Embed Size (px)

Citation preview

1

PRE102: Optimizing Your Medical Practice: Current and Future Financial Performance Preconference

Owen J. Dahl, MBA, FACHE, LSSMBBAnnual Conference

October 6, 2013

2

3

Objectives

Complete the picture of total financial management for your practice

Improve your revenue circle

Identify issues with cost management

Identify and report key performance indicators compared to benchmarks

Prepare for future payment model changes

Provide tools and techniques necessary for future success

4

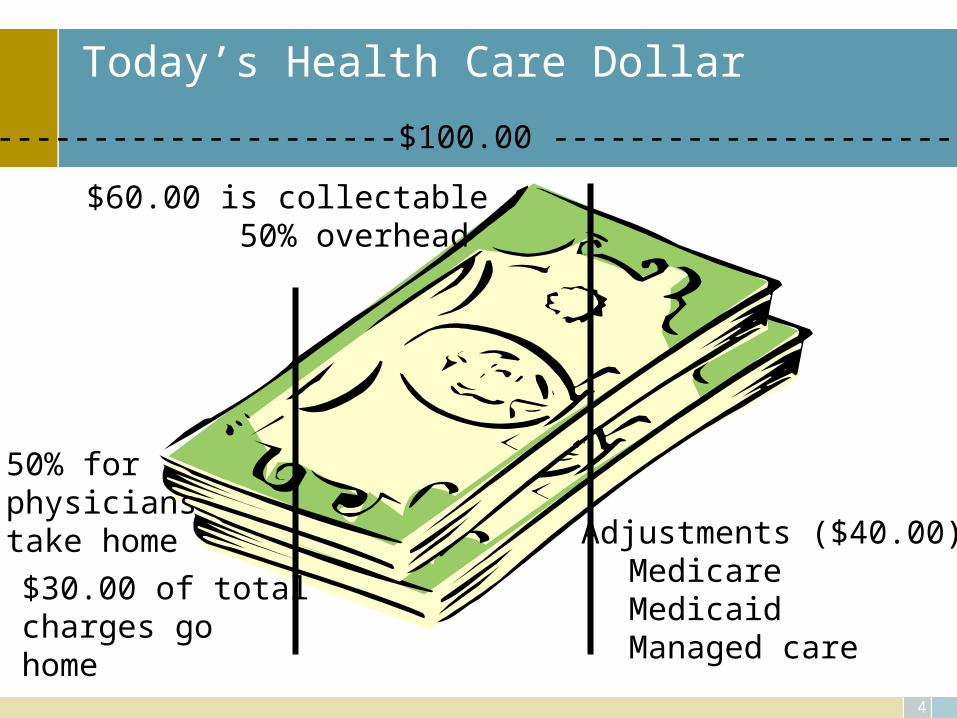

Today’s Health Care Dollar

Adjustments ($40.00):MedicareMedicaidManaged care

$60.00 is collectable 50% overhead

50% forphysicianstake home

$30.00 of totalcharges gohome

-------------------------$100.00 ---------------------------

5

What is your vision/mission/core business

• Office visits• Procedures• Ancillary revenue• All of the above• Type of patients seen

– Diagnostic– Treatment– Chronic

6

Accounting 101

• Cash– Record activities when cash is in hand

• Accrual– Record activities when the transaction occurs

7

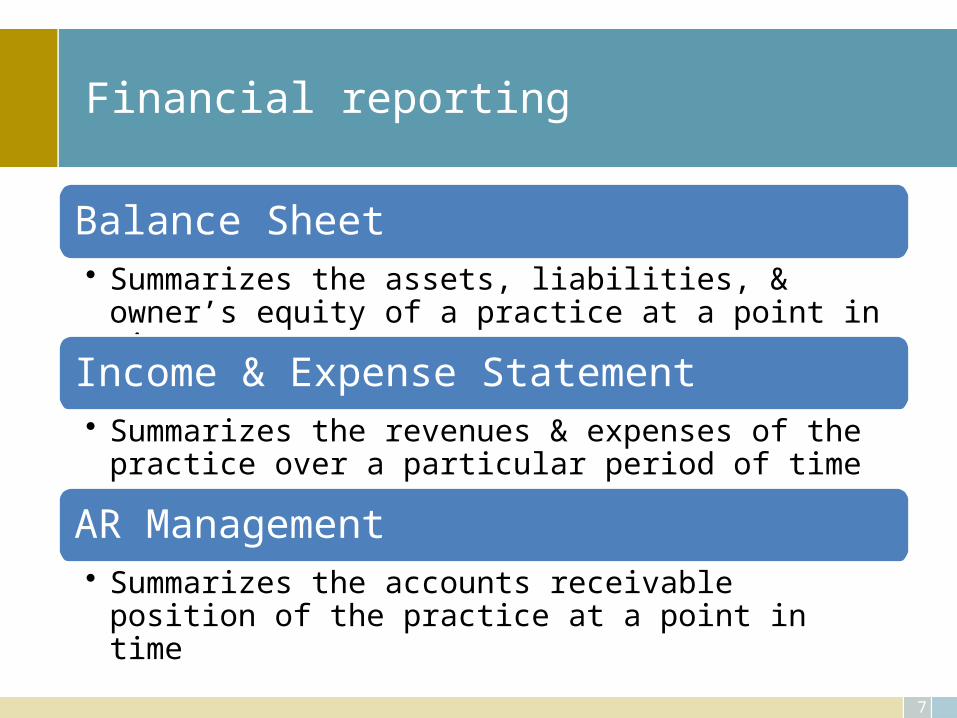

Financial reporting

Balance Sheet• Summarizes the assets, liabilities, & owner’s equity of a

practice at a point in time

Income & Expense Statement• Summarizes the revenues & expenses of the practice over a

particular period of time

AR Management • Summarizes the accounts receivable position of the practice at

a point in time

8

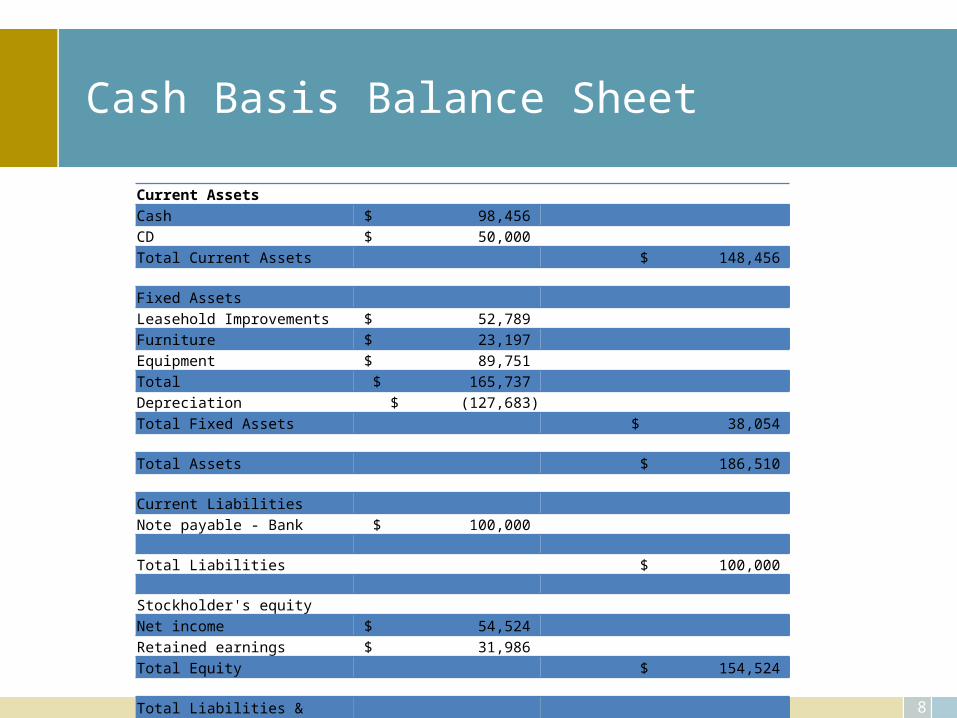

Cash Basis Balance Sheet

Current AssetsCash $ 98,456 CD $ 50,000 Total Current Assets $ 148,456

Fixed AssetsLeasehold Improvements $ 52,789 Furniture $ 23,197 Equipment $ 89,751 Total $ 165,737 Depreciation $ (127,683)Total Fixed Assets $ 38,054

Total Assets $ 186,510

Current LiabilitiesNote payable - Bank $ 100,000

Total Liabilities $ 100,000

Stockholder's equityNet income $ 54,524 Retained earnings $ 31,986 Total Equity $ 154,524

Total Liabilities & Equity $ 186,510

9

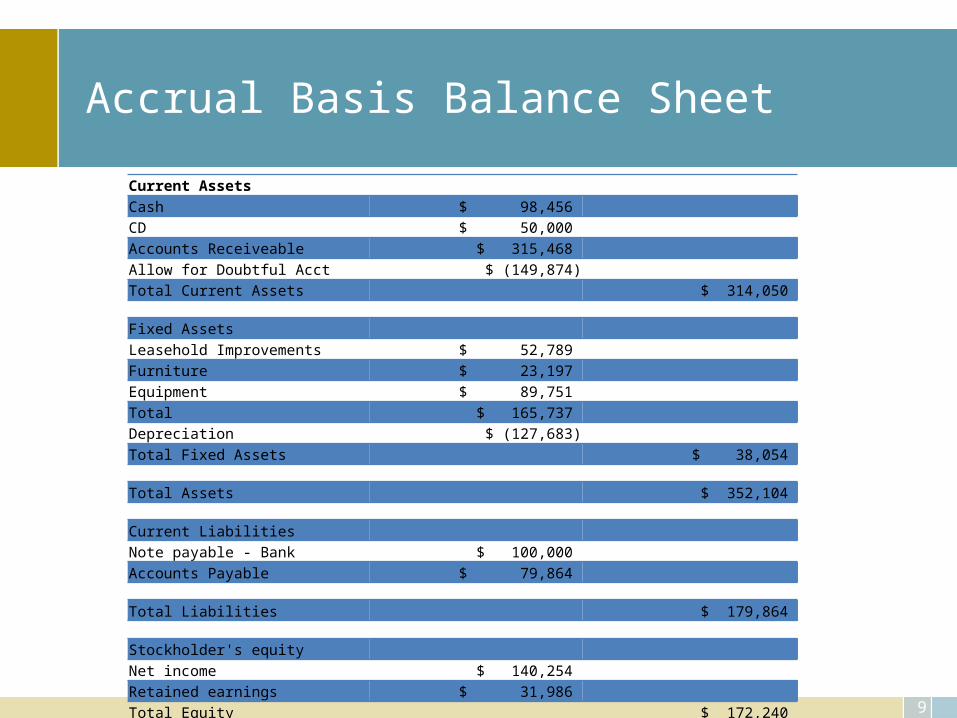

Accrual Basis Balance Sheet

Current AssetsCash $ 98,456 CD $ 50,000 Accounts Receiveable $ 315,468 Allow for Doubtful Acct $ (149,874)Total Current Assets $ 314,050

Fixed AssetsLeasehold Improvements $ 52,789 Furniture $ 23,197 Equipment $ 89,751 Total $ 165,737 Depreciation $ (127,683)Total Fixed Assets $ 38,054

Total Assets $ 352,104

Current LiabilitiesNote payable - Bank $ 100,000 Accounts Payable $ 79,864

Total Liabilities $ 179,864

Stockholder's equityNet income $ 140,254 Retained earnings $ 31,986 Total Equity $ 172,240

Total Liabilities & Equity $ 352,104

10

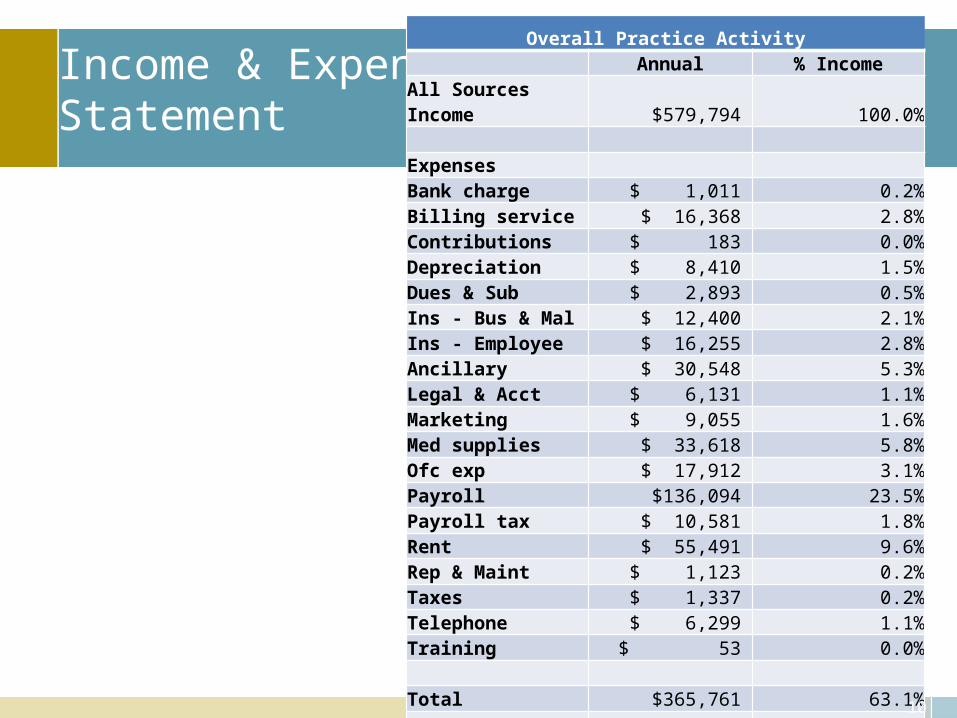

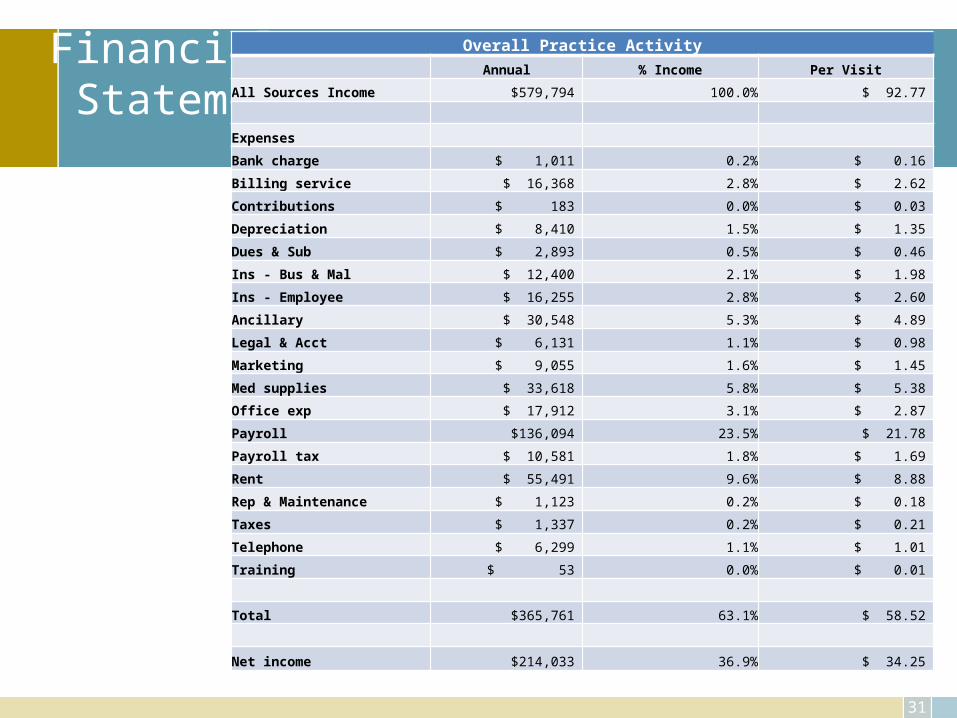

Income & ExpenseStatement

Overall Practice Activity Annual % Income

All Sources Income $579,794 100.0% Expenses Bank charge $ 1,011 0.2%Billing service $ 16,368 2.8%Contributions $ 183 0.0%Depreciation $ 8,410 1.5%Dues & Sub $ 2,893 0.5%Ins - Bus & Mal $ 12,400 2.1%Ins - Employee $ 16,255 2.8%Ancillary $ 30,548 5.3%Legal & Acct $ 6,131 1.1%Marketing $ 9,055 1.6%Med supplies $ 33,618 5.8%Ofc exp $ 17,912 3.1%Payroll $136,094 23.5%Payroll tax $ 10,581 1.8%Rent $ 55,491 9.6%Rep & Maint $ 1,123 0.2%Taxes $ 1,337 0.2%Telephone $ 6,299 1.1%Training $ 53 0.0% Total $365,761 63.1% Net income $214,033 36.9%

11

Benchmark

• Evaluate your practice in terms of best practice leading to improving some aspect of performance, function, financial or process improvement

• Methodology– Identify problem areas– Identify how you did it before (how others do it)– Identify “leading edge” practices– Implement new and improved business practices

12

Revenue

13

What can I make?

• Fee schedule• Sources of income

– Medicare/Medicaid– Managed care– Traditional insurance– Patient

14

Revenue – Top line

• Driven by – Contracts– Time involved

• Hours to sell• Others to support your effort

– Services provided• Diagnostic procedures• Treatment • Niche market

15

Top Line

• New patients– Recruit– Advertise– Referral sources– Managed care contracts

16

Top Line

• New services– Expand by offering something totally new– Enhance by improving what is currently offered– Factors:

• Experimental• Reimbursement• Training• Capital expenditure

17

Top Line

• Improve revenue– Collections– Managed care contract negotiations

• Identify what contractual rates you are willing to receive, is Medicare sufficient?

– Coding for service provided

18

Top Line

• Patient retention– Cost of loosing a patient– Common for business to loose 15 - 20% per year

• Another use of protocols– Determine when patients should return, track

• How– What benefits the patient?– “free visits”

19

Expense

20

Bottom Line

• Cost management– Per service– Per visit– ABC– RVU

• What things are you doing that make money?• What things loose money?• What is the desired target return?

21

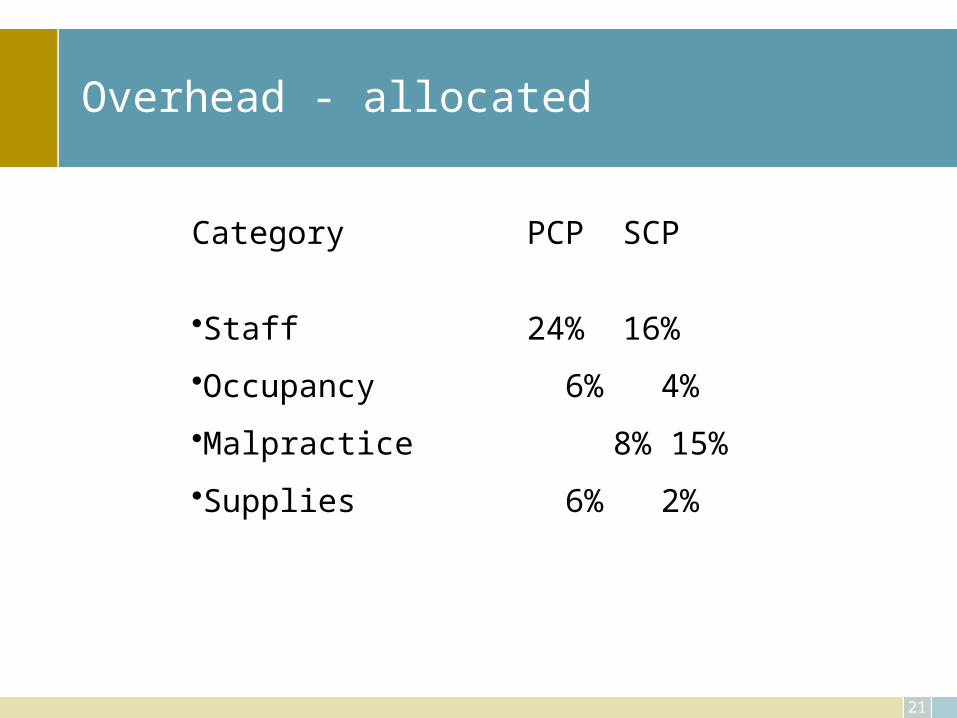

Overhead - allocated

Category PCP SCP

•Staff 24% 16%

•Occupancy 6% 4%

•Malpractice 8% 15%

•Supplies 6% 2%

22

Bottom Line

• Financial statement– Salaries – Occupancy costs – Malpractice – Supplies – Telephone

• Phone• Marketing

– All other

• Percentages– 20%+– 6 - 8%– 3 - 12%– 1 - 8%– 2 - 5%

• 1%• 2%

– to total 50% (or greater)

23

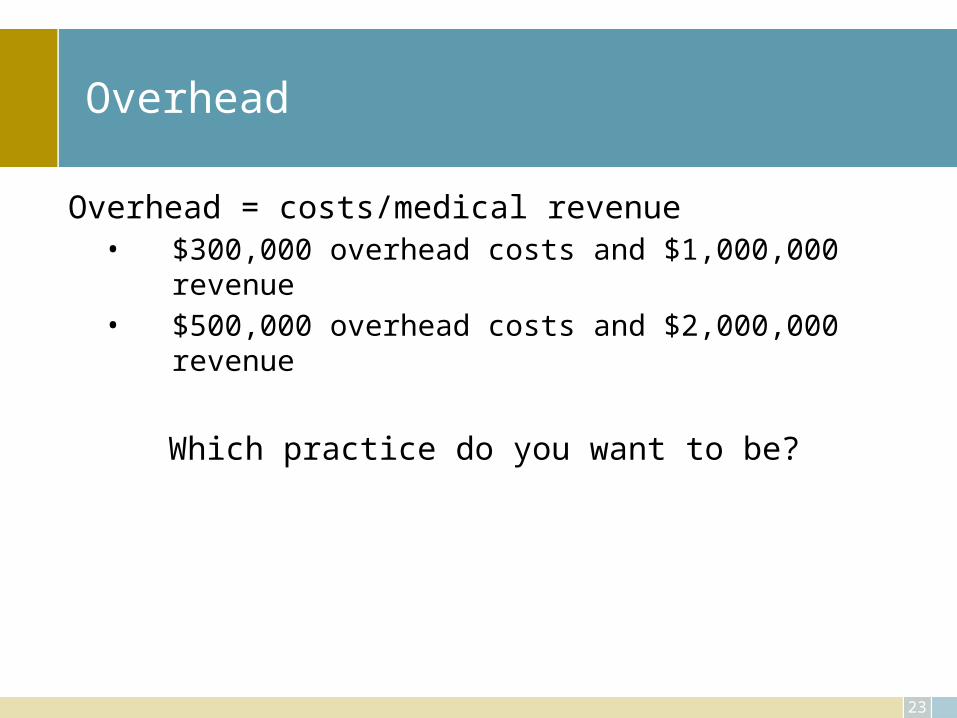

Overhead

Overhead = costs/medical revenue• $300,000 overhead costs and $1,000,000 revenue• $500,000 overhead costs and $2,000,000 revenue

Which practice do you want to be?

24

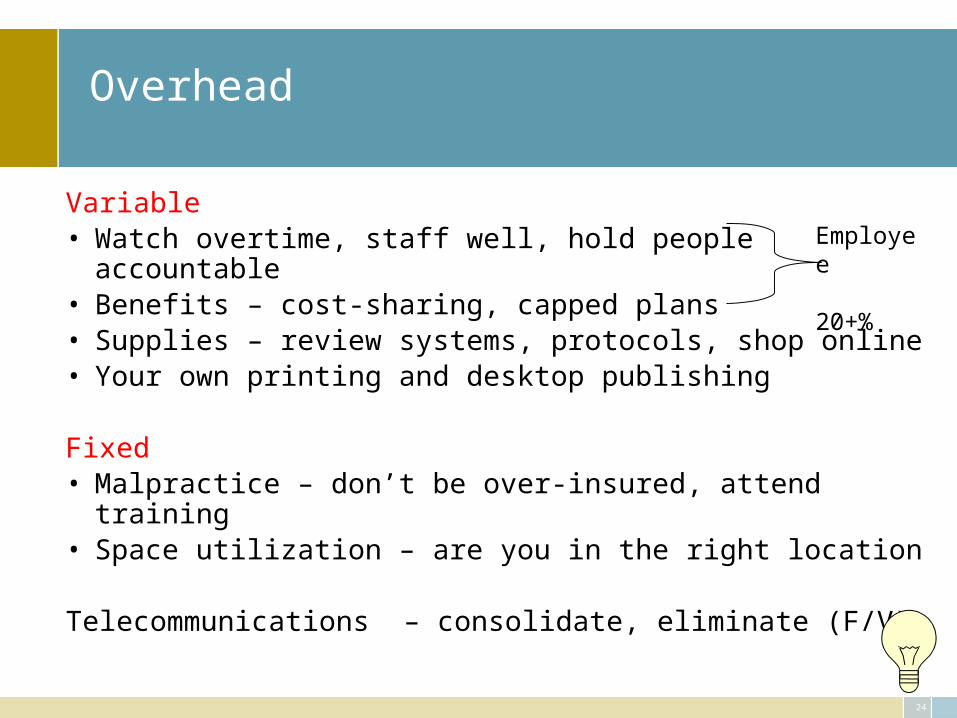

Overhead

Variable• Watch overtime, staff well, hold people accountable • Benefits – cost-sharing, capped plans • Supplies – review systems, protocols, shop online• Your own printing and desktop publishing

Fixed• Malpractice – don’t be over-insured, attend training• Space utilization – are you in the right location

Telecommunications – consolidate, eliminate (F/V)

Employee

20+%

25

Overhead

• Is the doctor overhead? A cost?• Overhead is your cost of doing business

– In your practice is it too much?– Is it just right?

• Measure by determining if you are getting the most out of your cost, the most from your staffing, etc.

26

How much does it cost to see a patient?

