Embed Size (px)

Citation preview

Industry overview

and economic

impact

assessment for

the South African

medical

technology

industry

Prepared for the South African

Medical Device Industry

Association (SAMED)

Glossary

ANVISA Agencia Nacional de Vigilancia Sanitaria [National Health Surveillance Agency]

ARGMD Australian Regulatory Guidelines for Medical Devices

ARTG Australian Register of Therapeutic Goods

BBBEE Broad Based Black Economic Empowerment

CAGR Compound Annual Growth Rate

CE Conformité Européenne [European Conformity]

CSIR Council for Scientific and Industrial Research

DBSA Development Bank of Southern Africa

DST Department of Science and Technology

DTI Department of Trade and Industry

EUCOMED European Confederation of Medical Suppliers Association

EIA Economic Impact Assessment

FDA Food and Drug Administration (USA)

GHTF Global Harmonization Task Force

GMDN Global Medical Device Nomenclature

GMP Good Manufacturing Practice

HTA Health Technology Assessment

IDC Industrial Development Corporation

IMDRF International Medical Device Regulators Forum

ISO International Organisation for Standardisation

MCC Medicines Control Council

MRC Medical Research Council

NDOH National Department of Health

NDP National Development Plan

NHI National Health Insurance

PBS Pharmaceutical Benefits Scheme [Australia]

PIC Public Investment Corporation

PFMA Public Finance Management Act

R&D Research & Development

ROI Return On Investment

SABS South African Bureau of Standards

SADC Southern African Development Community

SAHPRA South African Health Products Regulatory Authority

SALDA South African Laboratory Diagnostics Association

SAMED South African Medical Device Industry Association

SHIP Strategic Health Innovation Partnership

SME Small and Medium Enterprises

TGA Therapeutics Goods Administration [Australia]

TIA Technology Innovation Agency

TUV Technischer Uberwachungsverein [Technical Inspection Association]

WHO World Health Organisation

Executive Summary

About medical technology

Medical technologies are described as medical devices, in vitro diagnostics, imaging equipment and

e-health solutions used to diagnose, monitor, assess predispositions and treat patients suffering from

a wide range of conditions1. It covers a broad range of products like wheelchairs, hip prosthesis,

cardiac stents, syringes and MRI-scanners to name a few. Medical technology helps people live

healthier and longer lives and is an indispensable necessity to any health system. Moreover

continuous innovations in medical technology enhance the effectiveness and quality of care.

Why this document?

SAMED has commissioned KPMG to estimate the size of the medical technology market in South

Africa, the medical technology market’s impact on the economy and to explore what lessons can be

learnt from other countries in terms of regulating the medical technology industry. The information

presented in this document is based on survey results of 47 medical technology companies.

Global medical technology market

The global medical technology market is estimated at a value of US $ 270 billion. Drivers for growth

in the medical technology market are; demographic trends in both developed (ageing) and developing

countries (move from communicable to non-communicable diseases); convergence across all

segments of healthcare and innovation in technology.

South African medical technology market

The South African medical technology market has an estimated value of US $ 1.0 billion and

constitutes 0.4% of the global medical technology market. The average revenue for multinational

medical technology companies (R 283 million per annum, per company) is more than the revenue for

local medical technology companies (R 75.2 million per annum, per company). The majority of

companies import medical technology products from other parts of the world. It is therefore no

surprise that the volume of imported products exceed the volume of exported products in monetary

terms. In terms of exports, most products are exported to other African countries (80% of total

export of medical technology products).

South Africa’s health system is described as a dichotomous system with well-developed private

sector and a burdened public sector. The medical technology market derives most of its revenues

from clients in the private sector (70%) when compared with clients in the public sector (30%). The

medical technology industry employs over 3 600 people and medical technology companies are on

average BBBEE level 4 contributors. The average BBBEE rating is lower for local manufacturers when

compared to multinationals. Medical technology companies spent a total of R 23.7 million on

sponsorship and R 31.7 million on training healthcare professionals that use their products.

Sector contribution

Medical technology industry respondents to the industry survey raised concerns regarding the import

of substandard medical technology products. According to respondents this hampers fair

competition, specifically on price for quality products, and is exacerbated by the lack of a quality

regulator for medical devices in South Africa. The majority of medical technology companies would

support the establishment of a quality regulator. Other matters raised by respondents include the lack

of transparency in government tender processes, delayed payment from major public sector clients,

the relative power of private sector healthcare funders in approving reimbursement for medical

technology products or not, the limited appreciation for and availability of funds for Research &

Development (R&D) of medical technology products in South Africa.

Economic impact

The medical technology industry’s overall contribution to the national economy is estimated at R 3.88

billion. The associated economic multiplier is calculated at 1.25, this means that for every additional R

1 spent in the national economy by the medical technology industry, an additional 25 cents is

1 Medical Technology – Contribution to Europe’s Health, Innovation and Economy, MedTech Europe, 2013.

generated in economic activity. Capital and operational expenditure by the medical technology

industry resulted in supporting a total of 20 901 jobs. Lastly, the tax revenue generated by the

medical technology industry during the period under review is estimated at R 1.86 billion. All the

numbers presented above are the consequence of direct, indirect and induced impact expenditures

of the medical technology industry have on the broader economy. Besides economic impact, medical

technology adds value to patients, healthcare professionals and, more generally, the health system.

Regulation

The South African medical technology industry is mainly unregulated, except for a few regulated

medical technology product categories (e.g. products that emit a radio frequency and electromagnetic

products). Although the government intends to establish a national quality regulator, SAHPRA (South

African Health Products Regulatory Authority), it is uncertain at this point in time when this regulatory

body will be established and start operating. Although most respondents of the survey strongly

support the implementation of quality regulation, most oppose price regulation. Brazil and Australia

are two countries included in this report to serve as a benchmark for quality regulation. Lessons

learnt from these countries (i.e. regulations implemented that had a positive impact on the medical

technology industry) are the establishment of a quality regulator, forming free trade zones with

neighbouring countries (Brazil), and a highly educated population (Australia).

Conclusion

This document contains three takeaways for the broader health economy:

■ Continue the drive for quality regulation.

■ Use existing innovation-platforms and incentivise industry to grow R&D investments

■ Unite, collaborate and share insights with key stakeholders and the population.

SAMED invested significantly in this project and hence the following applies; for those who wish to obtain a

copy of the report:

■ One hard copy of the report will be provided free of charge to those who participated in the survey.

■ The cost of additional hard copies for participants will be R 500 per copy.

■ SAMED members who did not participate, but wish to have a copy will be charged R 500 per copy.

■ For all other parties, the cost of a hard copy will be R 2 000.

Contents

1 Introduction 1

1.1 Why this report? 1

1.2 Reading guide for this report 1

1.3 The information used in this report 1

1.4 Limitations of scope 2

1.5 Disclaimer 2

2 Industry Analysis 3

2.1 Introduction 4

2.2 South Africa’s healthcare system 4

2.3 What is medical technology? 6

2.4 The global medical technology market 9

2.5 The South African medical technology market 11

3 Economic Impact Assessment 27

3.1 Overview of approach 28

3.2 Introduction to the economic modelling impact results 31

3.3 The value medical technology brings to people’s lives, beyond economic impact on

the country 34

3.4 Economic Impact on the National development plan 35

4 Regulatory Environment 37

4.1 Introduction 38

4.2 South African regulatory environment 38

4.3 A brief overview of the countries involved 42

4.4 Brazil 43

4.5 Australia 45

4.6 Lessons learnt 46

5 Conclusion 48

5.1 Three key takeaways 49

5.2 Closing remarks 50

Appendix 1 Background information on National Health Insurance (NHI) 52

Appendix 2 Survey 54

Appendix 3 Theory and application of macroeconomic

impact assessments 65

Figures

Figure 1 - Comparison between public and private healthcare expenditure, ......................................... 5

Figure 2 - Number of hospitals in public and private sector .................................................................... 5

Figure 3 - Product ranges in medical technology .................................................................................... 8

Figure 4 - The Global Medical Technology market (2006 - 2015) ............................................................ 9

Figure 5 - The Global Medical Technology market (2006 - 2015 / percentage) .................................... 10

Figure 6 - Revenue per company split between multinationals and local companies .......................... 12

Figure 7 – Nature of business survey responses .................................................................................. 12

Figure 8 - Revenue per Province ........................................................................................................... 13

Figure 9 - average revenue per product category ................................................................................. 14

Figure 10 - classification of medical technology products .................................................................... 15

Figure 11 - Employment split per employment skills level ................................................................... 17

Figure 12 - Employment split per race medical technology .................................................................. 18

Figure 13 - BBBEE levels medical technology sector ........................................................................... 19

Figure 14 - Expenditure on training medical technology ....................................................................... 20

Figure 15: Split of total operational spend ............................................................................................ 25

Figure 16 - How the Economic Impact Model works ........................................................................... 29

Figure 17: Description of economic linkages ........................................................................................ 30

Figure 18 - Survey respondents views on quality and price regulation ................................................ 40

Figure 19 - Quality management systems ............................................................................................ 41

Figure 20 - product quality standards .................................................................................................... 42

