Embed Size (px)

Citation preview

• Azvalor occupies an under-populated niche of the asset management matrix juxtaposing duration ofcapital with size with a deliberate focus on maximising opportunity set through disciplined growth inorder to promote quality of Partner capital.

• Regulatory shifts, changing liquidity patterns in chief markets bode well for this strategy, particularly asthe competitive playing field for smaller managers shrinks and top-down risk management that equatesrisk with volatility take root at competing firms.

• Azvalor’s presence in London capitalises on the intensive bottom-up nature of research and investmentembedded in Company’s ethos – London is the financial capital of the world and allows both analystsand PMs to access differentiated primary data and intelligence.

• Value investing has endured a torrid period due to a combination of fund flows away from activemanagers towards passive structures married to an environment of financial repression in the ratesspace, the time is therefore ideal to capitalise on the intelligence on offer through the London office.

• High levels of valuation dispersion, absence of competition and wide gaps between price and valuewithin certain sub-sectors of the market – often deemed too “un-investible” for conventional managersis a prime area of focus at this time.

• The trinity of excellent people, process and critically partners creates the necessaryfoundation for successful long-term compounding of partner capital in value investing.

• Azvalor is in the minority of managers who intentionally limit asset size in order to maximize opportunity set.Such an approach is only possible with long term investors.

LARGE

AUM

SMALL

AUM

LONG DURATION INVESTOR CAPITAL

SHORT DURATION INVESTOR CAPITAL

Long Duration Capital

but strategy necessarily

focussed on large caps

due to large AUM.

Few managers in this

quadrant.

Short duration capital chasing

high liquidity products, such

as daily/weekly UCITs vehicles

that rarely compound at

elevated levels. Returns are

historically poor and managers

suffer from misalignment of

stakeholder interest. High

number of managers occupy

this quadrant.

Short duration capital

invested with Firms

whose assets never

grow substantially,

populated by managers

with assets <$50mm

0,88

2,66

3,87

5,19

Universe

>$5m ADV

>$20m ADV

>$50m ADV

EUROPE HIGHER COUNT,

LOWER LIQUIDITY

• European market infrastructure changes: growing and changing barriers to accessing value in Europe.

