Embed Size (px)

Citation preview

Polyamide & Intermediates

Darrel Collier

Tecnon OrbiChem Seminar at KICHEM 2012Seoul - 2 November, 2012

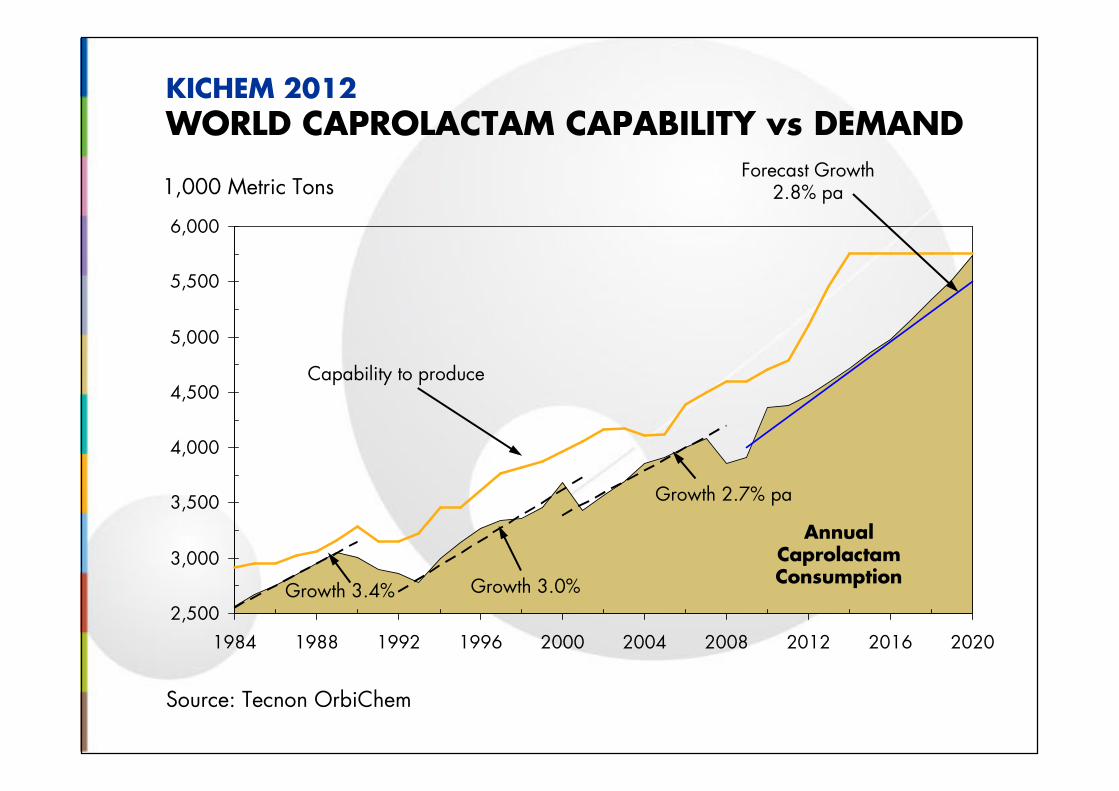

Source: Tecnon OrbiChem

KICHEM 2012WORLD CAPROLACTAM CAPABILITY vs DEMAND

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Forecast Growth 2.8% pa

Growth 3.4% Growth 3.0%

Growth 2.7% pa

Capability to produce

Annual CaprolactamConsumption

1,000 Metric Tons

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

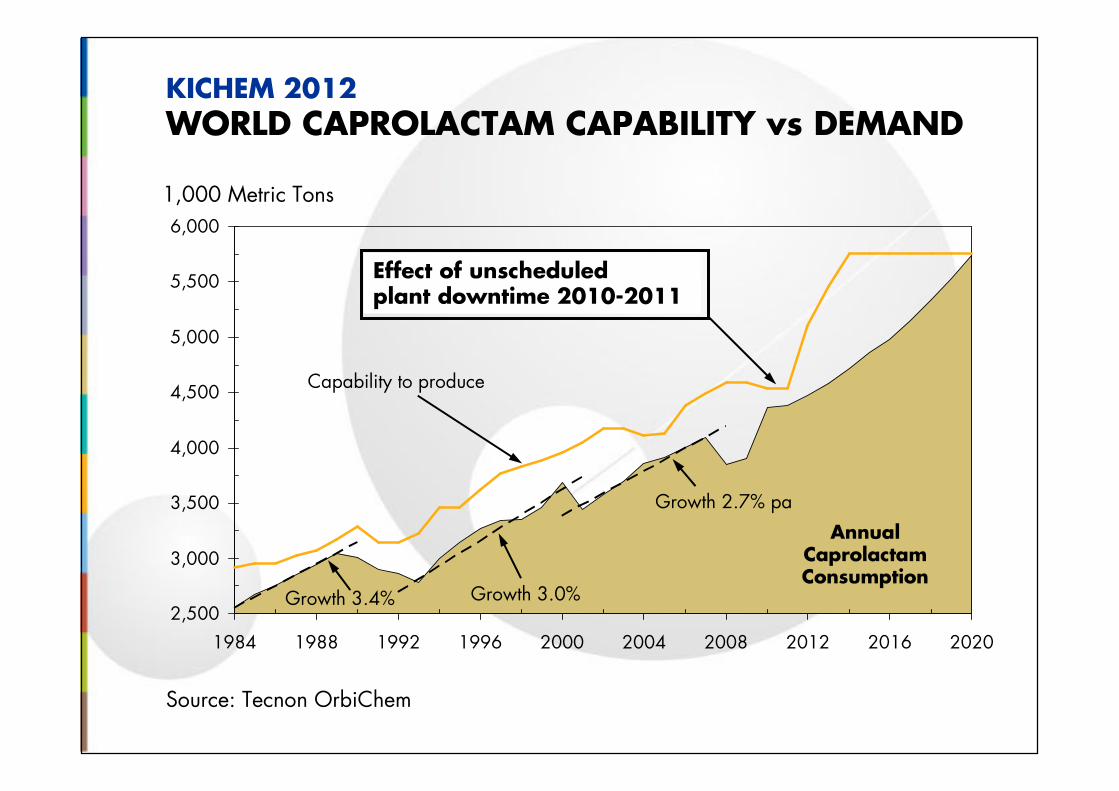

Source: Tecnon OrbiChem

KICHEM 2012WORLD CAPROLACTAM CAPABILITY vs DEMAND

Growth 3.4% Growth 3.0%

Growth 2.7% pa

Capability to produce

Annual CaprolactamConsumption

1,000 Metric Tons

Effect of unscheduledplant downtime 2010-2011

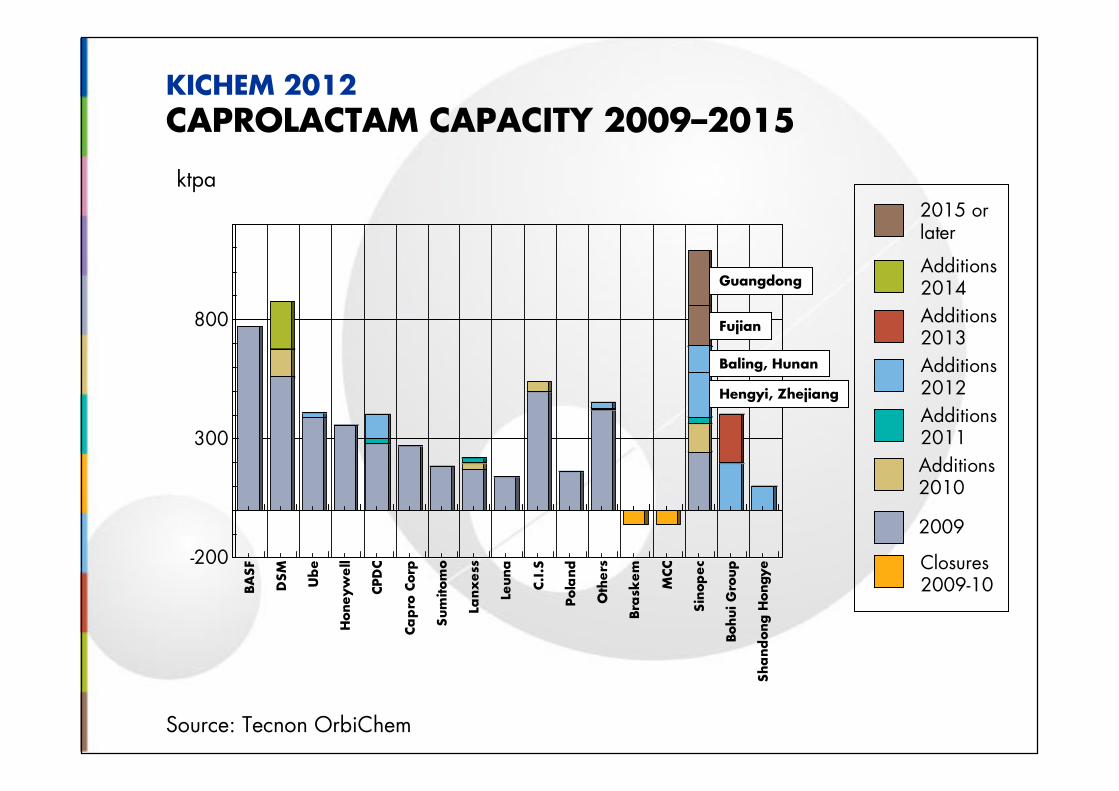

BA

SF

DSM

Ub

e

Honeyw

ell

CPD

C

Ca

pro

Corp

Sum

itom

o

Lanx

ess

Leuna

C.I

.S

Pola

nd

Oth

ers

Bra

skem

MCC

Sin

op

ec

Bohui G

roup

Sha

nd

ong H

ongye-200

300

800

Baling, Hunan

Guangdong

Hengyi, Zhejiang

Fujian

KICHEM 2012CAPROLACTAM CAPACITY 2009–2015

Source: Tecnon OrbiChem

ktpa

Additions 2010

2009

Closures 2009-10

Additions 2011

Additions 2012

Additions 2013

Additions 2014

2015 orlater

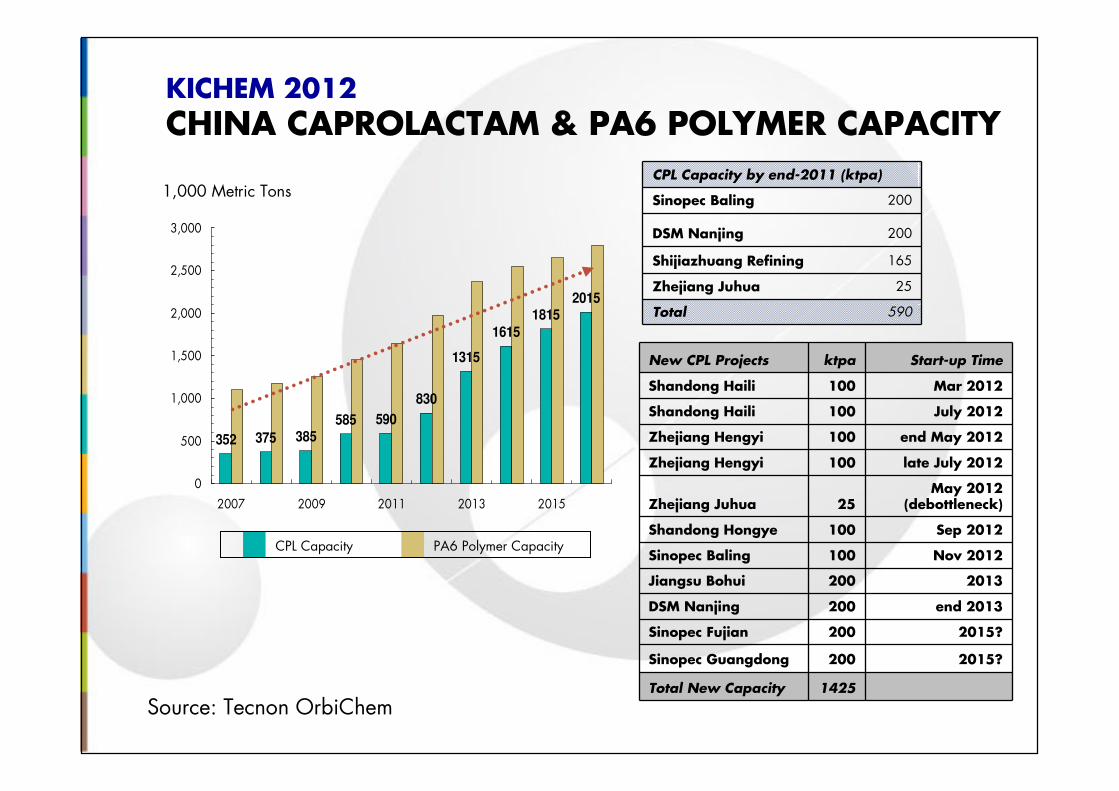

KICHEM 2012CHINA CAPROLACTAM & PA6 POLYMER CAPACITY

Source: Tecnon OrbiChem

1,000 Metric TonsCPL Capacity by end-2011 (ktpa)

Sinopec Baling 200

DSM Nanjing 200

Shijiazhuang Refining 165

Zhejiang Juhua 25

Total 590

352 375 385

585 590

830

1315

1615

1815

2015

0

500

1,000

1,500

2,000

2,500

3,000

2007 2009 2011 2013 2015

CPL Capacity PA6 Polymer Capacity

New CPL Projects ktpa Start-up Time

Shandong Haili 100 Mar 2012

Shandong Haili 100 July 2012

Zhejiang Hengyi 100 end May 2012

Zhejiang Hengyi 100 late July 2012

Zhejiang Juhua 25May 2012

(debottleneck)

Shandong Hongye 100 Sep 2012

Sinopec Baling 100 Nov 2012

Jiangsu Bohui 200 2013

DSM Nanjing 200 end 2013

Sinopec Fujian 200 2015?

Sinopec Guangdong 200 2015?

