Embed Size (px)

Citation preview

July 2017

Forward Looking Statements & Non-GAAP Measures

Forward-Looking Statements

This presentation contains, and oral statements made from time to time by our representatives may contain, “forward-

looking statements”. Forward-looking statements include statements under “Outlook” and other statements identified by

words such as “could,” “may,” “might,” “will,” “likely,” “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,”

“expects,” “continues,” “projects” and similar references to future periods, or by the inclusion of forecasts or projections.

Forward-looking statements are based on our current expectations and assumptions regarding capital market conditions,

our business, the economy and other future conditions. Because forward-looking statements relate to the future, by their

nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a

result, our actual results may differ materially from those contemplated by the forward-looking statements. Important

factors that could cause actual results to differ materially from those in the forward-looking statements include regional,

national or global political, economic, business, competitive, market and regulatory conditions, including risk regarding,

our ability to manage inventory or anticipate consumer demand; changes in consumer confidence and spending; our

competitive environment; our failure to open new profitable stores or successfully enter new markets and other factors set

forth under “Risk Factors” in the Form 10-K, as amended, filed with the U.S. Securities and Exchange Commission on April

28, 2017. Any forward-looking statement made in this presentation speaks only as of the date on which it is made. J.Jill

undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new

information, future developments or otherwise.

Non-GAAP Measures

This presentation includes certain non-GAAP financial measures, including Adjusted EBITDA and Adjusted EBITDA Margin.

Non-GAAP financial measures such as Adjusted EBITDA and Adjusted EBITDA Margin should be considered only as

supplemental to, and not as superior to, financial measures prepared in accordance with GAAP. Other companies may use

similarly titled non‐GAAP financial measures that are calculated differently from the way we calculate such measures.

Accordingly, our non‐GAAP financial measures may not be comparable to similar measures used by other companies. We

caution investors not to place undue reliance on such non‐GAAP measures, but instead to consider them with the most

directly comparable GAAP measure. Non‐GAAP financial measures have limitations as analytical tools, and should not be

considered in isolation, or as a substitute for our results as reported under GAAP. A reconciliation of non‐GAAP measures to

the most directly comparable financial measure prepared in accordance with GAAP is included as an appendix to this

presentation.

1

43%

57%

(1) Represents the fiscal year ended January 28, 2017

(2) Represents net sales from our full-price stores, open for more than 52 weeks, and our direct channel

(3) Please refer to the reconciliation in the appendix

Net Sales $639M

Comparable Sales 11.2%

# Stores 275

Adjusted EBITDA $106M

% Margin 16.6%

Profitable Omni-Channel Model

FY2016 Financials

Direct

Retail

• Proven, Profitable Omni-Channel Model That

Positions Us for Share Gains and Margin

Increases

• Data-Centric Approach That Guides Our Success

• Strong Relationship With Our Affluent, Highly

Loyal Customers

• Distinct, Well-Recognized Brand That Resonates

With Our Customers

• Aligned, Customer-Focused Product Strategy

Driving Superior Margins

• Clear, Sustainable Growth Strategies

• Team, Culture and Investments to Deliver

Consistent, Profitable Growth

Who we are

(Net Sales by Channel (1))

(2)

(3)

2

(1)

$297 $338

$363

$158

$192

$245 $28

$31

$31

$483

$562

$639

33%

34%

38%

2014 2015 2016E

E-commerce Sales E-comm Sales % of Total

645

275

Peer MedianJ.Jill

17%43%

Peer MedianJ.Jill

(Direct Sales % of Total Revenue)

Source: Company filings, publicly available information and Euromonitor

(1) Based on last fiscal year for peers. Peers include ASNA, CHS, EXPR, FRAN, GPS, J Crew, KATE, LB, LULU, Talbots and URBN. Median calculation

excludes J.Jill

Our Proven Omni-Channel Model Positions Us for Share Gains and Margin Increases

We Are Well

Positioned to Take Share

J.Jill E-commerce Channel Has Grown

at a 25% CAGR Since 2014

($ in millions)

And Underpenetrated in Retail

(1)

(1)Retail Sales Catalog Sales

Strong Penetration in Direct

(Retail Doors)

50%

375

Potential

3

Our Channels Complement and Drive Traffic to One Another

Catalog

Direct

43% of Net Sales (1)

