Embed Size (px)

Citation preview

Consumer Analyst Group of New York

(CAGNY) Conference

February 20, 2013

Jacek Olczak

Chief Financial Officer

Philip Morris International

2

Forward-Looking and Cautionary Statements

● This presentation and related discussion contain forward-looking statements. Achievement of projected

results is subject to risks, uncertainties and inaccurate assumptions, and PMI is identifying important

factors that, individually or in the aggregate, could cause actual results to differ materially from those

contained in any forward-looking statements made by PMI

● PMI’s business risks include: significant increases in cigarette-related taxes; the imposition of

discriminatory excise tax structures; fluctuations in customer inventory levels due to increases in product

taxes and prices; increasing marketing and regulatory restrictions, often with the goal of reducing or

preventing the use of tobacco products; health concerns relating to the use of tobacco products and

exposure to environmental tobacco smoke; litigation related to tobacco use; intense competition; the

effects of global and individual country economic, regulatory and political developments; changes in adult

smoker behavior; lost revenues as a result of counterfeiting, contraband and cross-border purchases;

governmental investigations; unfavorable currency exchange rates and currency devaluations; adverse

changes in applicable corporate tax laws; adverse changes in the cost and quality of tobacco and other

agricultural products and raw materials; and the integrity of its information systems. PMI’s future

profitability may also be adversely affected should it be unsuccessful in its attempts to produce products

with the potential to reduce the risk of smoking-related diseases; if it is unable to successfully introduce

new products, promote brand equity, enter new markets or improve its margins through increased prices

and productivity gains; if it is unable to expand its brand portfolio internally or through acquisitions and the

development of strategic business relationships; or if it is unable to attract and retain the best global talent

● PMI is further subject to other risks detailed from time to time in its publicly filed documents, including the

Form 10-Q for the quarter ended September 30, 2012. PMI cautions that the foregoing list of important

factors is not a complete discussion of all potential risks and uncertainties. PMI does not undertake to

update any forward-looking statement that it may make from time to time, except in the normal course of

its public disclosure obligations

● A glossary of terms and reconciliations of non-GAAP measures included in this presentation to the most

comparable GAAP measures are provided at the end of this presentation and are posted on our web site

at www.pmi.com

3

Agenda

● Strong performance in 2012

● Tobacco industry remains attractive

● PMI should continue to outperform

● Incremental growth opportunities

● Strong emphasis on returning cash to our shareholders

4

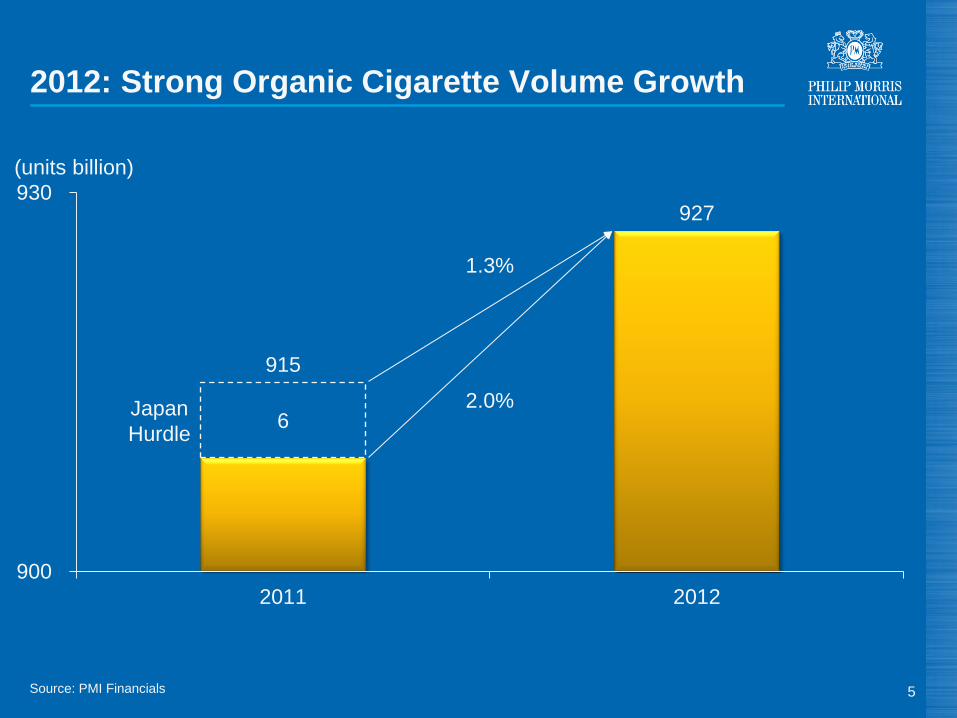

2012: Another Solid Year for PMI

● Strong organic volume growth

● Key brands performed well

● Pricing power remained strong

● Moderate cost increases largely offset by productivity

gains

● Continued investments in our business

● EPS growth at top end of target range

● $12 billion returned to our shareholders

6

915

927

900

930

2011 2012

2012: Strong Organic Cigarette Volume Growth

5

(units billion)

Japan

Hurdle

1.3%

2.0%

Source: PMI Financials

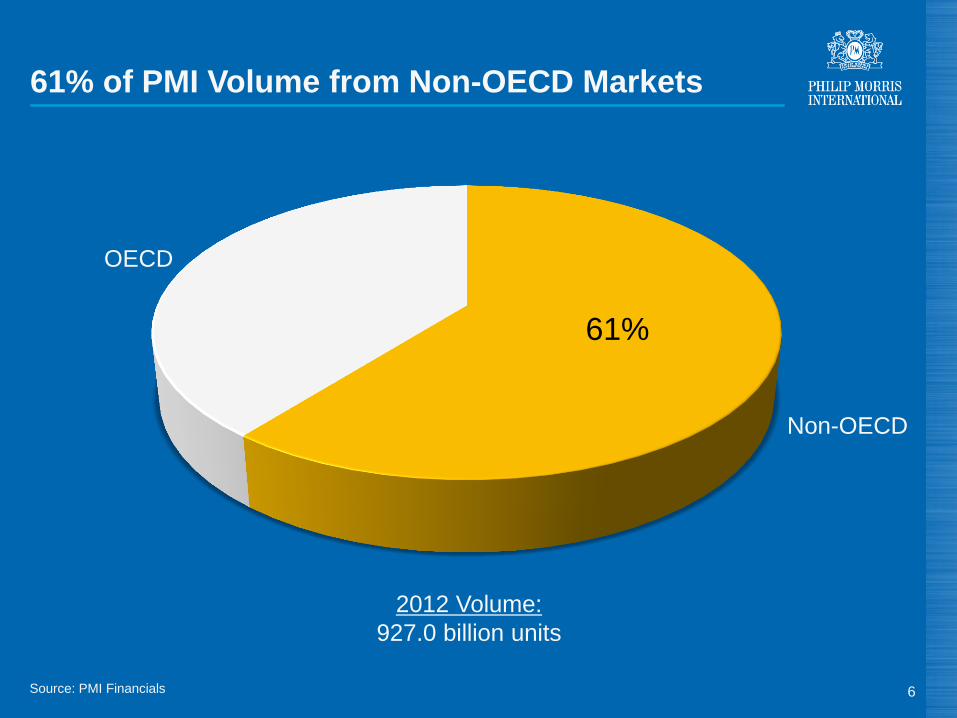

61% of PMI Volume from Non-OECD Markets

6

2012 Volume:

927.0 billion units

Non-OECD

OECD

Source: PMI Financials

61%

7

Source: PMI Financials

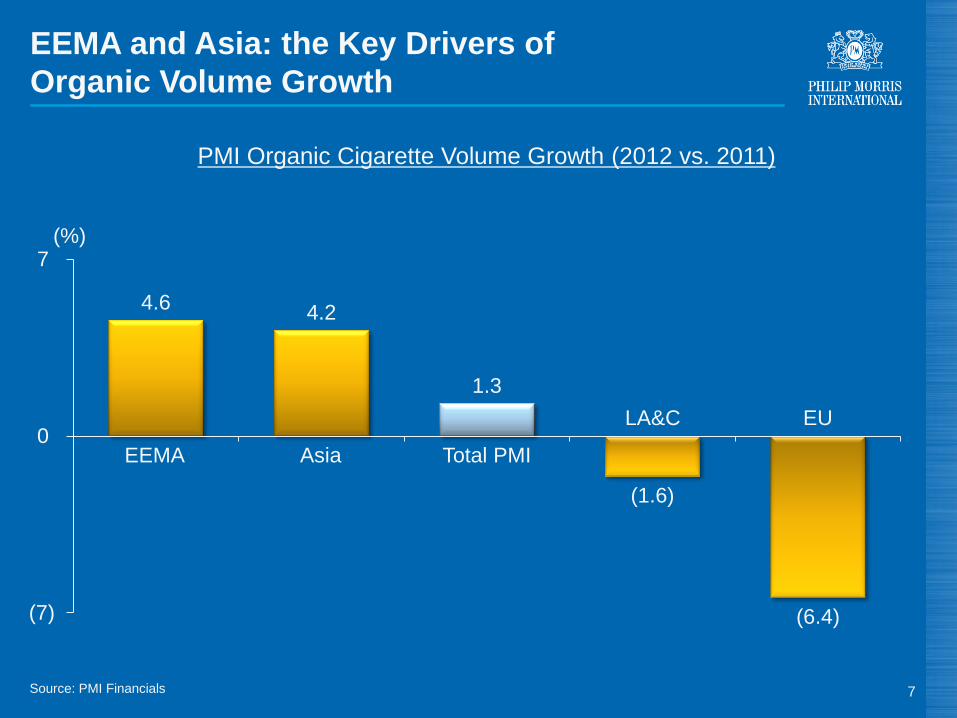

EEMA and Asia: the Key Drivers of

Organic Volume Growth

4.6 4.2

1.3

(1.6)

(6.4) (7)

0

7

PMI Organic Cigarette Volume Growth (2012 vs. 2011)

EEMA Asia

Total PMI

(%)

LA&C EU

(a) Excluding China

(b) Also excluding the USA

Source: PMI estimates 8

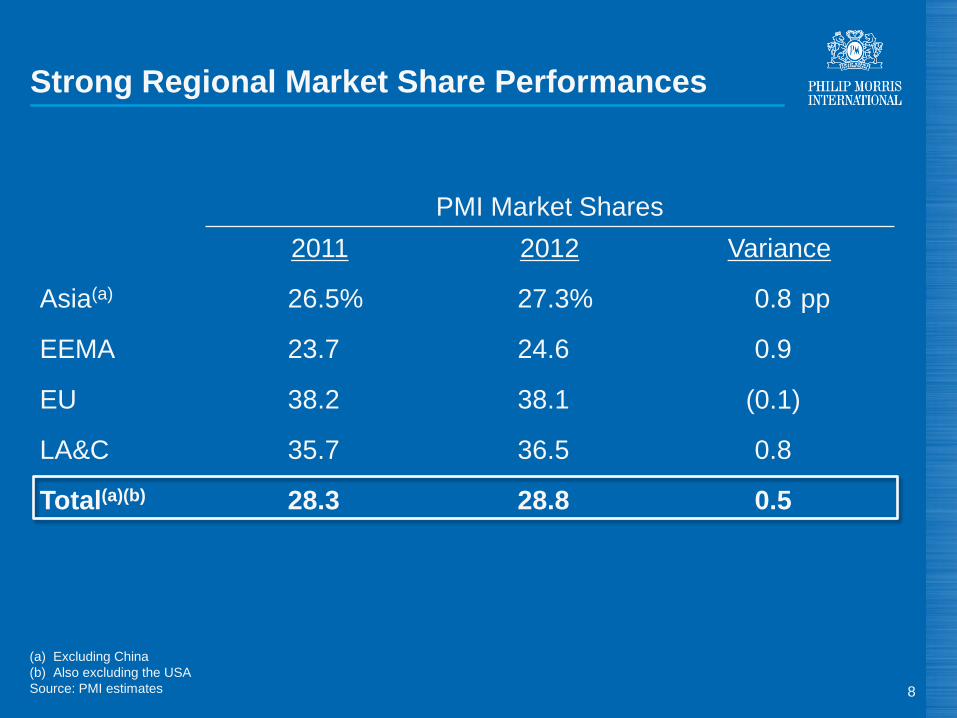

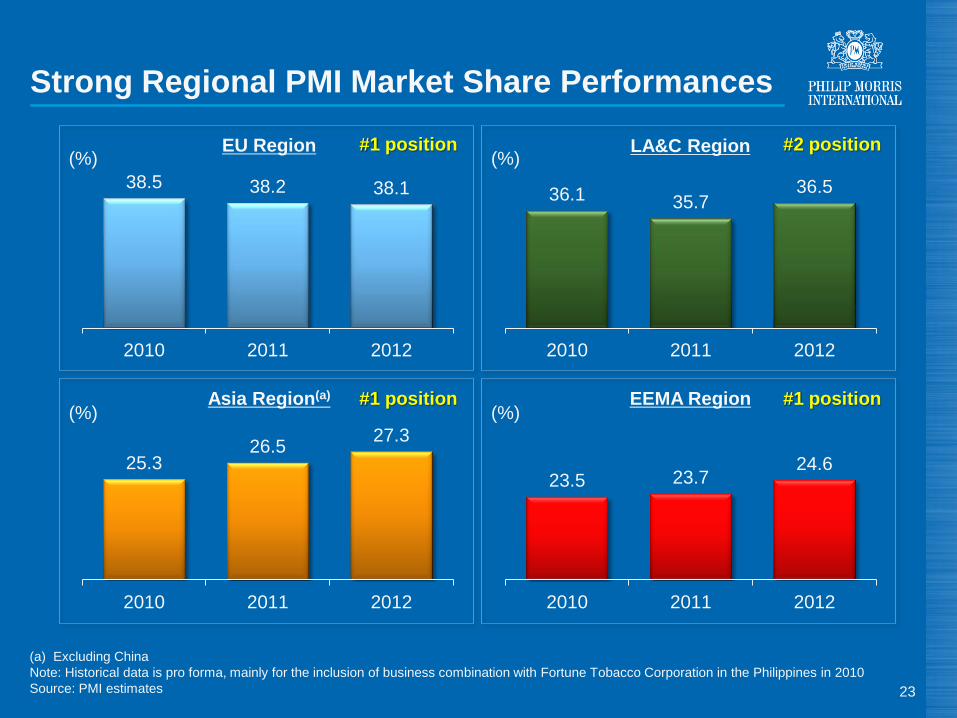

Strong Regional Market Share Performances

PMI Market Shares

2011 2012 Variance

Asia(a) 26.5% 27.3% 0.8)pp

EEMA 23.7 24.6 0.9

EU 38.2 38.1

LA&C 35.7 36.5 0.8

Total(a)(b) 28.3 28.8 0.5

(0.1)

9

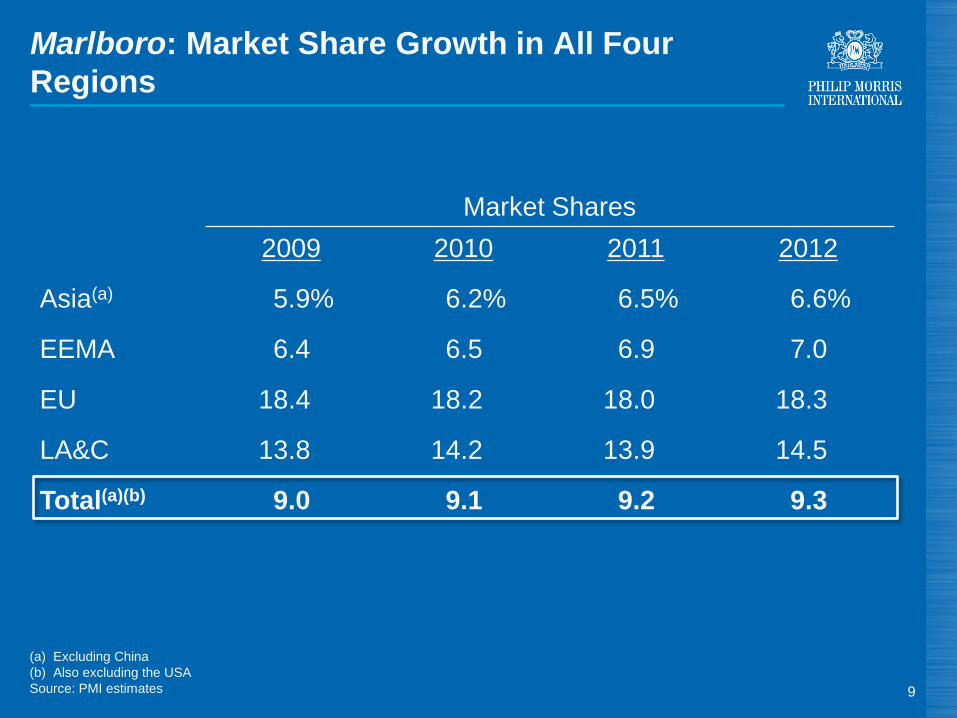

Marlboro: Market Share Growth in All Four

Regions

Market Shares

2009 2010 2011 2012

Asia(a) 5.9% 6.2% 6.5% 6.6%

EEMA 6.4 6.5 6.9 7.0

EU 18.4 18.2 18.0 18.3

LA&C 13.8 14.2 13.9 14.5

Total(a)(b) 9.0 9.1 9.2 9.3

(a) Excluding China

(b) Also excluding the USA

Source: PMI estimates

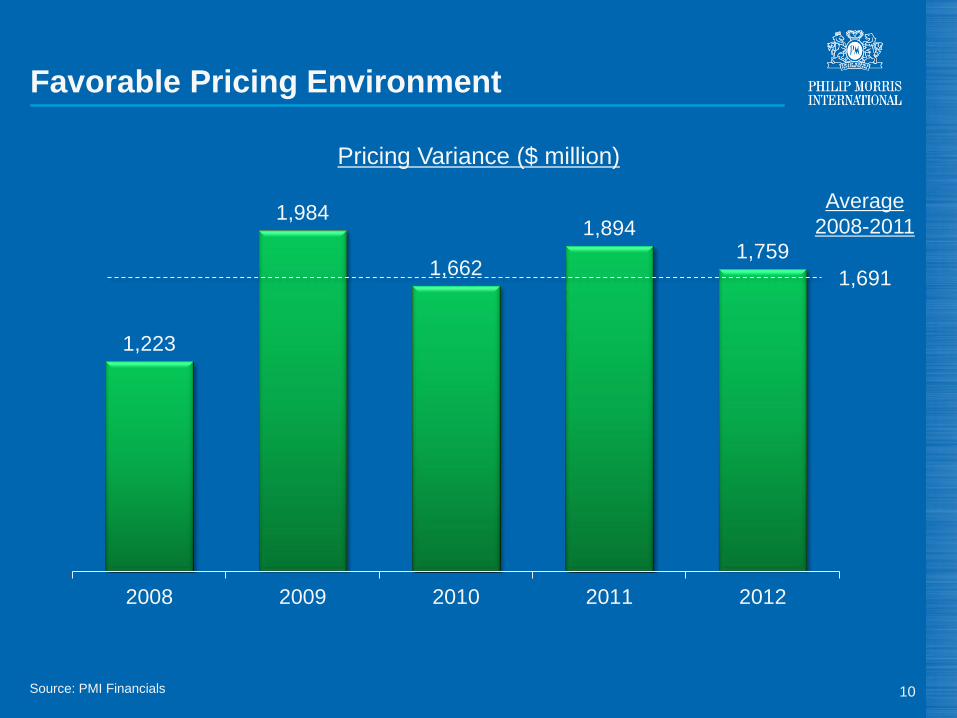

Source: PMI Financials

1,223

1,984

1,662

1,894 1,759

2008 2009 2010 2011 2012

Pricing Variance ($ million)