New patient

Established patient

Hospital visit

By procedure

Injection

Weekend activity

Others in your practice

27

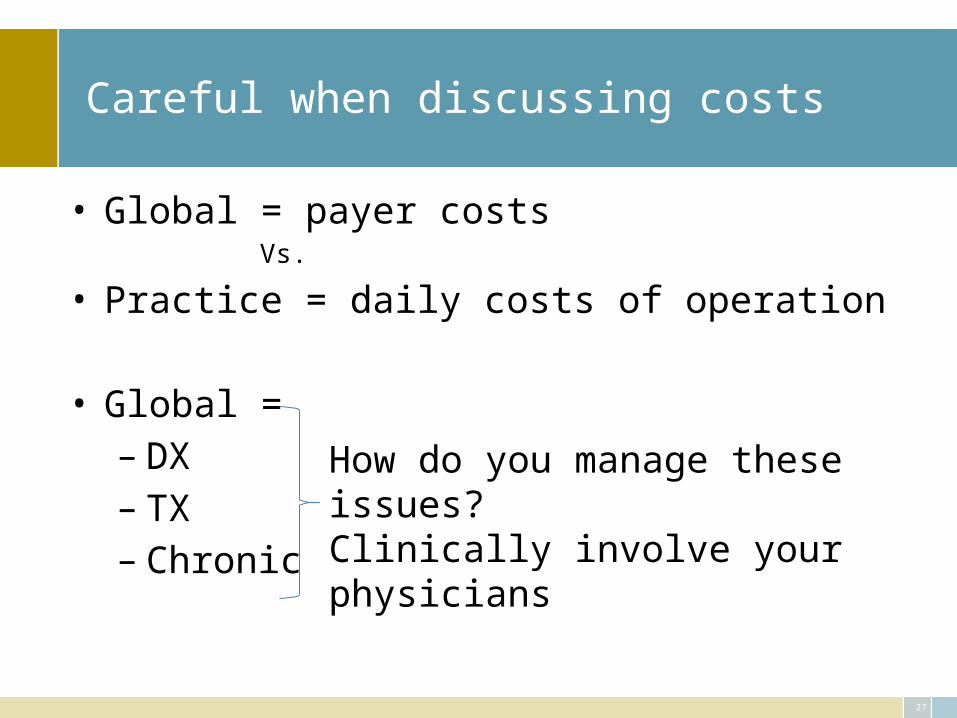

Careful when discussing costs

• Global = payer costsVs.

• Practice = daily costs of operation

• Global = – DX– TX– Chronic

How do you manage these issues?Clinically involve your physicians

28

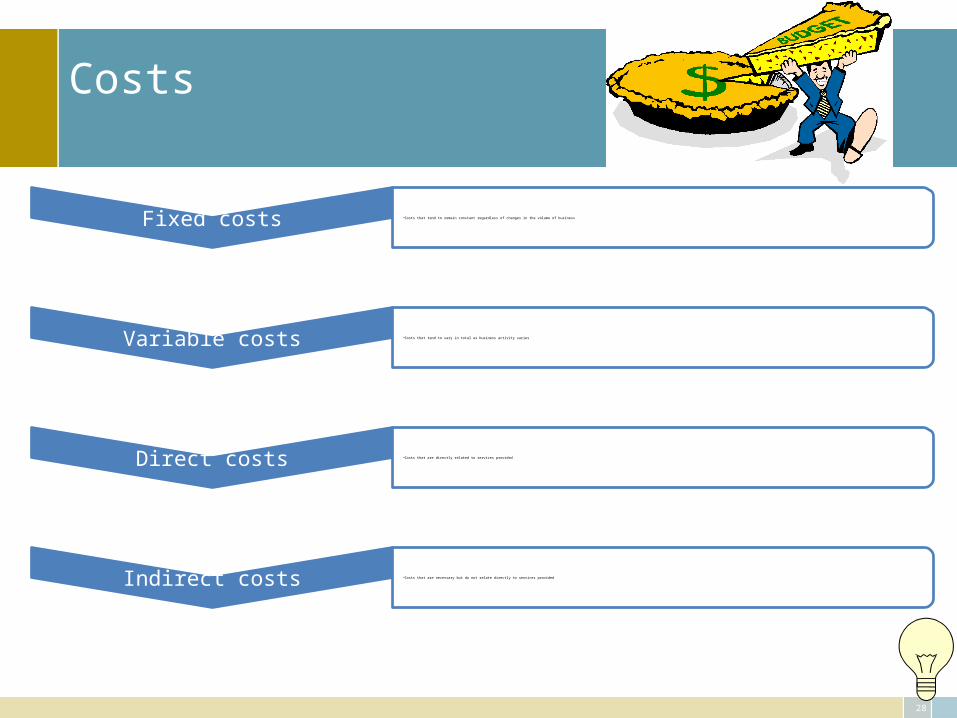

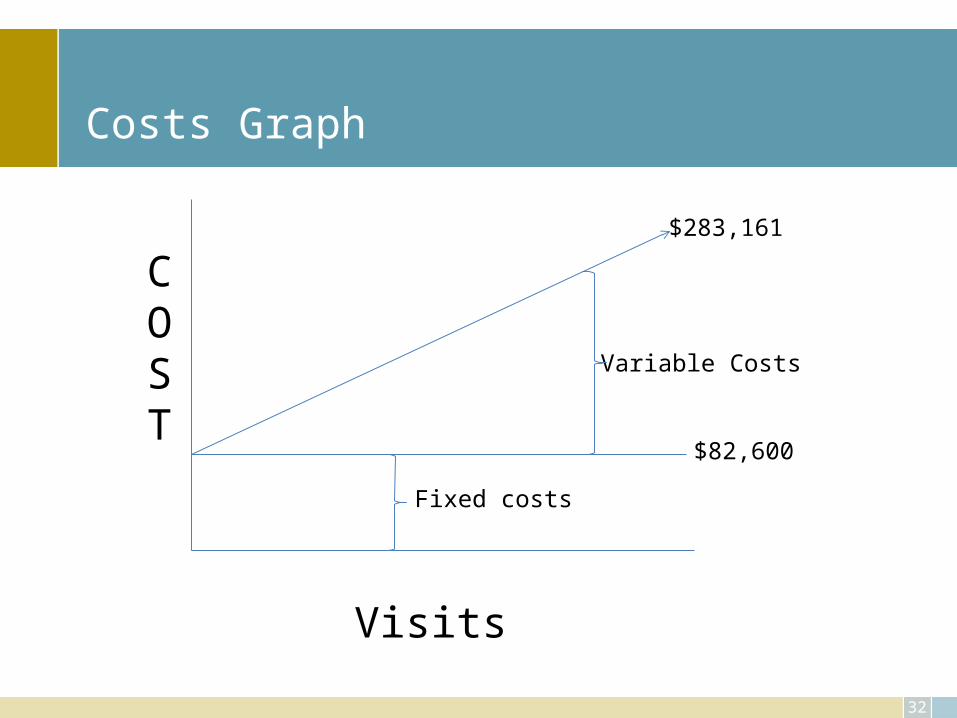

Costs

Fixed costs •Costs that tend to remain constant regardless of changes in the volume of business

Variable costs •Costs that tend to vary in total as business activity varies

Direct costs •Costs that are directly related to services provided

Indirect costs •Costs that are necessary but do not relate directly to services provided

29

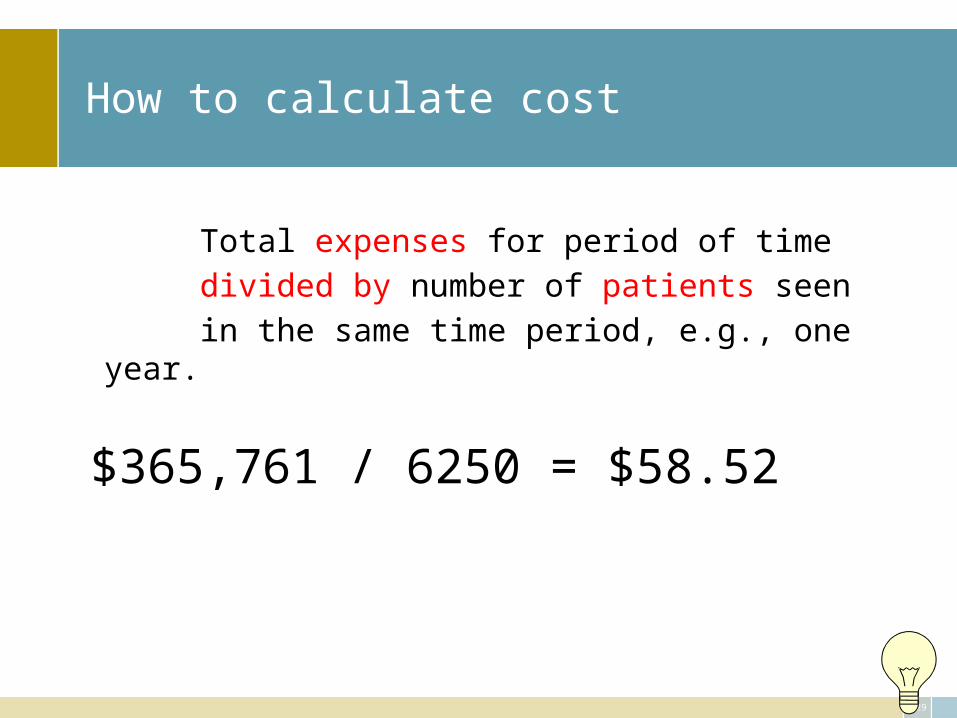

How to calculate cost

Total expenses for period of time

divided by number of patients seen

in the same time period, e.g., one year.

$365,761 / 6250 = $58.52

30

Assumptions

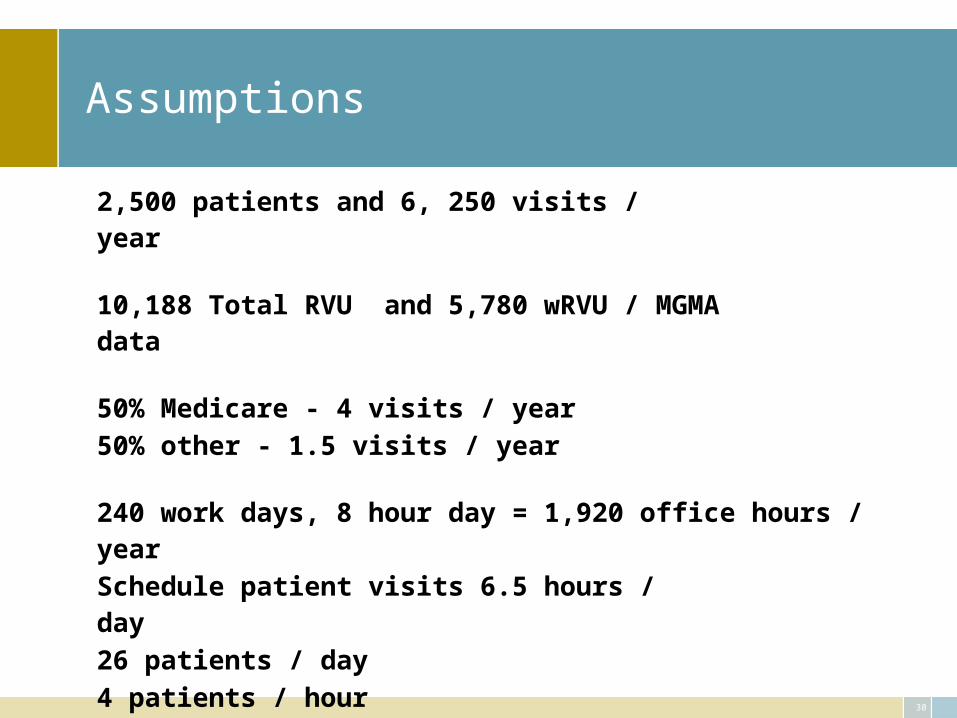

2,500 patients and 6, 250 visits / year

10,188 Total RVU and 5,780 wRVU / MGMA data

50% Medicare - 4 visits / year50% other - 1.5 visits / year

240 work days, 8 hour day = 1,920 office hours / yearSchedule patient visits 6.5 hours / day26 patients / day4 patients / hourOne new patient / work day25 established patients / day

Established patients scheduled - 15 min visits; new pts – 30 min

31

Financial Statement

Overall Practice Activity

Annual % Income Per Visit

All Sources Income $579,794 100.0% $ 92.77

Expenses

Bank charge $ 1,011 0.2% $ 0.16

Billing service $ 16,368 2.8% $ 2.62

Contributions $ 183 0.0% $ 0.03

Depreciation $ 8,410 1.5% $ 1.35

Dues & Sub $ 2,893 0.5% $ 0.46

Ins - Bus & Mal $ 12,400 2.1% $ 1.98

Ins - Employee $ 16,255 2.8% $ 2.60

Ancillary $ 30,548 5.3% $ 4.89

Legal & Acct $ 6,131 1.1% $ 0.98

Marketing $ 9,055 1.6% $ 1.45

Med supplies $ 33,618 5.8% $ 5.38

Office exp $ 17,912 3.1% $ 2.87

Payroll $136,094 23.5% $ 21.78

Payroll tax $ 10,581 1.8% $ 1.69

Rent $ 55,491 9.6% $ 8.88

Rep & Maintenance $ 1,123 0.2% $ 0.18

Taxes $ 1,337 0.2% $ 0.21

Telephone $ 6,299 1.1% $ 1.01

Training $ 53 0.0% $ 0.01

Total $365,761 63.1% $ 58.52

Net income $214,033 36.9% $ 34.25

32

Costs Graph

$82,600

$283,161

COST

Visits

Fixed costs

Variable Costs

33

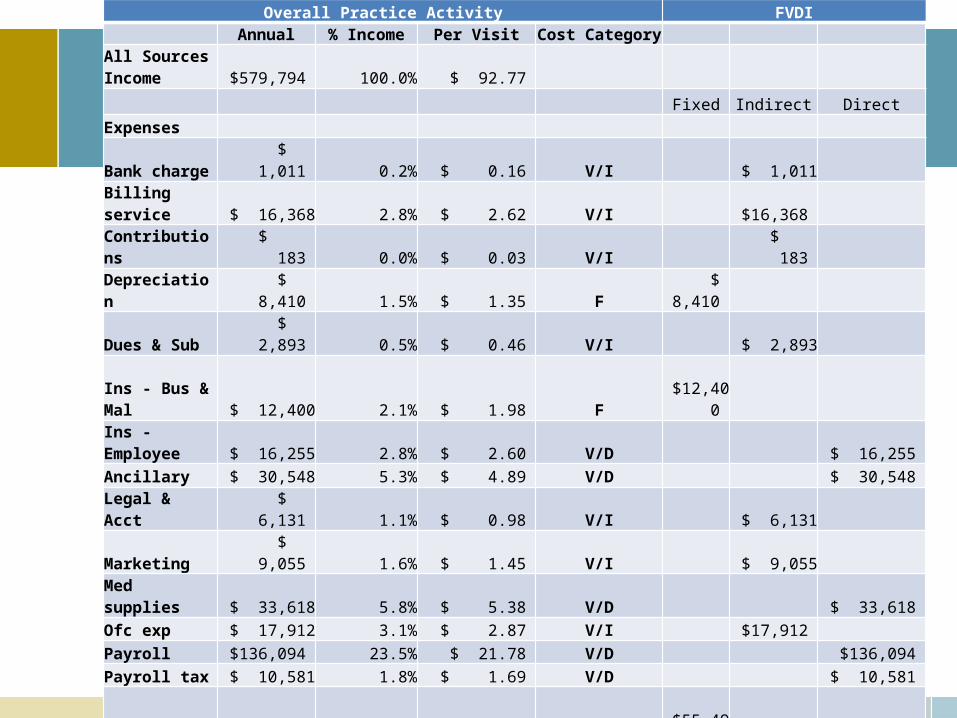

Overall Practice Activity FVDI Annual % Income Per Visit Cost Category

All Sources Income $579,794 100.0% $ 92.77

Fixed Indirect Direct

Expenses

Bank charge $ 1,011 0.2% $ 0.16 V/I $ 1,011

Billing service $ 16,368 2.8% $ 2.62 V/I $16,368

Contributions $ 183 0.0% $ 0.03 V/I $ 183

Depreciation $ 8,410 1.5% $ 1.35 F $ 8,410

Dues & Sub $ 2,893 0.5% $ 0.46 V/I $ 2,893 Ins - Bus & Mal $ 12,400 2.1% $ 1.98 F $12,400

Ins - Employee $ 16,255 2.8% $ 2.60 V/D $ 16,255

Ancillary $ 30,548 5.3% $ 4.89 V/D $ 30,548

Legal & Acct $ 6,131 1.1% $ 0.98 V/I $ 6,131

Marketing $ 9,055 1.6% $ 1.45 V/I $ 9,055

Med supplies $ 33,618 5.8% $ 5.38 V/D $ 33,618

Ofc exp $ 17,912 3.1% $ 2.87 V/I $17,912

Payroll $136,094 23.5% $ 21.78 V/D $136,094

Payroll tax $ 10,581 1.8% $ 1.69 V/D $ 10,581

Rent $ 55,491 9.6% $ 8.88 F $55,491

Rep & Maint $ 1,123 0.2% $ 0.18 V/I $ 1,123

Taxes $ 1,337 0.2% $ 0.21 V/I $ 1,337

Telephone $ 6,299 1.1% $ 1.01 F $ 6,299

Training $ 53 0.0% $ 0.01 V/D $ 53

Total $365,761 63.1% $ 58.52 $82,600 $56,013 $227,149

13.22 8.96 36.34

Net income $214,033 36.9% $ 34.25 22.6% 15.3% 62.1%

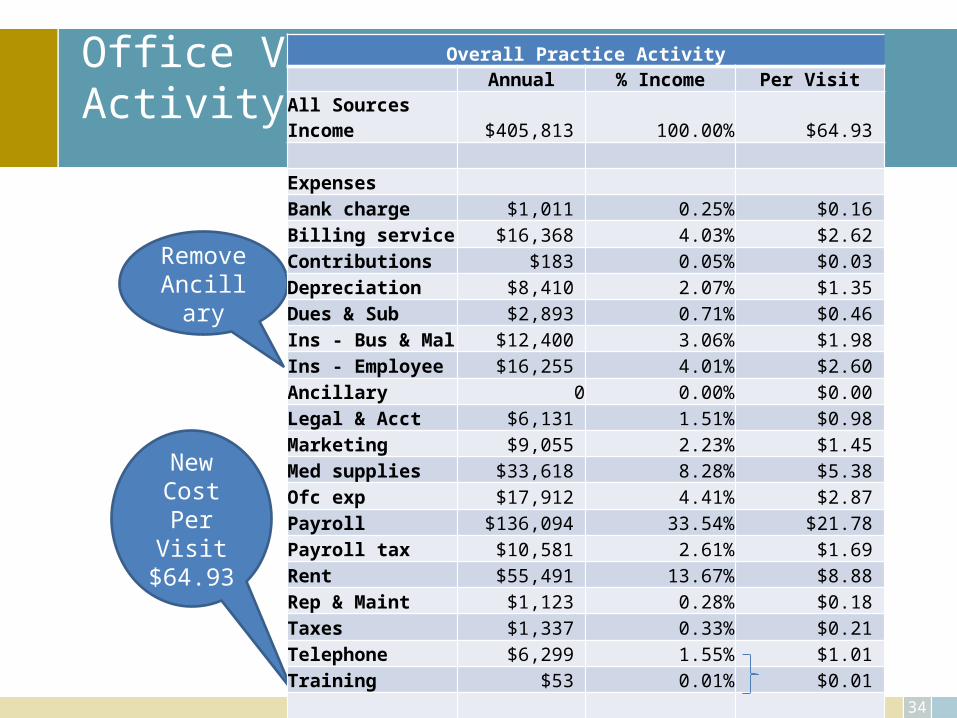

Office Visit Activity Only

34

New Cost Per Visit$64.93

RemoveAncillary

Overall Practice Activity Annual % Income Per Visit

All Sources Income $405,813 100.00% $64.93 Expenses Bank charge $1,011 0.25% $0.16 Billing service $16,368 4.03% $2.62 Contributions $183 0.05% $0.03 Depreciation $8,410 2.07% $1.35 Dues & Sub $2,893 0.71% $0.46 Ins - Bus & Mal $12,400 3.06% $1.98 Ins - Employee $16,255 4.01% $2.60 Ancillary 0 0.00% $0.00 Legal & Acct $6,131 1.51% $0.98 Marketing $9,055 2.23% $1.45 Med supplies $33,618 8.28% $5.38 Ofc exp $17,912 4.41% $2.87 Payroll $136,094 33.54% $21.78 Payroll tax $10,581 2.61% $1.69 Rent $55,491 13.67% $8.88 Rep & Maint $1,123 0.28% $0.18 Taxes $1,337 0.33% $0.21 Telephone $6,299 1.55% $1.01 Training $53 0.01% $0.01

Total $335,213 82.60% $53.63 Net income $70,600 17.40% $11.30

35

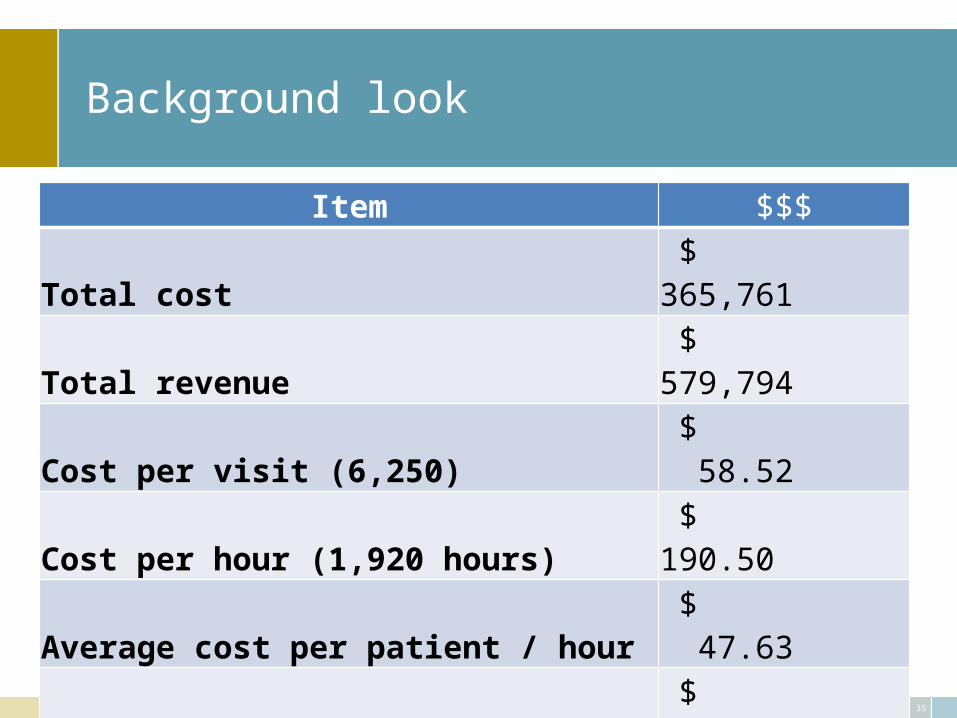

Background look

Item $$$Total cost $ 365,761 Total revenue $ 579,794

Cost per visit (6,250) $ 58.52

Cost per hour (1,920 hours) $ 190.50

Average cost per patient / hour $ 47.63

Revenue per hour $ 301.98

Cost per RVU $ 35.90

Cost per wRVU $ 63.28

36

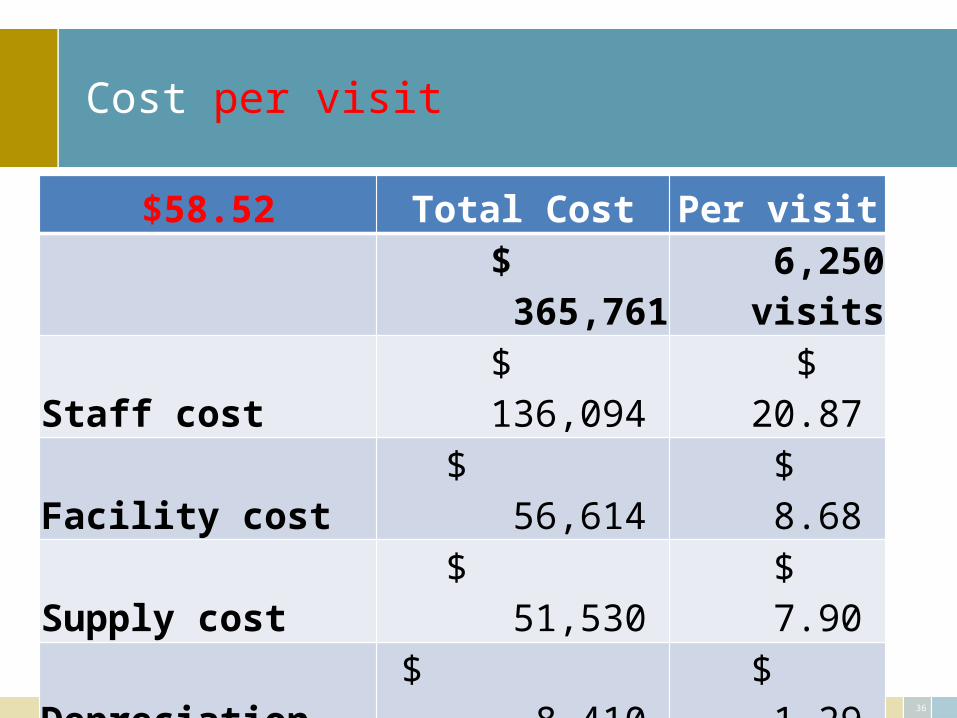

Cost per visit

$58.52 Total Cost Per visit

$ 365,761 6,250

visits

Staff cost $ 136,094 $ 20.87

Facility cost $ 56,614 $ 8.68

Supply cost $ 51,530 $ 7.90

Depreciation $ 8,410 $ 1.29

Communication $ 6,299 $ 0.97

Physician $ 214,033 $ 32.83

37

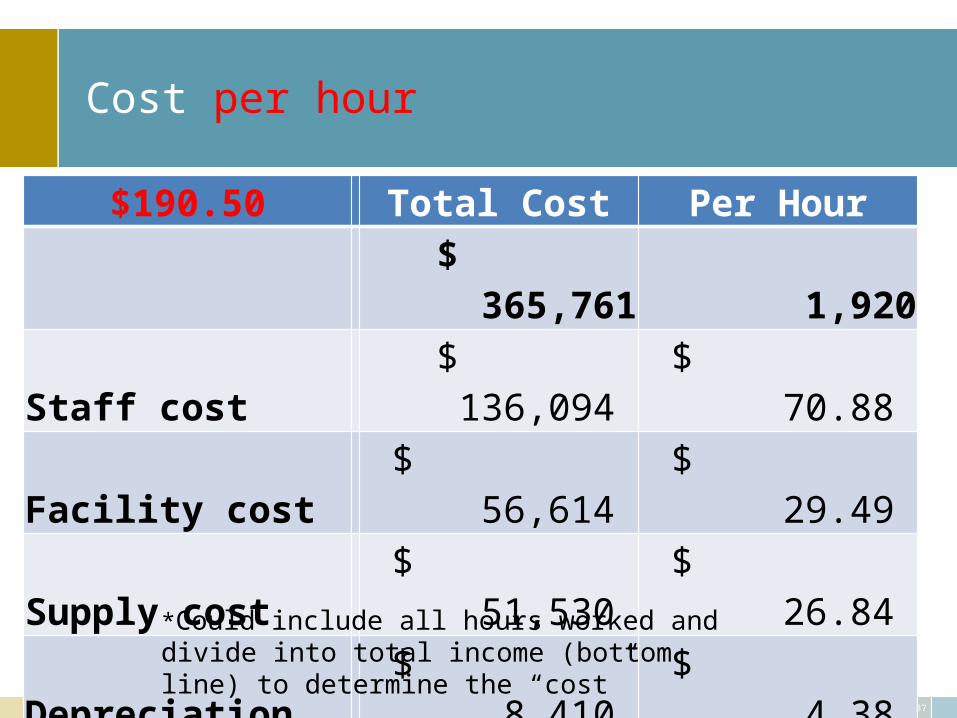

Cost per hour

$190.50 Total Cost Per Hour$ 365,761 1,920

Staff cost $ 136,094 $ 70.88

Facility cost $ 56,614 $ 29.49

Supply cost $ 51,530 $ 26.84

Depreciation $ 8,410 $ 4.38

Communication $ 6,299 $ 3.28

Physician* $ 214,033 $ 111.48

*Could include all hours worked and divide into total income (bottom line) to determine the “cost”

