Embed Size (px)

Citation preview

Why settle for simply outsourcing Cash Balance actuarial work when you can form a powerful business partnership with the national Cash Balance leader? At Kravitz Back Office Solutions, we deliver so much more than actuarial expertise: innovative plan designs at no cost, sales and marketing support, Cash Balance training, business-building tools and strategy. You control the client relationship, while we work behind the scenes to help you expand your plans and expand your business. Because when you succeed, we succeed.

Your Cash Balance Partner n KravitzBackOffice.com n 877 CB-Plans

LOS ANGELES • NEW YORK • CHICAGOAtlanta • Las Vegas • Denver • Portland • Phoenix • Salt Lake City • San Diego • Ann Arbor • Charleston • Naples • Honolulu

The Cash Balance AuthorityRetirement Plans that Save Today and Build Tomorrow

CASH BALANCE DESIGNYour Resource for Everything Cash Balance

BACK OFFICE SOLUTIONSYour Cash Balance PartnerExpand your Plans. Expand Your Business.

The Cash Balance AuthorityRetirement Plans that Save Today and Build Tomorrow

CASH BALANCE DESIGNYour Resource for Everything Cash Balance

BACK OFFICE SOLUTIONSYour Cash Balance PartnerExpand your Plans. Expand Your Business.

The Power ofPartnership.

A n o f f i c i a l p u b l i c a t i o n o f A S P P A

SPRING 2016

IRS Employee Plans — The ‘New Normal’

Takeovers and Conversions

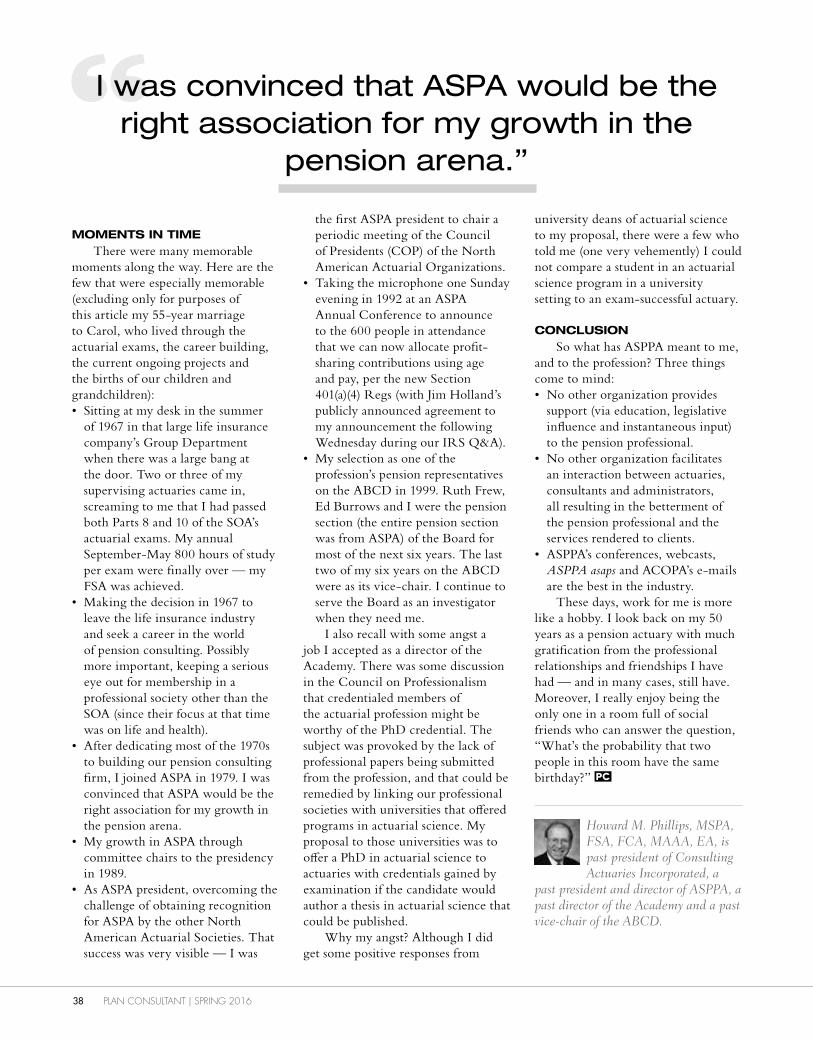

My 50 Years as a Pension Actuary

PLA

N C

ON

SU

LTA

NT • G

EN

ER

ATIO

N N

OW

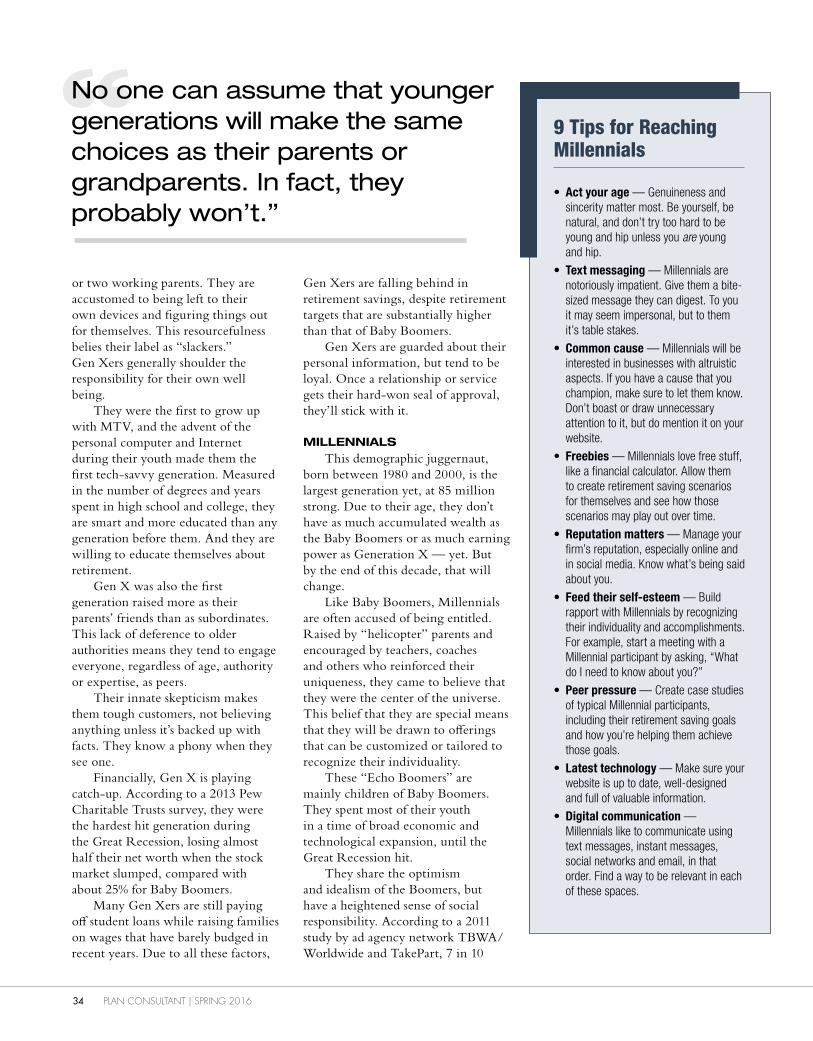

How to connect with allgenerations of participants

HOW DO I GET STARTED?*

Our dedicated resources and flexible solutions help you take care of past employees while reducing plan expenses in 3 easy steps.

CompleteChange ContactAdd/RolloverTransfer

Calculate

Select/ChooseOpenInvest SignResearch

HelpEducateDiscoverDownload Glossary

Submit Time/How Long Tools

Step 1: Sign Service Agreement

CompleteChange ContactAdd/RolloverTransfer

Calculate

Select/ChooseOpenInvest SignResearch

HelpEducateDiscoverDownload Glossary

Submit Time/How Long Tools Step 2: Send Us Participant Information

CompleteChange ContactAdd/RolloverTransfer

Calculate

Select/ChooseOpenInvest SignResearch

HelpEducateDiscoverDownload Glossary

Submit Time/How Long Tools

Step 3: Transfer Funds to Millennium to Establish an IRA

OUR AUTOMATIC ROLLOVER SOLUTION REALLY IS THAT EASY

Visit our new website at www.mtrustcompany.com

* Plan Sponsor must make appropriate disclosures and notifications to plan participants, and may utilize the notification services of Millennium Trust Company to satisfy safe harbor requirements. Millennium Trust Company performs the duties of a custodian and, as such, does not provide any investment advice, nor offer any tax or legal advice.

YEARS OFBUSINESS

proudly celebrating

Plan Consultant_3Steps_Ad_08-2015.indd 1 8/28/2015 1:48:07 PM

Faster Training• Easy access – online and mobile ready

• Modular content – the topics you need,

when you need them

• Less reading, more application

Stronger,leaner,faster.

The New RPF

ASPPA’S Retirement Plan Fundamentals Course

Stronger Instruction• Interactive practice, scenarios

and targeted feedback• Learning strategies backed by principles of Instructional Design

• Developed by ASPPA Industry Experts

Leaner Content• Selected to meet performance needs

• The skills you use the most

• Updated for current practices

The RPF certificate is the

trusted education program,

used by thousands to start

their retirement plan careers.

For more information, contact the SAM [email protected]

1WWW.ASPPA-NET.ORG

Generation NowHow to connect with all three generations of participants.

BY CAM MARSTON

COVER STORY

30

SPRING 2016Contents

26 Plan Takeovers and Conversions: Pitfalls and Pointers (Part 2)

Steps to takeover success.

BY ROBERT E. (BOB) MEYER, JR.

FEATURE STORIES

6 From the President JOSEPH A. NICHOLS

7 ASPPA Conferences

11 ASPPA History Website Now Online

51 New and Recently Credentialed Members

60 Government Affairs Update CRAIG P. HOFFMAN

ASPPA IN ACTION

36 50 Years as a Pension Actuary

A past president looks back on how his 50 years in the industry intertwined with ASPPA’s history.