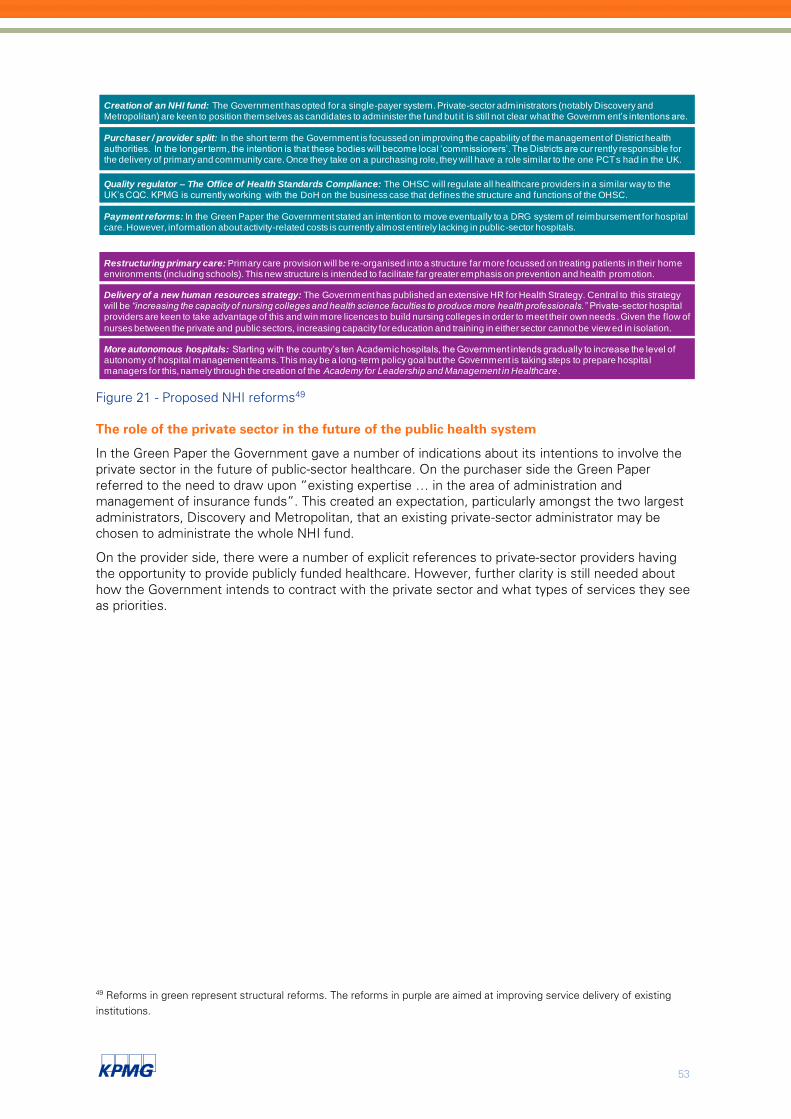

Figure 21 - Proposed NHI reforms ........................................................................................................ 53

Figure 22: Determining the Leontief inverse matrix ............................................................................. 66

Figure 23: Flow of income as represented by a SAM .......................................................................... 66

Figure 24: Determining the relationship between sectors in the SAM ................................................ 67

Figure 25: The multiplier effect ............................................................................................................. 67

Tables

Table 1 - Scheme membership change from 2010 to 2012 ................................................................... 6

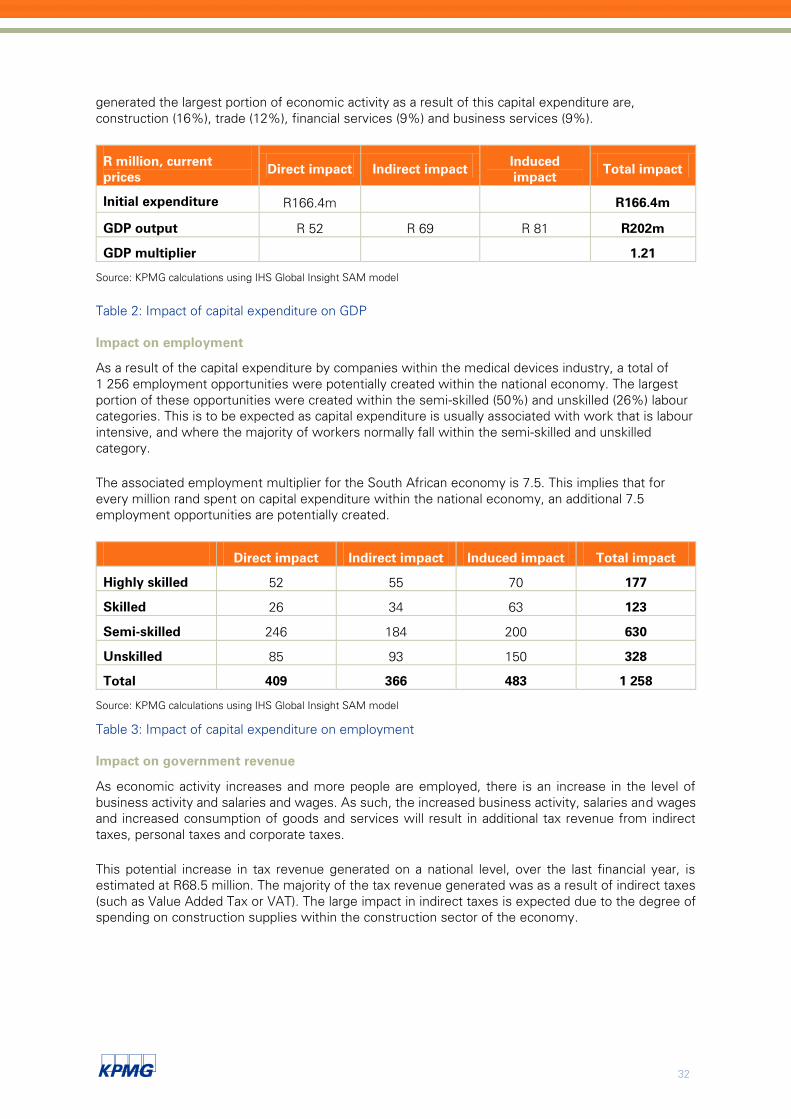

Table 2: Impact of capital expenditure on GDP..................................................................................... 32

Table 3: Impact of capital expenditure on employment ........................................................................ 32

Table 4: Impact of capital expenditure on Government revenue .......................................................... 33

Table 5: Impact of operational expenditure on GDP ............................................................................. 33

Table 6: Impact of operational expenditure on employment ................................................................ 34

Table 7: Impact of operational expenditure on Government revenue .................................................. 34

Table 8 - Overview of health indicators South Africa, Brazil and Australia ........................................... 43

1

1 Introduction

Introduction

1

1

1.1 Why this report?

The South African Medical Device Industry Association (further “SAMED”) seeks to continuously

engage with its stakeholders, to ensure a sustainable medical technology industry in South Africa.

This report estimates the size of the medical technology market in South Africa and, more

importantly, demonstrates the potential impact the industry has had on the broader economy and the

country as a whole. Lastly, current medical technology regulations in other countries are used to

provide insights and potential considerations for South Africa in possibly creating a business

environment where both the patient, the government and the industry could benefit.

As such, this report forms part of SAMED’s ongoing endeavours to inform and involve government,

SAMED’s members and other stakeholders on the medical technology industry.

SAMED has commissioned KPMG Services (Pty) Ltd (further “KPMG”) to undertake this

assessment. This report is prepared by KPMG, in collaboration with SAMED Board Members and

Secretariat.

1.2 Reading guide for this report

Section 2 – Industry Analysis

Before going into the detail of the South African medical technology market, an overview is given of

what is generally understood as ‘medical technology’ and a brief overview of the global medical

technology market. A summary of the South African healthcare market is included for the reader to

understand the environment medical technology companies operate in. Lastly, this section of the

report sketches the industry profile, using information provided by SAMED members. Data points

that are included in this analysis are, amongst others; company structure; product range; levels of

import and export; and lastly, SAMED members’ views on the sector contribution to South Africa’s

economy.

Section 3 – Economic Impact Assessment

The question answered in this section of the report is what the direct and indirect impact of the

industry is in South Africa. The macroeconomic variables included in this assessment are: Gross

Domestic Product (GDP); job creation; tax revenue and the impact that the industry indirectly has on

other industries. In addition, the section summarises how the industry contributes to the

achievement of government policy initiatives such as the Industry Policy Action Plan and the National

Development Plan.

Section 4 – Regulatory environment

The medical technology industry is heavily regulated in other parts of the world like the United States

(US) and the European Union. This section sets out what local regulation applies to the industry in

South Africa and seeks to gain insights from legislation and regulation from Brazil and Australia. It

furthermore includes the industry’s views on how regulation on price and quality could, or could not,

act as a driver for growth for the industry.

1.3 The information used in this report

A representation of SAMED and SALDA members have responded to a survey sent out by KPMG on

behalf of SAMED. The information in this report is presented at an aggregated level to ensure no data

could be traced back to individual companies. The information acquired through this survey is used

throughout the different sections in the report and is complemented with additional information from

market intelligence databases KPMG has access to. Where applicable this information was verified

through KPMG’s international network of member firms.

