Embed Size (px)

Citation preview

Portfolio Facing Headwind

The Wharf (Holdings) Limited

2019 Interim Results

8 Aug 2019

1

Overview

- Mainland China Assets

• Over RMB100B/ About 70% of Group Business Assets

• Contribute ~80% of Group Profit

- The Roller-coaster Sino-US Conflict - Profound Impact on both Economies & HK’s

- RMB -0.4% vs HKD in 1H19 & Faces Continued Uncertainty

- In HK, Weak Demand has been Further Weakened by Travel Advisories, Economic Slowdown, Contracting

Exports/Re-exports, Falling Retail Sales, Stock Market Jitters & the Threat to Employment

- Profit Attributable to Equity Shareholders for 1H19 -14%

- FY Outlook Uncertain

2

Highlights

Overview

3

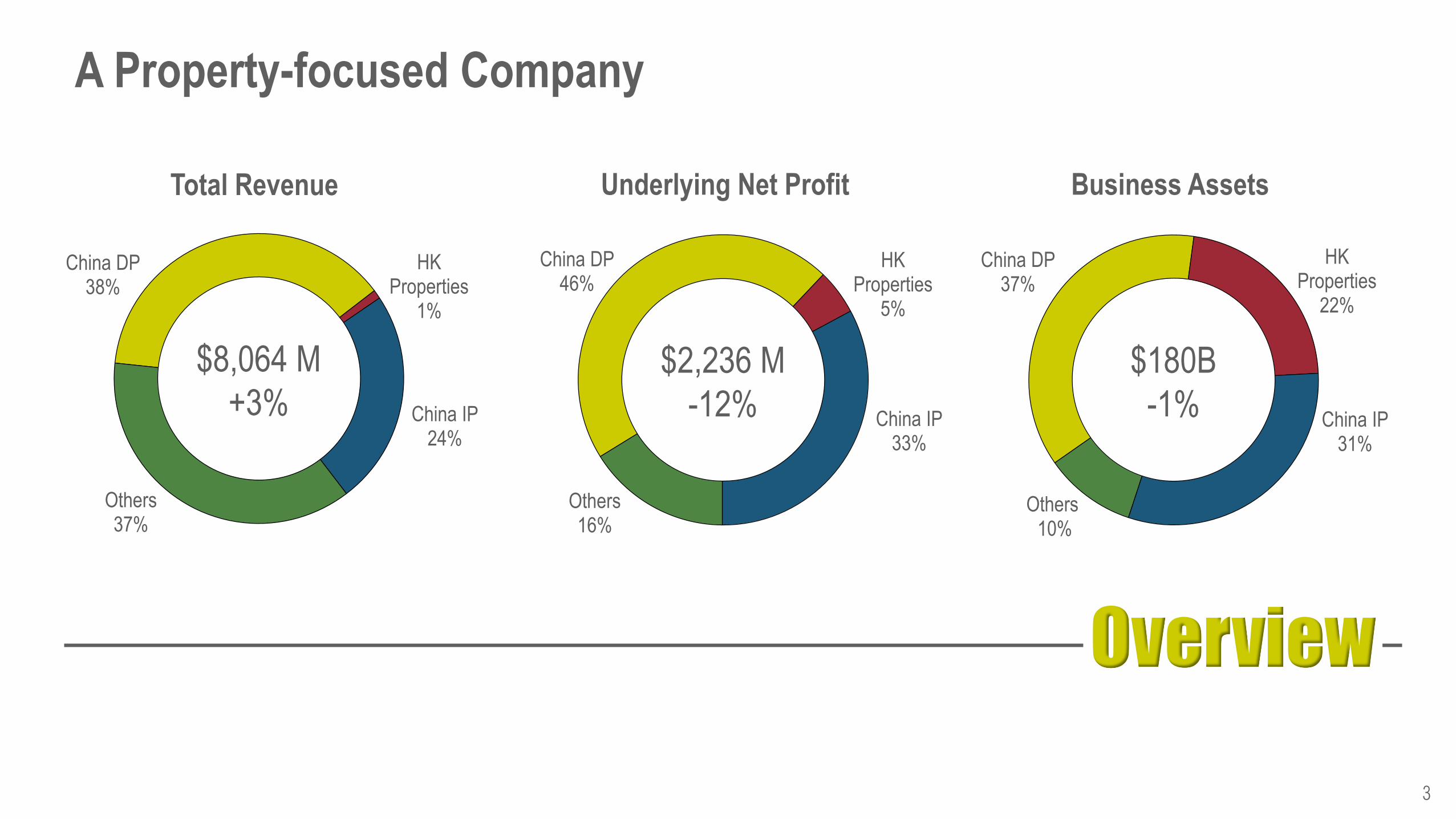

A Property-focused Company

China DP 38%

HK Properties

1%

China IP 24%

Others 37%

$8,064 M

+3%

China DP 46%

HK Properties

5%

China IP 33%

Others 16%

$2,236 M

-12%

China DP 37%

HK Properties

22%

China IP 31%

Others 10%

$180B

-1%

Total Revenue Underlying Net Profit Business Assets

Overview

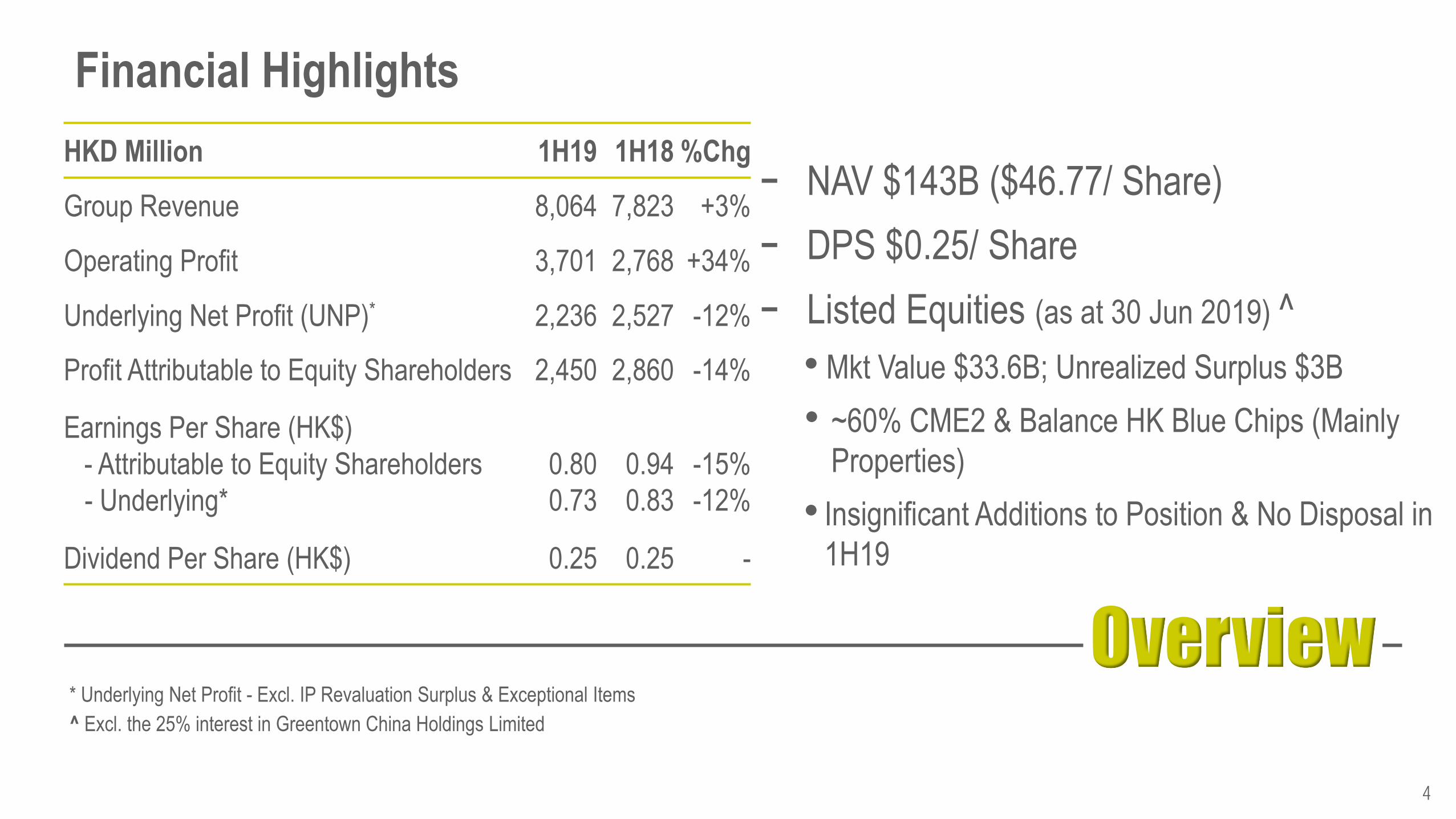

- NAV $143B ($46.77/ Share)

- DPS $0.25/ Share

- Listed Equities (as at 30 Jun 2019) ^

• Mkt Value $33.6B; Unrealized Surplus $3B

• ~60% CME2 & Balance HK Blue Chips (Mainly

Properties)

• Insignificant Additions to Position & No Disposal in

1H19

4

Financial Highlights

HKD Million 1H19 1H18 %Chg

Group Revenue 8,064 7,823 +3%

Operating Profit 3,701 2,768 +34%

Underlying Net Profit (UNP)* 2,236 2,527 -12%

Profit Attributable to Equity Shareholders 2,450 2,860 -14%

Earnings Per Share (HK$)

- Attributable to Equity Shareholders

- Underlying*

0.80

0.73

0.94

0.83

-15%

-12%

Dividend Per Share (HK$) 0.25 0.25 -

* Underlying Net Profit - Excl. IP Revaluation Surplus & Exceptional Items

^ Excl. the 25% interest in Greentown China Holdings Limited

Asset Turns

Recurring Income

Services

Financial Management

5

Asset Turns

Return-enhancing Strategy

HKDP

- Luxury-focused

- Landbank ~3M s.f *

China DP

- Key Cities: Hangzhou, Beijing,

Shanghai & Suzhou

- Landbank 3.6M s.m

6

Selective Landbanking

* Incl. IPs in HK

Hong Kong

Shanghai

Suzhou

Hangzhou

Beijing

Asset Turns

- Prestigious Peak Project

- Symbol of Luxury & Scarcity

- Among the Most Valuable in Asia

7

Quality Projects – Mount Nicholson

Asset Turns

- 10 Projects: ~80% of Total Sales

- Sound Reputation & Good Demand

- 3 New Projects Launched in 1H19

8

Quality Projects – China

Shanghai One Jingan

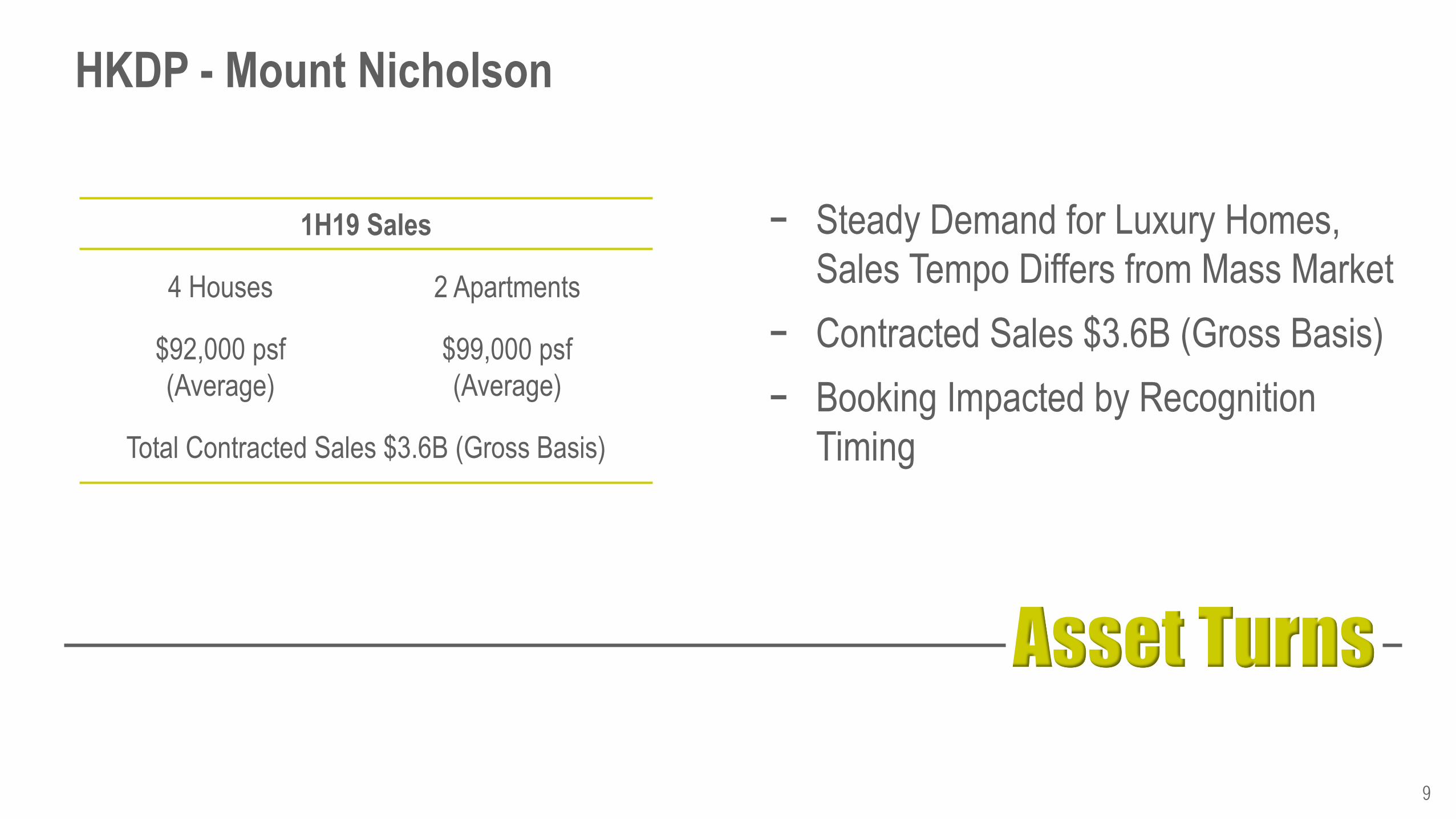

Asset Turns

- Steady Demand for Luxury Homes,

Sales Tempo Differs from Mass Market

- Contracted Sales $3.6B (Gross Basis)

