Embed Size (px)

Citation preview

Presentation of NORDEN | 1 Our business is global tramp shipping

PRESENTATION OF NORDEN

Jyske Bank

Company Day

27 November 2014

CFO Michael Tønnes Jørgensen

Presentation of NORDEN | 2 Our business is global tramp shipping

AGENDA

NORDEN at a glance

Group highlights

Financials

Dry Cargo

Tankers

2014 expectations

Q & A

Presentation of NORDEN | 3 Our business is global tramp shipping

0

25

50

75

100

125

150

175

200

225

250

275

300

1871

1874

1877

1880

1883

1886

1889

1892

1895

1898

1901

1904

1907

1910

1913

1916

1919

1922

1925

1928

1931

1934

1937

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2011

2014

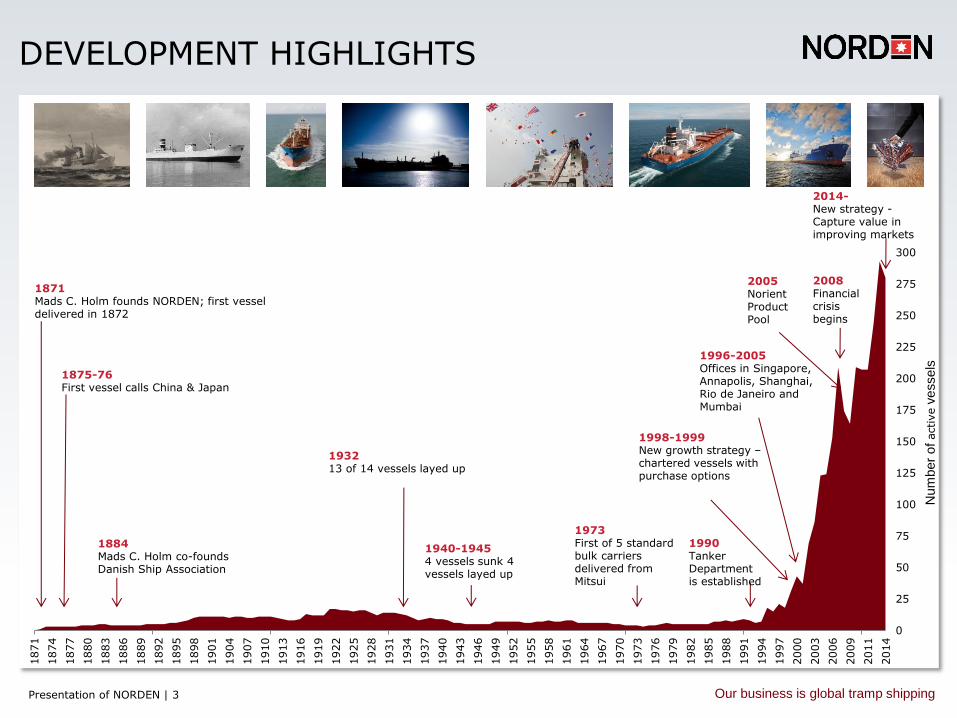

DEVELOPMENT HIGHLIGHTS

Num

ber

of active v

essels

2005 Norient Product Pool

1871 Mads C. Holm founds NORDEN; first vessel delivered in 1872

1875-76 First vessel calls China & Japan

1990 Tanker Department is established

1884 Mads C. Holm co-founds Danish Ship Association

1996-2005 Offices in Singapore, Annapolis, Shanghai, Rio de Janeiro and Mumbai

1973 First of 5 standard bulk carriers delivered from Mitsui

1998-1999 New growth strategy – chartered vessels with purchase options

1932 13 of 14 vessels layed up

1940-1945 4 vessels sunk 4 vessels layed up

2008 Financial crisis begins

2014- New strategy - Capture value in improving markets

Presentation of NORDEN | 4 Our business is global tramp shipping

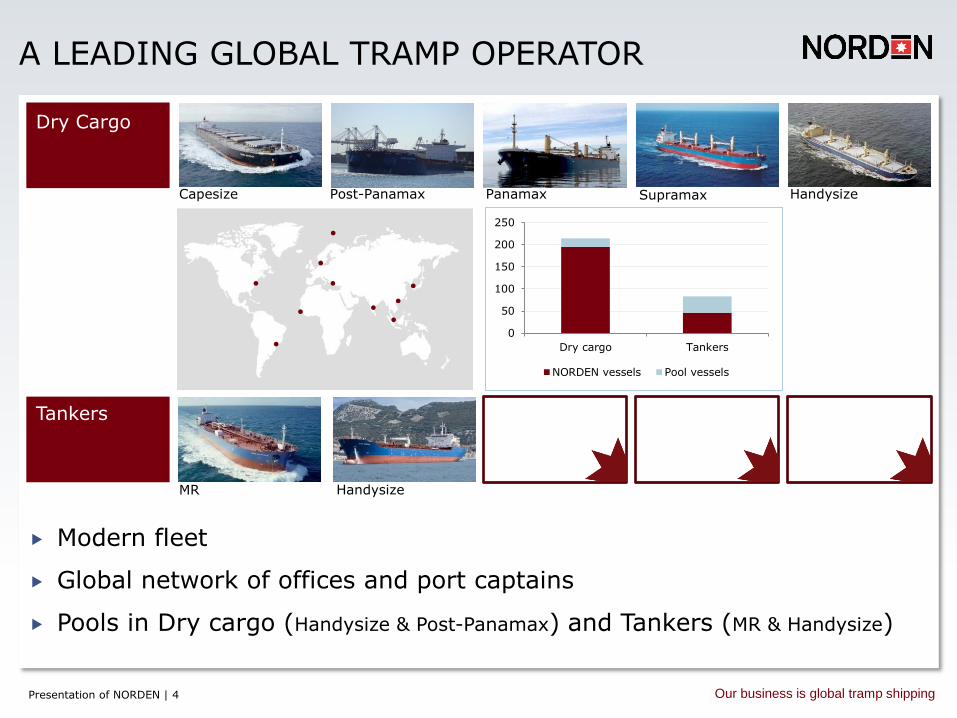

A LEADING GLOBAL TRAMP OPERATOR

Modern fleet

Global network of offices and port captains

Pools in Dry cargo (Handysize & Post-Panamax) and Tankers (MR & Handysize)

Capesize Post-Panamax Panamax Supramax Handysize

Dry Cargo

MR

Tankers

Handysize

0

50

100

150

200

250

Dry cargo Tankers

NORDEN vessels Pool vessels

Presentation of NORDEN | 5 Our business is global tramp shipping

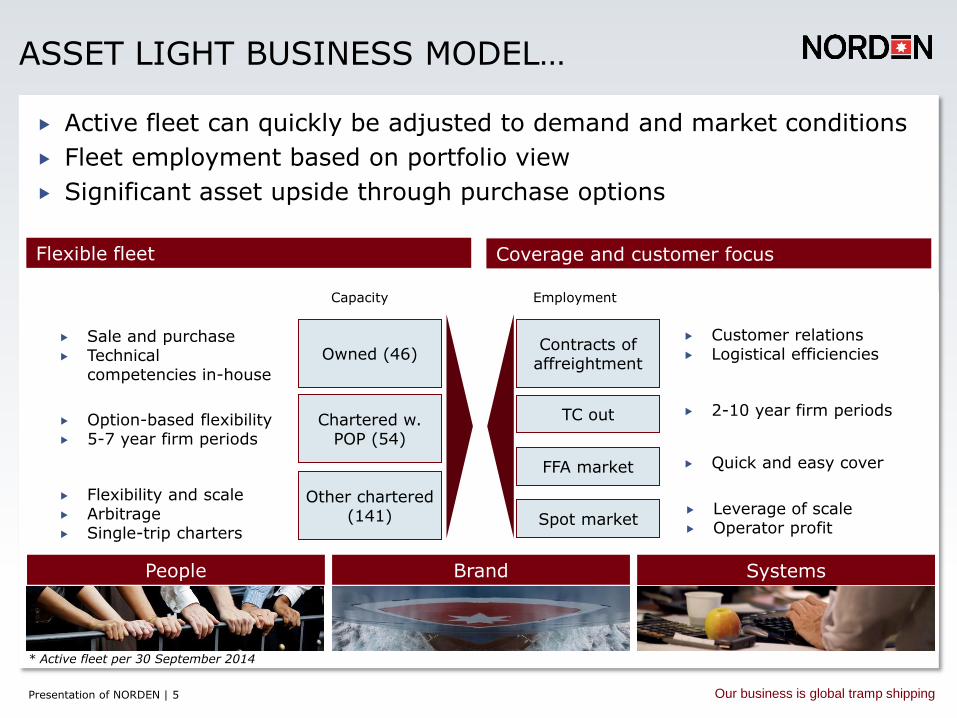

ASSET LIGHT BUSINESS MODEL…

Sale and purchase Technical

competencies in-house

Owned (46)

