Embed Size (px)

Citation preview

Nam B. Nguyen 1

Passive investing might deliver a better return,

but do not discount active investing just yet

Position paper

Nam B. Nguyen

CERGE-EI, Czech Republic

5 February 2016

1. Introduction

Whether active or passive investing is a

superior investment strategy is a long-lasting

and much heated debate among investment

professionals and academic researchers. This

debate is closely related to the efficient

market hypothesis (EMH) developed by

Eugene Fama, an economist professor who

won the Nobel Prize in Economics in 2013.

This theory claims that it is impossible to

achieve a rate of return higher than that of the

market as all the relevant information has

already been accounted for in the stock price

by rational investors. Investors therefore

would be better off buying and holding an

index that replicates the market portfolio for

the purpose of matching its performance as

close as possible (passive investing) rather

than attempting to outperform it by explicitly

selecting stocks and timing the market (active

investing) (Fama, 1970). Robert Shiller, who

shared the Nobel Prize with Fama, disagrees

with him on the efficiency of the market

Figure 1: Shiller and Fama

Nam B. Nguyen 2

based on the results of his behavioral finance

research. His counterargument is that stock

price is driven by human psychology, which

is not always rational. Stock prices therefore

do not always fairly reflect the economic

fundamentals of companies, which presents

opportunities for investors to take advantage

of market inefficiencies through active

investing (Shiller, 2003).

An overwhelming majority of academic

literature has sided with passive investing

and shown that most active managers cannot

beat the market on a consistent basis

(Whitehead, 2012). In an attempt to ground

the debate with concrete data, Morningstar, a

leading independent research firm, released

the Active/Passive Barometer, a performance

comparison tool, which concludes that

passive index funds have generally

outperformed their actively managed

counterparts, particularly over longer time

horizons (Johnson, Boccellari, Bryan, &

Rawson, 2015). Although passive investing

might deliver a better long-run return on

average, active investing should not be

discounted just yet for three reasons:

Active investing provides important

indirect benefits beyond financial

returns.

Despite its many benefits, passive

investing is not free of risks.

There are systematic risks associated

with the hyper growth of index funds

and exchange-traded funds (ETFs).

This paper makes the case for core-satellite

investing - a strategy that combines the best

benefits of the two approaches instead of

favoring one over the other.

2. What is passive investing and how

did it become so popular?

2.1. What is passive investing?

Passive investing or indexed investing is to

track the return of a particular index such as

the S&P 500 via index funds or ETFs. The

key distinction between passive and active

investing lies in the investment objective.

The objective of investing passively is to

match the performance of the benchmark

index. This involves buying the same

proportion of all constituent securities in the

benchmark index and “rebalancing” -

keeping the original weights of the securities

in the index when the value of these securities

changes (Vanguard, 2015). The aim of active

investing, however, is to beat the benchmark

index after taking into account all the costs

Nam B. Nguyen 3

(Philips, Kinniry, Walker, Schlanger, & Hirt,

2015).

Since the financial crisis in 2008, index funds

and ETFs have grown rapidly at the expense

of actively managed funds (see figure 2). In

2015, $365 billion has flown into low-cost

index funds and ETFs, while $147 billion has

been withdrawn from active funds. Passive

index funds and ETFs currently occupy a

third of mutual fund asset under management

(see figure 3). Bank of America Merrill

Lynch expects this trend to persist in the

years to come (Verhage, 2015).

2.2. How did passive investing become so

popular?

The underperformance of active investing

The primary reason for the proliferation of

passive investing is that the inability of most

active managers to match the performance of

their benchmark indexes has prompted

investors to look for alternative investment

strategies that can. In the paper “The bumpy

road to outperformance”, Wimmer, Chhabra,

and Wallick (2013) analyzed the fifteen-year

performance of 1,540 actively managed U.S.

mutual funds that were available to investors

at the beginning of 1998. The results of their

research have shown that only 275 or 18% of

the original 1,540 funds survived the full

period and outperformed their benchmark

indexes (see figure 4). Among these

Figure 3: Active versus passive funds breakdown

Figure 2: Cumulative flows into passive vs. active

funds ($mn)

Source: Bloomberg (2015). These charts show the

astounding rise in passive management.

