Embed Size (px)

Citation preview

NORDEN – ANNUAL REPORT 2016 RESULTS | 1 Custodians of smarter global trade

NORDEN

RESULTS

Annual Report 2016

Copenhagen, Denmark

1 March 2017

NORDEN – ANNUAL REPORT 2016 RESULTS | 2 Custodians of smarter global trade

AGENDA

� Group highlights

� Financials

� Dry Cargo

� Tankers

� 2017 expectations

� Q & A

NORDEN – ANNUAL REPORT 2016 RESULTS | 3 Custodians of smarter global trade

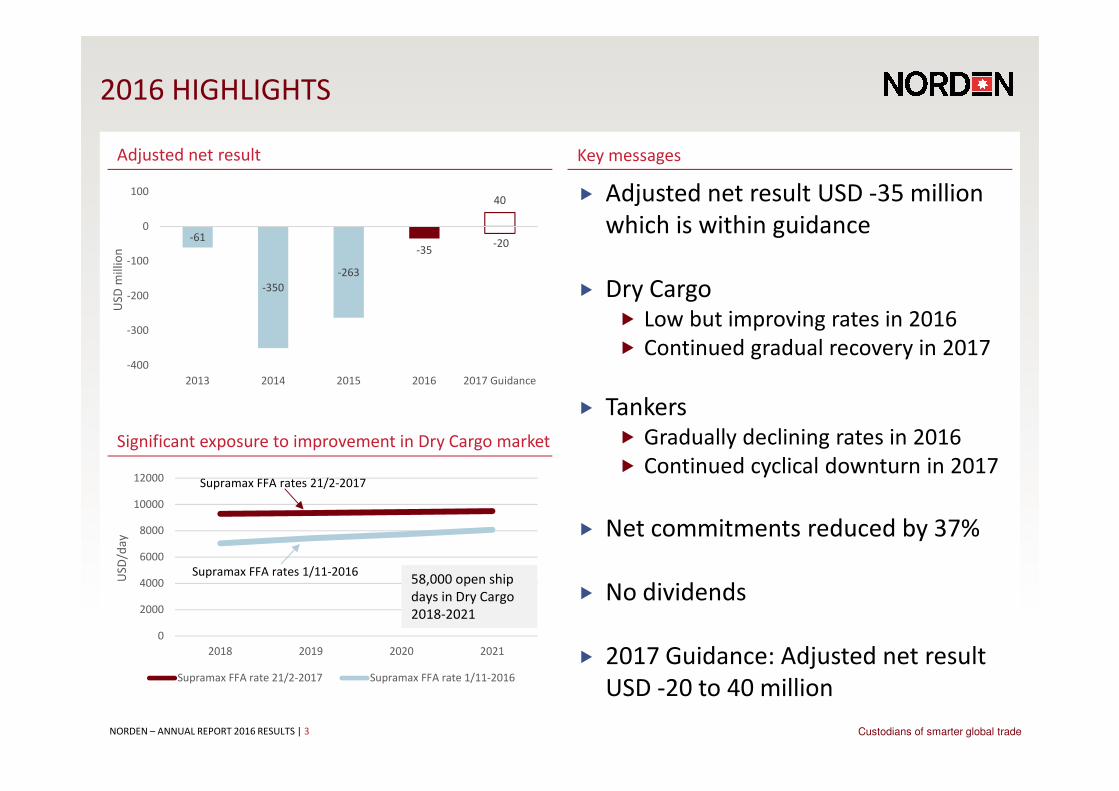

2016 HIGHLIGHTS

� Adjusted net result USD -35 million

which is within guidance

� Dry Cargo� Low but improving rates in 2016

� Continued gradual recovery in 2017

� Tankers� Gradually declining rates in 2016

� Continued cyclical downturn in 2017

� Net commitments reduced by 37%

� No dividends

� 2017 Guidance: Adjusted net result

USD -20 to 40 million

Key messagesAdjusted net result

Significant exposure to improvement in Dry Cargo market

-61

-350

-263

-35-20

40

-400

-300

-200

-100

0

100

2013 2014 2015 2016 2017 Guidance

US

D m

illi

on

0

2000

4000

6000

8000

10000

12000

2018 2019 2020 2021

US

D/d

ay

Supramax FFA rate 21/2-2017 Supramax FFA rate 1/11-2016

58,000 open ship

days in Dry Cargo

2018-2021

Supramax FFA rates 21/2-2017

Supramax FFA rates 1/11-2016

NORDEN – ANNUAL REPORT 2016 RESULTS | 4 Custodians of smarter global trade

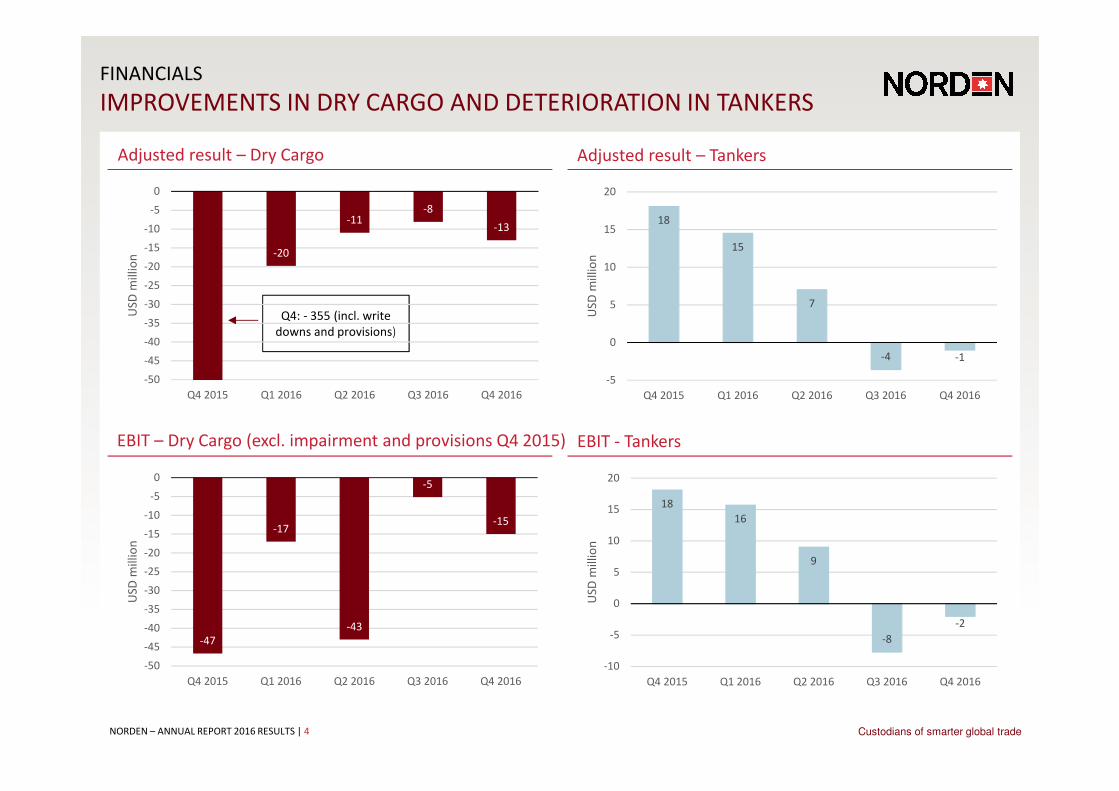

FINANCIALS

IMPROVEMENTS IN DRY CARGO AND DETERIORATION IN TANKERS

Adjusted result – Tankers

EBIT - Tankers

Adjusted result – Dry Cargo

EBIT – Dry Cargo (excl. impairment and provisions Q4 2015)

Q4: - 355 (incl. write

downs and provisions)

-20

-11-8

-13

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

US

D m

illi

on

18

15

7

-4 -1

-5

0

5

10

15

20

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

US

D m

illi

on

18

16

9

-8

-2

-10

-5

0

5

10

15

20

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

US

D m

illi

on

-47

-17

-43

-5

-15

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

US

D m

illi

on

NORDEN – ANNUAL REPORT 2016 RESULTS | 5 Custodians of smarter global trade

0

200

400

600

800

1,000

1,200

1,400

2014 2015 2016

UD

S m

illi

on -37%

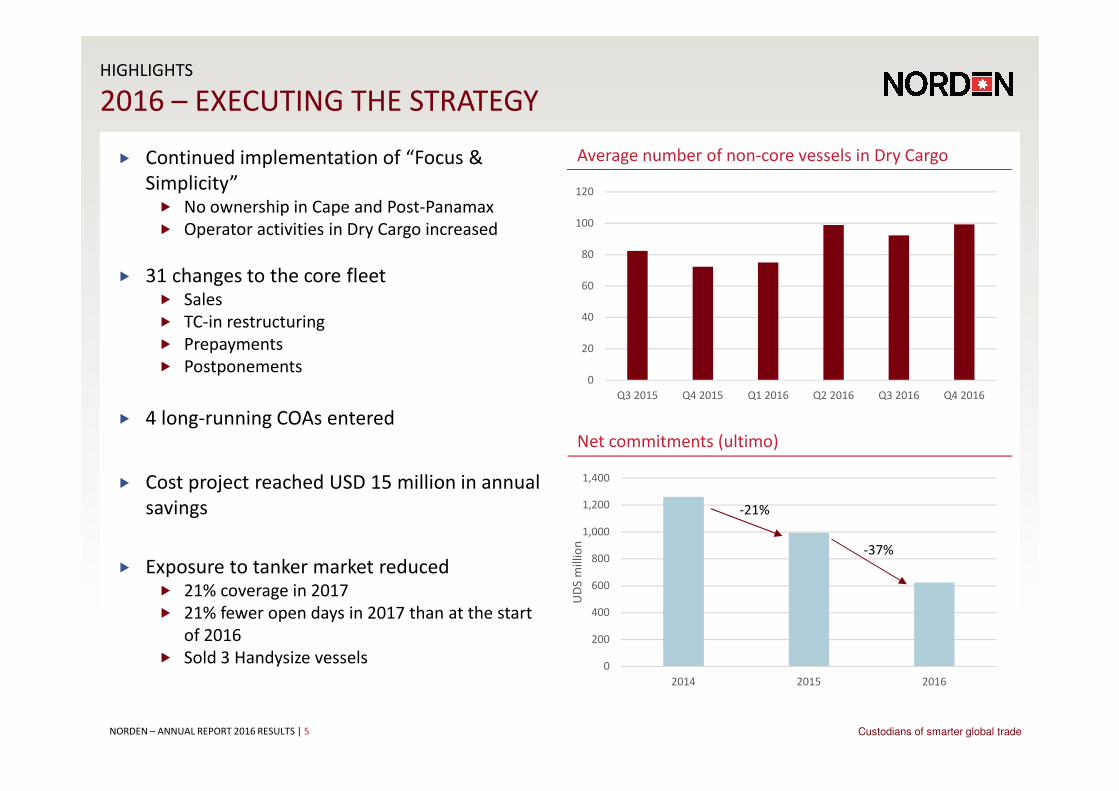

HIGHLIGHTS

2016 – EXECUTING THE STRATEGY

Average number of non-core vessels in Dry Cargo

Net commitments (ultimo)

