Embed Size (px)

Citation preview

1

www.igcseaccounts.com

Prepared by D. El-Hoss

IGCSE Accounting

Depreciation

All questions are the copyright of Cambridge International Examination Board.

2

1 Peter bought a non-current asset for $5000 and depreciated it at 10% per annum on the straight line basis. At the end of year 2 he sold it for $4100.

What was the profit or loss on disposal?

Answer: D. $100 profit

2 Safir bought a machine for $10 000 and depreciated it at the rate of 30% per annum on the reducing (diminishing) balance basis.

What was the net book value at the end of year 2?

Answer: B. $4900

3 Why is depreciation provided?

Answer: D. to spread the cost of an asset over its useful life

3

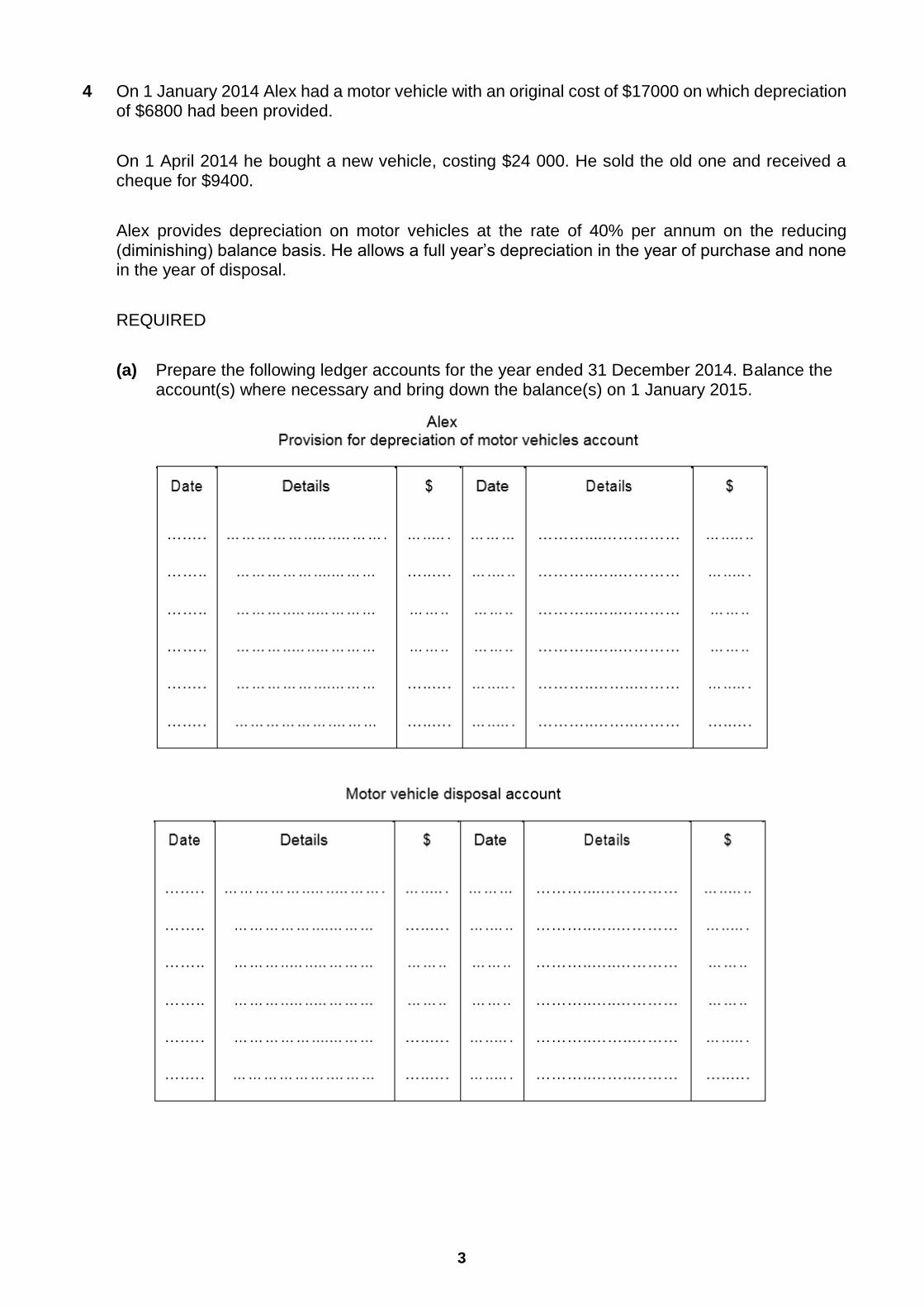

4 On 1 January 2014 Alex had a motor vehicle with an original cost of $17000 on which depreciation of $6800 had been provided.

On 1 April 2014 he bought a new vehicle, costing $24 000. He sold the old one and received a cheque for $9400.

Alex provides depreciation on motor vehicles at the rate of 40% per annum on the reducing (diminishing) balance basis. He allows a full year’s depreciation in the year of purchase and none in the year of disposal.

REQUIRED

(a) Prepare the following ledger accounts for the year ended 31 December 2014. Balance the account(s) where necessary and bring down the balance(s) on 1 January 2015.

4

Answer: (b) Prepare an extract from the statement of financial position at 31 December 2014 showing the entries for motor vehicles.

Alex Statement of Financial Position (extract) at 31 December 2014

Answer:

5

(c) Calculate the depreciation which will be provided on the new vehicle in the year ending 31 December 2015.

Answer: 14 400 × 40% = 5 760

(d) Name the two books of prime entry used in preparing the disposal account.

Answer: 1. general journal

2. cash book

(e) State the meaning of the term revenue expenditure. Give one example.

Answer: Money spent on day to day running expenses

Suitable example

5 (a) State two causes of depreciation of non-current assets. Answer: Physical deterioration Economic reasons Passage of time Depletion (b) Explain the straight line method of depreciation.

6

Answer: The depreciation is calculated on the net cost price and the same amount is written off each year.

(c) Explain the reducing (diminishing) balance method of depreciation.

Answer: The same percentage is written off each year but it is calculated on the net book value of the

asset.

(d) Explain how charging depreciation is an example of the application of the principle of prudence.

