Embed Size (px)

Citation preview

PPP Americas 2010Funding for PPPsCassio SchmittSantander Global Banking & Markets

Confidential | May 2010

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg2

AgendaPPP Americas 2010

PPP Projects – Investment Opportunities

Sources of Financing for PPPs in Brazil

Risk Mitigation and Guarantees

Case Study: Line 4 of the SP Metro

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg3

Investment OpportunitiesPPP Americas 2010

First phase - Investment in PPP Proyects

The PPP Law was approved in Brazil at the end of 2004, officially instituting the public-private partnership program in Brazil.

PPP interest has gone through different phases in the last years, from great expectations to difficult practical implementation issues.

A few number of projects have been auctioned or structured until now:

Metro - Line 4 of the São Paulo Metro (State level)

Water & Sewage – Rio das Ostras (Municipality level)

Road Concession – MG 050 (State level)

“Prison” – Itaquitinga Integrate Ressocialization Center - PE (State level)

Hospital – Hospital do Suburbio – BA (State level)

Irrigation – Pontal/PE Irrigation Project (State level)

What is the perception on PPPs as a “brand name”? General view is not positive. There is yet a lot do, and need to start presenting results.

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg4

Investment OpportunitiesPPP Americas 2010

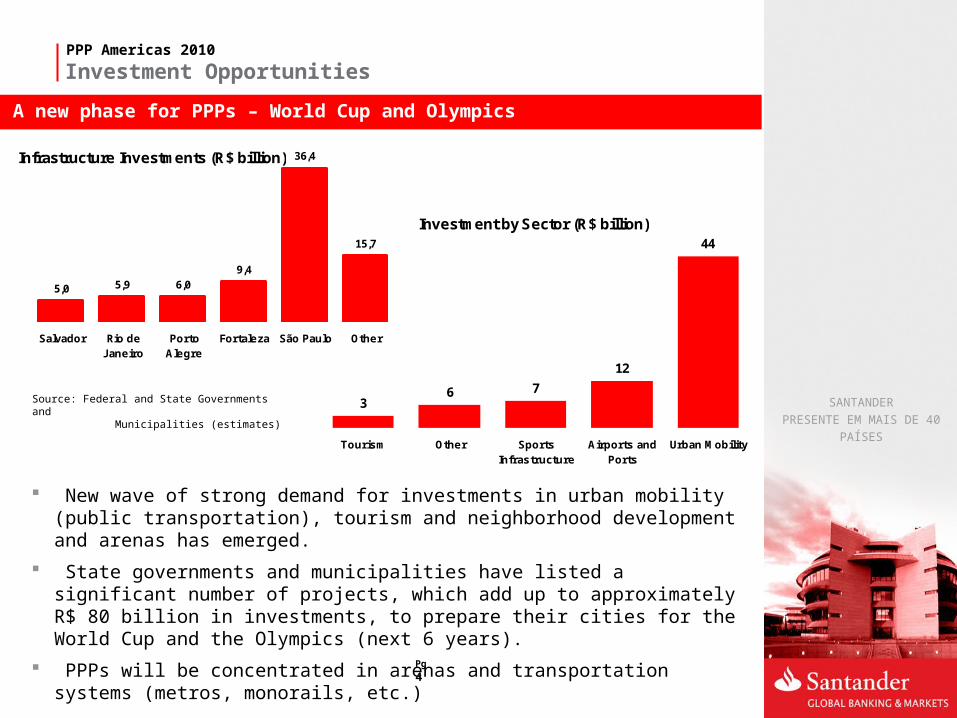

A new phase for PPPs – World Cup and Olympics

New wave of strong demand for investments in urban mobility (public transportation), tourism and neighborhood development and arenas has emerged.

State governments and municipalities have listed a significant number of projects, which add up to approximately R$ 80 billion in investments, to prepare their cities for the World Cup and the Olympics (next 6 years).

PPPs will be concentrated in arenas and transportation systems (metros, monorails, etc.)

Source: Federal and State Governments and Municipalities (estimates)

Investment by Sector (R$ billion)

36 7

12

44

Tourism Other SportsInfrastructure

Airports andPorts

Urban Mobility

Infrastructure Investments (R$ billion)

