Embed Size (px)

Citation preview

Preparing Australia’s future oil and gas workforce THREE SCENARIOS FOR WORKFORCE CHANGE

Registered office:Australian Resources Research Centre Level 3, 26 Dick Perry Avenue Kensington WA 6151

ABN 24 609 540 285

This report was commissioned by NERA (National Energy Resources Australia) and prepared by AlphaBeta. All information is derived from AlphaBeta analysis using both proprietary research and publicly available data and uses statistical techniques to provide insights on some of the drivers of defined scenarios, but is not intended to be statistically rigorous. Where information has been obtained from third-party sources, this is clearly referenced in the footnotes.

NERA is one of six Growth Centres established by the Australian Government under the Industry Growth Centres Initiative. It is an incorporated not-for-profit company governed by a board of industry experts to help drive projects to benefit the whole energy ecosystem in Australia. Through a national focus, NERA’s role is to grow collaboration and innovation to assist the energy resources industry manage cost structures and productivity, direct research to industry needs, deliver the future work skills required and promote fit for purpose regulation.

T: 1300 589 310E: [email protected]: www.nera.org.au

@NERAnetwork NERA – National Energy Resources Australia

EXECUTIVE SUMMARY 4

AUSTRALIA’S OIL AND GAS WORKFORCE HAS DOUBLED OVER THE LAST DECADE 8The direct oil and gas industry employs 19,000 people 9

Every job in the oil and gas industry sustains another 10 jobs elsewhere in the economy 10

The oil and gas workforce has doubled since 2006 11

The mix of roles in the oil and gas industry has changed 12

Case study 1: Legacy assets and the oil and gas workforce 16

How automation technology is changing the oil and gas workforce 16

PREPARING AUSTRALIA’S OIL AND GAS WORKFORCE FOR THE FUTURE 20Scenario-planning as a tool to manage uncertainty 21

Constructing scenarios based on past workforce changes 22

THREE SCENARIOS FOR THE FUTURE OIL AND GAS WORKFORCE 28Operational efficiency: companies will need more workers with operational, maintenance and technology skills 29

Case study 2: How maintenance roles may change in an operational efficiency scenario 31

Case study 3: How field operator roles may change in an operational efficiency scenario 33

Industry growth: rapid expansion may lead to a worker shortage and the need to lift workforce skills 35

Case study 4: How workers would operate in a highly automated LNG plant 38

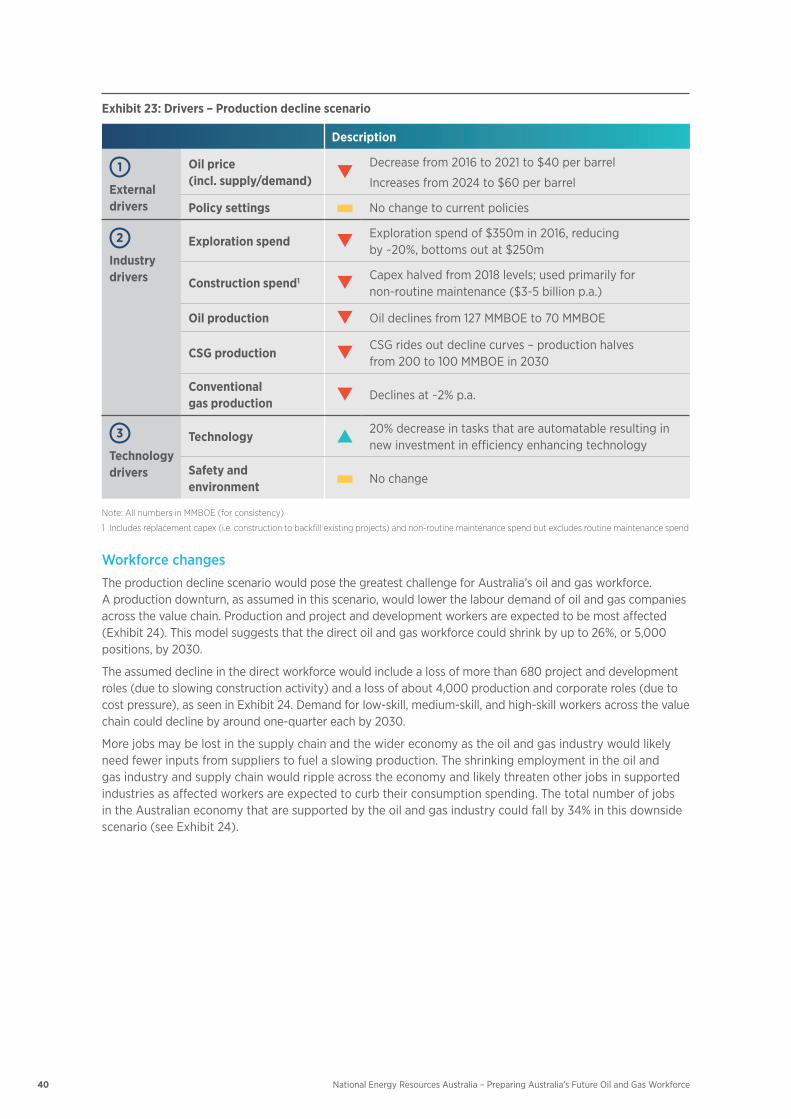

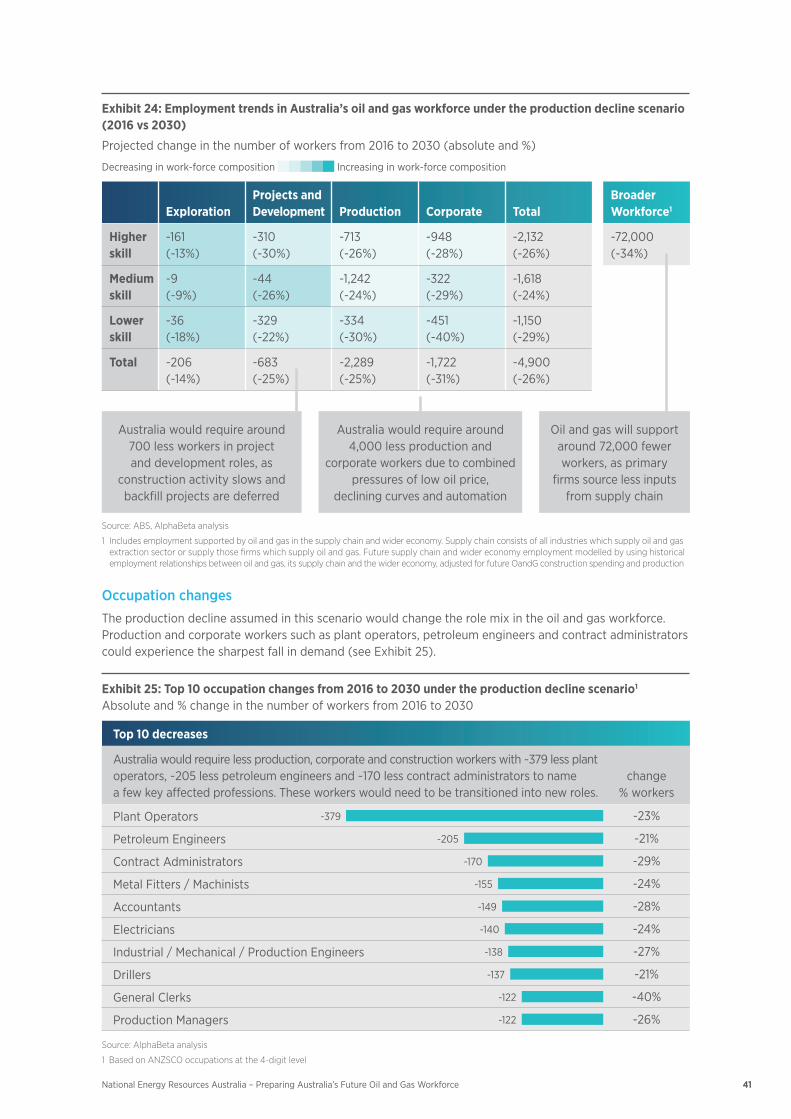

Production decline: downturn could require a large number of workers to leave the industry 39

Case study 5: Transitioning workers in the oil and gas industry 42

Roles in the oil and gas workforce will continue to change due to greater use of new energy, automation, and decommissioning of plants 43

HOW NERA WILL USE THESE SCENARIOS 44Inform the sector of potential workforce change 45

