Embed Size (px)

Citation preview

POWER OF ATTORNEY EQUITY RELEASE

GIVE FAMILY MEMBERS OR SOMEONE ELSE YOU TRUST THE LEGAL POWER TO MAKE DECISIONS ON YOUR BEHALFEach of us hopes to remain healthy and independent for as long as possible. But there may come a time when we are no longer physically or mentally capable of making decisions for ourselves, or we may simply want someone else to handle our financial affairs for us. For this reason, it is worth planning well in advance so someone you know and trust can manage your affairs for you if the need arises.

Under the Mental Capacity Act 2005, an individual must have mental capacity to enter into a contract. This includes applying for Partnership’s Enhanced Lifetime Mortgage. However, if an individual lacks mental capacity, a third party may make this decision on their behalf, provided they have been granted the legal power to do so. This power is known as ‘Power of Attorney’ (PoA). The person granting the power is called the Donor and the person to whom the power to act is given is called the Donee or the Attorney.

If you are considering an Enhanced Lifetime Mortgage, it may be worthwhile to consider setting up a PoA. Without a PoA, even close family members may not have the authority to make decisions on your behalf regarding your financial welfare or your assets such as your property, should you lack the physical or mental capacity to do so yourself. Never assume that a person will be able to act for you simply because they are an immediate family member.

There are different types of PoA in the United Kingdom, each giving different powers to manage the affairs of someone who is physically or mentally incapacitated. Authority may be granted by the Donor while mental capacity exists or be assigned by the Court of Protection in cases where an individual lacks mental capacity.

