Embed Size (px)

Citation preview

Rich Weiss

Senior Vice President

Senior Portfolio Manager

Portfolio Construction:

Rethinking Global Asset Allocation

ACI-1010142

Agenda

It’s a Changed World

Game Changers

A Leading-Edge Approach

2 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

CDO MBS

SIV CLO

BB / CCC / CC / C / D

The Financial Bailout

A Simple Flowchart

CPA, CFP or a CFA

APR on ARMs

FNMA FHLMC

GSEs

CPI, PPI, GDP IPD,

et. al. … FDIC

FED, FOMC,

ECB, BofJ, &

SEC

PDQ

WSJ FHFA

LTVs BS, LEH, AIG

FUBAR …

FASB /

GAAP:

EPS, ROE,

ROI, P/E,

etc.

H1N1

I.O.U.

3 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

In the past 40 years, how many times has the U.S. been the best performing equity market?

a. 27

b. 13

c. 4

d. 1

Pop Quiz – Building a Global Portfolio

4 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Performance Rankings by CountryBased on Annual Returns of MSCI Indices, 2002 - 2015

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

NEW ZEALAND GREECE AUSTRIA ISRAEL SPAIN FINLAND JAPAN NORWAY SWEDEN IRELAND BELGIUM GREECE ISRAEL DENMARK

AUSTRIA SWEDEN NORWAY JAPAN PORTUGAL HONG KONG ISRAEL AUSTRALIA DENMARK NEW ZEALAND DENMARK FINLAND USA IRELAND

AUSTRALIA GERMANY GREECE AUSTRIA IRELAND ISRAEL SWITZERLAND SINGAPORE HONG KONG USA SINGAPORE IRELAND NEW ZEALAND BELGIUM

NORWAY SPAIN BELGIUM DENMARK SINGAPORE GERMANY USA SWEDEN SINGAPORE UNITED KINGDOM GERMANY USA DENMARK ISRAEL

ITALY ISRAEL IRELAND NORWAY NORWAY GREECE SPAIN HONG KONG JAPAN SWITZERLAND NEW ZEALAND GERMANY HONG KONG JAPAN

JAPAN AUSTRIA SWEDEN FINLAND SWEDEN NORWAY FRANCE BELGIUM USA NORWAY HONG KONG SPAIN BELGIUM AUSTRIA

SWITZERLAND NEW ZEALAND NEW ZEALAND SWITZERLAND DENMARK SINGAPORE GERMANY ISRAEL AUSTRALIA BELGIUM AUSTRIA NETHERLANDS SINGAPORE ITALY

SINGAPORE AUSTRALIA ITALY GREECE BELGIUM AUSTRALIA SINGAPORE NEW ZEALAND SWITZERLAND AUSTRALIA AUSTRALIA BELGIUM IRELAND FINLAND

PORTUGAL DENMARK DENMARK AUSTRALIA AUSTRIA DENMARK DENMARK SPAIN NORWAY NETHERLANDS SWEDEN JAPAN SWITZERLAND NETHERLANDS

BELGIUM NORWAY AUSTRALIA SINGAPORE GERMANY PORTUGAL NETHERLANDS UNITED KINGDOM FINLAND SPAIN FRANCE SWITZERLAND FINLAND PORTUGAL

UNITED KINGDOM IRELAND SPAIN NETHERLANDS GREECE SPAIN UNITED KINGDOM AUSTRIA AUSTRIA JAPAN NETHERLANDS FRANCE AUSTRALIA USA

SPAIN PORTUGAL HONG KONG SWEDEN FRANCE NETHERLANDS SWEDEN NETHERLANDS UNITED KINGDOM SWEDEN SWITZERLAND DENMARK NETHERLANDS SWITZERLAND

DENMARK FRANCE PORTUGAL GERMANY ITALY FRANCE ITALY PORTUGAL GERMANY DENMARK NORWAY SWEDEN JAPAN FRANCE

HONG KONG HONG KONG SINGAPORE FRANCE NETHERLANDS NEW ZEALAND AUSTRALIA DENMARK NEW ZEALAND HONG KONG USA UNITED KINGDOM SPAIN HONG KONG

