given that they represent the majority of the traded volume globally, we will concentrate in three of the most active

derivatives markets: FX, Interest Rates, and Commodities.

We will delve into what are the reasons driving companies and countries to enter into financial derivative transactions and

what the evolution in the use of Financial Derivatives has been in the region

We will conclude by outlining our prognostics with regards to the future of the industry and our opinions on possible

developments

1 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

Agenda

2

Derivatives - What Are We Talking About ?

2

The Use of Financial Derivatives 5

Implementing Risk Management Policy 21

Annex A: Basic Derivative Product Descriptions 31

Annex B: JPM Commodity Capabilities 36

T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

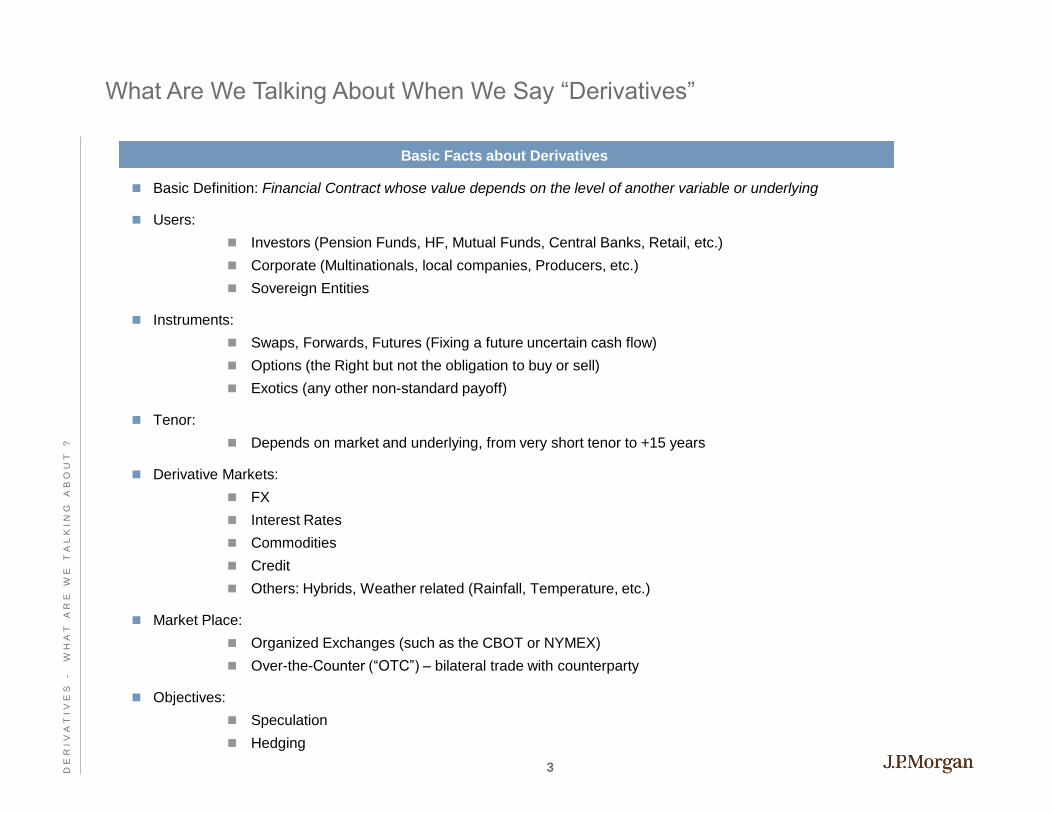

What Are We Talking About When We Say “Derivatives”

Basic Facts about Derivatives

Basic Definition: Financial Contract whose value depends on the level of another variable or underlying

Users:

Investors (Pension Funds, HF, Mutual Funds, Central Banks, Retail, etc.)

Corporate (Multinationals, local companies, Producers, etc.)

Sovereign Entities

Instruments:

Swaps, Forwards, Futures (Fixing a future uncertain cash flow)

Options (the Right but not the obligation to buy or sell)

Exotics (any other non-standard payoff)

Tenor:

Depends on market and underlying, from very short tenor to +15 years

Derivative Markets:

FX

Interest Rates

Commodities

Credit

Others: Hybrids, Weather related (Rainfall, Temperature, etc.)

Market Place:

Organized Exchanges (such as the CBOT or NYMEX)

Over-the-Counter (“OTC”) – bilateral trade with counterparty

Objectives:

Speculation

Hedging

3 D E

R I V

A T

I V

E S

-

W H

A T

A

R E

W

E

T A

L K

I N

G

A B

O U

T ?