38

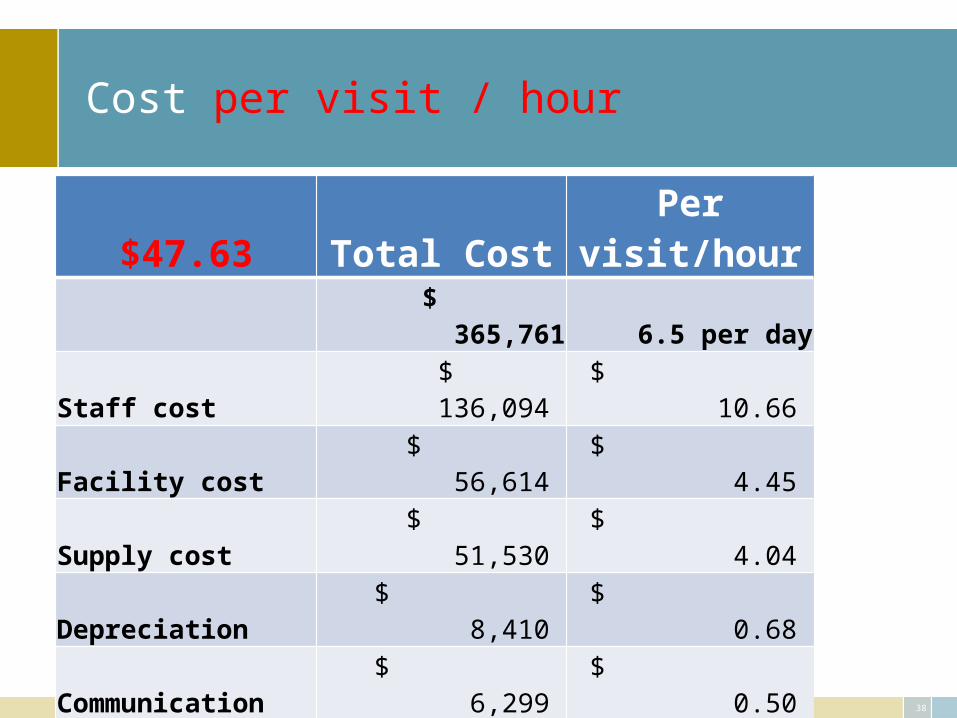

Cost per visit / hour

$47.63 Total Cost Per visit/hour$ 365,761 6.5 per day

Staff cost $ 136,094 $ 10.66

Facility cost $ 56,614 $ 4.45

Supply cost $ 51,530 $ 4.04

Depreciation $ 8,410 $ 0.68

Communication $ 6,299 $ 0.50

Physician $ 214,033 $ 16.74

Cost per hour

25 Established Pts / day X 6 hrs = 4.2 per hour $ 45.36

1 New Pt / day $ 95.25

39

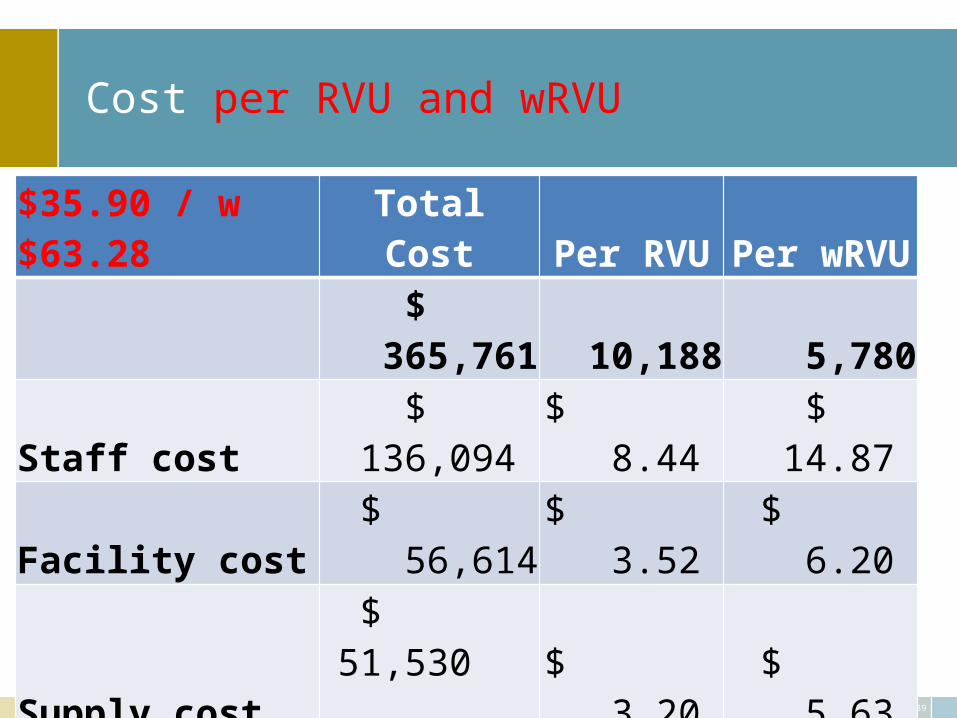

Cost per RVU and wRVU

$35.90 / w $63.28 Total Cost Per RVU Per wRVU

$ 365,761 10,188 5,780

Staff cost $ 136,094 $ 8.44 $ 14.87

Facility cost $ 56,614 $ 3.52 $ 6.20

Supply cost$ 51,530

$ 3.20 $ 5.63

Depreciation $ 8,410 $ 0.54 $ 0.95

Communication $ 6,299 $ 0.39 $ 0.70

Physician $ 214,033 $ 13.25 $ 23.35

40

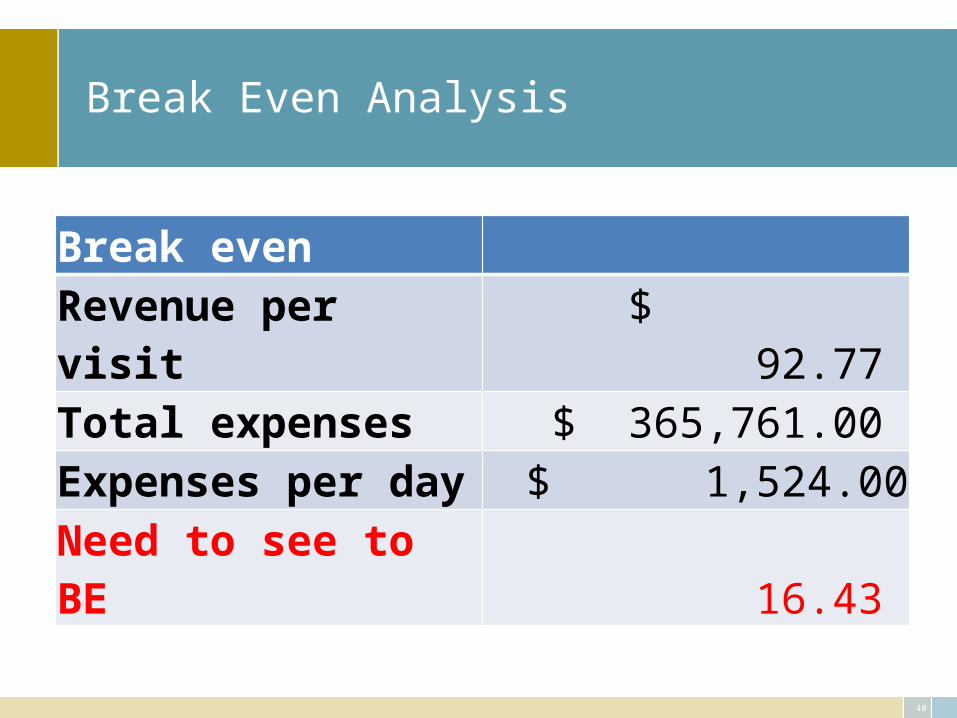

Break Even Analysis

Break evenRevenue per visit $ 92.77 Total expenses $ 365,761.00 Expenses per day $ 1,524.00 Need to see to BE 16.43

41

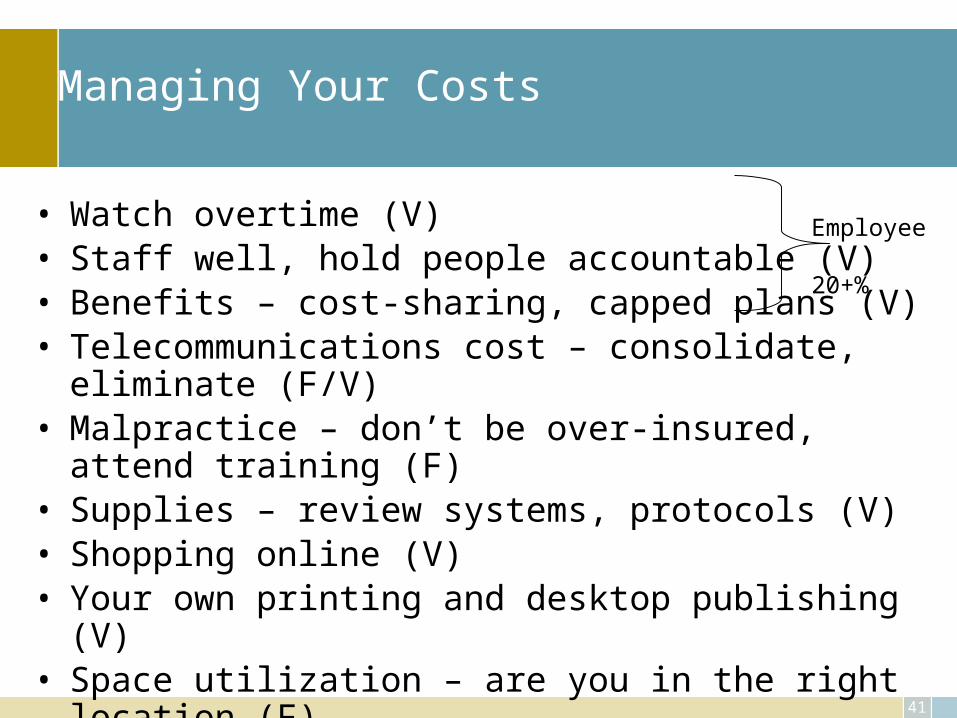

Managing Your Costs

• Watch overtime (V)• Staff well, hold people accountable (V)• Benefits – cost-sharing, capped plans (V)• Telecommunications cost – consolidate, eliminate (F/V)• Malpractice – don’t be over-insured, attend training (F)• Supplies – review systems, protocols (V)• Shopping online (V)• Your own printing and desktop publishing (V)• Space utilization – are you in the right location (F)

Employee

20+%

42

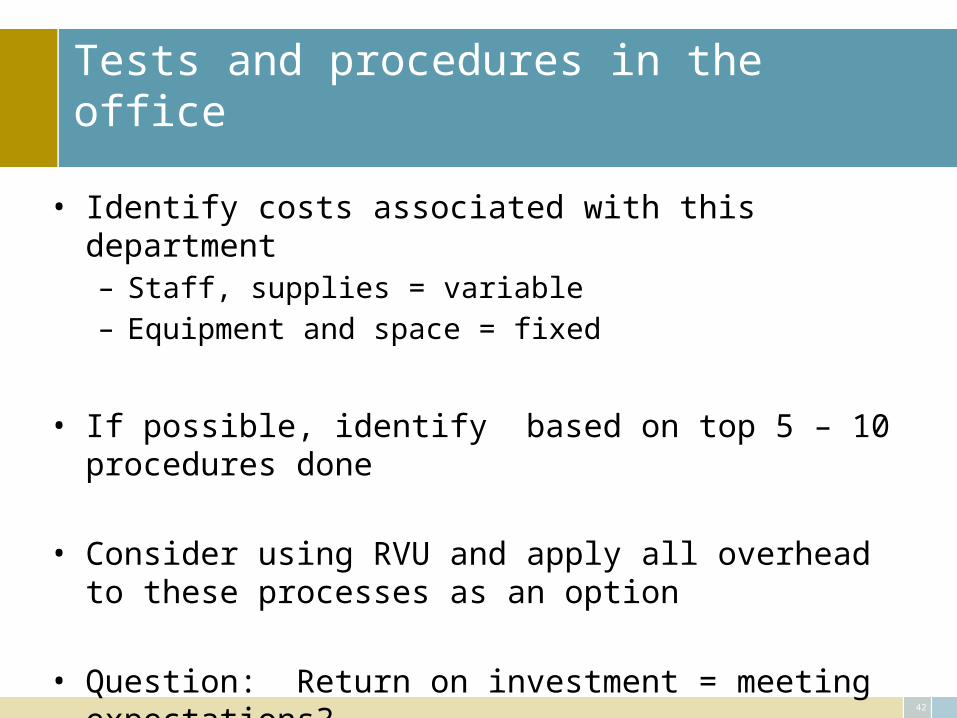

Tests and procedures in the office

• Identify costs associated with this department– Staff, supplies = variable– Equipment and space = fixed

• If possible, identify based on top 5 – 10 procedures done

• Consider using RVU and apply all overhead to these processes as an option

• Question: Return on investment = meeting expectations?

43

Hospital activity

• Carve out MA and most other clinic support• Retain billing costs• Key factor is time associated with visits• Consider the use of RVU• Questions:

– Is the time to walk/drive back and forth factored in and does this service bring value to the practice?

– Real question of cost benefit related to time: remember $190.50 is the total cost per hour (slide 21)

– Is this a marketing effort or a direct financial return?

44

Surgical Procedure

• Goal: Total cost of this procedure

• Number of visits– Office pre and post– Hospital

• Time in operating room• Allocation of “overhead”

• Awareness of options related to “total costs”, e.g., ambulatory center vs. hospital and the fact of who controls the decision

• Protocol for global treatment plan = national standards or group standards?• Therapy – in office, separate cost vs. total cost

45

Program for cost management

• Understand costs – create a culture of monitoring cost• Establish cost reduction/control goals• Benchmark• Utilize data available internally as well• Identify drivers of costs• Drill down into the processes• Insure that cost reduction/control goals are consistent with the

overall vision and organizational goals

46

Cost focus

What is the core business, are all cost aligned with this

• Right number, right skills, right job descriptions and duty assignments

Staffing

• Who orders, who inventories, who approves, who pays and when

Supplies

• When are each looked at, annually? Near end of contract?

Fixed costs• Investment in right services consistent with Core business • Include staff• Include ancillary• Review previous investments

Use of capital

47

Future revenue

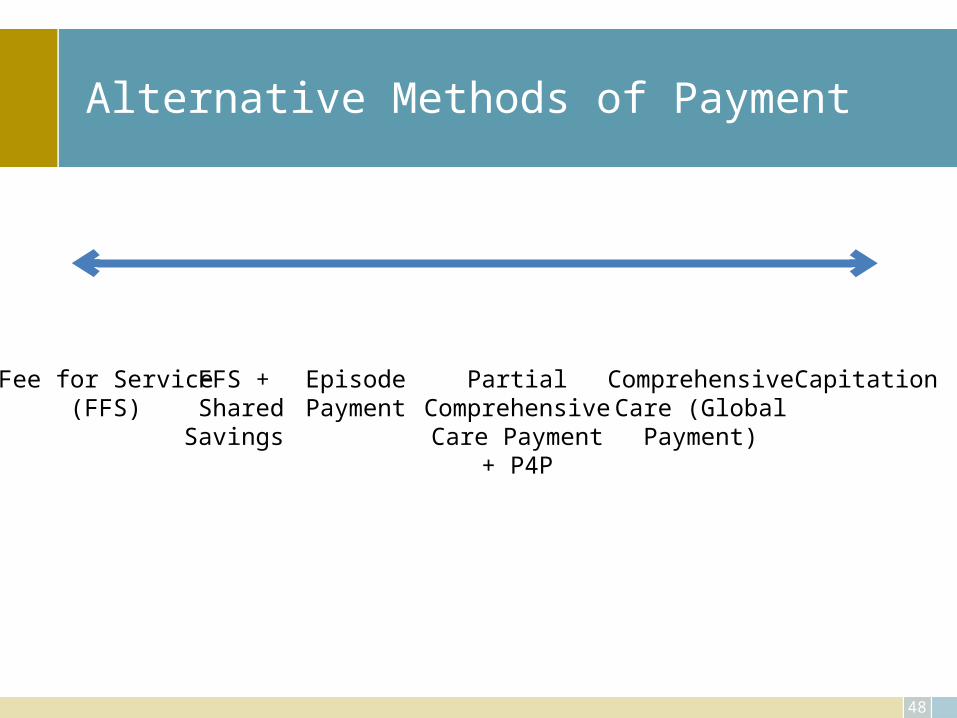

Alternative Methods of Payment

48

Fee for Service(FFS)

FFS + SharedSavings

EpisodePayment

PartialComprehensiveCare Payment

+ P4P

ComprehensiveCare (Global

Payment)

Capitation

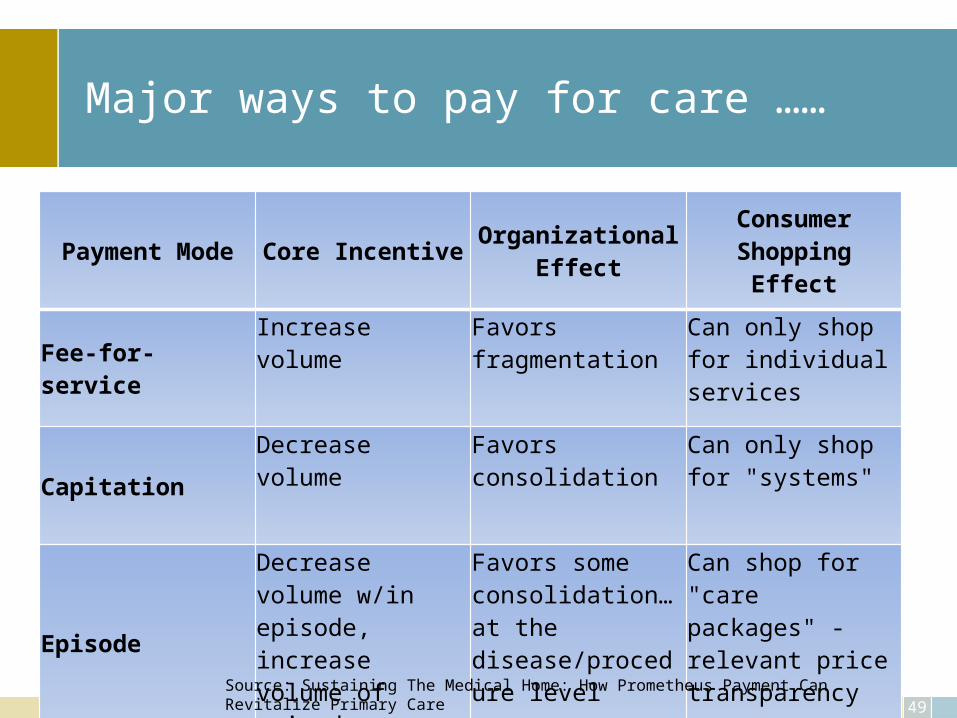

Major ways to pay for care ……

Payment Mode Core Incentive Organizational Effect Consumer Shopping Effect

Fee-for-service

Increase volume Favors fragmentation Can only shop for individual services

Capitation

Decrease volume Favors consolidation Can only shop for "systems"

Episode

Decrease volume w/in episode, increase volume of episodes

Favors some consolidation…at the disease/procedure level

Can shop for "care packages" - relevant price transparency

49Source: Sustaining The Medical Home: How Prometheus Payment Can Revitalize Primary Care

Set Payment Levels

• Regulation = Medicare• Price setting by Large payers = Medicare as base• Negotiation between payers and providers• Competition by providers• Evidence based estimation – cost of each

component estimated and combined

50

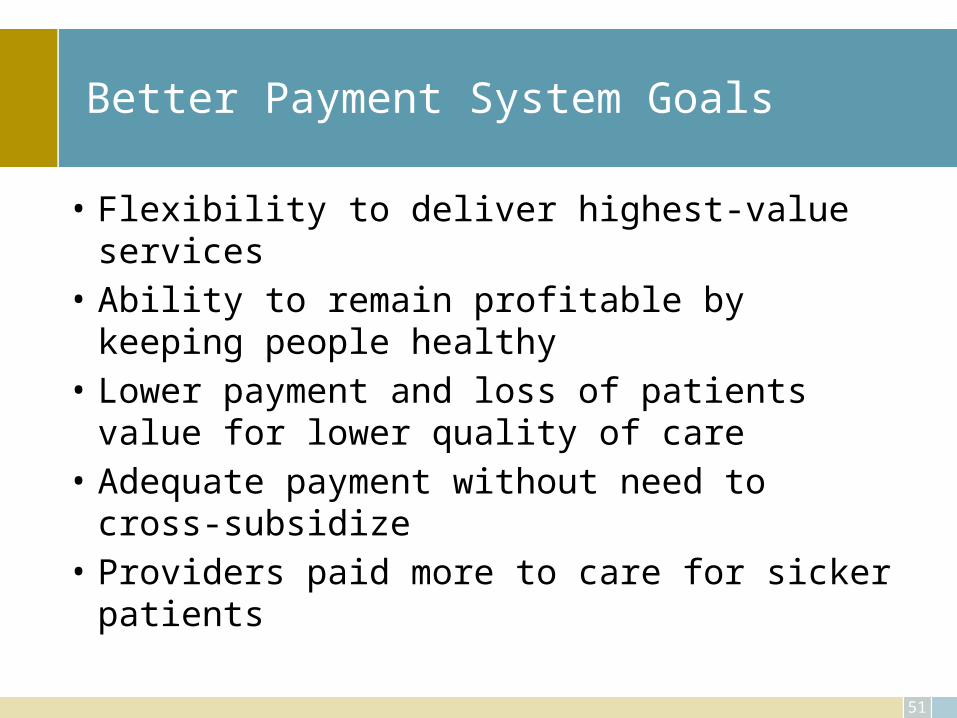

Better Payment System Goals

• Flexibility to deliver highest-value services• Ability to remain profitable by keeping people

healthy• Lower payment and loss of patients value for lower

quality of care• Adequate payment without need to cross-subsidize• Providers paid more to care for sicker patients

