Embed Size (px)

Citation preview

This document is downloaded from DR‑NTU (https://dr.ntu.edu.sg)Nanyang Technological University, Singapore.

Political corruption and corporate earningsmanagement

Zhang, Jin

2017

Zhang, J. (2017). Political corruption and corporate earnings management. Doctoral thesis,Nanyang Technological University, Singapore.

http://hdl.handle.net/10356/72893

https://doi.org/10.32657/10356/72893

Downloaded on 29 Jan 2022 17:47:12 SGT

POLITICAL CORRUPTION AND CORPORATE EARNINGS MANAGEMENT

ZHANG JIN

NANYANG BUSINESS SCHOOL

2017

POLITICAL CORRUPTION AND CORPORATE EARNINGS MANAGEMENT

ZHANG JIN

NANYANG BUSINESS SCHOOL

A thesis submitted to Nanyang Technological University in partial fulfillment of the

requirements for the degree of Doctor of Philosophy

2017

Acknowledgement

First and foremost, I would like to express my sincere gratitude towards my thesis advisor

Prof. Huai Zhang, for his continuous support during my PhD study. His wisdom, knowledge,

and commitment to high-quality research guide me through this progressive and stimulating

journey. He helps me prepare for an academic career by improving my research capacity,

communication skills, and teaching ability.

I am also deeply grateful for my thesis committee and oral defense committee members:

Prof. Huasheng Gao, Prof. Yen Hee Tong, Prof. Kevin Koh, and Prof. Yachang Zeng, for

their insightful comments and invaluable suggestions. I also want to thank Prof. Rui Shen,

Prof. Terence Ng, Prof. Huaxiang Yin, Prof. Hun-Tong Tan, and other faculty members, for

their sharp and helpful comments in my brownbag seminar.

Special thanks go to my co-authors: Prof. Po-Hsuan Hsu and Prof. Kai Li, for guiding me

to be an academic writer, a professional presenter and a collegiate scholar.

My appreciation also extends to my office colleagues: Mr. Lukas Helikum, Mr Truc

Thuc Do, Mr. Kenny Phua, Ms. Xiaoran Huang, Mr. Chongwu Xia, Mr Tongrui Cao and Mr.

Pingyi Lou. I truly benefit a lot from their advice, encouragement, information sharing, and

technical assistance.

I am also grateful for the help from the admin staff at Nanyang Business School: Ms.

Adeline Tang, Ms. Bee Hua Quek, Ms. Karen Barlaan, and Ms. Tsai Ting Hu. Thank you for

being there and always ready to help.

Last but not the least, I want to thank my family for their love and consistent support

throughout my life.

Contents Abstract ............................................................................................................................... 1

1. Introduction ..................................................................................................................... 2

2. Literature Review and Hypothesis Development ............................................................ 8

3. Research Design ............................................................................................................ 10

3.1 Baseline Model ........................................................................................................ 10

3.2 Measure of Earnings Management .......................................................................... 11

3.3 Measure of Political Corruption .............................................................................. 12

3.4 Control variables ..................................................................................................... 13

4. Sample Formation and Descriptive Statistics ............................................................... 15

4.1 Sample Formation ................................................................................................... 15

4.2 Descriptive Statistics ............................................................................................... 16

5. Empirical Results .......................................................................................................... 18

5.1 Baseline Regression ................................................................................................ 18

5.2 Subsample Analyses ................................................................................................ 19

5.2.1 Geographic Concentration ................................................................................ 19

5.2.2 Political Connections ........................................................................................ 20

5.2.3 Costs of Downward Earnings Management ..................................................... 21

6. Robustness checks ........................................................................................................ 22

6.1 Alternative Measures of Corruption ........................................................................ 22

6.1.1 Alternative Measures Based on Corruption Convictions ................................. 22

6.1.2 Alternative Measures Based on Perception ...................................................... 23

6.2 Restatement Analysis .............................................................................................. 24

6.3 Accounting Policy Analysis .................................................................................... 25

6.4 Instrument Variable Approach ................................................................................ 27

6.5 Difference-in-Differences Analysis ........................................................................ 28

6.6 Tax Avoidance Analysis ......................................................................................... 29

6.7 Party Affiliation ....................................................................................................... 30

6.8 High-Profile Political Corruption Case and Earnings Management ....................... 30

7. Conclusion .................................................................................................................... 32

Reference ........................................................................................................................... 35

Appendix A Variable Definition ....................................................................................... 40

Appendix B Summary Statistics for Corruption by State ................................................. 42

Appendix C Gravity-based Centered Index for Spatial Concentration (GCISC2) ........... 44

Appendix D High-Profile Political Corruption Case and Earnings Management............. 45

Figure 1 Map of the State Average Corruption ................................................................. 47

Table 1 Descriptive Statistics ............................................................................................ 48

Table 2 Baseline Regression ............................................................................................. 50

Table 3 Geographic Concentration ................................................................................... 52

Table 4 Political Connection ............................................................................................. 54

Table 5 Costs of Downward Earnings Management ......................................................... 56

Table 6 Alternative Measures of Corruption ..................................................................... 58

Table 7 Restatement Likelihood ....................................................................................... 61

Table 8 Accounting Policy Analysis ................................................................................. 62

Table 9 Instrument Variable Approach Based on Population Concentration ................... 64

Table 10 Difference-in-Differences Analyses Based on Re-Location .............................. 66

Table 11 Tax Avoidance ................................................................................................... 68

Table 12 State Party Affiliation ........................................................................................ 70

1

Abstract

Using U.S. Department of Justice data on political corruption convictions, I examine how

political corruption affects firms’ earnings management. I find that companies headquartered

in more corrupt states manipulate earnings downwards. The findings are robust to six

alternative corruption measures, the restatement analysis, the accounting policy analysis, the

instrumental variable approach, the difference-in-differences analysis, and an event study. In

addition, I find that the effect of corruption on earnings management is more pronounced for

firms whose operations concentrate in their headquarter states and for firms without political

connections, but is not significant for firms on the edge of missing earnings benchmarks or

firms facing tight debt covenants. In sum, my findings suggest that firms respond to

corruption by managing earnings downwards.

Keywords: Earnings Management, Political Corruption, Rent Seeking

JEL Classification: M41; G38

2

1. Introduction

Political corruption is pervasive and the U.S. is not immune to this problem. In its 2012

Global State of Mind Report, Gallup reports that the percentage of adults who perceive

corruption as a widespread problem in their government is greater than 50%, for 108 out of

129 countries. The percentage for the U.S. stands at 73%1. Consistent with these statistics,

there are plenty of anecdotal evidence of political corruption in the U.S. For example, Don

Siegelman, the former Alabama governor, appointed the CEO of HealthSouth to a state

regulatory board after taking a bribe of $500,000. For another example, several officials of

the Defense Logistics Agency awarded government contracts to United Logistic in exchange

for $800,000.

How does political corruption affect firms’ accounting choices? Given the pervasiveness

of political corruption, this is an important question that has implications for academics,

regulators and the public. However, this question has received scant attention from prior

literature, and I attempt to address this gap.

Following Butler et al. (2009), I define political corruption as agency issues between

elected or appointed government officials and their constituents, which manifest in rent-

seeking by government officials. Public officials can extract rents from firms through the

threat of additional regulations and targeted taxation (McChesney, 1987). According to the

positive accounting theory (Watts and Zimmerman, 1986), downward earnings management

weakens the argument for such government actions, and shields firms from the rent-seeking

of corrupt officials. Besides, if corrupt officials directly solicit bribes, the amount of bribe is

subject to a firm’s profitability (Svensson, 2003). Therefore, I hypothesize that firms facing

high corruption are incentivized to manipulate earnings downwards.

1

The report is available at http://www.gallup.com/file/poll/165497/GlobalStateMind_Report_10-

13_mh.pdf.

3

This hypothesis is not without tension. Numerous studies have shown that political favors

increase firm value (Fisman, 2001; Faccio et al., 2006; Claessens et al., 2008; Goldman, et al.,

2009; Duchin and Sosyura, 2012; Tahoun, 2014), and corruption offers opportunities for

firms to bribe their way into an advantageous position. Expenses related to illicit dealings

with government officials are likely hidden from the public (Gul, 2006). Since these expenses

can’t be reasonably expected by investors, they are likely to result in actual earnings falling

short of the market’s expectation. To avoid these negative surprises, firms have incentives to

manipulate earnings upwards.

Using a sample of 56,096 observations, I take the question to the data. To measure

corruption, I follow the common practice in related economics and finance literature

(Fredricksson et al., 2003; Glaeser and Saks 2006; Butler et al., 2009; Campante and Do,

2014; Smith 2016). Specifically, I obtain U.S. Department of Justice data on the number of

corruption convictions involving public officials in each of the 94 federal judicial districts in

the U.S. I aggregate the cases to the state level. The number of convictions per capita in each

state (i.e., the variable Corruption) is used as the main measure of political corruption. A

higher value indicates a more corrupt environment.

In my main test, I measure earnings management with performance-matched

discretionary accrual. I regress it on Corruption and a battery of control variables. My control

variables include general firm characteristics, firm characteristics associated with capital

market incentives and contracts-based incentives, and state characteristics related with local

corruption.