Total New Capacity 1425

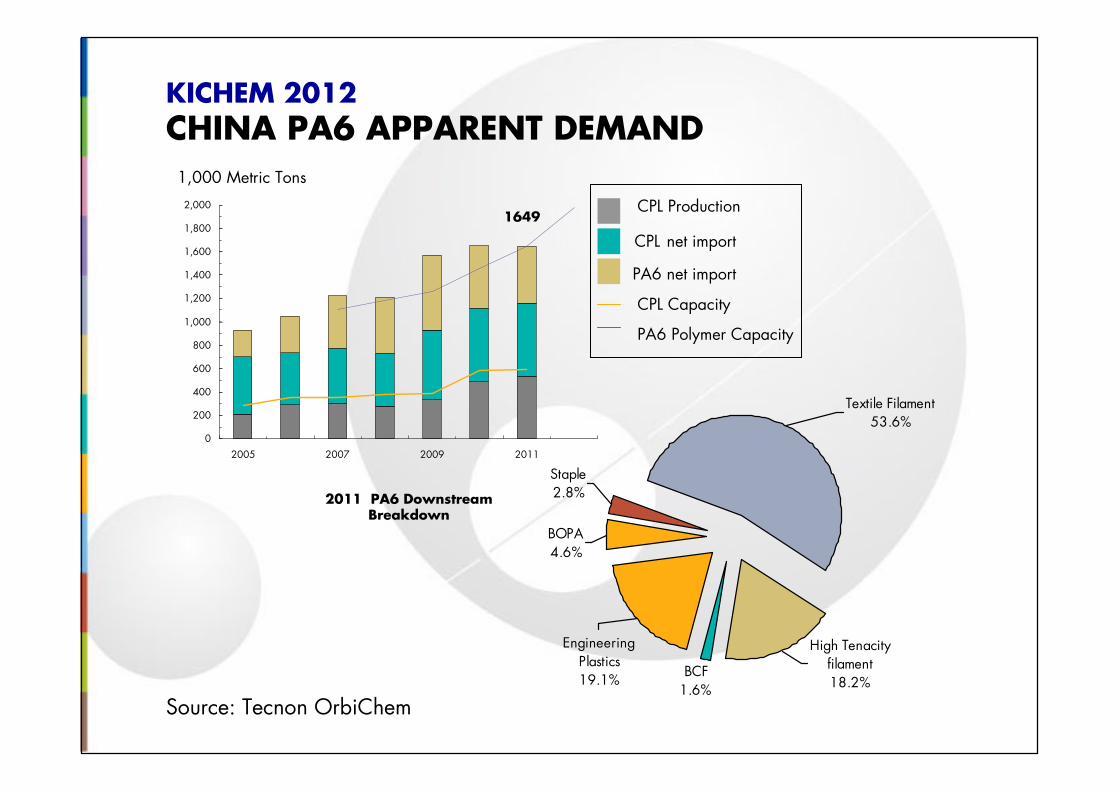

KICHEM 2012CHINA PA6 APPARENT DEMAND

Source: Tecnon OrbiChem

1,000 Metric Tons

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2005 2007 2009 2011

1649

BOPA4.6%

EngineeringPlastics19.1%

Textile Filament53.6%

High Tenacityfilament18.2%

Staple2.8%

BCF1.6%

2011 PA6 Downstream Breakdown

PA6 net import

CPL net import

CPL Production

CPL Capacity

PA6 Polymer Capacity

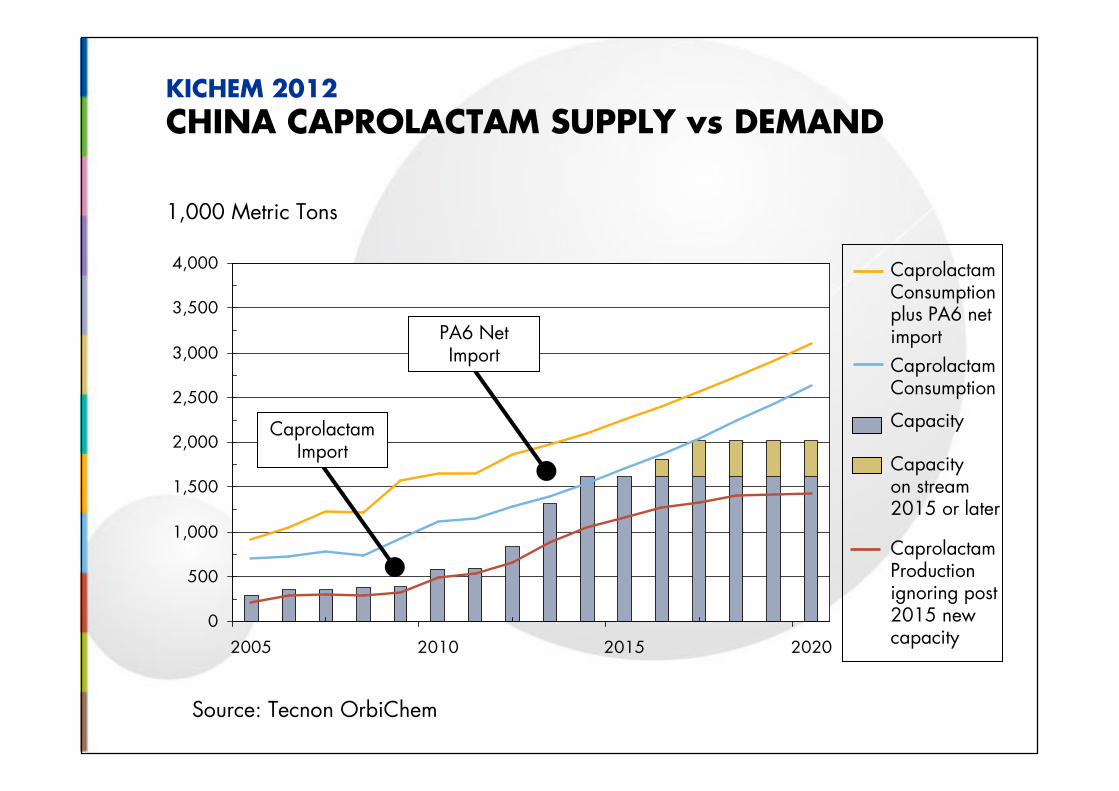

KICHEM 2012

CHINA CAPROLACTAM SUPPLY vs DEMAND

Source: Tecnon OrbiChem

CaprolactamConsumption

CaprolactamConsumptionplus PA6 netimport

Capacity on stream2015 or later

Capacity

CaprolactamProductionignoring post 2015 new capacity

1,000 Metric Tons

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2010 2015 2020

CaprolactamImport

PA6 NetImport

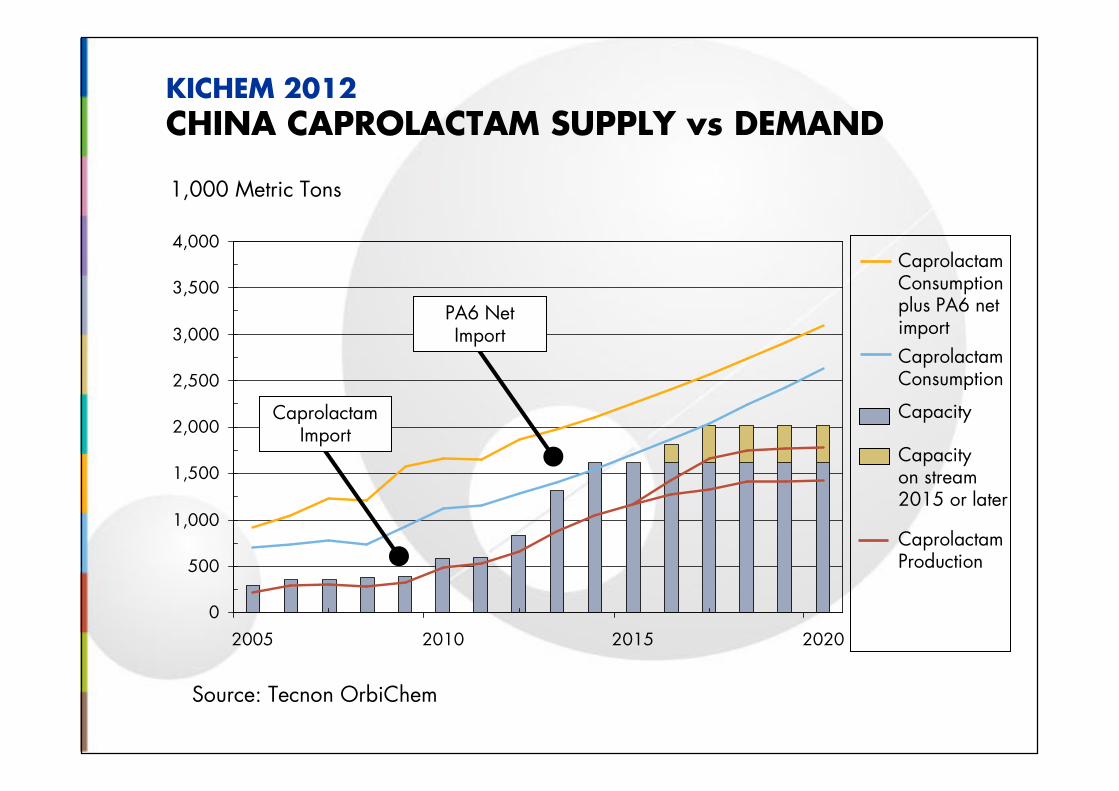

KICHEM 2012CHINA CAPROLACTAM SUPPLY vs DEMAND

Source: Tecnon OrbiChem

1,000 Metric Tons

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2010 2015 2020

CaprolactamImport

PA6 NetImport

CaprolactamConsumption

CaprolactamConsumptionplus PA6 netimport

Capacity on stream2015 or later

Capacity

CaprolactamProduction

ktpa

Source: Tecnon OrbiChem

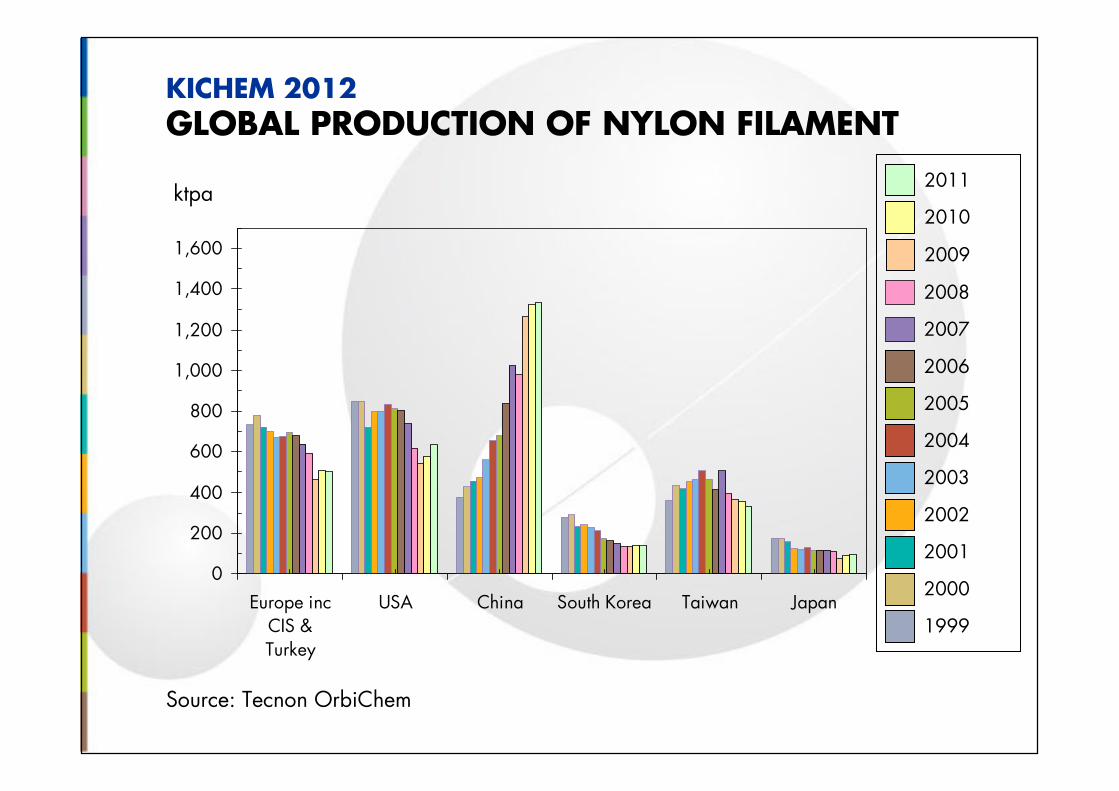

KICHEM 2012GLOBAL PRODUCTION OF NYLON FILAMENT

0

200

400

600

800

1,000

1,200

1,400

1,600

Europe incCIS &Turkey

USA China South Korea Taiwan Japan

2003

2004

2005

2006

1999

2000

2001

2002

2008