2

1.4 Limitations of scope

We have relied upon the sources of information referred to in this report. Except where specifically

stated, we have not sought to establish the reliability of those sources. We have however reviewed

the information and have sought explanations for key trends and salient features identified by us. We

have also satisfied ourselves, as far as possible, that the information presented is consistent with

other information obtained by us in the course of the work undertaken to prepare this report.

Our engagement does not comprise a due diligence review or constitute an audit or review, other

assurance engagement or an agreed-upon procedures engagement, performed in accordance with

International Standards on Auditing (ISAs), International Standards on Review Engagements (ISAEs)

or International Standards on Related Services (ISRS). Consequently, an audit opinion or assurance

conclusion will not be expressed nor will there be a report on factual findings. As such, this report

may not necessarily disclose all significant matters about the project or reveal errors or irregularities,

if any, in the information and representations made to us in order to undertake the valuation and upon

which we have relied.

Estimations made embody assumptions on the behaviour of factors in the macro and micro

economy, and the project itself. These assumptions were based on evidence available as at the time

of this report. Users of the forecasts may consider other assumptions to be more appropriate, which

may materially change the outcome of the forecasts. Please note that any advice, opinion, statement

of expectation, forecast or recommendation supplied by us as part of the service shall not amount to

any form of guarantee that we have determined or predicted future events or circumstances.

1.5 Disclaimer

This report has been compiled by KPMG for the sole and exclusive use of SAMED. It should not be

quoted in whole or in part, by any party other than SAMED, without our prior written consent.

KPMG’s findings in connection with this report are intended solely and exclusively for the benefit,

information, and use by SAMED. No party, other than SAMED, may rely on the findings, either in

whole or in part. KPMG (including its directors or employees or anybody or entity controlled, owned

or associated with KPMG) accepts no liability or responsibility whatsoever, resulting directly or

indirectly from the disclosure of our findings to any third party and/or the reliance of any third party on

the findings, either in whole or in part. KPMG’s findings are related to prevailing conditions and

information available at the time of issuing our report.

3

2 Industry Analysis

Industry Analysis

2

4

2.1 Introduction

When talking “medical technology”, one needs to understand what it exactly entails and within what

environment the medical technology market operates. This specifically refers to the relationship

between a country’s health system and medical technology. This section therefore starts with an

introduction into South Africa’s health system. It then continues with a brief overview of the global

medical technology market before unpacking the South African medical technology industry’s size

and value using the survey results.

2.2 South Africa’s healthcare system

South Africa’s two healthcare markets

South Africa’s healthcare spend is 8.9% of GDP2, which is often quoted as being comparable to the

spending of many developing countries and even some well-developed health systems, like

Australia3. However, this hides disparity between the public and private sectors, as 4% of GDP is

spent by the Government on the public health system, which meets the needs of approximately 80%

of the population4. Yet, even the increasingly public debate about the disparity between private and

public sector resourcing hides critical issues of the capability and capacity of management at a

Provincial Government level, where the public health systems are operationally managed. Over the

past 12 – 18 months these management issues have increasingly come to the fore and the National

Department of Health has placed pressure on Provincial Departments of Health to improve, even

putting some Provincial Departments of Health under administration, including the Limpopo and

Gauteng Department of Health.

The South African healthcare system suffers from the ‘growing pains’ characteristic of many

emerging economies – strong economic growth, a young population and a growing and demanding

middle class. In the public sector, challenges in making the best use of available capacity result in

poor access to healthcare. This, combined with poor infrastructure and problems with the availability

of staff, medicines and medical technology, create a strong public perception that the public sector

lacks capacity and is under-resourced. There is growing pressure on politicians and health sector

leaders at all levels to deliver better services.

The above strongly contrasts with a private sector that is well-funded and well-equipped, serving

almost nine million people, but using half of the healthcare expenditure in the country. However,

there is currently a great deal of pressure on the cost of private healthcare, both from the

Government and from consumers – and medical schemes through their members – who are

becoming increasingly aware of the high and rising costs of healthcare and who are becoming

increasingly selective about the level and type of health insurance they purchase. Healthcare pricing

is not currently regulated but the Government has recently announced an inquiry into the competitive

aspects in the healthcare sector through the Competition Commission.

The health sector in South Africa is often characterised as being split between entirely separate

public and private systems. However, this ignores the realities of a clinical workforce that commonly

works in both sectors and increasingly large sections of society that are combining limited health

insurance packages with public sector provision to cover the rest of their needs. The two systems

are closely interdependent. This is likely to increase in the coming years with joint regulation and,

potentially, large-scale private sector provision of publicly funded healthcare potentially under a NHI

umbrella.

2 WHO, NHA Indicators 2012

3 Based on World Bank data, www.worldbank.org, accessed in November 2013.

4 Business Monitor International, 2013.

5

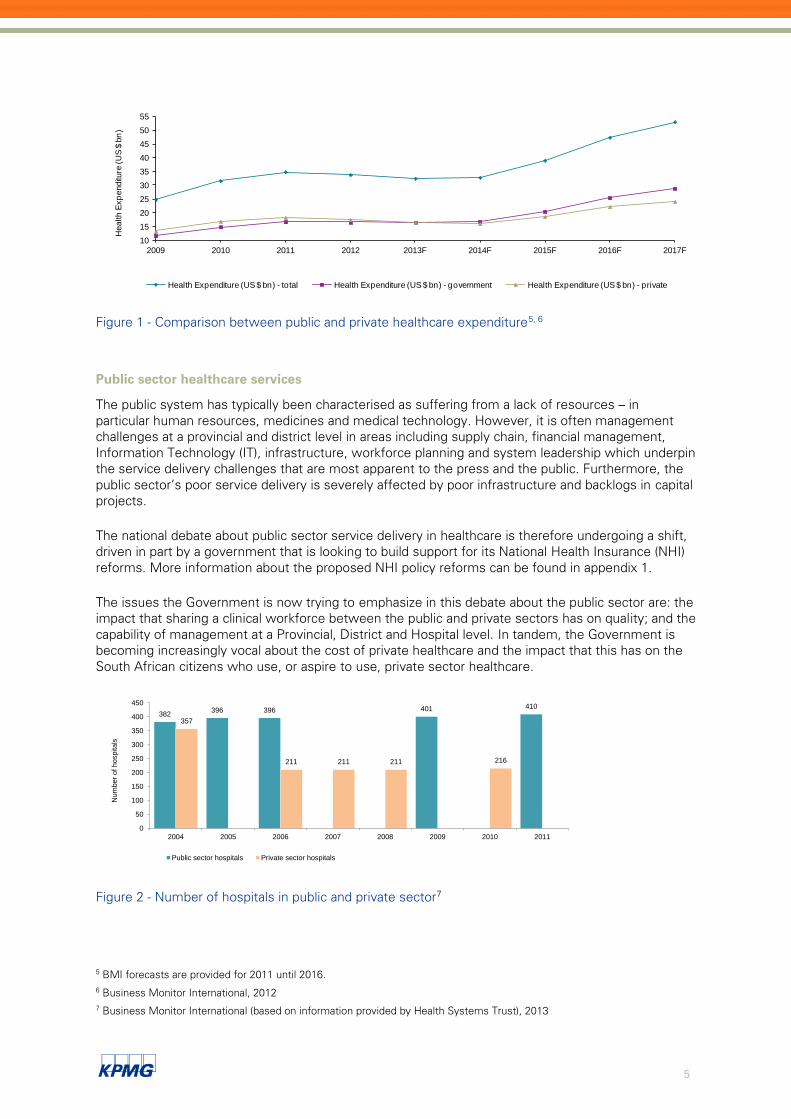

Figure 1 - Comparison between public and private healthcare expenditure5, 6

Public sector healthcare services

The public system has typically been characterised as suffering from a lack of resources – in

particular human resources, medicines and medical technology. However, it is often management

challenges at a provincial and district level in areas including supply chain, financial management,

Information Technology (IT), infrastructure, workforce planning and system leadership which underpin

the service delivery challenges that are most apparent to the press and the public. Furthermore, the

public sector’s poor service delivery is severely affected by poor infrastructure and backlogs in capital

projects.

The national debate about public sector service delivery in healthcare is therefore undergoing a shift,

driven in part by a government that is looking to build support for its National Health Insurance (NHI)

reforms. More information about the proposed NHI policy reforms can be found in appendix 1.

The issues the Government is now trying to emphasize in this debate about the public sector are: the

impact that sharing a clinical workforce between the public and private sectors has on quality; and the

capability of management at a Provincial, District and Hospital level. In tandem, the Government is

becoming increasingly vocal about the cost of private healthcare and the impact that this has on the

South African citizens who use, or aspire to use, private sector healthcare.

Figure 2 - Number of hospitals in public and private sector7

5 BMI forecasts are provided for 2011 until 2016.

6 Business Monitor International, 2012

7 Business Monitor International (based on information provided by Health Systems Trust), 2013

10

15

20

25

30

35

40

45

50

55

2009 2010 2011 2012 2013F 2014F 2015F 2016F 2017F

Health

Exp

enditu

re (U

S $

bn

)

Health Expenditure (US $ bn) - total Health Expenditure (US $ bn) - government Health Expenditure (US $ bn) - private

382396 396 401 410

357

211 211 211 216

0

50

100

150

200

250

300

350

400

450

2004 2005 2006 2007 2008 2009 2010 2011

Num

ber

of hospitals

Public sector hospitals Private sector hospitals

6

Private sector healthcare services

At the moment, only 17% of the South African population is able to afford private health insurance

and this has remained fairly stagnant over the past decade8.