- Booking Impacted by Recognition

Timing

9

HKDP - Mount Nicholson

1H19 Sales

4 Houses 2 Apartments

$92,000 psf

(Average)

$99,000 psf

(Average)

Total Contracted Sales $3.6B (Gross Basis)

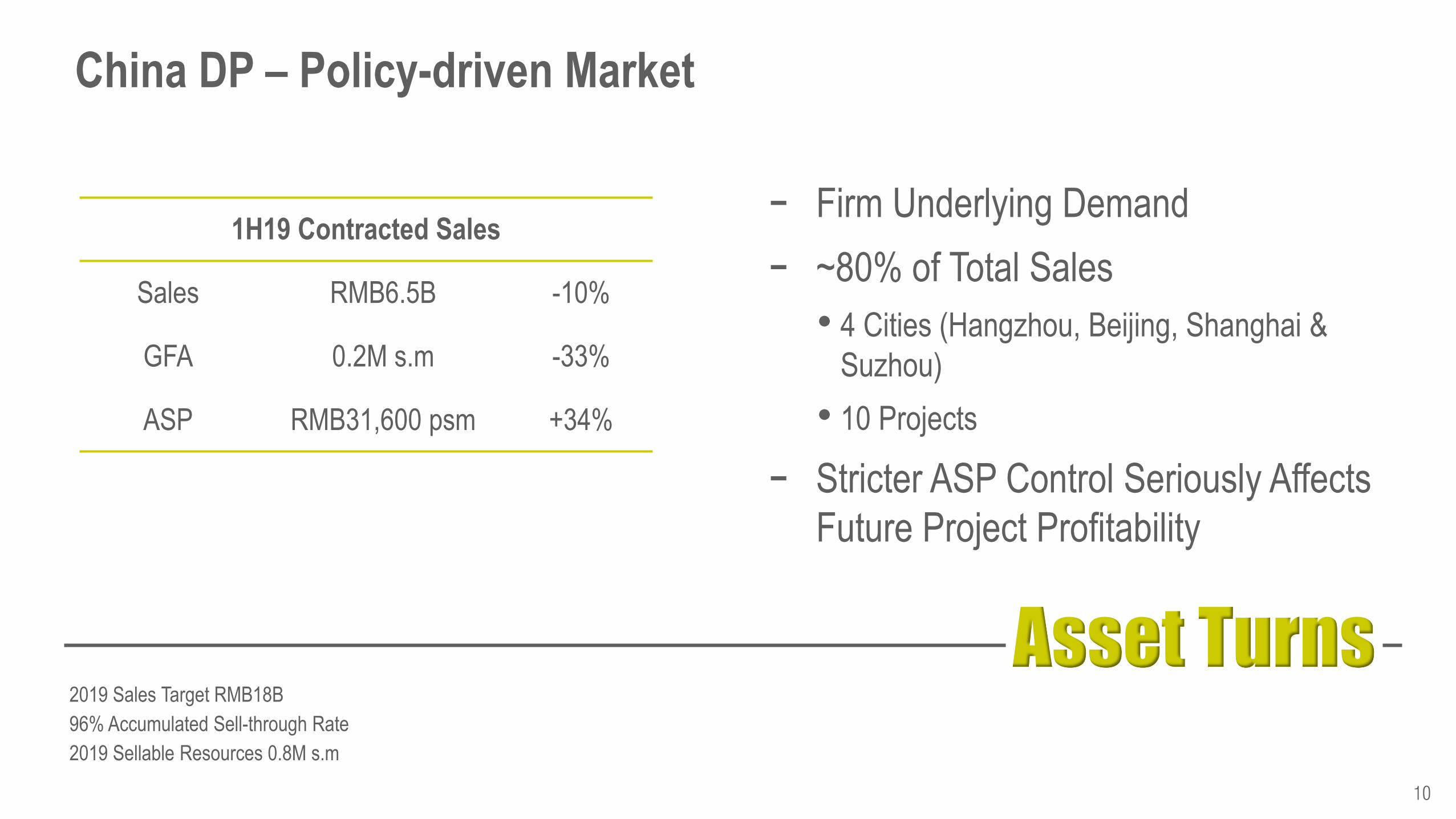

Asset Turns

- Firm Underlying Demand

- ~80% of Total Sales

• 4 Cities (Hangzhou, Beijing, Shanghai &

Suzhou)

• 10 Projects

- Stricter ASP Control Seriously Affects

Future Project Profitability

10

China DP – Policy-driven Market

1H19 Contracted Sales

Sales RMB6.5B -10%

GFA 0.2M s.m -33%

ASP RMB31,600 psm +34%

2019 Sales Target RMB18B

96% Accumulated Sell-through Rate

2019 Sellable Resources 0.8M s.m

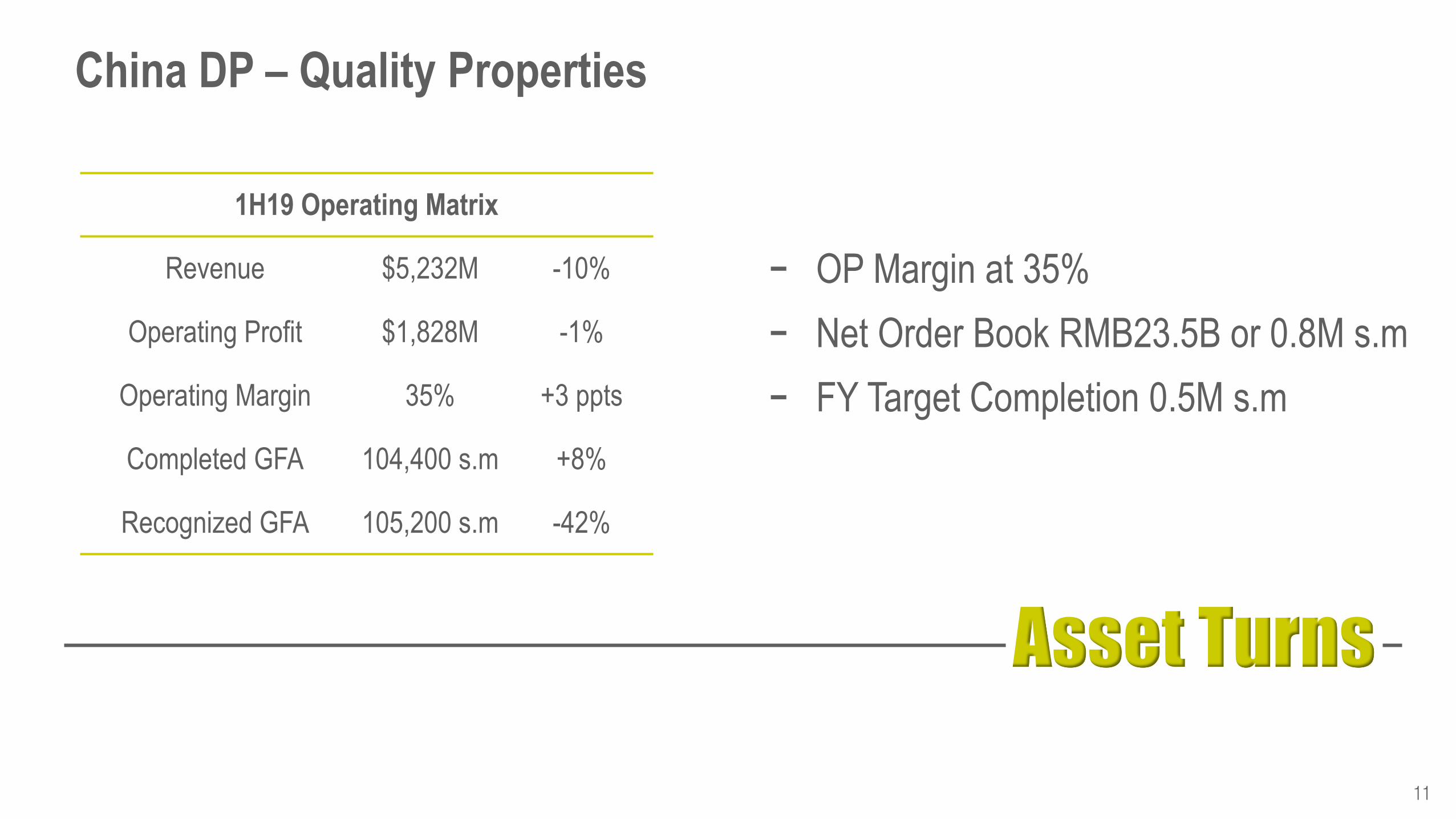

Asset Turns

- OP Margin at 35%

- Net Order Book RMB23.5B or 0.8M s.m

- FY Target Completion 0.5M s.m

11

China DP – Quality Properties

1H19 Operating Matrix

Revenue $5,232M -10%

Operating Profit $1,828M -1%

Operating Margin 35% +3 ppts

Completed GFA 104,400 s.m +8%

Recognized GFA 105,200 s.m -42%

Asset Turns

Recurring Income

Services

Financial Management

12

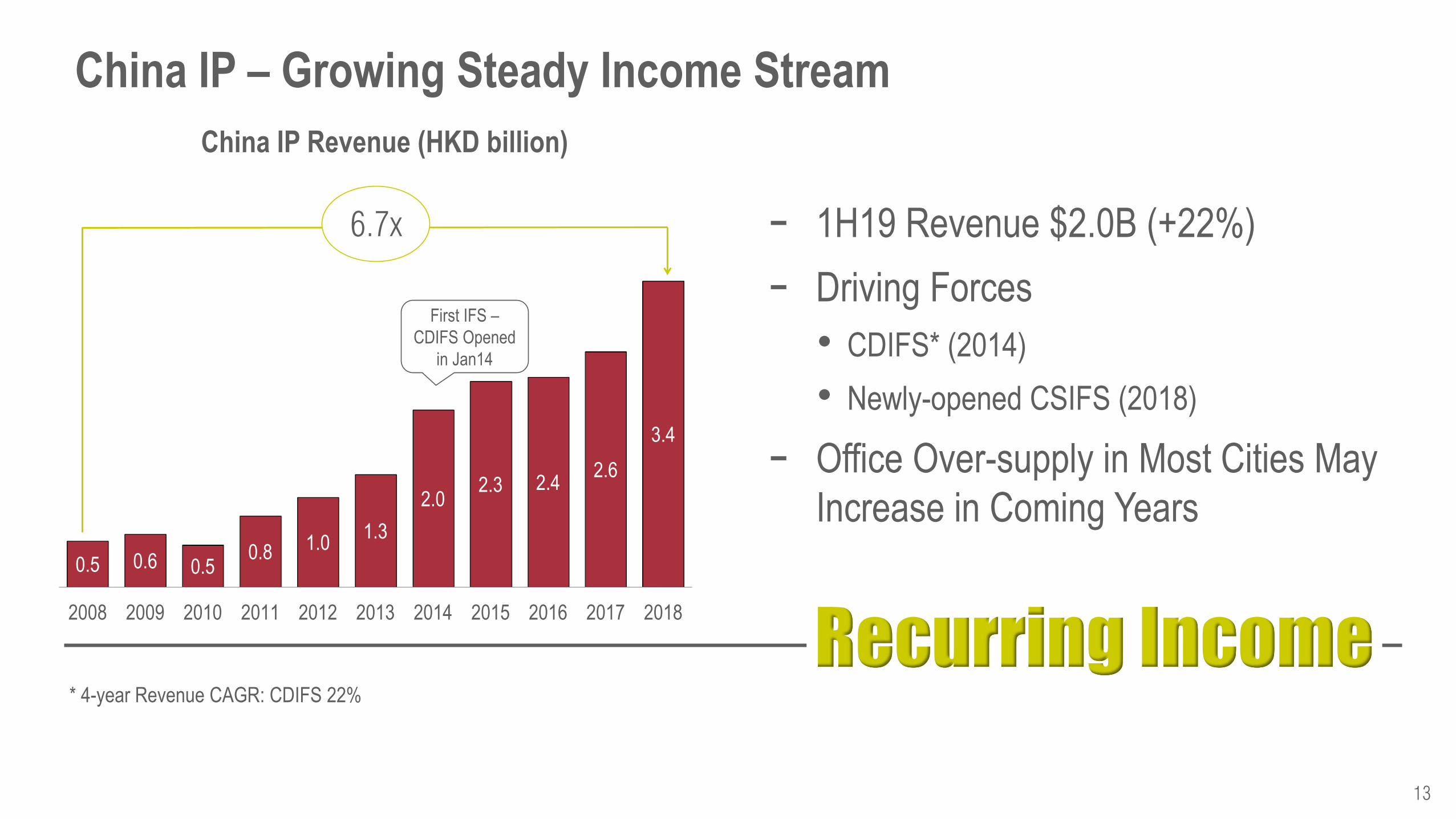

Recurring Income

- 1H19 Revenue $2.0B (+22%)

- Driving Forces

• CDIFS* (2014)

• Newly-opened CSIFS (2018)

- Office Over-supply in Most Cities May

Increase in Coming Years

13

China IP – Growing Steady Income Stream

0.5 0.6 0.5 0.8 1.0

1.3

2.0 2.3 2.4

2.6

3.4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

China IP Revenue (HKD billion)