Basic Overview of Financial Derivatives

Fixing Future Cash Flows through Futures, Forwards or Swaps

Futures, Swaps and Forwards are financial contracts that allow the user to fix an uncertain future cash flow

Why uncertain ? Because the future price level is not known yet and will depend on many unforeseeable factors. Examples:

Libor rate in 180 days or in 5.2 years

Imports on March 20 2012, denominated in EUR or JOY

Copper exports to happen during 2H12

10 Year Treasury Level relevant for a new bond issuance in 2 months time

By using Forwards or Swaps these future uncertain cash flows can be “fixed”, thus fully known in advance

Benefits vs. Risks:

Price Certainty versus Opportunity Cost

Other risks:

Legal risks

Operational risk (execution, transfers, etc)

Counterparty risk, etc. (bankruptcy of counterparty)

Financial Options

In contrast to Swaps (or Forwards), options provide an asymmetric payoff (downside and upside are not similar)

For the right to participate in a certain price movement, the buyer has to pay a premium in order to avoid being exposed to

the opposite price movement

By combining different option types (Calls, Puts) different profiles could be obtained, depending on needs, views, etc.

Exotics (non-standard payoffs very common)

4 D E

R I V

A T

I V

E S

-

W H

A T

A

R E

W

E

T A

L K

I N

G

A B

O U

T ?

Agenda

5

The Use of Financial Derivatives

5

Derivatives - What Are We Talking About ? 2

Implementing Risk Management Policy 21

Annex A: Basic Derivative Product Descriptions 31

Annex B: JPM Commodity Capabilities 36

T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

Derivative Use across Sectors is Very High for Fortune 500 Companies Worldwide

Source: ISDA News Release April 23, 2009

6 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Firms are Increasingly Using Derivatives Markets to Hedge Financial Risks

Commentary

Source: 2009 ISDA survey for Global Fortune 500 companies

Current usage of derivatives

Do not use

derivatives

6%

Use derivatives

94%

Historically, a significant number of large companies have

been utilizing financial instruments for risk management

purposes

Based on an ISDA survey conducted in 2009, 94% of

top large companies currently use derivatives (up from

92% in 2003)

Over the course of the last 5 years, the total outstanding

notional amount has increased significantly

Mix from swaps to options has increased of late with a

drop in option volatility

85% 84%

96%

72%

86% 85%92%

88%

70%

81%

94%

80%86%

75%

86%92%

79%

39%

63%

8%

37% 35%

15%

83%

Basic materials Consumer goods Financial Healthcare Industrial goods Services Technology Utilities

% Using FX % Using interest rate % Using commodity

Source: ISDA news release published on April 23, 2009

Current derivative usage by the world’s largest companies

7 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Peer Max Tenor Disclosed Commodities Exposures Hedged

Barrick 60 months Interest Rate Swaps, FX Forwards (AUD, CAD, CLP, EUR, PGK), Base Metals Zero Cost Options Collars

(Copper), Energy Swaps (Diesel, Propane, Natural Gas, Electricity)

Goldcorp 6-12 months FX Forwards & Options (CAD, MXN), Base Metals Swaps & Zero Cost Options Collars (Copper, Zinc, Lead),

Energy Swaps (Heating Oil)

Newmont 60 months FX Forwards (AUD, NZD, IDR), Energy Swaps (Diesel), Interest Rate Swaps

Kinross 36 months Precious Metals Forwards & Options (Gold, Silver), FX Forwards (BRL, CLP, RUB, CAD, EUR), Energy

Swaps (Crude Oil)

Agnico-Eagle 12 months FX Forwards (CAD), Base Metals Zero Cost Options Collars (Zinc)

IAMGOLD 36 months Precious Metals Zero Cost Options Collars (Gold), FX Options & Forwards (CAD, EUR), Energy Options and

Swaps (Heating Oil), Base Metals Options (Aluminum)

Hecla Mining 36 months Base Metals Swaps (Zinc, Lead)

Jaguar Mining 6 months FX Forwards (BRL), Precious Metals Zero Cost Options Collars (Gold)

Capstone

Mining

48 months Base Metals Swaps (Copper, Lead, Zinc)

Breakwater

Resources

12 months Base Metals Options (Copper, Lead, Zinc), Precious Metals Options (Gold, Silver)

Century

Aluminum

12 months Energy Swaps (Natural Gas), Base Metals Swaps & Zero Cost Options Collars (Aluminum)

Alpha Natural

Resources

12 months Energy Swaps & Options (Diesel, Natural Gas), Interest Rate Swaps

Disclosed Hedging of North American Mining Companies

Disclosed Hedging of North American Mining Companies

Sources: Third Quarter 2010 Financial Reports of each company 8 T

H E

U

S E

O

F

F I N

A N

C I A

L

D E

R I V

A T

I V

E S

Size of Foreign Exchange (FX) OTC Derivatives Market Worldwide Continuous to Grow

BIS 2010 Data

In the past 10 years the global OTC FX market has more than doubled.

While the Spot and Swaps markets still represent the bulk of the trading volume, there has been a significant increase in the

Options and Forwards markets as well.

Swaps volume has been greater than spot volume every year for the past 12 years, showing how the usage of derivatives is

becoming a central part of business transactions and gaining traction as a solution to mitigate risk exposure.

