Embed Size (px)

Citation preview

Portfolio Risk Management with VIXreg Futures and Options

6 March 2018

Edward Szado PhD CFA

Associate Professor of Finance Providence College Director of Research INGARM (Institute for Global Asset and Risk Management)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

1

Author of the Study

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

2

Edward Szado PhD CFA

Edward Szado is Associate Professor of Finance Providence College He is also the Director of Research at the Institute for Global Asset and Risk Management and received his PhD in Finance from the Isenberg School of Management University of Massachusetts Amherst He has taught Risk Management at the Boston University School of Management Derivatives at Clark University and a range of finance courses at the University of Massachusetts Amherst He is a former Option trader and his experience includes product development in the areas of volatility based investments and structured investment products He is also a Chartered Financial Analyst and has consulted for the Option Industry Council the Cboereg the CFA Institute the Chartered Alternative Investment Analyst Association and the Commodity Futures Trading Commission

Overview

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

3

1 Long VIXreg Futures and Long VIXreg Call based Strategies in Two Key Years ndash 2008 and 2016

2 Inverse VIXreg Futures and VIXreg Call Writing based Strategies in Two Key Years ndash 2008 and 2016

3 Performance of Long Term Buy and Hold Long and Inverse VIXreg based Strategies (2242006 to 12312017)

4 Open Interest and Volume of VIXreg options and futures

VIXreg Futures and Options Based Strategies in Two Key Years

4

bull Cost of holding futures in contango (when spot price is below futures price) suggests that long VIX futures and long VIX call option positions may be best suited to strategic uses rather than buy and hold

bull However the convex relationship and strong negative conditional correlation between the VIX index and the SampP 500 suggests long VIX futures and call options may provide an effective hedge for traditional portfolios

bull The following section considers the impact of a small allocation of VIX futures and options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods favorable to long positions in VIX futures and call options (2008) and generally unfavorable to long positions in VIX futures and call options (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

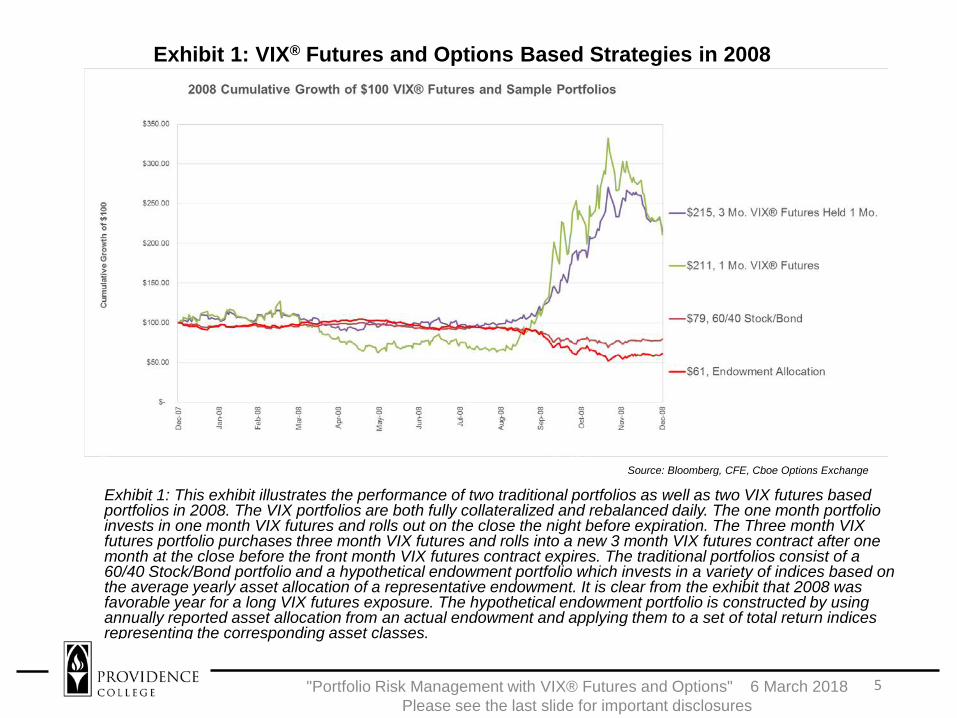

Exhibit 1 VIXreg Futures and Options Based Strategies in 2008

5Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 1 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was favorable year for a long VIX futures exposure The hypothetical endowment portfolio is constructed by using annually reported asset allocation from an actual endowment and applying them to a set of total return indices representing the corresponding asset classes

Source Bloomberg CFE Cboe Options Exchange

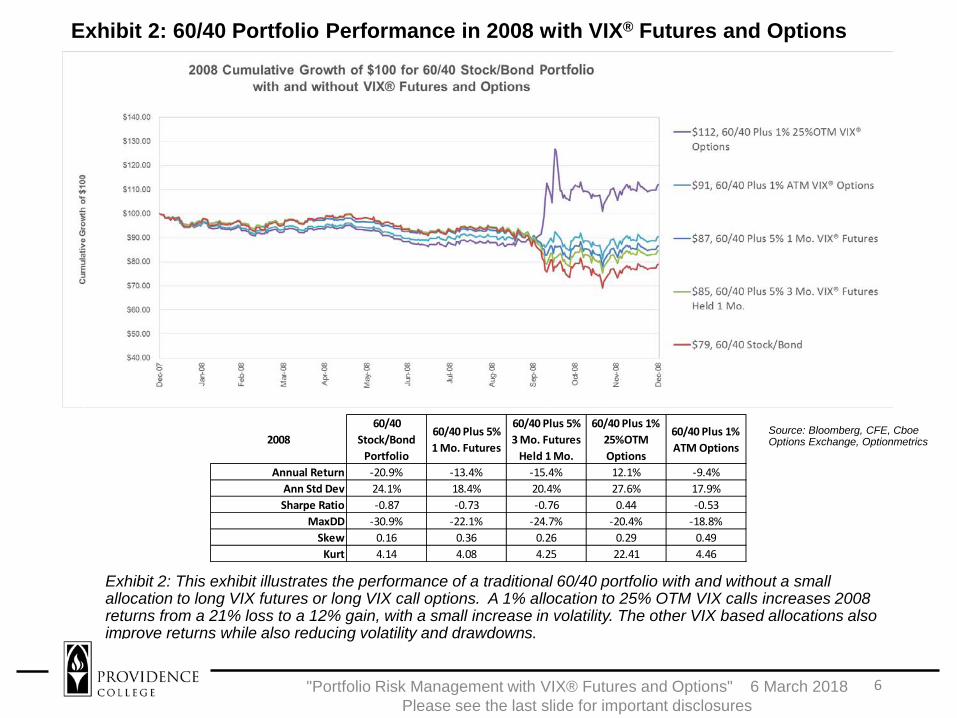

Exhibit 2 6040 Portfolio Performance in 2008 with VIXreg Futures and Options

6Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 2 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options A 1 allocation to 25 OTM VIX calls increases 2008 returns from a 21 loss to a 12 gain with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE CboeOptions Exchange Optionmetrics2008

6040 StockBond

Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return -209 -134 -154 121 -94Ann Std Dev 241 184 204 276 179Sharpe Ratio -087 -073 -076 044 -053

MaxDD -309 -221 -247 -204 -188Skew 016 036 026 029 049

Kurt 414 408 425 2241 446

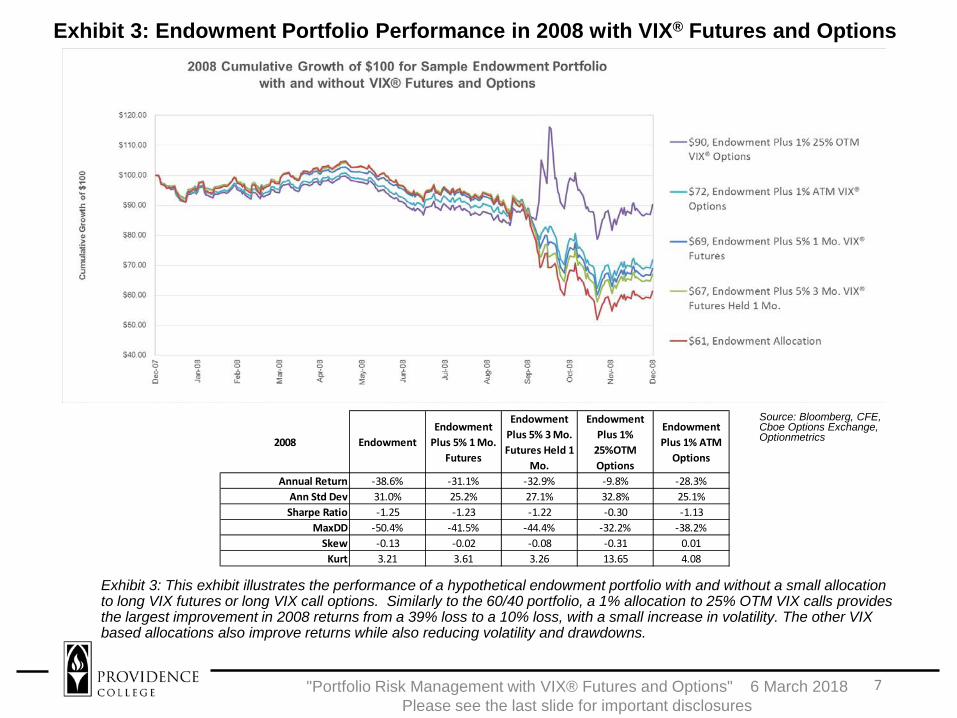

Exhibit 3 Endowment Portfolio Performance in 2008 with VIXreg Futures and Options

7Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 3 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocationto long VIX futures or long VIX call options Similarly to the 6040 portfolio a 1 allocation to 25 OTM VIX calls provides the largest improvement in 2008 returns from a 39 loss to a 10 loss with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE Cboe Options Exchange Optionmetrics2008 Endowment

Endowment Plus 5 1 Mo

Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return -386 -311 -329 -98 -283Ann Std Dev 310 252 271 328 251Sharpe Ratio -125 -123 -122 -030 -113