■ Offers full range of styles, colors and sizes

■ A full representation of our brand and features:

― Updates on new collections

― Guidance on how to wear and match

products

― Ability to chat live with a customer

representative

■ E-commerce serves as an efficient inventory

clearance vehicle

Retail

57% of Net Sales (1)

■ 275 stores nationwide, 52% located within

lifestyle centers and 48% within premium malls (1)

■ Merchandise showcases newest collection,

reflecting our brand concept and promoting full-

price selling

■ 64% of new customers make their first purchase

through our retail store

■ In-store concierge service to order and ship any

item

One of our primary marketing vehicles to drive customer acquisition and engagement across channels

Produce 25 annual editions

(1) Represents the fiscal year ended January 28, 2017 4

48%52%

Our Retail Store Base Is Profitable and Well-Positioned for Growth

PremiumMallsLifestyle

Centers

Growing Presence in Lifestyle Centers Store Design Elevates Shopping Experience

■ Introduced a store design that brings the J.Jill brand

concept to life

― Showcases our brand concept and elevates, yet

simplifies, the J.Jill shopping experience

― Provides a welcoming, easy-to-shop format that

guides her through clearly merchandised product

stories

We are in the best centers in America where traffic remains healthy

5

(1)

(1) Represents the fiscal year ended January 28, 2017

Industry Leading DatabaseCustomer Acquisition and Retention

■ Utilize data insights to strategically expand marketing

investment and to acquire and retain customers

Product and Merchandising

■ Leverage customer feedback to develop products and

identify new category opportunities

Omni-Channel Portfolio

■ Combine market demographics with customer purchase

behavior to frame our store portfolio

■ Leverage both quantitative and qualitative data

sources to deliver a best-in-class omni experience

■ Personal Identifiers

■ Demographic Overlay

■ Contact History

■ Transaction History

■ Channel History

1.7MM active customers and

can match ~97% of

transactions to an identifiable

customer

Our Data-Centric Approach Guides Our Success

What We Capture/ Track

Marketing Investment and Mix of Medium

■ On-going optimization of spend (e.g. catalog, digital

marketing) toward more effective and targeted

communications

Data Guides Our Success

6

Population Breakdown by Age (2015)

10%

20%

26%

33%35%

37%35% 34%

27%25%

17%

9%

15-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75+

Target Customer

Source: U.S. Census Bureau

% of U.S. Households Earning More than $100K / year by Age

We Target an Attractive, Highly Loyal Customer

We Target the Largest Segment

of the Female Population

She Has Tremendous Spending Power

18%

13%

20%

34%

15%

Children

(0-14 years)

Youth

(15-24 years)

Adults

(25-39 years)

JJ Customers

(40-65 years)

Seniors

(66 years+)

Target Customer■ We can match 97% of our transactions

to an identifiable customer

■ Extensive customer database allows us

to build and maintain relationships with

her to drive optimum value

■ Our customer is college educated,

works outside the home and has an

average household income > $150,000

We Know Our Customer…

…And She Is Extremely Loyal

7 Years

Average Customer Tenure

7

1. Grow Size and Value of Our

Active Customer Base

2. Increase Direct Sales

3. Strengthen Omni-Channel

Capabilities

4. Profitably Expand Our Store Base

5. Enhance Product Assortment

We Are Just Getting Started

Clear, Sustainable Growth Strategies Significant Whitespace Opportunity

SportswearFemales/Age 40+

$42.0B

$0.6B

79.0M

1.7M

NPD Market Size Customers

Market Opportunity

Source: NPD, US Census data, publicly reported sales

We Have Less Than 2% of Market Share

8

Active Customer Base Growth

■ Drive growth of our customer base by using data

to efficiently increase marketing Investment

■ Compelling customer acquisition economics for

sustained long-term growth

■ Optimize investment to drive customer retention

and lifetime value

Siz

e

■ Migrate single channel customers to omni-

channel customers

― Omni-channel customers spend 3x as much

and 3x as frequently per year

■ J.Jill credit card penetration of 53% of sales drives

loyalty and spend per customer

■ Leverage our data analytics as well as our brand

voice and customer segmentation initiative

― Identify highest value customer

segmentation and focus targeted

marketing to drive value

Key Drivers

Va

lue

Annual Spend per Customer (1)

CAGR +3%

CAGR +11%

Grow Size and Value of Customer Base

(in 000’s)

(1) Calculated as net sales divided by total customers9

1,387

1,549

1,723

2014 2015 2016

$348

$363

$371

2014 2015 2016

~$300

>$800

Single Channel Omni-Channel

Orders 1X 3X

Annual Spend by Customer TypeCustomer Growth’14 -’16

CAGR

Omni+19%

Single

10%

We Are Increasing Our Omni-Channel

Customers Faster…

…Driving Meaningful Sales Uplift

% Omni

Total11%

(in 000’s)

10

Grow Size and Value of Customer Base (Cont.)

