Embed Size (px)

Citation preview

POSITIONING BUSINESS MOBILE DEPOSIT TO WIN WITH SMBS THE DEVIL’S IN THE DETAILS

Bob Meara

August 23, 2016

This report was commissioned by Deluxe Corporation, at whose request Celent developed this research. The analysis and conclusions are Celent’s alone, and Deluxe had no editorial control over report contents.

For more information, please contact Celent through

our website (www.celent.com) or [email protected].

CONTENTS

Executive Summary ........................................................................................................ 1

Key Research Questions ............................................................................................. 1

Defining Business Mobile Deposit ................................................................................... 4

A Snapshot of US Small Businesses............................................................................... 7

Check Acceptance among SMBs .............................................................................. 10

Banking Relationships and Deposit Behavior ................................................................ 12

Product Usage .......................................................................................................... 12

Branch and ATM Deposit Behavior............................................................................ 17

Bank Engagement .................................................................................................... 19

SMB Reactions to Business Mobile Deposit .................................................................. 22

Attribute Importance .................................................................................................. 22

Pricing Expectations.................................................................................................. 27

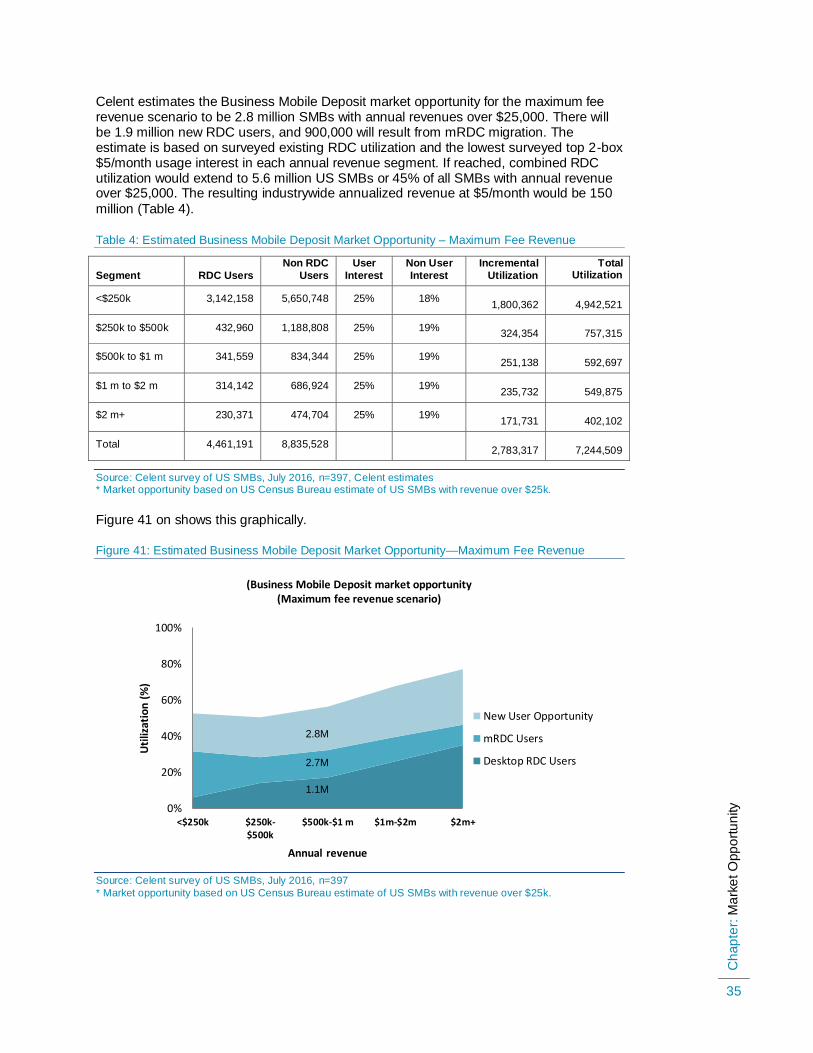

Market Opportunity ....................................................................................................... 32

Recommendations........................................................................................................ 36

Appendix I: Research Methodology............................................................................... 38

Appendix II: Survey Instrument ..................................................................................... 39

Leveraging Celent’s Expertise ...................................................................................... 44

Support for Financial Institutions ............................................................................... 44

Support for Vendors .................................................................................................. 44

Related Celent Research .............................................................................................. 45

EXECUTIVE SUMMARY

The small and medium size business (SMB) market is of increasing interest among US financial institutions as an important and profitable customer segment. So is the idea of migrating expensive branch transactions to self-service channels. The advent of Business Mobile Deposit, which became generally available in 2015, offers banks a unique opportunity to “kill two birds with one stone.” But doing so is tricky. This is

because:

The SMB market is diverse, with widely varying affinity for Business Mobile Deposit. Product positioning will need to uniquely fit for the value proposition to resonate.

Banks have taught SMBs to expect free stuff. Thus, most SMBs expect business Mobile Deposit to be free, or at least have a very low price point.

A significant percentage of SMBs already use Desktop Deposit (a.k.a. commercial remote deposit capture). While this doesn’t rule out Business Mobile Deposit for

these customers, different product attributes will need to be highlighted.

KEY RESEARCH QUESTIONS This report seeks to answer these three questions:

1 What is RDC adoption among US SMBs? 2

What Business Mobile Deposit features resonate with SMBs?

3 What is the market opportunity for Business Mobile Deposit?

To address these questions, Celent and Deluxe Corporation collaborated to survey US SMBs in June 2016. Respondents were recruited from among Deluxe Corporation’s 20,000+ SMB clients via email. Deluxe sells a variety of products and services to US small businesses, including business supplies and forms, checks, retail packaging, and a variety of marketing services. Survey results provide a comprehensive view of SMB usage and attitudes toward Desktop and Business Mobile Deposit across multiple market segments and annual revenue tiers. These much needed insights can equip financial

institutions to position Business Mobile Deposit to win with SMBs.

Findings

A number of findings are apparent from the survey results, including:

Lots of SMBs get checks. On average, SMBs receive about two checks per day, with significant variation from business to business. Traditional merchants with physical locations receive 6.5 checks per day, and those operating online stores in addition to physical locations receive nearly nine checks per day.

Check deposits continue to drive branch traffic, with 93% of surveyed SMBs making branch deposits. Non-RDC users made 2.1 branch deposits per week on average, compared to just 1.2 deposits for RDC users. The presence of cash in a minority of deposits keeps some RDC-using SMBs returning to the branch – albeit less frequently. This presence of cash in branch deposits means that widespread RDC adoption won’t eliminate branch deposit activity. On average, RDC cuts the

frequency of branch deposits in half.

Ch

ap

ter:

Exe

cutive S

um

ma

ry

2

Overall, 17% of surveyed SMBs use commercial Desktop RDC for their business. Usage is predictably related to where the checks are. That is, the larger the business (the more checks it receives), the greater the desktop RDC utilization. Thirty-five percent of SMBs with annual revenues over $2 million are Desktop RDC users, compared to just 6% of micro-businesses. Among surveyed businesses with over $5 million in revenue (8% of the sample), 48% use Desktop Deposit.

Mobile deposit utilization varies significantly between personal and business accounts. While 25% of surveyed SMBs use mobile RDC (mRDC) for business purposes, twice that many (46%) use mRDC for personal accounts. Personal use of mRDC does not correlate with the size of the business, but business utilization does. The smallest SMBs were the most likely to use mRDC for both personal and business accounts, consistent with their higher utilization of Mobile Banking.

Based solely on a brief product description and without the ability to clarify their understanding of various product attributes (as would be the case in a sales situation), respondents were asked to indicate how important each attribute would be to their decision to use Business Mobile Deposit for their business. SMBs offer a clear attribute rating hierarchy with the ability to capture multiple checks in a single deposit judged as the most important attribute.

SMBs regard several attributes similarly: multi-check deposits; the option to deposit using a desktop scanner, smartphone, or both (an integrated product); automatic accounting system updates; and research/reporting. By comparison, attributes addressing multiple users within the company scored poorly. For example, separation of duties (having one person scan checks and another person review and deposit) was viewed as least important among the Business Mobile Deposit attributes.

SMBs don’t speak with their bankers often, nor do they wish to. Fully half of surveyed SMBs “rarely if ever” speak with a banker about products or services that might benefit their business, and only 20% of SMBs speak with their banker quarterly or more often. When asked “About how often would you want your bank to contact you about products or services that might benefit your business?” about two-thirds of SMBs said they would want to hear from their bank annually or somewhat more frequently. Only 1 in 10 SMBs interact with their banker more than quarterly, or even want to.

Despite the diversity in how often SMBs would like to hear from their banks, there was clear consensus on how they would like to engage. Email is the overwhelmingly

preferred mechanism—preferred by two-thirds of SMBs across all segments.

Market Opportunity According to the US Census Bureau’s 2012 Survey of Small Businesses, there are a total of 27,626,000 small businesses in the US. Just over 12.5 million of them have annual revenues of $25,000 or more. Accounting for the roughly 25% of Desktop Deposit users that are also using Mobile Deposit, 4.5 million US SMBs (36%) with revenues over

$25,000 may be currently using some form of RDC .

Celent estimates the SMB Business Mobile Deposit market opportunity to be 4 million incremental SMBs. If reached, combined RDC utilization would extend to 8.3 million

SMBs or 67% of those with annual revenue over $25,000.

If Business Mobile Deposit carries a fee of $5/month, surveyed usage drops sharply. In this scenario, Celent estimates the market opportunity to be 2.8 million additional SMBs with annual revenues over $25,000. Of these, 1.9 million will be new RDC users and 900,000 will result from mRDC migration from free to a fee based product. If reached, combined RDC utilization would extend to 7.2 million US SMBs or 58% of all SMBs with annual revenue over $25,000. The resulting industrywide annualized revenue at

$5/month would be approximately $170 million.

Ch

ap

ter:

Exe

cutive S

um

ma

ry

3

Recommendations Regardless of a bank’s strategic intent, maximizing the value of Business Mobile Deposit to the institution will involve product, positioning, pricing, and promotion. We offer

recommendations in each area.

Product: Maximizing the market opportunity requires a product offering that supports

both SMBs that use Mobile Banking as well as those that do not. Celent advocates a two-tier product design. Some institutions may wish to create more distinct product differentiation by limiting certain capabilities on the less expensive product. Embracing a two-tier product offering is important because it allows institutions to offer a low-cost solution for SMBs with low average daily check volumes and a higher-priced solution for larger businesses having both desktop and mobile check acceptance. This latter product could be offered to both SMB and commercial/corporate market segments with less risk

of cannibalization by the lower-priced offering.

Positioning: Even banks seeking to maximize RDC utilization as part of a transaction

migration strategy won’t want to leave revenue on the table. For this reason, Celent recommends banks position each of the above products distinctly. Most SMBs will be attracted to the “entry-level” Business Mobile Deposit product, particularly if offered as a no-fee option on the Mobile Banking app. SMBs with higher average daily check volume are more likely to already use Desktop Deposit and are less likely to be enrolled in Mobile Banking. Clearly defined positioning like this will enhance banks’ ability to charge a monthly fee on the more advanced product—both among larger SMBs as well as within

commercial, middle market, and corporate market segments.

Pricing: While each institution must make its own decision, Celent views the branch channel cost saving opportunity that broad SMB RDC adoption affords to be more compelling than a modest fee revenue stream. For this reason, Celent recommends differentiated pricing based on the two-tier positioning advocated above. Offering an entry-level product free of charge alongside a modestly priced and clearly differentiated alternative will likely maximize overall utilization and minimize unintentional cannibalization. This outcome maximizes transaction migration to self-service channels

without leaving money on the table.

Promotion: Use email marketing as the centerpiece, with focused direct sales efforts

where it will be most effective. Specifically, Celent recommends segmenting prospects based on historic deposit behavior, with specifically tailored promotions and sales campaigns for low-volume and high-volume depositors. This segmentation would likely

be more successful than one based on business model or annual revenue.

After a definition of Business Mobile Deposit, this report begins with a snapshot of the US small business market, with a focus on check acceptance, deposit behavior, and product usage. An analysis of surveyed SMB reactions to Business Mobile Deposit concepts follows, along with a market opportunity assessment and recommendations for financial

institutions offering or intending to offer Business Mobile Deposit to SMB clients.

Ch

ap

ter:

Defin

ing

Bu

sin

ess

Mob

ile D

epo

sit

4

DEFINING BUSINESS MOBILE DEPOSIT

According to FI Navigator, through March 2016, over 4,000 US banks and credit unions offered mobile RDC (mRDC) capability within their consumer mobile banking apps. Before mRDC was available, thousands of banks launched desktop commercial RDC, aimed primarily at commercial and corporate clients. What is Business Mobile Deposit

and how does it compare to Commercial Desktop Deposit and consumer mRDC?

Said simply, Business Mobile Deposit refers to a product category that uses a mobile device for check deposit image capture. Unlike consumer mRDC, which is typically a

Mobile Banking app function, Business Mobile Deposit is being deployed in several ways:

Integrated to an institution’s Business Mobile Banking app. In this configuration,

all aspects of deposit management (image capture, deposit review, searching historic deposits, etc.) are accomplished within the Mobile Banking app.

As a stand-alone single-function app. For speed to market and as a way to offer

mobile capture capability to multiple users within a business without granting access to other Mobile Banking functionality, some banks offer stand-alone Business Mobile Deposit apps. An HVAC installation and maintenance firm, for example, may represent an ideal use case for this Business Mobile Deposit configuration.

Offered alongside Desktop Deposit. This allows Business Mobile and Commercial

Desktop RDC to be used in a coordinated way by a firm that may accept checks both in the field as well as in the back-office. Alternatively, firms that do not utilize Mobile Banking could use Business Mobile Deposit for image capture and perform all other

deposit administration functions within Online Banking.

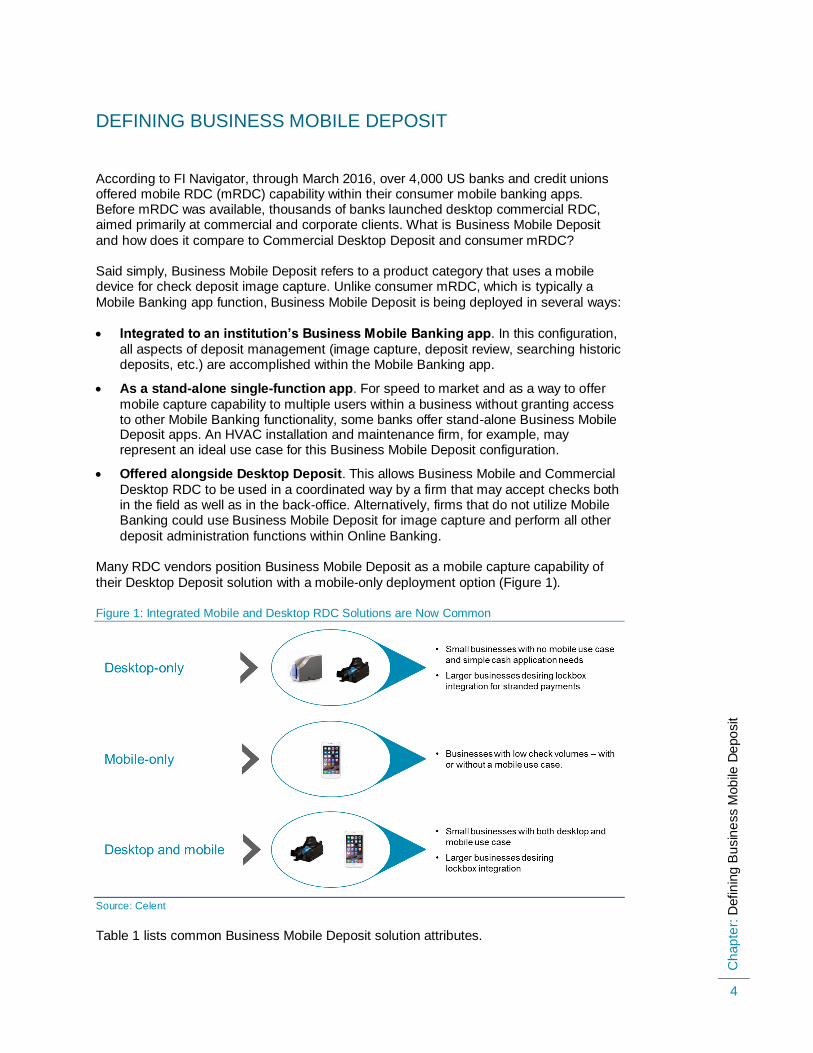

Many RDC vendors position Business Mobile Deposit as a mobile capture capability of

their Desktop Deposit solution with a mobile-only deployment option (Figure 1).

Figure 1: Integrated Mobile and Desktop RDC Solutions are Now Common

Source: Celent

Table 1 lists common Business Mobile Deposit solution attributes.

Ch

ap

ter:

Defin

ing

Bu

sin

ess

Mob

ile D

epo

sit

5

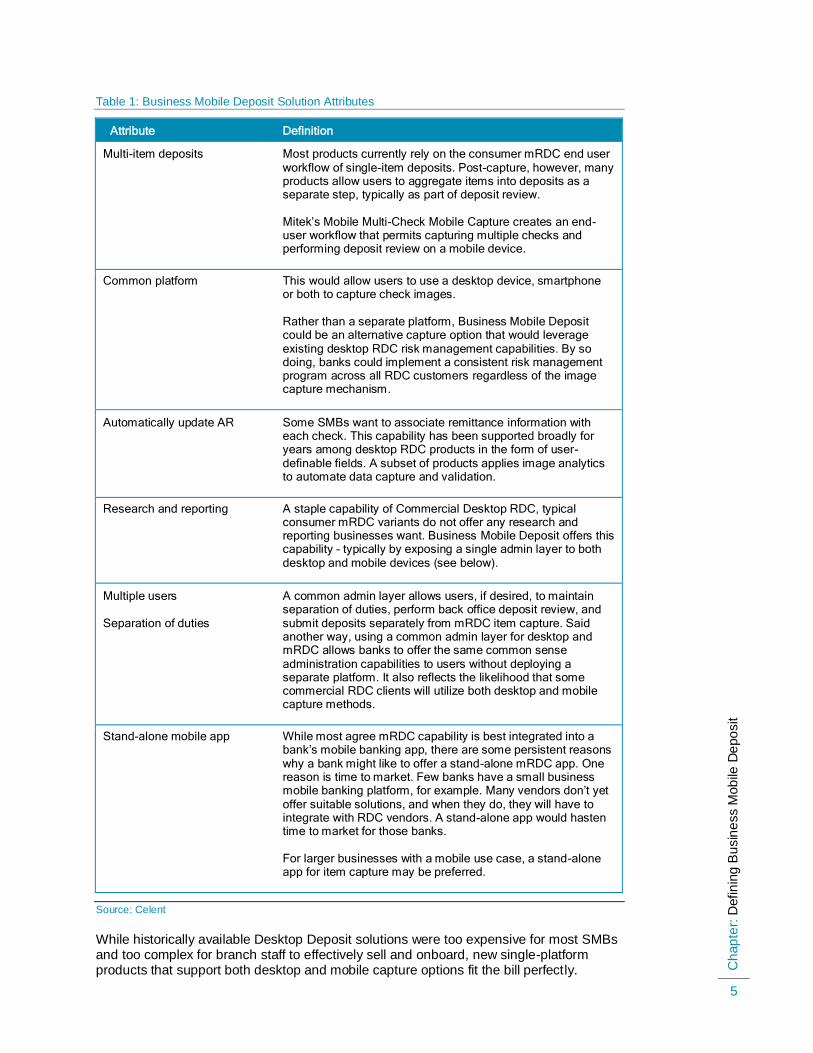

Table 1: Business Mobile Deposit Solution Attributes

Attribute Definition

Multi-item deposits Most products currently rely on the consumer mRDC end user workflow of single-item deposits. Post-capture, however, many products allow users to aggregate items into deposits as a separate step, typically as part of deposit review. Mitek’s Mobile Multi-Check Mobile Capture creates an end-user workflow that permits capturing multiple checks and performing deposit review on a mobile device.

