Embed Size (px)

Citation preview

I7-§

98th Congress S PRT 98-1872d Session JOINT COMMITEE PRINT

POLICIES FOR INDUSTRIAL GROWTHIN A COMPETITIVE WORLD

A VOLUME OF ESSAYS

PREPARED FOR THE USE OF THE

SUBCOMMITTEE ON ECONOMIC GOALS ANDINTERGOVERNMENTAL POLICY

OF THE

JOINT ECONOMIC COMMITTEECONGRESS OF THE UNITED STATES

28-489 0

APRIL 27, 1984

Printed for the use of the Joint Economic Committee

U.S. GOVERNMENT PRINTING OFFICE

WASHINGTON: 1984

For sale by the Superintendent of Documents, U.S. Government Printing OfficeWashington, D.C. 20402

JOINT ECONOMIC COMMITIEE

[Created pursuant to sec. 5(a) of Public Law 304, 79th Congress]

SENATEROGER W. JEPSEN, Iowa, ChairmanWILLIAM V. ROTH, JR., DelawareJAMES ABDNOR, South DakotaSTEVEN D. SYMMS, IdahoMACK MATTINGLY, GeorgiaALFONSE M. D'AMATO, New YorkLLOYD BENTSEN, TexasWILLIAM PROXMIRE, WisconsinEDWARD M. KENNEDY, MassachusettsPAUL S. SARBANES, Maryland

HOUSE OF REPRESENTATIVESLEE H. HAMILTON, Indiana, Vice Chau7nanGILLIS W. LONG, LouisianaPARREN J. MlCHELL, MarylandAUGUSTUS F. HAWKINS, CaliforniaDAVID R. OBEY, WisconsinJAMES H SCHEUER, New YorkCHALMERS P. WYLIE, OhioMARJORIE S. HOLT, MarylandDANIEL E. LUNGREN, CaliforniaOLYMPIA J. SNOWE, Maine

CHARLMS H. BRADFoRD, Acting Ezecutiue DirectorJAms K. GALBRAH, Deputy Director

SuBCOMMrrEE ON ECONOMIC GOALS AND INTERGOVERNMENTAL PoucY

HOUSE OF REPRESENTATIVESLEE H. HAMILTON, Indiana, ChairmanAUGUSTUS F. HAWKINS, CaliforniaOLYMPIA J. SNOWE, Maine

SENATELLOYD BENTSEN, Texas, Vce ChairmanROGER W. JEPSEN, IowaALFONSE M. D'AMATO, New York

(U)

LETTERS OF TRANSMITTAL.

APRIL 25, 1984.Hon. ROGER W. JEPSEN,Chairman, Joint Economic Committee,Congress of the United States, Washington, D.C.

DEAR MR. CHAIRMAN: I transmit herewith a volume of essays en-titled "Policies for Industrial Growth in a Competitive World."This volume was prepared for the Subcommittee on EconomicGoals and Intergovernmental Policy under the auspices of theOverseas Development Council. It represents a unique collaborativeeffort between the Subcommittee and that organization, which hasproduced an important contribution to a growing national debate.

The volume covers the major practical issues of policies to pro-mote industrial competitiveness-issues which must be facedwhether the United States eventually adopts a formal "industrialpolicy" or not. These issues are: investment policy, technologypolicy, trade policy, labor market policy and antitrust policy. Eachreceives treatment here in a separate, wide-ranging, dispassionateessay. The essays draw on the unique international perspective ofscholars associated with the Overseas Development Council, andprovide readers with a valuable source of comparative informationon the industrial competitiveness efforts of our major allies andtrading partners.

The essays were edited by Richard Newfarmer, formerly of theOverseas Development Council and now with the World Bank. TheSubcommittee is grateful to Dr. Newfarmer, his colleagues and as-sociates at the ODC, and to the contributing authors-KennethFlamm, Lee Price, Michael Podgursky, and David Martin-fortheir work in developing a superior and timely volume of papers.

Editing of these papers was carried out in close association withthe Subcommittee, under the supervision of James K. Galbraith,Deputy Director of the Joint Economic Committee, who has alsocontributed a foreword. Comments on particular essays were pre-pared by Richard Kaufman, Bill Buechner, George Tyler, MaryEccles, and Sandra Masur, of the Committee staff. The views ex-pressed are solely those of the authors, and do not necessarily rep-resent the views of the Overseas Development Council, the WorldBank, any institutions with which individual authors may be affili-ated, or the Joint Economic Committee or its Members.

Sincerely,LEE H. HAMILTON,

Chairman, Subcommittee on Economic Goalsand Intergovernmental Policy.

(liii

Iv

APRIL 19, 1984.Hon. LEE H. HAMILTON,Chairman, Subcommittee, on Economic Goals and Intergovernmen-

tal Policy, Joint Economic Committee, Congress of the UnitedStates, Washington, D.C

DEAR MR. CHAIRMAN: This project originated under the auspicesof the Overseas Development Council. It has been prepared for theJoint Economic Committee under the able editorship of RichardNewfarmer, formerly of the ODC and now with the World Bank.

The Council's interest in industrial policy stems from the factthat the distinction between U.S. domestic and foreign policy inter-ests has become increasingly blurred. The way in which the UnitedStates responds to its domestic economic problems spills over intointernational markets, and strongly affects developing countries,their prospects for growth, and U.S. national interests in ThirdWorld development. The ODC thus felt it would be useful to ad-dress what are at first blush primarily domestic concerns, but withstrong implications for the rest of the world.

Many people have helped with these papers. John Sewell, Presi-dent of the ODC, has been especially supportive. He, together withJohn Lewis, the Director of Studies at ODC and Professor of Eco-nomics at Princeton, provided much useful guidance. In addition,several people have provided extensive comments and encourage-ment: Michael Aho, Douglas Bennet, Douglas Bennett, MichaelBoretsky, William Diebold, Richard Feinberg, John Jackson, Wil-Had Mueller, Leonard Rapping, Daniel Sharp, Kenneth Sharpe,Andrew Wechsler, and Leonard Woodcock.

Special thanks go to Kathy Lynn of the ODC who efficiently andexpeditiously handled much of the administrative burden of theproject and copy edited the final manuscript.

Sincerely,JAMEs K. GALBRArrH,

Deputy Director, Joint Economic Committee.

FOREWORD

By James K. GalbraithDeputy Director, Joint Economic Committee

Not too long ago, the concept of industrial policy was obscure, itsadvocates few in number, their views peripheral to the main cur-rents of economics. Today, industrial policy is at the center of aspirited national debate. Its advocates have captured the imagina-tion of many political leaders, of influential constituencies amongboth business and labor, and of the press. Its opponents have beenobliged to take a forceful, clearly articulated position, in defense ofwhat were once the accepted verities: the optimality of market-place solutions to allocative problems, the sufficiency of good mac-roeconomic policy for the achievement of macroeconomic ends.

It is not difficult to understand the origins of this debate. Main-stream macroeconomic management deserves its poor reputation.It has failed to conquer inflation, even temporarily, except at anintolerable cost in joblessness and lost production. It has failed tomitigate the costs of adjustment of our industrial structure to newtechnologies and the emergence of developed industries in otherparts of the world. Yet the traditional measures of intervention-including incomes policies as conventionally conceived-have alsoproved unsustainable in the face of widespread political oppositionto their implementation and doubts about whether their benefitsoutweigh their costs. So, industrial policy has emerged as an alter-native: a policy approach concerned with the structure of industry,with the "supply side", which offers some hope of meeting the di-verse needs-for competitiveness, for adjustment, for employmentopportunities, for productivity gains-that seemed to be imposed onus by changing competitive conditions around the world.

Viewed dispassionately, most industrial policy platforms do notrepresent a fundamental departure from the past. Rather, they at-tempt to identify past experiences of successful industrial develop-ment policy-such as some believe the Reconstruction Finance Cor-poration to have been-and to combine the revival of such effortswith action on issues which have been continually on the publicagenda for many years: trade policy, technology developmentpolicy, labor market adjustment policy, capital formation policy,and antitrust. The appeal of industrial policy to its supporters-and the source of apprehension felt by opponents-lies in the prom-ise of coherence and political force that might be brought to theentire menu of such policies by a common conception of their goals.

In defining those goals, advocates of industrial policy point to theexperience of other countries, developed and developing, who havearticulated industrial development policies. There was a greatflowering of such policies in the nineteen-seventies, in response to

(V)

VI

the transformed patterns of demand wrought by OPEC, the oilshocks, and the more general loss of dynamism in Western econo-mies by comparison with East Asia and parts of the developingworld. In some cases, the goals of industrial policies which seemedappropriate for, say, Japan in the sixties or Brazil in the seventies,were based on a perceived need to emulate successes of still earlierindustrial development in the United States. These may not be ap-propriate for the United States itself as we face, not any need torecreate our own past, but an unknown and uncertain future. Inother cases, such as West Germany and France in the seventies,the goals of industrial policy may have been unduly oriented towhat were then rapidly growing export markets, such as in LatinAmerica, whose medium-term future is now under a cloud. Thesewould also not be good models for the present-day United States.Still, advocates of industrial policy maintain that lessons can bedrawn from the experience of other nations, and it would be philis-tine, not to say chauvinist, to ignore those lessons if their true mes-sage can be divined.

Given these two great sources of the industrial policy debate-our own past and present interventionist agenda and the experi-ence of foreign countries-a compelling need remains for reliable,dispassionate information about both. There is no shortage of selec-tive analyses in which information is presented in support of oneposition or another. The unmet demand is, instead, for a wide-rang-ing, readable survey of the major issues encompassed and sub-sumed by today's industrial policy debate.

This volume of essays will help meet this demand. A review of thecontents will show its exceptional range; a reading of each essay willshow the clarity and professionalism with which each has beenprepared.

Investment Policy, in the United States and overseas, is the sub-ject of the first chapter, which is authored by Richard Newfarmer.Newfarmer finds that existing U.S. investment policies revolvearound subsidies and tax expenditures designed to achieve goalsother than international competitiveness-such as increasedowner-occupied housing, national defense, and environmental pro-tection. I believe readers will find Newfarmer's summaries of theconduct of investment policies overseas to be a valuable source ofinformation and references, and his analysis of their importance(or lack of it) to U.S. interests, incisive.

Technology Policy is the topic of Kenneth Flamm's fine essay inChapter Two. Flamm points out what is at the same time well-known and oft-forgotten-that this area has been historically oneof U.S. pre-eminence, only recently challenged by foreign effortslargely modeled in our own. Such policy, Flamm points out, is for-mulated largely at the Department of Defense, and oriented to itsnational objectives; in some instances this works against nationalgoals. It is also an area on which there is a vast amount of extanteconomic research, from which-a rare thing in economics-sensi-ble conclusions about policy priorities can readily be drawn.