Chartered w. POP (54)

Other chartered (141)

Capacity

Option-based flexibility 5-7 year firm periods

Flexibility and scale Arbitrage Single-trip charters

Contracts of affreightment

TC out

FFA market

Employment

Spot market

Customer relations Logistical efficiencies

2-10 year firm periods

Quick and easy cover

* Active fleet per 30 June 2011

Active fleet can quickly be adjusted to demand and market conditions

Fleet employment based on portfolio view

Significant asset upside through purchase options

Coverage and customer focus Flexible fleet

Brand People Systems

* Active fleet per 30 September 2014

Leverage of scale Operator profit

Presentation of NORDEN | 6 Our business is global tramp shipping

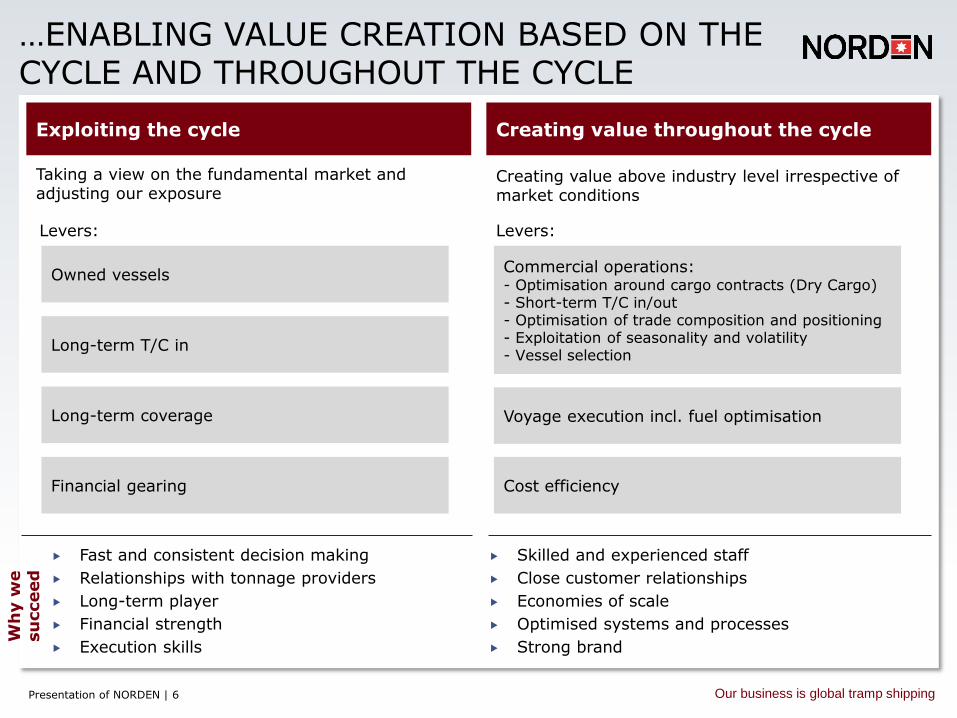

…ENABLING VALUE CREATION BASED ON THE CYCLE AND THROUGHOUT THE CYCLE

Taking a view on the fundamental market and adjusting our exposure

Exploiting the cycle Creating value throughout the cycle

Owned vessels

Long-term T/C in

Long-term coverage

Financial gearing

Levers:

Creating value above industry level irrespective of market conditions

Wh

y w

e

su

cceed

Fast and consistent decision making

Relationships with tonnage providers

Long-term player

Financial strength

Execution skills

Skilled and experienced staff

Close customer relationships

Economies of scale

Optimised systems and processes

Strong brand

Commercial operations: - Optimisation around cargo contracts (Dry Cargo) - Short-term T/C in/out - Optimisation of trade composition and positioning - Exploitation of seasonality and volatility - Vessel selection

Voyage execution incl. fuel optimisation

Cost efficiency

Levers:

Presentation of NORDEN | 7 Our business is global tramp shipping

LAST 5 YEARS PERFORMANCE

Return on equity

Dividend yield

Earnings per share (USD)

Cash flows, operations and investments (USDm)

5,2 5,8

2,1

-6,8

-1,2

2009 2010 2011 2012 2013

12,4% 12,9%

4,4%

-15,1%

-2,9%

2009 2010 2011 2012 2013

160

298

120 122 -9

-80

-380 -355

7

-103

2009 2010 2011 2012 2013

Cash from operations Net cash from investments

3,3%

4,0%

3,0%

1,8% 1,8%

2009 2010 2011 2012 2013

Presentation of NORDEN | 8 Our business is global tramp shipping

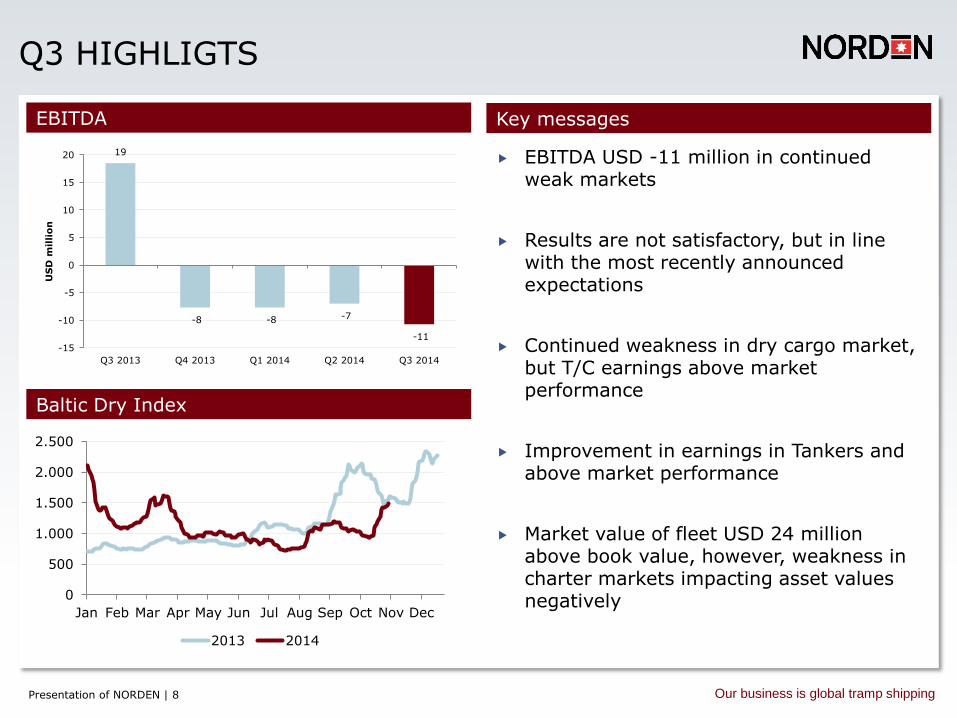

Q3 HIGHLIGTS

EBITDA USD -11 million in continued weak markets

Results are not satisfactory, but in line with the most recently announced expectations

Continued weakness in dry cargo market, but T/C earnings above market performance

Improvement in earnings in Tankers and above market performance

Market value of fleet USD 24 million above book value, however, weakness in charter markets impacting asset values negatively