Now, let’s compare how Latin American markets are tracking the rest of the world…

1998 2001 2004 2007 2010

Spot 568 386 631 1,005 1,490

Forwards 128 130 209 362 475

FX Swaps 744 663 975 1,745 1,808

Options 87 60 119 212 207

Total 1,527 1,239 1,934 3,324 3,980

Source:BIS 2010

OTC FX Markets Worldwide (Billions US$/Day)

9 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

ISDA Shows Granular Impact of Past Crisis in the Derivative Use, by Category

Source: ISDA Market Survey 2010

10 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Where are FX Derivatives Traded?

For financial derivatives, transaction costs tend to lower when volume increases, this in turn further increases the traded

volume for that asset, creating a virtuous cycle of volume and liquidity.

As Latin America has historically not been a center for financial derivative transactions, it has failed to gain traction as a

mayor powerhouse in total volume traded.

As it can be observed in the pie chart below, geographical areas with far lesser economic size (e.g. Australia, Switzerland

and Hong Kong) have significant higher proportions of FX turnover than Latin America.

11 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Global Interest Rate Derivatives Use by Instrument Shows Strong Preference to

Swaps

Source: BIS, Triennial Central Bank Survey, April 2010

12 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

The Use of Derivatives has Increased Rapidly in the Last 15 years: Summary

14 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

The Use of Derivatives has Increased Rapidly in the Last 15 years: Summary

15 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

ISDA 2010 End User Survey Shows Strong Use of FX, Interest Rate and Commodities

During July and August 2010, ISDA conducted a survey of over-the-counter (OTC) derivatives end-users, including non-

financial corporations, asset managers and other financial institutions295 respondents from North America and Europe who use

OTC derivatives participated in the survey. Of these:80% or 234 used interest rate swaps (IRS)

59% or 174 used currency/FX swaps,

27% or 80 used credit default swaps (CDS),

25% or 74 used equity swaps and

32% or 94 used commodity/energy swaps.

Respondents were asked their opinions only on those OTC derivatives that they said they have used

On a 1 to 5 scale, 62% rate IRS price competitiveness at a 4 or 5

Only 10% of IRS end-users rate it at a 1 or 2

Electronic Trading: A majority of those surveyed (77%) believe electronic trading of IRS is beneficial

The majority of surveyed IRS end-users give high remarks to the current level of pre-trade price transparency

71% of IRS end-users rank it same as or better than FX. 69% rank it same as or better than equities. 83% rank it equal to or

better than corporate bonds. 87% rank it same as or better than ABS

Source: ISDA End-User Survey: Interest Rate Swaps, October 2010

13 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Size of OTC Derivatives in Latin America

Latin American derivatives markets have almost tripled in size in the past 12 years…

… but they still represent less than 1% of the global market for derivatives

In fact, Latin America share of the world’s transactions hasn’t changed significantly in the last 12 years.

FX Rates Total

1998 2001 2004 2007 2010 1998 2001 2004 2007 2010 1998 2001 2004 2007 2010

Argentina 2.2 0.0 0.7 1.1 1.6 0.0 0.0 0.0 0.0 0.0 2.2 0.0 0.7 1.1 1.6

Brazil 5.1 5.5 3.8 5.8 14.2 0.0 0.3 0.9 0.1 7.5 5.1 5.8 4.7 5.9 21.7

Chile 1.3 2.3 2.5 4.0 5.5 0.0 0.0 0.0 0.0 0.2 1.3 2.3 2.5 4.0 5.7

Colombia 0.0 0.4 0.8 1.9 2.8 0.0 0.0 0.0 0.0 0.0 0.0 0.4 0.8 1.9 2.8

Mexico 8.7 8.6 15.3 15.3 17.0 0.2 0.4 1.4 2.9 1.4 8.9 9.0 16.7 18.2 18.4

Peru 0.0 0.2 0.3 0.8 1.4 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.3 0.8 1.4

Total Latam 17.3 17.0 23.4 28.9 42.5 0.2 0.7 2.3 3.0 9.1 17.5 17.7 25.7 31.9 51.6

Total World 2,099 1,692 2,609 4,281 5,056 344 676 1,331 2,173 2,698 2,443 2,368 3,940 6,454 7,754

Source:BIS 2010

OTC Derivatives Markets in Latin America (Billions US$/Day)

16 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Mexico FX Market by Product

Source:BIS 2010

Mexican OTC FX Market

17 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Colombia FX Market

Source:BIS 2010

Colombia OTC FX Market by Product Colombia OTC FX Market por plazo

18 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Chile: Policy Makers Have Expressed Continuous Interest in the Development of

Local Derivative Markets

Source: IMF Working paper

19 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Macro Hedging on Country Level has Experienced Particular Interest During the