� Continued implementation of “Focus &

Simplicity”� No ownership in Cape and Post-Panamax

� Operator activities in Dry Cargo increased

� 31 changes to the core fleet� Sales

� TC-in restructuring

� Prepayments

� Postponements

� 4 long-running COAs entered

� Cost project reached USD 15 million in annual

savings

� Exposure to tanker market reduced� 21% coverage in 2017

� 21% fewer open days in 2017 than at the start

of 2016

� Sold 3 Handysize vessels

-21%

0

20

40

60

80

100

120

Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

NORDEN – ANNUAL REPORT 2016 RESULTS | 6 Custodians of smarter global trade

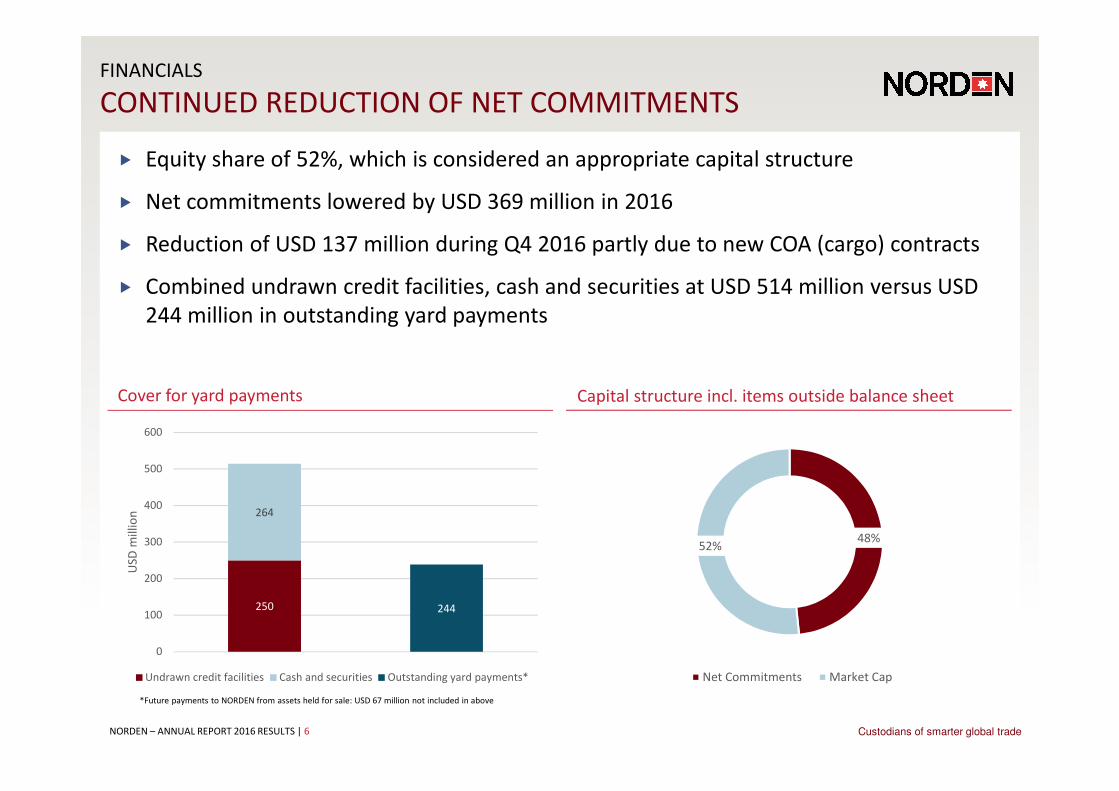

FINANCIALS

CONTINUED REDUCTION OF NET COMMITMENTS

Capital structure incl. items outside balance sheetCover for yard payments

� Equity share of 52%, which is considered an appropriate capital structure

� Net commitments lowered by USD 369 million in 2016

� Reduction of USD 137 million during Q4 2016 partly due to new COA (cargo) contracts

� Combined undrawn credit facilities, cash and securities at USD 514 million versus USD

244 million in outstanding yard payments

48%52%

Net Commitments Market Cap

250

264

244

0

100

200

300

400

500

600

US

D m

illi

on

Undrawn credit facilities Cash and securities Outstanding yard payments*

*Future payments to NORDEN from assets held for sale: USD 67 million not included in above

NORDEN – ANNUAL REPORT 2016 RESULTS | 7 Custodians of smarter global trade

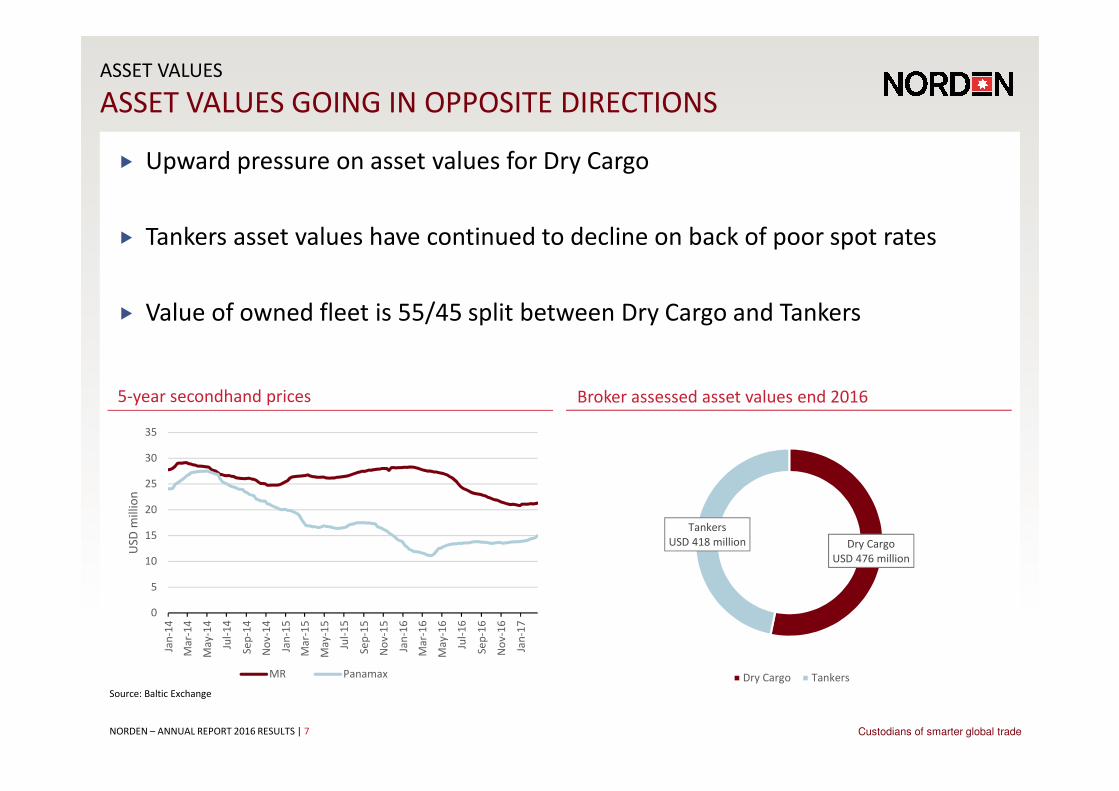

ASSET VALUES

ASSET VALUES GOING IN OPPOSITE DIRECTIONS

Broker assessed asset values end 20165-year secondhand prices

� Upward pressure on asset values for Dry Cargo

� Tankers asset values have continued to decline on back of poor spot rates

� Value of owned fleet is 55/45 split between Dry Cargo and Tankers

Source: Baltic Exchange

0

5

10

15

20

25

30

35

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-

15

Se

p-1

5

No

v-1

5

Jan

-16

Ma

r-1

6

Ma

y-1

6

Jul-

16

Se

p-1

6

No

v-1

6

Jan

-17

US

D m

illi

on

MR Panamax

Dry Cargo

USD 476 million

Tankers

USD 418 million

Dry Cargo Tankers

NORDEN – ANNUAL REPORT 2016 RESULTS | 8 Custodians of smarter global trade

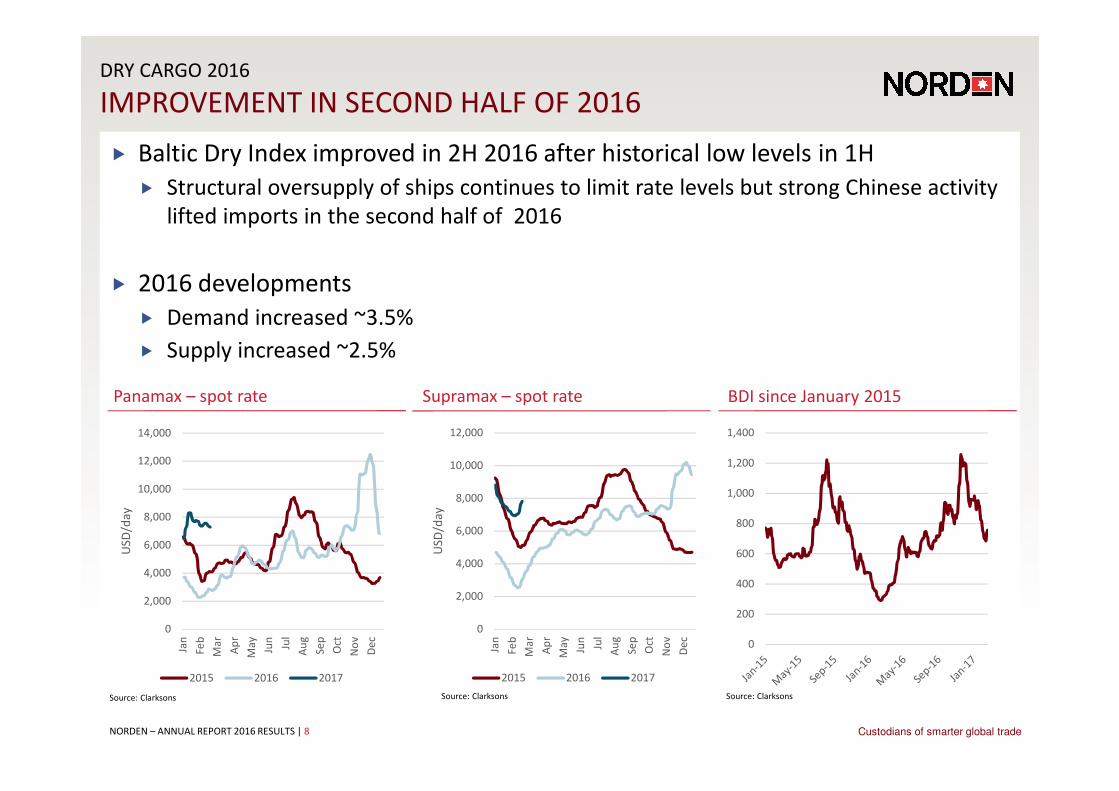

DRY CARGO 2016

IMPROVEMENT IN SECOND HALF OF 2016

Supramax – spot ratePanamax – spot rate BDI since January 2015

� Baltic Dry Index improved in 2H 2016 after historical low levels in 1H

� Structural oversupply of ships continues to limit rate levels but strong Chinese activity

