Embed Size (px)

Citation preview

© 2005 Prentice Hall Business Publishing© 2005 Prentice Hall Business Publishing Survey of Economics, 2/eSurvey of Economics, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Prepared by: Jamal Husein

C H A P T E R

1515Money, the Banking System, andthe Federal Reserve

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 2

What Is Money?What Is Money?What Is Money?What Is Money?

Money is anything that is regularly used in economic transactions or exchanges.

People are willing to accept money as a medium of exchange because of its recognizable value. We trust that the money we receive will also be accepted by others in lieu of payment.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 3

What Is Money?What Is Money?What Is Money?What Is Money?

In addition to currency, we also accept checks because checks can also be used to make payments.

Throughout history, many different items have played the role of money.

Precious metals, stones, gold bars, and even cigarettes have played the role of money.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 4

What Is Money?What Is Money?What Is Money?What Is Money?

In addition to recognizable value, other desirable properties of money include durability and divisibility.

Money serves several functions, all related to making economic exchanges easier:

Money serves as a medium of exchange Money serves as a unit of account Money serves as a store of value

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 5

Three Properties of MoneyThree Properties of MoneyThree Properties of MoneyThree Properties of Money

1. Money serves as a medium of exchange: Instead of using money, we could barter—or trade

goods directly for goods. But when compared to barter, money is clearly more efficient.

Barter requires a double coincidence of wants. Barter requires you to find someone who has precisely what you are looking for and wants to buy precisely what you are willing to offer in exchange.

The probability of a double coincidence of wants occurring is very, very tiny. Money solves that problem.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 6

Three Properties of MoneyThree Properties of MoneyThree Properties of MoneyThree Properties of Money

2. Money serves as a unit of account: Money provides a convenient

measuring rod when prices for all goods are quoted in money terms.

Money serves as the unit of account, or standard unit which can be used to compare the relative value of goods, making it easier to carry out economic transactions.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 7

Three Properties of MoneyThree Properties of MoneyThree Properties of MoneyThree Properties of Money

3. Money serves as a store of value: Money can be used to store value before it

is used to carry out transactions. From the time you receive a payment

until the time you make a payment, you can use money to store value.

However, money is an imperfect store of value, particularly in an inflationary economy, when the real value of a nominal amount of money decreases.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 8

Measuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. Economy

The most basic measure of money in the United States is called M1.

Components of M1, January 2003 (billions $)

Currency held by the public $630

Demand deposits 295

Other checkable deposits 279

Travelers’ checks 8

Total of M1 $1,212

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 9

Measuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. Economy Since there are approximately 280 million

people in the United States, the $630 billion of currency held by the public amounts to $2,250 per person.

In fact, most people don’t hold such a large amount of cash. Much of this currency is held abroad by wealthy people who hold part of their wealth in U.S. dollars; some circulates in other countries along with the official currency; and some is used in illegal transactions.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 10

Measuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. EconomyMeasuring Money in the U.S. Economy

A broader definition of money, known as M2, includes assets that are sometimes used in economic exchanges or can be readily turned into M1, such as deposits in money market mutual funds and savings accounts.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 11

Banks As Financial IntermediariesBanks As Financial IntermediariesBanks As Financial IntermediariesBanks As Financial Intermediaries

A typical commercial bank accepts funds from savers in the form of deposits, and uses the money to make loans to businesses.

A simplified balance sheet for a commercial bank has two sides:

Liabilities are the sources of funds. The bank is “liable” for returning funds to depositors.

Assets are the uses of funds. Assets generate income for the bank. Loans are assets for the bank because a borrower must pay interest to the bank.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 12

Balance Sheet for a Commercial BankBalance Sheet for a Commercial BankBalance Sheet for a Commercial BankBalance Sheet for a Commercial Bank

Assets LiabilitiesReserves $ 200 Deposits $2,000

Loans 2,000 Net worth 200______________ ______________

Total: $2,200 Total: $2,200

Net worth = assets – liabilities

Net worth refers to the bank’s initial funds contributed by its owners.

Net worth is entered on the liabilities side because it is also a source of funds.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 13

Balance Sheet for a Commercial BankBalance Sheet for a Commercial BankBalance Sheet for a Commercial BankBalance Sheet for a Commercial Bank

Reserves are assets that are not lent out. Banks are required by law to hold a

fraction of their deposits as reserves and not make loans with it. This fraction is called required reserves.

The bank may choose to hold additional reserves beyond what is required; these are called excess reserves.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 14

The Process of Money CreationThe Process of Money CreationThe Process of Money CreationThe Process of Money Creation Currency and checking deposits are included in the

money supply. When a customer makes a $1,000 cash deposit to open

a checking account, currency held by the public decreases and checking deposits increase. The money supply remains unchanged, but the bank’s reserves increase.

First Bank of Hollywood

Assets LiabilitiesReserves $100 Deposits $1,000

Loans 900

Assume that the bank holds no excess reserves and the required reserve ratio equals 10% of deposits.