1,124

1,349

263

374 1,387

1,723

2014

19%

2016

22%

4%

15%

Global Apparel Sales Global Apparel

E-commerce Sales

…And the Sector is Expected to

Continue Growing Rapidly

(’15 – ’20 CAGR)Expected Global Apparel Sales Growth

15%

25%

Global Apparel

E-commerce Sales

J.Jill

Our Growth Has Outpaced the

Apparel E-commerce Sector…

Increase Direct Sales

Source: Euromonitor

(’14 – ’16 CAGR)

Global E-commerce Apparel Sales Growth

11

We are well positioned to capitalize on the rapidly growing

e-commerce apparel sector growth

Expand InternationallyLeverage MobileEnhance E-commerce Platform

■ Personalize for the customer

― Improve navigation

― Implement guiding service

― Streamline checkout

process

■ Optimize for all device types

■ Estimated completion Fall

2017

■ Enhance and support

omni-channel

customer experience

■ Connect with

customers on mobile

via re-platformed

website

― Social media

― In-store push

notifications

■ Leverage new web

platform to expand

internationally

■ Expand geographic

reach, similar to other

global apparel

businesses

12

Increase Direct Sales (Cont.)

Our strategic initiatives will assist in driving further sales growth

in our Direct channel

Strengthen Omni-Channel Capabilities

Create Personalized Experiences

■ Omni-channel product recommendations

■ Wardrobing features / services in store and online

■ Enhanced product selection tools and features

Enable Seamless

Product Discovery

■ Customer visibility to in-store inventory

■ Reserve online, pickup in store

■ Buy online, pickup in store

Enhance Purchase and Post-Purchase

Service Experience

■ Responsive / device “agnostic” digital design

■ Omni-channel order history and “My Account” features

■ Alternate payment methods, mobile payments

■ Clientelling for in-store customers

What We Will Do What It Will Bring

13

Profitably Expand Our Store Base

Well Positioned to Grow Store BaseDisciplined, Analytical Approach

■ Grow retail store base by up to 100 stores

― 10-15 new stores per year

― New locations in lifestyle centers and

premium malls

■ Market-based approach to targeting

centers using internal and external data

such as customer demographics and

purchasing history, center quality and

tenant mix

■ 64% of new customers make their first

purchase through our retail store

Net Store Growth

J.Jill Store Count

Attractive New Store Model (1)

Net Sales ($ '000s) $1,000

Square Feet 3,600

4-Wall Contribution ($ '000s) $270

Payback Period 2 years

Cash-on-Cash Return 50%

13 14 ~100

14(1) Reflects company target new store model

10

261 275

~375

285

2015 2016 2017(f) Potential

Enhance Product Assortment

Expand Categories

■ Selectively broaden and enhance

assortment across our sub-brands, Pure Jill

and Wearever

■ Leverage strong demand for our extended

sizes

― Expand Women’s offerings to select

stores

■ Leverage our data to fuel growth

Optimize Assortment

■ Leverage our customer database as

well as our data capture capabilities

■ Determine optimal mix of assortment by

geography and by store

■ Ensure each of our monthly offerings

delivers right mix of fashion and basics

We will continue delivering high-quality, customer-focused product assortments across

each of our channels while strengthening visual merchandising

15

We Deliver

We Drive Superior Financial Results

Net Sales Adjusted EBITDA (1)

(1) Please refer to the Adjusted EBITDA reconciliation in the appendix

(2) Represents, for any period, Adjusted EBITDA as a percentage of net sales

MarginTotal Comp.