Trade Issues are covered by Lee Price in Chapter Three. First,Price reviews the rationales which have been advanced for incorpo-rating a program of limited trade intervention into an industrialpolicy. Then, he summarizes the actual past roles of U.S. tradepolicy, in the GATT and in domestic policy response to the trade

VII

and intervention policies of our trading partners. -Price's argumentlinks the justifications for further U.S. intervention provided in thefirst part of his paper to the actual policy described in the secondand outlines the further evolution of U.S. trade policy that wouldflow from acceptance of his premises. His conclusion is that thereis a fundamental need for trade policy alternatives that do notforce workers into a crude choice between raw adjustment withoutassistance, and raw protection without adjustment.

Labor Market Adjustment Policy is covered by Michael Pod-gursky's essay in Chapter Four. Podgursky provides a thoroughreview of the various needs which have led to the present compli-cated structure of policies. He shows how U.S. expenditures on itsunemployed have gone down at precisely the time when labor ad-justment measures are most needed. His historical summary andinternational comparisons provide a stark reminder of the deficien-cies of U.S. practice in this area, and he provides a specific list offeasible reforms.

Antitrust Policy is the fifth chapter, by David Dale Martin.Martin provides a counter to those who would view industrialpolicy as a means to effect a retreat from competition and to aban-don the protections afforded consumers and entrepreneurs by theexisting framework of anti-trust. His essay makes a case whichAmerican advocates of the free market should find congenial: thatour success has been based in the past on a competitive spirit fun-damentally superior to that of our competitor nations, who havebeen forced to engage the cartelizing energies of government so asto marshall forces to overtake our lead.

These are essays with a point of view. In each case, the authorshave taken the interventionist position, and sought to portray thatposition in a favorable light. What distinguishes these essays, how-ever, is the breadth of analytical vision, the balanced judgment,and the reasoned clarity with which each case is put.

I believe that advocates of industrial policy will find much hereto help define and specify their case. At the same time, opponentsof the more extreme claims for industrial policy will find muchthat supports their call for a reasonable, limited, incremental ap-proach, taken in the context of sensible macroeconomic policies,active development policies, and efforts to sustain a free and opentrading system and the international financial order.

CONTENTS

PageLetters of Transmittal ..............................................................Foreword-James K. Galbraith .................. . .v

I. Investment Policy-Richard Newfarmer ......................................................... 1Are investment policies important? . ................................. 3Foreign industrial policies: An international comparison . .: 4

The Federal Republic of Germany ........................................................ 5The United Kingdom ........................................................... .5France......................................................................................................... 6Japan........................................................................................................... 7The United States ............................................................ 7The role of developing countries............................................................ 9Brazil........................................................................................................... 9Mexico......................................................................................................... 10South Korea ........................................................... 11

Levels, forms, and trends of investment policies compared . . 12Aggregate subsidies and taxation . ......................................................... 12Industrial targeting ............................. .............................. 15Summary patterns.................................................................................... 16

Conclusions and policy implications............................................................. 17References.......................................................................................................... 21

H. Technology Policy in International Perspective-Kenneth Flamm .. 23Introduction....................................................................................................... 23The limitations of the market........................................................................ 25

Some qualifications................................................................................... 26Other problems in high technology activities . . 27

A historical perspective................................................................................... 28An international perspective.......................................................................... 34

Technology and industrial policy in the United States . . 35Technology policy in Europe ........................................................... 39Japanese technology development . ........................................................ 41Technology policy in the Third World . ................................................. 42Some lessons of historical experience . .................................................. 44

Toward a rational technology policy............................................................. 45The international dimension.......................................................................... 47.References.......................................................................................................... 50

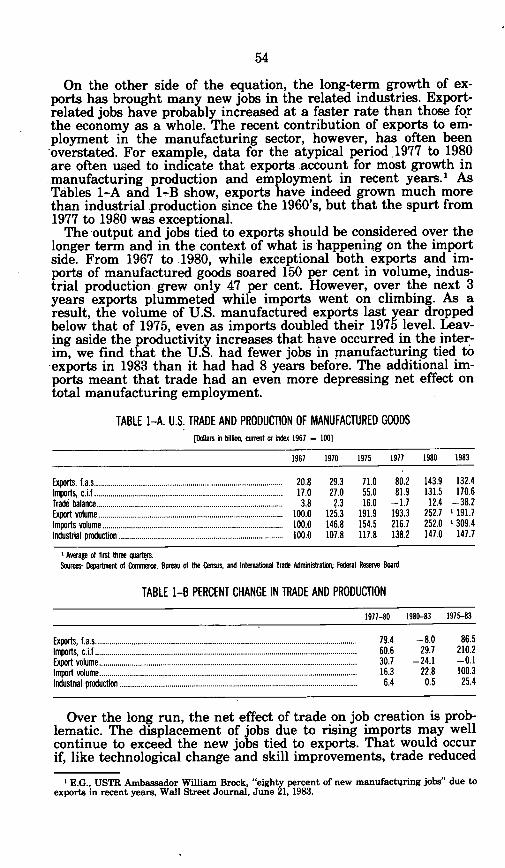

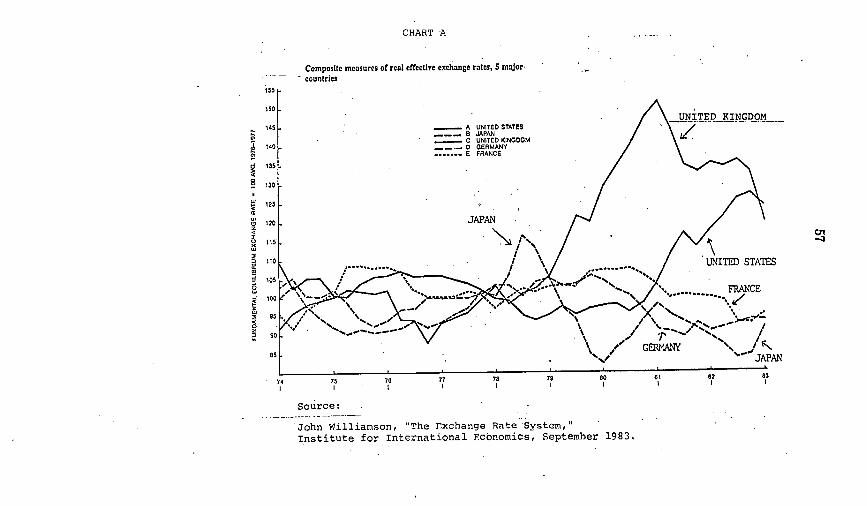

III. Trade Issues in U.S. Industrial Policy-Lee Price . ............................................ 52Overview............................................................................................................. 52The historical backdrop................................................................................... 52Sources of trade instability....................................................................: ........ 55

Exchange rates and volatile capital flows . ........................................... 55Oil prices..................................................................................................... 58Wage-based competition ........................ .. ............................. 58Changing Government-business relations. . 58Transnational enterprises....................................................................... 59-Implications for macroeconomic policy, income distribution and

employment............................................................................................ 60. The foundations of U.S. trade policy............................................................ 61

fix)

x

III. Trade Issues in U.S. Industrial Policy-Lee Price-Continued PageThe United States in the GATT: Proponent of limited govern-

ment ............................................................ 62The United States at home: Defender against foreign govern-

ments ............................................................ 64Toward a comprehensive trade policy: The opportunity provided by

the Safeguards Code ............................................................ 65Conclusion.......................................................................................................... 68References.......................................................................................................... 69

IV. Labor Market Policy and Structural Adjustment-Michael Podgursky ....... 71The changing structure of employment ....................................................... 71