51

52

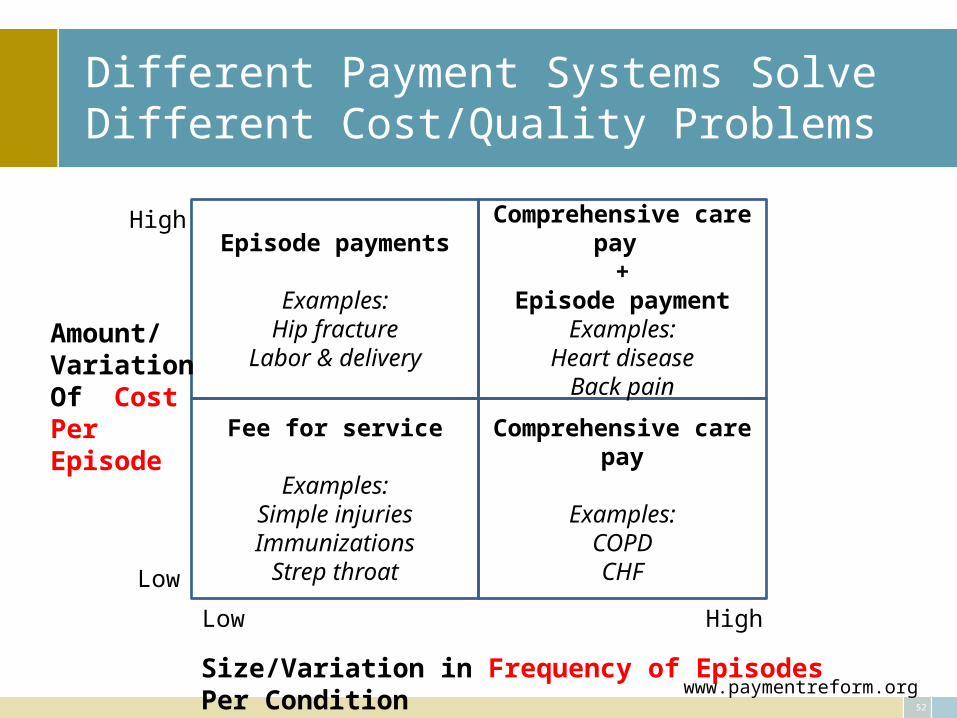

Different Payment Systems Solve Different Cost/Quality Problems

Episode payments

Examples:Hip fracture

Labor & delivery

Comprehensive care pay

Examples:COPDCHF

Comprehensive care pay

+Episode payment

Examples:Heart disease

Back pain

Fee for service

Examples:Simple injuriesImmunizations

Strep throat

High

High

Low

Low

Size/Variation in Frequency of Episodes Per Condition

Amount/VariationOf CostPerEpisode

www.paymentreform.org

53

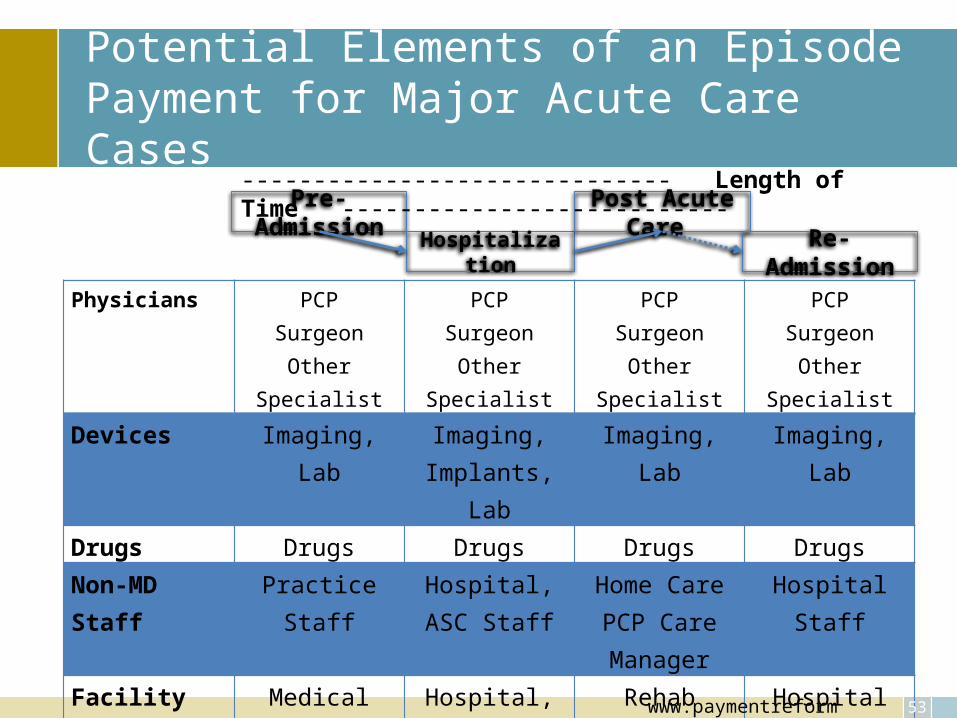

Potential Elements of an Episode Payment for Major Acute Care Cases

Physicians PCPSurgeon

Other Specialist

PCPSurgeon

Other Specialist

PCPSurgeon

Other Specialist

PCPSurgeon

Other Specialist

Devices Imaging, Lab Imaging, Implants, Lab

Imaging, Lab Imaging, Lab

Drugs Drugs Drugs Drugs DrugsNon-MD Staff Practice Staff Hospital, ASC

StaffHome CarePCP Care Manager

Hospital Staff

Facility Medical Office Hospital, ACE Rehab FacilityLong term

Care

Hospital

Pre-Admission

Hospitalization

Post Acute Care

Re-Admission

------------------------------ Length of Time ---------------------------

www.paymentreform.org

54

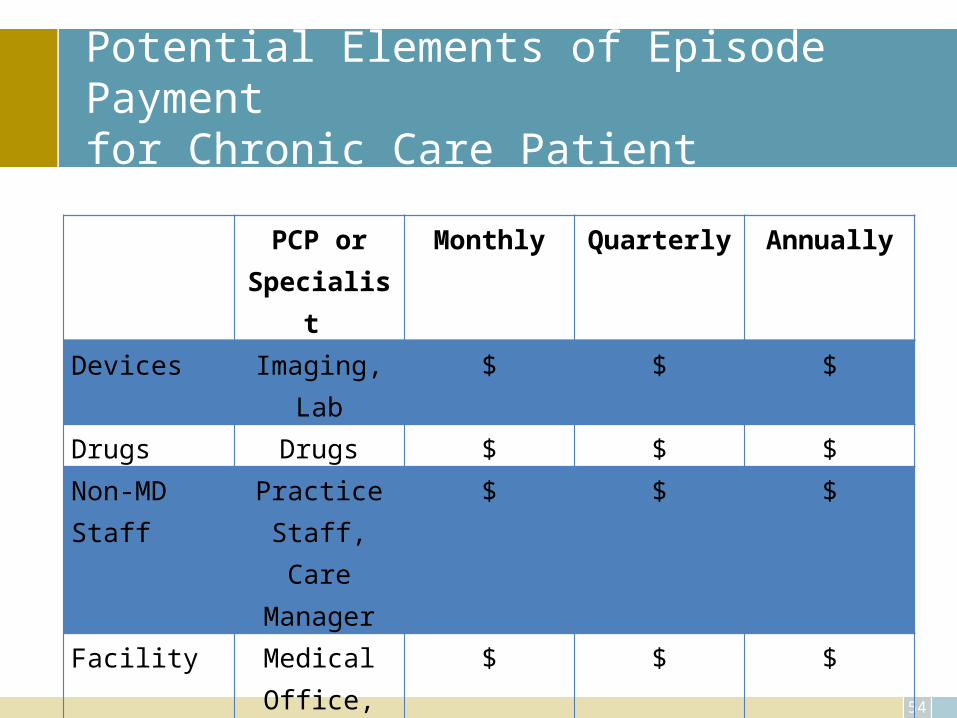

Potential Elements of Episode Payment for Chronic Care Patient

PCP or Specialist

Monthly Quarterly Annually

Devices Imaging, Lab $ $ $

Drugs Drugs $ $ $

Non-MD Staff

Practice Staff, Care Manager

$ $ $

Facility Medical Office,

Hospital, Long Term

Care

$ $ $

55

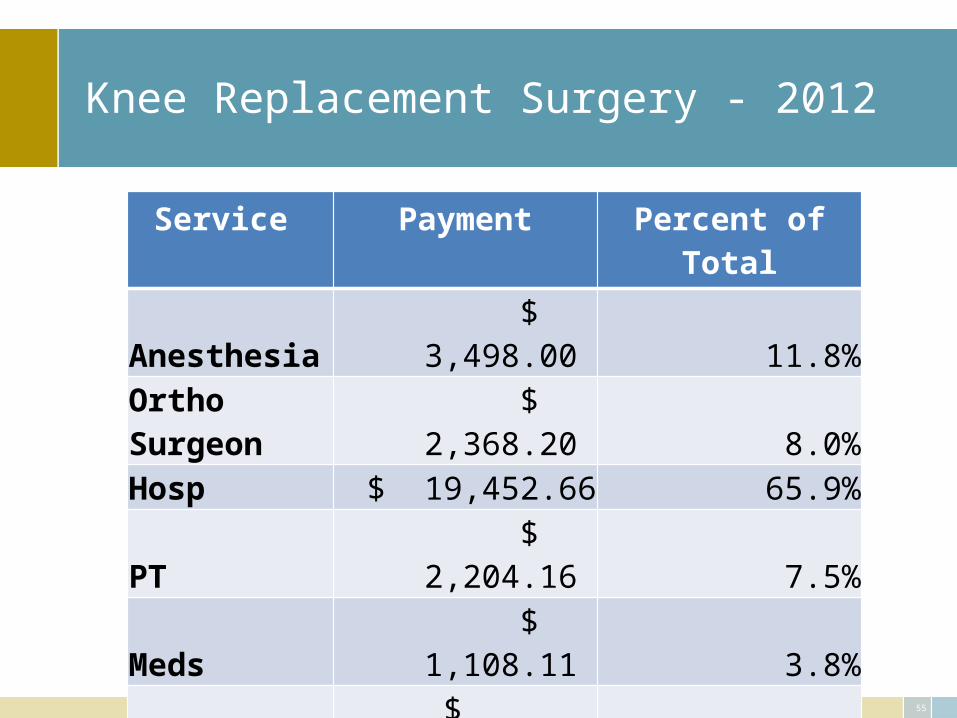

Knee Replacement Surgery - 2012

Service Payment Percent of TotalAnesthesia $ 3,498.00 11.8%Ortho Surgeon $ 2,368.20 8.0%Hosp $ 19,452.66 65.9%PT $ 2,204.16 7.5%Meds $ 1,108.11 3.8%Ortho $ 243.15 0.8%PCP $ 165.48 0.6%X-ray $ 34.50 0.1%Lab $ 464.51 1.6%Total $ 29,538.77 100.0%

56

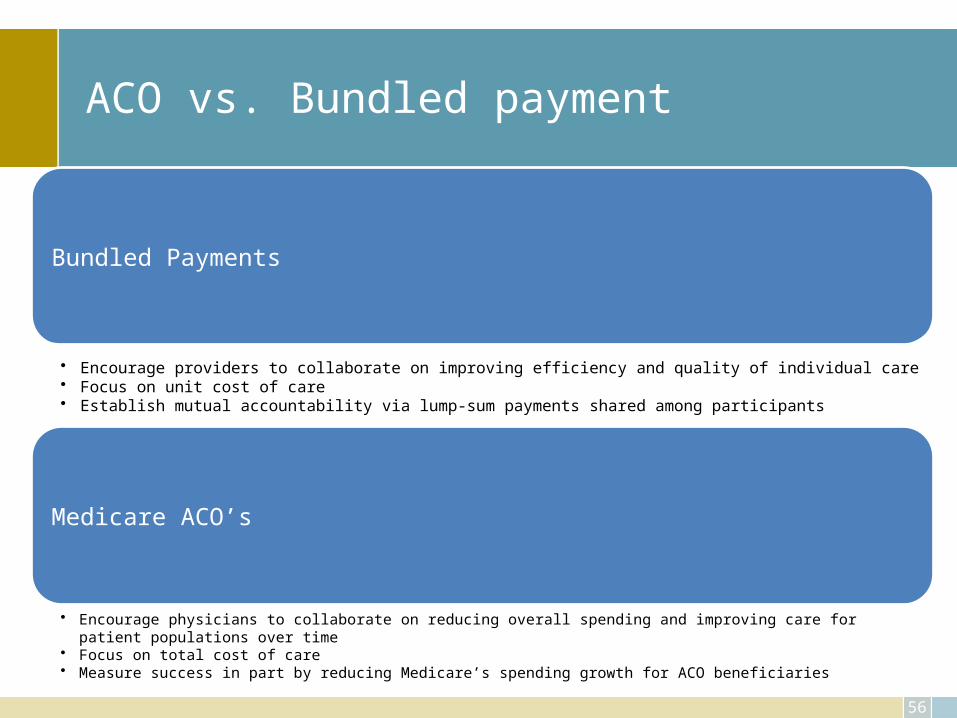

ACO vs. Bundled payment

Bundled Payments

• Encourage providers to collaborate on improving efficiency and quality of individual care• Focus on unit cost of care• Establish mutual accountability via lump-sum payments shared among participants

Medicare ACO’s

• Encourage physicians to collaborate on reducing overall spending and improving care for patient populations over time• Focus on total cost of care• Measure success in part by reducing Medicare’s spending growth for ACO beneficiaries

57

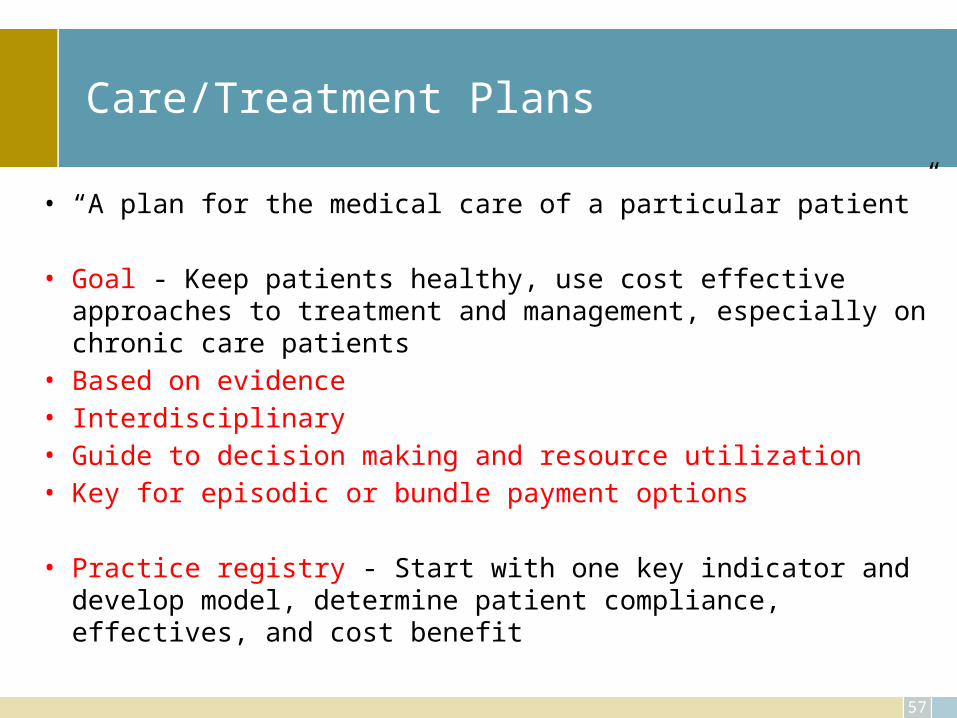

Care/Treatment Plans

• “A plan for the medical care of a particular patient”

• Goal - Keep patients healthy, use cost effective approaches to treatment and management, especially on chronic care patients

• Based on evidence• Interdisciplinary • Guide to decision making and resource utilization• Key for episodic or bundle payment options

• Practice registry - Start with one key indicator and develop model, determine patient compliance, effectives, and cost benefit

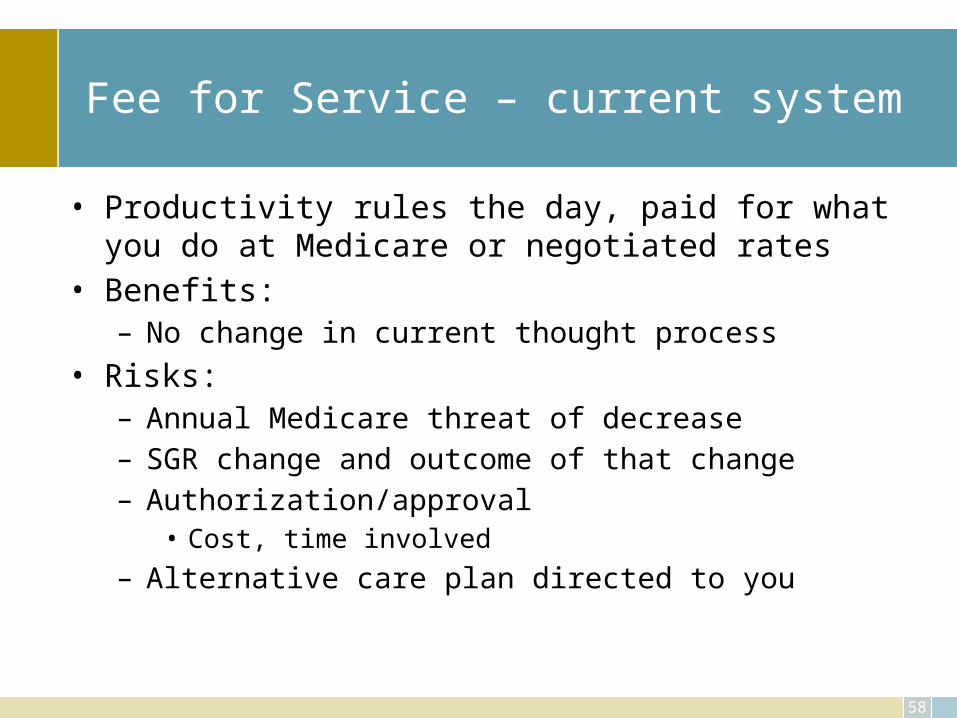

Fee for Service – current system

• Productivity rules the day, paid for what you do at Medicare or negotiated rates

• Benefits:– No change in current thought process

• Risks:– Annual Medicare threat of decrease– SGR change and outcome of that change– Authorization/approval

• Cost, time involved– Alternative care plan directed to you

58

Capitation – the way it was/is

• PMPM• If 100% cap, maximum dollars known• Work to reduce costs or• Increase patient numbers

59

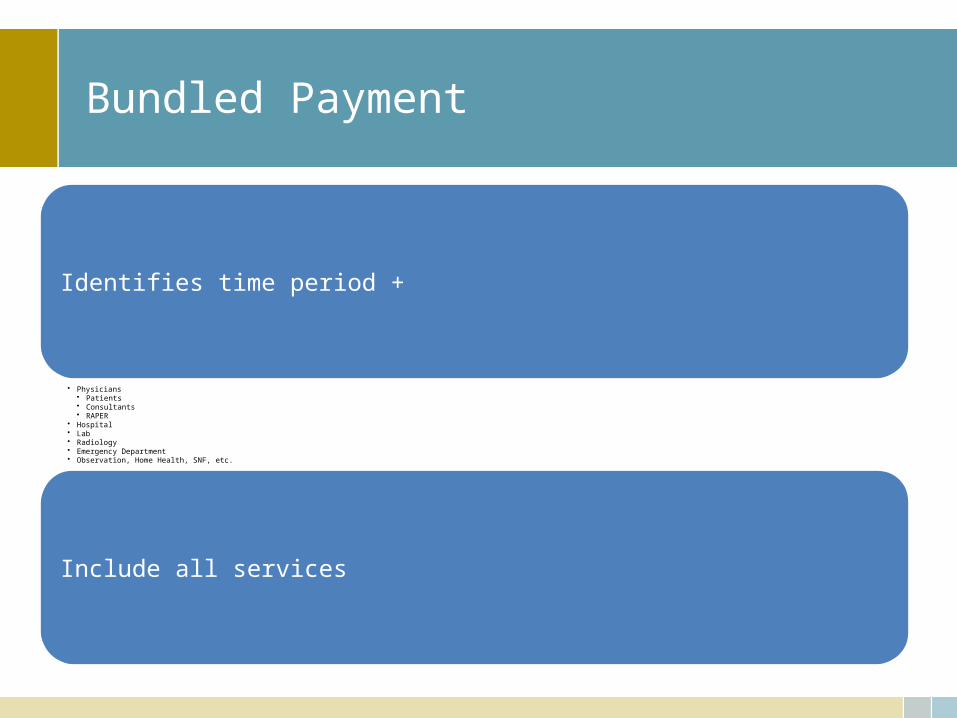

Bundled Payment

Identifies time period +

• Physicians• Patients • Consultants• RAPER

• Hospital• Lab• Radiology• Emergency Department• Observation, Home Health, SNF, etc.

Include all services

Middle of the road

• Episodic or Comprehensive Care (Global) fee• Requires treatment (care) plan• Internal development and management

– Compliance issue• Perspective greater and change in approach significant for

all providers• No need for: prior authorization, concurrent review, post-

pay audits, evaluation of visit levels, medical necessity test reviews, pharmacy benefit reviews