The $1,000 deposit changes the bank’s balance sheet as follows:

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 15

The Process of Money CreationThe Process of Money CreationThe Process of Money CreationThe Process of Money Creation

The First Bank of Hollywood makes a $900 loan which is used to open a checking account in the Second Bank of Burbank, with a balance of $900.

Second Bank of Burbank

Assets LiabilitiesReserves $ 90 Deposits $900

Loans 810 The Second bank of

Burbank makes loans in the amount of $810, which are deposited in the Third Bank of Venice, and the process continues.

The balance sheet of the Second Bank of Burbank changes as follows:

Third Bank of Venice

Assets LiabilitiesReserves $ 81 Deposits $810

Loans 729

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 16

The Deposit Creation FormulaThe Deposit Creation FormulaThe Deposit Creation FormulaThe Deposit Creation Formula

The original $1,000 cash deposit has created checking account balances equal to:

$1,000 + $900 + $810 + $729 + $656.10 +.…= $10,000

The general formula for deposit creation is:

The increase in the money supply, M1, resulting from the increase in the $1,000 deposit equals $10,000 - $1,000 = $9,000.

increase in checking account balances 1

reserve ratio initial deposit x

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 17

The Money MultiplierThe Money MultiplierThe Money MultiplierThe Money Multiplier

This term in the deposit creation formula is called the money multiplier.

The money multiplier shows the total increase in checking account deposits for any initial cash deposit.

The initial cash deposit triggers additional rounds of deposits and lending by banks, which leads to a multiple expansion of deposits.

1

reserve ratio

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 18

The Money MultiplierThe Money MultiplierThe Money MultiplierThe Money Multiplier

The money multiplier for the United States is between 2 and 3. It is much smaller than the value in our example because, in reality, people hold part of their loans as cash. This cash is not available for the banking system to lend.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 19

The Money MultiplierThe Money MultiplierThe Money MultiplierThe Money Multiplier The money multiplier also works in reverse.

Assuming a reserve ratio of 10%, a withdrawal of $1,000 reduces reserves by $100, and results in $900 less the bank will have to lend out.

Finally, it is important to note that when one individual writes a check to another, and the other deposits the check in the bank, the money supply will not change. Instead, the expansion in one bank’s reserves will offset the contraction in the reserves of the other.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 20

Open Market OperationsOpen Market OperationsOpen Market OperationsOpen Market Operations

The Federal Reserve, our central bank, has the power to change the total amount of reserves in the banking system.

The most important tool to change the total amount of reserves in the banking system, and therefore the money supply, is called Open Market Operations — the purchase and sale of government securities to the private sector.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 21

Open Market OperationsOpen Market OperationsOpen Market OperationsOpen Market Operations

Suppose the Fed purchases $1 million worth of government bonds from the private sector.

The Fed writes a check for $1 million and presents it to the party who sold the bonds. The Fed now owns those bonds, and the party who sold the bonds has a check for $1 million.

Checks written against the Fed count as reserves for banks. If the reserve ratio is 10%, the bank must keep $100,000 in new reserves, but can make loans for $900,000. And so, the process of money creation begins.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 22

Open Market OperationsOpen Market OperationsOpen Market OperationsOpen Market Operations

Open market purchases increase the money supply; and open market sales decrease it.

The Fed has unlimited ability to create money. It can write checks against itself to purchase the government bonds without having any explicit “funds.” Banks accept it because these checks count as reserves for the bank.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 23

Other Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary Policy

Other tools the Fed has available to change the money supply, although less important and not used as often as Open Market Operations are:

Changes in the reserve requirement: banks are asked to hold a smaller or larger fraction of their deposits as reserves.

Changes in the discount rate, or the rate at which banks borrow from the Fed.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 24

Other Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary Policy

The Fed does not increase the reserve requirement often because it can be disruptive to the banking system. Banks would be forced to call in or cancel many of its loans.

Before banks borrow from the Fed, they try to borrow from each other through the federal funds market, a market in which banks lend or borrow reserves from each other, overnight.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 25

Other Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary PolicyOther Tools of Monetary Policy

In practice, the Fed keeps the discount rate close to the federal funds rate to avoid large swings in borrowed reserves by banks.

The Fed conducts monetary policy by setting targets for the federal funds rate. Once it has set those targets, it uses open market operations to keep the actual federal funds rate on target.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 26

The Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal Reserve

The Federal Reserve System was created in 1913 following a series of financial panics in the United States.

Congress created the Federal Reserve to be a central bank, serving as a banker’s bank.

One of the Fed’s primary jobs was to serve as a lender of last resort—lending funds to banks that suffered from panic runs, thereby reducing some of the adverse consequences of the panics.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 27

The Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal Reserve

The United States was divided into 12 Federal Reserve districts, each of which has a Federal Reserve Bank.