Answer: Ensures that non-current assets are shown at more realistic values. Ensures that the profit for the year is not overstated.

(e) Name one other accounting principle which is applied when charging depreciation.

Answer: Accruals (matching).

6 On 1 October 2013 Natasha Salim started a business altering and mending clothes. On that date she purchased a machine, $4000, paying by cheque.

On 1 January 2014 she purchased another machine, $6000, on credit from ABC Machines.

She decided to depreciate the machines using the reducing (diminishing) balance method at 20% per annum. A whole year’s depreciation was to be charged in the year of purchase, but no depreciation in the year of sale.

On 1 February 2015 Natasha Salim decided that the machine purchased on 1 October 2013 was no longer required. She sold it for $2100, cash.

REQUIRED

(a) Prepare the following accounts in the ledger of Natasha Salim for each of the two years ended 30 September 2014 and 30 September 2015.

Balance the accounts and bring down the balances on 1 October 2014 and 1 October 2015. See next page.

7

Natasha Salim

Machinery account

Provision for depreciation of machinery account

8

Answer:

(b) Calculate the profit or loss on the disposal of the machine on 1 February 2015.

Answer: Proceeds of Sale

Provision for depreciation

Less Cost Price

Profit/Loss on disposal

9

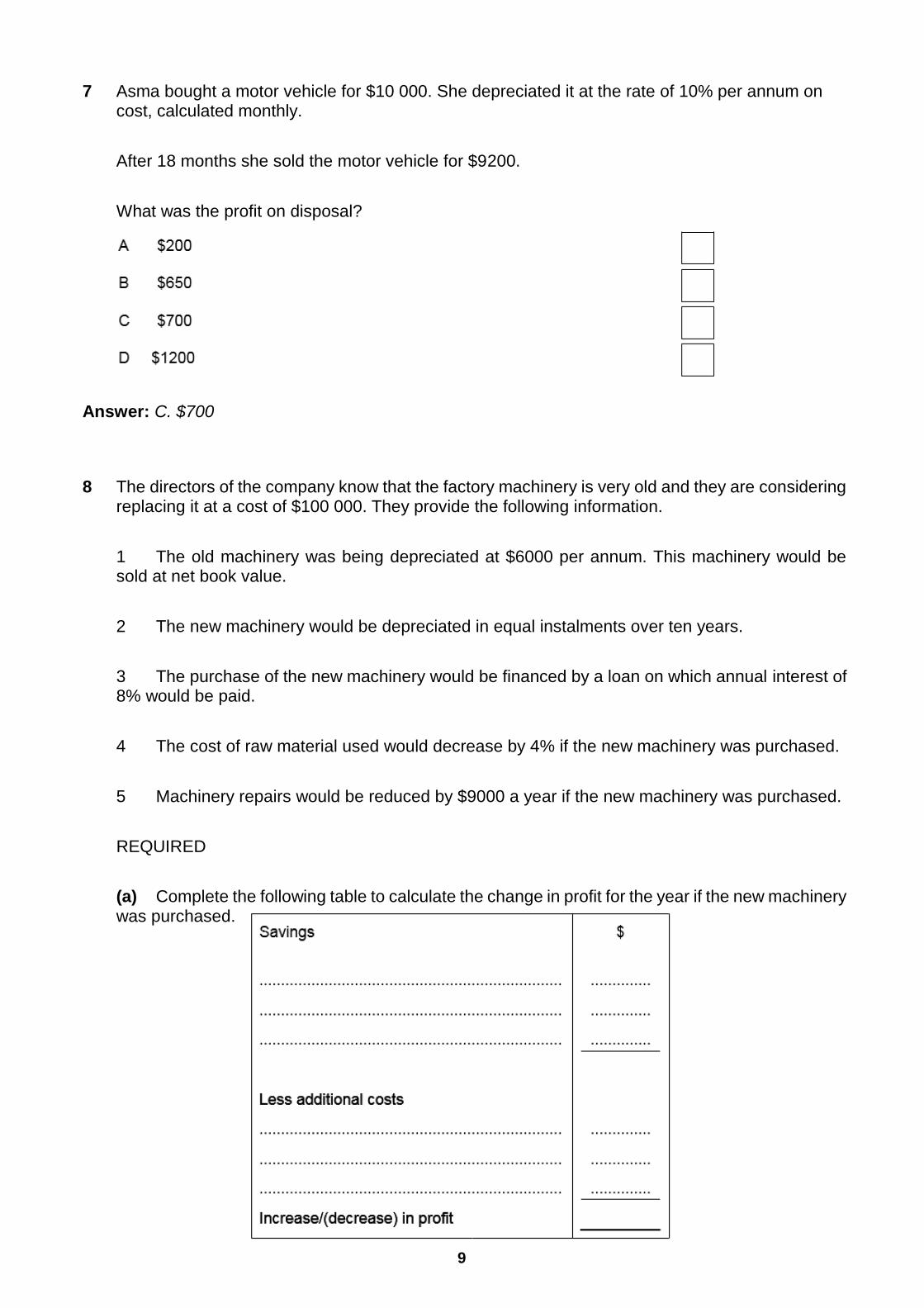

7 Asma bought a motor vehicle for $10 000. She depreciated it at the rate of 10% per annum on cost, calculated monthly.

After 18 months she sold the motor vehicle for $9200.

What was the profit on disposal?

Answer: C. $700

8 The directors of the company know that the factory machinery is very old and they are considering replacing it at a cost of $100 000. They provide the following information.

1 The old machinery was being depreciated at $6000 per annum. This machinery would be sold at net book value.

2 The new machinery would be depreciated in equal instalments over ten years.

3 The purchase of the new machinery would be financed by a loan on which annual interest of 8% would be paid.

4 The cost of raw material used would decrease by 4% if the new machinery was purchased.

5 Machinery repairs would be reduced by $9000 a year if the new machinery was purchased.

REQUIRED

(a) Complete the following table to calculate the change in profit for the year if the new machinery was purchased.