Source: Vanguard (2013). The bumpy road to

outperformance

Figure 4: Categorization of the 1,540 funds based

on performance

Nam B. Nguyen 4

successful funds, 181 funds experienced at

least three consecutive years of

underperformance (Wimmer et al., 2013).

This demonstrates how challenging it is for

active funds to survive, let alone to

outperform their benchmarks.

Diversification benefit of passive investing

Maintaining portfolio diversification is

integral to the success of an investment plan.

Figure 5 shows the performance of a

diversified portfolio compared to other

individual asset classes over the last 15 years.

The annualized return of the asset allocation

1 The weights of the “Asset Allocation” portfolio is as

follows: 25% in the S&P 500, 10% in the Russell 2000,

15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the

Barclays Aggregate, 5% in the Barclays 1-3m Treasury, 5%

portfolio 1 over the last 15 years is 4.8%,

which measures up relatively well compared

to other asset classes. More importantly, this

portfolio is able to achieve that return with a

higher stability than some major asset classes

(Liu, 2016). In brief, diversification allows

investors to achieve a good return with lower

volatility. When buying a multi-asset class

index, investors buy into a wide range of

asset classes and hundreds of securities

within them, which diminishes the

idiosyncratic risk of individual asset classes

and securities (Vanguard, 2015).

in the Barclays Global High Yield Index, 5% in the

Bloomberg Commodity Index and 5% in the NAREIT

Equity REIT Index.

Figure 5: Asset class returns – 2000 to 2015

Source: J.P. Morgan (2016). Investing with composure in volatile markets

Nam B. Nguyen 5

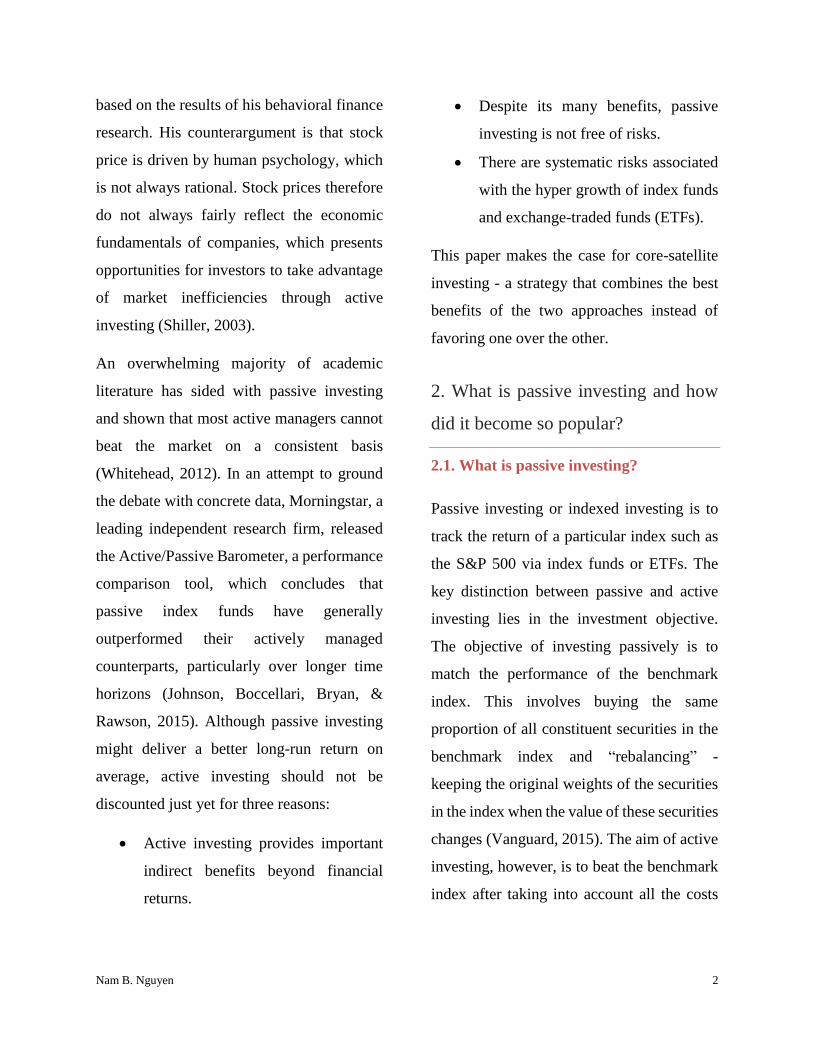

Low cost of passive investing

In his signature paper “The arithmetic of

active management”, Sharpe (1991) states

that active investing is a “zero-sum” game,

by which he means that for every winner who

outperforms in the market there must be a

loser who underperforms. The distribution of

investment return is therefore bell-shaped

and symmetrical as can be seen in figure 6.