First IFS –

CDIFS Opened

in Jan14

6.7x

* 4-year Revenue CAGR: CDIFS 22%

Recurring Income

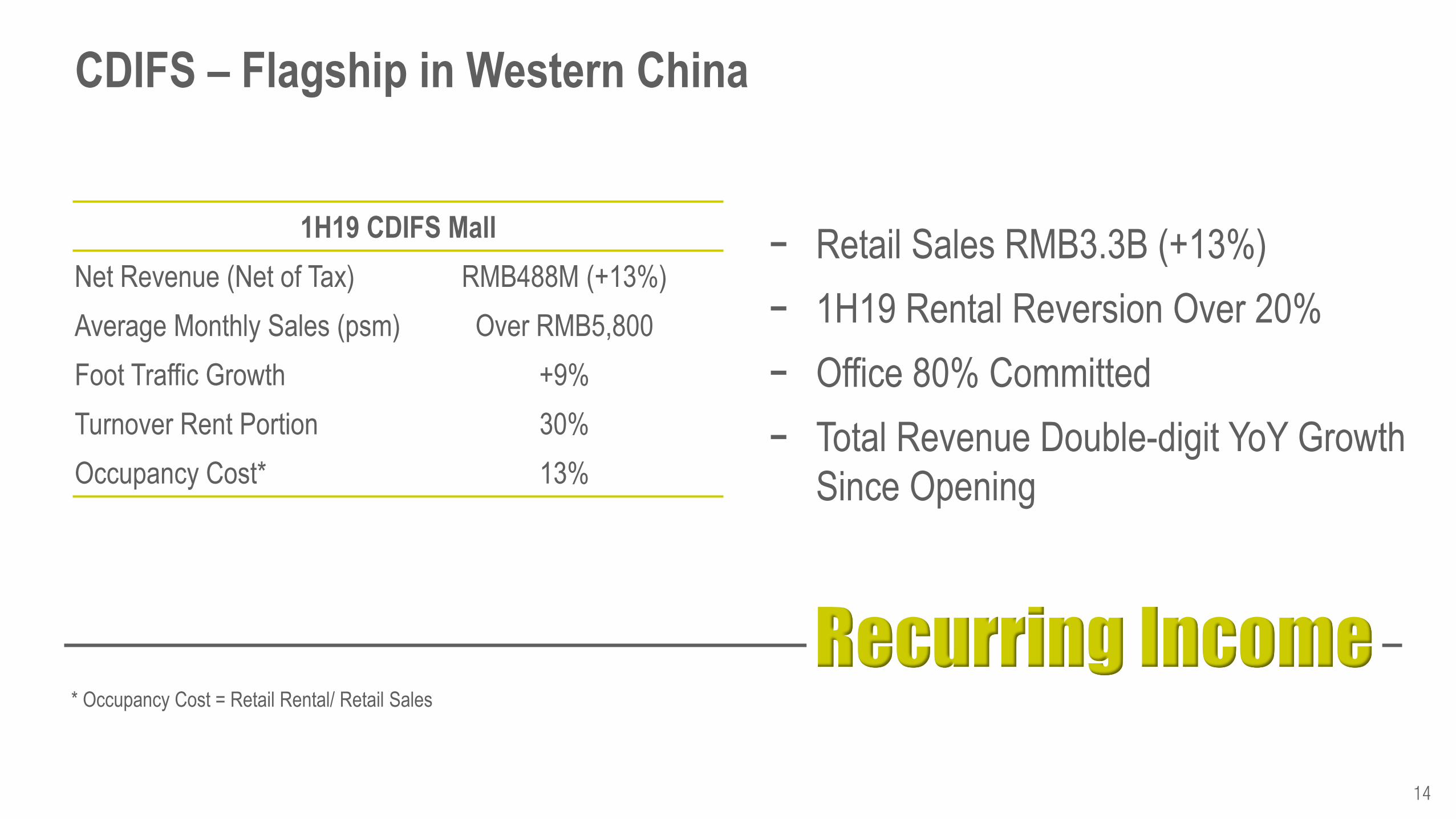

- Retail Sales RMB3.3B (+13%)

- 1H19 Rental Reversion Over 20%

- Office 80% Committed

- Total Revenue Double-digit YoY Growth

Since Opening

14

CDIFS – Flagship in Western China

1H19 CDIFS Mall

Net Revenue (Net of Tax) RMB488M (+13%)

Average Monthly Sales (psm) Over RMB5,800

Foot Traffic Growth +9%

Turnover Rent Portion 30%

Occupancy Cost* 13%

* Occupancy Cost = Retail Rental/ Retail Sales

Recurring Income

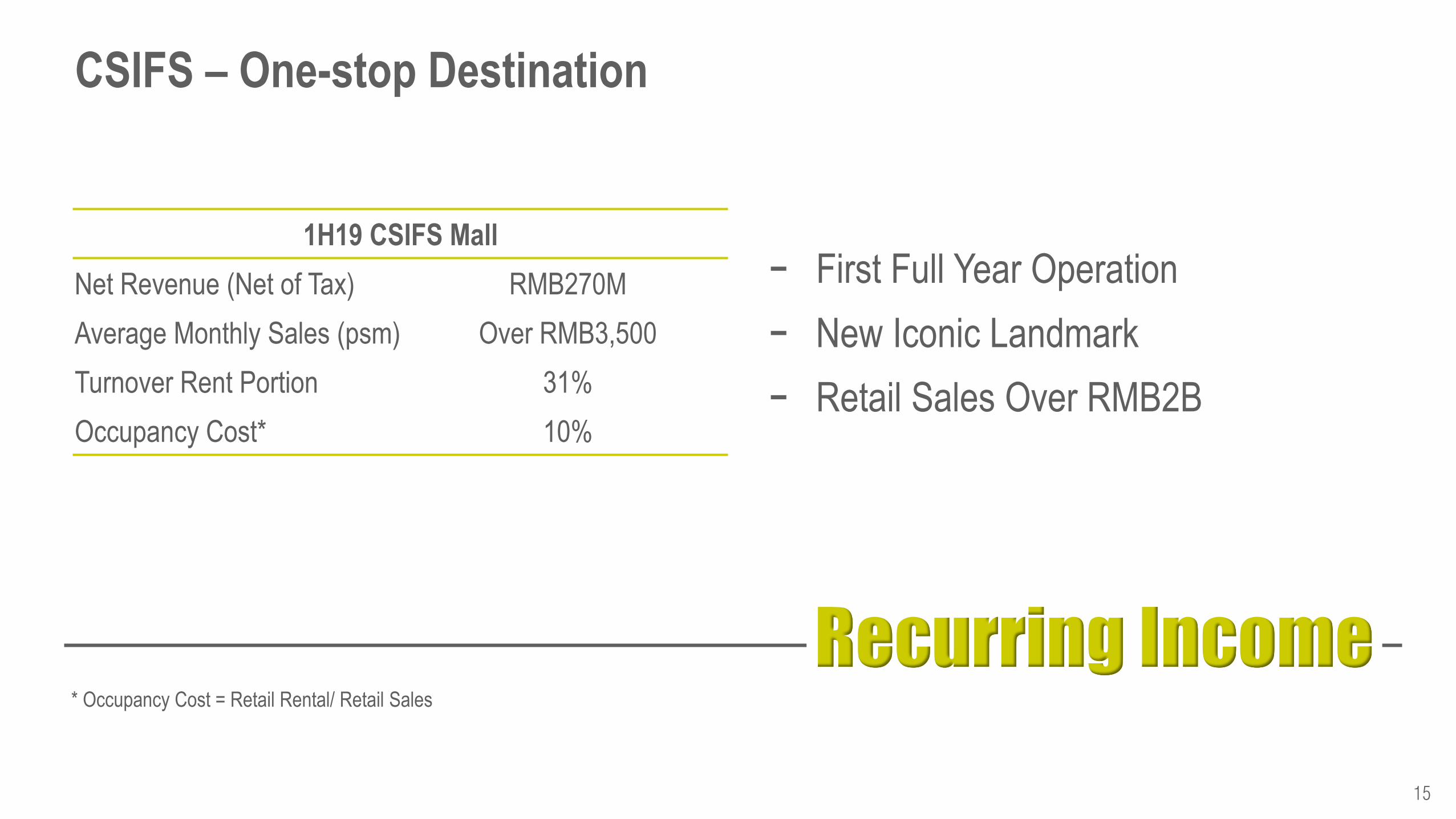

- First Full Year Operation

- New Iconic Landmark

- Retail Sales Over RMB2B

15

CSIFS – One-stop Destination

1H19 CSIFS Mall

Net Revenue (Net of Tax) RMB270M

Average Monthly Sales (psm) Over RMB3,500

Turnover Rent Portion 31%

Occupancy Cost* 10%

* Occupancy Cost = Retail Rental/ Retail Sales

Recurring Income

Marco Polo

Since 1986

Classic Brand

Provides Upscale Full-service

13 Owned & Managed in HK, China & the Philippines

16

Wharf Hotels – Enriched Portfolio

Niccolo

Since 2015

Award-winning, Contemporary Chic

Inspired by Luxury Fashion

4 in HK & China

Brand Enhancement

Recurring Income

17

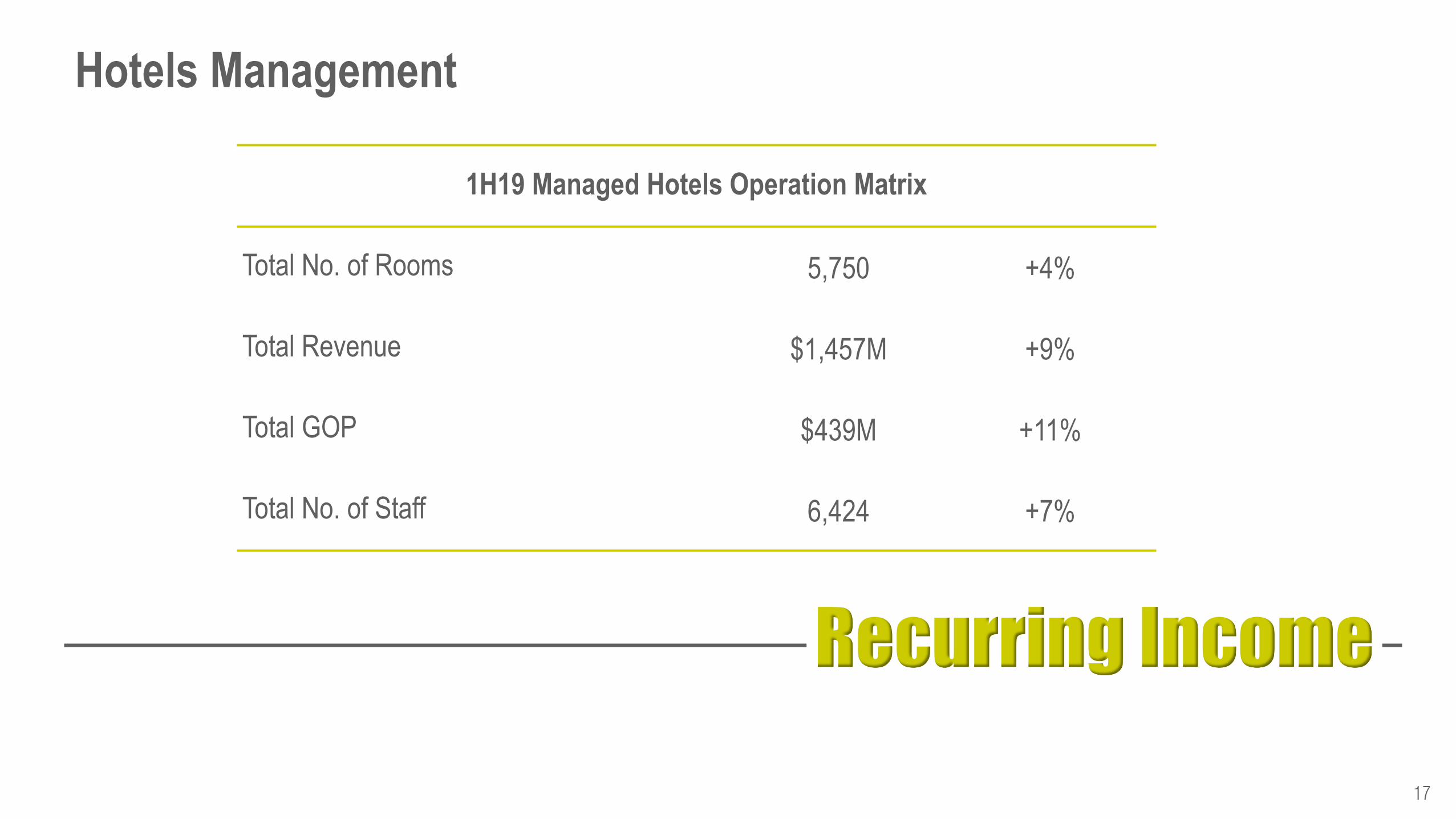

Hotels Management

1H19 Managed Hotels Operation Matrix

Total No. of Rooms 5,750 +4%

Total Revenue $1,457M +9%

Total GOP $439M +11%

Total No. of Staff 6,424 +7%

Recurring Income

18

Niccolo – Internationally-acclaimed

Performance Against Competitive Set (Ranking)