Sales

($ in millions) ($ in millions)

17

(2)

$44

$54

$66

$82

$106

2012

10.2%

2013

11.9%

2014

13.6%

2015

14.6%

2016

16.6%

Continued Momentum in 2017

18

- Total Sales Growth of 12.5%

- Comparable Sales Growth of 9.9%

- 90 basis points Gross Margin

Expansion

- Adjusted EPS growth of 50%

(1) Reference appendix for reconciliation of GAAP to Adjusted EPS

% ConversionFree Cash Flow

(1) Free Cash Flow defined as Adjusted EBITDA less Gross Capital Expenditures

(2) Conversion defined as Free Cash Flow divided by Adjusted EBITDA

Strong Free Cash Flow Generation and Conversion

Strong Free Cash Flow Generation While Investing in Growth

Free Cash Flow and % Conversion (1)(2)

(Free Cash Flow in $ millions)

Gross Capital Expenditures

Store Capital Expenditures Technology Other

($ in millions)

19

$29 $28

$42$48

$70

2012 2013 2014 2015 2016

69% 51% 64% 57% 66%

$13

$27

$24

$35 $36

2012 2013 2014 2015 2016

($MMs) Amount Maturity Pricing

$40mm ABL Facility $0 05/08/2020 L + 150bps

$290mm Term Loan $277(1) 05/08/2022 L + 500bps

Cash $5

Net Debt $272

LTM Q3’16 Adjusted EBITDA $99

Net Debt / Adjusted EBITDA 2.8x

Adjusted Debt (2) / Adjusted EBITDAR (3) 4.5x

Balance Sheet That Provides Significant Liquidity and Financial Flexibility

(1) Does not include voluntary pre-payment on Term loan of $10.1mm on January 19, 2017

(2) Capitalized at 8x rent expense with FY2015 rent expense of $48.9mm

(3) Adjusted EBITDAR defined as Adjusted EBITDA plus rent expense 20

Positioned to Deliver 2017 Financial Goals

Total Company

Comp Sales

High Single Digits

(7% to 9%)

Adjusted EPS $0.27 to $0.29

21

*Based on 52-week year

Adjusted EPS $0.80 to $0.84

Total Company

Comp Sales

High Single Digits

(7% to 9%)