2009

2010

2011

2007

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2000

2005

2010

2015

2020

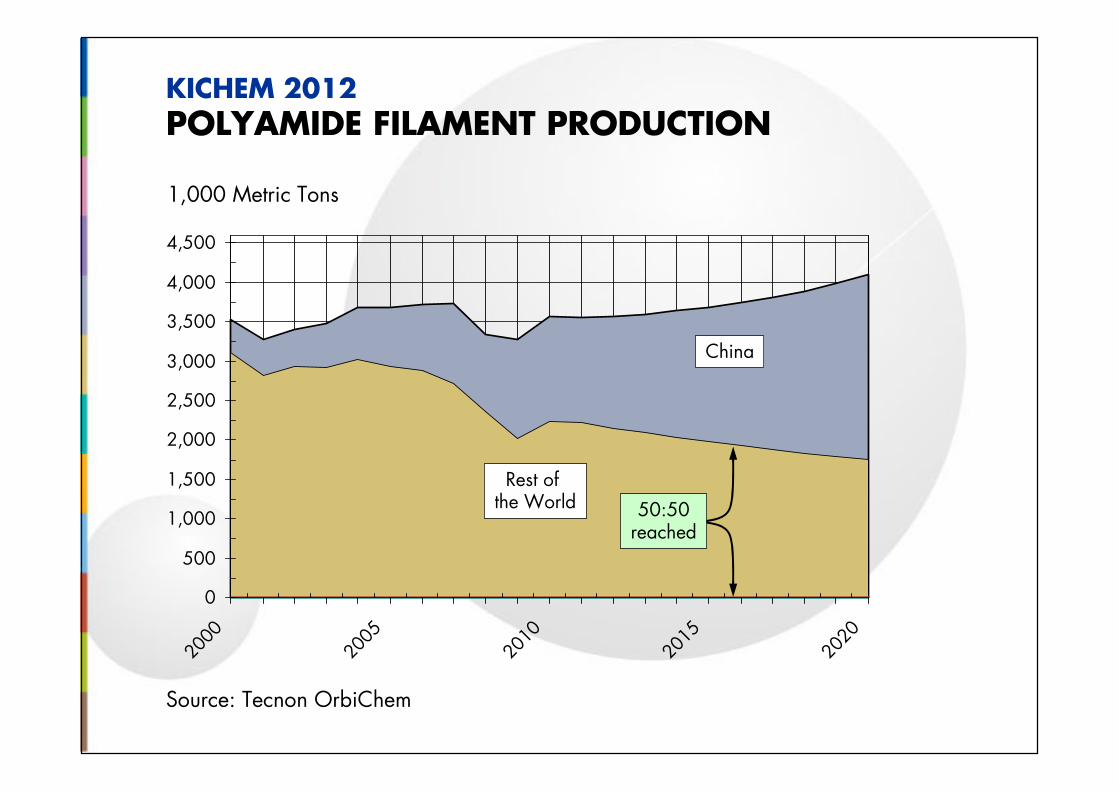

Rest of the World

KICHEM 2012POLYAMIDE FILAMENT PRODUCTION

Source: Tecnon OrbiChem

China

50:50reached

1,000 Metric Tons

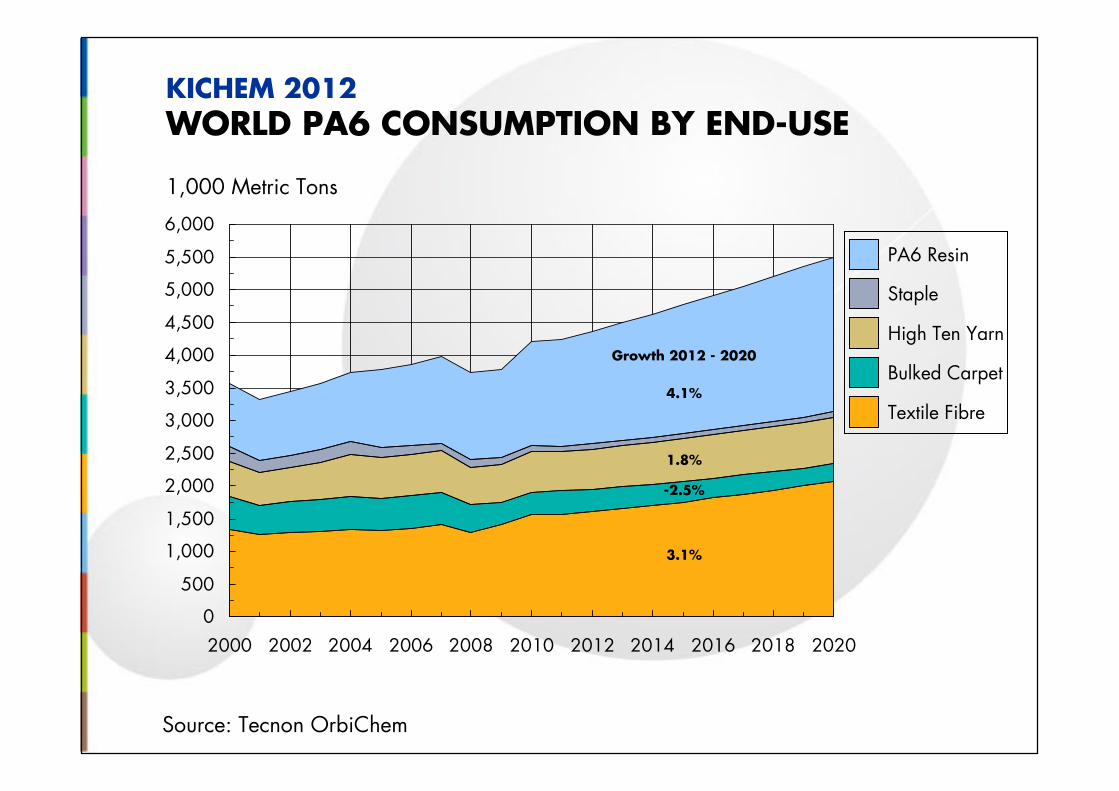

KICHEM 2012WORLD PA6 CONSUMPTION BY END-USE

Source: Tecnon OrbiChem

1,000 Metric Tons

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Textile Fibre

Bulked Carpet

High Ten Yarn

Staple

PA6 Resin

Growth 2012 - 2020

3.1%

1.8%

4.1%

-2.5%

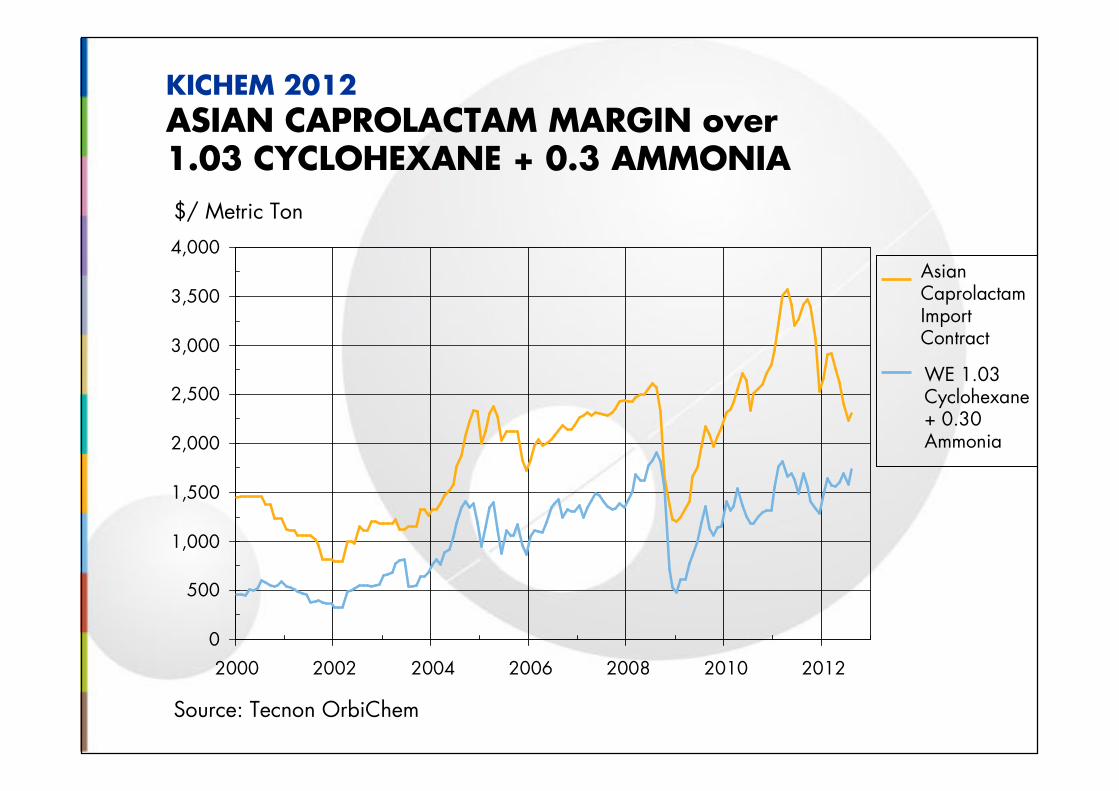

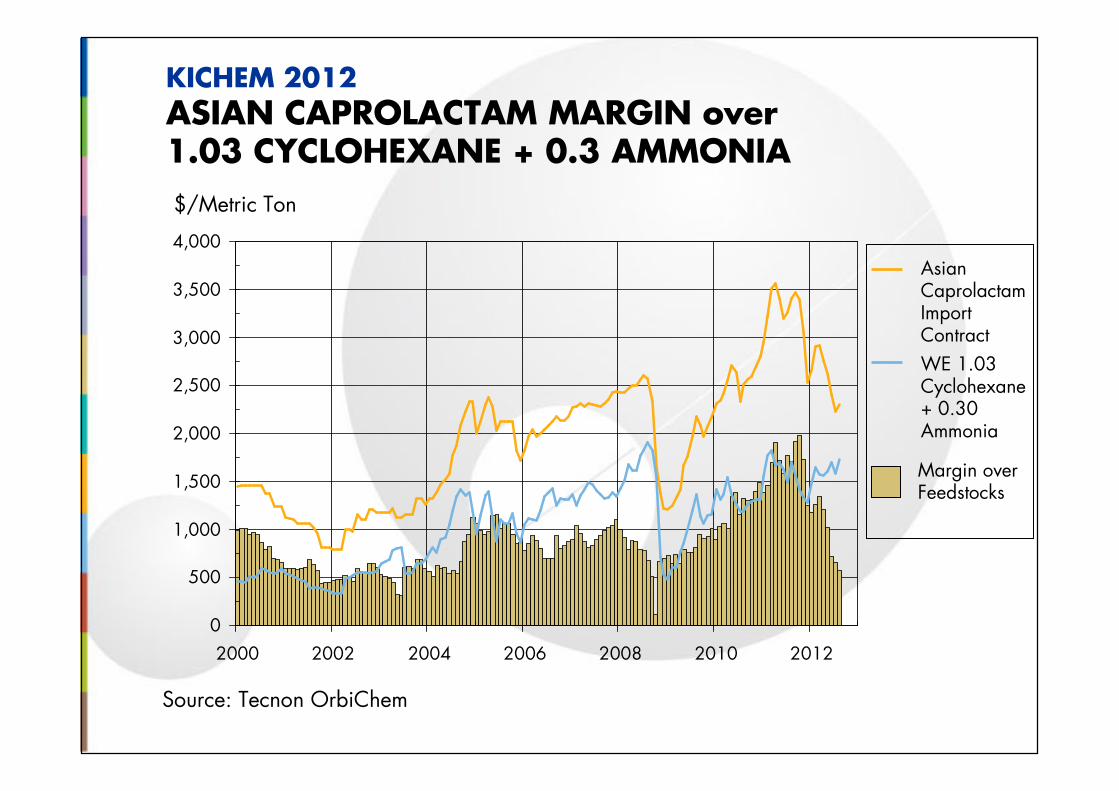

KICHEM 2012ASIAN CAPROLACTAM MARGIN over 1.03 CYCLOHEXANE + 0.3 AMMONIA

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

$/ Metric Ton

WE 1.03 Cyclohexane+ 0.30 Ammonia

Asian CaprolactamImport Contract

Source: Tecnon OrbiChem

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

$/Metric Ton

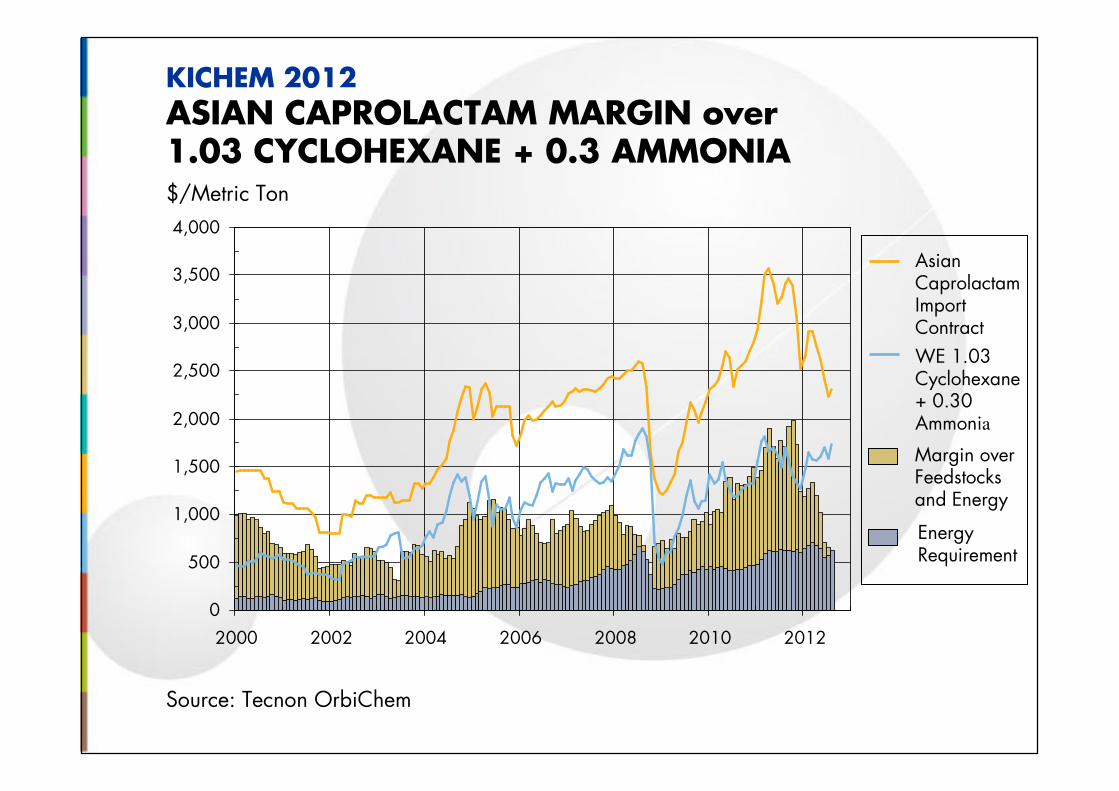

KICHEM 2012ASIAN CAPROLACTAM MARGIN over 1.03 CYCLOHEXANE + 0.3 AMMONIA

Margin over Feedstocks

WE 1.03 Cyclohexane+ 0.30 Ammonia

Asian CaprolactamImport Contract

Source: Tecnon OrbiChem

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

$/Metric Ton

KICHEM 2012ASIAN CAPROLACTAM MARGIN over 1.03 CYCLOHEXANE + 0.3 AMMONIA

Source: Tecnon OrbiChem

WE 1.03 Cyclohexane+ 0.30 Ammonia

Asian CaprolactamImport Contract

Margin overFeedstocksand Energy

Energy Requirement

