Embed Size (px)

Citation preview

PowerPoint slides by:

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada

Michael L. Hockenstein Commerce Department • Vanier College

Intermediate Accounting

Thomas H. BeechySchulich School of Business, York University

Joan E. D. ConrodFaculty of Management,

Dalhousie University

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-2

Criteria for Accounting Choices

Chapter 2

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-3

Introduction

This chapter looks at the financial statement concepts and principles that guide accounting choices

These concepts and principles underlie the exercise of professional judgement

It is the these sets of principles that provide the criteria that distinguish professional judgement from the exercise of uninformed opinion or bias

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-4

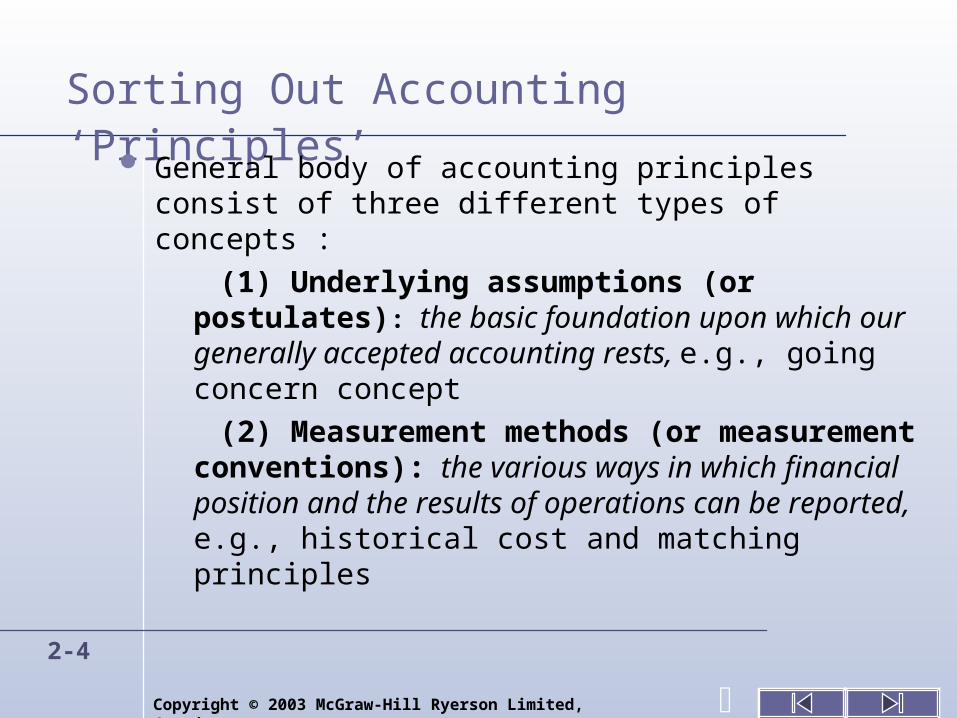

Sorting Out Accounting ‘Principles’ General body of accounting principles consist of three

different types of concepts :

(1) Underlying assumptions (or postulates): the basic foundation upon which our generally accepted accounting rests, e.g., going concern concept

(2) Measurement methods (or measurement conventions): the various ways in which financial position and the results of operations can be reported, e.g., historical cost and matching principles

