Embed Size (px)

Citation preview

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Presented By

For Plan Sponsor Use Only

Investment Review For Period Ending

Tim Duncan

December 31, 2009

Prepared Exclusively For

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

2

Section I

Section II

Section III

Section IV

Section V

Section VI

Section VII

Section VIII

Section IX

Executive Summary Investment Summary Plan Summary Performance Matrix Fees & Expenses Proposed Investment Options Market Commentary Definitions Disclosure

Table of Contents

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

3

Contact Information

Servicing Contact Email Address Phone Number

Portfolio Manager: Tim Duncan 816-360-3774 [email protected] Relationship Manager: David Sims 816-360-3762 [email protected]

Section I: Executive Summary4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Executive Summary As of December 31, 2009

5

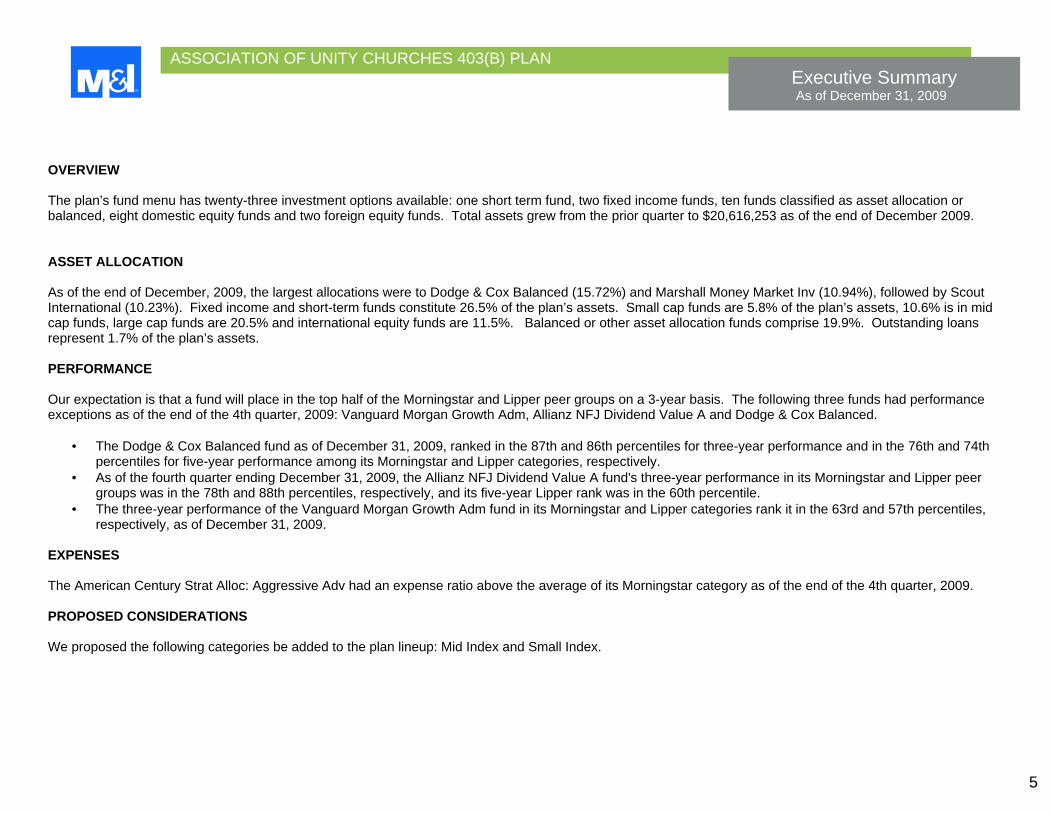

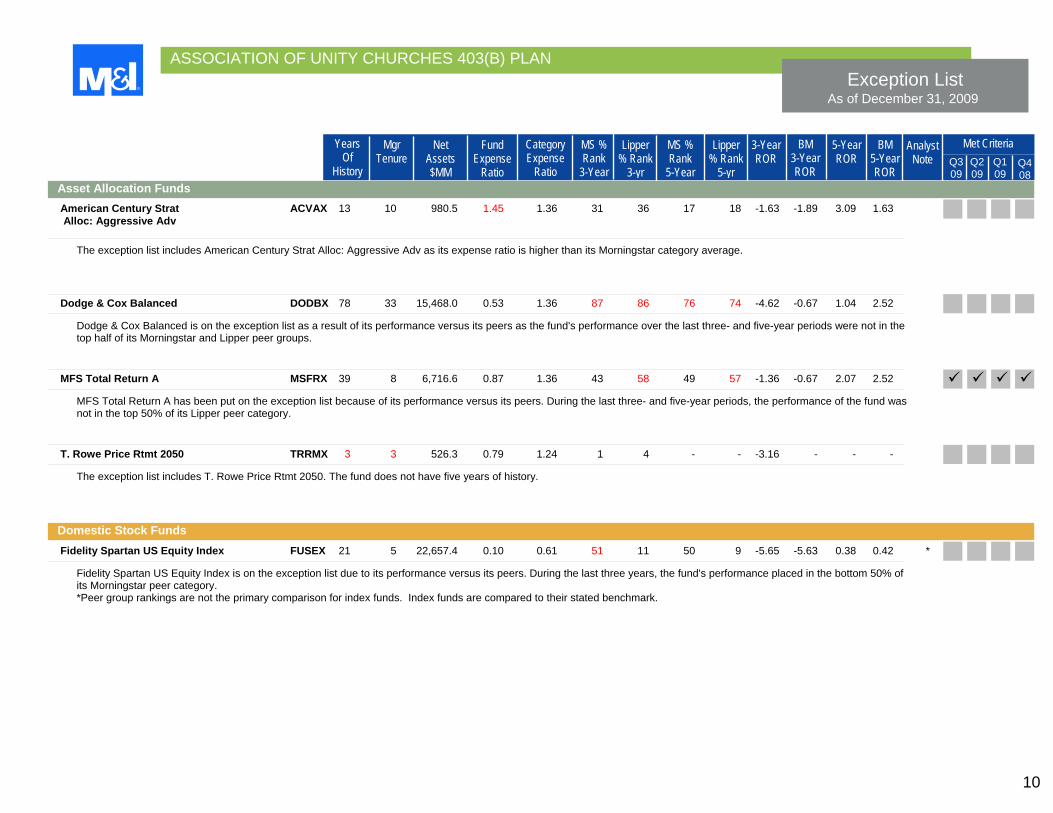

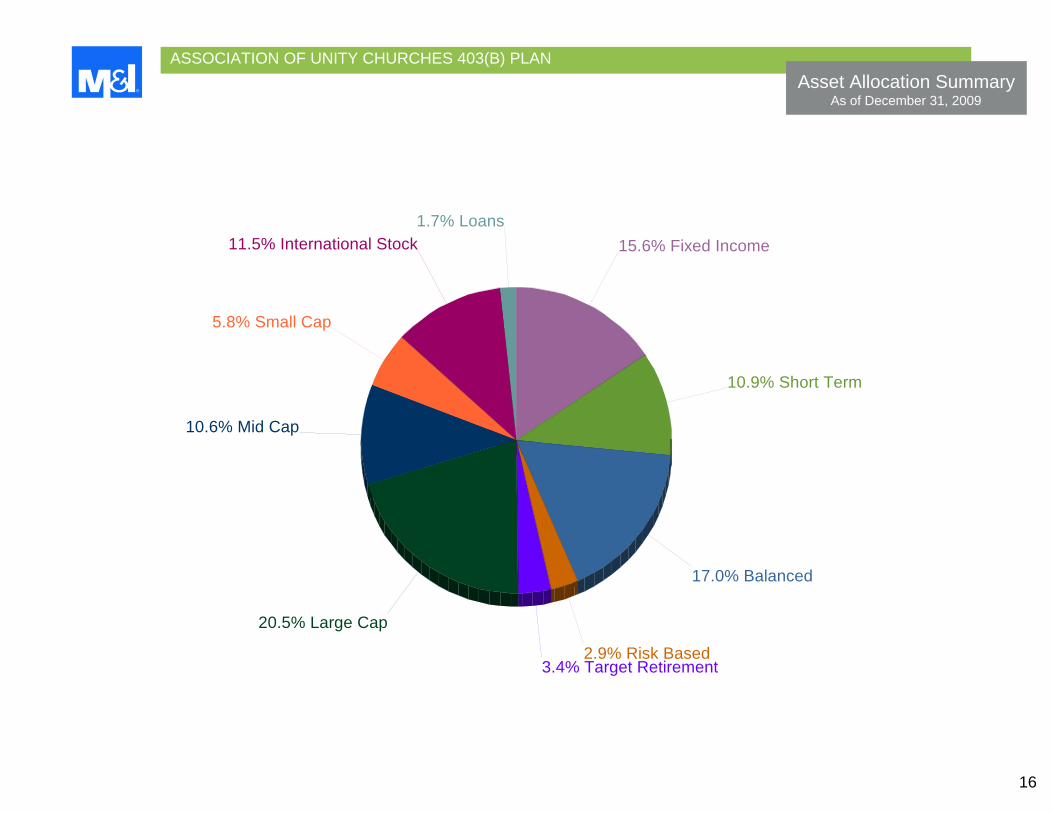

OVERVIEW The plan’s fund menu has twenty-three investment options available: one short term fund, two fixed income funds, ten funds classified as asset allocation or balanced, eight domestic equity funds and two foreign equity funds. Total assets grew from the prior quarter to $20,616,253 as of the end of December 2009. ASSET ALLOCATION As of the end of December, 2009, the largest allocations were to Dodge & Cox Balanced (15.72%) and Marshall Money Market Inv (10.94%), followed by Scout International (10.23%). Fixed income and short-term funds constitute 26.5% of the plan’s assets. Small cap funds are 5.8% of the plan’s assets, 10.6% is in mid cap funds, large cap funds are 20.5% and international equity funds are 11.5%. Balanced or other asset allocation funds comprise 19.9%. Outstanding loans represent 1.7% of the plan’s assets. PERFORMANCE Our expectation is that a fund will place in the top half of the Morningstar and Lipper peer groups on a 3-year basis. The following three funds had performance exceptions as of the end of the 4th quarter, 2009: Vanguard Morgan Growth Adm, Allianz NFJ Dividend Value A and Dodge & Cox Balanced.

• The Dodge & Cox Balanced fund as of December 31, 2009, ranked in the 87th and 86th percentiles for three-year performance and in the 76th and 74th percentiles for five-year performance among its Morningstar and Lipper categories, respectively.

• As of the fourth quarter ending December 31, 2009, the Allianz NFJ Dividend Value A fund's three-year performance in its Morningstar and Lipper peer groups was in the 78th and 88th percentiles, respectively, and its five-year Lipper rank was in the 60th percentile.

• The three-year performance of the Vanguard Morgan Growth Adm fund in its Morningstar and Lipper categories rank it in the 63rd and 57th percentiles, respectively, as of December 31, 2009.

EXPENSES The American Century Strat Alloc: Aggressive Adv had an expense ratio above the average of its Morningstar category as of the end of the 4th quarter, 2009. PROPOSED CONSIDERATIONS We proposed the following categories be added to the plan lineup: Mid Index and Small Index.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Executive Summary As of December 31, 2009

6

SUMMARY As of the end of the 4th quarter, 2009, the investment options offered in the plan are generally performing as expected, notwithstanding the short-term underperformance to be discussed at the next committee meeting. We propose that the committee consider adding the following categories to the plan lineup: Mid Index and Small Index.

7

Section II: Investment Summary4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

8

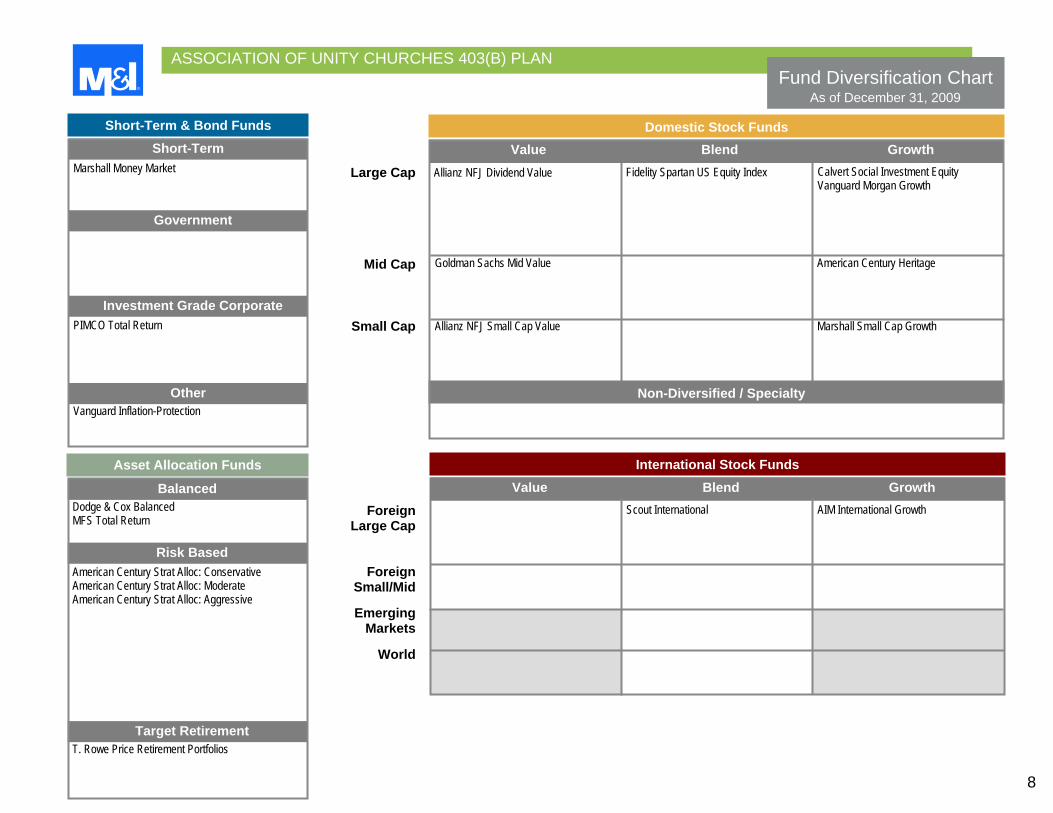

Fund Diversification Chart

Asset Allocation Funds

Short-Term & Bond Funds Short-Term

Government

Investment Grade Corporate

Balanced

Risk Based

Target Retirement

Domestic Stock Funds

International Stock Funds

Non-Diversified / Specialty

Large Cap

Mid Cap

Small Cap

ForeignLarge Cap

ForeignSmall/Mid

EmergingMarkets

World

Value Blend Growth

As of December 31, 2009

Marshall Money Market

PIMCO Total Return

Dodge & Cox Balanced MFS Total Return

American Century Strat Alloc: Conservative American Century Strat Alloc: Moderate American Century Strat Alloc: Aggressive

T. Rowe Price Retirement Portfolios

Allianz NFJ Dividend Value

Goldman Sachs Mid Value

Allianz NFJ Small Cap Value

Fidelity Spartan US Equity Index

Calvert Social Investment EquityVanguard Morgan Growth

American Century Heritage

Marshall Small Cap Growth

Scout International

AIM International Growth

Other Vanguard Inflation-Protection

Value Blend Growth

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Investment Policy Status Report As of December 31, 2009

9

Standard

Top Half Above Benchmark

Years of

History

Fund Name MgrTenure

Net Assets$MM

Category Expense

Ratio

MS % Rank

3-Year

Lipper% Rank

3-yr

MS %Rank

5-Year

Lipper% Rank

5-yr

BM3-Year ROR

5-YearROR

BM5-Year ROR

3-YearROR

100.05 Top Half Category Avg 5

Fund Expense

Ratio

Ticker Symbol

Marshall Money Market Inv MARXX 17 16 4,952.4 0.45 - - 7 - 6 2.86 2.22 3.19 2.88 PIMCO Total Return Admin PTRAX 15 23 199,462.3 0.71 0.97 2 2 2 2 8.91 6.04 6.58 4.97 Vanguard Inflation Protection Secs VIPSX 9 10 27,578.6 0.25 0.85 39 42 28 33 6.30 6.69 4.36 4.64 American Century Strat Alloc: Conservative Adv ACCAX 13 10 608.0 1.25 1.31 45 15 47 30 1.00 1.67 3.02 3.43 American Century Strat Alloc: Moderate Adv ACOAX 13 10 1,619.3 1.32 1.36 25 37 20 24 -0.40 -0.67 3.30 2.52 American Century Strat Alloc: Aggressive Adv ACVAX 13 10 980.5 1.45 1.36 31 36 17 18 -1.63 -1.89 3.09 1.63 Dodge & Cox Balanced DODBX 78 33 15,468.0 0.53 1.36 87 86 76 74 -4.62 -0.67 1.04 2.52 MFS Total Return A MSFRX 39 8 6,716.6 0.87 1.36 43 58 49 57 -1.36 -0.67 2.07 2.52 T. Rowe Price Rtmt 2010 TRRAX 7 7 4,819.2 0.64 1.10 32 31 6 5 0.00 - 3.70 - T. Rowe Price Rtmt 2020 TRRBX 7 7 9,091.8 0.73 1.22 24 24 2 4 -1.59 - 3.21 - T. Rowe Price Rtmt 2030 TRRCX 7 7 6,939.5 0.78 1.23 13 14 1 3 -2.84 - 2.87 - T. Rowe Price Rtmt 2040 TRRDX 7 7 4,258.4 0.79 1.25 7 8 1 3 -3.16 - 2.69 - T. Rowe Price Rtmt 2050 TRRMX 3 3 526.3 0.79 1.24 1 4 - - -3.16 - - - Fidelity Spartan US Equity Index FUSEX 21 5 22,657.4 0.10 0.61 51 11 50 9 -5.65 -5.63 0.38 0.42 Allianz NFJ Dividend Value A PNEAX 8 10 6,836.3 1.06 1.28 78 88 33 60 -9.12 -8.96 0.76 -0.25 Calvert Social Investment Equity A CSIEX 22 11 1,188.7 1.21 1.36 34 39 38 31 -1.85 -1.89 1.65 1.63 Vanguard Morgan Growth Adm VMRAX 8 6 7,687.2 0.29 1.36 63 57 38 49 -3.79 -1.89 1.62 1.63 Goldman Sachs Mid Value A GCMAX 12 9 5,704.3 1.19 1.39 33 37 28 39 -4.76 -6.62 2.35 1.98 American Century Heritage Adv ATHAX 12 3 2,133.1 1.26 1.48 7 7 1 1 2.15 -3.18 8.70 2.40 Allianz NFJ Small Cap Value A PCVAX 12 18 6,099.3 1.24 1.53 7 14 9 13 -1.10 -8.22 4.82 -0.01 Marshall Small Cap Growth Inv MRSCX 13 6 265.9 1.44 1.60 7 7 8 6 0.09 -4.00 4.58 0.87 Scout International UMBWX 16 16 4,951.6 1.02 1.50 2 4 8 6 -0.37 -8.66 7.52 0.85 AIM International Growth A AIIEX 17 15 3,279.1 1.45 1.55 19 19 6 14 -2.89 -4.78 6.60 3.65

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Exception List As of December 31, 2009

10

MgrTenure

Net Assets$MM

Category Expense

Ratio

MS % Rank

3-Year

Lipper % Rank

3-yr

MS %Rank

5-Year

Lipper% Rank

5-yr

BM3-Year ROR

5-YearROR

BM5-YearROR

3-YearROR

Fund Expense

Ratio

YearsOf

History

Met Criteria AnalystNote Q3

09Q2 09

Q1 09

Q4 08

Asset Allocation Funds American Century Strat ACVAX 13 10 980.5 1.45 1.36 31 36 17 18 -1.63 -1.89 3.09 1.63 Alloc: Aggressive Adv

The exception list includes American Century Strat Alloc: Aggressive Adv as its expense ratio is higher than its Morningstar category average.

Dodge & Cox Balanced DODBX 78 33 15,468.0 0.53 1.36 87 86 76 74 -4.62 -0.67 1.04 2.52 Dodge & Cox Balanced is on the exception list as a result of its performance versus its peers as the fund's performance over the last three- and five-year periods were not in the top half of its Morningstar and Lipper peer groups.

MFS Total Return A MSFRX 39 8 6,716.6 0.87 1.36 43 58 49 57 -1.36 -0.67 2.07 2.52 MFS Total Return A has been put on the exception list because of its performance versus its peers. During the last three- and five-year periods, the performance of the fund was not in the top 50% of its Lipper peer category.

T. Rowe Price Rtmt 2050 TRRMX 3 3 526.3 0.79 1.24 1 4 - - -3.16 - - - The exception list includes T. Rowe Price Rtmt 2050. The fund does not have five years of history.