10

Answer:

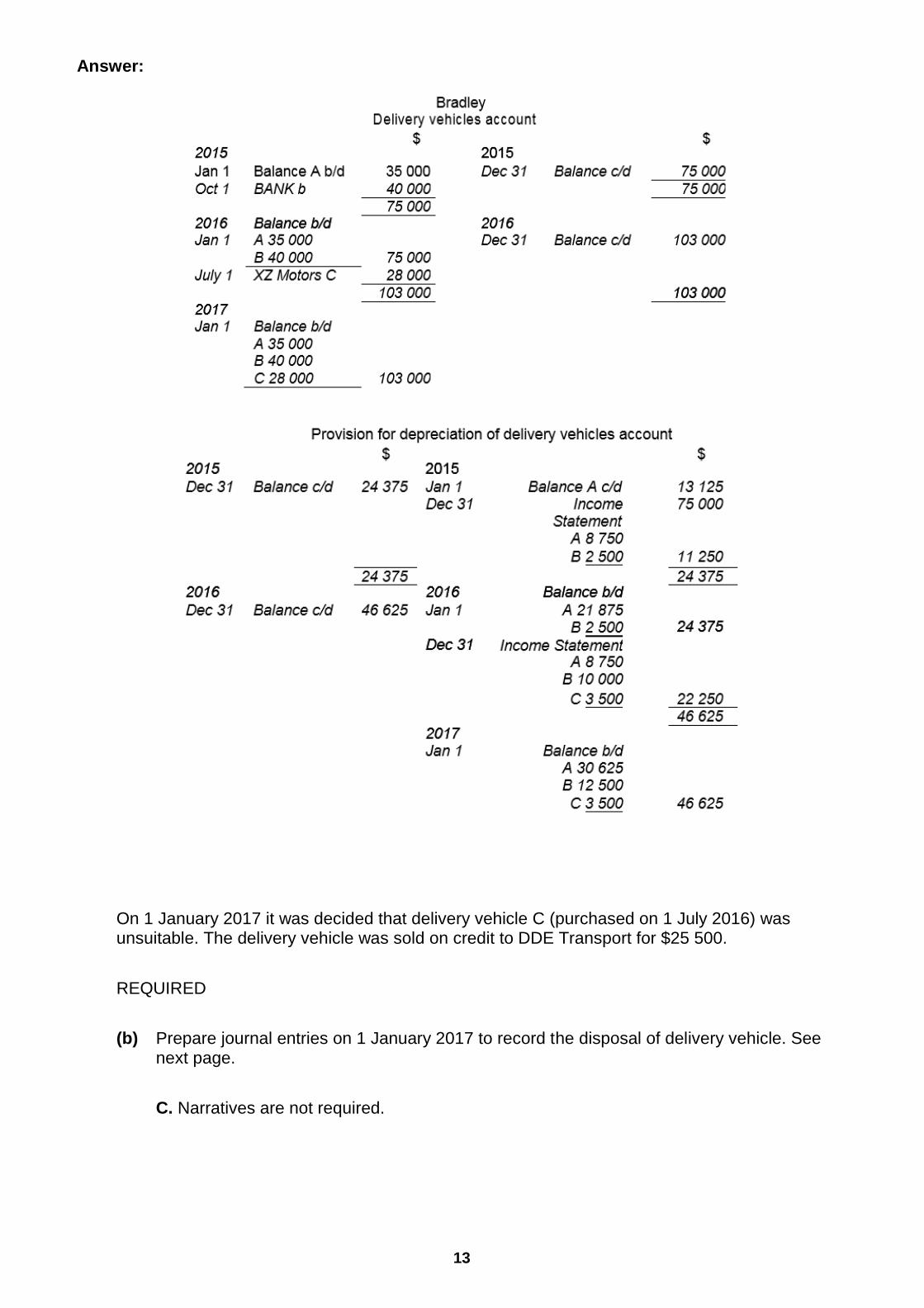

9 Bradley is a wholesaler. His financial year ends on 31 December.

On 1 January 2015 Bradley had a delivery vehicle A which had cost $35 000 and had been depreciated by $13 125.

On 1 October 2015 he purchased delivery vehicle B for $40 000 by cheque.

On 1 July 2016 he purchased delivery vehicle C on credit from XZ Motors for $28 000.

All the delivery vehicles are depreciated by 25% per annum on cost calculated from the date of purchase.

REQUIRED

(a) Prepare the following accounts for each of the years ended 31 December 2015 and 31 December 2016.

Balance the accounts and bring down the balances on 1 January 2016 and 1 January 2017.

See next page.

11

Bradley

Delivery vehicles account

12

Provision for depreciation of delivery vehicles account

13

Answer:

On 1 January 2017 it was decided that delivery vehicle C (purchased on 1 July 2016) was unsuitable. The delivery vehicle was sold on credit to DDE Transport for $25 500.

REQUIRED

(b) Prepare journal entries on 1 January 2017 to record the disposal of delivery vehicle. See next page.

C. Narratives are not required.

14

Bradley Journal

Answer:

10 The financial year of Doshi Manufacturing Company ends on 31 January. The following trial balance was extracted from the books on 31 January 2017.

15

REQUIRED

(a) Select the relevant figures and prepare the manufacturing account for the year ended 31 January 2017. See next page.

16

Doshi Manufacturing Company

Manufacturing Account for the year ended 31 January 2017

(b) Select the relevant figures and prepare the income statement for the 31 January 2017.

See next page.

17

Doshi Manufacturing Company

Income Statement for the year ended 31 January 2017

Answer:

18

(c) Suggest one reason why the loose tools are revalued at the end of each financial year rather than by using the straight line (equal instalment) or reducing (diminishing) balance method of depreciation.

Answer: Low value items which are not easy to depreciate separately/Not practical to keep detailed records of such assets/other.

11 Sonia started her business on 1 January 2015. She decided on the following depreciation policy.

Motor vehicles were to be depreciated at the rate of 25% per annum using the reducing (diminishing) balance method.

Equipment was to be depreciated at the rate of 10% per annum using the straight line (equal instalment) method.

A full year’s depreciation was to be provided in the year of purchase.

Sonia provided the following information about her purchases of assets.

19

REQUIRED

(a) Complete the following table. Indicate with a tick (3) in which column of a trial balance each ledger account balance would appear.

