Embed Size (px)

Citation preview

October 12, 2018

PORTUGAL

ECONOMICS & STATE FUNDING

Portugal has turned the corner from the European crisis, with economicrebalancing and structural reforms underpinning the recovery

Source: EC, IGCP

2

Executive summary

1. Economic revitalization, following a sustained recovery in the past 4 years. Currently, Portugal stands as one of the fastest-growing economies of the EA

2. Strong growth foundations led to the correction of macroeconomic imbalances, resulting in successive current and capital account surpluses since 2013

3. Private sector turnaround, following an extensive deleveraging process and balance sheet strengthening

4. Fiscal stabilization, based on sizable fiscal adjustments, successive primary surplus and lower interest charges, resulting in a sustained downward trend of GG debt

5. Resilient public debt structure, enhancing shock-absorptive capacities

6. Improving market conditions, based on lower financing costs and broadening investor base

Outline

2

6

10

14

18

-15

-10

-5

0

5

1995 1998 2001 2004 2007 2010 2013 2016 2019

% la

bo

ur

forc

e

% G

DP

Current account balance (LHS)Primary balance (LHS)Primary balance, excl BES/Banif resolutions (LHS)Unemployment rate (RHS)

Boom Slump CrisisBalancedGrowth

EC f

ore

cast

s

Outline

3

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

1.

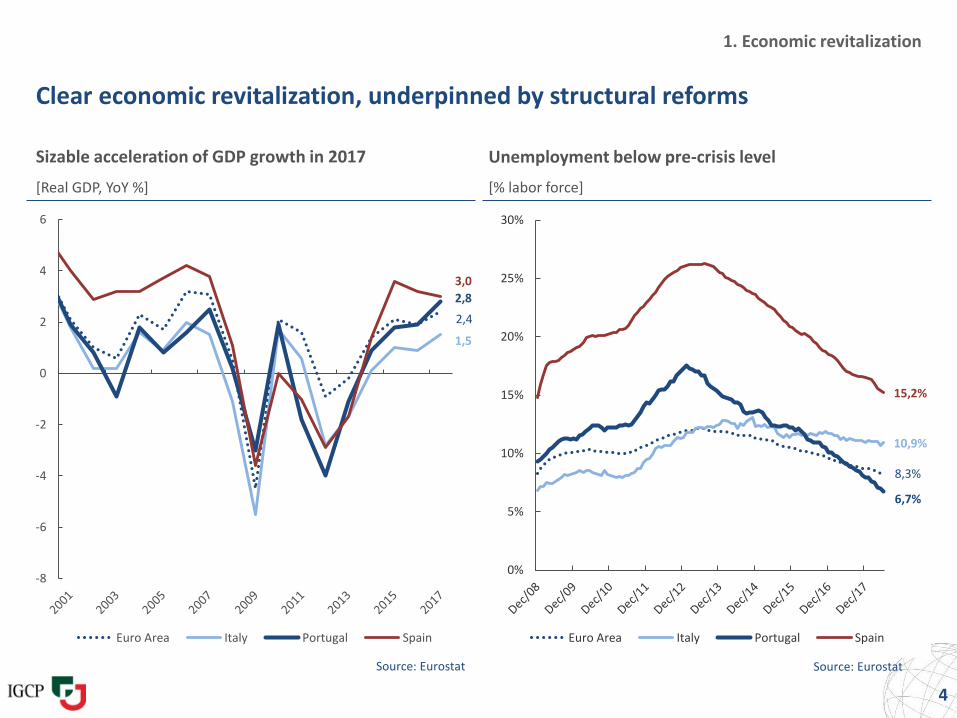

1. Economic revitalization

Clear economic revitalization, underpinned by structural reforms

Source: Eurostat

4

[Real GDP, YoY %]

Unemployment below pre-crisis level

[% labor force]

Source: Eurostat

Sizable acceleration of GDP growth in 2017

2,4

1,5

2,8

3,0

-8

-6

-4

-2

0

2

4

6

Euro Area Italy Portugal Spain

8,3%

10,9%

6,7%

15,2%

0%

5%

10%

15%

20%

25%

30%

Euro Area Italy Portugal Spain

1. Economic revitalization

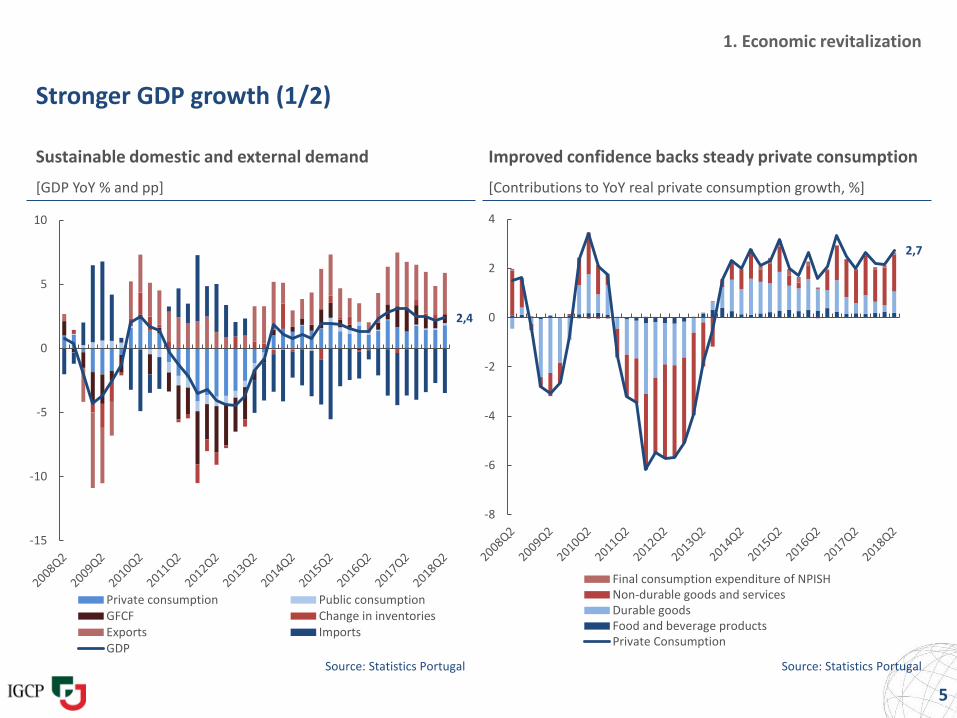

Stronger GDP growth (1/2)

[GDP YoY % and pp] [Contributions to YoY real private consumption growth, %]

Source: Statistics Portugal Source: Statistics Portugal

5

Sustainable domestic and external demand Improved confidence backs steady private consumption

2,4

-15

-10

-5

0

5

10

Private consumption Public consumptionGFCF Change in inventoriesExports ImportsGDP

2,7

-8

-6

-4

-2

0

2

4

Final consumption expenditure of NPISHNon-durable goods and servicesDurable goodsFood and beverage productsPrivate Consumption

1. Economic revitalization

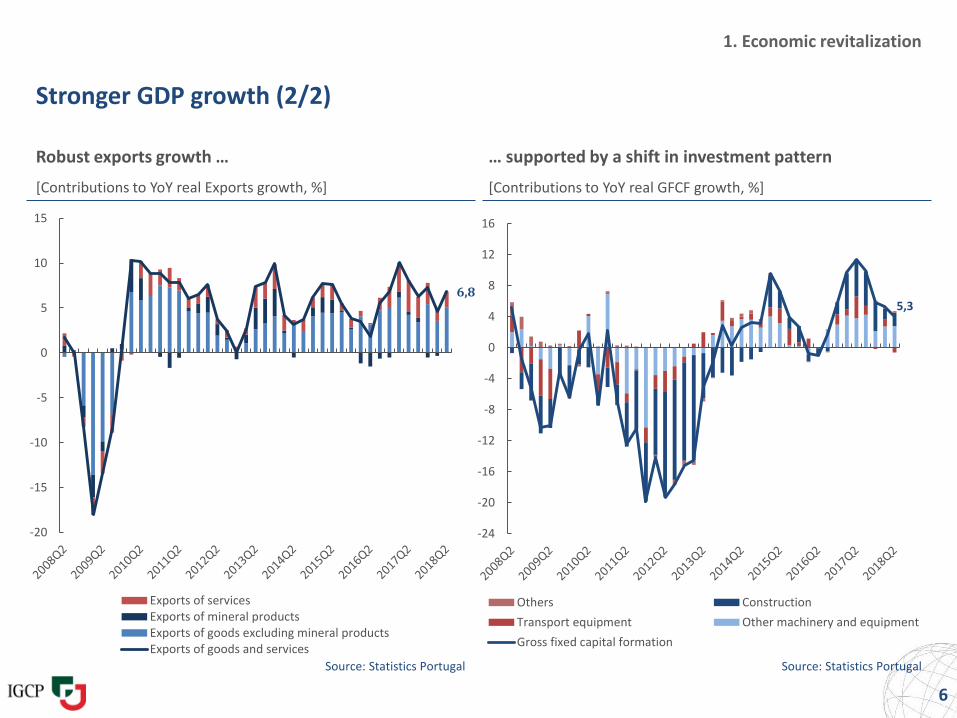

Stronger GDP growth (2/2)

Robust exports growth … … supported by a shift in investment pattern

[Contributions to YoY real Exports growth, %] [Contributions to YoY real GFCF growth, %]

Source: Statistics Portugal Source: Statistics Portugal

6

6,8

-20

-15

-10

-5

0

5

10

15

Exports of servicesExports of mineral productsExports of goods excluding mineral productsExports of goods and services

5,3

-24

-20

-16

-12

-8

-4

0

4

8

12

16

Others Construction

Transport equipment Other machinery and equipment

Gross fixed capital formation

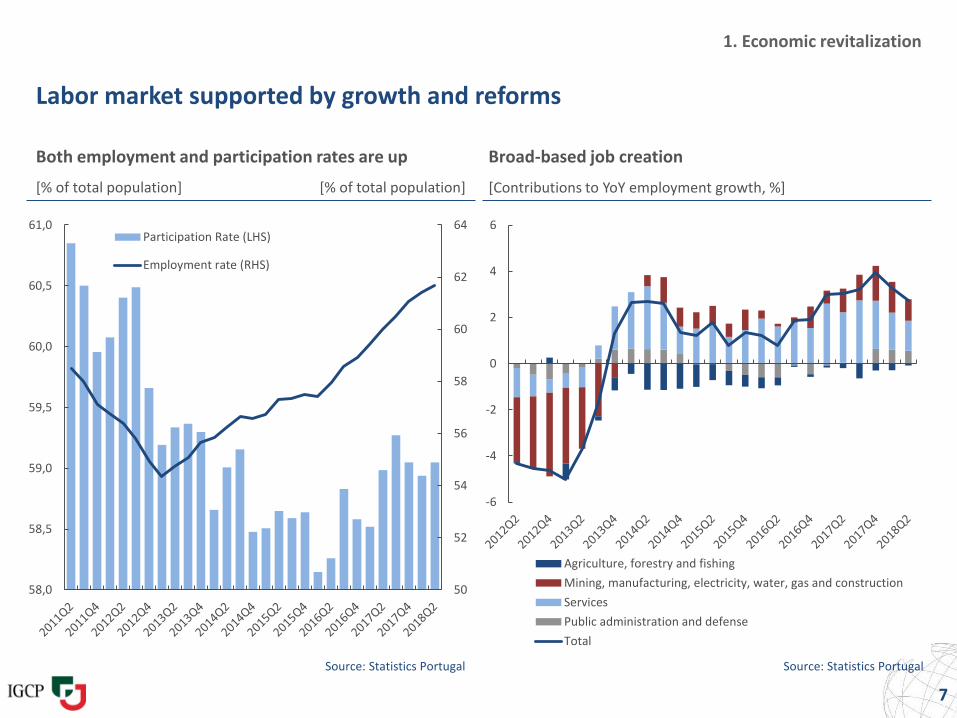

Labor market supported by growth and reforms

Broad-based job creation

[% of total population] [Contributions to YoY employment growth, %]

7

1. Economic revitalization

Both employment and participation rates are up

Source: Statistics Portugal Source: Statistics Portugal

[% of total population]

-6

-4

-2

0

2

4

6

Agriculture, forestry and fishing

Mining, manufacturing, electricity, water, gas and construction

Services

Public administration and defense

Total

50

52

54

56

58

60

62

64

58,0

58,5

59,0

59,5

60,0

60,5

61,0Participation Rate (LHS)

Employment rate (RHS)

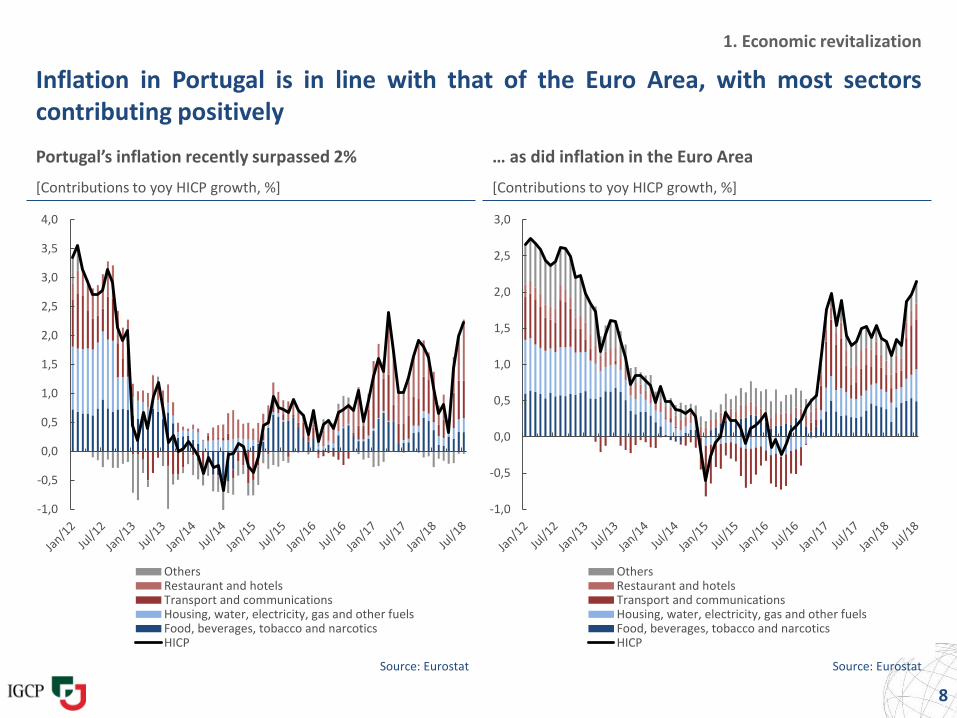

Inflation in Portugal is in line with that of the Euro Area, with most sectorscontributing positively

Portugal’s inflation recently surpassed 2% … as did inflation in the Euro Area

[Contributions to yoy HICP growth, %]

Source: Eurostat Source: Eurostat

8

1. Economic revitalization

[Contributions to yoy HICP growth, %]

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

OthersRestaurant and hotelsTransport and communicationsHousing, water, electricity, gas and other fuelsFood, beverages, tobacco and narcoticsHICP

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

OthersRestaurant and hotelsTransport and communicationsHousing, water, electricity, gas and other fuelsFood, beverages, tobacco and narcoticsHICP

1. Economic revitalization

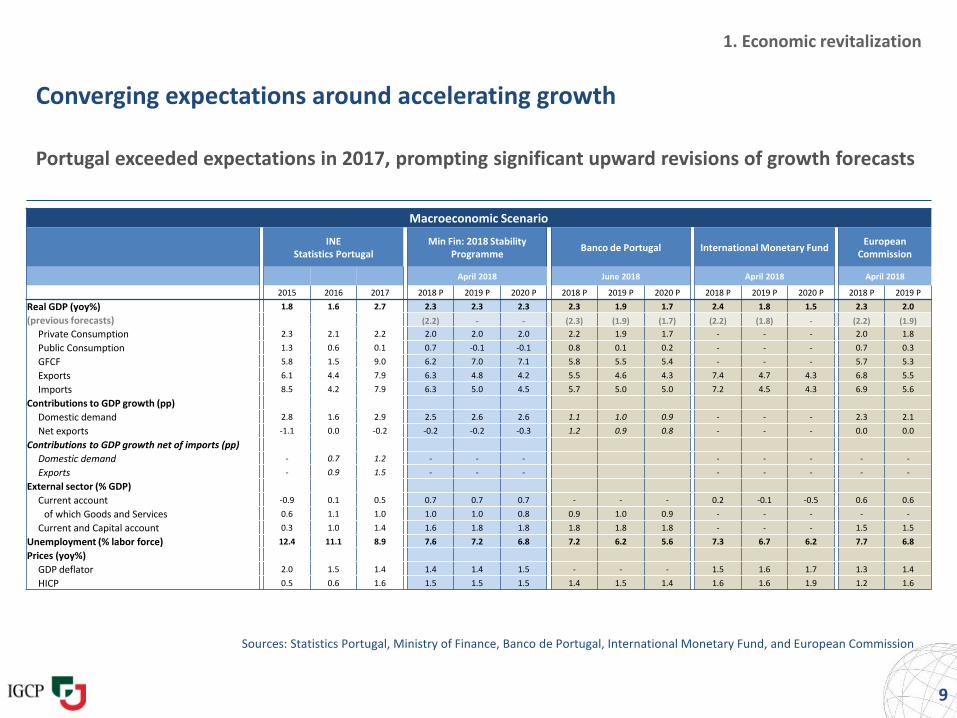

Converging expectations around accelerating growth

Portugal exceeded expectations in 2017, prompting significant upward revisions of growth forecasts

Sources: Statistics Portugal, Ministry of Finance, Banco de Portugal, International Monetary Fund, and European Commission

9

Macroeconomic Scenario

INEStatistics Portugal

Min Fin: 2018 Stability Programme

Banco de Portugal International Monetary FundEuropean

Commission

April 2018 June 2018 April 2018 April 2018

2015 2016 2017 2018 P 2019 P 2020 P 2018 P 2019 P 2020 P 2018 P 2019 P 2020 P 2018 P 2019 P

Real GDP (yoy%) 1.8 1.6 2.7 2.3 2.3 2.3 2.3 1.9 1.7 2.4 1.8 1.5 2.3 2.0

(previous forecasts) (2.2) - - (2.3) (1.9) (1.7) (2.2) (1.8) - (2.2) (1.9)

Private Consumption 2.3 2.1 2.2 2.0 2.0 2.0 2.2 1.9 1.7 - - - 2.0 1.8

Public Consumption 1.3 0.6 0.1 0.7 -0.1 -0.1 0.8 0.1 0.2 - - - 0.7 0.3

GFCF 5.8 1.5 9.0 6.2 7.0 7.1 5.8 5.5 5.4 - - - 5.7 5.3

Exports 6.1 4.4 7.9 6.3 4.8 4.2 5.5 4.6 4.3 7.4 4.7 4.3 6.8 5.5

Imports 8.5 4.2 7.9 6.3 5.0 4.5 5.7 5.0 5.0 7.2 4.5 4.3 6.9 5.6

Contributions to GDP growth (pp)

Domestic demand 2.8 1.6 2.9 2.5 2.6 2.6 1.1 1.0 0.9 - - - 2.3 2.1

Net exports -1.1 0.0 -0.2 -0.2 -0.2 -0.3 1.2 0.9 0.8 - - - 0.0 0.0

Contributions to GDP growth net of imports (pp)

Domestic demand - 0.7 1.2 - - - - - - - -

Exports - 0.9 1.5 - - - - - - - -

External sector (% GDP)

Current account -0.9 0.1 0.5 0.7 0.7 0.7 - - - 0.2 -0.1 -0.5 0.6 0.6

of which Goods and Services 0.6 1.1 1.0 1.0 1.0 0.8 0.9 1.0 0.9 - - - - -

Current and Capital account 0.3 1.0 1.4 1.6 1.8 1.8 1.8 1.8 1.8 - - - 1.5 1.5

Unemployment (% labor force) 12.4 11.1 8.9 7.6 7.2 6.8 7.2 6.2 5.6 7.3 6.7 6.2 7.7 6.8

Prices (yoy%)

GDP deflator 2.0 1.5 1.4 1.4 1.4 1.5 - - - 1.5 1.6 1.7 1.3 1.4

HICP 0.5 0.6 1.6 1.5 1.5 1.5 1.4 1.5 1.4 1.6 1.6 1.9 1.2 1.6

Outline

10

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

2.