Prepare the sector for a variety of outcomes 45

Enable firms in the industry to collaborate and plan for the future 45

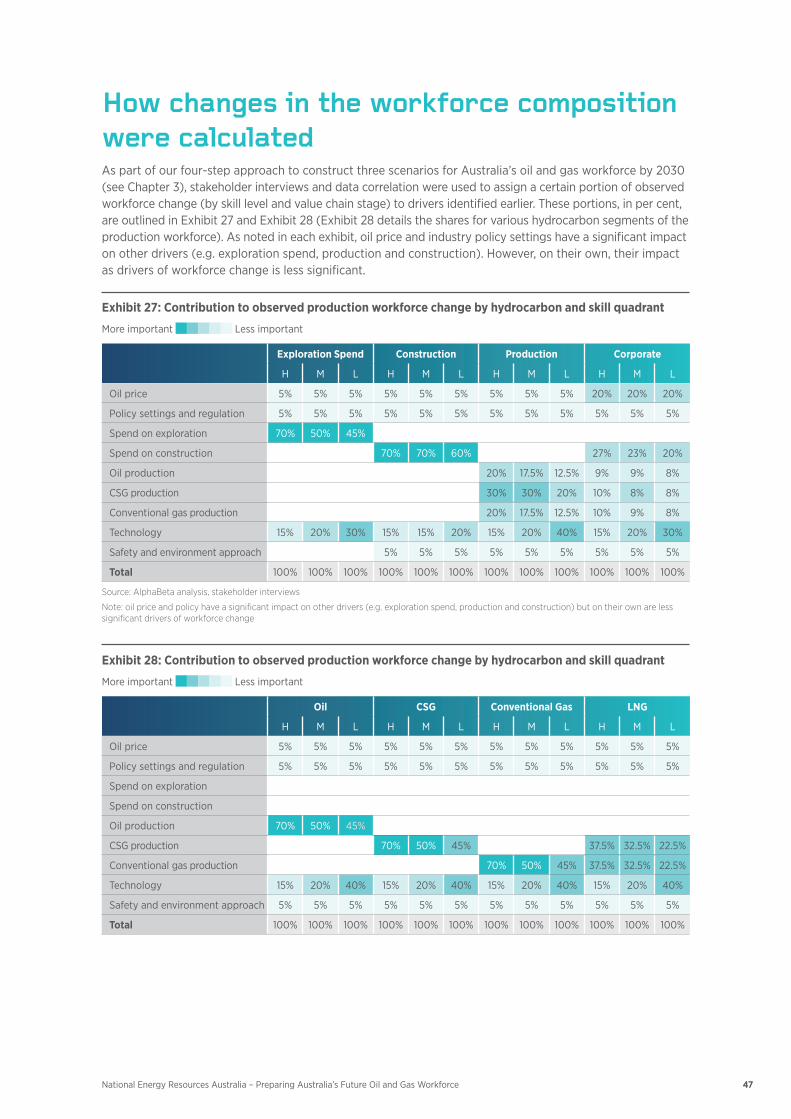

TECHNICAL APPENDIX 46How changes in the workforce composition were calculated 47

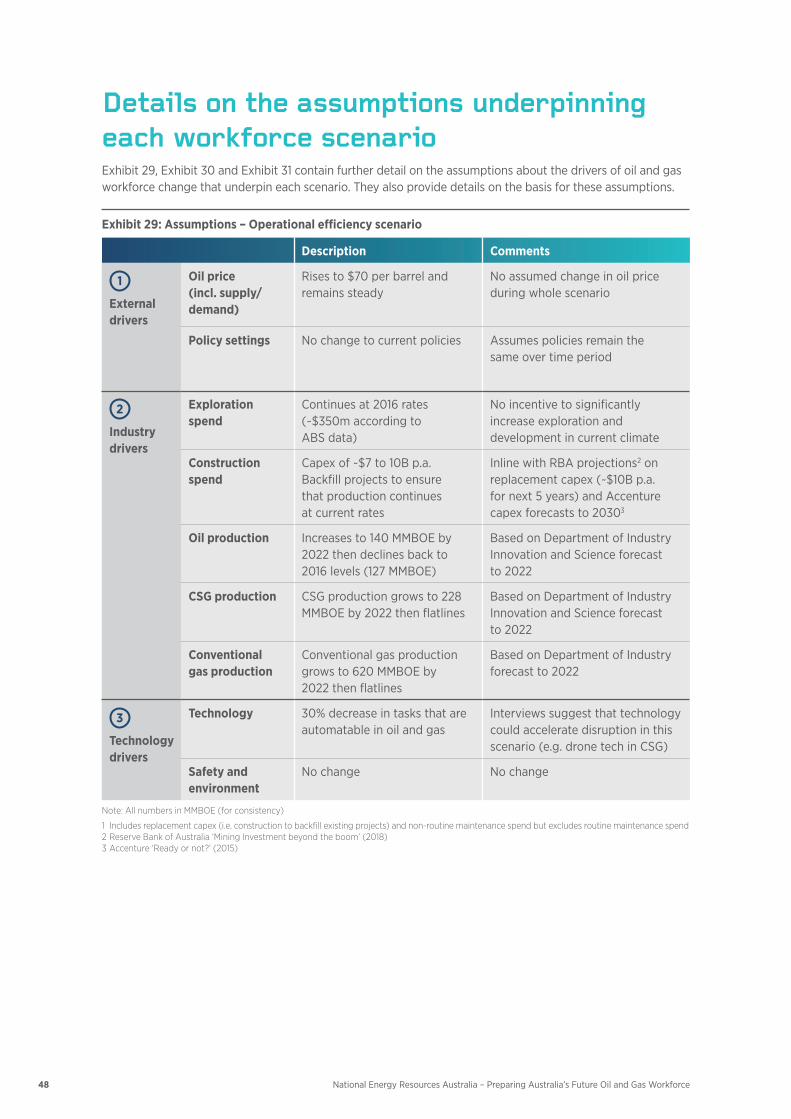

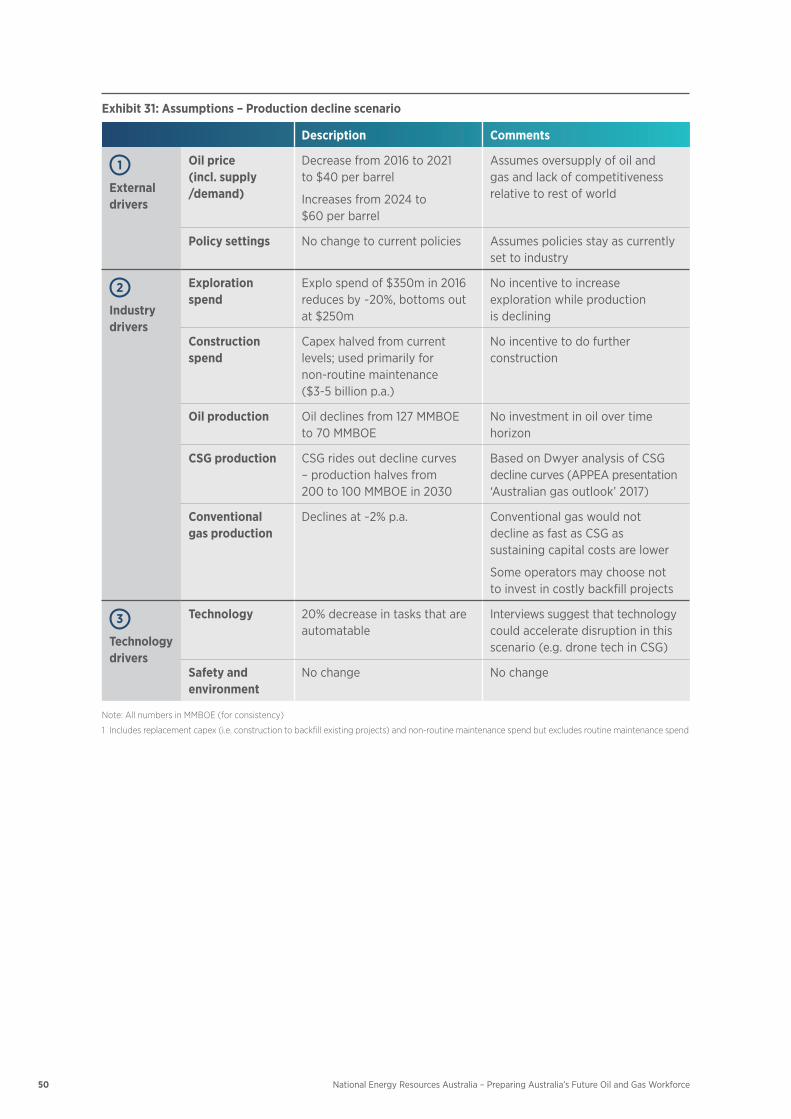

Details on the assumptions underpinning each workforce scenario 48

Supply chain and wider economy employment 51

Contents

3

Australia has developed one of the strongest natural gas industries in the world and is on track to become the biggest exporter of liquefied natural gas (LNG) globally following an unparalleled investment boom. Between 2009 and 2017, resources companies invested an estimated A$320 billion into new oil and gas extraction projects across Australia, including developing a completely new coal seam gas (CSG) industry in Queensland.1 As a result, the country’s LNG processing capacity has tripled since 2012. Today, the oil and gas industry contributes $28 billion to the Australian economy, or roughly 1.6% of the total GDP.2

The strong expansion of the LNG industry has caused Australia’s core oil and gas workforce to more than double from 9,000 workers in 2006 to 19,000 workers in 2016. More importantly, the indirect employment created by the oil and gas industry is substantial.3 Analysis used in this report shows that each oil and gas worker in Australia currently sustains another 10 jobs across the supply chain and wider economy – generating five times more indirect employment than an average worker in other industries. Oil and gas workers are also among the highest qualified in the country, with 44% employed in high-skill occupations, such as subsea engineers, geophysicists and production superintendents.

However, the future of the oil and gas workforce is uncertain. The industry’s ability to create new jobs has always been heavily dependent on a range of external factors that are difficult to predict, including the oil price, global supply and demand, and government policy. For example, the oil price has been highly volatile over the past five years and workforce growth has plateaued. An ongoing debate over CSG exploration and proposed resources taxes is affecting corporate investment decisions. As these sources of uncertainty are set to persist, it is challenging to reliably forecast the workforce needs of the oil and gas industry over the long, or even medium term.

This report, commissioned by NERA (National Energy Resources Australia), intends to offer guidance in uncertain times. Designed as a scenario-planning tool, it seeks to map the potential trajectory of the oil and gas workforce in Australia in the years ahead, so that companies, workers and policymakers can make informed decisions and prepare for a volatile future.

NERA, as an industry growth centre, has a mandate to foster collaboration and innovation, so that the oil and gas industry can deliver the future skills it requires. This includes informing the sector about expected workforce trends, liaising with education and training providers to ensure they are building and maintaining an adequate pipeline of skilled personnel, and helping the current workforce master periods of change driven by economic and technological trends.

This report uses scenario analysis to describe how Australia’s oil and gas workforce might look in 2030. It sets out three scenarios to estimate the potential direction of industry growth and employment. The three scenarios are by no means an attempt to predict the future. Rather, they should be seen as an exercise to test how the oil and gas workforce might react in a range of situations – from a sharp drop in oil prices to a reversal of current government policy.

1 Australian Bureau of Statistics (ABS), 2010 to 2018, Private new capital exp. and expected exp., cat. no. 5625.0. 2 Industry Gross Value Added for December 2017. See: ABS (March 2018), Australian National Accounts: National Income, Expenditure and Product,

cat. no. 5206.0. 3 This report defines the direct (core) oil and gas workforce as people directly employed by oil and gas extraction or production companies, while

the indirect workforce comprises of people in the supply chain and wider economy whose jobs indirectly rely on the oil and gas industry.

Executive Summary

4 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

4 The average price for Brent crude since the start of 2018 to end of June 2018 was US$67.33/barrel, according to Statista. See: HYPERLINK “http://www.statista.com/statistics/262860/uk-brent-crude-oil-price-changes-since-1976/” www.statista.com/statistics/262860/uk-brent-crude-oil-price-changes-since-1976/.

The upside and downside scenarios have been chosen to test the extremes and bracket the possible future at a time of ongoing uncertainty and global resource price volatility. In fact, the sharp swings in the oil price over the past decade suggest that not one, but all three scenarios may play out in some form in coming years through 2030. NERA has commissioned this report to help the industry prepare for this risk.

The scenarios, devised from over 30 interviews with industry experts across Australia, account for nine drivers of workforce change (including changes in oil prices and industry policy, as well as technological progress). Using historical workforce changes as a guideline, three scenarios were constructed.

Operational efficiency scenario (business as usual)

• Continuousinvestmentin‘operationalefficiency’isthemostlikelyscenarioandtheonethatmostcloselymirrors today’s situation. Assuming the oil price stays within the most recent range of US$60 to $80 per barrel,4 and Australian governments keep current policy settings steady (e.g. moratoria on CSG exploration remain in place), primary producers will likely remain focused on achieving greater production efficiency. Operators are expected to continue to upgrade and automate their operations using data analytics and predictive maintenance and technology such as advanced sensors.

• Inthisscenario,thesizeofthedirectoilandgasworkforcewouldnotchangegreatlyby2030.Aslightdecline of 5%, or approximately 1,000 direct full-time jobs (primarily low- and medium-skilled corporate and production roles), would be offset by an estimated increase of around 3,000 jobs (+3%) in the supply chain, leaving the overall workforce supported by the oil and gas industry with a net gain of 2,000 jobs by 2030. This job growth would occur as the entire oil and gas industry becomes more competitive and increases demand for inputs from suppliers.

• Companieswouldrequireahealthypipelineofworkerswithstrongoperational,maintenanceandtechnology skills to achieve greater production efficiency.

Industry growth scenario (upside)

• The‘industrygrowth’scenarioassumesthatanincreaseintheoilprice(toUS$100perbarrelorhigher) and favourable policy changes (such as lifting moratoria) provide a strong boost to the Australian oil and gas industry. It assumes that companies will continue to use automation technology to lower costs.

• Theproductionupswinginthisscenariohasthepotentialtocreatearound29,000newjobs(+14%)across the Australian economy by 2030. It is assumed that the majority of these new jobs (26,000) would emerge as indirect employment in the oil and gas supply chain and in the wider economy.

• However,thedramaticindustrygrowthinthisscenariocouldleadtotalentshortages(inexploration,inconstruction and in operational roles) and create a strong need to improve the skills of the current workforce.

Production decline scenario (downside)

• AsharpandsustainedfallintheoilpricetobetweenUS$40andUS$60perbarrelisthebasicassumptionofthe‘productiondeclinescenario’(thedownsidecase).Thisdeclinewouldbetheresultofstrongcompetition from other gas producers, such as Qatar, Russia and East Africa. The scenario assumes that governments keep current policy settings steady and that companies continue to adopt new technology to lower costs and increase their operational productivity.

• Inthisworst-casescenario,thedirectoilandgasworkforcecoulddeclinebyasmuchas26%,or5,000jobs, (primarily corporate and production roles), accompanied by an even larger fall in employment across the supply chain and wider economy. In this extreme downside scenario, the total workforce supported by oil and gas in 2030 could be 34% smaller than in 2016.

• Theassumedbusinessdownturninthisscenariomightrequireinterventionfromgovernmentandindustry to help transition a potentially large number of workers into new employment.

5National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

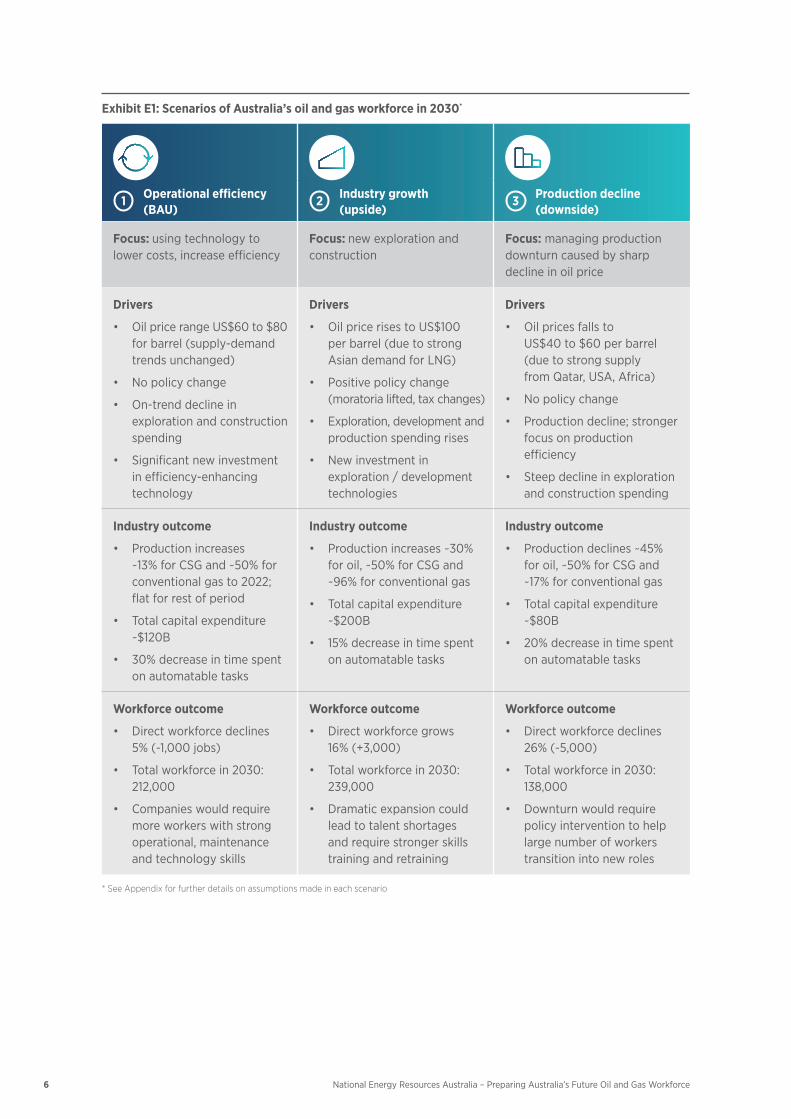

Exhibit E1: Scenarios of Australia’s oil and gas workforce in 2030*

1 Operational efficiency (BAU)

2 Industry growth (upside)

3 Production decline (downside)

Focus: using technology to lower costs, increase efficiency

Focus: new exploration and construction

Focus: managing production downturn caused by sharp decline in oil price

Drivers

• OilpricerangeUS$60to$80for barrel (supply-demand trends unchanged)

• Nopolicychange

• On-trenddeclineinexploration and construction spending

• Significantnewinvestmentin efficiency-enhancing technology

Drivers

• OilpricerisestoUS$100 per barrel (due to strong Asian demand for LNG)

• Positivepolicychange(moratoria lifted, tax changes)

• Exploration,developmentandproduction spending rises

• Newinvestmentinexploration / development technologies

Drivers

• Oilpricesfallsto US$40 to $60 per barrel (due to strong supply from Qatar, USA, Africa)

• Nopolicychange

• Productiondecline;strongerfocus on production efficiency

• Steepdeclineinexplorationand construction spending

Industry outcome

• Productionincreases ~13% for CSG and ~50% for conventionalgasto2022;flat for rest of period

• Totalcapitalexpenditure~$120B

• 30%decreaseintimespenton automatable tasks

Industry outcome

• Productionincreases~30%for oil, ~50% for CSG and ~96% for conventional gas

• Totalcapitalexpenditure~$200B

• 15%decreaseintimespenton automatable tasks

Industry outcome

• Productiondeclines~45% for oil, ~50% for CSG and ~17% for conventional gas

• Totalcapitalexpenditure~$80B

• 20%decreaseintimespenton automatable tasks

Workforce outcome

• Directworkforcedeclines 5% (-1,000 jobs)

• Totalworkforcein2030:212,000

• Companieswouldrequiremore workers with strong operational, maintenance and technology skills

Workforce outcome

• Directworkforcegrows 16% (+3,000)

• Totalworkforcein2030:239,000

• Dramaticexpansioncouldlead to talent shortages and require stronger skills training and retraining

Workforce outcome

• Directworkforcedeclines26% (-5,000)

• Totalworkforcein2030:138,000

• Downturnwouldrequirepolicy intervention to help large number of workers transition into new roles

* See Appendix for further details on assumptions made in each scenario

6 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

7National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

The scenarios have been developed with significant industry input, based on what is possible and most relevant. The upside and downside case represent theoretical extremes that are meant to bracket a range of future outcomes. In fact, it is likely that the oil and gas industry will need to brace for all three scenarios to play out to some extent in coming years. Heavy swings in the oil price over the past decade (from around US$61 per barrel in 2009 to more than US$111 per barrel in 2011 and back to around US$43 in 2016) show just how unpredictable some of the drivers of the Australian oil and gas workforce are.

Regardless of the scenario, this report expects that a number of new occupations will emerge in the oil and gas industry, for example in specialist roles related to technology (Artificial Intelligence (AI)/machine learning specialists). The decommissioning of plants is seen as a growing business, which will create new jobs. Further job growth is likely if the industry decides to embrace opportunities around renewables and carbon capture, as well as other forms of unconventional energy to complement existing oil and gas extraction methods.

