Embed Size (px)

Citation preview

Portfolio Committee on Public Enterprises

Securing coal resources for power generation

23 April 2013

1. Evolution of Eskom’s coal contracting and portfolio of contracts

2. Eskom’s stock day recovery process

3. Developments in the South African steam coal market

4. Eskom’s future coal requirements

5. International coal regulation benchmarks

6. Overview of key coal supply challenges for domestic electricity supply

7. Proposed enablers for securing coal for Eskom in the future

Content

Era

Predominant new contract type

Examples

“Development of the electricity infrastructure”

“Over-capacity and promotion of coal exports”

“Electricity and coal supply shortage”

1960 – mid 1980’s Mid 1980’s – mid 2000’s 2008 - 2018

Negotiating climate

Limited Eskom negotiating power

• Urgency• Unsophisticated mine

planning and analytical tools• Sanctions and limited foreign

investment• High interest rates• Abundant cheap coal with low

risk

Stronger Eskom negotiating power

• Commissioning of the coal export line opened up export opportunities

• This provided additional profit opportunities for several of Eskom’s cost-plus mines

• Plenty cheap dumps available as top-up

Limited Eskom negotiating power

• Urgency• Real coal supply shortage• Global credit crunch, skills

shortages and recent cost ‘explosions’ in mining contribute to extreme risk aversion

• Volatile export prices• Logistics a serious issue• BEE a strong driver• Global trend to lower qualities

• Cost plus with 30% - 40% Eskom capital contribution

• Eskom takes risk on geology

• Conversion of several cost plus contracts to fixed price contracts based on the marginal cost of producing Eskom coal

• Short term for emergency supplies

• Long term to be determined

• Matla• Kriel• Arnot• Khutala

• Optimum• Duvha

• >20 new long term contracts to be negotiated

History of Eskom’s coal contracts

• Long term contracts (cost plus & fixed price) are contracts generally not less than 10 years in duration and often up to 40 years in duration, some with options to extend

• Eskom undertakes a due diligence process in terms of ensuring environmental compliance of its suppliers

• With the coal mines this covers mining authorisations, approved mine plans and Environmental Management Programmes and Water Use licences

• 27 of Eskom’s 46 supply collieries have WUL’s while 19 have submitted applications

Eskom has a portfolio of long, medium and short term coal contracts

Cost plus contractsFixed price contracts with

escalationShort/medium term contracts

• Both parties contribute initial capital

• Eskom pays the supplier for the full operational costs and a pre-determined net return on its capital contribution

• Any additional capital requirements and/or cost increases are for Eskom’s account

• Coal reserves are dedicated to Eskom – ensures security of supply

• Cost, volumes and qualities are managed monthly

• Coal is sold to Eskom at a pre-determined base price

• The base price is escalated annually by applying an escalation formula

• The supplier incurs penalties for not meeting quality specifications

• Coal reserves are not dedicated to Eskom

• Eskom makes no capital contribution and theoretically has no exposure to new capital requirements or cost overruns

• The volume and quality of the coal supplied drives the management of the costs as the price is pre-determined

• Coal is sold to Eskom at a pre-determined base price

• The base price is escalated annually by applying an escalation formula

• The other criteria are similar to that of fixed price contracts

• The volume of the coal supplied drives the management of the costs as the price is pre-determined

• These contracts are concluded mainly with the Junior (Emerging) Miners

• Eskom has implemented a pre-certification procedures for quality management which ensures compliance to Eskom requirements

5

2008

53%

26%

2007

57%

26%

Cost plus

Fixed price

Short/med

2012 Budget

46%

24%

2011

47%

24%

2010

50%

25%

2009

49%

22%

Coal purchases volume breakdown (in %)

• Performance of cost plus mines has decreased over the past few years• Increased number of short/medium term purchases had to be transported by road – negative

impact on roads• Rail performance is improving – from 3.8 Mt in FY 2006/7 to 10.1 Mt in FY2012/13

• Performance of cost plus mines has decreased over the past few years• Increased number of short/medium term purchases had to be transported by road – negative

impact on roads• Rail performance is improving – from 3.8 Mt in FY 2006/7 to 10.1 Mt in FY2012/13

