Embed Size (px)

Citation preview

Poseidon Concepts• North American investors will remember the case of Poseidon Concepts(http://www.theglobeandmail.com/report-on-business/rob-magazine/the-13-billion-fraud-bay-street-forgot/article32651690/)

• Poseidon developed and leased out pools used by oil and gas customers to store dirty fracking water

• The stock went from over 16 DOLLARS to 16 CENTS in ~5 mos, wiping out well over $1 billion of market value

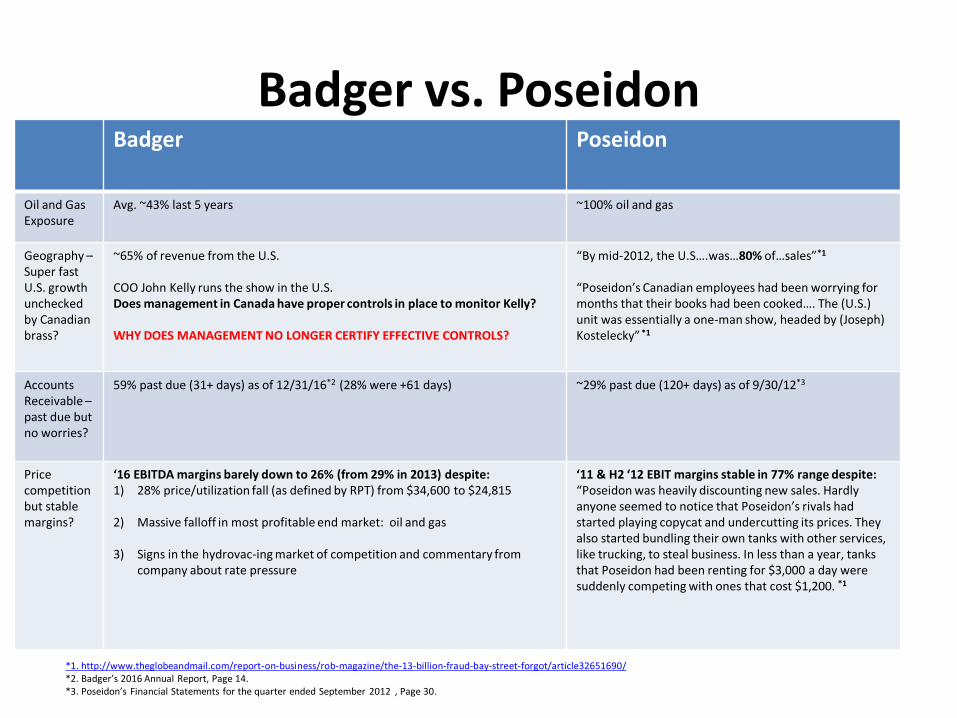

Badger vs. PoseidonBadger Poseidon

Oil and Gas Exposure

Avg. ~43% last 5 years ~100% oil and gas

Geography –Super fast U.S. growth unchecked by Canadianbrass?

~65% of revenue from the U.S.

COO John Kelly runs the show in the U.S. Does management in Canada have proper controls in place to monitor Kelly?

WHY DOES MANAGEMENT NO LONGER CERTIFY EFFECTIVE CONTROLS?

“By mid-2012, the U.S….was…80% of…sales”*1

“Poseidon’s Canadian employees had been worrying for months that their books had been cooked…. The (U.S.)unit was essentially a one-man show, headed by (Joseph) Kostelecky” *1

AccountsReceivable –past due but no worries?

59% past due (31+ days) as of 12/31/16*2 (28% were +61 days) ~29% past due (120+ days) as of 9/30/12*3

Pricecompetition but stable margins?

‘16 EBITDA margins barely down to 26% (from 29% in 2013) despite: 1) 28% price/utilization fall (as defined by RPT) from $34,600 to $24,815

2) Massive falloff in most profitable end market: oil and gas

3) Signs in the hydrovac-ing market of competition and commentary from company about rate pressure

‘11 & H2 ‘12 EBIT margins stable in 77% range despite:“Poseidon was heavily discounting new sales. Hardly anyone seemed to notice that Poseidon’s rivals had started playing copycat and undercutting its prices. They also started bundling their own tanks with other services, like trucking, to steal business. In less than a year, tanks that Poseidon had been renting for $3,000 a day were suddenly competing with ones that cost $1,200. *1

*1. http://www.theglobeandmail.com/report-on-business/rob-magazine/the-13-billion-fraud-bay-street-forgot/article32651690/*2. Badger’s 2016 Annual Report, Page 14.*3. Poseidon’s Financial Statements for the quarter ended September 2012 , Page 30.