How NERA will use these scenariosThese scenarios have been devised to be used as an educational and planning tool for the industry, government, current and future workers and general public.

Inform industry and public. This report will be disseminated widely and launched on the NERA website with a simple and interactive occupation-level tool that will allow workers to plan their own futures and firms to prepare for workforce change.

Prepare for workforce transitions. The scenarios will also help firms in the industry plan to build a strong pipeline of skilled workers, inform the upskilling decisions that may be needed and the workforce transitions that may occur.

Enable further collaboration. The scenarios in this report will allow further industry-wide collaboration to improve training initiatives, competency frameworks, infrastructure planning and engagement of the supply chain.

8

Australia’s oil and gas workforce has doubled over the last decade

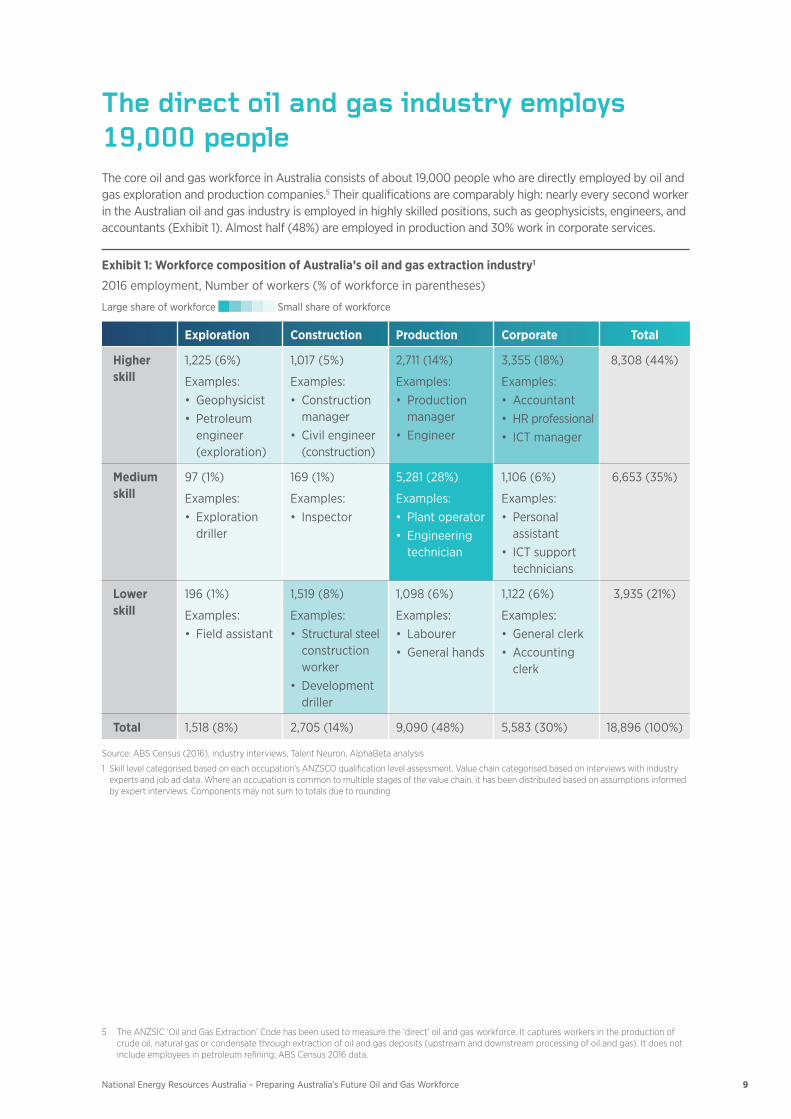

The direct oil and gas industry employs 19,000 peopleThe core oil and gas workforce in Australia consists of about 19,000 people who are directly employed by oil and gas exploration and production companies.5 Their qualifications are comparably high: nearly every second worker in the Australian oil and gas industry is employed in highly skilled positions, such as geophysicists, engineers, and accountants (Exhibit 1). Almost half (48%) are employed in production and 30% work in corporate services.

Exhibit 1: Workforce composition of Australia’s oil and gas extraction industry1

2016 employment, Number of workers (% of workforce in parentheses)

Large share of workforce Small share of workforce

Exploration Construction Production Corporate Total

Higher skill

1,225 (6%) 1,017 (5%) 2,711 (14%) 3,355 (18%) 8,308 (44%)

Examples:• Geophysicist• Petroleum

engineer (exploration)

Examples:• Construction

manager• Civilengineer

(construction)

Examples:• Production

manager• Engineer

Examples:• Accountant• HRprofessional• ICTmanager

Medium skill

97 (1%) 169 (1%) 5,281 (28%) 1,106 (6%) 6,653 (35%)

Examples:• Exploration

driller

Examples:• Inspector

Examples:• Plantoperator• Engineering

technician

Examples:• Personal

assistant• ICTsupport

technicians

Lower skill

196 (1%) 1,519 (8%) 1,098 (6%) 1,122 (6%) 3,935 (21%)

Examples:• Fieldassistant

Examples:• Structuralsteel

construction worker

• Developmentdriller

Examples:• Labourer• Generalhands

Examples:• Generalclerk• Accounting

clerk

Total 1,518 (8%) 2,705 (14%) 9,090 (48%) 5,583 (30%) 18,896 (100%)

Source: ABS Census (2016), industry interviews, Talent Neuron, AlphaBeta analysis

1 Skill level categorised based on each occupation’s ANZSCO qualification level assessment. Value chain categorised based on interviews with industry experts and job ad data. Where an occupation is common to multiple stages of the value chain, it has been distributed based on assumptions informed by expert interviews. Components may not sum to totals due to rounding

9National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

5 The ANZSIC ‘Oil and Gas Extraction’ Code has been used to measure the ‘direct’ oil and gas workforce. It captures workers in the production of crude oil, natural gas or condensate through extraction of oil and gas deposits (upstream and downstream processing of oil and gas). It does not include employees in petroleum refining; ABS Census 2016 data.

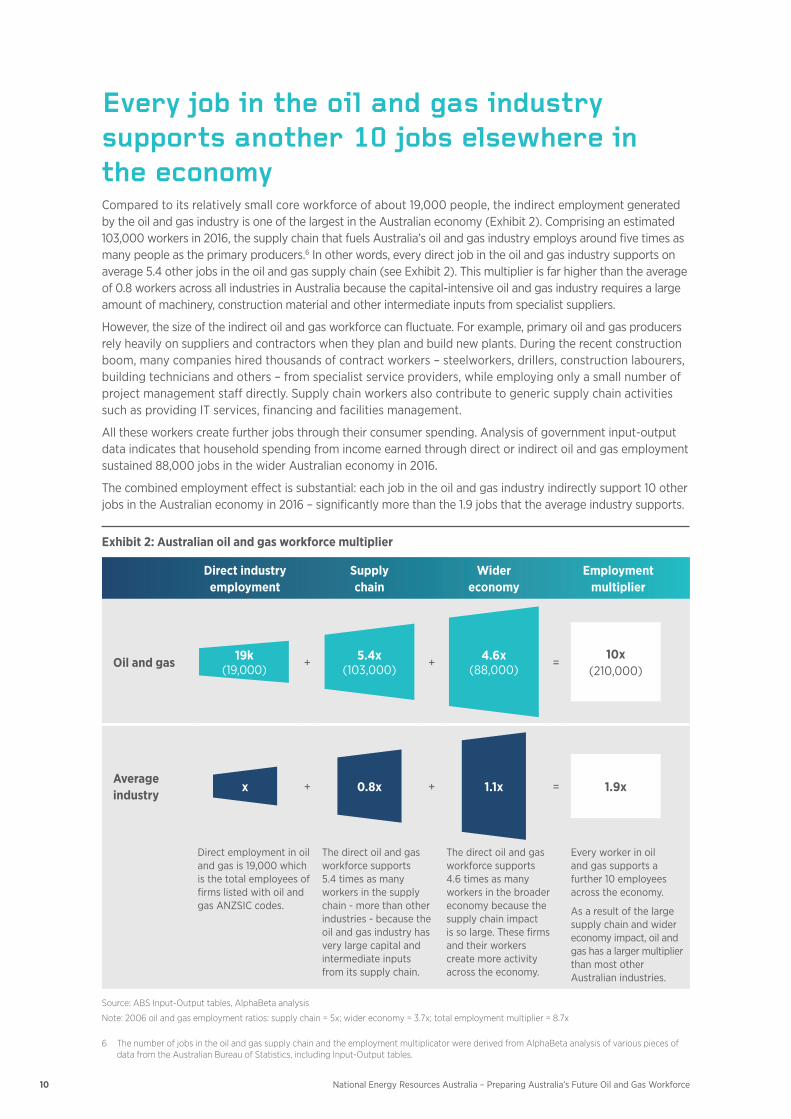

Every job in the oil and gas industry supports another 10 jobs elsewhere in the economyCompared to its relatively small core workforce of about 19,000 people, the indirect employment generated by the oil and gas industry is one of the largest in the Australian economy (Exhibit 2). Comprising an estimated 103,000 workers in 2016, the supply chain that fuels Australia’s oil and gas industry employs around five times as many people as the primary producers.6 In other words, every direct job in the oil and gas industry supports on average 5.4 other jobs in the oil and gas supply chain (see Exhibit 2). This multiplier is far higher than the average of 0.8 workers across all industries in Australia because the capital-intensive oil and gas industry requires a large amount of machinery, construction material and other intermediate inputs from specialist suppliers.

However,thesizeoftheindirectoilandgasworkforcecanfluctuate.Forexample,primaryoilandgasproducersrely heavily on suppliers and contractors when they plan and build new plants. During the recent construction boom, many companies hired thousands of contract workers – steelworkers, drillers, construction labourers, building technicians and others – from specialist service providers, while employing only a small number of project management staff directly. Supply chain workers also contribute to generic supply chain activities such as providing IT services, financing and facilities management.

All these workers create further jobs through their consumer spending. Analysis of government input-output data indicates that household spending from income earned through direct or indirect oil and gas employment sustained 88,000 jobs in the wider Australian economy in 2016.

The combined employment effect is substantial: each job in the oil and gas industry indirectly support 10 other jobs in the Australian economy in 2016 – significantly more than the 1.9 jobs that the average industry supports.

Exhibit 2: Australian oil and gas workforce multiplier

Direct industry employment

Supply chain

Wider economy

Employment multiplier

Oil and gas 19k (19,000) + 5.4x

(103,000) + 4.6x (88,000) =

10x (210,000)

Average industry

x + 0.8x + 1.1x = 1.9x

Direct employment in oil and gas is 19,000 which is the total employees of firms listed with oil and gas ANZSIC codes.

The direct oil and gas workforce supports 5.4 times as many workers in the supply chain - more than other industries - because the oil and gas industry has very large capital and intermediate inputs from its supply chain.

The direct oil and gas workforce supports 4.6 times as many workers in the broader economy because the supply chain impact is so large. These firms and their workers create more activity across the economy.

Every worker in oil and gas supports a further 10 employees across the economy.

As a result of the large supply chain and wider economy impact, oil and gas has a larger multiplier than most other Australian industries.

Source: ABS Input-Output tables, AlphaBeta analysis

Note: 2006 oil and gas employment ratios: supply chain = 5x; wider economy = 3.7x; total employment multiplier = 8.7x

10 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

6 The number of jobs in the oil and gas supply chain and the employment multiplicator were derived from AlphaBeta analysis of various pieces of data from the Australian Bureau of Statistics, including Input-Output tables.

11National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

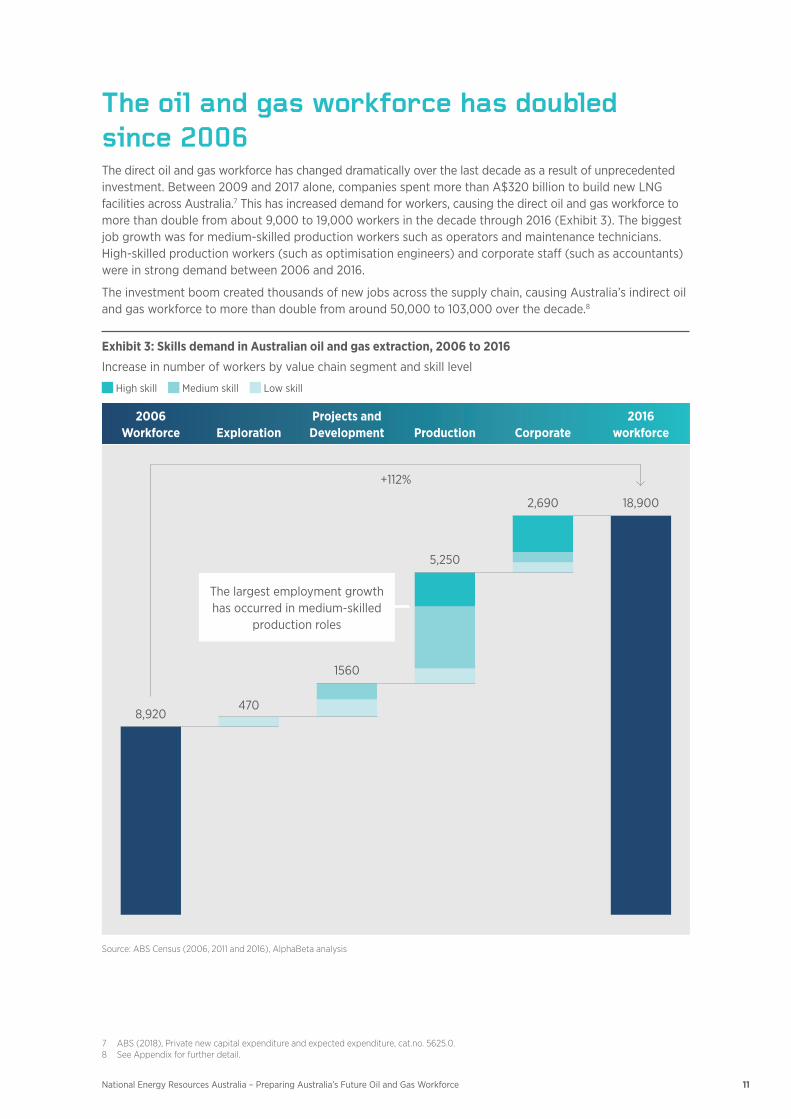

The oil and gas workforce has doubled since 2006The direct oil and gas workforce has changed dramatically over the last decade as a result of unprecedented investment. Between 2009 and 2017 alone, companies spent more than A$320 billion to build new LNG facilities across Australia.7 This has increased demand for workers, causing the direct oil and gas workforce to more than double from about 9,000 to 19,000 workers in the decade through 2016 (Exhibit 3). The biggest job growth was for medium-skilled production workers such as operators and maintenance technicians. High-skilled production workers (such as optimisation engineers) and corporate staff (such as accountants) were in strong demand between 2006 and 2016.