Key messages EBITDA

Baltic Dry Index

19

-8 -8 -7

-11

-15

-10

-5

0

5

10

15

20

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

US

D m

illi

on

0

500

1.000

1.500

2.000

2.500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

Presentation of NORDEN | 9 Our business is global tramp shipping

10

-14 -15

-6

-16 -20

-15

-10

-5

0

5

10

15

Q3 13 Q4 13 Q1 14 Q2 14 Q3 14

US

D m

illi

on

Dry Cargo

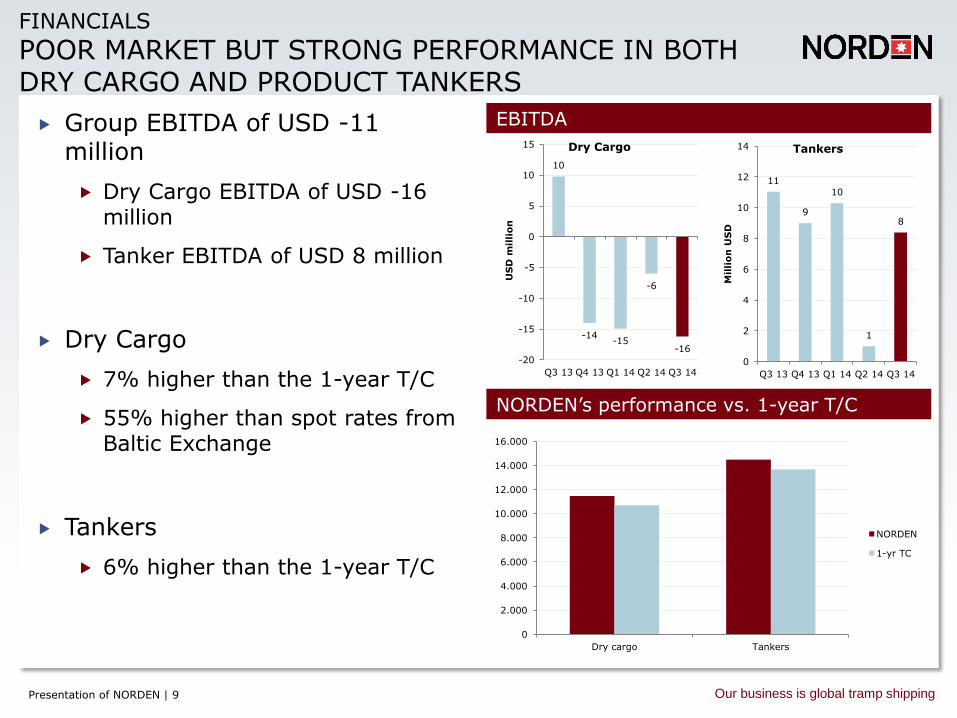

FINANCIALS

POOR MARKET BUT STRONG PERFORMANCE IN BOTH DRY CARGO AND PRODUCT TANKERS

EBITDA

NORDEN’s performance vs. 1-year T/C

Group EBITDA of USD -11 million

Dry Cargo EBITDA of USD -16 million

Tanker EBITDA of USD 8 million

Dry Cargo

7% higher than the 1-year T/C

55% higher than spot rates from Baltic Exchange

Tankers

6% higher than the 1-year T/C

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

Dry cargo Tankers

NORDEN

1-yr TC

11

9

10

1

8

0

2

4

6

8

10

12

14

Q3 13 Q4 13 Q1 14 Q2 14 Q3 14

Mil

lio

n U

SD

Tankers

Presentation of NORDEN | 10 Our business is global tramp shipping

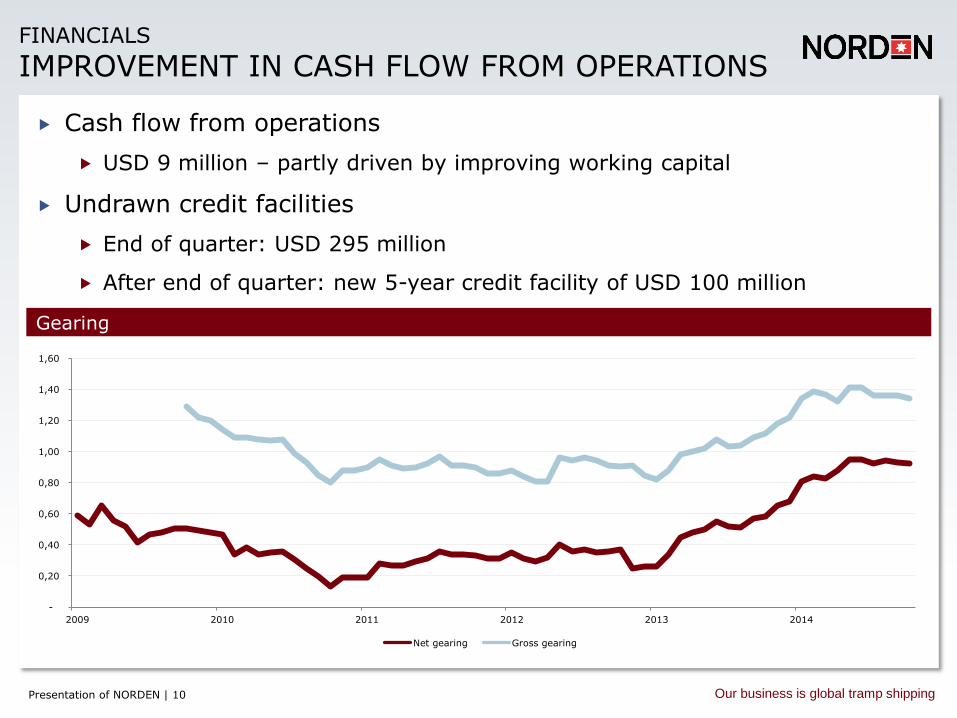

FINANCIALS

IMPROVEMENT IN CASH FLOW FROM OPERATIONS

Gearing

Cash flow from operations

USD 9 million – partly driven by improving working capital

Undrawn credit facilities

End of quarter: USD 295 million

After end of quarter: new 5-year credit facility of USD 100 million

-

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

2009 2010 2011 2012 2013 2014

Net gearing Gross gearing

Presentation of NORDEN | 11 Our business is global tramp shipping

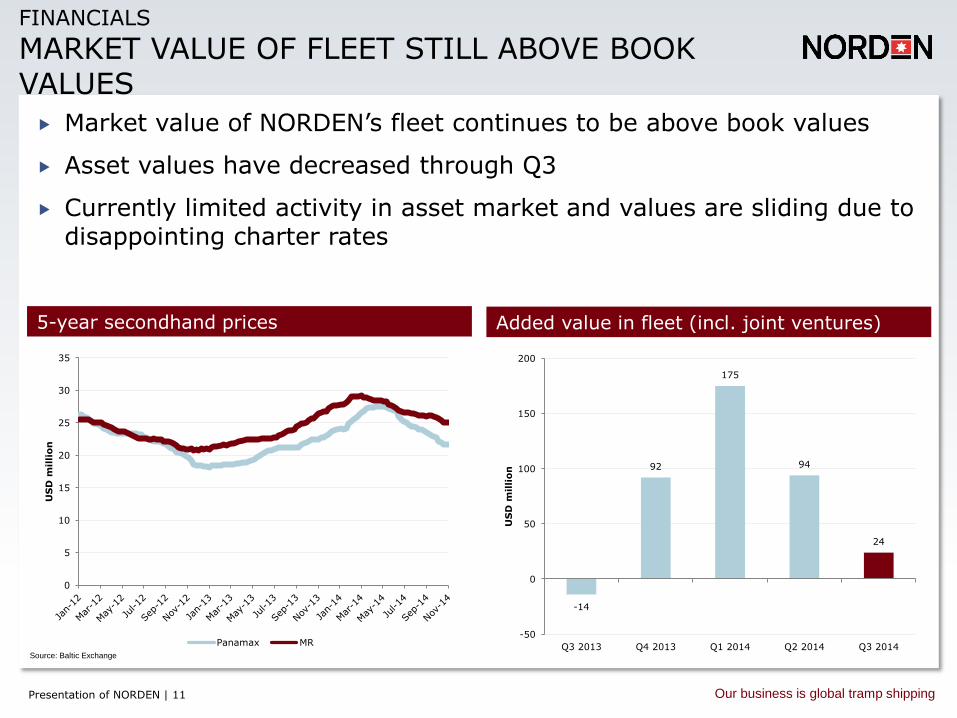

FINANCIALS

MARKET VALUE OF FLEET STILL ABOVE BOOK VALUES

Added value in fleet (incl. joint ventures) 5-year secondhand prices

Market value of NORDEN’s fleet continues to be above book values

Asset values have decreased through Q3

Currently limited activity in asset market and values are sliding due to disappointing charter rates