What happened with Poseidon’s AR?Poseidon’s 2011 Annual Report, Page 42 on Revenue Recognition:

• Fracturing fluid tank rental revenues are generally derived from the provision of rentals and related services which are based on contracts that include fixed or determinable prices based on daily rental rates. Revenue is recognized when there is persuasive evidence of an arrangement, tank rentals and related services are provided, the rate is fixed and determinable and collectability is reasonably assured.

SEC v. Joseph A. Kostelecky, Filed 2/6/2015, Page 6

• There was no basis, however, to book a material amount of the revenues from these contracts because the purported take-or-pay contracts simply did not exist or were otherwise uncollectible.

WHAT WAS THE OUTCOME?

SEC v. Joseph A. Kostelecky, Filed 2/6/2015, Page 9

• an independent member of Poseidon’s board of directors learned that the Operations Controller believed that at least $70 million of the company’s take-or-pay receivables were uncollectable.

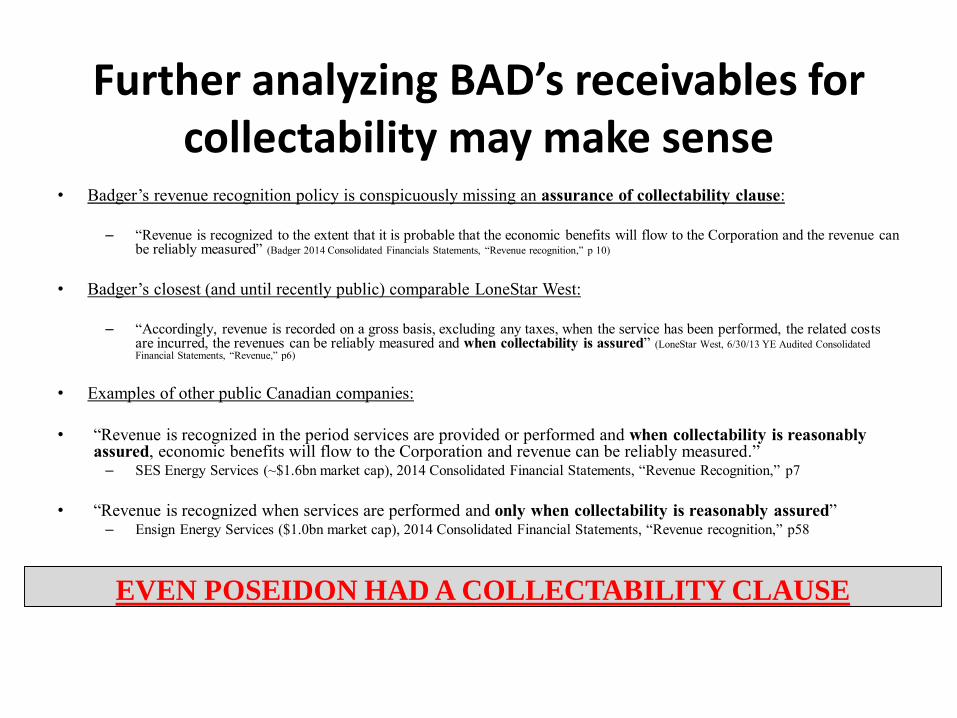

Further analyzing BAD’s receivables for collectability may make sense

• Badger’s revenue recognition policy is conspicuously missing an assurance of collectability clause:

– “Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Corporation and the revenue can be reliably measured” (Badger 2014 Consolidated Financials Statements, “Revenue recognition,” p 10)

• Badger’s closest (and until recently public) comparable LoneStar West:

– “Accordingly, revenue is recorded on a gross basis, excluding any taxes, when the service has been performed, the related costs are incurred, the revenues can be reliably measured and when collectability is assured” (LoneStar West, 6/30/13 YE Audited Consolidated Financial Statements, “Revenue,” p6)

• Examples of other public Canadian companies:

• “Revenue is recognized in the period services are provided or performed and when collectability is reasonably assured, economic benefits will flow to the Corporation and revenue can be reliably measured.” – SES Energy Services (~$1.6bn market cap), 2014 Consolidated Financial Statements, “Revenue Recognition,” p7