Common platform This would allow users to use a desktop device, smartphone or both to capture check images. Rather than a separate platform, Business Mobile Deposit could be an alternative capture option that would leverage existing desktop RDC risk management capabilities. By so doing, banks could implement a consistent risk management program across all RDC customers regardless of the image capture mechanism.

Automatically update AR Some SMBs want to associate remittance information with each check. This capability has been supported broadly for years among desktop RDC products in the form of user-definable fields. A subset of products applies image analytics to automate data capture and validation.

Research and reporting A staple capability of Commercial Desktop RDC, typical consumer mRDC variants do not offer any research and reporting businesses want. Business Mobile Deposit offers this capability – typically by exposing a single admin layer to both desktop and mobile devices (see below).

Multiple users Separation of duties

A common admin layer allows users, if desired, to maintain separation of duties, perform back office deposit review, and submit deposits separately from mRDC item capture. Said another way, using a common admin layer for desktop and mRDC allows banks to offer the same common sense administration capabilities to users without deploying a separate platform. It also reflects the likelihood that some commercial RDC clients will utilize both desktop and mobile capture methods.

Stand-alone mobile app While most agree mRDC capability is best integrated into a bank’s mobile banking app, there are some persistent reasons why a bank might like to offer a stand-alone mRDC app. One reason is time to market. Few banks have a small business mobile banking platform, for example. Many vendors don’t yet offer suitable solutions, and when they do, they will have to integrate with RDC vendors. A stand-alone app would hasten time to market for those banks. For larger businesses with a mobile use case, a stand-alone app for item capture may be preferred.

Source: Celent

While historically available Desktop Deposit solutions were too expensive for most SMBs and too complex for branch staff to effectively sell and onboard, new single-platform products that support both desktop and mobile capture options fit the bill perfectly.

Ch

ap

ter:

Defin

ing

Bu

sin

ess

Mob

ile D

epo

sit

6

Leveraging mRDC for both mobile and low-volume use cases benefits both banks and

their SMB customers by offering:

The lowest possible product cost (no scanner, lower cost license) for the majority of SMBs that receive check payments in relatively low volumes.

An upgrade path for higher-volume check depositors desiring the speed and efficiency of desktop scanners.

An integrated mobile / desktop product for businesses that capture check payments both in the back-office and in the field, or for businesses that otherwise do not utilize

their bank’s Mobile Banking app.

Armed with an understanding of how generally available Business Mobile Deposit products can support all common SMB use cases, the next section looks at the US small

business market through the lens of check payments.

Ch

ap

ter:

A S

nap

sho

t o

f U

S S

ma

ll B

usin

esse

s

7

A SNAPSHOT OF US SMALL BUSINESSES

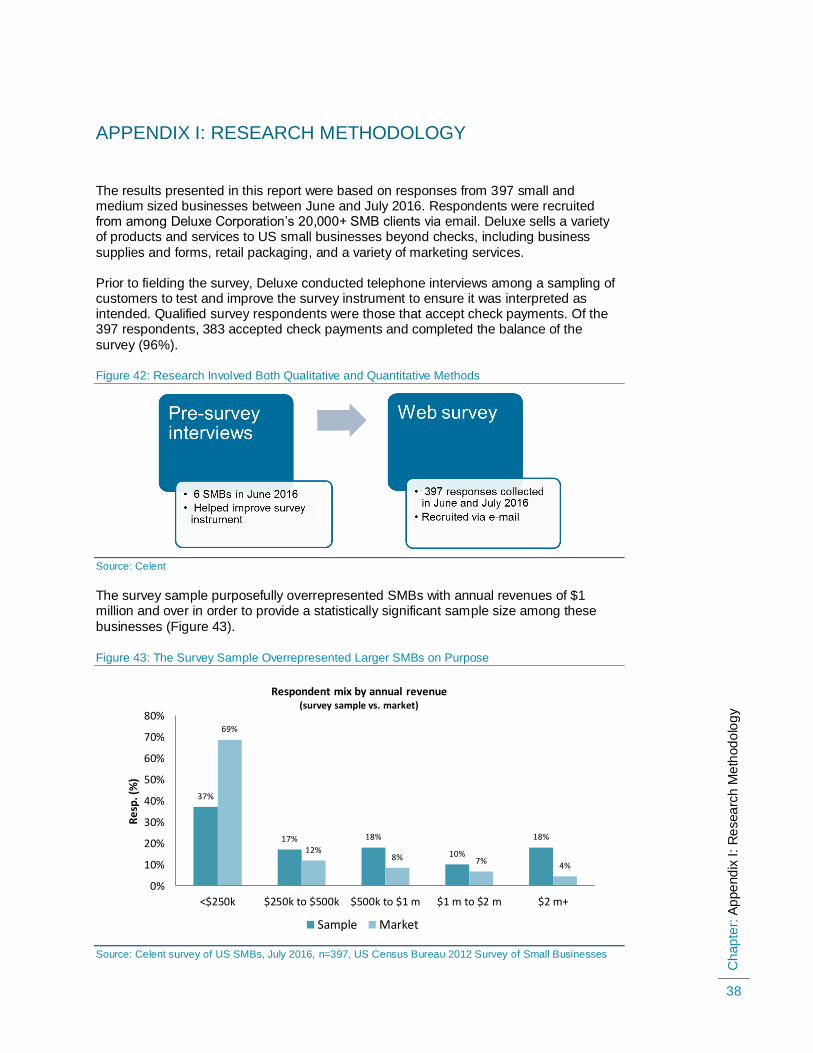

US SMBs are a relatively well researched segment. US Census Bureau, the US Small Business Administration (SBA), and Small Business & Entrepreneurship (SBE) Council all publish statistics of US SMBs, for example. However, these resources, as useful as they are, do not provide much insight specifically related to check payments and Business Mobile Deposit. Our June 2016 survey of US SMBs sought to provide this

needed insight.

Before seeking to understand SMB’s affinity towards Business Mobile Deposit, the survey sought to explore readily identifiable segments that would likely correlate to how SMBs

would value Business Mobile Deposit. Specifically:

Annual revenue

Business model—how they conduct business

Accounting system used

Check acceptance and average daily volume

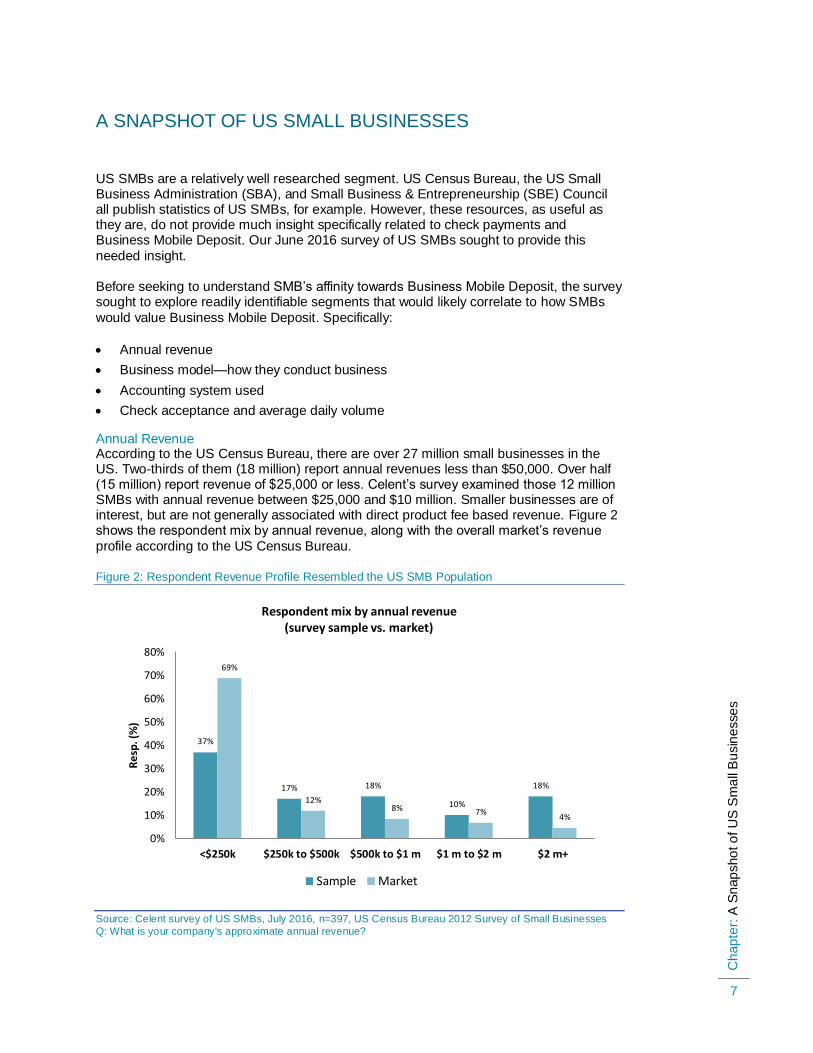

Annual Revenue According to the US Census Bureau, there are over 27 million small businesses in the US. Two-thirds of them (18 million) report annual revenues less than $50,000. Over half (15 million) report revenue of $25,000 or less. Celent’s survey examined those 12 million SMBs with annual revenue between $25,000 and $10 million. Smaller businesses are of interest, but are not generally associated with direct product fee based revenue. Figure 2 shows the respondent mix by annual revenue, along with the overall market’s revenue

profile according to the US Census Bureau.

Figure 2: Respondent Revenue Profile Resembled the US SMB Population

Source: Celent survey of US SMBs, July 2016, n=397, US Census Bureau 2012 Survey of Small Businesses

Q: What is your company's approximate annual revenue?

37%

17% 18%

10%

18%

69%

12% 8% 7%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

<$250k $250k to $500k $500k to $1 m $1 m to $2 m $2 m+

Re

sp. (

%)

Respondent mix by annual revenue (survey sample vs. market)

Sample Market

Ch

ap

ter:

A S

nap

sho

t o

f U

S S

ma

ll B

usin

esse

s

8

Many institutions segment businesses by annual revenue, with larger businesses (typically those with annual revenues over $1 million) assigned to specific business bankers and smaller businesses served exclusively by the branch network. The survey purposefully over-sampled businesses over $1 million in annual revenue in order to have

statistically significant results across all annual revenue segments.

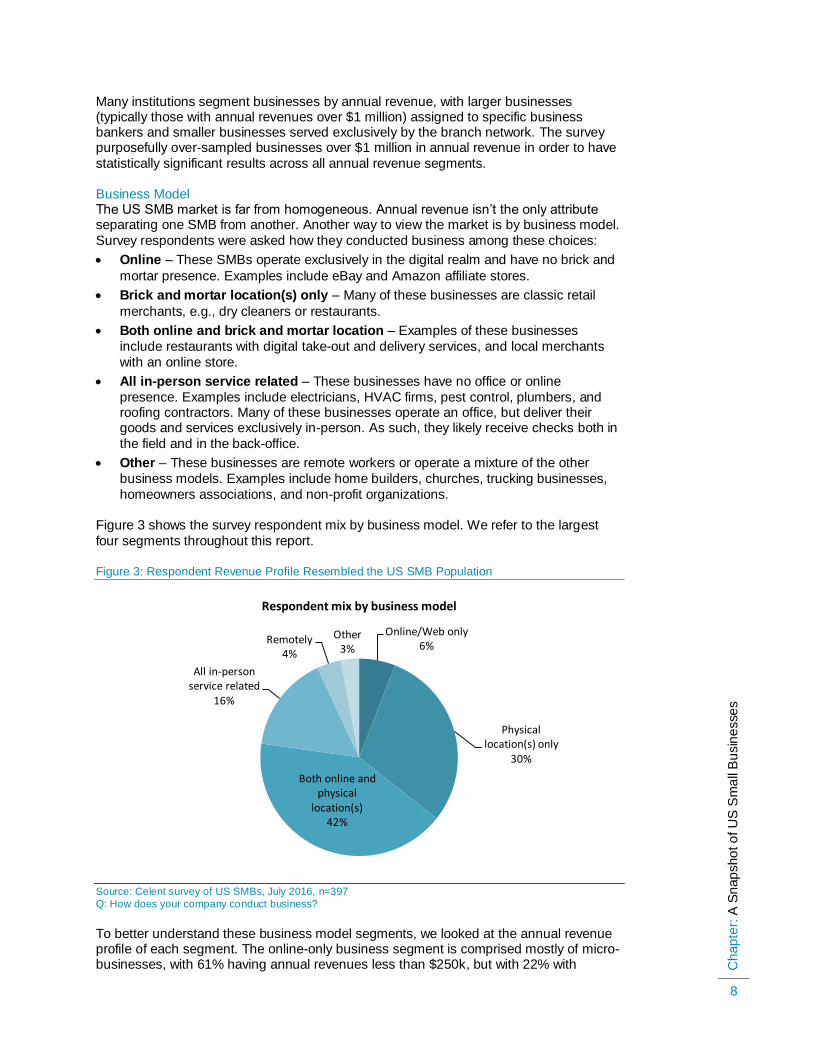

Business Model The US SMB market is far from homogeneous. Annual revenue isn’t the only attribute separating one SMB from another. Another way to view the market is by business model.

Survey respondents were asked how they conducted business among these choices:

Online – These SMBs operate exclusively in the digital realm and have no brick and

mortar presence. Examples include eBay and Amazon affiliate stores.

Brick and mortar location(s) only – Many of these businesses are classic retail

merchants, e.g., dry cleaners or restaurants.

Both online and brick and mortar location – Examples of these businesses

include restaurants with digital take-out and delivery services, and local merchants

with an online store.

All in-person service related – These businesses have no office or online

presence. Examples include electricians, HVAC firms, pest control, plumbers, and roofing contractors. Many of these businesses operate an office, but deliver their goods and services exclusively in-person. As such, they likely receive checks both in

the field and in the back-office.

Other – These businesses are remote workers or operate a mixture of the other

business models. Examples include home builders, churches, trucking businesses,

homeowners associations, and non-profit organizations.

Figure 3 shows the survey respondent mix by business model. We refer to the largest

four segments throughout this report.

Figure 3: Respondent Revenue Profile Resembled the US SMB Population

Source: Celent survey of US SMBs, July 2016, n=397

Q: How does your company conduct business?

To better understand these business model segments, we looked at the annual revenue profile of each segment. The online-only business segment is comprised mostly of micro-businesses, with 61% having annual revenues less than $250k, but with 22% with

Online/Web only 6%

Physical location(s) only

30%

Both online and physical

location(s) 42%

All in-person service related

16%

Remotely 4%

Other 3%

Respondent mix by business model

Ch

ap

ter:

A S

nap

sho

t o

f U

S S

ma

ll B

usin

esse

s

9

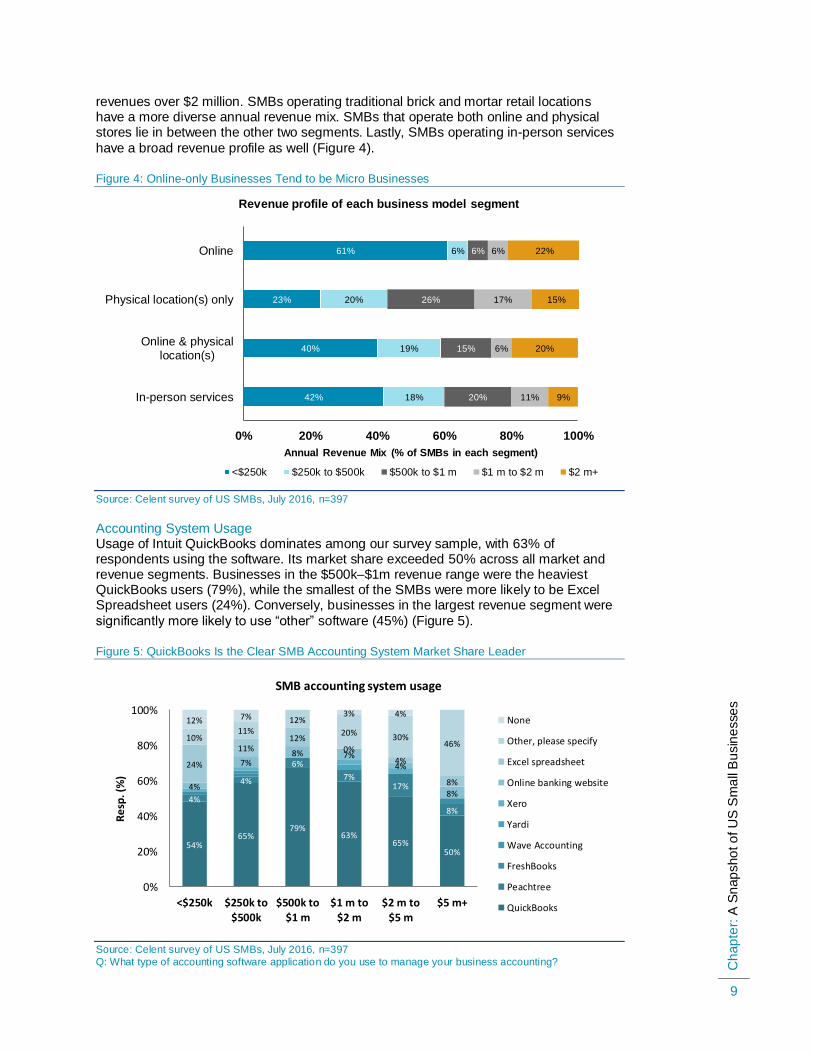

revenues over $2 million. SMBs operating traditional brick and mortar retail locations have a more diverse annual revenue mix. SMBs that operate both online and physical stores lie in between the other two segments. Lastly, SMBs operating in-person services

have a broad revenue profile as well (Figure 4).