Favorable Pricing Environment

10

Average

2008-2011

1,691

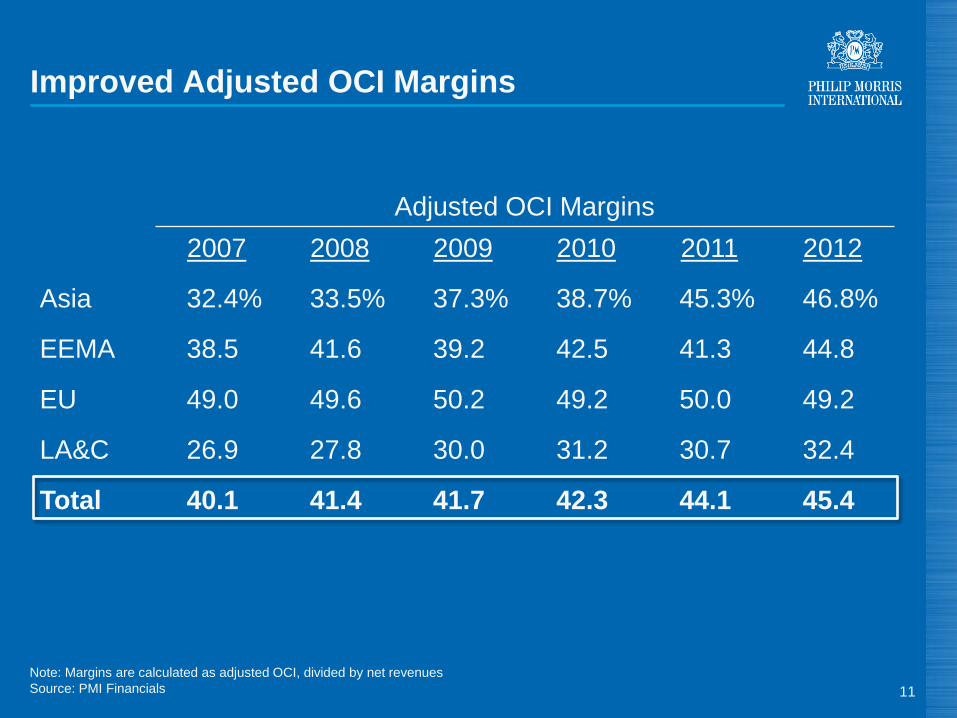

11

Adjusted OCI Margins

2007 2008 2009 2010 2011 2012

Asia 32.4% 33.5% 37.3% 38.7% 45.3% 46.8%

EEMA 38.5 41.6 39.2 42.5 41.3 44.8

EU 49.0 49.6 50.2 49.2 50.0 49.2

LA&C 26.9 27.8 30.0 31.2 30.7 32.4

Total 40.1 41.4 41.7 42.3 44.1 45.4

Improved Adjusted OCI Margins

Note: Margins are calculated as adjusted OCI, divided by net revenues

Source: PMI Financials

(a) Excluding currency and acquisitions

(b) Excluding currency

Source: PMI Financials

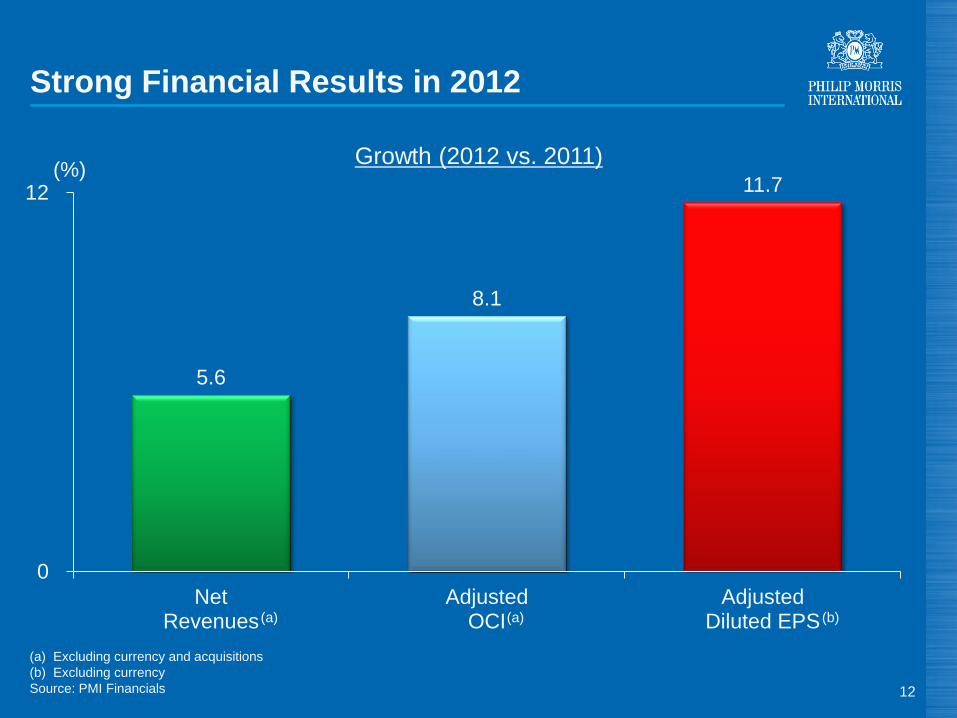

5.6

8.1

11.7

0

12

NetRevenues

AdjustedOCI

AdjustedDiluted EPS

Strong Financial Results in 2012

12

(a)

(%)

(a) (b)

Growth (2012 vs. 2011)

13

Tobacco Industry: An Attractive Sector

● Favorable pricing environment:

- Governments look to increase their revenues and lower tobacco

consumption based on higher cigarette prices

- Elasticity of demand is relatively low

14

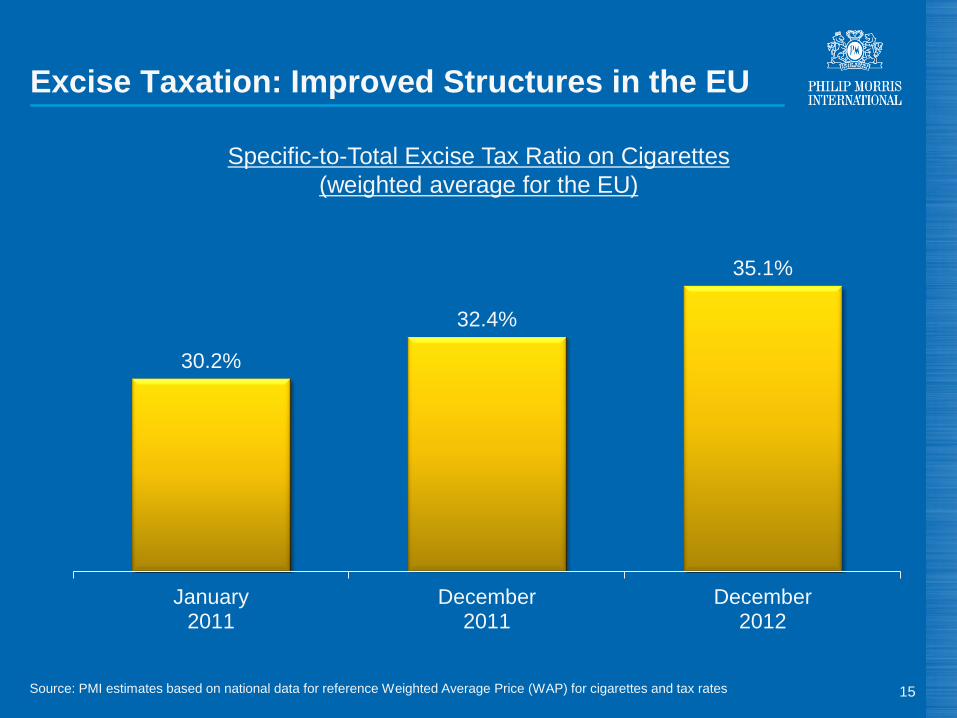

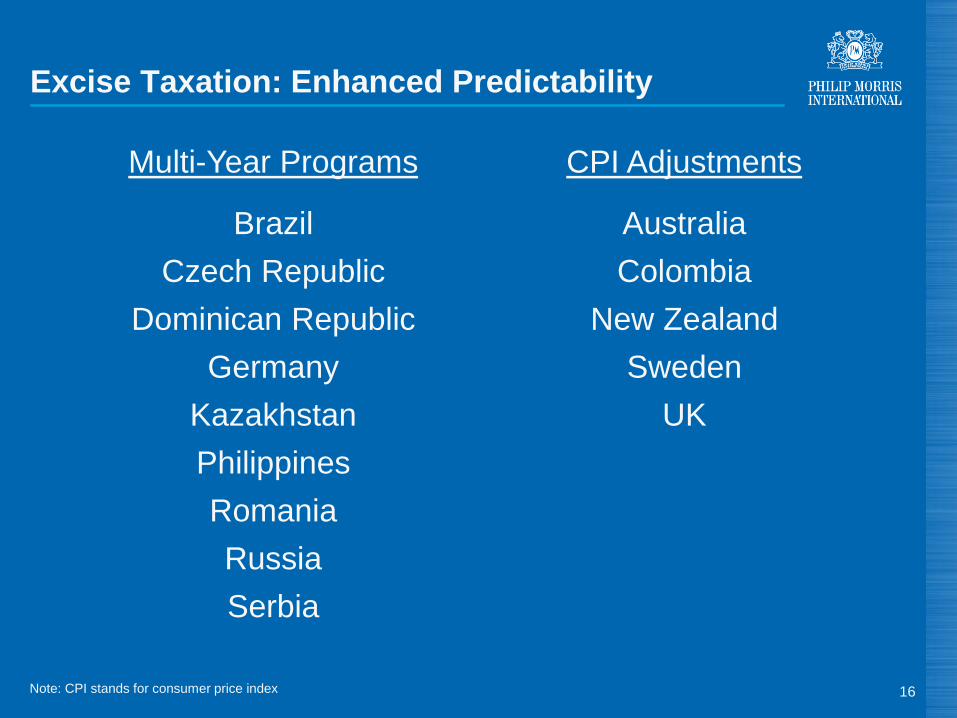

Tobacco Industry: An Attractive Sector

● Favorable pricing environment:

- Governments look to increase their revenues and lower tobacco

consumption based on higher cigarette prices

- Elasticity of demand is relatively low

● Rational excise tax environment:

- Governments recognize revenue predictability enhanced by:

• Regular, reasonable increases

• High proportion of specific elements in excise tax structure

• Multi-year programs

• Inflation indexation

• Harmonization of taxation between cigarettes and fine cut

Source: PMI estimates based on national data for reference Weighted Average Price (WAP) for cigarettes and tax rates

30.2%

32.4%

35.1%

January2011

December2011

December2012

Excise Taxation: Improved Structures in the EU

15

Specific-to-Total Excise Tax Ratio on Cigarettes

(weighted average for the EU)

Excise Taxation: Enhanced Predictability

16

Multi-Year Programs CPI Adjustments

Brazil Australia

Czech Republic Colombia

Dominican Republic New Zealand

Germany Sweden

Kazakhstan UK

Philippines

Romania

Russia

Serbia

Note: CPI stands for consumer price index

17

Tobacco Industry: An Attractive Sector

● Favorable pricing environment:

- Governments look to increase their revenues and lower tobacco

consumption based on higher cigarette prices

- Elasticity of demand is relatively low

● Rational excise tax environment:

- Governments recognize revenue predictability enhanced by:

• Regular, reasonable increases

• High proportion of specific elements in excise tax structure

• Multi-year programs

• Inflation indexation

• Harmonization of taxation between cigarettes and fine cut

- Exception in 2013 is the Philippines

18

Tobacco Industry: An Attractive Sector

● Favorable pricing environment:

- Governments look to increase their revenues and lower tobacco

consumption based on higher cigarette prices

- Elasticity of demand is relatively low

● Rational excise tax environment:

- Governments recognize revenue predictability enhanced by:

• Regular, reasonable increases

• High proportion of specific elements in excise tax structure

• Multi-year programs

• Inflation indexation

• Harmonization of taxation between cigarettes and fine cut

- Exception in 2013 is the Philippines

● Challenging but manageable regulatory environment

19

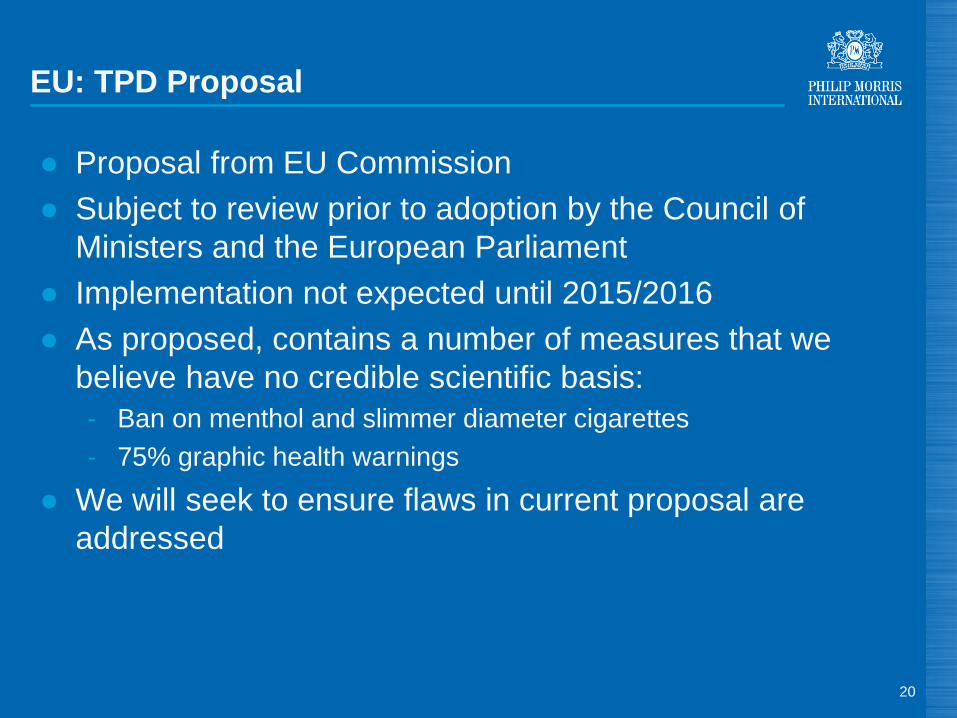

Plain Packaging: Summary

● 6 of 7 High Court judges in Australia recognized that plain

packaging law deprived tobacco companies of valuable

intellectual properties

● Plain packaging is not mandated in the proposed EU

Tobacco Products Directive ("TPD")

20

● Proposal from EU Commission

● Subject to review prior to adoption by the Council of

Ministers and the European Parliament

● Implementation not expected until 2015/2016

● As proposed, contains a number of measures that we

believe have no credible scientific basis:

- Ban on menthol and slimmer diameter cigarettes

- 75% graphic health warnings

● We will seek to ensure flaws in current proposal are

addressed

EU: TPD Proposal

21

PMI Should Continue to Outperform

● Overall market leadership and broad global footprint

● Superior brand portfolio

● Favorable market trends

● Higher conversion of revenues into free cash flow

(a) Excluding China and the USA

Source: PMI estimates

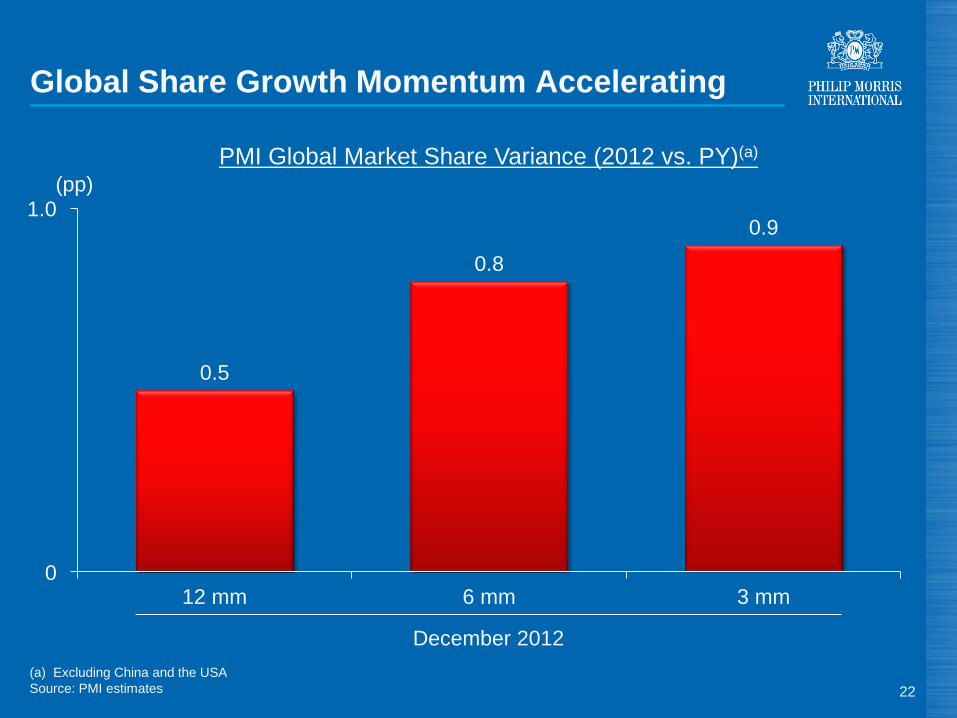

0.5

0.8

0.9

0.0

1.0

12 mm 6 mm 3 mm

Global Share Growth Momentum Accelerating

22

PMI Global Market Share Variance (2012 vs. PY)(a)

0

1.0 (pp)

December 2012

Strong Regional PMI Market Share Performances

23

38.5 38.2 38.1

2010 2011 2012

36.1 35.7 36.5

2010 2011 2012

25.3 26.5

27.3

2010 2011 2012

23.5 23.7 24.6

2010 2011 2012

LA&C Region

EEMA Region Asia Region(a)

EU Region #1 position (%) (%)

(%) (%)

#2 position

#1 position #1 position

(a) Excluding China

Note: Historical data is pro forma, mainly for the inclusion of business combination with Fortune Tobacco Corporation in the Philippines in 2010

Source: PMI estimates

Source: PMI estimates

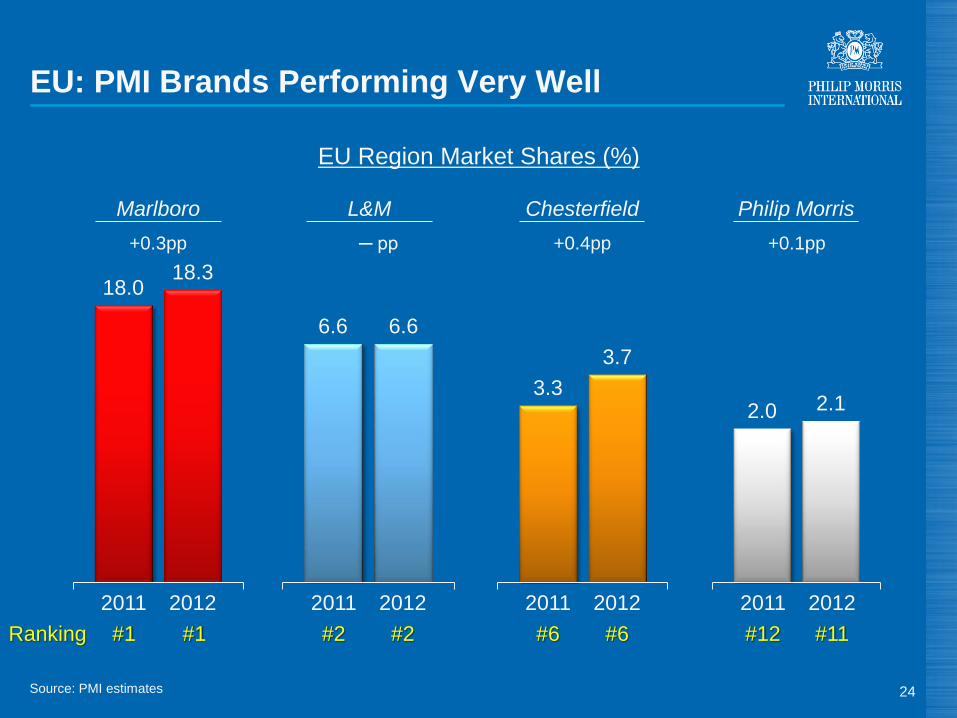

18.0 18.3

EU: PMI Brands Performing Very Well

24

EU Region Market Shares (%)

6.6 6.6

3.3

3.7

2.0 2.1

2011 2012

+0.3pp ─ pp +0.4pp +0.1pp

Marlboro L&M Chesterfield Philip Morris

2011 2012 2011 2012 2011 2012

#1 #1 #2 #2 #6 #6 #12 #11 Ranking

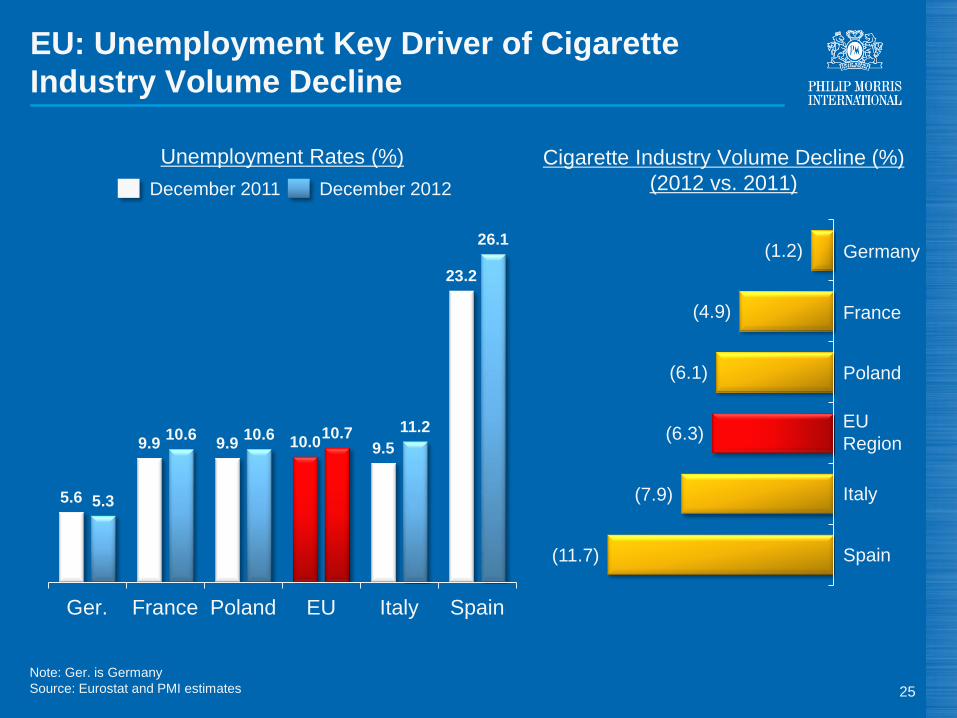

EU: Unemployment Key Driver of Cigarette

Industry Volume Decline

25

Note: Ger. is Germany

Source: Eurostat and PMI estimates

Unemployment Rates (%) Cigarette Industry Volume Decline (%)

(2012 vs. 2011)

Germany

Poland

France

Spain

5.6

9.9 9.9 10.0 9.5

23.2

5.3

10.6 10.6 10.7 11.2

26.1

Ger. France Poland EU Italy Spain

(11.7)

(7.9)

(6.3)

(6.1)

(4.9)

(1.2)

Italy

EU

Region

December 2011 December 2012

(a) Cigarette, OTP and dual smokers

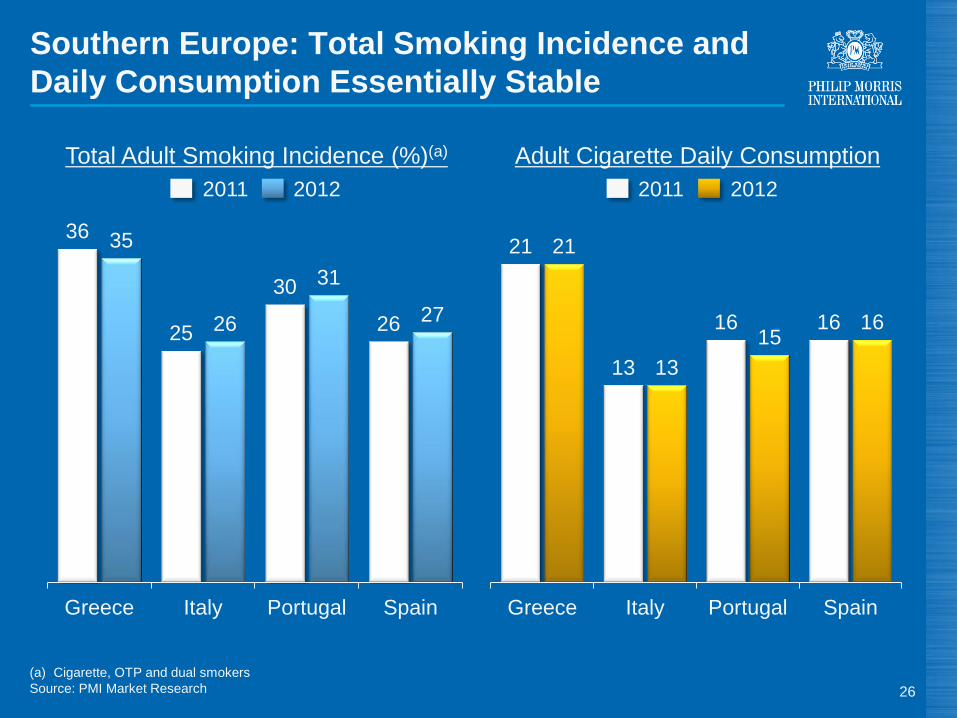

Source: PMI Market Research

21

13

16 16

21

13

15 16

Greece Italy Portugal Spain

Southern Europe: Total Smoking Incidence and

Daily Consumption Essentially Stable

26

36

25

30

26

35

26

31

27

Greece Italy Portugal Spain

Total Adult Smoking Incidence (%)(a) Adult Cigarette Daily Consumption

2011 2012 2011 2012

Source: PMI estimates (in-market sales)

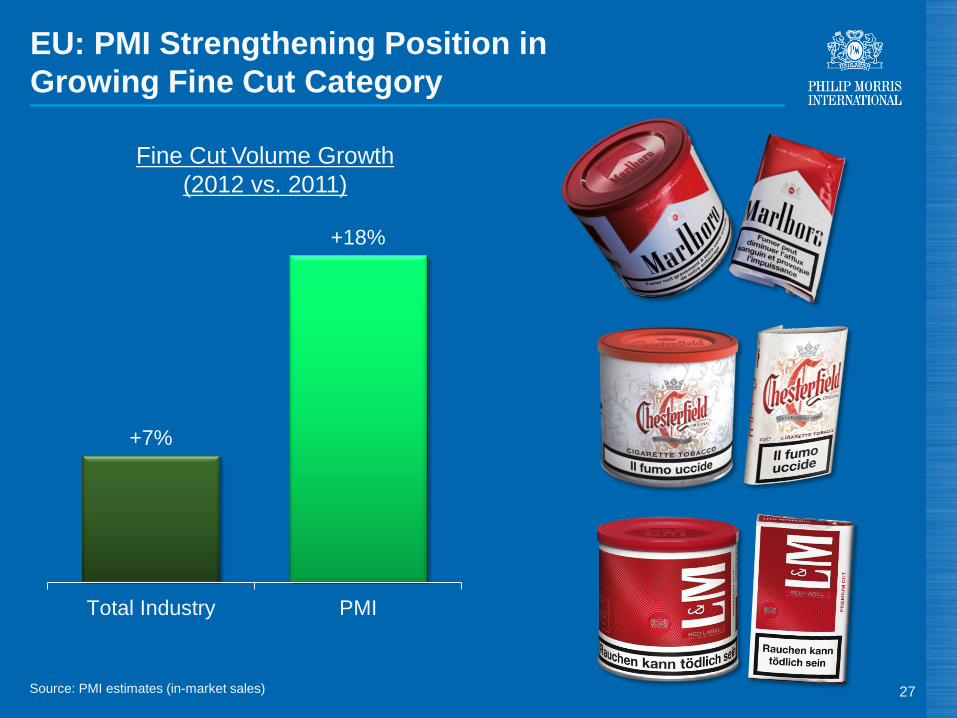

EU: PMI Strengthening Position in

Growing Fine Cut Category

27

+7%

+18%

Total Industry PMI

Fine Cut Volume Growth

(2012 vs. 2011)

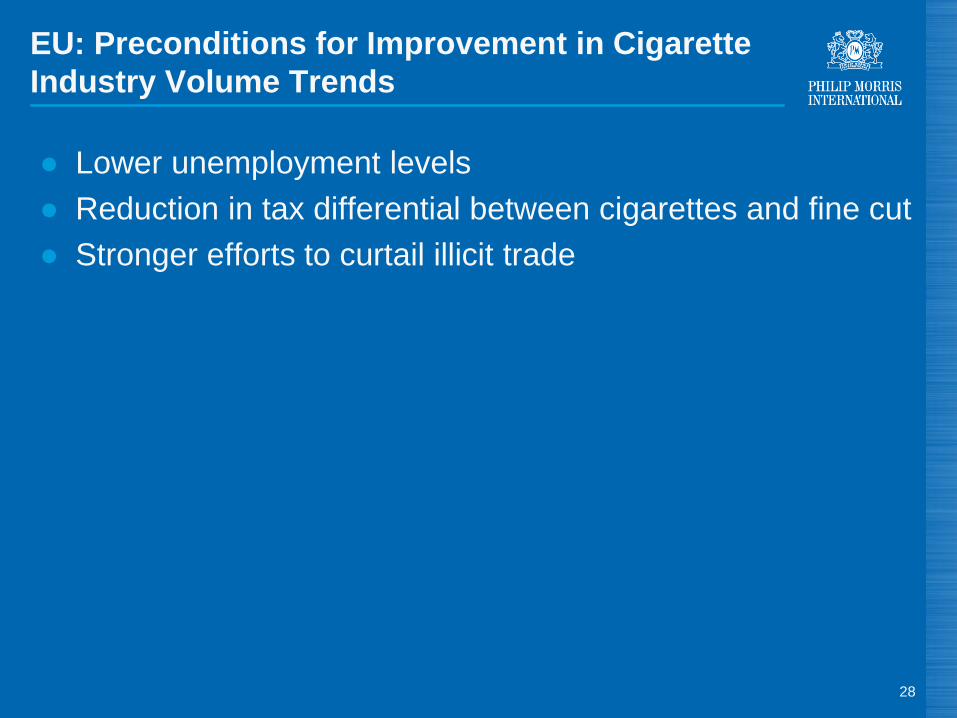

EU: Preconditions for Improvement in Cigarette

Industry Volume Trends

● Lower unemployment levels

● Reduction in tax differential between cigarettes and fine cut

● Stronger efforts to curtail illicit trade

28

Source: PMI estimates

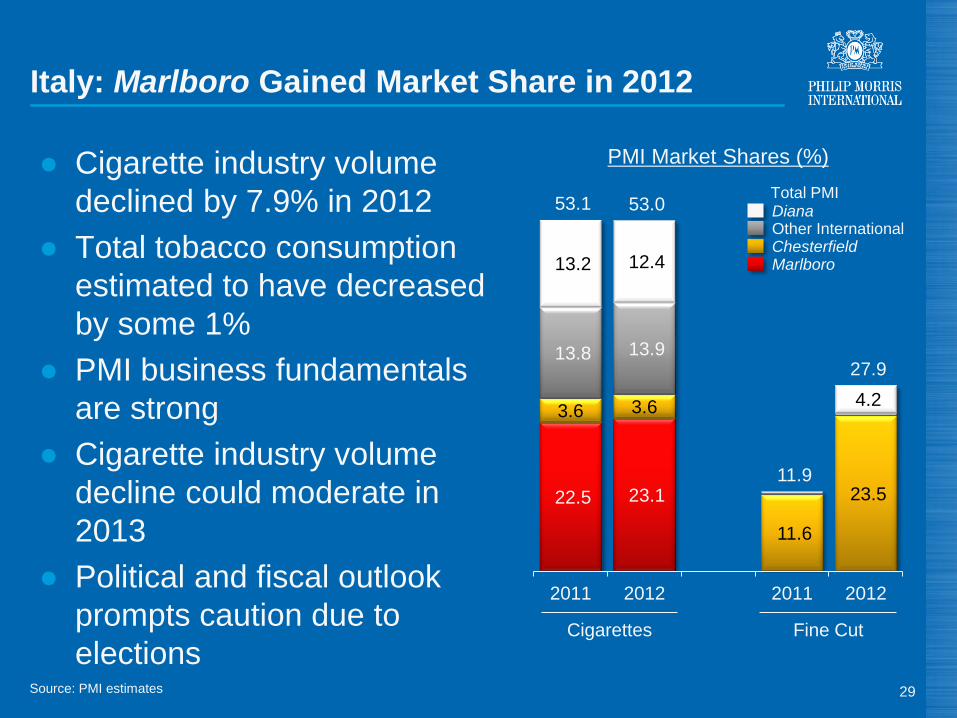

Italy: Marlboro Gained Market Share in 2012

29

22.5 23.1

11.6

23.5

3.6 3.6 4.2

13.8 13.9

13.2 12.4

53.1 53.0

11.9

27.9

2011 2012 2011 2012

● Cigarette industry volume

declined by 7.9% in 2012

● Total tobacco consumption

estimated to have decreased

by some 1%

● PMI business fundamentals

are strong

● Cigarette industry volume

decline could moderate in

2013

● Political and fiscal outlook

prompts caution due to

elections

PMI Market Shares (%)