Answer:

(b) Complete the following table showing the depreciation charges, the accumulated depreciation and the net book values of the different assets on the dates shown. A space is provided for your workings. See next page.

20

Answer:

21

(c) Prepare the extract from the statement of financial position at 31 December 2016 showing full details of the value of motor vehicles and equipment.

Sonia

Statement of Financial Position (extract) at 31 December 2016

Answer:

(d) Name the section of the statement of financial position where motor vehicles and equipment appear.

Answer: Non-current assets.

12 Bayani depreciates his fixtures and fittings using the straight line (equal instalment) method of depreciation. He provides a full year’s depreciation in the year of purchase and none in the year of disposal. He provided the following information.

22

REQUIRED

(a) Calculate the rate of depreciation Bayani is applying.

Answer:

Additional information

On 1 May 2015 Bayani bought new fixtures and fittings, cost $12 000, paying by cheque.

On 1 August 2016 he sold old fixtures and fittings, which had cost $10 000 and on which four years’ depreciation had been provided. The purchaser paid Bayani in cash.

REQUIRED

(b) Name the books of prime (original) entry used on 1 May 2015 and 1 August 2016.

1 May 2015

1 August 2016

Answer: 1 May 2015: Cash book

1 August 2016: 1. Nominal (general) journal

2. Cash book

23

(c) Complete the following table by inserting the amounts to be shown in the financial statements. Show your workings in the spaces provided.

Answer:

(d) State the double entry needed to record the depreciation charge for the year ended 31 December 2015.

Answer:

workings $

fixtures and fittings at cost on

31 December 2015

fixtures and fittings at cost on

31 December 2016

depreciation charge for the year

ended 31 December 2015

accumulated depreciation at

31 December 2015

depreciation charge for the year

ended 31 December 2016

accumulated depreciation at

31 December 2016

24

(e) State the double entry needed to eliminate the accumulated depreciation on the fixtures and fittings sold on 1 August 2016.

Answer:

(f) Name one method of depreciation, other than the straight line (equal instalment) method, and explain how it is calculated.

Name of method .......................................................................................................................

Method of calculation ................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

Answer: Reducing (diminishing) balance method.

Annual percentage rate is applied to the net book value of the asset.

OR

Revaluation method.

The difference between the opening and closing valuations is taken and adjusted for any purchases or disposals.

Additional information

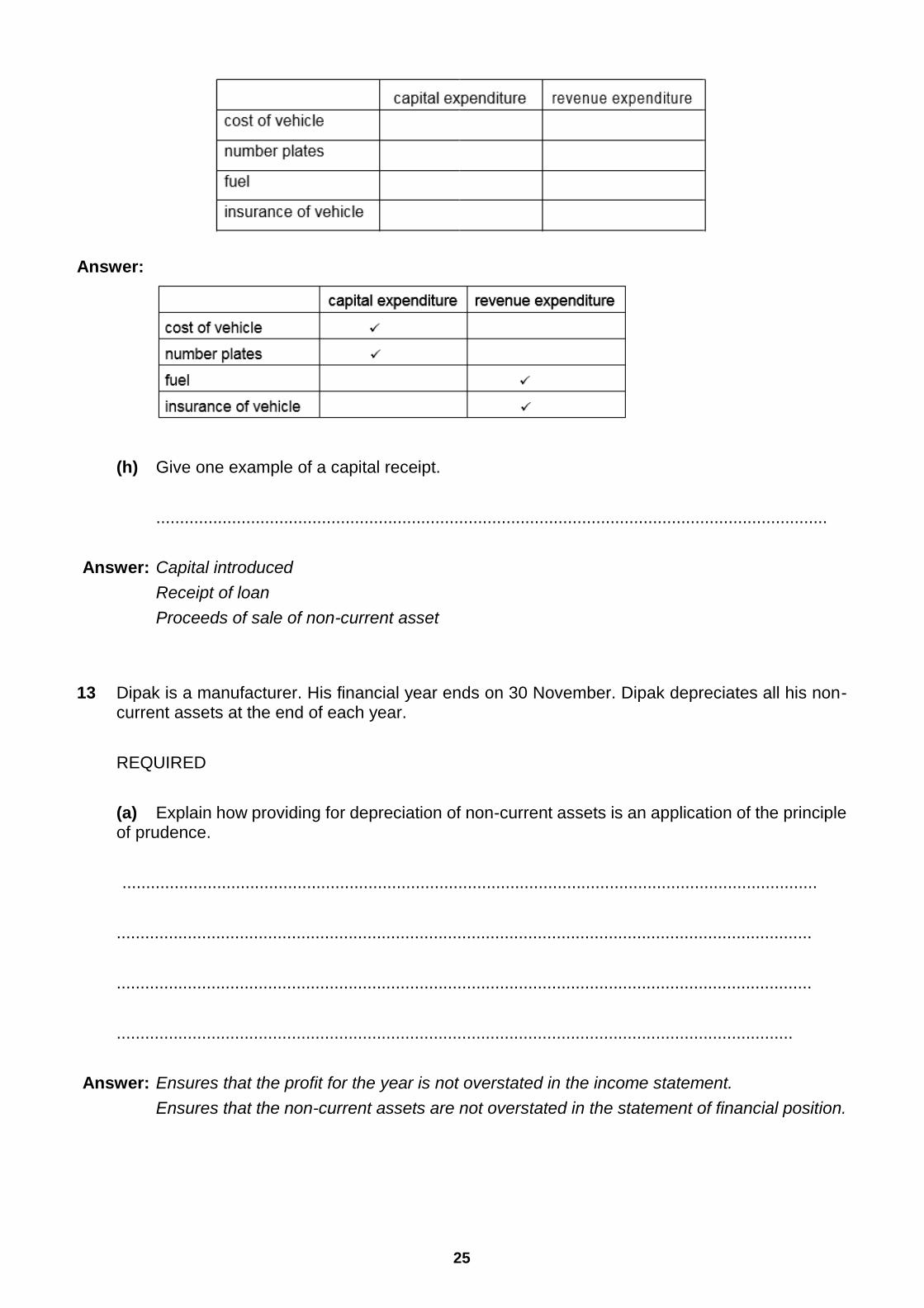

Bayani also bought a motor vehicle. The costs relating to the purchase were as follows:

REQUIRED

(g) Complete the following table, indicating with a tick (3) whether each item is a capital expenditure or a revenue expenditure.