Chengdu Chongqing Changsha

Room Yield 1st 3rd 3rd

Room Rate 1st 2nd 2nd

Changsha Chongqing

1H19 YoY Change

Chengdu Chongqing Changsha*

Room Yield +14% +31% NA

Room Rate +12% +6% NA

* Opened in Oct-18

Chengdu

Asset Turns

Recurring Income

Services

Financial Management

19

Services

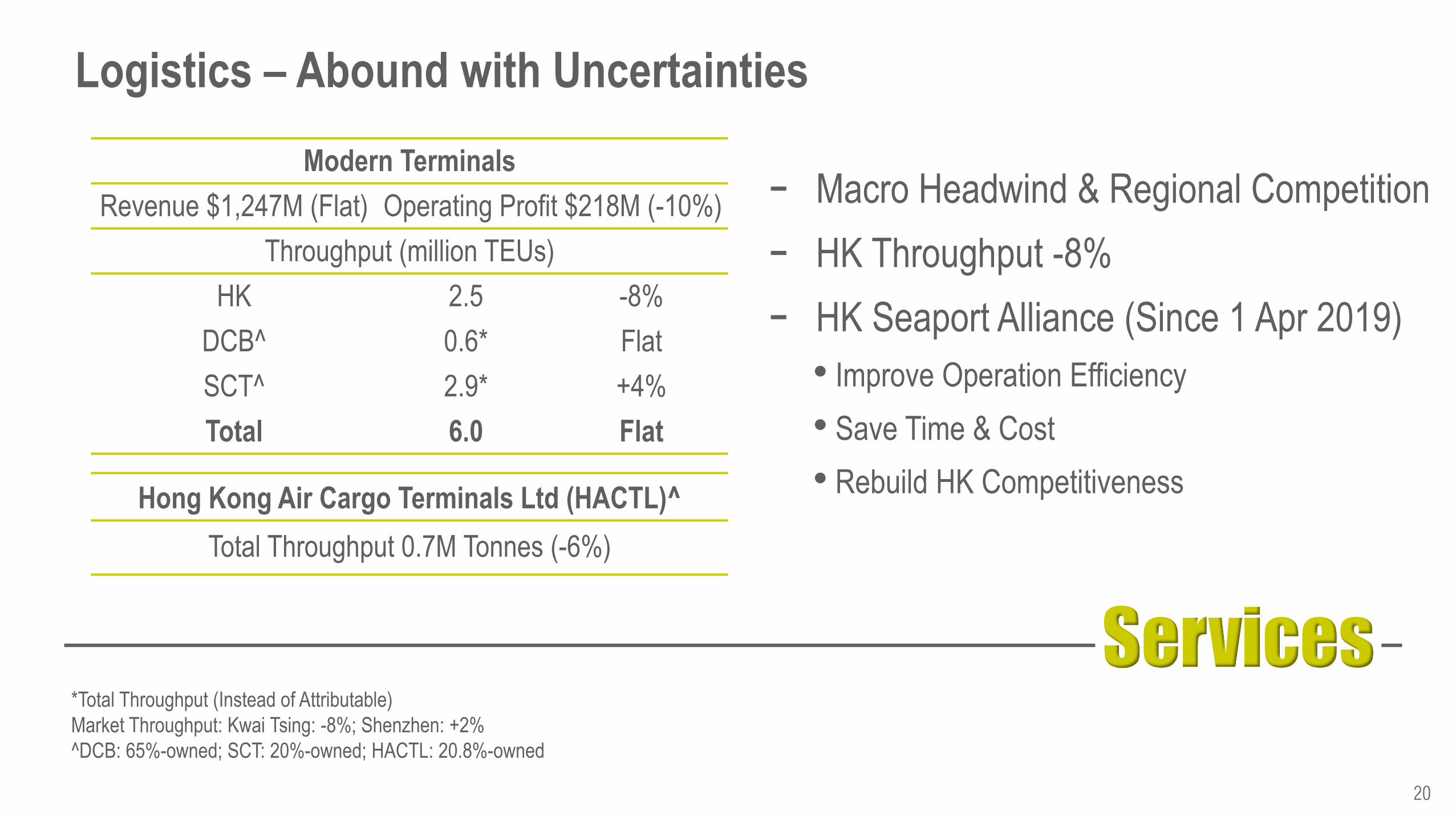

- Macro Headwind & Regional Competition

- HK Throughput -8%

- HK Seaport Alliance (Since 1 Apr 2019)

• Improve Operation Efficiency

• Save Time & Cost

• Rebuild HK Competitiveness

20

Logistics – Abound with Uncertainties

Modern Terminals

Revenue $1,247M (Flat) Operating Profit $218M (-10%)

Throughput (million TEUs)

HK 2.5 -8%

DCB^ 0.6* Flat

SCT^ 2.9* +4%

Total 6.0 Flat

Hong Kong Air Cargo Terminals Ltd (HACTL)^

Total Throughput 0.7M Tonnes (-6%)

*Total Throughput (Instead of Attributable)

Market Throughput: Kwai Tsing: -8%; Shenzhen: +2%

^DCB: 65%-owned; SCT: 20%-owned; HACTL: 20.8%-owned

Asset Turns

Recurring Income

Services

Financial Management

21

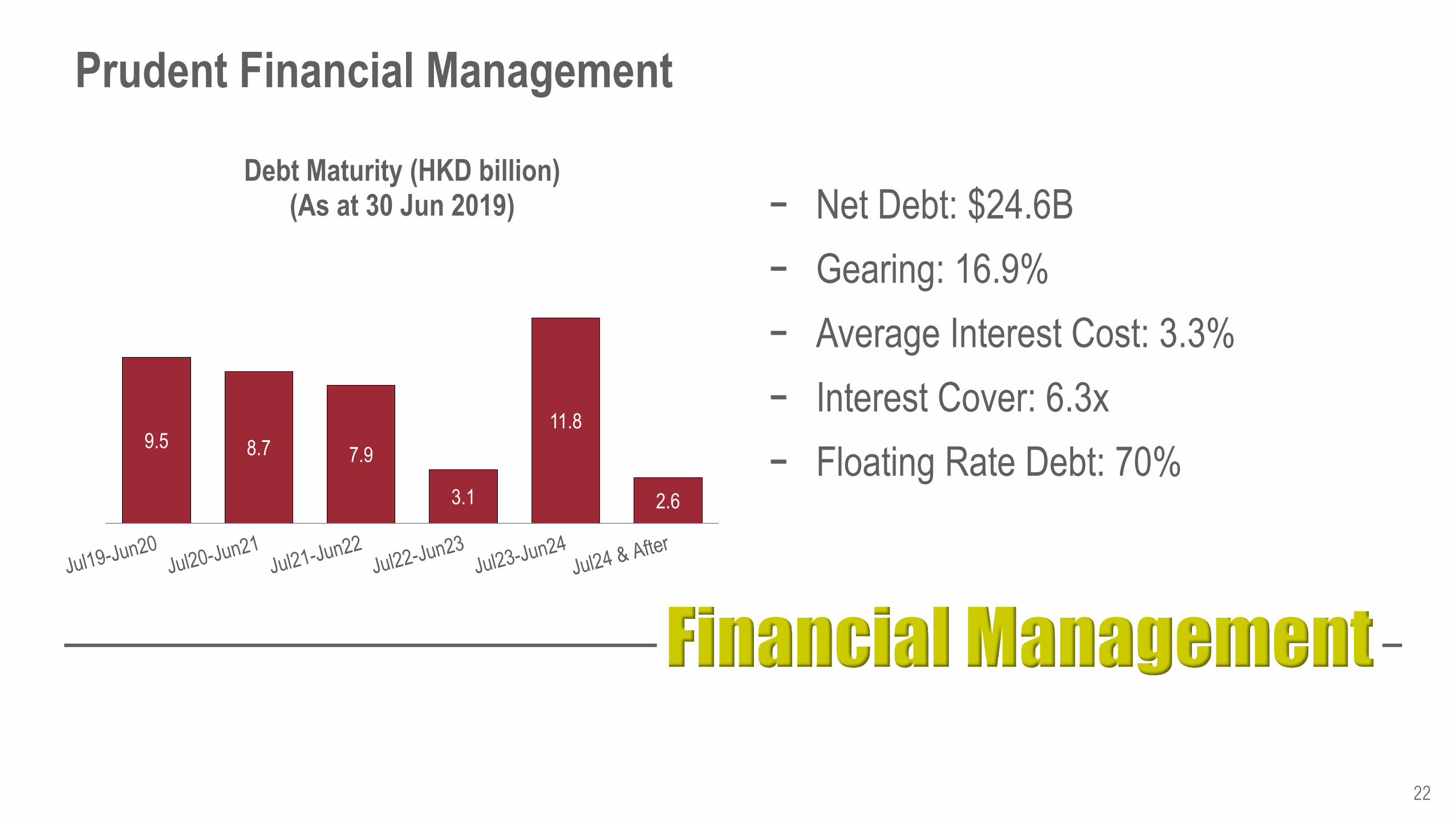

Financial Management

- Net Debt: $24.6B

- Gearing: 16.9%

- Average Interest Cost: 3.3%

- Interest Cover: 6.3x

- Floating Rate Debt: 70%

22

Prudent Financial Management

9.5 8.7 7.9

3.1

11.8

2.6

Debt Maturity (HKD billion) (As at 30 Jun 2019)

Outlook

23

Outlook

24

Cautious Outlook

- Sino-US Trade Disputes

- European Political Instability/ Brexit

- Global Currency & Interest Rate Movements

- Weak Global Demand

Sustainability

25

Sustainability

26

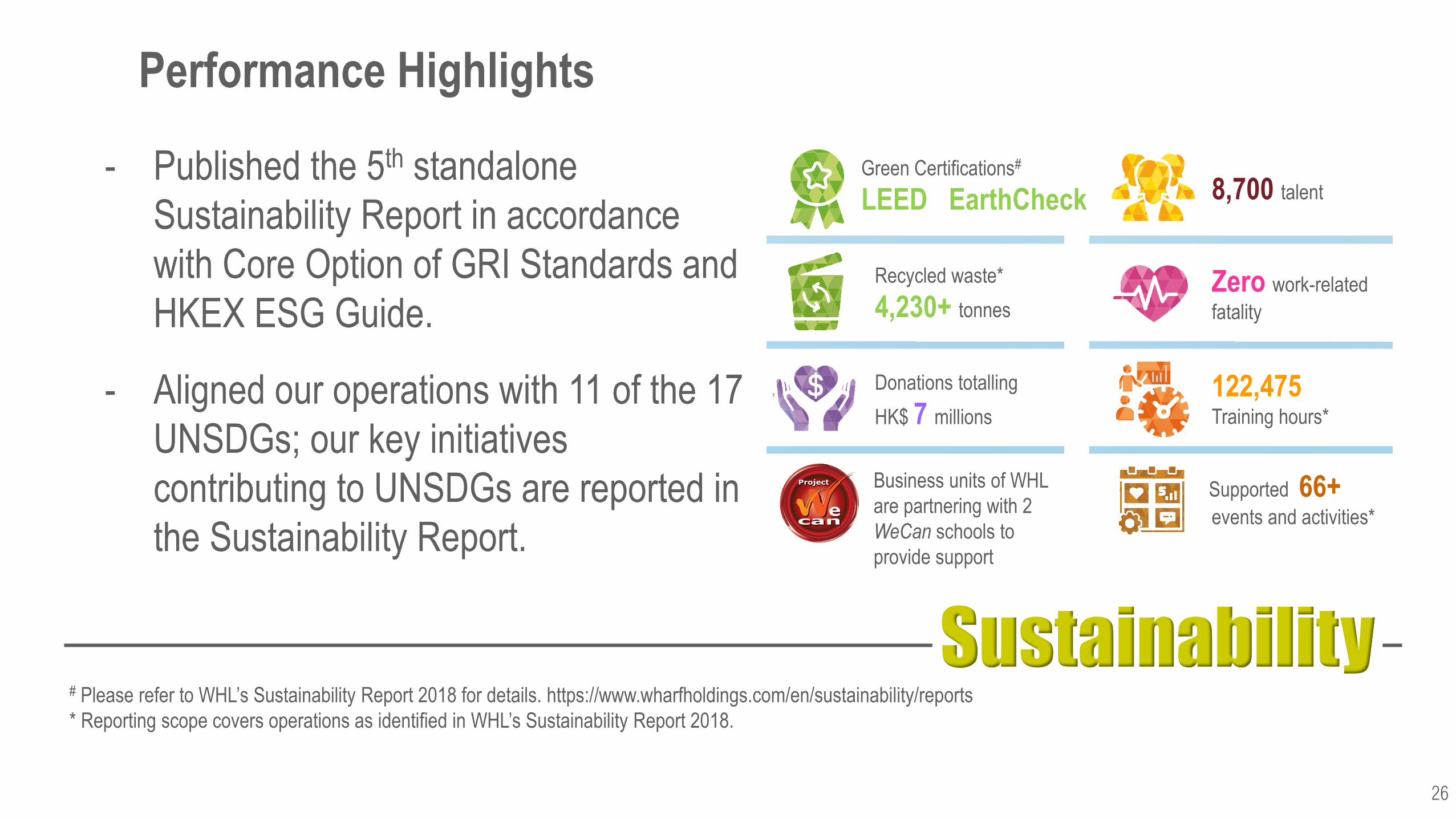

- Published the 5th standalone

Sustainability Report in accordance

with Core Option of GRI Standards and

HKEX ESG Guide.

- Aligned our operations with 11 of the 17

UNSDGs; our key initiatives

contributing to UNSDGs are reported in

the Sustainability Report.

Performance Highlights

8,700 talent

Zero work-related

fatality

122,475 Training hours*

Supported 66+ events and activities*

Recycled waste*

4,230+ tonnes

Green Certifications#

LEED & EarthCheck

Donations totalling

HK$ 7 millions

Business units of WHL

are partnering with 2

WeCan schools to

provide support

# Please refer to WHL’s Sustainability Report 2018 for details. https://www.wharfholdings.com/en/sustainability/reports

* Reporting scope covers operations as identified in WHL’s Sustainability Report 2018.

Supported

Sustainability

27

- Constituent member of Hang Seng

Corporate Sustainability Index

- CSR Index Plus

- 5 Years+ Caring Company Logo

- Has raised its first Green Loan Facility

in the amount of HK$2 billion to

refinance Chengdu IFS, the Group’s

first IFS flagship project in China.