NETHERLANDS ITALY ISRAEL BELGIUM AUSTRALIA UNITED KINGDOM HONG KONG FRANCE ISRAEL FRANCE UNITED KINGDOM ITALY UNITED KINGDOM GERMANY

FRANCE SINGAPORE UNITED KINGDOM HONG KONG UNITED KINGDOM ITALY PORTUGAL ITALY NETHERLANDS SINGAPORE FINLAND AUSTRIA SWEDEN SWEDEN

USA JAPAN FRANCE UNITED KINGDOM HONG KONG USA NEW ZEALAND USA BELGIUM GERMANY ITALY NEW ZEALAND ITALY NEW ZEALAND

GREECE BELGIUM GERMANY USA FINLAND SWITZERLAND FINLAND SWITZERLAND FRANCE PORTUGAL JAPAN HONG KONG FRANCE UNITED KINGDOM

IRELAND SWITZERLAND JAPAN SPAIN SWITZERLAND AUSTRIA NORWAY GERMANY PORTUGAL ITALY IRELAND PORTUGAL GERMANY AUSTRALIA

FINLAND UNITED KINGDOM SWITZERLAND ITALY NEW ZEALAND SWEDEN GREECE GREECE ITALY ISRAEL GREECE ISRAEL NORWAY NORWAY

SWEDEN USA NETHERLANDS NEW ZEALAND USA BELGIUM BELGIUM IRELAND IRELAND FINLAND PORTUGAL NORWAY AUSTRIA SPAIN

ISRAEL NETHERLANDS USA PORTUGAL JAPAN JAPAN AUSTRIA FINLAND SPAIN AUSTRIA SPAIN AUSTRALIA PORTUGAL SINGAPORE

GERMANY FINLAND FINLAND IRELAND ISRAEL IRELAND IRELAND JAPAN GREECE GREECE ISRAEL SINGAPORE GREECE GREECE

Global Investing – Country Rankings

5

Data reflects rankings based on annual returns of indices of MSCI World country constituents at the end of each annual period

Source: MSCI, Zephy r Sty leAdv isor

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Shift in Economic Influence

6 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014

Gross Domestic Product(in $Billions)

United States Non-U.S.

Data from 12/31/1970 to 12/31/2014Source: World Bank

World Markets Have Become More Correlated

7 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Correlation Between S&P 500 and International Equity Markets

Rolling 60-Month CorrelationApril 1950 - December 2015

Source: Wolfe Trahan & Co. , FactSet. This information is for illustrative purposes only and is not intended to represent any particular investment product.

Traditional Approach to Asset Allocation Portfolios

8 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

S&P 500

60/40 Balanced Portfolio

4

5

6

7

8

9

10

4 6 8 10 12 14 16 18 20

Re

turn

(A

nn

ualize

d %

)

Risk (Standard Deviation)

Ten-Year Risk/Return

Source: Morningstar Direct60/40 Balanced Portfolio represented by 50% S&P 500 Index, 10% MSCI EAFE Index, 40% Barclays Aggregate Bond Index. Rebalanced monthly. Data as of 12/31/2015This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved. This information should not be relied upon as a specific recommendation to buy or sell securities.

Game Changers

1. Sector diversification is as important as country diversification

2. Alternative investments are helping to optimize the risk/return trade-off

3. Volatility instruments offer the potential to limit downside risk

9 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

1. Sector diversification is as important as country diversification

Game Changers

10 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

United States Japan United Kingdom

Hong Kong Switzerland France

Germany Canada Australia

South Korea Taiwan Netherlands

Spain Others < 1.0%

MSCI World Index: Country Weights

Data as of 12/31/2015Source: FactSet

Consumer Discretionary Consumer Staples

Energy Financials

Health Care Industrials

Information Technology Materials

Telecommunication Services Utilities

MSCI World Index: Sector Weights

By definition, country allocation/rotation implies sector allocation/rotation. They are two sides of the

same coin.