Domestic Stock Funds Fidelity Spartan US Equity Index FUSEX 21 5 22,657.4 0.10 0.61 51 11 50 9 -5.65 -5.63 0.38 0.42 *

Fidelity Spartan US Equity Index is on the exception list due to its performance versus its peers. During the last three years, the fund's performance placed in the bottom 50% of its Morningstar peer category. *Peer group rankings are not the primary comparison for index funds. Index funds are compared to their stated benchmark.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Exception List As of December 31, 2009

11

MgrTenure

Net Assets$MM

Category Expense

Ratio

MS % Rank

3-Year

Lipper % Rank

3-yr

MS %Rank

5-Year

Lipper% Rank

5-yr

BM3-Year ROR

5-YearROR

BM5-YearROR

3-YearROR

Fund Expense

Ratio

YearsOf

History

Met Criteria AnalystNote Q3

09Q2 09

Q1 09

Q4 08

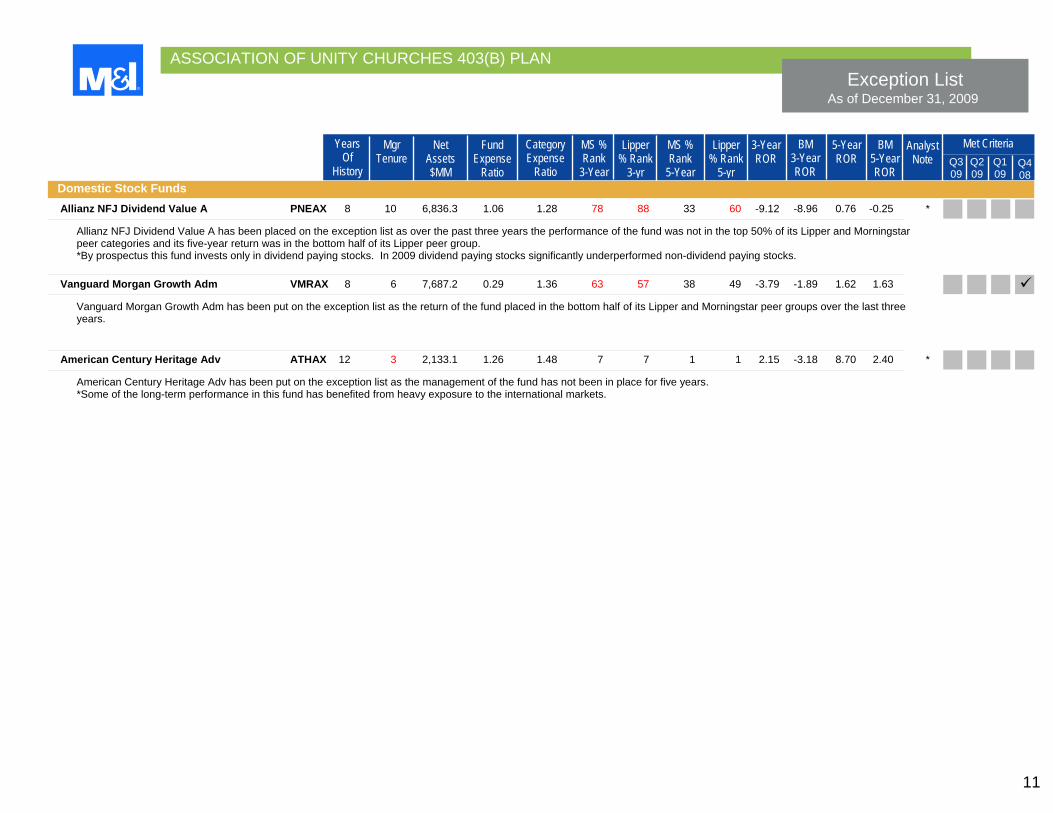

Domestic Stock Funds Allianz NFJ Dividend Value A PNEAX 8 10 6,836.3 1.06 1.28 78 88 33 60 -9.12 -8.96 0.76 -0.25 *

Allianz NFJ Dividend Value A has been placed on the exception list as over the past three years the performance of the fund was not in the top 50% of its Lipper and Morningstar peer categories and its five-year return was in the bottom half of its Lipper peer group. *By prospectus this fund invests only in dividend paying stocks. In 2009 dividend paying stocks significantly underperformed non-dividend paying stocks.

Vanguard Morgan Growth Adm VMRAX 8 6 7,687.2 0.29 1.36 63 57 38 49 -3.79 -1.89 1.62 1.63 Vanguard Morgan Growth Adm has been put on the exception list as the return of the fund placed in the bottom half of its Lipper and Morningstar peer groups over the last three years.

American Century Heritage Adv ATHAX 12 3 2,133.1 1.26 1.48 7 7 1 1 2.15 -3.18 8.70 2.40 * American Century Heritage Adv has been put on the exception list as the management of the fund has not been in place for five years. *Some of the long-term performance in this fund has benefited from heavy exposure to the international markets.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

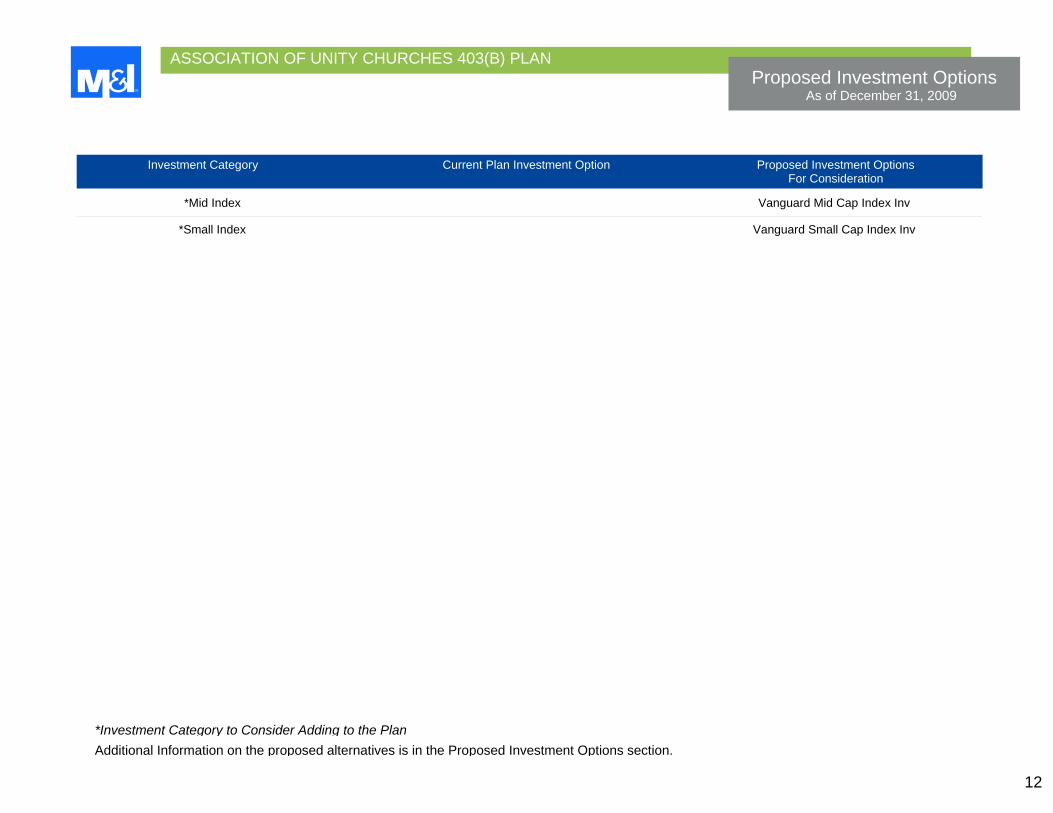

Proposed Investment Options As of December 31, 2009

12

Investment Category Current Plan Investment Option Proposed Investment Options For Consideration

*Mid Index Vanguard Mid Cap Index Inv *Small Index Vanguard Small Cap Index Inv

*Investment Category to Consider Adding to the PlanAdditional Information on the proposed alternatives is in the Proposed Investment Options section.

13

Section III: Plan Summary 4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

14

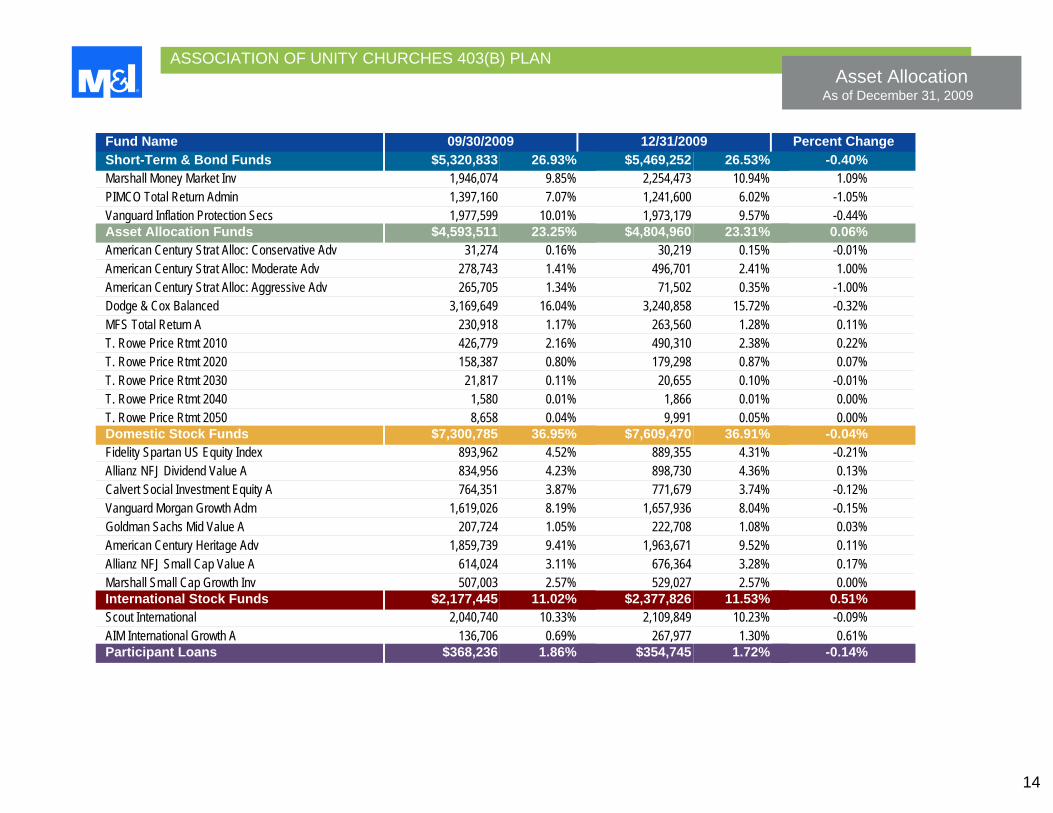

Asset Allocation As of December 31, 2009

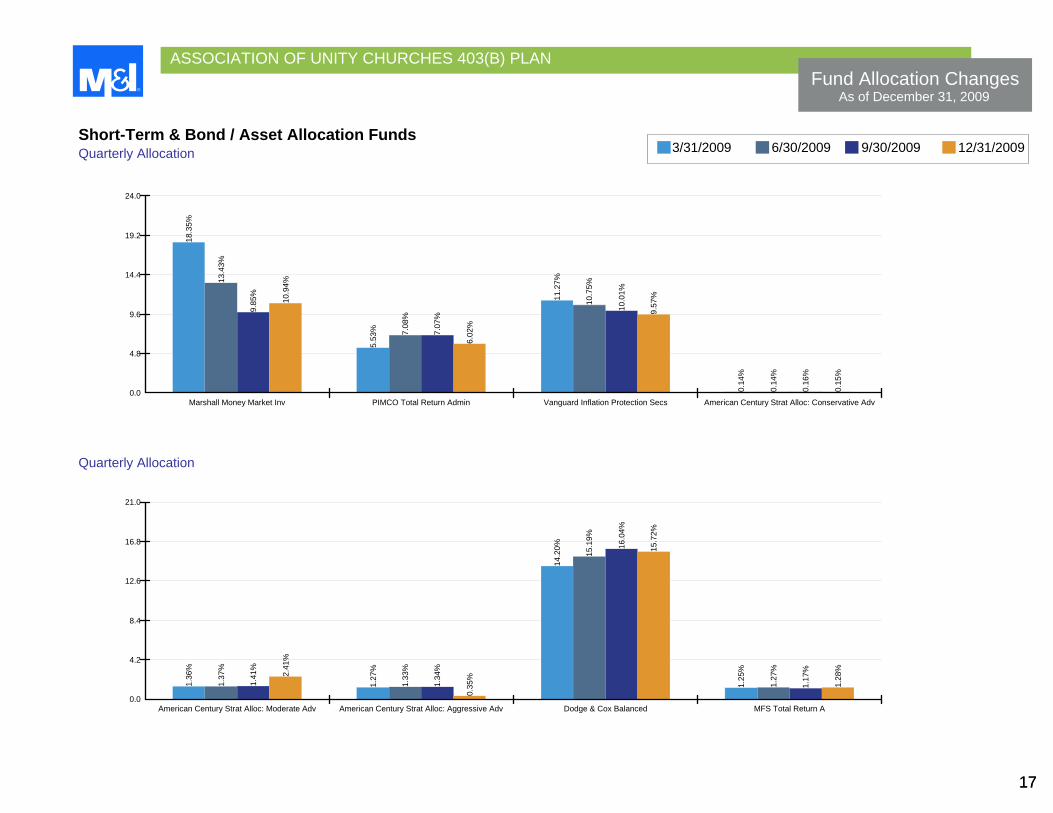

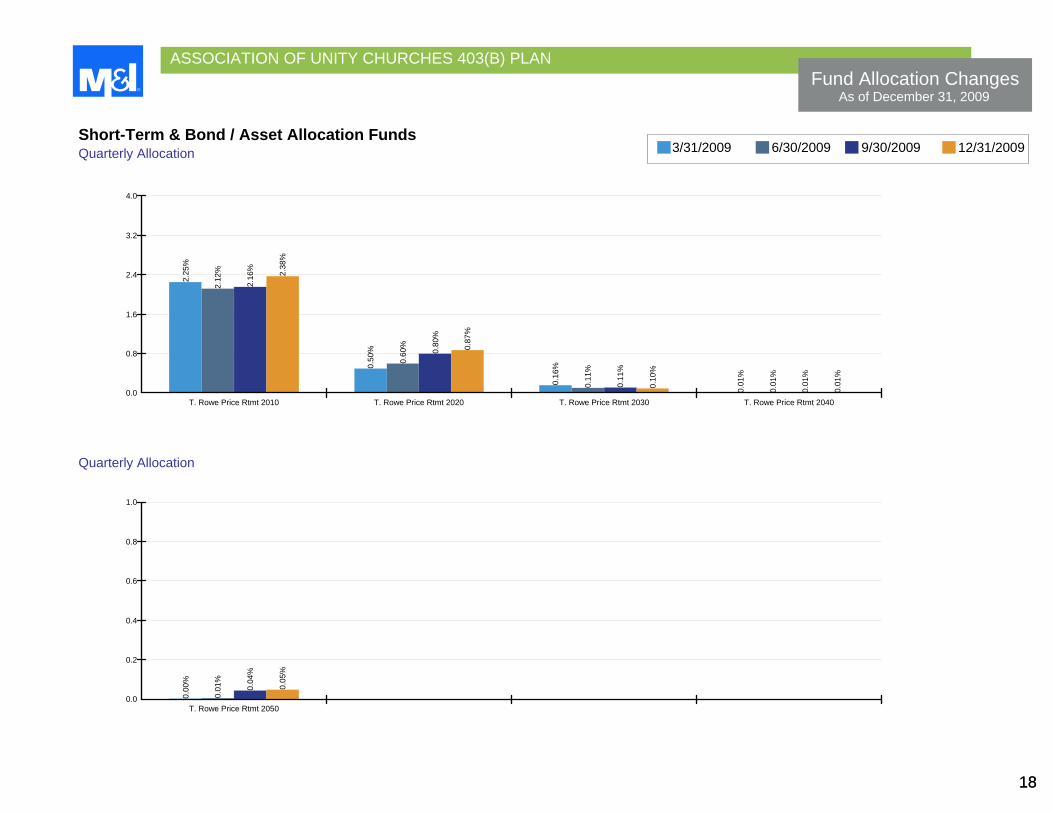

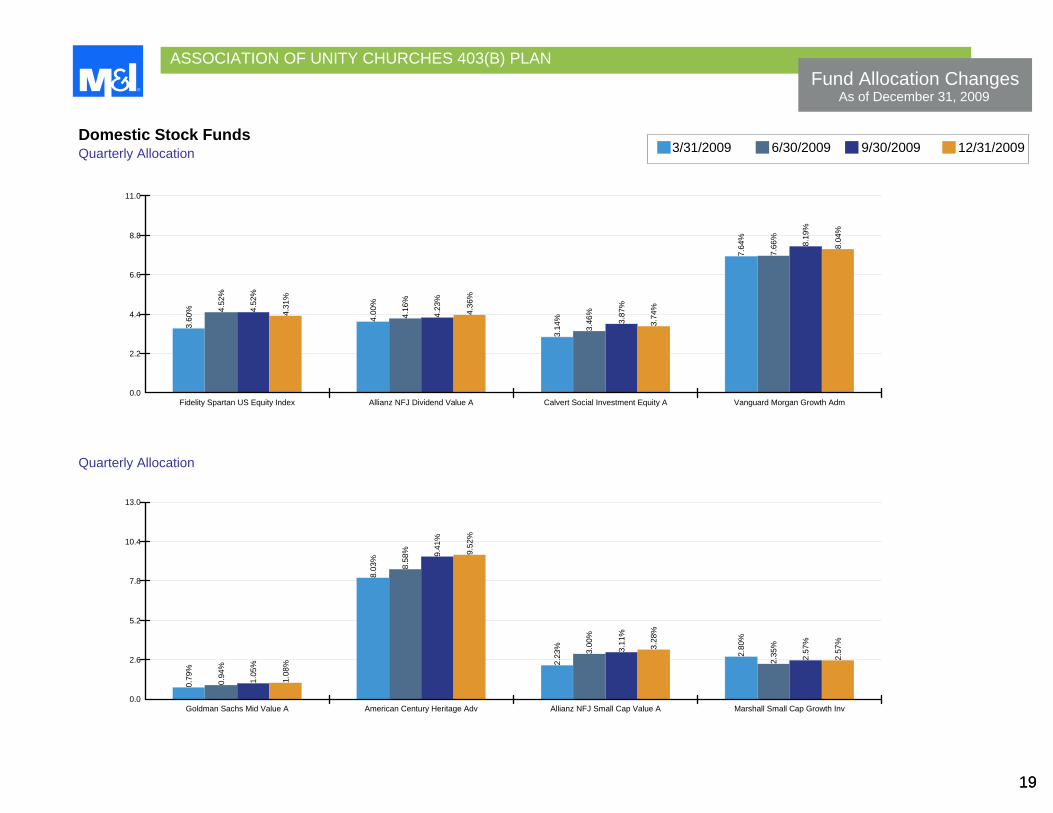

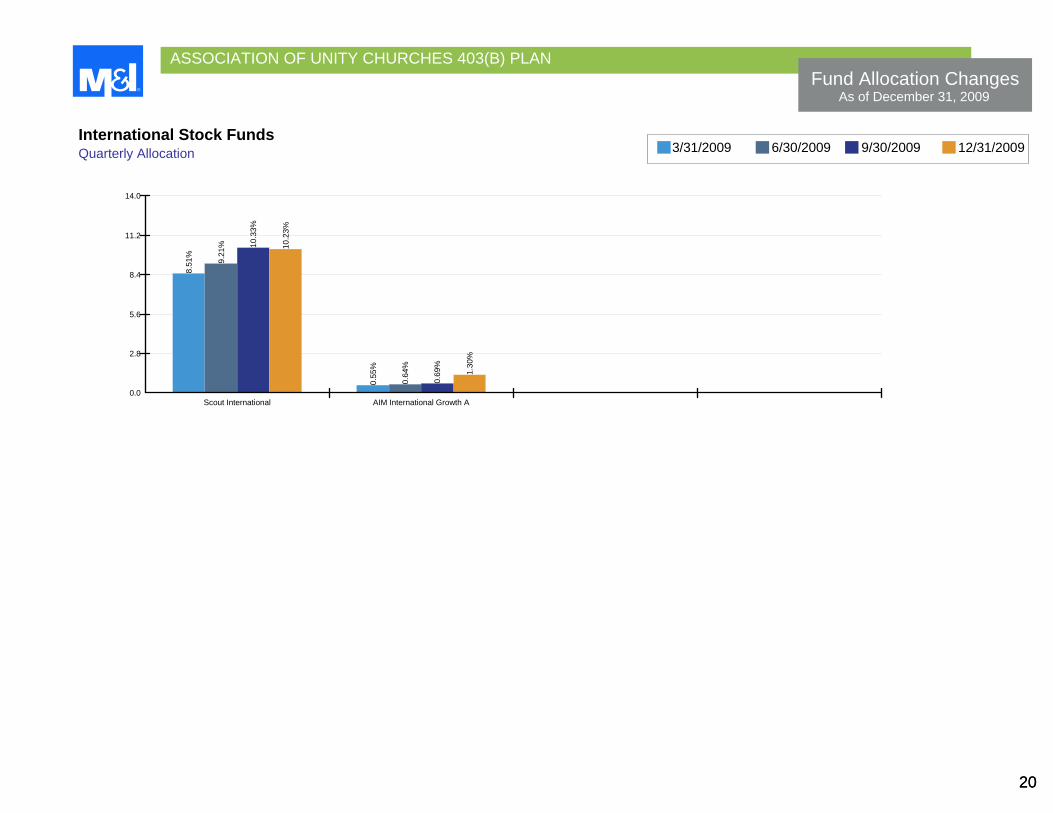

Fund Name 09/30/2009 12/31/2009 Percent Change Short-Term & Bond Funds $5,320,833 26.93% $5,469,252 26.53% -0.40%Marshall Money Market Inv 1,946,074 9.85% 2,254,473 10.94% 1.09%PIMCO Total Return Admin 1,397,160 7.07% 1,241,600 6.02% -1.05%Vanguard Inflation Protection Secs 1,977,599 10.01% 1,973,179 9.57% -0.44%Asset Allocation Funds $4,593,511 23.25% $4,804,960 23.31% 0.06%American Century Strat Alloc: Conservative Adv 31,274 0.16% 30,219 0.15% -0.01%American Century Strat Alloc: Moderate Adv 278,743 1.41% 496,701 2.41% 1.00%American Century Strat Alloc: Aggressive Adv 265,705 1.34% 71,502 0.35% -1.00%Dodge & Cox Balanced 3,169,649 16.04% 3,240,858 15.72% -0.32%MFS Total Return A 230,918 1.17% 263,560 1.28% 0.11%T. Rowe Price Rtmt 2010 426,779 2.16% 490,310 2.38% 0.22%T. Rowe Price Rtmt 2020 158,387 0.80% 179,298 0.87% 0.07%T. Rowe Price Rtmt 2030 21,817 0.11% 20,655 0.10% -0.01%T. Rowe Price Rtmt 2040 1,580 0.01% 1,866 0.01% 0.00%T. Rowe Price Rtmt 2050 8,658 0.04% 9,991 0.05% 0.00%Domestic Stock Funds $7,300,785 36.95% $7,609,470 36.91% -0.04%Fidelity Spartan US Equity Index 893,962 4.52% 889,355 4.31% -0.21%Allianz NFJ Dividend Value A 834,956 4.23% 898,730 4.36% 0.13%Calvert Social Investment Equity A 764,351 3.87% 771,679 3.74% -0.12%Vanguard Morgan Growth Adm 1,619,026 8.19% 1,657,936 8.04% -0.15%Goldman Sachs Mid Value A 207,724 1.05% 222,708 1.08% 0.03%American Century Heritage Adv 1,859,739 9.41% 1,963,671 9.52% 0.11%Allianz NFJ Small Cap Value A 614,024 3.11% 676,364 3.28% 0.17%Marshall Small Cap Growth Inv 507,003 2.57% 529,027 2.57% 0.00%International Stock Funds $2,177,445 11.02% $2,377,826 11.53% 0.51%Scout International 2,040,740 10.33% 2,109,849 10.23% -0.09%AIM International Growth A 136,706 0.69% 267,977 1.30% 0.61%Participant Loans $368,236 1.86% $354,745 1.72% -0.14%

