Embed Size (px)

Citation preview

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 1/24

N e w s l e t t e r v o l u m e 1

Pre Budget Analysis

2009-2010SIBM, Bangalore

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 2/24

The Budget is the most awaited financial

document for the year. The Union Budget

of India lays down guidelines and pro-

nouncements on different types of taxes,

financial allocations for various heads as

well as developmental plans for different

sectors. The Budget is also an important

source of information on government fi-

nances that shows which way it‘s heading.

Every year, before the Budget is presented,

there are expectations of people all over

the country, industry and the masses alike.

There are a few concerns and challenges

such as inflationary pressure from food and

oil, slowdown in the growth rate of the

economy from the previous years and in-

creasing fiscal pressure. The budget which

is slated for July 6th in the midst of raging

recession will be truly a masterpiece of

budget. It will combine the populism of a

newly re-elected government with the

pragmatism of fiscal deficit and recession

threatening to sweep the country‘s health

away.

We, the Research Committee at SIBM, Ban-

galore bring before you the pre-budget

analysis. The content that follows discusses 7

different sectors. We give insights about the in-

dustry, current scenario of the industry, expec-

tations from the upcoming budget and the stocks

you should watch for to invest. Criticisms are

welcome, though we wouldn‘t mind compli-

ments either!!!

Student Research Committee

SIBM, Bangalore

N e w s l e t t e r v o l u m e 1

EditorialS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 3/24

SIBM since 1978 has been synonymous with

progress, and it has continued this trend by

being the first to set up its offshore campus

at Bangalore. The world is changing and

SIBM, Bangalore is poised to be the perfect

catalyst to drive this change. SIBM is consis-

tently ranked among the top ten institutes

in the country. Encouragement provided for

analytical research creates the intellectual

capital which is highly sought after. The

program here provides a holistic approach

to management and this goes a long way in

creating a dynamic identity.

VISION

To be recognized globally as the preferred desti-

nation for all future leaders, where the spirit of

inquiry and enterprise will drive growth through

innovation.

MISSION

To create a centre of academic excellence with

a collaborative environment, which fosters ex-

perimental learning that can be applied towards

social, economic and global development.

N e w s l e t t e r v o l u m e 1

About SIBMS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 4/24

Macro-Economic Overview Com-

mentary

In the annals of socio-economic history,

never has there been the story of a billion

people massively struggling to rewrite their

economic destinies with vigor as un-

matched as India‘s. The much anticipated

budget of this year is largely seen as a con-

tinuation of the Government‘s effortsaimed at providing stability to an economy

ailing with the distresses of an economic

recession coupled with a fiscal deficit of

almost 11% GDP (State and Central Govern-

ment figures put together) and a looming

drought. The budget is expected to an-

nounce several bold measures to enhance

economic growth in an 'inclusive' manner as

well as to introduce much needed struc-

tural reforms.

For the country to achieve a growth rate of

8%, as against the projected figures of

6.7%, the Government would require to

tweak the various economic levers to en-

sure that there is massive spending in the

social sector that would include increased

allocation to various infrastructure related

sectors- roads, ports, etc, yet at the same

time ensuring that the fiscal deficit doesnot go out of hand. A deficit any more than

the existing range would have seriously

negative repercussions denting the cur-

rency stability brought about painstakingly

by the RBI.

The Government in three installments have

provided massive infusions of liquidity in

the form of stimulus packages and tax cuts,

hence inflation-expectations for the nextyear will be at historical highs and running

a tight monetary policy will be a pre-requisite.

This runs contrary to the current need of running

a rather liberal interest rate regime to boost

investments and ensuring a visible increase in

the credit-off take. The Budget will be closely

monitored to see if the Government sacrificesits prudent fiscal policies to advance growth. As

the RBI states in its Annual Policy Statement for

the year 2009-2010, ―Unlike the WPI based infla-

tion, CPI based inflation in India, remains high,

with recent evidence of very modest moderation

and this has emerged as an important issue in

the conduct of Reserve Bank's monetary policy‖.

Hence the need of the hour will be to balance

the reduction of the high fiscal deficit with poli-cies that promote growth.

Additionally, righting the wrongs of non-

expansion of critically important social sectors

will be schemes such as NREGA, Bharath Nirman

and JnNURM , this in turn requires massive infu-

sion of funds which in spite of all of the ills asso-

ciated with them are meant for the voiceless

whose marginalization is disastrously dangerous

for the nation while it attempts to achieve an

enhanced status in the league of nations-

extraordinaire.

While it may look bleak everything is not lost as

the present government has come in with in-

creased seat strength and the government can

push forward with many structural reforms

which was not be possible in the last few years

due to coalition pressures. Let us see, if Pranab

Mukherjee, our finance minister is able to fulfill

the historic mandate given to him.

N e w s l e t t e r v o l u m e 1

The Indian EconomyS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 5/24

Industry Overview

The automotive sector in India mainly com-

prises of two wheelers, light motor vehi-

cles, and heavy vehicles which include

buses and lorries. The major players in this

sector include Hero Honda, TVS, Bajaj, Ma-

ruti, Tata Motors, Ashok Leyland, Hyundai

etc and there are many more foreign firms

eagerly waiting to join the league.The past one year was a momentous occa-

sion for the Indian automotive industry with

the launch of the ultra cheap ―Tata Nano‖

car at Rs 1 lakh which astounded the entire

international automobile industry.

The previous budget of 2008-09 had re-

duced excise duties on two and three

wheelers. The duty was reduced to 14.0

percent from the existing 24.0 percent on

hybrid cars and from 16.0 percent to 12.0

percent on small cars thus making them

cheaper. With a reduction in duties on

these cars, the lagging demand for small

cars was anticipated to pick up and this was

expected to boost sales. Thus the auto ma-

jors were provided a stimulus to undertake

capacity expansion and they were expected

to make India a hub for small cars.