• “Revenue is recognized when services are performed and only when collectability is reasonably assured”– Ensign Energy Services ($1.0bn market cap), 2014 Consolidated Financial Statements, “Revenue recognition,” p58

EVEN POSEIDON HAD A COLLECTABILITY CLAUSE

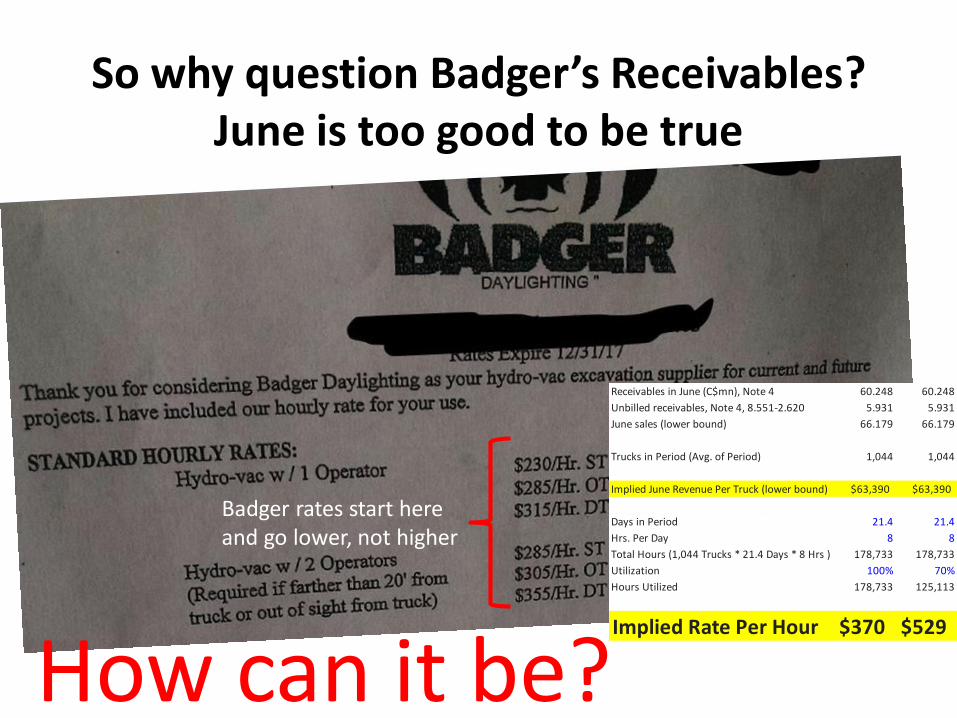

So why question Badger’s Receivables?June is too good to be true

How can it be?

Receivables in June (C$mn), Note 4 60.248 60.248

Unbilled receivables, Note 4, 8.551-2.620 5.931 5.931

June sales (lower bound) 66.179 66.179

Trucks in Period (Avg. of Period) 1,044 1,044

Implied June Revenue Per Truck (lower bound) $63,390 $63,390

Days in Period 21.4 21.4

Hrs. Per Day 8 8

Total Hours (1,044 Trucks * 21.4 Days * 8 Hrs ) 178,733 178,733

Utilization 100% 70%

Hours Utilized 178,733 125,113

Implied Rate Per Hour $370 $529

Badger rates start here and go lower, not higher

So why question Badger’s Receivables?

2014 2015 2016 Q1:17

Badger Daylighting

Trade Receivables (Avg. Over Period) 98.9 94.8 85.9

Allow ance for Doubtful Accts 1.0 2.1 1.5

Allowances / Trade Receivables 1.0% 2.2% 1.7%

Lonestar West

Trade Receivables (Avg. Over Period) 12.4 16.0 12.8 8.2

Allow ance for Doubtful Accts 0.2 1.5 0.0 0.2

Allowances / Trade Receivables 1.2% 9.3% 0.0% 3.0%

Bad Debt Exp. 0.3 1.4 0.8 0.2

Bad Debt Exp. / Trade Receivables 2.1% 8.8% 6.5% 3.0%

Lonestar & T-Rex write offs have been driven by Large Projects…

Badger worked on the Same Projects with more trucks on site…

How Much of Badger’s A/R is Impaired Due to Broke Customers?