Figure 4: Online-only Businesses Tend to be Micro Businesses

Source: Celent survey of US SMBs, July 2016, n=397

Accounting System Usage Usage of Intuit QuickBooks dominates among our survey sample, with 63% of respondents using the software. Its market share exceeded 50% across all market and revenue segments. Businesses in the $500k–$1m revenue range were the heaviest QuickBooks users (79%), while the smallest of the SMBs were more likely to be Excel Spreadsheet users (24%). Conversely, businesses in the largest revenue segment were

significantly more likely to use “other” software (45%) (Figure 5).

Figure 5: QuickBooks Is the Clear SMB Accounting System Market Share Leader

Source: Celent survey of US SMBs, July 2016, n=397

Q: What type of accounting software application do you use to manage your business accounting?

61%

23%

40%

42%

6%

20%

19%

18%

6%

26%

15%

20%

6%

17%

6%

11%

22%

15%

20%

9%

0% 20% 40% 60% 80% 100%

Online

Physical location(s) only

Online & physicallocation(s)

In-person services

Annual Revenue Mix (% of SMBs in each segment)

Revenue profile of each business model segment

<$250k $250k to $500k $500k to $1 m $1 m to $2 m $2 m+

54% 65%

79% 63%

65% 50%

4%

4%

6%

7% 17%

8%

4%

7% 8% 7%

4%

8%

24%

11% 12%

0% 4%

8%

10% 11%

12%

20% 30%

46%

12% 7% 3% 4%

0%

20%

40%

60%

80%

100%

<$250k $250k to$500k

$500k to$1 m

$1 m to$2 m

$2 m to$5 m

$5 m+

Re

sp. (

%)

SMB accounting system usage

None

Other, please specify

Excel spreadsheet

Online banking website

Xero

Yardi

Wave Accounting

FreshBooks

Peachtree

QuickBooks

Ch

ap

ter:

A S

nap

sho

t o

f U

S S

ma

ll B

usin

esse

s

10

As far as small business RDC goes, the only accounting system integration that matters is QuickBooks. Users of other accounting systems could be accommodated with file

export capability.

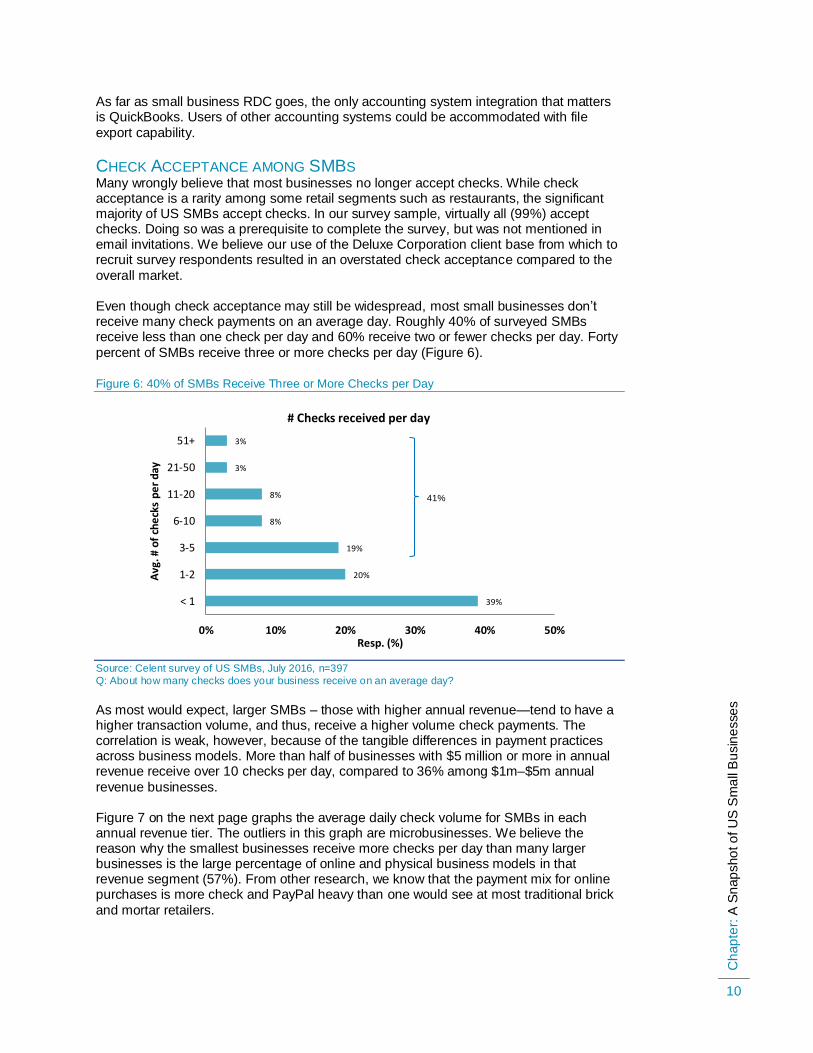

CHECK ACCEPTANCE AMONG SMBS Many wrongly believe that most businesses no longer accept checks. While check acceptance is a rarity among some retail segments such as restaurants, the significant majority of US SMBs accept checks. In our survey sample, virtually all (99%) accept checks. Doing so was a prerequisite to complete the survey, but was not mentioned in email invitations. We believe our use of the Deluxe Corporation client base from which to recruit survey respondents resulted in an overstated check acceptance compared to the

overall market.

Even though check acceptance may still be widespread, most small businesses don’t receive many check payments on an average day. Roughly 40% of surveyed SMBs receive less than one check per day and 60% receive two or fewer checks per day. Forty

percent of SMBs receive three or more checks per day (Figure 6).

Figure 6: 40% of SMBs Receive Three or More Checks per Day

Source: Celent survey of US SMBs, July 2016, n=397

Q: About how many checks does your business receive on an average day?

As most would expect, larger SMBs – those with higher annual revenue—tend to have a higher transaction volume, and thus, receive a higher volume check payments. The correlation is weak, however, because of the tangible differences in payment practices across business models. More than half of businesses with $5 million or more in annual revenue receive over 10 checks per day, compared to 36% among $1m–$5m annual

revenue businesses.

Figure 7 on the next page graphs the average daily check volume for SMBs in each annual revenue tier. The outliers in this graph are microbusinesses. We believe the reason why the smallest businesses receive more checks per day than many larger businesses is the large percentage of online and physical business models in that revenue segment (57%). From other research, we know that the payment mix for online purchases is more check and PayPal heavy than one would see at most traditional brick

and mortar retailers.

39%

20%

19%

8%

8%

3%

3%

0% 10% 20% 30% 40% 50%

< 1

1-2

3-5

6-10

11-20

21-50

51+

Resp. (%)

Avg

. # o

f ch

eck

s p

er

day

# Checks received per day

41%

Ch

ap

ter:

A S

nap

sho

t o

f U

S S

ma

ll B

usin

esse

s

11

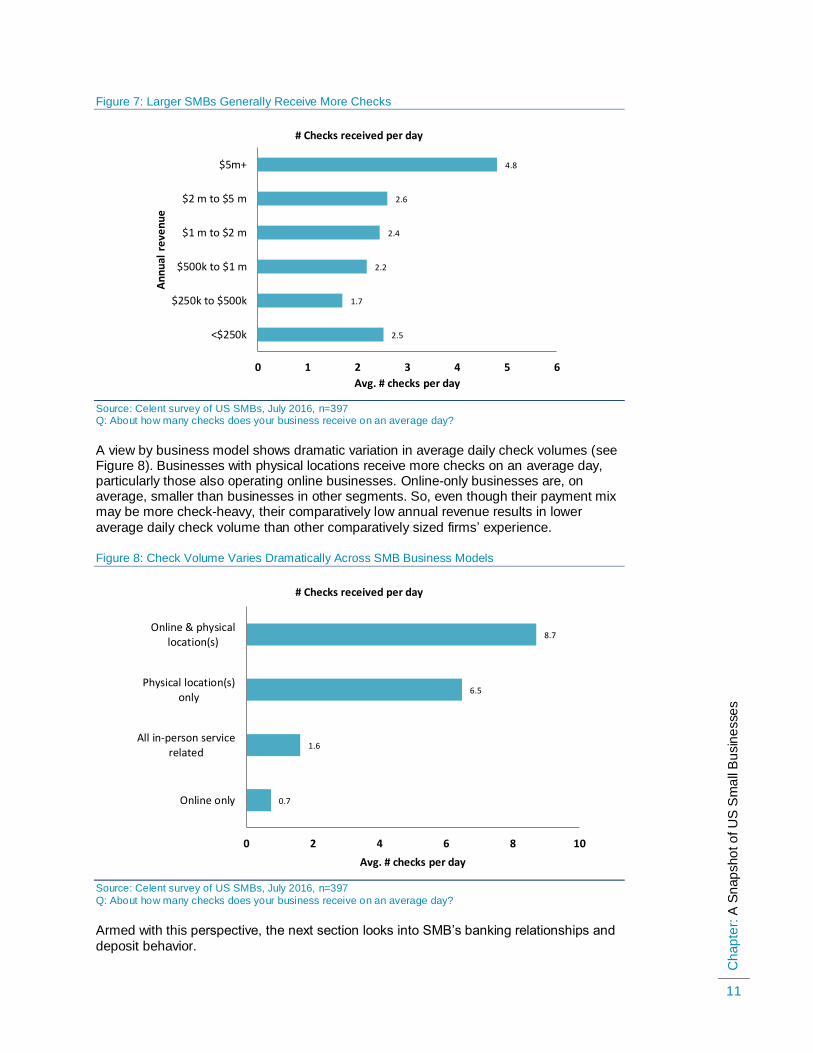

Figure 7: Larger SMBs Generally Receive More Checks

Source: Celent survey of US SMBs, July 2016, n=397 Q: About how many checks does your business receive on an average day?

A view by business model shows dramatic variation in average daily check volumes (see Figure 8). Businesses with physical locations receive more checks on an average day, particularly those also operating online businesses. Online-only businesses are, on average, smaller than businesses in other segments. So, even though their payment mix may be more check-heavy, their comparatively low annual revenue results in lower

average daily check volume than other comparatively sized firms’ experience.

Figure 8: Check Volume Varies Dramatically Across SMB Business Models

Source: Celent survey of US SMBs, July 2016, n=397

Q: About how many checks does your business receive on an average day?

Armed with this perspective, the next section looks into SMB’s banking relationships and

deposit behavior.

2.5

1.7

2.2

2.4

2.6

4.8

0 1 2 3 4 5 6

<$250k

$250k to $500k

$500k to $1 m

$1 m to $2 m

$2 m to $5 m

$5m+

Avg. # checks per day

An

nu

al r

eve

nu

e

# Checks received per day

0.7

1.6

6.5

8.7

0 2 4 6 8 10

Online only

All in-person servicerelated

Physical location(s)only

Online & physicallocation(s)

Avg. # checks per day

# Checks received per day

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

12

BANKING RELATIONSHIPS AND DEPOSIT BEHAVIOR

This section looks at bank products used by US SMBs, their deposit behavior and frequency of, and preference for, interacting with their banks. These aspects are

important for their ability to assist banks’ position and sell Business Mobile Deposit.

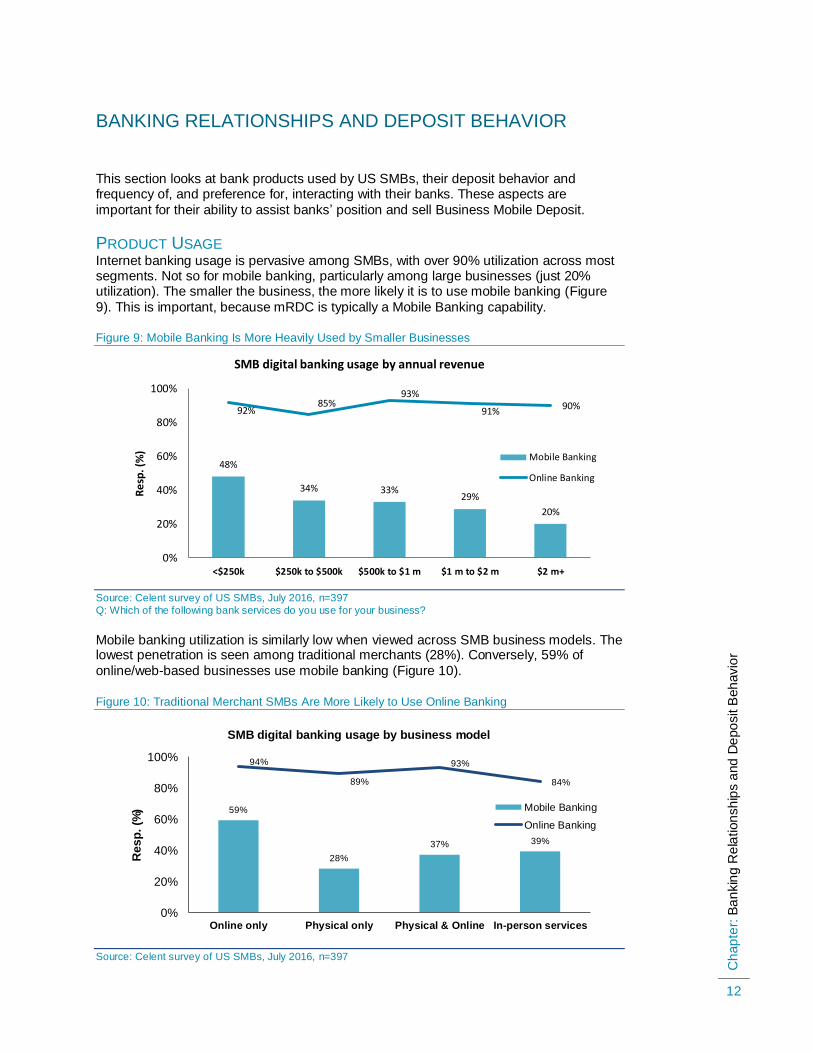

PRODUCT USAGE Internet banking usage is pervasive among SMBs, with over 90% utilization across most segments. Not so for mobile banking, particularly among large businesses (just 20% utilization). The smaller the business, the more likely it is to use mobile banking (Figure

9). This is important, because mRDC is typically a Mobile Banking capability.

Figure 9: Mobile Banking Is More Heavily Used by Smaller Businesses

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

Mobile banking utilization is similarly low when viewed across SMB business models. The lowest penetration is seen among traditional merchants (28%). Conversely, 59% of

online/web-based businesses use mobile banking (Figure 10).

Figure 10: Traditional Merchant SMBs Are More Likely to Use Online Banking

Source: Celent survey of US SMBs, July 2016, n=397

20%

29% 33% 34%

48%

90% 91%

93% 85%

92%

0%

20%

40%

60%

80%

100%

$2 m+$1 m to $2 m$500k to $1 m$250k to $500k<$250k

Re

sp. (

%)

SMB digital banking usage by annual revenue

Mobile Banking

Online Banking

39% 37%

28%

59%

84%

93%

89%

94%

0%

20%

40%

60%

80%

100%

In-person servicesPhysical & OnlinePhysical onlyOnline only

Re

sp

. (%

)

SMB digital banking usage by business model

Mobile Banking

Online Banking

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

13

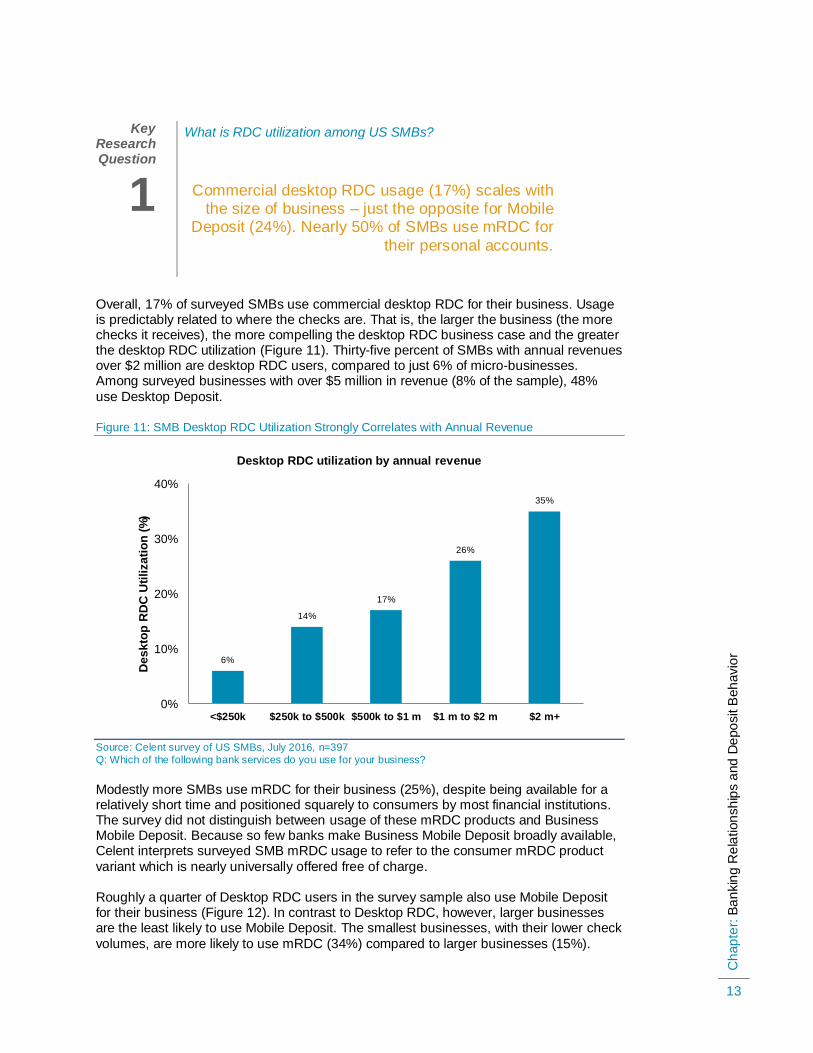

Overall, 17% of surveyed SMBs use commercial desktop RDC for their business. Usage is predictably related to where the checks are. That is, the larger the business (the more checks it receives), the more compelling the desktop RDC business case and the greater the desktop RDC utilization (Figure 11). Thirty-five percent of SMBs with annual revenues over $2 million are desktop RDC users, compared to just 6% of micro-businesses. Among surveyed businesses with over $5 million in revenue (8% of the sample), 48%

use Desktop Deposit.

