Embed Size (px)

Citation preview

1

Possible Barriers and Threats to Foreigner Direct

Investment (FDI) in Saudi Arabia: Pegged Exchange Rate,

Political Risks and Islamic Banking - Evaluation of the

Strategic Solutions.

By

Mohammed Binkhamis

PhD Candidate, Finance and Economic Depertment at De Montfort University

Supervised By

Dr. Yulia Rodionova

Senior Lecturer in Finance at De Montfort University

2

Key Words:

FDI

Political Risks

Pegged Exchange Rate

Saudi Arabia

Abstract

The purpose of study is to examine problems and restrictions that the overseas investors face

in doing business in Saudi Arabia.

Moreover, to examine the impact of political issues of radical organizations threats and

relationship with Iran on Foreign Direct Investment.

The researcher will study the influence of fixed exchange rate of Saudi riyals on Foreign

Direct Investment into the Saudi Market.

Also, the thesis will search for the strategic solutions that help foreign investors to predict the

potential risks of Saudi Market.

Research Question and Aims:

Research Question

3

• How can the political issues such as radical organisations’ threats, relationship with

Iran and the Arab spring revolution in the Middle East influence Foreign Direct

Investment for entering Saudi market?

• How can the previous political risks limit existing FDI to expand in Saudi Market?

• What are the impact of global terrorist on macroeconomic affect the growth of

economy and flow of FDI?

• As result of previous question, how can reduction of US dollar value influence the

flow of FDI to Saudi Arabia?

• Which Strategic solutions can be applied to challenge and predict the potential risks?

Research Aims:

To examine problems and restrictions that the overseas investors face in doing

business in Saudi Arabia.

To examine the impact of political issues related to radical organizations’ threats,

Relationship with Iran and the Arab Spring revolution in the Middle East on Foreign

Direct Investment.

To study the influence of fixed exchange rate of Saudi riyal on Foreign Direct

Investment into the Saudi economy.

Also, the thesis will search for the strategic solutions that help foreign investors to

predict the potential risks of Saudi Market.

Literature Review

4

1.0 General view of Saudi Market

1.1 Barriers and Attractors for Entering Saudi Market:

Davidson (1980), Moore (1998) and Braunerhjelm and Svensson (1996) suggest that the size

of the country’s market captures demand and scale effects. Bajo-Rubio and Sosvilla- Rivero

(1994) and Loree and Guisinger (1995) argue that different types of FDI will be influenced to

different degrees by the host market where market-oriented FDI may be more concerned with

the market size than export-oriented FDI. Two types of variables are often used either

separately or jointly, as measures of market size in empirical models: the GDP variable and

its rate of growth where they are stipulated to have a positive relationship to FDI. The growth

rate has an effect since if the host country market expands more rapidly than home country

markets, the host country market becomes more attractive and home country’s firms become

more willing to enter the host (Abdel-Rahman, 2010).

Busse and Hefeker (2007) examine investment flows to eighty three developing countries

over a number of years. In the cross-sectional section of their analysis, they discover the

survival of democracies, religion, and government stability to be significant. Pooling states

over time, they find internal conflict, external conflict, law and order, and bureaucratic value

to be important too (Clare and Gang, 2010).

According to Aleqt.com (2006) there is confirmation on the existence of several problems

and challenges in the field of investment. However, in 2005 have started beginnings of

distinct and important developments in the field of improving investment surroundings in the

Kingdom, such as:

1. The state approved specific arrangements for developing the law lords, establishing

new commercial courts and increasing the number of judges to speed up the the

judgment of cases. That was the most important issue highlighted by the General

Investment Authority in its report to the council of ministry in requirements

of improving the investment situation in the Kingdom.

2. The Minister of Foreign Affairs issued a strong orientation to embassies to issue

visas to investors within 24 hours. Furthermore, the council of

5

ministry approves on the issuance of visas from the airports to investors from certain

countries.

3. the Ministry of Finance has reduced the profits tax from 45 per cent to 20 per

cent, while allowing the deportation of the losses to unspecified number of years, for

the companies that facing some problems at the beginning of the application.

4. the state has been raising the capital loan funds, including the fund of Industrial

development and expand its lending to different areas. Incidentally, the Industrial

development fund has provided loans more than the funds that provided

by capital loan funds in other Arab countries.

5. The Ministry of Justice held seminars and training courses for notaries and judges on

investment regulations. As well, the Ministry of Interior provided seminar to

immigration staff at airports, in order to develop the provided services to investors

and the methods of dealing with them.

6. The Ministry of Commerce and Industry have declared the period of completing the

trade documentation and industrial licensing is minimized. In addition, the Ministry of

Transport has reduced the period of procedures completion in the ports.

However, According to Hafiz (2009) Classified the constraints of attracting direct

investment to the Kingdom of Saudi Arabia, to: (1) constraints related

to organizational and procedural sides. (2) barriers of legislation and regulations. (3) the

limitation of information availability systems. (4) impediments of costs of

private investment. (5) specific restrictions of economic policies.

For the constraints of organizational and procedural sides, it has been categorized to: (1) the

complexities of obtaining entrance visas to work and invest. (2) the time taken of issuance

business licenses and approvals. (3) ignore the visuals of private sector in the process of

government decision-making that related to foreigner investment. (4) the slowness of customs

clearance procedures. (5) the flexibility lack of sponsorship system.

6

For the barriers of legislation and regulations, it has been divided to: (1) the slow

implementing of the sentences. (2) the absence of effective judicial systems that able to

resolve disputes. (3) the lack of regulations to protect new investments and products from

imported fake products. (4) the slow procedure of litigation. (5) the lack of regulations to

protect property rights.

For the limitation of information availability systems, it has been classified to: (1) the limited

information of market size. (2) the weakness information of investment opportunities.

For the impediments of costs of private investment, it has been sorted to: (1) lack of qualified

administrators in the labor market. (2) the high cost of getting energy, electricity and fuel. (3)

high cost of manpower training. (4) the high cost of labours in Saudi Arabia.

For the specific restrictions of economic policies, it has been listed to: (1) the high rate

of inflation. (2) the existence of inappropriate infrastructure.