Last Decade in Latin America

20 T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

Agenda

21

Implementing Risk Management Policy

21

Derivatives - What Are We Talking About ? 2

The Use of Financial Derivatives 5

Annex A: Basic Derivative Product Descriptions 31

Annex B: JPM Commodity Capabilities 36

T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

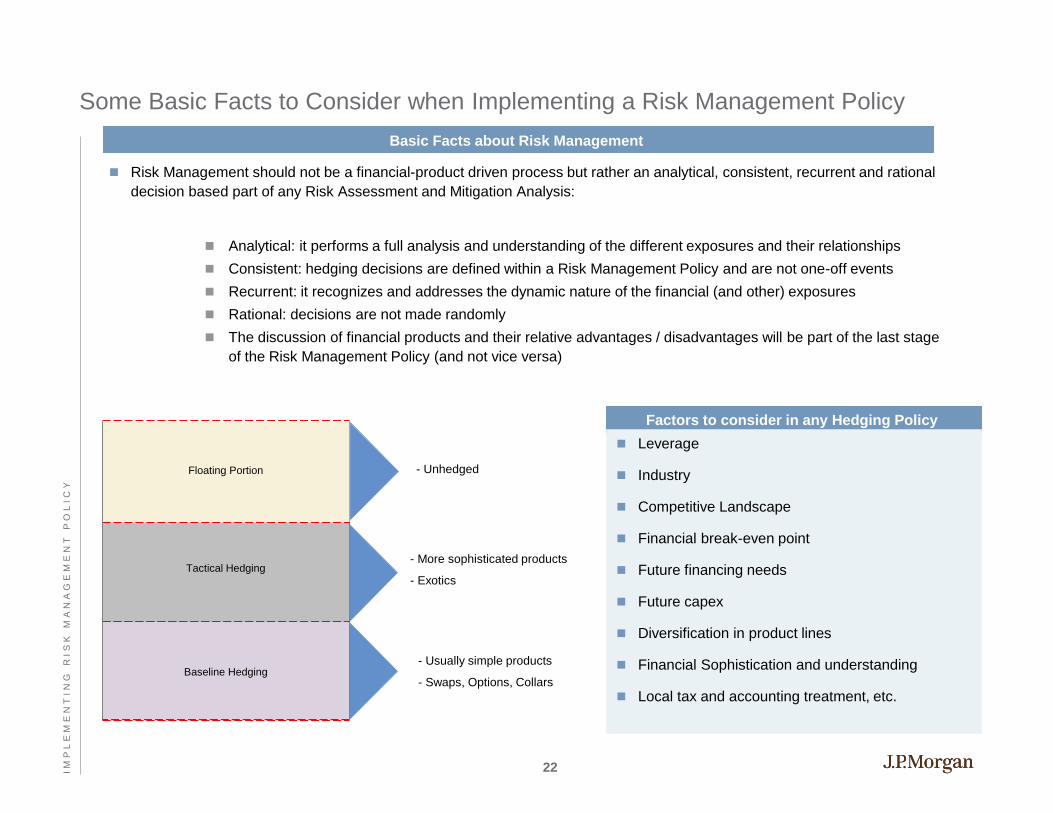

Some Basic Facts to Consider when Implementing a Risk Management Policy

Risk Management should not be a financial-product driven process but rather an analytical, consistent, recurrent and rational

decision based part of any Risk Assessment and Mitigation Analysis:

Analytical: it performs a full analysis and understanding of the different exposures and their relationships

Consistent: hedging decisions are defined within a Risk Management Policy and are not one-off events

Recurrent: it recognizes and addresses the dynamic nature of the financial (and other) exposures

Rational: decisions are not made randomly

The discussion of financial products and their relative advantages / disadvantages will be part of the last stage

of the Risk Management Policy (and not vice versa)

Tactical Hedging

Baseline Hedging

Floating Portion Floating Portion - Unhedged

- More sophisticated products

- Exotics

- Usually simple products

- Swaps, Options, Collars

Basic Facts about Risk Management

Factors to consider in any Hedging Policy

Leverage

Industry

Competitive Landscape

Financial break-even point

Future financing needs

Future capex

Diversification in product lines

Financial Sophistication and understanding

Local tax and accounting treatment, etc.

22 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

R I

S K

M

A N

A G

E M

E N

T P

O L

I C

Y

Decision to

hedge

Key drivers of the Hedging Decision

Business

viability

risk?

Hedge

Are competitors

hedging financial

risks?

Meaningful

impact to value? Hedge

Hedge

Are any

exposures at

opportunistic

levels to hedge?

Hedge Do not hedge

Yes

Yes

Yes

Yes

No

No

No

No

23 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

$30

$80

$130

Jan-2007 Apr-2007 Jul-2007 Oct-2007 Jan-2008 Apr-2008 Jul-2008 Oct-2008 Jan-2009 Apr-2009 Jul-2009

Pri

ce

( $

/ b

bl)

WTI Crude Oil Price Performance vs. 2 – Standard Deviation Risk Cone (Assuming Jan 2, 2008 Market Data)