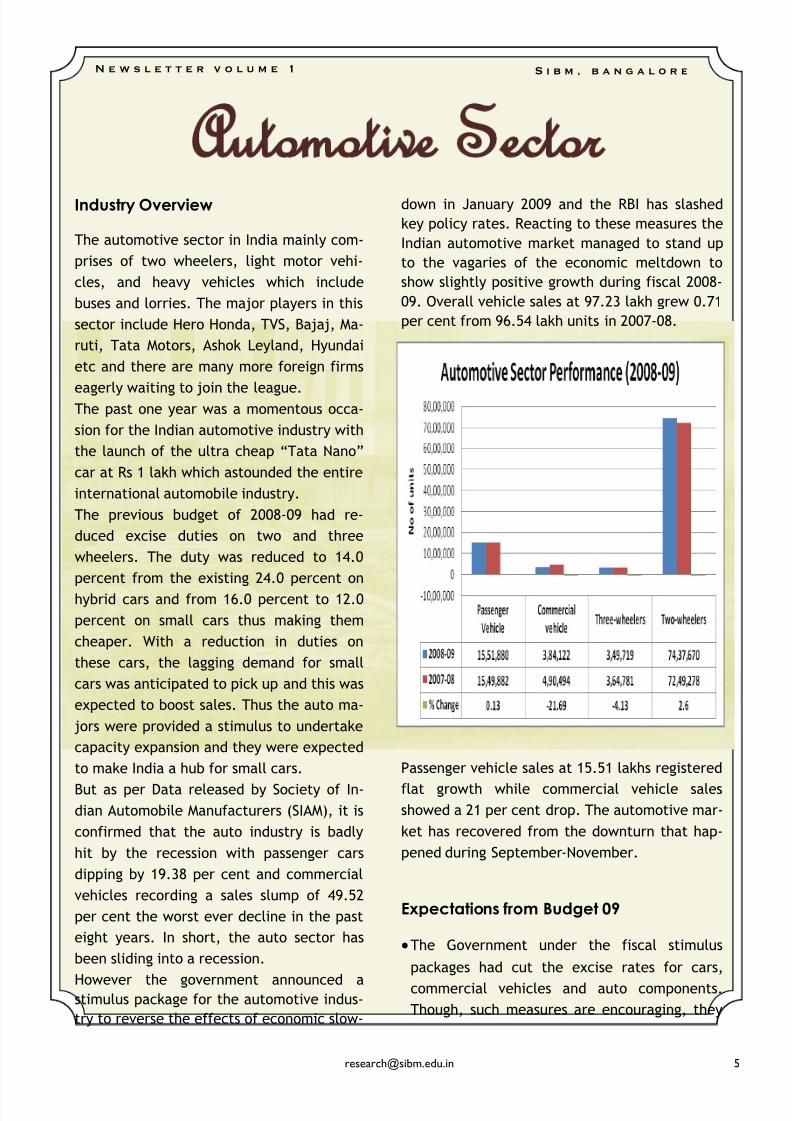

But as per Data released by Society of In-dian Automobile Manufacturers (SIAM), it is

confirmed that the auto industry is badly

hit by the recession with passenger cars

dipping by 19.38 per cent and commercial

vehicles recording a sales slump of 49.52

per cent the worst ever decline in the past

eight years. In short, the auto sector has

been sliding into a recession.

However the government announced astimulus package for the automotive indus-

try to reverse the effects of economic slow-

down in January 2009 and the RBI has slashed

key policy rates. Reacting to these measures the

Indian automotive market managed to stand up

to the vagaries of the economic meltdown to

show slightly positive growth during fiscal 2008-

09. Overall vehicle sales at 97.23 lakh grew 0.71

per cent from 96.54 lakh units in 2007-08.

Passenger vehicle sales at 15.51 lakhs registered

flat growth while commercial vehicle salesshowed a 21 per cent drop. The automotive mar-

ket has recovered from the downturn that hap-

pened during September-November.

Expectations from Budget 09

The Government under the fiscal stimulus

packages had cut the excise rates for cars,

commercial vehicles and auto components.

Though, such measures are encouraging, they

N e w s l e t t e r v o l u m e 1

Automotive SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 6/24

haven‘t completely bailed out the auto

industry. Radical actions are expected to

be taken keeping in view the long term

perspective of making India the hub of the

auto manufacturing.

Creation of special auto-component parks

with specific direct & indirect tax bene-

fits. For Auto parts manufacturers the im-

port duty for certain components stands

at 7.5 per cent. It is likely to increase soas to provide scope for Auto components

parks.

Banks can be asked to reduced the inter-

est rates charged on automobile loans.SBI

has already gone ahead in this measure by

charging 8% interest on car loans. Many

other banks are expected to follow suit.

Export is an area of grave concern given

the global economic crisis. Continuance oftax holiday for Export Oriented Units

(EOUs), deductions for profits on exports

for Small & Medium sector non- EOUs are

expected for the survival for many auto

component manufacturers.

For promoting use of environment friendly

fuel efficient cars, incentives for develop-

ment of technology for hybrids and reduc-

tion in custom rates on import of energyefficient completely built units are also

expected.

Incentives are expected for improving the

demand for commercial vehicles, by pro-

viding incentive to scrap old vehicles and

buy new ones like the enhanced deprecia-

tion benefit scheme etc.

While small cars attract 8 per cent excise

duty, the effective manufacturing duty onlarge cars and utility vehicles is 22-24 per

cent so we can expect that there will be some

reduction in the excise duty.

We also expect the VAT structure to get ration-

alized across all states .Now it varies from 12.5

% in Delhi to 15% in other states.