BY HOWARD M. PHILLIPS

40 IRS Employee Plans — the ‘New Normal’

Restructuring and budget cuts bring change.

BY RICHARD A. HOCHMAN

2 PLAN CONSULTANT | SPRING 2016

44 Operational Self Audits: How to Avoid the Financial Pitfalls of Qualified Plans WORKING WITH PLAN SPONSORSJOEL SHAPIRO

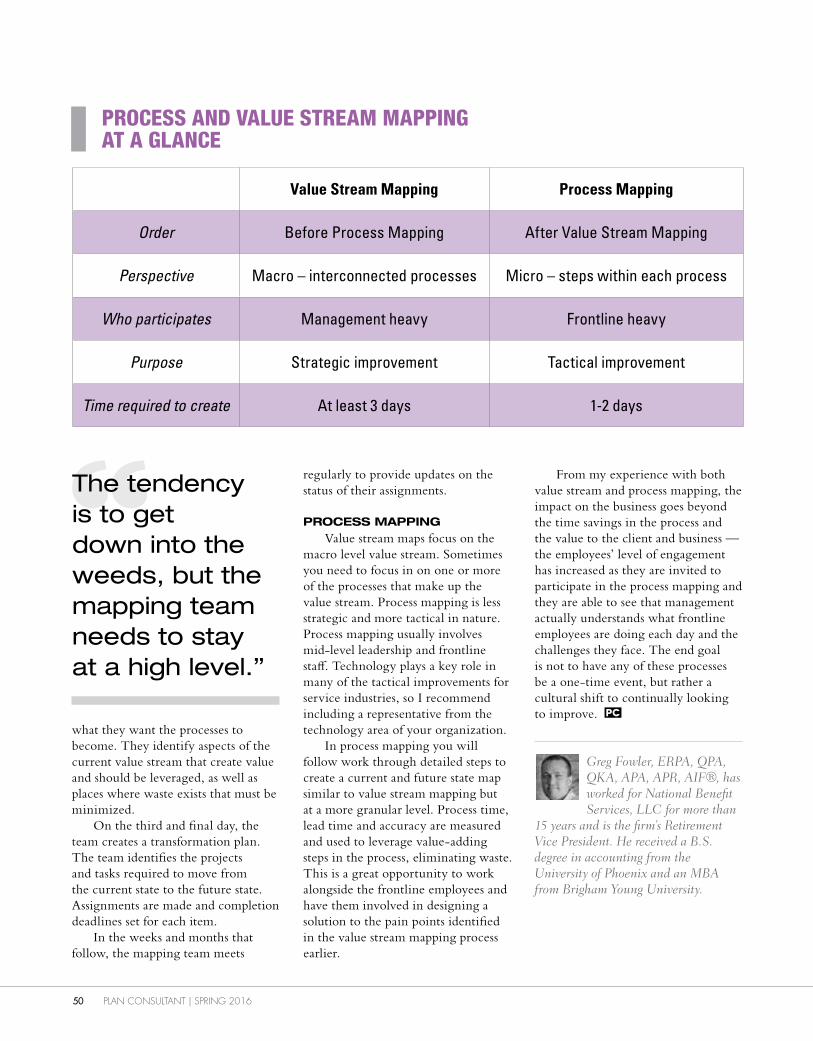

48 Mapping Your Business Workflows BUSINESS PRACTICES

GREG FOWLER

52 Want Your Employees To Be Productive, Faster? EDUCATION

BRIAN FURGALA

54 Reporting Professional Misconduct (Part 2) ETHICS

LAUREN BLOOM

56 QACAs: Making Retirement Veggies More Than Palatable SUCCESS STORIES

JOHN IEKEL

58 Work Smarter by Leveraging Cheap Tech TECHNOLOGY

YANNIS P. KOUMANTAROS AND ADAM C. POZEK

04 Letter from the Editor

08 Cross-Tested Plans in the Crosshairs (Again) REGULATORY/LEGISLATIVE UPDATE

BRIAN H. GRAFF

10 Year-End Tax and Spending Bill Has Retirement Implications LEGISLATIVE

12 A Fresh Look at After-Tax Contributions COMPLIANCE

KELSEY N.H. MAYO AND KELLY MARIE HURD

16 Coping with the Changes to ASOP 35 ACTUARIAL

WILLIAM D. KARBON

20 What’s Next for Pre-approved Plan Documents? LEGAL

DAVID N. LEVINE

22 Key Issues in 403(b) Plan Takeovers RECORD KEEPING

JOHN JEFFREY

584420COLUMNS

TECHNICAL ARTICLES

PRACTICE MANAGEMENT ARTICLES

Published by

Editor in ChiefBrian H. Graff, Esq., APM

Plan Consultant CommitteeMary L. Patch, QKA, QPFC, Co-chair

David J. Witz, Co-chairGary D. Blachman

John D. Blossom, Jr., MSPA, QPFCJason D. Brown

Kelton Collopy, QKAKimberly A. Corona, MSPAJohn A. Feldt, CPC, QPAJohn Frisvold, QPA, QKA

Catherine J. Gianotto, QPA, QKABrian J. Kallback, QKAPhillip J. Long, APM

Kelsey H. MayoRobert E. Meyer, Jr, QKAMichelle C. Miller, QKARobert G. Miller, QPFC

Eric W. Smith

EditorJohn Ortman

Associate EditorTroy L. Cornett

Senior WriterJohn Iekel

Graphic DesignerIan Bakar

Technical Review BoardMichael Cohen-Greenberg

Sheri Fitts Drew Forgrave, MSPA

Grant Halvorsen, CPC, QPA, QKA Jennifer Lancello, CPC, QPA, QKA

Robert Richter, APM

Advertising SalesErik Vanderkolk

ASPPA Officers

PresidentJoseph A. Nichols, MSPA

President-ElectRichard A. Hochman, APM

Vice PresidentAdam C. Pozek, QPA, QKA, QPFC

Immediate Past PresidentKyla M. Keck, CPC, QPA, QKA

Plan Consultant is published quarterly by the American Society of Pension Professionals & Actuaries, 4245 North

Fairfax Drive, Suite 750, Arlington, VA 22203. For subscription information, advertising, and customer service contact ASPPA

at the address above or 800.308.6714, [email protected]. Copyright 2016. All rights reserved.

This magazine may not be reproduced in whole or in part without written permission of the publisher. Opinions

expressed in signed articles are those of the authors and do not necessarily reflect the official policy of ASPPA.

Postmaster: Please send change-of-address notices for Plan Consultant to ASPPA, 4245 North Fairfax Drive, Suite 750,

Arlington, VA 22203.

4 PLAN CONSULTANT | SPRING 2016

ASPPA History Now Online

A new website dedicated to ASPPA’s rich history at the forefront of the retirement industry is now online, at asppa50.org/.

Designed to complement the ASPPA history book currently in progress, the website includes material uncovered in the course of researching, writing and editing the book, including:

• Photos from ASPPA Annual Conferences going back to 1974, and more.

• Documents from the ASPPA archives and other sources, including the 1966 certificate of incorporation, articles from The Pension Actuary by prominent leaders of the past, and more.

• Videos, starting with ones marking ASPPA’s 25th anniversary in 1991 (and featuring founder Harry T. Eidson) and previewing this year’s 50th anniversary celebration.

We’ll be adding photos, documents and new videos on a regular basis. When we do, we’ll let you know in an ASPPA Connect post. Check it all out at asppa50.org/, or click on “ASPPA History” in the “About” section of ASPPA Net’s nav bar.

L E T T E R F R O M T H E E D I T O RPC

Yet in the face of those dire circumstances, it’s clear that society cares about Millennials’ financial situation in general and their retirement prospects in particular — led by the retirement industry’s fairly recent focus on this generation of future savers.

More importantly, it looks like Millennials themselves are starting to show signs of having the “right stuff” when it comes to managing their finances. Increasingly, retirement industry surveys and studies are showing that Millennials’ views of their financial future, especially regarding saving for retirement, are distinctly realistic and positive. And when they do save, they tend to be risk averse.

Realistic, positive and risk averse. Sounds like a pretty good foundation to build a financial future on to me. Perhaps what this all means is that for Millennials, financial responsibility is officially becoming… cool.

Doubt it? In a new music video about student debt, rapper Dee-1 proclaims his happiness at finally finishing “paying Sallie Mae back.” The lyrics include references to checking his credit on Equifax and working two jobs to pay off his loans.

For a deeper dive into how Millennials — as well as Boomers and Gen Xers — are different, check out this month’s cover story by generational authority Cam Marston.

Comments, questions, bright ideas? Contact me at [email protected].

burden of student debt, but also including stagnant wages, the rising cost of child care and fewer opportunities to build wealth in the same manner as previous generations did. This includes saving for retirement. A Young Invincibles survey found that about half of employed, low-income Millennials don’t have access to a retirement plan at work. In New York State, AARP research indicates, that figure is north of 60%.

eed some good news? Try this on for size.

Back in February, AARP and Young Invincibles, a national nonprofit, nonpartisan organization that advocates

on behalf of 18- to 34-year-olds, cosponsored a happy hour event in New York City’s Greenwich Village called “Cheers to Your Future.” The focus: young people’s retirement prospects.

Now recall what you know about Boomers and Gen Xers when they were in their 20s. Retirement solutions weren’t even on their radar. But for today’s 85 million Millennials — those born between 1980 and 2000 — things are different.

Millennials are facing multiple economic pressures, especially the

JOHN ORTMANEDITOR-IN-CHIEF

What’s Different About Millennials?

NIt looks like Millennials are starting to show signs of having the ‘right stuff’ when it comes to managing their finances.”

Assessments performed by CefeX, Centre for fiduCiAry eXCellenCe, llC.

For more information on the certification program, please call 416.693.9733.

