Embed Size (px)

Citation preview

PRACTICAL ISSUES IN ISLAMIC FINANCE

3RD. ISLAMIC FINANCE INTELLECTUAL DISCOURSE (IFID)

HJ. ABDUL RAHMAN BIN MOHD YUSOFF CPIF. MIM-CPT

• Deputy President, Chartered Institute of Islamic Finance Professional (CIIF)

• Head Islamic Product & Business Development, OCBC Al-Amin Bank Berhad

• Chartered Professional in Islamic Finance (CPIF)

• Chartered Professional Trainer (MIM-CPT)

• Master of Science in Islamic Finance (INCEIF)

• Chartered Islamic Finance Professional (INCEIF)

• Master in Business Administration (KENTUCKY, USA)

• Bachelor of Science in Finance (INDIANA, USA)

• BSc. Finance (INDIANA, USA) 2

TRAINER’S PROFILE

FCSBF 3

What’s on the plate...

01 Islamic Finance Framework

02

03 Practical Issues in Shariah

04

Prohibition and Pillars

Lessons Learned & Moving Forward

FCSBF 4

The Islamic Finance Framework

#01

5

The Financial System Structure

Surplus units Financial

Intermediaries Deficit units

$ vs % $ vs %

• Individual

• Corporation

• GLCs

• Financial Inst.

• Deposits / Liabilities

• Financing / Assets

• Conventional / Islamic

• Fixed / Floating rates

• Types of products

• Individual

• Corporation

• GLCs

• Financial Inst.

“Issues in locking-in fixed & modest return with principal guaranteed to depositors whilst simultaneously

structuring a floating rate financing to customers with flexible collateral terms and conditions”

INTERNAL

6

Differences between Islamic Banking & Conventional Banking

“Challenges in creating public awareness on the conceptual differences and practical aspect

in Islamic Banking & Finance”

INTERNAL

7

Correct Usage of Islamic Banking Terminologies

Conventional Banking Terminologies Islamic Banking Terminologies

Lending Financing

Borrower Customer

Lender Bank/Financier

Interest Profit

Interest Rate Profit Rate

Loan Financing

Repayment Payment

Total Repayment Total Payment

Monthly Repayment Monthly Payment

Penalty Charges Compensation Charges

Insurance Takaful

Insurance Premium Takaful Contribution

Mortgage Reducing Term Assurance

(MRTA)

Mortgage Reducing Term Takaful

(MRTT)

Base Lending Rate Base Financing Rate

“Challenges of using inter-changeable terminologies in websites, documents, brochures etc.” INTERNAL

8

Islamic Window/Subsidiary

ADVANTAGES

Reduced cost of operations in terms of manpower, premises & shared services

Wider reach of mass market

Competitive advantages

Leveraging on same data base – alternative products for customers

Capital outlay minimized for new start-up

DISADVANTAGES

Difficulty to command trust of customers – Displaced Commercial Risk

Not completely Shariah-compliant in terms capital, co-mingling of funds and knowledge

of staff is limited

More or price takers rather than price makers

May lead to cannibalization between parent & subsidiary

Similar scenario for subsidiary except on the degree of impact

For full-fledge Islamic Bank – high capital outlay is overcome from M&A

“Challenges in ensuring Shariah-compliant due to single platforms, marketing

paraphernalia , shared-services, regulatory etc.”

INTERNAL

9

Development of Legal Framework Governing Islamic Banking Industry

10

PROVISION 28

DUTY OF INSTITUTION TO

ENSURE COMPLIANCE WITH

SHARIAH

Islamic Financial Services Act 2013

11

Duty of Institution to Ensure Compliance with Shariah

What constitute Shariah-compliance products, transactions & activities?

Why is Shariah-compliance so important – religious duty or regulatory obligation?

12

Who in the institution to identify that the activity is not in compliance with Shariah?

Duty of Institution to Ensure Compliance with Shariah, cont.

13

IFSA Vs BNM SGS – what’s the difference & which is more important?

Why do we need SGF in Islamic Banking?