Stocks to watch out for

Tata Motors, Ashok Leyland, Maruti and M&M

Conclusion

Despite the slowdown, the prospects of growth

for the Indian auto industry are perceived to be

strong, given that the country has a much lower

vehicle population as compared to the devel-

oped nations. Most of the auto giants have ex-pressed confidence in the Indian markets and

are continuing with their India investment/

expansion plans. However, consumers demand

for new passenger cars are known to be discre-

tionary and hence, can dip in an uncertain eco-

nomic environment. Similarly, the fortune of the

commercial vehicles segment is closely linked to

the industrial production. But, we do expect

that the government will definitely undertakeconcrete measures to help Auto Industry regain

its lost glory.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 7/24

Industry Overview

The Indian banking sector has acquired a

greater degree of resilience due to the fi-

nancial reforms implemented in a gradual

and sequential manner under the watchful

eyes of Reserve Bank of India and Ministry

of Finance. This was implemented by a par-

ticipative process aimed at reduction in

statutory pre-emption.An assessment of the banking sector per-

formance shows that banks in India have

experienced strong balance sheet growth in

the post-reform period in an environment

of operational flexibility. Improvement in

the financial health of banks, reflected in

significant improvement in capital ade-

quacy and improved asset quality, is dis-

tinctly visible. These significant gains have

been achieved even while renewing the

goals of social banking by maintaining the

wide reach of the banking system and di-

rected credit.

Current Scenario

Banks in India have always played a pivotal

role in providing a thrust to the develop-

ment of the country by assisting in the de-velopment of the priority sector in India

which includes agriculture as well as in the

industrial and infrastructural development.

Changes in these sectors are essential to

boost comprehensive growth and revival of

the economy. Thus, in the current challeng-

ing times of economic stagnation affecting

these sectors, it becomes all the more nec-

essary to provide the much required fiscal

support to the banking industry.

The risk aversion which has crept into the do-

mestic banking sector on account of the interna-

tional banking crisis has created a situation of

deep concern and threat for the real economy

and all the players in it. Challenges facing the

Indian Banking sector this year include: compli-ance with Basel II norms and competition from

foreign banks.

There has been a lackluster demand for credit

despite sufficient liquidity in the system and

lowering of interest rates by banks, following

the phased reductions in cash reserve ratio and

policy rates by the Reserve Bank of India. The

reduction in PLR required cut in deposit rates as

well. Credit targets of public sector banks had

been revised upwards to reflect the needs of the

economy, which called for a recapitalization

plan for banks to improve their soundness and

their ability to withstand sudden shocks—like the

ongoing global crisis that has devastated many

of top-notch US banks.

There is a negative impact on the banking sector

due to lending at fixed ceiling rates to focus sec-

tors. Margins have been hurt as the banking sys-

tem has raised a large portion of its liabilities athigh rates in the recent past.

N e w s l e t t e r v o l u m e 1

Banking SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 8/24

With economic slowdown being the major

issue at present, the bankers' main concern

is to fund growth without facing any hur-

dles. The obvious choice, according to

bankers, which has to be acted upon, is in-

frastructure funding. Though there has

been a revival of economic growth and a

pick up in the pace investment cycle, the

banking sector expects several positive

measures in the Budget 2009-10, so thatthey can continue to play a vital role in

intermediating between the demand and

supply of funds.

Expectations from the Budget

Banks may be given full tax exemption on

the interest earned from long-term loans

to infrastructure projects in order to pro-

vide them with the much needed invest-

ment thrust. This would additionally help

in reducing the interest rates charged by

banks on infrastructure projects having

long gestation periods.

Allowance for deduction based on provi-

sioning for bad and doubtful debts in the

books will ensure that banks are taxed on

profits that are similar to their accounting

profits.

De-regulation of the fixed deposit lock-in

clause and the small savings rate which

would give banks more flexibility to lower

deposit rates, meaning lower cost of funds

for banks, helping them protect their net

interest margins to an extent.

The government is expected to announce

more social welfare schemes which are

going to be financed by the banks, putting

the nationalized banks under more pressure.

Stocks to Watch Out for Infrastructure/housing lenders – HDFC Bank, SBI,

PNB and other Public Sector Banks

Conclusion Thus, key measures in Budget 2009-10 which are

expected to have a positive impact on the sector

are the de-regulation of the small savings rate,reduction in the lock-in period for FDs, qualify-

ing for tax deductions and tax breaks for infra-

structure and housing lenders.

Key measures expected to have a negative im-

pact on the sector is lending at some ceiling

rates to specific sectors and activities – agricul-

ture, infrastructure, SMEs, exporters, education

and affordable housing.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 9/24

Industry Overview

―Education for all‖ is the motto of the pre-

sent UPA government. The government‘s

vision is to convert our country‘s huge

population into skilled resources and help

India compete in the global market. To en-

sure this the government is focusing on the

three Ps of the Education Sector: Participa-

tion, Performance and Proportion. Thoughgovernment has taken a number of initia-

tives, funds have always been a problem.

The solution to the problem of education

infrastructure is through participation – pri-

vate players should be allowed to partici-

pate and contribute to this sector in a more

unfettered manner. Performance – im-

provement in the quality of education pro-

vided to students. Proportion – larger

amount of money from the budget needs to

be allocated, as it is really an investment in

India's future.

Increased demand for education has re-

sulted in major changes on the supply side

especially in the higher education arena.

Universities that had virtual monopolies for

decades are now dealing with a range of

competitors – that are vying for revenues

and surplus.

Current Scenario

Education is an important indicator of so-

cial development. It is increasingly becom-

ing the primary determinant of overall de-

velopment in the emerging knowledge

economy. India has a large number of

schools, colleges and universities across the

whole country. India houses many big edu-cational institutes like IITs, IIMs, JNU, DU

and other

MBA col-

l e g e s .