5,0 5,9 6,09,4

36,4

15,7

Salvador Rio deJaneiro

PortoAlegre

Fortaleza São Paulo Other

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg5

Investment OpportunitiesPPP Americas 2010

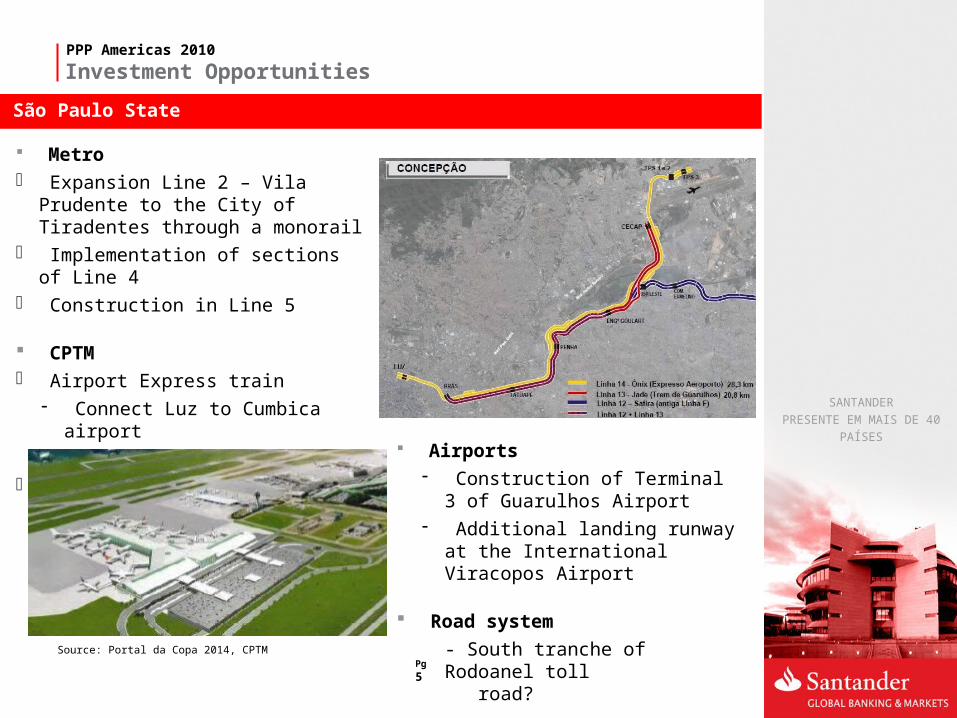

Metro- Expansion Line 2 – Vila Prudente to the

City of Tiradentes through a monorail- Implementation of sections of Line 4- Construction in Line 5

CPTM- Airport Express train

- Connect Luz to Cumbica airport- Extension - 28 Km

- Modernization of Lines 7 and 12

São Paulo State

Source: Portal da Copa 2014, CPTM

Airports- Construction of Terminal 3 of

Guarulhos Airport- Additional landing runway at the

International Viracopos Airport

Road system

- South tranche of Rodoanel toll road?

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg6

PPP Americas 2010

Investment Opportunities

PPP Challenges

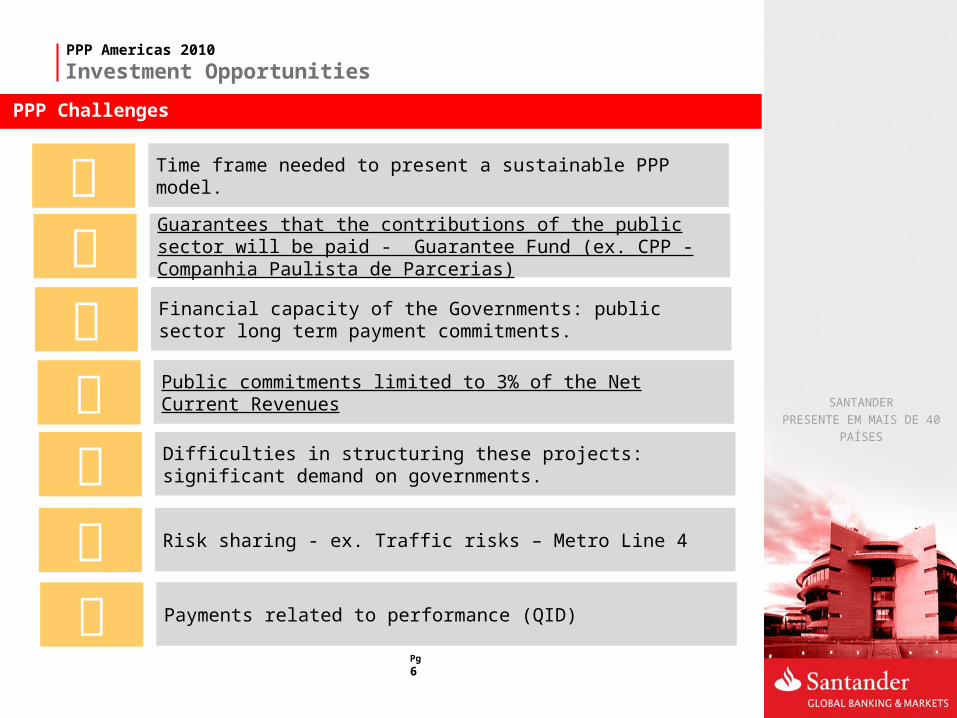

Time frame needed to present a sustainable PPP model.

Risk sharing - ex. Traffic risks – Metro Line 4Payments related to performance (QID)

Guarantees that the contributions of the public sector will be paid - Guarantee Fund (ex. CPP - Companhia Paulista de Parcerias)Financial capacity of the Governments: public sector long term payment commitments.Public commitments limited to 3% of the Net Current RevenuesDifficulties in structuring these projects: significant demand on governments.