22% 24% 23%

4%7%5%

26%18%14%

Conveyor

Rail

Road

2012 Budget

70%

2011

71%

2010

74%

2009

71%

3%

2008

79%

4%

2007

83%

3%

Delivery of purchases (in %)

Declining volumes from long term contracts has prompted greater short/medium term purchases, most of which is delivered by road

Source:Eskom PED; Barlow Jonker

• Similar quality reserves to Waterberg but the coal seam dips at ~12 degrees

• However, not much is known about these reserves and prospecting taking place

• Very far from existing power stations

• Have significant coal reserves, however the area requires a new method of mining as

– Reserves are too deep for O/C mining (at depths of 300m or greater)

– Roof strata is too soft for U/G mining

• Large reserves similar to Waterberg

• However, area is very expensive to mine as the coal seams dip at ~12 degrees ( e.g., Tshikondeni current cost of mining is ~R600/t)

Nongoma, Kangwane and Somkhele

• Good coal has been mined out

• Reserves left occur in small patches

• Significant portion is also anthracitic

• High quality coal but seams are too thin to mine in large quantities

• Hence, uneconomical to mine in high quantities that Eskom needs

• Reserves were mined in early 1900s

• Coal is of very poor quality (less than 16MJ/kg) and the seams are too thin

• Very long distance relative to other available fields

• Shallow areas are currently being mined (New Vaal and Sigma)

• Other mineable areas have been mined out for the old Taaibos and Highveld power stations

• Significant portions of reserves have also been sterilised from gold mining (e.g., reserves below Welkom)

• Majority of the reserves are to the south where it is very deep and more suited for UCG

• Coal reserves are mostly anthracitic

• Remaining reserves contain lean coal and the volatiles are too low for Eskom use

• Large reserves

• Very difficult mining conditions (faults, dykes, gas, spontaneous combustion, etc.)

• Coal reserves are also quite deep

• Accounts for over 80% of the country’s coal production

• Output will peak around 2025 and then decline quite rapidly

• Estimated ~30 years remaining economic life at current production rates

• Most potential of remaining SA coalfields

• Has large reserves which are economically viable to mine for electricity generation

• Over 90 years resource life at full production potential

• However, environmentally sensitive area and no rail link to Mpumalanga power stations

The Mpumalanga basin and Waterberg are two of the most important coalfields for power generation

Location of power stations Power Stations Main Supplier

MMS Colliery

Hendrina3 Optimum- Fixed Price

Arnot 1 Exxaro – Cost Plus

Kendal4 BECSA – Cost Plus

Duvha 2 BECSA – Fixed Price

Komati Various medium term

Grootvlei Various medium term

Kriel6 AAIC1 - Cost Plus

Lethabo7 Anglo – Cost Plus

Majuba8 Various medium term

Matimba9 Exxaro- Fixed Price

Matla Exxaro- Cost Plus

Camden Various medium term

1010

14

13

12

Tutuka Anglo – Cost Plus1111

Optimum Colliery

Arnot Colliery

Khutala Colliery

No tied mine

No tied mine

Kriel Colliery

New Vaal Colliery

No tied mine

Grootegeluk Colliery

Matla Colliery

No tied mine

New Denmark Colliery

Colliery Name

New build projects: 1) Medupi Power Station – long term agreement has been signed with Exxaro 2) Kusile Power Station – long term agreement will be signed with Anglo

The majority of the long term contracts are held by three large mining houses

Note: 1) AAIC – Anglo American Inyosi Coal

Post 2008, a new stock holding policy was implemented to ensure significant increase the stock days

• In 2008 the stock holding policy was reviewed and Minimum, Alarm and Expected stock levels for each power station determined. Based on this the expected system stock days is 42 days

• Stock days still reflect a seasonal profile1, however since 2008 we have managed to increase the average stock days around the expected level of 42 days

• The steady progress in improving stock levels is assisted by medium and short term coal contracts, improved contract management and focus on effective logistics operations

Note: 1) winter, rainy season, Easter and December festive season

Lower than budget and contract performance on the cost plus mines results in increased short / medium term purchases at higher prices

9

20102008 20122007

54

2009 2013

54

2011

6768

63

7068

65 65

60

62

6059

53

Actual

Budget

3031

36 37

2007 2008 2009 2010 2011 2012

38

20 20

31

26

2013

38

4645

40

36

Actual

Budget

Cost Plus Mines Short / Medium Term Contracts

• The cost plus mines’ production rapidly deteriorated since 2007.