02

CONTENTS

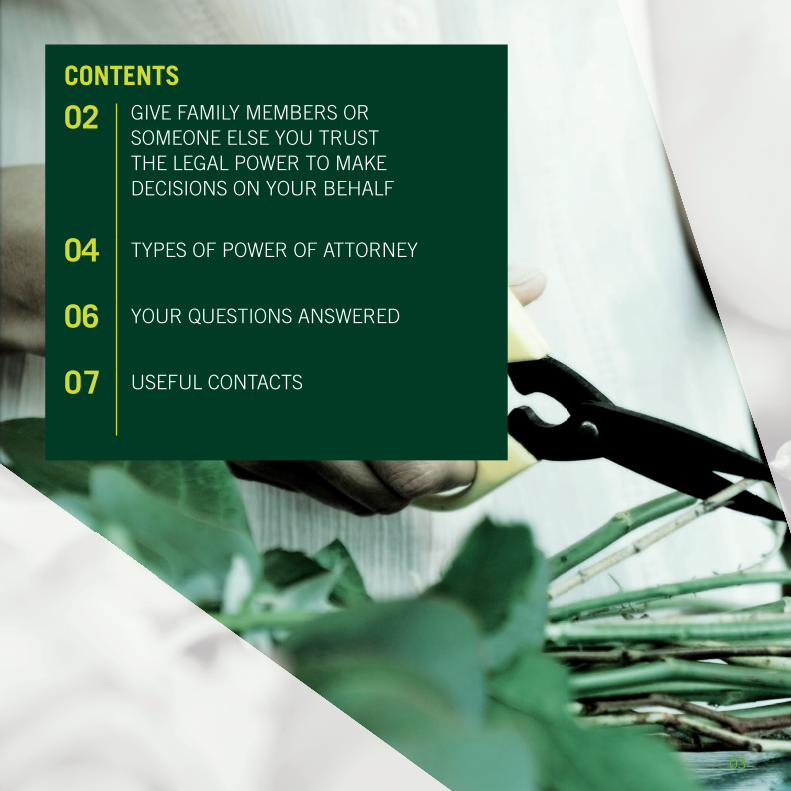

02 GIVE FAMILY MEMBERS OR SOMEONE ELSE YOU TRUST THE LEGAL POWER TO MAKE DECISIONS ON YOUR BEHALF

04 TYPES OF POWER OF ATTORNEY

06 YOUR QUESTIONS ANSWERED

07 USEFUL CONTACTS

03

POWER OF ATTORNEYEQUITY RELEASE

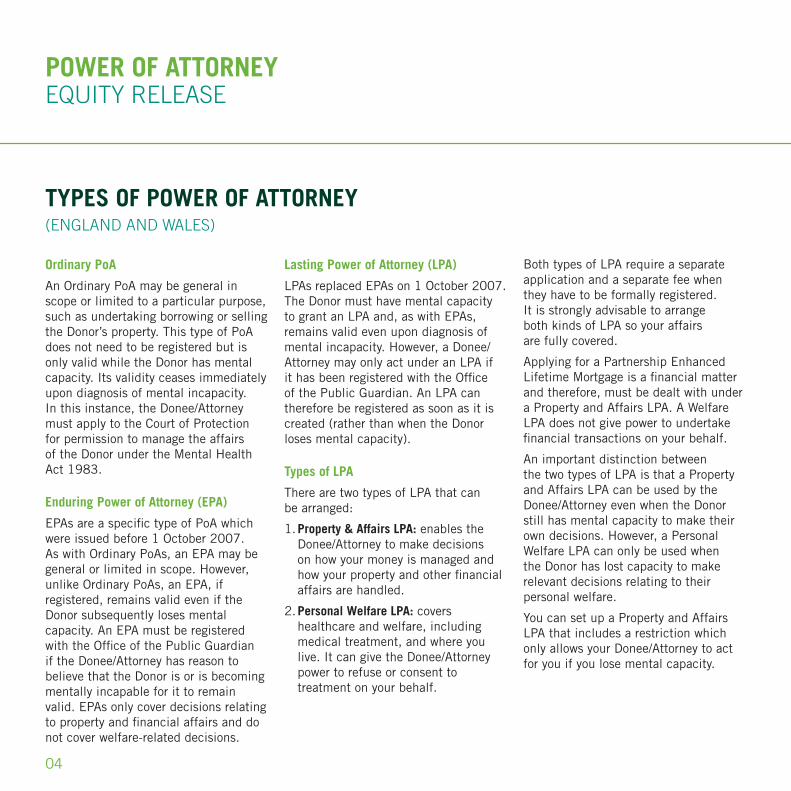

TYPES OF POWER OF ATTORNEY (ENGLAND AND WALES)

Ordinary PoA

An Ordinary PoA may be general in scope or limited to a particular purpose, such as undertaking borrowing or selling the Donor’s property. This type of PoA does not need to be registered but is only valid while the Donor has mental capacity. Its validity ceases immediately upon diagnosis of mental incapacity. In this instance, the Donee/Attorney must apply to the Court of Protection for permission to manage the affairs of the Donor under the Mental Health Act 1983.

Enduring Power of Attorney (EPA)

EPAs are a specific type of PoA which were issued before 1 October 2007. As with Ordinary PoAs, an EPA may be general or limited in scope. However, unlike Ordinary PoAs, an EPA, if registered, remains valid even if the Donor subsequently loses mental capacity. An EPA must be registered with the Office of the Public Guardian if the Donee/Attorney has reason to believe that the Donor is or is becoming mentally incapable for it to remain valid. EPAs only cover decisions relating to property and financial affairs and do not cover welfare-related decisions.

Lasting Power of Attorney (LPA)

LPAs replaced EPAs on 1 October 2007. The Donor must have mental capacity to grant an LPA and, as with EPAs, remains valid even upon diagnosis of mental incapacity. However, a Donee/Attorney may only act under an LPA if it has been registered with the Office of the Public Guardian. An LPA can therefore be registered as soon as it is created (rather than when the Donor loses mental capacity).

Types of LPA

There are two types of LPA that can be arranged:

1. Property & Affairs LPA: enables the Donee/Attorney to make decisions on how your money is managed and how your property and other financial affairs are handled.

2. Personal Welfare LPA: covers healthcare and welfare, including medical treatment, and where you live. It can give the Donee/Attorney power to refuse or consent to treatment on your behalf.

Both types of LPA require a separate application and a separate fee when they have to be formally registered. It is strongly advisable to arrange both kinds of LPA so your affairs are fully covered.

Applying for a Partnership Enhanced Lifetime Mortgage is a financial matter and therefore, must be dealt with under a Property and Affairs LPA. A Welfare LPA does not give power to undertake financial transactions on your behalf.

An important distinction between the two types of LPA is that a Property and Affairs LPA can be used by the Donee/Attorney even when the Donor still has mental capacity to make their own decisions. However, a Personal Welfare LPA can only be used when the Donor has lost capacity to make relevant decisions relating to their personal welfare.

You can set up a Property and Affairs LPA that includes a restriction which only allows your Donee/Attorney to act for you if you lose mental capacity.

04

POWER OF ATTORNEYEQUITY RELEASE

Both types of LPA document must be registered at the Office of the Public Guardian (OPG) before they can be used. This can be done before or after the Donor loses the mental capacity to make their own decisions. If you wish to, you may register the LPA while you still have capacity to do so, to avoid any delay when it needs to be used.

Court of Protection (COP)

The COP has wide powers and can make orders about the property of a person lacking mental capacity, as well as their personal welfare. Where the COP is satisfied that a person lacks mental capacity, a decision is made to appoint a Deputy or Deputies to manage the individual’s affairs. The Deputy will be a person or body whom the COP deems trustworthy.

Scotland

There are also various types of Power of Attorney in Scotland.