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

$/Metric Ton

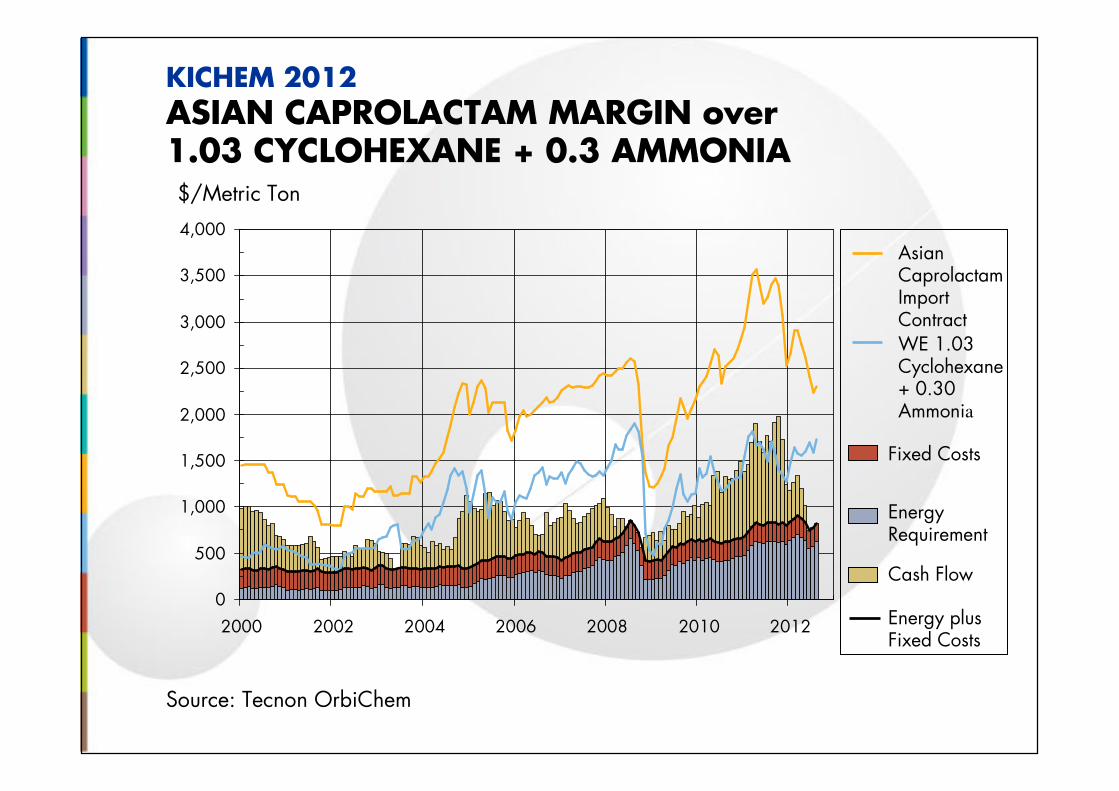

KICHEM 2012ASIAN CAPROLACTAM MARGIN over 1.03 CYCLOHEXANE + 0.3 AMMONIA

Source: Tecnon OrbiChem

WE 1.03 Cyclohexane+ 0.30 Ammonia

Asian CaprolactamImport Contract

Fixed Costs

Energy Requirement

Energy plus Fixed Costs

Cash Flow

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

$/Metric Ton

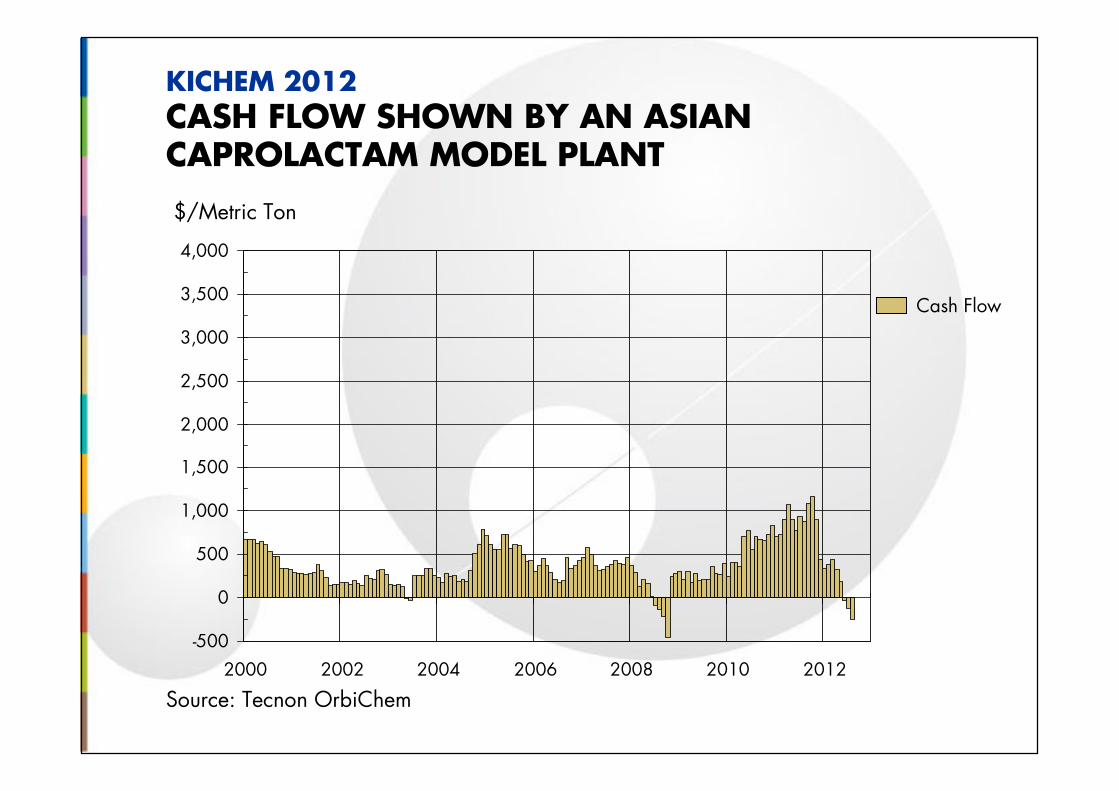

KICHEM 2012CASH FLOW SHOWN BY AN ASIANCAPROLACTAM MODEL PLANT

Source: Tecnon OrbiChem

Cash Flow

Source: Tecnon OrbiChem

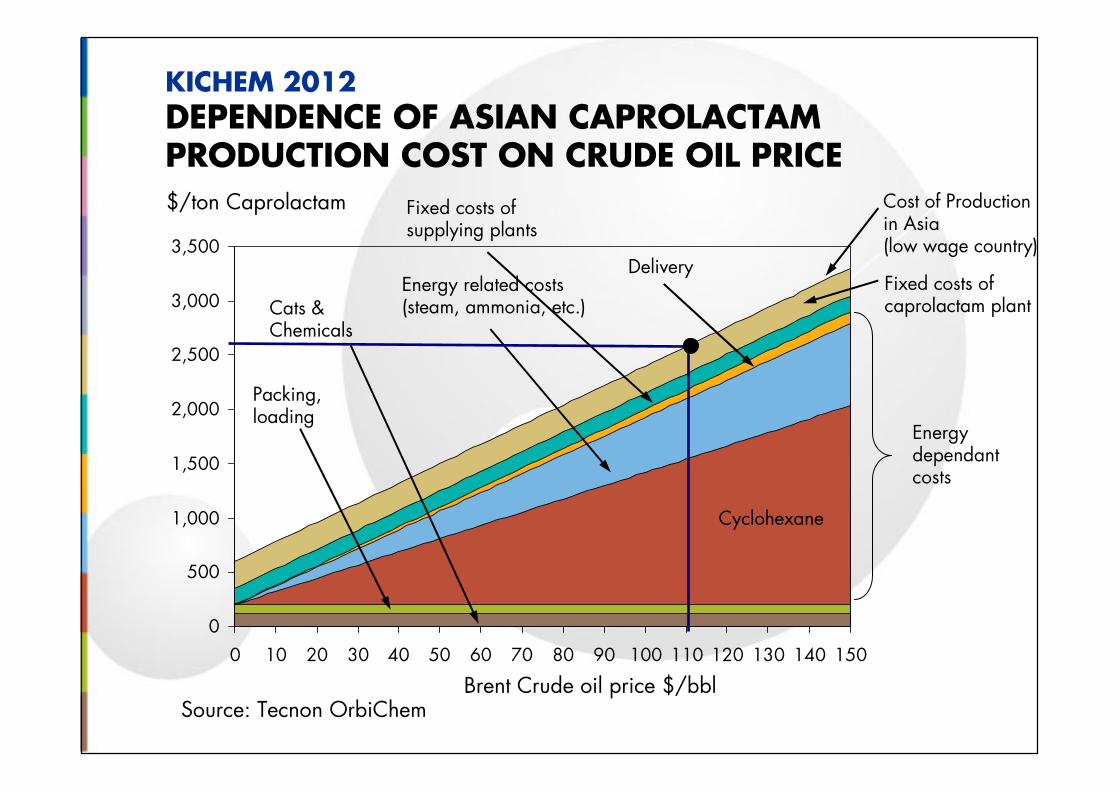

KICHEM 2012DEPENDENCE OF ASIAN CAPROLACTAM PRODUCTION COST ON CRUDE OIL PRICE

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

$/ton Caprolactam

Brent Crude oil price $/bbl

Cyclohexane

Energy related costs (steam, ammonia, etc.)

Delivery

Energy dependant costs

Packing, loading

Fixed costs of supplying plants

Cats & Chemicals

Fixed costs of caprolactam plant

Cost of Production in Asia (low wage country)

Source: Tecnon OrbiChem

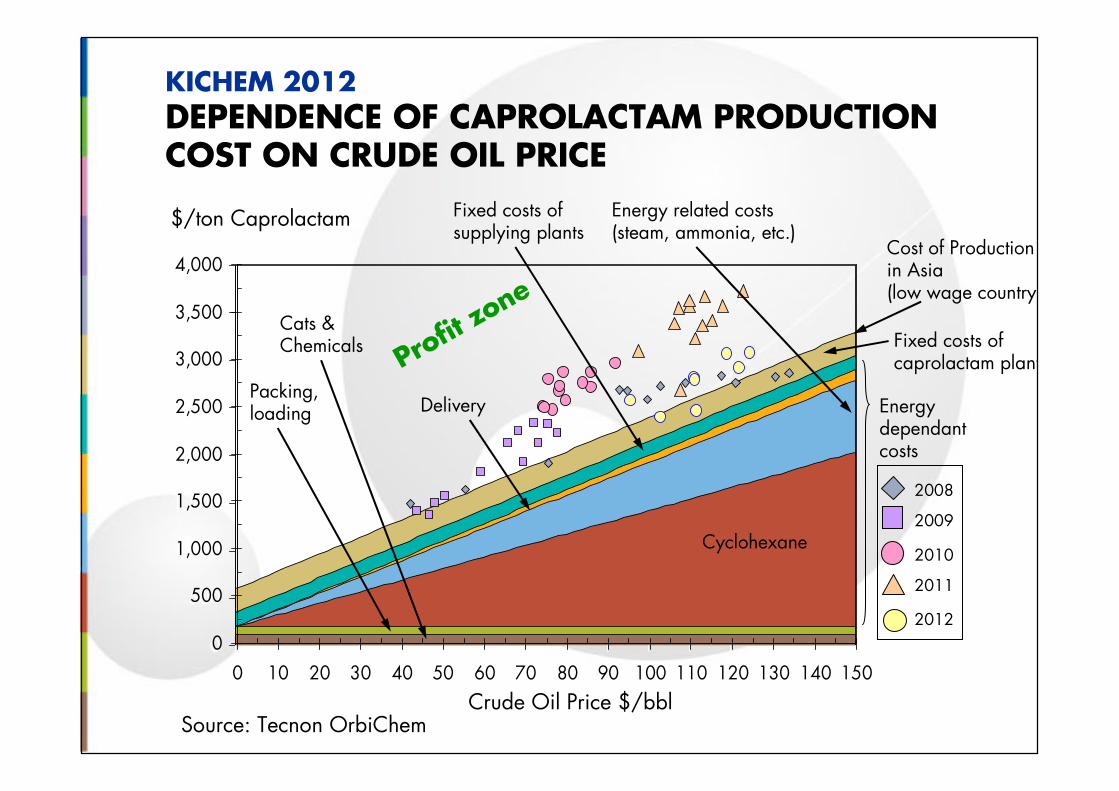

KICHEM 2012DEPENDENCE OF CAPROLACTAM PRODUCTION COST ON CRUDE OIL PRICE

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

$/ton Caprolactam

Cyclohexane

Packing, loading

Fixed costs of supplying plants

Cats & Chemicals Fixed costs of

caprolactam plant

Cost of Production in Asia (low wage country)

Energy dependant costs

Crude Oil Price $/bbl

Delivery

Energy related costs (steam, ammonia, etc.)