Moreover, Alamri (2011) agrees that it has been discovered that the huge foreign direct

investment that entered Saudi market from 2006 to the mid of 2010 reached to 462 billion

riyals. Although, the incomes that has been achieved by the national economist form the FDI

extremely low. Moreover, the balance of payment from Saudi Monetary Agency has

confirmed that, even though with increasing of FDI flows, doesn’t accompany that any

significant growing in the national employment of manpower as much as the dramatic rates

rising of recruitment of foreign labour. Subsequence, the gradually increasing of transferring

money out of the border by foreigner labour, which approximate from 57.3 billion riyals in

2006 to more than 96.3 billion and estimated to be about 117 billion riyals in 2010. To this

point, Aggravate economic leakage has increased from 9.5 percent in 2006 to more than 14.1

percent by the end of 2010.

1.2 Methods of Entering Saudi Market:

7

Entry strategy plays a significant function when MNCs enter foreign markets with the aim of

exploiting resources or capabilities. MNCs now expand to all over foreign markets with

different reasons by a multitude of forms. MNCs' achievement of strategy is often influenced

by their external environment. It may be concluded, then, that company wants to develop

more flexible systems of resource portion so that they are able to react quickly to adjust in

their environment; this is especially accurate for firms operating in emerging markets.

Certainly, those characteristics particular to the institutional environment in emerging

economies significantly influence the operations of foreign MNCs (Chiao, Lo and Yu, 2010).

Strategic alliances and mergers and acquisitions (M&As) became well-known organizational

implements through which firms could raise their market influenced, enter into new markets

or improve their capabilities. In the same time, R&D estimates rose three times as fast as

spending on fixed assets. This is why firms can no longer, on their own, meet all the

expenditure or increase all the dissimilar capabilities required for a totally independent

strategy (Grosu, n.d.).

Mergers and Acquisitions of two or more firms have been used as leading business strategies

to search for fast growth and diversification. A merger develops the competitive position of

the amalgamated firm as it can command improved market share. The amalgamated firms can

also try to find drop in the risk level through diversification of the business operations

(Shukla, 2010).

Strategic alliances are partnerships of two or more corporations or business parts that work

jointly to reach strategically major objectives that are equally beneficial. The prospective of

strategic alliances strategy is massive. If applied suitably, some authors claim it can

dramatically develop a corporation's operations and competitiveness (Brucellaria, 1997, p.

1998).

Traditionally, FDI in the KSA mostly assumed one of three forms: Joint ventures, Greenfield

investments, and investments related to the Offset Programs. Joint ventures were the

predominant form prior to the New Investment Law and involved ventures jointly with KSA

government institutions or KSA firms. Greenfield investments in KSA production, and

distribution facilities were relatively new being spurred by the New Investment Law. Mergers

and Acquisitions (M&A) by foreign companies are almost unknown. Joint ventures – the

present predominant form - could theoretically be either Equity Joint Ventures (EJV) or

Contractual Joint Ventures (CJV). Of these two forms EJVs seem to be the predominant form

8

in KSA’s FDI where the foreign side generally contributed equipment, industrial property

rights including technology, and funds while the Saudi counterpart contributed land, plant,

equipment and the local component of currency and funds. In addition to these forms, the

KSA also instituted an Offset program with foreign partners, which was tied to its defence

purchases (Abdel-Rahman, 2010).

2.0 Political Factors

2.1 Terrorism Feature

2.1.1 Terrorism Definition

According to Barkat (2005) defines terrorism is the intimidation and to be unable to find the

security in order to achieve certain benefits). The terrorism has been defined internationally

as the attack for creaming, but the differences in the legal nature of this work between

political crime and terrorist crime depend on the political nature of target of this terrorism

action. Conversely, political sociology identifies terrorism as the each act or behaviour of a

human tendency to use as much of the coercive force, including coercion, physical abuse,

unlawful use of force and torture techniques of traditional and modern violation against of the

basic human rights that approved by the religions laws and international conventions in

dealing with the administration of human relations. This including differences in the cultural,

social, economic and political order to achieve the goals in those areas between subjugation,

pressure, editing, and marginalization, also may affects others were not being targeted. This

behaviour is forced human non-peaceful occurs between individuals, groups and authorities

to each other within the a particular community or among certain communities and certain.

According to Maximilian Robespierre about the terrorism in the economic perspective,

cannot be applied only when it leads to the creation of chaos and ignore public freedoms,

which means that the terrorism is phenomenon and amalgamated product of factors that

related to the internal environment or the intervention of external environment factors or

both. So economic factors take part in an important role of guiding the conduct of terrorism

when the people and human societies. The necessitated for economic cannot be alternated by

any possible substitute, also the increasing of economic problems inevitably direct to the

destruction of civilization and the foundations of the social structure. In addition to, affect the

9

general members of society, because the economic structure causes growth in particular

social relations. Such as, the unity societies and cohesion are related to saturated economic is,

nevertheless the opposite was born aggressive behavior and violence societies (Barkat, 2005)

2.1.2 The impact of global terrorism on Saudi economy

It is common to most of countries in the general implications of any international variable

and, accordingly, distinguishes each community a number of economic characteristics, social

and cultural rights. The vulnerability of any country in international changes is vary

according to their agreement or disagreement with others in these properties. Therefore, the

effects of terrorism can be negative in all levels of long-term economical strategies. While

that, in the short term there may be negative and positive impacts, domestically or regionally.

However, these impacts not dependable for the economic policies. In addition, the

investments and capital regularly move to safe places in the world. As well, the effect of

global terrorism can be significant on the all general levels.

Almeshal and Albahoth (2004) have classified number of negative and positive effects on the

Saudi economy

The negative effects on the Saudi economy by the events of September can be observed as

direct and indirect effects, including:

1. Increase the speculation of real estate:

Because the absorptive capacity of the Saudi economy doesn’t able to hold all that

money belonging to either Saudi Arabia or the Arabian Gulf citizens. This has led to

common real estate speculation in Saudi market significantly. as well, the

phenomenon of the real estate contributions backs again to Saudi market that

dominated in the past days of economic high growth in the nineties Hijri.

Consequently, this phenomenon becomes the most pronounced at the local level for

investing money, assembled with several direct negative economic effects and

indirect. Perhaps, the most effective of withholding money for real investment

opportunities, and real participation in the development to increase Settlement of

employment for Saudi youth.