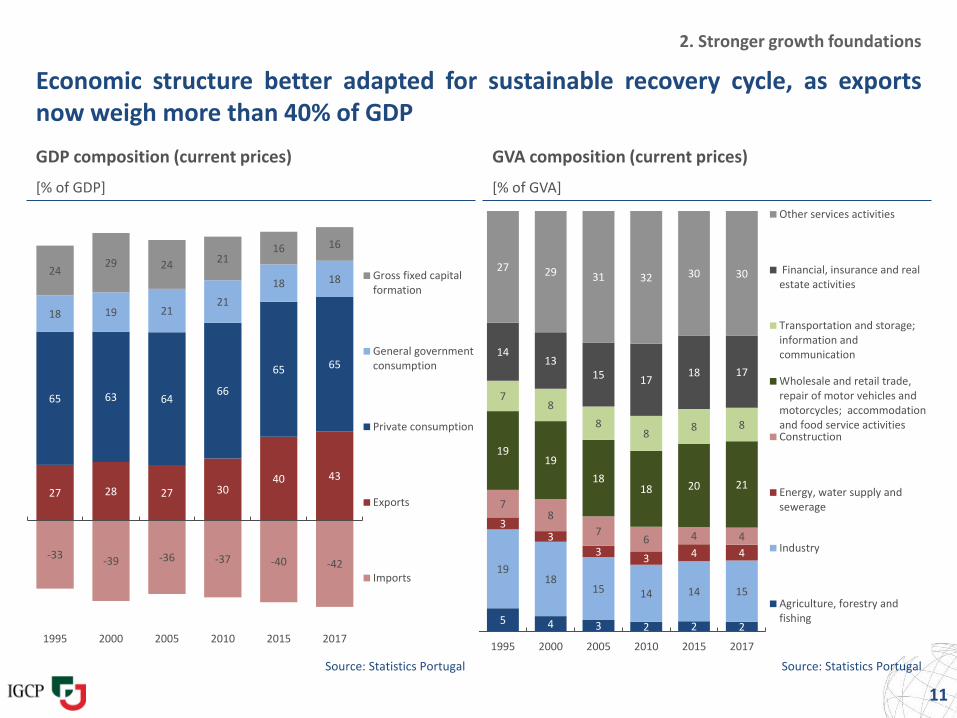

Economic structure better adapted for sustainable recovery cycle, as exportsnow weigh more than 40% of GDP

GDP composition (current prices) GVA composition (current prices)

[% of GDP] [% of GVA]

Source: Statistics Portugal Source: Statistics Portugal

11

2. Stronger growth foundations

-33-39 -36 -37 -40 -42

27 28 27 3040 43

65 63 6466

65 65

18 19 2121

18 1824

29 24 2116 16

1995 2000 2005 2010 2015 2017

Gross fixed capitalformation

General governmentconsumption

Private consumption

Exports

Imports

5 4 3 2 2 2

1918

15 14 14 15

33

33 4 4

78

76 4 4

1919

1818 20 21

78

88

8 8

1413

15 1718 17

27 29 31 32 30 30

1995 2000 2005 2010 2015 2017

Other services activities

Financial, insurance and realestate activities

Transportation and storage;information andcommunication

Wholesale and retail trade,repair of motor vehicles andmotorcycles; accommodationand food service activitiesConstruction

Energy, water supply andsewerage

Industry

Agriculture, forestry andfishing

2. Stronger growth foundations

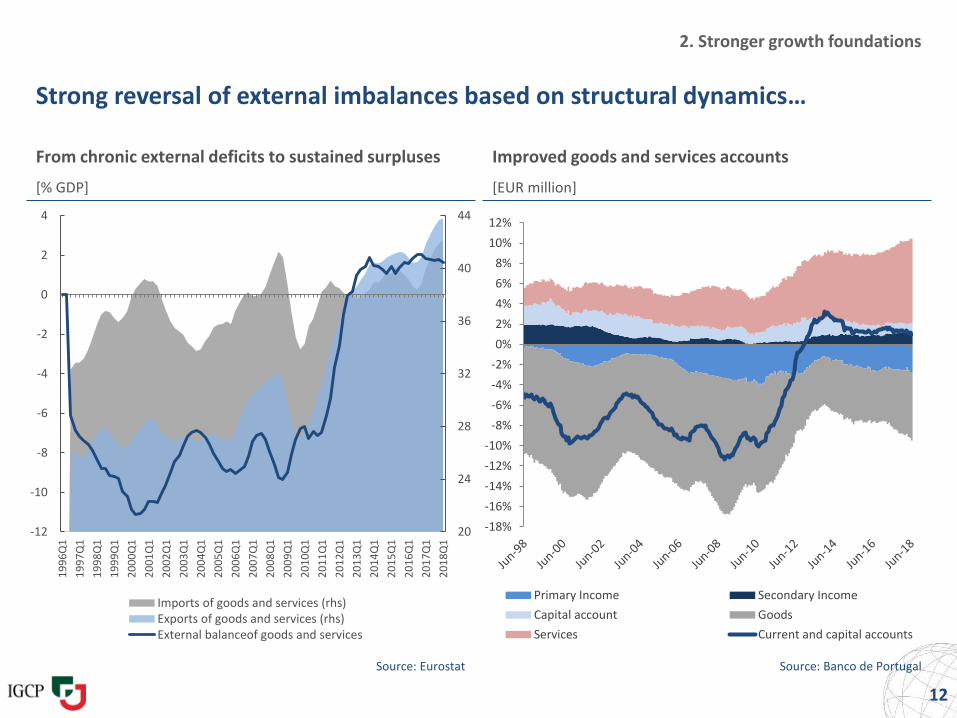

Strong reversal of external imbalances based on structural dynamics…

From chronic external deficits to sustained surpluses Improved goods and services accounts

[% GDP] [EUR million]

12

Source: Eurostat Source: Banco de Portugal

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Primary Income Secondary Income

Capital account Goods

Services Current and capital accounts

20

24

28

32

36

40

44

-12

-10

-8

-6

-4

-2

0

2

4

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

Imports of goods and services (rhs)Exports of goods and services (rhs)External balanceof goods and services

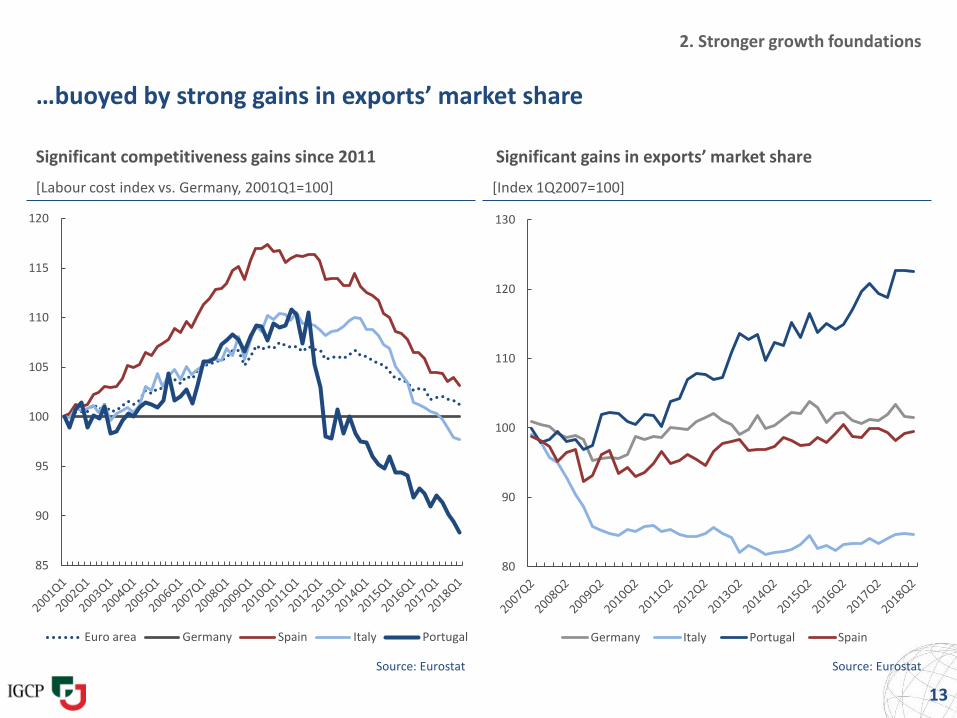

…buoyed by strong gains in exports’ market share

2. Stronger growth foundations

13

Significant gains in exports’ market share

[Index 1Q2007=100]

Source: Eurostat

[Labour cost index vs. Germany, 2001Q1=100]

Significant competitiveness gains since 2011

Source: Eurostat

85

90

95

100

105

110

115

120

Euro area Germany Spain Italy Portugal

80

90

100

110

120

130

Germany Italy Portugal Spain

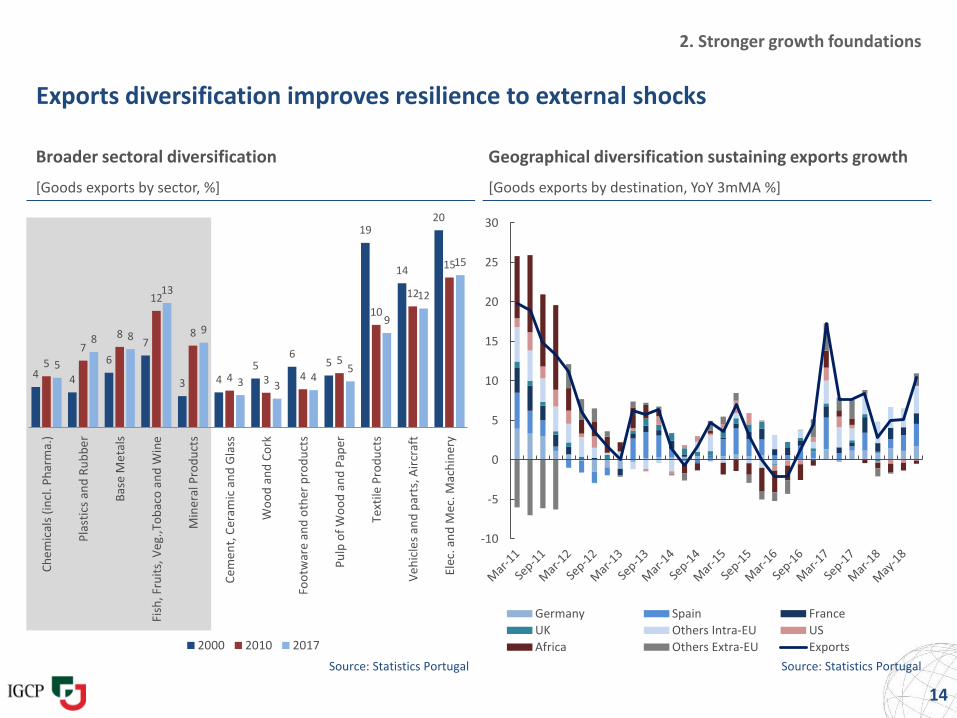

Exports diversification improves resilience to external shocks

Broader sectoral diversification

[Goods exports by sector, %]

Source: Statistics Portugal

14

2. Stronger growth foundations

Source: Statistics Portugal

Geographical diversification sustaining exports growth

[Goods exports by destination, YoY 3mMA %]

4 4

6

7

3 45

65

19

14

20

5

78

12

8

4 3 4

5

10

12

15

5

8 8

13

9

3 34

5

9

12

15

Ch

em

ical

s (i

ncl

. Ph

arm

a.)

Pla

stic

s an

d R

ub

be

r

Bas

e M

eta

ls

Fish

, Fru

its,

Ve

g.,T

ob

aco

an

d W

ine

Min

era

l Pro

du

cts

Ce

me

nt,

Cer

amic

an

d G

lass

Wo

od

an

d C

ork

Foo

twar

e an

d o

ther

pro

du

cts

Pu

lp o

f W

oo

d a

nd

Pap

er

Text

ile P

rod

uct

s

Ve

hic

les

and

par

ts, A

ircr

aft

Elec

. an

d M

ec. M

ach

iner

y

2000 2010 2017

-10

-5

0

5

10

15

20

25

30

Germany Spain France

UK Others Intra-EU US

Africa Others Extra-EU Exports

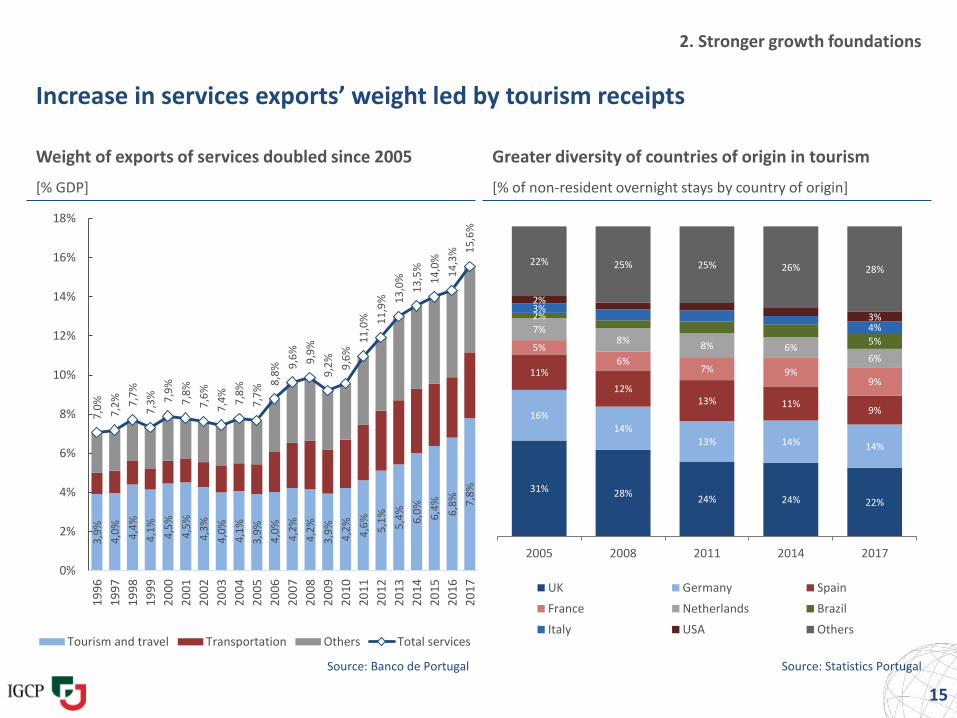

Increase in services exports’ weight led by tourism receipts

Weight of exports of services doubled since 2005 Greater diversity of countries of origin in tourism

[% GDP] [% of non-resident overnight stays by country of origin]

Source: Banco de Portugal Source: Statistics Portugal

15

2. Stronger growth foundations

31% 28%24% 24% 22%

16%14%

13% 14% 14%

11%

12%13% 11%

9%

5%

6%7% 9%

9%

7%8%

8% 6%6%

2%

5%

3%

4%

2%

3%

22% 25% 25% 26% 28%

2005 2008 2011 2014 2017

UK Germany Spain

France Netherlands Brazil

Italy USA Others

3,9

%

4,0

%

4,4

%

4,1

%

4,5

%

4,5

%

4,3

%

4,0

%

4,1

%

3,9

%

4,0

%

4,2

%

4,2

%

3,9

%

4,2

%

4,6

%

5,1

%

5,4

%

6,0

%

6,4

%

6,8

% 7,8

%

7,0

%

7,2

% 7,7

%

7,3

% 7,9

%

7,8

%

7,6

%

7,4

%

7,8

%

7,7

%

8,8

% 9,6

%

9,9

%

9,2

%

9,6

%

11

,0% 11

,9% 1

3,0

%

13

,5%

14

,0%

14

,3% 1

5,6

%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Tourism and travel Transportation Others Total services

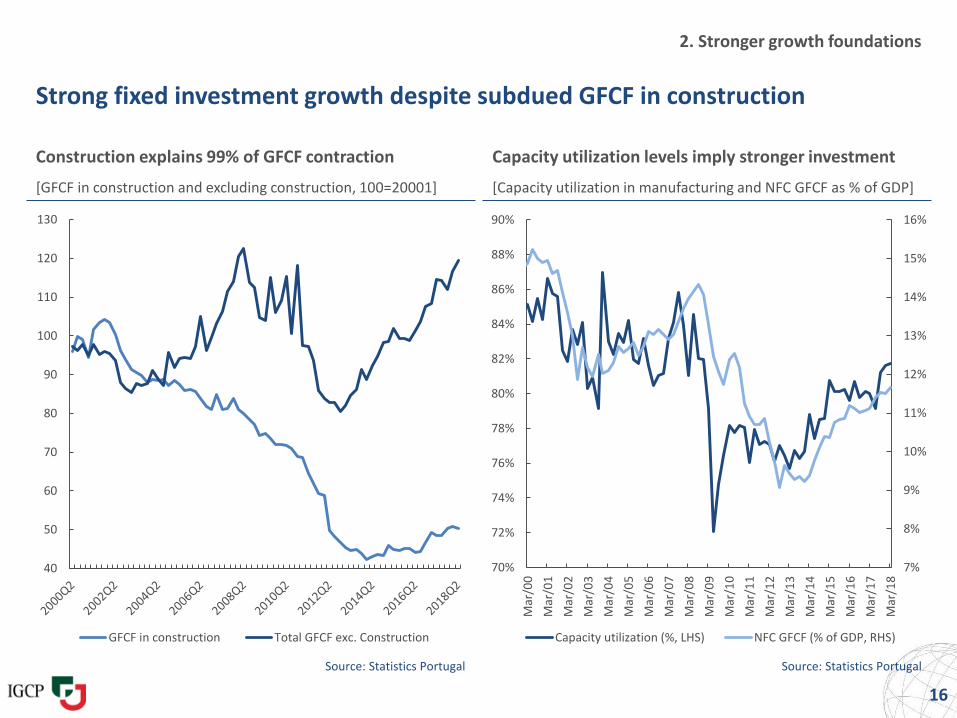

Strong fixed investment growth despite subdued GFCF in construction

Construction explains 99% of GFCF contraction

[GFCF in construction and excluding construction, 100=20001]

Source: Statistics Portugal Source: Statistics Portugal

16

2. Stronger growth foundations

Capacity utilization levels imply stronger investment

[Capacity utilization in manufacturing and NFC GFCF as % of GDP]

40

50

60

70

80

90

100

110

120

130

GFCF in construction Total GFCF exc. Construction

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

70%

72%

74%

76%

78%

80%

82%

84%

86%

88%

90%

Mar

/00

Mar

/01

Mar

/02

Mar

/03

Mar

/04

Mar

/05

Mar

/06

Mar

/07

Mar

/08

Mar

/09

Mar

/10

Mar

/11

Mar

/12

Mar

/13

Mar

/14

Mar

/15

Mar

/16

Mar

/17

Mar

/18

Capacity utilization (%, LHS) NFC GFCF (% of GDP, RHS)

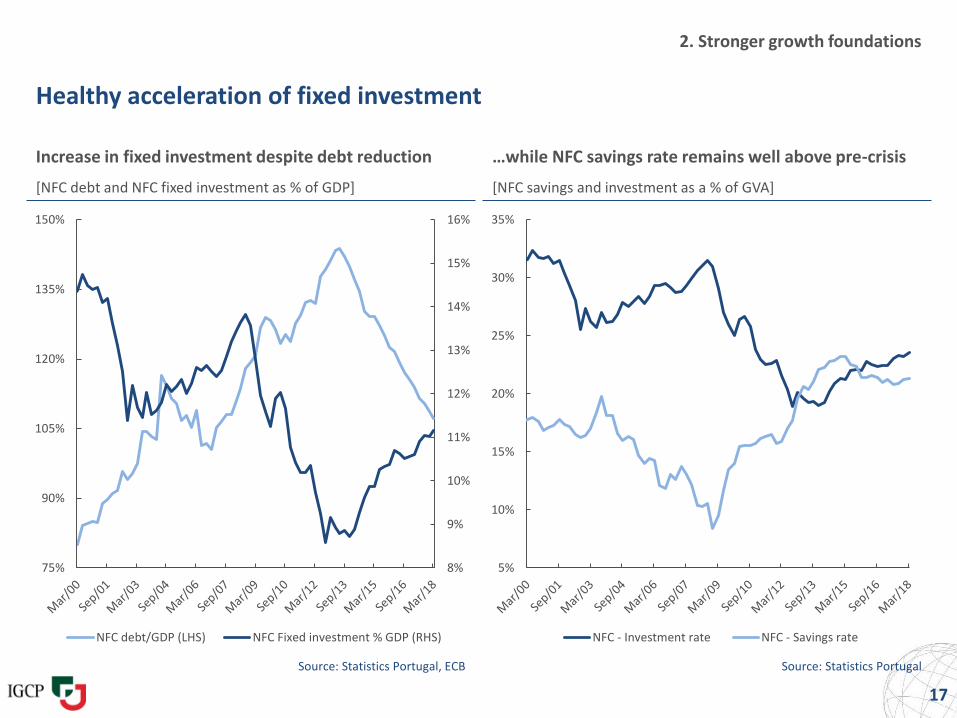

Healthy acceleration of fixed investment

Increase in fixed investment despite debt reduction

[NFC debt and NFC fixed investment as % of GDP]

Source: Statistics Portugal, ECB Source: Statistics Portugal

17

2. Stronger growth foundations

…while NFC savings rate remains well above pre-crisis

[NFC savings and investment as a % of GVA]

8%

9%

10%

11%

12%

13%

14%

15%

16%

75%

90%

105%

120%

135%

150%

NFC debt/GDP (LHS) NFC Fixed investment % GDP (RHS)

5%

10%

15%

20%

25%

30%

35%

NFC - Investment rate NFC - Savings rate

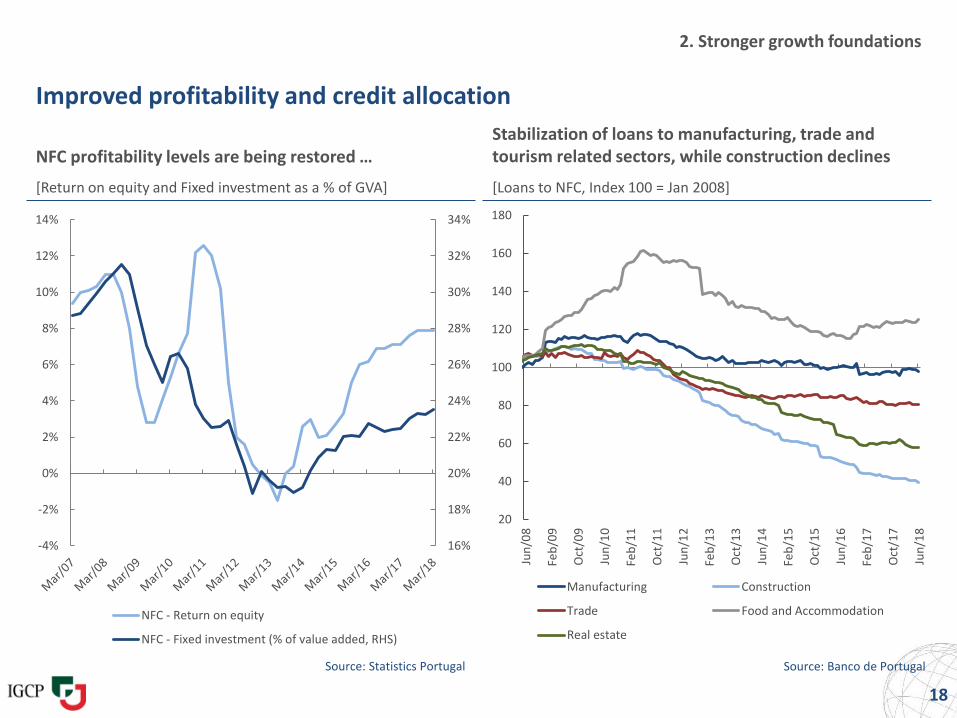

Improved profitability and credit allocation

NFC profitability levels are being restored …

[Return on equity and Fixed investment as a % of GVA]

Source: Statistics Portugal

18

2. Stronger growth foundations

Stabilization of loans to manufacturing, trade and tourism related sectors, while construction declines

[Loans to NFC, Index 100 = Jan 2008]

Source: Banco de Portugal

20

40

60

80

100

120

140

160

180

Jun

/08

Feb

/09

Oct

/09

Jun

/10

Feb

/11

Oct

/11

Jun

/12

Feb

/13

Oct

/13

Jun

/14

Feb

/15

Oct

/15

Jun

/16

Feb

/17

Oct

/17

Jun

/18

Manufacturing Construction

Trade Food and Accommodation

Real estate

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

NFC - Return on equity

NFC - Fixed investment (% of value added, RHS)

Outline

19

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

3.