The results show that a one standard deviation increase in Corruption is associated with a

reduction of 2.1 percentage points in performance-matched discretionary accrual. This effect

is economically significant, considering that the mean value of discretionary accrual in the

sample is only -2.4 percentage points. Overall, the results are consistent with the hypothesis.

4

To test whether the results are indeed related to rent-seeking by corrupt officials, I

conduct several subsample analyses. Public officials have higher ability to seek rents from

companies that mainly operate in their jurisdictions, because these firms face higher costs to

shift operations to non-corrupt states than geographically dispersed firms (Bai et al., 2015).

Therefore, I expect that the impact of local political corruption on earnings management is

more pronounced for geographically concentrated firms. I test this expectation by dividing

the sample into two subsamples based on their geographic concentration. Consistent with my

expectation, the effect of corruption on discretionary accruals is indeed more significant for

firms with more concentrated operations.

Firms without political connections are more vulnerable to expropriations by politicians,

such as bribe solicitations (Clarke and Xu, 2004). Thus, I predict that the impact of political

corruption on earnings management is more pronounced for these firms. Following Cooper et

al. (2010) and Kim and Zhang (2015), I use the establishment of corporate political action

committee (PAC) to identify political connection, and my empirical results lend support to

my prediction.

There is a tension between the costs of downward earnings management and the benefits

of downward earnings management (Bova, 2013). Compared with companies that are faced

with lower costs of downward earnings management, companies faced with higher costs of

downward earnings management are less likely to do so. I test this prediction by diving the

sample into two subsamples based on their costs of downward earnings management.

Following prior literature (i.e., DeFond and Jiambalvo, 1994; Skinner and Sloan, 2002), I

deem firms on the edge of missing earnings benchmarks or facing tight debt covenants as

firms with high costs of downward earnings management. I find that the effect of political

corruption on discretionary accrual is not pronounced for these firms.

5

The results are robust to six alternative political corruption measures that are suggested

by prior literature. These first three measures are the number of corruption conviction cases

per government employee, the per capita corrupt convictions weighted by firms’ operations

in each state, and the raw number of corruption convictions, respectively. The next three

measures are respectively based on the ranking of the state in the 2013 BGA-Alper Integrity

Index, the ranking of the state in the 2012 State Integrity Investigation, and the perception of

the level of corruption by State House reporters.

I also test whether my conclusion is robust by focusing on an alternative measure of

earnings management, i.e. restatement. I find that companies located in more corrupt states

are more likely to understate their earnings. Then, I continue to study how political corruption

affects corporate accounting policy choices. I document that companies headquartered in

more corrupt states are more likely to choose accelerated depreciation method and their

depreciation reserves are higher. Although these companies do not differ from other

companies in the likelihood of choosing LIFO as the primary inventory valuation method,

they do report higher LIFO reserves. My findings are consistent with the notion that

companies located in more corrupt areas report lower earnings.

To address the endogeneity concern and establish a causal relation between political

corruption and downward earnings management, I adopt an instrumental variable approach.

The instrumental variable (IV) is the isolation of state capital from its populace. Campante

and Do (2014) show that states with isolated capital cities are more corrupt, because

politicians in isolated capital cities are less effectively monitored by the public. This

instrumental variable is positively related with political corruption but is unlikely to be

correlated with local firms’ earnings management except through the channel of corruption. I

find that the relation between instrumented corruption and discretionary accrual remains

negative and significant.

6

In addition, I conduct a difference-in-differences test by focusing on firms that move

between corrupt and non-corrupt states. A state is deemed as corrupt (non-corrupt), if its

time-series mean value of Corruption is above (below) the median of all the states. For each

treatment firm (i.e., a firm that moves between corrupt and non-corrupt states), I match it to a

control company (i.e., a firm that does not move) that is in the same 2-digit SIC industry,

located in the same state, and with most similar ROA. The results show that treatment firms

that move to a more (less) corrupt state experience a decline (an increase) in discretionary

accruals, relative to control firms.

Besides, I provide some evidence by studying how a high-profile corruption case affects

firms’ discretionary accruals. High-profile corruption cases help deter the rent-seeking

behaviors of local politicians, by elevating their assessment of the likelihood of being caught

and penalized. Consistent with my expectation, I find that companies located in Alabama

increase their discretionary accruals after a former Alabama governor was sent to prison, and

decrease their discretionary accruals after the person was released in advance.

One alternative explanation is that my findings reflect the relation between political

corruption and tax avoidance (Ayyagari et al., 2014), which is achieved through downward

earnings management (Chen and Daley, 1996). To test this alternative hypothesis, I test how

political corruption affects book-tax difference. I find that political corruption does not

significantly affect book-tax difference, suggesting that the alternative explanation is unlikely.

Another alternative explanation is that my measure of corruption may be a proxy for state

party affiliation, since party affiliation may affect the Department of Justice’s decision to

prosecute a case (Meier and Holbrook, 1992). To test this alternative hypothesis, I conduct a

subsample analysis based on state party affiliation. The results suggest that the negative

relation between political corruption and discretionary accrual is unlikely to be affected by

state party affiliation.

7

This paper contributes to the literature in the following ways. First, this paper adds to the

understanding of the effect of political costs on firms’ accounting practices. The positive

accounting theory predicts that companies have incentives to manipulate earnings downwards

to minimize political costs (Watts and Zimmerman, 1986). While prior studies document

empirical evidence of the impact from other types of political costs (Liberty and Zimmerman,

1986; Han and Wang, 1998; Johnston and Rock, 2005; Grace and Leverty, 2010; Bova 2013),

the impact of political corruption has received scant attention. Given the importance and

pervasiveness of political corruption, this paper addresses an important gap in the literature.

Second, this paper contributes to the literature on corruption. Prior literature in finance

and economics has studied how corruption influences innovation, cost of capital, and firms’

operating decisions (Butler et al., 2009; Borisov et al., 2015; Smith, 2016; Ellis et al., 2016).2

I extend this line of enquiry to firms’ accounting choices, offering results from a novel and

less-explored perspective.

In addition, this paper contributes to prior research that investigates the relation between

corruption and earnings quality in the international setting. Leuz et al. (2003) and Gupta et al.

(2008) show that firms in countries with weaker legal enforcement (a measure partially based

on a cross-country corruption index) exhibit lower earnings quality. Countries differ

substantially in terms of culture and institutional features, and international studies are

subject to the criticism that uncontrolled/unobservable country-specific factors account for

the results. Since the sample in this paper consists of only U.S. firms that are faced with a

homogenous institutional environment, the results are less exposed to the criticism. What’s

more, while these studies suggest that firms manipulate earnings more in countries with

higher corruption, the direction of earnings management is unclear. This paper helps cover

the blank.

2 Dass et al. (2016) use unsigned discretionary accrual as a proxy for information transparency. They find

that companies located in areas of high political corruption are opaquer. Their study however offers no

prediction on the direction of earnings management, which is the focus of this study.

8

The rest of the paper proceeds as follows. Section 2 reviews prior literature and develops

hypothesis. Section 3 discusses research methodology. Section 4 reports sample formation

and descriptive statistics. Section 5 tests the hypothesis. Section 6 checks robustness. Section

7 concludes.

2. Literature Review and Hypothesis Development

The accounting literature has long recognized the importance of political costs on firms’

accounting choices. Watts and Zimmerman (1986) hypothesize that firms facing high

political costs have incentives to manipulate earnings downwards. This hypothesis has been

tested in different settings. Liberty and Zimmerman (1986) examine earnings management

around labor negotiations but they find no evidence that the management manipulates

earnings downwards to increase its negotiation power. Jones (1991) documents that affected

firms manage earnings downwards during import relief investigations by the U.S.

International Trade Commission. Han and Wang (1998) show that oil companies manipulate

earnings downwards to reduce their political costs during the 1990 Persian Gulf Crisis, when

the rapid rising oil price raises the prospects of wind-fall taxes on oil firms. Johnston and

Rock (2005) find that firms under investigation by the government for potential

environmental damages manage earnings downwards to minimize their future clean-up and

transaction costs. Bova (2013) reports that unionized firms are more likely to miss analysts’

consensus forecasts, consistent with that unionized firms seek to lower the threat of wage

increases by manipulating profitability signals. Overall, the empirical evidence so far

predominantly supports the positive accounting theory that managers deem downward

earnings management an effective way to reduce the political costs.

9

Public officials can extract rents from firms through the threat of regulations and targeted

taxation (McChesney, 1987), imposing additional costs on these firms. Svensson (2003)

suggests that the amount of bribe is determined in a bargaining process between a rent-

maximizing public official and a firm. The firm’s higher profitability reduces its bargaining

power, since the official can require a higher amount of bribe and the firm can afford to pay

the bribe. In sum, firms have incentives to manage earnings downwards, because poor

financial results offer powerful arguments against additional regulations, taxations, and bribe

solicitations.

Downward earnings management is not costless. Companies that disappoint the capital

market will face negative capital market consequences (Skinner and Sloan, 2002). A tension

exists between the costs of downward earnings management and the benefits of downward

earnings management (Bova, 2013). So, companies located in less corrupt areas, who are

faced with lower risk of expropriation by corrupt officials, have less incentive to manipulate

earnings downwards.

The above discussion gives rise to the following hypothesis.