The tan region represents the market, while

the vertical red line represents the market

return. Before costs, 50% of investors

outperform the market, and 50%

underperform the market. After accounting

for the various costs of investing such as

broker commissions, management fees,

administrative costs, etc., the distribution of

return would shift to the left (see figure 7).

The original red region to the right of the

vertical red line (area of outperformance) has

shrunk to a smaller orange region. The

returns of the majority of investors as

represented by the light yellow region are

now below the aggregate return. The point

here is that cost makes a crucial contribution

to investment success.

The frequency of trading associated with

passive investing is much lower compared to

active investing; therefore, the trading cost of

passive investing is significantly lower.

Additionally, active managers often charge

higher management fees for their service.

The average expense ratio of a typical index

fund was 0.14%, which is six times lower

than the average actively managed fund fee

of 0.93%. The effect of this difference can be

quite substantial due to the power of

compounding. Had an investor invested in an

S&P 500 index fund 20 years ago for a fee of

0.14%, he/she would have accumulated a

return of 371%. If the fee were 0.93%, the

return would be only 303% (O’Shaughnessy

et al., 2013).

3. Do not undermine active investing

Despite the significant benefits of passive

investing, investors should not discount

active investing just yet for the following

reasons.

Figure 6: Distribution of investor returns before cost

Figure 7: Distribution of investor returns after cost

Source: Vanguard (2015). Active and passive investing -

What you need to know

Nam B. Nguyen 6

3.1. Active investing provides important

indirect benefits beyond financial returns.

Ellis (2015) points out that the critics of

active investing with a narrow focus on

“beating the market” are missing the broader

picture - the indirect benefits of active

investing for societies and economies as a

whole. A crucial function of active investing

is to make the capital market efficient by

continuously trading on stock mispricings.

Efficient capital markets have proven to be

beneficial to society in many ways. Higher

efficiency of the market makes investors

more confident in entering the market and

investing their savings as it provides the

assurance that securities are fairly priced for

both buyers and sellers. Higher confidence of

investor in the capital market reduces the cost

of capital and makes it cheaper for companies

to raise funds for value-enhancing and

socially productive projects (Ellis, 2015). An

equally important function of active

managers is to help with the allocation of

scarce resources by directing capital towards

promising companies and away from weaker

ones.

3.2. Despite its many benefits, passive

investing is not free of risks.

A key weakness of index funds and ETFs is

that most of them are “market-cap weighted”

meaning that the weight of a stock in an index

is based on its market capitalization or market

value. Capitalization-weighted indexes force

investors to buy into “yesterday’s winners” -

the large-cap stocks that have performed well

in the recent periods but might not perform

well in the future. The concentration in large-

cap companies makes index investors

susceptible to their underperformance (Jones,

2014). For instance, more than 30% of the

total value of the S&P 500 was occupied by

the energy sector in the 1970s and by

technology and telecommunications in the

1990s, and just several years ago 20% of the

index was invested in financials. The

downfall of these sectors led to major losses

for the investors whose portfolios are

concentrated in these sectors (Whitehead,

2012). Felder (2016) put it perfectly: “Market

behavior suggests that an entire generation of

passive investors is about to discover the

downside risk of holding highly concentrated

positions that have flown blind, free of price

discovery”.

Apart from concentration risk, empirical

evidence has indicated that it is a losing

strategy to buy stocks based solely on their

market capitalization (O’Shaughnessy et al.,

2013). This is because passive investors buy

the stocks with expensive valuations and sell

cheap ones, which contradicts the successful

Nam B. Nguyen 7

“buy low, sell high” strategy of renowned

investors such as Benjamin Graham and

Warren Buffett (Jones, 2014). Additionally,

when buying an index, investors buy all the

stocks included in the index indiscriminately.