25

Answer:

(h) Give one example of a capital receipt.

..............................................................................................................................................

Answer: Capital introduced

Receipt of loan

Proceeds of sale of non-current asset

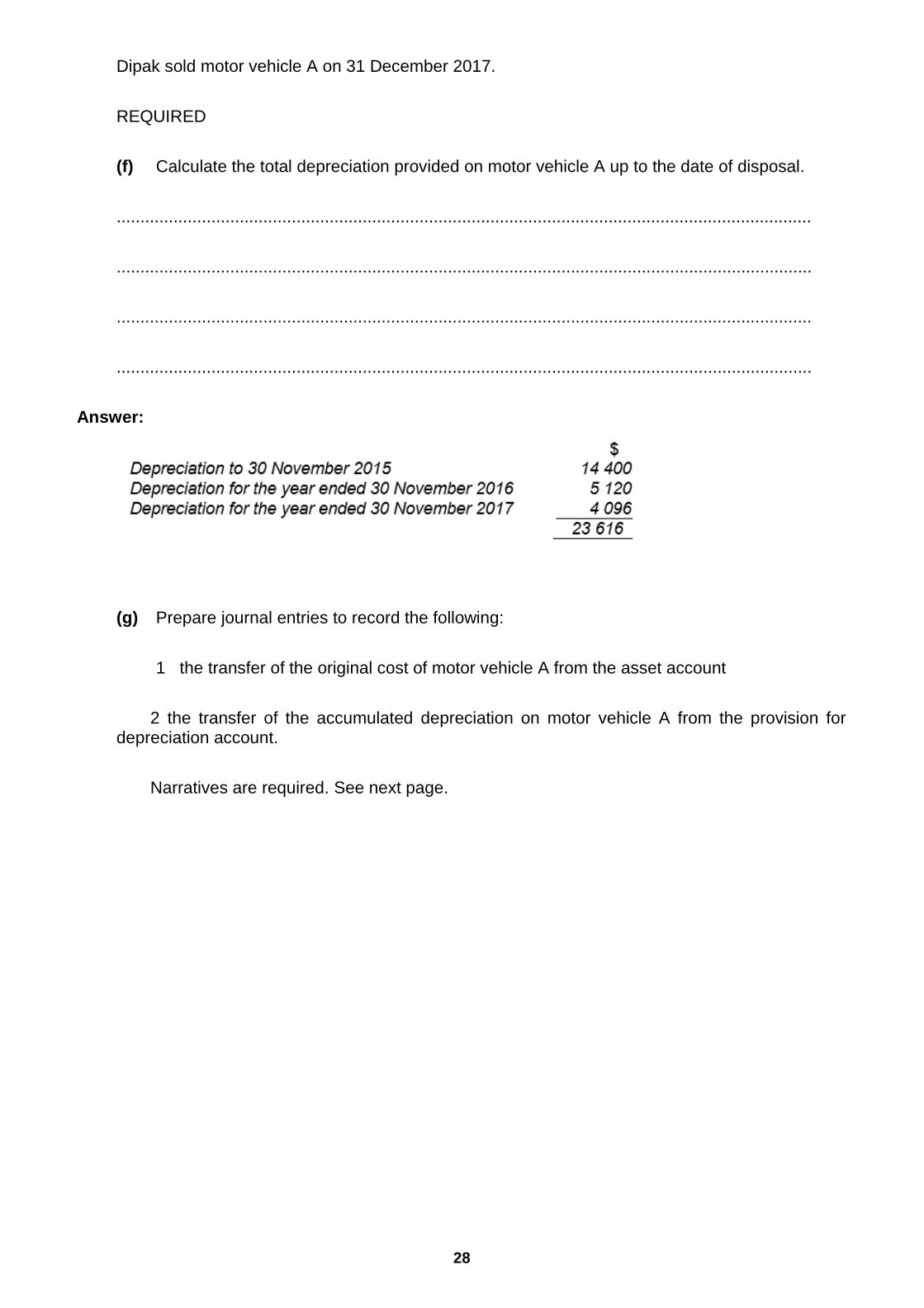

13 Dipak is a manufacturer. His financial year ends on 30 November. Dipak depreciates all his non-current assets at the end of each year.

REQUIRED

(a) Explain how providing for depreciation of non-current assets is an application of the principle of prudence.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

Answer: Ensures that the profit for the year is not overstated in the income statement.

Ensures that the non-current assets are not overstated in the statement of financial position.