There are

many insti-

tutions that

also cater

for many

d i s t a n c e -

l e a r n i n gcourses. In

fact, India

is a home for education. There are over 300 Uni-

versities and 45,000 colleges of various types in

the country. India has made huge progress in

terms of increasing primary education atten-

dance rate and expanding literacy to approxi-

mately two thirds of the population. However,

education is still far behind developing countriessuch as China or Thailand. There is no focus on

the quality of education in terms of the depth

and dimensions of teaching and in terms of syl-

labi, though technical education does have some

quality control.

Looking at the industry perspective, there is no

link, whatsoever, between the producers and

users of manpower with the result that institu-

tions of learning, essentially at the secondary

and technical levels, are not exactly aware of

the end result and use of their manpower out-

put. There has to be a complete synchronization

and rapport between the two sets: the produc-

ers and the users, as happens in most of the

countries, including the developing ones.

Expectations from the Budget

Allocation for National Skill Development Cor-poration to increase.

N e w s l e t t e r v o l u m e 1

Education SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 10/24

There is a need to set up more number of

higher secondary schools as well as col-

leges to match with the primary schools.

Budget expected School Education:

Rs.1100 crores. Number of schools:

50,000.

Focus on women and adult education in

the rural areas.

Major announcement for educations and

higher technical educations for new

higher education‘s institutes at various

places of country. Budget expectation for

higher education: Rs.150 crores. Number

of colleges: 400.

Two IITs, six IIMs, 10 NITs and 14 universi-

ties are still to be launched.

Schemes to be announced for the welfare

of the minorities including a multi sec-

toral development plan to be drawn for

each of the minority concentration dis-

trict and a scheme for modernizing ma-

drassa education. Expected budget alloca-

tion is: minorities department : Rs.520

crores, number of madrasas: 550.

Private university regulatory bill

Foreign university regulatory bill

Setting up National Commission for Higher

Education and Research which will be an

apex body in education

Allowing Foreign Direct Investment into

Education Sector

Increasing funds for SSA (Sarva Shiksha

Abhiyan), Mid-day meal scheme. Expected

budget for SSA is Rs.13, 100 Crores. And

for national program of Mid-Day Meal

Scheme – Rs. 8000 Crores

Increasing funds to Kasturba Gandhi Balika

Vidyalaya

National Means-cum-Merit Scholarship

1% of GDP may be spent of R&D

Stocks to Watch Out for Educomp, NIIT, Environ, Pearson Conclusion It is quite evident that the higher education sec-

tor in India faces a number of challenges and

constraints which need to be overcome through

various focused initiatives. Although the Govern-

ment‘s focus on the development of higher edu-

cation is increasing; much still needs to be done

to ensure that the targeted enrolment rates are

achieved. It is also clear that the expansion of

the higher education system in India would not

be possible without sufficient levels of private

sector funding. With a clear gap in the availabil-

ity of this private sector funding there is a need

to look at partnerships to create progress on this

front in the near term. Overall we believe the

budget allocations and higher spending by the

Indian middle class are expected to fuel growth

of private education companies in India.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 11/24

Industry Overview

According to FICCI, India FMCG sector is all

set to grow at 16% during 2008-09, from a

base of INR 85,470 crores. An increase in

disposable income, across rural and urban

consumers, has led many rural consumers

to shift from traditional unorganized un-

branded products to branded FMCG prod-

ucts and urban fraternity to splurge onvalue added and lifestyle products.

In the current economic downturn and

global financial turmoil, the FMCG industry

in India should be able to continue to grow,

albeit at a slower pace due to robust do-

mestic market. Increasing penetration and

low per capita consumption would help to

achieve the volume growth. However the

rate of growth may come down due to

higher base effect and falling commodity

price.

FMCG has inherent characteristics of neces-

sity and inelastic products used for daily

consumption. Also the demand from rural

India, which constitutes about 50% of the

total FMCG market in India, is expected to

remain strong as it has been boosted by

hikes in minimum support prices for agri-

cultural commodities and farm loan waiv-ers, rising consumerism and better penetra-

tion of FMCG sector. However the errant

monsoon has started giving sleepless nights

to fast moving consumer goods (FMCG) ma-

jors; poor rains could play havoc with de-

mand for their products, especially from

the rural markets. India has a tremendous

potential for development of food process-

ing industry. This is primarily due to chang-ing preferences towards healthy lifestyle,

Increase in disposable incomes, breakup of

joint families into nuclear families, double in-

come families and robust growth in organized

retail which is all leading to increased demand

for the processed food items in India.

Current Scenario

Overall sales growth in the FMCG sector contin-

ues at 20% plus with the balance tilted towards

price growth in large categories. However, re-

cent product price cuts mean that future growth

will be dominated by volumes.

Unorganized/regional competition has become

more active as expected, and this is partiallyresponsible for the dent in the market share of

larger players.

Although gross margins will expand, the quan-

tum of expansion will be lower than originally

estimated due to the recent rally in commodity

prices.

Focus on cost control should become even more

important in light of reduced scope for gross

margin improvement.

N e w s l e t t e r v o l u m e 1

FMCG SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 12/24

Expectations from the Budget

There is a possibility of tax incentives for

R&D in food processing industry which

would help the companies to invest in

R&D and evolve new standards and prac-

tices in food processing.

The government may raise the excise duty

on cigarettes. If excise duties increased

more than 10% might hurt cigarette vol-umes as companies pass on all tax hikes to

consumers.

We believe that the government may roll

back part of the reduction in overall ex-

cise duties for the sector (say by 200-400

bps). In the event of a rollback of excise

duties, all FMCG companies would be af-

fected. However, FMCG companies would

likely raise prices to offset the impact ofa potential increase in costs.

The government may reduce in VAT from

12% to 4% for biscuit Industry.