The rise in private medical costs over the past decade is of growing concern, not just for the

government, but also for private payers – i.e. the medical schemes – who are keen to grow their

member populations but are facing significant challenges in doing so in a way that is sustainable. The

large medical aid administrators are beginning to implement more innovative commissioning models

to try to drive down the costs of acute care and, consequently, allow them to offer lower-cost health

insurance products to a broader spectrum of the population. This is largely achieved through

designated service provider (DSP) arrangements. However, the scale and impact of these products

remain constrained by the costs of hospital care and some of these lower-cost options are currently

running at a loss to the administrators.

In addition to the constraints that high medical costs put on medical schemes’ abilities to tap into

new segments of the population, medical schemes and administrators are also concerned about the

level of cover that new members are choosing and the risk profile of those members. Medical

schemes have seen many new members buying only very limited cover. This is particularly true for

the ‘emerging middle class’ members who may not have the financial support of previous

generations to allow them to buy comprehensive cover at a young age and therefore buy (and retain)

only limited cover.

Table 1 - Scheme membership change from 2010 to 20129

2.3 What is medical technology?

Global organisations use different definitions to describe and define the medical technology industry.

Some definitions commonly used are summed below.

The International Medical Device Regulators Forum (IMDRF, previously the Global Harmonization

Task Force, GHTF) describes Medical Devices as:

“...any instrument, apparatus, implement, machine, appliance, implant, reagent for in vitro use,

software, material or other similar or related article, intended by the manufacturer to be used, alone

or in combination, for human beings, for one or more of the specific medical purpose(s) of:

■ diagnosis, prevention, monitoring, treatment or alleviation of disease;

8 Council for Medical Scheme annual report 2012.

9 Council for Medical Scheme data, 2011, 2012, 2013

Type of scheme Type of membership 2010 2011 2012

Principal members 2 172 723 2 182 562 2 197 454

Dependants 2 627 192 2 577 552 2 562 540

Beneficiaries 4 799 915 4 760 114 4 759 994

Principal members 1 439 339 1 548 003 1 617 977

Dependants 2 076 464 2 218 292 2 301 502

Beneficiaries 3 515 803 3 766 295 3 919 479

Principal members 3 612 062 3 730 565 3 815 431

Dependants 4 703 656 4 795 844 4 864 042

Beneficiaries 8 315 718 8 526 409 8 679 473

Open schemes

Restricted schemes

Total schemes

7

■ diagnosis, monitoring, treatment, alleviation of or compensation for an injury;

■ investigation, replacement, modification, or support of the anatomy or of a physiological process;

■ supporting or sustaining life;

■ control of conception;

■ disinfection of medical devices;

■ providing information by means of in vitro examination of specimens derived from the human

body; and,

■ does not achieve its primary intended action by pharmacological, immunological or metabolic

means, in or on the human body, but which may be assisted in its intended function by such

means.”10

The World Health Organisation tends to follow this definition in its publications11 12.

Espicom, a renowned global market intelligence firm describes medical equipment as “...any piece of

equipment or apparatus used to treat or diagnose an illness, which comes into direct contact with the

patient”13

.

The US Food and Drug Administration (FDA) describes medical devices as “an instrument, apparatus,

implement, machine, contrivance, implant, in vitro reagent, or other similar or related article, including

a component part, or accessory which is:

■ recognized in the official National Formulary, of the Unites States Pharmacopoeia, or any

supplement to them,

■ intended for use in the diagnosis of disease or other conditions, or in the cure, mitigation,

treatment, or prevention of disease, in man or other animals, or

■ intended to affect the structure or any function of the body of man or other animals, and which

does not achieve its primary intended purposes through chemical action within or on the body of

man or other animals and which is not dependent upon being metabolized for the achievement of

any of its primary intended purposes”14

.

The European Commission defines a medical device as “...any instrument, apparatus, appliance,

software, material or other article, whether used alone or in combination, together with any

accessories, including the software intended by its manufacturer to be used specifically for diagnostic

and/or therapeutic purposes and necessary for its proper application, intended by the manufacturer to

be used for human beings for the purpose of:

■ diagnosis, prevention, monitoring, treatment or alleviation of disease,

■ diagnosis, monitoring, treatment alleviation or compensation for an injury or handicap,

■ investigation, replacement or modification of the anatomy or a physiological process,

■ control of conception,

10 GHTF, Definition of the Terms ‘Medical Device’ and ‘In Vitro Diagnostic (IVD) Medical Device’, 2012.

11 Medical Device Regulation – Global Overview and Guiding Principles, WHO, 2003.

12 Local Production and Technology Transfer to Increase Access to Medical Devices, WHO, 2012.

13 Medistat – Worldwide Medical Market Forecasts to 2015, Espicom, 2010.

14 FDA website, accessed 25 November 2013,

http://www.fda.gov/medicaldevices/deviceregulationandguidance/overview/classifyyourdevice/ucm051512.htm

8

and which does not achieve its principal intended action in or on the human body by pharmacological,

immunological or metabolic means, but which may be assisted in its function by such means”15

.

To summarise the above definitions one can say that there is a strong overlap between them.

Recurring themes include that medical technology is used for human beings (or patients), it is a

medical solution or has a medical purpose. Medical technology is furthermore used for diagnostic,

preventative, monitoring, alleviating and therapeutic purposes. Lastly, it is explicitly not technology

that is pharmacological.

In this document, the description put forward by EUCOMED (European Confederation of Medical

Suppliers Association) is used:

“Medical technologies are medical devices, in vitro diagnostics, imaging equipment and e-

health solutions used to diagnose, monitor, assess predispositions and treat patients suffering

from a wide range of conditions”16

.

Medical technology covers a broad, diverse range of products currently estimated to surpass the

number of 500 000 products. As such the global medical technology community has established

Global Medical Device Nomenclature consisting of sixteen categories. Again, in this report however,

the classification as put forward by EUCOMED is followed and displayed in the figure below.

Figure 3 - Product ranges in medical technology17

Class A represents low-hazard products such as bandages, tongue depressors, hospital beds, splints,

stethoscopes, syringes without needles, handheld mirrors, impression trays, reusable scalpels,

15 Directive 2007/47/EC of the European Parliament and the Council, 2007.

16 Medical Technology – Contribution to Europe’s Health, Innovation and Economy, MedTech Europe, 2013.

17 The European Medical Technology Industry in Figures. MedTech Europe, 2013.

Class C

Class D

Class B

Class A

9

forceps, wheelchairs, patient chairs, corrective glasses and frames, incision drapes, conductive gels,

non-invasive electrodes, etc.

Class B represents low-moderate products such as hypodermic needles, suction equipment, tracheal

tubes, orthodontic wires, needles for suturing, suckers, staplers, spinal needles, clamps, bridges and

crowns, muscle stimulators, cryosurgery equipment, powered drills, hearing aids, ultrasound, etc.

Class C represents moderate high-hazard products. Examples are lung ventilator, bone fixation plate,

blood bags, urethral stents, insulin pens, ligaments, internal closure devices, shunts, warming

blankets, blood warmers, surgical lasers, suction equipment, etc.

Lastly, class D represents high-hazard products such as heart valves, implantable defibrillators,

cardiovascular catheters, neurological catheters, cortical electrodes, cardiac output probes, biological

adhesives, spinal stents, intra-aortic balloon pumps, absorbable sutures, bioactive implants (surface

coatings), breast implants, infusion pumps, etc.

The classes above were included in the survey and are reported on in section 2.5 of this report.

Additional categorisation was surveyed and based on KPMG’s global segmentation of the medical

technology market supplemented with additional insights from SAMED. The results of this are set

out in the section mentioned above.