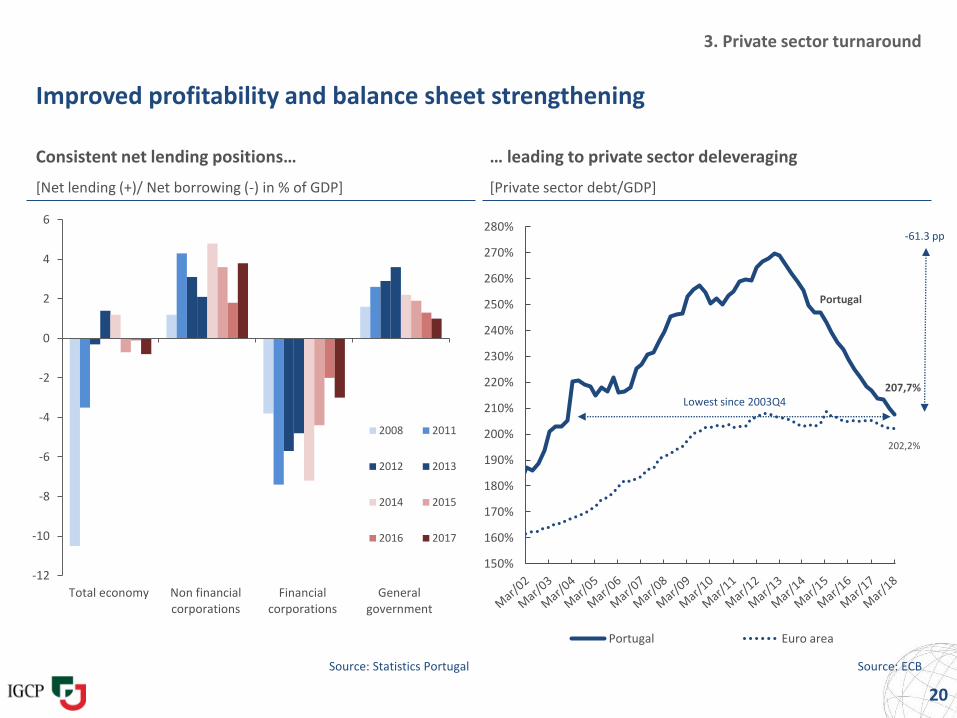

3. Private sector turnaround

Improved profitability and balance sheet strengthening

20

[Net lending (+)/ Net borrowing (-) in % of GDP]

Consistent net lending positions…

[Private sector debt/GDP]

… leading to private sector deleveraging

Source: Statistics Portugal Source: ECB

Portugal

207,7%

202,2%

150%

160%

170%

180%

190%

200%

210%

220%

230%

240%

250%

260%

270%

280%

Portugal Euro area

Lowest since 2003Q4

-61.3 pp

-12

-10

-8

-6

-4

-2

0

2

4

6

Total economy Non financialcorporations

Financialcorporations

Generalgovernment

2008 2011

2012 2013

2014 2015

2016 2017

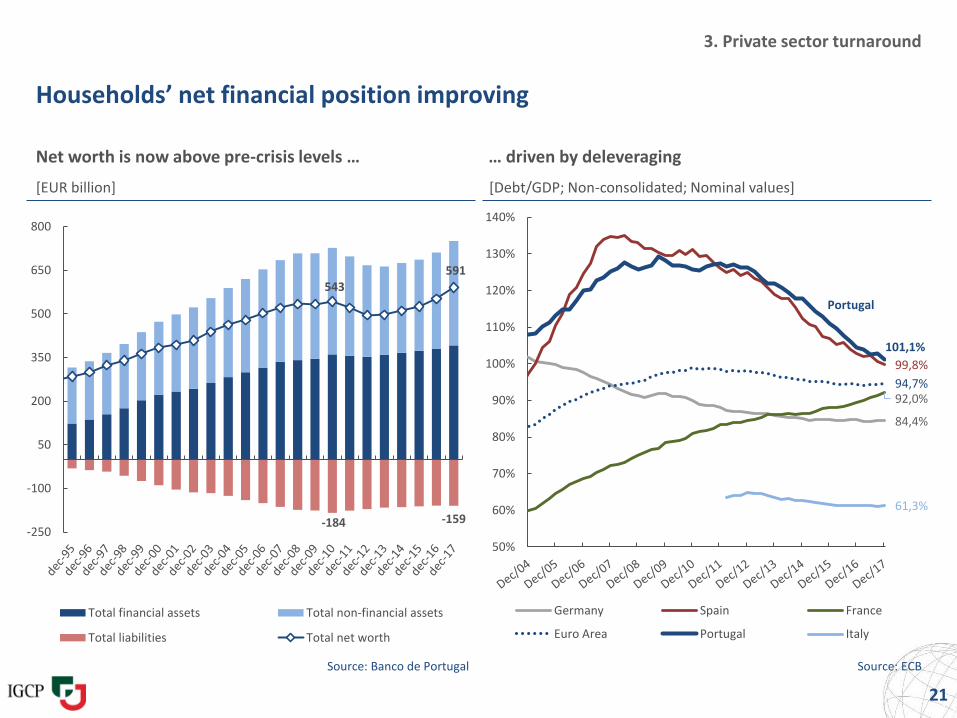

Households’ net financial position improving

Net worth is now above pre-crisis levels … … driven by deleveraging

[EUR billion]

Source: Banco de Portugal Source: ECB

21

3. Private sector turnaround

[Debt/GDP; Non-consolidated; Nominal values]

-184 -159

543591

-250

-100

50

200

350

500

650

800

Total financial assets Total non-financial assets

Total liabilities Total net worth

84,4%

99,8%

92,0%94,7%

Portugal

101,1%

61,3%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Germany Spain France

Euro Area Portugal Italy

Strengthening of corporates’ capital structure

Strong decline of debt stock

[Debt/GDP; Non-consolidated]

Source: ECB Source: Banco de Portugal

22

3. Private sector turnaround

Improved solvency position

[Capital ratio = Equity/Assets]

Portugal

107,2%

96,1%

134,2%

77,8%

62,5%

107,4%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

Portugal Spain France

Italy Germany Euro Area

30%

31%

32%

33%

34%

35%

36%

37%

38%

3. Private sector turnaround

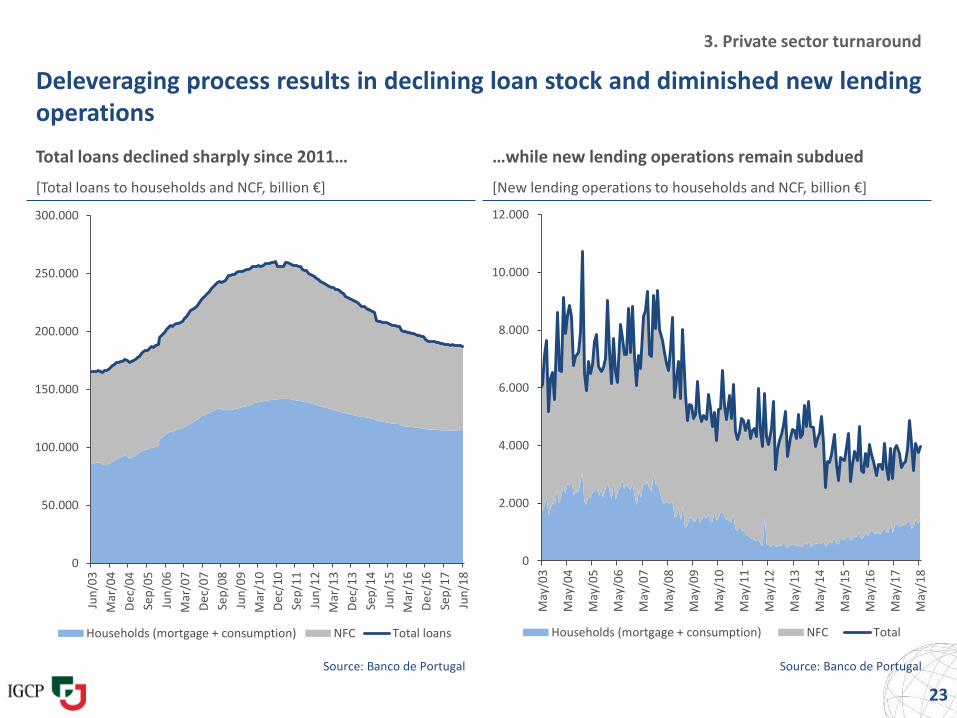

Deleveraging process results in declining loan stock and diminished new lendingoperations

Total loans declined sharply since 2011… …while new lending operations remain subdued

[Total loans to households and NCF, billion €] [New lending operations to households and NCF, billion €]

Source: Banco de Portugal Source: Banco de Portugal

23

0

50.000

100.000

150.000

200.000

250.000

300.000

Jun

/03

Mar

/04

De

c/0

4

Sep

/05

Jun

/06

Mar

/07

De

c/0

7

Sep

/08

Jun

/09

Mar

/10

De

c/1

0

Sep

/11

Jun

/12

Mar

/13

De

c/1

3

Sep

/14

Jun

/15

Mar

/16

De

c/1

6

Sep

/17

Jun

/18

Households (mortgage + consumption) NFC Total loans

0

2.000

4.000

6.000

8.000

10.000

12.000

May

/03

May

/04

May

/05

May

/06

May

/07

May

/08

May

/09

May

/10

May

/11

May

/12

May

/13

May

/14

May

/15

May

/16

May

/17

May

/18

Households (mortgage + consumption) NFC Total

150,7

135,1

122,6

111,8

102,1

96,1 95,592,5

2010 2011 2012 2013 2014 2015 2016 2017

3. Private sector turnaround

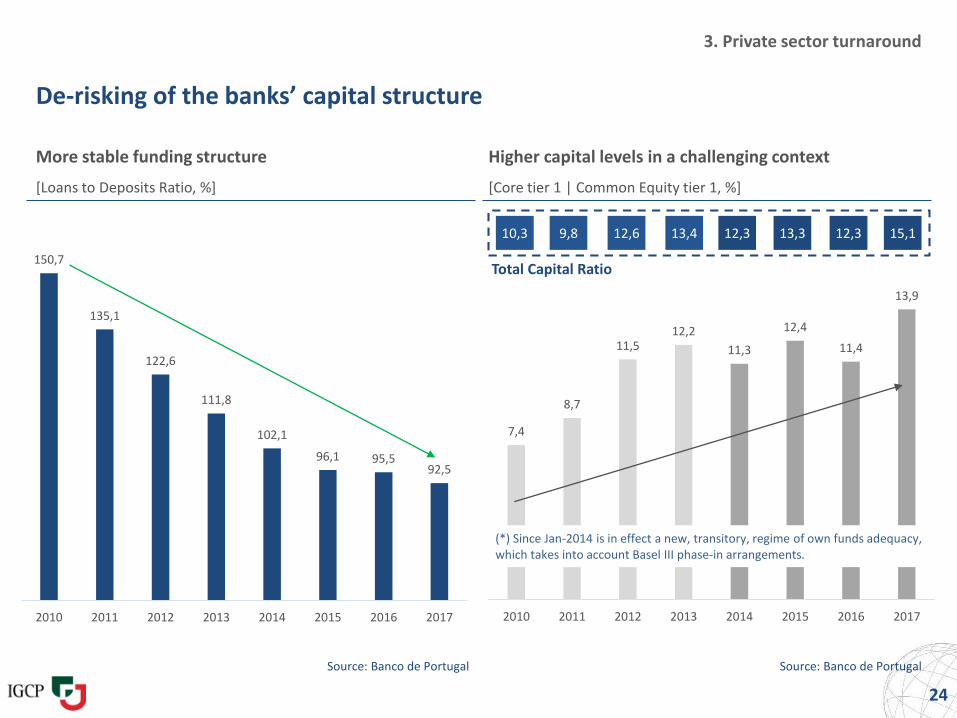

De-risking of the banks’ capital structure

24

[Loans to Deposits Ratio, %]

More stable funding structure

[Core tier 1 | Common Equity tier 1, %]

Higher capital levels in a challenging context

Source: Banco de PortugalSource: Banco de Portugal

7,4

8,7

11,512,2

11,3

12,4

11,4

13,9

2010 2011 2012 2013 2014 2015 2016 2017

13,4 12,3 13,3 12,3

Total Capital Ratio

12,69,810,3

(*) Since Jan-2014 is in effect a new, transitory, regime of own funds adequacy, which takes into account Basel III phase-in arrangements.

15,1

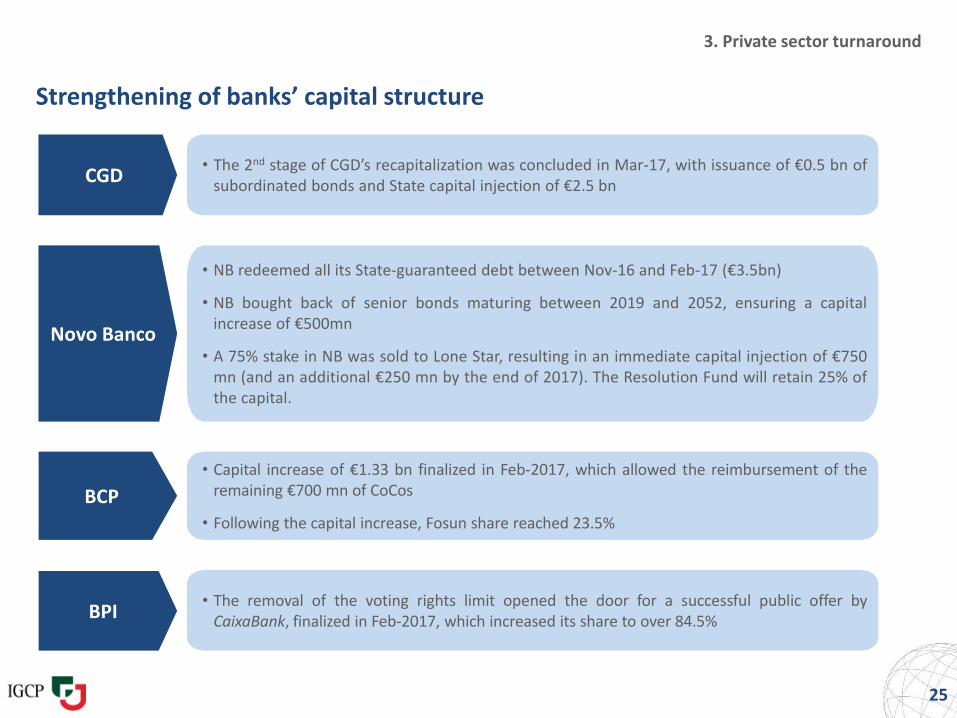

Strengthening of banks’ capital structure

25

• The 2nd stage of CGD’s recapitalization was concluded in Mar-17, with issuance of €0.5 bn ofsubordinated bonds and State capital injection of €2.5 bn

CGD

3. Private sector turnaround

• NB redeemed all its State-guaranteed debt between Nov-16 and Feb-17 (€3.5bn)

• NB bought back of senior bonds maturing between 2019 and 2052, ensuring a capitalincrease of €500mn

• A 75% stake in NB was sold to Lone Star, resulting in an immediate capital injection of €750mn (and an additional €250 mn by the end of 2017). The Resolution Fund will retain 25% ofthe capital.

Novo Banco

BCP

• Capital increase of €1.33 bn finalized in Feb-2017, which allowed the reimbursement of theremaining €700 mn of CoCos

• Following the capital increase, Fosun share reached 23.5%

BPI• The removal of the voting rights limit opened the door for a successful public offer by

CaixaBank, finalized in Feb-2017, which increased its share to over 84.5%

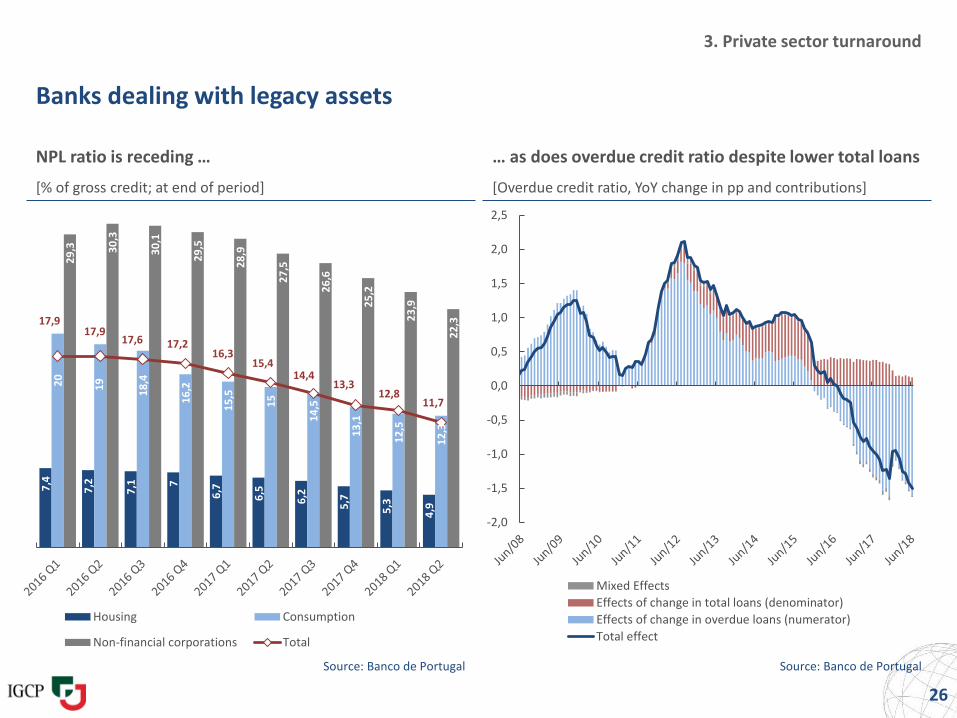

Banks dealing with legacy assets

NPL ratio is receding …

[% of gross credit; at end of period]

Source: Banco de Portugal

26

3. Private sector turnaround

… as does overdue credit ratio despite lower total loans

[Overdue credit ratio, YoY change in pp and contributions]

Source: Banco de Portugal

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

Mixed Effects

Effects of change in total loans (denominator)

Effects of change in overdue loans (numerator)

Total effect

7,4

7,2

7,1 7

6,7

6,5

6,2

5,7

5,3

4,9

20

19

18

,4

16

,2

15

,5

15

14

,5

13

,1

12

,5

12

,3

29

,3 30

,3

30

,1

29

,5

28

,9

27

,5

26

,6

25

,2

23

,9

22

,317,917,9

17,6 17,216,3

15,414,4

13,312,8

11,7

Housing Consumption

Non-financial corporations Total

27

3. Private sector turnaround

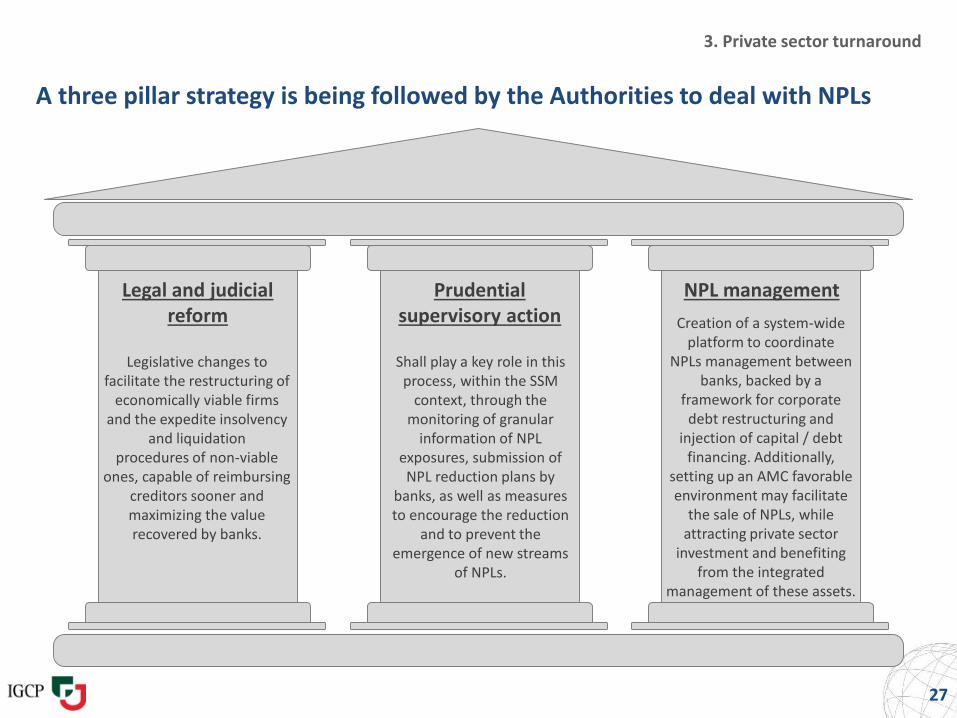

A three pillar strategy is being followed by the Authorities to deal with NPLs

Legal and judicial reform

NPL managementPrudential supervisory action

Legislative changes tofacilitate the restructuring of

economically viable firms and the expedite insolvency

and liquidationprocedures of non-viable

ones, capable of reimbursing creditors sooner and maximizing the value recovered by banks.