• Every year, in total, the cost plus mines performed below their own budgets.

• Since 2010 cost plus mines in total performed below contractual. This under-delivery had to be made up by expensive import coal.

17%*

18%*

* unit cost ( R / ton) increases

10

1. Under-investment in the coal mining sector in SA and rising production costs will force alignment in the domestic and export prices:•Cost of building new mines increased substantially and more and more suppliers are demanding export linked market prices with one to two year price re-openers

2. Operating costs within the coal mining industry have been much higher than CPI in the last decade. Higher input costs puts pressure on domestic coal prices. Costs are driven by:•Cyclical commodity based inputs•Rising labour costs•Declining yields and strip ratios

3. Frost and Sullivan identified several challenges to coal mining in South Africa:

• Poor road networks, logistical constraints and high transportation costs impact supply to domestics markets and puts pressure on delivered coal prices

• Depleted coal deposits puts pressure on coal availability and domestic coal prices

• Transformation of the coal industry – indecision on nationalisation hampers new investments

4. The South African coal market requires substantial investment and recapitalisation to meet both domestic and export requirements as the current mining capacity will not meet the growing demand

•No major new mining developments have been forthcoming to meet growing demand in the last decade

There have been several developments in the South African and global steam coal market (1/3)

Mining Wage Settlements are above inflation

Source: Andrew Levy Employment, RMB Morgan Stanley Research

Geological Factors are driving costs upwards

Source: Wood Mackenzie, RMB Morgan Stanley Research

Producers of coal have not been able to expand operations to meet the increased demand for coal due rising costs of mining

11

5. TFR has recently announced major capital investment projects which will increase rail export capacity:

• There are opportunities in the coal export infrastructure capacity; currently, the design capacity has not been met

• Transnet expects to increase their export rail (RBCT rail line) from 68 Mt to 75 Mt per annum with the view to expand to 81 Mt in the next three years

• TFR is in progress of constructing the rail link to Swaziland from Ermelo to divert general freight traffic from the coal line and provide extra capacity to RBCT – more export capacity puts pressure on coal availability for domestic use and prices trend to EPP

6. Analysts indicate that the upward trend of South African coal exports should continue until 2016:

•Scarcity of coal supply for domestic use and domestic users will be expected to pay EPP

7. SA steam coal exports continue to favour the Asian market, with major demand originating from India for Eskom grade coal:

• 25% of steam coal exports go to India – (power stations on the west coast of India are designed to burn lower grade coal)

• India is expected to represent ~ 82% of the market share for South African coal by 2020

• Indian Boilers favour lower grades of coal with CV values of c.3,300 kcal/kg. India’s coal imports are expected to rise to 185Mt by 2017

There have been several developments in the South African and global steam coal markets (2/3)

Source: Richards Bay Coal Terminal7

RBCT Coal Exports (Mtpa)

India dominates SA’s coal exports

Source : 1. Wood Mackenzie forecast; Intelligence brief PED 2012-07-30 vol 1 issue 1

TFR expanding rail capacity to ports will put increased pressure on the availability of coal for domestic use and render domestic users to pay EPP

8. The current lower prices for Richards Bay Coal should not hamper opportunities in the export market as export prices are still favourable for South African coal miners compared to domestic prices

9. RB3, the lower quality coal grade (~5,500kcal/kg, ~23MJ/kg) has been legitimised in recent months signifying that RB3 is a tradable commodity. RB3 competes directly with Eskom’s coal requirements:

• Coal Brokerage globalCOAL updated its Standard Coal Trading Agreement (SCoTA) in March 2012 to a new trading contract for Richards Bay (5,500 kcal/kg NAR; total moisture 14%; maximum ash 23% and 1% sulphur on as-received basis)

10. RB3 has been included as a product on the Coal Reserves and Resources Study conducted by the Council for Geoscience

There have been several developments in the South African and global steam coal markets (3/3)

IHS McCloskey Monthly Average Steam Coal Spot Prices (USD/ton)

Source: IHS McCloskey

Source: IHS McCloskey.Richards Bay: basis = 6,000 kilocalories per kilogram net as received free on board (FOB).Newcastle: basis 6,700 kilocalories gross air-dried FOB.