The investment boom created thousands of new jobs across the supply chain, causing Australia’s indirect oil and gas workforce to more than double from around 50,000 to 103,000 over the decade.8

Exhibit 3: Skills demand in Australian oil and gas extraction, 2006 to 2016

Increase in number of workers by value chain segment and skill level

High skill Medium skill Low skill

2006 Workforce Exploration

Projects and Development Production Corporate

2016 workforce

8,920470

1560

5,250

2,690 18,900

The largest employment growth has occurred in medium-skilled

production roles

+112%

Source: ABS Census (2006, 2011 and 2016), AlphaBeta analysis

7 ABS (2018), Private new capital expenditure and expected expenditure, cat.no. 5625.0. 8 See Appendix for further detail.

The mix of roles in the oil and gas industry has changedThe workforce changes over the last decade have largely been driven by a massive expansion of the industry. Oil and gas companies increased their spending on exploration, construction and production (Exhibit 4), as the oil price soared from around US$65 per barrel in 2006 to a peak of US$111 per barrel in 2011.9

Exhibit 4: Australian oil and gas workforce compared to exploration and capital spend and total production

Overall oil and gas workforce

(workers)

30,000

20,000

10,000

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exploration spend

($ million)

1,500

1000

500

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Capital spend

($ billion)

60

40

20

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (oil, CSG and other LNG)

(MMBOE)

800

700

600

500

4002006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: Employment – ABS Census interpolated with Labour Force survey (calendar year average); exploration spend – ABS data; capital spend - Accenture estimates, ABS Capex Survey, BIS Oxford Economics, AlphaBeta analysis; production - Department of Industry historical data; Interviews

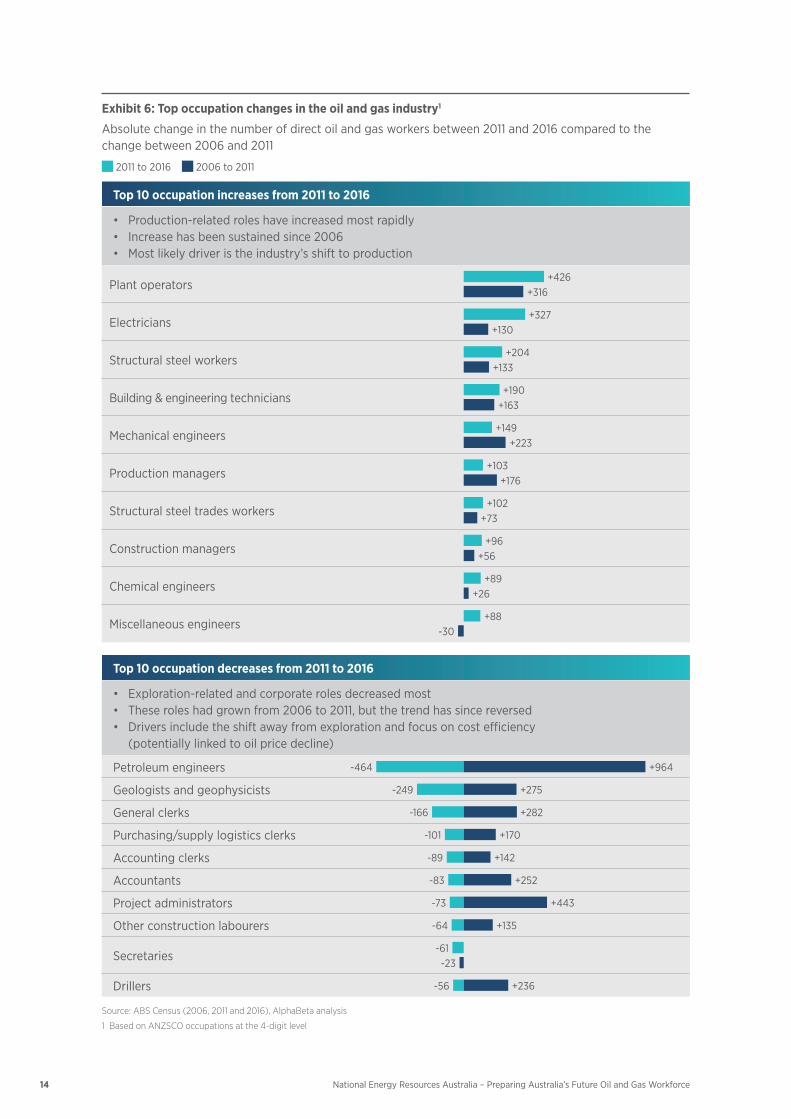

Between 2006 and 2011, the direct oil and gas workforce grew significantly across the value chain (exploration, project development and construction, production and corporate roles). Employment in exploration increased particularly strongly by 100% in medium skilled roles and 120% in high skilled roles. Project and development employment increased even more over the same period by 140% in high skilled roles and 220% in medium skilled roles (Exhibit 5).

12 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

9 The price of gas largely follows the oil price. See https://www.statista.com/statistics/262860/uk-brent-crude-oil-price-changes-since-1976/ for details.10 The project and development workforce in this analysis refers to staff directly employed by primary producers to oversee the planning, development

and construction of oil and gas projects. It does not include the substantial number of construction workers hired as contractors through the supply chain during peak construction periods.

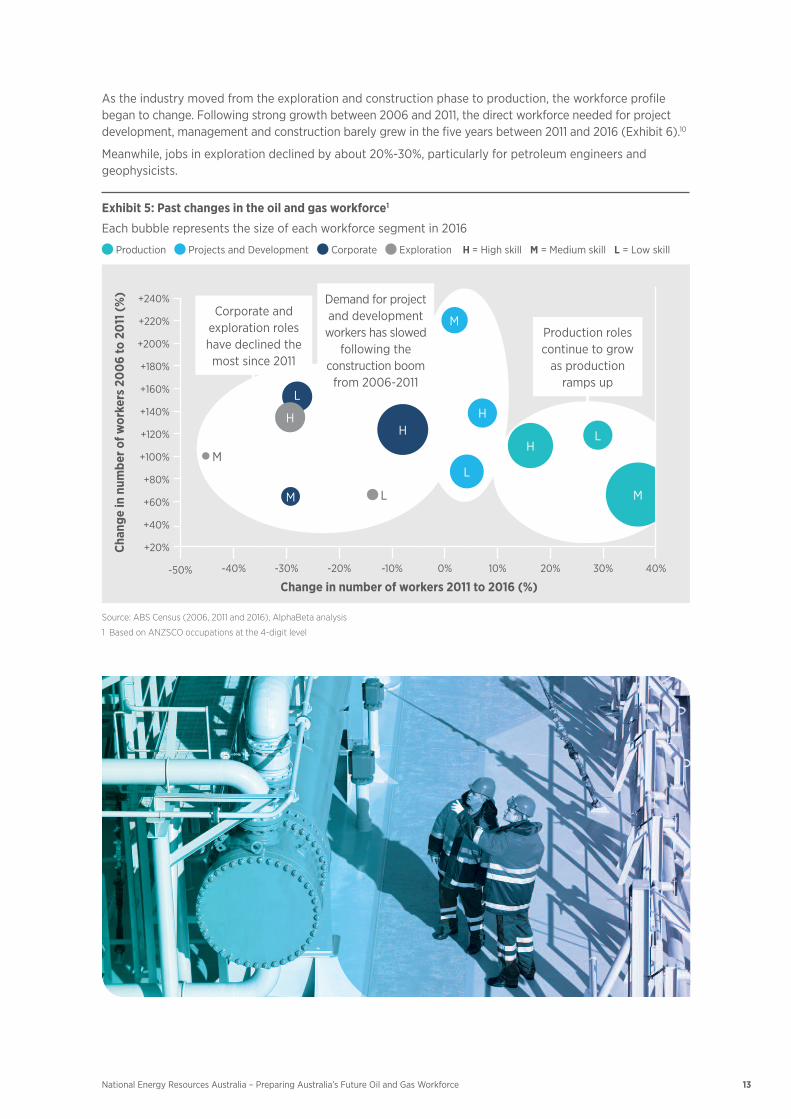

As the industry moved from the exploration and construction phase to production, the workforce profile began to change. Following strong growth between 2006 and 2011, the direct workforce needed for project development, management and construction barely grew in the five years between 2011 and 2016 (Exhibit 6).10

Meanwhile, jobs in exploration declined by about 20%-30%, particularly for petroleum engineers and geophysicists.

Exhibit 5: Past changes in the oil and gas workforce1

Eachbubblerepresentsthesizeofeachworkforcesegmentin2016

Production Projects and Development Corporate Exploration H = High skill M = Medium skill L = Low skill

LH

H

M

L

H

LM

H

L

M

M

Production roles continue to grow

as production ramps up

Corporate and exploration roles have declined the most since 2011

Demand for project and development

workers has slowed following the

construction boom from 2006-2011

Chan

ge in

num

ber o

f wor

kers

20

06

to 2

011 (

%) +240%

+220%

+200%

+180%

+160%

+140%

+120%

+100%

+80%

+60%

+40%

+20%

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40%

Change in number of workers 2011 to 2016 (%)

Source: ABS Census (2006, 2011 and 2016), AlphaBeta analysis

1 Based on ANZSCO occupations at the 4-digit level

13National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

14 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Exhibit 6: Top occupation changes in the oil and gas industry1

Absolute change in the number of direct oil and gas workers between 2011 and 2016 compared to the change between 2006 and 2011

2011 to 2016 2006 to 2011

Top 10 occupation increases from 2011 to 2016

• Production-relatedroleshaveincreasedmostrapidly• Increasehasbeensustainedsince2006• Mostlikelydriveristheindustry’sshifttoproduction

Plant operators+426

+316

Electricians+327

+130

Structural steel workers+204

+133

Building & engineering technicians+190

+163

Mechanical engineers+149

+223

Production managers+103

+176

Structural steel trades workers+102

+73

Construction managers+96

+56

Chemical engineers+89

+26

Miscellaneous engineers-30

+88

Top 10 occupation decreases from 2011 to 2016

• Exploration-relatedandcorporaterolesdecreasedmost• Theseroleshadgrownfrom2006to2011,butthetrendhassincereversed• Driversincludetheshiftawayfromexplorationandfocusoncostefficiency

(potentially linked to oil price decline)

Petroleum engineers -464 +964

Geologists and geophysicists -249 +275

General clerks -166 +282

Purchasing/supply logistics clerks -101 +170

Accounting clerks -89 +142

Accountants -83 +252

Project administrators -73 +443

Other construction labourers -64 +135

Secretaries-61-23

Drillers -56 +236

Source: ABS Census (2006, 2011 and 2016), AlphaBeta analysis

1 Based on ANZSCO occupations at the 4-digit level

15National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

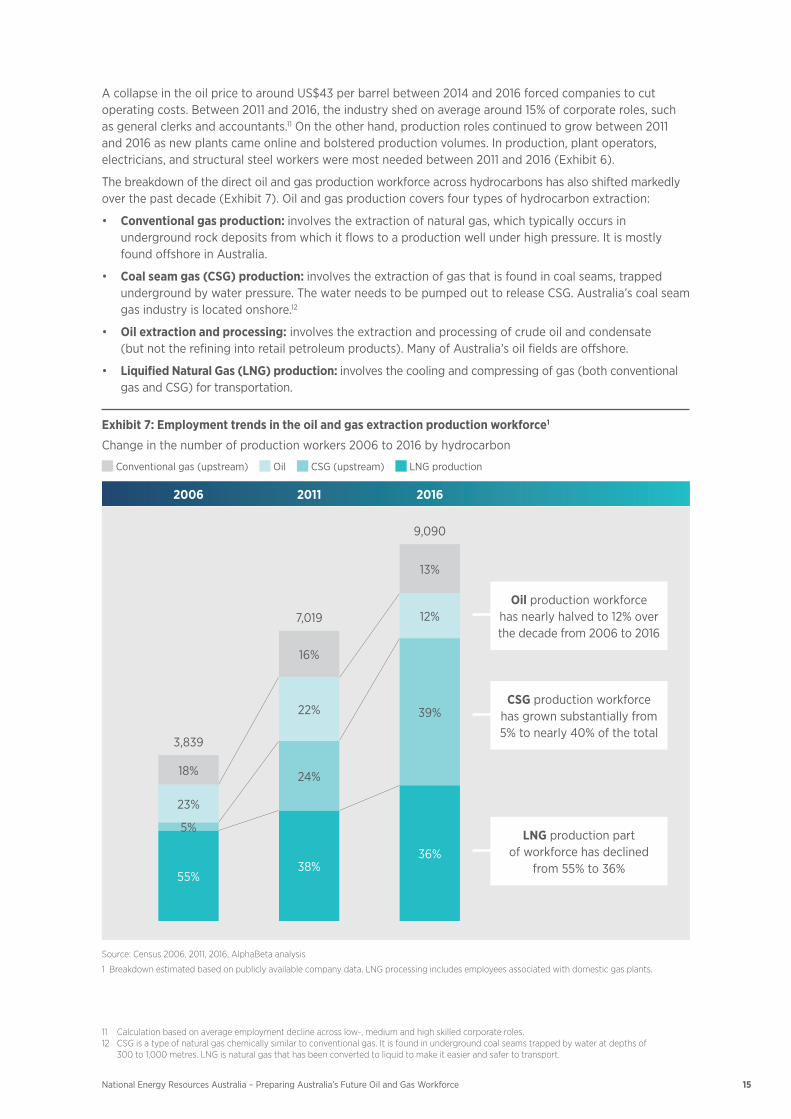

A collapse in the oil price to around US$43 per barrel between 2014 and 2016 forced companies to cut operating costs. Between 2011 and 2016, the industry shed on average around 15% of corporate roles, such as general clerks and accountants.11 On the other hand, production roles continued to grow between 2011 and 2016 as new plants came online and bolstered production volumes. In production, plant operators, electricians, and structural steel workers were most needed between 2011 and 2016 (Exhibit 6).

The breakdown of the direct oil and gas production workforce across hydrocarbons has also shifted markedly over the past decade (Exhibit 7). Oil and gas production covers four types of hydrocarbon extraction:

• Conventional gas production: involves the extraction of natural gas, which typically occurs in underground rock deposits from which it flows to a production well under high pressure. It is mostly found offshore in Australia.

• Coal seam gas (CSG) production: involves the extraction of gas that is found in coal seams, trapped underground by water pressure. The water needs to be pumped out to release CSG. Australia’s coal seam gas industry is located onshore.12

• Oil extraction and processing: involves the extraction and processing of crude oil and condensate (but not the refining into retail petroleum products). Many of Australia’s oil fields are offshore.