10

2. Low rate of economic growth:

The high peg between Saudi economy and U.S. economy, especially as the United

States of America is the largest trading partner with Saudi Arabia beside European

Union and Japan (accounting for the U.S. market by about 20% of exports, Saudi

Arabia). This has led to the vulnerability of the Saudi economy to what is happening

to the U.S. economy. Thus, the economic recession that has pressed the U.S. economy

was a major impact on the Saudi economy. as a result that has led to slow growth of

rates. Moreover, the U.S. currency (dollar) is the currency of international pricing of

oil, which represents 89% of Saudi exports. Along with, if include to that the Saudi

economy is characterized by general low rate of GDP growth compared to population

growth rate, which did not exceed the growth rate of GDP 00.1% during the sixth plan

(1995-1999). While that, the average growth rate of the Saudi population through the

same period about 3.5%.

3. Decline in the actual value of external financial assets:

Decline in the value of financial assets that owned by Saudis in abroad because of a

number of reasons, including:

- Losses in the U.S. stock market with collapse of many technology companies.

- Significant decreases in real estate market.

- freezing of a amount of deposited bank in U.S. banks.

The amount of funds that owned by Saudis and deposited in U.S. banks between (100-

400) billion dollars. The Arab Institution for Investment Guarantee losses has

estimated the total Arab investments abroad during 2000 and 2001, about (400)

billion dollars.

4. Interference in the internal affairs of the Saudi economy:

This intervention is usually required by international institutes to recognize all the

documents and data that related to bank accounts of individuals and institutions within

the Saudi banks. Allegedly, prevent the sources of financing terrorism and terrorist

organizations.

5. Negative impact on the charitable sector:

This has included the impact on the charitable sector in the Kingdom, with various

aspects of humanitarian, advocacy and investment. The restrictions on charitable work

11

and programs, also, the launching of suspicions and accusations towards it. These

have led to the decline in this sector and diminish its roles locally and globally.

Furthermore, it has led to fright and reluctance many businesses to donate and

contribute to charity, to protect their money and accounts from freezing and liability.

It can be summarized the most important positive economic effects of international

terrorist events, especially the events of September on Saudi economy in the following

points:

1. Return many of Capitals:

After the events of international terrorist in 11th

of September has oriented more

towards the of Saudi capital to resettlement, either through the return of some of them,

or through stop the others from leaving the channels of local economy. In addition to,

the events of September has dominates the principle of security rather than

profitability, the both principles are controlling and moving capitals. This has forced

investors and business to search for safe money markets, although isn’t necessarily to

be more profitable. This is normal characteristic for capital movements in the crisis

situation.

2. Recovery of financial markets:

to international events have contributed in alleviating the precipitate of a number of

Saudi investors to U.S. stock market in particular, which has easily access to it

through the global information network (Internet). As well as stimulated a lot of them

to distribute their investments through other parts of the world locally and regionally.

This positive attitude of distribution investment has been reflected on the Saudi stock

market, which recorded considerable increasing in the index. The highest point in its

history was (2, 9272 points) in 20/05/2002, and it has continued thereafter to reached

at the end of 2003 (58, 4437 points). As a result of the large return of capital inflows

to local market and high levels of liquidity. One study estimates that the Arabs

investors are investing in their stock markets more than one hundred and fifty billion

dollars of market share, the proportion of Saudi capital about 50%. However, it can’t

be accepted that, the rise of the Saudi stock market to high recorded levels is caused

by the return of capital from outside to Saudi market. Because the great proportion of

12

returned money engaged to real estate investment, which is considered for many

investors as safe place for investments.

3. Resettlement of Tourism:

the major positive effect of international contemporary events is the resettlement of

tourism. It has been emerged that Saudi tourists more preference to domestic tourism,

even for whose able to afford abroad tourism, which is the most support factor for the

tourism sector. In Saudi Arabia, has been noted during the past years, the spread of

festivals tourism, through the regions of the kingdom. This is indicated to positive

changes of the experience of Saudi tourists.

The research centre and tourist information of the Supreme Commission for Tourism

(MAS) has estimated the total expenditure of tourists (local and foreigner) about 5.63

billion riyals. Furthermore, the total contribution of the tourism sector in the

gross GDP amounted to 6.4% in 2002, where the added value of tourism (2.32 billion)

to the real GDP, which stood at (698) billion riyals for that year.

4. Accelerate the development of many systems:

the events of 11 September has contributed to speed the adoption of several

regulations and domestic economic reforms; including the issuance of the financial

market and the insurance system. Moreover, the lunching of telecommunications

company in the Saudi stock market, and privatized number of government facilities.

This has a direct relationship to open investment channels and new markets among

the economic reforms that planned previously. Although the rapidity of the events of

September has accelerated theses applications.

5. The hasty reaction of western governments against the wave of terrorism has

contributed to create more complex international situation than the past. It has been

increased the tensions in the Middle East as a result of the U.S. wars in Iraq and

Afghanistan, which led to suspend Iraq's oil production. As well as, the decreasing of

oil production from Venezuela and Nigeria about 40 per cent and 30 per cent

respectively, attributable to the striking of oil workers. It has also formed a low level

of U.S. crude oil inventories, which made additional pressure on oil prices. These

factors were caused by the rushed reactions of western governments to the events of

September 11have contributed for rising oil prices. The prices have been increased

13

about 5.5 per cent in 2002 from what it was in 2001. Along with, the increased of

tension in the world has pushed the prices of oil to reached as in 05/19/2008 to $126,

compared to 22 dollars per barrel in 2001(Aleqt.com, 2008).

As a result of these developments of high oil prices, have led to increase the revenues

that in turn raised the Saudi economy. The trade balance in the general budget and the

balance of payments is recorded a large surplus for first time after registering a deficit

for two decades. The total surplus has recorded an increasing in 2005 about 217billion

riyals, which is equivalent 18 per cent of GDP. The Foundation of Monetary expected

the total surplus rises to 405 billion riyals in 2008. Besides, these positive

developments have contributed to concentrate on the biggest problem of the Saudi

economy, namely the problem of public debt. Which reached in 1999 to 119 per cent

of GDP and surpassing the international standards accepted (60 per cent of gross

domestic product). It has been directed the proportion of the surplus funds to reduce

the size of the public debt, which assist to drop to 267 billion riyals in 2007 by 27 per

cent comparing with 2006. Presently, the amount of the public debt ratio to GDP is

about 19 per cent comparing with 119 per cent in 1999 (Aleqt.com, 2008).

