Embed Size (px)

Citation preview

Corporate Taxation Chapter Twelve: Corporate Attributes Professors Wells

Presentation:

April 12, 2017

2

Fundamental provisions are as follows: 1) §381 – target corporation’s tax attributes follow its assets in a tax-

free reorganization (other than B and E reorganizations) and tax-free liquidations of subsidiaries.

2) §382 & §383 – restrict the carryforward of NOLs and other other losses and credits following a change of ownership.

3) §269 – allows IRS authority to disallow deductions, credits, or other allowances where target corporation stock or assets are acquired with a principle purpose of obtaining tax attributes.

Chapter Twelve p.563 Basic Overview

3

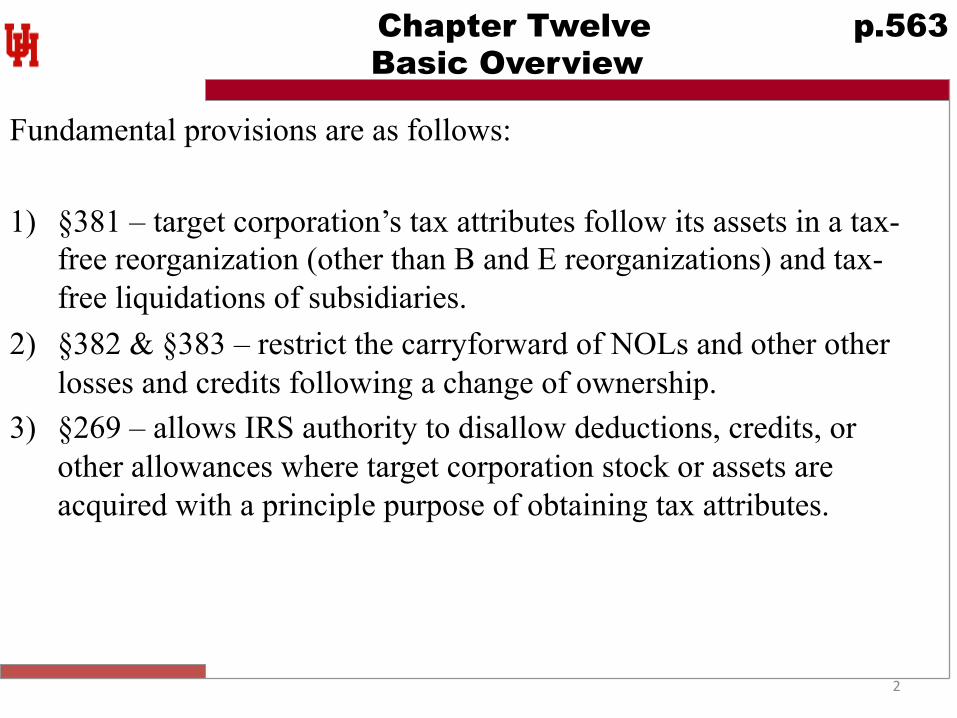

Section 381 Carryover Rules p.564

General Rule of §381(a): tax attributes of target carryover to acquierer in asset reorganizations and tax-free liquidations.

Exception in §381(c)(2): hovering deficit rule. Target’s acquired E&P deficit cannot be used to offset pre-acquisition positive E&P of Acquiring.

1. Target deficit can only offset post-acquisition Accumulated E&P. 2. Note that post-acquisition current E&P is not offset by

Accumulated E&P and would have nimble dividend.

Profit Co

Loss Co A Reorg.

E&P Deficit= <$100x> Pre-Acq. E&P = $100x

Shareholder

100x

4

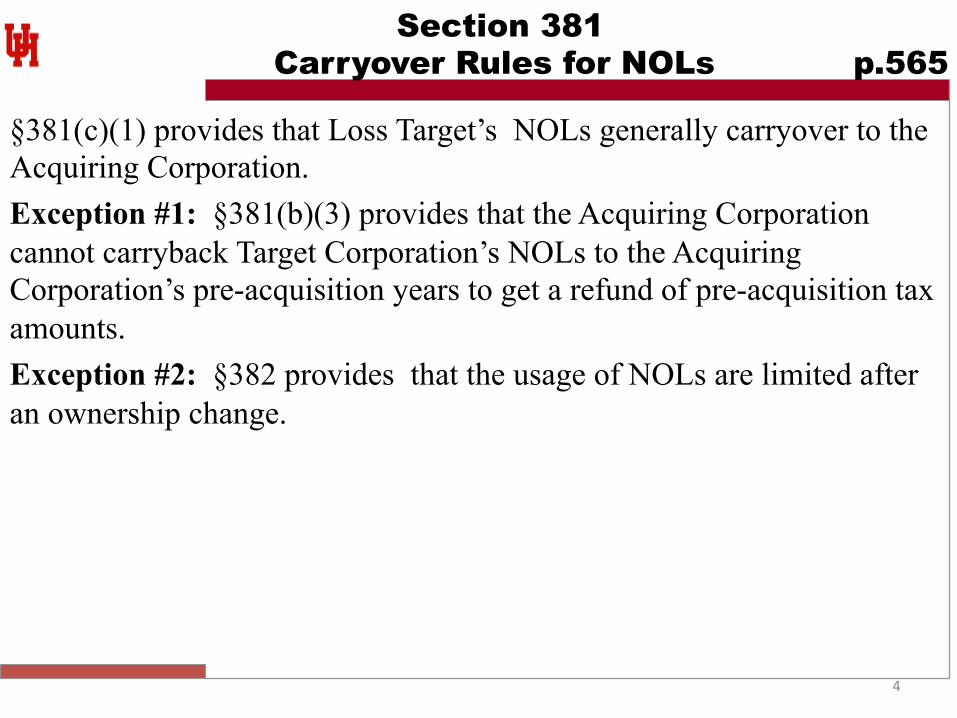

Section 381 Carryover Rules for NOLs p.565

§381(c)(1) provides that Loss Target’s NOLs generally carryover to the Acquiring Corporation. Exception #1: §381(b)(3) provides that the Acquiring Corporation cannot carryback Target Corporation’s NOLs to the Acquiring Corporation’s pre-acquisition years to get a refund of pre-acquisition tax amounts. Exception #2: §382 provides that the usage of NOLs are limited after an ownership change.

5

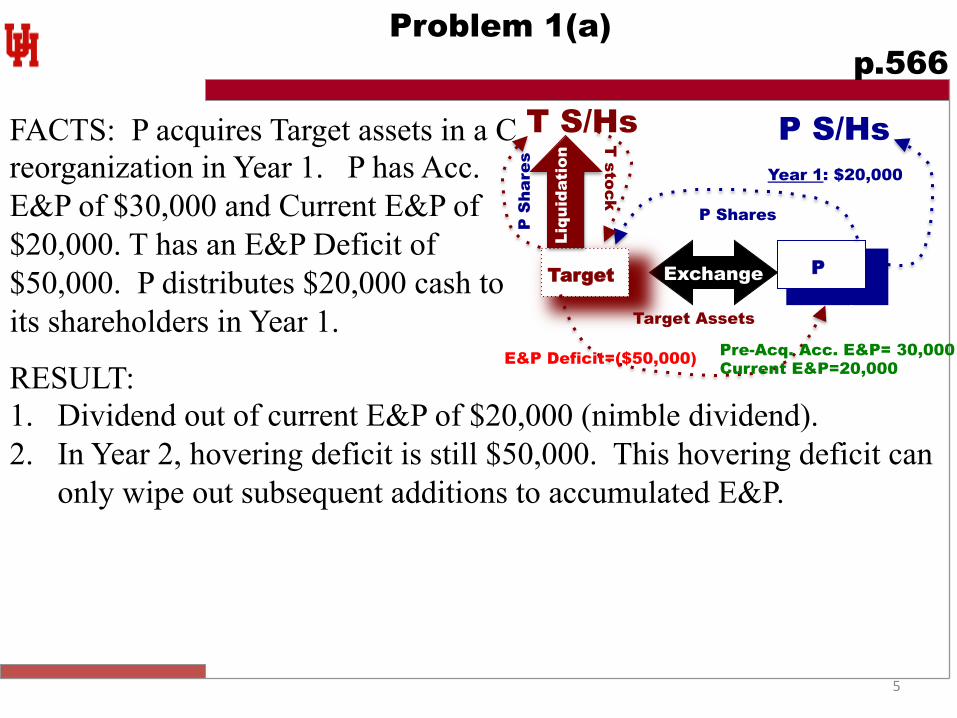

Problem 1(a) p.566

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets FACTS: P acquires Target assets in a C reorganization in Year 1. P has Acc. E&P of $30,000 and Current E&P of $20,000. T has an E&P Deficit of $50,000. P distributes $20,000 cash to its shareholders in Year 1.

RESULT: 1. Dividend out of current E&P of $20,000 (nimble dividend). 2. In Year 2, hovering deficit is still $50,000. This hovering deficit can

only wipe out subsequent additions to accumulated E&P.

P S/Hs

Year 1: $20,000

E&P Deficit=($50,000) Pre-Acq. Acc. E&P= 30,000 Current E&P=20,000

6

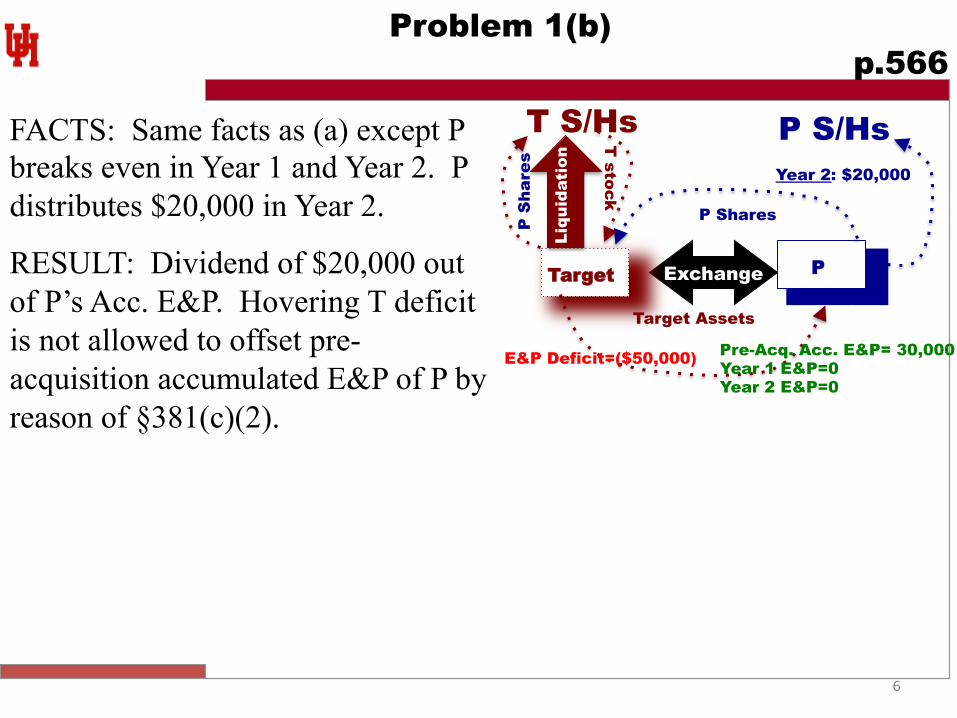

Problem 1(b) p.566

FACTS: Same facts as (a) except P breaks even in Year 1 and Year 2. P distributes $20,000 in Year 2.

RESULT: Dividend of $20,000 out of P’s Acc. E&P. Hovering T deficit is not allowed to offset pre-acquisition accumulated E&P of P by reason of §381(c)(2).

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets P S/Hs

Year 2: $20,000

E&P Deficit=($50,000) Pre-Acq. Acc. E&P= 30,000 Year 1 E&P=0 Year 2 E&P=0

7

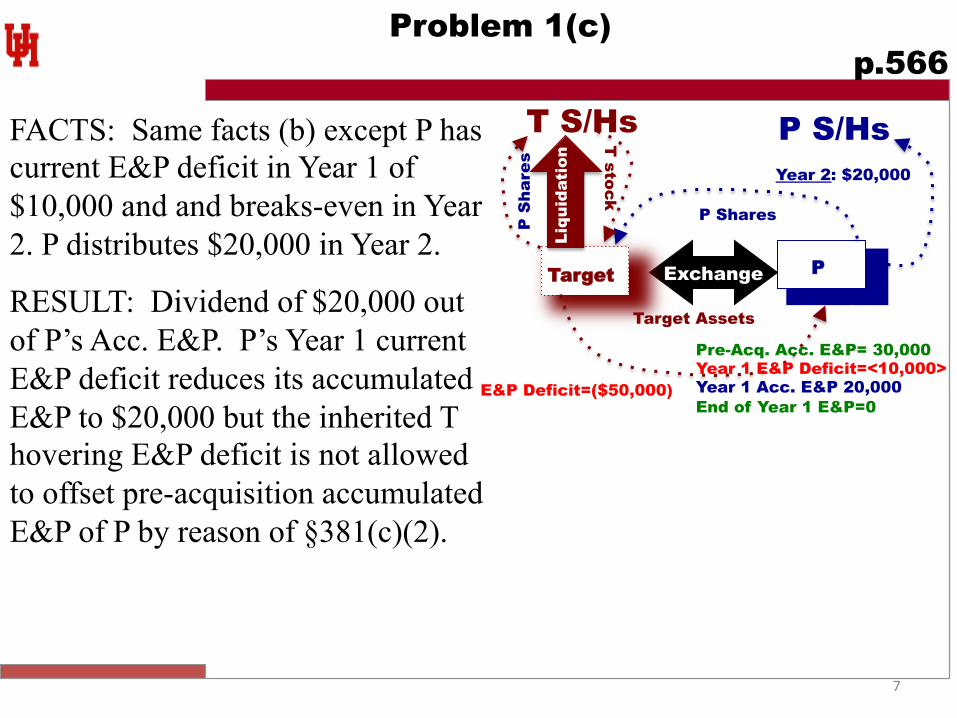

Problem 1(c) p.566

FACTS: Same facts (b) except P has current E&P deficit in Year 1 of $10,000 and and breaks-even in Year 2. P distributes $20,000 in Year 2.

RESULT: Dividend of $20,000 out of P’s Acc. E&P. P’s Year 1 current E&P deficit reduces its accumulated E&P to $20,000 but the inherited T hovering E&P deficit is not allowed to offset pre-acquisition accumulated E&P of P by reason of §381(c)(2).

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets P S/Hs

Year 2: $20,000

E&P Deficit=($50,000)

Pre-Acq. Acc. E&P= 30,000 Year 1 E&P Deficit=<10,000> Year 1 Acc. E&P 20,000 End of Year 1 E&P=0

8

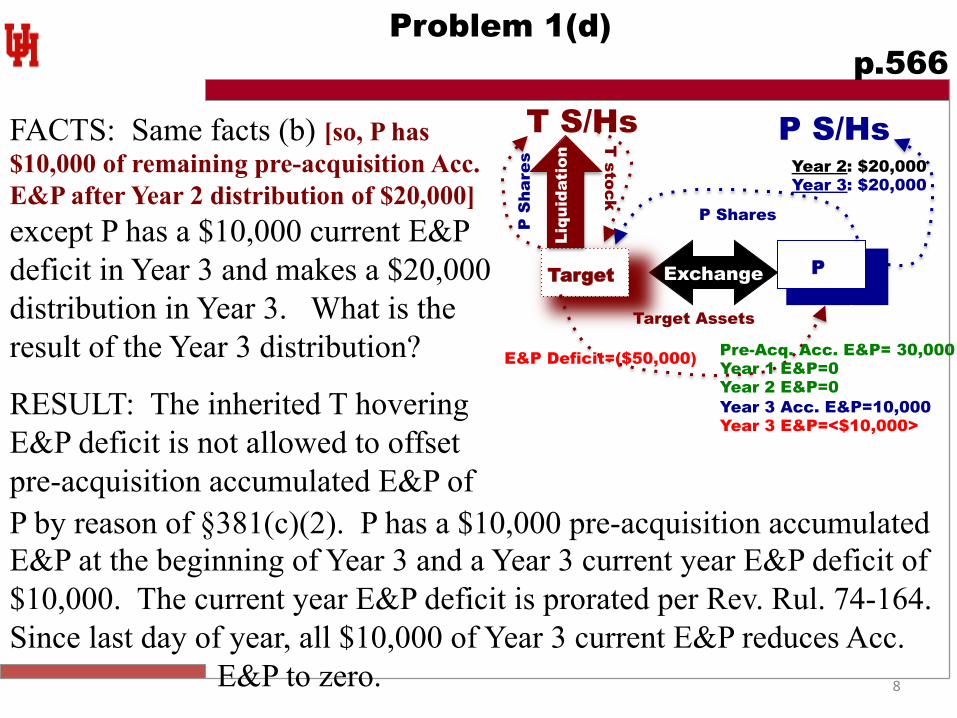

Problem 1(d) p.566

FACTS: Same facts (b) [so, P has $10,000 of remaining pre-acquisition Acc. E&P after Year 2 distribution of $20,000] except P has a $10,000 current E&P deficit in Year 3 and makes a $20,000 distribution in Year 3. What is the result of the Year 3 distribution?