Market Moves Greater than Two-Standard Deviations are not Unseen Events in

Commodity Markets – In Fact, They Have Occurred Repeatedly in the Recent Past

2 - Standard Deviation

Potential Move

WTI

Within a 10-month period,

WTI had a +2 and -2 standard

deviation move

Source: JPMorgan

24 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

$1.4

$1.6

$1.8

$2.0

$2.2

$2.4

$2.6

Jan-

2006

Apr

-200

6

Jul-2

006

Oct

-200

6

Jan-

2007

Apr

-200

7

Jul-2

007

Oct

-200

7

Jan-

2008

Apr

-200

8

Jul-2

008

Oct

-200

8

Jan-

2009

Apr

-200

9

Jul-2

009

Oct

-200

9

Jan-

2010

Apr

-201

0

Jul-2

010

Oct

-201

0

Jan-

2011

Apr

-201

1

Jul-2

011

Ex

ch

an

ge

Ra

te U

SD

BR

L)

Exchange rate USDBRL vs. 2 – Standard Deviation Risk Cone (Assuming Jan 2, 2007 Market Data)

The Same is True for FX and Interest Rates Markets

2 - Standard Deviation

Potential Move

USDBRL

Within a 10-month period,

BRL had a +2 and -2 standard

deviation move

Source: JPMorgan

25 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

Analysts Forecasting Commodity Prices Have Shown Low Accuracy in the

Recent Past

Monthly crude oil price forecast published by a well-known international consulting firm has shown low accuracy when

compared versus ex-post (real) prices, not only for long forecast horizons (12-18 months) but also in the short term (1-3

month period). Based on monthly published reports from 2002 - 2010

To base financial decisions on published forecasts could potentially become a dangerous proposal given that historically

financial analysts have exhibited low predictive powers, not only in Commodities but across different asset classes

-120.00%

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Source: JPMorgan

Month out

Perc

enta

ge F

ore

cast

Err

or

25% Percentile

75% Percentile

Maximum

Minimum

26 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q (current

quarter)

2Q 3Q 4Q 5Q 6Q

Hedge: Rolling and Layering as a Consistent Way to Lower Overall Cash Flow Volatility

J.P. Morgan recommends a policy that mandates discipline in hedging forecasted cash flows. The policy could also allow for

a measure of discretion within that discipline

Discretion on whether Client hedges to the minimum required by its policy or up to the maximum allowed in any given

quarter

Some discretion on layering trades intra-quarter: When does Client add a layer and how much?

Ability to layer further out than required

Discretion between minimum and maximum mandated by policy Minimum mandated by policy

Layer E

Layer D

Layer C

Layer B

Layer A

Layer E

Layer D

Layer C

Layer B

Layer E

Layer D

Layer c

Layer E

Layer D

Mandatory

% Hedged 50% 40% 30% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 (current quarter) Q2 Q3 Q4 Q5 Q6

[***] Assumptions: sliding scale minimum base level, decreasing discretionary maximum level, 15-month hedging tenor

Layer E

10%

How much discretion should your risk policy permit?

27 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

($5.00)

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

May-96 May-97 May-98 May-99 May-00 May-01 May-02 May-03 May-04

Difference WTI Hedged Profile 1 Hedge Profile 2 Hedge Profile 3

Rebalancing Effects of Different Consistent Hedging Policies – Crude Oil 1996 - 2004

Different Hedging Profiles Produce Different Reductions in Volatilities

28 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

($30.00)

($10.00)

$10.00

$30.00

$50.00

$70.00

$90.00

$110.00

$130.00

$150.00

Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10

Difference WTI Hedged Profile 1 Hedged Profile 2 Hedged Profile 3

Rebalancing Effects of Different Consistent Hedging Policies – Crude Oil 2004 - 2010

Different Hedging Profiles Produce Different Reductions in Volatilities

29 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

Historical Evolution in the Use of Financial Derivatives in Latin America

In the 1980’s few clients used Derivatives to hedge exposures, the exception to this usually in the agricultural space (through

Futures in the US) and to some extent FX Forwards, when available

During the 1990’s, for several reasons (PC’s, networks, education, sophistication pushed by international banks in local

markets) a widespread boom took off, across different asset classes, be it FX, Interest Rates, Commodities, etc.

From first generation derivatives (standard swaps and options) to second generation and beyond (“exotics”, such as barriers,

and extendible structures to more complex products, such as credit linked transactions) became quickly available – no limit in

terms of pricing, booking and marketing capabilities

Since the introduction of FAS 133 (and other similar accounting standards) corporate users, when affected, have gone back

to more simple structures due to adverse mark-to-market treatment for exotic products

In some jurisdictions tax treatment is (still) not fully clear, such as derivative loss deduction in the income statement, or

withholding tax issues

On average, sophistication has grown strongly across countries and sectors – customers that 10-15 years ago didn’t trade

any derivatives nowadays trade through Bloomberg electronically swaps (or other electronic platforms) and close other

sophisticated trades

Trades are being booked locally as well as with offshore entities (Banks), under standardized local and ISDA Master

Agreement

Sovereign entities have grown in sophistication as well and macro hedges are not uncommon any more (FX, Commodities,

Rates) in the region

As a general tendency, Derivatives are being used as part of more complex transactions – Capital Markets driven bond

issuance in other local markets and swapped back into local currency, commodity prepays, tax efficient funding structures,

etc.