There can be provision for Fringe Benefit

Tax (FBT) dilution. All FMCG companies

will have positive impact of that, as they

incur lot of expenditure on travel etc for

product promotions.

FMCG companies expect the governmentto boost the rural economy by increasing

allocation for various agriculture-centric

and employment generating schemes. In-

crease income in the hands of rural con-

sumers will increase rural consumption.

All FMCG companies are expected to

benefit from strong rural growth.

Stocks to Watch Out for We think is there it is very unlikely that this sec-

tor will get positive reforms so our view is bear-

ish on this sector.

Conclusion FMCG is expected to grow at a CAGR of a little

over 10% for the next few years to reach a size

of US$ 51 billion (Rs. 240,000 crore) by 2015.

But volume growth is all set to drive top line

profits, backed by new products and rural con-

sumer demand. For FMCG controlling overhead

costs is more important than ever.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 13/24

Industry Overview

India is referred to the ‗back office of the

world ‘ in the IT & ITES Sector. ITeS, which

started with basic data entry tasks over a

decade ago, is witnessing an expansion in

its scope of services to include increasingly

complex processes involving rule-based de-

cision making and even research services

requiring informed individual judgment. Itnow offers services such as knowledge

process outsourcing (KPO), legal process

outsourcing (LPO), games process outsourc-

ing (GPO) and design outsourcing among

others.

Indian IT and IT-enabled services industry is

expected to grow at 10.8 per cent in 2009,

the lowest in the last five years, due to the

global economic meltdown. The overall IT/

ITeS industry is expected to grow at 13.9

per cent (CAGR 2008-2013) to touch over

USD 110 billion in 2013.The domestic IT and

IT-enabled services (ITeS) revenue is slated

to touch about Rs 2, 06,398 crore by 2013

from Rs 99,254 crore in 2008, growing at a

CAGR of Rs 15.8 per cent, the study said.

India has the second lowest ITeS/BPO salary

base of about US$ 7,500-US$ 8,500, just

little above China's base of US$ 7,000-US$8,000. The other positive for India is that

the country is one of the largest producers

of English-speaking graduates, including

engineers and management graduates.

Current Scenario

The sector has faced significant challenges

in FY09. Growth in exports dropped from

30% in FY08 to about 16%. The economic

turmoil in developed nations impacted and

continues to impact demand for Indian IT / BPOvendors. While there are initial signs of the

situation easing in those economies, it is still

early to determine whether they have turned

the corner. Indian companies have seen some

signs of stabilization in the form of fewer pro-

ject deferrals, fewer pricing negotiations and

visits from new clients.

Another problem with the IT sector in India is

that there is a great amount of dependency on

the US market. Indian companies are now look-

ing to explore new and emerging markets such

as the Middle East and Australia.

Realizing its potential of this ever growing sec-

tor, after IT Parks and IT special economic zone

(SEZs), the government has cleared a proposal

for creating much larger Information Technology

Investment Regions (ITIRs) to give a fillip to the

country's growing IT and ITeS sector. But unfor-

tunately it is yet to be implemented and is cur-rently facing bureaucracy hassles.

N e w s l e t t e r v o l u m e 1

IT SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 14/24

In this backdrop, the budget is expected to

focus on maintaining an environment con-

ducive to the future growth of this largely

export-oriented industry.

Expectations from the Budget

As this is a job generating and export ori-

ented sector , Govt. will look to encour-

age sector for boosting export growth. Sofor that Government can give Tax exemp-

tion Under Section 10A and section 10B.

Till date this exemption is till 2010 gov-

ernment may expand period beyond 2010.

The industry has also submitted that FBT

be removed. Removal of FBT will have a

positive impact on the sector in terms of

cost control and competitiveness.

The industry also expects an Amendmentin Section 10AA of IT Act. Section 10AA(7)

states that only a portion of profits of IT

special economic zones (SEZ) profits will

be tax exempt as proportionate to the ex-

port contribution of that unit to the com-

pany‘s total exports. This nullifies to a

large extent, the logic of doing new busi-

ness via SEZs as they are meant to be tax-

free zones. Thus there might be some res-

pite to the industry in that respect. Prime

Minister Manmohan Singh has already ex-

pressed his keenness in correcting this

anomaly.

The industry also anticipates the programs

for Nationwide broadband rollout and fo-

cus on skill building to be launched during

this budget. This will ensure long term

competitiveness of the IT industry.

Stocks to Watch Out for Infosys, Mphasis, KPIT Infosystems

Conclusion The government reforms in this sector will cer-

tainly provide a fillip to the sagging profit mar-

gins of the IT industry. Thus it will provide for

the lesser layoffs and create more jobs in this

sector. The sector which is one of the largest

source of employment in this country is certainly

looking with bated breath towards this year‘s

annual budget.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 15/24

Industry Overview

Infrastructure is a very broad term which

encompasses everything from roads, rail-

ways, ports, bridges to power, irrigation,

water supply to housing, hospitals, schools

etc. It includes everything which is not part

of the manufacturing, service and agricul-

ture sector.

For any country growth mainly depends onits infrastructure facility which in turn

helps in industrial growth. India has been

wanting in infrastructure from independ-

ence; lacking the most basic of amenities.

It has only been since the last 10-15 years

that government has really started paying

attention to infrastructure. India‘s infra-

structure sector is mainly financed by gov-

ernment funds but nowadays Public Private

Partnership (PPP) projects are also in

vogue.

The major flagship schemes of the govern-

ment towards infrastructure building:

Bharat Nirman: This is the Government‘s

flagship program to provide houses, elec-

trification, telephony and irrigation facili-

ties for the rural poor and providing good

road connectivity to their areas. Indira Awaas Yojana: The objective of In-

dira Awaas Yojana is to help in construc-

tion of dwelling units for members of

Scheduled Castes/Scheduled Tribes, freed

bonded laborers and also rural poor below

the poverty line.