1. A General Power of Attorney is similar to an Ordinary PoA in England and Wales. It either gives the Donee/Attorney general power to do anything which the Donor might do (subject to certain exceptions) or may be more limited in scope. As with an Ordinary PoA, a General PoA is only valid whilst the Donor has mental capacity.

2. A Continuing Power of Attorney gives the Donee/Attorney power over the Donor’s property and finances. Such power may start immediately and will continue even when the Donor begins to lose mental capacity. You may also choose for it to begin at a later date, for example, when you lose mental capacity.

3. A Welfare Power of Attorney gives the Donee/Attorney power over decisions that need to be taken regarding the Donor’s health and welfare. This power can only begin when the Donor becomes mentally incapable. A Welfare PoA is often contained in the same document as a Continuing PoA.

NB: A Welfare PoA does not give power to undertake financial matters such as applying for a Partnership Enhanced Lifetime Mortgage. This would have to be dealt with under a Scottish Continuing PoA.

For further information, you should contact the Office of the Public Guardian Scotland (contact details provided overleaf).

05

POWER OF ATTORNEYEQUITY RELEASE

YOUR QUESTIONS ANSWEREDWhat if I don’t have a PoA in place when I apply for a Partnership Enhanced Lifetime Mortgage?

Arranging a PoA is the only way to ensure the people you choose will be able to handle your affairs when you can no longer do so.

If a PoA is not in place when you become mentally incapacitated, you may be registered with the COP. One or more Deputies may be appointed by the Court with power to make welfare and financial decisions on your behalf, including release of funds from bank accounts, sale of property and your medical treatment.

It is possible for family members to apply to the COP to become a Deputy but this can take time and cost money. Also their powers may be more limited than under an LPA.

If I am applying for a Partnership Enhanced Lifetime Mortgage, when should I set up a PoA?

Ideally, you should have a PoA in place when you send your Application to us. If a relative or friend signs your Application because they assist you with day to day business transactions

we will not be able to proceed with your Application unless such persons have legal power to act on your behalf. If cases where we require access to your medical records, we are not permitted to write to your GP unless you, or someone who has legal power to act as your Attorney, sign the Application.

What happens if I sign the Application Form and there is a diagnosis of mental incapacity in my medical reports or my solicitor does not believe I have the mental capacity to enter into a contract?

We will require a PoA document before entering into a contract with you. If you already have a PoA in place, the Attorney(s) will need to sign the Application Form and send a copy of the registered PoA document. If the PoA is not already registered with the Office of the Public Guardian, it will have to be registered before we can enter into the contract with you.

If you do not already have a PoA in place, the COP will need to be notified and a Deputy appointed to act on your behalf. We will require a copy of the registered COP Order before entering into the contract.

How long does it take to set up the Enhanced Lifetime Mortgage with Partnership?

Your adviser can prepare an illustration for you based on the answers you give about your health and property details. If you decide to apply and you are able to proceed straight away, it usually takes around seven working days for a professional valuation of your property to be carried out.

When we receive the valuation, we will provide you with an Offer of Loan, which will be valid for 21 days.

The process typically takes eight to ten weeks from sending in your Application to receiving the Enhanced Lifetime Mortgage funds. There are, however, some things that can cause delays, such as, if your GP or solicitor advises us of mental incapacity, and we reserve the right to withdraw the offer, or postpone it until a suitable PoA is in place. Therefore, it is advisable to setup a PoA sooner rather than later to avoid any delays.

06

USEFUL CONTACTSTo find a solicitor:

www.lawsociety.org.uk Telephone no. 020 7242 1222 www.lawscot.org.uk Telephone no. 0131 226 7411

For further guidance and to download the LPA forms:

www.direct.gov.uk Telephone no. 0300 456 0300

Office of the Public Guardian (Scotland)

Hadrian House Callendar Business Park Callendar Road Falkirk, FK1 1XR Telephone: 01324 678300 Fax: 01324 678301 Email: [email protected] Website: www.publicguardian-scotland.gov.uk

07

Regent House, 1-3 Queensway, Redhill, Surrey RH1 1QT.

Adviser line: 0845 108 7237* (local call rates apply)Email: [email protected]: www.partnership.co.uk

*Telephone calls may be recorded for training and monitoring purposes.

If you require this document in an alternative format please contact us.

Partnership is the trading name of the Partnership Group of Companies, which includes: Partnership Life Assurance Company Limited (registered in England and Wales No. 05465261) and Partnership Home Loans Limited (registered in England and Wales No. 05108846).

Partnership Life Assurance Company Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Partnership Home Loans Limited is authorised and regulated by the Financial Conduct Authority.

The registered office for both companies is 5th Floor, 110 Bishopsgate, London EC2N 4AY.

ELM2102 12.14 V2