26

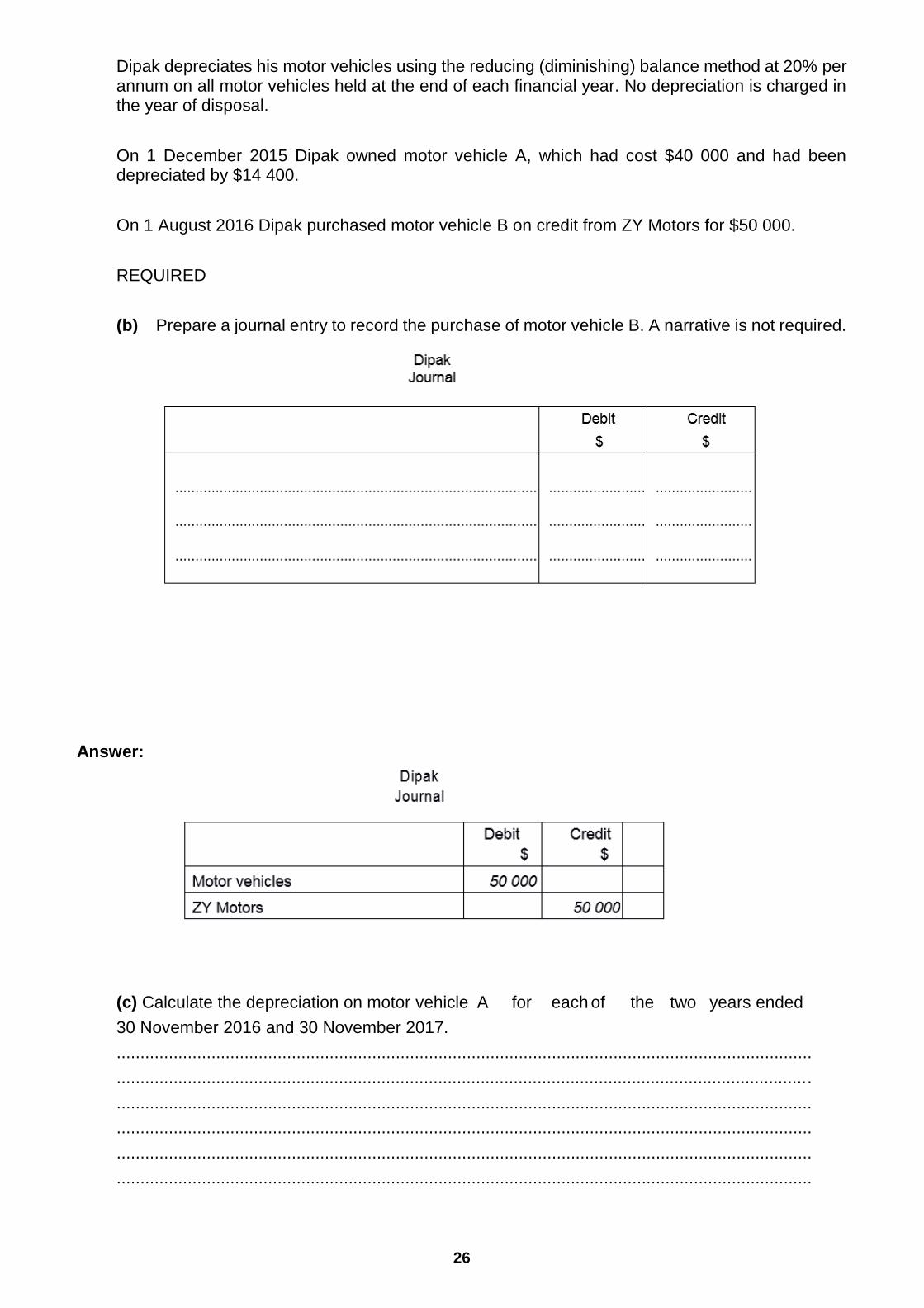

Dipak depreciates his motor vehicles using the reducing (diminishing) balance method at 20% per annum on all motor vehicles held at the end of each financial year. No depreciation is charged in the year of disposal.

On 1 December 2015 Dipak owned motor vehicle A, which had cost $40 000 and had been depreciated by $14 400.

On 1 August 2016 Dipak purchased motor vehicle B on credit from ZY Motors for $50 000.

REQUIRED

(b) Prepare a journal entry to record the purchase of motor vehicle B. A narrative is not required.

Answer:

(c) Calculate the depreciation on motor vehicle A for each of the two years ended

30 November 2016 and 30 November 2017.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

27

Answer:

(d) Calculate the depreciation on motor vehicle B for each of the two years ended 30 November 2016 and 30 November 2017.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

Answer:

(e) Prepare a journal entry to record the transfer to the income statement of the total depreciation on motor vehicles for the year ended 30 November 2017.

A narrative is not required.

28

Dipak sold motor vehicle A on 31 December 2017.

REQUIRED

(f) Calculate the total depreciation provided on motor vehicle A up to the date of disposal.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

Answer:

(g) Prepare journal entries to record the following:

1 the transfer of the original cost of motor vehicle A from the asset account

2 the transfer of the accumulated depreciation on motor vehicle A from the provision for depreciation account.

Narratives are required. See next page.

29

Answer:

14 Jamil started a business on 1 January 2014. He considered using the straight line (equal instalment) method to depreciate all his non-current assets.

REQUIRED

(a) Name one other method Jamil could use to depreciate his non-current assets.

...............................................................................................................................................

30

Answer: Reducing (diminishing) balance method

Revaluation method

(b) Suggest two reasons why the straight line (equal instalment) method would not be a suitable method of depreciation to apply to the hand tools used in Jamil’s factory.

1 ................................................................................................................................................

...................................................................................................................................................

2 ................................................................................................................................................

...............................................................................................................................................

Answer: Principle of materiality – not practical/too many items/too difficult/too costly to depreciate each item separately .

Do not depreciate by an equal amount each year.

May be certain amount of loss of tools each year.

Jamil decided to depreciate his office machinery at 20% per annum using the straight line (equal instalment) method calculated on a month-by-month basis from the date of purchase to the date of disposal.

He provided the following information.

REQUIRED

(c) Calculate the depreciation on office machinery for the year ended 31 December 2016. Show your calculations and insert your answers in the spaces provided. See next page

31

Calculation of depreciation for the year ended 31 December 2016

Answer:

(d) Calculate the depreciation on office machinery for the year ended 31 December 2017. Show your calculations and insert your answers in the spaces provided.

32

Answer:

(e) Prepare the following accounts in the ledger of Jamil for each of the two years ended 31 December 2016 and 31 December 2017.

Balance the accounts and bring down the balances on 1 January 2017 and 1 January 2018.

Jamil

Office machinery account

33

Provision for depreciation of office machinery account

Answer:

34

(f) Calculate the profit or loss on the disposal of office machine A.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

Answer:

35

15 Agatha depreciates her fixtures and fittings at the rate of 10% per annum.

On 1 January 2015 she bought new fixtures and fittings costing $800. In error she debited the repairs account with the purchase.

What was the effect of this error on the profit for the year ended 31 December 2015?