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

15

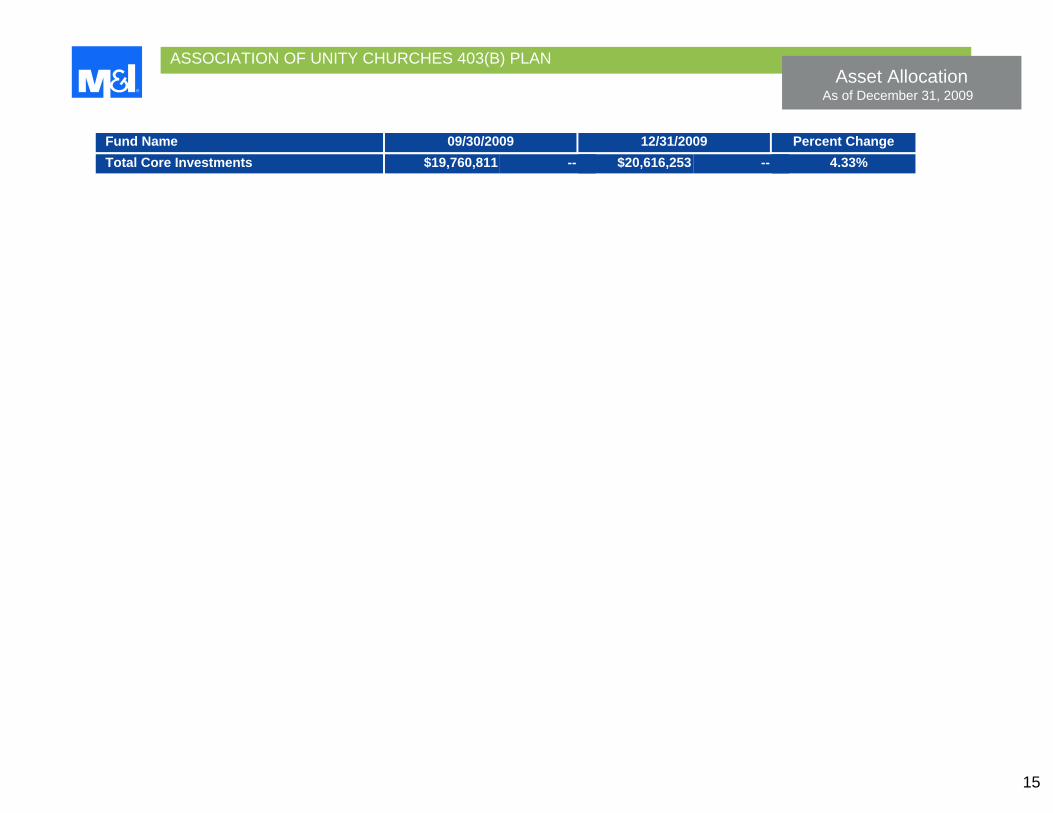

Asset Allocation As of December 31, 2009

Fund Name 09/30/2009 12/31/2009 Percent Change Total Core Investments $19,760,811 -- $20,616,253 -- 4.33%

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Asset Allocation Summary As of December 31, 2009

16

1.7% Loans11.5% International Stock

5.8% Small Cap

10.6% Mid Cap

20.5% Large Cap

3.4% Target Retirement2.9% Risk Based

17.0% Balanced

10.9% Short Term

15.6% Fixed Income

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

17

Fund Allocation Changes As of December 31, 2009

17

18.3

5%

13.4

3%

9.85

%

10.9

4%

5.53

% 7.08

%

7.07

%

6.02

%

11.2

7%

10.7

5%

10.0

1%

9.57

%

0.14

%

0.14

%

0.16

%

0.15

%

0.0

4.8

9.6

14.4

19.2

24.0

Marshall Money Market Inv PIMCO Total Return Admin Vanguard Inflation Protection Secs American Century Strat Alloc: Conservative Adv

Short-Term & Bond / Asset Allocation Funds

1.36

%

1.37

%

1.41

%

2.41

%

1.27

%

1.33

%

1.34

%

0.35

%

14.2

0%

15.1

9%

16.0

4%

15.7

2%

1.25

%

1.27

%

1.17

%

1.28

%

0.0

4.2

8.4

12.6

16.8

21.0

American Century Strat Alloc: Moderate Adv American Century Strat Alloc: Aggressive Adv Dodge & Cox Balanced MFS Total Return A

Quarterly Allocation

Quarterly Allocation

3/31/2009 6/30/2009 9/30/2009 12/31/2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

18

Fund Allocation Changes As of December 31, 2009

18

2.25

%

2.12

%

2.16

% 2.38

%

0.50

%

0.60

%

0.80

%

0.87

%

0.16

%

0.11

%

0.11

%

0.10

%

0.01

%

0.01

%

0.01

%

0.01

%

0.0

0.8

1.6

2.4

3.2

4.0

T. Rowe Price Rtmt 2010 T. Rowe Price Rtmt 2020 T. Rowe Price Rtmt 2030 T. Rowe Price Rtmt 2040

Short-Term & Bond / Asset Allocation Funds

0.00

%

0.01

%

0.04

%

0.05

%

0.0

0.2

0.4

0.6

0.8

1.0

T. Rowe Price Rtmt 2050

Quarterly Allocation

Quarterly Allocation

3/31/2009 6/30/2009 9/30/2009 12/31/2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

19

Fund Allocation Changes As of December 31, 2009

19

3.60

% 4.52

%

4.52

%

4.31

%

4.00

%

4.16

%

4.23

%

4.36

%

3.14

%

3.46

%

3.87

%

3.74

%

7.64

%

7.66

%

8.19

%

8.04

%

0.0

2.2

4.4

6.6

8.8

11.0

Fidelity Spartan US Equity Index Allianz NFJ Dividend Value A Calvert Social Investment Equity A Vanguard Morgan Growth Adm

Domestic Stock Funds

0.79

%

0.94

%

1.05

%

1.08

%

8.03

%

8.58

% 9.41

%

9.52

%

2.23

% 3.00

%

3.11

%

3.28

%

2.80

%

2.35

%

2.57

%

2.57

%

0.0

2.6

5.2

7.8

10.4

13.0

Goldman Sachs Mid Value A American Century Heritage Adv Allianz NFJ Small Cap Value A Marshall Small Cap Growth Inv

Quarterly Allocation

Quarterly Allocation

3/31/2009 6/30/2009 9/30/2009 12/31/2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

20

Fund Allocation Changes As of December 31, 2009

20

8.51

%

9.21

% 10.3

3%

10.2

3%

0.55

%

0.64

%

0.69

%

1.30

%

0.0

2.8

5.6

8.4

11.2

14.0

Scout International AIM International Growth A

International Stock Funds

Quarterly Allocation

3/31/2009 6/30/2009 9/30/2009 12/31/2009

21

Section IV: Performance Matrix4th Quarter, 2009

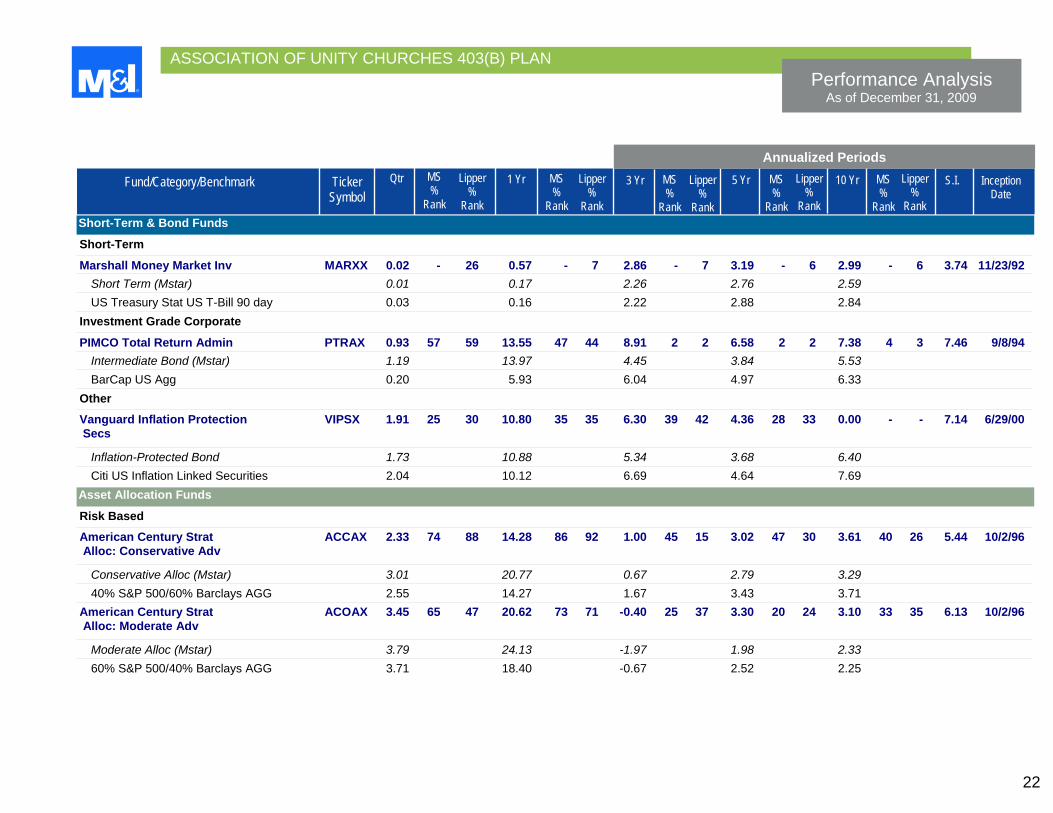

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

22

Qtr Fund/Category/Benchmark MS %

Rank

Lipper%

Rank

MS%

Rank

Lipper%

Rank

1 Yr Ticker Symbol

MS%

Rank

Lipper%

Rank

3 Yr MS%

Rank

Lipper%

Rank

5 Yr MS%

Rank

Lipper%

Rank

10 Yr S.I.

Inception Date

Annualized Periods

Short-Term & Bond Funds

Short-Term

Marshall Money Market Inv MARXX 0.02 - 26 0.57 - 7 2.86 - 7 3.19 - 6 2.99 - 6 3.74 11/23/92 Short Term (Mstar) 0.01 0.17 2.26 2.76 2.59 US Treasury Stat US T-Bill 90 day 0.03 0.16 2.22 2.88 2.84

Investment Grade Corporate

PIMCO Total Return Admin PTRAX 0.93 57 59 13.55 47 44 8.91 2 2 6.58 2 2 7.38 4 3 7.46 9/8/94 Intermediate Bond (Mstar) 1.19 13.97 4.45 3.84 5.53 BarCap US Agg 0.20 5.93 6.04 4.97 6.33

Other

Vanguard Inflation Protection VIPSX 1.91 25 30 10.80 35 35 6.30 39 42 4.36 28 33 0.00 - - 7.14 6/29/00 Secs

Inflation-Protected Bond 1.73 10.88 5.34 3.68 6.40 Citi US Inflation Linked Securities 2.04 10.12 6.69 4.64 7.69

Asset Allocation Funds

Risk Based

American Century Strat ACCAX 2.33 74 88 14.28 86 92 1.00 45 15 3.02 47 30 3.61 40 26 5.44 10/2/96 Alloc: Conservative Adv

Conservative Alloc (Mstar) 3.01 20.77 0.67 2.79 3.29 40% S&P 500/60% Barclays AGG 2.55 14.27 1.67 3.43 3.71 American Century Strat ACOAX 3.45 65 47 20.62 73 71 -0.40 25 37 3.30 20 24 3.10 33 35 6.13 10/2/96 Alloc: Moderate Adv

Moderate Alloc (Mstar) 3.79 24.13 -1.97 1.98 2.33 60% S&P 500/40% Barclays AGG 3.71 18.40 -0.67 2.52 2.25

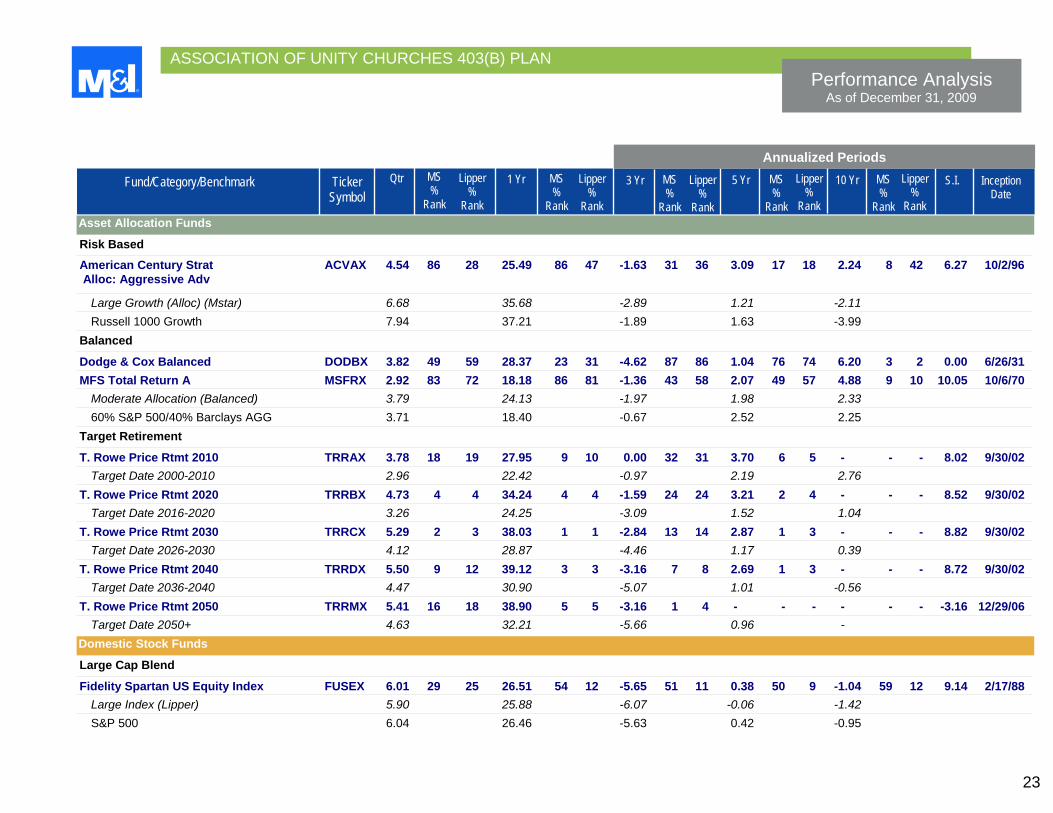

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

23

Qtr Fund/Category/Benchmark MS %

Rank

Lipper%

Rank

MS%

Rank

Lipper%

Rank

1 Yr Ticker Symbol

MS%

Rank

Lipper%

Rank

3 Yr MS%

Rank

Lipper%

Rank

5 Yr MS%

Rank

Lipper%

Rank

10 Yr S.I.

Inception Date

Annualized Periods

Asset Allocation Funds

Risk Based

American Century Strat ACVAX 4.54 86 28 25.49 86 47 -1.63 31 36 3.09 17 18 2.24 8 42 6.27 10/2/96 Alloc: Aggressive Adv

Large Growth (Alloc) (Mstar) 6.68 35.68 -2.89 1.21 -2.11 Russell 1000 Growth 7.94 37.21 -1.89 1.63 -3.99

Balanced

Dodge & Cox Balanced DODBX 3.82 49 59 28.37 23 31 -4.62 87 86 1.04 76 74 6.20 3 2 0.00 6/26/31 MFS Total Return A MSFRX 2.92 83 72 18.18 86 81 -1.36 43 58 2.07 49 57 4.88 9 10 10.05 10/6/70 Moderate Allocation (Balanced) 3.79 24.13 -1.97 1.98 2.33 60% S&P 500/40% Barclays AGG 3.71 18.40 -0.67 2.52 2.25

Target Retirement

T. Rowe Price Rtmt 2010 TRRAX 3.78 18 19 27.95 9 10 0.00 32 31 3.70 6 5 - - - 8.02 9/30/02 Target Date 2000-2010 2.96 22.42 -0.97 2.19 2.76 T. Rowe Price Rtmt 2020 TRRBX 4.73 4 4 34.24 4 4 -1.59 24 24 3.21 2 4 - - - 8.52 9/30/02 Target Date 2016-2020 3.26 24.25 -3.09 1.52 1.04 T. Rowe Price Rtmt 2030 TRRCX 5.29 2 3 38.03 1 1 -2.84 13 14 2.87 1 3 - - - 8.82 9/30/02 Target Date 2026-2030 4.12 28.87 -4.46 1.17 0.39 T. Rowe Price Rtmt 2040 TRRDX 5.50 9 12 39.12 3 3 -3.16 7 8 2.69 1 3 - - - 8.72 9/30/02 Target Date 2036-2040 4.47 30.90 -5.07 1.01 -0.56 T. Rowe Price Rtmt 2050 TRRMX 5.41 16 18 38.90 5 5 -3.16 1 4 - - - - - - -3.16 12/29/06 Target Date 2050+ 4.63 32.21 -5.66 0.96 -

Domestic Stock Funds

Large Cap Blend

Fidelity Spartan US Equity Index FUSEX 6.01 29 25 26.51 54 12 -5.65 51 11 0.38 50 9 -1.04 59 12 9.14 2/17/88 Large Index (Lipper) 5.90 25.88 -6.07 -0.06 -1.42 S&P 500 6.04 26.46 -5.63 0.42 -0.95

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

24

Qtr Fund/Category/Benchmark MS %

Rank

Lipper%

Rank

MS%

Rank

Lipper%

Rank

1 Yr Ticker Symbol

MS%

Rank

Lipper%

Rank

3 Yr MS%

Rank

Lipper%

Rank

5 Yr MS%

Rank

Lipper%

Rank

10 Yr S.I.

Inception Date

Annualized Periods

Domestic Stock Funds

Large Cap Value

Allianz NFJ Dividend Value A PNEAX 7.66 5 14 12.91 95 91 -9.12 78 88 0.76 33 60 - - - 5.45 10/31/01 Large Value (Mstar) 4.83 24.13 -7.32 0.02 2.54 Russell 1000 Value 4.22 19.69 -8.96 -0.25 2.47

Large Cap Growth

Calvert Social Investment CSIEX 4.50 87 94 33.41 56 57 -1.85 34 39 1.65 38 31 3.07 4 2 7.04 8/24/87 Equity A

Vanguard Morgan Growth Adm VMRAX 7.43 32 29 36.31 39 51 -3.79 63 57 1.62 38 49 -0.73 30 - 1.35 5/14/01 Large Growth (Mstar) 6.68 35.68 -2.89 1.21 -2.11 Russell 1000 Growth 7.94 37.21 -1.89 1.63 -3.99

Mid Cap Value

Goldman Sachs Mid Value A GCMAX 5.72 8 34 32.70 51 63 -4.76 33 37 2.35 28 39 9.65 10 10 7.37 8/15/97 Mid Value (Mstar) 5.21 35.41 -5.35 1.36 6.92 Russell Midcap Value 5.21 34.21 -6.62 1.98 7.58

Mid Cap Growth

American Century Heritage Adv ATHAX 4.91 66 70 36.51 63 69 2.15 7 7 8.70 1 1 3.65 20 17 6.44 7/11/97 Mid Growth (Mstar) 5.68 39.11 -3.09 1.76 0.34 Russell Midcap Growth 6.69 46.29 -3.18 2.40 -0.52

Small Cap Value

Allianz NFJ Small Cap Value A PCVAX 5.90 13 18 23.94 71 78 -1.10 7 14 4.82 9 13 11.57 11 5 9.72 1/20/97 Small Value (Mstar) 4.00 31.32 -6.13 0.67 8.64 Russell 2000 Value 3.63 20.58 -8.22 -0.01 8.27

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

25

Qtr Fund/Category/Benchmark MS %

Rank

Lipper%

Rank

MS%

Rank

Lipper%

Rank

1 Yr Ticker Symbol

MS%

Rank

Lipper%

Rank

3 Yr MS%

Rank

Lipper%

Rank

5 Yr MS%

Rank

Lipper%

Rank

10 Yr S.I.

Inception Date

Annualized Periods

Domestic Stock Funds

Small Cap Growth

Marshall Small Cap Growth Inv MRSCX 8.60 2 3 46.81 13 16 0.09 7 7 4.58 8 6 3.07 26 17 7.09 9/4/96 Small Growth (Mstar) 4.79 35.46 -4.89 0.37 0.60 Russell 2000 Growth 4.14 34.47 -4.00 0.87 -1.37