Shall play a key role in this process, within the SSM

context, through the monitoring of granular

information of NPL exposures, submission of NPL reduction plans by

banks, as well as measures to encourage the reduction

and to prevent the emergence of new streams

of NPLs.

Creation of a system-wide platform to coordinate

NPLs management between banks, backed by a

framework for corporate debt restructuring and

injection of capital / debt financing. Additionally,

setting up an AMC favorable environment may facilitate

the sale of NPLs, while attracting private sector

investment and benefiting from the integrated

management of these assets.

Outline

28

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

4.

EC

projections

EC

projections

4. Fiscal stabilization

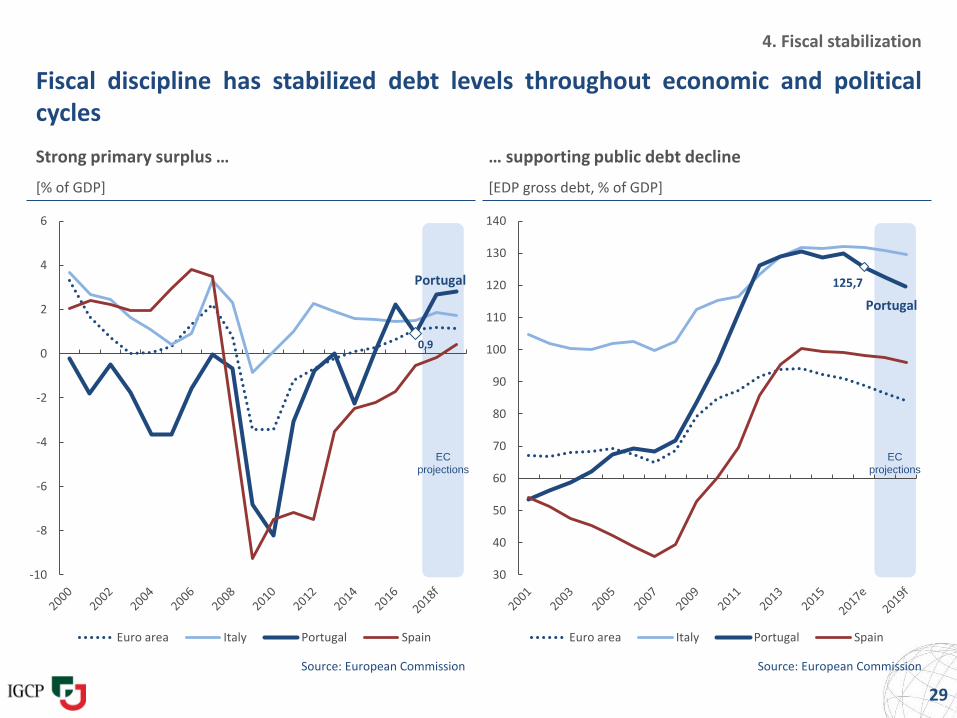

Fiscal discipline has stabilized debt levels throughout economic and politicalcycles

29

[% of GDP]

Strong primary surplus …

[EDP gross debt, % of GDP]

… supporting public debt decline

Source: European Commission Source: European Commission

0,9

Portugal

-10

-8

-6

-4

-2

0

2

4

6

Euro area Italy Portugal Spain

125,7

Portugal

30

40

50

60

70

80

90

100

110

120

130

140

Euro area Italy Portugal Spain

38%

40%

42%

44%

46%

48%

50%

52%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

2010 2012 2014 2016 2018 P 2020 P 2022 P

Total revenue (RHS)

Total expenditure excl NB, Banif and CGD (RHS)

Overall balance excl NB, Banif and CGD

4. Fiscal stabilization

Source: Statistics Portugal and Ministry of Finance Source: Statistics Portugal and Ministry of Finance

30

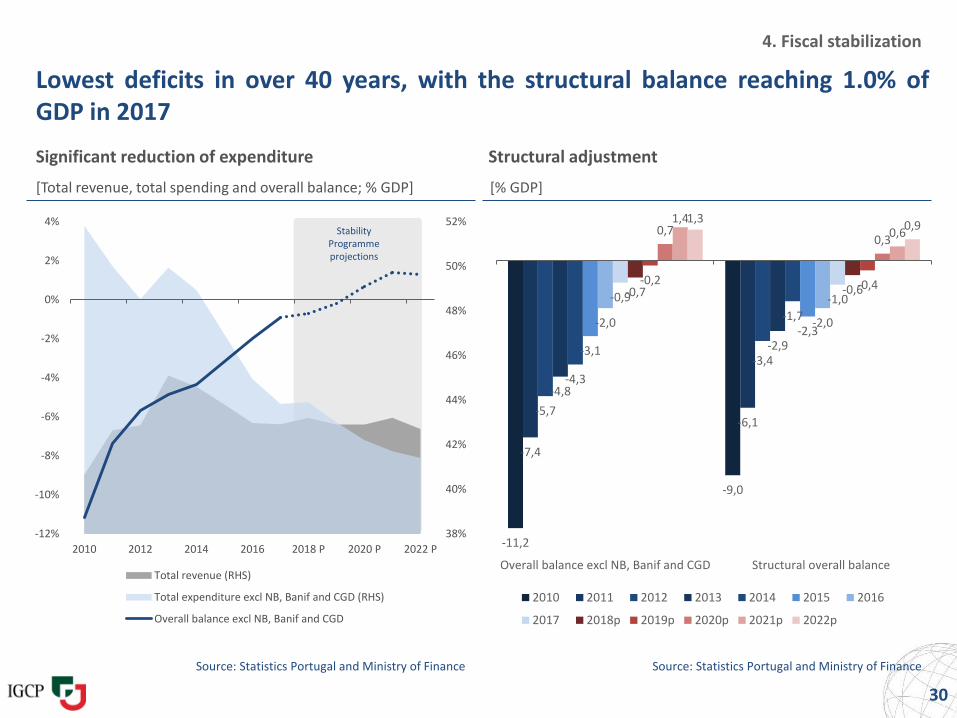

Lowest deficits in over 40 years, with the structural balance reaching 1.0% ofGDP in 2017

Structural adjustment

[% GDP][Total revenue, total spending and overall balance; % GDP]

Significant reduction of expenditure

Stability Programme projections

-11,2

-9,0

-7,4

-6,1-5,7

-3,4

-4,8

-2,9

-4,3

-1,7

-3,1

-2,3-2,0 -2,0

-0,9 -1,0-0,7 -0,6

-0,2 -0,4

0,70,3

1,40,6

1,30,9

Overall balance excl NB, Banif and CGD Structural overall balance

2010 2011 2012 2013 2014 2015 2016

2017 2018p 2019p 2020p 2021p 2022p

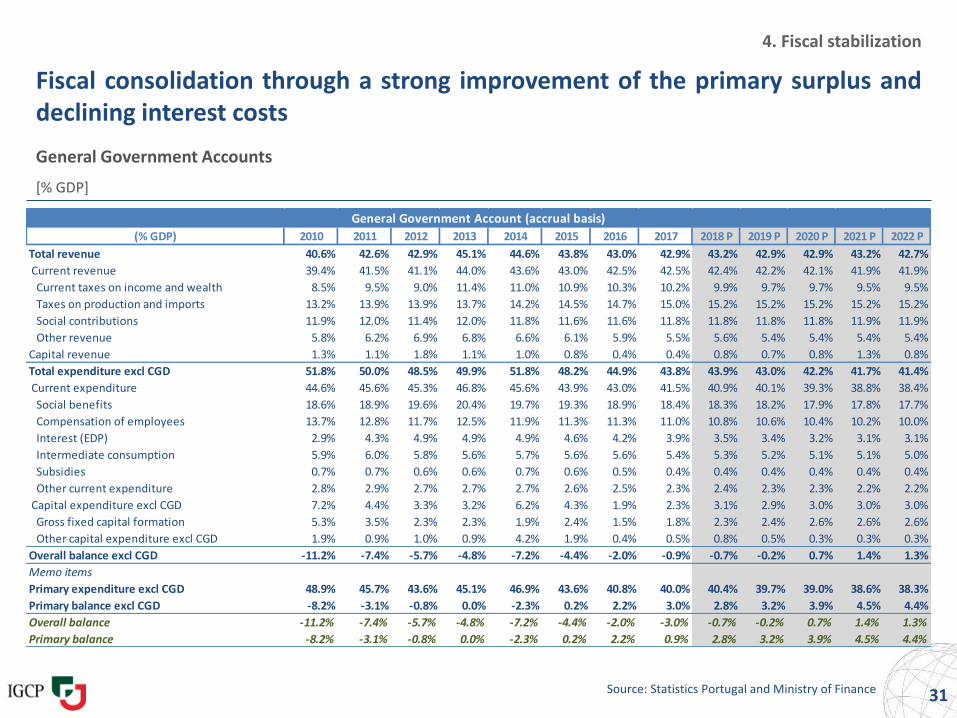

Fiscal consolidation through a strong improvement of the primary surplus anddeclining interest costs

General Government Accounts

[% GDP]

Source: Statistics Portugal and Ministry of Finance 31

4. Fiscal stabilization

General Government Account (accrual basis)

(% GDP) 2010 2011 2012 2013 2014 2015 2016 2017 2018 P 2019 P 2020 P 2021 P 2022 P

Total revenue 40.6% 42.6% 42.9% 45.1% 44.6% 43.8% 43.0% 42.9% 43.2% 42.9% 42.9% 43.2% 42.7%

Current revenue 39.4% 41.5% 41.1% 44.0% 43.6% 43.0% 42.5% 42.5% 42.4% 42.2% 42.1% 41.9% 41.9%

Current taxes on income and wealth 8.5% 9.5% 9.0% 11.4% 11.0% 10.9% 10.3% 10.2% 9.9% 9.7% 9.7% 9.5% 9.5%

Taxes on production and imports 13.2% 13.9% 13.9% 13.7% 14.2% 14.5% 14.7% 15.0% 15.2% 15.2% 15.2% 15.2% 15.2%

Social contributions 11.9% 12.0% 11.4% 12.0% 11.8% 11.6% 11.6% 11.8% 11.8% 11.8% 11.8% 11.9% 11.9%

Other revenue 5.8% 6.2% 6.9% 6.8% 6.6% 6.1% 5.9% 5.5% 5.6% 5.4% 5.4% 5.4% 5.4%

Capital revenue 1.3% 1.1% 1.8% 1.1% 1.0% 0.8% 0.4% 0.4% 0.8% 0.7% 0.8% 1.3% 0.8%

Total expenditure excl CGD 51.8% 50.0% 48.5% 49.9% 51.8% 48.2% 44.9% 43.8% 43.9% 43.0% 42.2% 41.7% 41.4%

Current expenditure 44.6% 45.6% 45.3% 46.8% 45.6% 43.9% 43.0% 41.5% 40.9% 40.1% 39.3% 38.8% 38.4%

Social benefits 18.6% 18.9% 19.6% 20.4% 19.7% 19.3% 18.9% 18.4% 18.3% 18.2% 17.9% 17.8% 17.7%

Compensation of employees 13.7% 12.8% 11.7% 12.5% 11.9% 11.3% 11.3% 11.0% 10.8% 10.6% 10.4% 10.2% 10.0%

Interest (EDP) 2.9% 4.3% 4.9% 4.9% 4.9% 4.6% 4.2% 3.9% 3.5% 3.4% 3.2% 3.1% 3.1%

Intermediate consumption 5.9% 6.0% 5.8% 5.6% 5.7% 5.6% 5.6% 5.4% 5.3% 5.2% 5.1% 5.1% 5.0%

Subsidies 0.7% 0.7% 0.6% 0.6% 0.7% 0.6% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4%

Other current expenditure 2.8% 2.9% 2.7% 2.7% 2.7% 2.6% 2.5% 2.3% 2.4% 2.3% 2.3% 2.2% 2.2%

Capital expenditure excl CGD 7.2% 4.4% 3.3% 3.2% 6.2% 4.3% 1.9% 2.3% 3.1% 2.9% 3.0% 3.0% 3.0%

Gross fixed capital formation 5.3% 3.5% 2.3% 2.3% 1.9% 2.4% 1.5% 1.8% 2.3% 2.4% 2.6% 2.6% 2.6%

Other capital expenditure excl CGD 1.9% 0.9% 1.0% 0.9% 4.2% 1.9% 0.4% 0.5% 0.8% 0.5% 0.3% 0.3% 0.3%

Overall balance excl CGD -11.2% -7.4% -5.7% -4.8% -7.2% -4.4% -2.0% -0.9% -0.7% -0.2% 0.7% 1.4% 1.3%

Memo items

Primary expenditure excl CGD 48.9% 45.7% 43.6% 45.1% 46.9% 43.6% 40.8% 40.0% 40.4% 39.7% 39.0% 38.6% 38.3%

Primary balance excl CGD -8.2% -3.1% -0.8% 0.0% -2.3% 0.2% 2.2% 3.0% 2.8% 3.2% 3.9% 4.5% 4.4%

Overall balance -11.2% -7.4% -5.7% -4.8% -7.2% -4.4% -2.0% -3.0% -0.7% -0.2% 0.7% 1.4% 1.3%

Primary balance -8.2% -3.1% -0.8% 0.0% -2.3% 0.2% 2.2% 0.9% 2.8% 3.2% 3.9% 4.5% 4.4%

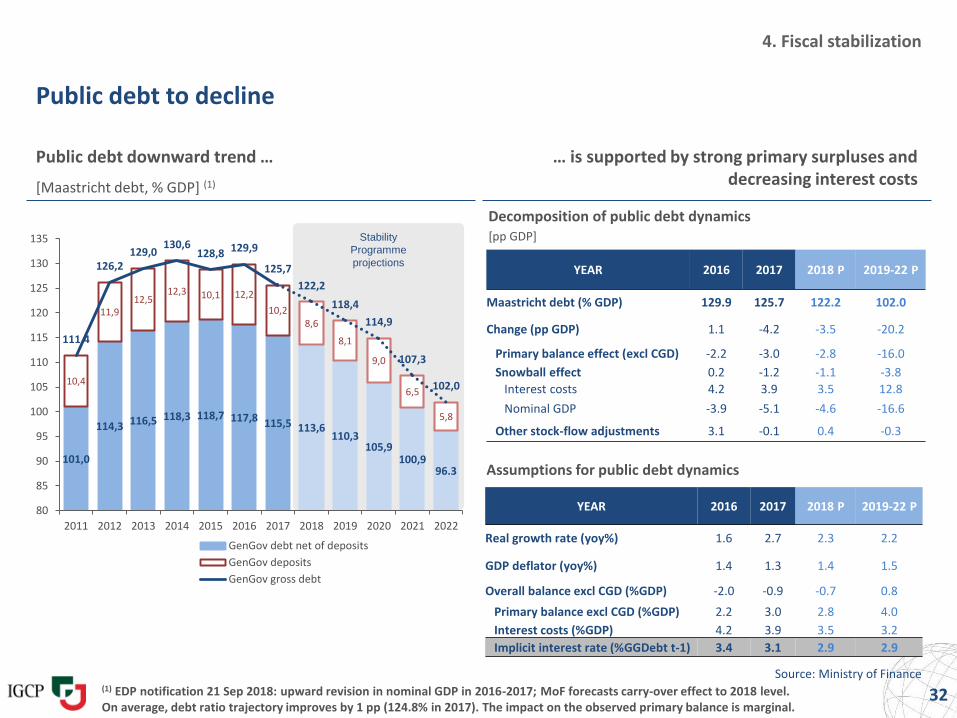

Public debt to decline

Public debt downward trend …

[Maastricht debt, % GDP] (1)

32Source: Ministry of Finance

Decomposition of public debt dynamics[pp GDP]

… is supported by strong primary surpluses and decreasing interest costs

4. Fiscal stabilization

Assumptions for public debt dynamics

YEAR 2016 2017 2018 P 2019-22 P

Real growth rate (yoy%) 1.6 2.7 2.3 2.2

GDP deflator (yoy%) 1.4 1.3 1.4 1.5

Overall balance excl CGD (%GDP) -2.0 -0.9 -0.7 0.8

Primary balance excl CGD (%GDP) 2.2 3.0 2.8 4.0

Interest costs (%GDP) 4.2 3.9 3.5 3.2

Implicit interest rate (%GGDebt t-1) 3.4 3.1 2.9 2.9

YEAR 2016 2017 2018 P 2019-22 P

Maastricht debt (% GDP) 129.9 125.7 122.2 102.0

Change (pp GDP) 1.1 -4.2 -3.5 -20.2

Primary balance effect (excl CGD) -2.2 -3.0 -2.8 -16.0

Snowball effect 0.2 -1.2 -1.1 -3.8

Interest costs 4.2 3.9 3.5 12.8

Nominal GDP -3.9 -5.1 -4.6 -16.6

Other stock-flow adjustments 3.1 -0.1 0.4 -0.3

Stability

Programme

projections

101,0

114,3 116,5 118,3 118,7 117,8 115,5 113,6110,3

105,9100,9

96.3

10,4

11,912,5

12,3 10,1 12,2

10,28,6

8,1

9,0

6,5

5,8

111,4

126,2129,0

130,6128,8 129,9

125,7

122,2

118,4

114,9

107,3

102,0

80

85

90

95

100

105

110

115

120

125

130

135

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

GenGov debt net of deposits

GenGov deposits

GenGov gross debt

(1) EDP notification 21 Sep 2018: upward revision in nominal GDP in 2016-2017; MoF forecasts carry-over effect to 2018 level.On average, debt ratio trajectory improves by 1 pp (124.8% in 2017). The impact on the observed primary balance is marginal.

Outline

33

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

5.