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg7

Sources of Financing for PPPsPPP Americas 2010

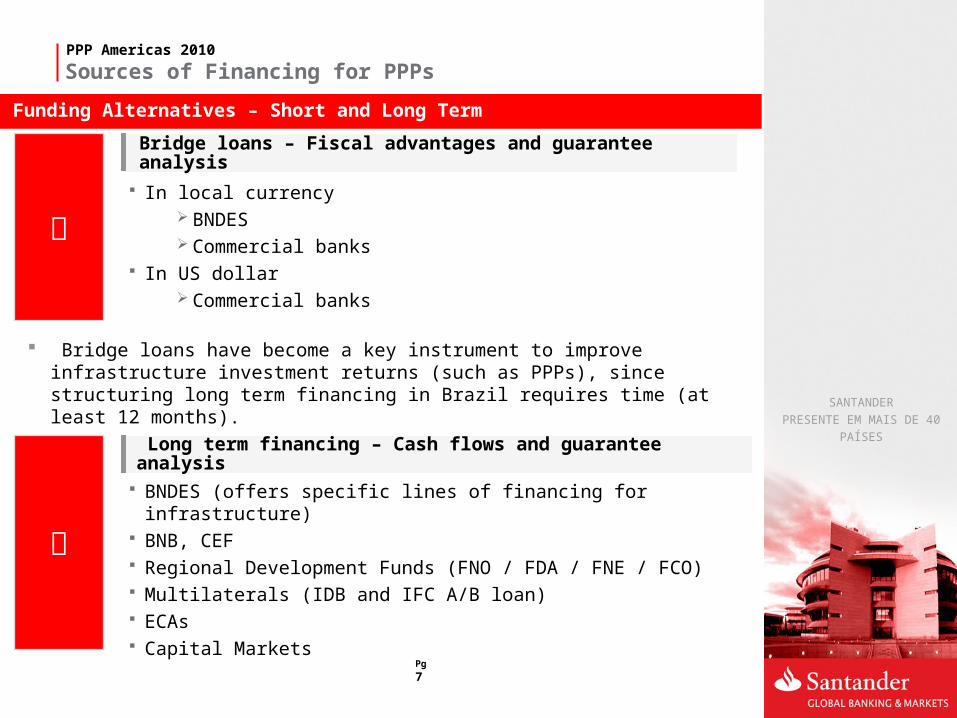

In local currency

BNDES Commercial banks

In US dollar Commercial banks

Bridge loans – Fiscal advantages and guarantee analysis

BNDES (offers specific lines of financing for infrastructure) BNB, CEF Regional Development Funds (FNO / FDA / FNE / FCO) Multilaterals (IDB and IFC A/B loan) ECAs Capital Markets

Long term financing – Cash flows and guarantee analysis

Funding Alternatives – Short and Long Term

Bridge loans have become a key instrument to improve infrastructure investment returns (such as PPPs), since structuring long term financing in Brazil requires time (at least 12 months).

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg8

Sources of Financing for PPPsPPP Americas 2010

Debt Structures in Brazil

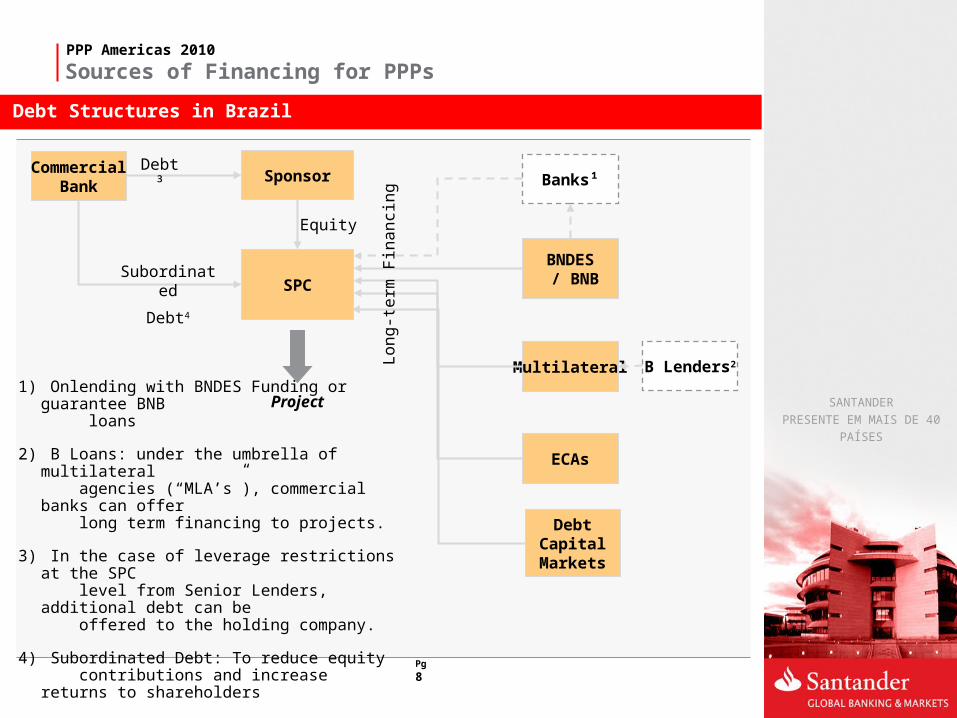

1) Onlending with BNDES Funding or guarantee BNB loans

2) B Loans: under the umbrella of multilateral agencies (“MLA’s”), commercial banks can offer

long term financing to projects.

3) In the case of leverage restrictions at the SPC level from Senior Lenders, additional debt can be offered to the holding company.

4) Subordinated Debt: To reduce equity contributions and increase returns to shareholders