International Stock Funds

Foreign Large Cap Blend

Scout International UMBWX 3.99 17 60 35.54 25 45 -0.37 2 4 7.52 8 6 4.50 8 10 9.27 9/14/93 Foreign Lg Blend (Mstar) 2.64 31.24 -6.15 3.58 0.62 MSCI EAFE 1.80 27.75 -8.66 0.85 -1.07

Foreign Large Cap Growth

AIM International Growth A AIIEX 6.00 14 11 34.93 60 48 -2.89 19 19 6.60 6 14 0.72 43 40 8.13 4/7/92 Foreign Lg Growth (Mstar) 4.48 38.02 -4.93 4.25 0.16 MSCI EAFE Growth 4.17 29.36 -4.78 3.65 -1.31

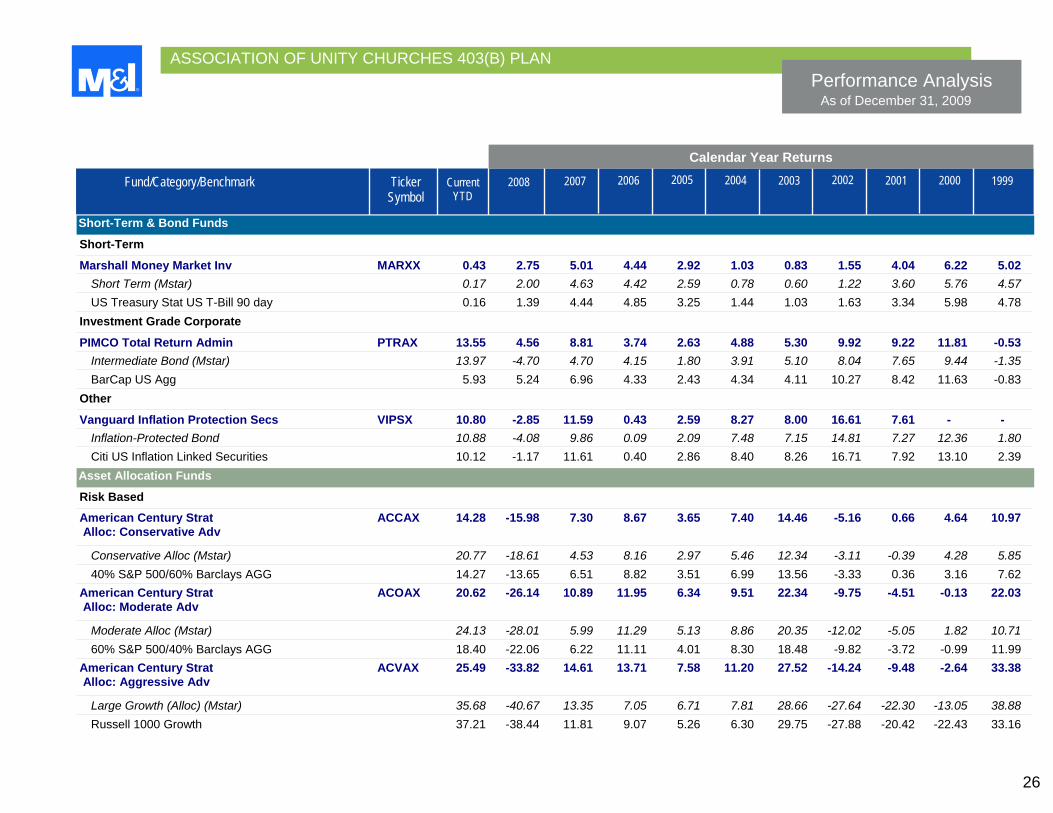

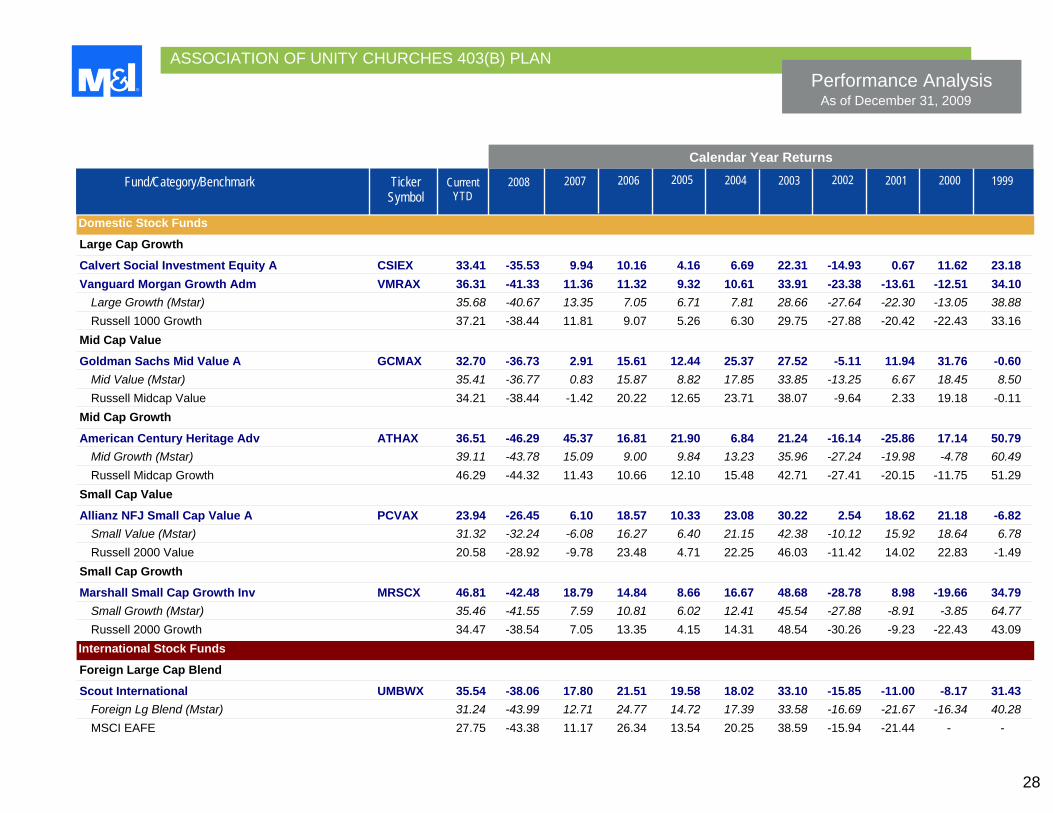

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

26

CurrentYTD

Fund/Category/Benchmark 2008 2006 2005 2007 Ticker Symbol

2003 2002 2004 2000 2001 1999

Calendar Year Returns

Short-Term & Bond Funds

Short-Term

Marshall Money Market Inv MARXX 0.43 2.75 5.01 4.44 2.92 1.03 0.83 1.55 4.04 6.22 5.02 Short Term (Mstar) 0.17 2.00 4.63 4.42 2.59 0.78 0.60 1.22 3.60 5.76 4.57 US Treasury Stat US T-Bill 90 day 0.16 1.39 4.44 4.85 3.25 1.44 1.03 1.63 3.34 5.98 4.78

Investment Grade Corporate

PIMCO Total Return Admin PTRAX 13.55 4.56 8.81 3.74 2.63 4.88 5.30 9.92 9.22 11.81 -0.53 Intermediate Bond (Mstar) 13.97 -4.70 4.70 4.15 1.80 3.91 5.10 8.04 7.65 9.44 -1.35 BarCap US Agg 5.93 5.24 6.96 4.33 2.43 4.34 4.11 10.27 8.42 11.63 -0.83

Other

Vanguard Inflation Protection Secs VIPSX 10.80 -2.85 11.59 0.43 2.59 8.27 8.00 16.61 7.61 - - Inflation-Protected Bond 10.88 -4.08 9.86 0.09 2.09 7.48 7.15 14.81 7.27 12.36 1.80 Citi US Inflation Linked Securities 10.12 -1.17 11.61 0.40 2.86 8.40 8.26 16.71 7.92 13.10 2.39

Asset Allocation Funds

Risk Based

American Century Strat ACCAX 14.28 -15.98 7.30 8.67 3.65 7.40 14.46 -5.16 0.66 4.64 10.97 Alloc: Conservative Adv

Conservative Alloc (Mstar) 20.77 -18.61 4.53 8.16 2.97 5.46 12.34 -3.11 -0.39 4.28 5.85 40% S&P 500/60% Barclays AGG 14.27 -13.65 6.51 8.82 3.51 6.99 13.56 -3.33 0.36 3.16 7.62 American Century Strat ACOAX 20.62 -26.14 10.89 11.95 6.34 9.51 22.34 -9.75 -4.51 -0.13 22.03 Alloc: Moderate Adv

Moderate Alloc (Mstar) 24.13 -28.01 5.99 11.29 5.13 8.86 20.35 -12.02 -5.05 1.82 10.71 60% S&P 500/40% Barclays AGG 18.40 -22.06 6.22 11.11 4.01 8.30 18.48 -9.82 -3.72 -0.99 11.99 American Century Strat ACVAX 25.49 -33.82 14.61 13.71 7.58 11.20 27.52 -14.24 -9.48 -2.64 33.38 Alloc: Aggressive Adv

Large Growth (Alloc) (Mstar) 35.68 -40.67 13.35 7.05 6.71 7.81 28.66 -27.64 -22.30 -13.05 38.88 Russell 1000 Growth 37.21 -38.44 11.81 9.07 5.26 6.30 29.75 -27.88 -20.42 -22.43 33.16

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

27

CurrentYTD

Fund/Category/Benchmark 2008 2006 2005 2007 Ticker Symbol

2003 2002 2004 2000 2001 1999

Calendar Year Returns

Asset Allocation Funds

Balanced

Dodge & Cox Balanced DODBX 28.37 -33.57 1.73 13.86 6.59 13.30 24.44 -2.94 10.05 15.14 12.06 MFS Total Return A MSFRX 18.18 -22.63 4.98 11.56 3.29 11.37 16.85 -5.56 -0.63 19.03 2.31 Moderate Allocation (Balanced) 24.13 -28.01 5.99 11.29 5.13 8.86 20.35 -12.02 -5.05 1.82 10.71 60% S&P 500/40% Barclays AGG 18.40 -22.06 6.22 11.11 4.01 8.30 18.48 -9.82 -3.72 -0.99 11.99

Target Retirement

T. Rowe Price Rtmt 2010 TRRAX 27.95 -26.72 6.65 12.84 6.25 11.11 23.75 - - - - Target Date 2000-2010 22.42 -22.47 5.22 8.58 3.68 6.82 13.67 -4.11 -0.54 2.70 9.09 T. Rowe Price Rtmt 2020 TRRBX 34.24 -33.48 6.73 14.66 7.17 12.82 27.41 - - - - Target Date 2016-2020 24.25 -29.46 6.02 11.95 5.80 9.61 21.84 -13.42 -9.85 -4.21 18.34 T. Rowe Price Rtmt 2030 TRRCX 38.03 -37.79 6.83 16.14 8.12 14.15 29.98 - - - - Target Date 2026-2030 28.87 -36.04 6.50 13.60 6.81 10.95 23.89 -14.20 -10.47 -5.93 18.32 T. Rowe Price Rtmt 2040 TRRDX 39.12 -38.85 6.77 16.24 8.14 14.11 29.99 - - - - Target Date 2036-2040 30.90 -37.94 6.21 14.67 7.41 11.71 26.65 -16.99 -13.81 -10.06 20.85 T. Rowe Price Rtmt 2050 TRRMX 38.90 -38.80 6.82 - - - - - - - - Target Date 2050+ 32.21 -38.86 5.94 15.51 8.76 12.60 25.73 -16.09 - - -

Domestic Stock Funds

Large Cap Blend

Fidelity Spartan US Equity Index FUSEX 26.51 -37.03 5.43 15.72 4.85 10.73 28.50 -22.21 -12.05 -9.18 20.66 Large Index (Lipper) 25.88 -37.29 4.92 15.19 4.36 10.25 27.87 -22.52 -12.39 -9.51 20.31 S&P 500 26.46 -37.00 5.49 15.79 4.91 10.88 28.68 -22.10 -11.88 -9.11 21.04

Large Cap Value

Allianz NFJ Dividend Value A PNEAX 12.91 -36.25 4.27 24.13 11.48 13.88 27.61 -7.06 16.03 - - Large Value (Mstar) 24.13 -37.09 1.42 18.15 5.95 12.97 28.44 -18.69 -4.99 7.87 6.72 Russell 1000 Value 19.69 -36.85 -0.17 22.25 7.05 16.49 30.03 -15.52 -5.59 7.02 7.35

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

28

CurrentYTD

Fund/Category/Benchmark 2008 2006 2005 2007 Ticker Symbol

2003 2002 2004 2000 2001 1999

Calendar Year Returns

Domestic Stock Funds

Large Cap Growth

Calvert Social Investment Equity A CSIEX 33.41 -35.53 9.94 10.16 4.16 6.69 22.31 -14.93 0.67 11.62 23.18 Vanguard Morgan Growth Adm VMRAX 36.31 -41.33 11.36 11.32 9.32 10.61 33.91 -23.38 -13.61 -12.51 34.10 Large Growth (Mstar) 35.68 -40.67 13.35 7.05 6.71 7.81 28.66 -27.64 -22.30 -13.05 38.88 Russell 1000 Growth 37.21 -38.44 11.81 9.07 5.26 6.30 29.75 -27.88 -20.42 -22.43 33.16

Mid Cap Value

Goldman Sachs Mid Value A GCMAX 32.70 -36.73 2.91 15.61 12.44 25.37 27.52 -5.11 11.94 31.76 -0.60 Mid Value (Mstar) 35.41 -36.77 0.83 15.87 8.82 17.85 33.85 -13.25 6.67 18.45 8.50 Russell Midcap Value 34.21 -38.44 -1.42 20.22 12.65 23.71 38.07 -9.64 2.33 19.18 -0.11

Mid Cap Growth

American Century Heritage Adv ATHAX 36.51 -46.29 45.37 16.81 21.90 6.84 21.24 -16.14 -25.86 17.14 50.79 Mid Growth (Mstar) 39.11 -43.78 15.09 9.00 9.84 13.23 35.96 -27.24 -19.98 -4.78 60.49 Russell Midcap Growth 46.29 -44.32 11.43 10.66 12.10 15.48 42.71 -27.41 -20.15 -11.75 51.29

Small Cap Value

Allianz NFJ Small Cap Value A PCVAX 23.94 -26.45 6.10 18.57 10.33 23.08 30.22 2.54 18.62 21.18 -6.82 Small Value (Mstar) 31.32 -32.24 -6.08 16.27 6.40 21.15 42.38 -10.12 15.92 18.64 6.78 Russell 2000 Value 20.58 -28.92 -9.78 23.48 4.71 22.25 46.03 -11.42 14.02 22.83 -1.49

Small Cap Growth

Marshall Small Cap Growth Inv MRSCX 46.81 -42.48 18.79 14.84 8.66 16.67 48.68 -28.78 8.98 -19.66 34.79 Small Growth (Mstar) 35.46 -41.55 7.59 10.81 6.02 12.41 45.54 -27.88 -8.91 -3.85 64.77 Russell 2000 Growth 34.47 -38.54 7.05 13.35 4.15 14.31 48.54 -30.26 -9.23 -22.43 43.09

International Stock Funds

Foreign Large Cap Blend

Scout International UMBWX 35.54 -38.06 17.80 21.51 19.58 18.02 33.10 -15.85 -11.00 -8.17 31.43 Foreign Lg Blend (Mstar) 31.24 -43.99 12.71 24.77 14.72 17.39 33.58 -16.69 -21.67 -16.34 40.28 MSCI EAFE 27.75 -43.38 11.17 26.34 13.54 20.25 38.59 -15.94 -21.44 - -

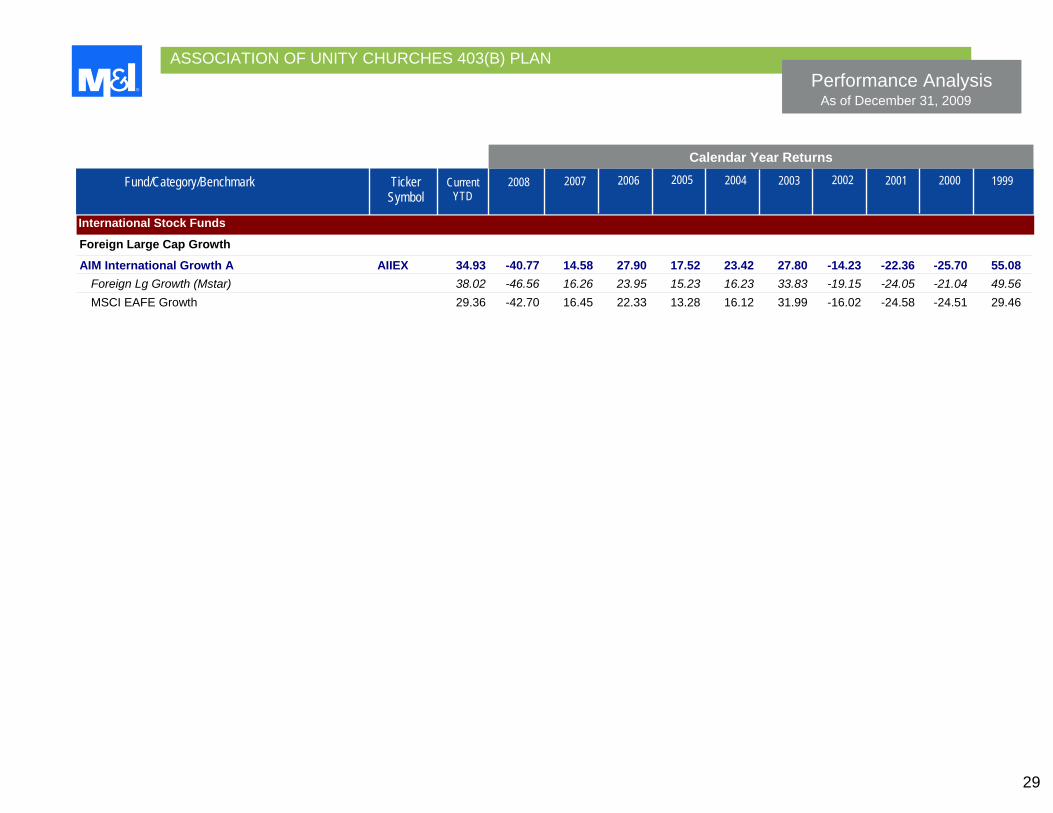

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

29

CurrentYTD

Fund/Category/Benchmark 2008 2006 2005 2007 Ticker Symbol

2003 2002 2004 2000 2001 1999

Calendar Year Returns

International Stock Funds

Foreign Large Cap Growth

AIM International Growth A AIIEX 34.93 -40.77 14.58 27.90 17.52 23.42 27.80 -14.23 -22.36 -25.70 55.08 Foreign Lg Growth (Mstar) 38.02 -46.56 16.26 23.95 15.23 16.23 33.83 -19.15 -24.05 -21.04 49.56 MSCI EAFE Growth 29.36 -42.70 16.45 22.33 13.28 16.12 31.99 -16.02 -24.58 -24.51 29.46

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

30

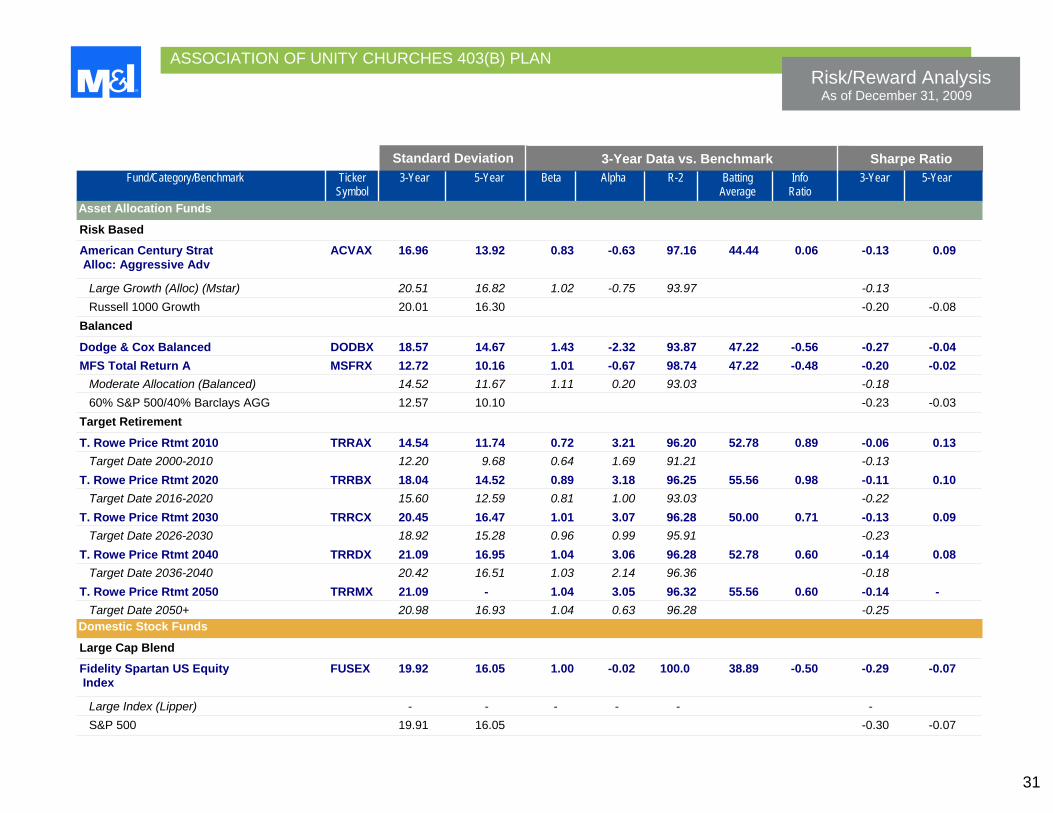

Risk/Reward Analysis As of December 31, 2009

Sharpe Ratio 3-Year Data vs. Benchmark Standard Deviation Fund/Category/Benchmark Ticker 3-Year 5-Year Beta Alpha R-2 Batting Info 3-Year 5-Year Symbol Average Ratio