• Liquified Natural Gas (LNG) production: involves the cooling and compressing of gas (both conventional gas and CSG) for transportation.

Exhibit 7: Employment trends in the oil and gas extraction production workforce1

Change in the number of production workers 2006 to 2016 by hydrocarbon

Conventional gas (upstream) Oil CSG (upstream) LNG production

2006 2011 2016

Oil production workforce has nearly halved to 12% over the decade from 2006 to 2016

9,090

13%

12%

39%

36%

7,019

16%

22%

24%

38%

3,839

18%

23%

55%

5%

CSG production workforce has grown substantially from 5% to nearly 40% of the total

LNG production part of workforce has declined

from 55% to 36%

Source: Census 2006, 2011, 2016, AlphaBeta analysis

1 Breakdown estimated based on publicly available company data. LNG processing includes employees associated with domestic gas plants.

11 Calculation based on average employment decline across low-, medium and high skilled corporate roles. 12 CSG is a type of natural gas chemically similar to conventional gas. It is found in underground coal seams trapped by water at depths of

300 to 1,000 metres. LNG is natural gas that has been converted to liquid to make it easier and safer to transport.

16 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

The CSG production workforce grew particularly rapidly between 2006 and 2016, increasing from 5% to nearly 40% of all oil and gas workers in Australia as three new plants on Curtis Island in Queensland came online. Compared to offshore oil and gas, the onshore upstream CSG industry is comparatively labour-intensive, requiring considerable numbers of workers to drill, service and operate thousands of onshore wells and gas facilities that are often spread over large distances.13

While the LNG production workforce continued to grow in absolute terms over the past decade, it reduced as a percentage of the total oil and gas production workforce in Australia. This is partly due to the emerging dominance of the CSG industry but also a result of the growing number of modern, high-tech LNG plants such as Pluto, Wheatstone and Gorgon, which require comparatively smaller workforces. The oil workforce has decreased from around 23% of Australia’s total oil and gas production workforce to nearly 10%, due to more efficient technology and declining production levels.

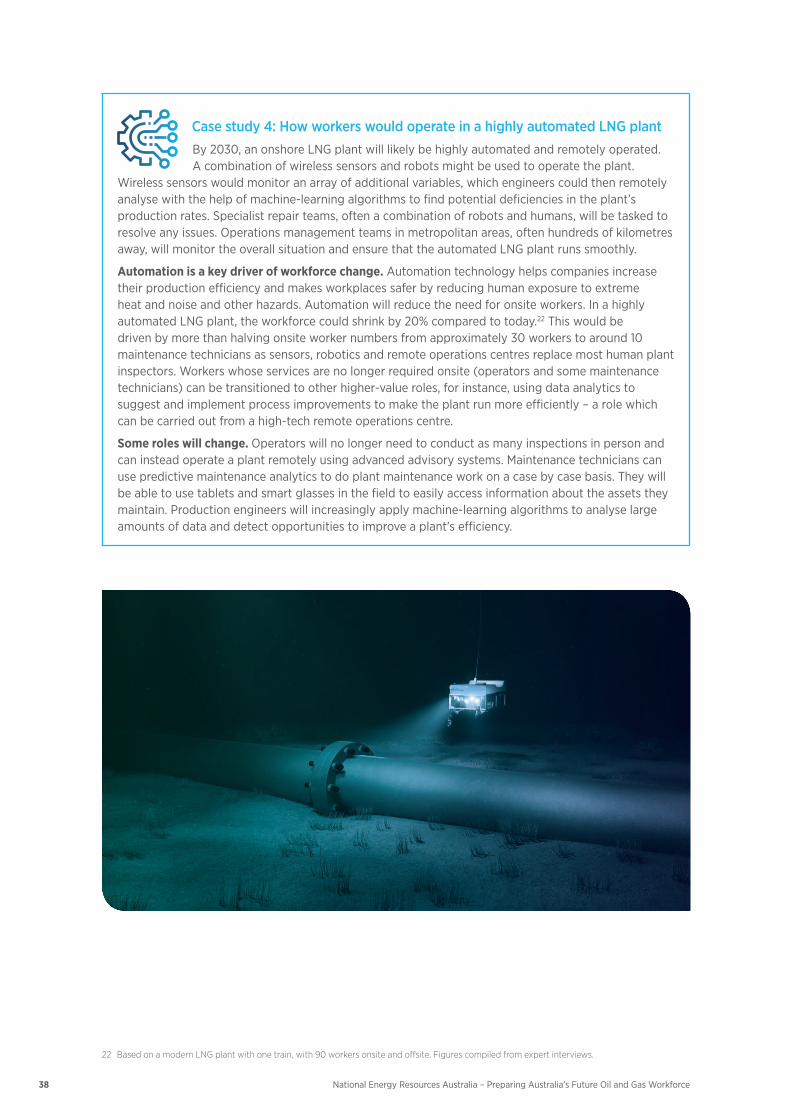

Case study 1: Legacy assets and the oil and gas workforceA substantial number of workers in Australian oil and gas production are currently employed in mature facilities. Automation technology could change this.

Despite the recent construction boom, around 50% of the LNG plants are more than a decade old.14 Such older LNG plants make up approximately 30% of all LNG plants in Australia and include Woodside’s Karratha and ConocoPhillip’s Darwin plant. The situation is similar in the CSG industry where around 30% of extraction workers perform tasks at legacy wells and gas facilities, even though these assets make up only 15% of all wells and facilities.15

There are several reasons for the relatively large workforce in older assets. Older assets typically require more frequent maintenance and hence more workers to repair and replace ageing parts. Older assets also tend to be less automated, which means they still rely predominantly on humans, rather than sensors and robots, to operate them. Companies will perform a cost-benefit analysis at each plant on a case-by-case basis to decide whether to retrofit ageing plants with updated automation technology.16 By contrast, newer assets are more easily automated because they are more likely to have been designed with new technology in mind.

How automation technology is changing the oil and gas workforceAutomation is changing the oil and gas workforce. New technologies, such as sensor technology and machine learning, are beginning to transform the way the industry operates and also changing the way workers do their jobs. For example, maintenance technicians are now likely to use data to determine which pieces of equipment require attention instead of working to pre-set schedules. In future, the ability to use and interpret data will only become more important for oil and gas occupations.

This report considers about 15 different technologies that have the potential to significantly increase the productivity and efficiency of oil and gas operations (see table below).

13 Upstream CSG production is defined as CSG field facilities including drilling, plant and pipeline components of the project.14 Estimates based on expert interviews and publicly available information. 15 Estimates based on expert interviews. 16 Such analysis has not been carried out in this report due to a lack of data.

17National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Oil and gas technologies considered in this project

Phase Technology Description

AI and connected ecosystem

Exploration Machine learning applied to seismic data

Faster processing of seismic data using machine-learning algorithms.

Development Intelligent design software (including digital twinning)

Use of algorithms to optimise processing plant design (e.g. to reduce total piping required) and to re-design rigs following reduction of human workers.

Production Predictive maintenance

Use of real-time and historical data to anticipate issues with offshore, onshore and subsea assets.

Production Machine learning / data analytics

Application of historical and real-time data to optimise the resource-to-market chain.

Operational hardware

Development Unmanned, intelligent drilling

Automation of already highly automated drilling process, supplemented by data analysis for more efficient drilling.

Production 4D seismic imaging Acquisition, processing and interpretation of repeated seismic surveys of a producing field to analyse the seismic impact of production.

Exploration Autonomous vehicles

Autonomous vehicles (aerial and subsea) powered by renewable energy and currents collecting data on exploration targets.

Production Subsea processing and subsea tie-backs

Processing oil and gas on the seafloor rather than on a fixed or floating platform, where fields are located in harsh / deepwater conditions.

Production 3D printing Additive manufacturing (3D printing) to construct spare and bespoke parts for platforms and plants.

Production Inspection and caretaker robots

Autonomous robots (land, subsea, aerial and amphibious) for dangerous / remote maintenance work and data gathering.

Production Autonomised, digitised sensor networks

Wireless sensor networks that collect physical, chemical and other data, converting it into a digital format for decision-making.

Connected worker

Production Use of wearables Technologies that enable workers to interact with the sensors, robots and systems around them, or otherwise augment the worker.

Production Remote operations centres

Monitoring / operation of equipment from a remote operations centre or other safe location, using advanced IT systems and virtual-reality technologies.

18 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

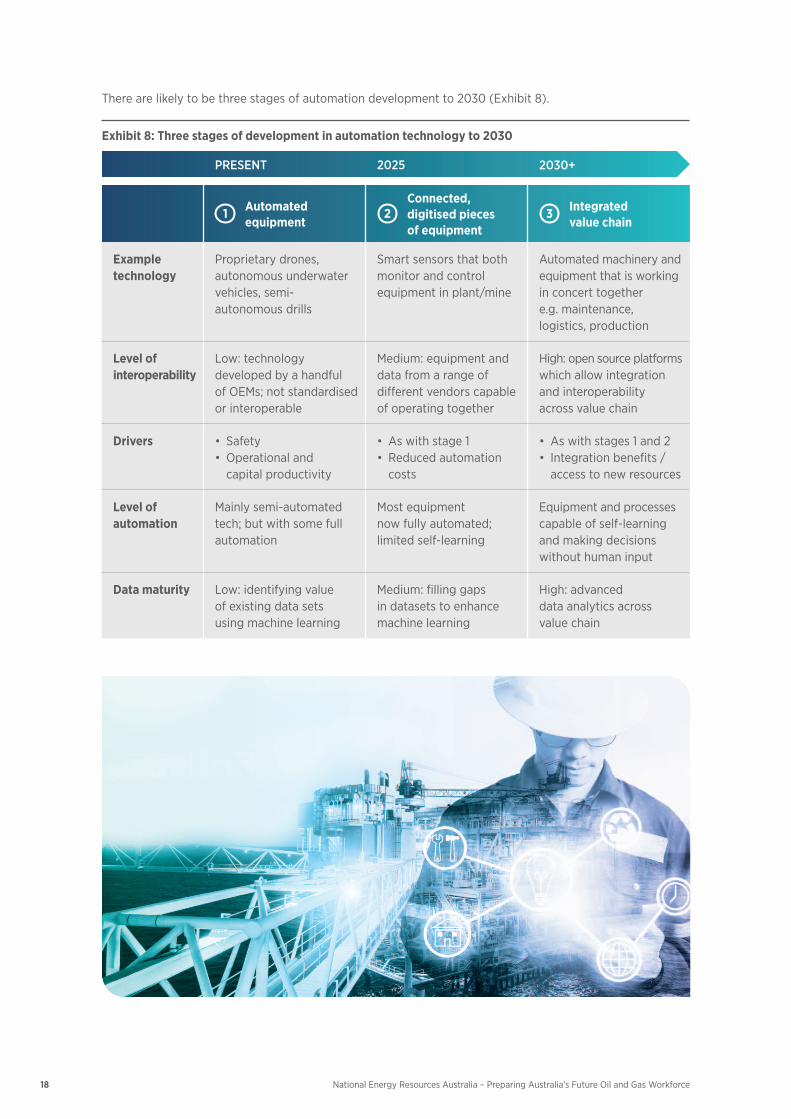

There are likely to be three stages of automation development to 2030 (Exhibit 8).

Exhibit 8: Three stages of development in automation technology to 2030

PRESENT 2025 2030+

1 Automated equipment

2Connected, digitised pieces of equipment

3 Integrated value chain

Example technology

Proprietary drones, autonomous underwater vehicles, semi-autonomous drills

Smart sensors that both monitor and control equipment in plant/mine

Automated machinery and equipment that is working in concert together e.g. maintenance, logistics, production

Level of interoperability

Low: technology developed by a handful ofOEMs;notstandardisedor interoperable

Medium: equipment and data from a range of different vendors capable of operating together

High: open source platforms which allow integration and interoperability across value chain

Drivers • Safety• Operationaland

capital productivity

• Aswithstage1• Reducedautomation

costs

• Aswithstages1and2• Integrationbenefits/

access to new resources

Level of automation

Mainly semi-automated tech;butwithsomefullautomation

Most equipment nowfullyautomated; limited self-learning

Equipment and processes capable of self-learning and making decisions without human input

Data maturity Low: identifying value of existing data sets using machine learning

Medium: filling gaps in datasets to enhance machine learning

High: advanced data analytics across value chain

19National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Phase 1 (today): Individual equipment automation Most of today’s oil and gas assets are being transformed by the digitisation of individual pieces of equipment. For example, sensors can monitor equipment by constantly collecting activity data and alerting staff of irregularities in running an operation. They can capture information about the effectiveness of a drill rig by measuring the drill hole or detect corrosion on an underwater pipe. However, operation of the individual pieces of equipment cannot always be integrated, as much of the advanced equipment is still sourced from a handful of original equipment manufacturers (OEMs) and technology from different manufacturers still does not easily interact. In this phase, automation is partial and not complete. For example, underwater vehicles are often tele-operated, but still require substantial involvement from humans. A lack of IT capability and incomplete data also means that the full potential of real-time data analytics is not achieved.

Phase 2: Connecting equipment By about 2025, oil and gas companies will have likely entered a new phase in their efforts to create the fully integrated and automated mine or plant. While the technology uptake in the first phase was primarily characterised by digitisation of individual pieces of equipment, the second phase will be marked by the growing interoperability of that equipment and adoption of automation technology. By 2025, most oil and gas plants will be fitted with an array of wireless smart sensors that monitor and control the movement of machines and operation of plants.

Technology manufacturers will spur this development by increasing the standardisation of their products, pressured by large producers who need their equipment to be interoperable. This is expected to open up the market for new competitors and lead to growing use of unbranded automation technology. It should also bring about new opportunities for companies in the supply chain. As the market for automation technology expands and technological progress becomes more entrenched, the data quality will improve along with the ability to analyse data using machine learning and artificial intelligence.

Phase 3: Connecting whole value chainIn a final phase, potentially starting in and around 2030, companies will continue to automate their production as they seek to realise very large benefits from technology integration. At this stage, many technologies will be highly interoperable across the entire value chain, from drilling through to shipping. Different pieces of equipment are now able to work in concert to perform highly complex tasks with unprecedented efficiency. Most equipment is expected to be fully autonomous by 2030, and most companies will be capable of using advanced data analytics and self-learning software to continuously improve product quality and operational efficiency. The increasing digitisation and integration of mining and oil and gas operations will substantially improve productivity.

20

Preparing Australia’s oil and gas workforce for the future

21National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Scenario-planning as a tool to manage uncertaintyForecasting the future of the oil and gas workforce over the medium and long term is challenging because the industry is subject to considerable volatility and uncertainty. Employment often ebbs and flows as the industry moves through cycles of expansion or contraction. For instance, jobs in oil and gas exploration increased by 107% between 2006 and 2011 and then decreased by 30% between 2011 and 2016.