Global Sector Allocation

11 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

MSCI United States Index

Consumer Discretionary Consumer Staples Energy

Financials Health Care Industrials

Information Technology Materials Telecommunication Services

Utilities

Data as of 12/31/2015Source: FactSet

MSCI Japan Index MSCI New Zealand Index

MSCI Country Sector Weights

12 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Sector Diversification as Important as Country Diversification

Source: "The Rise of Sector Effects in Major Equity Markets", by Baca, Garbe, and Weiss, Financial Analysts Journal, Sept/Oct 2000, pages 34-40

13 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

14

Data from MSCI confirm that the relative strength of countries and industries in explaining global stock returns has become roughly

equivalent through 2010.

Global Sector Rotation – Additional Evidence

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

MA

D (

\Pe

rce

nt

Mo

nth

ly)

Countries (World) Industries (World)

Results are based on cap-weighted regressions and cap-weighted segment averages.Data from April 2011. Source: MSCI

Mean Absolute Deviation for 48-Country Global Model

Central banks lower interest

rates to spur growth,

stimulating the financials

sector.

1

Lower interest rates

generate greater

consumption and

production, revitalizing the

consumer goods

sectors.

2

Higher demand for

consumer goods in turn

boosts activity in the

services sector and

subsequently the

industrials sector.

3

Heightened demand in the

industrials sectors intensifies

demand for raw materials,

stimulating the resources

sectors.

4

Rising demand eventually

causes inflation to

accelerate at a global level.

In response, central banks

raise interest rates. With the

onset of recession, the

defensive characteristics of

the utilities sector grow

increasingly attractive.

5

In time, central banks again

lower interest rates to promote

expansion, and a new cycle

begins.

6

Classic Economic Sector Rotation Cycle

15

Consumer

Goods

Services

Resources

Industrials

Financials

Utilities

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Quantitatively-Disciplined Global Sector Return Forecasts

16

Fundamental Valuation Measures

Dividend yields 1

2

3

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Economically Driven Factors

Cyclical momentum

Industrial production

Interest rates

Inflation

Yield spreads

Credit spreads

Technical Indicators

Volatility

Sector-specific momentum

Current Global Sector Forecasts

17 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Proprietary Equity Sector Return ExpectationsExcess Returns Relative to MSCI ACWI

Current Previous

Data as of 1/31/2016. Global equity sector forecasts based on proprietary asset allocation models. Forecasts show normalized excess returns relative to the MSCI ACWI. Source: American Century Investments, MSCI

2. Alternative investments are helping to optimize the risk/return trade-off

Game Changers

18 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Liquid alternatives

Alternative strategies

packaged in vehicles that

provide daily or weekly

pricing and liquidity in accord

with U.S. and European

regulations for investments

that are broadly marketed to

the public.

40 Act Mutual Funds,

ETFs

SMAs

UCITS

Listed securities such as

closed-end funds

Asset Class Framework

19

Illiquid Alternatives

Liquid Alternatives

Extended

Traditional

Large cap equity

Mid/small cap equity

International equity

Core fixed income

Emerging markets equity

REITs/Global REITs

International fixed income

Emerging markets debt

High yield bonds

TIPS

Sector funds

Market neutral

130/30

Global macro

Managed futures

Commodities – CTA, ETN

Currency

Direct real estate

Private equity

Infrastructure

Hedge funds

Collectibles (Art, Coins, Wine)

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

The World of International Investing

192 Countries

20

Source: Shutterstock

Image ID: 64143952

Used with permission.

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Global Equity Markets

Nepal

Panama

Papua New Guinea

Paraguay

Serbia

Montenegro

Sri Lanka

Tanzania

Uganda

Uruguay

Uzbekistan

West Bank

Gaza

Cayman Islands

United States

Japan

United Kingdom

France

Germany

Canada

Hong Kong

Italy

Switzerland

Spain

Australia

Taiwan

South Korea

Saudi Arabia

Netherlands

India

Sweden

China

Brazil

Russia

Belgium

South Africa

Singapore

Mexico

Finland

Malaysia

Norway

Denmark

U.A.E.