Cigarettes Fine Cut

Chesterfield

Total PMI Diana

Marlboro

Other International

Source: PMI estimates

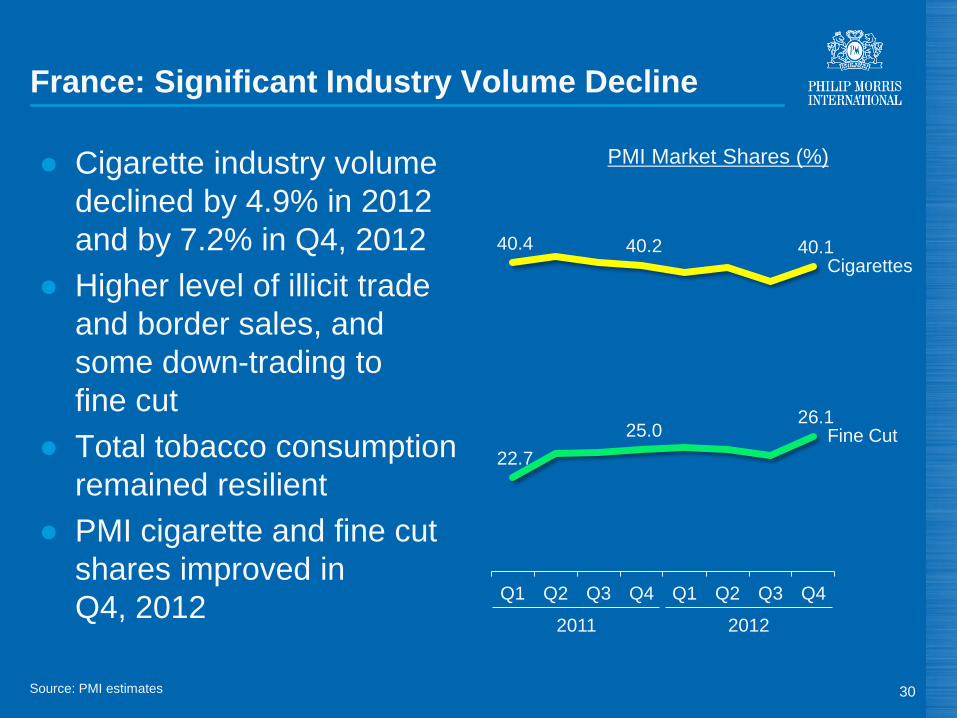

France: Significant Industry Volume Decline

30

● Cigarette industry volume

declined by 4.9% in 2012

and by 7.2% in Q4, 2012

● Higher level of illicit trade

and border sales, and

some down-trading to

fine cut

● Total tobacco consumption

remained resilient

● PMI cigarette and fine cut

shares improved in

Q4, 2012

40.4 40.2 40.1

22.7

25.0 26.1

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Cigarettes

Fine Cut

2012 2011

PMI Market Shares (%)

Source: PMI estimates

Germany: Strong Position in Resilient Market

31

● Cigarette industry volume

down by 1.2% and fine cut

up by 2.2% in 2012

● Competitor trade inventories

increased in December 2012

● Underlying decline in

cigarette volume estimated

at around 2%

● PMI has a strong competitive

position

21.4 21.3

2.2 2.9

10.4 10.5

5.5 5.3

35.9 35.8

14.0 14.7

2011 2012 2011 2012

PMI Market Shares (%)

L&M

Total PMI

Marlboro

Other

Cigarettes Fine Cut

Source: PMI Financials

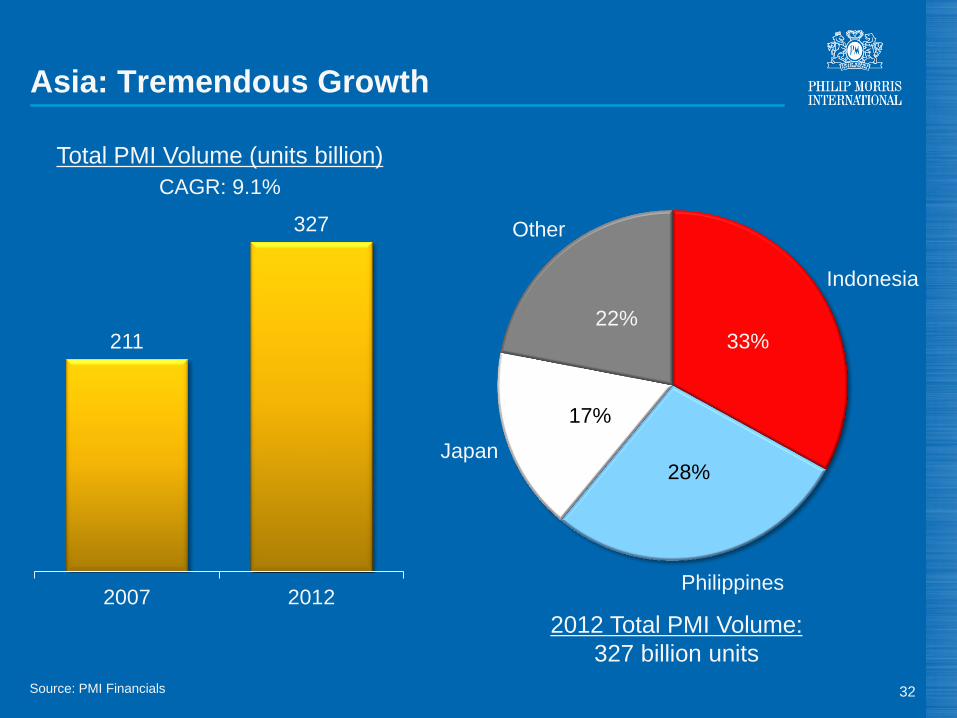

Asia: Tremendous Growth

32

33%

28%

17%

22%

2012 Total PMI Volume:

327 billion units

Indonesia

Philippines

Japan

Other

211

327

2007 2012

Total PMI Volume (units billion)

CAGR: 9.1%

Source: PMI estimates (based on expanded Nielsen coverage) and PMI Financials

● Cigarette industry volume

grew by 8.2% in 2012

● Going forward, we expect

5-6% growth

● PMI volume surged by

17.5% in 2012

● PMI share growth driven by:

- Consumer uptrading

- Best brand portfolio

- Superior national distribution

- Best sales field force

Indonesia: Expanding Share in Growing Market

33

30.2 30.9

32.8

35.6

2009 2010 2011 2012

PMI Market Share (%)

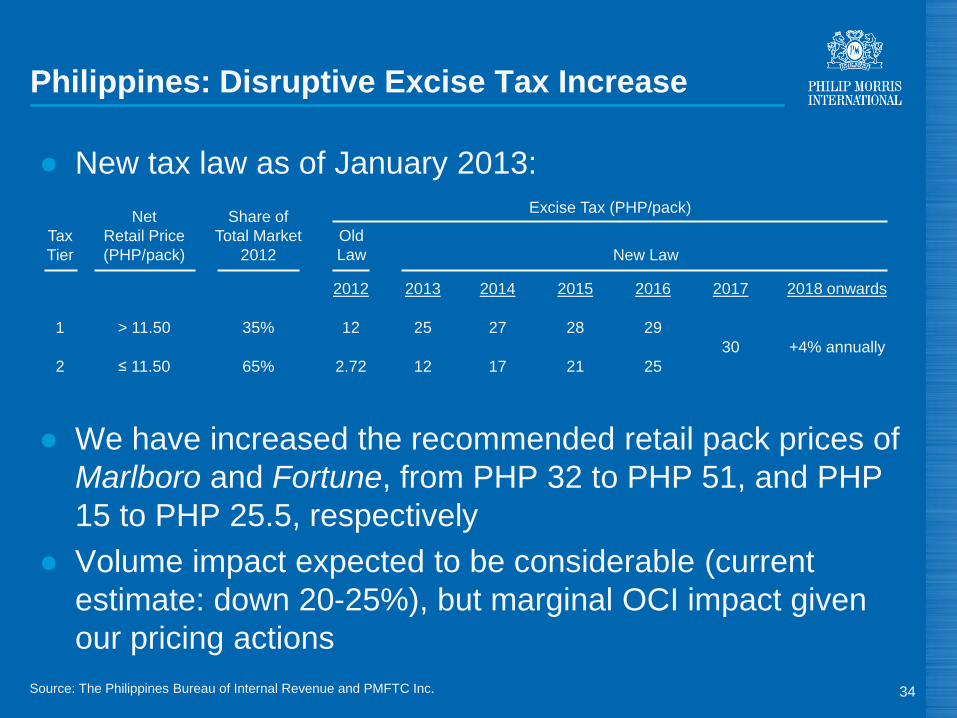

● New tax law as of January 2013:

● We have increased the recommended retail pack prices of

Marlboro and Fortune, from PHP 32 to PHP 51, and PHP

15 to PHP 25.5, respectively

● Volume impact expected to be considerable (current

estimate: down 20-25%), but marginal OCI impact given

our pricing actions

Source: The Philippines Bureau of Internal Revenue and PMFTC Inc.

Philippines: Disruptive Excise Tax Increase

34

Tax

Tier

Net

Retail Price

(PHP/pack)

Share of

Total Market

2012

New Law

2012 2013 2014 2015 2016 2017 2018 onwards

1 > 11.50 35% 12 25 27 28 29

30 +4% annually

2 ≤ 11.50 65% 2.72 12 17 21 25

Excise Tax (PHP/pack)

Old

Law

Source: PMI estimates and Tobacco Institute of Japan

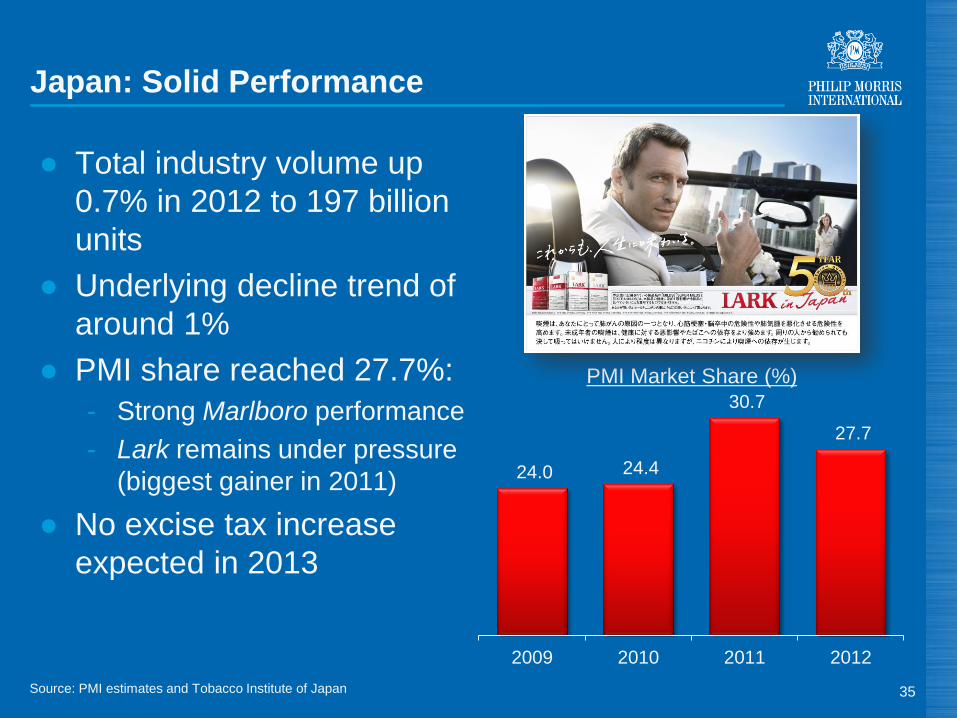

Japan: Solid Performance

35

24.0 24.4

30.7

27.7

2009 2010 2011 2012

● Total industry volume up

0.7% in 2012 to 197 billion

units

● Underlying decline trend of

around 1%

● PMI share reached 27.7%:

- Strong Marlboro performance

- Lark remains under pressure

(biggest gainer in 2011)

● No excise tax increase

expected in 2013

PMI Market Share (%)

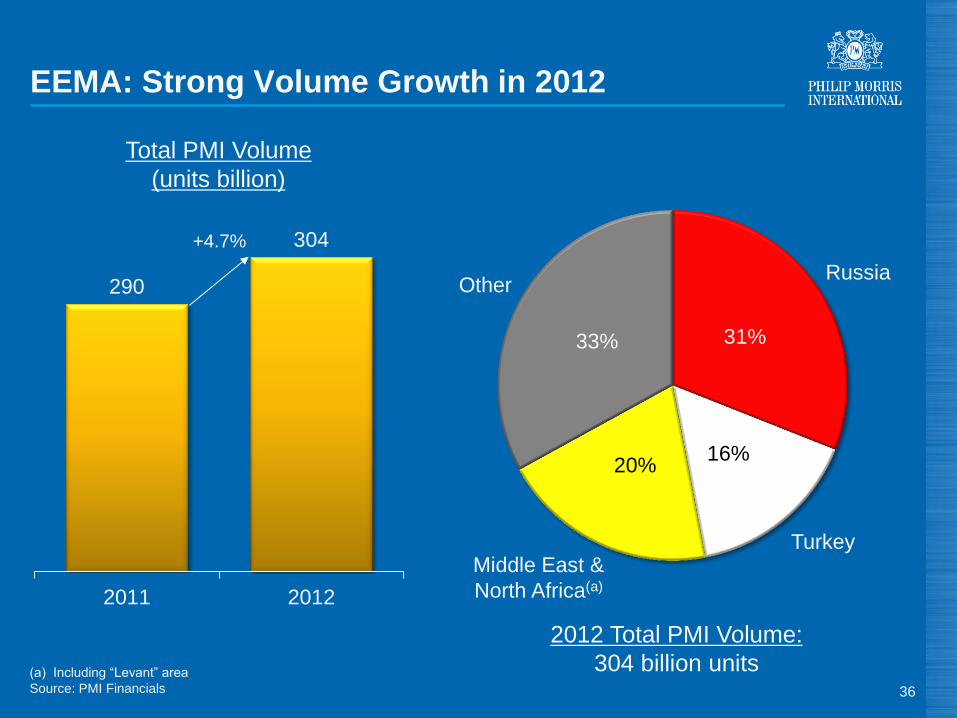

(a) Including “Levant” area

Source: PMI Financials

EEMA: Strong Volume Growth in 2012

36

31%

16% 20%

33%

2012 Total PMI Volume:

304 billion units

Russia

Turkey

Other 290

304

2011 2012

Total PMI Volume

(units billion)

+4.7%

Middle East &

North Africa(a)

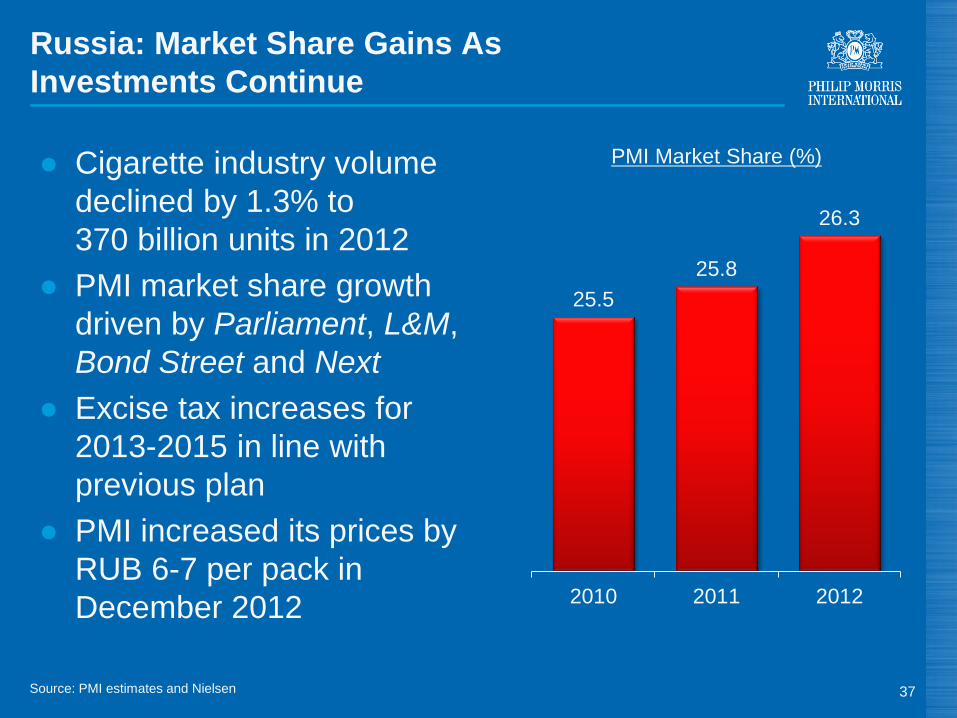

Russia: Market Share Gains As

Investments Continue

37

25.5

25.8

26.3

2010 2011 2012

PMI Market Share (%)

Source: PMI estimates and Nielsen

● Cigarette industry volume

declined by 1.3% to

370 billion units in 2012

● PMI market share growth

driven by Parliament, L&M,

Bond Street and Next

● Excise tax increases for

2013-2015 in line with

previous plan

● PMI increased its prices by

RUB 6-7 per pack in

December 2012

Turkey: Record Market Share and Improved Mix

38

19.7 21.1 20.8

5.8 6.3 6.7

16.6 17.4 18.2

42.1 44.8 45.7

2010 2011 2012

PMI Market Share (%)