H1: Compared to companies located in less corrupt states, companies located in more

corrupt states manipulate earnings downwards.

This hypothesis is not without tension. Shleifer and Vishny (1994) argue that corruption is

an efficient arrangement, which allows firms to cut through bureaucracies. According to this

view, it is optimal for firms to purchase political favors through bribes. There is plenty of

evidence that political favors increase firm value. Fisman (2001) documents that politically

dependent companies in Indonesia under President Suharto experience significant drops in

value when there are negative rumors related to Suharto’s health, suggesting the benefit of

political support. Subsequent studies show that politically favored firms are more likely to be

10

bailed out (Faccio et al., 2006; Duchin and Sosyura, 2012), experience higher returns

(Claessens et al., 2008; Goldman et al., 2009), win more government contracts (Tahoun,

2014), and are less likely to be the targets of the SEC’s enforcement actions (Correia, 2014).

These evidences help buttress the case that bribing corrupt officials is an optimal choice for

managers seeking to maximize shareholder value.

If firms indeed pay bribes to corrupt officials, I expect that these illicit expenditures are

more substantial for firms facing a higher level of corruption. Since these expenditures can’t

be revealed to the public (Gul, 2006), they can’t be reasonably anticipated by investors and

likely result in actual earning falling short of investors’ expectations. Therefore, firms have

incentives to manipulate earnings upwards to avoid the shortfall. This argument predicts that

firms in more corrupt areas manipulate earnings upwards.

3. Research Design

3.1 Baseline Model

I test whether firms in more corrupt states choose to manipulate earnings downwards by

running the following OLS regression:

𝐷𝐴𝑖𝑠𝑡 = 𝛼0 + 𝛼1𝐶𝑜𝑟𝑟𝑢𝑝𝑡𝑖𝑜𝑛𝑠𝑡 + 𝛼2𝐹𝑖𝑟𝑚 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖𝑠𝑡 + 𝛼3𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡

+ 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝜀𝑖𝑠𝑡 (1),

The dependent variable 𝐷𝐴𝑖𝑠𝑡 is discretionary accrual of firm i in year t. The independent

variable is 𝐶𝑜𝑟𝑟𝑢𝑝𝑡𝑖𝑜𝑛𝑠𝑡 , a measure of the local corruption level in state s in year t. The

details of these two variables are provided in Section 3.2 and Section 3.3. The model includes

a set of firm characteristics that affect earnings management, as well as state characteristics

that may be related with local corruption.

11

The model includes industry fixed effects, as some industries are more vulnerable to

political corruption (Svensson, 2003). It also includes year fixed effects, so as to capture the

economic-wide shocks. Since the independent variable (Corruption) is measured at state-year

level, I cluster the standard errors by state-year (Butler et al., 2009)3.

3.2 Measure of Earnings Management

I follow Kothari et al. (2005) and use the performance-matched discretionary accruals as

a proxy for earnings management. Specifically, I run the modified Jones (1991) model as

described in Dechow et al. (1995) for each two digit SIC-year combination as follows:

𝐴𝐶𝐶𝑅𝑈𝐴𝐿𝑖𝑡

𝐴𝑆𝑆𝐸𝑇𝑆𝑖,𝑡−1= 𝛽0 + 𝛽1

1

𝐴𝑆𝑆𝐸𝑇𝑆𝑖,𝑡−1+ 𝛽2

∆𝑅𝐸𝑉𝑖𝑡 − ∆𝐴𝑅𝑖𝑡

𝐴𝑆𝑆𝐸𝑇𝑆𝑖,𝑡−1+ 𝛽3

𝑃𝑃𝐸𝑖𝑡

𝐴𝑆𝑆𝐸𝑇𝑆𝑖,𝑡−1+ 𝜀𝑖𝑡 (2),

where ACCRUAL is accruals, computed as earnings before extraordinary items and

discontinued operations minus cash flow from operating activities from the statement of cash

flows (Hribar and Collins, 2002; Cohen et al., 2008). ASSET is total assets, REV is total

revenue, AR is accounts receivable, and PPE is gross property, plant, and equipment.

To measure accruals more accurately, I follow the method of Reichelt and Wang (2010)

and use all the available observations from Compustat U.S. universe to estimate Equation (2).

The residual from Equation (2) is the discretionary accrual measure. Following Kothari et al.

(2005), I calculate firm i’s performance-matched discretionary accrual in year t as firm i’s

discretionary accrual minus the discretionary accrual of the firm from the same industry-year

combination with the closest ROA.

3 If I cluster the standard errors by state and year, the results still hold.

12

3.3 Measure of Political Corruption

The main political corruption measure, Corruption, is the number of corruption

convictions divided by the number of population (in 100,000s) in the state. The U.S.

Department of Justice Public Integrity Section (PIN) reports annual public corruption

conviction numbers for the 94 U.S. federal district courts in its yearly Report to Congress on

the Activities and Operations of the Public Integrity Section4. Most convicted cases are

handled by the U.S. Attorney’s Office in the originating district, while some are handled by

PIN directly. The crimes reported include bribery, extortion, election scandals, conspiracy,

and criminal conflicts of interest. As discussed in Smith (2016), the data do not allow

researchers to identify cases directly impacting firms. Therefore, I implicitly assume that a

higher number of conviction cases in a district reflects a more corruption culture that firms in

the district have to face.

The data are used widely in finance and economics literature to measure corruption in the

U.S. (Fredricksson et al. 2003; Glaeser and Saks 2006, Butler et al. 2009; Campante and Do,

2014; Smith 2016). The researchers suggest that the data are objective and verifiable, and

therefore they are superior to survey data.

One plausible concern with the data is that a corruption conviction depends on not only

the existence of corruption, but also the detection of the misdeed. In fact, a lower number of

convicted cases could reflect the absence of strong oversight and effective law enforcement,

rather than a less corrupt environment in the particular area. This concern can be alleviated

in the following ways. First, Glaeser and Saks (2006) argue that the federal judicial system,

which is responsible for most cases, should be above the influence of local corruption and

therefore, the enforcement is more or less equal across the country. Second, Smith (2016)

4 If, in the rare cases, the number of convictions in a district is missing, I use the average number of

convictions in the adjacent years as the conviction number for the missing year.

13

shows that the number of convictions is aligned with intuition and anecdotal evidence in

identifying the most and least corrupt areas in the U.S. Third, I test the robustness of the

results by using survey-based measures of corruption. The results continue to hold.

Since a state may have more than one districts, I aggregate the number of convicted cases

to the state level. I then standardize the number by the state population data obtained from the

U.S. Census Bureau.

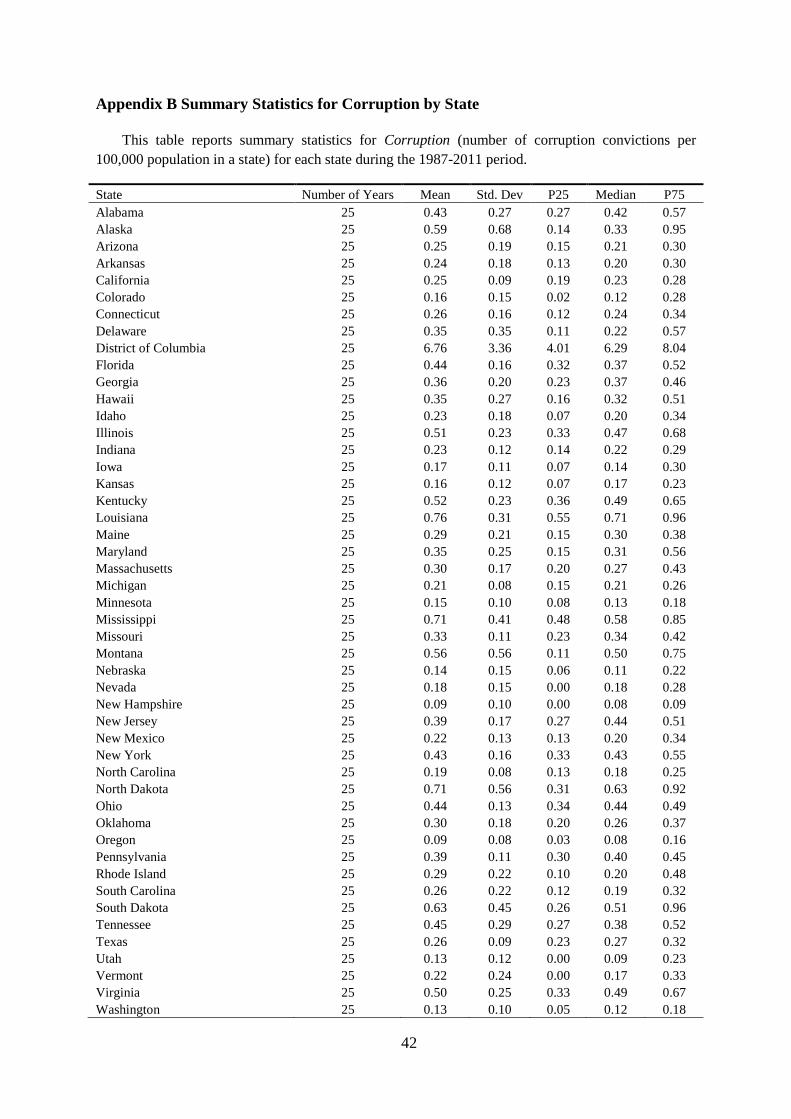

Appendix B reports summary statistics for Corruption by state for the period from 1987

to 2011. As indicated by the mean values of Corruption, Washing D.C., Louisiana, North

Dakota, and Mississippi are the most corrupt states, while Oregon, New Hampshire, Utah,

and Washington are the least corrupt ones. The value of Corruption for Washington D.C. is

exceptionally high. This is not surprising, since D.C. is a political centre with fewer residents.