In this way, they might be forced to buy the

bad stocks that have a weak momentum or

high past volatility, which were observed to

deliver disappointing results in the past

(Blitz, 2014).

3.3. There are systematic risks associated

with the hyper growth of index funds and

ETFs.

Mismatch between price and value and

market illiquidity

The market can only be efficient if a

sufficient number of investors believe it to be

inefficient and take actions to eliminate these

inefficiencies (Lorie & Hamilton, 1973, cited

in Blitz, 2014). In other words, in order for

the capital market to function efficiently,

there must exist a good proportion of active

managers. It is active managers who ensure

that the price fully reflects the economic

fundamentals and the true value of a

company and that the market is liquid by

constantly looking for and arbitraging away

market inefficiencies. Passive investors, who

are referred to as “free riders” by Blitz

(2014), just take the valuation work done by

active managers as granted and mechanically

follow the market index without attempting

to determine the intrinsic value of a security.

If all investors choose to invest passively,

there would be two serious consequences:

large discrepancies between price and value,

and illiquidity of the capital market (Blitz,

2014). Several analysts and scholars have

pointed out that the stocks included in an

index are overvalued compared to their non-

index counterparts. For instance, Sovran Self

Storage and Public Storage are two thriving

self-storage businesses with similar earnings

quality. Being included in the S&P 500,

Public Storage trades at a price-earnings ratio

of 36.9, while Sovran, not in the index, trades

at 31.7 times earnings (Alster, 2015).

Overvaluations like this could lead to price

bubbles, in which the price of stocks inside

index funds falls faster and further than that

of those outside of index funds. Another

damaging consequence of the massive shift

to passive investing is the lack of trading

volume, which will force investors to ask for

a liquidity premium to compensate them for

taking on liquidity risk. This in turn raises

the cost of capital for companies making it

more expensive for them to finance projects

and expansion (Cooper, 2015). To guard

against mispricing and illiquidity, the world

needs active managers.