Full Year Outlook*

Q2 Outlook

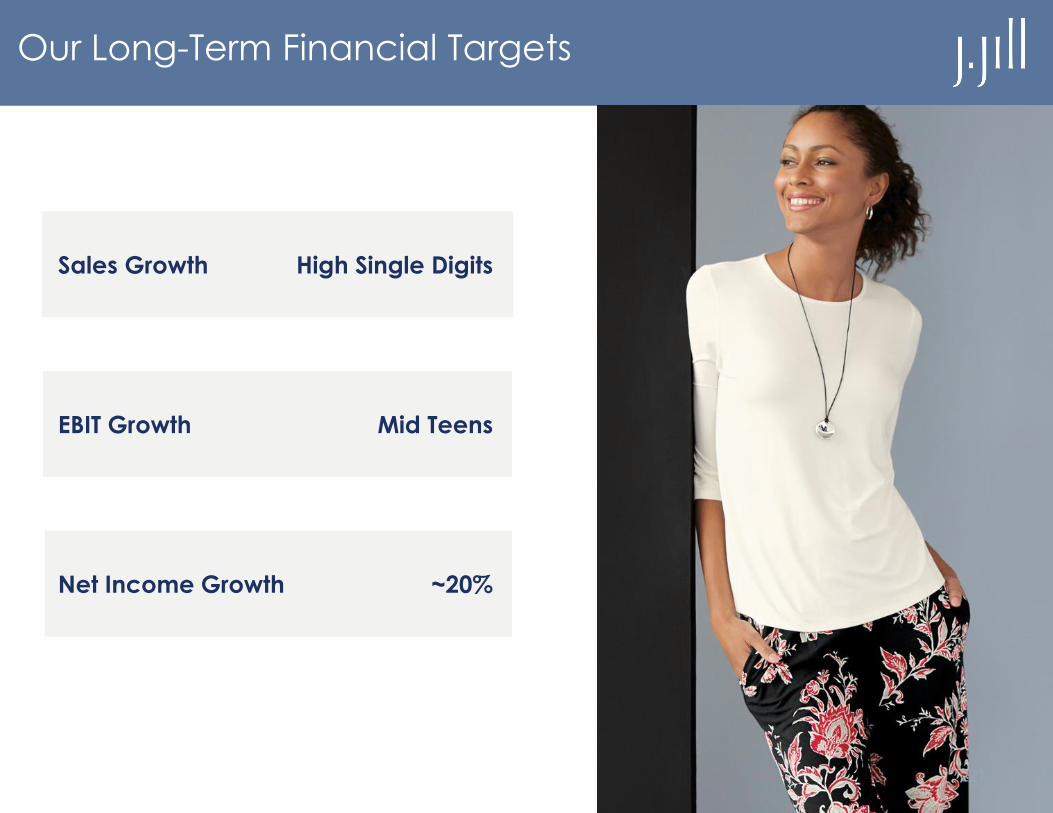

Our Long-Term Financial Targets

Sales Growth High Single Digits

EBIT Growth Mid Teens

Net Income Growth ~20%

221

9Appendix

Non-GAAP Measure – Adjusted EBITDA

J.Jill, Inc. Reconciliation of GAAP Net Income to Adjusted EBITDA

(Unaudited)

(Amounts in thousands)

For the Thirteen Weeks Ended

April 29, 2017 April 30, 2016

Net income $ 8,027 $ 6,073

Interest expense 4,945 4,112

Provision for income taxes 5,603 4,249

Depreciation and amortization 8,799 10,261

Equity-based compensation expense (a) 24 75

Write-off of property and equipment (b) 2 -

Other non-recurring expenses (c) 3,585 1,108

Adjusted EBITDA $ 30,985 $ 25,878

(a): Represents expenses associated with equity incentive instruments granted to our management. Incentive instruments are accounted for as

equity-classified awards with the related compensation expense recognized based on fair value at the date of the grants.

(b): Represents net gain or loss on the disposal of fixed assets.

(c): Represents items management believes are not indicative of ongoing operating performance. These expenses are primarily composed of

legal and professional fees associated with the initial public offering completed March 9, 2017.

24

Non-GAAP Measure – Adjusted Net Income & EPS

J.Jill, Inc.Reconciliation of GAAP Net Income to Adjusted Net Income

(Unaudited)

(Amounts in thousands)

For the Thirteen Weeks Ended

April 29, 2017 April 30, 2016

Net income and total comprehensive income $ 8,027 $ 6,073

Add: Provision for income taxes 5,603 4,249

Income before provision for income taxes 13,630 10,322

Add: Other non-recurring expenses(a)

3,585 1,108

Adjusted Income before provision for income taxes 17,215 11,430

Less: Adjusted Tax Provision(b)

6,886 4,572

Adjusted net income $ 10,329 $ 6,858

Adjusted net income per common share attributable to common shareholders

Basic $ 0.24 $ 0.16

Diluted $ 0.24 $ 0.16

Weighted average number of common shares outstanding

Basic 42,518,143 43,747,944

Diluted 43,680,485 43,747,944

(a): Represents items management believes are not indicative of ongoing operating performance. These expenses are primarily

composed of legal and professional fees associated with the initial public offering completed March 9, 2017.

(b): The adjusted tax provision for adjusted net income is estimated by applying 40% to the adjusted income before provision for