RESULT: The inherited T hovering E&P deficit is not allowed to offset pre-acquisition accumulated E&P of

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets P S/Hs

Year 2: $20,000 Year 3: $20,000

E&P Deficit=($50,000) Pre-Acq. Acc. E&P= 30,000 Year 1 E&P=0 Year 2 E&P=0 Year 3 Acc. E&P=10,000 Year 3 E&P=<$10,000>

P by reason of §381(c)(2). P has a $10,000 pre-acquisition accumulated E&P at the beginning of Year 3 and a Year 3 current year E&P deficit of $10,000. The current year E&P deficit is prorated per Rev. Rul. 74-164. Since last day of year, all $10,000 of Year 3 current E&P reduces Acc.

E&P to zero.

9

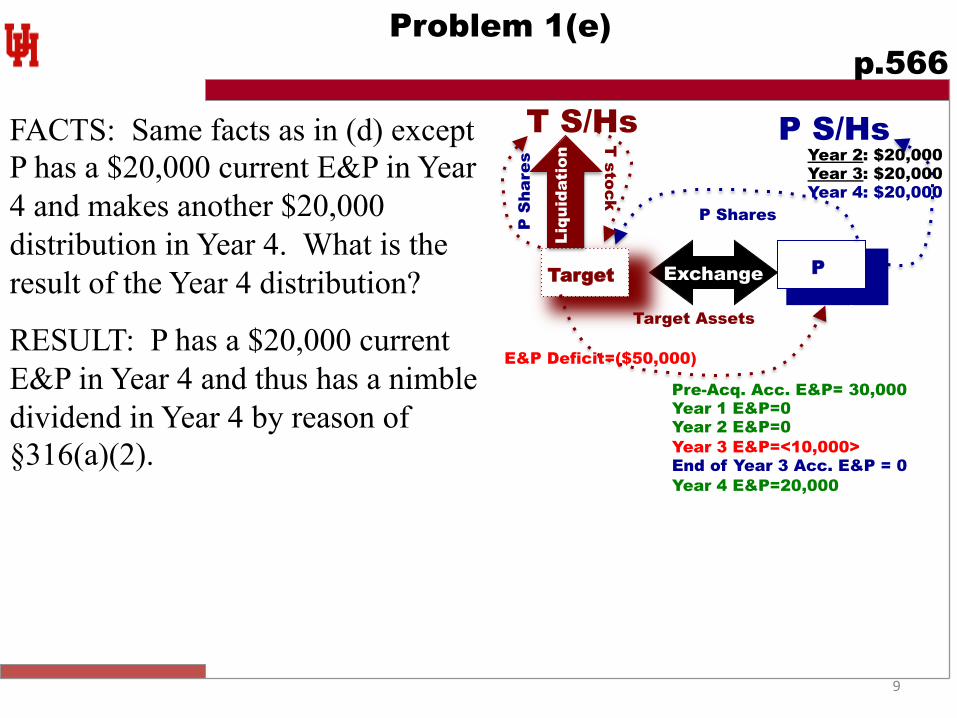

Problem 1(e) p.566

FACTS: Same facts as in (d) except P has a $20,000 current E&P in Year 4 and makes another $20,000 distribution in Year 4. What is the result of the Year 4 distribution?

RESULT: P has a $20,000 current E&P in Year 4 and thus has a nimble dividend in Year 4 by reason of §316(a)(2).

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets P S/Hs

Year 2: $20,000 Year 3: $20,000 Year 4: $20,000

E&P Deficit=($50,000)

Pre-Acq. Acc. E&P= 30,000 Year 1 E&P=0 Year 2 E&P=0 Year 3 E&P=<10,000> End of Year 3 Acc. E&P = 0 Year 4 E&P=20,000

10

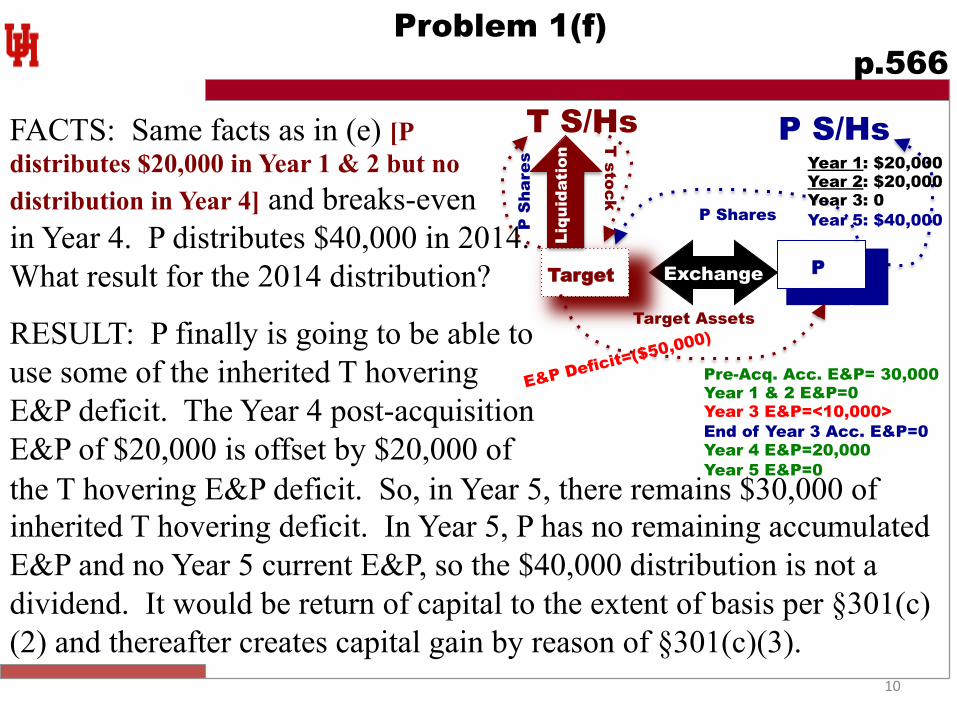

Problem 1(f) p.566

FACTS: Same facts as in (e) [P distributes $20,000 in Year 1 & 2 but no distribution in Year 4] and breaks-even in Year 4. P distributes $40,000 in 2014. What result for the 2014 distribution?

RESULT: P finally is going to be able to use some of the inherited T hovering E&P deficit. The Year 4 post-acquisition E&P of $20,000 is offset by $20,000 of

P Shares

Exchange

Target Assets

Target

P

T S/Hs

P S

hare

s

Liqu

idat

ion

T stock

T A

ssets P S/Hs

Year 1: $20,000 Year 2: $20,000 Year 3: 0 Year 5: $40,000

E&P Deficit=($50,000)

Pre-Acq. Acc. E&P= 30,000 Year 1 & 2 E&P=0 Year 3 E&P=<10,000> End of Year 3 Acc. E&P=0 Year 4 E&P=20,000 Year 5 E&P=0

the T hovering E&P deficit. So, in Year 5, there remains $30,000 of inherited T hovering deficit. In Year 5, P has no remaining accumulated E&P and no Year 5 current E&P, so the $40,000 distribution is not a dividend. It would be return of capital to the extent of basis per §301(c)(2) and thereafter creates capital gain by reason of §301(c)(3).

11

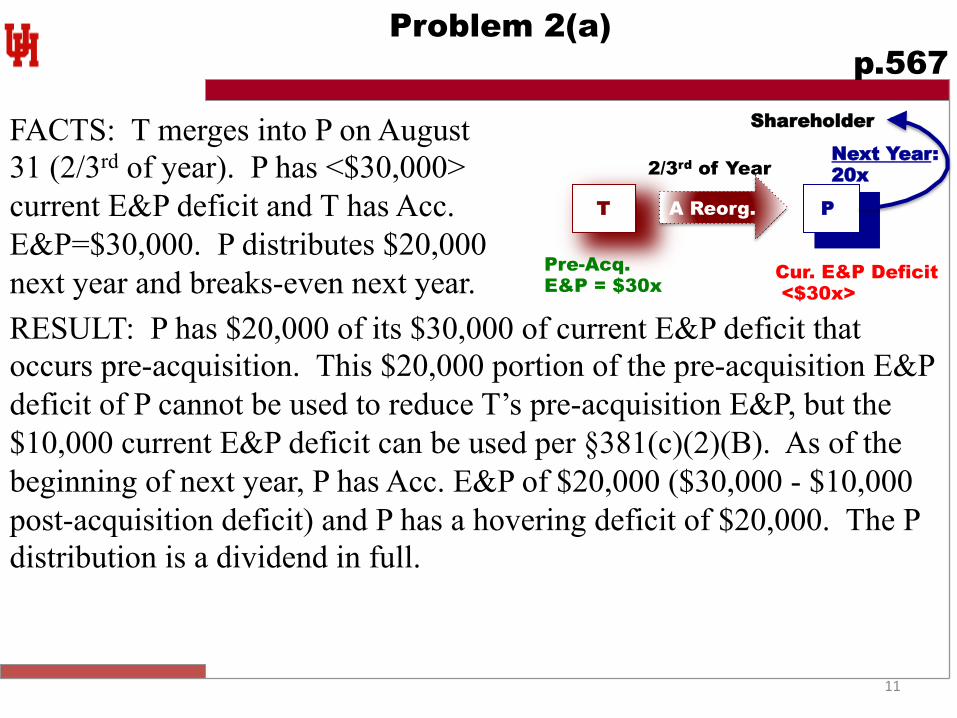

Problem 2(a) p.567

P

T A Reorg.

Cur. E&P Deficit <$30x>

Pre-Acq. E&P = $30x

Shareholder

Next Year: 20x

FACTS: T merges into P on August 31 (2/3rd of year). P has <$30,000> current E&P deficit and T has Acc. E&P=$30,000. P distributes $20,000 next year and breaks-even next year. RESULT: P has $20,000 of its $30,000 of current E&P deficit that occurs pre-acquisition. This $20,000 portion of the pre-acquisition E&P deficit of P cannot be used to reduce T’s pre-acquisition E&P, but the $10,000 current E&P deficit can be used per §381(c)(2)(B). As of the beginning of next year, P has Acc. E&P of $20,000 ($30,000 - $10,000 post-acquisition deficit) and P has a hovering deficit of $20,000. The P distribution is a dividend in full.

2/3rd of Year

12

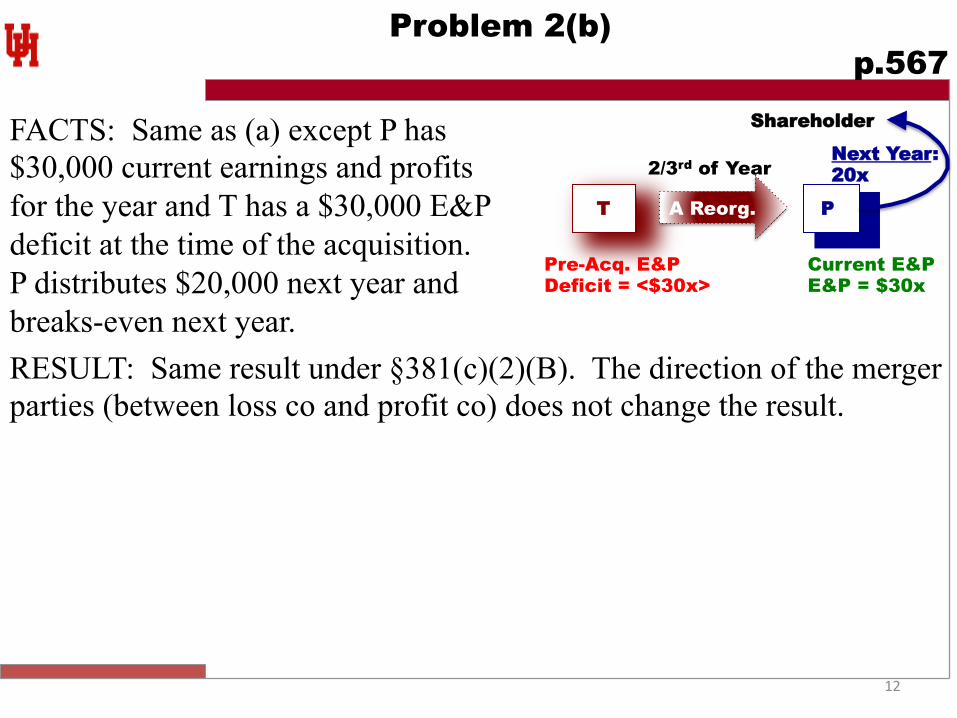

Problem 2(b) p.567

FACTS: Same as (a) except P has $30,000 current earnings and profits for the year and T has a $30,000 E&P deficit at the time of the acquisition. P distributes $20,000 next year and breaks-even next year.

P

T A Reorg.

Pre-Acq. E&P Deficit = <$30x>

Current E&P E&P = $30x

Shareholder

Next Year: 20x 2/3rd of Year

RESULT: Same result under §381(c)(2)(B). The direction of the merger parties (between loss co and profit co) does not change the result.

13

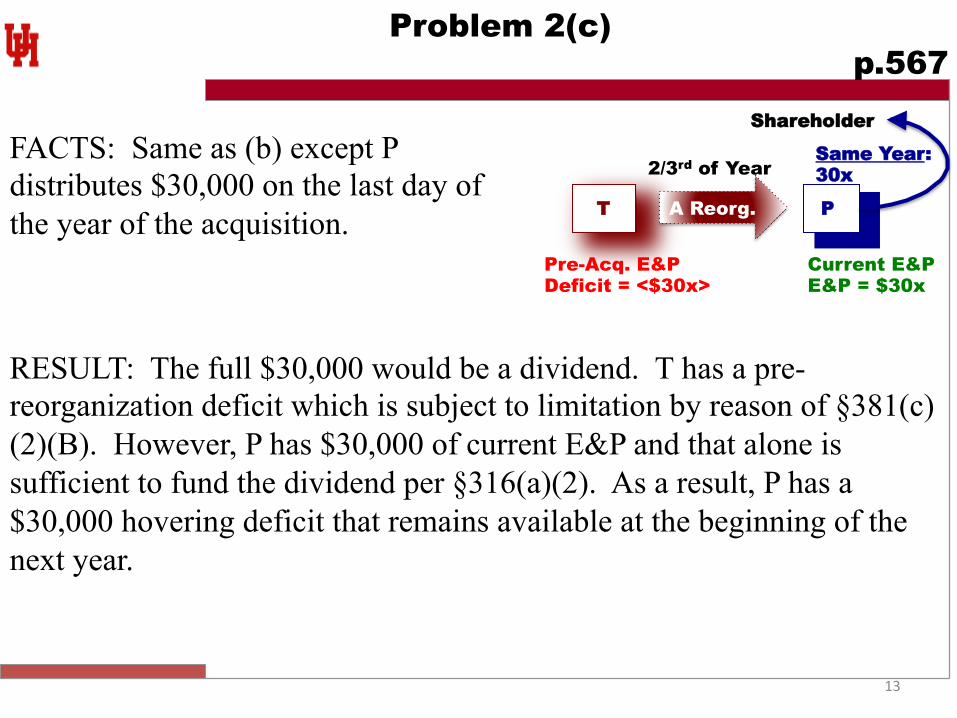

Problem 2(c) p.567

FACTS: Same as (b) except P distributes $30,000 on the last day of the year of the acquisition.