Short-Term & Bond Funds

Short-Term

Marshall Money Market Inv MARXX 0.55 0.49 - - - 88.89 3.77 3.70 1.73 Short Term (Mstar) - - - - - - US Treasury Stat US T-Bill 0.56 0.52 0.92 -0.76 90 day

Investment Grade Corporate

PIMCO Total Return Admin PTRAX 4.90 4.27 1.00 2.72 71.81 72.22 1.08 1.34 0.85 Intermediate Bond (Mstar) 5.13 4.27 0.99 -1.39 58.69 0.52 BarCap US Agg 4.17 3.70 0.92 0.57

Other

Vanguard Inflation Protection VIPSX 8.91 7.36 1.00 -0.35 99.19 52.78 -0.49 0.51 0.24 Secs

Inflation-Protected Bond 8.86 7.30 1.00 -1.25 94.49 0.41 Citi US Inflation Linked 8.90 7.38 0.55 0.28 Securities

Asset Allocation Funds

Risk Based

American Century Strat ACCAX 9.18 7.43 1.00 -0.66 97.79 50.00 -0.49 -0.06 0.07 Alloc: Conservative Adv

Conservative Alloc (Mstar) 10.10 8.02 1.08 -0.73 85.24 -0.05 40% S&P 500/60% Barclays AGG 9.07 7.30 -0.06 0.08 American Century Strat ACOAX 13.48 11.01 1.05 0.47 95.83 55.56 0.09 -0.11 0.10 Alloc: Moderate Adv

Moderate Alloc (Mstar) 14.52 11.67 1.11 0.20 93.03 -0.18 60% S&P 500/40% Barclays AGG 12.57 10.10 -0.23 -0.03

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

31

Risk/Reward Analysis As of December 31, 2009

Sharpe Ratio 3-Year Data vs. Benchmark Standard Deviation Fund/Category/Benchmark Ticker 3-Year 5-Year Beta Alpha R-2 Batting Info 3-Year 5-Year Symbol Average Ratio

Asset Allocation Funds

Risk Based

American Century Strat ACVAX 16.96 13.92 0.83 -0.63 97.16 44.44 0.06 -0.13 0.09 Alloc: Aggressive Adv

Large Growth (Alloc) (Mstar) 20.51 16.82 1.02 -0.75 93.97 -0.13 Russell 1000 Growth 20.01 16.30 -0.20 -0.08

Balanced

Dodge & Cox Balanced DODBX 18.57 14.67 1.43 -2.32 93.87 47.22 -0.56 -0.27 -0.04 MFS Total Return A MSFRX 12.72 10.16 1.01 -0.67 98.74 47.22 -0.48 -0.20 -0.02 Moderate Allocation (Balanced) 14.52 11.67 1.11 0.20 93.03 -0.18 60% S&P 500/40% Barclays AGG 12.57 10.10 -0.23 -0.03

Target Retirement

T. Rowe Price Rtmt 2010 TRRAX 14.54 11.74 0.72 3.21 96.20 52.78 0.89 -0.06 0.13 Target Date 2000-2010 12.20 9.68 0.64 1.69 91.21 -0.13 T. Rowe Price Rtmt 2020 TRRBX 18.04 14.52 0.89 3.18 96.25 55.56 0.98 -0.11 0.10 Target Date 2016-2020 15.60 12.59 0.81 1.00 93.03 -0.22 T. Rowe Price Rtmt 2030 TRRCX 20.45 16.47 1.01 3.07 96.28 50.00 0.71 -0.13 0.09 Target Date 2026-2030 18.92 15.28 0.96 0.99 95.91 -0.23 T. Rowe Price Rtmt 2040 TRRDX 21.09 16.95 1.04 3.06 96.28 52.78 0.60 -0.14 0.08 Target Date 2036-2040 20.42 16.51 1.03 2.14 96.36 -0.18 T. Rowe Price Rtmt 2050 TRRMX 21.09 - 1.04 3.05 96.32 55.56 0.60 -0.14 - Target Date 2050+ 20.98 16.93 1.04 0.63 96.28 -0.25

Domestic Stock Funds

Large Cap Blend

Fidelity Spartan US Equity FUSEX 19.92 16.05 1.00 -0.02 100.0 38.89 -0.50 -0.29 -0.07 Index

Large Index (Lipper) - - - - - - S&P 500 19.91 16.05 -0.30 -0.07

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

32

Risk/Reward Analysis As of December 31, 2009

Sharpe Ratio 3-Year Data vs. Benchmark Standard Deviation Fund/Category/Benchmark Ticker 3-Year 5-Year Beta Alpha R-2 Batting Info 3-Year 5-Year Symbol Average Ratio

Domestic Stock Funds

Large Cap Value

Allianz NFJ Dividend Value A PNEAX 21.37 17.42 0.97 -0.37 95.46 44.44 -0.04 -0.43 -0.02 Large Value (Mstar) 20.37 16.40 0.94 1.14 94.56 -0.35 Russell 1000 Value 21.40 17.27 -0.52 -0.18

Large Cap Growth

Calvert Social Investment CSIEX 19.83 15.99 0.97 -0.08 95.15 55.56 0.01 -0.09 0.01 Equity A

Vanguard Morgan Growth Adm VMRAX 20.65 16.98 1.03 -1.76 98.79 44.44 -0.82 -0.18 0.02 Large Growth (Mstar) 20.51 16.82 1.02 -0.75 93.97 -0.13 Russell 1000 Growth 20.01 16.30 -0.20 -0.08

Mid Cap Value

Goldman Sachs Mid Value A GCMAX 21.87 17.87 0.84 0.24 94.75 61.11 0.29 -0.20 0.07 Mid Value (Mstar) 23.02 18.64 0.92 0.68 94.08 -0.18 Russell Midcap Value 25.37 20.37 -0.35 -0.04

Mid Cap Growth

American Century Heritage Adv ATHAX 24.82 21.14 0.97 5.39 91.18 52.78 0.72 0.13 0.37 Mid Growth (Mstar) 22.99 19.23 0.92 0.32 92.09 -0.09 Russell Midcap Growth 24.35 20.10 -0.22 -0.02

Small Cap Value

Allianz NFJ Small Cap Value A PCVAX 20.47 17.23 0.75 4.36 90.52 63.89 0.78 -0.05 0.20 Small Value (Mstar) 24.46 20.24 0.95 1.91 93.81 -0.19 Russell 2000 Value 25.98 21.62 -0.40 -0.13

Small Cap Growth

Marshall Small Cap Growth Inv MRSCX 24.20 21.09 0.92 3.66 91.73 63.89 0.56 0.04 0.19 Small Growth (Mstar) 24.01 20.51 0.95 -1.02 93.71 -0.15 Russell 2000 Growth 25.20 21.78 -0.25 -0.09

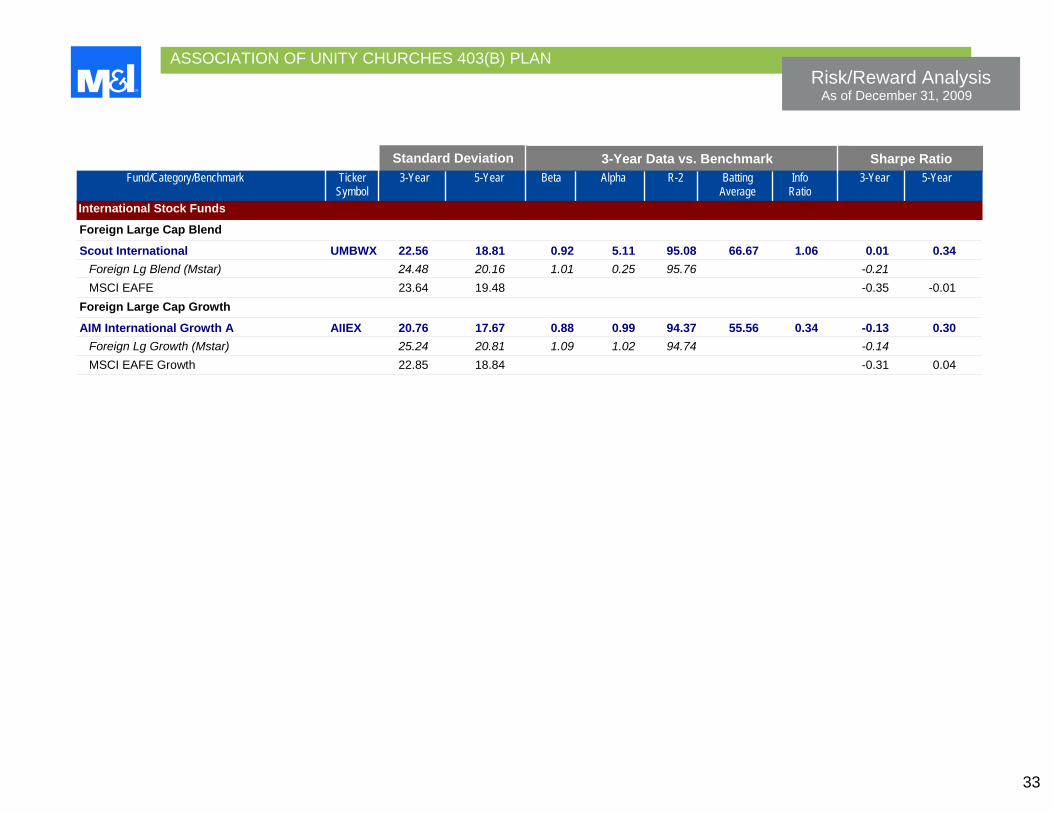

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

33

Risk/Reward Analysis As of December 31, 2009

Sharpe Ratio 3-Year Data vs. Benchmark Standard Deviation Fund/Category/Benchmark Ticker 3-Year 5-Year Beta Alpha R-2 Batting Info 3-Year 5-Year Symbol Average Ratio

International Stock Funds

Foreign Large Cap Blend

Scout International UMBWX 22.56 18.81 0.92 5.11 95.08 66.67 1.06 0.01 0.34 Foreign Lg Blend (Mstar) 24.48 20.16 1.01 0.25 95.76 -0.21 MSCI EAFE 23.64 19.48 -0.35 -0.01

Foreign Large Cap Growth

AIM International Growth A AIIEX 20.76 17.67 0.88 0.99 94.37 55.56 0.34 -0.13 0.30 Foreign Lg Growth (Mstar) 25.24 20.81 1.09 1.02 94.74 -0.14 MSCI EAFE Growth 22.85 18.84 -0.31 0.04

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

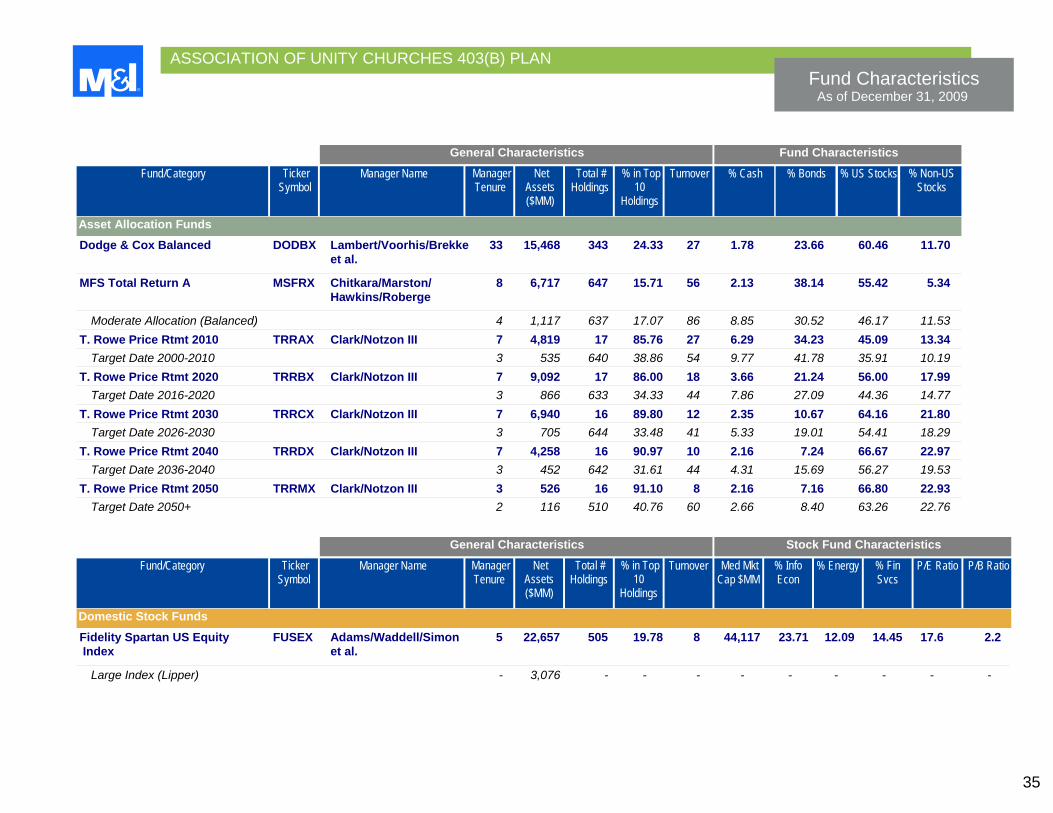

Fund Characteristics As of December 31, 2009

34

General Characteristics Bond Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover Wtd Avg Qual

Wtd Avg Cpn

Wtd Avg YTM

Wtd Avg Mty

Wtd Avg Dur

Short-Term & Bond Funds

Marshall Money Market Inv MARXX Richard M. Rokus 16 4,952 62 34.18 0 - - 0.57 - - Short Term (Mstar) - - 531 7.56 82 - 1.83 - - - PIMCO Total Return Admin PTRAX Gross, William H. 23 199,462 18271 42.14 300 AA 5.33 5.20 5.80 4.79 Intermediate Bond (Mstar) 6 1,431 592 44.19 230 AA 5.22 4.32 5.91 4.37 Vanguard Inflation Protection VIPSX Volpert/Hollyer 10 27,579 26 60.05 28 AAA 2.24 1.71 9.10 4.24 Secs

Inflation-Protected Bond 3 1,201 419 76.38 224 AAA 2.74 1.51 7.02 6.15

General Characteristics Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover % Cash % Bonds % US Stocks % Non-US Stocks

Asset Allocation Funds

American Century Strat ACCAX Chang/Tyler/Wittman/ 10 608 925 23.14 168 6.88 48.83 34.74 9.15 Alloc: Conservative Adv Torelli

Conservative Alloc (Mstar) 4 550 620 47.51 77 11.95 58.80 21.05 4.78 American Century Strat ACOAX Chang/Tyler/Torelli 10 1,619 1282 16.83 163 6.36 31.97 44.56 16.73 Alloc: Moderate Adv

Moderate Alloc (Mstar) 4 1,117 637 17.07 86 8.85 30.52 46.17 11.53 American Century Strat ACVAX Chang/Tyler/Wittman/ 10 980 1103 13.06 146 4.12 19.69 53.66 22.25 Alloc: Aggressive Adv Torelli

Large Growth (Alloc) (Mstar) 5 1,080 569 29.95 111 2.43 1.00 85.89 10.25

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fund Characteristics As of December 31, 2009

35

General Characteristics Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover % Cash % Bonds % US Stocks % Non-US Stocks

Asset Allocation Funds

Dodge & Cox Balanced DODBX Lambert/Voorhis/Brekke 33 15,468 343 24.33 27 1.78 23.66 60.46 11.70 et al.

MFS Total Return A MSFRX Chitkara/Marston/ 8 6,717 647 15.71 56 2.13 38.14 55.42 5.34 Hawkins/Roberge

Moderate Allocation (Balanced) 4 1,117 637 17.07 86 8.85 30.52 46.17 11.53 T. Rowe Price Rtmt 2010 TRRAX Clark/Notzon III 7 4,819 17 85.76 27 6.29 34.23 45.09 13.34 Target Date 2000-2010 3 535 640 38.86 54 9.77 41.78 35.91 10.19 T. Rowe Price Rtmt 2020 TRRBX Clark/Notzon III 7 9,092 17 86.00 18 3.66 21.24 56.00 17.99 Target Date 2016-2020 3 866 633 34.33 44 7.86 27.09 44.36 14.77 T. Rowe Price Rtmt 2030 TRRCX Clark/Notzon III 7 6,940 16 89.80 12 2.35 10.67 64.16 21.80 Target Date 2026-2030 3 705 644 33.48 41 5.33 19.01 54.41 18.29 T. Rowe Price Rtmt 2040 TRRDX Clark/Notzon III 7 4,258 16 90.97 10 2.16 7.24 66.67 22.97 Target Date 2036-2040 3 452 642 31.61 44 4.31 15.69 56.27 19.53 T. Rowe Price Rtmt 2050 TRRMX Clark/Notzon III 3 526 16 91.10 8 2.16 7.16 66.80 22.93 Target Date 2050+ 2 116 510 40.76 60 2.66 8.40 63.26 22.76

General Characteristics Stock Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover Med Mkt Cap $MM

% Info Econ

% Energy % Fin Svcs

P/E Ratio P/B Ratio

Domestic Stock Funds

Fidelity Spartan US Equity FUSEX Adams/Waddell/Simon 5 22,657 505 19.78 8 44,117 23.71 12.09 14.45 17.6 2.2 Index et al.

Large Index (Lipper) - 3,076 - - - - - - - - -

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fund Characteristics As of December 31, 2009

36

General Characteristics Stock Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover Med Mkt Cap $MM

% Info Econ

% Energy % Fin Svcs

P/E Ratio P/B Ratio

Domestic Stock Funds

Allianz NFJ Dividend Value PNEAX Fischer/Mckinney/ 10 6,836 47 32.77 43 26,610 15.72 20.30 15.81 13.2 1.8 A Oliver/Magnuson

Large Value (Mstar) 5 1,065 639 23.78 70 42,375 17.31 14.62 19.66 15.3 1.7 Calvert Social Investment CSIEX England/Hackney, 11 1,189 74 37.94 38 33,655 28.35 9.33 10.99 20.3 2.6 Equity A III/Irvin

Vanguard Morgan Growth Adm VMRAX McCarragher/Marrkand/ 6 7,687 344 23.15 87 21,296 39.05 7.80 7.33 20.2 3.1 Knightly

Large Growth (Mstar) 5 1,080 569 29.95 111 41,116 31.23 8.36 10.47 20.8 2.9 Goldman Sachs Mid Value A GCMAX Carroll/Bamford/Butkus 9 5,704 116 19.48 104 5,706 12.81 11.86 27.94 17.2 1.6 et al.

Mid Value (Mstar) 5 523 562 19.25 107 5,791 13.13 8.67 23.80 17.1 1.4 American Century Heritage ATHAX Walsh/Hollond 3 2,133 115 17.63 172 5,271 26.24 6.23 9.35 21.7 3.1 Adv

Mid Growth (Mstar) 5 473 615 15.50 137 5,188 24.51 6.71 12.19 20.0 2.5 Allianz NFJ Small Cap PCVAX Magnuson/Mckinney/ 18 6,099 121 13.43 33 1,865 1.74 10.97 15.37 12.3 1.6 Value A Campbell/Fischer

Small Value (Mstar) 5 376 538 19.38 86 1,347 12.89 5.89 24.29 12.9 1.2 Marshall Small Cap Growth MRSCX Gundlach/Salmon 6 266 87 28.47 233 611 47.09 8.31 4.13 14.9 2.2 Inv

Small Growth (Mstar) 5 322 476 21.34 132 1,525 27.94 5.32 9.95 20.5 2.4

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fund Characteristics As of December 31, 2009

37

General Characteristics International Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover Market Maturity % Developed

Market Maturity % Emerging

% Asia Dev

% Japan % Europe Dev

% United Kingdom

International Stock Funds

Scout International UMBWX Moffett/Anderson 16 4,952 96 15.95 16 89.80 10.20 6.06 10.97 47.77 9.57 Foreign Lg Blend (Mstar) 4 1,212 736 16.96 97 92.96 7.05 6.30 15.10 42.10 18.40 AIM International Growth A AIIEX Sides/Olsson/Dennis 15 3,279 79 27.51 38 90.61 9.39 9.26 6.33 36.67 23.49 et al.