Nam B. Nguyen 8

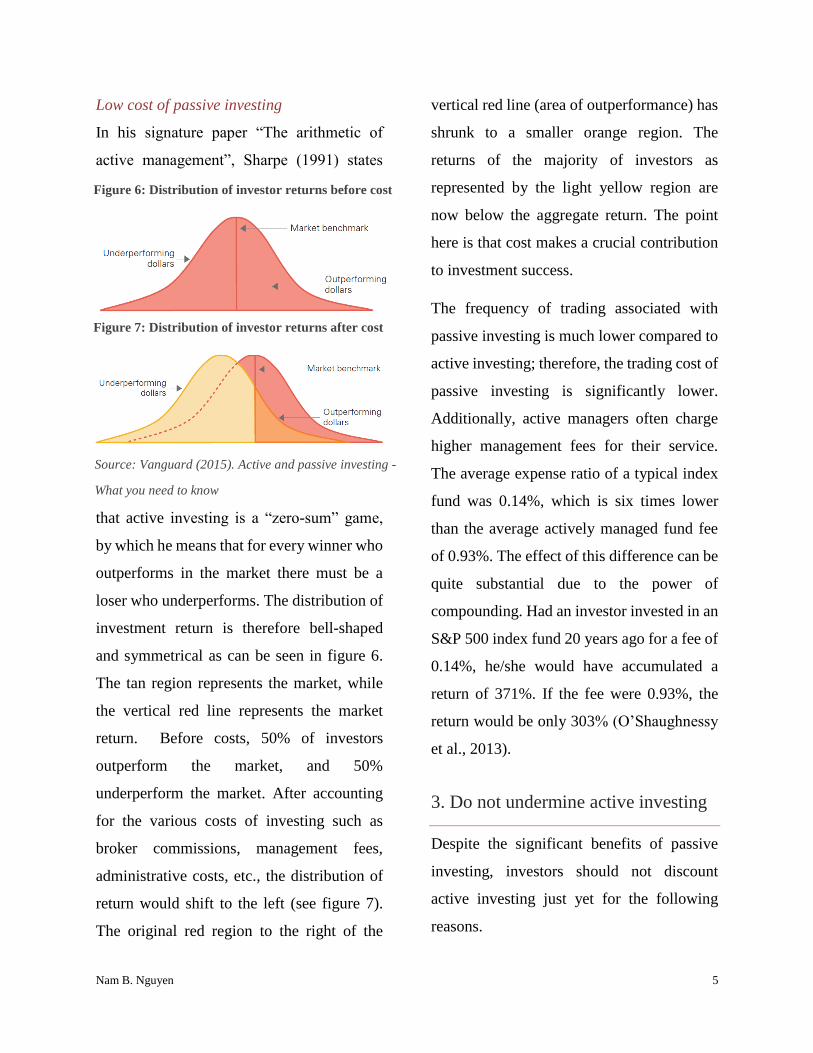

Increased volatility and lower diversification

The transition from active investing to

passive investing might entail a significant

systematic risk. The rising proportion of

index funds causes average stock

correlations, the degree to which share prices

move together, to increase as investors trade

the same index stocks simultaneously (see

figure 8) (Jones, 2014). Theoretically, to

achieve diversification, a portfolio should

include the asset classes and securities that

have low correlations with one another so

that when some asset classes or securities in

this portfolio go down in value, the other

asset classes or securities will go up to

maintain the desirable return. Therefore,

higher correlations caused by the rise of

passive investing might reduce the

diversification benefit of index portfolios.

Additionally, increased correlations also led

to sharp rises in the volatility of stocks with

large capitalizations as observed in the US

market (see figure 9) (Jones, 2014).