Austria

Greece

Chile

Turkey

Thailand

Ireland

Kuwait

Israel

Indonesia

Qatar

Poland

Portugal

Argentina

Egypt

New Zealand

Czech Republic

Pakistan

Philippines

Hungary

Jordan

Colombia

Luxembourg

Morocco

Peru

Ukraine

Iceland

Bahrain

Romania

Nigeria

Oman

Croatia

Cyprus

Lithuania

Venezuela

Slovenia

Jamaica

Kenya

Slovakia

Botswana

Trinidad

Lebanon

Tunisia

Estonia

Zimbabwe

Malta

Mauritius

Bulgaria

Latvia

Bermuda

Ghana

Zambia

Barbados

Swaziland

Malawi

Vietnam

Argentina

Armenia

Bangladesh

Bolivia

Costa Rica

Cote d'lvoire

Ecuador

El Salvador

Fiji

Georgia

Guyana

Iran

Kazakhstan

Kyrgyz Republic

Macedonia

Moldova

Mongolia

Namibia

116 Countries: 50,000 Equity Securities

21

As of 12/31/2012

Source: MSCI

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Emerging Markets - Equity Market Capitalization ($U.S. Billions)

Data as of 3/31/2016

Source: FactSet

Emerging Markets - Equity Market Capitalization

22 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

$0

$10

$20

$30

$40

$50

$60

$70

$80

Frontier Markets - Equity Market Capitalization ($U.S. Billions)

Data as of 3/31/2016; Data for Bill Gates' estimated net worth as of 3/31/2016

Source: FactSet, Bloomberg

“Frontier” Markets - Equity Market Capitalization

23 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

“BRIC” (Brazil / Russia / India / China)

“Malarkey” (Malaysia / Turkey)

“Thailitius” (Thailand / Mauritius)

“Chileconcarne” (Chile / Morocco / Ukraine)

“Upper Colon” (Upper Estonia / Colombia / Lebanon)

Emerging Market Investing

Rule of Thumb

Avoid Nicknames (e.g. “BRIC”, “Lefty”)

24 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Lower portfolio volatility