*As of September 5, 2014

AsppA retirement plan service provider

The following firms are certified* within the prestigious

ASPPA Service Provider Certification program. They have

been independently assessed to the ASPPA Standard of

Practice. These firms demonstrate adherence to the industry’s

best practices, are committed to continuous improvement and

are well-prepared to serve the needs of investment fiduciaries.

Actuarial Consultants, Inc.

Alliance Benefit Group North Central States, Inc.

Alliance Benefit Group of Illinois

Alliant Employee Benefits, a division of

Alliant Insurance Services, Inc.

American Benefits Systems, Inc. d.b.a.

Simpkins & Associates

American Pensions

Aspire Financial Services, LLC

Associated Benefit Planners, Ltd.

Atessa Benefits, Inc.

Atlantic Pension Services, Inc.

Benefit Management Inc. dba United

Retirement Plan Consultants

Benefit Planning Consultants, Inc.

Benefit Plans Plus, LLC

Benefit Plans, Inc.

Benefits Administrators, LLC

Blue Ridge ESOP Associates

BlueStar Retirement Services, Inc.

Creative Plan Designs Ltd.

Creative Retirement Systems, Inc.

DailyAccess Corporation

DWC ERISA Consultants, LLC

First Allied Retirement Services /

Associates in Excellence

Great Lakes Pension Associates, Inc.

Ingham Retirement Group

Intac Actuarial Services, Inc.

July Business Services, Inc.

Kidder Benefits Consultants, Inc.

Moran Knobel

National Benefit Services, LLC

North American KTRADE Alliance, LLC.

Pension Associates International

Pension Financial Services, Inc.

Pension Planning Consultants, Inc

Pension Solutions, Inc.

Pentegra Retirement Services

Pinnacle Financial Services Inc.

Preferred Pension Planning Corporation

Professional Capital Services, LLC

QRPS, Inc.

Qualified Plan Solutions, LC

Retirement Planning Services, Inc.

Retirement Strategies, Inc.

Rogers Wealth Group, Inc.

RPG Consultants

Securian Retirement

SI Group Certified Pension Consultants

SLAVIC401K.COM

Summit Benefit & Actuarial Services, Inc.

TPS Group

Trinity Pension Group, LLC

*as of August 24, 2015

6 PLAN CONSULTANT | SPRING 2016

F R O M T H E P R E S I D E N TPC

This is the main task of the 2016 ASPPA Leadership Council — to determine a path for strategic planning to maintain the passion. Notice I did not say, “develop a plan,” but rather determine a path for the planning. As passionate as our LC members are (and believe me, there is no shortage of passion during our meetings), they also have day jobs, and the important work involved in understanding what motivates our members cannot be done in a couple of phone calls. And it is important. We are trying to figure out how this incredible association can keep its passionate energy going for many years to come.

So as we continue to celebrate our 50th anniversary, think about what drives your ASPPA passion. Share your thoughts with me at [email protected]. And think especially about how (or if ) that passion changed throughout your career, either within the same firm or as you moved from firm to firm.

Most of all, thank you, everyone, for your ASPPA passion!

Joseph A. Nichols, MSPA, ASA, EA, MAAA, is ASPPA’s 2016 President. A senior director with FTI Consulting’s Pension Consulting Services group, he has provided pension actuarial services to a wide range of plan sponsors for more than 25 years.

growth since those days, that “working hard because we are the little guy” element still exists today.

Throughout the years, there have been many challenges that have tested ASPPA. Sometimes the passion gets in our way, but in the end, it guides us to be a stronger association. For just one example, ASPPA’s impassioned but reasoned response to the IRS’ small-plan audit initiative in the early 1990s forged a dynamic image for the organization.

My own ASPPA passion started in the second half of the 1990s when, while I was working on my first small business defined benefit plan, my colleague (and good friend to this day) Janet Thompson introduced me to ASPPA. My passion started with teaching local ASPPA courses, jumped to being an ASPPA rep for the Joint Board exam writing committee, and continued as I helped out in committee and leadership positions.

Most ASPPA presidents probably think that in their year, the association is at a crossroad. I cannot think of a year recently in which something monumental did not happen, either within ASPPA or our industry.

To me, here’s the crossroad we face in 2016: Now that we are settled into our role as a sister organization within the American Retirement Association, are better able to focus on the needs of our members and future members, and have realized that the makeup of our industry is shifting through growth, consolidation and attrition, what path do we choose to maintain the ASPPA passion?

s we wind down another Winter busy season (getting ready for the Spring busy season), I cannot help but think about how we got here. Not how we got here on this crazy rock circling

a flaming gas ball, but how ASPPA got where we are.

We know it all started with three guys writing down some goals on a bar napkin. We also know that there has always been a tremendous amount of passion and devotion to our profession driving us along the path we are traveling. That’s when it dawned on me — it’s the passion.

Passion drives ASPPA in many different ways. To some, passion for ASPPA means loyally attending the Annual Conference year after year, not only to keep up on PE requirements, but also to see our other passionate ASPPA friends. To others, passion means writing a check to ASPPA PAC year after year because the root of our existence depends on ASPPA’s Government Affairs staff and volunteers engaging with elected officials. And to still others, passion means being on a committee to plan a conference, draft an ASPPA asap or help run a local ASPPA Benefits Council (ABC) year after year.

Note the common themes in the above paragraph — passion and year after year.

So, what drives the passion? At the time three pension professionals in Texas founded ASPPA in 1966, I think the passion existed because many actuaries’ professional lives were at stake. And despite our monumental

ASPPA PassionHow do we keep the passion alive going forward?

A

BY JOSEPH A. NICHOLS

7WWW.ASPPA-NET.ORG

UPCOMING CONFERENCES

MAY 2016

May 19–20 ASPPA RegionalConference: Philadelphia Philadelphia, PA

JUNE 2016

June 6–9 Women Business Leaders Forum New Orleans, LA

June 16–17 ASPPA RegionalConference: Chicago Chicago, IL

JULY 2016

July 14–15 ASPPA RegionalConference: Boston Boston, MA

July 19–22 Western Benefits Conference Seattle, WA

AUGUST 2016

August 12–13 ACOPA Actuarial SymposiumChicago, IL

BOSTON JULY 14–15, 2016

HILTON BACK BAY

CHICAGO JUNE 16–17, 2016

HOTEL CHICAGO

PHILADELPHIA MAY 19–20, 2016 MARRIOTT DOWNTOWN

CINCINNATINOV. 16–17, 2016

NORTHERN KENTUCKY CONVENTION CENTER

REGIONALC O N F E R E N C E S

AMERICAN SOCIETY OF

PENSION PROFESSIONALS

& ACTUARIES

NOVEMBER 2016

Nov. 16–17ASPPA Regional Conference: Cincinnati Covington, KY

OCTOBER 2016

Oct. 23–26ASPPA Annual ConferenceNational Harbor, MD

8 PLAN CONSULTANT | SPRING 2016

workforce. It’s jarring that this proposal was unveiled the very same week that the Obama administration publicly came out in support of another proposal to open up private multiple employer plans to any unrelated employer, ostensibly to encourage small businesses to adopt retirement plans and increase retirement plan coverage in the private workforce.

As the Obama administration notes, millions of private sector workers do not have access to a retirement savings plans provided through the workplace. And moderate-income workers without access to a workplace based retirement savings plan rarely save for retirement. Small businesses employ many of these workers.

We need to do everything we can to increase access to retirement plans at work, especially among small businesses. The Treasury proposal is a classic case of the left hand of the federal government not knowing what the right hand is doing. This proposal is a step in the wrong direction — and needs to be rejected.

Brian H. Graff, Esq., APM, is the executive director of ASPPA.

would impose new costs on the small businesses that have these plans and scare away small businesses that are considering adopting these plans.

These cross-tested plans are some of the most popular defined contribution plan designs being used today in the small plan market. Needlessly damaging this effective plan design ultimately hurts the rank-and-file employees who have access to these plans. Remember, rank and file workers enjoy meaningful benefits under the current nondiscrimination rules — which have been in place for more than 10 years — since cross-tested plans need to satisfy the minimum allocation gateway rules.

The gateway allocation rules require that non-highly compensated employees get an annual contribution of 5% of pay in a defined contribution plan (or one-third of the allocation rate of highly compensated employees).

Additionally, if a company has a defined benefit plan in combination with a defined contribution plan, this minimum rate increases on a sliding scale up to 7.5% of pay (also depending on the allocation rate of highly compensated employees). Therefore, rank-and-file workers get more employer cash under these widely used arrangements — which are now seriously at risk — than they do under the common safe harbor plan designs that are not subject to nondiscrimination testing.

The Treasury proposal flies in the face of the Obama administration’s effort to increase retirement plan coverage in the private sector

mall business retirement plans are again under attack. Buried in a Treasury Department proposal to make it easier for large corporations to close their defined benefit plans to new

entrants is a provision that will make it harder for small businesses to form new retirement plans or maintain their current ones.

The proposal imposes a new “reasonable classification” requirement on highly compensated employee rate groups that will make it significantly harder for plans that allocate these rate groups on an individual or specific basis to pass the general nondiscrimination test used for cross-tested defined contribution plans under Section 401(a)(4) of the Internal Revenue Code.

There are major problems with this new requirement. First, determining “reasonable classification” is inherently a subjective process based on the facts and circumstances of each business in question. This subjective test removes the objective purely numerical nondiscrimination testing regime that has been in place for more than two decades. The result is to increase the uncertainty and complexity of an already complicated process.

Second, the new requirement unfairly burdens small businesses because they will likely have very small rate groups. So Treasury is in essence forcing small businesses to test on a ratio percentage basis rather than an average benefits basis, which

A new proposal from the Treasury Department is a step in the wrong direction — and needs to be rejected.