Highways: One of the most ambitious pro-

jects of the government launched under

National Highways Development Project(NHDP) by Golden Quadrilateral is a high-

way network in India connecting Delhi, Mum-

bai, Kolkata and Chennai, thus forming a quad-

rilateral of sorts. It consists of building 5,846

kilometers of four/six lane express highways at

a cost of Rs. 60,000 crores.

The corpus of Rural Infrastructure Develop-

ment Fund (RIDF-XIV) has been raised to

Rs14,000 crore, with a separate window for

rural roads.

National Maritime Development Programme

(NMDP) to boost infrastructure at major ports

in the next 10 years. The programme is ex-

pected to increase the port capacity from

389.5 MT to 917.5 MT by 2014.

In the power sector the government has many

schemes which include Rajiv Gandhi Grameen

Vidyutikaran which has a capital subsidy associ-

ated with it and Accelerated Power Develop-

ment and Reforms Project (APDRP).

Current Scenario

This sector is currently facing a host of issues

that needs timely attention from the govern-

ment:

Land acquisition is turning out to be a big prob-

lem for the infra companies which have re-

sulted in the delay or cancellation of many in-frastructure projects which include the much

vaunted SEZ projects.

There are many procedural clearances such as

environmental regulations and rules which are

hampering the growth of the industry.

Access to capital is one of the major problems

of the infrastructure industry. With long gesta-

tion period involved banks are usually reluctant

to lend to infra companies. The infra compa-nies would expect the budget to encourage

N e w s l e t t e r v o l u m e 1

Infrastructure SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 16/24

banks to lend to infra companies.

Infrastructure industries have to face a lot

of political problems while undertaking

projects.

Infra companies have issues with regard to

payments from government agencies in

case of cash contracts and annuity based

projects. Delay in payments for projects

have adverse impact on profitability of

companies

Machinery and equipment imported from

abroad at very high rates which ultimately

increase the total price of the project.

Industries like shipping are greatly af-

fected by the sharp drop in exports. They

would expect a stimulus package to boost

buying of more marine assets and the re-

moval of tax anomalies vis-à-vis foreign

companies.

Expectations from the Budget

The President's Address to Parliament on

June 4, 2009 had outlined the broad con-

tours of the socio-economic agenda the

UPA government plans to pursue in its sec-

ond term with emphasis on more effective

implementation of various infrastructure

projects and social schemes.

In an environment of economic slowdown

and deficient monsoons with accompanying

decline in rural income the government will

be seriously stressed to boost public spend-

ing on basic infrastructure for urban devel-

opment and under the ‗Bharat Nirman‘ pro-

gramme for the rural areas. Fiscal deficit

which is pegged at 5.5 % of the GDP, de-

clining tax revenues is also expected to be

a major dampener on government spending

on infrastructure. But the government will not

desist from investing in infrastructure as it will

not only create more employment avenues but

also revive the economy by boosting spending

power of the general public and also encourage

the growth of construction and allied industries

like cement, steel, etc.

The major expectations from the budget are:

It is expected that government will give banks

tax relief on interest earned on infrastructurelending in the budget to enable them to lend

more to the sector. This would be very neces-

sary as government is already in the midst of

an ever galloping fiscal deficit and the govern-

ment is under severe pressure to announce

more sops for the industry.

The GOI had announced Rs 99,000 crore for

infrastructure spending during the interim

budget of 2009-10; we expect this sum to in-crease by almost 10% in the full budget.

The housing sector is expected to get a major

boost with special incentives and low interest

schemes for ―affordable‖ housing. There will

be special announcement for low income group

for housing scheme.

Government is expected to give a major boost

to their welfare schemes like NREGS and other

rural welfare programmes which will be usedto improve productivity of land and build rural

infrastructure. The present government is

thought to have won on the premises of rural

prosperity and the looming drought and resul-

tant rural unemployment is threatening to

hamper the picture. So we do expect substan-

tially more investment in the rural welfare

schemes.

We expect the government to announce vari-

ous PPP partnership proposals in roads, sea

ports and airports.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 17/24

The government is also expected to an-

nounce major urban reforms and in-

creased spending on urban infrastructure

programmes for water supply and sanita-

tion like JNNURM, UIDSSMT etc.

We expect the announcement of construc-

tion of new airports and ports under PPP

partnership programs.

New mega power plants and nuclear

plants (under the US- India nuclear part-

nership) are also expected to be an-

nounced in this budget.

More reforms are expected in the power

sector including the opening of T& D busi-

ness to private players

Concessions in import duties on construc-

tion equipment can be expected.

Stocks to Watch Out for Larsen & Turbo, IVRCL Infra, Ramkey, Gam-

mon India, Reliance Infra, GMR Infra, NCC,

IRB Infra, Patel Engineering.

Infrastructure shares have been hot com-

modities for domestic/foreign funds in India

after the recent elections as the new gov-

ernment lays out plans to improve the

country's overburdened roads and bridges.While such expectations have helped infra-

structure shares surge twice as fast as In-

dia's benchmark index since mid-May.

However we would advice restraint on the

part of the investors not to get over enthu-

siastic over infrastructure stocks as the

market has already considered the heavy

spending embarked for infrastructure and

the expectations of further increase in

spending during the new budget. The gov-

ernment will be hard pressed for funds this

year as fiscal deficit is already at 5.5 % and any

further increase in spending will worsen the fi-

nancial situation.

We expect the government to announce a slewof projects with private participation i.e. PPP

projects.PPP projects transfer the associated

risk and financial burden to the private parties

and the revenue is spread over a longer period

of time. Thus on a short term infrastructure

companies will experience volatility as the

budget will not meet up the heightened expec-

tations from the budget, but in the long run in-

fra companies are a very good bet.