Foreign Lg Growth (Mstar) 5 1,169 757 12.00 101 84.85 15.16 6.70 11.70 36.80 19.20

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

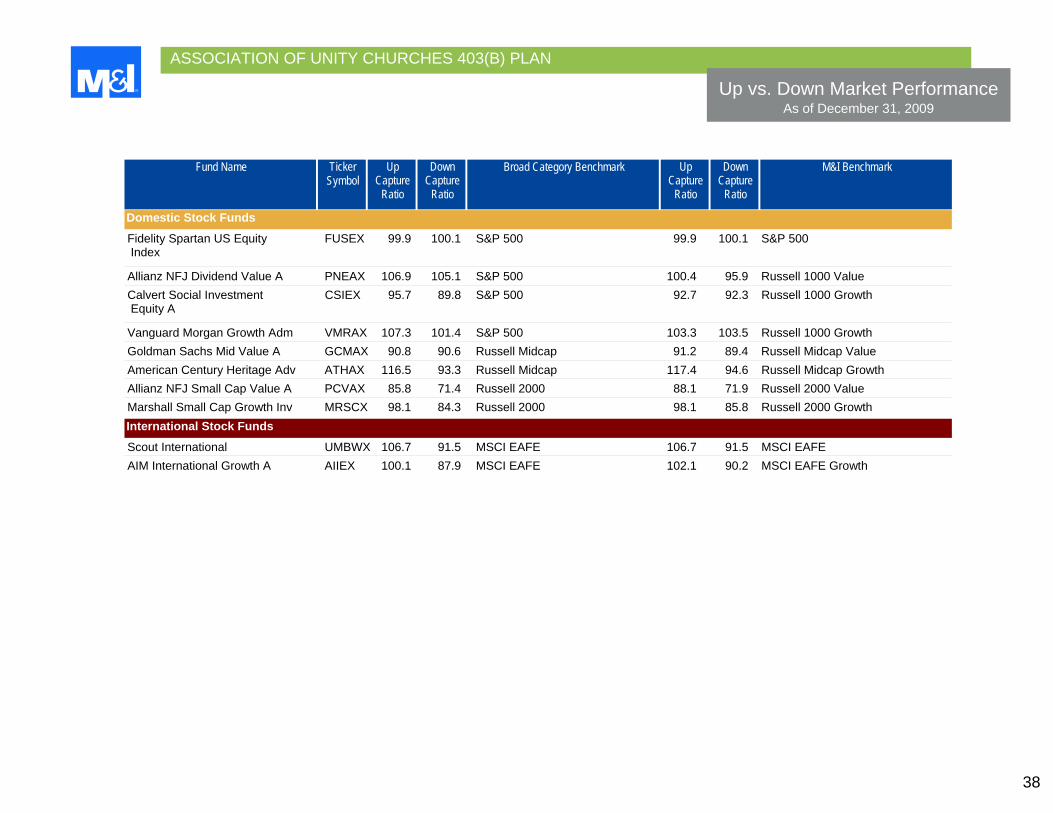

Up vs. Down Market Performance As of December 31, 2009

38

Fund Name Ticker Symbol

Up Capture

Ratio

Down Capture

Ratio

Broad Category Benchmark Up Capture

Ratio

Down Capture

Ratio

M&I Benchmark

Domestic Stock Funds

Fidelity Spartan US Equity FUSEX 99.9 100.1 S&P 500 99.9 100.1 S&P 500 Index

Allianz NFJ Dividend Value A PNEAX 106.9 105.1 S&P 500 100.4 95.9 Russell 1000 Value Calvert Social Investment CSIEX 95.7 89.8 S&P 500 92.7 92.3 Russell 1000 Growth Equity A

Vanguard Morgan Growth Adm VMRAX 107.3 101.4 S&P 500 103.3 103.5 Russell 1000 Growth Goldman Sachs Mid Value A GCMAX 90.8 90.6 Russell Midcap 91.2 89.4 Russell Midcap Value American Century Heritage Adv ATHAX 116.5 93.3 Russell Midcap 117.4 94.6 Russell Midcap Growth Allianz NFJ Small Cap Value A PCVAX 85.8 71.4 Russell 2000 88.1 71.9 Russell 2000 Value Marshall Small Cap Growth Inv MRSCX 98.1 84.3 Russell 2000 98.1 85.8 Russell 2000 Growth

International Stock Funds

Scout International UMBWX 106.7 91.5 MSCI EAFE 106.7 91.5 MSCI EAFE AIM International Growth A AIIEX 100.1 87.9 MSCI EAFE 102.1 90.2 MSCI EAFE Growth

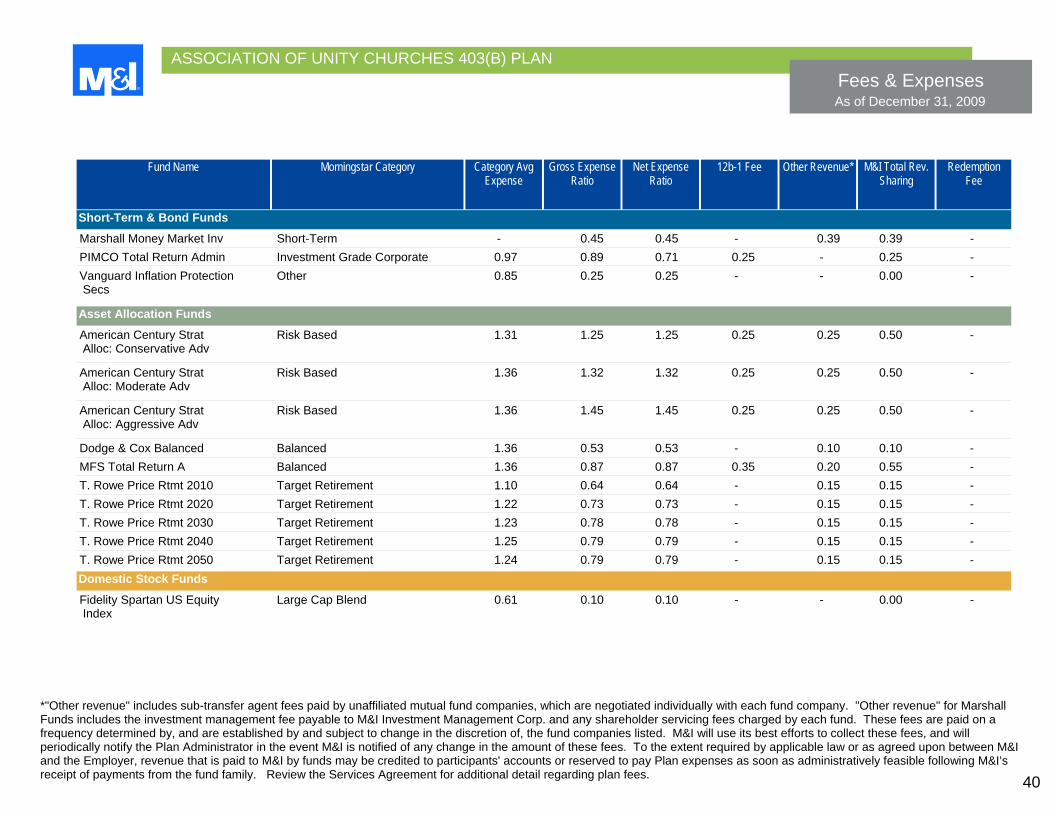

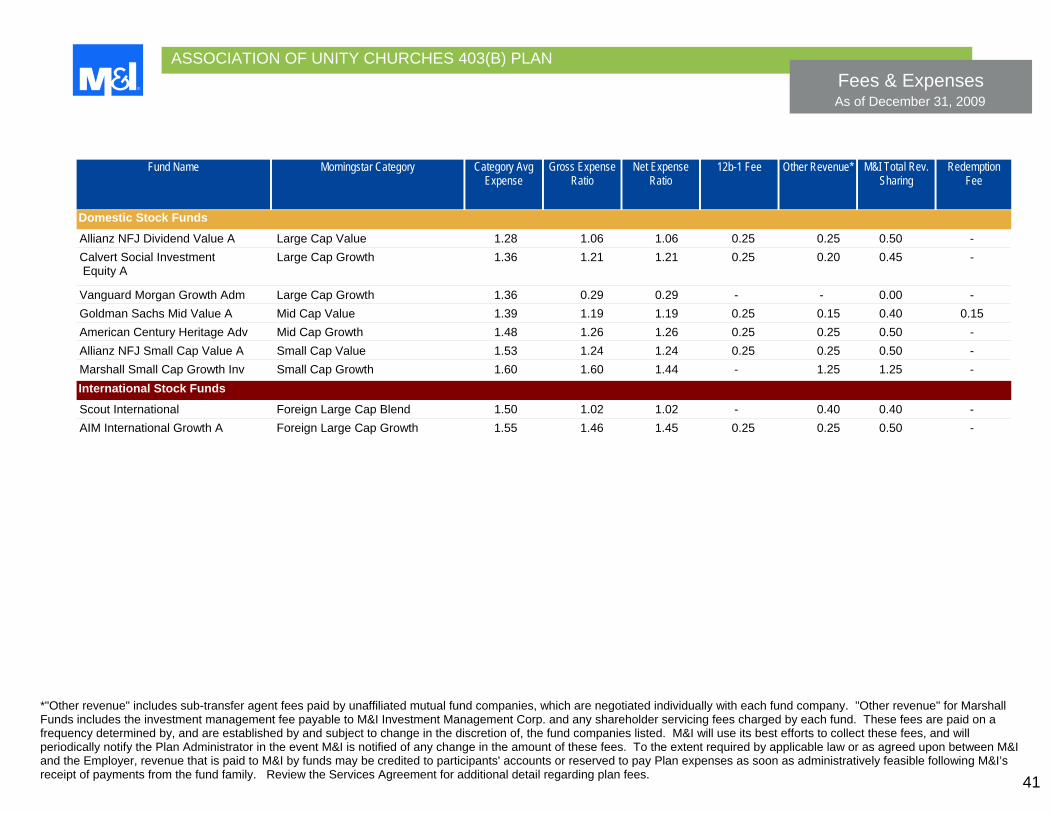

Section V: Fees & Expenses4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fees & Expenses As of December 31, 2009

40

*"Other revenue" includes sub-transfer agent fees paid by unaffiliated mutual fund companies, which are negotiated individually with each fund company. "Other revenue" for Marshall Funds includes the investment management fee payable to M&I Investment Management Corp. and any shareholder servicing fees charged by each fund. These fees are paid on a frequency determined by, and are established by and subject to change in the discretion of, the fund companies listed. M&I will use its best efforts to collect these fees, and will periodically notify the Plan Administrator in the event M&I is notified of any change in the amount of these fees. To the extent required by applicable law or as agreed upon between M&I and the Employer, revenue that is paid to M&I by funds may be credited to participants' accounts or reserved to pay Plan expenses as soon as administratively feasible following M&I’s receipt of payments from the fund family. Review the Services Agreement for additional detail regarding plan fees.

Fund Name Morningstar Category Category Avg Expense

Gross Expense Ratio

Net Expense Ratio

12b-1 Fee Other Revenue* M&I Total Rev. Sharing

Redemption Fee

Short-Term & Bond Funds

Marshall Money Market Inv Short-Term - 0.45 0.45 - 0.39 0.39 - PIMCO Total Return Admin Investment Grade Corporate 0.97 0.89 0.71 0.25 - 0.25 - Vanguard Inflation Protection Other 0.85 0.25 0.25 - - 0.00 - Secs

Asset Allocation Funds

American Century Strat Risk Based 1.31 1.25 1.25 0.25 0.25 0.50 - Alloc: Conservative Adv

American Century Strat Risk Based 1.36 1.32 1.32 0.25 0.25 0.50 - Alloc: Moderate Adv

American Century Strat Risk Based 1.36 1.45 1.45 0.25 0.25 0.50 - Alloc: Aggressive Adv

Dodge & Cox Balanced Balanced 1.36 0.53 0.53 - 0.10 0.10 - MFS Total Return A Balanced 1.36 0.87 0.87 0.35 0.20 0.55 - T. Rowe Price Rtmt 2010 Target Retirement 1.10 0.64 0.64 - 0.15 0.15 - T. Rowe Price Rtmt 2020 Target Retirement 1.22 0.73 0.73 - 0.15 0.15 - T. Rowe Price Rtmt 2030 Target Retirement 1.23 0.78 0.78 - 0.15 0.15 - T. Rowe Price Rtmt 2040 Target Retirement 1.25 0.79 0.79 - 0.15 0.15 - T. Rowe Price Rtmt 2050 Target Retirement 1.24 0.79 0.79 - 0.15 0.15 -

Domestic Stock Funds

Fidelity Spartan US Equity Large Cap Blend 0.61 0.10 0.10 - - 0.00 - Index

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fees & Expenses As of December 31, 2009

41

*"Other revenue" includes sub-transfer agent fees paid by unaffiliated mutual fund companies, which are negotiated individually with each fund company. "Other revenue" for Marshall Funds includes the investment management fee payable to M&I Investment Management Corp. and any shareholder servicing fees charged by each fund. These fees are paid on a frequency determined by, and are established by and subject to change in the discretion of, the fund companies listed. M&I will use its best efforts to collect these fees, and will periodically notify the Plan Administrator in the event M&I is notified of any change in the amount of these fees. To the extent required by applicable law or as agreed upon between M&I and the Employer, revenue that is paid to M&I by funds may be credited to participants' accounts or reserved to pay Plan expenses as soon as administratively feasible following M&I’s receipt of payments from the fund family. Review the Services Agreement for additional detail regarding plan fees.

Fund Name Morningstar Category Category Avg Expense

Gross Expense Ratio

Net Expense Ratio

12b-1 Fee Other Revenue* M&I Total Rev. Sharing

Redemption Fee

Domestic Stock Funds

Allianz NFJ Dividend Value A Large Cap Value 1.28 1.06 1.06 0.25 0.25 0.50 - Calvert Social Investment Large Cap Growth 1.36 1.21 1.21 0.25 0.20 0.45 - Equity A

Vanguard Morgan Growth Adm Large Cap Growth 1.36 0.29 0.29 - - 0.00 - Goldman Sachs Mid Value A Mid Cap Value 1.39 1.19 1.19 0.25 0.15 0.40 0.15 American Century Heritage Adv Mid Cap Growth 1.48 1.26 1.26 0.25 0.25 0.50 - Allianz NFJ Small Cap Value A Small Cap Value 1.53 1.24 1.24 0.25 0.25 0.50 - Marshall Small Cap Growth Inv Small Cap Growth 1.60 1.60 1.44 - 1.25 1.25 -

International Stock Funds

Scout International Foreign Large Cap Blend 1.50 1.02 1.02 - 0.40 0.40 - AIM International Growth A Foreign Large Cap Growth 1.55 1.46 1.45 0.25 0.25 0.50 -

Section VI: Proposed Investment Options4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

43

Qtr Fund/Category/Benchmark MS %

Rank

Lipper%

Rank

MS%

Rank

Lipper%

Rank

1 Yr Ticker Symbol

MS%

Rank

Lipper%

Rank

3 Yr MS%

Rank

Lipper%

Rank

5 Yr MS%

Rank

Lipper%

Rank

10 Yr S.I.

Inception Date

Annualized Periods

Domestic Stock Funds

Mid Cap Blend

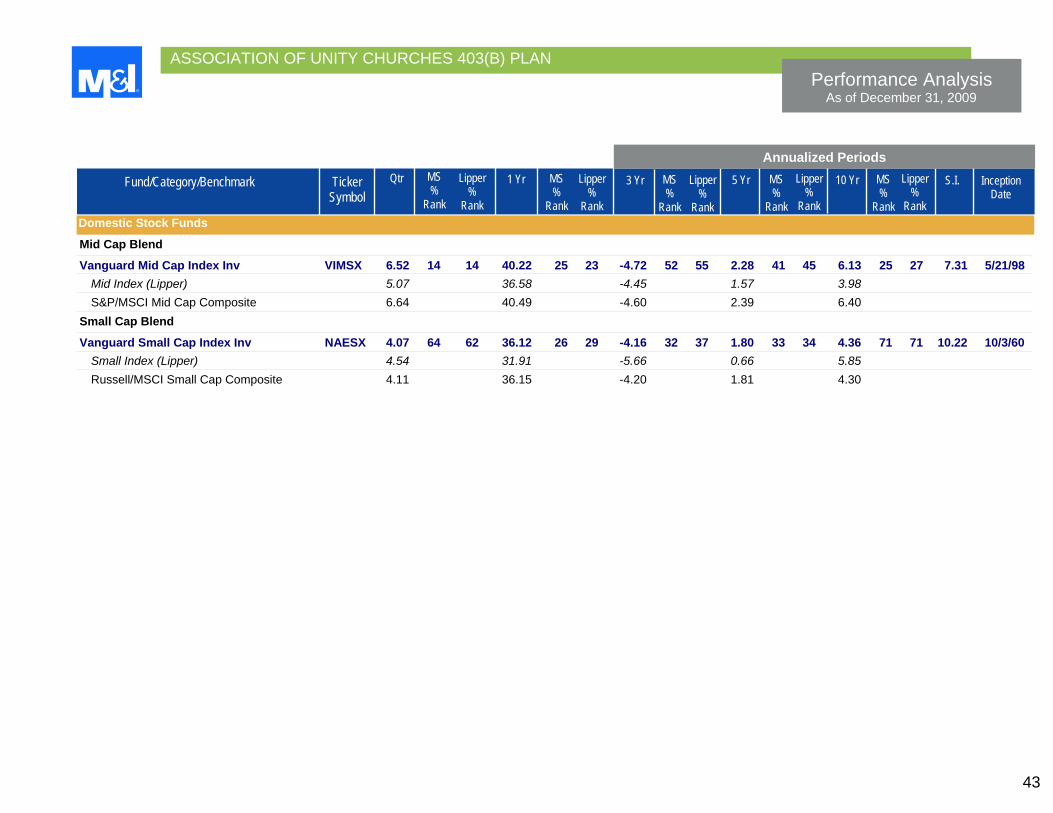

Vanguard Mid Cap Index Inv VIMSX 6.52 14 14 40.22 25 23 -4.72 52 55 2.28 41 45 6.13 25 27 7.31 5/21/98 Mid Index (Lipper) 5.07 36.58 -4.45 1.57 3.98 S&P/MSCI Mid Cap Composite 6.64 40.49 -4.60 2.39 6.40

Small Cap Blend

Vanguard Small Cap Index Inv NAESX 4.07 64 62 36.12 26 29 -4.16 32 37 1.80 33 34 4.36 71 71 10.22 10/3/60 Small Index (Lipper) 4.54 31.91 -5.66 0.66 5.85 Russell/MSCI Small Cap Composite 4.11 36.15 -4.20 1.81 4.30

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Performance Analysis As of December 31, 2009

44

CurrentYTD

Fund/Category/Benchmark 2008 2006 2005 2007 Ticker Symbol

2003 2002 2004 2000 2001 1999

Calendar Year Returns

Domestic Stock Funds

Mid Cap Blend

Vanguard Mid Cap Index Inv VIMSX 40.22 -41.82 6.02 13.60 13.93 20.35 34.14 -14.61 -0.50 18.10 15.32 Mid Index (Lipper) 36.58 -37.94 6.02 11.44 11.65 16.78 36.80 -15.88 - - - S&P/MSCI Mid Cap Composite 40.49 -41.80 6.19 13.75 13.94 20.52 37.31 -14.51 -0.61 17.51 14.72

Small Cap Blend

Vanguard Small Cap Index Inv NAESX 36.12 -36.07 1.16 15.66 7.36 19.90 45.63 -20.02 3.10 -2.67 23.13 Small Index (Lipper) 31.91 -34.77 -1.51 16.18 5.26 19.28 42.69 -18.64 - - - Russell/MSCI Small Cap Composite 36.15 -36.20 1.20 15.77 7.48 20.01 46.86 -20.48 2.49 -3.02 21.26

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

45

Risk/Reward Analysis As of December 31, 2009

Sharpe Ratio 3-Year Data vs. Benchmark Standard Deviation Fund/Category/Benchmark Ticker 3-Year 5-Year Beta Alpha R-2 Batting Info 3-Year 5-Year Symbol Average Ratio

Domestic Stock Funds

Mid Cap Blend

Vanguard Mid Cap Index Inv VIMSX 24.24 19.87 1.00 1.47 99.99 100.00 5.96 -0.16 0.08 Mid Index (Lipper) - - - - - - S&P/MSCI Mid Cap Composite 24.25 19.87 -0.28 -0.02

Small Cap Blend

Vanguard Small Cap Index Inv NAESX 26.16 21.70 1.00 1.50 99.99 100.00 6.83 -0.11 0.06 Small Index (Lipper) - - - - - - Russell/MSCI Small Cap 26.16 21.69 -0.25 -0.05 Composite

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fund Characteristics As of December 31, 2009

46

General Characteristics Stock Fund Characteristics

Fund/Category Ticker Symbol

Manager Name Manager Tenure

Net Assets ($MM)

Total # Holdings

% in Top 10

Holdings

Turnover Med Mkt Cap $MM

% Info Econ

% Energy % Fin Svcs

P/E Ratio P/B Ratio

Domestic Stock Funds

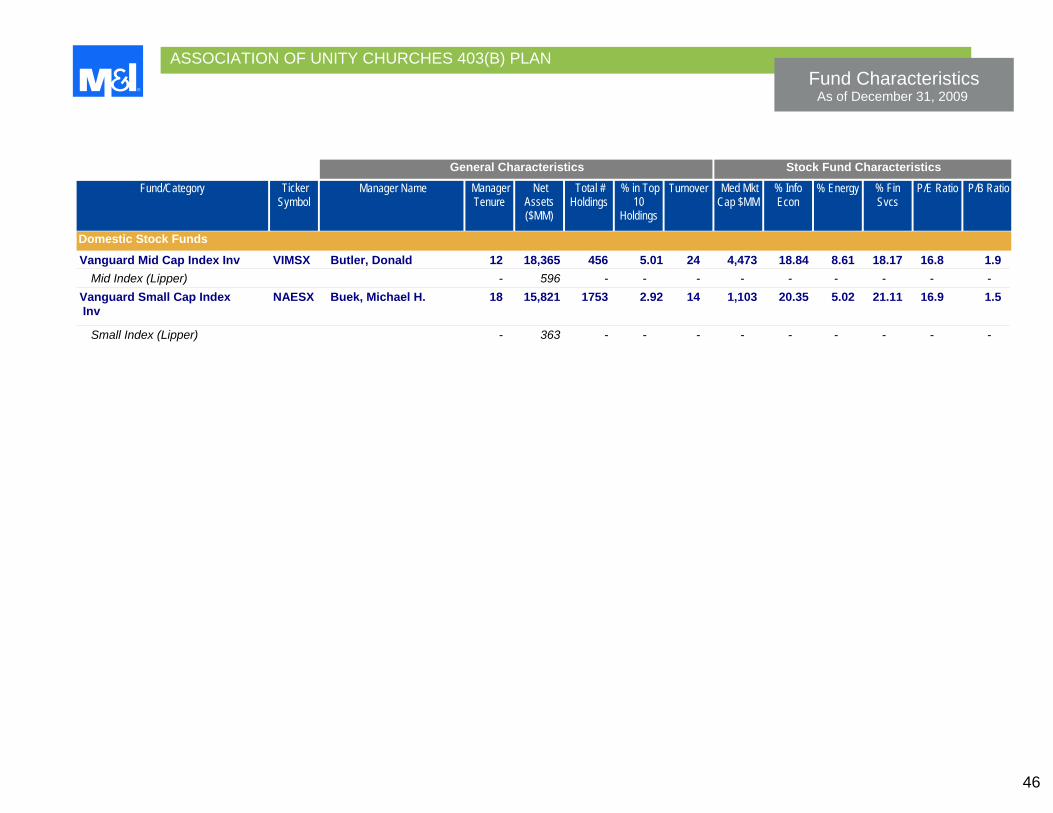

Vanguard Mid Cap Index Inv VIMSX Butler, Donald 12 18,365 456 5.01 24 4,473 18.84 8.61 18.17 16.8 1.9 Mid Index (Lipper) - 596 - - - - - - - - - Vanguard Small Cap Index NAESX Buek, Michael H. 18 15,821 1753 2.92 14 1,103 20.35 5.02 21.11 16.9 1.5 Inv