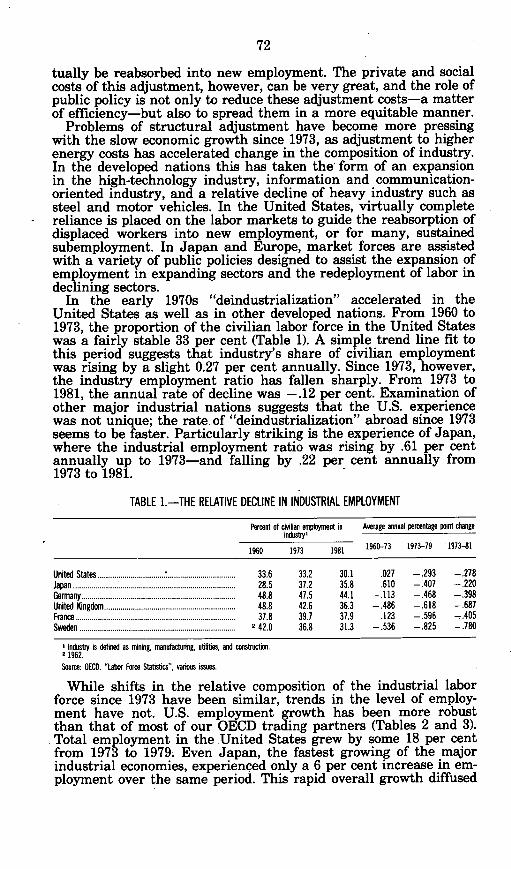

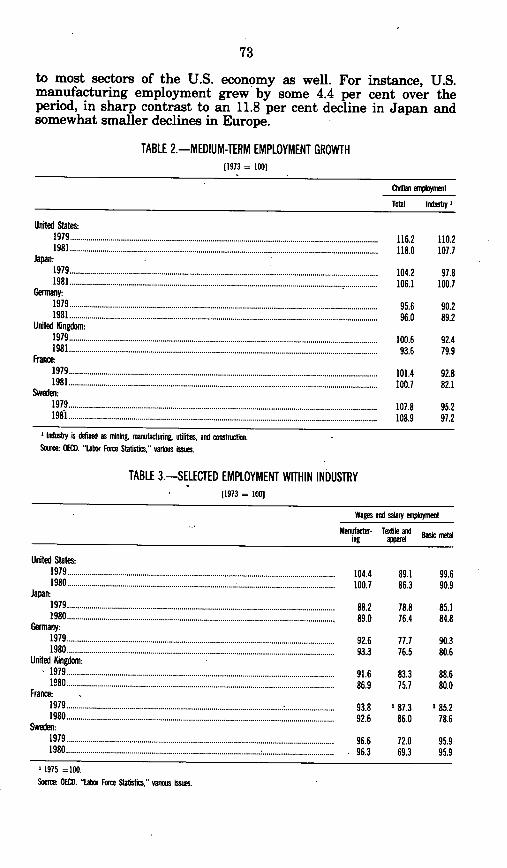

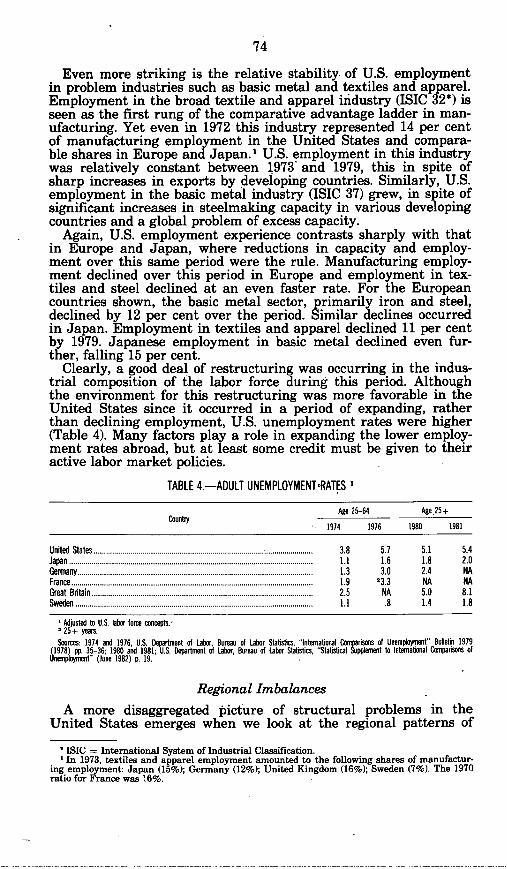

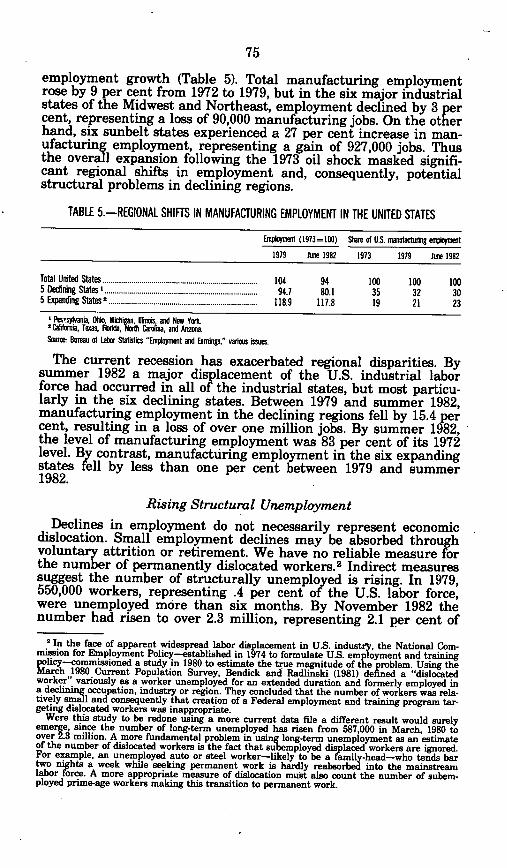

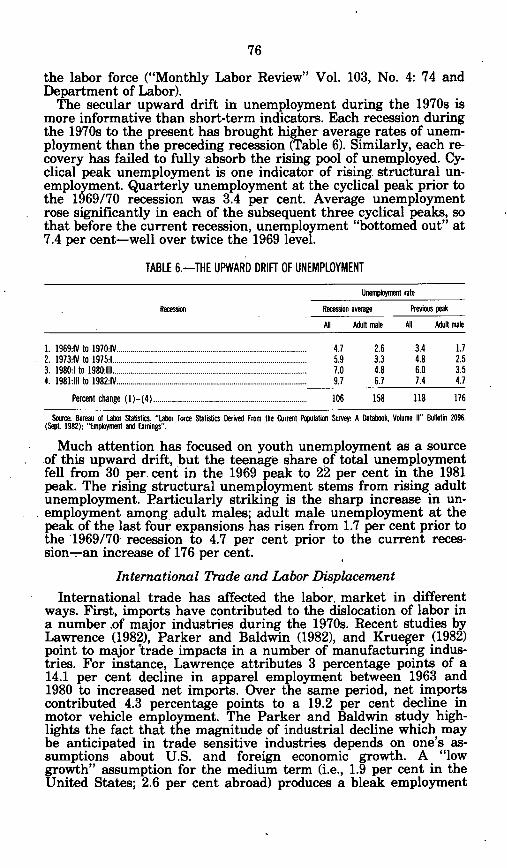

The decline of industry............................................................................ 71Regional imbalances................................................................................. 74Rising structural unemployment ........................................................... 75International trade and labor displacement ........................................ 76

Active labor market policy..................................................................................... 77Training and adjustment...................:.................................................................... 78

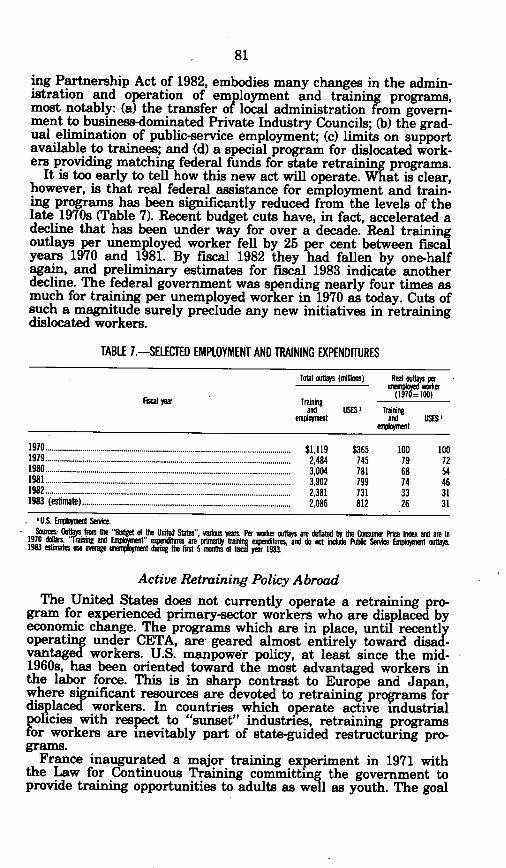

U.S. policy since 1962 ............................................................ 79Active retraining policy abroad............................................................. 81

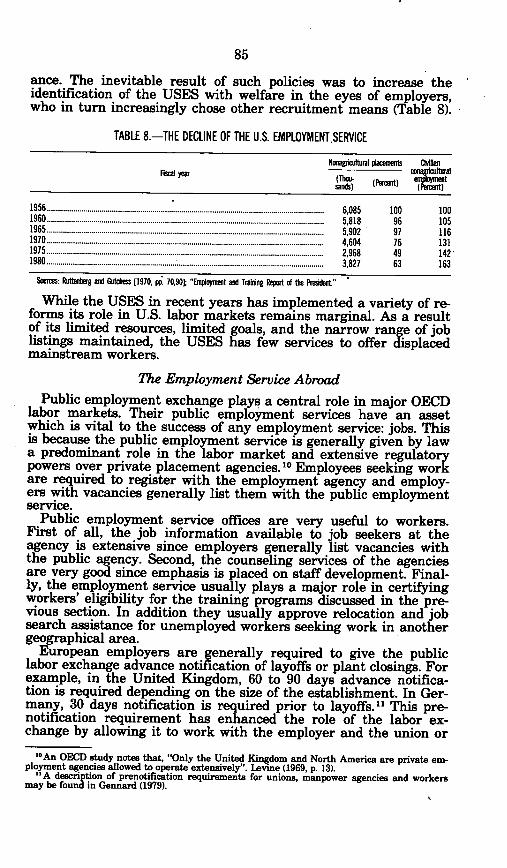

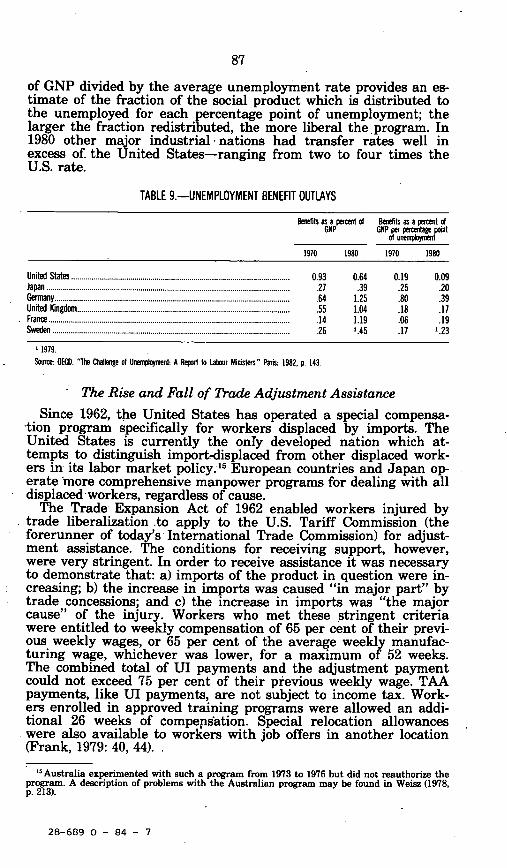

The Public Employment Office...................................................................... 83The shifting mandate of the U.S. Employment Service .................... 84The employment service abroad ............................................................ 85