BNM Shariah Governance Framework 2010

14

Islamic Banking Framework & Governance

FCSBF 4

Prohibition & Pillars

#02

16

Riba

(Interest)

Gharar

(Uncertainty)

Maysir

(Gambling)

Haram Items/Activities

(Prohibited Items/Activities)

Avoidance of the 4 Prohibited Elements

17

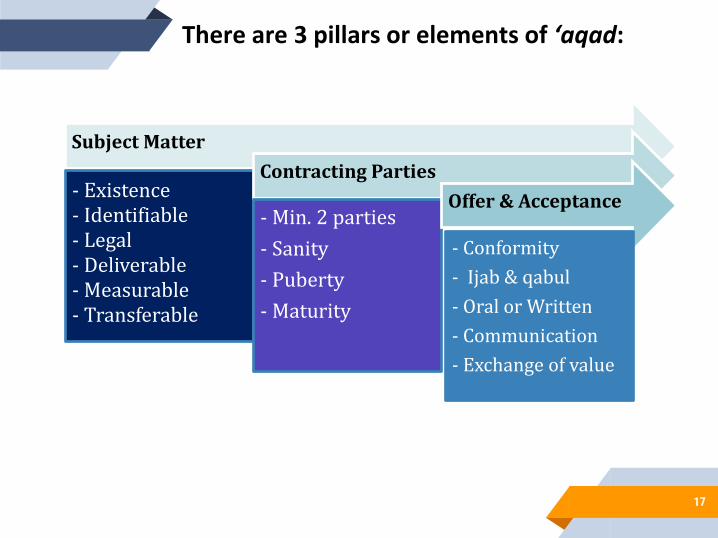

There are 3 pillars or elements of ‘aqad:

Subject Matter

- Existence - Identifiable - Legal - Deliverable - Measurable - Transferable

Contracting Parties

- Min. 2 parties

- Sanity

- Puberty

- Maturity

Offer & Acceptance

- Conformity

- Ijab & qabul

- Oral or Written

- Communication

- Exchange of value

FCSBF 4

Practical Issues in Shariah

#03

19

GOVERNANCE PRODUCTS

PEOPLE PROCESS & INFRA

PRACTICAL ISSUES

Islamic Finance encapsulates end-to-end activities from product development to maturity

which must be supported by good governance, shariah knowledge and readiness of people

as well as the process and infrastructure.

As financial intermediaries, the issues on Shariah-compliance are crucial as per its

commitments and duties to customers in ensuring that its revenue from business is Halal &

purified from any tainted elements.

Despite having craftily structured Islamic products, IFIs are normally exposed to various

Shariah Non-Compliance Events (SNCE) arising from the operationalization of Shariah in its

products, process, infra and the human errors due to incompetency or negligence.

Practical Issues in Islamic Finance

20

Areas of concerns:

Independence: issuance of fatwa – SAC resolution vs bank’s SC endorsement

Competency: banking operation – knowledge on credit, treasury, trade financing etc.

Confidentiality: product innovation – sharing of fatwas on product structure?

Consistency: SC’s endorsement – may not be industry-wide practices

Accountability: scope of duties – Shariah structure, Aqad, documentation, SOP etc?

Responsibility: business vs compliance – Shariah-compliance & yet business minded

Commitment: performance appraisal – Head of Shariah, Shariah Review to CEO/SC?

Continuing Professional Development (CPD): Tertiary vs Professional – CB, CPIF, CSA/CSP

Governance – Corporate & Shariah

21

Areas of concerns:

Replication: Forms vs Substance – A chicken is still a chicken?

Innovation: Risk-sharing a hard-sell to banks – focusing only Sale-based

Uniqueness: only on the Aqad? What about the Maqasid (objective), process?

Documentation: cumbersome & complicated? How about the cost vs benefit?

Marketability: Islamic First vs Islamic Must or remain optional to all?

Recovery chances – Case precedent

High capex – Customization

Issuance of Policy Documents (PDs) – frequency of issuance

Shariah Non-Compliance – penalties & monetary losses

Products – Replication vs Innovation

22

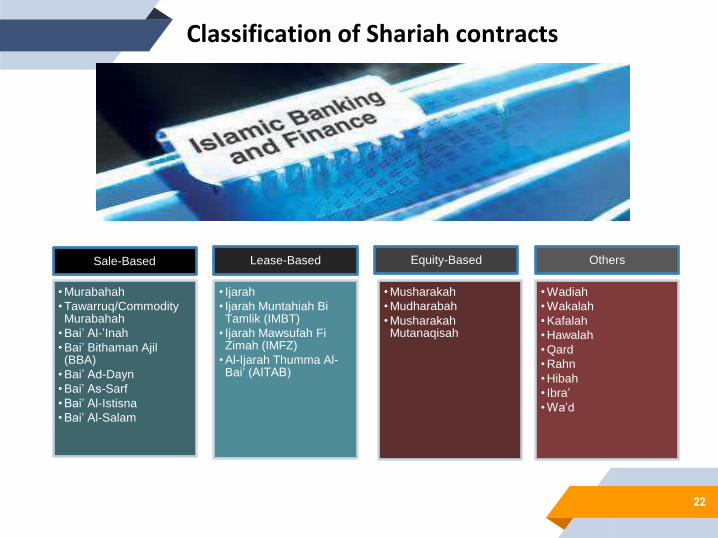

Sale-Based

• Murabahah

• Tawarruq/Commodity Murabahah

• Bai’ Al-’Inah

• Bai’ Bithaman Ajil (BBA)