income taxes.25

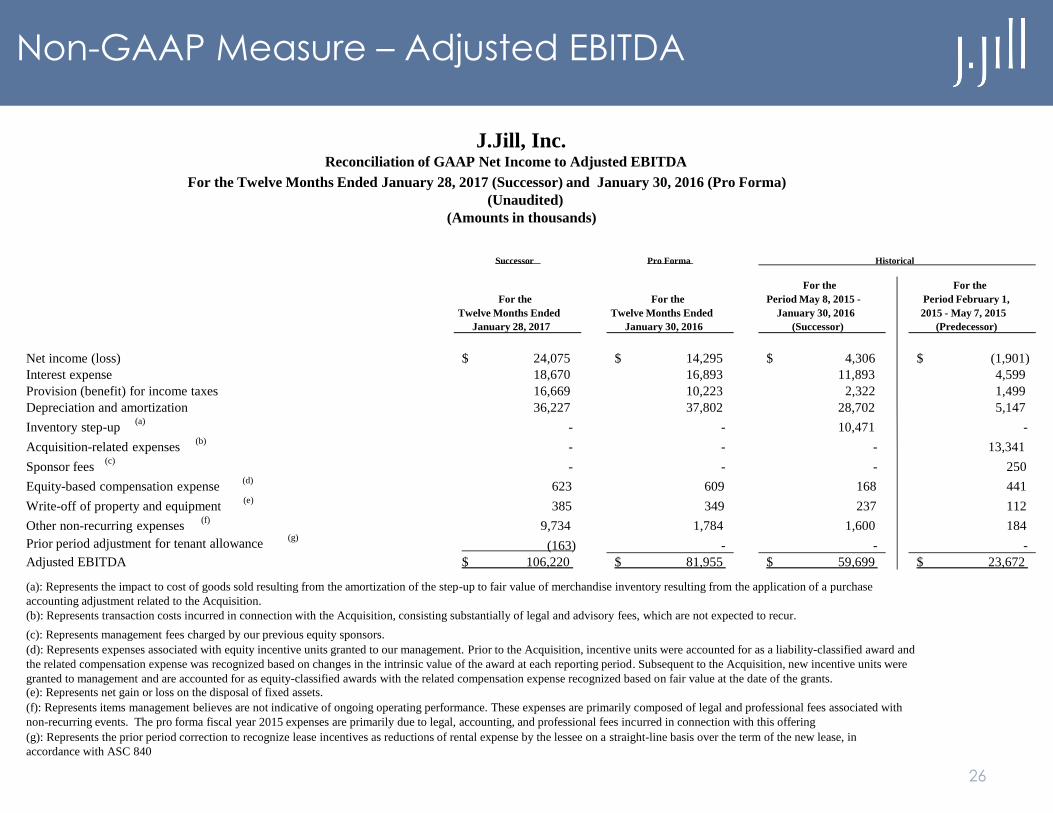

Non-GAAP Measure – Adjusted EBITDA

26

Successor Pro Forma Historical

For the

Twelve Months Ended

January 28, 2017

For the

Twelve Months Ended

January 30, 2016

For the

Period May 8, 2015 -

January 30, 2016

(Successor)

For the

Period February 1,

2015 - May 7, 2015

(Predecessor)

Net income (loss) 24,075$ 14,295$ 4,306$ (1,901)$

Interest expense 18,670 16,893 11,893 4,599

Provision (benefit) for income taxes 16,669 10,223 2,322 1,499

Depreciation and amortization 36,227 37,802 28,702 5,147

Inventory step-up (a)

- - 10,471 -

Acquisition-related expenses(b)

- - - 13,341

Sponsor fees(c)

- - - 250

Equity-based compensation expense(d)

623 609 168 441

Write-off of property and equipment(e)

385 349 237 112

Other non-recurring expenses(f)

9,734 1,784 1,600 184

Prior period adjustment for tenant allowance(g)

(163) - - -

Adjusted EBITDA 106,220$ 81,955$ 59,699$ 23,672$

J.Jill, Inc.Reconciliation of GAAP Net Income to Adjusted EBITDA

For the Twelve Months Ended January 28, 2017 (Successor) and January 30, 2016 (Pro Forma)

(Unaudited)

(Amounts in thousands)

(a): Represents the impact to cost of goods sold resulting from the amortization of the step-up to fair value of merchandise inventory resulting from the application of a purchase

accounting adjustment related to the Acquisition.

(b): Represents transaction costs incurred in connection with the Acquisition, consisting substantially of legal and advisory fees, which are not expected to recur.

(c): Represents management fees charged by our previous equity sponsors.

(d): Represents expenses associated with equity incentive units granted to our management. Prior to the Acquisition, incentive units were accounted for as a liability-classified award and

the related compensation expense was recognized based on changes in the intrinsic value of the award at each reporting period. Subsequent to the Acquisition, new incentive units were

granted to management and are accounted for as equity-classified awards with the related compensation expense recognized based on fair value at the date of the grants.

(e): Represents net gain or loss on the disposal of fixed assets.