Conclusion This budget would continue the trend of the

previous budgets in investing more funds in in-

frastructure and this trend would be expected to

grow for many more years to come especially in

the light of the huge gap between India and the

developed countries in infrastructure. Also a

slew of reforms and correction of the existing

anomalies would be expected in this budget.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 18/24

Industry Overview

Size

Generation capacity of 122 GW; 590 bil-

lion units produced (1 unit = 1kwh)

CAGR of 4.6% over the last four years.

India has the fifth largest electricity gen-

eration capacity in the world.

Low per capita consumption at 606 units;less than half of China

T & D network of 5.7 million circuit km –

the 3rd largest in the world

Coal-fired plants constitute 57% of the

installed generation capacity, followed by

25% from hydel power, 10% gas based, 3%

from nuclear energy and 5% from renew-

able sources

Structure

Majority of Generation, Transmission and

Distribution capacities are with either pub-

lic sector companies or with State Electric-

ity Boards (SEBs). Private sector participa-

tion is increasing especially in Generation

and Distribution. Distribution licenses for

several cities are already with the private

sector. Many large generation projects havebeen planned in the private sector.

Current Scenario

Policy

100% FDI permitted in Generation, Trans-

mission & Distribution - the Government is

keen to draw private investment into the

sectorPolicy framework in place: Electricity Act

2003 and National Electricity Policy 2005

Incentives: Income tax holiday for a block of 10

years in the first 15 years of operation; waiver

of capital goods import duties on mega powerprojects (above 1,000 MW generation capacity)

Independent Regulators: Central Electricity

Regulatory Commission for Central PSUs and

inter-State issues. Each State has its own Elec-

tricity Regulatory Commission.

Opportunity

India requires an additional 100,000 MW of

generation capacity by 2012.

Opportunities in Transmission network ventures

- additional 60,000 circuit km of transmission

network expected by 2012. A corresponding

investment is required in transmission and dis-

tribution networks.

Hydel power potential of 150,000 MW is un-

tapped.

Total investment opportunity of about US$ 200

billion over a seven year horizon.

Over 90,000 MW of new generation capacity is

N e w s l e t t e r v o l u m e 1

Power SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 19/24

required in the next seven years.

Power costs need to be reduced from the

current high of 8-10 cents/unit by a com-

bination of lower AT & C losses, increased

generation efficiencies and added low

cost generating capacity.

Large demand-supply gap: All India aver-

age energy shortfall of 7% and peak de-

mand shortfall of 12%.

―Open Access‖ to transmission and distri-

bution network. Distribution circles to be

privatized. Tariff reforms by regulatory

authorities.

Expectations from the Budget

Infrastructure Bonds: To garner funds for

infrastructure, interest on infrastructurebonds to be included under 80C.

Withholding tax to be removed on foreign

borrowings. This may not be applicable

for NTPC

To garner funds, ECB relaxation to bor-

rowing limits may be given.

Extension to 80IA tax benefit may be

given beyond 2010

Subsidy to Naphtha, a raw material for

turbines, is possible.

Approvals to additional Power projects,

including nuclear plants is possible. Huge

investments possible.

Renovation, modernization, up-rating and

life extension of old thermal and hydro

power plants.

Stocks to Watch Out for

Torrent Power, Jaiprakash Hydro-Power Ltd,

GVK Power & Infra, Gujarat Industries Power

Co., Neyveli Lignite Corporation Ltd., Power

Grid Corporation of India Ltd, Tata Power, En-

ergy Development Co., Indowind Energy and Re-

liance Power.In the last one month, shares of power compa-

nies have performed well after the govt. ex-

tended the exemption of basic custom duty on

naphtha import for generation of electricity.

Conclusion India‘s current GDP growth of 6.7% is the second

fastest, globally. India's high investment rate

(more than 35%) has been largely responsible inIndia achieving a high GDP growth rate. Power

Sector is expected to receive continued atten-

tion and funding (approx Rs 20 trillion). Power

Ministry desires to be able to add power genera-

tion capacity of about 78,000 MW by 2012. It

also wants to reach its target of providing elec-

tricity to about 118,000 villages at the earliest

(60000 villages already covered). Speedier im-

plementation will make these plans more effec-tive.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 20/24

Industry Overview

The Indian Telecom industry is said to be in

a ‗hyper growth‘ mode and is set to pip

China to the post by becoming the largest

telecom market till 2013. Currently India is

ranked second in the world in terms of sub-

scriber base behind China.

For all those who are statistically inclined it

can be noted that:

India added 113.26 million new custom-

ers in 2008, the largest globally thus hav-

ing a cellular base growth of almost 50%

As per TRAI, the total number of tele-

phone connections (mobile as well as

fixed) had touched 385 million as of De-

cember 2008. This means that one out of

every three Indians has a telephone con-

nection.

It is projected that the industry will

generate revenues worth US$ 43 billion in

2009-10.

Foreign direct investment (FDI) is one of

the important sources to meet the huge

funds that are required for rapid network

expansion. At present, 74% to 100% FDI is

permitted for various telecom services.

The total FDI equity inflows in telecom

sector have been 1261 million USD during

2007-08 which constitutes about 9% of the

total FDI Inflow in India during the same

period.

The next big thing in telecom is the rural

market - Rural telephones have gone up

from 12.3 million in March 2004 to 109.05

million in October 2008 with a tele-density

of 13.04%. Tele-density here is 10% as com-

pared to a national tele-density of 21%

thereby providing a huge potential for telecomcompanies.

In Feb this year, Government of India introduced

3G services in the country with which India en-

tered into a new era of telecommunication. This

was done when BSNL was awarded one block of

3G spectrum 6 months before the actual auction

for all other private players take place.