The reason for creating 12 separate, semiautonomous regional banks was to avoid monopoly and concentration of power in a single area or financial center.

District banks provide advice and take part in monetary policy decisions, and provide a liaison between the Fed and the banks in their districts.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 28

Federal Reserve BanksFederal Reserve BanksFederal Reserve BanksFederal Reserve Banks

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 29

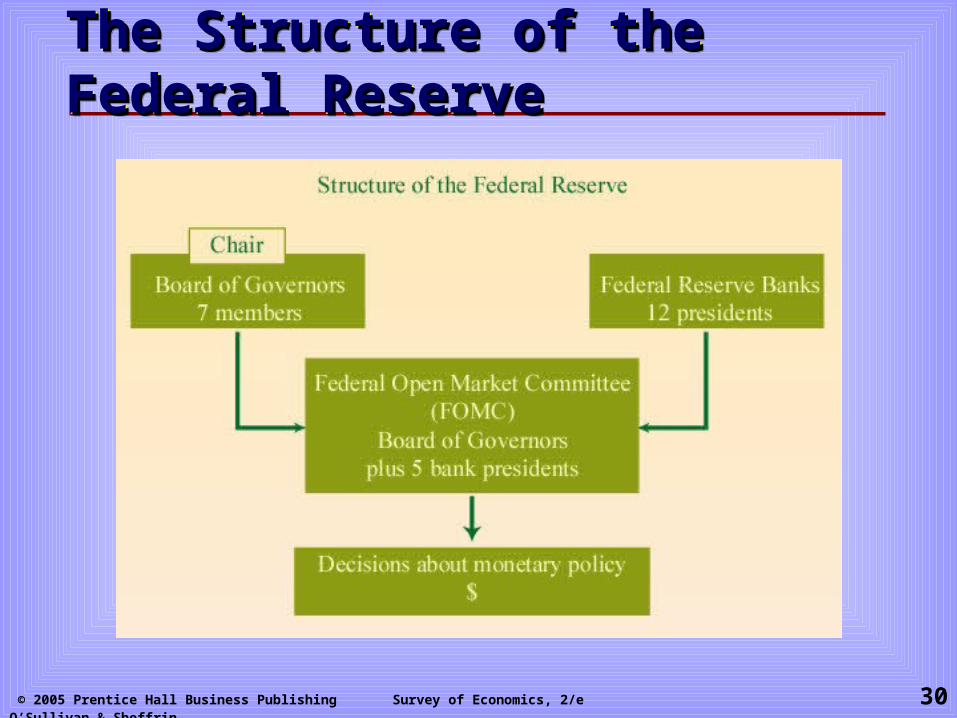

The Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal Reserve

The structure of the Federal Reserve today consists of three distinct subgroups:

Federal Reserve Banks The Board of Governors, and The Federal Open Market Committee

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 30

The Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal ReserveThe Structure of the Federal Reserve

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 31

The Board of GovernorsThe Board of GovernorsThe Board of GovernorsThe Board of Governors

The Board of Governors of the Federal Reserve is the true seat of power over the monetary system.

Headquartered in Washington, DC, the seven members of the board are appointed for staggered 14-year terms by the President and must be confirmed by the Senate.

The chairperson serves a four-year term and is the principal spokesperson for monetary policy in the U.S. What he speaks is carefully observed, or anticipated, by financial markets.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 32

The Federal Open Market Committee The Federal Open Market Committee (FOMC)(FOMC)The Federal Open Market Committee The Federal Open Market Committee (FOMC)(FOMC)

The Federal Open Market Committee (FOMC) is a 12-person board consisting of the seven members of the Board of Governors, the president of the New York Federal Reserve Bank, plus the presidents of four other regional Federal Reserve Banks. These four presidents serve on a rotating basis.

The seven nonvoting bank presidents attend the meetings and provide their views. The chairperson of the Board of Governors also serves as the chairperson of the FOMC.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 33

Central Bank IndependenceCentral Bank IndependenceCentral Bank IndependenceCentral Bank Independence

The matter of central bank independence from political authorities is a lively debate among economists.

Monetary discipline is important for the performance of the economy. Countries with greater central independence tend to have lower inflation rates.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 34

Central Bank IndependenceCentral Bank IndependenceCentral Bank IndependenceCentral Bank Independence

In the United States, the Board of Governors of the Federal Reserve operates with considerable independence.

Presidents and members of Congress can bring political pressures on the Board of Governors, but the 14-year terms provide some insulation from external pressures.

© 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O’Sullivan & Sheffrin 35

Central Bank IndependenceCentral Bank IndependenceCentral Bank IndependenceCentral Bank Independence

There are both supporters and opponents of the current system which allows bank presidents to play an important role in the determination of monetary policy. These presidents are neither appointed by elected officials nor confirmed by the Senate.

The Fed is a subject of significant public interest because the Fed exercises ultimate control of the money supply, which gives it substantial power over the economy.