The regression results remain similar, if I remove all the firms located in D.C. from my

sample.

I provide a visual illustration of Corruption in Figure 1. I calculate the mean value of

Corruption in each state across the sample period, and plot these values in the map. Figure 1

shows that there is a significant variation in Corruption across different states. The figure

also suggests that there is no obvious geographic cluster in terms of political corruption.

3.4 Control variables

I control for Ln(total assets), as larger firms are more politically visible (Watts and

Zimmerman, 1986). I control for CFO (cash flow from operating activities scaled by lagged

total assets) and ROA (income before extraordinary items divided by lagged total assets) to

capture the effect of firm performance on discretionary accruals (e.g., Kothari et al., 2005). I

control for R&D (research and development expenses divided by lagged total assets), because

14

firms with high R&D expenditure suffer from information asymmetry and have the incentive

to signal good accounting quality (Aboody and Lev, 2000; Godfrey and Hamilton, 2005).

Following the suggestions by prior studies (Bebchuk et al., 2011; Koh and Reeb, 2015), I set

missing R&D as zero and include a dummy variable R&D missing, which equals 1 when

R&D is reported as missing in Compustat, and 0 otherwise.

I control for Acquisition, an indicator for M&A involvement, because acquisitive

activities have a significant influence on financial accounting (Ali and Zhang, 2015). I also

control for Issuance, an indicator for external financing, because companies may manipulate

earnings upwards before external financing (Teoh et al., 1998; DuCharme et al., 2004; Carter

et al., 2007).

I control for Institution (the percentage of shares held by institutional investors) and

Ln(Analyst) (the logged number of analysts covering the firm), Big N (an indicator for Big N

auditor) and Leverage (long-term debt plus debt in current liabilities, divided by lagged total

assets), because institutional investors, analysts, auditors and debt holders could impede

earnings management (Matsumoto, 2002; Yu, 2008; Francis and Krishnan, 1999; Khan and

Watts, 2009).

I control for Tight covenant (an indicator for proximity to debt covenant violation) and

Meet/Beat (an indicator for meeting or beating earnings benchmarks by a small margin), as

managers may manipulate earnings to avoid debt covenant violation and to meet or beat

earnings benchmarks (DeFond and Jiambalvo, 1994; Sweeney, 1994; Burgstahler and Dichev,

1997; Graham et al., 2005).

I then control for firm growth by including Sales growth and M/B (the market-to-book

ratio) in the model, because high-growth firms are faced with severe penalty for missing

15

earnings benchmarks and thus have the incentive to manipulate earnings upwards (Skinner

and Sloan, 2002).

Barton and Simko (2002) show that firms with a bloated balance sheet are less capable of

upward earnings manipulation. I therefore control for NOA (net operating assets divided by

lagged sales), a measure of bloatedness of the balance sheet. I control for Sales Volatility

(standard deviation of the ratio of total sales to total assets in the prior five years) and

Operating cycle ([Average Inventory/(Cost of Sales/365)]+[Average Accounts

Receivable/(Sales/365)]), because companies with larger operating volatility and longer

operating cycle have more flexibility in earnings manipulations.

I additionally control for state characteristics. Specifically, I control for Per capita

income (personal income per capita), Education (the percentage of labor-force residents who

have finished four-year’s college education), and Hightech (the percentage of high tech

companies in the state). I calculate the percentage of high-tech firms based on the firms in

Compustat U.S. universe. Prior studies show that wealthier states and better educated states

are less corrupt (Glaeser and Saks, 2006), and that innovative companies are more likely to

be the targets of political corruption (Murphy et al., 1993).

Detailed variable definitions are provided in Appendix A.

4. Sample Formation and Descriptive Statistics

4.1 Sample Formation

I start with all U.S. public firms in the Compustat database. I only include companies that

are incorporated and headquartered in the U.S. I exclude firms in financial industries (SIC

codes 6000-6999) or utility industries (SIC codes 4900-4999), as they are under different

regulatory oversights. I require at least 10 observations in each industry-year combination

16

(industry is based on a two-digit SIC code). Following Heider and Ljungqvist (2015), I use

historical location and incorporation data from the SEC’s EDGAR service from May 1996

onwards, and use historical location and incorporation data from the Compact Disclosure

before May 1996. The SEC’s EDGAR data are provided by Bill McDonald5.

I obtain debt covenant data from the Dealscan database and institutional shareholding

data from Thomson Reuters Institutional (13f) Holdings. I collect analyst coverage, analyst

forecast, and actual earnings per share data from the I/B/E/S unadjusted detailed files.

I collect corruption conviction data from the Department of Justice Public Integrity

Section. I obtain data on each state’s personal income per capita from the Bureau of

Economic Analysis, and state education information from the Integrated Public Use

Microdata Series (Flood et al., 2015).

Following Hribar and Collins (2002)’s suggestion, I use the cash flow method to measure

total accrual. The sample period starts in 1987, the year when cash flow statements became

available. The sample period ends in 2011, since the Dealscan-Compustat linking is only

available before 2011 (Chava and Roberts, 2008). I delete all the firm-year observations with

negative book value of equity or with missing information for the variables included in

Equation (1), as specified in Section 3.1. The final sample consists of 56,096 firm-year

observations from 1987 to 2011.

4.2 Descriptive Statistics

Table 1 Panel A provides summary statistics for the full sample. The mean value of DA is

-2.39 % and its median value is -0.92%. It is slightly different from zero, because not all the

observations used in the estimation of discretionary accruals are included in the final sample.

5 The data can be obtained from http://www3.nd.edu/~mcdonald/10-K_Headers/10-K_Headers.html.

17

The mean value of Corruption is 0.31, indicating that every 100,000 people are faced with

0.31 corruption convictions in an average state. The average firm in the sample has total

assets of $1.80 billion, with an ROA of 0.61%, CFO and R&D of 6.75% and 6.41% of lagged

total assets, respectively. About 20% (28%) of sample observations are involved in mergers

and acquisitions (debt or equity issuance). On average, institutional investors hold about

49.73% of sample firms’ shares and my sample firms are followed by 8.63 analysts. About 11%

of the sample firms face tight debt covenants and 16% of them meet or beat earnings

benchmarks by a small margin. The mean market-to-book ratio is 3.25 and the net operating

assets averages about 75% of lagged sales. The mean value of sales volatility is about 21.90%

and the operating cycle on average is 130.76 days. The mean value of Big N shows that 90%

of sample firms are audited by Big N auditors. The states where the sample firms are

headquartered have a mean personal income per capita of $30,800. About 15 % of firms

headquartered in these states are high tech firms, and about 27% of labor-force residents in

these states have finished four years’ college education.

Table 1 Panel B provides descriptive statistics by the level of corruption. A firm-year

observation is in the most corrupt (least corrupt) group, if it is in the top (bottom) quartile of

all the observations. The mean value of DA is -1.52% in the least corrupt group, and -2.12%

in the most corrupt group. The difference is significant at the 10% level. On average,

companies in the most corrupt group are located in states where every 100,000 people are

faced with 0.61 corruption convictions in a year, and companies in the least corrupt group are

located in states where every 100,000 people are faced with only 0.11 corruption convictions

in a year. The difference is significant at the 1% level.

Many variables are significantly different between the two groups. Specifically,

companies in the most corrupt group are associated with higher cash flow from operations,

better firm performance, lower R&D expenditure, higher market-to-book ratio, higher

18

leverage, and are more likely to be involved in M&A activities and financing activities. These

differences give rise to the need to control these variables in the analyses.

5. Empirical Results

5.1 Baseline Regression

Table 2 reports the results from estimating model (1). Column (1) reports the results

where I control for all the firm-level and state-level characteristics. Column (2) shows the

results after I further control for year fixed effects. Column (3) reports the results after I

further include industry fixed effects.

The results in these three columns are similar. Since the model specification in Column

(3) is the most comprehensive, I focus on Column (3). The coefficient on Corruption is -

0.021, significant at the 1% level, suggesting that a one standard deviation increase in

Corruption (0.19) is associated with -2.1% decrease in discretionary accrual. The economic

magnitude is sizeable, as it is almost more than three times the mean value of ROA. The

coefficients are significantly negative for CFO, R&D, Acquisition, Ln(Analyst), and Big N,

consistent with prior literatures, e.g., DuCharme et al. (2004), Ali and Zhang (2005), and

Chen et al. (2015).

In sum, the results suggest that political corruption results in downward earnings

management, consistent with H1.

19

5.2 Subsample Analyses

5.2.1 Geographic Concentration

I predict that the impact of corruption on earnings management is more pronounced for

firms whose operations concentrate in their headquarter states. Political officials have

stronger ability to seek rents, when their jurisdiction is the only place for a company’s

operation (Smith, 2016). Besides, geographically dispersed companies face lower costs when

they shift operations to low-corrupt areas (Bai et al., 2015). The low costs of shifting increase

a firm’s bargaining power when it is faced with bribe solicitation (Svensson, 2003).