SINCE 2008 WE HAVE SEEN A STEADY STREAM

OF NEW REGULATION, WITH INTENDED AND

UNINTENDED CONSEQUENCES

REGULATORS ARE LOOKING FOR GREATER

ACCOUNTABILITY AND TRANSPARENCY

REQUIRES INCREASED FOCUS AND

INVESTMENTS IN DATA MANAGEGMENT FROM

WHICH TO REPORT FROM

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

AIFMD

EMIR

ESMA SSR

MIFID 2

GDPR

MARKET

ABUSE

ANNEX 4

CRS

COVERAGEPOORLY COVERED

PARTLY COVERED

WELL COVERED

64%EUROPEAN STOCKS COVERED BY

1 ANALYST OR LESS

21%EUROPEAN STOCKS COVERED BY

MORE THAN 5 ANALYSTS

15%EUROPEAN STOCKS

COVERED BY

2 THROUGH 5

ANALYSTS

LIMITED COVERAGE,

INCREASED OPPORTUNITY

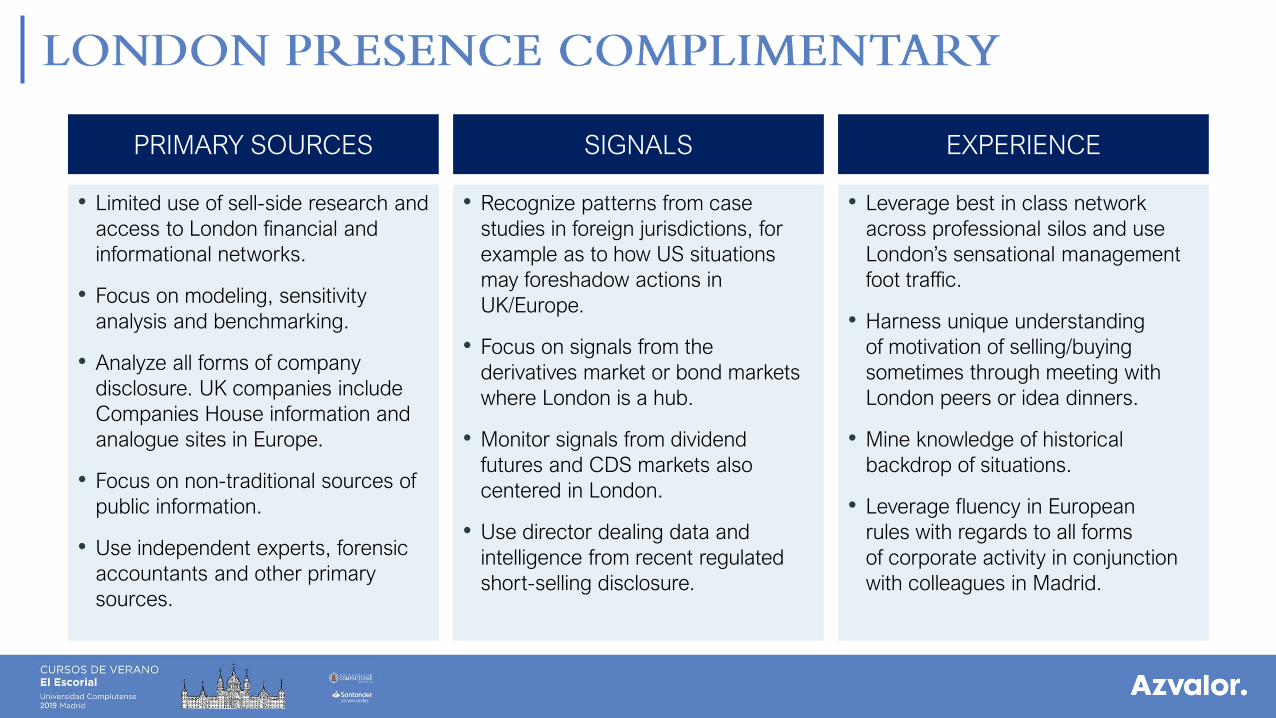

• Limited use of sell-side research and

access to London financial and

informational networks.

• Focus on modeling, sensitivity

analysis and benchmarking.

• Analyze all forms of company

disclosure. UK companies include

Companies House information and

analogue sites in Europe.

• Focus on non-traditional sources of

public information.

• Use independent experts, forensic

accountants and other primary

sources.

• Recognize patterns from case

studies in foreign jurisdictions, for

example as to how US situations

may foreshadow actions in

UK/Europe.

• Focus on signals from the

derivatives market or bond markets

where London is a hub.

• Monitor signals from dividend

futures and CDS markets also

centered in London.

• Use director dealing data and

intelligence from recent regulated

short-selling disclosure.

• Leverage best in class network

across professional silos and use

London’s sensational management

foot traffic.

• Harness unique understanding

of motivation of selling/buying

sometimes through meeting with

London peers or idea dinners.

• Mine knowledge of historical

backdrop of situations.

• Leverage fluency in European

rules with regards to all forms

of corporate activity in conjunction

with colleagues in Madrid.