2.1.3 Terrorism and Foreigner Direct Investment:

If terrorism is a local phenomenon, capital will tend to flow to destinations without a terrorist

threat, reducing net foreign investment in the economies affected by terrorism. Even if

terrorism is a global threat, international investment will respond to differences in the

expected intensity of terrorism across countries (Abadie and Gardeazabal, 2007).

Surveys of international corporate investors provide direct evidence of the importance of

terrorism on foreign investment. Corporate investors rate terrorism as one of the most

important factors influencing their foreign direct investment decisions (Global Business

Policy Council, 2004).

Yamani (2010) agrees that the terrorism has negative effects of on various aspects of people's

lives. Perhaps the most important aspect is economic, the negative effects of terrorism on

economic and FDI are divided to several areas:

14

First: damaging the proportional ability of the local economy for attracting foreigner

investments, because the terrorism provides a repellent environment for investments

regardless to the nature of the infrastructure and legislation. In addition, despite of the

approving of economic and social conditions cannot only attract investments. Because the

terrorism voids the programs, plans, economic policies and development from its contents.

Second: as result from the foregoing, the society will be deprived from the benefit of foreign

expertise and competencies in various disciplines. That is not limited to particular area, so the

universities, scientific research centres, hospitals and others will be affected, as well as

companies and the different productive sectors.

Third: the decline in the flow of investment by terrorism will lead to reduce employment

opportunities and the low level of training and rehabilitation for the local employees.

Fourth: The depletion of community capabilities and weighted towards for fighting against

terrorism, rather than spent to support the development routes. This means that instead of

building roads, expenditure on the establishment of schools, hospitals, and vital projects, the

spending will be toward to combat terrorism programs, so the cancellation of many of

development programs .

Fifth: some sectors are affected directly by the terrorist operations, such as the tourism sector,

which is usually an important vital sector of society because it offers huge opportunities of

jobs and incomes.

The process of measuring the impact of terrorist acts on the functioning of the economy and

take into account the direct and indirect effects. As well as, take into the consideration the

public or private sector and the production or consumption.

In addition consider the measurement standards in several pictures, including: the number of

jobs lost as a result of terrorism, the amount of new job opportunities decreasing, the size of

15

the risen in the cost of production which can be attributed to terrorist operations, the amount

of the in sales volumes declining, the production and profit levels, the size of capital outflows

from the country, and other criteria.

Aldukheil (2004) agrees that, as result of involving Saudi citizens in the events of eleven of

September. It is clearly to observe that from the social situation and the current political. The

view of foreigner to Saudis is not satisfactory, whether in the eyes of the leaders or the

general public. The existence of discrimination feeling among some foreigners because

they get less respectful treatment and rights recognition comparing to other countries is an

important problem, which diminish the effectiveness of the government's efforts to achieve

a high position of motivating foreign investment.

In addition to, the recent explosions in Riyadh, that targeted a specific segment of

foreigners in particular. This has led to exacerbate the problem, thus, some of the foreigners

in the kingdom, especially Americans and Westerners feel that the threats are surrounded

them and they aren’t protected. On the other hand, it can be observed that find that the

access to basic services such as health facilities and higher education is limited for foreigners.

Consequently, this situation may direct to obstruct the movement of foreign investment in the

predictable future at the Kingdom, so it is expected to remain below the level of

potential available.

In contrast, Abu Fatim (2003) argues that, Saudi market is one of the largest markets in the

Middle East and the Arab market due to the reserve of consumer power more than 700 billion

riyals a year, which supports the growth of commercial transactions in the Kingdom. Along

with this boosting, the growth in demand for real estate investment, which is estimated the

size market for it more than 60 billion Riyals per annum. Furthermore the growth in

this sector investment was due to the orientation of citizens and the benefit of economic

growth in the Kingdom this year. It is reflecting a clear indication of the non-affected on

small and large investors from terrorist attacks and the political ramifications of the region.

The national economy was performing well this year because of the Kingdom’s economic

and financial policies. Plus the availability of financial liquidity in the market has contributed

significantly to the support many economic sectors. This is reflected positively on the

national economy and achieved excellent results. The challenges that faced by the Saudi

during this year, especially the terrorist attacks doesn’t prevent its inception and growth with

good quality. Which is expected to reach the growth size in Saudi economy at the private

16

sector about 4%. The investors in the past years were transferring their savings to the

foreigner markets due to high returns. Nevertheless through these few years, it has been an

evolution in the local market, which attracts Saudi money to stay in market as a result of the

low interest rates on the dollar and euro, as the dollar interest rate drop to 1.25 per cent. The

very low rate doesn’t attract investors. As well as the radical security process that initiated by

European and American countries fright the investors from Saudi Arabia. As result, provided

a huge liquidity in the domestic market and the Kingdom is a good land for investment

environment and opportunities with high returns which contributed to the consolidation of the

investment sector in Saudi market.

2.2 Relationship with Iran

According to Abed (2010) regardless of the fact that Iran is neighbouring gulf countries,

combines them with demographics as a result of sharing coasts with Arabian Gulf states,

cultural cooperation, trade exchanges and similarity of civilization. as well as, the repeated

requests of the GCC countries from Iran to respect neighbours within international

conventions for assisting in the region's security and stability, also the request for changing

the language in the channel of communication. However the radical situation of Iran and its

excesses in the occupation of UAE islands, also the using of the force logic, with arrogance

and hostility view of Iran to the Gulf Cooperation Council (GCC countries) and not trying to

find interfaces balanced of relationships with the GCC countries. This hard-line stance of Iran

from some Gulf States can be as result of the failure of Iran entry into the regional military

alliances, and the decisions of some of gulf states to sign alliances and bilateral defence

agreements with western countries.

in addition the role of Iran is important for the Strait of Hormuz, because of the central

position and view on strait, also, the occupation of three UAE islands. Thus, Iran has over

control of the shipping lanes in the Arabian Gulf because 76% of the full oil production from

four countries in the Gulf and Saudi Arabia is exported through Strait of Hormuz.

Finally, the trepidation is shown by the international community of Iran, which is questioned

about the peaceful intentions of Iran's nuclear program. Added to, Iran's potential to product

plutonium able to use in the production of nuclear weapon.