Appendix

28

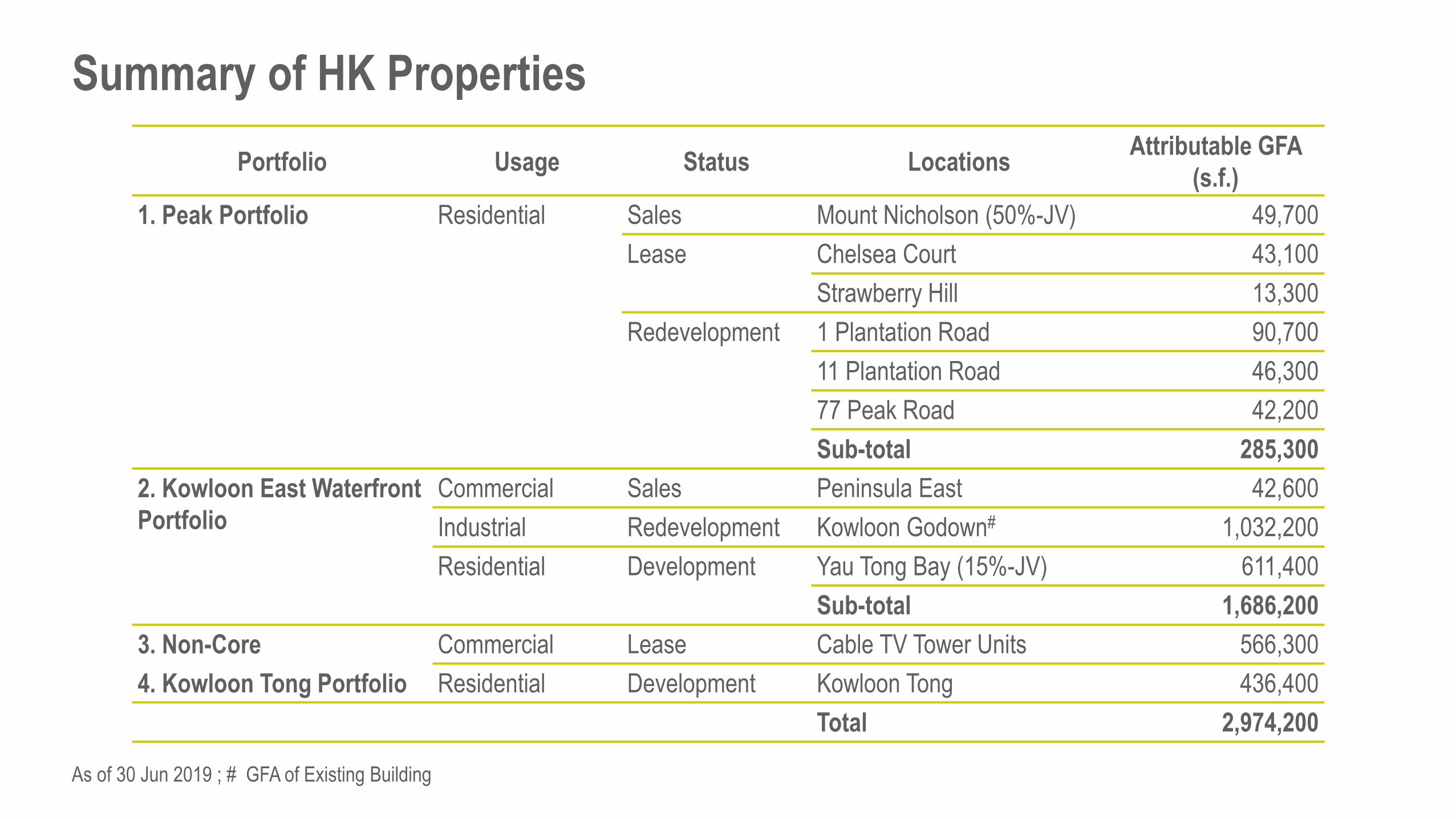

Portfolio Usage Status Locations Attributable GFA

(s.f.)

1. Peak Portfolio Residential Sales Mount Nicholson (50%-JV) 49,700

Lease Chelsea Court 43,100

Strawberry Hill 13,300

Redevelopment 1 Plantation Road 90,700

11 Plantation Road 46,300

77 Peak Road 42,200

Sub-total 285,300

2. Kowloon East Waterfront

Portfolio

Commercial Sales Peninsula East 42,600

Industrial Redevelopment Kowloon Godown# 1,032,200

Residential Development Yau Tong Bay (15%-JV) 611,400

Sub-total 1,686,200

3. Non-Core Commercial Lease Cable TV Tower Units 566,300

4. Kowloon Tong Portfolio Residential Development Kowloon Tong 436,400

Total 2,974,200

As of 30 Jun 2019 ; # GFA of Existing Building

Summary of HK Properties

30

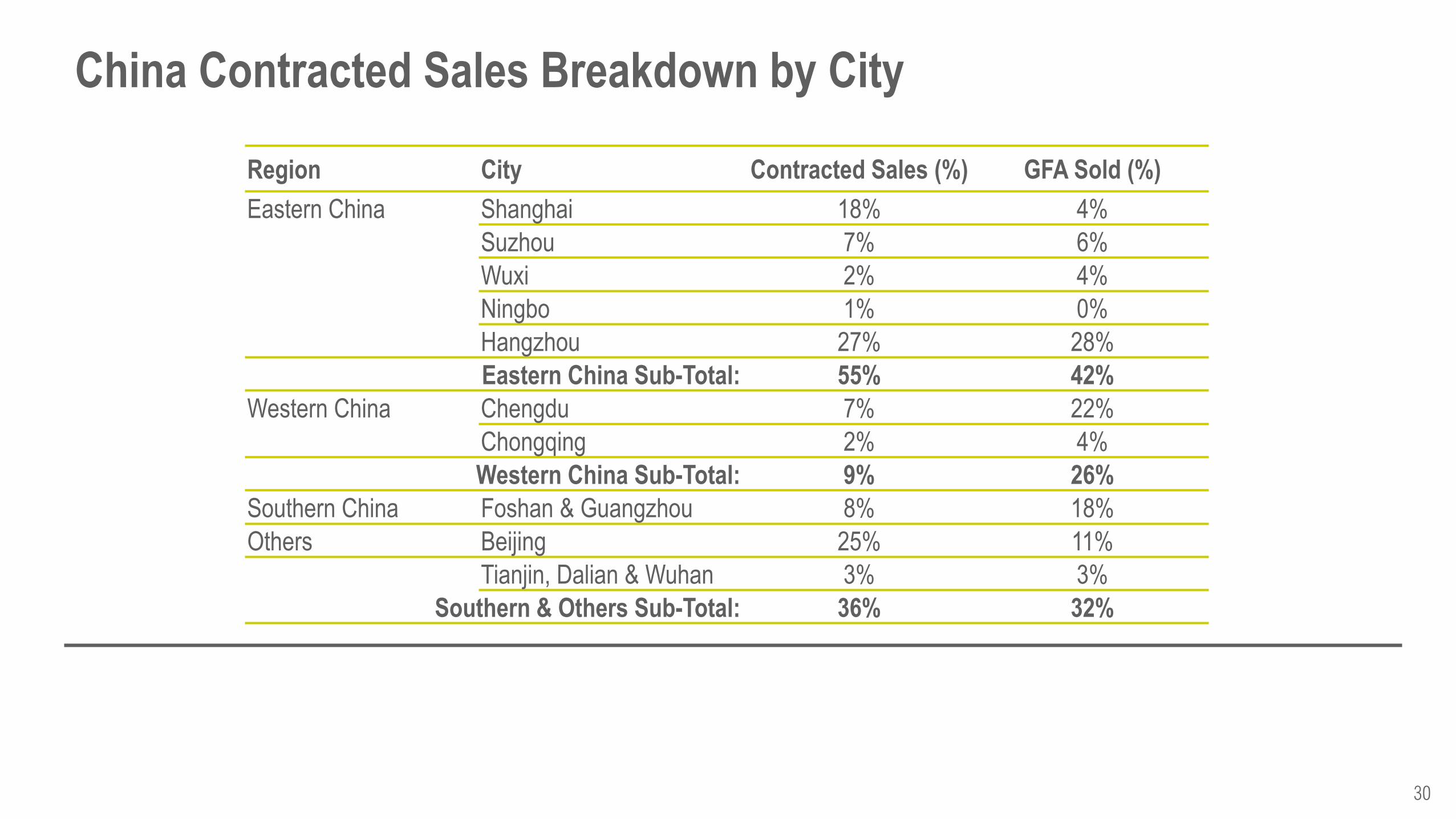

China Contracted Sales Breakdown by City

Region City Contracted Sales (%) GFA Sold (%)

Eastern China Shanghai 18% 4%

Suzhou 7% 6%

Wuxi 2% 4%

Ningbo 1% 0%

Hangzhou 27% 28%

Eastern China Sub-Total: 55% 42%

Western China Chengdu 7% 22%

Chongqing 2% 4%

Western China Sub-Total: 9% 26%

Southern China Foshan & Guangzhou 8% 18%

Others Beijing 25% 11%

Tianjin, Dalian & Wuhan 3% 3%

Southern & Others Sub-Total: 36% 32%

31

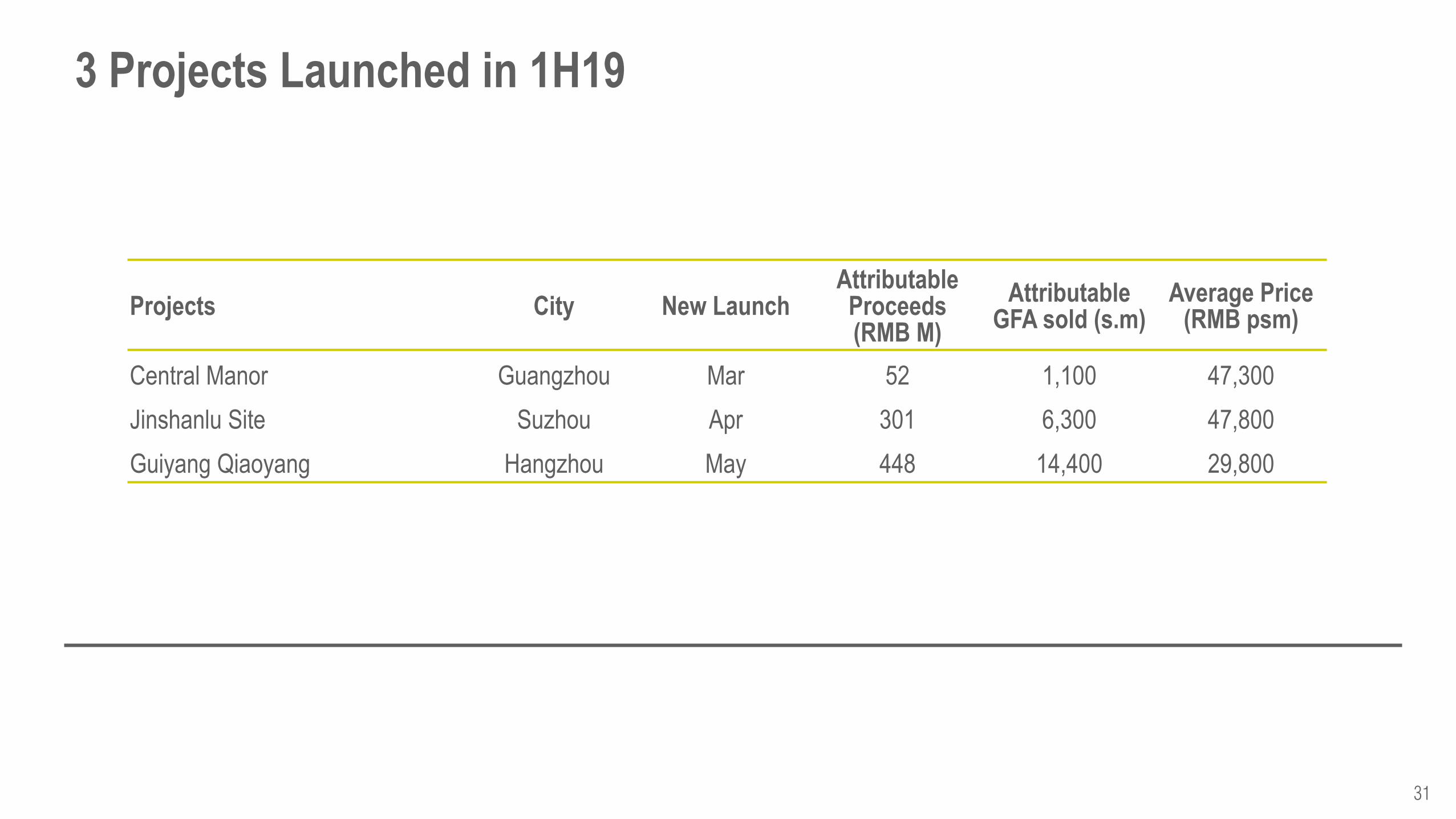

3 Projects Launched in 1H19

Projects City New Launch Attributable

Proceeds (RMB M)

Attributable GFA sold (s.m)

Average Price (RMB psm)

Central Manor Guangzhou Mar 52 1,100 47,300

Jinshanlu Site Suzhou Apr 301 6,300 47,800

Guiyang Qiaoyang Hangzhou May 448 14,400 29,800

32

China Key Projects on Sales in 1H19

Projects City Attributable Proceeds (RMB M)

Attributable GFA sold (s.m)

Average Price (RMB psm)