Source: Baltic Exchange

-14

92

175

94

24

-50

0

50

100

150

200

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

US

D m

illi

on

0

5

10

15

20

25

30

35

US

D m

illi

on

Panamax MR

Presentation of NORDEN | 12 Our business is global tramp shipping

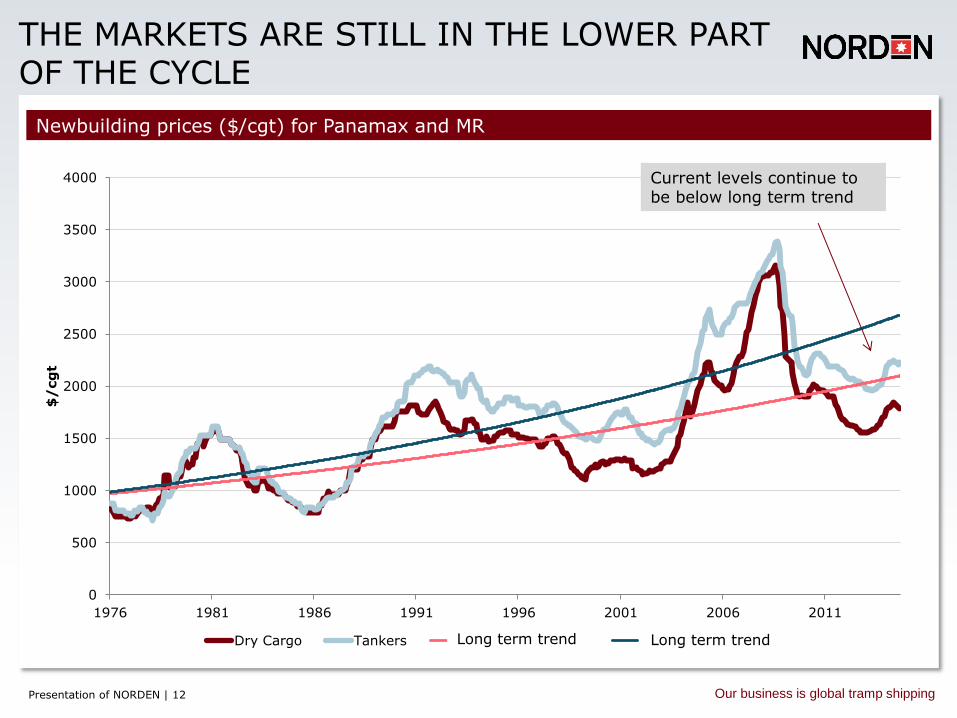

THE MARKETS ARE STILL IN THE LOWER PART OF THE CYCLE

Newbuilding prices ($/cgt) for Panamax and MR

0

500

1000

1500

2000

2500

3000

3500

4000

1976 1981 1986 1991 1996 2001 2006 2011

$/

cg

t

Dry Cargo Tankers Expon. (Dry Cargo) Expon. (Tankers)Long term trend Long term trend

Current levels continue to be below long term trend

Presentation of NORDEN | 13 Our business is global tramp shipping

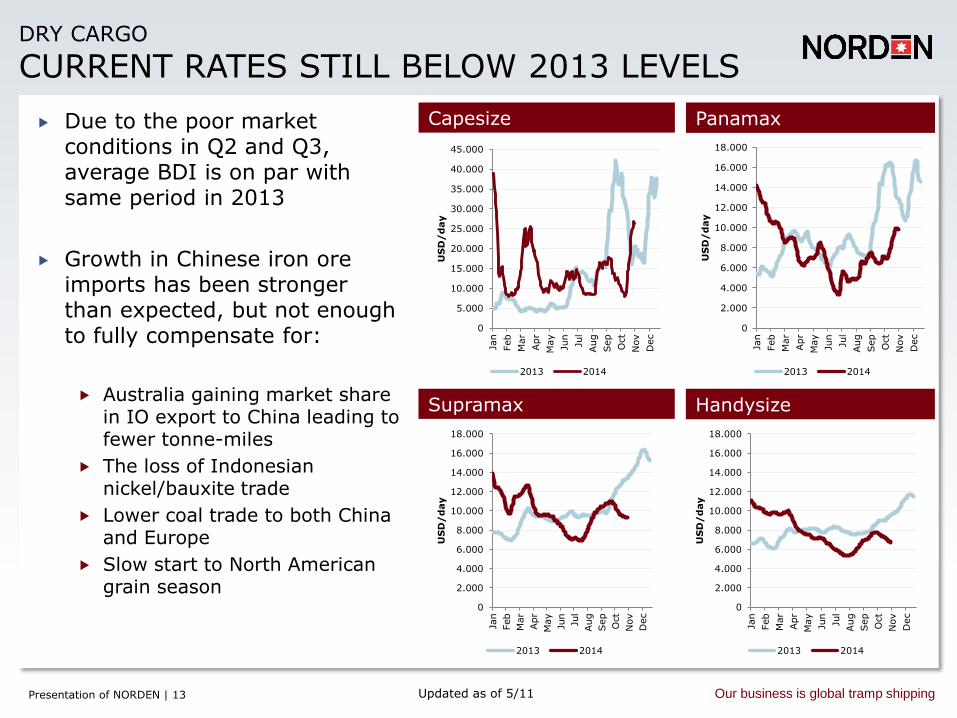

DRY CARGO

CURRENT RATES STILL BELOW 2013 LEVELS

Capesize Panamax Due to the poor market conditions in Q2 and Q3, average BDI is on par with same period in 2013

Growth in Chinese iron ore imports has been stronger than expected, but not enough to fully compensate for:

Australia gaining market share in IO export to China leading to fewer tonne-miles

The loss of Indonesian nickel/bauxite trade

Lower coal trade to both China and Europe

Slow start to North American grain season

Supramax Handysize

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

US

D/

day

2013 2014

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

US

D/

day

2013 2014

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

US

D/

day

2013 2014

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

US

D/

day

2013 2014

Updated as of 5/11

Presentation of NORDEN | 14 Our business is global tramp shipping

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-40

-20

-

20

40

60

80

100

2011 2012 2013 2014e 2015e

Realised deliveries Expected deliveries

Realised scrapping Expected scrapping

Net fleet growth (RHS)

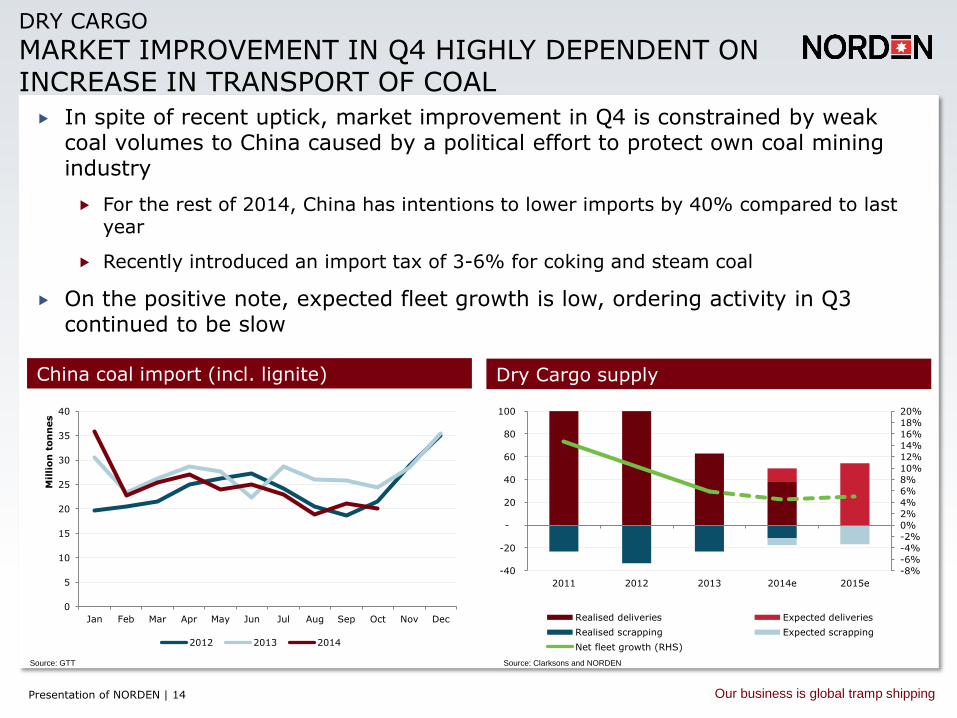

DRY CARGO

MARKET IMPROVEMENT IN Q4 HIGHLY DEPENDENT ON INCREASE IN TRANSPORT OF COAL

Dry Cargo supply China coal import (incl. lignite)