– Lower correlation

– Increased diversification

Separation of Alpha versus Beta

Earn an illiquidity premium

Benefits of Alternative Investments

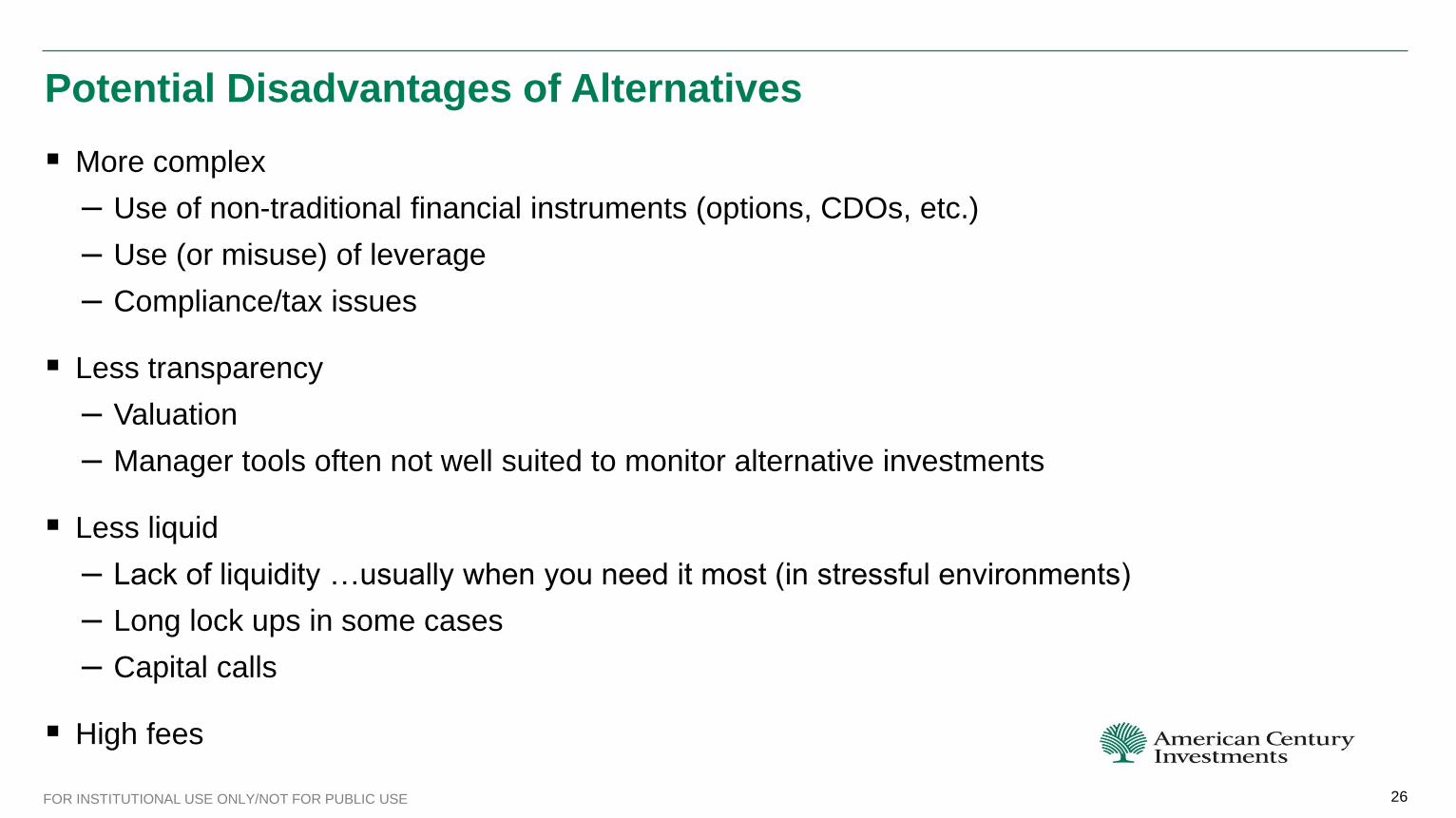

25 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

More complex

– Use of non-traditional financial instruments (options, CDOs, etc.)

– Use (or misuse) of leverage

– Compliance/tax issues

Less transparency

– Valuation

– Manager tools often not well suited to monitor alternative investments

Less liquid

– Lack of liquidity …usually when you need it most (in stressful environments)

– Long lock ups in some cases

– Capital calls

High fees

Potential Disadvantages of Alternatives

26 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Commodities

27 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0

50

100

150

200

250

1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Bloomberg Commodity Index Returns December 1969 to December 2015

Source: Bloomberg, Federal Reserve Bank of St. Louis, American Century

Annualized excess return Jan 1970 – Dec 2007: 5.4% Correlation with U.S. Stocks: 2%

Annualized excess return Jan 2008 - Dec 2015: -10.2%Correlation with U.S. Stocks: 54%

Roll returns diminished

after 1991,

commensurate with an

increase in the availability

and demand for

commodity-linked

products

Roll Cost and Diversification Benefits of Commodities

28 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

DJ-UBS Return Decomposition

Roll Return

Data as of 12/31/2015Source: Bloomberg, Federal Reserve Bank of St. Louis, American Century

Roll Cost and Diversification Benefits of Commodities

29 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bloomberg Commodity Index and MSCI Emerging MarketsRolling 36-Month Correlation - January 1991 - December 2015

Source: Bloomberg, Federal Reserve Bank of St. Louis, American Century

Emerging Market Debt

30

Return (%) Std Dev (%) Sharpe Ratio Correlations to

EM Debt

S&P 500 8.90 13.92 0.55 0.64

Russell 2000 10.16 18.86 0.47 0.59

MSCI EAFE Index 7.95 17.24 0.39 0.77

Barclays U.S. Aggregate 4.31 3.44 0.87 0.39

Citigroup Non-USD World Government Bond

Index 3.83 8.04 0.31 0.59

BofA Merrill Lynch U.S. High Yield 8.30 9.59 0.73 0.66

MSCI U.S. REIT 11.46 23.95 0.42 0.59

S&P GSCI -4.08 24.07 -0.22 0.41

MSCI EM (Emerging Markets) 11.04 22.40 0.43 0.80

JPMorgan GBI-EM Global Diversified Unhedged

USD 6.72 11.89 0.46 1.00

Source: Zephyr StyleADVISOR

Risk/Return Table Annualized Summary Statistics: January 2003-December 2015

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Emerging Markets Debt

31 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0%

5%

10%

15%

20%

25%

Emerging Markets DebtFive-Year Annualized Standard Deviations as of 12/31/2015

Currency Debt

Average FX Volatility: 10.29%Average Debt Volatility: 5.39%

Source: FactSet

3. Volatility instruments offer the potential to limit downside risk

Game Changers

32 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Volatility as an Asset Class