Small Index (Lipper) - 363 - - - - - - - - -

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Up vs. Down Market Performance As of December 31, 2009

47

Fund Name Ticker Symbol

Up Capture

Ratio

Down Capture

Ratio

Broad Category Benchmark Up Capture

Ratio

Down Capture

Ratio

M&I Benchmark

Domestic Stock Funds

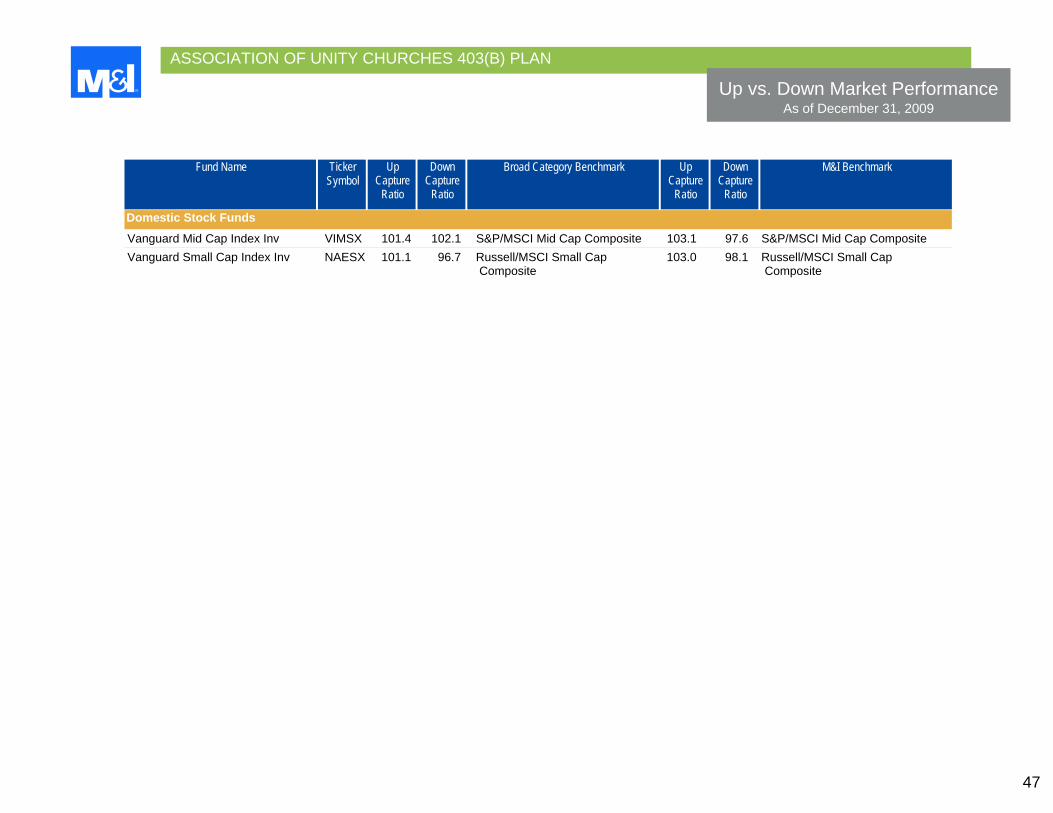

Vanguard Mid Cap Index Inv VIMSX 101.4 102.1 S&P/MSCI Mid Cap Composite 103.1 97.6 S&P/MSCI Mid Cap Composite Vanguard Small Cap Index Inv NAESX 101.1 96.7 Russell/MSCI Small Cap 103.0 98.1 Russell/MSCI Small Cap Composite Composite

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Fees & Expenses As of December 31, 2009

48

*"Other revenue" includes sub-transfer agent fees paid by unaffiliated mutual fund companies, which are negotiated individually with each fund company. "Other revenue" for Marshall Funds includes the investment management fee payable to M&I Investment Management Corp. and any shareholder servicing fees charged by each fund. These fees are paid on a frequency determined by, and are established by and subject to change in the discretion of, the fund companies listed. M&I will use its best efforts to collect these fees, and will periodically notify the Plan Administrator in the event M&I is notified of any change in the amount of these fees. To the extent required by applicable law or as agreed upon between M&I and the Employer, revenue that is paid to M&I by funds may be credited to participants' accounts or reserved to pay Plan expenses as soon as administratively feasible following M&I’s receipt of payments from the fund family. Review the Services Agreement for additional detail regarding plan fees.

Fund Name Morningstar Category Category Avg Expense

Gross Expense Ratio

Net Expense Ratio

12b-1 Fee Other Revenue* M&I Total Rev. Sharing

Redemption Fee

Domestic Stock Funds

Vanguard Mid Cap Index Inv Mid Cap Blend 1.32 0.27 0.27 - - 0.00 - Vanguard Small Cap Index Inv Small Cap Blend 1.50 0.28 0.28 - - 0.00 -

Section VII: Market Commentary4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

50

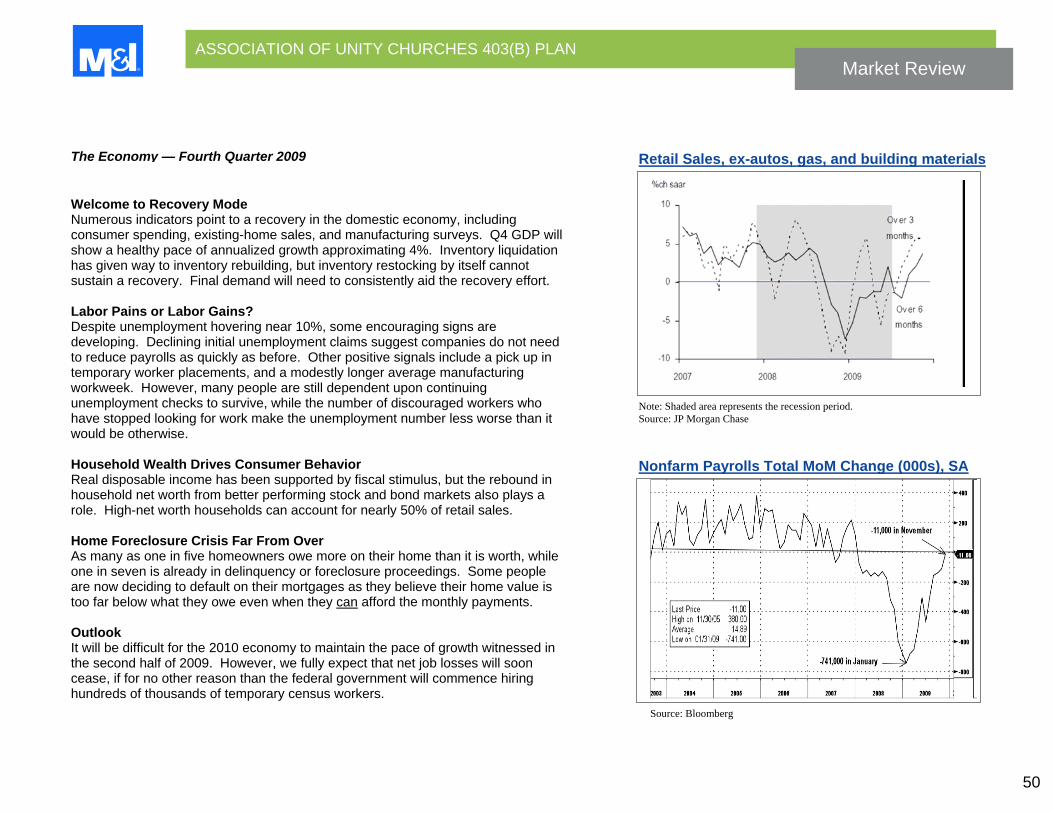

Source: Bloomberg

Retail Sales, ex-autos, gas, and building materials

Note: Shaded area represents the recession period. Source: JP Morgan Chase

Nonfarm Payrolls Total MoM Change (000s), SA

The Economy — Fourth Quarter 2009

Welcome to Recovery Mode Numerous indicators point to a recovery in the domestic economy, including consumer spending, existing-home sales, and manufacturing surveys. Q4 GDP will show a healthy pace of annualized growth approximating 4%. Inventory liquidation has given way to inventory rebuilding, but inventory restocking by itself cannot sustain a recovery. Final demand will need to consistently aid the recovery effort. Labor Pains or Labor Gains? Despite unemployment hovering near 10%, some encouraging signs are developing. Declining initial unemployment claims suggest companies do not need to reduce payrolls as quickly as before. Other positive signals include a pick up in temporary worker placements, and a modestly longer average manufacturing workweek. However, many people are still dependent upon continuing unemployment checks to survive, while the number of discouraged workers who have stopped looking for work make the unemployment number less worse than it would be otherwise. Household Wealth Drives Consumer Behavior Real disposable income has been supported by fiscal stimulus, but the rebound in household net worth from better performing stock and bond markets also plays a role. High-net worth households can account for nearly 50% of retail sales. Home Foreclosure Crisis Far From Over As many as one in five homeowners owe more on their home than it is worth, while one in seven is already in delinquency or foreclosure proceedings. Some people are now deciding to default on their mortgages as they believe their home value is too far below what they owe even when they can afford the monthly payments. Outlook It will be difficult for the 2010 economy to maintain the pace of growth witnessed in the second half of 2009. However, we fully expect that net job losses will soon cease, if for no other reason than the federal government will commence hiring hundreds of thousands of temporary census workers.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

51

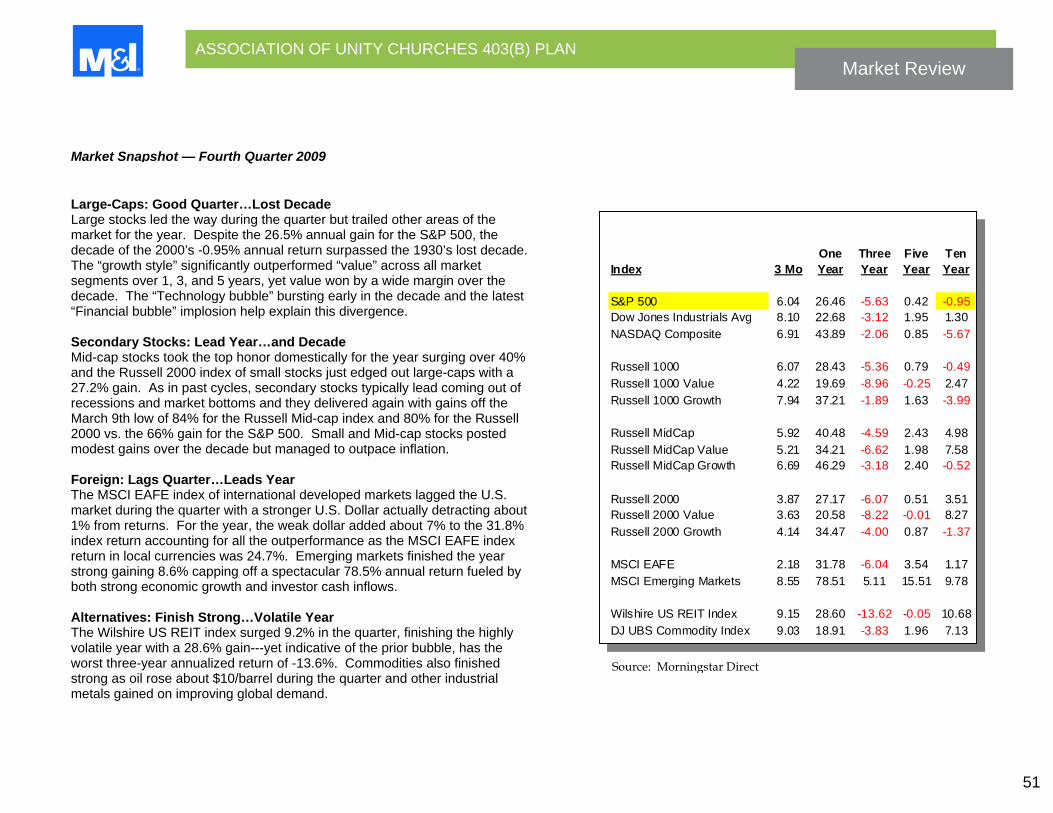

Source: Morningstar Direct

Index 3 MoOne Year

Three Year

Five Year

Ten Year

S&P 500 6.04 26.46 -5.63 0.42 -0.95Dow Jones Industrials Avg 8.10 22.68 -3.12 1.95 1.30NASDAQ Composite 6.91 43.89 -2.06 0.85 -5.67

Russell 1000 6.07 28.43 -5.36 0.79 -0.49Russell 1000 Value 4.22 19.69 -8.96 -0.25 2.47Russell 1000 Growth 7.94 37.21 -1.89 1.63 -3.99

Russell MidCap 5.92 40.48 -4.59 2.43 4.98Russell MidCap Value 5.21 34.21 -6.62 1.98 7.58Russell MidCap Growth 6.69 46.29 -3.18 2.40 -0.52

Russell 2000 3.87 27.17 -6.07 0.51 3.51Russell 2000 Value 3.63 20.58 -8.22 -0.01 8.27Russell 2000 Growth 4.14 34.47 -4.00 0.87 -1.37

MSCI EAFE 2.18 31.78 -6.04 3.54 1.17MSCI Emerging Markets 8.55 78.51 5.11 15.51 9.78

Wilshire US REIT Index 9.15 28.60 -13.62 -0.05 10.68DJ UBS Commodity Index 9.03 18.91 -3.83 1.96 7.13

Market Snapshot — Fourth Quarter 2009

Large-Caps: Good Quarter…Lost Decade Large stocks led the way during the quarter but trailed other areas of the market for the year. Despite the 26.5% annual gain for the S&P 500, the decade of the 2000’s -0.95% annual return surpassed the 1930’s lost decade. The “growth style” significantly outperformed “value” across all market segments over 1, 3, and 5 years, yet value won by a wide margin over the decade. The “Technology bubble” bursting early in the decade and the latest “Financial bubble” implosion help explain this divergence. Secondary Stocks: Lead Year…and Decade Mid-cap stocks took the top honor domestically for the year surging over 40% and the Russell 2000 index of small stocks just edged out large-caps with a 27.2% gain. As in past cycles, secondary stocks typically lead coming out of recessions and market bottoms and they delivered again with gains off the March 9th low of 84% for the Russell Mid-cap index and 80% for the Russell 2000 vs. the 66% gain for the S&P 500. Small and Mid-cap stocks posted modest gains over the decade but managed to outpace inflation. Foreign: Lags Quarter…Leads Year The MSCI EAFE index of international developed markets lagged the U.S. market during the quarter with a stronger U.S. Dollar actually detracting about 1% from returns. For the year, the weak dollar added about 7% to the 31.8% index return accounting for all the outperformance as the MSCI EAFE index return in local currencies was 24.7%. Emerging markets finished the year strong gaining 8.6% capping off a spectacular 78.5% annual return fueled by both strong economic growth and investor cash inflows. Alternatives: Finish Strong…Volatile Year The Wilshire US REIT index surged 9.2% in the quarter, finishing the highly volatile year with a 28.6% gain---yet indicative of the prior bubble, has the worst three-year annualized return of -13.6%. Commodities also finished strong as oil rose about $10/barrel during the quarter and other industrial metals gained on improving global demand.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

52

Bond Market Performance

Source: Barclays

Index 1Mo 3Mo YTD 1Yr

Barclays Aggregate -1.56 0.20 5.93 5.93

Barclays Government -2.27 -1.00 -2.20 -2.20

Barclays Credit -1.00 1.03 16.04 16.04

Barclays Mortgage -1.41 0.57 5.89 5.89

Barclays High Yield Index 3.28 6.19 58.20 58.20

Barclays 1 - 10 Yr Muni -0.14 -0.09 7.18 7.18

Yield Curve Performance

Source: Barclays

Rate QuarterlyU.S. Treasury 09/30/09 12/31/09 Change Return

3 Month 0.11 0.05 -0.06 0.04

6 Month 0.17 0.18 0.01 0.072 Year 0.94 1.13 0.19 0.16

3 Year 1.42 1.67 0.25 0.06

5 Year 2.31 2.68 0.37 -0.6410 Year 3.30 3.83 0.53 -3.60

30 Year 4.05 4.63 0.58 -8.46

U.S. Bond Market — Fourth Quarter 2009

Once-in-a-Lifetime Returns The riskiest parts of the bond market performed relatively well in Q4 but were spectacular in the context of the entire year. Corporate bonds performed in record fashion versus Treasury debt. On a duration-matched basis, investment grade corporate sector performance exceeded that of Treasuries by close to 20%! Uncle Sam Acts as Both Buyer and Seller The bond market was swamped by record amounts of new Treasury issuance amounting to $2.1 trillion. Government security yields rose across the board, with long-term yields rising the most (a bearish steepening pattern). Usually mortgage rates rise when Treasury yields go higher. Thanks to a Federal Reserve commitment to purchase up to $1.25 trillion in mortgage-backed securities (MBS), MBS had their second best performance year ever vs. Treasuries. Now Everyone is a Fed-Watcher By necessity, investors must pay very close attention to the behavior of the Federal Reserve. Short-term interest rates have been held near zero for more than a year. Despite language indicating rates are to be kept “exceptionally low for an extended period”, the bond market will anticipate and build in assumptions as to future Fed policy moves well before an actual change is made. We expect volatility surrounding the short-end of the yield curve will rise in 2010.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

53

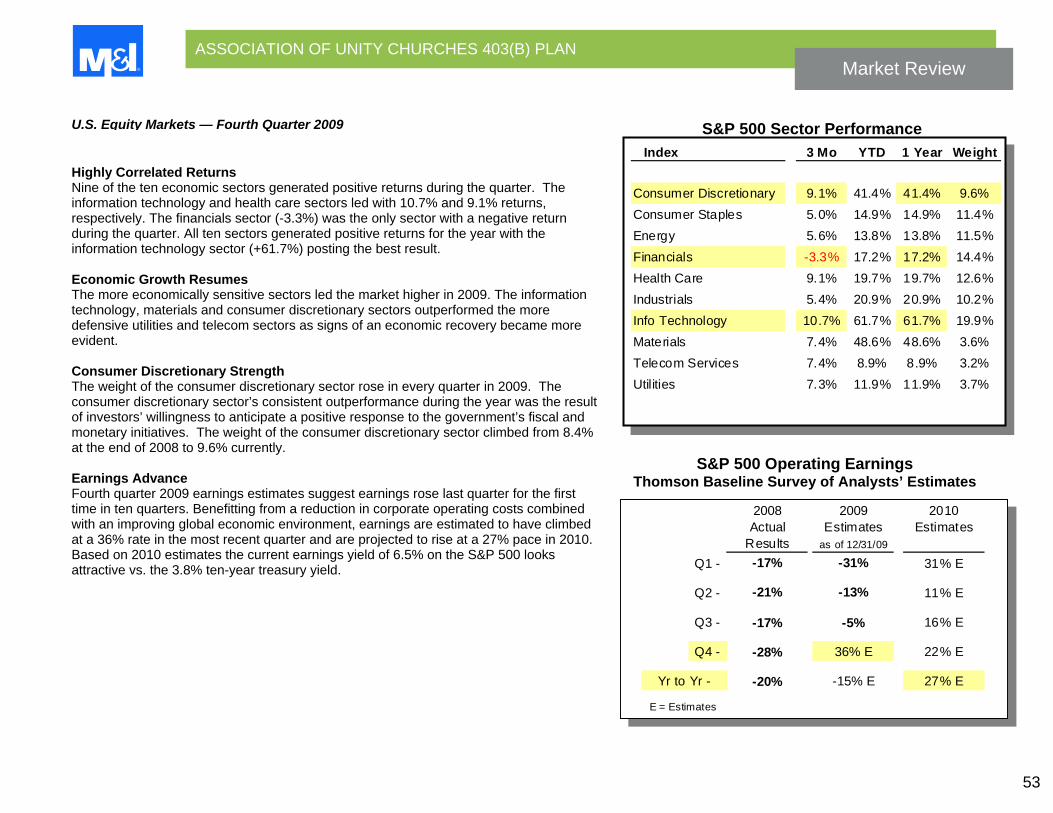

Source: Baseline

Source: Baseline

S&P 500 Operating Earnings Thomson Baseline Survey of Analysts’ Estimates

2008 2009 2010Actual Estimates Estimates

Results as of 12/31/09

Q1 - -17% -31% 31% E

Q2 - -21% -13% 11% E

Q3 - -17% -5% 16% E

Q4 - -28% 36% E 22% E

-20% -15% E 27% E

E = Estimates

Yr to Yr -

S&P 500 Sector Performance Index 3 Mo YTD 1 Year Weight

Consumer Discretionary 9.1% 41.4% 41.4% 9.6%Consumer Staples 5.0% 14.9% 14.9% 11.4%Energy 5.6% 13.8% 13.8% 11.5%Financials -3.3% 17.2% 17.2% 14.4%Health Care 9.1% 19.7% 19.7% 12.6%Industrials 5.4% 20.9% 20.9% 10.2%Info Technology 10.7% 61.7% 61.7% 19.9%Materials 7.4% 48.6% 48.6% 3.6%Telecom Services 7.4% 8.9% 8.9% 3.2%Utilities 7.3% 11.9% 11.9% 3.7%