Source: PMI estimates and Nielsen

● Total industry volume grew

by 8.8% in 2012 to

99 billion units

● PMI share increased and

mix improved

● PMI increased retail prices

by TRL 1.00 per pack

following January 2013

tax increase

● Relatively stable

underlying industry volume

trend

Premium

Mid

Low

Source: PMI estimates and PMI Financials

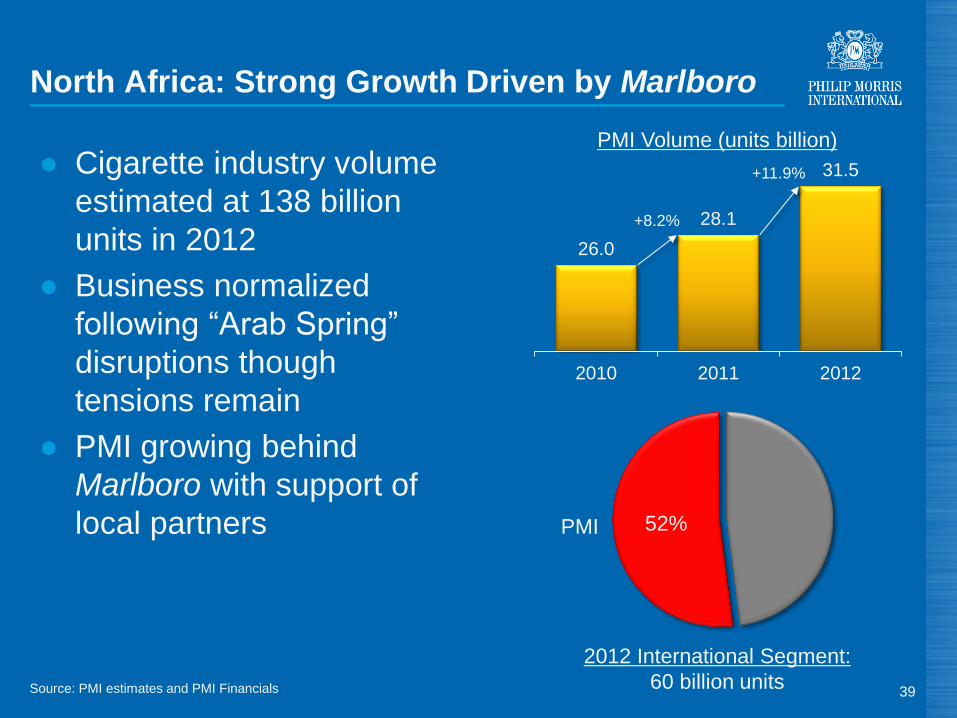

52%

26.0

28.1

31.5

2010 2011 2012

North Africa: Strong Growth Driven by Marlboro

39

● Cigarette industry volume

estimated at 138 billion

units in 2012

● Business normalized

following “Arab Spring”

disruptions though

tensions remain

● PMI growing behind

Marlboro with support of

local partners

PMI Volume (units billion)

2012 International Segment:

60 billion units

+8.2%

+11.9%

PMI

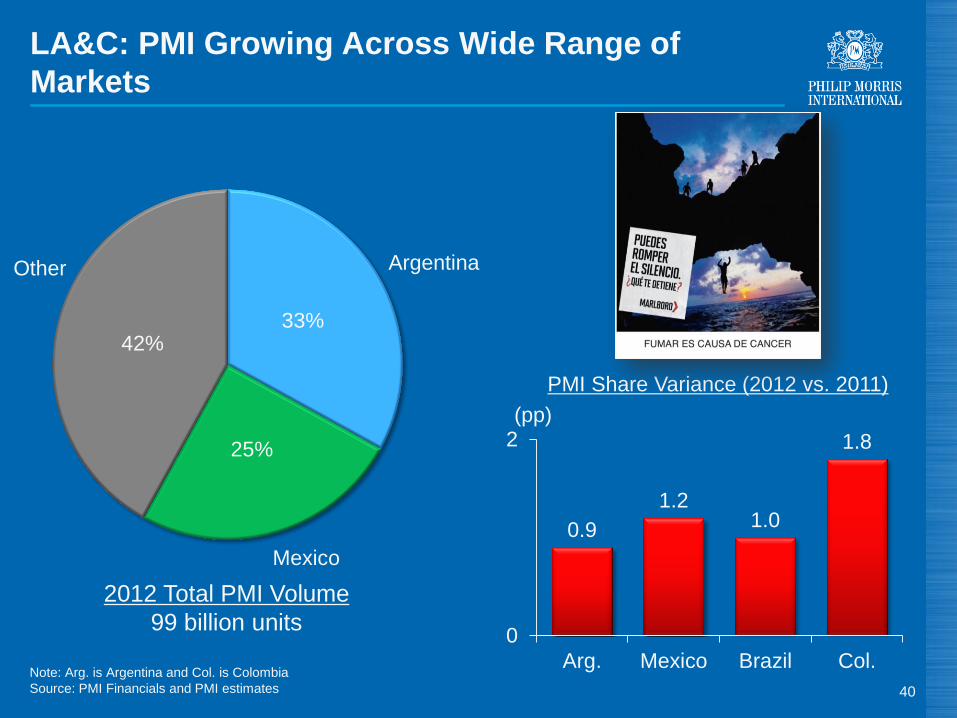

Note: Arg. is Argentina and Col. is Colombia

Source: PMI Financials and PMI estimates

LA&C: PMI Growing Across Wide Range of

Markets

40

0.9

1.2 1.0

1.8

0

2

Arg. Mexico Brazil Col.

PMI Share Variance (2012 vs. 2011)

Argentina

(pp)

33%

25%

42%

2012 Total PMI Volume

99 billion units

Mexico

Other

PMI: Superior Brand Portfolio

Mid-Price

Premium

& Above

Local Heritage International

Low-Price

Note: Pack designs are for illustrative purposes only 41

42

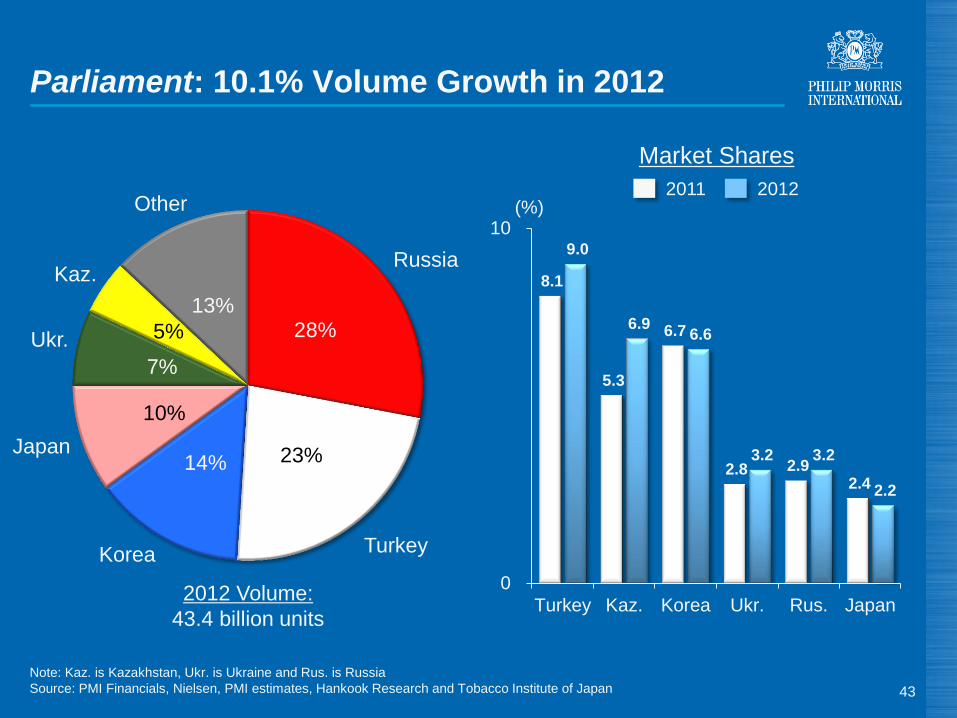

Note: Kaz. is Kazakhstan, Ukr. is Ukraine and Rus. is Russia

Source: PMI Financials, Nielsen, PMI estimates, Hankook Research and Tobacco Institute of Japan

Parliament: 10.1% Volume Growth in 2012

43

28%

23% 14%

10%

7%

5%

13%

Ukr.

Japan

Russia

Turkey

Kaz.

Korea

Other

8.1

5.3

6.7

2.8 2.9 2.4

9.0

6.9 6.6

3.2 3.2

2.2

0

10

Turkey Kaz. Korea Ukr. Rus. Japan

Market Shares

(%)

2012 Volume:

43.4 billion units

2011 2012

44

(a) Includes above premium

(b) Data currently under review following expansion of Nielsen coverage

(c) Excluding China and duty free

Note: SoM stands for share of market

Source: PMI estimates and Nielsen

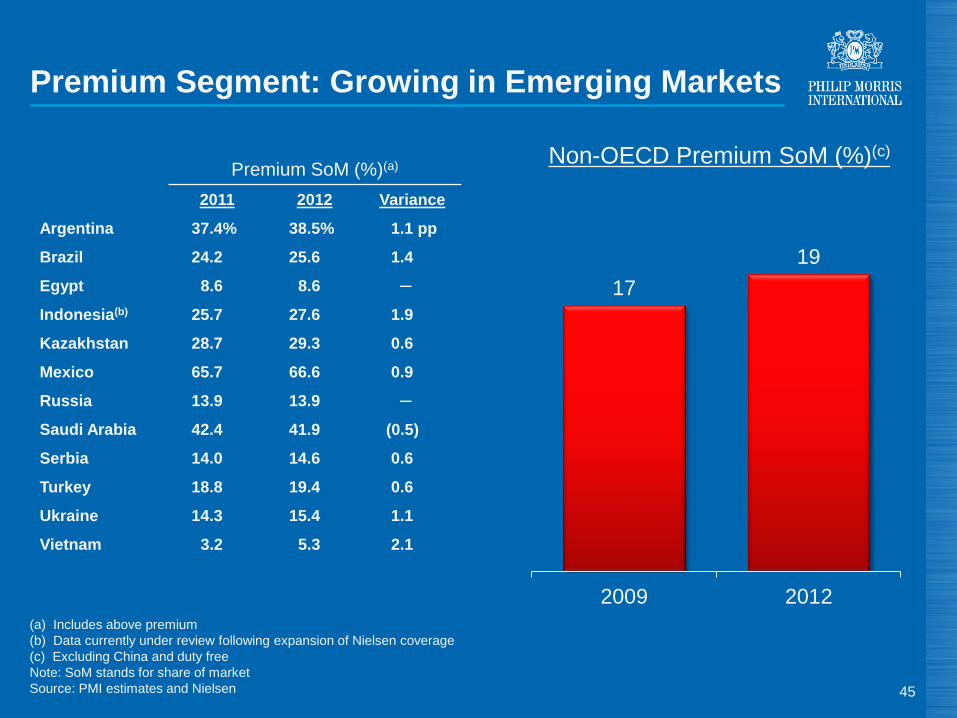

Premium Segment: Growing in Emerging Markets

45

17

19

2009 2012

Non-OECD Premium SoM (%)(c)

Premium SoM (%)(a)

2011 2012 Variance

Argentina 37.4% 38.5% 1.1 pp

Brazil 24.2 25.6 1.4

Egypt 8.6 8.6 ─

Indonesia(b) 25.7 27.6 1.9

Kazakhstan 28.7 29.3 0.6

Mexico 65.7 66.6 0.9

Russia 13.9 13.9 ─

Saudi Arabia 42.4 41.9

Serbia 14.0 14.6 0.6

Turkey 18.8 19.4 0.6

Ukraine 14.3 15.4 1.1

Vietnam 3.2 5.3 2.1

(0.5)

(a) Includes above premium

(b) Data currently under review following expansion of Nielsen coverage

Note: Arg. is Argentina, Indon. is Indonesia, Kaz. is Kazakhstan, Mex. is Mexico, Rus. is Russia, Saudi is Saudi Arabia and Ukr. is Ukraine

Source: PMI estimates and Nielsen

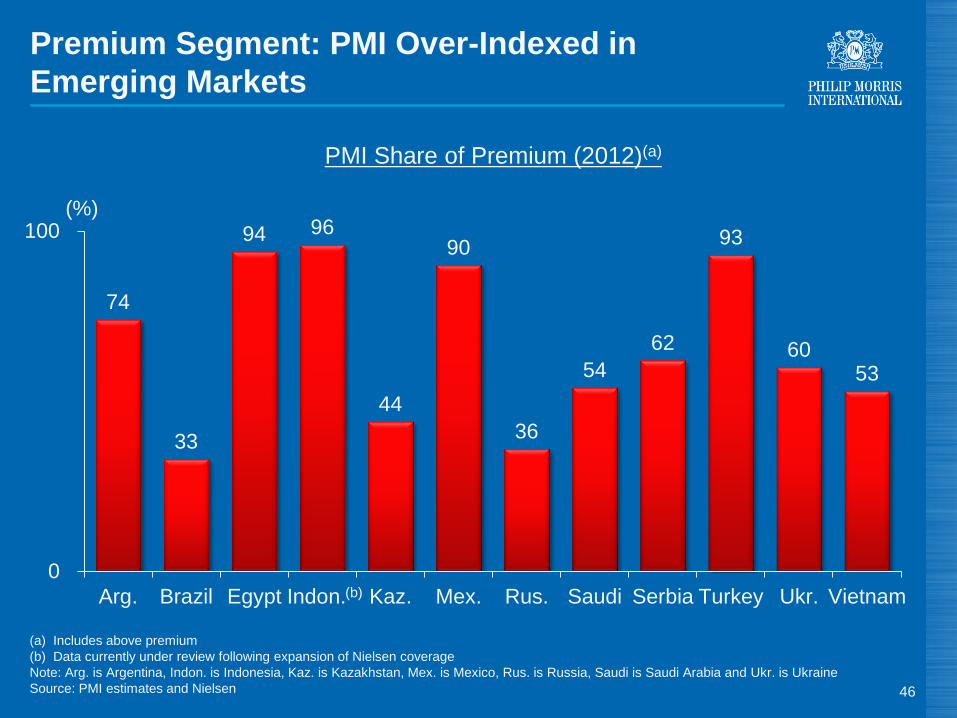

Premium Segment: PMI Over-Indexed in

Emerging Markets

46

74

33

94 96

44

90

36

54

62

93

60 53

0

100

Arg. Brazil Egypt Indon. Kaz. Mex. Rus. Saudi Serbia Turkey Ukr. Vietnam

PMI Share of Premium (2012)(a)

(%)

(b)

(a) Includes above premium

Source: PMI estimates

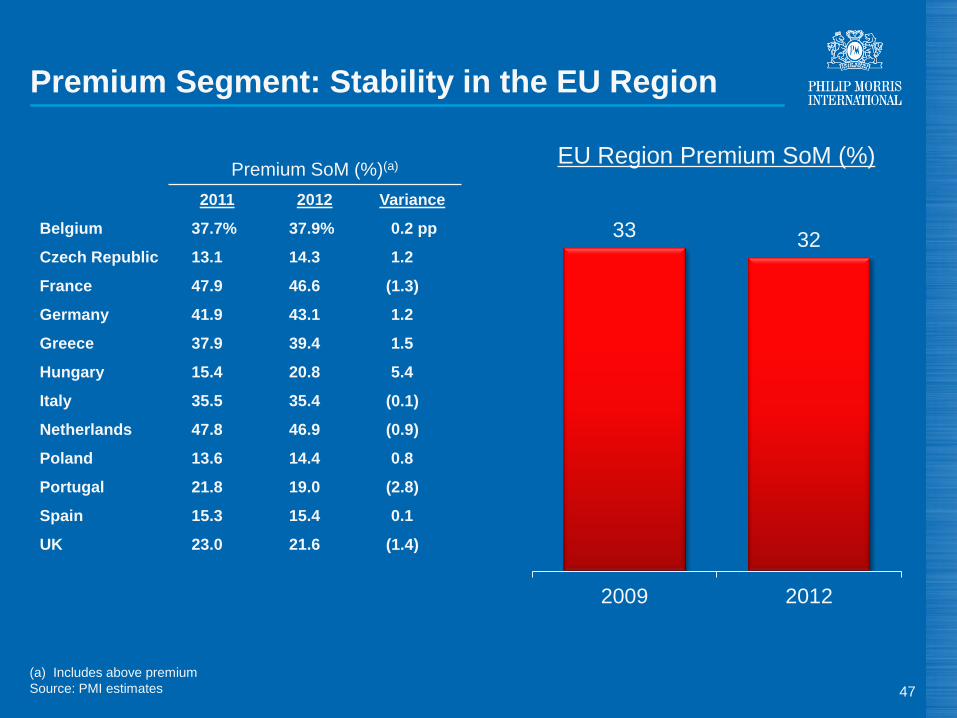

Premium Segment: Stability in the EU Region

Premium SoM (%)(a)

2011 2012 Variance

Belgium 37.7% 37.9% 0.2 pp

Czech Republic 13.1 14.3 1.2

France 47.9 46.6

Germany 41.9 43.1 1.2

Greece 37.9 39.4 1.5

Hungary 15.4 20.8 5.4

Italy 35.5 35.4

Netherlands 47.8 46.9

Poland 13.6 14.4 0.8

Portugal 21.8 19.0

Spain 15.3 15.4 0.1

UK 23.0 21.6

47

33 32

2009 2012

EU Region Premium SoM (%)

(1.3)

(0.1)

(0.9)

(2.8)

(1.4)