lifted imports in the second half of 2016

� 2016 developments

� Demand increased ~3.5%

� Supply increased ~2.5%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

US

D/d

ay

2015 2016 2017

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

US

D/d

ay

2015 2016 2017

0

200

400

600

800

1,000

1,200

1,400

Source: Clarksons Source: Clarksons Source: Clarksons

NORDEN – ANNUAL REPORT 2016 RESULTS | 9 Custodians of smarter global trade

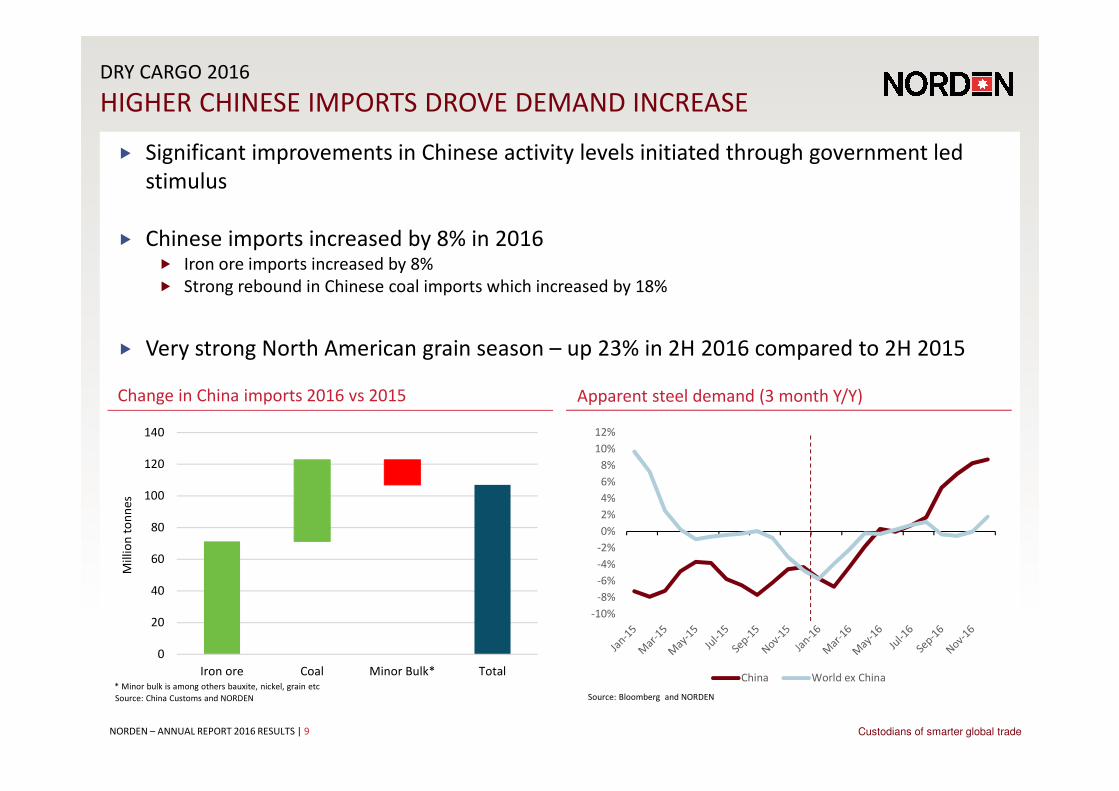

DRY CARGO 2016

HIGHER CHINESE IMPORTS DROVE DEMAND INCREASE

Apparent steel demand (3 month Y/Y)Change in China imports 2016 vs 2015

� Significant improvements in Chinese activity levels initiated through government led

stimulus

� Chinese imports increased by 8% in 2016� Iron ore imports increased by 8%

� Strong rebound in Chinese coal imports which increased by 18%

� Very strong North American grain season – up 23% in 2H 2016 compared to 2H 2015

Source: China Customs and NORDEN Source: Bloomberg and NORDEN

0

20

40

60

80

100

120

140

Iron ore Coal Minor Bulk* Total

Mil

lio

n t

on

ne

s

* Minor bulk is among others bauxite, nickel, grain etc

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

China World ex China

NORDEN – ANNUAL REPORT 2016 RESULTS | 10 Custodians of smarter global trade

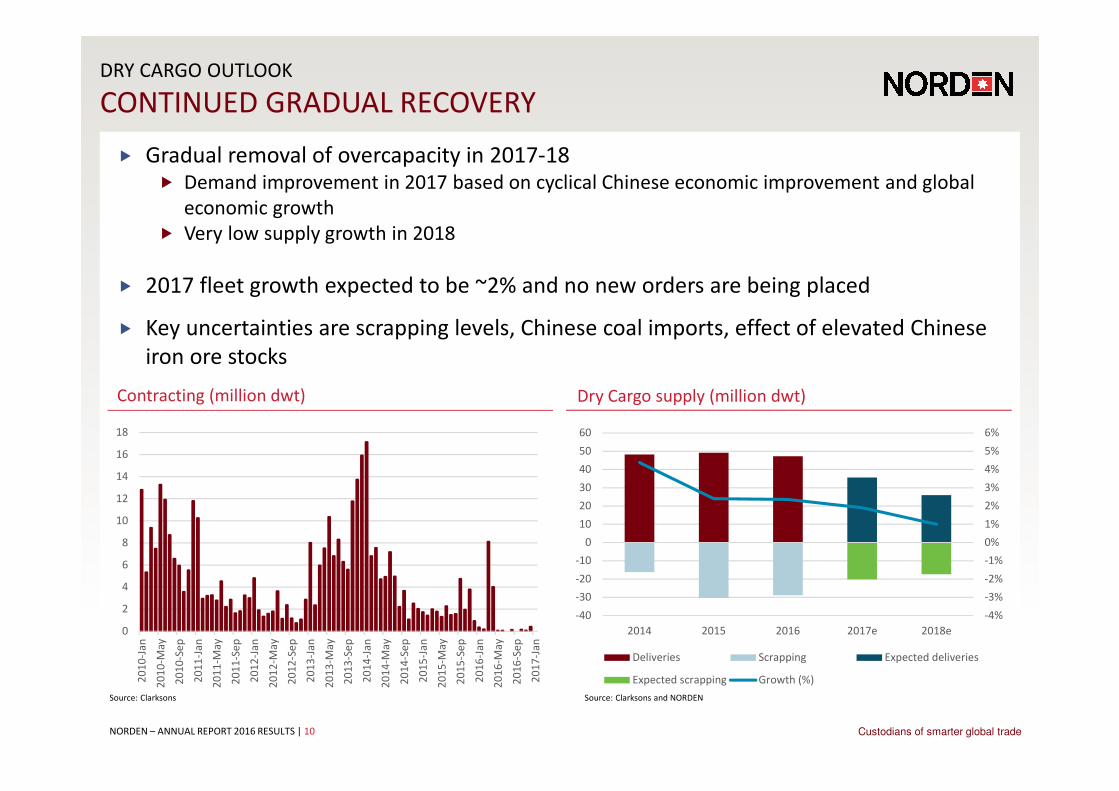

DRY CARGO OUTLOOK

CONTINUED GRADUAL RECOVERY

Dry Cargo supply (million dwt)Contracting (million dwt)

� Gradual removal of overcapacity in 2017-18� Demand improvement in 2017 based on cyclical Chinese economic improvement and global

economic growth

� Very low supply growth in 2018

� 2017 fleet growth expected to be ~2% and no new orders are being placed

� Key uncertainties are scrapping levels, Chinese coal imports, effect of elevated Chinese

iron ore stocks

Source: Clarksons Source: Clarksons and NORDEN

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

-40

-30

-20

-10

0

10

20

30

40

50

60

2014 2015 2016 2017e 2018e

Deliveries Scrapping Expected deliveries

Expected scrapping Growth (%)

0

2

4

6

8

10

12

14

16

18

20

10

-Ja

n

20

10

-Ma

y

20

10

-Se

p

20

11

-Ja

n

20

11

-Ma

y

20

11

-Se

p

20

12

-Ja

n

20

12

-Ma

y

20

12

-Se

p

20

13

-Ja

n

20

13

-Ma

y

20

13

-Se

p

20

14

-Ja

n

20

14

-Ma

y

20

14

-Se

p

20

15

-Ja

n

20

15

-Ma

y

20

15

-Se

p

20

16

-Ja

n

20

16

-Ma

y

20

16

-Se

p

20

17

-Ja

n

NORDEN – ANNUAL REPORT 2016 RESULTS | 11 Custodians of smarter global trade

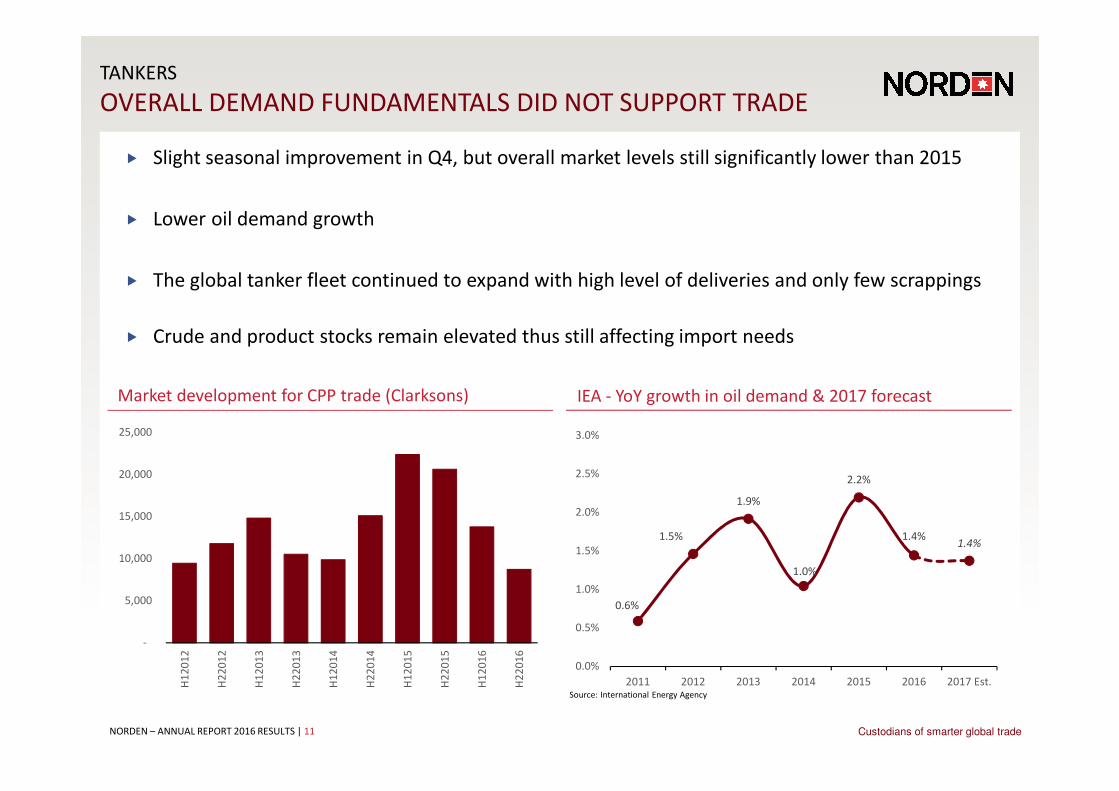

TANKERS

OVERALL DEMAND FUNDAMENTALS DID NOT SUPPORT TRADE

IEA - YoY growth in oil demand & 2017 forecast

0.6%

1.5%

1.9%

1.0%

2.2%

1.4%1.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2011 2012 2013 2014 2015 2016 2017 Est.