Sponsor

SPC

BNDES / BNB

Banks¹

Multilateral

ECAs

B Lenders2

Equity

ProjectL

on

g-t

erm

Fin

an

cin

g

Debt Capital Markets

CommercialBank

Debt³

Subordinated

Debt4

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg9

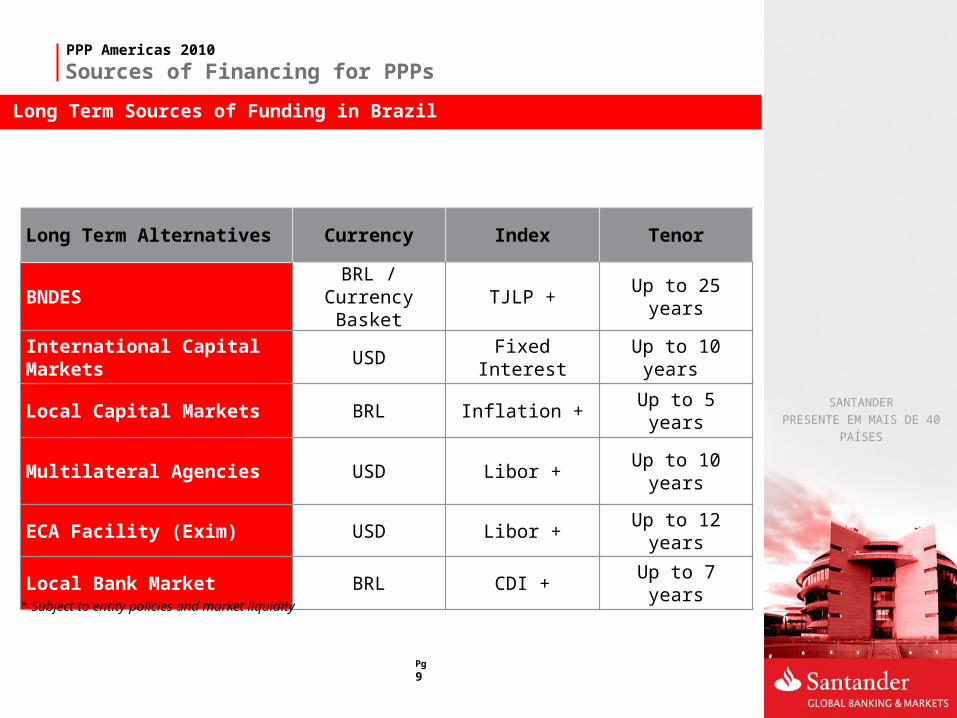

Sources of Financing for PPPsPPP Americas 2010

Long Term Alternatives Currency Index Tenor

BNDES BRL / Currency Basket TJLP + Up to 25 years

International Capital Markets USD Fixed Interest Up to 10 years

Local Capital Markets BRL Inflation + Up to 5 years

Multilateral Agencies USD Libor + Up to 10 years

ECA Facility (Exim) USD Libor + Up to 12 years

Local Bank Market BRL CDI + Up to 7 years

* Subject to entity policies and market liquidity

Long Term Sources of Funding in Brazil

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg10

Sources of Financing for PPPs

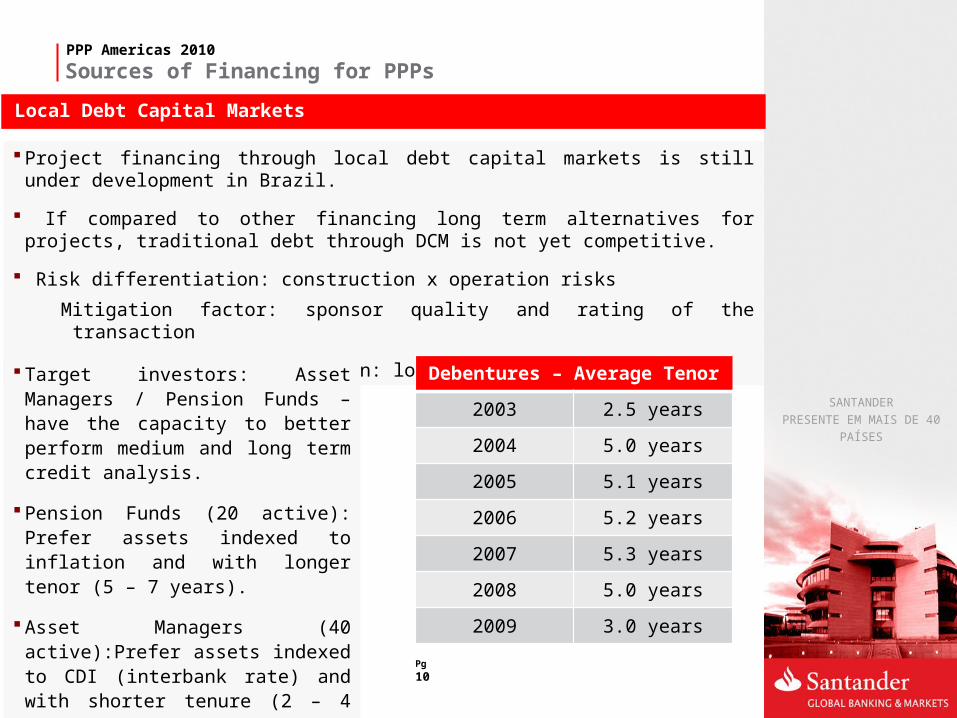

Project financing through local debt capital markets is still under development in Brazil.

If compared to other financing long term alternatives for projects, traditional debt through DCM is not yet competitive.

Risk differentiation: construction x operation risks

Mitigation factor: sponsor quality and rating of the transaction

Market and demand concentration: low asset liquidity

PPP Americas 2010

Local Debt Capital Markets

Target investors: Asset Managers / Pension Funds – have the capacity to better perform medium and long term credit analysis.

Pension Funds (20 active): Prefer assets indexed to inflation and with longer tenor (5 – 7 years).

Asset Managers (40 active):Prefer assets indexed to CDI (interbank rate) and with shorter tenure (2 – 4 years).