P

T A Reorg.

Pre-Acq. E&P Deficit = <$30x>

Current E&P E&P = $30x

Shareholder

Same Year: 30x 2/3rd of Year

RESULT: The full $30,000 would be a dividend. T has a pre-reorganization deficit which is subject to limitation by reason of §381(c)(2)(B). However, P has $30,000 of current E&P and that alone is sufficient to fund the dividend per §316(a)(2). As a result, P has a $30,000 hovering deficit that remains available at the beginning of the next year.

14

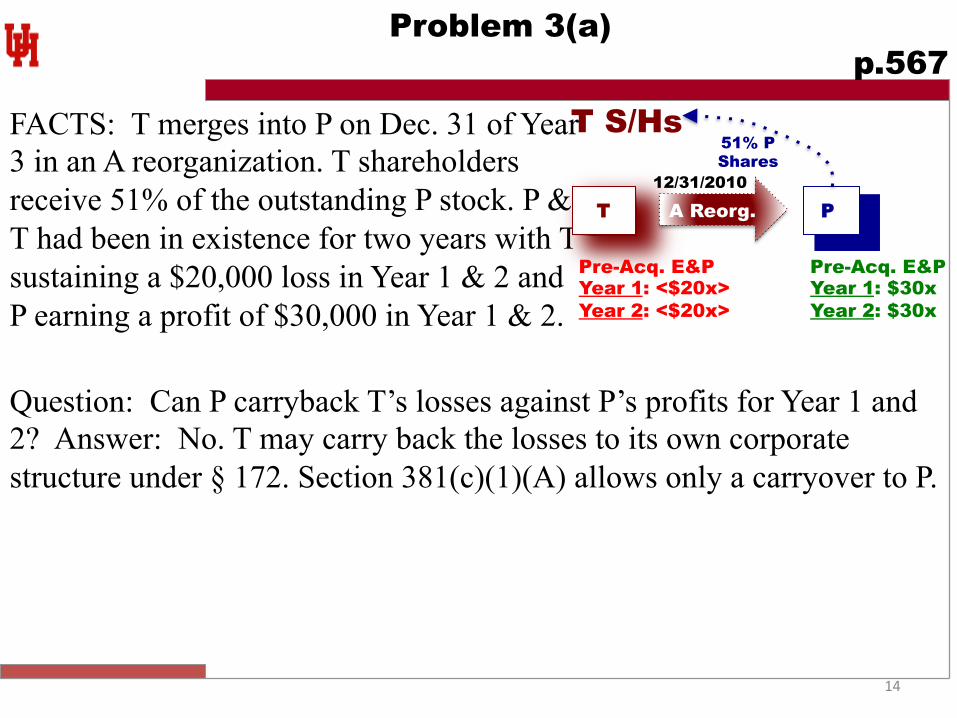

Problem 3(a) p.567

FACTS: T merges into P on Dec. 31 of Year 3 in an A reorganization. T shareholders receive 51% of the outstanding P stock. P & T had been in existence for two years with T sustaining a $20,000 loss in Year 1 & 2 and P earning a profit of $30,000 in Year 1 & 2.

P

T A Reorg.

Pre-Acq. E&P Year 1: <$20x> Year 2: <$20x>

Pre-Acq. E&P Year 1: $30x Year 2: $30x

T S/Hs 51% P Shares

Question: Can P carryback T’s losses against P’s profits for Year 1 and 2? Answer: No. T may carry back the losses to its own corporate structure under § 172. Section 381(c)(1)(A) allows only a carryover to P.

12/31/2010

15

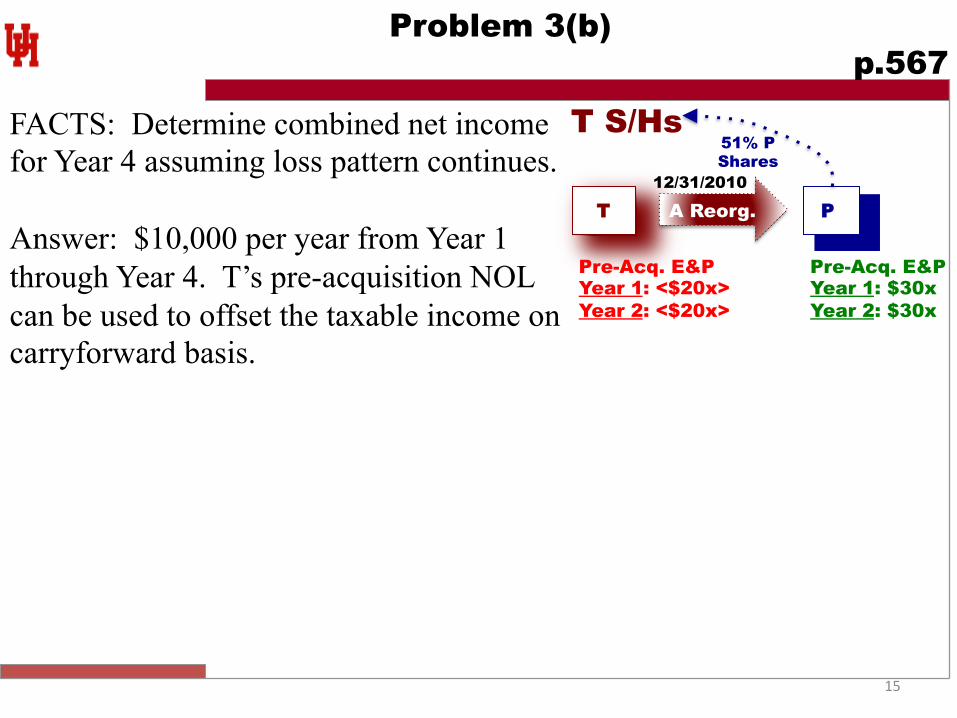

Problem 3(b) p.567

FACTS: Determine combined net income for Year 4 assuming loss pattern continues. Answer: $10,000 per year from Year 1 through Year 4. T’s pre-acquisition NOL can be used to offset the taxable income on carryforward basis.

P

T A Reorg.

Pre-Acq. E&P Year 1: <$20x> Year 2: <$20x>

Pre-Acq. E&P Year 1: $30x Year 2: $30x

T S/Hs 51% P Shares

12/31/2010

16

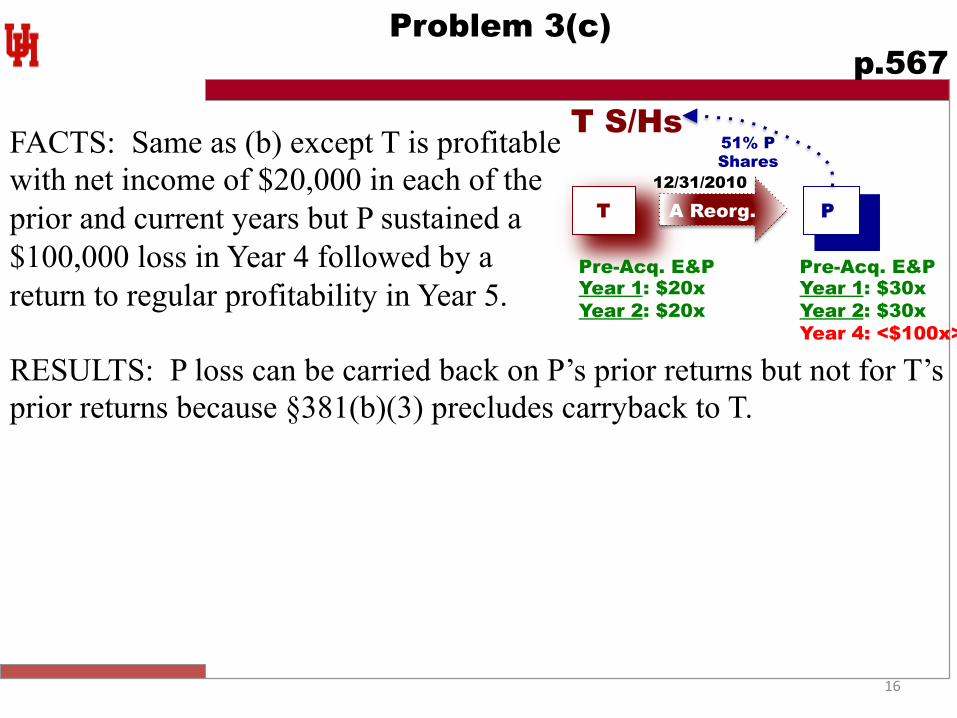

Problem 3(c) p.567

FACTS: Same as (b) except T is profitable with net income of $20,000 in each of the prior and current years but P sustained a $100,000 loss in Year 4 followed by a return to regular profitability in Year 5.

P

T A Reorg.

Pre-Acq. E&P Year 1: $20x Year 2: $20x

Pre-Acq. E&P Year 1: $30x Year 2: $30x Year 4: <$100x>

T S/Hs 51% P Shares

12/31/2010

RESULTS: P loss can be carried back on P’s prior returns but not for T’s prior returns because §381(b)(3) precludes carryback to T.

17

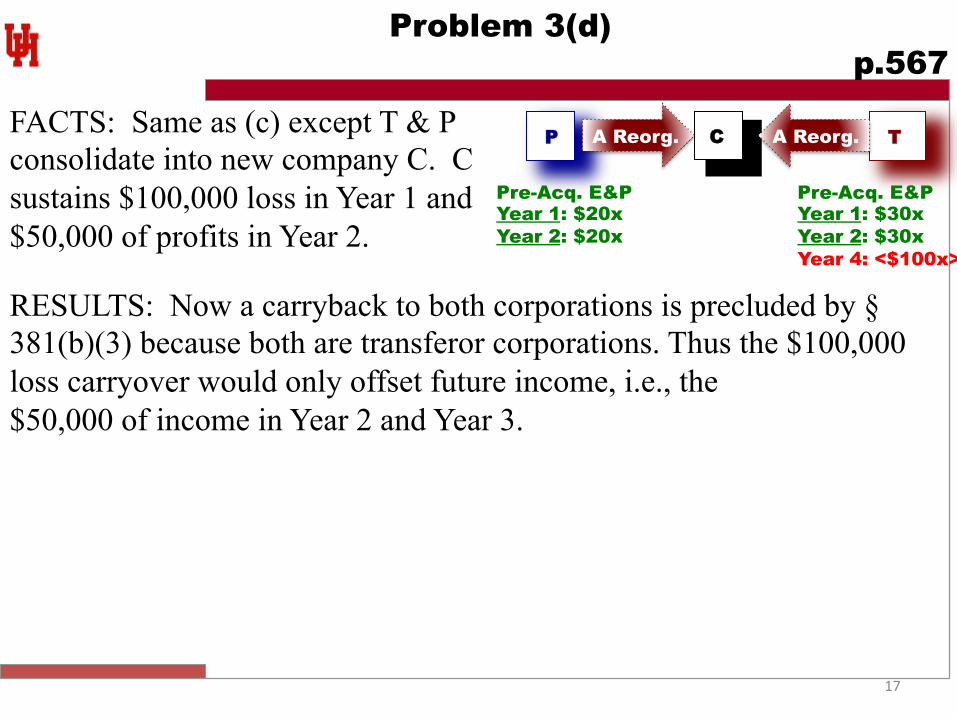

Problem 3(d) p.567

P

C

T A Reorg. A Reorg. FACTS: Same as (c) except T & P consolidate into new company C. C sustains $100,000 loss in Year 1 and $50,000 of profits in Year 2.

Pre-Acq. E&P Year 1: $20x Year 2: $20x

Pre-Acq. E&P Year 1: $30x Year 2: $30x Year 4: <$100x>

RESULTS: Now a carryback to both corporations is precluded by § 381(b)(3) because both are transferor corporations. Thus the $100,000 loss carryover would only offset future income, i.e., the $50,000 of income in Year 2 and Year 3.

18

Section 382 Limitation on NOL Carryforwards p.568

Policy Concern: Congress does not want trafficking in Loss Companies or to have Profitable Companies to be overly motivated to buy the tax attributes of Loss Companies. Congressional Response: §382 limits the ongoing usage of net operating losses if the Loss Company has experienced an Ownership Change.

19

Section 382 Ownership Change p.571

§382(g) provides that an ownership change occurs if there is either an “owner shift” involving 5% shareholders or an “equity structure shift.”

A. Owner Shift of 5% Shareholders: The percentage ownership of a Loss Corporation by 5% or greater shareholders is increased by 50% over the lowest percentage of stock of the loss corporation owned by such shareholders. 1. Ownership shift can occur by reason of purchase, redemptions,

§351 transfers, issuances of stock, and recapitalizations. 2. However, owner shifts by reason of gift, death, or divorce are not

counted. See §382(l)(3)(B).

B. Equity Structure Shift: Includes any reorganization including taxable acquisitions and public offerings that creates an owner shift See §382(g)(2) and (4)(B).

20

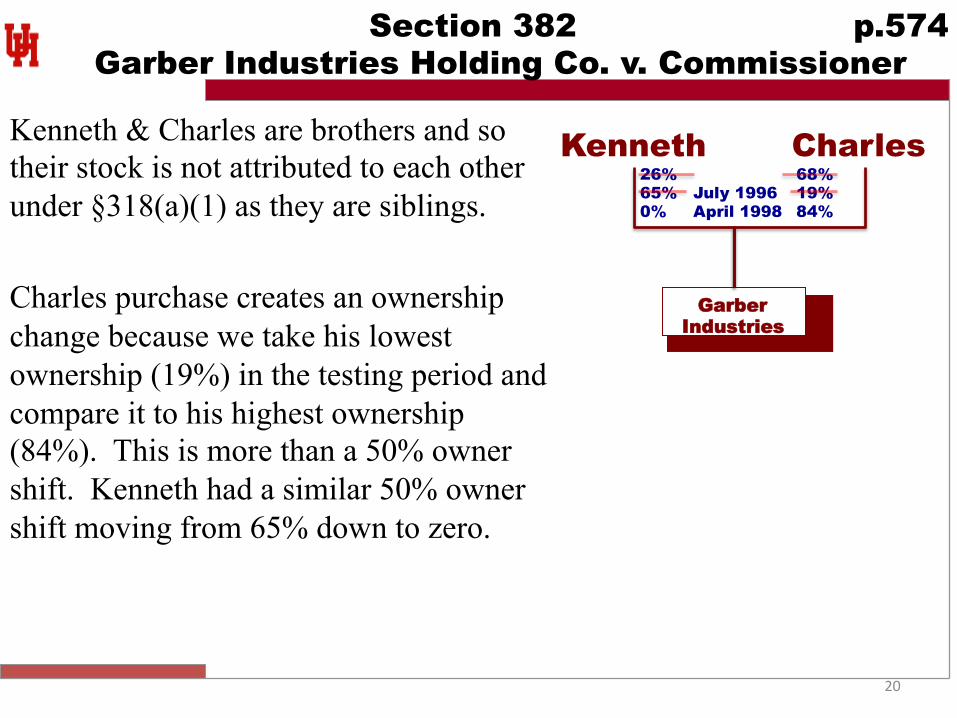

Section 382 p.574 Garber Industries Holding Co. v. Commissioner

Kenneth & Charles are brothers and so their stock is not attributed to each other under §318(a)(1) as they are siblings. Charles purchase creates an ownership change because we take his lowest ownership (19%) in the testing period and compare it to his highest ownership (84%). This is more than a 50% owner shift. Kenneth had a similar 50% owner shift moving from 65% down to zero.

Garber Industries

Kenneth Charles 68% 19% 84%

26% 65% July 1996 0% April 1998

21

Section 382 NOL Poison Pill Plan

If any shareholder acquires 4.9% or more stock without pre-approval by the board of directors of the company, then all other historic remaining shareholders have the right to acquire stock at 50% of its FMV to keep the new shareholder from becoming a 5% shareholder.