Such abrupt changes are typically caused by external factors that are difficult to predict and that influence a company’s exploration spending, construction spending and production levels (Exhibit 9). For example, the oil price – the key driver of profitability in the gas industry – has been highly volatile in recent years (falling by 60% between 2014 and 2016) and influenced by geopolitics and global supply and demand. Domestic policy settings can also have a significant impact on growth in the oil and gas industry. Key areas of uncertainty include moratoria, exploration regulation and taxes.

Exhibit 9: Key drivers of the oil and gas industry

DriversLevel of uncertainty Comments

1

External drivers

Oil price (incl. supply/ demand)

HighSignificantvolatilityhistorically;impactedbygeopolitics, supply, demand, government policy

Policy settings MediumKey areas of uncertainty include the policy around moratoria, exploration regulations, accelerated depreciation rules, remote lands taxation, ringfencing

2

Industry drivers

Exploration spend

HighDownward trend over last 5 years, but significant divergence of views on forward outlook and highly dependent on government policy

Construction spend

MediumTrending downwards following construction boom, with uncertainty regarding commercial viability of future developments (e.g. Browse) to and beyond 2022

Oil production MediumDownward trend over last 3 years, with some projectedfuturegrowthfromcondensates;productionexpansion prospects highly influenced by oil price

CSG production HighSignificant uncertainty regarding policy position on exploration and production in NSW, NT, Vic, as well as commercial viability in a low gas price environment

Conventional gas production

MediumAs noted above in construction, uncertainty regarding commercial viability of future projects beyond backfilling existing plants

3

Technology drivers

Technology MediumKey areas of uncertainty include rate of tech development and industry adoption (highly conservative industry, possible complacency in high oil price)

Safety and environment

Low Continued focus on safety and environment

The high degree of uncertainty around key drivers of the oil and gas industry means it is impossible to make a reliable forecast of the industry’s future workforce needs. Recognising this challenge, this report uses scenario-planning to help stakeholders understand the potential trajectory of Australia’s oil and gas workforceoverthenext12years.Thenextsectionsetsoutthreedifferentscenarios(‘operationalefficiency’,an‘upside’and‘downside’case)forthepotentialdirectionoftheindustryanditsworkforce.

22 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

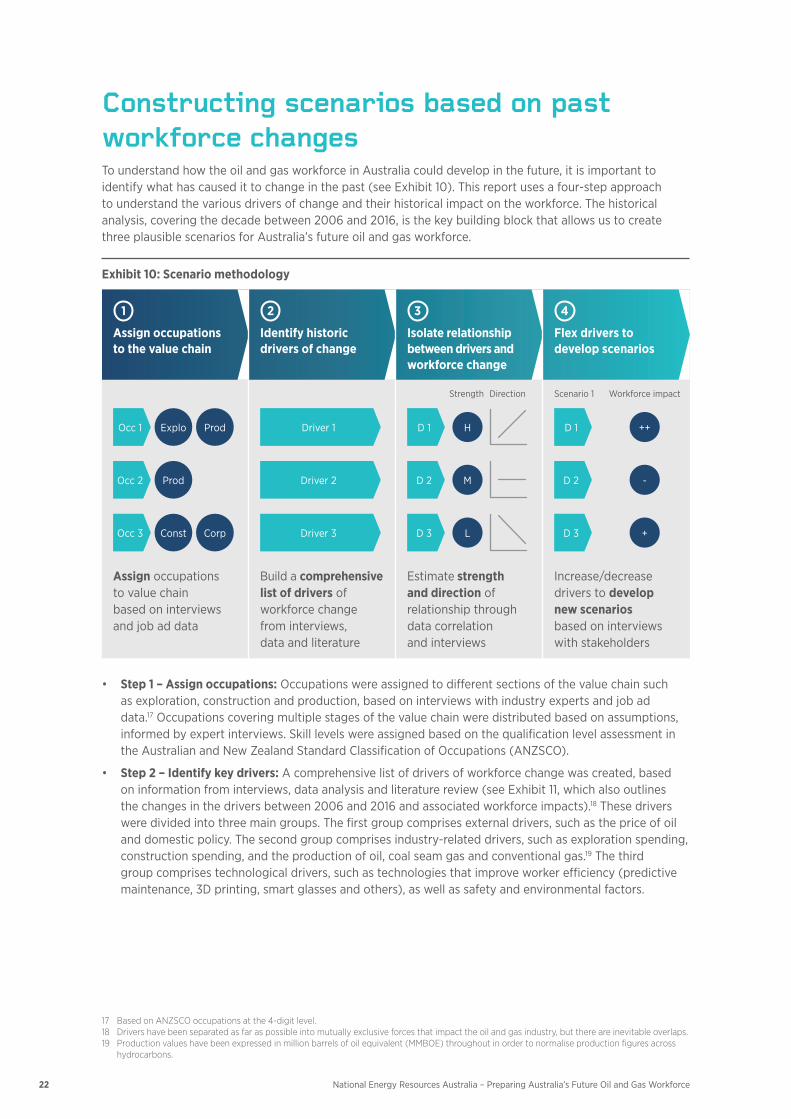

Constructing scenarios based on past workforce changesTo understand how the oil and gas workforce in Australia could develop in the future, it is important to identify what has caused it to change in the past (see Exhibit 10). This report uses a four-step approach to understand the various drivers of change and their historical impact on the workforce. The historical analysis, covering the decade between 2006 and 2016, is the key building block that allows us to create three plausible scenarios for Australia’s future oil and gas workforce.

Exhibit 10: Scenario methodology

1

Assign occupations to the value chain

2

Identify historic drivers of change

3

Isolate relationship between drivers and workforce change

4

Flex drivers to develop scenarios

Strength Direction Scenario 1 Workforce impact

Explo ProdOcc 1 Driver 1 HD 1 ++D 1

ProdOcc 2 Driver 2 MD 2 -D 2

Const CorpOcc 3 Driver 3 LD 3 +D 3

Assign occupations to value chain based on interviews and job ad data

Build a comprehensive list of drivers of workforce change from interviews, data and literature

Estimate strength and direction of relationship through data correlation and interviews

Increase/decrease drivers to develop new scenarios based on interviews with stakeholders

• Step 1 – Assign occupations: Occupations were assigned to different sections of the value chain such as exploration, construction and production, based on interviews with industry experts and job ad data.17 Occupations covering multiple stages of the value chain were distributed based on assumptions, informed by expert interviews. Skill levels were assigned based on the qualification level assessment in the Australian and New Zealand Standard Classification of Occupations (ANZSCO).

• Step 2 – Identify key drivers: A comprehensive list of drivers of workforce change was created, based on information from interviews, data analysis and literature review (see Exhibit 11, which also outlines the changes in the drivers between 2006 and 2016 and associated workforce impacts).18 These drivers were divided into three main groups. The first group comprises external drivers, such as the price of oil and domestic policy. The second group comprises industry-related drivers, such as exploration spending, construction spending, and the production of oil, coal seam gas and conventional gas.19 The third group comprises technological drivers, such as technologies that improve worker efficiency (predictive maintenance, 3D printing, smart glasses and others), as well as safety and environmental factors.

17 Based on ANZSCO occupations at the 4-digit level.18 Drivers have been separated as far as possible into mutually exclusive forces that impact the oil and gas industry, but there are inevitable overlaps.19 Production values have been expressed in million barrels of oil equivalent (MMBOE) throughout in order to normalise production figures across

hydrocarbons.

23National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

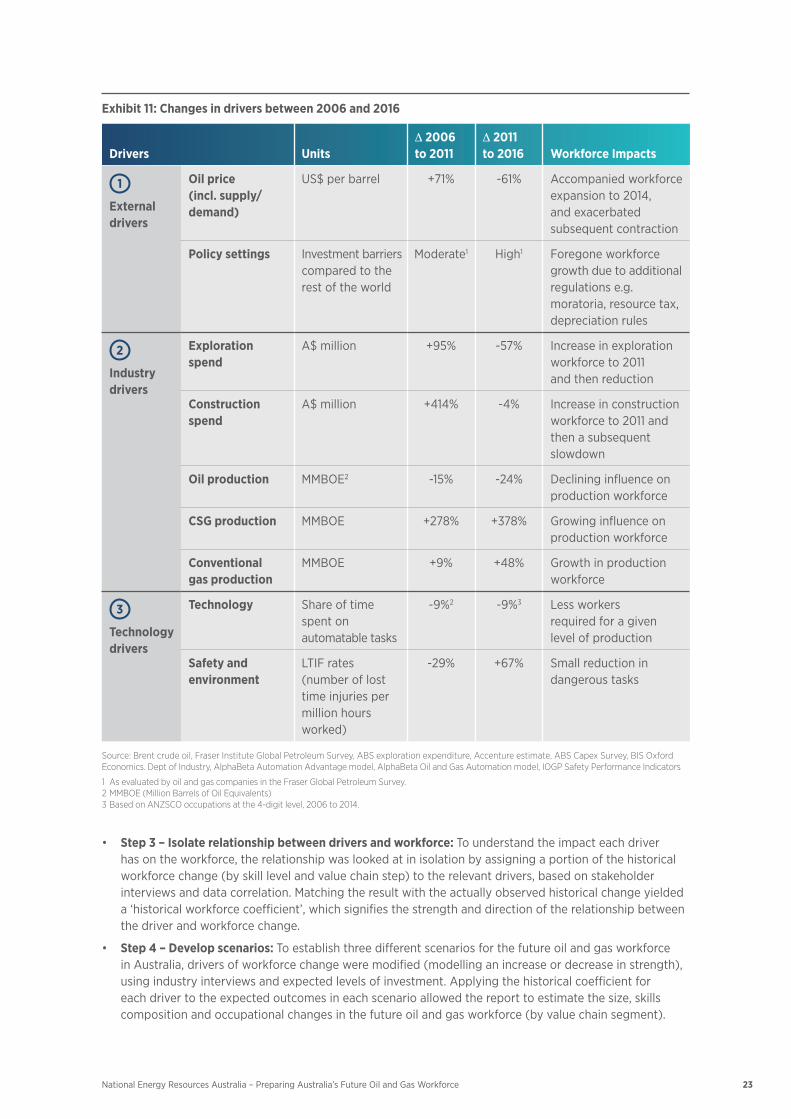

Exhibit 11: Changes in drivers between 2006 and 2016

Drivers Units∆ 2006 to 2011

∆ 2011 to 2016 Workforce Impacts

1

External drivers

Oil price (incl. supply/ demand)

US$ per barrel +71% -61% Accompanied workforce expansion to 2014, and exacerbated subsequent contraction

Policy settings Investment barriers compared to the rest of the world

Moderate1 High1 Foregone workforce growth due to additional regulations e.g. moratoria, resource tax, depreciation rules

2

Industry drivers

Exploration spend

A$ million +95% -57% Increase in exploration workforce to 2011 and then reduction

Construction spend

A$ million +414% -4% Increase in construction workforce to 2011 and then a subsequent slowdown

Oil production MMBOE2 -15% -24% Declining influence on production workforce

CSG production MMBOE +278% +378% Growing influence on production workforce

Conventional gas production

MMBOE +9% +48% Growth in production workforce

3

Technology drivers

Technology Share of time spent on automatable tasks

-9%2 -9%3 Less workers required for a given level of production

Safety and environment

LTIF rates (number of lost time injuries per million hours worked)

-29% +67% Small reduction in dangerous tasks

Source: Brent crude oil, Fraser Institute Global Petroleum Survey, ABS exploration expenditure, Accenture estimate, ABS Capex Survey, BIS Oxford Economics. Dept of Industry, AlphaBeta Automation Advantage model, AlphaBeta Oil and Gas Automation model, IOGP Safety Performance Indicators

1 As evaluated by oil and gas companies in the Fraser Global Petroleum Survey.2 MMBOE (Million Barrels of Oil Equivalents)3 Based on ANZSCO occupations at the 4-digit level, 2006 to 2014.

• Step 3 – Isolate relationship between drivers and workforce: To understand the impact each driver has on the workforce, the relationship was looked at in isolation by assigning a portion of the historical workforce change (by skill level and value chain step) to the relevant drivers, based on stakeholder interviews and data correlation. Matching the result with the actually observed historical change yielded a‘historicalworkforcecoefficient’,whichsignifiesthestrengthanddirectionoftherelationshipbetweenthe driver and workforce change.

• Step 4 – Develop scenarios: To establish three different scenarios for the future oil and gas workforce in Australia, drivers of workforce change were modified (modelling an increase or decrease in strength), using industry interviews and expected levels of investment. Applying the historical coefficient for eachdrivertotheexpectedoutcomesineachscenarioallowedthereporttoestimatethesize,skillscomposition and occupational changes in the future oil and gas workforce (by value chain segment).

24 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

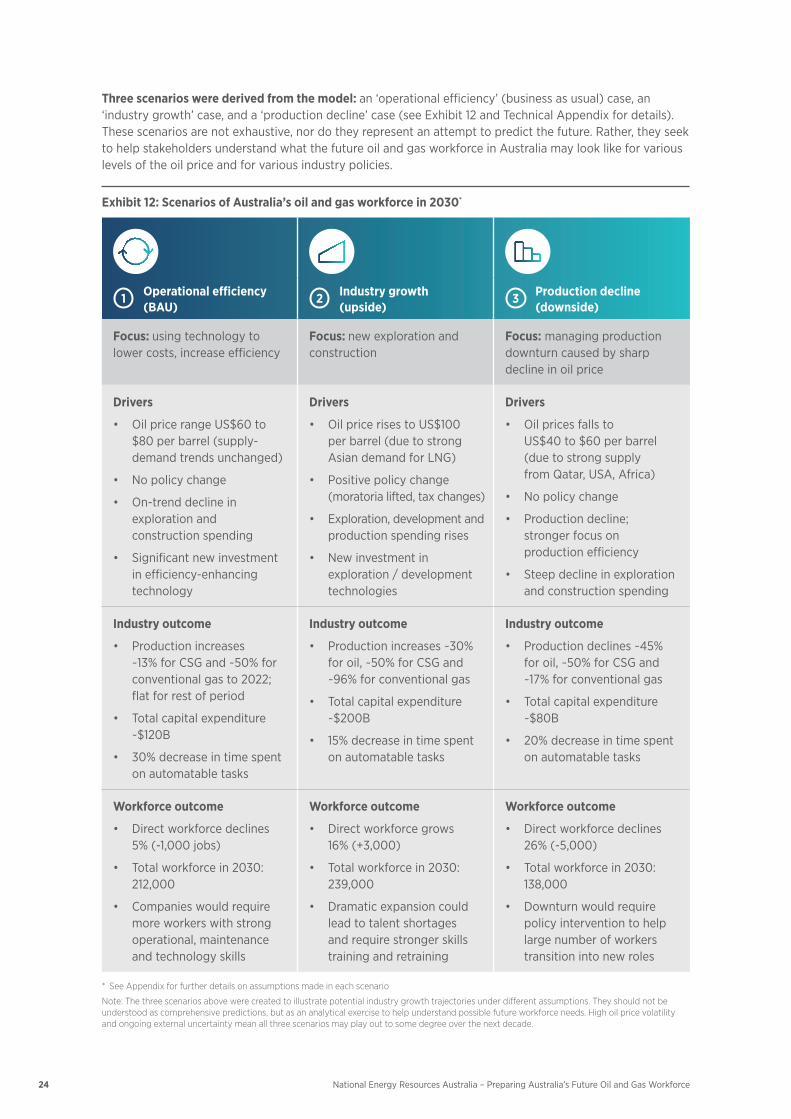

Three scenarios were derived from the model: an‘operationalefficiency’(businessasusual)case,an‘industrygrowth’case,anda‘productiondecline’case(seeExhibit12andTechnicalAppendixfordetails).These scenarios are not exhaustive, nor do they represent an attempt to predict the future. Rather, they seek to help stakeholders understand what the future oil and gas workforce in Australia may look like for various levels of the oil price and for various industry policies.