Profit zo

ne

2009

2008

2010

2011

2012

0

500

1000

1500

2000

2500

3000

3500

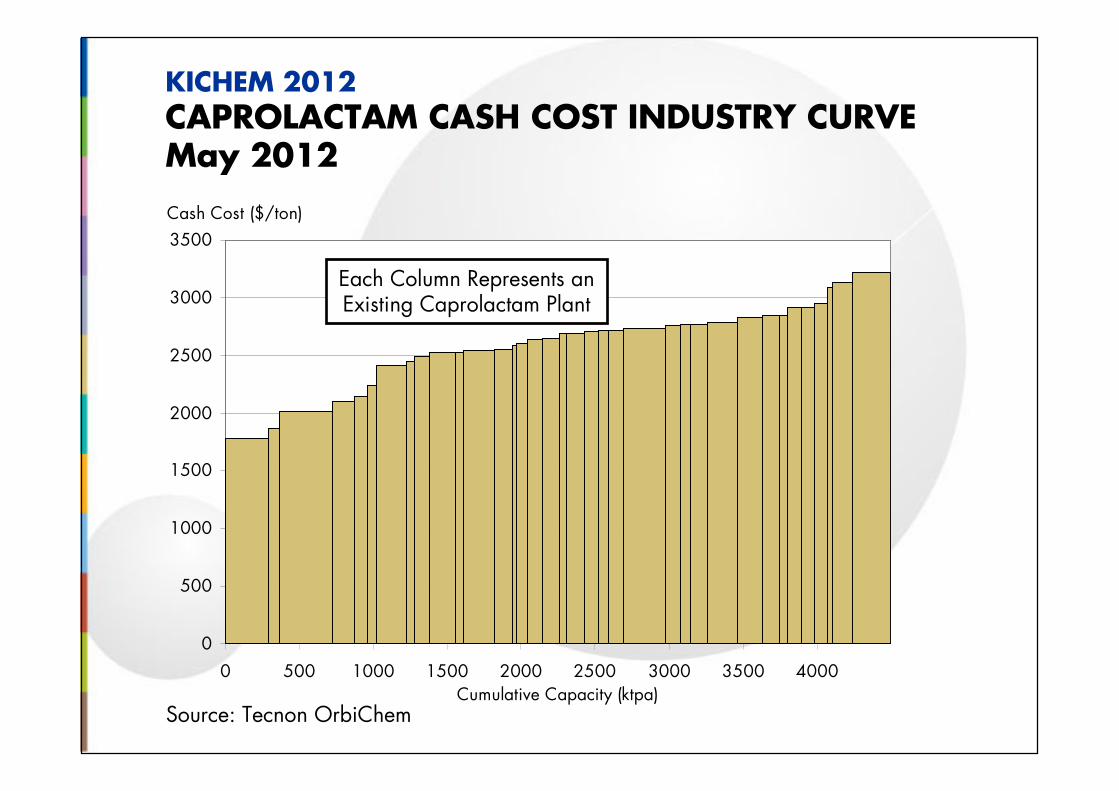

0 500 1000 1500 2000 2500 3000 3500 4000Cumulative Capacity (ktpa)

Cash Cost ($/ton)