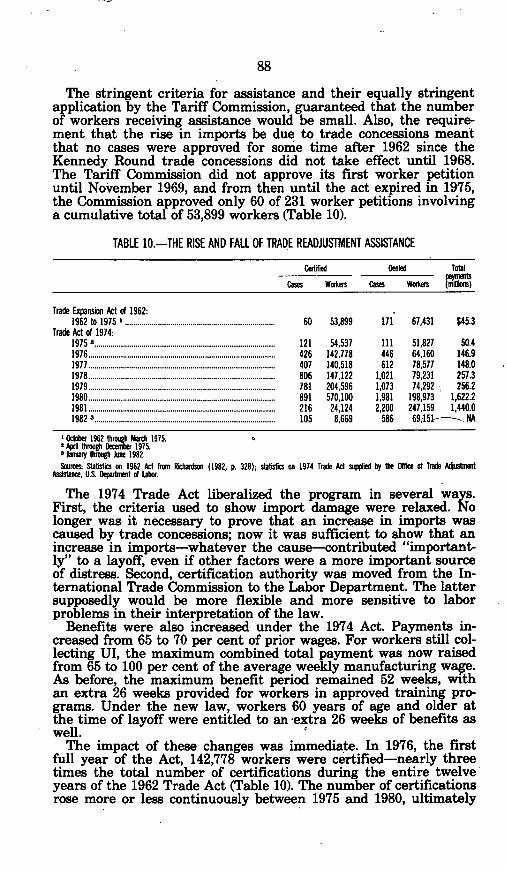

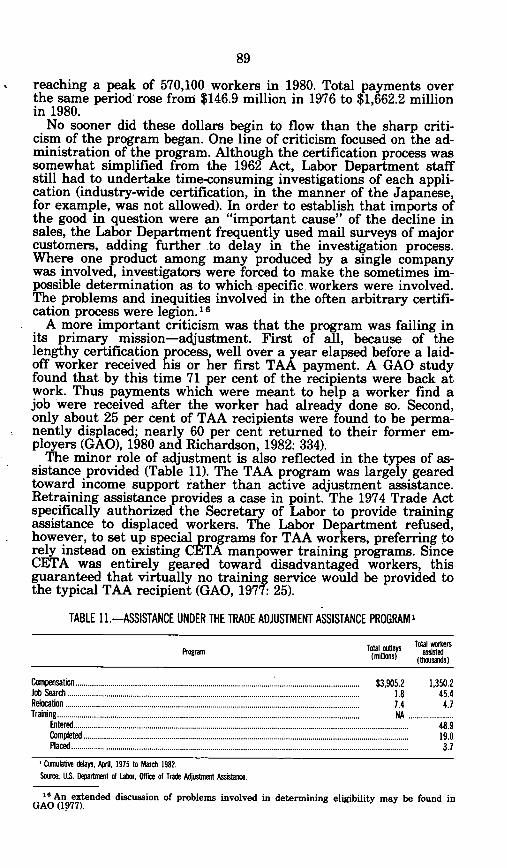

Income maintenance and adjustment ........................................................... 86The rise and fall of trade adjustment assistance ........................................ 87Conclusions and policy recommendations .................................................... 91

General policy recommendations ........................................................... 91Some specific recommendations............................................................. 92

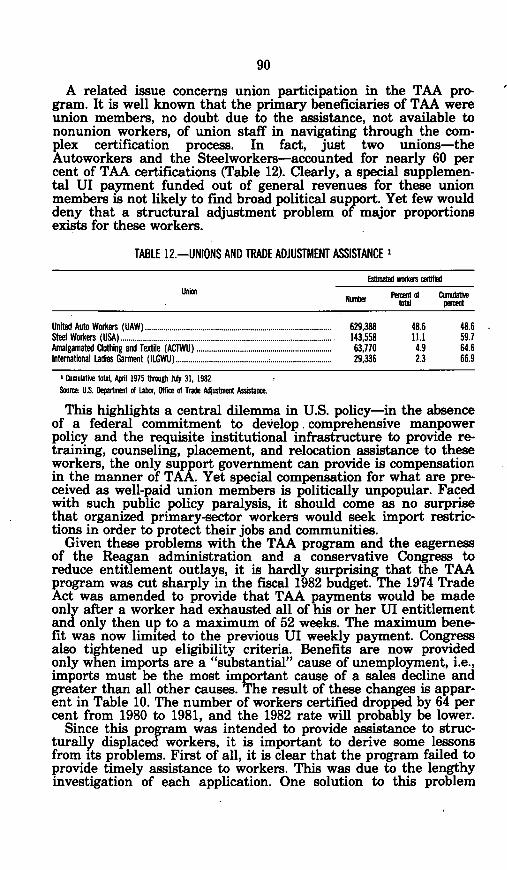

References.......................................................................................................... 94V. The Role of Antitrust in the Industrial Policies of the United States-

David Dale Martin ........................................................... 97International competition and new arguments to abandon antitrust .... 98Reconsidering the Industrial Policy-Antitrust Interface ........................ 103

Jurisdictional limitations ...................................... ..................... 103Governmental restraints on competition ..................................................... 105Possible changes in U.S. antitrust policy ..................................................... 106

The Export Trading Company Act ........................................................ 107Joint ventures in research and development ...................................... 109Harmonization and coordination ........................................................... 110

Conclusions ............................................................ 111Appendix ............................................................ 111

I. INVESTMENT POLICY

By Richard Newfarmer*World Bank

As the international economy has faltered and the U.S. positionrelative to other advanced countries has declined, concern forAmerica's competitive position has widened. Public attention hasgone beyond traditional trade measures to extend to the process ofcapital and technology formation itself. The 1980 Presidential cam-paign brought forth so-called "supply side" measures to increasethe rate of investment and capital formation to halt the slide inproductivity growth. More recent debate has focused on investmentin particular industries, notably steel and autos, as well as high-technology industries.

To be sure, there is considerable dispute over U.S. competitive-ness. The recently released "Economic Report of the President"(1983:53) states "The overall performance of the United States ...does not suggest a long-term problem of competitiveness." Rather,the administration asserts that "the United States has not experi-enced a persistent loss of ability to sell its products on internation-al markets . . ." (1983:52). It cites statistics for 1973 and 1980 com-paring the United States with other OECD countries' rates ofgrowth in GDP, relative export shares, and employment to buttressits case. Changes in the U.S. competitive position "are more theresult of changes in U.S. saving and investment position than ofslow productivity growth" (1983:53). Nonetheless, critics argue thepolicies associated with "Reaganomics"-large tax cuts, high deficitspending, tight monetary policy, and redistribution of the taxburden toward the low-income. groups-did not ameliorate the deeprecession of 1979-83 nor stem the tide of increasing unemployment.These policies have overlooked long-term changes in the sectoralcomposition of production and trade.

While most proponents of industrial policy underscore the need"to get macroeconomic policies right", they emphasize that thisalone will be insufficient to cope with the "pervasive problemsposed by structural adjustment" (Diebold, 1982; Pinder, 1982). Wil-liam Diebold writes: "The new realism emphasizes not only theneed to supplement macroeconomic policy . .. but also the suspi-cion that one of the reasons for the lack of success of the more gen-eral economic policies is that there is some accumulation of struc-tural difficulties . ." (1982:193).

'The author wishes to thank Kathy Lynn for her editorial and administrative help andRobert Pillar for his thorough and conscientious research assistance. This was written while theauthor was a Senior Fellow at the Overseas Development Council; does not reflect views here inthe official position of either the Council or the World Bank.

(1)

2

Several writers advocate new measures to channel investmentinto industry to promote American competitiveness. Felix Rohatyn(1981) has called for a Reconstruction Finance Corporation whichwould provide cheap capital for the rebuilding of selected Ameri-can industries. Business Week (1980) and Lester Thurow (1980) ad-vocate a national development bank that would funnel subsidizedcredit to promote new high-technology industries, but not to"sunset" industries. Ronald Muller (1980) has advocated and advi-sory investment board that would suggest industrial priorities anda development bank that would provide access to cheap capital topromote their development. Gar Alperovitz (1981) has called for a'committed public investment strategy." All of these proposals

seek to change the current incentive structure facing businessmenthrough capital markets. Almost all contain an implicit or explicitsubsidy or subsidy-cum-regulation. Magaziner and Reich (1982)present a variation of this idea by arguing that the United Statesalready subsidizes selected industries, but that the current patternof subsidies ought to be reordered to promote more rapid industrialgrowth. Since the U.S. economy is' embedded in a larger interna-tional economy, these changes are designed to influence the rateand location of new investment relative to other nations, relativeproductivity growth, and thus U.S. international competitiveness.

There are several reasons for the public sector to control or stim-ulate investment in a particular industry. Industries may be neces-sary for national defense. Plant closings may hit one region withparticular severity, an example of when the real social costs of pri-vate transactions are much higher than the costs to particularfirms. Or capital markets may be imperfect-oversupplying fundsto large established firms while undersupplying venture capital tonew firms; or financial markets may perceive some projects as toorisky because of large size or with pay-offs too far in the future,such as nuclear power, agricultural technology, or investments intechnology generally. Or product markets may be imperfect, allow-ing foreign firms to exploit their market power in ways not open totheir American competitors. In each one of these cases, the deci-sion to override market signals is fundamentally a political one be-cause policymakers believe that the verdict of the market is incon-sistent with social goals.

However compelling the above reasons may be for special policiestoward a particular industry, this paper treats another reason fre-quently given for an activist U.S. investment policy: the activist in-dustrial policies of other governments. One approach to this ques-tion would be to analyze in comparative fashion the macroeco-nomic determinants of investment, particularly rates of savingsand growth. While acknowledging the fundamental importance ofmacroeconomic policy, this paper instead focuses on specific invest-ment policies which affect an industry's long-term competitive posi-tion-capital allocation, industrial targeting, subsidies to technol-ogy development, tax expenditures for capital and technology, and,to a lesser extent, performance requirements. These investmentpolicies are discussed in three ways. An opening section charts theinterplay between industrial policies, changes in the internationaleconomy, and the GATT. A second part briefly compares the poli-cies of selected OECD countries and developing countries to discern

3

purpose, trends and extent of interventions, and their consequencesfor international competitiveness. The concluding section discussespossible U.S. responses along with some detailed exploration of theimplications of alternative programs for the developing countries.

Two debates are found woven into this discussion of investmentpolicy: Should the United States insist that other countries aban-don their investment policies in favor of circumscribed governmentintervention or should the United States adopt its own industrialpolicies in response to those abroad? And, what should be the bal-ance between resources devoted to preserving existing domestic in-dustry and those devoted to accelerating the process of developingnew industries?

ARE INVESTMENT POLICIES IMPORTANT?

For a range of new industries, the global location of comparativeadvantage is not tied to particular resource or location-specific en-dowments, but primarily based upon capital and technology (seeZysman, 1982). For these products, comparative advantage is large-ly arbitrary and becoming more so. The location of comparative ad-Vantage becomes increasingly arbitrary as transportation costs fall,as industrial products become more important in world trade, andas traded products have a higher value-added relative to non-trada-bles. Therefore according to this argument, politics in the form ofpolicies to provide subsidies to capital and technology formationplay an ever more important role in allocating world industry. Acorollary for the United States is that as capital and technologyshift to lower-wage countries, the new trade composition andinterdependence will exert a downward pressure on the averageAmerican wage if new employment opportunities are not createdin alternative, higher value-added industries.