Figure 11: SMB Desktop RDC Utilization Strongly Correlates with Annual Revenue

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

Modestly more SMBs use mRDC for their business (25%), despite being available for a relatively short time and positioned squarely to consumers by most financial institutions. The survey did not distinguish between usage of these mRDC products and Business Mobile Deposit. Because so few banks make Business Mobile Deposit broadly available, Celent interprets surveyed SMB mRDC usage to refer to the consumer mRDC product

variant which is nearly universally offered free of charge.

Roughly a quarter of Desktop RDC users in the survey sample also use Mobile Deposit for their business (Figure 12). In contrast to Desktop RDC, however, larger businesses are the least likely to use Mobile Deposit. The smallest businesses, with their lower check

volumes, are more likely to use mRDC (34%) compared to larger businesses (15%).

6%

14%

17%

26%

35%

0%

10%

20%

30%

40%

<$250k $250k to $500k $500k to $1 m $1 m to $2 m $2 m+

De

sk

top

RD

C U

tili

za

tio

n (

%)

Desktop RDC utilization by annual revenue

Key Research Question

1

What is RDC utilization among US SMBs?

Commercial desktop RDC usage (17%) scales with the size of business – just the opposite for Mobile

Deposit (24%). Nearly 50% of SMBs use mRDC for

their personal accounts.

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

14

Figure 12: Desktop and Mobile RDC Utilization Are Mirror Images

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

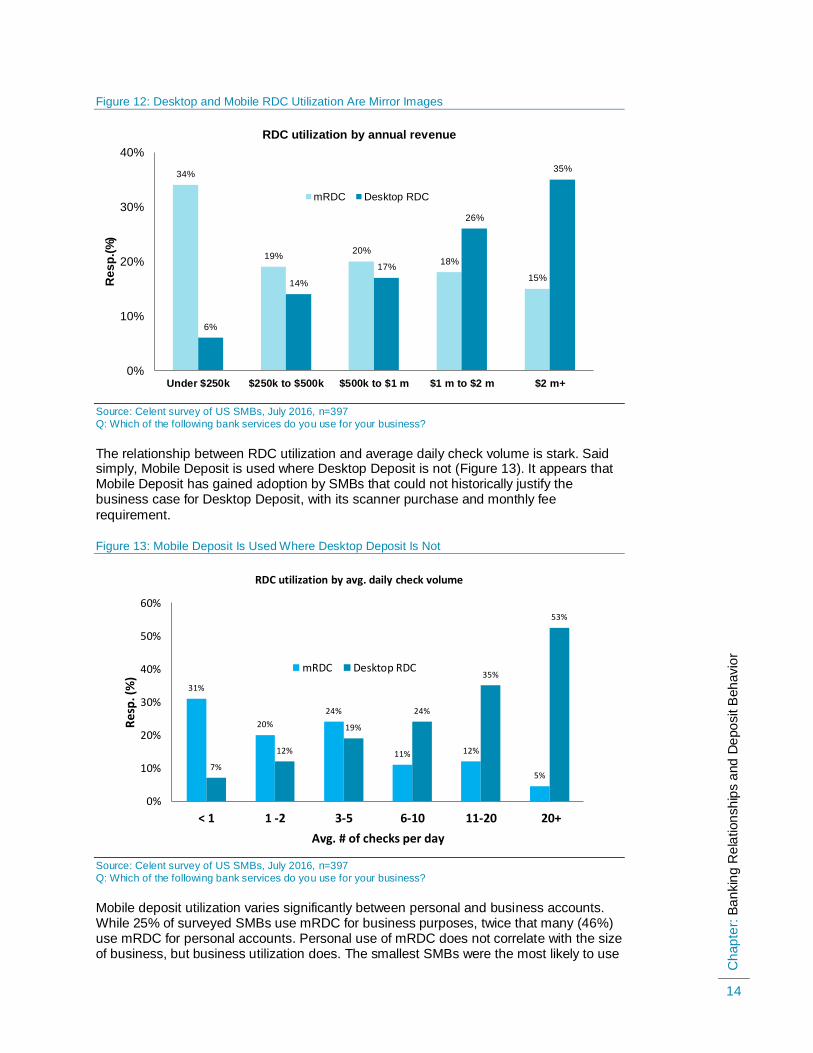

The relationship between RDC utilization and average daily check volume is stark. Said simply, Mobile Deposit is used where Desktop Deposit is not (Figure 13). It appears that Mobile Deposit has gained adoption by SMBs that could not historically justify the business case for Desktop Deposit, with its scanner purchase and monthly fee

requirement.

Figure 13: Mobile Deposit Is Used Where Desktop Deposit Is Not

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

Mobile deposit utilization varies significantly between personal and business accounts. While 25% of surveyed SMBs use mRDC for business purposes, twice that many (46%) use mRDC for personal accounts. Personal use of mRDC does not correlate with the size of business, but business utilization does. The smallest SMBs were the most likely to use

34%

19% 20%

18%

15%

6%

14%

17%

26%

35%

0%

10%

20%

30%

40%

Under $250k $250k to $500k $500k to $1 m $1 m to $2 m $2 m+

Re

sp

.(%

)

RDC utilization by annual revenue

mRDC Desktop RDC

31%

20%

24%

11% 12%

5% 7%

12%

19%

24%

35%

53%

0%

10%

20%

30%

40%

50%

60%

< 1 1 -2 3-5 6-10 11-20 20+

Res

p. (

%)

Avg. # of checks per day

RDC utilization by avg. daily check volume

mRDC Desktop RDC

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

15

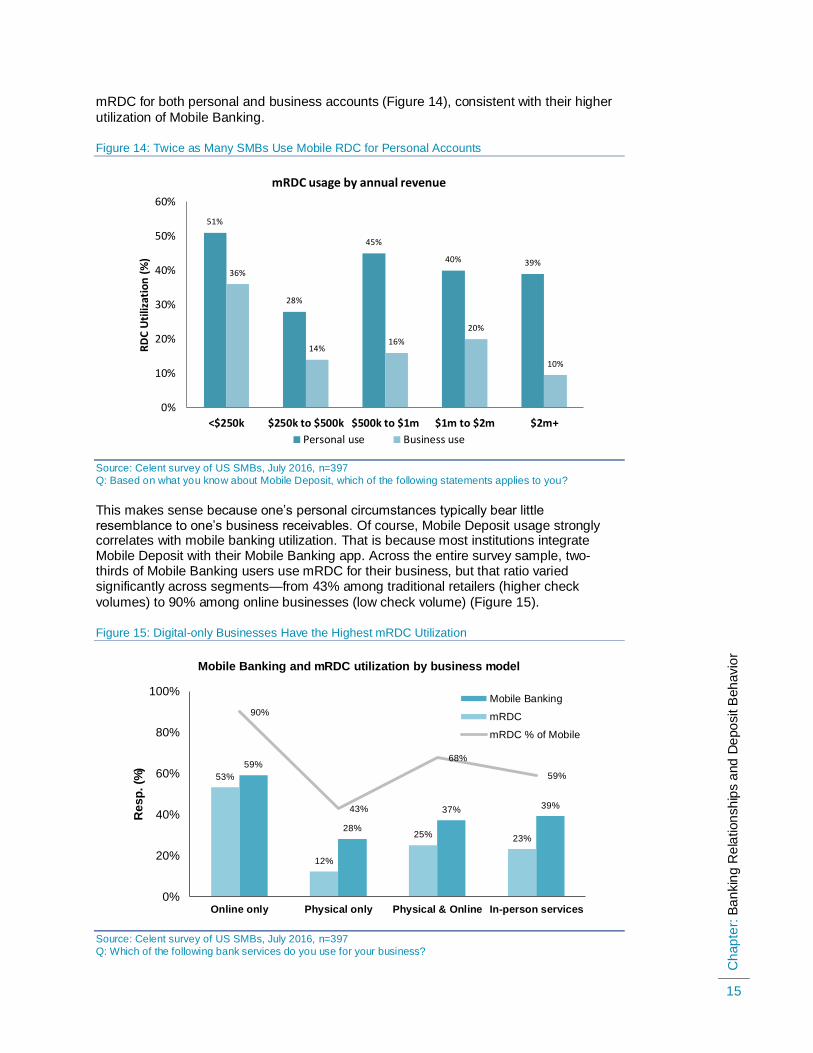

mRDC for both personal and business accounts (Figure 14), consistent with their higher

utilization of Mobile Banking.

Figure 14: Twice as Many SMBs Use Mobile RDC for Personal Accounts

Source: Celent survey of US SMBs, July 2016, n=397

Q: Based on what you know about Mobile Deposit, which of the following statements applies to you?

This makes sense because one’s personal circumstances typically bear little resemblance to one’s business receivables. Of course, Mobile Deposit usage strongly correlates with mobile banking utilization. That is because most institutions integrate Mobile Deposit with their Mobile Banking app. Across the entire survey sample, two-thirds of Mobile Banking users use mRDC for their business, but that ratio varied significantly across segments—from 43% among traditional retailers (higher check

volumes) to 90% among online businesses (low check volume) (Figure 15).

Figure 15: Digital-only Businesses Have the Highest mRDC Utilization

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

51%

28%

45%

40% 39% 36%

14% 16%

20%

10%

0%

10%

20%

30%

40%

50%

60%

<$250k $250k to $500k $500k to $1m $1m to $2m $2m+

RD

C U

tiliz

atio

n (

%)

mRDC usage by annual revenue

Personal use Business use

39% 37%

28%

59%

23% 25%

12%

53% 59%

68%

43%

90%

0%

20%

40%

60%

80%

100%

In-person servicesPhysical & OnlinePhysical onlyOnline only

Re

sp

. (%

)

Mobile Banking and mRDC utilization by business model

Mobile Banking

mRDC

mRDC % of Mobile

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

16

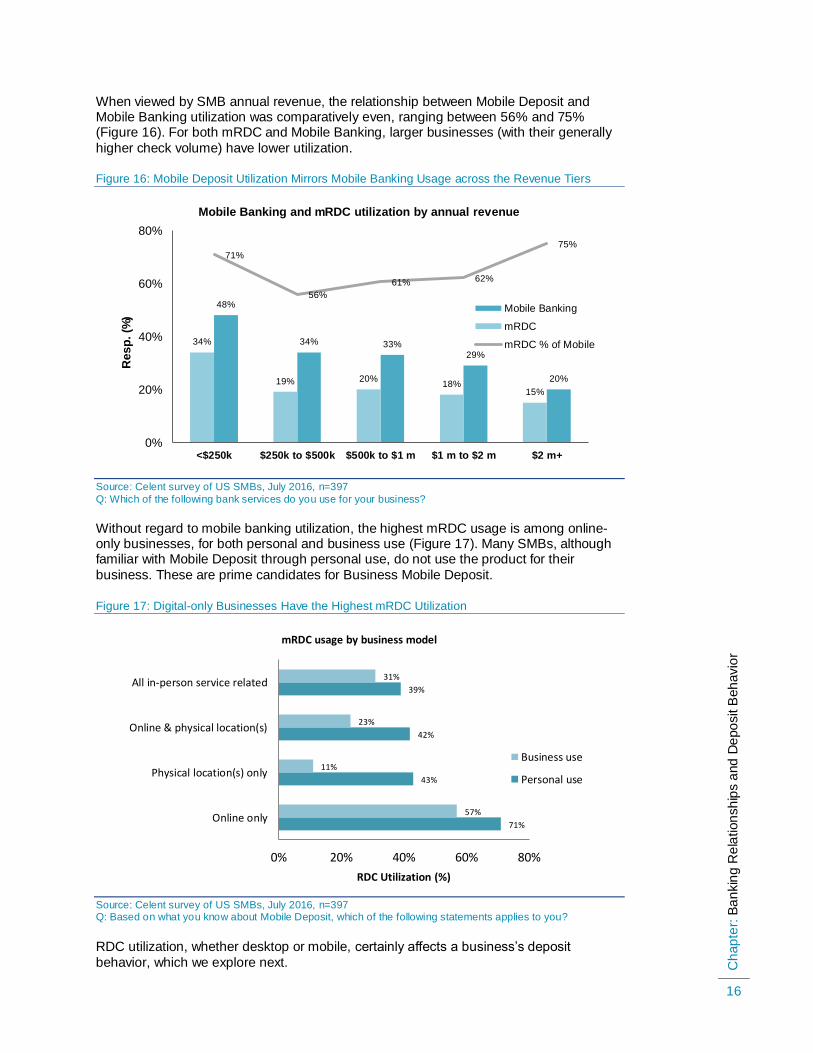

When viewed by SMB annual revenue, the relationship between Mobile Deposit and Mobile Banking utilization was comparatively even, ranging between 56% and 75% (Figure 16). For both mRDC and Mobile Banking, larger businesses (with their generally

higher check volume) have lower utilization.

Figure 16: Mobile Deposit Utilization Mirrors Mobile Banking Usage across the Revenue Tiers

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following bank services do you use for your business?

Without regard to mobile banking utilization, the highest mRDC usage is among online-only businesses, for both personal and business use (Figure 17). Many SMBs, although familiar with Mobile Deposit through personal use, do not use the product for their

business. These are prime candidates for Business Mobile Deposit.

Figure 17: Digital-only Businesses Have the Highest mRDC Utilization

Source: Celent survey of US SMBs, July 2016, n=397 Q: Based on what you know about Mobile Deposit, which of the following statements applies to you?

RDC utilization, whether desktop or mobile, certainly affects a business’s deposit

behavior, which we explore next.

20%

29% 33% 34%

48%

15% 18%

20% 19%

34%

75%

62% 61%

56%

71%

0%

20%

40%

60%

80%

$2 m+$1 m to $2 m$500k to $1 m$250k to $500k<$250k

Re

sp

. (%

)

Mobile Banking and mRDC utilization by annual revenue

Mobile Banking

mRDC

mRDC % of Mobile

71%

43%

42%

39%

57%

11%

23%

31%

0% 20% 40% 60% 80%

Online only

Physical location(s) only

Online & physical location(s)

All in-person service related

RDC Utilization (%)

mRDC usage by business model

Business use

Personal use

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

17

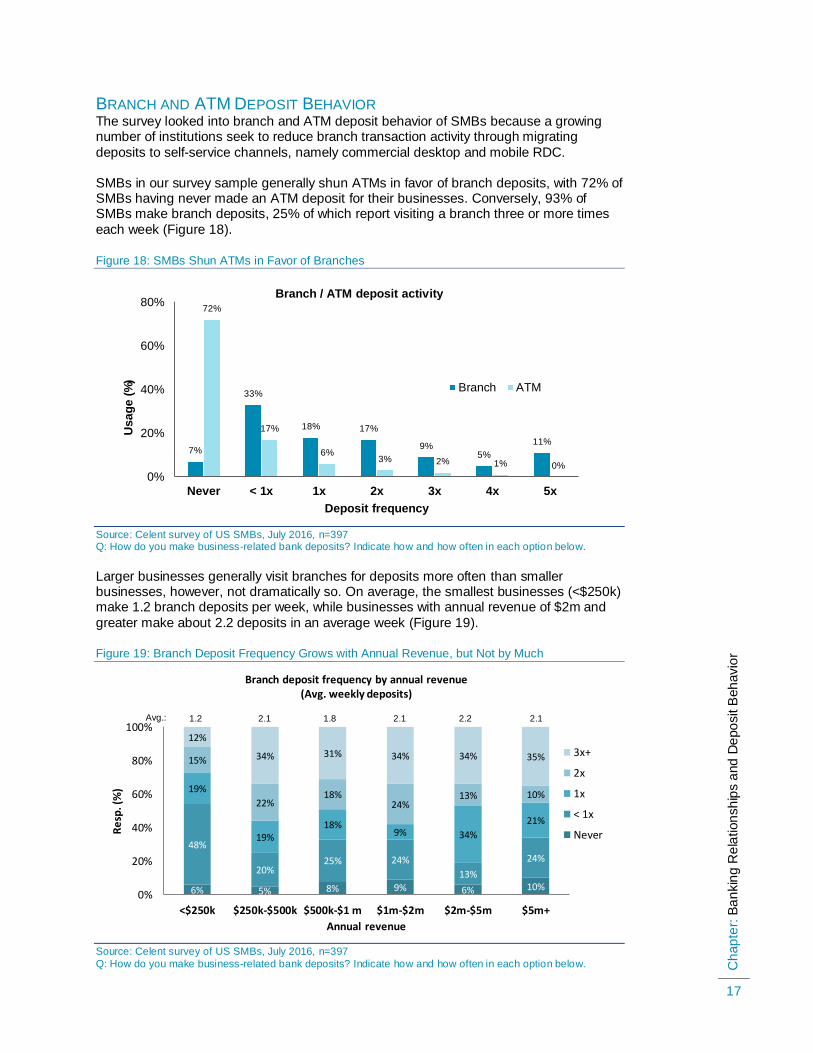

BRANCH AND ATM DEPOSIT BEHAVIOR The survey looked into branch and ATM deposit behavior of SMBs because a growing number of institutions seek to reduce branch transaction activity through migrating

deposits to self-service channels, namely commercial desktop and mobile RDC.

SMBs in our survey sample generally shun ATMs in favor of branch deposits, with 72% of SMBs having never made an ATM deposit for their businesses. Conversely, 93% of SMBs make branch deposits, 25% of which report visiting a branch three or more times

each week (Figure 18).

Figure 18: SMBs Shun ATMs in Favor of Branches

Source: Celent survey of US SMBs, July 2016, n=397 Q: How do you make business-related bank deposits? Indicate how and how often in each option below.

Larger businesses generally visit branches for deposits more often than smaller businesses, however, not dramatically so. On average, the smallest businesses (<$250k) make 1.2 branch deposits per week, while businesses with annual revenue of $2m and

greater make about 2.2 deposits in an average week (Figure 19).

Figure 19: Branch Deposit Frequency Grows with Annual Revenue, but Not by Much

Source: Celent survey of US SMBs, July 2016, n=397

Q: How do you make business-related bank deposits? Indicate how and how often in each option below.