Current Scenario

There is a huge pressure on average revenue per

user due to the soaring network infrastructure

costs. But the sheer number of subscriber is the

reason for the growth that we have witnessed. It

is high time that we stop depending on the vol-

ume game and thus calls for reduction of the

basic infrastructure costs. Another reason is the

profit sharing requirement set by the ministry.

As of now the telecom companies share 25-30%of the profits with the government that is result-

N e w s l e t t e r v o l u m e 1

Telecom SectorS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 21/24

ing in upward pressure on the average cost

per user.

The competitors have been involved in a

price war with each mobile network pro-

vider trying to woo the user with their low

tariff rates. As of now these companies

have succeeded in maintaining their profits

over the years but if this price war contin-

ues the sector may see tough times ahead.

Also there has been a long standing differ-ence between the Telecom ministry and

Finance ministry regarding the 3G reserve

price.

Currently, telecom industry is subject to

service tax, license fees including universal

service obligation fees, spectrum charges.

Besides, the states levy additional taxes

such as octroi, VAT, stamp duty, entry tax

and levies on towers. The total of all theabove levies on telecom industry works out

to around 30% of their total revenues,

which is one of the highest in the world.

Telecom Industry in other developing coun-

tries like Malaysia, Sri Lanka and Pakistan

pay less than 7% and in China it is around

3%.

Expectations from the Budget

The industry wish list as far as the telecom

sector is concerned is very long.

Rationalizing of various taxes levied on the

industry has been top on this list for quite

some time now. The telecommunications

industry has repeatedly requested that the

multifarious taxes, charges and fees appli-

cable to the industry should be unified and

a single levy on revenue should be col-

lected.

There are talks also of extending the Tax

Holiday under section 80-IA in case of mergers/

amalgamations. Currently it is available to all

companies who have commenced operations be-

fore April 2005. There is a strong industry de-

mand to extend it till Dec 2010. We believe thatthis will not get the Finance Ministry Approval in

this year‘s budget. But here is a list of things

that we believe will be implemented:

Increase in FDI Cap: The most important an-

nouncement that is expected is the increase in

FDI caps in telecom sector. Cat present 74% FDI

is allowed in this sector. The government be-

lieves that the sector has matured very rapidly

and hence can deal with an increased FDI limit

even up to 100%.

Listing of BSNL Likely: The government will

certainly take some concrete steps towards the

listing of Bharat Sanchar Nigam Limited (BSNL).

This was on the agenda in the last budget as

well but thanks to the Left party this couldn‘t

materialize. When this happens it is expected

to be the largest public offer in India and is

expected to fetch approx $10 billion

Reduction of taxes, fees and duties: The li-

cense fee and spectrum charges prevalent in

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 22/24

India are the highest in the world. But it is

expected that there will be some respite

in this area come July 6. We might see a

reduction or even scraping of the Univer-

sal Service Obligation Fee (USO). This is

the fee charged on only the private play-

ers for offering services. The total of all

the taxes, fees and levies works out to be

30% of their total revenues which is an

unprecedented number. For all other de-veloping economies like Malaysia, Sri

Lanka it is around 7% where as in China it

is 3%. An overall reduction is highly prob-

able in this area. Also there is a strong

possibility of the excise duty on domestic

telecom products reduced. It is currently

at 16%.

Provisions and procedures for 3G Auc-

tions: There is likely to be announce-ments regarding the early execution of 3G

Auctions. Also it will be ensured that fair

procedures and regulations are in place

before the auction begins. This will en-

able the ministry to raise huge amount of

funds.

Reduction of network infrastructure

costs: The cost of infrastructure for these

telecom companies is almost sure to comedown. We expect reduction is cost of cus-

tom duty on fibre optic cables. Also the

price of mobile handsets is likely to come down. Stocks to Watch Out for Bharti Airtel, Reliance Communication

Conclusion To summarize, the overall impact that the

budget will have is that it will encourage more

foreign players into India and thus create a more

competitive environment. The telecom ministry

has already hinted about the reduction of call

rates especially STD calls. A huge rural market

to tap powered by reduced costs along with a

whole gamut of services to offer to the mobile-

savvy Indians is certainly a mouth watering pros-

pect for the telecom companies. All-in-all the

budget 2010 augurs well for the future of tele-

com in India and finally it is the consumer that

will benefit.

N e w s l e t t e r v o l u m e 1 S i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 23/24

The upcoming budget would be very impor-

tant for the overall direction of the market.

The key market performance would depend

on whether the government can spur

growth while balancing an increasing fiscal

deficit. A strong policy action is needed by

the new government to tackle the fiscal

situation and growth through investment in

infrastructure.

However, given the macroeconomic con-

straints on the economy, especially growing

inflationary pressures and the dramatic rise

in fiscal deficit, the expectations from the

Budget may be too high to fulfill. Only time

will tell if the wish list of the all the Sec-

tors, people and students like you and me will

be fulfilled.

While details would be known soon, the one

thing that would remain unchanged even post

Budget is the fact that India has embarked on a

growth path that is certain and clear, notwith-

standing the near-term pressures as a result of

the global economic slowdown and we, as Fu-

ture Managers of India would continue to con-

tribute towards this growth.

N e w s l e t t e r v o l u m e 1

Final ThoughtsS i b m , b a n g a l o r e

8/8/2019 Pre Budget Analysis

http://slidepdf.com/reader/full/pre-budget-analysis 24/24

Aditya Ambekar

Apurv Dhingra

Ashu Bhardwaj

Dej Hegde

Divya Mittal

Gaurav Khetan

K Mythreya

Mogili Sindhu

Milind Suryavanshi

Nishit Mehta

Prashanna Sivaraman

Prem Mohan

Rajiv Govindan

Rahul Sopanrao Ghodke

Sejal Solanki

Swati Banthiya

N e w s l e t t e r v o l u m e 1

Student Research TeamS i b m , b a n g a l o r e