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-5

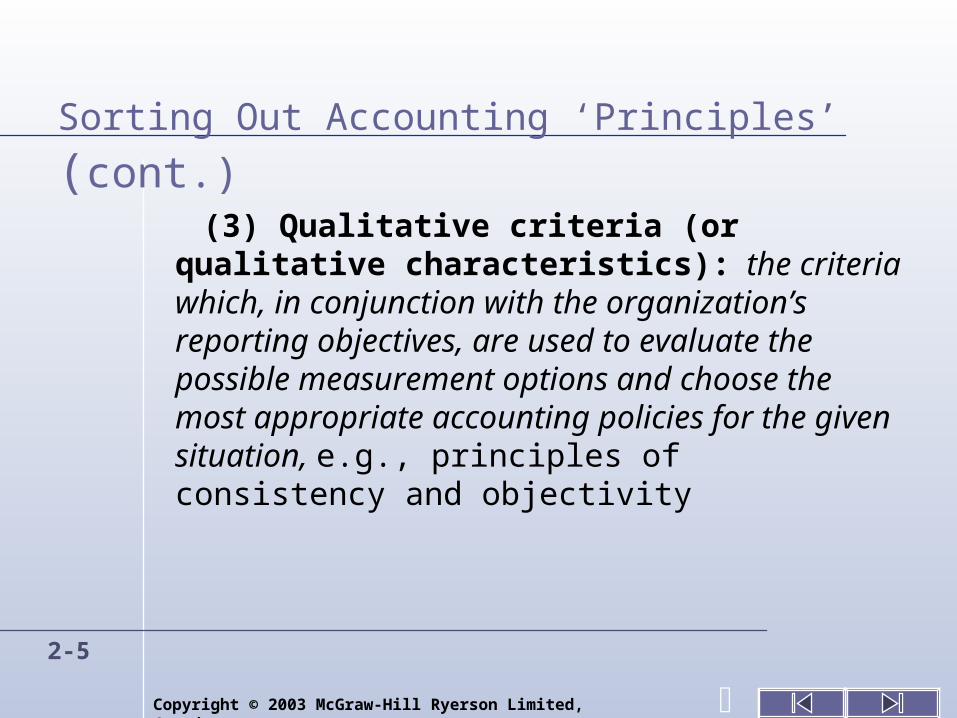

Sorting Out Accounting ‘Principles’ (cont.)

(3) Qualitative criteria (or qualitative characteristics): the criteria which, in conjunction with the organization’s reporting objectives, are used to evaluate the possible measurement options and choose the most appropriate accounting policies for the given situation, e.g., principles of consistency and objectivity

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-6

Sorting Out Accounting ‘Principles’ (cont.)

To construct financial statements for a particular enterprise, it is necessary:

to establish the facts of the business and its operating and economic environment

to determine the objectives of financial reporting

to develop the statements by using situation-appropriate accounting policies to measure the elements of the financial statements

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-7

General Purpose Statements

General purpose statements: those prepared for distribution to a well, undefined public

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-8

Professional Judgement In Accounting In any specific situation, an accountant exercises professional judgement about alternative measurement methods, (both accounting policies and accounting estimates) by taking into account several factors: the users of the financial statements, and

their specific information needs the motivations of managers the organization’s operations its reporting constraints, if any, e.g., audit

requirements, reporting to securities regulators, constraints imposed by foreign owners, etc.

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-9

Underlying Assumptions

Six basic assumptions significantly affect the recording, measuring, and reporting of accounting information: time-period assumptionseparate entity assumptioncontinuity assumptionpropriety assumptionunit of measure assumptionnominal dollar capital maintenance assumption

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-10

Time Period Assumption

Time period assumption: changes in a business’s financial position reported over a series of shorter time periods

Accruals: the accounting recognition of assets and liabilities that have not yet been realized as a cash flow

Deferrals: the delayed recognition of costs and receipts that have been realized through cash flows but have not yet contributed to the earnings process as expenses and revenues

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-11

Separate Entity Assumption

Separate entity assumption: all accounting records and reports are developed from the viewpoint of a single entity, whether it is a proprietorship, a partnership, or a corporation

The assumption is that an individual's transactions are distinguishable from those of the business he or she might own.

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-12

Separate Entity Assumption (cont.)

A corporation is an entity that is legally and for taxation purposes quite distinct from its owners, even if the corporation is a private family corporation or has a single shareholder

Partnerships and sole proprietorships do not share the legal and tax status of separate entities; in law and in taxation, they are viewed as an extension of their owners

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-13

Continuity Assumption

Continuity assumption (going-concern assumption): the business entity is expected not to liquidate but to continue operations for the foreseeable future

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-14

Proprietary Assumption (Concept)

The proprietary concept: an organization’s financial condition and results of operations are reported from the point of view of the owners, or proprietors in an economic sense

The entity concept: the owners are just one of many participants in the enterprise

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-15

Proprietary Assumption (cont.)

The fund concept: the basic accounting function is to trace the flow of funds in the organization

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-16

Unit of Measure Assumption

Unit of measure assumption: results of a business's economic activities can be reported in terms of a standard monetary unit throughout the financial statements

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-17

Nominal Dollar Capital Maintenance Assumption

The relative value of a currency can be measured in two ways: in relation to the value of other currencies (its

exchange rate) in relation to the amount of goods and services that

it will buy (its purchasing power) In Canada and the United States, accounting is

performed under the assumption that every dollar of revenue and expense has the same value

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-18

Nominal Dollar Capital Maintenance Assumption(cont.)

