Embed Size (px)

Citation preview

Politics of Public Fund Investing Part I Colorado County Treasurer’s Association June 26, 2012

Benjamin Finkelstein, CFA

Should a public fund manage money like Wall Street?

4

Preservation vs. Performance

Portfolio Manager: “I have great news for the Board of County

Commissioners! Our unit of local government is in the top 1% quartile of all professional money managers who use the Merrill Lynch 1-3 yr Government index.

“We realized only a 3.00% portfolio loss while the Merrill Lynch benchmark lost 3.50%.”

5

When managing a public fund portfolio what is the most significant risk you face?

Job Risk

6

Job Risk

7

When managing a public fund portfolio what is the most important skill you can possess?

8

Communication Skill

9

The Game Plan

Begin to show how a public fund with limited time, resources, and staff, can professionally manage the investment portfolio

10

“Politics” is used to describe a structure for thinking how Main Street should manage, measure and report investment portfolio performance

11

Two Types Of Portfolio Risk

POLITICAL Principal Preservation • Objectives

– Safety – Liquidity

ECONOMIC Enhance Earnings • Objectives

– Optimize Income

12

Dilemma How To Balance Competing Objectives Preserving Principal while Optimizing Income

What Differentiates Main Street from Wall Street?

14

I. Philosophy

II. Mission

III. Risk Objectives

IV. Management Style

V. Performance Measurement

15

Risk Management

Return Management

I. Philosophy

Manage risk not return

Main Street Political

Wall Street Economic

16

Principal Focus Preservation

Return of Investment Principal Focus Performance

Return on Investment

II. Mission Preserve and Protect

Main Street Political

Wall Street Economic

17

Be the market Political Uncertainty $Pain not = $Gain

GASB 31 vs. Budget Budget Stability

Beat the market Economic Uncertainty

$Pain = $Gain Risk vs. Reward Market Volatility

III. Risk Objectives To Be or to Beat

Main Street Political

Wall Street Economic

18

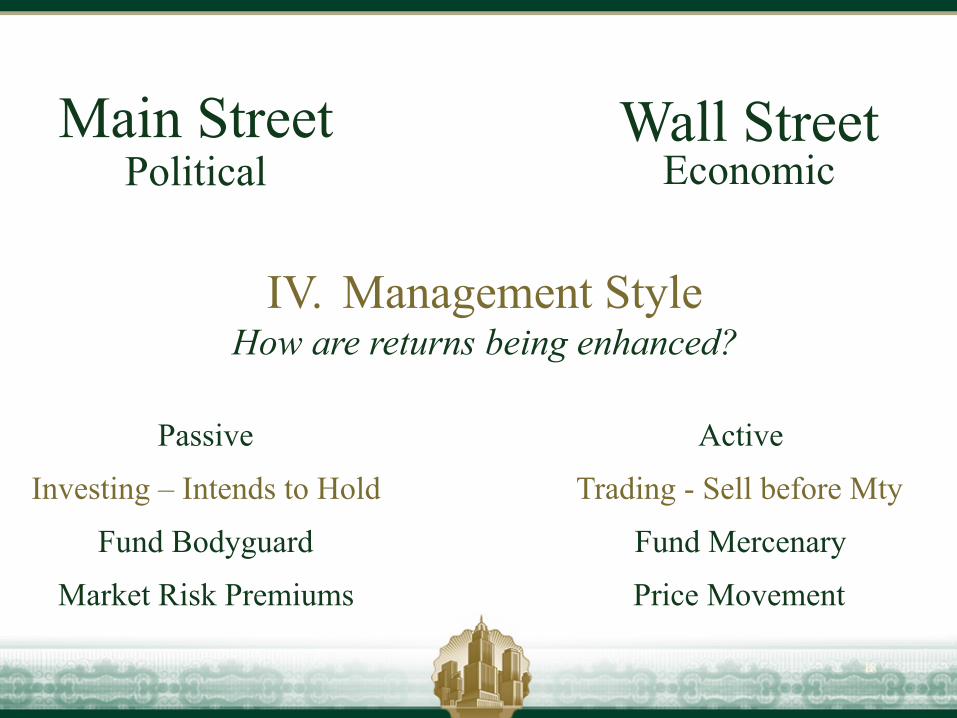

Passive

Investing – Intends to Hold

Fund Bodyguard

Market Risk Premiums

Active

Trading - Sell before Mty

Fund Mercenary

Price Movement

IV. Management Style How are returns being enhanced?

Main Street Political

Wall Street Economic

19

Market Rate of Return

Fiduciary Benchmark

No Peer Group

Suitability

No Historical Returns

Total Return

Market Benchmark

Peer Group Comparisons

Relative Returns

Historical Returns

V. Performance Measurement Accountability

Main Street Political

Wall Street Economic

20

Summary

What differentiates Main Street from Wall Street

21

Public Funds Are Not Pension Funds

Philosophy Manage risk not return

Mission Preservation dominates performance

Objective To be not beat the market / Income not Growth Management Style

Investors not Traders / Passive not Active Performance Reporting

Measuring Suitability / Not Market Indices

22

Building A Politically Correct Portfolio Part II

23

The Policy - Rank The Risk

SAFETY %

LIQUIDITY %

INCOME % Total: 100 %

24

What is the most frequent question asked about the portfolio? Is investment practice following investment policy if only one policy objective is the focus and that objective is the least important of the three?