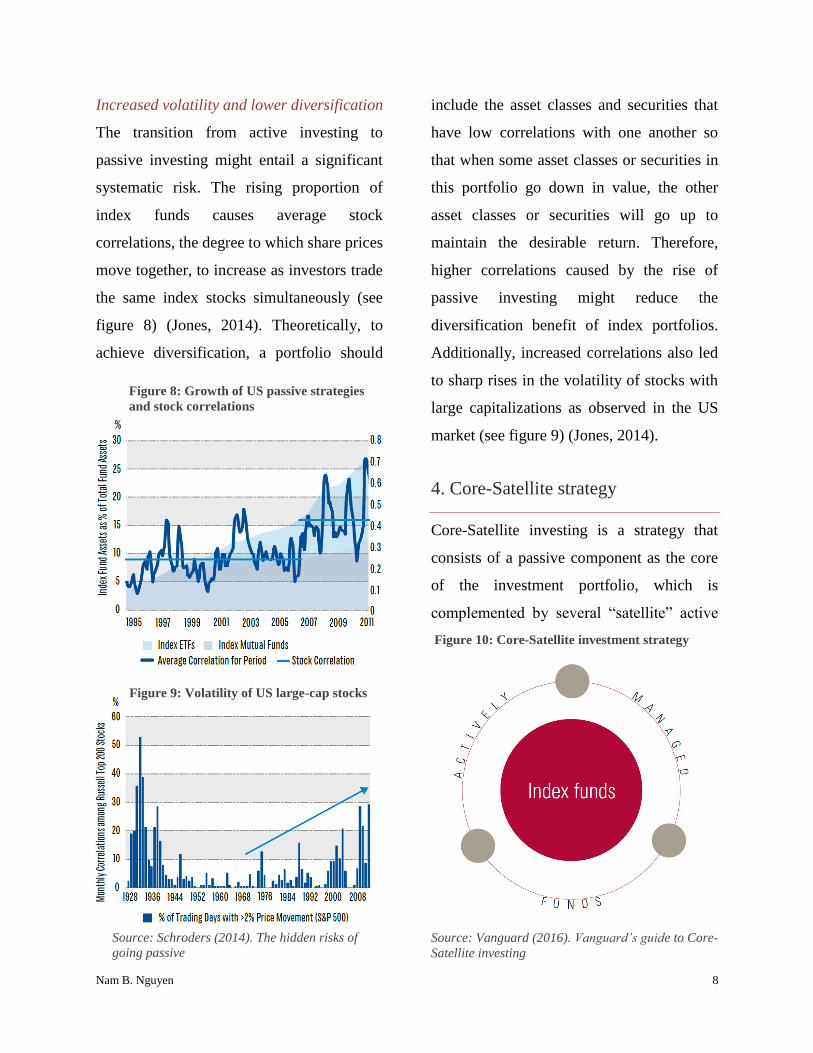

4. Core-Satellite strategy

Core-Satellite investing is a strategy that

consists of a passive component as the core

of the investment portfolio, which is

complemented by several “satellite” active

Figure 9: Volatility of US large-cap stocks

Source: Schroders (2014). The hidden risks of

going passive Source: Vanguard (2016). Vanguard’s guide to Core-

Satellite investing

Figure 10: Core-Satellite investment strategy

Figure 8: Growth of US passive strategies

and stock correlations

Nam B. Nguyen 9

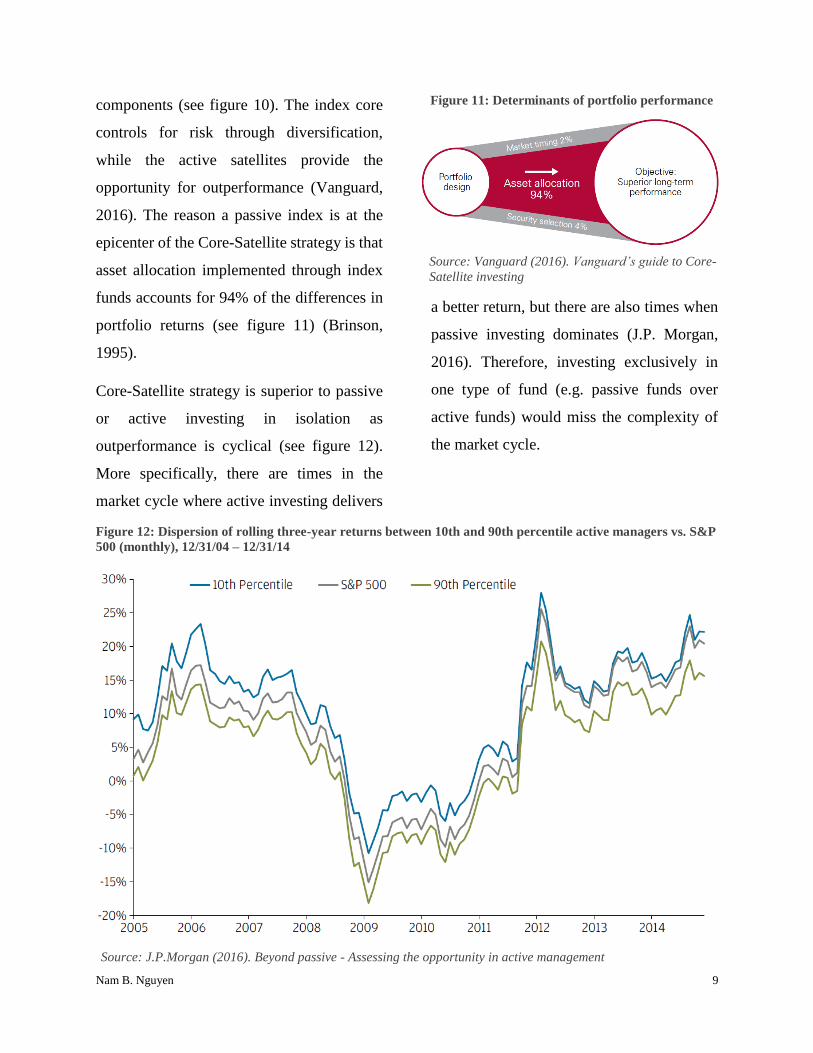

components (see figure 10). The index core

controls for risk through diversification,

while the active satellites provide the

opportunity for outperformance (Vanguard,

2016). The reason a passive index is at the

epicenter of the Core-Satellite strategy is that

asset allocation implemented through index

funds accounts for 94% of the differences in

portfolio returns (see figure 11) (Brinson,

1995).