7%

33%

18% 17%

9% 5%

11%

72%

17%

6% 3% 2% 1% 0%

0%

20%

40%

60%

80%

Never < 1x 1x 2x 3x 4x 5x

Usa

ge

(%

)

Deposit frequency

Branch / ATM deposit activity

Branch ATM

6% 5% 8% 9% 6% 10%

48%

20% 25% 24%

13%

24%

19%

19% 18%

9% 34%

21%

15%

22% 18%

24% 13% 10%

12%

34% 31% 34% 34% 35%

0%

20%

40%

60%

80%

100%

<$250k $250k-$500k $500k-$1 m $1m-$2m $2m-$5m $5m+

Re

sp. (

%)

Annual revenue

Branch deposit frequency by annual revenue (Avg. weekly deposits)

3x+

2x

1x

< 1x

Never

Avg.: 1.2 2.1 1.8 2.1 2.2 2.1

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

18

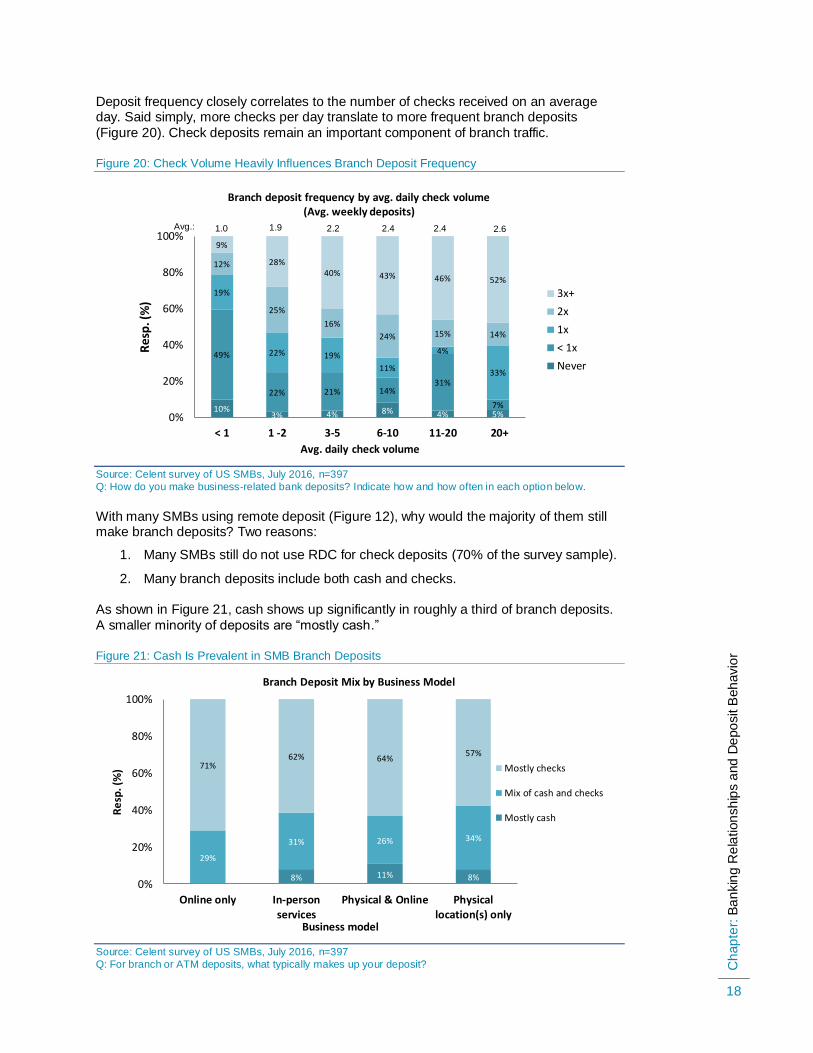

Deposit frequency closely correlates to the number of checks received on an average day. Said simply, more checks per day translate to more frequent branch deposits

(Figure 20). Check deposits remain an important component of branch traffic.

Figure 20: Check Volume Heavily Influences Branch Deposit Frequency

Source: Celent survey of US SMBs, July 2016, n=397

Q: How do you make business-related bank deposits? Indicate how and how often in each option below.

With many SMBs using remote deposit (Figure 12), why would the majority of them still make branch deposits? Two reasons:

1. Many SMBs still do not use RDC for check deposits (70% of the survey sample).

2. Many branch deposits include both cash and checks.

As shown in Figure 21, cash shows up significantly in roughly a third of branch deposits.

A smaller minority of deposits are “mostly cash.”

Figure 21: Cash Is Prevalent in SMB Branch Deposits

Source: Celent survey of US SMBs, July 2016, n=397

Q: For branch or ATM deposits, what typically makes up your deposit?

10% 3% 4% 8% 4% 5%

49%

22% 21% 14% 31%

7%

19%

22% 19%

11%

4%

33%

12%

25%

16%

24% 15% 14%

9%

28% 40% 43% 46% 52%

0%

20%

40%

60%

80%

100%

< 1 1 -2 3-5 6-10 11-20 20+

Res

p. (

%)

Avg. daily check volume

Branch deposit frequency by avg. daily check volume (Avg. weekly deposits)

3x+

2x

1x

< 1x

Never

8% 11% 8%

29%

31% 26% 34%

71% 62% 64%

57%

0%

20%

40%

60%

80%

100%

Online only In-personservices

Physical & Online Physicallocation(s) only

Re

sp. (

%)

Business model

Branch Deposit Mix by Business Model

Mostly checks

Mix of cash and checks

Mostly cash

1.0 1.9 2.2 2.4 2.4 2.6 Avg.:

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

19

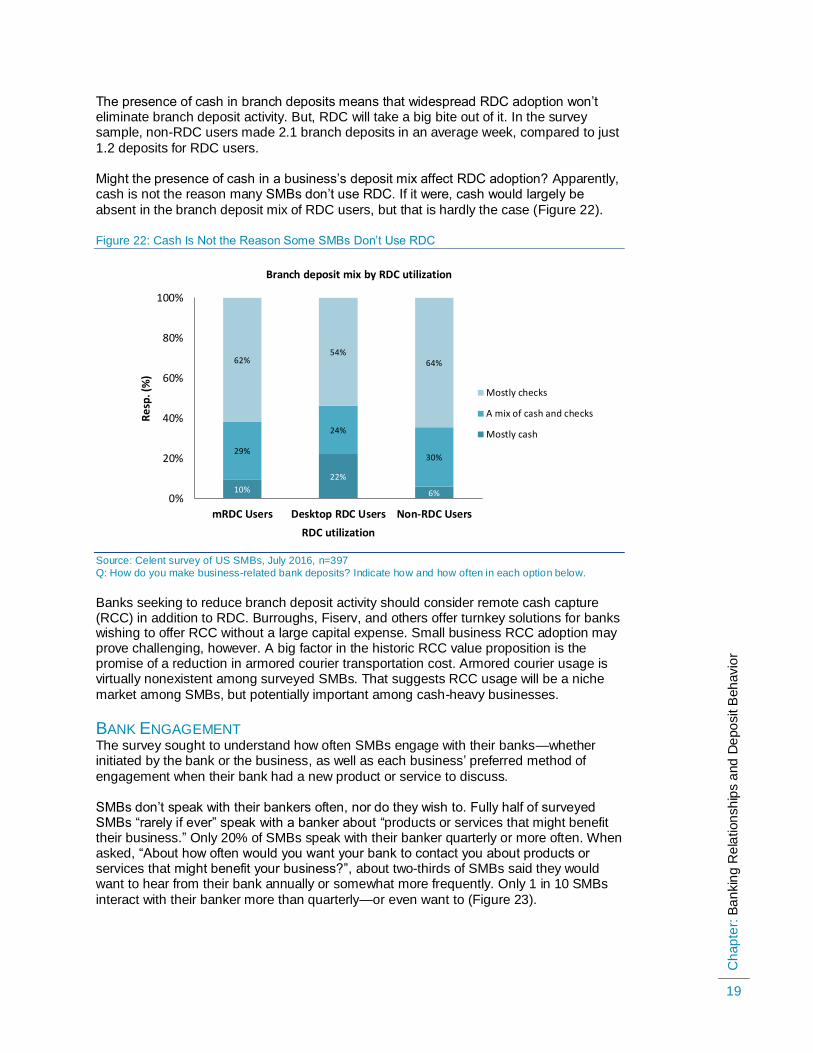

The presence of cash in branch deposits means that widespread RDC adoption won’t eliminate branch deposit activity. But, RDC will take a big bite out of it. In the survey sample, non-RDC users made 2.1 branch deposits in an average week, compared to just

1.2 deposits for RDC users.

Might the presence of cash in a business’s deposit mix affect RDC adoption? Apparently, cash is not the reason many SMBs don’t use RDC. If it were, cash would largely be

absent in the branch deposit mix of RDC users, but that is hardly the case (Figure 22).

Figure 22: Cash Is Not the Reason Some SMBs Don’t Use RDC

Source: Celent survey of US SMBs, July 2016, n=397

Q: How do you make business-related bank deposits? Indicate how and how often in each option below.

Banks seeking to reduce branch deposit activity should consider remote cash capture (RCC) in addition to RDC. Burroughs, Fiserv, and others offer turnkey solutions for banks wishing to offer RCC without a large capital expense. Small business RCC adoption may prove challenging, however. A big factor in the historic RCC value proposition is the promise of a reduction in armored courier transportation cost. Armored courier usage is virtually nonexistent among surveyed SMBs. That suggests RCC usage will be a niche

market among SMBs, but potentially important among cash-heavy businesses.

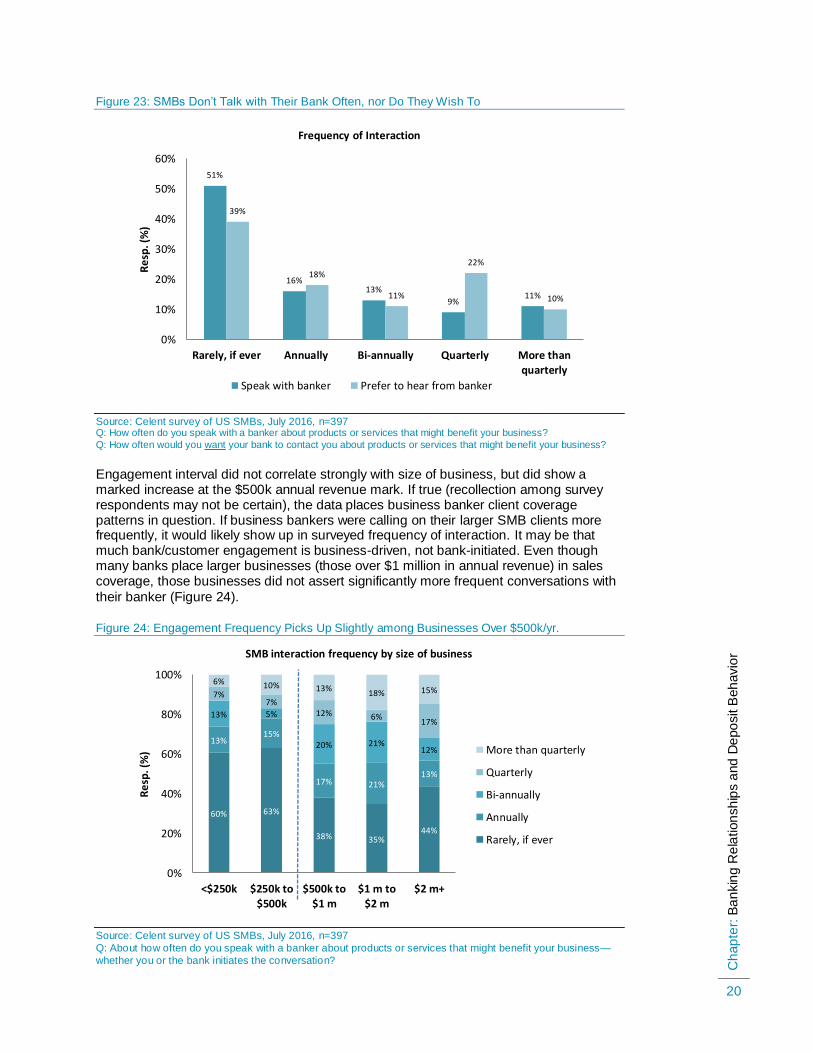

BANK ENGAGEMENT The survey sought to understand how often SMBs engage with their banks—whether initiated by the bank or the business, as well as each business’ preferred method of

engagement when their bank had a new product or service to discuss.

SMBs don’t speak with their bankers often, nor do they wish to. Fully half of surveyed SMBs “rarely if ever” speak with a banker about “products or services that might benefit their business.” Only 20% of SMBs speak with their banker quarterly or more often. When asked, “About how often would you want your bank to contact you about products or services that might benefit your business?”, about two-thirds of SMBs said they would want to hear from their bank annually or somewhat more frequently. Only 1 in 10 SMBs

interact with their banker more than quarterly—or even want to (Figure 23).

10%

22%

6%

29%

24%

30%

62% 54%

64%

0%

20%

40%

60%

80%

100%

mRDC Users Desktop RDC Users Non-RDC Users

Re

sp. (

%)

RDC utilization

Branch deposit mix by RDC utilization

Mostly checks

A mix of cash and checks

Mostly cash

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

20

Figure 23: SMBs Don’t Talk with Their Bank Often, nor Do They Wish To

Source: Celent survey of US SMBs, July 2016, n=397 Q: How often do you speak with a banker about products or services that might benefit your business?

Q: How often would you want your bank to contact you about products or services that might benefit your business?

Engagement interval did not correlate strongly with size of business, but did show a marked increase at the $500k annual revenue mark. If true (recollection among survey respondents may not be certain), the data places business banker client coverage patterns in question. If business bankers were calling on their larger SMB clients more frequently, it would likely show up in surveyed frequency of interaction. It may be that much bank/customer engagement is business-driven, not bank-initiated. Even though many banks place larger businesses (those over $1 million in annual revenue) in sales coverage, those businesses did not assert significantly more frequent conversations with

their banker (Figure 24).

Figure 24: Engagement Frequency Picks Up Slightly among Businesses Over $500k/yr.

Source: Celent survey of US SMBs, July 2016, n=397

Q: About how often do you speak with a banker about products or services that might benefit your business—

whether you or the bank initiates the conversation?

51%

16% 13%

9% 11%

39%

18%

11%

22%

10%

0%

10%

20%

30%

40%

50%

60%

Rarely, if ever Annually Bi-annually Quarterly More thanquarterly

Re

sp. (

%)

Frequency of Interaction

Speak with banker Prefer to hear from banker

60% 63%

38% 35% 44%

13% 15%

17% 21% 13%

13% 5%

20% 21% 12%

7% 7%

12% 6% 17%

6% 10% 13% 18% 15%

0%

20%

40%

60%

80%

100%

<$250k $250k to$500k

$500k to$1 m

$1 m to$2 m

$2 m+

Re

sp. (

%)

SMB interaction frequency by size of business

More than quarterly

Quarterly

Bi-annually

Annually

Rarely, if ever

Ch

ap

ter:

Ba

nkin

g R

ela

tion

sh

ips a

nd

De

po

sit B

eh

avio

r

21

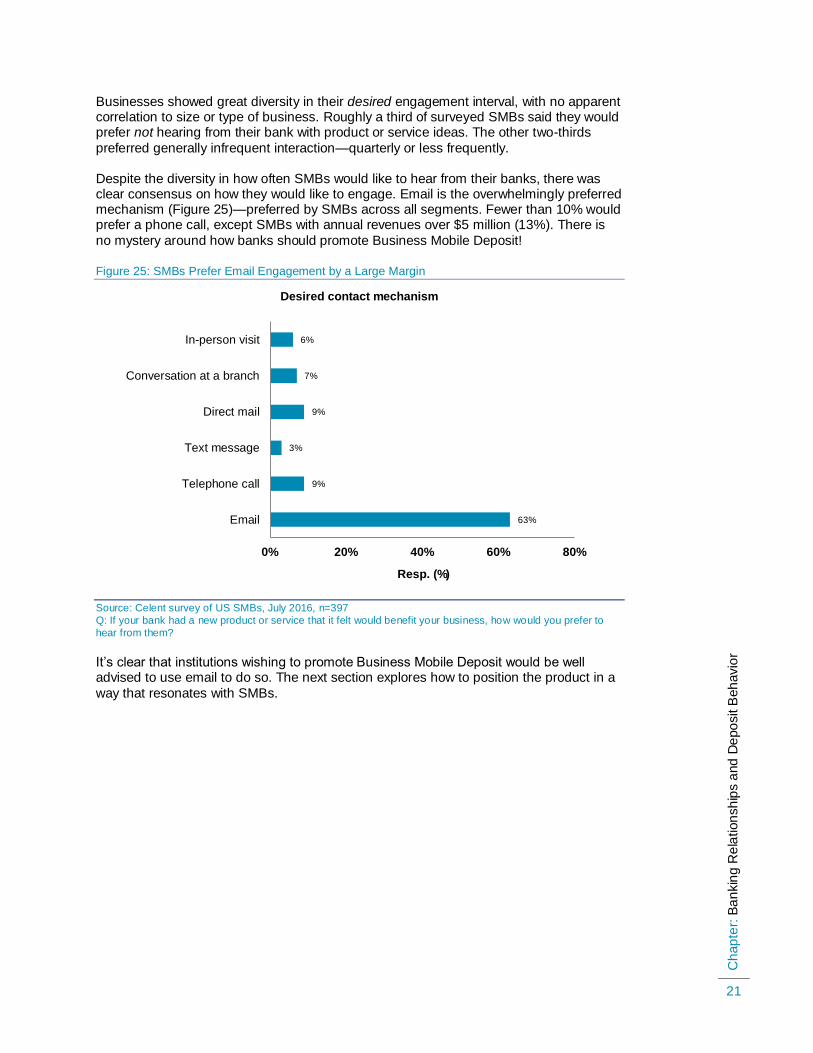

Businesses showed great diversity in their desired engagement interval, with no apparent correlation to size or type of business. Roughly a third of surveyed SMBs said they would prefer not hearing from their bank with product or service ideas. The other two-thirds

preferred generally infrequent interaction—quarterly or less frequently.

Despite the diversity in how often SMBs would like to hear from their banks, there was clear consensus on how they would like to engage. Email is the overwhelmingly preferred mechanism (Figure 25)—preferred by SMBs across all segments. Fewer than 10% would prefer a phone call, except SMBs with annual revenues over $5 million (13%). There is

no mystery around how banks should promote Business Mobile Deposit!

Figure 25: SMBs Prefer Email Engagement by a Large Margin

Source: Celent survey of US SMBs, July 2016, n=397

Q: If your bank had a new product or service that it felt would benefit your business, how would you prefer to

hear from them?

It’s clear that institutions wishing to promote Business Mobile Deposit would be well advised to use email to do so. The next section explores how to position the product in a

way that resonates with SMBs.