In spite of recent uptick, market improvement in Q4 is constrained by weak coal volumes to China caused by a political effort to protect own coal mining industry

For the rest of 2014, China has intentions to lower imports by 40% compared to last year

Recently introduced an import tax of 3-6% for coking and steam coal

On the positive note, expected fleet growth is low, ordering activity in Q3 continued to be slow

Source: GTT Source: Clarksons and NORDEN

0

5

10

15

20

25

30

35

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n t

on

nes

2012 2013 2014

Presentation of NORDEN | 15 Our business is global tramp shipping

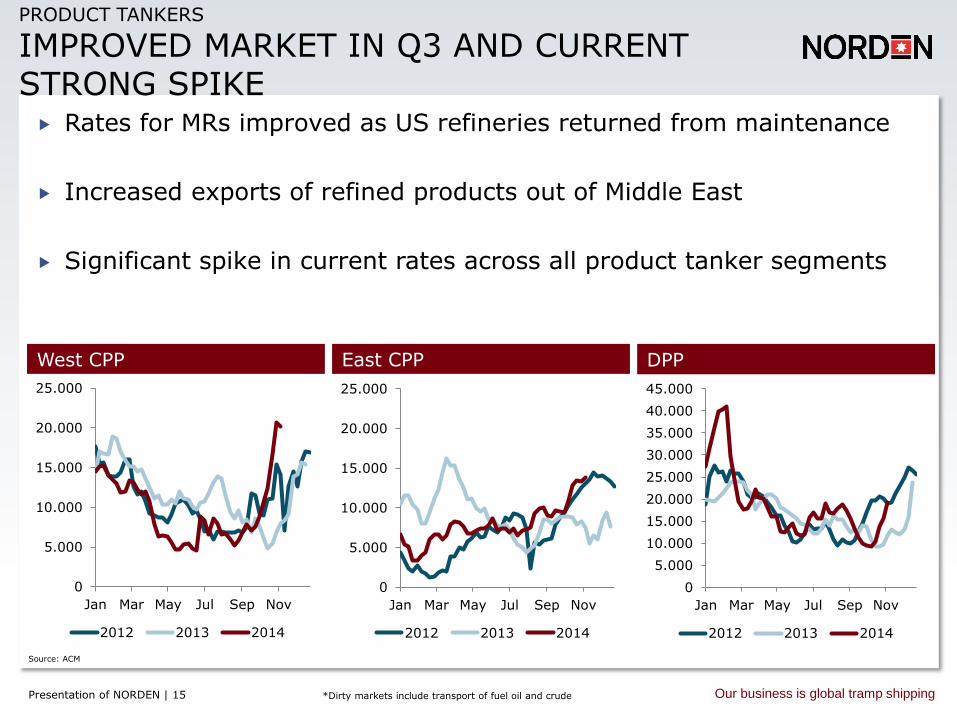

PRODUCT TANKERS

IMPROVED MARKET IN Q3 AND CURRENT STRONG SPIKE

East CPP West CPP DPP

Rates for MRs improved as US refineries returned from maintenance

Increased exports of refined products out of Middle East

Significant spike in current rates across all product tanker segments

Source: ACM

*Dirty markets include transport of fuel oil and crude

0

5.000

10.000

15.000

20.000

25.000

Jan Mar May Jul Sep Nov

2012 2013 2014

0

5.000

10.000

15.000

20.000

25.000

Jan Mar May Jul Sep Nov

2012 2013 2014

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

Jan Mar May Jul Sep Nov

2012 2013 2014

Presentation of NORDEN | 16 Our business is global tramp shipping

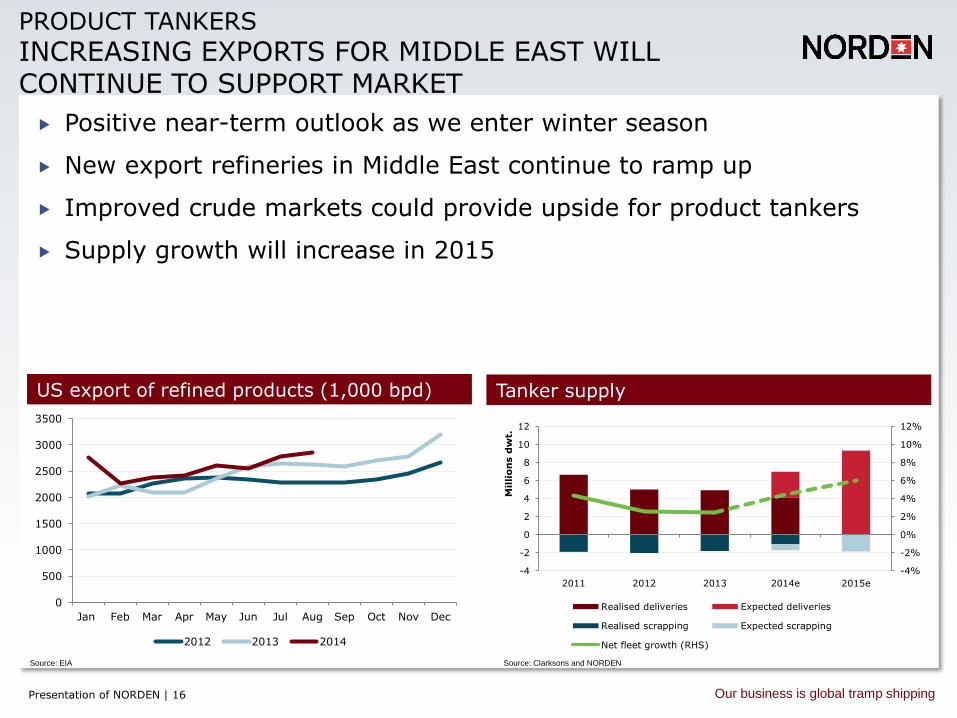

Positive near-term outlook as we enter winter season

New export refineries in Middle East continue to ramp up

Improved crude markets could provide upside for product tankers

Supply growth will increase in 2015

PRODUCT TANKERS

INCREASING EXPORTS FOR MIDDLE EAST WILL CONTINUE TO SUPPORT MARKET

Tanker supply US export of refined products (1,000 bpd)

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

-4

-2

0

2

4

6

8

10

12

2011 2012 2013 2014e 2015e

Mil

lio

ns d

wt.

Realised deliveries Expected deliveries

Realised scrapping Expected scrapping

Net fleet growth (RHS)