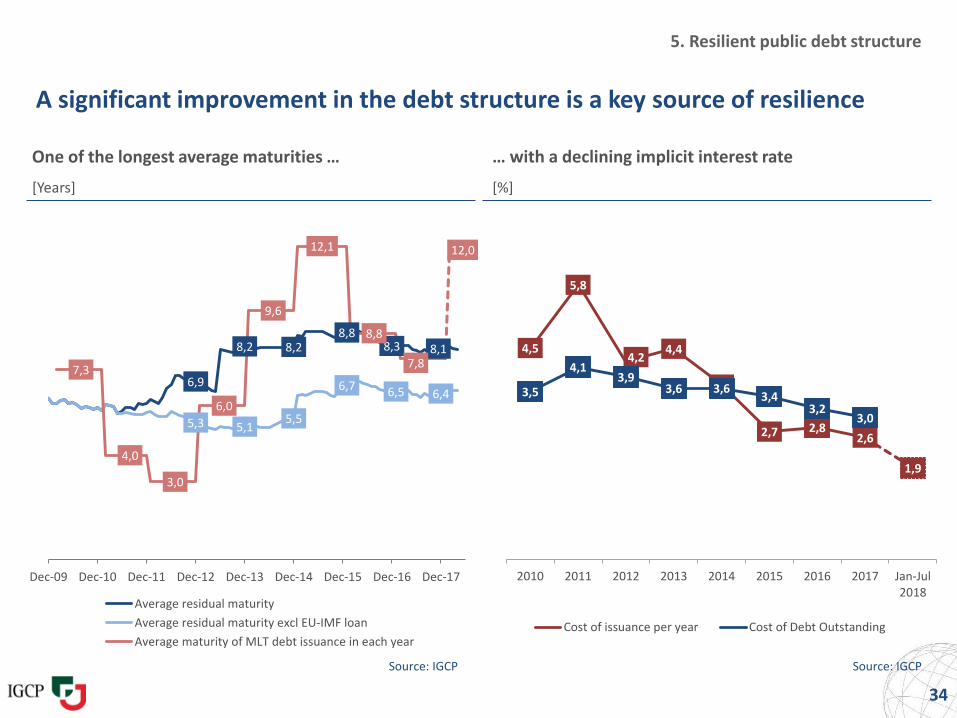

5. Resilient public debt structure

A significant improvement in the debt structure is a key source of resilience

34

One of the longest average maturities …

[Years]

Source: IGCP

6,9

8,2 8,28,8

8,3 8,1

5,3 5,15,5

6,7 6,5 6,4

7,3

4,0

3,0

6,0

9,6

12,1

8,8

7,8

12,0

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Average residual maturity

Average residual maturity excl EU-IMF loan

Average maturity of MLT debt issuance in each year

… with a declining implicit interest rate

[%]

Source: IGCP

4,5

5,8

4,24,4

3,7

2,7 2,82,6

1,9

3,5

4,13,9

3,6 3,63,4

3,23,0

2010 2011 2012 2013 2014 2015 2016 2017 Jan-Jul2018

Cost of issuance per year Cost of Debt Outstanding

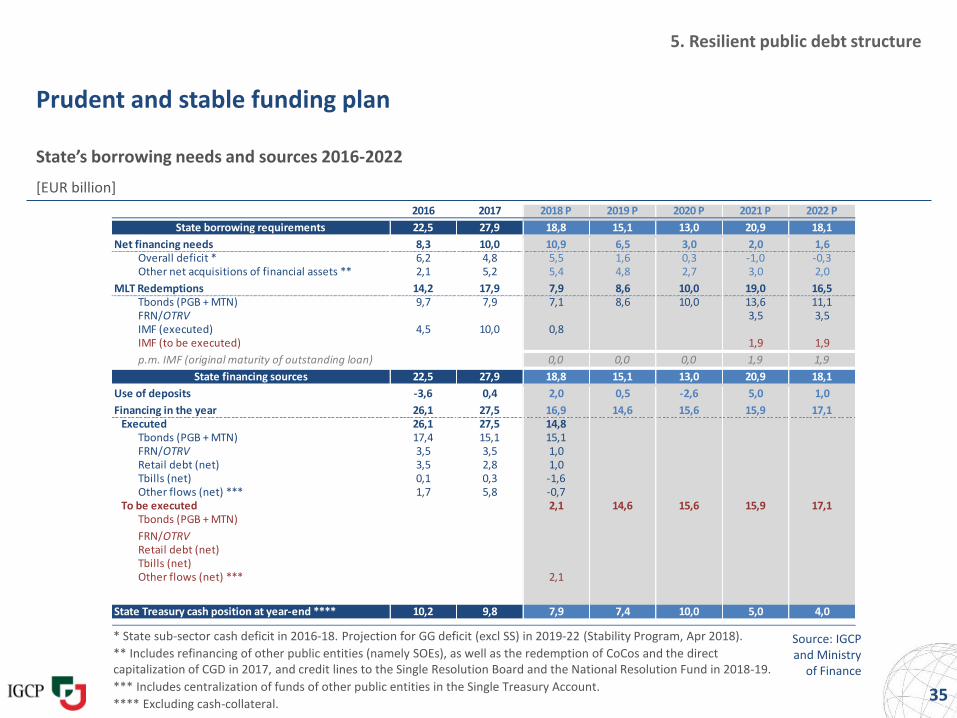

Prudent and stable funding plan

State’s borrowing needs and sources 2016-2022

[EUR billion]

Source: IGCPand Ministry

of Finance

35

5. Resilient public debt structure

* State sub-sector cash deficit in 2016-18. Projection for GG deficit (excl SS) in 2019-22 (Stability Program, Apr 2018).

** Includes refinancing of other public entities (namely SOEs), as well as the redemption of CoCos and the direct capitalization of CGD in 2017, and credit lines to the Single Resolution Board and the National Resolution Fund in 2018-19.

*** Includes centralization of funds of other public entities in the Single Treasury Account.

**** Excluding cash-collateral.

2016 2017 2018 P 2019 P 2020 P 2021 P 2022 P

State borrowing requirements 22,5 27,9 18,8 15,1 13,0 20,9 18,1

Net financing needs 8,3 10,0 10,9 6,5 3,0 2,0 1,6 Overall deficit * 6,2 4,8 5,5 1,6 0,3 -1,0 -0,3 Other net acquisitions of financial assets ** 2,1 5,2 5,4 4,8 2,7 3,0 2,0

MLT Redemptions 14,2 17,9 7,9 8,6 10,0 19,0 16,5 Tbonds (PGB + MTN) 9,7 7,9 7,1 8,6 10,0 13,6 11,1 FRN/OTRV 3,5 3,5 IMF (executed) 4,5 10,0 0,8 IMF (to be executed) 1,9 1,9

p.m. IMF (original maturity of outstanding loan) 0,0 0,0 0,0 1,9 1,9

State financing sources 22,5 27,9 18,8 15,1 13,0 20,9 18,1

Use of deposits -3,6 0,4 2,0 0,5 -2,6 5,0 1,0

Financing in the year 26,1 27,5 16,9 14,6 15,6 15,9 17,1Executed 26,1 27,5 14,8

Tbonds (PGB + MTN) 17,4 15,1 15,1 FRN/OTRV 3,5 3,5 1,0 Retail debt (net) 3,5 2,8 1,0 Tbills (net) 0,1 0,3 -1,6 Other flows (net) *** 1,7 5,8 -0,7

To be executed 2,1 14,6 15,6 15,9 17,1 Tbonds (PGB + MTN)

FRN/OTRV Retail debt (net) Tbills (net) Other flows (net) *** 2,1

State Treasury cash position at year-end **** 10,2 9,8 7,9 7,4 10,0 5,0 4,0

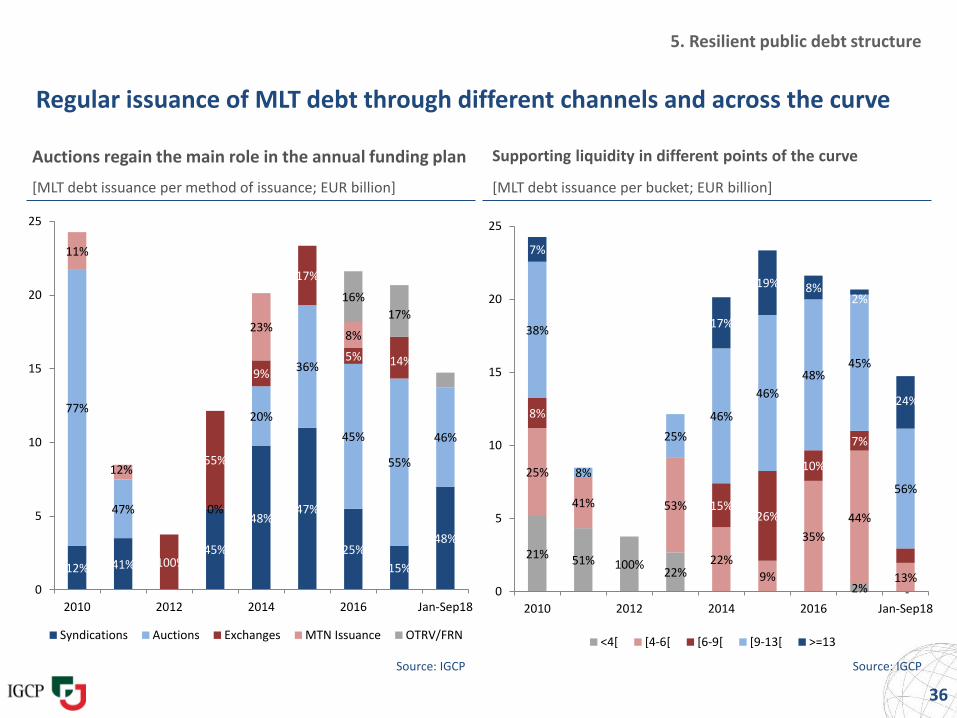

12% 41%45%

48%47%

25%

15%

48%

77%

47% 0%

20%

36%

45%

55%

46%

100%

55%

9%

17%

5% 14%…

11%

12%

23%8%

16%

17%

0

5

10

15

20

25

2010 2012 2014 2016 Jan-Sep18

Syndications Auctions Exchanges MTN Issuance OTRV/FRN

21% 51% 100%22%

2% -

25%

41% 53%

22%

9%

35%

44%

13%

8%

15%26%

10%

7%

38%

8%

25%

46%

46%

48%45%

56%

7%

17%

19% 8%2%

24%

0

5

10

15

20

25

2010 2012 2014 2016 Jan-Sep18

<4[ [4-6[ [6-9[ [9-13[ >=13

Regular issuance of MLT debt through different channels and across the curve

Auctions regain the main role in the annual funding plan Supporting liquidity in different points of the curve

[MLT debt issuance per method of issuance; EUR billion] [MLT debt issuance per bucket; EUR billion]

Source: IGCP Source: IGCP

36

5. Resilient public debt structure

The diversification of investors ensures a stable base of debt holders (1/2)

Progressively regaining traditional investors

Source: IGCP

37

Distribution by Geography Distribution by Investor Type

5. Resilient public debt structure

[Distribution by geography and investor type of 10-year syndications from 2010 to 2018]

2010

2013

2018

Asia

France

Germany/Austria/Switzerland

Nordics

North America

Other

Other EU

Portugal

Spain

UK

2010

2013

2018

Asset Managers

Banks

Official Institutions

Hedge Funds

Insurance / Pension Funds

Others

[% of total State debt securities]

Source: IGCP Source: IGCP

38

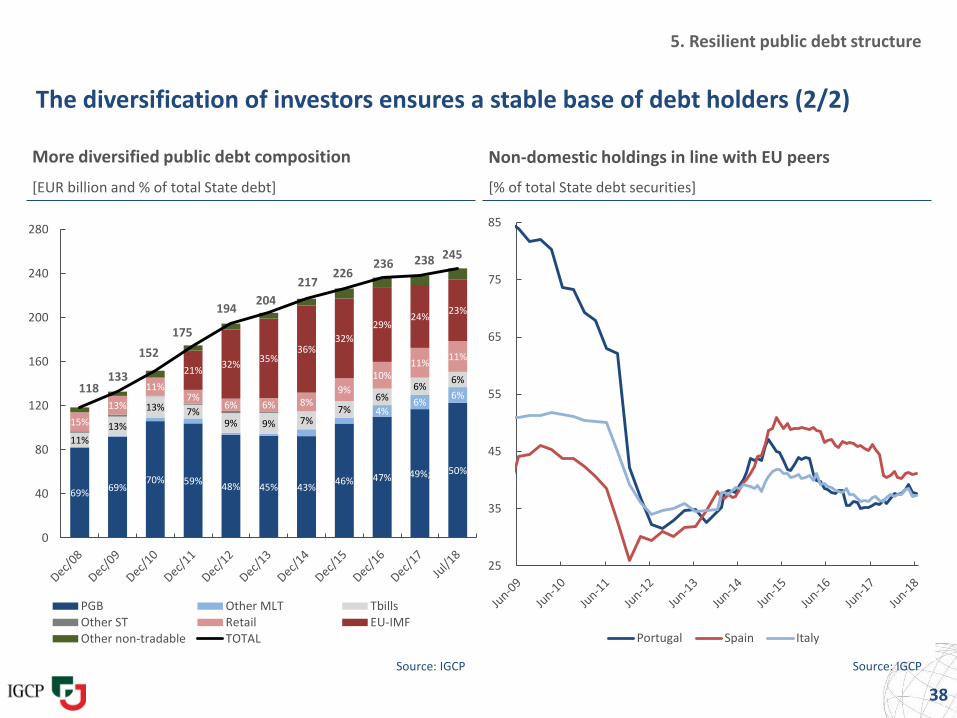

5. Resilient public debt structure

More diversified public debt composition

[EUR billion and % of total State debt]

Non-domestic holdings in line with EU peers

The diversification of investors ensures a stable base of debt holders (2/2)

69%69%

70% 59%48% 45% 43%

46% 47% 49%; 50%

4%6%

6%

11%

13%

13% 7%9% 9% 7%

7%6%

6%6%

15%

13%

11%7%

6% 6% 8%9%

10%11%

11%

21%32%

35%36%

32%

29%24%

23%

118133

152

175

194204

217226

236 238 245

0

40

80

120

160

200

240

280

PGB Other MLT TbillsOther ST Retail EU-IMFOther non-tradable TOTAL

25

35

45

55

65

75

85

Portugal Spain Italy

39

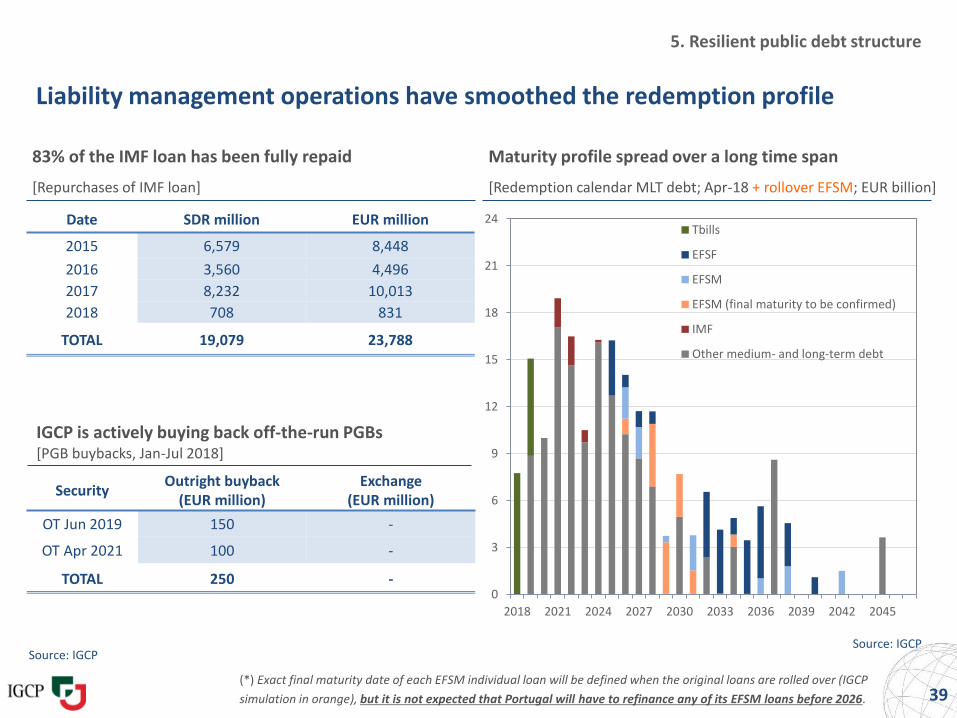

Liability management operations have smoothed the redemption profile

[Redemption calendar MLT debt; Apr-18 + rollover EFSM; EUR billion]

Source: IGCP

Maturity profile spread over a long time span

5. Resilient public debt structure

(*) Exact final maturity date of each EFSM individual loan will be defined when the original loans are rolled over (IGCP

simulation in orange), but it is not expected that Portugal will have to refinance any of its EFSM loans before 2026.

IGCP is actively buying back off-the-run PGBs

83% of the IMF loan has been fully repaid

[PGB buybacks, Jan-Jul 2018]

[Repurchases of IMF loan]

SecurityOutright buyback

(EUR million)Exchange

(EUR million)

OT Jun 2019 150 -

OT Apr 2021 100 -

TOTAL 250 -

Source: IGCP

Date SDR million EUR million

2015 6,579 8,448

2016 3,560 4,496

2017 8,232 10,013

2018 708 831

TOTAL 19,079 23,788

0

3

6

9

12

15

18

21

24

2018 2021 2024 2027 2030 2033 2036 2039 2042 2045

Tbills

EFSF

EFSM

EFSM (final maturity to be confirmed)

IMF

Other medium- and long-term debt

Outline

40

1.

1. Economic revitalization

2. Stronger growth foundations

3. Private sector turnaround

4. Fiscal stabilization

5. Resilient public debt structure

6. Improving market conditions

6.

6. Improving market conditions

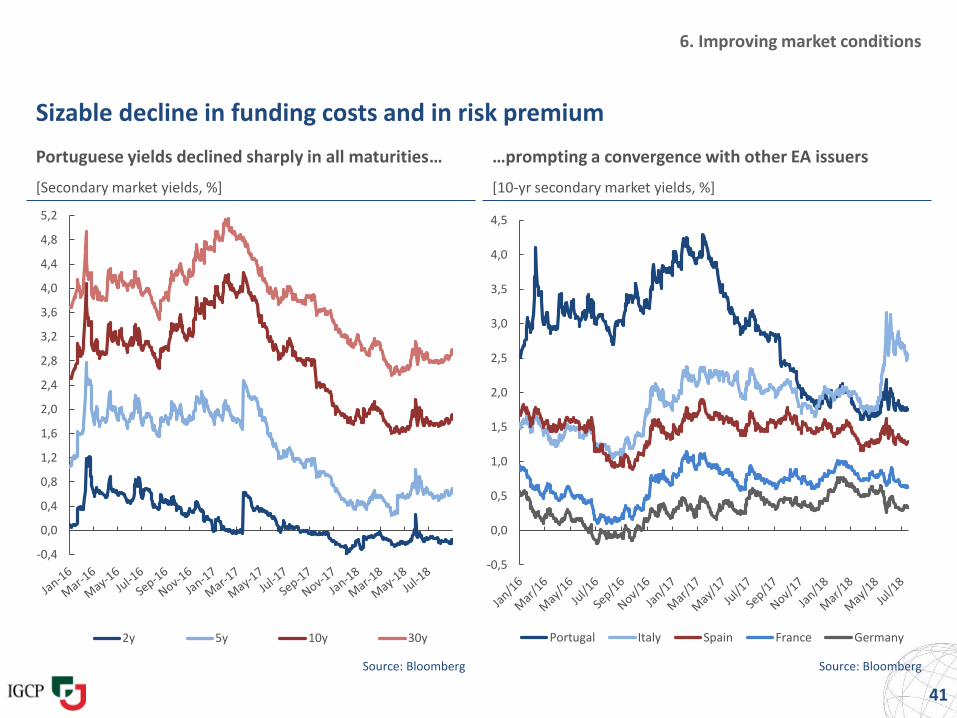

Sizable decline in funding costs and in risk premium

Portuguese yields declined sharply in all maturities… …prompting a convergence with other EA issuers

[Secondary market yields, %] [10-yr secondary market yields, %]

Source: Bloomberg Source: Bloomberg

41

-0,4

0,0

0,4

0,8

1,2

1,6

2,0

2,4

2,8

3,2

3,6

4,0

4,4

4,8

5,2

2y 5y 10y 30y

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

Portugal Italy Spain France Germany

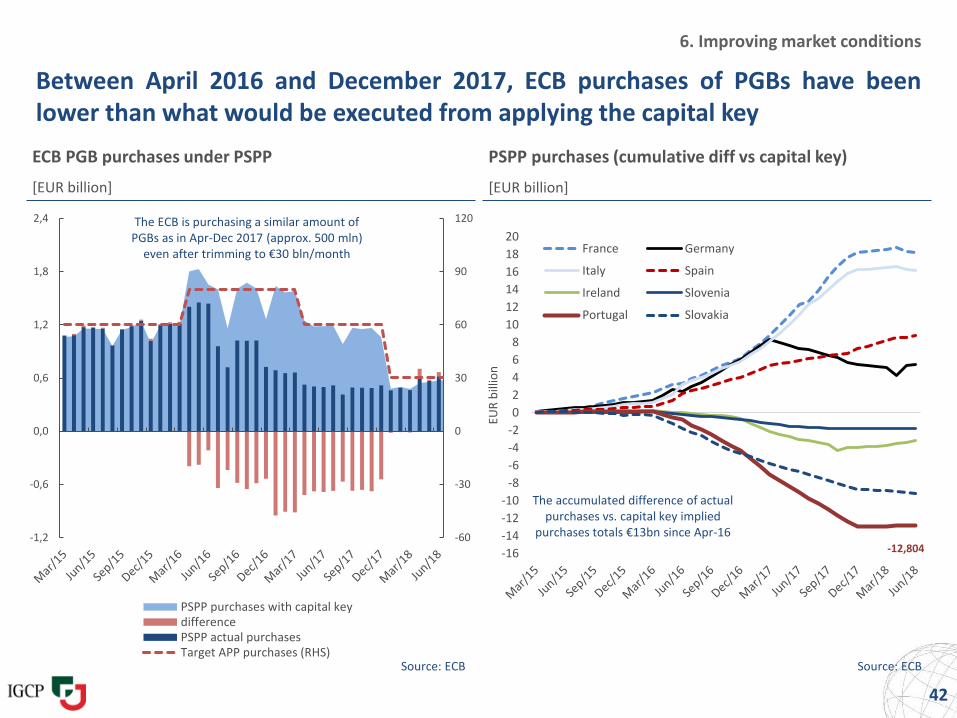

Between April 2016 and December 2017, ECB purchases of PGBs have beenlower than what would be executed from applying the capital key

Source: ECB Source: ECB

42

PSPP purchases (cumulative diff vs capital key)ECB PGB purchases under PSPP

[EUR billion][EUR billion]

6. Improving market conditions

-12,804-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

16

18

20

EUR

bill

ion

France Germany

Italy Spain

Ireland Slovenia

Portugal Slovakia

-60

-30

0

30

60

90

120

-1,2

-0,6

0,0

0,6

1,2

1,8

2,4

PSPP purchases with capital keydifferencePSPP actual purchasesTarget APP purchases (RHS)