63%

9%

3%

9%

7%

6%

0% 20% 40% 60% 80%

Telephone call

Text message

Direct mail

Conversation at a branch

In-person visit

Resp. (%)

Desired contact mechanism

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

22

SMB REACTIONS TO BUSINESS MOBILE DEPOSIT

Awareness of mobile deposit is high (80%), with relatively little variation across size of business or business models. Banks that offer mRDC have done a good job getting the word out. Just 17% of surveyed SMBs say their bank doesn’t offer mRDC, and another 12% are aware of mRDC but don’t use it. No doubt, the high awareness and usage of

mRDC for personal accounts influences SMB attitudes towards mRDC for their business.

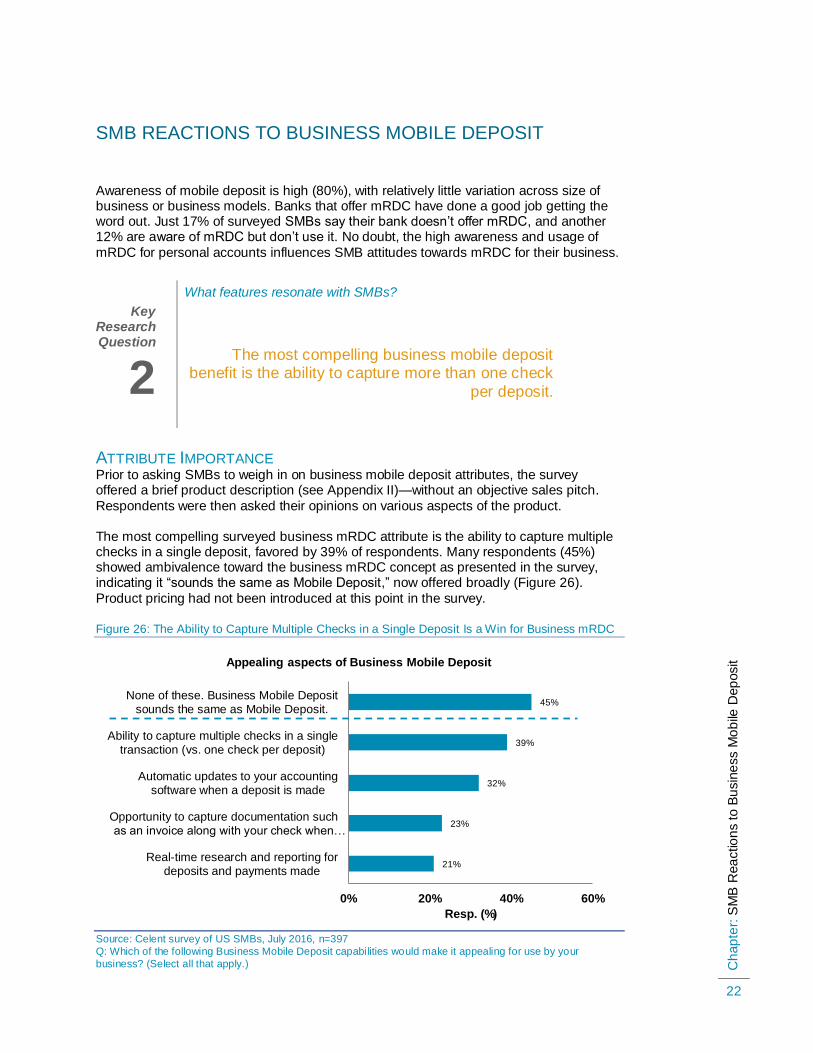

ATTRIBUTE IMPORTANCE Prior to asking SMBs to weigh in on business mobile deposit attributes, the survey offered a brief product description (see Appendix II)—without an objective sales pitch.

Respondents were then asked their opinions on various aspects of the product.

The most compelling surveyed business mRDC attribute is the ability to capture multiple checks in a single deposit, favored by 39% of respondents. Many respondents (45%) showed ambivalence toward the business mRDC concept as presented in the survey, indicating it “sounds the same as Mobile Deposit,” now offered broadly (Figure 26).

Product pricing had not been introduced at this point in the survey.

Figure 26: The Ability to Capture Multiple Checks in a Single Deposit Is a Win for Business mRDC

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following Business Mobile Deposit capabilities would make it appealing for use by your

business? (Select all that apply.)

21%

23%

32%

39%

45%

0% 20% 40% 60%

Real-time research and reporting fordeposits and payments made

Opportunity to capture documentation suchas an invoice along with your check when…

Automatic updates to your accountingsoftware when a deposit is made

Ability to capture multiple checks in a singletransaction (vs. one check per deposit)

None of these. Business Mobile Depositsounds the same as Mobile Deposit.

Resp. (%)

Appealing aspects of Business Mobile Deposit

Key Research Question

2

What features resonate with SMBs?

The most compelling business mobile deposit benefit is the ability to capture more than one check

per deposit.

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

23

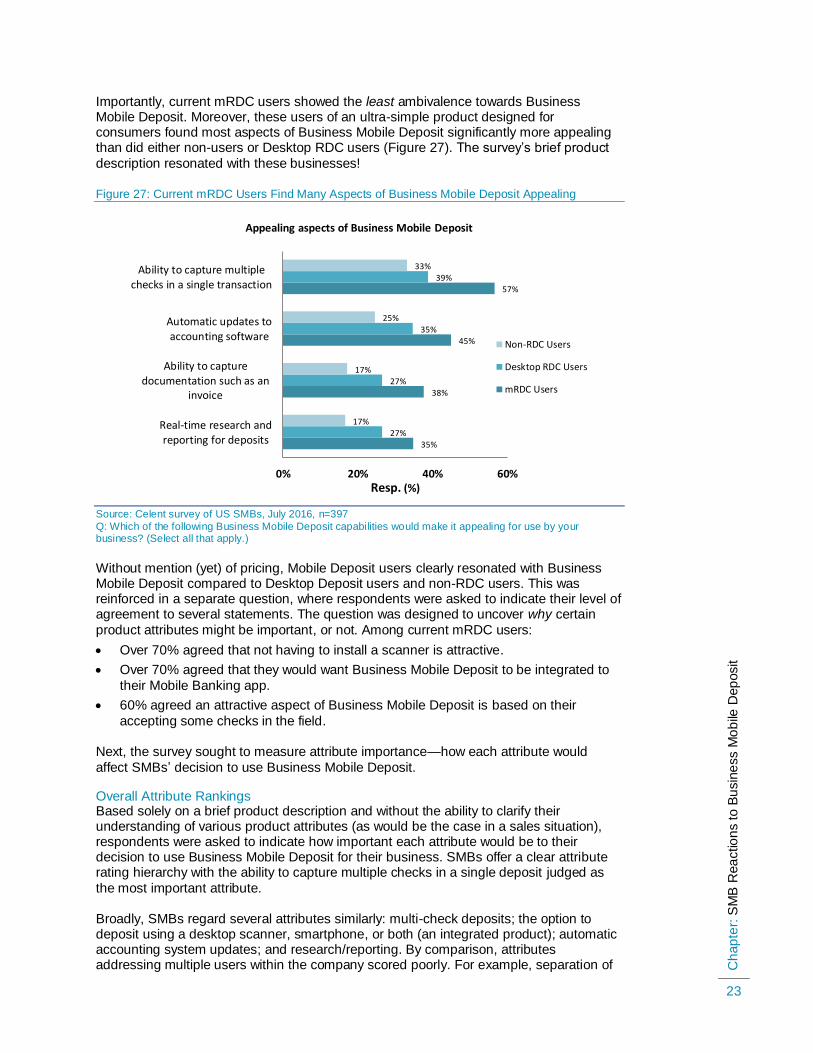

Importantly, current mRDC users showed the least ambivalence towards Business Mobile Deposit. Moreover, these users of an ultra-simple product designed for consumers found most aspects of Business Mobile Deposit significantly more appealing than did either non-users or Desktop RDC users (Figure 27). The survey’s brief product

description resonated with these businesses!

Figure 27: Current mRDC Users Find Many Aspects of Business Mobile Deposit Appealing

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following Business Mobile Deposit capabilities would make it appealing for use by your business? (Select all that apply.)

Without mention (yet) of pricing, Mobile Deposit users clearly resonated with Business Mobile Deposit compared to Desktop Deposit users and non-RDC users. This was reinforced in a separate question, where respondents were asked to indicate their level of agreement to several statements. The question was designed to uncover why certain

product attributes might be important, or not. Among current mRDC users:

Over 70% agreed that not having to install a scanner is attractive.

Over 70% agreed that they would want Business Mobile Deposit to be integrated to

their Mobile Banking app.

60% agreed an attractive aspect of Business Mobile Deposit is based on their

accepting some checks in the field.

Next, the survey sought to measure attribute importance—how each attribute would

affect SMBs’ decision to use Business Mobile Deposit.

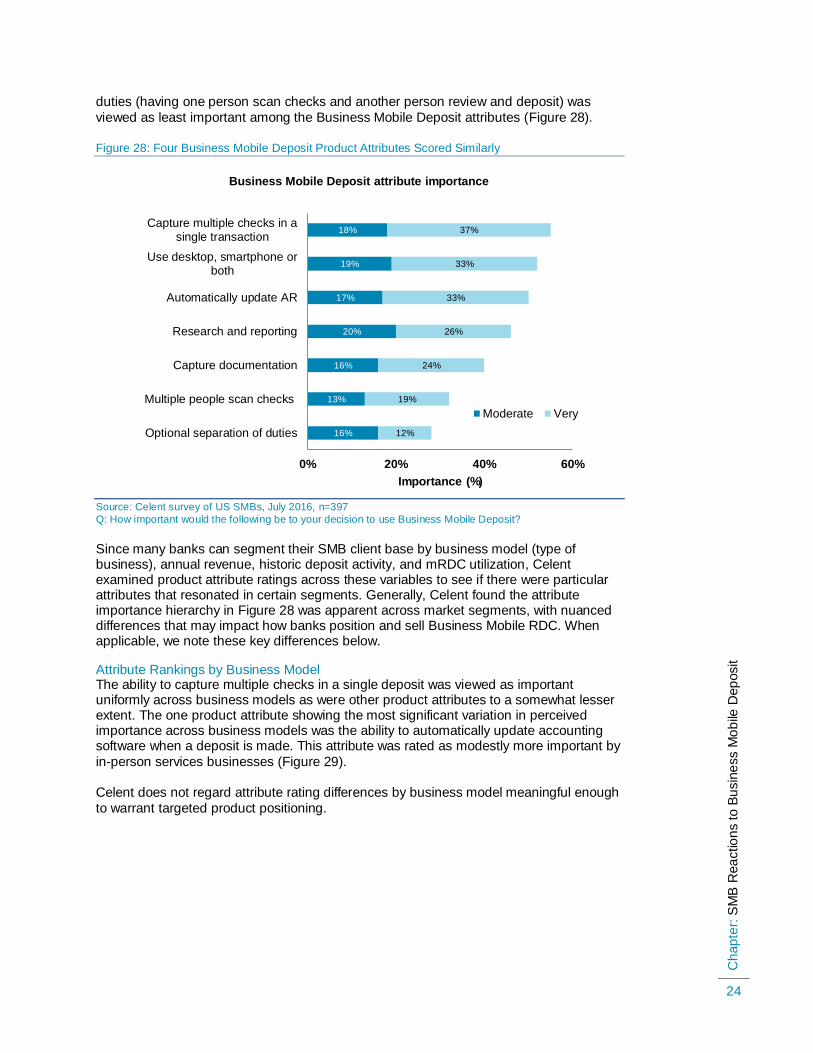

Overall Attribute Rankings Based solely on a brief product description and without the ability to clarify their understanding of various product attributes (as would be the case in a sales situation), respondents were asked to indicate how important each attribute would be to their decision to use Business Mobile Deposit for their business. SMBs offer a clear attribute rating hierarchy with the ability to capture multiple checks in a single deposit judged as

the most important attribute.

Broadly, SMBs regard several attributes similarly: multi-check deposits; the option to deposit using a desktop scanner, smartphone, or both (an integrated product); automatic accounting system updates; and research/reporting. By comparison, attributes addressing multiple users within the company scored poorly. For example, separation of

35%

38%

45%

57%

27%

27%

35%

39%

17%

17%

25%

33%

0% 20% 40% 60%

Real-time research andreporting for deposits

Ability to capturedocumentation such as an

invoice

Automatic updates toaccounting software

Ability to capture multiplechecks in a single transaction

Resp. (%)

Appealing aspects of Business Mobile Deposit

Non-RDC Users

Desktop RDC Users

mRDC Users

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

24

duties (having one person scan checks and another person review and deposit) was

viewed as least important among the Business Mobile Deposit attributes (Figure 28).

Figure 28: Four Business Mobile Deposit Product Attributes Scored Similarly

Source: Celent survey of US SMBs, July 2016, n=397

Q: How important would the following be to your decision to use Business Mobile Deposit?

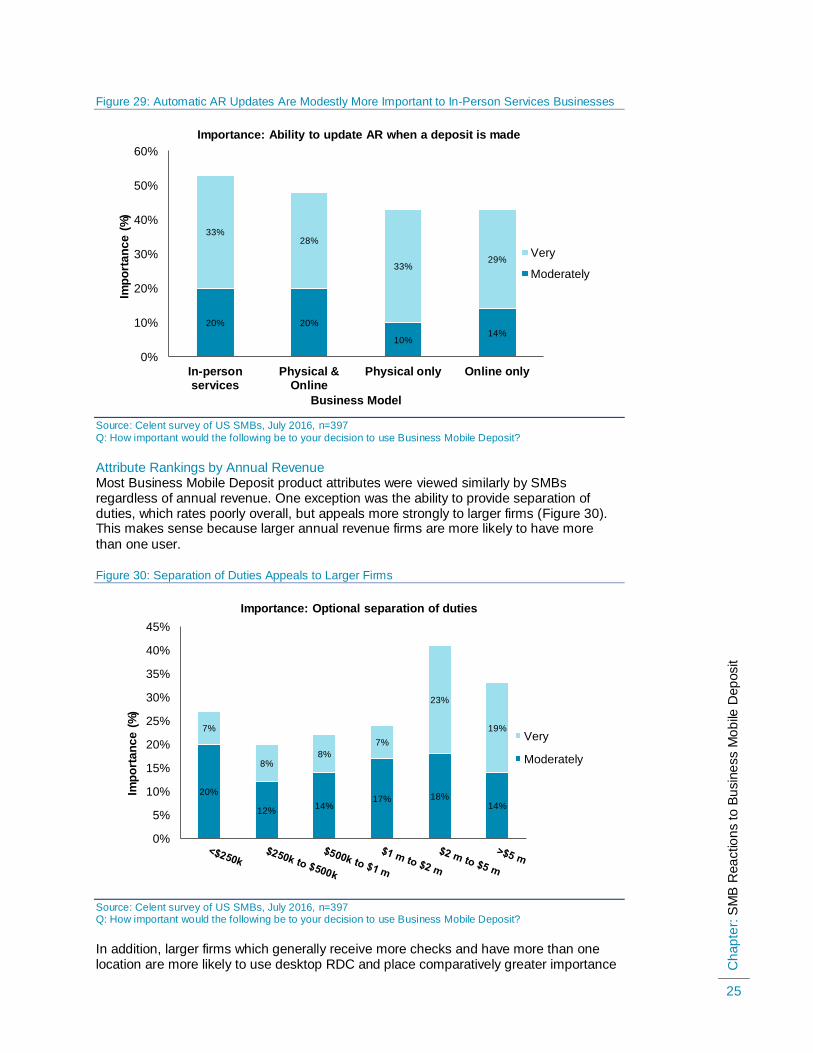

Since many banks can segment their SMB client base by business model (type of business), annual revenue, historic deposit activity, and mRDC utilization, Celent examined product attribute ratings across these variables to see if there were particular attributes that resonated in certain segments. Generally, Celent found the attribute importance hierarchy in Figure 28 was apparent across market segments, with nuanced differences that may impact how banks position and sell Business Mobile RDC. When applicable, we note these key differences below.

Attribute Rankings by Business Model The ability to capture multiple checks in a single deposit was viewed as important uniformly across business models as were other product attributes to a somewhat lesser extent. The one product attribute showing the most significant variation in perceived importance across business models was the ability to automatically update accounting software when a deposit is made. This attribute was rated as modestly more important by

in-person services businesses (Figure 29).

Celent does not regard attribute rating differences by business model meaningful enough

to warrant targeted product positioning.

16%

13%

16%

20%

17%

19%

18%

12%

19%

24%

26%

33%

33%

37%

0% 20% 40% 60%

Optional separation of duties

Multiple people scan checks

Capture documentation

Research and reporting

Automatically update AR

Use desktop, smartphone orboth

Capture multiple checks in asingle transaction

Importance (%)

Business Mobile Deposit attribute importance

Moderate Very

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

25

Figure 29: Automatic AR Updates Are Modestly More Important to In-Person Services Businesses

Source: Celent survey of US SMBs, July 2016, n=397

Q: How important would the following be to your decision to use Business Mobile Deposit?

Attribute Rankings by Annual Revenue Most Business Mobile Deposit product attributes were viewed similarly by SMBs regardless of annual revenue. One exception was the ability to provide separation of duties, which rates poorly overall, but appeals more strongly to larger firms (Figure 30). This makes sense because larger annual revenue firms are more likely to have more

than one user.

Figure 30: Separation of Duties Appeals to Larger Firms

Source: Celent survey of US SMBs, July 2016, n=397 Q: How important would the following be to your decision to use Business Mobile Deposit?

In addition, larger firms which generally receive more checks and have more than one location are more likely to use desktop RDC and place comparatively greater importance

20% 20%

10% 14%

33% 28%

33% 29%

0%

10%

20%

30%

40%

50%

60%

In-personservices

Physical &Online

Physical only Online only

Imp

ort

an

ce

(%

)

Business Model

Importance: Ability to update AR when a deposit is made

Very

Moderately

20%

12% 14%

17% 18% 14%

7%

8% 8%

7%

23%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Imp

ort

an

ce

(%

)

Importance: Optional separation of duties

Very

Moderately

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

26

on separation of duties as well as the ability to capture using a desktop or mobile device, or both. The <$250k micro business segment is surprisingly pro-business mRDC, rating

several attributes significantly higher than modestly larger businesses. In summary:

SMBs across all segments value the ability to capture more than one check in a

deposit.

Attributes suggesting a bundled mobile/desktop solution appeal to larger SMBs,

many of whom already use Desktop RDC.

In Celent’s view, an annual revenue view of SMBs is of some value in positioning and selling Business Mobile Deposit, but a more useful segmentation looks at where the

checks are.