Source: EIA Source: Clarksons and NORDEN

0

500

1000

1500

2000

2500

3000

3500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013 2014

Presentation of NORDEN | 17 Our business is global tramp shipping

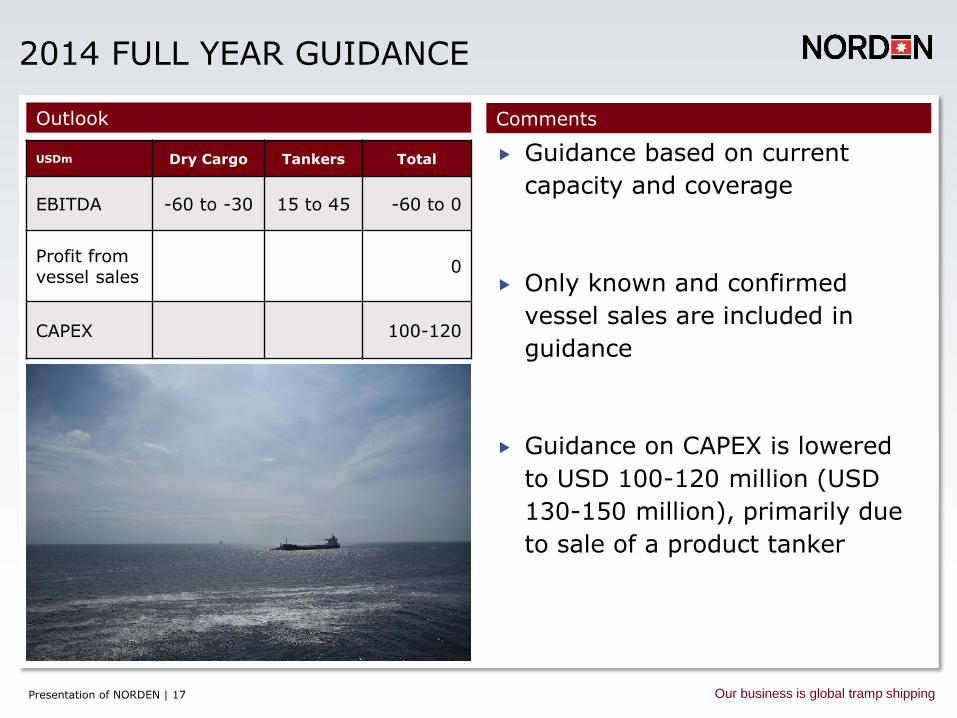

2014 FULL YEAR GUIDANCE

Guidance based on current

capacity and coverage

Only known and confirmed

vessel sales are included in

guidance

Guidance on CAPEX is lowered

to USD 100-120 million (USD

130-150 million), primarily due

to sale of a product tanker

Comments Outlook

USDm Dry Cargo Tankers Total

EBITDA -60 to -30 15 to 45 -60 to 0

Profit from vessel sales

0

CAPEX 100-120

Presentation of NORDEN | 18 Our business is global tramp shipping

FORWARD LOOKING STATEMENTS

This presentation contains certain forward-looking statements reflecting the management’s present judgment of future events and financial

results.

Statements relating to the remainder of 2014 and subsequent years are subject to uncertainty, and NORDEN’s actual results may therefore differ from the projections. Factors that may cause such variance include, but are not limited to, changes in macro-economic and political conditions,

particularly in the Company’s principal markets; changes to the Company’s rate assumptions and operating costs; volatility in rates and

tonnage prices; regulatory changes; any disruptions to traffic and operations as a result of external events, etc.

Presentation of NORDEN | 19 Our business is global tramp shipping

Dampskibsselskabet NORDEN A/S 52, Strandvejen DK-2900 Hellerup Denmark Phone: +45 3315 0451 www.ds-norden.com

Get mobile version of NORDEN’s website. Scan and add to home screen. Or go to m.ds-norden.com