MaxDD -504 -415 -444 -322 -382Skew -013 -002 -008 -031 001

Kurt 321 361 326 1365 408

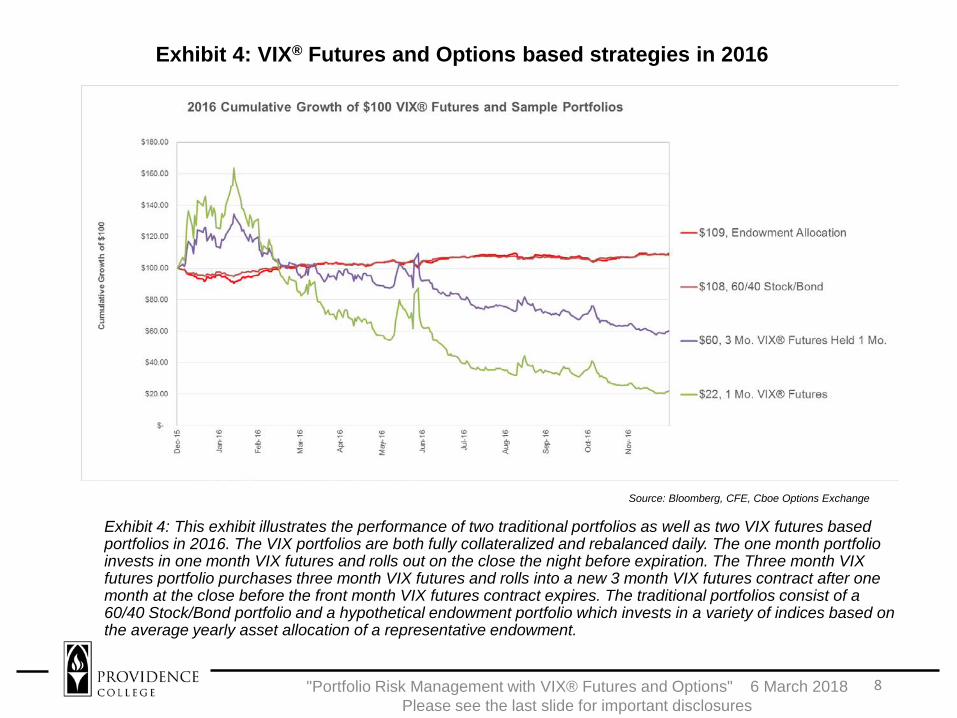

Exhibit 4 VIXreg Futures and Options based strategies in 2016

8Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 4 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment

Source Bloomberg CFE Cboe Options Exchange

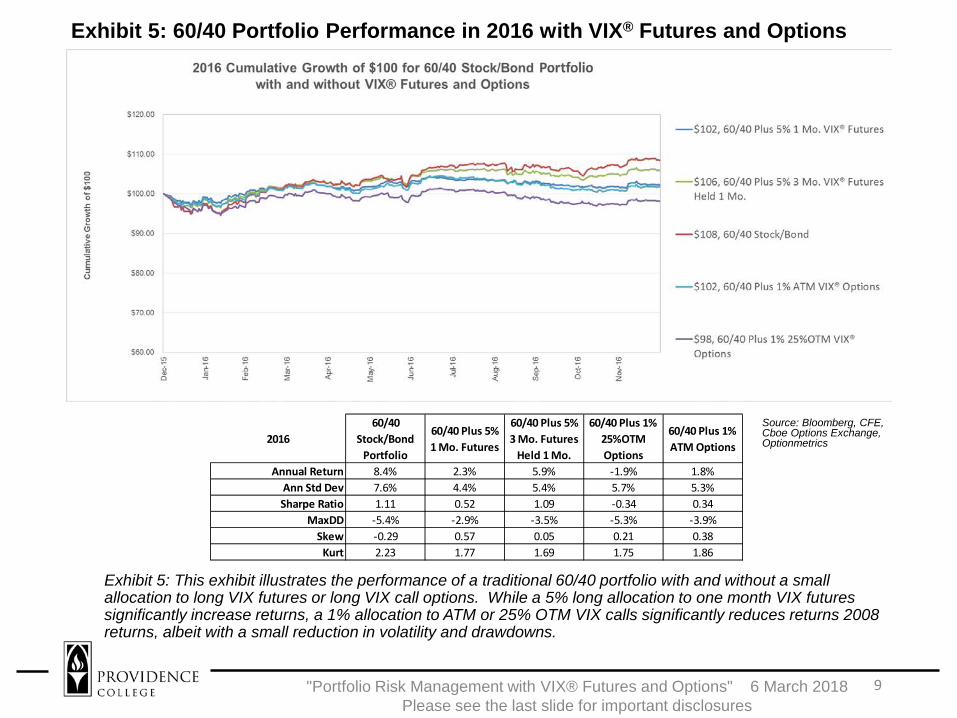

Exhibit 5 6040 Portfolio Performance in 2016 with VIXreg Futures and Options

9Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 5 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options While a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

20166040

StockBond Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return 84 23 59 -19 18Ann Std Dev 76 44 54 57 53Sharpe Ratio 111 052 109 -034 034

MaxDD -54 -29 -35 -53 -39Skew -029 057 005 021 038

Kurt 223 177 169 175 186

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

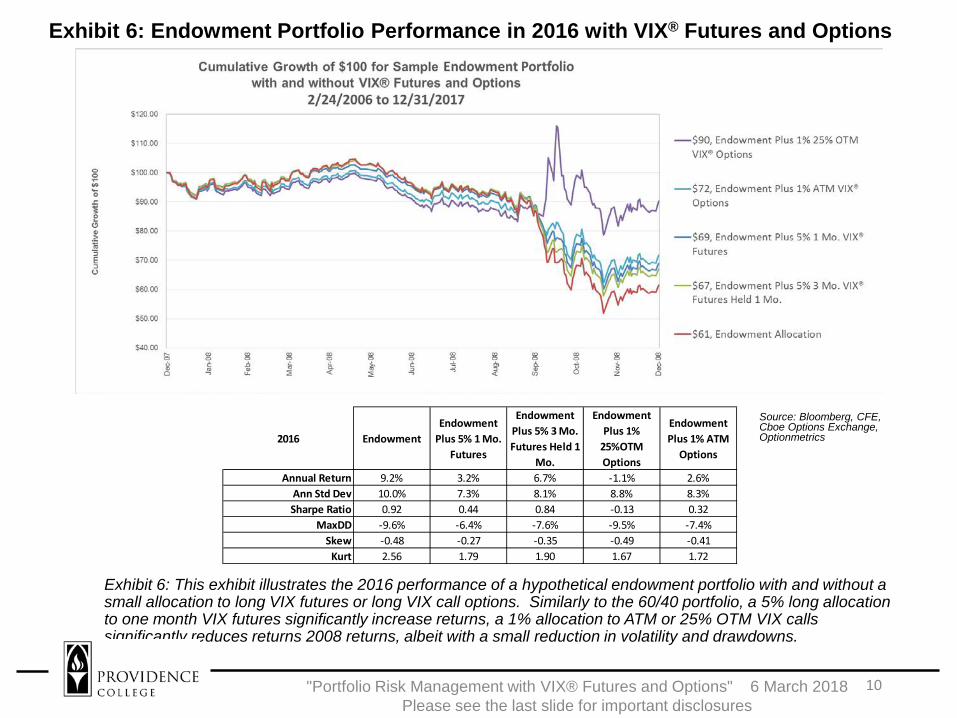

Exhibit 6 Endowment Portfolio Performance in 2016 with VIXreg Futures and Options

10Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 6 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or long VIX call options Similarly to the 6040 portfolio a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

2016 EndowmentEndowment

Plus 5 1 Mo Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return 92 32 67 -11 26Ann Std Dev 100 73 81 88 83Sharpe Ratio 092 044 084 -013 032

MaxDD -96 -64 -76 -95 -74Skew -048 -027 -035 -049 -041

Kurt 256 179 190 167 172

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Short (Inverse) VIXreg Futures in two key years

11

bull Cost of holding futures in contango suggests that VIX futures and options may be best suited to strategic uses rather than buy and hold

bull Periods of strong contango may generate high returns to short (inverse) VIX futures or VIX call option writing strategies if a volatility event does not occur

bull However a volatility event may result in catastrophic losses to inverse VIX futures or written VIX call option positions

bull The following section considers the impact of a small allocation of inverse VIX futures and written call options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods generally unfavorable for inverse VIX positions (2008) and generally favorable for inverse VIX positions (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

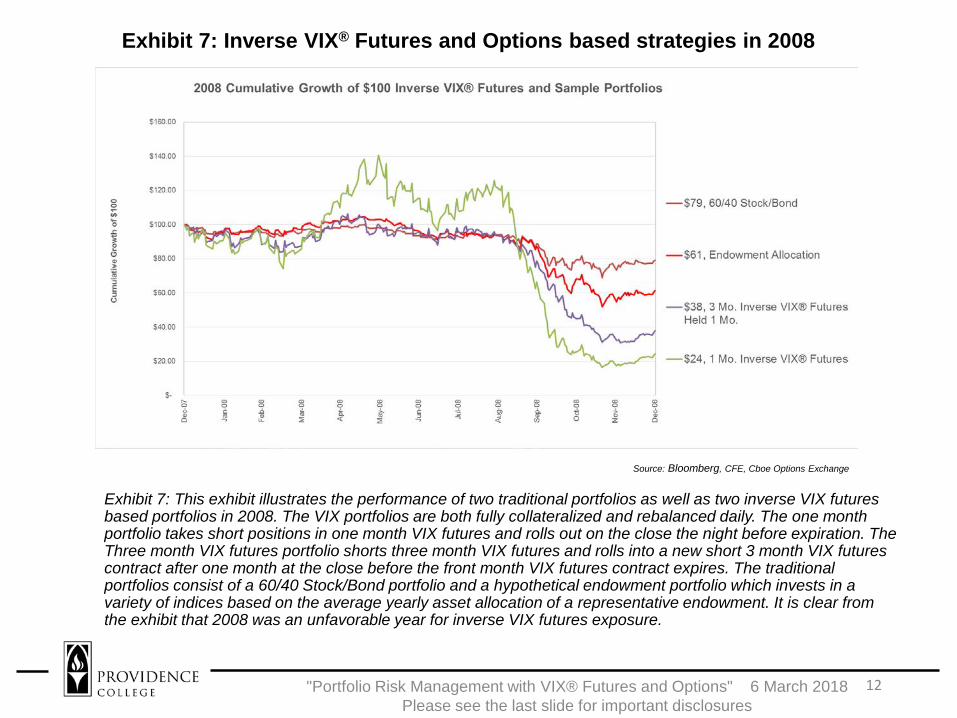

Exhibit 7 Inverse VIXreg Futures and Options based strategies in 2008

12Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 7 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was an unfavorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