Rationale: Prevent risk of creating an ownership change that would cause a Section 382 limitation on the NOLs of the company.

Notable NOL Right Plans: Citibank, General Motors, Ford, JC Penny, AIG.

Delaware Court of Chancery decision has upheld such rights plans was a reasonable means to defend the company’s value. See Selectica, Inc. v. Versata, Inc., Civ. A. No. 4241, 2010 WL 703062 (Del. Ch. 2010).

22

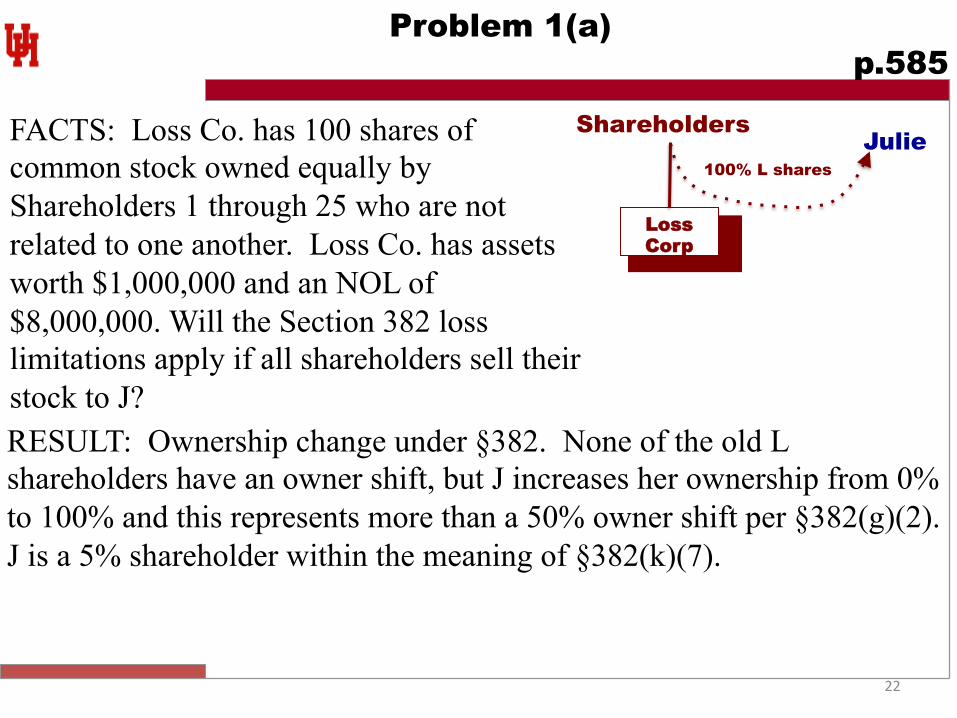

Problem 1(a) p.585

FACTS: Loss Co. has 100 shares of common stock owned equally by Shareholders 1 through 25 who are not related to one another. Loss Co. has assets worth $1,000,000 and an NOL of $8,000,000. Will the Section 382 loss limitations apply if all shareholders sell their stock to J? RESULT: Ownership change under §382. None of the old L shareholders have an owner shift, but J increases her ownership from 0% to 100% and this represents more than a 50% owner shift per §382(g)(2). J is a 5% shareholder within the meaning of §382(k)(7).

Loss Corp

Shareholders Julie

100% L shares

23

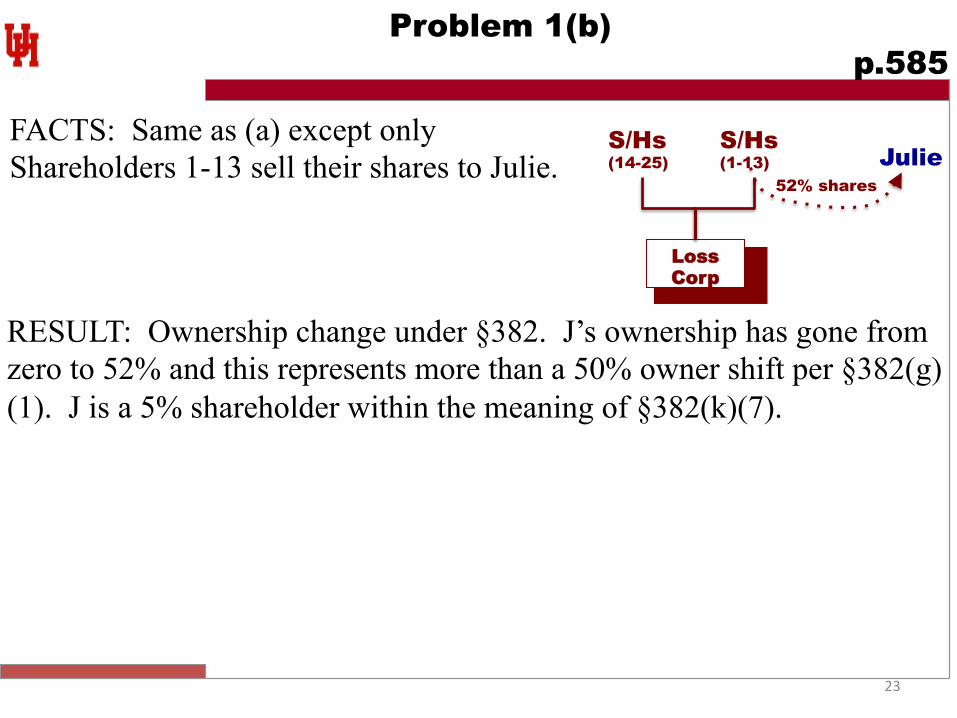

Problem 1(b) p.585

FACTS: Same as (a) except only Shareholders 1-13 sell their shares to Julie.

RESULT: Ownership change under §382. J’s ownership has gone from zero to 52% and this represents more than a 50% owner shift per §382(g)(1). J is a 5% shareholder within the meaning of §382(k)(7).

Loss Corp

S/Hs (14-25)

S/Hs (1-13) Julie

52% shares

24

Problem 1(c) p.585

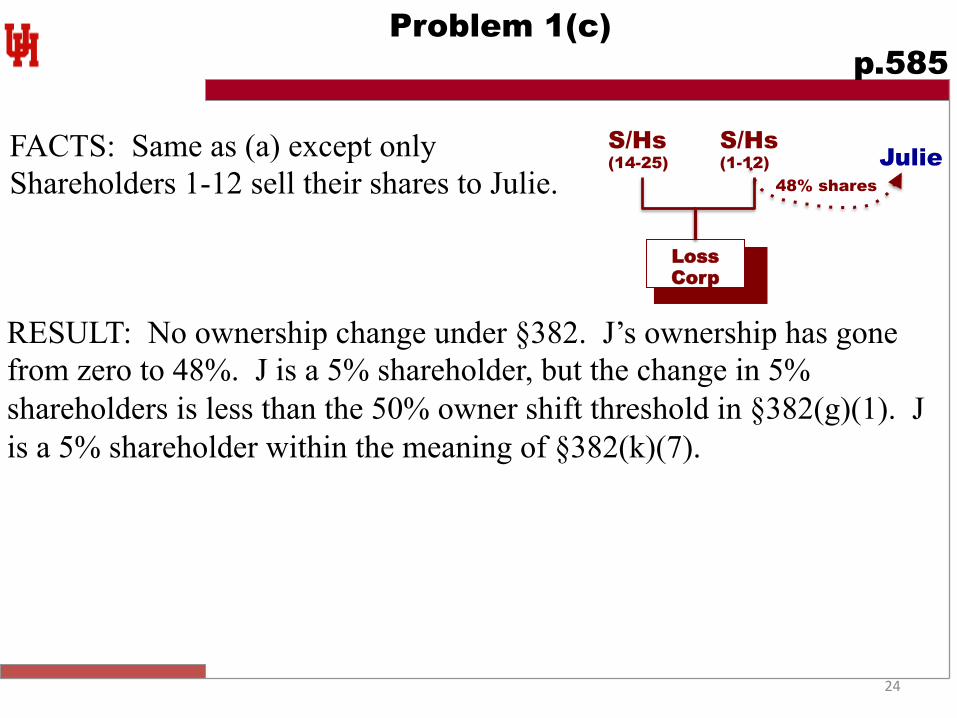

FACTS: Same as (a) except only Shareholders 1-12 sell their shares to Julie.

RESULT: No ownership change under §382. J’s ownership has gone from zero to 48%. J is a 5% shareholder, but the change in 5% shareholders is less than the 50% owner shift threshold in §382(g)(1). J is a 5% shareholder within the meaning of §382(k)(7).

Loss Corp

S/Hs (14-25)

S/Hs (1-12) Julie

48% shares

25

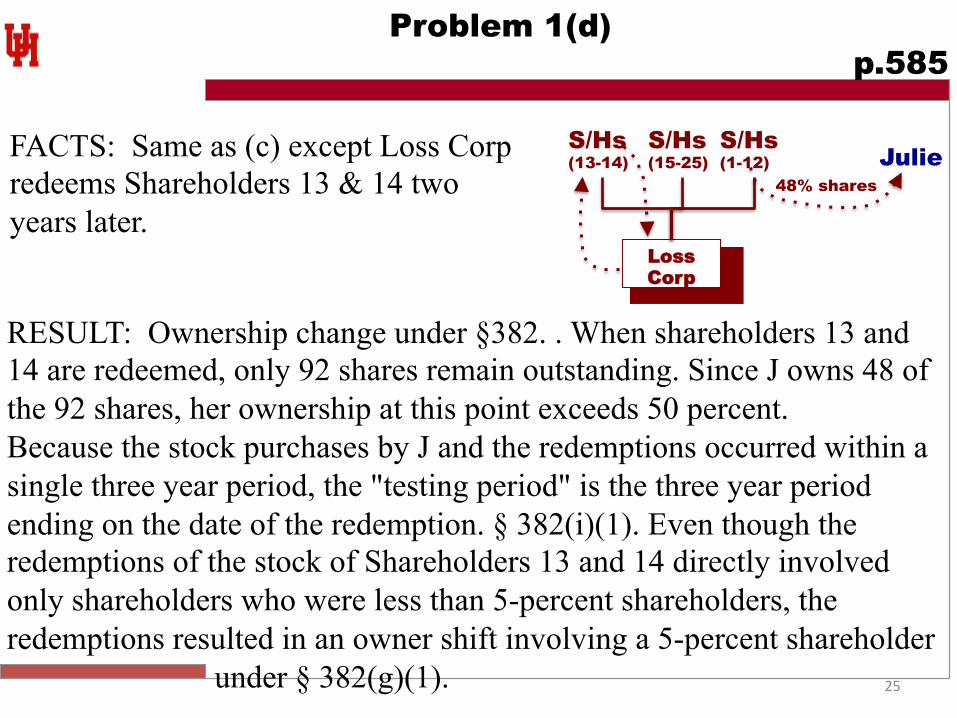

Problem 1(d) p.585

FACTS: Same as (c) except Loss Corp redeems Shareholders 13 & 14 two years later.

RESULT: Ownership change under §382. . When shareholders 13 and 14 are redeemed, only 92 shares remain outstanding. Since J owns 48 of the 92 shares, her ownership at this point exceeds 50 percent. Because the stock purchases by J and the redemptions occurred within a single three year period, the "testing period" is the three year period ending on the date of the redemption. § 382(i)(1). Even though the redemptions of the stock of Shareholders 13 and 14 directly involved only shareholders who were less than 5-percent shareholders, the redemptions resulted in an owner shift involving a 5-percent shareholder

under § 382(g)(1).

Loss Corp

S/Hs (13-14)

S/Hs (1-12) Julie

48% shares

S/Hs (15-25)

26

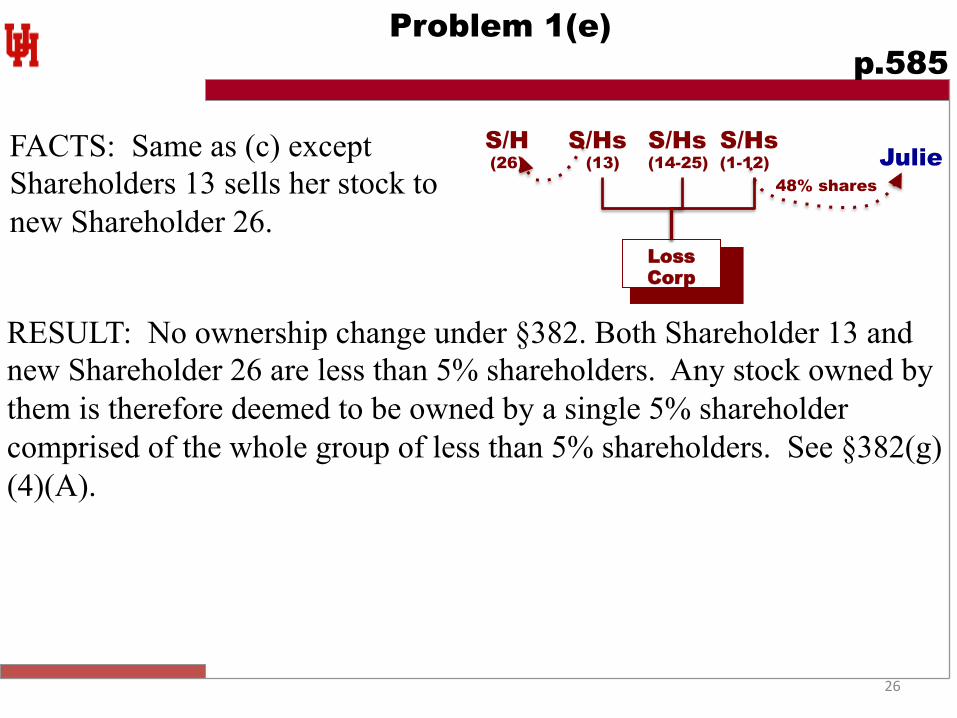

Problem 1(e) p.585

FACTS: Same as (c) except Shareholders 13 sells her stock to new Shareholder 26.

Loss Corp

S/Hs (13)

S/Hs (1-12) Julie

48% shares

S/Hs (14-25)

S/H (26)

RESULT: No ownership change under §382. Both Shareholder 13 and new Shareholder 26 are less than 5% shareholders. Any stock owned by them is therefore deemed to be owned by a single 5% shareholder comprised of the whole group of less than 5% shareholders. See §382(g)(4)(A).

27

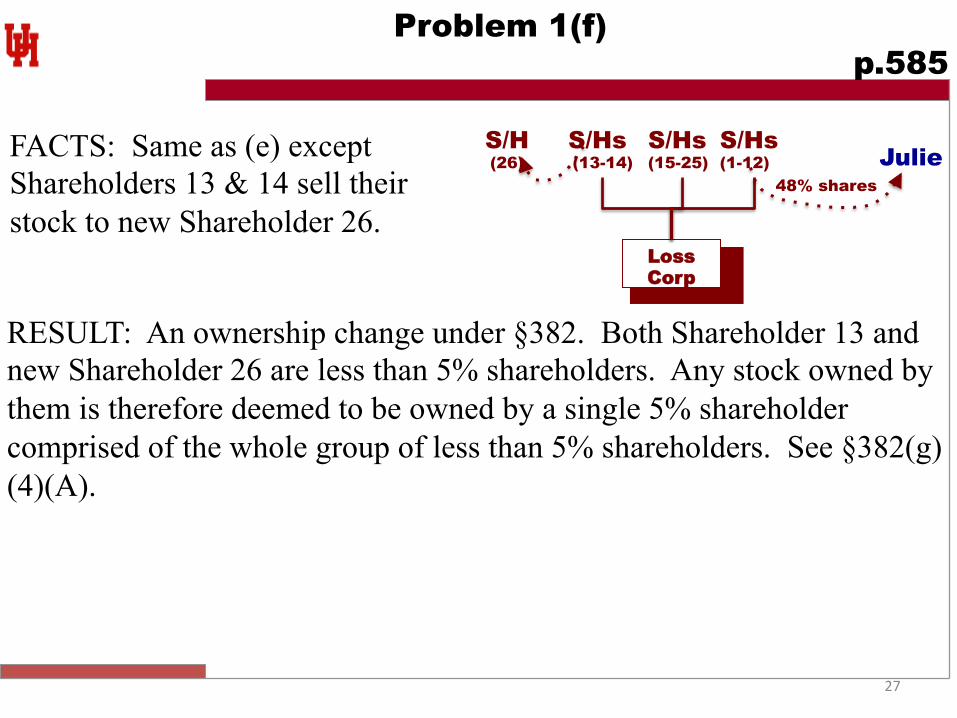

Problem 1(f) p.585

FACTS: Same as (e) except Shareholders 13 & 14 sell their stock to new Shareholder 26.