Ownership

West Manor Beijing 1,050 13,700 76,700 80%

Shanghai Pudong Huangpujiang (E18) Shanghai 727 4,500 118,800 100%

Longfor Jade Mansion Hangzhou 645 14,800 43,300 26%

Junting Hangzhou 518 22,400 23,100 100%

Jingan Garden Shanghai 474 3,800 126,100 55%

Guiyu Chaoyang Hangzhou 448 14,400 29,800 50%

Times City Chengdu 403 31,500 12,800 100%

One LiangMa Beijing 327 3,300 98,500 40%

Jinshanlu Site Suzhou 301 6,300 47,800 30%

Crown Land Beijing 186 3,600 52,200 25%

33

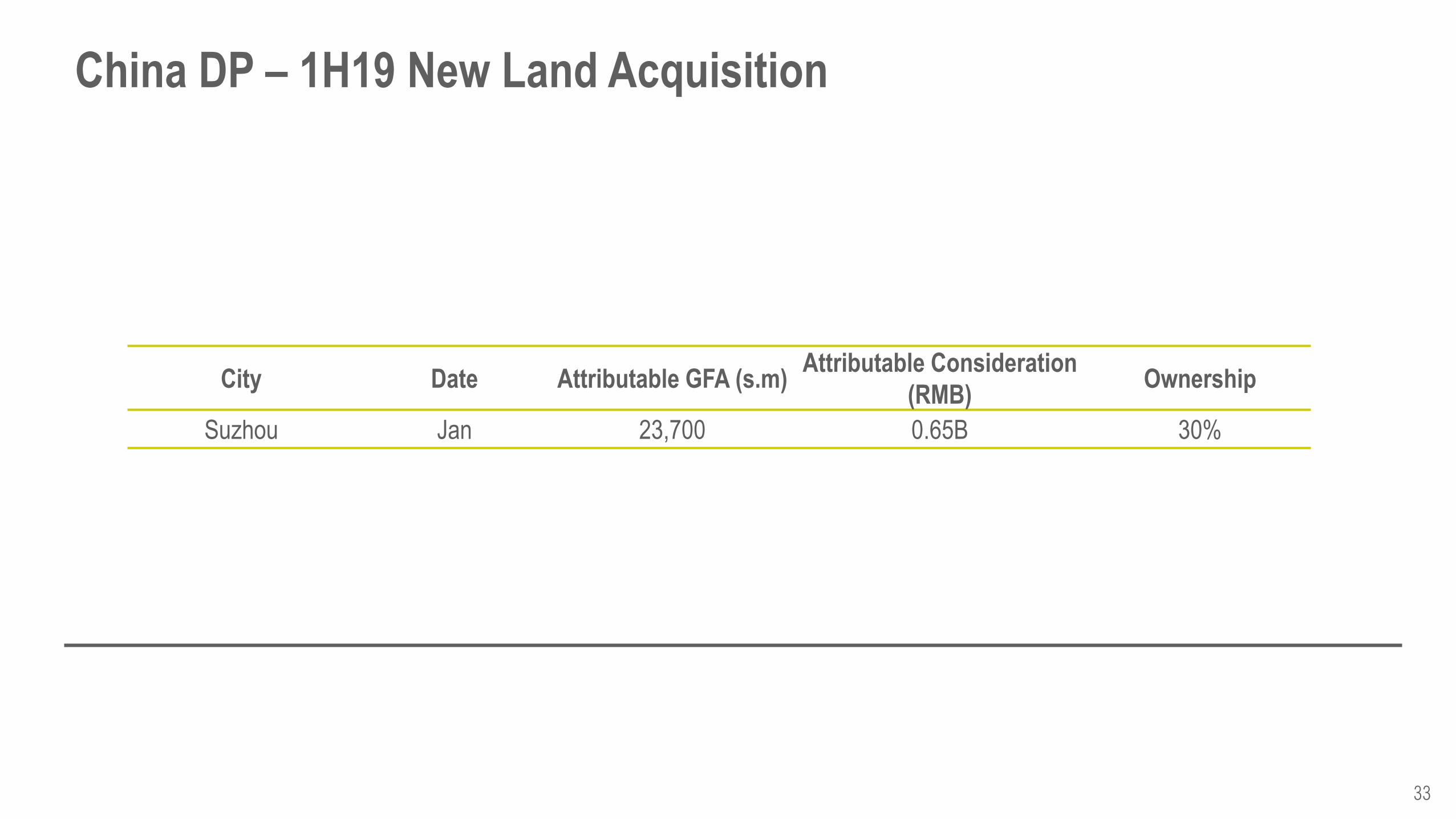

China DP – 1H19 New Land Acquisition

City Date Attributable GFA (s.m) Attributable Consideration

(RMB) Ownership

Suzhou Jan 23,700 0.65B 30%

34

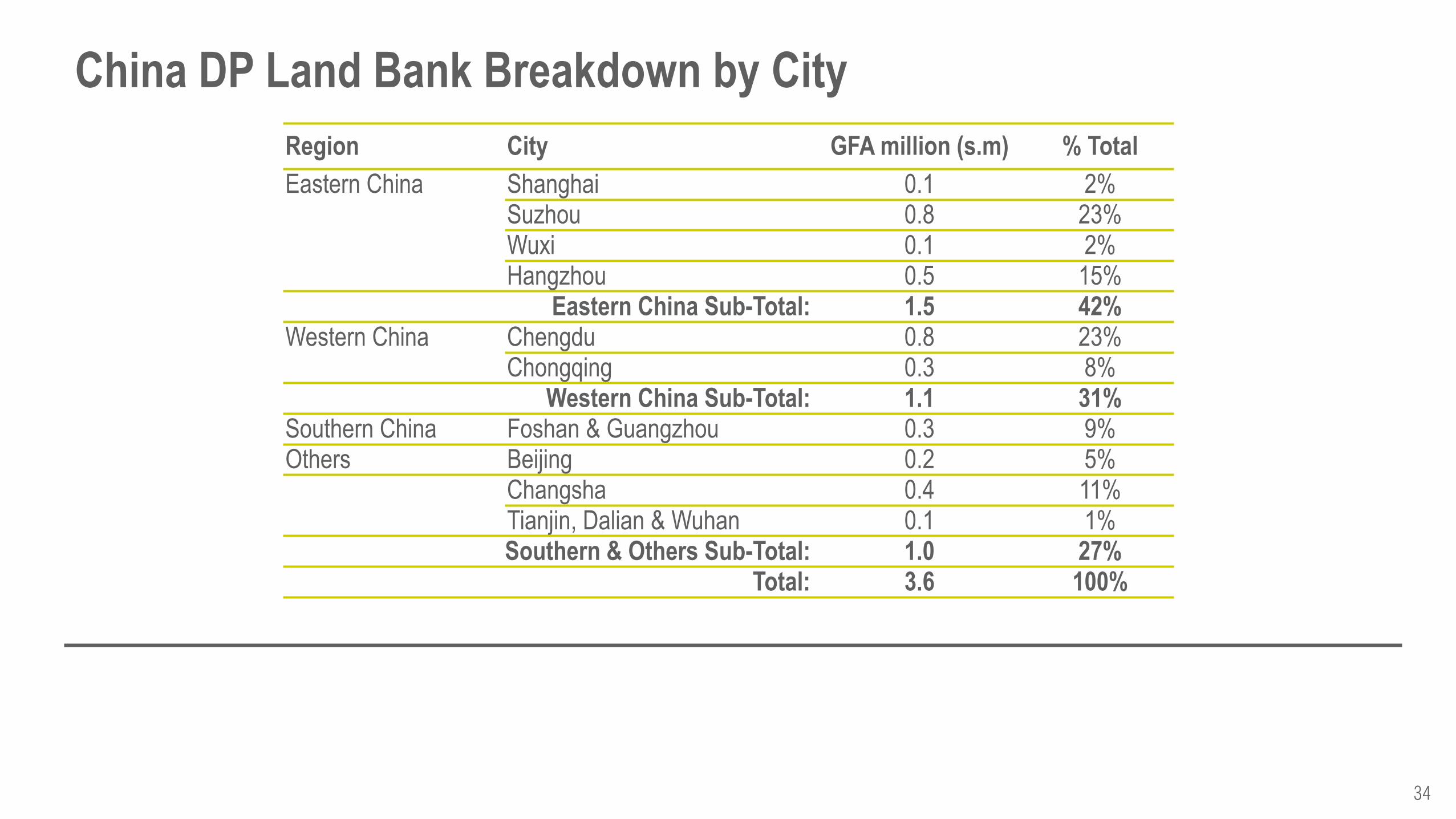

China DP Land Bank Breakdown by City

Region City GFA million (s.m) % Total

Eastern China Shanghai 0.1 2% Suzhou 0.8 23% Wuxi 0.1 2% Hangzhou 0.5 15%

Eastern China Sub-Total: 1.5 42% Western China Chengdu 0.8 23%

Chongqing 0.3 8% Western China Sub-Total: 1.1 31%

Southern China Foshan & Guangzhou 0.3 9% Others Beijing 0.2 5%

Changsha 0.4 11% Tianjin, Dalian & Wuhan 0.1 1% Southern & Others Sub-Total: 1.0 27%

Total: 3.6 100%

35

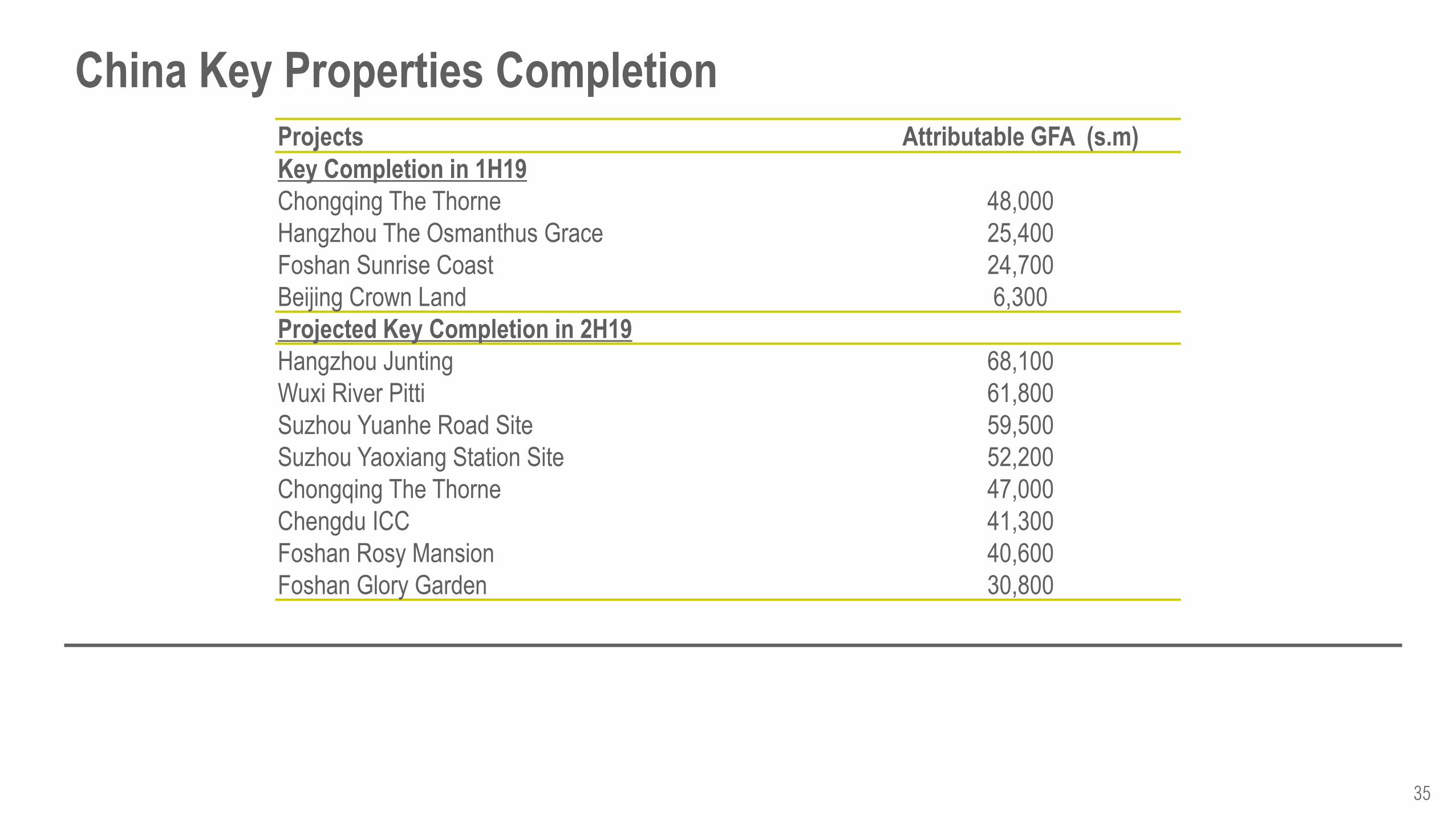

China Key Properties Completion

Projects Attributable GFA (s.m)