Market development for CPP trade (Clarksons)

� Slight seasonal improvement in Q4, but overall market levels still significantly lower than 2015

� Lower oil demand growth

� The global tanker fleet continued to expand with high level of deliveries and only few scrappings

� Crude and product stocks remain elevated thus still affecting import needs

Source: International Energy Agency

-

5,000

10,000

15,000

20,000

25,000

H1

20

12

H2

20

12

H1

20

13

H2

20

13

H1

20

14

H2

20

14

H1

20

15

H2

20

15

H1

20

16

H2

20

16

NORDEN – ANNUAL REPORT 2016 RESULTS | 12 Custodians of smarter global trade

TANKERS OUTLOOK

CONTINUED CYCLICAL DOWNTURN THROUGH 2017

Contracting (million dwt)Yearly net fleet growth and forecast 2017 (%, dwt)

� Market levels not expected to recover in 2017

� High fleet growth again in 2017 - total tanker fleet growth of 4-5%� Net growth for 2017 expected drop to 2-3% in product tankers

� Lower oil demand growth and high inventories limit tanker demand growth

� Contracting remains well below historical figures

0%

1%

2%

3%

4%

5%

6%

7%

8%

2012 2013 2014 2015 2016 2017 (F)

Ye

arl

y n

et

gro

wth

(%

)

Product Crude Total Tank

Source: SSY, Clarksons, NORDEN

0

2

4

6

8

10

12

20

13

-Jan

20

13

-Ma

y

20

13

-Se

p

20

14

-Jan

20

14

-Ma

y

20

14

-Se

p

20

15

-Jan

20

15

-Ma

y

20

15

-Se

p

20

16

-Jan

20

16

-Ma

y

20

16

-Se

p

Source: Clarksons Platou, all tankers +10k dwt

NORDEN – ANNUAL REPORT 2016 RESULTS | 13 Custodians of smarter global trade

2017 FULL YEAR GUIDANCE

CommentsOutlook

USDm Dry Cargo Tankers Total

Adjusted

results for

the year

-15 to 45 -15 to 15 -20 to 40

� Adjusted net result USD -20 to 40

million

� Corresponds to EBIT of USD -5 to

55 million

� Improving market conditions in

dry cargo

� Continued poor tanker market

NORDEN – ANNUAL REPORT 2016 RESULTS | 14 Custodians of smarter global trade

FORWARD LOOKING STATEMENTSFORWARD LOOKING STATEMENTS

This presentation contains certain forward-looking statements reflecting the

management’s present judgment of future events and financial results.

Statements relating to the remainder of 2017 and subsequent years are subject to

uncertainty, and NORDEN’s actual results may therefore differ from the

projections. Factors that may cause such variance include, but are not limited to,

changes in macro-economic and political conditions, particularly in the

Company’s principal markets; changes to the Company’s rate assumptions and

operating costs; volatility in rates and tonnage prices; regulatory changes; any

disruptions to traffic and operations as a result of external events, etc.

NORDEN – ANNUAL REPORT 2016 RESULTS | 15 Custodians of smarter global trade

Dampskibsselskabet NORDEN A/S

52, Strandvejen

DK-2900 Hellerup

Denmark

Phone: +45 3315 0451

www.ds-norden.com

http://www.linkedin.com/company/ds-norden/

http://twitter.com/DS_NORDEN

http://www.facebook.com/shippingtrainee.com

http://www.facebook.com/dampskibsselskabetnorden

Thank you for your attention

NORDEN – ANNUAL REPORT 2016 RESULTS | 16 Custodians of smarter global trade

FORWARD LOOKING STATEMENTSBACK UP SLIDES

NORDEN – ANNUAL REPORT 2016 RESULTS | 17 Custodians of smarter global trade

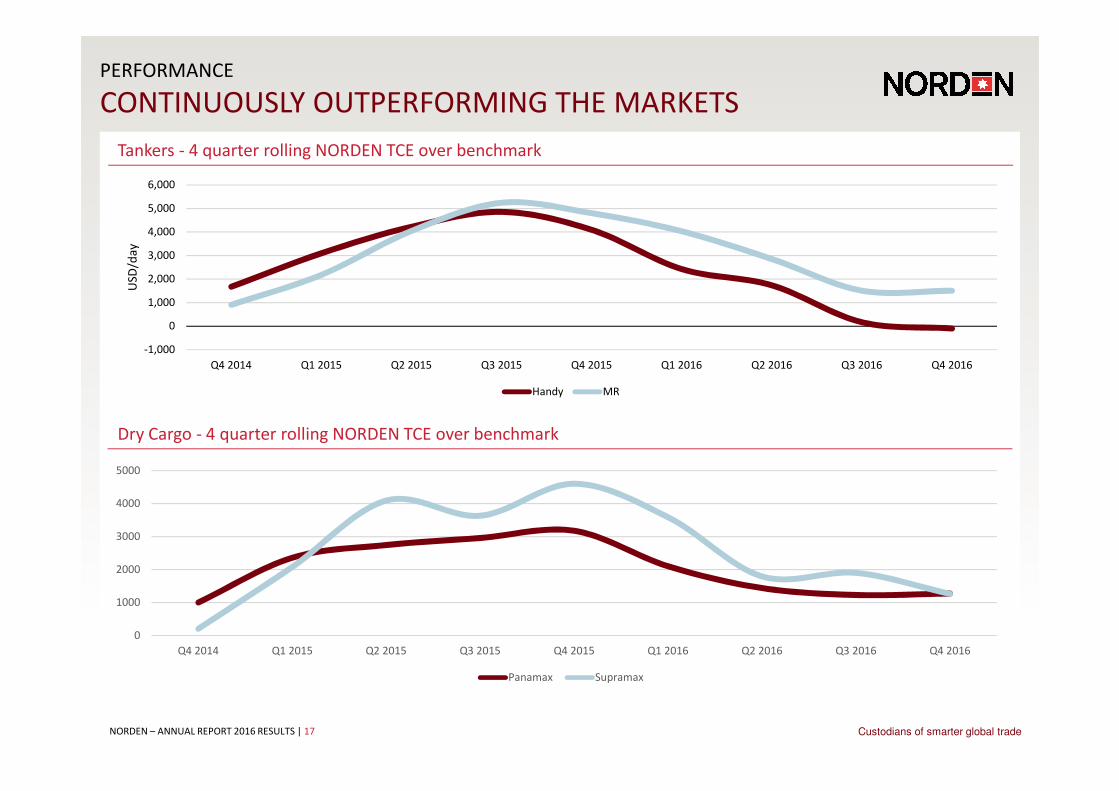

PERFORMANCE

CONTINUOUSLY OUTPERFORMING THE MARKETS

Dry Cargo - 4 quarter rolling NORDEN TCE over benchmark

Tankers - 4 quarter rolling NORDEN TCE over benchmark

0

1000

2000

3000

4000

5000

Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

Panamax Supramax

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

US

D/d

ay

Handy MR

NORDEN – ANNUAL REPORT 2016 RESULTS | 18 Custodians of smarter global trade

� 2 Segments - focus on vessel types where we can make a difference

� Dry Cargo

� Tankers

� Full scale operational setup - Direct customer contact

� Portfolio of time charter-in contracts and earnings coverage

� Long track record of overperformance in Dry Cargo and Tankers

� Healthy balance sheet

� Transparency and clear Corporate Governance

WHAT MAKES NORDEN DIFFERENT?

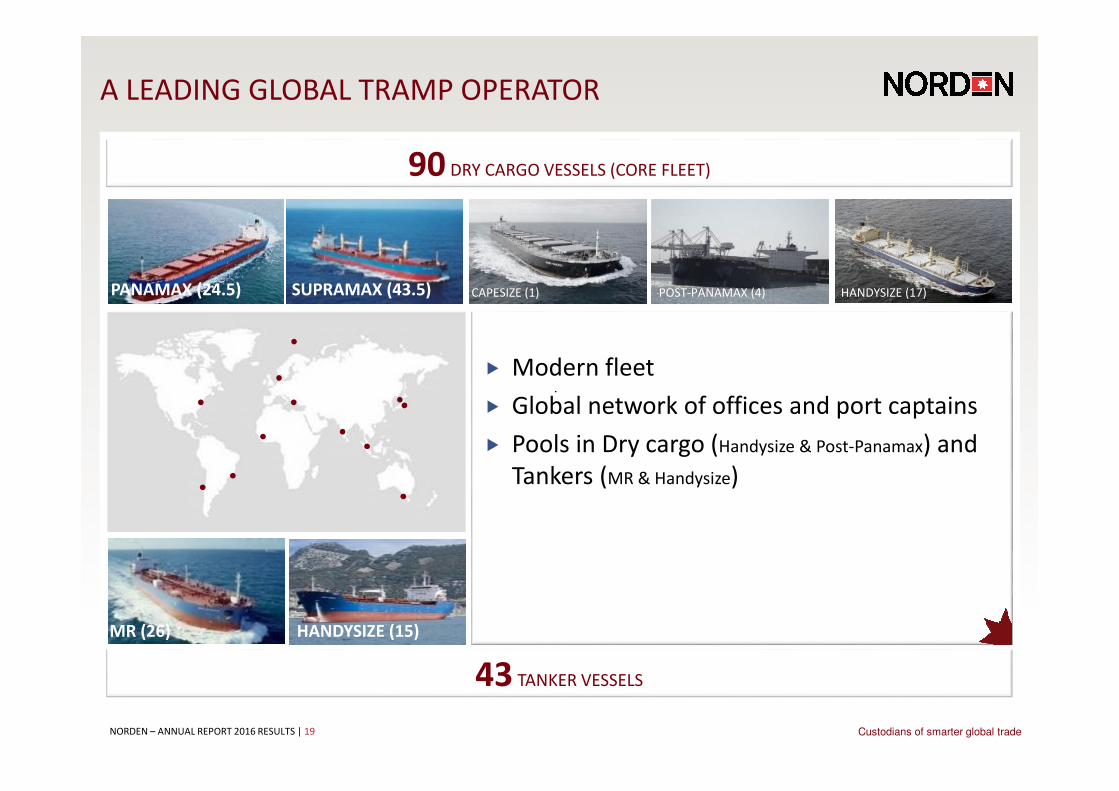

NORDEN – ANNUAL REPORT 2016 RESULTS | 19 Custodians of smarter global trade

A LEADING GLOBAL TRAMP OPERATOR

Tankers

43 TANKER VESSELS

CAPESIZE (1) POST-PANAMAX (4) PANAMAX (24.5) SUPRAMAX (43.5) HANDYSIZE (17)