Source: Tecnon OrbiChem

KICHEM 2012CAPROLACTAM CASH COST INDUSTRY CURVEMay 2012

Each Column Represents an Existing Caprolactam Plant

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

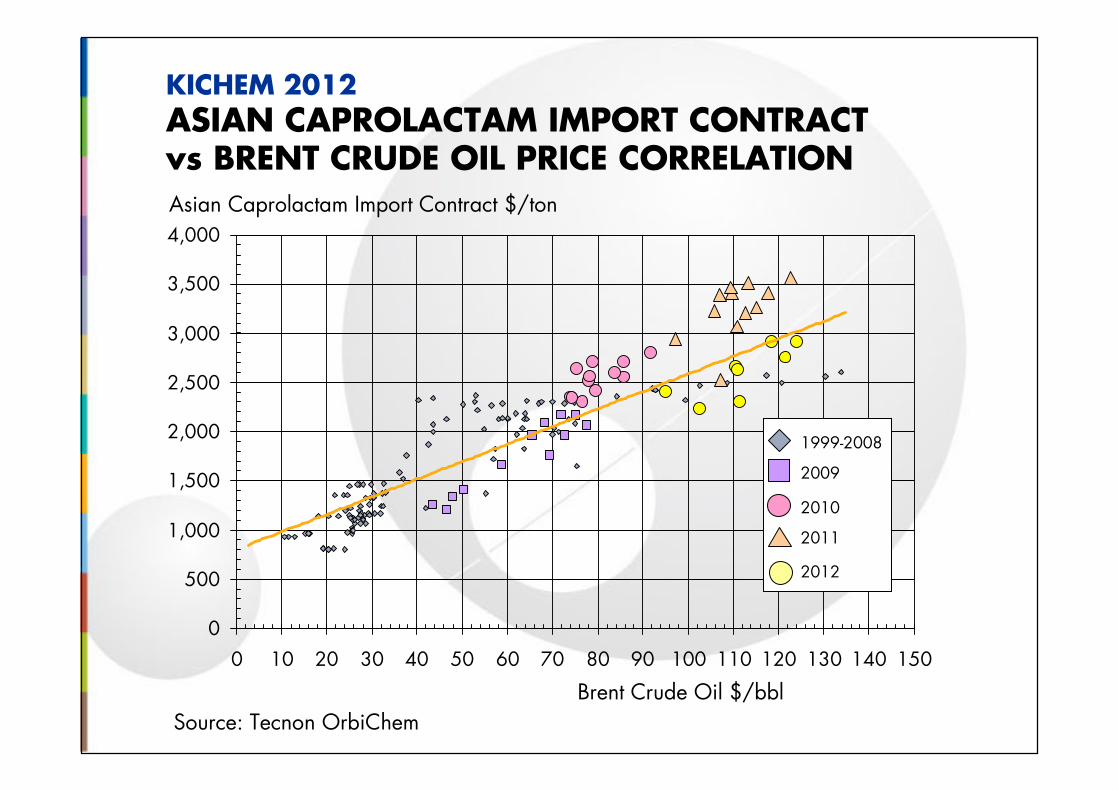

KICHEM 2012ASIAN CAPROLACTAM IMPORT CONTRACTvs BRENT CRUDE OIL PRICE CORRELATION

Source: Tecnon OrbiChem

Brent Crude Oil $/bbl

Asian Caprolactam Import Contract $/ton

2009

1999-2008

2010

2011

2012

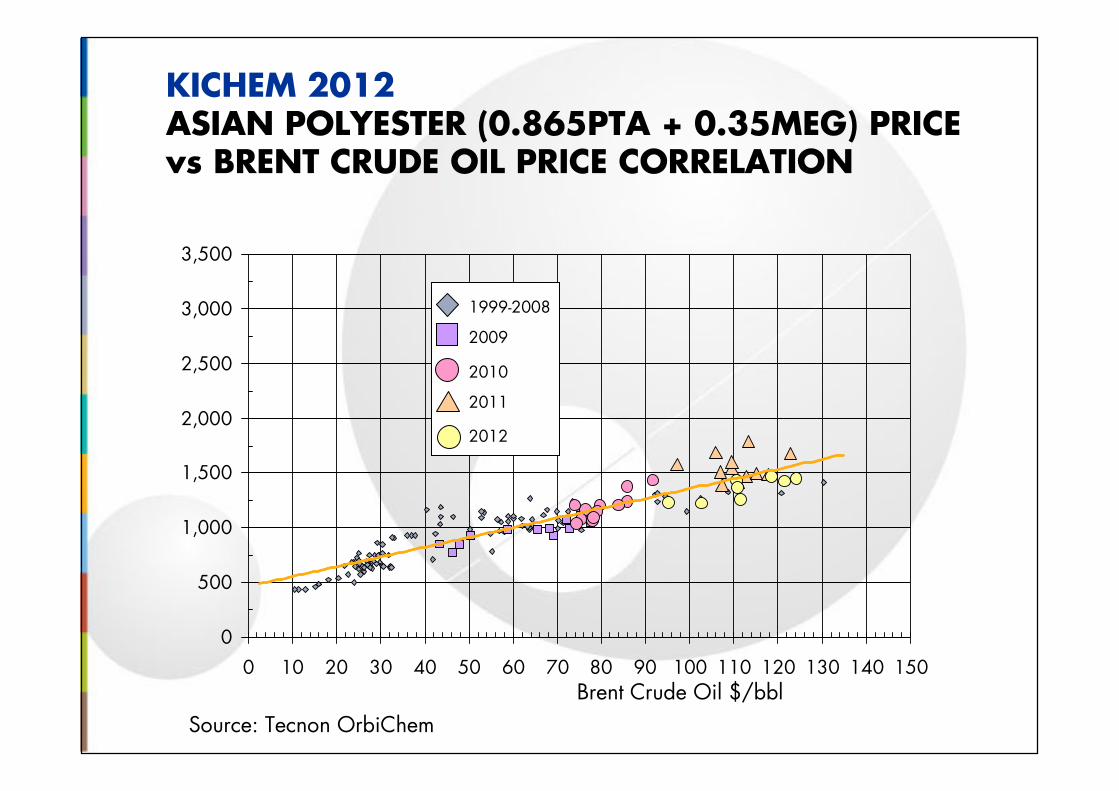

KICHEM 2012ASIAN POLYESTER (0.865PTA + 0.35MEG) PRICEvs BRENT CRUDE OIL PRICE CORRELATION

Source: Tecnon OrbiChem

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150Brent Crude Oil $/bbl

2009

1999-2008

2010

2011

2012

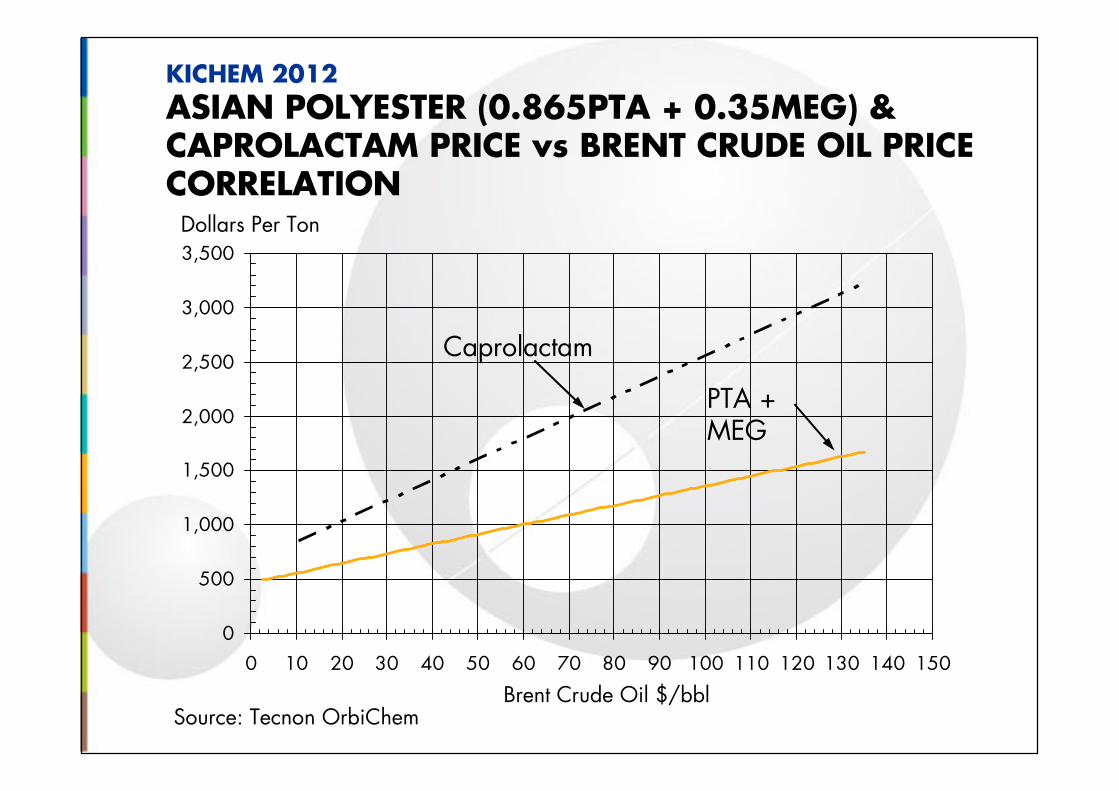

KICHEM 2012

ASIAN POLYESTER (0.865PTA + 0.35MEG) & CAPROLACTAM PRICE vs BRENT CRUDE OIL PRICE CORRELATION

Source: Tecnon OrbiChem

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

Brent Crude Oil $/bbl

Caprolactam

PTA + MEG

Dollars Per Ton

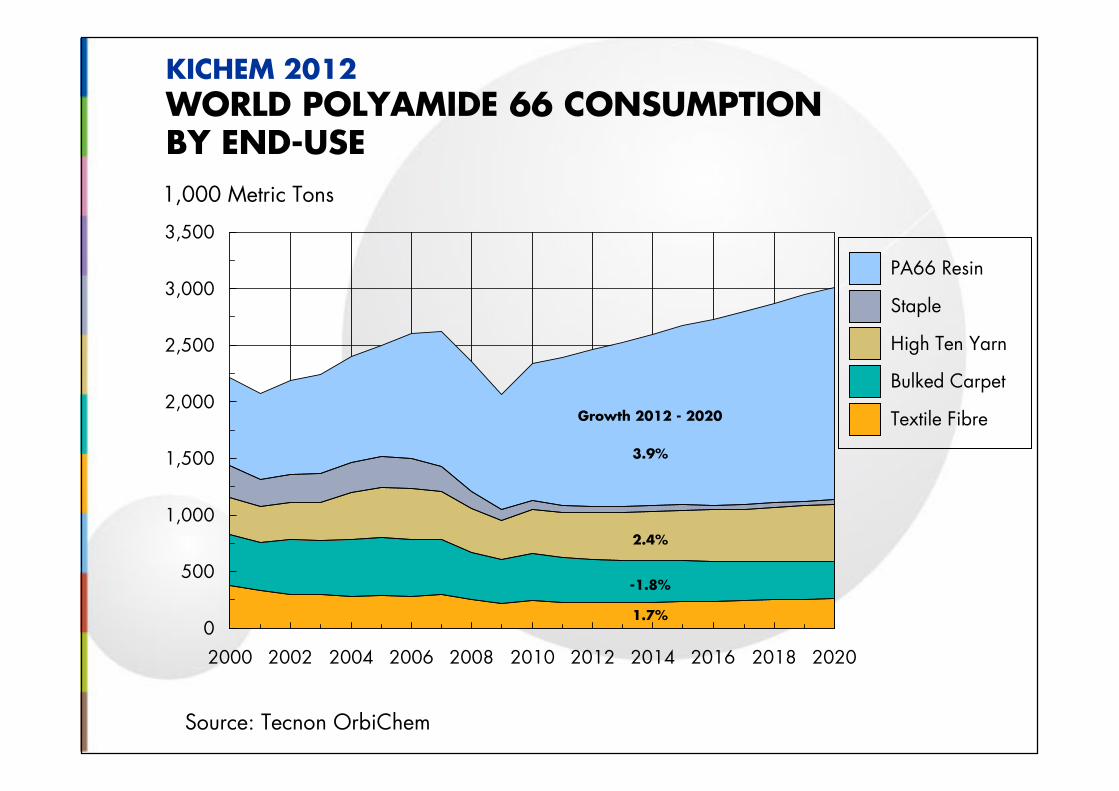

KICHEM 2012 WORLD POLYAMIDE 66 CONSUMPTIONBY END-USE

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Source: Tecnon OrbiChem

1,000 Metric Tons

Textile Fibre

Bulked Carpet

High Ten Yarn

Staple

PA66 Resin

Growth 2012 - 2020

1.7%

2.4%

3.9%

-1.8%

Source: Tecnon OrbiChem

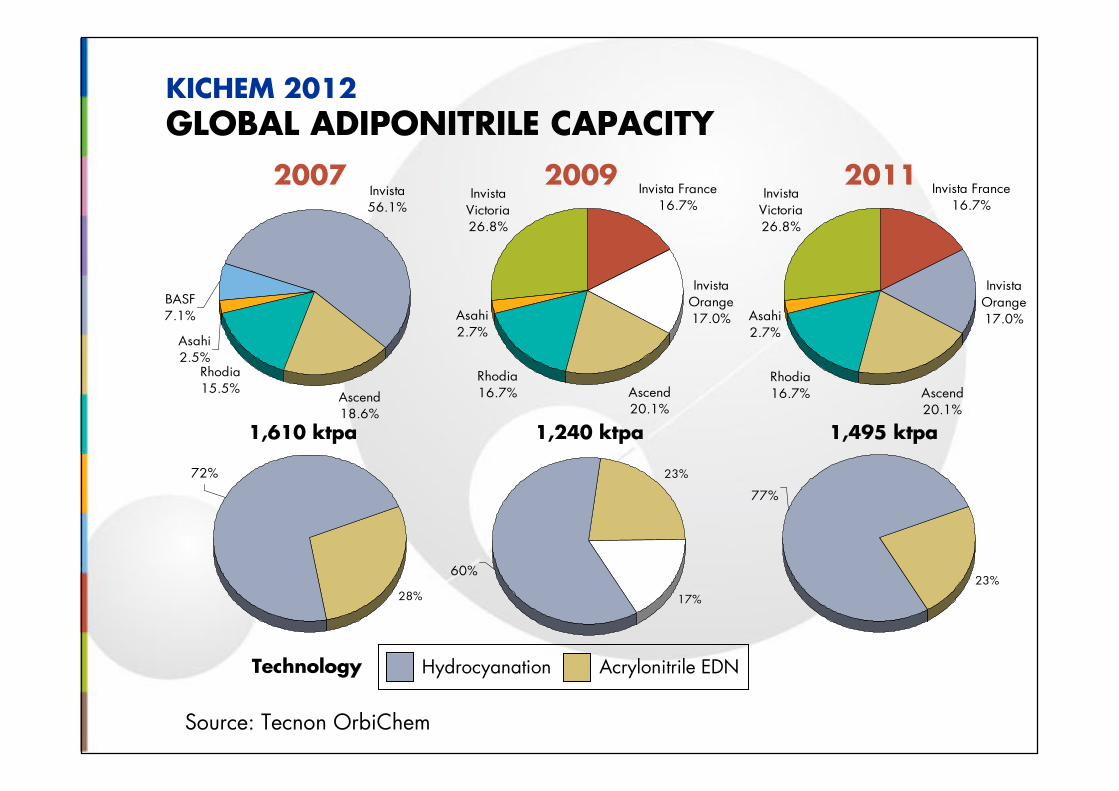

KICHEM 2012GLOBAL ADIPONITRILE CAPACITY

Invista Orange17.0%

Ascend 20.1%

Rhodia 16.7%

Asahi 2.7%

Invista Victoria26.8%

Invista France16.7%

28%

72%

Invista56.1%

Ascend 18.6%

Rhodia 15.5%

BASF 7.1%

Asahi 2.5%

1,240 ktpa

Technology

2009

Invista Orange17.0%

Ascend 20.1%

Rhodia 16.7%

Asahi 2.7%

Invista Victoria26.8%

Invista France16.7%

23%

77%

1,610 ktpa 1,495 ktpa

20112007

Hydrocyanation Acrylonitrile EDN

23%

17%

60%

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

4,000

2000 2002 2004 2006 2008 2010 2012

$/Metric Ton

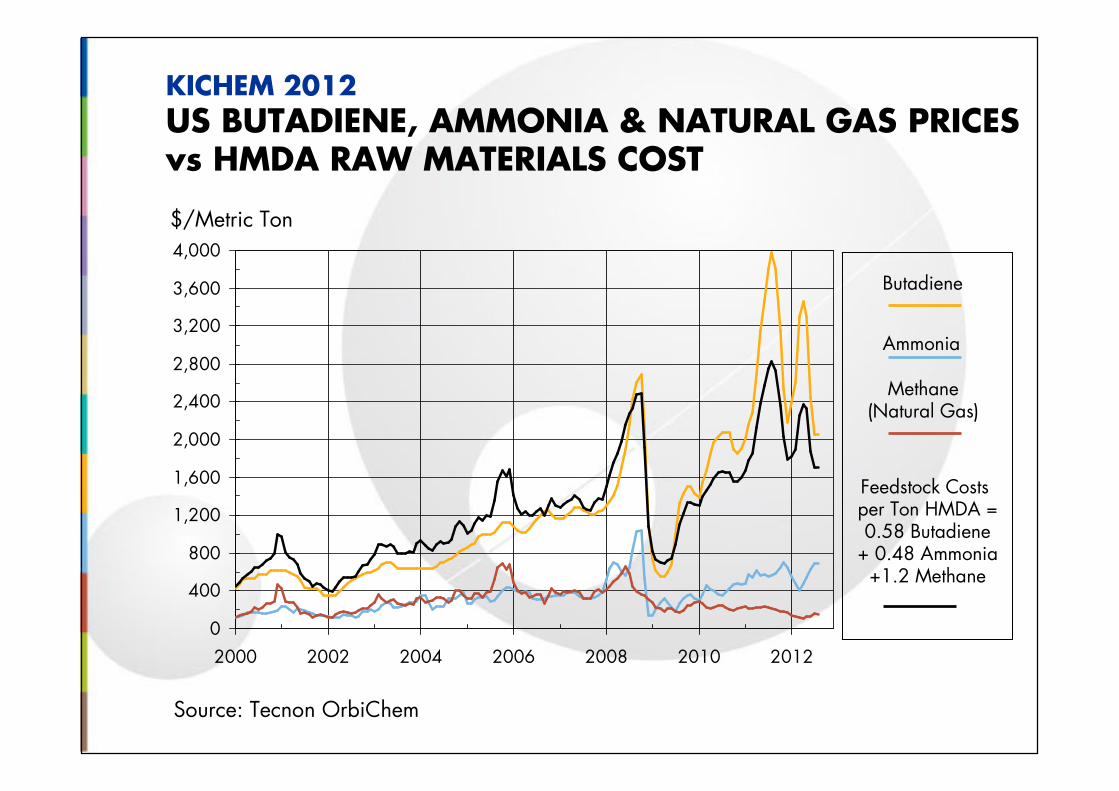

KICHEM 2012US BUTADIENE, AMMONIA & NATURAL GAS PRICES vs HMDA RAW MATERIALS COST

Source: Tecnon OrbiChem

Ammonia

Methane (Natural Gas)

Butadiene

Feedstock Costs per Ton HMDA =0.58 Butadiene

+ 0.48 Ammonia+1.2 Methane

Source: Tecnon OrbiChem

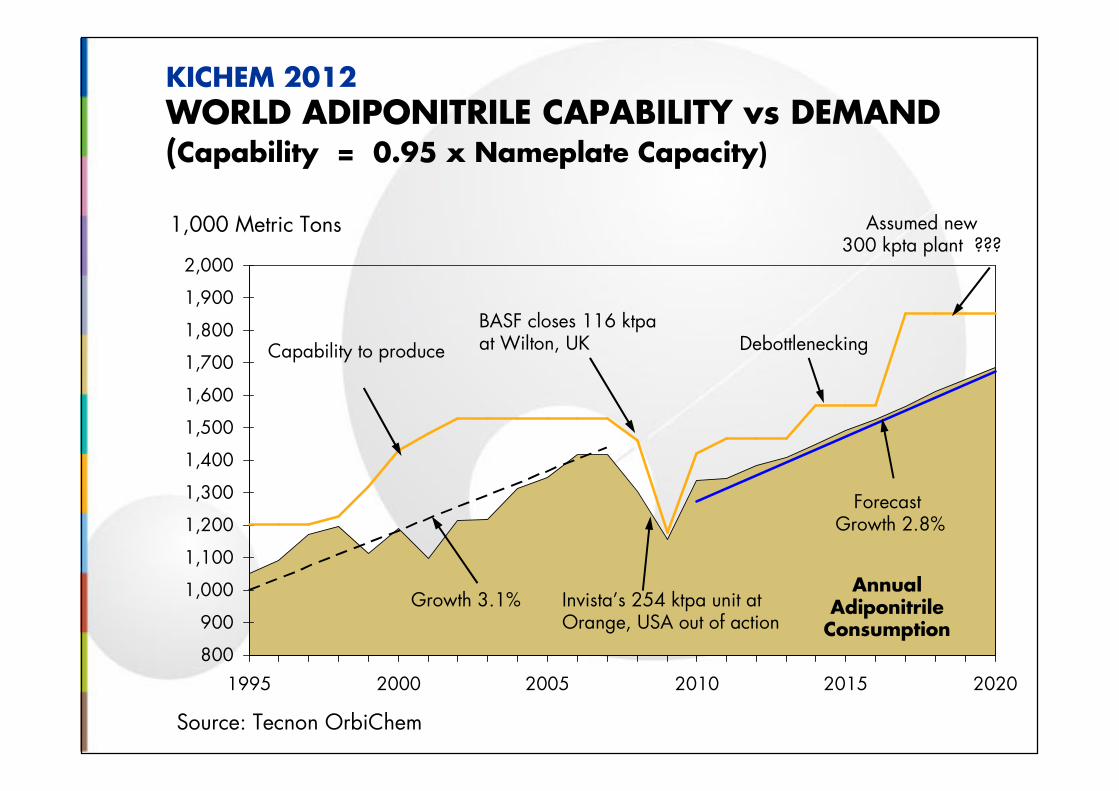

KICHEM 2012WORLD ADIPONITRILE CAPABILITY vs DEMAND (Capability = 0.95 x Nameplate Capacity)

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

1995 2000 2005 2010 2015 2020

Annual Adiponitrile

Consumption

Capability to produce

BASF closes 116 ktpaat Wilton, UK

Growth 3.1% Invista’s 254 ktpa unit atOrange, USA out of action

Assumed new300 kpta plant ???