48

Source: PMI Financials

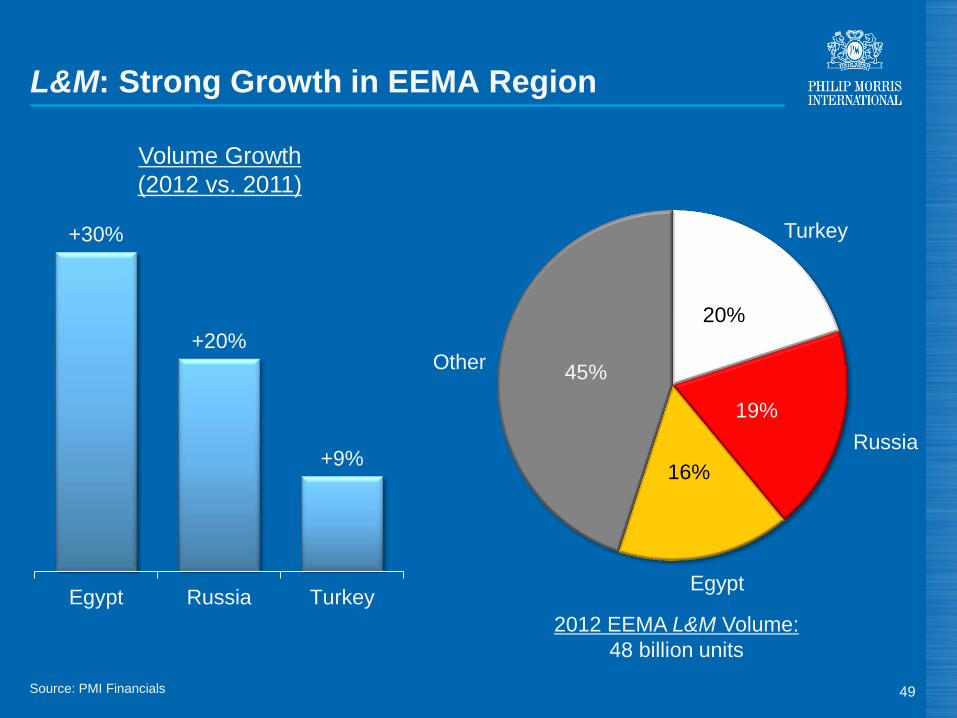

L&M: Strong Growth in EEMA Region

49

20%

19%

16%

45%

2012 EEMA L&M Volume:

48 billion units

Turkey

Russia

Egypt

Other

+30%

+20%

+9%

Egypt Russia Turkey

Volume Growth

(2012 vs. 2011)

Additional Growth Opportunities for PMI

● Geographic expansion

● Reduction in illicit trade

● Next Generation Products ("NGPs")

50

Source: PMI estimates and Nielsen

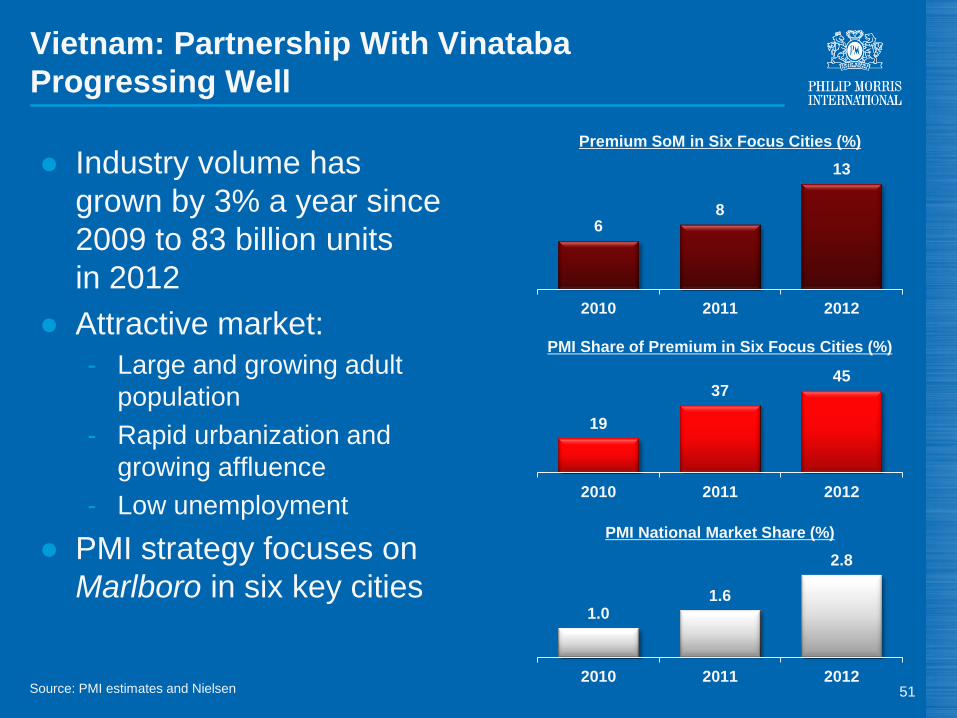

Vietnam: Partnership With Vinataba

Progressing Well

51

● Industry volume has

grown by 3% a year since

2009 to 83 billion units

in 2012

● Attractive market:

- Large and growing adult

population

- Rapid urbanization and

growing affluence

- Low unemployment

● PMI strategy focuses on

Marlboro in six key cities 1.0

1.6

2.8

2010 2011 2012

19

37 45

2010 2011 2012

6 8

13

2010 2011 2012

Premium SoM in Six Focus Cities (%)

PMI Share of Premium in Six Focus Cities (%)

PMI National Market Share (%)

Illicit Trade: Both an Opportunity and a Risk

● Estimated volume worldwide: 600 billion units

● Growing illicit trade category is “illicit whites”

52

Note: “Illicit whites” are branded cigarettes manufactured purely for export and resale without paying any taxes

Source: PMI estimates

Illicit Trade: Multi-Faceted Strategy

● Comprehensive approach by private and public sectors is

essential

● Need to tackle supply and demand

● PMI agreements with OLAF and INTERPOL

● WHO FCTC protocol on illicit trade

● Educational programs

53

Note: OLAF refers to the European Anti-Fraud Office. INTERPOL refers to the International Criminal Police Organization. WHO FCTC refers to the

WHO Framework Convention on Tobacco Control

NGPs: Steady Progress

● Clinical studies

● Perception and behavioral research

● Establishment of production facilities

● Addressing the regulatory environment

54

Platform 1 Platform 2 Platform 3

Free Cash Flow: Outlook

● Anticipate strong increase in currency-neutral free cash

flow in 2013

● Project free cash flow growth rate to exceed that of net

earnings in 2013

● Capex will increase over next few years:

- Additional capacity in Indonesia

- NGP manufacturing

● Forestalling-related inventory requirements expected to

fluctuate

55

Source: PMI Forecasts

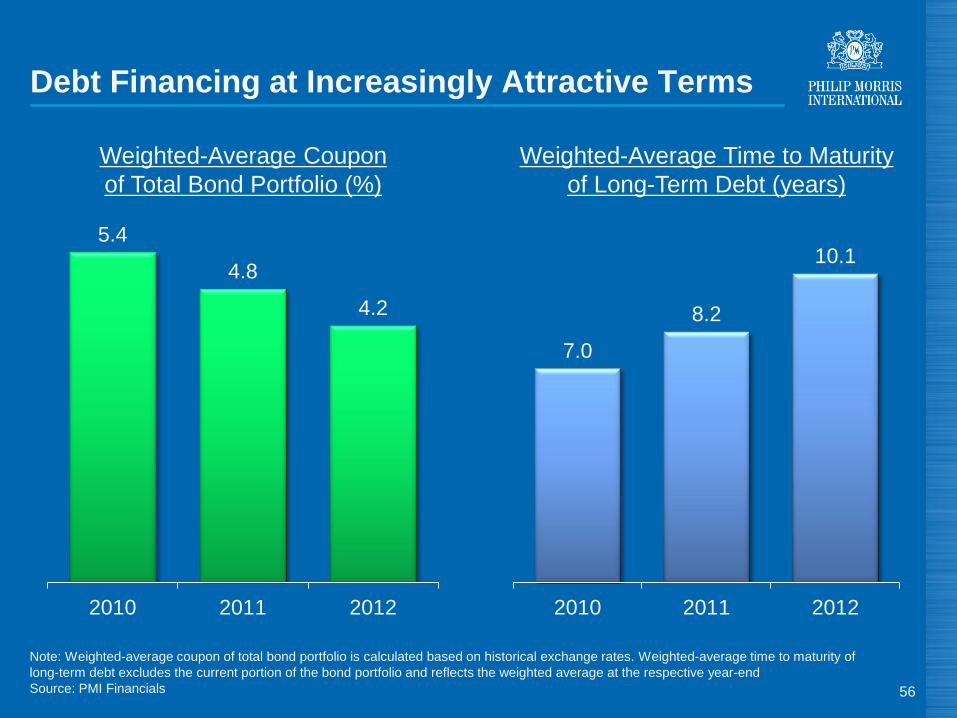

Debt Financing at Increasingly Attractive Terms

56

7.0

8.2

10.1

2010 2011 2012

5.4

4.8

4.2

2010 2011 2012

Weighted-Average Coupon

of Total Bond Portfolio (%)

Weighted-Average Time to Maturity

of Long-Term Debt (years)

Note: Weighted-average coupon of total bond portfolio is calculated based on historical exchange rates. Weighted-average time to maturity of

long-term debt excludes the current portion of the bond portfolio and reflects the weighted average at the respective year-end

Source: PMI Financials

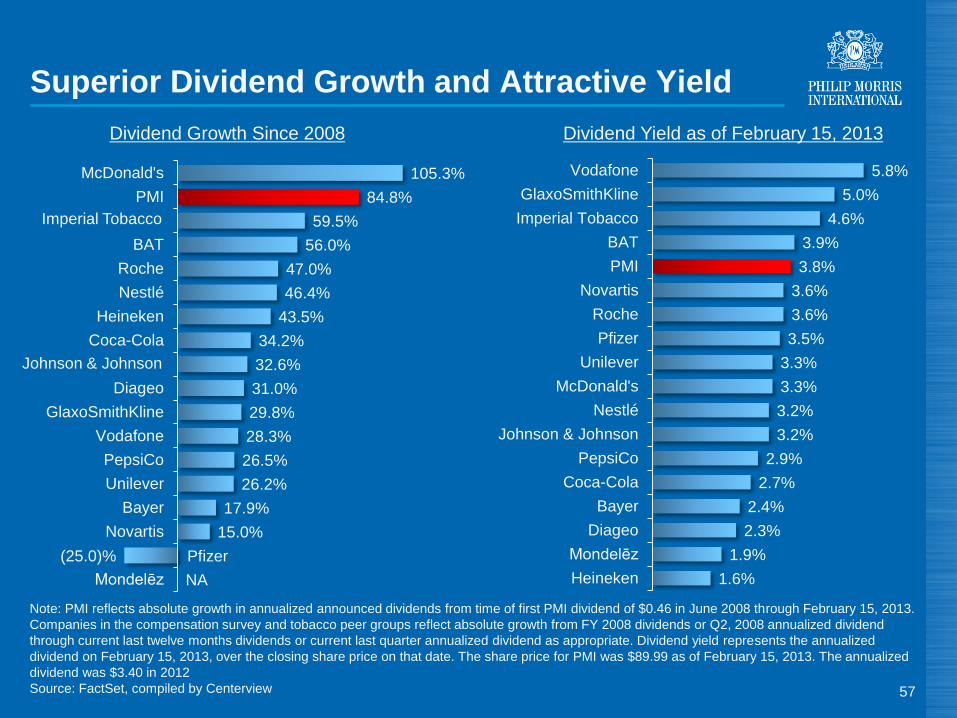

NA

(25.0)%

15.0%

17.9%

26.2%

26.5%

28.3%

29.8%

31.0%

32.6%

34.2%

43.5%

46.4%

47.0%

56.0%

59.5%

84.8%

105.3%

Mondelēz

Novartis

Bayer

Unilever

PepsiCo

Vodafone

GlaxoSmithKline

Diageo

Coca-Cola

Heineken

Nestlé

Roche

BAT

PMI

McDonald's

Superior Dividend Growth and Attractive Yield

57

Note: PMI reflects absolute growth in annualized announced dividends from time of first PMI dividend of $0.46 in June 2008 through February 15, 2013.

Companies in the compensation survey and tobacco peer groups reflect absolute growth from FY 2008 dividends or Q2, 2008 annualized dividend

through current last twelve months dividends or current last quarter annualized dividend as appropriate. Dividend yield represents the annualized

dividend on February 15, 2013, over the closing share price on that date. The share price for PMI was $89.99 as of February 15, 2013. The annualized

dividend was $3.40 in 2012

Source: FactSet, compiled by Centerview

Dividend Growth Since 2008

Pfizer

Imperial Tobacco

Johnson & Johnson

1.6%

1.9%

2.3%

2.4%

2.7%

2.9%

3.2%

3.2%

3.3%

3.3%

3.5%

3.6%

3.6%

3.8%

3.9%

4.6%

5.0%

5.8%

Heineken

Mondelēz

Diageo

Bayer

Coca-Cola

PepsiCo

Johnson & Johnson

Nestlé

McDonald's

Unilever

Pfizer

Roche

Novartis

PMI

BAT

Imperial Tobacco

GlaxoSmithKline

Vodafone

Dividend Yield as of February 15, 2013

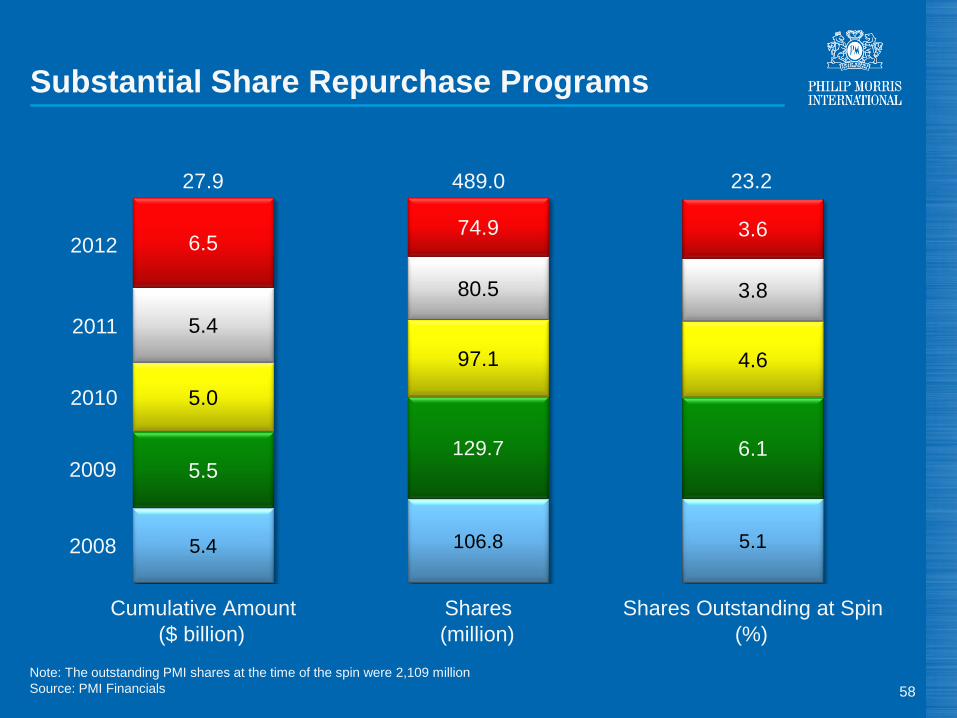

Substantial Share Repurchase Programs

58

Note: The outstanding PMI shares at the time of the spin were 2,109 million

Source: PMI Financials

5.4

5.5

5.0

5.4

6.5

Cumulative Amount

5.1

6.1

4.6

3.8

3.6

Shares Outstanding at Spin

27.9

($ billion)

23.2

(million) (%)

2010

2009

2008

489.0

106.8

129.7

97.1

80.5

74.9

Shares

2011

2012

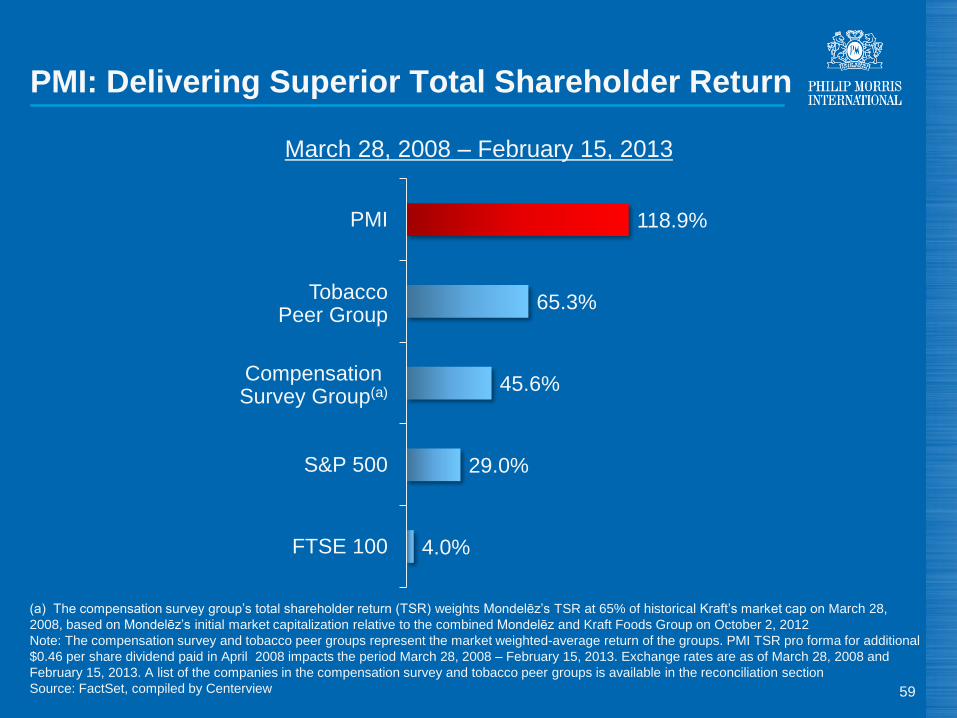

PMI: Delivering Superior Total Shareholder Return

59

4.0%

29.0%

45.6%

65.3%

118.9%

FTSE 100

S&P 500

PMI

Compensation Survey Group(a)

(a) The compensation survey group’s total shareholder return (TSR) weights Mondelēz’s TSR at 65% of historical Kraft’s market cap on March 28,

2008, based on Mondelēz’s initial market capitalization relative to the combined Mondelēz and Kraft Foods Group on October 2, 2012

Note: The compensation survey and tobacco peer groups represent the market weighted-average return of the groups. PMI TSR pro forma for additional