17

2.2.1 The influence of Iran relations on FDI in Saudi Arabia and Gulf Countries

the economic experts have confirmed that the international high tension between Iran and the

Western countries will not affect the ability of the oil-rich countries (GCC) to attract foreign

investment. As a result of the stability of their economies and the high liquidity that they

have.

Holdar (2007) “deputy director of Moody's Investors Services” confirm that, the Gulf region

is in high-quality situation and is unlikely to change this condition. If it is believed that there

is any risk because of the war in Iran, the projects will be retreated. Many of the foreign

capital aim to enter Gulf region for investing and financing, especially from international

banks, because of the economic and high commercial growth in these countries.

Moreover, Dr. Abu-Dahesh (2007) “expert and economics writer” proves that the gulf states

are aspirated by many of the foreign capital, many of international and western banks plan

and keen to enter this market in order to finance the growth economic and participate in

infrastructure. this will be spent by the Gulf states billions of dollars in the coming years. In

contrast, the case of nuclear programs, the development of nuclear weapons didn’t affect the

attraction of investments in South Korea and other countries. Thus, The Iran’s nuclear

programs will not affect Gulf states in attracting western investment, also GCC is now in

great economic growth.

furthermore, Dr Al Barrak (2007) Assistant Professor of Finance, confirms that the current

political tension between Iran and Western nations would not be as expulsion factor for the

Western investment in the Gulf region. In particular in Saudi Arabia, because it has great

political stability besides economic growth. Many of capitals are seeking to have the

opportunity to invest in the Gulf States and will not hesitate to enter. Although, some foreign

companies want to invest in the Gulf could plan to wait for six months to observe the case in

the future. It can be observed that, the political and economic situation in the Gulf States are

stable, vibrant and impartial. This is evident through the admission of the Kingdom, which is

a big state in the Gulf as a neutral and participate as mediator character to relate the views.

The reason of the tension in the Gulf region is the standoff with the Western countries over

Tehran's nuclear program and its refusal to suspend uranium enrichment activities. along

18

with, Washington accuses Iran of seeking to this program of nuclear armament. Regarding to

the view of economists, the huge oil revenues and annoy of spending on infrastructure for

supporting economic diversification in the Gulf States. These prevent the possible

implications of the geopolitical instability at the regional level (Aleqt.com, 2007).

2.2.2 Proposition: If Saudi Develops Nuclear Weapon

Many analysts hypothesize that Saudi Arabia will develop nuclear weapons if Iran succeeds

in acquiring such weapons because the two countries have a history of hostility, intensified

with the establishment of the Islamic Revolution in Iran in 1979, and since then, watching

Saudi Arabia rising Iranian influence with concern, and next to this historic animosity, the

two countries considered adversaries regional, where it is seen to Saudi Arabia as the capital

of Sunni Islam, while is the Shiite regime in Iran in the heart of the "Shiite Crescent", and

shows Saudi officials expressed concern that the growing political influence of the Shiites in

the surrounding areas of kingdom will turn into an existential threat aimed at the regime's

survival Governor also are concerned also that Iran is gaining more influence in places such

as Afghanistan, Lebanon and Iraq, and they then may threaten the security of Saudi Arabia,

as well as the possibility that Tehran strengthening its ties with the Shiites in the eastern

region of Saudi Arabia, that they could lead to challenge the authority of the Saudi

regime means Saudi officials mainly the impact that might have an Iran with a nuclear

program to the security of their country, developments taking place in Iran's nuclear program

is seen in Saudi Arabia as the physical evidence of the growing danger the Shiite in the

region, despite the lack of clarity nuclear intentions of Iran, the Saudis are afraid that in the

case of Iran's possession of nuclear weapons, this may represent a subversion of the security

of the Saudi national, however there is no evidence that Saudi leaders have decided the fact

that possession of nuclear deterrence as a reaction to Iran's nuclear activities, but if Iran

succeeds in acquiring nuclear weapons, the Saudi position may change (Amlin, 2008) .

In a similar vein, other analysts purport that Saudi Arabia is unlikely to develop nuclear

weapon due to the international condemnation that the Saudi Kingdom would face after

developing nuclear weapons. According to Etel Solingen (2007), states run by leaders that are

“internationalizing,” or seek greater access to international markets and increased foreign

investment in order to strengthen their own regime, are more likely to forgo the development

19

of nuclear weapons. Internationalizing leaders worry that proliferating would hurt their state’s

political and economic relations with other countries.

Applying this logic to Saudi Arabia, a recent population boom has weakened the Saudi

economy, raising unemployment rates and lowering per capita incomes in the Kingdom,

despite high oil prices on the international market. Partially to confront these issues, the Saudi

government has tried to vastly increase the levels of foreign direct investment coming into its

country. Increased foreign direct investment acts as a disincentive to Saudi Arabia building a

nuclear arsenal, as potential investors would likely not support such a decision. Furthermore,

as part of an effort to reform its economy and integrate into international markets, Saudi

Arabia joined the World Trade Organization in 2005. Bahgat argues that joining more

international organizations and making further reforms to its economy will “reduce incentives

for aggressive foreign and security policies and improve the chances for adherence to the

non-proliferation regime.” Saudi Arabia has been a member of the Nuclear Non-Proliferation

Treaty (NPT) since 1988, and signed a comprehensive safeguards agreement with the

International Atomic Energy Agency (IAEA) in 2005. The recent conclusion of a safeguards

agreement may demonstrate that Saudi officials are becoming more cognizant of international

non-proliferation norms. Lippman echoes the idea that Saudi leaders are internalizing

international norms, and that “the Saudis’ weapons of choice are cash and diplomacy.”

(Amlin, 2008)

Lippman (2008) thus concludes that Saudi Arabia is unlikely to proliferate – either through

domestic development of weapons or through buying nuclear bombs from countries such as

Pakistan – since the Kingdom would face substantial political and economic backlash after

developing the weapons.