25

What Is Politically Correct?

I. Portfolio maintains a prudent balance between preserving principal while achieving a market rate of return.

II. Suitability of portfolio can be both quantified and monitored for compliance.

26

Construction Steps I. Develop investment plan

Policy – Plan – Portfolio II. Define management style

Trader – Investor – Buy and Hold III. Determine risk tolerance targets

Liquidity – Interest Rate Risk – MRR IV. Designate portfolios

Liquidity – Income

Developing An Investment Plan

29

Policy Words General Static

Plan Portfolio Specific Dynamic

w Policy’s describe legal not suitable w Policy’s cannot be marked to market w Policy’s provide no cash flows w Policy’s do not pay obligations

Policy Is Not A Plan

30

Policy Objectives Safety Liquidity Income

Plan Priorities Liquidity Income Safety

Liquidity Risk or the premature sale of a security to meet an unexpected obligation creates the greatest political / principal risk to a portfolio and career

Rulebook versus Playbook

31

What is an Investment Plan?

The investment plan is a portfolio interpretation of the investment policy. It quantifies what is a suitable portfolio.

32

Policy Plan

Portfolio

Legal to Suitable

Policy – Plan – Portfolio

33

Investment Plan

1. Fiduciary Benchmark

2. Establishes an investment decision making discipline throughout budget and market cycles

3. Creates a compliance framework for monitoring and reporting the portfolio’s suitability

34

Defining Management Style Trader – Investor – Buy and Hold

35

Trader versus Investor

• Trader seeks to enhance portfolio returns by buying low and selling high. Strategy is founded on selling security before maturity.

• Investor seeks to enhance portfolio returns using the markets liquidity, structure, and/or credit premiums.

36

Active Trader

• Active is a total return style of portfolio management which recognizes and realizes gains and losses.

• Active management styles rely on price change and market benchmark comparisons

• Active management styles typically make budget concessions to offset market volatility and uncertainty

37

Passive Investor

• Passive management does not simply buy and hold investments until maturity.

• Passive management actively rebalances the portfolio current holdings with the investment plan to achieve a market rate of return throughout budget and market cycles.

• What distinguishes passive from active is a rebalance strategy which consist of a simultaneous buy and sell.

38

Buy And Hold Investor

• Buy and Hold investor does not rebalance • Buy and Hold investors have a “set it and

forget it” portfolio strategy

• Buy and Hold investors ignore their portfolio strengths and weaknesses relative to current market conditions

• Buy and Hold investors add no value to

portfolio management process

39

Determine Risk Tolerance Targets

Ability and Willingness Liquidity – Interest Rate Risk – MRR

40

Risk Tolerance - Objective

• Determine funds ability to take risk – Historical liquidity due diligence – Interest rate risk due diligence – Capital market risk premiums

41

Risk Tolerance - Subjective

• What’s funds willingness to take risk? – Expertise of portfolio manager – Investment committee sophistication – Defining Portfolio Purpose

• GASB 31 vs. Budget • Sleep well vs. Eat well

42

Liquidity Due Diligence

• Establish a due diligence process for supporting portfolio’s liquidity targets

• Example: Liquidity Estimator – Three year historical look back by month – Lowest month for collections (incl. portfolio) – Highest month of disbursements – Lowest bank balance net is your liquidity floor. – Liquidity level is X times your liquidity floor

43

Interest Rate Risk

• Interest rate risk quantifies a public funds willingness to take principal risk in pursuit of a market rate of return (#3 policy objective)

• The Plan’s duration is a risk constraint chosen to reflect how much the principal value of the portfolio will be expected to change with changes in interest rate risk (not total return).

44

GFOA Sample Investment Policy

Yield: “The investment portfolio shall be designed

with the objective of attaining a market rate of return throughout budgetary and economic cycles taking into account the investment risk constraints and liquidity needs.”

45

Market Rate of Return

• Market Rate of Return: 12-month moving average of the 2yr USTN auction yield.