Local Derivatives have become deeper and with longer maturities as well, similar to the ones seen in some mature markets:

FX and Rates in Chile, Mexico, Brazil

30 I M

P L

E M

E N

T I N

G

R I S

K

M A

N A

G E

M E

N T

P

O L

I C

Y

Agenda

31

Annex A: Basic Derivative Product Descriptions

31

Derivatives - What Are We Talking About ? 2

The Use of Financial Derivatives 5

Implementing Risk Management Policy 21

Annex B: JPM Commodity Capabilities 36

T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

Market Price

Net Price Unhedged Hedged

Buying a Fixed Price Swap

Key considerations Illustrative example

Objective

To lock in a forward price

Description

Client locks in the price over a predetermined period by

buying a fixed price swap from J.P.Morgan

The monthly settlement price is the average of each day’s

settlement in a given month and compared to the swap

price

– If settlement price is higher than the swap price, Client

receives the difference between the settlement price and

the swap price

– If settlement price is lower than the swap price, Client

pays the difference between the swap price and the

settlement price

Advantages

The Client locks in a price over a designated time period

and is protected from any price increase above the swap

price

Price increases in the physical market are compensated by

hedging gains

No upfront premium required

Disadvantages

The Client loses the potential gain from downward price

moves below the swap price

Price declines in the physical market are offset by hedging

losses

Potential gains

Potential costs

Client pays

difference

Client receives

difference

32 A N

N E

X

A :

B A

S I C

D

E R

I V

A T

I V

E

P R

O D

U C

T

D E

S C

R I P

T I O

N S

Market Price

Net Price Unhedged Hedged

Buying a Call Option

Key considerations Illustrative example

Objective

Buying insurance to protect against price increases by

paying premium upfront

Description

A call option creates a cap price in exchange for upfront

premium, which reflects the likelihood that the option will be

exercised. The farther the strike price is from trading levels,

the lower the amount of premium paid upfront. The call

option will reference a published price

The monthly settlement price is the average of each day’s

settlement in a given month and compared to the “option”

strike price

– If the settlement price is higher than the strike price,

Client receives the difference between the strike price

and settlement price. This payment offsets higher prices

in the physical market

– Otherwise, the purchased option expires worthless, but

Client benefits from lower prices in the physical market

Advantages

Client participates fully in downward price movements

while protecting against price increases above the call level

Disadvantages

There is an upfront cost associated with this strategy.

However, this strategy may prove to be more cost effective

than locking in a fixed price

Potential gains

Potential costs

Client receives

difference

Premium paid

Call Strike

33 A N

N E

X

A :

B A

S I C

D

E R

I V

A T

I V

E

P R

O D

U C

T

D E

S C

R I P

T I O

N S

Consumer Zero Cost Collar

Key considerations Illustrative example

Objective

To hedge at zero cost and still retain some benefit from

lower prices

Description

Client buys a call option and finances it by selling a put

option for the same time period at zero upfront cost. The

put and call options will reference a published price

The monthly settlement price is the average of each day’s

settlement in a given month and compared to the strike

levels of the monthly put and call

– If the settlement price is higher than call strike, the

Client receives the difference between the settlement

price and the call strike

– If the settlement price is lower than put strike, the Client

pays the difference between the put strike and the

settlement price

– Otherwise, no payments are made

Advantages

Zero upfront cost method of hedging against upward price

moves while maintaining some downside participation

Disadvantages

If the market price falls below the put strike, the Client will

pay the difference

Client has upward price exposure from the current swap

level to the call strike

Market Price

Net Price Unhedged Hedged

Potential gains

Potential costs

Client pays

difference

Put Strike

Call Strike

Client receives

difference

34 A N

N E

X

A :

B A

S I C

D

E R

I V

A T

I V

E

P R

O D

U C

T

D E

S C

R I P

T I O

N S

Hedge: Recommended Financial Instruments – the Risk Spectrum

Each of the available hedge alternatives offers different risk profiles

Low Risk High Risk

Call options Zero-Cost

Collars Swaps

Enhanced value

strategies

Written

options

Lock in forward price

Consumer receives

difference between

actual price and swap

price, if actual price is

higher than swap

price. Otherwise,

pays the difference

Full protection from

any price increases

above the swap price

No upfront premium

required

Forfeits potential

participation if prices

fall below swap price

Guaranteed cap level

in exchange for

upfront premium

Bespoke settlement

Full protection against

price increase above

the cap level

Full participation in

downward price

movements

Premium paid to

finance hedging

Guaranteed cap

level financed by

selling put options

for the same

time period

Zero upfront

premium cost

Maintain some

downward

participation

Downward

participation capped

at sold put strike

price

Upward price

exposure to calls

strike price

No upfront cost

relative to swap

Locks in more

favorable price today

Unknown potential

cash outflow if

market prices

change significantly

Limited participation in

downward price

movements to the sold

put strike price

Maximum benefit is

upfront premium

Downward

participation capped at

sold put strike price

Fully exposed to price

increases

Medium Risk

Premium

Collars

Guaranteed cap level

partially financed by

selling put options for

the same time period

Cheaper than outright

call purchase

Maintain some

downward

participation

Downward

participation capped at

sold put strike price

Upward price

exposure to calls

strike price

35 A N

N E

X

A :