1,000 Metric Tons

ForecastGrowth 2.8%

Debottlenecking

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1995 1999 2003 2007 2011 2015 2019

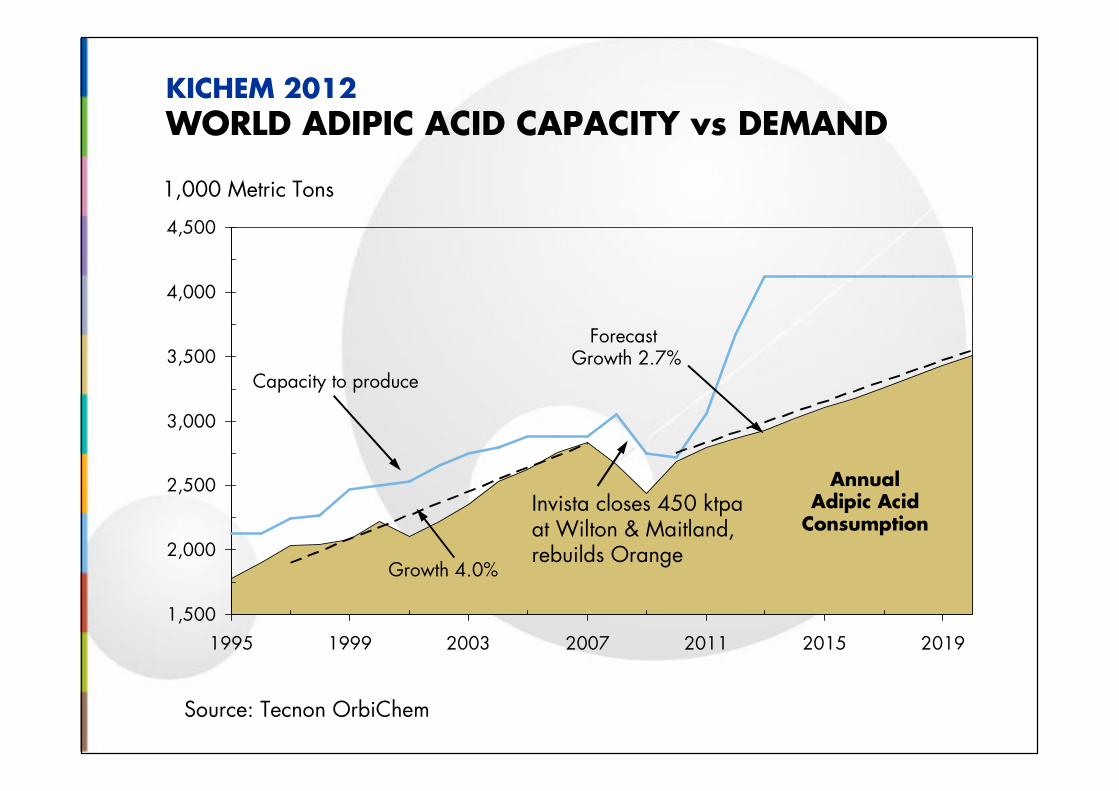

Source: Tecnon OrbiChem

AnnualAdipic Acid

Consumption

ForecastGrowth 2.7%

Capacity to produce

Invista closes 450 ktpaat Wilton & Maitland, rebuilds Orange

Growth 4.0%

1,000 Metric Tons

KICHEM 2012WORLD ADIPIC ACID CAPACITY vs DEMAND

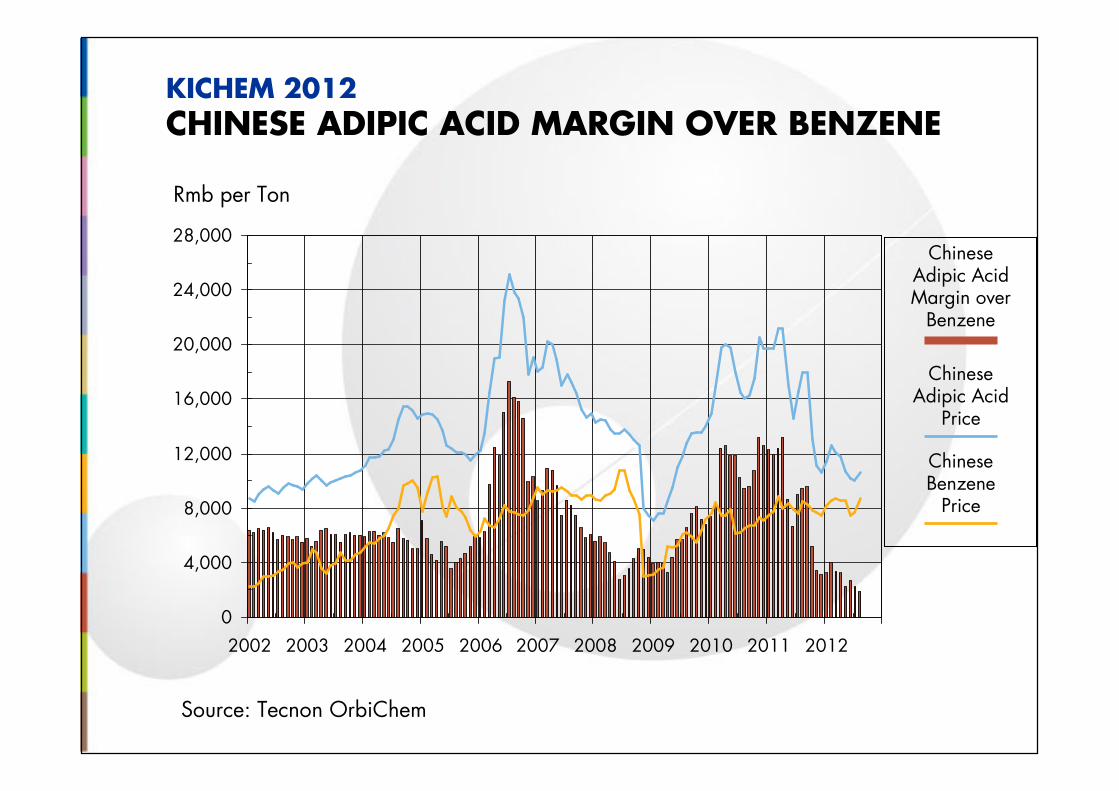

Rmb per Ton

ChineseAdipic Acid Margin over

Benzene

ChineseAdipic Acid

Price

Source: Tecnon OrbiChem

KICHEM 2012CHINESE ADIPIC ACID MARGIN OVER BENZENE

ChineseBenzene

Price

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

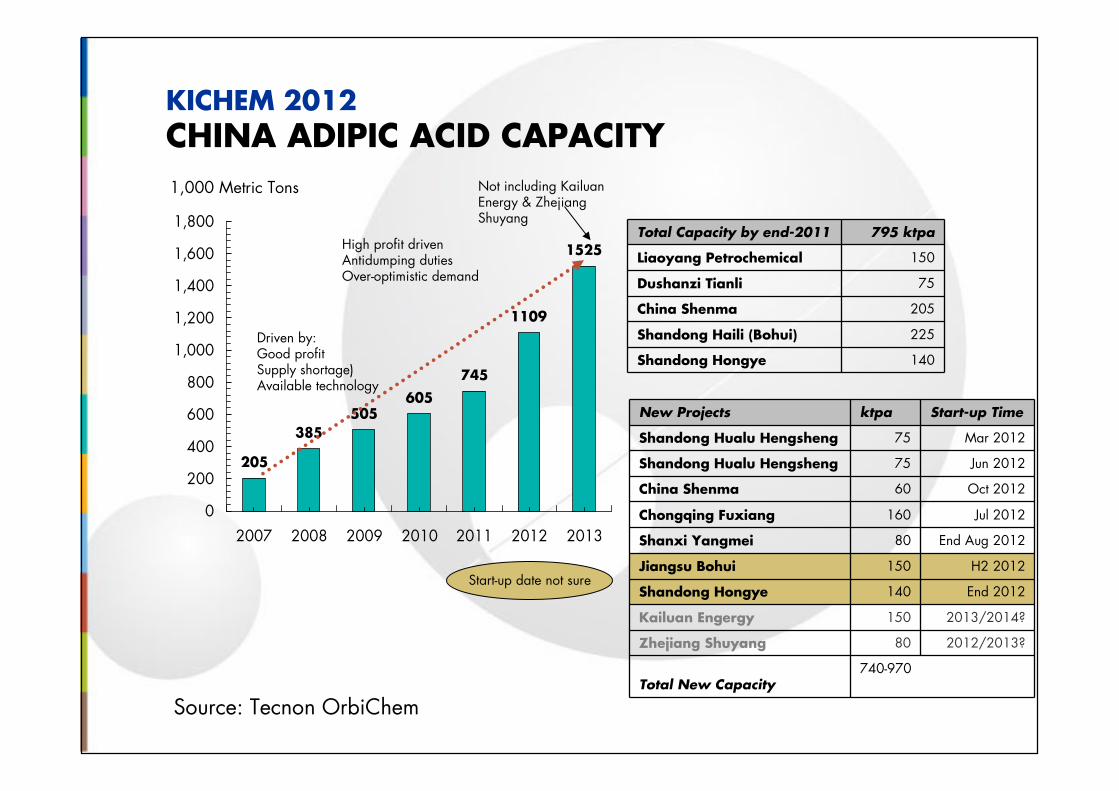

KICHEM 2012CHINA ADIPIC ACID CAPACITY

Source: Tecnon OrbiChem

Total Capacity by end-2011 795 ktpa

Liaoyang Petrochemical 150

Dushanzi Tianli 75

China Shenma 205

Shandong Haili (Bohui) 225

Shandong Hongye 140

New Projects ktpa Start-up Time

Shandong Hualu Hengsheng 75 Mar 2012

Shandong Hualu Hengsheng 75 Jun 2012

China Shenma 60 Oct 2012

Chongqing Fuxiang 160 Jul 2012

Shanxi Yangmei 80 End Aug 2012

Jiangsu Bohui 150 H2 2012

Shandong Hongye 140 End 2012

Kailuan Engergy 150 2013/2014?

Zhejiang Shuyang 80 2012/2013?

Total New Capacity740-970

205

385505

605

745

1109

1525

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2007 2008 2009 2010 2011 2012 2013

Driven by:Good profit Supply shortage)Available technology

High profit drivenAntidumping dutiesOver-optimistic demand

1,000 Metric Tons Not including KailuanEnergy & Zhejiang Shuyang

Start-up date not sure

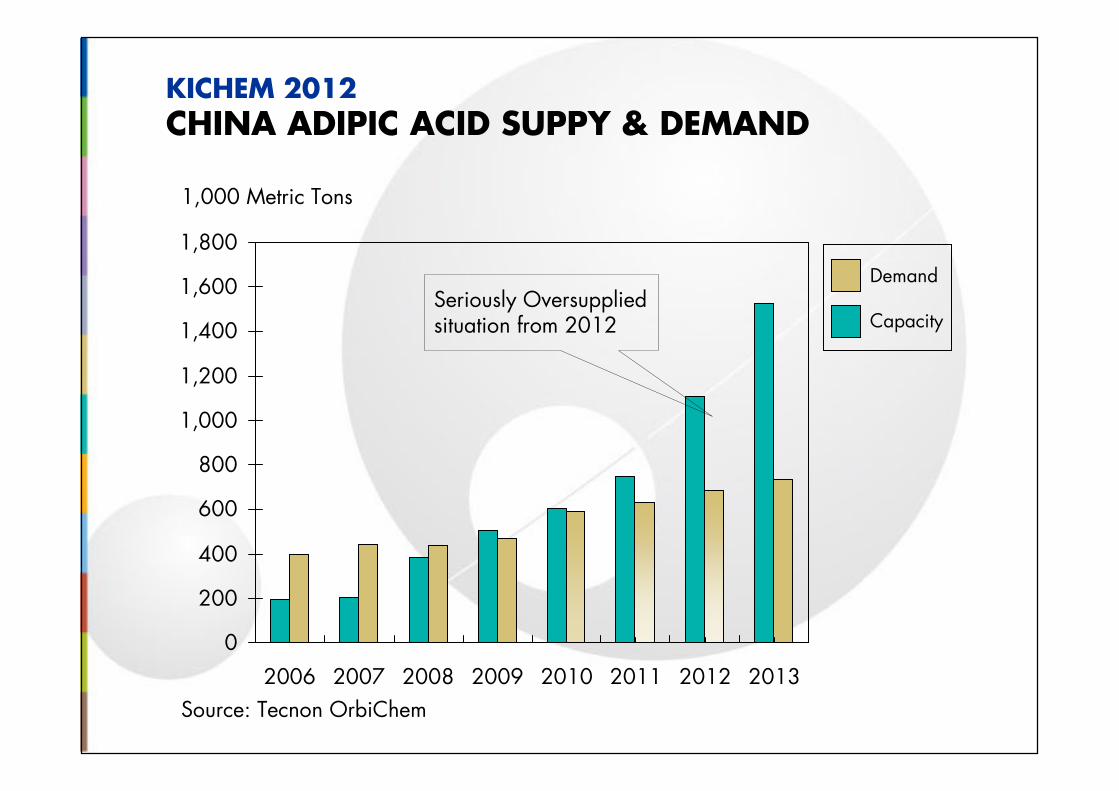

KICHEM 2012CHINA ADIPIC ACID SUPPY & DEMAND

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2006 2007 2008 2009 2010 2011 2012 2013