As trade has integrated economies, national investment policiesto influence production have spilled over into the internationaleconomy with potential injury to other countries. The trade conse-quences of these public investment policies can be conceptually sep-arated into those which affect the short-term market share of acountry and those that affect the long-term (quasi-permanent)market share, which we might define as "international competi-tiveness." Present trade law does not make this temporal distinc-tion, focusing solely on observable changes in import market shareand domestic profitability and employment. But these may be ofshort duration. Once the export subsidies are removed (or offset),the increase in foreign market share may shrink as domestic pro-duction again becomes economical.

Of greater consequence are policies with long-term effects. A sub-sidy (or other policy) has enduring effects if domestic productiondoes not become economical after the policy has ended. It is evenpossible that the trade consequences may occur after the produc-tion and technology subsidy have ended. The key is whether somebarrier to entry-learning curves, scale, technology, or capitalcosts-is present after the policy ends. Foreign producers, with thehelp of the investment or technology subsidy, may establish an in-dustry, gain a technological advantage, price low to capture marketshare, and displace domestic capacity before the importing country

4

can replicate the investment. Foreign sellers are then in a positionto set new higher prices at the entry-forestalling level, but stillabove the competitive rate, although this does not have to followfor a loss to occur to a country's competitive position.

Some have argued that investment policy in an era of floatingexchange rates makes little difference to the net international com-petitive position since changes in the foreign exchange rate offsetany subsidy effects (e.g., Cooper, 1978). The increase in exports isoffset by appreciation in the value of the currency and a subse-quent increase in imports. The only change is in the relative pricesof tradables and thus in the sectoral composition of production inboth countries. There are three problems ' with this argument:First, governmental controls in capital flows and exchange marketscan stave off changes in the exchange rate for lengthy periods, per-haps long enough to drive out capacity in the host country. Even ifexchange markets are relatively unencumbered, large inflows ofcapital can strengthen currencies and depress exports for pro-longed periods, driving out domestic production capacity thatcannot be easily reinstated when the currency falls. Second, chang-ing the sectoral composition of output and hence employment isitself a major investment and trade problem. Displaced labor oftenhas a difficult time finding employment in other industries even ifoutput is expanding. Third, over the long run, industries withhigher growth potential, higher barriers for entry, and potentialfor higher growth in productivity will produce gains in terms oftrade for the exporting country. All countries therefore wouldprefer to specialize in these exports. Of course, it cannot be predict-ed with certainty which product lines will be in demand. However,almost all countries look to the technology-intensive industries tobe safer bets than primary products. Investment policies that alterthe long-term division of labor are therefore of immense potentialimportance even though the short-term aggregate effects are par-tially offset through the exchange rate.

Let us then consider several countries' investment policies.

FOREIGN INDUSTRIAL PouciES: AN INTERNATIONAL COMPARISON

In briefly sketching seven countries' industrial programs, severalimpressions emerge: First, there is some evidence that govern-ments everywhere are becoming increasingly involved in subsidiz-ing their domestic industries. Second, governments appear to be in-creasingly active in promoting new industrial development, thusorienting policy toward accelerating structural change. Third, thepurpose and policies of developing countries are considerably differ-ent than those of the developed countries. The latter see theirfuture comparative advantage in knowledge-intensive industriesand have focused public efforts on high-technology industries; theadvanced developing countries are making considerable effort toclose the technological gap, but have made their largest gains in

I Seamus O'Cleiracain of the State University of New York has pointed out another to me:If nonprice factors such as availability, delivery dates, quality, etc., are important in deter-

mining trade flows, and if an industrial policy can affect these, there is no reason to expect thata flexible exchange rate regime will produce a relative price which exactly offsets the non-costinfluences of subsidies-especially when the exchange rate is being determined in some portfoliomodel manner rather through the trade account.

5

basic industries. Finally, the level of government expenditures topromote industry appears to be less of a predictor of success in es-tablishing international competitiveness than other institutionalfactors, especially industrial targeting.

Consider, then, key features of the industrial policies of Ger-many, the United Kingdom, France, the United States as well asBrazil, Mexico, and South Korea.

The Federal Republic of Germany

Business has generally worked more closely with government inWest Germany than in the United States, but the federal systemaccords a strong role to the states. The government has effectivelybrought several organized groups-labor, employer associations,etc.-into the political process through "concerted action," the lib-eral concept of the social market economy predominant in the1950s and 1960s. This produces no overall plan, but does lead tosectoral agreements and regional programs.

The guiding principles include the stabilization of income in de-clining industries and promoting the development of high-technol-ogy industries. This has been linked up with a protectionist sec-toral policy in industries such as coal, textiles, and shipbuilding.The government has extended protection to industries such asautos, while encouraging mergers. Subsidies have been extendedfor research and development in oil, aircraft, and more recently,computers.

The subsidy element of investment policy appears to be increas-ing. The total subsidies (including tax allowances) amounted toabout 1 per cent of GDP in 1975 and about 7 per cent of gross fixedcapital formation (de Carmoy, 1978). Mutti (1982:14) using a slight-ly different definition, reports a figure of 3.7 per cent of GDP for1976. The German Kreditanstalt reported that preferential capitalin the form of loans, loan guarantees, and grants increased three-fold between 1970 and 1981 while GNP only doubled. Between 1980and 1981 alone, this form of subsidy increased as a share of GNPby 13 per cent.

The United Kingdom

The activities of the British government in promoting its indus-try have evolved less organically than in West Germany becausepolicies have changed rather abruptly with the advent of a newparty in power. Moreover, investment policy has by and large beendirected at maintaining employment and controlling balance-of-payments disequilibria rather than developing new industries.

Accordingly to the Industry Act of 1975, the government wasgiven selective power to offer financial assistance to industry andorganize "voluntary planning agreements." The act established theNational Enterprise Board to administer one billion pounds of sub-sidies to aid in restructuring British industry and in the creation of"national champions." This board was the administrative sequel tothe Industrial Reorganization Corporation founded in 1967 by alabor government and later killed by a conservative government.

Under the 1975 program subsidies were granted (together withprotection) to the British textile industry, shipbuilding, steel, alu-

6

minum smelting, aircraft, computers, and automobiles. In all indus-tries, the government tried to reorganize fragmented industriesinto a few strong firms or create new technologically sophisticatedfirms (in computers and aircraft) to compete with foreign firms.

Government subsidies amounted to about 1.2 per cent of GDP in1974 and about 10 per cent of gross fixed capital formation (deCarmoy, 1978). Subsidies shown in national income accounts grewuntil about 1976. The election of Margaret Thatcher and the con-servatives changed policy abruptly toward reducing substantiallythe scope of government participation in the economy. TheConservative government has tried to "denationalize" several sec-tors. The net result has probably been to reduce the extent of fundschanneled to select industries on the basis of policy.

Frnce

The French state has historically played a more pervasive role ineconomic development than most of the other European countries(see Zysman, 1978). Industrial policy has therefore been far moreaggressive. The Commissariat au Plan brings together representa-tives of both public and private enterprises as well as governmentofficials to insure close cooperation in policy formation. All indus-try falls under the economic "tutelage" of a ministerial depart-ment, most under the Ministry of Industry and Research. The neteffect is more to coordinate private and public activities ratherthan strictly plan investment. France is the only OECD country be-sides Japan which publicly announces the sectors it will encourageor discourage (Franko, 1980).

The Fifth Plan (1966-70) emphasized the creation of one or twofirms of international scale in most industries, promoting nationalchampions through mergers on oil, chemicals, and aircraft. TheSixth Plan (1971-75) emphasized growth in four sectors-equip-ment goods, chemicals, electronics, and food and agriculture. TheSeventh Plan (1976-80) adopted a more protectionist stand in theface of severe recession, but continued to provide aid to targetedsectors, including autos and steel. Selective credit policies are a pri-mary instrument of channelling credit to dynamic industries andrestructuring declining industries (Joint Economic Committee,1982). The government allocated 5 billion francs for a five-year pro-gram in telecommunications and computers. Aircraft and energy,especially nuclear power, where government spending during thelate 1970s was 6 billion francs annually, are also targeted sectors.In declining industries-textiles, shoes, handbags, clothing, andwatches-the government has "managed decline" by using high in-terest rates, gradual reduction of subsidies, and before 1980, a will-ingness to tolerate unemployment.

With the advent of the Mitterrand government in 1980, the statehas extended its economic role in the economy. Implicit subsidiesthrough preferential capital to state enterprise have undoubtedlyincreased. The well-publicized goal of "reconquering domestic mar-kets," aimed primarily at textiles, electrical appliances, and furni-ture, tends to increase protection. Industry Minister Pierre Dreyfusdisclaimed, however, any intention of rescuing nationalized but de-clining sectors. The official purpose is "to restore the competitive

7

edge of industry" (Mosley, 1982). Mitterrand is interested in devel-oping new sectors via aid schemes. These include: professional andhousehold electronics, glassmaking, and electronic and computer-ized office equipment. Some sectors where government involvementwas high when Mitterrand assumed office should expect expandedstate help: metallurgy, base chemicals, and armaments (Mosley,1982). At the same time, there is a strong tendency to dismantlethe structure of generalized controls and subsidies and stimulatelocal capital markets. Thus, French policy has moved from one ofsevere protection to protecting selected industries and using invest-ment policy to create new internationally competitive industries.

JapanJapanese industrial policy has evolved through several rather

long phases-through the period of post-war readjustment (1945-52), industrial nationalization and restructuring (1952-60), theperiod of internationalization, with expanded trade and foreign ex-change liberalization (1960-73), and post-oil policy (after 1973).Each of these phases has been marked by a close, though fluctuat-ing, relationship between business and the state, and by a strongdrive to industrialize and close the technology gap (Magaziner andHout, 1980). Subsidies as an instrument of investment policy playedan important role in the first two periods, though less so in thethird (Namiki, 1978). They appear to have stabilized as a share ofGDP in the fourth period.

The Japanese government exercises a leadership role throughthe Ministry of Trade and Industry (MITI). Together with repre-sentatives of the business community, MITI formulated medium-and long-term national plans (although these do not encompass allsectors, omitting for example, housing and land use). The effective-ness of the program is more to signal public support of key indus-tries rather than to actually plan the flow of capital to each sector.

Post-1973 planning has targeted a set of technologically intensiveindustries to help reduce Japan's dependence on energy-intensiveindustries. These include aircraft parts, nuclear power, electroniccomputers, seabed and aerospace development (Namiki, 1978; Bar-anson and Malmgren, 1981). Industrial robotics also appears to beanother industry that will receive official government support. Inresponse to the Reagan administration's prodding, it also appearsthat the government will increase its allocation to national de-fense, and will undoubtedly increase funds devoted to military-re-lated technology. In summary, many of the new subsidies will bedestined for technology development and technology-intensive in-dustry.