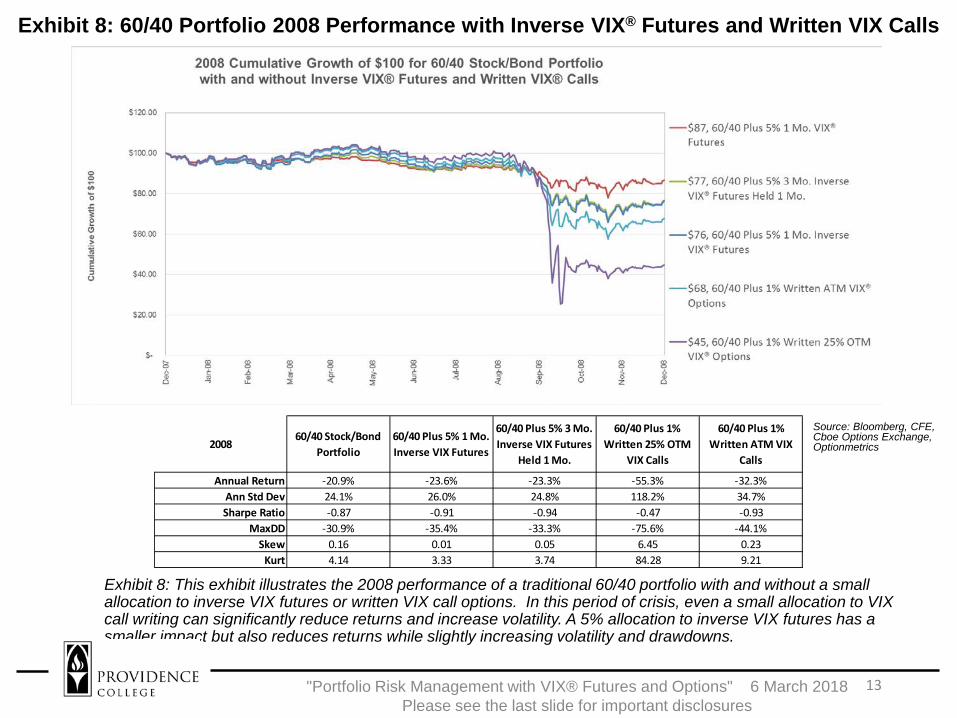

Exhibit 8 6040 Portfolio 2008 Performance with Inverse VIXreg Futures and Written VIX Calls

13Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 8 This exhibit illustrates the 2008 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

20086040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

Calls

Annual Return -209 -236 -233 -553 -323Ann Std Dev 241 260 248 1182 347Sharpe Ratio -087 -091 -094 -047 -093

MaxDD -309 -354 -333 -756 -441Skew 016 001 005 645 023

Kurt 414 333 374 8428 921

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

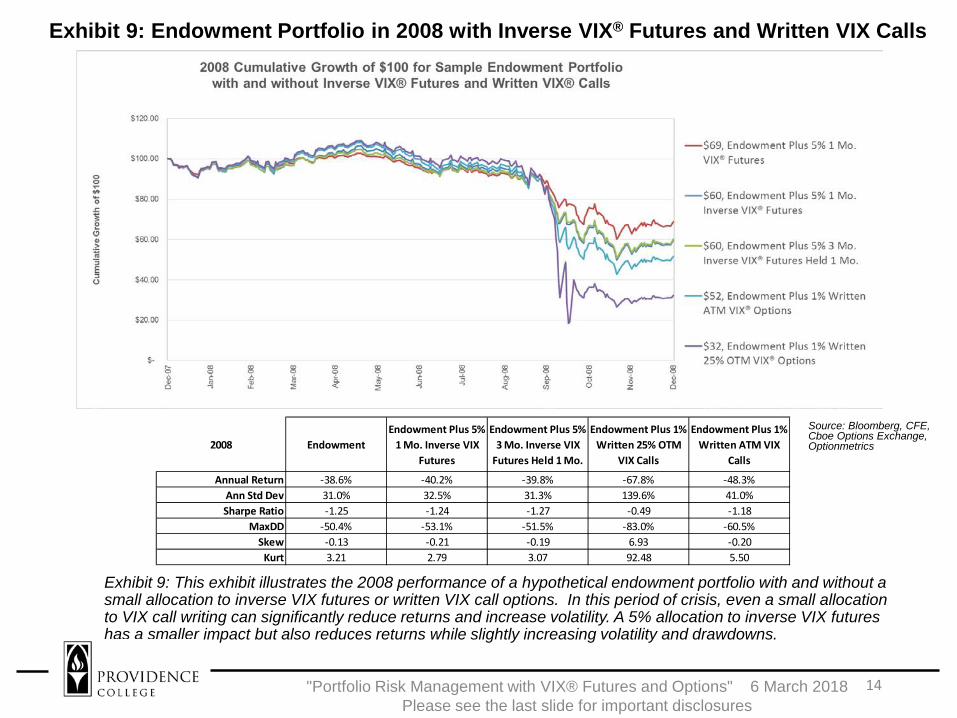

Exhibit 9 Endowment Portfolio in 2008 with Inverse VIXreg Futures and Written VIX Calls

14Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 9 This exhibit illustrates the 2008 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

2008 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

Calls

Annual Return -386 -402 -398 -678 -483Ann Std Dev 310 325 313 1396 410Sharpe Ratio -125 -124 -127 -049 -118

MaxDD -504 -531 -515 -830 -605Skew -013 -021 -019 693 -020

Kurt 321 279 307 9248 550

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

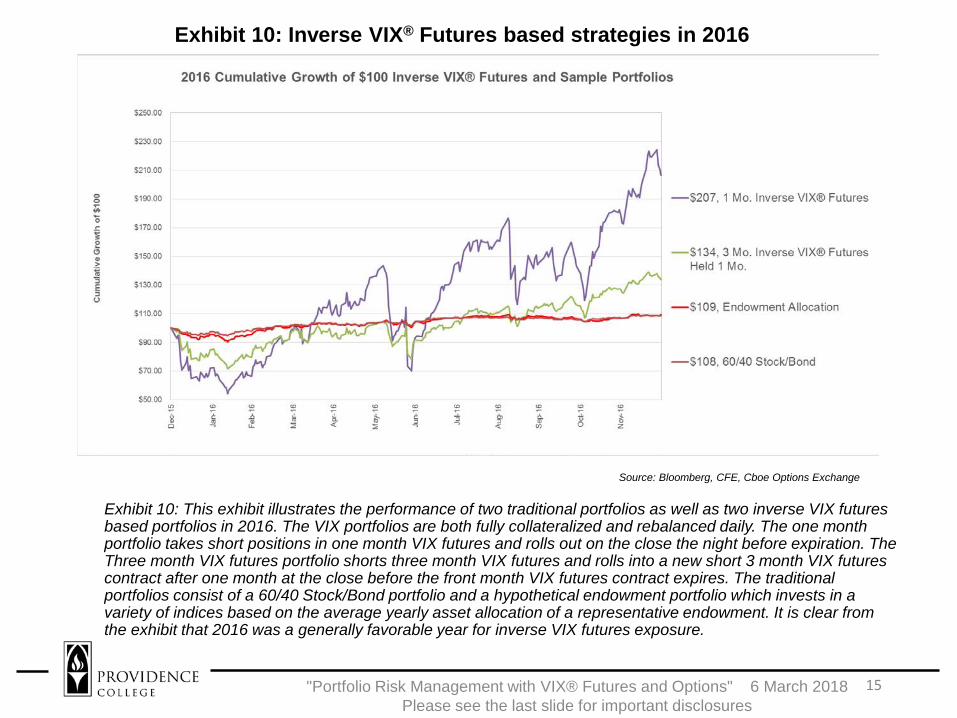

Exhibit 10 Inverse VIXreg Futures based strategies in 2016

15Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 10 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2016 was a generally favorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

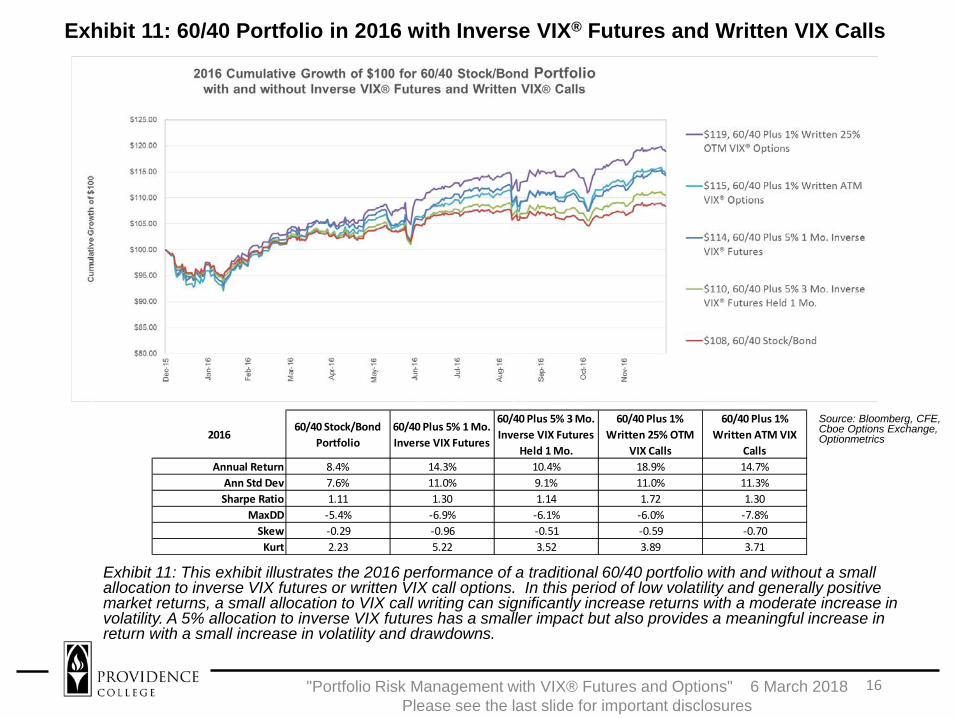

Exhibit 11 6040 Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

16Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 11 This exhibit illustrates the 2016 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of low volatility and generally positive market returns a small allocation to VIX call writing can significantly increase returns with a moderate increase in volatility A 5 allocation to inverse VIX futures has a smaller impact but also provides a meaningful increase in return with a small increase in volatility and drawdowns