Thank you for your attention

Presentation of NORDEN | 20 Our business is global tramp shipping

BACK UP

Presentation of NORDEN | 21 Our business is global tramp shipping

OVERALL RESULTS

USDm Q3 2013 Q2 2014 Q3 2014

EBITDA - Dry Cargo 10 -6 -16

EBITDA - Tankers 11 1 8

Unallocated -2 -3 -3

EBITDA - Group 19 -7 -11

Depreciation -21 -16 -19

EBIT Group -1 -27 -28

Net profit 1 -42 -46

Cash from operations 4 -29 9

Net Cash flow 29 -110 -31

Cash and securities 529 323 279

Presentation of NORDEN | 22 Our business is global tramp shipping

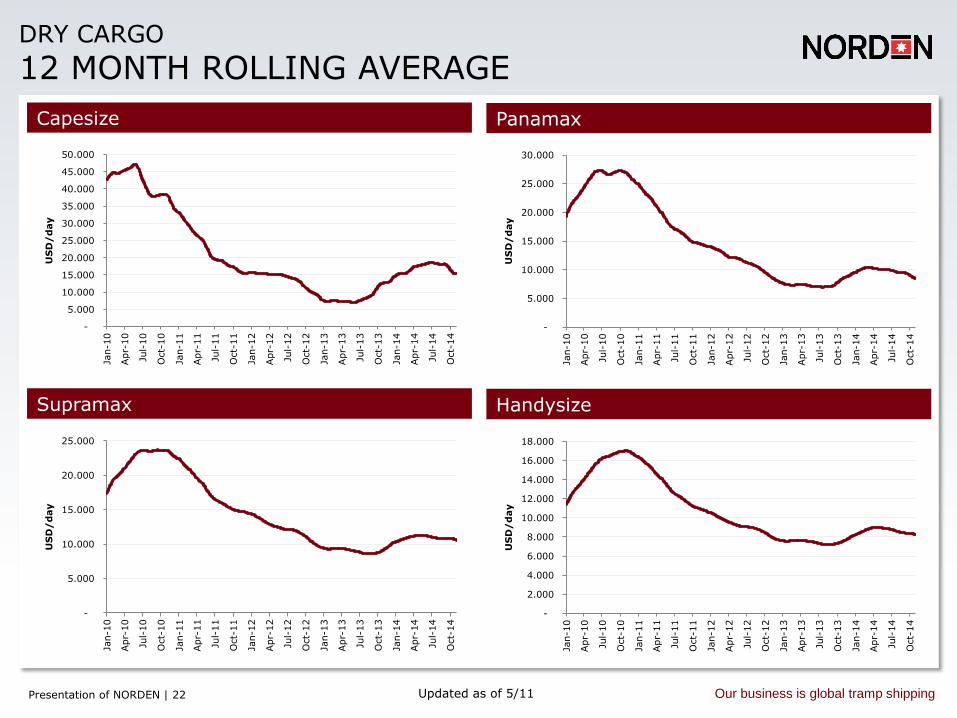

DRY CARGO

12 MONTH ROLLING AVERAGE

Panamax

Handysize

Capesize

Supramax

Updated as of 5/11

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

US

D/

day

-

5.000

10.000

15.000

20.000

25.000

30.000

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

US

D/

day

-

5.000

10.000

15.000

20.000

25.000

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

US

D/

day

-

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

US

D/

day

Presentation of NORDEN | 23 Our business is global tramp shipping

-10.000

-5.000

0

5.000

10.000

15.000

20.000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

US

D/

day

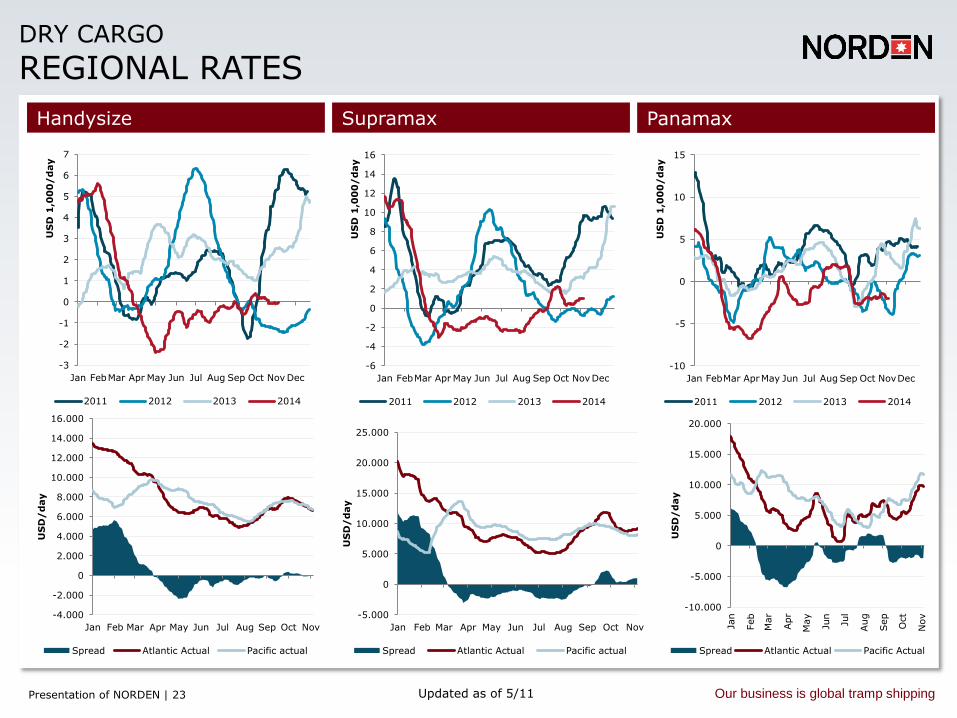

Spread Atlantic Actual Pacific Actual

DRY CARGO

REGIONAL RATES

Supramax Handysize Panamax

Updated as of 5/11

-10

-5

0

5

10

15

Jan FebMar AprMay Jun Jul Aug Sep Oct NovDec

US

D 1

,00

0/

day

2011 2012 2013 2014

-6

-4

-2

0

2

4

6

8

10

12

14

16

Jan FebMar Apr May Jun Jul Aug Sep Oct NovDec

US

D 1

,00

0/

day

2011 2012 2013 2014

-5.000

0

5.000

10.000

15.000

20.000

25.000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

US

D/

day

Spread Atlantic Actual Pacific actual

-3

-2

-1

0

1

2

3

4

5

6

7

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

US

D 1

,00

0/

day

2011 2012 2013 2014

-4.000

-2.000

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

US

D/

day

Spread Atlantic Actual Pacific actual

Presentation of NORDEN | 24 Our business is global tramp shipping

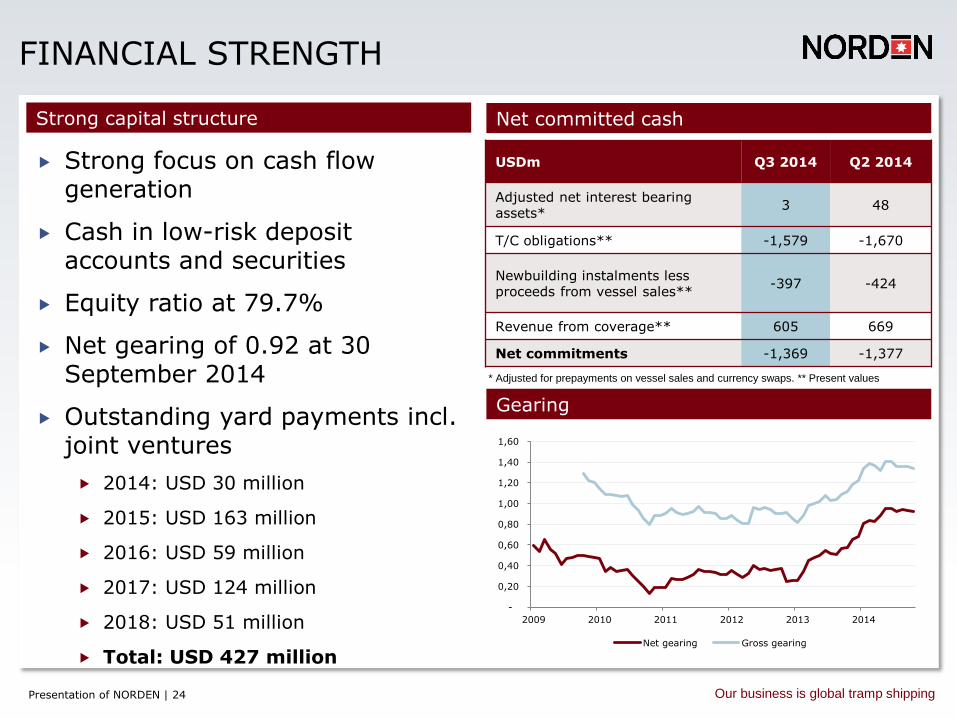