33 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0%

20%

40%

60%

80%

100%

120%

1/4/1897 12/6/1904 10/28/1912 2/17/1921 1/17/1929 12/17/1936 10/25/1944 9/17/1952 7/13/1960 5/13/1968 4/7/1976 2/8/1984 12/17/1991 10/27/1999 9/21/2007 6/29/2015

Dow Jones Industrials Historical VolatilityRolling 30-Day Annualized Standard Deviation

November 291929 November 27

1987

November 142008

Data from 1/1/1987 to 12/31/2015Source: Factset

CBOE Volatility Index® (VIX) created in 1993

Measures implied or “expected” volatility of the stock market using options prices

Barometer of investor sentiment (“fear” gauge)

VIX in the Mix: The “Godfather” Asset Class

34 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

0

10

20

30

40

50

60

70

80

90

0

500

1000

1500

2000

2500

Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15

VIX

S&

P 5

00

CBOE Volatility Index (VIX) with S&P500

S&P 500

VIX

Data from December 2008 to December 2015Source: FactSet

VIX

The Relationship Between Equities and VIX

35

Monday Tuesday Wednesday Thursday

8 Market falls on first

full day of trading after

S&P downgraded U.S.

credit rating

9

Market rises after first

regularly scheduled

Federal Reserve meeting

following U.S. downgrade.

10 Market falls on European

debt default concerns

11

Market rises on positive

U.S. economic news

S&P 500: -6.7%

VIX®: +50.0%

S&P 500: +4.7%

VIX®: -26.9%

S&P 500: -4.4%

VIX®: +22.6%

S&P 500: +4.6%

VIX®: -9.3%

August, 2011

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Autocorrelation (trending)

Mean-reverting (varies around some “normal”/historical level)

Information in term-structure

Characteristics of VIX

36 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 >=40

Re

turn

VIX Level

VIX Level vs. Future Returns

1-Mo Return 3-Mo Return 6-Mo Return 1-Yr Return

Data from January 1990 to December 2015Source: FactSet

January 1990 to December 2015

VIX is a mathematical formula, not an investment vehicle

VIX Index is not directly tradable

Volatility is volatile – (roughly 4x the volatility of market)

Beta, cost, and liquidity of swaps, futures, options, ETNs, and ETFs

VIX Implementation Hurdles

37 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

U.S.-Listed VIX Futures-Linked Volatility Indices

Source: ProShares, Barclays, UBS, VelocityShares

Investment Vehicles

38

VIXY

VIXM

VXX

XXV

IVO

VXZ

VZZ

TVIX

XIV

VIIZ

TVIZ

ZIV

XVIX

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

VIX in the Mix

39 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Global Balanced

Global Balanced with

10% Insurance Package

2

3

4

5

6

7

8

2 4 6 8 10 12 14 16 18 20

Re

turn

(A

nn

ualize

d %

)

Risk (Standard Deviation)

Risk/Return

Data from January 2006 to December 2015. Weights: Global Balanced: 17.50% Russell 3000, 18.00% MSCI EAFE, 5.50% MSCI Emerging Markets, 9.00% Barclays U.S. Aggregate Bond, 12.00% Barclays Global Treasury ex-U.S., 5.00% Barclays Intermediate U.S. HY, 10.00% MSCI ACWI REIT, 8.00% S&P GSCI, 3% BofA Merrill Lynch Global Emerging Markets Sovereign & Credit Bond, 3% London Fix Gold PM, and 9.00% Barclays 1-3 month T-Bill; "Volatility Insurance Package”: Equally weighted portfolio comprised of VIX, Oil VIX, Gold VIX and Euro VIX . Global Balanced and Global Balanced with 10% MidTerm VIX Futures are not actual portfolios available for investment. Source: Zephyr StyleAdvisor, BloombergPerformance results provided are hypothetical. Hypothetical performance results have many inherent limitations. Hypothetical trading does not involve financial risk, and no hypothetical trading record can