20166040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

CallsAnnual Return 84 143 104 189 147

Ann Std Dev 76 110 91 110 113Sharpe Ratio 111 130 114 172 130

MaxDD -54 -69 -61 -60 -78Skew -029 -096 -051 -059 -070

Kurt 223 522 352 389 371

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

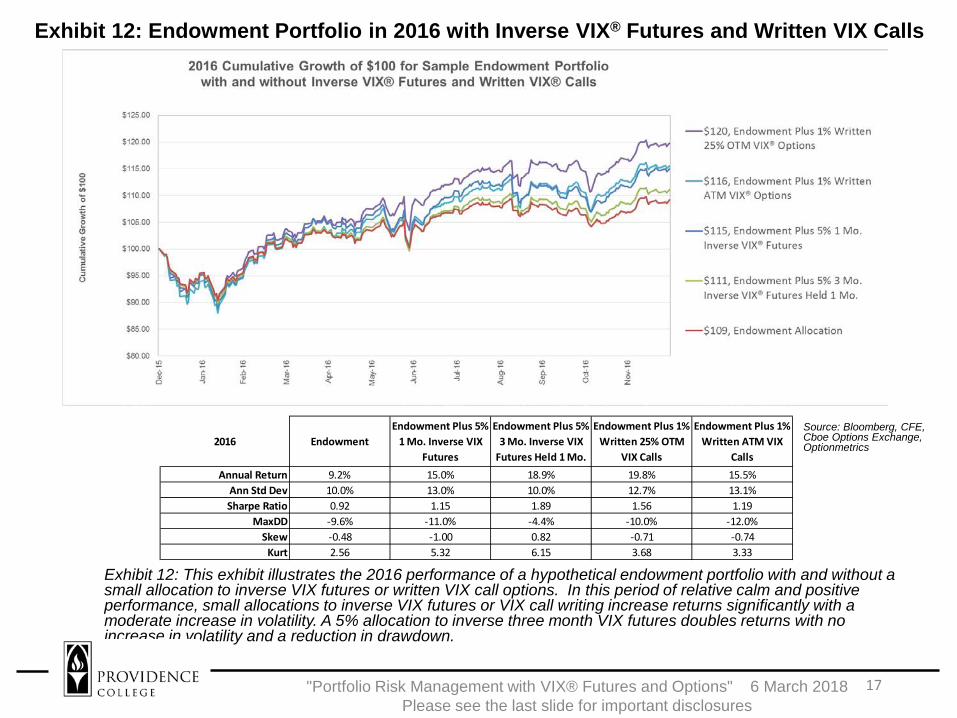

Exhibit 12 Endowment Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

17Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 12 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of relative calm and positive performance small allocations to inverse VIX futures or VIX call writing increase returns significantly with a moderate increase in volatility A 5 allocation to inverse three month VIX futures doubles returns with no increase in volatility and a reduction in drawdown

2016 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

CallsAnnual Return 92 150 189 198 155

Ann Std Dev 100 130 100 127 131Sharpe Ratio 092 115 189 156 119

MaxDD -96 -110 -44 -100 -120Skew -048 -100 082 -071 -074

Kurt 256 532 615 368 333

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

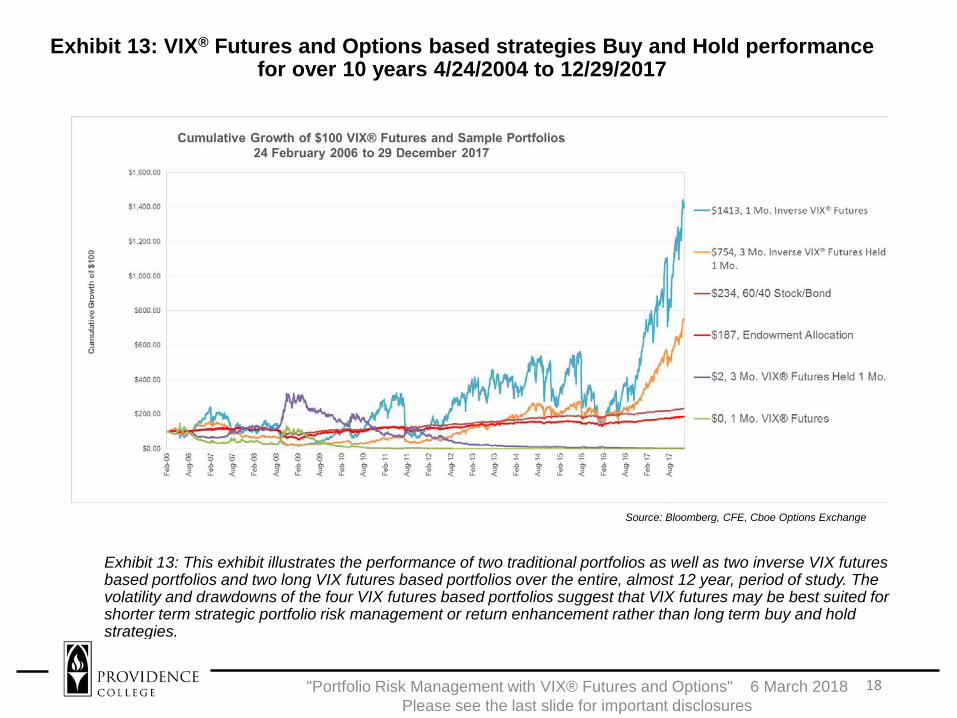

Exhibit 13 VIXreg Futures and Options based strategies Buy and Hold performance for over 10 years 4242004 to 12292017

18Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 13 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios and two long VIX futures based portfolios over the entire almost 12 year period of study The volatility and drawdowns of the four VIX futures based portfolios suggest that VIX futures may be best suited for shorter term strategic portfolio risk management or return enhancement rather than long term buy and hold strategies

Source Bloomberg CFE Cboe Options Exchange

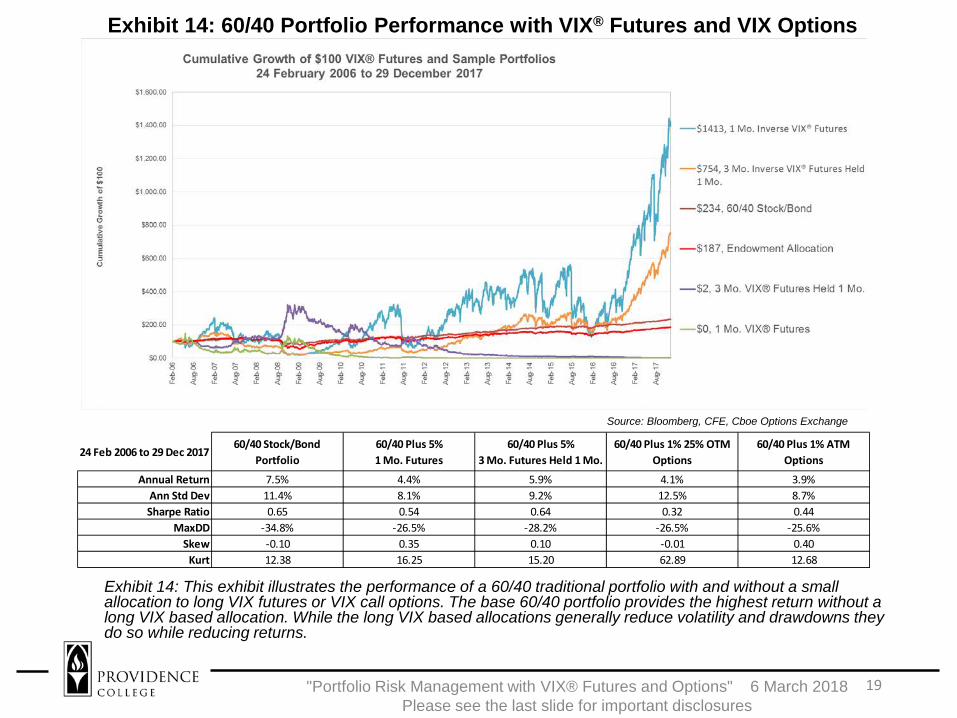

Exhibit 14 6040 Portfolio Performance with VIXreg Futures and VIX Options

19Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 14 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to long VIX futures or VIX call options The base 6040 portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations generally reduce volatility and drawdowns they do so while reducing returns

Source Bloomberg CFE Cboe Options Exchange

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures Held 1 Mo

6040 Plus 1 25 OTM Options

6040 Plus 1 ATM Options

Annual Return 75 44 59 41 39Ann Std Dev 114 81 92 125 87Sharpe Ratio 065 054 064 032 044

MaxDD -348 -265 -282 -265 -256Skew -010 035 010 -001 040

Kurt 1238 1625 1520 6289 1268

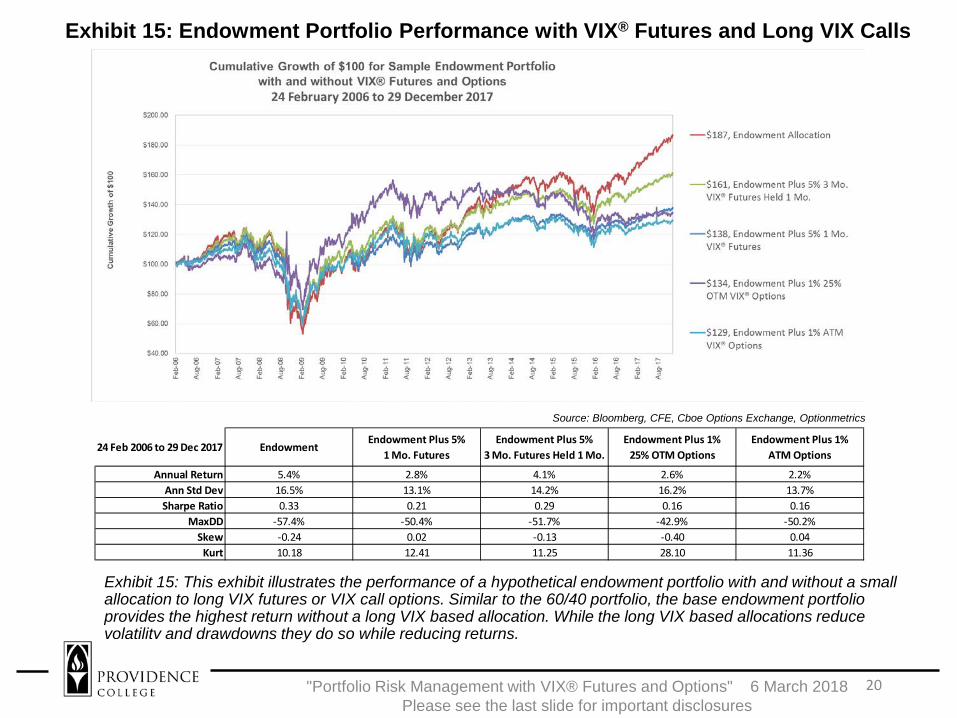

Exhibit 15 Endowment Portfolio Performance with VIXreg Futures and Long VIX Calls

20Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 15 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or VIX call options Similar to the 6040 portfolio the base endowment portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations reduce volatility and drawdowns they do so while reducing returns

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5

1 Mo FuturesEndowment Plus 5

3 Mo Futures Held 1 MoEndowment Plus 1

25 OTM OptionsEndowment Plus 1

ATM Options

Annual Return 54 28 41 26 22Ann Std Dev 165 131 142 162 137Sharpe Ratio 033 021 029 016 016