• Bai’ Ad-Dayn

• Bai’ As-Sarf

• Bai’ Al-Istisna

• Bai’ Al-Salam

Lease-Based

• Ijarah

• Ijarah Muntahiah Bi Tamlik (IMBT)

• Ijarah Mawsufah Fi Zimah (IMFZ)

• Al-Ijarah Thumma Al-Bai’ (AITAB)

Equity-Based

• Musharakah

• Mudharabah

• Musharakah Mutanaqisah

Others

• Wadiah

• Wakalah

• Kafalah

• Hawalah

• Qard

• Rahn

• Hibah

• Ibra’

• Wa’d

Classification of Shariah contracts

23

Shariah contracts using Murabahah

Murabahah

Tawarruq/Commodity Murabahah

Bai’ Al-’Inah

Bai’ Bithaman Ajil (BBA)

Bai’ Ad-Dayn

Bai’ As-Sarf

Bai’ Al-Istisna

Bai’ Al-Salam

Practical Issues in Murabahah

Identification & attributes of subject matter (SM)

Any recourse is on the sale-contract not loans

Non-existence of SM – gharar al-fahish (Void)

Transfer of ownership – sequencing is documented

Selling Price – Fixed throughout the tenor

Asset-Sale Agreement (ASA) /Murabahah Sale Contract (MSC) are transaction docs to the Aqad

Commodity Murabahah – E-certs & Master Listing on Block dealings with Commodity Trader

Termination of contract is required to claim the whole outstanding balance of the sale price less ibra’ (rebate)

Shariah Contracts in Sale-based

24

Product Issues in Ijarah

Identification & attributes of subject matter (SM)

Any recourse is on the Wa’d (undertaking) to purchase the asset upon failure to meet the lease payment

Usufruct of SM – to justify the lease amount paid

Transfer of ownership – sequencing is documented

Lease Rental can be varied throughout the tenor

Asset-Purchase Agreement (APA), Ijarah Agreement, Wa’d are transaction docs required in the Aqad

Invocation of the Wa’d is required to claim the whole outstanding balance.

Proceed of sale to 3rd.party if inadequate shall be claimed from the lessee.

Shariah Contracts in Lease-based

Shariah contracts using Ijarah

Ijarah

Ijarah Muntahiah Bi Tamlik (IMBT)

Ijarah Mawsufah Fi Zimmah (IMFZ)

Al-Ijarah Thumma Al-Bai (AITAB)

25

Practical Issues in Musyarakah

Identification & attributes of subject matter (SM)

Any recourse is on the Wa’d (undertaking) to purchase the remaining ownership share of the partnership

Transfer of ownership on gradual & proportionate basis

Rental portion can be varied throughout the tenor but equity (principal) portion remains fixed

Musyarakah Agreement & Wa’d are transaction docs required in the Aqad

Invocation of the Wa’d is required to claim the remaining ownership share of the partnership

Proceed of sale to 3rd.party if inadequate shall be claimed from the defaulting partner

Shariah Contracts in Equity-based

Shariah contracts using Musyarakah

Musyarakah

Mudarabah

Musyarakah Mutanaqisah (MM)

26

Areas of concerns:

Sales & Marketing – cross-selling allowed? Dress code & Etiquette

Marketing paraphernalia – images, shared brochures/pamphlets

Marketing channels – is ok to sell Hijab at Zioux i.e. by an entertainer?

Marketing expenses – Lucky draw, claims on liquor & haram F&B?

Competency – Operationalization beyond Shariah principles

Outsourcing structure – SLA on accountability & transparency

Responsibility – business vs compliance

Continuing Professional Development (CPD) – Certification program?

People – Flexibility and Multi-tasking?