PRIMARY SOURCES SIGNALS EXPERIENCE

100

150

200

250

300

350

31/03/2009 31/03/2010 31/03/2011 31/03/2012 31/03/2013 31/03/2014 31/03/2015 31/03/2016 31/03/2017 31/03/2018 31/03/2019

MSCI Global Value MSCI Global Growth

-400

-300

-200

-100

0

100

200

300

400

500

2012 2013 2014 2015 2016 2017 2018

Active Passive

FLOW DATA IN USD BILLIONS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

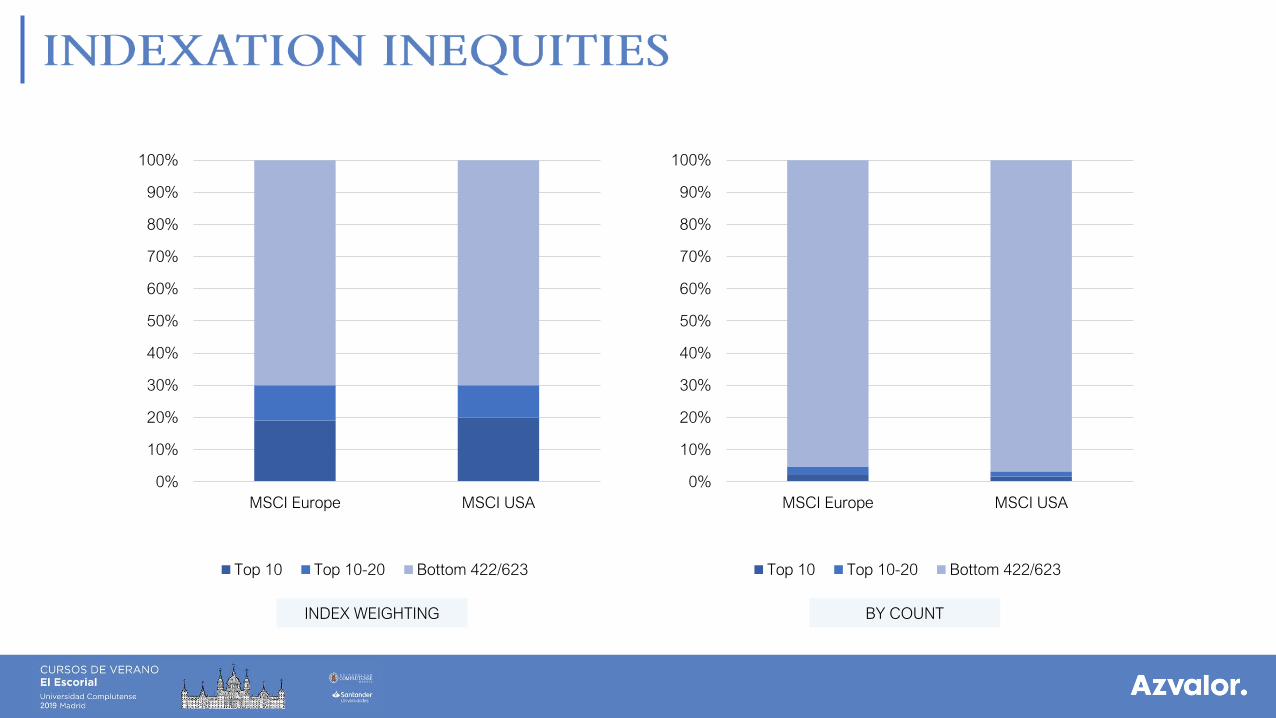

100%

MSCI Europe MSCI USA

Top 10 Top 10-20 Bottom 422/623

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MSCI Europe MSCI USA

Top 10 Top 10-20 Bottom 422/623

INDEX WEIGHTING BY COUNT

• There is a generational opportunity in value investing for winners of attrition like Azvalor who havepreferential capital.

• The past decade has been characterised by financial repression, central bank interference and multipleexpansion for a small coterie of securities which created a two tier market.

• Price is not value. There is an extraordinary amount of value in under-loved parts of the market whichare not accessible to many investors due to regulation and other external factors.

• Volatility is not risk. Azvalor believes that permanent impairment of capital is risk. Other marketopportunities that have bid assets to absurd absolute and relative valuations may find themselves withenormous irreparable capital impairment.

• Rates are at record low levels and valuation dispersion is at record high levels and significantlyincreases the chances of positive future value performance.

•