Export Steam Coal Price Forecasts – USD/metric ton

ForecastForecast

Medium term

Source : GTIS, Macquarie Research, March 2011

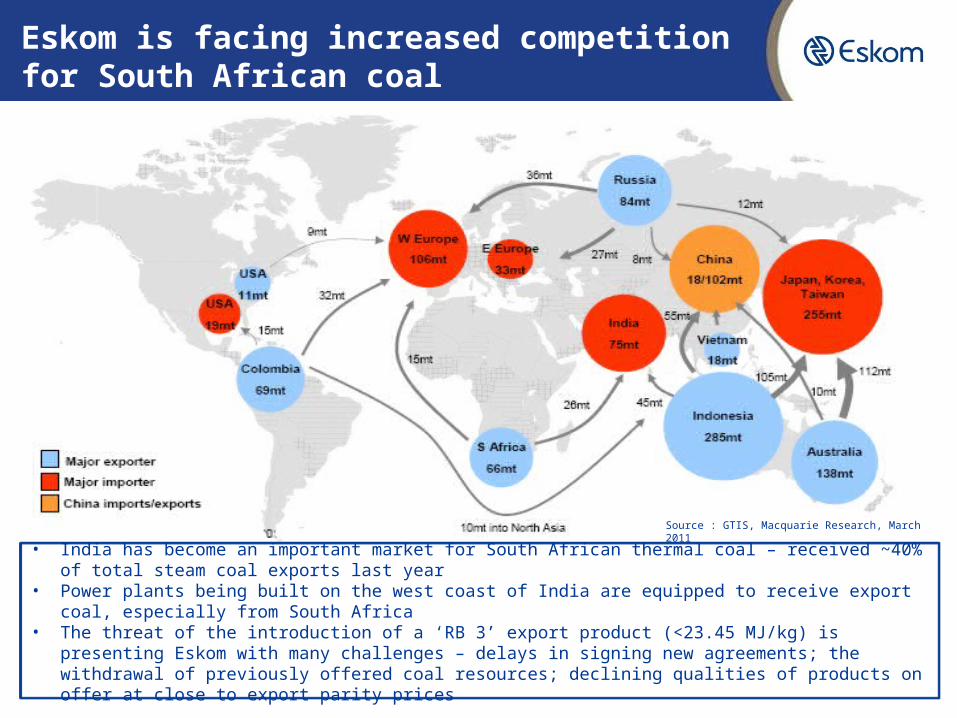

• India has become an important market for South African thermal coal – received ~40% of total steam coal exports last year

• Power plants being built on the west coast of India are equipped to receive export coal, especially from South Africa

• The threat of the introduction of a ‘RB 3’ export product (<23.45 MJ/kg) is presenting Eskom with many challenges – delays in signing new agreements; the withdrawal of previously offered coal resources; declining qualities of products on offer at close to export parity prices

Eskom is facing increased competition for South African coal

Impact of coal prices on electricity prices

IHS McCloskey weekly average spot prices for thermal coal – USD/metric ton

Contemporary prices ~ 83-87 USD/ton (EPP: R445-R453/ton)Prices continue on a downward trend due to the following:•Oversupply of coal stimulated by low gas prices•Coal stocks at Chinese ports and power stations are currently high •Japanese power demand has decreased (lower GDP, energy savings and higher temperatures)