Three other alternative approaches to this problem:

nominal dollar capital maintenance (or maintenance of financial capital)

constant dollar capital maintenanceproductive capacity capital maintenance

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-19

Qualitative Criteria

Relevance Reliability Understandability Comparability Objectivity Conservatism The Trade-off between

Cost and Benefit

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-20

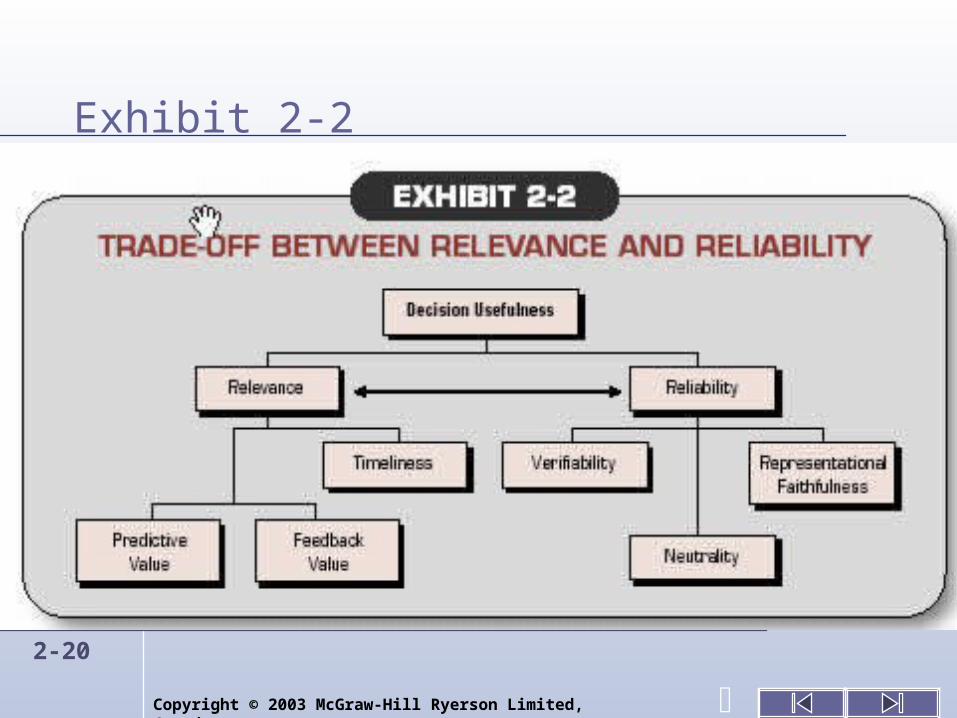

Exhibit 2-2

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-21

Relevance

Theoretically, relevance is the most important qualitative characteristic. If accounting information is to be of any use, it must:

be relevant for its intended use make a difference to the external decision-makers

who use financial reports

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-22

Relevance (cont.)

Additional characteristics that relate to relevance are:

timelinesspredictive value feedback value

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-23

Relevance (cont.)

Timeliness

Accounting information should be timely if it is to be useful to users for making decisions

Lack of timeliness reduces relevance

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-24

Relevance (cont.)

Predictive value Accounting information should be helpful to external

decision-makers by increasing their ability to make predictions about the outcome of future events

Decision-makers working from accounting information that has little or no predictive value are merely speculating intuitively

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-25

Relevance (cont.)