The ECB is purchasing a similar amount of PGBs as in Apr-Dec 2017 (approx. 500 mln)

even after trimming to €30 bln/month

The accumulated difference of actual purchases vs. capital key implied

purchases totals €13bn since Apr-16

0

20

40

60

80

100

120

140

160

02/01/2015 02/01/2016 02/01/2017 02/01/2018

10Y 5Y

0

500

1.000

1.500

2.000

Over-the-counter OT Platforms OT

OT 12M Moving Average

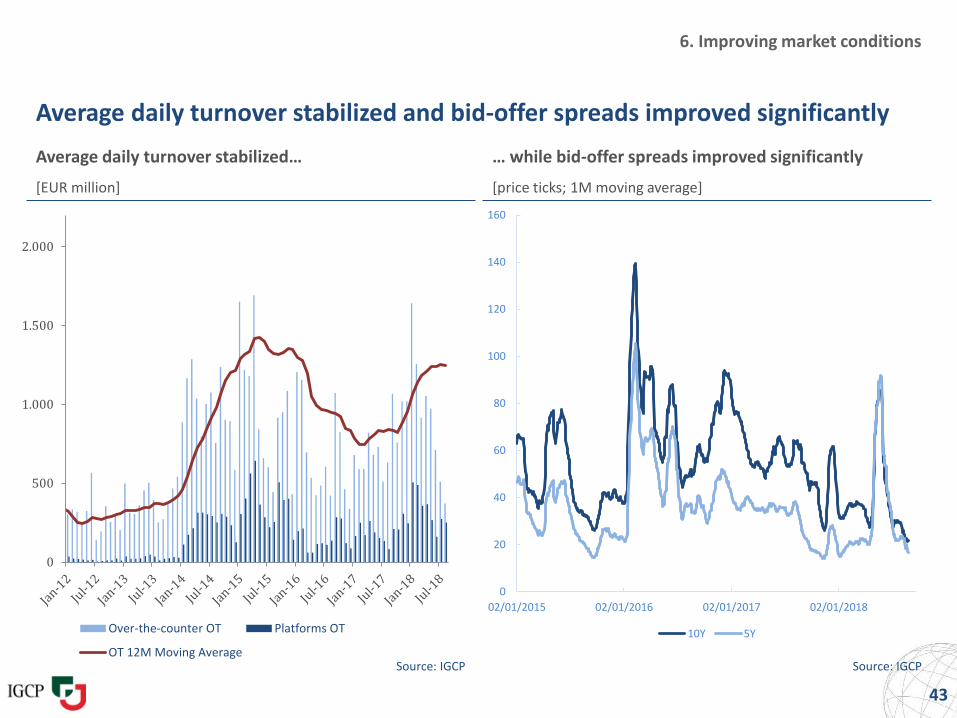

6. Improving market conditions

Average daily turnover stabilized and bid-offer spreads improved significantly

Average daily turnover stabilized… … while bid-offer spreads improved significantly

[EUR million] [price ticks; 1M moving average]

Source: IGCP Source: IGCP

43

-5.000

-4.000

-3.000

-2.000

-1.000

0

1.000

2.000

3.000

4.000

Dec/15 Mar/16 Jun/16 Sep/16 Dec/16 Mar/17 Jun/17 Sep/17 Dec/17 Mar/18 Jun/18

Banks Central Bank & Other Public Entity Pension Fund Insurance Company Fund Manager Hedge Fund Retail

6. Improving market conditions

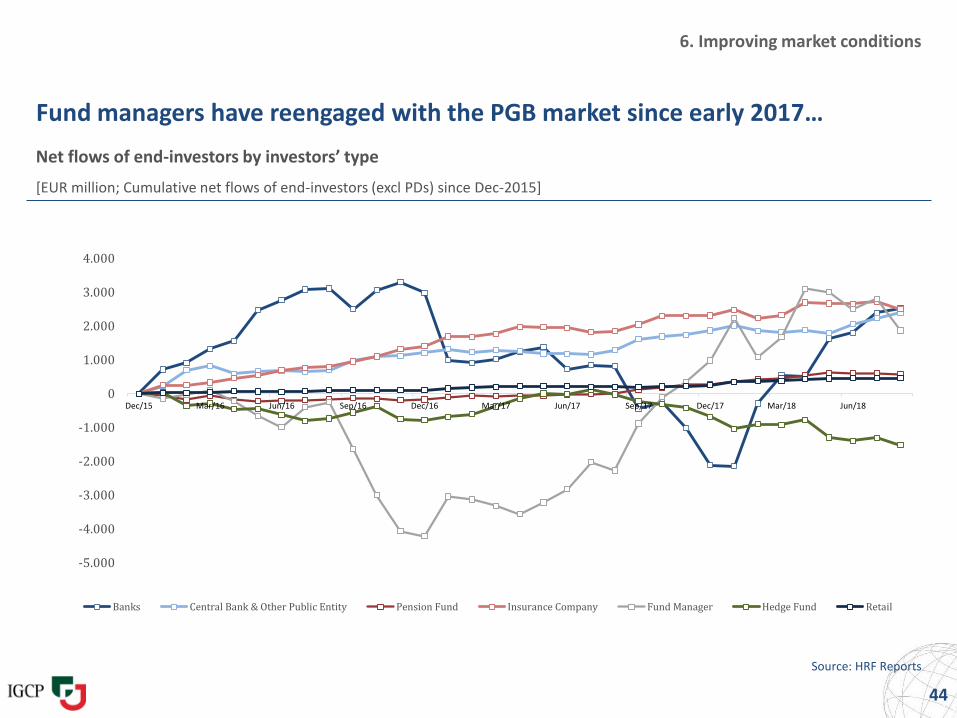

Fund managers have reengaged with the PGB market since early 2017…

Net flows of end-investors by investors’ type

[EUR million; Cumulative net flows of end-investors (excl PDs) since Dec-2015]

Source: HRF Reports

44

-3.000

-2.500

-2.000

-1.500

-1.000

-500

0

500

1.000

1.500

2.000

2.500

Germany/Austria/Swit North AmericaAsia BeneluxOther Nordics

-4.000

-3.000

-2.000

-1.000

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

Spain Other EU France Portugal UK

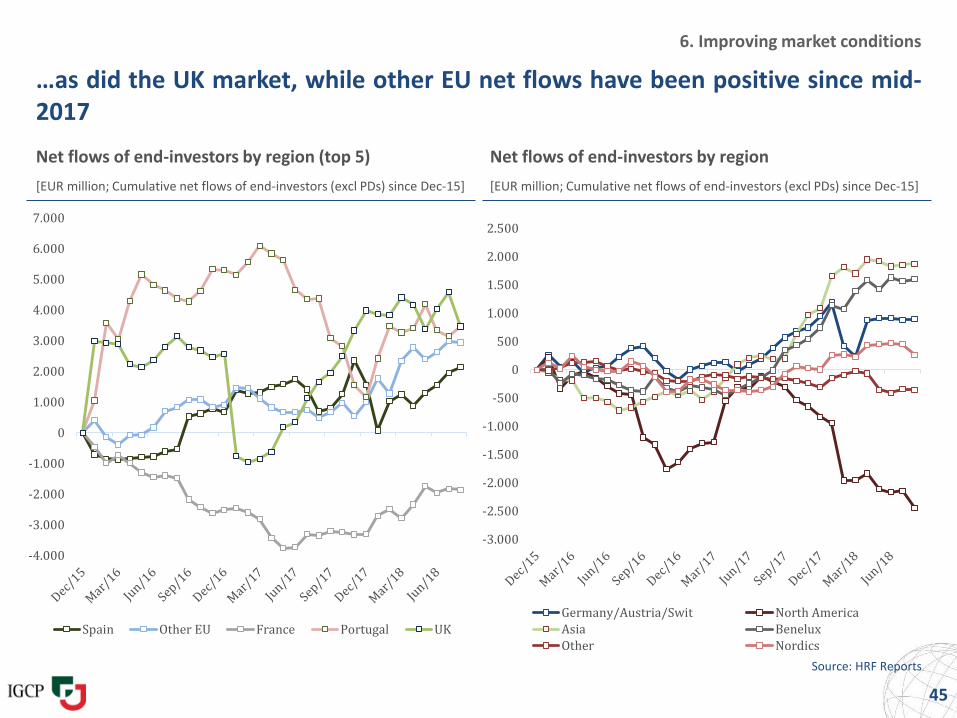

…as did the UK market, while other EU net flows have been positive since mid-2017

45

Net flows of end-investors by region (top 5)

[EUR million; Cumulative net flows of end-investors (excl PDs) since Dec-15] [EUR million; Cumulative net flows of end-investors (excl PDs) since Dec-15]

Net flows of end-investors by region

6. Improving market conditions

Source: HRF Reports

6. Improving market conditions

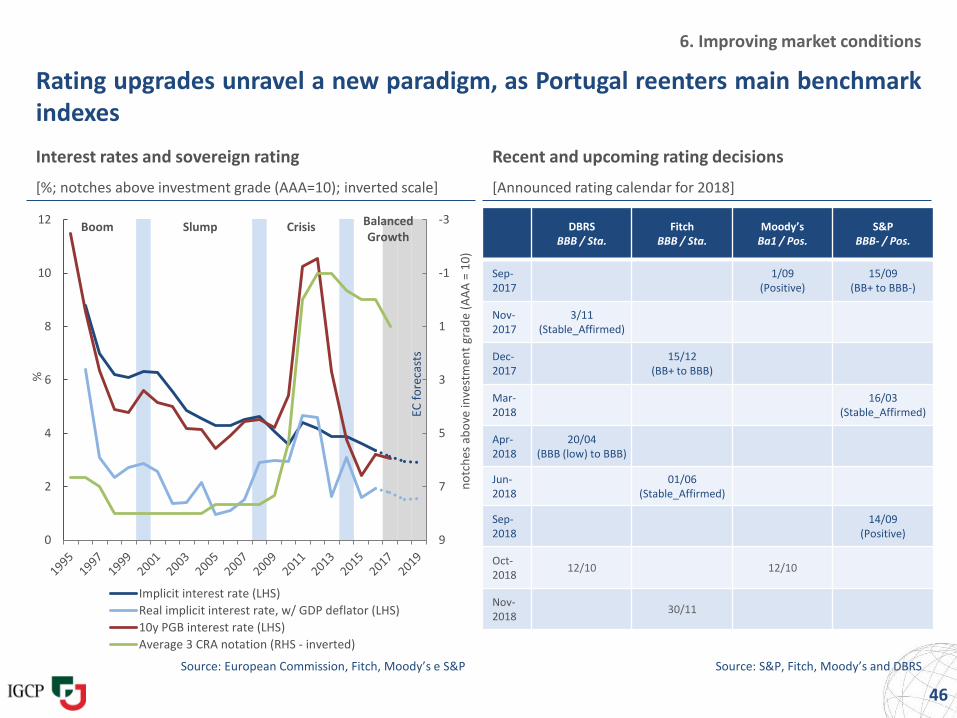

Rating upgrades unravel a new paradigm, as Portugal reenters main benchmarkindexes

Interest rates and sovereign rating Recent and upcoming rating decisions

[%; notches above investment grade (AAA=10); inverted scale] [Announced rating calendar for 2018]

Source: European Commission, Fitch, Moody’s e S&P Source: S&P, Fitch, Moody’s and DBRS

46

-3

-1

1

3

5

7

90

2

4

6

8

10

12

no

tch

es a

bo

ve in

vest

men

t gr

ade

(AA

A =

10

)

%

Implicit interest rate (LHS)

Real implicit interest rate, w/ GDP deflator (LHS)

10y PGB interest rate (LHS)

Average 3 CRA notation (RHS - inverted)

Boom Slump Crisis BalancedGrowth

EC f

ore

cast

s

DBRSBBB / Sta.

FitchBBB / Sta.

Moody’sBa1 / Pos.

S&PBBB- / Pos.

Sep-2017

1/09(Positive)

15/09(BB+ to BBB-)

Nov-2017

3/11(Stable_Affirmed)

Dec-2017

15/12(BB+ to BBB)

Mar-2018

16/03(Stable_Affirmed)

Apr-2018

20/04 (BBB (low) to BBB)

Jun-2018

01/06(Stable_Affirmed)

Sep-2018

14/09(Positive)

Oct-2018

12/10 12/10

Nov-2018

30/11

Appendix

47

A. Macroeconomic indicators

B. Structural reforms

C. Fiscal indicators

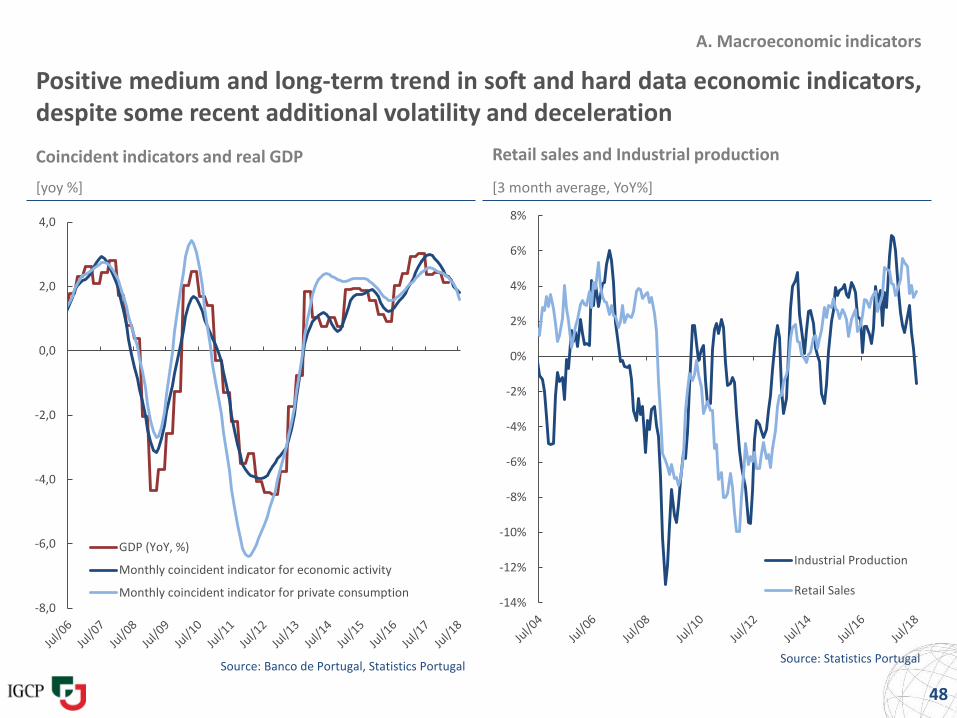

Positive medium and long-term trend in soft and hard data economic indicators,despite some recent additional volatility and deceleration

Coincident indicators and real GDP Retail sales and Industrial production

[yoy %] [3 month average, YoY%]

Source: Banco de Portugal, Statistics PortugalSource: Statistics Portugal

48

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Industrial Production

Retail Sales

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

GDP (YoY, %)

Monthly coincident indicator for economic activity

Monthly coincident indicator for private consumption

A. Macroeconomic indicators

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

Diff Euro area (19 countries) Portugal

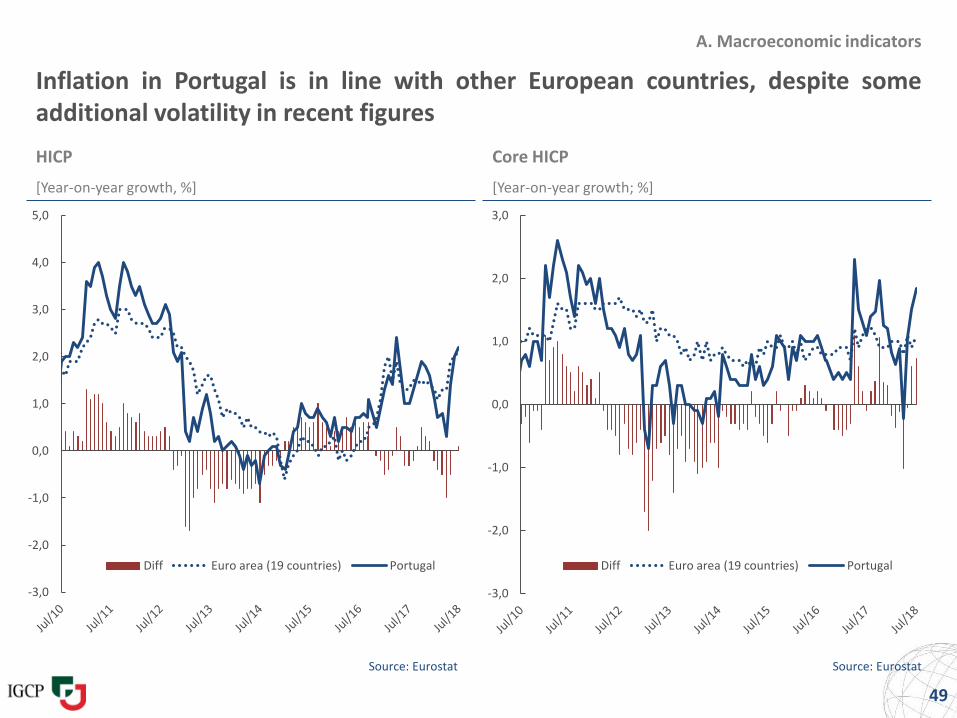

Inflation in Portugal is in line with other European countries, despite someadditional volatility in recent figures

HICP Core HICP

[Year-on-year growth, %] [Year-on-year growth; %]

Source: Eurostat Source: Eurostat

49

A. Macroeconomic indicators

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

Diff Euro area (19 countries) Portugal

A. Macroeconomic indicators

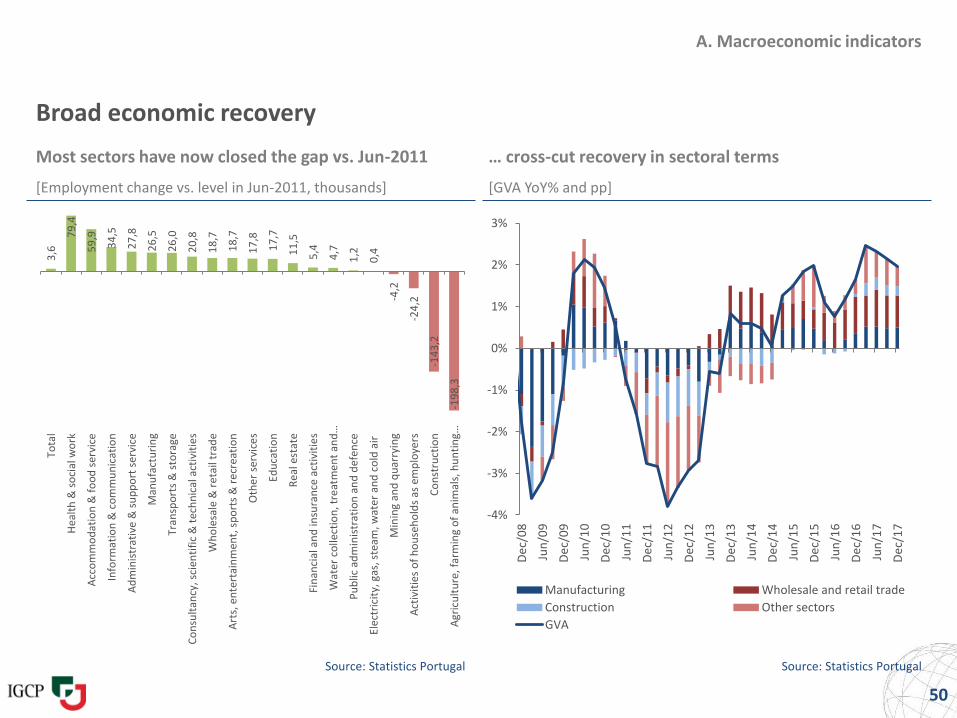

Broad economic recovery

Most sectors have now closed the gap vs. Jun-2011

[Employment change vs. level in Jun-2011, thousands]

Source: Statistics Portugal Source: Statistics Portugal

50

[GVA YoY% and pp]