A firm is deemed as a concentrated (dispersed) firm if the proportion of operations in its

headquarter state is above (below) sample median in the year. Following Garcia and Norli

(2012) and Smith (2016), I measure the proportion of a firm’s operations in each state as the

number of times the state is mentioned in the firm’s 10-K filing in the year divided by the

total number of times all states are mentioned. The relevant data is obtained from Diego

Garcia.6 Then, I re-estimate Equation (1) for the two subsamples that are formed based on

geographic concentration. Because of sample selection in Garcia and Norli (2012), the data

are not available for all the companies.

Table 3 reports the results. In the subsample of geographically concentrated firms, the

coefficient on Corruption is -0.037, significant at the 1% level. In contrast, in the subsample

of geographically dispersed firms, the coefficient on Corruption is -0.009, much smaller in

magnitude and not significant. A Chow test rejects the null hypothesis of no difference in the

coefficients for concentrated and dispersed companies at the 10% level (Chow 1960).

6 The data can be obtained from http://leeds-faculty.colorado.edu/garcia/page3.html.

20

Overall, the results from Table 3 suggest that the impact of political corruption on

downward earnings management is stronger for firms whose operations concentrate in their

headquarter states.

5.2.2 Political Connections

I predict that the impact of corruption on earnings management is less pronounced for

firms with political connections. Political connections protect these firm from local officials’

expropriations and these firms are less incentivized to manage earnings downwards (Clarke

and Xu, 2006). Following Cooper et al. (2010) and Kim and Zhang (2015), I use the

establishment of corporate political action committee (PAC) to measure political connection.

A firm is deemed as politically connected if it registered a PAC in November of the year.

I obtain the PAC data from the Federal Election Commission (FEC) Committee Master Files.

The database provides the name of the company that is connected to each PAC. I then match

company names from FEC to company names from Compustat by using the fuzzy merge

method developed by Wasi and Flaaen (2015). I use the historical company name data

provided by Bill McDonald to adjust for historical name change7. Then I re-estimate

Equation (1) for the two subsamples that are formed based on whether the firm has a PAC.

The sample consists of 56, 096 observations.

Table 4 reports the results. In the subsample of politically connected firms, the coefficient

on Corruption is 0.005 and not significant. In contrast, in the subsample of firms without

political connections, the coefficient on Corruption is -0.024, significant at the 1% level. The

difference in the coefficients is significant at the 10% level.

7 The data can be obtained from http://www3.nd.edu/~mcdonald/10-K_Headers/10-K_Headers.html.

21

Overall, the results from Table 4 lends support to the prediction that the impact of

corruption on earnings management is more pronounced for firms without political

connections.

5.2.3 Costs of Downward Earnings Management

Missing earnings benchmarks and violating debt covenants are both very costly (DeFond

and Jiambalvo, 1994; Skinner and Sloan, 2002). Compared with companies that are faced

with lower costs of downward earnings management, companies faced with higher costs of

downward earnings management are less likely to manipulate earnings downwards. I

therefore expect that the impact of political corruption is less pronounced for these firms.

I test this expectation by dividing the sample into two subsamples based on their costs of

downward earnings manipulation. A firm is deemed with high costs of downward earnings

manipulation, if it meets or beats earnings benchmarks at a small margin, of if it is faced with

tight debt covenant, and is deemed with low costs otherwise. Following Cohen et al. (2008), I

deem a company meets or beats earnings benchmarks by a small margin, if the net income

before extraordinary items scaled by total assets lies in [0,0.005) or the change in net income

before extraordinary items scaled by total assets lies in [0,0.005), or EPS beats analyst

forecasts by one cent per share or less. I deem a company with tight debt covenant, if the

tightest slack of the company is smaller than the sample median in the year, and equals 0 if

the tightest slack of the company is larger than the sample median in the year, or if the

company is not limited by debt covenant in the year, or if the company’s tightest slack is

negative. Following Dou et al. (2016), I measure slack as [(maximum threshold-actual) /

maximum threshold] for maximum threshold covenants, and [(actual-minimum threshold)/

absolute value of minimum threshold] for minimum threshold covenants.

22

Table 5 report the results. In the subsample of firms with low costs of manipulating

earnings downwards, the coefficient on Corruption is -0.024, significant at the 1% level. In

contrast, in the subsample of firms with high costs of manipulating earnings downwards, the

coefficient on Corruption is not significant. The results from Table 5 support the prediction

that the impact of corruption on downward earnings management is not pronounced for firms

with high costs of downward earnings manipulation.

6. Robustness checks

6.1 Alternative Measures of Corruption

6.1.1 Alternative Measures Based on Corruption Convictions

The number of political corruption convictions may be proportional to the number of

officials, rather than the number of population. Following Cordis and Warren (2014), I use an

alternative measure Corruption per government employee. This measure is calculated as the

number of corruption convictions per 100,000 full-time equivalent state and local government

employees8. I obtain the government employment data from the U.S. Census Bureau.

The main measure of corruption is based on the headquarter state and it may not capture

the political corruption faced by a company that operates in several states. To address this

concern, following Smith (2016), I construct Weighted corruption, which is the weighted

average of Corruption in all states where the firm operates in and the weight is determined by

the proportion of the firm’s operations in that state. The measure of the proportion is

discussed in Section 5.2.1.

8 According to the U.S. Census Bureau, the number of full-time equivalent government employees is equal

to the number of full-time government employees plus the number of part-time government employee working

hours divided by the standard number of working hours of a full-time government employee.

23

The third measure is Number of convictions, calculated as the raw number of corruption

convictions divided by 1,000, irrespective of the size of the population in the state.

I then re-estimate Equation (1) by replacing Corruption with these three alternative

measures and report regression results in Table 6 Panel A. Because the operation distribution

data are not available for all the companies, the sample size is smaller in Column (2). Across

all the three columns, the coefficients on the alternative measures are negative and significant

at least at 5% level, suggesting that the baseline regression results are robust to various

alternative measures based on corruption convictions.

6.1.2 Alternative Measures Based on Perception

Although the main measure of corruption is objective, this ex post measure may not

accurately portrait political corruption. In this subsection, I address this concern by using

three alternative measures that are based on perception.

The first two measures are based on the strength of state institutions that safeguard

against political corruption. Two non-government organizations, the Better Government

Association and the Centre for Public Integrity, separately issued reports that ranked states

based on transparency, accountability and anti-corruption mechanisms. I obtain the former

ranking data from the 2013 BGA-Alper Integrity Index and the latter ranking data from the

2012 State Integrity survey. I define Low integrity_BGA as a dummy variable that equals 1 if

the state ranks in the bottom quartile of all the states in the 2013 BGA-Alper Integrity Index,

and 0 otherwise. I define Low integrity_SII as a dummy variable that equals 1 if the state

ranks in the bottom quartile of all the states in the 2012 State Integrity Survey, and 0

otherwise. Both variables are cross-sectional, and are not available for Washington D.C.

24

The third measure is State House reporters’ perception of corruption. I obtain the data

from the survey conducted by Boylan and Long (2003) in 1999. I define Perceived

corruption as the corruption scale from Table 2 of Boylan and Long (2003). This variable is

not available for Massachusetts, New Hampshire, New Jersey, and Washington D.C.

I re-estimate Equation (1) by replacing Corruption with these three alternative measures

and report regression results in Table 6 Panel B. Because the three measures are not

available for all the companies, the sample size is smaller in these three columns. Table 4

Panel B shows that the coefficients on the three measures are negative and significant. Which

suggests that the baseline regression results are also robust to various subjective measures of

corruption.

6.2 Restatement Analysis

I also test whether the results are robust to an alternative measure of earnings

management, i.e. earnings restatement. Specifically, I run the following regression.

% 𝑜𝑓 𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔 𝐹𝑖𝑟𝑚𝑠𝑠𝑡 = 𝛼0 + 𝛼1𝐶𝑜𝑟𝑟𝑢𝑝𝑡𝑖𝑜𝑛𝑠𝑡 + 𝛼2𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡 +

𝑆𝑡𝑎𝑡𝑒 𝐹𝐸 + 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝜀𝑠𝑡 (3),

Where % 𝑜𝑓 𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔 𝐹𝑖𝑟𝑚𝑠𝑠𝑡 is the number of companies with restated earnings

divided by the number of companies located in state s in year t. A company is deemed as

understates (overstates) earning if the original net income is lower (higher) than restated net

income. I include all the companies in the Compustat U.S. universe. Among the 226,507

observations from 1987 to 2011, 1.81% understates their net income, and 6.94% overstates

their net income. Because there is not enough within-firm variation in terms of earnings

understatement, I conduct the analysis in state level, rather than firm level. The sample

consists of 1,275 state-year observations. The results are reported in Table 7.

25

Table 7 Column (1) reports the result when the focus is income-increasing restatement

(i.e., the restated earnings is higher than the originally reported earnings), which results from

downward earnings management. The coefficient on Corruption is positive and significant at

the 10% level, suggesting that the percentage of firms that understate earnings increases with

the level of political corruption. This is consistent with my conclusion that firms manipulate

earnings downwards to protect themselves against the expropriation by corrupt officials.