Loss Corp

S/Hs (13-14)

S/Hs (1-12) Julie

48% shares

S/Hs (15-25)

S/H (26)

RESULT: An ownership change under §382. Both Shareholder 13 and new Shareholder 26 are less than 5% shareholders. Any stock owned by them is therefore deemed to be owned by a single 5% shareholder comprised of the whole group of less than 5% shareholders. See §382(g)(4)(A).

28

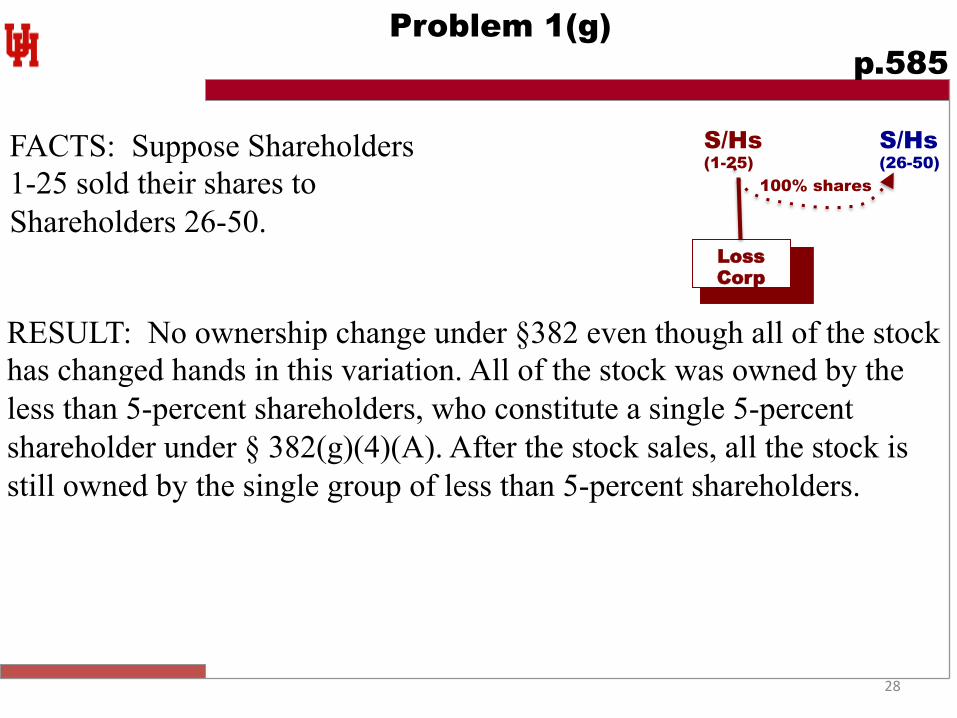

Problem 1(g) p.585

FACTS: Suppose Shareholders 1-25 sold their shares to Shareholders 26-50.

Loss Corp

S/Hs (26-50)

100% shares

S/Hs (1-25)

RESULT: No ownership change under §382 even though all of the stock has changed hands in this variation. All of the stock was owned by the less than 5-percent shareholders, who constitute a single 5-percent shareholder under § 382(g)(4)(A). After the stock sales, all the stock is still owned by the single group of less than 5-percent shareholders.

29

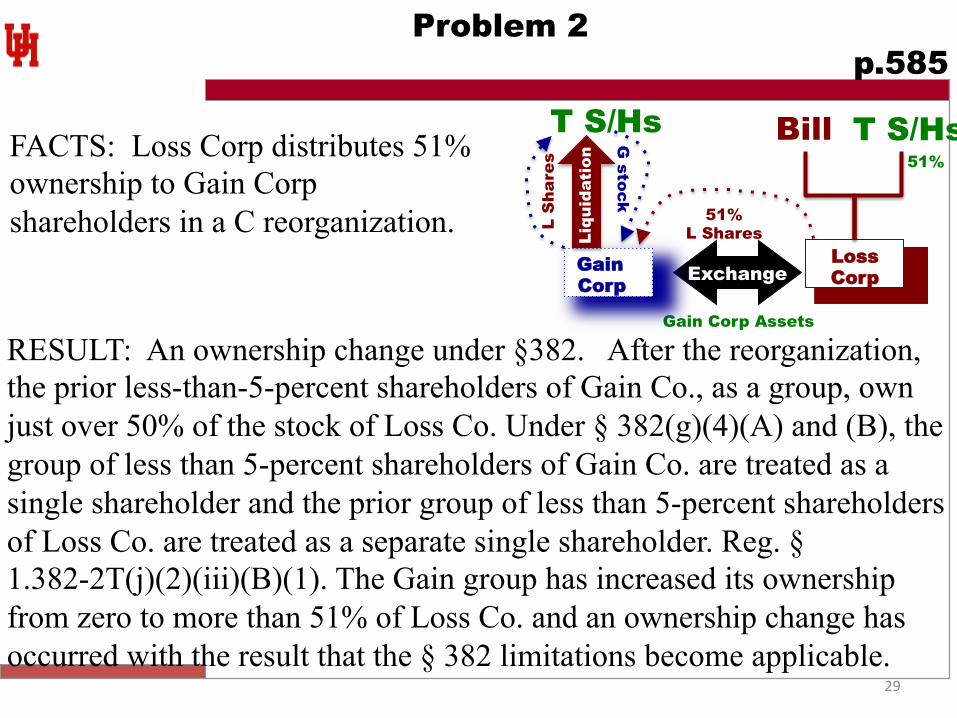

51% L Shares

Exchange

Gain Corp Assets

Gain Corp

T S/Hs

L S

hare

s

Liqu

idat

ion

G stock

Bill

Loss Corp

T S/Hs FACTS: Loss Corp distributes 51% ownership to Gain Corp shareholders in a C reorganization.

Problem 2 p.585

RESULT: An ownership change under §382. After the reorganization, the prior less-than-5-percent shareholders of Gain Co., as a group, own just over 50% of the stock of Loss Co. Under § 382(g)(4)(A) and (B), the group of less than 5-percent shareholders of Gain Co. are treated as a single shareholder and the prior group of less than 5-percent shareholders of Loss Co. are treated as a separate single shareholder. Reg. § 1.382-2T(j)(2)(iii)(B)(1). The Gain group has increased its ownership from zero to more than 51% of Loss Co. and an ownership change has occurred with the result that the § 382 limitations become applicable.

51%

30

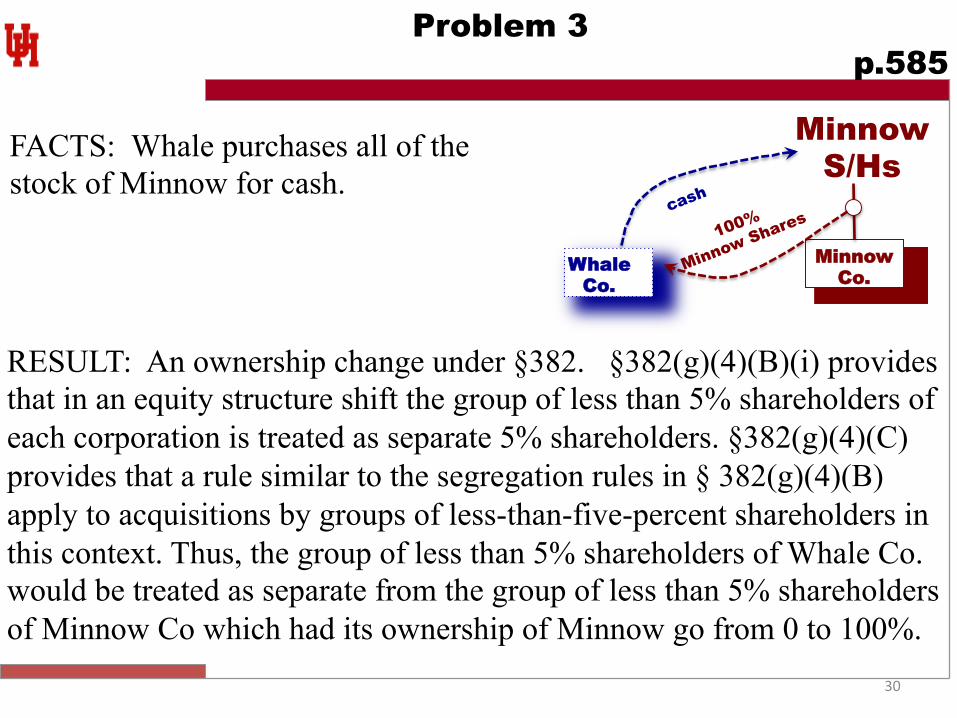

Whale Co.

Minnow S/Hs

Minnow Co.

FACTS: Whale purchases all of the stock of Minnow for cash.

Problem 3 p.585

RESULT: An ownership change under §382. §382(g)(4)(B)(i) provides that in an equity structure shift the group of less than 5% shareholders of each corporation is treated as separate 5% shareholders. §382(g)(4)(C) provides that a rule similar to the segregation rules in § 382(g)(4)(B) apply to acquisitions by groups of less-than-five-percent shareholders in this context. Thus, the group of less than 5% shareholders of Whale Co. would be treated as separate from the group of less than 5% shareholders of Minnow Co which had its ownership of Minnow go from 0 to 100%.

31

Section 382 Results of an Ownership Change p.585

Policy Concern: Congress does not want trafficking in Loss Companies or to have Profitable Companies to be overly motivated to buy the tax attributes of Loss Companies. But, Congress wanted to allow the corporation to use its losses to offset the income from its own business. §382 does this through two limitations: Continuity of Business Enterprise Limit (§382(c)): Disallows NOLs if the old loss corporation business is not continued for at least two years after the ownership change. §382 Limitation: NOLs can only be used in any “post-change period” only to the extent of the value of the Loss Corporation multiplied by the long-term tax-exempt rate.

32

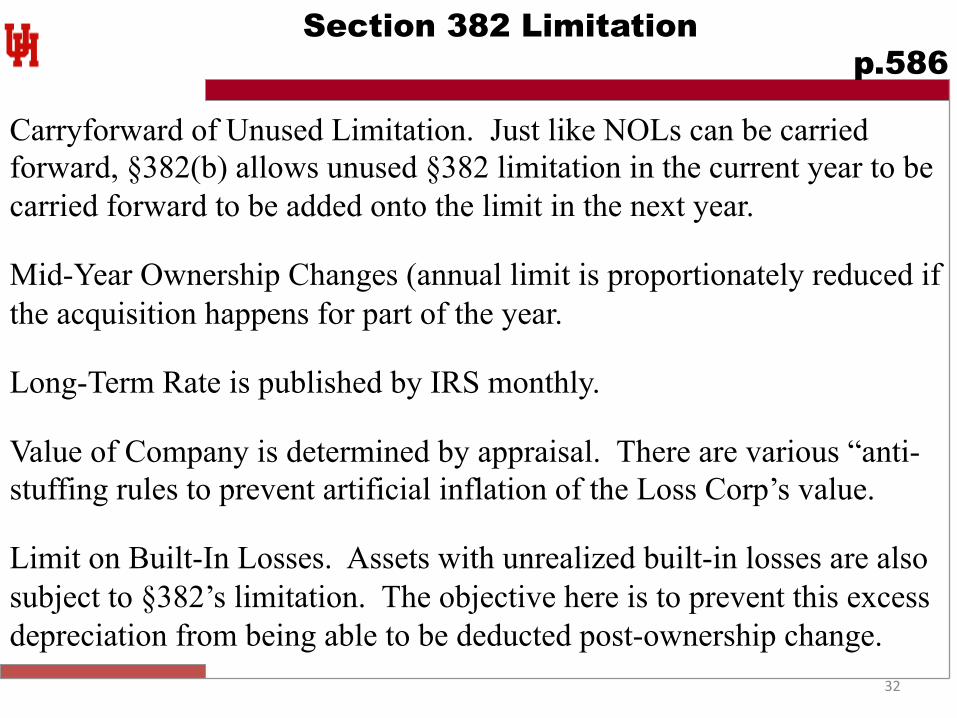

Section 382 Limitation p.586

Carryforward of Unused Limitation. Just like NOLs can be carried forward, §382(b) allows unused §382 limitation in the current year to be carried forward to be added onto the limit in the next year.

Mid-Year Ownership Changes (annual limit is proportionately reduced if the acquisition happens for part of the year.

Long-Term Rate is published by IRS monthly.

Value of Company is determined by appraisal. There are various “anti-stuffing rules to prevent artificial inflation of the Loss Corp’s value.

Limit on Built-In Losses. Assets with unrealized built-in losses are also subject to §382’s limitation. The objective here is to prevent this excess depreciation from being able to be deducted post-ownership change.

33

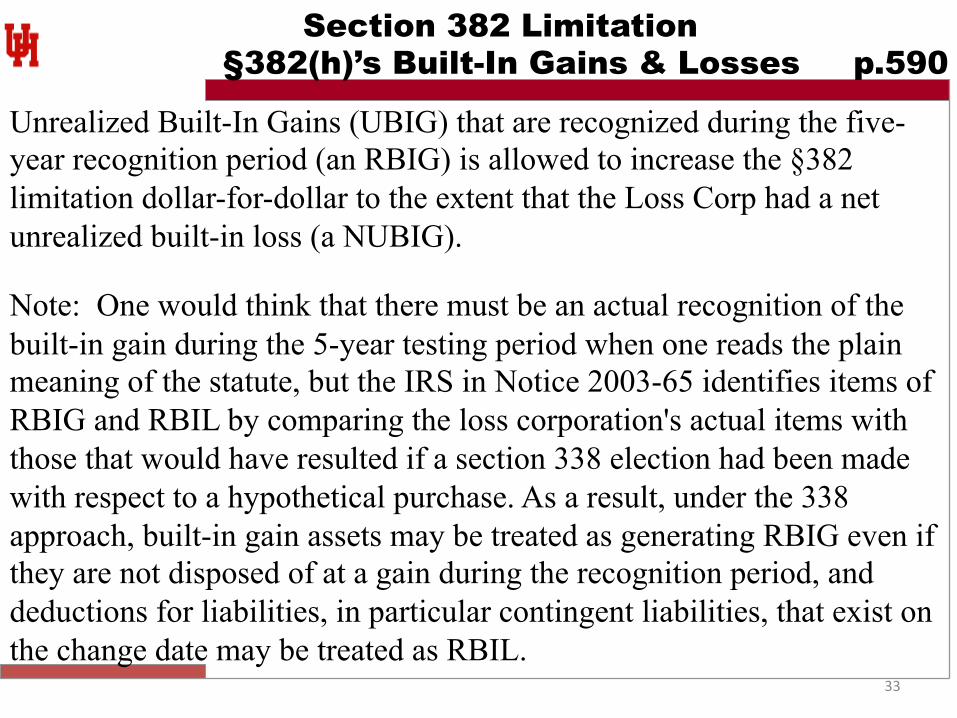

Section 382 Limitation §382(h)’s Built-In Gains & Losses p.590

Unrealized Built-In Gains (UBIG) that are recognized during the five-year recognition period (an RBIG) is allowed to increase the §382 limitation dollar-for-dollar to the extent that the Loss Corp had a net unrealized built-in loss (a NUBIG).