… cross-cut recovery in sectoral terms

-4%

-3%

-2%

-1%

0%

1%

2%

3%

De

c/0

8

Jun

/09

De

c/0

9

Jun

/10

De

c/1

0

Jun

/11

De

c/1

1

Jun

/12

De

c/1

2

Jun

/13

De

c/1

3

Jun

/14

De

c/1

4

Jun

/15

De

c/1

5

Jun

/16

De

c/1

6

Jun

/17

De

c/1

7

Manufacturing Wholesale and retail trade

Construction Other sectors

GVA

3,6

79

,4

59

,9

34

,5

27

,8

26

,5

26

,0

20

,8

18

,7

18

,7

17

,8

17

,7

11

,5

5,4

4,7

1,2

0,4

-4,2

-24

,2

-14

3,2

-19

8,3

Tota

l

Hea

lth

& s

oci

al w

ork

Acc

om

mo

dat

ion

& f

oo

d s

ervi

ce

Info

rmat

ion

& c

om

mu

nic

atio

n

Ad

min

istr

ativ

e &

su

pp

ort

se

rvic

e

Man

ufa

ctu

rin

g

Tran

spo

rts

& s

tora

ge

Co

nsu

ltan

cy, s

cien

tifi

c &

tec

hn

ical

act

ivit

ies

Wh

ole

sale

& r

eta

il tr

ade

Art

s, e

nte

rtai

nm

ent,

sp

ort

s &

re

crea

tio

n

Oth

er

serv

ice

s

Edu

cati

on

Rea

l est

ate

Fin

anci

al a

nd

insu

ran

ce a

ctiv

itie

s

Wat

er c

olle

ctio

n, t

reat

me

nt

and

…

Pu

blic

ad

min

istr

atio

n a

nd

def

ence

Elec

tric

ity,

gas

, ste

am, w

ate

r an

d c

old

air

Min

ing

and

qu

arry

ing

Act

ivit

ies

of

ho

use

ho

lds

as e

mp

loye

rs

Co

nst

ruct

ion

Agr

icu

ltu

re, f

arm

ing

of

anim

als,

hu

nti

ng…

100%-10,7%

-8,0%

-7,7%

-7,4%

-5,4%

-4,2%-4,2%

-3,6%-2,2%

-1,6% -1,1% 44%

Dec

-08

Man

ufa

ctu

rin

g, M

inin

g an

d q

uar

ryin

g

Elec

tric

ity,

gas

, wat

er

Wh

ole

sale

an

d r

etai

l tra

de

, re

pai

r o

fve

hic

les

Tech

nic

al, c

on

sult

ancy

an

d o

ther

act

ivit

ies

Tran

spo

rtat

ion

an

d s

tora

ge

Co

nst

ruct

ion

Rea

l est

ate

Acc

om

mo

dat

ion

, Fo

od

an

d b

eve

rage

Edu

cati

on

, he

alth

an

d o

the

r se

rvic

es

Info

rmat

ion

an

d c

om

mu

nic

atio

n

Agr

icu

ltu

re, f

ore

stry

an

d f

ish

ing

Dec

-12

44% -1,0% -0,4% -0,2%

65%

0,8% 1,2% 1,5% 1,9%2,5%

3,8%

5,5%

5,5%

Dec

-12

Elec

tric

ity,

gas

, wat

er

Co

nst

ruct

ion

Info

rmat

ion

an

d c

om

mu

nic

atio

n

Edu

cati

on

, he

alth

an

d o

the

r se

rvic

es

Agr

icu

ltu

re, f

ore

stry

an

d f

ish

ing

Tran

spo

rtat

ion

an

d s

tora

ge

Acc

om

mo

dat

ion

, Fo

od

an

d b

eve

rage

Rea

l est

ate

Wh

ole

sale

an

d r

etai

l tra

de

, re

pai

r o

f ve

hic

les

Man

ufa

ctu

rin

g, M

inin

g an

d q

uar

ryin

g

Tech

nic

al, c

on

sult

ancy

an

d o

ther

act

ivit

ies

Dec

-16

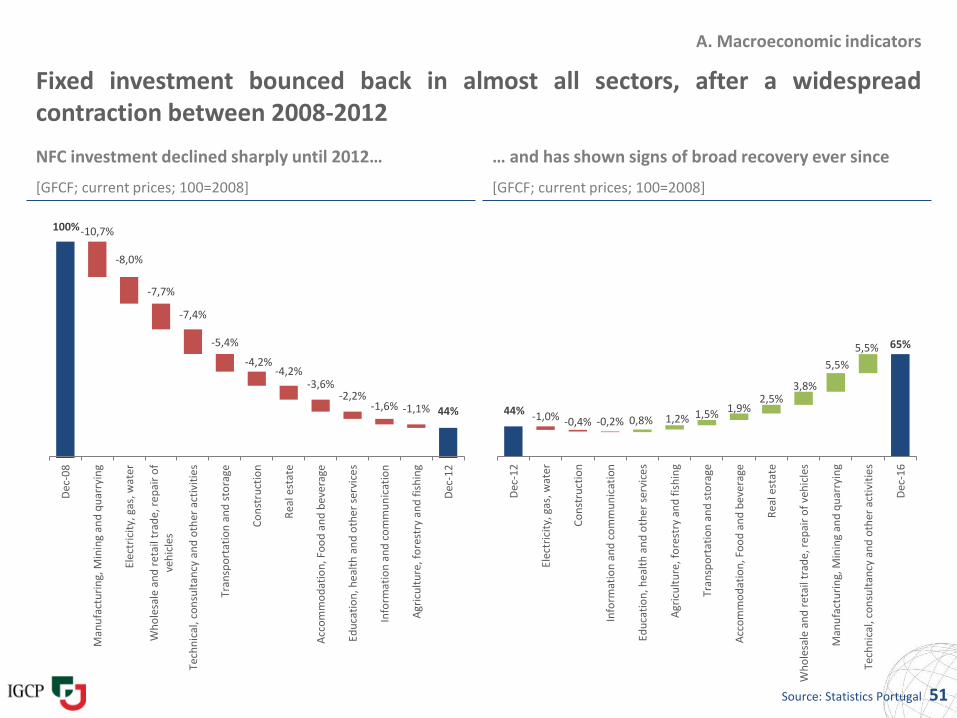

Fixed investment bounced back in almost all sectors, after a widespreadcontraction between 2008-2012

NFC investment declined sharply until 2012… … and has shown signs of broad recovery ever since

[GFCF; current prices; 100=2008] [GFCF; current prices; 100=2008]

Source: Statistics Portugal 51

A. Macroeconomic indicators

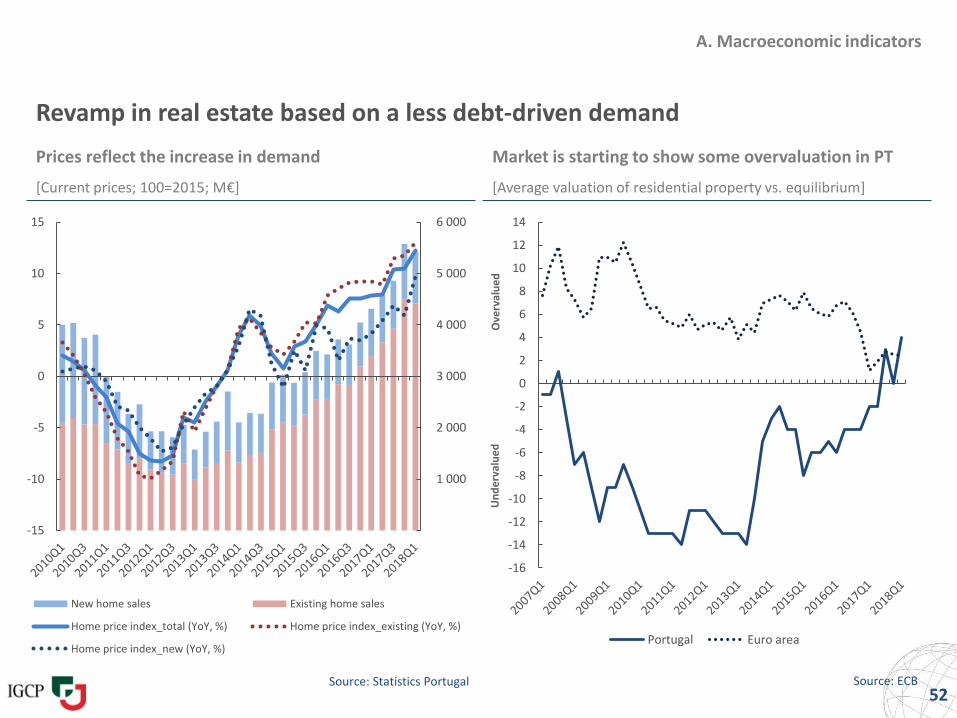

Revamp in real estate based on a less debt-driven demand

Prices reflect the increase in demand Market is starting to show some overvaluation in PT

[Current prices; 100=2015; M€] [Average valuation of residential property vs. equilibrium]

Source: ECB52

A. Macroeconomic indicators

Source: Statistics Portugal

1 000

2 000

3 000

4 000

5 000

6 000

-15

-10

-5

0

5

10

15

New home sales Existing home sales

Home price index_total (YoY, %) Home price index_existing (YoY, %)

Home price index_new (YoY, %)

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

Portugal Euro area

Un

de

rval

ue

dO

verv

alu

ed

-106,7

-81,3

-8,5

-140,0

-120,0

-100,0

-80,0

-60,0

-40,0

-20,0

0,0

Portugal Spain Italy

A. Macroeconomic indicators

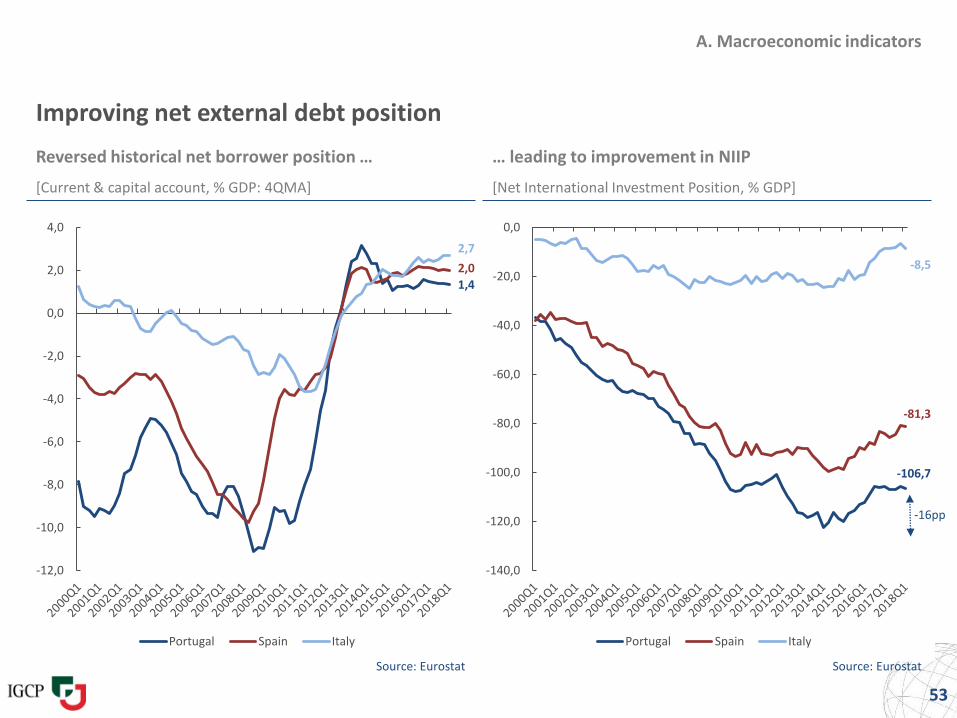

Improving net external debt position

Reversed historical net borrower position … … leading to improvement in NIIP

[Current & capital account, % GDP: 4QMA] [Net International Investment Position, % GDP]

53

-16pp

Source: Eurostat Source: Eurostat

1,4

2,0

2,7

-12,0

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

Portugal Spain Italy

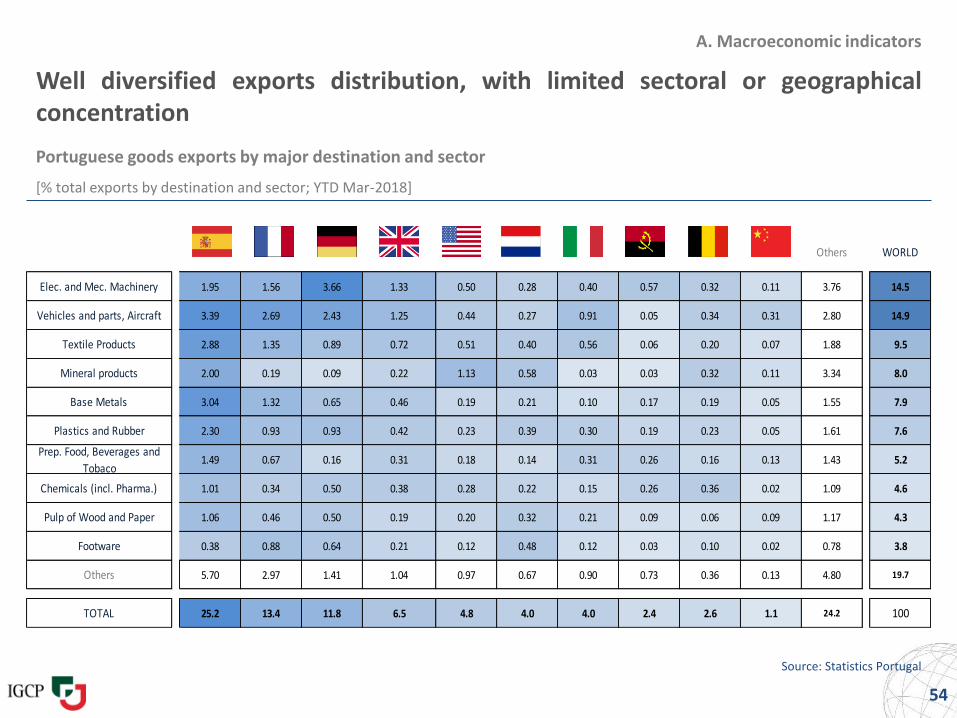

Well diversified exports distribution, with limited sectoral or geographicalconcentration

Portuguese goods exports by major destination and sector

[% total exports by destination and sector; YTD Mar-2018]

Source: Statistics Portugal

54

A. Macroeconomic indicators

Others WORLD

Elec. and Mec. Machinery 1.95 1.56 3.66 1.33 0.50 0.28 0.40 0.57 0.32 0.11 3.76 14.5

Vehicles and parts, Aircraft 3.39 2.69 2.43 1.25 0.44 0.27 0.91 0.05 0.34 0.31 2.80 14.9

Textile Products 2.88 1.35 0.89 0.72 0.51 0.40 0.56 0.06 0.20 0.07 1.88 9.5

Mineral products 2.00 0.19 0.09 0.22 1.13 0.58 0.03 0.03 0.32 0.11 3.34 8.0

Base Metals 3.04 1.32 0.65 0.46 0.19 0.21 0.10 0.17 0.19 0.05 1.55 7.9

Plastics and Rubber 2.30 0.93 0.93 0.42 0.23 0.39 0.30 0.19 0.23 0.05 1.61 7.6

Prep. Food, Beverages and

Tobaco1.49 0.67 0.16 0.31 0.18 0.14 0.31 0.26 0.16 0.13 1.43 5.2

Chemicals (incl. Pharma.) 1.01 0.34 0.50 0.38 0.28 0.22 0.15 0.26 0.36 0.02 1.09 4.6

Pulp of Wood and Paper 1.06 0.46 0.50 0.19 0.20 0.32 0.21 0.09 0.06 0.09 1.17 4.3

Footware 0.38 0.88 0.64 0.21 0.12 0.48 0.12 0.03 0.10 0.02 0.78 3.8

Others 5.70 2.97 1.41 1.04 0.97 0.67 0.90 0.73 0.36 0.13 4.80 19.7

TOTAL 25.2 13.4 11.8 6.5 4.8 4.0 4.0 2.4 2.6 1.1 24.2 100

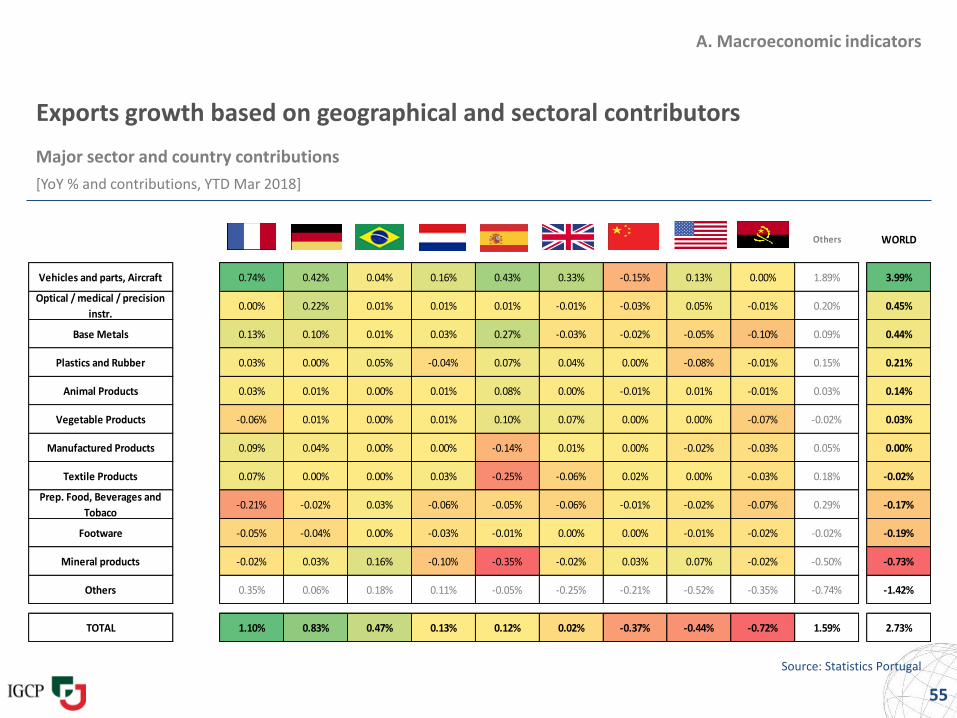

Exports growth based on geographical and sectoral contributors

Major sector and country contributions

[YoY % and contributions, YTD Mar 2018]

Source: Statistics Portugal

55

A. Macroeconomic indicators

France Germany Brazil Netherlands Spain United Kingdom China United States Angola Others WORLD

Vehicles and parts, AircraftVehicles,

aircraft, 0.74% 0.42% 0.04% 0.16% 0.43% 0.33% -0.15% 0.13% 0.00% 1.89% 3.99%

Optical / medical / precision

instr.

Optical,

photogra0.00% 0.22% 0.01% 0.01% 0.01% -0.01% -0.03% 0.05% -0.01% 0.20% 0.45%

Base MetalsBase

metals 0.13% 0.10% 0.01% 0.03% 0.27% -0.03% -0.02% -0.05% -0.10% 0.09% 0.44%

Plastics and RubberPlastics

and 0.03% 0.00% 0.05% -0.04% 0.07% 0.04% 0.00% -0.08% -0.01% 0.15% 0.21%

Animal ProductsLive

animals; 0.03% 0.01% 0.00% 0.01% 0.08% 0.00% -0.01% 0.01% -0.01% 0.03% 0.14%

Vegetable ProductsVegetabl

e -0.06% 0.01% 0.00% 0.01% 0.10% 0.07% 0.00% 0.00% -0.07% -0.02% 0.03%

Manufactured ProductsMiscella

neous 0.09% 0.04% 0.00% 0.00% -0.14% 0.01% 0.00% -0.02% -0.03% 0.05% 0.00%

Textile ProductsTextiles

and 0.07% 0.00% 0.00% 0.03% -0.25% -0.06% 0.02% 0.00% -0.03% 0.18% -0.02%

Prep. Food, Beverages and

Tobaco

Prepared

foodstuff-0.21% -0.02% 0.03% -0.06% -0.05% -0.06% -0.01% -0.02% -0.07% 0.29% -0.17%

FootwareFootwea

r, -0.05% -0.04% 0.00% -0.03% -0.01% 0.00% 0.00% -0.01% -0.02% -0.02% -0.19%

Mineral productsMineral

products-0.02% 0.03% 0.16% -0.10% -0.35% -0.02% 0.03% 0.07% -0.02% -0.50% -0.73%

Others 0.35% 0.06% 0.18% 0.11% -0.05% -0.25% -0.21% -0.52% -0.35% -0.74% -1.42%

TOTAL Total 1.10% 0.83% 0.47% 0.13% 0.12% 0.02% -0.37% -0.44% -0.72% 1.59% 2.73%

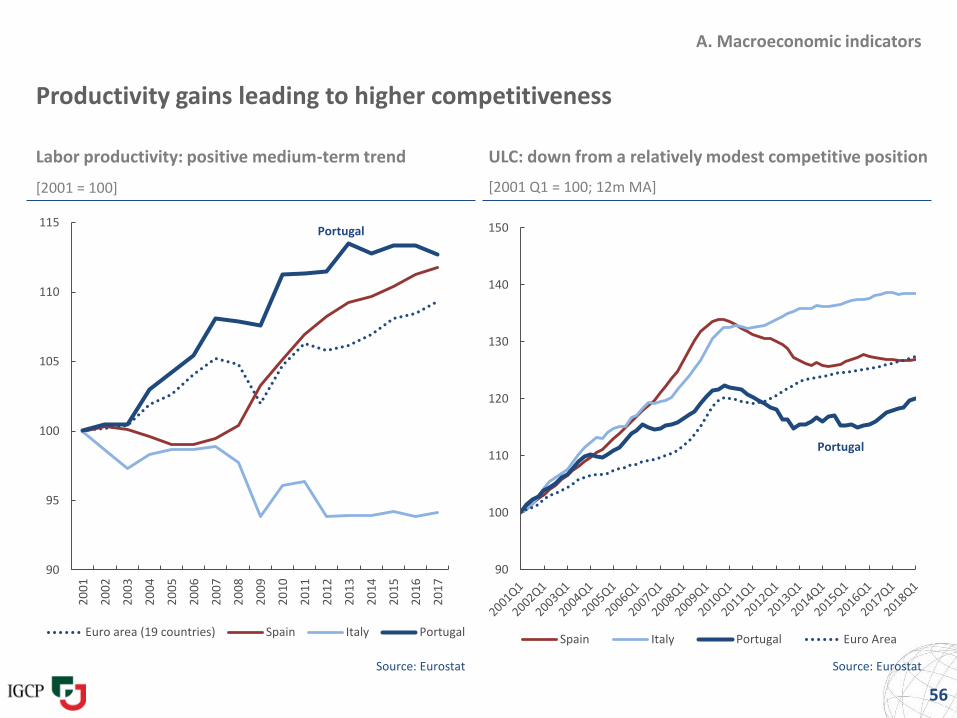

Productivity gains leading to higher competitiveness

Labor productivity: positive medium-term trend ULC: down from a relatively modest competitive position

[2001 = 100] [2001 Q1 = 100; 12m MA]