Long termMedium term

2013-2017 2017-2030

±87 USD/ton(R816/ton)EPP: R476/ton

±105 USD/ton(R985/ton)EPP: R596/ton

±105 USD/ton(R985/ton)EPP: R596/ton

±121 USD/ton(R1 135/ton)EPP: R704/ton

Downside Risk:•US west coast ports obstructed •Indonesian domestic market obligation grows / export ban•Strict carbon policy spreads globallyUpside Risk:•China power market reform

Upside Risk:•Unconventional gas in China grows rapidly •Rapid supply/infrastructure build out in China•Large exchange rate variation

Taking a closer look at the Expected Export Price Movements ex Richards Bay

South African coal exports continue to benefit from a weakened Rand despite falling prices

An increase in the price of the 30 million tons per annum of short term coal purchases, from the current levels to an Export Parity Price of R600/t delivered will lead to a 5% increase in total operating cost from 56.4 c/kWh.

The changing coal supply environment requires a new approach to secure the resources for future needs

• Eskom is on average 80% contracted for the next 5 years – price stability and volume and quality predictability

• Consolidation of the supplier market into 4 main suppliers

• The SA coal market requires substantial investment and recapitalisation to meet requirements in the future

• There are several challenges to coal mining in SA:• logistical constraints • depleted coal deposits

• TFR has recently announced major capital investment projects which will increase rail export capacity

• SA steam coal exports continue to favour the Asian market, with major demand originating from India for Eskom grade coal

The environment in which Eskom is operating, is changing

Contracted Un-contracted

0

20

40

60

80

100

120

140

160

180

205120492033202520182012

~2 100 Mt

~1 970 Mt

Eskom Coal Supply for the next 40 years

Shortages of up to 40 Mtpa of coal after 2018 are expected

A 40 Mtpa requirement translates into 10 X 4 Mtpa mines that need to be opened up in SA for domestic supply alone

Estimated capital required to open new mines to meet the supply the shortages over the next few years

Estimated cost to open new mines in the future

Brazil

• The new basic mining codes under discussion will:• Create a National Council of Mineral Policy and Regulatory Agency• Change rules granting mineral titles to ensure better monitoring, supervision and management by the managing

agency• Introduce a limitation of 35 years for concessions• Change financial compensation for the exploration of new mineral resources• Increased attention to community and environment al factors upfront

Australia• Government legislated 30% tax on iron ore and coal. This is due to increasing demand for Australian coal and iron ore

from India and China• This tax affects approximately 30 mining companies in Australia.

Argentina

• The new legislation guaranteed investors tax stability for 30 years, granted 100% deduction of exploration costs from income taxes, and capped the maximum royalty payment to the government at 3%.

• In 2002, a resolution was passed by the government that would establish some amount of export taxes on companies that came to Argentina after that year.

• In October 2011 the government imposed restrictions on oil and mining companies that mandated the repatriation of export profits and later introduced broad sweeping administrative hurdles to purchase foreign exchange

• Mining industry currently focused on project start ups

• Captive mining policy was introduced in 1993 as an interregnum to full and unrestricted opening of coal sector to private investment.

• Over 90 % of domestic coal production coming from government controlled mines• Government has allocated over 200 coal blocks for development by private / public entities out side the government

owned coal companies

India

Indonesia

• To restrict the exports of thermal coal, the Indonesian government has or will implement the following restrictive policies or changes with respect to thermal coal domestic production

• Domestic Market Obligation (DMO) - DMO is a new mining law passed in Indonesia requiring mining companies to sell a portion of their production to local customers

• Benchmark price regulation - guidelines are provided to determine the minimum selling price of coal into both domestic and export markets

• Export tax to be implemented - a tax on coal exports will be applicable at a 25% rate this year and a 50% rate next year

Benchmarking of Coal Regulatory Environment

Electricity supply

challenges

Coal resources• Deteriorating quality• Diminishing quantity• Increased competition