MR (26) HANDYSIZE (15)

90 DRY CARGO VESSELS (CORE FLEET)

� Modern fleet

� Global network of offices and port captains

� Pools in Dry cargo (Handysize & Post-Panamax) and

Tankers (MR & Handysize)

NORDEN – ANNUAL REPORT 2016 RESULTS | 20 Custodians of smarter global trade

0

25

50

75

100

125

150

175

200

225

250

275

300

18

71

18

74

18

77

18

80

18

83

18

86

18

89

18

92

18

95

18

98

19

01

19

04

19

07

19

10

19

13

19

16

19

19

19

22

19

25

19

28

19

31

19

34

19

37

19

40

19

43

19

46

19

49

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

12

20

15

20

16

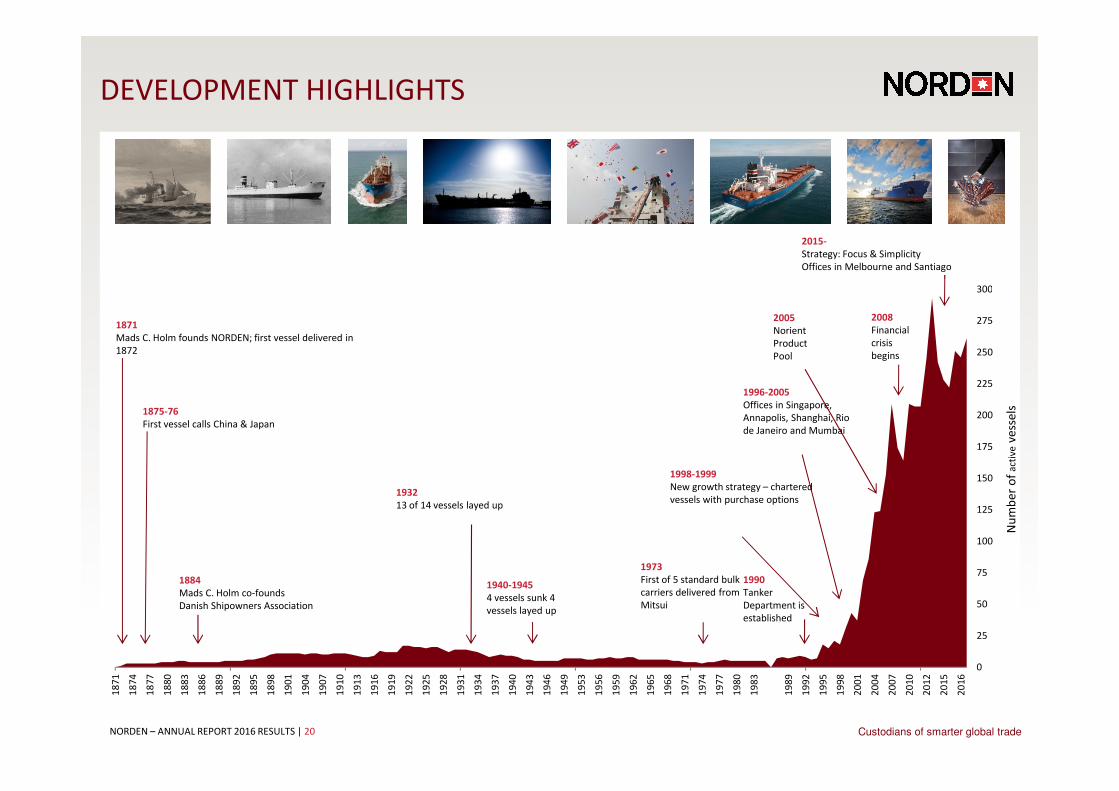

DEVELOPMENT HIGHLIGHTS

Nu

mb

er

of

act

ive

vess

els

2005

Norient

Product

Pool

1871

Mads C. Holm founds NORDEN; first vessel delivered in

1872

1875-76

First vessel calls China & Japan

1990

Tanker

Department is

established

1884

Mads C. Holm co-founds

Danish Shipowners Association

1996-2005

Offices in Singapore,

Annapolis, Shanghai, Rio

de Janeiro and Mumbai

1973

First of 5 standard bulk

carriers delivered from

Mitsui

1998-1999

New growth strategy – chartered

vessels with purchase options1932

13 of 14 vessels layed up

1940-1945

4 vessels sunk 4

vessels layed up

2008

Financial

crisis

begins

2015-

Strategy: Focus & Simplicity

Offices in Melbourne and Santiago

NORDEN – ANNUAL REPORT 2016 RESULTS | 21 Custodians of smarter global trade

ASSET LIGHT BUSINESS MODEL…

� Sale and purchase

� Technical competencies in-

house

Owned (47.5)

Chartered > 13

months (81.5)

Chartered < 13

months (132)

Capacity

� Option-based flexibility

� Some with purchase options

� Flexibility and scale

� Arbitrage

� Single-trip charters

Contracts of

affreightment

TC out

FFA market

Employment

Spot market

� Customer relations

� Logistical efficiencies

� 2-10 year firm periods

� Quick and easy cover

* Active fleet per 30 June 2011

� Active fleet can quickly be adjusted to demand and market conditions

� Fleet employment based on portfolio view

Coverage and customer focusFlexible fleet

BRANDPEOPLE SYSTEMS

* Active fleet per 31 December 2016

� Leverage of scale

� Operator profit

CORE FLEET

NORDEN – ANNUAL REPORT 2016 RESULTS | 22 Custodians of smarter global trade

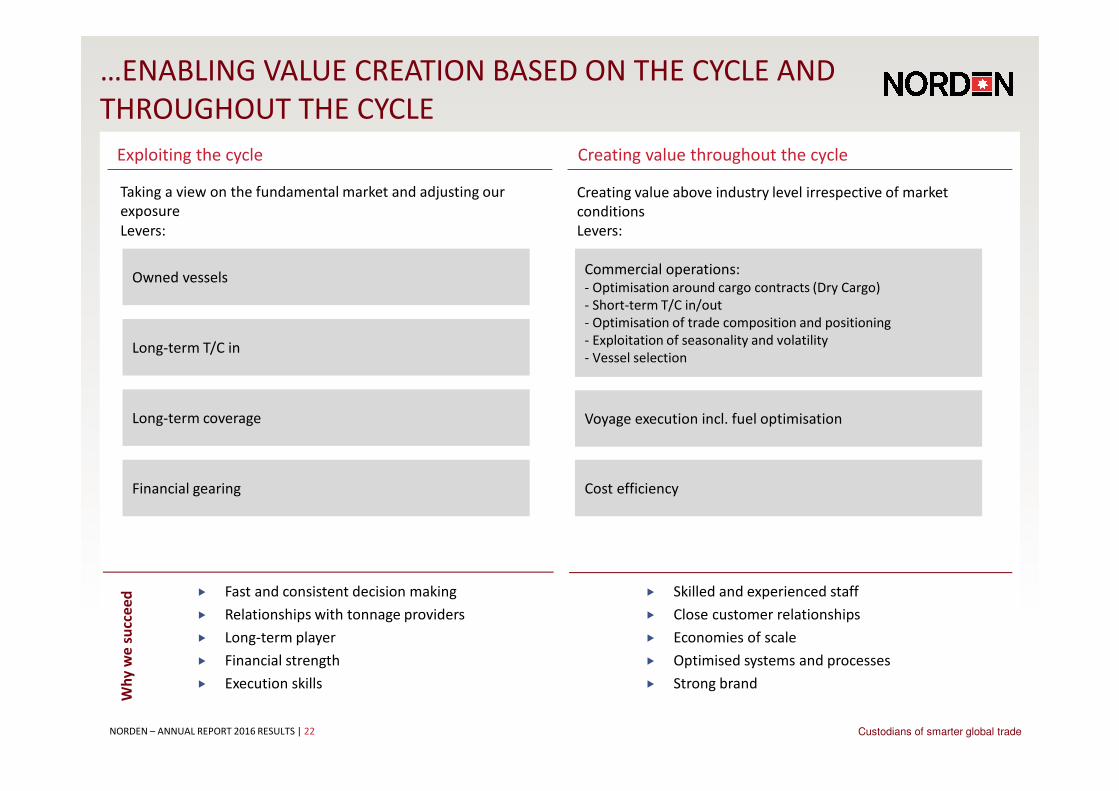

…ENABLING VALUE CREATION BASED ON THE CYCLE AND

THROUGHOUT THE CYCLE

Creating value throughout the cycle

Creating value above industry level irrespective of market

conditions

Exploiting the cycle

� Fast and consistent decision making

� Relationships with tonnage providers

� Long-term player

� Financial strength

� Execution skills

� Skilled and experienced staff

� Close customer relationships

� Economies of scale

� Optimised systems and processes

� Strong brand

Owned vessels

Long-term T/C in

Long-term coverage

Financial gearing

Levers:

Wh

y w

e s

ucc

ee

d

Commercial operations:

- Optimisation around cargo contracts (Dry Cargo)

- Short-term T/C in/out

- Optimisation of trade composition and positioning

- Exploitation of seasonality and volatility

- Vessel selection

Voyage execution incl. fuel optimisation

Cost efficiency

Levers:

Taking a view on the fundamental market and adjusting our

exposure

NORDEN – ANNUAL REPORT 2016 RESULTS | 23 Custodians of smarter global trade

OVERALL RESULTS

USD million Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Total 2016

EBITDA - Dry Cargo -149.0 -12.5 -4.5 -1.9 -4 -24

EBITDA - Tankers 28.0 23.9 16.7 6.0 8 55

EBITDA - Group -120.0 11.4 12.2 4.1 2.9 30.6

Depreciation -197.4 -13.3 -13.8 -11.6 -10.8 -49.6

EBIT Group -368.6 -1.3 -34 -12.9 -16.3 -64.5

Result for the period -379.0 4.6 -24 -14.1 -12.1 -45.6

Adjusted result for the period -338.0 -5.3 -3.5 -11.7 -14.0 -34.6

Cash flow from operations 18.2 6.6 -16 -29 -41.3 -79.7

Net cash flow 35.2 9.2 -42.9 -23.4 -5.8 -62.9

Cash and securities 365.7 375.5 345.5 294.2 263.9 263.9

NORDEN – ANNUAL REPORT 2016 RESULTS | 24 Custodians of smarter global trade

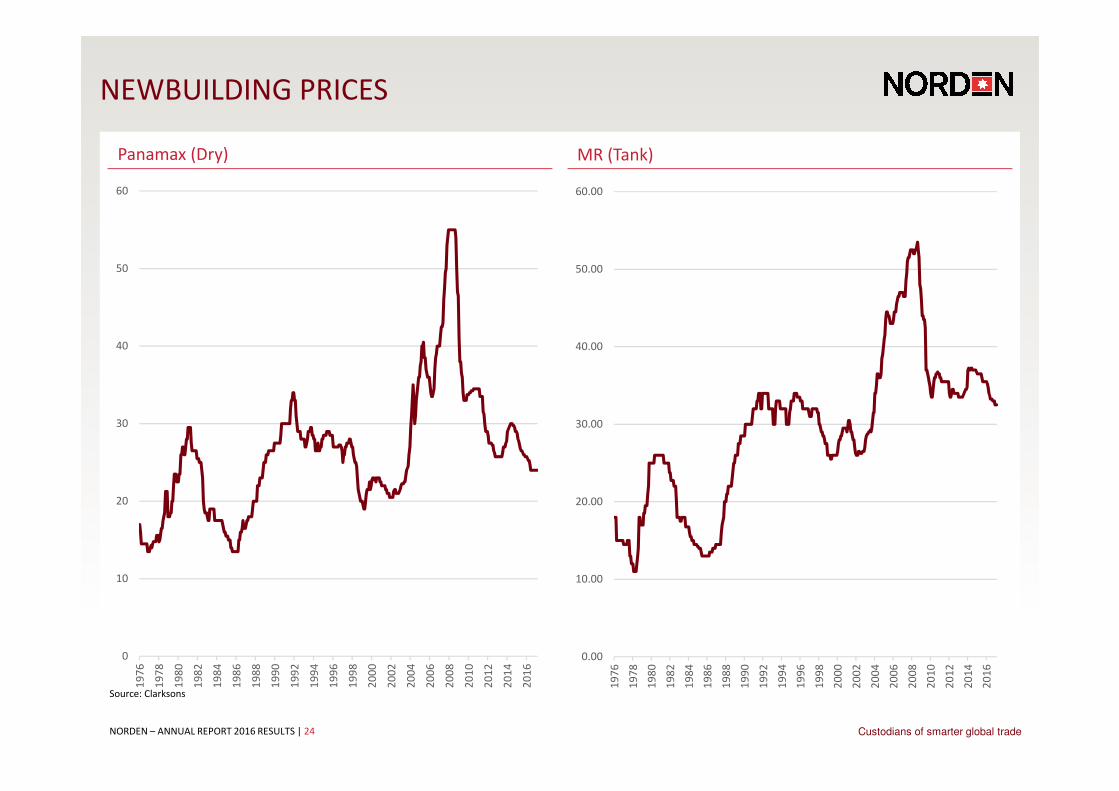

NEWBUILDING PRICES

MR (Tank)Panamax (Dry)

Source: Clarksons

0

10

20

30

40

50

60

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

0.00

10.00

20.00

30.00

40.00

50.00

60.00

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

NORDEN – ANNUAL REPORT 2016 RESULTS | 25 Custodians of smarter global trade

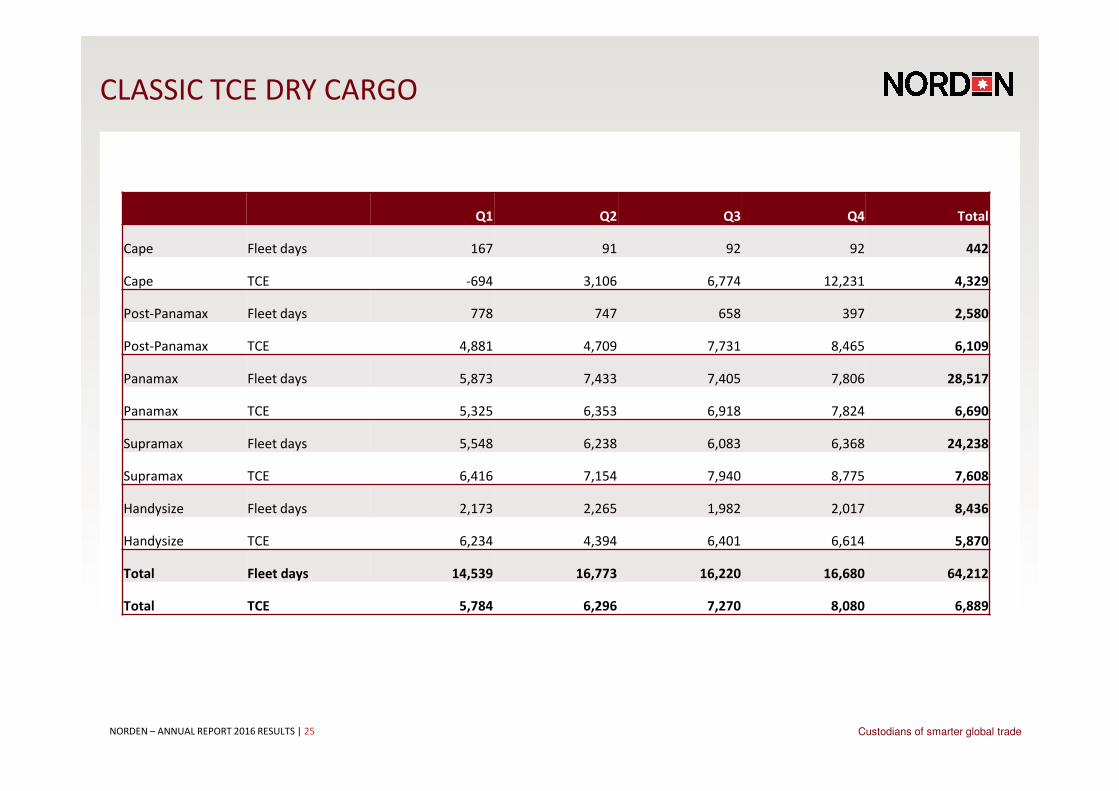

CLASSIC TCE DRY CARGO

Q1 Q2 Q3 Q4 Total

Cape Fleet days 167 91 92 92 442

Cape TCE -694 3,106 6,774 12,231 4,329

Post-Panamax Fleet days 778 747 658 397 2,580

Post-Panamax TCE 4,881 4,709 7,731 8,465 6,109

Panamax Fleet days 5,873 7,433 7,405 7,806 28,517

Panamax TCE 5,325 6,353 6,918 7,824 6,690

Supramax Fleet days 5,548 6,238 6,083 6,368 24,238

Supramax TCE 6,416 7,154 7,940 8,775 7,608

Handysize Fleet days 2,173 2,265 1,982 2,017 8,436

Handysize TCE 6,234 4,394 6,401 6,614 5,870

Total Fleet days 14,539 16,773 16,220 16,680 64,212

Total TCE 5,784 6,296 7,270 8,080 6,889

NORDEN – ANNUAL REPORT 2016 RESULTS | 26 Custodians of smarter global trade

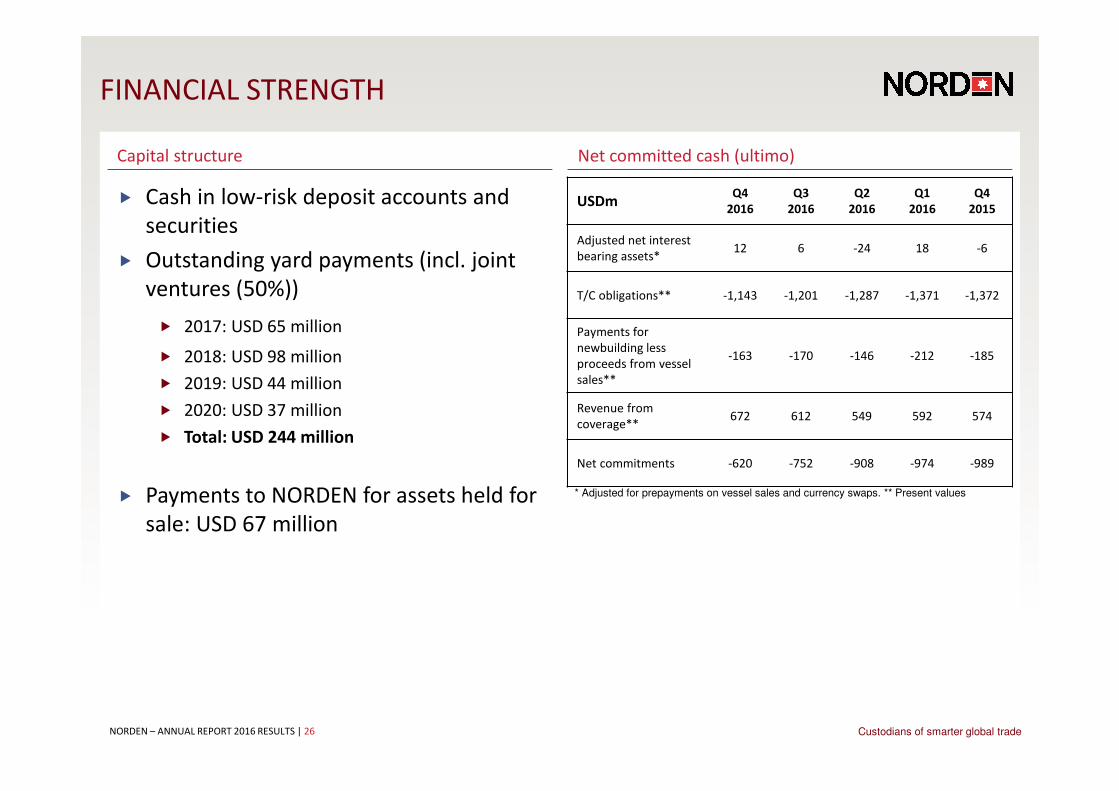

FINANCIAL STRENGTH

Net committed cash (ultimo)

� Cash in low-risk deposit accounts and

securities

� Outstanding yard payments (incl. joint

ventures (50%))