Source: Eurostat Source: Eurostat

56

A. Macroeconomic indicators

Portugal

90

95

100

105

110

115

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Euro area (19 countries) Spain Italy Portugal

Portugal

90

100

110

120

130

140

150

Spain Italy Portugal Euro Area

Appendix

57

A. Macroeconomic indicators

B. Structural indicators

C. Fiscal indicators

Structural reforms key to sustain a balanced growth environment

58

What has been achieved: Underway:

B. Structural indicators

• Improved efficiency of credit allocation by banks

• Resolution Fund: State loan extended for up to 30y, with maturity contingent on final outstanding amount (after NB sale)

Financial sector

• Social Security reform

• Improved effectiveness: reduction of civil servants (-10% since 2011) and SOEs restructuring

• Simplified tax compliance + reduced fraud and fiscal evasion

• New Budgetary Framework Law

• Privatization program

• Judicial system reform

Public sector

• Reduced firms’ administrative burden (e.g. licensing)

• Lower costs of context (e.g. communications, railways, ports)

• Rental market reform

Product market

• Reduced severance payments and unemployment benefits

• More flexible working arrangements

Labor market

• Program Capitalizar: promote reduction of indebtedness levels and increase capital holdings

• Initiative Indústria 4.0: designed to revitalize most traditional sectors (agroindustry, auto, fashion, retail and tourism)

• Program Semente: new fiscal framework to promote Start Up investment

Corporate sector

• Program Simplex+: improve efficient use of public resourcesand simplify administrative burden

• Spending review focused on: (i) health and education sectors; (ii) procurement; (iii) real estate; and (iv) SOEs

• Automatic income declaration for Personal Income Tax

Public sector

• NPLs: working group preparing measures to facilitate debt restructuring, including fiscal treatment of write-offs

• Improve efficiency of insolvency and debt restructuring frameworks

Financial sector

B. Structural indicators

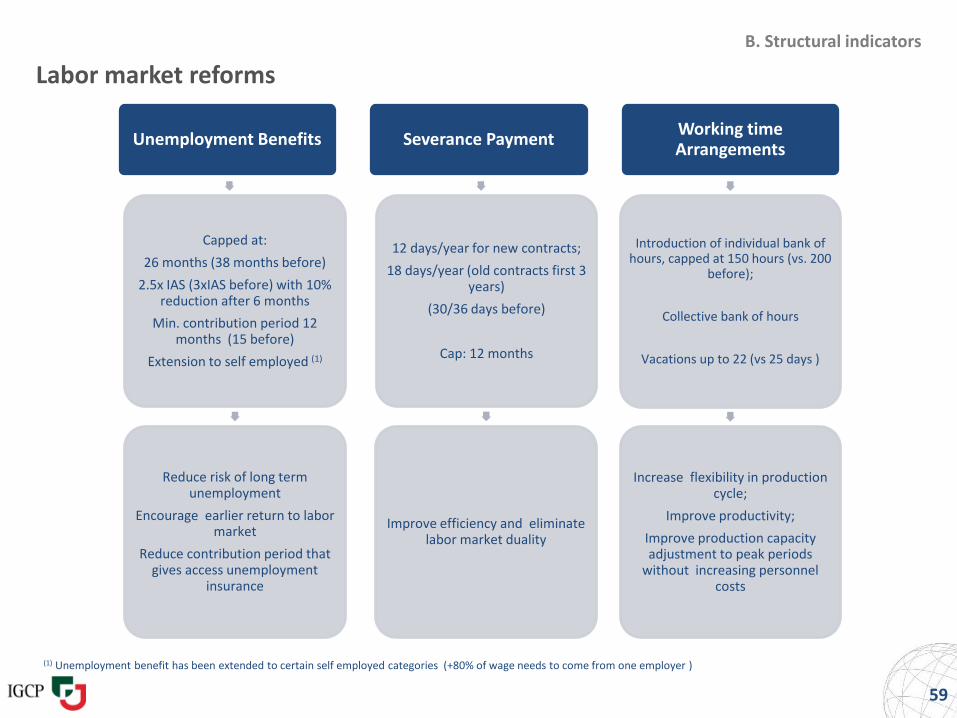

Labor market reforms

59

(1) Unemployment benefit has been extended to certain self employed categories (+80% of wage needs to come from one employer )

Unemployment Benefits

Capped at:

26 months (38 months before)

2.5x IAS (3xIAS before) with 10% reduction after 6 months

Min. contribution period 12 months (15 before)

Extension to self employed (1)

Reduce risk of long term unemployment

Encourage earlier return to labor market

Reduce contribution period that gives access unemployment

insurance

Severance Payment

12 days/year for new contracts;

18 days/year (old contracts first 3 years)

(30/36 days before)

Cap: 12 months

Improve efficiency and eliminate labor market duality

Working time Arrangements

Introduction of individual bank of hours, capped at 150 hours (vs. 200

before);

Collective bank of hours

Vacations up to 22 (vs 25 days )

Increase flexibility in production cycle;

Improve productivity;

Improve production capacity adjustment to peak periods

without increasing personnel costs

B. Structural indicators

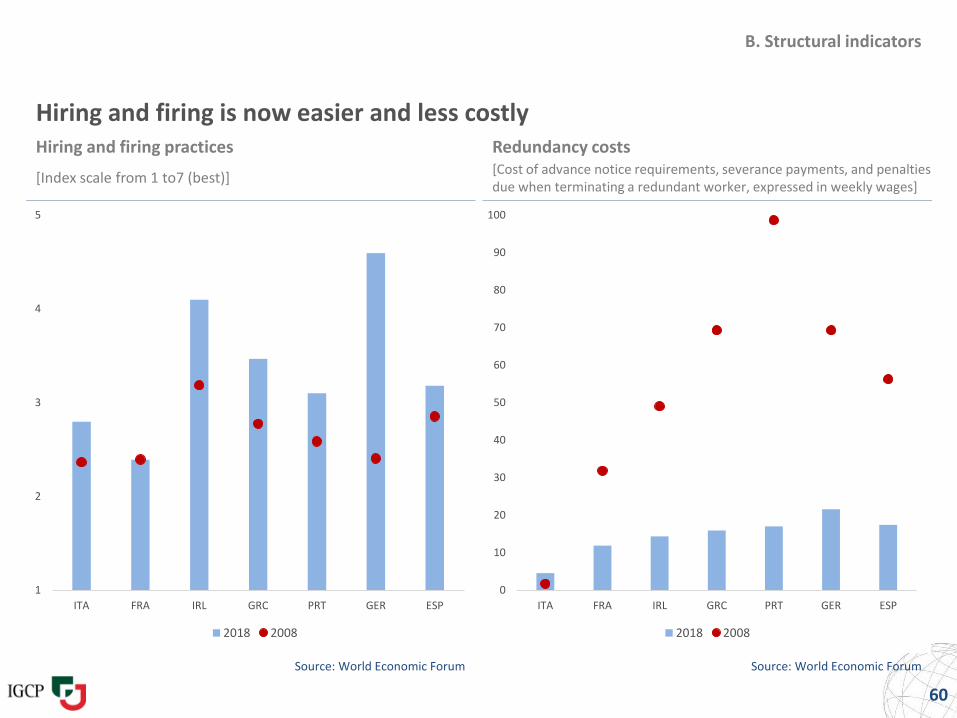

Hiring and firing is now easier and less costly

Source: World Economic Forum Source: World Economic Forum

60

Hiring and firing practices

[Index scale from 1 to7 (best)]

Redundancy costs[Cost of advance notice requirements, severance payments, and penalties due when terminating a redundant worker, expressed in weekly wages]

1

2

3

4

5

ITA FRA IRL GRC PRT GER ESP

2018 2008

0

10

20

30

40

50

60

70

80

90

100

ITA FRA IRL GRC PRT GER ESP

2018 2008

Appendix

61

A. Macroeconomic indicators

B. Structural reforms

C. Fiscal indicators

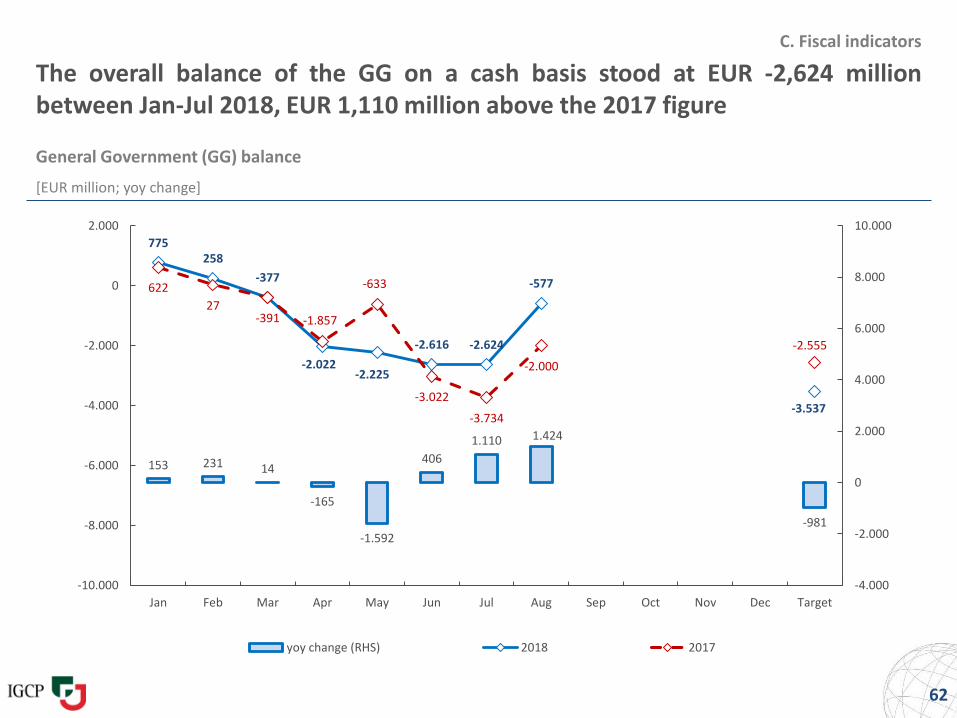

The overall balance of the GG on a cash basis stood at EUR -2,624 millionbetween Jan-Jul 2018, EUR 1,110 million above the 2017 figure

General Government (GG) balance

[EUR million; yoy change]

62

C. Fiscal indicators

153 231 14

-165

-1.592

406

1.110 1.424

-981

775258

-377

-2.022-2.225

-2.616 -2.624

-577

-3.537

622

27-391 -1.857

-633

-3.022

-3.734

-2.000

-2.555

-4.000

-2.000

0

2.000

4.000

6.000

8.000

10.000

-10.000

-8.000

-6.000

-4.000

-2.000

0

2.000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Target

yoy change (RHS) 2018 2017

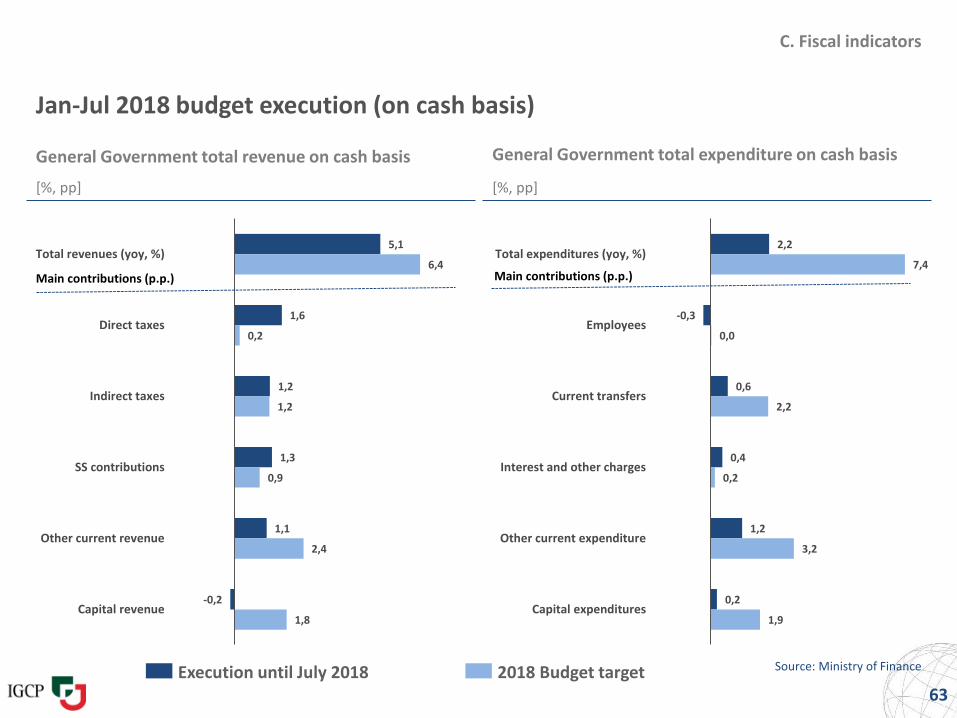

2,2

-0,3

0,6

0,4

1,2

0,2

7,4

0,0

2,2

0,2

3,2

1,9

Total expenditures (yoy, %)

Employees

Current transfers

Interest and other charges

Other current expenditure

Capital expenditures

Main contributions (p.p.)

5,1

1,6

1,2

1,3

1,1

-0,2

6,4

0,2

1,2

0,9

2,4

1,8

Total revenues (yoy, %)

Direct taxes

Indirect taxes

SS contributions

Other current revenue

Capital revenue

Main contributions (p.p.)

Jan-Jul 2018 budget execution (on cash basis)

General Government total revenue on cash basis General Government total expenditure on cash basis

[%, pp] [%, pp]

Source: Ministry of Finance

63Execution until July 2018 2018 Budget target

C. Fiscal indicators

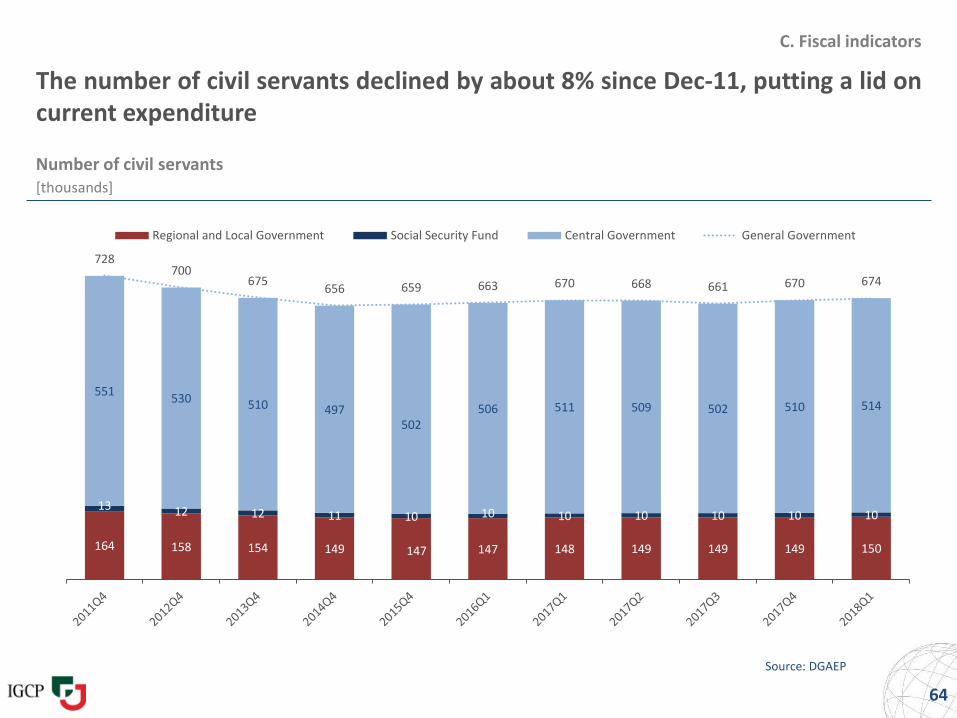

The number of civil servants declined by about 8% since Dec-11, putting a lid oncurrent expenditure

Number of civil servants[thousands]

Source: DGAEP

64

C. Fiscal indicators

164 158 154 149 147 147 148 149 149 149 150

13 12 12 11 10 10 10 10 10 10 10

551530 510 497

502506 511 509 502 510 514

728700

675656 659 663 670 668 661 670 674

Regional and Local Government Social Security Fund Central Government General Government

C. Fiscal indicators

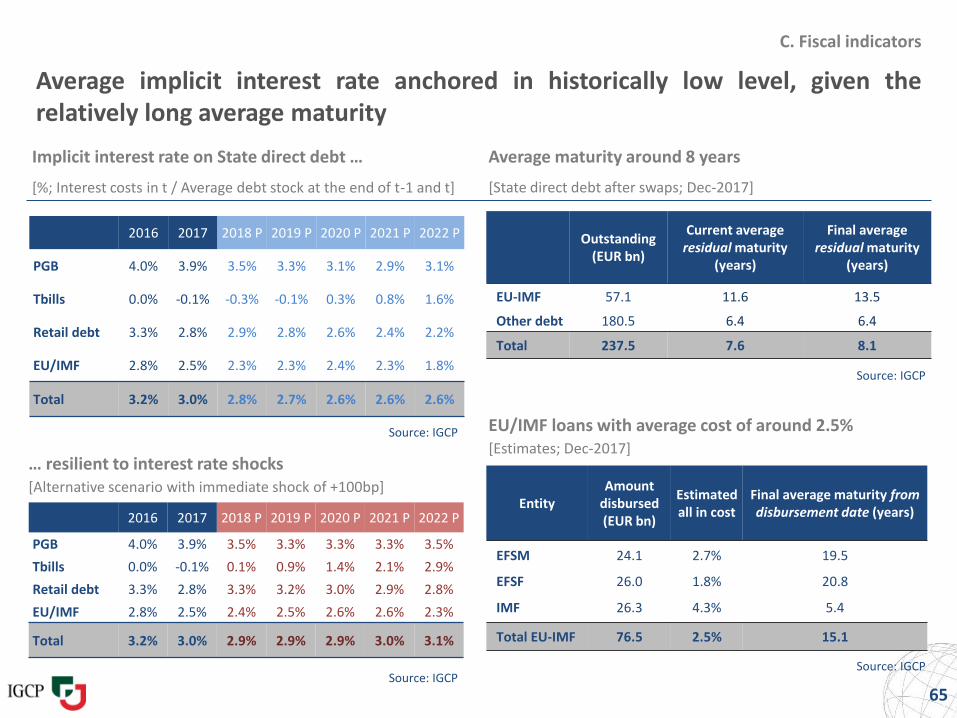

Average implicit interest rate anchored in historically low level, given therelatively long average maturity

Average maturity around 8 yearsImplicit interest rate on State direct debt …

[State direct debt after swaps; Dec-2017][%; Interest costs in t / Average debt stock at the end of t-1 and t]

Source: IGCP

Source: IGCP

65

EntityAmount

disbursed (EUR bn)

Estimated all in cost

Final average maturity from disbursement date (years)

EFSM 24.1 2.7% 19.5

EFSF 26.0 1.8% 20.8

IMF 26.3 4.3% 5.4

Total EU-IMF 76.5 2.5% 15.1

EU/IMF loans with average cost of around 2.5%[Estimates; Dec-2017]

Outstanding (EUR bn)

Current average residual maturity

(years)

Final average residual maturity

(years)

EU-IMF 57.1 11.6 13.5

Other debt 180.5 6.4 6.4

Total 237.5 7.6 8.1

2016 2017 2018 P 2019 P 2020 P 2021 P 2022 P

PGB 4.0% 3.9% 3.5% 3.3% 3.1% 2.9% 3.1%

Tbills 0.0% -0.1% -0.3% -0.1% 0.3% 0.8% 1.6%

Retail debt 3.3% 2.8% 2.9% 2.8% 2.6% 2.4% 2.2%

EU/IMF 2.8% 2.5% 2.3% 2.3% 2.4% 2.3% 1.8%

Total 3.2% 3.0% 2.8% 2.7% 2.6% 2.6% 2.6%

… resilient to interest rate shocks[Alternative scenario with immediate shock of +100bp]

2016 2017 2018 P 2019 P 2020 P 2021 P 2022 P

PGB 4.0% 3.9% 3.5% 3.3% 3.3% 3.3% 3.5%

Tbills 0.0% -0.1% 0.1% 0.9% 1.4% 2.1% 2.9%

Retail debt 3.3% 2.8% 3.3% 3.2% 3.0% 2.9% 2.8%

EU/IMF 2.8% 2.5% 2.4% 2.5% 2.6% 2.6% 2.3%

Total 3.2% 3.0% 2.9% 2.9% 2.9% 3.0% 3.1%

Source: IGCP

Source: IGCP

Web site: www.igcp.ptBloomberg pages: IGCPReuters pages: IGCP01

66

Disclaimer

The information and opinions contained in this presentation have been compiled or arrived at from sources believed to be reliable and ingood faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness.

All opinions and estimates contained in this document are published for the assistance of recipients, but are not to be relied upon asauthoritative or taken in substitution for the exercise of judgment by a recipient and, therefore, do not form the basis of any contract orcommitment whatsoever.

IGCP does not accept any liability whatsoever for any direct or consequential loss arising from any use of this document or its contents.

![PORTUGAL - IGCP, E.P.E. - IGCP€¦ · …buoyed by strong gains in exports’market share 2. Stronger growth foundations 12 Significant gains in exports’ market share [Index 2007Q1=100]](https://img.pdfslide.net/doc/110x75/5f0c30927e708231d4342edd/portugal-igcp-epe-igcp-buoyed-by-strong-gains-in-exportsamarket-share.jpg)