Debentures – Average Tenor

2003 2.5 years

2004 5.0 years

2005 5.1 years

2006 5.2 years

2007 5.3 years

2008 5.0 years

2009 3.0 years

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg11

Risk Mitigation and GuaranteesPPP Americas 2010

Project Risk Management

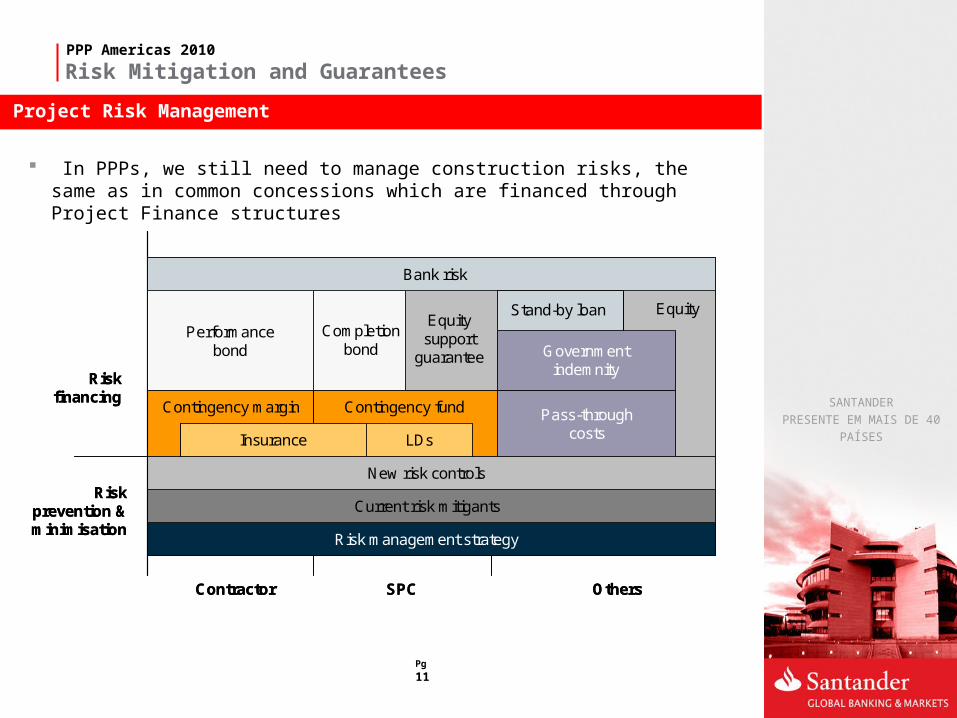

In PPPs, we still need to manage construction risks, the same as in common concessions which are financed through Project Finance structures

Risk management strategy

Current risk mitigants

New risk controls

Insurance

Contractor SPC Others

Performancebond

Contingency margin Contingency fund

Equity

Risk financing

Government indemnity

LDs

Risk prevention & minimisation

Equity support

guarantee

Completion bond

Bank risk

Stand-by loan

Pass-through costs

Risk management strategy

Current risk mitigants

New risk controls

InsuranceInsurance

Contractor SPC Others

Performancebond

Contingency margin Contingency fund

Equity

Risk financing

Government indemnity

LDs

Risk prevention & minimisation

Equity support

guarantee

Completion bond

Bank risk

Stand-by loan

Pass-through costs

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg12

Risk Mitigation and GuaranteesPPP Americas 2010

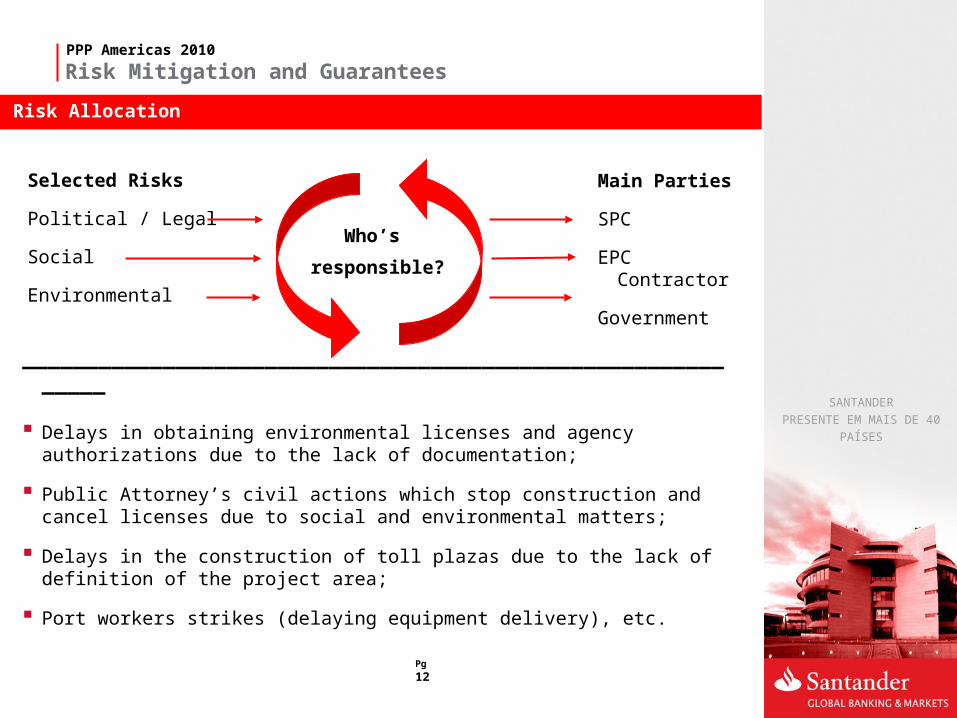

Risk Allocation

Main Parties

SPC

EPC Contractor

Government

Selected Risks

Political / Legal

Social

Environmental

Who’s

responsible?