2.4 The global medical technology market

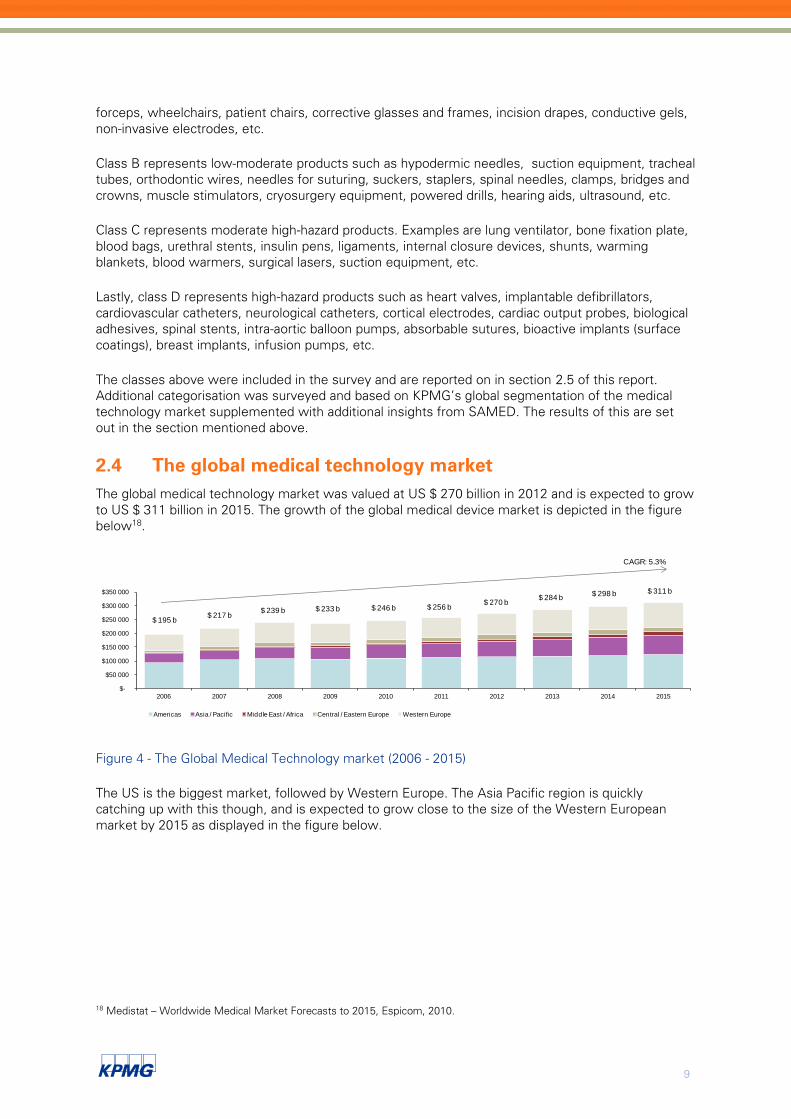

The global medical technology market was valued at US $ 270 billion in 2012 and is expected to grow

to US $ 311 billion in 2015. The growth of the global medical device market is depicted in the figure

below18

.

Figure 4 - The Global Medical Technology market (2006 - 2015)

The US is the biggest market, followed by Western Europe. The Asia Pacific region is quickly

catching up with this though, and is expected to grow close to the size of the Western European

market by 2015 as displayed in the figure below.

18 Medistat – Worldwide Medical Market Forecasts to 2015, Espicom, 2010.

$-

$50 000

$100 000

$150 000

$200 000

$250 000

$300 000

$350 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Americas Asia / Pacific Middle East / Africa Central / Eastern Europe Western Europe

$ 195 b$ 217 b

$ 239 b $ 233 b $ 246 b $ 256 b$ 270 b

$ 284 b$ 298 b $ 311 b

CAGR: 5.3%

10

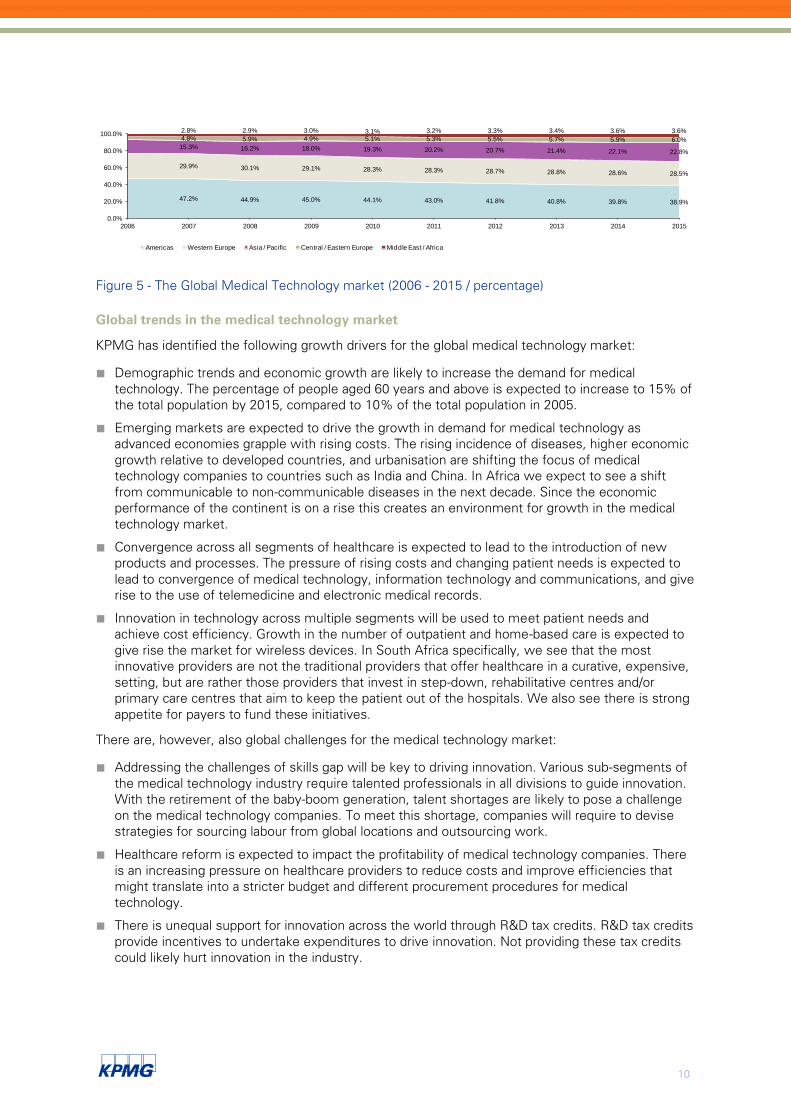

Figure 5 - The Global Medical Technology market (2006 - 2015 / percentage)

Global trends in the medical technology market

KPMG has identified the following growth drivers for the global medical technology market:

■ Demographic trends and economic growth are likely to increase the demand for medical

technology. The percentage of people aged 60 years and above is expected to increase to 15% of

the total population by 2015, compared to 10% of the total population in 2005.

■ Emerging markets are expected to drive the growth in demand for medical technology as

advanced economies grapple with rising costs. The rising incidence of diseases, higher economic

growth relative to developed countries, and urbanisation are shifting the focus of medical

technology companies to countries such as India and China. In Africa we expect to see a shift

from communicable to non-communicable diseases in the next decade. Since the economic

performance of the continent is on a rise this creates an environment for growth in the medical

technology market.

■ Convergence across all segments of healthcare is expected to lead to the introduction of new

products and processes. The pressure of rising costs and changing patient needs is expected to

lead to convergence of medical technology, information technology and communications, and give

rise to the use of telemedicine and electronic medical records.

■ Innovation in technology across multiple segments will be used to meet patient needs and

achieve cost efficiency. Growth in the number of outpatient and home-based care is expected to

give rise the market for wireless devices. In South Africa specifically, we see that the most

innovative providers are not the traditional providers that offer healthcare in a curative, expensive,

setting, but are rather those providers that invest in step-down, rehabilitative centres and/or

primary care centres that aim to keep the patient out of the hospitals. We also see there is strong

appetite for payers to fund these initiatives.

There are, however, also global challenges for the medical technology market:

■ Addressing the challenges of skills gap will be key to driving innovation. Various sub-segments of

the medical technology industry require talented professionals in all divisions to guide innovation.

With the retirement of the baby-boom generation, talent shortages are likely to pose a challenge

on the medical technology companies. To meet this shortage, companies will require to devise

strategies for sourcing labour from global locations and outsourcing work.

■ Healthcare reform is expected to impact the profitability of medical technology companies. There

is an increasing pressure on healthcare providers to reduce costs and improve efficiencies that

might translate into a stricter budget and different procurement procedures for medical

technology.

■ There is unequal support for innovation across the world through R&D tax credits. R&D tax credits

provide incentives to undertake expenditures to drive innovation. Not providing these tax credits

could likely hurt innovation in the industry.

47.2% 44.9% 45.0% 44.1% 43.0% 41.8% 40.8% 39.8% 38.9%

29.9% 30.1% 29.1% 28.3% 28.3% 28.7% 28.8% 28.6% 28.5%

15.3% 16.2% 18.0% 19.3% 20.2% 20.7% 21.4% 22.1% 22.8%

4.8% 5.9% 4.9% 5.1% 5.3% 5.5% 5.7% 5.9% 6.0%

2.8% 2.9% 3.0% 3.1% 3.2% 3.3% 3.4% 3.6% 3.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Americas Western Europe Asia / Pacific Central / Eastern Europe Middle East / Africa

11

2.5 The South African medical technology market

This part of the report includes information on the South African medical technology market. Where

possible we have compared the outcomes of the survey with market intelligence reports that were

available to KPMG and with other publicly available information. We report back on sections 1, 2, 4

and 5 from the survey. The survey is included in appendix 2 of this report.

Survey response

The survey was sent to 159 companies consisting of SAMED and SALDA19

members. Companies

that are not a member of the aforementioned bodies but that showed an appetite to participate in

this market investigation also received the survey. A total of 47 surveys (30%) were returned. From

the 47 companies that responded, 35 (74%) are SAMED members, 5 (11%) are SALDA members

and 7 (15%) or not members of SAMED or SALDA.

In the graphs displayed below, where applicable, the results are split between multinational

companies and local companies. The following definition is used to describe multinational companies:

all companies that operate in South Africa and distribute their own products manufactured abroad

and/or in South Africa. Local companies are described as all companies that originated and are based

in South Africa that distribute locally manufactured products and/or act as distributors/agents for

multinational companies that do not operate in South Africa. Multinationals with local manufacturing

capacity are regarded as multinationals. From the 47 surveys received, 23 (49%) came from

multinational companies and the remaining 24 (51%) are from local companies. The figures

presented below are based on the information provided by the survey participants. All figures are

based on the aggregated data of 47 companies unless otherwise stated.