Note: One would think that there must be an actual recognition of the built-in gain during the 5-year testing period when one reads the plain meaning of the statute, but the IRS in Notice 2003-65 identifies items of RBIG and RBIL by comparing the loss corporation's actual items with those that would have resulted if a section 338 election had been made with respect to a hypothetical purchase. As a result, under the 338 approach, built-in gain assets may be treated as generating RBIG even if they are not disposed of at a gain during the recognition period, and deductions for liabilities, in particular contingent liabilities, that exist on the change date may be treated as RBIL.

34

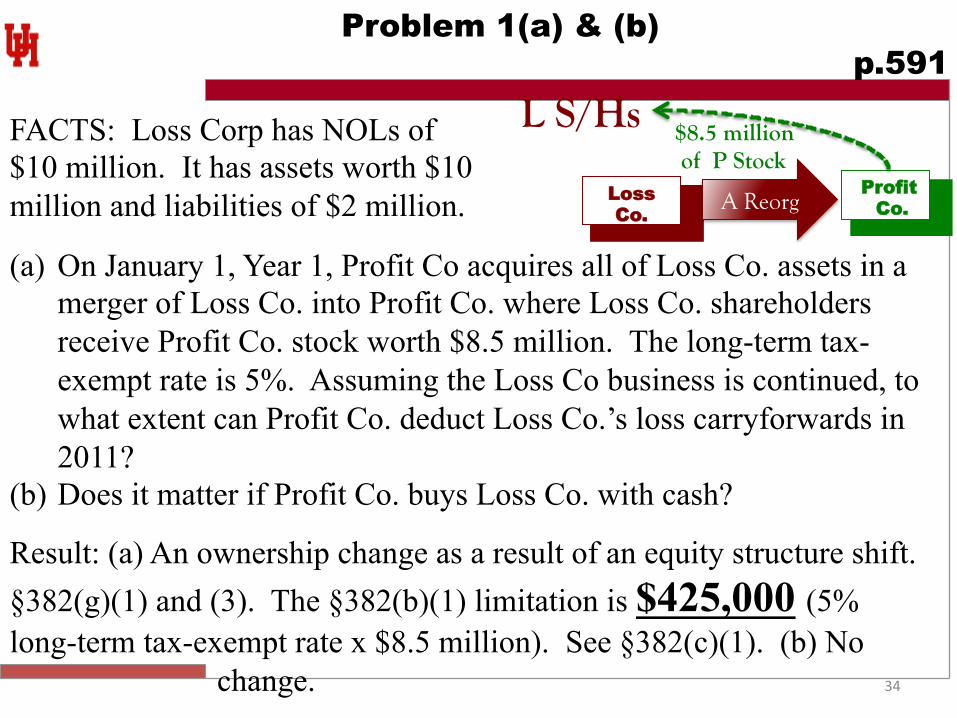

Problem 1(a) & (b) p.591

Profit Co.

Loss Co.

A Reorg

FACTS: Loss Corp has NOLs of $10 million. It has assets worth $10 million and liabilities of $2 million.

(a) On January 1, Year 1, Profit Co acquires all of Loss Co. assets in a merger of Loss Co. into Profit Co. where Loss Co. shareholders receive Profit Co. stock worth $8.5 million. The long-term tax-exempt rate is 5%. Assuming the Loss Co business is continued, to what extent can Profit Co. deduct Loss Co.’s loss carryforwards in 2011?

(b) Does it matter if Profit Co. buys Loss Co. with cash?

Result: (a) An ownership change as a result of an equity structure shift. §382(g)(1) and (3). The §382(b)(1) limitation is $425,000 (5% long-term tax-exempt rate x $8.5 million). See §382(c)(1). (b) No

change.

L S/Hs $8.5 million of P Stock

35

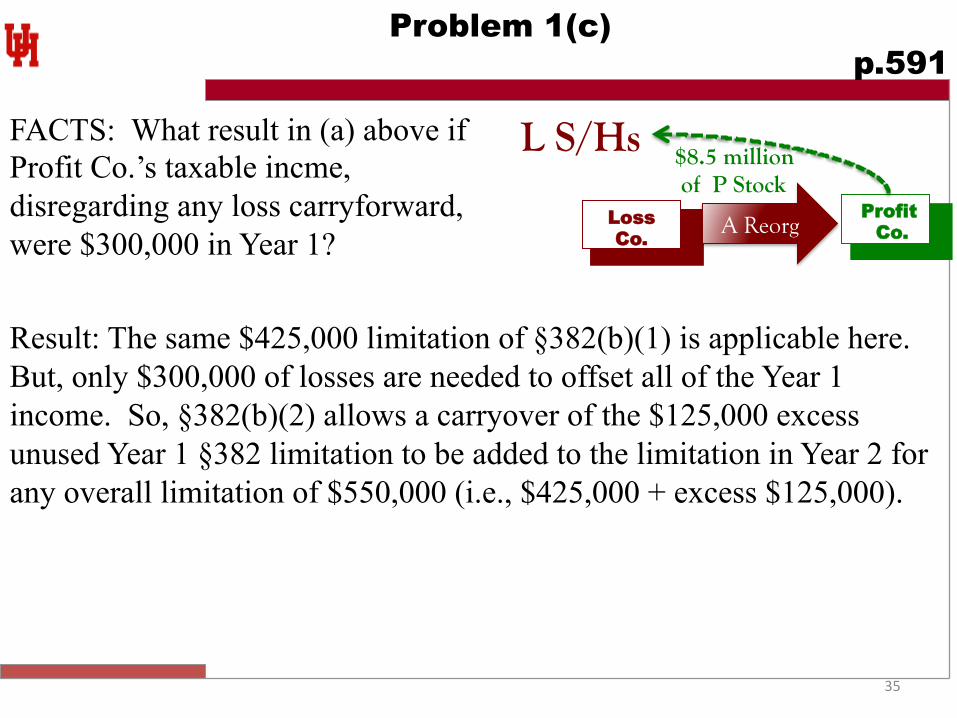

Problem 1(c) p.591

FACTS: What result in (a) above if Profit Co.’s taxable incme, disregarding any loss carryforward, were $300,000 in Year 1?

Result: The same $425,000 limitation of §382(b)(1) is applicable here. But, only $300,000 of losses are needed to offset all of the Year 1 income. So, §382(b)(2) allows a carryover of the $125,000 excess unused Year 1 §382 limitation to be added to the limitation in Year 2 for any overall limitation of $550,000 (i.e., $425,000 + excess $125,000).

Profit Co.

Loss Co.

A Reorg

L S/Hs $8.5 million of P Stock

36

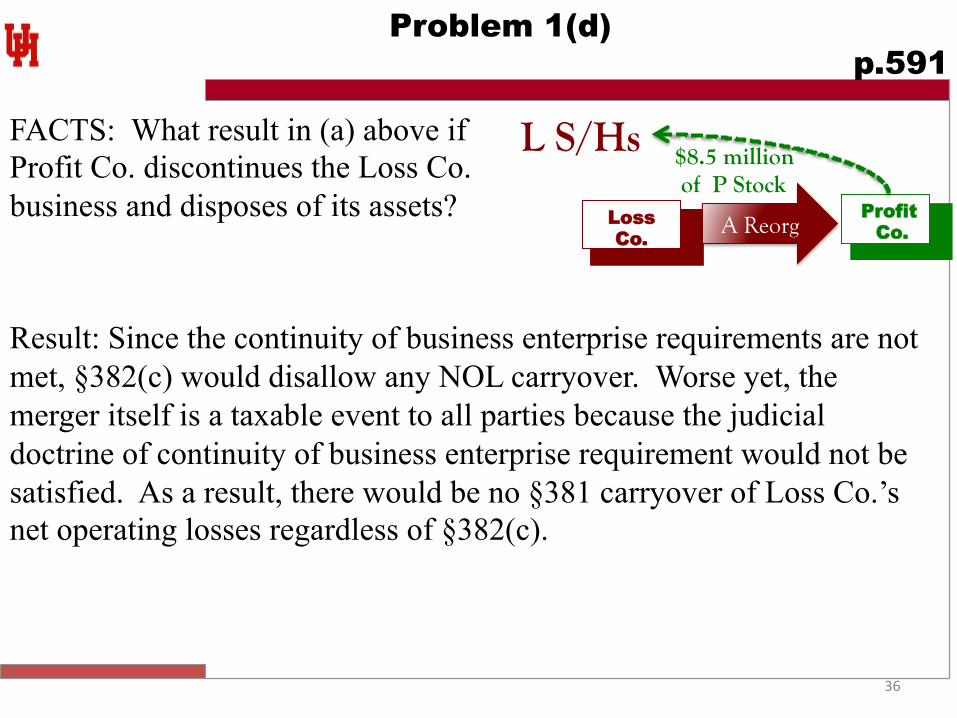

Problem 1(d) p.591

FACTS: What result in (a) above if Profit Co. discontinues the Loss Co. business and disposes of its assets?

Result: Since the continuity of business enterprise requirements are not met, §382(c) would disallow any NOL carryover. Worse yet, the merger itself is a taxable event to all parties because the judicial doctrine of continuity of business enterprise requirement would not be satisfied. As a result, there would be no §381 carryover of Loss Co.’s net operating losses regardless of §382(c).

Profit Co.

Loss Co.

A Reorg

L S/Hs $8.5 million of P Stock

37

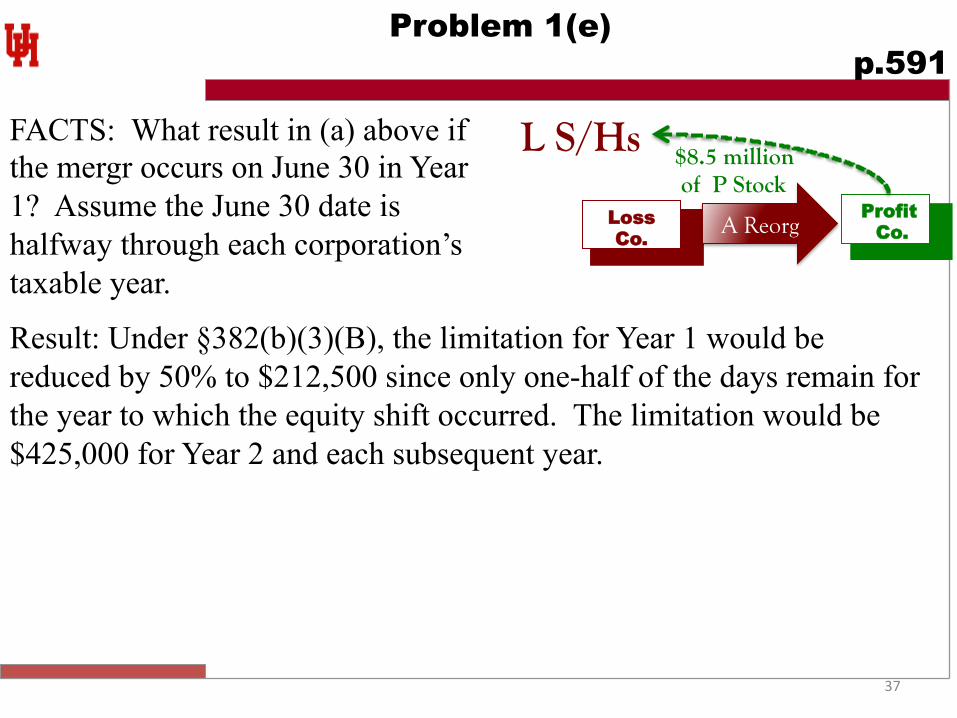

Problem 1(e) p.591

FACTS: What result in (a) above if the mergr occurs on June 30 in Year 1? Assume the June 30 date is halfway through each corporation’s taxable year. Result: Under §382(b)(3)(B), the limitation for Year 1 would be reduced by 50% to $212,500 since only one-half of the days remain for the year to which the equity shift occurred. The limitation would be $425,000 for Year 2 and each subsequent year.

Profit Co.

Loss Co.

A Reorg

L S/Hs $8.5 million of P Stock

38

Problem 2(a) p.591

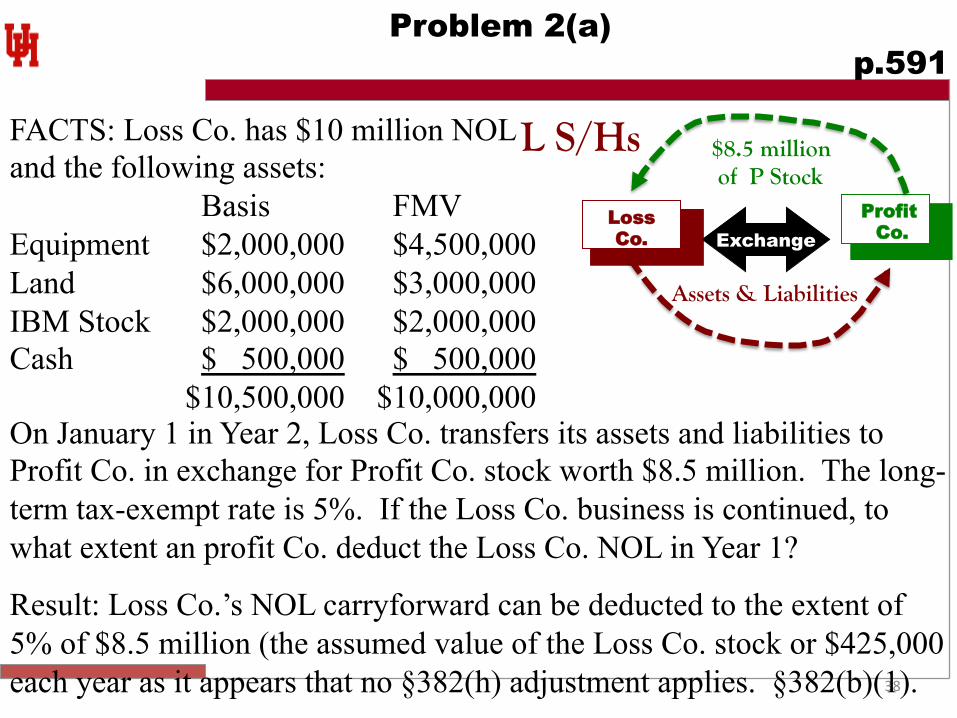

FACTS: Loss Co. has $10 million NOL and the following assets:

Basis FMV Equipment $2,000,000 $4,500,000 Land $6,000,000 $3,000,000 IBM Stock $2,000,000 $2,000,000 Cash $ 500,000 $ 500,000

$10,500,000 $10,000,000 On January 1 in Year 2, Loss Co. transfers its assets and liabilities to Profit Co. in exchange for Profit Co. stock worth $8.5 million. The long-term tax-exempt rate is 5%. If the Loss Co. business is continued, to what extent an profit Co. deduct the Loss Co. NOL in Year 1?

Result: Loss Co.’s NOL carryforward can be deducted to the extent of 5% of $8.5 million (the assumed value of the Loss Co. stock or $425,000 each year as it appears that no §382(h) adjustment applies. §382(b)(1).