MaxDD -574 -504 -517 -429 -502Skew -024 002 -013 -040 004

Kurt 1018 1241 1125 2810 1136

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

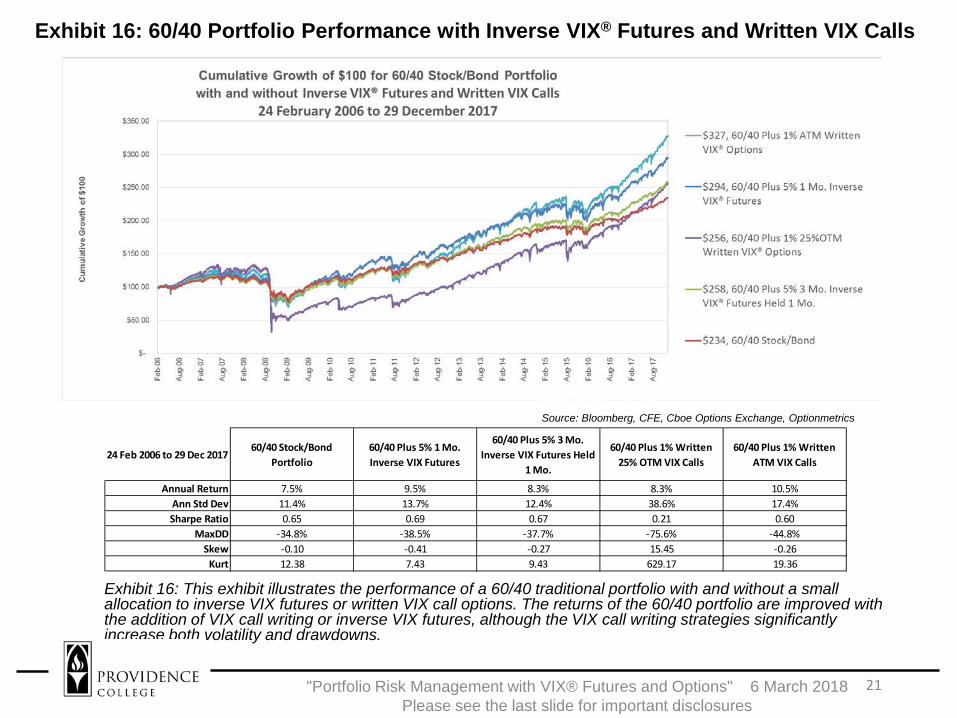

Exhibit 16 6040 Portfolio Performance with Inverse VIXreg Futures and Written VIX Calls

21Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 16 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the 6040 portfolio are improved with the addition of VIX call writing or inverse VIX futures although the VIX call writing strategies significantly increase both volatility and drawdowns

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures Held

1 Mo

6040 Plus 1 Written 25 OTM VIX Calls

6040 Plus 1 Written ATM VIX Calls

Annual Return 75 95 83 83 105Ann Std Dev 114 137 124 386 174Sharpe Ratio 065 069 067 021 060

MaxDD -348 -385 -377 -756 -448Skew -010 -041 -027 1545 -026

Kurt 1238 743 943 62917 1936

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

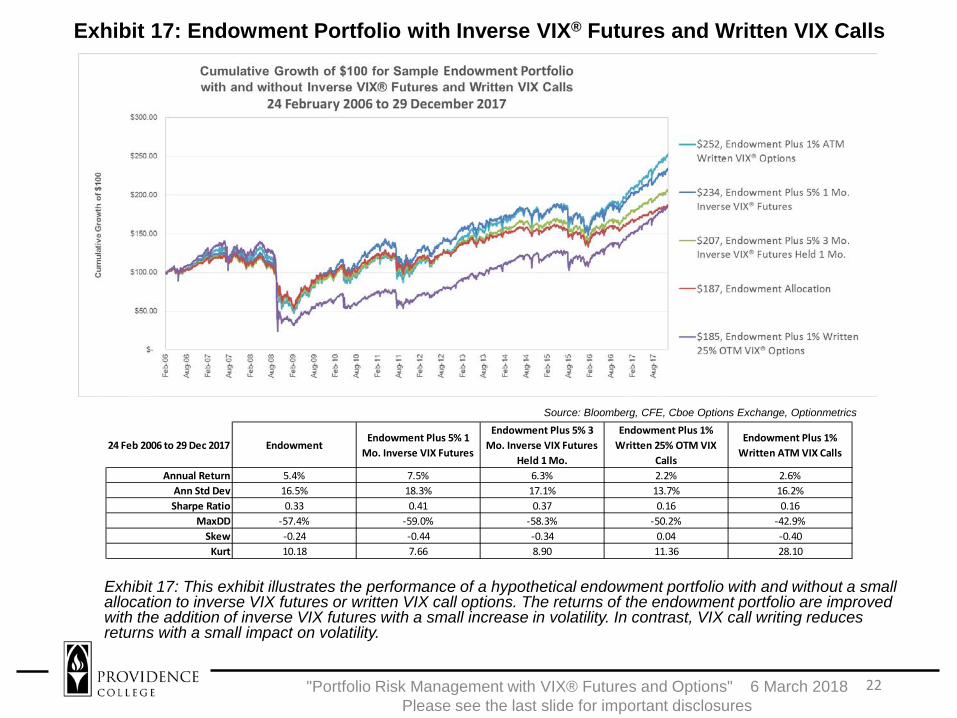

Exhibit 17 Endowment Portfolio with Inverse VIXreg Futures and Written VIX Calls

22Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 17 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the endowment portfolio are improved with the addition of inverse VIX futures with a small increase in volatility In contrast VIX call writing reduces returns with a small impact on volatility

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5 1

Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

Endowment Plus 1 Written 25 OTM VIX

Calls

Endowment Plus 1 Written ATM VIX Calls

Annual Return 54 75 63 22 26Ann Std Dev 165 183 171 137 162Sharpe Ratio 033 041 037 016 016

MaxDD -574 -590 -583 -502 -429Skew -024 -044 -034 004 -040

Kurt 1018 766 890 1136 2810

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Open Interest and Volume of VIXreg Futures and Options

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

23

Volume and Open Interestbull VIX Futures and Options Volume have both increased

significantly in recent years coinciding with lower levels of VIXbull VIX Futures and Options Open Interest have also significantly

increased coinciding with lower levels of VIXbull Lower levels of VIX tend to correspond with a shift of option

volume towards puts and away from callsbull In recent years at low VIX levels non-commercial (speculative)

traders have significantly increased their short (inverse) position open interest as a proportion of total short open interest

bull Commercial (hedging) traders have recently increased their long positions as a proportion of total short open interest although these positions are at historically low levels

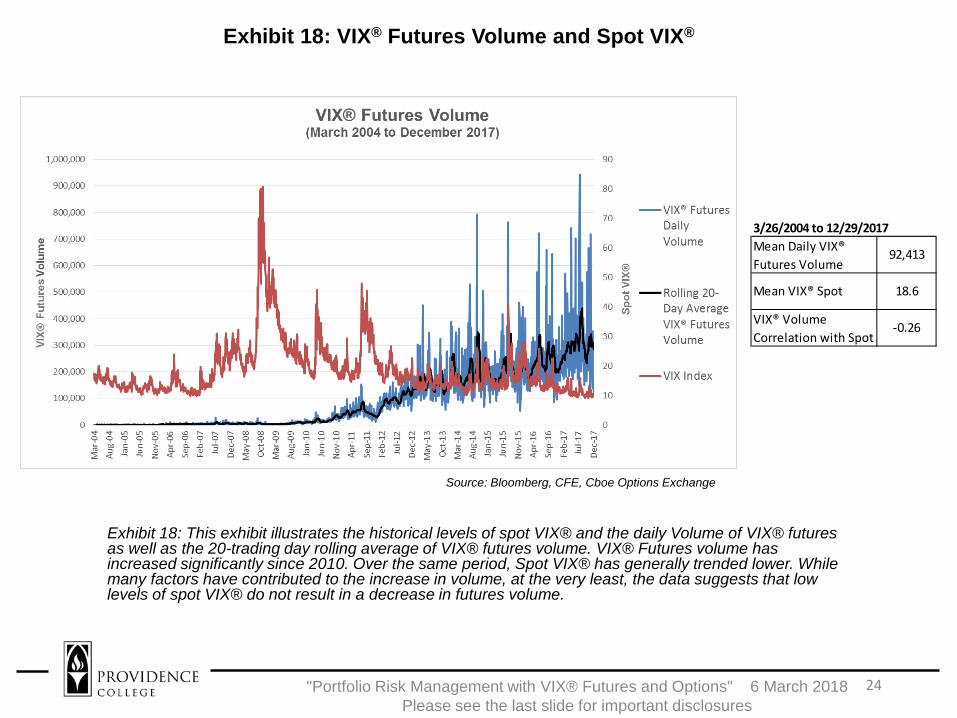

Exhibit 18 VIXreg Futures Volume and Spot VIXreg

Exhibit 18 This exhibit illustrates the historical levels of spot VIXreg and the daily Volume of VIXreg futures as well as the 20-trading day rolling average of VIXreg futures volume VIXreg Futures volume has increased significantly since 2010 Over the same period Spot VIXreg has generally trended lower While many factors have contributed to the increase in volume at the very least the data suggests that low levels of spot VIXreg do not result in a decrease in futures volume

24

3262004 to 12292017Mean Daily VIXreg Futures Volume

Mean VIXreg Spot

VIXreg Volume Correlation with Spot

92413

186

-026

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange

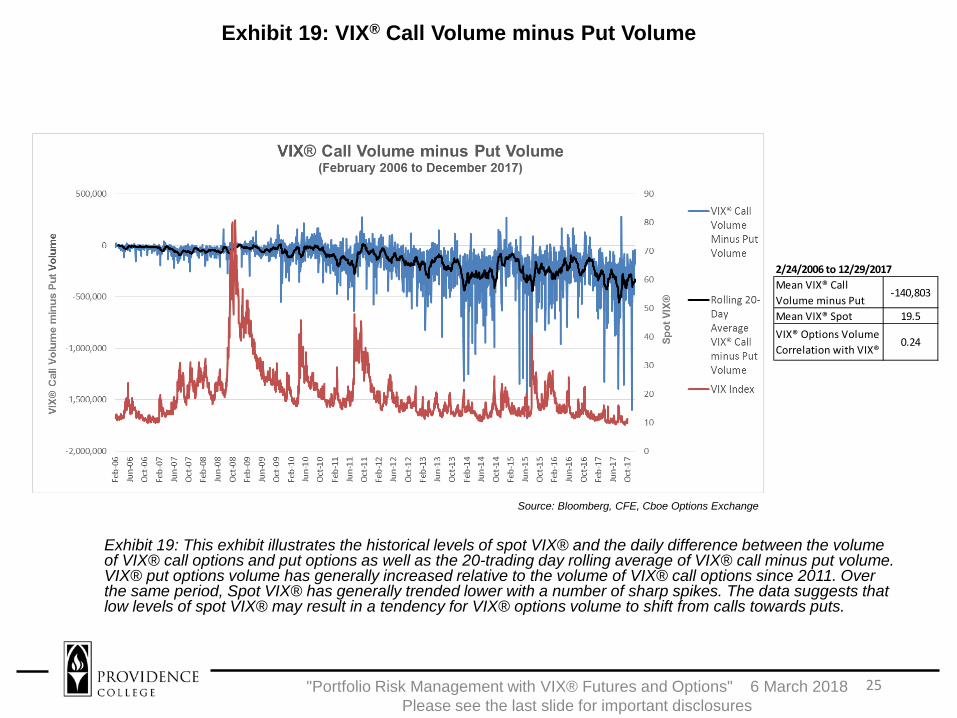

Exhibit 19 VIXreg Call Volume minus Put Volume

Exhibit 19 This exhibit illustrates the historical levels of spot VIXreg and the daily difference between the volume of VIXreg call options and put options as well as the 20-trading day rolling average of VIXreg call minus put volume VIXreg put options volume has generally increased relative to the volume of VIXreg call options since 2011 Over the same period Spot VIXreg has generally trended lower with a number of sharp spikes The data suggests that low levels of spot VIXreg may result in a tendency for VIXreg options volume to shift from calls towards puts

