Embed Size (px)

Citation preview

Presentation name www.hamptons.co.uk

Full steam ahead?

Fionnuala EarleyResidential Research Director, Hamptons International

Presentation name www.hamptons.co.uk

• The economic and housing market context

• Pent up demand

• The impact of regulation

• Summary and questions

Presentation name www.hamptons.co.uk

The Economy

• The Good News–IMF expects UK to have fastest growth in G7–Employment growing –Real wage growth positive – after five years–Inflation back on target–Interest rates expected to stay low till 2015

• The Not So Good News–High household debt–More austerity cuts to come–Election......

Presentation name www.hamptons.co.uk

Housing market recovery began 12 months ago

4

• Prices up 6.2% year on year in UK

• Price growth led by London – up 14.2%

• Transactions up by 18% in 2013

• Transactions at 64% of 2007 peak

Ave

rag

e H

ou

se

Pri

ce

Presentation name www.hamptons.co.uk

Price growth led by London and South East

• Strongest recovery in London and the South East

• Outside London and the South East higher value markets have recovered more quickly

• Some inner London Boroughs 50% above previous peak

Feb 2013 house price compared to 2007 peak

Presentation name www.hamptons.co.uk

Average house worth 94% of 2007 value

Presentation name www.hamptons.co.uk

Growth in transactions led by top of the market

7

• Recovery in transactions strongest in the higher price bands – not just driven by London

• Below £250k flat

• Recovery of domestic markets over 2014 should see growth of transactions in lower price bands pick up

Presentation name www.hamptons.co.uk

A recovery led by mortgage finance?

8

UK

Mort

gag

e l

en

din

g

(£b

n)

• Mortgage lending up 18% year on year in value terms. Still 50% below 2007 levels

• Lending to first time buyers doubled between 2008 and 2013 in percentage terms

Presentation name www.hamptons.co.uk

Ch

an

ge (

20

07

-2

01

3)

Yorks & Humber

East Midlands East

London South East

South West

West Midlands

North West Wales Scotland

• Cash buyers now account for around 1 in 3 transactions, while at the peak of the market in 2007 just 1 in 5 sales was to a cash buyer

• Housing markets in London and the South East are have seen an influx of cash buyers despite these regions traditionally relying more heavily on mortgage finance

Or a recovery led by cash buyers?

Presentation name www.hamptons.co.uk

Change (

Feb ‘

13

– F

eb ‘

14

) in

sto

ck

Yorks & Humber

East Midlands

East

LondonSouth East

South West

West Midlands

North West

Wales

Scotland

North East

• Number of properties for sale in London down 20%+ year on year

• Increased mortgage lending to cash and first time buyers means there are more buyers without property to sell

• Average time to sell fell by 2 weeks in 2013 – down to 8.3

Mismatch between supply and demand

Presentation name www.hamptons.co.uk

Sustainable or blowing bubbles?

11

Ave

rag

e m

on

thly

mort

gag

e r

ep

aym

en

ts (

20

14

p

rice

s)

• Homeowners are benefitting from low interest rates.

• For those buyers with a 10% deposit average mortgage repayments are at 2002 levels (adjusted for inflation).

• For existing owners housing is at its most affordable level for 10 years

Presentation name www.hamptons.co.uk

Pent up Demand

• Based on 2008 household projections c 350,000 pent up households

• Number of 20 to 34-year-olds living with their parents increased by 25 per cent since 1996

• Concealed households up by 70% in 10 years

• More in London and the South

• Migration of households from North to South

Presentation name www.hamptons.co.uk

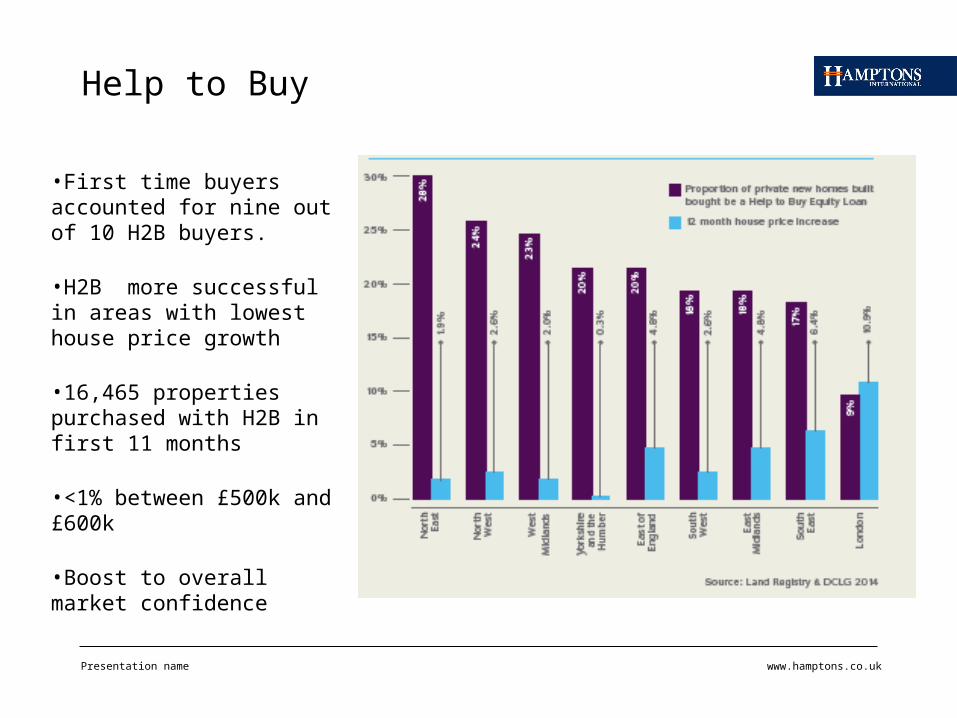

Help to Buy

•First time buyers accounted for nine out of 10 H2B buyers.

•H2B more successful in areas with lowest house price growth

•16,465 properties purchased with H2B in first 11 months

•<1% between £500k and £600k

•Boost to overall market confidence

Presentation name www.hamptons.co.uk

Risks

• Even with rates at +5% payments lower than in 2007 in real terms

• But essential spending is higher too squeezing real disposable income

• Expectations – pick up in Buy to Let advances

•Elections add uncertainty

Presentation name www.hamptons.co.uk

Three pronged attack of the TLAs

• MMR – stricter affordability tests to be documented

• PRA – tighter capital requirements if sign of risk to financial stability

• FPC – stress test powers on interest rates

• And the Chancellor

Presentation name www.hamptons.co.uk

Presentation name www.hamptons.co.uk

Thank You and Questions