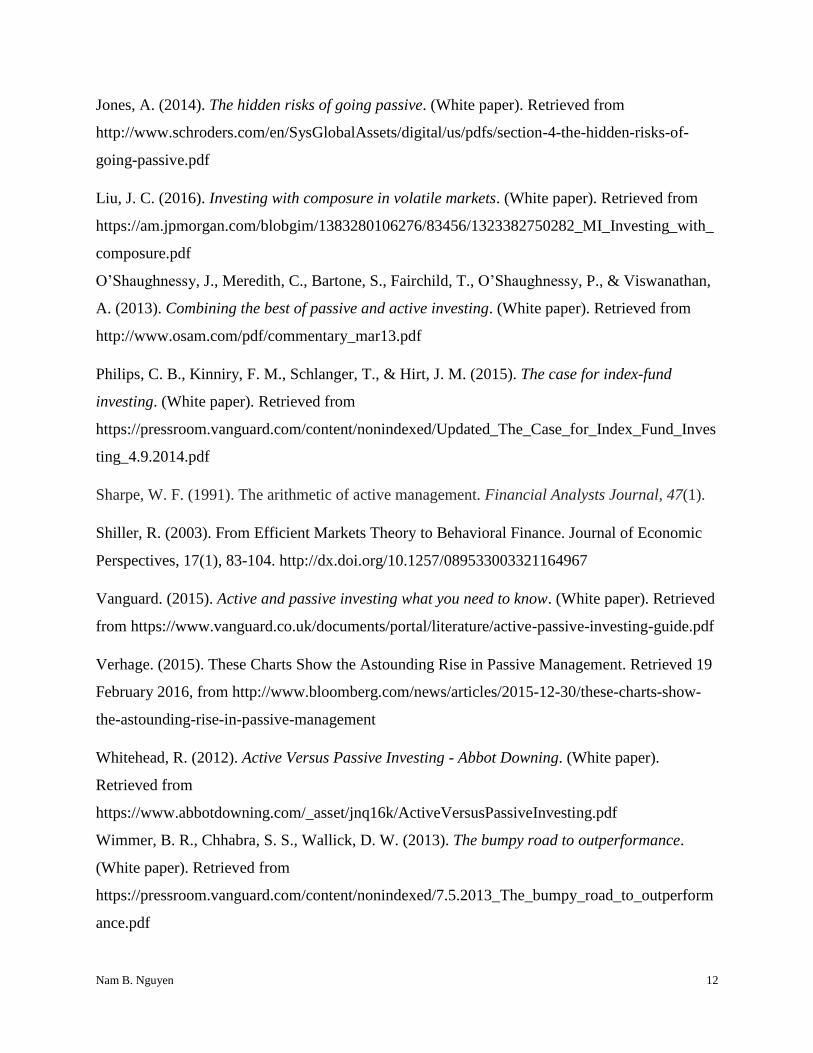

Core-Satellite strategy is superior to passive

or active investing in isolation as

outperformance is cyclical (see figure 12).

More specifically, there are times in the

market cycle where active investing delivers

a better return, but there are also times when

passive investing dominates (J.P. Morgan,

2016). Therefore, investing exclusively in

one type of fund (e.g. passive funds over

active funds) would miss the complexity of

the market cycle.

Source: Vanguard (2016). Vanguard’s guide to Core-

Satellite investing

Figure 11: Determinants of portfolio performance

Figure 12: Dispersion of rolling three-year returns between 10th and 90th percentile active managers vs. S&P

500 (monthly), 12/31/04 – 12/31/14

Source: J.P.Morgan (2016). Beyond passive - Assessing the opportunity in active management

Nam B. Nguyen 10

5. Conclusion and recommendations

There are significant benefits associated with

passive investing strategies including

diversification and low cost. Additionally, it

has been proven empirically that passive

investing delivers a better return than active

investing on average. However, this paper

advises against undermining the importance

of active investing because of three factors:

the important indirect benefits of active

investing, the risks associated with passive

investing, and the consequences related to the

massive shift from active to passive

investing. Firstly, active investing is essential

to the functioning of the capital market as it

ensures the fair pricing of frequent trading of

securities. Without active investing, stock

prices would not accurately reflect the true

value of the companies that they represent

and there would be lower trading volume.

The consequence is price bubbles and higher

cost of capital. Secondly, there are certain

risks associated with investing passively

including concentration risk and systematic

risk. Concentration risk is the result of index

portfolios being weighted by market

capitalization, which are tilted towards those

companies with higher value. These

companies have high value as they perform

well in recent periods, but there is no

guarantee that they will perform well in the

future. Thirdly, the transition from active to

passive investing might involve a systematic

risk, which is reflected in higher volatility

and weaker diversification.

Given the benefits and risks of both passive

investing, this paper recommends the Core-

Satellite investment strategy, which

combines best characteristics of the two

approaches with a core index fund at the

center of the portfolio that hedges against

risks and satellite active funds that provides

the potential for outperformance.