S

Cross-Tested Plans in the Crosshairs (Again)

REGULATORY/LEGISLATIVEUPDATE

BY BRIAN H. GRAFF

9WWW.ASPPA-NET.ORG

ERISATHE

OUTLINE BOOK

2016

Sal L. Tripodi, J.D., LL.M.

www.asppa.org/EOB800.308.6714

Print & Online Editions Available

10 PLAN CONSULTANT | SPRING 2016

LEGISLATIVE

H.R. 2029 affects IRAs, church plans and more.

Year-End Tax and Spending Bill Has Retirement Implications

On Dec. 18, 2015, President Obama signed into law H.R. 2029, a massive year-end spending and tax bill containing a number of provisions affecting health and retirement plans.

H.R. 2029 includes both an omnibus appropriations bill that funds the government through Sept. 30, 2016 (the Consolidated Appropriations Act, 2016, or “CAA”) and an “extender” (in some cases, a permanent one) of a large number of expiring or expired tax incentives (the Protecting Americans from Tax Hikes Act of 2015, or “PATH Act”). While most employers have probably focused on aspects like the legislation’s two-year delay of the high-cost employer-sponsored health coverage excise tax (a.k.a. the “Cadillac tax”), H.R. 2029 also includes the following retirement-related provisions.

CHARITABLE DISTRIBUTIONS FROM IRAsThe PATH Act permanently extends the ability

of individuals at least 70½ years of age to exclude from gross income qualified charitable distributions from IRAs, effective for 2015 and later years. However, that exclusion may not exceed $100,000 per taxpayer in any tax year.

CHURCH PLAN CHANGESThe PATH Act includes a long-pending package of

church plan changes, including:• a provision that the IRS cannot aggregate certain church

plans together for purposes of the nondiscrimination rules;• flexibility for church plans to choose other church plans

with which they associate;• prevention of certain grandfathered church defined benefit

plans from having to meet certain requirements relating to maximum benefit accruals;

• allowing defined contribution church plans to offer automatic enrollment;

• streamlining the rules for merging and reorganizing church plans; and

• allowing church plans to invest in 81-100 collective trusts.

ROLLOVERS TO SIMPLE IRAsThe PATH Act allows participants to roll over their

accounts from an employer sponsored retirement plan to a SIMPLE IRA, provided the participant’s SIMPLE IRA is at least two years old. Previously, SIMPLE IRAs were not permitted to accept such rollovers at all.

11WWW.ASPPA-NET.ORG

The ASPPA History Site is Now Online

ASPPA History Site Now OnlineASPPA History Site

Featuring videos, photos from the ASPPA archives and documents from past presidents, members and other sources, the ASPPA history website celebrates our contributions to the pension and retirement industry and the actuarial

profession – and the people who made it all happen. It’s designed to complement the ASPPA history book currently in progress, and includes photos and documents uncovered in the course of researching, writing and editing the book.

A new website dedicated to ASPPA’s rich history at the forefront of the retirement industry is now online!

asppa50.org

Photos from ASPPA Annual Conferences going back to the 1974

conference, held a month after ERISA was signed into law, and more.

Documents from the ASPPA archives and other sources, including the 1966

certifi cate of incorporation, ASPPA Presidents’ speeches, scripts of tributes to Chet Salkind and Ed Burrows, articles from The Pension Actuary by prominent

leaders of the past, and more.

Videos starting with ones marking ASPPA’s 25th anniversary in 1991 (and featuring founder Harry T.

Eidson) and previewing this year’s 50th anniversary celebration.

You’ll also fi nd a little background on the work-in-progress ASPPA history book, Leading the Evolution: ASPPA’s 50 Years at the Forefront of the Retirement Industry, coming in October.

Check it all out at asppa50.org/, or click on “ASPPA History” in the “About” section of the ASPPA Net nav bar.

should make U.S. real estate investments more attractive to non-U.S. pension plans.

AIRLINE EMPLOYEE IRA ROLLOVERS

The PATH Act corrects an effective date problem affecting rollovers to IRAs of amounts received by qualified airline employees as a result of certain airline bankruptcies. Those distributions generally may be rolled over within 180 days of receipt or, if later, within 180 days of the Dec. 18, 2014 enactment of the changes.

FILING OF WAGE REPORTING FORMS

Beginning with the 2017 tax year, Forms W-2, W-3 and 1099-MISC must be provided no later than Jan. 31 of the year following the calendar year to which the tax return applies.

The PATH Act includes a long-pending package of church plan changes.”

EXTENDED EARLY WITHDRAWAL RELIEF FOR PUBLIC SAFETY OFFICERS

The PATH act extends the current relief from the 10% penalty on early withdrawals from retirement plans and accounts for qualified public safety employees to include nuclear materials couriers, U.S. Capitol Police, Supreme Court Police, and diplomatic security special agents of the State Department for withdrawals made after 2015.

FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA)

The PATH Act adds an exemption to withholding under FIRPTA for the disposition of U.S. real property held directly (or indirectly through one or more partnerships) by certain foreign pension funds and made after enactment. This new exemption

12 PLAN CONSULTANT | SPRING 2016

COMPLIANCE

hese days, most of the attention on post-tax contributions is focused on Roth contributions. Newer consultants in our industry may never have heard of (or certainly never worked with) traditional after-tax contributions. However, traditional after-tax contributions have started to get a bit more attention recently.

In this article, we will review the renewed interest in after-tax contributions and the types of taxable contributions before discussing the pros and cons of after-tax contributions and closing with strategies for using after-tax contributions.

Like they say, what’s old is new again.

T

A Fresh Look at After-Tax Contributions

BY KELSEY N.H. MAYO AND KELLY MARIE HURD

13WWW.ASPPA-NET.ORG

However, the investment earnings on after-tax contributions are taxed as ordinary income, while investment earnings on Roth contributions are distributed tax-free (assuming it is a qualified distribution).

Consider the following example: An employee defers $10,000 in after-tax contributions. That $10,000 is included in the employee’s ordinary income. That amount grows to $50,000 by the time that employee retires. The $10,000 basis is not taxable. However, the $40,000 investment gain is included as ordinary income with any and all distributions from the plan. If that contribution had been a Roth contribution instead of an after-tax contribution, the entire amount could be distributed tax-free (assuming the Roth rules for a qualified distribution are met).

The math underlying this scenario is provided in Table 1. As it illustrates, an employee might end up paying five times more in taxes with the after-tax contribution — $15,000 in taxes vs. $3,000. So one can clearly see the advantage of using Roth contributions to reduce taxation.

least age 50), whereas the maximum Roth deferral to a qualified plan is $18,000 ($24,000 with catch-up if at least age 50). In addition, Roth IRAs are not available to high-income earners (for 2016, individuals who earn over $132,000 or joint filers over $194,000), but there is no income limit for a Roth feature in a qualified plan.

There also are the seemingly ancient after-tax contributions (also known as voluntary employee contributions or post-tax contributions). These after-tax contributions were developed as a way for employees to make contributions to employer sponsored retirement plans from their paychecks and predate the current 401(k) regulations.

Like Roth contributions, after-tax contributions are included in the employee’s taxable income when deferred into the plan, and the amount will grow with investment gains without taxation. The difference between Roth and after-tax contributions lies at the time of distribution. In either case, the original contribution, or basis, is not taxed when distributed from the plan.

RENEWED INTEREST IN AFTER-TAX CONTRIBUTIONS

Part of the recent interest in after-tax contributions comes from IRS Notice 2014-54, which offered guidance on the processing of distributions from retirement plans. This guidance made it easier to continue the advantageous tax treatment of after-tax contributions. In short, the IRS has rules concerning distributions, including that each distribution is a proportionate share of the participant’s pre-tax and after-tax amounts and the entire amount distributed at any one time is a single distribution. This single distribution rule led to confusion about how to roll over a distribution that was a mix of pre- and post-tax amounts. Notice 2014-54 made it clear that the after-tax portion of the distribution could be rolled into a Roth IRA and the taxable portion could be rolled into a traditional IRA.

Secondly, and perhaps more importantly, the recent addition of in-plan Roth conversions has led to a renewed interest in after-tax contributions. With this option, introduced in the 2012 “fiscal cliff” legislation, non-Roth funds (including after-tax contributions) may be converted into Roth funds within the plan. As discussed below, this results in significantly more favorable tax treatment for the converted after-tax contributions.

TAXABLE CONTRIBUTIONSAs a brief review, there are two

types of taxable contributions that employees can make to retirement plans. The newest and most common of these, as we are now familiar, are Roth contributions. Roth contributions were allowed into 401(k) and 403(b) plans starting Jan. 1, 2006. Although Roth IRAs are widely available, a Roth feature in the qualified plan is often more advantageous because the qualified plan permits more Roth contributions than a Roth IRA. The maximum Roth IRA contribution is $5,500 in 2016 ($6,500 with catch-up if at

After-tax Contribution Roth Contribution

Contribution $10,000 $10,000

Tax on Contribution $3,000 $3,000

Total Initial Investment $13,000 $13,000

Investment Gains $40,000 $40,000

Tax on Investment Gains $12,000 $0

Net Distribution at Retirement $38,000 $50,000

Total Tax Paid $15,000 $3,000

TABLE 1: ROTH VS. AFTER-TAX CONTRIBUTIONS

14 PLAN CONSULTANT | SPRING 2016

THE ADVANTAGES OF AFTER-TAX CONTRIBUTIONS

For starters, after-tax contributions are not subject to the Code Section 402(g) limit. Participants may contribute the maximum elective deferrals ($18,000 + $6,000 catch-up in 2016) plus after-tax contributions above that amount, only subject to the Section 415 limits. This allows participants who are able to defer income to save significantly more each year. An example is illustrated in Table 2.

Allowing for after-tax contributions in a plan also opens up the option of recharacterizing contributions in a testing failure situation. In this situation, pre-tax elective deferrals, which are generally included on the ADP test, may be recharacterized as after-tax contributions, which are included on the ACP test, to allow a plan to improve testing results.

A consultant who is familiar with after-tax contributions might be able to use these strategies to help clients find the best solution for retirement savings and/or keep a plan in the best testing position possible.