20

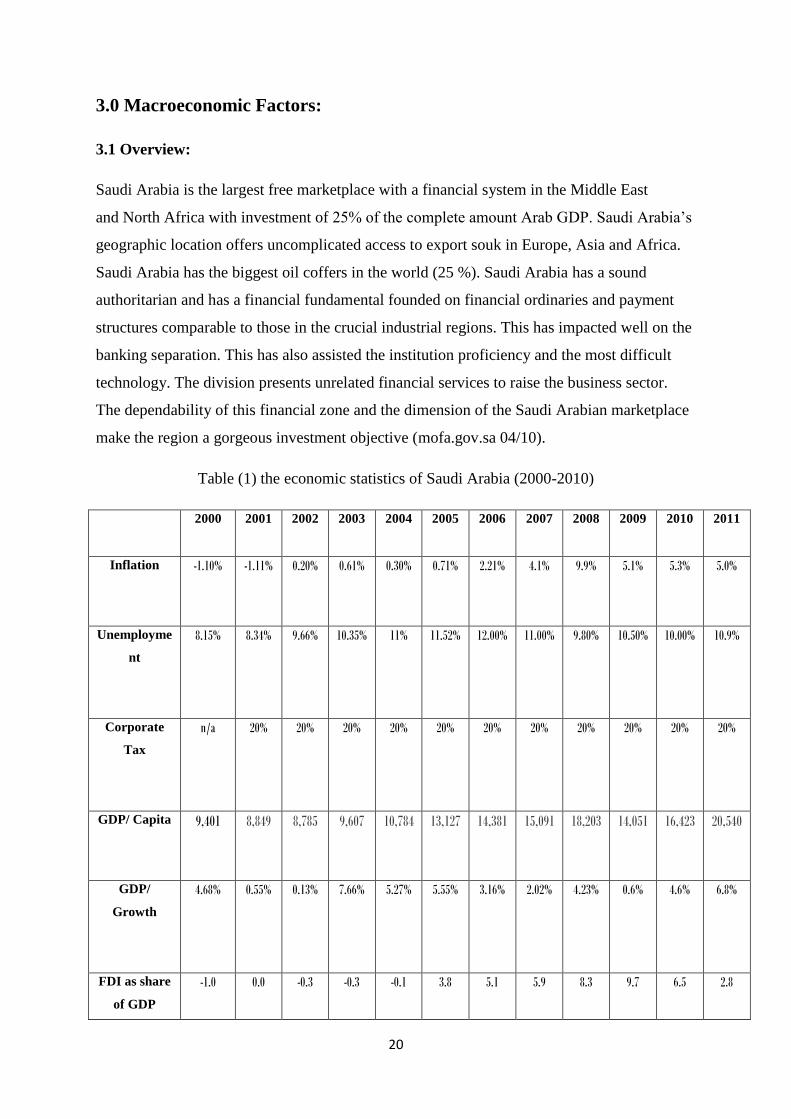

3.0 Macroeconomic Factors:

3.1 Overview:

Saudi Arabia is the largest free marketplace with a financial system in the Middle East

and North Africa with investment of 25% of the complete amount Arab GDP. Saudi Arabia’s

geographic location offers uncomplicated access to export souk in Europe, Asia and Africa.

Saudi Arabia has the biggest oil coffers in the world (25 %). Saudi Arabia has a sound

authoritarian and has a financial fundamental founded on financial ordinaries and payment

structures comparable to those in the crucial industrial regions. This has impacted well on the

banking separation. This has also assisted the institution proficiency and the most difficult

technology. The division presents unrelated financial services to raise the business sector.

The dependability of this financial zone and the dimension of the Saudi Arabian marketplace

make the region a gorgeous investment objective (mofa.gov.sa 04/10).

Table (1) the economic statistics of Saudi Arabia (2000-2010)

2000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Inflation

-1.10% -1.11% 0.20% 0.61% 0.30% 0.71% 2.21% 4.1% 9.9% 5.1% 5.3% 5.0%

Unemployme

nt

8.15% 8.34% 9.66% 10.35% 11% 11.52% 12.00% 11.00% 9.80% 10.50% 10.00% 10.9%

Corporate

Tax

n/a 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%

GDP/ Capita

9,401 8,849 8,785 9,607 10,784 13,127 14,381 15,091 18,203 14,051 16,423 20,540

GDP/

Growth

4.68% 0.55% 0.13% 7.66% 5.27% 5.55% 3.16% 2.02% 4.23% 0.6% 4.6% 6.8%

FDI as share

of GDP

-1.0 0.0 -0.3 -0.3 -0.1 3.8 5.1 5.9 8.3 9.7 6.5 2.8

21

Source: Saudi Arabian Monetary Agency, Trading Economics, Index Mundi and Department

of Zakat and Income Tax

3.2 Fixed Currency

International capital flows have been found to depend on the degree of financial development

in a country (Albuquerque, Loayza and Serven, 2005).

In a general sense, stock markets facilitate the flow of a significant share of foreign direct

investment. Furthermore, newly established foreign firms, both those acquired through the

stock market and those established as foreign direct investments, require financial services.

Thus, as they make investment decisions foreign investors should account for the degree of

development of a country's financial sector, and particularly the development of the banking

sector, as both of these factors will affect the returns of their investments (Abadie and

Gardeazabal, 2007).

Exchange rate fluctuations affect international capital flows and stocks of foreign investment.

Risk averse firms may decide not to invest in a country if exchange rate volatility is high

(Campa, 1993).

With regard to the economy of Saudi Arabia, it has been the impacted by terrorism on

number of economic sectors. Relating to exchange rates, it has been decreased the exchange

rate of Saudi riyal next to the currencies of major trading partners. Along with the reason for

this the peg to U.S. dollar, which has been suffered to steady decline against major currencies

since the U.S. occupation of Iraq and Afghanistan with an estimated decline of the dollar by

more than 35 per cent. This negative development of the dollar has led to low exchange rate

of the Saudi Riyal. Consequence, it leads to a rise the imports cost for the Kingdom. Saudi

economy has suffered from increasing import prices of food commodities, which constitute

about 26 per cent of the index price. It had recorded until 17th

March 2008, increasing in food

commodities were denominated by dollars of 62 per cent compared to last year. Which is

reflected negatively on the balance of payments, as well to a decrease in the value of money

earned from exports. That means the double of negative impact of exchange rate depreciation

of the dollar. According to study prepared by the Bank (SAMBA), the Kingdom has lost

22

during the period between 2003 and 2004, more than four billion riyals as a result of

exchange rate depreciation of the dollar. Based on the adopted standard of SAMBA’s report,

is expected to reach the sustained losses of the Saudi economy nearly 30 billion riyals,

because of the low dollar exchange rate, since 2003 until now.