25

2242006 to 12292017

-140803

195

024

Mean VIXreg Call Volume minus Put Mean VIXreg SpotVIXreg Options Volume Correlation with VIXreg

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange

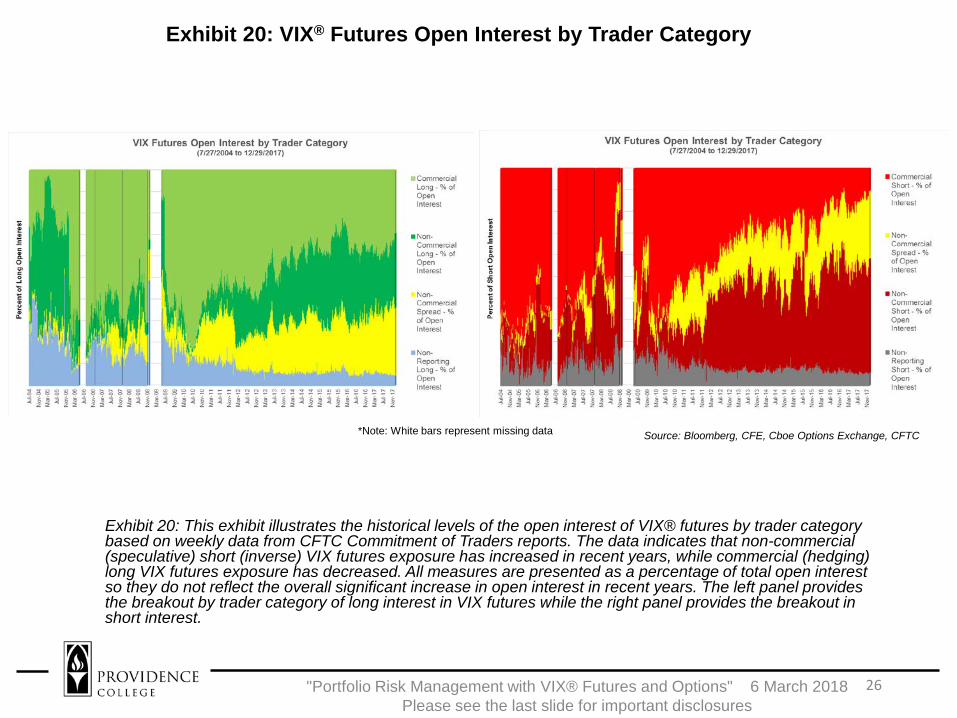

Exhibit 20 VIXreg Futures Open Interest by Trader Category

Exhibit 20 This exhibit illustrates the historical levels of the open interest of VIXreg futures by trader category based on weekly data from CFTC Commitment of Traders reports The data indicates that non-commercial (speculative) short (inverse) VIX futures exposure has increased in recent years while commercial (hedging) long VIX futures exposure has decreased All measures are presented as a percentage of total open interest so they do not reflect the overall significant increase in open interest in recent years The left panel provides the breakout by trader category of long interest in VIX futures while the right panel provides the breakout in short interest

26

Note White bars represent missing data

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange CFTC

Cboe Exchange Inc provided financial support for the research for this paper Options involve risk and are not suitable for all investors Prior to buying or selling an option a person must receive a copy of Characteristics and Risks of Standardized Options Copies are available from your broker or from The Options Clearing Corporation at wwwtheocccom Futures trading is not suitable for all investors and involves the risk of loss The risk of loss in futures can be substantial You should therefore carefully consider whether such trading is suitable for you in light of your circumstances and financial resources For additional information regarding futures trading risks see the Risk Disclosure Statement set forth in CFTC Regulation sect155(b) The information in these materials are provided for general education and information purposes only No statement within these materials should be construed as a recommendation to buy or sell a security or future or to provide investment advice Past performance is not indicative of future results Parameters relating to past performance of strategies discussed are not capable of being duplicated These materials contain performance data based on back-testing ie calculations of how a sample portfolio might have performed Back-tested performance information is purely hypothetical and is provided in these materials solely for informational purposes Back-tested performance does not represent actual performance and should not be interpreted as an indication of actual performance No representation is being made that any investment will or is likely to achieve a performance record similar to that shown The views of third party speakers and their materials are their own and do not necessarily represent the views of Cboe Third party speakers are not affiliated with Cboe These materials should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe product or service described in these materials Cboereg and VIXreg are registered trademarks and RMCSM is a service mark of Cboe Exchange Inc SampP 500reg is a registered trademark of Standard and Poors Financial Services LLC Financial products based on SampP indices are not sponsored endorsed sold or promoted by Standard amp Poorrsquos and neither Standard ampPoorrsquos nor Cboe make any representation regarding the advisability of investing in such products All other trademarks and service marks are the property of their respective owners More information is or will be available at wwwcboecomfunds Please email comments to eszadoprovidenceedu or institutionalcboecom

27Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Author of the Study

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

2

Edward Szado PhD CFA

Edward Szado is Associate Professor of Finance Providence College He is also the Director of Research at the Institute for Global Asset and Risk Management and received his PhD in Finance from the Isenberg School of Management University of Massachusetts Amherst He has taught Risk Management at the Boston University School of Management Derivatives at Clark University and a range of finance courses at the University of Massachusetts Amherst He is a former Option trader and his experience includes product development in the areas of volatility based investments and structured investment products He is also a Chartered Financial Analyst and has consulted for the Option Industry Council the Cboereg the CFA Institute the Chartered Alternative Investment Analyst Association and the Commodity Futures Trading Commission

Overview

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

3

1 Long VIXreg Futures and Long VIXreg Call based Strategies in Two Key Years ndash 2008 and 2016

2 Inverse VIXreg Futures and VIXreg Call Writing based Strategies in Two Key Years ndash 2008 and 2016

3 Performance of Long Term Buy and Hold Long and Inverse VIXreg based Strategies (2242006 to 12312017)

4 Open Interest and Volume of VIXreg options and futures

VIXreg Futures and Options Based Strategies in Two Key Years

4

bull Cost of holding futures in contango (when spot price is below futures price) suggests that long VIX futures and long VIX call option positions may be best suited to strategic uses rather than buy and hold

bull However the convex relationship and strong negative conditional correlation between the VIX index and the SampP 500 suggests long VIX futures and call options may provide an effective hedge for traditional portfolios

bull The following section considers the impact of a small allocation of VIX futures and options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods favorable to long positions in VIX futures and call options (2008) and generally unfavorable to long positions in VIX futures and call options (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 1 VIXreg Futures and Options Based Strategies in 2008

5Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 1 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was favorable year for a long VIX futures exposure The hypothetical endowment portfolio is constructed by using annually reported asset allocation from an actual endowment and applying them to a set of total return indices representing the corresponding asset classes

Source Bloomberg CFE Cboe Options Exchange

Exhibit 2 6040 Portfolio Performance in 2008 with VIXreg Futures and Options

6Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 2 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options A 1 allocation to 25 OTM VIX calls increases 2008 returns from a 21 loss to a 12 gain with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE CboeOptions Exchange Optionmetrics2008

6040 StockBond

Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return -209 -134 -154 121 -94Ann Std Dev 241 184 204 276 179Sharpe Ratio -087 -073 -076 044 -053

MaxDD -309 -221 -247 -204 -188Skew 016 036 026 029 049

Kurt 414 408 425 2241 446

Exhibit 3 Endowment Portfolio Performance in 2008 with VIXreg Futures and Options

7Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 3 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocationto long VIX futures or long VIX call options Similarly to the 6040 portfolio a 1 allocation to 25 OTM VIX calls provides the largest improvement in 2008 returns from a 39 loss to a 10 loss with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE Cboe Options Exchange Optionmetrics2008 Endowment

Endowment Plus 5 1 Mo

Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return -386 -311 -329 -98 -283Ann Std Dev 310 252 271 328 251Sharpe Ratio -125 -123 -122 -030 -113

MaxDD -504 -415 -444 -322 -382Skew -013 -002 -008 -031 001

Kurt 321 361 326 1365 408

Exhibit 4 VIXreg Futures and Options based strategies in 2016

8Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 4 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment

Source Bloomberg CFE Cboe Options Exchange

Exhibit 5 6040 Portfolio Performance in 2016 with VIXreg Futures and Options

9Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 5 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options While a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

20166040

StockBond Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return 84 23 59 -19 18Ann Std Dev 76 44 54 57 53Sharpe Ratio 111 052 109 -034 034

MaxDD -54 -29 -35 -53 -39Skew -029 057 005 021 038

Kurt 223 177 169 175 186

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 6 Endowment Portfolio Performance in 2016 with VIXreg Futures and Options

10Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 6 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or long VIX call options Similarly to the 6040 portfolio a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

2016 EndowmentEndowment

Plus 5 1 Mo Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return 92 32 67 -11 26Ann Std Dev 100 73 81 88 83Sharpe Ratio 092 044 084 -013 032

MaxDD -96 -64 -76 -95 -74Skew -048 -027 -035 -049 -041

Kurt 256 179 190 167 172

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Short (Inverse) VIXreg Futures in two key years

11

bull Cost of holding futures in contango suggests that VIX futures and options may be best suited to strategic uses rather than buy and hold

bull Periods of strong contango may generate high returns to short (inverse) VIX futures or VIX call option writing strategies if a volatility event does not occur

bull However a volatility event may result in catastrophic losses to inverse VIX futures or written VIX call option positions

bull The following section considers the impact of a small allocation of inverse VIX futures and written call options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods generally unfavorable for inverse VIX positions (2008) and generally favorable for inverse VIX positions (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 7 Inverse VIXreg Futures and Options based strategies in 2008

12Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 7 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was an unfavorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

Exhibit 8 6040 Portfolio 2008 Performance with Inverse VIXreg Futures and Written VIX Calls

13Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 8 This exhibit illustrates the 2008 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

20086040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

Calls

Annual Return -209 -236 -233 -553 -323Ann Std Dev 241 260 248 1182 347Sharpe Ratio -087 -091 -094 -047 -093

MaxDD -309 -354 -333 -756 -441Skew 016 001 005 645 023

Kurt 414 333 374 8428 921

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 9 Endowment Portfolio in 2008 with Inverse VIXreg Futures and Written VIX Calls

14Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 9 This exhibit illustrates the 2008 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

2008 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

Calls

Annual Return -386 -402 -398 -678 -483Ann Std Dev 310 325 313 1396 410Sharpe Ratio -125 -124 -127 -049 -118