$0.46 per share dividend paid in April 2008 impacts the period March 28, 2008 – February 15, 2013. Exchange rates are as of March 28, 2008 and

February 15, 2013. A list of the companies in the compensation survey and tobacco peer groups is available in the reconciliation section

Source: FactSet, compiled by Centerview

Tobacco Peer Group

March 28, 2008 – February 15, 2013

PMI: Why We Are An Attractive Investment

● Tobacco sector has attractive business fundamentals

● PMI outperformance based on:

- Volume growth and share momentum

- World-class portfolio of brands

- Truly global footprint with leading position in emerging markets

- Innovation

- Superior conversion of revenues into cash

- Robust capital structure

● Steadfast commitment to shareholder value: over $50

billion returned to our shareholders since 2008 through a

balanced program of higher dividends and substantial

share repurchases

60

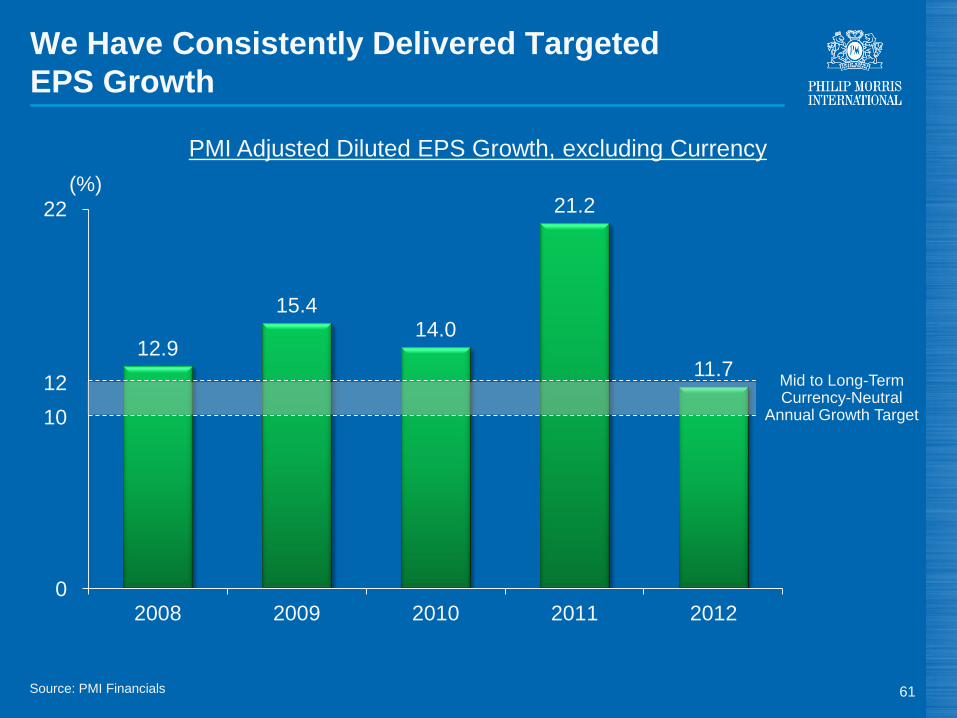

We Have Consistently Delivered Targeted

EPS Growth

61

12.9

15.4 14.0

21.2

11.7

0

22

2008 2009 2010 2011 2012

Mid to Long-Term Currency-Neutral

Annual Growth Target

PMI Adjusted Diluted EPS Growth, excluding Currency

Source: PMI Financials

10

12

0

22

(%)

62

Consumer Analyst Group of New York

(CAGNY) Conference

February 20, 2013

Jacek Olczak

Chief Financial Officer

Philip Morris International

Glossary and Reconciliation of

Non-GAAP Measures

65

Glossary

● Unless otherwise stated, results are compared with those of the same period

in the preceding year

● PMI stands for Philip Morris International Inc. and its subsidiaries

● PMI volumes refer to PMI cigarette shipment data, unless otherwise stated

● References to total international cigarette market, total cigarette market, total

market and market shares reflect our best estimates based on a number of

international and external sources

● Organic volume refers to volume excluding acquisitions

● Acquisitions, for the purposes of this presentation, also include our business

combination with Fortune Tobacco Corporation in the Philippines

● Net revenues exclude excise taxes

● OCI stands for Operating Companies Income, which is defined as operating

income before general corporate expenses and the amortization of

intangibles. OCI growth rates are on an adjusted basis which excludes asset

impairment, exit and other costs

● Adjusted OCI is defined as reported OCI adjusted for asset impairment, exit

and other costs

66

Glossary

● The Japan hurdle refers to the 6.3 billion units of additional volume shipped in

the second quarter of 2011 as a result of the disruption of our principal

competitor's supply chain following the natural disaster in March 2011

● OECD stands for Organisation for Economic Co-operation and Development

● EEMA refers to the Eastern Europe, Middle East & Africa Region

● EU refers to the European Union Region

● LA&C refers to the Latin America & Canada Region

● EU TPD stands for the EU Tobacco Products Directive

● Free cash flow is defined as net cash provided by operating activities less

capital expenditures

● Southern Europe includes Andorra, Canary Islands, Cyprus, Greece, Italy,

Malta, Portugal and Spain

● OTP stands for other tobacco products, including cigars, cigarillos, fine cut,

pipe tobacco and snus

● Fine cut includes Make Your Own (MYO), MYO Volume Tobacco and Roll

Your Own (RYO)

● Fine cut converted to cigarette equivalent on the basis of 0.60g per unit for

MYO Volume Tobacco and RYO, and 0.73g per unit for MYO

Glossary

67

● Illicit trade refers to domestic non-tax paid products

● The Middle East includes Azerbaijan, Bahrain, Iran, Iraq, Kuwait, Oman,

Qatar, Saudi Arabia, United Arab Emirates (UAE) and Yemen

● North Africa includes Algeria, Egypt, Libya, Morocco and Tunisia

● Levant area includes Jordan, Lebanon, the Palestine Authority Area (PAA)

and Syria

● SoM stands for share of market

PMI Peer Groups

- BAT

- Bayer

- Coca-Cola

- Diageo

- GlaxoSmithKline

- Heineken

- Imperial Tobacco

- Johnson & Johnson

- Kraft(a)

- McDonald’s

- Mondelēz International(b)

- Nestlé

- Novartis

- PepsiCo

- Pfizer

- Roche

- Unilever

- Vodafone

Compensation Survey Group

- Altria

- BAT

- Imperial Tobacco

- Japan Tobacco

- Lorillard

- Reynolds American

Tobacco Peer Group

(a) Effective until September 30, 2012

(b) Effective as of October 1, 2012 68

69

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Calculation of Adjusted Operating Companies Income Margins

($ in millions)

(Unaudited)

European Union 4,195$ (137)$ 4,332$ 26,829$ 17,994$ 8,835$ 49.0%

EEMA 2,431 (12) 2,443 12,166 5,820 6,346 38.5%

Asia 1,803 (28) 1,831 11,097 5,449 5,648 32.4%

Latin America & Canada 514 (18) 532 5,151 3,170 1,981 26.9%

PMI Total 8,943$ (195)$ 9,138$ 55,243$ 32,433$ 22,810$ 40.1%

European Union 4,738$ (66)$ 4,804$ 30,265$ 20,577$ 9,688$ 49.6%

EEMA 3,119 (1) 3,120 14,817 7,313 7,504 41.6%

Asia 2,057 (14) 2,071 12,222 6,037 6,185 33.5%

Latin America & Canada 520 (127) 647 6,336 4,008 2,328 27.8%

PMI Total 10,434$ (208)$ 10,642$ 63,640$ 37,935$ 25,705$ 41.4%

For the Year Ended December 31, 2008

Reported

Operating

Companies

Income

Less Asset

Impairment,

Exit Costs

and Other

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

Reported

Operating

Companies

Income

Less Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

For the Year Ended December 31, 2007

(a) Includes equity loss from RBH Legal Settlement ($124 million)

(a)

70

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Calculation of Adjusted Operating Companies Income Margins

($ in millions)

(Unaudited)

European Union 4,506$ (29)$ 4,535$ 28,550$ 19,509$ 9,041$ 50.2%

EEMA 2,663 - 2,663 13,865 7,070 6,795 39.2%

Asia 2,436 - 2,436 12,413 5,885 6,528 37.3%

Latin America & Canada 666 (135) 801 7,252 4,581 2,671 30.0%

PMI Total 10,271$ (164)$ 10,435$ 62,080$ 37,045$ 25,035$ 41.7%

European Union 4,311$ (27)$ 4,338$ 28,050$ 19,239$ 8,811$ 49.2%

EEMA 3,152 - 3,152 15,928 8,519 7,409 42.5%

Asia 3,049 (20) 3,069 15,235 7,300 7,935 38.7%

Latin America & Canada 953 - 953 8,500 5,447 3,053 31.2%

PMI Total 11,465$ (47)$ 11,512$ 67,713$ 40,505$ 27,208$ 42.3%

For the Year Ended December 31, 2009

Reported

Operating

Companies

Income

Less Asset

Impairment,

Exit Costs

and Other

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

For the Year Ended December 31, 2010

Reported

Operating

Companies

Income

Less Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

(a)

(a) Represents the 2009 Colombian Investment and Cooperation Agreement charge

71

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Calculation of Adjusted Operating Companies Income Margins

($ in millions)

(Unaudited)

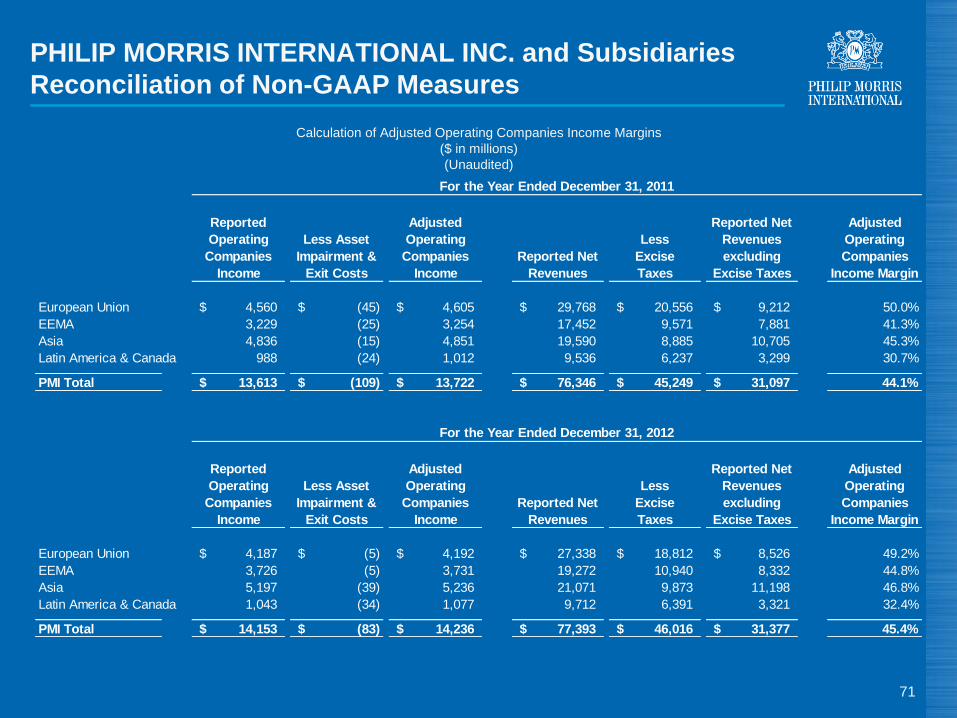

European Union 4,560$ (45)$ 4,605$ 29,768$ 20,556$ 9,212$ 50.0%

EEMA 3,229 (25) 3,254 17,452 9,571 7,881 41.3%

Asia 4,836 (15) 4,851 19,590 8,885 10,705 45.3%

Latin America & Canada 988 (24) 1,012 9,536 6,237 3,299 30.7%

PMI Total 13,613$ (109)$ 13,722$ 76,346$ 45,249$ 31,097$ 44.1%

European Union 4,187$ (5)$ 4,192$ 27,338$ 18,812$ 8,526$ 49.2%

EEMA 3,726 (5) 3,731 19,272 10,940 8,332 44.8%

Asia 5,197 (39) 5,236 21,071 9,873 11,198 46.8%

Latin America & Canada 1,043 (34) 1,077 9,712 6,391 3,321 32.4%

PMI Total 14,153$ (83)$ 14,236$ 77,393$ 46,016$ 31,377$ 45.4%

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

For the Year Ended December 31, 2012

Reported

Operating

Companies

Income

Less Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Adjusted

Operating

Companies

Income Margin

For the Year Ended December 31, 2011

Reported

Operating

Companies

Income

Less Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income

Reported Net

Revenues

Less

Excise

Taxes

72

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Adjustments for the Impact of Currency and Acquisitions

For the Years Ended December 31,

($ in millions)

(Unaudited)

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Less

Currency

Reported Net

Revenues

excluding

Excise Taxes &

Currency

Less

Acquisi-

tions

Reported Net

Revenues

excluding

Excise Taxes,

Currency &

Acquisitions

Reported Net

Revenues

Less

Excise

Taxes

Reported Net

Revenues

excluding

Excise Taxes

Reported

Reported

excluding

Currency

Reported

excluding

Currency &

Acquisitions

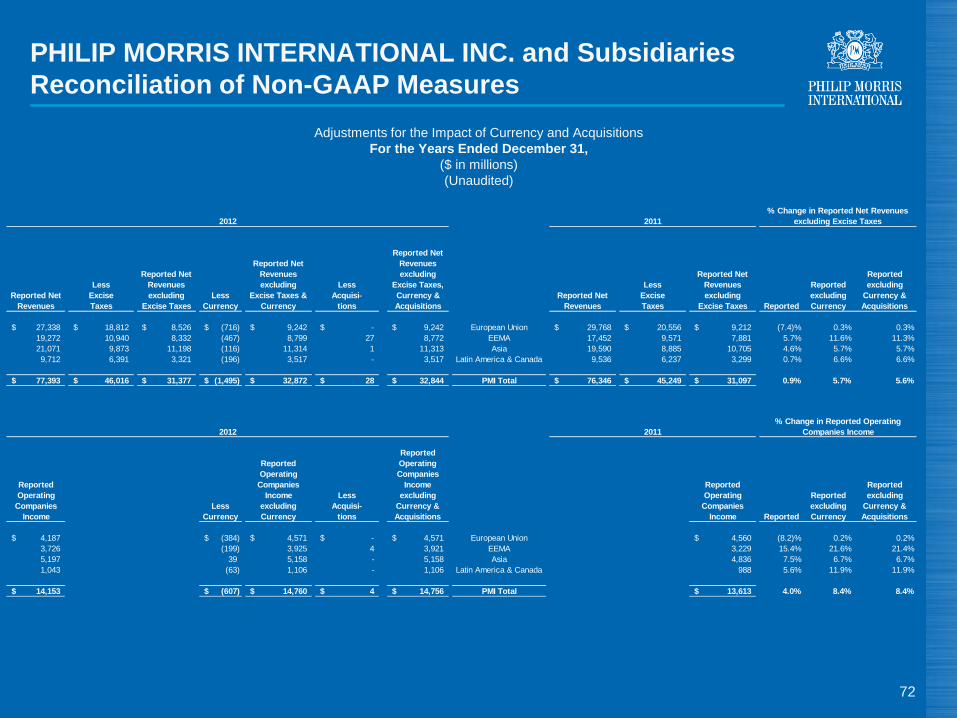

27,338$ 18,812$ 8,526$ (716)$ 9,242$ -$ 9,242$ European Union 29,768$ 20,556$ 9,212$ (7.4)% 0.3% 0.3%

19,272 10,940 8,332 (467) 8,799 27 8,772 EEMA 17,452 9,571 7,881 5.7% 11.6% 11.3%

21,071 9,873 11,198 (116) 11,314 1 11,313 Asia 19,590 8,885 10,705 4.6% 5.7% 5.7%

9,712 6,391 3,321 (196) 3,517 - 3,517 Latin America & Canada 9,536 6,237 3,299 0.7% 6.6% 6.6%

77,393$ 46,016$ 31,377$ (1,495)$ 32,872$ 28$ 32,844$ PMI Total 76,346$ 45,249$ 31,097$ 0.9% 5.7% 5.6%

Reported

Operating

Companies

Income

Less

Currency

Reported

Operating

Companies

Income

excluding

Currency

Less

Acquisi-

tions

Reported

Operating

Companies

Income

excluding

Currency &

Acquisitions

Reported

Operating

Companies

Income

Reported

Reported

excluding

Currency

Reported

excluding

Currency &

Acquisitions

4,187$ (384)$ 4,571$ -$ 4,571$ European Union 4,560$ (8.2)% 0.2% 0.2%

3,726 (199) 3,925 4 3,921 EEMA 3,229 15.4% 21.6% 21.4%

5,197 39 5,158 - 5,158 Asia 4,836 7.5% 6.7% 6.7%

1,043 (63) 1,106 - 1,106 Latin America & Canada 988 5.6% 11.9% 11.9%

14,153$ (607)$ 14,760$ 4$ 14,756$ PMI Total 13,613$ 4.0% 8.4% 8.4%

2012 2011

% Change in Reported Operating

Companies Income

2012 2011

% Change in Reported Net Revenues

excluding Excise Taxes

73

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Reconciliation of Reported Operating Companies Income to Adjusted Operating Companies Income &

Reconciliation of Adjusted Operating Companies Income Margin, excluding Currency and Acquisitions

For the Years Ended December 31,

($ in millions)

(Unaudited)