B A

S I C

D

E R

I V

A T

I V

E

P R

O D

U C

T

D E

S C

R I P

T I O

N S

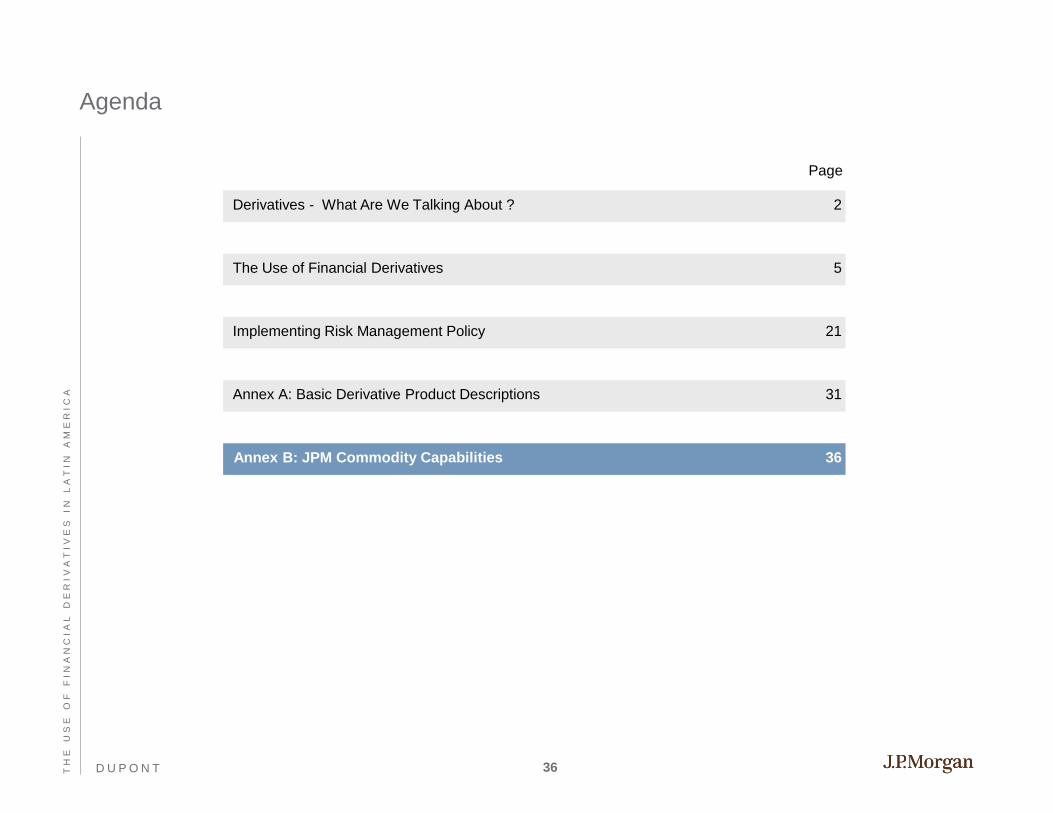

Agenda

Page

D U P O N T 36

Annex B: JPM Commodity Capabilities

36

Derivatives - What Are We Talking About ? 2

The Use of Financial Derivatives 5

Implementing Risk Management Policy 21

Annex A: Basic Derivative Product Descriptions 31

T H

E

U S

E

O F

F

I N

A N

C I A

L

D E

R I V

A T

I V

E S

I N

L

A T

I N

A

M E

R I C

A

J.P. Morgan Covers Commodities Across the Supply Chain

Futures & Options Global Commodities Research

OTC Metals, Energy and Ags

Warehousing Risk

Structured Products

Long Dated Contracts

Listed Futures and Options

Specialist Trading Desks

Global Clearing Solutions

Electronic Trading

Metals, Bulk Commodities

Energy and Power

Grains and Agricultural

Technical Analysis

Energy and

Power

Coal

Electricity

Natural Gas

Gasoline

Crude Oil

NGLs

Transportation

Freight

Base Metals

Steel

Nickel

Zinc

Tin

Copper

Aluminium

Lead

Aluminium Alloy

NASAAC

Precious Metals

Gold

Silver

Platinum

Palladium

Agricultural

Cattle

Dairy

Grains

Soybeans

Wheat

Corn

Softs

Coffee

Sugar

Cotton

Weather

Temperature

Precipitation

Wind

Hurricanes

Sunshine

Crop Yields

Environmental

Markets

Carbon

allowances and

offsets (e.g.,

RGGI; EUAs;

CERs; VERs)

Sulphur Dioxide

Nitrogen Oxides

Renewable

Energy Credits

Plastics

Ethylene

Polyethylene

Polypropylene

37 A N

N E

X

B :