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

39

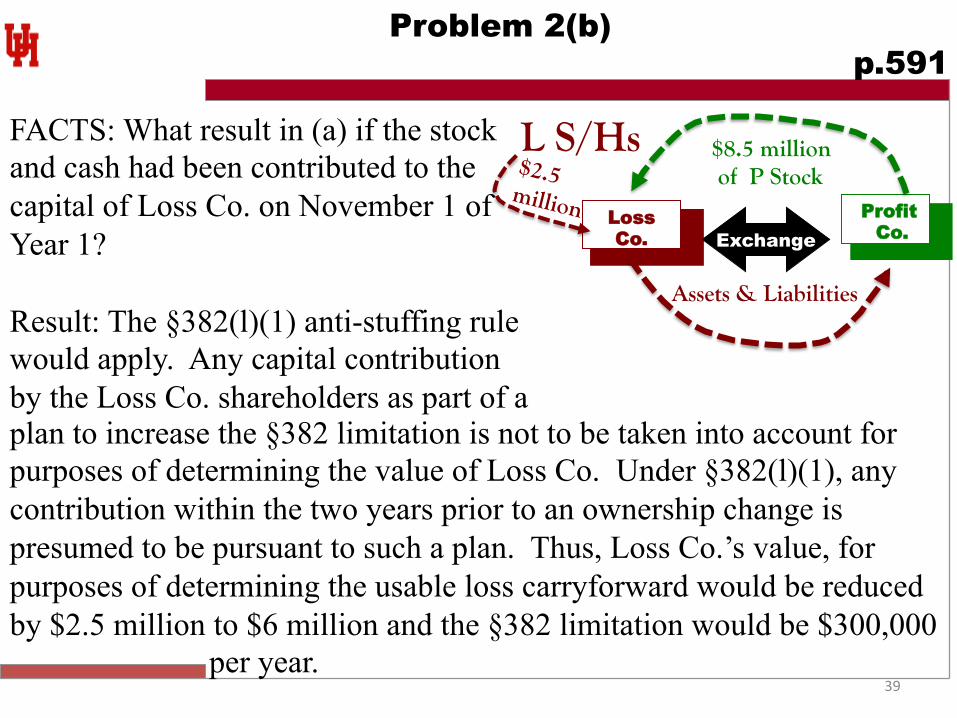

Problem 2(b) p.591

FACTS: What result in (a) if the stock and cash had been contributed to the capital of Loss Co. on November 1 of Year 1? Result: The §382(l)(1) anti-stuffing rule would apply. Any capital contribution by the Loss Co. shareholders as part of a plan to increase the §382 limitation is not to be taken into account for purposes of determining the value of Loss Co. Under §382(l)(1), any contribution within the two years prior to an ownership change is presumed to be pursuant to such a plan. Thus, Loss Co.’s value, for purposes of determining the usable loss carryforward would be reduced by $2.5 million to $6 million and the §382 limitation would be $300,000

per year.

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

40

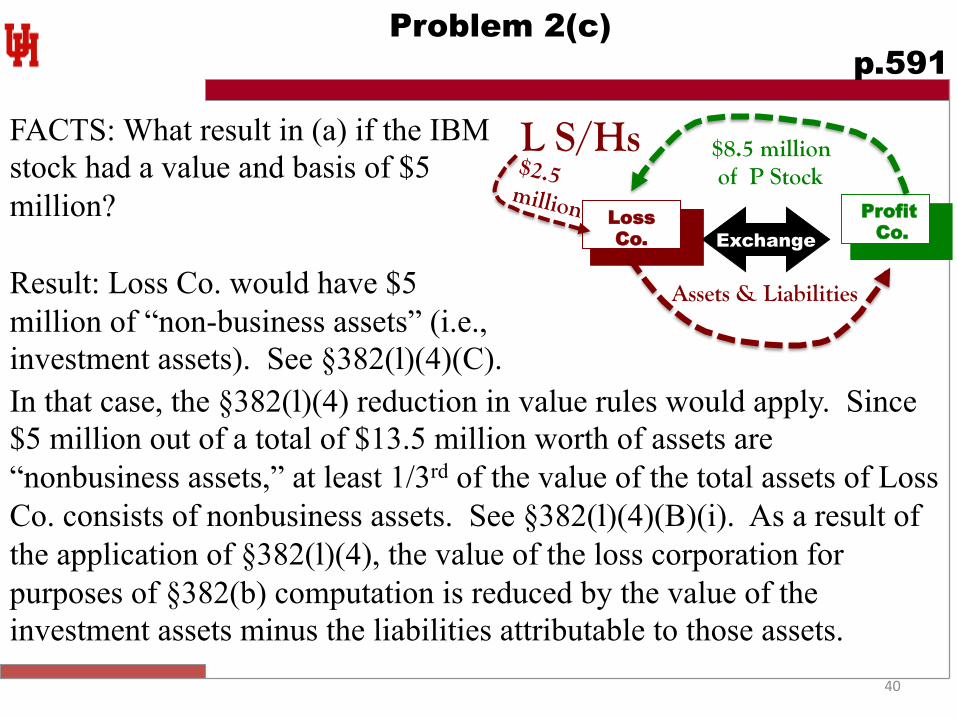

Problem 2(c) p.591

FACTS: What result in (a) if the IBM stock had a value and basis of $5 million? Result: Loss Co. would have $5 million of “non-business assets” (i.e., investment assets). See §382(l)(4)(C). In that case, the §382(l)(4) reduction in value rules would apply. Since $5 million out of a total of $13.5 million worth of assets are “nonbusiness assets,” at least 1/3rd of the value of the total assets of Loss Co. consists of nonbusiness assets. See §382(l)(4)(B)(i). As a result of the application of §382(l)(4), the value of the loss corporation for purposes of §382(b) computation is reduced by the value of the investment assets minus the liabilities attributable to those assets.

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

41

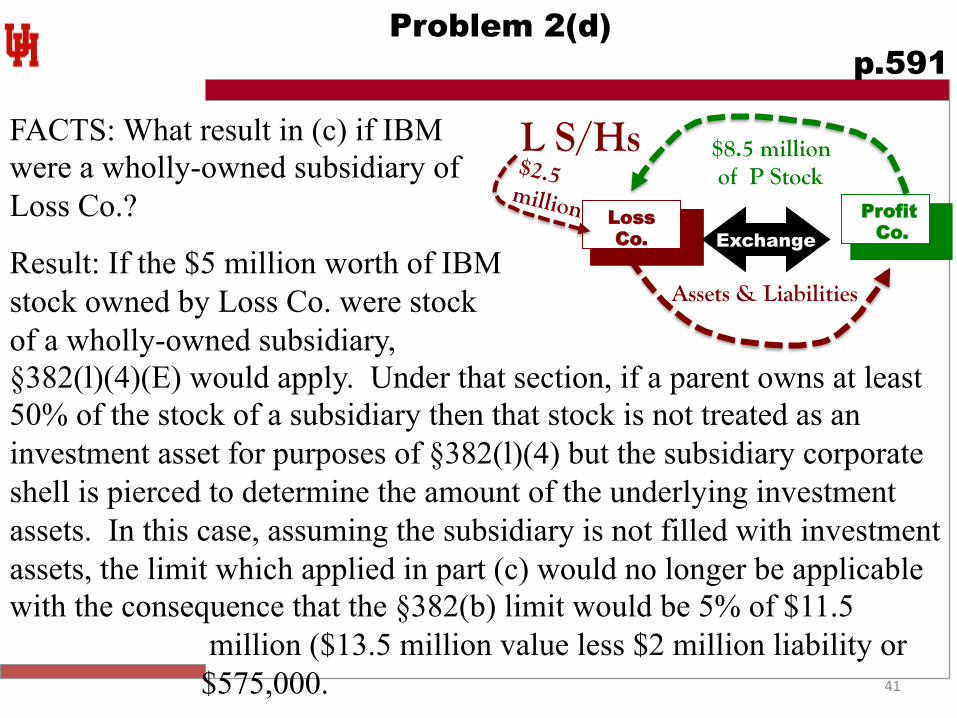

Problem 2(d) p.591

FACTS: What result in (c) if IBM were a wholly-owned subsidiary of Loss Co.?

Result: If the $5 million worth of IBM stock owned by Loss Co. were stock of a wholly-owned subsidiary, §382(l)(4)(E) would apply. Under that section, if a parent owns at least 50% of the stock of a subsidiary then that stock is not treated as an investment asset for purposes of §382(l)(4) but the subsidiary corporate shell is pierced to determine the amount of the underlying investment assets. In this case, assuming the subsidiary is not filled with investment assets, the limit which applied in part (c) would no longer be applicable with the consequence that the §382(b) limit would be 5% of $11.5

million ($13.5 million value less $2 million liability or $575,000.

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

42

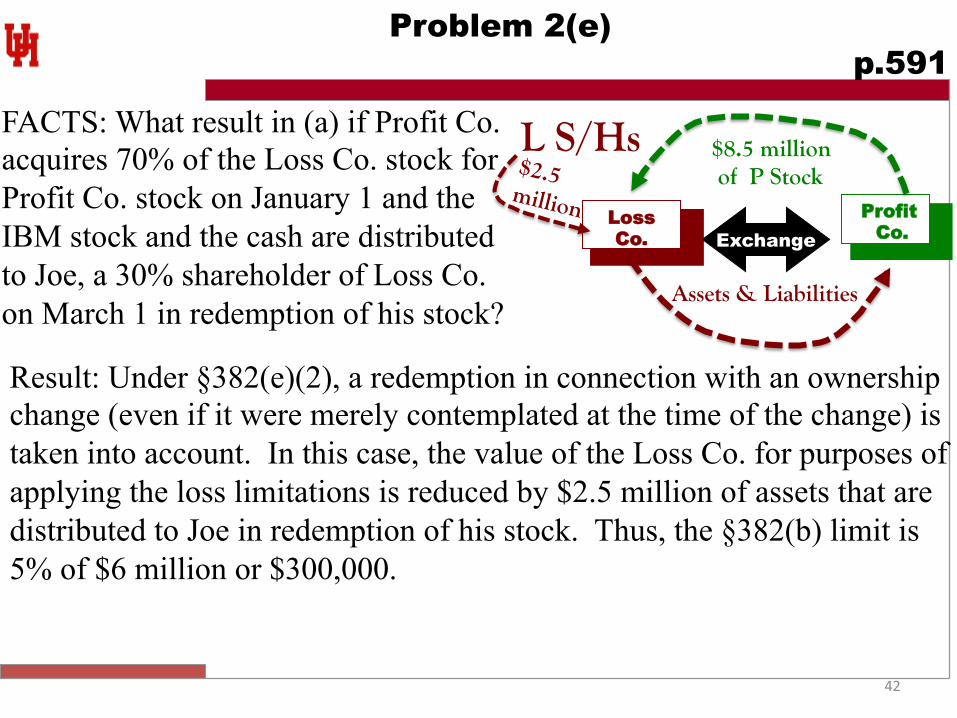

Problem 2(e) p.591

FACTS: What result in (a) if Profit Co. acquires 70% of the Loss Co. stock for Profit Co. stock on January 1 and the IBM stock and the cash are distributed to Joe, a 30% shareholder of Loss Co. on March 1 in redemption of his stock?

Result: Under §382(e)(2), a redemption in connection with an ownership change (even if it were merely contemplated at the time of the change) is taken into account. In this case, the value of the Loss Co. for purposes of applying the loss limitations is reduced by $2.5 million of assets that are distributed to Joe in redemption of his stock. Thus, the §382(b) limit is 5% of $6 million or $300,000.

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

43

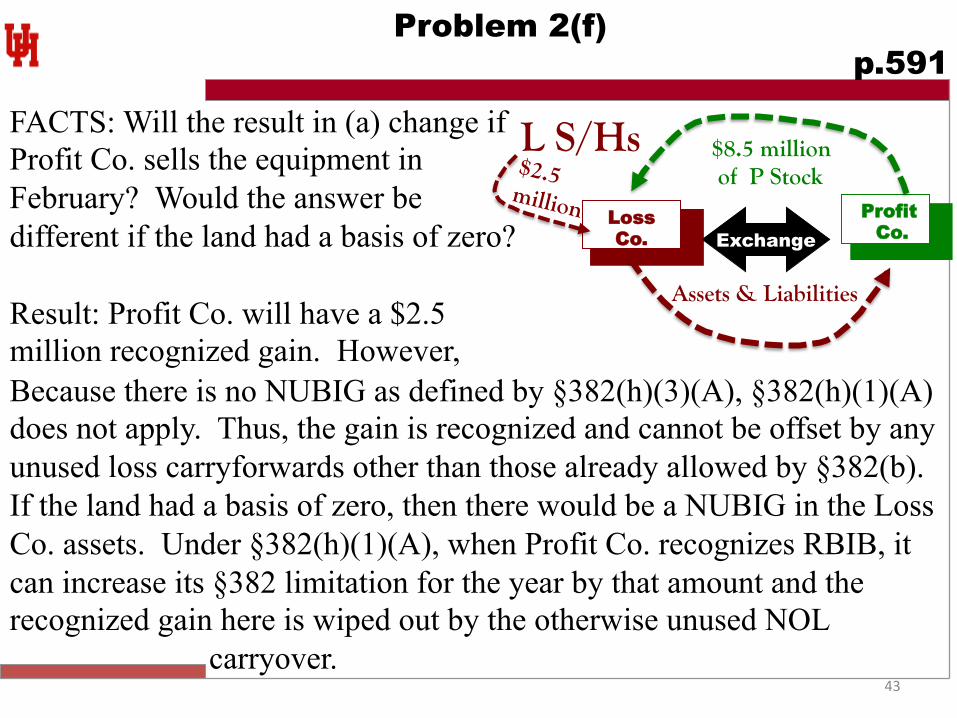

Problem 2(f) p.591

FACTS: Will the result in (a) change if Profit Co. sells the equipment in February? Would the answer be different if the land had a basis of zero? Result: Profit Co. will have a $2.5 million recognized gain. However, Because there is no NUBIG as defined by §382(h)(3)(A), §382(h)(1)(A) does not apply. Thus, the gain is recognized and cannot be offset by any unused loss carryforwards other than those already allowed by §382(b). If the land had a basis of zero, then there would be a NUBIG in the Loss Co. assets. Under §382(h)(1)(A), when Profit Co. recognizes RBIB, it can increase its §382 limitation for the year by that amount and the recognized gain here is wiped out by the otherwise unused NOL

carryover.

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

44

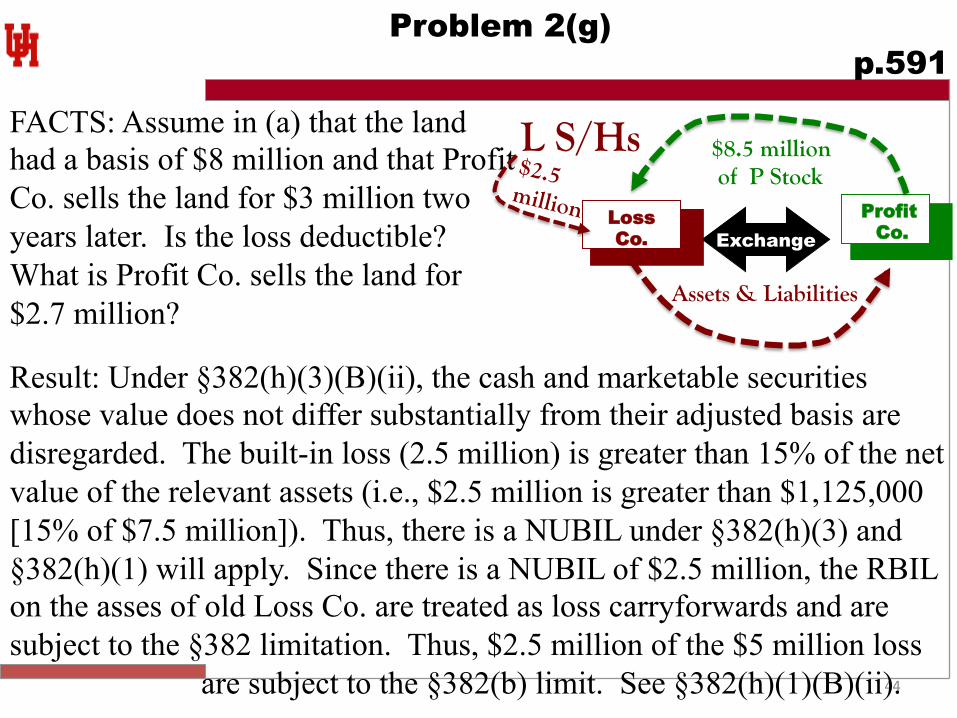

Problem 2(g) p.591

FACTS: Assume in (a) that the land had a basis of $8 million and that Profit Co. sells the land for $3 million two years later. Is the loss deductible? What is Profit Co. sells the land for $2.7 million?

Result: Under §382(h)(3)(B)(ii), the cash and marketable securities whose value does not differ substantially from their adjusted basis are disregarded. The built-in loss (2.5 million) is greater than 15% of the net value of the relevant assets (i.e., $2.5 million is greater than $1,125,000 [15% of $7.5 million]). Thus, there is a NUBIL under §382(h)(3) and §382(h)(1) will apply. Since there is a NUBIL of $2.5 million, the RBIL on the asses of old Loss Co. are treated as loss carryforwards and are subject to the §382 limitation. Thus, $2.5 million of the $5 million loss

are subject to the §382(b) limit. See §382(h)(1)(B)(ii).