27

Areas of concerns:

Keeping abreast with banking industry movement towards VBI, Fintech, Auto Intelligence (AI) etc

Overlapping process & procedure between Shariah Risks, Review, Audit

Remedial rates – penalty, compensation, judgment rates

Transparency of reporting

Robustness of training programs

Process – System & Infrastructure

FCSBF 4

Lessons Learned & Moving Forward

#04

29

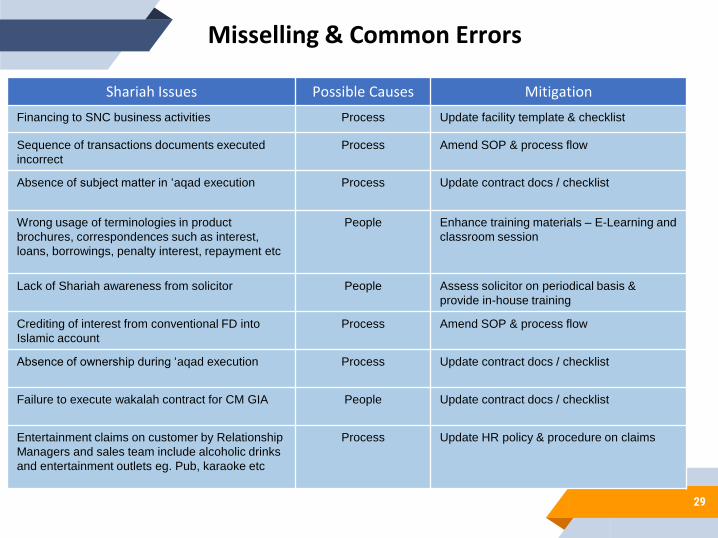

Shariah Issues Possible Causes Mitigation

Financing to SNC business activities Process Update facility template & checklist

Sequence of transactions documents executed

incorrect

Process

Amend SOP & process flow

Absence of subject matter in ‘aqad execution Process Update contract docs / checklist

Wrong usage of terminologies in product

brochures, correspondences such as interest,

loans, borrowings, penalty interest, repayment etc

People Enhance training materials – E-Learning and

classroom session

Lack of Shariah awareness from solicitor People

Assess solicitor on periodical basis &

provide in-house training

Crediting of interest from conventional FD into

Islamic account

Process

Amend SOP & process flow

Absence of ownership during ‘aqad execution Process

Update contract docs / checklist

Failure to execute wakalah contract for CM GIA People

Update contract docs / checklist

Entertainment claims on customer by Relationship

Managers and sales team include alcoholic drinks

and entertainment outlets eg. Pub, karaoke etc

Process Update HR policy & procedure on claims

Misselling & Common Errors

30

Shariah Issues Possible Causes Mitigation

E-cert number wrongly stated in the contract People

Update facility template & checklist

Commodity Murabahah was omitted on

Revolving Financing

People

Amend SOP & process flow

Subscribing insurance coverage instead of

Takaful for collateral

People

Amend SOP & process flow

Referral program for conventional parent

products for commission

Process / Infra

Amend SOP & process flow

Conventional branch staff doing sales activities

of conventional products at Islamic branch

premises

Process / Infra Shariah Awareness training & update policy

on shared-services

No regular engagement/meeting of Shariah

Committee with CEOi/management/Board

Governance Update internal policy on corporate &

shariah governance

Lack of Shariah knowledge amongst staff

following random interview &/or MCQ quizzes

given to them during your visit

People Enhance training materials – E-Learning and

classroom session

Branch premises displaying historical Fixed

Deposit rates

Infra Enhance training materials – E-Learning and

classroom session

contd. Misselling & Common Errors

31

Shariah Issues Possible Causes Mitigation

Islamic product marketing pamphlets using

conventional parent logo and portraying Shariah

non-compliance images

Process Shariah Awareness training & update policy

on marketing

From the sample of selected accounts, 3 financing

accounts were of mixed business activities and

income

Process Shariah Awareness training & update policy

on shared-services

Internal outsource business units under shared-

services eg. Finance, HR, IT, Business banking,

Consumer banking, Recovery etc. without Service

Level Agreement (SLA)

Process Shariah Awareness training & update policy

on shared-services

KPI of Head of Shariah (HOS) is set and assessed

by the CEOi – Islamic Bank

Governance Update internal policy on corporate &

shariah governance

Shariah Review reports direct to HOS

Governance Update internal policy on corporate &

shariah governance

All business plan & corporate strategy is under

Board of Directors & senior management with nil

engagement with SC Chairman

Governance Update internal policy on corporate &

shariah governance

Shariah Risk & Shariah Audit were not

represented in the monthly SC meeting

Governance Update internal policy on corporate &

shariah governance

contd. Misselling & Common Errors

32

Islamic Finance in Digital Era

“

33 33 FCSBF