THE DISADVANTAGES OF AFTER-TAX CONTRIBUTIONS

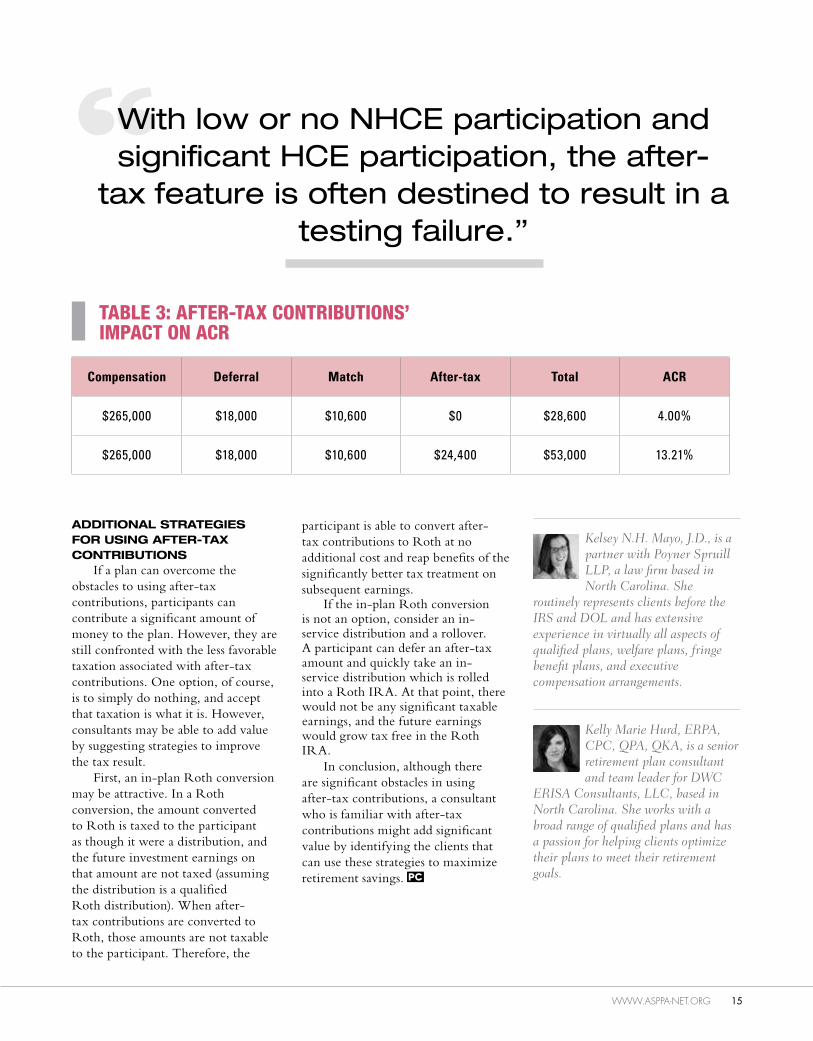

Naturally, there are also disadvantages to using after-tax contributions. The ACP test applies to after-tax contributions and is required even if the plan is safe harbor and would not otherwise be subject to testing. Because of the less favorable taxation associated with the after-tax contributions, participants will likely be less likely to utilize the after-tax feature (particularly if a Roth option is also available under the plan). Therefore, it is likely that only HCEs may take advantage of the after-tax feature in order to defer more than the limits on standard pre-tax and Roth contributions. With low or no NHCE participation and significant HCE participation, the after-tax feature is often destined to result in a testing failure.

Consider a plan with an HCE deferring the maximum $18,000 with a $10,600 match (and no after-tax contributions), the HCE has a total annual contribution of $28,600 and an ACR of 4%. As shown in Table 3, if that HCE contributed enough after-tax contributions to

meet the $53,000 Section 415 limit, an additional $24,400 contribution, her ACR would increase to 13.21%. Assuming a NHCE ACP of 4% (safe harbor matching formula) we can predict a potential refund of $19,100 to the HCE, because she would be maxed out at a 6% ACP contribution rate to pass testing.

ACP TESTING STRATEGIESWhile each situation is unique,

there are a few strategies to consider. For starters, encouraging the NHCEs to participate through communication and even not providing a Roth feature may improve testing results. One might also consider the top-paid group election, which might, with the right demographics, bump some of individuals who would otherwise be HCEs (and who might be participating in the after-tax feature) into the NHCE testing group and improve testing results. Also, limits could be placed on the after-tax contributions administratively, such as by projecting and communicating a permissible limit based on current trends or prior year testing, which might help to reduce or avoid large refunds after year end.

After-tax Permitted Not Permitted

Pre-tax Deferrals $8,000 $8,000

Roth Deferrals $10,000 $10,000

Matching Contribution $7,000 $7,000

After-tax Contribution $28,000 $0

Total Contributions $53,000 $25,000

Investment Gains $212,000 $100,000

Total Account at Retirement $265,000 $125,000

TABLE 2: THE ADVANTAGES OF AFTER-TAX CONTRIBUTIONS

If the in-plan Roth conversion is not an option, consider an in-service distribution and a rollover.”

15WWW.ASPPA-NET.ORG

Kelsey N.H. Mayo, J.D., is a partner with Poyner Spruill LLP, a law firm based in North Carolina. She

routinely represents clients before the IRS and DOL and has extensive experience in virtually all aspects of qualified plans, welfare plans, fringe benefit plans, and executive compensation arrangements.

Kelly Marie Hurd, ERPA, CPC, QPA, QKA, is a senior retirement plan consultant and team leader for DWC

ERISA Consultants, LLC, based in North Carolina. She works with a broad range of qualified plans and has a passion for helping clients optimize their plans to meet their retirement goals.

participant is able to convert after-tax contributions to Roth at no additional cost and reap benefits of the significantly better tax treatment on subsequent earnings.

If the in-plan Roth conversion is not an option, consider an in-service distribution and a rollover. A participant can defer an after-tax amount and quickly take an in-service distribution which is rolled into a Roth IRA. At that point, there would not be any significant taxable earnings, and the future earnings would grow tax free in the Roth IRA.

In conclusion, although there are significant obstacles in using after-tax contributions, a consultant who is familiar with after-tax contributions might add significant value by identifying the clients that can use these strategies to maximize retirement savings.

Compensation Deferral Match After-tax Total ACR

$265,000 $18,000 $10,600 $0 $28,600 4.00%

$265,000 $18,000 $10,600 $24,400 $53,000 13.21%

TABLE 3: AFTER-TAX CONTRIBUTIONS’ IMPACT ON ACR

With low or no NHCE participation and significant HCE participation, the after-

tax feature is often destined to result in a testing failure.”

ADDITIONAL STRATEGIES FOR USING AFTER-TAX CONTRIBUTIONS

If a plan can overcome the obstacles to using after-tax contributions, participants can contribute a significant amount of money to the plan. However, they are still confronted with the less favorable taxation associated with after-tax contributions. One option, of course, is to simply do nothing, and accept that taxation is what it is. However, consultants may be able to add value by suggesting strategies to improve the tax result.

First, an in-plan Roth conversion may be attractive. In a Roth conversion, the amount converted to Roth is taxed to the participant as though it were a distribution, and the future investment earnings on that amount are not taxed (assuming the distribution is a qualified Roth distribution). When after-tax contributions are converted to Roth, those amounts are not taxable to the participant. Therefore, the

16 PLAN CONSULTANT | SPRING 2016

e are now at that time of year when pension actuaries focus on providing services to clients with calendar plan/fiscal years. In doing so, an actuary needs to be aware of the revised principles now imposed by the Actuarial Standard of Practice (ASOP) No. 35, Selection of Demographic and Other Noneconomic Assumptions for Measuring Pension Obligations.

ASOP 35 affects the selection of demographic assumptions such as retirement, termination of employment, mortality and mortality improvement, disability and disability recovery and the election of optional forms of benefits.

To provide some history, in September 2013, the Actuarial Standards Board (ASB) issued an exposure draft of ASOP No. 35. Following comments on this exposure draft, the ASB issued the final revision of ASOP 35 during their September 2014 meeting.

The final revision to ASOP 35 is effective for any actuarial work product with a measurement date on or after June 30, 2015, which means that 2015 is the first calendar year cycle subject to the revised ASOP 35 principles.

The calendar year 2015 cycle is the first one subject to the revised ASOP 35 principles. Are you up to speed?

Coping with the Changes to ASOP 35

ACTUARIAL

BY WILLIAM G. KARBON

W

17WWW.ASPPA-NET.ORG

SIGNIFICANT CHANGESThe most significant revisions to

ASOP 35 address the following:• The guidelines for a reasonable

assumption are now consistent with the guidelines contained in ASOP 27, Selection of Economic Assumptions for Measuring Pension Obligations.

• The requirement to disclose the rationale for the demographic assumption selection.

CONSISTENCY WITH ASOP 27Section 3.3.5 of ASOP 35, which

addresses the selection of a reasonable assumption, is now consistent with ASOP 27. Under this section, an assumption is reasonable if it has the following characteristics:• It is appropriate for the purpose of

the measurement.• It reflects the actuary’s professional

judgment.• It takes into account historical and

current demographic data that is relevant as of the measurement date.

• It reflects the actuary’s estimate of future experience, the actuary’s observation of the estimates inherent in market data (if any) or a combination thereof.

• It has no significant bias (i.e., it is not significantly optimistic or pessimistic), except when provisions for adverse deviation or plan provisions that are difficult to measure are included or when alternative assumptions are used for the assessment of risk.

In selecting assumptions, the actuary needs to ensure that the combined effect of all nonprescribed assumptions selected by the actuary (both demographic and economic assumptions) are reasonable.

DISCLOSING RATIONALE FOR ASSUMPTION SELECTION

In an effort to create greater transparency, the ASB has imposed more robust communication standards with respect to the selection of demographic actuarial assumptions. Section 4.12 of ASOP 35 details

type of measurement. The general effects of the changes should be disclosed in words or by numerical data, as appropriate.