____________________________________________________________

Delays in obtaining environmental licenses and agency authorizations due to the lack of documentation;

Public Attorney’s civil actions which stop construction and cancel licenses due to social and environmental matters;

Delays in the construction of toll plazas due to the lack of definition of the project area;

Port workers strikes (delaying equipment delivery), etc.

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg13

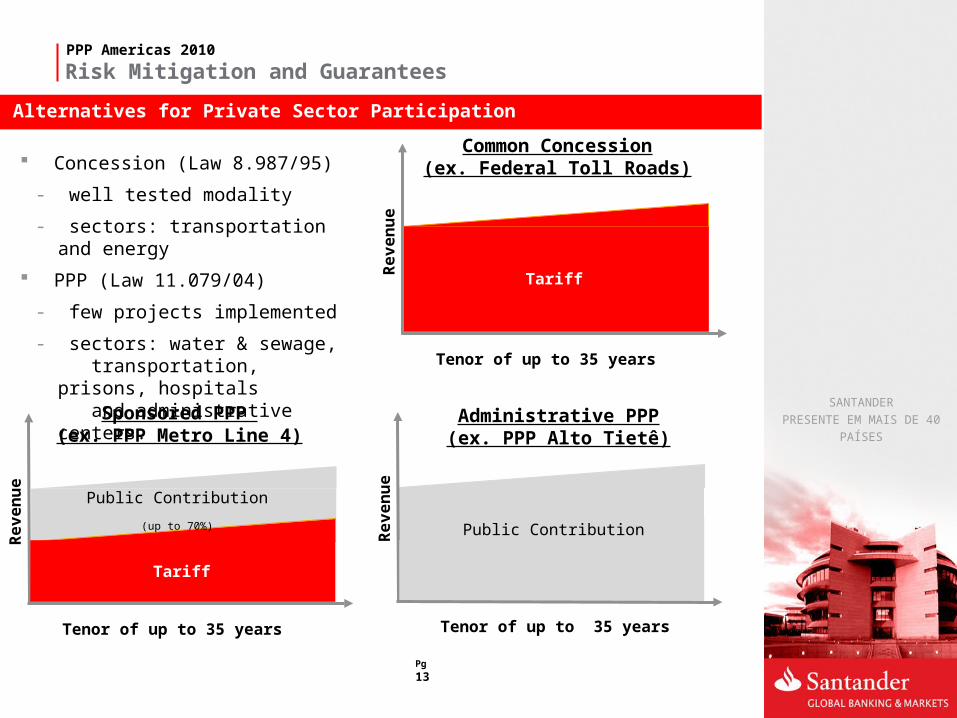

Risk Mitigation and GuaranteesPPP Americas 2010

Alternatives for Private Sector Participation

Tenor of up to 35 years

Reven

ue

Tariff

Reven

ue

Tenor of up to 35 years

Public Contribution

Common Concession(ex. Federal Toll Roads)

Administrative PPP(ex. PPP Alto Tietê)

Tenor of up to 35 years

Reven

ue

Public Contribution

(up to 70%)

Tariff

Sponsored PPP (ex. PPP Metro Line 4)

Concession (Law 8.987/95)

- well tested modality

- sectors: transportation and energy

PPP (Law 11.079/04)

- few projects implemented

- sectors: water & sewage, transportation, prisons, hospitals and administrative centers.

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg14

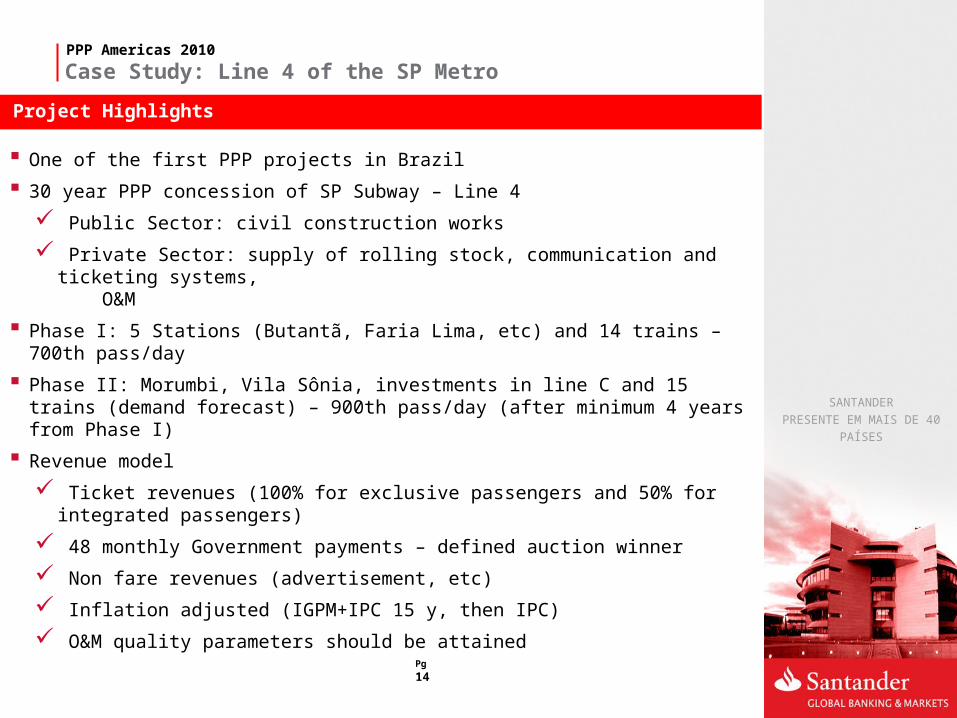

Case Study: Line 4 of the SP MetroPPP Americas 2010

Project Highlights

One of the first PPP projects in Brazil

30 year PPP concession of SP Subway – Line 4

Public Sector: civil construction works

Private Sector: supply of rolling stock, communication and ticketing systems, O&M