Feedback valueAccounting information should be helpful to external

decision-makers who are confirming past predictions or making updates, adjustments, or corrections to predictions

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-26

Reliability

Information is reliable if users can depend on it as a sufficiently accurate measure of what it is intended to measure

There are three components to reliability:Representational faithfulness

(including substance over form)VerifiabilityFreedom from bias (or neutrality)

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-27

Understandability

Information must be

understandable to be

useful to users in their

decision-making

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-28

Comparability Comparability: a characteristic of the relationship

between two pieces of information rather than of a particular piece of information by itself

Consistency: entails using the same accounting from year to year within a firm

Uniformity: companies with similar transactions and similar circumstances use the same accounting treatments

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-29

Objectivity – the ‘Missing’ Criterion

Objectivity can be viewed as being one or a combination of the following characteristics:

quantifiabilityverifiability freedom from biasnon-arbitrariness

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-30

Conservatism

When uncertainty exists, estimates of a conservative nature attempt to ensure that assets, revenues, and gains are not overstated

Conversely, liabilities, expenses, and losses should not be understated

Conservatism does not encompass the deliberate understatement of assets, revenues, and gains or the deliberate overstatement of liabilities, expenses, and losses [CICA 1000.21]

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-31

The Trade-off between Cost and Benefit

The concept of cost/benefit effectiveness: any accounting measurement or disclosure should result in greater benefits to the users than it costs to prepare and present

If there are no external users of a private company’s financial statements (other than Canada Customs and Revenue Agency), then there is no benefit to be derived from incurring higher accounting costs

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-32

Elements of Financial Statements

Elements: the building blocks of financial statements

They include:AssetsLiabilitiesOwners’ equityRevenueExpensesGains Losses

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-33

Recognition, Realization, and Accrual

Recognition: the process of measuring and including an item in the financial statements

The item is given a title and a numerical value

Recognition applies to all financial statement elements in all accounting entities

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-34

Recognition, Realization, and Accrual (cont.)

Realization: the process of converting an asset, liability, or commitment into a cash flow

A receivable is said to be realized when it is collected

Revenues are realized when received

Expenses and liabilities are realized when the cash payment occurs

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-35

Accrual Concept

Accrual Concept: the recognition of the effects of transactions and events prior to their realization

Assets are recognized when we have the right to receive their benefits, and liabilities are recognized when we take on the obligation to deliver cash (or other assets) or services in the future

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-36

Measurement Conventions

Measurement: the process of determining the amount at which an item is recognized in the financial statements

There are four pervasive measurement conventions:

Historical Cost Convention Revenue Recognition Convention Matching Convention Full Disclosure

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-37

Historical Cost Convention

The historical cost convention: the actual acquisition cost used for initial accounting recognition purposes

The cost principle: assumes that assets are acquired in business transactions conducted at arm's length

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-38

Historical Cost Convention (cont.)

If an asset is acquired via some means other than cash, the cost of the asset is based on the value of the consideration given

Consideration is whatever the buyer gives the seller

The cost principle provides guidance primarily at the initial acquisition date

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-39

Revenue Recognition Convention

The revenue recognition convention: the recognition and reporting of revenues when all three of the recognition criteriadefinition, measurability, and probability–are met

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-40

Revenue Recognition Convention (cont.)

Traditionally, four conditions must be met to satisfy the revenue recognition convention:

all significant acts required of the seller have been performed

consideration is measurablecollection is reasonably assured the risks and rewards of ownership have passed to

the buyer

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-41

Matching Convention Matching: all expenses incurred in earning

revenue should be recognized in the same period that the revenue is recognized, e.g., if revenue is carried over (deferred) for

recognition in a future period, any related expenses should also be carried over or deferred, since they are incurred in earning that revenue

If revenue is recognized in the current period but there are expenditures yet to be incurred in future periods, the expenses are recognized and a liability is created (e.g., the estimated provision for warranty costs)

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-42

Full Disclosure

Full disclosure: the financial statements should report all relevant information bearing on the economic affairs of a business enterprise

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-43

Full Disclosure (cont.)

A useful guide to deciding what to disclose is the following:Disclose items not in the regular or

normal activities of the businessDisclose items reflecting changes

in expectationsDisclose that which a statute or

contract requires to be disclosedDisclose new activities or major

changes in old ones

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-44

The Exercise Of Professional Judgement

Professional judgement permeates the work of a professional accountant, and it involves an ability to build accounting measurements that take into account: the objectives of financial reporting in each

particular situation the facts of the business environment and

operations the organization’s reporting constraints (if any)

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada 2-45

Making Choices In Accounting: The Exercise Of Professional Judgement (cont.)

Choices of accounting policies, accounting estimates, and accounting measurement methods are then based on tests of the validity of the underlying assumptions, followed by an evaluation of the various possible measurement methods with reference to the qualitative characteristics