MaxDD -504 -531 -515 -830 -605Skew -013 -021 -019 693 -020

Kurt 321 279 307 9248 550

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 10 Inverse VIXreg Futures based strategies in 2016

15Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 10 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2016 was a generally favorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

Exhibit 11 6040 Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

16Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 11 This exhibit illustrates the 2016 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of low volatility and generally positive market returns a small allocation to VIX call writing can significantly increase returns with a moderate increase in volatility A 5 allocation to inverse VIX futures has a smaller impact but also provides a meaningful increase in return with a small increase in volatility and drawdowns

20166040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

CallsAnnual Return 84 143 104 189 147

Ann Std Dev 76 110 91 110 113Sharpe Ratio 111 130 114 172 130

MaxDD -54 -69 -61 -60 -78Skew -029 -096 -051 -059 -070

Kurt 223 522 352 389 371

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 12 Endowment Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

17Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 12 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of relative calm and positive performance small allocations to inverse VIX futures or VIX call writing increase returns significantly with a moderate increase in volatility A 5 allocation to inverse three month VIX futures doubles returns with no increase in volatility and a reduction in drawdown

2016 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

CallsAnnual Return 92 150 189 198 155

Ann Std Dev 100 130 100 127 131Sharpe Ratio 092 115 189 156 119

MaxDD -96 -110 -44 -100 -120Skew -048 -100 082 -071 -074

Kurt 256 532 615 368 333

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 13 VIXreg Futures and Options based strategies Buy and Hold performance for over 10 years 4242004 to 12292017

18Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 13 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios and two long VIX futures based portfolios over the entire almost 12 year period of study The volatility and drawdowns of the four VIX futures based portfolios suggest that VIX futures may be best suited for shorter term strategic portfolio risk management or return enhancement rather than long term buy and hold strategies

Source Bloomberg CFE Cboe Options Exchange

Exhibit 14 6040 Portfolio Performance with VIXreg Futures and VIX Options

19Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 14 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to long VIX futures or VIX call options The base 6040 portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations generally reduce volatility and drawdowns they do so while reducing returns

Source Bloomberg CFE Cboe Options Exchange

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures Held 1 Mo

6040 Plus 1 25 OTM Options

6040 Plus 1 ATM Options

Annual Return 75 44 59 41 39Ann Std Dev 114 81 92 125 87Sharpe Ratio 065 054 064 032 044

MaxDD -348 -265 -282 -265 -256Skew -010 035 010 -001 040

Kurt 1238 1625 1520 6289 1268

Exhibit 15 Endowment Portfolio Performance with VIXreg Futures and Long VIX Calls

20Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 15 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or VIX call options Similar to the 6040 portfolio the base endowment portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations reduce volatility and drawdowns they do so while reducing returns

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5

1 Mo FuturesEndowment Plus 5

3 Mo Futures Held 1 MoEndowment Plus 1

25 OTM OptionsEndowment Plus 1

ATM Options

Annual Return 54 28 41 26 22Ann Std Dev 165 131 142 162 137Sharpe Ratio 033 021 029 016 016

MaxDD -574 -504 -517 -429 -502Skew -024 002 -013 -040 004

Kurt 1018 1241 1125 2810 1136

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 16 6040 Portfolio Performance with Inverse VIXreg Futures and Written VIX Calls

21Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 16 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the 6040 portfolio are improved with the addition of VIX call writing or inverse VIX futures although the VIX call writing strategies significantly increase both volatility and drawdowns

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures Held

1 Mo

6040 Plus 1 Written 25 OTM VIX Calls

6040 Plus 1 Written ATM VIX Calls

Annual Return 75 95 83 83 105Ann Std Dev 114 137 124 386 174Sharpe Ratio 065 069 067 021 060

MaxDD -348 -385 -377 -756 -448Skew -010 -041 -027 1545 -026

Kurt 1238 743 943 62917 1936

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 17 Endowment Portfolio with Inverse VIXreg Futures and Written VIX Calls

22Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 17 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the endowment portfolio are improved with the addition of inverse VIX futures with a small increase in volatility In contrast VIX call writing reduces returns with a small impact on volatility

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5 1

Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

Endowment Plus 1 Written 25 OTM VIX

Calls

Endowment Plus 1 Written ATM VIX Calls

Annual Return 54 75 63 22 26Ann Std Dev 165 183 171 137 162Sharpe Ratio 033 041 037 016 016

MaxDD -574 -590 -583 -502 -429Skew -024 -044 -034 004 -040

Kurt 1018 766 890 1136 2810

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Open Interest and Volume of VIXreg Futures and Options

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

23

Volume and Open Interestbull VIX Futures and Options Volume have both increased

significantly in recent years coinciding with lower levels of VIXbull VIX Futures and Options Open Interest have also significantly

increased coinciding with lower levels of VIXbull Lower levels of VIX tend to correspond with a shift of option

volume towards puts and away from callsbull In recent years at low VIX levels non-commercial (speculative)

traders have significantly increased their short (inverse) position open interest as a proportion of total short open interest

bull Commercial (hedging) traders have recently increased their long positions as a proportion of total short open interest although these positions are at historically low levels

Exhibit 18 VIXreg Futures Volume and Spot VIXreg

Exhibit 18 This exhibit illustrates the historical levels of spot VIXreg and the daily Volume of VIXreg futures as well as the 20-trading day rolling average of VIXreg futures volume VIXreg Futures volume has increased significantly since 2010 Over the same period Spot VIXreg has generally trended lower While many factors have contributed to the increase in volume at the very least the data suggests that low levels of spot VIXreg do not result in a decrease in futures volume

24

3262004 to 12292017Mean Daily VIXreg Futures Volume

Mean VIXreg Spot

VIXreg Volume Correlation with Spot

92413

186

-026

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange

Exhibit 19 VIXreg Call Volume minus Put Volume

Exhibit 19 This exhibit illustrates the historical levels of spot VIXreg and the daily difference between the volume of VIXreg call options and put options as well as the 20-trading day rolling average of VIXreg call minus put volume VIXreg put options volume has generally increased relative to the volume of VIXreg call options since 2011 Over the same period Spot VIXreg has generally trended lower with a number of sharp spikes The data suggests that low levels of spot VIXreg may result in a tendency for VIXreg options volume to shift from calls towards puts

25

2242006 to 12292017

-140803

195

024

Mean VIXreg Call Volume minus Put Mean VIXreg SpotVIXreg Options Volume Correlation with VIXreg

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange

Exhibit 20 VIXreg Futures Open Interest by Trader Category

Exhibit 20 This exhibit illustrates the historical levels of the open interest of VIXreg futures by trader category based on weekly data from CFTC Commitment of Traders reports The data indicates that non-commercial (speculative) short (inverse) VIX futures exposure has increased in recent years while commercial (hedging) long VIX futures exposure has decreased All measures are presented as a percentage of total open interest so they do not reflect the overall significant increase in open interest in recent years The left panel provides the breakout by trader category of long interest in VIX futures while the right panel provides the breakout in short interest

26

Note White bars represent missing data

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Source Bloomberg CFE Cboe Options Exchange CFTC

Cboe Exchange Inc provided financial support for the research for this paper Options involve risk and are not suitable for all investors Prior to buying or selling an option a person must receive a copy of Characteristics and Risks of Standardized Options Copies are available from your broker or from The Options Clearing Corporation at wwwtheocccom Futures trading is not suitable for all investors and involves the risk of loss The risk of loss in futures can be substantial You should therefore carefully consider whether such trading is suitable for you in light of your circumstances and financial resources For additional information regarding futures trading risks see the Risk Disclosure Statement set forth in CFTC Regulation sect155(b) The information in these materials are provided for general education and information purposes only No statement within these materials should be construed as a recommendation to buy or sell a security or future or to provide investment advice Past performance is not indicative of future results Parameters relating to past performance of strategies discussed are not capable of being duplicated These materials contain performance data based on back-testing ie calculations of how a sample portfolio might have performed Back-tested performance information is purely hypothetical and is provided in these materials solely for informational purposes Back-tested performance does not represent actual performance and should not be interpreted as an indication of actual performance No representation is being made that any investment will or is likely to achieve a performance record similar to that shown The views of third party speakers and their materials are their own and do not necessarily represent the views of Cboe Third party speakers are not affiliated with Cboe These materials should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe product or service described in these materials Cboereg and VIXreg are registered trademarks and RMCSM is a service mark of Cboe Exchange Inc SampP 500reg is a registered trademark of Standard and Poors Financial Services LLC Financial products based on SampP indices are not sponsored endorsed sold or promoted by Standard amp Poorrsquos and neither Standard ampPoorrsquos nor Cboe make any representation regarding the advisability of investing in such products All other trademarks and service marks are the property of their respective owners More information is or will be available at wwwcboecomfunds Please email comments to eszadoprovidenceedu or institutionalcboecom

27Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Overview

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

3

1 Long VIXreg Futures and Long VIXreg Call based Strategies in Two Key Years ndash 2008 and 2016

2 Inverse VIXreg Futures and VIXreg Call Writing based Strategies in Two Key Years ndash 2008 and 2016

3 Performance of Long Term Buy and Hold Long and Inverse VIXreg based Strategies (2242006 to 12312017)

4 Open Interest and Volume of VIXreg options and futures

VIXreg Futures and Options Based Strategies in Two Key Years

4

bull Cost of holding futures in contango (when spot price is below futures price) suggests that long VIX futures and long VIX call option positions may be best suited to strategic uses rather than buy and hold

bull However the convex relationship and strong negative conditional correlation between the VIX index and the SampP 500 suggests long VIX futures and call options may provide an effective hedge for traditional portfolios

bull The following section considers the impact of a small allocation of VIX futures and options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods favorable to long positions in VIX futures and call options (2008) and generally unfavorable to long positions in VIX futures and call options (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 1 VIXreg Futures and Options Based Strategies in 2008

5Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 1 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was favorable year for a long VIX futures exposure The hypothetical endowment portfolio is constructed by using annually reported asset allocation from an actual endowment and applying them to a set of total return indices representing the corresponding asset classes

Source Bloomberg CFE Cboe Options Exchange

Exhibit 2 6040 Portfolio Performance in 2008 with VIXreg Futures and Options

6Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 2 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options A 1 allocation to 25 OTM VIX calls increases 2008 returns from a 21 loss to a 12 gain with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE CboeOptions Exchange Optionmetrics2008

6040 StockBond

Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return -209 -134 -154 121 -94Ann Std Dev 241 184 204 276 179Sharpe Ratio -087 -073 -076 044 -053

MaxDD -309 -221 -247 -204 -188Skew 016 036 026 029 049

Kurt 414 408 425 2241 446

Exhibit 3 Endowment Portfolio Performance in 2008 with VIXreg Futures and Options

7Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 3 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocationto long VIX futures or long VIX call options Similarly to the 6040 portfolio a 1 allocation to 25 OTM VIX calls provides the largest improvement in 2008 returns from a 39 loss to a 10 loss with a small increase in volatility The other VIX based allocations also improve returns while also reducing volatility and drawdowns

Source Bloomberg CFE Cboe Options Exchange Optionmetrics2008 Endowment

Endowment Plus 5 1 Mo

Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return -386 -311 -329 -98 -283Ann Std Dev 310 252 271 328 251Sharpe Ratio -125 -123 -122 -030 -113

MaxDD -504 -415 -444 -322 -382Skew -013 -002 -008 -031 001

Kurt 321 361 326 1365 408

Exhibit 4 VIXreg Futures and Options based strategies in 2016

8Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 4 This exhibit illustrates the performance of two traditional portfolios as well as two VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio invests in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio purchases three month VIX futures and rolls into a new 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment

Source Bloomberg CFE Cboe Options Exchange

Exhibit 5 6040 Portfolio Performance in 2016 with VIXreg Futures and Options

9Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 5 This exhibit illustrates the performance of a traditional 6040 portfolio with and without a small allocation to long VIX futures or long VIX call options While a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

20166040

StockBond Portfolio

6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures

Held 1 Mo

6040 Plus 1 25OTM Options

6040 Plus 1 ATM Options

Annual Return 84 23 59 -19 18Ann Std Dev 76 44 54 57 53Sharpe Ratio 111 052 109 -034 034

MaxDD -54 -29 -35 -53 -39Skew -029 057 005 021 038

Kurt 223 177 169 175 186

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 6 Endowment Portfolio Performance in 2016 with VIXreg Futures and Options

10Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 6 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or long VIX call options Similarly to the 6040 portfolio a 5 long allocation to one month VIX futures significantly increase returns a 1 allocation to ATM or 25 OTM VIX calls significantly reduces returns 2008 returns albeit with a small reduction in volatility and drawdowns

2016 EndowmentEndowment

Plus 5 1 Mo Futures

Endowment Plus 5 3 Mo Futures Held 1

Mo

Endowment Plus 1

25OTM Options

Endowment Plus 1 ATM

Options

Annual Return 92 32 67 -11 26Ann Std Dev 100 73 81 88 83Sharpe Ratio 092 044 084 -013 032

MaxDD -96 -64 -76 -95 -74Skew -048 -027 -035 -049 -041

Kurt 256 179 190 167 172

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Short (Inverse) VIXreg Futures in two key years

11

bull Cost of holding futures in contango suggests that VIX futures and options may be best suited to strategic uses rather than buy and hold

bull Periods of strong contango may generate high returns to short (inverse) VIX futures or VIX call option writing strategies if a volatility event does not occur

bull However a volatility event may result in catastrophic losses to inverse VIX futures or written VIX call option positions

bull The following section considers the impact of a small allocation of inverse VIX futures and written call options to a traditional stock and bond portfolio and a hypothetical endowment portfolios

bull Two years were chosen to represent periods generally unfavorable for inverse VIX positions (2008) and generally favorable for inverse VIX positions (2016)

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 7 Inverse VIXreg Futures and Options based strategies in 2008

12Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 7 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2008 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2008 was an unfavorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

Exhibit 8 6040 Portfolio 2008 Performance with Inverse VIXreg Futures and Written VIX Calls

13Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 8 This exhibit illustrates the 2008 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

20086040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

Calls

Annual Return -209 -236 -233 -553 -323Ann Std Dev 241 260 248 1182 347Sharpe Ratio -087 -091 -094 -047 -093

MaxDD -309 -354 -333 -756 -441Skew 016 001 005 645 023

Kurt 414 333 374 8428 921

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 9 Endowment Portfolio in 2008 with Inverse VIXreg Futures and Written VIX Calls

14Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 9 This exhibit illustrates the 2008 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of crisis even a small allocation to VIX call writing can significantly reduce returns and increase volatility A 5 allocation to inverse VIX futures has a smaller impact but also reduces returns while slightly increasing volatility and drawdowns

2008 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

Calls

Annual Return -386 -402 -398 -678 -483Ann Std Dev 310 325 313 1396 410Sharpe Ratio -125 -124 -127 -049 -118

MaxDD -504 -531 -515 -830 -605Skew -013 -021 -019 693 -020

Kurt 321 279 307 9248 550

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 10 Inverse VIXreg Futures based strategies in 2016

15Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 10 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios in 2016 The VIX portfolios are both fully collateralized and rebalanced daily The one month portfolio takes short positions in one month VIX futures and rolls out on the close the night before expiration The Three month VIX futures portfolio shorts three month VIX futures and rolls into a new short 3 month VIX futures contract after one month at the close before the front month VIX futures contract expires The traditional portfolios consist of a 6040 StockBond portfolio and a hypothetical endowment portfolio which invests in a variety of indices based on the average yearly asset allocation of a representative endowment It is clear from the exhibit that 2016 was a generally favorable year for inverse VIX futures exposure

Source Bloomberg CFE Cboe Options Exchange

Exhibit 11 6040 Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

16Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 11 This exhibit illustrates the 2016 performance of a traditional 6040 portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of low volatility and generally positive market returns a small allocation to VIX call writing can significantly increase returns with a moderate increase in volatility A 5 allocation to inverse VIX futures has a smaller impact but also provides a meaningful increase in return with a small increase in volatility and drawdowns

20166040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

6040 Plus 1 Written 25 OTM

VIX Calls

6040 Plus 1 Written ATM VIX

CallsAnnual Return 84 143 104 189 147

Ann Std Dev 76 110 91 110 113Sharpe Ratio 111 130 114 172 130

MaxDD -54 -69 -61 -60 -78Skew -029 -096 -051 -059 -070

Kurt 223 522 352 389 371

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 12 Endowment Portfolio in 2016 with Inverse VIXreg Futures and Written VIX Calls

17Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 12 This exhibit illustrates the 2016 performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options In this period of relative calm and positive performance small allocations to inverse VIX futures or VIX call writing increase returns significantly with a moderate increase in volatility A 5 allocation to inverse three month VIX futures doubles returns with no increase in volatility and a reduction in drawdown

2016 EndowmentEndowment Plus 5

1 Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX

Futures Held 1 Mo

Endowment Plus 1 Written 25 OTM

VIX Calls

Endowment Plus 1 Written ATM VIX

CallsAnnual Return 92 150 189 198 155

Ann Std Dev 100 130 100 127 131Sharpe Ratio 092 115 189 156 119

MaxDD -96 -110 -44 -100 -120Skew -048 -100 082 -071 -074

Kurt 256 532 615 368 333

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 13 VIXreg Futures and Options based strategies Buy and Hold performance for over 10 years 4242004 to 12292017

18Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 13 This exhibit illustrates the performance of two traditional portfolios as well as two inverse VIX futures based portfolios and two long VIX futures based portfolios over the entire almost 12 year period of study The volatility and drawdowns of the four VIX futures based portfolios suggest that VIX futures may be best suited for shorter term strategic portfolio risk management or return enhancement rather than long term buy and hold strategies

Source Bloomberg CFE Cboe Options Exchange

Exhibit 14 6040 Portfolio Performance with VIXreg Futures and VIX Options

19Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 14 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to long VIX futures or VIX call options The base 6040 portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations generally reduce volatility and drawdowns they do so while reducing returns

Source Bloomberg CFE Cboe Options Exchange

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Futures

6040 Plus 5 3 Mo Futures Held 1 Mo

6040 Plus 1 25 OTM Options

6040 Plus 1 ATM Options

Annual Return 75 44 59 41 39Ann Std Dev 114 81 92 125 87Sharpe Ratio 065 054 064 032 044

MaxDD -348 -265 -282 -265 -256Skew -010 035 010 -001 040

Kurt 1238 1625 1520 6289 1268

Exhibit 15 Endowment Portfolio Performance with VIXreg Futures and Long VIX Calls

20Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 15 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to long VIX futures or VIX call options Similar to the 6040 portfolio the base endowment portfolio provides the highest return without a long VIX based allocation While the long VIX based allocations reduce volatility and drawdowns they do so while reducing returns

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5

1 Mo FuturesEndowment Plus 5

3 Mo Futures Held 1 MoEndowment Plus 1

25 OTM OptionsEndowment Plus 1

ATM Options

Annual Return 54 28 41 26 22Ann Std Dev 165 131 142 162 137Sharpe Ratio 033 021 029 016 016

MaxDD -574 -504 -517 -429 -502Skew -024 002 -013 -040 004

Kurt 1018 1241 1125 2810 1136

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 16 6040 Portfolio Performance with Inverse VIXreg Futures and Written VIX Calls

21Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 16 This exhibit illustrates the performance of a 6040 traditional portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the 6040 portfolio are improved with the addition of VIX call writing or inverse VIX futures although the VIX call writing strategies significantly increase both volatility and drawdowns

24 Feb 2006 to 29 Dec 20176040 StockBond

Portfolio6040 Plus 5 1 Mo Inverse VIX Futures

6040 Plus 5 3 Mo Inverse VIX Futures Held

1 Mo

6040 Plus 1 Written 25 OTM VIX Calls

6040 Plus 1 Written ATM VIX Calls

Annual Return 75 95 83 83 105Ann Std Dev 114 137 124 386 174Sharpe Ratio 065 069 067 021 060

MaxDD -348 -385 -377 -756 -448Skew -010 -041 -027 1545 -026

Kurt 1238 743 943 62917 1936

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Exhibit 17 Endowment Portfolio with Inverse VIXreg Futures and Written VIX Calls

22Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

Exhibit 17 This exhibit illustrates the performance of a hypothetical endowment portfolio with and without a small allocation to inverse VIX futures or written VIX call options The returns of the endowment portfolio are improved with the addition of inverse VIX futures with a small increase in volatility In contrast VIX call writing reduces returns with a small impact on volatility

24 Feb 2006 to 29 Dec 2017 EndowmentEndowment Plus 5 1

Mo Inverse VIX Futures

Endowment Plus 5 3 Mo Inverse VIX Futures

Held 1 Mo

Endowment Plus 1 Written 25 OTM VIX

Calls

Endowment Plus 1 Written ATM VIX Calls

Annual Return 54 75 63 22 26Ann Std Dev 165 183 171 137 162Sharpe Ratio 033 041 037 016 016

MaxDD -574 -590 -583 -502 -429Skew -024 -044 -034 004 -040

Kurt 1018 766 890 1136 2810

Source Bloomberg CFE Cboe Options Exchange Optionmetrics

Open Interest and Volume of VIXreg Futures and Options

Portfolio Risk Management with VIXreg Futures and Options 6 March 2018 Please see the last slide for important disclosures

23

Volume and Open Interestbull VIX Futures and Options Volume have both increased

significantly in recent years coinciding with lower levels of VIXbull VIX Futures and Options Open Interest have also significantly

increased coinciding with lower levels of VIXbull Lower levels of VIX tend to correspond with a shift of option