Phase I: 5 Stations (Butantã, Faria Lima, etc) and 14 trains – 700th pass/day

Phase II: Morumbi, Vila Sônia, investments in line C and 15 trains (demand forecast) – 900th pass/day (after minimum 4 years from Phase I)

Revenue model

Ticket revenues (100% for exclusive passengers and 50% for integrated passengers)

48 monthly Government payments – defined auction winner

Non fare revenues (advertisement, etc)

Inflation adjusted (IGPM+IPC 15 y, then IPC)

O&M quality parameters should be attained

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg15

Case Study: Line 4 of the SP MetroPPP Americas 2010

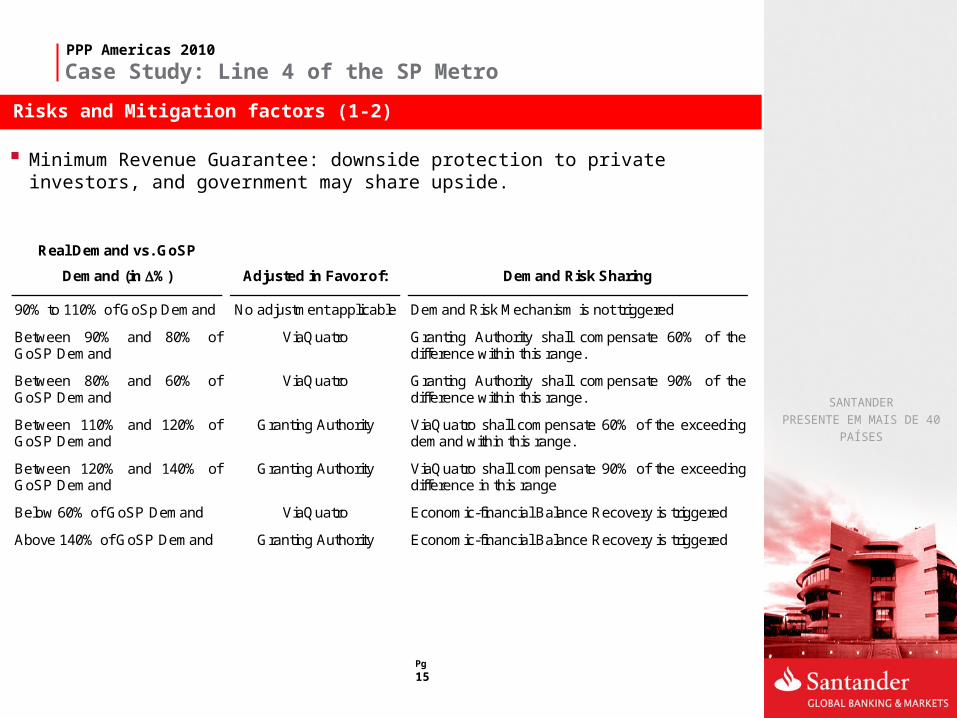

Risks and Mitigation factors (1-2)

Minimum Revenue Guarantee: downside protection to private investors, and government may share upside.

Real Demand vs. GoSP

Demand (in %)

Adjusted in Favor of:

Demand Risk Sharing

90% to 110% of GoSp Demand No adjustment applicable Demand Risk Mechanism is not triggered

Between 90% and 80% of GoSP Demand

ViaQuatro Granting Authority shall compensate 60% of the difference within this range.

Between 80% and 60% of GoSP Demand

ViaQuatro Granting Authority shall compensate 90% of the difference within this range.

Between 110% and 120% of GoSP Demand

Granting Authority ViaQuatro shall compensate 60% of the exceeding demand within this range.

Between 120% and 140% of GoSP Demand

Granting Authority ViaQuatro shall compensate 90% of the exceeding difference in this range

Below 60% of GoSP Demand ViaQuatro Economic-financial Balance Recovery is triggered

Above 140% of GoSP Demand Granting Authority Economic-financial Balance Recovery is triggered