(f): Represents items management believes are not indicative of ongoing operating performance. These expenses are primarily composed of legal and professional fees associated with

non-recurring events. The pro forma fiscal year 2015 expenses are primarily due to legal, accounting, and professional fees incurred in connection with this offering

(g): Represents the prior period correction to recognize lease incentives as reductions of rental expense by the lessee on a straight-line basis over the term of the new lease, in

accordance with ASC 840

Non-GAAP Measure – Adjusted Net Income & EPS

27

Successor Pro Forma Historical

For the

Twelve Months Ended

January 28, 2017

For the

Twelve Months Ended

January 30, 2016

For the

Period May 8, 2015 -

January 30, 2016

(Successor)

For the

Period February 1,

2015 - May 7, 2015

(Predecessor)

Net income (loss) 24,075$ 14,295$ 4,306$ (1,901)$

Adjustment: Prior period adjustment for tenant allowance(c)

(163) - - -

Adjustment: Other non-recurring expenses(b)

9,734 1,784 1,600 184

Adjustment: Tax Provision(a) (3,915) (744) (561) 686

Adjusted net income (loss) 29,731$ 15,335$ 5,345$ (1,031)$

Adjusted net income (loss) per share attributable to common stockholders

Basic 0.68$ 0.12$ (0.02)$

Diluted 0.68$ 0.12$ (0.02)$

Weighted average number of common shares outstanding

Basic 43,747,944 43,747,944 43,747,944

Diluted 43,747,944 43,747,944 43,747,944

J.Jill, Inc.Reconciliation of GAAP Net Income to Adjusted Net Income

For the Twelve Months Ended January 28, 2017 (Successor) and January 30, 2016 (Pro Forma)

(Unaudited)

(Amounts in thousands)

(a): The tax provision adjustment for adjusted net income is estimated by applying the effective tax rate for that period to the adjustment

(b): Represents items management believes are not indicative of ongoing operating performance. These expenses are primarily composed of legal and professional fees associated with

non-recurring events. The pro forma fiscal year 2015 expenses are primarily due to legal, accounting, and professional fees incurred in connection with this offering

(c): Represents the prior period correction to recognize lease incentives as reductions of rental expense by the lessee on a straight-line basis over the term of the new lease, in

accordance with ASC 840

Non-GAAP Measure – Historical Adjusted EBITDA

28

Predecessor Successor

Pro Forma

(unaudited)

For the Fiscal

Year Ended

February 2, 2013

For the Fiscal

Year Ended

February 1, 2014

For the Fiscal

Year Ended

January 31, 2015

For the Period

February 1, 2015

to May 7, 2015

For the Period

May 8, 2015 to

January 30, 2016

For the Fiscal

Year Ended

January 30, 2016(in thousands)

NET INCOME/(LOSS) $ (3,601) $ 4,498 $ 10,296 $ (1,901) $ 4,306 $ 14,295

Income tax expense/(benefit) (2,583) 3,884 10,860 1,499 2,322 10,223

Total Interest expense 19,183 19,064 17,895 4,599 11,893 16,893

Depreciation & Amortization 27,333 22,910 19,051 5,147 28,702 37,802

(a) Amortization of inventory step up - - - - 10,471 -

(b) Transaction fees, costs and expenses - - - 13,341 - -

(c) Sponsor fees 1,000 1,000 1,000 250 - -

(d) Stock-based compensation 417 1,930 5,152 441 168 609

(e) Write-off of assets 250 386 58 112 237 349

(f) Other Non-recurring costs 1,914 569 1,408 184 1,600 1,784

Adjusted EBITDA $43,913 $54,241 $65,720 $23,672 $59,699 $81,955

(a) Impact to cost of sales for inventory step-up related to the Acquisition by TowerBrook

(b) Represents transaction costs that have been incurred related to the Acquisition by TowerBrook

(c) For predecessor periods, this includes management fees paid to Arcapita and Golden Gate. For the successor period, it represents expenses reimbursed to

TowerBrook for travel related expenses.

(d) Amount relates to the expense associated with equity incentive units granted to management. Prior to the 2015 acquisition the incentive units were

accounted for as a liability based award and revalued at each reporting period to current fair value. Subsequent to the acquisition by TowerBrook, the units are

accounted for as equity based awards, and are expensed using fair value at the date of the grants.

(e) Represents gain or loss on the disposal of assets

(f) Represents items which management believes are not indicative of our ongoing operating performance. These expenses are primarily composed of outside legal and professional

fees associated with non-recurring events. The 2012 and 2014 costs are primarily associated with legal fees in connection with entering into a forbearance agreement with our lends

for the term loan and revolving credit facility. The 2014 expenses were primarily driven by outside legal and professional services associated with the sale of the company that

occurred in 2015. The 2015 expenses are primarily due to legal, accounting, and professional fees incurred in connection with the Initial Public Offering.