Table 7 Column (2) reports the result when the focus is income-decreasing restatement

(i.e., the restate earnings is lower than the originally reported earnings), resulting from

upward earnings management. The coefficient on Corruption is not significant, indicating

that political corruption does not affect firms’ likelihood of overstating income.

In sum, this analysis based on restatement suggests that the findings in baseline

regression is robust to an alternative measure of earnings management.

6.3 Accounting Policy Analysis

I test the robustness of my baseline regression results by focusing on the choices of

inventory valuation methods and depreciation methods. I first test the impact of political

corruption on the choice of inventory valuation methods by running the following Logit

model.

𝐼𝑛𝑣 𝑚𝑒𝑡ℎ𝑜𝑑𝑖𝑠𝑡 = 𝛼0 + 𝛼1𝐶𝑜𝑟𝑟𝑢𝑝𝑡𝑖𝑜𝑛𝑠𝑡 + 𝛼2𝐹𝑖𝑟𝑚 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖𝑠𝑡

+ 𝛼3𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝜀𝑖𝑠𝑡 (4),

Where the dependent variables is INV method, a dummy variable that equals 1 if the firm

adopts FIFO (first-in, first-out) as the primary inventory valuation method, and 0 if the firm

adopts LIFO (last-in, first-out) or average cost method as the primary inventory valuation

method. Table 8 Column (1) reports the results. The coefficient on Corruption is not

26

significantly different from zero, suggesting no association between political corruption and

the choice of inventory valuation method.

Then I examine the relation between Corruption and LIFO reserve. LIFO reserve is the

difference between LIFO and FIFO carrying values (Penman and Zhang, 2002). All the firms

using LIFO are required to disclose this value (Jennings et al., 1996). I re-run Equation (1)

where, LIFO reserve, the value of LIFO reserve divided by lagged total assets, is the

dependent variable. The results are reported in Table 8 Column (2). The coefficient on

Corruption is positive and significant at 1%, indicating that LIFO-using firms in more corrupt

areas would have reported much higher earnings if they switch from LIFO to FIFO.

Next, I test firms’ choices of depreciation methods. I re-run Equation (4) by replacing

INV method with DEP method, a dummy variable that equals 1 if the firm adopts accelerated

depreciation method, and 0 if the firm adopts straight-line depreciation method, or the mix of

accelerated depreciation method and straight-line depreciation method. The results are

reported in Table 8 Column (3). The results suggest that companies located in more corrupt

states are more likely to choose accelerated depreciation method.

Further, I test how political corruption affects depreciation reserve, the excess amount of

accumulated depreciation (Penman and Zhang, 2016). I re-run Equation (1) with DEP reserve

as the dependent variable. It is estimated by multiplying the gross amount of PPE by the

difference of the accumulated-depreciation-to-gross-PPE ratio and the median accumulated-

depreciation-to-gross-PPE ratio of all firms within the same industry-year combination,

divided by lagged total assets. The regression results are reported in Table 8 Column (4). The

coefficient on Corruption is significantly positive, suggesting that firms in more corrupt areas

record a higher amount of accumulated depreciation.

27

Overall, above analyses suggest that companies located in more corrupt areas are more

likely to choose income-decreasing accounting policies.

6.4 Instrument Variable Approach

I address the endogeneity concerns by using an instrumental variable approach. The

instrumental variable is the isolation of state capital from its populace, measured by the size-

normalized version of Gravity-based Centered Index for Spatial Concentration (GCISC2)

from Campante and Do (2014). The measure ranges from zero to one, with zero indicating

minimum isolation where all individuals live close to the state house, and one indicating

maximum isolation where all individuals live as far from the state house as possible.

Campante and Do (2014) find that states with isolated capital cities are associated with

greater political corruption. They attribute it to less oversight and scrutiny.

Following Campante and Do (2014), I compute GCISC2 for each state in each year. The

details of the calculation are shown in Appendix C. I obtain the geospatial data and

population data from the U.S. Census Bureau. Because the geospatial data are not available

for Alaska, Hawaii, and Washington D.C., the sample size is reduced slightly to 55,850

observations. The F-statistic for weak instrument test is 105.41 (Kleibergen and Paap, 2006),

exceeding the Stock and Yogo (2005) 10% maximal IV size critical value of 16.38. Therefore,

I can reject the null hypothesis that the instrument is weak.

Table 9 reports the second stage regression results. The coefficient on the instrumented

value of Corruption is -0.042, significant at the 5% level. The results suggest that the baseline

finding is unlikely to be driven by endogeneity.

28

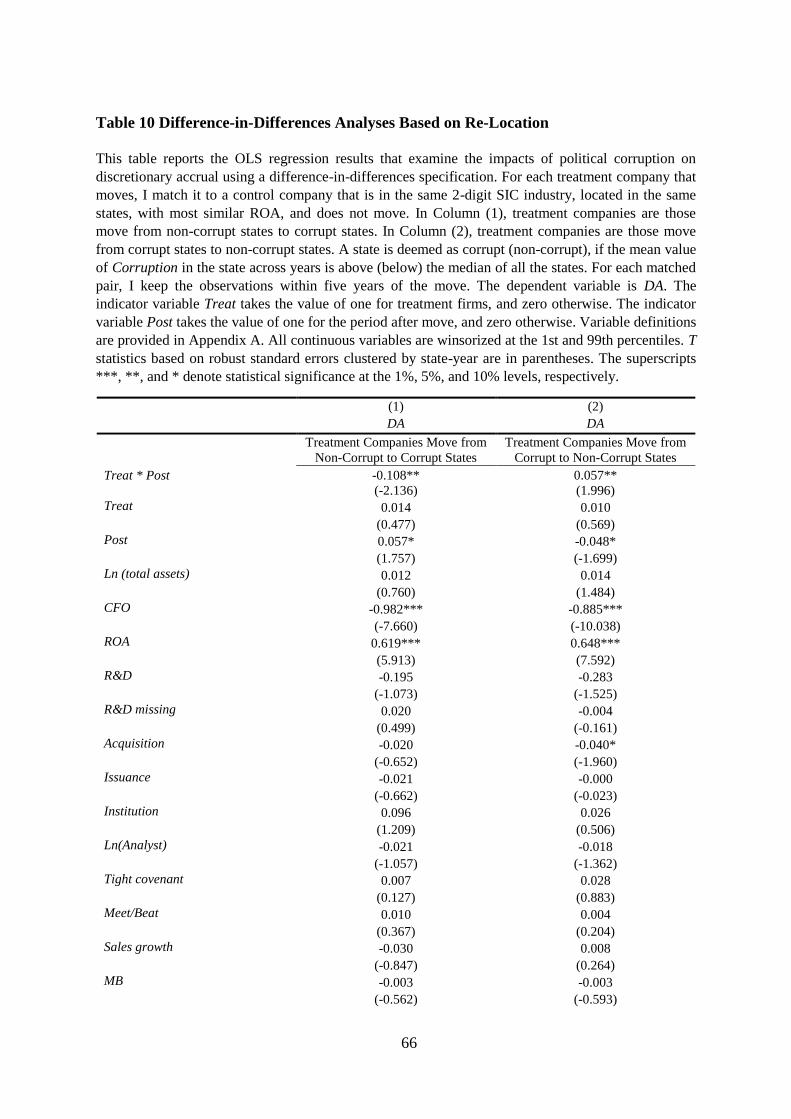

6.5 Difference-in-Differences Analysis

To further address the endogeneity concern, I conduct a difference-in-differences test by

focusing on companies that move between corrupt and non-corrupt states. This test

effectively controls for non-time-varying firm characteristics and time-series trends having

similar influences on treatment and control firms. Specifically, a state is deemed as corrupt

(non-corrupt), if the mean value of Corruption in the state across years is above (below) the

median of all the states. For each treatment company that moves between corrupt and non-

corrupt states, I match it to a control company (i.e., a firm that does not move) which is in the

same 2-digit SIC industry, located in the same state, and with most similar ROA. For each

matched pair, I keep the observations from five years before to five years after the move. I

then run the following regression.

𝐷𝐴𝑖𝑠𝑡 =

𝛼0 + 𝛼1𝑇𝑟𝑒𝑎𝑡𝑖 ×

𝑃𝑜𝑠𝑡𝑖𝑡+ 𝛼2𝑇𝑟𝑒𝑎𝑡𝑖+ 𝛼3𝑃𝑜𝑠𝑡𝑖𝑡+ 𝛼4𝐹𝑖𝑟𝑚 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖𝑠𝑡+ 𝛼5𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡 +

𝑃𝑎𝑖𝑟 𝐹𝐸 + 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝜀𝑖𝑠𝑡 (5),

Where 𝑇𝑟𝑒𝑎𝑡𝑖 is a dummy variable that takes the value one if the company is a treatment

company, and zero if it is a control firm. 𝑃𝑜𝑠𝑡𝑖𝑡 is a dummy variable that takes the value one

for the years after the move, and zero for the years before the move. I control for pair fixed

effects, to avoid the correlated omitted variable problem (Cram et al., 2009).