U.S. Equity Markets — Fourth Quarter 2009

Highly Correlated Returns Nine of the ten economic sectors generated positive returns during the quarter. The information technology and health care sectors led with 10.7% and 9.1% returns, respectively. The financials sector (-3.3%) was the only sector with a negative return during the quarter. All ten sectors generated positive returns for the year with the information technology sector (+61.7%) posting the best result. Economic Growth Resumes The more economically sensitive sectors led the market higher in 2009. The information technology, materials and consumer discretionary sectors outperformed the more defensive utilities and telecom sectors as signs of an economic recovery became more evident. Consumer Discretionary Strength The weight of the consumer discretionary sector rose in every quarter in 2009. The consumer discretionary sector’s consistent outperformance during the year was the result of investors’ willingness to anticipate a positive response to the government’s fiscal and monetary initiatives. The weight of the consumer discretionary sector climbed from 8.4% at the end of 2008 to 9.6% currently. Earnings Advance Fourth quarter 2009 earnings estimates suggest earnings rose last quarter for the first time in ten quarters. Benefitting from a reduction in corporate operating costs combined with an improving global economic environment, earnings are estimated to have climbed at a 36% rate in the most recent quarter and are projected to rise at a 27% pace in 2010. Based on 2010 estimates the current earnings yield of 6.5% on the S&P 500 looks attractive vs. the 3.8% ten-year treasury yield.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

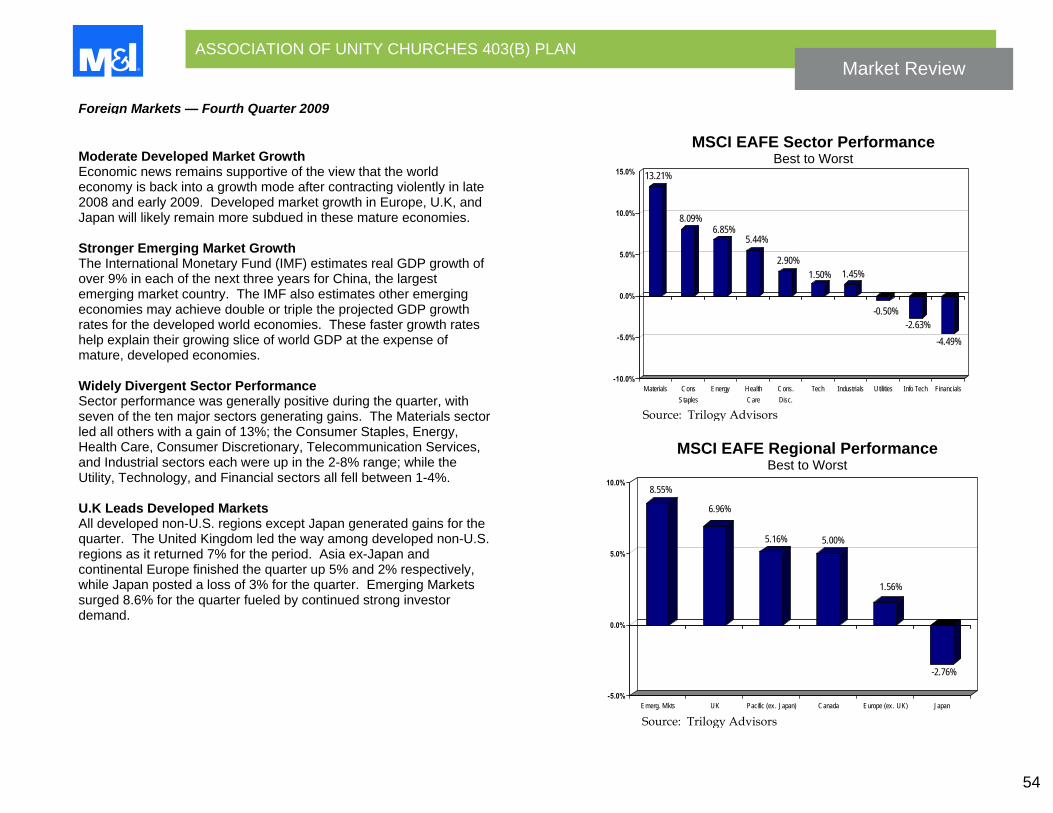

54

13.21%

8.09%6.85%

5.44%

2.90%1.50% 1.45%

-0.50%-2.63%

-4.49%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Materials ConsStaples

Energy HealthCare

Cons.Disc.

Tech Industrials Utilities Info Tech Financials

Source: Trilogy Advisors

MSCI EAFE Regional Performance Best to Worst

8.55%

6.96%

5.16% 5.00%

1.56%

-2.76%

-5.0%

0.0%

5.0%

10.0%

Emerg. Mkts UK Pacific (ex. Japan) Canada Europe (ex. UK) Japan

Source: Trilogy Advisors

MSCI EAFE Sector Performance Best to Worst

Foreign Markets — Fourth Quarter 2009

Moderate Developed Market Growth Economic news remains supportive of the view that the world economy is back into a growth mode after contracting violently in late 2008 and early 2009. Developed market growth in Europe, U.K, and Japan will likely remain more subdued in these mature economies. Stronger Emerging Market Growth The International Monetary Fund (IMF) estimates real GDP growth of over 9% in each of the next three years for China, the largest emerging market country. The IMF also estimates other emerging economies may achieve double or triple the projected GDP growth rates for the developed world economies. These faster growth rates help explain their growing slice of world GDP at the expense of mature, developed economies. Widely Divergent Sector Performance Sector performance was generally positive during the quarter, with seven of the ten major sectors generating gains. The Materials sector led all others with a gain of 13%; the Consumer Staples, Energy, Health Care, Consumer Discretionary, Telecommunication Services, and Industrial sectors each were up in the 2-8% range; while the Utility, Technology, and Financial sectors all fell between 1-4%. U.K Leads Developed Markets All developed non-U.S. regions except Japan generated gains for the quarter. The United Kingdom led the way among developed non-U.S. regions as it returned 7% for the period. Asia ex-Japan and continental Europe finished the quarter up 5% and 2% respectively, while Japan posted a loss of 3% for the quarter. Emerging Markets surged 8.6% for the quarter fueled by continued strong investor demand.

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

55

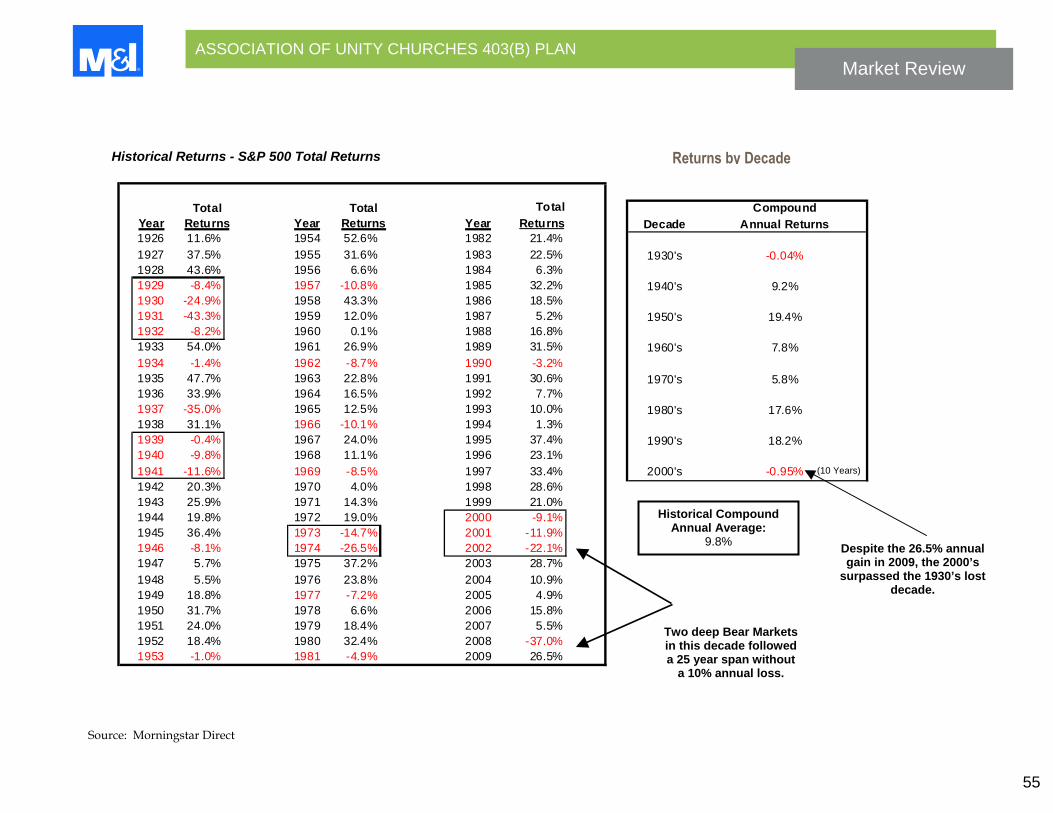

Historical Returns - S&P 500 Total Returns

Two deep Bear Markets in this decade followed a 25 year span without

a 10% annual loss.

Returns by Decade

Despite the 26.5% annual gain in 2009, the 2000’s

surpassed the 1930’s lost decade.

Historical CompoundAnnual Average:

9.8%

(10 Years)

Source: Morningstar Direct

Year Year YearTotal

Returns1926 11.6% 1954 52.6% 1982 21.4%1927 37.5% 1955 31.6% 1983 22.5%1928 43.6% 1956 6.6% 1984 6.3%1929 -8.4% 1957 -10.8% 1985 32.2%1930 -24.9% 1958 43.3% 1986 18.5%1931 -43.3% 1959 12.0% 1987 5.2%1932 -8.2% 1960 0.1% 1988 16.8%1933 54.0% 1961 26.9% 1989 31.5%1934 -1.4% 1962 -8.7% 1990 -3.2%1935 47.7% 1963 22.8% 1991 30.6%1936 33.9% 1964 16.5% 1992 7.7%1937 -35.0% 1965 12.5% 1993 10.0%1938 31.1% 1966 -10.1% 1994 1.3%1939 -0.4% 1967 24.0% 1995 37.4%1940 -9.8% 1968 11.1% 1996 23.1%1941 -11.6% 1969 -8.5% 1997 33.4%1942 20.3% 1970 4.0% 1998 28.6%1943 25.9% 1971 14.3% 1999 21.0%1944 19.8% 1972 19.0% 2000 -9.1%1945 36.4% 1973 -14.7% 2001 -11.9%1946 -8.1% 1974 -26.5% 2002 -22.1%1947 5.7% 1975 37.2% 2003 28.7%1948 5.5% 1976 23.8% 2004 10.9%1949 18.8% 1977 -7.2% 2005 4.9%1950 31.7% 1978 6.6% 2006 15.8%1951 24.0% 1979 18.4% 2007 5.5%1952 18.4% 1980 32.4% 2008 -37.0%1953 -1.0% 1981 -4.9% 2009 26.5%

Total Returns

Total Returns Decade

Compound Annual Returns

1930's -0.04%

1940's 9.2%

1950's 19.4%

1960's 7.8%

1970's 5.8%

1980's 17.6%

1990's 18.2%

2000's -0.95%

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

56

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

57

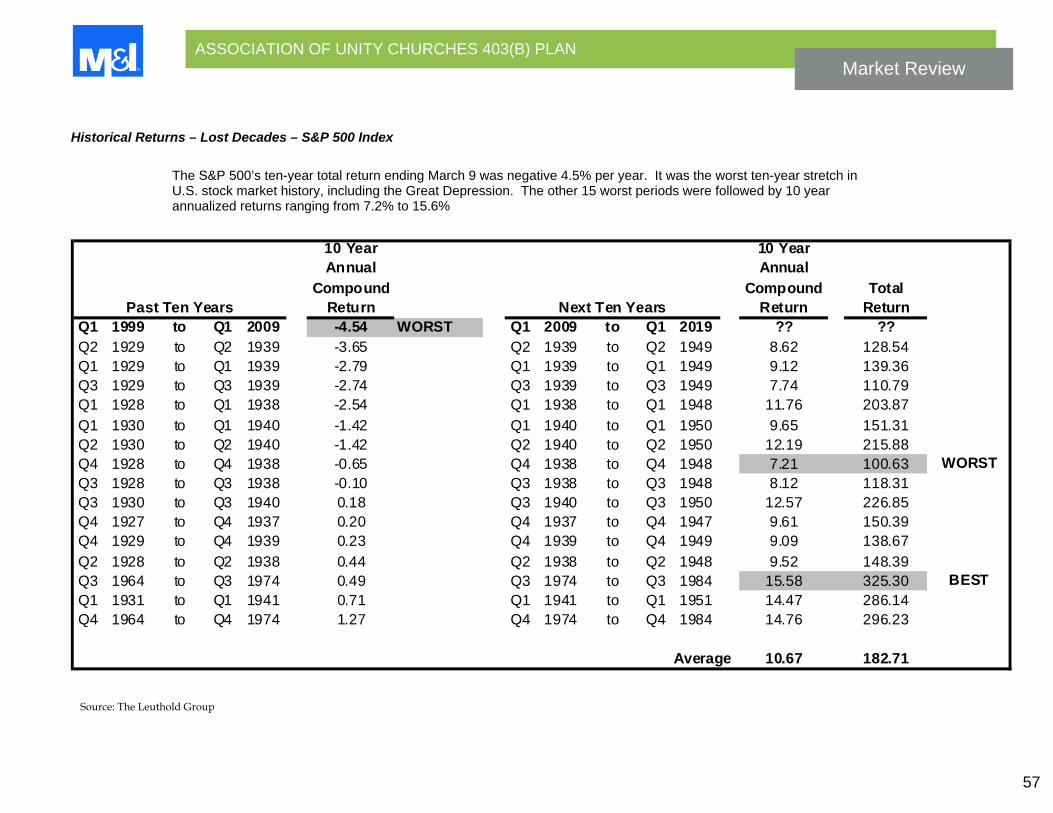

10 YearAnnual

Compound Return

10 YearAnnual

Compound Return

TotalReturn

Q1 1999 to Q1 2009 -4.54 WORST Q1 2009 to Q1 2019 ?? ??Q2 1929 to Q2 1939 -3.65 Q2 1939 to Q2 1949 8.62 128.54Q1 1929 to Q1 1939 -2.79 Q1 1939 to Q1 1949 9.12 139.36Q3 1929 to Q3 1939 -2.74 Q3 1939 to Q3 1949 7.74 110.79Q1 1928 to Q1 1938 -2.54 Q1 1938 to Q1 1948 11.76 203.87Q1 1930 to Q1 1940 -1.42 Q1 1940 to Q1 1950 9.65 151.31Q2 1930 to Q2 1940 -1.42 Q2 1940 to Q2 1950 12.19 215.88Q4 1928 to Q4 1938 -0.65 Q4 1938 to Q4 1948 7.21 100.63 WORSTQ3 1928 to Q3 1938 -0.10 Q3 1938 to Q3 1948 8.12 118.31Q3 1930 to Q3 1940 0.18 Q3 1940 to Q3 1950 12.57 226.85Q4 1927 to Q4 1937 0.20 Q4 1937 to Q4 1947 9.61 150.39Q4 1929 to Q4 1939 0.23 Q4 1939 to Q4 1949 9.09 138.67Q2 1928 to Q2 1938 0.44 Q2 1938 to Q2 1948 9.52 148.39Q3 1964 to Q3 1974 0.49 Q3 1974 to Q3 1984 15.58 325.30 BESTQ1 1931 to Q1 1941 0.71 Q1 1941 to Q1 1951 14.47 286.14Q4 1964 to Q4 1974 1.27 Q4 1974 to Q4 1984 14.76 296.23

Average 10.67 182.71

Past Ten Years Next Ten Years

Historical Returns – Lost Decades – S&P 500 Index

The S&P 500’s ten-year total return ending March 9 was negative 4.5% per year. It was the worst ten-year stretch in U.S. stock market history, including the Great Depression. The other 15 worst periods were followed by 10 year annualized returns ranging from 7.2% to 15.6%

Source: The Leuthold Group

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN Market Review

58

Disclosure

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested. Investments can not be made in an index. Past performance is not necessarily a guide to future performance. Investment products are: Not FDIC Insured | No Bank Guarantee | May Lose Value © 2010 Marshall & Ilsley Corporation

Section VIII: Definitions 4th Quarter, 2009

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Definitions

60

12b-1 An extra fee charged by some mutual funds to cover promotion, distributions, marketing expenses, and sometimes commissions to brokers. 12b-1 fee information is disclosed in a fund’s prospectus, is included in the stated expense ratio, and is usually less than 1%. Alpha Alpha is a risk (beta adjusted) measurement. Officially, alpha measures the difference between a portfolio's actual returns and what it might be expected to deliver based on its level of risk. Higher risk generally means higher reward. A positive alpha means the fund has beaten expectations. A negative alpha means that the manager failed to match performance with risk. If two managers had the same return but one had a lower beta, that manager would have a higher alpha. Annualized Periods Adjusting an income or return to an annual basis. Also called annualized return. Asset Allocation The mix of investment classes – equities, fixed income and cash – for an investor’s portfolio. The appropriate balance is based on the anticipated return and relative risk of each asset category as well as the investor’s personal factors such as risk tolerance, age, current asset allocation and asset level. Asset Allocation Funds An investment strategy that aims to balance

risk and reward by apportioning a portfolio’s assets according to an individual’s goals, risk tolerance and investment horizon. Risk Based

“Risk-based” asset allocation funds usually have a mix of stocks, bonds and cash equivalent securities. At the inception of the portfolio, a static allocation is established based on an expected risk/return profile. Because the value of assets can change given market conditions, the portfolio periodically needs to be re-adjusted to meet the allocation policy.

Target-Date

“Life-cycle” or “target-date” funds, which are often used in retirement plans, usually have a mix of stocks, bonds and cash equivalent securities that starts out with a higher risk-return position and gradually become less risky as the investor ages and/or nears retirement.

Average Effective Duration A measure of a fund's interest-rate sensitivity--the longer a fund's duration, the more sensitive the fund is to shifts in interest rates. Duration is determined by a formula that includes coupon rates and bond maturities. Small coupons tend to increase duration, while shorter maturities and higher coupons shorten duration. The relationship between funds with different durations is straightforward: A fund with a duration of 10 years is twice as volatile as a fund with a five-

year duration. Morningstar prints an average effective duration statistic that incorporates call, put, and prepayment possibilities. Average Effective Maturity Average effective maturity is a weighted average of all the effective maturities of the bonds in a portfolio. Effective maturity takes into consideration mortgage prepayments, puts, calls, adjustable coupons, and other features of individual bonds and is thus a more accurate measure of interest-rate sensitivity. Longer-maturity funds are generally considered more interest-rate sensitive than their shorter counterparts. Average Credit Quality An average of all the credit quality positions for a fund’s bond holdings. For corporate-bond and municipal bond funds, Morningstar also shows the percentage of fixed-income securities that fall within each credit-quality rating, as assigned by Standard & Poor's or Moody's. Because it's rare to find individual bonds in a portfolio with a rating below B, the average credit quality of bond funds in Morningstar's database ranges from AAA (highest) to B (lowest). U.S. Government bonds carry the highest credit rating, while bonds issued by speculative or bankrupt companies usually carry the lowest credit ratings. Anything at or below BB is considered a high-yield or "junk" bond. Balanced A mutual fund that buys a combination of common stock, preferred stock, bonds, and

ASSOCIATION OF UNITY CHURCHES 403(B) PLAN

Definitions

61

short-term bonds, to provide both income and capital appreciation while avoiding excessive risk. The purpose of balanced funds (also sometimes called hybrid funds) is to provide investors with a single mutual fund that combines both growth and income objectives, by investing in both stocks (for growth) and bonds (for income). Batting Average The batting average of the manager vs. a benchmark is the ratio between the number of periods where the manager outperforms the benchmark and the total number of periods. Benchmark A market index typically used to measure relative performance of a mutual fund or investment strategy. Broad Category Benchmark

A market index representing a broad asset class, such as large cap, small cap, or international. This index does not reflect stylistic biases.

M&I Benchmark

A market index used to compare a fund’s performance based on both a similar asset class and style bias – e.g., small cap value, foreign large growth.

Beta Beta represents the systematic risk of a portfolio and measures its historical sensitivity to a benchmark. A portfolio with a beta of one

Category

Morningstar Morningstar, Inc. is a leading provider of independent investment research in North America, Europe, Australia, and Asia. Morningstar is a source for information on stocks, mutual funds, variable annuities, closed-end funds, exchange-traded funds, separate accounts, hedge funds, and 529 college savings plans. With operations in 18 countries, they currently provide data on more than 290,000 investment offerings worldwide.

Morningstar Classification In an effort to distinguish funds by what they own, as well as by their prospectus objectives and styles, Morningstar developed the Morningstar Categories. While the prospectus objective identifies a fund’s investment goals based on the wording in the fund prospectus, the Morningstar Category identifies funds based on their actual investment styles as measured by their underlying portfolio holdings (portfolio statistics and compositions over the past three years). If the fund is new and has no portfolio, Morningstar estimates where it will fall before assigning a more permanent category. When necessary, Morningstar may change a category assignment based on current information. Lipper Lipper, a Reuters company, is a global leader in supplying mutual fund information, analytical tools, and