The United StatesAlthough more reliant perhaps on the market system than other

OECD countries, the United States government has historicallypromoted the growth of its private sector. Diebold (1982:160) notesthat during the 18th century "there was a certain coherence" toU.S. industrial policy: It relied on selective protection to limit de-pendence on imports, expand the domestic market, and promote ag-riculture. Producer interests were dominant. The government

28-689 0 - 84 - 2

8

helped build the eastern canal system and then the railroads lawsanctioned the birth of the indefinite-life corporation in the 1880sand large scale industrial businesses began to flourish. Antitrustlaw, a thread of industrial policy, emerged between 1890 and 1914as a reaction to the abuse of economic power. The Great Depressionand the Second World War dramatically expanded the role of gov-ernment in industrial development. Since then, defense, space,atomic power, energy, and the environment have occupied centerstage as the primary concern for government activity.

As one indication of trends, Magaziner and Reich (1982:241-48)estimate that U.S. expenditures solely on industrial developmentrose from 3.4 per cent of GNP in 1920, to 9.2 per cent in 1950, andto 13.9 per cent in 1980. Tax exemptions and procurement almosttripled as a percentage of GNP betwen 1950 and 1980. Tax expendi-tures were targeted to housing, petroleum, coal and timber. Pro-curement policy benefitted aviation, maritime, semiconductors, andpetroleum, among others.2

These numbers are open to dispute, but the level of public re-sources directly or indirectly benefiting selected industries has un-doubtedly been increasing in the United States. The decontrol of oiland gas prices during the Reagan administration has reduced animportant element of subsidy (to downstream industries), but thishas been offset by increases in military procurement and financingof research and development, the near elimination of the corporateincome tax, new subsidies for nuclear power development, and thereincarnation of agricultural price supports in key commodities.

In contrast to many countries, the U.S. pattern of promoting spe-cific industries is not oriented to enhancing international competi-tiveness. This is not to say U.S. policy is incoherent; rather it "co-heres" around other goals, such as national defense, the promotionof particular national concerns, e.g., housing and energy.

2 R. N. Cooper (1978: 109) lists subsidies that are more directly related to export competitive-ness (in approximate order of importance):

Aid to developing countries tied to the purchase of American goodsThe Domestic International Sales Corporation which permit U.S. corrations to defer profits

on exports until dividends are remitted to the parent corporations;The U.S. government subsidies to both the construction and operation of merchant vessels

under U.S. registry;The Export-import Bank provision of medium-term credit for American exports at lower-than-

market interest rates;Congressional legislation providing subsidies for the export of agricultural products; until 1973

subsidies had been employed through the Commodity Credit Corporation as part of the U.S. do-mestic price support program. With the fall in commodity prices after 1979, the program hasbeen reinstituted;

A 10% U.S. investment tax credit for investment in new plants and equipment;Federal spending on services used to support private business, such as airports, air traffic con-

trol, harbor maintenance, and postal services; this spending, net of user charges, undoubtedlyincreases business activity;

Price controls on domestically produced oil and gas amount to an upstream subsidy for energyusing producers;

Government procurement may subsidize domestic industry through Buy American tariff pro-visions, full cost pricing in high overhead (including R&D) product lines;

Other regulations, such as the minimum wage, environmental protection laws, child laborlaws, etc., which increase the costs of particular industries constitute a subsidy for unaffectedindustries to the extent the foreign exchange rate is the adiustment mechanism.

This list is hardly exhaustive. One might add the subsidies to the ill-fated synfuel project, thespace program, military grants and contracts for research and development and others.

9

The Role of Developing CountriesAs relatively late starters in the industrialization process, most

newly industrializing developing countries (NICs) have relied heav-ily on the government to promote growth. This has occurred in amuch more conscious way than in most developed countries. Na-tional policies to encourage capital formation and technological de-velopment commonly began with an inward looking import substi-tution in the 1950s, but by the.1970s, most had become export-ori-ented. As national strategies shifted toward an export orientation,state enterprise subsidies for exports (often to offset overvalued for-eign exchange rates), production subsidies (often through preferen-tial foreign exchange), and performance requirements have beencommon policies.

BrazilBrazilian government direction of national growth grew rapidly

in the post-war period. A first phase, from 1950 to 1961, extendedthe process of import substitution begun during the Depression andWorld War II. Tariff protection and several other incentives weregranted to manufacturing industries. Several state enterpriseswere born, including electrical utilities, steel companies, and thenational development bank. Beginning in 1955, foreign firms weregranted special incentives to import capital equipment to set upfactories, and they responded with dramatic increases in invest-ment. But by 1961, growth rates fell and the' import substitutiondynamic was exhausted, resulting in a political crisis that broughton a succession of military governments.

The governments enacted a stabilization program that lastedfrom 1964 to 1967, during which time a crawling peg exchange ratewas introduced, indexing for inflation, and an end to subsidies inpublic enterprise. Beginning in 1968, growth resumed, this timebased upon an export drive of manufactured products. Exports ofmanufactured products grew from a small share of total exports toabout 25 per cent by 1973 (Tyler, 1980). Throughout this period, na-tional planning was improved, incentives created for exports andinvestments in industry.

After the oil crisis of 1973, policy shifted to emphasize greaterimport substitution (to offset the greater cost of oil), a more rapidexpansion of exports, (especially agricultural exports), and greatertargeting for technologically sophisticated industries, such as petro-chemicals, nuclear power, telecommunications, and capital goods.

The state enterprise sector expanded rapidly, growing from 22per cent to 27 per cent of equity holdings between 1970 and 1980.This included growth in technologically sophisticated industriesslich as mineral production, railroad equipment, aircraft, andci. micals. Since these now occupy positions of considerable eco-nomic weight in industry as suppliers and buyers, the governmenthas tried (with mixed results) to use them as a policy lever to pro-mote backward linkage industries.

The government relied heavily on subsidies and regulations ofvarious forms throughout the 1970s. In the post-1973 period, for ex-ample, cheap credit has been made available to agriculture, to na-tionally-owned enterprises through the National Development

10

Bank, and to selected industries such as those in the sugar alcoholprogram and petrochemical industries. State-owned enterprisesbecame vehicles to keep prices lower than the rate of inflationduring the 1975-78 period, benefiting downstream user industries,most notably, agricultural chemicals, steel, and glassmaking indus-tries, and final consumers. Increases in the price of petroleumlagged the world market increases for many months after 1973 butwere eventually increased.

Steel prices too were kept low. All- of this postponed the adjust-ment process but did not circumvent it. Eventually prices'had to beraised and inflation began to increase (by 1980 it reached 100 percent). Third, export subsidies were increased throughout the period,in large measure to offset an overvalued exchange. These includeddirect incentives through the BEFIEX program and tax rebates ofthe value-added tax on manufactured products. The level of overallsubsidies is difficult to quantify; subsidies probably amounted toconsiderably more than those evident in the United States, perhapsin the range of those found in France. Fourth, the government hasbargained assertively with foreign investors over the terms ofaccess to the Brazilian market seeking to promote more rapid tech-nological transfer, reduce its net cost, promote Brazilian-controlledenterprise, and promote exports. Thus, bargaining produced a na-tionally integrated auto industry, a telecommunications industry,the successful state-owned aircraft industry, and several viable cap-ital goods industries. Performance requirements (mainly local con-tents) have been used in autos, petrochemicals, pharmaceuticals,and most recently (though not altogether successfully) in comput-ers.

Mexico

The national government has taken a strong role in economic de-velopment beginning with Cardenas era in the 1930s. In 1938 theholdings of American oil companies were nationalized to form thefirst major state enterprise. But a concerted effort at import-substi-tution industrialization did not begin until the 1960s. During theDiaz Ordaz administration (1964-70), Mexico continued the expan-sion of the state enterprise that had taken place in the recession-ary period after 1958 and subsequent upsurge in nationlism thatculminated in the takeover of several key sectors. Import-substitu-tion manufacturing produced growth of 9.1 per cent while the over-all growth rate was over 7 per cent for the 1960s. 4

While some observers have called Mexico "a land of planners"(Hufbauer, et al., 1981), the country confined its efforts to sectoralplans until 1979 when it issued its National Industrial Develop-ment Plan, soon followed by the Global Plan in 1980. The idea ofboth programs is to increase the growth rate, increase exports, es-pecially manufactured exports, and reduce agricultural imports.Manufactured exports had grown fairly dramatically from 37.7 percent of total exports in 1966 to 53.8 per cent in 1974; with the sub-sequent growth in oil exports, the share of manufactured exportsfell to 16.5 per cent in 1980. Part of the rapid export growth hadbeen due to the Border Industries Program which was establishedin 1965. In addition, several industries were targeted for special

11

state-aided growth: petrochemical fertilizers, autos, and heavy elec-trical equipment.

The government and subsidies have been an integral part of theindustrialization strategy. First, the state enterprise sector account-ed for about .16 per cent of assets of the 300 largest manufacturingfirms in 1972 (Newfarmer and Mueller, 1975:55). After 1974, pricesof products sold by state enterprises-including petroleum and gas-oline, railroads, electricity, steel, and even tortillas-were heavilysubsidized. Railroad subsidies were estimated at $715 million in1980, electrical utilities at $2.1 billion, and the food distributionsystem at $1.4 billion (Castillo, 1981). The subsidies to the petro-leum sector were made via lower-than-world-market prices to con-sumers and amounted to at least $3 billion, depending on the basisfor calculation. Export subsidies equal to 100 per cent of the valueof tariffs on imported inputs were rebated to exporters, and playedan integral part in the expansion of exports during the period.Total subsidies were estimated at about 5.7 per cent in 1980 (Cas-tillo, 1981).

Performance requirements proliferate: Auto companies were re-quired in 1977 to increase exports until they equaled imports by1982; pharmaceutical companies are compelled to sell undifferenti-ated drugs to the government for distribution; the state-owned elec-trical utility is using its monopsonistic power to create a capitalgoods industry; and the government petroleum firm has negotiatedwith the international petrochemical firms to create a domestic in-dustry. Computers are also the subject of bilateral bargaining.

With the fall in petroleum prices, the advent of the financialcrisis in late 1982, and the subsequent agreement with the IMF,government participation in investment regulation and subsidiza-tion will undoubtedly be reduced. The government agreed to reducethe fiscal deficit from about 13 per cent of GDP to under 8 per centas part of the agreement.