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg16

Case Study: Line 4 of the SP MetroPPP Americas 2010

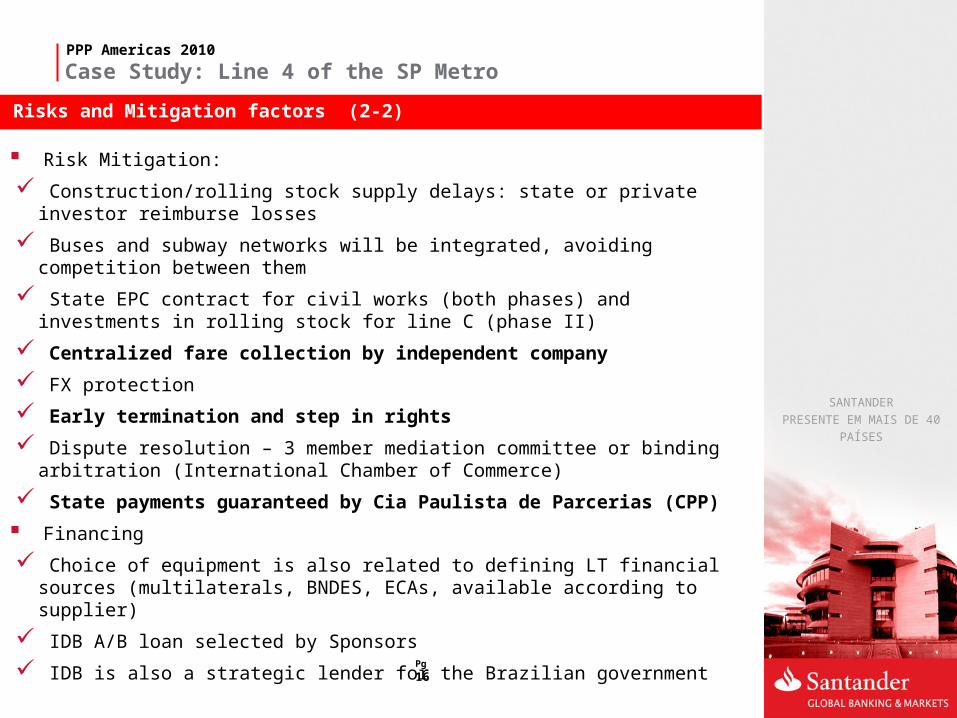

Risks and Mitigation factors (2-2)

Risk Mitigation:

Construction/rolling stock supply delays: state or private investor reimburse losses

Buses and subway networks will be integrated, avoiding competition between them

State EPC contract for civil works (both phases) and investments in rolling stock for line C (phase II)

Centralized fare collection by independent company

FX protection

Early termination and step in rights

Dispute resolution – 3 member mediation committee or binding arbitration (International Chamber of Commerce)

State payments guaranteed by Cia Paulista de Parcerias (CPP)

Financing

Choice of equipment is also related to defining LT financial sources (multilaterals, BNDES, ECAs, available according to supplier)

IDB A/B loan selected by Sponsors

IDB is also a strategic lender for the Brazilian government

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pg17

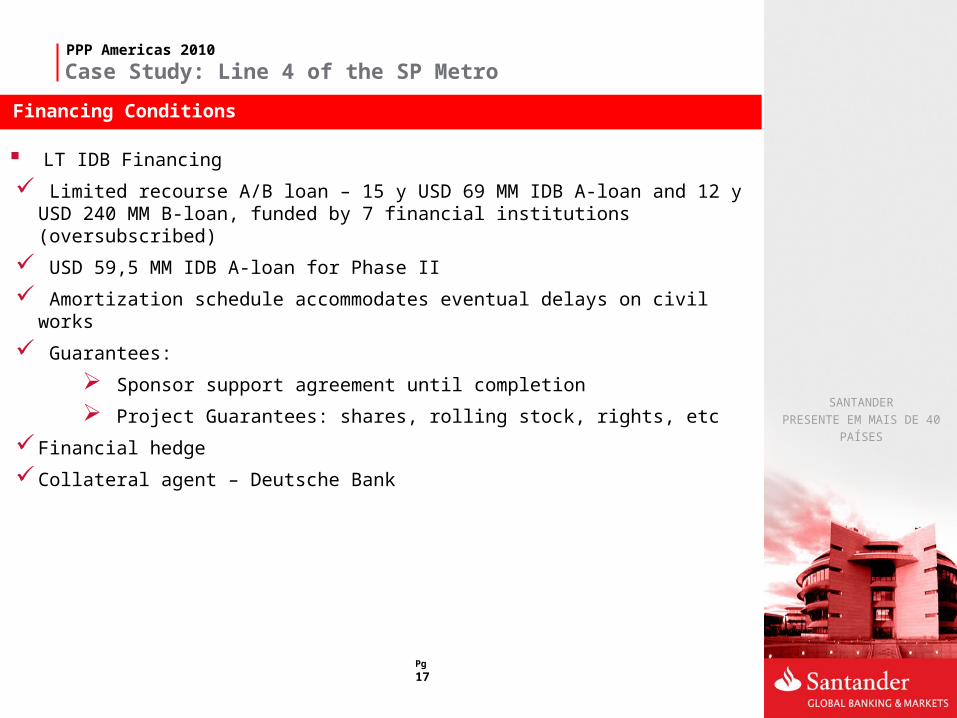

Case Study: Line 4 of the SP MetroPPP Americas 2010

Financing Conditions

LT IDB Financing

Limited recourse A/B loan – 15 y USD 69 MM IDB A-loan and 12 y USD 240 MM B-loan, funded by 7 financial institutions (oversubscribed)

USD 59,5 MM IDB A-loan for Phase II

Amortization schedule accommodates eventual delays on civil works

Guarantees:

Sponsor support agreement until completion

Project Guarantees: shares, rolling stock, rights, etc

Financial hedge

Collateral agent – Deutsche Bank

SANTANDERPRESENTE EM MAIS DE 40 PAÍSES

Pág18

Contact DetailsPPP Americas 2010

Todas as informações apresentadas neste documento são de natureza genérica e não têm por finalidade abordar as circunstâncias de nenhum indivíduo específico ou entidade. Embora tenhamos nos empenhado para prestar informações precisas e atualizadas, não há nenhuma garantia de sua exatidão na data em que forem recebidas nem de que tal exatidão permanecerá no futuro. Essas informações não devem servir de base para se empreender qualquer ação sem orientação profissional qualificada, precedida de um exame minucioso da situação em pauta.

Cassio Schmitt

Project & Acquisition Finance – Head

Santander Global Banking & MarketsAv. Juscelino Kubitscheck, 2235, 27th floor04543-011 - São Paulo, SP – Brazil

![Cassio Melo [cassio.ufpe at gmail]](https://img.pdfslide.net/doc/110x75/56814781550346895db4b3be/cassio-melo-cassioufpe-at-gmail.jpg)