Saudi Government has expressed its concern about low dollar exchange rate in the words of

Minister of Petroleum and Mineral Resources, where he said: "The level of the dollar is

concerned and the decline is impacts the purchasing power of oil producers of OPEC."

The depreciation of the dollar has contributed to decline the actual value of financial assets of

Saudi Arabia at home and abroad. SAMA (Saudi Arabian Monetary Agency) has estimated

the decline of assets in out of the country about $301 billion in 2007 and the assets invested

in the home under the supervision of the Public Investment Fund was estimated around $214

billion (Aleqt.com, 2008).

As a result of peg the Saudi currency to U.S. dollars, the decline in the dollar exchange rate

has a significant impact on the Saudi economy in many ways; including: the cost of Saudi

products will be more competitive in international markets and the foreign imports will be

higher prices in the domestic market. Theoretically, this will motivate for increasing exports

and decreasing imports, thus will improve the balance of trade with other countries except the

United States. However, this theoretical proposal is confronted with number of facts and

practical challenges, the most important fact is the flexibility of demand. Explicitly, the

demand for exports and imports must be responsive to the changes of prices. In addition, the

dynamic of time of taking the movements of exchange rates that affect the trade balance.

Even more, the balance of trade could depreciate due to the decline of the exchange rate

because exports become more expensive. The improvement of the trade balance is associated

with the increasing amount of exports and the reduction in the imports amount (Almeshal and

Albahoth, 2004).

During this situation of the low exchange rate of U.S. dollar, the Kingdom of Saudi Arabia

will pay more money for importing, while the earned money from its exports is low. So, the

impact of the dollar depreciation will be a double on Saudi economy. One study estimates the

losses economic of the Kingdom during 2003 because of the devaluation of U.S. dollar

23

around 10.4 billion riyals.

It is a significant fact that, the trade growth and trade balance are determined by changes in

the level of competitive prices, the rates of economic growth for trading partners and the

growth income in particular countries. The changes that take place in exchange rates are

leading to change the level of competition between prices and income growth (Almeshal and

Albahoth, 2004).

3.3 The effect of fixed currency on FDI

Russ (2007) estimates the direction of the effect of exchange rate volatility on flows of FDI

rests on two premises. First, it assumes that there is a repeated sunk cost involved in

production at home and overseas some fixed overhead cost such as legal retainers, rental and

maintenance contracts, or a property tax that is paid, negotiated, or legislated in advance. In

this respect, the model draws on the option value literature sparked by Pindyck (1998), Dixit

and Pindyck (1994), and Campa (1993), as well as on trade models incorporating

multinational firms with plant-level fixed costs (Horstmann and Markusen, 1992 and

Brainard, 1997) and sunk costs, which are defined here as fixedcosts that must be paid before

the realization of a random shock (Grossman and Razin, 1985 and Helpman et al., 2004).

Because the sunk cost is paid or negotiated in one period under a given exchange rate, but

revenues are earned and repatriated at a later date, firms care about fluctuations in the value

of the host-country currency.

Second, it is assumed that there are common macroeconomic forces that influence both the

exchange rate and the volume of sales by overseas branches. These forces could involve

productivity growth or any number of unobservable variables governing the international

asset market. However, the fluctuations in the growth rate of the money supply as the

mechanism influencing both realizations of the exchange rate and, due to sticky prices, the

demand for consumption goods in the host country. The exchange rate is a function of the

ratio of the home (host-country) and foreign (native-country) money supply. It ovaries

negatively with the host country's demand for goods, as a positive shock to the home money

supply weakens the value of the home currency but simultaneously increases real income—

and therefore sales by both domestically owned firms and multinationals operating in the

home market.

Alheji (2007) addresses the negative and positive impact of raising the exchange rate of Saudi

Riyals:

24

Advantage of raising the riyal's exchange rate: increase the value of the assets and

returns of foreign companies in the Kingdom, especial the companies that lunched its

investments to Saudi with U.S. dollar. As well, it has applies for Saudi investors who

have turned their investments into the Kingdom in the past three years.

Disadvantages of raising the riyal's exchange rate: a significant decline in new foreign

investments, as the revaluation of Saudi riyal will raise the costs

of direct investment in the Kingdom. This impact will be greater on the foreign

companies that entering the Saudi market for the first time, compared to

companies that entered before and benefited from the rising value of their assets as a

result of Riyal revaluation. Moreover, the revaluation will also contribute

to discourage some investors from Saudi Arabia to transfer their investments from

foreigner market to Saudi market.

25

References

Abed, S (2010) Iran - the perspective of Geostrategic [Online] Available at:

http://www.alriyadh.com/2010/10/14/article567840.html [Access on: 21/02/2011]

Abadie, A and Gardeazabal, J (2007) Terrorism and the World Economy [Online] Available

at: www.hks.harvard.edu/fs/aabadie/twe.pdf [Access on 12/02/2011].

Abdel-Rahman, A (2010) Determinants of Foreign Direct Investment in the Kingdom of

Saudi Arabia [Online] available at

cba.ksu.edu.sa/member/file/research/edoc_1263800116.pdf [Access on 10/02/2011]

Abu Fatim, M (2003) Saudi economy to achieve a fiscal surplus is estimated at 60 billion

riyals, despite the Iraq war and terrorism [Online] Available at:

http://www.alriyadh.com/Contents/11-12-2003/Economy/EcoNews_9030.php [Access on

16/02/2011]

Ahmad, A and Hassan, M (2009) Legal and regulatory issues of Islamic finance in Australia.

International Journal of Islamic and Middle Eastern Finance and Management.