FINANCIAL STRENGTH

Net committed cash

Gearing

Strong focus on cash flow generation

Cash in low-risk deposit accounts and securities

Equity ratio at 79.7%

Net gearing of 0.92 at 30 September 2014

Outstanding yard payments incl. joint ventures

2014: USD 30 million

2015: USD 163 million

2016: USD 59 million

2017: USD 124 million

2018: USD 51 million

Total: USD 427 million

Strong capital structure

USDm Q3 2014 Q2 2014

Adjusted net interest bearing assets*

3 48

T/C obligations** -1,579 -1,670

Newbuilding instalments less proceeds from vessel sales**

-397 -424

Revenue from coverage** 605 669

Net commitments -1,369 -1,377

* Adjusted for prepayments on vessel sales and currency swaps. ** Present values

-

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

2009 2010 2011 2012 2013 2014

Net gearing Gross gearing

Presentation of NORDEN | 25 Our business is global tramp shipping

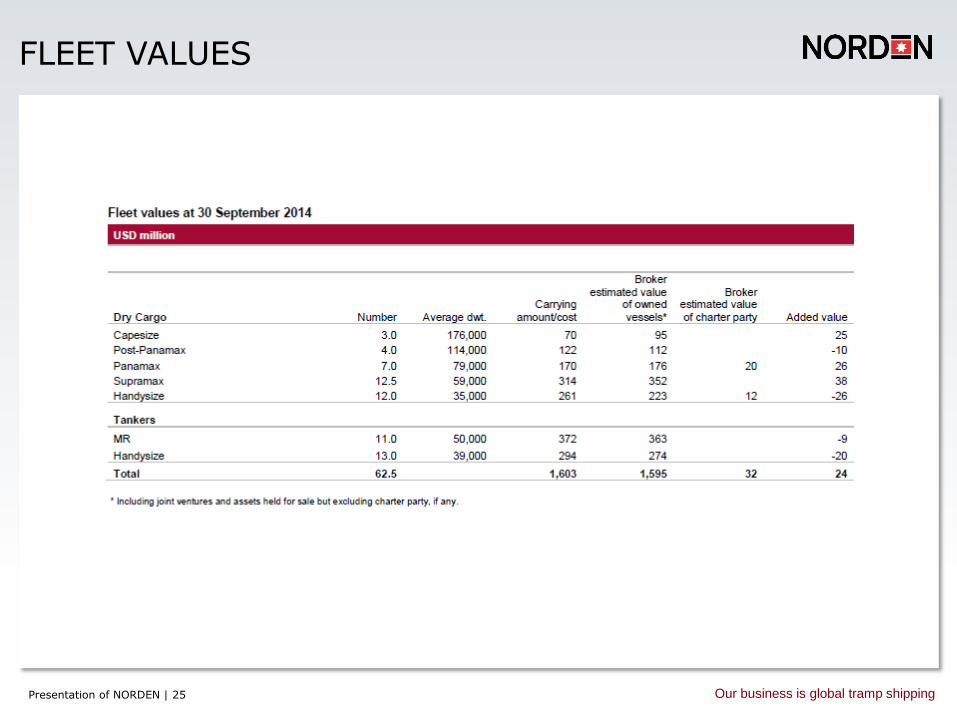

FLEET VALUES

Presentation of NORDEN | 26 Our business is global tramp shipping

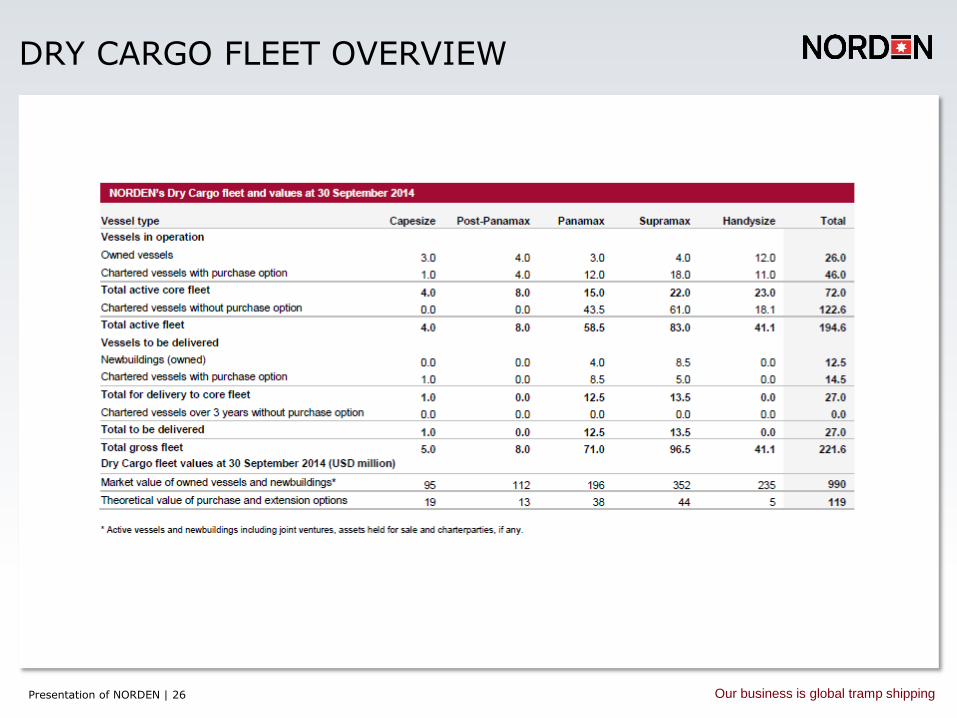

DRY CARGO FLEET OVERVIEW

Presentation of NORDEN | 27 Our business is global tramp shipping

PRODUCT TANKER FLEET OVERVIEW

Presentation of NORDEN | 28 Our business is global tramp shipping

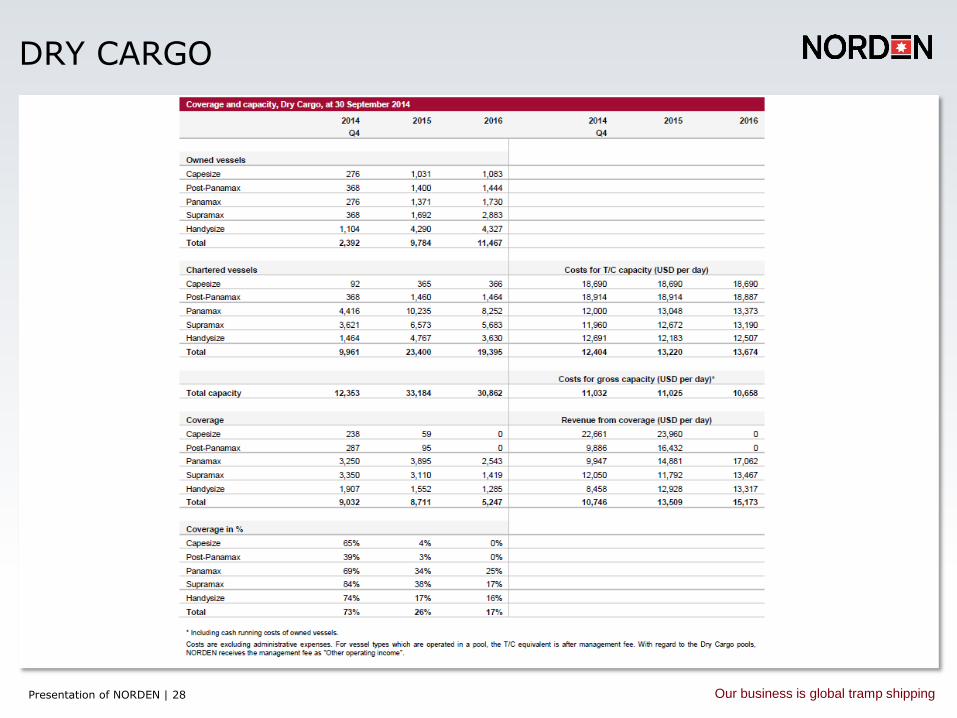

DRY CARGO

Presentation of NORDEN | 29 Our business is global tramp shipping

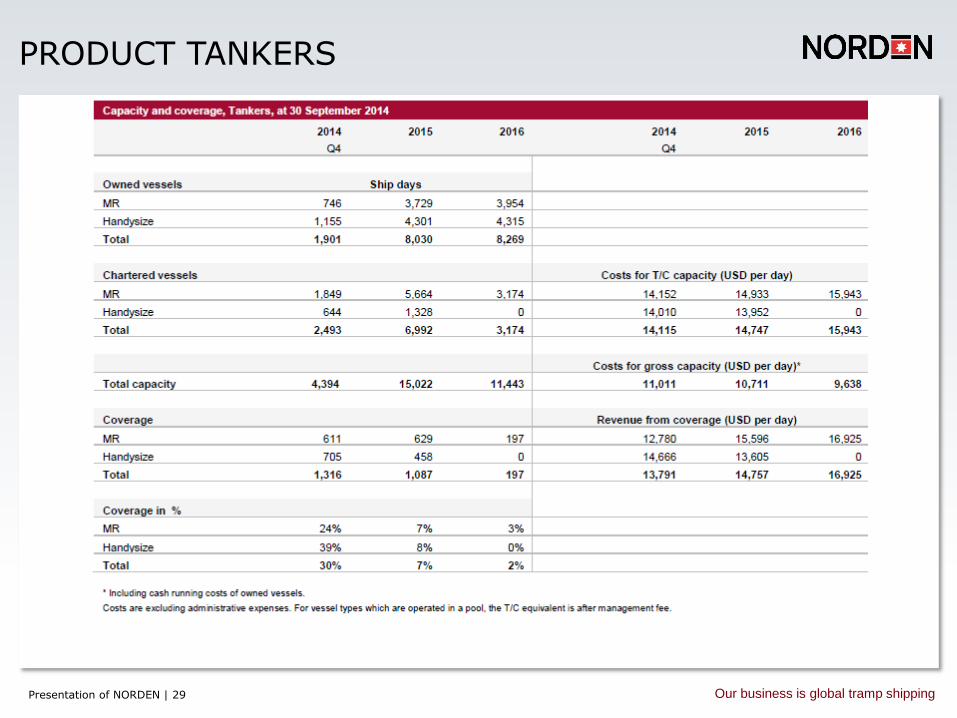

PRODUCT TANKERS

Presentation of NORDEN | 30 Our business is global tramp shipping

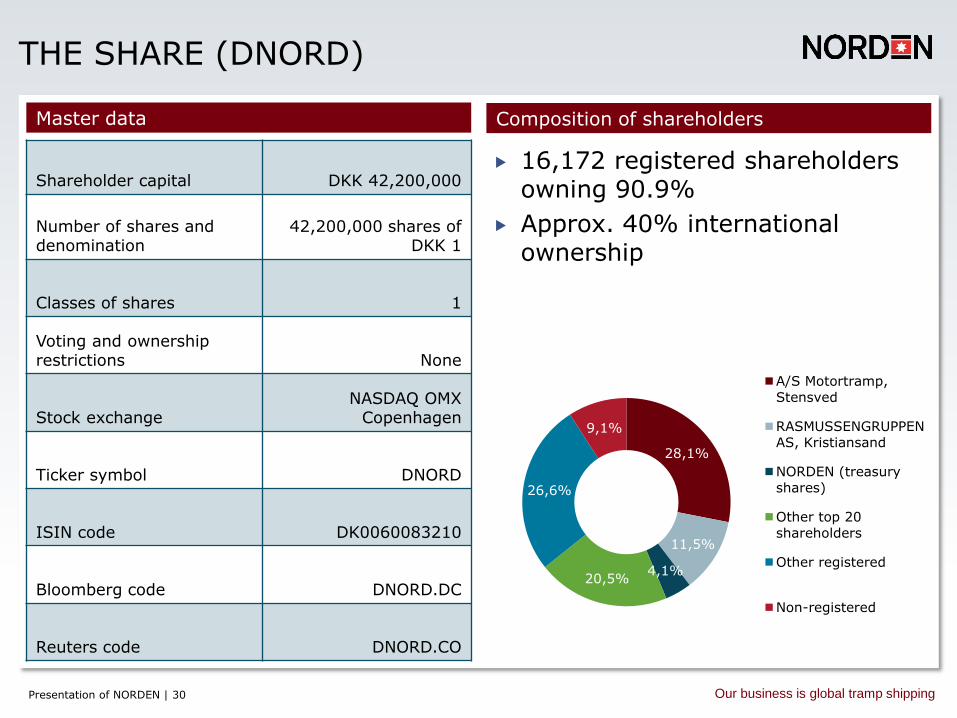

THE SHARE (DNORD)

Composition of shareholders Master data

Shareholder capital DKK 42,200,000

Number of shares and denomination

42,200,000 shares of DKK 1

Classes of shares 1

Voting and ownership restrictions None

Stock exchange NASDAQ OMX

Copenhagen

Ticker symbol DNORD

ISIN code DK0060083210

Bloomberg code DNORD.DC

Reuters code DNORD.CO

16,172 registered shareholders owning 90.9%

Approx. 40% international ownership

28,1%

11,5%

4,1% 20,5%

26,6%

9,1%

A/S Motortramp,

Stensved

RASMUSSENGRUPPEN

AS, Kristiansand

NORDEN (treasury

shares)

Other top 20

shareholders

Other registered

Non-registered