Medical technology industry profile

Various sources estimate the total size of the South African market for medical technology to be

around the R 10 billion mark (US $ 1 billion, 0.4% of the global medical technology market)20 21 22

.

Total revenue based on the outcome of the survey adds up to R 8.3 billion. Based on the earlier

survey carried out in 2009, this is an increase of R 1.3 billion (19%)23

.

If we extrapolate the revenue, based on SAMED members that participated in the survey against the

total number of SAMED members, we calculate the total revenue of SAMED to be in the region of

about R12.1 billion24

25

. We can therefore fairly accurately comment on a sizeable part of the medical

technology market.

How companies’ revenue is split between multinationals and local companies is demonstrated in the

figure below.

19 Southern African Laboratory Diagnostics Association

20 Medistat – Worldwide Medical Market Forecasts to 2015, Espicom, 2010.

21 Manufacture of Medical and Surgical Equipment and Orthopaedic Appliances, Siccode 3741, Who Owns Whom, 2012

22 Extrapolation of SAMED membership data

23 Sample size in 2009 was 49 companies.

24 The extrapolation process only included companies that responded to the survey and are a member of SAMED. Using the

number of SAMED members per revenue category range [information provided by SAMED, based on the full list of SAMED

members, i.e. not only those that responded to the survey] we were able to extrapolate the survey revenue data into the same

revenue categories. Once we identified which revenue category each of the survey respondents fell into, we then calculated

how many of each revenue category responded to the survey. We then calculated the average revenue for each non-

responder within each revenue band and multiplied that by the number of non-responders within each revenue category. This

enabled us to provide a rough estimate of revenue unaccounted for by non-responders, which we calculated to be about R5.2

billion, whereas the total revenue of SAMED members that responded to the survey amounted to R6.95 billion.

25 The highest response rates to the questionnaire fell within the he higher revenue categories. Hence we are confident that

the survey provides accurate information for 75%-80% of the total market size.

12

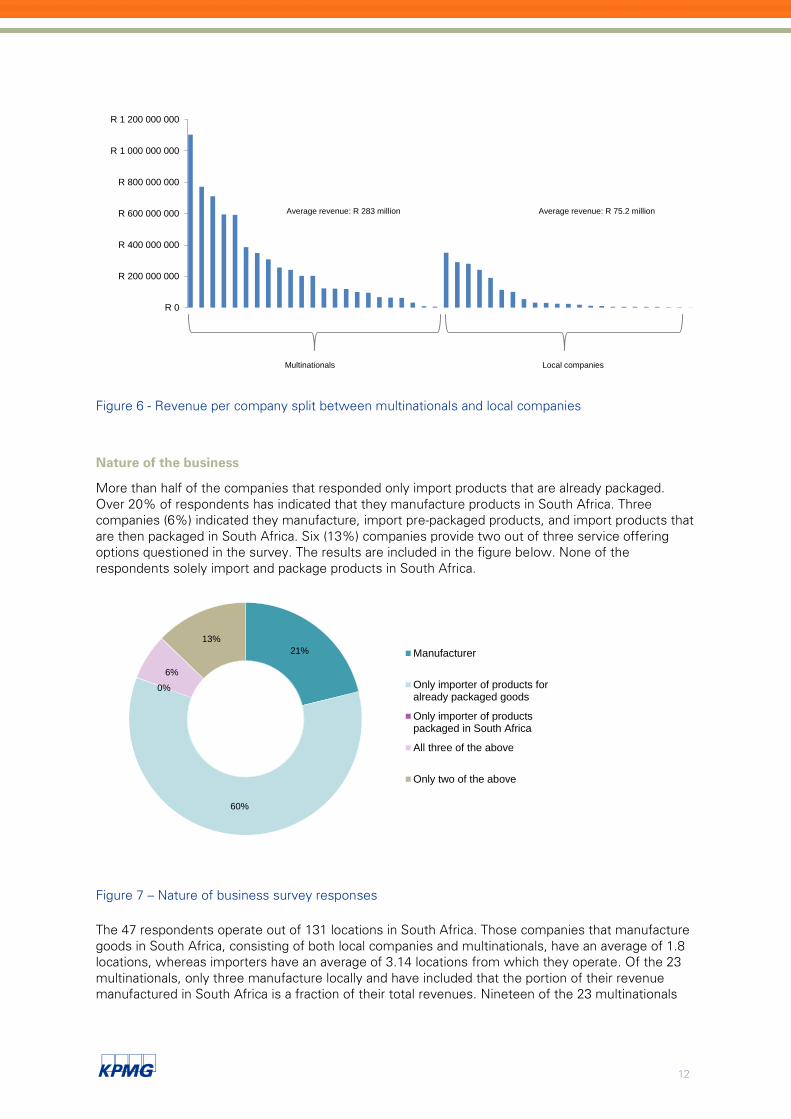

Figure 6 - Revenue per company split between multinationals and local companies

Nature of the business

More than half of the companies that responded only import products that are already packaged.

Over 20% of respondents has indicated that they manufacture products in South Africa. Three

companies (6%) indicated they manufacture, import pre-packaged products, and import products that

are then packaged in South Africa. Six (13%) companies provide two out of three service offering

options questioned in the survey. The results are included in the figure below. None of the

respondents solely import and package products in South Africa.

Figure 7 – Nature of business survey responses

The 47 respondents operate out of 131 locations in South Africa. Those companies that manufacture

goods in South Africa, consisting of both local companies and multinationals, have an average of 1.8

locations, whereas importers have an average of 3.14 locations from which they operate. Of the 23

multinationals, only three manufacture locally and have included that the portion of their revenue

manufactured in South Africa is a fraction of their total revenues. Nineteen of the 23 multinationals

R 0

R 200 000 000

R 400 000 000

R 600 000 000

R 800 000 000

R 1 000 000 000

R 1 200 000 000

Multinationals Local companies

Average revenue: R 283 million Average revenue: R 75.2 million

21%

60%

0%

6%

13%

Manufacturer

Only importer of products foralready packaged goods

Only importer of productspackaged in South Africa

All three of the above

Only two of the above

13

only import products into South Africa. The local companies consist of local manufacturers (9 out of

24) and importers (also 9 out of 24). The remaining 6 offer a mixture of services.

National footprint

The participants in the survey have been running operations in South Africa for an average of 26.5

years. One participant has been resident in South Africa for as long as 150 years, whereas the

youngest company was established just over a year ago. This average is higher for multinationals (38

years) compared to local companies (15 years).

The respondents were asked to split their revenue per province as presented in the figure below.

Figure 8 - Revenue per Province

Most revenue is generated in those provinces where most economic activity is centred, i.e. in

Gauteng, Western Cape and KwaZulu-Natal. The numbers are fairly consistent between

multinationals and local companies.

Product categories

There are several product categorisation mechanisms that are used globally. Probably the most well-

known is the Global Medical Device Nomenclature system that categorises medical technology

products into sixteen categories. However, following discussions with SAMED, it was decided to use

a more detailed categorisation, splitting the medical technology products into the overarching

categories of ‘wound care’, ‘implants’, ‘surgical equipment’, ‘non-surgical equipment’ and ‘other’ like

active medical devices, IVD, disinfecting devices and imaging devices, amongst others. The results

presented on the next page show the percentage revenue per product category for 46 respondents.

Based on the information provided, most revenue is generated through IVD products. The biggest

combined product range, in terms of revenue, is implants – whether that be orthopaedic, cardiac or

other implants. Surgical devices are the third in row with an average of 10% revenue. The ‘other’

category is made up of sterilisation packaging and monitoring devices, mobile clinics, dialysis

equipment and radioactive implants. On average, companies sell products in three different

categories. Thirteen companies (28%) have indicated that they only sell products in one product

category, i.e. advanced wound care. Those respondents that have products ranging over multiple

categories can typically be grouped at higher level, i.e. “implants” or “surgical devices”. International

publications show that the global medical technology sector is dominated by small and medium

enterprises (SMEs) and that companies within the industry are typically small companies employing

40 people on average26

.

26 Technical Barriers to Trade: Evaluating the Trade Effects of Supplier’s Declaration of Conformity, OECD Trade Policy Working

Paper No 78, 2008.

5% 7%

43%

16%

2% 3% 2% 3%

21%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Average revenue percentage

Eastern Cape Free State Gauteng Kwa-Zulu Natal Limpopo Mpumalanga Northern Cape North West Western Cape

14

Figure 9 - average revenue per product category

13%

11%

10%

9%

8%

7%

6%

6%

6%

4%

3%

3%

2%

2%

2%

2%

1%

1%

1%

1%

0%

0%

0%

0%

0%

0%

0%

0% 2% 4% 6% 8% 10% 12% 14% 16%

15

In addition to the grouping discussed above, respondents were also asked to split their revenue

according to the four product classifications as per the GHTF risk categorisations. These four

categories overlap with the ones in figure 4 in this report. The results shown in the figure below only

include the responses of 46 respondents.