Answer: B. $720 understated

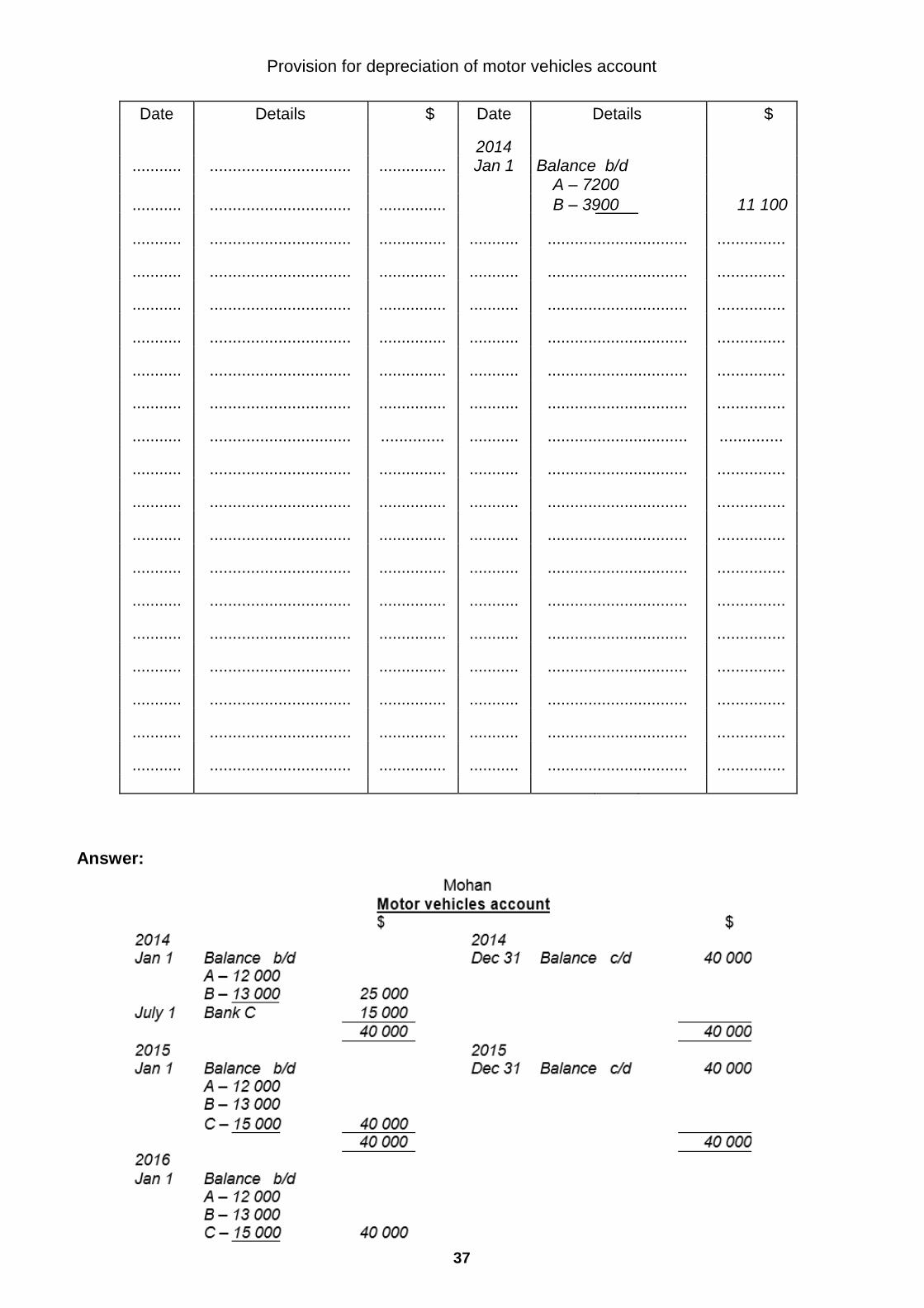

16 Mohan is a trader. His financial year ends on 31 December.

Mohan depreciates his motor vehicles at 20% per annum on cost, calculated from the date of purchase.

The following information was available on 1 January 2014.

REQUIRED

(a) Prepare the following accounts for each of the two years ended 31 December 2014 and 31 December 2015.

Balance the accounts and bring down the balances on 1 January 2015 and 1 January 2016. See next page.

36

37

Provision for depreciation of motor vehicles account

Date Details $ Date Details $

2014

........... ............................... ............... Jan 1 Balance b/d

A – 7200

........... ............................... ............... B – 3900 11 100

............................... ............... ...........

...............

........... ...............................

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... .............. ........... ............................... ..............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

........... ............................... ............... ........... ............................... ...............

Answer:

38

On 1 January 2016 Motor vehicle B was sold for $2900, cash.

REQUIRED

(b) Calculate the depreciation on Motor vehicle B up to the date of disposal.

...................................................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

Answer:

39

Answer:

17 A club records its equipment at valuation.

How does it calculate its depreciation?

Answer: C. value at start of year + equipment purchased – value at end of year

40

18 David and Harold are in partnership. The partnership agreement states that David is to receive an annual salary of $12 000 and that profits and losses are to be shared in the ratio 2:1.

The following balances were extracted from the partnership books on 31 March 2016.

Additional information

1 Other operating expenses included $500 for insurance which was paid in advance at 31 March 2016.

2 Inventory on 31 March 2016 amounted to $26 800.

3 Fixtures and fittings are depreciated at the rate of 10% per annum on the straight line basis. A full year’s depreciation is provided in the year of purchase. The current year’s depreciation has not yet been provided.

4 All the fixtures and fittings were purchased when the partnership was formed.

REQUIRED

(a) Calculate how many years’ depreciation had been charged.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

41

Answer:

(b) Prepare the income statement for the year ended 31 March 2016.

$ $

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

42

Answer:

(c) Prepare the appropriation account for the year ended 31 March 2016.

David and Harold

Appropriation Account for the year ended 31 March 2016 $ $

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

........................................................................... ......................... .........................

Answer:

43

19 Virginia depreciates motor vehicles at the rate of 25% per annum using the reducing (diminishing) balance method. She provides a full year’s depreciation in the year of purchase and none in the year of disposal. Her accounting year end is 31 December.

She purchased a motor vehicle, cost $10 000, on 1 April 2013, and sold it on 28 May 2015 for $7210 cash. On the same date she bought a new motor vehicle for $17 000, paying by cheque.

REQUIRED

(a) Calculate the depreciation which had been provided on the old motor vehicle at the date of disposal.

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

Answer:

44

Answer:

45

(c) Name the financial statement in which the provision for depreciation appears. State in which section it appears.

Name of financial statement .....................................................................................................

Section ..................................................................................................................................