• Adapts to the fiscal year budget cycle

• Unlike total returns, a market rate of return when compared to portfolio purchase yield produces a more stable and realistic snapshot of portfolio performance within budget cycle

46

(6.00)

(4.00)

(2.00)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

08/3

1/98

- 08

/31/

99

02/2

8/99

- 02

/29/

00

08/3

1/99

- 08

/31/

00

02/2

9/00

- 02

/28/

01

08/3

1/00

- 08

/31/

01

02/2

8/01

- 02

/28/

02

08/3

1/01

- 08

/31/

02

02/2

8/02

- 02

/28/

03

08/3

1/02

- 08

/31/

03

02/2

8/03

- 02

/29/

04

08/3

1/03

- 08

/31/

04

02/2

9/04

- 02

/28/

05

08/3

1/04

- 08

/31/

05

02/2

8/05

- 02

/28/

06

08/3

1/05

- 08

/31/

06

02/2

8/06

- 02

/28/

07

08/3

1/06

- 08

/31/

07

02/2

8/07

- 02

/29/

08

08/3

1/07

- 08

/31/

08

02/2

9/08

- 02

/28/

09

08/3

1/08

- 08

/31/

09

Tota

l Ret

urn

Date

Total Return Component Analysis: 1Yr Annualized Returns 1YrTotRtnAnn-G1A0

1YrPrcRtnAnn-G1A0 1YrCpnRtnAnn-G1A0 12MoMovAvg-G1A0

Focus on Budget Stability

48

Designate Strategic Portfolios

Primary – Secondary – Income

49

Constructing PC Portfolio

1. Divide total investment portfolio – Strategic liquidity – Income portfolio.

2. Divide strategic liquidity – Primary liquidity – Secondary liquidity

50

Orange County, CA When Practice Didn’t Follow Policy

• Putting all your liquidity eggs in one basket makes a basket case

• Diversify (more than one) primary liquidity

51

• Liquidity focused solely on insuring cash management is able to meet current obligations without prematurely selling a security; absolutely no market risk

• Liquidity positioned to convert a security or investment to cash at or near it’s original cost or NAV; no principal loss

Primary Liquidity 0-Days

52

Secondary Liquidity 1-360 Days

• CYA liquidity “expects the unexpected”

• CYA liquidity allows portfolio manager to combine diversification of liquidity with a focus on income enhancement (Rated 3c-7 or 1.00 NAV funds)

53

• Liquidity Rule #1: Diversification • Liquidity Rule #2: Divide • Liquidity Rule #3: Job Risk

Job risk is forgetting liquidity rules 1 & 2

Cash Management Rules

54

Creating Income Portfolio

55

Diversification Suitable diversification will focus on two

critical measures, liquidity and issuers.

1. State Pools should not be the only source for primary liquidity

2. Individual security holdings should not exceed XX % of portfolio market value

3. Individual corporate issuers other than federal agency’s should not exceed XX % of portfolio holdings

56

Income Portfolio

Total Portfolio – Strategic Liquidity = Income Portfolio

100 % – 30 % = 70 %

57

Income Portfolio • Income portfolio represents the core

investment portfolio. • Optimizing income not liquidity is the key

characteristic of a income portfolio. • Minimizing risk means minimize principal

risk. For public funds this means enhance income with minimum price volatility.

58

Income Politics

Why should each public fund portfolio manager expect to recognize a principal loss?

59

Because the investment policy mandates it!

Avoiding risk is

not managing risk!

60

Why have Yield as an investment policy objective?

61

1. Offer more public services 2. Cover operational cost 3. Mitigate tax burden

To Satisfy the Public’s Three Most Wanted List

Concluding Thoughts “performance reporting”

Ø The key question to be answered - is the

portfolio manager a good steward of the public’s money?

Ø How good is the portfolio manger at both protecting principal and earning a reasonable market rate of return?

Performance Measurement “quantifying stewardship”

Ø The key distinction of a fiduciary benchmark or investment plan is it will capture all policy objectives in policy priority.

Ø The plan or fiduciary benchmark measures performance in the context of not only what is legal but also what is suitable.

Suitability 1. Sufficient liquidity to pay obligations without selling a

security before maturity

2. Portfolio maintains the appropriate level of interest rate risk

3. Portfolio is diversified (no concentration risk)

4. Portfolio holdings are legal

5. Portfolio earns a market rate of return

Disclaimer

This information is for discussion purposes. By accepting this information you agree not to copy, reproduce or otherwise disclose its contents to any third party without our prior consent.

Although the information is obtained from sources we believe to be reliable, we cannot

guarantee it is accurate or complete and it may not be relied upon as such. Neither the information nor any opinion expressed constitutes a solicitation by us for the purchase or sale of any security or >inancial instrument, or is advice or an expression of our views as to whether a particular investment is suitable and appropriate for you or meets your >inancial objectives.

The information does not constitute legal, tax, accounting, regulatory, or investment

advice. Any decision to purchase or sell securities should be based upon consultation with your legal, >inancial, tax, accounting and other advisors as to how such transactions affect you.