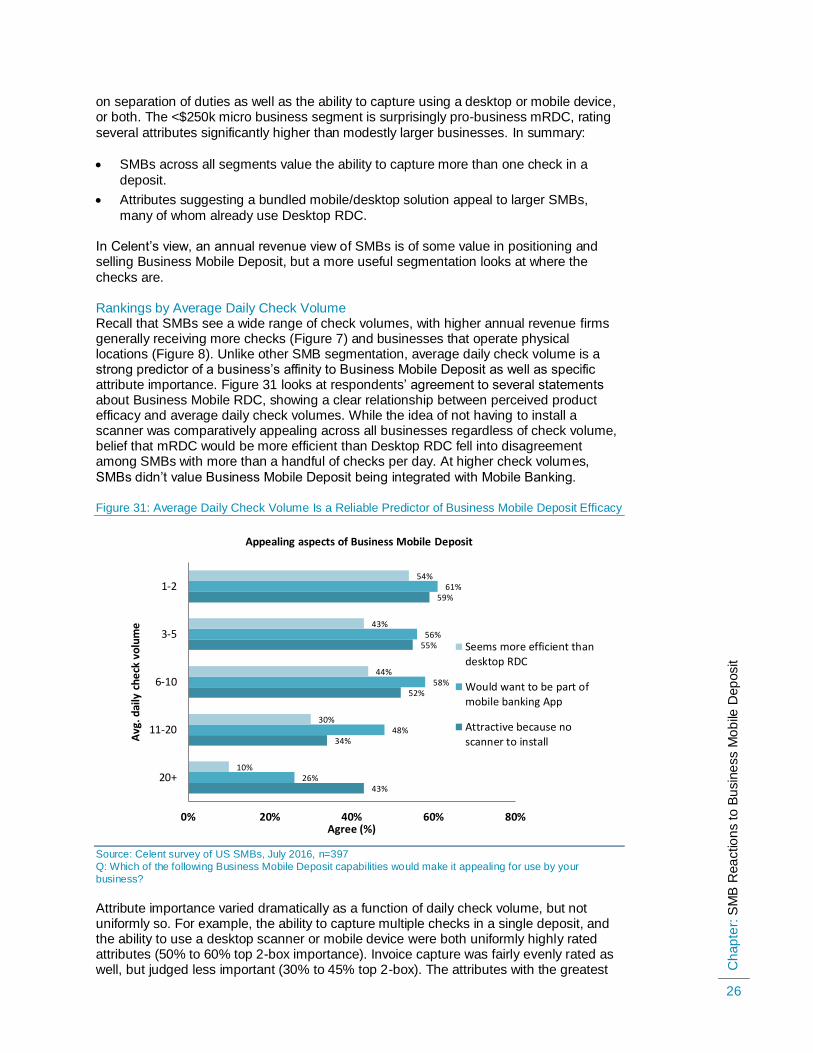

Rankings by Average Daily Check Volume Recall that SMBs see a wide range of check volumes, with higher annual revenue firms generally receiving more checks (Figure 7) and businesses that operate physical locations (Figure 8). Unlike other SMB segmentation, average daily check volume is a strong predictor of a business’s affinity to Business Mobile Deposit as well as specific attribute importance. Figure 31 looks at respondents’ agreement to several statements about Business Mobile RDC, showing a clear relationship between perceived product efficacy and average daily check volumes. While the idea of not having to install a scanner was comparatively appealing across all businesses regardless of check volume, belief that mRDC would be more efficient than Desktop RDC fell into disagreement among SMBs with more than a handful of checks per day. At higher check volumes,

SMBs didn’t value Business Mobile Deposit being integrated with Mobile Banking.

Figure 31: Average Daily Check Volume Is a Reliable Predictor of Business Mobile Deposit Efficacy

Source: Celent survey of US SMBs, July 2016, n=397

Q: Which of the following Business Mobile Deposit capabilities would make it appealing for use by your

business?

Attribute importance varied dramatically as a function of daily check volume, but not uniformly so. For example, the ability to capture multiple checks in a single deposit, and the ability to use a desktop scanner or mobile device were both uniformly highly rated attributes (50% to 60% top 2-box importance). Invoice capture was fairly evenly rated as well, but judged less important (30% to 45% top 2-box). The attributes with the greatest

43%

34%

52%

55%

59%

26%

48%

58%

56%

61%

10%

30%

44%

43%

54%

0% 20% 40% 60% 80%

20+

11-20

6-10

3-5

1-2

Agree (%)

Avg

. dai

ly c

he

ck v

olu

me

Appealing aspects of Business Mobile Deposit

Seems more efficient thandesktop RDC

Would want to be part ofmobile banking App

Attractive because noscanner to install

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

27

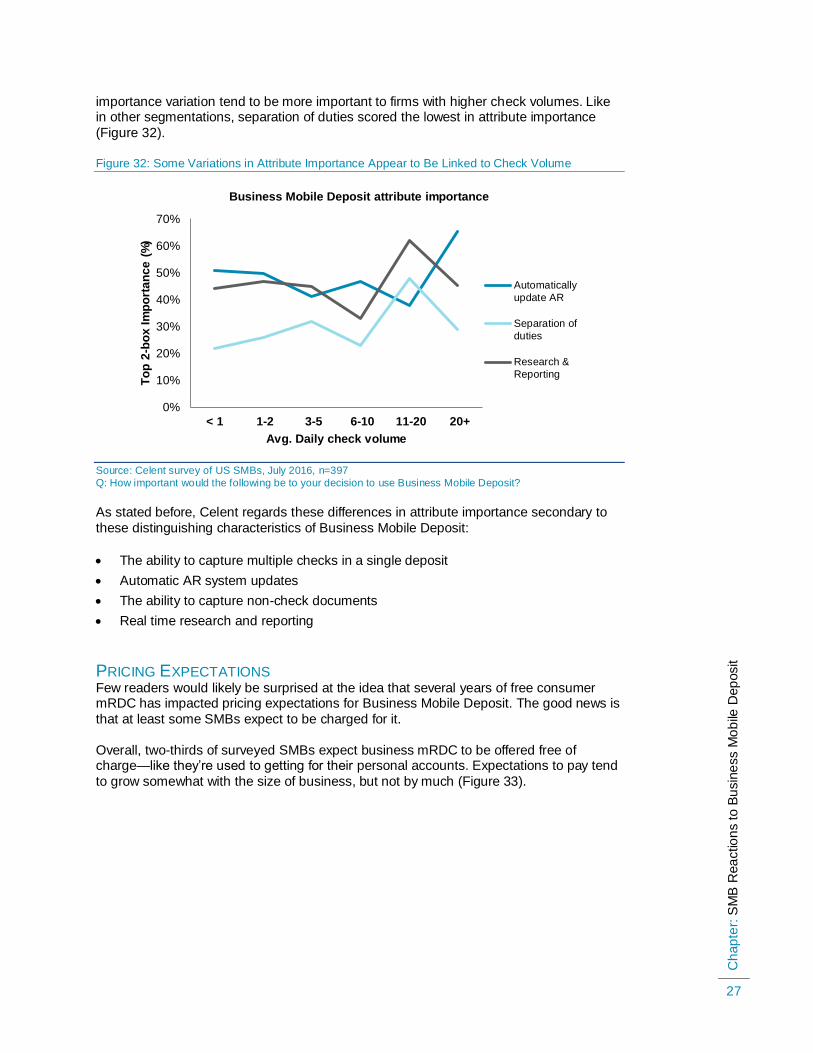

importance variation tend to be more important to firms with higher check volumes. Like in other segmentations, separation of duties scored the lowest in attribute importance

(Figure 32).

Figure 32: Some Variations in Attribute Importance Appear to Be Linked to Check Volume

Source: Celent survey of US SMBs, July 2016, n=397

Q: How important would the following be to your decision to use Business Mobile Deposit?

As stated before, Celent regards these differences in attribute importance secondary to

these distinguishing characteristics of Business Mobile Deposit:

The ability to capture multiple checks in a single deposit

Automatic AR system updates

The ability to capture non-check documents

Real time research and reporting

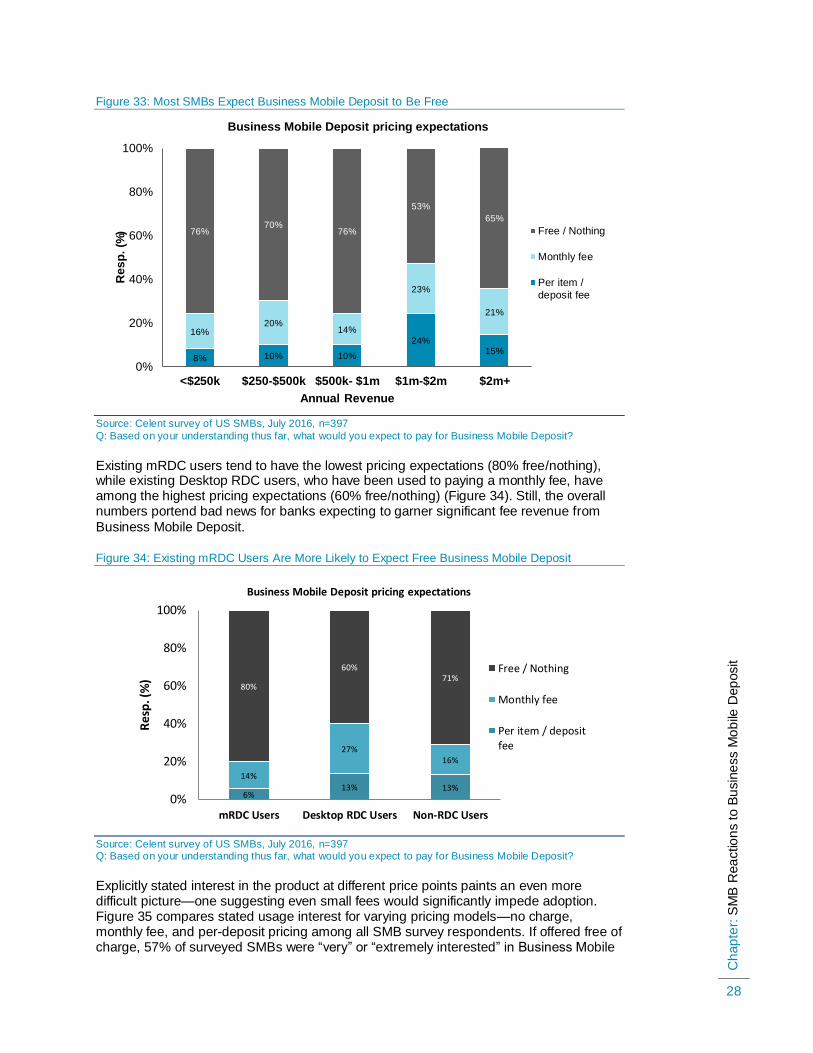

PRICING EXPECTATIONS Few readers would likely be surprised at the idea that several years of free consumer mRDC has impacted pricing expectations for Business Mobile Deposit. The good news is

that at least some SMBs expect to be charged for it.

Overall, two-thirds of surveyed SMBs expect business mRDC to be offered free of charge—like they’re used to getting for their personal accounts. Expectations to pay tend

to grow somewhat with the size of business, but not by much (Figure 33).

0%

10%

20%

30%

40%

50%

60%

70%

< 1 1-2 3-5 6-10 11-20 20+

To

p 2

-bo

x I

mp

ort

an

ce

(%

)

Avg. Daily check volume

Business Mobile Deposit attribute importance

Automatically

update AR

Separation of

duties

Research &

Reporting

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

28

Figure 33: Most SMBs Expect Business Mobile Deposit to Be Free

Source: Celent survey of US SMBs, July 2016, n=397

Q: Based on your understanding thus far, what would you expect to pay for Business Mobile Deposit?

Existing mRDC users tend to have the lowest pricing expectations (80% free/nothing), while existing Desktop RDC users, who have been used to paying a monthly fee, have among the highest pricing expectations (60% free/nothing) (Figure 34). Still, the overall numbers portend bad news for banks expecting to garner significant fee revenue from

Business Mobile Deposit.

Figure 34: Existing mRDC Users Are More Likely to Expect Free Business Mobile Deposit

Source: Celent survey of US SMBs, July 2016, n=397 Q: Based on your understanding thus far, what would you expect to pay for Business Mobile Deposit?

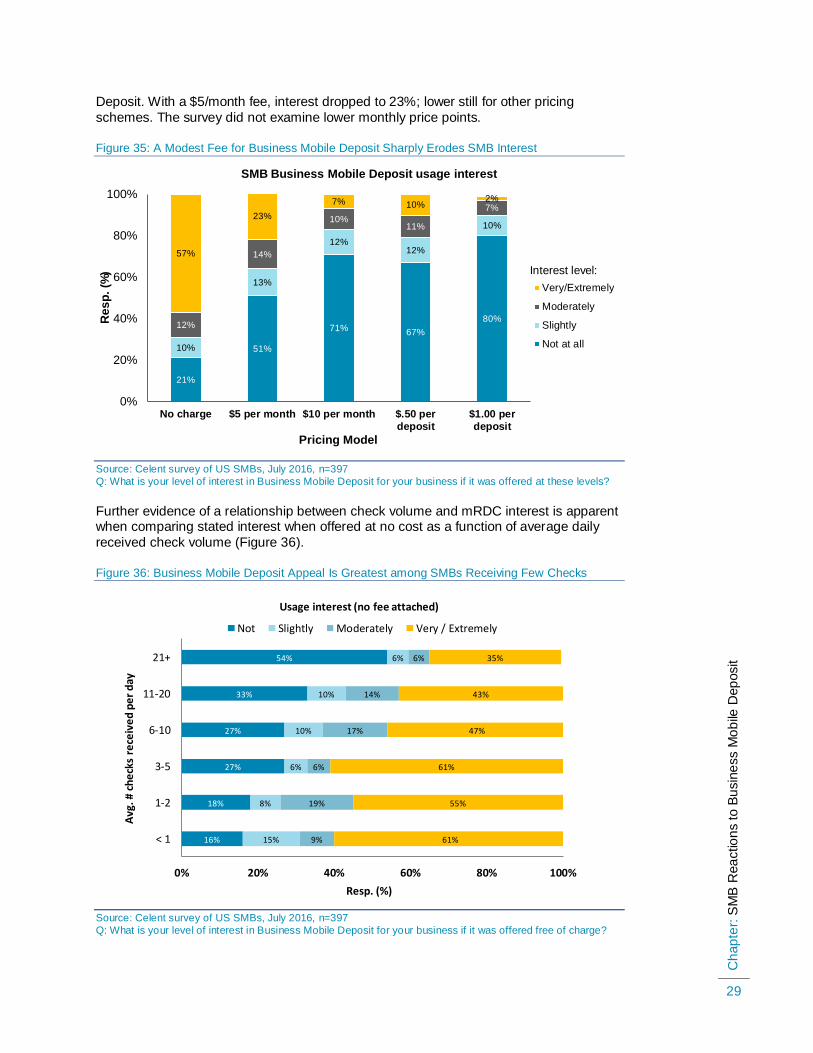

Explicitly stated interest in the product at different price points paints an even more difficult picture—one suggesting even small fees would significantly impede adoption. Figure 35 compares stated usage interest for varying pricing models—no charge, monthly fee, and per-deposit pricing among all SMB survey respondents. If offered free of charge, 57% of surveyed SMBs were “very” or “extremely interested” in Business Mobile

8% 10% 10%

24% 15%

16% 20%

14%

23%

21%

76% 70%

76%

53%

65%

0%

20%

40%

60%

80%

100%

<$250k $250-$500k $500k- $1m $1m-$2m $2m+

Re

sp

. (%

)

Annual Revenue

Business Mobile Deposit pricing expectations

Free / Nothing

Monthly fee

Per item /

deposit fee

6% 13% 13%

14%

27% 16%

80%

60% 71%

0%

20%

40%

60%

80%

100%

mRDC Users Desktop RDC Users Non-RDC Users

Res

p. (

%)

Business Mobile Deposit pricing expectations

Free / Nothing

Monthly fee

Per item / depositfee

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

29

Deposit. With a $5/month fee, interest dropped to 23%; lower still for other pricing

schemes. The survey did not examine lower monthly price points.

Figure 35: A Modest Fee for Business Mobile Deposit Sharply Erodes SMB Interest

Source: Celent survey of US SMBs, July 2016, n=397

Q: What is your level of interest in Business Mobile Deposit for your business if it was offered at these levels?

Further evidence of a relationship between check volume and mRDC interest is apparent when comparing stated interest when offered at no cost as a function of average daily

received check volume (Figure 36).

Figure 36: Business Mobile Deposit Appeal Is Greatest among SMBs Receiving Few Checks

Source: Celent survey of US SMBs, July 2016, n=397

Q: What is your level of interest in Business Mobile Deposit for your business if it was offered free of charge?