� 2017: USD 65 million

� 2018: USD 98 million

� 2019: USD 44 million

� 2020: USD 37 million

� Total: USD 244 million

� Payments to NORDEN for assets held for

sale: USD 67 million

Capital structure

USDmQ4

2016

Q3

2016

Q2

2016

Q1

2016

Q4

2015

Adjusted net interest

bearing assets*12 6 -24 18 -6

T/C obligations** -1,143 -1,201 -1,287 -1,371 -1,372

Payments for

newbuilding less

proceeds from vessel

sales**

-163 -170 -146 -212 -185

Revenue from

coverage**672 612 549 592 574

Net commitments -620 -752 -908 -974 -989

* Adjusted for prepayments on vessel sales and currency swaps. ** Present values

NORDEN – ANNUAL REPORT 2016 RESULTS | 27 Custodians of smarter global trade

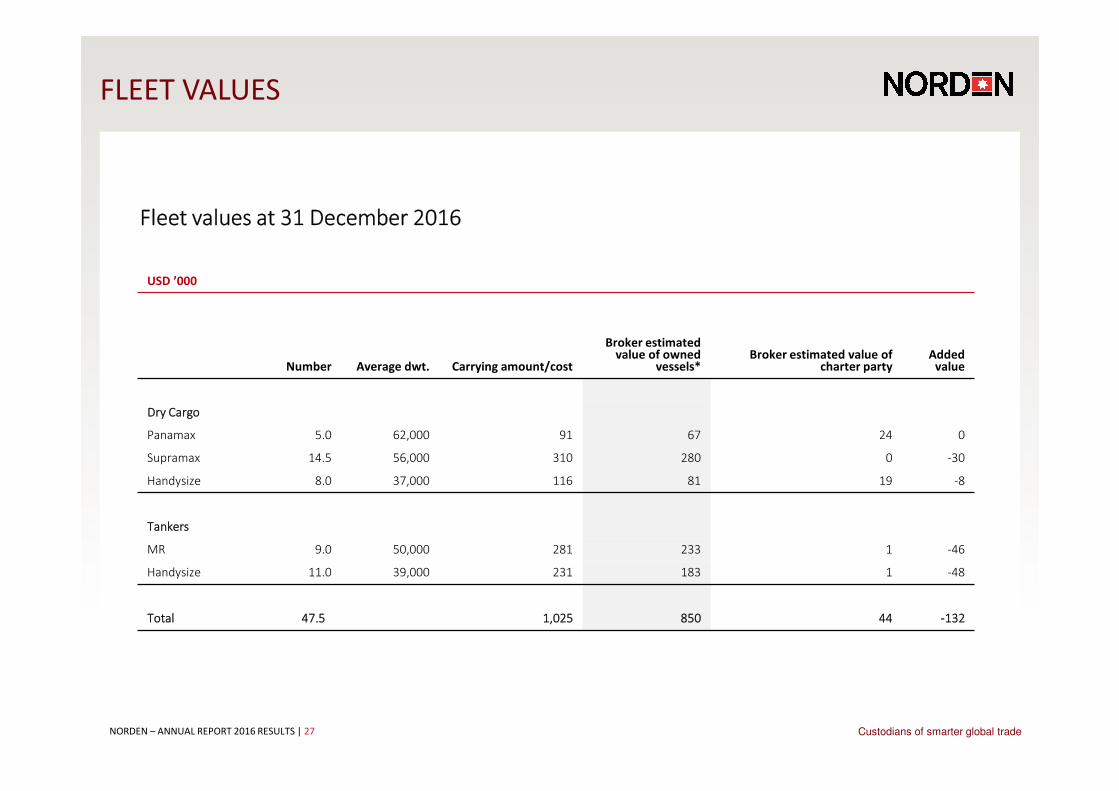

FLEET VALUES

USD ’000

Number Average dwt. Carrying amount/cost

Broker estimated value of owned

vessels*Broker estimated value of

charter partyAdded

value

Dry Cargo

Panamax 5.0 62,000 91 67 24 0

Supramax 14.5 56,000 310 280 0 -30

Handysize 8.0 37,000 116 81 19 -8

Tankers

MR 9.0 50,000 281 233 1 -46

Handysize 11.0 39,000 231 183 1 -48

Total 47.55 1,025 850 44 -132

Fleet values at 31 December 2016

NORDEN – ANNUAL REPORT 2016 RESULTS | 28 Custodians of smarter global trade

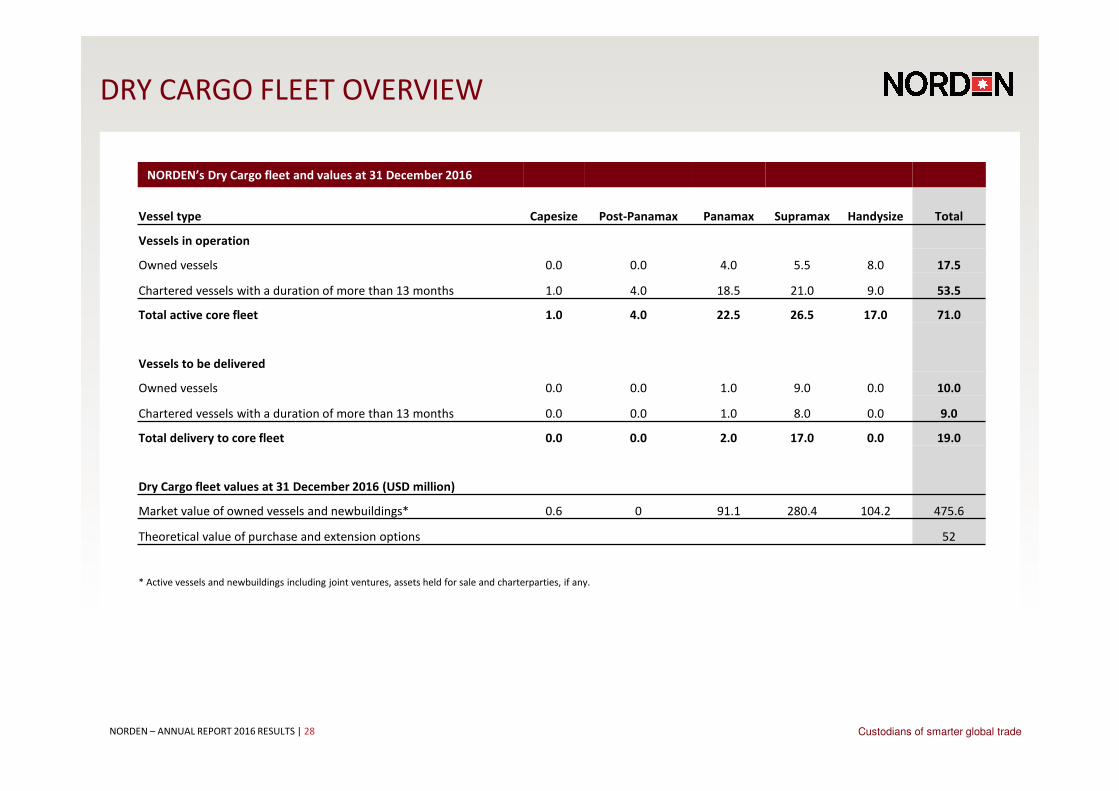

DRY CARGO FLEET OVERVIEW

NORDEN’s Dry Cargo fleet and values at 31 December 2016

Vessel type Capesize Post-Panamax Panamax Supramax Handysize Total

Vessels in operation

Owned vessels 0.0 0.0 4.0 5.5 8.0 17.5

Chartered vessels with a duration of more than 13 months 1.0 4.0 18.5 21.0 9.0 53.5

Total active core fleet 1.0 4.0 22.5 26.5 17.0 71.0

Vessels to be delivered

Owned vessels 0.0 0.0 1.0 9.0 0.0 10.0

Chartered vessels with a duration of more than 13 months 0.0 0.0 1.0 8.0 0.0 9.0

Total delivery to core fleet 0.0 0.0 2.0 17.0 0.0 19.0

Dry Cargo fleet values at 31 December 2016 (USD million)

Market value of owned vessels and newbuildings* 0.6 0 91.1 280.4 104.2 475.6

Theoretical value of purchase and extension options 52

* Active vessels and newbuildings including joint ventures, assets held for sale and charterparties, if any.

NORDEN – ANNUAL REPORT 2016 RESULTS | 29 Custodians of smarter global trade

PRODUCT TANKER FLEET OVERVIEW

NORDEN’s Tanker fleet and values at 31 December 2016

Vessel type LR1 MR Handysize Total

Vessels in operation

Owned vessels 0 9 11 20

Chartered vessels with a duration of more than 13 months 0 13 0 13

Total active core fleet 0 22 11 33

Chartered vessels with a duration of less than 13 months 0 0 4 4

Total active fleet 0 22 15 37

Vessels to be delivered

Owned vessels 0 0 0 0

Chartered vessels with a duration of more than 13 months 2 4 0 6

Total delivery to core fleet 2 4 0 6

Tanker fleet values at 30 September 2016 (USD million)

Market value of owned vessels and newbuildings* 0 235 184 418

Theoretical value of purchase and extension options 1.4

* Active vessels and newbuildings including joint ventures, assets held for sale and charter parties, if any.