Vol. 2, Iss. 4; pg. 305

Alamri, A (2011) foreign investment... Are we actually its need?! [Online] Available at:

http://www.alriyadh.com/2011/02/09/article602735.html [Access on 07/02/2011]

Aldukheil, A (2004) foreign direct investment in the Kingdom of complicated

procedures take more time, Report of the Advisory Centre for Finance and Investment

[Online] Available at: http://www.arabiyat.com/forums/showthread.php?t=91018 [Access on

03/02/2011]

26

Aleqt.com (2006) Obstacles to investment... The right word [Online] Available at:

http://www.aleqt.com/2006/02/22/article_27979.html [Access on 10/02/2011]

Aleqt.com (2007) Disagreement between Iran and the West will not hinder the flow

of investment to the Gulf [Online] Available at:

http://www.aleqt.com/2007/02/24/article_79543.html [Access on: 19/02/2011]

Aleqt.com (2008) The effects of terrorism in the Saudi economy [Online] Available at

http://www.aleqt.com/2008/05/21/article_142026.html [Access on 20/02/2011]

Alheji, F (2007) The Revaluation of the riyal and oil’s revenues: the

benefits and disadvantages [Online] Available at:

http://www.alaswaq.net/views/2007/06/05/8451.html [Access on: 22/03/2011]

Almeshal, K and Albahoth, A (2004) the economic effects of international terrorism with a

focus on the events of eleven of September [Online], Available at:

www.murajaat.com/researches_files/177.doc [Access on 07/02/2011]

Al-Otaibi, M (n.d.)On the compatibility of Higher Education Output with the Labour Market

Requirements in Saudi Arabia [Online] Available at:

faculty.ksu.edu.sa/5173/Documents/المؤامة.doc [Access on 20/02/2011]

Al-Roubaie, A and Alvi, S (2009) Islamic Banking and Finance; Critical Concepts in

Economic. Routledge Taylor & Francis Group [Online] Available From:

http://media.routledgeweb.com/pdf/9780415485760/9780415485760.pdf Accessed on

08/04/10

27

Al-Zahrani, A (2010) Poor harmonization of higher education outputs Saudi reality, causes,

effects and solutions [Online] Available at:

http://www.aleqt.com/2010/04/30/article_386303.html [Access on: 11/02/2011]

Amlin, K (2008) Will Saudi Arabia Acquire Nuclear Weapons? [Online] Available at:

http://www.nti.org/e_research/e3_40a.html [Access on: 24/02/2011]

Barkat, Y (2005) Terrorism in the economic perspective...Consequences and solutions

[Online] Available at: http://www.annabaa.org/nbahome/nba78/index.htm [Access On

18/02/2011]

Chiao,Y. Lo, F and Yu, C (2010) Choosing between wholly-owned subsidiaries and joint

ventures of MNCs from an emerging market. Emerald Group Publishing Limited, Vol: 27,

No: 3, pp: 338-365

Clare, G and Gang, I (2010) Exchange Rate and Political Risks, Again. Emerging Markets

Finance and Trade, Vol. 46, No. 3, pp. 46–58.

Department of Zakat and Income Tax (2011) Corporate Income tax: Tax Rates [Online]

Available at: http://www.dzit.gov.sa/en/NewIncomeTaxLaw/NewIncomeTaxLaw2_2.shtml

[Access on 15/03/2011]

Ebrahim, M and Safadi, A (1995) Behavioral norms in the Islamic doctrine of economics: A

comment. Journal of Economic Behavior and Organization, Vol: 27, pp: 151-157.

El-Hawary, D. Grais, W and Iqbal, Z (2007) Diversity in the regulation of Islamic Financial

Institutions. The Quarterly Review of Economics and Finance, Vol: 46, pp: 778–800

28

Elmuti, D and Kathawala, Y (2001) An overview of strategic alliances. MCB UP Ltd, Vol:

39, No: 1, pp: 205-218.

Grosu, F( n.d.) STRATEGIC ALLIANCES VS. MERGERS & ACQUISITIONS IN CENTRAL

AND EASTERN EUROPE - ALTERNATIVE SOURCES OF INNOVATION [Online]

Available from: http://www.asecu.gr/files/RomaniaProceedings/28.pdf [ Accessed On

01/06/2010]

Hafiz, T (2009) Impediments to investment in Saudi Arabia [Online] Available at

http://www.alaswaq.net/views/2009/03/26/22218.html [Access on 01/02/2011]

Harab, S (n.d) Islamic banks in the eyes of the West [Online] Available at:

http://www.balagh.com/islam/vs0ua8bk.htm [Access on 01/06/2011]

Index Mundi (2010) Saudi Arabia GDP - per capita [Online] Available on:

http://www.indexmundi.com/saudi_arabia/gdp_per_capita_(ppp).html [access on:

12/03/2011]

Kamla, K (2009) Critical insights into contemporary Islamic accounting. Critical

Perspectives on Accounting, Vol: 20, pp: 921–932

Karbhari, Y. Naser, K and Shahin, Z (2004) Problems and Challenges Facing the Islamic

Banking System in the West: The Case of the UK. Thunderbird International Business

Review, Vol. 46, No: 5, pp: 521-543

Khan, M and Bhatti, M (2008) Islamic banking and finance: on its way to globalization.

Emerald Group Publishing Limited, VOL: 34, No: 10, pp: 708-725

29

Ministry of foreign Affairs (n.d.) Economy and Resources [Online] Available From:

http://www.mofa.gov.sa/Detail.asp?InSectionID=3977&InNewsItemID=34476 Accessed on

01/04/10

Quarterly Inflation Report (2007-2010) Saudi Arabian Monetary Agency [Online] Available

at: http://www.sama.gov.sa/ReportsStatistics/Reports/Pages/InflationList.aspx [access on

13/03/2011]

Russ, K (2007) The endogeneity of the exchange rate as a determinant of FDI: A model of

entry and multinational firms. Journal of International Economics, Vol: 71, Issue: 2, pp: 344-

372.

Shukla, A (2010) Effects of Multinational Mergers and Acquisitions on Shareholders’ Wealth

and Corporate Performance. The IUP Journal of Accounting Research and Audit Practices,

Vol: IX, pp: 44-62.

Smith, A (1994) The Wealth of Nations, Modern Library. Dover Publications, United State.

Trading Economics (2011) Saudi Arabian GDP Growth Rate [Online] Available at:

http://www.tradingeconomics.com/Economics/GDP-Growth.aspx?symbol=SAR [Access on

16/03/2011]

The Forty-Six Annual Report (2010) Saudi Arabian Monetary Agency [Online] Available at:

http://www.sama.gov.sa/ReportsStatistics/Pages/AnnualReport.aspx [access on 13/03/2011]

Yamani, M (2010) Terrorism and the depletion of community resources [Online] Available

at: http://www.alukah.net/Web/rommany/0/22943/ [Access on 15/02/2011].