Figure 10 - classification of medical technology products

Please note that the answers received to this question in the survey have not been answered

consistently and the results in the figure above should therefore be interpreted with caution.

Import and export

We have asked what percentage of the companies’ products are imported and exported, as a share

of total revenue. 46 respondents answered the question related to import and the results show that,

on average, 76% of products is imported. When looking at absolute numbers, 33 of the 46

companies import more than 80% of their products. These are predominantly multinationals. A WHO

publication estimates the value of medical technology imports in South Africa to be US $ 670

million.27

When it comes to exports, an average of 14.3% of revenues is generated by exporting products. This

was 8% in the 2009 survey. This average is higher for local companies (17.3%) compared to

multinationals (11.1%). There is quite a large variance in the revenues generated by exports between

the respondents: One company generates 90% of its revenues through exporting products, where

the minimum percentage of revenue consisting of exports for another is 0.5%. Out of the top ten

exporting companies that participated in the survey, six are local companies and four are

multinationals. For these top ten, export, on average, makes up 46% of their revenues. Of the total

exports, almost 80% is exported to other African countries – as such one can say that South Africa

plays an important role in providing medical technology to the rest of the continent. Products are

furthermore exported to the US, Europe, Latin America, the Middle East and the Indian Ocean

islands.

27 World Health Organization, Local Production and Technology Transfer to Increase Access to Medical Devices – Addressing

the barriers and challenges in low- and middle-income countries, 2012.

Class A - Low Hazard

31%

Class B - Low Moderate

22%

Class C - Moderate High Hazard

20%

Class D - High Hazard

27%

16

Public versus private sector clients

An average of 70% of revenues was earned through sales in the private sector, 30% through public

sector. These numbers are based on 34 respondents and don’t differ significantly compared with the

numbers collected in 2009 survey. The results seem to be consistent between multinationals and

local companies.

Employment

The 46 respondents that answered this section of the survey currently provide employment for 3 655

people. The top 10 largest companies in terms of staff numbers, employ 2 582 people (71% of the

total). This top 10 consists of 7 multinationals and 3 local companies. Included in the total number of

3 842, are 294 temporary employees. A further breakdown per job level and race is provided in the

figures on the following pages. Based on these figures one can see that the industry is dominated by

female employees (58.5% of the total), a phenomenon that is seen throughout the healthcare

industry. The medical technology is also predominantly a ‘white’ industry with 44% of employees

being white (53% in 2009), 30% are African (27.3% in 2009), 15% Coloured (8.7% in 2009) and 11%

Indian (11% in 2009).

17

Figure 11 - Employment split per employment skills level

8 9

38

117

177

121

42

4 7 19 37 54

31

11

3 11 26

78

31

4 7

80

75

187

276

26

2 16

2 8

29

123

105

209

96

3 8

33 5

8

56

146

83

8 11 3

1

95

44

40

1329

87

211

466

107

4

26

0

50

100

150

200

250

300

350

400

450

500

Top management Senior management Professionally qualified andexperienced specialists and

mid-management

Skilled technical andacademically qualified

workers, juniormanagement, supervisors,

foremen andsuperintendents

Semi-skilled anddiscretionary decision

makers

Unskilled and defineddecision makers

Temporary employees

African Male Coloured Male Indian Male White Male African Female Coloured Female Indian Female White Female Foreign nationals - male Foreign nationals - female

3.9% 6.0% 15.9% 34.4% 16.4% 15.3% 8.0%

18

Figure 12 - Employment split per race medical technology

8 4 3

80

2 3 8

29

5 19 7 11

75

8 8 11

87

3 2

38

19 26

187

29 33

31

211

6 2

117

37

78

276

123

58

95

466

5 2

177

54

31

26

105

56

44

107

0 0

121

31

4 2

209

146

40

4 1 0

42

11

7 16

96

83

13 26

0 0

0

50

100

150

200

250

300

350

400

450

500

African Male Coloured Male Indian Male White Male African Female Coloured Female Indian Female White Female Foreign nationals -male

Foreign nationals -female

Top management

Senior management

Professionally qualified and experienced specialists and mid-management

Skilled technical and academically qualified workers, junior management, supervisors, foremen and superintendents

Semi-skilled and discretionary decision makers

Unskilled and defined decision makers

Temporary employees

14.0% 4.5% 4.4% 18.1% 15.6% 10.6% 6.6%

25.4%

0.5% 0.2%

19

BBBEE Levels

Further to the conclusions presented above, top management in the medical technology industry is

largely white. Total top and senior management, based on 46 surveys, consists of 364 people. From

this number, 271 are white (74%), 27 are African (7%), 22 are coloured (6%), 33 are Indian (9%) and

11 are foreign nationals (3%). These numbers are reflected in the average BBBEE levels in the

industry as shown in the figure below. Compared to the 2009 industry overview, where total top and

senior management was 83% white, one can conclude that the industry is transforming, though be

at a steady pace.

Figure 13 - BBBEE levels medical technology sector

There are four medical technology companies that do not comply with BBBEE regulation. Most

companies (32%) are a level 4 contributor. When splitting these numbers between multinationals and

local companies, the mode for multinationals is a level 5 contributor whereas the mode for local

manufacturers is a level 4 contributor28

. Local companies also score higher, in absolute terms, on the

BBBEE levels 2 and 3. A cautious conclusion that can be drawn is that local companies are perhaps

better aware and have a better understanding of BBBEE regulation compared to multinational

companies. Another reason provided by multinationals is that to move beyond level 5 they would

need to sell equity which is something multinationals are reluctant to do due to the way their

business is structured and organised. When asked if respondents expect their BBBEE levels to

increase next year a majority answered ‘no’ (32 respondents, or 68%). The main reasons mentioned

in this regard were:

■ New BBBEE codes, that are considered to be ‘stricter’, that come into effect within the next

twelve months. The new targets of these codes are 88% blacks in junior management, 75% in

middle management and 60% in senior management; and,

■ The argument raised above relating to multinationals that are restricted in selling their equity.

The companies that indicate that their BBBEE levels will improve use the following arguments for it:

■ Planned restructuring of the business that will include a heavier investment on bursaries;

■ Employing more black staff in senior positions; and,

■ More investments in partnerships and social development.

28 The mode is the value that appears most often in the dataset.

01

8

15

9

5

0

54

BB

BE

E le

vel 1

con

trib

uto

r

BB

BE

E le

vel 2

con

trib

uto

r

BB

BE

E le

vel 3

con

trib

uto

r

BB

BE

E le

vel 4

con

trib

uto

r

BB

BE

E le

vel 5

con

trib

uto

r

BB

BE

E level 6

con

trib

uto

r

BB

BE

E le

vel 7

con

trib

uto

r

BB

BE

E le

vel 8

con

trib

uto

r

Non c

om

plia

nt

20

Investment in sponsorship and training

The respondents spent a total of R 23.7 million on sponsorship in the last audited financial year. This

is an average of R 504 000 per company if all companies – also those that do not spend any money

on sponsorships – are taken into account. When excluding companies that do not spend money on

sponsorship, the average is R 696 772. We found no correlation between total company revenue and

expenditure on training. Of the ten companies with the highest expenditure on sponsorship, seven

are multinationals.

Further to the expenditure on sponsorship, survey respondents have also shared their expenditure on

training split between the five categories in the figure below.

Figure 14 - Expenditure on training medical technology

Total expenditure on training is R 31.7 million. As can be seen in the figure above, half of it goes to

CME training for doctors in the private sector, followed by CME training for doctors in the public

sector. Consequently, over 80% of training is spent on training doctors. The remainder is set aside

for the training of allied health professionals in both the public and private sector. The category ‘other’

consists of specific training for employees. The expenditure on training by multinationals is

significantly higher (R 20.5 million) when compared with local companies (R 11.3 million). In section

3.3 of this report we further set out the value the medical technology delivers beyond its impact on

economic indicators. As can be seen in the figure above, the industry invests over R 30 million in

training health professionals and, as is further set out in section 3.3 of this report, this is but one of

the values the industry brings for health professionals.

Medical Technology sector contribution to South Africa – discussion

The survey is purposely designed to capture the – perhaps more qualitative and emotional –

arguments on the industry’s contribution to South Africa. With regards to this, we have agreed with

SAMED in the preparation of this survey, to ask the following four questions:

1. In your opinion, how can the contribution to the South African economy by the Medical

Device industry be increased?

2. What barriers should be removed to enable the expansion of the Medical Device industry in

South Africa?

Continuing Medical Education (CME ) training

for doctors in private sector50%

Continuing Medical Education (CME) training

for allied health professionals in the private

sector 8%

Continuing Medical Education (CME) training for doctors in public sector

31%

Continuing Medical Education (CME) training

for allied health professionals in the public

sector 7%

Other4%

R 15.8 million

R 2.6 million

R 9.8 million

R 2.1 million

R 1.4 million

21

3. In your opinion, how do you think the Medical Device industry contributes to Research &

Development in South Africa?

4. What barriers should be removed, to increase Research & Development spending in South

Africa?

No less than 44 respondents answered these open-ended questions of which the most common

themes brought forward by the respondents are summarised below.

2.5.1 Question 1: In your opinion, how can the contribution to the South African economy by

the Medical Device industry be increased?