NORDEN – ANNUAL REPORT 2016 RESULTS | 30 Custodians of smarter global trade

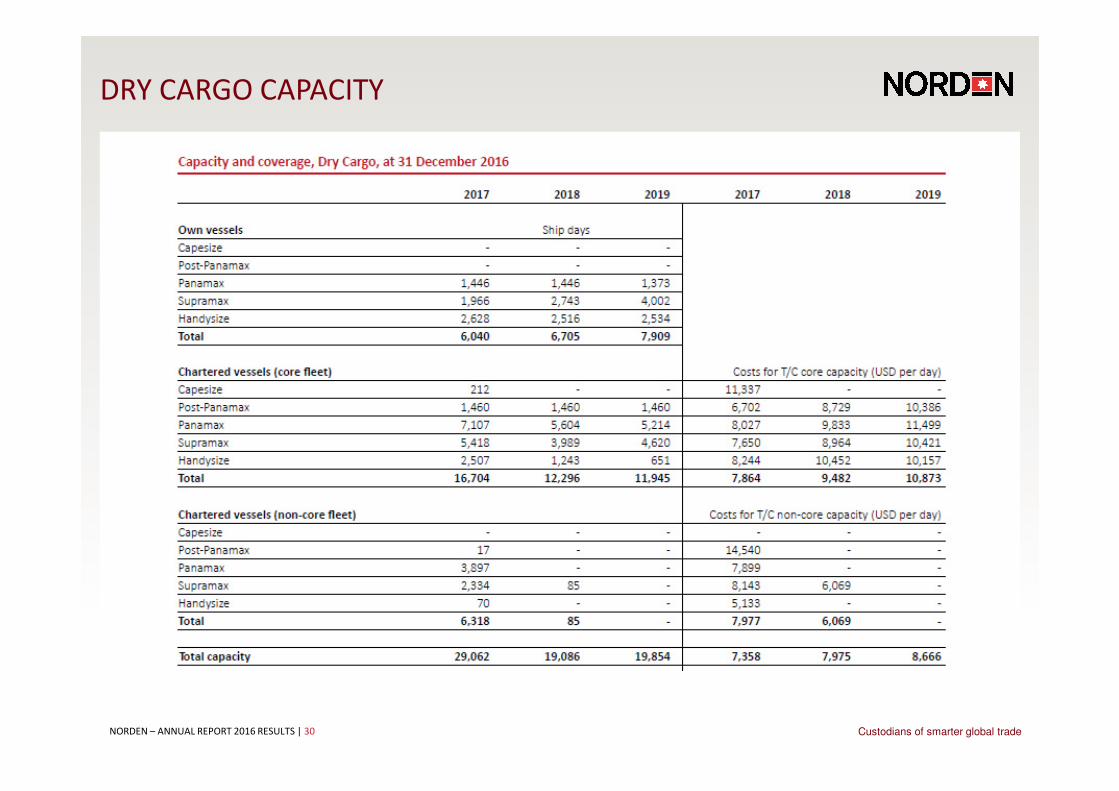

DRY CARGO CAPACITY

NORDEN – ANNUAL REPORT 2016 RESULTS | 31 Custodians of smarter global trade

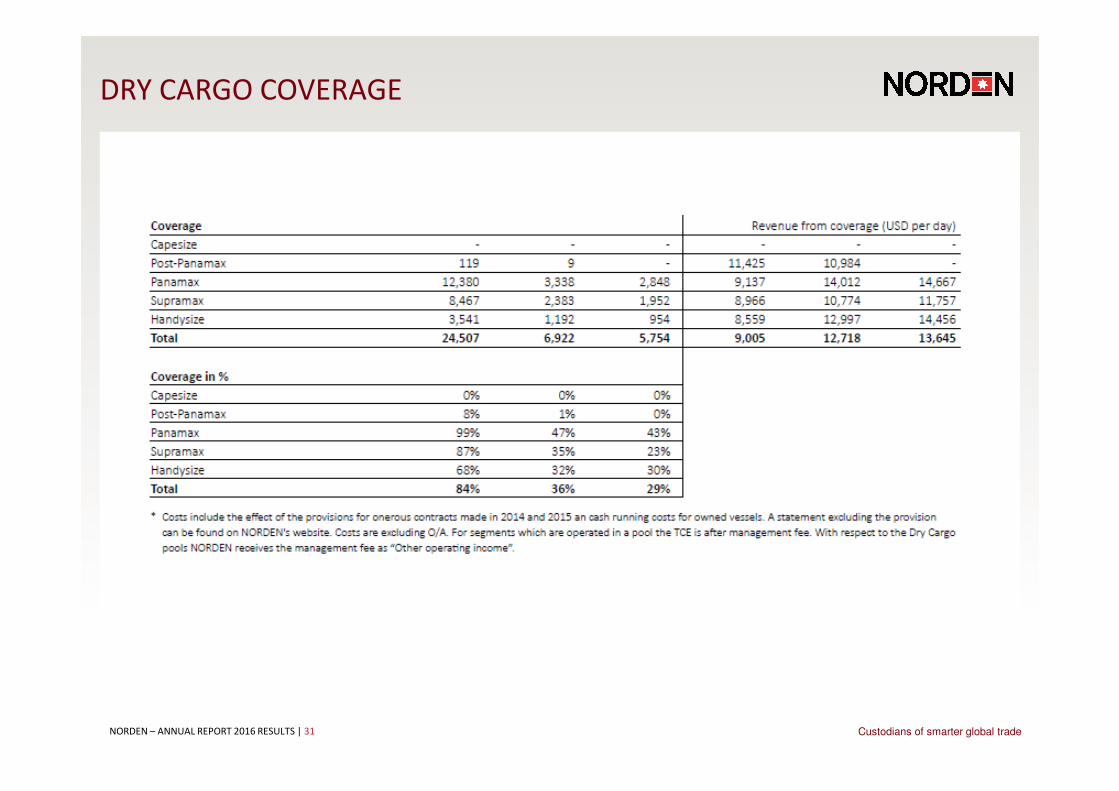

DRY CARGO COVERAGE

NORDEN – ANNUAL REPORT 2016 RESULTS | 32 Custodians of smarter global trade

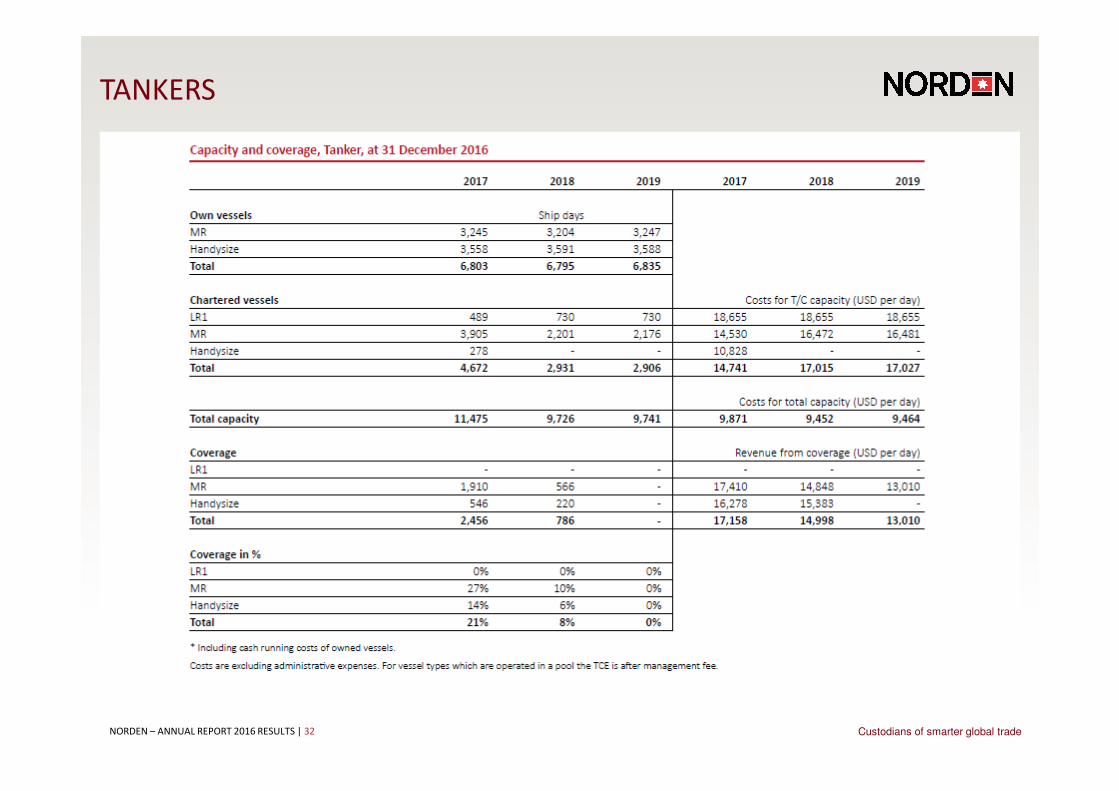

TANKERS

NORDEN – ANNUAL REPORT 2016 RESULTS | 33 Custodians of smarter global trade

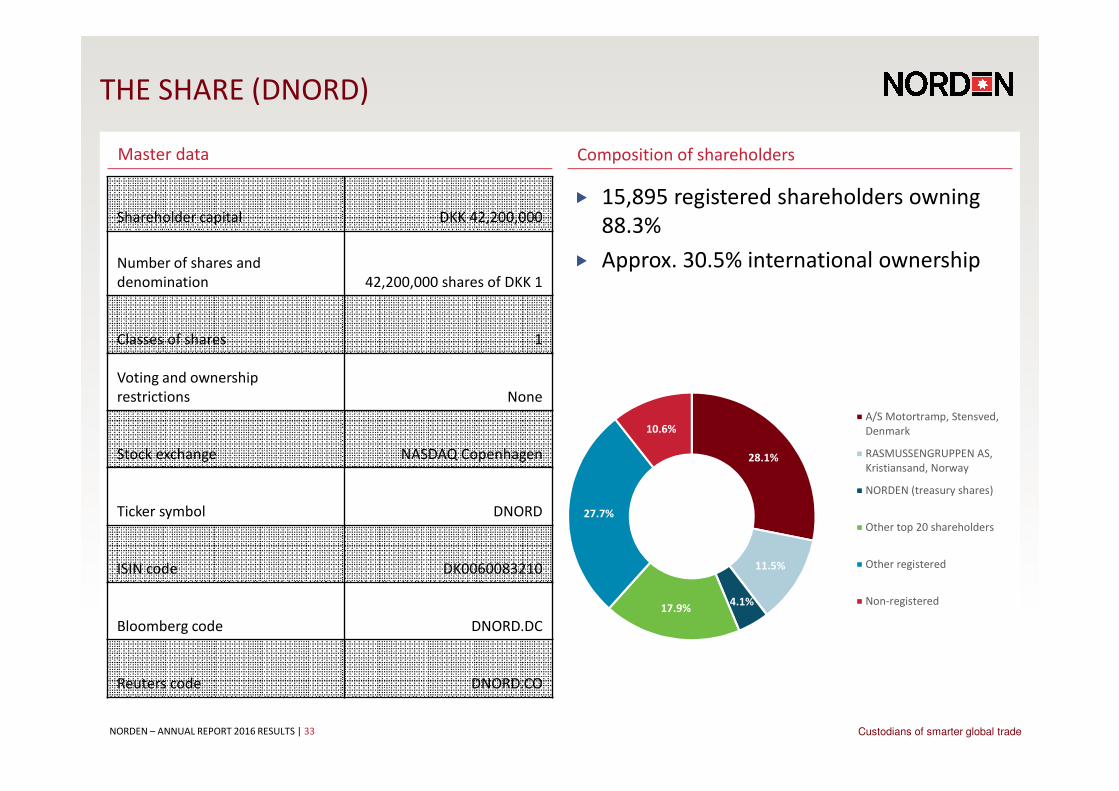

THE SHARE (DNORD)

Composition of shareholdersMaster data

Shareholder capital DKK 42,200,000

Number of shares and

denomination 42,200,000 shares of DKK 1

Classes of shares 1

Voting and ownership

restrictions None

Stock exchange NASDAQ Copenhagen

Ticker symbol DNORD

ISIN code DK0060083210

Bloomberg code DNORD.DC

Reuters code DNORD.CO

� 15,895 registered shareholders owning

88.3%

� Approx. 30.5% international ownership

28.1%

11.5%

4.1%17.9%

27.7%

10.6%A/S Motortramp, Stensved,

Denmark

RASMUSSENGRUPPEN AS,

Kristiansand, Norway

NORDEN (treasury shares)

Other top 20 shareholders

Other registered

Non-registered