Exhibit 12: Scenarios of Australia’s oil and gas workforce in 2030*

1 Operational efficiency (BAU)

2 Industry growth (upside)

3 Production decline (downside)

Focus: using technology to lower costs, increase efficiency

Focus: new exploration and construction

Focus: managing production downturn caused by sharp decline in oil price

Drivers

• OilpricerangeUS$60to $80 per barrel (supply-demand trends unchanged)

• Nopolicychange

• On-trenddeclineinexploration and construction spending

• Significantnewinvestmentin efficiency-enhancing technology

Drivers

• OilpricerisestoUS$100 per barrel (due to strong Asian demand for LNG)

• Positivepolicychange(moratoria lifted, tax changes)

• Exploration,developmentandproduction spending rises

• Newinvestmentinexploration / development technologies

Drivers

• Oilpricesfallsto US$40 to $60 per barrel (due to strong supply from Qatar, USA, Africa)

• Nopolicychange

• Productiondecline; stronger focus on production efficiency

• Steepdeclineinexplorationand construction spending

Industry outcome

• Productionincreases ~13% for CSG and ~50% for conventionalgasto2022;flat for rest of period

• Totalcapitalexpenditure~$120B

• 30%decreaseintimespenton automatable tasks

Industry outcome

• Productionincreases~30%for oil, ~50% for CSG and ~96% for conventional gas

• Totalcapitalexpenditure~$200B

• 15%decreaseintimespenton automatable tasks

Industry outcome

• Productiondeclines~45% for oil, ~50% for CSG and ~17% for conventional gas

• Totalcapitalexpenditure~$80B

• 20%decreaseintimespenton automatable tasks

Workforce outcome

• Directworkforcedeclines 5% (-1,000 jobs)

• Totalworkforcein2030:212,000

• Companieswouldrequiremore workers with strong operational, maintenance and technology skills

Workforce outcome

• Directworkforcegrows 16% (+3,000)

• Totalworkforcein2030:239,000

• Dramaticexpansioncouldlead to talent shortages and require stronger skills training and retraining

Workforce outcome

• Directworkforcedeclines26% (-5,000)

• Totalworkforcein2030:138,000

• Downturnwouldrequirepolicy intervention to help large number of workers transition into new roles

* See Appendix for further details on assumptions made in each scenario

Note: The three scenarios above were created to illustrate potential industry growth trajectories under different assumptions. They should not be understood as comprehensive predictions, but as an analytical exercise to help understand possible future workforce needs. High oil price volatility and ongoing external uncertainty mean all three scenarios may play out to some degree over the next decade.

25National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

The scenarios have been developed with significant industry input, based on what is possible and most relevant. The upside and downside scenarios represent theoretical extremes that are meant to bracket a range of future outcomes. In fact, it is likely that the oil and gas industry will need to brace for all three scenarios to play out to some extent in coming years. Heavy swings in the oil price over the past decade (from around US$61 per barrel in 2009 to more than US$111 per barrel in 2011 and back to around US$43 in 2016) show just how unpredictable some of the drivers of the Australian oil and gas workforce are.

This report does not consider any scenario that would reflect a large structural change in the use of energy by 2030. Industry stakeholders deemed such a structural change less likely (over the modelled time frame) and uncertain in consequences. For simplicity reasons, the report assumes that differences between the oil workforce and the gas workforce are limited.

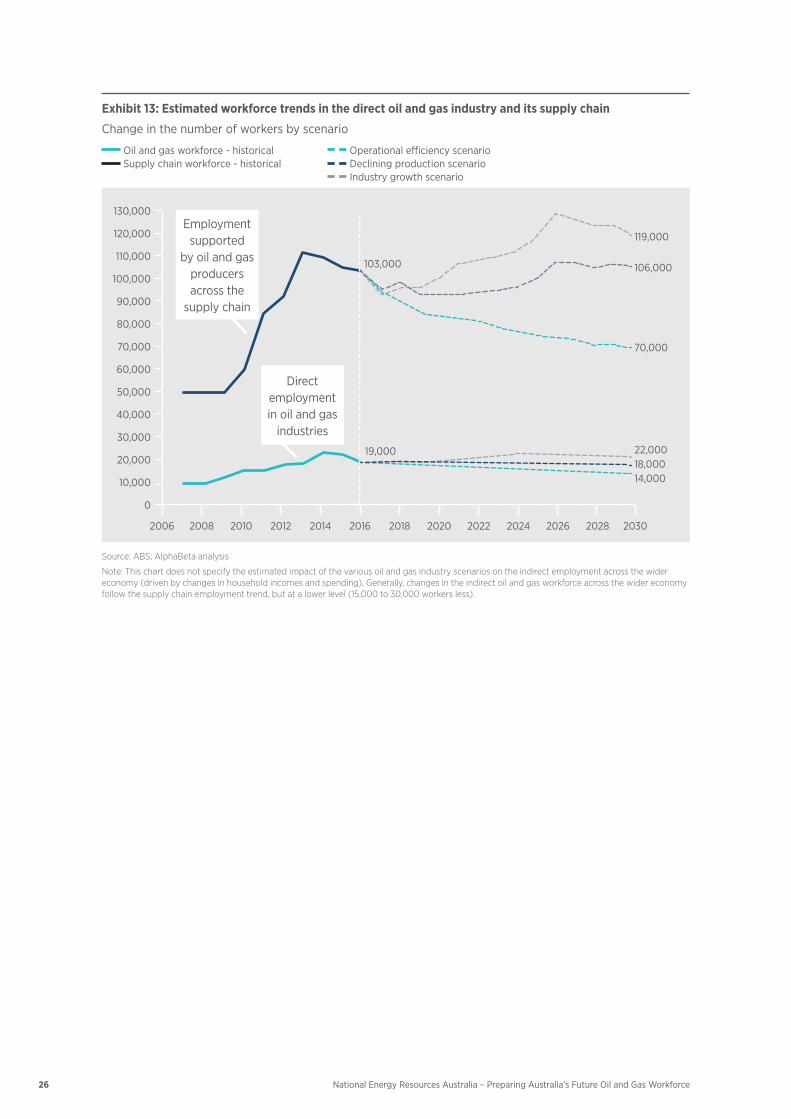

Each scenario implies different challenges for Australia’s oil and gas workforce (see Exhibit 13 and Exhibit 14).

• Inthe‘operational efficiency scenario’ (business as usual), which assumes the oil price remains within a range of US$60 to $80 per barrel and companies continue to use latest technology to make operations more cost-effective, the direct oil and gas workforce would shrink by 1,000 workers, or 5%. However, this slight decline would be offset by growing employment across the supply chain, resulting in a potential net gain of +2,000 new jobs and an increase in the total workforce supported by the oil and gas industry to 212,000 by 2030.

• The‘growth scenario’ assumes that an increase in the oil price to US$100 per barrel or higher and positive policy changes, such as lifting of moratoria, will spur strong production growth. In this case, the total number of jobs supported by the oil and gas industry (including in the supply chain and the wider economy) is expected to increase by 29,000 people, or 14%, to 239,000 in the years to 2030.

• However,asharpdeclineintheoilpricetoaslowasUS$40to$60perbarrelcouldleadtoanegativeemploymentoutcome,asseeninthe‘decline scenario’, which illustrates the risk that the core oil and gas workforce could shrink by 5,000 (26%) in the years to 2030 – with an even more substantial employment decline across the oil and gas supply chain and wider economy.

26 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Exhibit 13: Estimated workforce trends in the direct oil and gas industry and its supply chain

Change in the number of workers by scenario Oil and gas workforce - historical Operational efficiency scenario Supply chain workforce - historical Declining production scenario

Industry growth scenario

Employment supported

by oil and gas producers across the

supply chain

Direct employment in oil and gas

industries

103,000

119,000

106,000

70,000

22,00018,00014,000

19,000

130,000

120,000

110,000

100,000

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Source: ABS; AlphaBeta analysis

Note: This chart does not specify the estimated impact of the various oil and gas industry scenarios on the indirect employment across the wider economy (driven by changes in household incomes and spending). Generally, changes in the indirect oil and gas workforce across the wider economy follow the supply chain employment trend, but at a lower level (15,000 to 30,000 workers less).

27National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Exhibit 14: Estimated employment trends under various oil and gas industry scenarios

Number of workers, 2016 and 2030

Employment generated by O&G in the wider economy Employment generated by O&G in supply chain Direct O&G workforce

2016

Operational Efficiency

2030

Industry Growth

2030

Declining Production

2030

+29,000

138,000

239,000

212,000210,000

70,000

14,000

55,000

98,000

119,000

22,000

88,000

106,000

18,000

88,000

103,000

19,000

Source: ABS; AlphaBeta analysis

Note: Supply chain consists of all industries which supply oil and gas extraction sector or supply those firms which supply oil and gas. Future supply chain and wider economy employment modelled by using historical employment relationships between oil and gas, its supply chain and the wider economy, adjusted for future OandG construction spending and production

28

Three scenarios for the future oil and gas workforce

29National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Operational efficiency: companies will need more workers with operational, maintenance and technology skills

SUMMARY • Underthisscenariooilandgascompanieswillcontinuethedeploymentofemergingtechnology

to maximise production efficiency. The oil price is assumed to remain at a moderate level of US$60 to $80 per barrel.

• Thesizeofthefutureoilandgasworkforcewouldbesimilartotoday.Primaryproducerswouldrequire around 1,000 workers less in 2030 compared to 2016, mostly shedding low to medium skilled corporate and production roles such as drillers, project development workers and clerks.

• Thedirectworkforcedeclinewouldbeoffsetbygrowingemploymentinthesupplychainasprimaryfirms would become more competitive and demand more inputs. The result would be a net gain of 2,000 jobs supported by the oil and gas industry in 2030.

• Thetrendtowardsahigherproductionefficiencywouldrequireoilandgasworkerstobecomemoretechnologically adept and improve their operations management skills.

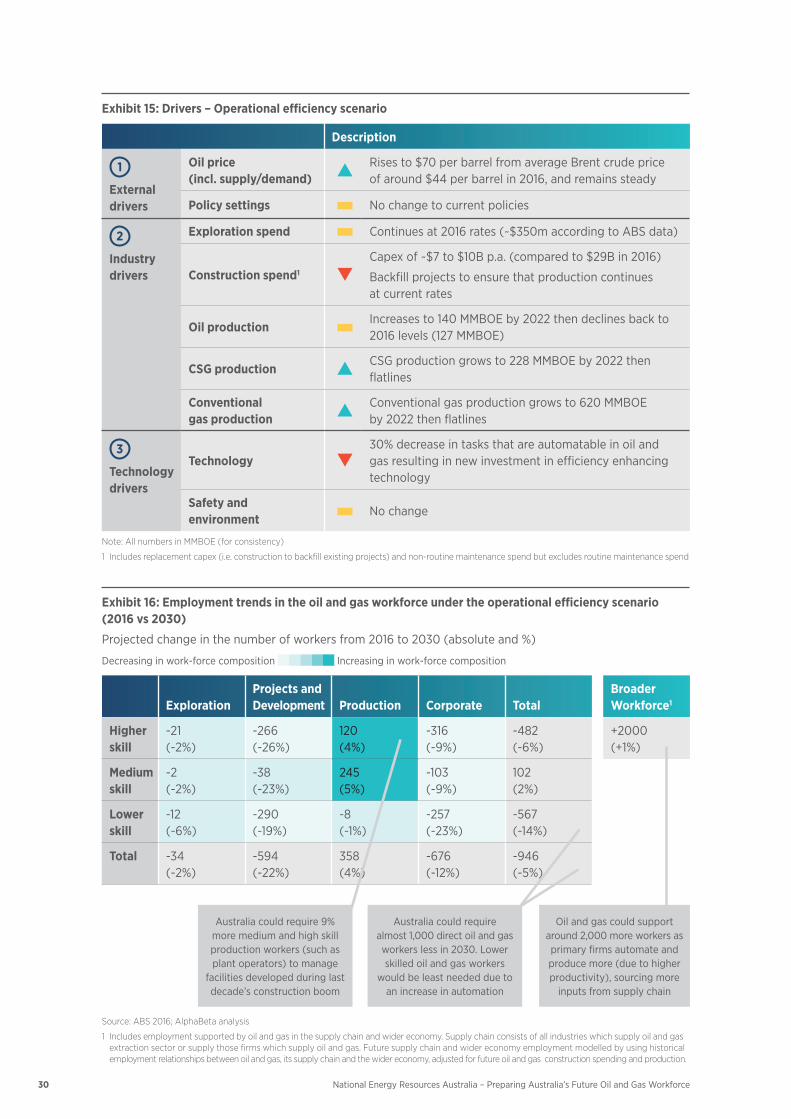

DriversThe key driver in the operational efficiency scenario is a relatively steady oil price in the years to 2030 (see Exhibit 15).20 The scenario assumes that federal and state governments keep their current policy settings (moratoria, taxes etc.) unchanged, meaning the incentives for companies to increase exploration spending are low. As a result, companies are expected to focus on maximising production returns from existing assets, rather than expanding further. To achieve this, primary companies are expected to continue to invest heavily in automation technology (such as advanced sensors).

Workforce changesIntheoperationalefficiencyscenario,theimpactofchangeonthesizeandcompositionoftheworkforcewould be muted (Exhibit 16). As primary companies continue to automate and refrain from further investments in exploration and construction, their direct workforce demand could fall by almost 1,000 workers by 2030, mostly driven by a lower need for low-skilled workers (see Exhibit 16).