South KoreaAfter 1953, Korea emphasized import substitution industrializa-

tion as it reconstructed its economy. While this generated a strongand fairly consistent impulse for economic growth, eventually thesmall market size and limited natural resources led to a reorienta-tion of import substitution policy in 1964 toward export promotion.Reforms included a uniform exchange rate, unrestricted access tointermediate and capital goods, imports, tax exemptions for export-ers, reduced prices on inputs, and access to credit for investment(Bradford, 1982; Wade and Kim, 1978). Economic planning, whichbegan as part of this phase of industrial growth with the first five-year plan (1962-67), was consistently strengthened and became anintegral tool for government policy. By many accounts, planningwas a major contributor to the success of Korean developmentduring the period (Brown, 1973; Wade and Kim, 1978).

Subsidies through credit to selected industries were usedthroughout the 1970s to encourage capital formation (although ear-lier the overvalued currency had also been a direct stimulant to in-vestment in imported machinery). In addition, the numerous stateenterprises also sold their output at below-market rates for much

12

of the 1970s. This appears to have changed with the adoption of theFourth Five-Year Plan in 1977. Export subsidies were enacted inthe 1960s and incorporated into the planning process as part ofpledges to export (Bradford, 1982).

LEVELS, FORMS, AND TRENDS OF INVESTMENT POLICIES COMPARED

Aggregate Subsidies and Taxation

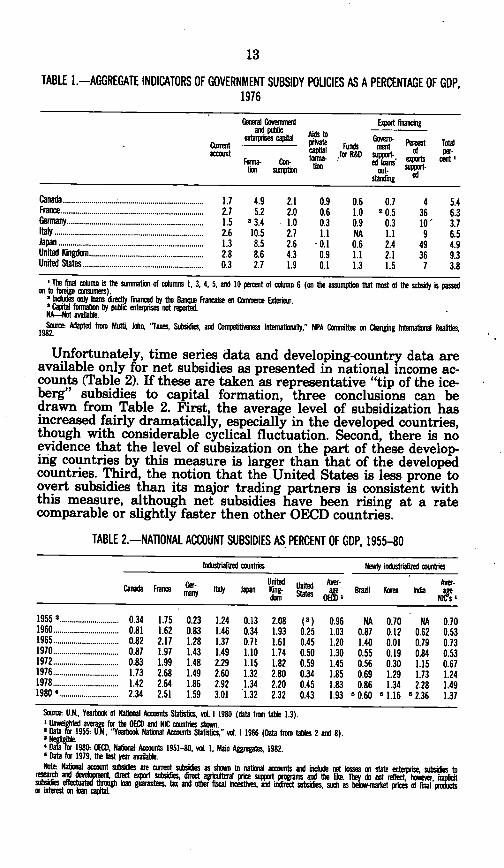

Leaving aside the institutional framework for the moment, acomparison of the aggregate level of subsidies and tax incentivesoffers some indication of the relative governmental roles in attract-ing (or creating) international capital and technology. Quantitativecomparisons quickly lose rigor in the face of differences in nationalaccounts, asymmetries in regulatory practices, and the opaquenessof investment subsidies. Nonetheless, several studies have attempt-ed careful comparisons and their findings are worth recounting.

Mutti (1982), presents cross-national comparisons of six catego-ries of subsidies as a percentage of GDP for seven OECD countries(Table 1). In addition to the caveats adumbrated above, the dataare imperfect in one other respect: they do not include subsidies in-herent in the defense programs of the countries involved. Column 1represents the operating subsidies to firms, frequently in the publicsector. The relatively high levels of France, the United Kingdom,and Italy are attributable to agricultural subsidies and to the largeshare of public ownership in utilities and basic industry relative tothe United States. Column 2 represents the government share innew investment; this figure is overstated because it does not ex-clude user fees from public activities, a major source of revenue.Here too the United States ranks lowest among all seven countries.Column 3 is the depreciation of publicly owned capital; eventhough this represents past funding from previous tax payments,this can be taken as a proxy for the currently available benefitsfrom government investment. Government grants and loans forprivate investment are included in column 4; by this measure theUnited States ranks comparably with Japan and just below Ger-many. Such is not the case for funds expended on research and de-velopment where the United States spends the most. The finalcolumn is the summation of columns 1, 3, 4, and 5 and 10 per centof column 6 (on the assumption that most of the subsidy is passedon to foreign consumers). This total indicates that the United King-dom, Italy, and France are among subsidized economies, while theUnited States is second only to Germany as the country with thelowest subsidy ratio in the 1970s.

These rankings do not correlate with rapid growth or less precisenotions of international competitiveness. Governments in theUnited Kingdom, Italy, and France subsidize their industry to thegreatest extent, yet only France arguably has made consistentgains. Japan, seen as the most competitive, ranks fifth. While thesubsidy rate is notably higher than Germany and the UnitedStates, the Japanese still subsidize at a rate far below the Europe-ans. If these broad orders of magnitudes are correct, one has to ex-plain Japanese economic performance on the basis of less quantifi-able subsidies, greater marginal efficiency of subsidized investment,or institutional and economic factors in addition to subsidies.

13

TABLE 1.-AGGREGATE INDICATORS OF GOVERNMENT SUBSIDY POLICIES AS A PERCENTAGE OF GDP,1976

Geeral Govemnent Export financing_ apta Aids to Govern-

_ _rrent pHWt Funds ment Percent Totalamcount capiot ofR&fo per-

rm- Con, tWC e loan' notnots centXtin sumptin dot

standing

Canada .. ............... 1.7 4.9 2.1 0.9 0.6 0.7 4 5.4France ...................................................................... 2.7 5.2 2.0 0.6 1.0 2 0.5 36 6.3Germany ................................................................... 1.5 3 3.4 1.0 0.3 0.9 0.3 10' 3.7Italy ......................................................................... 2.6 10.5 2.7 1.1 NA 1.1 9 6.5Japan 1.3 8.5 2.6 -0.1 0.6 2.4 49 4.9United lingdom........................................................ 2.8 8.6 4.3 0.9 1.1 2.1 36 9.3United States......................................................... 0.3 2.7 1.9 0.1 1.3 1.5 7 3.8

X The final column is the summation of columns 1, 3, 4, 5, and 10 percent of couomn 6 (on the assumption that nost of tie subsidy is passedon to oreign consumers).Incldies ony loaos drety financed by tile Baie Francatse en Commnerce Eteior.

fCaptaI onriation by public enterprises not reported.HA Io availabto.SuMrc. Adapted fon Mutti, John, "Taxs, Suboeiies, and ICmpelo Interatioally," NPA Comonittee on aCanging Inteationoal Realities,

1982.

Unfortunately, time series data and developing-country data areavailable only for net subsidies as presented in national income ac-counts (Table 2). If these are taken as representative "tip of the ice-berg" subsidies to capital formation, three conclusions can bedrawn from Table 2. First, the average level of subsidization hasincreased fairly dramatically, especially in the developed countries,though with considerable cyclical fluctuation. Second, there is noevidence that the level of subsization on the part of these develop-ing countries by this measure is larger than that of the developedcountries. Third, the notion that the United States is less prone toovert subsidies than its major trading partners is consistent withthis measure, although net subsidies have been rising at a ratecomparable or slightly faster then other OECD countries.

TABLE 2.-NATIONAL ACCOUNT SUBSIDIES AS PERCENT OF GDP, 1955-80

Inoustniaizad countries Newy industrialized countries

Canada ftu Ger- Un~Vite l ed Ame- Aver-Canada rona G- Italy Japan ring- sttes ox Brazil Korea IniA re

1955 0. ........... 0.34 1.75 0.23 1.24 0.13 2.08 (0) 0.96 NA 0.70 NA 0.701960 ........... 0.81 1.62 0.83 1.46 0.34 1.93 0.25 1.03 0.87 0.12 0.62 0.531965 ........... 0.82 2.17 1.28 1.37 0.71 1.61 0.45 1.20 1.40 0.01 0.79 0.731970 ........... 0.87 1.97 1.43 1.49 1.10 1.74 0.50 1.30 0.55 0.19 0.84 0.531972 ........... 0.83 1.99 1.48 2.29 1.15 1.82 0.59 1.45 0.56 0.30 1.15 0.671976 ........... 1.73 2.68 1.49 2.60 1.32 2.80 0.34 1.85 0.69 1.29 1.73 1.241978 ........... 1.42 2.64 1.86 2.92 1.34 2.20 0.45 1.83 0.86 1.34 2.28 1.491980 *. ........... 2.34 2.51 1.59 3.01 1.32 2.32 0.43 1.93 5 0.60 61.16 5 2.36 1.37

Sounc. U.N., Yearbookof National Accounts Statistics, voL 1980 (data Iron tatbe 1.3).'U=Wntod aveag for tie OEMl and NIC countris fo.wo

Data for 195 i U.N., "Yeartook National Accounts Statistics," vol. 1 1966 (Data fon tables 2 and 8).

M1980: OECD, National Accounts 1951-80, vol. 1, Main Aggregates 1982.Data for 1979, the tot tear available.

Note- National acount sut are current sobide as sto in n oationa accounts and innude net tosses an state enterprise, sutois toresearh dvamnent. direct exor sutsides diret a cof prurM oort prgowams and the l u They do not ref.ecL homeri f u nitSutsi effechoted bv loan guarantees, tax and other fiscal Yesntiesd indirect subtsies, such as teoow et prices of finaltor mterest 0o lan capital

14

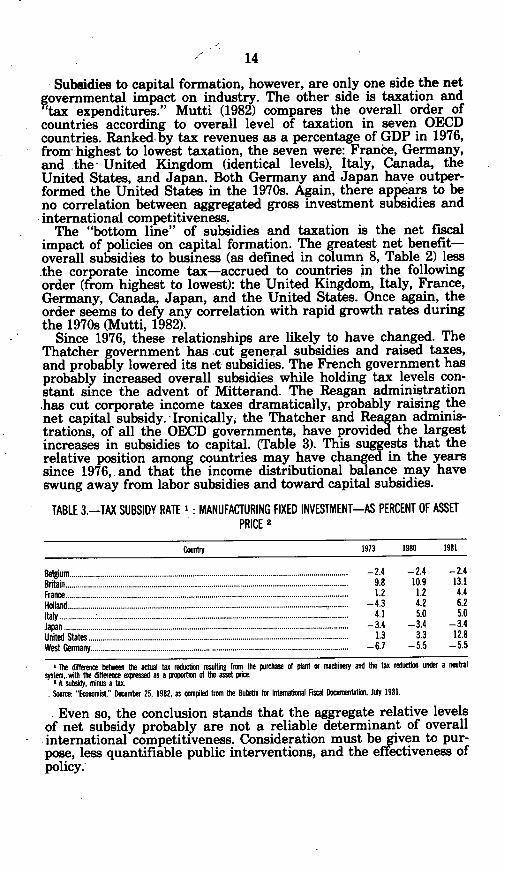

Subsidies to capital formation, however, are only one side the netgovernmental impact on industry. The other side is taxation and'tax expenditures." Mutti (1982) compares the overall order of

countries according to overall level of taxation in seven OECDcountries. Ranked by tax revenues as a percentage of GDP in 1976,from-highest to lowest taxation, the seven were: France, Germany,and the United Kingdom (identical levels), Italy, Canada, theUnited States, and Japan. Both Germany and Japan have outper-formed the United States in the 1970s. Again, there appears to beno correlation between aggregated gross investment subsidies andinternational competitiveness.