21%

51%

71% 67%

80%

10%

13%

12% 12%

10%

12%

14%

10% 11%

7%

57%

23%

7% 10% 2%

0%

20%

40%

60%

80%

100%

No charge $5 per month $10 per month $.50 per

deposit

$1.00 per

deposit

Re

sp

. (%

)

Pricing Model

SMB Business Mobile Deposit usage interest

Very/Extremely

Moderately

Slightly

Not at all

16%

18%

27%

27%

33%

54%

15%

8%

6%

10%

10%

6%

9%

19%

6%

17%

14%

6%

61%

55%

61%

47%

43%

35%

0% 20% 40% 60% 80% 100%

< 1

1-2

3-5

6-10

11-20

21+

Resp. (%)

Avg

. # c

he

cks

rece

ive

d p

er

day

Usage interest (no fee attached)

Not Slightly Moderately Very / Extremely

Interest level:

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

30

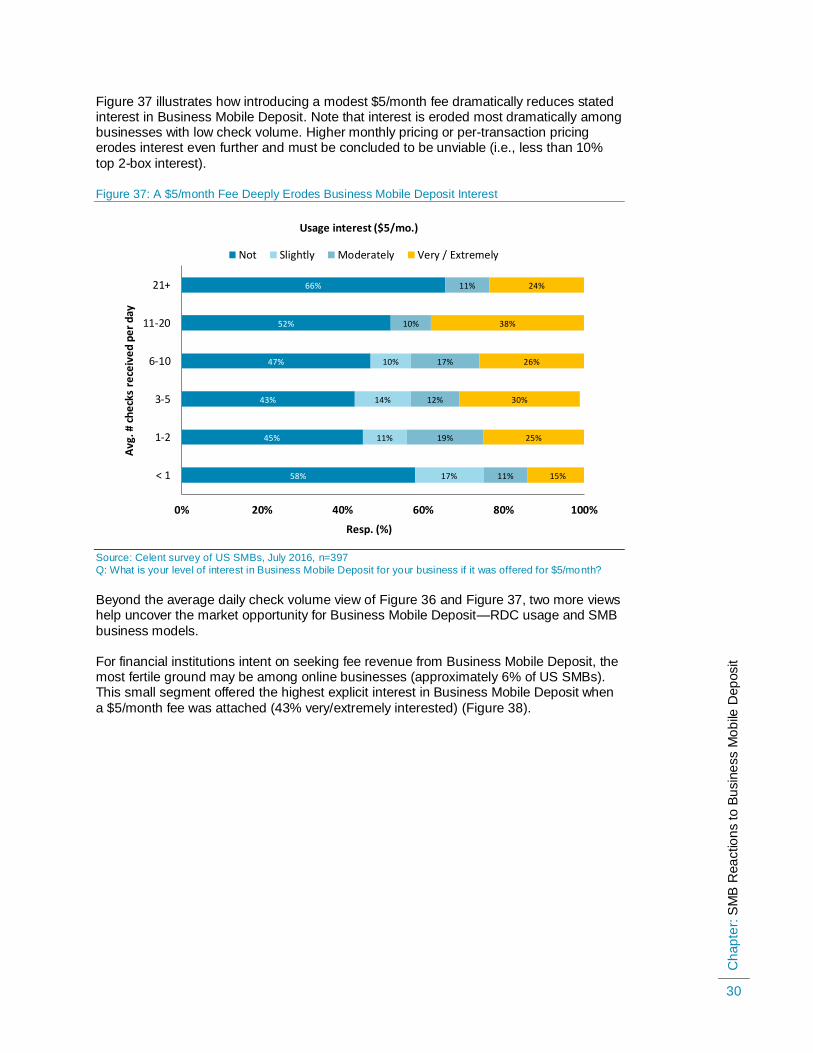

Figure 37 illustrates how introducing a modest $5/month fee dramatically reduces stated interest in Business Mobile Deposit. Note that interest is eroded most dramatically among businesses with low check volume. Higher monthly pricing or per-transaction pricing erodes interest even further and must be concluded to be unviable (i.e., less than 10%

top 2-box interest).

Figure 37: A $5/month Fee Deeply Erodes Business Mobile Deposit Interest

Source: Celent survey of US SMBs, July 2016, n=397

Q: What is your level of interest in Business Mobile Deposit for your business if it was offered for $5/month?

Beyond the average daily check volume view of Figure 36 and Figure 37, two more views help uncover the market opportunity for Business Mobile Deposit—RDC usage and SMB

business models.

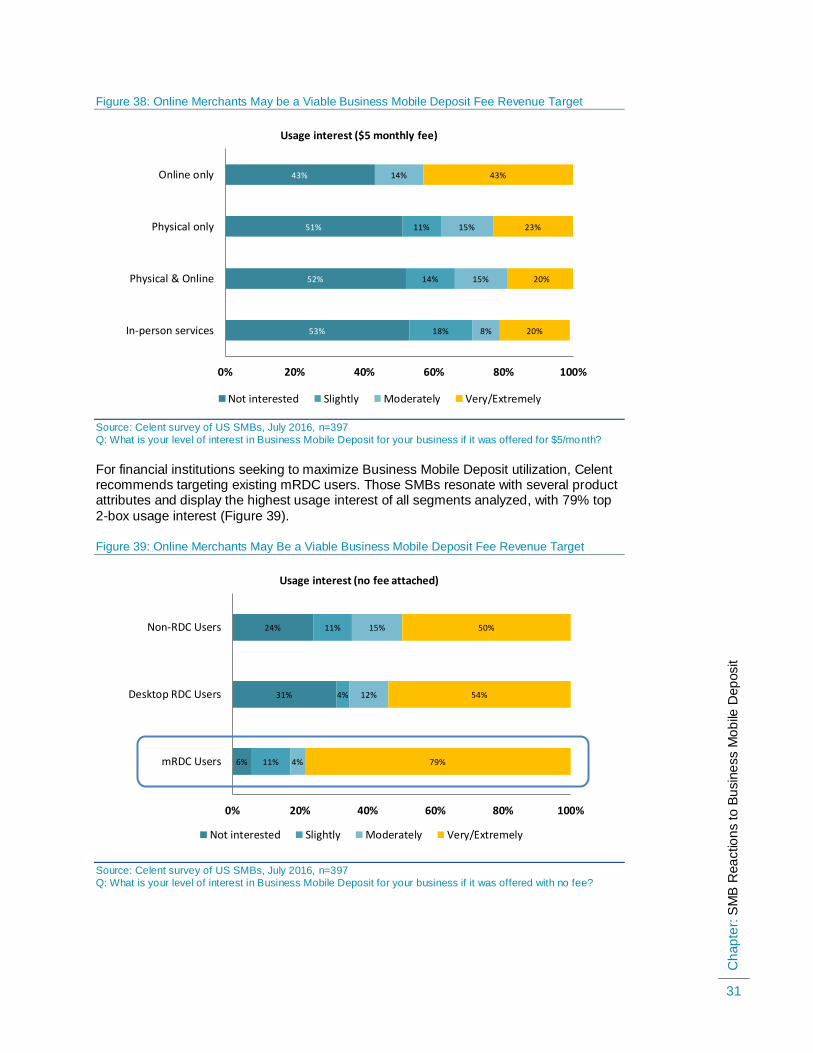

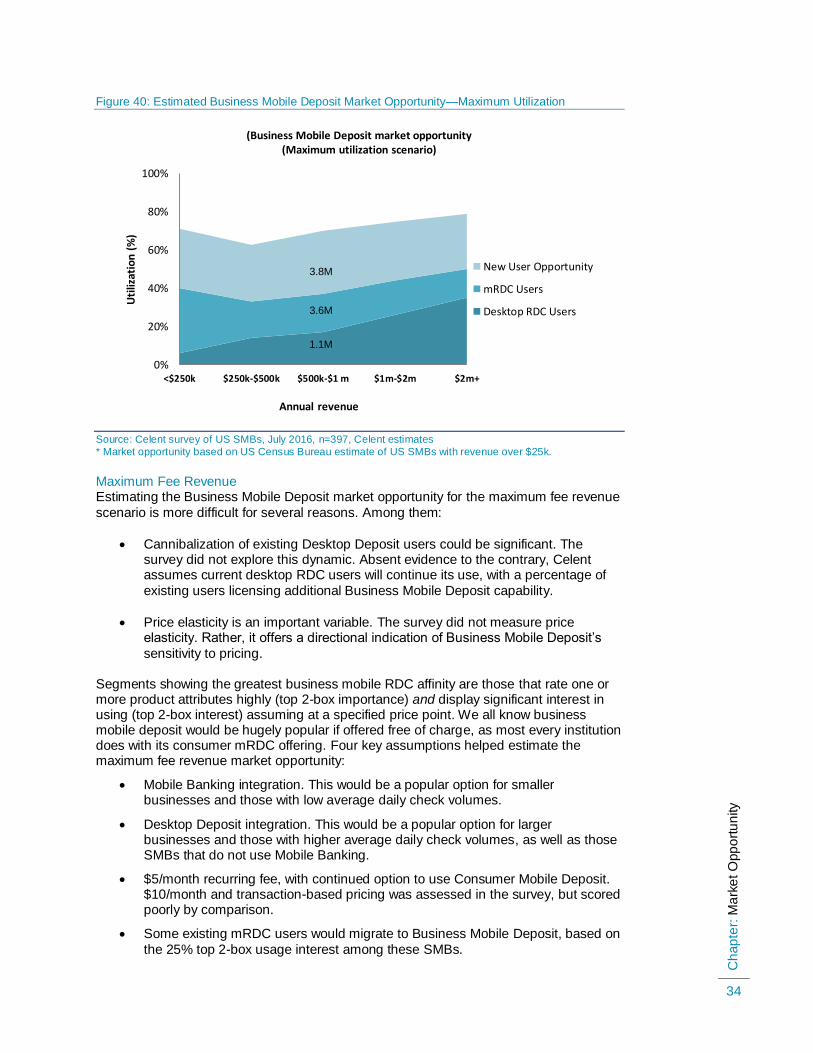

For financial institutions intent on seeking fee revenue from Business Mobile Deposit, the most fertile ground may be among online businesses (approximately 6% of US SMBs). This small segment offered the highest explicit interest in Business Mobile Deposit when

a $5/month fee was attached (43% very/extremely interested) (Figure 38).

58%

45%

43%

47%

52%

66%

17%

11%

14%

10%

11%

19%

12%

17%

10%

11%

15%

25%

30%

26%

38%

24%

0% 20% 40% 60% 80% 100%

< 1

1-2

3-5

6-10

11-20

21+

Resp. (%)

Avg

. # c

he

cks

rece

ive

d p

er

day

Usage interest ($5/mo.)

Not Slightly Moderately Very / Extremely

Ch

ap

ter:

SM

B R

ea

ctio

ns

to B

usin

ess M

ob

ile D

ep

osit

31

Figure 38: Online Merchants May be a Viable Business Mobile Deposit Fee Revenue Target

Source: Celent survey of US SMBs, July 2016, n=397

Q: What is your level of interest in Business Mobile Deposit for your business if it was offered for $5/month?

For financial institutions seeking to maximize Business Mobile Deposit utilization, Celent recommends targeting existing mRDC users. Those SMBs resonate with several product attributes and display the highest usage interest of all segments analyzed, with 79% top

2-box usage interest (Figure 39).

Figure 39: Online Merchants May Be a Viable Business Mobile Deposit Fee Revenue Target

Source: Celent survey of US SMBs, July 2016, n=397

Q: What is your level of interest in Business Mobile Deposit for your business if it was offered with no fee?

53%

52%

51%

43%

18%

14%

11%

8%

15%

15%

14%

20%

20%

23%

43%

0% 20% 40% 60% 80% 100%

In-person services

Physical & Online

Physical only

Online only

Usage interest ($5 monthly fee)

Not interested Slightly Moderately Very/Extremely

6%

31%

24%

11%

4%

11%

4%

12%

15%

79%

54%

50%

0% 20% 40% 60% 80% 100%

mRDC Users

Desktop RDC Users

Non-RDC Users

Usage interest (no fee attached)

Not interested Slightly Moderately Very/Extremely

Ch

ap

ter:

Ma

rke

t O

pp

ort

un

ity

32

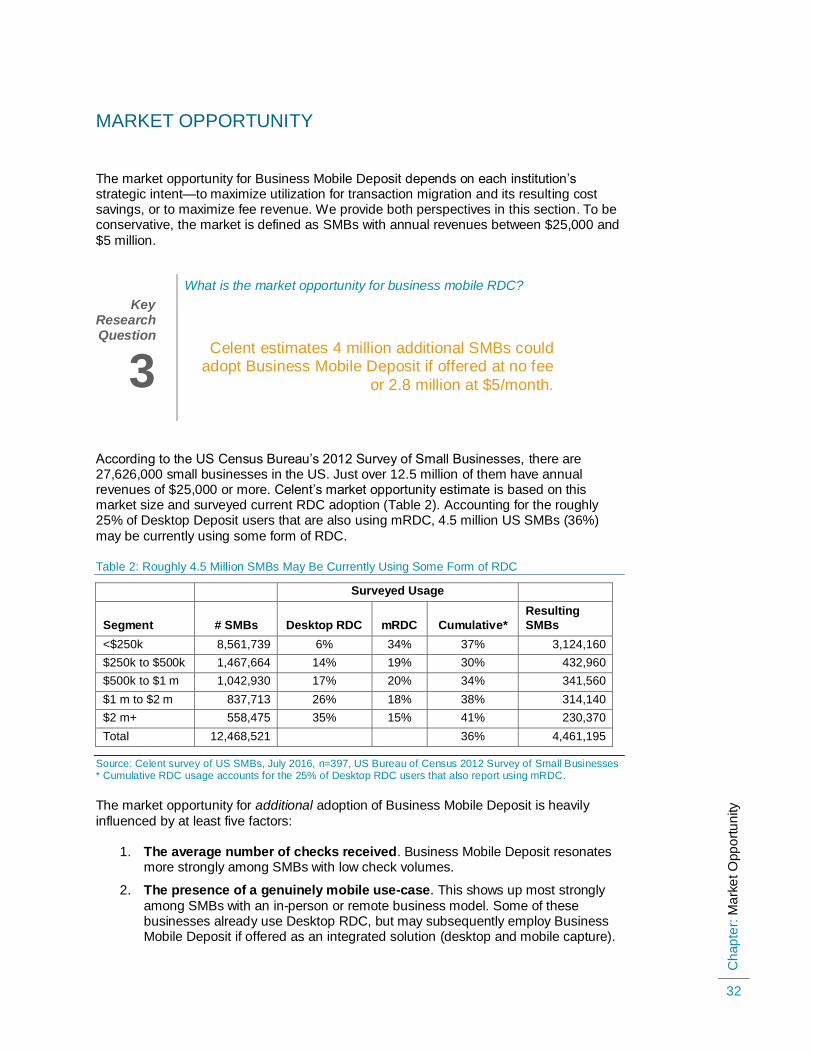

MARKET OPPORTUNITY

The market opportunity for Business Mobile Deposit depends on each institution’s strategic intent—to maximize utilization for transaction migration and its resulting cost savings, or to maximize fee revenue. We provide both perspectives in this section. To be conservative, the market is defined as SMBs with annual revenues between $25,000 and

$5 million.

According to the US Census Bureau’s 2012 Survey of Small Businesses, there are 27,626,000 small businesses in the US. Just over 12.5 million of them have annual revenues of $25,000 or more. Celent’s market opportunity estimate is based on this market size and surveyed current RDC adoption (Table 2). Accounting for the roughly 25% of Desktop Deposit users that are also using mRDC, 4.5 million US SMBs (36%)

may be currently using some form of RDC.

Table 2: Roughly 4.5 Million SMBs May Be Currently Using Some Form of RDC

Surveyed Usage

Segment # SMBs Desktop RDC mRDC Cumulative*

Resulting

SMBs

<$250k 8,561,739 6% 34% 37% 3,124,160

$250k to $500k 1,467,664 14% 19% 30% 432,960

$500k to $1 m 1,042,930 17% 20% 34% 341,560

$1 m to $2 m 837,713 26% 18% 38% 314,140

$2 m+ 558,475 35% 15% 41% 230,370

Total 12,468,521 36% 4,461,195

Source: Celent survey of US SMBs, July 2016, n=397, US Bureau of Census 2012 Survey of Small Businesses * Cumulative RDC usage accounts for the 25% of Desktop RDC users that also report using mRDC.

The market opportunity for additional adoption of Business Mobile Deposit is heavily

influenced by at least five factors:

1. The average number of checks received. Business Mobile Deposit resonates more strongly among SMBs with low check volumes.

2. The presence of a genuinely mobile use-case. This shows up most strongly

among SMBs with an in-person or remote business model. Some of these businesses already use Desktop RDC, but may subsequently employ Business Mobile Deposit if offered as an integrated solution (desktop and mobile capture).

Key Research Question

3

What is the market opportunity for business mobile RDC?

Celent estimates 4 million additional SMBs could adopt Business Mobile Deposit if offered at no fee

or 2.8 million at $5/month.

Ch

ap

ter:

Ma

rke

t O

pp

ort

un

ity

33

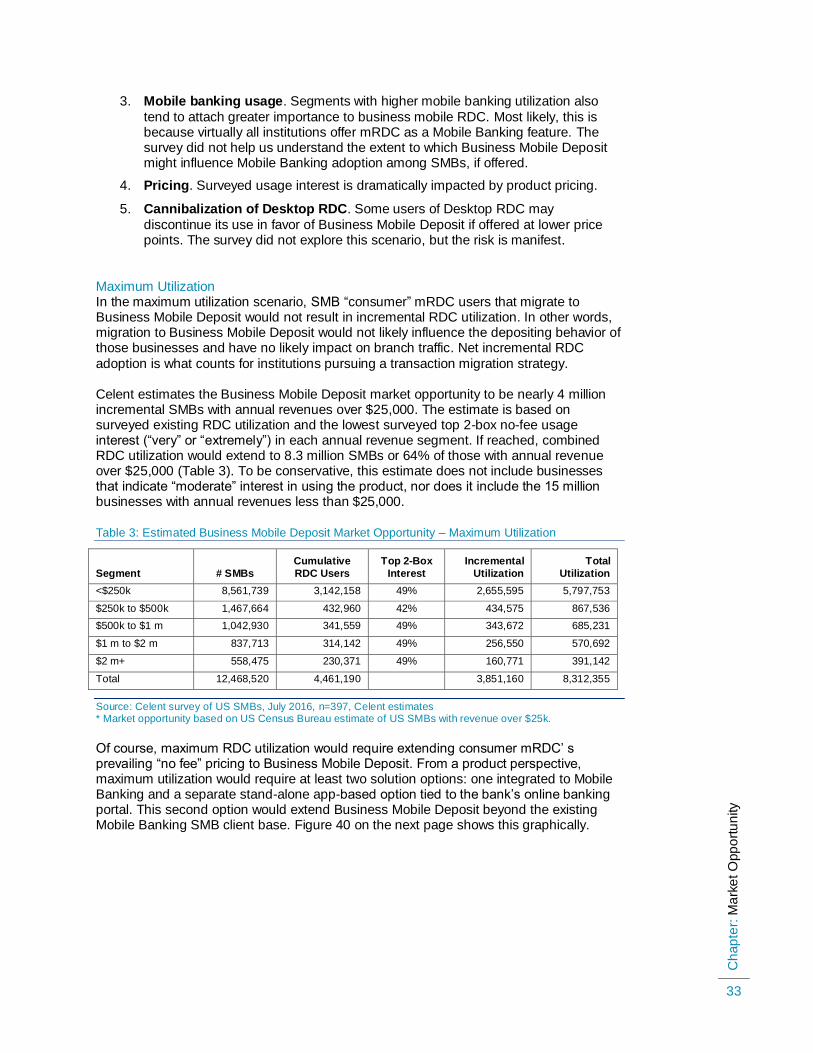

3. Mobile banking usage. Segments with higher mobile banking utilization also

tend to attach greater importance to business mobile RDC. Most likely, this is because virtually all institutions offer mRDC as a Mobile Banking feature. The survey did not help us understand the extent to which Business Mobile Deposit might influence Mobile Banking adoption among SMBs, if offered.

4. Pricing. Surveyed usage interest is dramatically impacted by product pricing.

5. Cannibalization of Desktop RDC. Some users of Desktop RDC may

discontinue its use in favor of Business Mobile Deposit if offered at lower price points. The survey did not explore this scenario, but the risk is manifest.