61

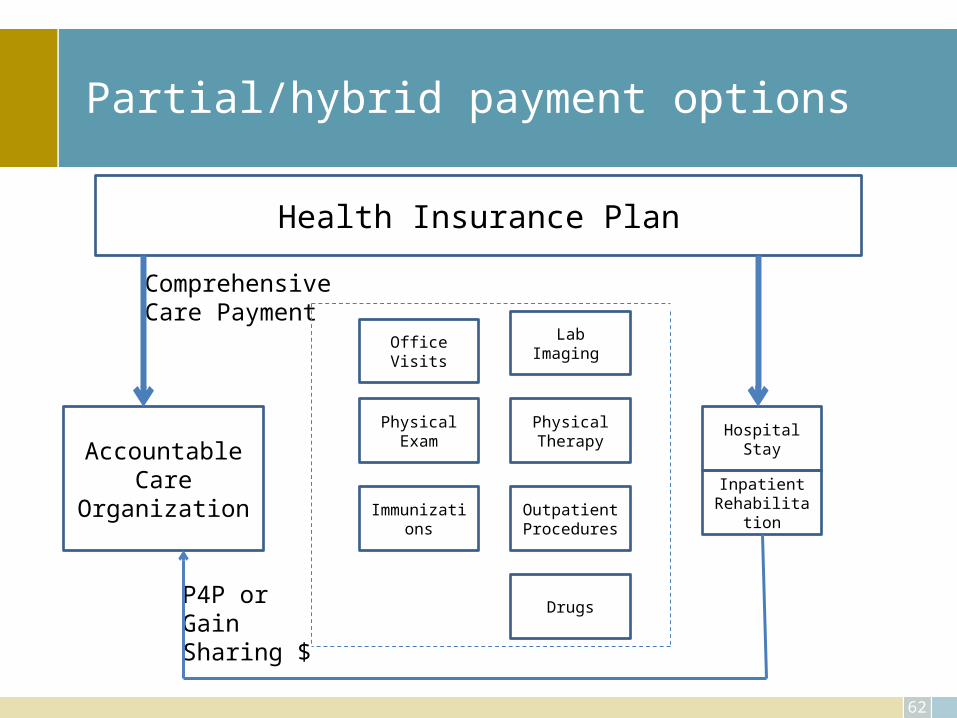

Partial/hybrid payment options

62

Health Insurance Plan

AccountableCare

Organization

OfficeVisits

PhysicalExam

Immunizations

Drugs

OutpatientProcedures

PhysicalTherapy

HospitalStay

LabImaging

InpatientRehabilitation

P4P orGain Sharing $

ComprehensiveCare Payment

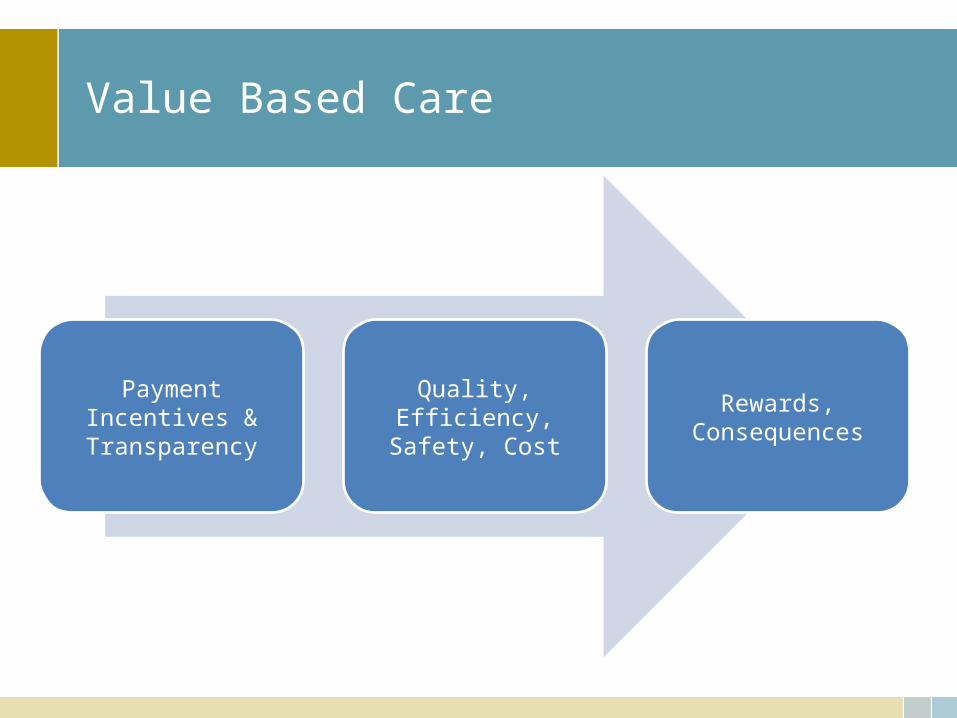

Value Based Care

Payment Incentives & Transparency

Quality, Efficiency, Safety, Cost

Rewards, Consequences

Information on Outcomes

Standardized

Comparative

Transparent

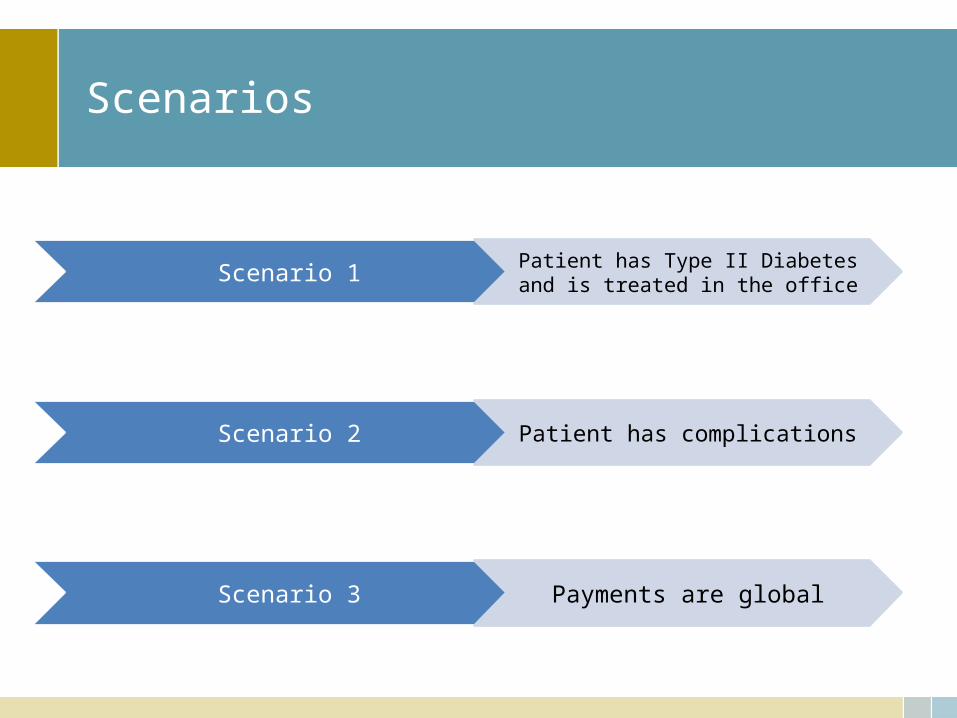

Scenarios

Scenario 1 Patient has Type II Diabetes and is treated in the office

Scenario 2 Patient has complications

Scenario 3 Payments are global

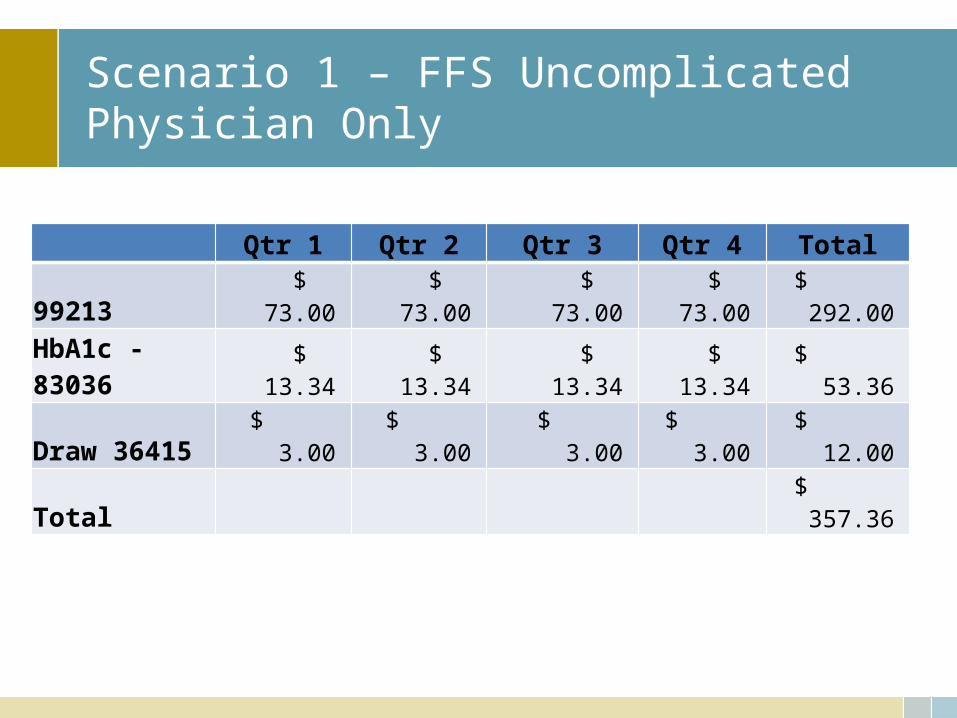

Scenario 1 – FFS UncomplicatedPhysician Only

Qtr 1 Qtr 2 Qtr 3 Qtr 4 Total99213 $ 73.00 $ 73.00 $ 73.00 $ 73.00 $ 292.00

HbA1c - 83036 $ 13.34 $ 13.34 $ 13.34 $ 13.34 $ 53.36

Draw 36415 $ 3.00 $ 3.00 $ 3.00 $ 3.00 $ 12.00

Total $ 357.36

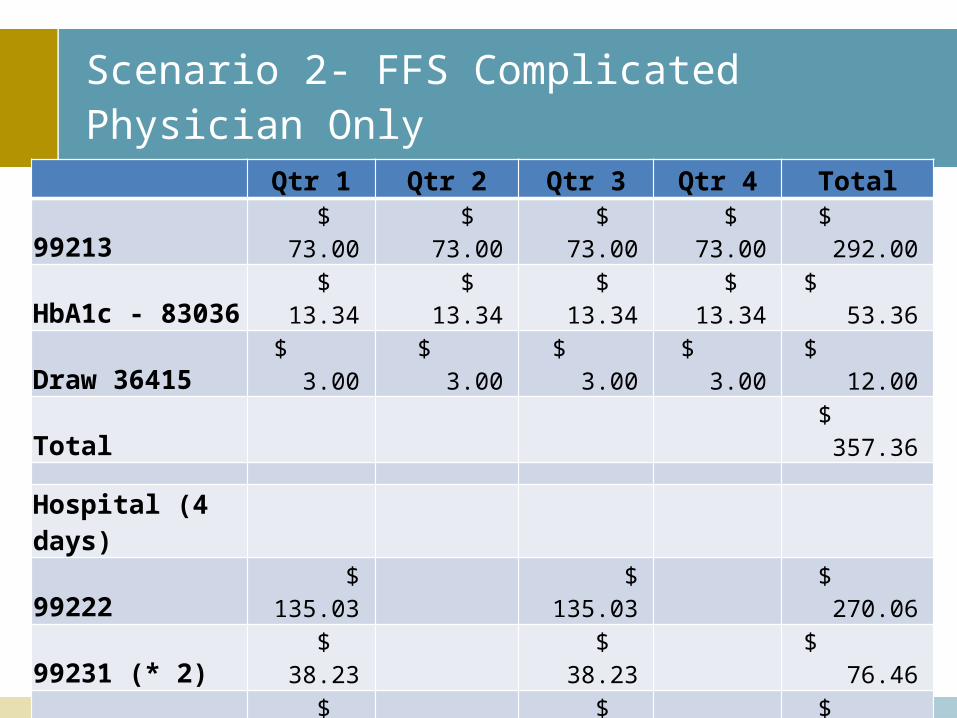

Scenario 2- FFS ComplicatedPhysician Only

Qtr 1 Qtr 2 Qtr 3 Qtr 4 Total99213 $ 73.00 $ 73.00 $ 73.00 $ 73.00 $ 292.00

HbA1c - 83036 $ 13.34 $ 13.34 $ 13.34 $ 13.34 $ 53.36

Draw 36415 $ 3.00 $ 3.00 $ 3.00 $ 3.00 $ 12.00

Total $ 357.36

Hospital (4 days)99222 $ 135.03 $ 135.03 $ 270.06

99231 (* 2) $ 38.23 $ 38.23 $ 76.46

99238 $ 71.03 $ 71.03 $ 142.06

Four day stay $ 282.52 $ 282.52 $ 565.04

Total $ 526.81 $ 526.81 $ 1,053.62

Emergency 99283 $ 60.05 $ 60.05 $ 60.05 $ 60.05 $ 240.20

Total $ 1,651.18

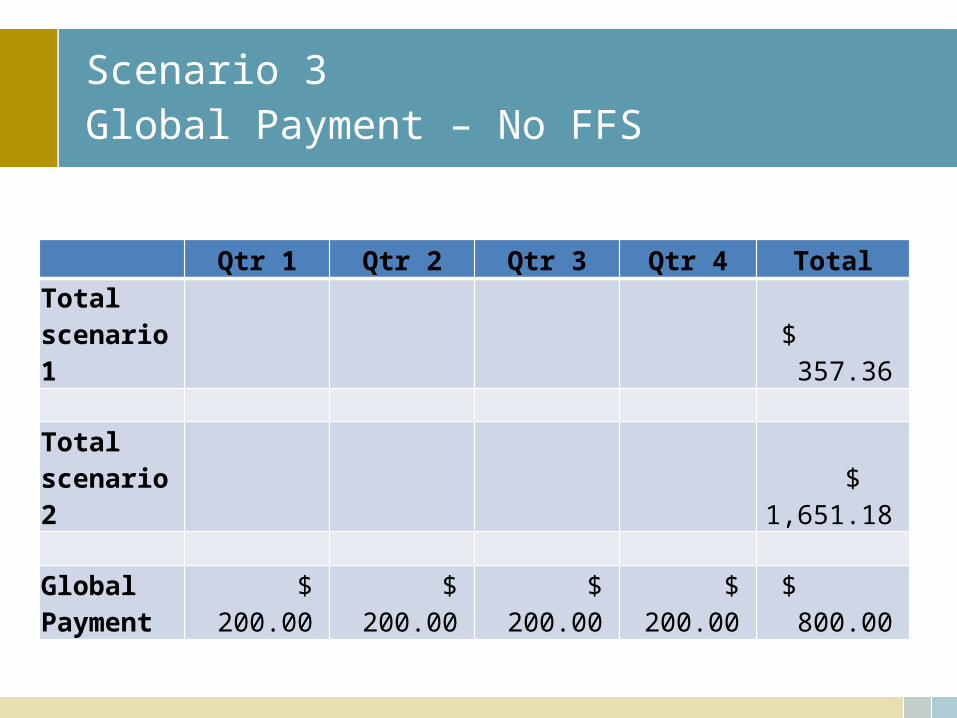

Scenario 3Global Payment – No FFS

Qtr 1 Qtr 2 Qtr 3 Qtr 4 TotalTotal scenario 1 $ 357.36

Total scenario 2 $ 1,651.18

Global Payment $ 200.00 $ 200.00 $ 200.00 $ 200.00 $ 800.00

Approach to future

• Patient involvement • Access, quality, cost control• Mission

– Safe, affordable, effective, patient centered, evidence based care

• Not mission– Duplicate care, treatments, eliminate overuse, misuse

of treatment options• Baseline – diabetes, heart: CAD, CHF, failure, COPD,

hypertension, prevention69

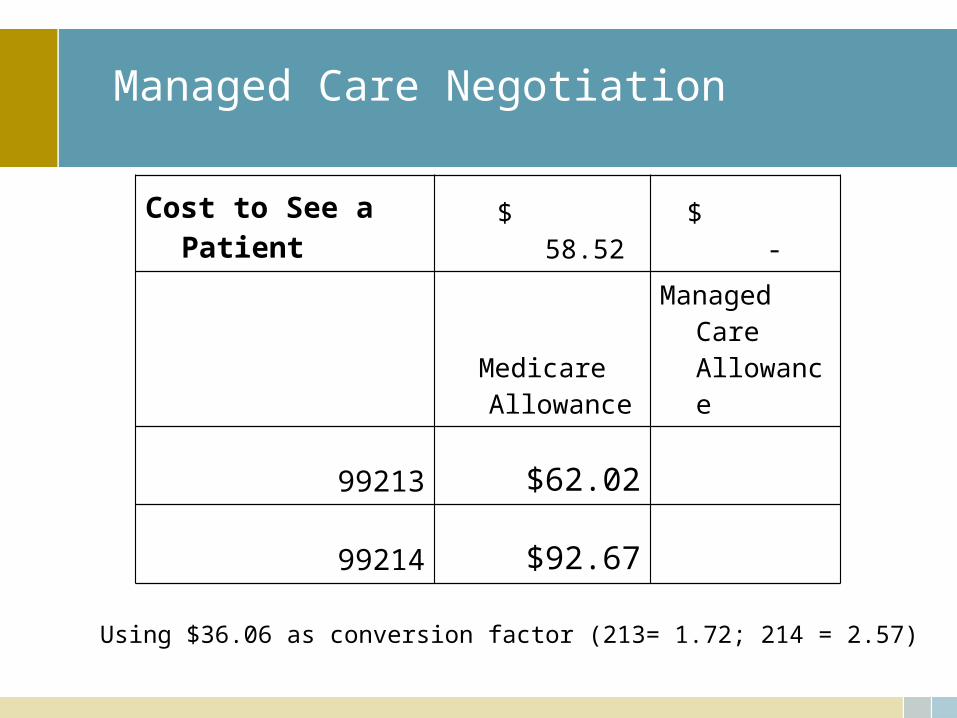

Managed Care Negotiation

Cost to See a Patient $ 58.52 $ -

Medicare Allowance

Managed Care Allowance

99213 $62.02

99214 $92.67

70

Using $36.06 as conversion factor (213= 1.72; 214 = 2.57)

71

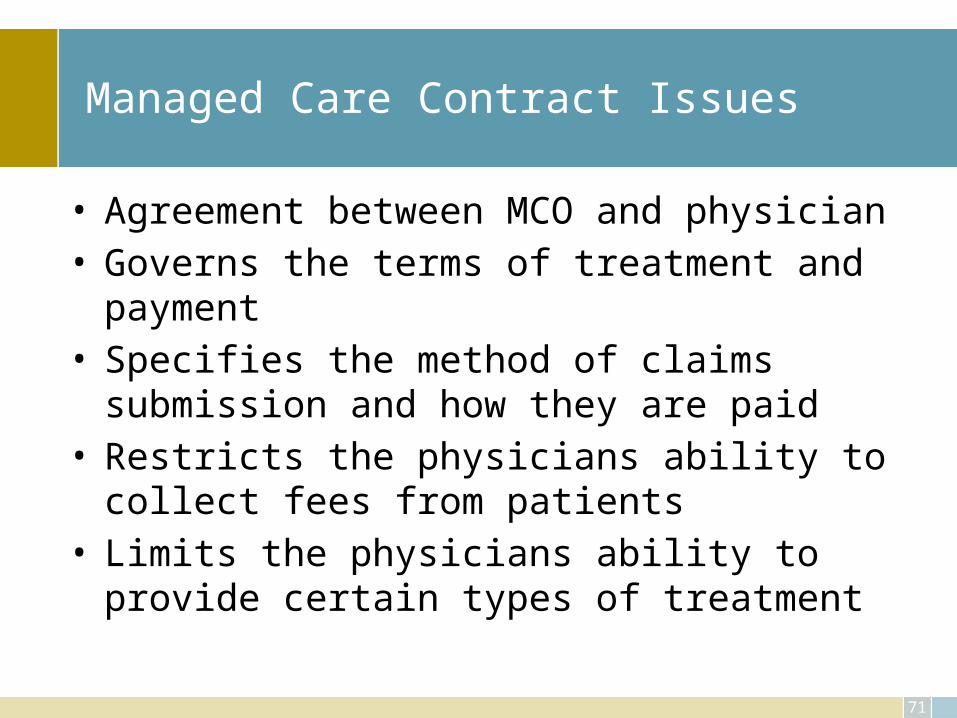

Managed Care Contract Issues

• Agreement between MCO and physician• Governs the terms of treatment and payment• Specifies the method of claims submission and how they

are paid• Restricts the physicians ability to collect fees from patients• Limits the physicians ability to provide certain types of

treatment

72

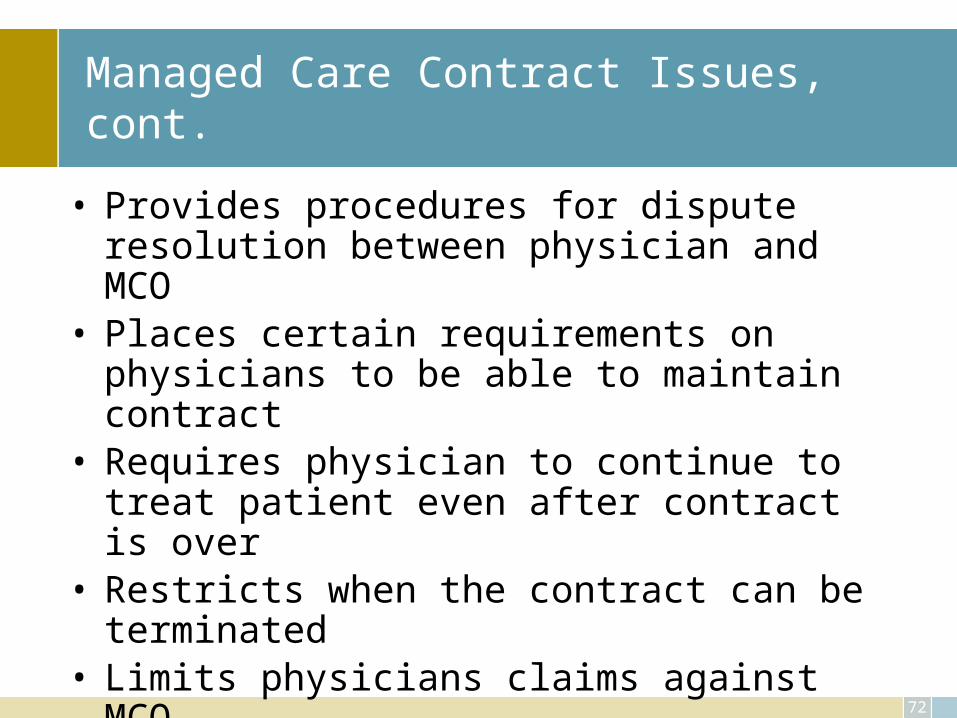

Managed Care Contract Issues, cont.

• Provides procedures for dispute resolution between physician and MCO

• Places certain requirements on physicians to be able to maintain contract

• Requires physician to continue to treat patient even after contract is over

• Restricts when the contract can be terminated• Limits physicians claims against MCO

73

Budget

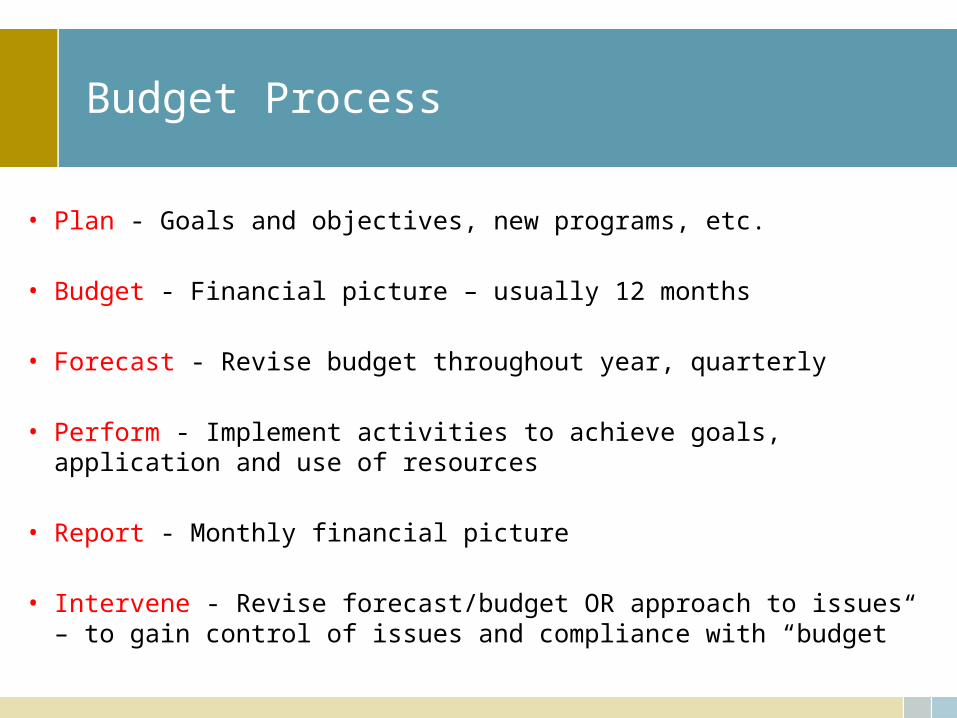

Budget Process

• Plan - Goals and objectives, new programs, etc.

• Budget - Financial picture – usually 12 months

• Forecast - Revise budget throughout year, quarterly

• Perform - Implement activities to achieve goals, application and use of resources

• Report - Monthly financial picture

• Intervene - Revise forecast/budget OR approach to issues – to gain control of issues and compliance with “budget”

Factors to consider in budget

• Uncertainty and volatility of the market

• Key drivers – metrics

• Trend analysis

• Gaps – business as unusual

• Forecast

• Decision support

76

Uncertainty/risk/probability

• Uncertain – indefinite, not known beyond doubt, not clearly identified or defined

• Risk – possibility of loss or injury, the chance that an (investment …) will lose value

• Probability – the ratio of the number of outcomes in an exhaustive set of equally likely outcomes that produce a given event to the total number of possible outcomes

• For example:– Weather today – 60% chance of rain (probability), should you have the

company picnic (uncertain), if not what will the cost be to re-schedule and the loss of the food, etc. already ordered?

Budgeting 101

• Revenue– Number of office visits and/or procedures [know what you need to

break even (3,943), track by month]– New services you might add– Services you’ll drop– Times of higher levels (e.g. Back to School)– Physician time off (watch cash flow after vacations, illness)

77

Budgeting 101

• Expenses– Increases in staff salary/benefits– Increases in staff– Investment in technology, equipment– Decreases in maintenance agreements, loan payments ending– Lower expenses thanks to technology investments

78

Budgeting 101

• Develop annually• Review monthly• Dig to understand variances. Not all savings are

good.