Key Completion in 1H19

Chongqing The Thorne 48,000

Hangzhou The Osmanthus Grace 25,400

Foshan Sunrise Coast 24,700

Beijing Crown Land 6,300

Projected Key Completion in 2H19

Hangzhou Junting 68,100

Wuxi River Pitti 61,800

Suzhou Yuanhe Road Site 59,500

Suzhou Yaoxiang Station Site 52,200

Chongqing The Thorne 47,000

Chengdu ICC 41,300

Foshan Rosy Mansion 40,600

Foshan Glory Garden 30,800

36

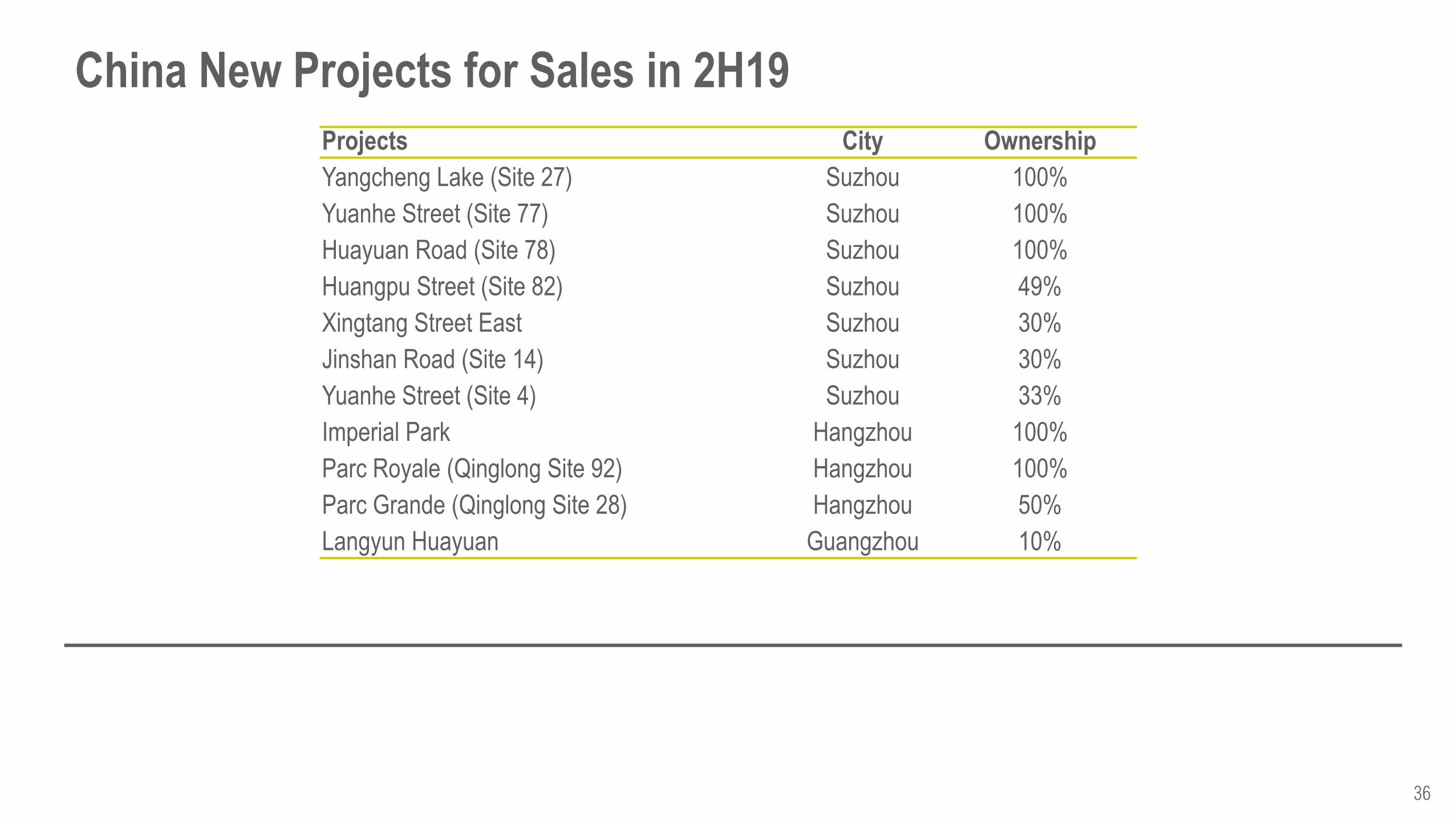

China New Projects for Sales in 2H19

Projects City Ownership

Yangcheng Lake (Site 27) Suzhou 100%

Yuanhe Street (Site 77) Suzhou 100%

Huayuan Road (Site 78) Suzhou 100%

Huangpu Street (Site 82) Suzhou 49%

Xingtang Street East Suzhou 30%

Jinshan Road (Site 14) Suzhou 30%

Yuanhe Street (Site 4) Suzhou 33%

Imperial Park Hangzhou 100%

Parc Royale (Qinglong Site 92) Hangzhou 100%

Parc Grande (Qinglong Site 28) Hangzhou 50%

Langyun Huayuan Guangzhou 10%

37

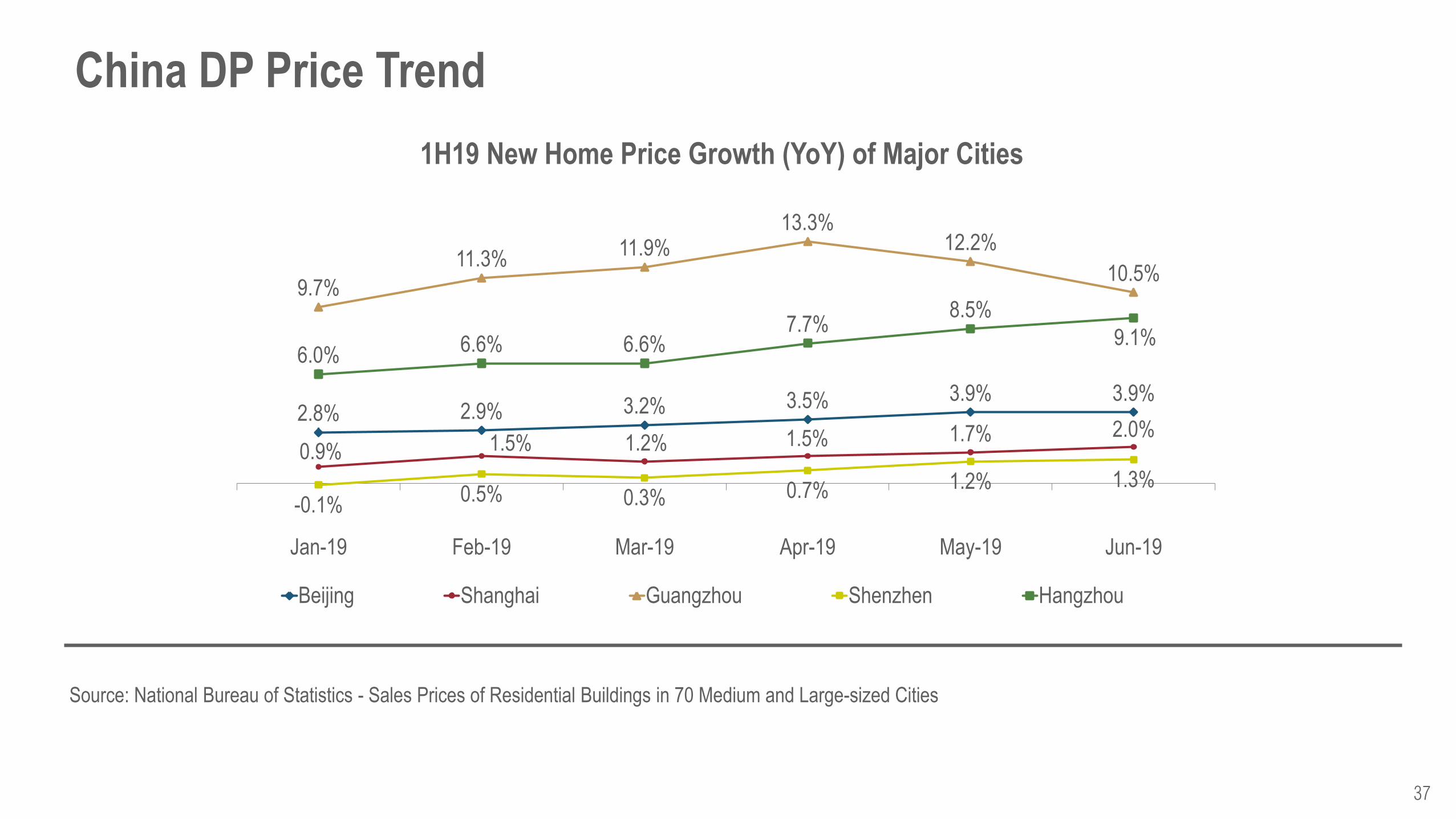

China DP Price Trend

2.8% 2.9% 3.2% 3.5% 3.9% 3.9%

0.9% 1.5% 1.2% 1.5% 1.7% 2.0%

9.7%

11.3% 11.9%

13.3% 12.2%

10.5%

-0.1% 0.5% 0.3% 0.7% 1.2% 1.3%

6.0% 6.6% 6.6%

7.7% 8.5%

9.1%

Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19

1H19 New Home Price Growth (YoY) of Major Cities

Beijing Shanghai Guangzhou Shenzhen Hangzhou

Source: National Bureau of Statistics - Sales Prices of Residential Buildings in 70 Medium and Large-sized Cities

38

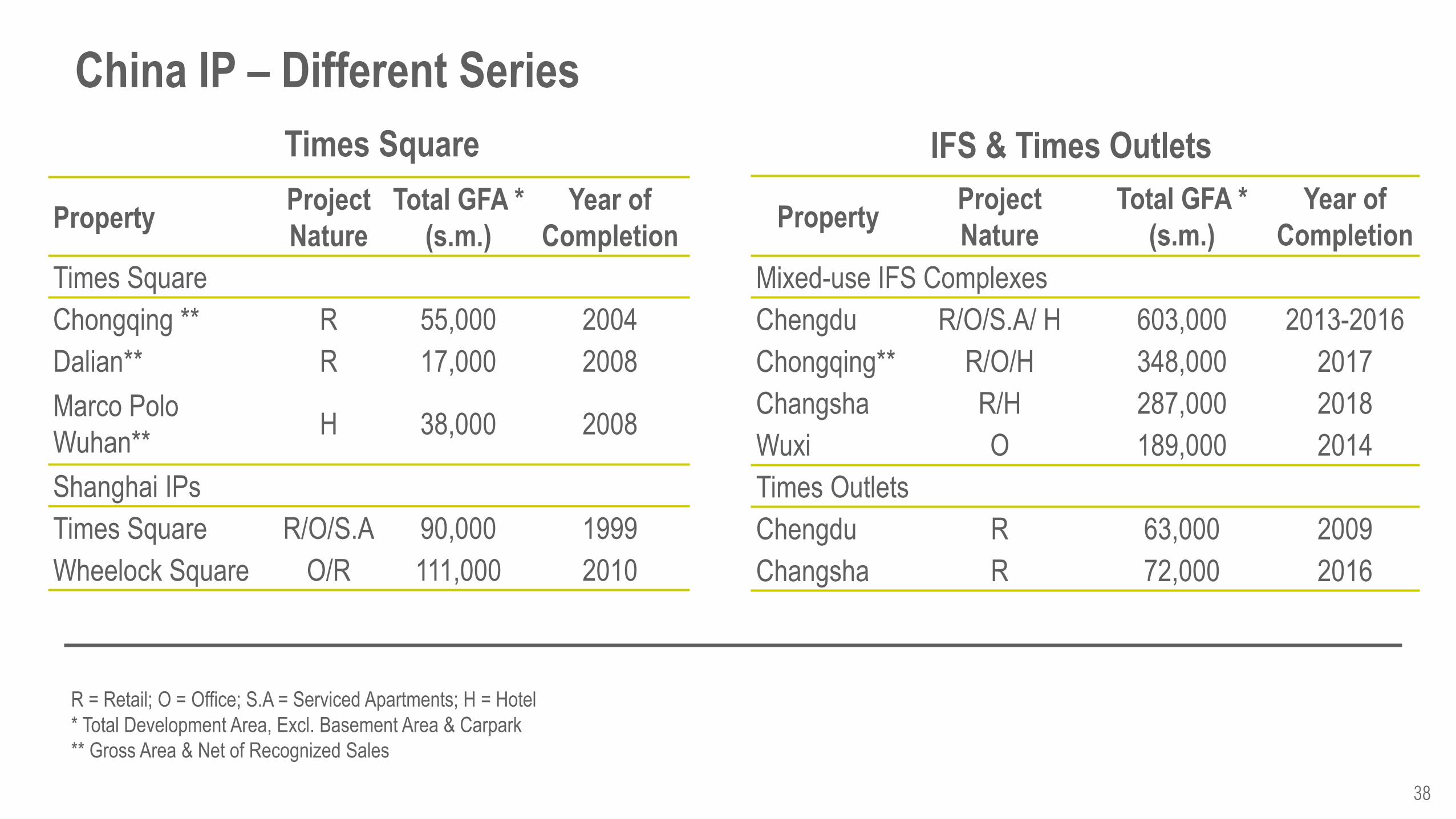

China IP – Different Series

Property Project

Nature

Total GFA *

(s.m.)

Year of

Completion

Times Square

Chongqing ** R 55,000 2004

Dalian** R 17,000 2008

Marco Polo

Wuhan** H 38,000 2008

Shanghai IPs

Times Square R/O/S.A 90,000 1999

Wheelock Square O/R 111,000 2010

R = Retail; O = Office; S.A = Serviced Apartments; H = Hotel

* Total Development Area, Excl. Basement Area & Carpark

** Gross Area & Net of Recognized Sales

Times Square

Property Project

Nature

Total GFA *

(s.m.)