• If the assumption is not a prescribed assumption, a method set by another party or a method set by law, then the actuary should include an explanation of the information and analysis that led to the change.

• The disclosure may be brief, but it should be pertinent to the plan’s circumstances and may reference any actuarial experience report or study performed.

EXAMPLEThe normal retirement age for the

XYZ Pension Plan is age 65. The plan also provides for early retirement after attainment of age 62 with 20 years of service. The early retirement benefit is the accrued benefit reduced 2% for each year the early retirement age precedes the normal retirement age. Furthermore, the employer provides post-retirement medical benefits from the time that participants reach early retirement age until they become eligible for Medicare.

The actuary assumes the following retirement probabilities:

Age 62 30% Age 63 20% Age 64 10% Age 65 100%

the new requirements for disclosing the rationale used in demographic assumption selection:

The actuary should disclose the information and analysis used in selecting each demographic assumption that has a significant effect on the measurement. The disclosure may be brief but should be pertinent to the plan’s circumstances. For example, the actuary may disclose any specific approaches used, sources of external advice, and how past experience and future expectations were considered. The disclosure may reference any actuarial experience report or study performed, including the date of the report or study. This section is not applicable to prescribed assumptions or methods set by another party or prescribed assumptions or methods set by law.

Furthermore, the actuary should include an assumption as to expected mortality improvement after the measurement date. This assumption should be disclosed even if the actuary concludes that an assumption of zero future improvement is reasonable.

The new disclosure requirements imposed by ASOP 35 are only imposed on assumptions that have a significant impact on the measurement. An assumption would have a significant impact on a measurement if its omission or misstatement could influence a decision of the intended user. If there is doubt as to the significance of an assumption, it would be prudent to treat it as significant in order to avoid any questions regarding transparency.

Though the ASOP has always required the disclosure of the rationale for assumption changes, the actuary should refer to Section 4.13 of the ASOP regarding the communication of any changes in assumptions. In communicating assumption changes:• The actuary should disclose

any changes in the significant demographic assumptions from those previously used for the same

The ASB has imposed more robust communication standards with respect to the selection of demographic actuarial assumptions.”

18 PLAN CONSULTANT | SPRING 2016

SHARING THE CHALLENGE

As we move forward to comply with the revised ASOP 35 principles, ACOPA members are encouraged to share their rationales for assumption selection on the ACOPA listserv. Sharing the challenges of meeting the revised ASOP 35 principles as we work on plans of varying size, plan design and type of plan sponsors would be a benefit to all ACOPA members.

Bill Karbon, MSPA, CPC, QPA, is a senior vice president, director of compliance with CBIZ

Benefits & Insurance Services, Inc. in Lawrenceville, N.J. He currently serves as the 2015-2016 executive vice president of the ASPPA College of Pension Actuaries (ACOPA).

The actuary may also disclose the sources of any external advice and how past and future experience was considered.

A sample rationale for this assumption for a small plan could be as follows:

Professional judgment was used to develop the retirement probabilities. It is anticipated that the highest rate of retirement will occur at the point that the early retirement benefit has the greatest actuarial value and medical benefits are available to the retiree. It is anticipated that the retirement rates will decline until full normal retirement benefits are provided by the plan.

How does the actuary disclose the rationale for this assumption as required by Section 4.12 of ASOP 35?

If the plan is large and the retirement rate assumption is based on a recent experience study, then the actuary should disclose the date of the experience study and the fact that the assumption is based on the results of the experience study. Absent an experience study, the actuary could state that professional judgment was used to set the retirement probability assumption. The judgment should be based on the plan design, the availability of income from social programs such as Social Security and other post-retirement benefits that are available to the retiree.

We understand your business and are committed to supporting

your needs. The John Hancock TPAessentials program offers

unique and relevant tools, programs and services based

on four key elements for a healthy business.

1 Operational Efficiency 2 Industry Education 3 Business Practice Optimization 4 Marketing Support

John Hancock Retirement Plan Services, LLC, Boston, MA 02210.

NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED | NOT INSURED BY ANY GOVERNMENT AGENCY

© 2016 All rights reserved G-I29772-GE 03/16-29772

For more details, contact your local John Hancock representative.

Partnering for success

Generate additional revenue and enhance your client service offering The new TPA Service Exchange tool can help you optimize your business practice by

making it easy to offer or outsource services within the TPAessentials community.

We understand your business and are committed to supporting

your needs. The John Hancock TPAessentials program offers

unique and relevant tools, programs and services based

on four key elements for a healthy business.

1 Operational Efficiency 2 Industry Education 3 Business Practice Optimization 4 Marketing Support

John Hancock Retirement Plan Services, LLC, Boston, MA 02210.

NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED | NOT INSURED BY ANY GOVERNMENT AGENCY

© 2016 All rights reserved G-I29772-GE 03/16-29772

For more details, contact your local John Hancock representative.

Partnering for success

Generate additional revenue and enhance your client service offering The new TPA Service Exchange tool can help you optimize your business practice by

making it easy to offer or outsource services within the TPAessentials community.

19WWW.ASPPA-NET.ORG

Western benefits conferenceWestern benefits conference

July 19-22, 2016 | Sheraton SeattleSeattle, Washington

Your road to a healthy retirement starts in the Emerald City

20 PLAN CONSULTANT | SPRING 2016

LEGAL

A look at five key factors that will affect the process going forward.

What’s Next for Pre-approved Plan Documents?BY DAVID N. LEVINE

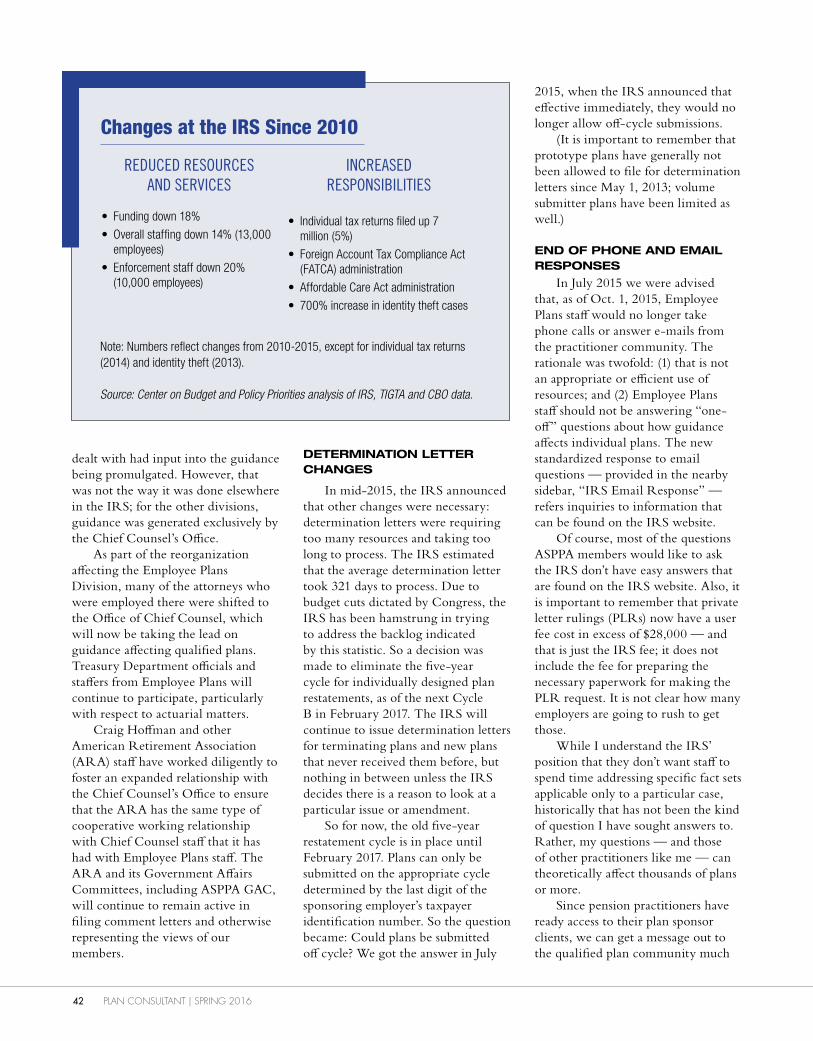

Plan consultants play many roles for their clients. A core service is helping them with the design of their plans and implementation with their third-party administrators and recordkeepers of their choice. As anyone who has ever dealt with design and implementation can attest, it can seem easy but can be full of pitfalls. Each year that passes, the pre-approved plan process gets more and more complex. Why is this the case? A few of the reasons are: • The IRS is exiting the world of individually designed plan determination

letters and is encouraging plan sponsors to move to pre-approved plan documents, driving more complex plans into this world.

• In many cases, pre-approved plan documents are a low-margin business where recordkeepers are already pressed on their margins, thus creating a significant need for plan consultant advice.

• Progressive features, such as automatic enrollment and automatic increase, require significant coordination between sponsors, payroll systems providers, recordkeepers and TPAs — which can lead to significant liabilities.

• Litigation continues to spread across the retirement landscape.• Open multiple employer plans hold the potential to add a whole new layer of

complexity to pre-approved plans.Let’s walk through each of these items.

21WWW.ASPPA-NET.ORG

are on the horizon that hold the potential to dramatically affect a large user of pre-approved plans — small employers. At first blush, one would assume that open MEPs will make utilizing pre-approved plans easier. In some ways they will make pre-approved plans easier because many of the core options selected by smaller employers will be selected by default by an open MEP provider. However, there are other challenges that plan consultants will need to work through with open MEPs. As smaller employers outsource more of their plan activities, it will be more important than ever to ensure that the features elected align with their automated systems.

WHAT’S THE FUTURE HOLD?Recognizing that there are

opportunities and challenges as part of the increasing complexity of pre-approved plans, where will the pre-approved plan program itself be headed?