79

80

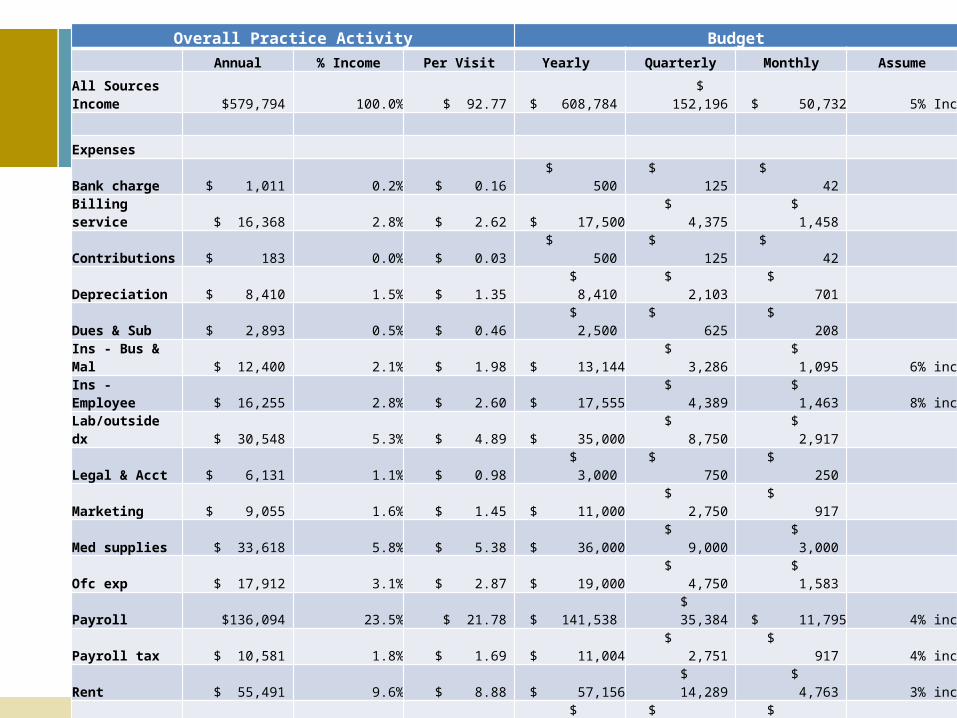

Overall Practice Activity Budget

Annual % Income Per Visit Yearly Quarterly Monthly Assume

All Sources Income $579,794 100.0% $ 92.77 $ 608,784 $ 152,196 $ 50,732 5% Inc

Expenses

Bank charge $ 1,011 0.2% $ 0.16 $ 500 $ 125 $ 42

Billing service $ 16,368 2.8% $ 2.62 $ 17,500 $ 4,375 $ 1,458

Contributions $ 183 0.0% $ 0.03 $ 500 $ 125 $ 42

Depreciation $ 8,410 1.5% $ 1.35 $ 8,410 $ 2,103 $ 701

Dues & Sub $ 2,893 0.5% $ 0.46 $ 2,500 $ 625 $ 208

Ins - Bus & Mal $ 12,400 2.1% $ 1.98 $ 13,144 $ 3,286 $ 1,095 6% inc

Ins - Employee $ 16,255 2.8% $ 2.60 $ 17,555 $ 4,389 $ 1,463 8% inc

Lab/outside dx $ 30,548 5.3% $ 4.89 $ 35,000 $ 8,750 $ 2,917

Legal & Acct $ 6,131 1.1% $ 0.98 $ 3,000 $ 750 $ 250

Marketing $ 9,055 1.6% $ 1.45 $ 11,000 $ 2,750 $ 917

Med supplies $ 33,618 5.8% $ 5.38 $ 36,000 $ 9,000 $ 3,000

Ofc exp $ 17,912 3.1% $ 2.87 $ 19,000 $ 4,750 $ 1,583

Payroll $136,094 23.5% $ 21.78 $ 141,538 $ 35,384 $ 11,795 4% inc

Payroll tax $ 10,581 1.8% $ 1.69 $ 11,004 $ 2,751 $ 917 4% inc

Rent $ 55,491 9.6% $ 8.88 $ 57,156 $ 14,289 $ 4,763 3% inc

Rep & Maint $ 1,123 0.2% $ 0.18 $ 1,500 $ 375 $ 125

Taxes $ 1,337 0.2% $ 0.21 $ 1,500 $ 375 $ 125

Telephone $ 6,299 1.1% $ 1.01 $ 6,500 $ 1,625 $ 542

Training $ 53 0.0% $ 0.01 $ 2,500 $ 625 $ 208

Total $365,761 63.1% $ 58.52 $ 385,807 $ 96,452 $ 32,151

Net income $214,033 36.9% $ 34.25 $ 222,977 $ 55,744 $ 18,581 4.2% inc

81

Annual % Income Per Visit One Two Three Assume

All Sources Income $579,794 100.00% $92.77 $550,804 $550,804 $521,815

Expenses

Bank charge $1,011 0.20% $0.16 $1,011 $1,011 $1,011

Billing service $16,368 2.80% $2.62 $16,368 $16,368 $16,368

Contributions $183 0.00% $0.03 $183 $183 $183

Depreciation $8,410 1.50% $1.35 $8,410 $8,410 $8,410

Dues & Sub $2,893 0.50% $0.46 $2,893 $2,893 $2,893

Ins - Bus & Mal $12,400 2.10% $1.98 $13,144 $13,144 $13,144 ***

Ins - Employee $16,255 2.80% $2.60 $17,555 $16,255 $16,255 8% inc

Lab/outside dx $30,548 5.30% $4.89 $30,548 $30,548 $30,548

Legal & Acct $6,131 1.10% $0.98 $6,131 $6,131 $6,131

Marketing $9,055 1.60% $1.45 $9,055 $9,055 $9,055

Med supplies $33,618 5.80% $5.38 $33,618 $33,618 $33,618

Ofc exp $17,912 3.10% $2.87 $17,912 $17,912 $17,912

Payroll $136,094 23.50% $21.78 $141,538 $136,094 $136,094 4% inc

Payroll tax $10,581 1.80% $1.69 $11,004 $10,581 $10,581

Rent $55,491 9.60% $8.88 $57,156 $57,156 $57,156 ***

Rep & Maint $1,123 0.20% $0.18 $1,123 $1,123 $1,123

Taxes $1,337 0.20% $0.21 $1,337 $1,337 $1,337

Telephone $6,299 1.10% $1.01 $6,299 $6,299 $6,299

Training $53 0.00% $0.01 $53 $53 $53

Total $365,762 63.10% $58.52 $375,338 $368,171 $368,171

Net income $214,032 36.90% $34.25 $175,466 $182,633 $153,644

% Income change -18.0% -14.7% -28.2%

$ needed to maintain $264,347

NoWage inc

5% decrease 10% decrease

82

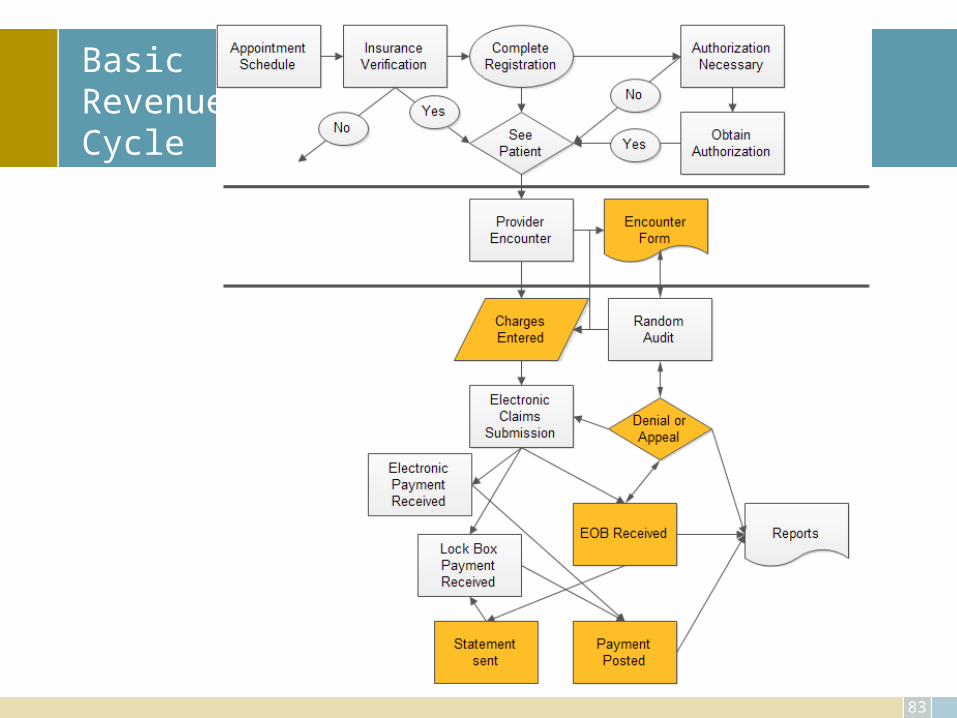

Managing the revenue cycle

83

Basic Revenue Cycle

84

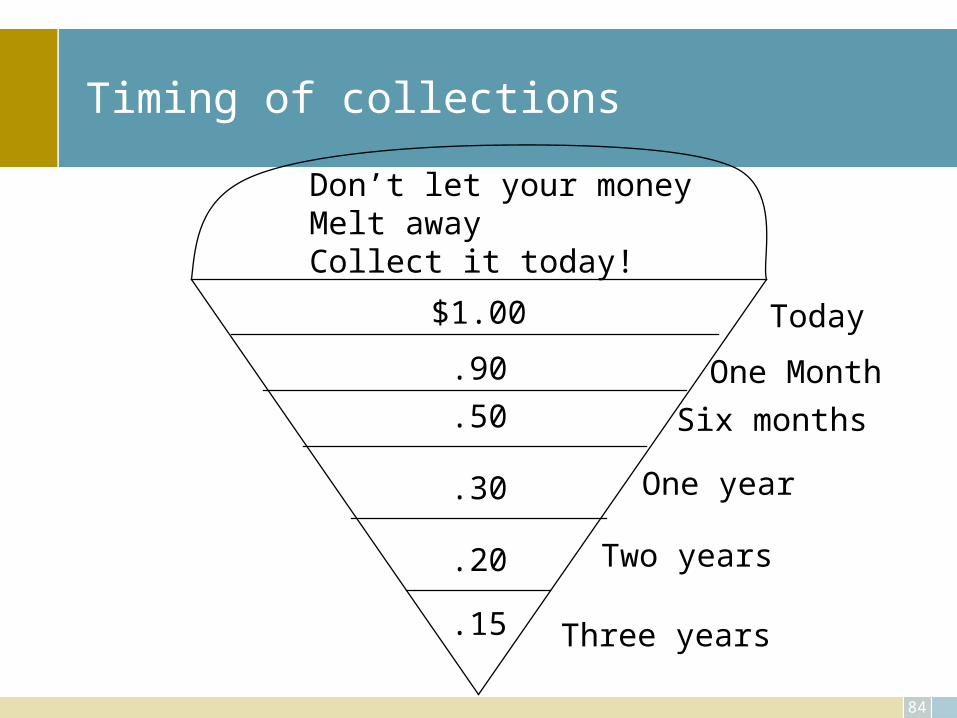

Timing of collections

$1.00

.90

.50

.30

.20

.15

Don’t let your moneyMelt awayCollect it today!

Today

One Month

Six months

One year

Two years

Three years

Pre-visit

• Schedule appointment!• Established financial policy• When do you get what information?

– New patient coordinator– Demographic, insurance and medical

• Verification (eligibility – which term?) of coverage– At every visit– Payment assurance process

• Reminder call with appointment time, location AND notice of co-pay and balance due

Time of Visit

• Define activity at the time of the patient visit– Payments will be made prior to or after the visit with

the physician? – Will you collect old balances in full or partially?– Consider “social norm” approach rather than

threaten– Physicians (all providers) should NOT become

involved with any discussion on payments, this is covered in the collection policy

87

Payments . . . TOV

• Super bill must be complete– Continuous number– Missing ticket report

• Must know deductibles and/or co-pay• Must know extent of coverage allowed• Must know procedure(s) done, e.g., down payment

required• Time of entry• Deposit ticket – shared duties

88

Deductible and co-pay changes beginning of each year

• Medicare Part B Deductible increases annually• Medicare traditional vs. Medicare Advantage Plans• Review contracts and ANY Letters received from payers,

check their web sites– Payer– Employer

Financial Policy

• A simple broad statement that is given to every patient that defines the patient responsibility in the management of their payments

• Communicate, expectations clear, consistency• Keep it simple yet broad to cover all patients• Train staff on contents and expectations of training• Give copy to each patient, have them sign, scan in signed

copy, • Include on your web site

Financial Policy - Content

• Introduction – what is in this policy• Patient is responsible for what they owe• When payments are expected• Fees for late payments, discount options• If they don’t pay what could happen• Allow for discounts for cash payments• Consider charging for sending statements (incentive to pay on time,

discount option)• Signature

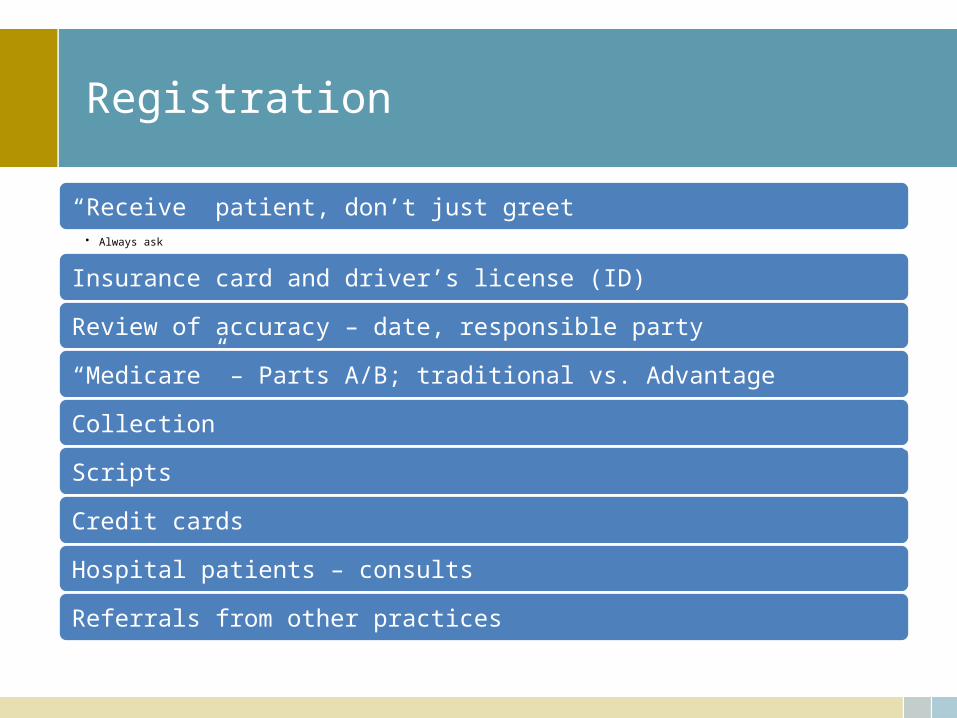

Registration

“Receive” patient, don’t just greet• Always ask

Insurance card and driver’s license (ID)

Review of accuracy – date, responsible party

“Medicare” – Parts A/B; traditional vs. Advantage

Collection

Scripts

Credit cards

Hospital patients – consults

Referrals from other practices

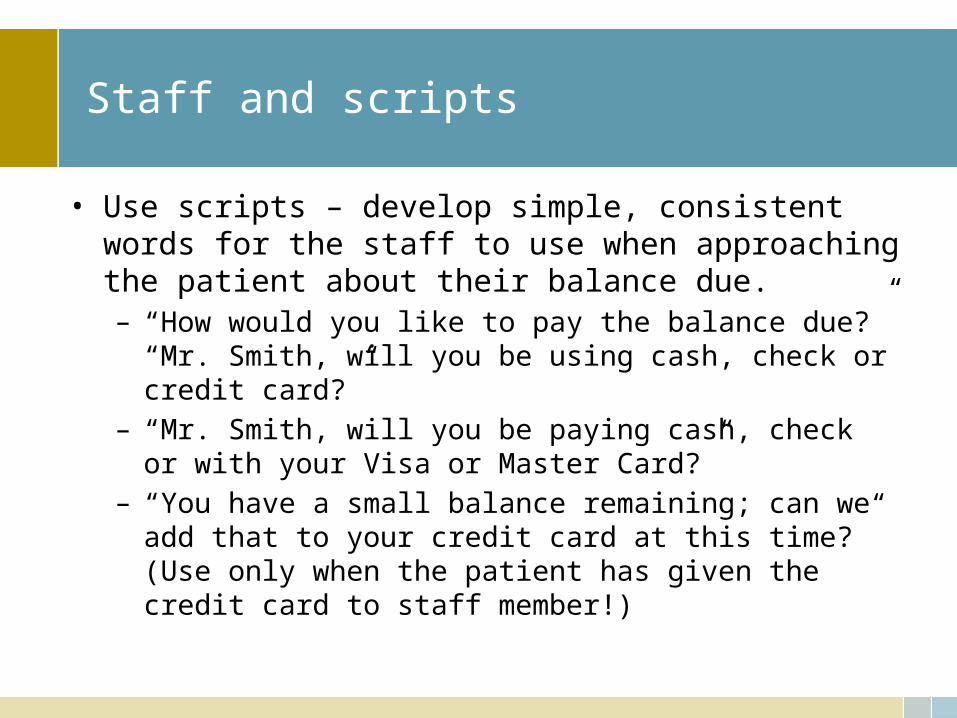

Staff and scripts

• Use scripts – develop simple, consistent words for the staff to use when approaching the patient about their balance due. – “How would you like to pay the balance due?” “Mr. Smith, will you be

using cash, check or credit card?” – “Mr. Smith, will you be paying cash, check or with your Visa or Master

Card?”– “You have a small balance remaining; can we add that to your credit

card at this time?” (Use only when the patient has given the credit card to staff member!)

93

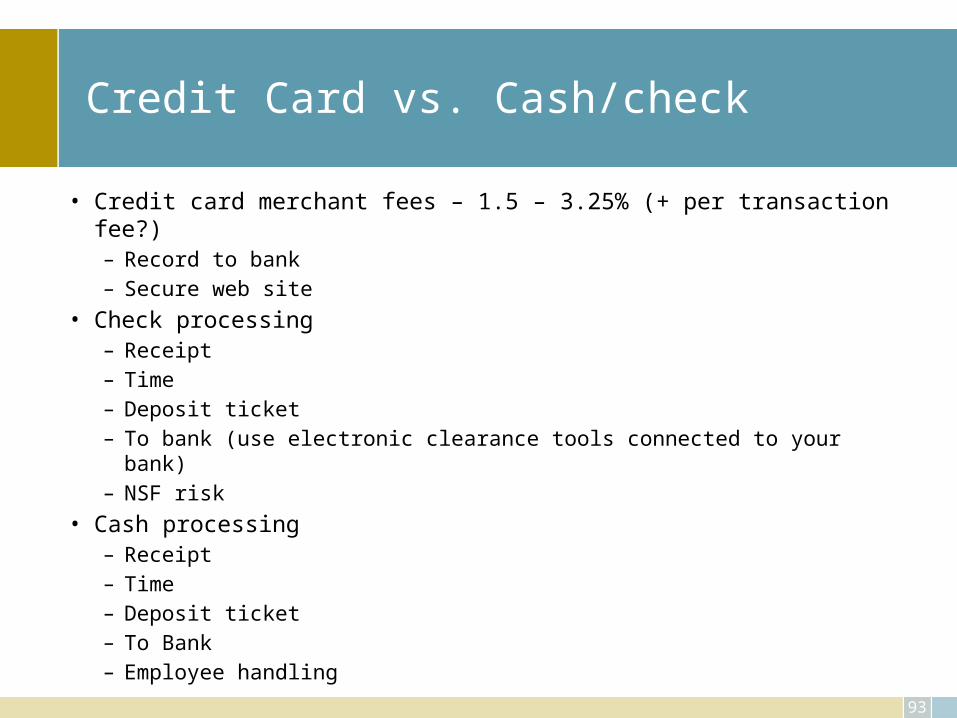

Credit Card vs. Cash/check

• Credit card merchant fees – 1.5 – 3.25% (+ per transaction fee?)– Record to bank– Secure web site

• Check processing– Receipt– Time– Deposit ticket– To bank (use electronic clearance tools connected to your bank)– NSF risk

• Cash processing– Receipt– Time – Deposit ticket– To Bank– Employee handling

94

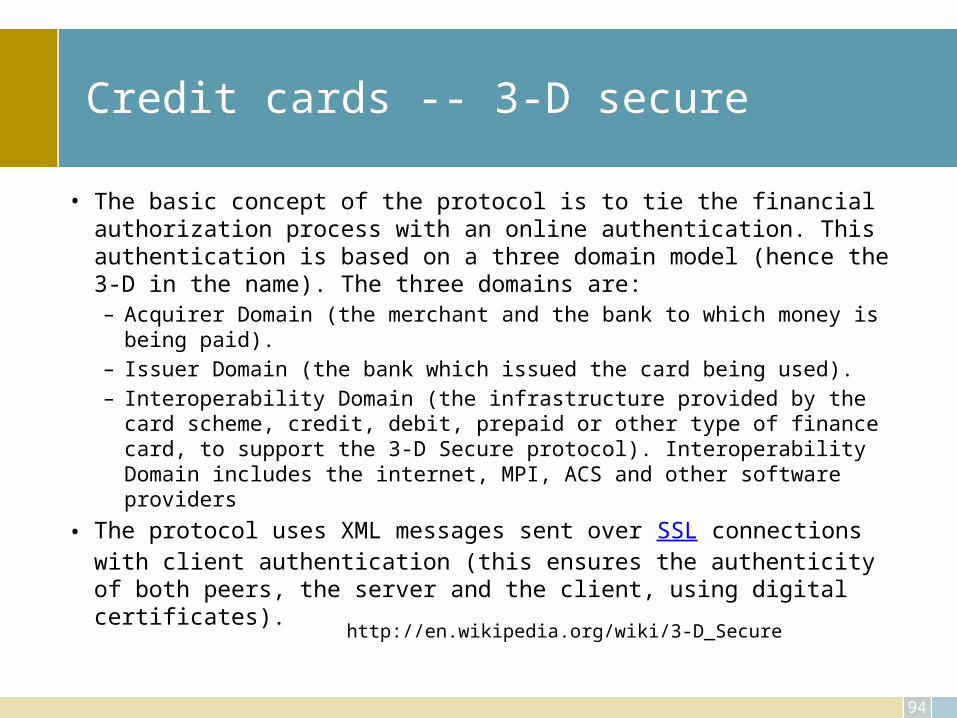

Credit cards -- 3-D secure

• The basic concept of the protocol is to tie the financial authorization process with an online authentication. This authentication is based on a three domain model (hence the 3-D in the name). The three domains are:– Acquirer Domain (the merchant and the bank to which money is being paid).– Issuer Domain (the bank which issued the card being used).– Interoperability Domain (the infrastructure provided by the card scheme,

credit, debit, prepaid or other type of finance card, to support the 3-D Secure protocol). Interoperability Domain includes the internet, MPI, ACS and other software providers

• The protocol uses XML messages sent over SSL connections with client authentication (this ensures the authenticity of both peers, the server and the client, using digital certificates).

http://en.wikipedia.org/wiki/3-D_Secure

95

Credit Card … Do’s

• Do:– Sign your cards as soon as they arrive. – Carry your cards separately from your wallet, in a zippered compartment, a business

card holder, or another small pouch. – Keep a record of your account numbers, their expiration dates, and the phone number

and address of each company in a secure place. – Keep an eye on your card during the transaction, and get it back as quickly as possible. – Void incorrect receipts. – Destroy carbons. – Save receipts to compare with billing statements. – Open bills promptly and reconcile accounts monthly, just as you would your checking

account. – Report any questionable charges promptly and in writing to the card issuer. – Notify card companies in advance of a change in address.

http://www.ftc.gov/bcp/edu/pubs/consumer/credit/cre07.shtm

96

Don’ts

• Don't:– Lend your card(s) to anyone. – Leave cards or receipts lying around. – Sign a blank receipt. When you sign a receipt, draw a line through any

blank spaces above the total. – Write your account number on a postcard or the outside of an

envelope. – Give out your account number over the phone unless you're making

the call to a company you know is reputable. If you have questions about a company, check it out with your local consumer protection office or Better Business Bureau.

Blame others . . .

• Get the blame away from you (staff)!

– “Our accountant will not allow us to carry these amounts on our books”

• Sign (use digital photo frame)

– “Your insurance company requires us to collect co-payments at the time of service”

Performance

• Monitor daily activity of the staff for collections –– Know how many patients with payments due - actually paid, goal

100%. – Know how many dollars could have been collected and the actual

amount collected, goal 100%. – For those accounts that payment was not received, ask the staff to

note why. – This can become a training tool on the issues, excuses, etc. that are

faced daily. – You can work through more “scripts” to handle these issues in the

future.

Coding and Charge Entry

• Timely coding– Day of service– Hospital/surgery charges

• Who does what?– CCI– LCD

• Claims scrubbing and edits• Audit

– Random– 10 charts per provider

100

Process

• Claims submission• Statements• Secondary's• Timing

Claims Processing & Payment Posting

• Electronic submission– Clean up process and tracking to determine source of

any common error issues

• Daily review

• Payment posting– Process of denial and/or appeal

102

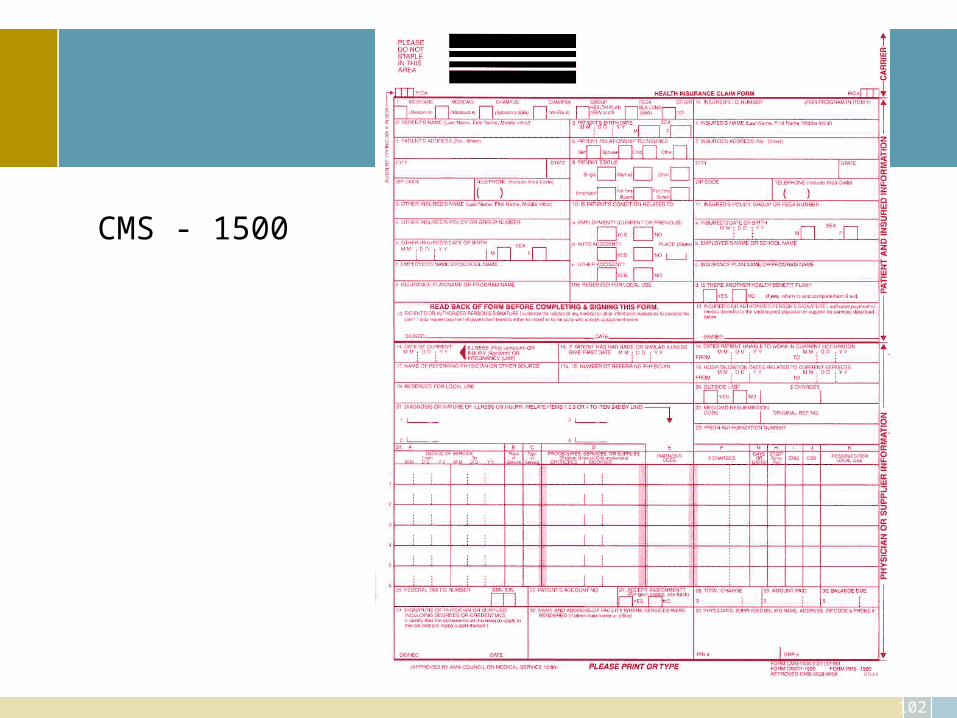

CMS - 1500

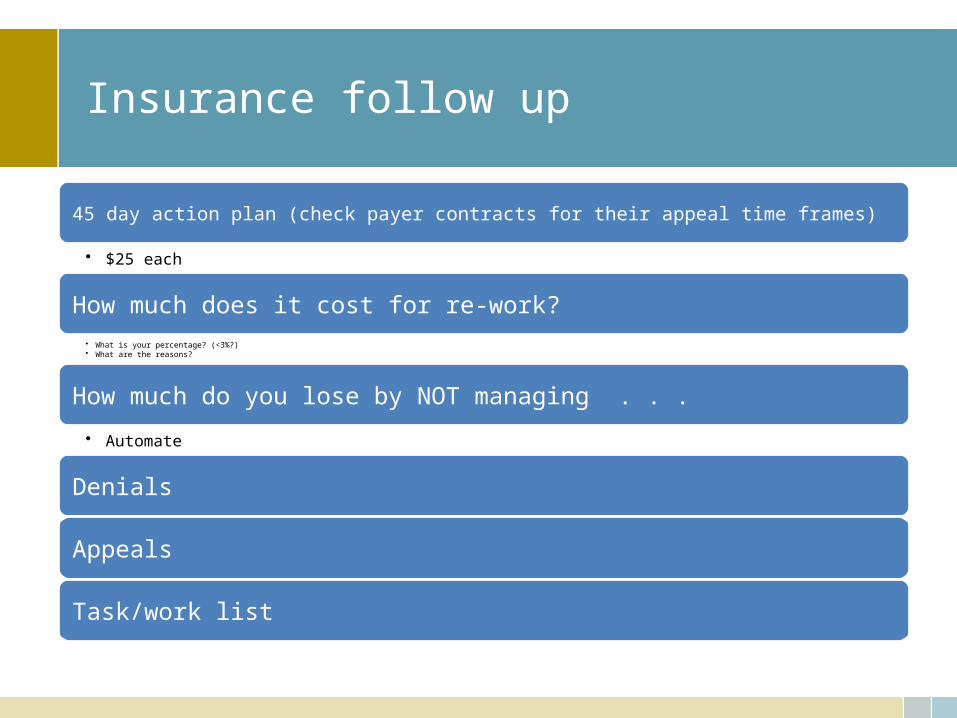

Insurance follow up

45 day action plan (check payer contracts for their appeal time frames)

• $25 each

How much does it cost for re-work?• What is your percentage? (<3%?) • What are the reasons?

How much do you lose by NOT managing . . .