However, the growing competitiveness and operational efficiency of primary producers would benefit suppliers, which – in this scenario – are expected to employ around 3,000 additional workers in 2030 to service the higher need for inputs from primary producers. This would result in a total net gain of 2,000 jobs supported by the oil and gas industry by 2030.

20 See technical Appendix for further details on the assumptions underpinning these drivers.

Exhibit 15: Drivers – Operational efficiency scenario

Description

1

External drivers

Oil price (incl. supply/demand)

Rises to $70 per barrel from average Brent crude price of around $44 per barrel in 2016, and remains steady

Policy settings No change to current policies

2

Industry drivers

Exploration spend Continues at 2016 rates (~$350m according to ABS data)

Construction spend1

Capex of ~$7 to $10B p.a. (compared to $29B in 2016)

Backfill projects to ensure that production continues at current rates

Oil productionIncreases to 140 MMBOE by 2022 then declines back to 2016 levels (127 MMBOE)

CSG productionCSG production grows to 228 MMBOE by 2022 then flatlines

Conventional gas production

Conventional gas production grows to 620 MMBOE by 2022 then flatlines

3

Technology drivers

Technology30% decrease in tasks that are automatable in oil and gas resulting in new investment in efficiency enhancing technology

Safety and environment

No change

Note: All numbers in MMBOE (for consistency)

1 Includes replacement capex (i.e. construction to backfill existing projects) and non-routine maintenance spend but excludes routine maintenance spend

Exhibit 16: Employment trends in the oil and gas workforce under the operational efficiency scenario (2016 vs 2030)

Projected change in the number of workers from 2016 to 2030 (absolute and %)

Decreasing in work-force composition Increasing in work-force composition

ExplorationProjects and Development Production Corporate Total

Broader Workforce1

Higher skill

-21 (-2%)

-266 (-26%)

120 (4%)

-316 (-9%)

-482 (-6%)

+2000 (+1%)

Medium skill

-2 (-2%)

-38 (-23%)

245 (5%)

-103 (-9%)

102 (2%)

Lower skill

-12 (-6%)

-290 (-19%)

-8 (-1%)

-257 (-23%)

-567 (-14%)

Total -34 (-2%)

-594 (-22%)

358 (4%)

-676 (-12%)

-946 (-5%)

Australia could require almost 1,000 direct oil and gas workers less in 2030. Lower skilled oil and gas workers

would be least needed due to an increase in automation

Australia could require 9% more medium and high skill production workers (such as plant operators) to manage

facilities developed during last decade’s construction boom

Oil and gas could support around 2,000 more workers as primary firms automate and produce more (due to higher productivity), sourcing more

inputs from supply chain

Source: ABS 2016; AlphaBeta analysis

1 Includes employment supported by oil and gas in the supply chain and wider economy. Supply chain consists of all industries which supply oil and gas extraction sector or supply those firms which supply oil and gas. Future supply chain and wider economy employment modelled by using historical employment relationships between oil and gas, its supply chain and the wider economy, adjusted for future oil and gas construction spending and production.

30 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

31National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Case study 2: How maintenance roles may change in an operational efficiency scenarioMaintenance technicians are a crucial part of the oil and gas workforce. They ensure

that a plant is running at maximum capacity and that all of its electrical and mechanical equipment are in good condition. A steady rise in new electronic equipment has led to significant growth in electrical and instrumental technician roles, and this trend is expected to continue. However, new technology could significantly shift the day-to-day activities of technicians over the next decade.

Maintenance technicians are typically split into two categories: electrical and instrumental technicians, who maintain monitoring, control and electrical equipment such as metering, power supply and generators and account for about 70% of maintenance roles, and mechanical technicians, who perform maintenance and repairs on equipment such as rotating equipment. Both tend to carry out similar activities: maintenance and testing, fault finding in systems and equipment, modifying, repairing and replacing parts, and preparing reports on the work done.

Historically, maintenance technicians have done a large amount of scheduled routine inspections to ensure equipment is working. In the future, much of that routine maintenance could be supported by robotics and supplemented with predictive maintenance technology. With the rise of advanced sensors and growing amounts of real-time data, workers could be required to only maintain equipment on a case-by-case basis when they receive a data alert. Advances in technology mean maintenance work will likely shift from scheduled routine maintenance to more diagnostic tasks and ad-hoc repairs. However, these changes are likely to have only a small impact on maintenance workers numbers as workers will shift towards more diagnostic activities (Exhibit 17).

Exhibit 17: Potential evolution of maintenance roles, now to 2016 (Production efficiency scenario)

Mechanical

Electrical & Instrumental Tool time (reactive)

Tool time (routine)

Tool time (predictive including diagnosis)

Logs

Permitry

2016 2030 2016 2030

65%

20%

80%

35%

30%

10%

20%

10%

24%

24%

12%

10%

50%

10%

Shift away from field mechanical rolesMaintenance roles will require

much less routine maintenance

32 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

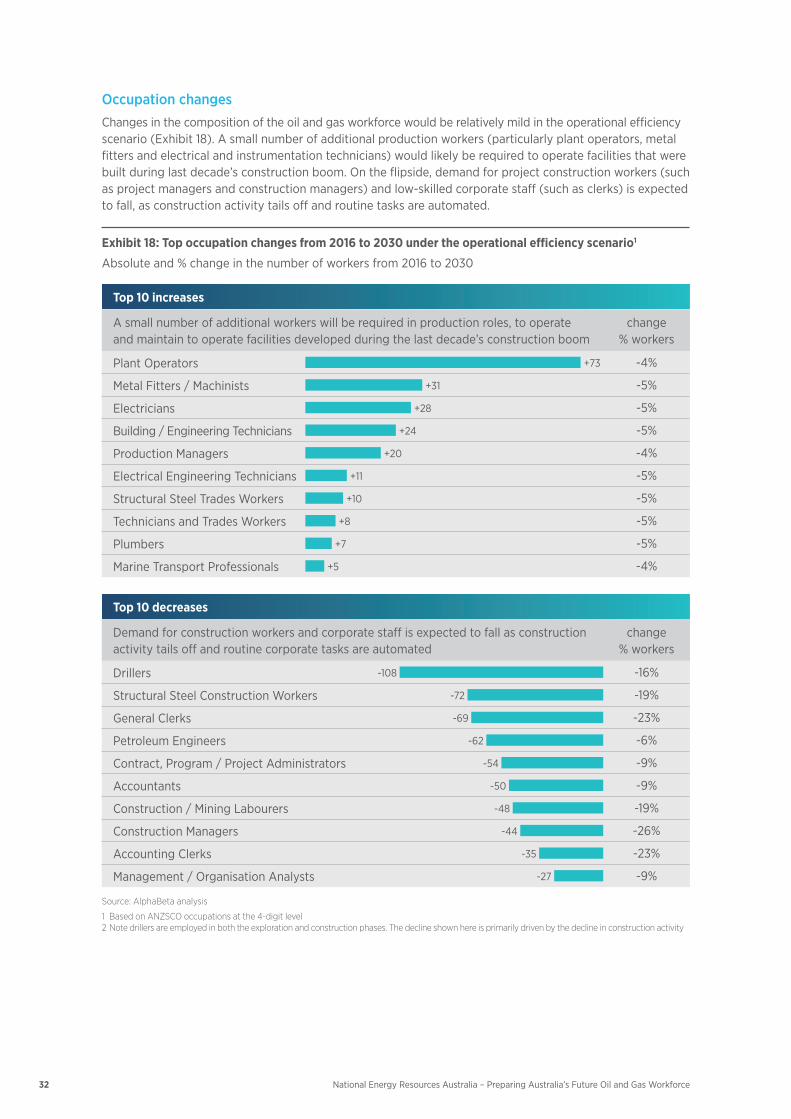

Occupation changesChanges in the composition of the oil and gas workforce would be relatively mild in the operational efficiency scenario (Exhibit 18). A small number of additional production workers (particularly plant operators, metal fitters and electrical and instrumentation technicians) would likely be required to operate facilities that were built during last decade’s construction boom. On the flipside, demand for project construction workers (such as project managers and construction managers) and low-skilled corporate staff (such as clerks) is expected to fall, as construction activity tails off and routine tasks are automated.

Exhibit 18: Top occupation changes from 2016 to 2030 under the operational efficiency scenario1

Absolute and % change in the number of workers from 2016 to 2030

Top 10 increases

A small number of additional workers will be required in production roles, to operate and maintain to operate facilities developed during the last decade’s construction boom

change% workers

Plant Operators +73 -4%

Metal Fitters / Machinists +31 -5%

Electricians +28 -5%

Building / Engineering Technicians +24 -5%

Production Managers +20 -4%

Electrical Engineering Technicians +11 -5%

Structural Steel Trades Workers +10 -5%

Technicians and Trades Workers +8 -5%

Plumbers +7 -5%

Marine Transport Professionals +5 -4%

Top 10 decreases

Demand for construction workers and corporate staff is expected to fall as construction activity tails off and routine corporate tasks are automated

change% workers

Drillers -108 -16%

Structural Steel Construction Workers -72 -19%

General Clerks -69 -23%

Petroleum Engineers -62 -6%

Contract, Program / Project Administrators -54 -9%

Accountants -50 -9%

Construction / Mining Labourers -48 -19%

Construction Managers -44 -26%

Accounting Clerks -35 -23%

Management / Organisation Analysts -27 -9%

Source: AlphaBeta analysis

1 Based on ANZSCO occupations at the 4-digit level2 Note drillers are employed in both the exploration and construction phases. The decline shown here is primarily driven by the decline in construction activity

33National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Case study 3: How field operator roles may change in an operational efficiency scenarioField operators form a major part of the current oil and gas workforce. They look after

the day-to-day running of oil and gas plants by streamlining production and keeping operations safe. Over the coming decade, new technologies could see the occupation mix within field operations shift as well as their day-to-day functions.

At present, field operators such as plant operators, undertake key activities such as monitoring plant processes, observing instruments and meters, starting and stopping equipment and inspecting the plant. To do these tasks, they need a range of skills and abilities. For example, plant operators need to be comfortable working with machines given their frequent interaction with machinery and equipment. Their jobs also demand good problem-solving skills and physical fitness as they patrol oil and gas plants and troubleshoot issues with plant equipment.

New technology will change the nature of field operations in the oil and gas industry. In 2016, field operators encompassed the majority of operations roles in oil and gas, comprising about 55% of these roles (Exhibit 19). Over the next decade, new technologies such as advanced sensors and automated testing will be able to perform field operations functions such as monitoring and controlling equipment e.g. doing gas tests. As a consequence, the number of field operators will likely decline. By 2030, field operators could only represent 30% of oil and gas operations roles.

Of the field operator roles that remain in 2030, their day-to-day activities will be quite different. Their work is already being influenced by technology. For example, tablets are now used to receive and send real-time data from their inspections, whereas previously they recorded observations manually. This is part of a broader movement toward reducing the volume of manual inspection activities and making plant operations more data driven. Eventually, advanced robotics could see an end to many of the taxing and risky physical tasks performed in oil and gas plants.

Exhibit 19: Potential evolution of operator roles, now to 2030 (Production efficiency scenario)

Flow of low/medium-skill workers from and within oil and gas between 2011 to 2016

Control room operators

Permitry

Field operators

Multi-skilled field operators

Checking plant

Running / fixing plant (with control operators)

Enabling work to happen

2016 2030 2016 2030

15%

55%

15%

15% 20%

35%

30%

15%

25%

40%

35%

70%

25%

5%

Shift away from field operator rolesField operator roles would involve

significantly less inspection

Source: Expert interviews

34 National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

In the operational efficiency scenario, core production roles such as plant operator and production manager would remain vital to primary companies, albeit with a shift in skills requirements.

The heavy use of automation technology would require production workers to develop stronger multi-disciplinary skills (to use technology and to manage and maintain increasingly automated production plants). Almost 1,000 workers, predominantly lower skilled employees in primary exploration, project and development and corporate roles, would be affected by the automation trend (see Exhibit 16). These workers would need support transitioning into new roles – ideally in the direct oil and gas industry or its supply chain. Workers in the supply chain would also need stronger technology skills to service rapidly automating primary firms.

Over the next 10 years, most workers will be able to gradually acquire the new skills required in the oil and gas plants of the future. Inevitably, there will be some job losses due to growing use of automation technology in remote,hazardousoperationsandforrepetitive,routinework.However,casestudies(seeCasestudy2,3and4on how specific roles might change) indicate that automation technology is first and foremost changing the tasks within an occupation, not the occupation itself. Moreover, it is expected that technological progress will cause new jobs to emerge in roles focusing on technology supervision, maintenance, data evaluation and training. This would increase the need for re-training and teaching new skills, particularly technology skills, to workers.

35National Energy Resources Australia – Preparing Australia’s Future Oil and Gas Workforce

Industry growth: rapid expansion may lead to a worker shortage and the need to lift workforce skills

SUMMARY • KeyassumptionofthisscenarioisasustainedperiodofexpansionintheAustralianoilandgas

industry, sparked by a strong increase in the oil price to US$100 per barrel or higher and favourable government policies (such as lifting of moratoria).

• Oilandgascompanieswillsubstantiallyincreasetheirexplorationactivitiesandstartnewprojectsinthe North West Shelf and East Coast, lifting overall production levels.

• Thestrongindustryexpansioncouldcreatearound29,000newjobsinthecoreoilandgasworkforceas well as indirectly across the supply chain and wider economy (see Exhibit 13).

• Theexpecteddramaticworkforceincreasecouldleadtoaskillsshortage,particularlyinexplorationand production. To increase the supply in specialist workers and to keep pace with the technological change in the industry, education and training opportunities would need to improve.

DriversThe key drivers in the industry growth scenario are a rising oil price due to strong global demand for LNG, as well as changes to federal and state government policies (such as lifting of CSG moratoria and changes to depreciation rules). Together, these two drivers are expected to encourage primary oil and gas companies to increase their spending on exploration, project development and construction. As a result, Australia’s hydrocarbon production, particularly production of CSG and conventional gas, is expected to soar (see Exhibit 20). This scenario assumes companies will invest in automation technology, particularly to lower exploration and construction costs. Technological progress is expected to reduce the number of automatable tasks performed by workers by 15%.21

Workforce changesThe expected changes that underpin the industry growth scenario would have a strong and positive impact on employment, increasing the total workforce supported by oil and gas to 29,000 in 2030 (see Exhibit 21). In this scenario, the direct oil and gas workforce could grow by around 3,000 workers by 2030, with the largest growth in medium and high skill production workers such as plant operators and petroleum engineers (increase of 27%, or more than 700 workers, as seen in Exhibit 21). Demand for highly skilled exploration workers, such as geologists and geophysicists, could increase by nearly 300, or 24%, as companies invest more heavily in exploration (Exhibit 21).