Reported

Operating

Companies

Income

Less

Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income

Less

Currency

Adjusted

Operating

Companies

Income

excluding

Currency

Less

Acquisi-

tions

Adjusted

Operating

Companies

Income

excluding

Currency &

Acquisitions

Reported

Operating

Companies

Income

Less

Asset

Impairment &

Exit Costs

Adjusted

Operating

Companies

Income Adjusted

Adjusted

excluding

Currency

Adjusted

excluding

Currency &

Acquisitions

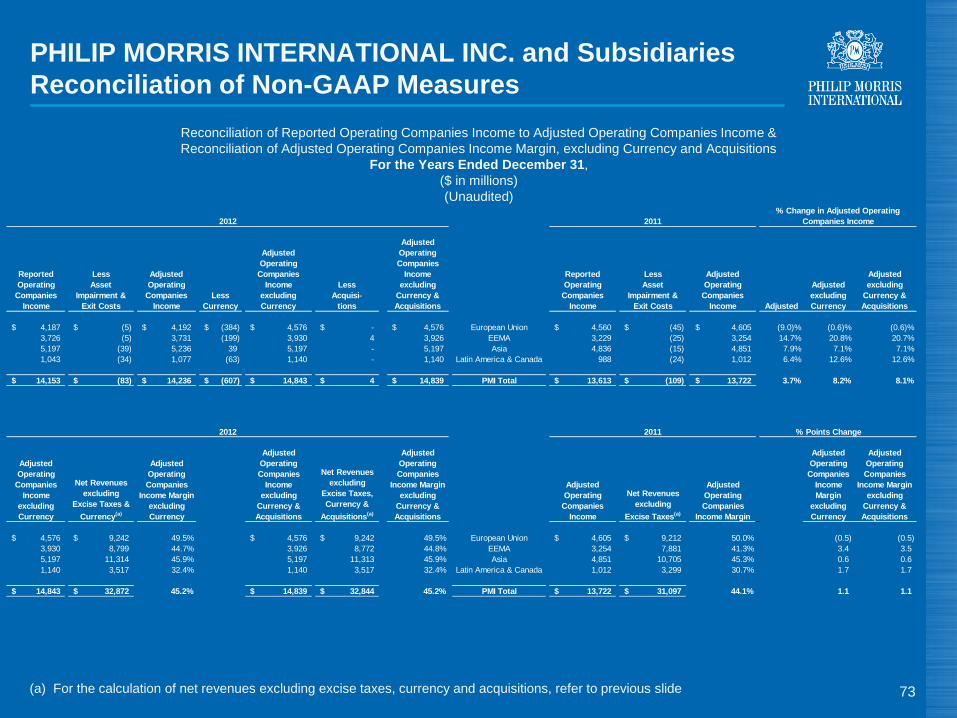

4,187$ (5)$ 4,192$ (384)$ 4,576$ -$ 4,576$ European Union 4,560$ (45)$ 4,605$ (9.0)% (0.6)% (0.6)%

3,726 (5) 3,731 (199) 3,930 4 3,926 EEMA 3,229 (25) 3,254 14.7% 20.8% 20.7%

5,197 (39) 5,236 39 5,197 - 5,197 Asia 4,836 (15) 4,851 7.9% 7.1% 7.1%

1,043 (34) 1,077 (63) 1,140 - 1,140 Latin America & Canada 988 (24) 1,012 6.4% 12.6% 12.6%

14,153$ (83)$ 14,236$ (607)$ 14,843$ 4$ 14,839$ PMI Total 13,613$ (109)$ 13,722$ 3.7% 8.2% 8.1%

% Points Change

Adjusted

Operating

Companies

Income

excluding

Currency

Net Revenues

excluding

Excise Taxes &

Currency(a)

Adjusted

Operating

Companies

Income Margin

excluding

Currency

Adjusted

Operating

Companies

Income

excluding

Currency &

Acquisitions

Net Revenues

excluding

Excise Taxes,

Currency &

Acquisitions(a)

Adjusted

Operating

Companies

Income Margin

excluding

Currency &

Acquisitions

Adjusted

Operating

Companies

Income

Net Revenues

excluding

Excise Taxes(a)

Adjusted

Operating

Companies

Income Margin

Adjusted

Operating

Companies

Income

Margin

excluding

Currency

Adjusted

Operating

Companies

Income Margin

excluding

Currency &

Acquisitions

4,576$ 9,242$ 49.5% 4,576$ 9,242$ 49.5% European Union 4,605$ 9,212$ 50.0% (0.5) (0.5)

3,930 8,799 44.7% 3,926 8,772 44.8% EEMA 3,254 7,881 41.3% 3.4 3.5

5,197 11,314 45.9% 5,197 11,313 45.9% Asia 4,851 10,705 45.3% 0.6 0.6

1,140 3,517 32.4% 1,140 3,517 32.4% Latin America & Canada 1,012 3,299 30.7% 1.7 1.7

14,843$ 32,872$ 45.2% 14,839$ 32,844$ 45.2% PMI Total 13,722$ 31,097$ 44.1% 1.1 1.1

2012 2011

2012 2011

% Change in Adjusted Operating

Companies Income

(a) For the calculation of net revenues excluding excise taxes, currency and acquisitions, refer to previous slide

74

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

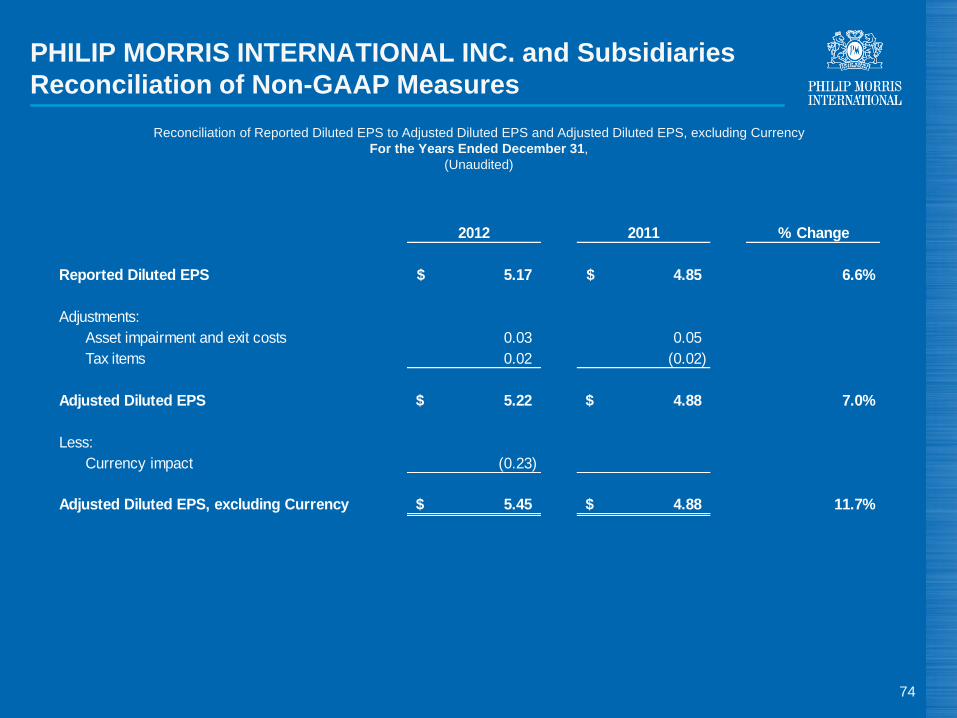

Reconciliation of Reported Diluted EPS to Adjusted Diluted EPS and Adjusted Diluted EPS, excluding Currency

For the Years Ended December 31,

(Unaudited)

2012 2011 % Change

Reported Diluted EPS 5.17$ 4.85$ 6.6%

Adjustments:

Asset impairment and exit costs 0.03 0.05

Tax items 0.02 (0.02)

Adjusted Diluted EPS 5.22$ 4.88$ 7.0%

Less:

Currency impact (0.23)

Adjusted Diluted EPS, excluding Currency 5.45$ 4.88$ 11.7%

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Reconciliation of Reported Diluted EPS to Adjusted Diluted EPS and Adjusted Diluted EPS, excluding Currency

For the Years Ended December 31,

(Unaudited)

75

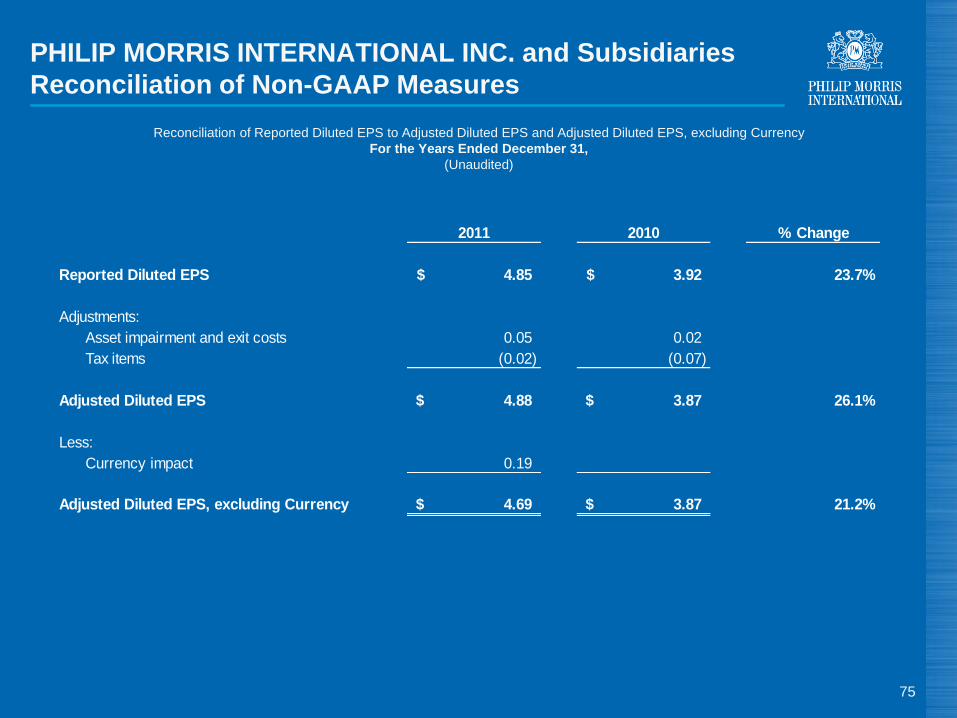

2011 2010 % Change

Reported Diluted EPS 4.85$ 3.92$ 23.7%

Adjustments:

Asset impairment and exit costs 0.05 0.02

Tax items (0.02) (0.07)

Adjusted Diluted EPS 4.88$ 3.87$ 26.1%

Less:

Currency impact 0.19

Adjusted Diluted EPS, excluding Currency 4.69$ 3.87$ 21.2%

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Reconciliation of Reported Diluted EPS to Adjusted Diluted EPS and Adjusted Diluted EPS, excluding Currency

For the Years Ended December 31,

(Unaudited)

76

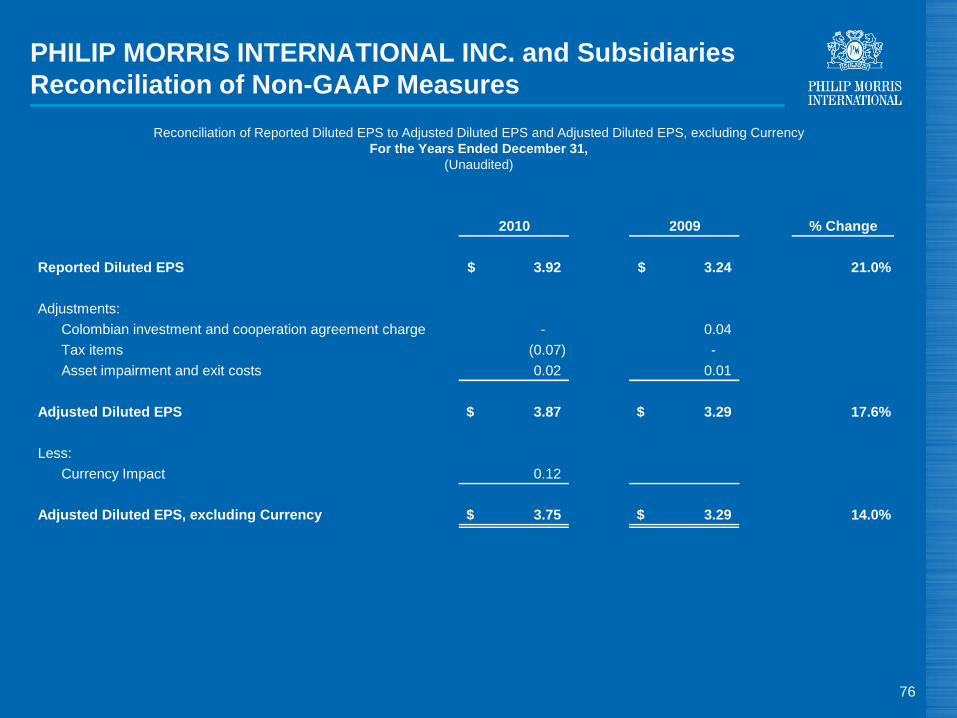

2010 2009 % Change

Reported Diluted EPS 3.92$ 3.24$ 21.0%

Adjustments:

Colombian investment and cooperation agreement charge - 0.04

Tax items (0.07) -

Asset impairment and exit costs 0.02 0.01

Adjusted Diluted EPS 3.87$ 3.29$ 17.6%

Less:

Currency Impact 0.12

Adjusted Diluted EPS, excluding Currency 3.75$ 3.29$ 14.0%

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Reconciliation of Reported Diluted EPS to Adjusted Diluted EPS and Adjusted Diluted EPS, excluding Currency

For the Years Ended December 31,

(Unaudited)

77

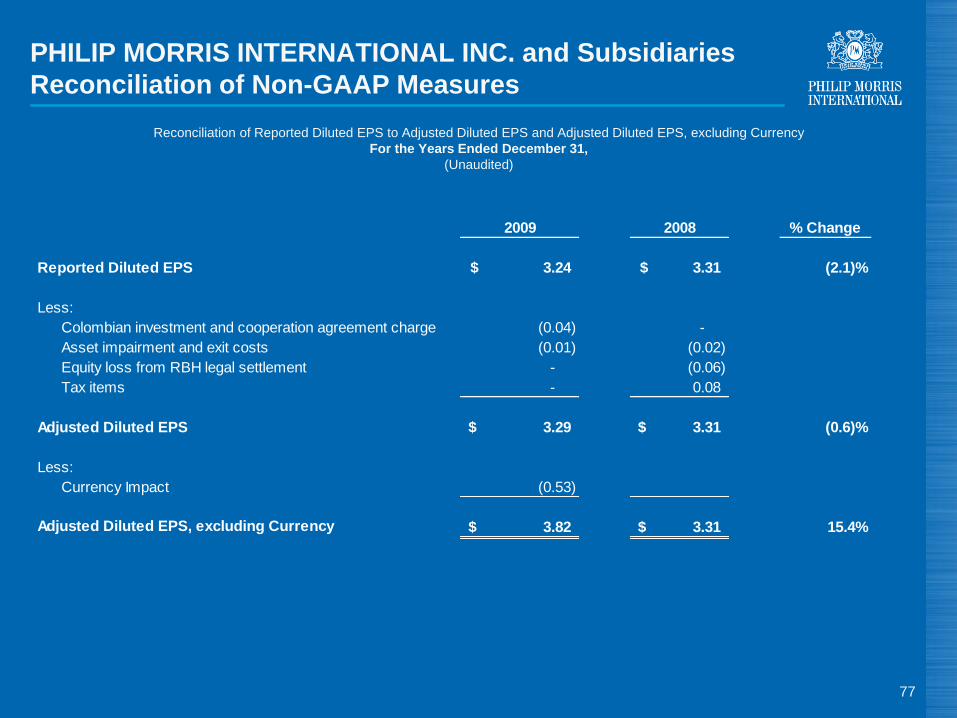

2009 2008 % Change

Reported Diluted EPS 3.24$ 3.31$ (2.1)%

Less:

Colombian investment and cooperation agreement charge (0.04) -

Asset impairment and exit costs (0.01) (0.02)

Equity loss from RBH legal settlement - (0.06)

Tax items - 0.08

Adjusted Diluted EPS 3.29$ 3.31$ (0.6)%

Less:

Currency Impact (0.53)

Adjusted Diluted EPS, excluding Currency 3.82$ 3.31$ 15.4%

78

PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries

Reconciliation of Non-GAAP Measures

Reconciliation of Reported Diluted EPS to Adjusted Diluted EPS &

Adjustments for the Impact of Currency and 2007 Pro Forma

For the Years Ended December 31,

(Unaudited)

Reported (a)(c)

Less Asset

Impairment &

Exit Costs /

Others Adjusted

Less

Currency

Adjusted

excluding

Currency Reported (a)(c)

Less Asset

Impairment &

Exit Costs /

Others Adjusted

Pro Forma (b)

Adjustments

Adjusted

Pro Forma Adjusted

Adjusted

excluding

Currency

3.31 $ - 3.31 $ 0.15 3.16 $ Diluted Earnings Per Share 2.86 $ (0.03) 2.89 $ (0.09) 2.80 $ 18.2% 12.9%

% Change on Diluted

Earnings Per Share 2008 2007

(a) Refer to schedule 11 and 12 in the 2008 Full Year Earnings Release

(b) For details on the pro forma adjustments, please refer to the schedule 14 in the 2008 Full Year Earnings Release

(c) Effective January 1, 2009, PMI adopted the provisions of amended FASB authoritative guidance which requires that unvested share-based

payment awards that contain non-forfeitable rights to dividends are participating securities and therefore shall be included in the earnings per

share calculation pursuant to the two-class method

$ $ $ $

Consumer Analyst Group of New York

(CAGNY) Conference

February 20, 2013

Jacek Olczak

Chief Financial Officer

Philip Morris International

![pm-june-2012 [Read-Only]tobaccoexhibits.musc.edu/wp-content/uploads/2013/11/pm-june-2012-R… · companies: Philip Morris Domestic, Philip Morris International and Philip Morris Industrial](https://img.pdfslide.net/doc/110x75/605e327ad336c824c43fb936/pm-june-2012-read-only-companies-philip-morris-domestic-philip-morris-international.jpg)