Electricity generation• New generation

infrastructure delays• Existing generation

infrastructure utilization

Mining industry• Not developing new

resources• Preference to export

Domestic electricity supply is facing several challenges

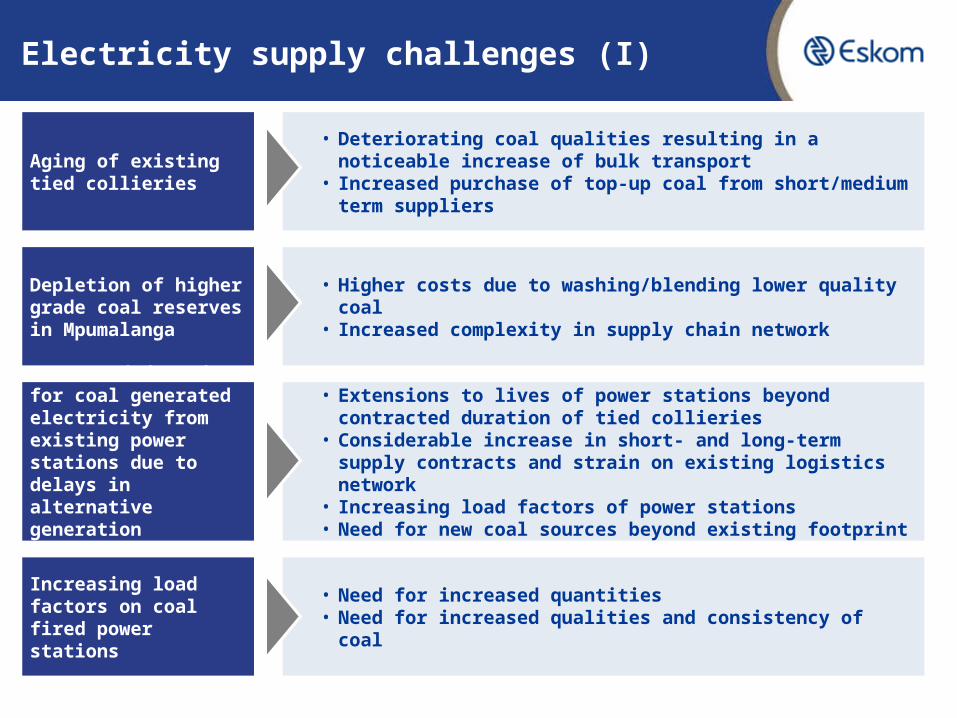

Electricity supply challenges (I)

Aging of existing tied collieries

• Deteriorating coal qualities resulting in a noticeable increase of bulk transport

• Increased purchase of top-up coal from short/medium term suppliers

Depletion of higher grade coal reserves in Mpumalanga

• Higher costs due to washing/blending lower quality coal• Increased complexity in supply chain network

Increased demand for coal generated electricity from existing power stations due to delays in alternative generation solutions

• Extensions to lives of power stations beyond contracted duration of tied collieries

• Considerable increase in short- and long-term supply contracts and strain on existing logistics network

• Increasing load factors of power stations• Need for new coal sources beyond existing footprint

Increasing load factors on coal fired power stations

• Need for increased quantities• Need for increased qualities and consistency of coal

Electricity supply challenges (II)

Mine productivity underperforming

• Under-performance of cost plus mines • Increased costs due to purchase of top up coal from

short/medium term suppliers, often located a considerable distance away from power stations

Mining projects behind schedule

• Timing of domestic coal requirements is not aligned with the mining houses

• The trend of the market is to only invest in mines for export and not for local supply

Price expectations/returns of suppliers significantly higher than previous estimates

• Potential for exports of lower quality coal to India has created direct competition for new coal sources that were previously only suitable for domestic use.

• Reduced bargaining power for domestic buyers

Some resources reduced due to more rigorous environmental compliance

• Stricter environmental compliance for coal mining has reduced the quantity of coal planned for supply to Eskom

Competition Tribunal raised broad public sector concerns and advised that trends “could be addressed by policy instruments"1

The Competition Tribunal has supported the challenges faced by Eskom in the coal supply market

Trends and developments in the coal industry

• Impending ending of certain Eskom long term coal contracts.• The anticipated increased coal demand from Eskom and its increased

buying on short term contracts• The anticipated increase in rail transport capacities for coal exports• The incentives of miners to export given higher coal export prices and

revenues• Increases in the export of coal and meaningful changes in the

composition of these exports, specifically the increased demand from countries that use lower quality coal (RB3) and thus increases in the exports of this coal from South Africa