A regular feature of IRS presentations is that the IRS’ employee plans resources have become extremely limited. The individually designed determination letter program was one of many first casualties of these resource limitations. However, pre-approved plans may not be immune from the reduced resources available to the IRS as the years continue to pass. The exact path forward is unclear, but it is definitely clear that interaction and resources from the IRS will continue to wane.

Plan consultants will need to be nimble and adapt to the complex challenges ahead. The future for many plan sponsors lies in pre-approved plans, but strong guidance from plan consultants will be more necessary than ever.

David N. Levine is a principal with the Groom Law Group, Chartered, in Washington, DC.

INCREASED USE OF PROGRESSIVE FEATURES

A key retirement focus in recent years has been to expand coverage and contribution levels through the use of automatic enrollment and automatic increase features. These features require significant coordination between service providers, often through a plan consultant, and can definitely achieve the coverage and contribution goals of many plan sponsors. In a pre-approved plan world, plan documents are drafted to provide a wide range of options, but reconciling elections with payroll processes and legal notice requirements holds the potential for significant operational failures. For example, employer payroll systems may not always align with how the adoption agreement provisions for a pre-approved plan apply the timing and manner of auto-escalation or auto-enrollment.

MORE LITIGATION Given the significant liabilities

that can result from inconsistencies between plan documents and plan operations, plan consultants implementing pre-approved plan documents will continue to face the threat of additional claims for liability when inevitable disconnects occur. Although service agreement terms and conditions may, in some cases, limit a plan consultant’s potential exposure, the continued focus on errors will likely increase risk to plan consultants and service providers.

OPEN MEPsOpen multiple employer plans

END OF THE IRS DETERMINATION LETTER PROGRAM

Over the past year, the IRS has been discussing and increasingly laying out its plan to eliminate the individually designed plan determination letter process. A key portion of this discussion has been the IRS’ efforts to encourage sponsors of individually designed plans to pre-approved plan documents. Although a majority of plans are already using pre-approved plans, the decision to transition potentially more complex plans from individually designed plans to pre-approved plans presents significant risks. Recognizing that adoption agreements are often long, complex documents, carefully coordinating this transition (including from one pre-approved plan document to another) carries significant risk of error and will require great care.

BUSINESS REALITIES RELATING TO PRE-APPROVED PLAN DOCUMENTS

As the data show, the costs of running a retirement plan continue to decline — especially in the area of TPA and recordkeeping fees. One item that is often a commoditized part of this process, and frequently outsourced by TPAs and recordkeepers, is the core pre-approved plan document. With these cost pressures, these documents, while maintained diligently by many providers (especially for Internal Revenue Code compliance items as part of the pre-approved plan process), do not always contain the level of detail in their fiduciary language often seen in complex individually designed plans. This distinction means that it is more important than ever, especially in a volume submitter world, that fiduciaries be properly identified in plan documents and that additional fiduciary provisions, as necessary, be considered for inclusion in supplemental provisions addendums as permitted under relevant pre-approved plan documents.

Each year that passes, the pre-approved plan process gets more and more complex.”

22 PLAN CONSULTANT | SPRING 2016

RECORDKEEPING

A look at three important concepts: eligible employers, ERISA exemptions and investment restrictions.

Key Issues in 403(b) Plan Takeovers

BY JOHN JEFFREY

In recent years, 403(b) plans have grown more similar to 401(k) plans as a result of changes in the Internal Revenue Code. However, it’s a faulty assumption to view a 403(b) plan as just another tax deferred savings option. The Code and ERISA still provide unique twists to 403(b) administration and plan design. While covering all of them is beyond the scope of this article, we’ll focus on three basic concepts relevant to every 403(b) new business client: employer eligibility, ERISA exemptions and investment restrictions.

23WWW.ASPPA-NET.ORG

determination letter confirming their tax exempt status. The letter will identify whether the entity qualifies for exempt status under Code Section 501(c)(3) or some other Code section.

ERISA EXEMPTIONSCertain 403(b) plans are

exempt from ERISA. Sponsors of these plans avoid many ERISA-imposed obligations, including the need to file Form 5500, large plan audits, ERISA 404a-5 participant disclosures, minimum age/service requirements and vesting restrictions. The following plans are exempt from ERISA coverage: • Government-sponsored 403(b)

plans. Congress excluded the federal government, states, their political subdivisions, agencies and instrumentalities from ERISA. This exemption is most frequently used by state colleges, universities or local school districts. Also, a state- or county-affiliated hospital may fall under this exemption. Each is considered an instrumentality of the state.

• Nonelecting church plans. ERISA excludes retirement plans established and maintained by a church or church-related organization. These employers may opt in to ERISA coverage by making a one-time irrevocable election under the Code.2 All other plans are exempt from ERISA and appropriately referred to as “non-electing” church plans.

• Minimal employer involvement (“deferral-only plans”). ERISA applies to retirement plans that are “established or maintained” by an employer. But does mere payroll deduction constitute establishment or maintenance of a plan? The DOL has addressed this question through a regulatory safe harbor.3 A plan is exempt from ERISA if all of the following criteria are met:

may offer 403(b) programs. The organization must be separate from the government and may not have regulatory or enforcement authority. Examples include county hospitals and libraries.

• For-profit subsidiaries cannot offer 403(b) plans. A taxable subsidiary of a 501(c)(3) organization cannot offer a 403(b) plan. A subsidiary that generates nonrelated business income must have its own “for-profit” plan, such as a 401(k). For example, assume that Hospital A owns Gift Shop B, Inc., which generates unrelated business income through the sale of merchandise. The employees of Gift Shop B cannot participate in Hospital A’s 403(b) plan.

Practice Pointer: Your service agreement should confirm the new client’s eligibility to offer a 403(b). If the client’s status is not clear, ask for its 501(c)(3) determination letter. Most nonprofit entities (other than churches) have obtained an IRS

EMPLOYER ELIGIBILITYThe Code defines the categories

of employers who may sponsor a 403(b) program. If an ineligible employer offers a 403(b), its employees are taxed on contributions and earnings. Eligible employers1 include: 1. educational organizations of a state,

a political subdivision of a state or its agency or instrumentality, and

2. charities qualifying under IRC 501(c)(3)

Employers in the first category are relatively easy to identify. They include state-sponsored universities and colleges as well as local public school districts. All are educational organizations that are instrumentalities of a state or a political subdivision.

On the other hand, charities may raise complications, including: • Not all non-profit entities are

charities. The Code provides tax exemption to numerous organizations such as labor unions, chambers of commerce, real estate boards, fraternal organizations, etc. These entities are exempt from income tax, but they are not charities as defined under Code Section 501(c)(3). Generally, a “charity” must be organized exclusively for religious, charitable, scientific, literary or educational purposes. Other tax exempt entities are not eligible to offer a 403(b). For example, a golf course is incorporated as a non-profit entity. It may be exempt from income taxation under Code Section 501(c)(4). However, the entity does not meet the Code Section 501(c)(3) definition of a charity and is not eligible to offer a 403(b) plan.

• Some governmental entities may be charities. The IRS has expanded the definition of a charity to include certain government-related entities with charitable purposes. These entities

1 In addition to these two categories, the Code includes a special category for religious ministers. They may defer income under section 403(b) regardless of whether their church sponsors a 403(b) program.

2 IRC §410(d). 3 DOL Reg. §2510.3-2(f ).

It’s a faulty assumption to view a 403(b) plan as just another tax deferred savings option. The Code and ERISA still provide unique twists to 403(b) administration and plan design.”

24 PLAN CONSULTANT | SPRING 2016

the employer cannot trigger the liquidation and wholesale transfer of plan assets. Each participant has control. If the participant doesn’t consent, the annuity remains with the insurance company. The employer can prevent future contributions to the annuity, but it is still a plan asset.

• Do the terms of the annuity prohibit transfer? Some annuity contracts contain provisions requiring liquidation over time. Even if the participant intends to transfer the proceeds to the new vendor, the contract can prevent it. For example, the annuity may require transfers to occur in installments over 10 years. Participants could transfer one-tenth of the contract value in Year 1, one-ninth in Year 2 and so on. The balance would remain locked up with the insurance company until the end of the transfer period.

• Will “stranded contracts” require an information sharing agreement? Whether the participant or the annuity terms prevent liquidation and transfer, the result is the same. The annuity is left behind with the original insurer. Unless it falls within an exception, the annuity is a plan asset requiring administration and an “information sharing agreement.”4 The agreement establishes procedures for sharing information between the employer and the insurer related to employment status, distributions, loans and tax reporting obligations. Often it will designate the new vendor as the party to coordinate this information.

• Are there surrender charges? Annuity contracts may have charges triggered upon liquidation of the contract.

• assuming control over hardships, distributions, loans and QDRO determinations.

Keep in mind that the safe harbor does not affect governmental and non-electing church 403(b)s. These plans are excluded from ERISA coverage by a statutory exemption based upon the status of the employer (i.e., government entity or church) and not the employer’s involvement in the plan.

Practice Pointer: Your service agreement should state whether the plan is exempt from ERISA and if so, the basis for the exemption. You should inquire about the plan’s ERISA status early in the new business process before discussions ensue about plan changes. If the plan relies upon the deferral-only safe harbor, encourage the employer to consult legal counsel if changing plan design or operation. The employer should understand the administrative and legal implications of moving from a non-ERISA plan to an ERISA plan. Also, many service contracts require the employer to determine eligibility for distributions, hardships, loans and QDROs. If the employer relies upon the deferral-only safe harbor, either you or some other third party (e.g., the annuity provider) must assume this responsibility.

INVESTMENT RESTRICTIONSThree types of funding vehicles

may be offered in a 403(b) plan: annuities, custodial accounts and retirement income accounts. Each funding arrangement comes with its own considerations. • Annuities. Annuities must be

offered by an insurance company and may consist of either group or individual annuity contracts. Four questions should be top of mind:• Do participants have control of the

transfer decision? Many annuity contracts require participant consent to liquidate. In that case, unlike a 401(k) plan,

• Deferral only: The plan cannot have a company match or nonelective contribution, direct or indirect. Match contributions to a separate 401(a) plan causes the 403(b) plan to lose safe harbor status.