Profit Co.

Loss Co.

L S/Hs $8.5 million of P Stock

Exchange

Assets & Liabilities

$2.5 million

45

Other Limitation Regimes p.593

§383: States that limitation regime of §382 that applies to NOLs should also apply to limit tax credits.

§269: Applies a subjective test to deny the usage of tax attributes if it is determined that the the principal purpose of an acquisition of Loss Crop was ‘‘evasion or avoidance of Federal income tax by acquiring the benefit of a deduction, credit, or other allowance.’’

§384: Restricts an acquiring corporation from using its preacquisition losses to offset built-in gains of an acquired corporation. Example: L has $100,000 NOL and acquires T in an A reorganization. T’s asset is sold for $100,000 of gain. §384 prevents Loss Corp from using its pre-acquisition NOL to offset the gain on the T asset that arose pre-acquisition.

46

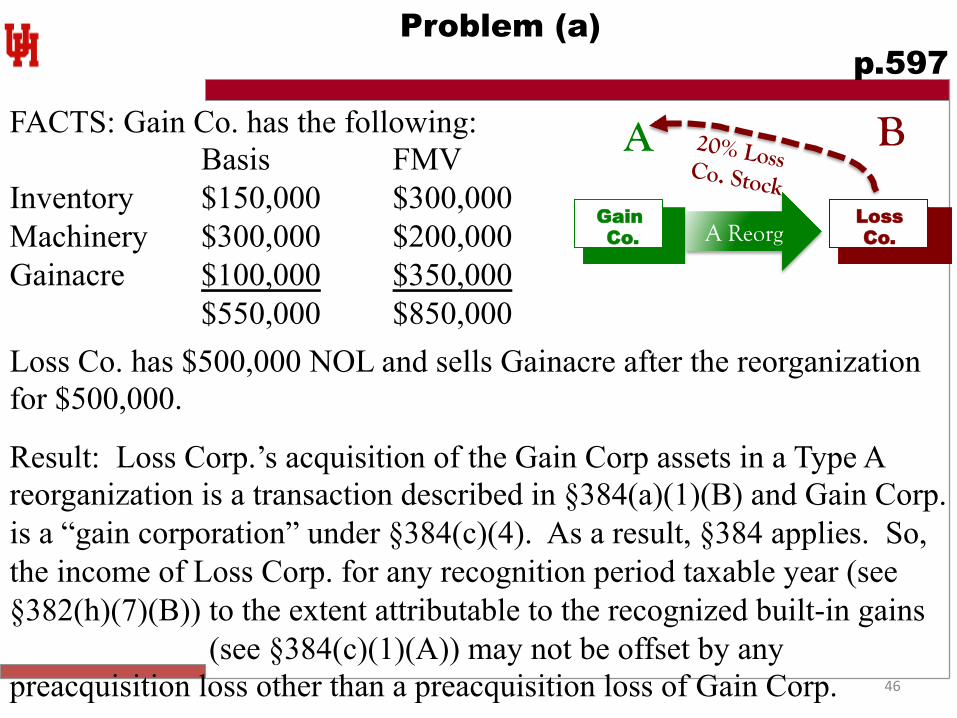

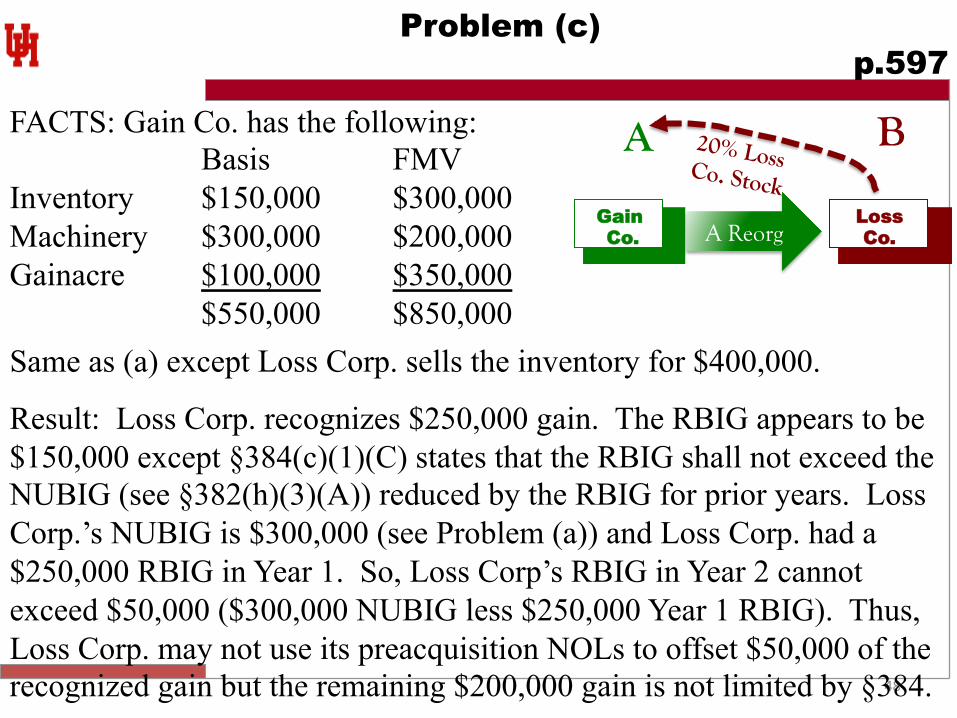

Problem (a) p.597

Loss Co. has $500,000 NOL and sells Gainacre after the reorganization for $500,000.

Result: Loss Corp.’s acquisition of the Gain Corp assets in a Type A reorganization is a transaction described in §384(a)(1)(B) and Gain Corp. is a “gain corporation” under §384(c)(4). As a result, §384 applies. So, the income of Loss Corp. for any recognition period taxable year (see §382(h)(7)(B)) to the extent attributable to the recognized built-in gains

(see §384(c)(1)(A)) may not be offset by any preacquisition loss other than a preacquisition loss of Gain Corp.

Gain Co.

Loss Co.

A 20% Loss Co. Stock

FACTS: Gain Co. has the following: Basis FMV

Inventory $150,000 $300,000 Machinery $300,000 $200,000 Gainacre $100,000 $350,000

$550,000 $850,000

B

A Reorg

47

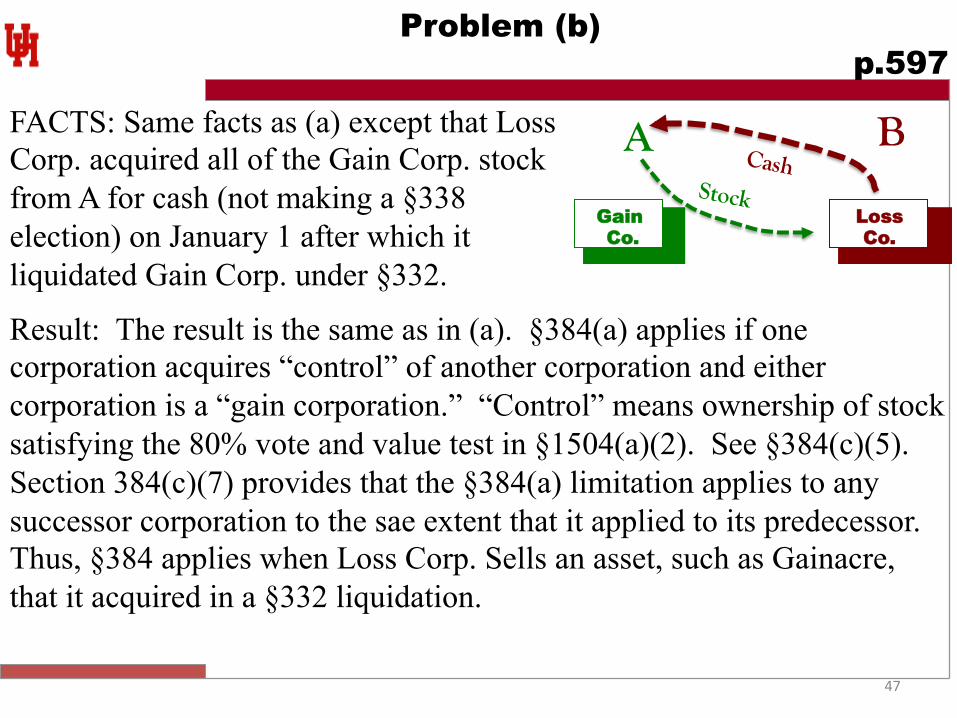

Problem (b) p.597

Result: The result is the same as in (a). §384(a) applies if one corporation acquires “control” of another corporation and either corporation is a “gain corporation.” “Control” means ownership of stock satisfying the 80% vote and value test in §1504(a)(2). See §384(c)(5). Section 384(c)(7) provides that the §384(a) limitation applies to any successor corporation to the sae extent that it applied to its predecessor. Thus, §384 applies when Loss Corp. Sells an asset, such as Gainacre, that it acquired in a §332 liquidation.

Gain Co.

Loss Co.

A Cash

FACTS: Same facts as (a) except that Loss Corp. acquired all of the Gain Corp. stock from A for cash (not making a §338 election) on January 1 after which it liquidated Gain Corp. under §332.

B Stock

48

Problem (c) p.597

Same as (a) except Loss Corp. sells the inventory for $400,000.

Result: Loss Corp. recognizes $250,000 gain. The RBIG appears to be $150,000 except §384(c)(1)(C) states that the RBIG shall not exceed the NUBIG (see §382(h)(3)(A)) reduced by the RBIG for prior years. Loss Corp.’s NUBIG is $300,000 (see Problem (a)) and Loss Corp. had a $250,000 RBIG in Year 1. So, Loss Corp’s RBIG in Year 2 cannot exceed $50,000 ($300,000 NUBIG less $250,000 Year 1 RBIG). Thus, Loss Corp. may not use its preacquisition NOLs to offset $50,000 of the recognized gain but the remaining $200,000 gain is not limited by §384.

Gain Co.

Loss Co.

A 20% Loss Co. Stock

FACTS: Gain Co. has the following: Basis FMV

Inventory $150,000 $300,000 Machinery $300,000 $200,000 Gainacre $100,000 $350,000

$550,000 $850,000

B

A Reorg

49

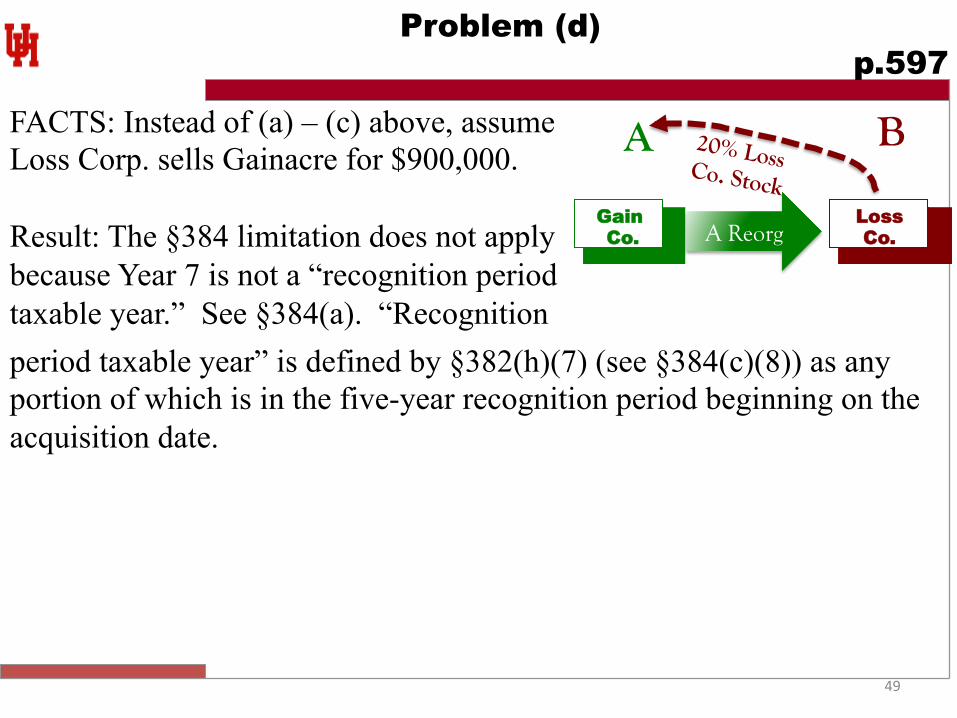

Problem (d) p.597

period taxable year” is defined by §382(h)(7) (see §384(c)(8)) as any portion of which is in the five-year recognition period beginning on the acquisition date.

Gain Co.

Loss Co.

A 20% Loss Co. Stock

FACTS: Instead of (a) – (c) above, assume Loss Corp. sells Gainacre for $900,000. Result: The §384 limitation does not apply because Year 7 is not a “recognition period taxable year.” See §384(a). “Recognition

B

A Reorg

50

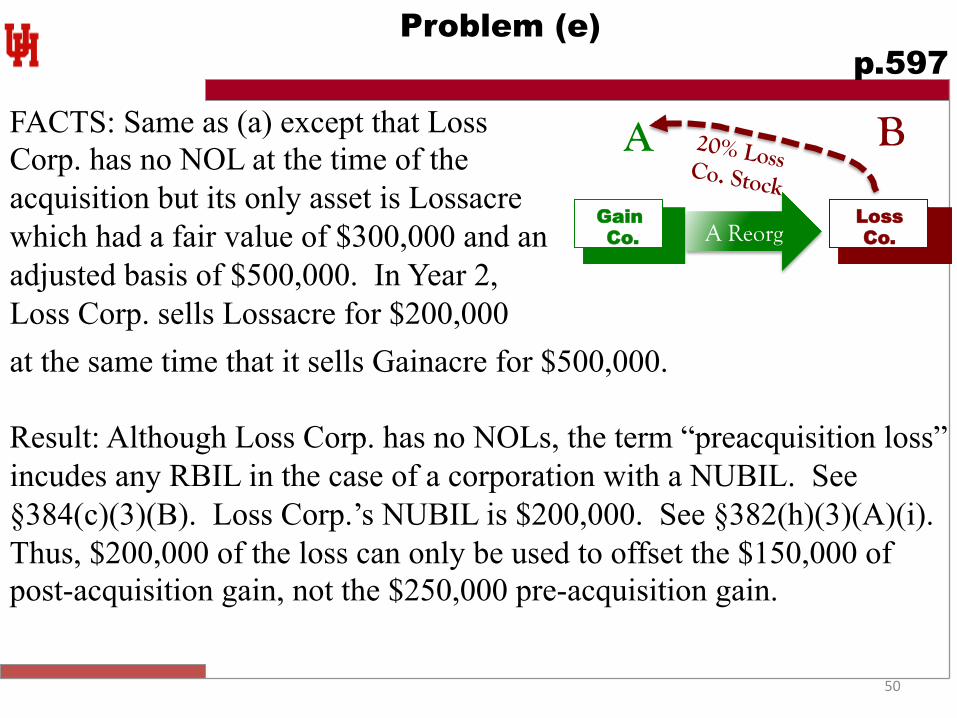

Problem (e) p.597

at the same time that it sells Gainacre for $500,000. Result: Although Loss Corp. has no NOLs, the term “preacquisition loss” incudes any RBIL in the case of a corporation with a NUBIL. See §384(c)(3)(B). Loss Corp.’s NUBIL is $200,000. See §382(h)(3)(A)(i). Thus, $200,000 of the loss can only be used to offset the $150,000 of post-acquisition gain, not the $250,000 pre-acquisition gain.

Gain Co.

Loss Co.

A 20% Loss Co. Stock

FACTS: Same as (a) except that Loss Corp. has no NOL at the time of the acquisition but its only asset is Lossacre which had a fair value of $300,000 and an adjusted basis of $500,000. In Year 2, Loss Corp. sells Lossacre for $200,000

B

A Reorg