J P

M

C O

M M

O D

I T

Y

C A

P A

B I L

I T

I E

S

J.P. Morgan named “2011 House of the Year” in Oil, Coal and Natural Gas

Oil and Products House of the Year

J.P. Morgan won EnergyRisk’s Oil and Products House in June 2011

Innovative financing deals with refiners and state-owned enterprises

demonstrated J.P. Morgan’s continued ability to provide first class

solutions to clients

J.P Morgan also showed the importance of maintaining strong

relationships with clients despite a challenging economic climate

Achieved greatest market penetration for over-the-counter energy

derivatives

Executed several large tailored transactions to meet clients risk

management needs

U.S. Natural Gas House of the Year

“Particularly over the last three years, it is fair to say that our

share of the wallet overall, in terms of flow and structured

transactions, has grown dramatically. I think there isn’t a

meaningful transaction or opportunity out there that we’re

not participating in or competing for.“

- Roy Salame, Global Head of Commodities Corporate Sales

EnergyRisk; June, 2011

Coal House of the Year

J.P. Morgan won EnergyRisk’s Coal House of the Year in June 2011

The magazine recognized J.P. Morgan for its “transformational

restructure” of its U.S Coal business highlighting:

Increase in offerings

International integration

Alignment with changing market fundamentals

Developing export market for thermal coal

J.P Morgan also demonstrated growth in product offering to European

and Asian clients

Increased marketing support, illustrates J.P. Morgan’s leadership within

the Commodities Industry

J.P. Morgan won EnergyRisk’s U.S. Natural Gas House of the Year

in June 2011

EnergyRisk highlighted J.P. Morgan’s robust deal-making activities

and purchase of RBS Sempra’s North America gas business

Resulting in expansion of the Firm’s ability to serve clients through

a diverse network of physical assets in North America

70 bcf/d of storage capacity

1.9 bcf/d of transportation capacity

6 bcf/d of gas marketing activities in 2010

J.P. Morgan also continued excellence in executing large,

structured transactions and risk managing capabilities

38 A N

N E

X

B :

J P

M

C O

M M

O D

I T

Y

C A

P A

B I L

I T

I E

S

J.P. Morgan named “2011 Best Commodities House” by Euromoney

Euromoney Awards for Excellence - June 2011

Diverse platform of financial and physical capabilities across product

areas – energy, metals, investor products, agriculture etc

Strong growth both organically and through strategic acquisitions,

multi-year agreements and large structured transactions

Integrated RBS Sempra business in 2010 to further develop a strong

and diversified platform across multiple commodity product types

Acquisition nearly doubled physical and financial power business

Expanded our presence in oil, power, gas and metals

Expanded global presence

Integration of US and Europe Coal and Freight Platform and a

long-term physical coal supply agreement into German coal fired

power-plant

Increased agricultural products presence in emerging market

regions

Established sales coverage in emerging markets such as Brazil,

South Africa and Middle East

Undertaken innovative projects to transform the J.P. Morgan

Commodities business

In February 2011, J.P. Morgan launched the Commodity-related

Project Finance business, a joint venture between Commodities

and Syndicated and Leveraged Finance Business

Moved the Commodities Research function into the business,

publishing some of the industry’s most thought-provoking analysis

Notable Structured Transactions

Large syndicated loan facility for a North African producer

In July 2011, J.P. Morgan acted as the lead arranger and

underwriter for a syndicated pre-export credit facility

J.P. Morgan’s leading commodity trading capability enabled

enhanced tailoring of oil hedges to fit with the client’s actual

exposure profile

Long term, large volume physical Natural Gas purchase with North

East producer

In February 2011, J.P. Morgan entered into a large volume, 10

year physical index sales agreement with a major North American

Natural Gas producer

This leverages J.P. Morgan’s existing platform in US and Canada,

providing the client with a credit worthy base load market and

access to potentially higher priced markets

J.P. Morgan acquired and restructured five wind power purchase

agreements to monetize the assets owned by a large renewable

energy client

Highlights J.P. Morgan’s continued leadership in executing large,

structured transactions across commodities

LNG delivery to the UK

J.P. Morgan executed delivery of Liquified Natural Gas (LNG)

across three continents, purchasing the cargo from a large Middle

Eastern gas and power company

Transaction represents the first import of LNG into the UK from

the US in over 50 years

39 A N

N E

X

B :

J P

M

C O

M M

O D

I T

Y

C A

P A

B I L

I T

I E

S

JPMorgan has Recently Won Every Commodity Award in the Industry

JPMorgan Named “Commodity Derivatives House” of 2009 by IFR

JPMorgan Named “Derivatives House of the Year” in 2010 by Energy Risk Magazine

JPMorgan ranked “Most Innovative in Commodities” in 2009 by The Banker

JPMorgan Named “Commodity Derivatives House of the Year” in 2009 by Risk

Magazine

JP Morgan Named “Quality Leader in US Commodities Corporate Energy” in 2010 by

Greenwich Associates

40 A N

N E

X

B :

J P

M

C O

M M

O D

I T

Y

C A

P A

B I L

I T

I E

S