Table 10 Column (1) reports the result when treatment companies move from non-

corrupt states to corrupt states. The coefficient on Treat×Post is -0.108 and significant at the

5% level. The result suggests that firms tend to manipulate earnings downwards after moving

to a more corrupt state.

29

Table 10 Column (2) reports the result when treatment companies move in the opposite

direction, i.e., from corrupt states to non-corrupt states. The coefficients on Treat×Post is

0.057 and significant at the 5% level. The results show that firms are more likely to

manipulate earnings upwards after moving to a less corrupt state.

Taken together, the results from Table 10 show that political corruption causally results

in downward earnings management.

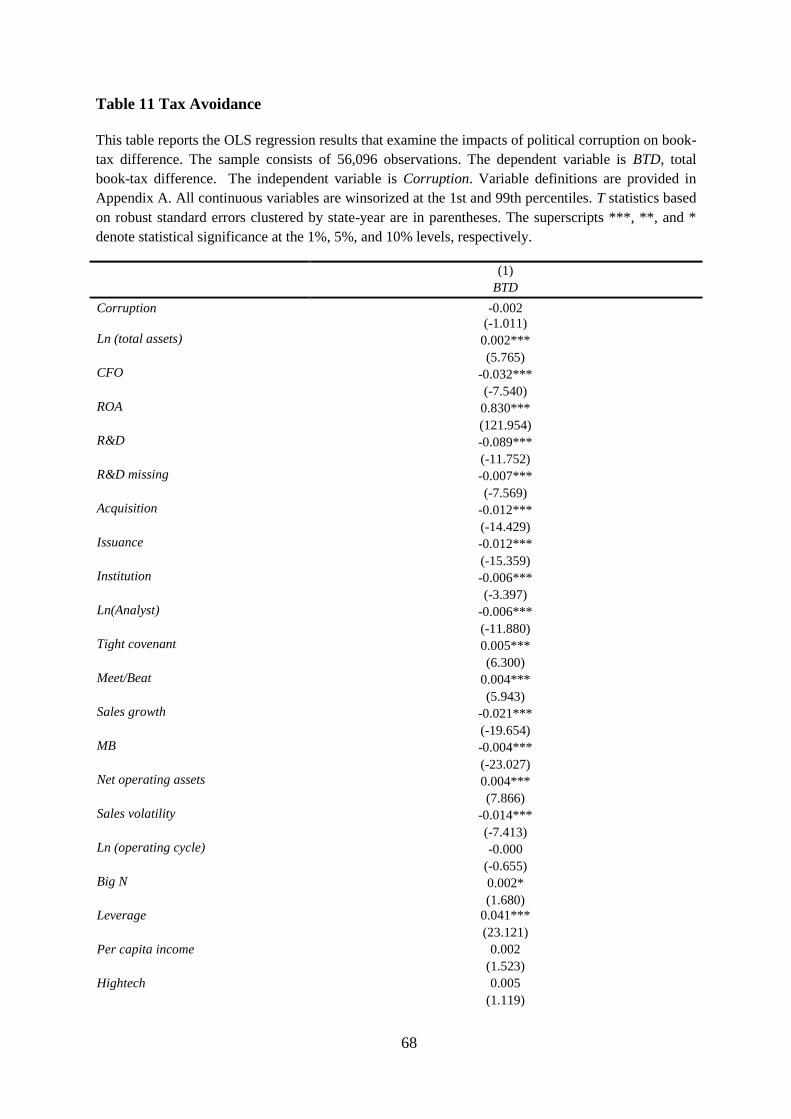

6.6 Tax Avoidance Analysis

Political corruption breaches the trust between governments and companies, leading to

tax avoidance (Ayyagari et al., 2014). Since companies may evade tax by manipulate

earnings downwards (Chen and Daley, 1996), my findings may only reflect the relation

between political corruption and tax avoidance.

To address this concern, I analyze how political corruption affects tax avoidance.

Following Frank et al. (2009), I use BTD (total book-tax difference) to capture corporate tax

avoidance. BTD is calculated as (𝑝𝑟𝑒 − 𝑡𝑎𝑥 𝑏𝑜𝑜𝑘 𝑖𝑛𝑐𝑜𝑚𝑒 – 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑡𝑎𝑥𝑎𝑏𝑙𝑒 𝑖𝑛𝑐𝑜𝑚𝑒)/

𝑙𝑎𝑔𝑔𝑒𝑑 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 , where 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑡𝑎𝑥𝑎𝑏𝑙𝑒 𝑖𝑛𝑐𝑜𝑚𝑒 is (𝑓𝑒𝑑𝑒𝑟𝑎𝑙 𝑖𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥𝑒𝑠 +

𝑓𝑜𝑟𝑒𝑖𝑔𝑛 𝑖𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥𝑒𝑠)/𝑈. 𝑆. 𝑠𝑡𝑎𝑡𝑢𝑡𝑜𝑟𝑦 𝑡𝑎𝑥 𝑟𝑎𝑡𝑒 . Following the suggestions of Dyreng

and Lindsey (2009), I calculate 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑡𝑎𝑥𝑎𝑏𝑙𝑒 𝑖𝑛𝑐𝑜𝑚𝑒 as (𝑡𝑜𝑡𝑎𝑙 𝑖𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥𝑒𝑠 −

𝑑𝑒𝑓𝑒𝑟𝑟𝑒𝑑 𝑖𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥𝑒𝑠)/𝑈. 𝑆. 𝑠𝑡𝑎𝑡𝑢𝑡𝑜𝑟𝑦 𝑡𝑎𝑥 𝑟𝑎𝑡𝑒, if either federal income taxes data or

foreign income taxes data are missing. I obtain financial data from Compustat, and statutory

tax rate data from the Internal Revenue Service.

Then I re-run Equation (1) by using total book-tax difference as the dependent variable.

Table 11 reports the regression results. The coefficient on Corruption is not significantly

30

different from zero. The regression results suggest that the reduction in discretionary accrual

is unlikely to be related with tax avoidance.

6.7 Party Affiliation

One concern for my study is that the number of political corruption convictions may be

proxy for state party affiliation. For example, Merier and Holbrook (1992) study the

prosecution of political corruption during the Reagan administration and find more intensive

prosecution of political corruption in Democratic states. To figure out whether my findings

are driven by state party affiliation, I conduct a subsample analysis based on state party

affiliation. I identify a state’s party affiliation with the party affiliation of the state governor.

A firm is in the Republican (Non-Republican) subsample, if the governor of the firm’s

headquarter state is a Republican (Non-Republican). I obtain state governor party affiliation

data from the National Governors Association.

Table 12 report the results. In the Republican subsample, the coefficient on Corruption

is -0.023, significant at the 5% level. In the Non-Republican subsample, the coefficient on

Corruption is -0.031, significant at the 1% level. These two coefficients are not significantly

different (p=0.581). The results suggest that no matter whether a state is Republican or not,

companies manipulate earnings downwards in response to political corruption.

6.8 High-Profile Political Corruption Case and Earnings Management

Another approach to identify the change in corruption is through the prosecution of high

profile corruption cases. These cases are likely to elevate local politicians’ assessment of the

likelihood of corrupt deeds being detected and penalized, and therefore deter their rent-

31

seeking activities. In this sub-section, I provide some evidence by studying how a high-

profile corruption case, the Siegelman case, affects firms’ discretionary accruals.

I choose this case because it involves the highest local official, the governor, and it has

two turning points, offering different implications. One point is in June 2007, when the U.S.

District Court for the Middle District of Alabama sentenced Siegelman, the former Alabama

governor, to 88 months in prison plus other penalties. The second point is in March 2008,

when the 11th U.S. Circuit Court of Appeals released him from prison, effectively cutting his

jail time from 88 months to 10 months.

The information from Google Trends suggests that both the sentence and the release of

Mr. Siegelman received tremendous public attention from the state Alabama. The

implications of the two events are distinct. While the sentencing and the related heavy

penalty are likely to lower local corruption, the drastic reduction in penalty indicated by the

early release has the opposite effect.

I utilize this event and run the following two regressions. I run Equation (6) with the data

from 2006 to 2007, and run Equation (7) with the data from 2007 to 2008.

𝐷𝐴𝑖𝑠𝑡 =

𝛼0 + 𝛼1𝐴𝑙𝑎𝑏𝑎𝑚𝑎𝑖 ×

𝑃𝑜𝑠𝑡_𝑠𝑒𝑛𝑡𝑒𝑛𝑐𝑒𝑡+ 𝛼2𝐴𝑙𝑎𝑏𝑎𝑚𝑎𝑖+ 𝛼3𝑃𝑜𝑠𝑡_𝑠𝑒𝑛𝑡𝑒𝑛𝑐𝑒𝑡+ 𝛼4𝐹𝑖𝑟𝑚 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖𝑠𝑡+ 𝛼5𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡 +

𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀𝑖𝑠𝑡 (6),

𝐷𝐴𝑖𝑠𝑡 =

𝛼0 + 𝛼1𝐴𝑙𝑎𝑏𝑎𝑚𝑎𝑖 ×

𝑃𝑜𝑠𝑡_𝑟𝑒𝑙𝑒𝑎𝑠𝑒𝑡+ 𝛼2𝐴𝑙𝑎𝑏𝑎𝑚𝑎𝑖+ 𝛼3𝑃𝑜𝑠𝑡_𝑟𝑒𝑙𝑒𝑎𝑠𝑒𝑡+ 𝛼4𝐹𝑖𝑟𝑚 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖𝑠𝑡+ 𝛼5𝑆𝑡𝑎𝑡𝑒 𝐶ℎ𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑠𝑡 +

𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀𝑖𝑠𝑡 (7),

32

Where 𝐴𝑙𝑎𝑏𝑎𝑚𝑎𝑖 is a dummy variable that equals 1 if the company is located in

Alabama, and zero if it is a control firm. 𝑃𝑜𝑠𝑡_𝑠𝑒𝑛𝑡𝑒𝑛𝑐𝑒𝑡 is a dummy variable that equals 1

for 2007, and 0 for 2006. 𝑃𝑜𝑠𝑡_𝑟𝑒𝑙𝑒𝑎𝑠𝑒𝑡 is a dummy variable that equals 1 for 2008, and 0

for 2007. Due to multi-collinearity, I do not include year fixed effects in the model.