Nam B. Nguyen 11

References

Alster, N. (2015). The Ease of Index Funds Comes With Risk. Nytimes.com. Retrieved 21

February 2016, from http://www.nytimes.com/2015/10/11/business/mutfund/the-ease-of-index-

funds-comes-with-risk.html?_r=1

Blitz, D. (2014). The dark side of passive investing. (White paper). Retrieved from

http://www.fundssociety.com/sites/default/files/opinion/downloads/darksiderobeco.pdf

Brinson, G. P., Hood, L. R., & Beebower, G. L. (1995). Determinants of portfolio performance.

Financial Analysts Journal, 51(1), 133-138.

Cooper, J. A. (2015). Part I: the unintended consequences of passive investing. (White paper).

Retrieved from

http://static1.squarespace.com/static/54526be5e4b0d0c07573e118/t/5582da5de4b01c221cf0d80b

/1434638941478/Part+I_Unintended+Consequences+of+Passive+Investing.pdf

Ellis, C. D. (2015). In Defense of Active Investing. Financial Analysts Journal, 71(4), 4-7.

Fama, E. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The

Journal of Finance, 25(2), 383. http://dx.doi.org/10.2307/2325486

Felder, J. (2016). Are Passive Investors Taking On Far More Risk Than They Realize?. The

Felder Report. Retrieved 19 February 2016, from

https://www.thefelderreport.com/2016/02/03/are-passive-investors-taking-on-far-more-risk-than-

they-realize/

J.P. Morgan. (2016). Beyond passive Assessing the opportunity in active management. (White

paper). Retrieved from https://www.ny529advisor.com/blobcontent/843/92/1323410725616_II-

ACTIVEMGT.pdf

Johnson, B., Boccellari, T., Bryan, A. & Rawson, M. (2015). Morningstar’s active/passive

barometer a new yardstick for an old debate. Retrieved from

http://corporate.morningstar.com/US/documents/ResearchPapers/MorningstarActive-

PassiveBarometerJune2015.pdf

Nam B. Nguyen 12

Jones, A. (2014). The hidden risks of going passive. (White paper). Retrieved from

http://www.schroders.com/en/SysGlobalAssets/digital/us/pdfs/section-4-the-hidden-risks-of-

going-passive.pdf

Liu, J. C. (2016). Investing with composure in volatile markets. (White paper). Retrieved from

https://am.jpmorgan.com/blobgim/1383280106276/83456/1323382750282_MI_Investing_with_

composure.pdf

O’Shaughnessy, J., Meredith, C., Bartone, S., Fairchild, T., O’Shaughnessy, P., & Viswanathan,

A. (2013). Combining the best of passive and active investing. (White paper). Retrieved from

http://www.osam.com/pdf/commentary_mar13.pdf

Philips, C. B., Kinniry, F. M., Schlanger, T., & Hirt, J. M. (2015). The case for index-fund

investing. (White paper). Retrieved from

https://pressroom.vanguard.com/content/nonindexed/Updated_The_Case_for_Index_Fund_Inves

ting_4.9.2014.pdf

Sharpe, W. F. (1991). The arithmetic of active management. Financial Analysts Journal, 47(1).

Shiller, R. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic

Perspectives, 17(1), 83-104. http://dx.doi.org/10.1257/089533003321164967

Vanguard. (2015). Active and passive investing what you need to know. (White paper). Retrieved

from https://www.vanguard.co.uk/documents/portal/literature/active-passive-investing-guide.pdf

Verhage. (2015). These Charts Show the Astounding Rise in Passive Management. Retrieved 19

February 2016, from http://www.bloomberg.com/news/articles/2015-12-30/these-charts-show-

the-astounding-rise-in-passive-management

Whitehead, R. (2012). Active Versus Passive Investing - Abbot Downing. (White paper).

Retrieved from

https://www.abbotdowning.com/_asset/jnq16k/ActiveVersusPassiveInvesting.pdf

Wimmer, B. R., Chhabra, S. S., Wallick, D. W. (2013). The bumpy road to outperformance.

(White paper). Retrieved from

https://pressroom.vanguard.com/content/nonindexed/7.5.2013_The_bumpy_road_to_outperform

ance.pdf