Customer

Date of

Filing

2016

Rock Hard Ex cav ating Jan-16

Harv est Mustang GP Ltd. (1)

Jan-16

Lemke Construction (Michael & Chelsey Lemke) Jan-16

Osage Ex ploration & Dev elopment Feb-16

Pipeline Energy Group Feb-16

Graham Brothers Construction Mar-16

Terra Energy Corp. Mar-16

JRS Industrial Inc. Apr-16

Chinook Pipeline Limited May -16

Ultra Petroleum May -16

NuWeld Inc. May -16

Abengoa Jun-16

C.C. My ers Inc. Jul-16

Louisiana Crane & Construction LLC Jul-16

H.B. White Canada Corp. Jul-16

NTS Inc. Aug-16

Light Tow er Rentals / LTR Aug-16

Tw in Butte Energy Ltd. Sep-16

Elite Construction & Fabrication LLC Sep-16

Warren Resources Oct-16

Northern Frontier Oct-16

Vortex Drain Tiling LLC Dec-16

2015

Furix Energy Jan-15

Palliser Oil & Gas (2)

Feb-15

BG Furniture Ltd. / Harv est Mustang GP Ltd. Jul-15

Adv anced Pipeline Serv ices Jul-15

Capriati Construction Corp. Oct-15

Camar Construction Dec-15

(1) Benko Sewer Service

(2) Fieldtek Ltd.

2015-2016 Bankruptcy Filings In Which Badger is Unsecured Creditor

Many of Badger’s Customers Have Gone Bankrupt…

Yet, Customers Going Broke & Other Operators Writing Off A/R from the Same Jobs as Badger Still Hasn’t Shown Up on Badger’s Aging A/R Book

What % of Badger’s $25mn of A/R > 60 Days Will Be Collected?

So what happened to Poseidon? Well, a lot…but we’ll keep it brief

Q3 2012 results showed EBITDA margins down from 84% to 65%*1

Come spring 2013 , Poseidon’s shares were worth practically nothing *2

More details can be found on Google or in the Globe and Mail article cited below.

*1. Poseidon’s Financial Statements for the quarter ended September 2012 .*2. http://www.theglobeandmail.com/report-on-business/rob-magazine/the-13-billion-fraud-bay-street-forgot/article32651690//

About UsAlder Lane Farm LLC publishes periodic, time sensitive, fact-based financial news and analysis to the public and its readers. Our reporting is designed to help the public interpret and understand publicly available information about the economic health ofparticular companies and their share value, and to understand the impact that a fuller disclosure of information may have on share prices. We publish when there are newsworthy items relevant to the companies analyzed.

We rely on public disclosures of the companies under review and other companies in the same or similar sectors. We also conductinterviews with employees, former employees, officers, and others associated with the companies we analyze, when possible. We review national and international news services, internet reporting, and social media and may rely on reporting by others to prepare our report. We discuss the companies with other analysts who may have positive or negative information and opinions about the companies under review and then analyze the information and opinions received to determine whether the information and opinions are based on available factual information or disclosures. We also may obtain information from, and rely on, information from sources who wish to remain confidential and whose information, but not identity, may be included in this report.

We welcome comments from the companies we review, from other newspapers or analysts, and from the public. We will publish corrections or explanations submitted if those are found to be based in fact and are credible. We conduct most of our analysis without active participation by, or with limited input from, the subject companies and thus we recognize that those companies may disagree with our conclusions or may believe there are facts that were not available to us when we published our report. We make efforts to obtain accurate and complete information in preparing this report. However, we do not warrant that the information and analysis is correct.

Comments or requests for corrections are therefore welcomed.

Any requests for corrections to this report should be directed to the publisher at PO Box 578, Pengrove, CA 94951. The request for correction should identify the statements challenged and a demand that the statements be corrected.

You should consider this report along with all other information and analysis that is available, as well as your own research. We are not responsible for any trading losses you believe may have been caused by your reliance on this report. It is not investment advice or a recommendation or solicitation to buy any securities. We are not registered as an investment advisor in any jurisdiction.

We take investment positions consistent with our own opinions in the companies we cover. If the report contains an overall negative assessment, then that means we stand to profit if the company’s stock declines. We may buy, sell, cover or otherwise change the form or substance of our position in the company and we do not publicly announce our investment decisions or changes in our investment positions.