The answers received are generally consistent and can be broken down into the following categories.

■ Promote local manufacturing

The vast majority of respondents, specifically the local companies, felt that an increase of local

manufacturing would have a significant impact on the nation’s economy in terms of supporting job

creation and its positive contribution to the balance of payments. The arguments most frequently

mentioned are further discussed hereafter.

Several companies have suggested that export incentives be created for products that are locally

manufactured. Besides creating incentives for locally manufacturing products, it would also nicely fit

into South Africa’s reputation in acting as a gateway for doing business in the rest of the continent

and specifically in the SADC countries. On the flipside and mentioned by several respondents is

penalising, through increasing tax or import levies, imported low and medium risk commodity

products that could have been manufactured locally. By only focussing on this product range it

excludes the more capital intensive products like CTs and MRIs. Other companies have argued that

incentives could be put in place by government to create an environment in which it is more

attractive, also for multinationals, to increase local manufacturing of medical technology. These

incentives could be put forward by the Department of Trade and Industry (dti). This Department could

play a role in prioritising the medical technology sector as was done previously by this Department for

the pharmaceuticals market. As such, dti could also create awareness of what the industry means for

the country’s economy. The respondents also suggest better and easier access for funds to invest in

R&D. Again, this could form part of incentives impose by government. However another example

mentioned in this respect is to set-up and invest in formal programmes at universities that exclusively

focus on medical technology.

■ Improve legislation/regulation

The second category of answers given by respondents is around improving legislation and regulation

in the industry. Several companies reason that less onerous labour legislation and a more stable

labour market are imperative for local manufacturers to be successful. Several companies mention

that regulation, and specifically registration of companies and/or products, of the industry would have

a positive impact specifically on quality of the medical devices. It prevents import of products that are

currently cheaper but are considered to be of sub-standard quality. In line with this reasoning, one

company strongly urged that MCC should improve its performance. Both local companies and

multinationals have commented on how BBBEE regulation in some cases hampers growth. The

smaller companies prefer a situation in which they would be subjected to stringent BBBEE models,

and/or, a situation in which BBBEE points are rewarded for those companies making local

investments. Multinationals agree with this as they believe that changes in ownership structures,

as was set in the previous section of this report, are not achievable.

There is a slight contradiction in the answers given as some companies indicate that less regulation

would benefit the economy and others argue more regulation is needed. Having said that, more

companies were in favour of ‘more regulation’ compared to ‘less regulation’.

22

■ Turnaround of the current practice and thinking for procurement and payment for our major payers

The major funders in private sector are the medical schemes that, in turn, have influence in what

medical technology is covered and thus preferred by patients and providers alike. Another important

payer is government. In general, respondents feel too much emphasis is placed on price and less so

on the long-term savings that new medical technology brings. In line with this reasoning; the

respondents feel there should be more focus on quality instead of price.

Many respondents have raised concerns related to delayed payments, or not paying according to

payment terms, by government. Indeed, this poses a financial risk for those companies whose main

clientele is within the public sector as cash flows become unpredictable resulting in a need to raise

finance that again results in additional, preventable, costs. This is a particular risk for small and

medium enterprises. Some respondents also commented on government procurement processes

saying that it could be improved in terms of transparency. Additionally, more focus should be placed

on quality and less on price and, so is felt in industry, also on BBBEE compliance. Lastly, respondents

claim that government indeed has a role play to increase the usage of locally manufactured products

and should therefore, in its procurement processes, award more credits to those companies that are

local manufacturers.

SAMED’s position on public procurement of medical technology is29

:

– Medical technology products are not commodities. They undergo rapid cycles of improvement

and variation to meet patient and doctor needs. A system in which low price alone prevails

over a combined consideration of cost and quality, fails to account for costs and value for the

entire episode of care. Many medical devices often remain in a patient or in use at a hospital

for many years. According to SAMED it favours older and simpler technology and does not

consider the long-term value and cost as replacing low-quality devices leads to additional

hospital expenditure and thus costs.

– When procuring medical technology, maintenance and the in- or exclusion of a maintenance

contract in price, should be considered. In the UK, for example, medical technology tenders are

evaluated not only on price but also on; functional characteristics; product support; quality; and,

delivery performance.

– Medical technology contracts should not be exclusive to one brand and/or product. This will

allow to cater for different patient, clinical and doctor needs. In addition, there should be a way

for new technology to be introduced during the term of the contract, this would specifically

apply to longer term contracts.

– Make contracting terms and conditions clear and transparent before publishing a tender to

increase competitiveness and create a level playing field between bidders.

– Procurement is most efficient when it is closer to the end-users and at the critical point of care.

As such, SAMED believes that decentralised procurement should be preferred over centralised

procurement; this will be specifically true for critical items. Another reason put forward by

SAMED is that central procurement would require a national database of all medical items

including stock-levels as procurement without such a system can lead to shortages or

oversupply.

– Competitive tendering should not artificially control the number of organisations that can exist

in a healthcare system. A maximum threshold should be established to limit the total monetary

value per tender. A way to circumvent this is to use multiple source contracts so that a diverse

range of brands, products and services is available to the clinical workforce.

■ Remaining issues

Not all the arguments provided by the survey respondents could be categorised. We do, however,

strongly feel that the remaining issues stated below are relevant and should be put forward in this

29 Draft SAMED position on public procurement of medical devices, 2012.

23

report. Several companies said that the main factor for growth for the medical technology industry is

the growth of the health sector in general, whether that be growth in private healthcare (through, for

example, GEMS) or in public sector (through NHI). Another company had a strong view that public

sector providers and the medical technology industry should improve collaboration to support and

revitalise the public sector hospitals. Through collaboration the medical technology industry could

lower costs and improve patient care in the public sector. There was one company who argued that

the trade association [SAMED] should aim, through its board members and secretariat

representation, to increase its visibility at government level.

Other remaining issues that were mentioned were related to increasing the training of health

professionals in actually using medical technology. Lastly, it was argued that South Africa is the

perfect place to create ‘domestic centres of global excellence’.

2.5.2 Question 2: What barriers should be removed to enable the expansion of the Medical

Device industry in South Africa?

The arguments put forward by the respondents are clearly in line with the arguments given under the

first question. The four main themes are reflected below:

■ Implement regulation and registration processes

The general tone in the answers provided to us is that there is a big need for more regulation and the

registration of products and companies that work in the sector. On the other hand, several

companies argue for less stringent regulation in the BBBEE space. One multinational specifically said

that removal of BBBEE legislation would allow multinationals to tender in NHI. There is only one

company that says less regulation would enable the expansion of the medical technology industry.

The main argument to increase regulation is to better regulate imported products and thus protect

patients from products that are of inferior quality. Multinationals tend to reason that they are reluctant

to invest in a country with a medical technology market that is minimally regulated. One company

suggested the creation of more free trade zones in Africa. For South Africa, this would create

incentives to export products manufactured in-country. Regarding the registration of products,

comments were made that the MCC should base its registration on the Health Technology

Assessment (HTA) framework and then specifically on the outcomes medical technology achieves,

rather than costs. Another company desired the processes to obtain CE-mark for locally

manufactured product to be simplified.

■ Incentivise the market

Lowering the cost-base for companies’ results in money being freed up for investments,

employment and profit. The market can be incentivised through, indeed, making sure the incurred

costs for companies decrease, through the creation of subsidies, grants and other ways of support.

The latter is further discussed under the following two questions related to R&D. Many companies

have stated that tax incentives can contribute significantly in terms of increasing investments in the

industry. Another argument shared is to remove import duties for raw materials used by local

manufacturers. Survey participants would welcome an investment fund set up by government.

Organisations that could play a role in providing investment funding are dti and the Department of

Science and Technology (DST), and parastatals like the Public Investment Corporation (PIC),

Development Bank of Southern Africa (DBSA), the Technology Innovation Agency (TIA) and the

Industrial Development Corporation (IDC) are well positioned to make medical technology a priority

industry as was done with pharmaceuticals in the last decade. One company explicitly mentioned

that public awareness of the industry should be a focal point, for example through the introduction of

a “made in SA” banner similar to the initiative in the food and retail industry with the “proudly South

African” logo.

There were a few companies that raised concerns about the relative power some dominant

healthcare funders (medical schemes) have in terms of approving medical technology products.

24

Some experience this environment, specifically to get medical technology on the ‘approved’ list of

medical devices, to be restricted. The main concern is around the limits set by funders. One

respondent said that ‘exclusion lists’ hamper the industry’s growth. In line with this argument, one

company suggested the creation of stronger links between HTA resource and reimbursement

models where HTA should rather focus on outcomes and longer-term cost impacts as opposed to

merely looking at current costs incurred.

■ Work more closely with government and raise general awareness of the medical technology

industry

A large portion of the respondents expressed concerns about the knowledge base with regards to

medical technology across the different spheres of government. According to the industry this has an

impact on national policies, but is also felt on a day-to-day basis when it comes to responding to

tenders and, once a tender is won, payment for services and products delivered. The feeling is that

there is a lack of transparency in the procurement process and some companies showed their

dissatisfaction if adjudication of a bid is delayed or cancelled.

Industry players indicated they’d appreciate a clear direction from government in terms of health

policies that is more open to innovation. Also, a clear path for the implementation of NHI is