Answer: Statement of financial position

Non-current assets

(d) State how providing depreciation is an application of the accounting principle of accruals (matching).

...................................................................................................................................................

...................................................................................................................................................

...............................................................................................................................................

Answer: The cost of the non-current asset and the revenues arising from its use are matched in an accounting period.

OR

The cost of the non-current asset is spread over its useful life.

46

(e) Name one other accounting principle which is applied when depreciation is provided.

...............................................................................................................................................

Answer: Prudence.

(f) State the type of asset for which the revaluation method of depreciation is suitable.

...............................................................................................................................................

Answer: Small items of equipment e.g. loose tools.

20 Tom’s financial year ends on 31 July. He depreciates his non-current assets using the reducing (diminishing) balance method.

REQUIRED

(a) Name one other method of depreciation which Tom could apply.

.............................................................................................................................................

Answer: Straight line/fixed instalment

Revaluation

(b) Explain how providing for depreciation of non-current assets is an application of the principle of accruals (matching).

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

.............................................................................................................................................

Answer: The loss in value of the non-current asset during the year is set against the revenue for the same period.

OR

The cost of the non-current asset is spread over the years which benefit from

the use of that asset.

47

(c) Name one other accounting principle which is applied when providing for depreciation of non-current assets.

.............................................................................................................................................

Answer: Prudence

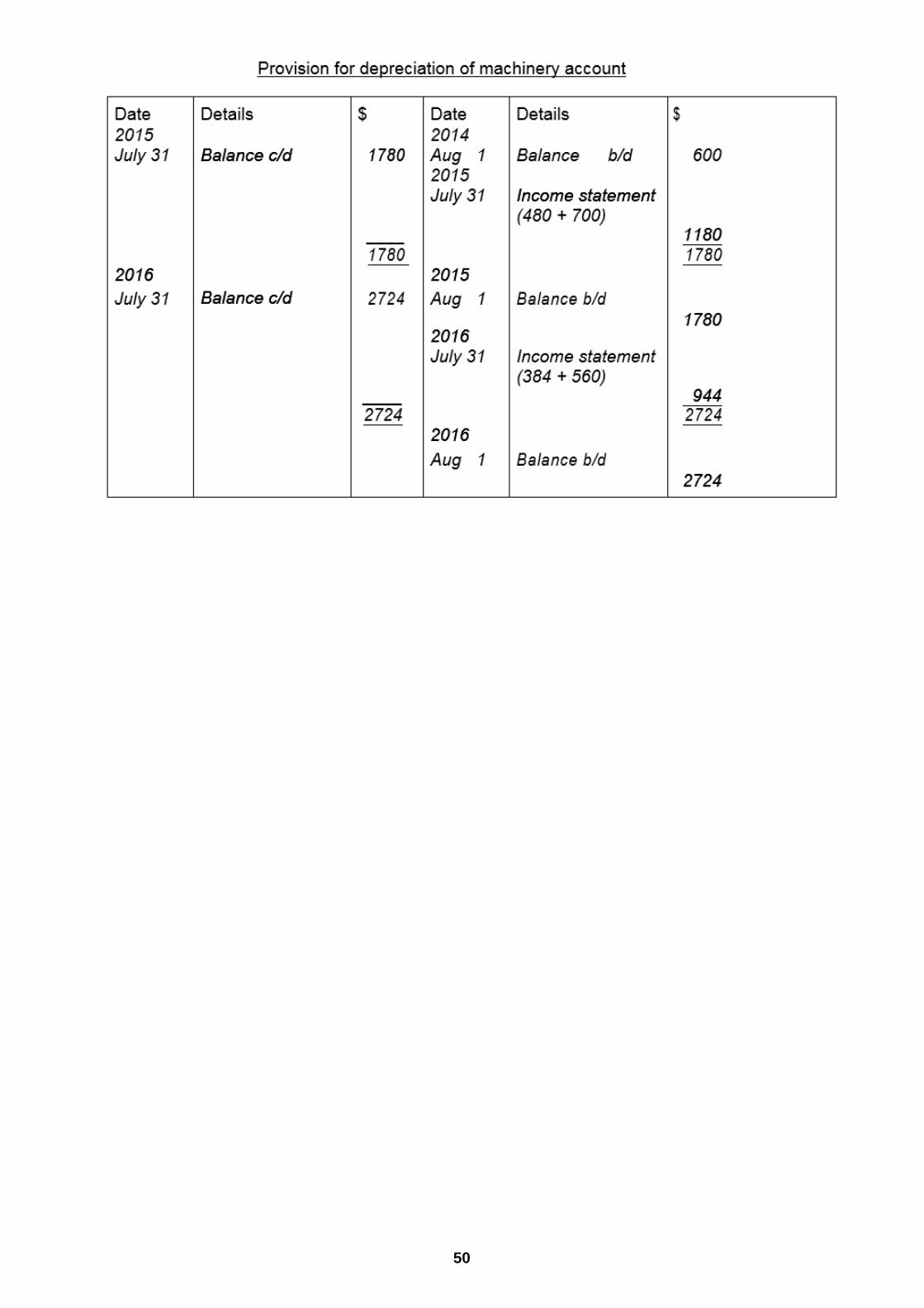

Tom depreciates his machinery using the reducing (diminishing) balance method at 20% per annum on all machinery held at the end of the year. No depreciation is charged in the year of disposal.

On 1 August 2014 he owned one machine (Machine A) which had cost $3000, and which had been depreciated by $600.

On 1 January 2015 Tom purchased another machine (Machine B) for $3500, paying by cheque.

REQUIRED

(d) (i) Calculate the depreciation of Machine A for each of the years ended 31 July 2015 and 31 July 2016.

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

Answer:

48

(ii) Calculate the depreciation of Machine B for each of the years ended 31 July 2015 and 31 July 2016.

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

Answer:

(e) Prepare the following accounts in the ledger of Tom.

(i) Machinery account

Balance the account on 31 July 2015 and bring down the balance on 1 August 2015.

Tom

Machinery account

49

(ii) Provision for depreciation of machinery account

Balance the account at the end of each year and bring down the balance on 1 August 2015 and 1 August 2016.

Answer:

50