Source: Tecnon OrbiChem

Demand

CapacitySeriously Oversupplied situation from 2012

1,000 Metric Tons

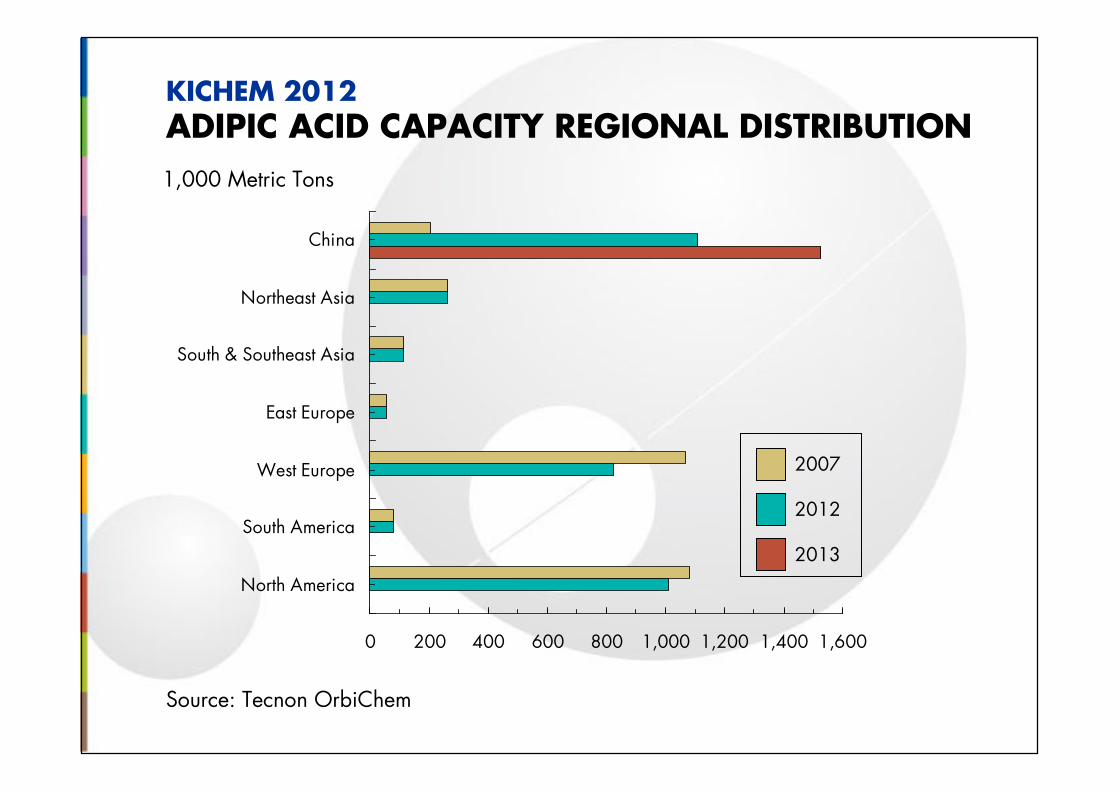

0 200 400 600 800 1,000 1,200 1,400 1,600

North America

South America

West Europe

East Europe

South & Southeast Asia

Northeast Asia

China

Source: Tecnon OrbiChem

KICHEM 2012ADIPIC ACID CAPACITY REGIONAL DISTRIBUTION

2012

2007

1,000 Metric Tons

2013

Source: Tecnon OrbiChem

KICHEM 2012WORLD ADIPIC ACID REGIONAL NET TRADE

-300

-250

-200

-150

-100

-50

0

50

100

150

200

S &

SE A

sia

E Euro

pe

W Eu

rope

N A

merica

S A

merica

ME &

Africa

NE A

sia

Chin

a

1,000 Metric Tons

Possible exporting outlets,

but fierce competition

2005

2004

2006

2008

2009

2010

2007

2011

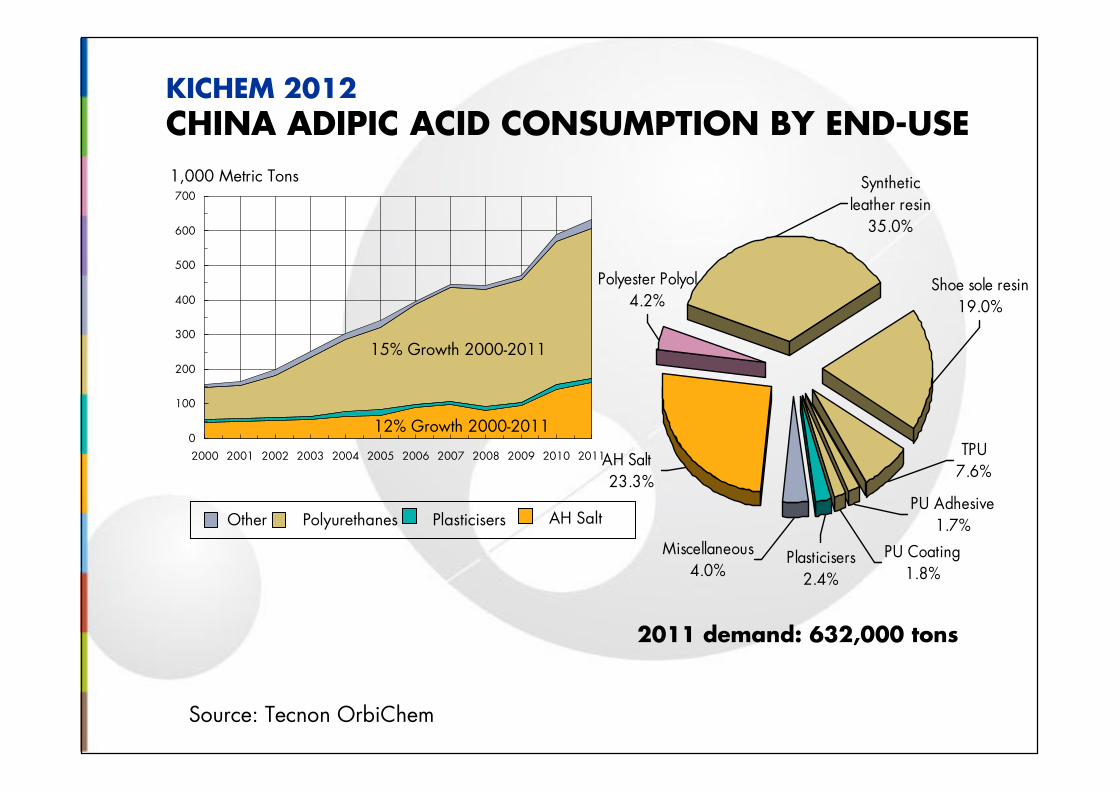

KICHEM 2012CHINA ADIPIC ACID CONSUMPTION BY END-USE

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

AH Salt PlasticisersPolyurethanesOther

Source: Tecnon OrbiChem

12% Growth 2000-2011

15% Growth 2000-2011

2011 demand: 632,000 tons

1,000 Metric Tons

Polyester Polyol 4.2%

AH Salt 23.3%

Miscellaneous4.0%

Plasticisers2.4%

TPU7.6%

PU Coating1.8%

PU Adhesive1.7%

Synthetic leather resin

35.0%

Shoe sole resin19.0%

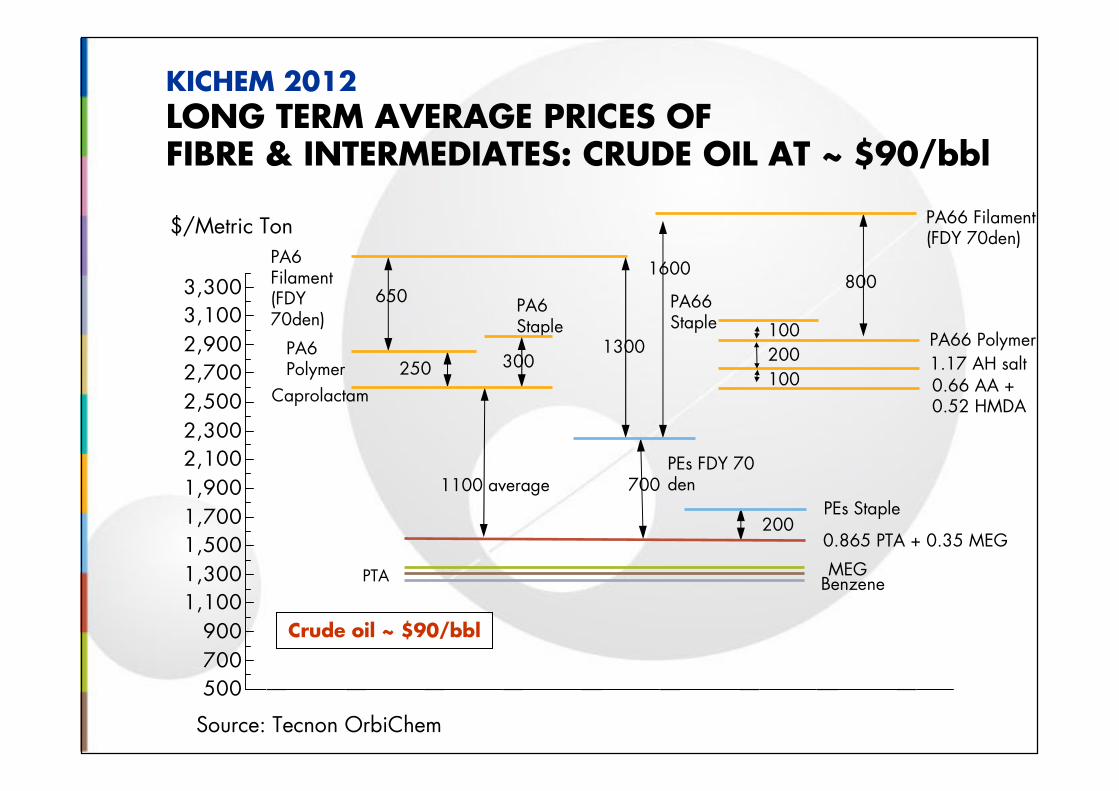

KICHEM 2012LONG TERM AVERAGE PRICES OF FIBRE & INTERMEDIATES: CRUDE OIL AT ~ $90/bbl

Source: Tecnon OrbiChem

500

700

900

1,1001,300

1,500

1,700

1,900

2,1002,300

2,500

2,700

2,900

3,1003,300

$/Metric Ton

Crude oil ~ $90/bbl

Caprolactam

1100 average

PA6Polymer 250 300

650

PA6Filament(FDY 70den)

PA6Staple

200

PA66Staple

800

100

200PEs Staple

700

1300

1600

PEs FDY 70 den

PA66 Filament(FDY 70den)

0.66 AA + 0.52 HMDA

PTA Benzene

100

0.865 PTA + 0.35 MEG

PA66 Polymer1.17 AH salt

MEG

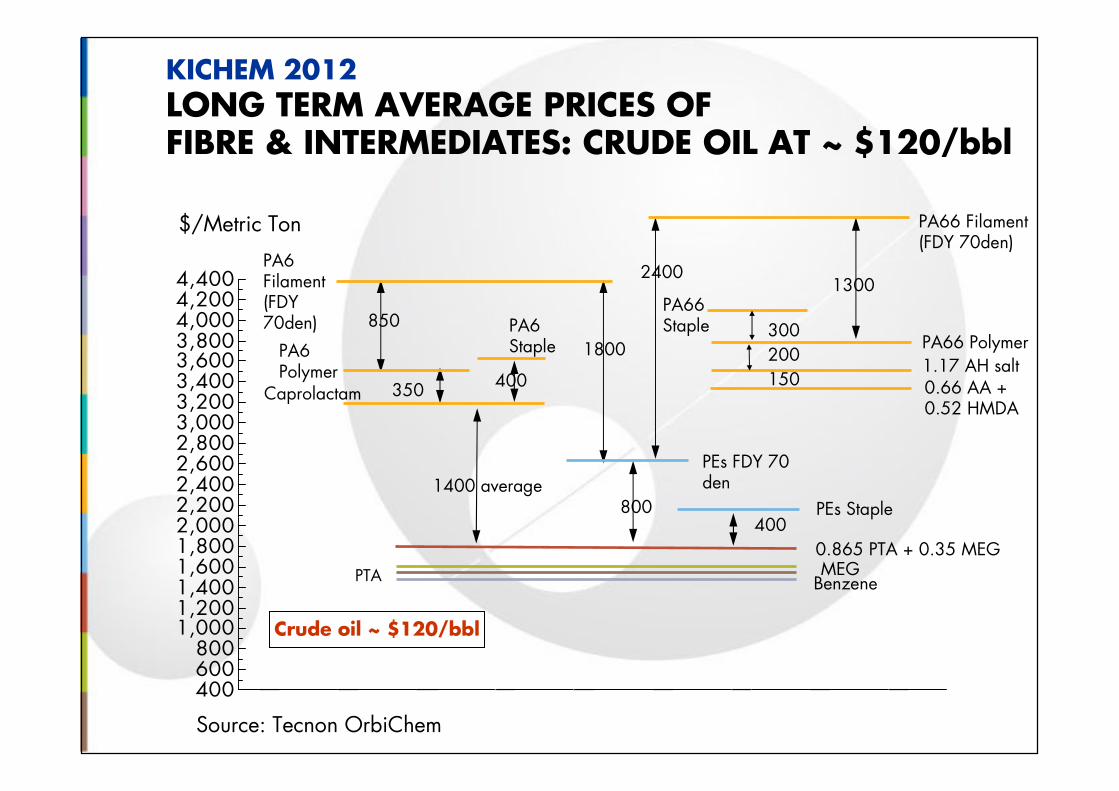

KICHEM 2012LONG TERM AVERAGE PRICES OF FIBRE & INTERMEDIATES: CRUDE OIL AT ~ $120/bbl

Source: Tecnon OrbiChem

400600800

1,0001,2001,4001,6001,8002,0002,2002,4002,6002,8003,0003,2003,4003,6003,8004,0004,2004,400

$/Metric Ton

Crude oil ~ $120/bbl

Caprolactam

1400 average

PA6Polymer

350 400

850

PA6Filament(FDY 70den) PA6

Staple

PA66Staple

1300

400PEs Staple800

1800

2400

PEs FDY 70 den

PA66 Filament(FDY 70den)

0.66 AA + 0.52 HMDA

PTA Benzene

0.865 PTA + 0.35 MEG

PA66 Polymer1.17 AH salt

MEG

200

150

300

KICHEM 2012CONCLUSIONS

• World caprolactam consumption bounced back in 2010, but then slowed considerably H2 2011 and H1 2012; World caprolactam growth will return to trend from 2012 onwards, at a long term rate of 2.8% per year

• The 2010 recovery was due to a surge in demand from China but this resulted from a pull forward of future demand, such that 2011 has seen almost zero growth in China

• A quick and large release of China new caprolactam capacity will lead to over-capacity over 2012-2015 but supply and demand will return to balance by 2016 if no further caprolactam plants are built

• Caprolactam showed excellent profitability in 2010 and most of 2011, but profits have collapsed in 2012 as Chinese polyamide growth has faltered combined with a large and rapid expansion of Chinese capacity

• PA6 and PA66 will be hard pressed by competition from polyester with an increasing crude oil price

Source: Tecnon OrbiChem

KICHEM 2012CONCLUSIONS

• PA66 producers have to grapple with high and volatile costs, especially on butadiene; High butadiene prices are likely to persist, damaging long term PA66 growth

• Some new investments in polyamide 66 was stimulated by good profit and short supply years ago, such as Huafeng Group (40 ktpa started up in May 2011) and Guorui Chemical (50 ktpa AH salt in H1 2012), but highADN/HMDA prices and relatively slow demand mean that they are struggling

• Polyamide 66 resin prices in China have been decreasing in H1 2012, even for a time close to the current nylon 6 resin prices, showing a big cost pressure for the nylon 66 producers

• Over-enthusiasm for adipic acid investment in China has led to gross overcapacity

• Adipic acid imports into China have been replaced -- except for high quality material -- and export opportunities are limited, so over-capacity will continue and domestic markets will be depressed for years to come

• Fierce competition could lead to a reshuffling in the adipic acid markets, in China and even overseas

Source: Tecnon OrbiChem

…..your source of expert chemical industry knowledge