• Automate

Denials

Appeals

Task/work list

104

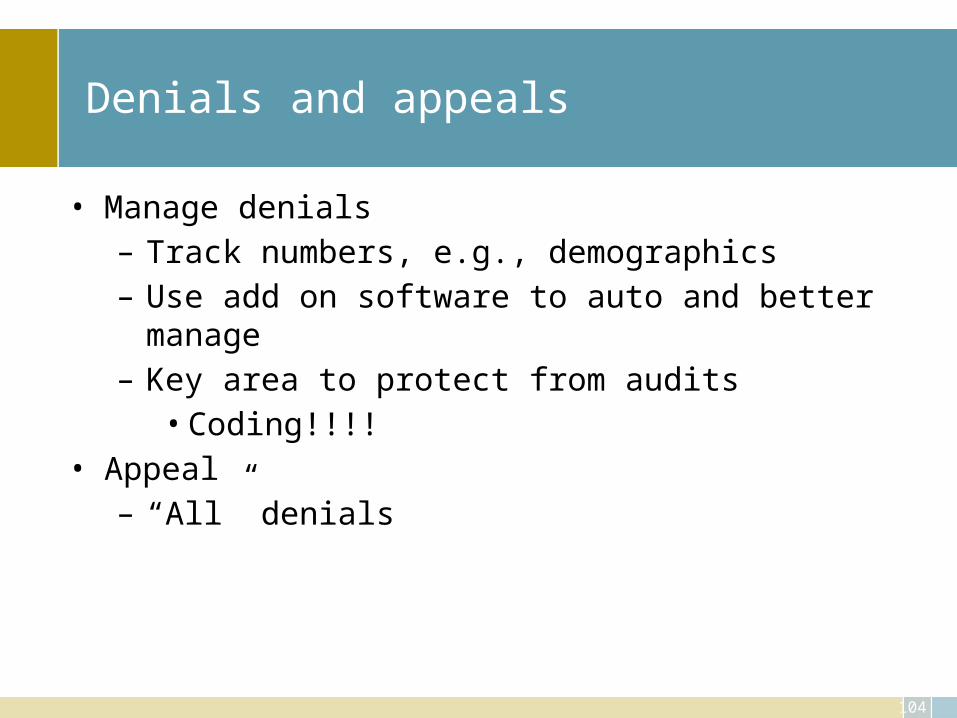

Denials and appeals

• Manage denials– Track numbers, e.g., demographics– Use add on software to auto and better manage– Key area to protect from audits

• Coding!!!!• Appeal

– “All” denials

105

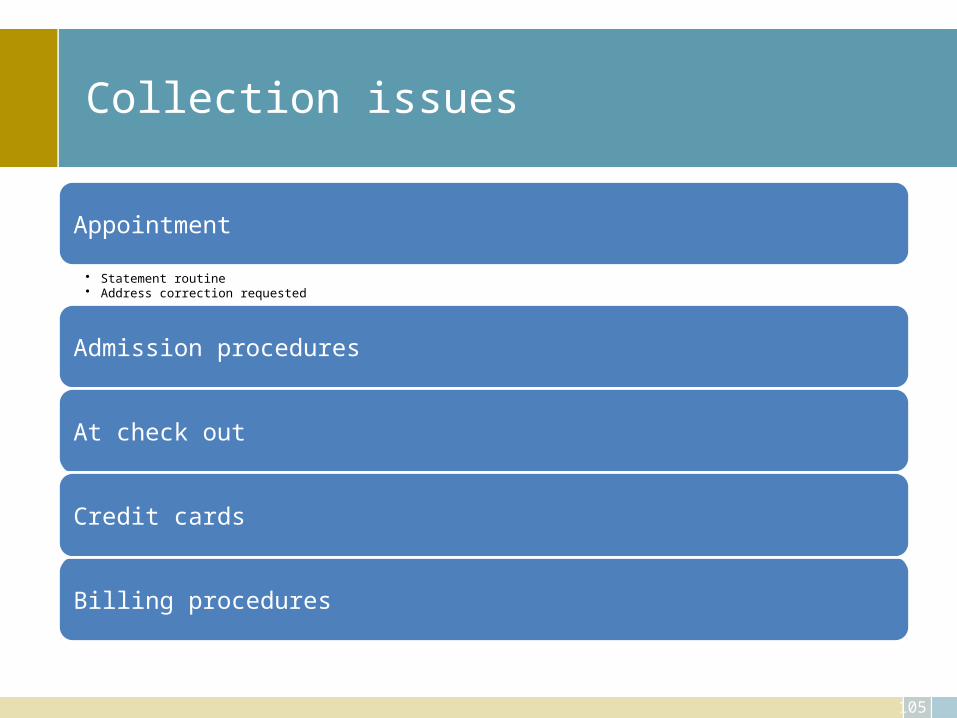

Collection issues

Appointment

• Statement routine• Address correction requested

Admission procedures

At check out

Credit cards

Billing procedures

106

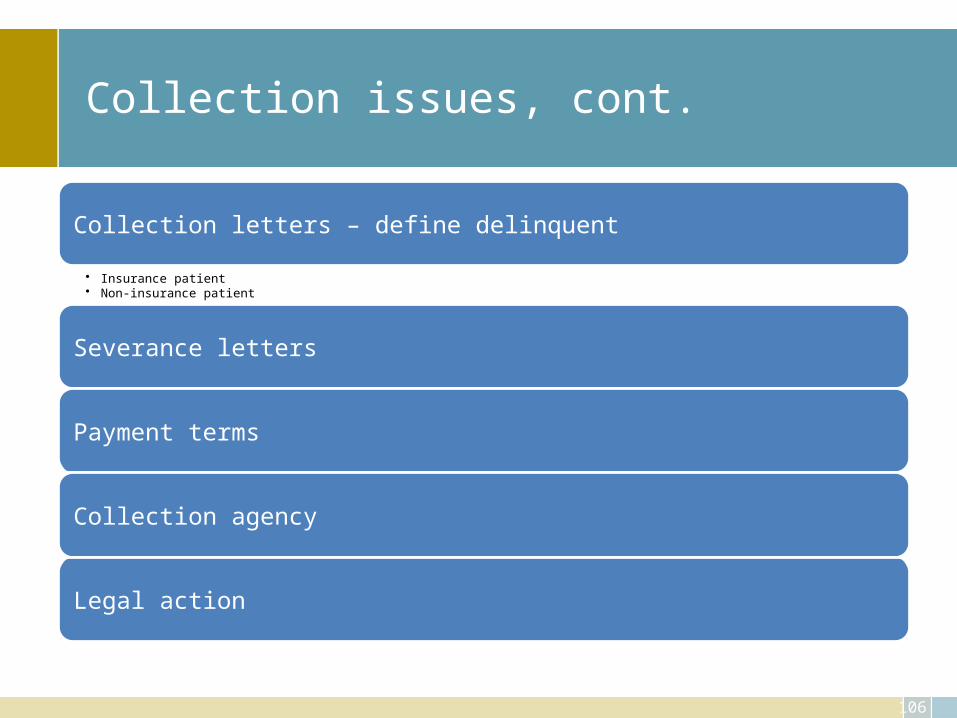

Collection issues, cont.

Collection letters – define delinquent

• Insurance patient• Non-insurance patient

Severance letters

Payment terms

Collection agency

Legal action

107

Payments . . . improve

• Accurate demographics• Complete super bill immediately• Collect at time of visit• Allow the use of credit cards• Make phone calls

– Day before visit– In collection process

• Systematic follow up

Patient Statements

• How much does it cost to send one?– $8.75 each

• Use weekly, cycle billing option• Small balance limit• Use Postal service “Address Service Requested”• Note of account status – delinquent, etc.• The goal is to get the patient to open the statement and KNOW that

they have a balance due for the high quality of service provided– Letter writing – Creative options

• Invitation size, style• Color paper• Humor

Delinquent Account

• Define what is a delinquent account – – Recommend two statements. – If you do not currently use the “cycle” statement option for your

billing, change. – Statements are sent the week that it is determined that the balance

remaining is the patient’s responsibility and then four weeks later. – If no payment is received, the account is now considered

delinquent. – You then activate the notes on statements or letter writing

campaign to inform that patient that if the balance is not paid by such and such date, action will be taken to collect the balance due.

Land Line (Telephone!)

• Use the telephone – – Remind the patient of their co-pay and/or balance due when the

appointment reminder call is made.– Also determine a minimum balance necessary to exercise the

personal request for payment. It may not be wise to call on every account but beneficial to call on those accounts with a balance greater than say $100, you decide what works best for you.

– This is the second most effective time to collect, time of visit being the most effective!

Payment plans

Retain copy of credit card, securely, and use it

Allow for payments on the web site

Payment plans – YOU are a bank

Charge interest

112

Consumer Credit Protection Acts

• Truth & Lending– Disclose terms and costs – “4”– Credit card– Dispute resolution

• Fair Credit Billing– Unfair billing

• Fair Debt Collection Practices– Communication– Harassment– False & Misleading

Use Web Site & Patient Portal

• Financial policy• Collection• Statements• Appointments• And so much more

– Post your fee schedule– Marketing of “specials”– And . . . .

Aggressive? Not?

• Determine how far you are willing to go to collect the balance due – Will you refer patients to a collection agency or write of the

balance? – Is there a dollar amount that you will write off? – Dr. A says this while Dr. B says that

• Who’s in the middle!– Expectation for patients must be very clear– Every one must act consistently to achieve the goal of improved

collections.

Guidelines from the Doctors

• Develop a collection policy – – All items noted here should be written, agreed upon and given to

the staff to use in their daily efforts to collect. – This policy should go beyond just the patient balances and

include the entire process of verification, authorization, claims submission, and the like,

– In other words this should define how the entire revenue cycle is managed.

116

Payments . . .Audits

Timeliness

• EOB check DOS, DOB, DOP

Error analysis

• Invalid numbers, demographic related

Denials

• Coding

Other

Costs to collect – review again!!!!

• Hardware/software• Statements - $8.75• Denial and appeal - $25 each time• Staff

– Wage & benefits– Time off and effect on processing– Knowledge development

118

Other Collection Issues

• Third party insurance, e.g., accident• Co-pay• Bankruptcy• Laws• Embezzlement• Medicaid• Medicare with no secondary

119

Revenue cycle focus

• Key performance indicators throughout office• Time of visit functions and effectiveness• Manage the contracts• Process claims

– Coding– Documentation– Pay levels– Timely submission

• Manage denials– Sources– Timely review – Internal vs. external failure

120

Audits

Recovery Audit Contractor – RAC

• HIPAA – business associate• HIPAA – designated record set• HIPAA – breach notification rule • Accounting of disclosure rules• Meaningful use

HITECH (part of American Recovery and Reinvestment Act 2009)

There will be more . . . .

121

Current and more. . .

• Fear of audits implies uncertainty in the practice• Recognition of audits as part of today’s medical practice is reality• Don’t stone wall or delay when audit requests appear• Do ask for clarification and insurance that the audit effort is

legitimate, Don’t say NO when asked by a appropriate source• If issues are found, review and determine what steps need to be

taken to address them• Review any and all sources of information to stay ahead of the

regulation changes and potential audits that are or may be on the horizon

122

Internal controls

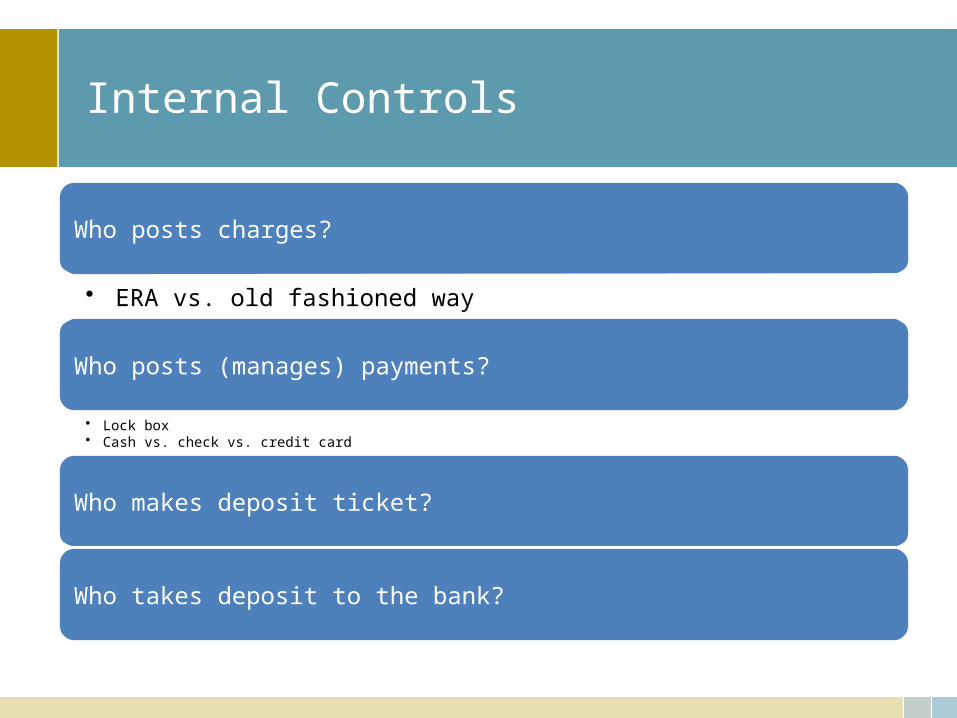

Internal Controls

Who posts charges?

• ERA vs. old fashioned way

Who posts (manages) payments?

• Lock box• Cash vs. check vs. credit card

Who makes deposit ticket?

Who takes deposit to the bank?

124

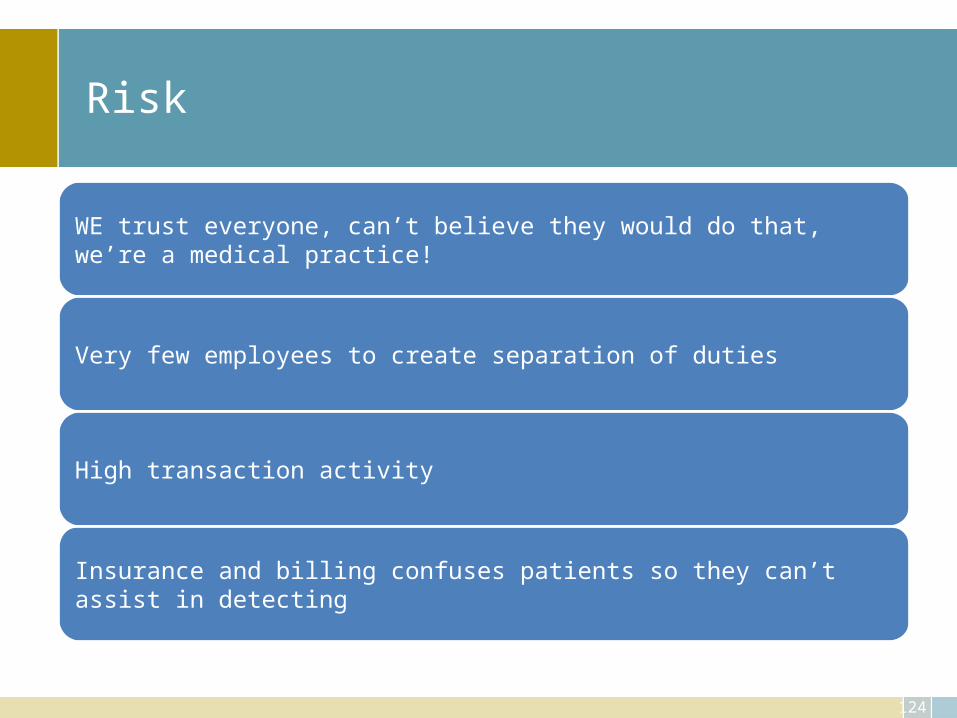

Risk

WE trust everyone, can’t believe they would do that, we’re a medical practice!

Very few employees to create separation of duties

High transaction activity

Insurance and billing confuses patients so they can’t assist in detecting

125

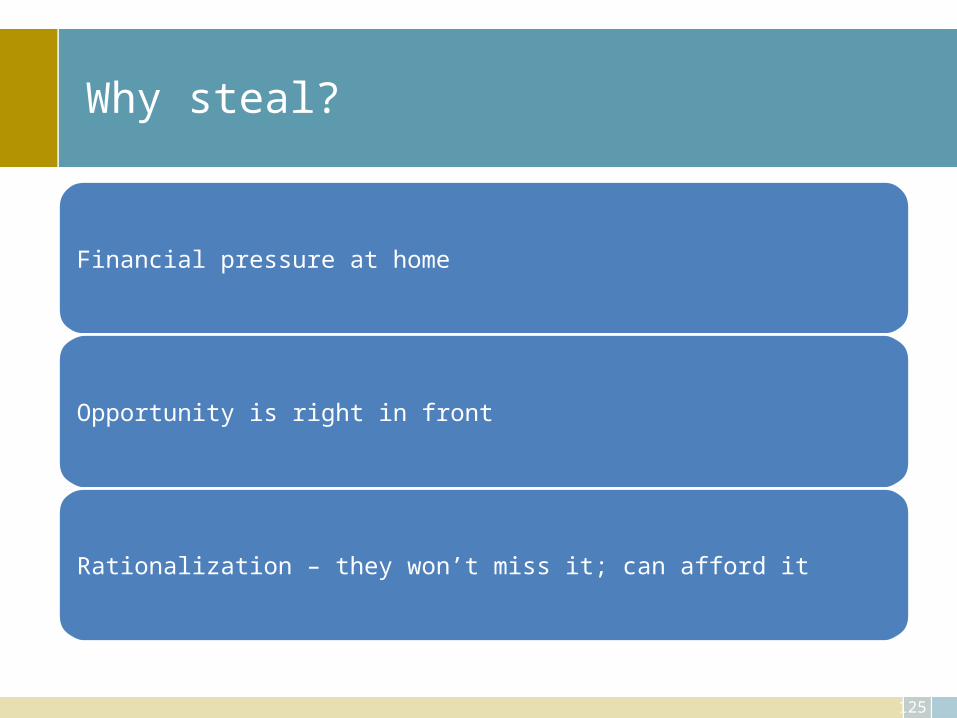

Why steal?

Financial pressure at home

Opportunity is right in front

Rationalization – they won’t miss it; can afford it

126

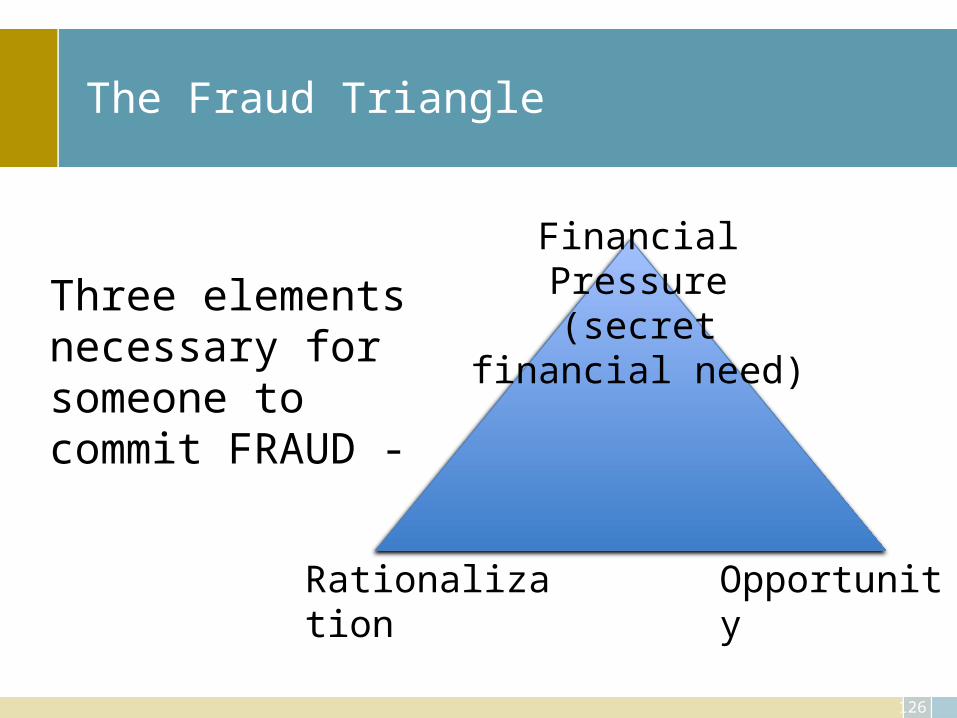

The Fraud Triangle

Financial Pressure(secret financial need)

OpportunityRationalization

Three elements necessary for someone to commit FRAUD -

127

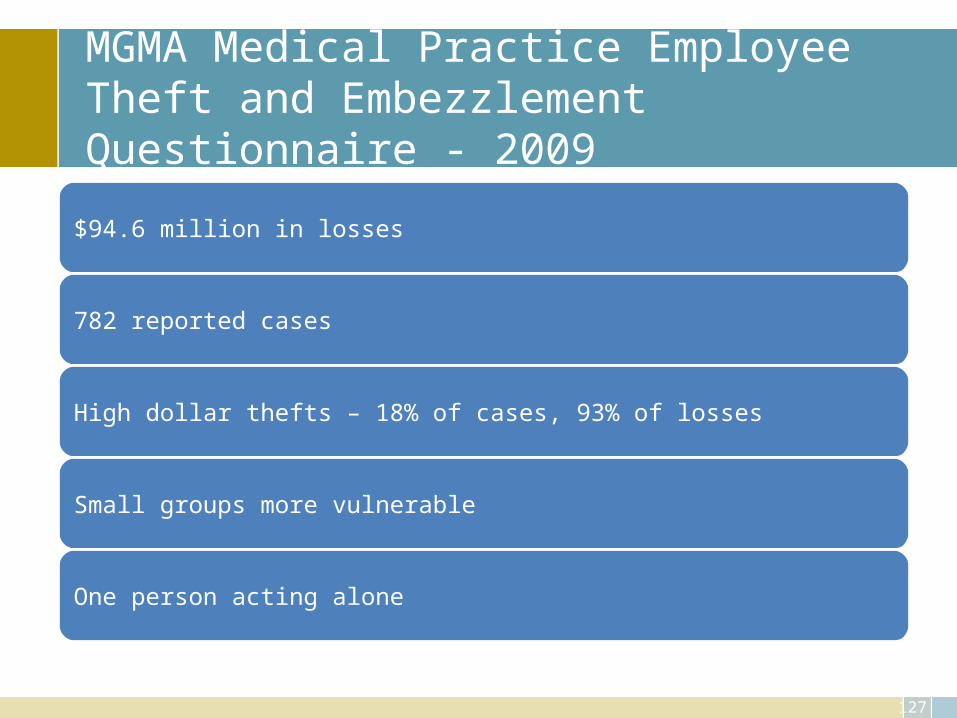

MGMA Medical Practice Employee Theft and Embezzlement Questionnaire - 2009

$94.6 million in losses

782 reported cases

High dollar thefts – 18% of cases, 93% of losses

Small groups more vulnerable

One person acting alone

128

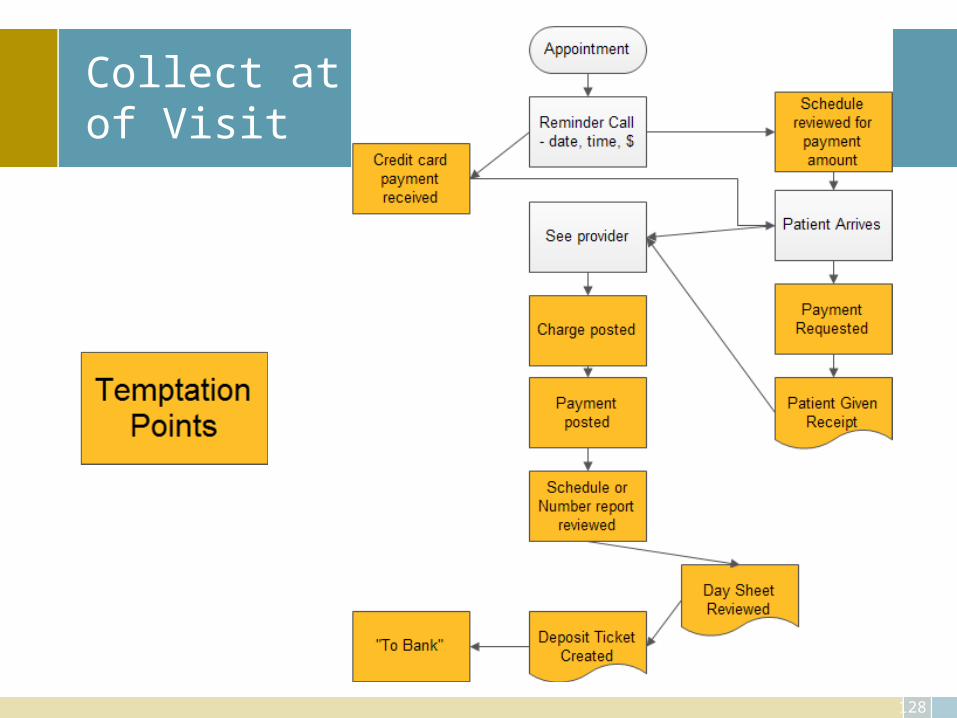

Collect at Time of Visit

129

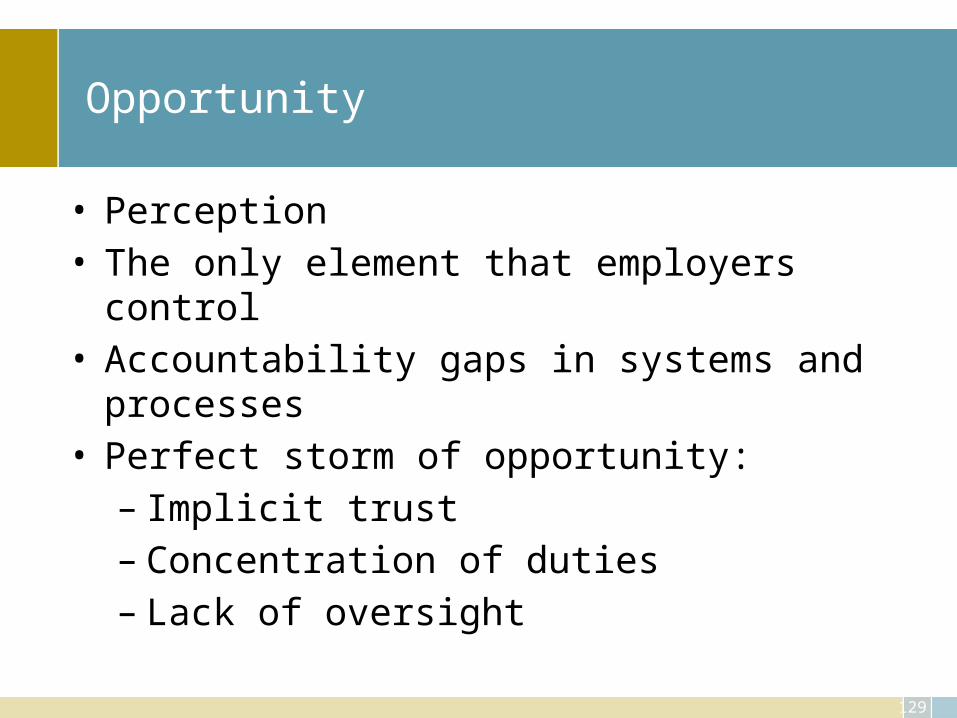

Opportunity

• Perception• The only element that employers control• Accountability gaps in systems and processes• Perfect storm of opportunity:

– Implicit trust– Concentration of duties– Lack of oversight

130

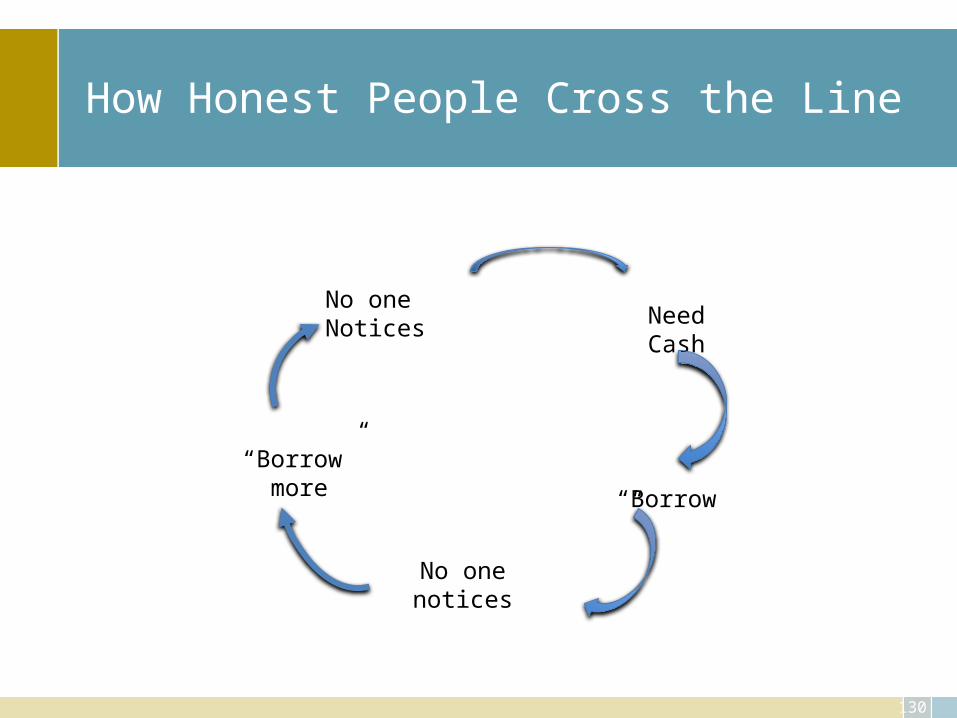

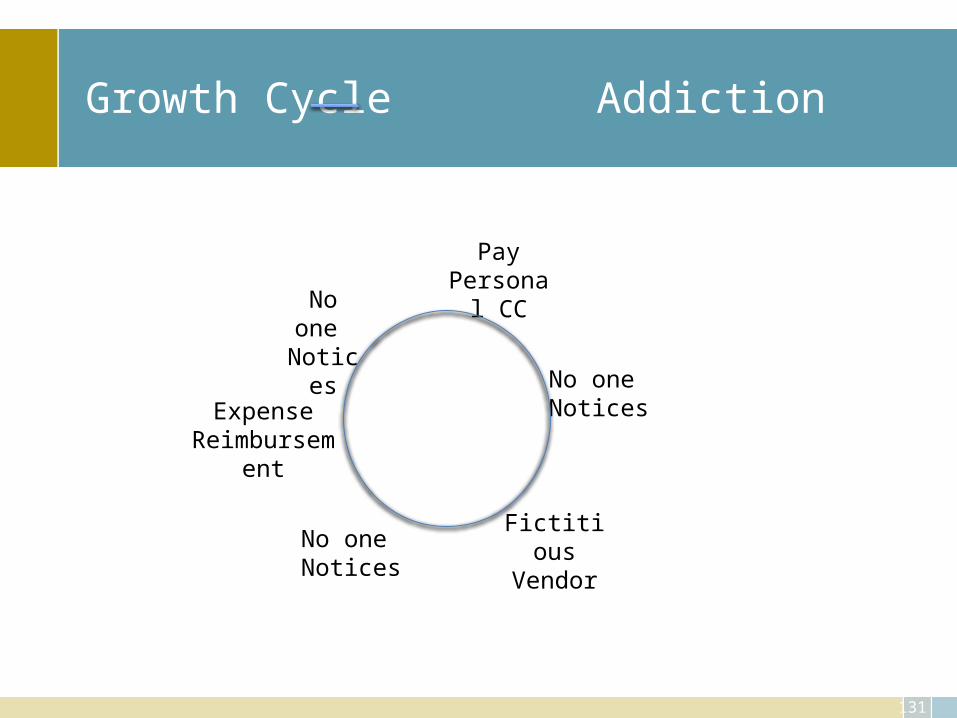

How Honest People Cross the Line

Need Cash

“Borrow”

No one notices

“Borrow” more

No one Notices

131

Growth Cycle Addiction

Pay Personal

CC

No one Notices

No one Notices

No one Notices

Fictitious Vendor

Expense Reimbursement

132

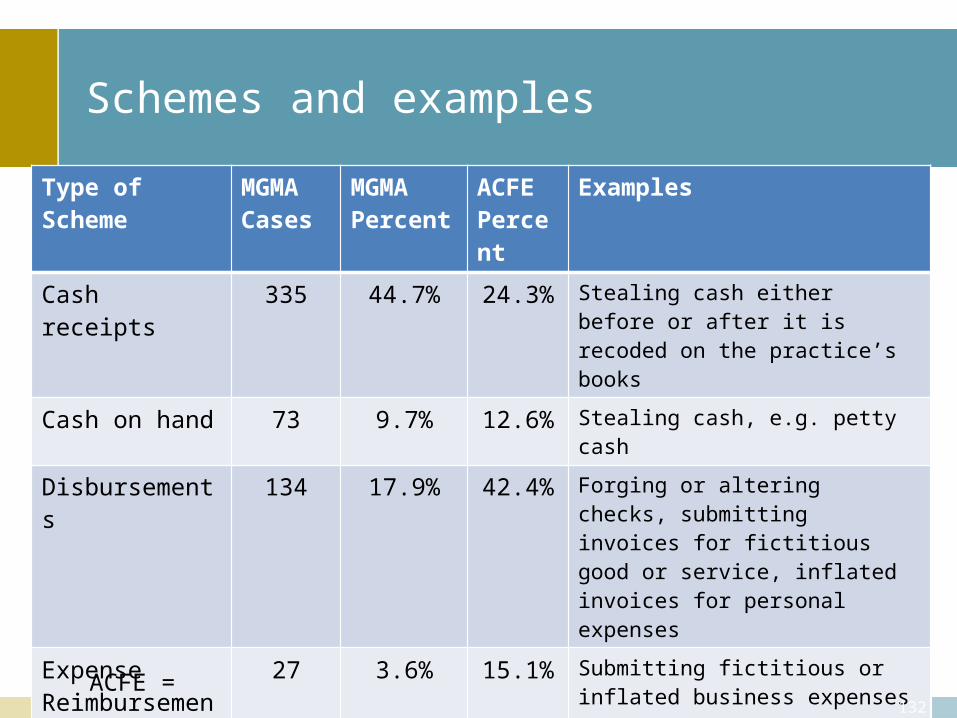

Schemes and examples

Type of Scheme MGMACases

MGMAPercent

ACFE Percent

Examples

Cash receipts 335 44.7% 24.3% Stealing cash either before or after it is recoded on the practice’s books

Cash on hand 73 9.7% 12.6% Stealing cash, e.g. petty cash

Disbursements 134 17.9% 42.4% Forging or altering checks, submitting invoices for fictitious good or service, inflated invoices for personal expenses

Expense Reimbursements

27 3.6% 15.1% Submitting fictitious or inflated business expenses

Payroll 46 6.1% 8.5% Creating fictitious employees, unauthorized bonuses or inflate pay

Non cash 56 7.5% 16.3% Stealing or misusing practices non cash assets such as supplies, equip

Other 78 10.4% Respondents reported thefts involving multiple schemes, patient refunds, billing schemes, identity theft, prescription theft

ACFE =

133

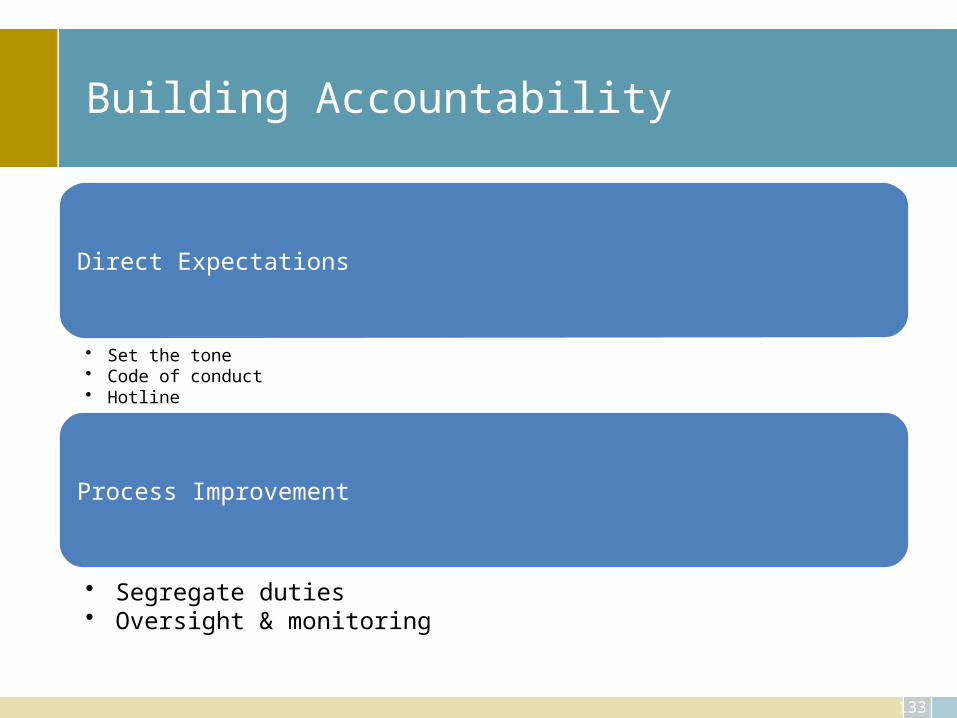

Building Accountability

Direct Expectations

• Set the tone• Code of conduct• Hotline

Process Improvement

• Segregate duties• Oversight & monitoring

134

Closing process gaps

• Segregate duties– No ONE controls a transaction from beginning to end

• Monitor– Create a “perception of detection”

• Review processes annually or when significant changes in personnel or systems occur

135

Cash Paid at Time of Service

• Skimming co-payments• Duration & loss depends on IT security• Discovered by accident or patient complaints

• Best practices– Receptionist/cashier security rights– Credit card processing– Missing ticket reports– Patient complaints– Reconcile receipt book – deposit – posted receipts

136

Checks and Mail Payments

• Billing office/business office• Diverting checks• Discovered by accident or by successor

• Best Practices– Separate deposit process from posting/insurance– Lockbox– Reconciliations– Monitoring contractual adjustments and write offs

137

Deposit processing

• Receive and open the mail• Endorse checks• Create record of checks• Prepare deposit• Take deposit to the bank• Record in accounting system• Receive bank statement• Reconcile bank statement• Reconcile deposits – receipts to general ledger

138

Disbursements

• Paying personal bills with practice funds• Gift cards• Fictitious vendors• Payroll

• Best practices– Monitor bank statements– Monitor credit card statements– Monitor direct deposit & payroll calculations– IT security – vendor and payroll files

139

Oversight and monitoring

Create a “perception of detection”

Intermittent and routine

Surprise audits

Job rotation

Mandatory vacations

Mandatory reconciliations

Surprise audits

140

Routine Reconciliations & Reviews

Deposits – revenue – collections

Refunds per billing system to accounting system

Merchant credit card statements

Physician review of bank statement

Scan check facsimiles

Deleted & modified transactions

Terminated employees

Direct deposit detail

141

IT Security/user rights

Merchant credit card security

Cashiers shouldn’t delete or write off accounts – monitor appointments

Limit addition of vendors in accounting system

Limit changes to payroll files

142

Job rotation & Mandatory vacations

One week

Cross training

Perform key duties

Behavior while on vacations

143

Surprise audits

Intermittent

Expected

Unannounced

Ask questions, review original documents

144

Long Term Trusted Employees

• 49% employed six years or more• 52% had college degrees• Losses increase with tenure

– Employed less than one year - $ 47,000– Employed over 10 years - $289,000

• Nearly 60% from accounting, operations, or executive/upper management

• First time offender – 93% no prior convictions– 10% terminated previously for fraud

Source: ACFE 2010 Report to the nations on Occupational Fraud & Abuse

145

Behavioral Red Flags

• Financial difficulties• Living beyond means• Control issues/unwillingness to share duties• Divorce/family problems• Wheeler dealer attitude• Unusually close association with vendor• Irritability, suspiciousness, or defensiveness• Addiction problems• Past employment/legal problems• Complain about inadequate pay• Instability in life circumstancesSource: ACFE 2010 Report to the nations on Occupational Fraud & Abuse

146

Process gaps

• Clearly outline expectations• Segregate duties• Hold accountable• Monitor and manage• Reports to insure outcomes achieved

Monitor staff activity

• Monitor daily activity of the staff for collections –– Know how many patients with payments due actually paid, goal 100%. – Know how many dollars could have been collected and the actual

amount collected, goal 100%. – For those accounts that payment was not received, ask the staff to

note why. – This can become a training tool on the issues, excuses, etc. that are

faced daily. – You can work through more “scripts” to handle these issues in the

future.

148

Reporting

149

Daily reporting

Who is tracking action daily?

“Executive Daily Dashboard”

What should be tracked daily and why?

150

Monthly reporting

Be consistent

Explain and educate

Utilize

dashboards to consolida

te

Utilize graphics and

pictures in

addition to the

actual financi

al statem

ents

151

Benchmark

• Evaluate your practice in terms of best practice leading to improving some aspect of performance, function, financial or process improvement

• Methodology– Identify problem areas– Identify how you did it before (how others do it)– Identify “leading edge” practices– Implement new and improved business practices

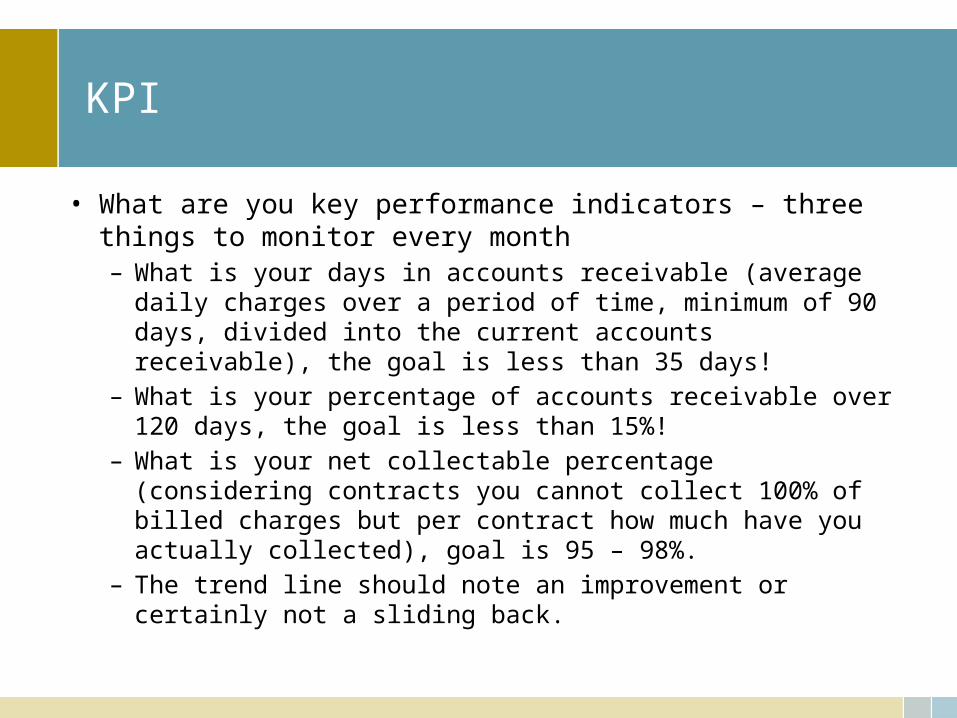

KPI

• What are you key performance indicators – three things to monitor every month– What is your days in accounts receivable (average daily charges over

a period of time, minimum of 90 days, divided into the current accounts receivable), the goal is less than 35 days!

– What is your percentage of accounts receivable over 120 days, the goal is less than 15%!

– What is your net collectable percentage (considering contracts you cannot collect 100% of billed charges but per contract how much have you actually collected), goal is 95 – 98%.

– The trend line should note an improvement or certainly not a sliding back.

153

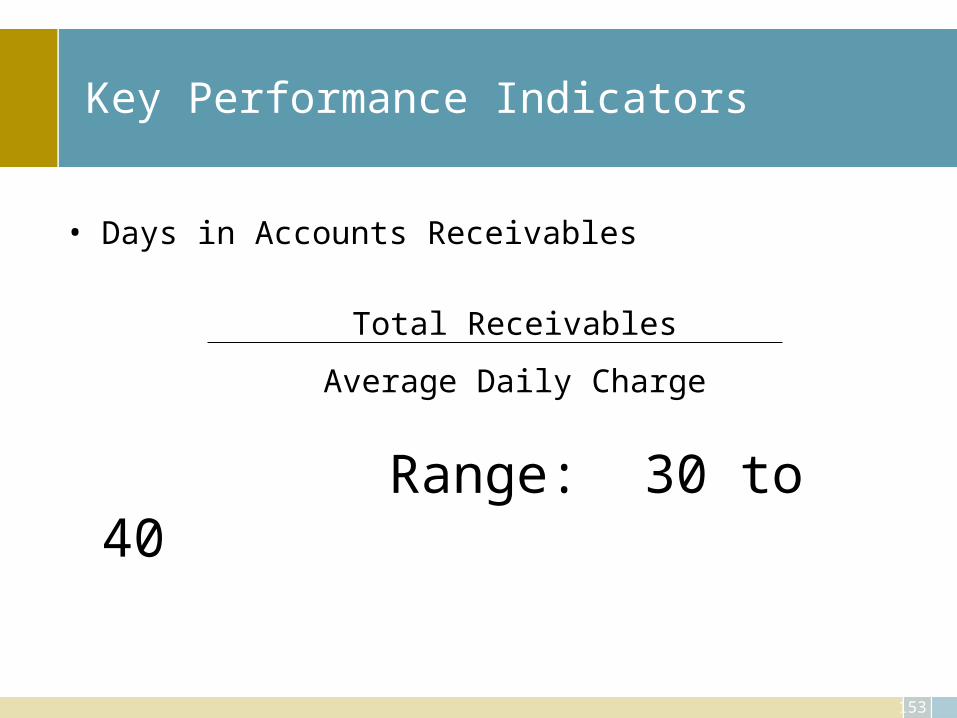

Key Performance Indicators

• Days in Accounts Receivables

Range: 30 to 40

Total Receivables

Average Daily Charge

154

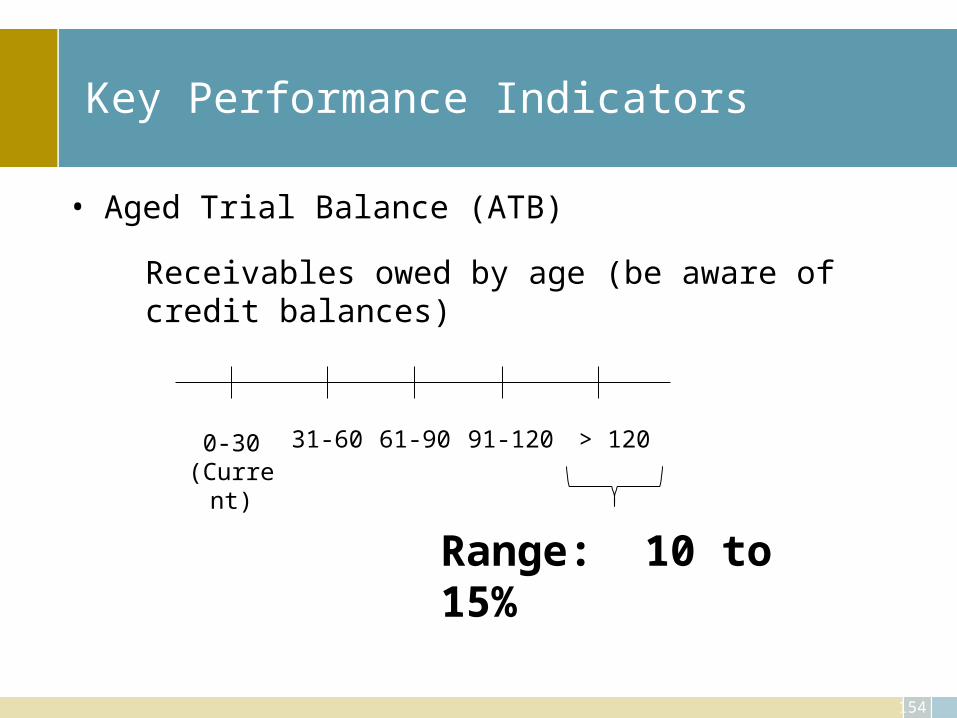

Key Performance Indicators

• Aged Trial Balance (ATB)

Receivables owed by age (be aware of credit balances)

0-30(Curren

t)

> 12061-90 91-12031-60

Range: 10 to 15%

155

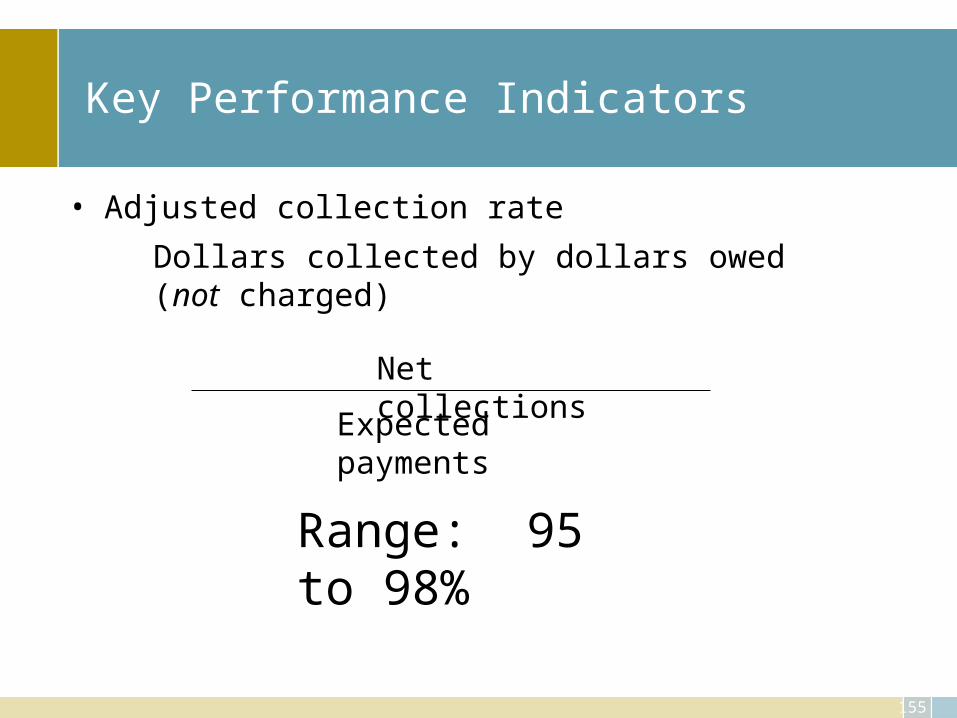

Key Performance Indicators

• Adjusted collection rate

Dollars collected by dollars owed (not charged)

Net collectionsExpected

payments

Range: 95 to 98%

Dashboard

156

– Benefits of using digital dashboards include:• Visual presentation of performance measures • Ability to identify and correct negative trends • Measure efficiencies/inefficiencies • Ability to generate detailed reports showing new trends • Ability to make more informed decisions based on collected business intelligence • Align strategies and organizational goals • Save time over running multiple reports

• Use in sequence– Practice wide– Department– Location– Doctor

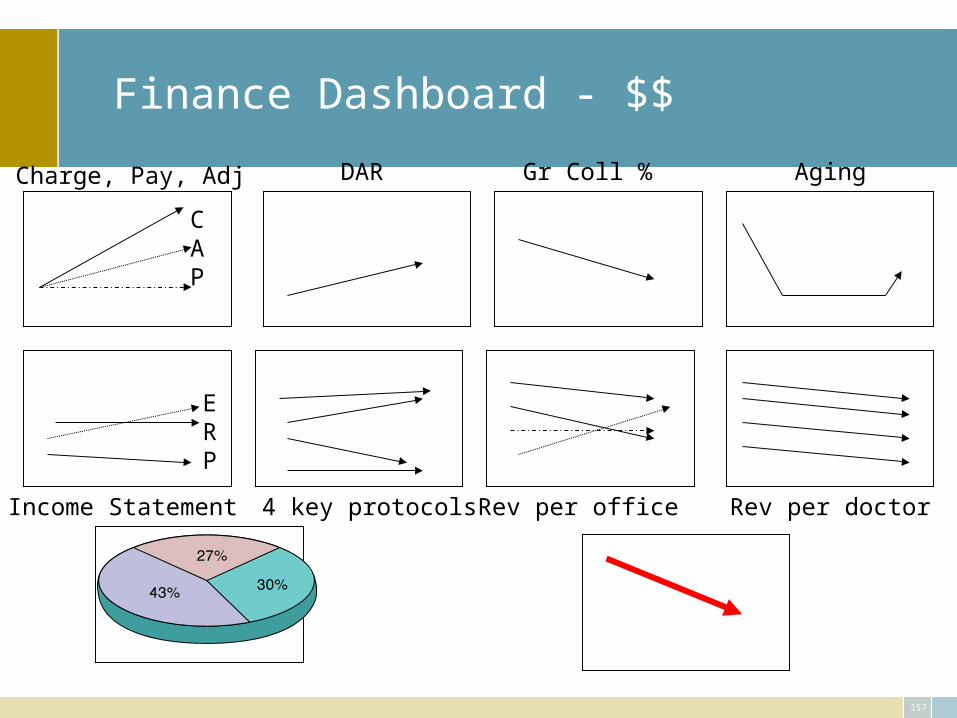

Finance Dashboard - $$

157

CAP

Charge, Pay, Adj DAR Gr Coll % Aging

ERP

Income Statement 4 key protocols Rev per office Rev per doctor

158

Key to the entire process: Accountability

• Defined as:– the quality or state of being accountable; especially: an obligation or

willingness to accept responsibility or to account for one's actions <public officials lacking accountability> http://www.merriam-webster.com/dictionary/accountability

• Define expectations• Set standards• Monitor results• Discipline or reward for outcomes

159

Next Practices – going beyond Best

• Set standards that are appropriate: recognize and reward when. . .– Exceed individual and department performance standards– Exceed external and internal benchmarking measures

• Hold self and staff accountable• Establish and adhere to a code of conduct based upon practice

mission and values– Culture of success– Culture of compliance– Culture of high quality, effective health care and appropriate, efficient

business practices

Staff training

• Train the staff –

– not once but often to insure that • they are aware of the issues at hand • they are doing• they can do to improve.

161

Case studies

Revenue cycle

Cost management

Internal controls

Budget

Contracting

162

Assignment

• Review your case• Answer the questions• Present your findings • Discussion

163

Action Plan

• Cannot overwhelm the staff• Events need to occur orderly• Pursue biggest pay back items first• Detail the plan to all staff• Get all follow up staff to buy in• Use tight time line, with report and end dates• Allow for slippage for things beyond control

164

Conclusion

• Review and tighten up the entire revenue cycle

• Utilize multiple staff and sources to protect and increase efficiency

• Clearly establish guidelines and standards• Hold yourself and all staff accountable

165

Conclusion

• Episodic, bundled or capitation will be part of our future

• Know what your COSTS are• Know the components of each cost category• Prepare for the future NOW• Control the right costs• Seek to improve operations• Patient first, profit will follow