• The trending of prices from the residual (short-term) market to international export prices

Domestic coal supply concerns

• Trends do not favour domestic coal users especially Eskom as the largest coal customer in South Africa

• These factors will have an impact on Eskom’s ability to procure coal and the price thereof and to produce competitively priced electricity

• Increasing prices to our domestic market is a serious concern given its effect on electricity prices and potential detrimental effects on economic growth, South Africa’s developmental goals and the entire economy

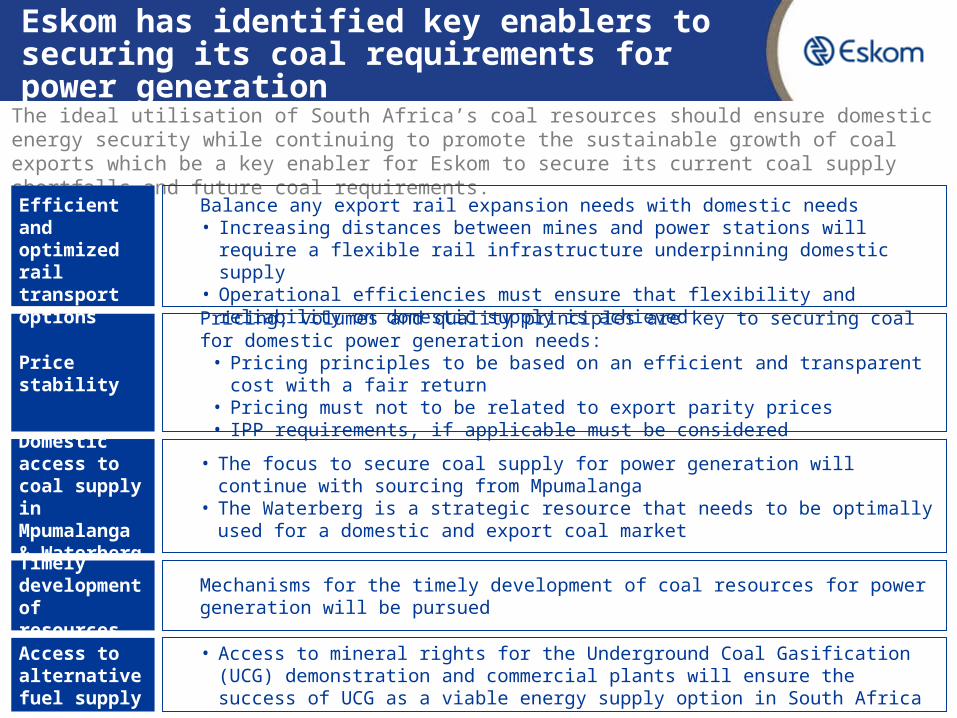

The ideal utilisation of South Africa’s coal resources should ensure domestic energy security while continuing to promote the sustainable growth of coal exports which be a key enabler for Eskom to secure its current coal supply shortfalls and future coal requirements.

Eskom has identified key enablers to securing its coal requirements for power generation

Domestic access to coal supply in Mpumalanga & Waterberg

• The focus to secure coal supply for power generation will continue with sourcing from Mpumalanga

• The Waterberg is a strategic resource that needs to be optimally used for a domestic and export coal market

Timely development of resources

Mechanisms for the timely development of coal resources for power generation will be pursued

Access to alternative fuel supply

• Access to mineral rights for the Underground Coal Gasification (UCG) demonstration and commercial plants will ensure the success of UCG as a viable energy supply option in South Africa

Pricing, volumes and quality principles are key to securing coal for domestic power generation needs:

• Pricing principles to be based on an efficient and transparent cost with a fair return• Pricing must not to be related to export parity prices• IPP requirements, if applicable must be considered

Price stability

Efficient and optimized rail transport options

Balance any export rail expansion needs with domestic needs• Increasing distances between mines and power stations will require a flexible rail

infrastructure underpinning domestic supply• Operational efficiencies must ensure that flexibility and reliability on domestic supply is

achieved