Year of

Completion

Mixed-use IFS Complexes

Chengdu R/O/S.A/ H 603,000 2013-2016

Chongqing** R/O/H 348,000 2017

Changsha R/H 287,000 2018

Wuxi O 189,000 2014

Times Outlets

Chengdu R 63,000 2009

Changsha R 72,000 2016

IFS & Times Outlets

39

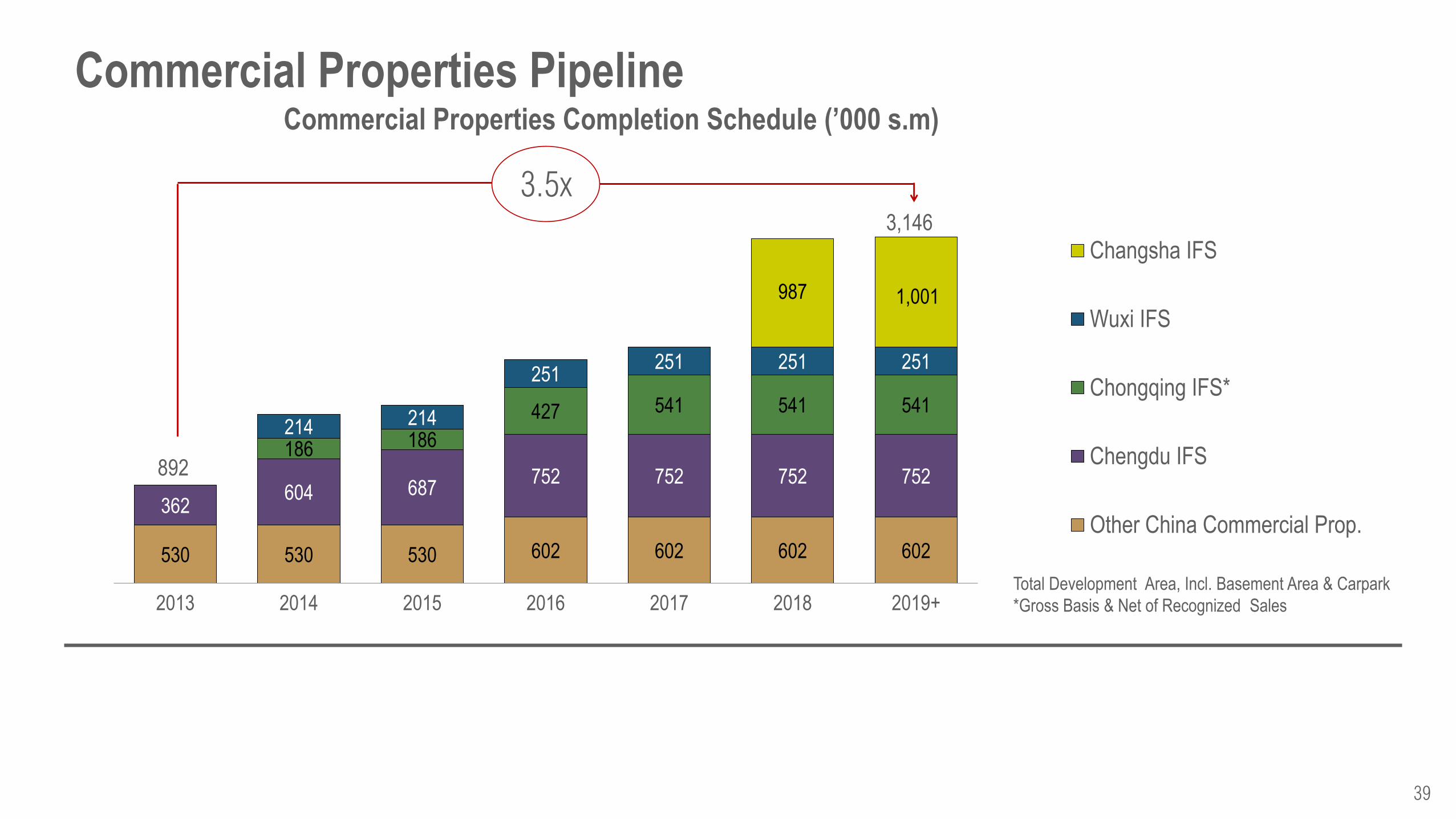

Commercial Properties Pipeline

530 530 530 602 602 602 602

362 604 687

752 752 752 752

186 186

427 541 541 541 214 214

251 251 251 251

987 1,001

2013 2014 2015 2016 2017 2018 2019+

Commercial Properties Completion Schedule (’000 s.m)

Changsha IFS

Wuxi IFS

Chongqing IFS*

Chengdu IFS

Other China Commercial Prop.

3,146

Total Development Area, Incl. Basement Area & Carpark

*Gross Basis & Net of Recognized Sales

892

3.5x

40

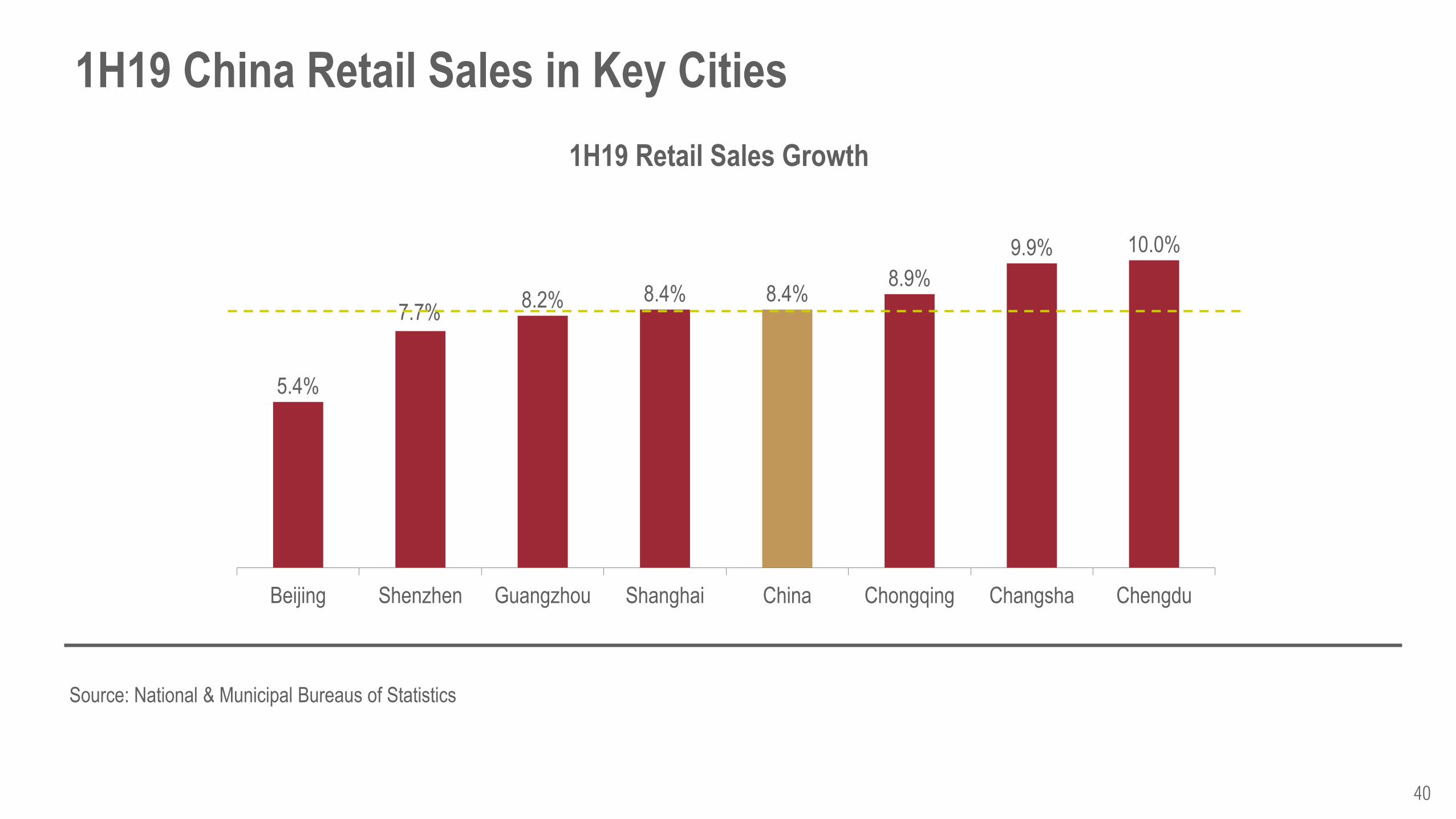

1H19 China Retail Sales in Key Cities

5.4%

7.7% 8.2% 8.4% 8.4%

8.9%

9.9% 10.0%

Beijing Shenzhen Guangzhou Shanghai China Chongqing Changsha Chengdu

1H19 Retail Sales Growth

Source: National & Municipal Bureaus of Statistics

41

Wharf Hotels Management

Niccolo

Hong Kong The Murray, Hong Kong, a Niccolo Hotel*

China Niccolo Chengdu

Niccolo Chongqing^

Niccolo Changsha

Niccolo Suzhou* (Opening in 2021)

Marco Polo

Hong Kong Marco Polo Hongkong Hotel*

Gateway Hotel*

Prince Hotel*

China Marco Polo Parkside, Beijing * Marco Polo Shenzhen* Marco Polo Wuhan Marco Polo Xiamen* Marco Polo Lingnan Tiandi, Foshan* Marco Polo Changzhou* Marco Polo Jinjiang*

Philippines Marco Polo Ortigas, Manila* Marco Polo Plaza, Cebu* Marco Polo Davao*

* Owned by Third Party

^ 50%-owned

42

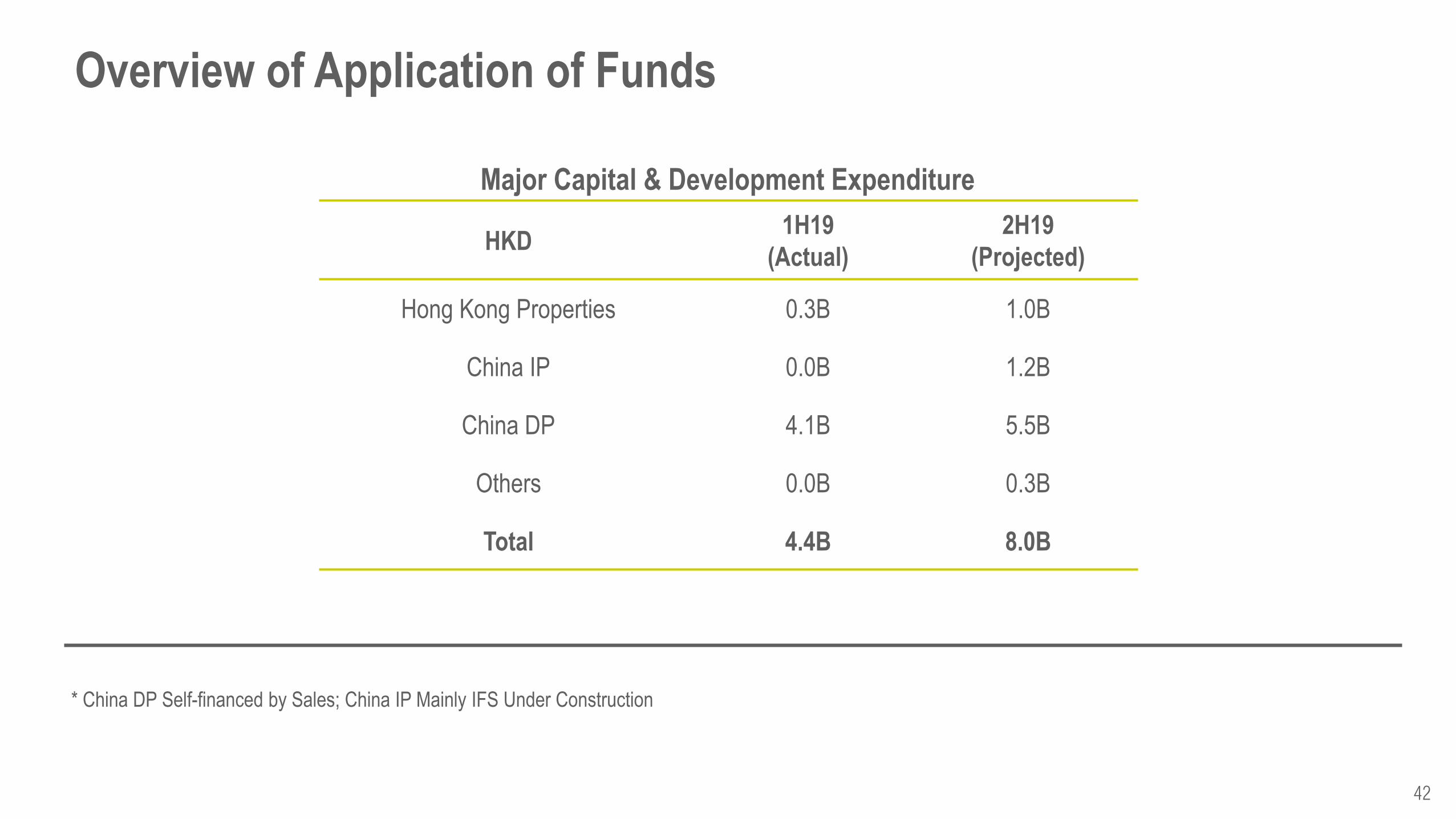

Overview of Application of Funds

HKD 1H19

(Actual)

2H19

(Projected)

Hong Kong Properties 0.3B 1.0B

China IP 0.0B 1.2B

China DP 4.1B 5.5B

Others 0.0B 0.3B

Total 4.4B 8.0B

* China DP Self-financed by Sales; China IP Mainly IFS Under Construction

Major Capital & Development Expenditure

43

Portfolio Facing Headwind

Thank You

44

End of Presentation

The Wharf (Holdings) Limited [HKEx Stock Code: 0004.HK]

Disclaimer

1) All information and data are provided for information purposes only. All opinions included herein constitute

Wharf’s judgment as of the date hereof and are subject to change without notice. The Group, its subsidiaries

and affiliates hereby disclaim (i) all express, implied, and statutory warranties of any kind to user and/or any

third party including warranties as to accuracy, timeliness, completeness, or fitness for any particular

purpose; and (ii) any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or

any part of the information and data contained herein.

2) The full-year statutory financial information of preceding financial years quoted in this presentation are

derived from statutory annual financial statements for that relevant financial years, each of which had been

delivered to Registrar of Companies in accordance with the prevailing Companies Ordinance and were

reported on by the auditors with relevant auditors’ reports without qualification or modification.