completely account for the impact of financial risk in actual trading. In addition, the hypothetical performance results do not represent actual recommendations or trading decisions, and they may not reflect the impact that economic and market factors might have had on the investment decision-making. For example, the ability to withstand losses, or to adhere to a particular trading program in spite of losses, can adversely affect actual results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program that cannot be fully accounted for in the preparation of hypothetical performance results, but which can adversely affect actual results.

Technical Filtering

State-of-the-Art Tactical Volatility Hedging

40

Forecasting Model

Developed multivariate

linear regression forecast:

–Consider historical

performance and current

market environment

–Evaluate mean-reverting

tendencies and other

characteristics of VIX to

predict future level of VIX

futures

VIX futures ETFs

selected for

implementation

(VIXM, VIXY)

Invest up to 5.0% of

portfolio in VIX

futures, depending

on forecast strength

Implementation

Designed timing

factor to identify

possible inflection

points in VIX’s

direction

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

A Leading-Edge Approach to Global Asset Allocation

41 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Alternatives

Alpha Strategies/

Cash

Fixed Income

Equity

Commodities

Global Real Estate

Mkt Neutral

Currencies Sector ETFs

Volatility

Instruments

EM Debt

High Yield Bonds

Non-U.S. BondsU.S. Bonds

Non-U.S. Equity

U.S. Equity

The New Recipe

42

Equity

Fixed Income

Source: American Century Investment Management

Alpha Strategies includes investments in non-U.S. currencies, bonds, exchange traded funds (ETFs) and futures that are designed to improve the fund's risk-adjusted

performance. Alpha is the excess return of a portfolio over its benchmark. An ETF is a security that tracks an index, commodity or basket of assets. Futures are agreements

to buy or sell a specific amount of a commodity or financial instrument at a particular price on a stipulated future date.

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Tactical Allocation Overlay: Alpha With Intelligent Risk Control

43 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

41%

29%

23%

7%

0%

10%

20%

30%

40%

50%

60%

Equity Fixed Income Alternatives Alpha Strategies/Cash

Asset Class Strategic Weights and Tactical RangesAmerican Century Global AllocationMarch 2015

New Pages for Your Playbook

Sector diversification perspective required in today’s integrated global markets.

Alternative investments may not only boost return potential, but also help improve portfolio

efficiency.

Volatility investments may help reduce downside risk.

Summary

44 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Pop Quiz

Volatility can be thought of as "The Godfather" asset class because:

a. "You want to keep your friends close, but your enemies closer"

b. “Fuggedaboudit”

c. (The unwritten law of 'Omerta' prevents me from telling you the answer)

d. Volatility One and Volatility Two were great, but Volatility Three sucked

45 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

A picture of a classic business cycle looks like this:

a. b.

c. d.

VISUAL DAILY

DOUBLE

46 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Pop Quiz

Consumer

Goods

Services

Resources

Industrials

Financials

Utilities

Pop Quiz

In light of increasing global economic and capital market integration, sector allocation

strategies represent a promising approach for performing global asset allocation going

forward.

a. True

b. False

c. Don’t know

d. Don’t care

e. All of the above

f. When is this over?

47 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Thank You

48 FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE

Performance focus for 50+ years

Pure play business model

Privately controlled and independent

Profits with a purpose

American Century Investments

49

American Century Investment Services, Inc., Distributor

©2016 American Century Proprietary Holdings, Inc. All rights reserved.

The contents of this American Century Investments presentation are protected by applicable copyright and trademark laws. No permission is granted to copy,

redistribute, modify, post or frame any text, graphics, images, trademarks, designs or logos.

FOR INSTITUTIONAL USE ONLY/NOT FOR PUBLIC USE