The "bottom line" of subsidies and taxation is the net fiscalimpact of policies on capital formation. The greatest net benefit-overall subsidies to business (as defined in column 8, Table 2) less.the corporate income tax-accrued to countries in the followingorder (from highest to lowest): the United Kingdom, Italy, France,Germany, Canada, Japan, and the United States. Once again, theorder seems to defy any correlation with rapid growth rates duringthe 1970s (Mutti, 1982).

Since 1976, these relationships are likely to have changed. TheThatcher government has .cut general subsidies and raised taxes,and probably lowered its net subsidies. The French government hasprobably increased overall subsidies while holding tax levels con-stant since the advent of Mitterand. The Reagan administrationhas cut corporate income taxes dramatically, probably raising thenet capital subsidy. Ironically, the Thatcher and Reagan adminis-trations, of all the OECD governments, have provided the largestincreases in subsidies to capital. (Table 3). This suggests that therelative position among countries may have changed in the yearssince 1976, and that the income distributional balance may haveswung away from labor subsidies and toward capital subsidies.

TABLE 3.-TAX SUBSIDY RATE ' MANUFACTURING FIXED INVESTMENT-AS PERCENT OF ASSETPRICE 2

Country 1973 1980 1981

Belgium ................................................................................................... . ................................... -2.4 -2.4 -2.4Britain... ....................................................................................................................................... 9.8 10.9 13.1France............................................................................................... ..................................... . 1.2 1.2 4.4Holland .................................. ,............,........,...........,.....,............,....,......,...........,........,............. - 4.3 4.2 6.2Italy . 4.1 5.0 5.0Japan .......................................................... -3.4 -3.4 -3.4United Ste s ......................................................... . 1.3 3.3 12.8West Germany ......................................................... -6.7 -5.5 -5.5

' The dce between the actual tax reduction resulting trom the purchase of plant or machinery and the tax redoction under a neutralnystein wit' the dfence eressed as a proportion of the asset pMic.' A nuhedy minas a tax.Source: "Economist," December 25, 1982, as compiled from the Bulletin for Intemafneal Fscal Decumentation, July 1981.

Even so, the conclusion stands that the aggregate relative levelsof net subsidy probably are not a reliable determinant of overallinternational competitiveness. Consideration must be given to pur-pose, less quantifiable public interventions, and the effectiveness ofpolicy.

15

Industrial Targeting

Targeting of investment policy has been central to the success ofJapan and, to a lesser extent, France. Based on government-busi-ness planning in the 1940s, Japan eventually built one of the mostefficient steel industries in the world, despite the fact that domesticsources for raw materials, energy, and technology were limited. Itselectrical equipment industry and consumer electronics industrywere built with close business-government planning. More recently,policy focuses on computer, optical fibers, robotics, microprocessors,and office machinery. French policy supports the development ofsix key sectors: electronic office equipment, underwater explorationequipment, biotechnology, robotics, consumer electronics, andenergy conservation equipment (Baranson and Malmgren, 1981).

These industries recently targeted by both governments share anumber of characteristics: they are knowledge-intensive, high bar-rier-to-entry, and have a high income elasticity of demand. Select-ing industries because they are knowledge-intensive allows coun-tries to build upon perceived potential for comparative advantageand rapid productivity gains. High barriers-to-entry imply thatonce an advantage is established it cannot easily be eroded; theymay also imply a need for some initial government participation tooffset the advantage of established foreign firms or to bring thetechnology into commercial production. The high income elasticityof demand characteristics ensure these industries will be growthindustries in the future. These programs have the greatest poten-tial for impact upon international trade patterns, even thoughtheir near-term trade effects may be minimal.

Governments in the United States and Western Europe also playan active role in steel, autos, textiles, and energy, although thesepolicies share a defensive character designed to preserve interna-tional market share and domestic employment rather than addingto world capacity. The United States has a markedly smaller rolein these industries, attributable to its large market, the historicalstrength of its private sector, and its aversion to industrial policy.

The advanced developing countries have focused on mature high-barrier industries-steel and shipbuilding-or high-barrier indus-tries controlled by multinational companies-autos, chemicals, pet-rochemicals, and capital goods. As a result, their share of world ex-ports in high-skill, low-capital-intensity products (rubber, printing,electrical machinery, nonelectrical machinery, and transportationequipment) has increased fairly dramatically (UNCTAD, 1982:75-87). Many newly industrializing countries see these industries asthe heart of a modern industrial base with abundant linkage ef-fects in skill development, employment, and demand for inputsfrom other industries. More recently they have, sought to entersome high-technology industries, primarily production, for their do-mestic markets.

The peculiar nature of the barriers to entry confronting firms inthe newly industrializing countries requires the use of different in-dustrial policies than commonly found in the developed countries.

16

In the heavy industries, barriers to international entry involveeconomies of scale, capital requirements, and international market-ing. Many countries have domestic markets that are too small tosupport firms of competitive scale, even though they would have aninherent cost advantage (wage rates) were they producing for worldmarkets. Similarly, the vertical or horizontal integration often ac-companying multinational ownership often constitutes a entry bar-rier to domestic production for export. In both of these instances,industrial policies relying upon state ownership, preferential capi-tal or subsidies, or performance requirements may be necessary torealize potential comparative advantage.

Summary Patterns

Several long-term patterns in the trends and purposes of indus-trial policies are apparent. First, within the OECD countries, indus-trial policies seem to have moved beyond the preservationist poli-cies of protecting weak industries toward "accelerationist" policiesof more aggressively creating and promoting high-technology indus-tries. At the same time, some governments have retreated fromdirect allocation of capital, preferring to make available cheap cap-ital for a select group of industries while encouraging the growth ofprivate capital markets. This may be the logical result of the devel-opment process. If Japan can be taken as a model, the planners atMITI arguably play a smaller role in the allocation of total invest-ment than they did 20 years ago. The French experience, however,might temper this generalization. Nonetheless, it seems reasonablethat with economic growth the pattern, and perhaps the scope, ofintervention should change-because capital markets become moredeveloped (and internationalized) while investment decisionsbecome more complex to manage publicly, because firms developan international interest that transcends domestic economies, andbecause the indirect, larger average size of firms brings an in-creased internal financing capability that makes them less depend-ent on government planners. Similarly, spending for research anddevelopment increased as a share of GNP between 1962 and 1978.

Second, policy within the OECD seems to converge on a sectoralbasis as well. Nearly all the OECD countries have strong publicpolicies to defend their auto, steel, shipbuilding, and aircraft indus-tries. Those countries with accelerationist policies toward high-technology industries have tended to overlap in the same indus-tries: computers, semiconductors, robotics, and office equipment.This convergence indicates that governments may begin to competewith each other in offering subsidies, tax incentives, incentives totechnological development, and the like to promote specific indus-tries.

Third, concomitant to the transition in industrial policy in theNorth has come a marked transition in the newly industrializingcountries of the South: the transition from the import-substitutionindustrialization, strategies of the early 1960s to the export-promo-tion programs that blossomed during the 1970s. Government poli-cies typically have used a variety of instruments to convert an in-dustrial base built upon import substitution to an internationallycompetitive, outward-oriented industry. This has required various

17

instruments: state enterprise, performance requirements, aggres-sive bargaining with multinationals, and export incentives. The in-dustrial targets tend to be mature industries in the developed coun-tries, but also some high-technology industries.

The industrial policies of developing countries are quite differentthan those of developed countries because the NICs confront differ-ent barriers to entry. These countries confront scale and interna-tional marketing barriers (often in addition to technology barriers)and they do so with the handicap of a much smaller private sector.This suggests that state participation will be more direct and moretargeted since industrial gaps are more obvious in countries withsmall industrial bases and it may take the form of bargaining withforeign multinationals since the latter frequently control market-ing channels and technology.

By their very nature, these policies are more likely to have directspillover effects on trade than are the indirect policies of the moreadvanced countries. Smaller domestic markets imply that in indus-tries with high-scale barriers, such as autos, tractors, and largepower generating equipment, international efficiency sooner orlater requires exporting. Second, the mature industries tend tohave slower growth so that new additions to capacity are more no-ticeable. Firms in the NICs in steel, petrochemicals and some min-erals were creating new capacity during the 1970s at a time whenthe major suppliers in the OECD countries were cutting back oncapacity. Third, the skill gap is much narrower than the wage gapbetween the advanced countries and the newly industrializingcountries for many industries. Thus wage rates may accord produc-tion facilities in the developing countries a substantial cost andproductivity advantage in many industries.

CONCLUSIONS AND POLICY IMPLICATIONS

Two quite different conflicts emerge over industrial policies. Thefirst is within the OECD. On the one hand, industrial policies arein conflict when. many countries have the industry and none iswilling to cede it to the other as market (or nonmarket) forceswould dictate. The evolving resolution of these protectionist con-flicts seems to be in the form of quasi-negotiated de facto sectoralarrangements as in steel, autos, and textiles-at least until theworld economy begins to grow convincingly. On the other hand,conflicts are increasingly surfacing over indirect, or even direct,support for particular high-technology industries. The semiconduc-tor suit and Houdaille petition are recent examples. The 1982GATT Ministerial failed to produce multilateral agreement to ad-dress these problems, and the onus has been effectively transferredto working parties for further action.

The second set of conflicts occurs between developed countriesand the NICs. The latter tend to pose a more destabilizing force tothe world trade hierarchy. On the one hand, they tend to resort to"unorthodox" policies (such as bargaining with state multination-als, state enterprise, and performance requirements) with greatertrade effects, and on the other they pose a competitive threat be-cause of the increasingly high ratio of skills to wages. Thesethreats are mitigated in the short run by the relatively small mag-

18

nitudes of exports from developing countries, but they will prob-ably grow as the NICs develop. Renewed economic growth can as-suage the conflict, but probably not eradicate it.