• Totally voluntary: Employees must be able to opt out of participation.

• Participant enforcement rights: All rights under an annuity or custodial account must be enforceable solely by the employee.

• Limited employer control over vendors: For administrative ease, an employer may designate a list of 403(b) vendors from which employees may choose. However, if the employer limits employees to a single vendor, it may lose the safe harbor protection.

• Limited employer discretion: The employer may not exercise discretion over plan operations such as hardships, distributions, loans or QDRO determinations. These discretionary decisions must reside with either the plan’s investment vendor or third- party administrator.

If the plan fails to meet the above criteria, it loses the presumption that it is exempt from ERISA. However, it does not automatically create an ERISA plan. In that case, the employer must prove it has not “established or maintained” a plan based upon the facts and circumstances surrounding the employer’s involvement and plan design.

Employers relying upon the safe harbor should consider ERISA implications any time they change plan design or operation, but especially when:• adding a company match or non-

elective contribution; • moving the plan to a single

custodian/vendor; or

4 IRS Rev. Proc. 2007-71 provides exceptions to the information sharing agreement requirement. Generally, the exception applies to annuity contracts that have not received contributions since Jan. 1, 2005, and to certain other contracts issued between Jan. 1, 2005 and Jan. 1, 2009.

25WWW.ASPPA-NET.ORG

• Retirement Income Accounts. Retirement income accounts may only be offered by church plans. The account must be maintained pursuant to a separate plan stating that it intends to constitute an income retirement account. The account is not subject to the restrictions of an annuity or custodial account. For example, unlike a custodial account, the income retirement account may invest in assets other than registered mutual funds. In addition, the employer may commingle the retirement income account in a common fund with other church assets so long as there is a separate accounting and the fund is used solely for benefit payments.

Practice Pointer: Some 403(b) prototype-like documents may have language addressing a church plan with a retirement income account. Nevertheless, because of its unique nature, encourage attorney review of the plan document and investment line up to assure the plan’s continued ERISA exemption and Code compliance.

CONCLUSIONEmployer eligibility, ERISA

exemption and investment restrictions are three of the many issues that remain unique to 403(b) plans. Having a general understanding of these areas will avoid surprises for the employer and assure a smoother transition for your new business 403(b) client.

John Jeffrey is the corporate counsel for Alerus Retirement Solutions, a division of Alerus Financial, N.A. As a

national bank, Alerus provides trustee and custodial services, record keeping and third party administration to plans nationwide.

• Custodial Accounts. The Code allows a 403(b) plan to use a custodial account similar to a 401(k) trust account if the plan only invests in registered mutual funds. This requirement poses a challenge when seeking a stable value product, especially when moving a plan from an annuity to a custodial arrangement. The annuity will often have a “fixed” account with a stated rate of interest and guaranteed principal. Unlike in a 401(k) takeover, the custodial account cannot use a stable value fund as a replacement for the fixed account. A stable value fund is a collective trust, not a registered mutual fund. Some advisors may point out that a 2011 Revenue Ruling5 permits the use of collective trusts for 403(b) custodial accounts. However, that ruling requires the collective trust to only invest in mutual funds. A traditional stable value fund invests in non-mutual fund assets such as Guaranteed Investment Contracts (GICs) and GICs with insurance wrappers (synthetic GICs). Thus, it is not permitted in a 403(b) custodial account.

Practice Pointer: Custodial accounts may need to offer a money market fund as the plan’s stable value investment alternative. However, a money market fund will have lower returns than most fixed accounts.

In the alternative, the plan could use a fixed annuity for the stable value investment alternative. The balance of the account would use mutual funds in a custodial account. Logistics in participant trading may be an issue, but some insurance companies have addressed the problem by designing a stable value annuity that trades similar to a stable value fund.

The amount and triggering events changes will vary and are included in the contract language. Often the charge will be a percentage of contract value and will trail off over time. For example, the charge may be 7% in Year 1 and lessen by a percentage point over the next 7 years.

Practice Pointer: You should inquire about the existence of annuity contracts early in the new business process. If they exist, encourage the employer to pose written questions to the insurer regarding the ability to transfer plan assets, the need for participant consent, the restrictions on transfers and surrender charges, if any. Upon request, many insurers will estimate the surrender charges prior to actual liquidation of the contract.

Do not suggest methods to avoid a surrender charge. Often, contracts will have complex provisions, including “look-back” periods designed to prevent participant end-runs. You may think that you understand the exceptions to the charge, only to be surprised at the time of transfer. Leave contract interpretation to the insurer or the plan’s attorney.

If annuities require individual participant consent to transfer, then obtain information regarding surrender charges, distribution forms and transfer procedures from the insurer. Making the transfer more understandable and easier for participants will limit the number of “stranded” contracts.

Identify which non-transferable contracts may require an information sharing agreement. Consider the added costs and logistics of handling the “stranded” contracts and price accordingly in your service agreement.

5 Rev. Rul. 2011-1.

Plan Takeovers and Conversions: Pitfalls and Pointers (Part 2)

BY ROBERT E. (BOB) MEYER, JR.

Editor’s note: This is the second of a two-part series of feature articles. Part 1 was published in the Winter 2016 issue.

FEATURE

One of the certainties in the life of every plan is a change in providers, whether an investment advisor, custodian, recordkeeper or TPA. The

purpose of this two-part article is to provide guidelines for TPAs going through the lengthy and detailed process of working with plan sponsors to effect a seamless transition.

In Part 1 of this series, we looked at the takeover process in terms of the TPA communicating with the sponsor and investment advisor and requesting the legal document, participant indicative information and plan financial records. In Part 2, we will examine how having this information plays out in the “life cycle” of a plan takeover.

There are three stages in the life cycle of a takeover: remote preparation, proximate preparation, and immediate preparation.

27WWW.ASPPA-NET.ORG

transferred in-kind, what forms need to be executed and by whom?

13. In the case of a transfer at or near the end of a plan year, who will perform recordkeeping and compliance services?Successful takeovers require

a good working relationship with the prior TPA. Knowing who is providing recordkeeping and compliance services can make the takeover simpler. As the takeover specialists grow in their experience, they get a feel for the quality of data provided from the various vendors, and this knowledge assists in the budgeting of time for the takeover and how it affects scheduling other takeovers that are in the pipeline. With every new takeover project, the TPA should be given the information on who currently holds the assets and who is performing recordkeeping and compliance services.

It is important for the successor TPA to know how the conversion data will be given to them. Ideally, the existing TPA can produce a test file with all the data that will be provided when the transfer occurs. Many providers will do so at no charge to the plan sponsor, and will disclose it in their deconversion agreements. If it is possible for the information to be sent electronically,

the test data should include a map of the files that are sent.

Very seldom will the existing provider not be able to generate and send electronic records; however, there are still some that will only produce hard copy reports. If the TPA designate knows this sooner rather than later, then necessary modifications to the schedule can be made with a minimum of dislocation and stress. If necessary, the sponsor, RIA and other interested parties should discuss any changes to the takeover schedule and negotiate fee alterations due to this situation.

It could be a daunting task to get the records and reports, especially if the relationship of the TPA with the plan sponsor is strained, but most TPAs are willing to assist their successors, as they may have to come looking for information from them on a takeover going the other way.

A valuable benefit that can be realized from a working relationship with the existing TPA is obtaining the previous year’s valuation reports. By comparing the census information in them to the census information given by the plan sponsor, terminated participants who still have plan balances can be identified earlier in the takeover process.

Special difficulties are encountered when the plan has outside brokerage accounts (often referred to as the “brokerage window”) as part of its investment lineup:1. There is no possibility of

obtaining these reports in a single electronic or hard copy file.

2. All of the individual brokerage statements from the beginning of the plan year have to be obtained, and the TPA is charged with reconstructing the plan year for each participant and each brokerage account they have.

3. The brokerage statements do not report activity and balances in each source of funding. It is imperative, then, that the new TPA receives not only all of

REMOTE PREPARATION

Remote preparation begins when the plan sponsor has committed to migrate the plan to a new provider. A good sign that the work is about to begin is the receipt of all the service agreements and fee schedules. The TPA makes the initial request for legal documents, census information and plan records.

In this stage, many other important questions and issues have to be resolved, even as the information requests are being made and followed up on. The sponsor, investment advisor and existing service providers must understand their roles in the transfer of the plan and know the answers to a number of questions, including the following:1. Is everyone in agreement on the

transfer date?2. Have the prior providers (TPA

and custodian) been notified?3. What are the old TPA’s fees for a

plan deconversion and how will they be paid?

4. Are there any issues with specific investments, such as guaranteed investment contracts or stable value funds, that might affect the transfer of the plan?

5. Does the prior custodian have a time standard, such as 45 or 60 days from date of notification, that will affect when the plan can be transferred?

6. If a blackout is necessary, when will the blackout period start and end?

7. Who will be responsible for drafting and distributing the notice?

8. Will the assets be liquidated or transferred in-kind?

9. Will holdings be “mapped” from one fund to another or invested according to investment elections set by the participant?

10. What is the lag time between the final liquidation of the assets and the wire transfer of the proceeds?

11. When will the final records be provided and to whom?

12. If there are any assets to be

It could be a daunting task to get the records and reports, especially if the relationship of the TPA with the plan sponsor is strained.”

28 PLAN CONSULTANT | SPRING 2016

the brokerage statements, but also the following information so that accurate records will be established and maintained.Overcoming these difficulties

requires the following:1. The prior year-end valuation

report in order to establish the beginning balances for each participant in each source.

2. A reconciliation of the balances reported on the year-end brokerage statements to the value reported on the valuation report, to account for any receivables or payables due at year end.

3. A report from the plan sponsor that details all the contributions and distributions made in the current plan year for each participant and each source of money.All the parties involved in