I report the results in Appendix D. The table shows that after the public sentencing of

Don Siegelman, companies located in Alabama increase their discretionary accruals. While

after Siegelman was released, companies located in Alabama reduces their discretionary

accruals. These results are consistent with my argument that companies manipulate earnings

downwards to shield their assets from political corruption.

7. Conclusion

Political corruption can be regarded as an inefficient form of taxation and firms have

incentives to avoid rent-seeking by corrupt officials. Since prior studies document that

downward earnings management is helpful in reducing political costs (Watts and Zimmerman,

1986; Han and Wang, 1998; Johnston and Rock, 2005; Grace and Leverty, 2010; Bova 2013),

I hypothesize that firms respond to political corruption by manipulating earnings downwards.

However, Shleifer and Vishny (1994) argue that corruption can be viewed as an efficient

mechanism to help firms cut through bureaucracies. Therefore, it may be optimal for firms to

bribe corrupt officials in exchange for political favors. In this case, firms may manage

earnings upwards to hide expense items related to illicit dealings with government officials.

Using a sample of 56,096 observations, I empirically investigate the relation between

political corruption and earnings management. Consistent with Glaeser and Saks (2006) and

Smith (2016), I use the number of corruption convictions per capita to measure political

corruption.

33

I find that corruption is negatively related to discretionary accruals, suggesting that

corruption leads to downward earnings management. Specifically, the performance-matched

discretionary accrual, is reduced by 2.1 percentage points, when Corruption increases by one

standard deviation. This effect is economically significant, since the mean value of

discretionary accrual in the sample is only -2.4 percentage points.

To test whether the results are indeed related to the rent-seeking by corrupt officials, I

examine whether the effect of corruption on earnings management is more pronounced for

firms whose operations concentrate in their headquarter states. Political corruption has lower

impact on geographically dispersed firms, because these firms’ cost of relocating to a less

corrupt state is lower (Bai et al., 2015). Consistent with the explanation of corruption, the

effect of political corruption on earnings management is more significant for firms whose

operations concentrate in their headquarter states. I also examine whether the impact of

corruption is more pronounced for firms without political connections. These firms are more

vulnerable to bribe demands (Clarke and Xu, 2006), and thus having stronger incentives to

manipulate earnings downwards. Consistent with my expectation, the impact of political

corruption on earnings manipulation is more significant for these firms. Besides, I test

whether the effect of corruption is weaker for firms with higher costs of downward earnings

management. Consistent with the view that companies are faced with the trade-off between

the costs of downward earnings management and the benefits of downward earnings

management (Bova, 2013), I find that the impact of political corruption on downward

earnings manipulation is not significant for firms faced with higher costs of downward

earnings management.

This negative relation between corruption and earnings management is robust to six

alternative measures of corruption, the earnings restatement analysis, the accounting policy

analysis, the instrumental variable approach, the difference-in-differences test, and an event

34

study. Additional tests also show that my findings are unlikely to be driven by tax avoidance

or state party affiliation. While I can’t completely rule out the possibility that omitted

correlated variables explain the findings, the predominance of my results suggests otherwise.

One limitation of the study is that there could be a time lag between corrupt behaviors

and corruption convictions. As a result, the number of corruption convictions in a given year

could be unrelated with the underlying political corruption level in that year. Subject to this

caveat, this study shows that when faced with high political corruption, firms manipulate

earnings downwards to shield their assets from expropriations by public officials. These

results contribute to both the literature on earnings management and the literature on political

corruption.

Future studies could further explore the interaction between corporate corruption and

political corruption. For example, managers in a company with corrupt culture may be happy

to use bribes to gain some competitive advantages.

35

Reference

Aboody, D., Lev, B., 2000. Information asymmetry, R&D, and insider gains. The Journal of

Finance 55, 2747-2766.

Ali, A., Zhang, W., 2015. CEO tenure and earnings management. Journal of Accounting and

Economics 59, 60-79.

Ayyagari, M., Demirgüç-Kunt, A., Maksimovic, V., 2014. Bribe payments and innovation in

developing countries: Are innovating firms disproportionately affected? Journal of Financial

and Quantitative Analysis 49, 51-75.

Bai, J., Jayachandran, S., Malesky, E.J., Olken, B.A., 2015. Does economic growth reduce

corruption? Theory and evidence from Vietnam. Massachusetts Institute of Technology

working paper.

Barton, J., Simko, P.J., 2002. The balance sheet as an earnings management constraint. The

Accounting Review 77, 1-27.

Bebchuk, L.A., Cremers, K.M., Peyer, U.C., 2011. The CEO pay slice. Journal of Financial

Economics 102, 199-221.

Borisov, A., Goldman, E., Gupta, N., 2016. The corporate value of (corrupt) lobbying. The

Review of Financial Studies 29, 1039-1071.

Bova, F., 2013. Labor unions and management’s incentive to signal a negative outlook.

Contemporary Accounting Research 30, 14-41.

Boylan, R.T., Long, C.X., 2003. Measuring political corruption in the American states: A

survey of state house reporters. State Politics & Policy Quarterly 3, 420-438.

Burgstahler, D., Dichev, I., 1997. Earnings management to avoid earnings decreases and

losses. Journal of Accounting and Economics 24, 99-126.

Butler, A.W., Fauver, L., Mortal, S., 2009. Corruption, political connections, and municipal

finance. Review of Financial Studies 22, 2673-2705.

Campante, F.R., Do, Q.-A., 2014. Isolated Capital Cities, Accountability, and Corruption:

Evidence from US States. The American Economic Review 104, 2456-2481.

Carter, M.E., Lynch, L.J., Tuna, I., 2007. The role of accounting in the design of CEO equity

compensation. The Accounting Review 82, 327-357.

Chava, S., Roberts, M.R., 2008. How does financing impact investment? The role of debt

covenants. The Journal of Finance 63, 2085-2121.

Chen, X., Cheng, Q., Wang, X., 2015. Does increased board independence reduce earnings

management? Evidence from recent regulatory reforms. Review of Accounting Studies 20,

899-933.

36

Chen, P., Daley, L., 1996. Regulatory capital, tax, and earnings management effects on loan

loss accruals in the Canadian banking industry. Contemporary Accounting Research 13, 91-

128.

Claessens, S., Feijen, E., Laeven, L., 2008. Political connections and preferential access to

finance: The role of campaign contributions. Journal of Financial Economics 88, 554-580.

Clarke, G., Xu, L.C., 2004. Privatization, competition, and corruption: How characteristics of

bribe takers and payers affect bribes to utilities. Journal of Public Economics 88, 2067-2097.

Chow, G.C., 1960. Tests of equality between sets of coefficients in two linear regressions.

Econometrica: Journal of the Econometric Society 28, 591-605.

Cohen, D.A., Dey, A., Lys, T.Z., 2008. Real and accrual-based earnings management in the

pre-and post-Sarbanes-Oxley periods. The Accounting Review 83, 757-787.

Cooper, M.J., Gulen, H., Ovtchinnikov, A.V., 2010. Corporate political contributions and

stock returns. The Journal of Finance 65, 687-724.

Cordis, A.S., Warren, P.L., 2014. Sunshine as disinfectant: The effect of state Freedom of

Information Act laws on public corruption. Journal of Public Economics 115, 18-36.

Correia, M.M., 2014. Political connections and SEC enforcement. Journal of Accounting and

Economics 57, 241-262.

Cram, D.P., Karan, V., Stuart, I., 2009. Three threats to validity of choice‐ based and

matched‐ sample studies in accounting research. Contemporary Accounting Research 26,

477-516.

Dass, N., Nanda, V., Xiao, S.C., 2016. Public Corruption in the United States: Implications

for Local Firms. The Review of Corporate Finance Studies 5, 102-138.

Dechow, P.M., Sloan, R.G., Sweeney, A.P., 1995. Detecting earnings management. The

Accounting Review 70, 193-225.

DeFond, M.L., Jiambalvo, J., 1994. Debt covenant violation and manipulation of accruals.

Journal of Accounting and Economics 17, 145-176.

Dou, Y., Khan, M., Zou, Y., 2016. Labor unemployment insurance and earnings management.

Journal of Accounting and Economics 61, 166-184.

DuCharme, L.L., Malatesta, P.H., Sefcik, S.E., 2004. Earnings management, stock issues, and